Embed Size (px)

DESCRIPTION

TJAGC Student Loan Repayment Program (JA-SLRP). Maj Christine Lamont Maj Darrel Johnson AF/JAX 26 May 2010. Air Force JAG Corps. W i s d o m - V a l o r - J u s t i c e. 1. Overview. JA-SLRP Overview Who is eligible? What loans are eligible? When do you apply? Collateral issues - PowerPoint PPT Presentation

Citation preview

TJAGC Student LoanRepayment Program

(JA-SLRP)

Maj Christine LamontMaj Darrel Johnson

AF/JAX 26 May 2010

W i s d o m - V a l o r - J u s t i c e

Air Force JAG Corps

1

W i s d o m - V a l o r - J u s t i c e 2

Overview

JA-SLRP Overview

Who is eligible?

What loans are eligible?

When do you apply?

Collateral issues

Tax issues

How to calculate your JA-SLRP payment

Should I apply for JA-SLRP?

W i s d o m - V a l o r - J u s t i c e 3

JA-SLRP Overview

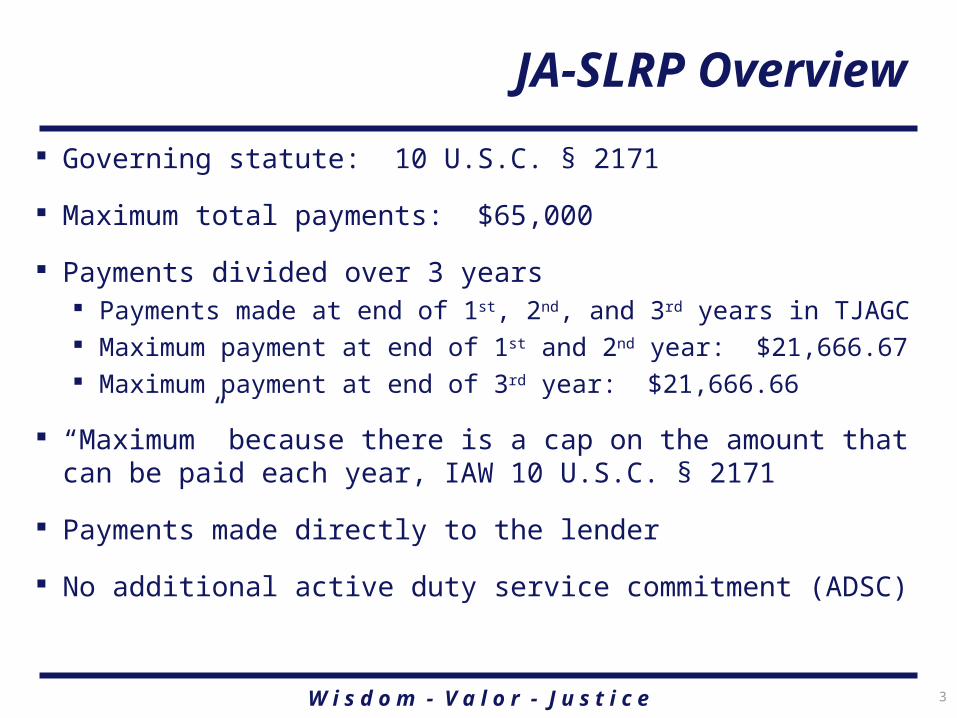

Governing statute: 10 U.S.C. § 2171

Maximum total payments: $65,000

Payments divided over 3 years Payments made at end of 1st, 2nd, and 3rd years in TJAGC Maximum payment at end of 1st and 2nd year: $21,666.67 Maximum payment at end of 3rd year: $21,666.66

“Maximum” because there is a cap on the amount that can be paid each year, IAW 10 U.S.C. § 2171

Payments made directly to the lender

No additional active duty service commitment (ADSC)

W i s d o m - V a l o r - J u s t i c e 4

Who Is Eligible?

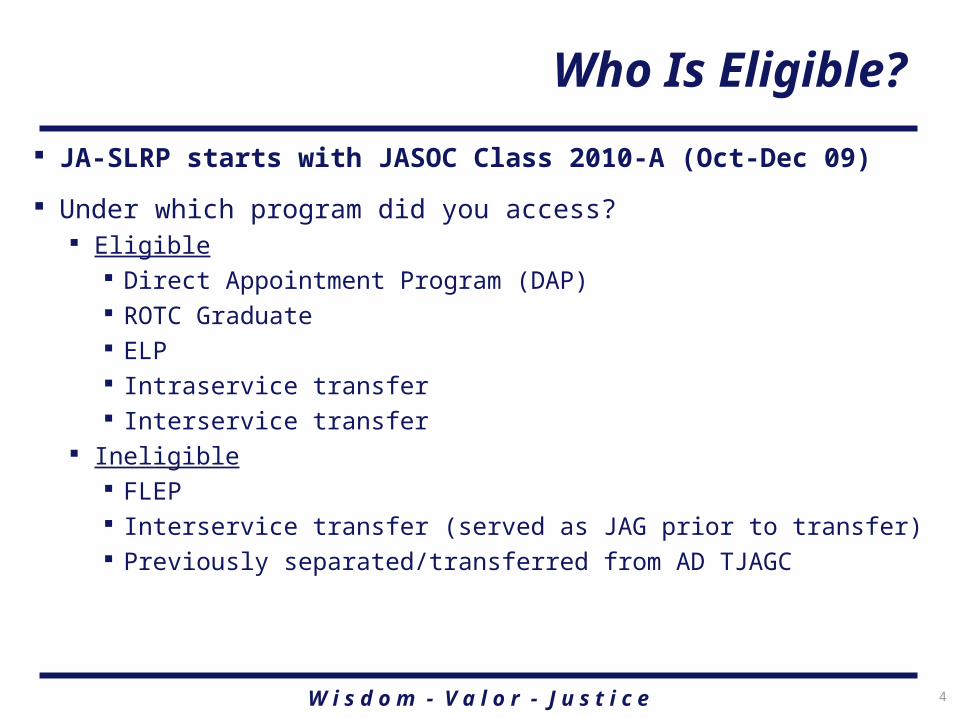

JA-SLRP starts with JASOC Class 2010-A (Oct-Dec 09)

