Embed Size (px)

Citation preview

Three Dutch State Aid Cases: Technolease, Group Interest Box and Starbucks

Prof. Dr. Peter Essers

Constituent elements forbidden state aid (Art. 107 (1) TFEU)

• Any aid in any form whatsoever (economic advantage) • An advantage can be understood as any economic benefit which an undertaking would not have obtained under normal market conditions, namely in the absence of State intervention

• Granted by a Member State or through State resources • The State includes all public authorities such as the legislator, the judiciary, regional authorities, public or private bodies designated by the State to grant aid

• Which distorts or threatens to distort competition • Not only actual distortion of competition is targeted, but also potential distortion

• By favoring certain undertakings or the production of certain goods • Undertakings who engage in economic activities, regardless of their legal status and the way in which they are financed • Only selective measures (de jure or de facto) can be considered

• In so far as it affects trade between Member States • De minimis aid (the aid granted per Member State to a single undertaking does not exceed €200.000 over any period of three fiscal years) is in general no State aid

2

1. Technolease case Philips-Rabobank

3

Electrologica BV

Know How (2,18 billion; 31-12-1992) +

Shares (0,58 mld)

Loan 1,6 billion with 7% interest

Transfer of shares (0,6 billion cash; 30-11-1993)

Rabo Merchant Bank NV

Leasecontract with respect to know how

F.U

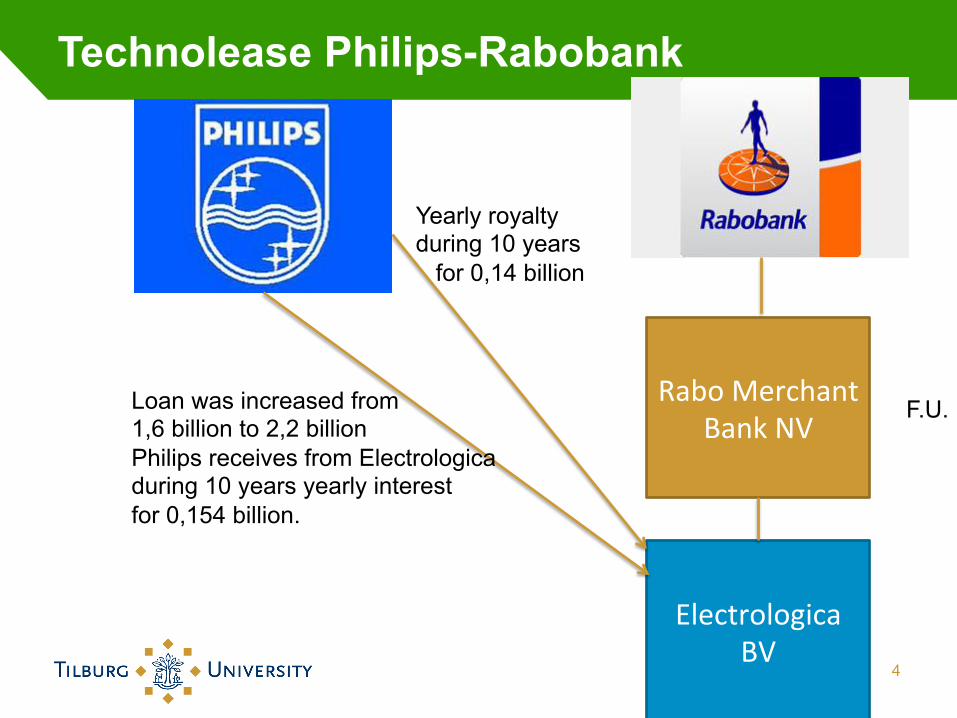

Technolease Philips-Rabobank

4

Electrologica BV

Rabo Merchant Bank NV

F.U. Loan was increased from 1,6 billion to 2,2 billion Philips receives from Electrologica during 10 years yearly interest for 0,154 billion.

