Embed Size (px)

Citation preview

1

To be the partner of choice

Franz MaierEVP Head of Sales

at the Deutsche Bank Swiss Equities conference17 May 2011

2STRAUMANN May 2011© by Straumann. All rights reserved.

Disclaimer

This presentation contains certain “forward-looking statements”, which can be identified by the use of terminology such as “will”, “guidance”, “would”, “prevailing”, “still be able to”, “should”, “confidence in achieving”, “turnaround”, “future”, “anticipated”, “continue”, “mid and long term”, “believes”, “outlook”, or similar wording. Such forward-looking statements reflect the current views of Management and are subject to known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements of the Group to differ materially from those expressed or implied. These include risks related to the success of and demand for the Group’s products, the potential for the Group’s products to become obsolete, the Group’s ability to defend its intellectual property, the Group’s ability to develop and commercialize new products in a timely manner, the dynamic and competitive environment in which the Group operates, the regulatory environment, changes in currency exchange rates, the Group’s ability to generate revenues and profitability, and the Group’s ability to realize its expansion projects in a timely manner. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in this report. Straumann is providing the information in this release as of this date and does not undertake any obligation to update any forward-looking statements contained in it as a result of new information, future events or otherwise.

The availability and indications/claims of the products illustrated and mentioned in this presentation may vary according to country.

2

3STRAUMANN May 2011© by Straumann. All rights reserved.

Highlights in 2011

Business performance

Eventful first-quarter

Outlook

Questions & answers

Agenda

Highlights in 2011

3

5STRAUMANN May 2011© by Straumann. All rights reserved.

Straumann achieves growth in all regions

Net revenue up 4.3% (l.c.) driven by implant volumes (Bone Level, Roxolid®) and lifted by new products (scanners and regeneratives)

APAC slightly impacted by disaster in Japan; future negative effects anticipated

Strong currency headwind, cutting CHF 19 million off top line

Strong presence at five international dental meetings to showcase innovative products, solutions and services

Collaborations with Dental Wings, 3M ESPE and VITA add further flexibility for CADCAM customers

Thomas Dressendörfer appointed as new CFO

6STRAUMANN May 2011© by Straumann. All rights reserved.

Despite recovery from recession, 2010/11 brought little improvement to unemployment, household income and access to credit

With consumer sentiment still fragile, dental practices reported no substantial pick-up in complex and elective dental procedures

Q1 figures point to gradual improvement in the tooth-replacement market; Robust emerging market growth continues

Regulatory requirements increasing

Further consolidation expected

New technologies; increase in digitalization

What is happening in the market?

4

Business performance

8STRAUMANN May 2011© by Straumann. All rights reserved.

