Embed Size (px)

Citation preview

Three Essays in International Finance andMacroeconomics

Thèse

Simplice Aimé Nono

Doctorat en économiquePhilosophiæ doctor (Ph.D.)

Québec, Canada

© Simplice Aimé Nono, 2017

Three Essays in International Finance andMacroeconomics

Thèse

Simplice Aimé Nono

Sous la direction de:

Kévin Moran, directeur de recherche

Résumé

Cette thèse examine l’effet de l’information sur la prévision macroéconomique. De façon spéci-fique, l’emphase est d’abord mise sur l’impact des frictions d’information en économie ouvertesur la prévision du taux de change bilatéral et ensuite sur le rôle de l’information issue desdonnées d’enquêtes de conjoncture dans la prévision de l’activité économique réelle. Issu duparadigme de la nouvelle macroéconomie ouverte (NOEM), le premier essai intègre des fric-tions d’informations et des rigidités nominales dans un modèle d’équilibre général dynamiquestochastique (DSGE) en économie ouverte. Il présente ensuite une analyse comparative desrésultats de la prévision du taux de change obtenu en utilisant le modèle avec et sans cesfrictions d’information. Tandis que le premier essai développe un modèle macroéconomiquestructurel de type DSGE pour analyser l’effet de la transmission des choc en informationincomplète sur la dynamique du taux de change entre deux économies, le deuxième et troi-sième essais utilisent les modèles factorielles dynamiques avec ciblage pour mettre en exerguela contribution de l’information contenu dans les données d’enquêtes de confiance (soit auniveau de l’économie nationale que internationale) sur la prévision conjoncturelle de l’activitééconomique réelle.

« The Forward Premium Puzzle : a Learning-based Explanation » (Essai 1) est une contribu-tion à la littérature sur la prévision du taux de change. Cet essai a comme point de départ lerésultat théorique selon lequel lorsque les taux d’intérêt sont plus élevés localement qu’ils lesont à l’étranger, cela annonce une dépréciation future de la monnaie locale. Cependant, lesrésultats empiriques obtenus sont généralement en contradiction avec cette intuition et cettecontradiction a été baptisée l’énigme de la parité des taux d’intérêt non-couverte ou encore «énigme de la prime des contrats à terme ». L’essai propose une explication de cette énigmebasée sur le mécanisme d’apprentissage des agents économiques. Sous l’hypothèse que leschocs de politique monétaire et de technologie peuvent être soit de type persistant et soit detype transitoire, le problème d’information survient lorsque les agents économiques ne sont pasen mesure d’observer directement le type de choc et doivent plutôt utiliser un mécanisme defiltrage de l’information pour inférer la nature du choc. Nous simulons le modèle en présencede ces frictions informationnelles, et ensuite en les éliminant, et nous vérifions si les donnéesartificielles générées par les simulations présentent les symptômes de l’énigme de la prime descontrats à terme. Notre explication à l’énigme est validée si et seulement si seules les données

iii

générées par le modèle avec les frictions informationnelles répliquent l’énigme.

« Using Confidence Data to Forecast the Canadian Business Cycle » (Essai 2) s’appuie surl’observation selon laquelle la confiance des agents économiques figure désormais parmi lesprincipaux indicateurs de la dynamique conjoncturelle. Cet essai analyse la qualité et laquantité d’information contenu dans les données d’enquêtes mesurant la confiance des agentséconomiques. A cet effet, il évalue la contribution des données de confiance dans la prévisiondes points de retournement (« turning points ») dans l’évolution de l’économie canadienne.Un cadre d’analyse avec des modèles de type probit à facteurs est spécifié et appliqué àun indicateur de l’état du cycle économique canadien produit par l’OCDE. Les variablesexplicatives comprennent toutes les données canadiennes disponibles sur la confiance des agents(qui proviennent de quatre enquêtes différentes) ainsi que diverses données macroéconomiqueset financières. Le modèle est estimé par le maximum de vraisemblance et les données deconfiance sont introduites dans les différents modèles sous la forme de variables individuelles,de moyennes simples (des « indices de confiance ») et de « facteurs de confiance » extraitsd’un ensemble de données plus grand dans lequel toutes les données de confiance disponiblesont été regroupées via la méthode des composantes principales,. Nos résultats indiquent que leplein potentiel des données sur la confiance pour la prévision des cycles économiques canadiensest obtenu lorsque toutes les données sont utilisées et que les modèles factoriels sont utilisés.

« Forecasting with Many Predictors: How Useful are National and International ConfidenceData? » (Essai 3) est basé sur le fait que dans un environnement où les sources de données sontmultiples, l’information est susceptible de devenir redondante d’une variable à l’autre et qu’unesélection serrée devient nécessaire pour identifier les principaux déterminants de la prévision.Cet essai analyse les conditions selon lesquelles les données de confiance constituent un desdéterminants majeurs de la prévision de l’activité économique dans un tel environnement.La modélisation factorielle dynamique ciblée est utilisé pour évaluer le pouvoir prédictif desdonnées des enquêtes nationales et internationales sur la confiance dans la prévision de lacroissance du PIB Canadien. Nous considérons les données d’enquêtes de confiance désagrégéesdans un environnement riche en données (c’est-à-dire contenant plus d’un millier de sériesmacro-économiques et financières) et évaluons leur contenu informatif au-delà de celui contenudans les variables macroéconomiques et financières. De bout en bout, nous étudions le pouvoirprédictif des données de confiance en produisant des prévisions du PIB avec des modèlesà facteurs dynamiques où les facteurs sont dérivés avec et sans données de confiance. Lesrésultats montrent que la capacité de prévision est améliorée de façon robuste lorsqu’on prenden compte l’information contenue dans les données nationales sur la confiance. En revanche,les données internationales de confiance ne sont utiles que lorsqu’elles sont combinées dans lemême ensemble avec celles issues des enquêtes nationales. En outre, les gains les plus pertinentsdans l’amelioration des prévisions sont obtenus à court terme (jusqu’à trois trimestres enavant).

iv

Abstract

This thesis examines the effect of information on macroeconomic forecasting. Specifically,the emphasis is firstly on the impact of information frictions in open economy in forecast-ing the bilateral exchange rate and then on the role of information from confidence surveydata in forecasting real economic activity. Based on the new open-economy macroeconomicsparadigm (NOEM), the first chapter incorporates information frictions and nominal rigiditiesin a stochastic dynamic general equilibrium (DSGE) model in open economy. Then, it presentsa comparative analysis of the results of the exchange rate forecast obtained using the modelwith and without these information frictions. While the first chapter develops a structuralmacroeconomic model of DSGE type to analyze the effect of shock transmission in incompleteinformation on exchange rate dynamics between two economies, the second and third chaptersuse static and dynamic factor models with targeting to highlight the contribution of informa-tion contained in confidence-based survey data (either at the national or international level)in forecasting real economic activity.

The first chapter is entitled The Forward Premium Puzzle: a Learning-based Explanation andis a contribution to the exchange rate forecasting literature. When interest rates are higher inone’s home country than abroad, economic intuition suggests this signals the home currencywill depreciate in the future. However, empirical evidence has been found to be at odds withthis intuition: this is the "forward premium puzzle." I propose a learning-based explanationfor this puzzle. To do so, I embed an information problem in a two-country open-economymodel with nominal rigidities. The information friction arises because economic agents do notdirectly observe whether shocks are transitory or permanent and must infer their nature usinga filtering mechanism each period. We simulate the model with and without this informationalfriction and test whether the generated artificial data exhibits the symptoms of the forwardpremium puzzle. Our leaning-based explanation is validated as only the data generated withthe active informational friction replicates the puzzle.

The second chapter uses dynamic factor models to highlight the contribution of the infor-mation contained in Canadian confidence survey data for forecasting the Canadian businesscycle: Using Confidence Data to Forecast the Canadian Business Cycle is based on the factthat confidence (or sentiment) is one key indicators of economic momentum. The chapter

v

assesses the contribution of confidence -or sentiment-data in predicting Canadian economicslowdowns. A probit framework is applied to an indicator on the status of the Canadianbusiness cycle produced by the OECD. Explanatory variables include all available Canadiandata on sentiment (which arise from four different surveys) as well as various macroeconomicand financial data. Sentiment data are introduced either as individual variables, as simpleaverages (such as confidence indices) and as confidence factors extracted, via principal com-ponents’ decomposition, from a larger dataset in which all available sentiment data have beencollected. Our findings indicate that the full potential of sentiment data for forecasting futurebusiness cycles in Canada is attained when all data are used through the use of factor models.

The third chapter uses dynamic factor models to highlight the contribution of the informationcontained in confidence survey data (either in Canadian or International surveys) for forecast-ing the Canadian economic activity. This chapter entitled Forecasting with Many Predictors:How Useful are National and International Confidence Data? is based on the fact that ina data-rich environment, information may become redundant so that a selection of forecast-ing determinants based on the quality of information is required. The chapter investigateswhether in such an environment; confidence data can constitute a major determinant of eco-nomic activity forecasting. To do so, a targeted dynamic factor model is used to evaluate theperformance of national and international confidence survey data in predicting Canadian GDPgrowth. We first examine the relationship between Canadian GDP and confidence and assesswhether Canadian and international (US) improve forecasting accuracy after controlling forclassical predictors. We next consider dis-aggregated confidence survey data in a data-richenvironment (i.e. containing more than a thousand macroeconomic and financial series) andassess their information content in excess of that contained in macroeconomic and financialvariables. Throughout, we investigate the predictive power of confidence data by producingGDP forecasts with dynamic factor models where the factors are derived with and withoutconfidence data. We find that forecasting ability is consistently improved by considering infor-mation from national confidence data; by contrast, the international counterpart are helpfulonly when combined in the same set with national confidence. Moreover most relevant gainsin the forecast performance come in short-horizon (up to three-quarters-ahead).

vi

Contents

Résumé iii

Abstract v

Contents viii

List of Tables xi

List of Figures xii

List of Abbreviations xiii

Remerciements xviii

Avant-propos xxii

1 The Forward Premium Puzzle: a Learning-based Explanation 11.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.2 Review of literature . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.3 The model economy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.3.1 Preferences . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51.3.2 Assets market and budget constraint . . . . . . . . . . . . . . . . . . 61.3.3 Firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.3.3.1 Domestic final goods . . . . . . . . . . . . . . . . . . . . . . 71.3.3.2 Domestic composite goods . . . . . . . . . . . . . . . . . . 71.3.3.3 Domestic basic goods . . . . . . . . . . . . . . . . . . . . . 8

1.3.4 Monetary policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91.4 Information frictions and filtering mechanism . . . . . . . . . . . . . . . . . 9

1.4.1 Technology shocks . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101.4.2 Monetary policy shocks . . . . . . . . . . . . . . . . . . . . . . . . . 101.4.3 Incomplete information and Kalman filter . . . . . . . . . . . . . . . 11

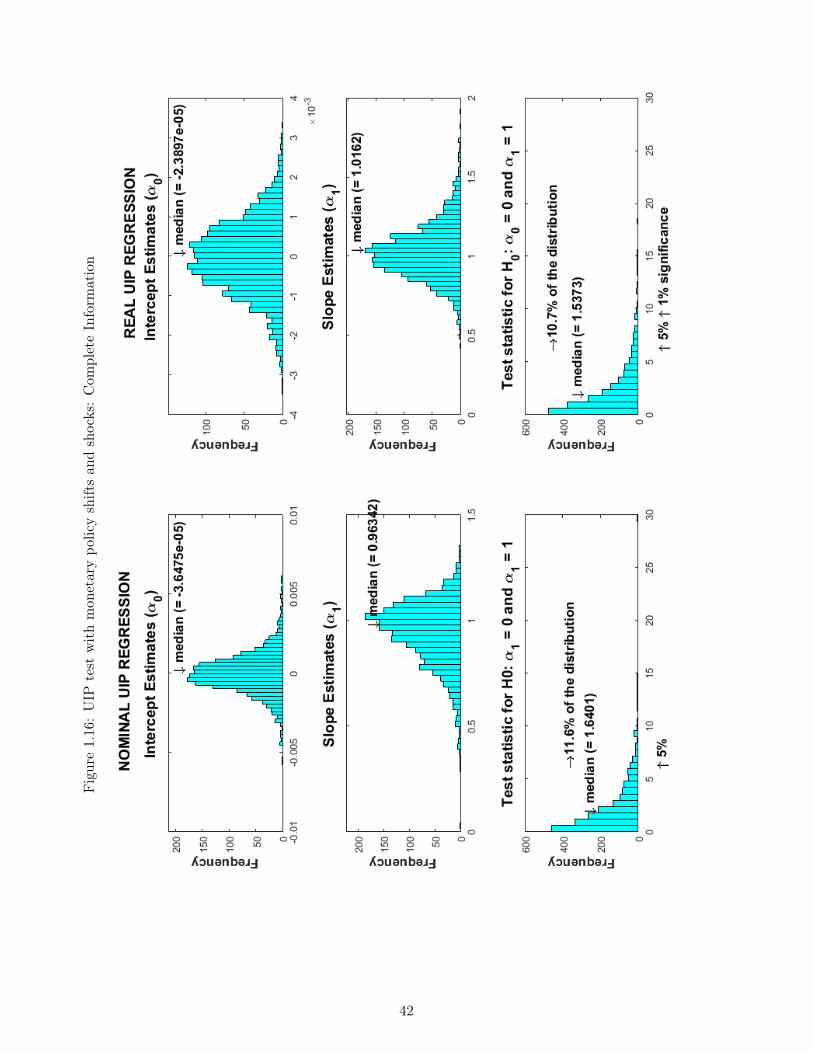

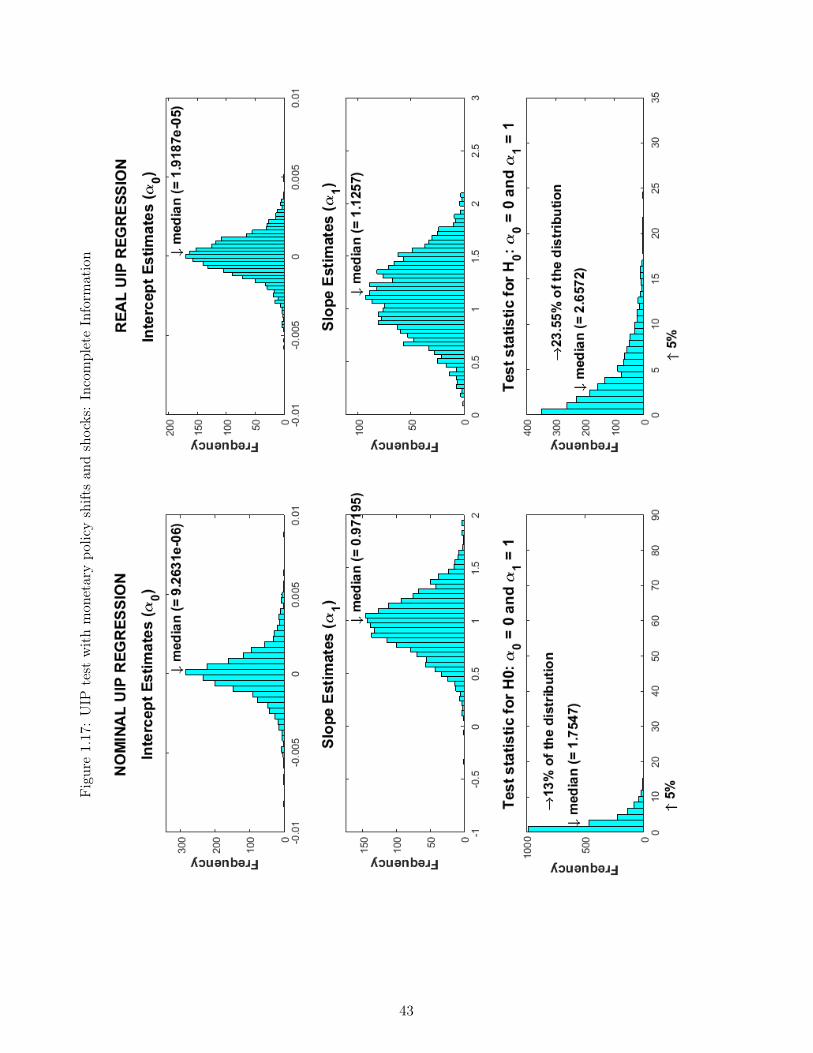

1.5 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121.5.1 Parameter calibration . . . . . . . . . . . . . . . . . . . . . . . . . . 121.5.2 Impulse response functions: Complete information . . . . . . . . . . 131.5.3 Impulse response functions: Complete versus incomplete information 171.5.4 Unbiasedness regression and the UIP . . . . . . . . . . . . . . . . . 19

