Embed Size (px)

Citation preview

Februar y 2018 ISSUE 65

NEWS REVIEWS COMMENT ANALYSIS

For today’s discerning financial and investment professional

This time next year Rodney

The disruptive rise of crypto?

The tax efficient investment market has changed significantly in recent years. There has never been a better time to get involved, as high value clients are gaining interest in this sector and it’s exactly where you can add tangible value. Complex structures and investments with higher risk profiles mean that clients would benefit from your advice. Without it, they may invest anyway and could make ill-informed decisions, whilst dis-intermediating you from the process and reducing your revenue potential.

Whether you’re already advising on SEIS, EIS, BPR or VCT products, or perhaps considering them for your clients’ portfolios then contact us at GrowthInvest. We’ll show you how you can consolidate historic investments onto our platform and build a diversified portfolio from a wide range of managed fund or single company investments. Through our intuitive online platform you’ll be able to offer your clients exclusive access to real portfolio growth, secure in the knowledge that these government-backed schemes offer unique tax efficiencies.

Visit us to learn about the products, the pitfalls and how best to advise on this dynamic and evolving sector. So make it your business, before someone else makes it theirs...

Find out more at growthinvest.com

Make ItYourBusiness

5 Ed's Welcome

6News

20Brian ToraDon’t overdo the gloom, says Brian Tora, because the global economy in 2018 is still fundamentally strong

24On balancePeter Sleep of 7IM weighs up ETFs against other options in portfolio management

30Global Advisers3 concepts fundamental to understanding cryptocurrencies

32Tony Catt

How much regulation does it take to treat customers fairly? A regulatory update from compliance consultant, Tony Catt

16 Ed's Rant

Mike Wilson explores the expansive world of crypto-currencies what with assets fast approaching $1 trillion

22Better Business

Make 2018 the year that you experience a real business transformation by putting these tips into practice

26Taking your marketing to the next level

Part 3 in the series from Sam Turner, on adding structure to your marketing approach

14ETF Securities Mixed outlook for commodities in 2018 – ETF Securities

CONTRIBUTORS

Brian Toraan Associate with investment managers JM Finn & Co.

Neil Martinhas been covering the global financial markets for over 20 years.

Richard Harveya distinguished independent PR and media consultant.

Michael WilsonEditor-in-Chiefeditor ifamagazine.com

Sue WhitbreadEditorsue.whitbread ifamagazine.com

Alex SullivanPublishing Directoralex.sullivan ifamagazine.com

IFA Magazine is published by IFA Magazine Publications Ltd, Arcade Chambers, 8 Kings Road, Bristol BS8 4AB Tel: +44 (0) 1179 089686

© 2018. All rights reserved

‘IFA Magazine’ is a trademark of IFA Magazine Publications Limited. No part of this publication may be reproduced or stored in any printed or electronic retrieval system without prior permission. All material has been carefully checked for accuracy, but no responsibility can be accepted for inaccuracies. Wherever appropriate, independent research and where necessary legal advice should be sought before acting on any information contained in this publication.

IFA Magazine is for professional advisers only. Full details and eligibility at: www.ifamagazine.com

Brett DavidsonFP Advance

46Career Opportunities

From Heat Recruitment

40Making the tax year-end less taxing for advisers

Les Cameron discusses the range of technical support and resources which are available to advisers and paraplanners

36EIS – A new dawn?Mark Brownridge analyses what the Budget changes mean for financial planners

44The Young OnesPensions aren’t boring. A message that Richard Harvey hopes more young people will latch on to in 2018

IFAmagazine.com

CONTENTS

Februar y 2018

3

SMARTER INDICES& QUALITY INCOME.OUR ETFs ARE AGAME CHANGER.

LET’S TALK HOW.

Investments should be made on the basis of the current prospectus, which is available along with the Key Investor Information Document and annual and semi-annual reports, freeof charge from our website, your broker or your financial adviser. The Fidelity UCITS ICAV is managed by FIL Fund Management (Ireland) Limited. The Fund is authorized in Irelandand regulated by the Central Bank of Ireland. FIL Fund Management (Ireland) Limited is authorized in Ireland and regulated by the Central Bank of Ireland. Issued by FinancialAdministration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and F symbols aretrademarks of FIL Limited. UKM1117/20936/CSO08568/0518.

In the search for sustainable income, a smart approach canpay dividends. Fidelity’s range of smart beta ETFs applyour investment team’s years of experience in selectingquality income stocks to the purpose-built indices we track.We focus on companies that have demonstrated goodprofitability, strong cashflows and consistent dividends.

• Fidelity Global Quality Income UCITS ETF

• Fidelity US Quality Income UCITS ETF

• Fidelity Europe Quality Income UCITS ETF

• Fidelity Emerging Markets Quality Income UCITS ETF

Change your approach to finding an income atfidelity-etfs.com

Past performance is not a reliable indicator of futurereturns. The value of investments and the income from themcan go down as well as up and clients may get back lessthan they invest. The funds may invest in overseas marketsand so the value of investments can be affected bychanges in currency exchange rates. The Fidelity EmergingMarkets Quality Income UCITS ETF invests in small andemerging markets which can be more volatile than othermore developed markets.

This advertisement is for investment professionals only

FIDELITY QUALITY INCOME UCITS ETFs

Job No: 55294-37 Publication: IFA Magazine Size: 297x210 Ins Date: 01.12.17 Proof no: 1 Tel: 020 7291 4700

5I FAmagazine.com

Februar y 2018

ED'S WELCOME

World fails to collapse as Santa Claus rally ends. Analysts distraught as rock-solid and reliable metrics all fail to deliver long-overdue global crisis. Valuations now running at twice the unsustainable ratios they were the last time that we had an unsustainable bout of unsustainability. Newspaper editors forced to choose between eating their hats and their words.

America discovers that handing out half a trillion dollars in tax breaks for business is really quite a good way to put new heart into US stock prices. Bitcoin stubbornly refuses to bite the tulip-field dust, as its first-ever exposure to shorting pressure results in a worldwide epidemic of – well, nothing much, really. By the third week of January it’s still sporting a year-on-year gain of 2,000%.

Back in Washington, Donald Trump breaks with his propaganda-meister Steve Bannon and gets an apology from the very same man who, a few weeks ago, called his son’s behaviour “treasonous”. State Secretary Rex Tillerson, who called Trump a “moron” last summer, now says that there’s no reason to doubt his self-proclaimed “very stable genius”. The Dow Jones index hits another record high, the S&P 500 has the best start to January since 1987.

Stocks continue to climb as North Korea’s Kim Jong Un responds to playground insults from Trump about who’s got the bigger button, with an announcement that his government is interested in teaming up with South Korea during the winter Olympics.

Nearer to home, Theresa May unexpectedly fails to get removed as Conservative Party leader, and promptly signals more of the same with a largely unchanged cabinet. Sterling strengthens, UK stocks continue to climb.

China’s leader Xi Jinping continues to crunch the political opposition into the ground and installs himself in the pantheon of the great, alongside Chairman Mao, by getting his personal thoughts embedded into the Chinese constitution. GDP growth projections for 2018 rise slightly to 7%. Shanghai stocks continue to climb.

Germany’s leader Angela Merkel picks herself up after being pitched into an unsustainable political situation. France’s President Emmanuel Macron ditto. Euro strengthens and FTSE Eurofirst 300 continues to climb.

Okay, are you getting the picture? And shall we stop embarrassing ourselves now? Are we, and the rest of the financial press, guilty of spreading the biggest bear myth since the 1970s? Is it really “different this time”?

Back to the Future

Have the laws of logic and mathematics turned themselves inside out, just for us? Have the stars and planets rearranged

themselves so as to rewrite the celestial horoscope? Indeed, have we somehow slipped through the space-and-time continuum so that we now inhabit an entirely different slice of time with entirely different outcomes, as Einstein postulated?

The heck we have. If you’re reading this magazine in early February, and if the world is still round and the sea is still wet and two and two still make four, the chances are that the underlying logic of the old place is still intact.

And that the Federal Reserve’s plans to raise rates, perhaps three times, will slow investment and restore the broken strength of the dollar, and pitch the perilously-valued bond markets into a competitive round of capital losses. And that we, the advisers and managers, are likely to find ourselves managing a rotation that’s been staring us in the face for the last three years. And that our clients will need us more than ever.

Michael WilsonEditor-in-Chief

Shock horror, hold the front page...

Alternative Truths

I FAmagazine.com6

Februar y 2018

NEWS

Ascot Lloyd and Bellpenny to become IFA under Ascot Lloyd brand

Following the merger of the two companies in July 2017, Ascot Lloyd Financial Services and Bellpenny have now become a single, fully independent financial advisory company under the unified brand Ascot Lloyd.