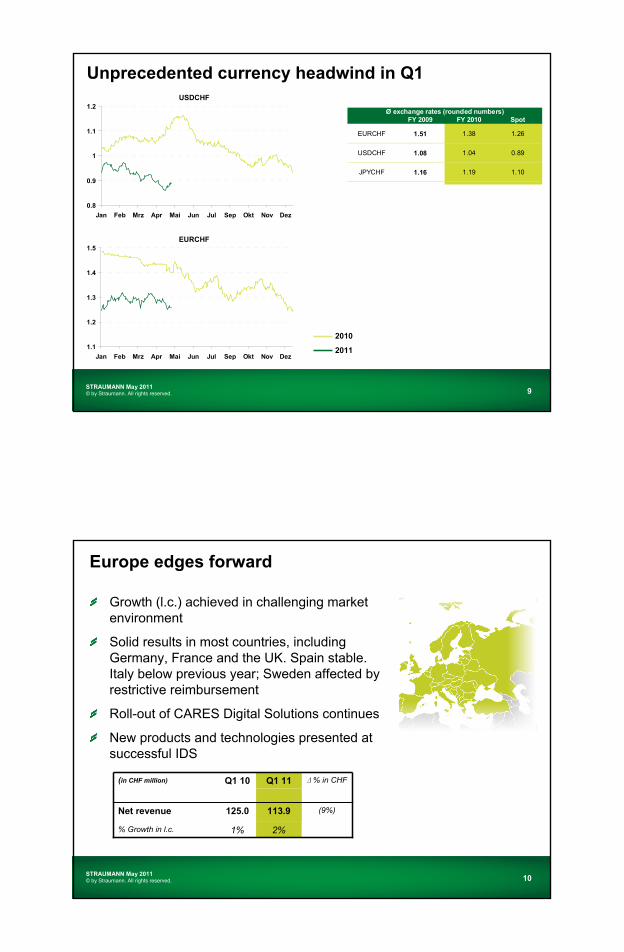

2%

8%

2%

17%

4%

-9%

-4%

0%

-5%

15%

Europe NorthAmerica

Asia/Pacific ROW Group

l.c. CHF

Stable growth in l.c. for five consecutive quarters

Group organic growth1 by quarter (l.c.)

1 ’Organic growth’ excludes FX effects and includes incremental revenue growth of an acquired business upon consolidation. There were no material M&A effects in the 12 months preceding the period under review.

2009 2010 2011

2%

-8%

-1% -1%

7%

4%

5%

3%3%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Growth by region

5

9STRAUMANN May 2011© by Straumann. All rights reserved.

USDCHF

0.8

0.9

1

1.1

1.2

Jan Feb Mrz Apr Mai Jun Jul Sep Okt Nov Dez

EURCHF

1.1

1.2

1.3

1.4

1.5

Jan Feb Mrz Apr Mai Jun Jul Sep Okt Nov Dez

Unprecedented currency headwind in Q1

2010

2011

FY 2009 FY 2010 Spot

EURCHF 1.51 1.38 1.26

USDCHF 1.08 1.04 0.89

JPYCHF 1.16 1.19 1.10

Ø exchange rates (rounded numbers)

10STRAUMANN May 2011© by Straumann. All rights reserved.

Europe edges forward

Growth (l.c.) achieved in challenging market environment

Solid results in most countries, including Germany, France and the UK. Spain stable. Italy below previous year; Sweden affected by restrictive reimbursement

Roll-out of CARES Digital Solutions continues

New products and technologies presented at successful IDS

1%

125.0

Q1 10

2%% Growth in l.c.

(9%)113.9Net revenue

∆ % in CHFQ1 11(in CHF million)

6

11STRAUMANN May 2011© by Straumann. All rights reserved.