Under which program did you access? Eligible

Direct Appointment Program (DAP) ROTC Graduate ELP Intraservice transfer Interservice transfer

Ineligible FLEP Interservice transfer (served as JAG prior to transfer) Previously separated/transferred from AD TJAGC

W i s d o m - V a l o r - J u s t i c e 5

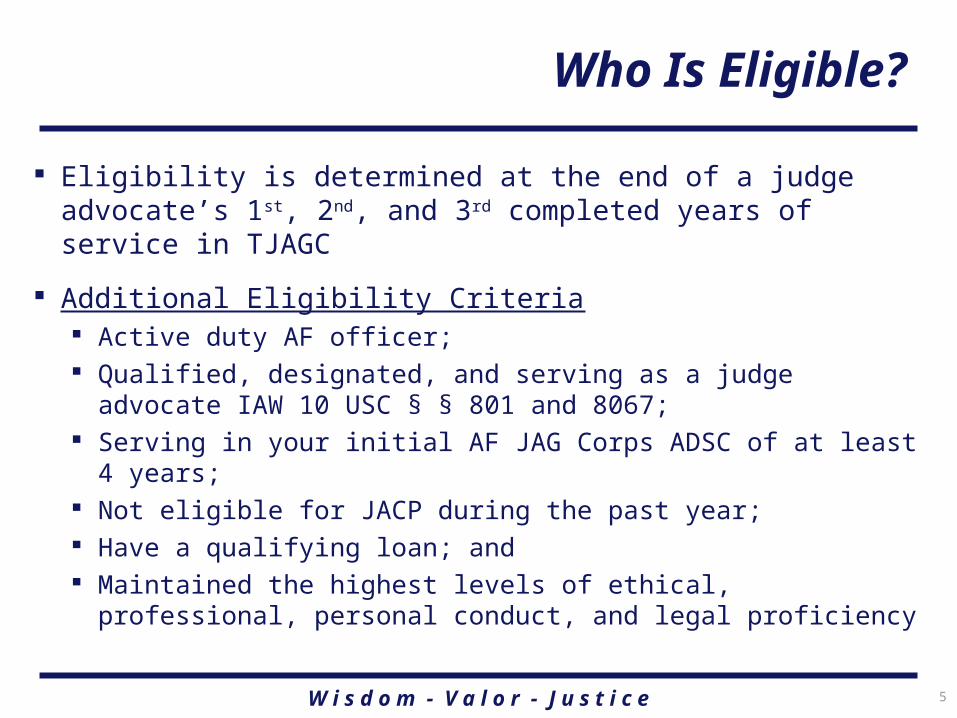

Who Is Eligible?

Eligibility is determined at the end of a judge advocate’s 1st, 2nd, and 3rd completed years of service in TJAGC

Additional Eligibility Criteria Active duty AF officer; Qualified, designated, and serving as a judge advocate IAW 10

USC § § 801 and 8067; Serving in your initial AF JAG Corps ADSC of at least 4 years; Not eligible for JACP during the past year; Have a qualifying loan; and Maintained the highest levels of ethical, professional, personal

conduct, and legal proficiency

W i s d o m - V a l o r - J u s t i c e 6

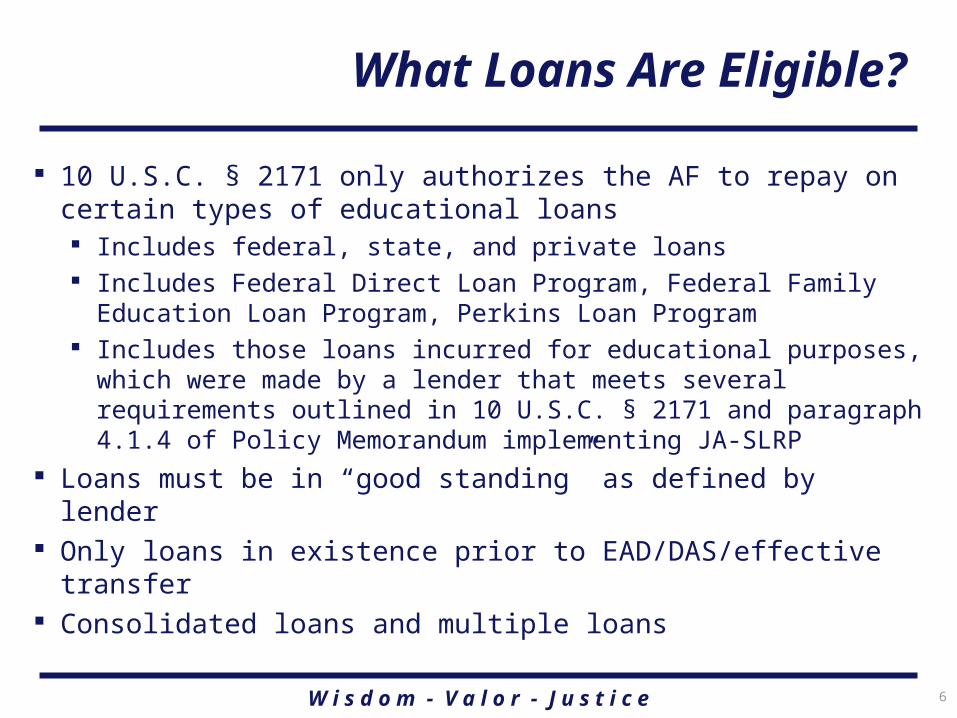

What Loans Are Eligible?

