Embed Size (px)

Citation preview

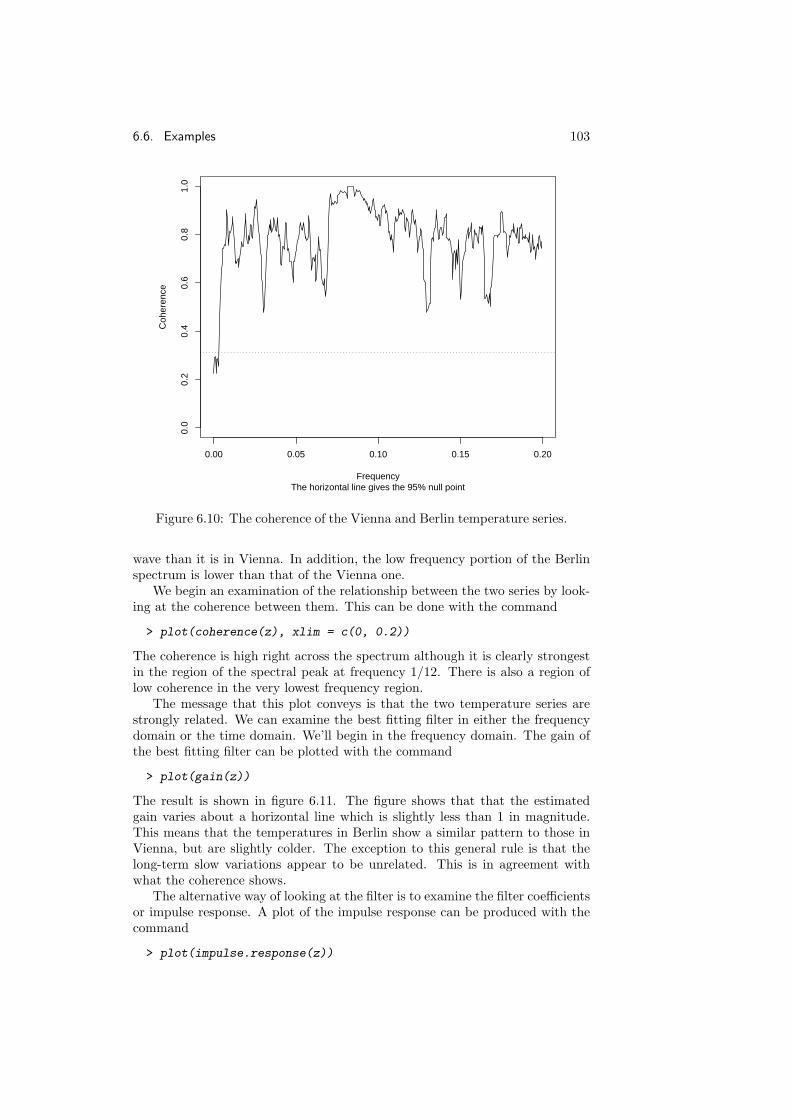

Time Series AnalysisLecture Notes for 475.726

Ross Ihaka

Statistics DepartmentUniversity of Auckland

April 14, 2005

ii

Contents

1 Introduction 11.1 Time Series . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2 Stationarity and Non-Stationarity . . . . . . . . . . . . . . . . . 11.3 Some Examples . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

1.3.1 Annual Auckland Rainfall . . . . . . . . . . . . . . . . . . 21.3.2 Nile River Flow . . . . . . . . . . . . . . . . . . . . . . . . 21.3.3 Yield on British Government Securities . . . . . . . . . . 21.3.4 Ground Displacement in an Earthquake . . . . . . . . . . 31.3.5 United States Housing Starts . . . . . . . . . . . . . . . . 31.3.6 Iowa City Bus Ridership . . . . . . . . . . . . . . . . . . . 3

2 Vector Space Theory 72.1 Vectors In Two Dimensions . . . . . . . . . . . . . . . . . . . . . 7

2.1.1 Scalar Multiplication and Addition . . . . . . . . . . . . . 72.1.2 Norms and Inner Products . . . . . . . . . . . . . . . . . 8

2.2 General Vector Spaces . . . . . . . . . . . . . . . . . . . . . . . . 92.2.1 Vector Spaces and Inner Products . . . . . . . . . . . . . 92.2.2 Some Examples . . . . . . . . . . . . . . . . . . . . . . . . 11

2.3 Hilbert Spaces . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122.3.1 Subspaces . . . . . . . . . . . . . . . . . . . . . . . . . . . 132.3.2 Projections . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.4 Hilbert Spaces and Prediction . . . . . . . . . . . . . . . . . . . . 142.4.1 Linear Prediction . . . . . . . . . . . . . . . . . . . . . . . 142.4.2 General Prediction . . . . . . . . . . . . . . . . . . . . . . 15

3 Time Series Theory 173.1 Time Series . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 173.2 Hilbert Spaces and Stationary Time Series . . . . . . . . . . . . . 183.3 The Lag and Differencing Operators . . . . . . . . . . . . . . . . 193.4 Linear Processes . . . . . . . . . . . . . . . . . . . . . . . . . . . 203.5 Autoregressive Series . . . . . . . . . . . . . . . . . . . . . . . . . 21

3.5.1 The AR(1) Series . . . . . . . . . . . . . . . . . . . . . . . 213.5.2 The AR(2) Series . . . . . . . . . . . . . . . . . . . . . . . 233.5.3 Computations . . . . . . . . . . . . . . . . . . . . . . . . . 26

3.6 Moving Average Series . . . . . . . . . . . . . . . . . . . . . . . . 293.6.1 The MA(1) Series . . . . . . . . . . . . . . . . . . . . . . 293.6.2 Invertibility . . . . . . . . . . . . . . . . . . . . . . . . . . 293.6.3 Computation . . . . . . . . . . . . . . . . . . . . . . . . . 30

iii

iv Contents

3.7 Autoregressive Moving Average Series . . . . . . . . . . . . . . . 303.7.1 The ARMA(1,1) Series . . . . . . . . . . . . . . . . . . . 313.7.2 The ARMA(p,q) Model . . . . . . . . . . . . . . . . . . . 323.7.3 Computation . . . . . . . . . . . . . . . . . . . . . . . . . 323.7.4 Common Factors . . . . . . . . . . . . . . . . . . . . . . . 34

3.8 The Partial Autocorrelation Function . . . . . . . . . . . . . . . 343.8.1 Computing the PACF . . . . . . . . . . . . . . . . . . . . 363.8.2 Computation . . . . . . . . . . . . . . . . . . . . . . . . . 37

4 Identifying Time Series Models 394.1 ACF Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . 394.2 PACF Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . 424.3 System Identification . . . . . . . . . . . . . . . . . . . . . . . . . 434.4 Model Generalisation . . . . . . . . . . . . . . . . . . . . . . . . . 45

4.4.1 Non-Zero Means . . . . . . . . . . . . . . . . . . . . . . . 454.4.2 Deterministic Trends . . . . . . . . . . . . . . . . . . . . . 474.4.3 Models With Non-stationary AR Components . . . . . . . 474.4.4 The Effect of Differencing . . . . . . . . . . . . . . . . . . 48

4.5 ARIMA Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

5 Fitting and Forecasting 515.1 Model Fitting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

5.1.1 Computations . . . . . . . . . . . . . . . . . . . . . . . . . 515.2 Assessing Quality of Fit . . . . . . . . . . . . . . . . . . . . . . . 545.3 Residual Correlations . . . . . . . . . . . . . . . . . . . . . . . . 585.4 Forecasting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

5.4.1 Computation . . . . . . . . . . . . . . . . . . . . . . . . . 595.5 Seasonal Models . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

5.5.1 Purely Seasonal Models . . . . . . . . . . . . . . . . . . . 615.5.2 Models with Short-Term and Seasonal Components . . . 635.5.3 A More Complex Example . . . . . . . . . . . . . . . . . 66

6 Frequency Domain Analysis 756.1 Some Background . . . . . . . . . . . . . . . . . . . . . . . . . . 75

6.1.1 Complex Exponentials, Sines and Cosines . . . . . . . . . 756.1.2 Properties of Cosinusoids . . . . . . . . . . . . . . . . . . 766.1.3 Frequency and Angular Frequency . . . . . . . . . . . . . 776.1.4 Invariance and Complex Exponentials . . . . . . . . . . . 77

6.2 Filters and Filtering . . . . . . . . . . . . . . . . . . . . . . . . . 786.2.1 Filters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 786.2.2 Transfer Functions . . . . . . . . . . . . . . . . . . . . . . 796.2.3 Filtering Sines and Cosines . . . . . . . . . . . . . . . . . 806.2.4 Filtering General Series . . . . . . . . . . . . . . . . . . . 806.2.5 Computing Transfer Functions . . . . . . . . . . . . . . . 816.2.6 Sequential Filtering . . . . . . . . . . . . . . . . . . . . . 81

6.3 Spectral Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . 826.3.1 The Power Spectrum . . . . . . . . . . . . . . . . . . . . . 826.3.2 The Cramer Representation . . . . . . . . . . . . . . . . . 836.3.3 Using The Cramer Representation . . . . . . . . . . . . . 856.3.4 Power Spectrum Examples . . . . . . . . . . . . . . . . . 86

Contents v

6.4 Statistical Inference . . . . . . . . . . . . . . . . . . . . . . . . . 886.4.1 Some Distribution Theory . . . . . . . . . . . . . . . . . . 886.4.2 The Periodogram and its Distribution . . . . . . . . . . . 906.4.3 An Example – Sunspot Numbers . . . . . . . . . . . . . . 916.4.4 Estimating The Power Spectrum . . . . . . . . . . . . . . 926.4.5 Tapering and Prewhitening . . . . . . . . . . . . . . . . . 956.4.6 Cross Spectral Analysis . . . . . . . . . . . . . . . . . . . 96

6.5 Computation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 996.5.1 A Simple Spectral Analysis Package for R . . . . . . . . . 996.5.2 Power Spectrum Estimation . . . . . . . . . . . . . . . . . 996.5.3 Cross-Spectral Analysis . . . . . . . . . . . . . . . . . . . 100

6.6 Examples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

vi Contents

Chapter 1

Introduction

1.1 Time Series

Time series arise as recordings of processes which vary over time. A recordingcan either be a continuous trace or a set of discrete observations. We willconcentrate on the case where observations are made at discrete equally spacedtimes. By appropriate choice of origin and scale we can take the observationtimes to be 1, 2, . . .T and we can denote the observations by Y1, Y2, . . . , YT .

There are a number of things which are of interest in time series analysis.The most important of these are:

Smoothing: The observed Yt are assumed to be the result of “noise” valuesεt additively contaminating a smooth signal ηt.

Yt = ηt + εt

We may wish to recover the values of the underlying ηt.

Modelling: We may wish to develop a simple mathematical model whichexplains the observed pattern of Y1, Y2, . . . , YT . This model may dependon unknown parameters and these will need to be estimated.

Forecasting: On the basis of observations Y1, Y2, . . . , YT , we may wish topredict what the value of YT+L will be (L ≥ 1), and possibly to give anindication of what the uncetainty is in the prediction.

Control: We may wish to intervene with the process which is producing theYt values in such a way that the future values are altered to produce afavourable outcome.

1.2 Stationarity and Non-Stationarity

A key idea in time series is that of stationarity. Roughly speaking, a timeseries is stationary if its behaviour does not change over time. This means, forexample, that the values always tend to vary about the same level and thattheir variability is constant over time. Stationary series have a rich theory and

1

2 Chapter 1. Introduction

their behaviour is well understood. This means that they play a fundamentalrole in the study of time series.