The company says that this change will enable the business to provide a broader product set and reflects the group’s ambitious growth strategy as one of the largest independent wealth managers in the UK. Following the merger in July 2017, the business saw strong growth in the second half of the year. The combined Ascot Lloyd now has a turnover in excess of £40m, over £6bn in funds under management, 80 personal advisers and 40,000 clients.

Nigel Stockton, CEO of Ascot Lloyd, commented: “At the heart of our success is a client driven business, and our move to become fully independent is in direct response to what our clients and advisers want, while also allowing us to offer a more comprehensive service.

“We have now established an outstanding platform, with significant scale and a trusted brand. Going forward we have considerable opportunities to expand our client base, deepen existing relationships and welcome new, high quality advisers. We look ahead to 2018 with great confidence.”

Februar y 2018

7I FAmagazine.com

Property demand levelling out

NEWS

House prices in London rose by just 1% during 2017, according to the latest survey from the Halifax mortgage lender – the slowest increase in six years, and markedly less than the UK national average of 2.7%, which was itself around half the level of 2016.

2018 is likely to see further rises of 1% to 1.5% (according to Nationwide) or 0% to 3% (Halifax). The general slowdown has been widely attributed to the effects of changes in taxation policy, which raised stamp duty and reduced the tax reductions available on buy-to-let properties – thus encouraging a sell-off by BTL owners. But much attention has also focused on the fact that many of last year’s fastest growth areas were provincial but “classy” locations such as Cheltenham (up 13%), Bristol,

Manchester and Birmingham. Are we seeing a long-term exodus of city types toward the less pressurised areas of the country, analysts wondered?

Halifax’s managing director, Russell Galley, characterised the 2017 situation as being essentially flat, with demand, supply, construction activity and even mortgage approvals all being suppressed by low consumer expectations of the country’s economic prospects, and of rising expectations that interest rates would soon rise.

It was not all gloom, however. Wales and the East Midlands both saw an 8% increase in house prices during 2017, the Halifax says, and the South West witnessed a 4.9% rise.

Scotland experienced a small/insignificant price fall of 0.2%, but localised pressure points such as Perth saw prices dropping by as much as 5.3%. Pity, however, the Northern Ireland property owners who suffered a 5.6% drop in values.

Will the situation be rescued by Chancellor Philip Hammond’s pledges of £44 billion in new money and new investment during the Autumn Budget statement, we wondered? We can certainly hope so. But we do need to remember that Hammond’s ambitious pledge of 300,000 new homes a year has been pencilled in for the mid-2020s. Right now, that seems a long time away.

Februar y 2018

I FAmagazine.com8

NEWS

The quiet (but oh, so decisive) arrival of the MiFID II rules in January has somehow managed to catch out a substantial number of funds which have unaccountably failed to meet the required KID (Key Information Document) standards introduced under the Packaged Retail and Insurance based Investment Products (Priips) regulations. As a result, Hargreaves Lansdown alone chopped 296 investment trusts from its platform within days of Priips coming into force on 1 January – and Bestinvest had sent another handful of funds to the naughty step.

The Priips requirements are part of an overall package of investor protection measures

that effectively formed part of the MiFID II programme. It isn’t clear yet how long the suspensions will last, because most of the British and European funds will now be working hard to bring their documentation up to speed. But the situation with US and Canadian funds may be different.

The Financial Times reported that as many as 1,200 ETFs had been similarly struck dumb by Hargreaves, including 900 from US corporations which presumably hadn’t been keeping up to date with their European requirements. Or which (equally likely) had no real intention of complying.

The FT reassured its readers that the new measures “do not affect certain mutual funds based in the EU known as Ucits funds, which includes a large volume of ETFs.”

Observers say that the failure to comply with the KID requirement will have only limited impact on UK investors., most of whom buy these North American funds through other funds or through regular savings plans. However, according to the FT, UK investors with existing holdings in such funds would find it hard to amend their savings amounts until such time as the funds produced the necessary KID paperwork.

Trouble with the KIDS again

I FAmagazine.com10

Februar y 2018

NEWS

A series of disappointing Christmas trading figures from UK retailers pointed toward a general downturn in British spending patterns – at least, from the conventional store chains. Only Next, whose sales rose, could really lighten the gloom, it appeared.

Toys R Us announced the closure of a quarter of its UK stores, in the face of relentless pressure from e-sales; M&S reported sharply lower Christmas food sales on top of its already lacklustre clothing sales; Tesco announced a modest rise which didn’t meet market expectations; John Lewis reported a higher Christmas turnover but agreed that it had been forced to absorb so many extra costs that profits would fall; and the mighty House of Fraser was reduced to asking its landlords for rent reductions.

Specialist chains seemed to have fared little better. Poundland and the Harveys furniture chain were squeezed after their South African parent Steinhoff was forced to restate its accounts; Moss Bros issued a warning in mid-January; and electronics retailer Maplin, with 2018 stores, faced the partial withdrawal of its credit insurance cover as its market suffered from e-commerce competitors.

Analysts agreed that the causes for the retail unease on the high street were many and various. On the one hand, inflation and a weak pound had boosted prices which had put shoppers off. On the other, many felt unwilling to extend their credit balances much further, especially while Brexit uncertainty was destabilising their job situations. Analysts said they were hopeful, however, that a successful negotiation of Brexit terms would improve the situation.

A Bleak Midwinter

11I FAmagazine.com

TITLE

Februar y 2018

NEWS

CAPE FearFinancial markets opened the year in fine style, with nearly all the major stock market indices attaining new records during the first two weeks of January. And all this despite – or perhaps because of? – displays of occasionally brutal strength from world leaders.

As detailed on page 5, Presidents Trump, Xi Jinping, Kim Jong-un and his southern Korean counterpart Moon Jae-in all took distinctive steps to stamp their political authority on their respective economies, and in lesser ways so did Prime Minister Theresa May and Germany’s Angela Merkel. (By contrast, there was little to be seen of President Vladimir Putin in Moscow, where the Micex

showed no clear sign of breaking out of last year’s turbulent slide.)

The World Bank picked up on the bullish sentiment with an upgrade in its global growth projection (3.2% in 2018, rising to 4.5% in emerging markets), and it also forecast a steep resurgence in commodity prices. You can read the summary at (https://tinyurl.com/yank2gs4).

But developed economies such as US were still running uncomfortably high numbers on Robert Shiller’s 10 year Cyclically Adjusted P/E (CAPE) ratio, which surpassed its 1929 maximum.

Academics remained divided as to whether CAPE was still valid, or whether it should

be amended to allow a kinder interpretation of fair value, since CAPE had been signalling an over-expensive US market for the whole of the last seven years.

A recent paper by Research Affiliates, entitled ‘CAPE Fear’ (https://tinyurl.com/y9w2ydmo), had argued for a review of the mechanism; other observers, meanwhile, pointed out that the current 10 year statistics are mathematically skewed by the memory of the 2008 crisis which had seen huge short-term drops in profits. Once those had passed out of the calculations in late 2018, they said, the picture would become somewhat less perilous. At present, the jury is still out.

I FAmagazine.com12

Februar y 2018

Award-winning financial planners Paradigm Norton continue to expand with the announcement of the merger between the firm and London-based The Red House Consulting Limited. Paradigm Norton now employs a team of 55 across its offices located in Bristol, Torquay and London.

The merger is part of its planned strategy to build a significant financial planning business focussed

on delivering great financial planning and life outcomes for its clients and creating a dynamic environment for its team to develop and grow.

Paradigm Norton’s Chief Executive Barry Horner commented: “We are absolutely thrilled to be merging with The Red House, a firm we have watched for a number of years, who share our values, passion and commitment to delivering an excellent client experience.”

Ruth Sturkey, Managing Director of The Red House, was also delighted to join forces with Paradigm Norton. She comments: “This merger is great news for both our clients and our team, bringing greater strength, depth and continuity to our offering. The integration of our teams, each of whom have an excellent track record of delivering innovative financial planning solutions, gives our mutual clients a range of additional resources, expertise and life skills”

Paradigm Norton continues to grow

NEWS

13I FAmagazine.com

Februar y 2018

This communication has been provided by ETF Securities (UK) Lim-ited (“ETFS UK”) which is authorised and regulated by the United King-dom Financial Conduct Authority (the “FCA”).

This communication is only targeted at qualified or professional in-vestors.

The information contained in this communication is for your general information only and is neither an offer for sale nor a solicitation of an of-fer to buy securities. This communication should not be used as the basis for any investment decision. Historical performance is not an indication of future performance and any investments may go down in value.