10 U.S.C. § 2171 only authorizes the AF to repay on certain types of educational loans

Includes federal, state, and private loans Includes Federal Direct Loan Program, Federal Family

Education Loan Program, Perkins Loan Program Includes those loans incurred for educational purposes, which

were made by a lender that meets several requirements outlined in 10 U.S.C. § 2171 and paragraph 4.1.4 of Policy Memorandum implementing JA-SLRP

Loans must be in “good standing” as defined by lender Only loans in existence prior to EAD/DAS/effective transfer Consolidated loans and multiple loans

W i s d o m - V a l o r - J u s t i c e 7

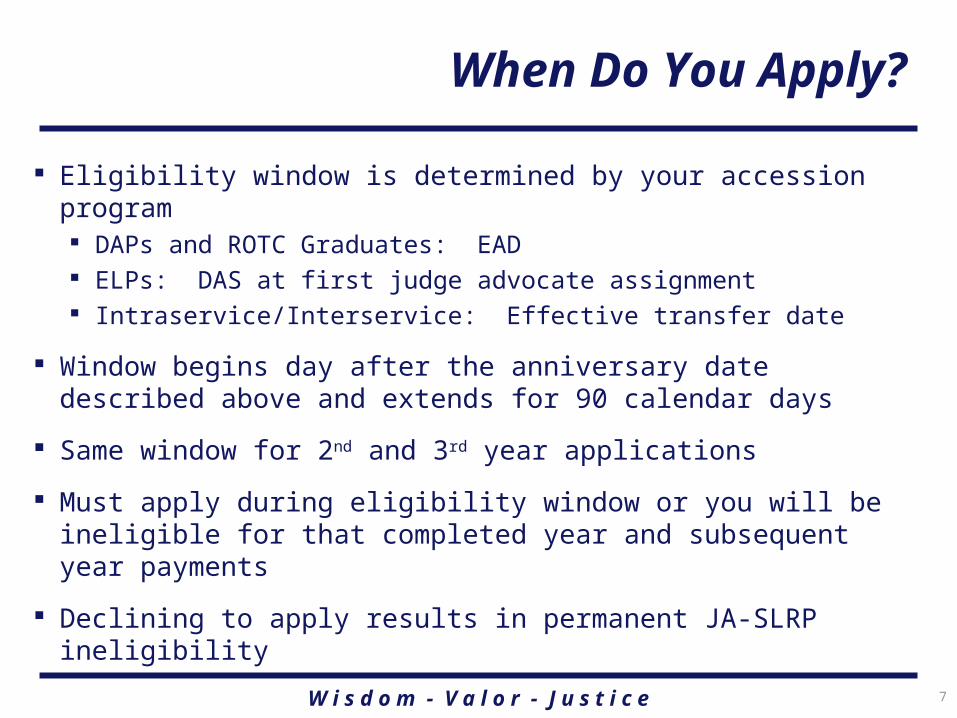

When Do You Apply?

Eligibility window is determined by your accession program DAPs and ROTC Graduates: EAD ELPs: DAS at first judge advocate assignment Intraservice/Interservice: Effective transfer date

Window begins day after the anniversary date described above and extends for 90 calendar days

Same window for 2nd and 3rd year applications

Must apply during eligibility window or you will be ineligible for that completed year and subsequent year payments

Declining to apply results in permanent JA-SLRP ineligibility

W i s d o m - V a l o r - J u s t i c e 8

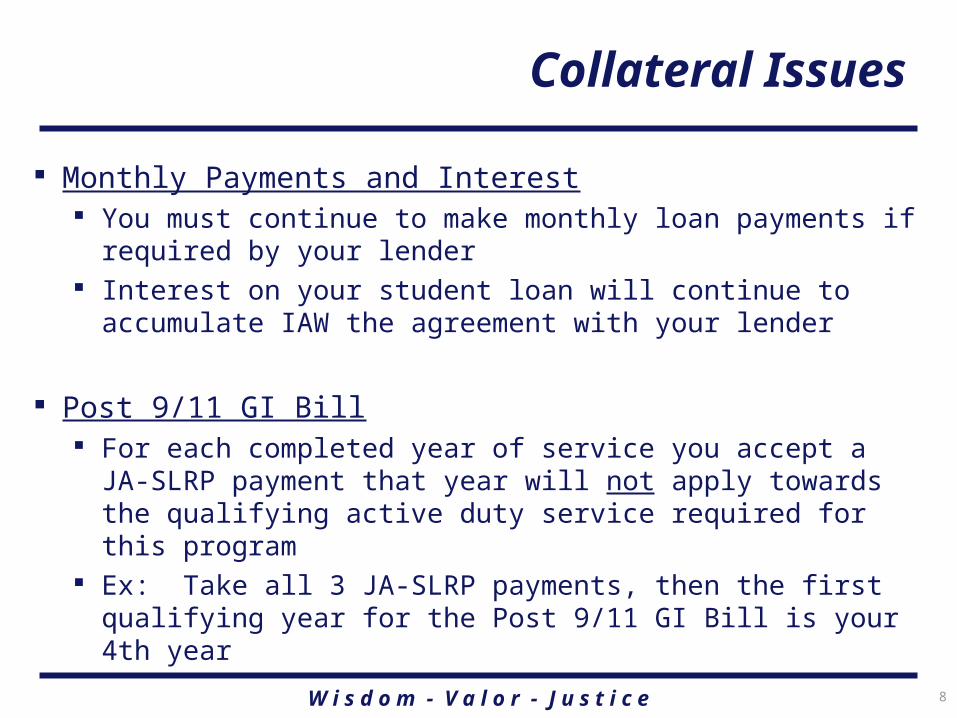

Collateral Issues

Monthly Payments and Interest You must continue to make monthly loan payments if required

by your lender Interest on your student loan will continue to accumulate IAW

the agreement with your lender

Post 9/11 GI Bill For each completed year of service you accept a JA-SLRP

payment that year will not apply towards the qualifying active duty service required for this program

Ex: Take all 3 JA-SLRP payments, then the first qualifying year for the Post 9/11 GI Bill is your 4th year

