Embed Size (px)

Citation preview

Tognum Investor PresentationNovember 2010

Dr. Ulrich DohleExecutive Vice President and CTO Technology and Operations

Frankfurt, November 18, 2010

Slide 2 | Tognum Investor Presentation | November 2010

Legal disclaimer

This presentation is for information purposes only and does not constitute an offer to sell or a solicitation for an offer to buy any securities. The shares of Tognum AG will not be registered under the U.S. Securities Act of 1933.

This presentation includes certain forward-looking statements. These forward-looking statements can be identified by the use of forward-looking terminology, including the words "believes", "estimates", "anticipates", "expects", "assumes", "predicts", "intends", "may", "will" or "should", and similar expressions. Such forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Such forward-looking statements do not represent any guarantees of future performance. Tognum's actual results of operations, including its financial condition and profitability as well as the development of the general economic conditions in which it operates, may differ materially from (and be more negative than) those made in or suggested by the forward-looking statements contained in this presentation.

This presentation also includes certain market and market share data. To our knowledge, there is no single, comprehensive source that reliably describes the overall market and its sub-markets or the competitive situation in the market breakdown presented herein. Unless indicated otherwise, all the statements herein concerning the market and competition are therefore based on our own estimates, some of which have in turn been derived from a variety of sources. It is possible that the actual market conditions and competition may differ from the situation described herein, or that other market participants may come up with different estimates of the market and competitive conditions.

Slide 3 | Tognum Investor Presentation | November 2010

Business model & outlook

Slide 4 | Tognum Investor Presentation | November 2010

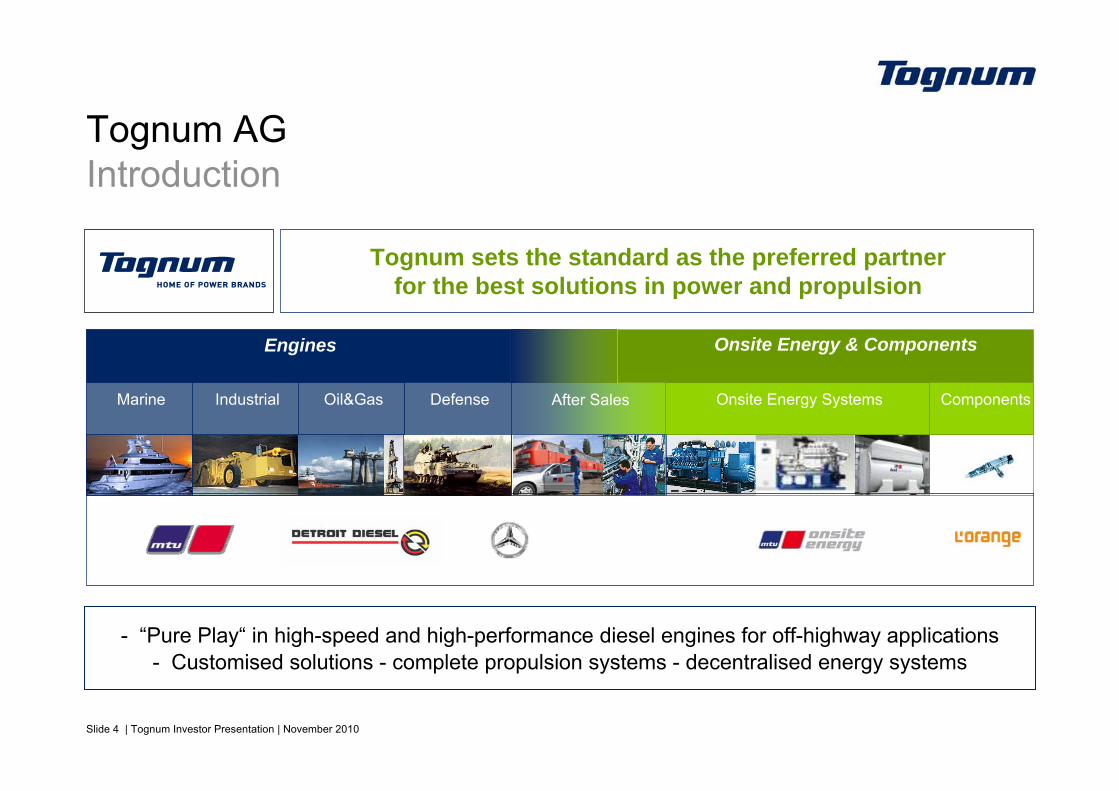

Tognum AGIntroduction

IndustrialMarine Oil&Gas After Sales Onsite Energy Systems

Engines Onsite Energy & Components

ComponentsDefense

Tognum sets the standard as the preferred partner for the best solutions in power and propulsion

- “Pure Play“ in high-speed and high-performance diesel engines for off-highway applications- Customised solutions - complete propulsion systems - decentralised energy systems

Slide 5 | Tognum Investor Presentation | November 2010

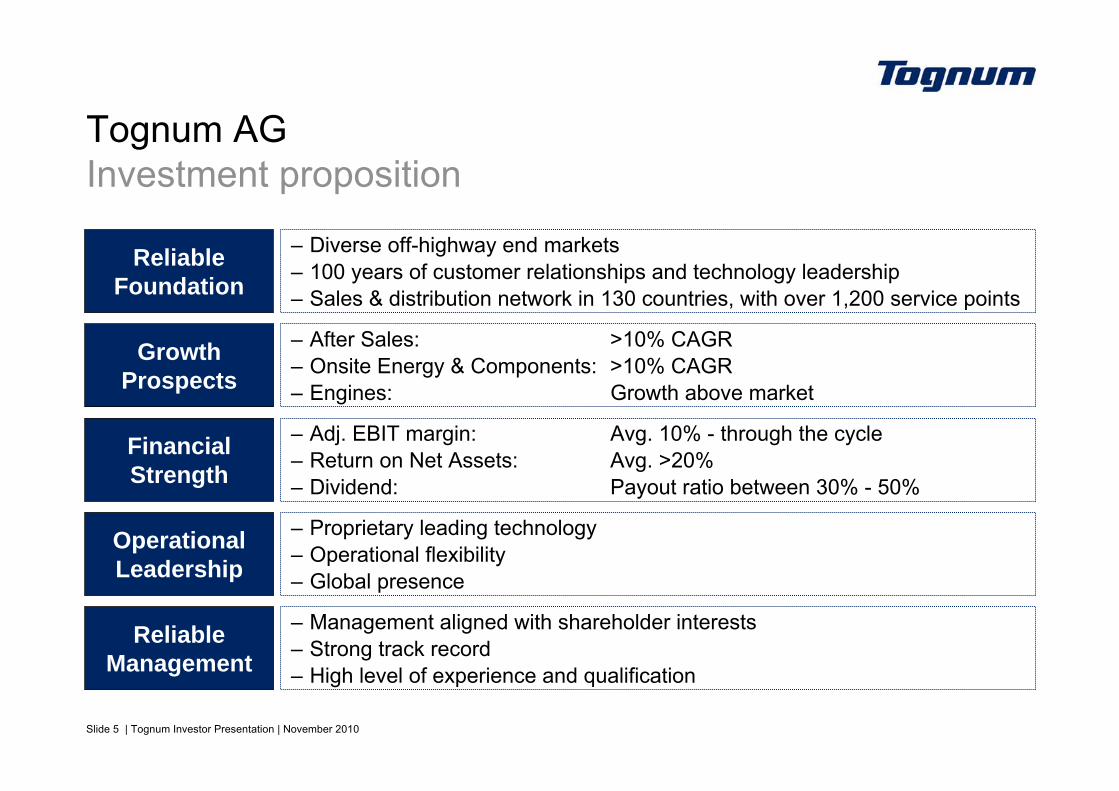

Tognum AG Investment proposition

Reliable Foundation

Growth Prospects

– Diverse off-highway end markets– 100 years of customer relationships and technology leadership– Sales & distribution network in 130 countries, with over 1,200 service points

Financial Strength

Operational Leadership

Reliable Management

– Management aligned with shareholder interests – Strong track record– High level of experience and qualification

– Proprietary leading technology– Operational flexibility– Global presence

– Adj. EBIT margin: Avg. 10% - through the cycle– Return on Net Assets: Avg. >20%– Dividend: Payout ratio between 30% - 50%

– After Sales: >10% CAGR– Onsite Energy & Components: >10% CAGR– Engines: Growth above market

Slide 6 | Tognum Investor Presentation | November 2010

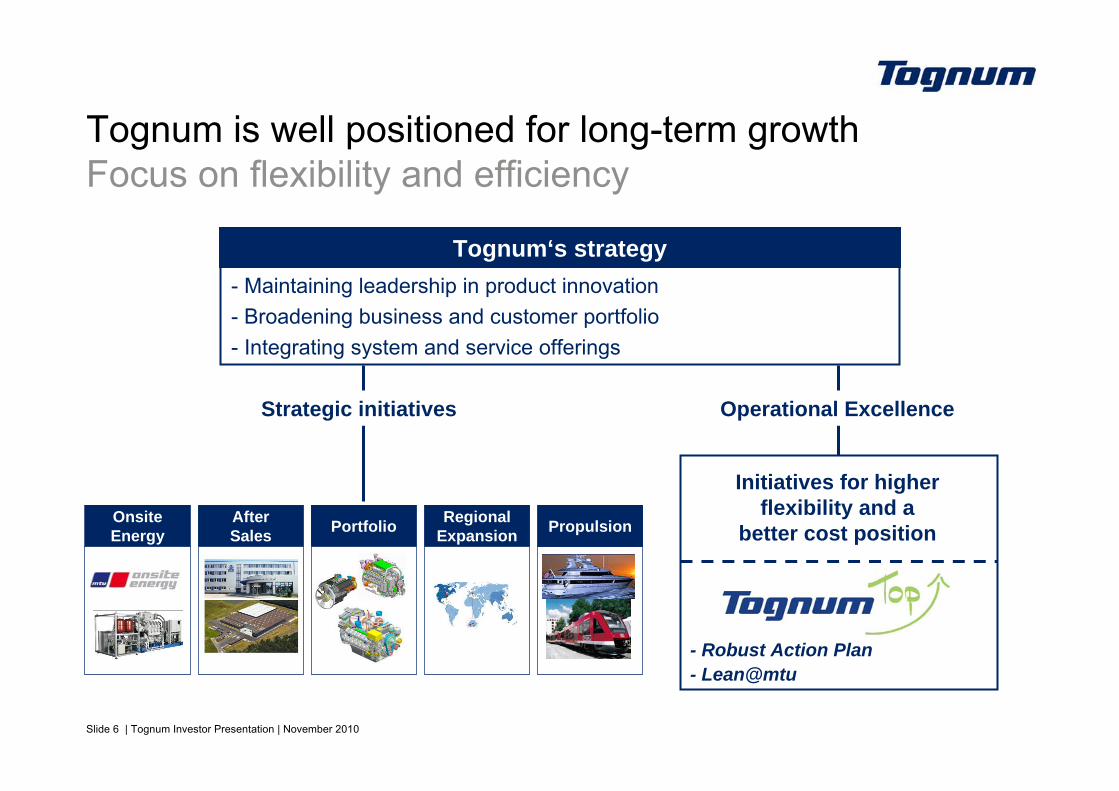

After Sales

Tognum is well positioned for long-term growthFocus on flexibility and efficiency

- Maintaining leadership in product innovation- Broadening business and customer portfolio- Integrating system and service offerings

Tognum‘s strategy

Operational Excellence

Portfolio

Strategic initiatives

Onsite Energy

Regional Expansion

- Robust Action Plan- Lean@mtu

Propulsion

Initiatives for higher flexibility and a

better cost position

Slide 7 | Tognum Investor Presentation | November 2010

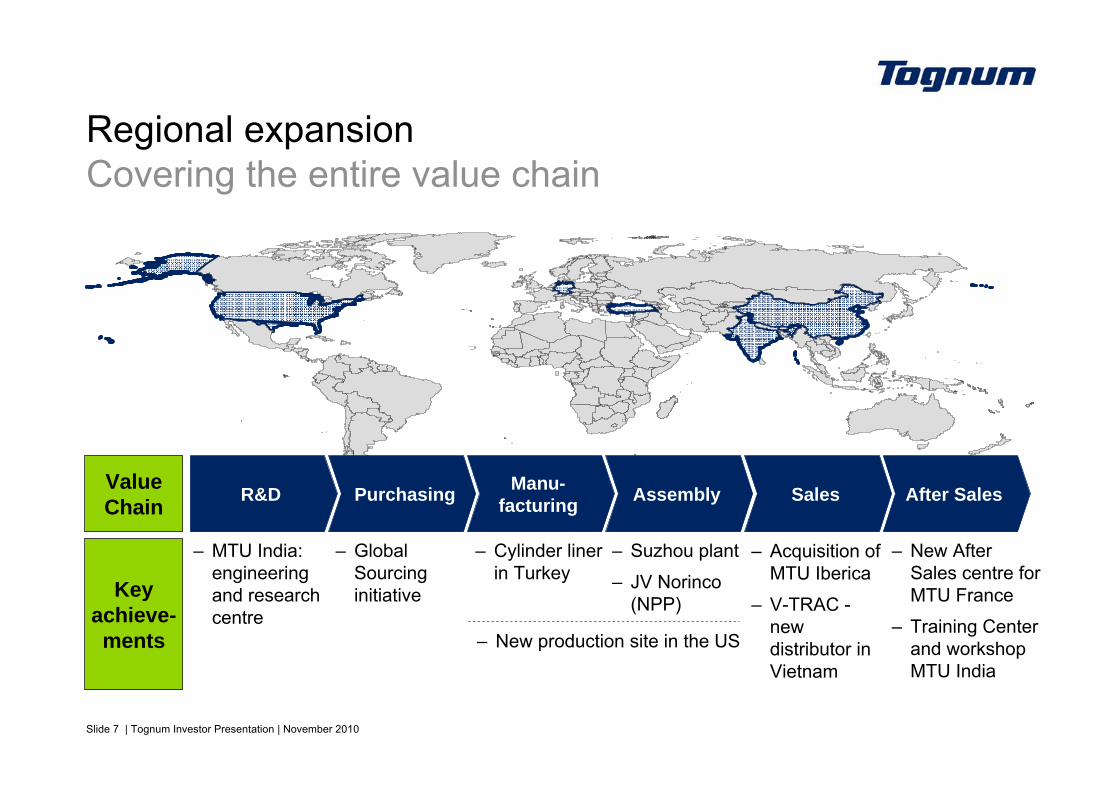

Regional expansionCovering the entire value chain

R&D Purchasing Manu-facturing Assembly Sales After Sales

– MTU India: engineering and research centre

– Global Sourcing initiative

– New production site in the US

– Acquisition of MTU Iberica

– V-TRAC -new distributor in Vietnam

– New After Sales centre for MTU France

– Training Center and workshop MTU India

– Cylinder liner in Turkey

– Suzhou plant

– JV Norinco(NPP)

ValueChain

Key achieve-ments

Slide 8 | Tognum Investor Presentation | November 2010

Intelligent R&D

Slide 9 | Tognum Investor Presentation | November 2010

Intelligent R&DManaging the emission challenge

► Efficient solutions to meet upcoming emission standards

► Tognum keeps key technology know-how in-house

► Focus to achieve optimised combustion process

► Developing new engine series (lower power range) and new engine generations (S 2000 / S 4000)

► Competitive advantage and optimum solutions in all our applications for our customer base

► Customer benefits through engines with superior fuel consumption and low total cost of ownership

