Embed Size (px)

Citation preview

TIM NASIONALPERCEPATAN PENANGGULANGAN KEMISKINAN

TNP2KWORKING PAPER

QUALITATIVE SURVEY OF CURRENT AND ALTERNATIVE G2P PAYMENT CHANNELS IN PAPUA

AND PAPUA BARAT

TNP2K WORKING PAPER 26-2015April 2015

MICHAEL JOYCE, SHELLEY SPENCER, JORDAN WEINSTOCK AND GRACE RETNOWATI

TNP2K WORKING PAPER 26-2015April 2015

MICHAEL JOYCE, SHELLEY SPENCER, JORDAN WEINSTOCK AND GRACE RETNOWATI

The TNP2K Working Paper Series disseminates the findings of work in progress to encourage discussion and exchange of ideas on poverty, social protection and development issues.

Support for this publication has been provided by the Australian Government through the Poverty Reduction Support Facility (PRSF).

The findings, interpretations and conclusions herein are those of the author(s) and do not necessarily reflect the views of the Government of Indonesia or the Government of Australia.

You are free to copy, distribute and transmit this work, for non-commercial purposes.

Suggested citation: Joyce, M., S. Spencer, J. Weinstock and G. Retnowati. 2015. ‘Qualitative Survey of Current and Alternative G2P Payment Channels in Papua and Papua Barat’. TNP2K Working Paper 26-2015. Jakarta, Indonesia: National Team for the Acceleration of Poverty Reduction (TNP2K).

To request copies of this paper or for more information, please contact the TNP2K - Knowledge Management Unit ([email protected]). This and other TNP2K publications are also available at the TNP2K website.

QUALITATIVE SURVEY OF CURRENT AND ALTERNATIVE G2P PAYMENT CHANNELS IN PAPUA

AND PAPUA BARAT

TNP2KGrand Kebon Sirih Lt.4,Jl.Kebon Sirih Raya No.35,Jakarta Pusat, 10110Tel: +62 (0) 21 3912812Fax: +62 (0) 21 3912513www.tnp2k.go.id

v

QUALITATIVE SURVEY OF CURRENT AND ALTERNATIVE G2P PAYMENT CHANNELS IN PAPUA AND PAPUA BARAT

Michael Joyce, Shelley Spencer, Jordan Weinstock And Grace Retnowati1

April 2015

ABSTRACT

Many Papuans are eligible for social assistance in the form of government-to-person (G2P) payments because the poverty levels in Papua and Papua Barat are among the highest in the country. However, disbursing these payments is difficult, costly and time-consuming. Recent developments in technology and regulatory environments in Indonesia mean that G2P payments could potentially be delivered using locally-based agents and low-cost payment instruments such as electronic money or branchless banking. This research provides a snapshot of current payment practices in 18 subdistricts in Papua and Papua Barat that have varying degrees of accessibility. It reveals that beneficiaries are interested in and willing to try alternative payment mechanisms. The research focuses on payments made from the Conditional Cash Transfer Programme for Poor Families (PKH) and the Cash Transfers for Poor Students programme (BSM) but also looked at other payment streams, including salaries for the civil servants and teachers living in the subdistricts studied.

The research shows that the costs of travelling to reach current payment points and the time this takes are major challenges for beneficiaries of these programmes and this situation could be alleviated if alternative payments channels were possible. The research presents a cost–benefit model that suggests potential pricing models for different payment locations. However, before these alternative payment channels can be introduced, Papua and Papua Barat need to have reliable power, transport and communications infrastructures throughout the subdistricts and this remains a major obstacle. Until this issue can be tackled, some areas will need to continue using existing payment methods for the foreseeable future.

1 The authors would like to thank all those who participated in this study and made it possible. We are grateful to the National Team for the Acceleration of Poverty Reduction (TNP2K) for providing the opportunity to conduct the research and for providing useful information on social assistance programmes in Indonesia. Particular thanks go to the Conditional Cash Transfer Programme for Poor Families (PKH) recipients and facilitators and Cash Transfers for Poor Students (BSM) recipients, Bank Papua and Bank Rakyat Indonesia (BRI) and the Indonesian post office (PT POS), as well as local government officials. The study was undertaken by OpenRevolution, NetHope, Inc. and MicroSave. The primary authors were Jordan Weinstock, OpenRevolution and Shelley Spencer, NetHope, with research conducted by MicroSave under the leadership of Grace Retnowati. The authors are grateful to Margo Bedingfield for her editorial assistance. The study was funded by the Poverty Reduction Support Facility (PRSF) and managed by GRM International on behalf of the Australian government.

vi

Table of Contents

Acronyms ....................................................................................................................................................... ixExecutive Summary ........................................................................................................................................ x1. Overview ................................................................................................................................................... 12. Research Objectives/Methodology...........................................................................................................23. District Assessment ................................................................................................................................... 4

Infrastructure analysis .............................................................................................................................. 7Payment point analysis ............................................................................................................................. 7

4. Field Research ........................................................................................................................................... 12Focus group participant profiles ............................................................................................................... 12In-depth participant profiles ..................................................................................................................... 15G2P payment streams in Papua and Papua Barat ..................................................................................... 17

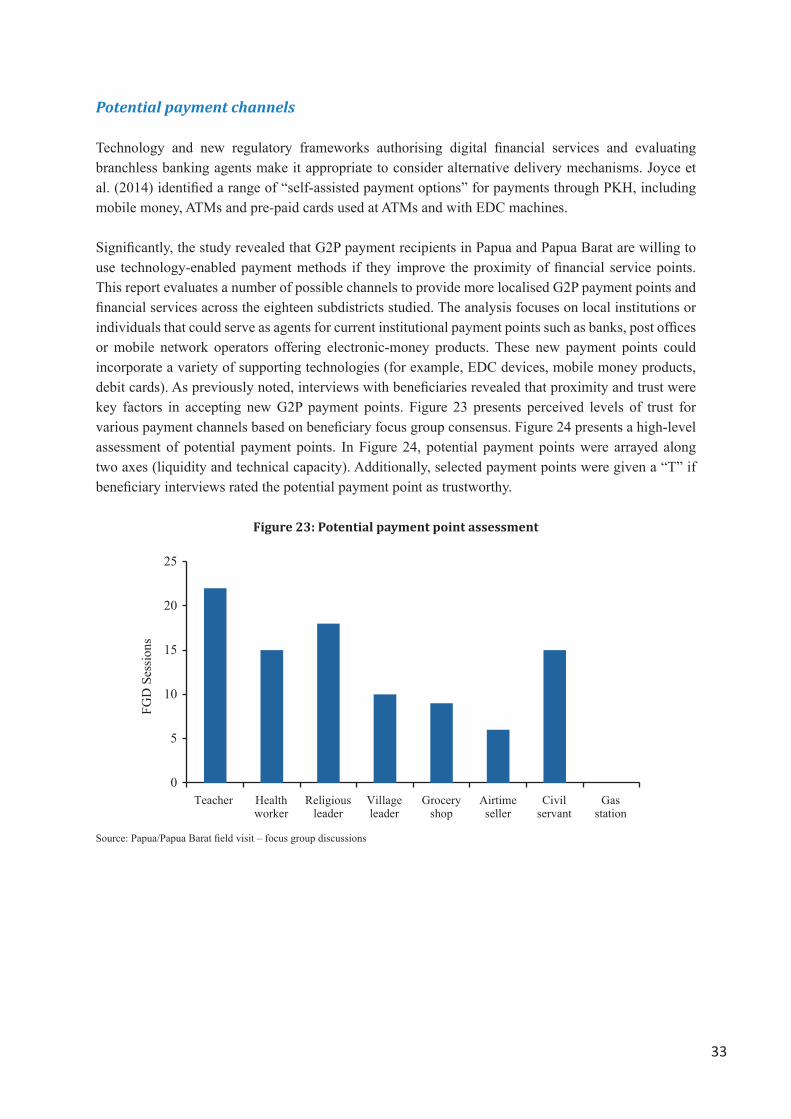

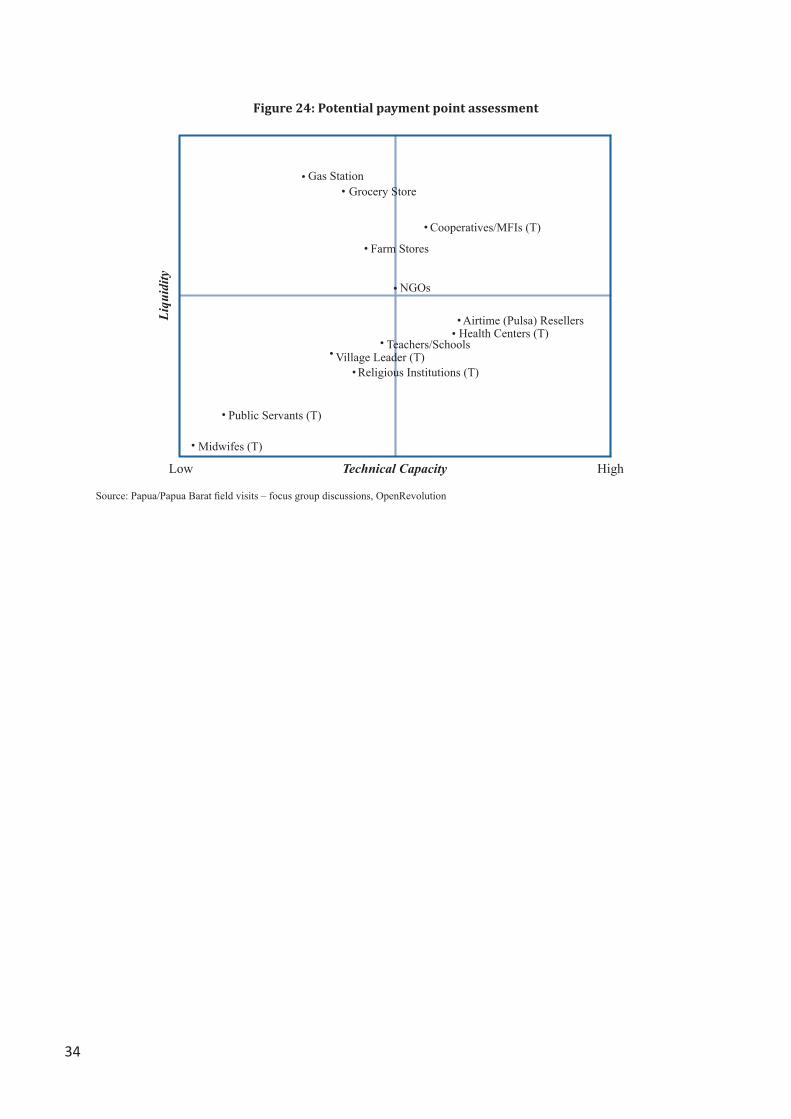

5. Findings ..................................................................................................................................................... 22Beneficiary focus groups ........................................................................................................................... 22Payer interviews........................................................................................................................................ 28Service providers ...................................................................................................................................... 30Infrastructure and facilities findings .........................................................................................................31Potential payment channels ..................................................................................................................... 33

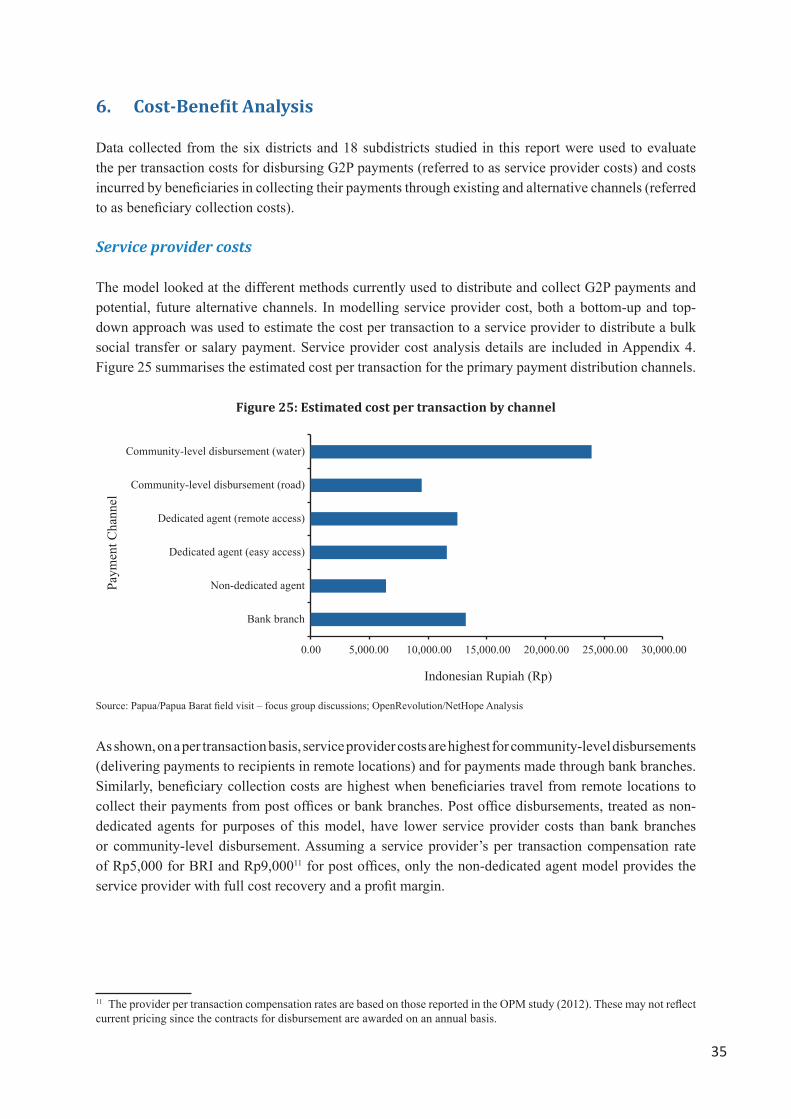

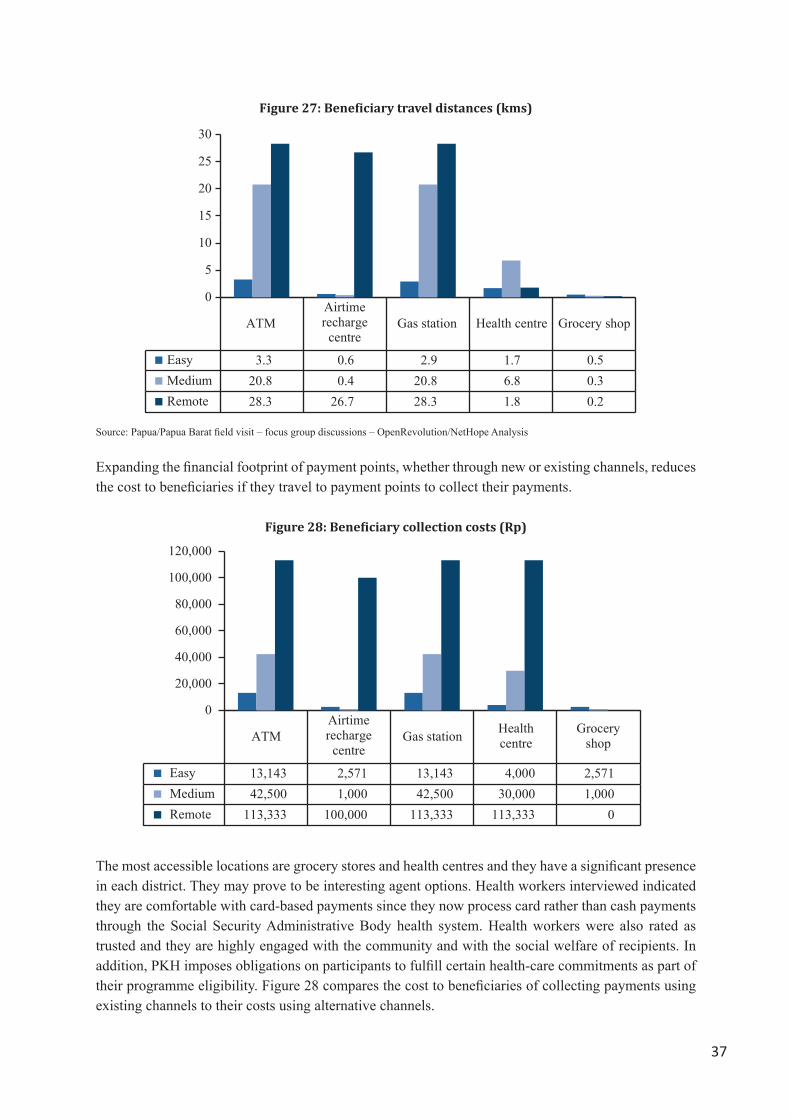

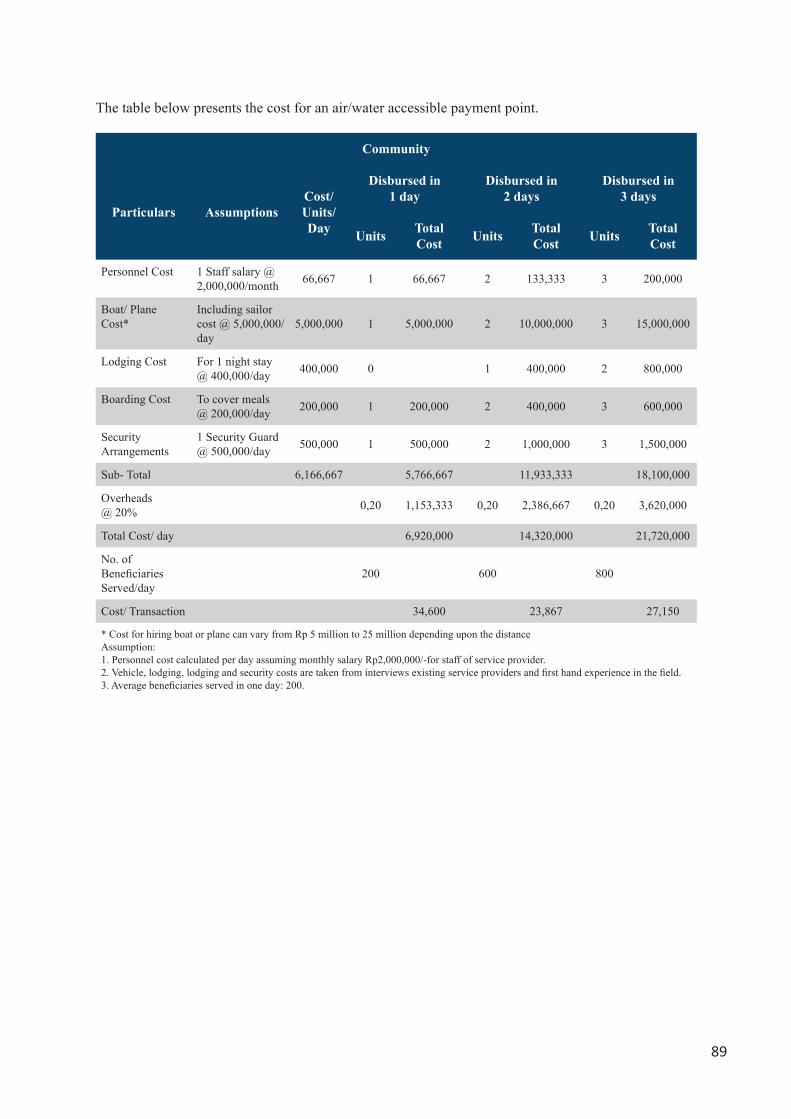

6. Cost-Benefit Analysis ................................................................................................................................ 35Service provider costs ............................................................................................................................... 35Beneficiary collection costs....................................................................................................................... 36Other benefits ........................................................................................................................................... 38

7. Challenges ................................................................................................................................................. 41Existing payment point challenges ...........................................................................................................41Alternative payment point challenges ......................................................................................................42

8. Recommendations and Summary .............................................................................................................449. G2P Pilot Recommendations .................................................................................................................... 47

Pilot overview ........................................................................................................................................... 47Pilot details ............................................................................................................................................... 49

Appendix 1: Desk study district details ........................................................................................................... 53Appendix 2: Focus group discussions and in-depth interviews: composition and locations .......................... 62Appendix 3: Focus group discussions and in-depth interviews: question sets ............................................... 64Appendix 4: Cost Analysis ............................................................................................................................... 81Appendix 5: Policy Brief .................................................................................................................................. 93Appendix 6: Payment Pilot Sample Statement of Work ................................................................................. 98References ...................................................................................................................................................... 101

vii

List of Tables

Table 1: District evaluation framework ...................................................................................................... 5Table 2: Existing payment points in Papua ................................................................................................. 8Table 3: Existing payment points in Papua Barat districts .......................................................................... 9Table 4: District composite rating .............................................................................................................. 11Table 5: Service provider interviews ..........................................................................................................16Table 6: G2P payment details .................................................................................................................... 20Table 7: Infrastructure and facilities summary .......................................................................................... 31Table 8: Pilot payment process .................................................................................................................. 48Table 9: Pilot attributes .............................................................................................................................. 49