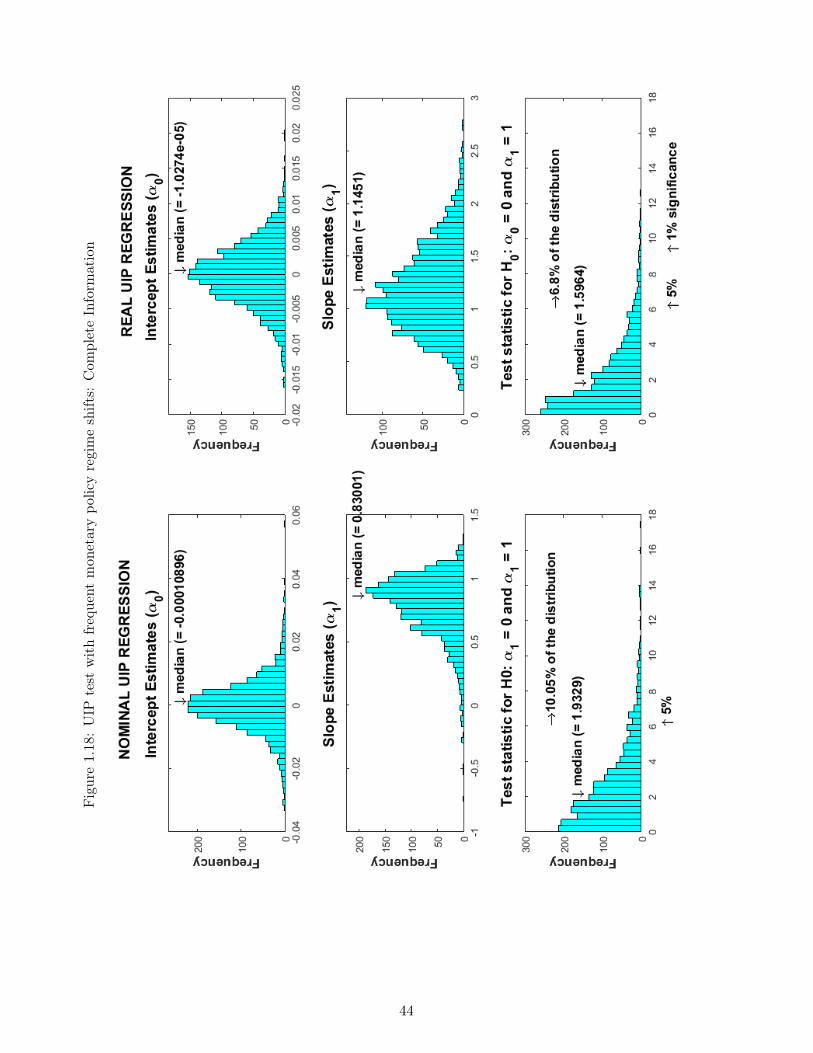

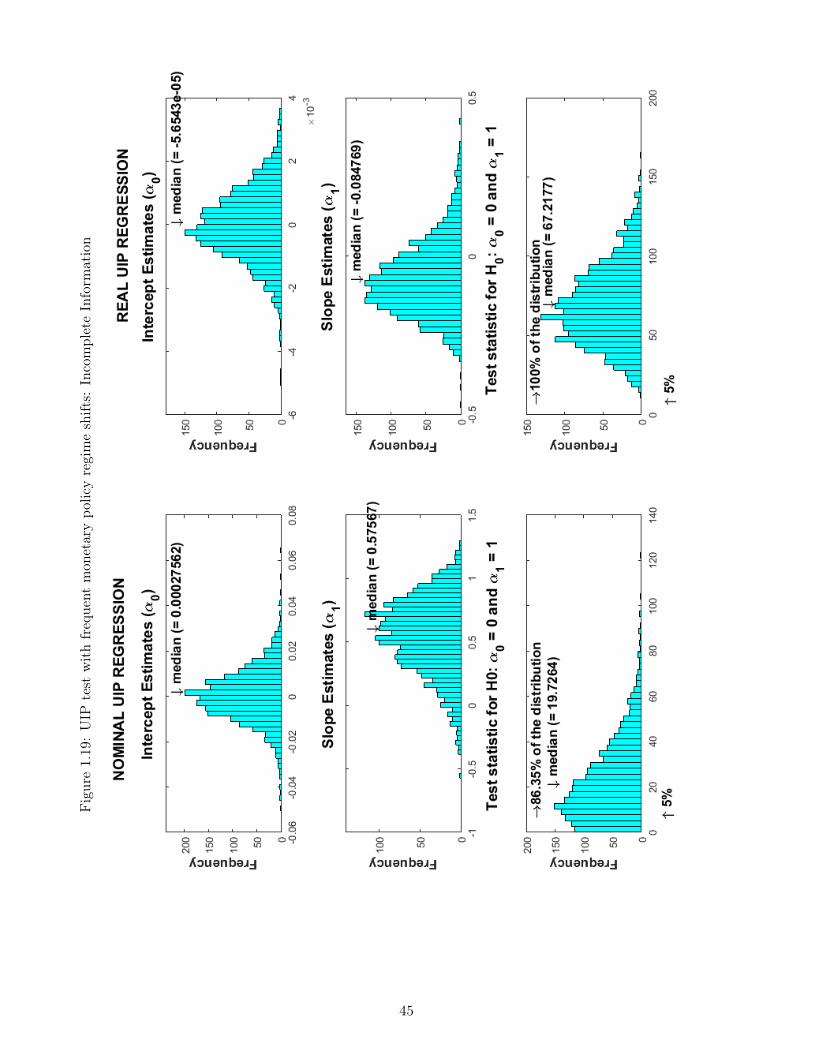

1.5.4.1 UIP with monetary policy regime shifts . . . . . . . . . . . 20

viii

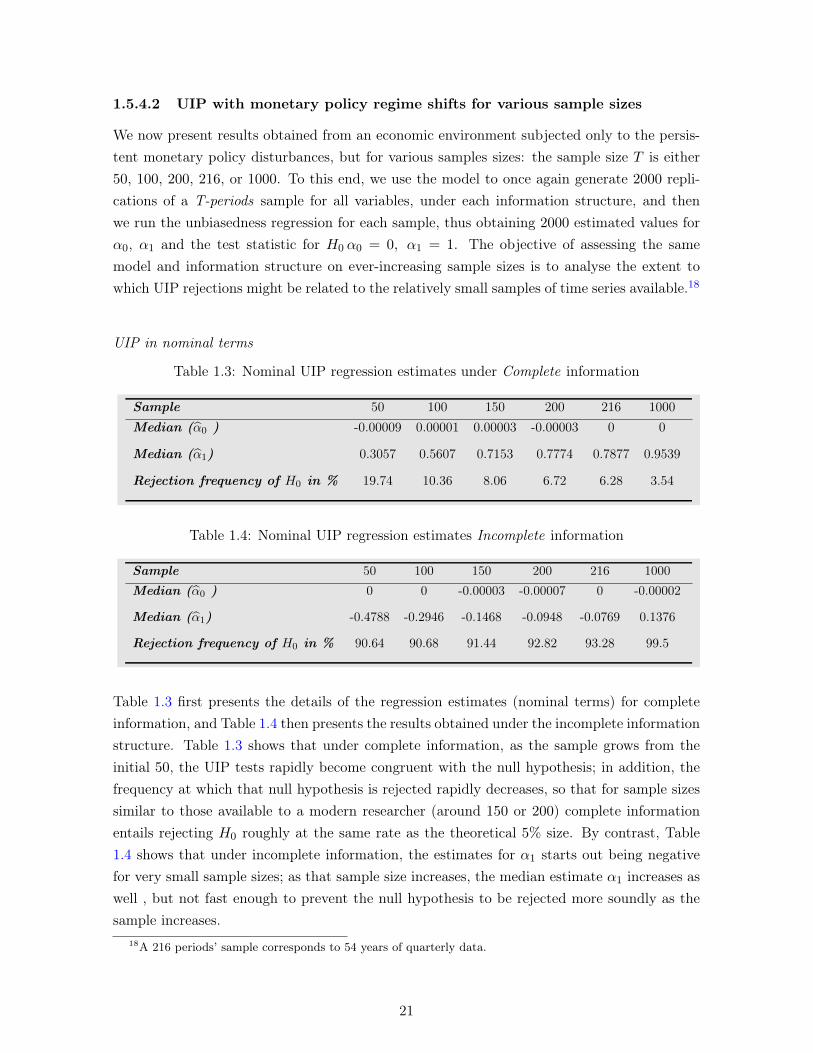

1.5.4.2 UIP with monetary policy regime shifts for various samplesizes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

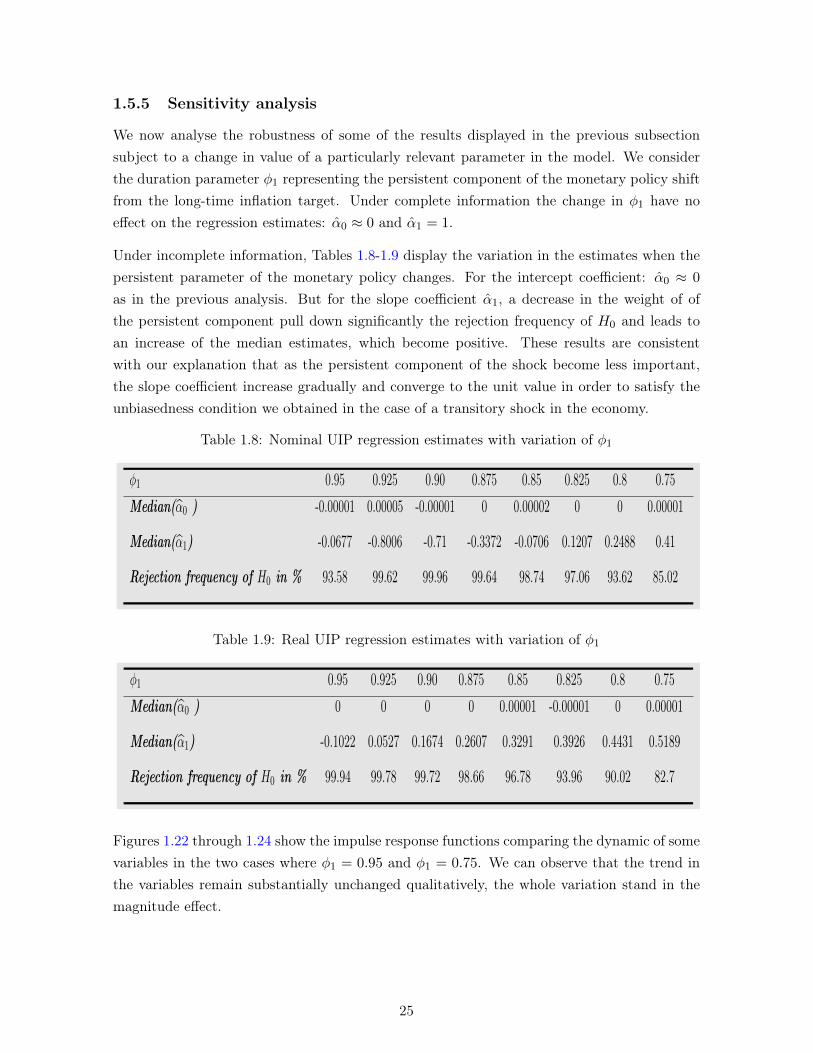

1.5.4.3 UIP with other shocks . . . . . . . . . . . . . . . . . . . . . 231.5.5 Sensitivity analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

1.6 Concluding Remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

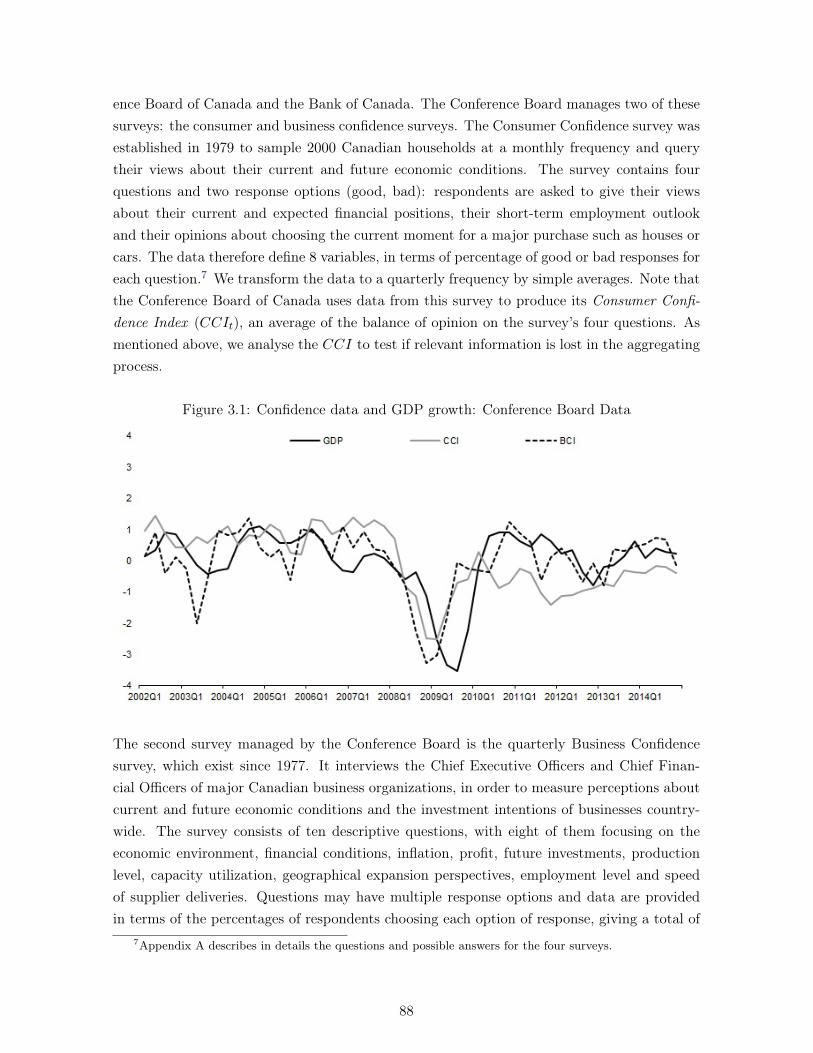

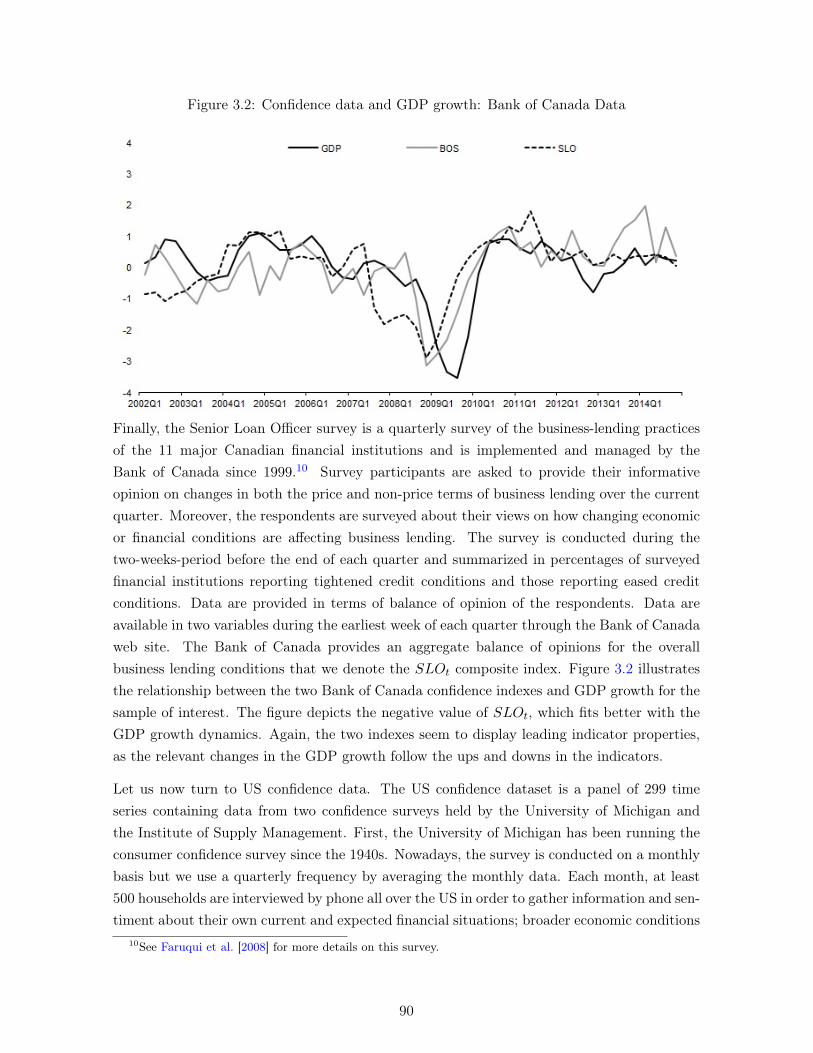

2 Using Confidence Data to Forecast the Canadian Business Cycle 522.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 532.2 Related Literature . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 542.3 Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 572.4 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

2.4.1 Canadian Business Cycles . . . . . . . . . . . . . . . . . . . . . . . . 582.4.2 Explanatory Variables . . . . . . . . . . . . . . . . . . . . . . . . . . 60

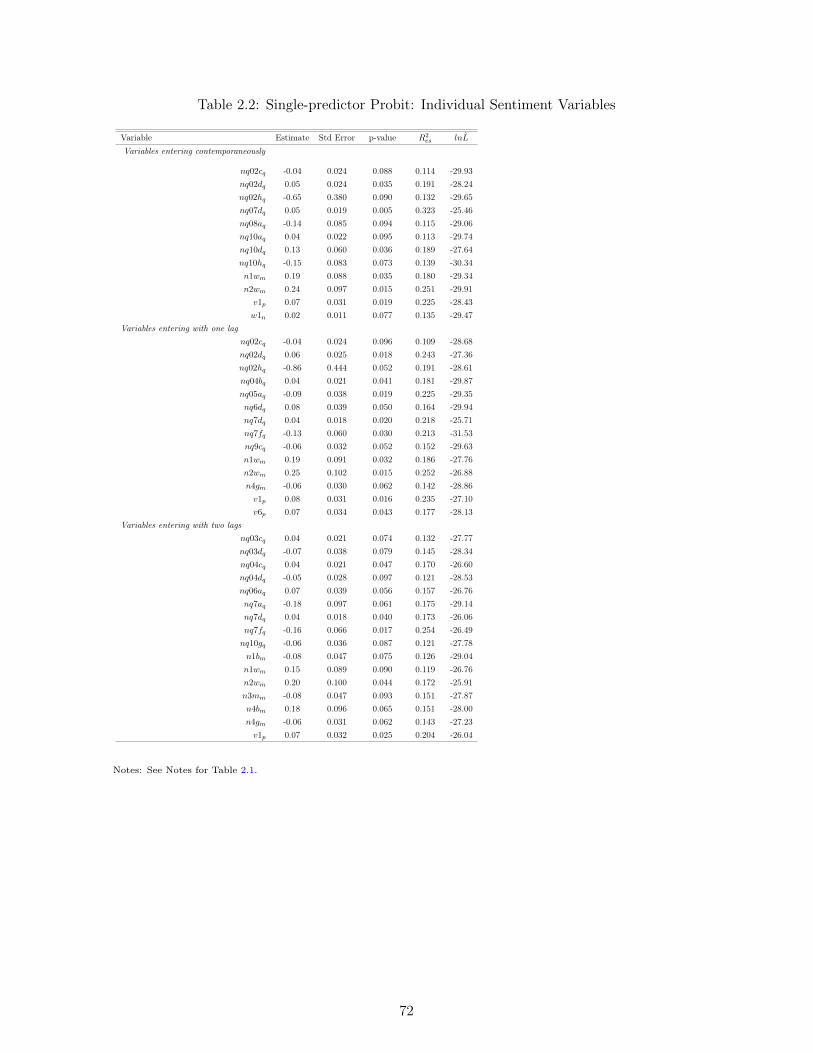

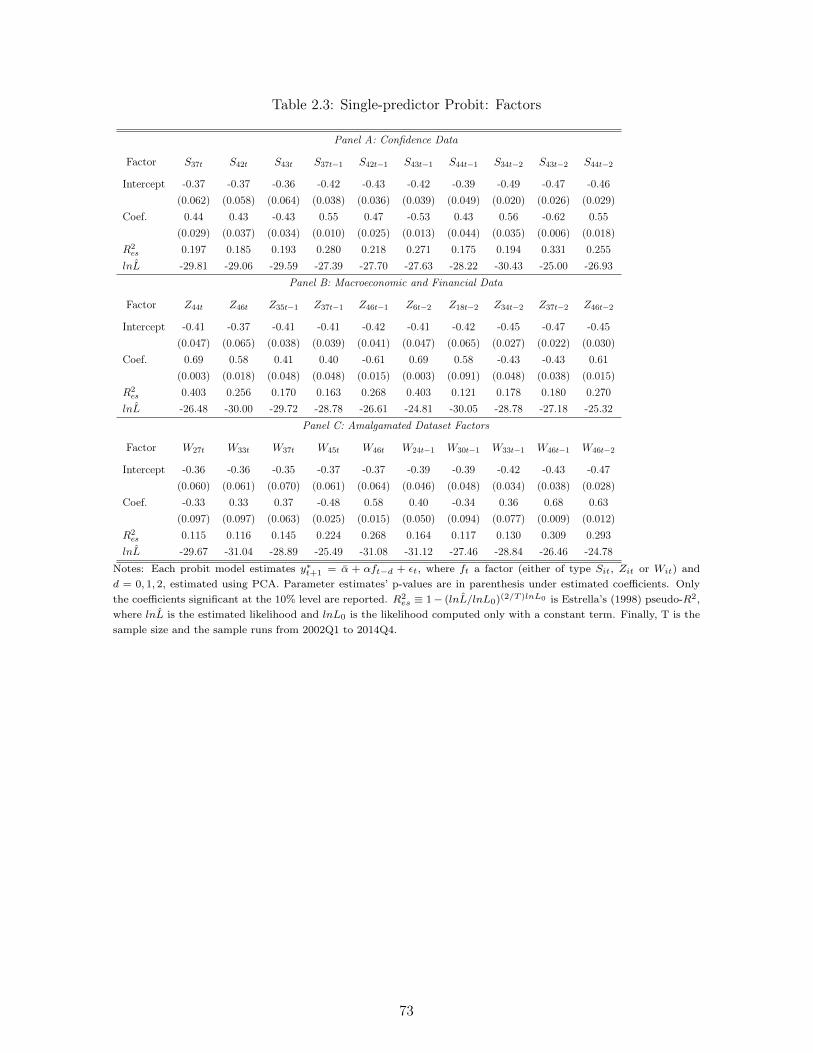

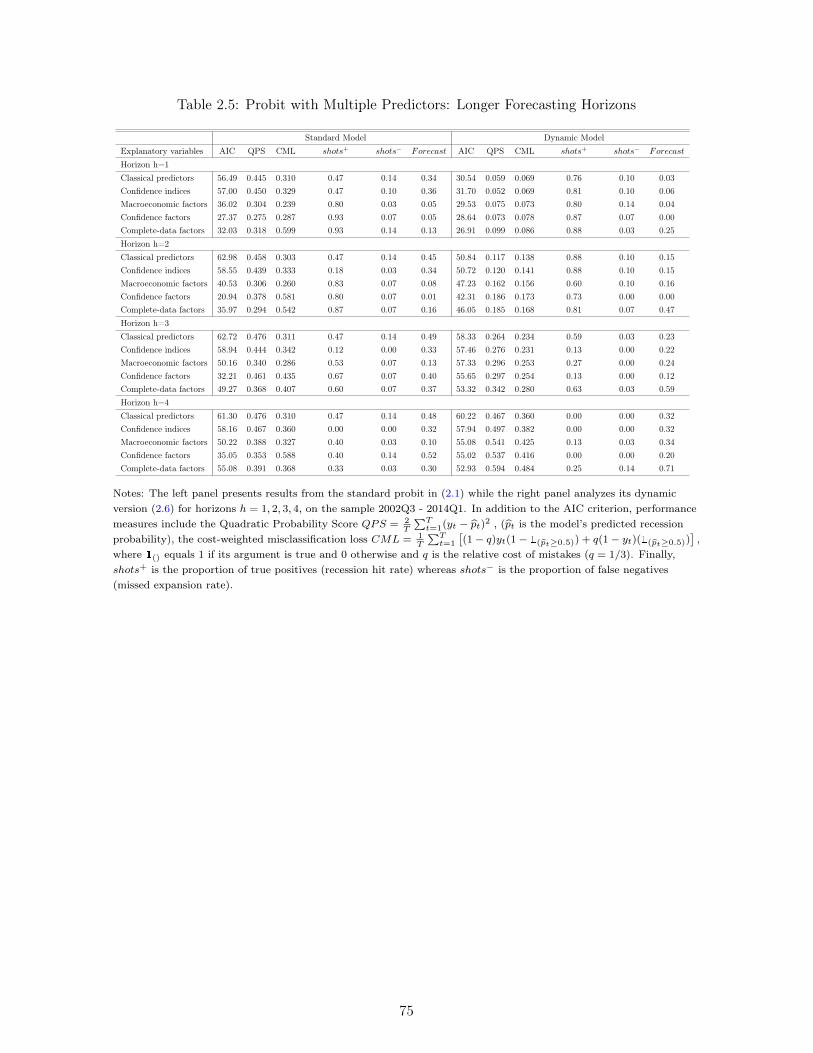

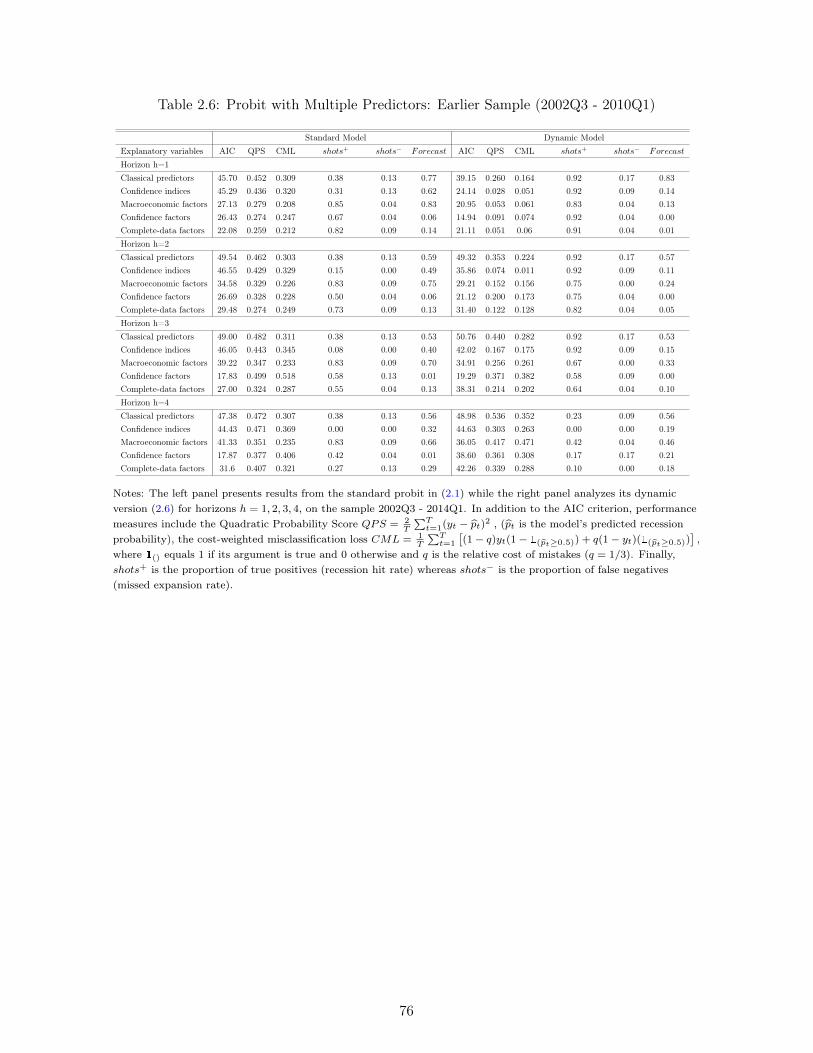

2.5 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 622.5.1 Single-predictor models . . . . . . . . . . . . . . . . . . . . . . . . . 622.5.2 Multiple-predictor models . . . . . . . . . . . . . . . . . . . . . . . . 652.5.3 Robustness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