Yearly royalty during 10 years for 0,14 billion

Additional information

• At the moment of the sale of the shares, the tax administration increased the value of the know how to 2,78 billion. As a result, the loan was increased to 2,2 billion.

• This loan had to be redeemed in 2005 either by transformation in shares in AK Electrologica BV or in cash

• After 10 years Rabo Merchant Bank NV had the right to sell back during 24 months the shares Electrologica BV to Philips for 50 million

• Electrologica BV was entitled to sub-license intangibles; Rabo Merchant Bank BV was entitled to 50% of the revenues of all sub-licenses granted since 1 January 1994

• Electrologica BV depreciates the know how degressively in 10 years. First 6 years: depreciation percentage of 25, in the last 4 years the remainder is depreciated in four equal terms

• If the sale of the shares had not occurred: Philips would have depreciated the know how in 4 years on the basis of a bookvalue of 2,2 billion

5

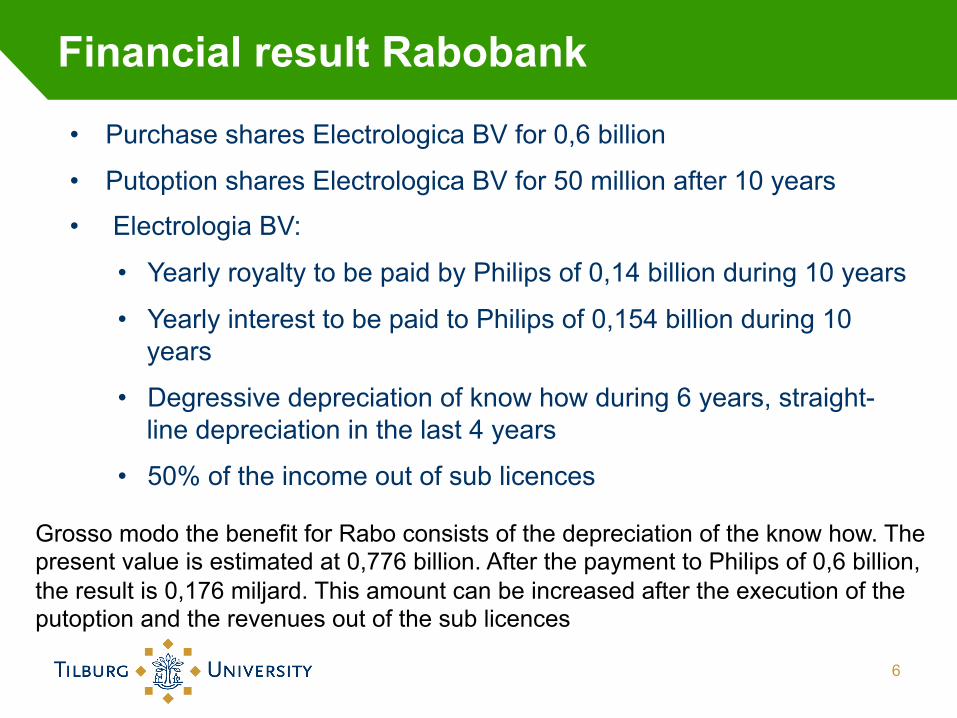

Financial result Rabobank

• Purchase shares Electrologica BV for 0,6 billion

• Putoption shares Electrologica BV for 50 million after 10 years

• Electrologia BV:

• Yearly royalty to be paid by Philips of 0,14 billion during 10 years

• Yearly interest to be paid to Philips of 0,154 billion during 10 years

• Degressive depreciation of know how during 6 years, straight-line depreciation in the last 4 years

• 50% of the income out of sub licences

6

Grosso modo the benefit for Rabo consists of the depreciation of the know how. The present value is estimated at 0,776 billion. After the payment to Philips of 0,6 billion, the result is 0,176 miljard. This amount can be increased after the execution of the putoption and the revenues out of the sub licences