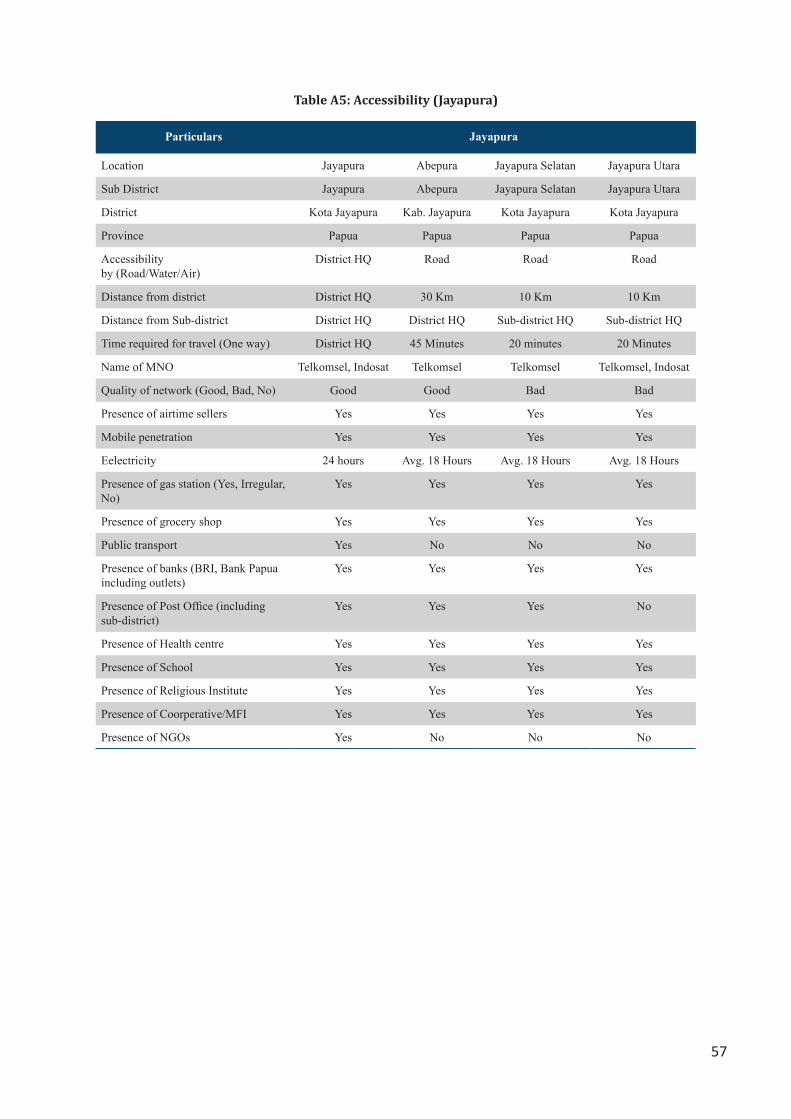

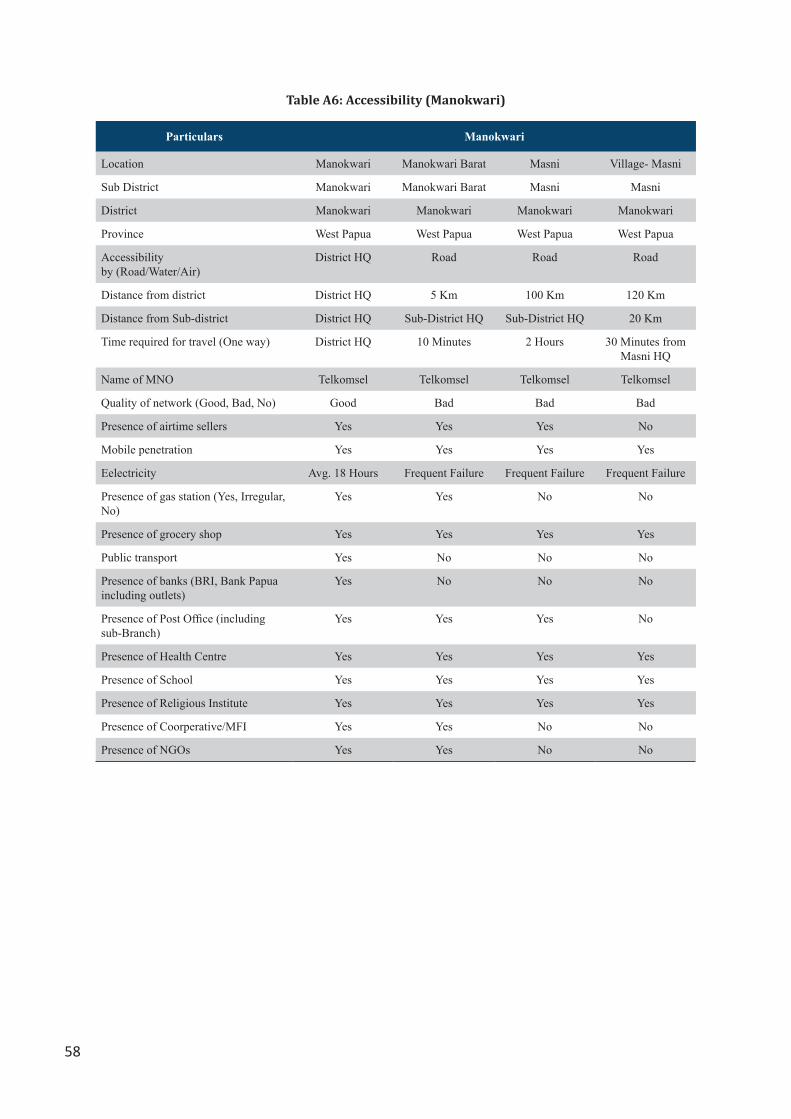

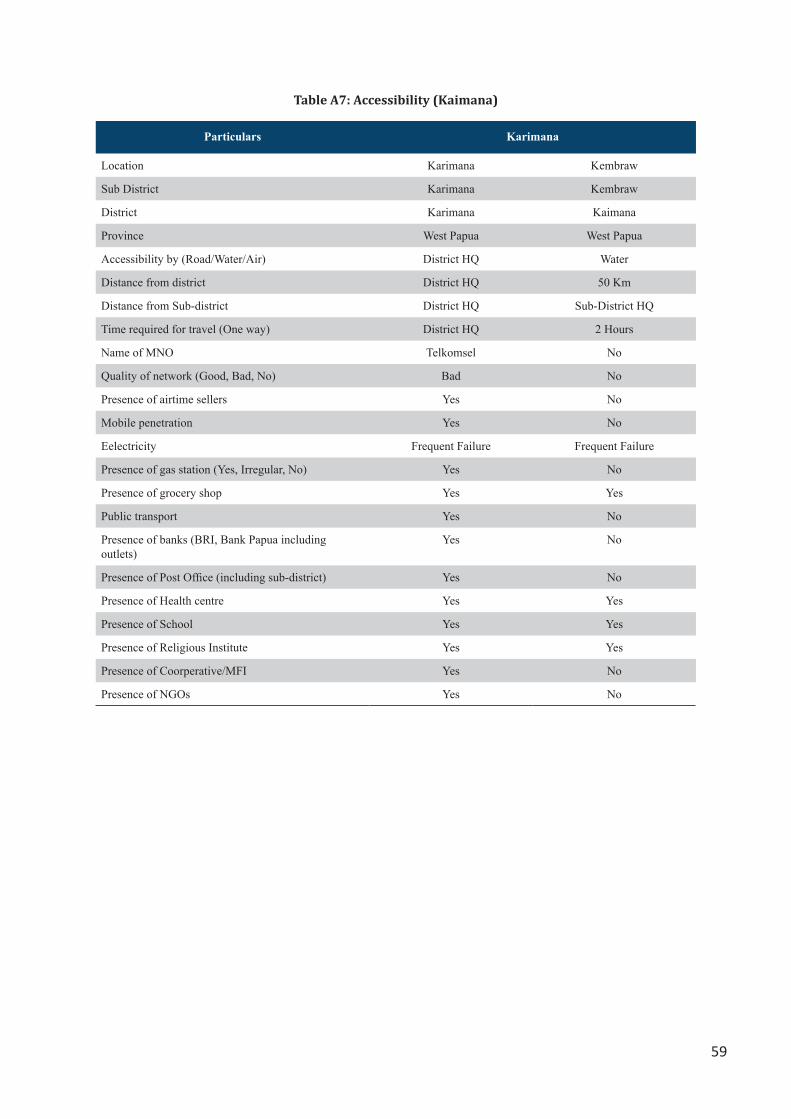

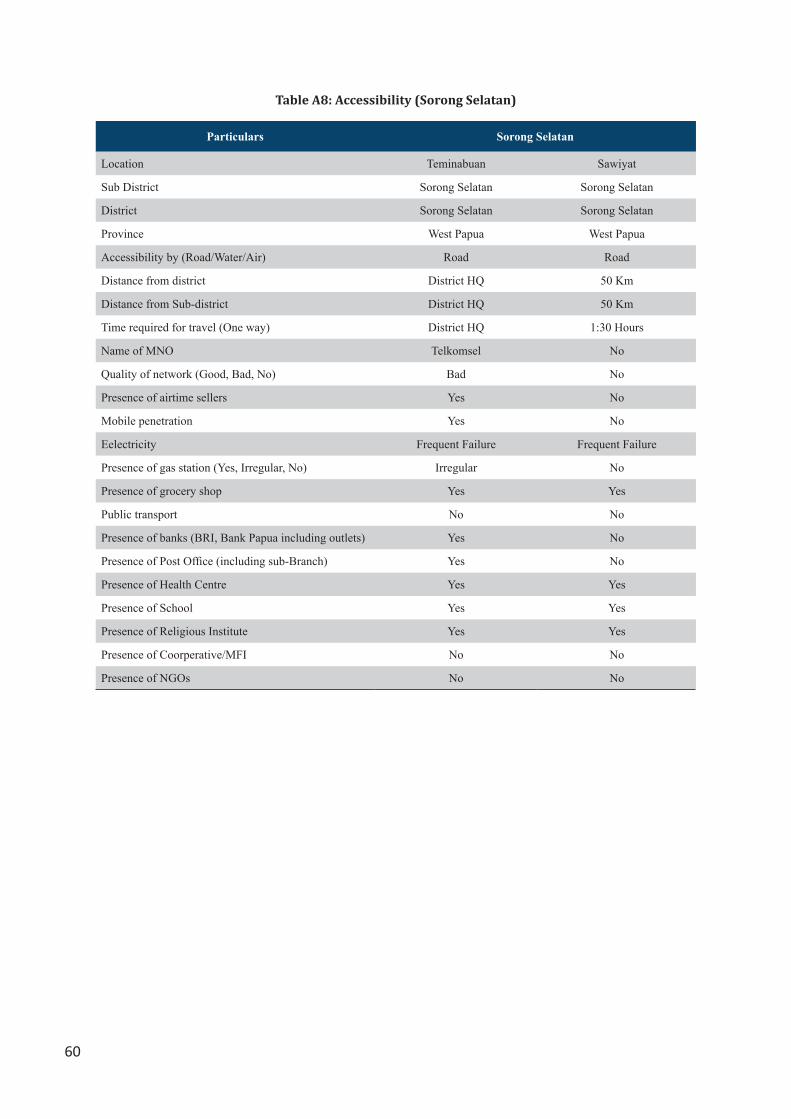

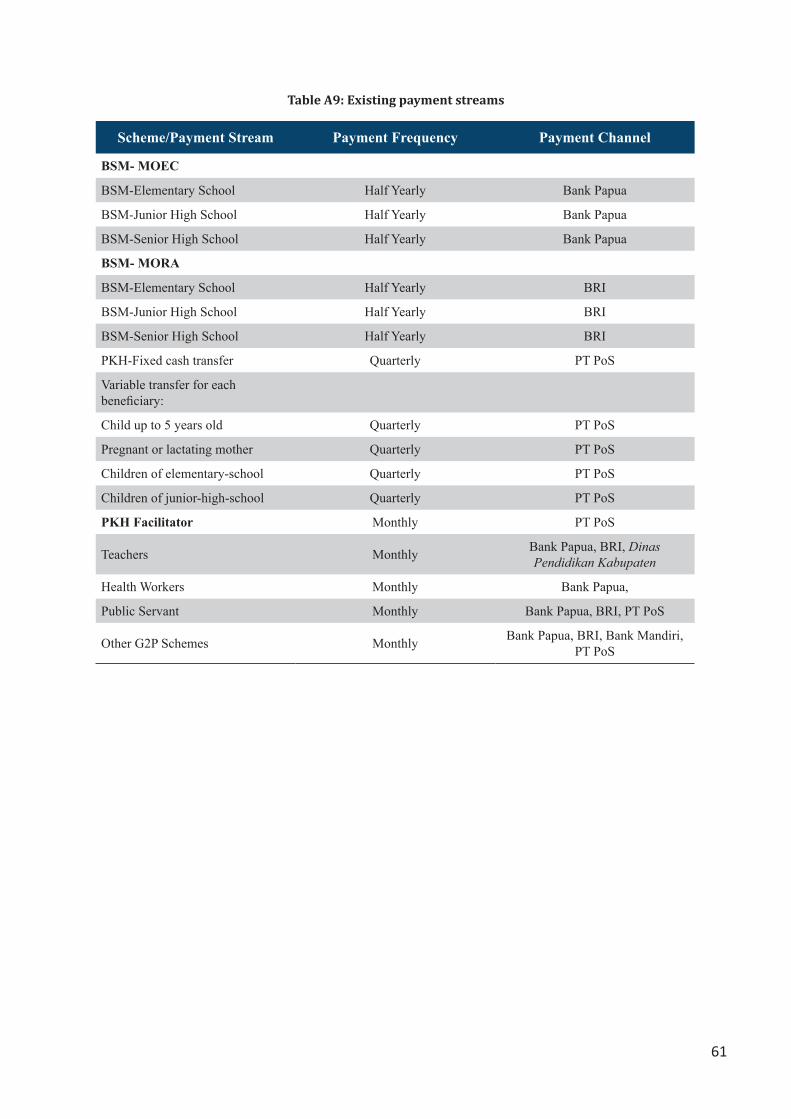

Table A1: Papua Payment Points .................................................................................................................. 53Table A2: West Papua payment points .........................................................................................................54Table A3: Accessibility (Biak) ....................................................................................................................... 55Table A4: Accessibility (Keerom) ................................................................................................................. 56Table A5: Accessibility (Jayapura) ................................................................................................................ 57Table A6: Accessibility (Manokwari) ............................................................................................................58Table A7: Accessibility (Kaimana) ................................................................................................................ 59Table A8: Accessibility (Sorong Selatan) ...................................................................................................... 60Table A9: Existing payment streams ............................................................................................................61

List of Figures

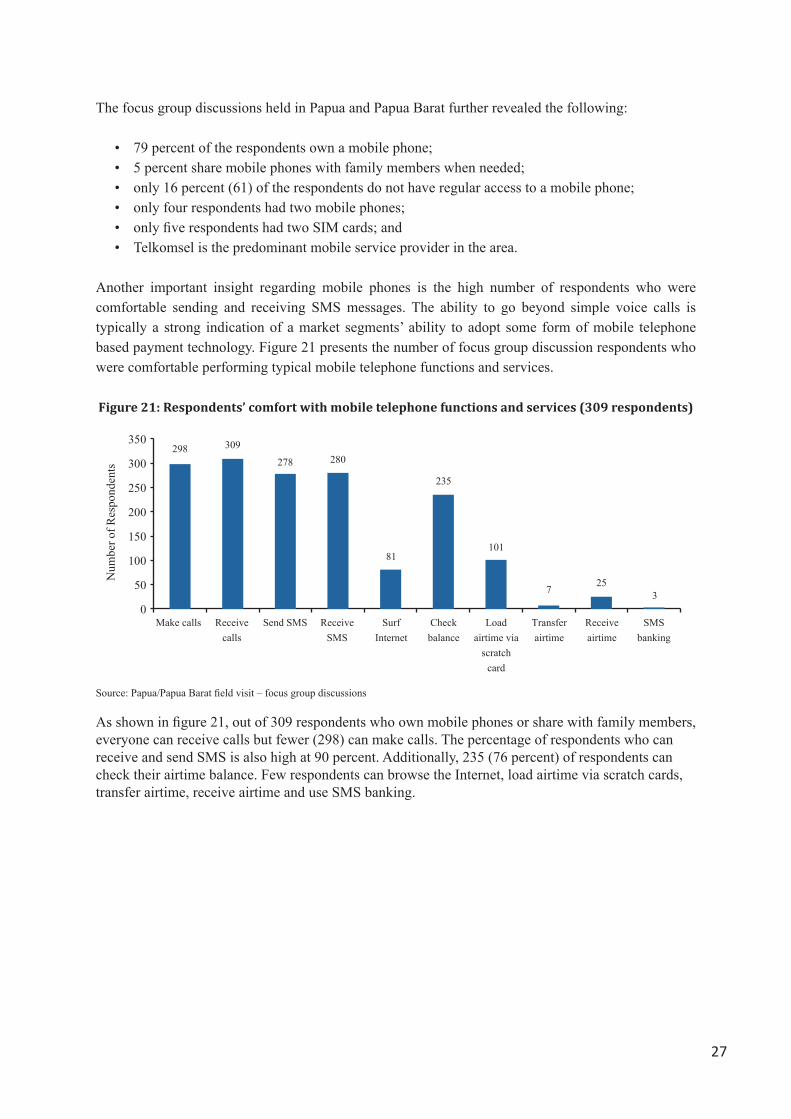

Figure 1: Time taken to collect a PKH payment ........................................................................................... xiFigure 2: Collecting education stipends ...................................................................................................... xiiFigure 3: Estimated cost per transaction by channel .................................................................................. xiiiFigure 4: Project framework ........................................................................................................................ 3Figure 5: Project approach .......................................................................................................................... 3Figure 6: Bank branches per 100,000 inhabitants ....................................................................................... 9Figure 7: Villages within 25kms of a bank branch ....................................................................................... 10Figure 8: Selected district summary ............................................................................................................12Figure 9: Demand-side focus group composition ........................................................................................ 13Figure 10: Focus group participant breakdown (programme or role, 370 respondents) .............................. 13Figure 11: Focus group participant breakdown (gender and age, 370 respondents) .................................... 14Figure 12: Focus group participant breakdown (literacy rates, 370 respondents) ........................................ 15Figure 13: Payer interviews ........................................................................................................................... 15Figure 14: PKH payment flow ........................................................................................................................ 18Figure 15: BSM payment flow ....................................................................................................................... 19Figure 16: Methods of receiving cash salary payments (percentages) .......................................................... 21Figure 17: Time taken to collect a PKH payment ........................................................................................... 23

viii

Figure 18: Bank account ownership – G2P payment recipients .................................................................... 25Figure 19: Bank account rationale ................................................................................................................. 26Figure 20: Mobile telephone ownership – gender breakdown ..................................................................... 26Figure 21: Respondents’ comfort with mobile telephone functions and services (309 respondents) .......... 27Figure 22: G2P payment scheme attributes .................................................................................................. 28Figure 23: Potential payment point assessment ........................................................................................... 33Figure 24: Potential payment point assessment ........................................................................................... 34Figure 25: Estimated cost per transaction by channel .................................................................................. 35Figure 26: Beneficiary collection costs (existing payment points) (Rp) ......................................................... 36Figure 27: Beneficiary travel distances (kms) ................................................................................................ 37Figure 28: Beneficiary collection costs (Rp) ................................................................................................... 37Figure 29: Beneficiary collection cost comparison (Rp) ................................................................................ 38Figure 30: Collecting education stipends ......................................................................................................39Figure 31: Collecting education stipends using branchless banking ............................................................. 44Figure 32: Proposed electronic payment process ......................................................................................... 48

ix

Acronyms

ATM : Automated teller machineBappenas : Badan Perencanaan dan Pembangunan Nasional (National Development Planning Agency)BFA : Bankable Frontiers AssociatesBKMM : Beasiswa Khusus Murid Miskin (Special Aid for Poor Students)BLSM : Bantuan Langsung Sementara Masyarakat (Temporary Unconditional Cash Transfers)BOS : Bantuan Operational Sekolah (School Operational Grants)BPS : Badan Pusat Statistik (Statistics Indonesia) BRI : Bank Rakyat IndonesiaBSM : Beasiswa untuk Siswa Miskin (Cash Transfers for Poor Students)BTN : Bank Tabungan NegaraEDC : Electronic data captureFGD : Focus group discussionG2P : Government to person payments GDP : Gross Domestic ProductGoI : Government of the Republic of IndonesiaKYC : know your customer (client information required)KPE : kartu pegawai elektronik (Electronic card for civil servants)MoEC : Ministry of Education and Culture MoSA : Ministry of Social AffairsPKH : Program Keluarga Harapan (Conditional Cash Transfer Programme for Families)PNPM : Program Nasional Pemberdayaan Masyarakat (National Programme for Community Empowerment)POP : Point of payment PT Pos : Indonesian post officePIN : Personal identification numberRESPEK : Rencana Strategi Pembangunan Ekonomi Kampung (Economic Development Strategy for Villages)Rp : Indonesian rupiahTNP2K : Tim Nasional Percepatan Penanggulangan Kemiskinan (National Team for the Acceleration of Poverty Reduction)

x

Executive Summary

The poverty levels in Papua and Papua Barat make many Papuans eligible for government assistance programmes, including the Conditional Cash Transfer Programme for Poor Families (hereafter referred to as PKH) and the Cash Transfers for Poor Students programme (hereafter referred to as BSM). Accordingly, government payments provide an important income stream to residents of Papua and Papua Barat. With the highest poverty rate among the provinces of Indonesia, timely and cost-effective delivery of government to people (hereafter referred to as G2P) payments are particularly important. Currently, disbursing and collecting government payments can be costly for all parties in the payment chain. Both those processing the payments and those receiving them face high costs at the set payment points. For beneficiaries, this reduces the net value of their payments. The National Team for the Acceleration of Poverty Reduction (TNP2K) commissioned this research to understand more about: current payment practices; the costs of delivering and receiving payments in Papua and Papua Barat; the availability of current payment points; and the potential for alternative channels to improve payment delivery. The research provides a snapshot of current payment practices and interest in alternative payment mechanisms in 18 subdistricts in Papua and Papua Barat with varying degrees of accessibility. The research focuses primarily on payments made from the PKH and BSM programmes but also looks at other payment streams, including civil servants and teachers’ salaries paid to residents in the subdistricts studied.

Current payment points provide insufficient reach

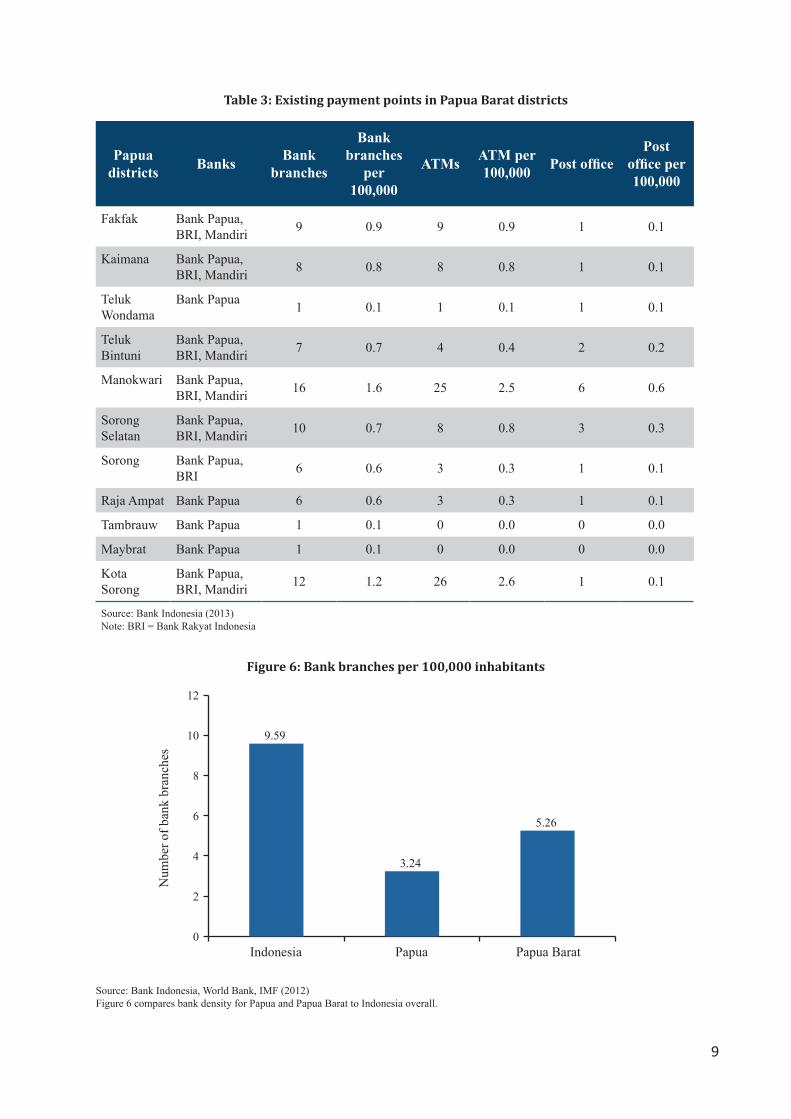

This research project began by collecting data on existing payment points in Papua and Papua Barat. Mapping current payment points based on publicly-available data indicates that most villages in the provinces are more than 25kms from a physical bank branch. This is confirmed by bank density levels for the areas. Bank density levels in Papua and Papua Barat are significantly lower than the level in Indonesia as a whole, reported as 9.59 bank branches per 100,000 inhabitants. Papua has 3.24 bank branches per 100,000 residents, while Papua Barat has a higher density with 5.26 bank branches per 100,000 inhabitants. Post offices serve as the payment distribution point for the PKH, while BSM payments are currently disbursed by banks. Post offices are more common at the district level in Papua Barat than in Papua (Bank Indonesia, World Bank, IMF 2012).

