Embed Size (px)

Citation preview

IN THIS ISSUE...

ASSOCIATION NEWS

1

YOUR BOTTOM LINE

10

GENERAL BUSINESS NEWS

15

CALENDAR

41

Registration StillClimbing for 2004Management Conference

Tile ManagementQuarterly

Vol. III, No. III September 2004

Published by

Remember toforward to your employees!

________________________________________________________________________________________________________________________________________________________________________________________________________

Registrations are still arriving dailyfor the 2004 Management Conferenceto be held November 4-7 in Cancun,Mexico. With 225 people alreadyregistered, it should be one of the morememorable events of CTDA's educationalyear.

World-class speakers such asCharlie Plumb, Jonathan Trivers, AlBates, and Jack Daly will be on handwith tips to grow your business andprepare for the changes ahead. But thehighlight of every CTDA event is theunique networking opportunitiesavailable during the conference. Notonly will the owners and managers ofthe top distribution companies in thecountry be in attendance, but the uppermanagement of the leadingmanufacturers will also be present. Addto this international associationrepresentatives, press, and invited guests,

and you have a who's who of the ceramictile industry.

CTDA's annual Hall of Fameinductions for Sam Widener and S.M.Van Kirk will be a part of Thursday'sschedule and you can try your luck atwinning $1,000,000 in the golf hole-in-one contest on Saturday.

In addition to the JW Marriott'snumerous amenities designed to fillyour free time, Cancun affordsManagement Conference attendees anumber of additional diversions: deepsea fishing, a snorkeling adventure withyour own watercraft, archeological tours,and a Saturday evening fiesta completewith games and prizes.

If you haven't registered yet, space isstill available!

For more information:Please visit our website at

www.ctdahome.org for completeconference information. See you there!

Tile Management Quarterly2

CTDA Holds the Summer Boardand Committee Meetings

In late August, members of the CTDA Board of Directorsand committees gathered in Chicago for the summer meetings.Held the weekend of the Chicago Air and Water Show, it gaveparticipants an opportunity for a family getaway too!

A very special ceremony was held for CTDA legal counselBill Ives. Many of you know of Mr. Ives' love of eating,especially chocolate (and Starbucks coffee too!). At thesummer meeting in 2003, Mr. Ives availed himself of theentire piece of chocolate cake from the group sampler dessertplatter at Smith and Wollensky. He was unable to attend thedinner there this year--we think he was afraid we would pullsome silly stunt reminiscent of his 2003 antics--so we decidedto bring the stunt to him the next morning.

Executive Director Rick Church presented Mr. Ives witha challenge: if he could eat an entire Smith and Wollenskychocolate cake (all 5 layers and 40 pounds of it) by 4:00 p.m.,he would be rewarded with a cash prize!

Much to our disappointment, Mr. Ives turned down thechallenge, but happily served everyone cake for the morningbreak!

We can't wait to see what he comes up with for retributionnext summer!

If you want to be there in person, sign up today toparticipate on a CTDA committee. Committees meet 4 timesa year: January (prior to Surfaces), May (prior to Coverings),August (in Chicago), and November (at the ManagementConference).

Tile Management Quarterly3

CTDA Sponsors Make It Happen

We are so very pleased to announcethe following sponsors for the 2004Management Conference. As you know,our conference is made possible eachyear by their commitment to educationin our industry.

Please thank them for theircontinued support!

PlatinumCeramic Tiles of ItalyCoveringsCrossville Ceramics CompanyDal-Tile Corp./American OleanLaticrete International, Inc.Laufen/USMAPEI CorporationTEC Specialty Products, Inc.Tile of SpainTurkish Ceramic Association

GoldAqua Mix, Inc.Azuvi/Classic Ceramic TileDancik International, Ltd.Kale EksportNational Gypsum CompanyProphet 21Schechner Lifson CorporationSchluter Systems L.P.United States Gypsum CorporationVitra USA

SilverBonsal/Fin PanFlorida TileSGM

BronzeGeorgia-PacificNational Metal ShapesNoble Company

Golf AwardsAqua Mix, Inc.

Golf HoleEPC America

Golf Beverage CartSchechner Lifson Corporation

Honorable MentionCeramic Tile and Stone Consultants

Tues, Nov 22:00pm - 5:00pm Executive Committee Meeting

Wed, Nov 38:00am - 9:30am CTDA Marketing/PR Committee9:30am - 10:45am CTDA Education Committee9:30am - 10:45am CTDA Convention Committee10:45am - 12:00am CTDA Membership & Benefits Committee10:45am - 12:00pm CTDA Certification Task Force Committee12:00pm - 1:00pm Lunch (committee members only)1:00pm - 4:00pm Board of Directors Meeting (directors only)5:00pm - 6:00pm New Member Orientation

Thur, Nov 47:30am - 8:30am Breakfast8:30am - 9:00am Hall of Fame Presentation #19:00am - 10:00am Keynote Address: Charlie Plumb10:00am - 10:30am Networking Break10:30am - 12:00pm Jonathan Trivers: The Costco Effect - What She Saves at

Costco/WalMart She Spends on Ceramic Tile12:00pm - 1:00pm Lunch1:00pm - 1:30pm Hall of Fame Presentation #21:30pm - 2:00pm CTDA Annual Business Meeting2:00pm - 3:30pm Al Bates: Challenges for the Industry - Inflation, Rising

Metal Costs, Rising Fuel Costs, and the Euro6:00pm - 7:30pm Opening Cocktail Reception

2004 Management Conference ScheduleFri, Nov 5

8:30am - 10:00am Distributor Forum (distributors only)10:00am - 10:30am Networking Break10:30am - 11:30am Company Performance Report: Al Bates11:30am - 12:30pm Jack Daly: Relationship Selling1:00pm - 4:00pm Jungle Cruise1:00pm - 5:30pm Deep Sea Fishing

Sat, Nov 68:00am - 11:00am Jack Daly: Building a World Class Sales Organization11:30am - 4:00pm Tulum Tour11:30am - 5:30pm Deep Sea Fishing12:00pm - 5:00pm Golf Tournament7:00pm - 10:00pm President's Fiesta Dinner Celebration

Sun, Nov 78:00am - 5:00pm Chichen Itza Tour

Tile Management Quarterly4

November 4-7, 2004

Tile Management Quarterly5

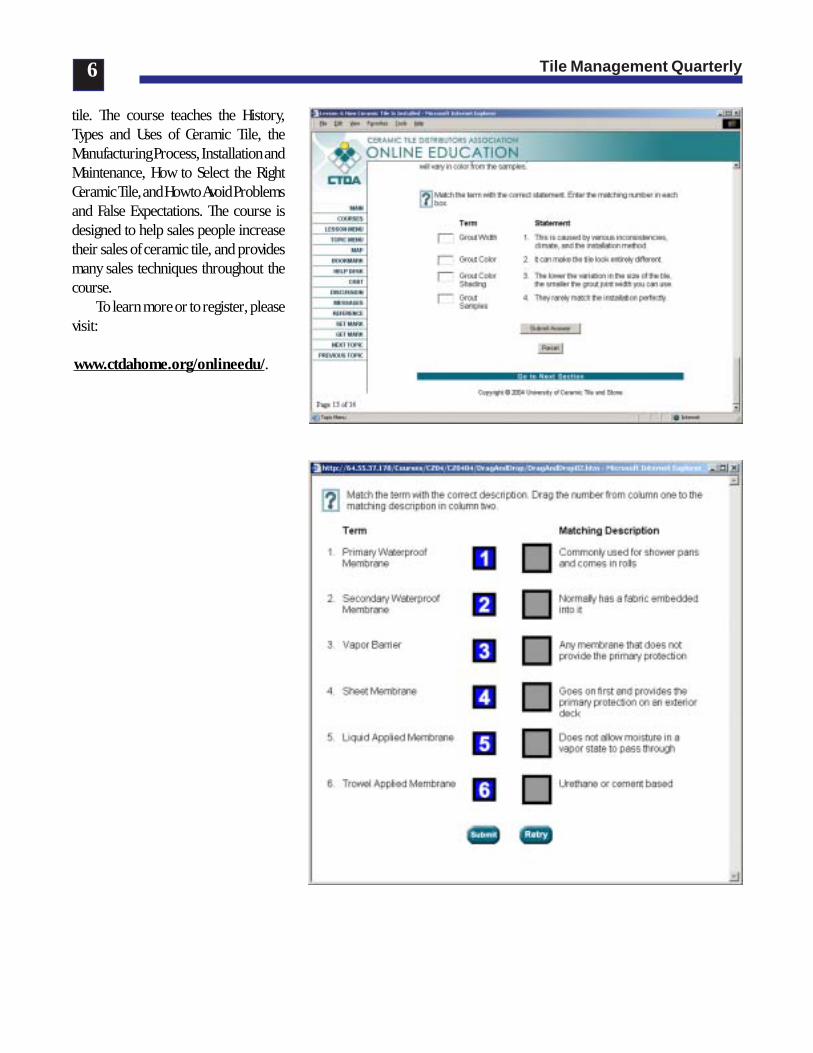

CTDA members have asked foreducational programs on ceramic tilethat they could offer to their employees,and now we have them as a discountedCTDA membership benefit. CTDA andthe University of Ceramic Tile and Stone(U of CTS) have joined to develop aseries of educational programs to helpceramic tile distributor and dealeremployees be more effective at theirjobs.

CTDA Online EducationalCourses:• Teach your employees the basics of

ceramic tile with selling tips• Give your employees credibility with

your customers• Sell more tile with more upgrades• Available on the internet for 14

days, 24/7 (any time at home or atwork)

• No lost employee productivity timeor travel expenses

• Self-paced interactive course - comeand go as you please at your ownrate.

• Enjoyable experience and veryeffective at teaching

• Student prints their own diplomaupon completion

• Group Managers get reports onstudents’ progress and results

• All you need is a computer andaccess to the internet

Understanding the Basics ofCeramic Tile is a ceramic tile coursefor new employees and those who haven’thad the opportunity to learn about thehistory and all the aspects of ceramic

CTDA Announces New On-LineCeramic Tile Training

Tile Management Quarterly6

tile. The course teaches the History,Types and Uses of Ceramic Tile, theManufacturing Process, Installation andMaintenance, How to Select the RightCeramic Tile, and How to Avoid Problemsand False Expectations. The course isdesigned to help sales people increasetheir sales of ceramic tile, and providesmany sales techniques throughout thecourse.

To learn more or to register, pleasevisit:

www.ctdahome.org/onlineedu/.

Tile Management Quarterly7

In August of this year, the CTDA Strategic Planning Committee met in Chicago, Illinois for two long days planning the futureof CTDA. At the end of the second day, a working document was finalized and approved by the Board of Directors in September.Below is the result of their work. Please review and forward any comments to the CTDA staff and be ready to do your partto help CTDA reach newer and greater heights in the years ahead.

CTDA is the leading source ofknowledge, networking and educational opportunities

to grow the ceramic tile and stone industry

Value Create recognition for the value CTDA delivers to its members.Objective #1: Increase awareness of all CTDA programs in 2005. Measure success by benchmarking against 2004 strategic

planning survey results.Objective #2: Achieve 85% or greater membership retention annually and achieve net 5% increase in membership annually.Objective #3: In all CTDA programs, develop awareness level of at least 80% by end of first year; 90% by end of second year.Objective #4: In 2005, research possibilities of group health insurance coverage for CTDA members. Report findings to

Board for consideration.

Networking Maximize networking opportunities for members.Objective #1: Annually host a Management Conference for distributors and suppliers of ceramic tile, stone and related

products.Objective #2: Annually participate in Coverings with a booth, reception and as a host of educational programming.Objective #3: Publish six issues of TileDealer magazine in 2005.Objective #4: Annually publish a directory listing all members of the association, their contact information and products

they make/sell.