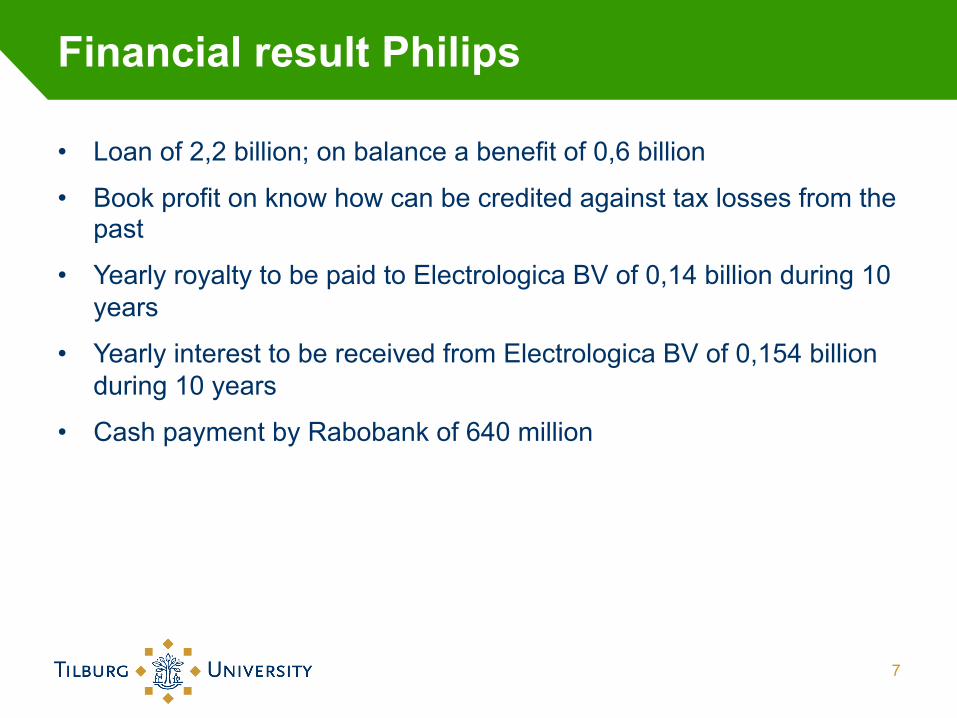

Financial result Philips

• Loan of 2,2 billion; on balance a benefit of 0,6 billion

• Book profit on know how can be credited against tax losses from the past

• Yearly royalty to be paid to Electrologica BV of 0,14 billion during 10 years

• Yearly interest to be received from Electrologica BV of 0,154 billion during 10 years

• Cash payment by Rabobank of 640 million

7

Decision European Commission 21 April 1999, C (1999) 1122

• After a thorough investigation of Dutch fiscal legislation and jurisprudence, the Commission found that the Netherlands' tax authorities did not exercise any discretionary power in the application of their general tax law to the technolease agreement

• Government interference was caused by the strong differences of opinions within the Tax Administration; Philips urged for legal certainty

• The general tax law had been applied

• The tax advantage of Rabobank was balanced against the tax disadvantage of Philips

• No revenue loss for the State

8

Some observations

• If before the sale of the shares, the economic lifetime of the know how for Philips was 4 years, why would Philips be willing to pay a royalty for the use of the know how for a period of 10 years? At arm’s length?

• What is the value of the put option after ten years? Was the 50 million realistic?

• Parties did expect revenues out of the sub licensing in the second part of the term of the contract. Realistic?

• De facto Philips had the exclusive right to use the know how in the first 4 years

• According to the Commission, at the moment of the technolease contract Philips did not have losses that could be compensated with profits. Also, the profit expectations for Philips were promising. Realistic?

• Should a ruling be granted if there are strong differences of opinion within the tax administration?

