Embed Size (px)

Citation preview

Today’s Agenda

Targets: State what factors affect insurance

rates

Apply insurance concepts and terminology to traffic accident cases

Insurance Lingo

Indemnity Places you back into the same

(financial) position you were in 1 second before the loss

Deductible A set amount the insured must pay

before the insurance company will pay benefits

Collision & Comprehensive Insurance

Insurance Lingo

Insured The person or persons covered by X

Insurance Company

Claimant The other individual involved in the loss,

not insured by X Insurance Company Arbitration

Settling a claim through a neutral party

Automobile Insurance Why do we need it?

Auto crashes - leading cause of death

Teens account for 20% of all accidents

Economic Cost - $150 billion/year

It’s required! Liability insurance

required in most states

What affects insurance rates?

What group of individuals pays the highest rates?

UNMARRIED MALE DRIVERS, AGES 16-25

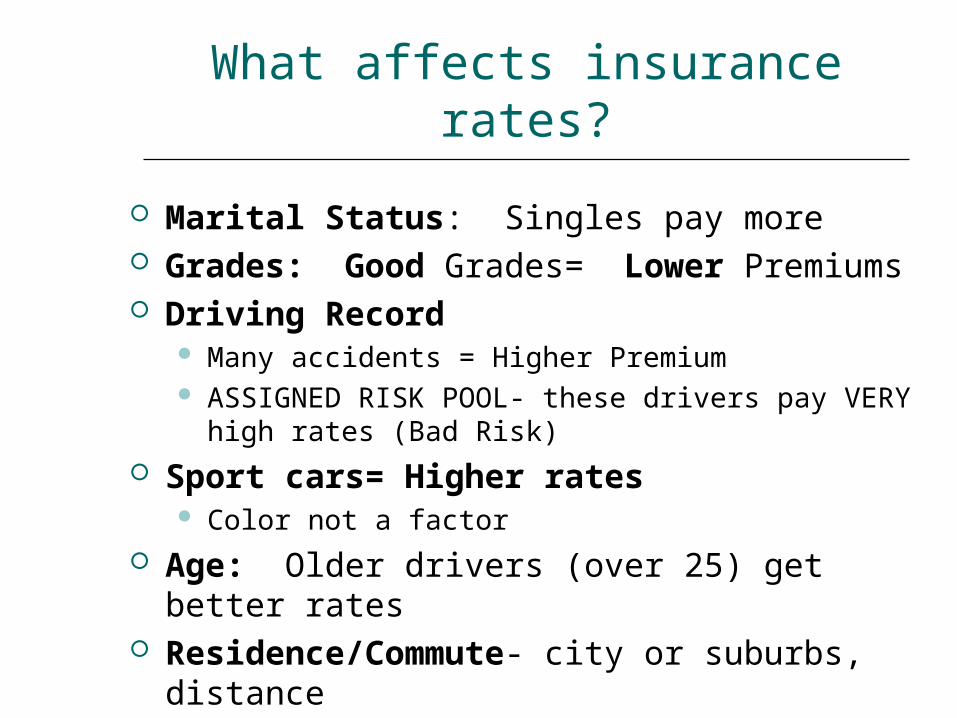

What affects insurance rates?

Marital Status: Singles pay more Grades: Good Grades= Lower Premiums Driving Record

Many accidents = Higher Premium ASSIGNED RISK POOL- these drivers pay VERY

high rates (Bad Risk) Sport cars= Higher rates

Color not a factor Age: Older drivers (over 25) get better rates Residence/Commute- city or suburbs,