W i s d o m - V a l o r - J u s t i c e 9

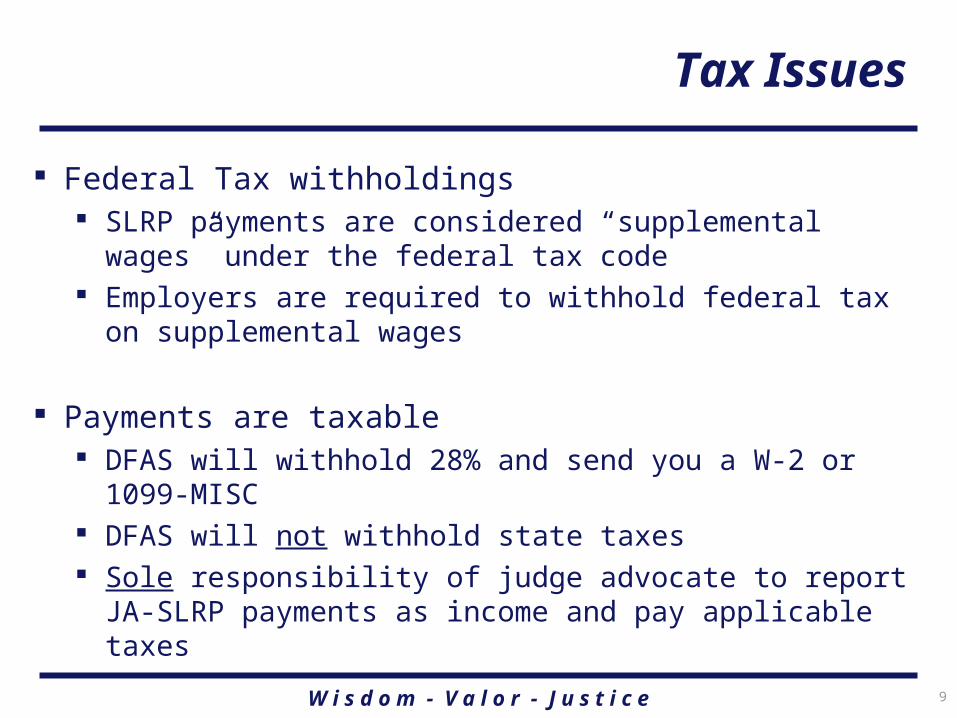

Tax Issues

Federal Tax withholdings SLRP payments are considered “supplemental wages” under

the federal tax code Employers are required to withhold federal tax on

supplemental wages

Payments are taxable DFAS will withhold 28% and send you a W-2 or 1099-MISC DFAS will not withhold state taxes Sole responsibility of judge advocate to report JA-SLRP

payments as income and pay applicable taxes

W i s d o m - V a l o r - J u s t i c e 10

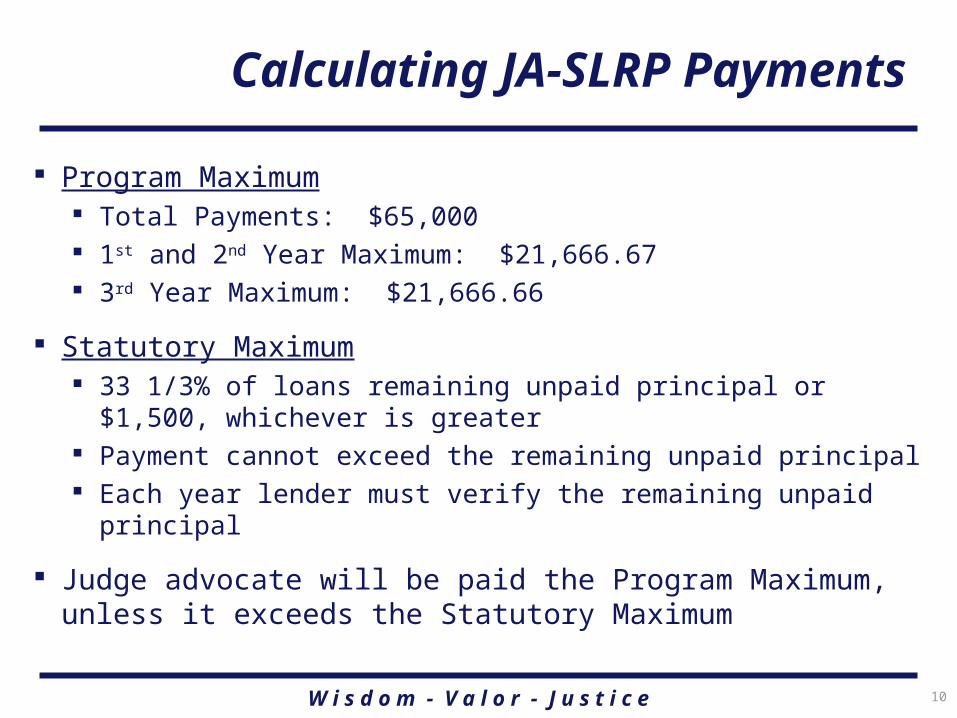

Calculating JA-SLRP Payments

Program Maximum Total Payments: $65,000 1st and 2nd Year Maximum: $21,666.67 3rd Year Maximum: $21,666.66

Statutory Maximum 33 1/3% of loans remaining unpaid principal or $1,500,

whichever is greater Payment cannot exceed the remaining unpaid principal Each year lender must verify the remaining unpaid principal

Judge advocate will be paid the Program Maximum, unless it exceeds the Statutory Maximum

