Embed Size (px)

Citation preview

Report of Independent Auditors and Financial Statements with

Supplementary Information for

Tillamook People’s Utility District

December 31, 2015 and 2014

CONTENTS PAGEBOARDOFDIRECTORS,ADMINISTRATIVESTAFF,ANDREGISTEREDAGENT 1REPORTOFINDEPENDENTAUDITORS 2–4MANAGEMENT’SDISCUSSIONANDANALYSIS 5–11FINANCIALSTATEMENTS Statementsofnetposition 12–13 Statementsofrevenues,expenses,andchangesinnetposition 14 Statementsofcashflows 15–16 Notestofinancialstatements 17–35REQUIREDSUPPLEMENTARYINFORMATION Scheduleoffundingprogressforretireehealthplan 36 ScheduleofproportionateshareofthenetpensionliabilityasofJune30,2015 37 ScheduleofcontributionsasofJune30,2015 38SUPPLEMENTARYINFORMATION Scheduleofchangesinelectricplantinservice 39 Scheduleofbondsandcertificatesdebtservicetransactions 40 Scheduleoffuturebondsandcertificatesdebtservicerequirements 41 Scheduleofoperatingexpenses 42–43REPORTOFINDEPENDENTAUDITORSONINTERNALCONTROLOVER FINANCIALREPORTINGANDONCOMPLIANCEANDOTHERMATTERS BASEDONANAUDITOFFINANCIALSTATEMENTSPERFORMEDIN ACCORDANCEWITHGOVERNMENTAUDITINGSTANDARDS 44–45REPORTOFINDEPENDENTAUDITORSONCOMPLIANCEANDINTERNAL CONTROLOVERFINANCIALREPORTINGBASEDONANAUDITOF FINANCIALSTATEMENTSPERFORMEDINACCORDANCEWITH OREGONAUDITSTANDARDS 46–47

1

TILLAMOOKPEOPLE’SUTILITYDISTRICTBOARDOFDIRECTORS,ADMINISTRATIVESTAFF,ANDREGISTEREDAGENT

Address Position

KenPhillips 4855SunsetDrive PresidentTillamook,Oregon

HarryE.Hewitt 1816NinthStreet VicePresidentTillamook,Oregon

BarbaraA.Trout 17640OldPacificHighway TreasurerRockawayBeach,Oregon

DougOlson POBox1000 SecretaryPacificCity,Oregon

EdwinL.Jenkins 6996BewleyCreekRoad DirectorTillamook,Oregon

Position

RaymonSieler GeneralManagerRobertS.White PowerServicesManagerJimMartin FinanceManagerMartyHolm CustomerServicesManagerBarbaraJohnson PublicRelationsManagerJohnLuquette InformationTechnologyManager

RaymonSieler 1115PacificAvenue Tillamook,Oregon

REGISTEREDAGENT

Name

BOARDOFDIRECTORS

ADMINISTRATIVESTAFF

Name

2

REPORTOFINDEPENDENTAUDITORSTheBoardofDirectorsTillamookPeople’sUtilityDistrictReportontheFinancialStatementsWehaveauditedtheaccompanyingfinancialstatementsofTillamookPeople'sUtilityDistrict(theDistrict),whichcomprisethestatementsofnetpositionasofDecember31,2015and2014,andtherelatedstatementsofrevenues,expensesandchangesinnetposition,andcashflowsfortheyearsthenended,andtherelatednotestothefinancialstatements.Management'sResponsibilityfortheFinancialStatementsManagement is responsible for the preparation and fair presentation of these financial statements inaccordancewithaccountingprinciplesgenerallyaccepted intheUnitedStatesofAmerica;this includesthedesign,implementation,andmaintenanceofinternalcontrolrelevanttothepreparationandfairpresentationoffinancialstatementsthatarefreefrommaterialmisstatement,whetherduetofraudorerror.Auditor'sResponsibilityOurresponsibilityistoexpressanopiniononthesefinancialstatementsbasedonouraudits.WeconductedourauditsinaccordancewithauditingstandardsgenerallyacceptedintheUnitedStatesofAmericaandthestandards applicable to financial audits contained in Government Auditing Standards, issued by theComptrollerGeneralof theUnitedStates.Those standards require thatweplanandperform theaudits toobtainreasonableassuranceaboutwhetherthefinancialstatementsarefreefrommaterialmisstatement.Anauditinvolvesperformingprocedurestoobtainauditevidenceabouttheamountsanddisclosuresinthefinancialstatements.Theproceduresselecteddependontheauditor'sjudgment,includingtheassessmentoftherisksofmaterialmisstatementofthefinancialstatements,whetherduetofraudorerror.Inmakingthoserisk assessments, the auditor considers internal control relevant to the entity's preparation and fairpresentation of the financial statements in order to design audit procedures that are appropriate in thecircumstances,butnotforthepurposeofexpressinganopinionontheeffectivenessoftheentity'sinternalcontrol.Accordingly,weexpressnosuchopinion.Anauditalso includesevaluating theappropriatenessofaccountingpoliciesusedandthereasonablenessofsignificantaccountingestimatesmadebymanagement,aswellasevaluatingtheoverallpresentationofthefinancialstatements.Webelievethattheauditevidencewehaveobtainedissufficientandappropriatetoprovideabasisforourauditopinion.

3

REPORTOFINDEPENDENTAUDITORS(continued)OpinionInouropinion,thefinancialstatementsreferredtoabovepresentfairly,inallmaterialrespects,thefinancialposition of Tillamook People's Utility District as of December 31, 2015 and 2014, and the results of itsoperationsand its cash flows for the years thenended in accordancewith accountingprinciples generallyacceptedintheUnitedStatesofAmerica.OtherMattersRequiredSupplementaryInformationAccounting principles generally accepted in the United States of America require that management'sdiscussion and analysis, schedule of proportionate share of the net pension liability, schedule ofcontributions,andthescheduleof fundingprogress forretireehealthplanbepresentedtosupplementthefinancial statements. Such information, although not a part of the financial statements, is required by theGovernmentalAccountingStandardsBoardwhoconsidersittobeanessentialpartoffinancialreportingforplacing the financial statements in an appropriate operational, economic, or historical context. We haveappliedcertain limitedprocedures to therequiredsupplementary information inaccordancewithauditingstandardsgenerally accepted in theUnitedStatesofAmerica,which consistedof inquiriesofmanagementabout the methods of preparing the information and comparing the information for consistency withmanagement'sresponsestoourinquiries,thefinancialstatements,andotherknowledgeweobtainedduringour audits of the financial statements. We do not express an opinion or provide any assurance on theinformationbecausethelimitedproceduresdonotprovideuswithsufficientevidencetoexpressanopinionorprovideanyassurance.SupplementaryInformationOurauditwasconductedforthepurposeofforminganopiniononthefinancialstatementsthatcollectivelycomprisetheDistrict’sfinancialstatements.Thesupplementaryinformation,listedinthetableofcontentsispresented for purposes of additional analysis and is not a required part of the financial statements. Suchinformationistheresponsibilityofmanagementandwasderivedfromandrelatesdirectlytotheunderlyingaccountingandotherrecordsusedtopreparethefinancialstatements.Suchinformationhasbeensubjectedtotheauditingproceduresappliedintheauditofthefinancialstatementsandcertainadditionalprocedures,including comparing and reconciling such information directly to the underlying accounting and otherrecords used to prepare the financial statements or to the financial statements themselves, and otheradditional procedures in accordance with auditing standards generally accepted in the United States ofAmerica.Inouropinion,thesupplementaryinformationisfairlystatedinallmaterialrespectsinrelationtothefinancialstatementsasawhole.

4

REPORTOFINDEPENDENTAUDITORS(continued)OtherReportingRequiredbyGovernmentAuditingStandardsInaccordancewithGovernmentAuditingStandards,wehavealsoissuedourreportdatedApril7,2016onourconsiderationoftheDistrict'sinternalcontroloverfinancialreportingandonourtestsofitscompliancewithcertainprovisionsoflaws,regulations,contracts,andgrantagreementsandothermatters.Thepurposeof that report is to describe the scope of our testing of internal control over financial reporting andcomplianceandtheresultsofthattesting,andnottoprovideanopinionontheinternalcontroloverfinancialreporting or on compliance. That report is an integral part of an audit performed in accordance withGovernment Auditing Standards in considering the District's internal control over financial reporting andcompliance.OtherReportingRequiredbyOregonAuditingStandardsInaccordancewiththeMinimumStandardsforAuditsofOregonMunicipalCorporations,wehaveissuedourreportdatedApril7,2016,onourconsiderationoftheDistrict’scompliancewithcertainprovisionsoflawsandregulations, including theprovisionsofOregonRevisedStatutesasspecified inOregonAdministrativeRules.Thepurposeofthatreportistodescribethescopeofourtestingofcomplianceandtheresultsofthattestingandnottoprovideanopiniononcompliance.JulieDesimone,PartnerforMossAdamsLLPPortland,OregonApril7,2016

TILLAMOOKPEOPLE’SUTILITYDISTRICTMANAGEMENT’SDISCUSSIONANDANALYSIS

5

TheManagement'sDiscussionandAnalysissectionoftheDistrict'sAnnualFinancialReportpresentsananalysisofthefinancialpositionandactivitiesofTillamookPeople'sUtilityDistrictfortheyearsendedDecember 31, 2015 and 2014. This report has been prepared by management and is a requiredcomponent of an annual financial report prepared in accordancewith generally accepted accountingprinciples. The discussion is designed to assist readers in understanding the accompanying financialstatements throughanobjectiveandeasilyreadableanalysisof theDistrict's financialactivitiesbasedoncurrentlyknownfactsandconditions.FinancialHighlightsComparisonof2015,2014and2013revenues&expenses:

Change ChangeFrom2014 From2013

2015 2014 to2015 2013 to2014

Revenues:Salesofelectrcity 34,382,271$ 33,850,825$ 531,446$ 34,736,010$ (885,185)$Otheroperatingrevenues 449,874 434,604 15,270 390,560 44,044Interestandotherincome 94,844 165,791 (70,947) 62,316 103,475

Totalrevenues 34,926,989 34,451,220 475,769 35,188,886 (737,666)

Expenses:Costofpower 17,192,295 17,785,638 (593,343) 17,293,955 491,683Distributionexpense:

Operation 3,810,331 3,876,278 (65,947) 3,995,055 (118,777)Maintenance 3,419,660 3,291,174 128,486 3,390,284 (99,110)

Customeraccounts 1,024,628 934,808 89,820 898,498 36,310Customerserviceandinfo 751,608 730,596 21,012 709,410 21,186Sales 123,074 125,251 (2,177) 132,501 (7,250)Administrativeandgeneral 3,077,676 2,882,982 194,694 3,103,674 (220,692)Depreciation 2,861,370 2,676,159 185,211 2,668,440 7,719Taxes 844,520 842,741 1,779 824,756 17,985Interestonlong‐termdebt 840,868 862,644 (21,776) 704,735 157,909Othercharges 15,566 15,566 ‐ 18,323 (2,757)

Totalexpenses 33,961,596 34,023,837 (62,241) 33,739,631 284,206

Netincome 965,393$ 427,383$ 538,010$ 1,449,255$ (1,021,872)$

RevenuesThewarmweatherin2015limitedrevenuesfromsalesofelectricitytoincreaseonly$531,446,orup1.6%in2015from2014.Thisinspiteofretailrateincreasesof3%inAugust2014,and5%inOctober2015.Totalenergy(kWh’s)soldwasdown4.1%in2015from2014.Revenues from sales of electricity decreased $885,185 or 2.5% in 2014 over 2013 also due tomildweather.2013wasrecordingnormalweather,while2014wasmild,and2015washistoricallywarm.Totalenergy(kWh’s)wasdown4.3%from2013to2014.Otheroperatingrevenues increased$44,044 in2014,mostlydueto the increasedrental income frompolecontactsofabout$30,000.