distance

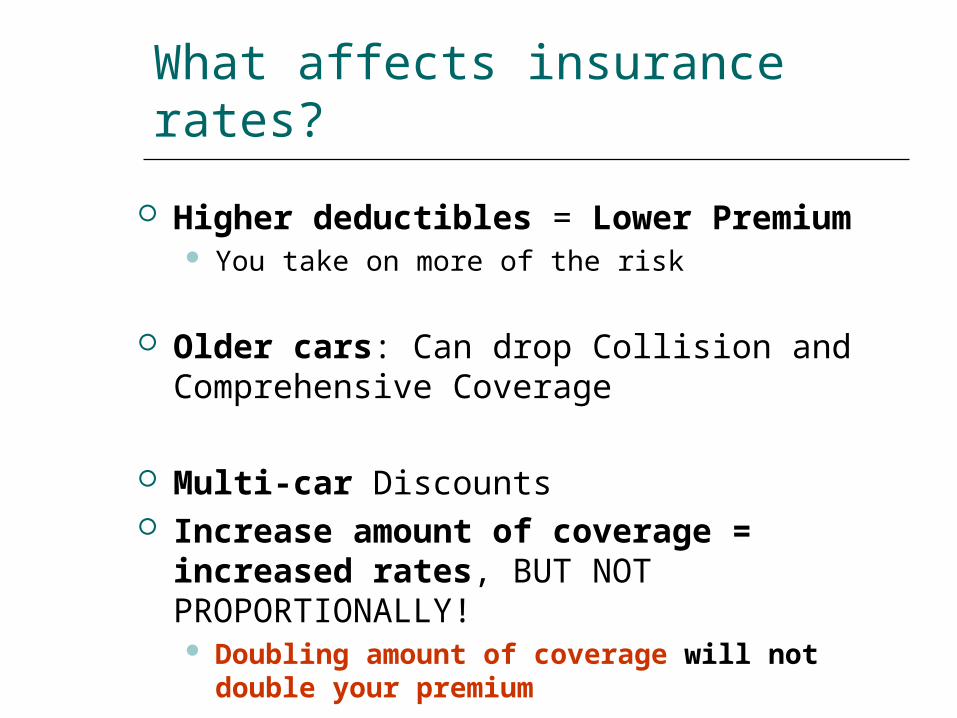

What affects insurance rates?

Higher deductibles = Lower Premium You take on more of the risk

Older cars: Can drop Collision and Comprehensive Coverage

Multi-car Discounts Increase amount of coverage =

increased rates, BUT NOT PROPORTIONALLY! Doubling amount of coverage will not

double your premium

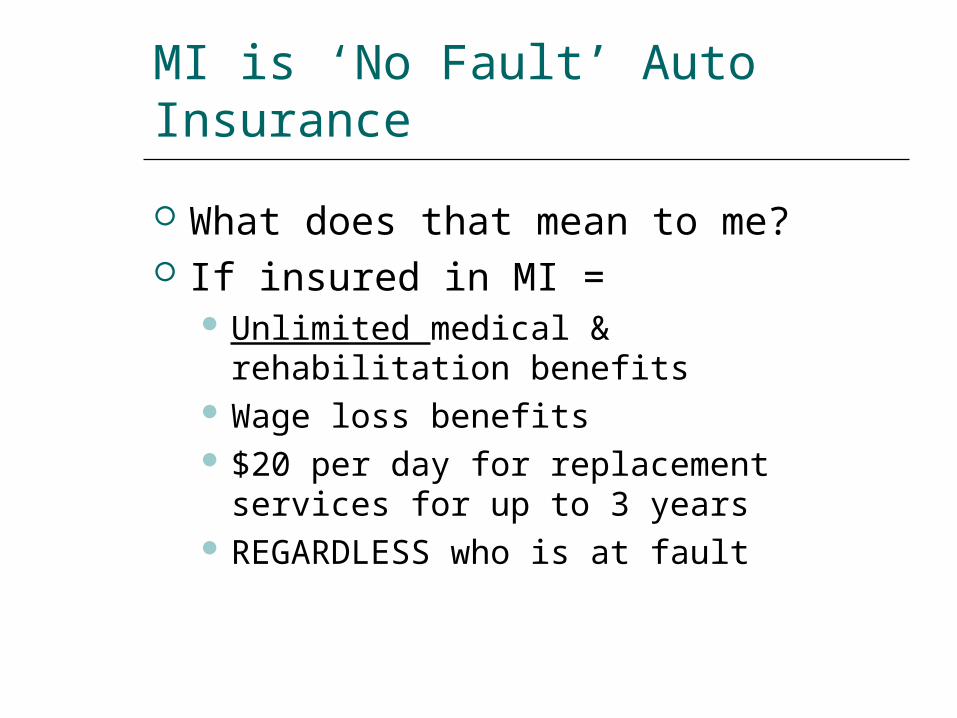

MI is ‘No Fault’ Auto Insurance

What does that mean to me? If insured in MI =

Unlimited medical & rehabilitation benefits

Wage loss benefits $20 per day for replacement services

for up to 3 years REGARDLESS who is at fault

Why do I need insurance?