Slide 10 | Tognum Investor Presentation | November 2010

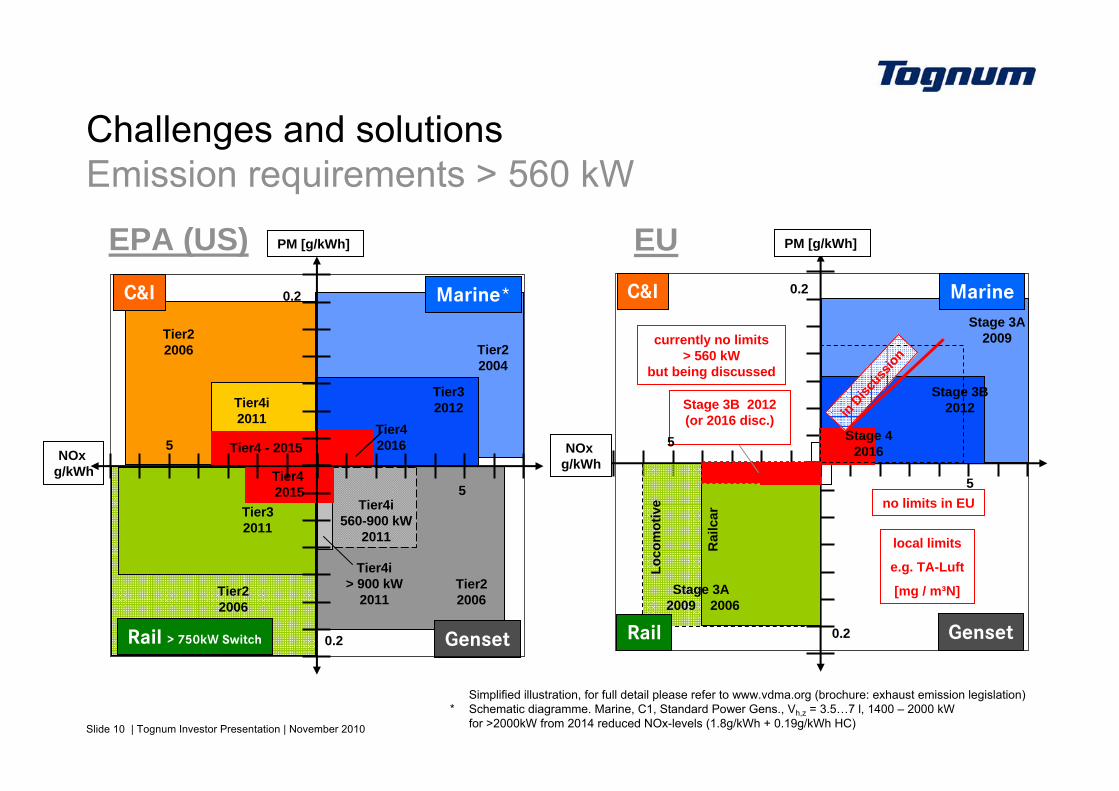

Simplified illustration, for full detail please refer to www.vdma.org (brochure: exhaust emission legislation)* Schematic diagramme. Marine, C1, Standard Power Gens., Vh,z = 3.5…7 l, 1400 – 2000 kW

for >2000kW from 2014 reduced NOx-levels (1.8g/kWh + 0.19g/kWh HC)

Challenges and solutions Emission requirements > 560 kW

C&I

RailLo

com

otiv

e

Rai

lcar

Marine

Genset

Stage 3A 2009 2006

Stage 3B 2012(or 2016 disc.)

EU

Stage 3A2009

Stage 3B2012in D

iscus

sion

currently no limits> 560 kW

but being discussed

no limits in EU

local limits

e.g. TA-Luft

[mg / m³N]

NOx g/kWh

PM [g/kWh]

5

5

0.2

0.2

Stage 42016

EPA (US)Marine*

Tier22004

Tier32012

Tier42016

NOx g/kWh

PM [g/kWh]

C&I

Tier22006

Tier4i2011

Tier4 - 20155

0.2

Genset

Tier22006

Tier4i560-900 kW

2011

Tier4i> 900 kW

2011

5

0.2Rail > 750kW Switch

Tier32011

Tier22006

Tier4 2015

Slide 11 | Tognum Investor Presentation | November 2010

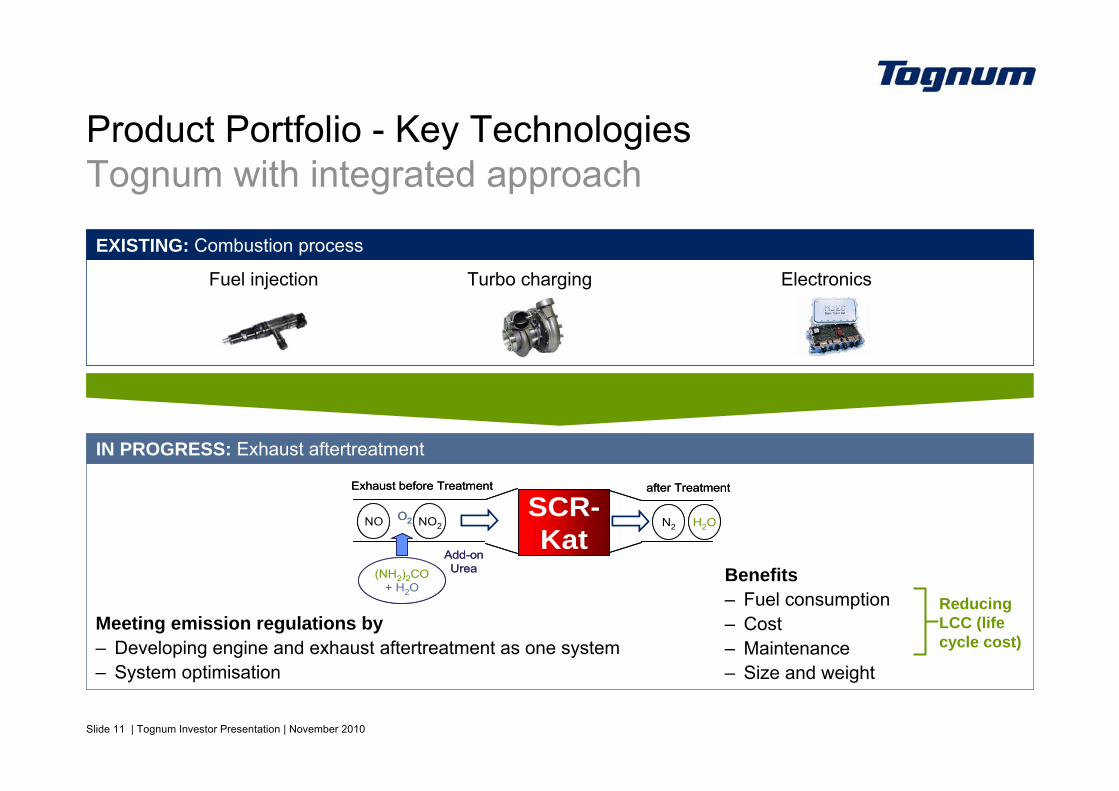

IN PROGRESS: Exhaust aftertreatment

Benefits– Fuel consumption– Cost– Maintenance– Size and weight

EXISTING: Combustion process

Fuel injection Turbo charging Electronics

Reducing LCC (life cycle cost)

NO2O2NO

Exhaust before Treatment

N2 H2O

after Treatment

SCR-Kat

(NH2)2CO+ H2O

Add-onUrea

NO2O2NO

Exhaust before Treatment

N2 H2O

after Treatment

SCR-Kat

(NH2)2CO+ H2O

Add-onUrea

Meeting emission regulations by – Developing engine and exhaust aftertreatment as one system– System optimisation

Product Portfolio - Key TechnologiesTognum with integrated approach

Slide 12 | Tognum Investor Presentation | November 2010

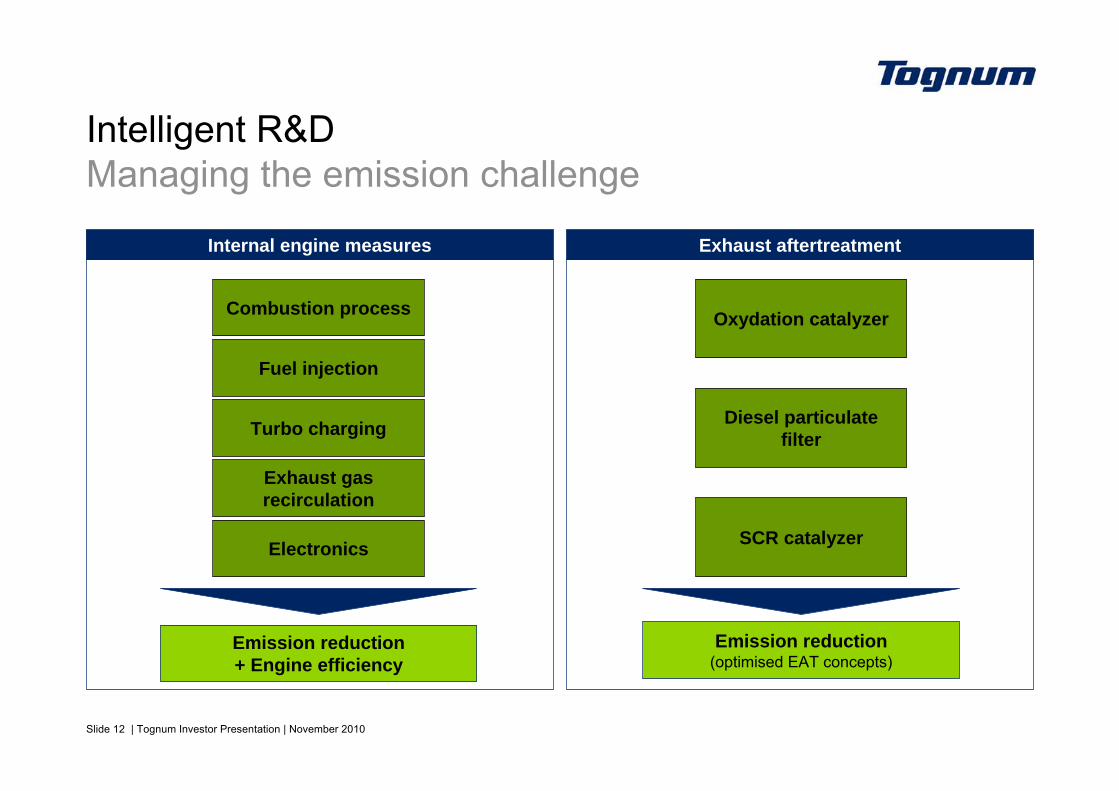

Intelligent R&DManaging the emission challenge

Internal engine measures

Combustion process

Exhaust gas recirculation

Turbo charging

Emission reduction+ Engine efficiency

Fuel injection

Electronics

Exhaust aftertreatment

Oxydation catalyzer

Diesel particulate filter

SCR catalyzer

Emission reduction(optimised EAT concepts)

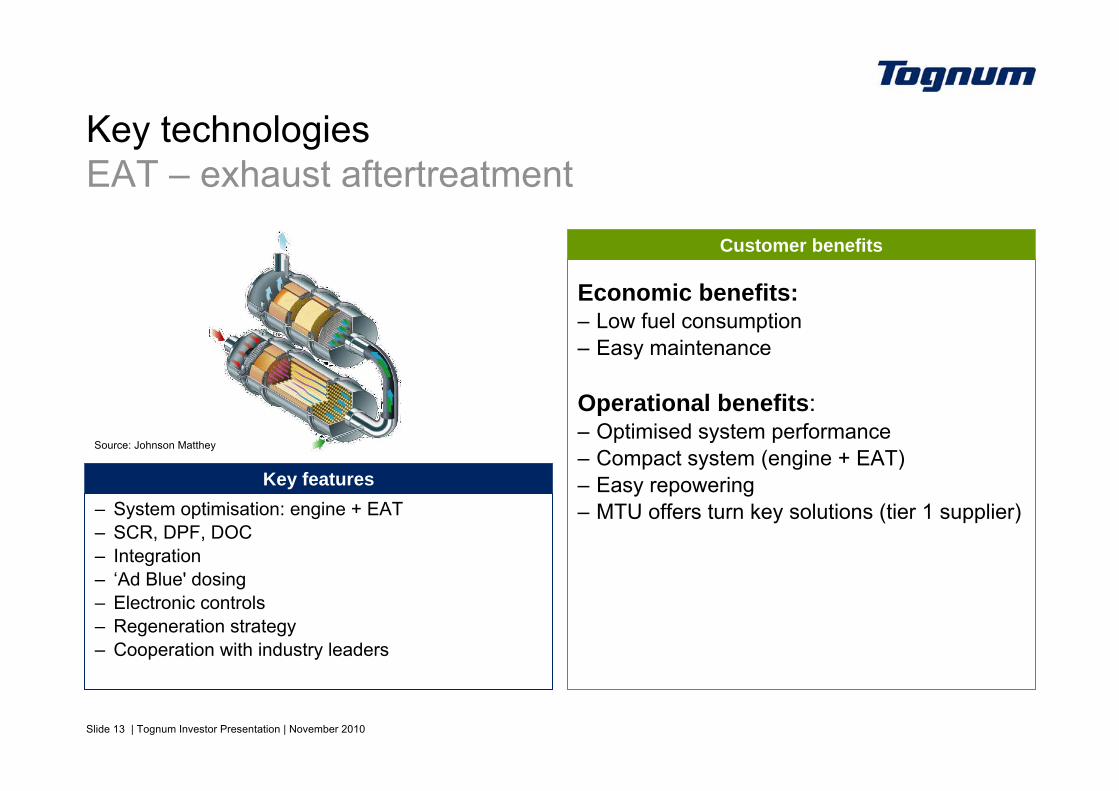

Slide 13 | Tognum Investor Presentation | November 2010

Key technologiesEAT – exhaust aftertreatment

Customer benefits

Key features– System optimisation: engine + EAT– SCR, DPF, DOC– Integration– ‘Ad Blue' dosing– Electronic controls– Regeneration strategy– Cooperation with industry leaders

Economic benefits:– Low fuel consumption– Easy maintenance

Operational benefits:– Optimised system performance– Compact system (engine + EAT)– Easy repowering– MTU offers turn key solutions (tier 1 supplier)

Source: Johnson Matthey

Slide 14 | Tognum Investor Presentation | November 2010

– Diesel particulate filter (DPF)– Railcar in service since Dec ‘06– Accumulated operational

experience > 200.000h– Reduction of PM: >90%

PM reduction – Rail PowerPack (S 1800)– Switcher Locomotive with 8V4000R41– Combined exhaust after treatment system (DPF/

SCR, MTU-design; fulfills EU IIIb (2012, ISO F))– Project “Locex”: 2006 - 2010– Field operating since July 2008: >2500h– Reduction of NOx: >88%– Reduction of PM: >>90%

NOx and PM reduction – Rail S 4000

Emission reduction technologiesProjects for innovative emission reduction solutions

EAT

Slide 15 | Tognum Investor Presentation | November 2010

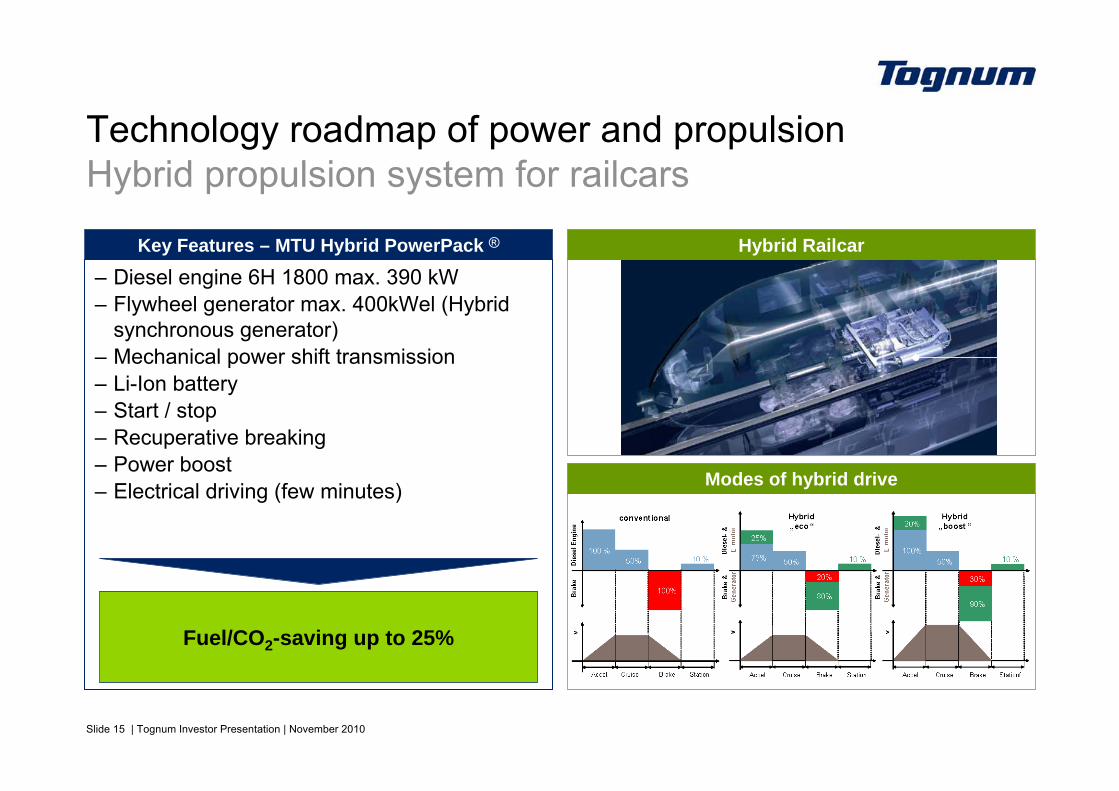

Technology roadmap of power and propulsionHybrid propulsion system for railcars

Key Features – MTU Hybrid PowerPack ®

– Diesel engine 6H 1800 max. 390 kW– Flywheel generator max. 400kWel (Hybrid

synchronous generator) – Mechanical power shift transmission– Li-Ion battery– Start / stop– Recuperative breaking– Power boost– Electrical driving (few minutes)