TILLAMOOKPEOPLE’SUTILITYDISTRICTMANAGEMENT’SDISCUSSIONANDANALYSIS

6

Revenues(continued)Interestandotherincomedecreasedin2015by$70,947mostlydueto2014beingtheexceptionwith$76,000 in revenue fromsanctions frompole contact attachments.These sanctionsarealso themainreasonfortheincreaseininterestandotherincomebeingover$103,475in2014over2013.PowerSupplyThe District’s cost of power decreased $593,343 in 2015 from 2014. The decrease was due tohistorically warm weather of 2015 and occurred even with a 6% BPA wholesale rate that becameeffectiveOctober2015.The District’s cost of power increased $491,683, or 2.8% in 2014 over 2013. The increase was acombinationofBPA’srateincrease,counteredbyadecreaseintotalenergypurchased.BPA’swholesalepowerincreaseof8.3%forpowerand9.3%fortransmissioneffectiveOctober2013madepowercostsgoup,whiletheenergy(kWh’s)purchasedactuallydecreased4.3%,resultinginanetincreaseof2.8%.ExpensesTheincreaseofDistributionexpense–Maintenanceof$128,486in2015wasduetotheDecember2015StormDamage.Thisstormwasofficiallydeclaredadisaster,andtheDistrict isworkingwithFEMAtodetermineiftherewillbeanydisasterrecoveryavailable.Thedecreaseof$220,692intheDistributionExpense–Maintenancein2014from2013wastheresultofpayrollrelatedcostschargedtoDistributionExpense‐Maintenancedecreasingin2014from2013.AdministrativeandGeneralExpensedecreased$220,692or7.1%from2013to2014.Thiswasduetoanumber of items but was led by Legal – General Counsel, which decreased about $90,000. Alsodecreasingin2014wasMaintenanceofPropertyandGroundsbyabout$67,000.After the decreases in Administrative and General in 2014 as discussed above, the Legal andMaintenance costs returned to normal in 2015 resulting in an overall increase inAdministrative andgeneralof$194,694,or6.7%.Depreciation expense increased by $185,211 in 2015 as a result of an increase in the amount ofdepreciationexpenseforsubstationDistributionAutomation.InterestonLong‐termDebtincreasedin2014by$157,909or22.4%asaresultofadding$7millionofdebtinearly2014.The$7millionRUSloanlockedinarateof3.05%over21years.TheotherRUSone‐yearvariableratescontinuedathistoricallowratestobringthetotalweightedaveragecostofdebttoabout2.6%in2015,2014,and2013.

TILLAMOOKPEOPLE’SUTILITYDISTRICTMANAGEMENT’SDISCUSSIONANDANALYSIS

7

StatementofNetPosition:

2015 Percent 2014 Percent 2013 Percent

ASSETS

TotalelectricPlant 97,036,587$ 94,508,951$ 92,181,955$Accumulatedprovisionfor

depreciation (30,300,669) (28,283,086) (26,613,426)

Netelectricplant 66,735,918 62.6% 66,225,865 63.7% 65,568,529 70.0%Notesreceivable 194,719 0.2% 214,596 0.2% 227,308 0.2%Investments 2,561,335 2.4% 2,829,862 2.7% 2,556,283 2.7%Currentassets 18,496,346 17.3% 18,817,178 18.1% 14,295,069 15.3%Othernoncurrentassets 17,592,163 16.5% 15,113,509 14.5% 10,741,678 11.5%Deferredoutflowsofresources 1,074,883 0.4% 697,962 0.7% 309,645 0.3%

Totalassetsanddeferredoutflowsofresources 106,655,364$ 99.3% 103,898,972$ 100.0% 93,698,512$ 100.0%

LIABILITIES&NETPOSITION

NetpositionNetinvestmetnincapitalassets 35,957,107$ 33.7% 33,725,132$ 32.5% 38,462,257$ 41.0%Restricted 3,387,376 3.2% 3,470,647 3.3% 3,172,392 3.4%Designated 3,400,000 3.2% 3,400,000 3.3% 3,400,000 3.6%Unrestricted 9,298,009 8.7% 10,481,320 10.1% 5,615,067 6.0%

Long‐termdebt 29,368,157 27.5% 31,050,640 29.9% 25,978,022 27.7%Currentliabilities 6,496,693 6.1% 6,138,806 5.9% 6,212,967 6.6%Othernoncurrentliabilities 6,250,266 5.9% 277,078 0.3% 250,568 0.3%Deferredinflowsofresources 12,497,756 11.7% 15,355,349 14.8% 10,607,239 11.3%

Totalliabilities,netpositionanddeferredinflowsofresources 106,655,364$ 100.0% 103,898,972$ 100.0% 93,698,512$ 100.0%

The statement of net position showsan increase in net electric plant of about $500,000 in 2015 and$650,000 in 2014. Our combined Construction costs along with electric plant additions and generalplantadditionslessourdepreciation,accountsfortheannualincreasesinnetelectricplantinboth2014and2015.Currentassetsincreasedconsiderablyin2014duetotheproceedsofthe$7millionRUSLoan.Othernoncurrentassetsincreasedbymorethan$4.3millionin2014asaresultofthenewaccountingrequiredbyGASB68forpensionliability.Long‐termdebtincreasedconsiderablyin2014asaresultofthe$7millionRUSLoan.Other noncurrent liabilities increased by almost $6 million in 2015, again as a result of the newaccountingrequiredbyGASB68forpensionliability.The new accounting of GASB 68 contributed to the fluctuations in Deferred inflows of resources – adecreaseofabout$2.9millionin2015andanincrease$4.7millionin2014.

TILLAMOOKPEOPLE’SUTILITYDISTRICTMANAGEMENT’SDISCUSSIONANDANALYSIS

8

CapitalAssetsTheDistrict'sinvestmentinnetelectricplantasofDecember31,2015amountedto$66,735,918,netofaccumulateddepreciationrepresenting62.6%oftotalassets.Investmentinelectricplantincludesland,structures,improvements,stationequipment,poles,conductor,metersandtransformers.LongTermDebtAsofDecember31,2015,theDistricthaddebtoutstandingof$29,256,887,netofcurrentmaturities.Ofthis amount, $4,945,000 is from the 2008 bond sale, $4,450,000 is from the 2010 bond sale, and$19,861,887consistsofrevenuecertificatesofindebtedness,issuedinlieuofbondsforloansfromtheRuralUtilitiesService.NextYear’sBudgetThe2016budgetforecastssignificantincreasesinbothSalesofelectricity,andPowerSupplyexpensecomparedto2015’sauditedrevenueandexpenses.Astheresultofawarm2015,alongwiththeOctober2015’s5%retailand6%wholesalerateincrease,2016(weathernormalized)isbudgetedtobeabout$2,98millionhigherinSalesofElectricity,and$2.21millionhigherinPowerSupplyexpensethan2015.Majorconstructionprojectsin2016includetheHeboFeederReconductor,budgetedat$1million.Mostprojects will be performed by District employees, and hired contractors, with the exception beingtransmissionprojects.AdditionstoLongTermDebt, intheformofRUSLoansorBondSales,havenotbeenbudgetedforinthe2016year.

TILLAMOOKPEOPLE’SUTILITYDISTRICTMANAGEMENT’SDISCUSSIONANDANALYSIS

9

FiveYearComparison,statedinpercentageoftotaloperatingrevenue

2015 2014 2013 2012 2011

OperatingrevenuesThousandsofdollars 34,832$ 34,285$ 35,127$ 33,835$ 32,844$

Percent 100.0% 100.0% 100.0% 100.0% 100.0%

Deduct:Costofpower 49.4% 51.9% 47.1% 48.9% 45.5%Otheroperatingexpenses 45.7% 44.8% 45.7% 47.4% 44.7%

Netoperatingrevenues 5.0% 3.3% 7.2% 3.7% 9.8%

Interestandotherincome 0.3% 0.5% 0.7% 0.8% 0.2%

Totalnetoperatingrevenues,interest,andotherincome 5.2% 3.8% 7.9% 4.5% 10.0%

Deduct:Interestandothercharges 2.5% 2.6% 2.0% 2.1% 2.3%

Netincome: 2.8% 1.2% 5.9% 2.4% 7.7%

FiveYearComparisonofFinancialRatiosTimesInterestEarnedRatio(TIER):Measures the extent towhich earnings are adequate tomeet the annual interest costs for bonds andcertificates.R.U.S.minimumis1.25.

2015 2014 2013 2012 2011

Netincome 965,393$ 427,383$ 1,449,255$ 794,303$ 2,531,702$Addinterestexpense 840,868 862,644 704,735 755,166 619,584Ratestabilizationfund(RSF)transfer ‐ ‐ ‐ 100,000 ‐

Subtotal 1,806,261 1,290,027 2,153,990 1,649,469 3,151,286Dividebyinterestexpense 840,868 862,644 704,735 755,166 619,584

TIER 2.15 1.50 3.06 2.18 5.09

OperatingTIER:SameasTIERabove,exceptusesNetoperatingrevenuesinsteadofNetincome.

2015 2014 2013 2012 2011

Netoperatingrevenues(netofRSFtransfers) 1,726,983$ 1,139,802$ 2,109,997$ 1,143,720$ 3,219,676$

Dividebyinterestexpense 840,868 862,644 704,735 755,166 619,584

OperatingTIER 2.05 1.32 2.99 1.51 5.20

TILLAMOOKPEOPLE’SUTILITYDISTRICTMANAGEMENT’SDISCUSSIONANDANALYSIS

10

FiveYearComparisonofFinancialRatios(continued)DebtServiceCoverage(DSC):MeasurestheDistrict’sabilitytocoveritsdebtserviceforbondsandcertificates.R.U.S.minimumis1.25.

2015 2014 2013 2012 2011

Netincome 965,393$ 427,383$ 1,449,255$ 794,303$ 2,531,702$Addinterestexpense 840,868 862,644 704,735 755,166 619,584Adddepreciationexpense 2,861,370 2,676,159 2,668,440 2,586,228 2,497,584RSFtransfers ‐ ‐ ‐ 100,000 ‐

Subtotal 4,667,631 3,966,186 4,822,430 4,235,697 5,648,870Dividebydebtservicematurities 1,737,488 1,621,105 1,313,096 1,889,773 1,744,939

DSC 2.69 2.45 3.67 2.24 3.24

OperatingDSC:SameasDSCabove,exceptusesNetoperatingrevenueinsteadofNetincome.

2015 2014 2013 2012 2011

Netoperatingrevenues 1,726,983$ 1,139,802$ 2,109,997$ 1,243,720$ 3,219,676$Adddepreciationexpense 2,861,370 2,676,159 2,668,440 2,586,228 2,497,584RSFtransfers ‐ ‐ ‐ 100,000 ‐

Subtotal 4,588,353 3,815,961 4,778,437 3,929,948 5,717,260Dividebydebtservicematurities 1,737,488 1,621,105 1,313,069 1,889,773 1,744,939

OperatingTIER 2.64 2.35 3.64 2.08 3.28

EquityLevel:Representshowmuchthecustomerhasfurnishedofthetotalassetsascomparedtotheportionborrowed.

