Embed Size (px)

Citation preview

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 115

Thoughts from a Renaissance manWhen will the EM FX sell-off be complete

Thoughts from aRenaissance manEconomics amp Strategy

28 September 2015

We see more downside in EM currencies into 2016 before low valuations improved CAs andhigher FDI change the trend We think frontier FX looks vulnerable too following EM

The BRL is not even close to its previous weakest level

A misleading headline is the necessary incentive for this economist to begin a rant which (a little surprisingly) has produced some

useful conclusions The headline referred to the BRL hitting record lows which is factually correct in nominal terms but is as

irrelevant as elderly folk (who I generally like) telling us they could buy a mansion in our financial capital city for the equivalent of

$10000 back in the 1970s Once we adjust for inflation the BRL was in fact far weaker in 2001-2002 The BRL would need to

be BRL6$ to truly be at a record low Similar applies to Russia where the RUB would need to be RUB114$ to be the equivalent

of the record weakest level of January 1999 ZAR152$ for SA TRY426$ for Turkey or INR100$ in India while in frontier we

would need to see PKR135$ in Pakistan KES266$ in Kenya or NGN618$ in Nigeria (the NGN level in 1995 once we adjust for

inflation ndash see page 3 for more explanation)

We assume more currency weakness leading to a big shift in fundamentals

EM investors of course want to see an end to the EM FX sell-off so we want to believe misleading headlines implying the bottom is nearBut while we reckon the aggressive sell-off over the summer is a little overdone in the short term we suspect second-round effects will send

many currencies weaker still into 2016 We expect external debt defaults to hit EM financials and corporates and higher import prices will

feed into weaker domestic demand and hurt GDP Economic stagnation and rising unemployment may feed the political limbo in Turkey

the impeachment talk in Brazil or lead to demonstrations elsewhere And this is leaving aside the impact on the West JCBrsquos and

Caterpillars decisions last week to make thousands redundant will not be the last time we see western companies react to EM

weakness Lastly we still have concerns about a US recession adding a leg down to commodities and global demand

Yet currency weakness is changing economic fundamentals and if it continues we think there will be a dramatic impact on EM

economies FX weakness is already helping Russiarsquos budget and CA boosting Turkeyrsquos exports to Europe and cutting SArsquos CA

to just 3 of GDP in 2Q15 Cheap EM exports will undercut higher cost production in the West and encourage western companies

to put FDI into EM either to sell into domestic markets or export back to the West itself The model of domestic consumption will

shift towards investment and export-led growth in our opinion

China has taken the lead here this reflects the big CNY appreciation against the RUB TRY and BRL From 0-1 of total FDI into

Russia over 2007-2013 and a peak of $06bn in 2013 we have seen Chinarsquos share rise to 6 ($13bn) in 2014 and 12 ($02bn)

in 1Q15 Chinese FDI into Turkey ranged from $0-10mn annually from 2002-2013 was $29mn in 2014 but over January-July

2015 has jumped to $434mn and could top $1bn this year (in a bank electricity and a port) Chinarsquos FDI to Brazil averaged $84mn

annually from 2001-2013 but in 2014 rose tenfold to $840mn Unfortunately SA does not produce FDI data

FX conclusions

REER calculations suggest Egyptrsquos currency should be closer to EGP10$ and with Peru and India constitute the three most

vulnerable to FX weakness in EM In EEMEA the ZAR is nearest to a record low The RUB is far stronger than its 1999 low but is

cheaper than its 20-year average REER implied rate of RUB59$ and is supported by a decent CA surplus Turkey is only a little

cheaper than its 20-year average of TRY287$ and far stronger than the TRY426$ lows The lira probably has further to go over

2016-2018 given our concerns over private sector debt Central European currencies are around long-term fair value in our view

In frontier Kenya looks most exposed to us with KES152$ implied by 20-year averages followed closely by Nigeria (NGN285$)

Bangladesh and perhaps Vietnam Morocco and Romania look closer to fair value while Kazakhstan is cheapest within 1 of its

all-time weakest level Of the Gulf currencies we think Oman looks most vulnerable to a devaluation

copy 2015 Renaissance Securities (Cyprus) Limited All rights reserved Regulated by the Cyprus Securities and Exchange Commission (Licence No KEPEY 05304)Hyperlinks to important information accessible at wwwrencapcom Disclosures and Privacy Policy Terms amp Conditions Disclaimer

Charles Robertson+44 (207) 367-8235CRobertsonrencapcom

Mobile +44 7747 118 756

RenCapMan

Vikram Lopez+44 (203) 379-7974 x8974

VLopezrencapcom

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 215

2

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

EM investors we meet are feeling pretty downbeat We spend more time discussing the

Syrian refugee crisis and the UK premierrsquos alleged predilection for roast pork than we do

discussing Russian inflation figures or SArsquos CA

The reason is obvious as Dan Salter pointed out in his Hindsight is a wonderful thing report published 13 April 2015 currency return is the second most important determinant

of total investor return ndash and currencies are getting crushed The BRL has collapsed from

BRL225$ in mid-2014 through BRL300$ in early 2015 and beyond BRL400$ in 3Q15

The ZAR has also been a very naughty currency breaking out (to the weaker side) of

what had become a relatively predictable four-year bearish channel

Figure 1 ZAR vs $

Source Bloomberg

Despite modest geopolitical improvements in Ukraine the RUB managed to lose all its

1H15 gains and weaken to beyond where it was in January when fighting was surging inUkraine and the US feared a Russian assault to create a land bridge to Crimea While all

of the above could be attributed in part to Chinarsquos slowdown and commodity prices

Turkey which should be a key beneficiary has seen its currency weaken sharply too

This recent currency weakness feels a litt le overdone to us in the short term but we doubt

the multi-year trend is over

We have yet to see the second-round effect of this currency weakness We expect to see

sovereign corporate or financial defaults on external debt as we explained in About that

1982 debt default published 4 September 2015 Weaker GDP could also intensify

problems domestically too via bank or corporate failures and rising unemployment

Politics represents a third threat via impeachment in Brazil political limbo in Turkey andthe risk of demonstrations against the authorities due to economic factors (such as the

wage disputes in SA over recent years) It is hard after over a decade in power to blame

economic problems on external factors alone

Indeed three of the four major EM currencies shown in the following chart are nowhere

near the lows seen in the five-year wake of the Asian crisis of 1997 Default weak GDP

and politics as well as the threat of a US recession (see our 13 January 2015 report SampP

500 at 1100 by March 2016) taking away a key leg in the global growth story could all

push EM currencies weaker still However after three-to-four years of REER depreciation

we think we might now be within a year or two of the bottom

6

7

8

9

10

1112

13

14

15

J a n - 1 1

F e b - 1 1

A p r - 1 1

J u n - 1 1

J u l - 1 1

S e p - 1 1

N o v - 1 1

D e c - 1 1

F e b - 1 2

M a r - 1 2

M a y - 1 2

J u l - 1 2

A u g - 1 2

O c t - 1 2

D e c - 1 2

J a n - 1 3

M a r - 1 3

M a y - 1 3

J u n - 1 3

A u g - 1 3

O c t - 1 3

N o v - 1 3

J a n - 1 4

M a r - 1 4

A p r - 1 4

J u n - 1 4

A u g - 1 4

S e p - 1 4

N o v - 1 4

J a n - 1 5

F e b - 1 5

A p r - 1 5

J u n - 1 5

J u l - 1 5

S e p - 1 5

Rand breaks out

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 315

3

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

Figure 2 EM currencies ndash REER (Dec 2007 = 100)

Note Bruegel uses CPI to adjust the index we have not made any CPI adjustment for June to September 2015

Source Bruegel Renaissance Capital (June to September 2015)

We need to explain the figure above and those below We have taken the REER numbersfrom Bruegel ndash which strips out consumer price inflation (CPI) from main trading partnersand the countries themselves ndash to give the ldquorealrdquo picture of currency valuation So while theBRL may now be weaker against the dollar than it was in 2002 there has been so muchmore inflation in Brazil than the US that comparing the exchange rate in 2002 and 2015really tells us very little The same applies to Nigeria Nigerias currency has never been asweak as NGN618 against the dollar but what the REER does is let us estimate what theNGN would have been in 1995 in todays money And the answer is NGN618

Note the Bruegel estimates stop in May 2015 ndash so for June to September 2015 we have

adjusted the index figure by currency moves but not by inflation This probably distorts the

figures by a percent or two but we donrsquot think this is significant enough to matter

So if we look at MSCI EM the graph below shows the highest REER rate a currency has

seen the lowest rate the May 2015 figure which is the last accurate REER reading and the

currency price on 22 September 2015 Lastly we add the long-term average REER rate

Colombia has a currency that is actually at its REER lows and well below its long-term

average Greece Chile and Taiwan also look competitive relative to their own histories