Localised data from 18 subdistricts with differing degrees of accessibility

Data on current payment practices were collected from focus group discussions (FGD) and in-depth interviews held in 12 subdistricts across six districts with three districts each in Papua and Papua Barat and two subdistricts in each district. The subdistricts were selected based on their classifications as remote and difficult to access, semi-urban with medium accessibility and easy to access urban areas. The 370 focus group discussion participants included a range of G2P recipients, mostly beneficiaries of the BSM and PKH programmes. Significantly, the PKH payment recipients interviewed reside in the more urban subdistricts of Jayapura and Manokwari Barat, while the BSM recipients surveyed live in more remote and semi-urban subdistricts with less accessibility. In addition to the focus groups, payer and service provider information was collected through a series of in-depth interviews.

xi

Travel cost and time to current payment points is the major challenge for G2P payment recipients

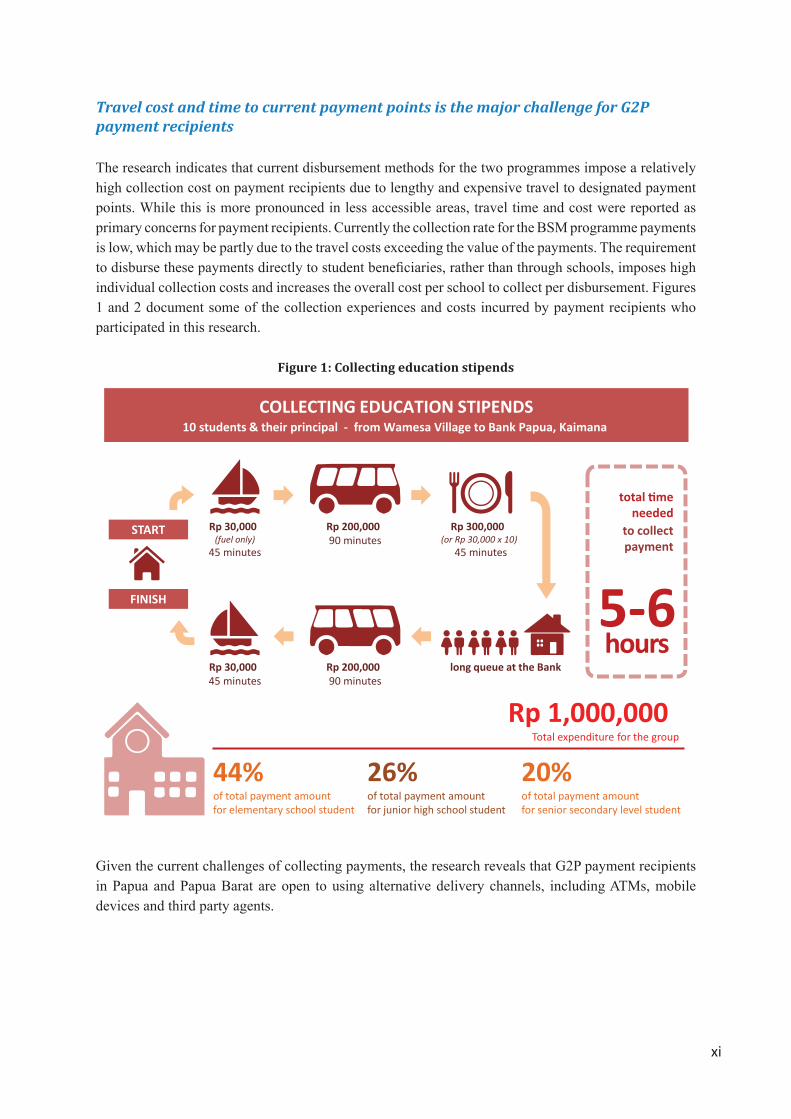

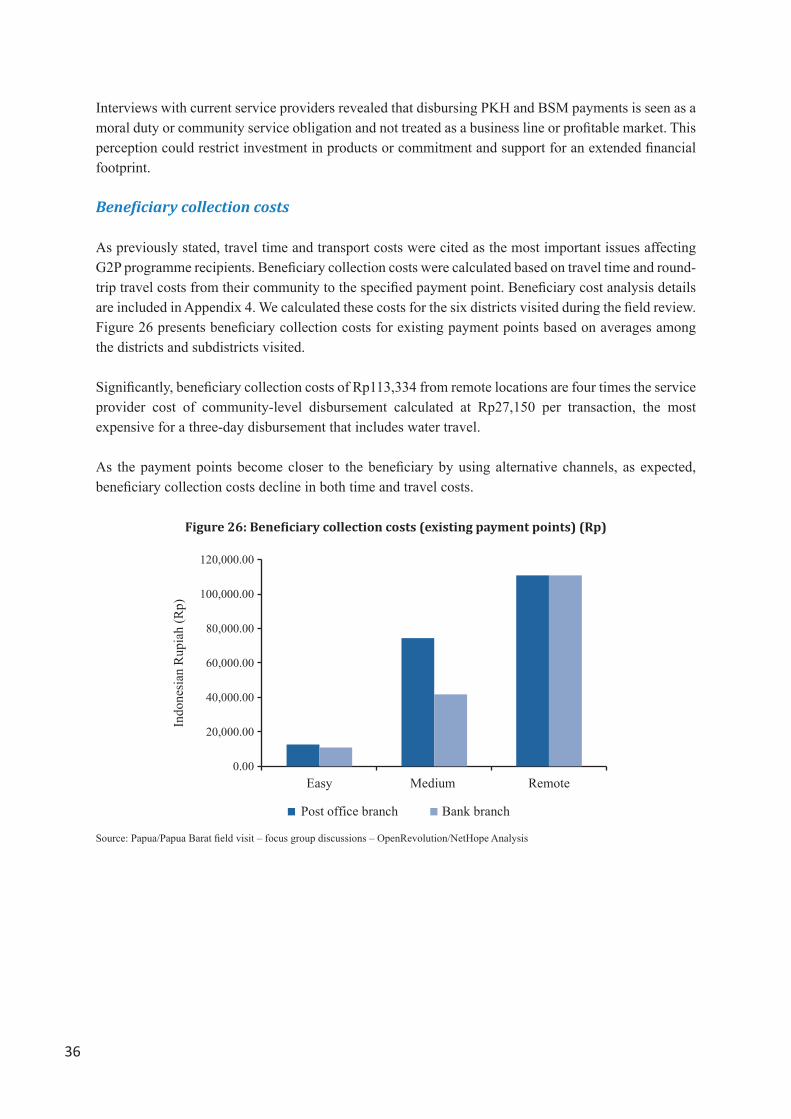

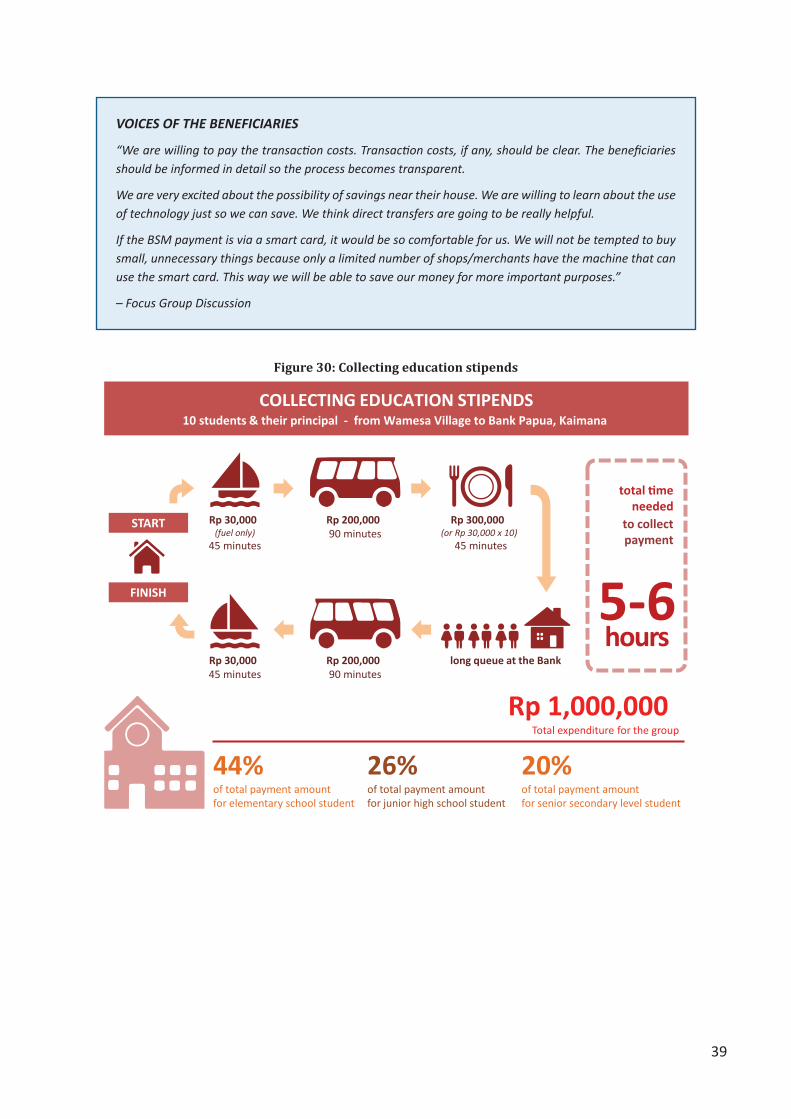

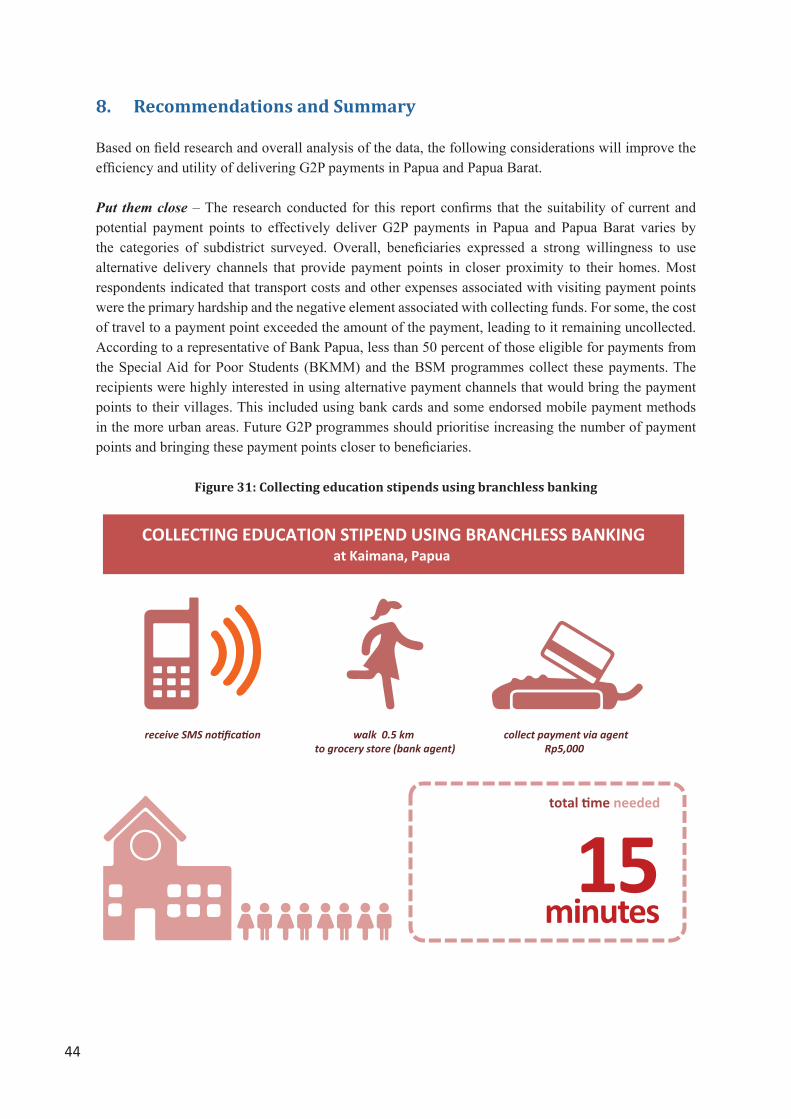

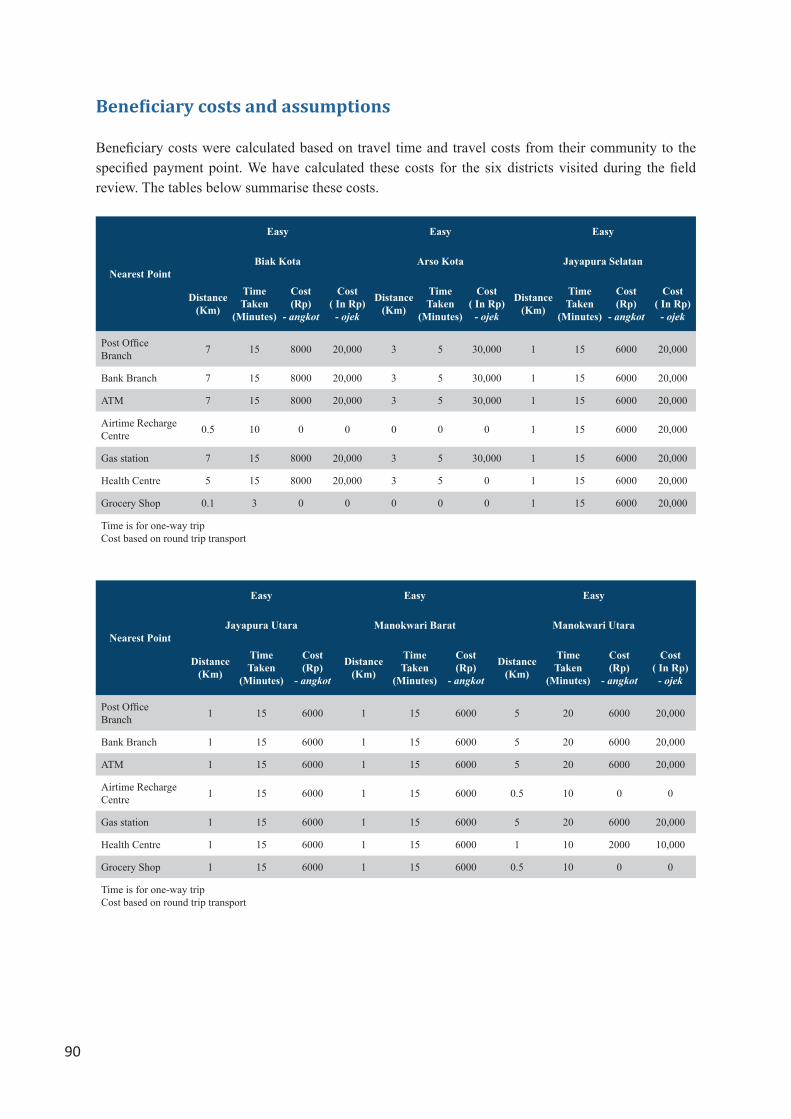

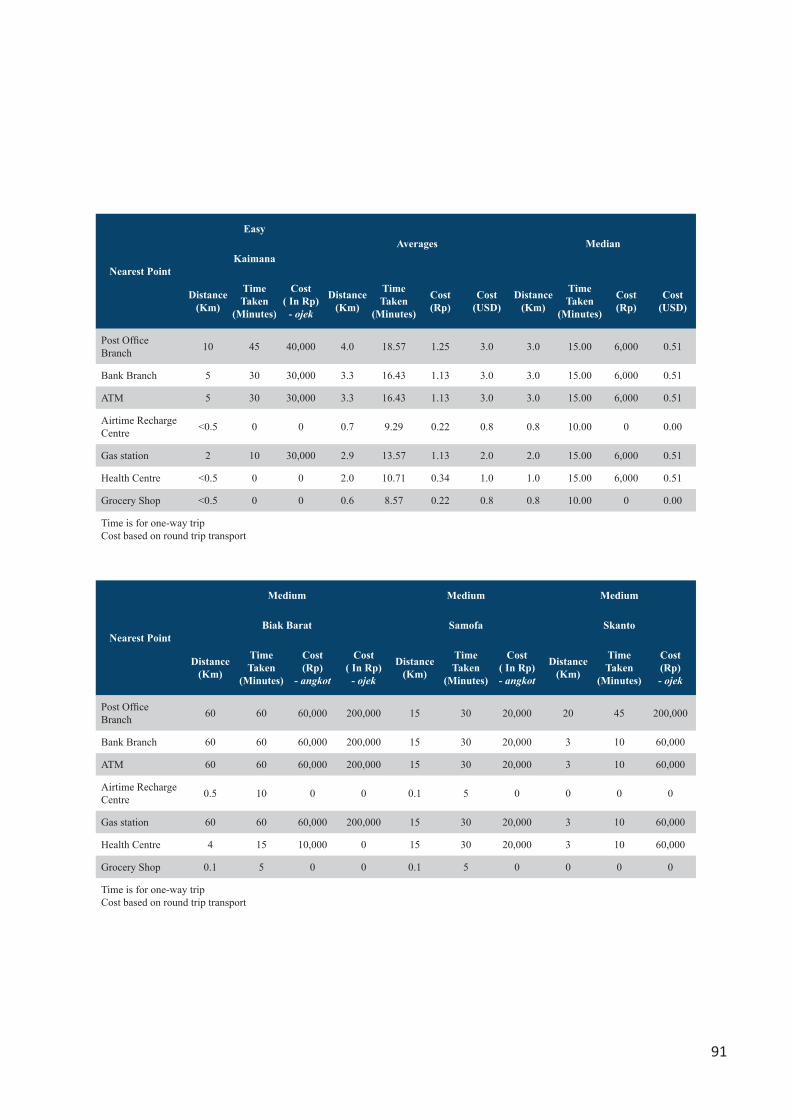

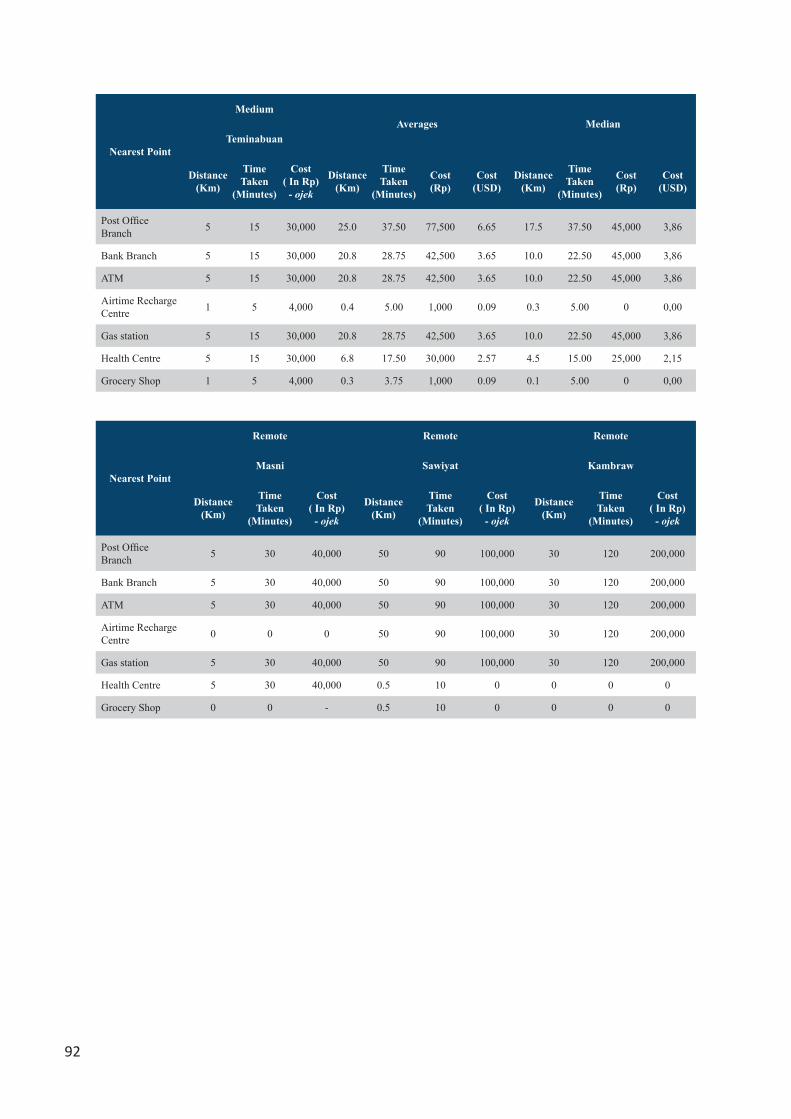

The research indicates that current disbursement methods for the two programmes impose a relatively high collection cost on payment recipients due to lengthy and expensive travel to designated payment points. While this is more pronounced in less accessible areas, travel time and cost were reported as primary concerns for payment recipients. Currently the collection rate for the BSM programme payments is low, which may be partly due to the travel costs exceeding the value of the payments. The requirement to disburse these payments directly to student beneficiaries, rather than through schools, imposes high individual collection costs and increases the overall cost per school to collect per disbursement. Figures 1 and 2 document some of the collection experiences and costs incurred by payment recipients who participated in this research.

Figure 1: Collecting education stipends

Given the current challenges of collecting payments, the research reveals that G2P payment recipients in Papua and Papua Barat are open to using alternative delivery channels, including ATMs, mobile devices and third party agents.

Rp 1,000,000 Total expenditure for the group

Rp 30,000(fuel only)

45 minutes

Rp 200,00090 minutes

Rp 300,000 (or Rp 30,000 x 10)

45 minutes

total timeneeded

to collectpayment

5-6Rp 200,00090 minutes

Rp 30,00045 minutes

long queue at the Bank

26%of total payment amount for junior high school student

44%of total payment amount for elementary school student

20%of total payment amount for senior secondary level student

hours

START

FINISH

COLLECTING EDUCATION STIPENDS10 students & their principal - from Wamesa Village to Bank Papua, Kaimana

xii

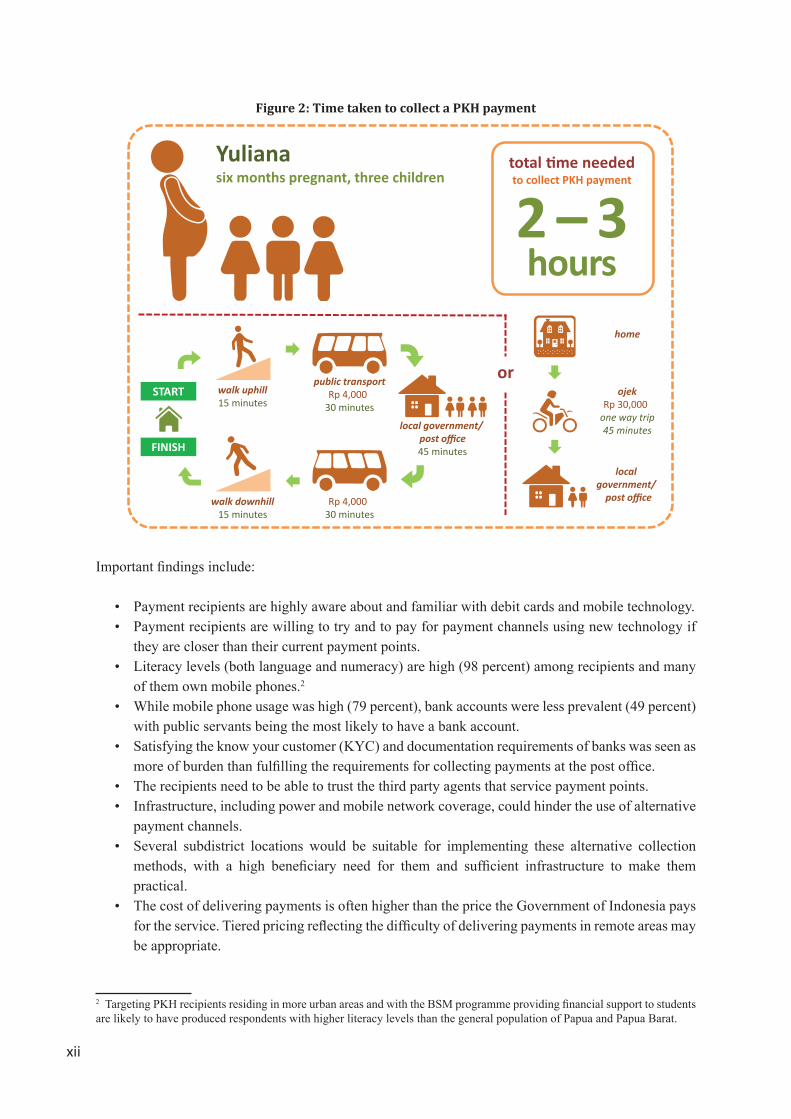

Figure 2: Time taken to collect a PKH payment

Important findings include:

• Payment recipients are highly aware about and familiar with debit cards and mobile technology.• Payment recipients are willing to try and to pay for payment channels using new technology if

they are closer than their current payment points.• Literacy levels (both language and numeracy) are high (98 percent) among recipients and many

of them own mobile phones.2

• While mobile phone usage was high (79 percent), bank accounts were less prevalent (49 percent) with public servants being the most likely to have a bank account.

• Satisfying the know your customer (KYC) and documentation requirements of banks was seen as more of burden than fulfilling the requirements for collecting payments at the post office.