Obviously, not all time series that we encouter are stationary. Indeed, non-stationary series tend to be the rule rather than the exception. However, manytime series are related in simple ways to series which are stationary. Two im-portant examples of this are:

Trend models : The series we observe is the sum of a determinstic trendseries and a stationary noise series. A simple example is the linear trendmodel:

Yt = β0 + β1t+ εt.

Another common trend model assumes that the series is the sum of aperiodic “seasonal” effect and stationary noise. There are many othervariations.

Integrated models : The time series we observe satisfies

Yt+1 − Yt = εt+1

where εt is a stationary series. A particularly important model of this kindis the random walk. In that case, the εt values are independent “shocks”which perturb the current state Yt by an amount εt+1 to produce a newstate Yt+1.

1.3 Some Examples

1.3.1 Annual Auckland Rainfall

Figure 1.1 shows the annual amount of rainfall in Auckland for the years from1949 to 2000. The general pattern of rainfall looks similar throughout the record,so this series could be regarded as being stationary. (There is a hint that rainfallamounts are declining over time, but this type of effect can occur over shortishtime spans for stationary series.)

1.3.2 Nile River Flow

Figure 1.2 shows the flow volume of the Nile at Aswan from 1871 to 1970. Theseare yearly values. The general pattern of this data does not change over timeso it can be regarded as stationary (at least over this time period).

1.3.3 Yield on British Government Securities

Figure 1.3 shows the percentage yield on British Government securities, monthlyover a 21 year period. There is a steady long-term increase in the yields. Overthe period of observation a trend-plus-stationary series model looks like it mightbe appropriate. An integrated stationary series is another possibility.

1.3. Some Examples 3

1.3.4 Ground Displacement in an Earthquake

Figure 1.4 shows one component of the horizontal ground motion resulting froman earthquake. The initial motion (a little after 4 seconds) corresponds to thearrival of the p-wave and the large spike just before six seconds corresponds tothe arrival of the s-wave. Later features correspond to the arrival of surfacewaves. This is an example of a transient signal and cannot have techniquesappropriate for stationary series applied to it.

1.3.5 United States Housing Starts

Figure 1.5 shows the monthly number of housing starts in the Unites States (inthousands). Housing starts are a leading economic indicator. This means thatan increase in the number of housing starts indicates that economic growth islikely to follow and a decline in housing starts indicates that a recession may beon the way.

1.3.6 Iowa City Bus Ridership

Figure 1.6 shows the monthly average weekday bus ridership for Iowa City overthe period from September 1971 to December 1982. There is clearly a strongseasonal effect suprimposed on top of a general upward trend.

4 Chapter 1. Introduction

Year

Ann

ual R

ainf

all (

cm)

1950 1960 1970 1980 1990 2000

80

100

120

140

160

180

200

Figure 1.1: Annual Auckland rainfall (in cm) from 1949 to 2000 (fromPaul Cowpertwait).

Year

Flo

w

1880 1900 1920 1940 1960

600

800

1000

1200

1400

Figure 1.2: Flow volume of the Nile at Aswan from 1871 to 1970 (fromDurbin and Koopman).

1.3. Some Examples 5

Month

Per

cent

0 50 100 150 200 250

2

4

6

8

Figure 1.3: Monthly percentage yield on British Government securitiesover a 21 year period (from Chatfield).

Seconds

Dis

plac

emen

t

0 2 4 6 8 10 12

−100

0

100

200

300

400

500

Figure 1.4: Horizontal ground displacement during a small Nevadaearthquake (from Bill Peppin).

6 Chapter 1. Introduction

Time

Hou

sing

Sta

rts

(000

s)

1966 1968 1970 1972 1974

50

100

150

200

Figure 1.5: Housing starts in the United States (000s) (from S-Plus).

Time

Ave

rage

Wee

kly

Rid

ersh

ip

1972 1974 1976 1978 1980 1982

4000

6000

8000

10000

Figure 1.6: Average weekday bus ridership, Iowa City (monthly ave)Sep 1971 - Dec 1982.

Chapter 2

Vector Space Theory

2.1 Vectors In Two Dimensions

The theory which underlies time series analysis is quite technical in nature.In spite of this, a good deal of intuition can be developed by approaching thesubject geometrically. The geometric approach is based on the ideas of vectorsand vector spaces.

2.1.1 Scalar Multiplication and Addition

A good deal can be learnt about the theory of vectors by considering the two-dimensional case. You can think of two dimensional vectors as being littlearrows which have a length and a direction. Individual vectors can be stretched(altering their length but not their direction) and pairs of vectors can be addedby placing them head to tail.

To get more precise, we’ll suppose that a vector v extends for a distance xin the horizontal direction and a distance y in the vertical direction. This givesus a representation of the vector as a pair of numbers and we can write it as

v = (x, y).

Doubling the length of the vector doubles the x and y values. In a similarway we can scale the length of the vector by any value, and this results in asimilar scaling of the x and y values. This gives us a natural way of definingmultiplication of a vector by a number.

cv = (cx, cy)

A negative value for c produces a reversal of direction as well as change of lengthof magnitude |c|.

Adding two vectors amounts to placing them head to tail and taking the sumto be the arrow which extends from the base of the first to the head of the second.This corresponds to adding the x and y values corresponding to the vectors. Fortwo vectors v1 = (x1, y1) and v2 = (x2, y2) the result is (x1 + x2, y1 + y2). Thiscorresponds to a natural definition of addition for vectors.

v1 + v2 = (x1 + x2, y1 + y2)

7

8 Chapter 2. Vector Space Theory

2.1.2 Norms and Inner Products

While coordinates give a complete description of vectors, it is often more usefulto describe them in terms of the lengths of individual vectors and the anglesbetween pairs of vectors. If we denote the length of a vector by ‖u‖, then byPythagoras’ theorem we know

‖u‖ =√x2 + y2.

Vector length has a number of simple properties:

Positivity: For every vector u, we must have ‖u‖ > 0, with equality if andonly if u = 0.

Linearity: For every scalar c and vector u we have ‖cu‖ = |c|‖u‖.

The Triangle Inequality: If u and v are vectors, then ‖u + v‖ 6 ‖u‖+ ‖v‖.

The first and second of these properties are obvious, and the third is simplya statement that the shortest distance between two points is a straight line.The technical mathematical name for the length of a vector is the norm of thevector.

Although the length of an individual vector gives some information aboutit, it is also important to consider the angles between pairs of vectors. Supposethat we have vectors v1 = (x1, y1) and v2 = (x2, y2), and that we want to knowthe angle between them. If v1 subtends an angle θ1 with the x axis and v2

subtends an angle θ2 with the x axis, simple geometry tells us that:

cos θi =xi

‖vi‖,

sin θi =yi

‖vi‖.

The angle we are interested in is θ1− θ2 and the cosine of this can be computedusing the formulae:

cos(α− β) = cosα cosβ + sinα sinβ

sin(α− β) = sinα cosβ − cosα sinβ,

so thatcos(θ1 − θ2) =

x1x2 + y1y2‖v1‖‖v2‖

sin(θ1 − θ2) =x2y1 − x1y2‖v1‖‖v2‖

.

Knowledge of the sine and cosine values makes it possible to compute the anglebetween the vectors.

There are actually two angles between a pair of vectors; one measured clock-wise and one measured counter-clockwise. Often we are interested in the smallerof these two angles. This can be determined from the cosine value (becausecos θ = cos−θ). The cosine is determined by the lengths of the two vectorsand the quantity x1x2 + y1y2. This quantity is called the inner product of thevectors v1 and v2 and is denoted by 〈v1,v2〉. Inner products have the followingbasic properties.

2.2. General Vector Spaces 9

Positivity: For every vector v, we must have 〈v,v〉 > 0, with 〈v,v〉 = 0 onlywhen v = 0.

Linearity: For all vectors u, v, and w; and scalars α and β; we must have〈αu + βv,w〉 = α〈u,w〉+ β〈v,w〉.

Symmetry: For all vectors u and v, we must have 〈u,v〉 = 〈v,u〉 (or in thecase of complex vector spaces 〈u,v〉 = 〈v,u〉, where the bar indicates acomplex conjugate).

It is clear that the norm can be defined in terms of the inner product by

‖v‖2 = 〈v,v〉.

It is easy to show that the properties of the norm ‖v‖ follow from those of theinner product.

Two vectors u and v are said to be orthogonal if 〈u,v〉 = 0. This meansthat the vectors are “at right angles” to each other.

2.2 General Vector Spaces

The theory and intuition obtained from studying two-dimensional vectors car-ries over into more general situations. It is not the particular representationof vectors as pairs of coordinates which is important but rather the ideas ofaddition, scalar multiplication and inner-product which are important.

2.2.1 Vector Spaces and Inner Products

The following concepts provide an abstract generalisation of vectors in two di-mensions.

1. A vector space is a set of objects, called vectors, which is closed underaddition and scalar multiplication. This means that when vectors arescaled or added, the result is a vector.

2. An inner product on a vector space is a function which takes two vectorsu and v and returns a scalar denoted by 〈 u,v 〉 which has the conditionsof positivity, linearity and symmetry described in section 2.1.2. A vectorspace with an associated inner product is called an inner product space.

3. The norm associated with an inner product space is defined in terms ofthe inner product as ‖u‖ =

√〈u,u〉.

These ideas can be applied to quite general vector spaces. Although it mayseem strange to apply ideas of direction and length to some of these spaces,thinking in terms of two and three dimensional pictures can be quite useful.

Example 2.2.1 The concept of two-dimensional vectors can be generalised bylooking at the set of n-tuples of the form u = (u1, u2, . . . , un), where each ui isa real number. With addition and scalar multiplication defined element-wise,

10 Chapter 2. Vector Space Theory

the set of all such n-tuples forms a vector space, usually denoted by Rn. Aninner product can be defined on the space by

〈u,v〉 =n∑

i=1

uivi,

and this produces the norm

‖u‖ =

(n∑

i=1

u2i

) 12

.

This generalisation of vector ideas to n dimensions provides the basis for agood deal of statistical theory. This is especially true for linear models andmultivariate analysis.

We will need a number of fundamental results on vector spaces. These followdirectly from the definition of vector space, inner-product and norm, and do notrely on any special assumptions about the kind of vectors being considered.

The Cauchy-Schwarz Inequality. For any two vectors u and v

|〈u,v〉| 6 ‖u‖‖v‖. (2.1)

Proof : For any two vectors u and v and scalars α and β,

0 6 ‖αu− βv‖2 = 〈αu− βv, αu− βv〉 = α2‖u‖2 − 2αβ〈u,v〉+ β2‖v‖2

Setting α = ‖v‖ and β = 〈u,v〉/‖v‖ yields

0 6 ‖u‖2‖v‖2 − 2〈u,v〉2 + 〈u,v〉2 = ‖u‖2‖v‖2 − 〈u,v〉2.

This can be rewritten as|〈u,v〉| 6 ‖u‖‖v‖.

The Triangle Inequality. For any two vectors u and v,

‖u + v‖ 6 ‖u‖+ ‖v‖.

Proof : For any u and v

‖u + v‖2 = 〈u + v,u + v〉= 〈u,u〉+ 〈u,v〉+ 〈v,u〉+ 〈v,v〉6 ‖u‖2 + 2‖u‖‖v‖+ ‖v‖2 (Cauchy-Schwarz)

= (‖u‖+ ‖v‖)2

The Angle Between Vectors. The Cauchy-Schwarz inequality means that

−1 6〈x,y〉‖x‖‖y‖

6 1.

This means that just as in the 2-d case we can define the angle betweenvectors u and v by

θ = cos−1 〈x,y〉‖x‖‖y‖

.