W i s d o m - V a l o r - J u s t i c e 11

Example – Year 1

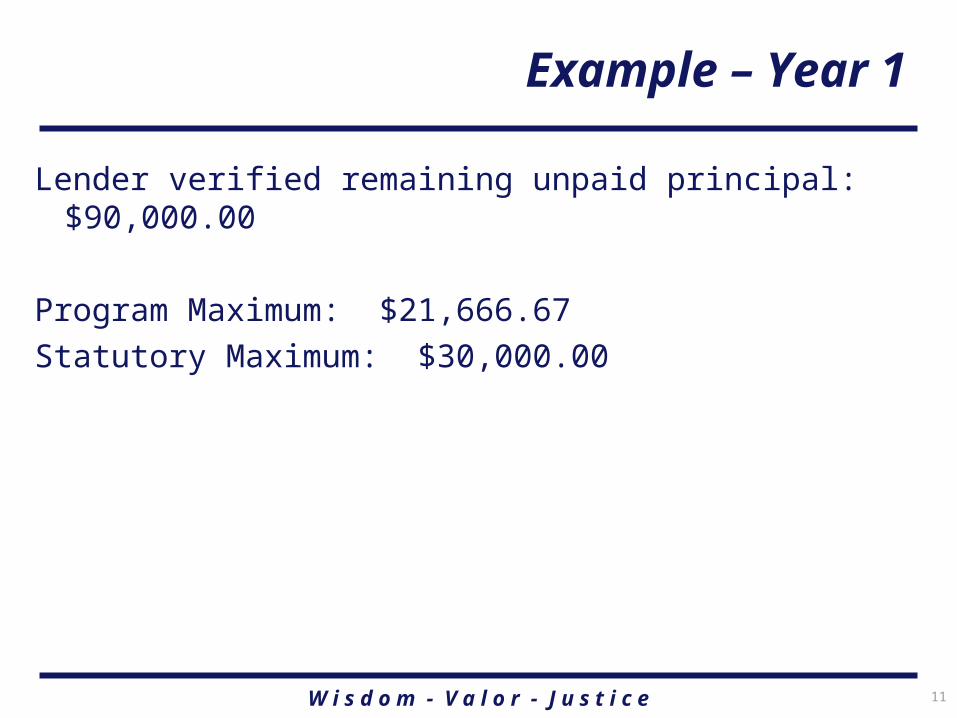

Lender verified remaining unpaid principal: $90,000.00

Program Maximum: $21,666.67

Statutory Maximum: $30,000.00

W i s d o m - V a l o r - J u s t i c e 12

Example – Year 1

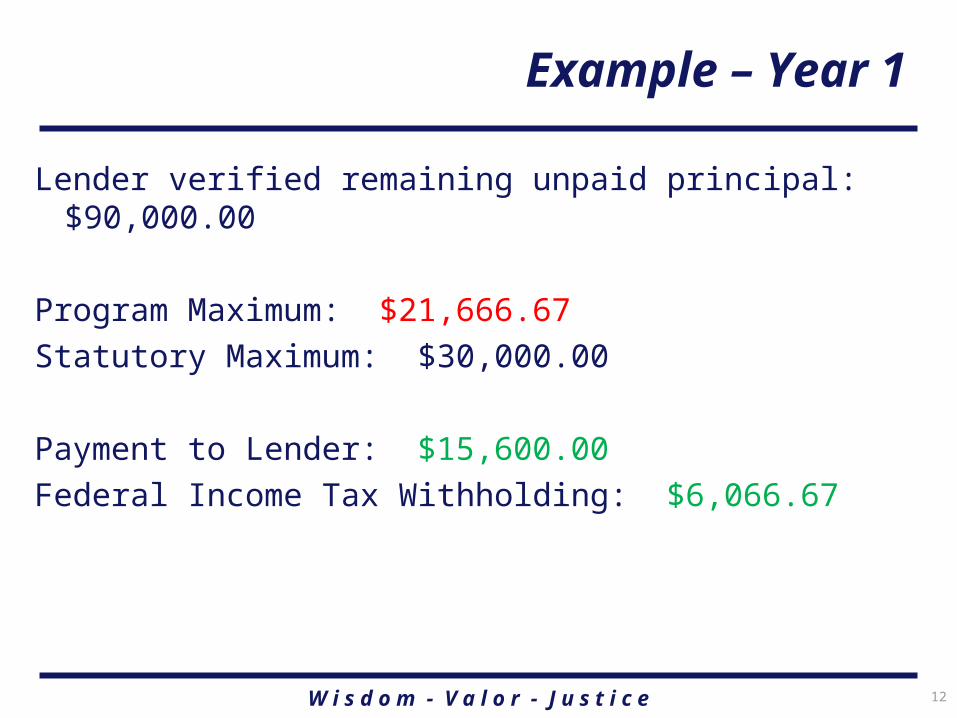

Lender verified remaining unpaid principal: $90,000.00

Program Maximum: $21,666.67

Statutory Maximum: $30,000.00

Payment to Lender: $15,600.00

Federal Income Tax Withholding: $6,066.67

W i s d o m - V a l o r - J u s t i c e 13

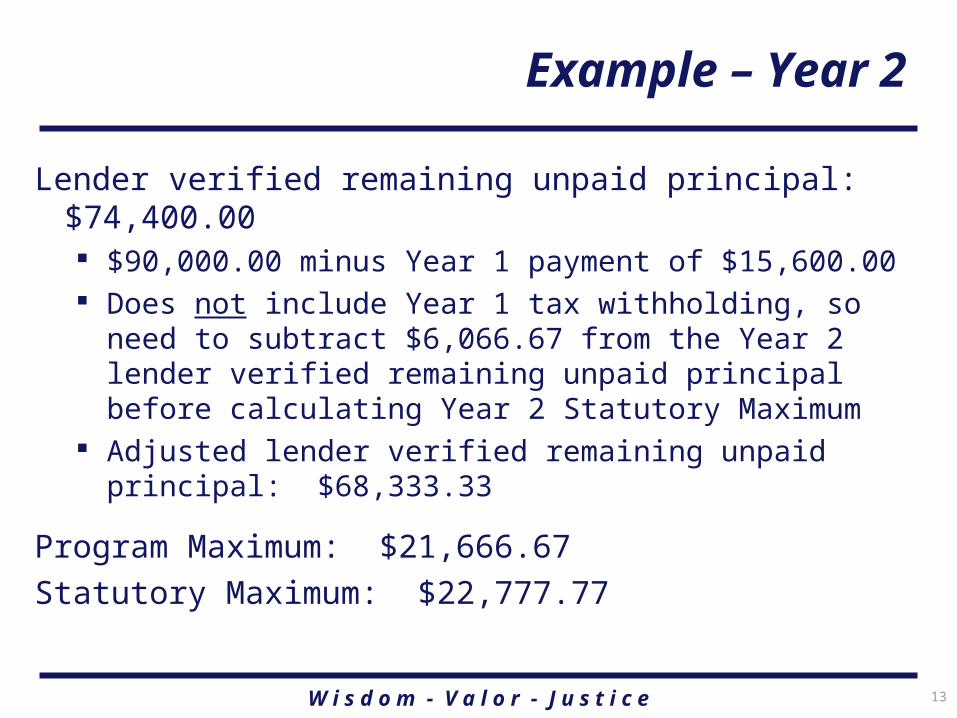

Example – Year 2

Lender verified remaining unpaid principal: $74,400.00 $90,000.00 minus Year 1 payment of $15,600.00 Does not include Year 1 tax withholding, so need to subtract