2.6 Concluding Remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

3 Forecasting with Many Predictors: How Useful are National and In-ternational Confidence Data? 793.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 803.2 Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

3.2.1 Forecasting Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . 823.2.2 Factor Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 833.2.3 Factor and Predictor targeting . . . . . . . . . . . . . . . . . . . . . 843.2.4 Forecast Evaluation Measures . . . . . . . . . . . . . . . . . . . . . . 86

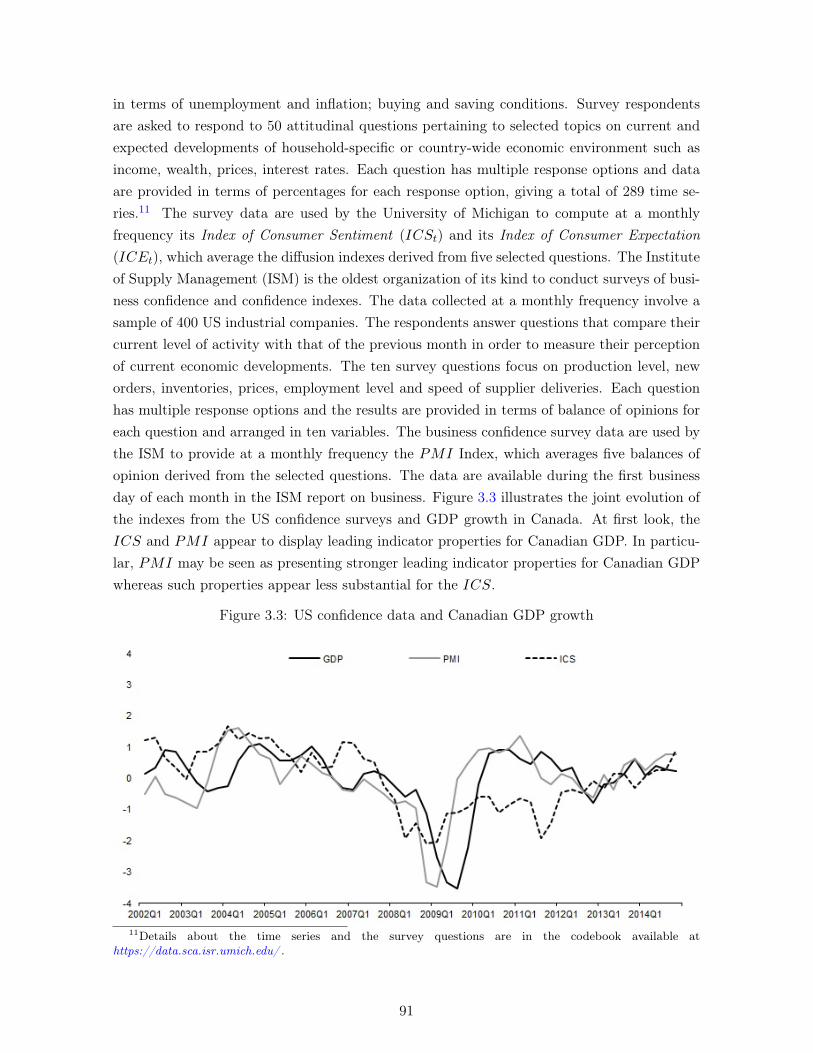

3.3 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 873.3.1 Confidence Variables . . . . . . . . . . . . . . . . . . . . . . . . . . . 873.3.2 Macroeconomic and Financial variables . . . . . . . . . . . . . . . . 92

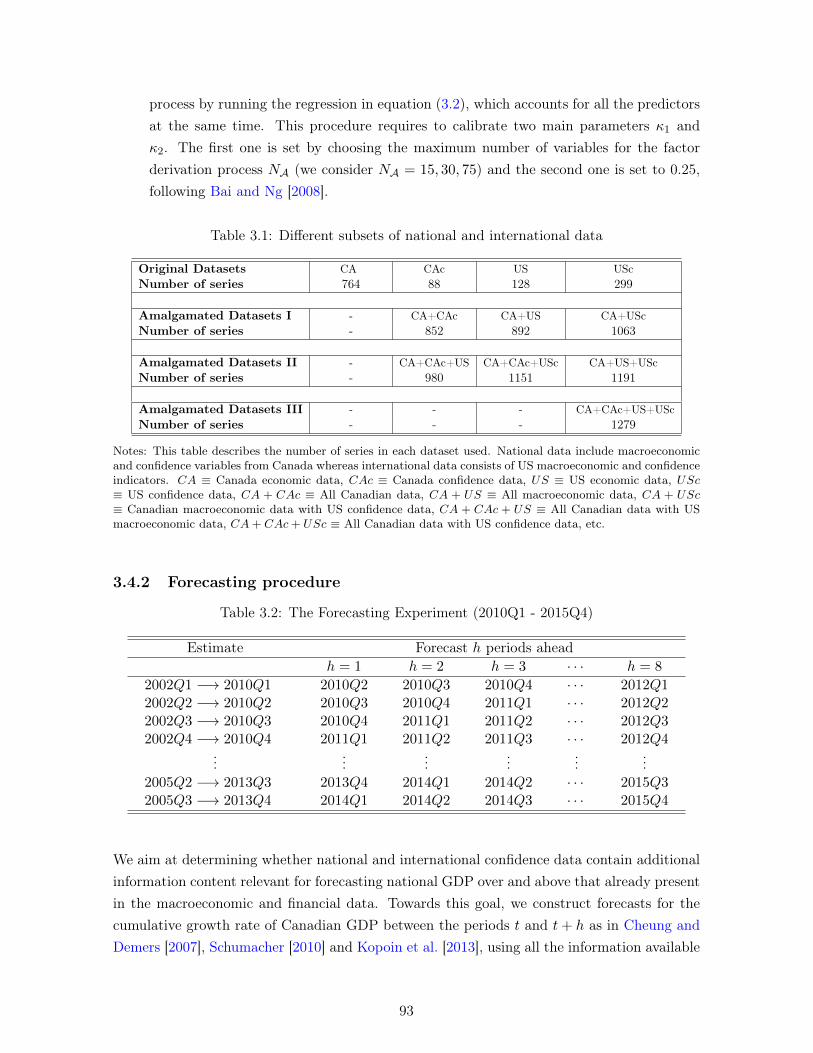

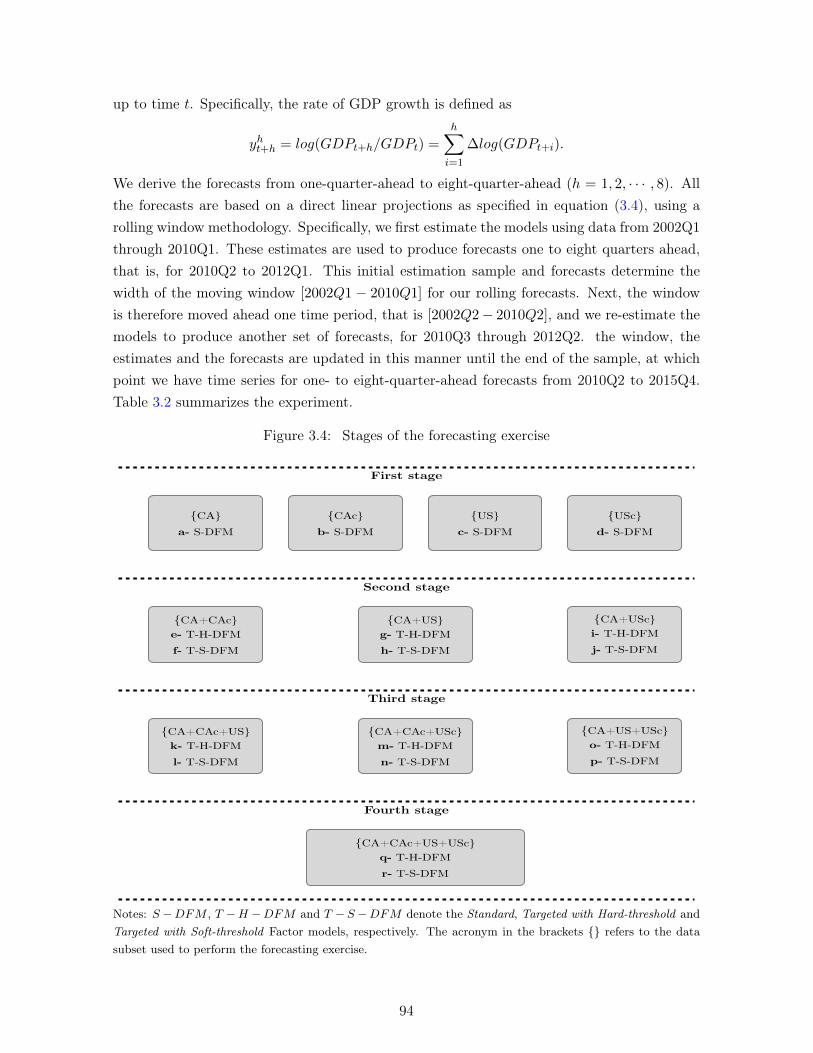

3.4 Empirical Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 923.4.1 Targeting procedure . . . . . . . . . . . . . . . . . . . . . . . . . . . 923.4.2 Forecasting procedure . . . . . . . . . . . . . . . . . . . . . . . . . . 933.4.3 Comparison exercise . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

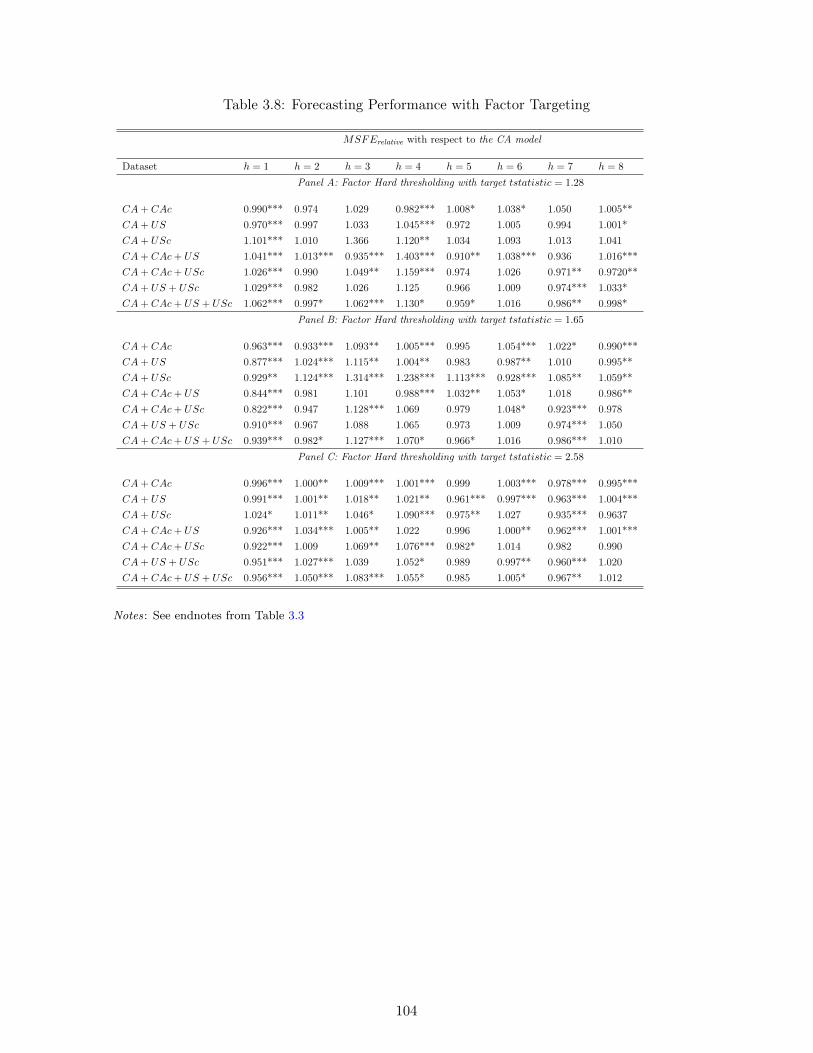

3.5 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 953.5.1 Forecasting Performance with no Targeting . . . . . . . . . . . . . . 953.5.2 Forecasting Performance with Predictor Hard Thresholding . . . . . 973.5.3 Forecasting Performance with Predictor Soft Thresholding . . . . . 983.5.4 Forecasting Performance with Factor Targeting . . . . . . . . . . . . 98

3.6 Concluding Remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99

Conclusion 106

A Survey Data on Sentiment 109A.1 Conference Board Consumer Confidence survey . . . . . . . . . . . . . . . . 109A.2 Conference Board Business Confidence Survey . . . . . . . . . . . . . . . . . 110A.3 Bank of Canada Business Outlook Survey . . . . . . . . . . . . . . . . . . . 113A.4 Bank of Canada Senior Loan Officer Survey . . . . . . . . . . . . . . . . . . 115