2.2. General Vector Spaces 11

2.2.2 Some Examples

The ideas in abstract vector space theory are derived from the concrete ideas ofvectors in 2 and 3 dimensions. The real power of vector space theory is that itapplies to much more general spaces. To show off the generality of the theorywe’ll now look at a couple of examples of less concrete spaces.

Example 2.2.2 The set F of all (real-valued) random variables with EX = 0and E|X|2 <∞ is a vector space, because for any choice of X1 and X2 from Fand scalars β1 and β2

E[β1X1 + β2X2] = 0

andE|β1X1 + β2X2|2 <∞.

It is possible to define an inner product on this vector space by

〈X,Y 〉 = EXY.

This in turn produces the norm

‖X‖ =(E|X|2

) 12 ,

which is just the standard deviation of X.The cosine of the angle between random variables is defined as

EXY√E|X|2E|Y |2

,

which is recognisable as the correlation between the X and Y .(There is a technical problem with uniqueness in this case. Any random

variable which has probability 1 of being zero will have 〈X,X〉 = 0, whichviolates the requirement that this only happen for X = 0. The workaround is toregard random variables as identical if they are the same with probability one.)

Example 2.2.3 The set of all continuous functions from [−1, 1] to R is a vectorspace because there is a natural definition of addition and scalar multiplicationfor such functions.

(f + g)(x) = f(x) + g(x)(βf)(x) = βf(x)

A natural inner-product can be defined on this space by

〈f, g〉 =∫ 1

−1

f(x)g(x) dx.

Vector space theory immediately gets us results such as∣∣∣∣∫ 1

−1

f(x)g(x) dx∣∣∣∣ 6 (∫ 1

−1

f(x)2 dx)1/2(∫ 1

−1

g(x)2 dx)1/2

,

which is just a restatement of the Cauchy-Schwarz inequality.

12 Chapter 2. Vector Space Theory

There is also a technical uniqueness problem in this case. This is handledby regarding functions f and g as equal if∫ 1

−1

|f(x)− g(x)|2 dx = 0.

This happens, for example, if f and g differ only on a finite or countably infiniteset of points. Integration theory gives a characterisation in terms of sets with“measure zero.”

2.3 Hilbert Spaces

The vector spaces we’ve looked at so far work perfectly well for performing finiteoperations such as forming linear combinations. However, there can be problemswhen considering limits.

Consider the case of example 2.2.3. Each of the functions fn defined by

fn(x) =

0, x < − 1

n,

nx+ 12

, − 1n

6 x 61n,

1, x >1n,

is continuous and the sequence obviously converges to the function

f(x) =

0, x < 0,1/2, x = 0,1, x > 0.

This limit function is not in the space under consideration because it is notcontinuous.

Hilbert spaces add a requirement of completeness to those for an inner prod-uct space. In Hilbert spaces, sequences that look like they are converging willactually converge to an element of the space. To make this precise we need todefine the meaning of convergence.

Convergence. Suppose that {un} is a sequence of vectors and u is a vectorsuch that ‖un − u‖ → 0, then un is said to converge to u and this is denotedby un → u.

If {un} is a sequence of vectors such that the un → u and v is any vectorthen, by the Cauchy-Schwarz inequality 〈un,v〉 → 〈u,v〉. In a similar way‖un‖ → ‖u‖. These properties are referred to as continuity of the inner productand norm.

A sequence for which limm,n→∞ ‖um−un‖ → 0 is called a Cauchy sequence.It is easy to see that every convergent sequence is a Cauchy sequence. If con-versely every Cauchy sequence converges to an element of the space, the spaceis said to be complete. A complete inner product space is called a Hilbert space.

Hilbert spaces preserve many of the important properties of Rn. In particularthe notions of length and direction retain their intuitive meanings. This makesit possible to carry out mathematical arguments geometrically and even to usepictures to understand what is happening in quite complex cases.

2.3. Hilbert Spaces 13

2.3.1 Subspaces

A subset M of a Hilbert space H is called a linear manifold if whenever u andv are elements of M then so is αu + βv. A linear manifold which contains thelimit of every Cauchy sequence of its elements is called a linear subspace of H.A linear subspace of a Hilbert space is itself a Hilbert space.

A vector v is orthogonal to a subspace M if 〈v,u〉 = 0 for every u ∈ M.The set all vectors which are orthogonal to M is itself a subspace denoted byM⊥ and called the orthogonal complement of M.

A set of vectors {vλ : λ ∈ Λ} is said to generate a linear subspace M if M isthe smallest subspace containing those vectors. It is relatively straightforwardto show that the subspace consists of all linear combinations of the vλs togetherwith the limits of all Cauchy sequences formed from these linear combinations.

We will use the notation sp{vλ : λ ∈ Λ} to indicate the subspace generatedby the random variables {vλ : λ ∈ Λ}.

2.3.2 Projections

If M is a subspace of a Hilbert space H and v is a vector not in M then thedistance from M to v is defined to be minu∈M ‖v − u‖. A crucial result inHilbert space theory tells us about how this minimum is attained.

The Projection Theorem. There is a unique vector PMv ∈M such that

‖v − PMv‖ = minu∈M

‖v − u‖.

The vector PMv satisfies PMv ∈M and v − PMv ∈M⊥. It is called theorthogonal projection of v on M.

When M is generated by a set of elements {uλ : λ ∈ Λ}, the conditionv−PMv ∈M⊥ is equivalent to the condition (v−PMv) ⊥ uλ for every λ ∈ Λ.In other words, 〈v−PMv,uλ〉 = 0 for every λ ∈ Λ. This produces the equations

〈PMv,uλ〉 = 〈v,uλ〉, λ ∈ Λ,

which together with the requirement PMv ∈M, completely determines PMv.When a subspace of a Hilbert space is generated by a countable set of or-

thogonal vectors {ξn}, the orthogonal projection has the form

PMv =∑

n

〈v, ξn〉‖ξn‖2

ξn

In the case of a finite set {ξ1, . . . , ξn} this is easy to see.

〈v, ξ1〉‖ξ1‖2

ξ1 + · · ·+ 〈v, ξn〉‖ξn‖2

ξn

In addition, the orthogonality of {ξ1, . . . , ξn} means⟨〈v, ξ1〉‖ξ1‖2

ξ1 + · · ·+ 〈v, ξn〉‖ξn‖2

ξn, ξi

⟩=〈v, ξi〉‖ξi‖2

〈ξi, ξi〉

= 〈v, ξi〉

14 Chapter 2. Vector Space Theory

so the conditions above are verified.The general (countable) case follows from the continuity of the norm and

inner product.

2.4 Hilbert Spaces and Prediction

Consider the Hilbert space H consisting of all finite-variance random variableson some probability space, with inner product defined by

〈X,Y 〉 = EXY .

We will now look at the problem of predicting a variable Y using zero, one ormore predicting random variables X1, . . . , Xn.

2.4.1 Linear Prediction

The problem can be stated as follows. Given a “response” random variable Yand predictor random variables X1, . . . , Xn, what is the best way of predictingY using a linear function of the Xs. This amounts to finding the coefficientswhich minimise the mean squared error

E|Y − β0 − β1X1 − · · · − βnXn|2,

or, in a Hilbert space setting,

‖Y − β0 − β1X1 − · · · − βnXn‖2.

The variables {1, X1, . . . , Xn} generate a subspace M of H, and the minimi-sation problem above amounts to finding the projection PMY . We’ll approachthis problem in steps, beginning with n = 0.

The subspace C generated by the constant random variable 1 consists of allconstant random variables. Using the result above, the projection of a randomvariable Y with mean µY and variance σ2

Y onto this subspace is

PCY =〈Y, 1〉‖1‖2

1 = EY = µY .

This tells us immediately that the value of c which minimises E[Y − c]2 is µY .Now consider the subspace L generated by 1 and a single random variable

X with mean µX and variance σ2X . This is clearly the same as the subspace

generated by 1 and X − EX. Since 1 and X − EX are orthogonal, we can usethe projection result of the previous section to compute the projection of Y ontoL.

PLY =〈Y, 1〉‖1‖2

1 +〈Y,X − EX〉‖X − EX‖2

(X − EX)

= EY +〈Y − EY,X − EX〉

‖X − EX‖2(X − EX) +

〈EY,X − EX〉‖X − EX‖2

(X − EX)

= EY +〈Y − EY,X − EX〉

‖X − EX‖2(X − EX)

2.4. Hilbert Spaces and Prediction 15

because 〈EY,X − EX〉 = 0.Now 〈Y − EY,X − EX〉 = cov(Y,X) which is in turn equal to ρY XσY σX ,

where ρYX is the correlation between Y and X. This means that

PLY = µY + ρYXσY

σX(X − µX).

PLY is the best possible linear prediction of Y based on X, because among allpredictions of the form β0 + β1X, it is the one which minimises

E(Y − β0 − β1X)2.

The general case of n predictors proceeds in exactly the same way, but ismore complicated because we must use progressive orthogonalisation of the setof variables {1, X1, . . . , Xn}. The final result is that the best predictor of Y is

PLY = µY + ΣYXΣ−1XX(X − µX),

where X represents the variables X1, . . . , Xn assembled into a vector, µX isthe vector made up of the means of the Xs, ΣYX is the vector of covariancesbetween Y and each of the Xs, and ΣXX is the variance-covariance matrix ofthe Xs.

2.4.2 General Prediction

It is clear that linear prediction theory can be developed using Hilbert spacetheory. What is a little less clear is that Hilbert space theory also yields ageneral non-linear prediction theory.

Linear prediction theory uses only linear information about the predictorsand there is much more information available. In the one variable case, theadditional information can be obtained by considering all possible (Borel) func-tions φ(X). These are still just random variables and so generate a subspaceM of H. The projection onto this subspace gives the best possible predictor ofY based on X1, . . . , Xn.

With some technical mathematics it is possible to show that this projectionis in fact just the conditional expectation E[Y |X]. More generally, it is possibleto show that the best predictor of Y based on X1, . . . , Xn is E[Y |X1, . . . , Xn].

Although this is theoretically simple, it requires very strong assumptionsabout the distribution of Y andX1, . . . , Xn to actually compute an explicit valuefor the prediction. The simplest assumption to make is that Y and X1, . . . , Xn

have a joint normal distribution. In this case, the general predictor and thelinear one are identical.

Because of this it is almost always the case that linear prediction is preferredto general prediction.

16 Chapter 2. Vector Space Theory

Chapter 3

Time Series Theory

3.1 Time Series

We will assume that the time series values we observe are the realisations ofrandom variables Y1, . . . , YT , which are in turn part of a larger stochastic process{Yt : t ∈ Z}. It is this underlying process that will be the focus for our theoreticaldevelopment.

Although it is best to distinguish the observed time series from the under-lying stochastic process, the distinction is usually blurred and the term timeseries is used to refer to both the observations and the underlying process whichgenerates them.

The mean and the variance of random variables have a special place in thetheory of statistics. In time series analysis, the analogs of these are the meanfunction and the autocovariance function.

Definition 3.1.1 (Mean and Autocovariance Functions): The mean functionof a time series is defined to be µ(t) = EYt and the autocovariance function isdefined to be γ(s, t) = cov(Ys, Yt).

The mean and the autocovariance functions are fundamental parameters andit would be useful to obtain sample estimates of them. For general time seriesthere are 2T + T (T − 1)/2 parameters associated with Y1, . . . , YT and it is notpossible to estimate all these parameters from T data values.

To make any progress at all we must impose constraints on the time serieswe are investigating. The most common constraint is that of stationarity. Thereare two common definitions of stationarity.

Definition 3.1.2 (Strict Stationarity): A time series {Yt : t ∈ Z} is said to bestrictly stationary if for any k > 0 and any t1, . . . , tk ∈ Z, the distribution of

(Yt1 , . . . , Ytk)

is the same as that for(Yt1+u, . . . , Ytk+u)

for every value of u.