This document is not, and under no circumstances is to be construed as, an advertisement or any other step in furtherance of a public offering of shares or securities in the United States or any province or territory thereof. Neither this document nor any copy hereof should be taken, transmitted or distributed (directly or indirectly) into the United States.

This communication may contain independent market commentary prepared by ETFS UK based on publicly available information. Although ETFS UK endeavours to ensure the accuracy of the content in this com-munication, ETFS UK does not warrant or guarantee its accuracy or cor-rectness. Any third party data providers used to source the information in this communication make no warranties or representation of any kind relating to such data. Where ETFS UK has expressed its own opinions related to product or market activity, these views may change. Neither ETFS UK, nor any affiliate, nor any of their respective officers, directors, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

ETFS UK is required by the FCA to clarify that it is not acting for you in any way in relation to the investment or investment activity to which this communication relates. In particular, ETFS UK will not provide any investment services to you and or advise you on the merits of, or make

any recommendation to you in relation to, the terms of any transaction. No representative of ETFS UK is authorised to behave in any way which would lead you to believe otherwise. ETFS UK is not, therefore, responsi-ble for providing you with the protections afforded to its clients and you should seek your own independent legal, investment and tax or other ad-vice as you see fit.

Short and/or leveraged exchange-traded products are only intended for investors who understand the risks involved in investing in a product with short and/or leveraged exposure and who intend to invest on a short term basis. Potential losses from short and leveraged exchange-traded products may be magnified in comparison to products that provide an unleveraged exposure. Please refer to the section entitled “Risk Factors” in the relevant prospectus for further details of these and other risks.

Will 2018 be a golden year?

etfsecurities.com/gold

Gold has begun 2018 strongly, helped by a weaker US Dollar and, amongst other factors, stronger demand for inflation hedged investments.

Access latest insights from Europe’s leading provider of gold ETPs

• Physical gold ETPs with zero credit risk and London or Zurich vaulting

• Currency hedged physical gold ETPs

• Short & leveraged gold ETPs

• Gold miners ETF

Gold-A4-2018.indd 1 12/01/2018 15:25

I FAmagazine.com14

Februar y 2018

Mixed outlook for commodities

in 2018 Advisers looking for value in the commodities sector may wish

to consider exposure to industrial metals within clients’ portfolios argues James Butterfill, Head of Research, ETF Securities

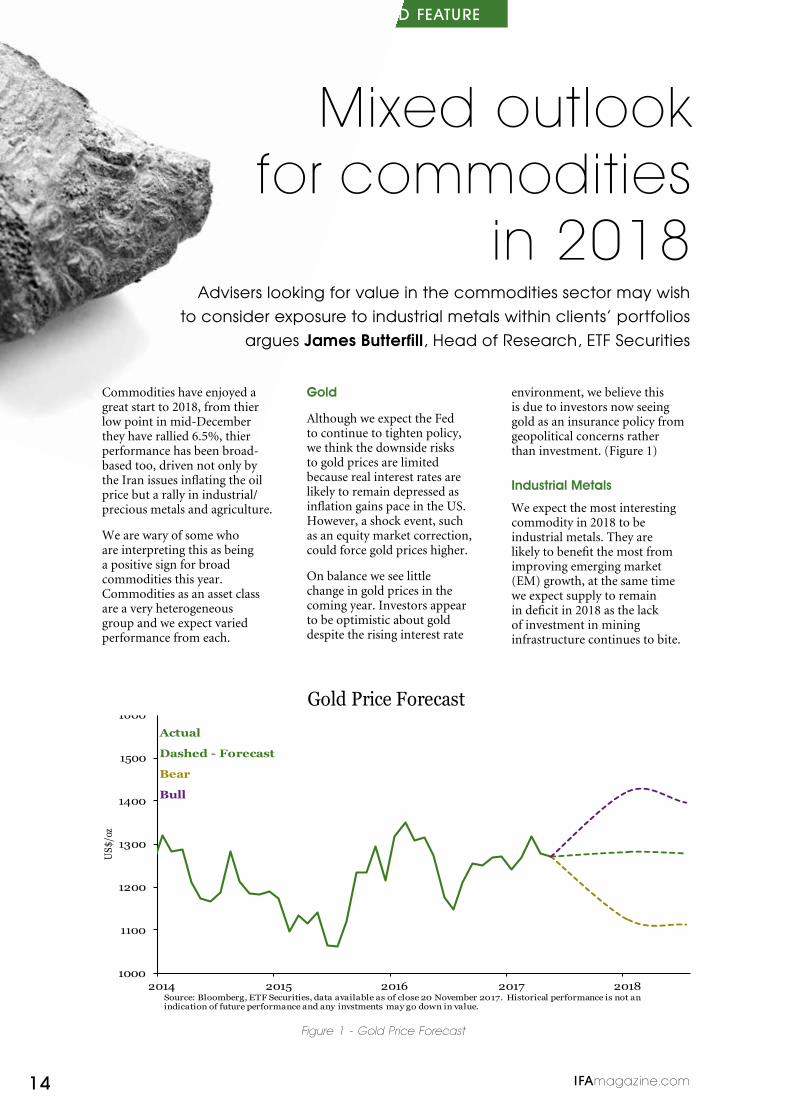

Commodities have enjoyed a great start to 2018, from thier low point in mid-December they have rallied 6.5%, thier performance has been broad-based too, driven not only by the Iran issues inflating the oil price but a rally in industrial/precious metals and agriculture.

We are wary of some who are interpreting this as being a positive sign for broad commodities this year. Commodities as an asset class are a very heterogeneous group and we expect varied performance from each.

Gold

Although we expect the Fed to continue to tighten policy, we think the downside risks to gold prices are limited because real interest rates are likely to remain depressed as inflation gains pace in the US. However, a shock event, such as an equity market correction, could force gold prices higher.

On balance we see little change in gold prices in the coming year. Investors appear to be optimistic about gold despite the rising interest rate

environment, we believe this is due to investors now seeing gold as an insurance policy from geopolitical concerns rather than investment. (Figure 1)

Industrial Metals

We expect the most interesting commodity in 2018 to be industrial metals. They are likely to benefit the most from improving emerging market (EM) growth, at the same time we expect supply to remain in deficit in 2018 as the lack of investment in mining infrastructure continues to bite.

1000

1100

1200

1300

1400

1500

1600

2014 2015 2016 2017 2018

US$

/oz

Gold Price Forecast

Source: Bloomberg, ETF Securities, data available as of close 20 November 2017. Historical performance is not an indication of future performance and any invstments may go down in value.

Actual

Dashed - Forecast

Bear

Bull

Figure 1 - Gold Price Forecast1000

1100

1200

1300

1400

1500

1600

2014 2015 2016 2017 2018

US$

/oz

Gold Price Forecast

Source: Bloomberg, ETF Securities, data available as of close 20 November 2017. Historical performance is not an indication of future performance and any invstments may go down in value.

Actual

Dashed - Forecast

Bear

Bull

SPONSORED FEATURE

I FAmagazine.com

Februar y 2018

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-2,500

-1,500

-500

500

1,500

2,500

3,500

4,500

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Min

ers margin

s (in %

)

Sup

ply

/Dem

and

bal

ance

in

'00

0 to

ns

Miners Margins vs Supply/Demand

World Refined Metals Balance (YoY '000 MT, LHS)

Mining company margins 2yr lead(YoY%, RHS)