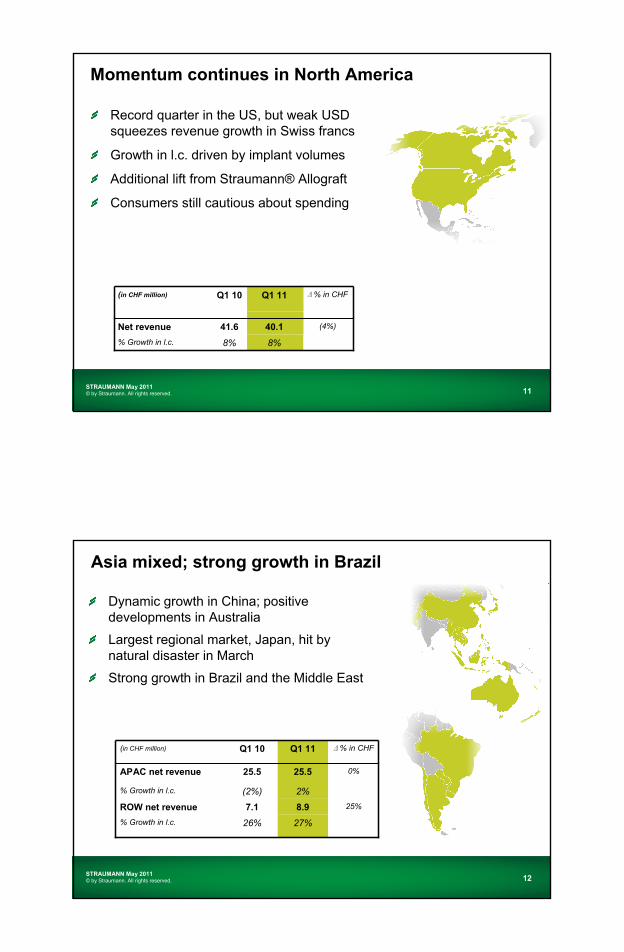

Momentum continues in North America

Record quarter in the US, but weak USD squeezes revenue growth in Swiss francs

Growth in l.c. driven by implant volumes

Additional lift from Straumann® Allograft

Consumers still cautious about spending

8%

41.6

Q1 10

8%% Growth in l.c.

(4%)40.1Net revenue

∆ % in CHFQ1 11(in CHF million)

12STRAUMANN May 2011© by Straumann. All rights reserved.

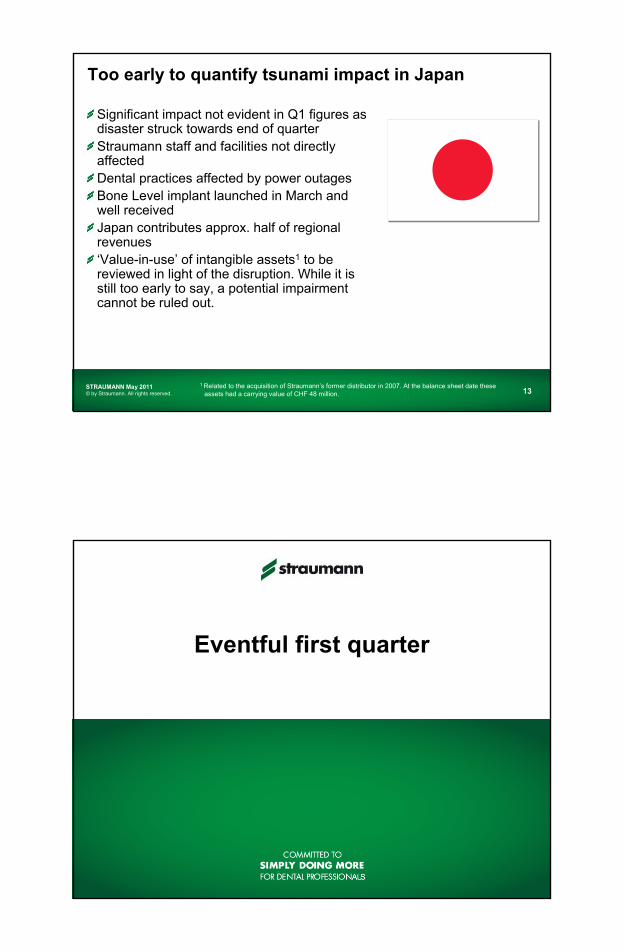

Asia mixed; strong growth in Brazil

Dynamic growth in China; positive developments in Australia

Largest regional market, Japan, hit by natural disaster in March

Strong growth in Brazil and the Middle East

27%

8.9

2%

25.5

Q1 11

26%

7.1

(2%)

25.5

Q1 10

25%ROW net revenue

% Growth in l.c.

% Growth in l.c.

0%APAC net revenue

∆ % in CHF(in CHF million)

7

13STRAUMANN May 2011© by Straumann. All rights reserved.

Too early to quantify tsunami impact in Japan

Significant impact not evident in Q1 figures as disaster struck towards end of quarterStraumann staff and facilities not directly affectedDental practices affected by power outagesBone Level implant launched in March and well receivedJapan contributes approx. half of regional revenues‘Value-in-use’ of intangible assets1 to be reviewed in light of the disruption. While it is still too early to say, a potential impairment cannot be ruled out.