2015 2014 2013 2012 2011

Netposition 52,042,492$ 51,077,099$ 50,649,716$ 49,200,461$ 47,592,699$Totalassetsanddeferredoutflows

ofresources 106,655,364 103,898,972 93,698,512 93,221,079 82,224,166

Equitylevel 48.8% 49.2% 54.1% 52.8% 57.9%

TILLAMOOKPEOPLE’SUTILITYDISTRICTMANAGEMENT’SDISCUSSIONANDANALYSIS

11

FiveYearComparisonofFinancialRatios(continued)WorkingCapital:Theamountofcurrentassetsabovecurrentliabilities.

2015 2014 2013 2012 2011

Currentassets 18,496,346$ 18,817,178$ 14,295,069$ 14,446,838$ 11,694,331$Lesscurrentliabilities 6,496,693 6,138,806 6,212,967 5,784,455 5,560,810

Workingcapital 11,999,653$ 12,678,372$ 8,082,102$ 8,662,383$ 6,133,521$

CurrentRatio:Currentassetscomparedtocurrentliabilities.

2015 2014 2013 2012 2011

Currentassets 18,496,346$ 18,817,178$ 14,295,069$ 14,446,838$ 11,694,331$Currentliabilities 6,496,693 6,138,806 6,212,967 5,784,455 5,560,810

Currentratio 2.85 3.07 2.30 2.50 2.10

RateofReturn:Netincomeasapercentageofnetutilityplant.

2015 2014 2013 2012 2011

Netincome 965,393$ 427,383$ 1,449,255$ 794,303$ 2,531,702$Netutilityplant 66,735,918 66,225,865 65,568,529 64,907,904 63,202,259

Rateofreturn 1.4% 0.6% 2.2% 1.2% 4.0%

Thispageintentionallyleftblank.

12 Seeaccompanyingnotes.

TILLAMOOKPEOPLE’SUTILITYDISTRICTSTATEMENTSOFNETPOSITION

2015 2014

ELECTRICPLANT:Inservice‐atcost 96,135,088$ 93,883,268$Acquisitionadjustment (126,384) (126,384)Constructionworkinprogress 1,027,883 752,067

Totalelectricplant 97,036,587 94,508,951Lessaccumulatedprovisionfordepreciation (30,300,669) (28,283,086)

Netelectricplant 66,735,918 66,225,865

NOTESRECEIVABLE 194,719 214,596

INVESTMENTS‐BONDRESERVEFUND 2,561,335 2,558,944

CURRENTASSETSCashandcashequivalents:

Cashandcashequivalents 8,126,316 9,345,057Principalredemptionfund 557,514 640,785Specialdepositsrelatedtobondinterest 65,699 74,193Ratestabilizationfund‐designated 3,400,000 3,400,000

Accountsreceivable(netofallowancefordoubtfulaccountsof$216,054and$195,883,respectively) 2,934,795 2,541,624

Unbilledrevenue 1,835,171 1,538,329Materialsandsupplies 1,159,320 1,127,679Prepayments 417,531 420,429

Totalcurrentassets 18,496,346 19,088,096

OTHERNONCURRENTASSETSRegulatoryasset‐contributionsinaid 11,015,804 10,664,870Regulatoryasset‐pensiondebit 6,514,541 1,929,677Netpensionasset ‐ 2,350,235Other 61,818 168,727

Totalothernoncurrentassets 17,592,163 15,113,509

DEFERREDOUTFLOWSOFRESOURCESDeferredoutflowsofresources‐pension 809,738 410,567Unamortizedlossonbondrefunding 265,145 287,395

Totaldeferredoutflowsofresources 1,074,883 697,962

Totalassetsanddeferredoutflowsofresources 106,655,364$ 103,898,972$

ASSETS

December31,

Seeaccompanyingnotes. 13

TILLAMOOKPEOPLE’SUTILITYDISTRICTSTATEMENTSOFNETPOSITION

2015 2014

NETPOSITIONNetinvestmentincapitalassets 35,957,107$ 33,725,132$Designatedforratestabilizationfund 3,400,000 3,400,000Restrictedforbonddebtservice 3,387,376 3,470,647Unrestricted 9,298,009 10,481,320

Totalnetposition 52,042,492 51,077,099

LONG‐TERMDEBTRevenuebonds,lesscurrentmaturities 9,395,000 10,060,000RUSrevenuecertificatesofindebtedness,lesscurrent

maturities 19,878,983 20,889,782Unamortizedrevenuebondpremium 94,174 100,858

Totallong‐termdebt 29,368,157 31,050,640

CURRENTLIABILITIESCurrentmaturitiesoflong‐termdebt 1,675,799 1,737,488Accountspayable 2,390,181 2,241,982Customerdeposits 341,393 327,207Accruedinterest 65,699 74,193Accruedvacationpay 823,948 781,307Otheraccruals 1,199,673 976,629

Totalcurrentliabilities 6,496,693 6,138,806

OTHERNONCURRENTLIABILITIESNetpensionliability 5,842,327 ‐Othernoncurrentliabilities 407,939 277,078

Totalnoncurrentliabilities 6,250,266 277,078

DEFERREDINFLOWSOFRESOURCESDeferredinflowsofresources‐pension 1,481,952 4,690,479Regulatoryliability–contributionsinaid 11,015,804 10,664,870

Totaldeferredinflowsofresources 12,497,756 15,355,349

Totalnetposition,liabilitiesanddeferredinflowsofresources 106,655,364$ 103,898,972$

NETPOSITION,LIABILITIESANDDEFERREDINFLOWSOFRESOURCES

December31,

14 Seeaccompanyingnotes.

TILLAMOOKPEOPLE’SUTILITYDISTRICTSTATEMENTSOFREVENUES,EXPENSES,ANDCHANGESINNETPOSITION

2015 2014

OPERATINGREVENUESSalesofelectricity:

Residential:Urbanandrural 14,417,792$ 14,206,124$Secondary 5,218,450 5,042,477

Commericial:Small 6,184,855 5,978,471Large 8,192,574 8,236,020

Arealighting 259,772 265,579Publiclighting 108,828 122,154Otheroperatingrevenues 449,874 434,604

Totaloperatingrevenues 34,832,145 34,285,429

OPERATINGEXPENSESCostofpower 17,192,295 17,785,638Distributionexpense:

Operation 3,810,331 3,876,278Maintenance 3,419,660 3,291,174

Customeraccountsexpense 1,024,628 934,808Customerserviceandinformationalexpense 751,608 730,596Salesexpense 123,074 125,251Administrativeandgeneralexpense 3,077,676 2,882,982Depreciation 2,861,370 2,676,159Taxes 844,520 842,741

Totaloperatingexpenses 33,105,162 33,145,627

NETOPERATINGREVENUES 1,726,983 1,139,802

NONOPERATINGREVENUES(EXPENSES)Interestandotherincome 83,594 89,002Interestonlong‐termdebt (840,868) (862,644)Otherincome(expense) 11,250 76,789Amortizationofdebtpremiumandloss (15,566) (15,566)

Totalnonoperatingexpenses (761,590) (712,419)

CHANGEINNETPOSITION 965,393 427,383

NETPOSITION,BEGINNINGOFYEAR 51,077,099 50,649,716

NETPOSITION,ENDOFYEAR 52,042,492$ 51,077,099$

YearsEndedDecember31,

Seeaccompanyingnotes. 15

TILLAMOOKPEOPLE’SUTILITYDISTRICTSTATEMENTSOFCASHFLOWS

2015 2014

CASHFLOWSFROMOPERATINGACTIVITIESCashreceivedfromcustomers 34,156,318$ 34,890,836$Cashpaymentsforpurchasedpower (17,143,340) (18,101,156)Cashpaymentstosuppliersforgoodsandservices (6,980,167) (6,998,011)Cashpaymentstoemployeesforservices (5,735,144) (5,794,945)

Netcashprovidedbyoperatingactivities 4,297,667 3,996,724

CASHFLOWSFROMCAPITALANDRELATEDFINANCINGACTIVITIESProceedsfromissuanceofcertificatesofindebtedness ‐ 7,000,000Principalpaymentsonbondsandcertificatesofindebtedness (1,737,488) (1,621,105)Interestpaymentsonlong‐termdebt,netofamountcapitalized (849,362) (862,644)Constructionandacquisitionofplant (4,441,990) (4,251,687)Contributionsinaidofconstruction 1,097,503 848,646Materialssalvagedfromretirements 130,319 145,911

Netcashprovidedby(usedin)capitalandfinancingactivities (5,801,018) 1,259,121

CASHFLOWSFROMINVESTINGACTIVITIESNetdecrease(increase)in:

Investments‐reservefund,net (2,391) (2,661)Principalredemptionfund,net 83,271 (24,676)Specialdepositsrelatedtobondinterest 8,494 8,661Notesreceivable 19,877 12,712

Interestandotherincomereceived 83,594 89,002

Netcash(usedin)providedbyinvestingactivities 192,845 83,038

NETINCREASE(DECREASE)INCASHANDCASHEQUIVALENTS (1,310,506) 5,338,883

CASHANDCASHEQUIVALENTS,beginningofyear 13,460,035 8,121,152

CASHANDCASHEQUIVALENTS,endofyear 12,149,529$ 13,460,035$

YearsEndedDecember31,

16 Seeaccompanyingnotes.

TILLAMOOKPEOPLE’SUTILITYDISTRICTSTATEMENTSOFCASHFLOWS

2015 2014YearsEndedDecember31,

Reconciliationofnetoperatingrevenuestonetcashprovidedbyoperatingactivities:

Netoperatingrevenues 1,726,983$ 1,139,802$Adjustmentstoreconcilenetoperatingrevenuestonetcash

providedbyoperatingactivities:Depreciation 2,861,370 2,676,159Decrease(increase)in:

Accountsreceivable (393,171) 409,698Unbilledrevenue (296,842) 161,915Materialsandsupplies (31,641) (31,291)Prepayments 2,898 5,534

Increase(decrease)in:Accountspayable 148,199 (463,082)Customerdepostits 14,186 33,794Accruedvacationpay 42,641 32,219Otheraccruals 223,044 31,976

Totaladjustments 2,570,684 2,856,922

Netcashprovdedbyoperatingactivities 4,297,667$ 3,996,724$

Noncashinvesting,capital,andfinancingactivitiesUnamortizedlossonbondrefunding 22,250$ 22,250$Unamortizedrevenuebondpremium (6,684) (6,684)Amortizationofdebtpremiumandloss (15,566) (15,566)

Totalnoncashinvesting,capital,andfinancingactivities ‐$ ‐$

RECONCILIATIONOFCASHANDCASHEQUIVALENTSCashandcashequivalents,current 8,126,316$ $9,074,139Principalredemptionfund,current 557,514 640,785Specialdepositsrelatedtobondinterest 65,699 74,193Ratestabilizationfund‐designated 3,400,000 3,400,000