Figure 2 - Miners Margins Vs Supply/Demand

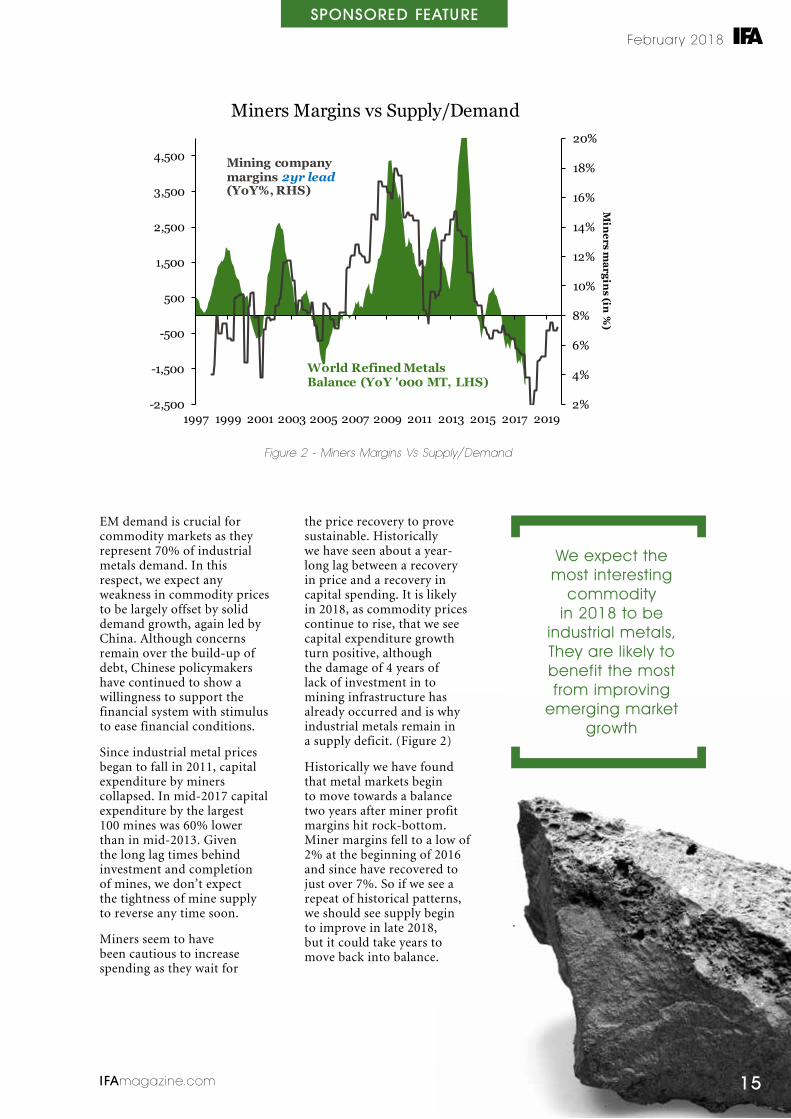

EM demand is crucial for commodity markets as they represent 70% of industrial metals demand. In this respect, we expect any weakness in commodity prices to be largely offset by solid demand growth, again led by China. Although concerns remain over the build-up of debt, Chinese policymakers have continued to show a willingness to support the financial system with stimulus to ease financial conditions.

Since industrial metal prices began to fall in 2011, capital expenditure by miners collapsed. In mid-2017 capital expenditure by the largest 100 mines was 60% lower than in mid-2013. Given the long lag times behind investment and completion of mines, we don’t expect the tightness of mine supply to reverse any time soon.

Miners seem to have been cautious to increase spending as they wait for

the price recovery to prove sustainable. Historically we have seen about a year-long lag between a recovery in price and a recovery in capital spending. It is likely in 2018, as commodity prices continue to rise, that we see capital expenditure growth turn positive, although the damage of 4 years of lack of investment in to mining infrastructure has already occurred and is why industrial metals remain in a supply deficit. (Figure 2)

Historically we have found that metal markets begin to move towards a balance two years after miner profit margins hit rock-bottom. Miner margins fell to a low of 2% at the beginning of 2016 and since have recovered to just over 7%. So if we see a repeat of historical patterns, we should see supply begin to improve in late 2018, but it could take years to move back into balance.

We expect the most interesting

commodity in 2018 to be

industrial metals, They are likely to benefit the most from improving

emerging market growth

15

SPONSORED FEATURE

This time next year Rodney…

Crypto-currency assets are fast approaching $1 trillion, says Michael Wilson. Anonymous, tax-untraceable

and floating on a global bed of popular support. Whatever might happen next?

In the inimitable words of Del Trotter himself: “This time next year, Rodney, we’ll both be millionaires…..”

“Naah, honestly. Strictly kushty. You can play the system, Rodney or you can play outside it. Sort of. Just find your own sort of people who share your own youthful values, and who trust each other, and then who cares what the boring old f@rts in the central banks say? Who needs <audible sneer> “fundamental analysis” anyway? We’ve heard what them baby boomers have said, and it’s all about protecting their own fat backsides, isn’t it? What have they ever left behind for us common people, eh? Answer me that, then, Trigger?”

In a weird kind of way, the crypto-currency people have a point. For the first time since the Age of Aquarius in the 1960s (“Harmony and understanding, sympathy and trust abounding, no more falsehoods or derisions, golden living dreams of visions, mystic crystal revelation and the mind's true liberation”… yeah, move along folks, there’s nothing here to see), the arrival of a wealth system based on something other than hard economic realities and cruel mathematical ratios is taking hold. And it’s making an embarrassing amount of money (sorry, Del, “wonga”) for the early believers. My Coindesk

subscription tells me that $895 of bitcoin in January 2017 is worth $12,000 today. Having been all the way up to $20,000, and then chaotically down again. Lovely jubbly, but a bit scary all the same.

Stronger than it looks

So should we, as industry professionals, be taking bitcoin and its crypto brethen seriously? Or is it all just a disaster waiting to happen? Should we, as advisers, be bracing ourselves for the inevitable plane crash and trying to anticipate where the wreckage is going to land? And just what do we say to our clients who are absolutely slavering for this dodgy new paradigm?

I have to warn you that the following news isn’t all easy to swallow. Bitcoin has now been accepted by a number of central banks, and its “blockchain” confirmation concept is being seriously studied by big institutions all around the world. More importantly, it’s recently been opened up to the searching scrutiny of the short-sellers’ markets. And you know what? It hasn’t collapsed.

Well, not yet anyway. There were a lot of people who said that bitcoin wouldn’t survive the opening of the Chicago futures contracts in December 2017 – because, they said, bitcoin had never needed to base its

valuation on anything other than that the numbers of people who wanted to buy it; and as for fundamental value, it had none anyway, so what would happen when somebody shorted it?

The question was intriguing. How do you short something that doesn’t have a fundamental value in the first place? If the buyer’s pitch is based on a loosely optimistic idea of future liquidity and the seller’s pitch centres around an equally intuitive but downmarket view of same, where are the two to meet?

The blockchain concept

I’m going to be perfectly honest here. I’m a traditional liberal artsy type who only scraped maths O level at school because I didn’t follow the inevitable logic of what other people were calling logic. Even today, my head starts to spin when I hear people making nearly-circular arguments about why one system is better/more logical than the others. But here’s what I’ve picked up about this thing that other people are calling blockchain.

The first thing is that blockchain doesn’t concern itself with who’s making what transactions, but focuses instead on ensuring that the identity of a unit of transaction (such as a bitcoin) is openly and publicly confirmed.

Februar y 2018

IFAmagazine.com16

ED'S RANT

Whenever a bitcoin transaction goes ahead, the blockchain sends out a “distributed ledger” notification to all and sundry to say that it’s happened, and that the bits-of-bitcoins have changed hands. That, in turn, should be enough to ensure that nobody will be able to claim that the dog ate his bitcoin, or that somehow an imposter has got away with it while his back was turned. And therein lies the security. Who needs a gold bar in the cellar when you’ve got that kind of confirmation of your claim to title?

The important thing, though, surely, is that the blockchain process doesn’t record who’s bought or sold the bitcoin. Anonymity is the absolute name of the game - which is why, unfortunately, bitcoin is still the currency of choice for fraudsters, pornographers, kidnappers, illegal Chinese currency brokers, and a whole lot of other bad people who the proponents of the New Age of Aquarius are trying to forget about.

But can the system ever break that chain of anonymity? There’s rather a lot riding on it. We’ll look at this question in a moment.

What’s a bitcoin worth anyway?

That’s a serious question, and we’re not going to find any answers in the textbooks. As long as we can get our heads round the fact that bitcoin and the like have no intrinsic value at all, but exist only as an aspiration in the searching hearts of their admirers, then we’re on the starting point for assessing the value of this strange new mechanism.

“Mechanism” is perhaps the right word. Supposedly invented by somebody called Satoshi Nakamoto, who now appears never to have existed, the general idea of bitcoin is that it floats upon the public consciousness

and derives its value from the level of demand at the time.

So [playing the young devil’s advocate here], how different is that from all the conventional currencies in the world? All right, you can plant a tulip bulb in the ground and get a flower from it, and you can wear a lump of gold around your neck, or maybe even make an electrical connector out of it. But tell me, could you say the same about a dollar, or a yen, or a euro? Aren’t they just what we call fiat currencies? (From the Latin word for “trust”) Aren’t they just a load of bull***t from a bunch of self-interested bankers who’ve set up the world to benefit their own system?”

You don’t have to agree with that sentiment to see where the logic’s coming from. Buying a bitcoin is a statement of solidarity with a millennial generation which feels that it’s been passed over by the wrinklies. And the possibility that there might be a different way of floating a currency on a bed of public confidence is bound to feel attractive, isn’t it?

How big is crypto?