17

18 Chapter 3. Time Series Theory

This definition says that the stochastic behaviour of the process does notchange through time. If Yt is stationary then

µ(t) = µ(0)

andγ(s, t) = γ(s− t, 0).

So for stationary series, the mean function is constant and the autocovariancefunction depends only on the time-lag between the two values for which thecovariance is being computed.

These two restrictions on the mean and covariance functions are enough fora reasonable amount of theory to be developed. Because of this a less restrictivedefinition of stationarity is often used in place of strict stationarity.

Definition 3.1.3 (Weak Stationarity): A time series is said to be weakly, wide-sense or covariance stationary if E|Yt|2 <∞, µ(t) = µ and γ(t+ u, t) = γ(u, 0)for all t and u.

In the case of Gaussian time series, the two definitions of stationarity areequivalent. This is because the finite dimensional distributions of the time seriesare completely characterised by the mean and covariance functions.

When time series are stationary it is possible to simplify the parameteri-sation of the mean and autocovariance functions. In this case we can definethe mean of the series to be µ = E(Yt) and the autocovariance function to beγ(u) = cov(Yt+u, Yt). We will also have occasion to examine the autocorrelationfunction

ρ(u) =γ(u)γ(0)

= cor(Yt+u, Yt).

Example 3.1.1 (White Noise) If the random variables which make up {Yt}are uncorrelated, have means 0 and variance σ2, then {Yt} is stationary withautocovariance function

γ(u) ={σ2 u = 0,0 otherwise.

This type of series is referred to as white noise.

3.2 Hilbert Spaces and Stationary Time Series

Suppose that {Yt : t ∈ Z} is a stationary zero-mean time series. We can considerthe Hilbert space H generated by the random variables {Yt : t ∈ Z} with innerproduct

〈X,Y 〉 = E(XY ),

and norm‖X‖2 = E|X|2.

At a given time t, we can consider the subspace M generated by the randomvariables {Yu : u 6 t}. This subspace represents the past and present of theprocess. Future values of the series can be predicted by projecting onto the

3.3. The Lag and Differencing Operators 19

subspace M. For example, Yt+1 can be predicted by PMYt+1, Yt+1 by PMYt+2

and so on.Computing these predictions requires a knowledge of the autocovariance

function of the time series and typically this is not known. We will spend agood deal of this chapter studying simple parametric models for time series. Byfitting such models we will be able to determine the covariance structure of thetime series and so be able to obtain predictions or forecasts of future values.

3.3 The Lag and Differencing Operators

The lag operator L is defined for a time series {Yt} by

LYt = Yt−1.

The operator can be defined for linear combinations by

L(c1Yt1 + c2Yt2) = c1Yt1−1 + c2Yt2−1

and can be extended to all of H by a suitable definition for limits.In addition to being linear, the lag operator preserves inner products.

〈LYs, LYt〉 = cov(Ys−1, Yt−1)= cov(Ys, Yt)= 〈Ys, Yt〉

(An operator of this type is called a unitary operator.)There is a natural calculus of operators on H. For example we can define

powers of L naturally by

L2Yt = LLYt = LYt−1 = Yt−2

L3Yt = LL2Yt = Yt−3

...

LkYt = Yt−k

and linear combinations by

(αLk + βLl)Yt = αYt−k + βYt−l.

Other operators can be defined in terms in terms of L. The differencingoperator defined by

∇Yt = (1− L)Yt = Yt − Yt−1

is of fundamental importance when dealing with models for non-stationary timeseries. Again, we can define powers of this operator

∇2Yt = ∇(∇Yt)= ∇(Yt − Yt−1)= (Yt − Yt−1)− (Yt−1 − Yt−2)= Yt − 2Yt−1 + Yt−2.

We will not dwell on the rich Hilbert space theory associated with time series,but it is important to know that many of the operator manipulations which wewill carry out can be placed on a rigorous footing.

20 Chapter 3. Time Series Theory

3.4 Linear Processes

We will now turn to an examination of a large class of useful time series models.These are almost all defined in terms of the lag operator L. As the simplestexample, consider the autoregressive model defined by:

Yt = φYt−1 + εt, (3.1)

where φ is a constant with |φ| < 1 and εt is a sequence of uncorrelated randomvariables, each with with mean 0 and variance σ2. From a statistical point ofview this“model”makes perfect sense, but is not clear that any Yt which satisfiesthis equation exists.

One way to see that there is a solution is to re-arrange equation 3.1 andwrite it in its operator form.

(1− φL)Yt = εt.

Formally inverting the operator (1− φL) leads to

Yt = (1− φL)−1εt

=∞∑

u=0

φuLuεt

=∞∑

u=0

φuεt−u.

The series on the right is defined as the limit as n→∞ ofn∑

u=0

φuεt−u.

Loosely speaking, this limit exists if

‖∞∑

u=n+1

φuεt−u‖2 → 0.

Since

‖∞∑

u=n+1

φuεt−u‖2 = var(∞∑

u=n+1

φuεt−u)

=∞∑

u=n+1

|φ|2uσ2

and |φ| < 1, there is indeed a well-defined solution of 3.1. Further, this solutioncan be written as an (infinite) moving average of current and earlier εt values.

This type of infinite moving average plays a special role in the theory of timeseries.

Definition 3.4.1 (Linear Processes) The time series Yt defined by

Yt =∞∑

u=−∞ψuεt−u

3.5. Autoregressive Series 21

where εt is a white-noise series and

∞∑u=−∞

|ψu|2 <∞

is called a linear process.

The general linear process depends on both past and future values of εt. Alinear process which depends only on the past and present values of εt is saidto be causal. Causal processes are preferred for forecasting because they reflectthe way in which we believe the real world works.

Many time series can be represented as linear processes. This provides aunifying underpinning for time series theory, but may be of limited practicalinterest because of the potentially infinite number of parameters required.

3.5 Autoregressive Series

Definition 3.5.1 (Autoregressive Series) If Yt satisfies

Yt = φ1Yt−1 + · · ·+ φpYt−p + εt

where εt is white-noise and the φu are constants, then Yt is called an autore-gressive series of order p, denoted by AR(p).

Autoregressive series are important because:

1. They have a natural interpretation — the next value observed is a slightperturbation of a simple function of the most recent observations.

2. It is easy to estimate their parameters. It can be done with standardregression software.

3. They are easy to forecast. Again standard regression software will do thejob.

3.5.1 The AR(1) Series

The AR(1) series is defined by

Yt = φYt−1 + εt. (3.2)

Because Yt−1 and εt are uncorrelated, the variance of this series is

var(Yt) = φ2var(Yt−1) + σ2ε .

If {Yt} is stationary then var(Yt) = var(Yt−1) = σ2Y and so

σ2Y = φ2σ2

Y + σ2ε . (3.3)

This implies thatσ2

Y > φ2σ2Y

and hence1 > φ2.

22 Chapter 3. Time Series Theory

There is an alternative view of this, using the operator formulation of equa-tion 3.2, namely

(1− φL)Yt = εt

It is possible to formally invert the autoregressive operator to obtain

(1− φL)−1 =∞∑

u=0

φuLu.

Applying this to the series {εt} produces the representation

Yt =∞∑

u=0

φuεt−u. (3.4)

If |φ| < 1 this series converges in mean square because∑|φ|2u <∞. The limit

series is stationary and satisfies equation 3.2. Thus, if |φ| < 1 then there isa stationary solution to 3.2. An equivalent condition is that the root of theequation

1− φz = 0

(namely 1/φ) lies outside the unit circle in the complex plane.If |φ| > 1 the series defined by 3.4 does not converge. We can, however,

rearrange the defining equation 3.2 in the form

Yt =1φYt+1 −

1φεt+1,

and a similar argument to that above produces the representation

Yt = −∞∑

u=0

φ−uεt+u.

This series does converge, so there is a stationary series Yt which satisfies 3.2.The resulting series is generally not regarded as satisfactory for modelling andforecasting because it is not causal, i.e. it depends on future values of εt.

If |φ| = 1 there is no stationary solution to 3.2. This means that for thepurposes of modelling and forecasting stationary time series, we must restrictour attention to series for which |φ| < 1 or, equivalently, to series for which theroot of the polynomial 1− φz lies outside the unit circle in the complex plane.

If we multiply both sides of equation 3.2 by Yt−u and take expectations weobtain

E(YtYt−u) = φE(Yt−1Yt−u) + E(εtYt−u).

The term on the right is zero because, from the linear process representation, εt

is independent of earlier Yt values. This means that the autocovariances mustsatisfy the recursion

γ(u) = φγ(u− 1), u = 1, 2, 3, . . . .

This is a first-order linear difference equation with solution

γ(u) = φuγ(0), u = 0, 1, 2, . . .

3.5. Autoregressive Series 23

φ1 = 0.7

0 2 4 6 8 10 12 14

−1.0

−0.5

0.0

0.5

1.0

φ1 = −0.7

AC

F

0 2 4 6 8 10 12 14

−1.0

−0.5

0.0

0.5

1.0

Figure 3.1: Autocorrelation functions for two of AR(1) models.

By rearranging equation 3.3 we find γ(0) = σ2ε/(1− φ2), and hence that

γ(u) =φuσ2

ε

1− φ2, u = 0, 1, 2, . . .

This in turn means that the autocorrelation function is given by

ρ(u) = φu, u = 0, 1, 2, . . .

The autocorrelation functions for the the AR(1) series with φ1 = .7 andφ1 = −.7 are shown in figure 3.1. Both functions show exponential decay.

3.5.2 The AR(2) Series

The AR(2) model is defined by

Yt = φ1Yt−1 + φ2Yt−2 + εt (3.5)

or, in operator form(1− φ1L− φ2L

2)Yt = εt.

As in the AR(1) case we can consider inverting the AR operator. To see whetherthis is possible, we can consider factorising the operator

1− φ1L− φ2L2

and inverting each factor separately. Suppose that

1− φ1L− φ2L2 = (1− c1L)(1− c2L),

24 Chapter 3. Time Series Theory

then it is clear that we can invert the operator if we can invert each factorseparately. This is possible if |c1| < 1 and |c2| < 1, or equivalently, if the rootsof the polynomial

1− φ1z − φ2z2

lie outside the unit circle. A little algebraic manipulation shows that this isequivalent to the conditions:

φ1 + φ2 < 1, −φ1 + φ2 < 1, φ2 > −1.

These constraints define a triangular region in the φ1, φ2 plane. The region isshown as the shaded triangle in figure 3.3.

The autocovariance function for the AR(2) series can be investigated bymultiplying both sides of equation 3.5 by Yt−u and taking expectations.

E(YtYt−u) = φ1E(Yt−1Yt−u) + φ2E(Yt−2Yt−u) + E(εtYt−u).

This in turns leads to the recurrence

γ(u) = φ1γ(u− 1) + φ2γ(u− 2)

with initial conditions

γ(0) = φ1γ(−1) + φ2γ(−2) + σ2ε

γ(1) = φ1γ(0) + φ2γ(−1).

or, using the fact that γ(−u) = γ(u),

γ(0) = φ1γ(1) + φ2γ(2) + σ2ε

γ(1) = φ1γ(0) + φ2γ(1).

The solution to these equations has the form

γ(u) = A1Gu1 +A2G

u2

where G−11 and G−1

2 are the roots of the polynomial

1− φ1z − φ2z2 (3.6)

and A1 and A2 are constants that can be determined from the initial conditions.In the case that the roots are equal, the solution has the general form

γ(u) = (A1 +A2u)Gu

These equations indicate that the autocovariance function for the AR(2) serieswill exhibit (exponential) decay as u→∞.