1 Related to the acquisition of Straumann’s former distributor in 2007. At the balance sheet date these assets had a carrying value of CHF 48 million.

Eventful first quarter

8

15STRAUMANN May 2011© by Straumann. All rights reserved.

Present dilemma: too many incompatible systems; confusion; limited growth opportunities

Straumann and 3M ESPE adopt DWOS and join forces with Dental Wings to establish a leading software standard in digital dentistry

Straumann announces intention to acquire a 30% stake in Dental Wings

dwos inside

Collaboration to create the leading standard

16STRAUMANN May 2011© by Straumann. All rights reserved.

Traditional prosthetic production is a time-consuming and labor intensive process

Dentist Dental technician

Physical impression taking

Veneering (Porcelain layer)

Digital connection Analogue workflow

Plaster model Modeling / wax up

Trimming cast / polishing

Casting framework

Molding / burnout

9

17STRAUMANN May 2011© by Straumann. All rights reserved.

Substitution of an unpleasant treatment step

(Digital) intra-oral scanning with the iTero handheld scanner

Analogue impression-taking in the dental practice

18STRAUMANN May 2011© by Straumann. All rights reserved.

Seamless connectivity with Straumann® CARES®

Dentist Dental technician Straumann CADCAM production

Intra-oral scan / digital impression

Physical impression taking

Implant

Planning

Product

Library

Model

Scanning

Prosthetic

Design

Lab

Management

Implant

Planning

Product

Library

Model

Scanning

Prosthetic

Design

Lab

Management

Digital modeling

Centralized milling

Veneering (Porcelain layer)

Extra-oral scanning

Plaster model

Digital connection Analogue workflow

10

19STRAUMANN May 2011© by Straumann. All rights reserved.

Leading material offering and application range

IPS e.max® CAD2

Zirconium dioxide abutment

zerion™

IPS Empress® CAD2

VITA Mark II2 ticon®

VITA TriLuxe3

Titanium abutment Polyamide

polycon® ae

polycon® cast

coron®

Ceramics1 Metals1 Polymers1

1 Products may require regulatory approvals and may not be available in all markets.2 IPS e.max®, IPS Empress® are registered trademarks of Ivoclar Vivadent AG, LI3 VITABLOCS® Mark II, -TriLuxe are registered trademarks and brands of Vita Zahnfabrik

20STRAUMANN May 2011© by Straumann. All rights reserved.

Variobase1 coping for selected non-Straumann implant platforms2

CADCAM – expanded applications

1 Products may require regulatory approvals and may not be available in all markets2 Camlog and Nobel Biocare Replace™

Straumann Variobasecoping

Competitor

Fully digital implant restoration workflow with new repositionable implant analog

Screw-retained bars and bridges

Full contour inlays, onlays and veneers1

11

21STRAUMANN May 2011© by Straumann. All rights reserved.

‘Peace of mind’ for clinicians and patients

Straumann® Classic1

Continued availability of prosthetic components for Straumann implants dating back to 1974

1 May not be available in all markets immediately and may require regulatory approvals

Straumann® warranty extendedClear warranty conditions for Straumann Dental Implant System and CARES® elements

Life-time warranty for implants and abutments in certain countries

Straumann® All-in-one Sets1

Kit contains all components for complete restoration

Easier ordering and storage

Convenient packaging for transfer from dentist to lab

Assurance that original components are used

Outlook 2011 and beyond

12

23STRAUMANN May 2011© by Straumann. All rights reserved.