ix

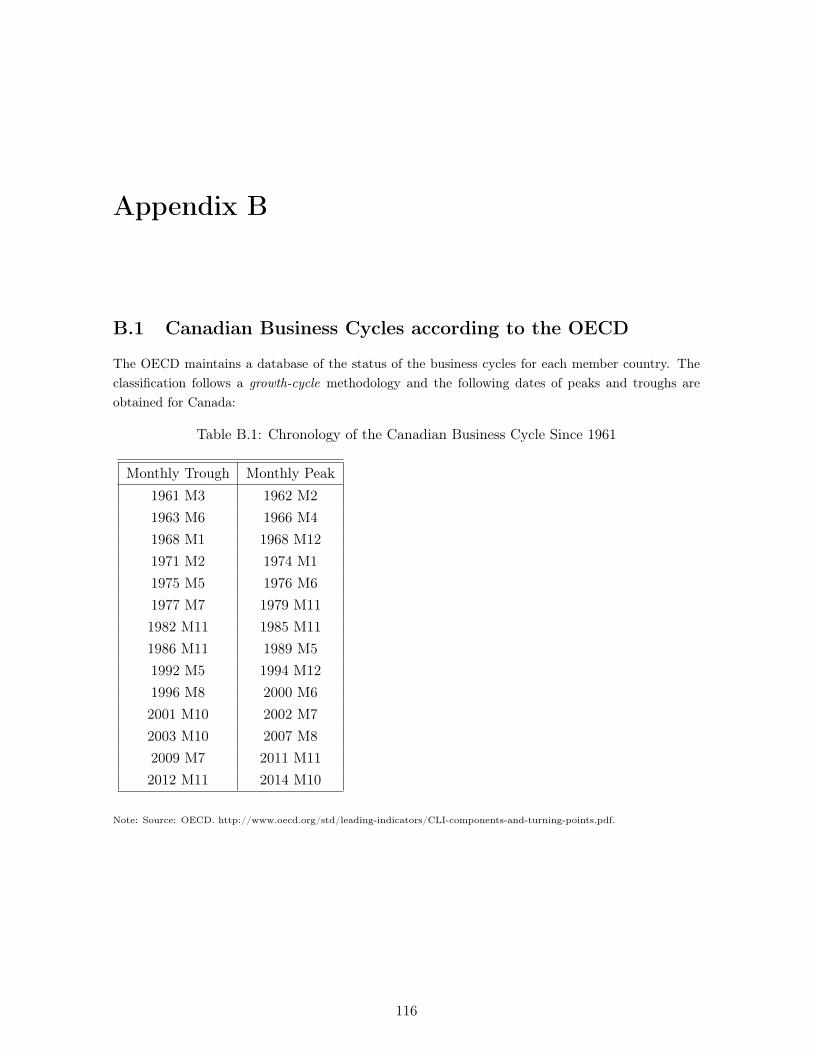

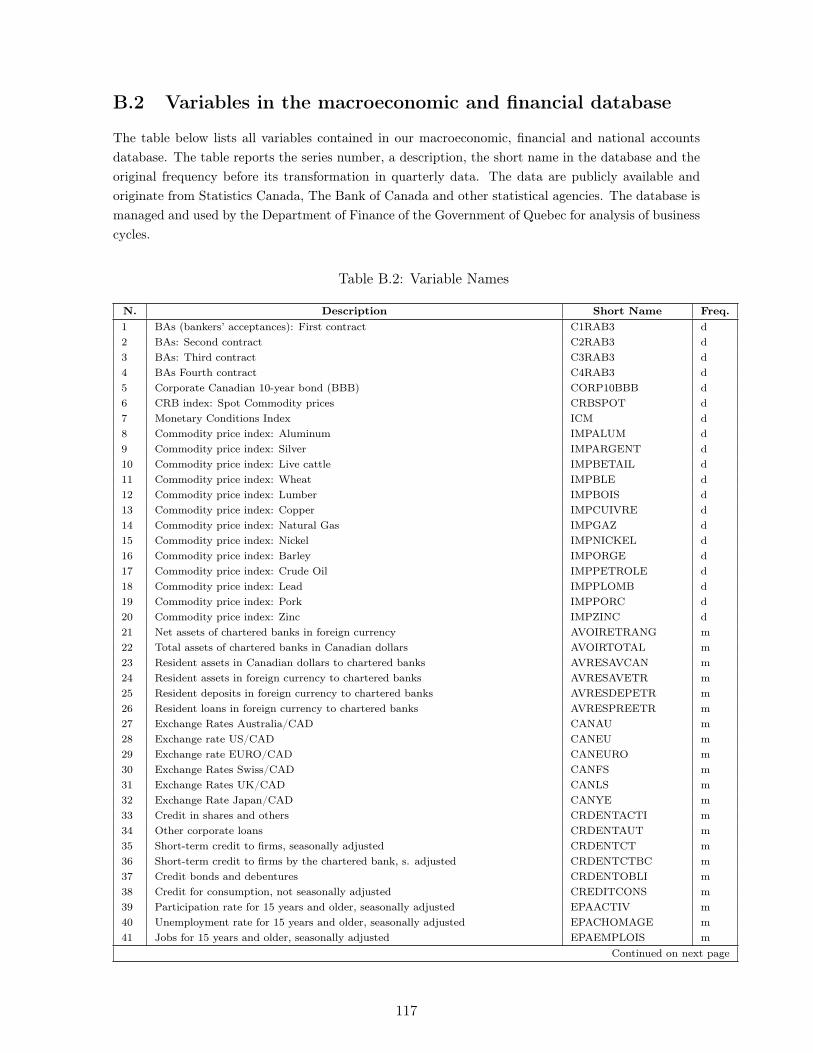

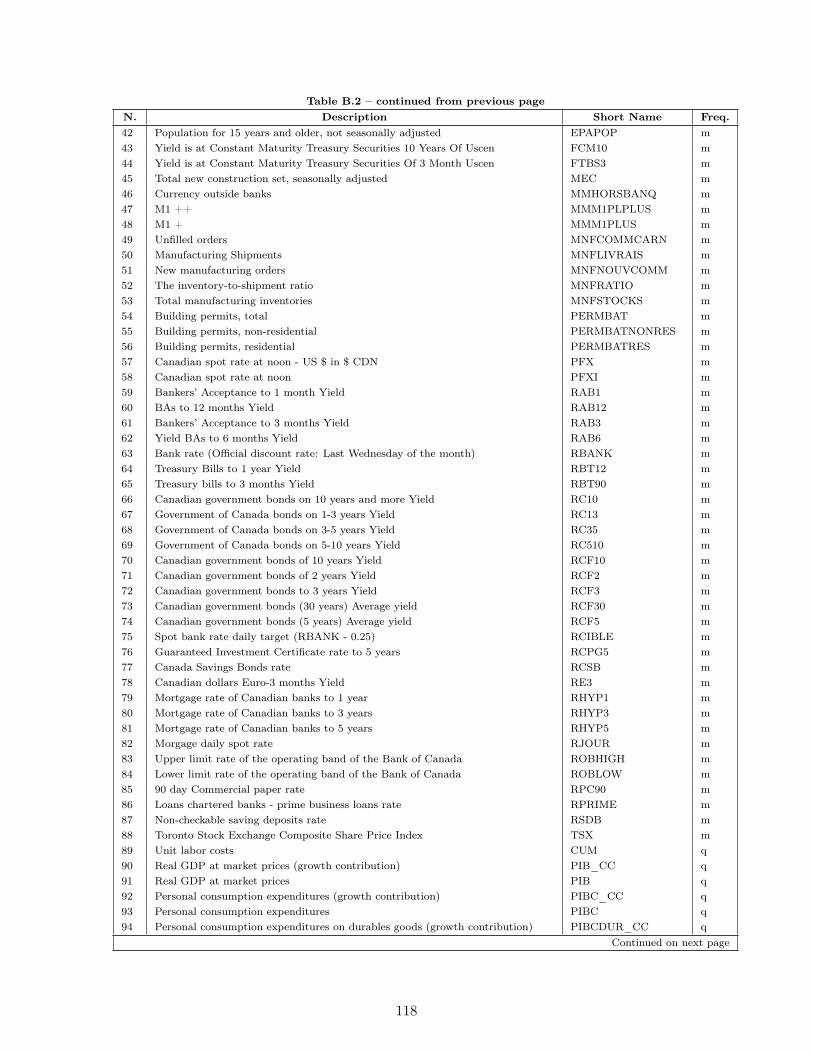

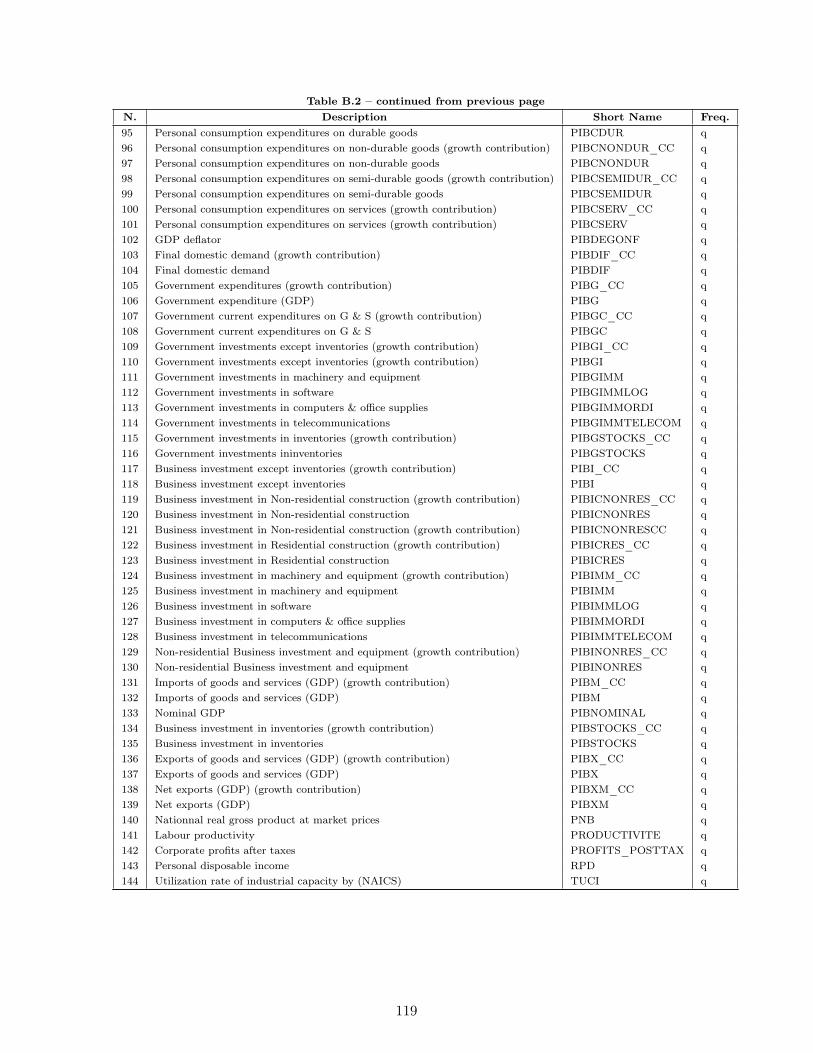

B 116B.1 Canadian Business Cycles according to the OECD . . . . . . . . . . . . . . 116B.2 Variables in the macroeconomic and financial database . . . . . . . . . . . . 117

Bibliography 121

x

List of Tables

1.1 Baseline estimates for the UIP regression under Complete information . . . . . 191.2 Baseline estimates for the UIP regression under Incomplete information . . . . 191.3 Nominal UIP regression estimates under Complete information . . . . . . . . . 211.4 Nominal UIP regression estimates Incomplete information . . . . . . . . . . . . 211.5 Real UIP regression estimates - Complete information . . . . . . . . . . . . . . 221.6 Real UIP regression estimates - Incomplete information . . . . . . . . . . . . . 221.7 Fisher effect test . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 231.8 Nominal UIP regression estimates with variation of φ1 . . . . . . . . . . . . . . 251.9 Real UIP regression estimates with variation of φ1 . . . . . . . . . . . . . . . . 25

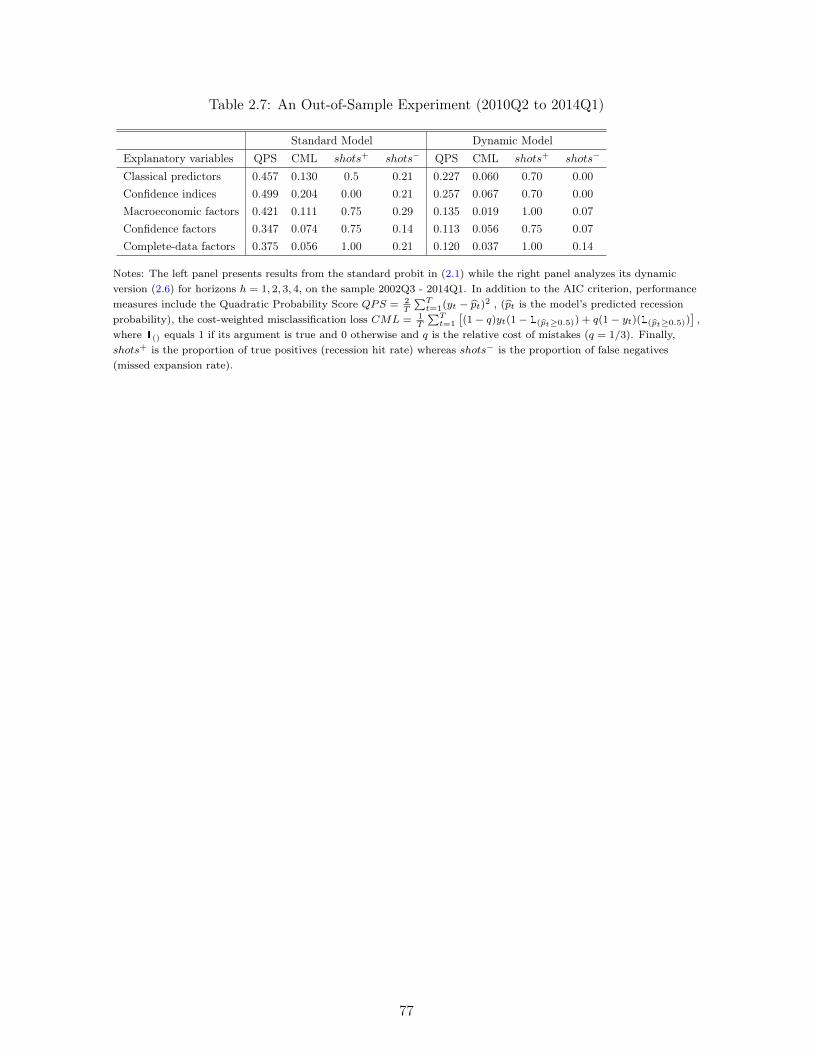

2.1 Single-predictor Probit: Classical predictors and Confidence indices . . . . . . . 712.2 Single-predictor Probit: Individual Sentiment Variables . . . . . . . . . . . . . 722.3 Single-predictor Probit: Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . 732.4 Probit with Multiple predictors: In-Sample Results . . . . . . . . . . . . . . . . 742.5 Probit with Multiple Predictors: Longer Forecasting Horizons . . . . . . . . . . 752.6 Probit with Multiple Predictors: Earlier Sample (2002Q3 - 2010Q1) . . . . . . 762.7 An Out-of-Sample Experiment (2010Q2 to 2014Q1) . . . . . . . . . . . . . . . . 77

3.1 Different subsets of national and international data . . . . . . . . . . . . . . . . 933.2 The Forecasting Experiment (2010Q1 - 2015Q4) . . . . . . . . . . . . . . . . . 933.3 Forecasting Performance with no targeting . . . . . . . . . . . . . . . . . . . . . 1003.4 Forecasting Performance with Targeting I: Hard-Thresholding with t? = 1.28 . 1013.5 Forecasting Performance with Targeting II: Hard-Thresholding with t? = 1.65 . 1013.6 Forecasting Performance with Targeting I: Hard-Thresholding with t? = 2.58 . 1023.7 Forecasting Performance with Predictor Soft-thresholding . . . . . . . . . . . . 1033.8 Forecasting Performance with Factor Targeting . . . . . . . . . . . . . . . . . . 104

B.1 Chronology of the Canadian Business Cycle Since 1961 . . . . . . . . . . . . . . 116B.2 Variable Names . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117

xi

List of Figures

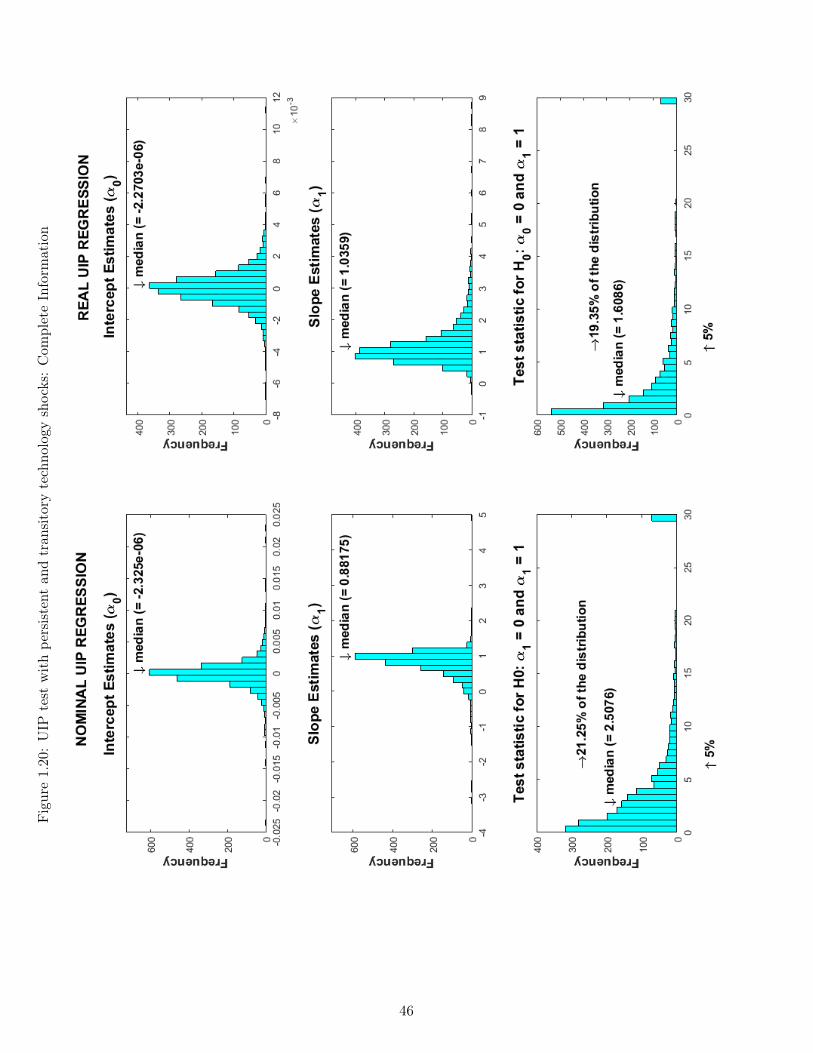

1.1 Responses to a transitory monetary policy shock I . . . . . . . . . . . . . . . . 271.2 Responses to a transitory monetary policy shock II . . . . . . . . . . . . . . . . 281.3 Responses to a transitory monetary policy shock III . . . . . . . . . . . . . . . 291.4 Responses to a persistent technological shock I . . . . . . . . . . . . . . . . . . 301.5 Responses to a persistent technological shock II . . . . . . . . . . . . . . . . . . 311.6 Responses to a persistent technological shock III . . . . . . . . . . . . . . . . . 321.7 Responses to a monetary policy shift I . . . . . . . . . . . . . . . . . . . . . . . 331.8 Responses to a monetary policy shift II . . . . . . . . . . . . . . . . . . . . . . 341.9 Responses to a monetary policy shift III . . . . . . . . . . . . . . . . . . . . . . 351.10 Monetary policy shift: Complete vs Incomplete Information I . . . . . . . . . . 361.11 Monetary policy shift: Complete vs Incomplete Information II . . . . . . . . . . 371.12 Monetary policy shift: Complete vs Incomplete Information III . . . . . . . . . 381.13 Monetary policy shift: Complete vs Incomplete Information IV . . . . . . . . . 391.14 UIP test with monetary policy regime shifts: Complete Information . . . . . . . 401.15 UIP test with monetary policy regime shifts: Incomplete Information . . . . . . 411.16 UIP test with monetary policy shifts and shocks: Complete Information . . . . 421.17 UIP test with monetary policy shifts and shocks: Incomplete Information . . . 431.18 UIP test with frequent monetary policy regime shifts: Complete Information . 441.19 UIP test with frequent monetary policy regime shifts: Incomplete Information . 451.20 UIP test with persistent and transitory technology shocks: Complete Information 461.21 UIP test with persistent and transitory technology shocks: Incomplete Infor-

mation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 471.22 Monetary policy shift: Incomplete Information-φ1 = 0.95 vs φ1 = 0.75 . . . . . 481.23 Monetary policy shift: Incomplete Information-φ1 = 0.95 vs φ1 = 0.75 . . . . . 491.24 Monetary policy shift: Incomplete Information-φ1 = 0.95 vs φ1 = 0.75 . . . . . 50

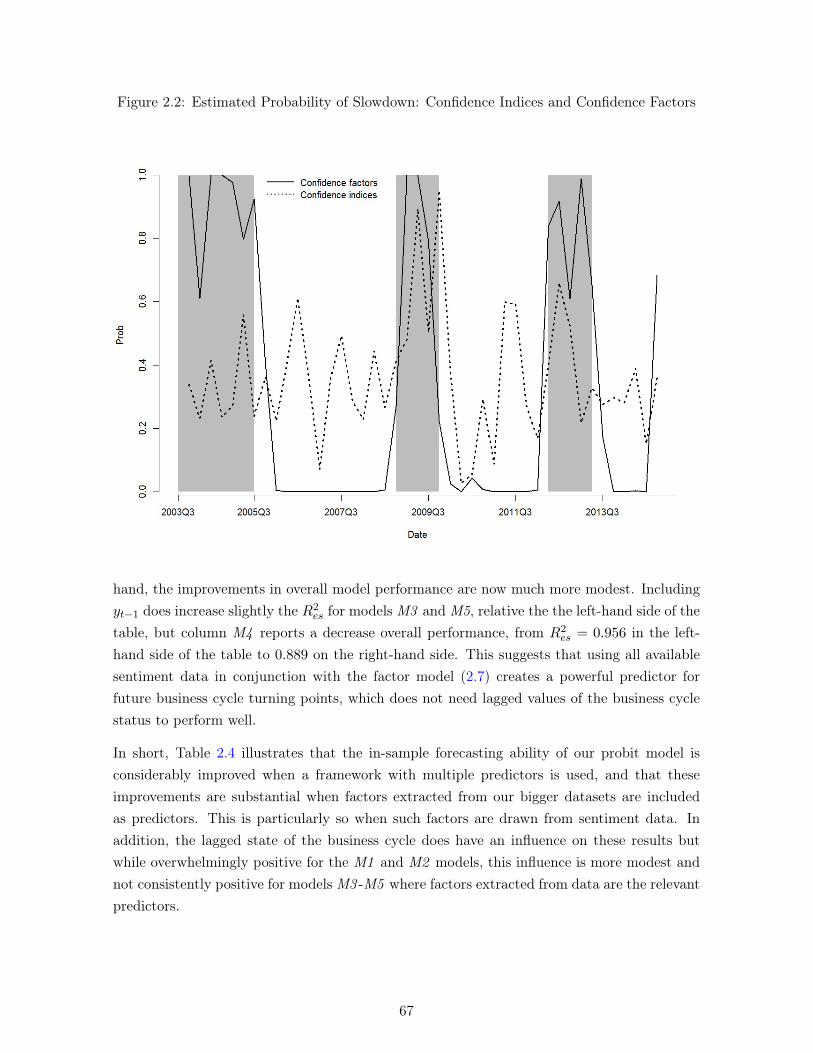

2.1 Canadian Recessions: OECD and C.D. Howe . . . . . . . . . . . . . . . . . . . 592.2 Estimated Probability of Slowdown: Confidence Indices and Confidence Factors 67

3.1 Confidence data and GDP growth: Conference Board Data . . . . . . . . . . . 883.2 Confidence data and GDP growth: Bank of Canada Data . . . . . . . . . . . . 903.3 US confidence data and Canadian GDP growth . . . . . . . . . . . . . . . . . . 913.4 Stages of the forecasting exercise . . . . . . . . . . . . . . . . . . . . . . . . . . 94

xii

List of Abbreviations

AIC Akaike Information CriterionBCI Business Confidence IndexBIC Bayesian Information CriterionBOS Business Outlook SurveyC.D. Howe Clarence Decatur Howe InstituteCCI Consumer Confidence IndexCEA Canadian Economic AssociationCIP Covered interest rate parityCML Cost-weighted Misclassification LossesCPI consumer price indexCRS constant returns to scaleCSI Canada’s Short-Term IndicatorDM Diebold and Mariano (1995) testDSGE Dynamic Stochastic General Equilibrium ModelFRED-MD Federal Reserve Economic Data - Monthly DatabaseGDP Gross Domestic ProductGW Giacomini and White (2006) testICE Index of Consumer ExpectationICS Index of Consumer SentimentISM Institute of Supply ManagementKPSS Kwiatkowski-Phillips-Schmidt-Shin testsLARS-EN Least Angle Regression Selection with Elastic NetMSFE Mean Squared Forecast ErrorNBER National Bureau of Economic ResearchNIPA National Income and Product AccountsNOEM New-Open Economy MacroeconomicsOECD Organisation for Economic Co-operation and DevelopmentPC Principal ComponentPCA Principal Component AnalysisPMI Purchasing Managers’ Indexes

xiii

QPS Quadratic Probability ScoreSCSE Société Canadienne de Sciences ÉconomiquesSLO Senior Loan OfficersSP/TSX Standard and Poor’s/Toronto Stock Exchange indexSPF Survey of Professional ForecastersUIP Uncovered Interest ParityUK United-KingdomUS United-StatesVAR Vector Autoregressive

xiv

To the loving memory of mygrandmother Jouego Luise.

xvi

Economics has then as itspurpose firstly to acquireknowledge for its own sake, andsecondly to throw light onpractical issues.

Alfred Marshall 1920, p. 33

xvii

Acknowledgments

I owe a debt of gratitude to several people for the realization of this thesis, but first of all, Iam grateful to the Almighty God for giving me the opportunity to pursue my doctoral studiesand for providing me with health and the needed resources to complete this thesis. I wouldlike to extend my deepest gratitude to all individuals and organizations that have providedme help and support throughout the whole period of my doctoral studies.

I express my gratitude first and foremost to my thesis advisor Prof. Kevin Moran for mentoringme over the course of my thesis. He provided me with essential tools in macroeconomicmodeling and gave a clear direction to my research when leaving me a full autonomy. Hisprofessional breadth throughout this research guided me to improve its technical aspects andhis experience led to this original proposal that analyzes a topical issue of social sciences in amore innovative way.