Education Provide quality educational events and tools to the industry.Objective #1: In 2005, implement online educational courses for CTDA members and their employees to learn the basics

of ceramic tile and stone.Objective #2: Continue to offer Tile Training in a Box and Shade Variation programs to members and non-members.Objective #3: In 2005, launch a certification program for ceramic tile and stone salespeople.Objective #4: Annually survey and publish aggregate operational and financial data of distributors. (CPR Report)Objective #5: Annually survey and publish aggregate profile data on distributor’s businesses including product trends,

company size, etc.Objective #6: In 2005, hold at least one session at Management Conference focused on specific industry issues like:

moisture intrusion, green building, installation techniques, etc.Objective #7: Charge Education Committee in 2005 with developing recommendations to deliver industry specific education

on environmental and installation issues.

CTDA Strategic Plan 2004

Tile Management Quarterly8

Stone Enhance existing tools and develop new ones for use by the stone segment of the industry.Objective #1: In 2005, develop a Committee to re-purpose all existing materials and tools to include stone and stone related

products.Objective #2: In 2005, consider renaming CTDA to more formally include stone.

Localization Deliver value to members through local/regional meetings and educationalevents.

Objective #1: Host four local one day conferences in 2005 with a minimum total attendance of 200.

Consumer Pull Through Create tools to develop consumer demand for products suppliedby the tile and stone industry.

Objective #1: In 2005, develop an online design center for consumers on CTDA’s website and connect consumers interestedin specific brands of tile with distributors that carry those brands.

Online Identify and plan for online opportunities that will create efficiencies and enhance thebusinesses of our members.

Objective #1: In 2005, develop a committee to develop, consider and recommend opportunities for online efficiencies tothe CTDA Board of Directors.

Objective #2: Online Committee should make several recommendations at least one of which is implemented by CTDA Boardin 2006 budget.

Objective #3: Establish ERC as the CEO desktop for the ceramic tile and stone industry by the end of 2005.

How Much Can You Put In One Box? We Put An Entire Industry In This One…

CTDA Training in a Box is an easy, affordable way to introduce a newcomer to the ceramic tile industry using a varietyof reading, audiovisual and sensory resource aids in an easy to use box, complete with a tabbed binder of information andresource information. Simply place the labels provided on your own tile, andtraining is ready to begin!

Training Guide Deluxe Program (with 4 videos)1-5 copies $189.00 each 1-5 copies $239.006-10 copies $129.00 each 6-10 copies $179.00 each11+ copies $99.00 each 11+ copies $149.00 each

Available to non-CTDA members at $399.00

Visit www.ctdahome.org to order your copy today!

Tile Management Quarterly9

Education CommitteeThe Education Committee finalized

plans for the on-line training and willhave the program available to membersby the Management Conference.

Membership & BenefitsCommitteeThe Membership and Benefits Committeecontinued their discussion ofcommunications with members and arelooking into new benefits to offer.

Marketing CommitteeThe Marketing Committee reviewed

TileDealer Magazine and offeredguidance for the 2005 editorial calendar.

Certification Task ForceThe Task Force has begun the beta-

testing phase of the CertificationProgram. Look for more informationcoming soon.

Convention PlanningCommittee

The committee finalized the detailsfor the November conference and begandiscussions on 2005.

They are also working on plans forthe booth and reception at Coverings2005. More details to come.

Board of DirectorsThe Board of Directors reviewed

the draft Strategic Planning and begandiscussions regarding the 2005 budgetto be adopted at their November meeting.

CTDA Board of Directors andCommittee Updates

2004 Fall Committee Meeting ScheduleAll meetings will be held in Cancun, Mexico. For more information, please

contact the CTDA office.Executive Committee Tuesday, November 3 2:00-6:00 p.m.Marketing/PR Committee Wednesday, November 4 8:00-9:30 a.m.Education Committee Wednesday, November 4 9:30-10:45 a.m.Convention Planning Committee Wednesday, November 4 9:30-10:45 a.m.Membership & Benefits Committee Wednesday, November 4 10:45 – 12:00

noonCertification Committee Wednesday, November 4 10:45 – 12:00 noonLuncheon Wednesday, November 4 12:00-1:00 p.m.Board of Directors Wednesday, November 4 1:00 – 4:00 p.m.

2005 Winter Committee Meeting ScheduleAll meetings will be held in Las Vegas, Nevada. For more information, please

contact the CTDA office.Executive Committee Tuesday, January 25 10:00 a.m.-1:00 p.m.Marketing/PR Committee Tuesday, January 25 1:00-2:30 p.m.Education Committee Tuesday, January 25 2:30-3:45 p.m.Convention Planning Committee Tuesday, January 25 2:30-3:45 p.m.Membership & Benefits Committee Tuesday, January 25 3:45 – 4:30 p.m.Certification Committee Tuesday, January 25 3:45 – 4:30 p.m.Board of Directors Tuesday, January 25 4:30 – 7:00 p.m.

If you are interested in serving on a committee, pleasecontact the CTDA office at 1-800-938-CTDA(2832), [email protected]

Tile Management Quarterly10

Most CTDA members continue tooperate under price pressures. Eventhough the economy has turned up,there is a relentless push by customersfor an extra discount. Far too manyfirms simply lower the price and moveon.

This report will examine two keyissues with regard to the price/volumerelationship:• The Sales Volume Challenge—

Measurement of the volume increaserequired by the typical CTDAmember to offset a price decrease.

• Holding the Line on Prices—Suggestions regarding specificprocedures for holding the line onprice.The first of these is extremely

quantitative. It demonstrates quiteclearly the futility of chasing additionalvolume. The second is much morequalitative in nature. It probes the areasof action that are likely to have thelargest payoff in controlling pricereductions.

The Sales Volume ChallengeFar too many decision makers view

price cutting benignly or even favorably.In part this is a function of the continualpressures on margin faced by firmsevery day. If everybody is asking forprice reductions, the concept becomesa way of life. It is also due to the fact thatsome firms that have successfully used

Profit Improvement Report:

price as a competitive tool. In particular,Wal-Mart and Dell Computer arecommonly presented in the businesspress as role models for success.

The truth is that CTDA membersface a very different cost structure thaneither Wal-Mart or Dell. The uniquestructure of expenses in the industrymakes it extremely difficult to employprice cutting successfully without asignificant change in operations.

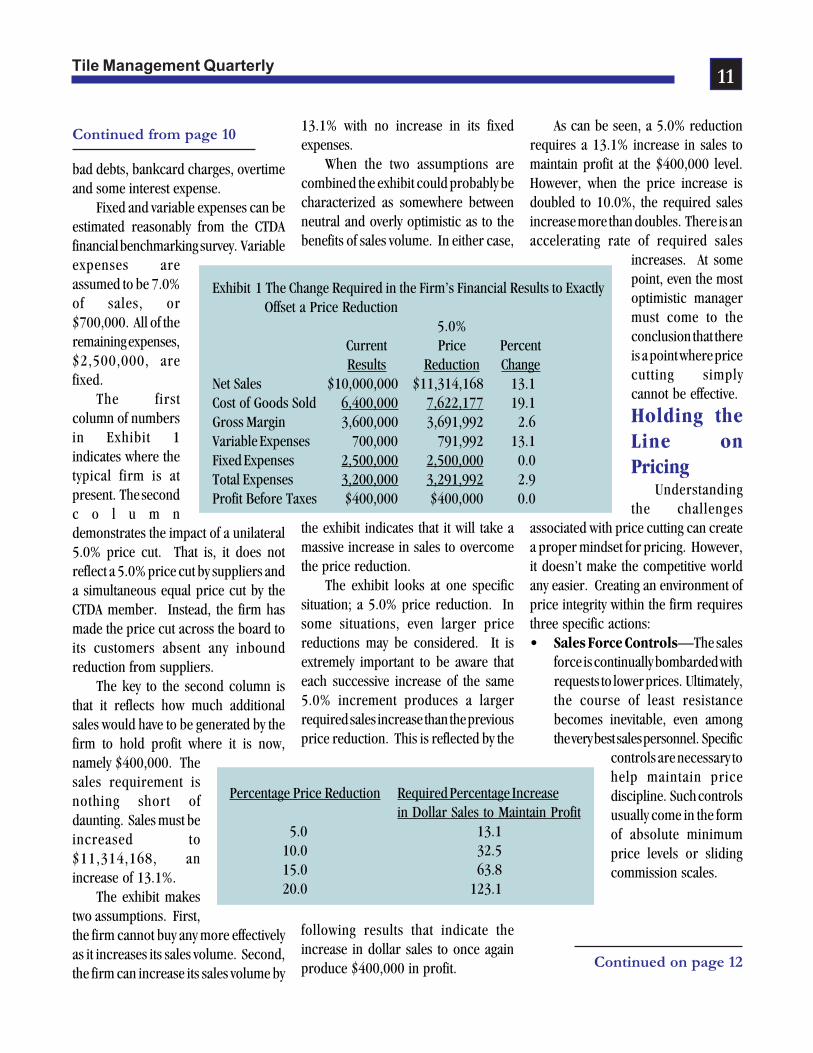

Exhibit 1 looks at the operation ofthe typical CTDA member. According tothe most recent CTDA financialbenchmarking survey, this firm generates$10,000,000 in sales volume, operateson a gross margin of 36.0% and producesa pre-tax profit of $400,000, or 4.0% ofsales.

In addition, the firm has both fixedand variable expenses as part of itsfinancial profile. Fixed expensesrepresent the commitments that mustbe made so that the firm can conductbusiness, including rent, maintenanceand related expenses. It also includesvirtually all salaries and associated fringebenefits.

In sharp contrast, variable expensesrepresent the incremental costs ofgenerating additional sales. Typically,these will include sales commissions,

Al Bates, Profit PlanningGroup, Inc.

YourBottomLine

Continued on page 11

Making It UpWith Volume

Tile Management Quarterly11

bad debts, bankcard charges, overtimeand some interest expense.

Fixed and variable expenses can beestimated reasonably from the CTDAfinancial benchmarking survey. Variableexpenses areassumed to be 7.0%of sales, or$700,000. All of theremaining expenses,$2,500,000, arefixed.

The firstcolumn of numbersin Exhibit 1indicates where thetypical firm is atpresent. The secondc o l u m ndemonstrates the impact of a unilateral5.0% price cut. That is, it does notreflect a 5.0% price cut by suppliers anda simultaneous equal price cut by theCTDA member. Instead, the firm hasmade the price cut across the board toits customers absent any inboundreduction from suppliers.

The key to the second column isthat it reflects how much additionalsales would have to be generated by thefirm to hold profit where it is now,namely $400,000. Thesales requirement isnothing short ofdaunting. Sales must beincreased to$11,314,168, anincrease of 13.1%.

The exhibit makestwo assumptions. First,the firm cannot buy any more effectivelyas it increases its sales volume. Second,the firm can increase its sales volume by

13.1% with no increase in its fixedexpenses.

When the two assumptions arecombined the exhibit could probably becharacterized as somewhere betweenneutral and overly optimistic as to thebenefits of sales volume. In either case,

the exhibit indicates that it will take amassive increase in sales to overcomethe price reduction.

The exhibit looks at one specificsituation; a 5.0% price reduction. Insome situations, even larger pricereductions may be considered. It isextremely important to be aware thateach successive increase of the same5.0% increment produces a largerrequired sales increase than the previousprice reduction. This is reflected by the

following results that indicate theincrease in dollar sales to once againproduce $400,000 in profit.

As can be seen, a 5.0% reductionrequires a 13.1% increase in sales tomaintain profit at the $400,000 level.However, when the price increase isdoubled to 10.0%, the required salesincrease more than doubles. There is anaccelerating rate of required sales

increases. At somepoint, even the mostoptimistic managermust come to theconclusion that thereis a point where pricecutting simplycannot be effective.

Holding theLine onPricing

Understandingthe challenges

associated with price cutting can createa proper mindset for pricing. However,it doesn’t make the competitive worldany easier. Creating an environment ofprice integrity within the firm requiresthree specific actions:• Sales Force Controls—The sales

force is continually bombarded withrequests to lower prices. Ultimately,the course of least resistancebecomes inevitable, even amongthe very best sales personnel. Specific

controls are necessary tohelp maintain pricediscipline. Such controlsusually come in the formof absolute minimumprice levels or slidingcommission scales.

