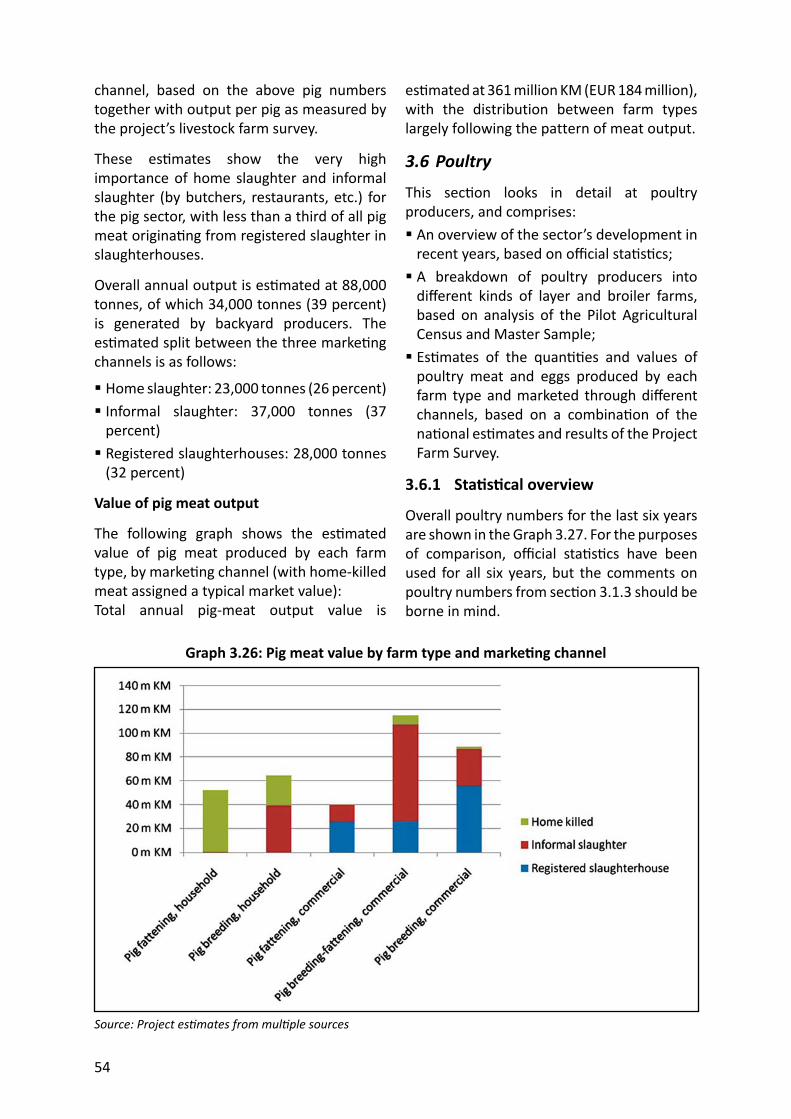

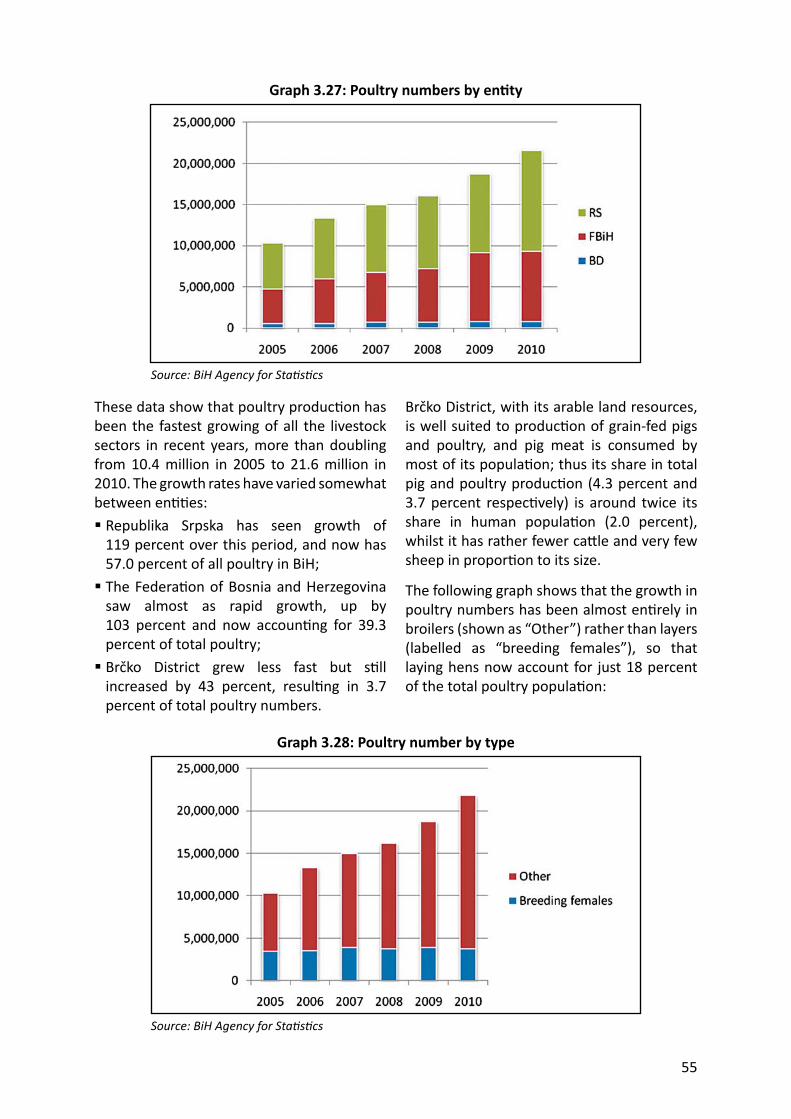

Embed Size (px)

Citation preview

The Meat and Dairy Sector in Bosnia and Herzegovina

Preparation of IPARD Sector Analyses in Bosnia and Herzegovina

2012

FAO Regional Of ice for Europe and Central Asia

FAO Regional Offi ce for Europe and Central Asia

31 August 2012

The

Mea

t and

Dai

ry S

ecto

r in

Bosn

ia a

nd H

erze

govi

na

This project is funded by the European Union

Please address comments and inquiries to:

Regional Offi ce for Europe and Central Asia Food and Agriculture Organiza on of the United Na ons (FAO)

Benczúr u. 34, 1068 Budapest, HungaryTelephone: (+36) 1 461 2000Fax: (+36) 1 351 7029Email: [email protected]: www.fao.org/europe/en

Electronic Version of the report: h p://www.fao.org/europe/publica ons/documents-and-reports/IPARD-BiH/

Cover photograph: ©FAO/Vlado Pijunovic

The Meat and Dairy Sector in Bosnia and Herzegovina

Prepara on of IPARD Sector Analyses in Bosnia and Herzegovina

GCP/BIH/007/ECContract number: 2010/256–560

Regional Offi ce for Europe and Central Asia Food and Agriculture Organiza on

of the United Na ons

This publica on has been produced with the assistance of the European Union. The contents of this publica on are the sole responsibility of the Regional Offi ce for Europe and Central Asia of the Food and Agriculture

Organiza on of the United Na ons and can in no way be taken to refl ect the views of the European Union.

The designa ons employed and the presenta on of material in this publica on do not imply the expression of any opinion whatsoever on the part of the Food and Agriculture Organiza on of the United Na ons (FAO) concerning the legal or development status of any country, territory, city or area or of its authori es, or concerning the delimita on of its fron ers or boundaries. The men on of specifi c companies or products of manufacturers, whether or not these have been patented, does not imply that these have been endorsed or recommended by FAO in preference to others of a similar nature that are not men oned.

All rights reserved. FAO encourages reproduc on and dissemina on of material in this publica on. Non-commercial uses will be authorized free of charge. Reproduc on for resale or other commercial purposes, including educa onal purposes, may incur fees. Applica ons for permission to reproduce or disseminate FAO copyright materials and all other queries on rights and licences, should be addressed by e-mail to [email protected] or to the Chief, Publishing Policy and Support Branch, Offi ce of Knowledge Exchange, Research and Extension, FAO,Viale delle Terme di Caracalla, 00153 Rome, Italy.

© FAO 2012

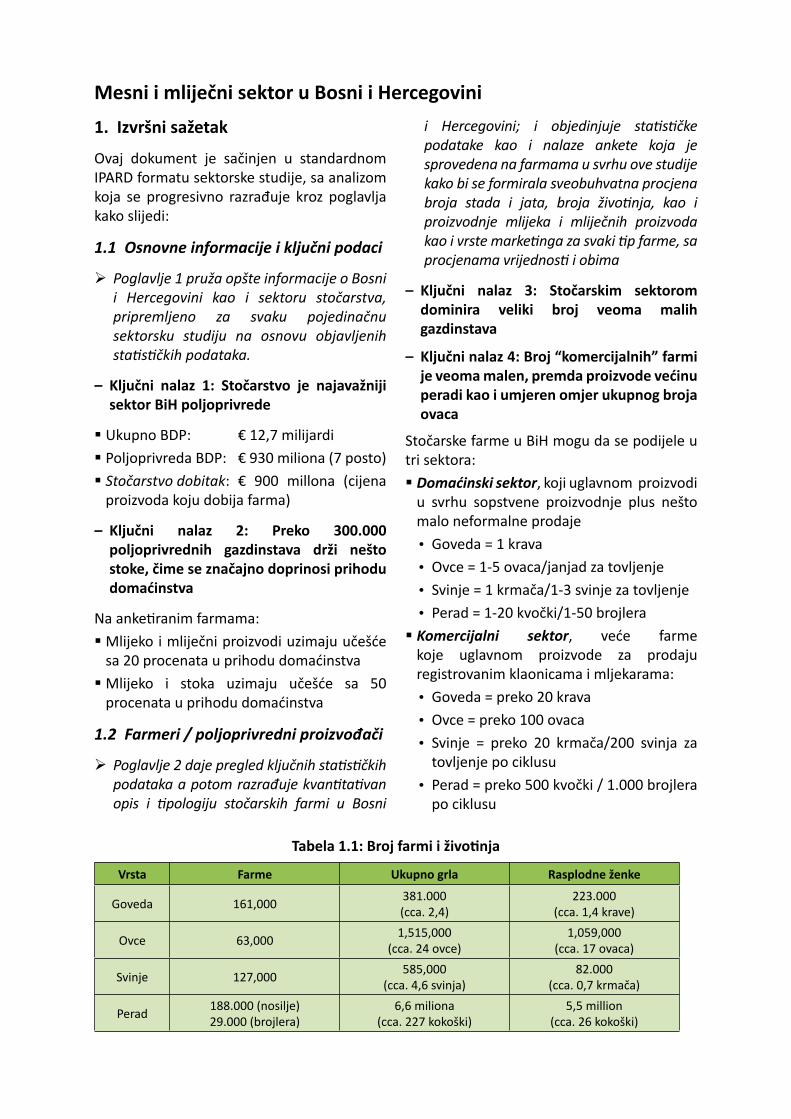

Mesni i mliječni sektor u Bosni i Hercegovini1. Izvršni sažetak

Ovaj dokument je sačinjen u standardnom IPARD formatu sektorske studije, sa analizom koja se progresivno razrađuje kroz poglavlja kako slijedi:

1.1 Osnovne informacije i ključni podaci

Poglavlje 1 pruža opšte informacije o Bosni i Hercegovini kao i sektoru stočarstva, pripremljeno za svaku pojedinačnu sektorsku studiju na osnovu objavljenih sta s čkih podataka.

– Ključni nalaz 1: Stočarstvo je najavažniji sektor BiH poljoprivrede

Ukupno BDP: € 12,7 milijardi Poljoprivreda BDP: € 930 miliona (7 posto) Stočarstvo dobitak: € 900 millona (cijena proizvoda koju dobija farma)

– Ključni nalaz 2: Preko 300.000 poljoprivrednih gazdinstava drži nešto stoke, čime se značajno doprinosi prihodu domaćinstva

Na anke ranim farmama: Mlijeko i mliječni proizvodi uzimaju učešće sa 20 procenata u prihodu domaćinstva Mlijeko i stoka uzimaju učešće sa 50 procenata u prihodu domaćinstva

1.2 Farmeri / poljoprivredni proizvođači

Poglavlje 2 daje pregled ključnih sta s čkih podataka a potom razrađuje kvan ta van opis i pologiju stočarskih farmi u Bosni

i Hercegovini; i objedinjuje sta s čke podatake kao i nalaze ankete koja je sprovedena na farmama u svrhu ove studije kako bi se formirala sveobuhvatna procjena broja stada i jata, broja živo nja, kao i proizvodnje mlijeka i mliječnih proizvoda kao i vrste marke nga za svaki p farme, sa procjenama vrijednos i obima

– Ključni nalaz 3: Stočarskim sektorom dominira veliki broj veoma malih gazdinstava

– Ključni nalaz 4: Broj “komercijalnih” farmi je veoma malen, premda proizvode većinu peradi kao i umjeren omjer ukupnog broja ovaca

Stočarske farme u BiH mogu da se podijele u tri sektora: Domaćinski sektor, koji uglavnom proizvodi u svrhu sopstvene proizvodnje plus nešto malo neformalne prodaje • Goveda = 1 krava• Ovce = 1-5 ovaca/janjad za tovljenje• Svinje = 1 krmača/1-3 svinje za tovljenje• Perad = 1-20 kvočki/1-50 brojlera Komercijalni sektor, veće farme koje uglavnom proizvode za prodaju registrovanim klaonicama i mljekarama:• Goveda = preko 20 krava• Ovce = preko 100 ovaca• Svinje = preko 20 krmača/200 svinja za

tovljenje po ciklusu • Perad = preko 500 kvočki / 1.000 brojlera

po ciklusu

Tabela 1.1: Broj farmi i živo nja

Vrsta Farme Ukupno grla Rasplodne ženke

Goveda 161,000 381.000(cca. 2,4)

223.000(cca. 1,4 krave)

Ovce 63,000 1,515,000(cca. 24 ovce)

1,059,000(cca. 17 ovaca)

Svinje 127,000 585,000(cca. 4,6 svinja)

82.000(cca. 0,7 krmača)

Perad 188.000 (nosilje)29.000 (brojlera)

6,6 miliona(cca. 227 kokoški)

5,5 million(cca. 26 kokoški)