I also thank Dr. Imad Rherrad who accepted to act as my supervisor during my three yearsat the Quebec Ministry of Finance as a PhD research fellow. He patiently guided me withhis precious comments and suggestions. His insight in economic research and analysis shapedthis document; may he find in these words my gratitude for all I have learned from him andfor his continuous support.

I would additionally like to thank Prof. Benoît Carmichael who has taught me in my doctoralcoursework in Macroeconomics and Prof. Stephen Gordon who has taught me in my doctoralcoursework in Econometrics and both accepted to be part of my thesis committee. I alsothank Prof. John W. Galbraith from McGill University who accepted to serve as the externalreviewer of this thesis. Their cogent comments and suggestions have improved the quality ofthis document.

I would also like to thank the Department of Economics of Université Laval and all its facultymembers for the quality of training I have received and for their availability and assistance overthe course of my studies. In particular, I thank Prof. Sylvain Dessy, who, as Chair of GraduateStudies in 2011, accepted my application to the PhD program and for his continuous support,encouragement and discussions over the last five years. His mentorship has been crucial in myacademic success and my journey in the program.

xviii

I also thank The Honourable Prof. Jean-Yves Duclos, who, as Chair of the Department ofEconomics offer me my first contract as lecturer and after him, Prof. Guy Lacroix for givingme the same trust and support for the same job. I also thank Prof. Philippe Barla andProf. Stephen Gordon, who, as chair of Graduate Studies successively, provided me timelinesssupport and assistance in renewing my immigration documents. I am grateful to Prof. CarlosOrdas Criado, who has taught me in my doctoral coursework in Econometrics, for his supportand advice.

I am also grateful to all the professors of the Department of Economics, who helped improvedthe quality of my work with their comments and guidance on how to communicate and writeefficiently a scientific document by attending my presentations at the Department. I am alsograteful to all the administrative staff of the Department of Economics and its research centerCIRPÉE for their kind collaboration and support.

I would like to thank conference participants at Laval University, Canadian Economics As-sociation Conference, Congrès annuel de la société canadienne de science économique, anddiscussants of my work at conferences. I am also grateful to all my macroeconomist colleaguesat the Ministry of Finance of Quebec for their advice and assistance, a special thanks to DanielFloréa and Raymond Fournier.

I would like to thank all the professors of the Department of Statistics at Padua University andthe Department of Mathematics at the University of Yaoundé I, where I obtained my Bachelorand Master’s degrees. These undergraduate years in discovering Economics and learningquantitative tools were decisive in my PhD journey. A special thanks to Prof. MassimilianoCaporin, Prof. Nunzio Cappuccio, Prof. Efrem Castelnuovo, Prof. Guglielmo Weber, Prof.Ottorino Chillemi and Prof. Giovanni Battista Di Masi.

I would also like to express my appreciation to my colleagues of the Department of Economicsfor their (and non-) academic discussions, patience, assistance and friendship over the last fiveyears. In particular, I am grateful to André-Marie Taptué for his time and support. I alsoexpress my gratitude to my elders Legrand Kana, Bouba Housseini, Alexendre Kopoin, HabibSome, Jerome Gagnon-April, Aboudrahim Savadogo and Rokaya Ndiaye for their advice.

I also thank my close friends and colleagues for their crucial support and continuous encour-agement throughout the whole period of my PhD studies. Many thanks to Gilles Koumou,Jean-Armand, Ali, Setou, Isaora, Mbea, Abdhalla, Elfried, Marie-Albertine, Bodel, Carollefor giving me crucial support and assistance.

I also extend my deepest gratitude to my family, in particular, to my late grandmother Louise,who set the path for all possible knowledge in my life. To my mother and siblings, my friendsin Quebec, Italy and Cameroon and all the persons who have always been there for me,physically or in thoughts. For their love, encouragement and continuous guidance to pursue

xix

my PhD studies, may all of these persons find in these words my deepest gratitude.

Finally, I gratefully acknowledge logistical and financial support from: the Department ofeconomics of Université Laval; the Faculty of Social Sciences of Université Laval, the CentreInteruniversitaire sur le Risque, les Politiques Économiques et l’Emploi (CIRPÉE) and theQuebec Ministry of Finance. I would also like to thank them for their logistical and financialsupport, including the sponsoring of my participation to various academic conferences andinternship. These activities have hugely boosted my research skills and interest in the areasof macroeconomic modeling, economic analysis and forecasting.

xx

Avant-propos

Cette thèse s’articule autour de trois chapitres indépendants qui s’inscrivent dans les champs dela macroéconomie, de la finance internationale et de prévision économique. Les trois chapitresconstituent des articles soumis ou à soumettre à des revues scientifiques avec comité de lecture.Je suis le principal auteur de chacun de ces trois articles.

Le premier chapitre est un article réalisé avec mon directeur de thèse, Kevin Moran. Il faitl’objet de quelques révisions pour être soumis à une revue scientifique avec comité de lecture.

Le deuxième chapitre est un article réalisé avec mon directeur de thèse, Kevin Moran, et monco-auteur, Imad Rherrad. Cet article, dont je suis le principal auteur, a été soumis pourpublication à une revue scientifique avec comité de lecture.

Le troisième chapitre est un article réalisé sous la direction de mon directeur de thèse, KevinMoran, et avec la collaboration de mon co-auteur Imad Rherrad. Cet article a été soumis pourpublication à une revue scientifique avec comité de lecture.

xxii

Chapter 1

The Forward Premium Puzzle: aLearning-based Explanation

Abstract

When interest rates are higher in one’s home country than they are abroad, standard arbi-trage arguments suggest this signals that the home currency will depreciate in the future.However, empirical evidence has regularly been found to be strongly at odds with thisintuition. This is the “forward premium puzzle”. This paper proposes a learning-basedexplanation for this puzzle. We embed an information problem in the two-country New-Open Economy Macroeconomics (NOEM) model with nominal rigidities. The informationfriction arises because the shocks affecting the model economy can be of either persistentor transitory types and economic agents do not directly observe the shocks’ types; insteadthey must infer their nature using a filtering mechanism. We simulate the model with andwithout this informational friction and test whether the generated artificial data exhibitsthe symptoms of the forward premium puzzle. Our leaning-based explanation is validatedif only the data generated with the active informational friction replicates the puzzle.

Keywords: monetary policy, learning, exchange rate, forward premium puzzle, open-economy,UIP, DSGE.

1

1.1 Introduction

Research in international finance has documented the presence of several empirical regularitiesthat pose significant challenges to standard open-economy models and arguments. Theseregularities, often described as “anomalies” or “puzzles”, are the subject of much active research.One important such anomaly is the forward premium puzzle. This puzzle arises becausesimple theories of international finance suggest that observing a premium between the domesticinterest rate and its foreign counterpart signals that the home currency will depreciate in thefuture. However, data on interest rates and realized exchange rate depreciations have stronglyand consistently refuted the implication of these theories.1

This paper proposes a learning-based explanation for the forward premium puzzle. To do so,we first embed an information friction in the New-Open Economy Macroeconomics (NOEMhenceforth) model with nominal rigidities.2 Specifically, we assume that monetary policy andtechnology shocks can each either be of a persistent or a transitory type, but that economicagents do not observe the type directly and must instead infer its nature using a filteringmechanism. We then simulate the model repeatedly, with and without this informationalfriction, and assess the generated artificial data to see if they exhibit the signs of the forwardpremium puzzle. Validation for our leaning-based explanation for the puzzle arises in the eventthat only the data generated with the active informational friction can replicate the puzzle.

The simulations undertaken with our model lead to these findings: the forward premiumpuzzle arises in an environment where investors face an information bias about the relevantnature of each shock hitting the economy. As the time-horizon increases the puzzle lessensand subsequently disappears in the medium-term of about two or three years. Only underincomplete information, we document a strong consistency with the regularities emerging frommost empirical studies in literature, namely the negative correlation between the interest ratedifferential and the foreign exchange rate changes overtime (the negative slope coefficient inthe Fama [1984] regression).

The rest of this paper is organized as follows. Section 2 presents a short literature review thatdiscusses the forward premium puzzle and the literature that analyses it and attempts to ra-tionalize it. Section 3 presents our model economy. Section 4 describe the information frictionthat we embed in the NOEM model and the filtering mechanism used to distinguish betweenpersistent and transitory shocks. Section 5 presents our simulation results and discusses them,while Section 6 concludes.

1The existence of this puzzle was documented in early contributions such as Hansen and Hodrick [1980]and Fama [1984] and confirmed since by several subsequent studies [Froot and Thaler, 1990, Gourinchas andTornell, 2004, Engel, 2014].

2The NOEM framework originates from Obstfeld and Rogoff [1995] and is an open-economy extension ofthe New Keynesian model. See Lane [2001] and Corsetti [2008] for surveys on the NOEM and Corsetti et al.[2010] for an analysis of optimal monetary policy within the model.

2

1.2 Review of literature

According to the efficient-market hypothesis, prices integrate all the information availableto market participants and there is no possibility for a trader to earn excess returns. Oneimplication of this hypothesis is that in foreign exchange markets, the covered interest rateparity condition (CIP) holds:

ft − et = it − i∗t , (1.1)

where it and i∗t are the returns on comparable domestic and foreign assets, respectively, be-tween time t and t + 1, ft denotes the logarithm of the forward exchange rate (the rate forforeign exchange delivered next period) and et is the spot exchange rate (the price of foreigncurrency in units of domestic currency). Equation (1.1) represents a no-arbitrage conditionbecause all the variables are known at time t. Several empirical analyses have confirmed thevalidity of the CIP condition using a large variety of currencies.3

The empirical evidence has not been as supportive of the uncovered interest parity condition,however. This condition arises by taking (1.1), assuming further that agents are risk neutralso that no risk premium is required by an agent choosing between a risky and a risk-free asset,that they have rational expectations and that forward rates equal expected future rates, sothat

Et(et+1 − et) ≈ it − i∗t , (1.2)

where Et(et+1) is the rational expectation of the future spot exchange rate et+1. Since bydefinition et+1 = Et(et+1) + ξt+1 with ξt+1 ∼ i.i.d N(0, σ), condition (1.2) can be rewritten as

et+1 − et = it − i∗t + ξt+1. (1.3)

The empirical validity of this condition is usually assessed by running the following regressionin nominal terms:

et+1 − et = α0 + α1 (it − i∗t ) + ξt+1, (1.4)

or in real terms:st+1 − st = α0 + α1 (rt − r∗t ) + ξt+1, (1.5)

where the real rate st = et ∗ Pt/P ∗t and testing the unbiasedness hypothesis H0 : α0 =

0 , α1 = 1. Under this null hypothesis, realized changes in the spot exchange rates shouldtherefore have a one to one correlation with the interest rate differential. However, resultsfrom the literature reject H0 decisively, with estimates α0 6= 0, α1 � 1 and many instances ofnegative estimates for α1.4 Such frequent rejection of H0 is referred to as the forward premium

3See Sarno and Taylor [2002], Chap. 2, for a detailed description and analysis of the CIP.4As indicated above, several authors report such evidence; among them, Froot and Thaler [1990], Backus

et al. [1993], Lewis [1995], Bansal and Dahlquist [2000], Moore and Roche [2002, 2008], Gourinchas and Tornell[2004] or Engel [2014].

3

puzzle. Froot and Thaler [1990], for example, survey more than 70 empirical contributionsthat analyse the puzzle and report that the average estimate of α1 is −0.88.

A large literature has proposed various explanations to rationalize the forward premium puzzle,among them, Bacchetta and Van Wincoop [2006], Kearns [2007], Benigno and Benigno [2008],Chakraborty and Evans [2008], Burnside et al. [2007], Evans [2010], Snaith et al. [2013], Hallet al. [2011], Martin [2011], Ilut [2012], Coudert and Mignon [2013], Yu [2013], Djeutem [2014]and Londono and Zhou [2015]. This literature and contributions have proposed two mainapproaches to explain the puzzle.

The first such approach originates in Fama [1984] and focuses on the existence of a riskpremium. This premium, when introduced either in capital asset pricing, portfolio balance, ifboth highly volatile and positively correlated with the interest rate differential it − i∗t couldaffect the estimation of (1.4) and help induce a small or even negative estimate for α1. Macklem[1991], Engel [1992] and Bekaert [1994] show that such class of models can indeed generate arisk premium, but that the quantitative magnitude of this premium is not sufficient to accountfor the high volatility in the data. This occurs because the implied variability in the inter-temporal marginal rate of substitution of the agents is too low. Using a general equilibrium,open-economy model similar to the one used here but with incomplete markets, Leduc [2002]shows that it can generate at best a degree volatility in the risk premium that is 30% of whatwould be necessary to rationalize the findings in the empirical literature.

Alternatively, Froot and Frankel [1989] propose to decompose the predictable excess returns(a fact closely associated to the presence of the foward premium puzzle) into currency riskpremium and expectation error components, using survey data to measure expectations. Theyshow that the forward premium puzzle is mostly associated with the expectation error com-ponent. Accordingly, the conclude that models based on risk premia may have less potentialto provide an explanation to the puzzle.

The second general approach thus relies on expectation errors. Froot and Frankel [1989], Lewis[1988, 1993], De Long et al. [1990] and Gourinchas and Tornell [1996] argue that the puzzlemay be due to systematic expectational errors on the part of investors. In addition, theypoint out that the presence of market speculators create informational heterogeneity betweentraders, which can lead to inefficient expectation errors, of that rational expectation errorsmay emerge from regime shifts and so called peso problems.5

The present paper contributes to this literature by investigates whether a general equilibrium,two-country model with rational and risk-averse agents can explain the forward premium puz-zle, in the information environment is such that agents cannot directly observe the persistence

5Yet another line of inquiry into the forward premium puzzle involves assuming and showing that sub-stantial non-linearities affect the regression (1.4). Mark and Moh [2002] illustrate that transaction costs andcentral bank interventions can indeed lead to a non-linear variance of the innovation term in (1.4). See alsoBaldwin [1990] and McCallum [1994].

4

of a given shock but must instead use a filtering mechanism to ascertain that persistence.Our methodological approach thus follows Lewis [1988, 1995] and Andolfatto et al. [2008] andrepeatedly simulates the economy with and without the information friction and then runningthe classic econometric tests of coefficients in the Fama (1984) regression, reporting the valueof each coefficient and the frequency at which the null hypothesis of unbiasedness is rejected.

1.3 The model economy

This section describes our two-country model economy. The model is part of the New Open-Economy Macroeconomics (NOEM) literature exemplified by Corsetti [2008] and Corsettiet al. [2010]. As indicated above, this model is drawn from the New Keynesian paradigmnwith monopolistic competition and nominal rigidities, extended to a two-country world. Theworld economy consists of two countries of equal size, denotedH(Home) and F (Foreign). Eachcountry specializes in one type of traded good produced in a number of varieties (or brands)defined over a continuum of unit mass. Brands of tradable goods are indexed by h ∈ [0, 1]

in the Home country and f ∈ [0, 1] in the Foreign country. Firms producing the goods aremonopolistic suppliers of one brand only and use labor as the only input to production. Thesefirms set nominal prices in local currency units and in staggered fashion, à la Calvo [1983].Finally, international asset markets are complete.6

1.3.1 Preferences

We describe the structure of the Home country, with the understanding that similar expressionscharacterize the Foreign country economy with obvious notational changes. We consider acashless economy in which the representative household (or Home agent) maximizes expectedlifetime utility :

W0 = E0

∞∑t=0

βtU [Ct, Lt], (1.6)

where instantaneous utility U is a function of the consumption index Ct and of leisure (1−Lt),as follows:

U [Ct, Lt] =C1−σt

1− σ+ κ

(1− Lt)1+η

1 + η, σ > 0. (1.7)

Households consume both domestically-produced and imported goods, aggregated in the bas-kets CH,t and CF,t respectively. We define Ct(h) as Home’s consumption of Home good h,and similarly, Ct(f) as Home’s consumption of imported Foreign good f . Each good h (or f)is an imperfect substitute for other varieties so that the baskets CH,t and CF,t are:

CH,t ≡[∫ 1

0Ct(h)

θθ−1dh

], CF,t ≡

[∫ 1

0Ct(f)

θθ−1df

], (1.8)

6Corsetti et al. [2010] also analyse a model version with incomplete asset markets.

5

with the constant elasticity of substitution θ > 1 common across baskets. The full consump-tion basket Ct aggregates both domestic and foreign baskets according to the following CESfunction:

Ct ≡[a

1/φH C

φ−1φ

H,t + a1/φF C

φ−1φ

F,t

] φφ−1

, φ > 0, (1.9)

where aH and aF are the weights of home and foreign goods in total Home consumption,respectively, and φ is the elasticity of substitution between CH,t and CF,t. As in Corsettiet al. [2010], the utility-based CPI associated with the consumption basket Ct is the resultminimizing total expenses in order to purchase one unit of Ct and entails

Pt =[aHP

1−θH,t + aFP

1−θF,t

] 11−θ

, (1.10)

where sub-indices PH,t and PF,t of home and foreign composites are

PH,t =

[∫ 1

0Pt(h)1−θdh

] 11−θ

; PF,t =

[∫ 1

0Pt(f)1−θdf

] 11−θ

. (1.11)

1.3.2 Assets market and budget constraint

In each time period t, Home households purchase Bt+1 units of contingent claims at the pricepbt,t+1. These assets represent a promise to pay one unit of local currency the next period foreach possible realization of the state of nature. Domestic households also derive income fromwork, WtLt, from their ownership of domestic firms, Π(h), with h ∈ [0, 1] and from bondsholdings Bt. Home’s disposable income is used to consume both home and foreign producedgoods or invested to transfer wealth in the next period. The budget constraint for the Home’sis therefore

PH,tCH,t + PF,tCF,t +

∫spbt,t+1Bt+1 ≤WtLt +Bt +

∫ 1

0Π(h) dh. (1.12)

Home household’s optimization problem can therefore be explicitly defined as

maxE0

∞∑t=0

βt[C1−σt

1− σ+ k

(1− Lt)1+η

1 + η

],

subject to (1.12).

Foreign households face a similar maximization problem, as in

maxE0

∞∑t=0

βt[C∗1−σt

1− σ+ k

(1− L∗t )1+η

1 + η

],

subject to

P ∗H,tC∗H,t + P ∗F,tC

∗F,t +

∫sp∗bt,t+1B

∗t+1 ≤W ∗t L∗t +B∗t +

∫ 1

0Π(f) df,

where P ∗H,t, C∗H,t, P

∗F,t, C

∗F,t are defined in analogous fashion to their domestic counterparts.

6

1.3.3 Firms

Three different types of firms are present in the home and foreign country, each producing aspecific type of good.

1.3.3.1 Domestic final goods

Domestic final good assemblers operate in a perfectly competitive environment and use thefollowing CRS production function:

Dt =

[a

1φ

HDφ−1φ

H,t + a1φ

FDφ−1φ

F,t

] φφ−1

,

where DH,t represents inputs of home-produced goods and DF,t inputs of foreign-producedgoods, respectively, with φ the elasticity of substitution between home and foreing goods inproduction. Profit maximisation for these firms entails

maxDH,t;DF,t

[PtDt − PH,tDH,t − PF,tDF,t] ,

with the optimality conditions leading to input-demand functions DH,t = Dt

(PH,tPt

)and

DF,t = Dt

(PF,tPt

). Further, imposing the zero-profit condition leads to equation (1.10).

1.3.3.2 Domestic composite goods

Domestic composite good assemblers operate under perfect competition, using the followingCRS technology:

DH,t =

[∫ 1

0Dt(h)

θ−1θ dh

] θθ−1

,

where Dt(h) represents their input demand for each of the differentiated domestic goods h.Their profit maximization problem is therefore as such:

maxDt(h)

[PH,tDH,t −

∫ 1

0Pt(h)Dt(h) dh

].

and from the optimality conditions and the zero-profit condition, one can derive

Dt(h) = DH,t

(Pt(h)

PH,t

)(1.13)

and

PH,t =

[∫ 1

0Pt(h)1−θdh

] 11−θ

. (1.14)

For assemblers of the foreign composite good, similar expressions obtain:

maxDt(f)

[PF,tDF,t −

∫ 1

0Pt(f)Dt(f) df

]s.t. DF,t =

[∫ 1

0Dt(f)

θ−1θ df

] θθ−1

,

7

withDt(f) = DF,t

(Pt(f)

PF,t

), (1.15)

and

PF,t =

[∫ 1

0Pt(f)1−θdf

] 11−θ

.

1.3.3.3 Domestic basic goods

Domestic producers of basic goods operate under monopolistic competition and employ do-mestic labor to produce a differentiated good h using the following linear production function:

Yt(h) = ZtLt(h), (1.16)

where Lt(h) is the demand for labor by the producer of good h and Zt is a technology shockcommon to all producers in the domestic country, which follows a statistical process to bespecified below.