12,149,529$ 13,189,117$

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

17

Note1–OrganizationandSummaryofSignificantAccountingPoliciesOrganization – TillamookPeople'sUtilityDistrict (theDistrict) is amunicipal corporation organizedunderOregonRevisedStatutesChapter261.TheDistrictisapowerdistributionutilityservingpatronsin almost all of Tillamook County and small portions of Yamhill and Clatsop counties. The District'sBoard of Directors has the authority to set rates and charges for services furnished. Substantially allrevenuesarederivedfromthesaleofelectricpowertoresidentialandcommercialcustomers.Reportingentity–ThefinancialstatementsoftheDistrictincludeallfinancialactivitiesforwhichtheBoardofDirectorsisfinanciallyaccountable.TheDistricthasnocomponentunits.Incometaxstatus–TheDistrictisapeople'sutilitydistrictorganizedunderOregonRevisedStatutesChapter261.AsapoliticalsubdivisionoftheStateofOregon,theDistrictisexemptfromtaxationundertheprovisionsofSection115oftheInternalRevenueCode.Basisofaccounting–TheDistrictisconsideredanenterpriseandoperatesasaproprietaryfund.Thefinancial statements of the District have been prepared using the “economic resourcesmeasurementfocus” and on the “accrual basis of accounting” in accordance with accounting principles generallyaccepted intheUnitedStatesofAmerica(GAAP)asappliedtogovernmentalunits.TheGovernmentalAccounting Standards Board (GASB) is the standard‐setting body for governmental accounting andfinancialreporting.Changeinaccountingprinciple–EffectiveJanuary1,2015,theDistrictadoptedGASBStatementNo.68,AccountingandFinancialReporting forPensionsandGASBStatementNo.71,PensionTransitionforContributionsMadeSubsequenttotheMeasurementDate.Thesestatementsprovideaccountingguidancefornetpensionliabilities/assets,alsodefiningbalancestobeincludedindeferredoutflowsofresourcesanddeferredinflowsofresources.AffecteditemswerepreviouslyreportedundertherequirementsofGASBStatementNo.27,AccountingforPensionsbyStateandLocalGovernmentalEmployers.Previousstandardsdefinedpension liabilities in termsof theAnnuallyRequiredContributions (ARC).Statement No. 68 defines the net pension liability as the portion of the actuarial present value ofprojected benefit payments attributed to past periods of employee service, net of the pension plan’sfiduciarynetposition.StatementNo. 68 also requires recognitionof deferredoutflowsof resources anddeferred inflowsofresources related to pensions. Items related to pensions to be presented as deferred outflows ofresourcesordeferredinflowsofresourcesinclude:differencesbetweenexpectedandactualexperience,changes of assumptions, net differences between projected and actual earnings on investments, andchangesintheproportionanddifferencesbetweenemployercontributionsandproportionateshareofcontributions. Deferred balances are to be recognized in pension expense over a five year period orusingasystematicandrationalmethodequaltotheaverageoftheexpectedremainingservicelivesofallemployeesprovidedwithpensionsthroughthepensionplandeterminedasofthebeginningofthemeasurementperiod.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

18

Note1–OrganizationandSummaryofSignificantAccountingPolicies(continued)InNovember2013,theGASBissuedStatementNo.71,amendingStatementNo.68.StatementsNo.71requirescontributionsmadebyparticipatingemployers topensionplansafter themeasurementdatefor thenet pension liability but before the endof the financial statement period for the employer bereportedasdeferredoutflowsofresources.Prioryearnetpositionhasnotbeenrestatedasaresultofthechangeinaccountingprincipleduetotheuseofregulatoryaccountingtodefertheimpactofpensionexpense.Useofestimates – Thepreparation of financial statements in conformitywith accountingprinciplesgenerally accepted in the United States of America requires management to make estimates andassumptionsthataffectthereportedamountsofassetsandliabilitiesanddisclosureofcontingentassetsandliabilitiesatthedateofthefinancialstatementsandthereportedamountsofrevenuesandexpensesduringthereportingperiod.Actualresultscoulddifferfromthoseestimates.Revenuerecognition–Operatingrevenuesgenerallyresultfromprovidingelectricsalesandservices.TheDistrictutilizescyclebillingandrecordsrevenuebilledtoitscustomerswhenthecycle’sreadsarepulledintothebillingsystem.Metersarereaddailyandcustomeraccountsarecyclebilledmonthly.TheDistrict also records unbilled revenue, revenues from electric power delivered but not yet billed. Allrevenuesnotmeetingthisdefinitionarereportedasnon‐operatingrevenues.Concentrationofcreditrisk–Financialinstrumentsthatareexposedtoconcentrationsofcreditriskconsistprimarilyofcash(seeNote3)andreceivables.Creditisextendedtocustomersgenerallywithoutcollateral requirements, however, deposits are obtained from certain customers and formal shut‐offproceduresareinplace.Electricplant–Electricplantisrecordedatoriginalcost(seeNote2).Thecostofadditions,renewalsandreplacementsofpropertywithanestimatedusefullifegreaterthanoneyearisaddedtoplant,andrepairs andmaintenance of property is charged to expense. Property units renewed or replaced areremovedfromtheplantattheirestimatedcost.Thecostofplantretired,plusremovalcost,lesssalvagevalue,ischargedtothedepreciationreserve.Provisionhasbeenmadefordepreciationoftransmissionplantatastraight‐lineannualcompositerateof 2.75 percent in 2015 and 2014. Provision has beenmade for depreciation of distribution plant atstraight‐lineannualcompositeratesof1.8percentin2015and2014.Generalplantdepreciationrateshavebeenappliedonastraight‐linebasiswithannualratesof3.0to14.4percentin2015and2014.Cashequivalentsandrestrictedcash –TheDistrict considers short‐term investmentswithoriginalmaturitiesofthreemonthsorlessanddemanddepositstobecashequivalents(seeNote3).Fairvalueoffinancial instruments–Thecarryingamountsofcurrentassets, includingunrestrictedandrestrictedcashandinvestments,andcurrentliabilitiesapproximatefairvalueduetotheshort‐termmaturityofthoseinstruments.ThefairvalueoftheDistrict’sinvestmentsanddebtareestimatedbasedonthequotedmarketpricesforthesameorsimilarissues.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

19

Note1–OrganizationandSummaryofSignificantAccountingPolicies(continued)Accountsreceivable–Accountsreceivablearerecordedwheninvoicesareissuedandarewrittenoffwhentheyaredeterminedtobeuncollectible.TheallowancefordoubtfulaccountsisestimatedbasedontheDistrict’shistoricallosses,reviewofspecificproblemaccounts,theexistingeconomicconditions,andthefinancialstabilityofitscustomers.Generally,theDistrictconsidersaccountsreceivablepastdueafter30days.Materials and supplies – Materials and supplies consist primarily of items for construction andmaintenanceoftheutilityplantandisstatedataveragecost.Investments–Investmentsarecarriedatfairvalue.Restrictedinvestmentsconsistofthebondreservefund,principalredemptionfundandspecialdepositsrelatedtobondinterest.Regulatory asset and regulatory liability – The District has established a regulatory asset and aregulatoryliabilityforthefollowingitem:

Contributions inaidofconstruction – Contributions in aid of construction represent customer

reimbursements received to cover the cost of certain plant additions. The regulatory liability isestablishedtoamortizethecontributionsatarateequaltotheDistrict’saveragedepreciationrateof3.3%.InaccordancewithestablishedRuralUtilityService(RUS)accountingrequirements,customerreimbursementsarenettedagainstthecostofplantadditions.Theregulatoryassetisestablishedtorecognize the impact of GASB No. 33, Accounting and Financial Reporting for NonexchangeTransactions,andamortizeitovertheusefullifeoftheasset.

Pensiondebits–Pensiondebitsrepresentaportionofthechangeinnetpensionitemsandpensionexpense, as defined under GASB Statement No. 68. Regulatory accounting is used to recognizepension expense in accordancewith the required employer contribution rates set by the OregonPublicEmployeesRetirementSystem.

Deferredoutflows–Deferredoutflowsconsistofthefollowingcomponent: Unamortizedlossonbondrefunding–Forcurrentandadvancerefundingresultingindefeasance

ofdebt,thedifferencebetweenthereacquisitionpriceandthenetcarryingamountoftheolddebt(gainorloss)isdeferredandamortizedasacomponentofinterestexpenseovertheremaininglifeof theolddebt or thenewdebt,whichever is shorter.These amounts are reported as a deferredoutflowonthestatementsofnetposition.

Pension–Deferredoutflowsofresourcesrelatedtopensionrepresentsdeferralsofchangesinnetpensionliability,asdefinedunderGASBStatementNo.68.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

20

Note1–OrganizationandSummaryofSignificantAccountingPolicies(continued)Deferredinflows–Deferredinflowsconsistofthefollowingcomponent: Contributions inaidofconstruction – Contributions in aid of construction represent customer

reimbursements received to cover the cost of certain plant additions. The regulatory liability isestablishedtoamortizethecontributionsatarateequaltotheDistrict’saveragedepreciationrateof3.3%.InaccordancewithestablishedRuralUtilityService(RUS)accountingrequirements,customerreimbursementsarenettedagainstthecostofplantadditions.Theregulatoryassetisestablishedtorecognize the impact of GASB No. 33, Accounting and Financial Reporting for NonexchangeTransactions,andamortizeitovertheusefullifeoftheasset.

Pensioncredits–Deferredinflowsofresourcesrelatedtopensionrepresentsdeferralsofchangesinnetpensionliability,asdefinedunderGASBStatementNo.68.

Netposition–Consistsofthefollowingcomponents: Netinvestmentincapitalassets–Thiscomponentofnetpositionconsistsofcapitalassets,netof

accumulated depreciation and outstanding balances of any bonds or debt obligations that areattributabletotheacquisition,construction,orimprovementofthoseassets.

Restricted – This component of net position on which constraints are placed as to their use.

Constraints includethoseimposedbycreditors(suchasthroughdebtcovenants),contributors,orlaws or regulation of other governments or constraints imposed by law through constitutionalprovisionsorthroughenablinglegislation.

Designated – This component of net position on which constraints are placed as to their use.

ConstraintsincludethoseimposedinternallybytheBoardofDirectors. Unrestricted – This component of net position consists of net position that does not meet the

definitionof“restricted”or“netinvestmentincapitalassets.”Reclassifications–Certainaccountsinthe2014financialstatementshavebeenreclassifiedtoconformtothepresentation inthe2015basic financialstatements.Suchreclassificationshavenoeffectonnetpositionorthechangesinnetposition.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

21

Note2–ElectricPlantElectricplantactivityfortheyearendedDecember31,2015wasasfollows:

Balance Balance1/1/2015 Additions Retirements 12/31/2015

Electricplantnotbeingdepreciated:Land 1,098,018$ ‐$ ‐$ 1,098,018$Intangibleplant 556 ‐ ‐ 556Constructioninprogress 752,067 2,811,846 2,536,030 1,027,883

Totalelectricplantnotbeingdepreciated 1,850,641 2,811,846 2,536,030 2,126,457

ElectricplantbeingdepreciatedTransmissionanddistribution 80,025,775 2,756,338 756,230 82,025,883General 12,758,919 316,630 64,918 13,010,631Acquisitionadjustment (126,384) ‐ ‐ (126,384)

Totalelectricplantbeingdepreciated 92,658,310 3,072,968 821,148 94,910,130

Lessaccumulateddepreciation 28,283,086 2,861,370 843,787 30,300,669

Totalelectricplantbeingdepreciated,net 64,375,224 211,598 (22,639) 64,609,461

Electricplant,net 66,225,865$ 3,023,444$ 2,513,391$ 66,735,918$

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

22

Note2–ElectricPlant(continued)ElectricplantactivityfortheyearendedDecember31,2014wasasfollows:

Balance Balance1/1/2014 Additions Retirements 12/31/2014

Electricplantnotbeingdepreciated:Land 1,098,018$ $‐ $‐ 1,098,018$Intangibleplant 556 ‐ ‐ 556Constructioninprogress 2,114,489 2,607,129 3,969,551 752,067