• The recipients need to be able to trust the third party agents that service payment points.• Infrastructure, including power and mobile network coverage, could hinder the use of alternative

payment channels.• Several subdistrict locations would be suitable for implementing these alternative collection

methods, with a high beneficiary need for them and sufficient infrastructure to make them practical.

• The cost of delivering payments is often higher than the price the Government of Indonesia pays for the service. Tiered pricing reflecting the difficulty of delivering payments in remote areas may be appropriate.

2 Targeting PKH recipients residing in more urban areas and with the BSM programme providing financial support to students are likely to have produced respondents with higher literacy levels than the general population of Papua and Papua Barat.

total time neededto collect PKH payment

2 – 3hours

Yulianasix months pregnant, three children

ojekRp 30,000

one way trip45 minutes

public transportRp 4,000

30 minutes

walk uphill15 minutes

or

local government/ post office45 minutes

Rp 4,00030 minutes

walk downhill15 minutes

home

local government/

post office

START

FINISH

xiii

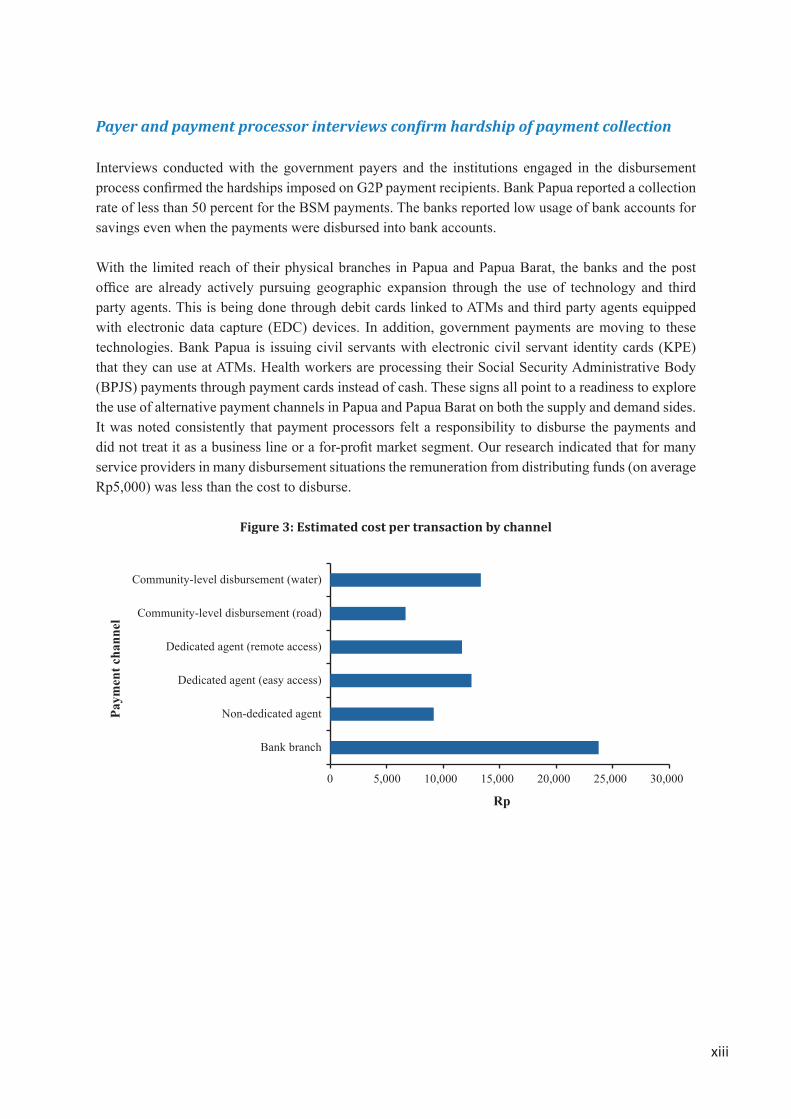

Payer and payment processor interviews confirm hardship of payment collection

Interviews conducted with the government payers and the institutions engaged in the disbursement process confirmed the hardships imposed on G2P payment recipients. Bank Papua reported a collection rate of less than 50 percent for the BSM payments. The banks reported low usage of bank accounts for savings even when the payments were disbursed into bank accounts.

With the limited reach of their physical branches in Papua and Papua Barat, the banks and the post office are already actively pursuing geographic expansion through the use of technology and third party agents. This is being done through debit cards linked to ATMs and third party agents equipped with electronic data capture (EDC) devices. In addition, government payments are moving to these technologies. Bank Papua is issuing civil servants with electronic civil servant identity cards (KPE) that they can use at ATMs. Health workers are processing their Social Security Administrative Body (BPJS) payments through payment cards instead of cash. These signs all point to a readiness to explore the use of alternative payment channels in Papua and Papua Barat on both the supply and demand sides. It was noted consistently that payment processors felt a responsibility to disburse the payments and did not treat it as a business line or a for-profit market segment. Our research indicated that for many service providers in many disbursement situations the remuneration from distributing funds (on average Rp5,000) was less than the cost to disburse.

Figure 3: Estimated cost per transaction by channel

Gin

i

Bank branch

Non-dedicated agent

Dedicated agent (easy access)

Dedicated agent (remote access)

Community-level disbursement (road)

Community-level disbursement (water)

0 5,000 10,000 15,000 20,000 25,000 30,000

Rp

Paym

ent c

hann

el

xiv

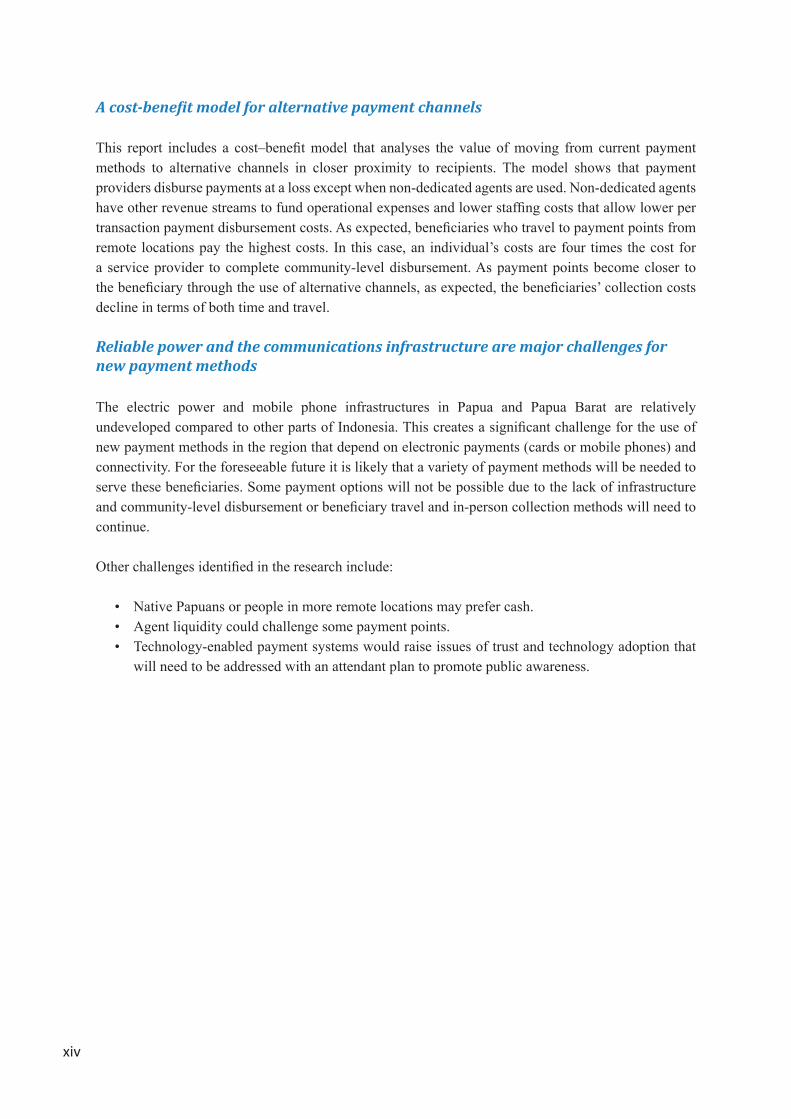

A cost-benefit model for alternative payment channels

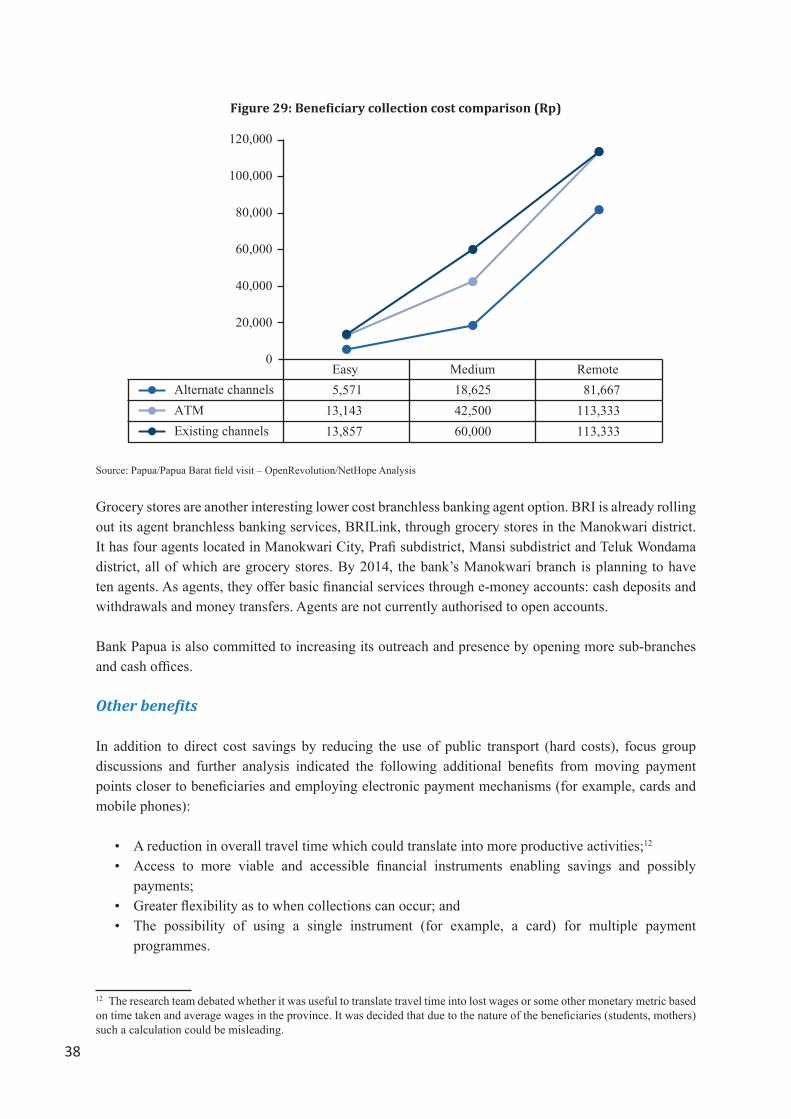

This report includes a cost–benefit model that analyses the value of moving from current payment methods to alternative channels in closer proximity to recipients. The model shows that payment providers disburse payments at a loss except when non-dedicated agents are used. Non-dedicated agents have other revenue streams to fund operational expenses and lower staffing costs that allow lower per transaction payment disbursement costs. As expected, beneficiaries who travel to payment points from remote locations pay the highest costs. In this case, an individual’s costs are four times the cost for a service provider to complete community-level disbursement. As payment points become closer to the beneficiary through the use of alternative channels, as expected, the beneficiaries’ collection costs decline in terms of both time and travel.

Reliable power and the communications infrastructure are major challenges for new payment methods

The electric power and mobile phone infrastructures in Papua and Papua Barat are relatively undeveloped compared to other parts of Indonesia. This creates a significant challenge for the use of new payment methods in the region that depend on electronic payments (cards or mobile phones) and connectivity. For the foreseeable future it is likely that a variety of payment methods will be needed to serve these beneficiaries. Some payment options will not be possible due to the lack of infrastructure and community-level disbursement or beneficiary travel and in-person collection methods will need to continue.

Other challenges identified in the research include:

• Native Papuans or people in more remote locations may prefer cash. • Agent liquidity could challenge some payment points.• Technology-enabled payment systems would raise issues of trust and technology adoption that

will need to be addressed with an attendant plan to promote public awareness.

xv

Next steps

Given plans to expand G2P payments in Papua and Papua Barat, it becomes imperative that more efficient payment mechanisms are developed and tested. Recent changes to the Agent Banking regulations and a commitment on the part of the Financial Services Authority of Indonesia (OJK) to expand the availability of financial services through agent banking, provide an opportunity to address the greatest challenge facing G2P beneficiaries: proximity to payment points. Additionally, the continued development of mobile technologies and the adoption of these technologies in Papua and Papua Barat provide a further foundation for alternative payment channels. Our findings indicate that multiple payment mechanisms will be required in Papua and Papua Barat with existing channels (bank branches and post offices), community disbursements and agent banking locations all playing a role in delivering G2P payments. Critical next steps include:

• Mapping expanded PKH and BSM programme payments for 2015/2016;• Selecting optimal geographies for an alternative channel payment pilot;• Developing detailed pilot requirements;• Discussing requirements with potential service providers;• Finalising contract requirements;• Executing the payment pilot;• Collecting and analysing the pilot metrics; and• Expanding the pilot to other geographies and other beneficiaries.

1

1. Overview

This report provides the findings of research commissioned by TNP2K to survey and evaluate current and potential payment options for disbursing government to people (hereafter referred to as G2P) social welfare payments to residents of Papua and Papua Barat. Based on research conducted in 18 subdistricts, the report analyses the needs for and costs of disbursing and collecting G2P payments in this region and provides a cost–benefit analysis of current and alternative electronic payment options. It also examines other payment streams, including salary payments to civil servants, teachers and health care workers. The report makes policy recommendations that TNP2K, the National Development Planning Agency (Bappenas), the Ministry of Education and Culture (MoEC), the Ministry of Social Affairs (MoSA) and other policy makers can use to develop effective disbursement mechanisms to meet the specific goals of the PKH and the BSM programmes as well as other G2P payments in Papua and Papua Barat. Additionally, the report includes a plan for an alternative payment pilot and specific guidelines on designing and executing the social welfare G2P pilot in selected areas in the region.

2

2. Research Objectives/Methodology

This report builds on earlier work commissioned by TNP2K in 2013 and 2014 that examined payment options for PKH in selected areas of Indonesia. In 2013, a study was commissioned to evaluate options for the government to distribute PKH payments directly to recipients’ bank accounts (OPM 2013).3 In a follow-on study in 2014, TNP2K and Bankable Frontiers Associates developed a PKH strategy and requirements matrix that identifies options for assisted and self-service programme payments or disbursements (using electronic payments, including mobile phones and ATM cards) (Joyce et al. 2014). The study recommended that district-level considerations be factored into the selection of payment disbursement methods for the revised and expanded programme. This research aimed to identify the district-level considerations in Papua and Papua Barat and better understand the demand-side (payment recipient) and supply-side considerations at the district and subdistrict level in Papua and Papua Barat. It also aimed to assess infrastructure readiness to support the delivery of G2P payments through current or alternative electronic payment channels. Open Revolution, MicroSave and NetHope were selected as the contracting team to conduct this research in April 2014.

G2P payments are an important payment stream in Papua and Papua Barat and are likely to continue and to increase as the government expands their programmes as part of an overall campaign to address the consistently high levels of poverty in the two provinces. Papua and Papua Barat have the largest poverty severity percentages (2.3 percent and 2.05 percent respectively) in Indonesia, more than five times the country’s average of 0.44 percent (BPS 2014).4 The poor are concentrated in the rural areas of the provinces that include 1.1 million of the 1.15 million people living below the poverty line – 38 percent of the rural population in Papua is poor. A slightly smaller percentage (36.62 percent) of rural residents in Papua Barat are poor.

These poverty levels make the timely and cost-effective delivery of G2P payments particularly important. In addition, the change in the BSM programme requiring payments to be disbursed directly to recipients, rather than through schools or school officials, will create challenges in the existing payment systems. With current disbursement methods, beneficiaries incur costs in collecting their payments. This reduces the value of the payments or even, in some cases, eliminates the benefit of collecting them. Service providers, in some cases, incur operational costs above the per transaction remuneration rate paid and so they often disburse these payments at a loss. The research reveals that the cost of disbursement and collection varies between urban and rural areas. This suggests that a diversified approach to payment disbursement may be necessary in Papua and Papua Barat to ensure optimal programme benefits.

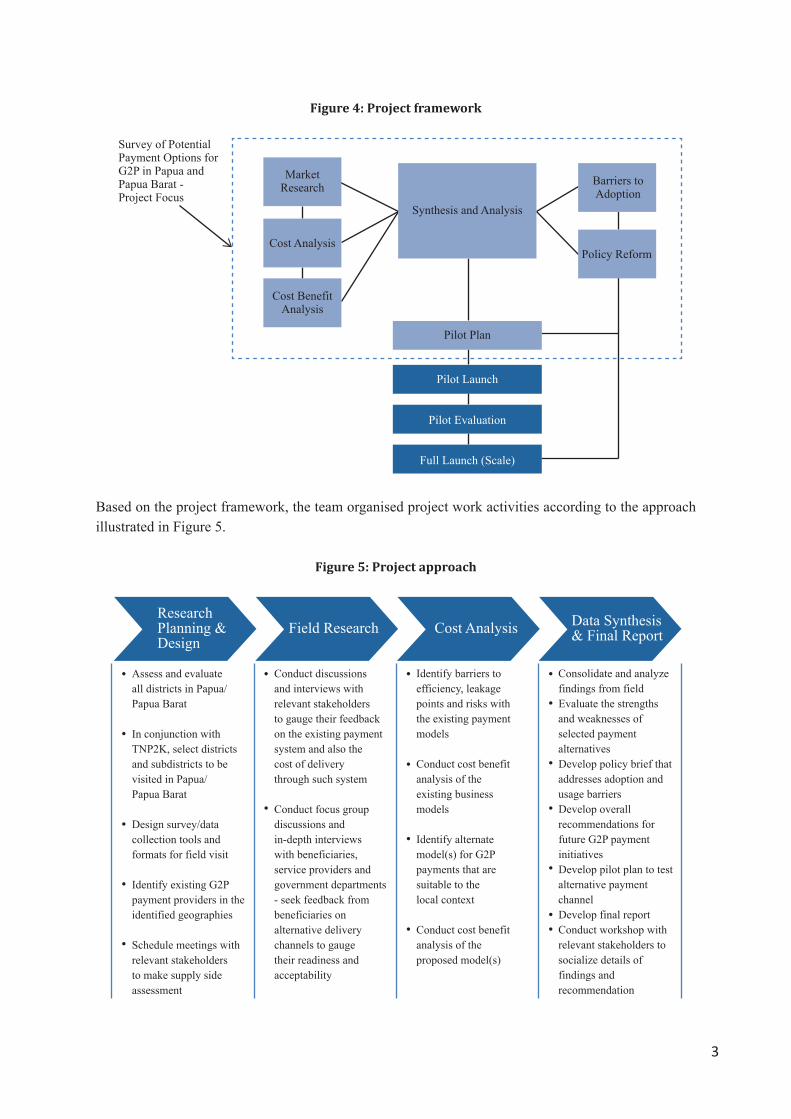

Based on the project objectives, the team developed a project framework that provided a high-level guide to the project and illustrated the linkages among various project-related activities. Figure 4 presents our overall project framework.

3 The study drew on findings from qualitative research collected through interviews with 209 programme recipients in the provinces of Gorontalo, Nanggroe Ached Darussalam, Nusa Tenggara Timur, Nusa Tenggara Barat, Sumatera Utara, Jawa Tengah, Bengkulu and Maluku Utara (hereafter referred to as the OPM study).4 Statistics Indonesia – the poverty severity index is used to measure poverty intensity and to what degree the lack of resources impacts on the poor.

3

Figure 4: Project framework

Based on the project framework, the team organised project work activities according to the approach illustrated in Figure 5.

Figure 5: Project approach

Survey of PotentialPayment Options forG2P in Papua andPapua Barat -Project Focus

MarketResearch

Cost Analysis

Cost BenefitAnalysis

Synthesis and Analysis

Pilot Plan

Pilot Launch

Pilot Evaluation

Full Launch (Scale)

Barriers toAdoption

Policy Reform

Assess and evaluate all districts in Papua/Papua Barat

In conjunction withTNP2K, select districtsand subdistricts to bevisited in Papua/Papua Barat

Design survey/datacollection tools andformats for field visit

Identify existing G2Ppayment providers in theidentified geographies

Schedule meetings withrelevant stakeholdersto make supply sideassessment

Conduct discussionsand interviews withrelevant stakeholdersto gauge their feedbackon the existing paymentsystem and also the cost of deliverythrough such system

Conduct focus groupdiscussions and in-depth interviews with beneficiaries,service providers andgovernment departments- seek feedback frombeneficiaries on alternative deliverychannels to gaugetheir readiness andacceptability

Identify barriers toefficiency, leakagepoints and risks withthe existing paymentmodels

Conduct cost benefitanalysis of the existing businessmodels

Identify alternatemodel(s) for G2Ppayments that are suitable to the local context

Conduct cost benefitanalysis of theproposed model(s)

Consolidate and analyzefindings from fieldEvaluate the strengths and weaknesses of selected payment alternativesDevelop policy brief thataddresses adoption andusage barriersDevelop overallrecommendations forfuture G2P paymentinitiativesDevelop pilot plan to testalternative payment channelDevelop final reportConduct workshop withrelevant stakeholders tosocialize details of findings and recommendation

ResearchPlanning &Design

Field Research Cost Analysis Data Synthesis& Final Report

4

3. District Assessment

Prior to selecting specific districts and subdistricts for field research, the team conducted a broad review of all 28 districts in Papua and 11 in Papua Barat. Using government offices, donor organisations and other sources, the team collected information on the following attributes:

• Area in square kilometres;• Population including male/female breakdown, households and population density;• Gross domestic product (GDP) per district and per capita;• Poverty rates;• Number of schools;• Number of teachers;• Number of health-care facilities;• Electricity usage;• Number of kilometres of road; and • Existing points.