Countries on the left from Egypt to China to the Gulf countries are close to the strongest

they have ever been

Figure 3 Latest REER vs all-time high and low (Dec 2007 = 100) in MSCI EM

Source Bruegel Bloomberg Renaissance Capital

40

50

60

70

80

90

100

110

120

130

140

1 9 9 5 M 0 1

1 9 9 5 M 0 9

1 9 9 6 M 0 5

1 9 9 7 M 0 1

1 9 9 7 M 0 9

1 9 9 8 M 0 5

1 9 9 9 M 0 1

1 9 9 9 M 0 9

2 0 0 0 M 0 5

2 0 0 1 M 0 1

2 0 0 1 M 0 9

2 0 0 2 M 0 5

2 0 0 3 M 0 1

2 0 0 3 M 0 9

2 0 0 4 M 0 5

2 0 0 5 M 0 1

2 0 0 5 M 0 9

2 0 0 6 M 0 5

2 0 0 7 M 0 1

2 0 0 7 M 0 9

2 0 0 8 M 0 5

2 0 0 9 M 0 1

2 0 0 9 M 0 9

2 0 1 0 M 0 5

2 0 1 1 M 0 1

2 0 1 1 M 0 9

2 0 1 2 M 0 5

2 0 1 3 M 0 1

2 0 1 3 M 0 9

2 0 1 4 M 0 5

2 0 1 5 M 0 1

2 0 1 5 M 0 9

Brazil Turkey Russia South Africa

WEAKER

STRONGER

0

20

40

60

80

100

120

140

160180

E g y p t

C h i n a

Q a t a r

P h i l i p p i n e s

U A E

P e r u

I n d i a

T h a i l a n d

T a i w a n

I n d o n e s i a

C z e c h

C h i l e

G r e e c e

K o r e a

M a l a y s i a

P o l a n d

H u n g a r y

M e x i c o

S A f r i c a

R u s s i a

T u r k e y

C o l o m b i a

B r a z i l

Estimated current REER REER High REER Low REER May 2015 LT Avg REER

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 415

4

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

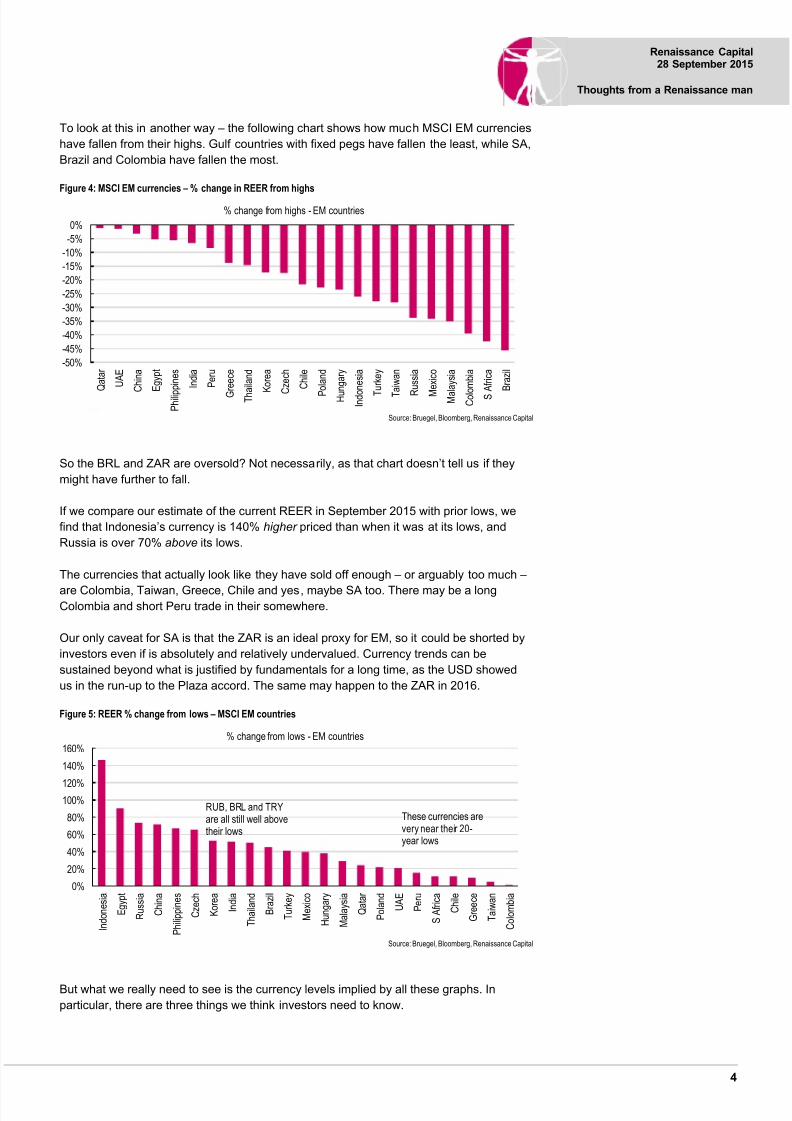

To look at this in another way ndash the following chart shows how much MSCI EM currencies

have fallen from their highs Gulf countries with fixed pegs have fallen the least while SA

Brazil and Colombia have fallen the most

Figure 4 MSCI EM currencies ndash change in REER from highs

Source Bruegel Bloomberg Renaissance Capital

So the BRL and ZAR are oversold Not necessarily as that chart doesnrsquot tell us if they

might have further to fall

If we compare our estimate of the current REER in September 2015 with prior lows we

find that Indonesiarsquos currency is 140 higher priced than when it was at its lows and

Russia is over 70 above its lows

The currencies that actually look like they have sold off enough ndash or arguably too much ndash

are Colombia Taiwan Greece Chile and yes maybe SA too There may be a longColombia and short Peru trade in their somewhere

Our only caveat for SA is that the ZAR is an ideal proxy for EM so it could be shorted by

investors even if is absolutely and relatively undervalued Currency trends can be

sustained beyond what is justified by fundamentals for a long time as the USD showed

us in the run-up to the Plaza accord The same may happen to the ZAR in 2016

Figure 5 REER change from lows ndash MSCI EM countries

Source Bruegel Bloomberg Renaissance Capital

But what we really need to see is the currency levels implied by all these graphs In

particular there are three things we think investors need to know

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

Q a t a r

U A E

C h i n a

E g y p t

P h i l i p

p i n e s

I n d i a

P e r u

G r e e c e

T h a i l a n d

K o r e a

C

z e c h

C h i l e

P

o l a n d

H u n g a r y

I n d o

n e s i a

T

u r k e y

T a i w a n

R

u s s i a

M

e x i c o

M a l a y s i a

C o l o

m b i a

S A f r i c a

B r a z i l

change from highs - EM countries

0

20

40

60

80

100120

140

160

I n d o n e s i a

E g y p t

R u s s i a

C h i n a

P h i l i p p i n e s

C z e c h

K o r e a

I n d i a

T h a i l a n d

B r a z i l

T u r k e y

M e x i c o

H u n g a r y

M a l a y s i a

Q a t a r

P o l a n d

U A E

P e r u

S A f r i c a

C h i l e

G r e e c e

T a i w a n

C o l o m b i a

change from lows - EM countries

These currencies arevery near their 20-year lows

RUB BRL and TRYare all still well abovetheir lows

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 515

5

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

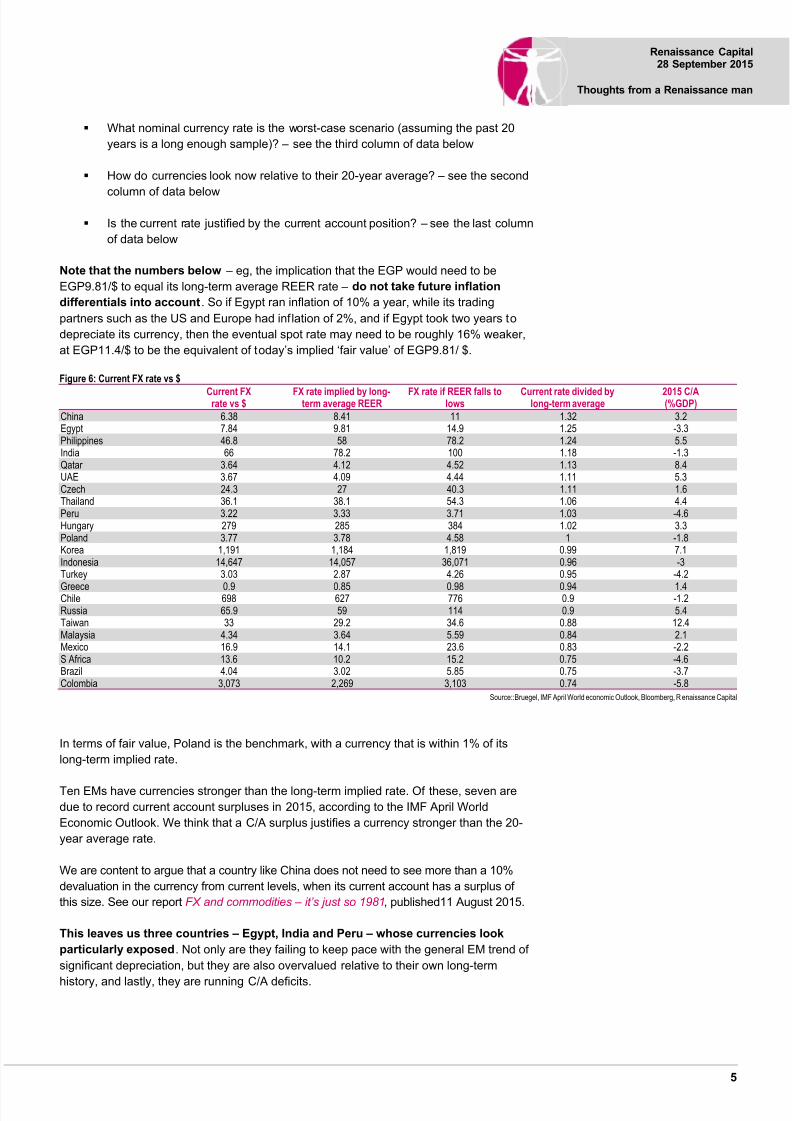

What nominal currency rate is the worst-case scenario (assuming the past 20

years is a long enough sample) ndash see the third column of data below

How do currencies look now relative to their 20-year average ndash see the second

column of data below

Is the current rate justified by the current account position ndash see the last column

of data below

Note that the numbers below ndash eg the implication that the EGP would need to be

EGP981$ to equal its long-term average REER rate ndash do not take future inflation

differentials into account So if Egypt ran inflation of 10 a year while its trading

partners such as the US and Europe had inf lation of 2 and if Egypt took two years to

depreciate its currency then the eventual spot rate may need to be roughly 16 weaker

at EGP114$ to be the equivalent of todayrsquos implied lsquofair valuersquo of EGP981 $