If Gk corresponds to a complex root, then

Gk = |Gk|eiθk

and henceGu

k = |Gk|ueiθku = |Gk|u(cos θku+ i sin θku)

Complex roots will thus introduce a pattern of decaying sinusoidal variationinto the covariance function (or autocorrelation function). The region of theφ1, φ2 plane corresponding to complex roots is indicated by the cross-hatchedregion in figure 3.3.

3.5. Autoregressive Series 25

φ1 = 0.5, φ2 = 0.3

Lag

0 2 4 6 8 10 12 14

−1.0

−0.5

0.0

0.5

1.0

φ1 = 1, φ2 = −0.5

Lag

AC

F

0 2 4 6 8 10 12 14

−1.0

−0.5

0.0

0.5

1.0

φ1 = −0.5, φ2 = 0.3

0 2 4 6 8 10 12 14

−1.0

−0.5

0.0

0.5

1.0

φ1 = −0.5, φ2 = −0.3

AC

F

0 2 4 6 8 10 12 14

−1.0

−0.5

0.0

0.5

1.0

Figure 3.2: Autocorrelation functions for a variety of AR(2) models.

26 Chapter 3. Time Series Theory

−2 −1 0 1 2

−1

0

1

φ1

φ2

Figure 3.3: The regions of φ1/φ2 space where the series produced by theAR(2) scheme is stationary (indicated in grey) and has complex roots(indicated by cross-hatching).

The AR(p) Series

The AR(p) series is defined by

Yt = φ1Yt−1 + · · ·+ φpYt−p + εt (3.7)

If the roots of1− φ1z − · · · − φpz

p (3.8)

lie outside the unit circle, there is a stationary causal solution to 3.7.The autocovariance function can be investigated by multiplying equation 3.7

by Yt−u and taking expectations. This yields

γ(u) = φ1γ(u− 1) + · · ·+ φpγ(u− p).

This is a linear homogeneous difference equation and has the general solution

γ(u) = A1Gu1 + · · ·+ApG

up

(this is for distinct roots), where G1,. . . ,Gp are the reciprocals of the rootsof equation 3.8. Note that the stationarity condition means that γ(u) → 0,exhibiting exponential decay. As in the AR(2) case, complex roots will introduceoscillatory behaviour into the autocovariance function.

3.5.3 Computations

R contains a good deal of time series functionality. On older versions of R (thoseprior to 1.7.0) you will need to type the command

3.5. Autoregressive Series 27

> library(ts)

to ensure that this functionality is loaded.The function polyroot can be used to find the roots of polynomials and so

determine whether a proposed model is stationary. Consider the model

Yt = 2.5Yt−1 − Yt−2 + εt

or, its equivalent operator form

(1− 2.5L+ L2)Yt = εt.

We can compute magnitudes of the roots of the polynomial 1− 2.5z + z2 withpolyroot.

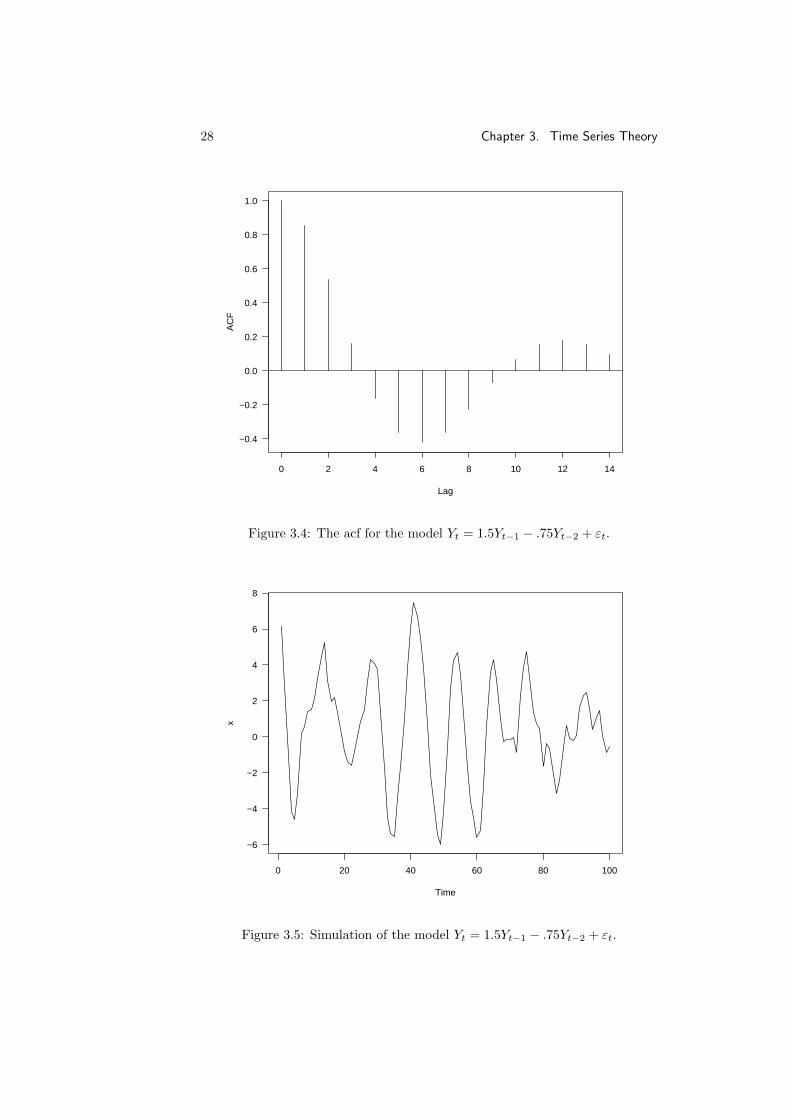

> Mod(polyroot(c(1,-2.5,1)))[1] 0.5 2.0

The roots have magnitudes .5 and 2. Because the first of these is less than 1 inmagnitude the model is thus not stationary and causal.

For the modelYt = 1.5Yt−1 − .75Yt−2 + εt

or its operator equivalent

(1− 1.5L+ .75L2)Yt = εt

we can check stationarity by examining the magnitudes of the roots of 1−1.5z+.75z2.

> Mod(polyroot(c(1,-1.5,.75)))[1] 1.154701 1.154701

Both roots are bigger than 1 in magnitude, so the series is stationary. We canobtain the roots themselves as follows.

> polyroot(c(1,-1.5,.75))[1] 1+0.5773503i 1-0.5773503i

Because the roots are complex we can expect to see a cosine-like ripple in theautocovariance function and the autocorrelation function.

The autocorrelation function for a given model can be computed using theARMAacf function. The acf for the model above can be computed and plottedas follows.

> plot(0:14, ARMAacf(ar=c(1.5,-.75), lag=14), type="h",xlab = "Lag", ylab = "ACF")

> abline(h = 0)

The result is shown in figure 3.4.Finally, it may be useful to simulate a time series of a given form. We can

create a time series from the model Yt = 1.5Yt−1− .75Yt−2 + εt and plot it withthe following statements.

> x = arima.sim(model = list(ar=c(1.5,-.75)), n = 100)> plot(x)

The result is shown in figure 3.5. Note that there is evidence that the seriescontains a quasi-periodic component with period about 12, as suggested by theautocorrelation function.

28 Chapter 3. Time Series Theory

0 2 4 6 8 10 12 14

−0.4

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

AC

F

Figure 3.4: The acf for the model Yt = 1.5Yt−1 − .75Yt−2 + εt.

Time

x

0 20 40 60 80 100

−6

−4

−2

0

2

4

6

8

Figure 3.5: Simulation of the model Yt = 1.5Yt−1 − .75Yt−2 + εt.

3.6. Moving Average Series 29

3.6 Moving Average Series

A time series {Yt} which satisfies

Yt = εt + θ1εt−1 + · · ·+ θqεt−q (3.9)

(with {εt} white noise) is said to be a moving average process of order q orMA(q) process. No additional conditions are required to ensure stationarity.

The autocovariance function for the MA(q) process is

γ(u) =

(1 + θ21 + · · ·+ θ2q)σ2 u = 0(θu + θ1θu+1 + · · ·+ θq−uθq)σ2 u = 1, . . . , q0 otherwise.

which says there is only a finite span of dependence on the series.Note that it is easy to distinguish MA and AR series by the behaviour of

their autocorrelation functions. The acf for MA series “cuts off” sharply whilethat for an AR series decays exponentially (with a possible sinusoidal ripplesuperimposed).

3.6.1 The MA(1) Series

The MA(1) series is defined by

Yt = εt + θεt−1. (3.10)

It has autocovariance function

γ(u) =

(1 + θ2)σ2 u = 0θσ2 u = 10 otherwise.

and autocorrelation function

ρ(u) =

θ

1 + θ2for u = 1,

0 otherwise.(3.11)

3.6.2 Invertibility

If we replace θ by 1/θ and σ2 by θσ2 the autocorrelation function given by 3.11is unchanged. There are thus two sets of parameter values which can explainthe structure of the series.

For the general process defined by equation 3.9, there is a similar identifia-bility problem. The problem can be resolved by requiring that the operator

1 + θ1L+ · · ·+ θqLq

be invertible – i.e. that all roots of the polynomial

1 + θ1z + · · ·+ θqzq

lie outside the unit circle.

30 Chapter 3. Time Series Theory

0 2 4 6 8 10 12 14

0.0

0.2

0.4

0.6

0.8

1.0

Lag

AC

F

Figure 3.6: The acf for the model Yt = εt + .9εt−1.

3.6.3 Computation

The function polyroot can be used to check invertibility for MA models. Re-member that the invertibility requirement is only so that each MA model is onlydefined by one set of parameters.

The function ARMAacf can be used to compute the acf for MA series. Forexample, the acf of the model

Yt = εt + 0.9εt−1

can be computed and plotted as follows.

> plot(0:14, ARMAacf(ma=.9, lag=14), type="h",xlab = "Lag", ylab = "ACF")

> abline(h = 0)

The result is shown in figure 3.6.A simulation of the series can be computed and plotted as follows.

> x = arima.sim(model = list(ma=.9), n = 100)> plot(x)

The result of the simulation is shown in figure 3.7.

3.7 Autoregressive Moving Average Series

Definition 3.7.1 If a series satisfies

Yt = φ1Yt−1 + · · ·+ φpYt−p + εt + θ1εt−1 + · · ·+ θqεt−q (3.12)

3.7. Autoregressive Moving Average Series 31

Time

x

0 20 40 60 80 100

−3

−2

−1

0

1

2

3

Figure 3.7: Simulation of the model Yt = εt + .9εt−1.

(with {εt} white noise), it is called an autoregressive-moving average series oforder (p, q), or an ARMA(p, q) series.

An ARMA(p, q) series is stationary if the roots of the polynomial

1− φ1z − · · · − φpzp

lie outside the unit circle.

3.7.1 The ARMA(1,1) Series

The ARMA(1,1) series is defined by

Yt = φYt−1 + εt + θεt−1. (3.13)

To derive the autocovariance function for Yt, note that

E(εtYt) = E[εt(φYt−1 + εt + θεt−1)]

= σ2ε

and

E(εt−1Yt) = E[εt−1(φYt−1 + εt + θεt−1)]

= φσ2ε + θσ2

ε

= (φ+ θ)σ2ε .

32 Chapter 3. Time Series Theory

Multiplying equation 3.13 by Yt−u and taking expectation yields:

γ(u) =

φγ(1) + (1 + θ(φ+ θ))σ2

ε u = 0

φγ(0) + θσ2ε u = 1

φγ(u− 1) u ≥ 2

Solving the first two equations produces

γ(0) =(1 + 2θφ+ θ2)

1− φ2σ2

ε =(1 + 2θφ+ θ2)

1− φ2σ2

ε

and using the last recursively shows

γ(u) =(1 + θφ)(φ+ θ)

1− φ2φu−1σ2

ε for u ≥ 1.

