Embed Size (px)

Citation preview

Title Slide

JUN 8 – 10, 2015

www.bermudacaptive.bm

Specialty Session – Technical Briefs: IFRS, GAAP, Tax, Solvency II, etc.

Agenda

• Captive Market Statistics

• Equivalence Designations

• E-Filings Initiative

• GAAP Updates– Financial Instruments– Insurnace Contracts– IFRS Updates– US GAAP Updates

The Panel

Moderator:

•Muhammad Khan, Partner, Deloitte.

Speakers:

•Leslie Robinson, Assistant Director, Bermuda Monetary Authority

•Jane Morley-Davies, Vice President, Aon Insurance Managers (Bermuda) Ltd.

•Greg Tyers, Senior Vice President, Marsh IAS Management Services (Bermuda) Ltd.

•Ann Culala, Senior Manager, KPMG

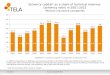

As at 31st December 2013*

Captive Market Statistics

Class of Insurer Gross Premiums Net Premiums Total Assets Capital & Surplus

Class 1 $3.6 billion $2.9 billion $16.3 billion $11.2 billion

Class 2 $9.1 billion $7.4 billion $56.0 billion $25.2 billion

Class 3 $34.8 billion $23.4 billion $87.3 billion $22.6 billion

Long Term Class A $0.5 billion $0.5 billion $1.5 billion $0.3 billion

Long Term Class B $0.1 billion $0.1 billion $0.2 billion $0.09 billion

Total $48.1 billion $34.3 billion $161.3 billion $59.4 billion

*Underwriting statistics quoted are from insurance company Statutory Financial Returns (SFRs) submitted for 31st December 2013. Companies submit filings on a phased basis throughout the year following their respective financial year-ends. The initial submission deadline for 2013 SFRs was April 2014. Due to this schedule, the most recent complete year-end figures for this overview are from 2013.

Class of Insurer 2014 %

Class 1 246 20.2%

Class 2 300 24.7%

Class 3 236 19.4%

Class 3A 108 8.9%

Class 3B 20 1.6%

Class 4 29 2.4%

Class A 3 0.2%

Class B 1 0.1%

Class C 74 6.1%

Class D 4 0.3%

Class E 20 1.6%

Special Purpose Insurer 111 9.1%

Dual Licenses 65 5.3%

Totals: 1,217 100%

Bermuda Insurer Register 2014

Class of Insurer 2014 Registrations %

Class 1 6 9.2%

Class 2 7 10.8%

Class 3 3 4.6%

Class 3A 7 10.8%

Class 3B 1 1.5%

Class 4 1 1.5%

Class A 0 0.0%

Class B 0 0.0%

Class C 5 7.7%

Class D 0 0.0%

Class E 4 6.2%

SPI 28 43.1%

Dual 3 4.6%

Totals: 65 100%

Analysis of 2014 Additions to the Register

• BMA continues to adhere to international standards – e.g. NAIC Qualified Jurisdiction Status

• Authority is committed to seeking the equivalence designation prior to the Solvency II implementation date of 1st January, 2016. Solvency II equivalence for commercial sector only: captive sector not in scope of Solvency II

• Active outreach to industry will be conducted as Authority concludes final work for assessment

Equivalence Designations

• Successful trial run at end of 2013 for e-filing of enhanced Statutory Financial Return

• Currently reviewing underlying platform supporting e-filing initiatives. Anticipate e-filing of enhanced statutory financial return to begin for year-end 2015 financials

• Authority will conduct intensive outreach with industry commencing Q3 2015

E-Filing Initiative

Financial Instruments

Classification and Measurement:

•Substantially retain the existing guidance for investments in debt securities and loans

•Equity investments to be measured at fair value through net income except for those:

• Accounted for under equity method of accounting; or• Without readily determinable fair values for which the entity has elected to

apply the practicability exception to measure them at cost, adjusted for impairment and observable price changes

•For financial liabilities where the fair value option has been elected, the change in fair value that is attributable to an instrument specific credit risk should be recognized in OCI

•Ability to elect to measure using fair value option will be retained in final standard

•Final standard expected to be issued in first half of 2015. This would indicate the standard would not be effective earlier than January 1, 2018 for calendar year-end companies

•Transition method – all outstanding instruments would apply guidance and record a cumulative-effect adjustment to opening retained earnings.

