Embed Size (px)

Citation preview

BEFORE THE AUTHORITY FOR ADVANCE RULINGS (INCOME TAX)

NEW DELHI

23rd day of July 2010

P R E S E N T

Mr.Justice P.V. Reddi (Chairman) Mr.J.Khosla, (Member)

Mr. V.K.Shridhar (Member)

A.A.R. No.836 of 2009

Name & Address of the applicant The Timken Company 1835 Dueber Avenue Sw., Canton, Ohio – 44706 0 0928, USA Commissioner concerned Director of Income-tax

(International Taxation) Kolkata.

Present for the applicant Mr.Percy Pardiwalla, Sr. Advocate M/s.Rajan Vora, K.T.Chandy,

Chavali Narayan, Chartered Accountants Ms. Preeti Goel, Advocate

Mr.Sridharan R., CFO Present for the Department None

RULING (By Mr. V.K.Shridhar)

The applicant is a Company formed under the laws of the State of Ohio, USA

and is a global manufacturer of engineered bearings, alloy and specialty steel related

components. It was initially a joint venture between Timken USA and Tata Iron and

Steel Company Limited (“TISCO”), subsequent to which the Company undertook a

1 http://www.itatonline.org

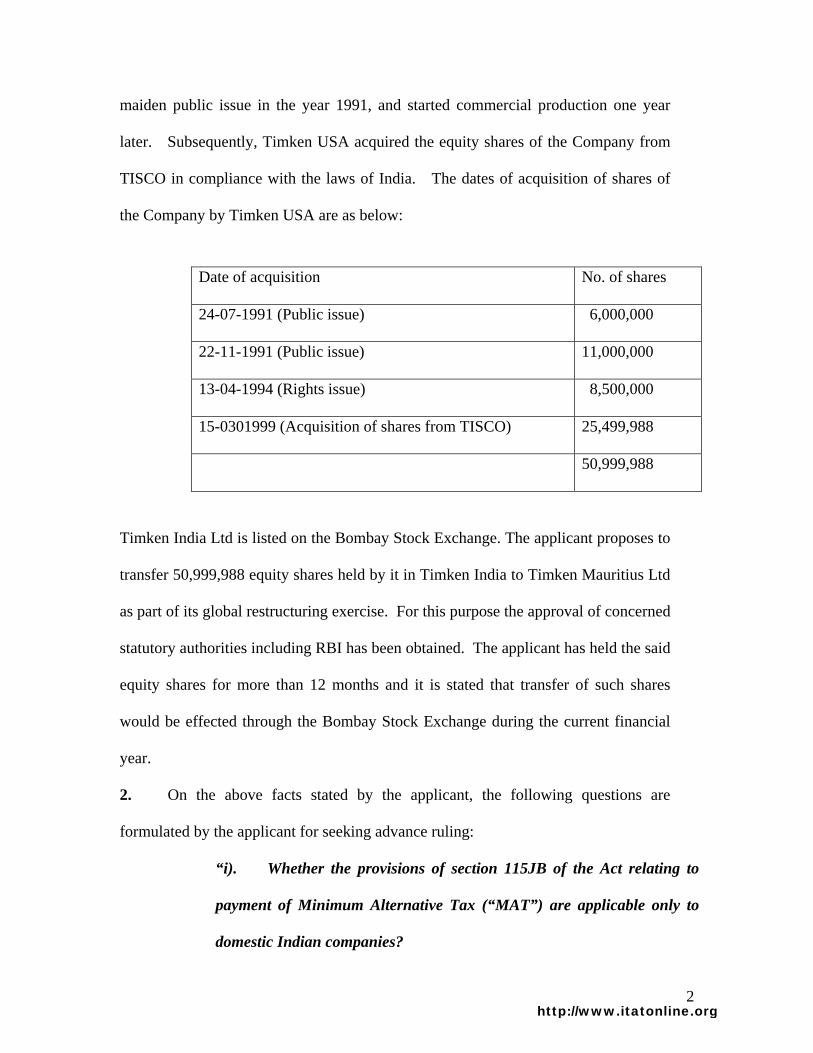

maiden public issue in the year 1991, and started commercial production one year

later. Subsequently, Timken USA acquired the equity shares of the Company from

TISCO in compliance with the laws of India. The dates of acquisition of shares of

the Company by Timken USA are as below:

Date of acquisition No. of shares

24-07-1991 (Public issue) 6,000,000

22-11-1991 (Public issue) 11,000,000

13-04-1994 (Rights issue) 8,500,000

15-0301999 (Acquisition of shares from TISCO) 25,499,988

50,999,988

Timken India Ltd is listed on the Bombay Stock Exchange. The applicant proposes to

transfer 50,999,988 equity shares held by it in Timken India to Timken Mauritius Ltd

as part of its global restructuring exercise. For this purpose the approval of concerned

statutory authorities including RBI has been obtained. The applicant has held the said

equity shares for more than 12 months and it is stated that transfer of such shares

would be effected through the Bombay Stock Exchange during the current financial

year.