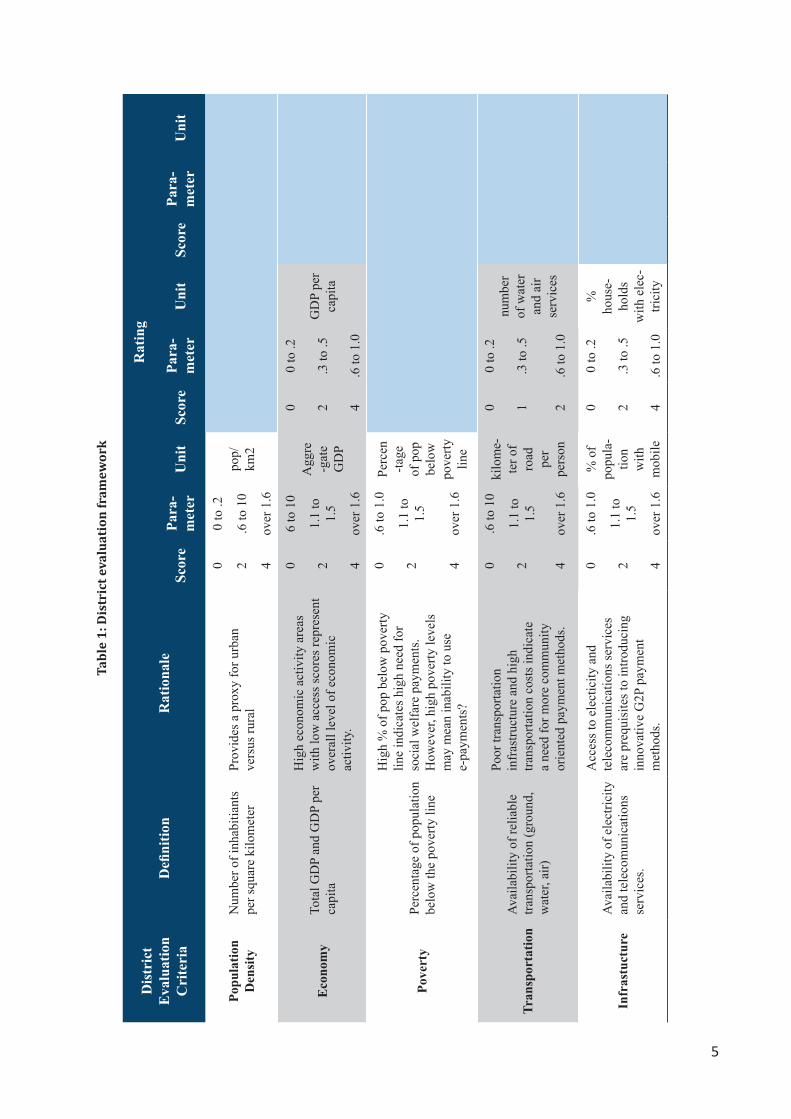

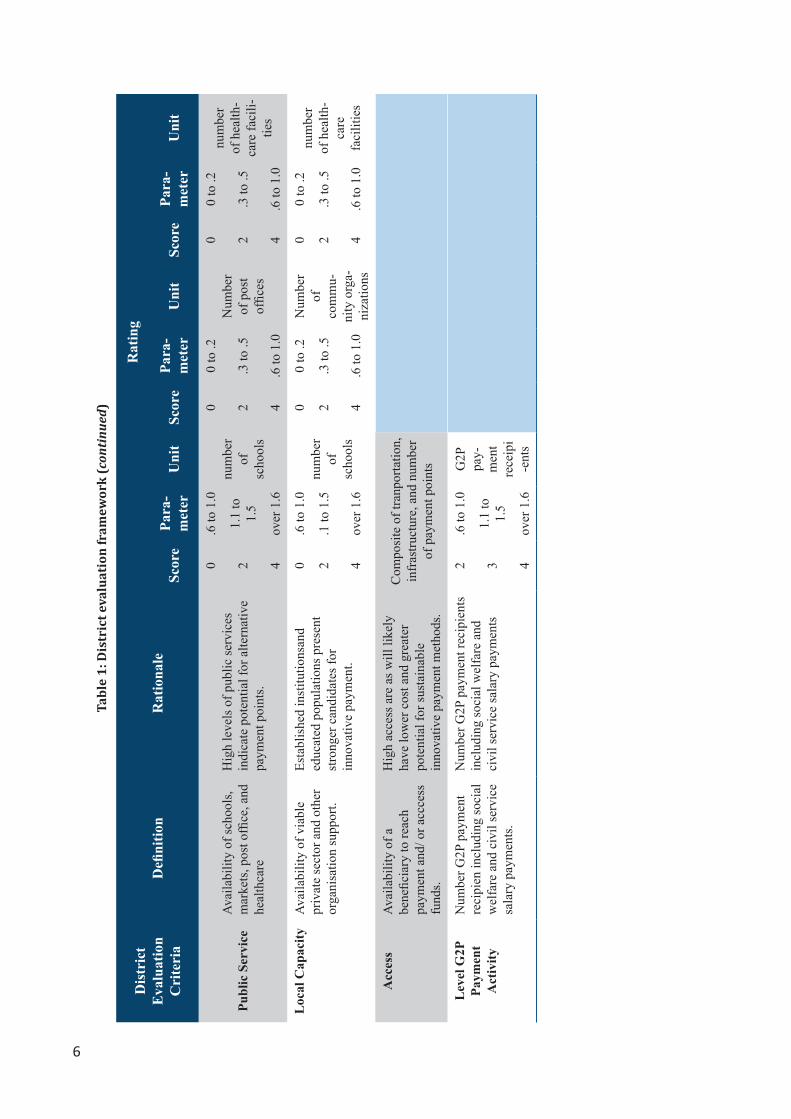

Specific criteria and parameters were then developed in order to assign ratings to districts. Table 1 presents the district evaluation framework. From this evaluation, the team developed a district assessment that assigned each district an accessibility rating (easy, moderate or difficult).

5

Tabl

e 1:

Dis

tric

t eva

luat

ion

fram

ewor

k

Dis

tric

t E

valu

atio

n C

rite

ria

Defi

nitio

nR

atio

nale

Rat

ing

Scor

ePa

ra-

met

erU

nit

Scor

ePa

ra-

met

erU

nit

Scor

ePa

ra-

met

erU

nit

Popu

latio

n D

ensi

tyN

umbe

r of i

nhab

itian

ts

per s

quar

e ki

lom

eter

Prov

ides

a p

roxy

for u

rban

ve

rsus

rura

l

00

to .2

pop/

km2

2.6

to 1

0

4ov

er 1

.6

Eco

nom

yTo

tal G

DP

and

GD

P pe

r ca

pita

Hig

h ec

onom

ic a

ctiv

ity a

reas

w

ith lo

w a

cces

s sco

res r

epre

sent

ov

eral

l lev

el o

f eco

nom

ic

activ

ity.

06

to 1

0A

ggre

-gat

eG

DP

00

to .2

GD

P pe

r ca

pita

21.

1 to

1.

52

.3 to

.5

4ov

er 1

.64

.6 to

1.0

Pove

rty

Perc

enta

ge o

f pop

ulat

ion

belo

w th

e po

verty

line

Hig

h %

of p

op b

elow

pov

erty

lin

e in

dica

tes h

igh

need

for

soci

al w

elfa

re p

aym

ents

. H

owev

er, h

igh

pove

rty le

vels

m

ay m

ean

inab

ility

to u

se

e-pa

ymen

ts?

0.6

to 1

.0Pe

rcen

-tage

of

pop

be

low

po

verty

lin

e

21.

1 to

1.

5

4ov

er 1

.6

Tran

spor

tatio

nAv

aila

bilit

y of

relia

ble

trans

porta

tion

(gro

und,

w

ater

, air)

Poor

tran

spor

tatio

n in

fras

truct

ure

and

high

tra

nspo

rtatio

n co

sts i

ndic

ate

a ne

ed fo

r mor

e co

mm

unity

or

ient

ed p

aym

ent m

etho

ds.

0.6

to 1

0ki

lom

e-

ter o

f ro

ad

per

pers

on

00

to .2

num

ber

of w

ater

an

d ai

r se

rvic

es

21.

1 to

1.

51

.3 to

.5

4ov

er 1

.62

.6 to

1.0

Infr

astu

ctur

eAv

aila

bilit

y of

ele

ctric

ity

and

tele

com

unic

atio

ns

serv

ices

.

Acc

ess t

o el

ectic

ity a

nd

tele

com

mun

icat

ions

serv

ices

ar

e pr

equi

site

s to

intro

duci

ng

inno

vativ

e G

2P p

aym

ent

met

hods

.

0.6

to 1

.0%

of

popu

la-

tion

with

m

obile

00

to .2

%

hous

e-ho

lds

with

ele

c-

trici

ty

21.

1 to

1.

52

.3 to

.5

4ov

er 1

.64

.6 to

1.0

6

Dis

tric

t E

valu

atio

n C

rite

ria

Defi

nitio

nR

atio

nale

Rat

ing

Scor

ePa

ra-

met

erU

nit

Scor

ePa

ra-

met

erU

nit

Scor

ePa

ra-

met

erU

nit

Publ

ic S

ervi

ceAv

aila

bilit

y of

scho

ols,

mar

kets

, pos

t offi

ce, a

nd

heal

thca

re

Hig

h le

vels

of p

ublic

serv

ices

in

dica

te p

oten

tial f

or a

ltern

ativ

e pa

ymen

t poi

nts.

0.6

to 1

.0nu

mbe

r of

sc

hool

s

00

to .2

Num

ber

of p

ost

offic

es

00

to .2

num

ber

of h

ealth

- ca

re fa

cili-

tie

s

21.

1 to

1.

52

.3 to

.52

.3 to

.5

4ov

er 1

.64

.6 to

1.0

4.6

to 1

.0

Loc

al C

apac

ityAv

aila

bilit

y of

via

ble

priv

ate

sect

or a

nd o

ther

or

gani

satio

n su

ppor

t.

Esta

blis

hed

inst

itutio

nsan

d ed

ucat

ed p

opul

atio

ns p

rese

nt

stro

nger

can

dida

tes f

or

inno

vativ

e pa

ymen

t.

0.6

to 1

.0nu

mbe

r of

sc

hool

s

00

to .2

Num

ber

of

com

mu-

ni

ty o

rga-

ni

zatio

ns

00

to .2

num

ber

of h

ealth

- ca

re

faci

litie

s

2.1

to 1

.52

.3 to

.5

2.3

to .5

4ov

er 1

.64

.6 to

1.0

4.6

to 1

.0

Acc

ess

Avai

labi

lity

of a

be

nefic

iary

to re

ach

paym

ent a

nd/ o

r acc

cess

fu

nds.

Hig

h ac

cess

are

as w

ill li

kely

ha

ve lo

wer

cos

t and

gre

ater

po

tent

ial f

or su

stai

nabl

e in

nova

tive

paym

ent m

etho

ds.

Com

posi

te o

f tra

npor

tatio

n,

infr

astru

ctur

e, a

nd n

umbe

r of

pay

men

t poi

nts

Lev

el G

2P

Paym

ent

Act

ivity

Num

ber G

2P p

aym

ent

reci

pien

incl

udin

g so

cial

w

elfa

re a

nd c

ivil

serv

ice

sala

ry p

aym

ents

.

Num

ber G

2P p

aym

ent r

ecip

ient

s in

clud

ing

soci

al w

elfa

re a

nd

civi

l ser

vice

sala

ry p

aym

ents

2.6

to 1

.0G

2P

pay-

m

ent

rece

ipi

-ent

s

31.

1 to

1.

5

4ov

er 1

.6

Tabl

e 1:

Dis

tric

t eva

luat

ion

fram

ewor

k (c

ontin

ued)

7

Infrastructure analysis

A key area of investigation was the quality and breadth of infrastructure. Our team focused on the following three infrastructure components:

• electricity;• telecommunications; and• road networks.

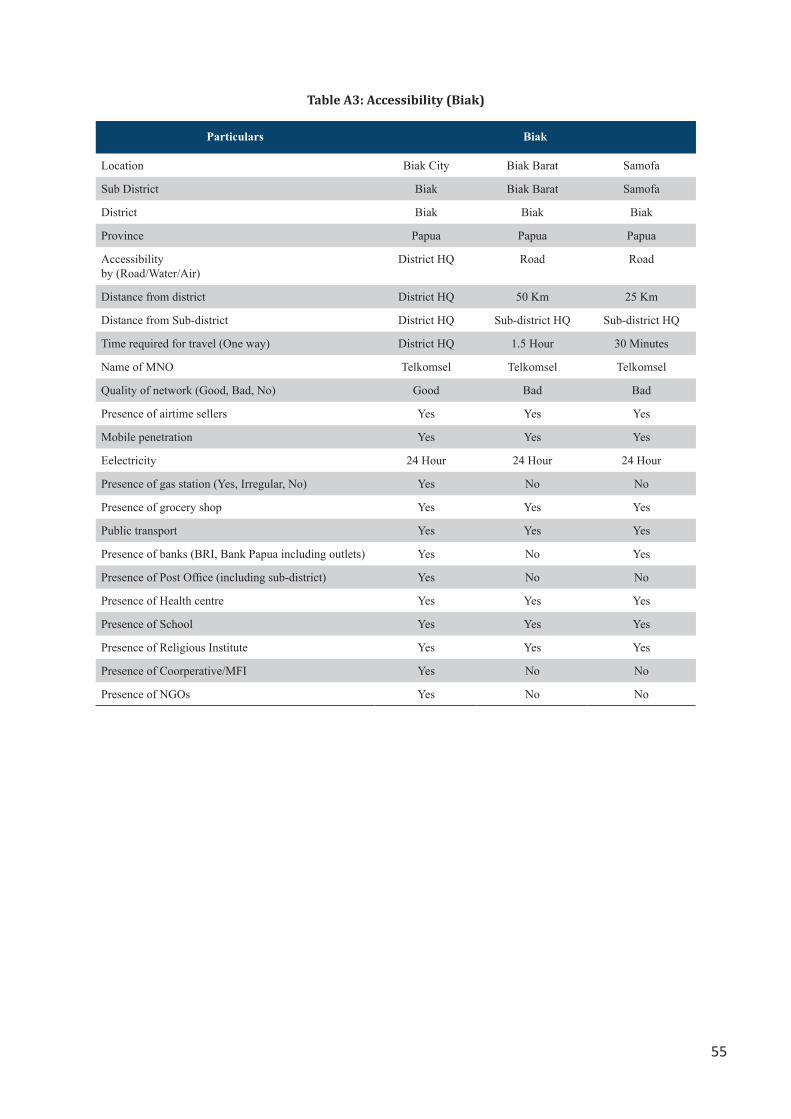

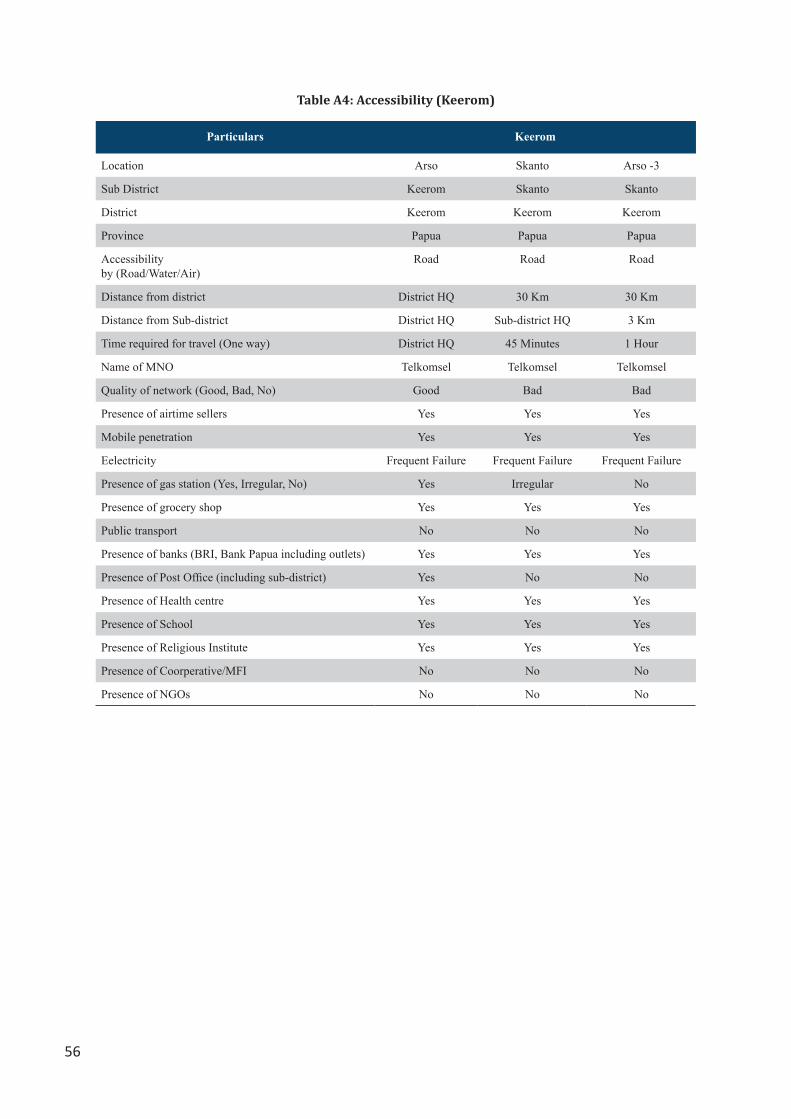

Reliable electricity at the payment point is a prerequisite for most payment technologies (for example, electronic data capture devices – hereafter referred to as EDCs). While generator and battery options can provide temporary capabilities, expanding the power grid in Papua and Papua Barat will be critical in developing comprehensive payment solutions. In the near-term, one criteria used to select future payment points will be the availability of reliable power. Connectivity, typically through mobile networks, is the other prerequisite for electronic payment solutions. EDCs, ATMs and mobile handsets all need to connect to back office systems in order to register the payment transaction. Our research confirmed that Telkomsel is the primary provider of telecommunications services in the region. Our research further confirmed that in many rural districts, coverage is poor. The final infrastructure element reviewed was the road network. Our findings indicated that the quality and reach of the road network directly impacted on travel time and travel costs for both payer and beneficiary. Details on the availability of infrastructure and other facilities in Papua and Papua Barat are given in Appendix 1.

Payment point analysis

Payment points and channels exist in Papua and Papua Barat and are used to disburse G2P payments. These payment points include bank branches, post office facilities and temporary community-level disbursement points that deliver cash payments to remote locations. ATMs also exist in the two provinces and can be used to access accounts serviced by a bank and, more recently, accounts with the post office linked through ATM Bersama (an inter-bank network). There are indications that residents of Papua are increasingly using ATM and debit cards. However, to date, card-based systems have not been used for G2P payments. The research did not identify the current offering of electronic-money services by mobile network operators. In addition, existing money transfer services, such as Western Union, were not included, given that G2P payment recipients are unfamiliar with these services and the services are generally expensive. For the region as a whole, this report maps the existing payment points as determined through secondary research and information available from public sources. The accessibility of banks and post offices varies in Papua and Papua Barat with more bank branches across the districts of Papua than post office facilities. By contrast, there is a post office in over 80 percent of the districts in Papua Barat. In Papua all districts, with the exception of Intan Jaya, have at least one bank branch while only 58 percent of the districts have a post office facility.

8

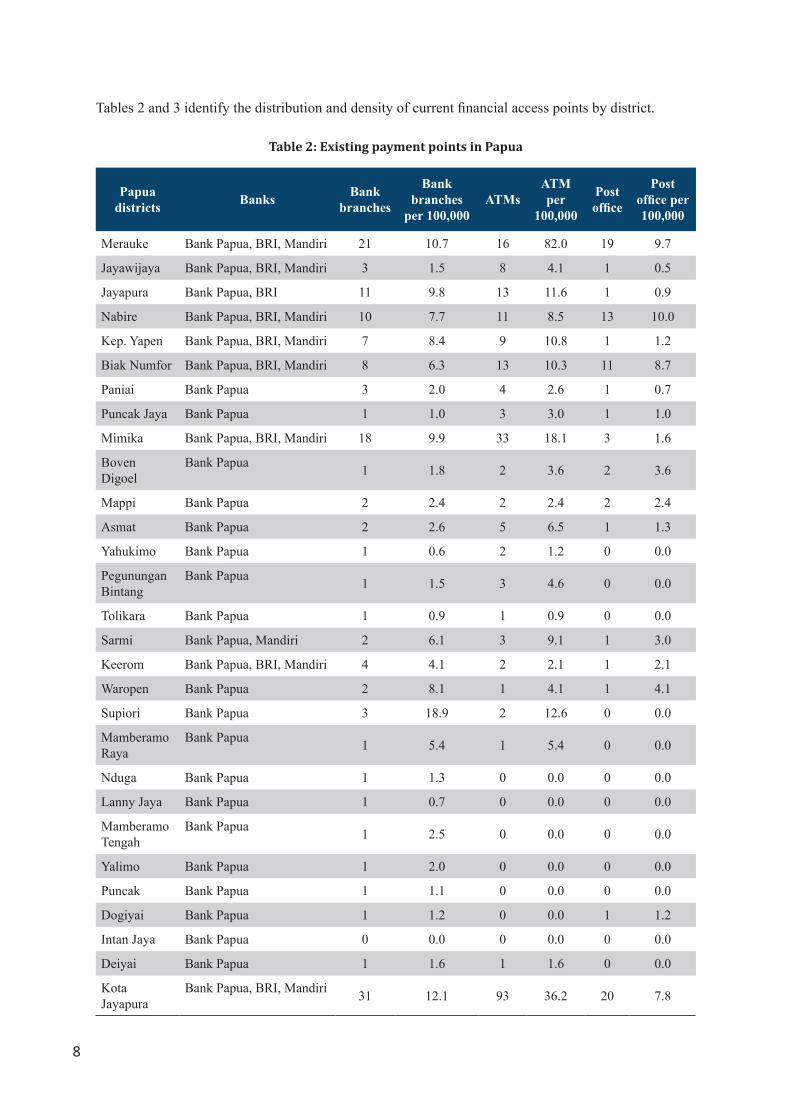

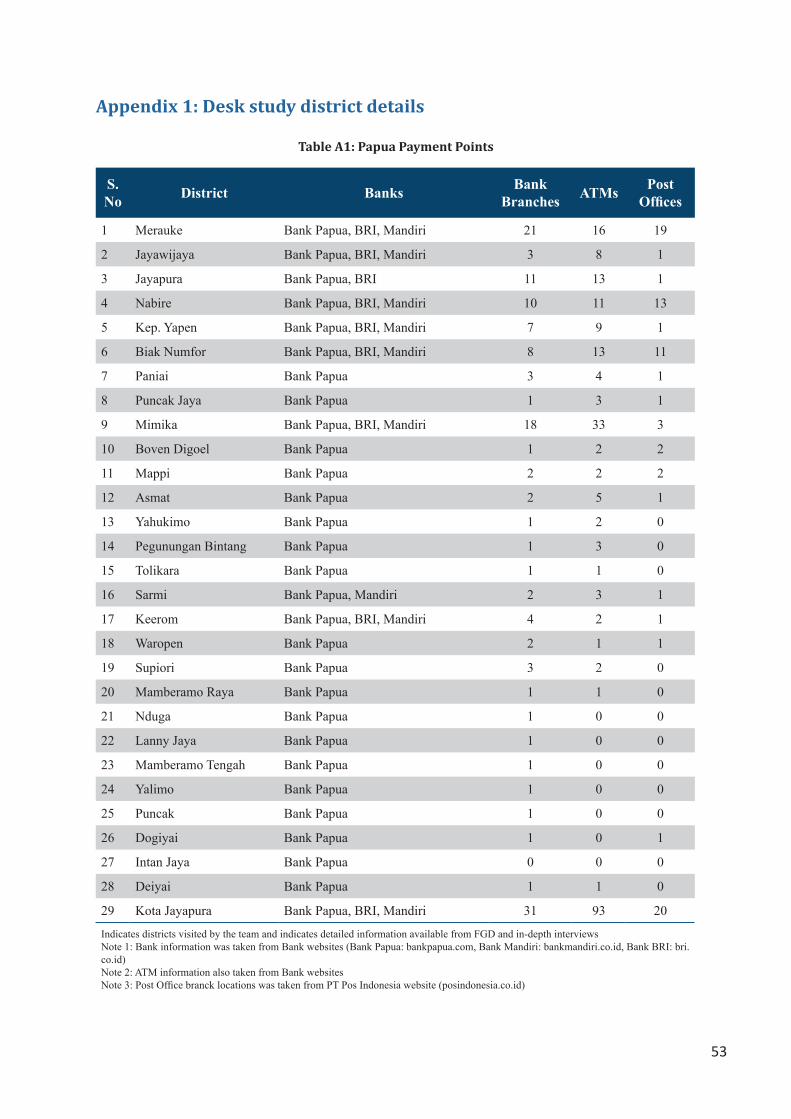

Tables 2 and 3 identify the distribution and density of current financial access points by district.