Figure 6 Current FX rate vs $

Current FXrate vs $

FX rate implied by long-term average REER

FX rate if REER falls tolows

Current rate divided bylong-term average

2015 CA(GDP)

China 638 841 11 132 32Egypt 784 981 149 125 -33Philippines 468 58 782 124 55India 66 782 100 118 -13Qatar 364 412 452 113 84UAE 367 409 444 111 53Czech 243 27 403 111 16Thailand 361 381 543 106 44Peru 322 333 371 103 -46Hungary 279 285 384 102 33Poland 377 378 458 1 -18Korea 1191 1184 1819 099 71Indonesia 14647 14057 36071 096 -3Turkey 303 287 426 095 -42

Greece 09 085 098 094 14Chile 698 627 776 09 -12Russia 659 59 114 09 54Taiwan 33 292 346 088 124Malaysia 434 364 559 084 21Mexico 169 141 236 083 -22S Africa 136 102 152 075 -46Brazil 404 302 585 075 -37Colombia 3073 2269 3103 074 -58

SourceBruegel IMF April World economic Outlook Bloomberg R enaissance Capital

In terms of fair value Poland is the benchmark with a currency that is within 1 of its

long-term implied rate

Ten EMs have currencies stronger than the long-term implied rate Of these seven are

due to record current account surpluses in 2015 according to the IMF April World

Economic Outlook We think that a CA surplus justifies a currency stronger than the 20-

year average rate

We are content to argue that a country like China does not need to see more than a 10

devaluation in the currency from current levels when its current account has a surplus of

this size See our report FX and commodities ndash itrsquos just so 1981 published11 August 2015

This leaves us three countries ndash Egypt India and Peru ndash whose currencies look

particularly exposed Not only are they failing to keep pace with the general EM trend of

significant depreciation but they are also overvalued relative to their own long-term

history and lastly they are running CA deficits

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 615

6

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

On the other side of the equation ndash Taiwan Russia Malaysia Greece and Korea

look relatively good value These currencies may be considerably more expensive than

their historical lows ndash Russia would need to see RUB114$ to equal January 1999 ndash but

each has a CA surplus and each is cheaper than their long-term 20-year average In

Greecersquos case ndash given it has the euro ndash this simply means that Greece is roughly 6more competitive today than it has been for most of the past 20 years which is a modest

positive for company earnings In Greecersquos case we do not see that as offsetting the

damage that may be done by the ideologically anti-market Syriza government

Taiwan and Korea look like strong buys from a currency perspective but they do have to

compete with Japan which at the current JPY1205$ is around its all-time low of

JPY1225$ Any bounce for these two would presumably require a stronger yen

For SA we would now expect to see the CA improve more than the 46 of GDP that the

IMF expected in April 2015 Indeed the 2Q15 figure was around 3 of GDP We think

similar improvement is likely in Brazil Colombia and Mexico

What about frontier

Below we analyse 12 countries in MSCI Frontier plus Saudi Arabia Iran and Georgia

What jumps out first is that so many of them have a currency level that is very near their

20-year record strongest level Frontier FX has clearly not depreciated in line with EM FX

A number of factors may explain this First frontier markets are less globally integrated

than EM so we might expect them to react later Second their financial markets are far

more shallow which means it is easier for the authorities to resist market pressure ndash even

if economic fundamentals tell us this may not be the right policy stance to take It also

means that it does not take much money in the way of foreign aid or IMF support to keepa currency stable Third perhaps the underlying economic structure in frontier markets is

changing more than in emerging markets so their current exchange rates should not be

compared with their history We are however sceptical about that excuse Fourth frontier

markets tend to be poorer than EM countries so REER measures may not be as

applicable (see below) Fifth a few of these countries such as Kuwait (off-index) Saudi

Arabia Bahrain and Oman have historical pegs that have not changed much in 20 years

or more bolstered by large sovereign wealth funds (less true of Oman)

Figure 7 A number of Frontier and Beyond Frontier markets are near their strongest levels of the past 20 years

Note Argentinas strongest point was 250 which is off the scaleSource Bruegel Bloomberg Renaissance Capital

0

20

40

60

80

100

120

140

160

180

B a n g l a d e s h

V i e t n a m

S a u d i A r a b i a

I r a n

N i g e r i a

O m a n

K e n y a

K u w a i t

P a k i s t a n

S r i L a n k a

M o r o c c o

G e o r g i a

R o m a n i a

A r g e n t i n a

K a z a k h s t a n

Latest REER vs all-time high and low (Dec 2007 = 100) - selected Frontier countriesEstimated current REER REER High REER Low REER May 2015

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 715

7

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

Only Morocco Argentina and Kazakhstan are at or near their lows ndash but we are sceptical

about Argentinean data The IMF does not trust Argentinarsquos inflation data so if Bruegel is

using Argentinarsquos official inflation figures these are likely to distort their calculations More

positively Kazakhstan looks a particularly interesting investment given these graphs

Figure 8 REER change from strongest level ndash MSCI FM

Source Bruegel Renaissance Capital Bloomberg

Even more dramatic is when we compare the currency levels today with the lowest levels

seen over the past 20 years

Nigeria still has a very strong currency which we think is hurting the Nigerian economy ndash

see Yvonne Mhangorsquos report The cost of defending NGN199$1 from 11 September

2015 We doubt that improved fiscal management can do enough to support this Former

central bank governor Lamido Sanusi estimated that Nigeria was losing about $20bn over

2011-2013 due to theft from the budget or roughly $6-7bn a year With the oil price nowcut in half we estimate Nigeria could be saving $3bn a year by rooting out corruption in

the oil sector ndash which is less than 1 of GDP We doubt this is enough to support the

current naira rate if oil remains in a $40-60bl range in the medium-term

Kenya also comes out poorly on these charts ndash although we must note that the IMF does

its own analysis and it argued as recently as 23 September 2015 that the KES real

exchange rate is ldquobroadly in line with fundamentalsrdquo

Figure 9 REER change from lows ndash MSCI Frontier countries

Source Bruegel Bloomberg Renaissance Capital

Nigeria and Kenya look particularly extreme here but Morocco also interests us It is

curious how little volatility there has been in this REER rate ndash its Bloomberg currency

-80

-70

-60

-50

-40

-30

-20

-10

0

B a n g l a d e s h

K u w

a i t

O m

a n

S a u d i A r a

b i a

P a k i s

t a n

V i e t n

a m

S r i L a n k a

M o r o c c o

N i g e r i a

K e n y a

R o m a

n i a

G e o r g i a

K a z a k h s

t a n

I r a n

A r g e n t i n a

change from highs

0

50

100

150

200

250

N i g e r i a

K e n y a

R o m a n i a

I r a n

G e o r g i a

V i e t n a m

B a n g l a d e s h

S r i L a n k a

K u w a i t

S a u d i A r a b i a

P a k i s t a n

O m a n

A r g e n t i n a

M o r o c c o

K a z a k h s t a n

change from lows - FM countries

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 815

8

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

code MAD could not be a greater misnomer This is particularly interesting given that

Morocco is the only country we know that of that has experienced a private sector boom

and subsequent slowdown without this distorting its exchange rate significantly Irsquom

increasingly keen to meet a Moroccan central bank governor or two

So when we put numbers to these graphs we find that Kenya and Nigeria have currencies

that are the most overvalued relative to their own histories Moreover the IMF now

forecasts that Kenya will run a significant 10 of GDP current account deficit in 2015-16

The IMF did not expect Nigeria to have a CA deficit when it made its April 2015 forecasts

but Yvonne Mhango thinks there will be a 3 of GDP deficit ndash and we trust her to be more

up to date Just to reach their 20-year average implied rate would require Kenya and

Nigeria to see depreciation to KES152$ and NGN285$ respectively

Vietnam looks expensive to us It had a chunky CA surplus in 2014 but it may want to

keep it that way by allowing further depreciation of the currency We will be visiting

Vietnam next month and expect to learn more about the authorities thinking on this

Bangladesh would need to see the currency at around BDT100$ and Pakistan at around

PKR120$ to match their 20-year average implied rate We see this as representing

depreciation risk to our PKR110$ forecast for June 2016 (see Reform Awakens

published 18 May 2015) and we will not argue strongly against investors suggesting

PKR120$ is more realistic

If any Gulf peg looks vulnerable we think it is Oman with a currency that is a little too

strong and a big CA deficit We have also previously noted in Dan Salterrsquos report When

Fed patience is a virtue published 19 December 2014 that its sovereign wealth fund is

very limited in size relative to others

Figure 10 Gulf sovereign wealth fund (SWF) assets to GDP 2014-15SWF assets ($bn) GDP $bn (2015E) SWF assets to GDP

Kuwait 592 134 440

UAE 1215 364 334Qatar 256 197 130Saudi Arabia 677 649 104Bahrain 11 31 34Oman 19 63 30Note SWF assets data for Kuwait Qatar Bahrain and Oman have not been updated since 2014 ndash it would be wise to assume these are lower now

Source Sovereign wealth fund institute Renaissance Capital

Saudi Arabia looks okay in our view and like Kuwait it has substantial reserves There

has been modest currency appreciation We assume Saudi Arabia will have to cut budget

spending and provoke disinflation to bring its currency back into alignment and push the

current account back to into surplus A devaluation would be more surprising to us than

the CHF move earlier this year

We do not see much to worry about in Romania or Morocco

Georgia also has a currency that is now near long-term fair value although its external

debt (see About that 1982 debt default ) and CA deficit warrant continued attention Our

economist Oleg Kouzmin argues that from here the GELrsquos direction will be driven by

moves in the RUB AZM and TRY Further depreciation of the TRY towards its all-time

lows would therefore pull the GEL weaker too unless the RUB appreciated to offset this