9 02/10/14

2. Group Interest Box case

• Group Interest Box was meant to reduce the different tax treatment of equity and debt within a group of companies and consequently the tax arbitrage leading to base erosion because of this different treatment

• If the received group interest exceeds the paid group interest: surplus is not taxed at the regular CIT-rate of 25,5% but at a rate of 5%; if the received group interest is lower than the paid group interest: deficit is deductible not at the regular CIT-rate of 25,5% but at 5%

• Several specific anti-abuse provisions • Group: parent should own more than 50% in subsidiary (later: de facto

control - direct or indirect - with respect to the financing of the subsidiary • First: only on a voluntary basis; later: compulsory • De jure (only companies being part of a group) and de facto (only

multinational entities benefit from this box): selectivity?

10

Decision European Commission 8 July 2009, C (2009) 4511

• With respect to debt financing activities: non-group companies are de jure and de facto not comparable with group companies

• Compulsory character guarantees that all group companies are treated equally

• No distinction should be made between national and cross-border situations • Specific regulations do not differ between national and cross-border

situations • Possible advantage is not caused by the low Dutch rate on received

interest but by the unlimited deduction in another country (which is also not financed by Dutch means)

• Enterprises are free to benefit from the different taxes in different countries

• Advantages are the result of disparities; they can not be considered in testing State aid rules

11

Some observations

• Group financing activities seem not to be selective

• State aid regulations seem not to be applicable with respect to regulations that benefit base erosion

• State aid regulations cannot be used to overcome disparities

• Consequences with respect to hybrid loans (interest deduction in debtor state, exemption in creditor state)?

12 02/10/14

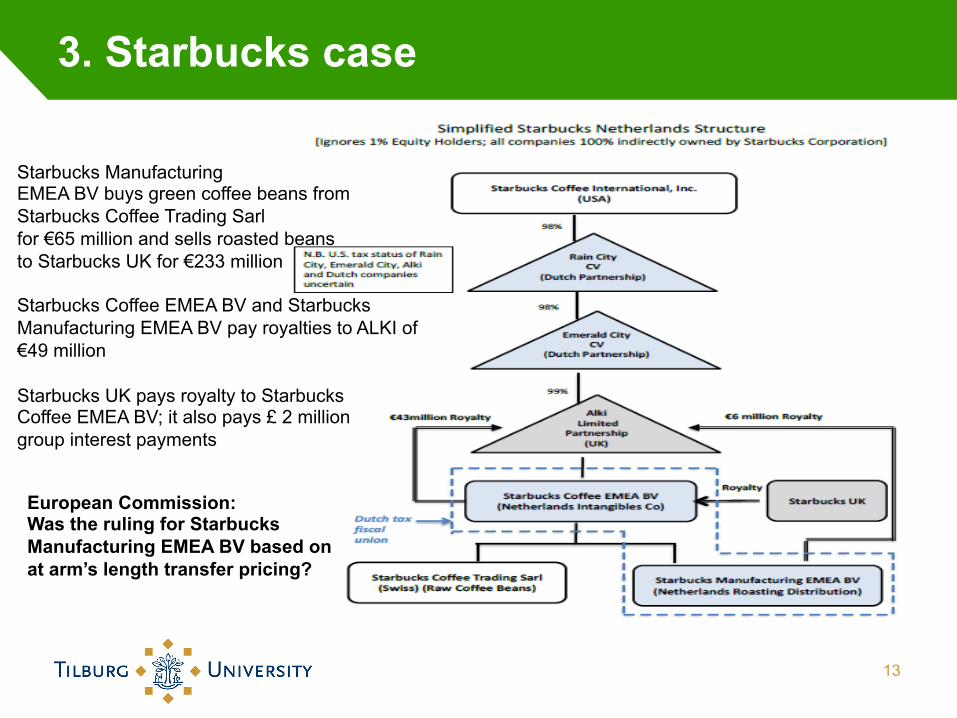

3. Starbucks case

13

Starbucks Manufacturing EMEA BV buys green coffee beans from Starbucks Coffee Trading Sarl for €65 million and sells roasted beans to Starbucks UK for €233 million Starbucks Coffee EMEA BV and Starbucks Manufacturing EMEA BV pay royalties to ALKI of €49 million Starbucks UK pays royalty to Starbucks Coffee EMEA BV; it also pays £ 2 million group interest payments European Commission: Was the ruling for Starbucks Manufacturing EMEA BV based on at arm’s length transfer pricing?