Table 2: Existing payment points in Papua

Papuadistricts Banks Bank

branches

Bank branches

per 100,000ATMs

ATM per

100,000

Post office

Post office per 100,000

Merauke Bank Papua, BRI, Mandiri 21 10.7 16 82.0 19 9.7

Jayawijaya Bank Papua, BRI, Mandiri 3 1.5 8 4.1 1 0.5

Jayapura Bank Papua, BRI 11 9.8 13 11.6 1 0.9

Nabire Bank Papua, BRI, Mandiri 10 7.7 11 8.5 13 10.0

Kep. Yapen Bank Papua, BRI, Mandiri 7 8.4 9 10.8 1 1.2

Biak Numfor Bank Papua, BRI, Mandiri 8 6.3 13 10.3 11 8.7

Paniai Bank Papua 3 2.0 4 2.6 1 0.7

Puncak Jaya Bank Papua 1 1.0 3 3.0 1 1.0

Mimika Bank Papua, BRI, Mandiri 18 9.9 33 18.1 3 1.6

Boven Digoel

Bank Papua 1 1.8 2 3.6 2 3.6

Mappi Bank Papua 2 2.4 2 2.4 2 2.4

Asmat Bank Papua 2 2.6 5 6.5 1 1.3

Yahukimo Bank Papua 1 0.6 2 1.2 0 0.0

Pegunungan Bintang

Bank Papua 1 1.5 3 4.6 0 0.0

Tolikara Bank Papua 1 0.9 1 0.9 0 0.0

Sarmi Bank Papua, Mandiri 2 6.1 3 9.1 1 3.0

Keerom Bank Papua, BRI, Mandiri 4 4.1 2 2.1 1 2.1

Waropen Bank Papua 2 8.1 1 4.1 1 4.1

Supiori Bank Papua 3 18.9 2 12.6 0 0.0

Mamberamo Raya

Bank Papua 1 5.4 1 5.4 0 0.0

Nduga Bank Papua 1 1.3 0 0.0 0 0.0

Lanny Jaya Bank Papua 1 0.7 0 0.0 0 0.0

Mamberamo Tengah

Bank Papua 1 2.5 0 0.0 0 0.0

Yalimo Bank Papua 1 2.0 0 0.0 0 0.0

Puncak Bank Papua 1 1.1 0 0.0 0 0.0

Dogiyai Bank Papua 1 1.2 0 0.0 1 1.2

Intan Jaya Bank Papua 0 0.0 0 0.0 0 0.0

Deiyai Bank Papua 1 1.6 1 1.6 0 0.0

Kota Jayapura

Bank Papua, BRI, Mandiri 31 12.1 93 36.2 20 7.8

9

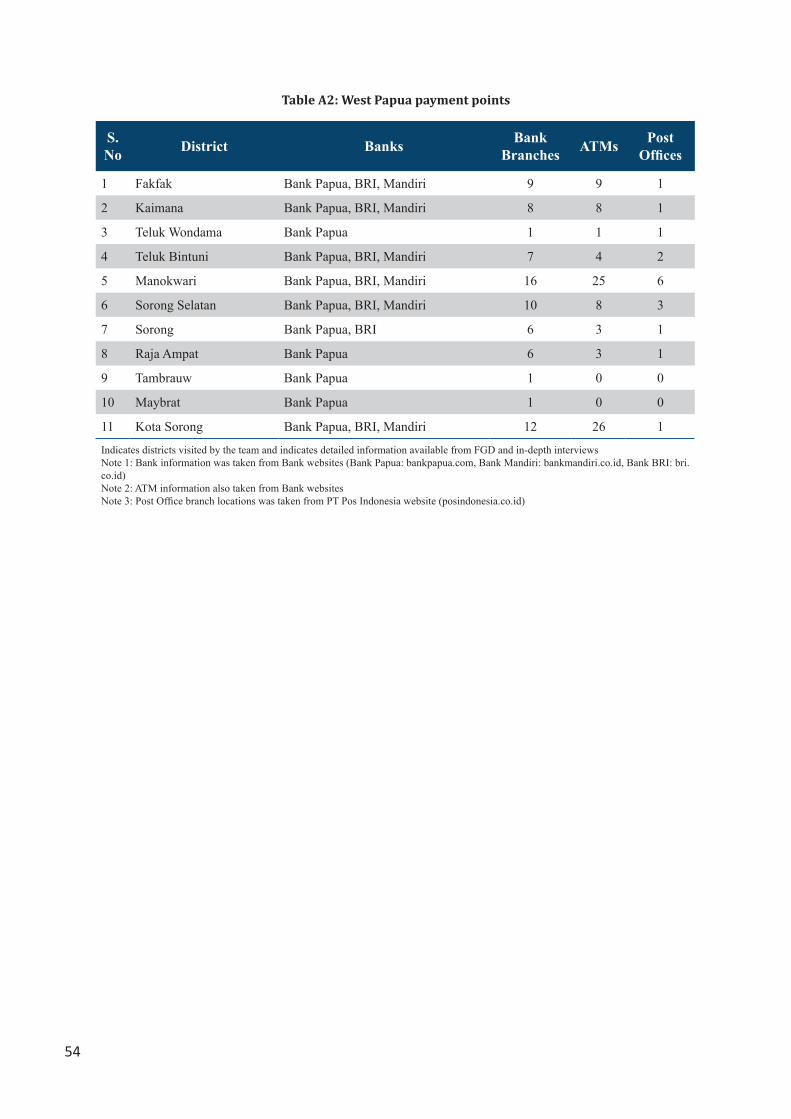

Table 3: Existing payment points in Papua Barat districts

Papuadistricts Banks Bank

branches

Bank branches

per 100,000

ATMs ATM per 100,000 Post office

Post office per 100,000

Fakfak Bank Papua, BRI, Mandiri 9 0.9 9 0.9 1 0.1

Kaimana Bank Papua, BRI, Mandiri 8 0.8 8 0.8 1 0.1

Teluk Wondama

Bank Papua 1 0.1 1 0.1 1 0.1

Teluk Bintuni

Bank Papua, BRI, Mandiri 7 0.7 4 0.4 2 0.2

Manokwari Bank Papua, BRI, Mandiri 16 1.6 25 2.5 6 0.6

Sorong Selatan

Bank Papua, BRI, Mandiri 10 0.7 8 0.8 3 0.3

Sorong Bank Papua, BRI 6 0.6 3 0.3 1 0.1

Raja Ampat Bank Papua 6 0.6 3 0.3 1 0.1

Tambrauw Bank Papua 1 0.1 0 0.0 0 0.0

Maybrat Bank Papua 1 0.1 0 0.0 0 0.0

Kota Sorong

Bank Papua, BRI, Mandiri 12 1.2 26 2.6 1 0.1

Source: Bank Indonesia (2013)Note: BRI = Bank Rakyat Indonesia

Figure 6: Bank branches per 100,000 inhabitants

Source: Bank Indonesia, World Bank, IMF (2012) Figure 6 compares bank density for Papua and Papua Barat to Indonesia overall.

9.59

3.24

5.26

0

2

4

6

8

10

12

Indonesia Papua Papua Barat

Num

ber o

f ban

k br

anch

es

10

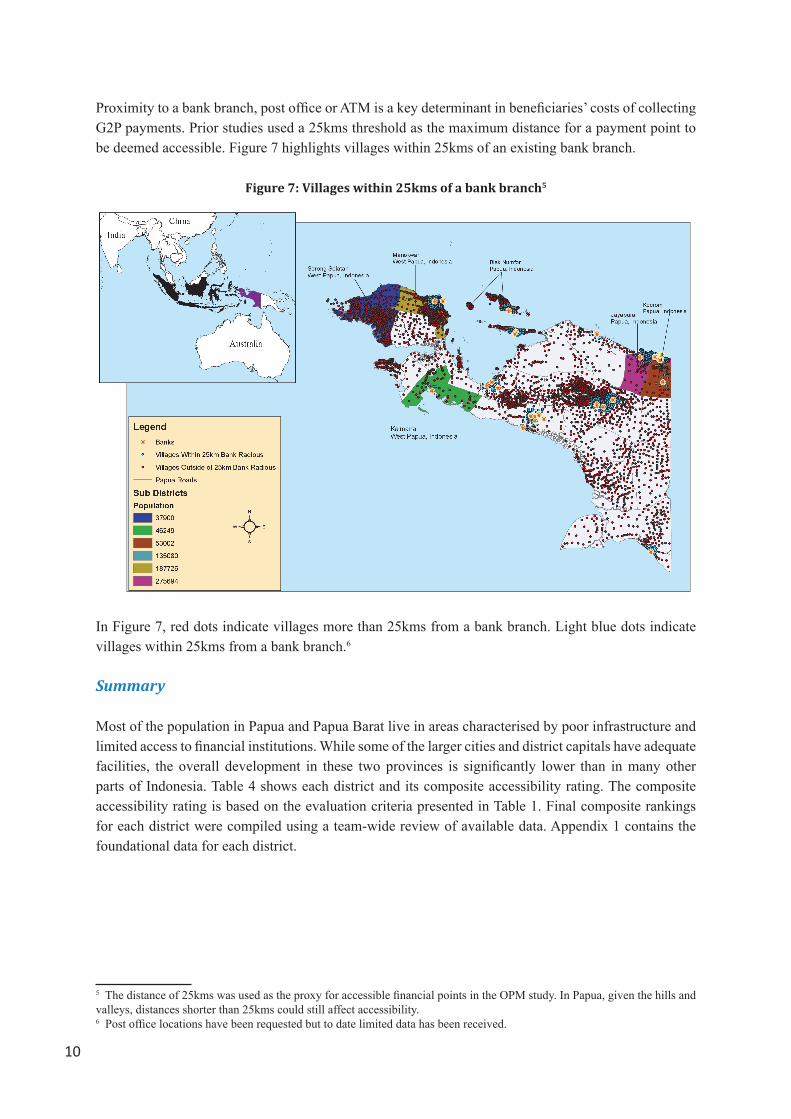

Proximity to a bank branch, post office or ATM is a key determinant in beneficiaries’ costs of collecting G2P payments. Prior studies used a 25kms threshold as the maximum distance for a payment point to be deemed accessible. Figure 7 highlights villages within 25kms of an existing bank branch.

Figure 7: Villages within 25kms of a bank branch5

In Figure 7, red dots indicate villages more than 25kms from a bank branch. Light blue dots indicate villages within 25kms from a bank branch.6

Summary

Most of the population in Papua and Papua Barat live in areas characterised by poor infrastructure and limited access to financial institutions. While some of the larger cities and district capitals have adequate facilities, the overall development in these two provinces is significantly lower than in many other parts of Indonesia. Table 4 shows each district and its composite accessibility rating. The composite accessibility rating is based on the evaluation criteria presented in Table 1. Final composite rankings for each district were compiled using a team-wide review of available data. Appendix 1 contains the foundational data for each district.

5 The distance of 25kms was used as the proxy for accessible financial points in the OPM study. In Papua, given the hills and valleys, distances shorter than 25kms could still affect accessibility.6 Post office locations have been requested but to date limited data has been received.

11

Table 4: District composite rating

Papua Papua Barat

Districts Composite Rating Districts Composite Rating

Merauke 2 Fakfak 3

Jayawijaya 1 Kaimana 1

Jayapura 3 Teluk wondawa 2

Nabire 2 Teluk Bintuni 3

Kep. Yapen 2 Manokwari 2

Biak Numfor 1 Sorong Selatan 2

Paniai 2 Sorong 2

Puncak Jaya 2 Raja Ampat 2

Mimika 1 Tambrauw 1

Bocen Digoel 2 Maybrat 1

Mappi 1 Kota Sorong 3

Asmat 1

Yahukimo 0

Pegunungan Bintang 2

Tolikara 0

Sarmi 2

Keerom 1

Waropen 3

Supiori 2

Mamberamo Raya 1

Nduga 0

Lanny Jaya 1

Mamberamo Tengah 1

Yalimo 1

Puncak 1

Dogiyai 1

Intan Jaya 1

Deiyai 1

Kota Jayapura 4

4 Indicates strong infrastructure, facilities, and accessibility0 Incicates weak infrastructure, facilities, and accessibility

12

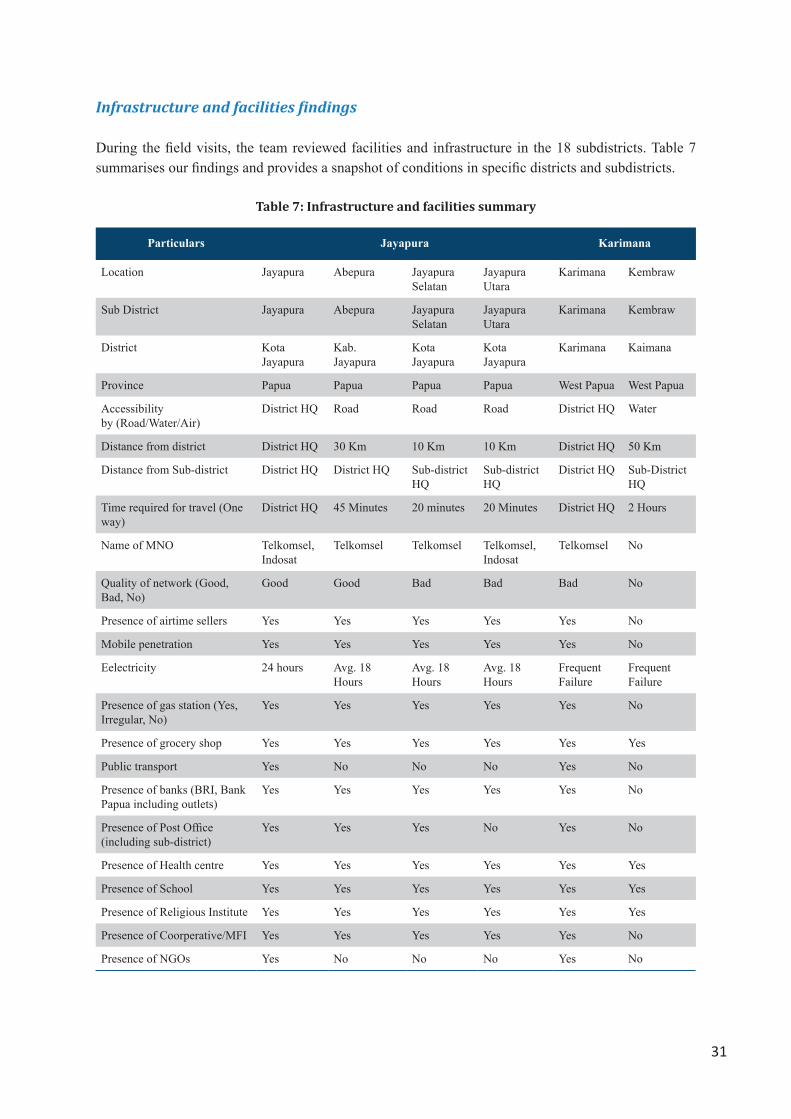

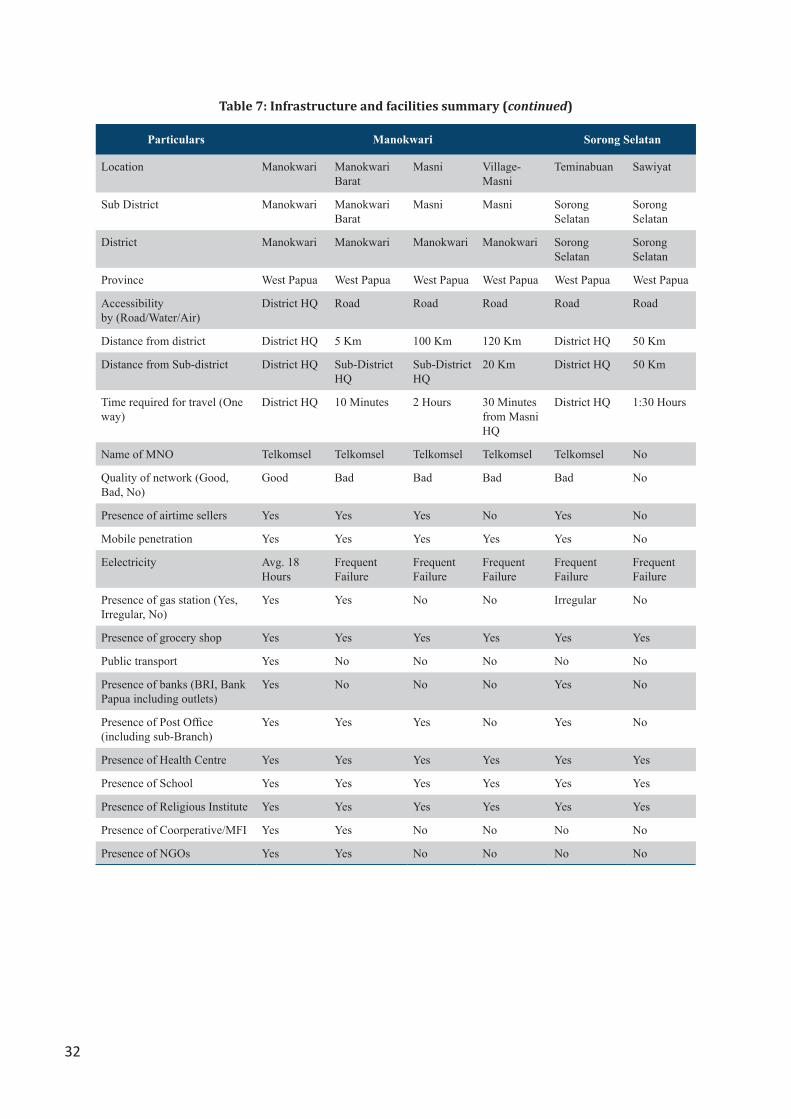

4. Field Research

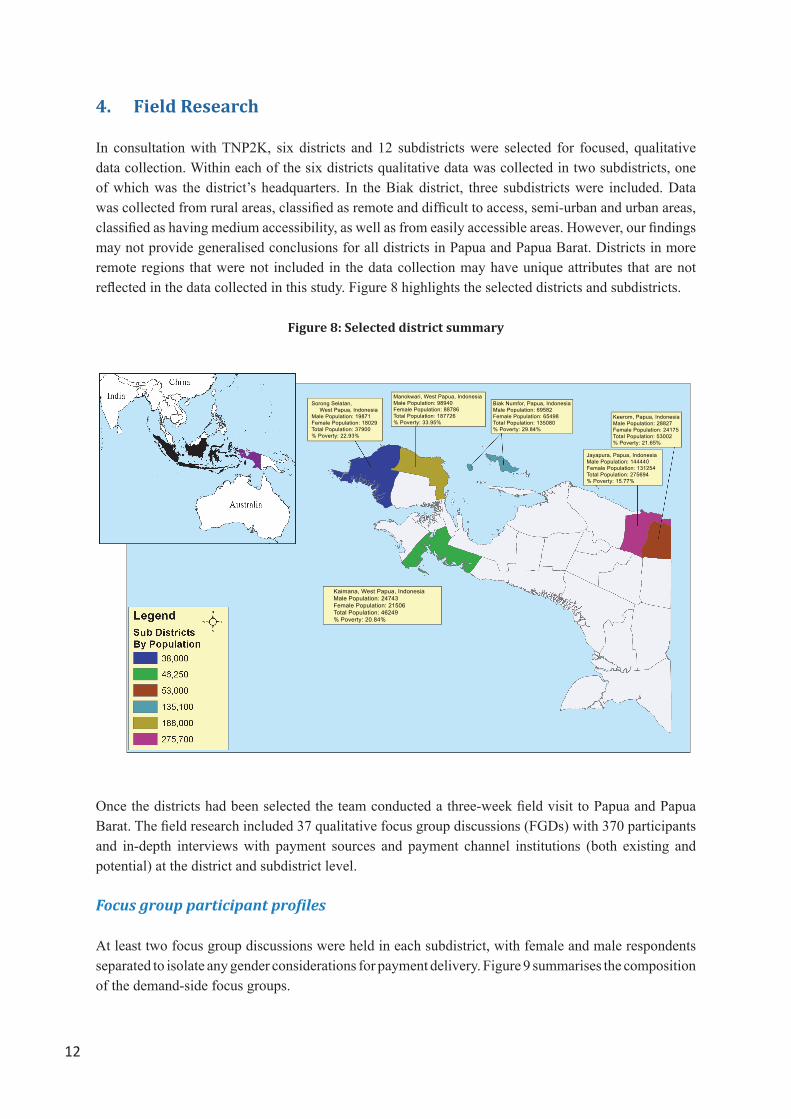

In consultation with TNP2K, six districts and 12 subdistricts were selected for focused, qualitative data collection. Within each of the six districts qualitative data was collected in two subdistricts, one of which was the district’s headquarters. In the Biak district, three subdistricts were included. Data was collected from rural areas, classified as remote and difficult to access, semi-urban and urban areas, classified as having medium accessibility, as well as from easily accessible areas. However, our findings may not provide generalised conclusions for all districts in Papua and Papua Barat. Districts in more remote regions that were not included in the data collection may have unique attributes that are not reflected in the data collected in this study. Figure 8 highlights the selected districts and subdistricts.

Figure 8: Selected district summary

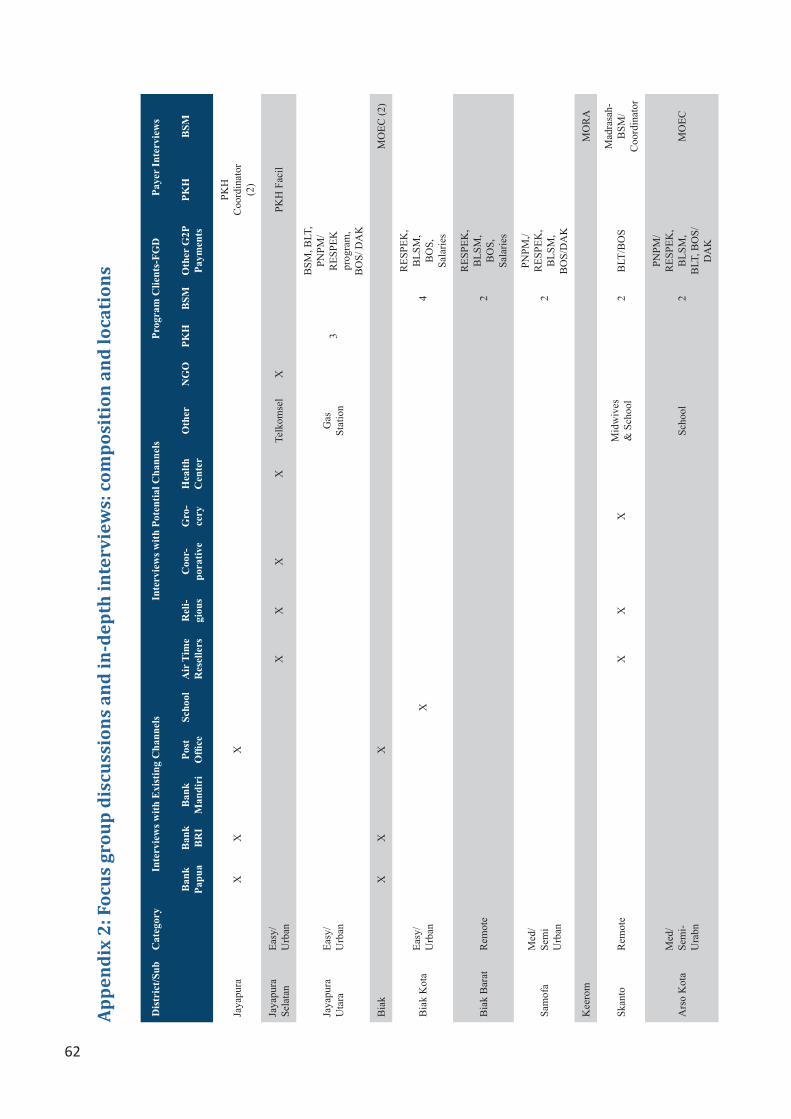

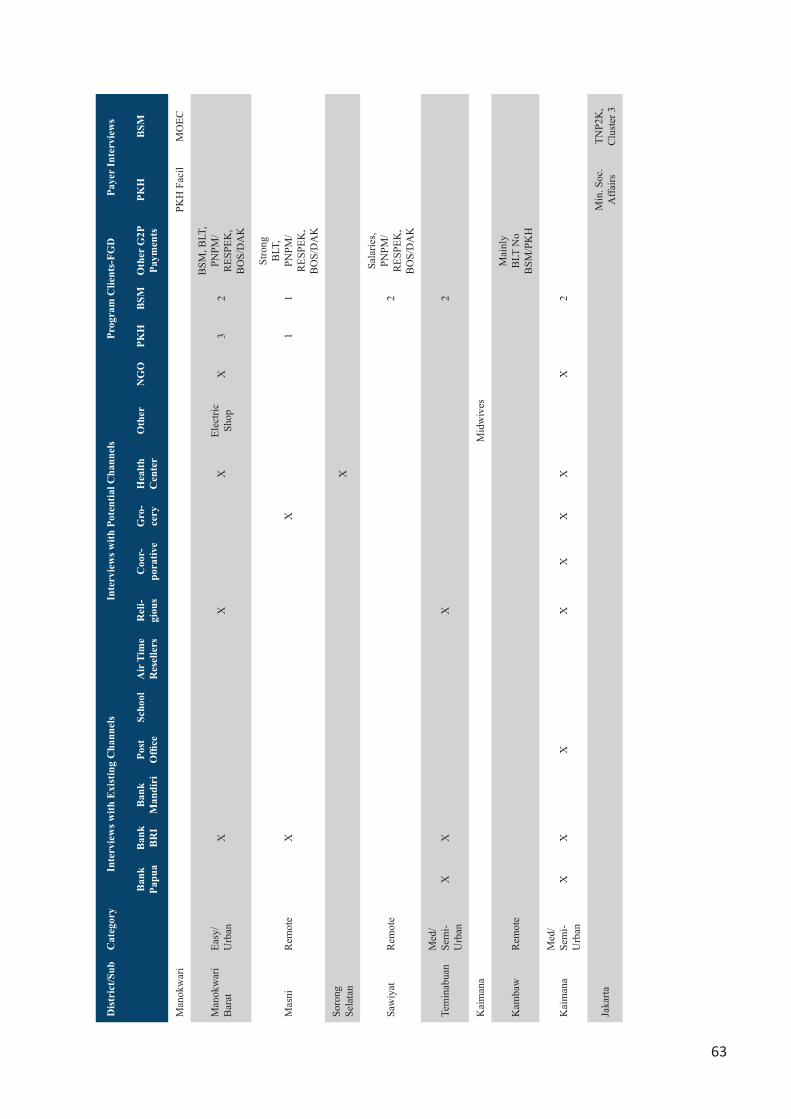

Once the districts had been selected the team conducted a three-week field visit to Papua and Papua Barat. The field research included 37 qualitative focus group discussions (FGDs) with 370 participants and in-depth interviews with payment sources and payment channel institutions (both existing and potential) at the district and subdistrict level.