Continued from page 10

Continued on page 12

Percentage Price Reduction Required Percentage Increasein Dollar Sales to Maintain Profit

5.0 13.110.0 32.515.0 63.820.0 123.1

Exhibit 1 The Change Required in the Firm’s Financial Results to Exactly Offset a Price Reduction

5.0%Current Price PercentResults Reduction Change

Net Sales $10,000,000 $11,314,168 13.1Cost of Goods Sold 6,400,000 7,622,177 19.1Gross Margin 3,600,000 3,691,992 2.6Variable Expenses 700,000 791,992 13.1Fixed Expenses 2,500,000 2,500,000 0.0Total Expenses 3,200,000 3,291,992 2.9Profit Before Taxes $400,000 $400,000 0.0

Tile Management Quarterly12

Continued from page 11

• Margin Enhancements—Most ofthe severe price competition isfocused on the commodity end ofthe product line. At the slow-moving end of the assortment thereare numerous opportunities to buildmargin back. There should be nohesitation in doing so in instanceswhere product availability on slowsellers is a major value being added.

• Employee Education—There issometimes the tendency to view thepricing challenge as being entirelythe responsibility of the sales force.In point of fact, numerousemployees impact margin in actionsranging from buying moreeffectively to controlling damagedgoods and shrinkage. Everyemployee needs to be aware of themargin issue.

Moving ForwardPrice pressures are not going to go

away any time soon. To continue to besuccessful, CTDA members must makesure that every decision maker in thefirm understands the impact that pricecutting has on performance and therather massive sales increase that itmandates.

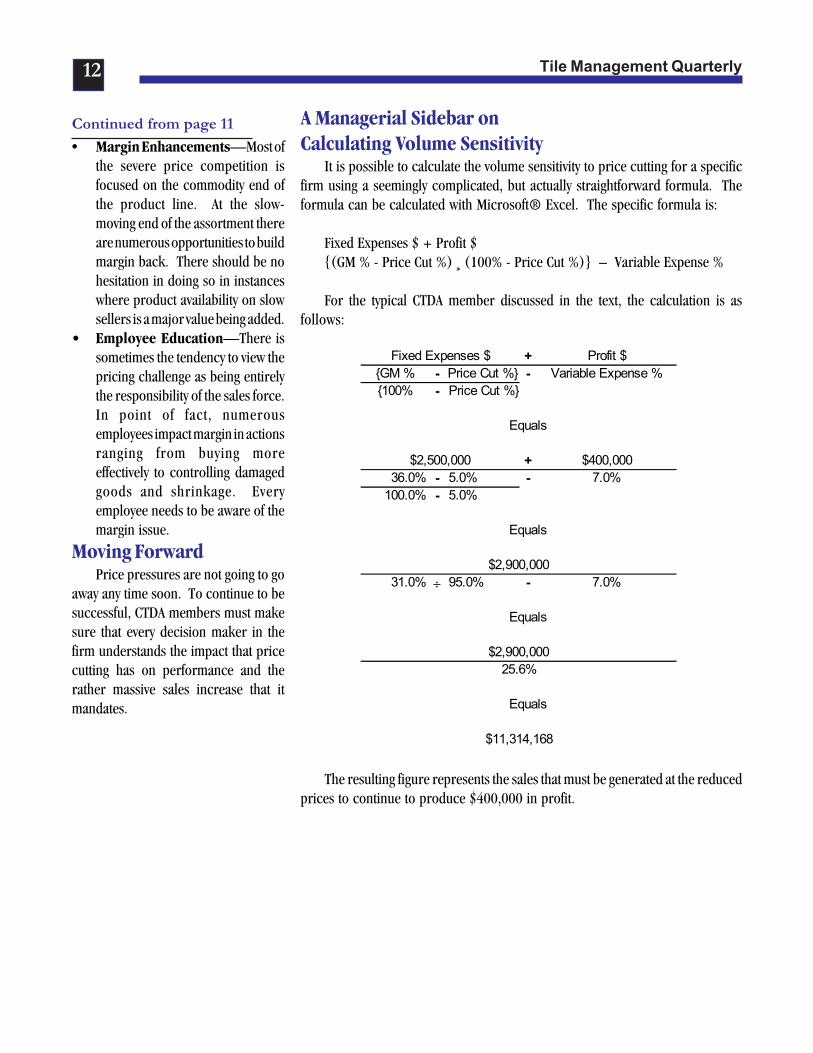

A Managerial Sidebar onCalculating Volume Sensitivity

It is possible to calculate the volume sensitivity to price cutting for a specificfirm using a seemingly complicated, but actually straightforward formula. Theformula can be calculated with Microsoft® Excel. The specific formula is:

Fixed Expenses $ + Profit ${(GM % - Price Cut %) ¸ (100% - Price Cut %)} – Variable Expense %

For the typical CTDA member discussed in the text, the calculation is asfollows:

The resulting figure represents the sales that must be generated at the reducedprices to continue to produce $400,000 in profit.

+{GM % - Price Cut %} -{100% - Price Cut %}

Equals

+36.0% - 5.0% -

100.0% - 5.0%

Equals

31.0% ÷ 95.0% -

Equals

Equals

Profit $

$2,500,000 $400,000

Variable Expense %

$11,314,168

25.6%

7.0%

7.0%$2,900,000

$2,900,000

Fixed Expenses $

Tile Management Quarterly13

cement tough

Cementitious core

Fiberglass mesh

Double wrappedEdgeTech® design

Cementitious core

Fiberglass mesh

Double wrappedEdgeTech® design

NationalGypsumhas the best

cementboardfor your next project.

NationalGypsumhas the best

cementboardfor your next project.

Applications• Tub surrounds• Shower enclosures• Garden tubs• Countertops• Floor underlayment• Radius construction

(with PermaBase Flex)

Features• Fastens closer to edge• Easiest to cut• Low water absorption• Interior and exterior

use• 30-year limited

warranty

For technical information, call: 1-800-NATIONAL

(1-800-628-4662)or visit our website at:www.nationalgypsum.com

Tile Management Quarterly14

Many of us have by now read JimCollins terrific business book Good toGreat. If you haven’t, we recommenddoing so. This article is not about thebook, but rather about the cover storyfrom the May issue of Fast Companymagazine, which keys on the five yearold JetBlue airline. The question posedis can CEO David Neeleman make itgreat?

A year ago, Fast Company published10 make-or-break questions thataddressed what a fast company is today.Here they are repeated:1. Does your company create an

emotional bond with itscustomers?

2. Does your strategy stand outfrom the crowd?

3. Is your company a fun place towork-and a fun organization todo business with?

4. Are you built to change?5. Do you embrace the value of

values?6. Are you as disciplined, as you

are creative?7. Are you winning the battle for

talent?8. Do you use technology to change

expectations and reshape yourbusiness?

9. Are you built for speed?10. Have you built a company of

leaders?Editor John Byrne believes Jet Blue

meets every one of these tests ( if you’veyet to experience the JetBlue airline, putit on your to-do list). John states it stillmust meet one more and most difficult

GOOD TO GREAT…ARE YOUAND YOUR COMPANY READY?Jack Daly www.ProfessionalSalesCoach.net

of all: 11. Can you Scale? Of the manyhundreds of articles I have read over thepast several months, this was one of thebest. Here are some of the take-aways:

JetBlue has put together 12consecutive profitable quarters, and isreporting among the industry’s bestoperating margins, the highestpercentage of seats filled, and one of thetop rates for on-time arrivals. It’sintroducing a new plane every 3 weeks-and next year will be adding one every 10days. Comparable growth companiescited include Starbucks, Dell, andAmazon. These companies depend onflexibility, speed, and a sense of intimacywith employees and customers alike.The challenge now is: is it scalable?

Some lessons learned-Do more for customers. “I don’t

care if they notice everything we do. Justas long as they notice something that’sdifferent about us.”

Only the paranoid survive.Neeleman is always on the lookout forcomplacency, particularly when thingsare going well. “When you’re makingmoney and good margins, you tend toget sloppy.”

Actions speak louder thanwords. Neeleman talks a lot aboutteamwork. When he flies, he helps flightattendants pass out snacks and staysbehind to clean the plane. “You can’task employees to do something youwouldn’t be willing to do yourself.”

The best culture polices itself.Competition is the ultimate

motivation. “People respond to thatchallenge.”

Employees have to understandthe business. “I always talk about thetripod- low costs, a great product, andcapitalization,” he says. “If everyonehere understands how important it is tomaintain each leg, you’ve got a verystable business model.”

Build a team of big thinkers.Since he has never run a large company,Neeleman has surrounded himself withsenior execs that have.

Don’t scale at the expense ofpeople. If a change hurts morale, it’snot worth it, because employees treatcustomers the way they’re treatedthemselves.

Stay small as you grow. JetBluetries to maintain the feel of a startup byhaving senior officers practice visibleleadership.

Propagate the culture. In a seriesof training courses, Neeleman and othersenior managers teach supervisors theprinciples they rely on to manage peopleand make decisions.

As it manages growth, the airlinemust standardize many other things itdoes to avoid starting from scratch everytime. For example, JetBlue has developeda checklist of what has to happenwhenever it enters a new market.Everyone has access to the list on thecompany intranet. Low costs remain anobsession. JetBlue’s reservation agents,for example, work from home ratherthan in an expensive call center.

Clearly Culture Rules. What are youdoing to proactively manage your culture?What systems and processes do you havein place to ensure an ongoing vibrantsuccess culture?

Tile Management Quarterly15

Housing Starts Return ToHighest Pace Of Year InAugust

Housing starts climbed back to thehighest pace of the year in August,reaching a seasonably adjusted annualrate of 2.0 million units, the U.S.Commerce Department reported.

The 2-million-unit pace, whichmatched the pace set in March, was 0.6percent above July’s upwardly revisedrate of 1.988 million. Total housingstarts were up by 10.4 percent on a year-to-date basis.

“Builders remain confident aboutthe market and are keeping up withstrong demand for single-family homesand condominiums,” said BobbyRayburn, president of the NationalAssociation of Home Builders (NAHB)and a home and apartment builder fromJackson, Miss. “However, builders aremanaging their production schedulescarefully and cutting back slightly on thenumber of new building permits.”

Issuance of total building permitsdecreased 5.5 percent from the upwardlyrevised July pace to a seasonably adjustedrate of 1.952 million units. However,permits are up by 10 percent on a year-to-date basis.

“The housing market recently hasbeen buoyed by a healthy combinationof strong demographics, improvingemployment and income growth and adownshift in long-term interest rates,”said NAHB Chief Economist DavidSeiders. “Naysayers talking about ahousing bubble should look at thefundamentals that are in place and seethat the national housing market isextremely sound.”

For the month, single-family housingstarts increased 0.4 percent to a pace of

GeneralBusinessNews

1.667 million. This was an 11.6 percentincrease over the August 2003 pace.Multifamily housing starts increased toa seasonally adjusted rate of 333,000units, 1.5 percent above the July pace,but 2.3 percent below a year earlier.

“Starts are likely to slip a bit in thefourth quarter as interest rates firm up,but it’s now clear that single-familyhome production will hit a new annualrecord in 2004,” Seiders added.

Construction of new homes andapartments increased across all regionsbut the West for the month. The Westdecreased 4.7 percent in August followinga surge in new construction the monthbefore. The Northeast increased 6.5percent, the Midwest increased 4.8percent and the South increased 1.0percent for the month.

Single-family permit issuancedecreased by 3.0 percent and multifamilypermits were down 13.8 percent fromthe July pace.

Builder Confidence Down,But Not Out In September

Following a strong bump-up inAugust, builder confidence in the marketfor new single-family homes edged downthis month but remained within thenarrow range maintained since this timelast year, according to the latest NationalAssociation of Home Builders/WellsFargo Housing Market Index (HMI).The seasonally adjusted monthly gaugeof builder sentiment registered a 68 forSeptember, down three points from itsmonth-ago reading.