2. On the above facts stated by the applicant, the following questions are

formulated by the applicant for seeking advance ruling:

“i). Whether the provisions of section 115JB of the Act relating to

payment of Minimum Alternative Tax (“MAT”) are applicable only to

domestic Indian companies?

2 http://www.itatonline.org

ii) If the answer to Question 1 is negative, whether the provisions of

section 115JB of the Act relating to payment of MAT are applicable to

only such foreign companies that have a physical business presence in

India?

iii) Based on the answer to Question (ii) since the Applicant, is a

foreign company who does not have any physical presence in India in the

form of an office or branch and also in the light of the declaration

provided by the Applicant that it does not have a permanent

establishment in India in terms of Article 5 of India-USA Double

Taxation Avoidance Agreement [Attachment VIII], whether the

provisions of section 115JB of the Act are applicable on the sale of

shares of a listed company viz Timken India Limited, by the applicant,

which has suffered securities transaction tax and accordingly, tax exempt

under section 10(38) of the Act?

iv) If the provisions of section 115JB of the Act are applicable to the

Applicant, whether the payments made to the Applicant on sale of the

shares would suffer any withholding tax under section 195 of the Act and

if yes, whether tax at 15% of the net capital gains would be required to be

withheld?

3. The applicant is of the view that the capital gains, if any, arising from the above

transaction would be exempt from tax under Section 10(38) of the Income Tax Act, 1961

(herein after referred to as Act) and therefore no tax is deductible under section 195. The

3 http://www.itatonline.org

applicant submits that the provisions of MAT contained in Section 115JB cannot be made

applicable to foreign companies who do not have any presence or PE in India.

4. The relevant provision of section 10(38) is extracted as under:

“10. In computing the total income of a previous year of any person, any

income falling within any of the following clauses shall not be

included -

(38) any income arising from the transfer of a long-term capital

asset, being an equity share in a company or a unit of an equity

oriented fund where –

(a) the transaction of sale of such equity share or unit is

entered into on or after the date on which Chapter VII of

the Finance (No.2) Act, 2004 comes into force; and

(b) such transaction is chargeable to securities transaction

tax under that Chapter :

[Provided that the income by way of long-term capital gain of

a company shall be taken into account in computing the book

profit and income-tax payable under section 115JB.]”

As per this section, the income arising on transfer of long term equity share in a

company fulfilling the requirements in clauses (a) and (b) would not be included in the

total income of a person. However, in the case of a company, it would be taken into

account in computing the book-profit and income tax payable under section 115JB.

Therefore, in a case where the income arising on transfer of long term equity share in a

company is taken into account in computing the book-profit, the book profit so

4 http://www.itatonline.org

determined should be such on which income tax should be payable under section 115JB.

Thus, if no income tax is payable under section 115JB even after including the income

arising on transfer of long term equity share in a company, the applicant would be eligible

to exclude such income from the total income as envisaged under section 10(38) of the

Act. There is no doubt that the proviso under a particular section controls the operation of

that section but its application cannot make the operative part of the section redundant. In

other words, section 10(38) cannot be construed to rule out its applicability to a

‘company’ to which section 115JB does not apply. We are of the view that the exemption

provided by section 10(38) of the Act is not taken away in the case of every company. The

context in which a company is defined needs to be taken into account.

5. The contentious issue involved in the case is: whether the provisions of MAT

contained in Section 115JB can be made applicable to foreign companies who do not have

any presence or PE in India, in view of the Proviso to Section 10(38). For an answer, we

have to refer to the provisions of Section 115JB of the Act.

The relevant portion of section 115JB of the Act is reproduced below:

“(1) Notwithstanding anything contained in any other provision of this Act, where in the

case of an assessee, being a company, the income-tax, payable on the total income

as computed under this Act in respect of any previous year relevant to the

assessment year commencing on or after the 1st day of April, 2007, is less than

fifteen per cent of its book profit, such book profit shall be deemed to be total

income of the assessee and the tax payable by the assessee on such total income

shall be the amount of income-tax @ of fifteen per cent.