Outlook 2011 (barring unforeseen circumstances)

Straumann assumes mid-single-digit market growth (in l.c.) for 2011

The Group is convinced it can again deliver above-market performance

Currency headwind has to be expected for some time in 2011

It is difficult to predict the impact of recent events in Japan. ‘Value-in-use’of intangible assets to be reviewed in light of these. It is still too early to say but an impairment of these assets cannot be ruled out

Excluding potential effects on sales and profits related to Japan, and in spite of the currency headwind and further investments in all franchises, innovation, and Marketing & Sales, Straumann is confident that its operating margin will remain at around 20% in 2011

Straumann is well positioned for full market recovery but it is still premature to foresee when that might be, as the economic outlook remains uncertain

24STRAUMANN May 2011© by Straumann. All rights reserved.

• New small diameter implant design

• New implant material• Soft tissue control• Implant maintenance

• Prosthetic & surgical flexibility

• Tooth-colored • Tissue control round implants• Implant rescue

2011

20132014

2012/13

Stocked pipeline despite recent introductions

Project Benefits Due1

• Enhanced bone graft

• Multi-unit implant restoration• New restorative materials • New abutment solutions • New materials for provisionals• Advanced digital versatility

• Improved digital workflowfor implant restoration

• Restorative options• Restorative options• Restorative options• Handling • Applications & workflow

efficiency• Process efficiency

• Enhanced remodeling & regeneration

20112011201120112011

2011

2012

1 Refers to planned initial market acceptance testing, controlled relese, or initial marketlaunch, depending on product type, clinical results and regulatory clearances/approvals. Further details on Straumann‘s product pipeline can be found in our Annual Report.

13

25STRAUMANN May 2011© by Straumann. All rights reserved.

Time-tested SLA surface enablesStraumann to compete effectively in the value segment

One-stage surgical proceduresaves time, costs and discomfort forpatients

Proven long-term reliability; 10-year data from randomized controlled clinical trial1

Excellent value and reliability

1 Fischer K: 10-year outcome of SLA implants in the edentulous maxilla. ITI World Symposium 15-17 April 2010, Geneva

10-year results

Question & answer session

14

27STRAUMANN May 2011© by Straumann. All rights reserved.

27 May Helvea Healthcare Trip Basel

29 June Investor roadshow London

30 June Nomura Healthcare conference London

16 August Half-Year results 2011 Basel

Calendar of upcoming events

Detailed calendar on www.straumann.com

28STRAUMANN May 2011© by Straumann. All rights reserved.

1 Including implants, abutments and toolsSource: MRG 2008/09, iDATA 2009, Straumann estimates

Implant dentistry1

Total market size CHF 3.4bn

19% <5% <5%

A leader in markets worth >CHF 5bn

Main competitors:3M ESPE, Sirona, Nobel Biocare,

Dentsply, 3shape

Main competitors:Geistlich/Osteohealth, Zimmer,

ACE, Dentsply

Main competitors:Nobel Biocare, Biomet/3i, Zimmer

Dentsply, Astra Tech

CADCAM dentistryTotal market size CHF 1.7bn Total

Regenerative dentistryTotal market size CHF 0.5bn

CADCAM

Conventional

15

29STRAUMANN May 2011© by Straumann. All rights reserved.