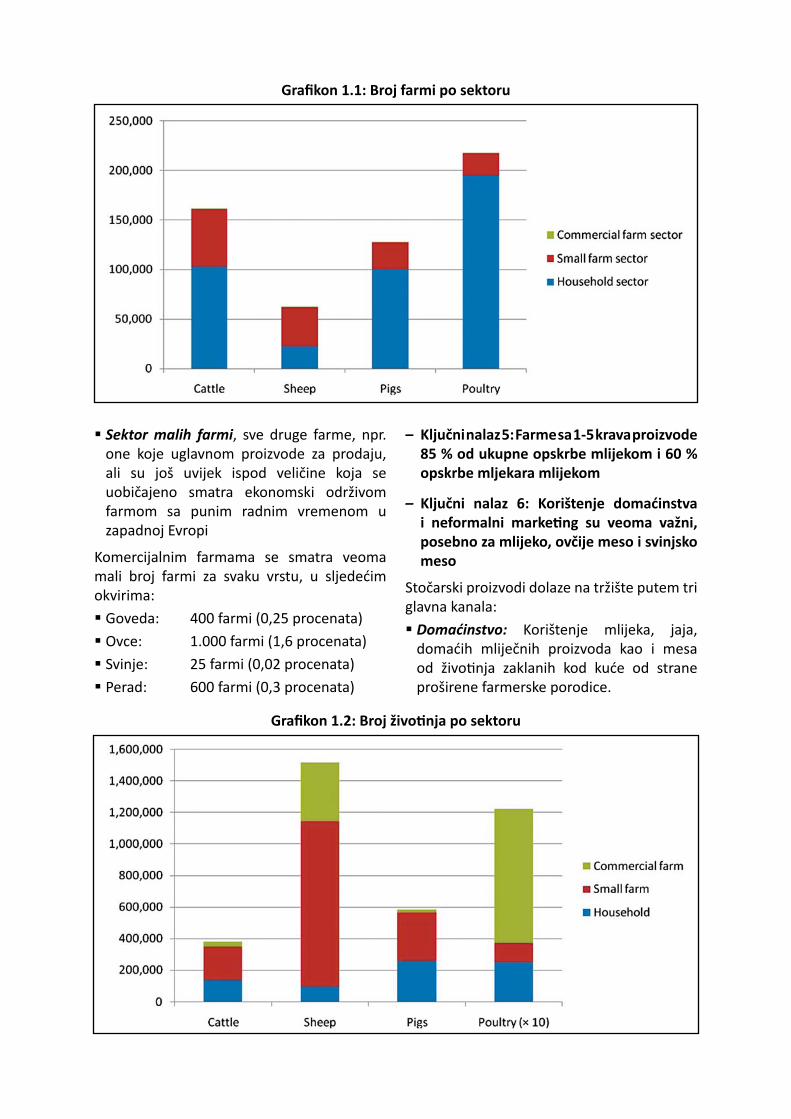

Sektor malih farmi, sve druge farme, npr. one koje uglavnom proizvode za prodaju, ali su još uvijek ispod veličine koja se uobičajeno smatra ekonomski održivom farmom sa punim radnim vremenom u zapadnoj Evropi

Komercijalnim farmama se smatra veoma mali broj farmi za svaku vrstu, u sljedećim okvirima: Goveda: 400 farmi (0,25 procenata) Ovce: 1.000 farmi (1,6 procenata) Svinje: 25 farmi (0,02 procenata) Perad: 600 farmi (0,3 procenata)

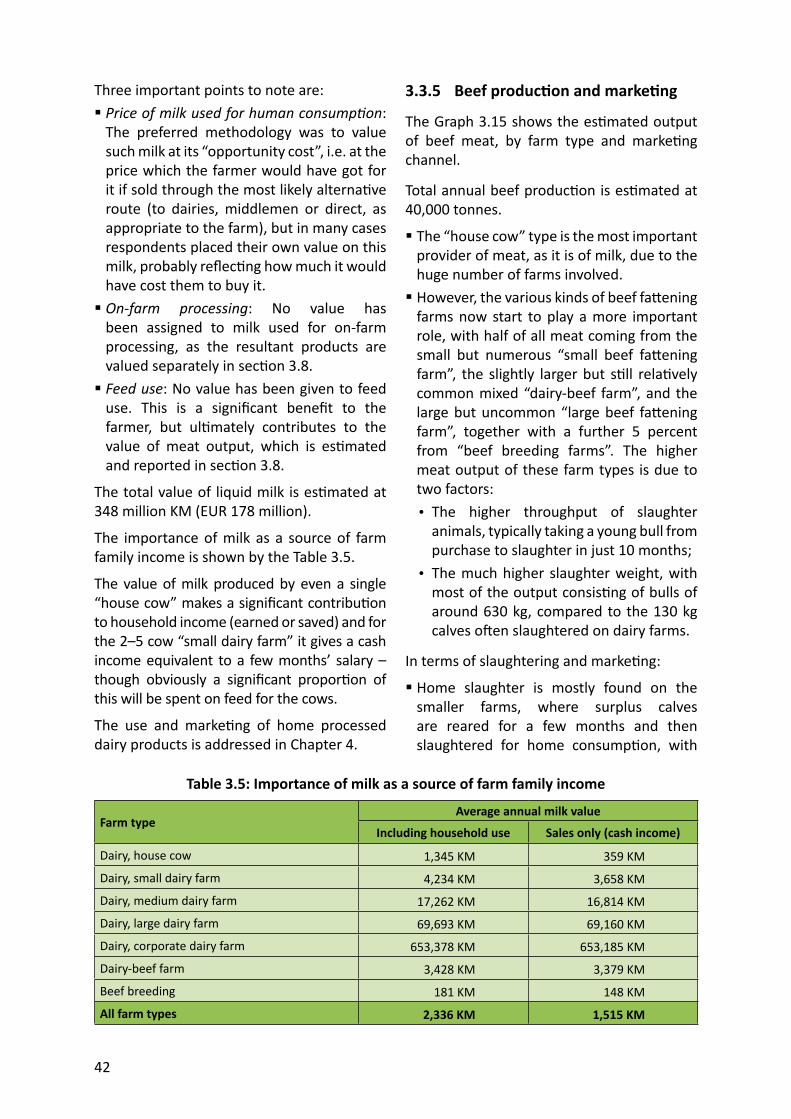

– Ključni nalaz 5: Farme sa 1-5 krava proizvode 85 % od ukupne opskrbe mlijekom i 60 % opskrbe mljekara mlijekom

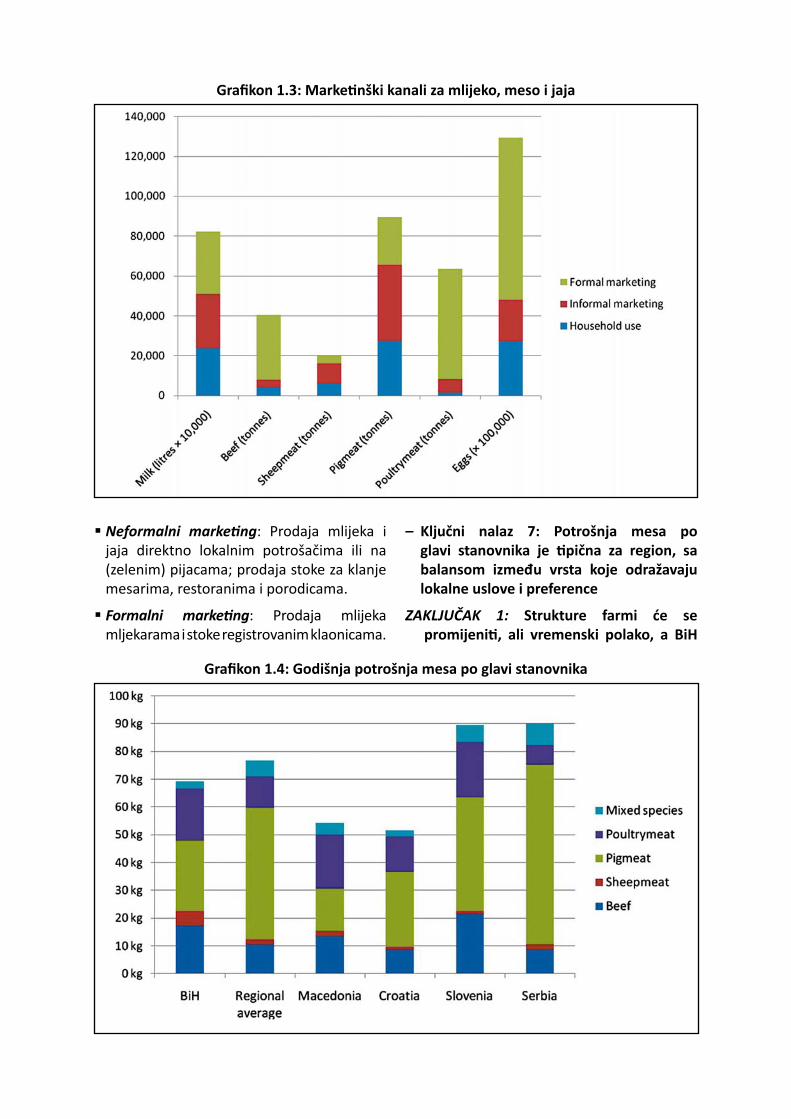

– Ključni nalaz 6: Korištenje domaćinstva i neformalni marke ng su veoma važni, posebno za mlijeko, ovčije meso i svinjsko meso

Stočarski proizvodi dolaze na tržište putem tri glavna kanala: Domaćinstvo: Korištenje mlijeka, jaja, domaćih mliječnih proizvoda kao i mesa od živo nja zaklanih kod kuće od strane proširene farmerske porodice.

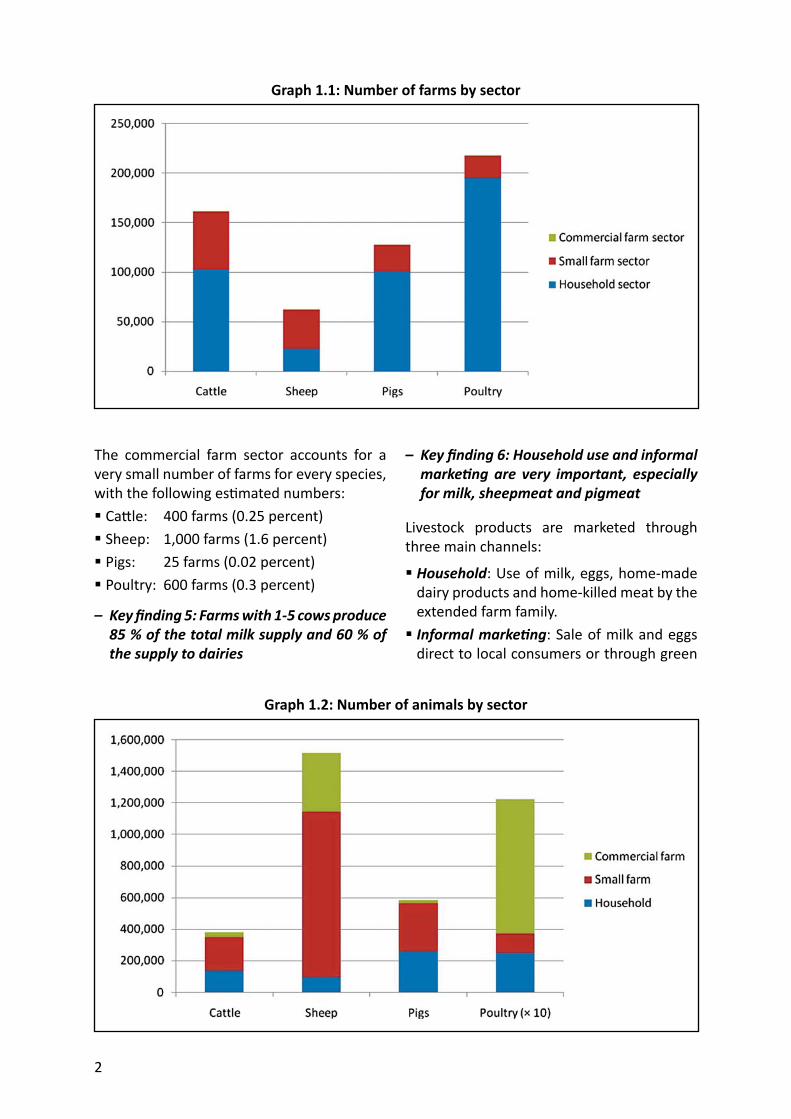

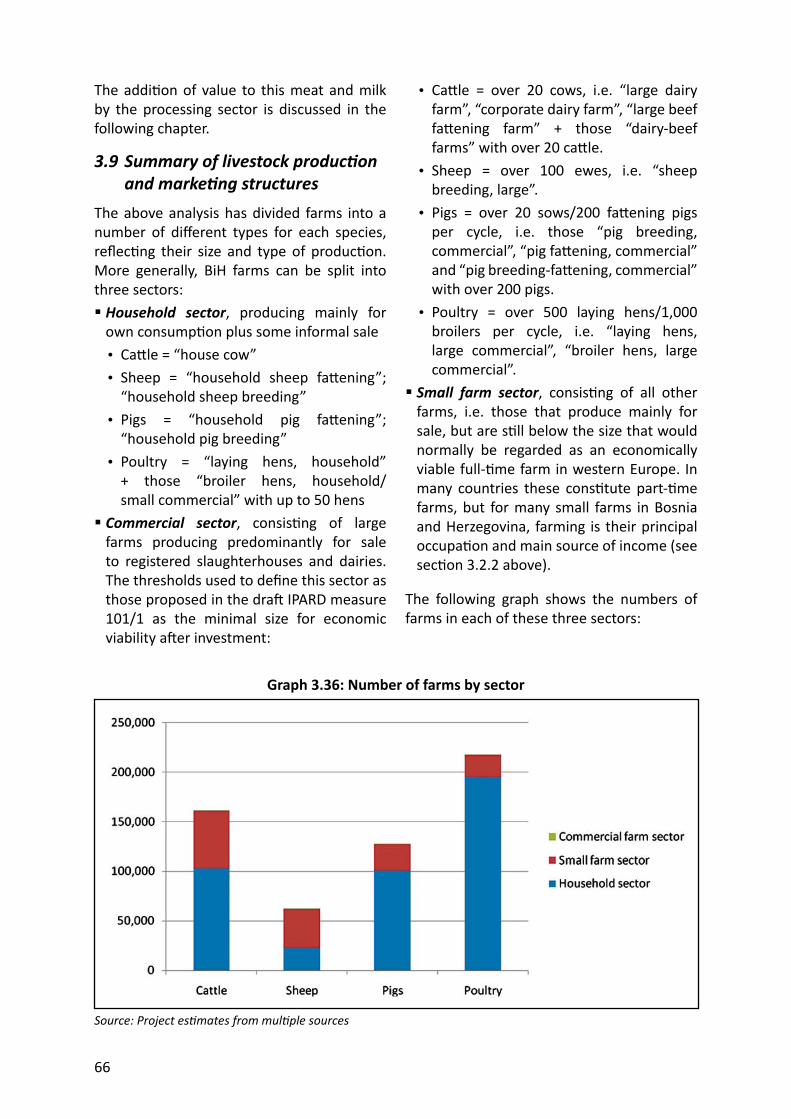

Grafi kon 1.1: Broj farmi po sektoru

Grafi kon 1.2: Broj živo nja po sektoru

Neformalni marke ng: Prodaja mlijeka i jaja direktno lokalnim potrošačima ili na (zelenim) pijacama; prodaja stoke za klanje mesarima, restoranima i porodicama.

Formalni marke ng: Prodaja mlijeka mljekarama i stoke registrovanim klaonicama.