5 http://www.itatonline.org

(2) Every assessee, being a company, shall, for the purposes of this section, prepare its

profit and loss account for the relevant previous year in accordance with the

provisions of Parts II and III of Schedule VI to the Companies Act, 1956 (1 of 1956):

Provided that while preparing the annual accounts including profit and loss account,-

(i) the accounting policies;

(ii) the accounting standards adopted for preparing such accounts including

profit and loss account;

(iii) the method and rates adopted for calculating the depreciation,

shall be the same as have been adopted for the purpose of preparing such accounts

including profit and loss account and laid before the company at its annual general

meeting in accordance with the provisions of section 210 of the Companies Act, 1956 (1

of 1956);

Provided further that where the company has adopted or adopts the

financial year under the Companies Act, 1956 (1 of 1956), which is different from the

previous year under this Act, -

(i) the accounting policies;

(ii) the accounting standards adopted for preparing such accounts including

profit and loss account;

(iii) the method and rates adopted for calculating the depreciation,

shall correspond to the accounting policies, accounting standards and the method and

rates for calculating the depreciation which have been adopted for preparing such

accounts including profit and loss account for such financial year or part of such

financial year falling within the relevant previous year.

6 http://www.itatonline.org

Explanation 1 – For the purposes of this section, “book profit” means the net profit as

shown in the profit and loss account for the relevant previous year prepared under sub-

section (2), as increased by –

a) to (h) . . . . .

If any amount referred to in clauses (a) to (h) is debited to the profit and loss account,

and as reduced by –

(i) to (viii) ………

Explanation 2 –

(4) xxx

(5) Save as otherwise provided in this section, all other provisions of this Act

shall apply to every assessee, being a company, mentioned in this section.”

6. Section 115JB of the Act applies notwithstanding anything contained in any

other provision of the Act. It is attracted when the income-tax payable on the total

income as computed under the Act is less than 15% of its book profit. In case the section

applies, tax payable shall be 15% of book profit. The section requires every company

assessee to prepare its profits and account (P & L account) for the relevant previous year

in accordance with the provisions of Parts II and III of Schedule VI of the Companies

Act. While preparing such annual accounts, the accounting policies, etc. should be the

same as have been adopted for the purpose of preparing such accounts, which are laid

before the company’s annual general meeting. Where the company has adopted or adopts

a financial year under the Companies Act, 1956, which is different from the previous year

under the Act, the accounting policies adopted for preparing such accounts and

calculating the book profit should correspond to the accounting policies adopted for

7 http://www.itatonline.org

preparing accounts for such financial year or part of such financial year falling within the

relevant previous year. All other provisions of the Act continue to apply to such company

covered by section 115JB.

6.1 The applicant submits that for the purposes of section 115JB while

interpreting the meaning of the word ‘Company’ as appearing therein, it would be

inappropriate to read only clause (ii) of section 2(17) without considering the opening

line of section 2. Under the Act the term ‘Company’ is defined as follows:

“In this Act, unless the context otherwise requires.”

“Company means

(i) any Indian company; or

(ii) any body corporate incorporated by or under the laws of a country outside

India; or….”

The applicant contended that the definition of “company” is qualified by the

expression ‘unless the context otherwise requires’. In CIT v. B C.Srinivasa Shetty (1981)

128 ITR 294, the Supreme Court held that the definitions in section 2 are subject to an

overall restrictive clause that is expressed in the opening words of the section “unless the

context otherwise requires”. Hence it would be necessary to enquire as to whether

contextually the expression capital asset as used in section 45 would include goodwill.

The apex Court in this regard held that goodwill cannot be described as an asset within

the meaning of section 45 and hence any capital gains arising on the transfer of such

goodwill cannot be subject to income-tax under the head capital gains. Thus, the

definition of ‘company’ in the applicant’s case requires the evaluation of the

circumstances in which the words as defined in the sub- sections (of section 2) have been

8 http://www.itatonline.org

used and if the circumstances do require otherwise, then the meanings as given to those

words by the said sub-sections are not to be resorted to.

6.2. In this regard, the applicant has drawn our attention to the notes on clauses

explaining the provisions of Finance Bill 2002, 254 ITR (St) 118, which provided for

some amendments to section 115JB, which read as follows:

“Clause 49 seeks to amend section 115JB of the Income-tax Act relating to special

provision for payment of tax by certain companies. The existing provisions of the

said section provide for levy of a minimum tax on domestic companies of an amount

equal to seven and one-half per cent of the book profit, if the tax payable on the total

income chargeable to tax as per the provisions of the Income-tax Act, 1961, is less

than seven and one-half per cent of the book profit …” (emphasis supplied)

The Notes explaining the provisions have accepted/clarified the law that

section 115JB is a levy of minimum tax on domestic companies. Thus, Government has

recognized that section 115JB is not applicable to foreign companies.