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 915

9

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

Figure 11 REER implied exchange rates in MSCI Frontier

Current FXrate vs $

FX rate impliedby long-term average REER

FX rate if REERfalls to lows

Current rate divided bylong-term average

2015 CA(GDP)

Kenya 106 152 266 143 -77Nigeria 199 285 618 143 07Vietnam 22470 29114 35506 130 48Bangladesh 777 992 117 128 -06Sri Lanka 141 166 205 118 -20Kuwait 030 035 042 117 157Oman 038 044 049 116 -150Pakistan 104 120 135 115 -13Romania 396 449 935 113 -11Saudi Arabia 375 424 505 113 -10Georgia 238 237 392 100 -66Morocco 974 926 992 095 -34Iran 29856 26224 60389 088 08Kazakhstan 270 216 272 080 -19

Argentina 939 519 108 055 -17Note We expect Nigerias current account deficit to be 3 of GDP in 2015 the IMF revised its Kenya forecast to -99 of GDP in September 2015

Source IMF April WEO Bruegel Bloomberg Renaissance Capital

We have one fundamental problem with the REER methodology that is applicable to

Kenya and Nigeria We think it is flawed because inflation rates between rich and poor

countries are not the same

US per capita GDP was nearly $55000 in 2014 while Kenyarsquos was around $1400 If we

see 1 inflation in the US and 10 in Kenya and if we use those per capita GDP figures

as a proxy for wages then in 2015 US wages would have risen by $550 and Kenyan

wages would have risen by $140 A REER comparison would tell us that i f the Kenyan

shilling did not move in nominal terms then Kenya has lost about 9 competitiveness

against the US (10 Kenyan inflation minus 1 US inflation) but for a company

employing people in the US and Kenya the absolute cost of employing a worker has risen

much less in Kenya than it has in the US Kenya would need to have seen inflation closer

to 30 for wages in both countries to have risen by the same absolute amount Moreoverwe can imagine that productivity is much easier to improve in Kenya than the US

The implication then is that REER methodologies are fine when we compare rich

countries to rich countries or poor countries to poor countries but not when we compare

rich to poor

This is a key reason why we are not about to alter Yvonne Mhangorsquos exchange forecasts

for the NGN or the KES with the figures implied by this work on REER rates

However our problem with REER figures for poor countries also apply to Pakistan

Bangladesh Georgia and others We do think the REER methodology helps us see

where the risks are greatest And in the frontier space that risk would appear to begreatest in both Nigeria and Kenya and much less dramatic in Pakistan or Romania

while the Kazakh tenge looks very good value to us

How will cheaper currencies improve the situation

Amidst all the doom and gloom about EM we should be careful not to throw the baby out

with the bath water It is right for chief investment officers (CIOs) to ask why they should

invest in economies growing slower than the US with worse corporate governance than

the US and in companies that donrsquot have the global success of a Google or an Apple

and in currencies that keep weakening against the US dollar We are also fully aware of

some of the negative common themes in certain emerging markets see The problem with

political longevity published 12 August 2013

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 1015

10

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

But there is reform in EM ndash see Reform Awakens in which we highlighted positive trends

in Pakistan Romania Egypt Ukraine and probably Nigeria Russia is not generally seen

as being at the forefront of reform but here the central bank has let the currency float

management in key firms is being replaced (we think in a bid to improve productivity)

while the government has lifted its position from 120th

in the Ease of Doing businesssurvey in 2012 to 62nd today and targets 20th place by 2018

Eventually valuations will convince CIOs ndash and indeed western companies ndash that EM cannot

be written off and that it is worth making this move from allocating to the US to EM The

currency is going to play a key role in this The competitiveness gain that EM is experiencing

will be hard to ignore EM demand is likely to be hurt by the higher cost of imported goods

and in time this should translate into import substitution (where possible) and some

additional export lift even if much of the competitiveness gains are between emerging

markets at present (Russian mining competing with Brazilian mining for example)

In addition when over 30 of US exports go to (depreciating) Canada and Mexico US

companies will have few choices open to them They can either cut US costs dramatically

but this will require nominal wage cuts which is hard to imagine or they can choose to

produce in Mexico and sell in Mexico or they can choose to produce in Mexico and sell

back to the US We expect to see US FDI to EM pick up

Figure 12 Currencies vs the $ (nominal change) Sept 2005 to Sept 2015

Source Bloomberg

China has seen its currency appreciate even more significantly against most EM

currencies We expect Chinese firms to take advantage of their strong currency to buy up

assets in EM Since 2005 in nominal terms some of the largest EM currency falls relative

to the CNY have been seen in the RUB ZAR BRL and TRY

Figure 13 Currencies vs CNY nominal change Sept 2005 to Sept 2015

Source Bloomberg

-80

-60

-40

-20

0

20

40

C N Y

P H P

S G D

T H B

P E N

T W D

H K D

C Z K

B G N

M Y R

K R W

P L N

C L P

C O P

H U F

R O N

I D R

I N R

M X N

B R L

Z A R

T R Y

R U B

A R S

C H F

A U D

J P Y

D K K

E U R

S E K

N Z D

C A D

G B P

N O K

-80

-70

-60

-50

-40

-30

-20

-10

0

10

P H

P

S G

D

T H

B

P E

N

T W

D

H K

D

C Z

K

B G

N

M Y

R

K R

W

P L

N

C L

P

C O

P

H U

F

R O

N

I D

R

I N

R

M X

N

B R

L

Z A

R

T R

Y

R U

B

A R

S

C H

F

U S

D

A U

D

J P

Y

D K

K

E U

R

S E

K

N Z

D

C A

D

G B

P

N O

K

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 1115

11

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

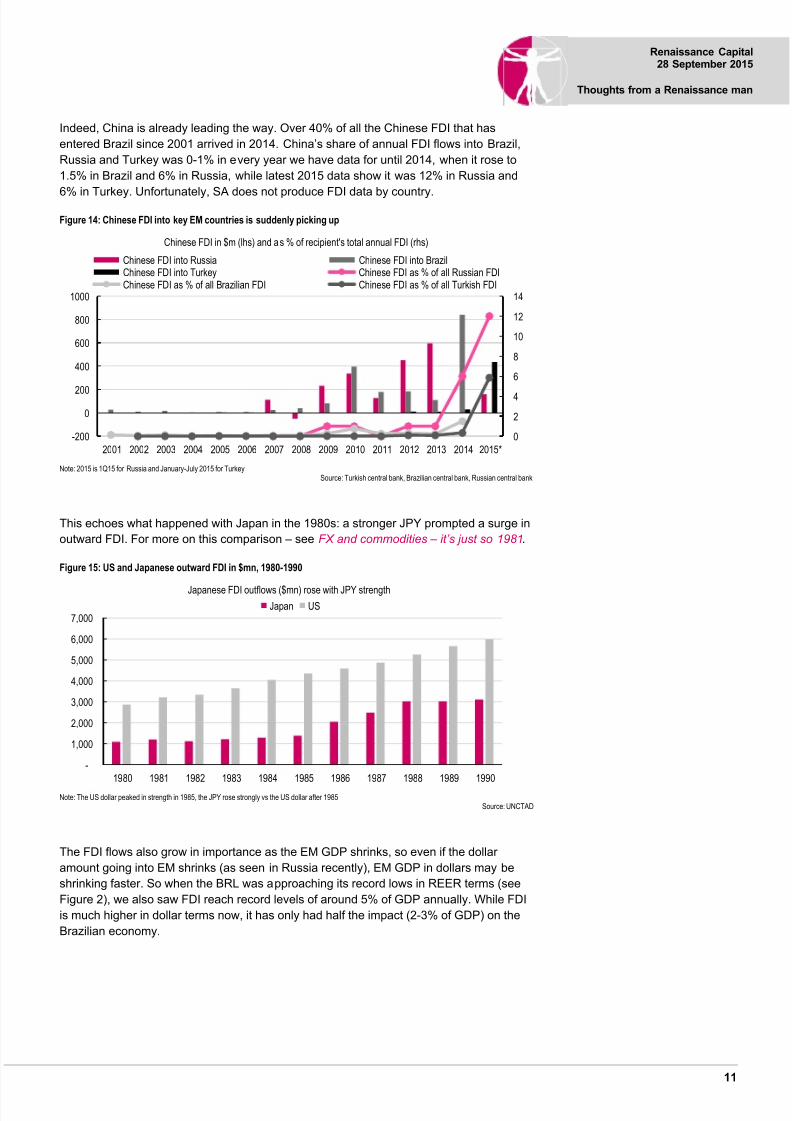

Indeed China is already leading the way Over 40 of all the Chinese FDI that has

entered Brazil since 2001 arrived in 2014 Chinarsquos share of annual FDI flows into Brazil

Russia and Turkey was 0-1 in every year we have data for until 2014 when it rose to

15 in Brazil and 6 in Russia while latest 2015 data show it was 12 in Russia and

6 in Turkey Unfortunately SA does not produce FDI data by country

Figure 14 Chinese FDI into key EM countries is suddenly picking up

Note 2015 is 1Q15 for Russia and January-July 2015 for TurkeySource Turkish central bank Brazilian central bank Russian central bank

This echoes what happened with Japan in the 1980s a stronger JPY prompted a surge in

outward FDI For more on this comparison ndash see FX and commodities ndash itrsquos just so 1981

Figure 15 US and Japanese outward FDI in $mn 1980-1990

Note The US dollar peaked in strength in 1985 the JPY rose strongly vs the US dollar after 1985Source UNCTAD

The FDI flows also grow in importance as the EM GDP shrinks so even if the dollar

amount going into EM shrinks (as seen in Russia recently) EM GDP in dollars may be

shrinking faster So when the BRL was approaching its record lows in REER terms (see

Figure 2) we also saw FDI reach record levels of around 5 of GDP annually While FDI

is much higher in dollar terms now it has only had half the impact (2-3 of GDP) on the

Brazilian economy

0

2

4

6

8

10

12

14

-200

0

200

400

600

800

1000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Chinese FDI in $m (lhs) and as of recipients total annual FDI (rhs)

Chinese FDI into Russia Chinese FDI into BrazilChinese FDI into Turkey Chinese FDI as of all Russian FDIChinese FDI as of all Brazilian FDI Chinese FDI as of all Turkish FDI