But none of these concerns are going to mean much unless we can get a proper sense of how large the crypto currency market actually is. Before we can assess the risk from the advancing army, we need to know how much gunpowder they’ve got.

The answer is illuminating. According to CoinMarketCap, the total value of crypto currencies in early January was $760 billion at current exchange rates. Of which perhaps half consists of bitcoins – the others include Ethereum, Litecoin, Swiftcoin, Bytecoin, Primecoin, Blackcoin, Auroracoin and nearly 1,400 more. (Do you see where this is heading?)

How does that $760 billion stack up against the global environment? It’s equivalent to a bit less than 1% of

the world’s stock market capitalisation. It amounts to around ten days’ worth of US Gross Domestic Product.

Small beer, then. And when compared with the $22 trillion cost of the 2008 crash, it would be hard not to conclude that a crypto collapse would be opening up buying opportunities as soon as the losses exceeded $1 trillion or so.

Except that the downforce from a bitcoin crash would vastly exceed the losses suffered by the unlucky speculators. Troubles are likely to happen because some institutions will have over-exposed themselves and will face liquidity issues, which will have knock-on counterparty effects all over the place. Bitcoin in itself won't be the cause of a financial avalanche, but it might well be the trigger for one if the preconditions are already in place elsewhere. And that’s the hard bit to calculate in advance.

“No income tax, no VAT, no money back, no guarantee…”

Can cryptos be taxed?

Here’s an interesting conundrum, courtesy of a contributor to an internet forum which I frequent. The contributor’s son, it seemed, had been given a gift of 250 bitcoins by a friend, many years ago, as a thank you for a small bit of research that he’d done toward a project. And how, with bitcoin at $16,000, his gift was suddenly worth $4 million, and what was he to do about it?

Should he be liable for income tax on what HMRC might well decide to regard as earned income? Or would tax be levied only on the value of the bitcoins at the time of transfer (probably less than $10,000). Or would the taxman be entitled to lay a top-rate tax claim to the entire sterling capital gain since the gift had been made?

17IFAmagazine.com

Februar y 2018

ED'S RANT

Or could he simply dismiss the whole matter as a gift, and not as earnings at all? And if he did none of those things, would the taxman ever find out that he’d ever received the bitcoins, in view of the aforementioned provisions about blockchain anonymity?

What price anonymity?

That’s not such an easy question to answer as it seems, apparently. The prized anonymity of bitcoin transactions has been taken pretty much for granted up till now – not least, by the hackers and scam artists who infect people’s computers and then demand ransom payments to disinfect them – invariably in bitcoin. But the Feds are now starting to close in on the crypto-currency exchanges themselves. And that’s where the bitcoin taxation issue starts to get interesting.

Last November, a court in San Francisco approved a demand by the American IRS tax agency that forces the Coinbase exchange to reveal traders’ identities whenever they trade (or simply receive) bitcoin to the value of $20,000 or more. According to the evidence considered by the court, some 14,350 Coinbase users had traded in such amounts between 2013 and 2015, but only 800-900 had declared gains to the US tax authorities.

Coinbase had opposed the IRS’s move on the grounds that its sweeping demand for information was a threat to privacy The court found that the IRS “has a legitimate interest in investigating” taxpayers who remain stumm about their

dealings – and the court ruled, according to Bloomberg, that the company “must turn over basic identifying information, records of account activity and period statements for accounts with the equivalent of $20,000 in any one transaction type during any single year from 2013 to 2015”. However, the court held back from ordering the surrender of other identifying data such as public keys that might allow the inspection of all accounts, wallets and vaults.

Courts in other countries, especially in Asia, are being less subtle about the increasing pressures that they’re bringing to bear on the exchanges to make them open up their records. Hardly a week goes by without some exchange being closed, suspended or generally leaned on. So is the cryptocurrency business ready to grow up and go mainstream?

First in, first out?

We’ll look at that question in a minute. But first, let’s ask a rather obvious question that’s been puzzling the US tax people. If you ask people to declare their bitcoin gains for capital gains tax purposes, how are you going to stop them from preferring last-in, last-out, so as to minimise the gains on which tax has to be paid?

I mean, if you buy a building or a distinct block of shares, or even a gold bar, it’s easy to see when you

bought that particular item and when you sold it. But when you’ve been adding to (and drawing from) a liquid pool of same-stuff crypto-coinage, the task of defining first in and first out becomes much more difficult. The word is that Congress is still scratching its head about how to stop taxpayers from kicking their bigger long-term capital gains down the road for as long as possible.

The market calls for regulation

And yet the market itself is gradually starting to see the logic of regulating itself a bit more transparently. If crypto-currencies are half-serious about taking the task of money-creation out of the hands of the world’s Central Banks (pause for effect…), and if they want to attract serious attention from businesses and bond markets, they need to ensure that the scarcity of their currencies (and therefore their value) remains tightly controlled.

So is the cryptocurrency business ready to grow up and go mainstream?

Februar y 2018

IFAmagazine.com18

ED'S RANT

And that, of course, can be a tall order if the global fleet of crypto-currency operators insists on hoisting the Jolly Roger. Nobody appreciates that more than the now-defunct Mt Gox, formerly the world’s biggest bitcoin exchange, which crashed in 2014 after it discovered that fraudsters had spent the last three years silently skimming off around 850,000 bitcoins to the (then) value of $450,000. A sum which would now be worth somewhere around $11 billion. Eek.

The Mt Gox fraudsters, as far as my feeble brain can decipher, had cracked the secret of persuading the trading system to give them a second go at a bitcoin transaction when their first attempt “failed” (ho ho). And by this simple strategy they had been buying one, getting one free for years while nobody noticed. Moreover, it hardly improved the market’s confidence when Mt. Gox subsequently ‘discovered’ a wad of 200,000 bitcoins that had been lying down the back of the digital sofa in a wallet where nobody had thought to look for it.

The point here is that when your money’s gone, it’s gone. Nobody will know who took it, and you certainly won’t get any depositor protection. A point that you may wish to make to your clients when they enthuse about the burgeoning digital cash machine.

Then there are the inside fraudsters at the exchanges themselves. Trading at one US exchange was suspended in December for what seemed to have been a classic pump ’n dump operation – ramping up their apparent turnover in readiness for offloading their shares in the exchange. Elsewhere, there have been fears that smaller crypto-currencies have also been snapped up by staffers so as to inflate their values and dump them on the unwary.

And all the while, of course, the Chinese government is still battling to shut down the hundreds of illegal

exchanges which exist to export yuan wealth from the country without anyone noticing. If they ever succeed, the volume of global trading is certain to plummet. And with it will go a huge slice of the demand.

How to advise your clients?

And so to the crunch question. Is there anything good to be said about bitcoin? Well, for some people there probably is. As you’ll probably have heard, you can buy fractions of bitcoins quite easily (including from vending machines!), and they make nice birthday presents as long as you regard them as a speculation, not an investment. The transaction charges are eye-watering, though.

You can buy into bitcoin values with an exchange traded note such as the ones marketed by Hargreaves Lansdown – and another one that focuses on Etherium instead. Other funds are available, but I am reliably informed that some of these trade at premiums of up to 35% against assets. Why? Because it can take two days to complete a bitcoin transaction, and the price can move an awful lot during those 48 hours.

And finally. If I were a hard-working millennial with no hope of ever scraping together a deposit for a house of my own, I might very well be inclined to think that putting a couple of thousand pounds into bitcoin would be more likely to fulfil my dreams than investing them in Ernie. We can’t know whether we’re at the market’s peak and getting ready for a sell-off and a fatal capitulation. But viewed from a young person’s perspective, you can see the logic of the situation. The IFA’s task, I suppose, is to try and instil a sense of perspective and proportion.

I’ll tell you one thing, though. If bitcoin does crash, there are going to be a heck of a lot of very disgruntled young people who've convinced themselves that bitcoin is the only kind of lottery ticket with a guaranteed 100,000 percent payout. I expect they'll find a way somehow to blame it all on the baby boomers.

Buying a bitcoin is a statement of solidarity with a

millennial generation which feels that it ’s

been passed over by the wrinklies

19IFAmagazine.com

Februar y 2018

ED'S RANT

I FAmagazine.com20

Februar y 2018

Planet Ear th 2018Don’t overdo the gloom, says Brian Tora, because the global economy in 2018 is still fundamentally strong. But do keep an eye on the risk factors

In the end, 2017 was kind to investors. The FTSE 100 Share Index ended the year at an all-time high, as did several other major markets. True, the overall increase was not as great as that seen in the US and Japan, but it was still a plus, and perhaps it leaves room for further progress in the current year.