Fuel/CO2-saving up to 25%

Modes of hybrid drive

Hybrid Railcar

Slide 16 | Tognum Investor Presentation | November 2010

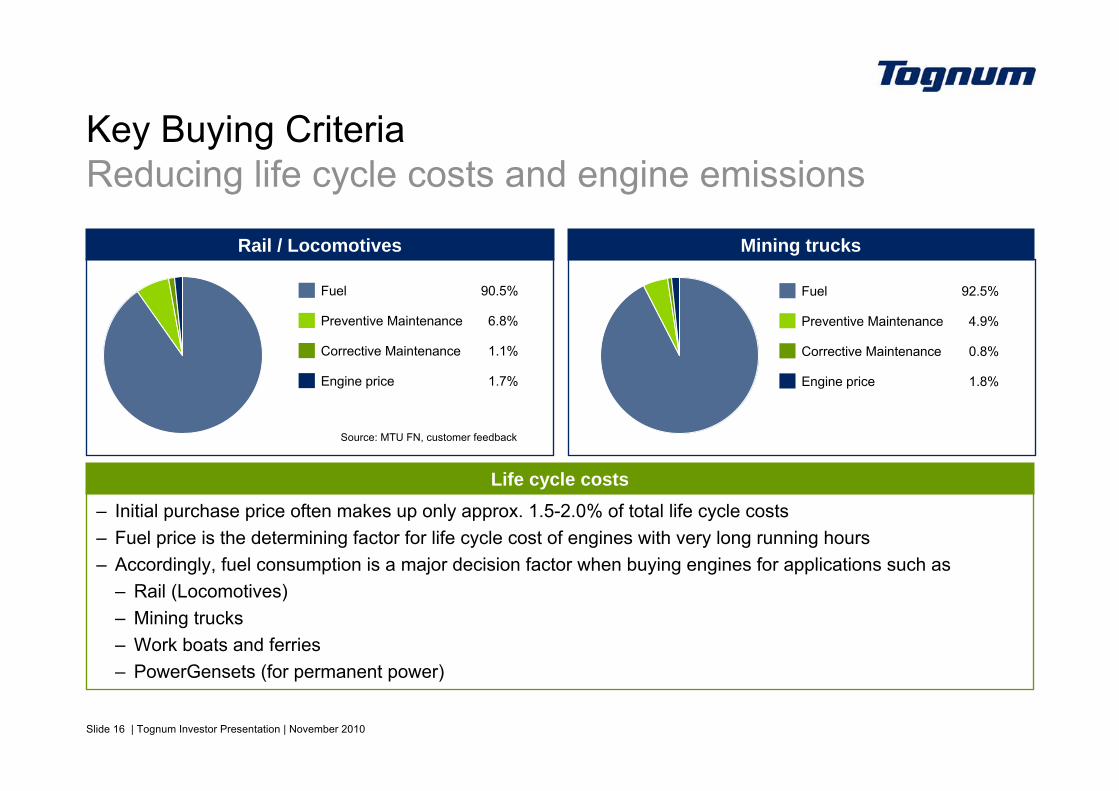

Rail / Locomotives Mining trucks

Life cycle costs

Key Buying CriteriaReducing life cycle costs and engine emissions

– Initial purchase price often makes up only approx. 1.5-2.0% of total life cycle costs– Fuel price is the determining factor for life cycle cost of engines with very long running hours – Accordingly, fuel consumption is a major decision factor when buying engines for applications such as

– Rail (Locomotives)– Mining trucks– Work boats and ferries– PowerGensets (for permanent power)

Fuel 90.5%

Preventive Maintenance 6.8%

Corrective Maintenance 1.1%

Engine price 1.7%

Fuel 92.5%

Preventive Maintenance 4.9%

Corrective Maintenance 0.8%

Engine price 1.8%

Source: MTU FN, customer feedback

Slide 17 | Tognum Investor Presentation | November 2010

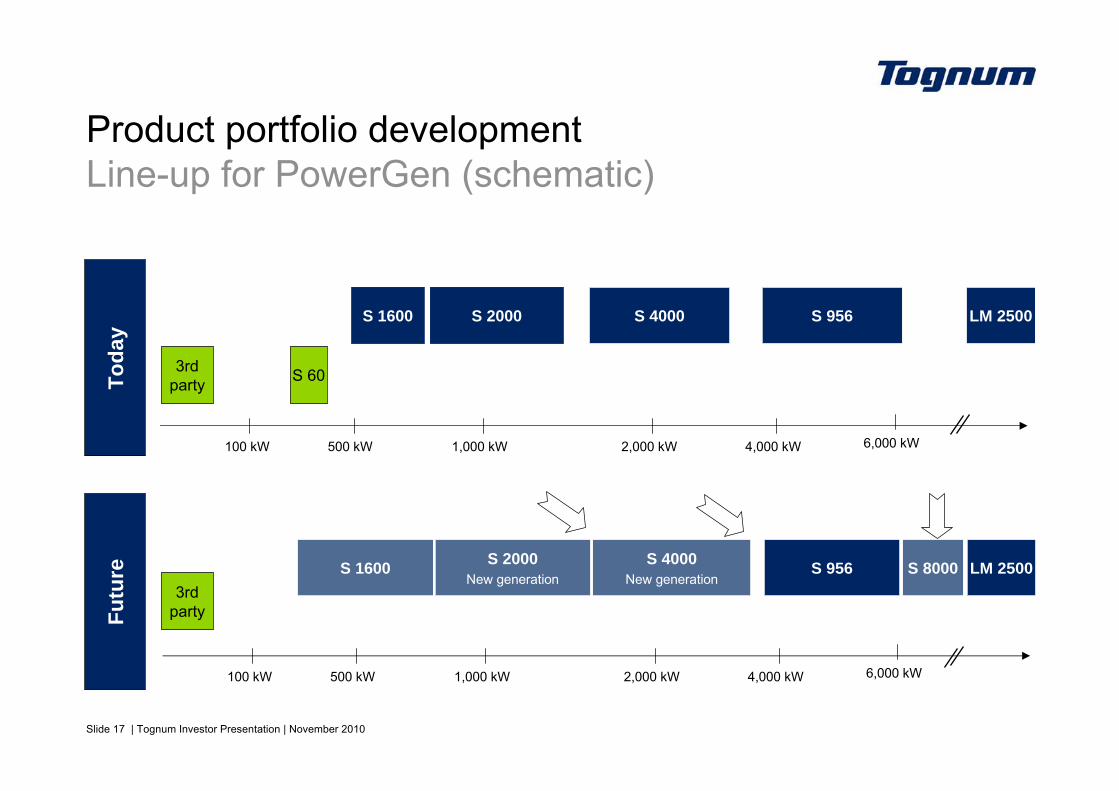

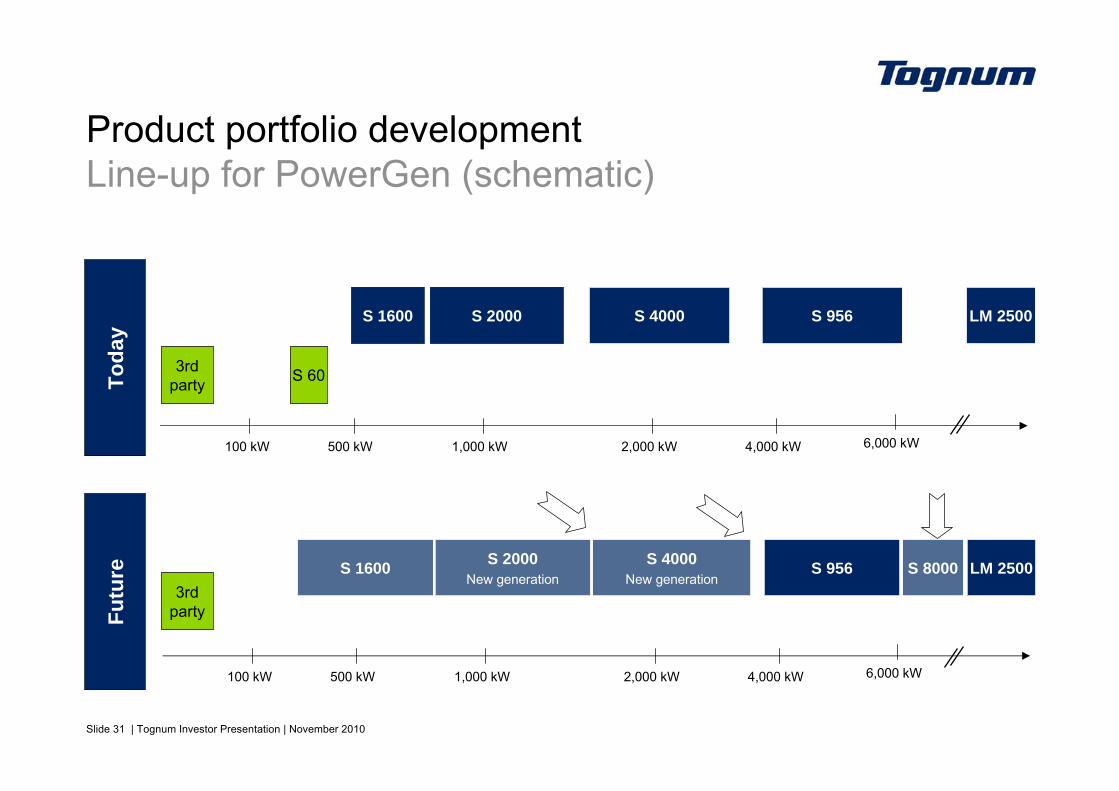

Product portfolio developmentLine-up for PowerGen (schematic)

Toda

y

S 4000S 2000

S 60

Futu

re S 4000New generation

S 2000New generation

S 1600

100 kW 500 kW 4,000 kW2,000 kW1,000 kW 6,000 kW

S 956

S 8000

100 kW 500 kW 4,000 kW2,000 kW1,000 kW 6,000 kW

S 956

S 1600

3rd party

3rd party

LM 2500

LM 2500

Slide 18 | Tognum Investor Presentation | November 2010

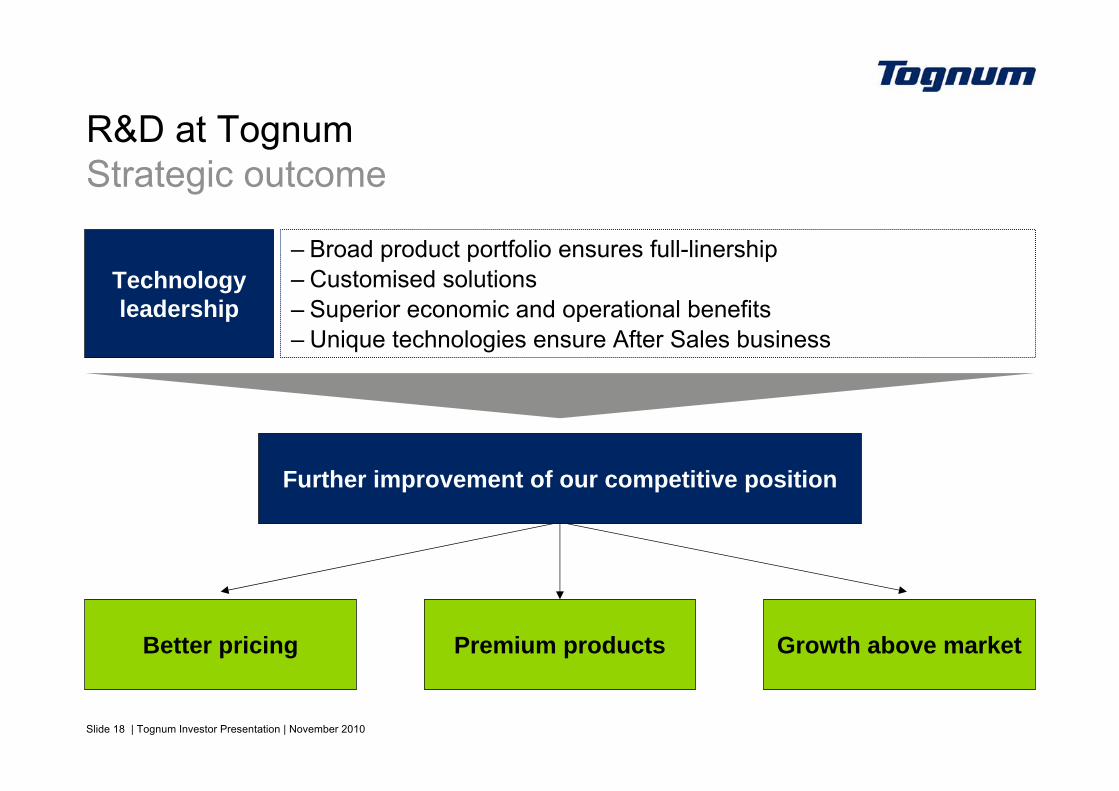

R&D at TognumStrategic outcome

Technology leadership

Further improvement of our competitive position

Growth above market

– Broad product portfolio ensures full-linership– Customised solutions – Superior economic and operational benefits – Unique technologies ensure After Sales business