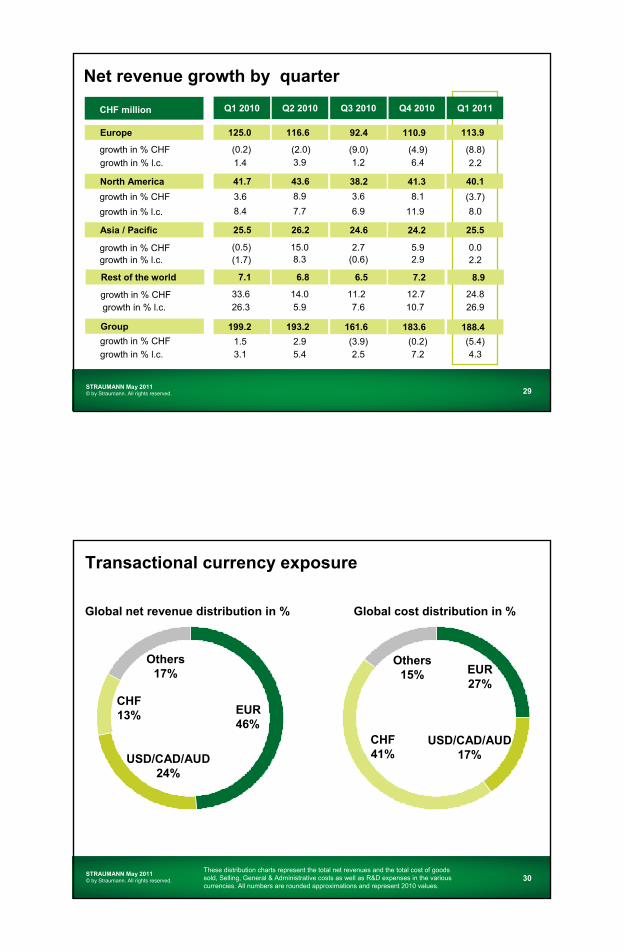

Rest of the world

North America

Europe

CHF million

Asia / Pacific

growth in % CHF

growth in % l.c.

growth in % CHF

growth in % l.c.

growth in % CHF

growth in % CHF

Group

growth in % CHF

growth in % l.c.

growth in % l.c.

growth in % l.c.

Q2 2010

193.2

6.8

26.2

43.6

116.6

5.4

(2.0)3.9

8.9

7.7

15.0

14.0

2.9

5.9

8.3

Q1 2010

199.2

7.1

25.5

41.7

125.0

3.1

(0.2)

1.4

3.6

8.4

(0.5)

33.6

1.5

26.3

(1.7)

Q3 2010

161.6

6.5

24.6

38.2

92.4

2.5

(9.0)1.2

3.6

6.9

2.7

11.2

(3.9)

7.6

(0.6)

Net revenue growth by quarter

Q4 2010

183.6

7.2

24.2

41.3

110.9

7.2

(4.9)6.4

8.1

11.9

5.9

12.7

(0.2)

10.7

2.9

Q1 2011

188.4

8.9

25.5

40.1

113.9

4.3

(8.8)

2.2

(3.7)

8.0

0.0

24.8

(5.4)

26.9

2.2

30STRAUMANN May 2011© by Straumann. All rights reserved.

Transactional currency exposure

These distribution charts represent the total net revenues and the total cost of goods sold, Selling, General & Administrative costs as well as R&D expenses in the various currencies. All numbers are rounded approximations and represent 2010 values.

Others 17%

USD/CAD/AUD 24%

CHF 13% EUR

46%

EUR 27%

USD/CAD/AUD 17%

CHF 41%

Others 15%

Global net revenue distribution in % Global cost distribution in %

16

31STRAUMANN May 2011© by Straumann. All rights reserved.

Your investor relations contacts

Fabian Hildbrand

Corporate Investor RelationsPhone +41 (0)61 965 13 27

Mobile +41 (0)79 392 80 32

Email [email protected]

Deborah Capobianco

Investor Relations CoordinationPhone +41 (0)61 965 12 66

Email [email protected]

32STRAUMANN May 2011© by Straumann. All rights reserved.

Portfolio manager summary

Market Capitalization USD 4.1bn

Return on equity 20%

Return on capital employed 47%

Equity ratio 82%; debt-free; cash & cash equivalents of CHF 350m

Free cash flow margin 21%

Employees 2 361

Payout ratio ~33% of net income

Index member SPI, SMIM, SPI Extra,

Dow Jones STOXX 600, Dow Jones STOXX Health Care etc.

Stock listing SIX Swiss exchange

Source, Thomson Reuters, key ratios as per end of 2010

NET REVENUE

5Y SHARE PRICE PERFORMANCE

20

70

120

170

2006 2007 2008 2009 2010 2011

StraumannNobel BiocareSwiss market index SMIMSCI World Healthcare Equ&Serv index (CHF)