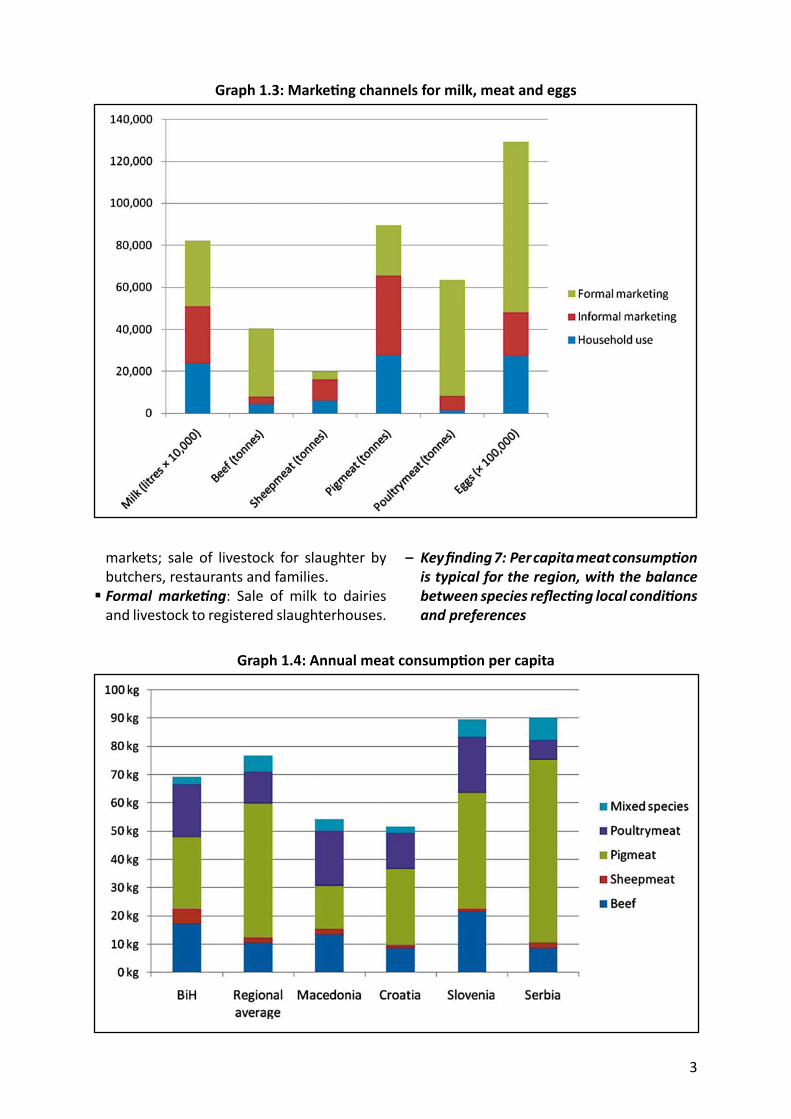

– Ključni nalaz 7: Potrošnja mesa po glavi stanovnika je pična za region, sa balansom između vrsta koje odražavaju lokalne uslove i preference

ZAKL JUČAK 1: Strukture farmi će se promijeni , ali vremenski polako, a BiH

Grafi kon 1.3: Marke nški kanali za mlijeko, meso i jaja

Grafi kon 1.4: Godišnja potrošnja mesa po glavi stanovnika

treba da planira ulazak u EU sa stočarskim sektorom kojim dominiraju male farme

ZAKL JUČAK 2: Broj farmi dovoljno velikih da budu uspješno konkurentne za IPARD grantove je mali, i većina farmi će zah jeva dodatne izvore inves ranja

1.3 Prerađivači

Poglavlje 3 daje sistemski opis formalne proizvodnje mlijeka i mliječnih proizvoda u Bosni i Hercegovini, a prvenstveno se zasniva na anke izvršenoj licem u lice sa proizvođačima od strane projektnog ma.

– Ključni nalaz 8: Prerađivački sektor se oporavio nakon rata, u nekim slučajevima čak uspijeva i da “prevaziđe” susjedne zemlje

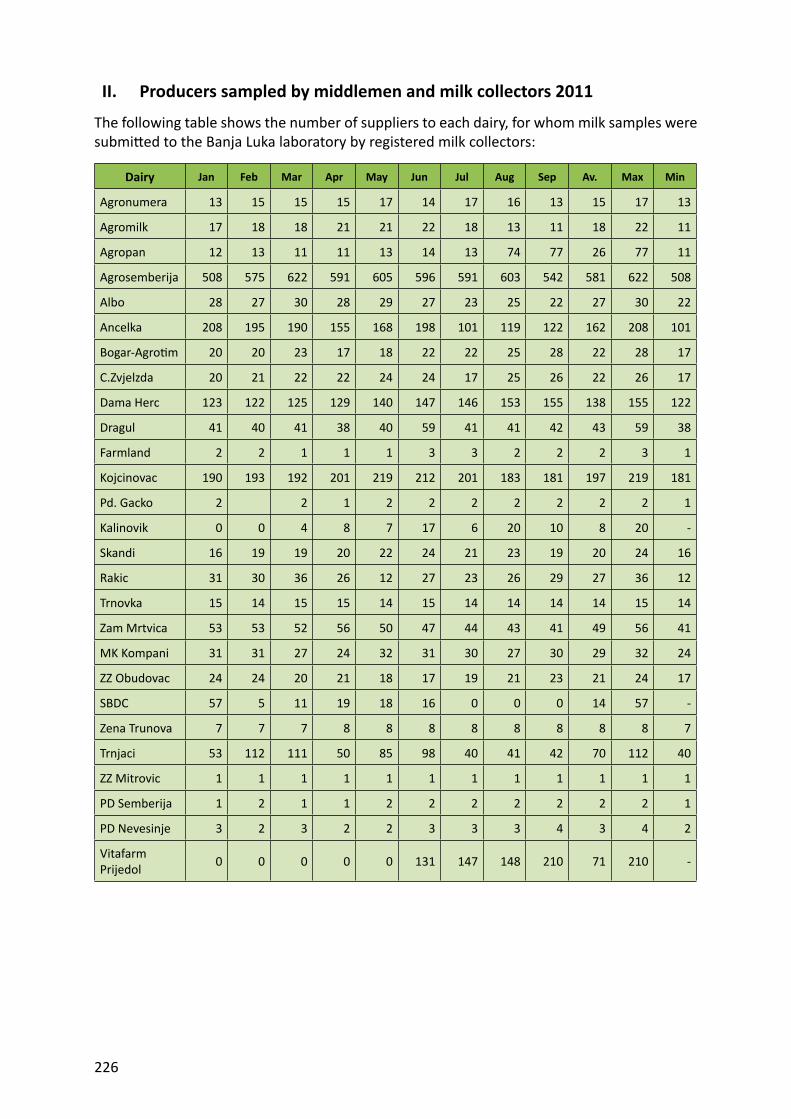

– Ključni nalaz 9: Prikupljanje mlijeka je raznovrsno, a uključuje otkupne centre i posrednike kao i direktno prikupljanje od strane mljekara, a određene količine sirovog mlijeka još uvijek nije rashlađeno

– Ključni nalaz 10: Dnevno prikupljanje mlijeka po farmi je neznatno (cca. 26 litara), čime se povećava jedinična cijena

– Ključni nalaz 11: Tes ranje sirovog mlijeka teče dobro u RS, ali ne i u FBiH

– Ključni nalaz 12: Proizvodnja mlijeka je dvomodna

Više od 75 % prikupljenog mlijeka obrađuje 7 mljekara Oko 50 mljekara, plus nepoznat broj mikro mljekara obrađuje preostalih 25 %

– Ključni nalaz 13: Većina mljekara se koncentrise na etablirane regionalne proizvode, sa većim mljekarama koje također proizvode UHT mlijeko

– Ključni nalaz 14: Većina mljekara je u dobrom stanju u tehničkom i fi nansijskom smislu, a gotove sve imaju HACCP ser fi kat

– Ključni nalaz 15: Osnovne potrebe se odnose na laboratorije, i posebno na odgovarajuće odlaganje tekućeg otpada

– Ključni nalaz 16: Prerada mlijeka kombinuje lokalne zalihe sa je inim uvozom

Proizvođači navode da: Meso lokalnih proizvođača je do 30 % skuplje nego uvoz Kvaliteta uveženog mesa je dosta adekvatna obradi Željeli bi da koriste više uveženog mesa

– Ključni nalaz 17: Asor man mesnih proizvoda je tradicionalan, usmjeren ka lokalnom i CEFTA tržištu, sa dobrom kontrolom kvaliteta i pakiranjem

– Ključni nalaz 18: Tvornice za mesnu preradu subrom stanju, ali neophodna su znatna ulaganja u klaonice za crveno meso

– Ključni nalaz 19: BiH nema odgovarajući sistem odlaganja otpada iz klaonica kao ni uginule ili oboljele stoke

ZAKL JUČAK 3: Mljekare i proizvođači mlijeka treba da učine svoj asor man raznolikijim kako bi prodrli na tržište EU – ali imaju male pods caje na inovacije bez pristupa tržištu

ZAKL JUČAK 4: Kako proces EU integracije povećava pristup je inijem uvoznom mesu, benefi cije od istog će osje prerađivači, ali će to stavi dodatni pri sak na proizvođače

ZAKL JUČAK 5: Najvažniji inves cioni prioritet u preradi koji je relevantan za IPARD je tretman tekućeg otpada i odlaganje otpada

1.4 Javna poli ka

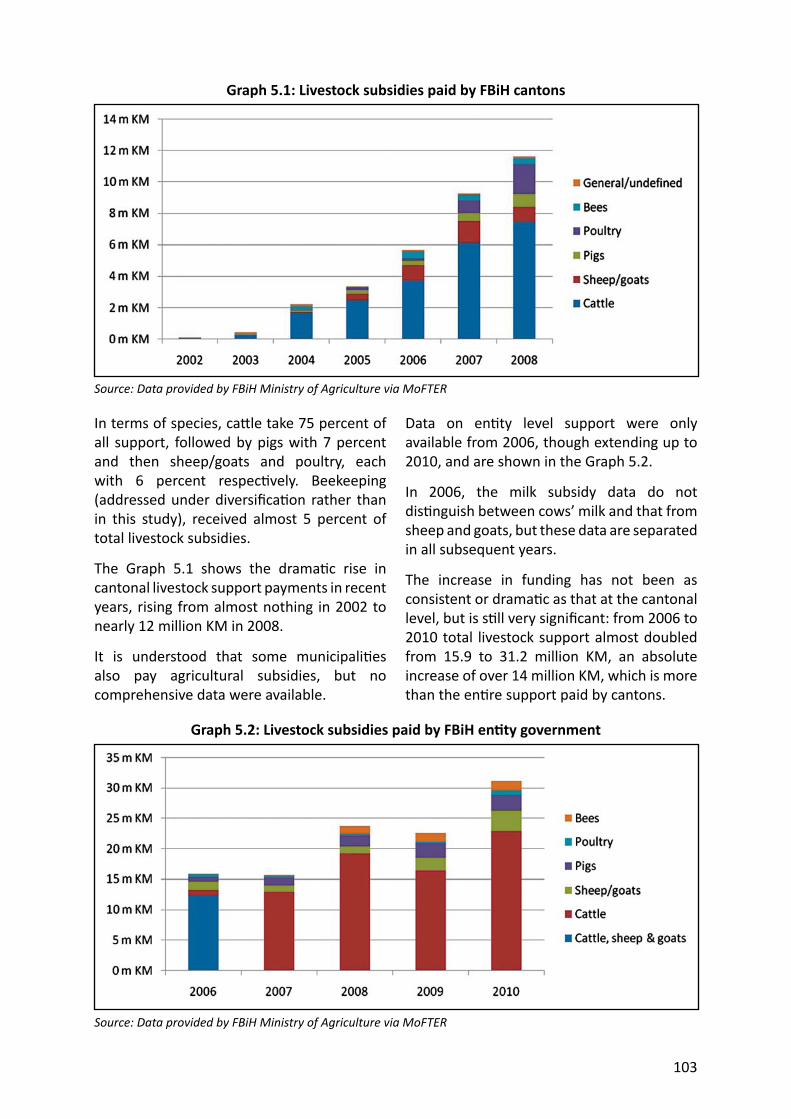

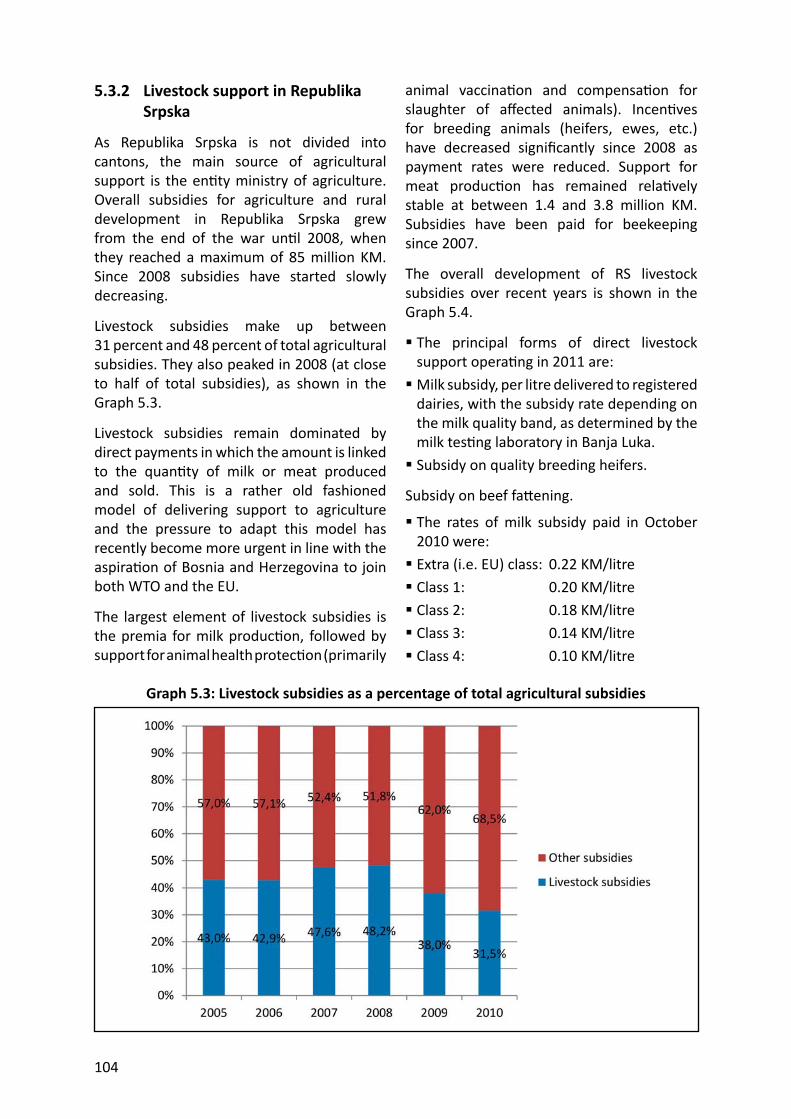

Poglavlje4 daje pregled državne podrške, regulatorne i trgovinske poli ke koje u ču stočarske farme i prerađivački; uključuje i opš uvod u strategije na državnom i en teskom nivou, koje su izrađene za svih pet sektorskih studija.