$6,066.67 from the Year 2 lender verified remaining unpaid principal before calculating Year 2 Statutory Maximum

Adjusted lender verified remaining unpaid principal: $68,333.33

Program Maximum: $21,666.67

Statutory Maximum: $22,777.77

W i s d o m - V a l o r - J u s t i c e 14

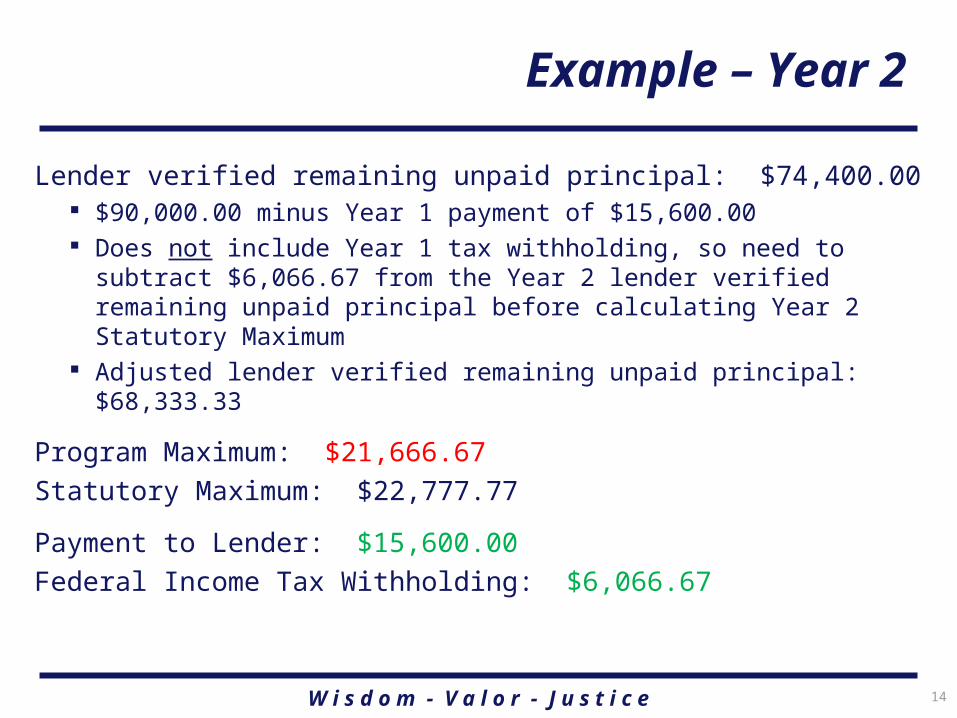

Example – Year 2

Lender verified remaining unpaid principal: $74,400.00 $90,000.00 minus Year 1 payment of $15,600.00 Does not include Year 1 tax withholding, so need to subtract

$6,066.67 from the Year 2 lender verified remaining unpaid principal before calculating Year 2 Statutory Maximum

Adjusted lender verified remaining unpaid principal: $68,333.33

Program Maximum: $21,666.67

Statutory Maximum: $22,777.77

Payment to Lender: $15,600.00

Federal Income Tax Withholding: $6,066.67

W i s d o m - V a l o r - J u s t i c e 15

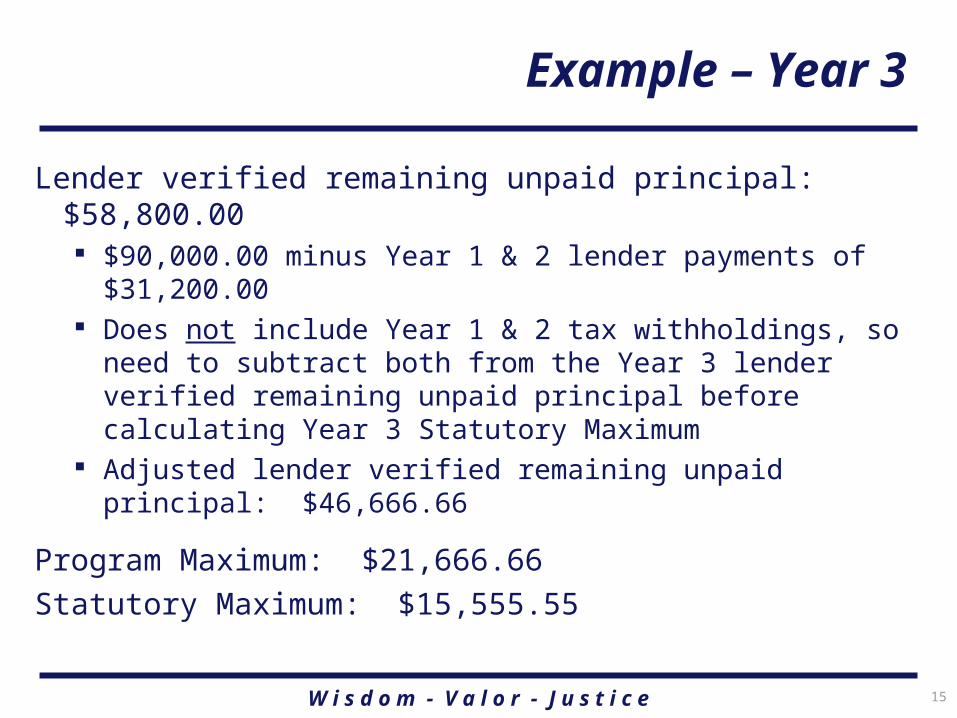

Example – Year 3

Lender verified remaining unpaid principal: $58,800.00 $90,000.00 minus Year 1 & 2 lender payments of $31,200.00 Does not include Year 1 & 2 tax withholdings, so need to

subtract both from the Year 3 lender verified remaining unpaid principal before calculating Year 3 Statutory Maximum