CBDT Circular No. 794 dated 9th August 2000(supra) explaining the newly

introduced provisions of section 115JB, reads as follows:

“The new provisions provide that all companies having book profits under the

companies act, prepared in accordance with Part II and Part III of Schedule VI to the

Companies Act, shall be liable to pay a minimum alternate tax at a lower rate of 7.5

per cent as against the existing effective rate of 10.5 percent of the book profits”.

It can be observed from the above CBDT Circular that the “existing effective rate” of

10.5% was arrived at by multiplying “30% of the Book Profits” [as under section 115JA]

9 http://www.itatonline.org

by the normal corporate tax rate of 35% (excluding surcharge), which was the rate of tax

applicable to domestic companies. In those years, the rate of tax applicable to foreign

companies was 48%. Thus in the CBDT circular, the effective rate of MAT has been

worked out with reference to domestic companies only, and it is evident that it was

understood by the CBDT that MAT applies only to domestic companies.

6.3 The applicant contended that it is well established that CBDT Circulars are not

only binding on the tax department but quite apart from their binding character, they are

clearly in the nature of contemporaneous exposition furnishing legitimate aid in the

construction of the provisions. In this regard, reliance can be placed on K.P.Verghese v.

ITO 131 ITR 597, wherein the Supreme Court has held as follows:

“These two circulars of the CBDT are, as we shall presently point out, binding on the

tax department in administering or executing the provision enacted in sub-s. (2), but

quite apart from their binding character, they are clearly in the nature of

contemporanea exposition furnishing legitimate aid in the construction of sub-s. (2).

The rule of construction by reference to contemporanea exposition is a well-

established rule for interpreting a statute by reference to the exposition it has

received from contemporary authority, though it must give way where the language of

the statute is plain and unambiguous …. It is clear from these two circulars that the

CBDT, which is the highest authority entrusted with the execution of the provisions of

the Act, understood sub-s (2) as limited to cases where the consideration for the

transfer has been understated by the assessee and this must be regarded as strong

circumstance supporting the construction which we are placing on that sub-section”.

10 http://www.itatonline.org

6.4 The applicant submits that by applying the rule of construction by reference to

contemporaneous exposition, it is clear from the Circular that the CBDT, which is the

highest authority entrusted with the execution of the provisions of the Act, understood

that section 115JB as applicable only to domestic companies. On various other occasions,

the Hon’ble Finance Minister in his speech had understood the MAT provisions to apply

only to domestic companies. This is evident from the following extracts of Finance

Minister’s speeches before the Parliament while introducing/amending various MAT

provisions and the Memorandum explaining these provisions in which it is observed that

the effective rates of MAT have been worked out with reference to domestic companies

only:

“ The various exemptions currently available while calculating Minimum Alternate

Tax (MAT) and the credit system has undermined the efficacy of the existing

provision and has also led to legal complications. To address these issues, I propose

that the Minimum Alternate Tax be now levied at the revised rate of 7.5% of the

“book profits” as determined under the Companies Act instead of the existing

effective rate of 10.5%”.

The Memorandum explaining the provisions of the Finance Bill 2000, 242 ITR

(St) 117, provides as follows:

“In its place, it is proposed to insert a new provision which is simpler in application.

The new provisions provide that all companies having book profits under the

Companies Act, prepared in accordance with Part –II and Part-III of Schedule-VI to

the Companies Act, shall be liable to pay a minimum alternate tax at a lower rate of

7.5%, as against the existing effective rate of 10.5% of the book profits.” The

11 http://www.itatonline.org

“existing effective rate” of 10.5% was arrived at by multiplying “30% of the Book

Profits” [as under section 115JB] by the normal corporate tax rate of 35% (excluding

surcharge) which was the rate of tax applicable to domestic companies. In those

years, the rate of tax applicable to foreign companies was 48%. Thus it is evident that

it was understood by the Finance Minister / CBDT that MAT applies only to domestic

companies.

The relevant extracts of the Finance Minister’s speech in the Parliament while placing

the Finance Bill 1996 are as follows:

“I propose to introduce a “Minimum Alternate Tax (MAT) on companies. In a case

where the total income of the company, as computed under the Income-tax Act after

availing of all eligible deductions is less than 30 percent, of the book profit, the total

income of such a company shall be deemed to be 30 percent. Of the book profit and

shall be charged to tax accordingly. The effective rate works out to 12 percent of

book profit calculated under the Companies Act.”

Thus, while introducing section 115JA, the Finance Minister stated that the effective

rate of tax was 12%. In the assessment year 1997-98, the tax rate applicable in case of

domestic company was 40%. Accordingly, the rate of tax was worked out at 12% of

book profits (as 30% of book profits was deemed to be the income). In case of a foreign

company, in the assessment year 1997-98, the rate of tax was 55%. Accordingly, if the

provisions were applicable to a foreign company, the rate of tax would be 16.5% and not

12%. It is evident from this distinction that the provisions of MAT, was not intended to

be applicable to a foreign company, going by the Explanatory Memorandum to the bill

and the speeches of Finance Minister.