– Ključni nalaz 20: Jedinstvena administra vna struktura BiH pruža posebne izazove u smislu kreiranja poli ka, implementacije kao i sprovođenja is h

– Ključni nalaz 21: Subvencije za stočarstvo u oba en teta favorizuju veće farme i uglavnom streme ka socijalnim a ne razvojnim ciljevima

ZAKL JUČAK 6: BiH će teško dobiti EU odobrenje za izvoz mesnih proizvoda bez osiguranja unifi ciranog sistema veterinarske kontrole

ZAKL JUČAK 7: Oba en teta treba da preusmjere svoju podršku stočarstvu na manje farme kako bi se pripremile ua pristupanje EU

1.5 Marke ng

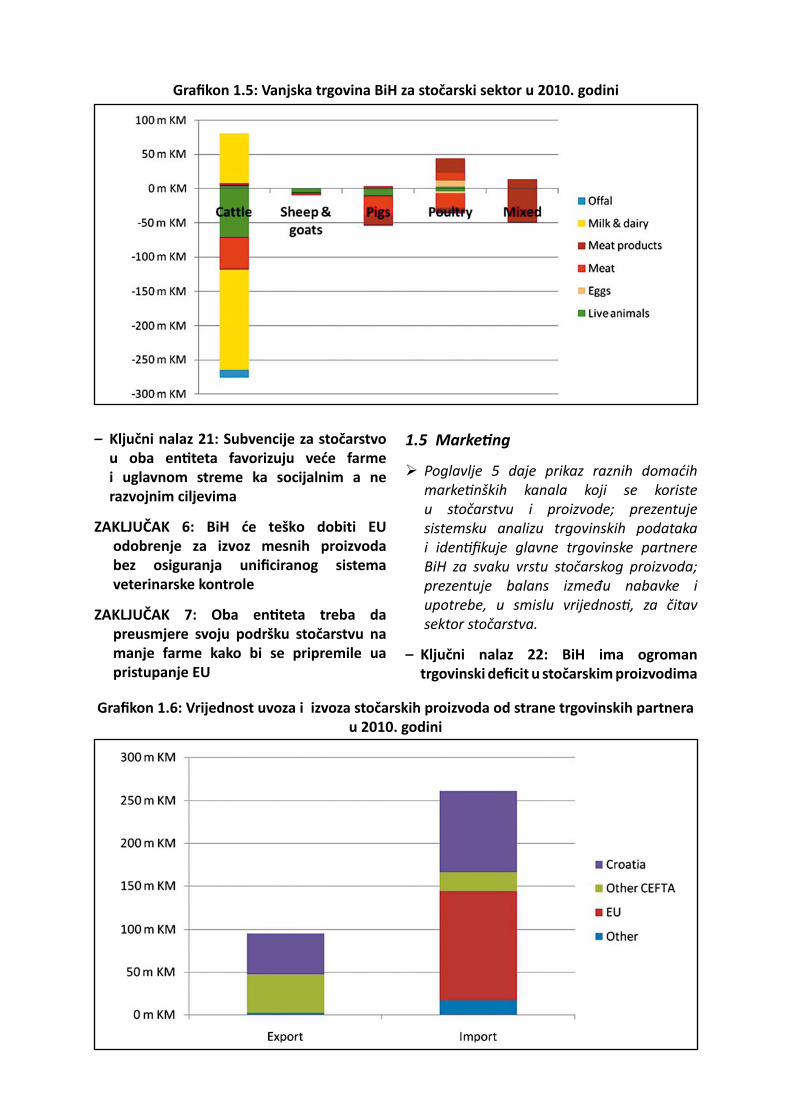

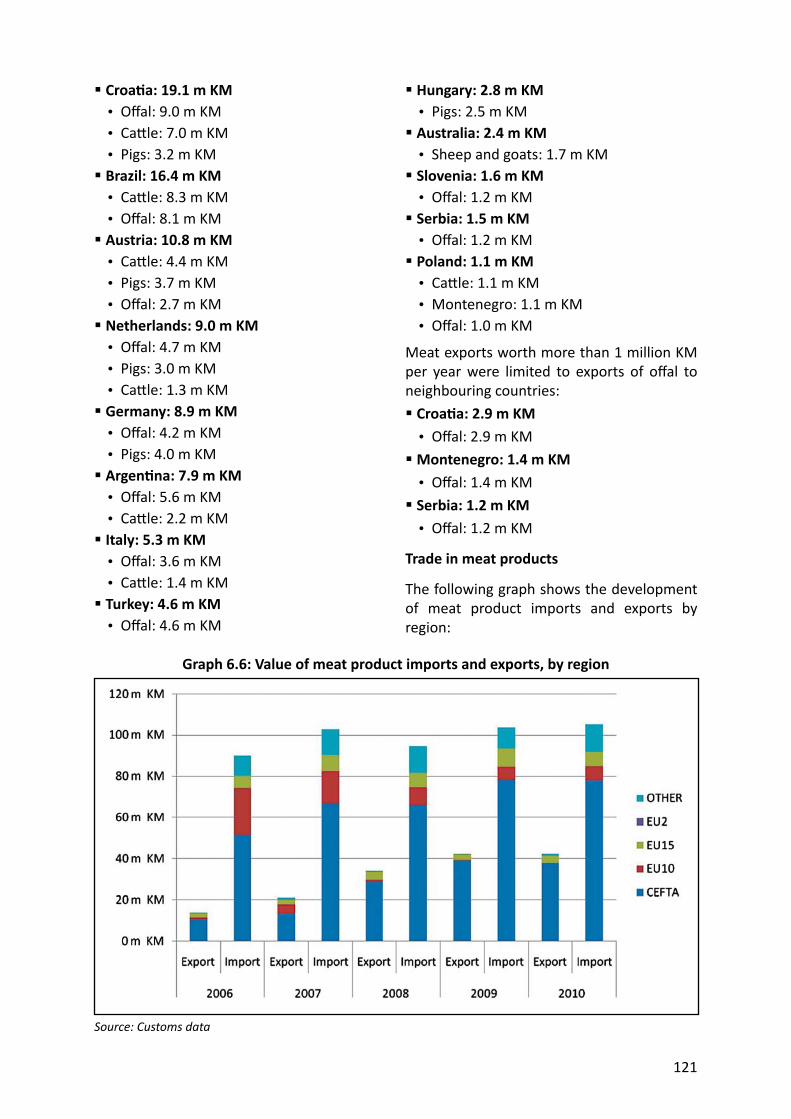

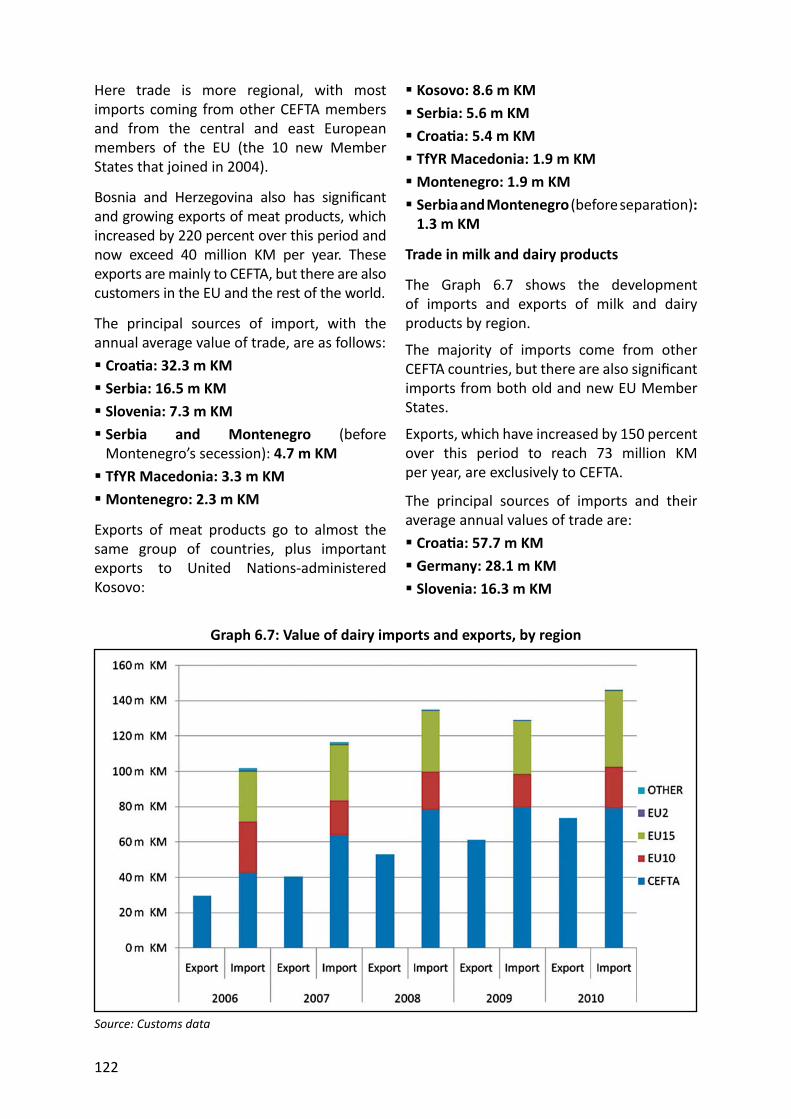

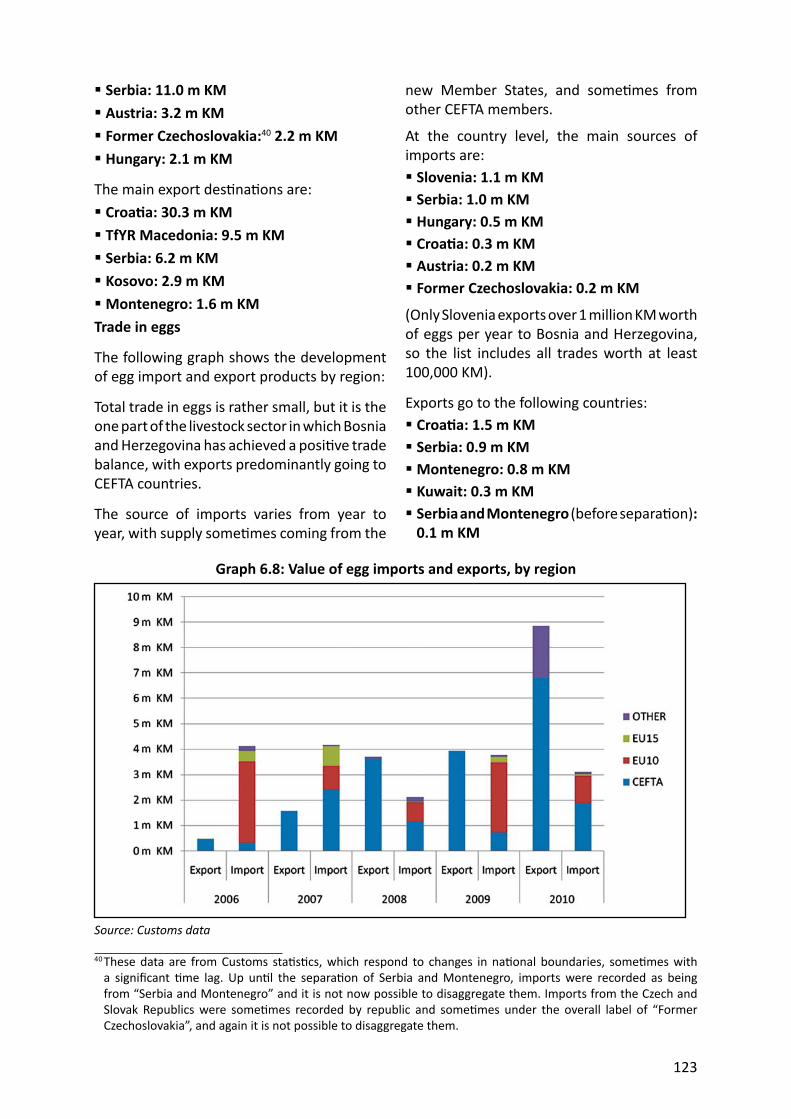

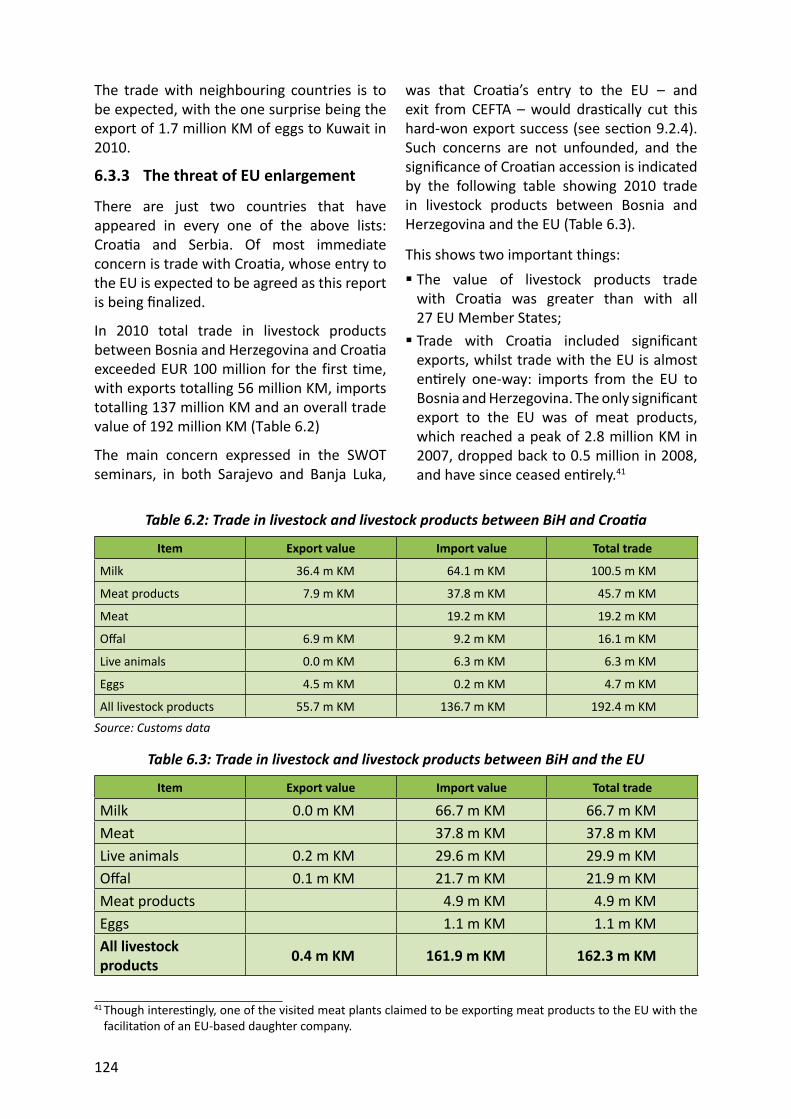

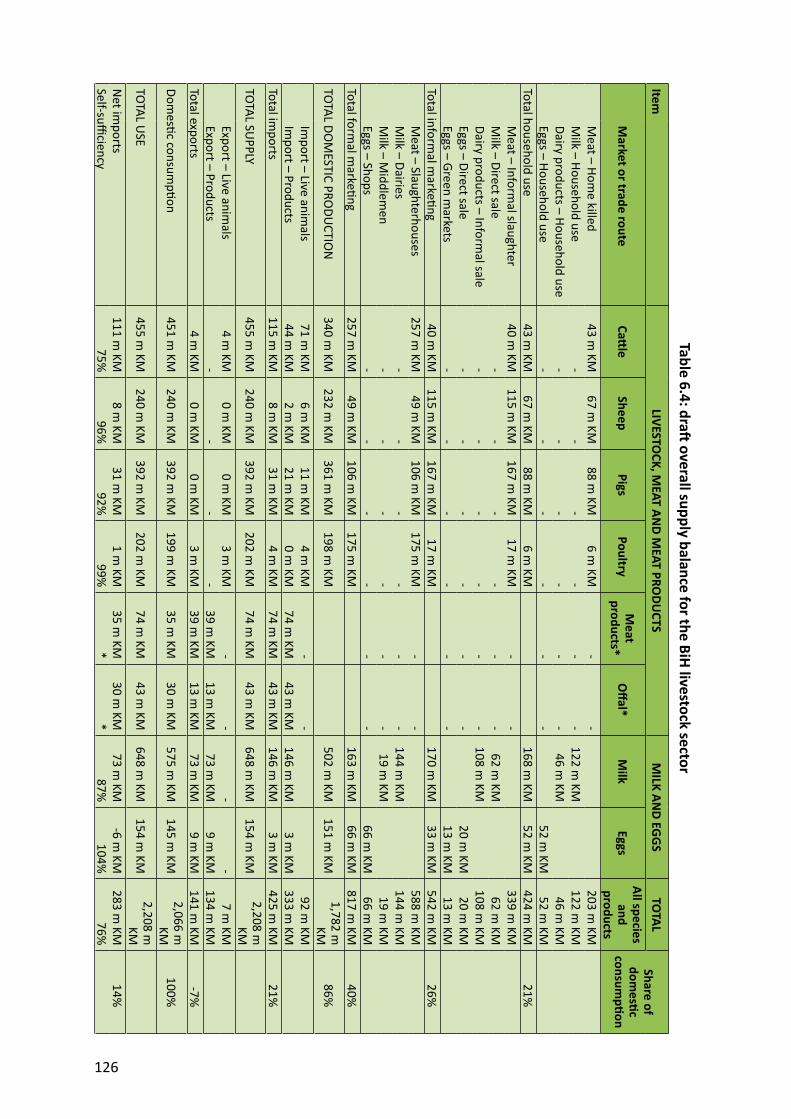

Poglavlje 5 daje prikaz raznih domaćih marke nških kanala koji se koriste u stočarstvu i proizvode; prezentuje sistemsku analizu trgovinskih podataka i iden fi kuje glavne trgovinske partnere BiH za svaku vrstu stočarskog proizvoda; prezentuje balans između nabavke i upotrebe, u smislu vrijednos , za čitav sektor stočarstva.