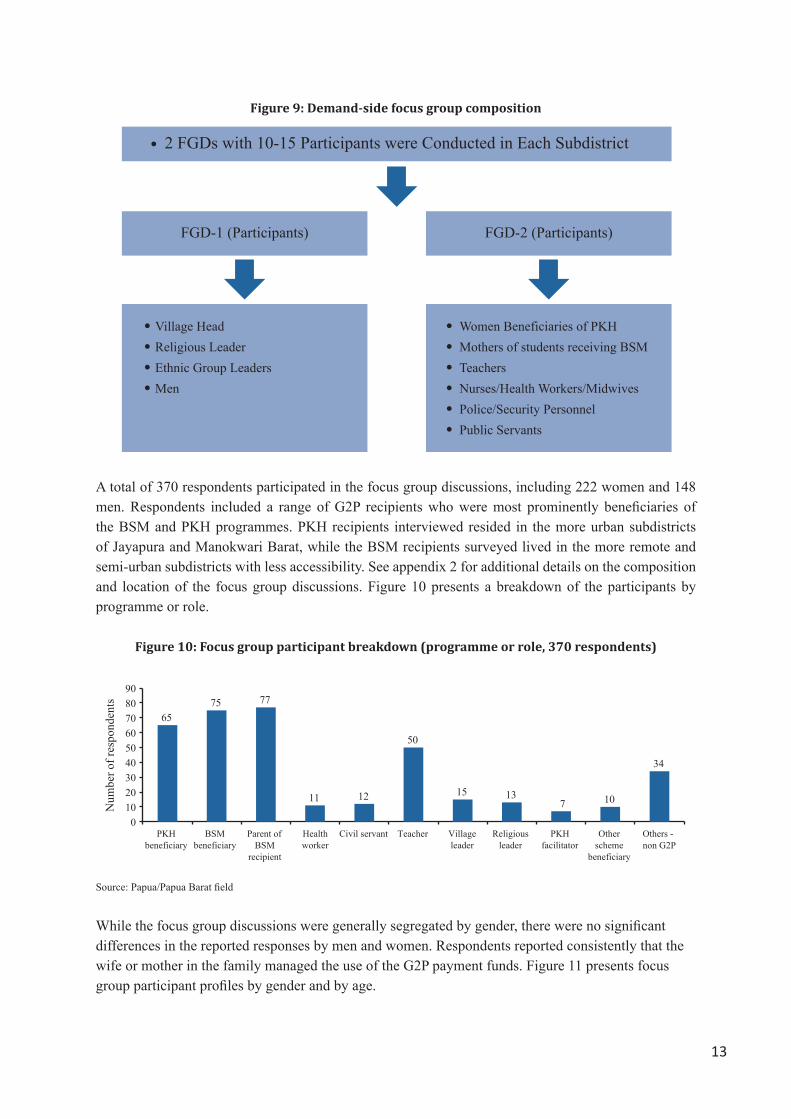

Focus group participant profiles

At least two focus group discussions were held in each subdistrict, with female and male respondents separated to isolate any gender considerations for payment delivery. Figure 9 summarises the composition of the demand-side focus groups.

Keerom, Papua, IndonesiaMale Population: 28827Female Population: 24175Total Population: 53002% Poverty: 21.65%

Jayapura, Papua, IndonesiaMale Population: 144440Female Population: 131254Total Population: 275694% Poverty: 15.77%

Biak Numfor, Papua, IndonesiaMale Population: 69582Female Population: 65498Total Population: 135080% Poverty: 29.84%

Manokwari, West Papua, IndonesiaMale Population: 98940Female Population: 88786Total Population: 187726% Poverty: 33.95%

Sorong Selatan, West Papua, IndonesiaMale Population: 19871Female Population: 18029Total Population: 37900% Poverty: 22.93%

Kaimana, West Papua, IndonesiaMale Population: 24743Female Population: 21506Total Population: 46249% Poverty: 20.84%

13

Figure 9: Demand-side focus group composition

A total of 370 respondents participated in the focus group discussions, including 222 women and 148 men. Respondents included a range of G2P recipients who were most prominently beneficiaries of the BSM and PKH programmes. PKH recipients interviewed resided in the more urban subdistricts of Jayapura and Manokwari Barat, while the BSM recipients surveyed lived in the more remote and semi-urban subdistricts with less accessibility. See appendix 2 for additional details on the composition and location of the focus group discussions. Figure 10 presents a breakdown of the participants by programme or role.

Figure 10: Focus group participant breakdown (programme or role, 370 respondents)

Source: Papua/Papua Barat field

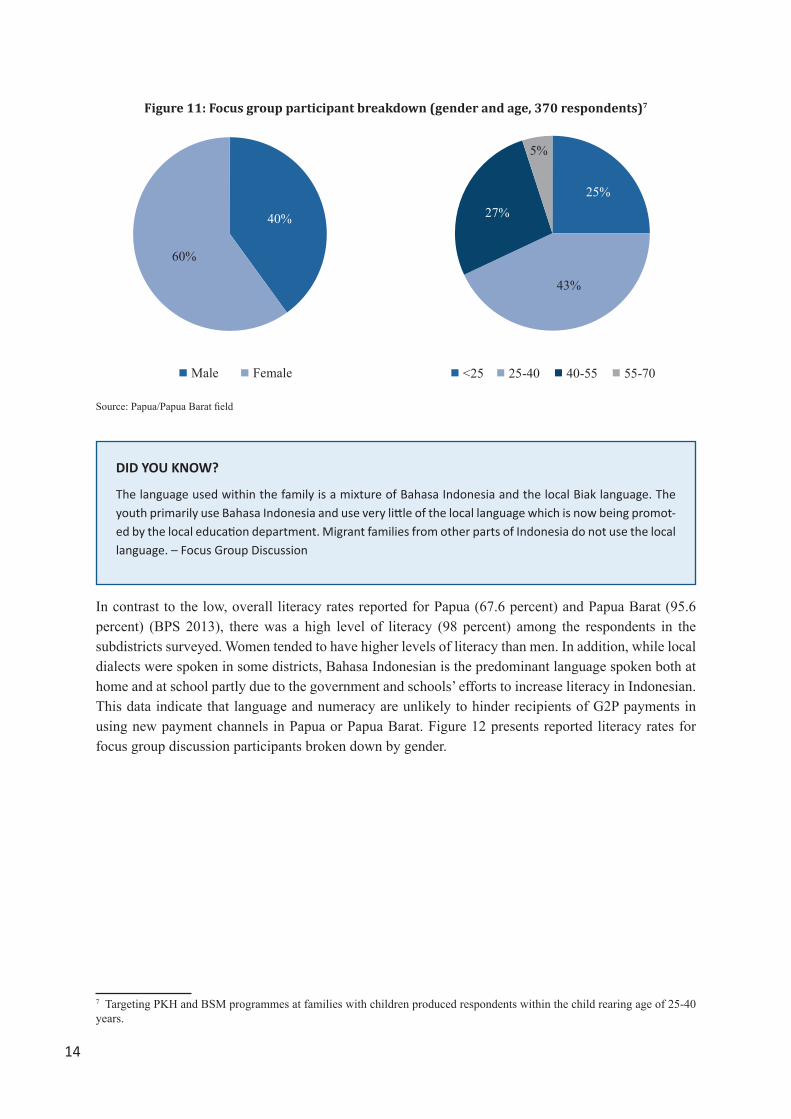

While the focus group discussions were generally segregated by gender, there were no significant differences in the reported responses by men and women. Respondents reported consistently that the wife or mother in the family managed the use of the G2P payment funds. Figure 11 presents focus group participant profiles by gender and by age.

2 FGDs with 10-15 Participants were Conducted in Each Subdistrict

FGD-1 (Participants) FGD-2 (Participants)

Women Beneficiaries of PKHMothers of students receiving BSMTeachersNurses/Health Workers/MidwivesPolice/Security PersonnelPublic Servants

Village HeadReligious LeaderEthnic Group LeadersMen

Num

ber o

f res

pond

ents

0102030405060708090

PKHbeneficiary

BSMbeneficiary

Parent ofBSM

recipient

Healthworker

Civil servant Teacher Villageleader

Religiousleader

PKHfacilitator

Otherscheme

beneficiary

Others - non G2P

6575 77

11 12

50

15 137 10

34

14

Figure 11: Focus group participant breakdown (gender and age, 370 respondents)7

Source: Papua/Papua Barat field

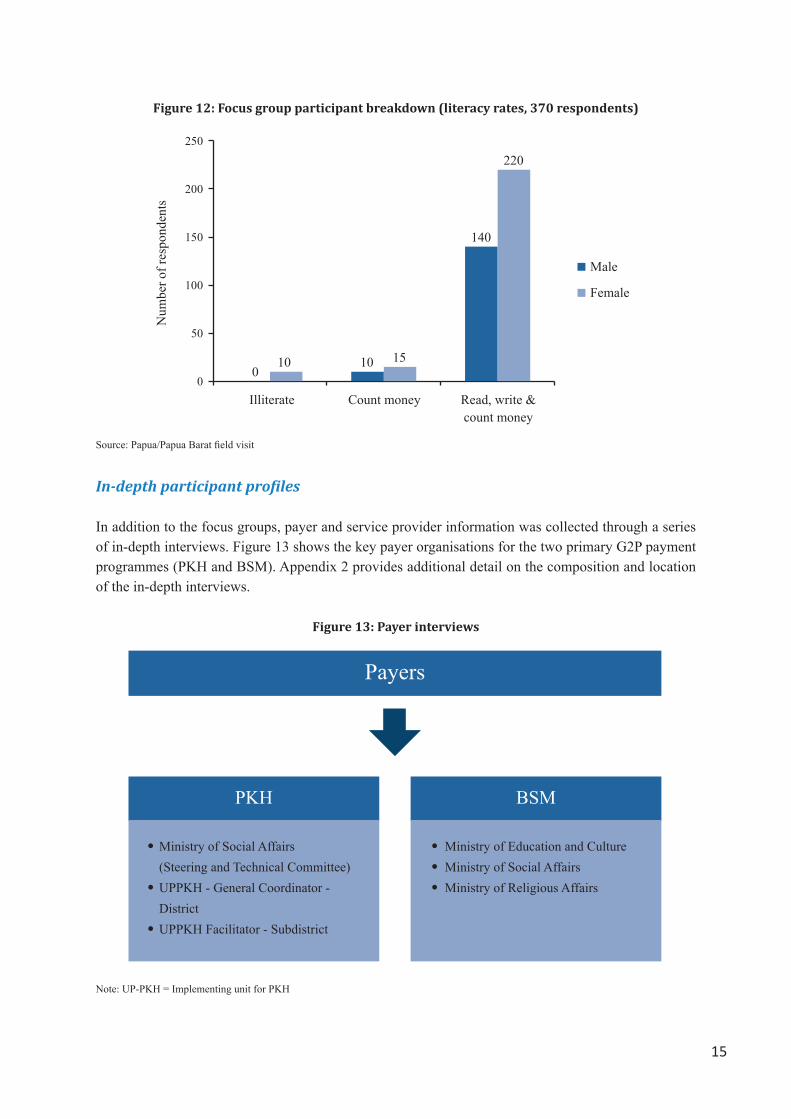

In contrast to the low, overall literacy rates reported for Papua (67.6 percent) and Papua Barat (95.6 percent) (BPS 2013), there was a high level of literacy (98 percent) among the respondents in the subdistricts surveyed. Women tended to have higher levels of literacy than men. In addition, while local dialects were spoken in some districts, Bahasa Indonesian is the predominant language spoken both at home and at school partly due to the government and schools’ efforts to increase literacy in Indonesian. This data indicate that language and numeracy are unlikely to hinder recipients of G2P payments in using new payment channels in Papua or Papua Barat. Figure 12 presents reported literacy rates for focus group discussion participants broken down by gender.

7 Targeting PKH and BSM programmes at families with children produced respondents within the child rearing age of 25-40 years.

40%

60%

Male Female

25%

43%

27%

5%

<25 25-40 40-55 55-70

DID YOU KNOW?

The language used within the family is a mixture of Bahasa Indonesia and the local Biak language. The youth primarily use Bahasa Indonesia and use very little of the local language which is now being promot-ed by the local education department. Migrant families from other parts of Indonesia do not use the local language. – Focus Group Discussion

15

Figure 12: Focus group participant breakdown (literacy rates, 370 respondents)

Source: Papua/Papua Barat field visit

In-depth participant profiles

In addition to the focus groups, payer and service provider information was collected through a series of in-depth interviews. Figure 13 shows the key payer organisations for the two primary G2P payment programmes (PKH and BSM). Appendix 2 provides additional detail on the composition and location of the in-depth interviews.

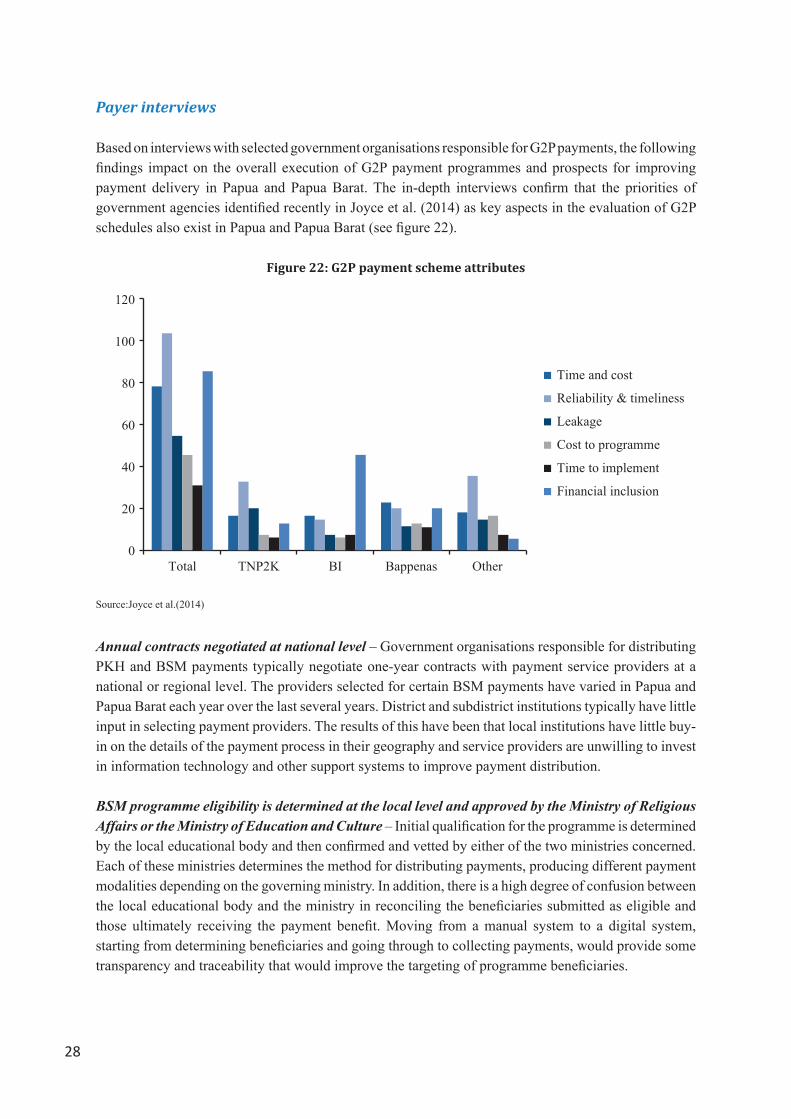

Figure 13: Payer interviews

Note: UP-PKH = Implementing unit for PKH

010

140

10 15

220

0

50

100

150

200

250

Illiterate Count money Read, write &count money

Num

ber o

f res

pond

ents

Male

Female

Payers

PKH BSM

Ministry of Education and CultureMinistry of Social AffairsMinistry of Religious Affairs

Ministry of Social Affairs(Steering and Technical Committee)UPPKH - General Coordinator - DistrictUPPKH Facilitator - Subdistrict

16

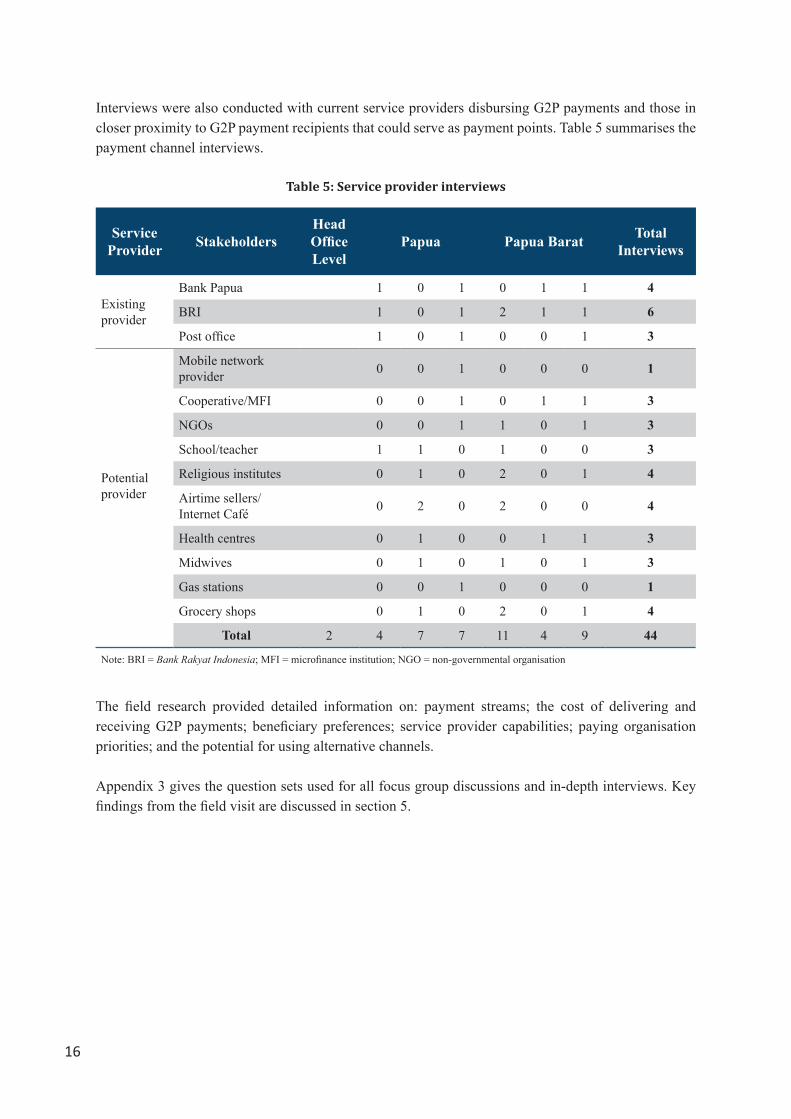

Interviews were also conducted with current service providers disbursing G2P payments and those in closer proximity to G2P payment recipients that could serve as payment points. Table 5 summarises the payment channel interviews.

Table 5: Service provider interviews

Service Provider Stakeholders

Head Office Level

Papua Papua Barat Total Interviews

Existing provider

Bank Papua 1 0 1 0 1 1 4

BRI 1 0 1 2 1 1 6

Post office 1 0 1 0 0 1 3

Potential provider

Mobile network provider

0 0 1 0 0 0 1

Cooperative/MFI 0 0 1 0 1 1 3

NGOs 0 0 1 1 0 1 3

School/teacher 1 1 0 1 0 0 3

Religious institutes 0 1 0 2 0 1 4

Airtime sellers/ Internet Café 0 2 0 2 0 0 4

Health centres 0 1 0 0 1 1 3

Midwives 0 1 0 1 0 1 3

Gas stations 0 0 1 0 0 0 1

Grocery shops 0 1 0 2 0 1 4

Total 2 4 7 7 11 4 9 44

Note: BRI = Bank Rakyat Indonesia; MFI = microfinance institution; NGO = non-governmental organisation

The field research provided detailed information on: payment streams; the cost of delivering and receiving G2P payments; beneficiary preferences; service provider capabilities; paying organisation priorities; and the potential for using alternative channels.

Appendix 3 gives the question sets used for all focus group discussions and in-depth interviews. Key findings from the field visit are discussed in section 5.

17

G2P payment streams in Papua and Papua Barat

PKH (Conditional Cash Transfer Programme for Families)The research focused primarily on G2P payments. It looked particularly at payments disbursed through PKH that gives financial assistance to women and poor families, and the BSM programme, that assists poor students with school-related costs. The research also identified other G2P schemes that generate payments flowing into the subdistricts, including salary payments. Payment streams that could be active in the subdistricts include:

• BSM (Cash Transfers for Poor Students) – Ministry of Education and Culture (MoEC) ◦ BSM – elementary school ◦ BSM – junior high school ◦ BSM – senior high school

• BSM – Ministry of Religious Affairs (MoRA) ◦ BSM – elementary school ◦ BSM – junior high school ◦ BSM – senior high school

• PKH – fixed conditional cash transfers ◦ Child up to 5 years old ◦ Pregnant woman or lactating mother ◦ Children in elementary school ◦ Children in junior high school

• PKH facilitators • Teachers’ salaries • Health workers’ salaries• Civil servants’ salaries• Other G2P scheme payments8

Some of the G2P payments, such as PKH, originate and are administered by the national government while other payments may originate more locally or are paid to the local government directly. In remote and rural areas, payments may be collected by the community leaders or school principals (with letters of authorisation) and then disbursed in kind or through the schools’ allocation of funds, rather than being collected individually by the beneficiaries. A recent change to the BSM programme will require disbursement of programme payments directly to the student recipients, a policy that will necessitate a change in some current disbursement and collection practices.