Some observations

• Very big difference between cost price of green coffee beans (€ 65 million) and the sales price for roasted coffee beans (€133 million). Total expenditures that year were only €17 million (salaries, depreciations and administrative costs). How to explain the other ‘costs’?

• Starbucks Coffee EMEA BV paid €342.000 CIT in the Netherlands • The royalty ruling (Starbucks Coffee EMEA BV) is apparently not

under investigation; however, is a royalty payment for a loss making license at arm’s length? Or wasn’t there a royalty ruling?

• Who is to blame? The UK, the Netherlands, Cayman Islands, US, Switzerland?

• Should the ruling be granted without taking into account the complete tax avoiding scheme of Starbucks?

14 02/10/14

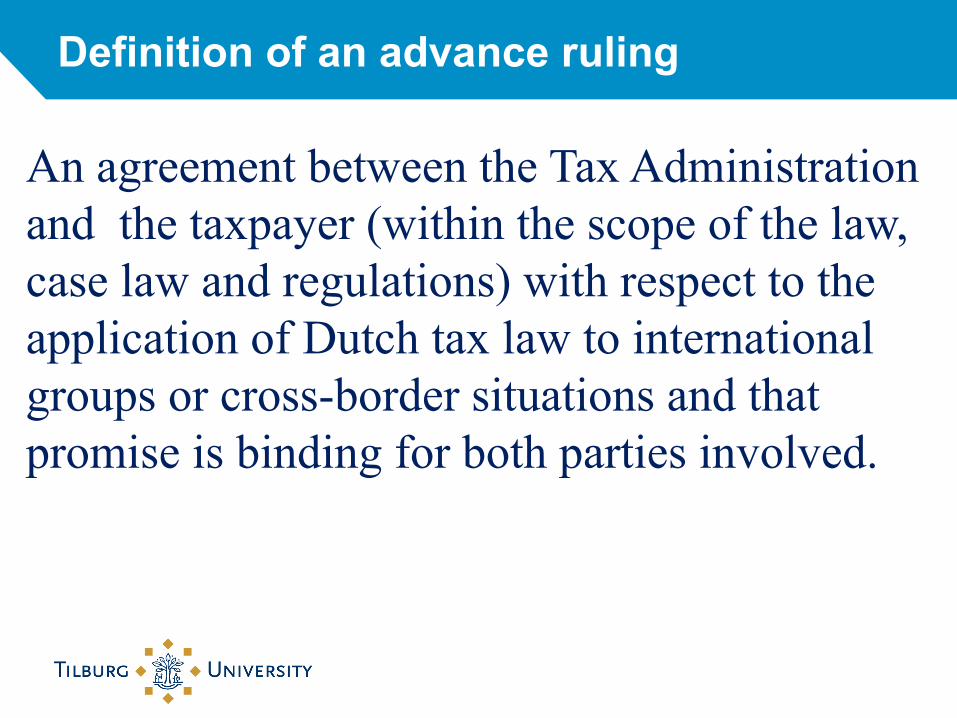

Definition of an advance ruling

An agreement between the Tax Administration and the taxpayer (within the scope of the law, case law and regulations) with respect to the application of Dutch tax law to international groups or cross-border situations and that promise is binding for both parties involved.