“This is exactly on par with theindex’s year-ago standing, and showsthat, in the midst of a particularlydevastating hurricane season, builderconfidence is essentially unshaken,” said

Continued on page 16

Tile Management Quarterly16

Bobby Rayburn, NAHB president and ahome and apartment builder fromJackson, Miss.

“Favorable financing conditions,sound house-price performance andreviving consumer confidence continueto propel the single-family market,”agreed NAHB Chief Economist DavidSeiders. “Builders are still reportinghealthy demand for new homes acrossmost markets, and that bodes well forsales in coming months.”

The NAHB/Wells Fargo HMI isderived from a monthly survey ofbuilders that NAHB has been conductingfor almost 20 years. Home builders areasked to rate current sales of single-family homes as “good,” “fair” or “poor.”They are also asked to rate traffic ofprospective buyers as “high to very high,”“average” or “low to very low.” Scoresfor responses to each component areused to calculate a seasonally adjustedindex, where any number over 50indicates that more builders view salesconditions as good than poor.

Following a four-point surge to 71in August, the HMI dropped back threepoints to the same range it has been infor the past year. Two out of three of thecomponent indexes – the one gaugingcurrent sales conditions and the onegauging traffic of prospective buyers –fell four points this time around, to 73and 52, respectively. The componentgauging expected sales in the next sixmonths declined three points to 75. Allare within close range of their year-agostandings in September 2003.

Continued from page 15

Continued on page 17

Builders Applaud NAFTASoftwood Ruling, Call ForQuick Elimination Of CostlyDuties

Hailing it as a major victory forhousing affordability and millions ofAmerican consumers who are feelingthe pinch of near-record lumber prices,the National Association of HomeBuilders (NAHB) today said that a NorthAmerican Free Trade Agreement paneldecision clears the way to removeburdensome tariffs on Canadian timber.

Countervailing and anti-dumpingduties totaling more than 27 percenthave been in place since May of 2002. Ofall the NAFTA and World TradeOrganization court rulings against thetariffs that have emerged since then,yesterday’s verdict represents by far themost significant development because ifthe U.S. can’t prove its contention thatCanadian lumber shipments threatenthe domestic industry, it must removethe duties it imposes on lumber fromCanada.

“For the third time, NAFTA hasunequivocally ruled that Canadian lumberimports present no harm to the domesticindustry. We call on the Administrationto refrain from any further legalmaneuvers or delays and allow thisdecision to be implemented within 10days, as ordered by the NAFTA panel.This would rescind the 27 percent levieson Canadian lumber and end the hiddentax imposed on American home buyersand renters,” said Bobby Rayburn,president of NAHB and a home andapartment builder from Jackson, Miss.

Twice previously, NAFTA haddetermined that the domestic lumberindustry’s threat of injury allegationswere baseless and contrary to law. In

each instance, the case was remandedback to the U.S. International TradeCommission.

In a strongly worded decisionreleased yesterday, the NAFTA panelclearly indicated that it had grown wearyof the ITC’s attempts to prove that U.S.lumber interests were harmed bycompetition from their northernneighbor.

The five-member NAFTA panel,which consists of three Americans andtwo Canadians, unanimously concludedthat the ITC was “simply unwilling toaccept this (NAFTA) panel’s review” and“has consistently ignored the authorityof this panel in an effort to preserve itsfinding of threat of material injury.”

The NAFTA panel ordered the ITC“to make a determination consistentwith the decision of this panel that theevidence on the record does not supporta finding of threat of material injury andto make that determination within 10days.”

Although the NAFTA panel notedthat the U.S. had no new evidence toback the claims of injury and that it“would be an exercise in futility” tofurther review the case, the U.S. couldstill appeal the ruling to an “extraordinarychallenge” committee.

“Such an action would merely be adelaying tactic,” said Rayburn, who notedthat NAFTA’s extraordinary challengeprovisions are only meant to be used formatters of gross misconduct, for whichthere is no legitimate claim in this case.

With the price of framing lumbernow at $473 per 1,000 board feet,according to Random Lengths – upmore than 40 percent from the beginningof the year and approaching the all-timehigh of $519 recorded in 1994 – Rayburn

Tile Management Quarterly17

Continued from page 16

noted that the NAFTA decision could nothave come at a better time.

“Rising building material costs,led by lumber, have added $5,000 to$7,000 to the cost of constructing anaverage new home,” he said. “The dutieshave artificially boosted lumber pricesand have helped line the pockets ofdomestic producers at the expense ofU.S. consumers. NAFTA hasunambiguously ruled that this case hasno merit. Therefore, the Administrationshould prevent this case from draggingout any further and allow these punitiveduties to disappear.”

Survey Reveals NationwideShortages Of Cement, OtherKey Building Materials

A shortage of cement and other keybuilding materials looms as the biggestthreat to the dynamic housing marketthat has produced record levels of newhome construction in the U.S., accordingto a recent survey conducted by theNational Association of Home Builders(NAHB).

“A nationwide survey conducted inJuly shows that builders are reportingshortages of cement, gypsum wallboard,oriented strand board (OSB), steelframing and insulating materials,” saidJerry Howard, executive vice presidentand CEO of NAHB. “Rising wholesaleprices of building materials have added$5,000 to $7,000 to the cost of buildingan average new home, and constructiondelays caused by supply shortages couldtranslate into further cost increases. Leftunchecked, these factors could result inserious disruptions to the housingmarket.”

Of most immediate concern iscement, with 41 percent of respondentsciting a shortage of this vital buildingmaterial. This is a huge jump from May,when 11 percent of those polled viewedthis as an issue. In March, only 3 percentof builders reported that cement was inshort supply.

To relieve the shortage, Howardcalled on the Administration to eliminatethe high anti-dumping duties on importsof Mexican cement.

Shortages first appeared this springin Florida, which imports about 40percent of its cement, compared with anationwide average of just 20 percent.Supplies subsequently tightened in otherregions partly because strong demandfrom China has diverted the amount ofcement available from other countriesand limited the number of cargo shipsthat can bring the product to U.S. ports.

Prohibitive duties have severelylimited supplies from Mexico, which isthe most logical source of supplementaryimports. A delivery from that countrytakes only four days, compared to anaverage of 44 days for a cement shipmentfrom Asia.

“With global shipping capacitystrained, the ability to import cementfrom Asia and Europe to meet thisshortfall has been significantly reduced,”said Howard. “Therefore, it makes senseto rescind the costly anti-dumping dutieson Mexican cement that are preventinga stable and reliable supply of importsto U.S. consumers.”

Twenty-six percent of those surveyedreported experiencing a shortage ofgypsum wall board, up from 11 percentlast October, 16 percent in March and19 percent in May.

Nearly one-third of respondentsare experiencing shortages of oriented

strand board and plywood, wood panelproducts used for wall sheathing, floorsand roofs. While this is a significantfigure, it is well below the peak of 52percent reported in last October’s survey.However, prices of those products remainhigh.

Insulation material is another sorespot for builders, as 20 percent noted alack of this product, compared to 10percent just four months earlier.

In a number of regions where brickis widely used, builders have reportedshortages of that material as well.

While framing lumber suppliesappear adequate, the larger concernamong builders in this area is pricevolatility. The price of 1,000 board feetof framing lumber hit a yearly high of$472 last week, up 52 percent from$311 a year ago, according to RandomLengths, a trade publication based inEugene, Ore.

Shortages of building materialshave also led to rising costs. During thepast six months, 90 percent ofrespondents reported paying higherprices for framing lumber and orientedstrand board, 88 percent for plywood,86 percent for cement, 80 percent forsteel, 75 percent for gypsum wall boardand 68 percent for insulation.

“A steady supply of buildingmaterials available at reasonable pricesis important to maintaining a vibranthousing market and to meeting thegrowing demand for affordable housing,”said Howard.

Tile Management Quarterly18

Continued on page 19

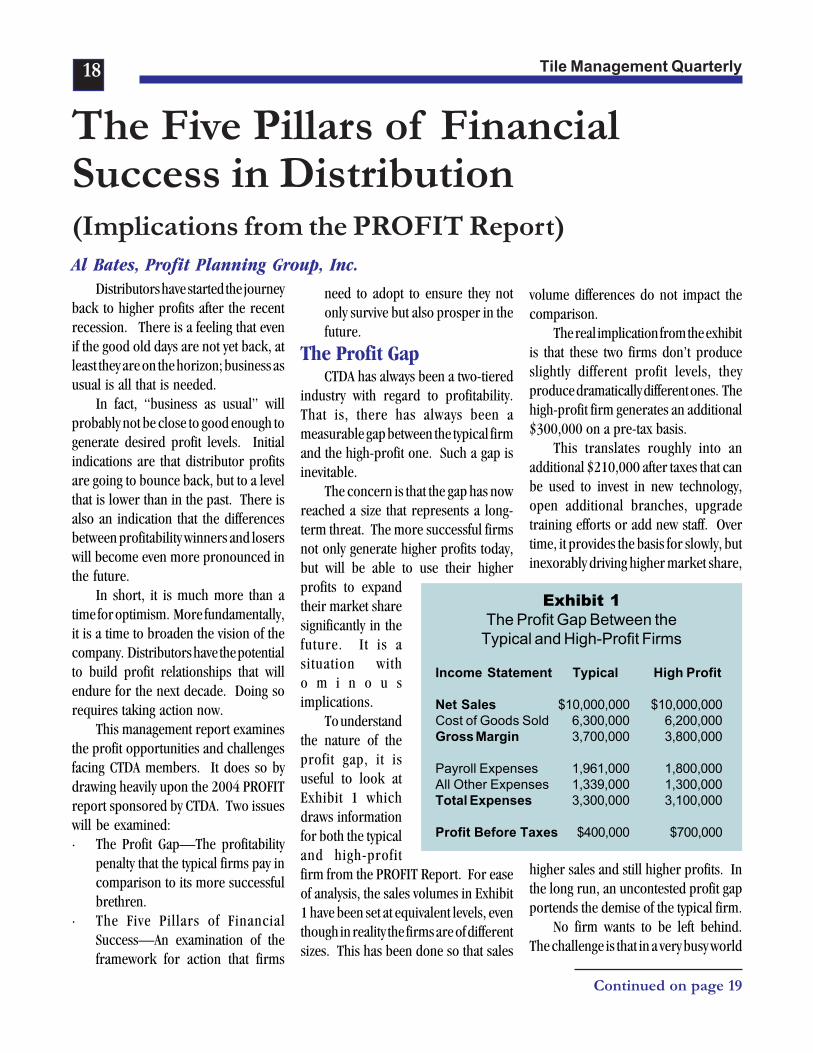

Distributors have started the journeyback to higher profits after the recentrecession. There is a feeling that evenif the good old days are not yet back, atleast they are on the horizon; business asusual is all that is needed.

In fact, “business as usual” willprobably not be close to good enough togenerate desired profit levels. Initialindications are that distributor profitsare going to bounce back, but to a levelthat is lower than in the past. There isalso an indication that the differencesbetween profitability winners and loserswill become even more pronounced inthe future.

In short, it is much more than atime for optimism. More fundamentally,it is a time to broaden the vision of thecompany. Distributors have the potentialto build profit relationships that willendure for the next decade. Doing sorequires taking action now.

This management report examinesthe profit opportunities and challengesfacing CTDA members. It does so bydrawing heavily upon the 2004 PROFITreport sponsored by CTDA. Two issueswill be examined:· The Profit Gap—The profitability

penalty that the typical firms pay incomparison to its more successfulbrethren.

· The Five Pillars of FinancialSuccess—An examination of theframework for action that firms

The Five Pillars of FinancialSuccess in Distribution(Implications from the PROFIT Report)Al Bates, Profit Planning Group, Inc.

need to adopt to ensure they notonly survive but also prosper in thefuture.

The Profit GapCTDA has always been a two-tiered

industry with regard to profitability.That is, there has always been ameasurable gap between the typical firmand the high-profit one. Such a gap isinevitable.