-

1000

2000

3000

4000

5000

6000

7000

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990

Japanese FDI outflows ($mn) rose with JPY strengthJapan US

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 1215

12

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

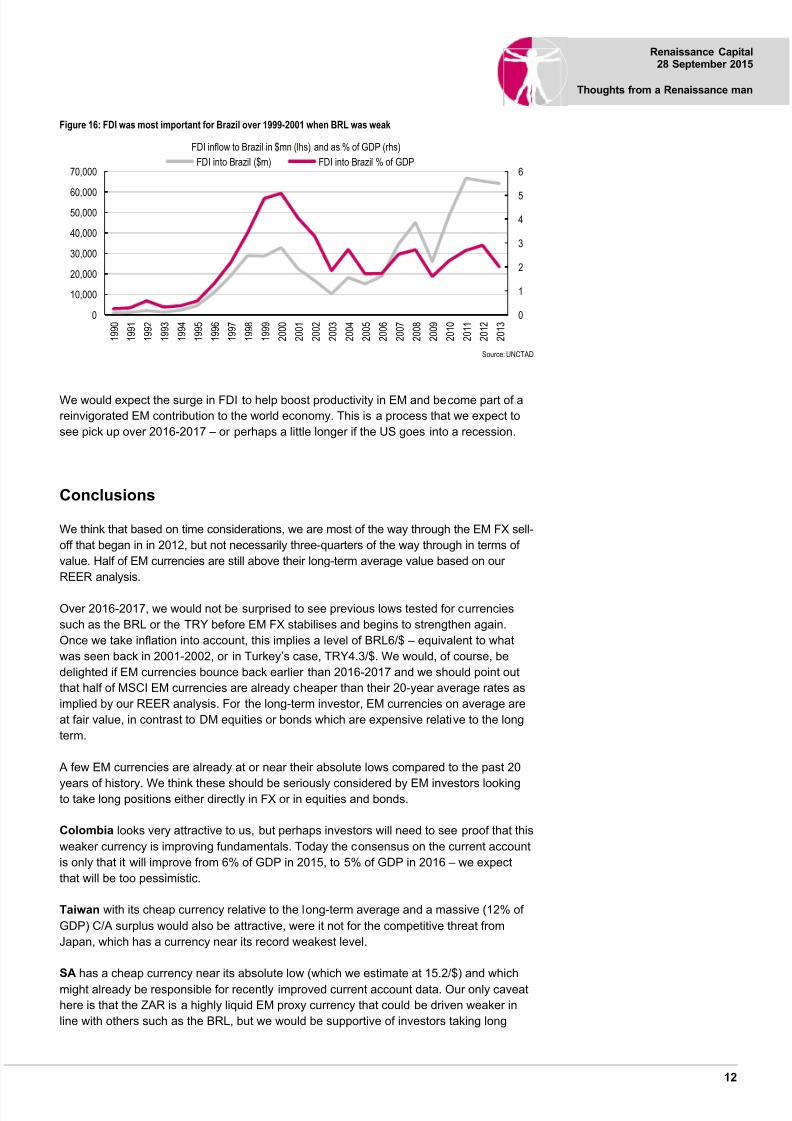

Figure 16 FDI was most important for Brazil over 1999-2001 when BRL was weak

Source UNCTAD

We would expect the surge in FDI to help boost productivity in EM and become part of a

reinvigorated EM contribution to the world economy This is a process that we expect to

see pick up over 2016-2017 ndash or perhaps a little longer if the US goes into a recession

Conclusions

We think that based on time considerations we are most of the way through the EM FX sell-

off that began in in 2012 but not necessarily three-quarters of the way through in terms of

value Half of EM currencies are still above their long-term average value based on our

REER analysis

Over 2016-2017 we would not be surprised to see previous lows tested for currencies

such as the BRL or the TRY before EM FX stabilises and begins to strengthen again

Once we take inflation into account this implies a level of BRL6$ ndash equivalent to what

was seen back in 2001-2002 or in Turkeyrsquos case TRY43$ We would of course be

delighted if EM currencies bounce back earlier than 2016-2017 and we should point out

that half of MSCI EM currencies are already cheaper than their 20-year average rates as

implied by our REER analysis For the long-term investor EM currencies on average are

at fair value in contrast to DM equities or bonds which are expensive relative to the long

term

A few EM currencies are already at or near their absolute lows compared to the past 20

years of history We think these should be seriously considered by EM investors lookingto take long positions either directly in FX or in equities and bonds

Colombia looks very attractive to us but perhaps investors will need to see proof that this

weaker currency is improving fundamentals Today the consensus on the current account

is only that it will improve from 6 of GDP in 2015 to 5 of GDP in 2016 ndash we expect

that will be too pessimistic

Taiwan with its cheap currency relative to the long-term average and a massive (12 of

GDP) CA surplus would also be attractive were it not for the competitive threat from

Japan which has a currency near its record weakest level

SA has a cheap currency near its absolute low (which we estimate at 152$) and which

might already be responsible for recently improved current account data Our only caveat

here is that the ZAR is a highly liquid EM proxy currency that could be driven weaker in

line with others such as the BRL but we would be supportive of investors taking long

0

1

2

3

4

5

6

0

10000

20000

30000

40000

5000060000

70000

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3

FDI inflow to Brazil in $mn (lhs) and as of GDP (rhs)

FDI into Brazil ($m) FDI into Brazil of GDP

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 1315

13

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

positions in SA around current or weaker FX levels It is also worth noting that SArsquos equity

market outperformed EM in the Asian crisis of 1997-98 the tech bubble crash of 2000-01

and the global financial crisis of 2007-08 helped by its funds

The short side of the equation is Egypt ndash where a currency level around EGP98$ is justif ied today but where Gulf inflows could help the authorities resist this for some

time We would also recommend selling India which also happens to be a widely-

owned overweight in GEM funds as this currency is stronger than its long-term average

and it runs a current account deficit The other most vulnerable currency we think is

Perursquos for the same reasons

Elsewhere in EEMEA we see Poland Hungary and the Czech Republic as offering

low-risk alternatives Currencies are close to their 20-year average levels and current

accounts are healthy

Greece is slightly cheap but we donrsquot see that offsetting the problem of having a Syriza

government in power ndash which is likely to be unfriendly to portfolio investors in private

companies

Russiarsquos currency looks cheap to us too ndash at RUB65$ against the 20-year average of

RUB59$ ndash and is supported by a decent current account surplus

In the Gulf the UAE and Qatar have somewhat expensive currencies but these have

never been that volatile in 20 years In addition they have SWF reserves which we

estimate at over 300 and 100 of GDP respectively We doubt the currency regimes

will be altered in either so the main downside stems from the impact of budget cuts

The story for Frontier FX is very different Very few currencies have seen significant

depreciation Half are near the strongest levels they have ever been in REER terms

By far the best value from our perspective is now Kazakhstan ndash with a currency at its

absolute lows in a country that we expect to run a current account surplus in 2016 ndash see

our report Kazakhstanrsquos devaluation Implications for frontier currencies published 20

August 2015 In addition the government has a dynamic reform agenda that has been

likened to what Singapore has done in the past ndash see Kazakhstan Impressive reform plan

initiated published 9 July 2015

We also like the look of Morocco which has an enviable record of currency stability Like

South Africa equities may be relatively expensive to its peers but for a decent reason

assuming the currency is stable

Romania carries modest currency risk in our view but is inside the EU envelope which

offers some protection and has a healthy CA

We see risks being higher in Pakistan where a 15 devaluation to PKR120$ is

plausible and higher still in Bangladesh where history implies that fair value is

BDT100$ Vietnam is trading even further from long-term fair value and might also be

getting more vulnerable since its CA entered deficit territory in 1Q15

We always doubt Gulf currencies will move significantly but we are concerned by Oman

The 2008-2009 crisis hit that country hard reserves are far lower than in other countries

(Omanrsquos sovereign wealth fund would not cover a budget deficit on the scale of Saudirsquos

for even 12 months) and we think the currency looks expensive

The most vulnerable currencies of all according to this REER analysis are in Kenyarunning an estimated 10 of GDP current account deficit this year and Nigeria Their

current exchange rates look hard to justify if this REER analysis is valid (as noted above

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 1415

14

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

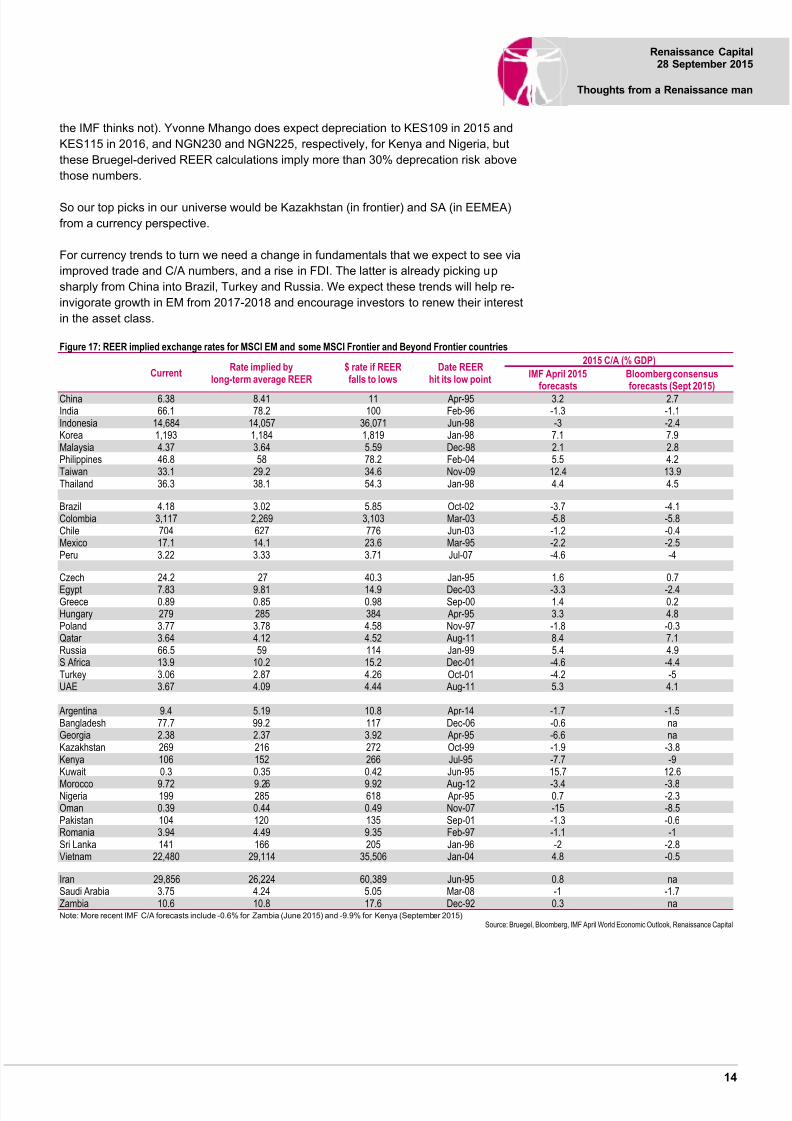

the IMF thinks not) Yvonne Mhango does expect depreciation to KES109 in 2015 and

KES115 in 2016 and NGN230 and NGN225 respectively for Kenya and Nigeria but

these Bruegel-derived REER calculations imply more than 30 deprecation risk above