12 http://www.itatonline.org

6.5 The applicant submits that for the purposes of determining the meaning the word

“Company’ as used in section 115JB of the Act, it is necessary to ascertain the context in

which it has been used in the other subsections of the section. In Section 115JB(2) of the

Act, it has been provided that for the purposes of section 115JB, every company has to

prepare its profit and loss account in accordance with the provisions of Part II and Part III

of Schedule VI of the Companies Act, 1956 for the relevant previous year. This literally

means that every foreign company is required to compile its entire global accounts in

accordance with Part II and Part III of Schedule VI of the Companies Act 1956, because

under section 2(17)(ii), company includes a foreign company. Recasting the entire global

accounts in this manner is itself a massive exercise. Secondly, for the purpose of

adjustments as provided in the Explanation below sub-section (2), as the net profits

disclosed by the global profit & loss account would be the starting point, a foreign

company may end up paying income-tax on its entire global income which may not have

accrued/arisen or received in India. In the absence of any specific guidance provided for

computation of book profits in the case of foreign companies in the statue, it is difficult to

accept that the Legislature had intended to make the foreign companies chargeable to

MAT.

6.6 The applicant took us to the provisions of section 115J (1A), inserted by

Finance Act 1989, which were identical to section 115JB (2). Section 115J (1A) reads as

follows:

“Every assessee, being a company shall, for the purpose of this section, prepare

its profit and loss account for the relevant previous year in accordance with the

13 http://www.itatonline.org

provisions of Parts II and III of Schedule VI to the Companies Act, 1956 (1 of

1956)”.

In this regard, reference to the CBDT’s Circular No. 50 dated 1 January

1990 182 ITR (St) 14 has been made, which reads as follows:

“Under the existing provisions, where the total income of a company is

less than 30 percent, of its book profits, the income chargeable to tax is deemed to be

30 percent of such book profits (section 115J). For the purposes of the aforesaid

provision, “book profits” means the net profit as shown in the profit and loss account

in the relevant previous year prepared in accordance with the provisions of Parts II

and III of the Sixth? Schedule to the Companies Act, 1956, subject to certain

adjustments, which increase or decrease the book profits. A large number of

companies interpreted the provisions to mean that in case they were following an

accounting year (under the Companies Act, 1956), which is different from the

previous year under the Income-tax Act (i.e. period ending on 31st March) then the

provisions of section 115J do not apply to them. This interpretation was based on

the understanding that section 115J does not make it mandatory for a company to

prepare its profit and loss account on 31st March of any year in case it is following an

accounting year which ends on a different date. As this was against the legislative

intent, the Amending Act has made it mandatory for all companies to prepare their

profits and loss account for the previous year ending 31st March to determine “book

profits” for the purposes of this section even if it is having a different accounting year

for the requirements under the Companies Act.

14 http://www.itatonline.org

This amendment will come into force with effect from 1st April 1989, and will,

accordingly, apply in relation to the assessment year 1989-90 and subsequent years.”

Thus, where the accounts are to be prepared in accordance with the special

requirements of other Acts and Part II and III of Schedule VI to Companies Act are

not applicable (as in the case of electricity, insurance and banking companies),

section 115JB cannot apply to such companies. Now, even in the case of foreign

companies, accounts are not required to be prepared as per Part II and III of Schedule

VI to Companies Act. Hence, the applicant’s counsel contends that MAT provisions

should also not apply to foreign companies.

6.7 Then, it is submitted that many foreign companies claim treaty protection under

section 90 of the Act and offer their different streams of income such as royalty, fees for

technical services, dividend, interest etc. for tax at concessional rates (as compared to

rates under the Act). In some cases, the foreign companies also claim complete

exemption from tax in India on the basis of DTAA. Thus, if the proposition that MAT

applies to foreign companies is accepted, then in every case, despite treaty protection, tax

under MAT will be payable @ 15%. It is argued by the Learned Counsel for the applicant

that simply because the opening sentence of Section 115JB begins with ‘notwithstanding

anything contained in any other provisions of this Act’, it cannot be interpreted to

override Section 90. In such event it leads to absurdity.