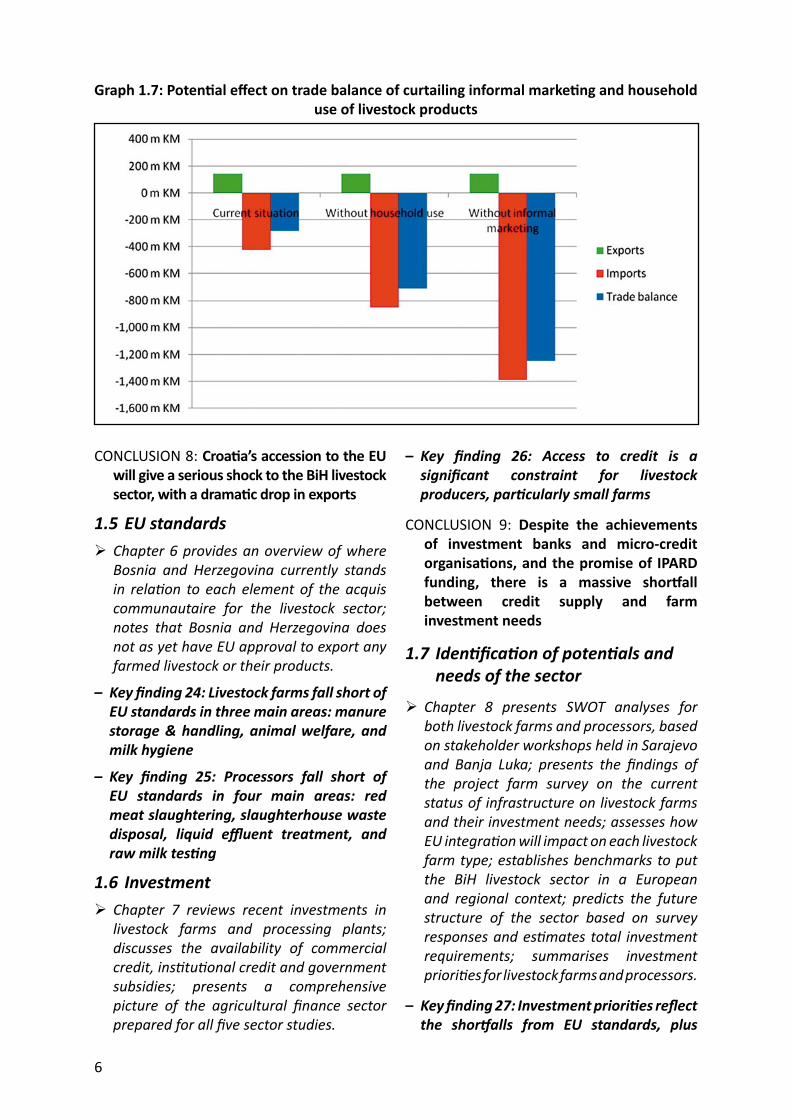

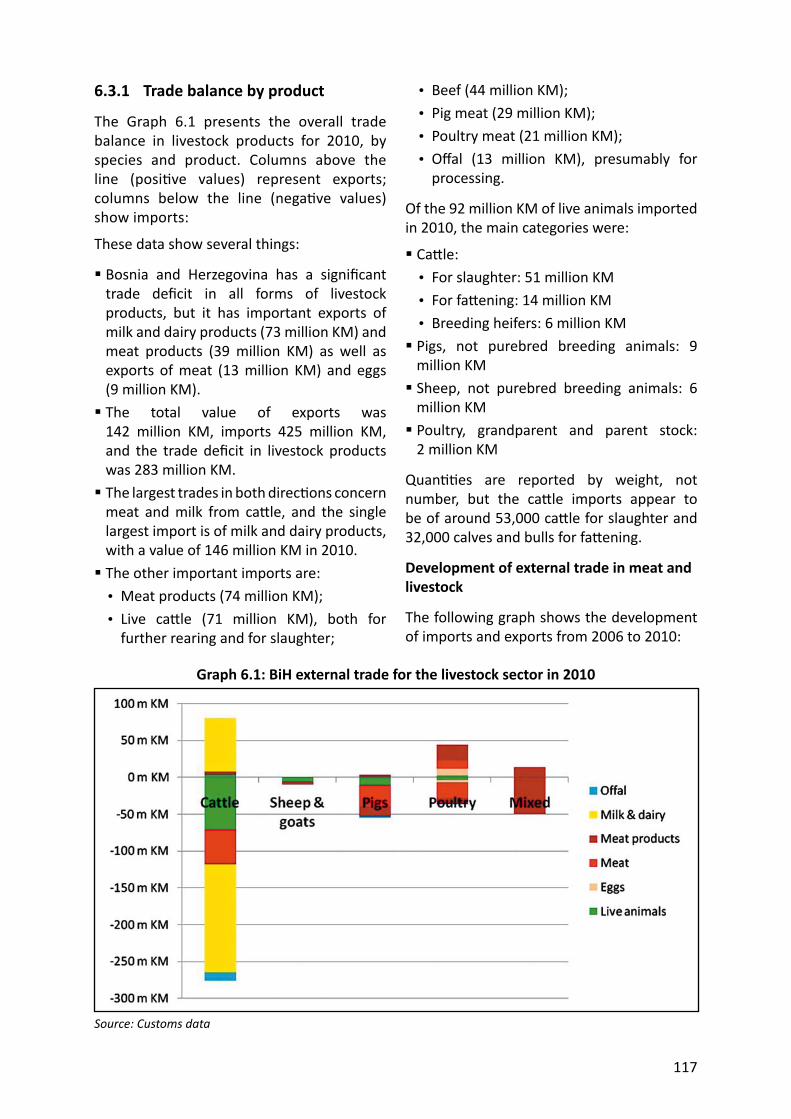

– Ključni nalaz 22: BiH ima ogroman trgovinski defi cit u stočarskim proizvodima

Grafi kon 1.5: Vanjska trgovina BiH za stočarski sektor u 2010. godini

Grafi kon 1.6: Vrijednost uvoza i izvoza stočarskih proizvoda od strane trgovinskih partnera u 2010. godini

i u velikoj mjeri zavisi od Hrvatske kao izvoznog tržišta

– Klju čni nalaz 23: Proizvodnja malog obima i neformalni marke ng mnogo doprinose državnoj opskrbi hranom i balansu

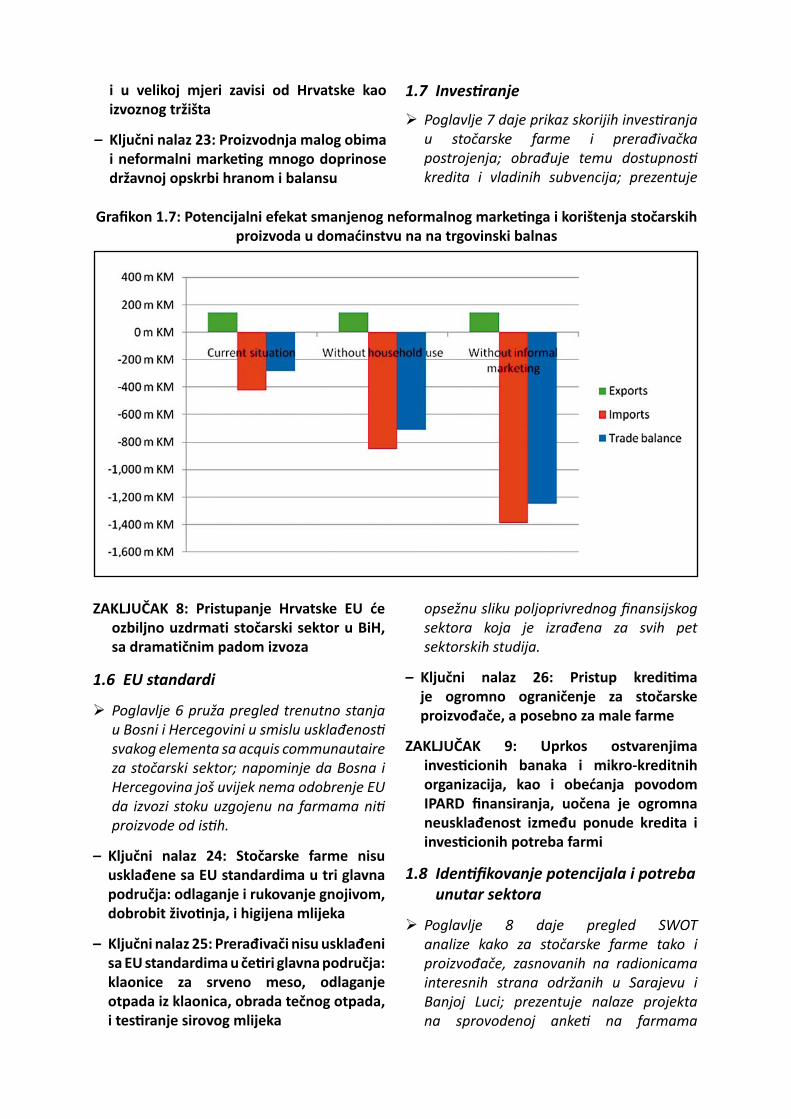

1.7 Inves ranje

Poglavlje 7 daje prikaz skorijih inves ranja u stočarske farme i prerađivačka postrojenja; obrađuje temu dostupnos kredita i vladinih subvencija; prezentuje

Grafi kon 1.7: Potencijalni efekat smanjenog neformalnog marke nga i korištenja stočarskih proizvoda u domaćinstvu na na trgovinski balnas

ZAKLJUČ AK 8: Pristupanje Hrvatske EU će ozbiljno uzdrmati stočarski sektor u BiH, sa dramatičnim padom izvoza

1.6 EU standardi

Poglavlje 6 pruža pregled trenutno stanja u Bosni i Hercegovini u smislu usklađenos svakog elementa sa acquis communautaire za stočarski sektor; napominje da Bosna i Hercegovina još uvijek nema odobrenje EU da izvozi stoku uzgojenu na farmama ni proizvode od is h.

– Ključni nalaz 24: Stočarske farme nisu usklađene sa EU standardima u tri glavna područja: odlaganje i rukovanje gnojivom, dobrobit živo nja, i higijena mlijeka

– Ključni nalaz 25: Prerađivači nisu usklađeni sa EU standardima u če ri glavna područja: klaonice za srveno meso, odlaganje otpada iz klaonica, obrada tečnog otpada, i tes ranje sirovog mlijeka

opsežnu sliku poljoprivrednog fi nansijskog sektora koja je izrađena za svih pet sektorskih studija.

– Ključni nalaz 26: Pristup kredi ma je ogromno ograničenje za stočarske proizvođače, a posebno za male farme

ZAKLJUČ AK 9: Uprkos ostvarenjima inves cionih banaka i mikro-kreditnih organizacija, kao i obećanja povodom IPARD fi nansiranja, uočena je ogromna neusklađenost između ponude kredita i inves cionih potreba farmi

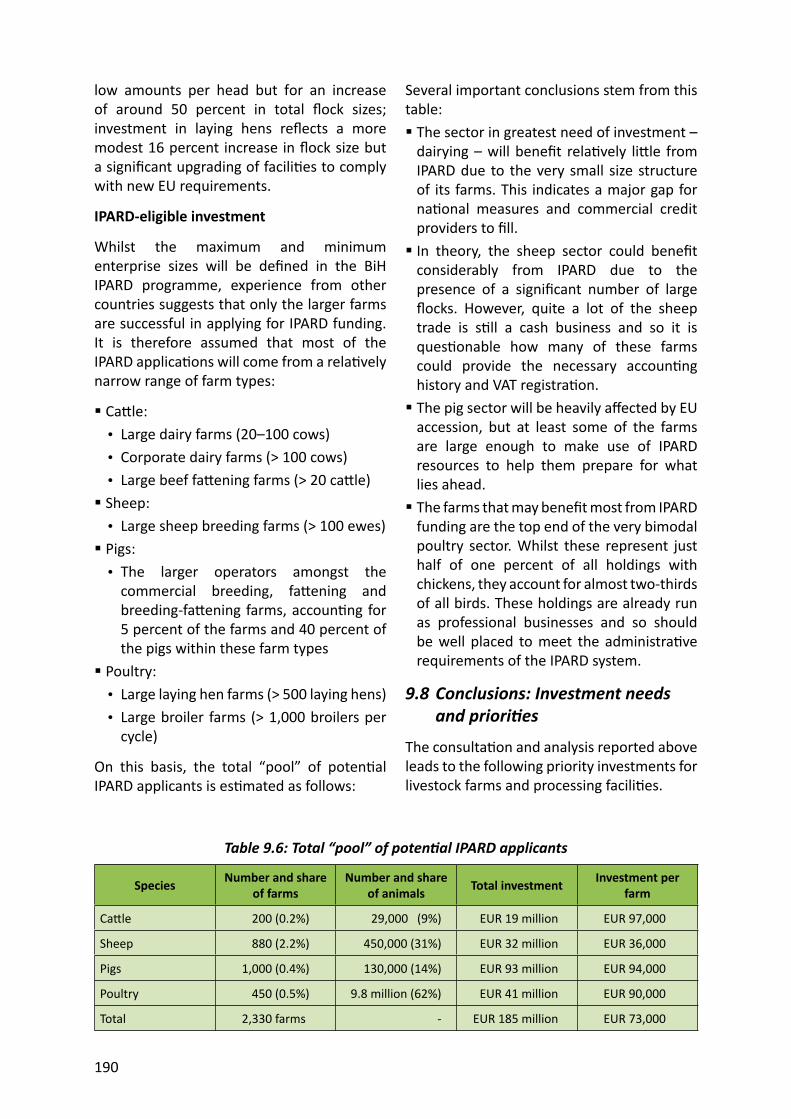

1.8 Iden fi kovanje potencijala i potreba unutar sektora

Poglavlje 8 daje pregled SWOT analize kako za stočarske farme tako i proizvođače, zasnovanih na radionicama interesnih strana održanih u Sarajevu i Banjoj Luci; prezentuje nalaze projekta na sprovodenoj anke na farmama

vezano za trenutno stanje infrastrukture i njihovim inves cionim potrebama; daje procjenu o tome kako će integracija u EU u ca na svaki p stočarske farme; uspostavlja referentne vrijednos kako bi se stočarski sektor u BiH stavio u evropski i regionalni kontekst; predviđa buduću strukturu sektora zasnovane na anektnim odgovorima i daje procjenu o ukupnim inves cionim zahtjevima; sumira inves cione prioritete za stočarske farme i prerađivače.