For a typical such producer, output satisfies a domestic and a foreign demand in that:

Yt(h) = Dt(h) +D∗t (h) (1.17)

where Dt(h) is the domestic demand for the good, expressed above in equation (1.14) andD∗t (h) is the foreign demand for the same good. Total real revenues for this firm are therefore:

Pt(h)Dt(h) + EtP ∗t (h)D∗t (h)

Pt,

where Et is the nominal exchange rate i.e. the price of the domestic currency in terms of theforeign one (increases in Et thus represent domestic depreciations). Firms are subject to nom-inal rigidities a la Calvo. Every period t, some firms receive a signal indicating they can seta new price. Each firm receiving this signal chooses its domestic and foreign-currency pricesPt(h) and P ∗t (h) knowing the same prices continue to apply in future periods with proba-bility α, while their real production cost will be mct (Dt(h) +D∗t (h)). 7 The intertemporalmaximization problem is then:

maxP (h),P ∗(h)

Et

{ ∞∑k=0

(αβ)kµt+kµt

(1

Pt+k

[Pt(h)Dt+k(h) + EtP ∗t (h)D∗t+k(h)

]−

MCt+kPt+k

[Dt+k(h) +D∗t+k(h)

] )} (1.18)

where µt+1

µtis the firm’s stochastic nominal discount factor between t and t + k.8 By the

first order condition of the producer’s problem, the optimal price Pt(h) in domestic currencycharged to domestic customers is:

Pt(h) =θ

θ − 1

Et∑∞

k=0(αβ)kµt+kmct+kPθH,t+kCH,t+k

Et∑∞

k=0(αβ)kµt+kPθH,t+k

CH,t+kPt+k

, (1.19)

7This specification of the production assumes that when firms update their prices, they do so simultaneouslyin the Home and in the Foreign market and in the respective currencies.

8µt is the Lagrange multiplicator in the Home’s firm maximisation problem

8

similarly, the optimal price P ∗t (h) in domestic currency charged to foreign customers is:

P ∗t (h) =θ

θ − 1

Et∑∞

k=0(αβ)kµ∗t+kmc∗t+kP

∗θH,t+kC

∗H,t+k

Et∑∞

k=0(αβ)kµ∗t+kP∗θH,t+k

C∗H,t+kP ∗t+k

.

Since all the producers allowed to set new prices in period t make the same choices Pt(h) = Pt,we obtain the following equation for PH,t and P ∗H,t:

P 1−θH,t = αP 1−θ

H,t−1 + (1− α)Pt(h)1−θ,

P ∗1−θH,t = αP ∗1−θH,t−1 + (1− α)P ∗t (h)1−θ,(1.20)

and we note that similar relations is applicable for the Foreign firms f .

For the goods market clearing condition in the Home economy, it follows that :

Dt = Ct , DH,t = CH,t , DF,t = CF,t.

We obtain dual relations in the Foreign economy.

1.3.4 Monetary policy

We complete the model by adding a policy rule for the domestic interest rate, which representsthe behavior of the monetary authority. Let it and πt denote the (net) nominal interest rateand the (net) inflation rate and let it , respectively. Further, let r and yt denote the steadystate value of the real interest rate and the natural rate of real GDP.9 The rule is then:

it = ρit−1 + (1− ρ) [r + πt + ψπ(πt − πt) + ψy(yt − y)] + εt. (1.21)

In (1.21), πt denotes the monetary authority’s date t ’s inflation target and εt denotes anexogenous monetary policy shock. We consider that the target πt varies occasionally becauseof infrequent shifts in targeted or mandated inflation. The parameter ρ ∈ [0, 1) represents thedegree of interest rate smoothing. According to (1.21), therefore, the central bank graduallyadjusts its interest rate instrument in response to domestic inflation and output gaps. Weconsider that the monetary authority in the foreign economy follows a similar policy rule.

1.4 Information frictions and filtering mechanism

This section describes how shocks affecting this economy, to the technology in production andto the monetary policy rule, both have persistent and transitory types. It also details howagents, who cannot directly observe the persistence of these shocks, instead use a filteringmechanism (the Kalman filter) to disentangle both components.

9“Natural” GDP is the production level that would obtain in the absence of nominal rigidities.

9

1.4.1 Technology shocks

We consider first the shock to multi-factor productivity Zt. We assume that Zt is affected bya persistent and by a transitory component, so that we have:

logZt = logZpt + logZτt , (1.22)

where Zpt is the persistent component and Zτt the transitory component. We assume furtherthat these components evolve according to:[

logZpt+1

logZτt+1

]=

[λp 0

0 λτ

].

[logZptlogZτt

]+

[νpt+1

ντt+1

], (1.23)

where λp and λτ represent the serial correlation of each component of the shock with λp >> λτ

and νpt+1 and ντt+1 follow iid zero-mean processes with standard deviations σpν and στν . Takentogether, (1.22) and (1.23) form a state-space system integral to our model solution.

1.4.2 Monetary policy shocks

For the shocks in monetary policy, the transitory component εt is imputable to the reactionof the monetary authority to various unexpected economic developments and is assumed tofollow the process:

εt = φ1εt−1 + eεt, (1.24)

with 0 ≤ |φ1| � 1 and eεt ∼ N(0, σ2e).

Following Andolfatto et al. [2008], let the persistent component of the monetary policy shocksarise from regime shifts to the inflation target πt. Let at ≡ πt − π denote an occasionaldeviation of the current target of monetary authorities πt from its very long run mean π. Themonetary regime shift at can be attributed to a new insight (revolutionary vision) about theeconomy or to preference changes with the monetary authority. We assume that at has thefollowing dynamic process:

at =

{at−1 with prob. φ2

gt with prob. (1− φ2) and gt ∼ N(0, σ2

g

) (1.25)

where φ2 reflects the persistence of any given regime in terms of duration and σ2g is the

importance of regime shifts in terms of size, when they do occur. Using the definition of at,the policy rule (1.21) can be rewritten:

it = ρit−1 + (1− ρ) [r + π + ψπ(πt − π) + ψy(yt − y)] + ut, (1.26)

whereut = εt + (1− ρ)(1− ψπ)at.

10

The observed shock to monetary policy ut is thus a combination of the transitory componentεt and the persistent component at . In our complete information environment, agents canobserve separately at and εt so that the rule is effectively as written in (1.21). The state-spacesystem for monetary policy shocks is therefore:[

at+1

εt+1

]=

[φ2 0

0 φ1

].

[at

εt

]+

[eat+1

eεt+1

], (1.27)

and

ut = [(1− ρ)(1− ψ) 1]

[at

εt

], (1.28)

with eat+1 defined as:

eat+1 =

{(1− φ2)at with prob. φ2

gt+1 − φ2at with prob. (1− φ2).

1.4.3 Incomplete information and Kalman filter

The overall state-space representation for the two shocks affecting the economy is:logZpt+1

logZτt+1

at+1

εt+1

=

λp 0 0 0

0 λτ 0 0

0 0 φ2 0

0 0 0 φ1

.logZptlogZτt

at

εt

+

νpt+1

ντt+1

eat+1

eεt+1

(1.29)

and

[logZt

ut

]=

[1 1 0 0

0 0 (1− ρ)(1− ψ) 1

]logZptlogZτt

at

εt

. (1.30)

Under complete information, agents know all structural parameters and directly observe thetwo components of each shock. Under incomplete information, by contrast, agents know allstructural parameters but cannot distinguish between the two components of each shock. Inthis case, we apply the Kalman filter to the state-space system (1.29) and (1.30) to determinethe expectations of the variables logZpt+1, logZ

τt+1, at+1 and εt+1, conditional to the set of infor-

mation available at time t. These forecasts illustrate how agents learn to use new informationavailable in the economy to infer the probable future values of shocks. The filter producesestimates for the unobserved variables logZpt , logZτt , at and εt, by updating sequentially asevery new information become available, as in the following:

11

EtlogZ

pt

EtlogZτt

Etat

Etεt

=

Et−1logZ

pt−1

Et−1logZτt−1

Et−1at−1

Et−1εt−1

+Kt

([logZt

ut

]− Et−1

[logZt−1

ut−1

])

where Kt is the Kalman gain.10 Thus, using (1.29) and (1.30) we compute the expectationsof unobserved variables:

EtlogZpt+1

EtlogZτt+1

Etat+1

Etεt+1

=

λp 0 0 0

0 λτ 0 0

0 0 φ2 0

0 0 0 φ1

.EtlogZ

pt

EtlogZτt

Etat

Etεt

and

Et

[logZt+1

ut+1

]=

[1 1 0 0

0 0 (1− ρ)(1− φπ) 1

]EtlogZ

pt+1

EtlogZτt+1

Etat+1

Etεt+1

.

1.5 Results

This section presents our results. First, we discuss how key model parameters are assignednumerical values (ie. calibrated). Second, we report a series of standard impulse responseexperiments studying the economy’s evolution, under full information, following three typesof shocks: the transitory monetary policy shock, the persistent technology shock, and thepersistent shift in the monetary authorities’ target for inflation. This is undertaken in orderto develop intuition about the model and verify that its implications are consistent with similarcontributions in the literature. Third, we then report the reaction of the economy followingthe monetary policy shift when we compare responses under full information and incompleteinformation. This illustrates how gradual learning about the persistence of a given shock canmodify the responses of key variables and entail departures from UIP in realized paths forinterest rates differentials and exchange rate depreciations. Fourth, we describe the procedurewhereby regressions are ran on simulated data and analyzed, to assess if they can reproduceresults from UIP tests conducted on actual data in the literature. Finally, we present a sectionwith a sensitivity analysis of our main results.

1.5.1 Parameter calibration

We parametrize the model to a quarterly frequency. We thus assume β = 0.99, which impliesa real annualized return on assets of about 4% in the steady state. We set the elasticity

10See Hamilton [1994], Chapter 13 for useful details.

12

of substitution between the brands, θ, to be 6, which implies a markup over the marginalcost equal to 20% at the steady state. The parameter α, governing the frequency of pricechanges, is equal to 0.75, which implies an average of four periods (one year) between twoprice adjustments. We set the parameter governing the curvature on labor disutility η, tobe equal to 1.5 and the parameter κ such that the hours worked are 1/3 of available timeat the steady state. Finally we assume an import share in consumption equal to aF = 0.4,corresponding to the import/GDP ratio in Canada.11

The calibration of the monetary policy rule (1.21) is adapted from Andolfatto et al. [2008].First, we set the coefficient governing the response to inflation deviations from target, ψπ,to 1.8 and the coefficient governing the inertia in interest rate, ρ, to 0.1. The calibration ofthe shock processes, which play a decisive role in the model, is next. To this end, note thatφ2 characterizes the mean duration of a given regime shift in monetary authorities’ inflationtarget and σg the standard deviation of the distribution governing the magnitude of suchregime shifts when they do occur. Following Andolfatto et al. [2008], we set φ1 = 0.0 andφ2 = 0.975, σg = 0.01 and σε = 0.005; these values entail Kalman filter gains that are similar tothose used by Erceg and Levin [2003] and Schorfheide [2005]. Note that these parameter valuesimply that monetary policy shifts occur infrequently (on average once every 40 quarters, or 10

years) and that when they do occur their magnitude is relatively high, changing the inflationtarget by a typical 4 points of percentage on an annualized basis (0.01·4). For the technologicalshocks, we similarly set λτ = 0.0 and λp = 0.95, as well as στ = 0.005 and σp = 0.0025. Weuse a similar calibration for the foreign economy’s monetary policy.