6.8 Then, it is pointed out that the two provisos to sub-section (1) provide that

depreciation shall be calculated using the same method and rates that have been adopted

for the purposes of preparing the profit and loss account for the purposes of laying down

the same before the Annual General Meeting of the company. A foreign company does

15 http://www.itatonline.org

not hold an annual general meeting in India and consequently the question of laying

down a Balance Sheet and Profit & Loss Account by the assessee in accordance with the

provisions of section 210 of the Companies Act, 1956 does not arise. The first and the

second proviso to Section 115JB, are meant for the purposes of compiling the profit and

loss account. In case of a foreign company, no profit and loss account is prepared in

accordance with the provisions of section 210 of the Companies Act, 1956 that is laid

before any annual general meeting. In other words, the first proviso cannot apply in case

of foreign company. If the first proviso does not apply, one cannot compile profit and

loss account for the purposes of the section.

6.9 Then, reference has been made to the Explanation below sub-section (2) various

adjustments/deductions are to be carried out in the net profit as shown by the Profit and

Loss Account. The deductions under chapter VIA of the Act are applicable only to an

Indian Company and/or other resident non-corporate assesses. Similarly, clause (vii) of

the Explanation provides that the profits of a sick industrial company under certain

circumstances shall not be subject to tax under section 115JB. It may be noted that

section 3(d) of the Sick Industrial Companies Act, 1985 defines a company as a company

as defined in section 3 of the Companies Act, 1956. Section 3(1) of the Companies act,

1956 defines a, company as a company formed and registered under the Companies Act,

1956 or an existing company as defined in section 3(ii). A foreign company is not a

company formed and registered under the Companies Act, 1956. Consequently, a

foreign company can never be considered as a Sick Industrial Company. Thus clause

(vii) to the Explanation 1 is also not applicable in the case of a foreign company. Many of

16 http://www.itatonline.org

the adjustments would not be applicable to foreign companies. Thus, it is evident that the

Legislature did not contemplate a foreign company for the purpose of levy of MAT.

To sum up, the applicant’s contention is that if due consideration is given to the

context in which the word ‘Company’ has been used, it can be seen that what is meant is

an Indian Company. At no place, does the context in which the word ‘Company’ has

been used in the section give an indication that it would include a foreign company.

Various reasons given above are also supported by CBDT Circulars, Finance Minister’s

speeches, Notes to clauses and Memorandum attached to the Finance Bill. Hence the

definition of ‘Company’ in section 2(17) in the context of section 115JB should be read

to exclude foreign company.

7. The contention of the deptt. is that the provisions of section 115JB(1) are applicable

in case of ‘any company’ and there is no demarcation as such between a ‘domestic

company’ and a ‘foreign company’. Therefore, the provisions should apply to foreign

companies as well. Its contention is that Explanation 1 of Section 115JB(2) of the Act

simply provides the mode of computation of “book profits” of a company. The “book

profit” as defined is nothing but the “net profit” of the company in the P/L account

prepared as per Part II and III of Schedule VI of the Companies Act after making

adjustments of certain items as enumerated in Explanation 1 of the said section. Even if it

is assumed that it may not be obligatory on a particular Foreign Company to prepare its

accounts as per Part II and III of the Schedule VI of the Companies Act, it cannot be the

case that the particular foreign company cannot prepare its accounts for its operations in

India as per Part II and III of Schedule VI of the Companies Act. It is stated that the

applicant files its return of income in India regularly as a Non resident Foreign Company

17 http://www.itatonline.org

(having PAN ; AABCT9658F) in the jurisdiction of ADIT (IT)-3(1), Kolkata. In the

returns so filed, it generally shows the income earned by it under the heads ‘Royalty’ and

‘Fee for Technical/Included Services’ which is offered for taxation on gross basis at the

rates applicable as per Indo-USA DTAA. Though no statement of accounts as per Part II

and III of the Schedule VI of the Companies Act are filed by the applicant with the

return, nothing prevents the applicant from doing so for the heads of income shown in the

return. The Department further contends that at the end of the day, Net Profit as per Part

II and III of the Schedule VI of the Companies Act is nothing but excess of income over

expenditure in the P/L account prepared in accordance with Part II and III of the

Schedule VI of the Companies Act. In the case of the applicant, if items of income are

credited in the P/L account without any corresponding debit of the expenditure in the

same then the whole of the income would qualify as ‘Net Profit’ in the P/L account of the

applicant as per Part II and III of the Schedule VI of the Companies Act. Now, for

computation of “Book Profits”, the Net Profit in the P/L account as per Part II and III of

the Schedule VI of the Companies Act has to be increased or reduced by certain items as

enumerated in Explanation 1 to section 115JB(2) of the Act. If these enumerated items

do not exist in the case of the applicant, then the ‘Net Profit’ in the P/L account as per

part II and III of the Schedule VI of the Companies Act would itself become the “Book

Profit” of the applicant as defined in Explanation 1 of section 115JB(2) of the Act.