The concern is that the gap has nowreached a size that represents a long-term threat. The more successful firmsnot only generate higher profits today,but will be able to use their higherprofits to expandtheir market sharesignificantly in thefuture. It is asituation witho m i n o u simplications.

To understandthe nature of theprofit gap, it isuseful to look atExhibit 1 whichdraws informationfor both the typicaland high-profitfirm from the PROFIT Report. For easeof analysis, the sales volumes in Exhibit1 have been set at equivalent levels, eventhough in reality the firms are of differentsizes. This has been done so that sales

volume differences do not impact thecomparison.

The real implication from the exhibitis that these two firms don’t produceslightly different profit levels, theyproduce dramatically different ones. Thehigh-profit firm generates an additional$300,000 on a pre-tax basis.

This translates roughly into anadditional $210,000 after taxes that canbe used to invest in new technology,open additional branches, upgradetraining efforts or add new staff. Overtime, it provides the basis for slowly, butinexorably driving higher market share,

higher sales and still higher profits. Inthe long run, an uncontested profit gapportends the demise of the typical firm.

No firm wants to be left behind.The challenge is that in a very busy world

Exhibit 1The Profit Gap Between the

Typical and High-Profit Firms

Income Statement Typical High Profit

Net Sales $10,000,000 $10,000,000Cost of Goods Sold 6,300,000 6,200,000Gross Margin 3,700,000 3,800,000

Payroll Expenses 1,961,000 1,800,000All Other Expenses 1,339,000 1,300,000Total Expenses 3,300,000 3,100,000

Profit Before Taxes $400,000 $700,000

Tile Management Quarterly19

where sometimes everything seemsimportant, there is difficulty in layingout a plan of action for the future.Closing the gap will require not onlypriorities for action, but an entirely newfocus on what the firm is trying to be.

The Pillars of FinancialSuccess

In closing the gap, there is aninevitable desire to find the silver bulletthat will drive the firm to improvedresults. Unfortunately, there are nosilver bullets for producing higher profitsin distribution. Instead, success willcome from doing a lot of things rightover an extended time period. Firmsmust have a clear strategy, operateefficiently, understand the needs ofcustomers, and engage in a myriad ofother activities as effectively as possible.

Even though there are no magicanswers, a detailed analysis of the PROFITReport and comparisons with otherindustries does suggest that there is adefinite “short list” of factors thatdistinguish the successful firms fromthe ordinary ones. Given theirimportance, these factors are beingreferred to here as the five pillars offinancial success.

They are not five actions to take andthen check off on a to-do list. Further,they are not five profit drivers to worryabout, such as sales, gross margin andinventory. Instead, they are fivefundamental characteristics of firms thatenjoy long-term success. The five factorslisted below are all strategic in nature.They describe the competitive andoperating environment the firm hascreated.

· Barriers to Entry—Competitivebattles are not fought on every itemon every transaction every singleday. Instead, competition is wagedbetween alternative businesssystems.

· De-Commoditization—The overallproduct assortment offered allowsfor both tonnage sales andreasonable margin opportunitiesfrom non-commodities.

· Employee Productivity—Newprocedures for controlling payrollexpense have been implemented.

· Profit Focus—The maximization ofdollar profits takes priority over themaximization of sales or theminimization of asset investment.

· Internal Profit Understanding—There is a clear understanding withinthe decision-making ranks of howprofit is generated or destroyed byemployee actions.

Focusing on these strategic factorsprovides no absolute guarantee ofsuccess. Brilliant strategies can becombined with ineffective operatingprocedures to produce marginal results.Instead, concentrating on these fivefactors creates an environment in whicheffective operations can deliver highprofits. Without such approaches, highprofits are distinctly unattainableregardless of operational efficiency.

Barriers to EntryEconomic theory contends that

barriers to entry are industry-wideconditions. If it is impossible, or atleast very difficult for new competitorsto enter an industry, then every firm inthe industry prospers. In fact, researchinto distribution profitability indicatesthat the single most important reasonwhy some industries produce higher

profits than others are such industry-wide barriers.1

The reality is that distribution firmscan’t unilaterally create industry-widebarriers to entry for their line of trade.Instead, they must find a way to erecttheir own unique barriers to entry at theindividual firm level. Such barriers aremuch more fragile than industry-widelegal or licensing barriers. However,they also are much easier to construct.

Examples of company-specificbarriers to entry abound in distribution,although they are not often thought of assuch. A few selected examples include:

· Proprietary Technology—Orderingsystems that link customers anddistributors, particularly in anautomatic reordering mode.

· Patronage Programs—Cumulativerebate programs that tend to tiecustomers to the firm.

· Tailored Assortments—Programsthat facilitate one-stop shopping.These are particularly effective inindustries where competitors aredramatically reducing inventory forcash flow reasons.

· Operational Effectiveness—Differentially high fill rates anddifferentially low error rates thatlower operating costs for customers.

Measuring the impact of barriers toentry is difficult when relying exclusivelyon available financial information. Ananalysis of profitability information fromPROFIT reports conducted in fortydifferent lines of trade in distributionsuggests three benefits (1) an enhancedgross margin, probably in the range ofone to two percentage points above theindustry norm, (2) five to ten percent in

Continued from page 18

Continued on page 20

Tile Management Quarterly20

additional sales volume, and (3) areduction in payroll of between one-halfand one percentage point.

It should be noted carefully thatevery line of trade is unique and thatsuch differences play out differentlyamong the various lines of trade.

Financial results from the PROFIT reportsuggest that CTDA members appear tofollow a pattern very close to the norm.

Exhibit 2 measures the profit impactof potential changes in performance forthe typical CTDA member. A typicalfirm, producing pre-tax profits of$400,000, has the opportunity toincrease profits by $302,000 or 75.5%if all three of the profit enhancementopportunities were realized fully.

The changes don’t impact resultsslightly. They move the firm into adifferent sphere of profitability. For allpractical purposes the firm is no longereven in the same industry. If barriers toentry can be thought of as manageabledefenses rather than an industry-widecondition over which the firm has nocontrol, there is no real limit to theprofitability levels that can be achieved.

De-Commoditization of theProduct Line

Firms in nearly every industry feelthat their products are, or are rapidlybecoming, commodities. This simply is

not the case. The product offer for CTDAmembers is diverse with numerousopportunities to avoid directcompetition. Even if the most basicSKUs are commodities, there are alwayssome extended product offerings to wraparound the commodity base.

The level of commoditization issecond only to barriers to entry as a

strategic determinant of profit indistribution. Interestingly, firms in thesame industry often have very differentviews about the extent to which they sellcommodities. Part of this is reality, buta large part is perception.

The distinction betweencommodities and non-commodities isimportant in that it produces a mind set

in the firm about the role of pricing.With true commodities, the naturalfeeling is that there is little that can bedone in the pricing arena. When themarket price declines, firms must meetthat price. If not, they are symbolicallywaving a flag indicating that their priceon every item is high.

Non-commodities call for a verydifferent set of rules. On these itemsthere is the perception that there issome breathing room on price. Theitems may still be price sensitive to alarge degree, but there is no requirementto meet every competitive price in everyinstance.

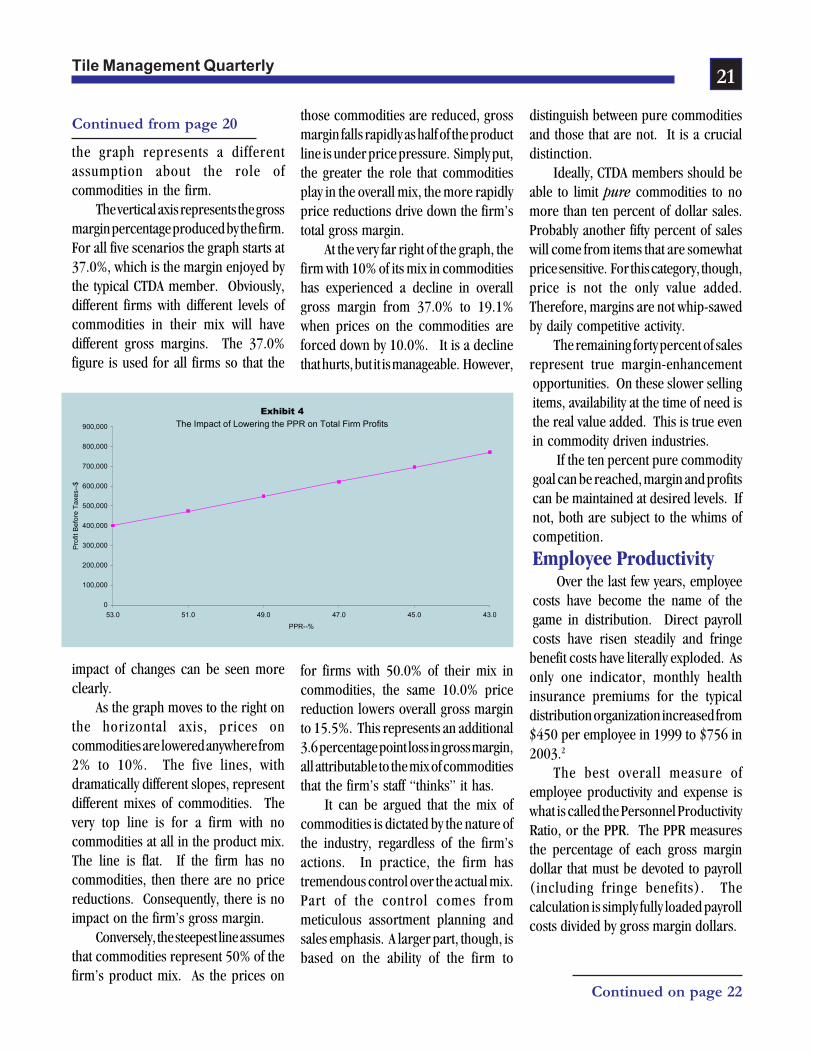

If one firm in the industry has aperception that virtually everything is acommodity while another feels thatonly a few items are commodities, thenthe two firms come to very differentpositions regarding pricing and grossmargin. Exhibit 3 presents the differentperceptions graphically.

The chart measures the gross margin“hit” the firm will experience if its

prices on commodities are forced downfrom 2% to 10%. Each of the lines on

Exhibit 3 The Impact of Commodities on Gross Margin

30.0

32.0

34.0

36.0

38.0

40.0

0 2 4 6 8 10

Price Cut--%

Tota

l Firm

Gro

ss M

argi

n--%

0.0 10.0 20.0 30.0 40.0 50.0Percent of Sales from Commodities:

Continued from page 19

Continued on page 21

Exhibit 2The Impact on Profit of Selected Changes in Performance

AdditionalArea of Change Improvement ProfitGross Margin Percentage One Percentage Point $100,000Net Sales Five Percent 152,000Payroll as a Percent of Sales One-Half Percentage Point 50,000Total Improvement Potential $302,000

Tile Management Quarterly21

the graph represents a differentassumption about the role ofcommodities in the firm.

The vertical axis represents the grossmargin percentage produced by the firm.For all five scenarios the graph starts at37.0%, which is the margin enjoyed bythe typical CTDA member. Obviously,different firms with different levels ofcommodities in their mix will havedifferent gross margins. The 37.0%figure is used for all firms so that the

impact of changes can be seen moreclearly.

As the graph moves to the right onthe horizontal axis, prices oncommodities are lowered anywhere from2% to 10%. The five lines, withdramatically different slopes, representdifferent mixes of commodities. Thevery top line is for a firm with nocommodities at all in the product mix.The line is flat. If the firm has nocommodities, then there are no pricereductions. Consequently, there is noimpact on the firm’s gross margin.

Conversely, the steepest line assumesthat commodities represent 50% of thefirm’s product mix. As the prices on

those commodities are reduced, grossmargin falls rapidly as half of the productline is under price pressure. Simply put,the greater the role that commoditiesplay in the overall mix, the more rapidlyprice reductions drive down the firm’stotal gross margin.