1.5.2 Impulse response functions: Complete information

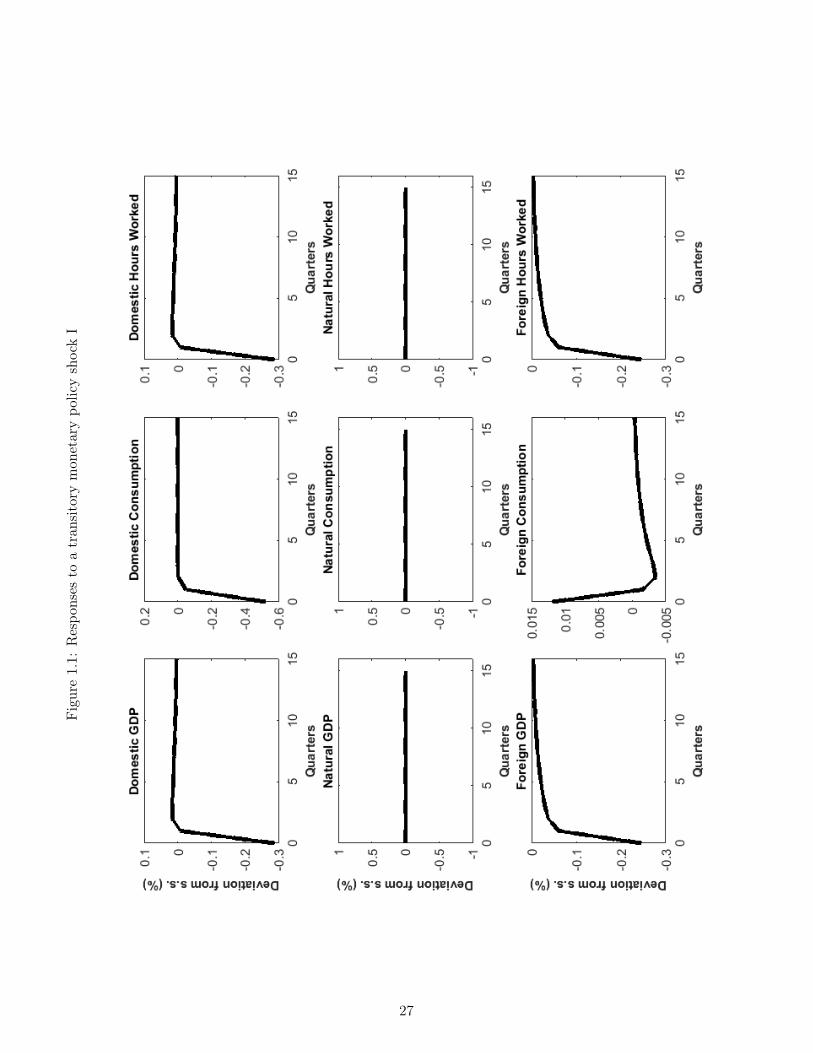

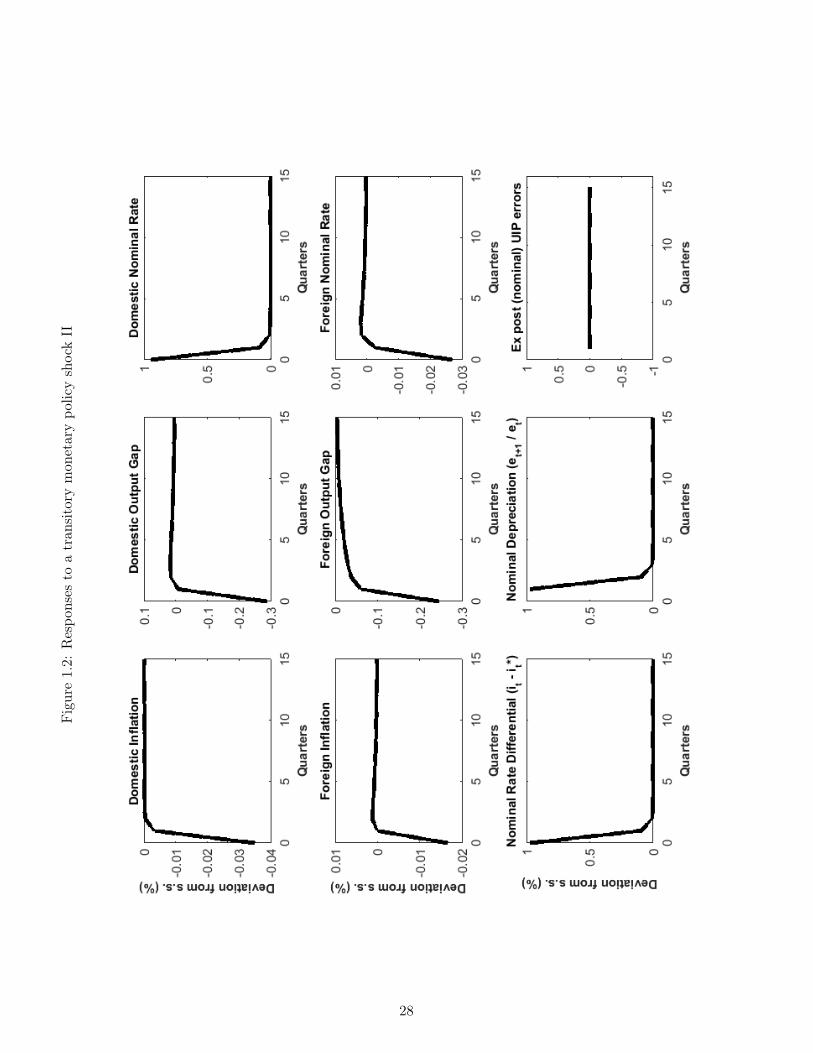

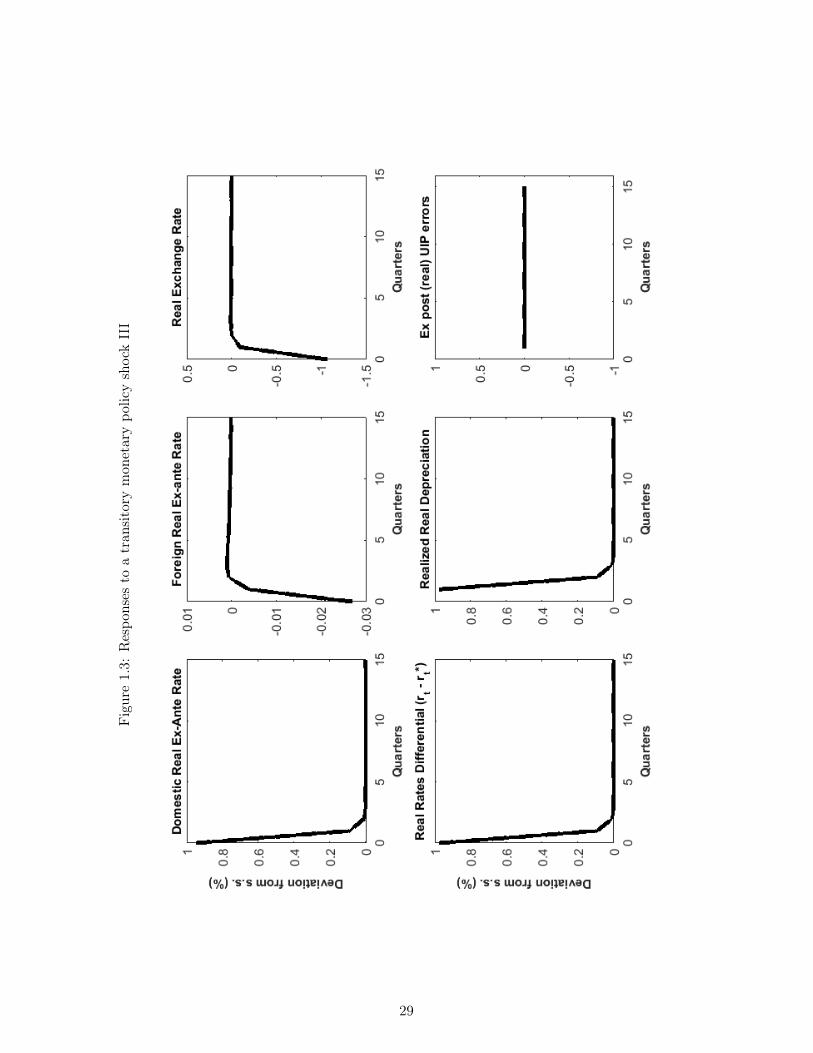

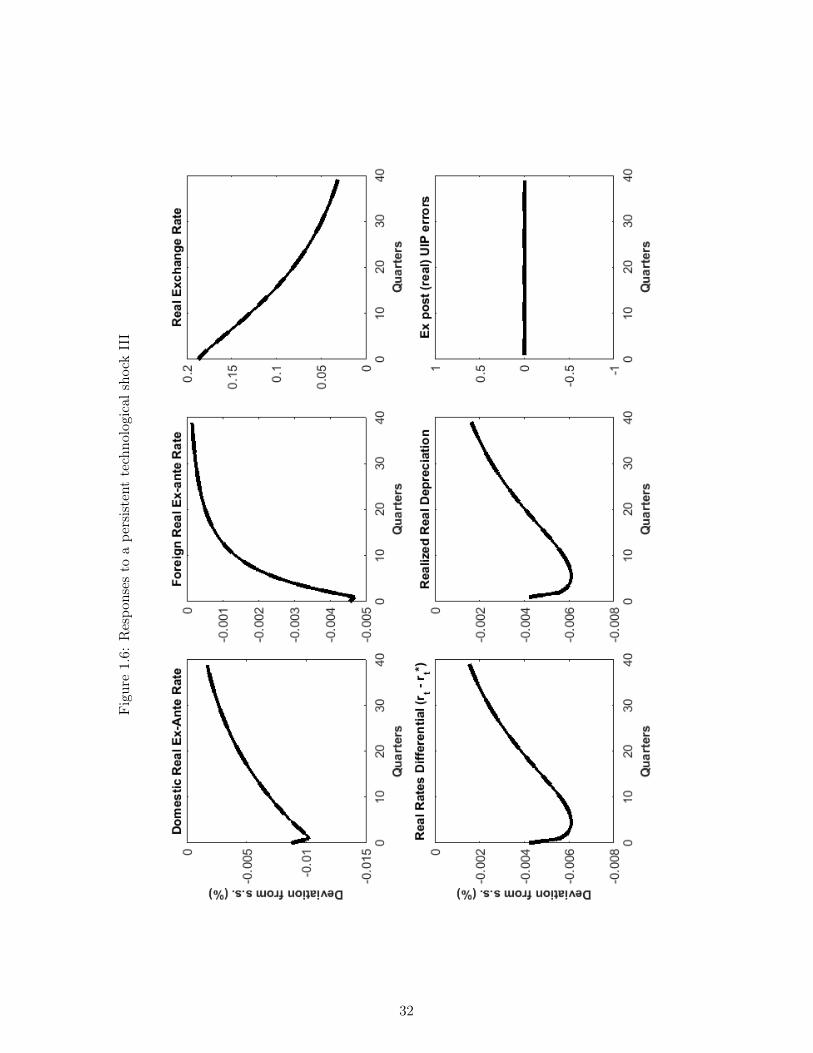

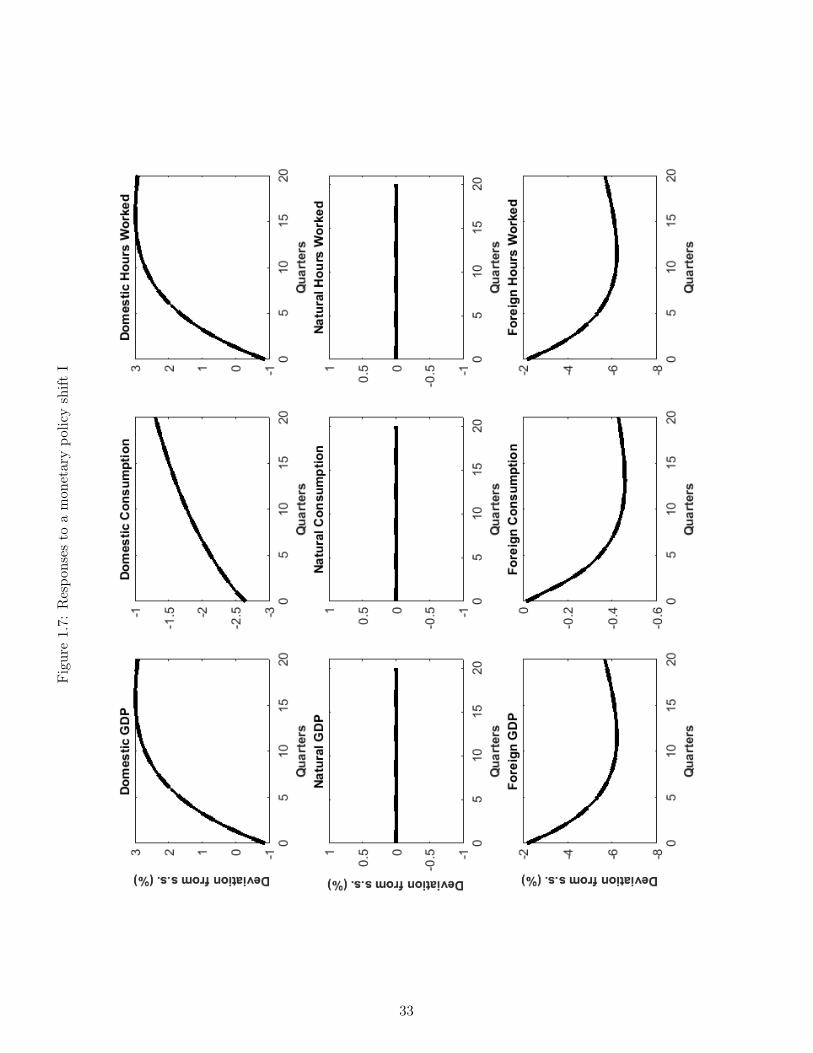

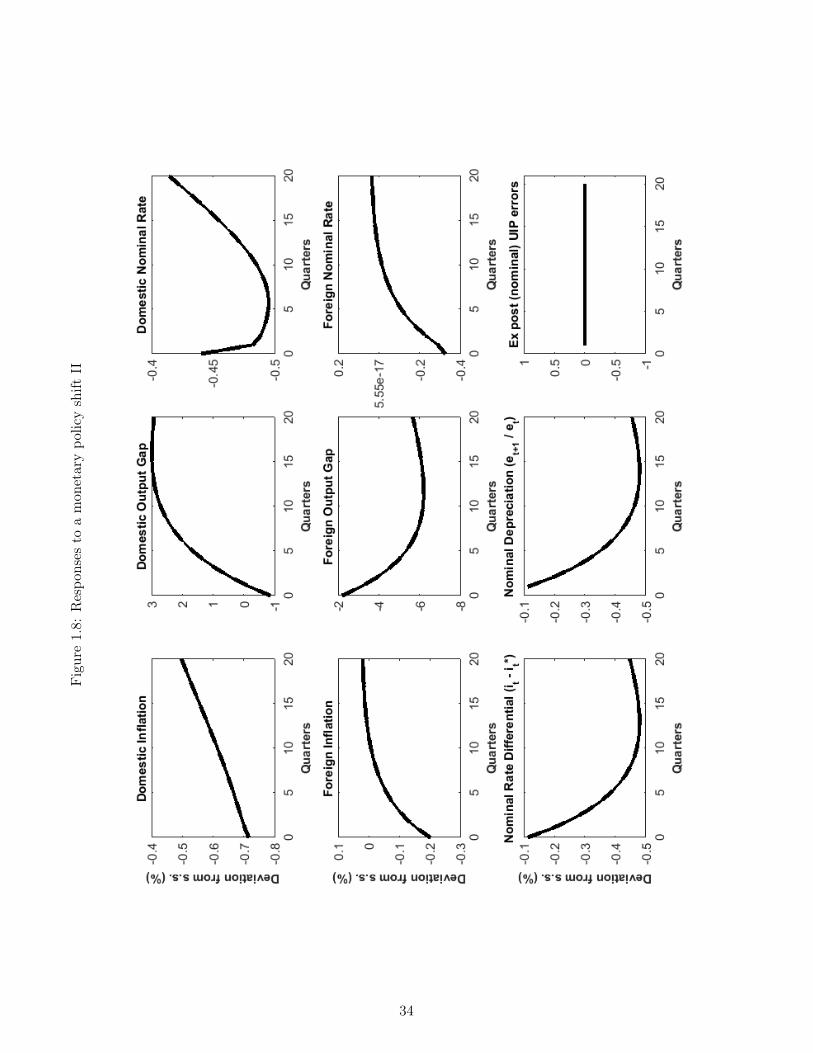

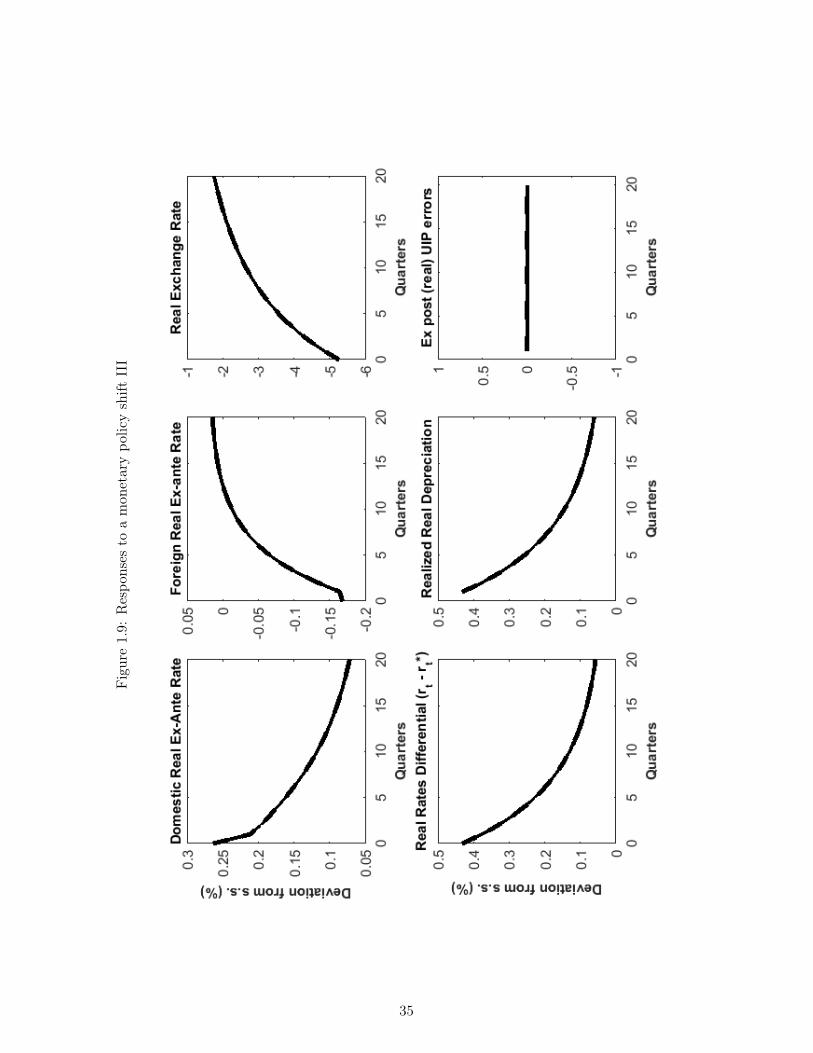

This subsection presents the impulse response functions of our model economy, under completeinformation, following the three major types of shocks affecting the economy. Figures 1.1-1.3 first report the effect of a one percent (positive) transitory monetary policy shock (eεt).Recall that such a shock represents a transitory positive displacement to (1.21), the domesticmonetary policy rule. Real activity variables are displayed in Figure 1.1 while Figure 1.2-1.3 report nominal and financial variables (interest rates, inflation, nominal exchange ratedepreciation) or their real counterparts (the real ex-ante interest rate, the real exchange rate,realized real depreciation, etc.). All responses are computed assuming complete informationin order to compare these results to other contributions in the NOEM literature. Finally, notethe presence of the UIP errors in the graphs: this simply refers to the difference betweeninterest rate differentials and realized depreciations, as in (1.4) and (1.5) under H0.

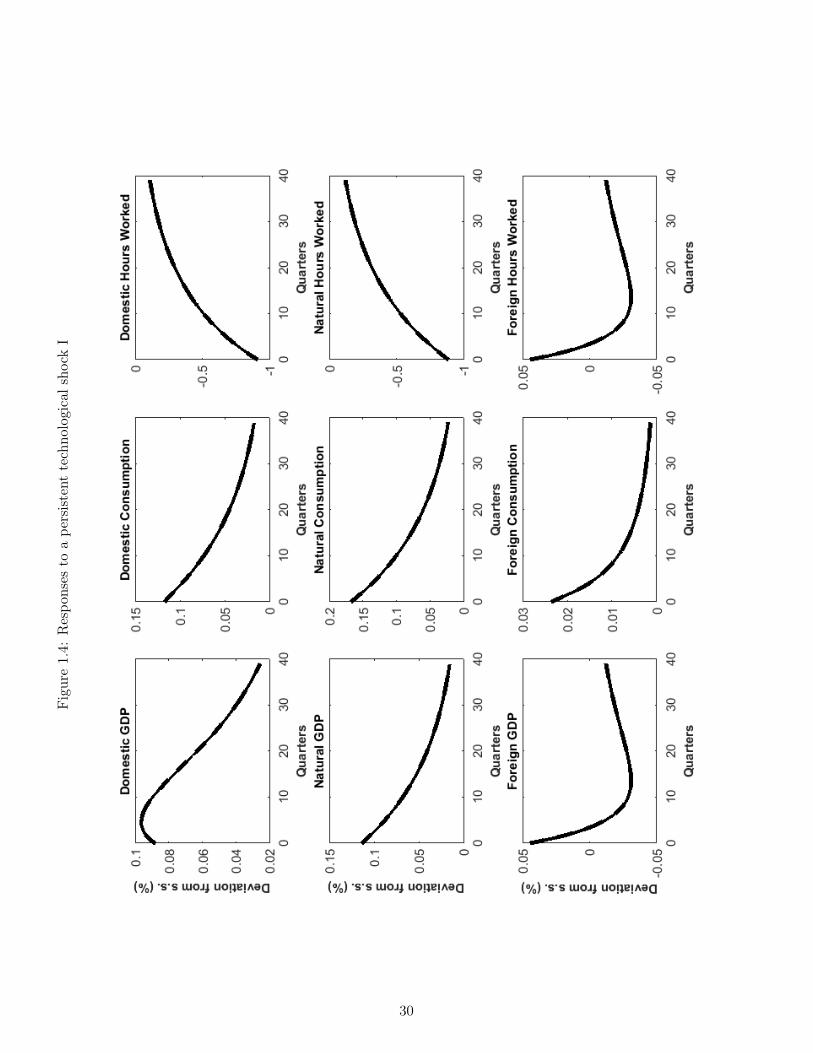

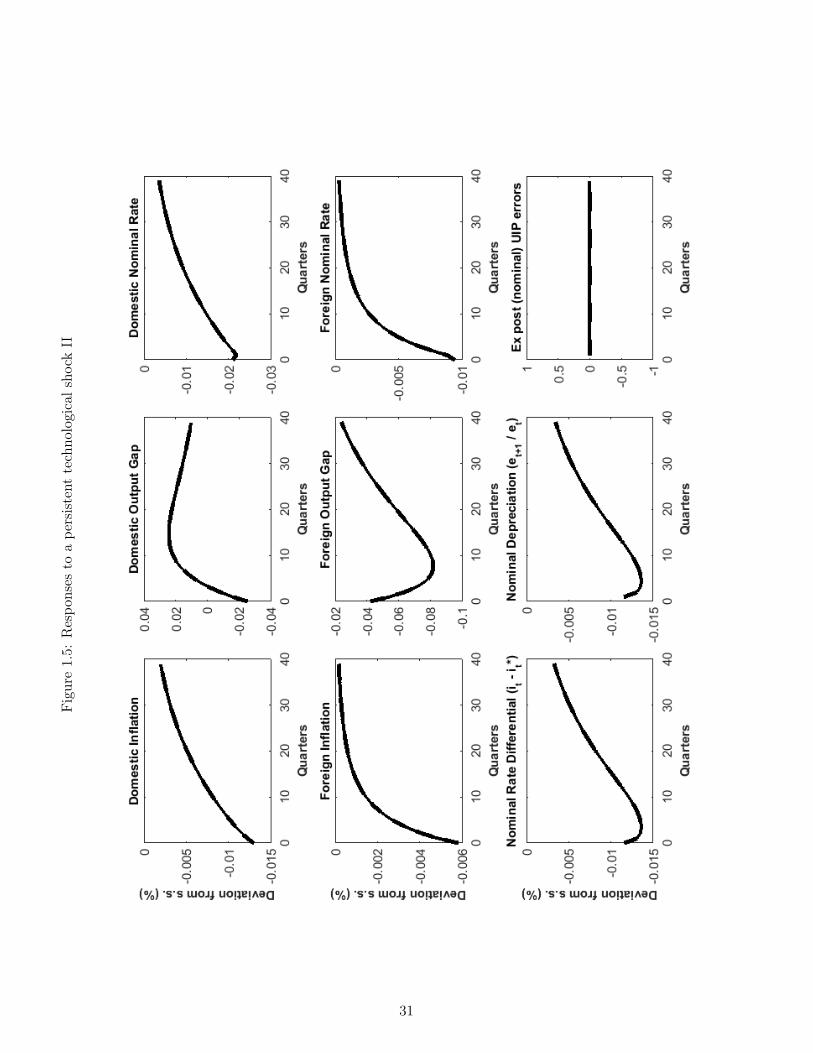

Next, Figures 1.4-1.6 record the responses following a favorable one percent persistent produc-tivity shock. Finally, Figures 1.7-1.9 display the dynamic properties of the economy arising

11These values are similar to those used in Corsetti et al. [2010], apart from the import share (which theycalibrate to a lower value).

13

from of a one percent negative persistent monetary policy shift. Recall that this entails adecline in at from (1.25) and thus such a shift implies that monetary authorities have loweredtheir target rate for inflation πt and that this decline will be persistent.

Monetary Policy Shocks

Figures 1.1-1.3 depict the economy’s response to a one percent (positive) transitory monetarypolicy shock (eεt). This represents a tightening of monetary policy in the domestic country;said otherwise, domestic monetary authorities choose a more aggressive stance than theirusual rule (1.21). Recall however that this aggressive stance will be short-lived, as we haveset the autocorrelation of monetary policy shocks φ1 to 0. Note also that when describingthe responses of the economy to the shock, both endogenous and exogenous aspects to themonetary policy rule (1.21) come into play: whereas the positive shock to (eεt) implies a tightermonetary policy, all things equal, the actual interest rate will continue to depend on inflationand the output gap through the endogenous coefficient ψπ.

The aggressive stance of the domestic monetary authorities increases both the domestic nom-inal interest rate, Figure 1.2, and the domestic real rate, Figure 1.3, because of the rigiditiesin the evolution of prices. Through its impact on consumption decisions, the increase in thereal ex-ante rate depresses domestic economic activity and thus labour demand, so that do-mestic consumption, hours worked and GDP decline on impact (Figure 1.1). Note that in thiseconomy monetary policy shocks can have real economic impacts only because of the pricerigidities’ presence. It is therefore not surprising that natural output, consumption and hoursworked do not react to the shock (Figure 1.1).12 Finally, note that as expected, the domesticmonetary tightening results in decreases in domestic inflation and the opening of a negativeoutput gap (Figure 1.2).

So far, the responses discussed are common to complete- and open-economy versions of theNew Keynesian model. We now discuss the transmission of the shock to international variables.The increase in domestic interest rates implies that all things equal, they will be higher thantheir international counterparts. Because UIP holds in the economy, this can only occur if anexpected path of currency depreciation opens up. Indeed positive interest rate differentials(between domestic rates and their foreign counterparts) manifest themselves, both measuredin nominal terms (Figure 1.2) and in real terms (Figure 1.3). Further, these interest ratedifferentials are accompanied by expected depreciations for the nominal and real exchangerate.13

12Recall that natural variables are computed by simulating responses from a “parallel” economy wherenominal rigidities are absent.

13Recall that our notation implies that an increase in the level of the exchange rate represents a depreciationof the domestic currency.

14

Because our open economy is relatively highly-integrated (recall our calibration of aF = 0.4)the shock also has important negative impacts on the foreign economy: Foreign GDP, hoursworked, and inflation all decline and a negative output gap also opens in the foreign econ-omy. Considering that the interest rate rule followed by the foreign monetary authority isof the same form as (1.21), the foreign interest rate responds to these depressed conditionswith a small decline. Finally, note that the real exchange rate appreciates on impact: thisoccurs because perfect risk sharing commands that this rate equal the ratio of domestic toforeign consumption, and domestic consumption has declined importantly. Said otherwise,the model rationalizes the fall in the foreign to domestic consumption ratio by increasing therelative price of domestic goods, ie. by appreciating the real exchange rate. As discussedabove, this contemporaneous, real appreciation is expected to undo itself in future periodsand the currency is thus expected to experience future depreciations. This pattern, whereby acontemporaneous real exchange rate appreciation is associated with future depreciations, realor nominal, is consistent with the classic Dornbush overshooting hypothesis and is discussedat length in Eichenbaum et al. [2017]. It will play a key role below when we discuss depar-tures from UIP under incomplete information. Here, under complete information, UIP holdsexactly however so that the positive interest rate differentials are exactly matched with thesubsequent depreciations and UIP errors are nil (Figure 1.2-Figure 1.3).

Technology Shocks

Next, Figures 1.4-1.6 report the impulse responses following a favourable shock to technology.Recall that such a shock is relatively persistent, as we calibrated λp to be 0.95. The shockmakes domestic goods cheaper to produce, so absent rigidities one would expect production andconsumption of these goods to increase and their relative price to decrease. Indeed, Figure 1.4does report that natural output and consumption increase. However, the presence of nominalrigidities means that domestic prices cannot decrease fast enough to accommodate this changein the relative competitiveness of domestic goods: as a result, one expects economic activityto initially increase by less than this new potential. Indeed, Figure 1.5 shows that a shortfallbetween realized and potential output opens up (ie. the domestic output gap is negative) inthe first few periods immediately after the onset of the shock.

Domestic monetary policy can compensate somewhat for the lack of flexibility in prices, byboosting money supply and reducing interest rates: Figure 1.5 shows this occurs to someextent, as the nominal and real domestic interest rates decrease; however, this is not enoughfor the output gap to be eliminated. Finally, as the favourable shock renders domestic goodscheap compared to foreign counterparts, the real exchange rate depreciates (Figure 1.6): assuch, it is up to the nominal exchange rate to make the necessary adjustments between therelative prices of domestic and foreign goods when actual money prices cannot change. Once

15

more, note that UIP continues to hold exactly: the negative differentials in interest rates areexactly matched by expected and realized depreciations and the UIP errors (Figure 1.5 - 1.6)are nil. Said otherwise, the contemporaneous real depreciation is associated with an expectedpath of future appreciations, a key negative correlation that is consistent with data [Burnsideet al., 2007] and that will imply departures from UIP under incomplete information, below.