8. The issue of applicability of Minimum Alternate Tax as per the provision of

Section 115JB of the Act came up before this Authority in the case reported as P.NO. 14

of 1997, in [234 ITR 335]. The Authority had the occasion to consider the issue whether

or not the Minimum Alternate Tax under Section 115JB is applicable to the foreign

18 http://www.itatonline.org

companies. In the said ruling, the Authority came to the conclusion that Section 115JA

(akin to section 115JB) applies to the foreign companies as well. We have perused the

said ruling and we find that the case is factually different from the present case due to the

following reasons.

8.1. In that case, the applicant was a company incorporated in the Netherlands having

a project office in India. It executed several dredging contracts in India since 1985 and

had a project office for executing contracts in India. The applicant was filing its returns

of income annually and reported losses every year on the contracts executed in India.

The losses were on account of depreciation claimed by the applicant on the dredgers and

equipment utilized in India for executing the contracts. The applicant had unabsorbed

losses, which were available for carry forward and set-off against the profits, which may

be earned by the applicant in its dredging operations. The applicant was preparing and

maintaining its accounts relating to the Indian projects at its project office. The applicant

was preparing its accounts in accordance with Part-II and III of Schedule VI to the

Companies Act, 1956, though it related only to the income and expenditure incurred out

of the Indian bank account. The depreciation was claimed at the rates provided under the

Income-tax Act. The applicant’s argument was as there were so many integral and

important provisions of Section 115JA, which cannot apply to a foreign company, foreign

company would not be covered by the provision under. This did not find favour with this

Authority. By making reference to the Memorandum explaining the purpose behind

introduction of Section 115JA and the Budget speech, this Authority took the view that

Section 115JA(4) applies to every assessee company and there was no reason to presume

that the legislature did not intend the provision of section 115JA to apply to an assessee

19 http://www.itatonline.org

which is a foreign company. The Authority was not convinced that there was any

difficulty to determine the profit and loss made by a foreign company in its Indian

business. Under the Companies Act, every foreign company has to maintain its books of

account relating to Indian business in the manner provided under section 209 and in each

calendar year it has to file its world account. Three copies of the world account are to be

delivered under section 594. Copies of balance sheet of Indian business account duly

audited have to be filed with the Registrar within 9 months of the close of financial year.

Even though Section 115JA contain drastic measures for taxing the income of a

company, this Authority held the view that provision will apply “notwithstanding

anything contained in any other provision of this Act”. It applies to all companies, which

will include a foreign company according to the definition given by section 2(17) of the

Act. When section 115JA speaks of a company, there is no reason to restrict the meaning

of a company to a domestic company. The fact that applicant company is a tax resident of

Netherlands and has got only a Permanent Establishment in India does not make any

difference to the position in law.

9. The considerations that have weighed in the ruling of this Authority referred supra

appears to be as under:

- that there was no difficulty in preparing the accounts in accordance with

Part-II and III of Schedule VI to the Companies Act, 1956;

- that the budget speech and memorandum explain the purpose behind

section 115JA;

- that there is a non-obstante clause in section 115JA;

20 http://www.itatonline.org

- that there is no specific exclusion of ‘foreign company’ under section

115JA;

- that the definition of ‘company’ given in section 2(17) means a ‘foreign

company’.

These considerations are based primarily on the peculiar facts of that case. In

the above-referred case the applicant was doing business and had a PE in India. Its

income was being assessed under the head “income from business and profession”. It

was required to maintain accounts under section 44AA of the IT Act and prepare

accounts under section 594 of the Companies Act, 1956. However, under section 591

of the Companies Act, only such foreign companies, who have established a place of

business within India, are required to make out a balance sheet and P&L Account as

required under section 594 of the Companies Act. In the case referred supra, as it had

a place of business by way of a PE in India, it was required to comply with Section

594 as if it was a company within the meaning of Companies Act, 1956. In order

therefore to comply with the requirement under section 115JA(2) to prepare P&L

Account in accordance with the provisions of Part II and III of Schedule VI of the

companies Act, 1956, it is essential that the foreign company should have a place of

business within India. Therefore, while giving ruling in the case referred supra, there

was no reason to look into the applicability of section 594 read with section 591. In

the present case as the applicant does not have an established place of business in

India, its preparation of P&L Account in accordance with the provisions of Part II &

III of Schedule VI of the Companies Act cannot be complied. This is the sine-qua-

non to comply with the provision under section 115JA.