those numbers

So our top picks in our universe would be Kazakhstan (in frontier) and SA (in EEMEA)

from a currency perspective

For currency trends to turn we need a change in fundamentals that we expect to see via

improved trade and CA numbers and a rise in FDI The latter is already picking up

sharply from China into Brazil Turkey and Russia We expect these trends will help re-

invigorate growth in EM from 2017-2018 and encourage investors to renew their interest

in the asset class

Figure 17 REER implied exchange rates for MSCI EM and some MSCI Frontier and Beyond Frontier countries

CurrentRate implied by

long-term average REER$ rate if REERfalls to lows

Date REERhit its low point

2015 CA ( GDP)

IMF April 2015forecasts

Bloomberg consensusforecasts (Sept 2015)

China 638 841 11 Apr-95 32 27India 661 782 100 Feb-96 -13 -11Indonesia 14684 14057 36071 Jun-98 -3 -24Korea 1193 1184 1819 Jan-98 71 79Malaysia 437 364 559 Dec-98 21 28Philippines 468 58 782 Feb-04 55 42Taiwan 331 292 346 Nov-09 124 139Thailand 363 381 543 Jan-98 44 45

Brazil 418 302 585 Oct-02 -37 -41Colombia 3117 2269 3103 Mar-03 -58 -58Chile 704 627 776 Jun-03 -12 -04Mexico 171 141 236 Mar-95 -22 -25Peru 322 333 371 Jul-07 -46 -4

Czech 242 27 403 Jan-95 16 07

Egypt 783 981 149 Dec-03 -33 -24Greece 089 085 098 Sep-00 14 02Hungary 279 285 384 Apr-95 33 48Poland 377 378 458 Nov-97 -18 -03Qatar 364 412 452 Aug-11 84 71Russia 665 59 114 Jan-99 54 49S Africa 139 102 152 Dec-01 -46 -44Turkey 306 287 426 Oct-01 -42 -5UAE 367 409 444 Aug-11 53 41

Argentina 94 519 108 Apr-14 -17 -15Bangladesh 777 992 117 Dec-06 -06 naGeorgia 238 237 392 Apr-95 -66 naKazakhstan 269 216 272 Oct-99 -19 -38Kenya 106 152 266 Jul-95 -77 -9Kuwait 03 035 042 Jun-95 157 126

Morocco 972 926 992 Aug-12 -34 -38Nigeria 199 285 618 Apr-95 07 -23Oman 039 044 049 Nov-07 -15 -85Pakistan 104 120 135 Sep-01 -13 -06Romania 394 449 935 Feb-97 -11 -1Sri Lanka 141 166 205 Jan-96 -2 -28Vietnam 22480 29114 35506 Jan-04 48 -05

Iran 29856 26224 60389 Jun-95 08 naSaudi Arabia 375 424 505 Mar-08 -1 -17Zambia 106 108 176 Dec-92 03 naNote More recent IMF CA forecasts include -06 for Zambia (June 2015) and -99 for Kenya (September 2015)

Source Bruegel Bloomberg IMF April World Economic Outlook Renaissance Capital

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 1515

Renaissance CapitalMoscowT + 7 (495) 258 7777

Renaissance Capital LtdLondonT + 44 (203) 379 7777

Renaissance CapitalJohannesburgT +27 (11) 750 1400

Renaissance Securities (Cyprus)LtdNicosiaT + 357 (22) 505 800

Renaissance Securities (Nigeria) LtdLagosT +234 (1) 448 5300

Renaissance CapitalNairobiT +254 (20) 368 2000

Renaissance CapitalIstanbulT +90 (212) 362 3500

Renaissance CapitalDubaiT +971 (4) 409 2000

A complete set of disclosure statements associated with the issuers discussed in this report is available using the lsquoStock Finderrsquo or lsquoBond Finderrsquo for individualissuers on the Renaissance Capital Research Portal at httpresearchrencapcomengdefaultasp

This Communication is for information purposes only The Communication does not form a fiduciary relationship or constitute advice and is not and should not be construed asa recommendation or an offer or a solicitation of an offer of securities or related financial instruments or an invitation or inducement to engage in investment activity and cannotbe relied upon as a representation that any particular transaction necessarily could have been or can be effected at the stated price The Communication is not anadvertisement of securities nor independent investment research and has not been prepared in accordance with legal requirements designed to promote the independence ofinvestment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research Opinions expressed therein may differ or be contrary toopinions expressed by other business areas or groups of the Renaissance Capital as a result of using different assumptions and criteria All such information is subject tochange without notice and neither Renaissance Capital nor any of its subsidiaries or affiliates is under any obligation to update or keep current the information contained in theCommunication or in any other medium

Descriptions of any company or issuer or their securities or the markets or developments mentioned in the Communication are not intended to be complete TheCommunication should not be regarded by recipients as a substitute for the exercise o f their own judgment as the Communication has no regard to the specific investmentobjectives financial situation or particular needs of any specific recipient The material (whether or not it states any opinions) is for general information purposes only and doesnot take into account your personal circumstances or objectives and nothing in this material is or should be considered to be financial investment or other advice on whichreliance should be placed Any reliance you place on such information is therefore strictly at your own risk The application of taxation laws depends on an investorrsquos individualcircumstances and accordingly each investor should seek independent professional advice on taxation implications before making any investment decision TheCommunication has been compiled or arrived at based on information obtained from sources believed to be reliable and in good faith Such information has not beenindependently verified is provided on an lsquoas isrsquo basis and no representation or warranty either expressed or implied is provided in relation to the accuracy completenessreliability merchantability or fitness for a particular purpose of such information except with respect to information concerning Renaissance Capital its subsidiaries andaffiliates All statements of opinion and all projections forecasts or statements relating to expectations regarding future events or the possible future performance ofinvestments represent Renaissance Capitalrsquos own assessment and interpretation of information available to them currently Any information relating to past performance of aninvestment does not necessarily guarantee future performance

The Communication is not intended for distribution to the public and may be confidential It may not be reproduced redistributed or published in whole or in part for anypurpose without the written permission of Renaissance Capital and neither Renaissance Capital nor any of its affiliates accepts any liability whatsoever for the actions of thirdparties in this respect The information may not be used to create any financial instruments or products or any indices Neither Renaissance Capital and its affiliates nor theirdirectors representatives or employees accept any liability for any direct or consequential loss or damage arising out of the use of all or any part of the Communication

copy 2015 Renaissance Securities (Cyprus) Limited All rights reserved Regulated by the Cyprus Securities and Exchange Commission (Licence No KEPEY 05304)

This research is for general information purposes only and should not be interpreted that Renaissance Capital is encouraging investment dealings ie buyingand selling securities in Iran Under US law ldquocriminal penalties for violations of the Iranian Transactions Regulations may result in a fine of up to $1000000 andnatural persons may be imprisoned for up to 20 yearsrdquo Under UK law criminal penalties for violating restrictions on investment in and certain financialtransactions with Iran may carry criminal penalties including up to 2 years in prison andor substantial fines

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 215

2

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

EM investors we meet are feeling pretty downbeat We spend more time discussing the

Syrian refugee crisis and the UK premierrsquos alleged predilection for roast pork than we do

discussing Russian inflation figures or SArsquos CA

The reason is obvious as Dan Salter pointed out in his Hindsight is a wonderful thing report published 13 April 2015 currency return is the second most important determinant

of total investor return ndash and currencies are getting crushed The BRL has collapsed from

BRL225$ in mid-2014 through BRL300$ in early 2015 and beyond BRL400$ in 3Q15

The ZAR has also been a very naughty currency breaking out (to the weaker side) of

what had become a relatively predictable four-year bearish channel

Figure 1 ZAR vs $

Source Bloomberg

Despite modest geopolitical improvements in Ukraine the RUB managed to lose all its

1H15 gains and weaken to beyond where it was in January when fighting was surging inUkraine and the US feared a Russian assault to create a land bridge to Crimea While all

of the above could be attributed in part to Chinarsquos slowdown and commodity prices

Turkey which should be a key beneficiary has seen its currency weaken sharply too

This recent currency weakness feels a litt le overdone to us in the short term but we doubt

the multi-year trend is over

We have yet to see the second-round effect of this currency weakness We expect to see

sovereign corporate or financial defaults on external debt as we explained in About that

1982 debt default published 4 September 2015 Weaker GDP could also intensify

problems domestically too via bank or corporate failures and rising unemployment

Politics represents a third threat via impeachment in Brazil political limbo in Turkey andthe risk of demonstrations against the authorities due to economic factors (such as the

wage disputes in SA over recent years) It is hard after over a decade in power to blame

economic problems on external factors alone

Indeed three of the four major EM currencies shown in the following chart are nowhere

near the lows seen in the five-year wake of the Asian crisis of 1997 Default weak GDP

and politics as well as the threat of a US recession (see our 13 January 2015 report SampP