Inflation Targets Shifts

Finally, Figure 1.7 through 1.9 display our open economy’s dynamic properties after a onepercent (negative) persistent monetary policy shock, ie. a decline in the long term inflationtarget of domestic monetary authorities. The sudden occurrence of this shift implies thatdomestic monetary authorities are now aiming for lower inflation and therefore will judgecurrent inflation in a more hawkish manner, tending to set higher interest rates, all thingsequal.14

In the short term this shift represents a tightening of domestic monetary policy and tends, allthings equal, to create a transitory economic slowdown in the domestic economy.15 This occursbecause of the monetary authority’s desire to have higher interest rates and the inflexibilityof domestic prices. This is illustrated in Figure 1.8 which shows that nominal domestic ratesdecrease but less, in magnitude, than domestic inflation, so that domestic real rates increase(Figure 1.9). This tightening creates a transitory economic slowdown in domestic productionand hours worked (Figure 1.7). The responses of the foreign monetary authorities are muchmore subdued, and a positive interest rate differential thus opens up when measured by the rateinterest rate (Figure 1.9) and is associated with future expected (and realized) depreciations.

Eventually however, the reality of a persistently lower rate of monetary expansion in thedomestic country starts to have beneficial long-term impacts and the direction of the economyreverses itself. Domestic output and hours worked become positive and stay above steady-state for several periods.16 Finally, as was the case for the other two shocks analysed above,UIP continues to hold: the differentials in interest rates are exactly matched by expected andrealized rates of appreciation or depreciation, so that the UIP errors in Figure 1.8 and Figure1.9 are nil.

14Recall that the shift is destined to be ultimately transitory, because sooner or later a new regime shift willcome to replace it; see (1.25). This creates a difficulty in graphing the impulse response function following theshift: how long should we make is persist? We solve this practical problem by producing the impulse responsefunction using the expected duration of the shift, which is governed by the parameter φ2.

15Recall that both the shift to the target and the monetary policy shock materialize themselves as increasesin the composite shock ut in (1.28). As such, the shift is a persistent version of the monetary policy tighteninganalyzed above in Figure 1.1-1.3.

16If the shift was truly permanent, these positive responses relative to the initial steady state would remain.

16

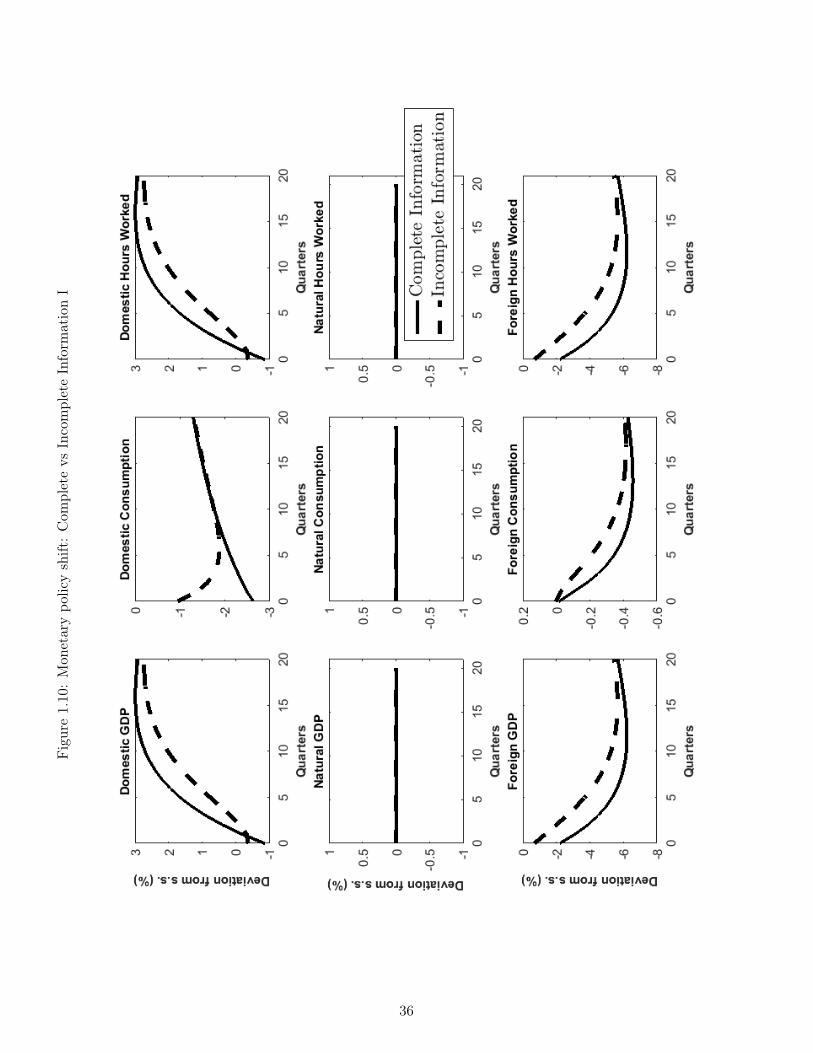

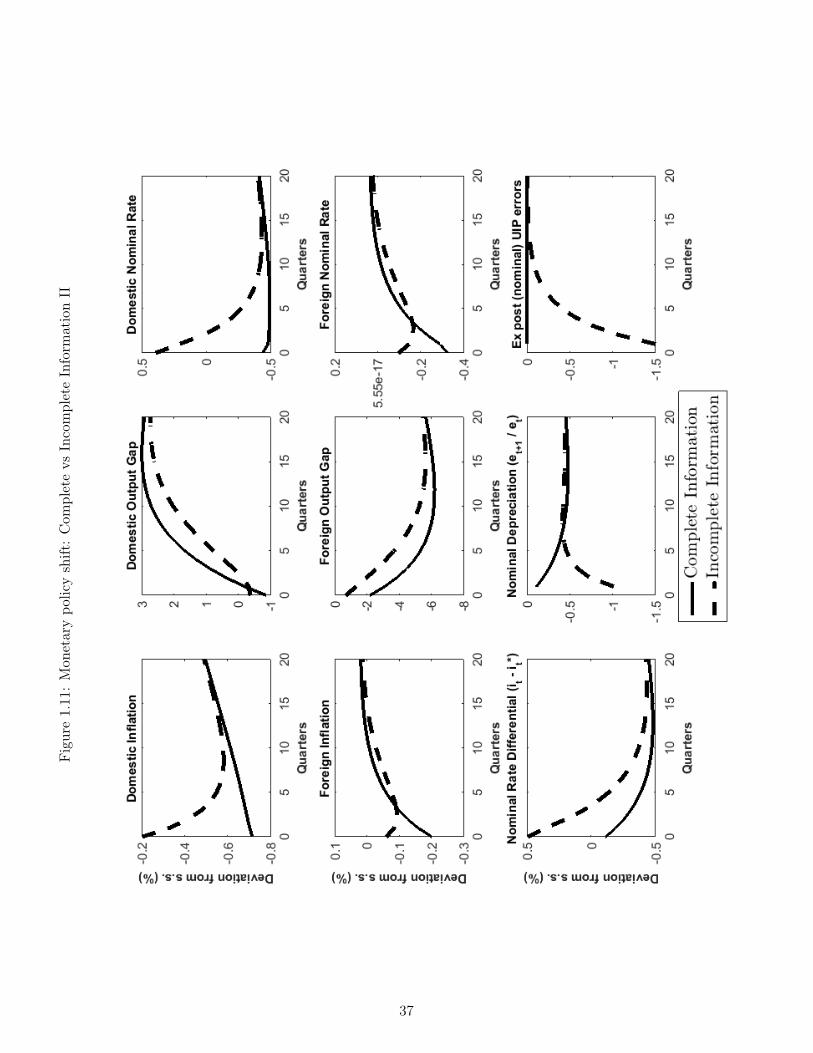

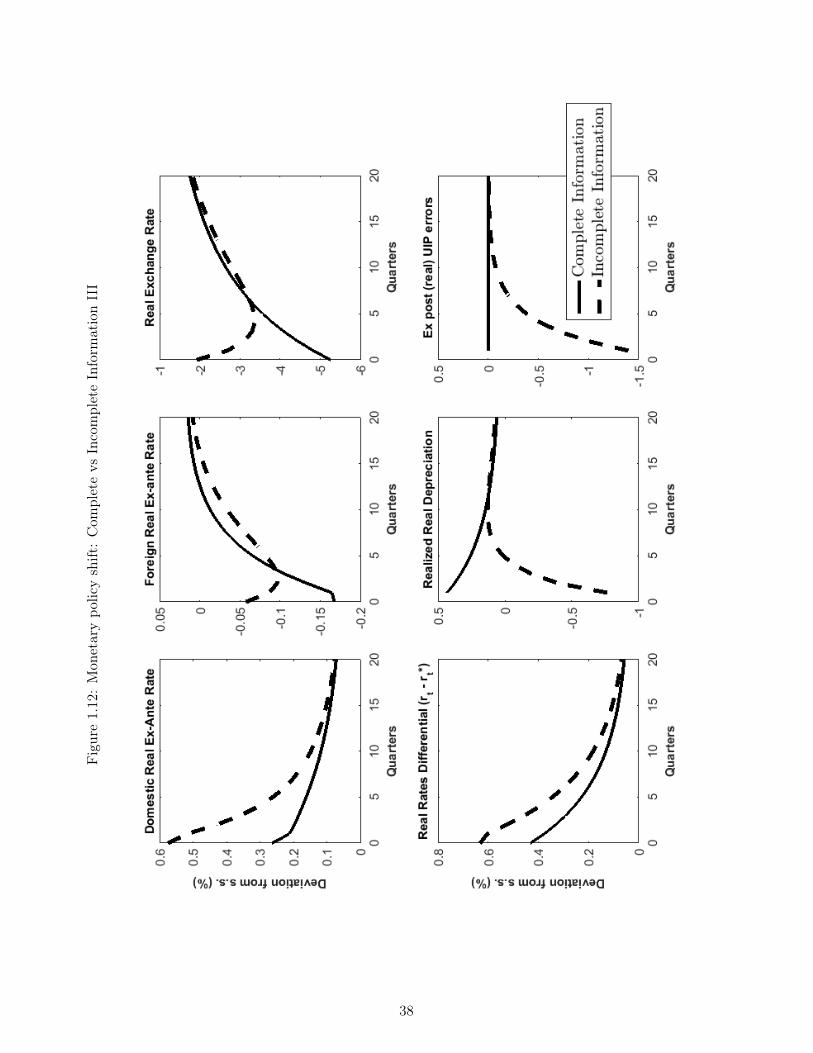

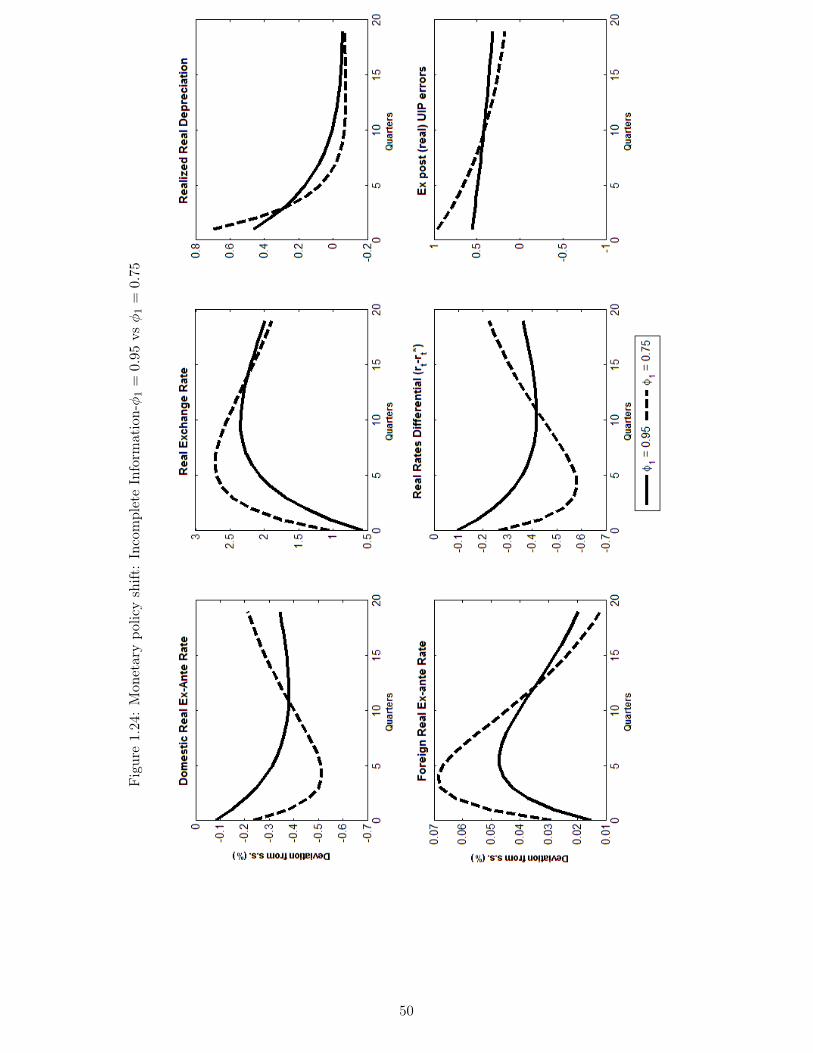

1.5.3 Impulse response functions: Complete versus incompleteinformation

We now contrast our economy’s responses to shocks under complete and incomplete informa-tion. To this end, we once again study the monetary policy shift described above, but nowintroduce the incomplete information responses. These arise when agents can only observethe composite monetary policy tightening ut in (1.28), but have to ascertain whether it oc-curred because of a temporary tightening (an increase in eεt) or because of a persistent declinein the inflation target (a decline in at). Under incomplete information, this learning occursvia a filtering mechanism; as such, agents will place positive probability weights on the eventthat the shift was transitory and will therefore be surprised, in subsequent periods, when thetightening persists. This surprise will then trigger departures from UIP.

Figure 1.10 - 1.12 report the impulse responses for both cases, where complete informationis displayed in full lines and incomplete information is in dashed lines.17 The key differencebetween the two cases is the perceived persistence of the tightening: full-information agentsknow it will be persistent, and thus price-setting reacts to a larger extent than it does underincomplete information, when agents view the shock as likely transitory. As a result, the con-temporaneous decline in inflation is substantial under complete information and very modestunder incomplete information.

This change of perception in turn modifies the rest of the economy’s responses. Since inflationhas declined substantially under complete information, monetary authorities’ new hawkishpreferences are satisfied and the nominal interest rates decreases (Figure 1.11) and the realrate increases only slightly (Figure 1.12). By contrast, the two figures show that under incom-plete information, monetary authorities react to the very mild decrease in inflation by furthertightening: the nominal rate actually increases, and the rise in the real rate is now substantial(Figure 1.12). Looking further, the harsher tightening under incomplete information also hasconsequences for the real economy: domestic consumption does not adjust fully to the newreality of a persistently lower inflation target, so the decline under incomplete informationis very small; this in turn implies that the real exchange rate (Figure 1.12), which shouldappreciate substantially, only does so modestly. The initial real exchange rate appreciationis expected to undo itself in subsequent periods, so agents expect future real depreciations,both under complete and incomplete information. On the nominal side, a similar story playsout: because of the price rigidities, the nominal rate does much of the adjusting and appre-ciates substantially (complete information) or just a little (incomplete information). Becausethe shock is expected to be very transitory under incomplete information, this appreciationis expected to undo itself and agents expect a nominal depreciation (a fact consistent withthe positive nominal interest rate differential - Figure 1.11). Under complete information bycontrast, agents know the shock will persist and the nominal exchange rate has already ad-

17The responses under complete information are the same as the ones displayed in Figures 1.4-1.6.

17

justed by a significant margin; as a consequence, they expect it to actually appreciate a littlein future periods, which is congruent with the negative interest rate differential in Figure 1.11.

The presence of incomplete information and gradual learning implies that the dashed linesin (Figure 1.10 - 1.12) reflect information that changes every period. Consider then whathappens in the second period: the persistent shift in the inflation target is still present, butagents under incomplete information, who considered it a transitory tightening, are surprised.In effect, this makes the second period on the graphs behave as if a further tightening shockoccurred. This entails that the UIP condition fails to hold with realized data: agents wereexpecting the depreciation announced by the initial tightening, but the second tightening nowimplies appreciating pressures on the real exchange rate. As a result, the real exchange ratedepreciates even further than its first-period state, which causes a substantial deviation fromUIP, as illustrated by the negative UIP “error” in Figure 1.12. In nominal terms, the nominalexchange rate, which agents expected to depreciate back to its original steady state afterthe first shock, further appreciates following this second, surprise bout of tightening. Takentogether, these two surprise imply that both UIP expressed in nominal terms (Figure 1.11)and in real terms (Figure 1.12) fails and the graph reports substantial deviations from thecondition. This pattern repeats itself in further periods, so that a third (and fourth and soon) surprise tightening episodes occur under incomplete information; however, both becauseagents are gradually learning about the shock’s type and because that shock itself is receding,responses from the incomplete and complete information cases gradually merge together.

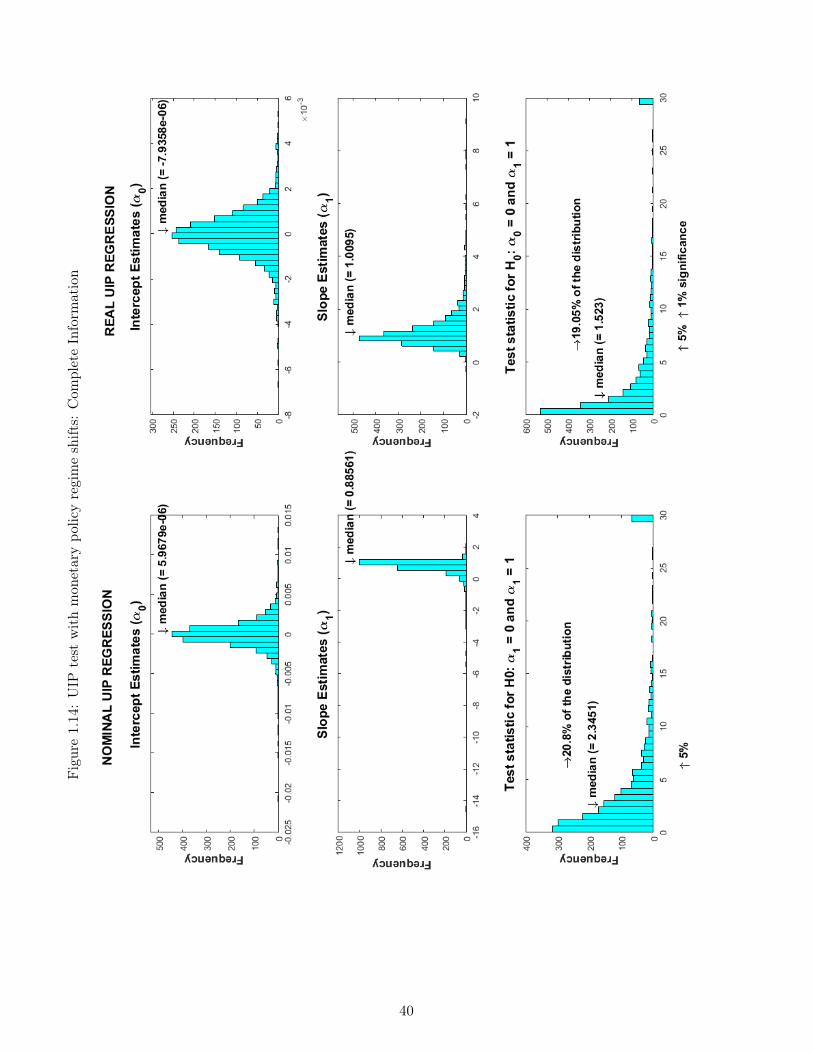

Figure 1.13 reports the UIP regressions implicit in the impulse responses in Figures 1.11-1.12. The figure depicts the combinations between interest rate differentials and realizedrates of depreciation, for the regression in nominal terms (left) and in real terms (right), andfor the cases of complete information (left panel) and incomplete information (right panel).As expected, for the complete information case, the theoretical regression (1.4) under H0,the actual regression line, and the scatter plot of the points all coincide perfectly. In theincomplete information case however, the substantial errors produced by the initial confusionbetween the transitory and persistent monetary policy shocks imply that over the 20-periodhorizon considered, the trajectory of interest rates differentials and realized depreciationsentails an estimated slope coefficient significantly lower than its value of 1 under H0. If thistype of gradual learning is pervasive in our model economy, such a pattern could be present insimulated data and thus contribute to generating regressions congruent with the UIP puzzle.

Table 1.1-1.2 below reproduce these results; the tables report the actual estimates for α0

and α1 in the regressions depicted graphically in Figure 1.13. As discussed, estimates undercomplete information coincide perfectly with the theoretical assumptions. In the incompleteinformation case, however, the results depart significantly from those predicted by the UIPcondition: for the regression run on nominal terms, the slope coefficient notably declinessubstantially and is around −0.43; for the regression run in real terms, this distortion is even

18

worse and the slope coefficient is close to −1.0.

Table 1.1: Baseline estimates for the UIP regression under Complete information

Estimates α0 α1

Nominal terms: Regressing (et+1 − et) on (it − it∗)Persistent shock 0 1Transitory shock 0 1

Real terms: Regressing (st+1 − st) on (rt − rt∗)Persistent shock 0 1Transitory shock 0 1

Table 1.2: Baseline estimates for the UIP regression under Incomplete information

Estimates α0 α1

Nominal terms: Regressing (et+1 − et) on (it − it∗)Persistent shock -0.5831 -0.4302Transitory shock 0.1483 1.4830

Real terms: Regressing (st+1 − st) on (rt − rt∗)Persistent shock 0.2684 -1.0223Transitory shock 0.1132 1.5850