The autocorrelation function can then be computed as

ρ(u) =(1 + θφ)(φ+ θ)(1 + 2θφ+ θ2)

φu−1 for u ≥ 1.

The pattern here is similar to that for AR(1), except for the first term.

3.7.2 The ARMA(p,q) Model

It is possible to make general statements about the behaviour of general ARMA(p,q)series. When values are more than q time units apart, the memory of the moving-average part of the series is lost. The functions γ(u) and ρ(u) will then behavevery similarly to those for the AR(p) series

Yt = φ1Yt−1 + · · ·+ φpYt−p + εt

for large u, but the first few terms will exhibit additional structure.

3.7.3 Computation

Stationarity can be checked by examining the roots of the characteristic poly-nomial of the AR operator and model parameterisation can be checked by ex-amining the roots of the characteristic polynomial of the MA operator. Bothchecks can be carried out with polyroot.

The autocorrelation function for an ARMA series can be computed withARMAacf. For the model

Yt = −.5Yt−1 + εt + .3εt−1

this can be done as follows

> plot(0:14, ARMAacf(ar=-.5, ma=.3, lag=14), type="h",xlab = "Lag", ylab = "ACF")

> abline(h = 0)

and produces the result shown in figure 3.8.Simulation can be carried out using arma.sim

> x = arima.sim(model = list(ar=-.5,ma=.3), n = 100)> plot(x)

producing the result in figure 3.9.

3.7. Autoregressive Moving Average Series 33

0 2 4 6 8 10 12 14

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

AC

F

Figure 3.8: The acf for the model Yt = −.5Yt−1 + εt + .3εt−1.

Time

x

0 20 40 60 80 100

−2

−1

0

1

2

Figure 3.9: Simulation of the model Yt = −.5Yt−1 + εt + .3εt−1.

34 Chapter 3. Time Series Theory

3.7.4 Common Factors

If the AR and MA operators in an ARMA(p, q) model possess common factors,then the model is over-parameterised. By dividing through by the commonfactors we can obtain a simpler model giving and identical description of theseries. It is important to recognise common factors in an ARMA model becausethey will produce numerical problems in model fitting.

3.8 The Partial Autocorrelation Function

The autocorrelation function of an MA series exhibits different behaviour fromthat of AR and general ARMA series. The acf of an MA series cuts of sharplywhereas those for AR and ARMA series exhibit exponential decay (with possi-ble sinusoidal behaviour superimposed). This makes it possible to identify anARMA series as being a purely MA one just by plotting its autocorrelation func-tion. The partial autocorrelation function provides a similar way of identifyinga series as a purely AR one.

Given a stretch of time series values

. . . , Yt−u, Yt−u+1, . . . , Yt−1, Yt, . . .

the partial correlation of Yt and Yt−u is the correlation between these randomvariables which is not conveyed through the intervening values.

If the Y values are normally distributed, the partial autocorrelation betweenYt and Yt−u can be defined as

φ(u) = cor(Yt, Yt−u|Yt−1, . . . , Yt−u+1).

A more general approach is based on regression theory. Consider predictingYt based on Yt−1, . . . , Yt−u+1. The prediction is

Yt = β1Yt−1 + β2Yt−2 · · · , βu−1Yt−u+1

with the βs chosen to minimise

E(Yt − Yt)2.

It is also possible to “think backwards in time” and consider predicting Yt−u

with the same set of predictors. The best predictor will be

Yi−u = β1Yt−u+1 + β2Yt−u+2 · · · , βu−1Yt−1.

(The coefficients are the same because the correlation structure is the samewhether the series is run forwards or backwards in time.

The partial correlation function at lag u is the correlation between the pre-diction errors.

φ(u) = cor(Yt − Yt, Yt−u − Yt−u)

By convention we take φ(1) = ρ(1).

3.8. The Partial Autocorrelation Function 35

It is quite straightforward to compute the value of φ(2). Using the resultsof section 2.4.1, the best predictor of Yt based on Yt−1 is just ρ(1)Yt−1. Thus

cov(Yt − ρ(1)Yt−1, Yt−2 − ρ(1)Yt−1) = σ2Y (ρ(2)− ρ(1)2 − ρ(1)2) + ρ(1)2)

= σ2Y (ρ(2)− ρ(1)2)

and

var(Yt − ρ(1)Yt−1) = σ2Y (1 + ρ(1)2 − 2ρ(1)2)

= σ2Y (1− ρ(1))2

This means that

φ(2) =ρ(2)− ρ(1)2

1− ρ(1)2(3.14)

Example 3.8.1 For the AR(1) series, recall that

ρ(u) = φu (u ≥ 0).

Substituting this into equation 3.14 we find

φ(2) =φ2 − φ2

1− φ2= 0.

Example 3.8.2 For the MA(1) series

ρ(u) =

θ

1 + θ2if u = 1,

0 otherwise.

Substituting this into 3.14 we find

φ(2) =0− (θ/(1 + θ2))2

1− (θ/(1 + θ2))2

=−θ2

(1 + θ2)2 − θ2

=−θ2

1 + θ2 + θ4.

More generally it is possible to show

φ(u) =−θu(1− θ2)1− θ2(u+1)

for u ≥ 0.

For the general AR(p) series, it is possible to show that φ(u) = 0 for allu > p. For such a series, the best predictor of Yt using Yt−1, . . . , Yt−u+1 foru > p is

φ1Yt−1 + · · ·+ φpYt−p.

36 Chapter 3. Time Series Theory

becauseYt − φ1Yt−1 + · · ·+ φpYt−p = εt

and εt is uncorrelated with Yt−1, Yt−2, . . ., so that the “fit” cannot be improved.The prediction error corresponding to the best linear predictor of Yt−u is

based on Yt−1, . . . , Yt−u+1 and so must be uncorrelated with εt. This showsthat φ(u) = 0.

For the general MA(q), it is possible to show that φ(u) decays exponentiallyas u→∞.

3.8.1 Computing the PACF

The definition of the partial autocorrelation function given in the previous sec-tion is conceptually simple, but it makes computations hard. In this sectionwe’ll see that there is an equivalent form which is computationally simple.

Consider the kth order autoregressive prediction of Yk+1

Yk+1 = φk1Yk + · · ·+ φkkY1 (3.15)

obtained by minimising E(Yk+1 − Yk+1)2. We will show that the kth partialautocorrelation values is given by φ(k) = φkk. The proof of this is a geometricone which takes places in the space H generated by the series {Yt}.

We begin by defining the subspace H1 = sp{Y2, . . . , Yk} and associatedprojection PH1 , the subspace H2 = sp{Y1 − PH1Y1} and the subspace Hk =sp{Y1, . . . , Yk}. Any Y ∈ H,

PHkY = PH1Y + PH2Y.

Thus

Yk+1 = PHkYk+1

= PH1Yk+1 + PH2Yk+1

= PH1Yk+1 + a(Y1 − PH1Y1),

wherea = 〈Yk+1, Y1 − PH1Y1〉/‖Y1 − PH1Y1‖2. (3.16)

Rearranging, we find

Yk+1 = PH1(Yk+1 − aY1) + aY1.

The first term on the right must be a linear combination of Y2, . . . , Yk, so com-paring with equation 3.15 we see that a = φkk.

Now, the kth partial correlation is defined as the correlation between theresiduals from the regressions of Yk+1 and Y1 on Y2, . . . , Yk. But this is just

cor(Yk+1 − PH1Yk+1, Y1 − PH1Y1)

= 〈Yk+1 − PH1Yk+1, Y1 − PH1Y1〉/‖Y1 − PH1Y1‖2

= 〈Yk+1, Y1 − PH1Y1〉/‖Y1 − PH1Y1‖2

= a

3.8. The Partial Autocorrelation Function 37

by equation 3.16.A recursive way of computing the regression coefficients in equation 3.15 from

the autocorrelation function was given by Levinson (1947) and Durbin (1960).The Durbin-Levinson algorithm updates the coefficients the from k − 1st ordermodel to those of the kth order model as follows:

φkk =

ρ(k)−k−1∑j=1

φk−1,jρk−j

1−k−1∑j=1

φk−1,jρj

φk,j = φk−1,j − φkkφk−1,k−j j = 1, 2, . . . , k − 1.

3.8.2 Computation

The R function ARMAacf can be used to obtain the partial autocorrelation func-tion associated with a stationary ARMA series. The call to ARMAacf is identicalto its use for obtaining the ordinary autocorrelation function, except it has theadditional argument pacf=TRUE.

The following code computes and plots the partial autocorrelation functionfor the ARMA(1,1) model with φ = −.5 and θ = .3.

> plot(1:14, ARMAacf(ar=-.5, ma=.3, lag=14, pacf=TRUE),type="h", xlab = "Lag", ylab = "ACF")

> abline(h = 0)

The resulting plot is shown in figure 3.10.

38 Chapter 3. Time Series Theory

2 4 6 8 10 12 14

−0.20

−0.15

−0.10

−0.05

0.00

0.05

Lag

AC

F

Figure 3.10: The partial acf for the model Yt = −.5Yt−1 + εt + .3εt−1.

Chapter 4

Identifying Time SeriesModels

4.1 ACF Estimation

We have seen that it is possible to distinguish between AR, MA and ARMAmodels by the behaviour of their acf and pacf functions. In practise, we don’tknow these functions and so we must estimate them.

Given a stretch of data Y1, . . . , YT , the usual estimate of the autocovariancefunction is

γ(u) =1T

T−u∑t=1

(Yt+u − Y )(Yt − Y )

Note that this estimator is biased — an unbiased estimator would have adivisor of T − u in place of T . There are two reasons for using this estimator.

The first of these reasons is that it produces a γ(u) which is positive definite.This means that for any constants c1, . . . , ck,

k∑u=1

k∑v=1

cucvγ(u− v) ≥ 0.

This ensures that our estimate of the variance ofk∑

u=1

cuXt−u

will be non-negative, something which might not be the case for the unbiasedestimate.

The second reason is that for many time series γ(u) → 0 as u → ∞. Forsuch time series, the biased estimate can have lower mean-squared error.

The estimate of ρ(u) based on γ(u) is

r(u) =γ(u)γ(0)

=∑

t(Yt+u − Y )(Yt − Y )∑t(Yt − Y )2

(Again, this can have better mean-squared error properties than the estimatebased on the unbiased estimate of γ(u).)

39

40 Chapter 4. Identifying Time Series Models

In order to say whether an observed correlation is significantly different fromzero, we need some distribution theory. Like most time series results, the theoryhere is asymptotic (as T →∞). The original results in this area were obtainedby Bartlett in 1947. We will look at results due to T. W. Anderson in 1971.

Suppose that

Yt = µ+∞∑

u=0

ψuεt−u

with the εt independent and identically distributed with zero mean and non-zerovariance. Suppose that

∞∑u=0

|ψu| <∞ and∞∑

u=0

u|ψu|2 <∞.

(This is true for all stationary ARMA series). The last condition can be replacedby the requirement that the {Yt} values have a finite fourth moment.

Under these conditions, for any fixed m, the joint distribution of√T (r(1)− ρ(1)),

√T (r(2)− ρ(2)), . . .

√T (r(m)− ρ(m))

is asymptotically normal with zero means and covariances

cuv =∞∑

t=0

(ρ(t+ u)ρ(t+ v) + ρ(t− u)ρ(t+ v)

− 2ρ(u)ρ(t)ρ(t+ v)− 2ρ(v)ρ(t)ρ(t+ u) (4.1)

+ 2ρ(u)ρ(v)ρ(t)2).