500 at 1100 by March 2016) taking away a key leg in the global growth story could all

push EM currencies weaker still However after three-to-four years of REER depreciation

we think we might now be within a year or two of the bottom

6

7

8

9

10

1112

13

14

15

J a n - 1 1

F e b - 1 1

A p r - 1 1

J u n - 1 1

J u l - 1 1

S e p - 1 1

N o v - 1 1

D e c - 1 1

F e b - 1 2

M a r - 1 2

M a y - 1 2

J u l - 1 2

A u g - 1 2

O c t - 1 2

D e c - 1 2

J a n - 1 3

M a r - 1 3

M a y - 1 3

J u n - 1 3

A u g - 1 3

O c t - 1 3

N o v - 1 3

J a n - 1 4

M a r - 1 4

A p r - 1 4

J u n - 1 4

A u g - 1 4

S e p - 1 4

N o v - 1 4

J a n - 1 5

F e b - 1 5

A p r - 1 5

J u n - 1 5

J u l - 1 5

S e p - 1 5

Rand breaks out

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 315

3

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

Figure 2 EM currencies ndash REER (Dec 2007 = 100)

Note Bruegel uses CPI to adjust the index we have not made any CPI adjustment for June to September 2015

Source Bruegel Renaissance Capital (June to September 2015)

We need to explain the figure above and those below We have taken the REER numbersfrom Bruegel ndash which strips out consumer price inflation (CPI) from main trading partnersand the countries themselves ndash to give the ldquorealrdquo picture of currency valuation So while theBRL may now be weaker against the dollar than it was in 2002 there has been so muchmore inflation in Brazil than the US that comparing the exchange rate in 2002 and 2015really tells us very little The same applies to Nigeria Nigerias currency has never been asweak as NGN618 against the dollar but what the REER does is let us estimate what theNGN would have been in 1995 in todays money And the answer is NGN618

Note the Bruegel estimates stop in May 2015 ndash so for June to September 2015 we have

adjusted the index figure by currency moves but not by inflation This probably distorts the

figures by a percent or two but we donrsquot think this is significant enough to matter

So if we look at MSCI EM the graph below shows the highest REER rate a currency has

seen the lowest rate the May 2015 figure which is the last accurate REER reading and the

currency price on 22 September 2015 Lastly we add the long-term average REER rate

Colombia has a currency that is actually at its REER lows and well below its long-term

average Greece Chile and Taiwan also look competitive relative to their own histories

Countries on the left from Egypt to China to the Gulf countries are close to the strongest

they have ever been

Figure 3 Latest REER vs all-time high and low (Dec 2007 = 100) in MSCI EM

Source Bruegel Bloomberg Renaissance Capital

40

50

60

70

80

90

100

110

120

130

140

1 9 9 5 M 0 1

1 9 9 5 M 0 9

1 9 9 6 M 0 5

1 9 9 7 M 0 1

1 9 9 7 M 0 9

1 9 9 8 M 0 5

1 9 9 9 M 0 1

1 9 9 9 M 0 9

2 0 0 0 M 0 5

2 0 0 1 M 0 1

2 0 0 1 M 0 9

2 0 0 2 M 0 5

2 0 0 3 M 0 1

2 0 0 3 M 0 9

2 0 0 4 M 0 5

2 0 0 5 M 0 1

2 0 0 5 M 0 9

2 0 0 6 M 0 5

2 0 0 7 M 0 1

2 0 0 7 M 0 9

2 0 0 8 M 0 5

2 0 0 9 M 0 1

2 0 0 9 M 0 9

2 0 1 0 M 0 5

2 0 1 1 M 0 1

2 0 1 1 M 0 9

2 0 1 2 M 0 5

2 0 1 3 M 0 1

2 0 1 3 M 0 9

2 0 1 4 M 0 5

2 0 1 5 M 0 1

2 0 1 5 M 0 9

Brazil Turkey Russia South Africa

WEAKER

STRONGER

0

20

40

60

80

100

120

140

160180

E g y p t

C h i n a

Q a t a r

P h i l i p p i n e s

U A E

P e r u

I n d i a

T h a i l a n d

T a i w a n

I n d o n e s i a

C z e c h

C h i l e

G r e e c e

K o r e a

M a l a y s i a

P o l a n d

H u n g a r y

M e x i c o

S A f r i c a

R u s s i a

T u r k e y

C o l o m b i a

B r a z i l

Estimated current REER REER High REER Low REER May 2015 LT Avg REER

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 415

4

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

To look at this in another way ndash the following chart shows how much MSCI EM currencies

have fallen from their highs Gulf countries with fixed pegs have fallen the least while SA

Brazil and Colombia have fallen the most

Figure 4 MSCI EM currencies ndash change in REER from highs

Source Bruegel Bloomberg Renaissance Capital

So the BRL and ZAR are oversold Not necessarily as that chart doesnrsquot tell us if they

might have further to fall

If we compare our estimate of the current REER in September 2015 with prior lows we

find that Indonesiarsquos currency is 140 higher priced than when it was at its lows and

Russia is over 70 above its lows

The currencies that actually look like they have sold off enough ndash or arguably too much ndash

are Colombia Taiwan Greece Chile and yes maybe SA too There may be a longColombia and short Peru trade in their somewhere

Our only caveat for SA is that the ZAR is an ideal proxy for EM so it could be shorted by

investors even if is absolutely and relatively undervalued Currency trends can be

sustained beyond what is justified by fundamentals for a long time as the USD showed

us in the run-up to the Plaza accord The same may happen to the ZAR in 2016

Figure 5 REER change from lows ndash MSCI EM countries

Source Bruegel Bloomberg Renaissance Capital

But what we really need to see is the currency levels implied by all these graphs In

particular there are three things we think investors need to know

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

Q a t a r

U A E

C h i n a

E g y p t

P h i l i p

p i n e s

I n d i a

P e r u

G r e e c e

T h a i l a n d

K o r e a

C

z e c h

C h i l e

P

o l a n d

H u n g a r y

I n d o

n e s i a

T

u r k e y

T a i w a n

R

u s s i a

M

e x i c o

M a l a y s i a

C o l o

m b i a

S A f r i c a

B r a z i l

change from highs - EM countries

0

20

40

60

80

100120

140

160

I n d o n e s i a

E g y p t

R u s s i a

C h i n a

P h i l i p p i n e s

C z e c h

K o r e a

I n d i a

T h a i l a n d

B r a z i l

T u r k e y

M e x i c o

H u n g a r y

M a l a y s i a

Q a t a r

P o l a n d

U A E

P e r u

S A f r i c a

C h i l e

G r e e c e

T a i w a n

C o l o m b i a

change from lows - EM countries

These currencies arevery near their 20-year lows

RUB BRL and TRYare all still well abovetheir lows

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 515

5

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

What nominal currency rate is the worst-case scenario (assuming the past 20

years is a long enough sample) ndash see the third column of data below

How do currencies look now relative to their 20-year average ndash see the second

column of data below

Is the current rate justified by the current account position ndash see the last column

of data below

Note that the numbers below ndash eg the implication that the EGP would need to be

EGP981$ to equal its long-term average REER rate ndash do not take future inflation

differentials into account So if Egypt ran inflation of 10 a year while its trading

partners such as the US and Europe had inf lation of 2 and if Egypt took two years to

depreciate its currency then the eventual spot rate may need to be roughly 16 weaker

at EGP114$ to be the equivalent of todayrsquos implied lsquofair valuersquo of EGP981 $

Figure 6 Current FX rate vs $

Current FXrate vs $

FX rate implied by long-term average REER

FX rate if REER falls tolows

Current rate divided bylong-term average

2015 CA(GDP)

China 638 841 11 132 32Egypt 784 981 149 125 -33Philippines 468 58 782 124 55India 66 782 100 118 -13Qatar 364 412 452 113 84UAE 367 409 444 111 53Czech 243 27 403 111 16Thailand 361 381 543 106 44Peru 322 333 371 103 -46Hungary 279 285 384 102 33Poland 377 378 458 1 -18Korea 1191 1184 1819 099 71Indonesia 14647 14057 36071 096 -3Turkey 303 287 426 095 -42

Greece 09 085 098 094 14Chile 698 627 776 09 -12Russia 659 59 114 09 54Taiwan 33 292 346 088 124Malaysia 434 364 559 084 21Mexico 169 141 236 083 -22S Africa 136 102 152 075 -46Brazil 404 302 585 075 -37Colombia 3073 2269 3103 074 -58

SourceBruegel IMF April World economic Outlook Bloomberg R enaissance Capital

In terms of fair value Poland is the benchmark with a currency that is within 1 of its

long-term implied rate

Ten EMs have currencies stronger than the long-term implied rate Of these seven are

due to record current account surpluses in 2015 according to the IMF April World

Economic Outlook We think that a CA surplus justifies a currency stronger than the 20-

year average rate

We are content to argue that a country like China does not need to see more than a 10

devaluation in the currency from current levels when its current account has a surplus of

this size See our report FX and commodities ndash itrsquos just so 1981 published11 August 2015

This leaves us three countries ndash Egypt India and Peru ndash whose currencies look

particularly exposed Not only are they failing to keep pace with the general EM trend of

significant depreciation but they are also overvalued relative to their own long-term

history and lastly they are running CA deficits

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 615

6

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

On the other side of the equation ndash Taiwan Russia Malaysia Greece and Korea

look relatively good value These currencies may be considerably more expensive than

their historical lows ndash Russia would need to see RUB114$ to equal January 1999 ndash but

each has a CA surplus and each is cheaper than their long-term 20-year average In