Financial Instruments (continued)

Impairment:

•The proposals would significantly change how entities measure and recognize credit impairment for most financial assets, as proposals change from incurred loss model to lifetime expected loss model.

•Debt securities held as AFS would continue with OTTI model, with targeted amendments:

• Recognized through an allowance account that would allow for reversals of previously recognized credit losses

• When evaluating whether a credit loss exists, time would not be a factor

• Disclosures on credit risk would be required• Allowance roll-forward would be required

•Final standard expected to be issued later in 2015. This would indicate the standard would not be effective earlier than January 1, 2018 for calendar year-end companies

•Whilst follow cumulative-effect adjustment on transition, there are varied transition methods depending on instrument

Financial Instruments (continued)

Completed standard substantially concludes project to replace IAS 39 Financial Instruments: Recognition and Measurement

Financial asset classification based on:

contractual cash flow characteristics; and

objective of business model in which assets are managed Asset measurement categories are: amortised cost; fair value

through other comprehensive income (FVOCI); and fair value through profit and loss (FVTPL)

New ‘expected credit loss’ model to replace current ‘incurred loss’ model

OverviewOverview

Financial assets: although categories are similar, basis of classification significantly different

Impairment allowance will cover both incurred credit losses and (some) expected future credit losses

Impairment trigger no longer required before impairment allowance is recognised

Dual method for impairment – 12 months or lifetime, depending on whether there has been a significant increase in credit risk

Differences from current practiceDifferences from current practice

31 December 2018: First annual financialstatements in which thestandard applies

24 July 2014: Standard published

1 January 2018: Effective date (early adoption permitted)

Financial Instruments (continued)

Expected impact for Insurance Industry

Reporting

Business

Systems / processes

People and change

Increase in number and complexity of judgments Change from incurred loss reporting basis to an

expected loss reporting basis Extensive new disclosures required in relation to

impairment of financial instruments

Understand changes and develop implementation strategy

Begin your business model assessment and plan to assess both your existing contracts and those you expect to enter into before 2018

Set up project team with representatives from credit risk management, accounting, tax, regulatory and IT teams

Immediate next stepsImmediate next steps

Bottom lineBottom line

Key impactsKey impacts

Potential to result in higher levels of impairment of financial assets

Potential for more financial assets to be recorded at FVTPL

Need for stakeholder communication Expert knowledge to implement changes

Insurance Contracts

Short duration contracts:

•FASB recently decided based on feedback from draft ASU that certain disclosures should be presented as supplementary information, rather than in notes to the financial statements. This included:

• Claims development table except for current reporting period and related disclosure on history of claims duration

•The Board also modified its disclosures about claims frequency and incurred but not reported liabilities.

•Other decisions were not changed.

•Retrospective application would be required, and be applicable for public companies for annual reporting periods beginning after December 15, 2015, and interim reporting periods the year after. All other entities have a one-year delay.

•FASB directed staff to proceed with a written ballot for the final standard.

Insurance Contracts (continued)

Long-duration contracts:

•FASB is deliberating on targeted improvements to accounting for long-duration contracts. Items covered thus far include:

• Assumptions - updated in Q4 annually, no provision for adverse deviation within, effects would be recognized in net income

• Discount rate – to be determined with reference to a portfolio of high-quality, fixed income investments

• Premium deficiency and loss recognition – eliminated for certain contracts

• Amortization of DAC – consistent approach where amortize over the expected life of a book of contracts in proportion to the balance of insurance inforce.

•FASB continuing deliberations, no indication on when these will complete.