Better pricing Premium products

Slide 19 | Tognum Investor Presentation | November 2010

Back-up Strategy, Production & Financials

Slide 20 | Tognum Investor Presentation | November 2010

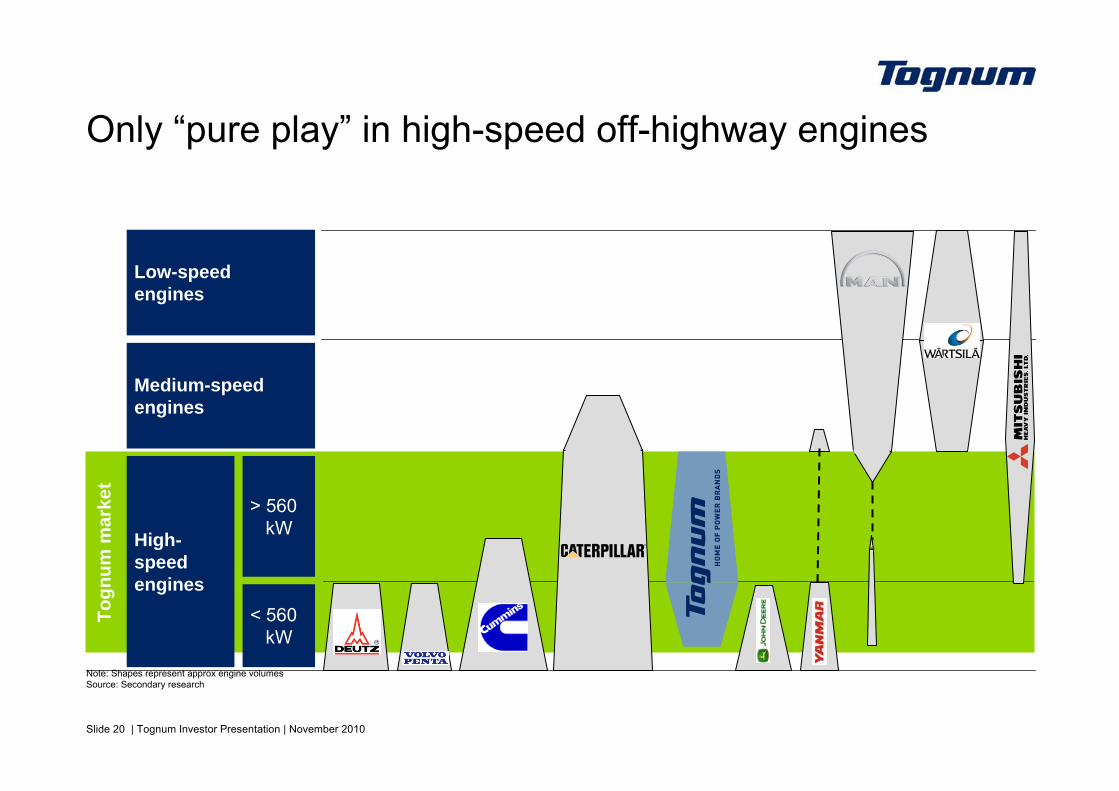

Only “pure play” in high-speed off-highway enginesTo

gnum

mar

ket

Low-speed engines

Medium-speed engines

> 560kW

< 560kW

High-speed engines

Note: Shapes represent approx engine volumesSource: Secondary research

Slide 21 | Tognum Investor Presentation | November 2010

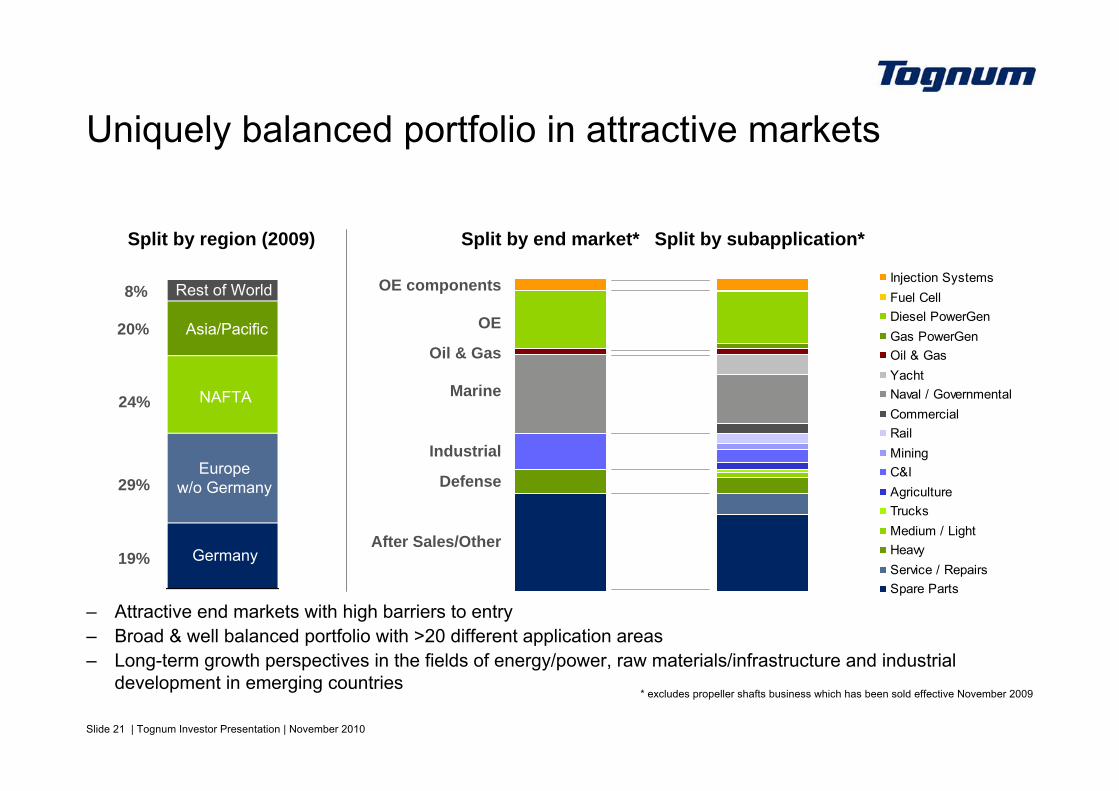

Injection SystemsFuel CellDiesel PowerGenGas PowerGenOil & GasYachtNaval / GovernmentalCommercialRailMiningC&IAgricultureTrucksMedium / LightHeavyService / RepairsSpare Parts

Uniquely balanced portfolio in attractive markets

Split by region (2009)

– Attractive end markets with high barriers to entry– Broad & well balanced portfolio with >20 different application areas– Long-term growth perspectives in the fields of energy/power, raw materials/infrastructure and industrial

development in emerging countries

29%

20%

24%

8%

19%

Rest of World

Europew/o Germany

Asia/Pacific

NAFTA

Germany

Split by end market* Split by subapplication*

OE components

OE

Oil & Gas

Marine

Industrial

Defense

After Sales/Other

* excludes propeller shafts business which has been sold effective November 2009

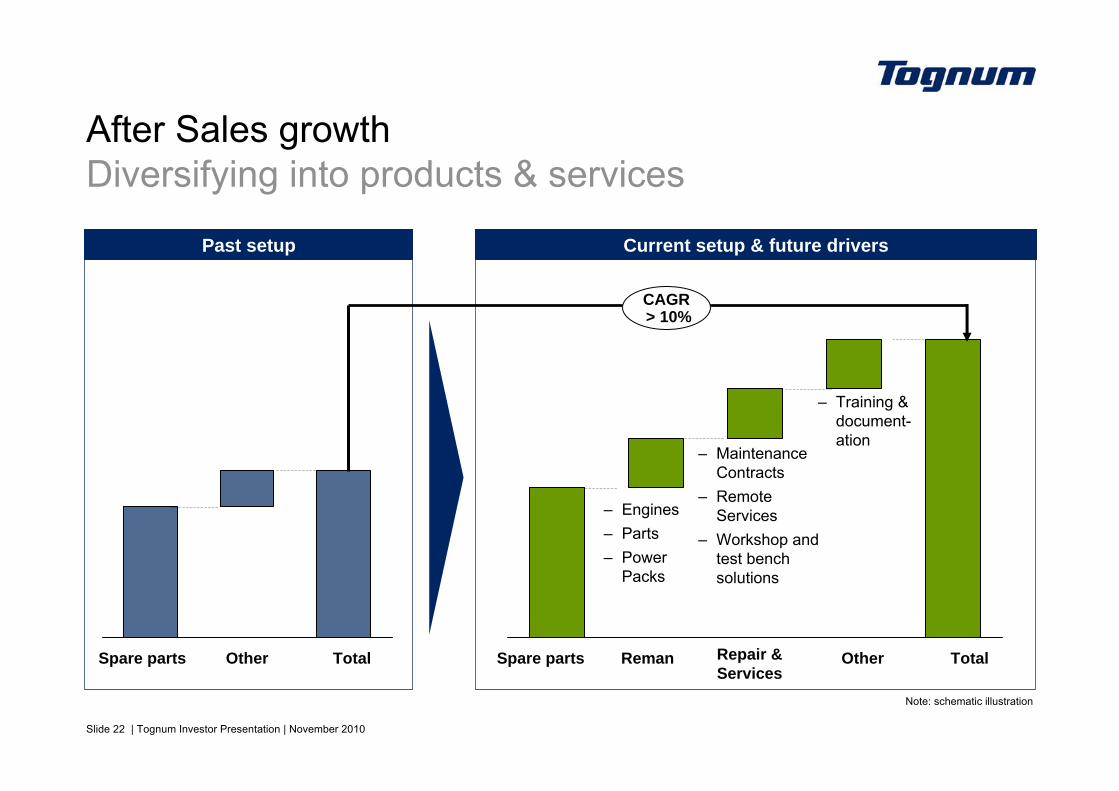

Slide 22 | Tognum Investor Presentation | November 2010

Current setup & future driversPast setup

TotalOtherRepair & Services

RemanSpare parts

– Maintenance Contracts

– Remote Services

– Workshop and test bench solutions

– Engines– Parts– Power

Packs

– Training & document-ation

TotalOtherSpare parts

CAGR> 10%

After Sales growthDiversifying into products & services

Note: schematic illustration

Slide 23 | Tognum Investor Presentation | November 2010

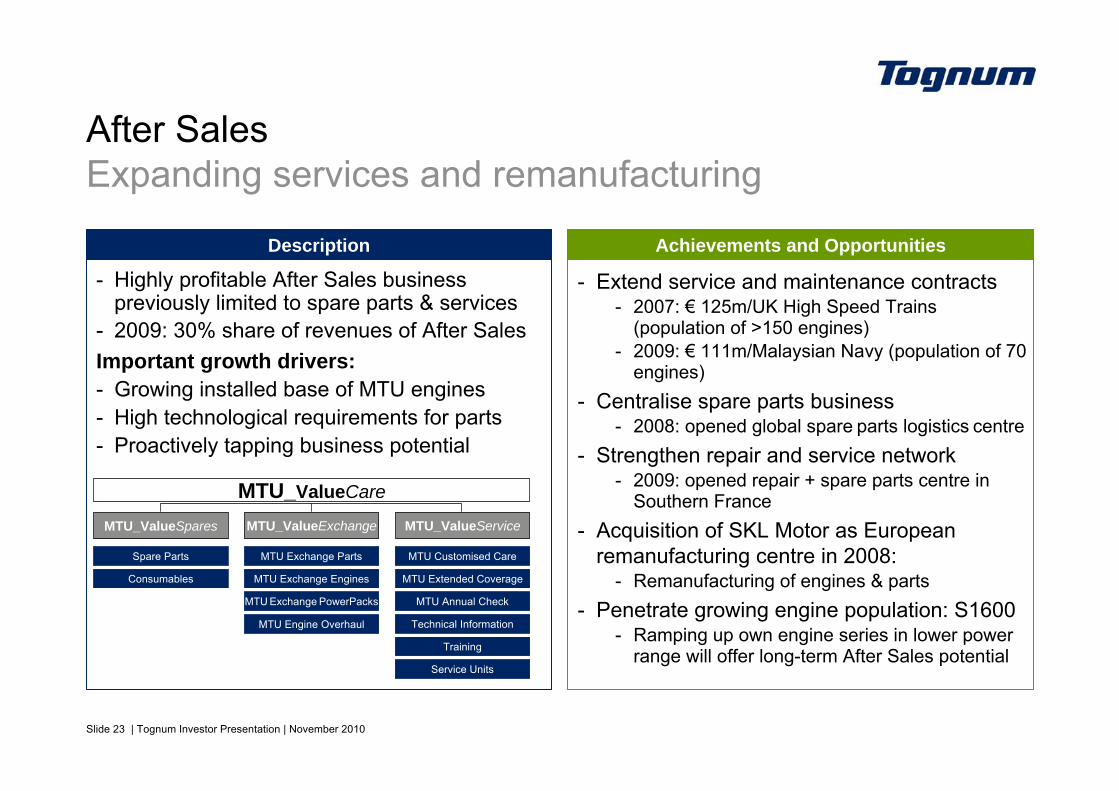

After SalesExpanding services and remanufacturing

- Highly profitable After Sales business previously limited to spare parts & services

- 2009: 30% share of revenues of After SalesImportant growth drivers:- Growing installed base of MTU engines- High technological requirements for parts- Proactively tapping business potential

Achievements and Opportunities

- Extend service and maintenance contracts- 2007: € 125m/UK High Speed Trains

(population of >150 engines)- 2009: € 111m/Malaysian Navy (population of 70

engines)- Centralise spare parts business

- 2008: opened global spare parts logistics centre- Strengthen repair and service network

- 2009: opened repair + spare parts centre in Southern France

- Acquisition of SKL Motor as European remanufacturing centre in 2008:

- Remanufacturing of engines & parts- Penetrate growing engine population: S1600

- Ramping up own engine series in lower power range will offer long-term After Sales potential

Description

MTU_ValueSpares MTU_ValueExchange MTU_ValueService

Spare Parts

Consumables

MTU Exchange Parts MTU Customised Care

MTU Exchange Engines

MTU Exchange PowerPacks

MTU Engine Overhaul

MTU Extended Coverage

MTU Annual Check

Technical Information

Training

Service Units

MTU_ValueCare

Slide 24 | Tognum Investor Presentation | November 2010

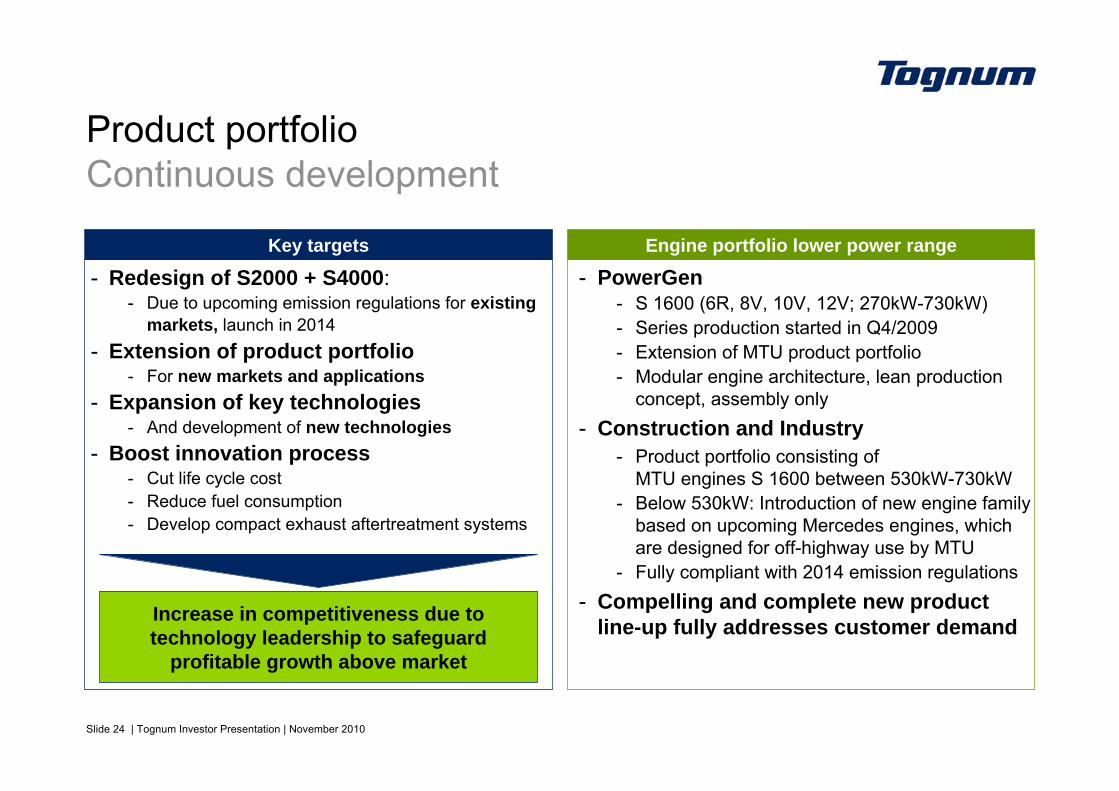

Product portfolioContinuous development

Engine portfolio lower power rangeKey targets

- Redesign of S2000 + S4000: - Due to upcoming emission regulations for existing

markets, launch in 2014- Extension of product portfolio

- For new markets and applications- Expansion of key technologies

- And development of new technologies- Boost innovation process

- Cut life cycle cost- Reduce fuel consumption- Develop compact exhaust aftertreatment systems

Increase in competitiveness due to technology leadership to safeguard

profitable growth above market

- PowerGen- S 1600 (6R, 8V, 10V, 12V; 270kW-730kW)- Series production started in Q4/2009- Extension of MTU product portfolio- Modular engine architecture, lean production

concept, assembly only- Construction and Industry

- Product portfolio consisting of MTU engines S 1600 between 530kW-730kW

- Below 530kW: Introduction of new engine family based on upcoming Mercedes engines, which are designed for off-highway use by MTU