Bear in mind, incidentally, that the Footsie was only about 10% above the level that it had reached eighteen years previously when the technology boom was driving markets into what turned out to be bubble territory. So should we be drawing comparisons between then – the end of the last millennium – and now?

There are some similarities, but the differences are particularly marked and worthy of examination. Both the political and geo-political landscapes are less predictable than they were in 1999. That ought to make investors more nervous, but in fact the economic picture has improved sufficiently to allow a degree of confidence to creep in.

Anyone for Top Trumps?

That said, there have been plenty of predictions that this long bull run, which started back in 2009, cannot last much longer. The biggest area of risk appears to be the United States, where probably the greatest political uncertainty lies.

President Trump remains an unknown quantity one year in to his first term. His programme of change to deliver an America First agenda has experienced considerable

problems getting off the ground, while controversy continues over the methods used to gain his ascendancy in the polls. While Trump’s tax cuts do seem to be on track (and they were into their final stages as we went to press), opinion is still divided as to how much of a boost this will be to markets?

One effect is likely to be the repatriation of corporate cash held overseas. How businesses might use this resource is currently hard to determine, but in the past share buybacks have been favoured by boardrooms.

In theory, this should boost markets by limiting supply, but past experience shows that this need not prove to be the case. Moreover, enhanced cash resources could fuel an acquisition boom – again, a potential short-term plus for investors, although again such an approach can be value-destroying for those companies launching their takeover strategies.

But the overall expectation is that the US should help to lead a strong upswing in global growth in 2018. Shares on the other side of the pond certainly do need a positive profits outlook if the demanding valuation levels are to be justified.

BRIAN TORA

21I FAmagazine.com

Februar y 2018

The end of cheap money

The major risk, from my perspective, remains the ending of very cheap money. The Federal Reserve Bank has already started to reverse its quantitative easing stance, which brings us to one of

the similarities with 1999/2000. Easy

money made available

ahead of

the new millennium found its way into technology shares, which tanked when this policy was withdrawn early in 2000.

Of course, it is difficult to be certain how much influence the cheap money approach has had on share ownership, but it would be naïve to believe that higher interest rates will not have some impact on markets. While the US and the UK are the only major central banks to have started putting interest rates up, the Bank of Japan and the European Central Bank are

likely to join the monetary tightening party as the

year progresses - even if we may have to wait

until 2019 before they feel brave enough to increase the cost of money.

One effect of this change of tack must be to reinforce inflationary pressures. Already inflation has risen markedly here in the UK, although we should add that this is down to a

falling exchange rate, rather

than suggesting consumer-led

upward pressure on prices. Indeed,

consumers here remain constrained by declining

living standards – a point which was underscored by the post-Christmas trading updates from some major retailers. The positive, on the other hand, must be that all this is necessarily slow burn – so that, given any unexpected shocks, markets should have time to adjust to what must be a changing environment as the year progresses.

An uncertain planet

The “known unknowns”, of course, are the many continuing geo-political issues which are as dangerous today as they have ever been in living memory. 18 years ago, Iraq was centre stage; today, however, it’s not just North Korea that casts a threatening shadow over world peace – in the Middle East, the proxy wars between Saudi Arabia and Iran, the continuing involvement of Russia in the Syrian conflict, and the evaporation of peace talk initiatives between the Israelis and the Palestinians also remind us that the cauldron that is the Middle East is as volatile as ever.

Which is where we return to the unpredictability that constitutes the Trump presidency. As the arguable leader of the West, we all hope for direction from the world’s largest economy. But Trump’s decision to withdraw from climate change initiatives, and his determination to make America more protectionist, both demonstrate that the President’s priorities may not accord with the rest of the developed world. This is not necessarily a negative for investors, but it does add to the degree of uncertainty that needs to be factored into portfolio strategy.

My conclusion is that advisers and their clients should not expect as benign an environment as that which characterised 2017, but that even so, the bullish sentiment that has supported markets may well have further to run.

Markets tend to anticipate, rather than follow, events. A setback could occur either if a geo-political explosion occurs, or if the Goldilocks economic scenario approaches the end of its road. Sadly, neither is capable of being forecast with any degree of accuracy.

BRIAN TORA

Financial Planning ‘done right’ is a thing of beauty. It can transform people’s lives, which in turn can have a major positive impact on society.

Does all of that sound a little too grandiose to you? Is it possible to have a strongly performing business, in the financial sense, without losing your social purpose (or soul) in the process?

Of course it is.

To prove this you don’t have to look much further than some of the best performing businesses in the Financial Planning space. Firms like:

• Capital Asset Management www.capital.co.uk

• The Red House www.theredhousefm.com

• Cooper Parry Wealth www.cooperparrywealth.com

• Carbon Financial www.carbonfinancial.co.uk

• Paradigm Norton Financial Planning www.paradigmnorton.co.uk

All of these firms are heavily values-based. They know who they are and who they serve. They believe strongly in the

social purpose that underlines what they do every day.

If you’re still on the financial advisory treadmill where you work too hard, you don’t have a client list full of ideal clients, and some days you’re not sure if this is the right profession for you, then there are two specific areas you can work on.

1 Get clear on ‘who you serve’

It almost doesn’t matter what stage of development you’re at for this to apply. I’ll cut you some slack if you’re in the first 12-24 months as a start up, but even then, having a clear idea of who you work best with is crucial.

The best firms know who they serve. That will include the obvious things like:

• A minimum level of investable assets

or

• A minimum level of annual earnings (i.e. the client’s annual earnings in their business, job, or profession)

At the very least it will involve a minimum level of income the client must pay to the firm to ‘get in the door’.

However, knowing who you serve is about the soft facts as well. At The Red House, in addition to some specific minimum criteria, they only work with people ‘that get what life’s about’. They know what that means when they meet a new client. It’s a way of looking at the world.

At Paradigm Norton they have defined their ideal client, ‘Paradigm Pete’, with (last time I saw it) something like 25 criteria for what good looks like.

At FP Advance we want to work with people that are nice. That gets overlaid on top of any other financial metrics we might use.

Love is all you need

It’s vital to get crystal clear on who you want to work with, rather than taking anyone who walks through the door.

Why?

Because that’s how you end up with a business full of clients you love and can help. The joy that comes from that helps you attract more of the same types of clients.

It’s so much easier to go the extra mile when it’s a client you love to work with. Going that extra

Better Business - Do the Right ThingMaking sure you work with the right clients and setting proper limits on how much time you spend at work are the ways to getting a successful financial planning business says Brett Davidson of FP Advance. Make 2018 the year that you experience a real business transformation by putting these tips into practice

I FAmagazine.com22

BETTER BUSINESS

Februar y 2018

mile for someone you can’t stand is almost unbearable, especially when the pressure is really on.

Freedom of choice

The beautiful part of running your own business is that ‘you get to choose’ who you work with. Don’t forgo that choice on a day-to-day basis. If you do, every time you fail to make a positive choice you are sowing the seeds of your own unhappiness in the future.

Don’t believe this small change can make a life-changing difference to your business?

Just call any one of the firms I’ve listed here and ask. They’ll all tell you it was one of the most important steps on their journey.

2 Put hard limits on your time

When there are challenges at work, what do most of us do?

We work harder and often that means working longer hours.

I’m sorry to burst your bubble, but working harder and longer doesn’t work. I can say that with great authority because I’ve tried it. You might have tried it too and are sitting there wondering why you haven’t quite got to where you wanted to be. Read on.

The only way to break through is to resolve the challenges that arise in your business.

However, the tricky part is identifying the real issue, not just the symptom.

The best way to solve this quickly, is to set time limits on the hours

you and your team will spend at work. By setting time limits you are forced to choose. You have to consciously decide on what you will do and what you won’t, because you can’t do it all.

Time matters

The biggest breakthrough I had in my Financial Planning business in Sydney came after I got married to Deb. There was a two-year period before that, where I was in at 7:30am and often didn’t leave until 7:30pm or 8:30pm. I also worked most Saturdays. After getting married we decided those hours were not going to work for us. We agreed on 8:00am to 6:00pm, which is still a fair day.

What happened was a revelation. At first, I left at 6:00pm whether all the work I wanted to get done was completed or not. Over the ensuing weeks and months it pushed me, and my team, to get smarter. It forced our hand on making choices. As a result we actually started solving the underlying problems that were holding us back.

Prior to that, working longer and harder had simply covered up those issues. For example, rather than identifying a technological solution to improve a process, we just stayed late and got nowhere.

Don’t do it.

Set some hard limits on your time, then let things blow up for a bit. You can then discuss the issues that cause the blow up as a team, agree on the real issue, and find a solution to it. That’s how you move forward.