Advance rulings

• Why? • Based on General Principles of Sound Administration (trust and

equal treatment) • All relevant facts must be disclosed • No rulings in case of fraus legis, infringement of good faith • No standard rulings, only tailor made rulings; essentials are

published • Rulings are divided in Advance Tax Rulings (ATRs) and Advance

Pricing Agreements (APAs) • The input to be provided by the taxpayer has been increased:

more substance requirements • Rulingteam at Tax Inspectorate Large Enterprises in Rotterdam • Duration: normally four years • Reflection procedure

APA’s

• Holding ruling • Financial ruling • Royalty ruling • Cost-plus ruling • Resale-minus ruling • Informal capital ruling • Head office-p.e. allocation ruling

ATR’s as of 1 April 2001

• Participation exemption

• Hybrids (financial instruments and legal forms)

• Permanent establishment in the Netherlands

Horizontal Supervision

• Shift from retrospective and repressive control to mutual respect, trust and transparancy

• Pilot Horizontal Supervision: to improve the relationship between the Tax Administration and corporate taxpayers and also to increase efficiency

• Based on trust and Tax Control Framework

Enforcement Covenants

Titel presentatie in Footer 20 02/10/14

• Enforcement (Compliance) Covenants • Agreement between Tax Administration and

executive board of the company • Company partly takes over tax supervision and

presents proactively tax risks and tax planning in exchange of advance certainty and less compliance costs

• Tax inspector and taxpayer discuss current instead of past events: less need for time-consuming retrospective audits by the Tax Administration or tax procedures

Advantages and Threats to Taxpayers ADVANTAGES • Less compliance costs • Less audits and questions • Reduction of tax advisory costs • Less tax procedures • Working in the present instead of in the past • More and sooner legal certainty

THREATS • More dependent on tax inspector • High-risk (if covenant is cancelled) • No optimal tax structures • Sooner tax assessments • Internal bureaucracy

Advantages and Threats to Tax Advisors

ADVANTAGES • Improvement of the quality of advices • Less procedures • More possibilities preliminary talks with tax inspector • Less liability risks THREATS • Less possibilities for exploring the boundaries of the law • More dependent on the tax inspector • More dependent on internal procedures of clients