- Fully compliant with 2014 emission regulations- Compelling and complete new product

line-up fully addresses customer demand

Slide 25 | Tognum Investor Presentation | November 2010

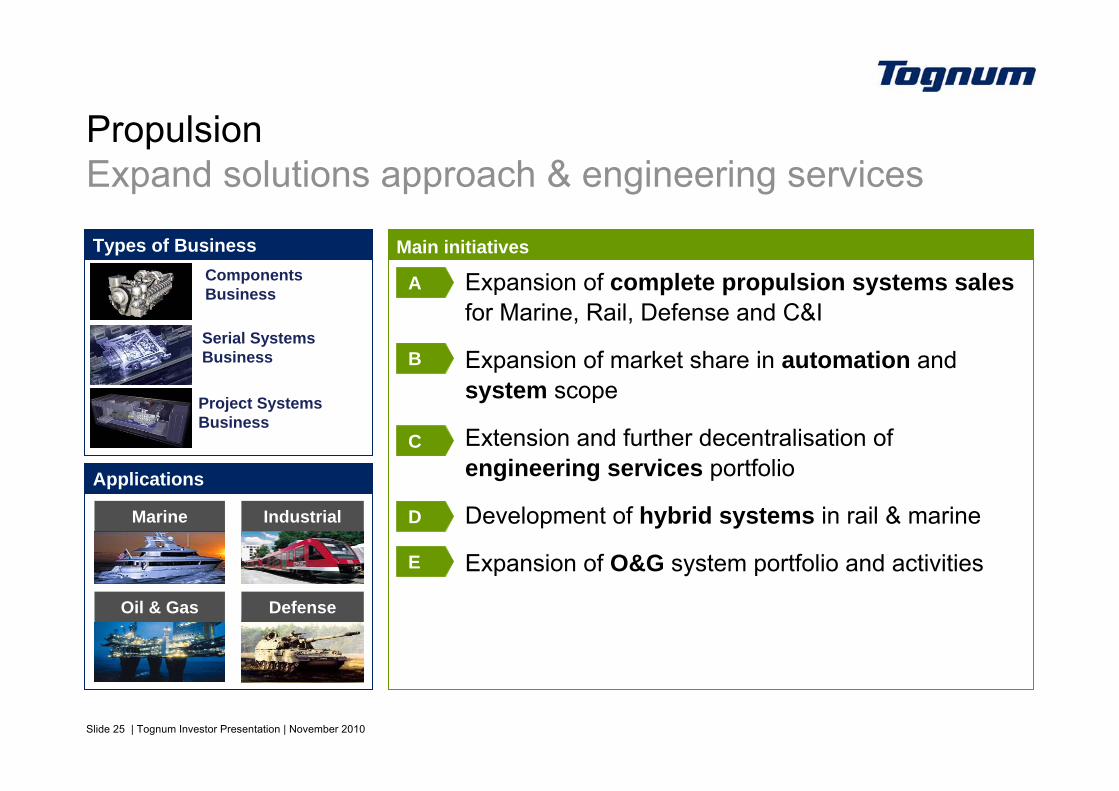

Expansion of complete propulsion systems salesfor Marine, Rail, Defense and C&I

Expansion of market share in automation and system scope

Extension and further decentralisation of engineering services portfolio

Development of hybrid systems in rail & marine

Expansion of O&G system portfolio and activities

PropulsionExpand solutions approach & engineering services

Types of Business Main initiatives

A

B

C

D

E

Components Business

Serial Systems Business

Project Systems Business

Applications

Marine Industrial

DefenseOil & Gas

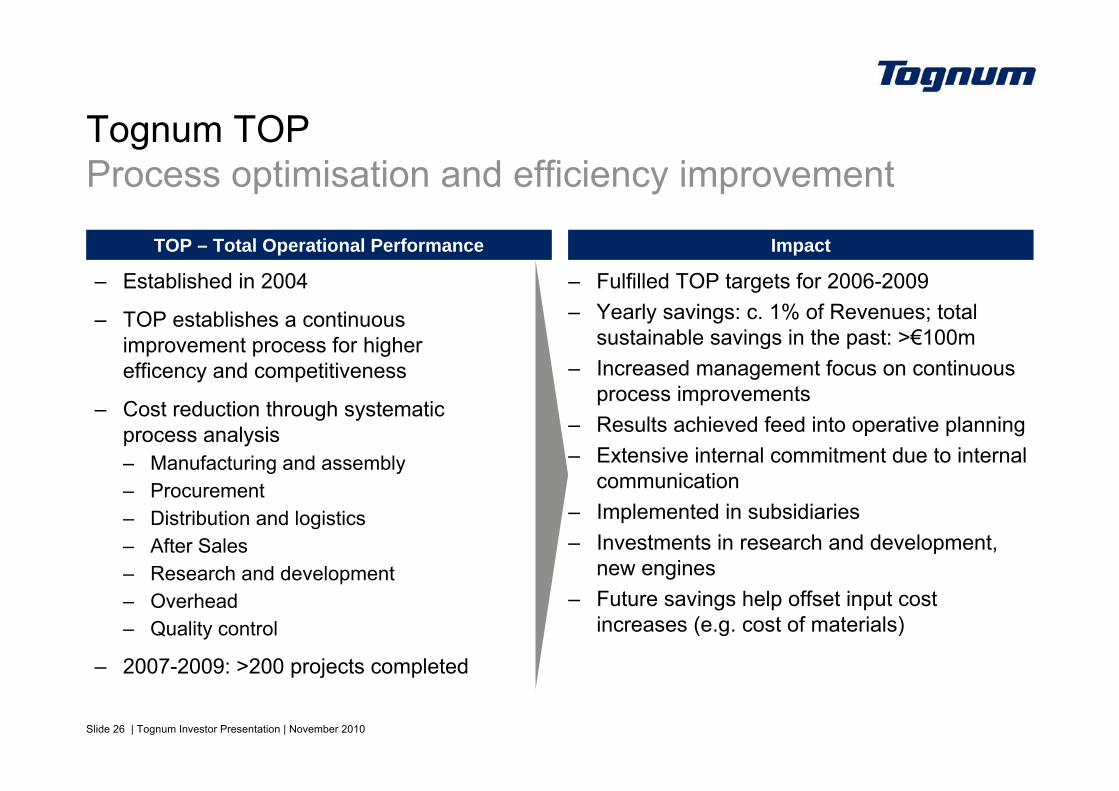

Slide 26 | Tognum Investor Presentation | November 2010

– Established in 2004

– TOP establishes a continuous improvement process for higher efficency and competitiveness

– Cost reduction through systematic process analysis – Manufacturing and assembly– Procurement– Distribution and logistics– After Sales– Research and development– Overhead– Quality control

– 2007-2009: >200 projects completed

– Fulfilled TOP targets for 2006-2009– Yearly savings: c. 1% of Revenues; total

sustainable savings in the past: >€100m– Increased management focus on continuous

process improvements – Results achieved feed into operative planning – Extensive internal commitment due to internal

communication– Implemented in subsidiaries– Investments in research and development,

new engines– Future savings help offset input cost

increases (e.g. cost of materials)

TOP – Total Operational Performance Impact

Tognum TOPProcess optimisation and efficiency improvement

Slide 27 | Tognum Investor Presentation | November 2010

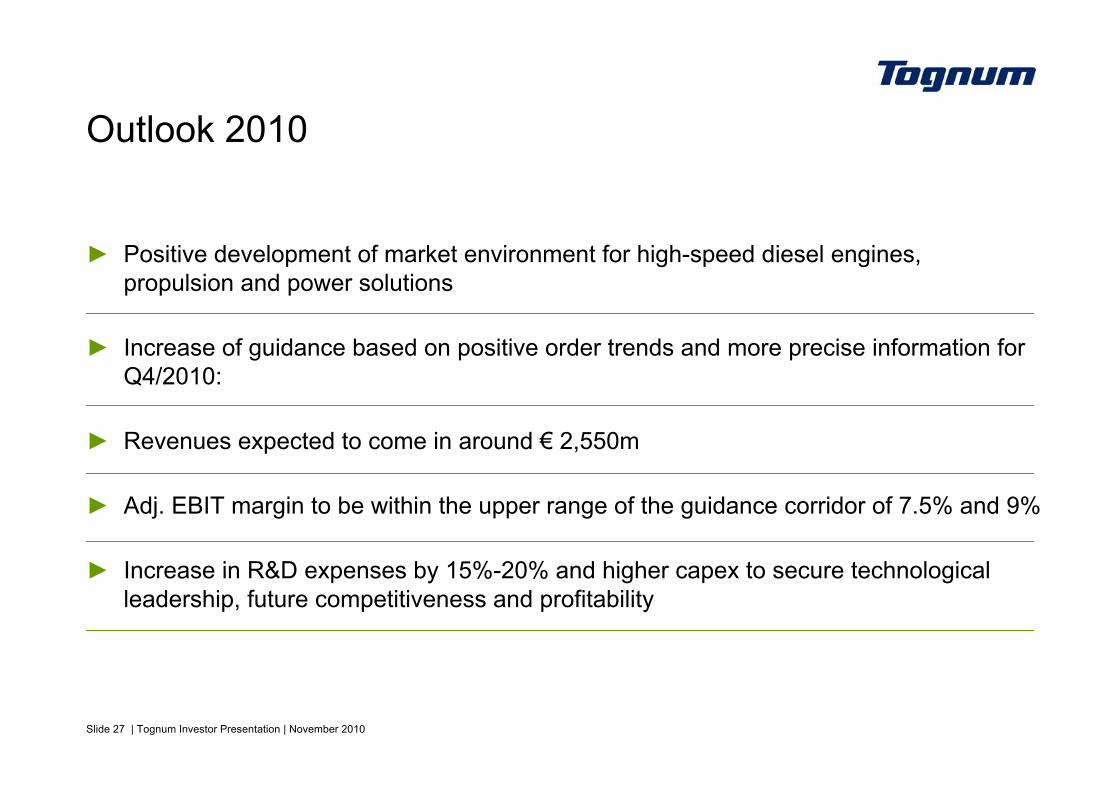

Outlook 2010

► Positive development of market environment for high-speed diesel engines, propulsion and power solutions

► Increase of guidance based on positive order trends and more precise information for Q4/2010:

► Revenues expected to come in around € 2,550m

► Adj. EBIT margin to be within the upper range of the guidance corridor of 7.5% and 9%

► Increase in R&D expenses by 15%-20% and higher capex to secure technological leadership, future competitiveness and profitability

Slide 28 | Tognum Investor Presentation | November 2010

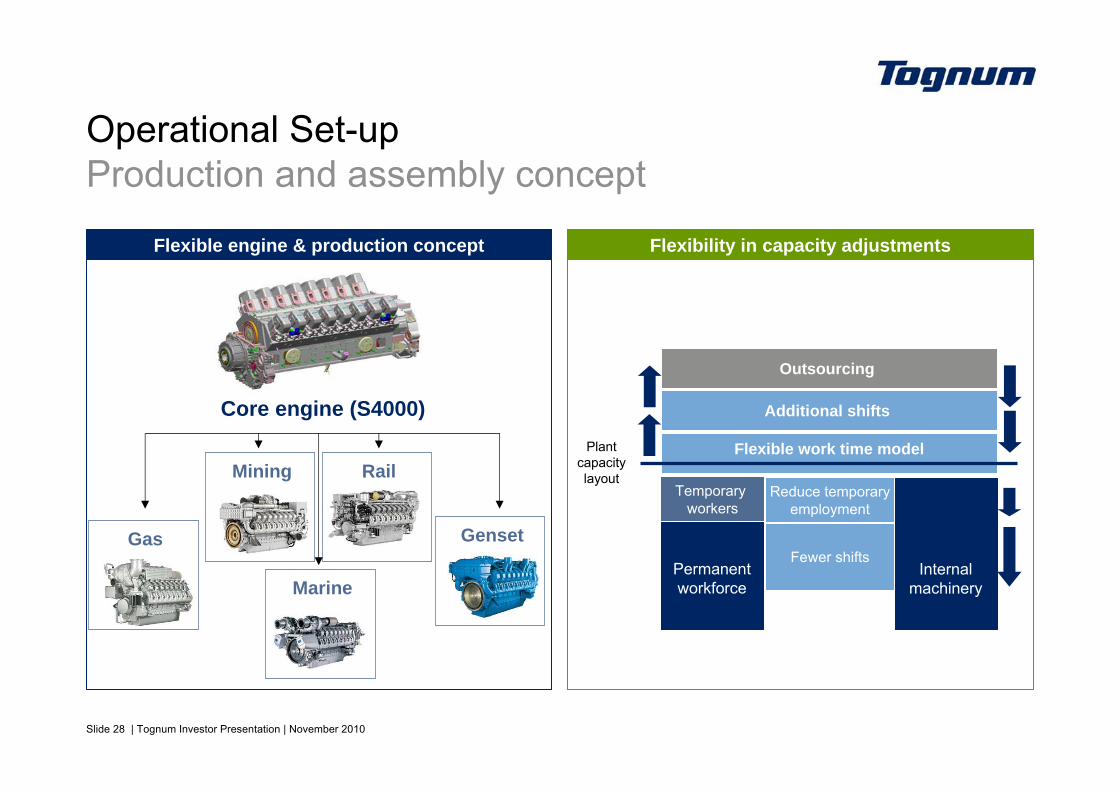

Operational Set-upProduction and assembly concept

Flexibility in capacity adjustmentsFlexible engine & production concept

Core engine (S4000)

Gas

Marine

Mining Rail

Genset

Permanent workforce

Temporary workers

Plant capacity layout

Additional shifts

Outsourcing

Reduce temporaryemployment

Fewer shifts

Flexible work time model

Internal machinery

Slide 29 | Tognum Investor Presentation | November 2010

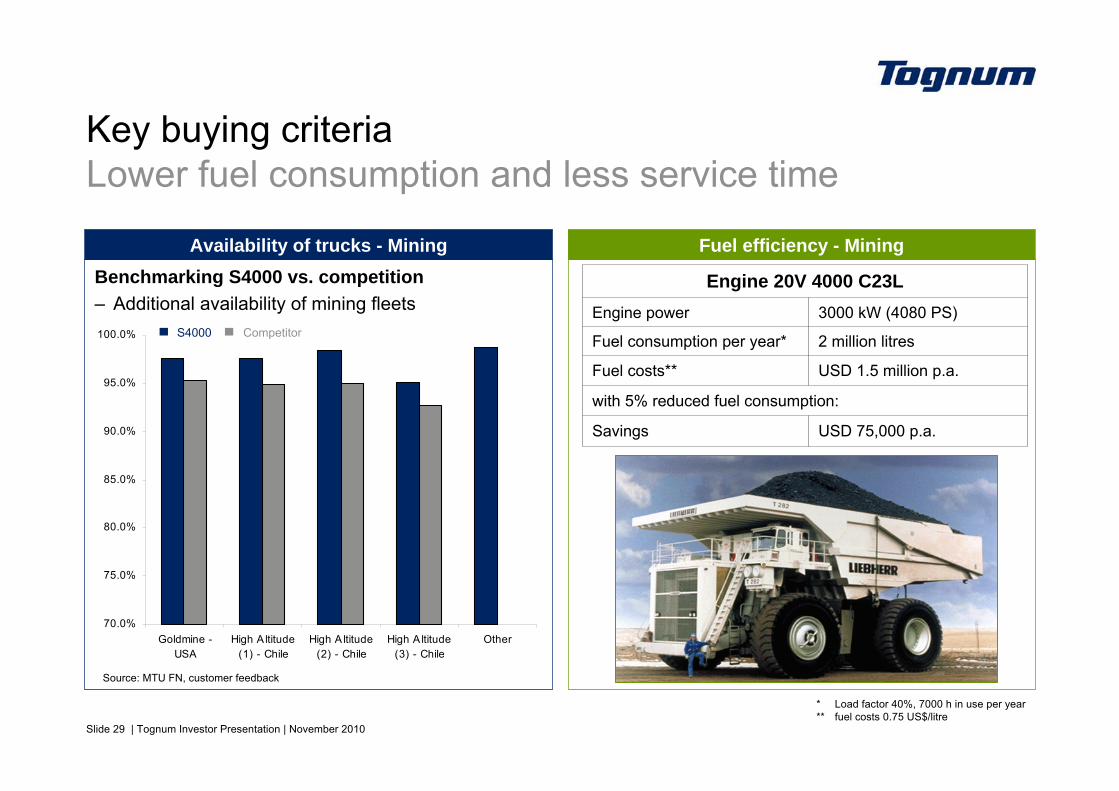

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

100.0%

Goldmine -USA

High A ltitude(1) - Chile

High A ltitude(2) - Chile

High A ltitude(3) - Chile

Other

Availability of trucks - Mining Fuel efficiency - Mining

Key buying criteriaLower fuel consumption and less service time

Benchmarking S4000 vs. competition– Additional availability of mining fleets

Source: MTU FN, customer feedback

CompetitorS4000

USD 75,000 p.a.Savings

with 5% reduced fuel consumption:

USD 1.5 million p.a.Fuel costs**

2 million litresFuel consumption per year*

3000 kW (4080 PS)Engine power

Engine 20V 4000 C23L

* Load factor 40%, 7000 h in use per year** fuel costs 0.75 US$/litre

Slide 30 | Tognum Investor Presentation | November 2010

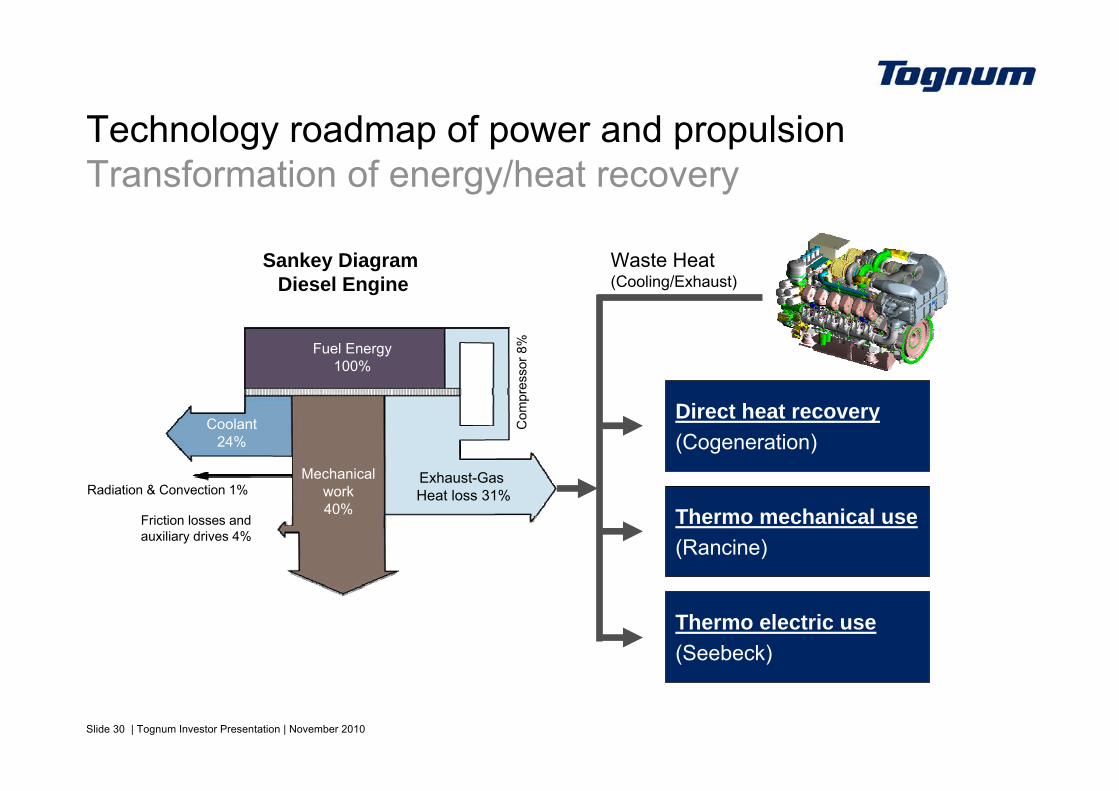

Technology roadmap of power and propulsionTransformation of energy/heat recovery

Sankey Diagram Diesel Engine

Radiation & Convection 1%

Com

pres

sor 8

%Friction losses and auxiliary drives 4%

Fuel Energy100%

Mechanicalwork40%

Coolant24%

Exhaust-Gas Heat loss 31%

Waste Heat(Cooling/Exhaust)

Thermo electric use(Seebeck)

Thermo mechanical use(Rancine)

Direct heat recovery(Cogeneration)

Slide 31 | Tognum Investor Presentation | November 2010

Product portfolio developmentLine-up for PowerGen (schematic)

Toda

y

S 4000S 2000

S 60

Futu

re S 4000New generation

S 2000New generation

S 1600

100 kW 500 kW 4,000 kW2,000 kW1,000 kW 6,000 kW

S 956

S 8000

100 kW 500 kW 4,000 kW2,000 kW1,000 kW 6,000 kW

S 956

S 1600

3rd party

3rd party

LM 2500

LM 2500

Slide 32 | Tognum Investor Presentation | November 2010

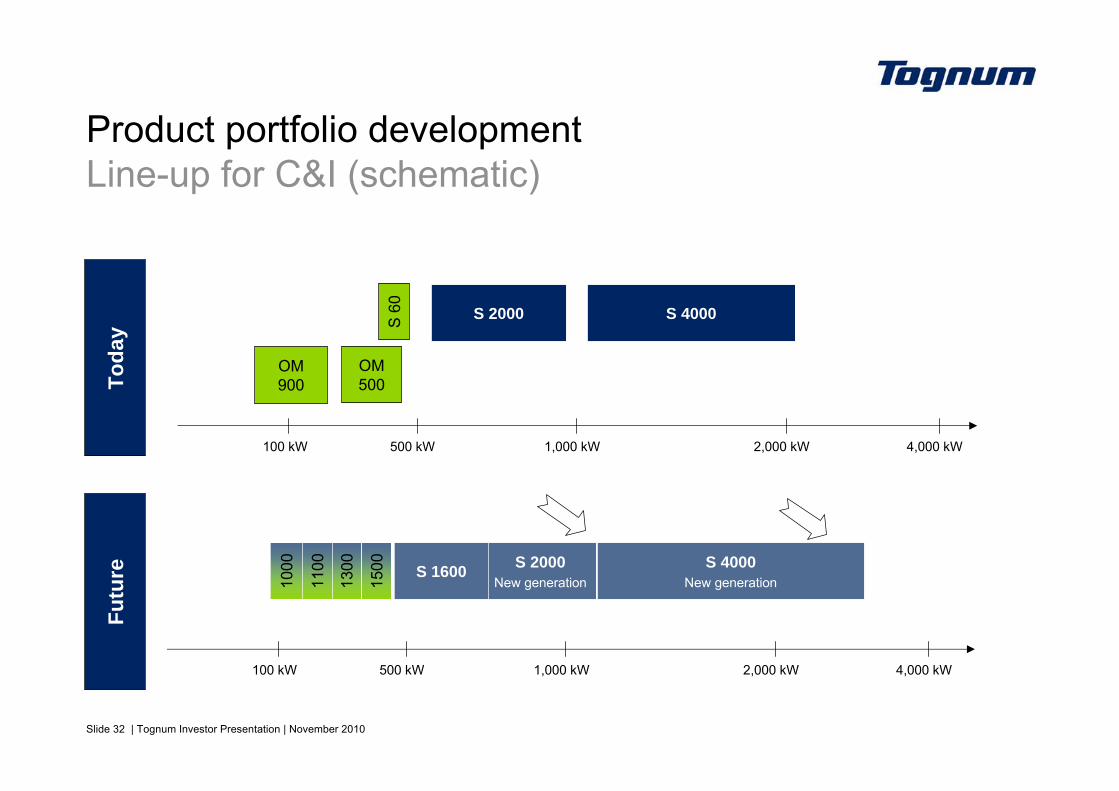

Product portfolio developmentLine-up for C&I (schematic)

Toda

y

OM900

OM500

S 4000S 2000S 60

100 kW 500 kW 4,000 kW2,000 kW1,000 kW

Futu

re S 4000New generation

S 2000New generation

S 1600

1000

1500

1300

1100

100 kW 500 kW 4,000 kW2,000 kW1,000 kW

Slide 33 | Tognum Investor Presentation | November 2010

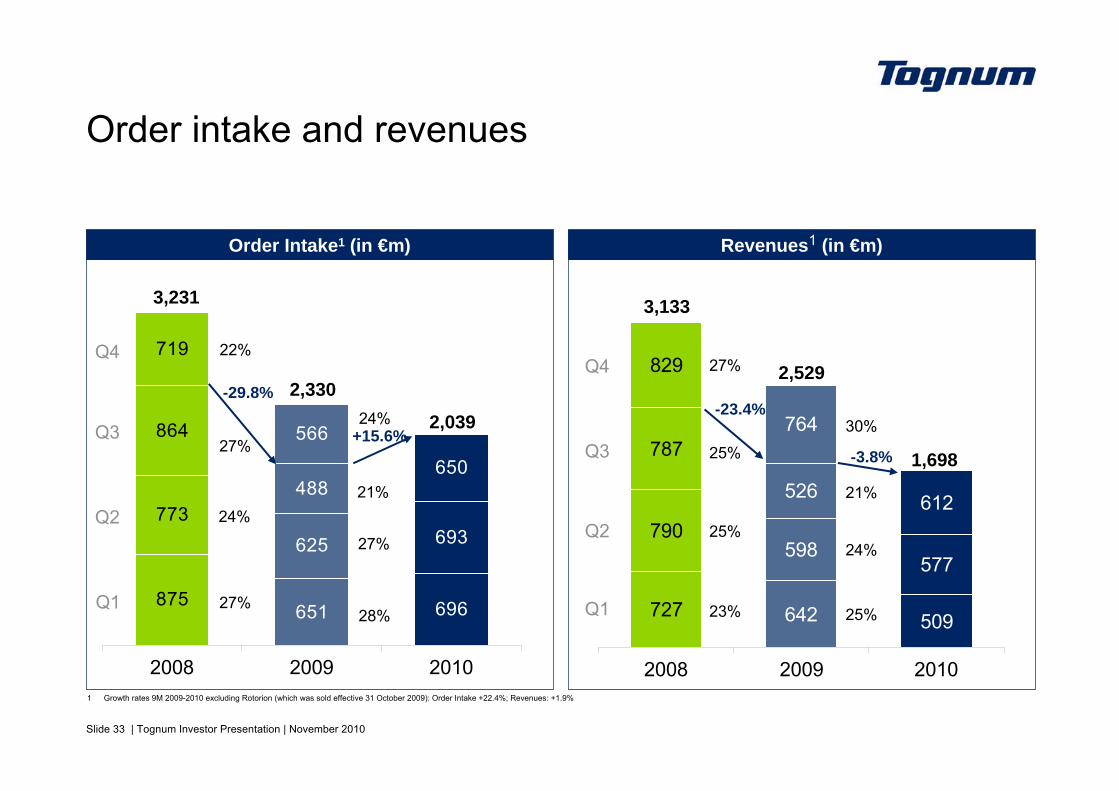

727

790

787

829

642 509

598577

526 612

764

2008 2009 2010

875

773

864

719

651 696

625 693

488650

566

2008 2009 2010

Revenues1 (in €m)

Order intake and revenues

Order Intake1 (in €m)

+15.6%

3,231

-3.8%

Q4

Q3

Q2

Q1

Q4

Q3

Q2

Q1

3,133

22%

27%

24%

27%

27%

25%

25%

23%

-23.4%-29.8% 2,330

2,529

24%

21%

27%

28%

30%

21%

24%

25%

2,039

1,698

1 Growth rates 9M 2009-2010 excluding Rotorion (which was sold effective 31 October 2009): Order Intake +22.4%; Revenues: +1.9%

Slide 34 | Tognum Investor Presentation | November 2010

58

75

69

62

22383113

3417

54

2008 2009 2010

100

100

124

83

64 43

19 5433

5683

2008 2009 2010

Q3

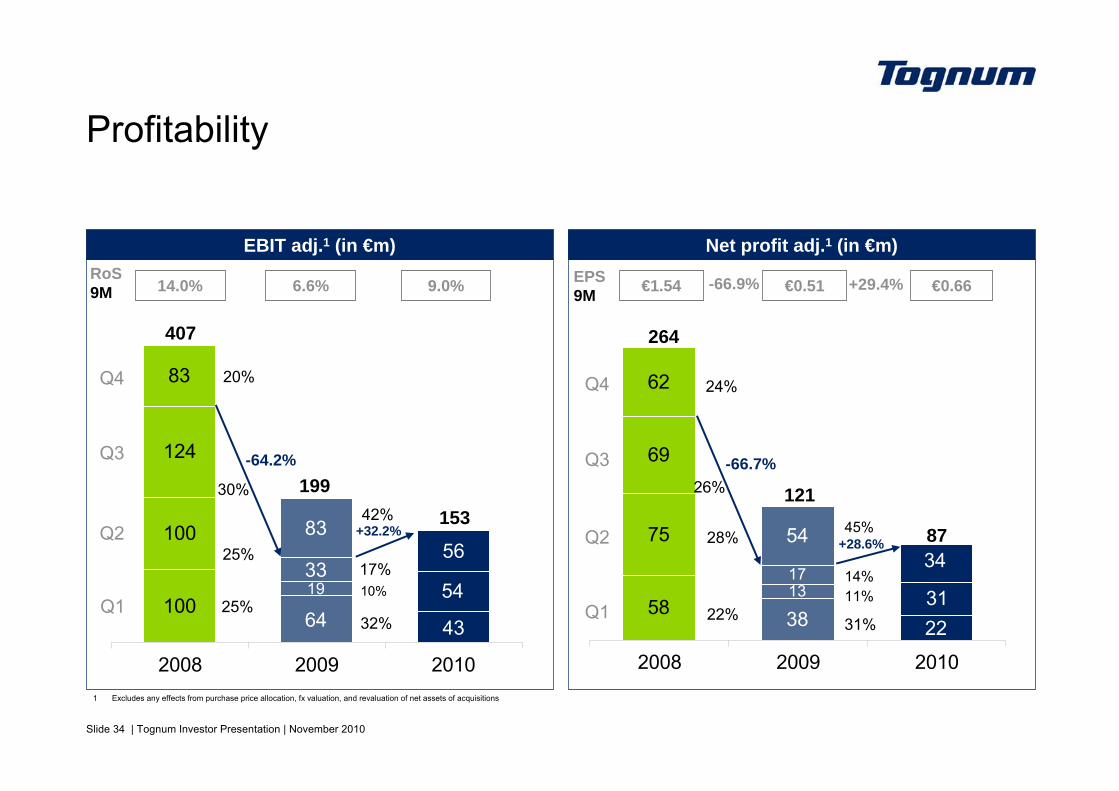

EBIT adj.1 (in €m) Net profit adj.1 (in €m)

Profitability

1 Excludes any effects from purchase price allocation, fx valuation, and revaluation of net assets of acquisitions

-66.7%

RoS9M 6.6% 9.0% EPS

9M €0.51 €0.66

-64.2%

407 264

Q4

Q2

Q1

Q4

Q3

Q2

Q1

24%

26%

28%

22%

20%

30%

25%

25%

+29.4%14.0%

+32.2%+28.6%

€1.54 -66.9%

12119942%

10%17%

32%

14%11%

31%

1538745%

Slide 35 | Tognum Investor Presentation | November 2010

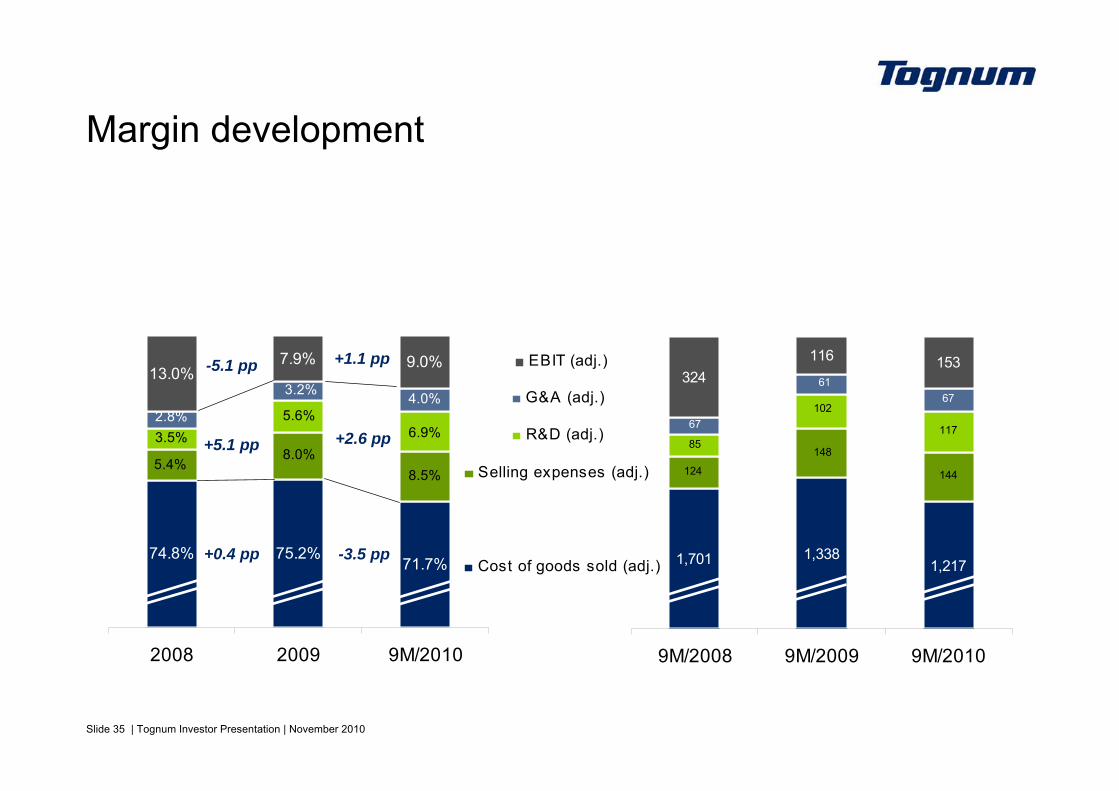

74.8% 75.2%71.7%

13.0%7.9% 9.0%

8.0%5.4%

8.5%

5.6%3.5% 6.9%2.8%

3.2% 4.0%

2008 2009 9M/2010

324116 153

1,2171,3381,701

148

124 144

102

8511767

6167

9M/2008 9M/2009 9M/2010

G&A (adj.)