Adjusted lender verified remaining unpaid principal: $46,666.66

Program Maximum: $21,666.66

Statutory Maximum: $15,555.55

W i s d o m - V a l o r - J u s t i c e 16

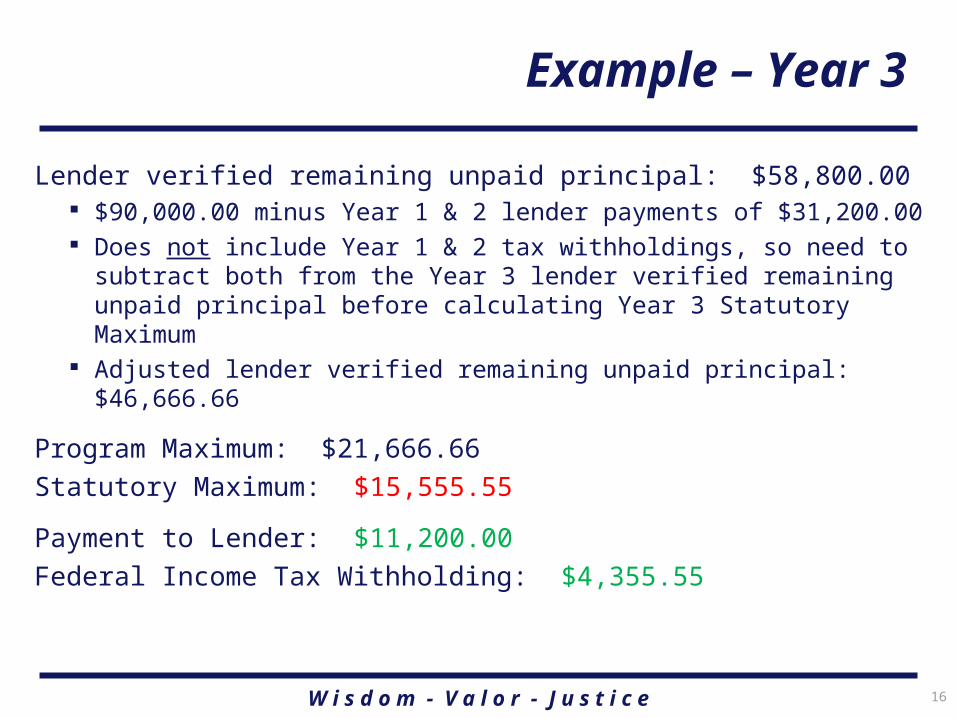

Example – Year 3

Lender verified remaining unpaid principal: $58,800.00 $90,000.00 minus Year 1 & 2 lender payments of $31,200.00 Does not include Year 1 & 2 tax withholdings, so need to

subtract both from the Year 3 lender verified remaining unpaid principal before calculating Year 3 Statutory Maximum

Adjusted lender verified remaining unpaid principal: $46,666.66

Program Maximum: $21,666.66

Statutory Maximum: $15,555.55

Payment to Lender: $11,200.00

Federal Income Tax Withholding: $4,355.55

W i s d o m - V a l o r - J u s t i c e 17

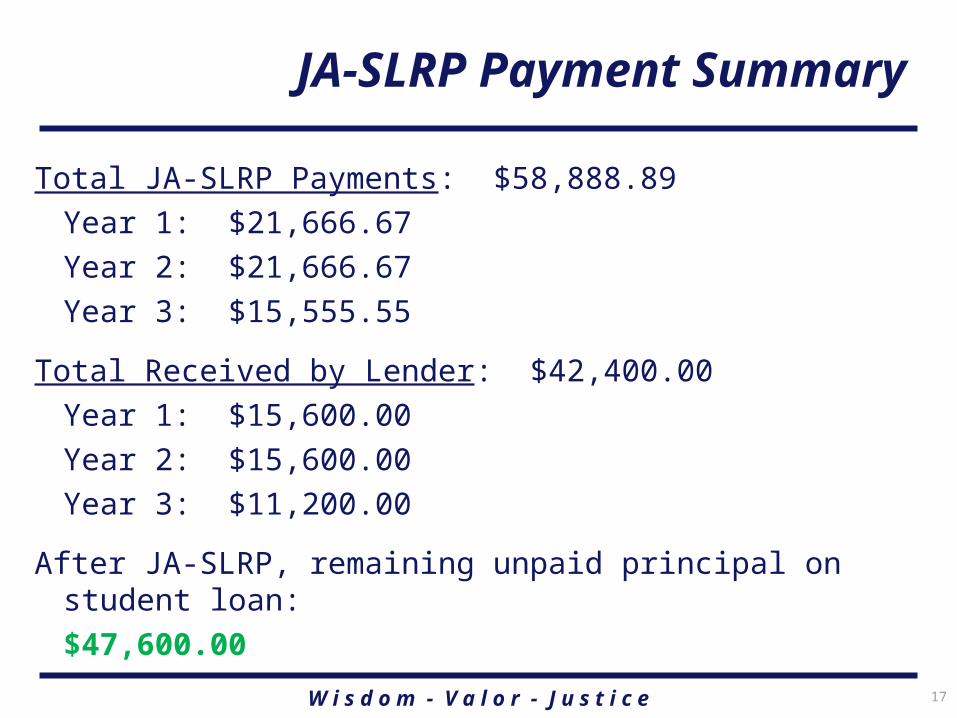

JA-SLRP Payment Summary

Total JA-SLRP Payments: $58,888.89

Year 1: $21,666.67

Year 2: $21,666.67

Year 3: $15,555.55

Total Received by Lender: $42,400.00

Year 1: $15,600.00

Year 2: $15,600.00

Year 3: $11,200.00

After JA-SLRP, remaining unpaid principal on student loan:

$47,600.00

W i s d o m - V a l o r - J u s t i c e 18

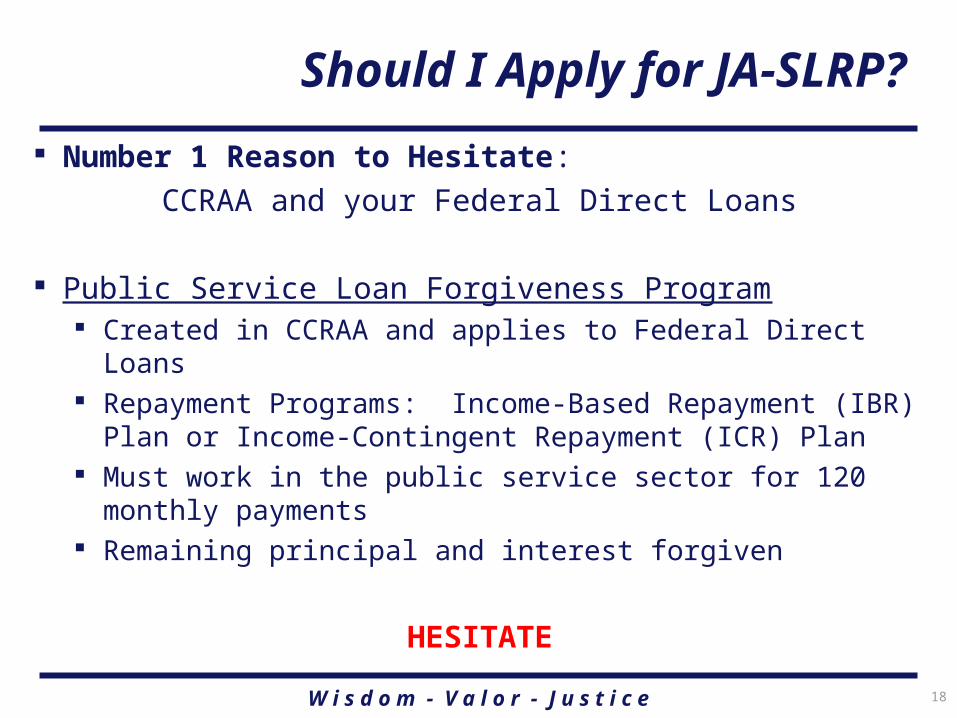

Should I Apply for JA-SLRP?

Number 1 Reason to Hesitate:

CCRAA and your Federal Direct Loans

Public Service Loan Forgiveness Program Created in CCRAA and applies to Federal Direct Loans Repayment Programs: Income-Based Repayment (IBR) Plan

or Income-Contingent Repayment (ICR) Plan Must work in the public service sector for 120 monthly

payments Remaining principal and interest forgiven

HESITATE

W i s d o m - V a l o r - J u s t i c e 19

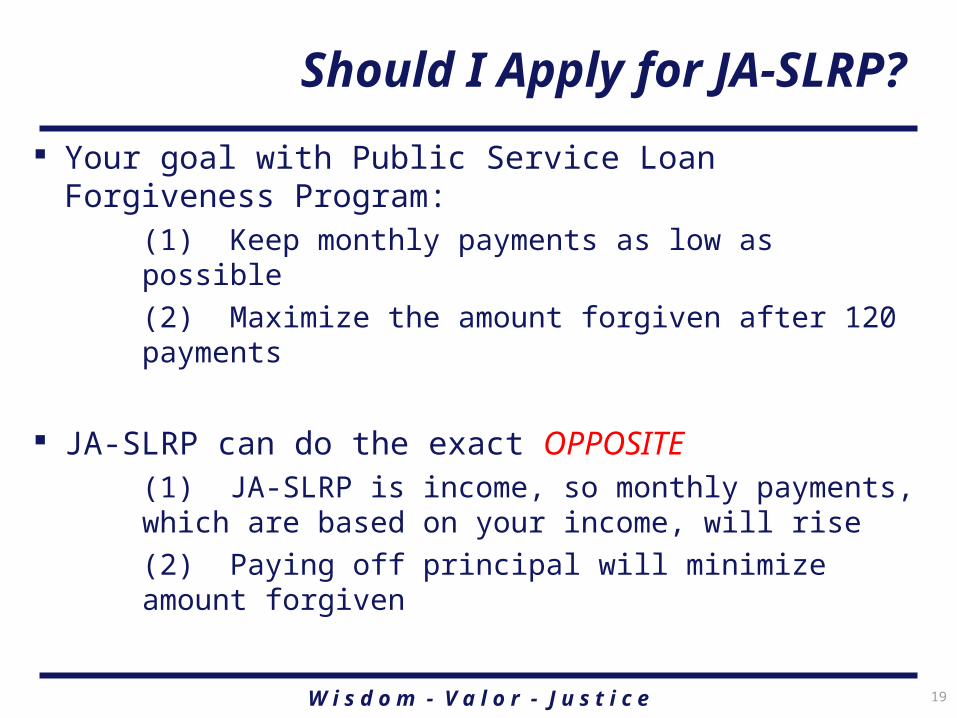

Should I Apply for JA-SLRP?

Your goal with Public Service Loan Forgiveness Program:(1) Keep monthly payments as low as possible

(2) Maximize the amount forgiven after 120 payments

JA-SLRP can do the exact OPPOSITE(1) JA-SLRP is income, so monthly payments, which are based on your income, will rise

(2) Paying off principal will minimize amount forgiven

W i s d o m - V a l o r - J u s t i c e 20

Should I Apply for JA-SLRP?

IBR monthly repayment calculator: http://www.finaid.org/calculators/ibr.phtml

ICR monthly repayment calculator: http://www.finaid.org/calculators/icr.phtml

Equal Justice Resource Center: http://www.equaljusticeworks.org

W i s d o m - V a l o r - J u s t i c e 21

Summary

Closely review the implementing Policy Memorandum

JA-SLRP System will launch on FLITE on 1 July 2010

When your eligibility window opens, contact JAX with any questions

W i s d o m - V a l o r - J u s t i c e 22

Questions?