I.e. for large T

r(u) ≈ N(0, cuu/T ) cor(r(u), r(v)

)≈ cuv√

cuucvv.

Notice that var r(u) ↓ 0 but that the correlations stay approximately constant.Equation 4.1 is clearly not easy to interpret in general. Let’s examine some

special cases.

Example 4.1.1 White Noise.The theory applies to the case that the Yt are i.i.d.

var r(u) ≈ 1T

cor(r(u), r(v)

)≈ 0

Example 4.1.2 The AR(1) Series.In this case ρ(u) = φu for u > 0. After a good deal of algebra (summinggeometric series) one finds:

var r(u) ≈ 1T

((1 + φ2)(1− φ2u)

1− φ2− 2uφ2u

).

In particular, for u = 1,

var r(1) ≈ 1− φ2

T.

4.1. ACF Estimation 41

Table 4.1: Large Sample Results for rk for an AR(1) Model.

φ√

var r(1)√

var r(2) cor(r(1), r(2)

) √var r(10)

0.9 0.44/√T 0.807/

√T 0.97 2.44/

√T

0.7 0.71/√T 1.12/

√T 0.89 1.70/

√T

0.5 0.87/√T 1.15/

√T 0.76 1.29/

√T

0.3 0.95/√T 1.08/

√T 0.53 1.09/

√T

0.1 0.99/√T 1.01/

√T 0.20 1.01/

√T

Notice that the closer φ is to ±1, the more accurate the estimate becomes.As u→∞, φ2u → 0. In that case

var r(u) ≈ 1T

(1 + φ2

1− φ2

).

For values of φ close to ±1 this produces large variances for the r(u).For 0 < u 6 v (after much algebra),

cuv =(φv−1 − φv+u)(1 + φ2)

1− φ2+ (v − u)φv−u − (v + u)φv+u.

In particular,

cor(r(1), r(2)

)≈ 2φ

(1− φ2

1 + 2φ2 − 3φ4

)1/2

Using these formulae it is possible to produce the results in table 4.1.

Example 4.1.3 The MA(1) SeriesFor the MA(1) series it is straightforward to show that

c11 = 1− 3ρ(1)2 + 4ρ(1)4

cuu = 1− 2ρ(1)2 u > 1

c12 = 2ρ(1)(1− ρ(1)2)

Using these results it is easy to produce the results in table 4.2.

Example 4.1.4 The General MA(q) SeriesIn the case of the general MA(q) series it is easy to see that

cuu = 1 + 2q∑

v=1

ρ(v)2, for u > q,

and hence that

var r(u) =1T

(1 + 2

q∑v=1

ρ(v)2), for u > q.

42 Chapter 4. Identifying Time Series Models

Table 4.2: Large Sample Results for rk for an MA(1) Model.

θ√

var r(1)√

var r(k) (k > 1) cor(r(1), r(2)

)0.9 0.71/

√T 1.22/

√T 0.86

0.7 0.73/√T 1.20/

√T 0.84

0.5 0.79/√T 1.15/

√T 0.74

0.4 0.84/√T 1.11/

√T 0.65

Notes

1. In practise we don’t know the parameters of the model generating the datawe might have. We can still estimate the variances and covariances of ther(u) by substituting estimates of ρ(u) into the formulae above.

2. Note that there can be quite large correlations between the r(u) values socaution must be used when examining plots of r(u).

4.2 PACF Estimation

In section 3.8.1 we saw that the theoretical pacf can be computed by solvingthe Durbin-Levinson recursion

φkk =

ρ(k)−k−1∑j=1

φk−1,jρ(k − j)

1−k−1∑j=1

φk−1,jρ(j)

φk,j = φk−1,j − φkkφk−1,k−j j = 1, 2, . . . , k − 1.

and setting φ(u) = φuu.In practice, the estimated autocorrelation function is used in place of the

theoretical autocorrelation function to generate estimates of the partial auto-correlation function.

To decide whether partial autocorrelation values are significantly differentfrom zero, we can use a (1949) result of Quenouille which states that if the trueunderlying model is AR(p), then the estimated partial autocorrelations at lagsgreater than p are approximately independently normal with means equal tozero and variance 1/T . Thus ±2/

√T can be used as critical limits on φ(u) for

u > p to test the hypothesis of an AR(p) model.

4.3. System Identification 43

Time

Diff

eren

ce In

Yie

ld

1962 1964 1966 1968 1970 1972 1974

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Figure 4.1: Monthly differences between the yield on mortgages andgovernment loans in the Netherlands, January 1961 to March 1974.

4.3 System Identification

Given a set of observations Y1, . . . , YT we will need to decide what the appro-priate model might be. The estimated acf and pacf are the tools which can beused to do this. If the acf exhibits slow decay and the pacf cuts off sharply afterlag p, we would identify the series as AR(p). If the pacf shows slow decay andthe acf show a sharp cutoff after lag q, we would identify the series as beingMA(q). If both the acf and pacf show slow decay we would identify the seriesas being mixed ARMA. In this case the orders of the AR and MA parts are notclear, but it is reasonable to first try ARMA(1,1) and move on to higher ordermodels if the fit of this model is not good.

Example 4.3.1 Interest Yields

Figure 4.1 shows a plot of the Monthly differences between the yield on mort-gages and government loans in the Netherlands, January 1961 to March 1974.The series appears stationary, so we can attempt to use the acf and pacf todecide whether an AR, MA or ARMA model might be appropriate.

Figures 4.2 and 4.3 show the estimated acf and pacf functions for the yieldseries. The horizontal lines in the plots are drawn at the y values ±1.96/

√159

(the series has 159 values). These provide 95% confidence limits for what canbe expected under the hypothesis of white noise. Note that these limits arepoint-wise so that we would expect to see roughly 5% of the values lying outsidethe limits.

The acf plot shows evidence of slow decay, while the pacf plot shows a“sharp

44 Chapter 4. Identifying Time Series Models

0.0 0.5 1.0 1.5

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

AC

F

Figure 4.2: The acf for the yield data.

0.5 1.0 1.5

0.0

0.2

0.4

0.6

0.8

Lag

Par

tial A

CF

Figure 4.3: The pacf for the yield data.

4.4. Model Generalisation 45

Time

Yie

ld

0 10 20 30 40 50 60 70

30

40

50

60

70

80

Figure 4.4: Yields from a chemical process (from Box and Jenkins).

cutoff” after lag 1. On the basis of these two plots we might hypothesise thatan AR(1) model was an appropriate description of the data.

Example 4.3.2 Box and Jenkins Chemical Yields

Figure 4.4 shows an example from the classic time series text by Box and Jenk-ins. This series contains consecutive yields recorded from a chemical process.Again, the series is apparently stationary so that we can consider identifying anappropriate model on the basis of the acf and pacf.

Again, the acf seems to show slow decay, this time with alternating signs.The pacf shows sudden cutoff after lag 1, suggesting that again an AR(1) modelmight be appropriate.

4.4 Model Generalisation

ARMA series provide a flexible class of models for stationary mean-zero series,with AR and MA series being special cases.

Unfortunately, many series are clearly not in this general class for models.It is worthwhile looking at some generalisation of this class.

4.4.1 Non-Zero Means

When a series {Yt} has a non-zero mean µ, the mean can be subtracted and thedeviations from the mean modeled as an ARMA series.

Yt − µ = φ1(Yt−1 − µ) + · · ·+ φp(Yt−p − µ) + εt + θ1εt−1 + · · ·+ θqεt−q

46 Chapter 4. Identifying Time Series Models

0 5 10 15

−0.4

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

AC

F

Figure 4.5: The acf for the chemical process data.

5 10 15

−0.4

−0.3

−0.2

−0.1

0.0

0.1

0.2

Lag

Par

tial A

CF

Figure 4.6: The pacf for the chemical process data.

4.4. Model Generalisation 47

Alternatively, the model can be adjusted by introducing a constant directly.

Yt = φ1Yt−1 + · · ·+ φpYt−p + θ0 + εt + θ1εt−1 + · · ·+ θqεt−q

The two characterisations are connected by

θ0 = µ− µ(φ1 + · · ·+ φp)

so thatµ =

θ01− φ1 − · · · − φp

orθ0 = µ(1− φ1 − · · · − φp).

4.4.2 Deterministic Trends

Consider the modelYt = f(t) + Zt,

where Zt is a stationary ARMA series and f(t) is a deterministic function of t.Considering Yt− f(t) reduces Yt to an ARMA series. (If f(t) contains unknownparameters we can estimate them.)

4.4.3 Models With Non-stationary AR Components

We’ve seen that any AR model with characteristic equation roots outside theunit circle will be non-stationary.

Example 4.4.1 Random WalksA random walk is defined by the equation

Yt = Yt−1 + εt

where {εt} is a series of uncorrelated (perhaps independent) random variables.In operator form this equation is

(1− L)Yt = εt.

The equation 1− z = 0 has a root at 1 so that Yt is non-stationary.

Example 4.4.2 Integrated Moving AveragesConsider the model

Yt = Yt−1 + εt + θεt−1.

This is similar to an ARMA(1,1) model, but again it is non-stationary.

Both these models can be transformed to stationarity by differencing —transforming to ∇Yt = Yt − Yt−1. In the first example we have,

∇Yt = εt,

which is the white noise model. In the second we have,

∇Yt = εt + θεt−1,

which is the MA(1) model.

48 Chapter 4. Identifying Time Series Models

4.4.4 The Effect of Differencing

Suppose that Yt has a linear trend

Yt = β0 + β1t+ Zt

where Zt is stationary with E(Zt) = 0.

∇Yt = β1 +∇Zt

Differencing has removed the trend. Now suppose that {Yt} has a deterministicquadratic trend

Yt = β0 + β1t+ β2t2 + Zt

then

∇Yt = (β0 + β1t+ β2t2)− (β0 + β1(t− 1) + β2(t− 1)2) +∇Zt

= β1 + β2(t2 − (t2 − 2t+ 1)) +∇Zt

= (β1 − β2) + 2β2t+∇Zt

= linear trend + stationary.

Differencing again produces

∇2Yt = 2β2 +∇2Zt.

In general, a polynomial trend of order k can be eliminated by differencing ktimes.

Now let’s consider the case of a “stochastic trend.” Suppose that

Yt = Mt + εt

where Mt is a random process which changes slowly over time. In particular,we can assume that Mt is generated by a random walk model.

Mt = Mt−1 + ηt

with ηt independent of εt. Then

∇Yt = ηt + εt − εt−1.

∇Yt is stationary and has an autocorrelation function like that of an MA(1)series.

ρ(1) =−1

2 + (ση/σε)2

More generally, “higher order” stochastic trend models can be reduced to sta-tionarity by repeated differencing.