Totalelectricplantnotbeingdepreciated 3,213,063 2,607,129 3,969,551 1,850,641

ElectricplantbeingdepreciatedTransmissionanddistribution 76,425,544 4,659,210 1,058,979 80,025,775General 12,669,732 266,601 177,414 12,758,919Acquisitionadjustment (126,384) ‐ ‐ (126,384)

Totalelectricplantbeingdepreciated 88,968,892 4,925,811 1,236,393 92,658,310

Lessaccumulateddepreciation 26,613,426 2,676,159 1,006,499 28,283,086

Totalelectricplantbeingdepreciated,net 62,355,466 2,249,652 229,894 64,375,224

Electricplant,net 65,568,529$ 4,856,781$ 4,199,445$ 66,225,865$

Note3–CashandInvestmentsCashandinvestmentsarecomprisedofthefollowingasofDecember31,2015and2014:

2015 2014

Workingfunds 2,050$ 2,050$Depositswithfinancialinstitutions 9,711,118 9,692,631DepositswithOregonLocalGovernmentInvestmentPool 2,436,361 3,765,354Investments 2,561,335 2,558,944

Totalcashandinvestments 14,710,864$ 16,018,979$

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

23

Note3–CashandInvestments(continued)Deposits–Depositswithfinancialinstitutionsincludebankdemandandtimecertificatedeposits.The Oregon State Treasurer is responsible formonitoring public funds held by bank depositories inexcessofFDICinsuredamounts,andforassuringthatpublicfundsondepositarecollateralizedtotheextentrequiredbyOregonRevisedStatutes(ORS)Chapter295.ORSChapter295requiresdepositorybankstoplaceandmaintainondepositwitha third‐partycustodianbanksecuritieshavingavalueof10%, 25%or 110%of public funds ondeposit dependingprimarily on the capitalization level of thedepositorybank.TheOregonLocalGovernmentInvestmentPoolisanopen‐ended,no‐loaddiversifiedportfoliopool.Thefair value of the District’s position in the pool is substantially the same as the value of the District’sparticipantbalance.The Oregon Local Government Investment Pool is an external investment pool which is part of theOregonShort‐TermFund(OSTF).InvestmentpoliciesaregovernedbytheOregonRevisedStatuesandtheOregonInvestmentCouncil(Council).TheStateTreasureristheinvestmentofficerfortheCouncil.Investments are further governed by portfolio guidelines issued by the OSTF Board. The GovernorappointsthemembersoftheCouncilandOSTFBoard.ThefairvalueoftheDistrict’spositioninthepoolis the same as the value of the pool shares. The OSTF does not receive credit quality ratings fromnationallyrecognizedstatisticalratingorganizations.FinancialstatementsfortheOSTFmaybeobtainedfromtheOregonStateTreasurer’swebsite.Interest rate risk is the risk that changes in interest rates will adversely affect the fair value of aninvestment.TheOregonShort‐TermFundmanagesthisriskbylimitingthematurityoftheinvestmentsheldbythefund.Custodialcreditriskfordepositsistheriskthatintheeventofabankfailure,theDistrict’sdepositsmaynotbereturned.TheDistrictdoesnothaveapolicyfordepositscustodialcreditrisk.The District created a rate stabilization fund as permitted by the District's bond resolution and isfundingitfromunrestrictedcashanddeposits.TheresolutionallowstheDistricttouseamountsinthisfundforitsdebtservicecoveragecalculationasdefinedintheDistrict'sbondresolution.Investments – State statutes authorize the District to invest in general obligations of the U.S.Government and its agencies, certain bonded obligations of Oregon municipalities, bank repurchaseagreements, bankers' acceptances, and theOregonLocalGovernment InvestmentPool, amongothers.TheDistricthasnoinvestmentpolicythatwouldfurtherlimititsinvestmentchoices.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

24

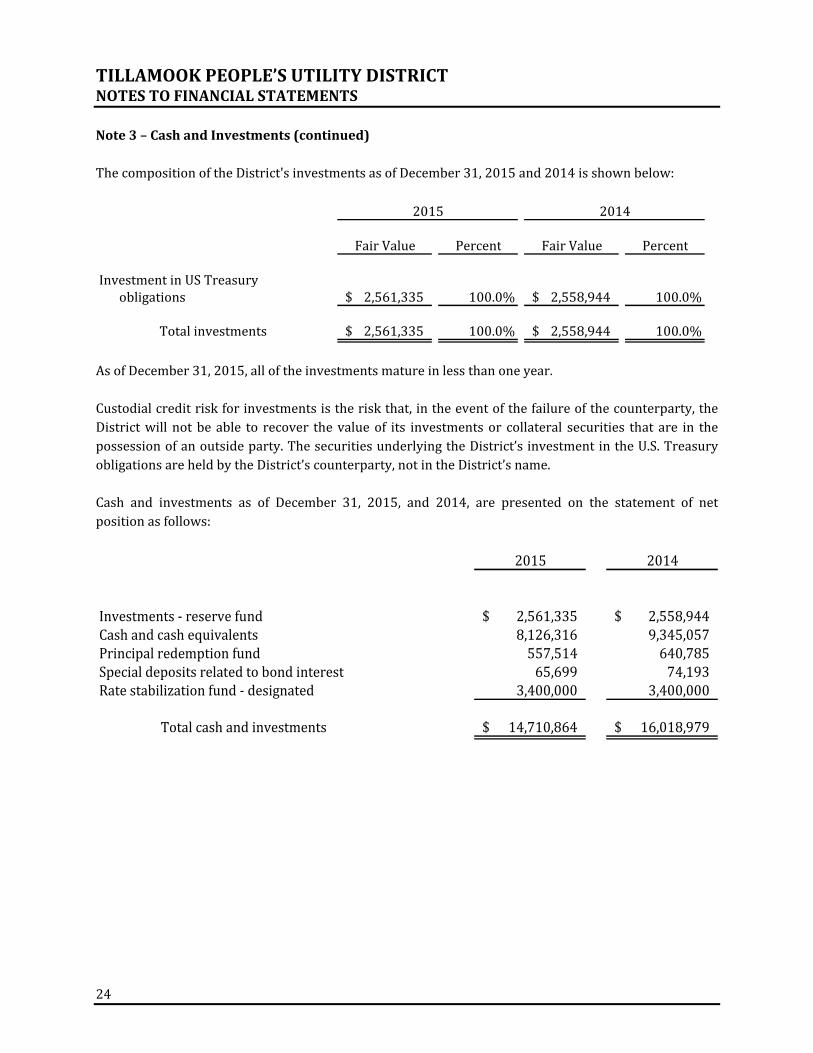

Note3–CashandInvestments(continued)ThecompositionoftheDistrict'sinvestmentsasofDecember31,2015and2014isshownbelow:

FairValue Percent FairValue Percent

InvestmentinUSTreasuryobligations 2,561,335$ 100.0% 2,558,944$ 100.0%

Totalinvestments 2,561,335$ 100.0% 2,558,944$ 100.0%

2015 2014

AsofDecember31,2015,alloftheinvestmentsmatureinlessthanoneyear.Custodialcreditriskforinvestmentsistheriskthat,intheeventofthefailureofthecounterparty,theDistrictwillnotbeable to recover thevalueof its investmentsor collateral securities that are in thepossessionofanoutsideparty.ThesecuritiesunderlyingtheDistrict’sinvestmentintheU.S.TreasuryobligationsareheldbytheDistrict’scounterparty,notintheDistrict’sname.Cash and investments as of December 31, 2015, and 2014, are presented on the statement of netpositionasfollows:

2015 2014

Investments‐reservefund 2,561,335$ 2,558,944$Cashandcashequivalents 8,126,316 9,345,057Principalredemptionfund 557,514 640,785Specialdepositsrelatedtobondinterest 65,699 74,193Ratestabilizationfund‐designated 3,400,000 3,400,000

Totalcashandinvestments 14,710,864$ 16,018,979$

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

25

Note4–Long‐TermDebtBonds and Certificates – Authority to issue revenue bonds is granted to the District under theprovisions of Chapter 261, Oregon Revised Statutes. Revenue certificates of indebtedness have beenissued in lieu of bonds for loans obtained from theRuralUtilities Service. Long‐termdebt covenantsspecify that District revenues are pledged for the retirement of long‐term debt. The proceeds of allbondsandcertificateswereusedforconstructionandacquisitionofcapitalassets.AtDecember31,2015and2014,bondsandcertificatespayableconsistofthefollowing:

2015 2014

Electricsystemrevenuebonds:Series2008 5,160,000$ 5,370,000$Series2010,refundingbonds 4,900,000 5,325,000

Totalelectricsystemrevenuebonds 10,060,000 10,695,000

RUSrevenuecertificatesofindebtedness:2.58%‐3.05%certificates 12,924,543 13,439,1635%certificates 580,000 765,000Variableratecertificates 7,385,239 7,788,107

TotalRUSrevenuecertificatesofindebtedness 20,889,782 21,992,270

Totalbondsandcertificatespayable 30,949,782 32,687,270Lesscurrentmaturities 1,675,799 1,737,488

Long‐termdebt 29,273,983$ 30,949,782$

The Electric System Revenue Bonds, Series 2008, are due annually through December 1, 2032, withinterestat4%to4.25%perannumpayablesemi‐annuallyonJune1andDecember1.The Electric System Revenue Refunding Bonds, Series 2010, are due annually through December1,2027,withinterestat2%to4%perannumpayablesemi‐annuallyonJune1andDecember1.TheRUSrevenuecertificatesofindebtednessareduesemi‐annuallyorannuallywithinterestat2.58%,3.05% or 5% per annum or a variable rate with a maximum rate of 7% per annum payable semi‐annuallyorquarterlyonJanuary1andJuly1oronMarch31,June30,September30andDecember31.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

26

Note4–Long‐TermDebt(continued)Principalandinterestactivityduringtheyears2015and2014wasasfollows:

InterestOutstanding Matured Outstanding Matured1/1/2015 Issued andPaid 12/31/2015 andPaid

Revenuebonds 10,695,000$ ‐$ 635,000$ 10,060,000$ 401,302$Certificatesofindebtedness 21,992,270 ‐ 1,102,488 20,889,782 439,566

Total 32,687,270$ ‐$ 1,737,488$ 30,949,782$ 840,868$

Principal

InterestOutstanding Matured Outstanding Matured1/1/2014 Issued andPaid 12/31/2014 andPaid

Revenuebonds 11,315,000$ ‐$ 620,000$ 10,695,000$ 421,947$Certificatesofindebtedness 15,993,375 7,000,000 1,001,105 21,992,270 440,697

Total 27,308,375$ 7,000,000$ 1,621,105$ 32,687,270$ 862,644$

Principal

Scheduledfuturematuritiesofprincipalandinterestareasfollows:

Year Principal Interest Principal Interest Principal Interest

2016 665,000$ 381,947$ 1,010,799$ 406,270$ 1,675,799$ 788,217$2017 685,000 359,789 1,073,881 383,523 1,758,881 743,3122018 710,000 336,918 1,104,365 360,271 1,814,365 697,1892019 735,000 313,095 1,057,831 339,857 1,792,831 652,9522020 755,000 287,101 1,088,412 319,000 1,843,412 606,101

2021‐25 3,485,000 987,749 5,915,887 1,267,192 9,400,887 2,254,9412026‐30 2,220,000 419,927 6,204,618 719,990 8,424,618 1,139,9172031‐32 805,000 48,787 3,433,989 187,254 4,238,989 236,041