21 http://www.itatonline.org

9.1 Regarding the Budget Speech, memorandum explaining the purpose

behind introduction of section 115JA and the legislative intent, our attention was

drawn to the decision of the Supreme Court in the case of K P Varghese in 131 ITR

597) (SC), wherein it was held that :

“Now, it is true that the speeches made by the Members of the Legislature on the

floor of the House when a Bill for enacting a statutory provision is being debated

are inadmissible for the purpose of interpreting the statutory provision but the

speech made by the mover of the Bill explaining the reason for the introduction of

the Bill can certainly be referred to for the purpose of ascertaining the mischief

sought to be remedied by the legislation and the object and purpose for which the

legislation was enacted.” This has been reiterated in the case of Kerala State

Industrial Development Corporation Ltd (259 ITR 51) as under:

“That the Finance Minister’s speech can be relied upon to throw light on the

object and purpose of the particular provisions introduction by the Finance Bill

has been recognized by this Court in K.P.Varghese vs. ITO (1981) 131 ITR 597

(SC), at 609.” Again in the case of R&B Falcon (A) Pty Ltd,301 ITR 209)(SC), it

was held that:

“Rules of executive construction in a situation of this nature may also be applied.

Where a representation is made by the maker of legislation at the time of

introduction of Bill or construction thereupon is put by the executive upon its

coming into force, the same carries great weight.”

These aspects have not been taken into account by this Authority while

deciding the above case.

22 http://www.itatonline.org

9.2 This brings us to the context in which company is defined under the Act. Under

the Act the term ‘Company’ is defined as follows:

“In this Act, unless the context otherwise requires.”

“Company means-

(iii) any Indian company; or

(iv) any body corporate incorporated by or under the laws of a country outside

India; or ……..”

For the purposes of section 115JB, if we apply the definition of “company” to a

‘foreign company’ without enquiring into the opening words used in the section “unless

the context otherwise requires”, section 115JB may become unworkable. The income,

which does not have a source in India, cannot be made part of the book profits. The

annual accounts, including the P&L Account, can not be prepared as per the first proviso

to section 115JB(2) in respect of the world income and laid before the company at its

AGM in accordance with the provision of Section 210 of the Companies Act. The speech

of Finance Minister and the memorandum explaining the provision also become out of

sync if the meaning of “company” appearing in section 115JB is adopted as ‘foreign

company”. Any other meaning would take away force and life from the true intent of the

makers of the Act. It must be said that it is a trite law that several provisions in the Act

must be read together and as parts of one larger scheme. Every clause of a statute is to be

construed with reference to the context and other clauses of the Act to make a consistent

enactment of the whole statute. Therefore, a construction that would render any part of

the statute ineffective would normally be rejected, as held in the case of V.Guruviah

Naidu & Sons 216 ITR 156 (Mad.). The department’s contention that there is no

23 http://www.itatonline.org

demarcation between a ‘domestic company’ and a ‘foreign company’ while applying the

provisions of section 115JB does not take into account the definition of a ‘company’

appearing in section 2(17) in the context of section 115JB. It has also not drawn its

attention to the fact that as the applicant did not have a place of business in India it was

not required to prepare its accounts under section 594 read with section 591 of the

Companies Act, 1956. That being so the applicant could not have prepared its accounts in

accordance with the provisions of Part II and III of Schedule VI of the companies Act,

1956. We therefore do not find any force in the contentions raised by the department.

We are therefore of the view that Section 115JB is not designed to be applicable

to the case of the applicant, a foreign company, who has no presence or PE in India.

10. In the light of the above discussion we answer Question No. (iii) in the

negative. In the facts and circumstances of the case as the applicant does not have any

physical presence in India in the form of an office or branch or a PE, the provisions of

section 115JB of the Act are not applicable on the sale of shares of a listed company

Timken India Limited, by the applicant, which has suffered securities transaction tax and

accordingly, tax exempt under section 10(38) of the Act.

In view of the above answer, the other questions need not be answered. It is

unnecessary and inappropriate to give a ruling thereon.

Pronounced by the Authority on this 23rd day of July 2010.

Sd/- Sd/- Sd/- (J. Khosla) (P.V. Reddi) (V.K.Shridhar)

Member Chairman Member F.No. AAR/836/2009 Dated 23.7.2010

(A) This copy is certified to be a true copy of the advance ruling and is sent to:

1. The applicant. 2. The Director of Income-tax (International Taxation), Kolkata. 3. The Joint Secretary (FT&TR-I), M/Finance, CBDT,Bhikaji Cama Place, New Delhi. 4. The Joint Secretary (FT&TR-II), M/Finance, CBDT,Bhikaji Cama Place, New Delhi 5. Guard file.

(B) In view of the provisions contained in Section 245S of the Act, this ruling should not be given for publication without obtaining prior permission of the Authority.

( Nidhi Srivastava )

Addl. Commissioner of Income-tax(AAR-IT

24 http://www.itatonline.org