Save your soul

So is it possible to have a strongly performing business,

in the financial sense, without losing your social purpose (or soul) in the process?

Yes it is, but there are some choices to be made on a daily basis in order to do so. The two ways I’ve outlined above are a great start.

Understand that not choosing who you serve and how long you work for each day, is in itself a choice to remain overwhelmed and to underperform.

Set limits on who you will work with (who you want to serve), and set limits on your time spent at work. These are the two fastest ways to build a business that you love without losing your social purpose or soul.

Brett is the Founder of FP Advance, the boutique consulting firm that helps financial planning professionals advise better and live better.

He is recognised as one of the leading consultants to financial advisers in the UK. Professional Adviser magazine has rated him one of the Top 50 Most Influential people in UK financial services on three occasions.

You can follow Brett online and via social media: Twitter: @brettdavidsonFacebook: www.facebook.com/FPAdvanceLtdLinkedIn: www.linkedin.com/in/davidsonbrettWebsite: www.fpadvance.com

23I FAmagazine.com

BETTER BUSINESS

Februar y 2018

A perennial question facing many advisers is how they might put together an investment portfolio for clients and use active funds or ETFs. Most advisers will agree that this is a bit like asking how long a piece of string is. It certainly doesn’t have to be an either / or scenario – as our own portfolios testify.

But frustratingly, the answer is not easy and it inevitably involves a lot of tooth sucking and head scratching. We do this because it is a difficult question and there is no clear answer, not because I want to be enigmatic or evasive.

Client first

Advisers will know all too well that putting together a portfolio is a very personal thing. It will depend on your client’s time horizon and whether they are willing to accept losses in exchange for long term returns - even then there is a high degree of uncertainly to build in. This is why advisers spend so much time with risk tolerance questionnaires. It is also where they can really add a lot of value. Perhaps one of the great conundrums facing advisers is the fact that whilst past performance is absolutely no guide to future returns, we can still draw on the past to try to gauge how that might inform the future.

Some of the best mathematical and computer science people in the world work in the savings and finance industry and I think they will all agree that there are no absolute correct answers for any investor or their adviser.

For the purposes of this article, I shall assume that you have had a long hard think about your client’s personal situation and that they have a very long time horizon, but that they do not really want to take a great deal of risk. A “balanced” investor might invest 50% of their portfolio in bonds and 50% in equities. Even though this sounds conservative, nearly all the ups and downs you suffer will probably come from the equities in the portfolio. The risk experts at 7IM tell me that about 85% of the volatility you will experience will probably come from the

equity components of your portfolio.

An adviser can really add value in this area by explaining

the risks upfront and by guiding their

clients through the market

downturns.

Weighing up ETFs against other

por tfolio optionsWhen it comes to portfolio construction and asset allocation, which

areas do ETFs tend to have the advantage? Peter Sleep, Senior Investment Manager, Seven Investment Management (7IM) gives his

opinion on how advisers can seek the best value approach for clients

BALANCING ETFS

I FAmagazine.com24

Februar y 2018

Active funds or ETFs?

Whether you should use active funds or ETFs seems to be the next question. Here I think personal preference is again key. Whilst with any age-old debate, there’s always that element of ‘six of one and half a dozen of the other’, there is much evidence to suggest that as a group, active managers find it difficult to add value. However, on the other hand, some might argue that you are guaranteed to underperform by the fees with an ETF. At least with an active manager you have the chance of outperforming and there is some value in that option.

Advantage ETFs?

At 7IM we tend to sit on the fence on the active versus passive argument. It is very hard to find an active manager who consistently outperforms in areas like government bonds, so it seems like a good idea to save your time and reduce fees by selecting ETFs in these areas. A holding in high grade, developed market global bonds is a key component of most portfolios, despite their low yields. Not always, but usually, when equity markets go down, high grade bonds generally go up and act as a bit of a cushion for your portfolio.

I say this knowing that this has not always been the case. In the bad old, high inflation days of the early 1970s, when bonds were known as “certificates of confiscation”, bonds were not great for balanced portfolios. Expect to pay between 0.1% and 0.2% for a government bond ETF and if there is an overseas component you may decide to look for a hedged ETF. To hedge or not to hedge is not clear cut, as hedging removes exposure to some of the world’s safe haven currencies like the US dollar and the Japanese yen, but on balance we believe that bonds are low risk assets and removing currency volatility through hedging can be a good thing.

When it comes to corporate bonds we think ETFs tend to win out. Generally, it is very hard to find an active manager in this area and an adviser might prefer to spend their efforts in other areas with greater added value. An ETF will cost around 0.2%, whereas an active fund will cost twice that.

Advantage active funds?

High yield, Emerging Market bond and convertible bond ETFs are generally priced at levels close to the active managers and these are areas where good fundamental research by an active manager can really pay off, so an adviser might want to spend some time trying to find a good active manager.

Equities are an area where an adviser can add value by trying to find active managers. This can be done by selecting a global equity manager or by a series of UK and country / regional portfolio managers. Historically investors have struggled to find active managers in the US – the argument being that the markets are “too efficient” for active managers to outperform. The reality may be that the market has been led higher by a few very large tech companies, whereas portfolio managers tend to prefer smaller stocks with room to grow. If you think that the large tech companies may have had their day in the sun, then it could be worthwhile looking for a US active manager who invests in smaller US stocks. The same is true for the other major markets like Europe, Japan and the Emerging Markets. We think it is generally worth spending time to find an active manager in these areas.

I have given a personal outline of how I think an adviser might combine ETFs and active funds. There is a lot of room to be creative within this outline by perhaps including some of the ethical or gender equality ETFs that are now emerging and gaining traction. However, perhaps the greatest added value comes from the adviser’s relationship with their clients. By ensuring that they are in the correct risk category and keeping those clients invested in the market through thick and thin, ensures that they can benefit

from the long term returns they need, in order to meet the all-important

objectives of their financial plan.

Peter Sleep 7IM Senior Investment Manager, EquitiesPeter joined 7IM in 2007. Having qualified as a chartered accountant, Peter audited company accounts, before joining Citibank as an internal auditor. After three years in that role, he worked for 11 years in Citibank/Citigroup as fund manager and analyst.

Prior to joining 7IM he worked as an analyst at Man Group. Specialist areas/responsibilities: portfolio strategy, quant funds, investment auditing, alternative assets / methodologies and Japanese equities.

BALANCING ETFS

25I FAmagazine.com

Februar y 2018

Taking your marketing to the next level - Par t 3

In this three part series, Sam Turner, Head of Digital at ClientsFirst, examines the factors that elevate marketing strategies from functional tick box exercises to plans that make a real difference for advisory firms’ bottom lines

Adding structure to your marketing approach

You’ve defined your marketing strategy, selected your marketing technology and possibly even chosen your niche. You’re full of exciting plans of how to reach your target audience.

Unfortunately though, it’s all too easy to go off all guns blazing, full of enthusiasm, only to discover in a few months’ time that your campaigns are not producing the results you‘d hoped for. In addition, despite your good intentions, ‘real’ work takes priority or clients insist on demanding your time!

We’ve learnt from experience with marketing projects that without a solid structure in place, even the best ideas will fail to get off the ground. That’s why we use a linear six stage structure which breaks up the process into useful chunks. This means it’s clear to everyone involved where you’re up to and what needs to happen next for a successful outcome.

Establish the infrastructure

Success comes from strong foundations. Take time at the outset to do some detailed planning. What are your business objectives? What assets do you currently have in place? What’s getting results for you and what could you be doing better? Think about your main challenges and how you would describe your USP. Conduct some client research to find out what they really think. At this stage, we draw up marketing personas of our client’s target audience so we can form a clearly defined marketing plan which will address their specific needs.

Develop the assets

With a plan and some personas in place, you can start to think about the appropriate collateral that will appeal to your carefully defined audience. To really engage with them, it needs to be value led, engaging and helpful. If you’re developing a piece of content

IFAmagazine.com26

Februar y 2018

MARKETING STRATEGY

with the purpose of generating leads, consider what people will view as valuable enough to exchange their contact details for. One of our own most successful pieces of content, for example, has been an SEO guide with 47 handy tips.

You have a range of options at your disposal:

online: guides, whitepapers, blogs, videos, infographics, landing pages, mailshots, case studies

offline: mailers, brochures, flyers, surveys, pitch documents, client facing documents

Reach your audience

You’ve defined your target audience and you know what you want to send them but how do you make sure your message reaches them and that they will interact with the content.

It’s crucial to think about what channels are most relevant for them. Where do they ‘hang out?’ What do they read? How do they search for information?