Totals 10,060,000$ 3,135,313$ 20,889,782$ 3,983,357$ 30,949,782$ 7,118,670$

TotalsCertificates

ofIndebtednessRevenueBonds

Scheduled interest maturities for RUS variable rate loans are based on the maximum rate of sevenpercentperannum,exceptforthe23rdSeries.The23rdSeriesareequalpaymentloansandscheduledprincipalandinterestmaturitiesarebasedonanestimatedvariablerateprovidedbyRUS.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

27

Note5–RetirementPlanPlandescription–AllqualifiedemployeesareeligibletoparticipateinoneoftheUtility’stwopensionplans administered by Public Employees Retirement System (PERS). The Oregon Public EmployeesRetirementFund (Tier1/Tier2) isa cost‐sharingmultiple‐employerdefinedbenefitpensionplan forqualifyingemployeeshiredbeforeAugust29,2003.TheOregonPublicServiceRetirementPlan(OPSRP)isahybridsuccessorplantoTier1/Tier2consistingoftwoprograms:adefinedbenefitpensionplanandadefinedcontributionprogram(theIndividualAccountProgramorIAP).TheOPSRPpensionplaniseffective forallnewemployeeshiredonorafterAugust29,2003.Theplanprovidesa lifepensionfundedbyemployercontributions.Benefitsarecalculatedbyaformulaformemberswhoattainnormalretirementage.Theformulatakesintoaccountfinalaveragesalary,yearsofserviceandtypeofservice(general or police/fire). Beginning January 1, 2004, all PERS member contributions go into the IAPportion of OPSRP. Tier 1/Tier 2 members retain their existing Tier 1/Tier 2 accounts, but futuremembercontributionsaredepositedintothemember’sIAPaccount.BenefitprovisionsunderthePlansareestablishedbyStatestatute.PERSissuespubliclyavailablereportsthatincludeafulldescriptionofthepensionplansregardingbenefitprovisions,assumptionsandmembership informationthatcanbefoundonthePERSwebsite.BenefitsProvided(Tier1/Tier2)–TheTier1/Tier2pensionplanprovidesretirement,disabilitybenefits, annual cost‐of‐living adjustments, and death benefits to planmembers,whomust be publicemployees and beneficiaries. The plan is closed to new members on or after August 29, 2003. Theretirement allowance is payable monthly for life and may be selected from 13 retirement benefitoptions.Theseoptionsincludesurvivorshipbenefitsandlump‐sumrefunds.Thebasicbenefitisbasedonyearsofserviceandfinalaveragesalary.Apercentage(1.67percentforgeneralserviceemployees)ismultipliedbythenumberofyearsofserviceandthefinalaveragesalary.Benefitsmayalsobecalculatedundereitheraformulaplusannuity(formemberswhowerecontributingbeforeAugust21,1981)oramoney match computation if a greater benefit results. A member is considered vested and will beeligible at minimum retirement age for a service retirement allowance if he or she has had acontribution in each of five calendar years or has reached at least 50 years of age before ceasingemploymentwithaparticipatingemployer.Generalserviceemployeesmayretireafterreachingage55.Tier1general serviceemployeebenefits are reduced if retirementoccursprior to age58with fewerthan30yearsofservice.Tier2membersareeligibleforfullbenefitsatage60.Uponthedeathofanon‐retiredmember,thebeneficiaryreceivesalump‐sumrefundofthemember’saccount balance (accumulated contributions and interest). In addition, the beneficiary will receive alump‐sum payment from employer funds equal to the account balance, provided one ormore of thefollowingconditionsaremet: ThememberwasemployedbyaPERSemployeratthetimeofdeath Thememberdiedwithin1200daysafterterminatedofPERS‐coveredemployment ThememberdiedasaresultofinjurysustainedwhileemployedinaPERS‐coveredjob ThememberwasonanofficialleaveofabsencefromaPERS‐coveredjobatthetimeofdeath.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

28

Note5–RetirementPlan(continued)Amemberwith 10 ormore years of creditable servicewho becomes disabled fromother than duty‐connected causesmay receiveanon‐dutydisabilitybenefit.Adisability resulting froma job‐incurredinjury or illness qualifies a member for disability benefits regardless of the length of PERS‐coveredservice. Upon qualifying for either a non‐duty or duty disability, service time is computed to age 58whendeterminingthemonthlybenefit.Under ORS 238.360 monthly benefits are adjusted annually through cost‐of‐living changes. Undercurrent law, the cap on the cost of living adjustments will vary based on 1.25 percent on the first$60,000ofannualbenefitand0.15percentonannualbenefitsover$60,000.BenefitsProvided(OPSRP)–TheOPSRPpensionplanprovidesretirement,disabilitybenefits,annualcost‐of‐living adjustments, and death benefits to planmembers, whomust be public employees andbeneficiaries. The plan is open to newmembers hired on or after August 29, 2003. This portion ofOPSRP provides a life pension funded by employer contributions. Benefits are calculated with thefollowing formula for members who attain normal retirement age: 1.5 percent is multiplied by thenumber of years of service and the final average salary. Normal retirement age for general servicemembersisage65,orage58with30yearsofretirementcredit.AmemberoftheOPSRPplanbecomesvestedon theearliestof the followingdates: thedate themember completes600hoursof service ineach of five calendar years, the date themember reaches normal retirement age, and, if the pensionprogramisterminated,thedateonwhichterminationbecomeseffective.Uponthedeathofanon‐retiredmember,thespouseorotherpersonwhoisconstitutionallyrequiredtobe treated in the samemanner as the spouse receives for life 50 percent of the pension thatwouldotherwisehavebeenpaidtothedeceasedmember.A member who has accrued 10 or more years of retirement credits before the member becomesdisabledoramemberwhobecomesdisabledduetoajob‐relatedinjuryshallreceiveadisabilitybenefitof 45percent of themember’s salary determined as of the last fullmonth of employment before thedisabilityoccurred.Under ORS 238A.210 monthly benefits are adjusted annually through cost‐of‐living changes. Undercurrentlaw,thecapontheCOLAwillvarybasedon1.25percentonthefirst$60,000ofannualbenefitand0.15percentonannualbenefitsabove$60,000.Contributions – PERS funding policy provides for monthly employer contributions at actuariallydetermined rates. These contributions, expressed as a percentage of coveredpayroll, are intended toaccumulatesufficientassetstopaybenefitswhendue.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

29

Note5–RetirementPlan(continued)Employer contribution rates during the period were based on the December 31, 2011 actuarialvaluationassubsequentlymodifiedby2013legislatedchangesinbenefitprovisions.Theratesbasedona percentage of payroll, first became effective July 1, 2013. The state of Oregon and certain schools,community colleges and political subdivisions have made lump sum payments to establish sideaccounts,andtheirrateshavebeenreduced.EmployercontributionsfortheyearendedDecember31,2015were$903,396,excludingamountstofundemployer‐specificliabilities.Pension asset, pension expense, and deferred outflows or resources and deferred inflows ofresourcesrelatedtopension–AtDecember31,2015theutilityreportedaliabilityof$5,842,327foritsproportionateshareofthenetpensionliability.AtDecember31,2014,theutilityreportedanassetof$2,350,235foritsproportionateshareofthenetpensionasset.ThenetpensionliabilitywasmeasuredasofJune30,2015andthetotalpensionliabilityforeachPlanusedtocalculatethenetpensionliabilitywasdeterminedbyanactuarialvaluationasofDecember31,2014rolledforwardtoJune30,2015usingstandardupdateprocedures.TheUtility’sproportionofthenetpensionassetwasbasedonaprojectionoftheUtility’slong‐termshareofcontributionstothePlansrelativetotheprojectedcontributionsforallparticipating employers, actuarially determined. The Utility’s proportionate share of the net pensionassetforthePlansasofJune30,2015was0.10175680%.For theyearendedDecember31,2015, theDistrict’sproportionate shareof systempensionexpensewas$5.4million.TheDistricthaselectedtouseregulatoryaccountingtorecognizepensionexpenseinconjunctionwiththerequiredemployercontributionrates.Accordingly,theDistrictrecognizedpensionexpenserelatedtoTierOne/TierTwoandOPSRPof$903,396.AsofDecember31,2015,theDistrictreporteddeferredoutflowsofresourcesanddeferredinflowsofresourcesrelatedtopensionsfromthefollowingsources:

Pensioncontributionssubsequenttomeasurementdate 494,690$ ‐$Differencesbetweenexpectedandactualexperience 315,048 ‐Differencesbetweenprojectedandactualearnings

onplaninvestments ‐ 1,224,684Changesinproportionateshare ‐ 33,099Differencesbetweenemployercontributionsandthe

employer'sproportionateshareofsystemcontributions ‐ 224,169

809,738$ 1,481,952$

DeferredOutflowsofResources

DeferredInflowsofResources

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

30

Note5–RetirementPlan(continued)$494,690 reported as deferred outflows of resources related to contributions subsequent to themeasurement date will be recognized as a reduction of the net pension liability in the year endedDecember31,2016.Otheramountsreportedasdeferredoutflowsofresourcesanddeferredinflowsofresourcesrelatedtopensionsaretobeamortizedaspensiondebitsandpensioncreditsasfollows:

YearsendingDecember31, 2016 (582,622)$2017 (582,622)2018 (582,623)2019 564,6492020 16,314

(1,166,904)$

ActuarialAssumptions–ThetotalpensionassetsintheDecember31,2013actuarialvaluationsweredeterminedusingthefollowingactuarialassumptions.ValuationDate December31,2013MeasurementDate June30,2015ActuarialCostMethod EntryAgeNormalActuarialAssumptions:

DiscountRate 7.75%Inflation 2.75%PayrollGrowth 3.75%ProjectedSalaryIncrease 3.75%InvestmentRateofReturn 7.75%

MortalityratesforhealthyretireesandbeneficiarieswerebasedontheRP‐2000Sex‐distincttables,asappropriate,withadjustmentsformortalityimprovementsbasedonScaleAA.Mortalityratesforactivemembersareapercentageofhealthyretireeratesthatvarybygroup,asdescribedinthevaluation.Fordisabled retirees,mortality rates are a percentage (65% formales, 90% for females) of theRP‐2000staticcombineddisabledmortalitysex‐distincttable.Actuarial valuations of an ongoing plan involve estimates of the value of projected benefits andassumptions about the probability of events far into the future. Actuarially determined amounts aresubjecttocontinualrevisionasactualresultsarecomparedtopastexpectationsandnewestimatesaremadeaboutthefuture.ExperiencestudiesareperformedasofDecember31ofevennumberedyears.Themethodsandassumptionsshownabovearebasedonthe2014ExperienceStudywhichreviewedexperienceforthefour‐yearperiodendedonDecember31,2014.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

31

Note5–RetirementPlan(continued)Discountrate–Thediscountrateusedtomeasurethetotalpensionliabilitywas7.75percentfortheDefinedBenefitPensionPlan.Theprojectionofcashflowsusedtodeterminethediscountrateassumedthat contributions from plan members and those of the contributing employers are made at thecontractuallyrequiredrates,asactuariallydetermined.Basedonthoseassumptions,thepensionplan’sfiduciary net positionwas projected to be available tomake all projected future benefit payments ofcurrentplanmembers.Therefore,thelong‐termexpectedrateofreturnonpensionplaninvestmentsfortheDefinedBenefitPensionPlanwasappliedtoallperiodsofprojectedbenefitpaymentstodeterminethetotalpensionliability.Todevelopananalyticalbasisfortheselectionofthelong‐termexpectedrateofreturnassumption,inJuly2013thePERSBoardreviewedlong‐termassumptionsdevelopedbybothMilliman’scapitalmarketassumptions team and the Oregon Investment Council’s (OIC) investment advisors. The table belowshowsMilliman’sassumptionsforeachoftheassetclassesinwhichtheplanwasinvestedatthattimebasedontheOIClong‐termtargetassetallocation.TheOIC’sdescriptionofeachassetclasswasusedtomapthetargetallocationtotheassetclassesshownbelow.Eachassetclassassumption isbasedonaconsistentsetofunderlyingassumptions,andincludesadjustmentfortheinflationassumption.These assumptions are not based on historical returns, but instead are based on a forward‐lookingcapitalmarketeconomicmodel.