At the very far right of the graph, thefirm with 10% of its mix in commoditieshas experienced a decline in overallgross margin from 37.0% to 19.1%when prices on the commodities areforced down by 10.0%. It is a declinethat hurts, but it is manageable. However,

for firms with 50.0% of their mix incommodities, the same 10.0% pricereduction lowers overall gross marginto 15.5%. This represents an additional3.6 percentage point loss in gross margin,all attributable to the mix of commoditiesthat the firm’s staff “thinks” it has.

It can be argued that the mix ofcommodities is dictated by the nature ofthe industry, regardless of the firm’sactions. In practice, the firm hastremendous control over the actual mix.Part of the control comes frommeticulous assortment planning andsales emphasis. A larger part, though, isbased on the ability of the firm to

distinguish between pure commoditiesand those that are not. It is a crucialdistinction.

Ideally, CTDA members should beable to limit pure commodities to nomore than ten percent of dollar sales.Probably another fifty percent of saleswill come from items that are somewhatprice sensitive. For this category, though,price is not the only value added.Therefore, margins are not whip-sawedby daily competitive activity.

The remaining forty percent of salesrepresent true margin-enhancementopportunities. On these slower sellingitems, availability at the time of need isthe real value added. This is true evenin commodity driven industries.

If the ten percent pure commoditygoal can be reached, margin and profitscan be maintained at desired levels. Ifnot, both are subject to the whims ofcompetition.

Employee ProductivityOver the last few years, employee

costs have become the name of thegame in distribution. Direct payrollcosts have risen steadily and fringebenefit costs have literally exploded. Asonly one indicator, monthly healthinsurance premiums for the typicaldistribution organization increased from$450 per employee in 1999 to $756 in2003.2

The best overall measure ofemployee productivity and expense iswhat is called the Personnel ProductivityRatio, or the PPR. The PPR measuresthe percentage of each gross margindollar that must be devoted to payroll(including fringe benefits). Thecalculation is simply fully loaded payrollcosts divided by gross margin dollars.

Exhibit 4 The Impact of Lowering the PPR on Total Firm Profits

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

53.0 51.0 49.0 47.0 45.0 43.0

PPR--%

Pro

fit B

efor

e Ta

xes-

-$

Continued from page 20

Continued on page 22

Tile Management Quarterly22

For the typical CTDA member fromExhibit 1, the calculation of the PPR is:

Payroll CostsGross Margin

=$1,961,000$3,700,000

=53.0%

This means that for every one dollarof gross margin that is generated, thefirm must spend 53.0 cents on payroll.The figure is too high for long-termfinancial success.

Exhibit 4 graphs the dollar profitsthe firm will generate as it begins tolower its PPR. As can be seen, therelationship is quite pronounced. If, forexample the firm could make a tenpoint reduction in the PPR, then dollarprofits would increase from the current$400,000 to $770,000.

A ten point cut is dramatic. However,the high-profit firms within CTDA operateon a PPR of only 55.0%, compared to53.0% for the typical firm. A programto move systematically towards the high-profit number is essential.

In trying to improve the PPR, firmshave three distinct opportunities:

· Actual Cost Levels—The amountspent per employee on payroll andfringe benefits.

· Productivity—The amount ofoutput that is generated per unit oflabor input.

· Workload—The number of orders,deliveries, invoices and the like thatmust be processed.

Historically, firms have focusedalmost exclusively on the first two—costs and productivity. As a result,efforts in these areas have reached apoint of diminishing (or possibly evenno) returns.

Cost reductions continue to be animportant strategy for firms that canengage in outsourcing. However, mostdistribution functions have to beperformed locally. In current parlance,it is hard to move the truck-drivingfunction to India.

While distribution firms are blockedon lowering payroll costs, they face analmost impossible battle on fringebenefits. Firms have engaged in somerearguard programs such as increasingco-pays and deductibles on healthinsurance. The best that can be hopedfor, though, is to reduce the rate ofincrease.

Enhanced productivity has been thefocal point of distributor activity inrecent years. Inevitably, this has lead toincreasing sophistication in terms oftechnology and operating systems. Theuse of technology to drive higher levelsof productivity has been the great successof distribution. At the same time, theimpact on the bottom line has beeninfuriatingly small.

The vast majority of employee-productivity technology has beenindustry wide. That is, new technologythrusts, such as bar coding andincreasingly, radio frequencyidentification, ultimately are widelyadopted by almost all distributors. Theresult is that costs go down for everybody.

If the story ended there, it wouldrepresent the proverbial happy ending.Unfortunately, as costs go down foreverybody, gross margins also tend to godown for everybody. This leaves CTDA

members more productive, but not moreprofitable.

It is probably time for distributorsto turn their attention to controlling theworkload. That is, they must managethe number of orders received, thenumber of deliveries made and the like.

For most managers, even thinkingabout workload controls is anathema.Distribution firms have built their entirebusiness around service. If anything,though, distributors are now over-servicing their customers. The costimplication is clearly negative fordistributors. Of strategic consequence,the cost implication is also negative forcustomers who waste their own employeetime by placing and processing too manysmall orders.

Controlling the workload involves acombination of better analysis of costsand more sophisticated selling:

· Analysis—Before excessive activitycan be eliminated, it must beidentified. Activity Based Costingtools are now cheap enough (withExcel or other spreadsheets) thatevery firm should know its costs toprocess an order or make a delivery.The cost-understanding issue is nolonger a barrier.

· Selling—Understanding is differentthan taking action. Programs mustbe in place to educate the salesforce, and ultimately customers, onthe essential need for fewer, largerorders throughout the channel.

Profit FocusTo accuse distributors of not having

a profit focus is to accuse them of beingun-American. The reality, though, isthat most firms do not focus on profits

Continued from page 21

Continued on page 23

Tile Management Quarterly23

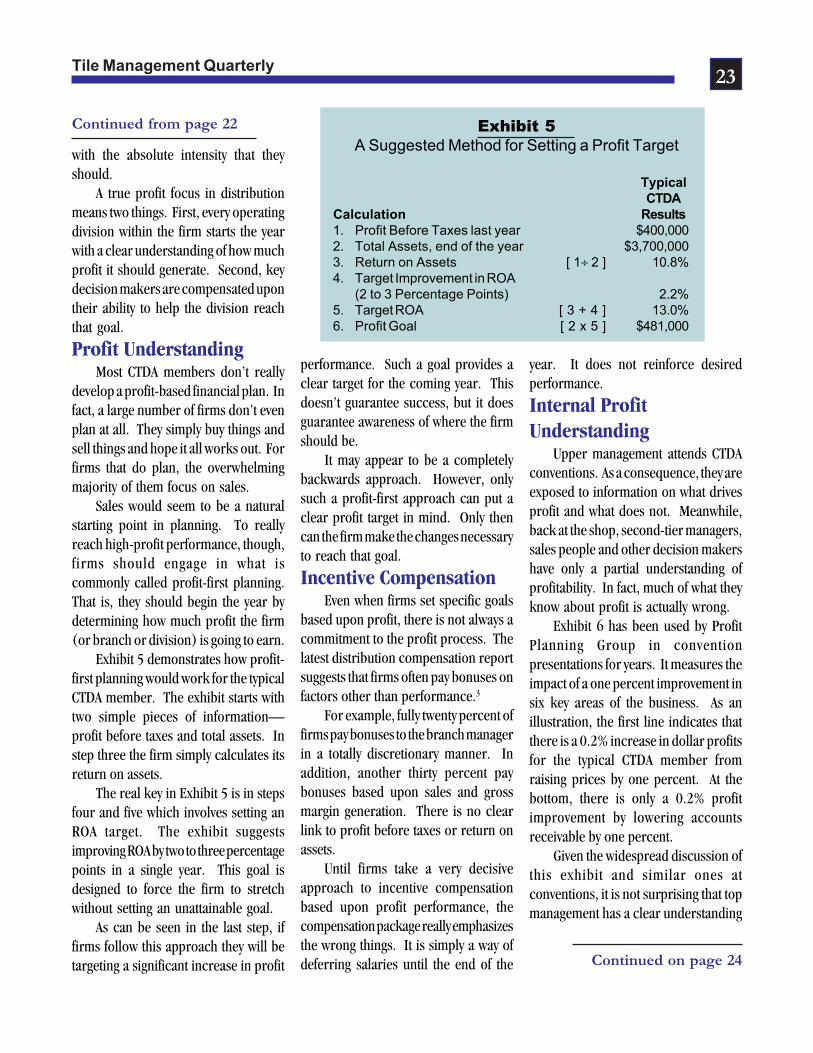

with the absolute intensity that theyshould.

A true profit focus in distributionmeans two things. First, every operatingdivision within the firm starts the yearwith a clear understanding of how muchprofit it should generate. Second, keydecision makers are compensated upontheir ability to help the division reachthat goal.

Profit UnderstandingMost CTDA members don’t really

develop a profit-based financial plan. Infact, a large number of firms don’t evenplan at all. They simply buy things andsell things and hope it all works out. Forfirms that do plan, the overwhelmingmajority of them focus on sales.

Sales would seem to be a naturalstarting point in planning. To reallyreach high-profit performance, though,firms should engage in what iscommonly called profit-first planning.That is, they should begin the year bydetermining how much profit the firm(or branch or division) is going to earn.

Exhibit 5 demonstrates how profit-first planning would work for the typicalCTDA member. The exhibit starts withtwo simple pieces of information—profit before taxes and total assets. Instep three the firm simply calculates itsreturn on assets.

The real key in Exhibit 5 is in stepsfour and five which involves setting anROA target. The exhibit suggestsimproving ROA by two to three percentagepoints in a single year. This goal isdesigned to force the firm to stretchwithout setting an unattainable goal.

As can be seen in the last step, iffirms follow this approach they will betargeting a significant increase in profit

performance. Such a goal provides aclear target for the coming year. Thisdoesn’t guarantee success, but it doesguarantee awareness of where the firmshould be.

It may appear to be a completelybackwards approach. However, onlysuch a profit-first approach can put aclear profit target in mind. Only thencan the firm make the changes necessaryto reach that goal.

Incentive CompensationEven when firms set specific goals

based upon profit, there is not always acommitment to the profit process. Thelatest distribution compensation reportsuggests that firms often pay bonuses onfactors other than performance.3

For example, fully twenty percent offirms pay bonuses to the branch managerin a totally discretionary manner. Inaddition, another thirty percent paybonuses based upon sales and grossmargin generation. There is no clearlink to profit before taxes or return onassets.

Until firms take a very decisiveapproach to incentive compensationbased upon profit performance, thecompensation package really emphasizesthe wrong things. It is simply a way ofdeferring salaries until the end of the

year. It does not reinforce desiredperformance.

Internal ProfitUnderstanding

Upper management attends CTDAconventions. As a consequence, they areexposed to information on what drivesprofit and what does not. Meanwhile,back at the shop, second-tier managers,sales people and other decision makershave only a partial understanding ofprofitability. In fact, much of what theyknow about profit is actually wrong.