The funds for PKH are currently disbursed through the post office and the programme provides a more structured support system for collecting payments than the BSM programme. It supports programme participants through facilitators whose role was highly rated by the participants in our survey. The facilitators help participants collect payments, notifying recipients when payments are available and assisting them at the disbursement points. In some cases, the facilitators travel with the cash to more remote villages and manage the disbursement directly. Sometimes they are required to accompany post

8 Other payment streams reported by participants in the survey included the following programmes: Economic Development Strategy for Villages (Rencana Strategi Pembangunan Ekonomi Kampung –RESPEK), Temporary Unconditional Cash Transfers (Bantuan Langsung Sementara Masyarakat – BLSM), School Operational Grants (Bantuan Operasional Sekolah – BOS) and National Programme for Community Development (Program Nasional Pemberdayaan Masyarakat – PNPM)

18

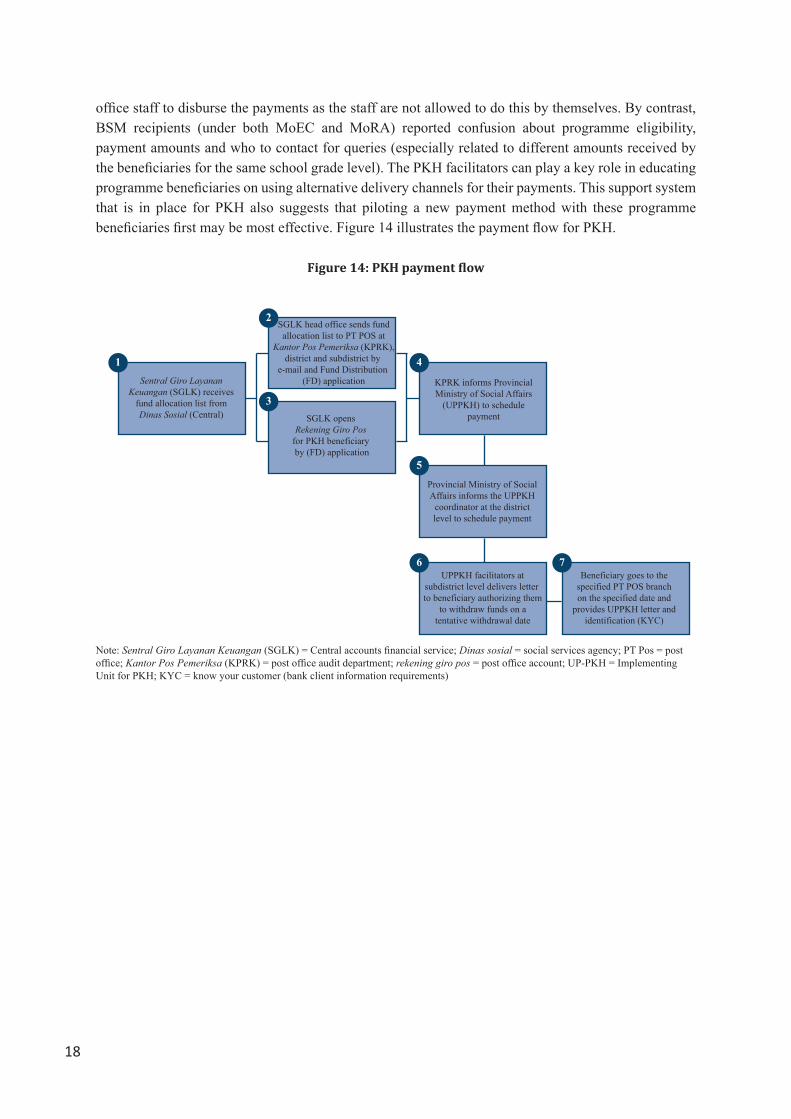

office staff to disburse the payments as the staff are not allowed to do this by themselves. By contrast, BSM recipients (under both MoEC and MoRA) reported confusion about programme eligibility, payment amounts and who to contact for queries (especially related to different amounts received by the beneficiaries for the same school grade level). The PKH facilitators can play a key role in educating programme beneficiaries on using alternative delivery channels for their payments. This support system that is in place for PKH also suggests that piloting a new payment method with these programme beneficiaries first may be most effective. Figure 14 illustrates the payment flow for PKH.

Figure 14: PKH payment flow

Note: Sentral Giro Layanan Keuangan (SGLK) = Central accounts financial service; Dinas sosial = social services agency; PT Pos = post office; Kantor Pos Pemeriksa (KPRK) = post office audit department; rekening giro pos = post office account; UP-PKH = Implementing Unit for PKH; KYC = know your customer (bank client information requirements)

1

2

3

4

5

6 7

Sentral Giro LayananKeuangan (SGLK) receives

fund allocation list fromDinas Sosial (Central)

SGLK head office sends fundallocation list to PT POS at

Kantor Pos Pemeriksa (KPRK),district and subdistrict by

e-mail and Fund Distribution (FD) application

SGLK opens Rekening Giro Pos

for PKH beneficiary by (FD) application

KPRK informs ProvincialMinistry of Social Affairs

(UPPKH) to schedulepayment

Provincial Ministry of SocialAffairs informs the UPPKH

coordinator at the districtlevel to schedule payment

UPPKH facilitators atsubdistrict level delivers letter to beneficiary authorizing them

to withdraw funds on atentative withdrawal date

Beneficiary goes to thespecified PT POS branchon the specified date and

provides UPPKH letter andidentification (KYC)

19

Figure 15 illustrates the BSM payment flow using Bank Papua:

Figure 15: BSM payment flow

Note: HO = head office; Dinas Pendidikan Kabupaten (DPK) = district education office

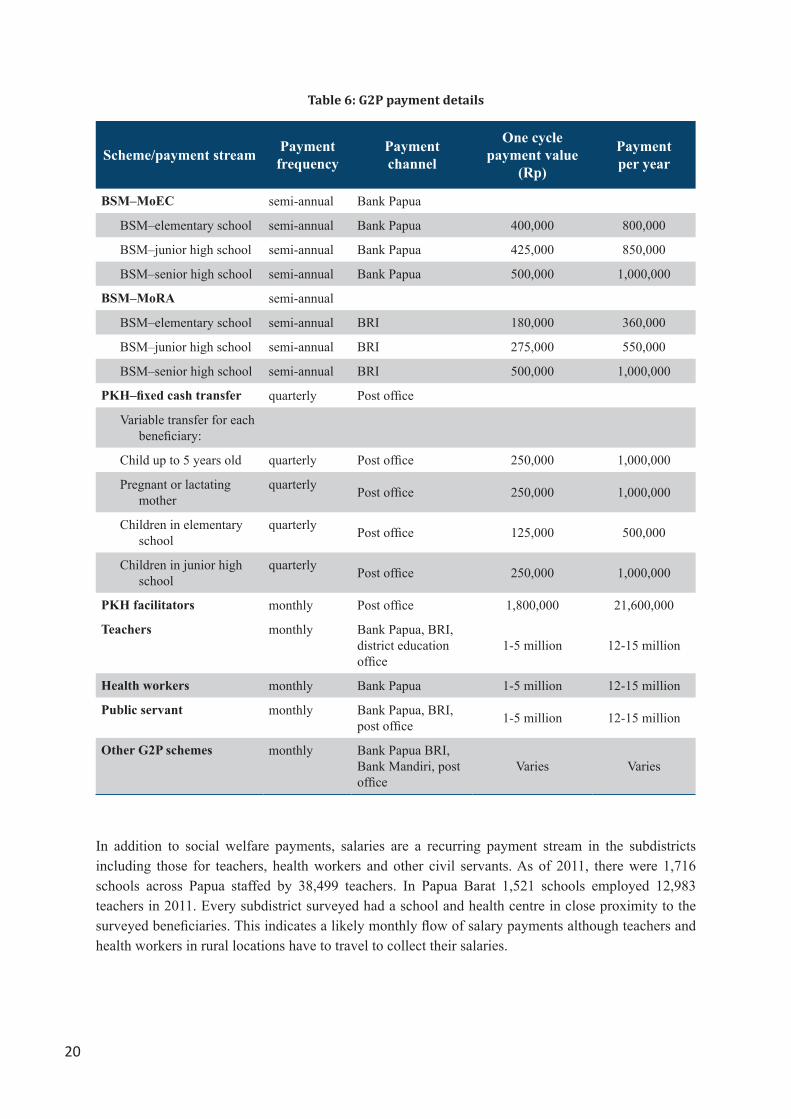

In the subdistricts surveyed payment streams funded by government revenues included payments for the programmes shown in Table 6. The payment amount and frequency varies by programme as does the payment point. The most frequent disbursements are monthly salary payments (which are also highest in value), followed by quarterly PKH payments and semi-annual BSM payments.9

9 Some of the BSM programme participants surveyed indicated they only received payments annually or received no payment when they believed they were eligible.

1 2

3

4

5

5A

6

Bank HO receives beneficiarylist and funds from MOEC

(central-level)

HO opens account for the beneficiary and provides

beneficiary list to thebranches (district and

subdistrict)

Bank branch provides DinasPendidikan Kabupaten (DPK)

beneficiary list - DPK theninforms the school

School informs thebeneficiary to receivepayment from bank

(Announced during morningschool session or call

to beneficiary)

Beneficiary visits bank branch, presents

identification and otherdocumentation and

collects funds*

If a school is in a remotearea, school organizes a

collective visit to the bankbranch or school staff visitbank branch and withdrawfunds on student’s behalf

Bank branch verifies the dataand provides beneficiary

with funds

*Documents Required: - For senior high school: copy of report, copy of family register, statement letter from school - For junior high school: copy of family register, copy of parent’s ID, copy of birth certificate, copy of report and certificate of graduation, letter of recommendation issued by district office of education

20

Table 6: G2P payment details

Scheme/payment stream Payment frequency

Payment channel

One cycle payment value

(Rp)

Paymentper year

BSM–MoEC semi-annual Bank Papua

BSM–elementary school semi-annual Bank Papua 400,000 800,000

BSM–junior high school semi-annual Bank Papua 425,000 850,000

BSM–senior high school semi-annual Bank Papua 500,000 1,000,000

BSM–MoRA semi-annual

BSM–elementary school semi-annual BRI 180,000 360,000

BSM–junior high school semi-annual BRI 275,000 550,000

BSM–senior high school semi-annual BRI 500,000 1,000,000

PKH–fixed cash transfer quarterly Post office

Variable transfer for each beneficiary:

Child up to 5 years old quarterly Post office 250,000 1,000,000

Pregnant or lactating mother

quarterly Post office 250,000 1,000,000

Children in elementary school

quarterly Post office 125,000 500,000

Children in junior high school

quarterly Post office 250,000 1,000,000

PKH facilitators monthly Post office 1,800,000 21,600,000

Teachers monthly Bank Papua, BRI, district education office

1-5 million 12-15 million

Health workers monthly Bank Papua 1-5 million 12-15 million

Public servant monthly Bank Papua, BRI, post office 1-5 million 12-15 million

Other G2P schemes monthly Bank Papua BRI, Bank Mandiri, post office

Varies Varies

In addition to social welfare payments, salaries are a recurring payment stream in the subdistricts including those for teachers, health workers and other civil servants. As of 2011, there were 1,716 schools across Papua staffed by 38,499 teachers. In Papua Barat 1,521 schools employed 12,983 teachers in 2011. Every subdistrict surveyed had a school and health centre in close proximity to the surveyed beneficiaries. This indicates a likely monthly flow of salary payments although teachers and health workers in rural locations have to travel to collect their salaries.

21

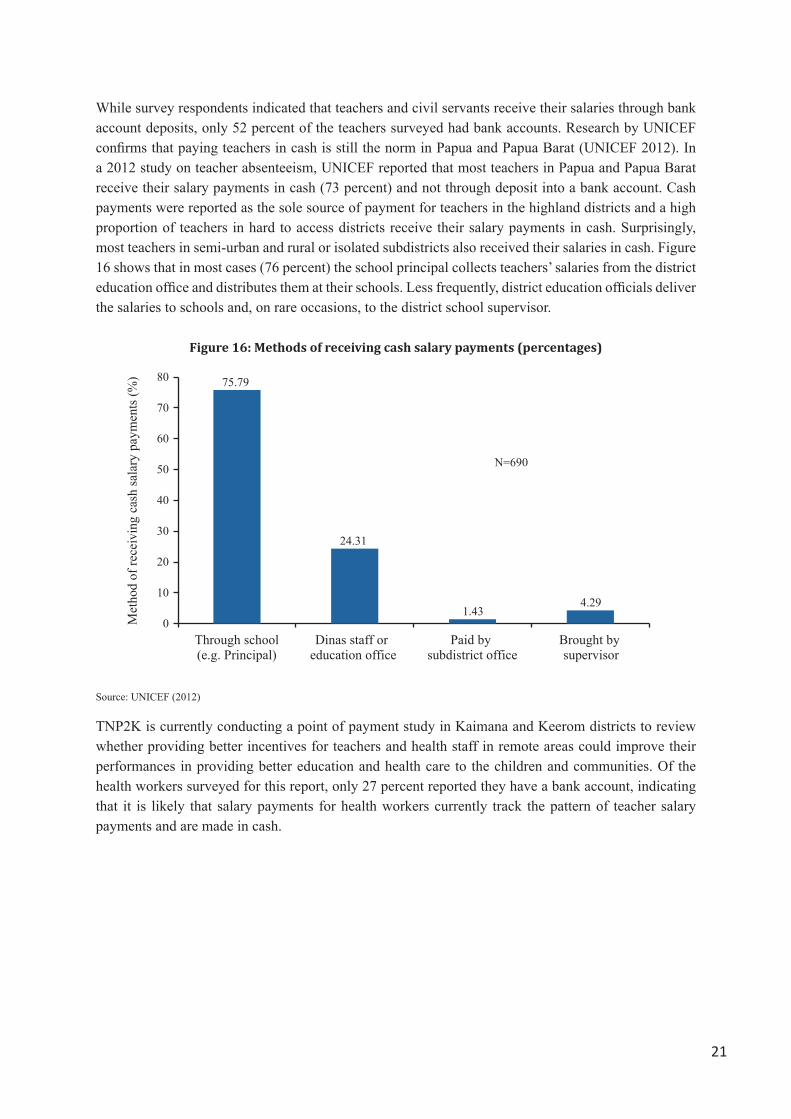

While survey respondents indicated that teachers and civil servants receive their salaries through bank account deposits, only 52 percent of the teachers surveyed had bank accounts. Research by UNICEF confirms that paying teachers in cash is still the norm in Papua and Papua Barat (UNICEF 2012). In a 2012 study on teacher absenteeism, UNICEF reported that most teachers in Papua and Papua Barat receive their salary payments in cash (73 percent) and not through deposit into a bank account. Cash payments were reported as the sole source of payment for teachers in the highland districts and a high proportion of teachers in hard to access districts receive their salary payments in cash. Surprisingly, most teachers in semi-urban and rural or isolated subdistricts also received their salaries in cash. Figure 16 shows that in most cases (76 percent) the school principal collects teachers’ salaries from the district education office and distributes them at their schools. Less frequently, district education officials deliver the salaries to schools and, on rare occasions, to the district school supervisor.

Figure 16: Methods of receiving cash salary payments (percentages)

Source: UNICEF (2012)

TNP2K is currently conducting a point of payment study in Kaimana and Keerom districts to review whether providing better incentives for teachers and health staff in remote areas could improve their performances in providing better education and health care to the children and communities. Of the health workers surveyed for this report, only 27 percent reported they have a bank account, indicating that it is likely that salary payments for health workers currently track the pattern of teacher salary payments and are made in cash.

75.79

24.31

1.434.29

0

10

20

30

40

50

60

70

80

Through school(e.g. Principal)

Dinas staff or education office

Paid by subdistrict office

Brought by supervisor

Met

hod

of re

ceiv

ing

cash

sala

ry p

aym

ents

(%)

N=690

22

5. Findings

The field visit findings are presented in this section and are organised into the following subsections:

• Beneficiary focus groups• Payer interviews• Service provider interviews• Potential payment channels

Beneficiary focus groups

As part of the focus group discussions, three foundational areas were explored:

• respondents’ experience in collecting social welfare payments from current payment points; • respondents’ experience with and access to financial institutions (banks); and • respondents’ experience with and access to mobile phone technology.

Information on respondents’ experience with banks provides insights into the usefulness of bank branches as payment points and the overall utility of linking G2P payments through banks to broader financial inclusion objectives. Mobile telephone usage provides information on the practicality of using mobile network based G2P payment delivery channels, including network and end user access issues.

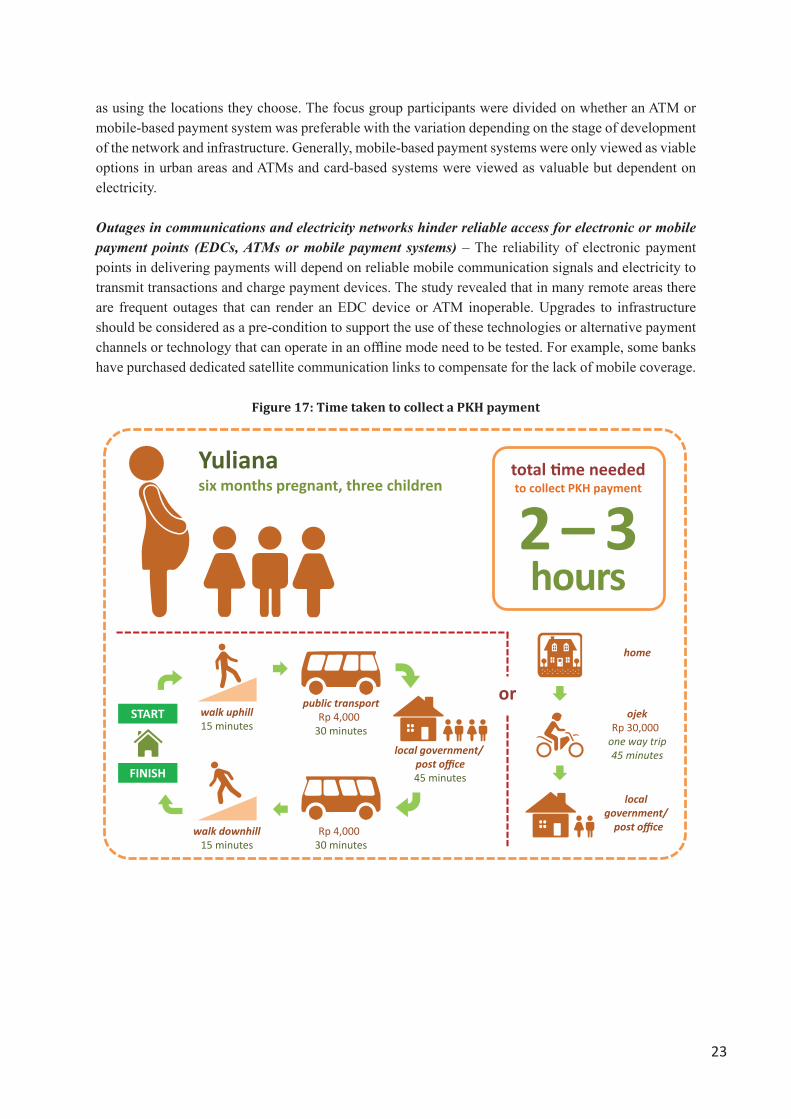

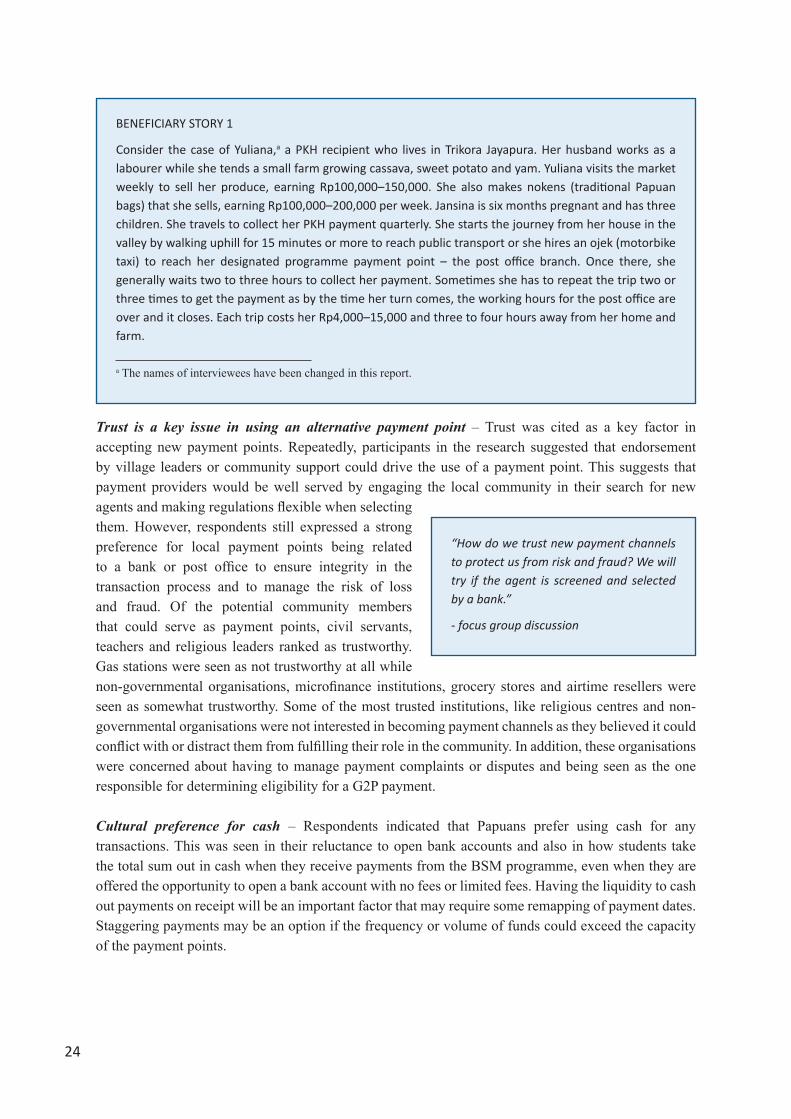

Recipient experiencesThe beneficiaries of G2P payments interviewed in the 18 subdistricts revealed that payment disbursement methods need to be improved to reduce the distance between the recipients and the payment points. The current situation discourages collection and reduces the value of the payments. The study found that beneficiaries were open to using alternative channels with trusted agents and the appropriate public awareness and training on the use of the new payment methods. The findings for the BSM and PKH beneficiaries differed slightly as the focus group discussions for the latter were held in more urban areas while the focus group discussions for the former were largely in remote or medium-access locations.

Beneficiaries of both the PKH and BSM programmes cited travel costs and other expenses associated with visiting payment points as a primary hardship with collecting funds – G2P payment recipients in Papua and Papua Barat face higher costs in collecting their social protection payments than those in more populous regions of Indonesia (OPM 2013). The travel costs and time required for payment collection were viewed negatively by the focus group discussion participants. There was a strong preference for improving the proximity of payment points to ease the burden of collection. For some more rural groups this included using community-level disbursement while others were ready to adopt new technologies and channels to reduce the travel distance and costs.

G2P beneficiaries are familiar with ATM cards and mobile technology – Payment recipients interviewed acknowledged an awareness and familiarity with debit cards and mobile technology. Recipients also recognised the convenience of accessing an ATM at a bank or post office outside office hours as well

23

as using the locations they choose. The focus group participants were divided on whether an ATM or mobile-based payment system was preferable with the variation depending on the stage of development of the network and infrastructure. Generally, mobile-based payment systems were only viewed as viable options in urban areas and ATMs and card-based systems were viewed as valuable but dependent on electricity.

Outages in communications and electricity networks hinder reliable access for electronic or mobile payment points (EDCs, ATMs or mobile payment systems) – The reliability of electronic payment points in delivering payments will depend on reliable mobile communication signals and electricity to transmit transactions and charge payment devices. The study revealed that in many remote areas there are frequent outages that can render an EDC device or ATM inoperable. Upgrades to infrastructure should be considered as a pre-condition to support the use of these technologies or alternative payment channels or technology that can operate in an offline mode need to be tested. For example, some banks have purchased dedicated satellite communication links to compensate for the lack of mobile coverage.

Figure 17: Time taken to collect a PKH payment

total time neededto collect PKH payment

2 – 3hours

Yulianasix months pregnant, three children

ojekRp 30,000

one way trip45 minutes

public transportRp 4,000

30 minutes

walk uphill15 minutes

or

local government/ post office45 minutes

Rp 4,00030 minutes

walk downhill15 minutes

home

local government/

post office

START

FINISH

24