AssetClass TargetCompoundAnnualReturn(Geometric)

CoreFixedIncome 7.20% 4.50%Short‐TermBonds 8.00% 3.70%Intermediate‐TermBonds 3.00% 4.10%HighYieldBonds 1.80% 6.66%LargeCapUSEquities 11.65% 7.20%MidCapUSEquities 3.88% 7.30%SmallCapUSEquities 2.27% 7.45%DevelopedForeignEquities 14.21% 6.90%EmergingForeignEquities 5.49% 7.40%PrivateEquity 20.00% 8.26%OpportunityFunds/AbsoluteReturn 5.00% 6.01%RealEstate(Property) 13.75% 6.51%RealEstate(REITS) 2.50% 6.76%Commodities 7.71% 6.07%

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

32

Note5–RetirementPlan(continued)Sensitivityanalysis–Belowisasensitivityanalysisaroundthediscountrateassumedintheactuarialassumptions:

Employers'NetPensionLiability(Asset) 1%Decrease6.75%CurrentDiscountRate7.75% 1%Increase8.75%

Definedbenefitpensionplan 1,070,600$ 5,842,327$ (1,839,300)$

Pensionplan fiduciarynetposition–Detailed information about each pension plan’s fiduciary netpositionisavailableintheseparatelyissuedOPERSfinancialreports.Payable to the pension plan – At December 31, 2015 and 2014, the District did not have anoutstandingamountofcontributionspayabletothepensionplan.Changesinplanprovisionsduringthemeasurementperiod–TheOregonSupremeCourtonApril30,2015ruledthattheprovisionsofSenateBill861,signedintolawinOctober2013,thatlimitedthepost‐retirementCOLAonbenefitsaccruedpriortothesigningofthelawwasunconstitutional.Benefitscouldbemodifiedprospectively,butnotretrospectively.Asaresult, thosewhoretiredbefore thebillwaspassedwillcontinuetoreceiveaCOLAtiedtotheConsumerPriceIndexnormallyresultingina2%increaseannually.Restorationpaymentswillbemadetothosebenefitrecipients.PERSmemberswhohave accruedbenefits before and after the effectivedatesof the2013 legislationwill have ablendedCOLAratewhentheyretire.This isachange inbenefit termssubsequentto themeasurementdateofJune30,2014andhasbeenreflectedinthecurrentmeasurementperiod.Changesinplanprovisionssubsequenttothemeasurementperiod–AtitsJuly31,2015meeting,thePERSBoardloweredthe“assumedrate”to7.5%effectiveJanuary1,2016.Theassumedrateistherateofinvestmentreturn(includinginflation)thatPERSFund’splansareexpectedtoearnoverthelongterm.OregonAdministrativeRule459‐007‐0001(2)statesthattheassumedrate“meanstheactuarialassumedrateofreturnoninvestmentsasadoptedbytheBoardforthemostrecentactuarialvaluation.”Note6–Post‐EmploymentHealthCareBenefitsPlandescription–TheDistrictadministersasingle‐employerdefinedbenefithealthcareplan.Theplanprovides postretirement healthcare benefits for eligible retirees until the retiree turns 65 or hasreceivedthesubsidyfor5years.BenefitprovisionsareestablishedthroughDistrictpolicy.TheDistrict’spost‐employmenthealthcareplandoesnotissueapubliclyavailablefinancialreport.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

33

Note6–Post‐EmploymentHealthCareBenefits(continued)Fundingpolicy–ContributionrequirementsareestablishedthroughDistrictpolicy.Retireesandtheirdependentsareeligibletoreceivethesamemedicalanddentalcoverageasactiveemployees.$350ofthemonthlymedicalpremiumispaidbytheemployer.Employer‐paidhealthcarebenefitswereclosedtonewentrantseffectiveJanuary1,2008.Theretireeisresponsibleforthedentalpremiums.Nospousalcoverageispaidforbytheemployer.Fundingisonapay‐as‐you‐gobasis.TheDistrict'scontributionstotheplanforthe2015,2014,and2013yearswere$31,324,$45,158,and$43,699respectively.AnnualOPEBcostandnetOPEBobligation –TheDistrict's annual other post‐employment benefit(OPEB)costiscalculatedbasedontheannualrequiredcontributionoftheemployer(ARC),anamountactuarially determined in accordance with the parameters of GASB Statement No. 45. The ARCrepresentsaleveloffundingthat,ifpaidonanongoingbasis,isprojectedtocovernormalcosteachyearandamortizeanyunfundedactuarialliabilitiesovera10yearperiod.The following table shows the components of the District’s annual OPEB cost for 2015 and 2014,amounts actually contributed to the plan, and changes in theDistrict’s netOPEB obligation,which isrecordedwithotheraccrualsonthestatementofnetposition:

2015 2014

Annualrequiredcontribution 63,493$ $59,840InterestonnetOPEBobligation 2,281 2,172Adjustmentstoannualrequiredcontribution (17,744) (13,747)

AnnualOPEBcost 48,030 48,265Contributionsmade (31,324) (45,158)

IncreaseinnetOPEBobligation 16,706 3,107

NetOPEBobligation,beginningofyear 65,177 62,070

NetOPEBobligation,endofyear 81,883$ $65,177

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

34

Note6–Post‐EmploymentHealthCareBenefits(continued)TheDistrict'sannualOPEBcost,thepercentageofannualOPEBcostcontributedtotheplan,andthenetOPEBobligationforthelastthreeyearswereasfollows:

PercentageofAnnual AnnualOPEB NetOPEBOPEBCost CostContributed Obligation

48,030$ 65% 81,883$48,265$ 94% 65,177$49,968$ 87% 62,070$

YearEnded

12/31/201512/31/201412/31/2013

Fundedstatusandfundingprogress–AsofAugust1,2014,themostrecentactuarialvaluation,theactuarialaccruedliabilityforbenefitswas$155,628andtheactuarialvalueofassetswas$0,resultinginan unfunded actuarial accrued liability (UAAL) of $155,628. The covered payroll (annual payroll ofactiveemployeescoveredbytheplan)was$845,000for2014andtheratiooftheUAALtothecoveredpayrollwas18.4%.Actuarial valuations of an ongoing plan involve estimates of the value of reported amounts andassumptions about the probability of occurrence of events far into the future. Examples includeassumptionsabout future employment,mortality and thehealthcare cost trend.Amountsdeterminedregarding the funded status of the plan and the annual required contributions of the employer aresubjecttocontinualrevisionsasactualresultsarecomparedwithpastexpectationsandnewestimatesaremadeaboutthefuture.Thescheduleoffundingprogress,presentedasrequiredsupplementaryinformationfollowingthenotestothefinancialstatements,presentsmultiyeartrendinformationaboutwhethertheactuarialvalueofplanassetsisincreasingordecreasingovertimerelativetotheactuarialaccruedliabilityforbenefits.Actuarialmethods and assumptions – Projections of benefits for financial reporting purposes arebased on the substantive plan (the plan as understood by the employer and the planmembers) andincludethetypesofbenefitsprovidedatthetimeofeachvaluationandthehistoricalpatternofsharingofbenefitcostsbetweentheemployerandtheplanmemberstothatpoint.Theactuarialmethodsandassumptionsusedincludetechniquesthataredesignedtoreducetheeffectsofshort‐termvolatilityinactuarialaccruedliabilitiesandtheactuarialvalueofassets,consistentwiththelong‐termperspectiveofthecalculations.IntheactuarialvaluationconductedasofAugust1,2014,theprojectedunitcreditactuarialcostmethodwas used. Actuarial assumptions included a discount rate of 3.5%. The unfunded actuarial accruedliabilityisbeingamortizedusingthelevel‐dollarmethodoveraclosed10‐yearperiod.

TILLAMOOKPEOPLE’SUTILITYDISTRICTNOTESTOFINANCIALSTATEMENTS

35

Note7–RiskManagementTheDistrict isexposedtovariousrisksof lossrelated to torts; theftof,damage to,anddestructionofassets; errors and omissions; and natural disasters. The District is a member of Special DistrictsInsurance Services (SDIS) and pays an annual premium to SDIS for risks of loss including generalliability, automobile liability, public official liability and property coverage. Under the membershipagreementwithSDIS,SDISistobeself‐sustainingthroughmemberpremiumsandwillreinsurethroughcommercial companies for claims in excessof certain limits. Settled claims resulting from these riskshavenotexceededinsurancecoverageinanyofthepastthreeyears.Note8–CommitmentsPowerpurchaseagreement–TheDistricthasexecutedaPowerSalesAgreementwiththeBonnevillePower Administration. Power deliveries under the agreement commenced on October 1, 2011 andcontinuethroughSeptember30,2028.TheagreementisforLoadFollowingservicecoupledwithanewTieredRateMethodology(TRM).TheTRMestablishesaninitialContractHighWaterMark(CHWM)loadthatqualifiesforserviceatBonnevillePowerAdministration’s(BPA)lowercostpower(Tier1)fromtheFederalBaseSystem(FBS).AnyrequirementabovetheCHWMloadisknownasAboveHighWaterMark(AHWM) load.TheAHWMloadobligation foreachyear isestablished inadvanceofeachrateperiod,whichspanstwoyears,baseduponloadforecastsandprojectedFBScapability.TheAHWMloadcanbeservedwith non‐federal resources or purchased fromBPA as Tier 2 power. Tier 2 power purchasedfromBPAisexpectedtobepricedatoraroundmarket.

REQUIREDSUPPLEMENTARYINFORMATION

36

TILLAMOOKPEOPLE’SUTILITYDISTRICTSCHEDULEOFFUNDINGPROGRESSFORRETIREEHEALTHPLAN

8/1/2014 8/1/2012 8/1/2010

Actuarialvalueofassets(a) ‐$ ‐$ ‐$Actuarialaccruedliability(b) 155,628 238,060 290,662

Unfundedactuarialaccruedliability(b‐a) 155,628$ 238,060$ 290,662$

Fundedratio(a/b) 0.0% 0.0% 0.0%

Coveredpayroll(c) 845,000$ 1,322,450$ 1,553,440$

Unfundedactuarialaccruedliabilityasapercentageofcoveredpayroll((b‐a)/c) 18.4% 18.0% 18.7%

ActuarialValuationDate

Employer‐paidhealthcarebenefitswereclosedtonewentrantseffectiveJanuary1,2008.AsofJanuary1,2008,activemembersweregivenachoiceofmaintainingeligibilityforfutureemployer‐paid retiree medical coverage or receiving a $7,500 one‐time contribution to a VEBA account. Onlymemberswhomaintainedeligibilityforfutureemployer‐paidretireemedicalcoverageareincludedintheAugust1,2008andsubsequentvaluations.