Greecersquos case ndash given it has the euro ndash this simply means that Greece is roughly 6more competitive today than it has been for most of the past 20 years which is a modest

positive for company earnings In Greecersquos case we do not see that as offsetting the

damage that may be done by the ideologically anti-market Syriza government

Taiwan and Korea look like strong buys from a currency perspective but they do have to

compete with Japan which at the current JPY1205$ is around its all-time low of

JPY1225$ Any bounce for these two would presumably require a stronger yen

For SA we would now expect to see the CA improve more than the 46 of GDP that the

IMF expected in April 2015 Indeed the 2Q15 figure was around 3 of GDP We think

similar improvement is likely in Brazil Colombia and Mexico

What about frontier

Below we analyse 12 countries in MSCI Frontier plus Saudi Arabia Iran and Georgia

What jumps out first is that so many of them have a currency level that is very near their

20-year record strongest level Frontier FX has clearly not depreciated in line with EM FX

A number of factors may explain this First frontier markets are less globally integrated

than EM so we might expect them to react later Second their financial markets are far

more shallow which means it is easier for the authorities to resist market pressure ndash even

if economic fundamentals tell us this may not be the right policy stance to take It also

means that it does not take much money in the way of foreign aid or IMF support to keepa currency stable Third perhaps the underlying economic structure in frontier markets is

changing more than in emerging markets so their current exchange rates should not be

compared with their history We are however sceptical about that excuse Fourth frontier

markets tend to be poorer than EM countries so REER measures may not be as

applicable (see below) Fifth a few of these countries such as Kuwait (off-index) Saudi

Arabia Bahrain and Oman have historical pegs that have not changed much in 20 years

or more bolstered by large sovereign wealth funds (less true of Oman)

Figure 7 A number of Frontier and Beyond Frontier markets are near their strongest levels of the past 20 years

Note Argentinas strongest point was 250 which is off the scaleSource Bruegel Bloomberg Renaissance Capital

0

20

40

60

80

100

120

140

160

180

B a n g l a d e s h

V i e t n a m

S a u d i A r a b i a

I r a n

N i g e r i a

O m a n

K e n y a

K u w a i t

P a k i s t a n

S r i L a n k a

M o r o c c o

G e o r g i a

R o m a n i a

A r g e n t i n a

K a z a k h s t a n

Latest REER vs all-time high and low (Dec 2007 = 100) - selected Frontier countriesEstimated current REER REER High REER Low REER May 2015

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 715

7

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

Only Morocco Argentina and Kazakhstan are at or near their lows ndash but we are sceptical

about Argentinean data The IMF does not trust Argentinarsquos inflation data so if Bruegel is

using Argentinarsquos official inflation figures these are likely to distort their calculations More

positively Kazakhstan looks a particularly interesting investment given these graphs

Figure 8 REER change from strongest level ndash MSCI FM

Source Bruegel Renaissance Capital Bloomberg

Even more dramatic is when we compare the currency levels today with the lowest levels

seen over the past 20 years

Nigeria still has a very strong currency which we think is hurting the Nigerian economy ndash

see Yvonne Mhangorsquos report The cost of defending NGN199$1 from 11 September

2015 We doubt that improved fiscal management can do enough to support this Former

central bank governor Lamido Sanusi estimated that Nigeria was losing about $20bn over

2011-2013 due to theft from the budget or roughly $6-7bn a year With the oil price nowcut in half we estimate Nigeria could be saving $3bn a year by rooting out corruption in

the oil sector ndash which is less than 1 of GDP We doubt this is enough to support the

current naira rate if oil remains in a $40-60bl range in the medium-term

Kenya also comes out poorly on these charts ndash although we must note that the IMF does

its own analysis and it argued as recently as 23 September 2015 that the KES real

exchange rate is ldquobroadly in line with fundamentalsrdquo

Figure 9 REER change from lows ndash MSCI Frontier countries

Source Bruegel Bloomberg Renaissance Capital

Nigeria and Kenya look particularly extreme here but Morocco also interests us It is

curious how little volatility there has been in this REER rate ndash its Bloomberg currency

-80

-70

-60

-50

-40

-30

-20

-10

0

B a n g l a d e s h

K u w

a i t

O m

a n

S a u d i A r a

b i a

P a k i s

t a n

V i e t n

a m

S r i L a n k a

M o r o c c o

N i g e r i a

K e n y a

R o m a

n i a

G e o r g i a

K a z a k h s

t a n

I r a n

A r g e n t i n a

change from highs

0

50

100

150

200

250

N i g e r i a

K e n y a

R o m a n i a

I r a n

G e o r g i a

V i e t n a m

B a n g l a d e s h

S r i L a n k a

K u w a i t

S a u d i A r a b i a

P a k i s t a n

O m a n

A r g e n t i n a

M o r o c c o

K a z a k h s t a n

change from lows - FM countries

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 815

8

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

code MAD could not be a greater misnomer This is particularly interesting given that

Morocco is the only country we know that of that has experienced a private sector boom

and subsequent slowdown without this distorting its exchange rate significantly Irsquom

increasingly keen to meet a Moroccan central bank governor or two

So when we put numbers to these graphs we find that Kenya and Nigeria have currencies

that are the most overvalued relative to their own histories Moreover the IMF now

forecasts that Kenya will run a significant 10 of GDP current account deficit in 2015-16

The IMF did not expect Nigeria to have a CA deficit when it made its April 2015 forecasts

but Yvonne Mhango thinks there will be a 3 of GDP deficit ndash and we trust her to be more

up to date Just to reach their 20-year average implied rate would require Kenya and

Nigeria to see depreciation to KES152$ and NGN285$ respectively

Vietnam looks expensive to us It had a chunky CA surplus in 2014 but it may want to

keep it that way by allowing further depreciation of the currency We will be visiting

Vietnam next month and expect to learn more about the authorities thinking on this

Bangladesh would need to see the currency at around BDT100$ and Pakistan at around

PKR120$ to match their 20-year average implied rate We see this as representing

depreciation risk to our PKR110$ forecast for June 2016 (see Reform Awakens

published 18 May 2015) and we will not argue strongly against investors suggesting

PKR120$ is more realistic

If any Gulf peg looks vulnerable we think it is Oman with a currency that is a little too

strong and a big CA deficit We have also previously noted in Dan Salterrsquos report When

Fed patience is a virtue published 19 December 2014 that its sovereign wealth fund is

very limited in size relative to others

Figure 10 Gulf sovereign wealth fund (SWF) assets to GDP 2014-15SWF assets ($bn) GDP $bn (2015E) SWF assets to GDP

Kuwait 592 134 440

UAE 1215 364 334Qatar 256 197 130Saudi Arabia 677 649 104Bahrain 11 31 34Oman 19 63 30Note SWF assets data for Kuwait Qatar Bahrain and Oman have not been updated since 2014 ndash it would be wise to assume these are lower now

Source Sovereign wealth fund institute Renaissance Capital

Saudi Arabia looks okay in our view and like Kuwait it has substantial reserves There

has been modest currency appreciation We assume Saudi Arabia will have to cut budget

spending and provoke disinflation to bring its currency back into alignment and push the

current account back to into surplus A devaluation would be more surprising to us than

the CHF move earlier this year

We do not see much to worry about in Romania or Morocco

Georgia also has a currency that is now near long-term fair value although its external

debt (see About that 1982 debt default ) and CA deficit warrant continued attention Our

economist Oleg Kouzmin argues that from here the GELrsquos direction will be driven by

moves in the RUB AZM and TRY Further depreciation of the TRY towards its all-time

lows would therefore pull the GEL weaker too unless the RUB appreciated to offset this

7252019 Thoughts From RenMan-280915(5)

httpslidepdfcomreaderfullthoughts-from-renman-2809155 915

9

Renaissance Capital28 September 2015

Thoughts from a Renaissance man

Figure 11 REER implied exchange rates in MSCI Frontier

Current FXrate vs $

FX rate impliedby long-term average REER

FX rate if REERfalls to lows

Current rate divided bylong-term average

2015 CA(GDP)

Kenya 106 152 266 143 -77Nigeria 199 285 618 143 07Vietnam 22470 29114 35506 130 48Bangladesh 777 992 117 128 -06Sri Lanka 141 166 205 118 -20Kuwait 030 035 042 117 157Oman 038 044 049 116 -150Pakistan 104 120 135 115 -13Romania 396 449 935 113 -11Saudi Arabia 375 424 505 113 -10Georgia 238 237 392 100 -66Morocco 974 926 992 095 -34Iran 29856 26224 60389 088 08Kazakhstan 270 216 272 080 -19

Argentina 939 519 108 055 -17Note We expect Nigerias current account deficit to be 3 of GDP in 2015 the IMF revised its Kenya forecast to -99 of GDP in September 2015

Source IMF April WEO Bruegel Bloomberg Renaissance Capital

We have one fundamental problem with the REER methodology that is applicable to

Kenya and Nigeria We think it is flawed because inflation rates between rich and poor

countries are not the same

US per capita GDP was nearly $55000 in 2014 while Kenyarsquos was around $1400 If we

see 1 inflation in the US and 10 in Kenya and if we use those per capita GDP figures

as a proxy for wages then in 2015 US wages would have risen by $550 and Kenyan

wages would have risen by $140 A REER comparison would tell us that i f the Kenyan

shilling did not move in nominal terms then Kenya has lost about 9 competitiveness

against the US (10 Kenyan inflation minus 1 US inflation) but for a company

employing people in the US and Kenya the absolute cost of employing a worker has risen

much less in Kenya than it has in the US Kenya would need to have seen inflation closer

to 30 for wages in both countries to have risen by the same absolute amount Moreoverwe can imagine that productivity is much easier to improve in Kenya than the US

The implication then is that REER methodologies are fine when we compare rich

countries to rich countries or poor countries to poor countries but not when we compare

rich to poor

This is a key reason why we are not about to alter Yvonne Mhangorsquos exchange forecasts

for the NGN or the KES with the figures implied by this work on REER rates

However our problem with REER figures for poor countries also apply to Pakistan