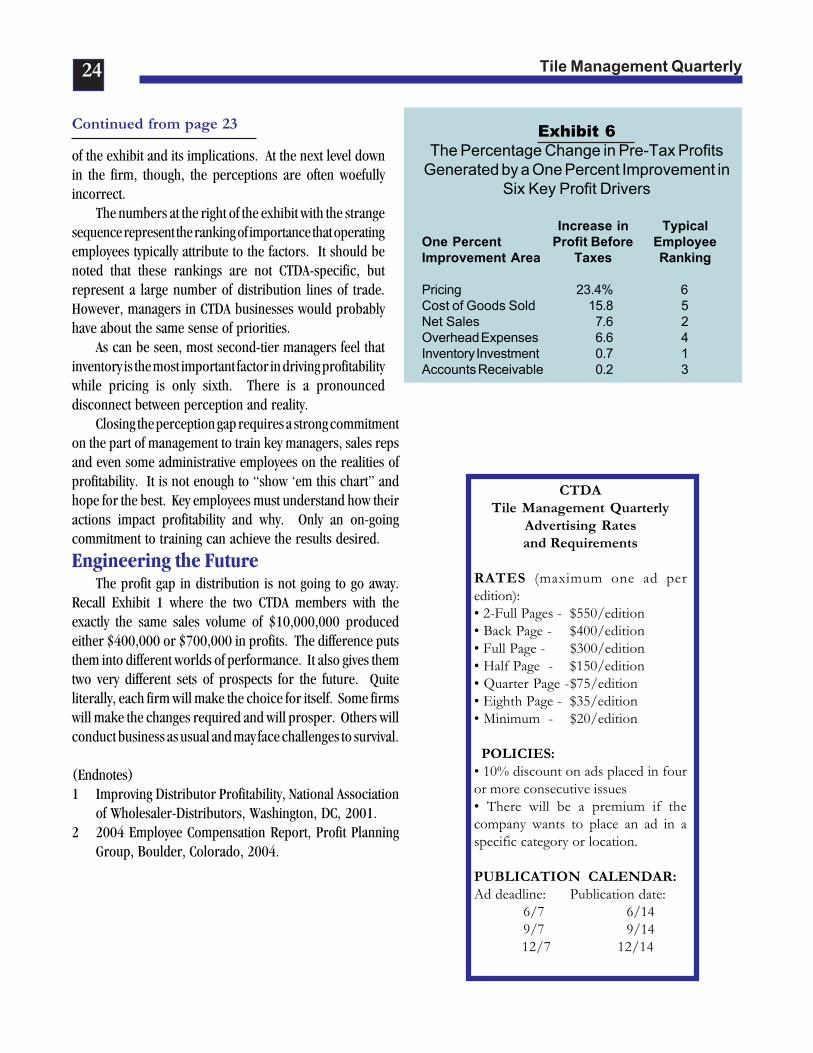

Exhibit 6 has been used by ProfitPlanning Group in conventionpresentations for years. It measures theimpact of a one percent improvement insix key areas of the business. As anillustration, the first line indicates thatthere is a 0.2% increase in dollar profitsfor the typical CTDA member fromraising prices by one percent. At thebottom, there is only a 0.2% profitimprovement by lowering accountsreceivable by one percent.

Given the widespread discussion ofthis exhibit and similar ones atconventions, it is not surprising that topmanagement has a clear understanding

Continued from page 22

Continued on page 24

Exhibit 5A Suggested Method for Setting a Profit Target

TypicalCTDA

Calculation Results1. Profit Before Taxes last year $400,0002. Total Assets, end of the year $3,700,0003. Return on Assets [ 1÷ 2 ] 10.8%4. Target Improvement in ROA

(2 to 3 Percentage Points) 2.2%5. Target ROA [ 3 + 4 ] 13.0%6. Profit Goal [ 2 x 5 ] $481,000

Tile Management Quarterly24

of the exhibit and its implications. At the next level downin the firm, though, the perceptions are often woefullyincorrect.

The numbers at the right of the exhibit with the strangesequence represent the ranking of importance that operatingemployees typically attribute to the factors. It should benoted that these rankings are not CTDA-specific, butrepresent a large number of distribution lines of trade.However, managers in CTDA businesses would probablyhave about the same sense of priorities.

As can be seen, most second-tier managers feel thatinventory is the most important factor in driving profitabilitywhile pricing is only sixth. There is a pronounceddisconnect between perception and reality.

Closing the perception gap requires a strong commitmenton the part of management to train key managers, sales repsand even some administrative employees on the realities ofprofitability. It is not enough to “show ‘em this chart” andhope for the best. Key employees must understand how theiractions impact profitability and why. Only an on-goingcommitment to training can achieve the results desired.

Engineering the FutureThe profit gap in distribution is not going to go away.

Recall Exhibit 1 where the two CTDA members with theexactly the same sales volume of $10,000,000 producedeither $400,000 or $700,000 in profits. The difference putsthem into different worlds of performance. It also gives themtwo very different sets of prospects for the future. Quiteliterally, each firm will make the choice for itself. Some firmswill make the changes required and will prosper. Others willconduct business as usual and may face challenges to survival.

(Endnotes)1 Improving Distributor Profitability, National Association

of Wholesaler-Distributors, Washington, DC, 2001.2 2004 Employee Compensation Report, Profit Planning

Group, Boulder, Colorado, 2004.

CTDATile Management Quarterly

Advertising Ratesand Requirements

RATES (maximum one ad peredition):• 2-Full Pages - $550/edition• Back Page - $400/edition• Full Page - $300/edition• Half Page - $150/edition• Quarter Page -$75/edition• Eighth Page - $35/edition• Minimum - $20/edition

POLICIES:• 10% discount on ads placed in fouror more consecutive issues• There will be a premium if thecompany wants to place an ad in aspecific category or location.

PUBLICATION CALENDAR:Ad deadline: Publication date: 6/7 6/14 9/7 9/14

12/7 12/14

Continued from page 23 Exhibit 6The Percentage Change in Pre-Tax Profits

Generated by a One Percent Improvement inSix Key Profit Drivers

Increase in TypicalOne Percent Profit Before EmployeeImprovement Area Taxes Ranking

Pricing 23.4% 6Cost of Goods Sold 15.8 5Net Sales 7.6 2Overhead Expenses 6.6 4Inventory Investment 0.7 1Accounts Receivable 0.2 3

Tile Management Quarterly25

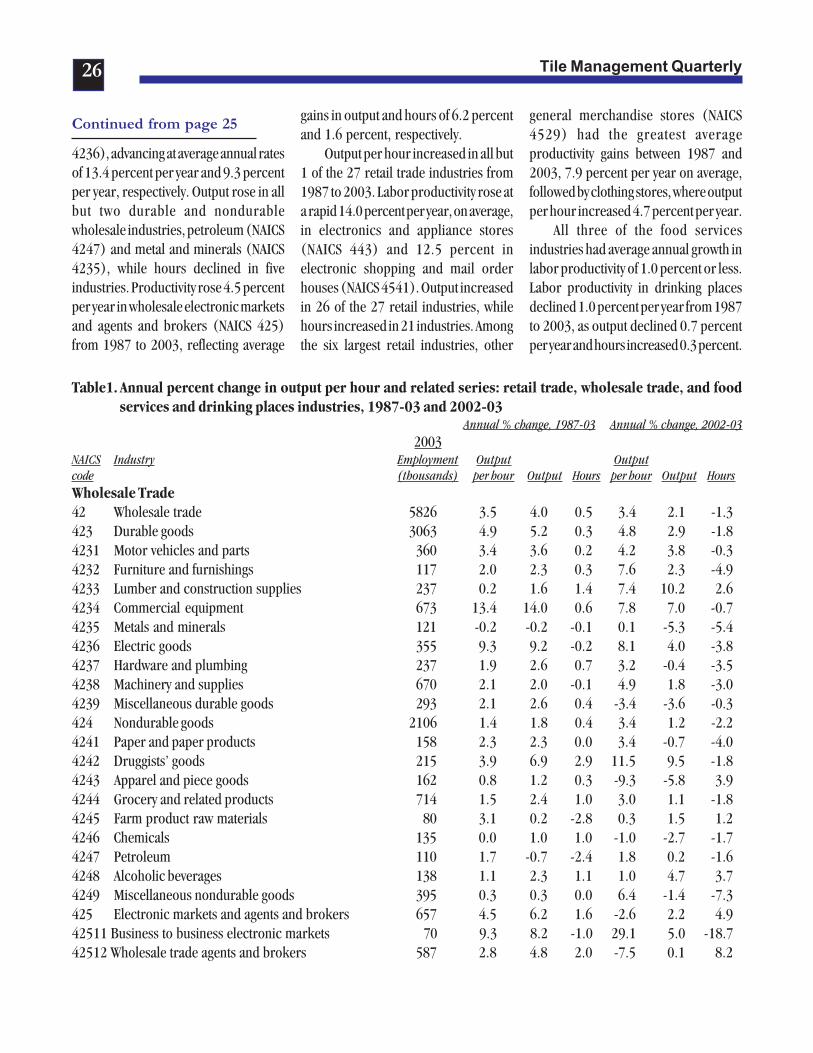

2003 PRODUCTIVITY BY INDUSTRY:

WHOLESALE TRADE, RETAIL TRADE, AND

FOOD SERVICES AND DRINKING PLACESThe Bureau of Labor Statistics of the

U.S. Department of Labor reported todayon labor productivity changes forwholesale trade, retail trade, and foodservices and drinking places. In 2003,labor productivity—defined as outputper hour—rose 3.4 percent for wholesaletrade, 5.1 percent for retail trade, and3.3 percent for food services and drinkingplaces. In both the retail and wholesaletrade sectors, output increased in 2003while hours declined. In food servicesand drinking places, both output andhours increased in 2003.

From 1987 to 2003, laborproductivity in the wholesale trade sectorrose an average of 3.5 percent per year.Output increased 4.0 percent per year,and hours increased 0.5 percent peryear. Labor productivity in retail tradeincreased 2.9 percent per year, whileoutput increased 3.9 percent, and hoursincreased 0.9 percent per year. In foodservices and drinking places, laborproductivity increased at an averageannual rate of 0.8 percent between 1987-2003, as output increased 2.4 percentand hours grew 1.6 percent per year.

Labor compensation and unit laborcosts are not reported in this releasebecause data to develop these measuresfor 2003 are not yet available. Industryproductivity and cost measures areproduced and published as source databecome available. Measures forindustries in other sectors have beenpublished in separate releases and can

Continued on page 26

be accessed online at http://www.bls.gov/schedule/archives/all_nr.htm.

2002-03 changeLabor productivity grew in 15 of the

18 durable and nondurable wholesaletrade industries measured in 2003. Eightof the nine durable goods and seven ofthe nine nondurable goods wholesaleindustries had productivity increases.Among the durable goods wholesaleindustries, the highest productivityincreases occurred for electrical goods(NAICS 4236) and commercialequipment (NAICS 4234), with outputper hour increases of 8.1 percent and7.8 percent, respectively. Two otherdurable wholesale industries, furnitureand furnishing (NAICS 4232) and lumberand construction supplies (NAICS 4233),had output per hour increases in 2003nearly as high, with gains of 7.6 percentand 7.4 percent, respectively. Amongthe nondurable wholesale tradeindustries, druggists’ goods (NAICS4242) had the highest productivityincrease (11.5 percent), followed bymiscellaneous nondurable goods (NAICS4249) with an increase of 6.4 percent.Output increased in 11 of the 18wholesale trade industries in 2003, whilehours declined in 14 industries. Laborproductivity declined 2.6 percent forwholesale electronic markets and agentsand brokers (NAICS 425), reflecting a2.2 percent increase in output with a 4.9percent increase in hours in 2003.

Labor productivity rose in 23 of the27 retail trade industries in 2003. Thehighest increases were 25.3 percent inelectronics and appliance stores (NAICS443) and 15.8 percent in electronicshopping and mail-order houses (NAICS4541). Productivity grew in five of thesix largest retail trade industries, thosewith more than 1,000,000 employees.Output grew in 22 of the 27 retailindustries, and all but two of theseindustries experienced productivityincreases. Hours declined in 17 retailindustries, 15 of which experiencedproductivity increases.

Labor productivity increased 3.3percent in food services and drinkingplaces in 2003. All four of the industriesin this subsector had productivity gains.The largest productivity gain occurredfor drinking places (NAICS 7224) —5.4percent. The two large industries in thisgroup, full-service restaurants (NAICS7221) and limited-service eating places(NAICS 7222), experienced productivitygains of 3.4 percent and 3.5 percent,respectively.