MI law Misdemeanor $200 to $300 fine And / or 1 year in jail Suspended license for 30 days

Sued and held personally liable Liable for all damages when in an

accident

Required Automobile Coverage

LIABILITY INSURANCE – 3 TYPES Personal Injury Protection (PIP)

Medical costs if hurt in auto accident Property Protection (PPI)

Up to $1 million for damage your car does in MI to other people’s property (buildings, fences, etc)

OOPS! SORRY!

Required Coverage Continued

Residual Bodily Injury and Property Damage Liability (BI / PD) Defense and damages if liable for auto

accident Min. limits 20/40/10

$20,000 max per person hurt or killed $40,000 max payout per accident for hurt /

killed $10,000 max property damage in another

state

Available Automobile Coverage

Collision – 3 types Protects against damage to YOUR

vehicle due to a traffic accident Not required by states, BUT required by

your lender! Insurance will only pay for damages up

to current value of your car TOTAL LOSS

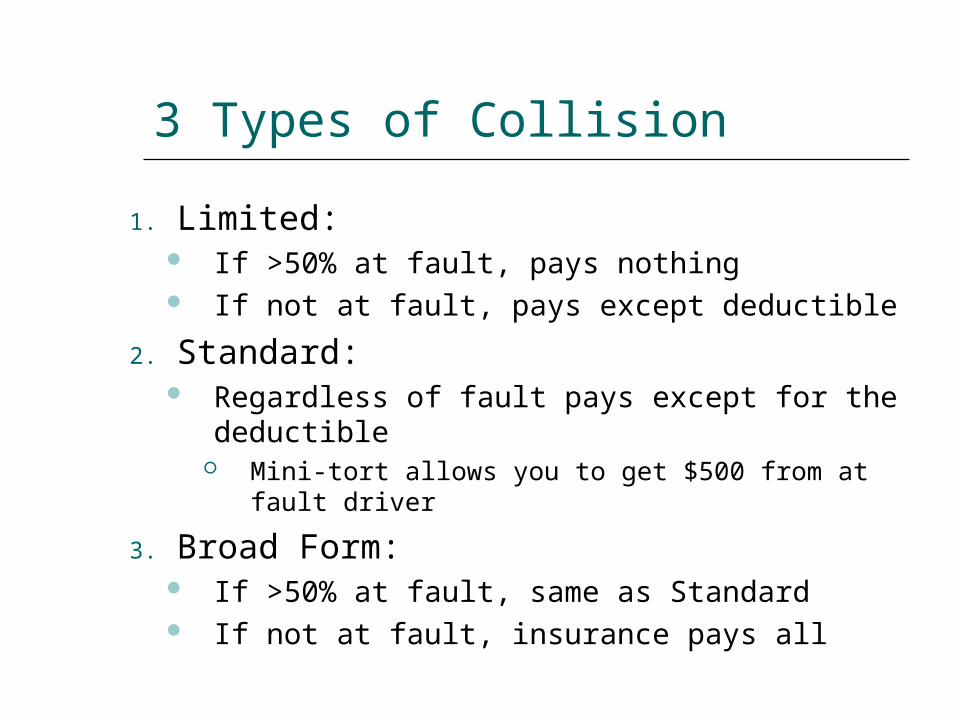

3 Types of Collision

1. Limited: If >50% at fault, pays nothing If not at fault, pays except deductible

2. Standard: Regardless of fault pays except for the

deductible Mini-tort allows you to get $500 from at fault

driver

3. Broad Form: If >50% at fault, same as Standard If not at fault, insurance pays all

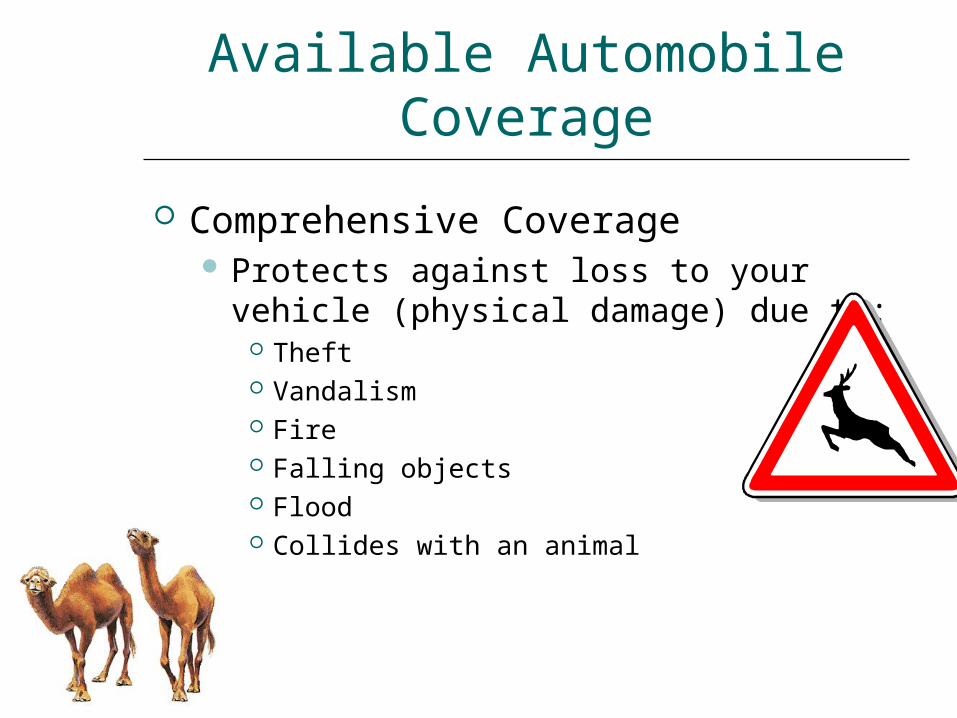

Available Automobile Coverage

Comprehensive Coverage Protects against loss to your vehicle

(physical damage) due to: Theft Vandalism Fire Falling objects Flood Collides with an animal

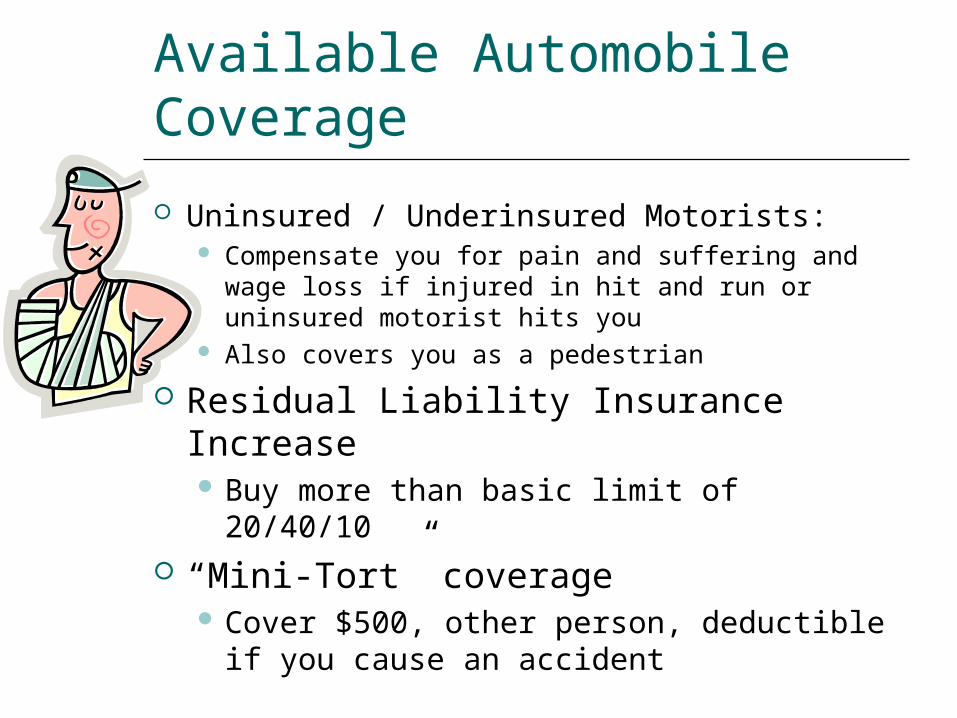

Available Automobile Coverage

Uninsured / Underinsured Motorists: Compensate you for pain and suffering and

wage loss if injured in hit and run or uninsured motorist hits you

Also covers you as a pedestrian

Residual Liability Insurance Increase Buy more than basic limit of 20/40/10

“Mini-Tort” coverage Cover $500, other person, deductible if

you cause an accident