Insurance Contracts (continued)

Introduction of a comprehensive accounting and measurement model for all insurance contracts

Proposals apply to all insurance contracts, rather than insurance entities, and to investment contracts with a DPF issued by insurers

Model is based on current fulfilment value, including four building blocks

Use of current assumptions and discount rates

Simplified (or ‘premium-allocation’) measurement approach for some short-duration contracts

Revised definition and accounting for acquisition costs

Participating contracts are still being re-deliberated

New presentation and disclosure requirements

OverviewOverview

1 January 2019: More likely earliest effective date

24 July 2013: Re-exposure draft published

1 January 2018: Earliest possible effective date

25 October 2013: Comment period ends

Insurance Contracts (continued)

Fulfilment cash flows and discount rates updated each reporting period

Effects of changes in discount rates will be an accounting policy choice, can be presented in OCI or profit and loss

Contractual service margin adjusted each reporting period

Other changes in insurance liabilities recognised in profit or loss

Need to track historical data – e.g. for contractual service margins and discount rates

Retrospective application with practical expedients if impracticable

Limited ability to redesignate some financial assets on initial application

Restatement of comparatives – including opening balance sheet

Increased volatility possible in profit or loss and equity

Measurement and reporting of operational performance will be impacted

Possible synergies and interaction with solvency and regulatory reporting

Interaction with IFRS 9: Different effective dates possible Limited ability to redesignate some financial

assets Extent of accounting mismatches / volatility

would depend on entity’s accounting for financial instruments

Broad business impacts possible – e.g. on product design, features and pricing

New systems and processes as well as additional resources may be necessary

Key impactsKey impactsApplication and transitionApplication and transition

Insurance Contracts (continued)

Expected impact for Insurance Industry

Reporting

Business

Systems / processes

People and change

Bottom lineBottom line

The proposals mark a major step forward towards implementing a common insurance reporting framework

Different drivers of profit or loss and increased volatility could impact your market position

Consider proactively assessing and planning for the new world now ...

Evaluate need to upgrade systems and actuarial models, to ensure that they can handle new requirements

Consider impact on data requirements Review product profile and product design Identify impacts on financial KPIs Establish high-level plan for dealing with

reporting changes Incorporate accounting change into planning for

solvency and regulatory reporting Identify need for additional resources – e.g.

actuaries, finance, IT – or training

Next stepsNext steps

IFRS Updates

• Newly effective IFRS Standards

Effective for years ending Standards

31 December 2014

Offsetting Financial Assets and Financial Liabilities (Amendments to IAS 32)

Recoverable Amount Disclosures for Non-Financial Assets (Amendments to IAS 36)

Novation of Derivatives and Continuation of Hedge Accounting (Amendments to IAS 39)

30 June 2015

Annual Improvements to IFRSs 2010-2012 Cycle – various standards

Annual Improvements to IFRSs 2011-2013 Cycle – various standards

IFRS Updates (continued)

IFRS Updates (continued)

• Standards not yet effective, but available for early adoption

Effective for years ending

Standards

31 December 2016

Accounting for Acquisitions of Interests in Joint Operations (Amendments to IFRS 11)

Equity Method in Separate Financial Statements (Amendments to IAS 27)

Sale or Contribution of Assets between an Investor and Its Associate or Joint Venture

Annual Improvements to IFRSs 2012-2014 Cycle – various standards

31 December 2017 IFRS 15 Revenue from Contracts with Customers

31 December 2018 IFRS 9 Financial Instruments

US GAAP Updates

Effective for years ending Standards

December 31, 2014

ASU 2013-04, Obligations Resulting from Joint and Several Liability Arrangements for which the Total Amount of the Obligation is Fixed at the Reporting Date

ASU 2013-05, Parent’s Accounting for Cumulative Translation Adjustment upon Derecognition of Certain Subsidiaries of Groups of Assets within a Foreign Entity or of an Investment in a Foreign Entity

ASU 2014-02, Accounting for Goodwill (a consensus of the Private Company Council)

ASU 2014-03, Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps—Simplified Hedge Accounting Approach (a consensus of the Private Company Council)

ASU 2014-17, Pushdown Accounting

31 December 2015

ASU 2014-16, Determining Whether the Host Contract in a Hybrid Financial Instrument Issued in the Form of a Share Is More Akin to Debt or to Equity

ASU 2014-18, Accounting for Identifiable Intangible Assets in a Business Combination

US GAAP Updates (continued)

• Standards not yet effective, but available for early adoption

Effective for years ending

Standards

31 December 2016 ASU 2014-13, Measuring the Financial Assets and the Financial Liabilities of a Consolidated Collateralized Financing Entity (a consensus of the FASB Emerging Issues Task

ASU 2015-02, Amendments to the Consolidation Analysis

31 December 2017 ASU 2014-09, Revenue from Contracts with Customers (ASC 606)