Long-term trendsLabor productivity increased in 16

of the 18 durable and nondurableindustries in the wholesale trade sectorfrom 1987 to 2003. Output per hourrose most rapidly in commercialequipment wholesalers (NAICS 4234)and in electric goods wholesalers (NAICS

Tile Management Quarterly26

4236), advancing at average annual ratesof 13.4 percent per year and 9.3 percentper year, respectively. Output rose in allbut two durable and nondurablewholesale industries, petroleum (NAICS4247) and metal and minerals (NAICS4235), while hours declined in fiveindustries. Productivity rose 4.5 percentper year in wholesale electronic marketsand agents and brokers (NAICS 425)from 1987 to 2003, reflecting average

Table1. Annual percent change in output per hour and related series: retail trade, wholesale trade, and foodservices and drinking places industries, 1987-03 and 2002-03

Annual % change, 1987-03 Annual % change, 2002-032003

NAICS Industry Employment Output Outputcode (thousands) per hour Output Hours per hour Output HoursWholesale Trade42 Wholesale trade 5826 3.5 4.0 0.5 3.4 2.1 -1.3423 Durable goods 3063 4.9 5.2 0.3 4.8 2.9 -1.84231 Motor vehicles and parts 360 3.4 3.6 0.2 4.2 3.8 -0.34232 Furniture and furnishings 117 2.0 2.3 0.3 7.6 2.3 -4.94233 Lumber and construction supplies 237 0.2 1.6 1.4 7.4 10.2 2.64234 Commercial equipment 673 13.4 14.0 0.6 7.8 7.0 -0.74235 Metals and minerals 121 -0.2 -0.2 -0.1 0.1 -5.3 -5.44236 Electric goods 355 9.3 9.2 -0.2 8.1 4.0 -3.84237 Hardware and plumbing 237 1.9 2.6 0.7 3.2 -0.4 -3.54238 Machinery and supplies 670 2.1 2.0 -0.1 4.9 1.8 -3.04239 Miscellaneous durable goods 293 2.1 2.6 0.4 -3.4 -3.6 -0.3424 Nondurable goods 2106 1.4 1.8 0.4 3.4 1.2 -2.24241 Paper and paper products 158 2.3 2.3 0.0 3.4 -0.7 -4.04242 Druggists’ goods 215 3.9 6.9 2.9 11.5 9.5 -1.84243 Apparel and piece goods 162 0.8 1.2 0.3 -9.3 -5.8 3.94244 Grocery and related products 714 1.5 2.4 1.0 3.0 1.1 -1.84245 Farm product raw materials 80 3.1 0.2 -2.8 0.3 1.5 1.24246 Chemicals 135 0.0 1.0 1.0 -1.0 -2.7 -1.74247 Petroleum 110 1.7 -0.7 -2.4 1.8 0.2 -1.64248 Alcoholic beverages 138 1.1 2.3 1.1 1.0 4.7 3.74249 Miscellaneous nondurable goods 395 0.3 0.3 0.0 6.4 -1.4 -7.3425 Electronic markets and agents and brokers 657 4.5 6.2 1.6 -2.6 2.2 4.942511 Business to business electronic markets 70 9.3 8.2 -1.0 29.1 5.0 -18.742512 Wholesale trade agents and brokers 587 2.8 4.8 2.0 -7.5 0.1 8.2

gains in output and hours of 6.2 percentand 1.6 percent, respectively.

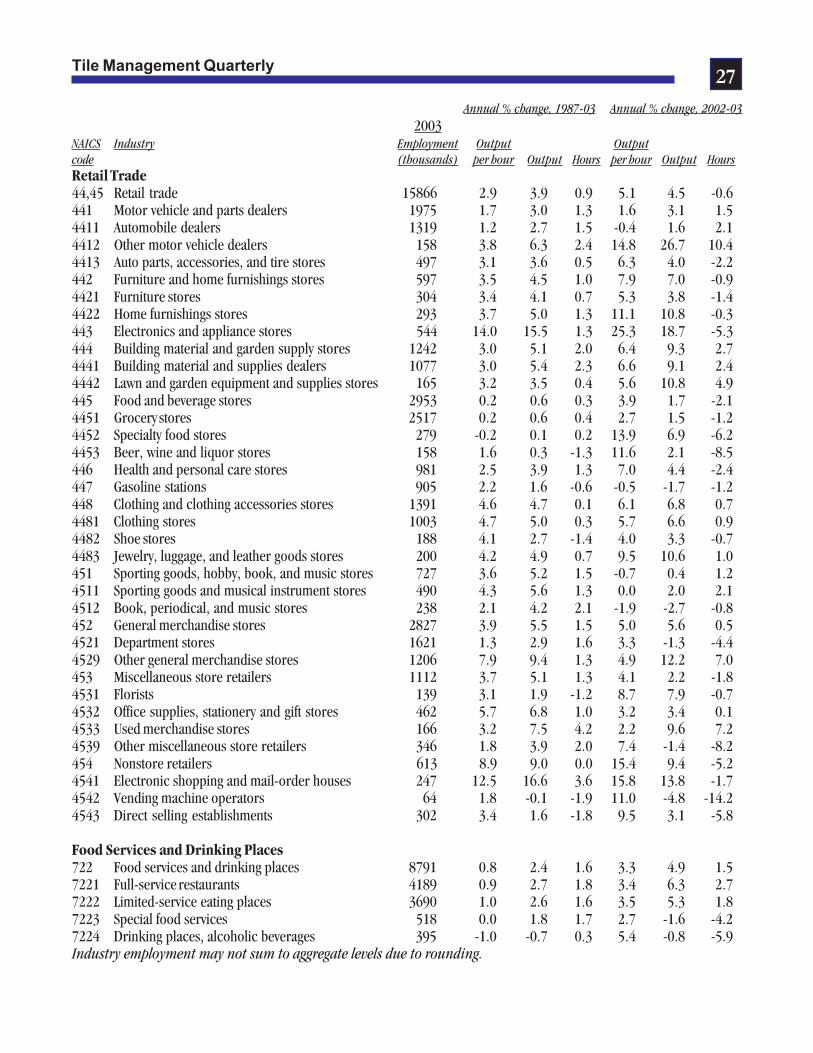

Output per hour increased in all but1 of the 27 retail trade industries from1987 to 2003. Labor productivity rose ata rapid 14.0 percent per year, on average,in electronics and appliance stores(NAICS 443) and 12.5 percent inelectronic shopping and mail orderhouses (NAICS 4541). Output increasedin 26 of the 27 retail industries, whilehours increased in 21 industries. Amongthe six largest retail industries, other

general merchandise stores (NAICS4529) had the greatest averageproductivity gains between 1987 and2003, 7.9 percent per year on average,followed by clothing stores, where outputper hour increased 4.7 percent per year.

All three of the food servicesindustries had average annual growth inlabor productivity of 1.0 percent or less.Labor productivity in drinking placesdeclined 1.0 percent per year from 1987to 2003, as output declined 0.7 percentper year and hours increased 0.3 percent.

Continued from page 25

Tile Management Quarterly27

Annual % change, 1987-03 Annual % change, 2002-032003

NAICS Industry Employment Output Outputcode (thousands) per hour Output Hours per hour Output HoursRetail Trade44,45 Retail trade 15866 2.9 3.9 0.9 5.1 4.5 -0.6441 Motor vehicle and parts dealers 1975 1.7 3.0 1.3 1.6 3.1 1.54411 Automobile dealers 1319 1.2 2.7 1.5 -0.4 1.6 2.14412 Other motor vehicle dealers 158 3.8 6.3 2.4 14.8 26.7 10.44413 Auto parts, accessories, and tire stores 497 3.1 3.6 0.5 6.3 4.0 -2.2442 Furniture and home furnishings stores 597 3.5 4.5 1.0 7.9 7.0 -0.94421 Furniture stores 304 3.4 4.1 0.7 5.3 3.8 -1.44422 Home furnishings stores 293 3.7 5.0 1.3 11.1 10.8 -0.3443 Electronics and appliance stores 544 14.0 15.5 1.3 25.3 18.7 -5.3444 Building material and garden supply stores 1242 3.0 5.1 2.0 6.4 9.3 2.74441 Building material and supplies dealers 1077 3.0 5.4 2.3 6.6 9.1 2.44442 Lawn and garden equipment and supplies stores 165 3.2 3.5 0.4 5.6 10.8 4.9445 Food and beverage stores 2953 0.2 0.6 0.3 3.9 1.7 -2.14451 Grocery stores 2517 0.2 0.6 0.4 2.7 1.5 -1.24452 Specialty food stores 279 -0.2 0.1 0.2 13.9 6.9 -6.24453 Beer, wine and liquor stores 158 1.6 0.3 -1.3 11.6 2.1 -8.5446 Health and personal care stores 981 2.5 3.9 1.3 7.0 4.4 -2.4447 Gasoline stations 905 2.2 1.6 -0.6 -0.5 -1.7 -1.2448 Clothing and clothing accessories stores 1391 4.6 4.7 0.1 6.1 6.8 0.74481 Clothing stores 1003 4.7 5.0 0.3 5.7 6.6 0.94482 Shoe stores 188 4.1 2.7 -1.4 4.0 3.3 -0.74483 Jewelry, luggage, and leather goods stores 200 4.2 4.9 0.7 9.5 10.6 1.0451 Sporting goods, hobby, book, and music stores 727 3.6 5.2 1.5 -0.7 0.4 1.24511 Sporting goods and musical instrument stores 490 4.3 5.6 1.3 0.0 2.0 2.14512 Book, periodical, and music stores 238 2.1 4.2 2.1 -1.9 -2.7 -0.8452 General merchandise stores 2827 3.9 5.5 1.5 5.0 5.6 0.54521 Department stores 1621 1.3 2.9 1.6 3.3 -1.3 -4.44529 Other general merchandise stores 1206 7.9 9.4 1.3 4.9 12.2 7.0453 Miscellaneous store retailers 1112 3.7 5.1 1.3 4.1 2.2 -1.84531 Florists 139 3.1 1.9 -1.2 8.7 7.9 -0.74532 Office supplies, stationery and gift stores 462 5.7 6.8 1.0 3.2 3.4 0.14533 Used merchandise stores 166 3.2 7.5 4.2 2.2 9.6 7.24539 Other miscellaneous store retailers 346 1.8 3.9 2.0 7.4 -1.4 -8.2454 Nonstore retailers 613 8.9 9.0 0.0 15.4 9.4 -5.24541 Electronic shopping and mail-order houses 247 12.5 16.6 3.6 15.8 13.8 -1.74542 Vending machine operators 64 1.8 -0.1 -1.9 11.0 -4.8 -14.24543 Direct selling establishments 302 3.4 1.6 -1.8 9.5 3.1 -5.8

Food Services and Drinking Places722 Food services and drinking places 8791 0.8 2.4 1.6 3.3 4.9 1.57221 Full-service restaurants 4189 0.9 2.7 1.8 3.4 6.3 2.77222 Limited-service eating places 3690 1.0 2.6 1.6 3.5 5.3 1.87223 Special food services 518 0.0 1.8 1.7 2.7 -1.6 -4.27224 Drinking places, alcoholic beverages 395 -1.0 -0.7 0.3 5.4 -0.8 -5.9Industry employment may not sum to aggregate levels due to rounding.

Tile Management Quarterly28

When I was a new business owner Iattended a management seminar, thespeaker said something that I have neverforgotten. “Your business is as good asyour worst employee.” What a soberingthought.

Paul Harvey said: “For a company’sadvertising strategy to work, it has to behandled not only corporately but alsoindividually.” Haven’t you ever walkedinto a hotel and felt like saying to thedesk clerk “Haven’t you seen yourcommercials, you’re supposed to benice to me” then walked into therestaurant and felt like deducting 15%for putting up with the lousy service?

I was parked in the Union SquareGarage in San Francisco, I asked theyoung man at the counter if I could havea token to use for the ladies room, hesaid “we are out”, I said “that’s not verygood customer service”, and thenstaggered, cross legging to my car. Acouple of months later, same garage,different young man, I was about to givethem $16.00 of my hard earned cash, Isaid “could I have a token for he ladiesroom please?” He said “we are out, butfollow me”, we walked a few yards to theladies room, he turned a lever and allthe tokens fell out, he gave one to meand took the rest back to the till for thenext customers. Can you imagine thefirst young man would not give me goodservice because he would have had towalk just a few steps?

Perhaps that young man was not aslucky as I was to be brought up in an

Everyone Represents YourCompanyPatricia Fripp, CSP, CPAE

entrepreneurial environment, that meanshis manager or supervisor should lethim know exactly what is expected.