– Ključni nalaz 27: Inves cioni priorite odražavaju uočene nedostatke u smislu neusklađenos sa EU standardima, plus potreba za povećanjem obima i tehničke efi kasnos

Proizvođači:• Povećanje stada/jata (posebno mljekare;

sa napomenom da se IPARD sredstva ne mogu koris za kupovinu stoke)

• Zgrade i oprema (posebno mljekare)• Mašinerija (posebno za krmu)• Odlaganje i rukovanje gnojivom (posebno

goveđim i svinjskim) Prerađivači mlijeka:• Unaprjeđenje postrojenja kako bi se

poboljšala opera vna efi kasnost i opseg proizvoda

• Laboratorije unutar postrojenja kako bi se unaprijedila kvaliteta proizvoda

• Skladištenje i tretman tekućeg otpada kako bi se ispunili standardi o zaš životne sredine

Prerađivači mesa:• Unaprjeđenje postrojenja kako bi se

poboljšala opera vna efi kasnost • Skladištenje, prevoz i odlaganje

živo njskog otpada

1.9 Iden fi kacija potreba za obučavanjem u sektoru

Poglavlje 9 daje pregled postojećih struktura koje pružaju obuku, savjete i informacije stočarskom sektoru; prezentuje kratak sažetak ključnih prioriteta za obučavanje

za različite grupe korisnika, uključujući farmere, prerađivače i inspektore.

– Ključni nalaz 28: Postojeće službe za pružanje savjetodavnih usluga u poljoprivredi se neadekvatne da pruže pomoć 300.000 stočarskim farmama kako bi ispunile EU standarde i poboljšale tehničku efi kasnost, upravljanje i marke ng

ZAKLJUČ AK 10: Uspostavljanje efek vnog brojnijeg sistema za pružanje usluga u poljoprivredi je prioritet broj jedan

1.10 Ishodi / Rezulta

Poglavlje 10 daje kratak sažetak ključnih faktora koje treba uze u obzir prilikom kreiranja inves cionih mjera za sektor BiH stočarstva; prezentuje prijedloge za šest specifi čnih mjera koje se fi nansiraju u sklopu IPARD programa.

– Ključni nalaz 29: Implikacije pristupanja EU po stočarske farme po ču direktno iz njihove strukture

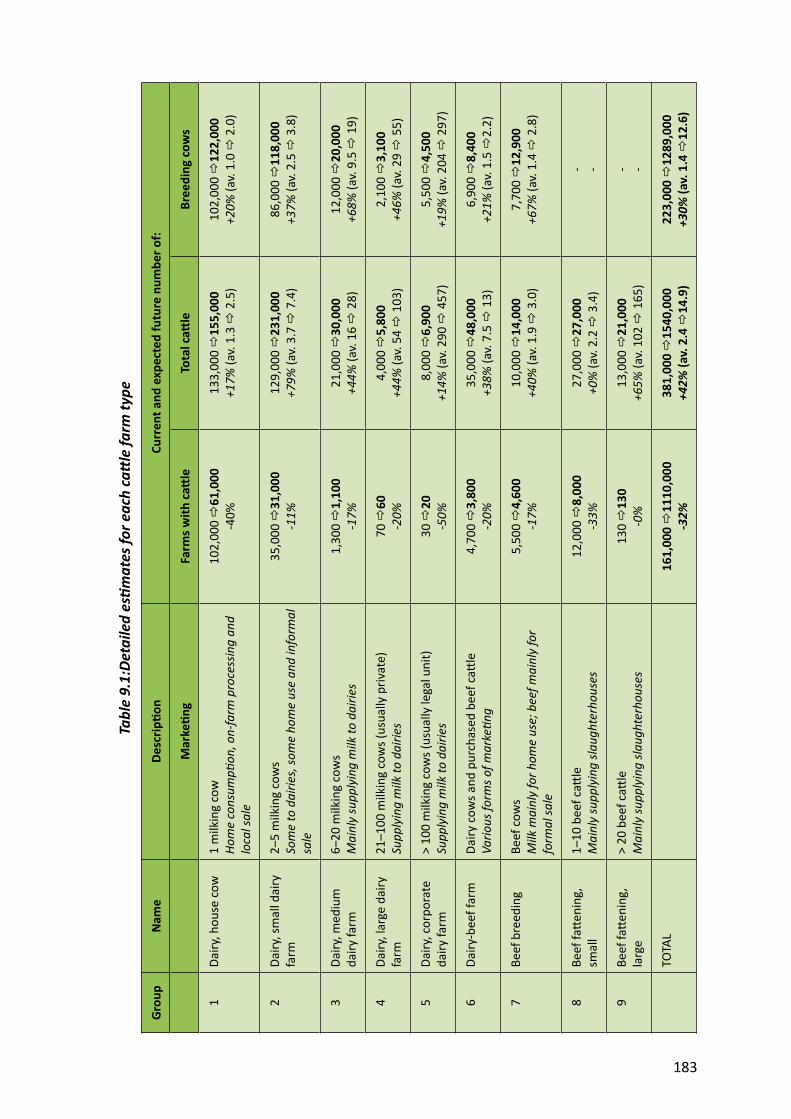

Goveda (160.000 gazdinstava)• Ogroman strukturalni problem u

mljekarskoj proizvodnji, sa potrebom pružanja pomoći manjim farmama da se adap raju promjenama; manje ozbiljan problem u proizvodnji govedine.

Ovce (50.000 gazdinstava)• Manje ozbiljan sturkturalni problem,

pošto i manje farme mogu da budu usklađene sa EU regula vom i održive u komercijalnom smislu, premda će samo veće farme vjerovatno učestvova u IPARD.

Svinje (130.000 gazdinstava)• Veliki problem konkurentnosti,

rezultat koje će vjerovatno biti prestanak proizvodnje na manjim svinjogojskim farmama; samo veće farme će vjerovatno imati dugoročniju komercijalnu budućnost, i one mogu u velikoj mjeri da izvuku ogromne koristi od IPARD pomoći.

Perad (220.000 gazdinstava)

• Kvočke: » Trenutna dvomodalna stuktura je održiva, pošto je veliki broj malih farmi u suš ni nekomercijalan; mnoge velike komercijalne farme će zah jeva značajnu podršku kako bi se uskladile sa EU standardima.

• Brojleri: » Manje farme brojlera imaju neznatnu komercijalnu budućnost; IPARD ulaganje treba da se fokusira na pomaganje velikim farmama brojlera da se usklade sa EU standardima, povećaju efi kasnost i da nastave da se šire.

– Ključni nalaz 30: 3 IPARD mjere su predložene za proizvođače a tri za prerađivače stočarskih proizvoda

Modernizacija poljoprivrednog gazdinstva (101):

a. 101/1: Unaprjeđenje i uvećanje poljoprivrednog gazdinstva

b. 101/2: Skladištenje i odlaganje gnojiva

c. 101/3: Mašinerija za krmno bilje

Obrada i marke ng poljoprivrednih proizvoda (103):

a. 103/1. Unaprjeđenje prerađivačkih postrojenja

b. 103/2: Skladištenje i odlaganje mljekarskog tekućeg otpada

c. 103/3: Sakupljanje i obrada živo njskog otpada

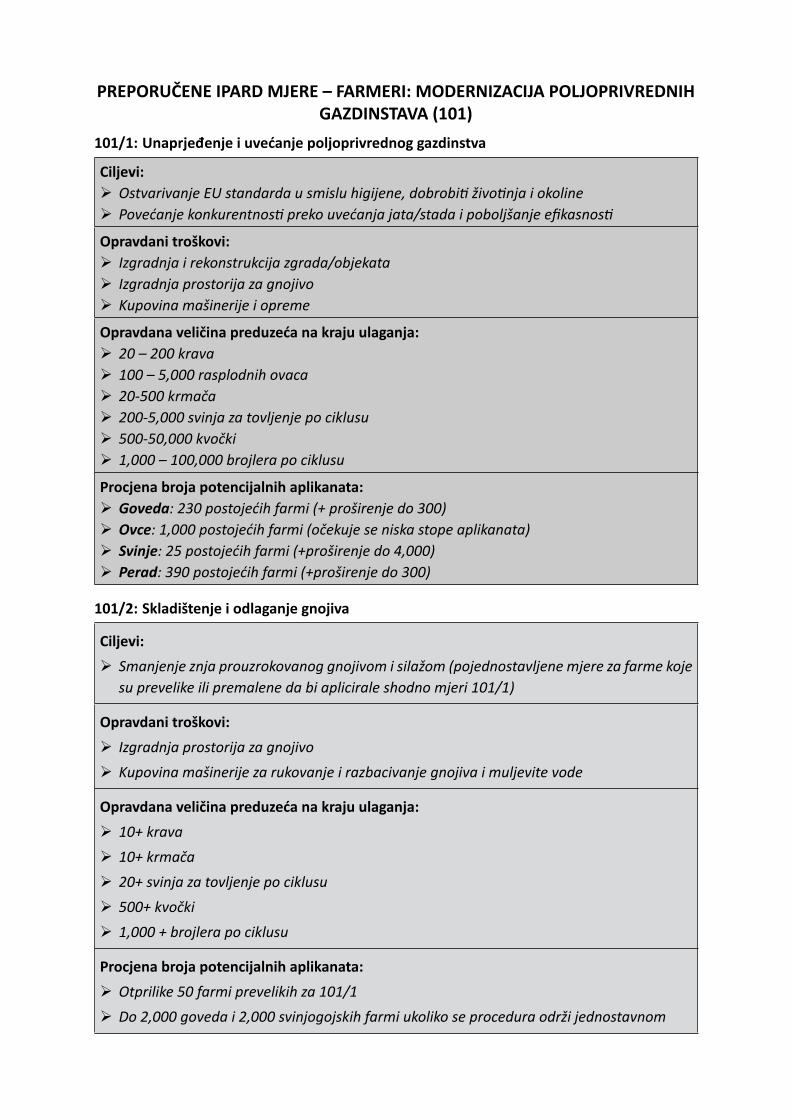

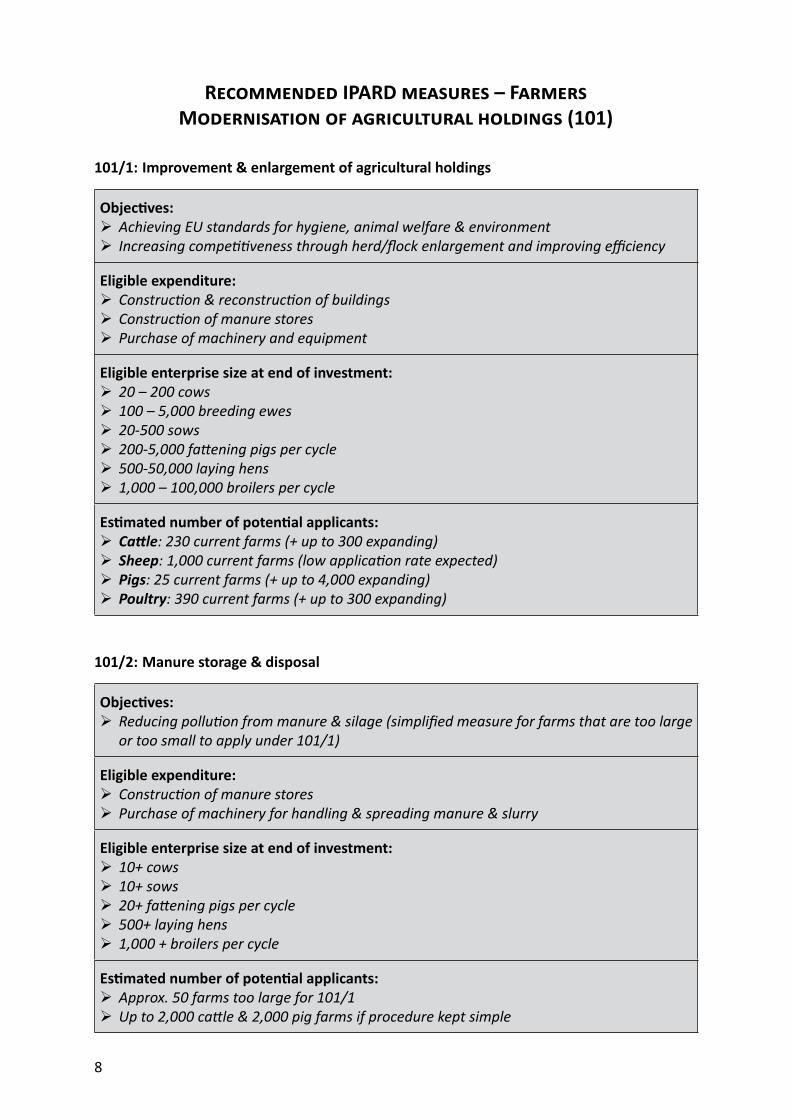

PREPORUČENE IPARD MJERE – FARMERI: MODERNIZACIJA POLJOPRIVREDNIH GAZDINSTAVA (101)

101/1: Unaprjeđenje i uvećanje poljoprivrednog gazdinstva

Ciljevi: Ostvarivanje EU standarda u smislu higijene, dobrobi živo nja i okoline Povećanje konkurentnos preko uvećanja jata/stada i poboljšanje efi kasnos

Opravdani troškovi: Izgradnja i rekonstrukcija zgrada/objekata Izgradnja prostorija za gnojivo Kupovina mašinerije i opreme

Opravdana veličina preduzeća na kraju ulaganja: 20 – 200 krava 100 – 5,000 rasplodnih ovaca 20-500 krmača 200-5,000 svinja za tovljenje po ciklusu 500-50,000 kvočki 1,000 – 100,000 brojlera po ciklusu

Procjena broja potencijalnih aplikanata: Goveda: 230 postojećih farmi (+ proširenje do 300) Ovce: 1,000 postojećih farmi (očekuje se niska stope aplikanata) Svinje: 25 postojećih farmi (+proširenje do 4,000) Perad: 390 postojećih farmi (+proširenje do 300)

101/2: Skladištenje i odlaganje gnojiva

Ciljevi: Smanjenje znja prouzrokovanog gnojivom i silažom (pojednostavljene mjere za farme koje su prevelike ili premalene da bi aplicirale shodno mjeri 101/1)

Opravdani troškovi: Izgradnja prostorija za gnojivo Kupovina mašinerije za rukovanje i razbacivanje gnojiva i muljevite vode

Opravdana veličina preduzeća na kraju ulaganja: 10+ krava 10+ krmača 20+ svinja za tovljenje po ciklusu 500+ kvočki 1,000 + brojlera po ciklusu

Procjena broja potencijalnih aplikanata: Otprilike 50 farmi prevelikih za 101/1 Do 2,000 goveda i 2,000 svinjogojskih farmi ukoliko se procedura održi jednostavnom