Margin development

-3.5 pp

+2.6 pp

+1.1 pp

+0.4 pp

+5.1 pp

-5.1 pp

R&D (adj.)

Selling expenses (adj.)

EBIT (adj.)

Cost of goods sold (adj.)

Slide 36 | Tognum Investor Presentation | November 2010

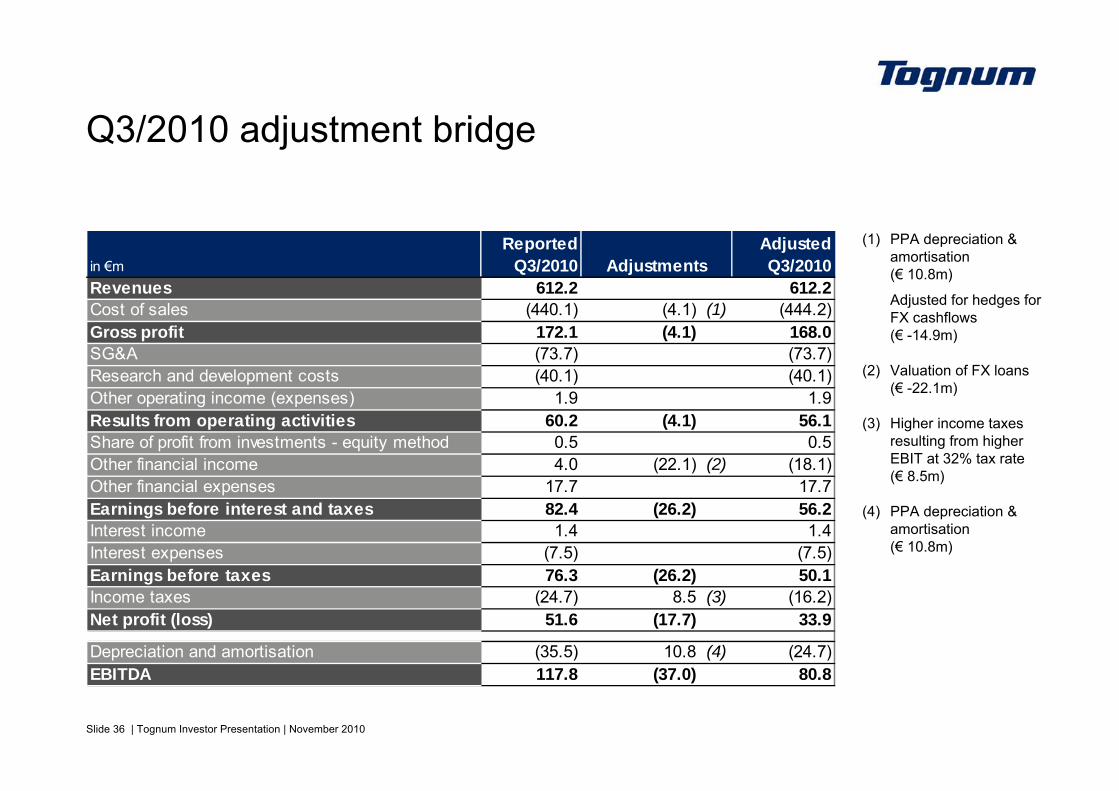

Q3/2010 adjustment bridge

(1) PPA depreciation & amortisation (€ 10.8m)

Adjusted for hedges for FX cashflows(€ -14.9m)

(2) Valuation of FX loans (€ -22.1m)

(3) Higher income taxes resulting from higher EBIT at 32% tax rate (€ 8.5m)

(4) PPA depreciation & amortisation (€ 10.8m)

in €mReported

Q3/2010Adjusted Q3/2010

Revenues 612.2 612.2Cost of sales (440.1) (4.1) (1) (444.2)Gross profit 172.1 (4.1) 168.0SG&A (73.7) (73.7)

(40.1) (40.1)1.9 1.9

60.2 (4.1) 56.10.5 0.5

Other financial income 4.0 (22.1) (2) (18.1)Other financial expenses 17.7 17.7

82.4 (26.2) 56.2Interest income 1.4 1.4Interest expenses (7.5) (7.5)Earnings before taxes 76.3 (26.2) 50.1Income taxes (24.7) 8.5 (3) (16.2)Net profit (loss) 51.6 (17.7) 33.9

Depreciation and amortisation (35.5) 10.8 (4) (24.7)EBITDA 117.8 (37.0) 80.8

Research and development costs

Results from operating activitiesShare of profit from investments - equity method

Other operating income (expenses)

Adjustments

Earnings before interest and taxes

Slide 37 | Tognum Investor Presentation | November 2010

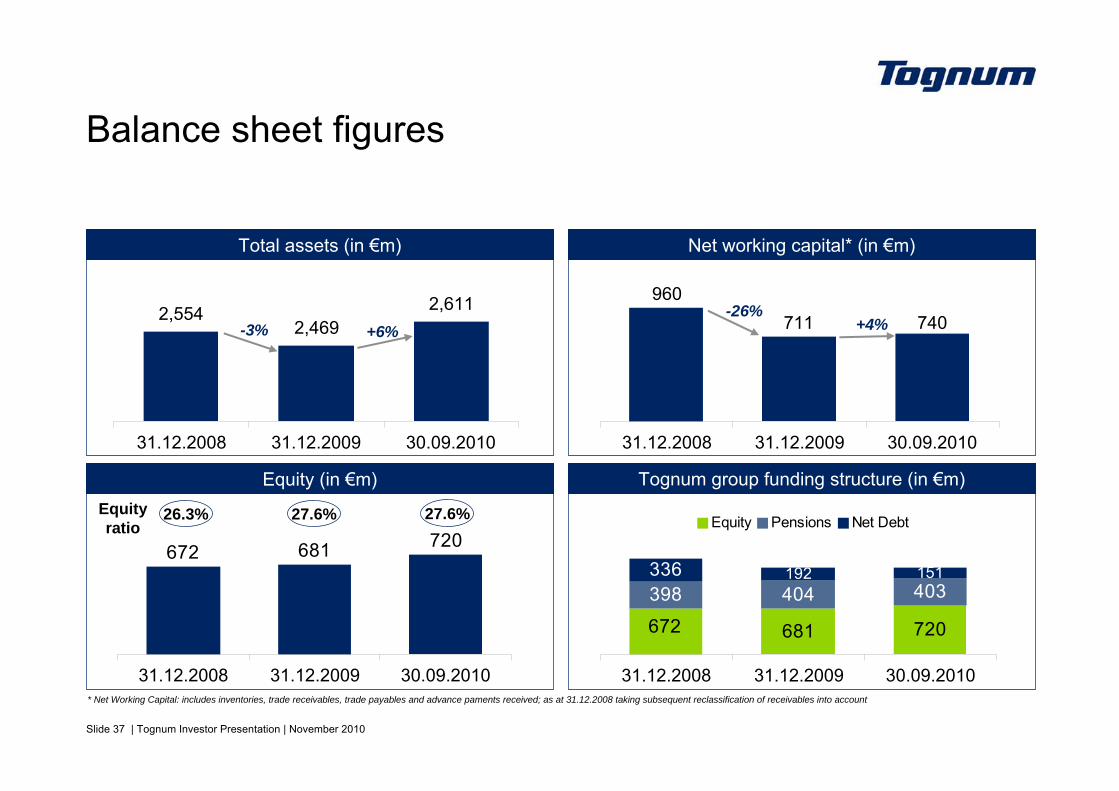

681 720

398 404 403336

672

151192

31.12.2008 31.12.2009 30.09.2010

Equity Pensions Net Debt720672 681

31.12.2008 31.12.2009 30.09.2010

740711960

31.12.2008 31.12.2009 30.09.2010

2,5542,469

2,611

31.12.2008 31.12.2009 30.09.2010

Total assets (in €m) Net working capital* (in €m)

Tognum group funding structure (in €m)Equity (in €m)

Balance sheet figures

Equityratio

-3% +4%+6%-26%

26.3% 27.6%

* Net Working Capital: includes inventories, trade receivables, trade payables and advance paments received; as at 31.12.2008 taking subsequent reclassification of receivables into account

27.6%

Slide 38 | Tognum Investor Presentation | November 2010

31.12.2008 31.12.2009 30.09.2010

(36.6)

(16.1)

(9.7) (12.5)(28.6)

(46.0)

(77.7)181.3

(150.8)

(192.2)

54.6

136.4

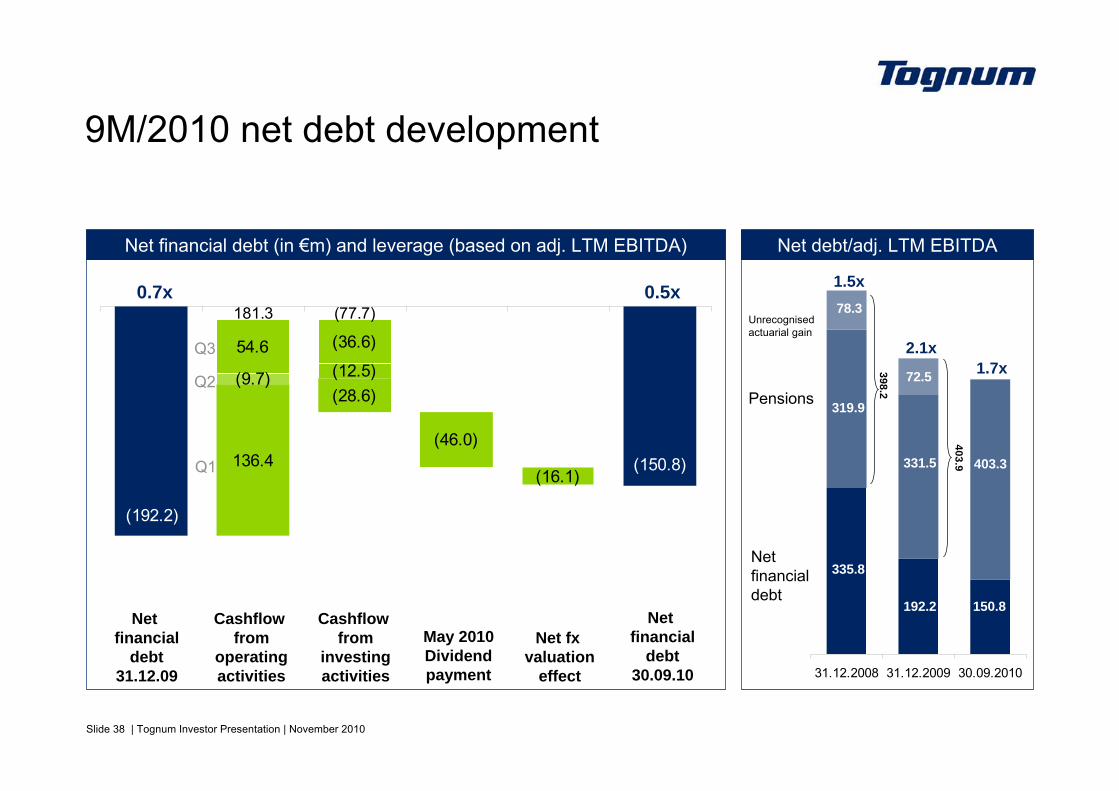

9M/2010 net debt development

Net financial debt (in €m) and leverage (based on adj. LTM EBITDA)