Are you going to reach them online or offline or through both? Online channels could include: SEO, PPC, email marketing, social media, outreach and banner ads, whereas offline could be: events, awards, PR. If you decide SEO is a good way of reaching your audience, a useful next step might be to conduct an SEO audit.

Not that we’re structure mad but we also use the inbound marketing model ‘Attract, Convert, Close, Delight’ in tandem with our six step process. This shows what sort of content will be most successful as your prospects move through the process.

27

Februar y 2018

IFAmagazine.com

MARKETING STRATEGY

Sam’s original article, on creating a marketing strategy for your advisory firm, can be found in the August issue of IFA Magazine or on www.IFAMagazine.com

ClientsFirst is a marketing agency which specialises in working with financial services firms.

Website: www.clients-first.co.uk

Engage

Once the data from your contacts is safely stored in your CRM, you can start to develop those all-important ongoing relationships with them. Your aim here is to move your contacts through the sales funnel from merely ‘interested’ to ‘invested’.

Use marketing automation to make life easier for you. Triggered email campaigns, surveys, LinkedIn or Twitter engagement all come into play here. You can also use engagement tools to react appropriately with interested prospects, monitor reactions and gain valuable feedback.

Create opportunities

This is what all the hard work has been about. All that engagement should now start to produce new business opportunities.

It’s important that you have a set of tools and processes in place to identify the hottest prospects and pass them to your sales department as quickly and efficiently as possible.

Done correctly, your campaigns should be producing a steady stream of relevant sales opportunities which will result in more new business.

Act on insight

You might think that‘s the end - your marketing activity has been successful and produced some opportunities. Your campaigns, however, will contain lots of useful data which can help you to make improvements for future projects. Measure everything. Collect feedback via tools such as Feefo, TrustPilot or Google reviews. Use A/B testing to test different ideas on different parts of your database. The joy of modern marketing systems means they give you a clear view of your key metrics so you know exactly what is performing and what isn’t. This will lead to even more opportunity and greater ROI next time round.

IFAmagazine.com28

Februar y 2018

MARKETING STRATEGY

I FAmagazine.com32

Februar y 2018

FORTUNE FAVOURS THE BOLD

BUT YOUR CLIENTS DON’T NEED BOLD

THEY NEED YOU TO DO THE RESEARCH

UNCOVER THE FACTS ON CRYPTO-ASSETS

CS

COINSHARES.CO.UK@COINSHARESCO

CoinShares

COINSHARES.CO.UK

WITH OVER £1 BILLION IN CRYPTO-ASSETS ACROSS A FAMILY OF

EXCHANGE TRADED PRODUCTS, COINSHARES GROUP IS THE EUROPEAN

LEADER IN CRYPTO-FINANCE. FIND OUT WHY AT COINSHARES.CO.UK

£1 BILLION FIGURE CALCULATED ON CLOSE OF MARKET 10-JAN 2018 | COPYRIGHT © 2018 COINSHARES | COINSHARES (UK) LIMITED IS AN APPOINTED REPRESENTATIVE OF SAPIA PARTNERS LLP, WHICH IS AUTHORISED AND REGULATED BY THE UK FINANCIAL CONDUCT AUTHORITY (FRN: 550103). THIS DOCUMENT HAS BEEN PREPARED AND ISSUED BY COINSHARES (UK) LIMITED AND IS BEING PROVIDED FOR INFORMATION PURPOSES ONLY. IT IS NOT INTENDED AS AN OFFER OR SOLICITATION TO ENTER INTO ANY PROPOSED TRANSACTION OR INVESTMENT. INVESTORS’ CAPITAL IS AT RISK, AND INVESTORS SHOULD ONLY INVEST IF THEY ARE ABLE TO AFFORD THE LOSS OF ALL CAPITAL INVESTED. THERE IS NO GUARANTEE THAT THE INVESTMENT OBJECTIVES WILL BE ACHIEVED AND PAST PERFORMANCE SHOULD NOT BE CONSTRUED AS AN INDICATOR OF FUTURE PERFORMANCE.

I FAmagazine.com30

Februar y 2018

Many traditional investors are intrigued by cryptocurrencies, but it’s difficult to determine where to start and what trends to watch. While bitcoin has captured headlines with its meteoric price increase and volatility, there are more than 1,000 other cryptocurrencies and crypto-assets; with around 50 more initial coin offerings hitting the market each month. Analyzing these can be challenging compared to conventional stocks, bonds, options, and futures. At CoinShares Research,

we aim to help separate the signal from the noise, and provide fundamental investment research for crypto-finance investors.

By way of an introduction – let’s start with a quick education on 3 core crypto-asset concepts.

What is a Crypto Coin?

Cryptocurrencies and crypto-assets are denominated in coins, most of which are mined as a part of the transaction

verification process. Mining exists to prove ‘loyalty’ to a system by requiring provably expensive input work in order to be allowed the privilege of verifying transactions (for which miners receive newly minted coins as a reward). As more and more miners compete for the freshly minted coins, the difficulty level automatically resets such that the block verification times always average out to the same length of time. More miners means a more secure protocol and an increased cost of

3 Concepts Fundamental To Understanding CryptocurrenciesBy CoinShares Research Team

SPONSORED FEATURE

31I FAmagazine.com

Februar y 2018

SPONSORED FEATURE

“forging” coins by tampering with the transaction history.

Traditional investors might conceptualize this as mining gold in a world where gold becomes increasingly difficult to mine as the remaining finite supply dwindles.

What is a Crypto Exchange?

Cryptocurrencies are traded on various exchanges. These are online platforms that enable a person to exchange one cryptocurrency for another crypto or fiat currency.

One could think of these exchanges like traditional stock exchanges, currency exchanges, or brokers, but they aren’t typically regulated by governments or insured in any way. Needless to say, investors must ensure that they’re doing business with an exchange that is secure and reputable.

Some of the most important factors to consider when evaluating a cryptocurrency exchange include:

• Liquidity – How liquid is the order book of the exchange?

• History – Is the exchange credible and secure with a strong track record?

• Regulatory Exposure – Is the exchange regulated by any governments, or do they have self-imposed regulations?

What is a Cryptocurrency ‘Network’?

The network represents the group of people using the coin, mining the coin, relaying and verifying transactions, and maintaining the underlying software.

Traditional investors should consider a cryptocurrency’s network characteristics for the same reason that they wouldn’t invest in a company just because of its market capitalization alone. An illiquid penny stock could have a large market capitalization, but that market capitalization is meaningless beyond pure speculation if there is no underlying business to support it. A cryptocurrency’s network can be, to some degree, compared to a company’s operations – it’s the valuable asset behind the hype.

Some important factors to consider when evaluating cryptocurrency networks are:

• Mining – What are the relative sizes of the mining networks between coins? Are they growing?

• Creators – Who are the developers supporting the cryptocurrency? How is new code created? What is the governance model?

• Technology – What type of cryptography does the cryptocurrency rely upon? Is the technology experimental or established?

The Bottom Line

Investors have become increasingly interested in cryptocurrencies, but it can be (and is) overwhelming to analyze them from an investment standpoint. That’s why we have built a professional research arm to help investors understand the complex dynamics of cryptocurrencies and help them make better investment decisions. To see the type of research we offer, read our most recent research here: H2 2017 Crypto Report.

I FAmagazine.com32

Februar y 2018

How much regulation does it take to treat customers fairly?Whilst most adviser businesses already operate on a putting clients first basis, compliance consultant, Tony Catt, talks us through current relevant regulatory changes and how they are likely to impact advisers

It would seem that most of the latter half of 2017 was spent trying to translate acronyms – MiFID II, SM&CR, IDD, GDPR. All of these represent regulations that are going to hit the UK in 2018 or 2019. Although, due to their complexity, actual adoption of them may be delayed.

Markets in Financial Instruments Directive II

At the time of writing, the only one of these that has come into force has been MiFID II on 3rd January.

This brings European advisers in line with advisers in the UK as far as the receipt of commission on business. UK advisers went through most of this pain with RDR of course.

In the UK, MiFID II has had more of an effect on fund managers, who need to report much more detail to the regulators than previously. This involves greater detail regarding the underlying costs of fund managers, including research and other costs, which have previously simply been bundled up. it is thought that this greater transparency will

promote greater choice for clients. It may also drive down the costs as fund managers can no longer hide them.

A 10% drop

What will affect advisers and fund managers more is the requirement that clients are advised when a fund drops by 10% in value. This would appear to be a good early warning and keep the clients informed regarding possibly losses, but this could be quite a problem to manage.

TONY CATT

33I FAmagazine.com

Februar y 2018

Some considerations are:

• Most advisers would not be happy for the fund managers to have direct contact with their clients.