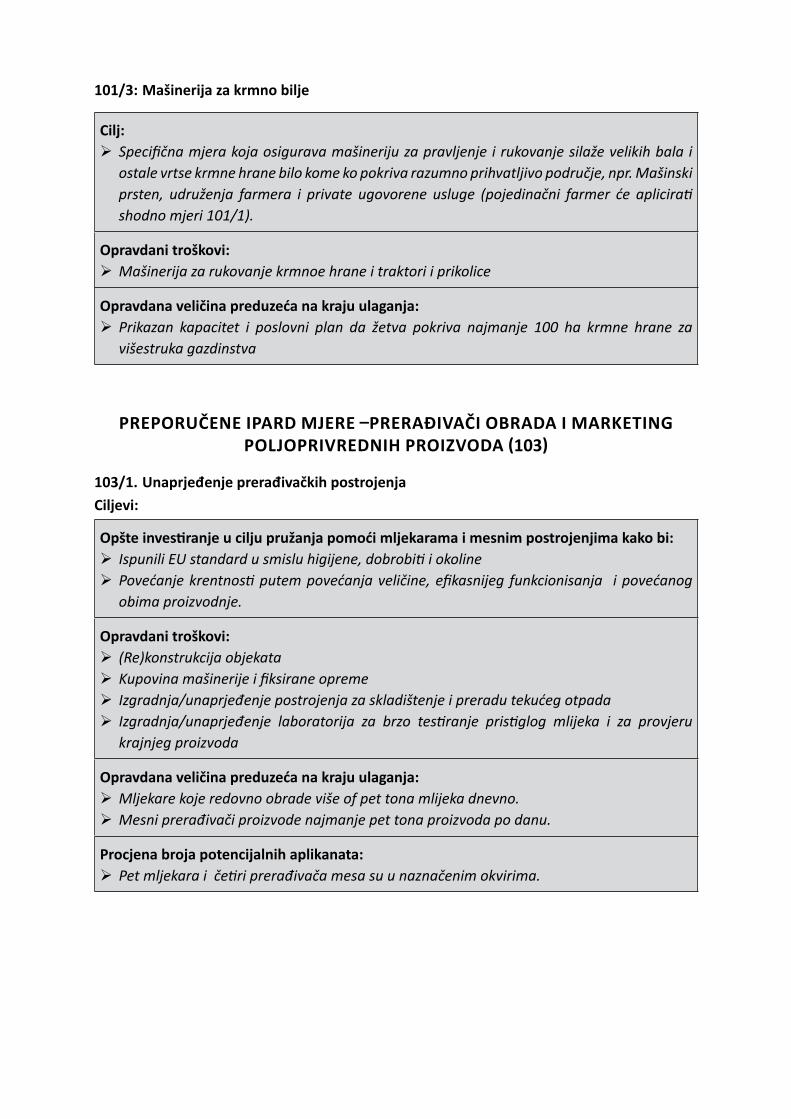

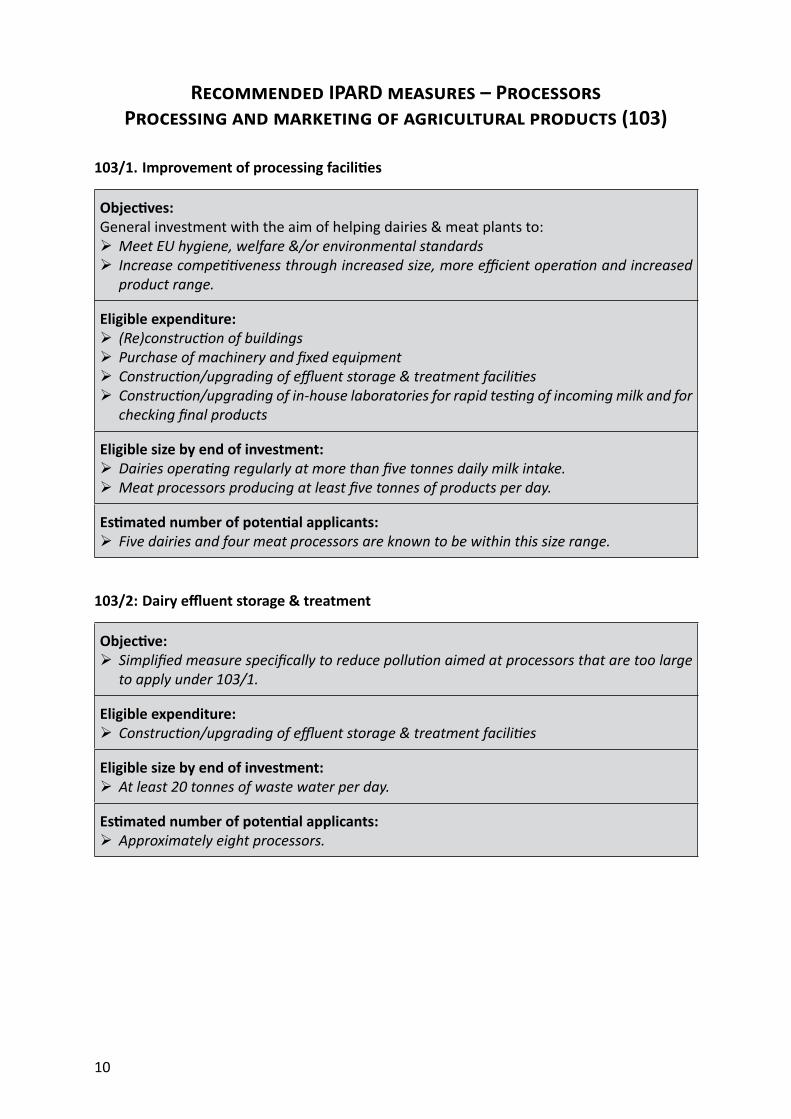

PREPORUČENE IPARD MJERE PRERAĐIVAČI OBRADA I MARKETING POLJOPRIVREDNIH PROIZVODA 103

103/1. Unaprjeđenje prerađivačkih postrojenja Ciljevi:

Opšte inves ranje u cilju pružanja pomoći mljekarama i mesnim postrojenjima kako bi: Ispunili EU standard u smislu higijene, dobrobi i okoline Povećanje krentnos putem povećanja veličine, efi kasnijeg funkcionisanja i povećanog obima proizvodnje.

Opravdani troškovi: (Re)konstrukcija objekata Kupovina mašinerije i fi ksirane opreme Izgradnja/unaprjeđenje postrojenja za skladištenje i preradu tekućeg otpada Izgradnja/unaprjeđenje laboratorija za brzo tes ranje pris glog mlijeka i za provjeru krajnjeg proizvoda

Opravdana veličina preduzeća na kraju ulaganja: Mljekare koje redovno obrade više of pet tona mlijeka dnevno. Mesni prerađivači proizvode najmanje pet tona proizvoda po danu.

Procjena broja potencijalnih aplikanata: Pet mljekara i če ri prerađivača mesa su u naznačenim okvirima.

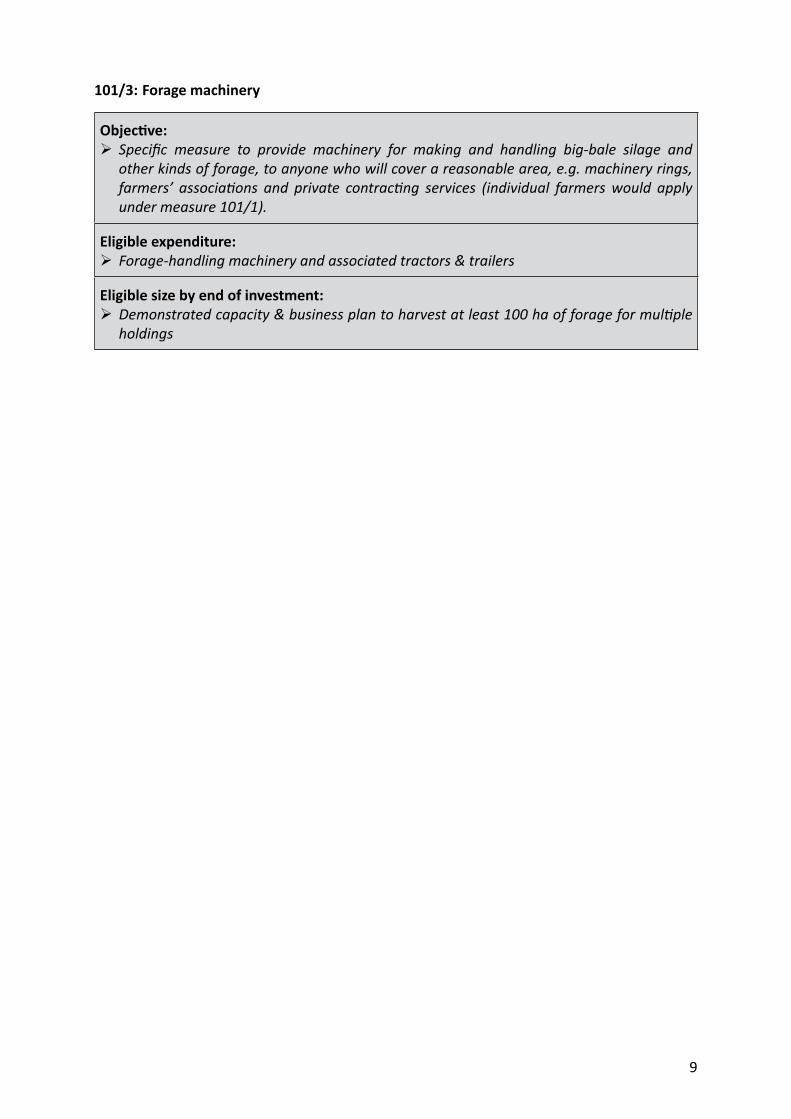

101/3: Mašinerija za krmno bilje

Cilj: Specifi čna mjera koja osigurava mašineriju za pravljenje i rukovanje silaže velikih bala i ostale vrtse krmne hrane bilo kome ko pokriva razumno prihvatljivo područje, npr. Mašinski prsten, udruženja farmera i private ugovorene usluge (pojedinačni farmer će aplicira shodno mjeri 101/1).

Opravdani troškovi: Mašinerija za rukovanje krmnoe hrane i traktori i prikolice

Opravdana veličina preduzeća na kraju ulaganja: Prikazan kapacitet i poslovni plan da žetva pokriva najmanje 100 ha krmne hrane za višestruka gazdinstva

103/2: Skladištenje i odlaganje mljekraskog tekućeg otpada

Cilj: Pojednostavljena mjera kako bi se smanjilo zagađenje a namijenjena za prerađivače koji su preveliki da bi aplicirali u skolopu mjere 103/1.

Opravdani troškovi: Izgradnja/unaprjeđenje postrojenja za skladištenje i preradu tekućeg otpada

Opravdana veličina preduzeća na kraju ulaganja: Najmanje 20 tona otpadnih voda po danu.

Procjena broja potencijalnih aplikanata: Otprilike osam prerađivača.

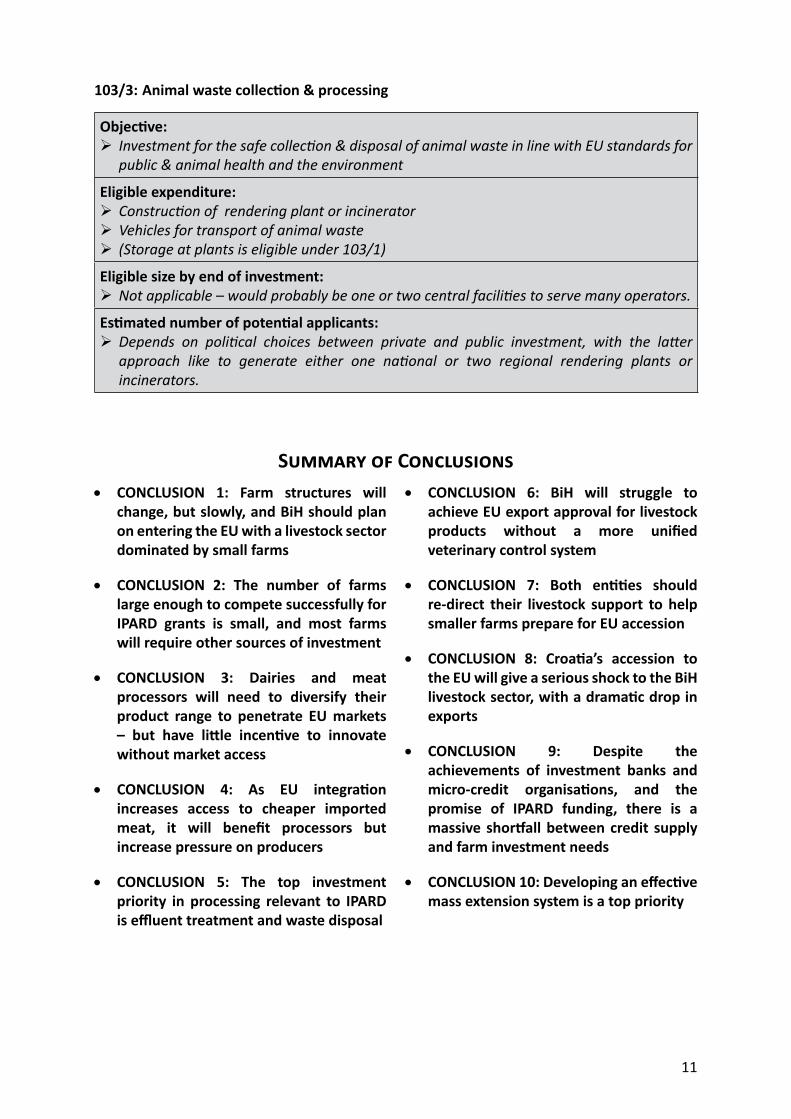

103/3: Sakupljanje i obrada živo njskog otpada

Cilj: Ulagedno prikupljanje i odalaganje živo njskog otpada u skladu sa EU standardima zbog javnog i živo njskog zdravlja kao i očuvanja okoline

Opravdani troškovi: Izgradnja postrojenjenja za uništavanje ili peći Vozila za prevoz živo njskog otpada (Skladište u postrojenjima je dozvoljeno shodno mjeri 103/1)

Opravdana veličina preduzeća na kraju ulaganja: Nije primjenljivo – vjerovatno će bi jedan ili dva centralna postrojenja koja će opsluživa mnogo operatera/korisnika.

Procjena broja potencijalnih aplikanata: Zavisi od poli čkih izbora između privatnih i javnih ulaganja, s m što će druga opcija sa velikom vjerovatnoćom generisa bilo jednu državnu ili dva regionalna postrojenja za uništavanje i peći.