0.7x 0.5x

Q1

Net financial

debt31.12.09

Cashflow from

operatingactivities

Net financial

debt30.09.10

Cashflow from

investingactivities

Net fxvaluation

effect

Net debt/adj. LTM EBITDA

Pensions

Netfinancialdebt

1.5x

2.1x

Unrecognisedactuarial gain

335.8

192.2

319.9

331.5

78.3

398.2

72.5

403.9

150.8

403.3

1.7xQ2

May 2010Dividendpayment

Q3

Slide 39 | Tognum Investor Presentation | November 2010

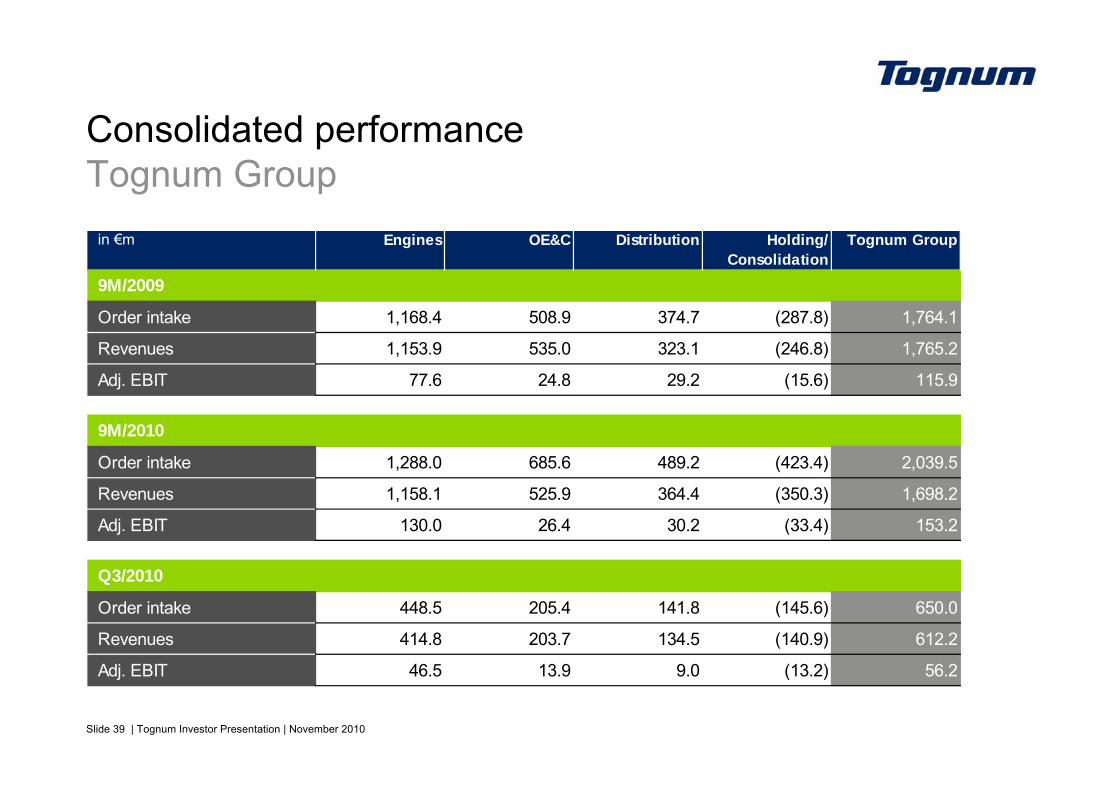

Consolidated performance Tognum Group

in €m Engines OE&C Distribution Holding/ Consolidation

Tognum Group

9M/2009

Order intake 1,168.4 508.9 374.7 (287.8) 1,764.1

Revenues 1,153.9 535.0 323.1 (246.8) 1,765.2

Adj. EBIT 77.6 24.8 29.2 (15.6) 115.9

9M/2010

Order intake 1,288.0 685.6 489.2 (423.4) 2,039.5

Revenues 1,158.1 525.9 364.4 (350.3) 1,698.2

Adj. EBIT 130.0 26.4 30.2 (33.4) 153.2

Q3/2010

Order intake 448.5 205.4 141.8 (145.6) 650.0

Revenues 414.8 203.7 134.5 (140.9) 612.2

Adj. EBIT 46.5 13.9 9.0 (13.2) 56.2

Slide 40 | Tognum Investor Presentation | November 2010

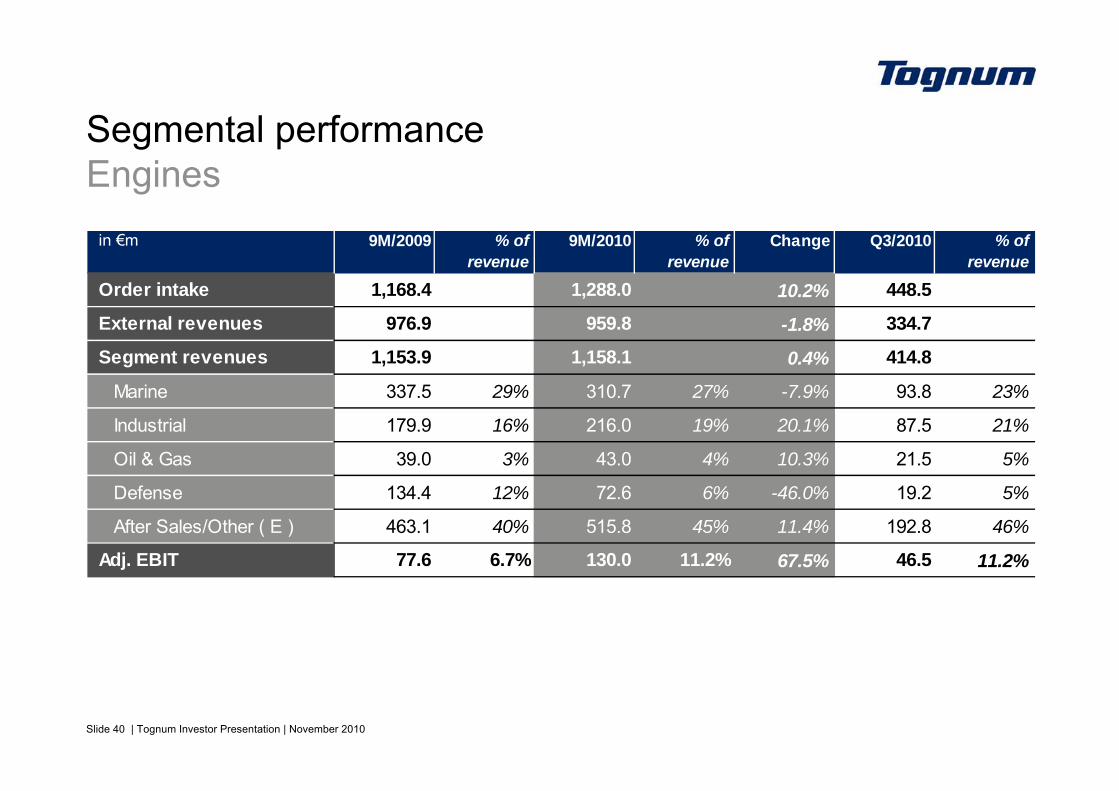

Segmental performanceEngines

in €m 9M/2009 % of revenue

9M/2010 % of revenue

Change Q3/2010 % of revenue

Order intake 1,168.4 1,288.0 10.2% 448.5

External revenues 976.9 959.8 -1.8% 334.7

Segment revenues 1,153.9 1,158.1 0.4% 414.8

Marine 337.5 29% 310.7 27% -7.9% 93.8 23%

Industrial 179.9 16% 216.0 19% 20.1% 87.5 21%

Oil & Gas 39.0 3% 43.0 4% 10.3% 21.5 5%

Defense 134.4 12% 72.6 6% -46.0% 19.2 5%

After Sales/Other ( E ) 463.1 40% 515.8 45% 11.4% 192.8 46%

Adj. EBIT 77.6 6.7% 130.0 11.2% 67.5% 46.5 11.2%

Slide 41 | Tognum Investor Presentation | November 2010

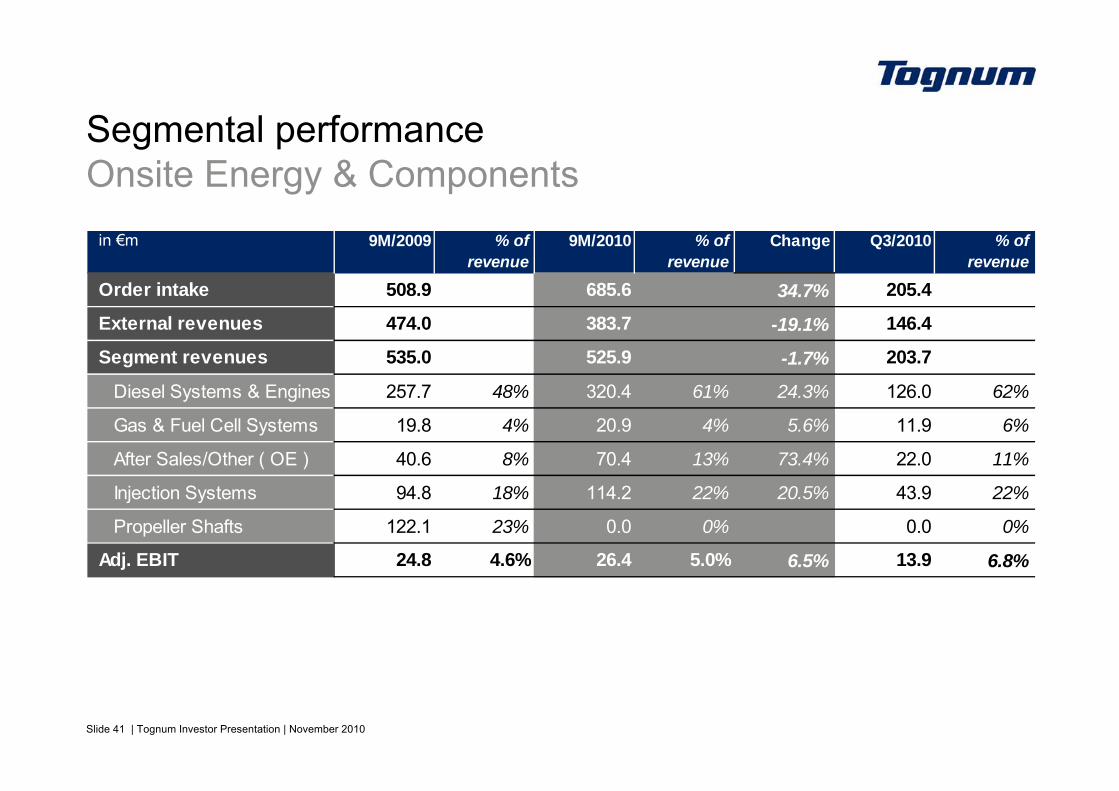

Segmental performance Onsite Energy & Components

in €m 9M/2009 % of revenue

9M/2010 % of revenue

Change Q3/2010 % of revenue

Order intake 508.9 685.6 34.7% 205.4

External revenues 474.0 383.7 -19.1% 146.4

Segment revenues 535.0 525.9 -1.7% 203.7

Diesel Systems & Engines 257.7 48% 320.4 61% 24.3% 126.0 62%

Gas & Fuel Cell Systems 19.8 4% 20.9 4% 5.6% 11.9 6%

After Sales/Other ( OE ) 40.6 8% 70.4 13% 73.4% 22.0 11%

Injection Systems 94.8 18% 114.2 22% 20.5% 43.9 22%

Propeller Shafts 122.1 23% 0.0 0% 0.0 0%

Adj. EBIT 24.8 4.6% 26.4 5.0% 6.5% 13.9 6.8%

Slide 42 | Tognum Investor Presentation | November 2010

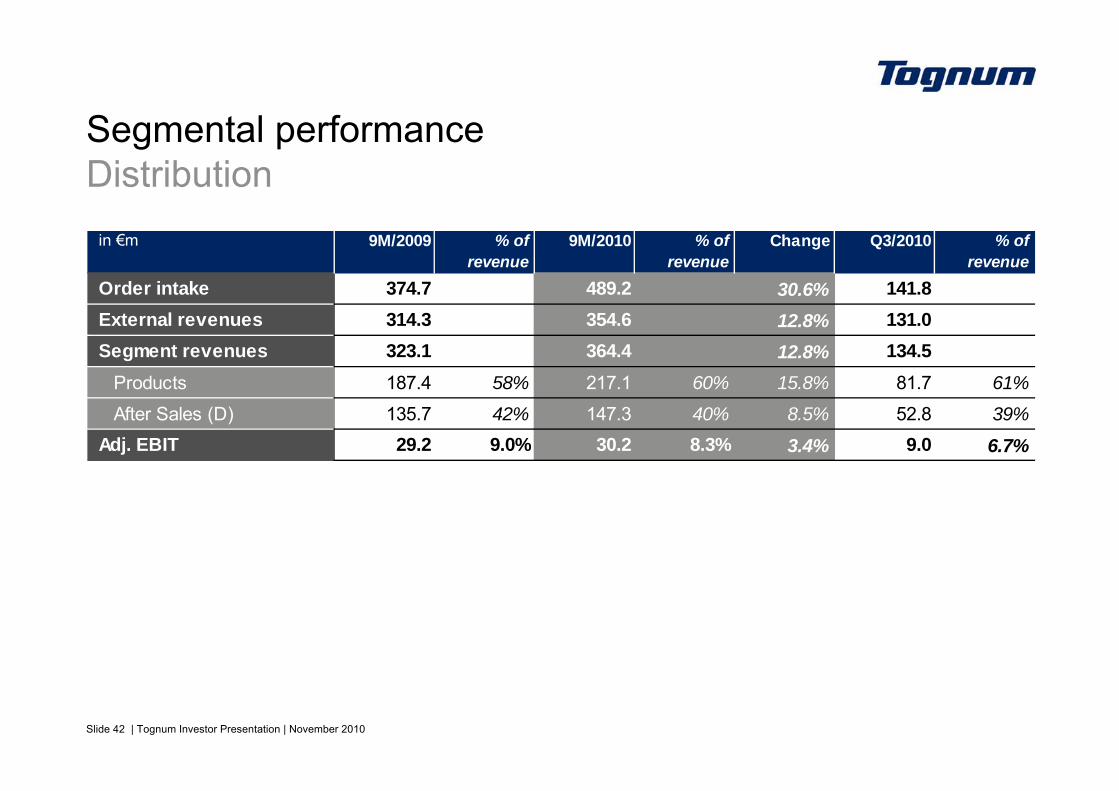

Segmental performance Distribution

in €m 9M/2009 % of revenue

9M/2010 % of revenue

Change Q3/2010 % of revenue

Order intake 374.7 489.2 30.6% 141.8External revenues 314.3 354.6 12.8% 131.0Segment revenues 323.1 364.4 12.8% 134.5

Products 187.4 58% 217.1 60% 15.8% 81.7 61%

After Sales (D) 135.7 42% 147.3 40% 8.5% 52.8 39%Adj. EBIT 29.2 9.0% 30.2 8.3% 3.4% 9.0 6.7%

Slide 43 | Tognum Investor Presentation | November 2010

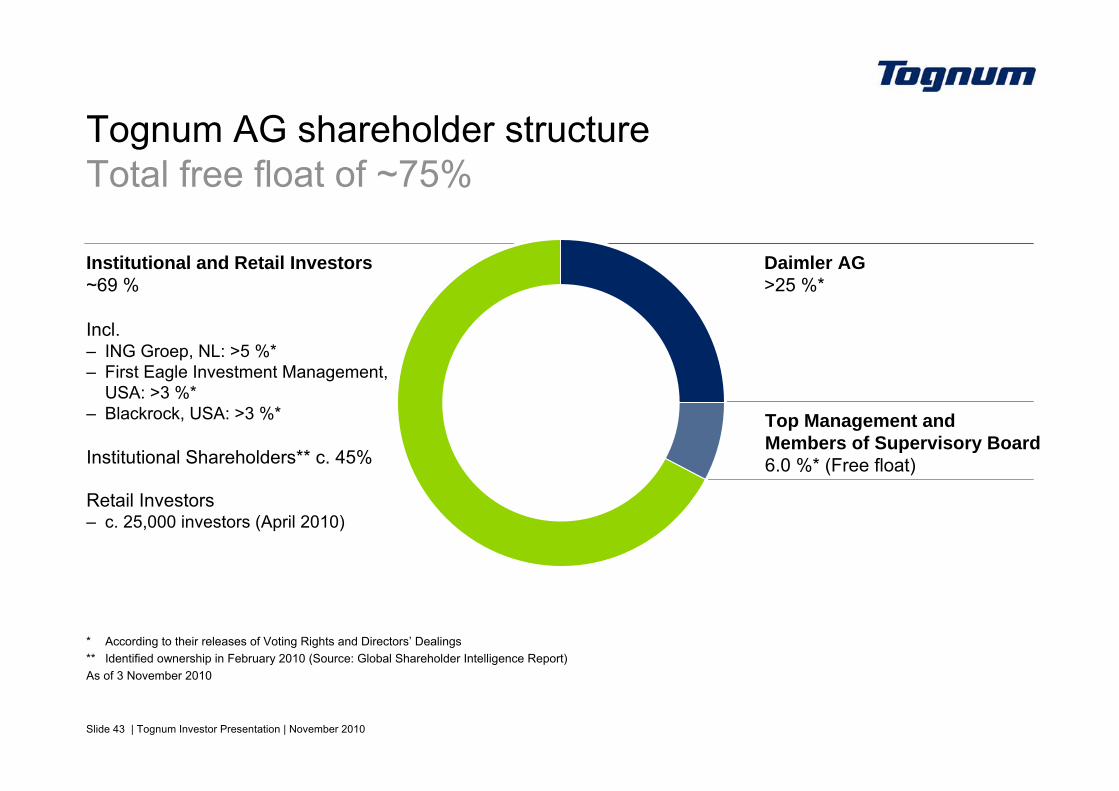

Tognum AG shareholder structureTotal free float of ~75%

Daimler AG>25 %*

Top Management and Members of Supervisory Board6.0 %* (Free float)

Institutional and Retail Investors~69 %

Incl.– ING Groep, NL: >5 %*– First Eagle Investment Management,

USA: >3 %*– Blackrock, USA: >3 %*

Institutional Shareholders** c. 45%

Retail Investors – c. 25,000 investors (April 2010)

* According to their releases of Voting Rights and Directors’ Dealings** Identified ownership in February 2010 (Source: Global Shareholder Intelligence Report)As of 3 November 2010

Investor contacts:Dieter RoyalHead of Corporate Finance & Investor Relations

Michael FrankDragica Sikić

Phone: + 49 (0)7541 90-3318Fax: + 49 (0)7541 9090-3318mailto:[email protected]://www.tognum.com

Tognum AG, 88040 Friedrichshafen / Germany

Thank you very much!

Financial calendar 2011*March 10 FY 2010 numbers & conference call

May 09 Q1/11 final report & conference call

May 11 Annual General Meeting 2011

August 04 Q2/11 final report & conference call

November 08 Q3/11 final report & conference call

* All dates are preliminary and subject to change