37

TILLAMOOKPEOPLE’SUTILITYDISTRICTSCHEDULEOFPROPORTIONATESHAREOFTHENETPENSIONLIABILITYASOFJUNE30,2015LASTTENYEARS*

2014 2015

Proportionofthenetpensionasset/(liability) 0.10368462% 0.10175680%

Proportionateshareofthenetpensionasset/(liability) 2,350,235$ (5,842,327)$

Covered‐employeepayroll 7,068,710$ 7,198,189$

Proportionateshareofthenetpensionasset/(liability)aspercentageofcovered‐employeepayroll 33% 81%

Plan'sfiduciarynetposition 65,401,492,664$ 64,923,626,094$

Planfiduciarynetpositionasapercentageofthetotalpensionasset(liability) 103.60% 91.90%

*10yeartrendinformationwillbepresentedprospectively

38

TILLAMOOKPEOPLE’SUTILITYDISTRICTSCHEDULEOFCONTRIBUTIONS

ASOFJUNE30,2015LASTTENYEARS*

2014 2015

Contractuallyrequiredcontribution(actuariallydetermined) 767,956$ 799,161$

Contributionsinrelationtotheactuariallydeterminedcontribution 767,956 799,161

Contributiondeficiency(excess) ‐$ ‐$

Covered‐employeepayroll 7,068,710$ 7,198,189$

Contributionsasapercentageofcovered‐employeepayroll 10.86% 11.10%

NotestoSchedule

Valuationdate: 12/31/2012,rolledforwardtoJune30,2014 12/31/2013,rolledforwardtoJune30,2015

Methodsandassumptionsusedtodeterminecontributionrates:

SingleandAgentEmployersExample Entryagenormal EntryagenormalExperiencestudyreport 2012,publishedSeptember2013 2014,publishedSeptember2015Amortizationmethod Levelpercentageofpayroll,closed Levelpercentageofpayroll,closedRemainingamortizationperiod TierOne/TierTwo‐20years;OPSRP‐16years TierOne/TierTwo‐20years;OPSRP‐16yearsAssetvaluationmethod Marketvalueofassets MarketvalueofassetsInflation 2.75% 2.75%Salaryincreases 3.75% 3.75%Investmentrateofreturn 7.75% 7.75%Retirementage 55forTier1/Tier2;65forOPSRP 55forTier1/Tier2;65forOPSRPMortality RP‐2000Sex‐distincttables RP‐2000Sex‐distincttablesDiscountrate 7.75% 7.75%

*10yeartrendinformationwillbepresentedprospectively

SUPPLEMENTARYINFORMATION

39

TILLAMOOKPEOPLE’SUTILITYDISTRICTSCHEDULEOFCHANGESINELECTRICPLANTINSERVICE

YEARENDEDDECEMBER31,2015

Balance Balance1/1/2015 Additions Retirements 12/31/2015

Intangibleplant:Miscellaneousintangibleplant $556 ‐$ ‐$ 556$

Transmissionanddistributionplant:Landandlandrights 621,008 ‐ ‐ 621,008Roadsandtrails 47,128 ‐ ‐ 47,128Stationequipment 11,368,469 26,983 156,000 11,239,452Poles,towers,andfixtures 15,693,590 1,674,841 242,676 17,125,755Overheadconductorsanddevices 15,376,049 586,744 282,277 15,680,516Undergroundconduit 1,481,261 60,681 10,861 1,531,081Undergroundconductorsanddevices 9,248,999 252,947 43,023 9,458,923Transformers,regulators,andcapacitors 14,676,719 376,611 275,826 14,777,504Services 7,042,010 179,149 60,405 7,160,754Metersanddevices 4,061,761 161,755 64,904 4,158,612Installationsoncustomers'premises 226,708 4,231 2,046 228,893Streetlightingequipment 238,525 4,234 1,951 240,808Constructioncompletednotclassified 611,367 423,268 611,365 423,270

Totaltransmissionanddistributionplant 80,693,594 3,751,444 1,751,334 82,693,704

Generalplant:Landandlandrights 430,199 ‐ ‐ 430,199Structuresandimprovements 5,455,886 ‐ ‐ 5,455,886Officefurnitureandequipment 92,549 ‐ ‐ 92,549Computerequipment 313,730 39,357 62,656 290,431Transportationequipment 5,064,680 197,362 5,262,042Storesequipment 110,638 9,920 ‐ 120,558Shopequipment 249,128 ‐ ‐ 249,128Laboratoryequipment 151,443 ‐ ‐ 151,443Heavyworkequipment 35,139 ‐ ‐ 35,139Communicationsequipment 695,289 ‐ ‐ 695,289Miscellaneousequipment 590,437 69,991 2,264 658,164

Totalgeneralplant 13,189,118 316,630 64,920 13,440,828

Totalelectricplantinservice $93,883,268 4,068,074$ 1,816,254$ 96,135,088$

40

TILLAMOOKPEOPLE’SUTILITYDISTRICTSCHEDULEOFBONDSANDCERTIFICATESDEBTSERVICETRANSACTIONSYEARENDEDDECEMBER31,2015

Interest Original Outstanding 2015 2015 Outstanding 2015 2015Rates Issue 1/1/2015 Issues Retirements 12/31/2015 Maturities Payments

Electricsystemrevenuebonds:24thseries,dated3/1/2008 4‐4.25% 6,625,000$ 5,370,000$ ‐$ 210,000$ 5,160,000$ 220,270$ 220,270$25thseries,dated3/1/2010 2‐4% 7,390,000 5,325,000 ‐ 425,000 4,900,000 182,906 182,906

RUSrevenuecertificatesofindebtedness:

13thseries,dated9/1/1980 5% 1,671,000 105,000 ‐ 105,000 ‐ ‐ ‐15thseries,dated3/1/1983 5% 864,000 220,000 ‐ 40,000 180,000 9,000 9,00018thseries,dated11/1/1988 5% 993,000 440,000 ‐ 40,000 400,000 20,000 20,00020thseries,dated7/1/1994 variable 2,920,000 2,090,000 ‐ 80,000 2,010,000 7,538 7,53821stseries,dated11/1/1996 variable 2,170,000 1,575,000 ‐ 55,000 1,520,000 3,800 3,80023rdseries,dated11/1/2003 variable 6,125,000 4,123,107 ‐ 267,868 3,855,239 31,324 31,32426thseries‐a,dated8/18/2011 2.58% 7,000,000 6,622,373 ‐ 259,743 6,362,630 159,651 159,65126thseries‐b,dated2/10/2014 3.05% 5,300,000 5,159,474 ‐ 192,930 4,966,544 147,941 147,94126thseries‐c,dated3/13/2014 3..05% 1,700,000 1,657,316 ‐ 61,947 1,595,369 7,587 7,587

Total 42,758,000$ 32,687,270$ ‐$ 1,737,488$ 30,949,782$ 790,017$ 790,017$

PrincipalTransactions InterestTransactions

41

TILLAMOOKPEOPLE’SUTILITYDISTRICTSCHEDULEOFFUTUREBONDSANDCERTIFICATESDEBTSERVICEREQUIREMENTS

YEARENDEDDECEMBER31,2015

Principal Interest Principal Interest Principal Interest

665,000 381,947$ 1,010,799$ 406,270$ 1,675,799$ 788,217$685,000 359,789 1,073,881 383,523 1,758,881 743,312710,000 336,918 1,104,365 360,271 1,814,365 697,189735,000 313,095 1,057,831 339,857 1,792,831 652,952755,000 287,101 1,088,412 319,000 1,843,412 606,101785,000 258,164 1,132,290 297,363 1,917,290 555,527810,000 229,231 1,165,960 275,234 1,975,960 504,465845,000 198,670 1,213,445 252,234 2,058,445 450,904510,000 167,245 1,186,261 231,704 1,696,261 398,949535,000 134,439 1,217,931 210,657 1,752,931 345,096550,000 124,705 1,251,246 189,085 1,801,246 313,790575,000 102,273 1,298,799 166,876 1,873,799 269,149350,000 79,350 1,349,818 143,994 1,699,818 223,344365,000 64,582 1,400,123 120,430 1,765,123 185,012380,000 49,017 904,632 99,605 1,284,632 148,622395,000 32,814 930,632 78,214 1,325,632 111,028410,000 15,973 811,732 56,601 1,221,732 72,574

‐ ‐ 834,447 34,393 834,447 34,393‐ ‐ 857,178 18,046 857,178 18,046

10,060,000$ 3,135,313$ 20,889,782$ 3,983,357$ 30,949,782$ 7,118,670$

20332034

20282027

2029203020312032

202420252026

2022

TotalFutureRequirementsElectricSystemRevenueBonds

Year

RUSRevenueCertificatesofIndebtedness

2023

201820172016

202120202019

Scheduled interest maturities for RUS variable rate loans are based on the maximum rate of sevenpercentperannum,exceptforthe23rdSeries.The23rdSeriesareequalpaymentloansandscheduledprincipalandinterestmaturitiesarebasedonanestimatedvariablerateprovidedbyRUS.

42

TILLAMOOKPEOPLE’SUTILITYDISTRICTSCHEDULEOFOPERATINGEXPENSES

2015 2014

Costofpower 17,192,295$ $17,785,638

Distributionexpense:Operation:

Stationexpenses 95,301 116,860Dispatching 117,694 115,228Operationoflines 2,726,784 2,695,575Meterexpenses 838,359 939,464Environmentalprograms 508 502Rents 31,685 8,649

Totaldistributionexpense‐operation 3,810,331 3,876,278

Maintenance:Stationequipment 159,723 202,338Overheadandundergroundlines 3,000,303 2,825,899Linetransformersanddevices 143,693 134,360Meters 19,641 29,354Streetlightingandsignalsystems 96,300 99,223

Totaldistributionexpense‐maintenance 3,419,660 3,291,174

Customeraccountsexpense:Meterreading 41 2,751Customerrecordsandcollection 997,172 897,761Uncollectibleaccounts 27,415 34,296

Totalcustomeraccountsexpense 1,024,628 934,808

Customerserviceandinformationalexpense:Customerassistance 468,768 462,733Informationalandinstructionexpense 282,840 267,863

Totalcustomerserviceandinformationalexpense 751,608 730,596

Salesexpense:Advertising 43,008 42,637Other 80,066 82,614

Totalsalesexpense 123,074 125,251

YearsEndedDecember31,

43

TILLAMOOKPEOPLE’SUTILITYDISTRICT

SCHEDULEOFOPERATINGEXPENSES

2015 2014YearsEndedDecember31,

Administrativeandgeneralexpense:Administrativeandgeneralsalaries 1,636,054$ 1,591,989$Officesuppliesandexpense 272,384 336,334Outsideservicesemployed 126,425 22,340Propertyinsurance 85,127 87,029Injuriesanddamages 4,354 (198)Employeepensionsandbenefits 178,050 174,059Miscellaneousgeneralexpenses 453,953 410,726Maintenanceofgeneralplant 321,329 260,703

Totaladministrativeandgeneralexpense 3,077,676 2,882,982

Depreciation:Distributionplant 2,549,777 2,402,810Generalplant 311,593 273,349

Totaldepreciation 2,861,370 2,676,159

Taxes:Property 805,452 813,565OregonDepartmentofEnergyAssessment 39,068 29,176

Totaltaxes 844,520 842,741

Totaloperatingexpenses 33,105,162$ $33,145,627

44

REPORTOFINDEPENDENTAUDITORSONINTERNALCONTROLOVERFINANCIALREPORTINGANDONCOMPLIANCEANDOTHERMATTERSBASEDONANAUDITOF

FINANCIALSTATEMENTSPERFORMEDINACCORDANCEWITHGOVERNMENTAUDITINGSTANDARDS