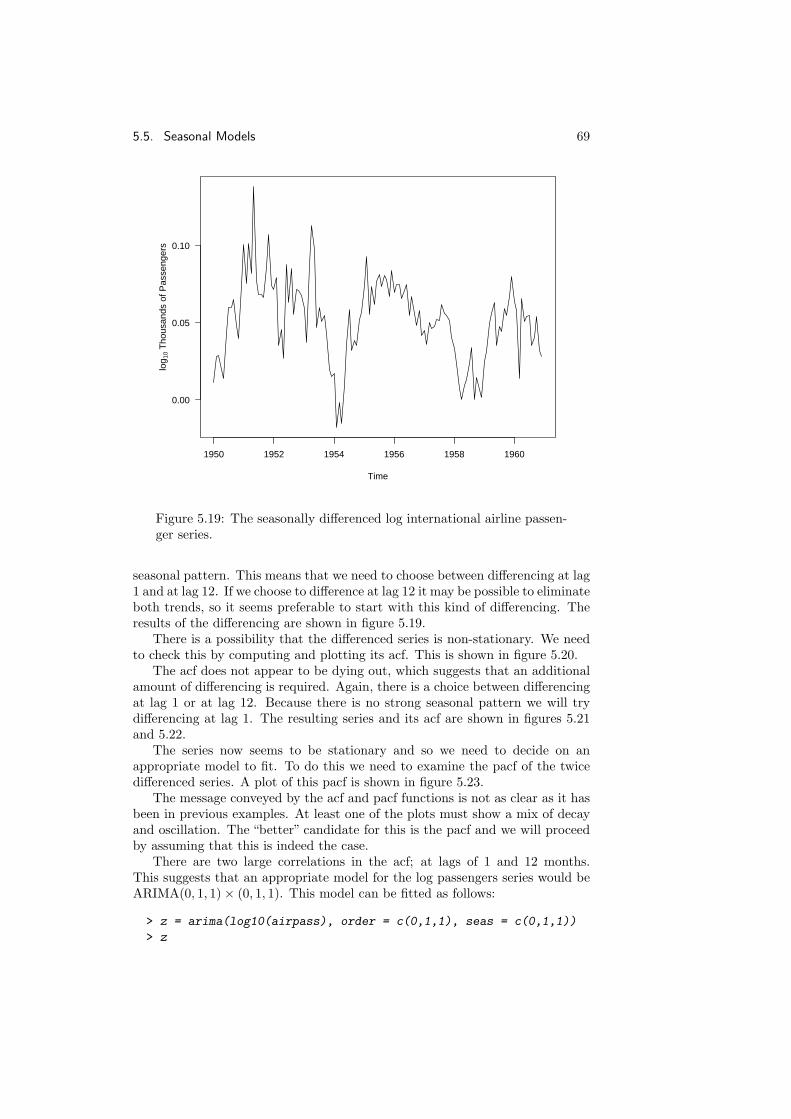

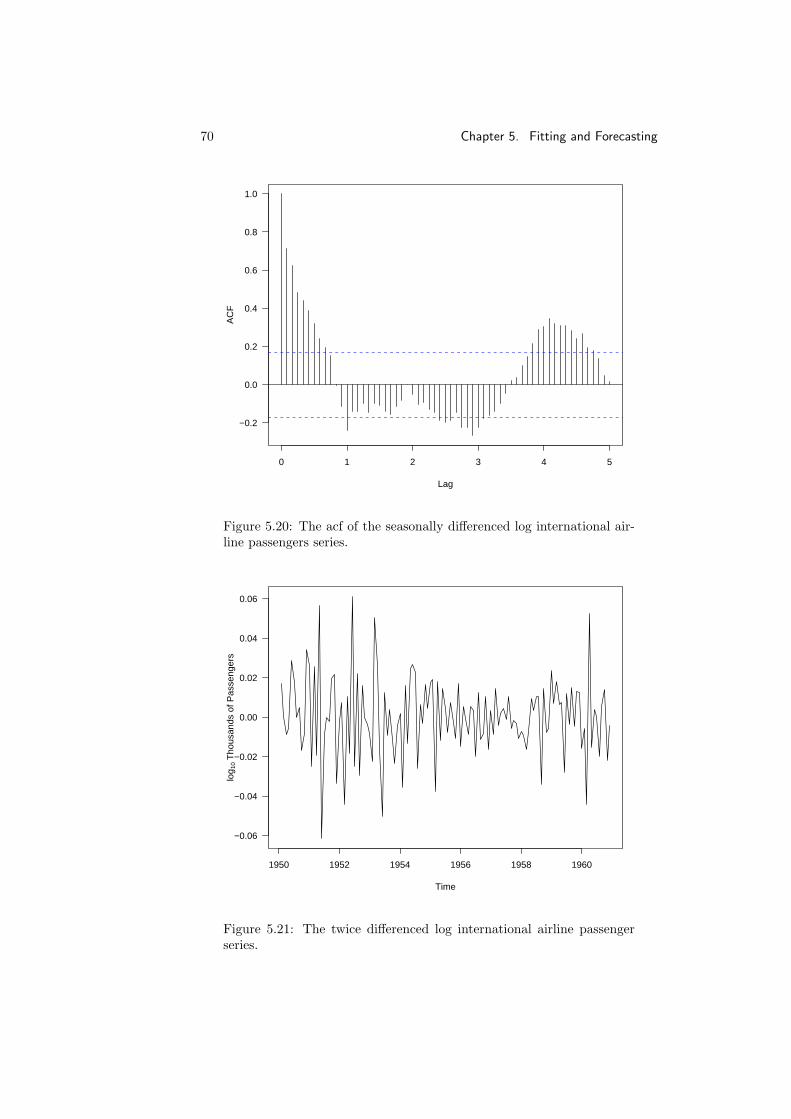

4.5. ARIMA Models 49

4.5 ARIMA Models

If Wt = ∇dYt is an ARMA(p,q) series than Yt is said to be an integrated autore-gressive moving-average (p, d, q) series, denoted ARIMA(p,d,q). If we write

φ(L) = 1− φ1L− · · · − φpLp

andθ(L) = 1 + θ1L+ · · ·+ θqL

q

then we can write down the operator formulation

φ(L)∇dYt = θ(L)εt.

Example 4.5.1 The IMA(1,1) Model This model is widely used in businessand economics. It is defined by

Yt = Yt−1 + εt + θεt−1.

Yt can be thought of as a random walk with correlated errors.Notice that

Yt = Yt−1 + εt + θεt−1

= Yt−2 + εt−1 + θεt−2 + εt + θεt−1

= Yt−2 + εt + (1 + θ)εt−1 + θεt−2

...

= Y−m + εt + (1 + θ)εt−1 + · · ·+ (1 + θ)ε−m + θε−m−1

If we assume that Y−m = 0 (i.e. observation started at time −m),

Yt = εt + (1 + θ)εt−1 + · · ·+ (1 + θ)ε−m + θε−m−1

This representation can be used to derive the formulae

var(Yt) =(1 + θ2 + (1 + θ)2(t+m)

)σ2

ε

cor(Yk, Yt−k

)=

1 + θ2 + (1 + θ)2(t+m− k)(var(Yt)var(Yt−k)

)1/2

=

√t+m− k

t+m

≈ 1

for m large and k moderate. (We are considering behaviour after “burn-in.”)This means that we can expect to see very slow decay in the autocorrelationfunction.

The very slow decay of the acf function is characteristic of ARIMA serieswith d > 0. Figures 4.7 and 4.8 show the estimated autocorrelation functionsfrom a simulated random walk and an integrated autoregressive model. Bothfunctions show very slow declines in the acf.

50 Chapter 4. Identifying Time Series Models

0 5 10 15 20

0.0

0.2

0.4

0.6

0.8

1.0

Lag

AC

F

Figure 4.7: The autocorrelation function of the ARIMA(0,1,0) (randomwalk) model.

0 5 10 15 20

0.0

0.2

0.4

0.6

0.8

1.0

Lag

AC

F

Figure 4.8: The autocorrelation function of the ARIMA(1,1,0) modelwith φ1 = .5.

Chapter 5

Fitting and Forecasting

5.1 Model Fitting

Suppose that we have identified a particular ARIMA(p,d,q) model which appearsto describe a given time series. We now need to fit the identified model andassess how well the model fits. Fitting is usually carried out using maximumlikelihood. For a given set of model parameters, we calculate a series of one-step-ahead predictions.

Yk+1 = PHkYk+1

where Hk is the linear space spanned by Y1, . . . , Yk. The predictions are ob-tained in a recursive fashion using a process known as Kalman filtering. Eachprediction results in a prediction error Yk+1 − Yk+1. These are, by construc-tion, uncorrelated. If we add the requirement that the {Yt} series is normallydistributed, the prediction errors are independent normal random variables andthis can be used as the basis for computing the likelihood.

The parameters which need to be estimated are the AR coefficients φ1, . . . , φp,the MA coefficients θ1, . . . , θq and a constant term (either µ or θ0 as outlinedin section 4.4.1). Applying maximum-likelihood produces both estimates andstandard errors.

5.1.1 Computations

Given a time series y in R, we can fit an ARMA(p,d,q) model to the series asfollows

> z = arima(y, order=c(p, d, q))

The estimation results can be inspected by printing them.

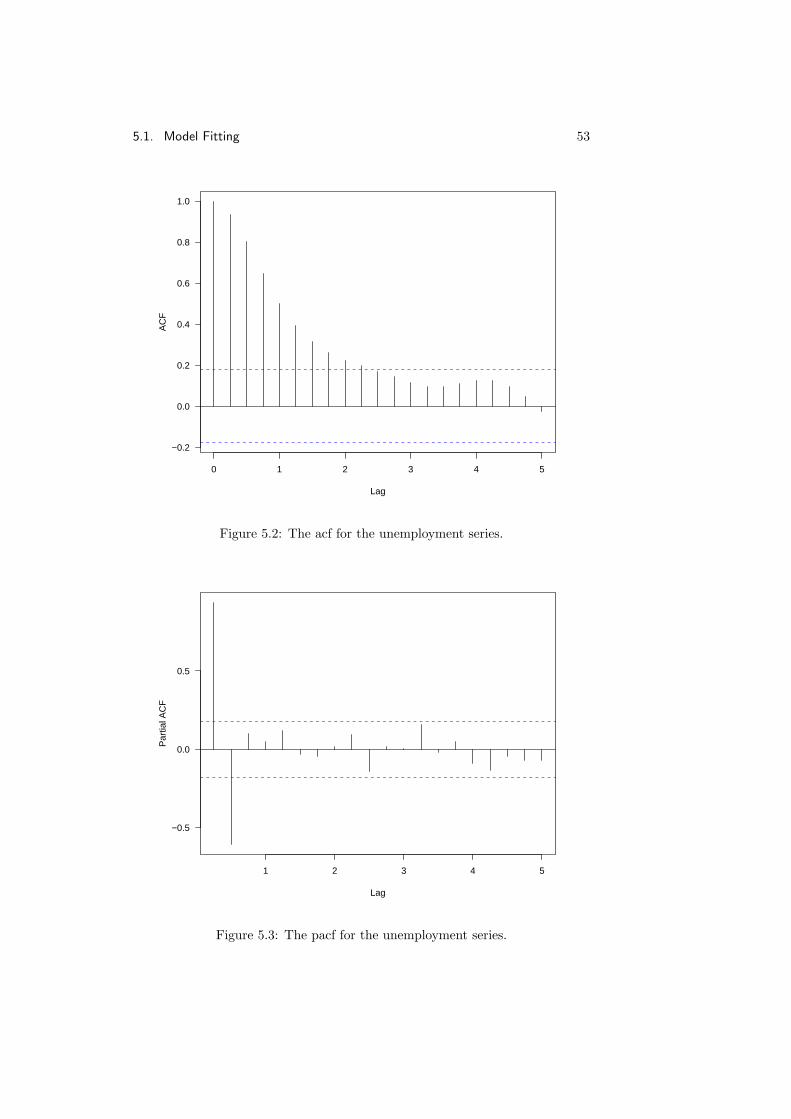

Example 5.1.1 U.S. Unemployment RatesFigure 5.1 shows a plot of the seasonally adjusted quarterly United States un-employment rates from the first quarter of 1948 to the first quarter of 1978.If the data is stored as a time series in the R data set unemp, the plot can beproduced with the command

> plot(unemp)

51

52 Chapter 5. Fitting and Forecasting

Time

unem

p

1950 1955 1960 1965 1970 1975

3

4

5

6

7

8