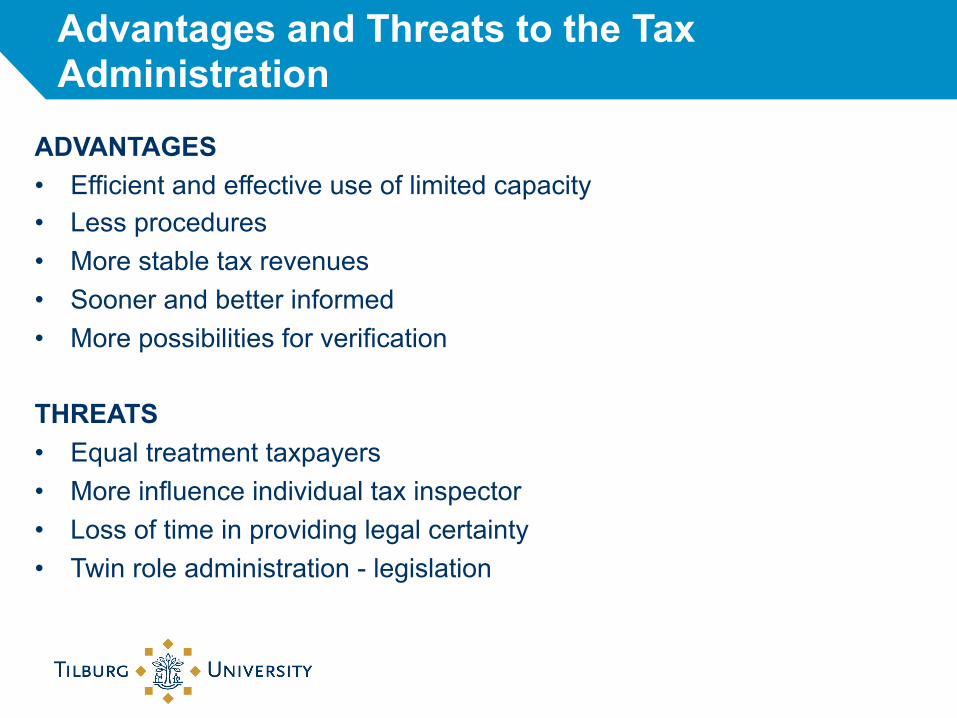

Advantages and Threats to the Tax Administration

ADVANTAGES • Efficient and effective use of limited capacity • Less procedures • More stable tax revenues • Sooner and better informed • More possibilities for verification THREATS • Equal treatment taxpayers • More influence individual tax inspector • Loss of time in providing legal certainty • Twin role administration - legislation

Advantages and Threats to the Legislator

ADVANTAGES • Less damage control legislation • Less legislative urgency • More attention for quality of laws • More attention for equality principle

THREATS • Taxation and legislation could become disconnected (‘fair share’

versus ‘fair play’) • Less incentives to amend laws or to implement new laws • Increased dominance of Ministry of Finance

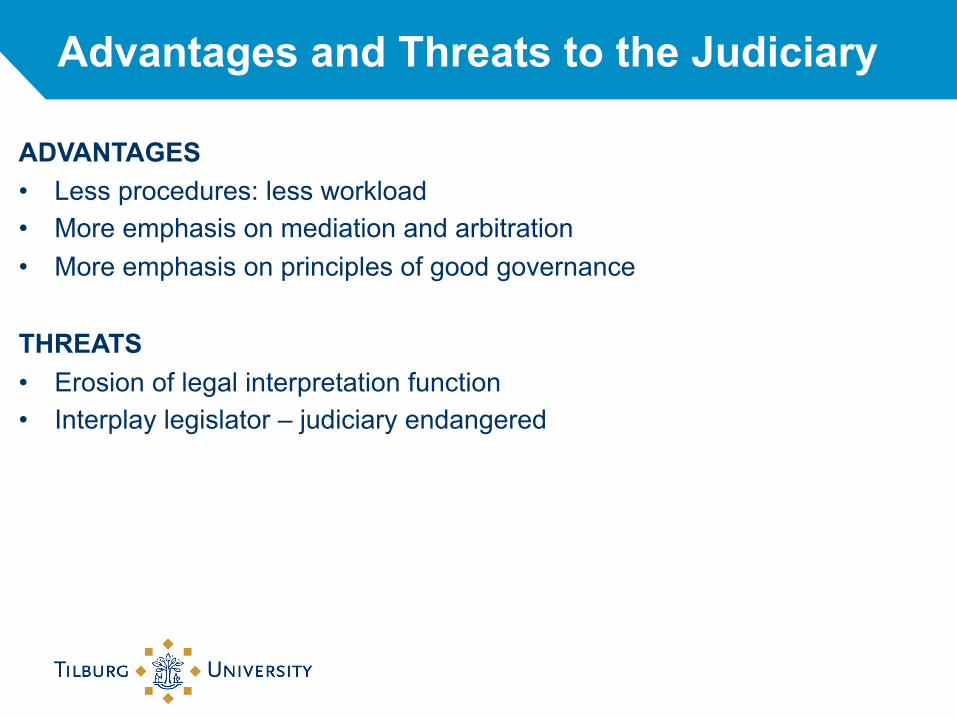

Advantages and Threats to the Judiciary

ADVANTAGES • Less procedures: less workload • More emphasis on mediation and arbitration • More emphasis on principles of good governance

THREATS • Erosion of legal interpretation function • Interplay legislator – judiciary endangered

Conclusions with respect to Horizontal Supervision

• Horizontal supervision has positive and negative aspects

• Dutch tradition and experiences promising for potential success

• Relationships within Trias Politica will change

• Increased need for supervision and monitoring of Ministery of Finance/Tax Administration

• Enforcement covenants might become the most important tax asset of the Netherlands