SAŽETAK ZAKLJUČAKA

ZAKLJUČAK 1: Strukture farmi će se promijeni , ali vremenski polako, a BiH treba da planira ulazak u EU sa stočarskim sektorom kojim dominiraju male farme

ZAKLJUČAK 2: Broj farmi dovoljno velikih da budu uspješno konkurentne za IPARD grantove je mali, i većina farmi će zah jeva dodatne izvore inves ranja

ZAKLJUČAK 3: Mljekare i proizvođači mlijeka treba da učine svoj asortiman raznolikijim kako bi prodrli na tržište EU – ali imaju male podsticaje na inovacije bez pristupa tržištu

ZAKLJUČAK 4: Kako proces EU integracije povećava pristup je inijem uvoznom mesu, benefi cije od istog će osje prerađivači, ali će to stavi dodatni pri sak na proizvođače

ZAKLJUČAK 5: Najvažniji inves cioni prioritet u preradi koji je relevantan za IPARD je tretman tekućeg otpada i odlaganje otpada

ZAKLJUČAK 6: BiH će teško dobi EU odobrenje za izvoz mesnih proizvoda bez osiguranja unifi ciranog sistema veterinarske kontrole

ZAKLJUČAK 7: Oba en teta treba da preusmjere svoju podršku stočarstvu na manje farme kako bi se pripremile ua pristupanje EU

ZAKLJUČAK 8: Pristupanje Hrvatske EU će ozbiljno uzdrma stočarski sektor u BiH, sa drama čnim padom izvo za

ZAKLJUČAK 9: Uprkos ostvarenjima inves cionih banaka i mikro-kreditnih organizacija, kao i obećanja povodom IPARD fi nansiranja, uočena je ogromna neusklađenost između ponude kredita i inves cionih potreba far mi

ZAKLJUČAK 10: Uspostavljanje efek vnog brojnijeg sistema za pružanje usluga u poljoprivredi je prioritet broj jedan

i

Table of Contents

ABBREVIATIONS AND ACRONYMS vii

INTRODUCTION ix

1. EXECUTIVE SUMMARY 1

1.1 B 11.1 F 11.2 P 41.3 P 41.4 M 51.5 EU 61.6 I 61.7 I 61.8 I 71.9 O 7

2. BACKGROUND AND KEY FIGURES 13

2.1 G B H 132.2 C 15

2.2.1 General context of the sector analyses: Prepara on for EU accession 152.2.2 Sector context 15

2.3 G B H 162.4 A 182.5 T B H 22

3. FARMERS 23

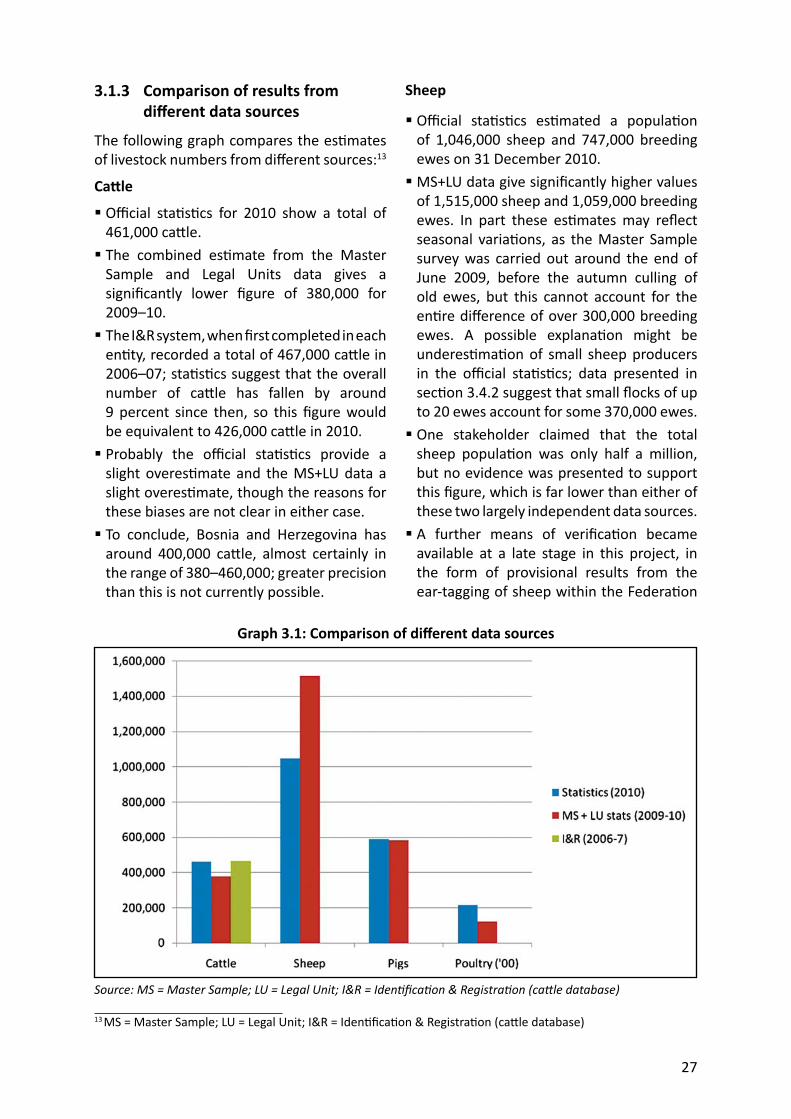

3.1 M 233.1.1 Strengths and weaknesses of each dataset 233.1.2 Methodology to combine data sources 243.1.3 Comparison of results from diff erent data sources 27

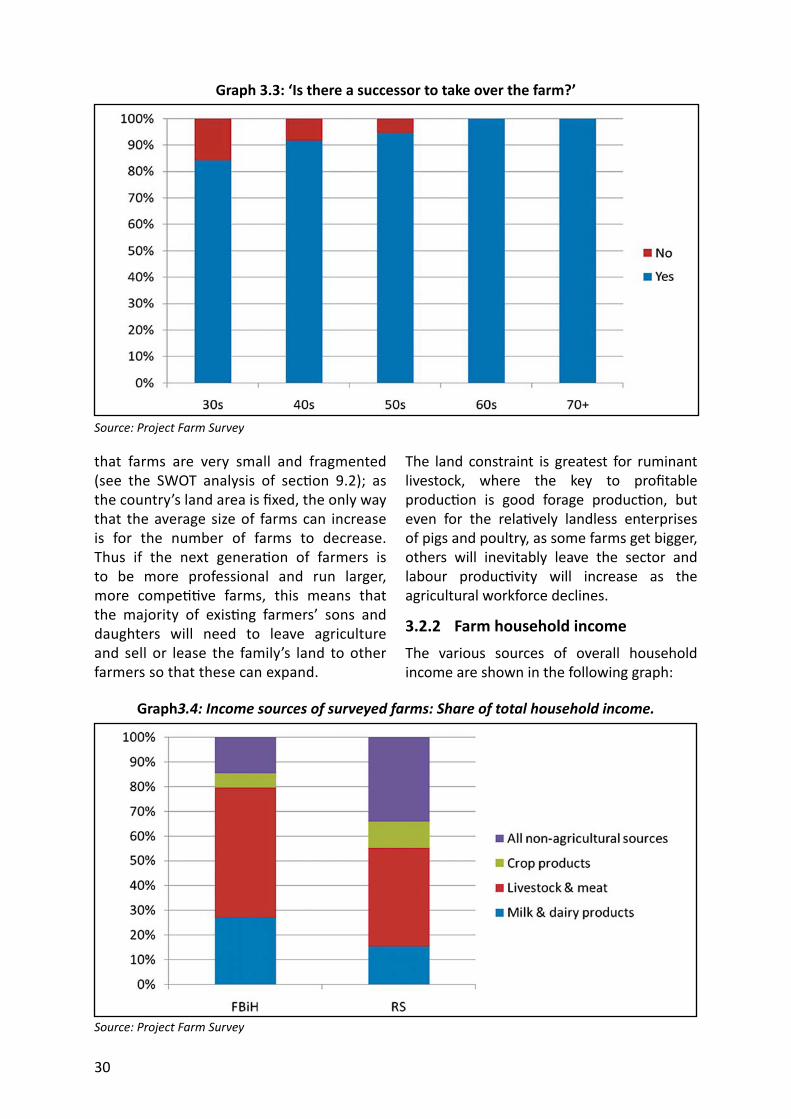

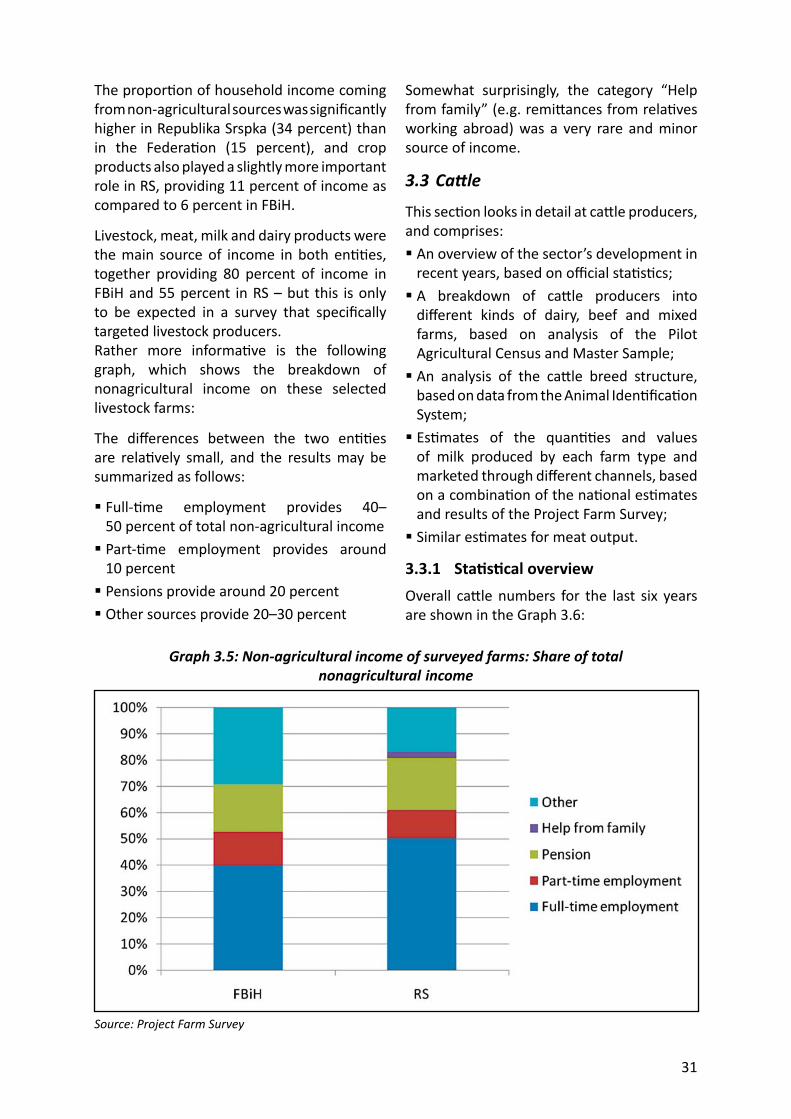

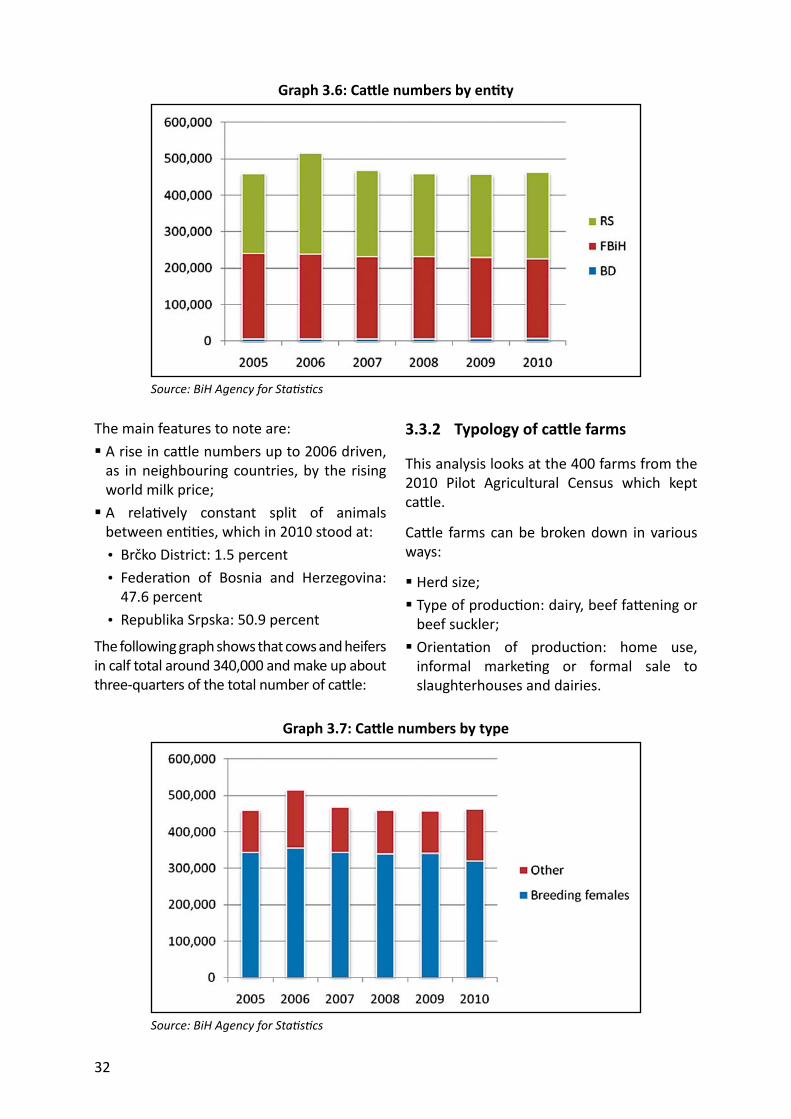

3.2 O 293.2.1 Age and succession 293.2.2 Farm household income 30

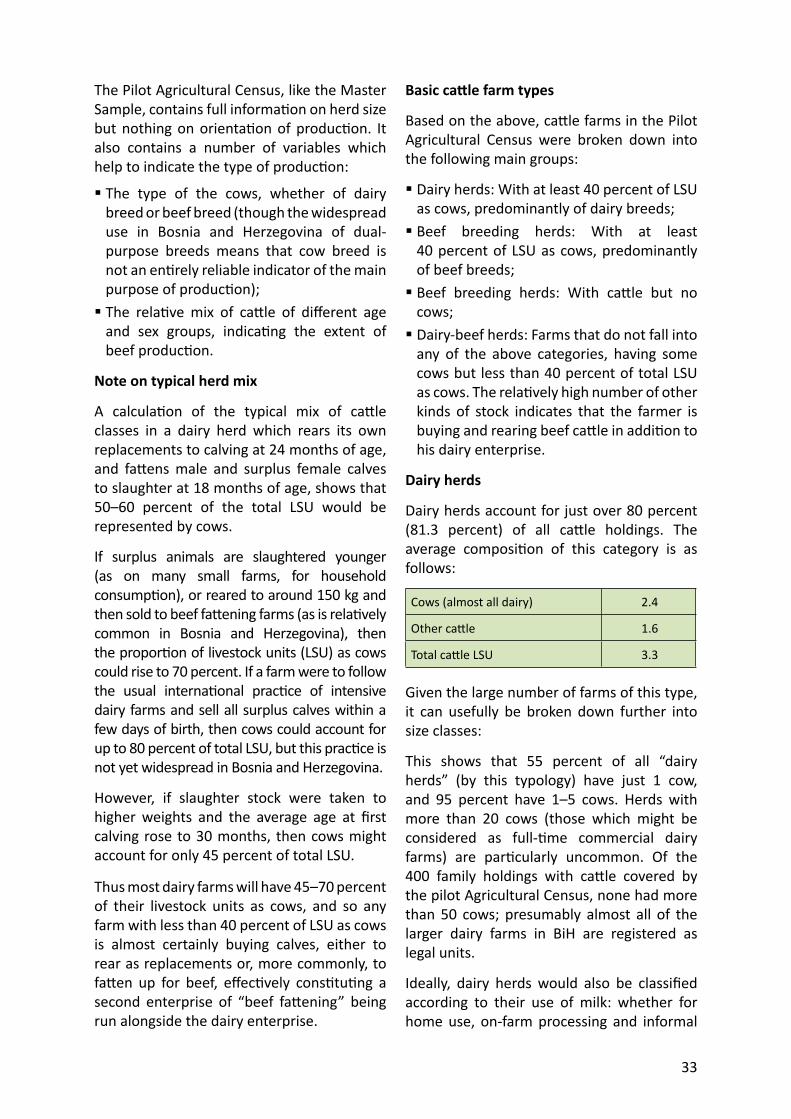

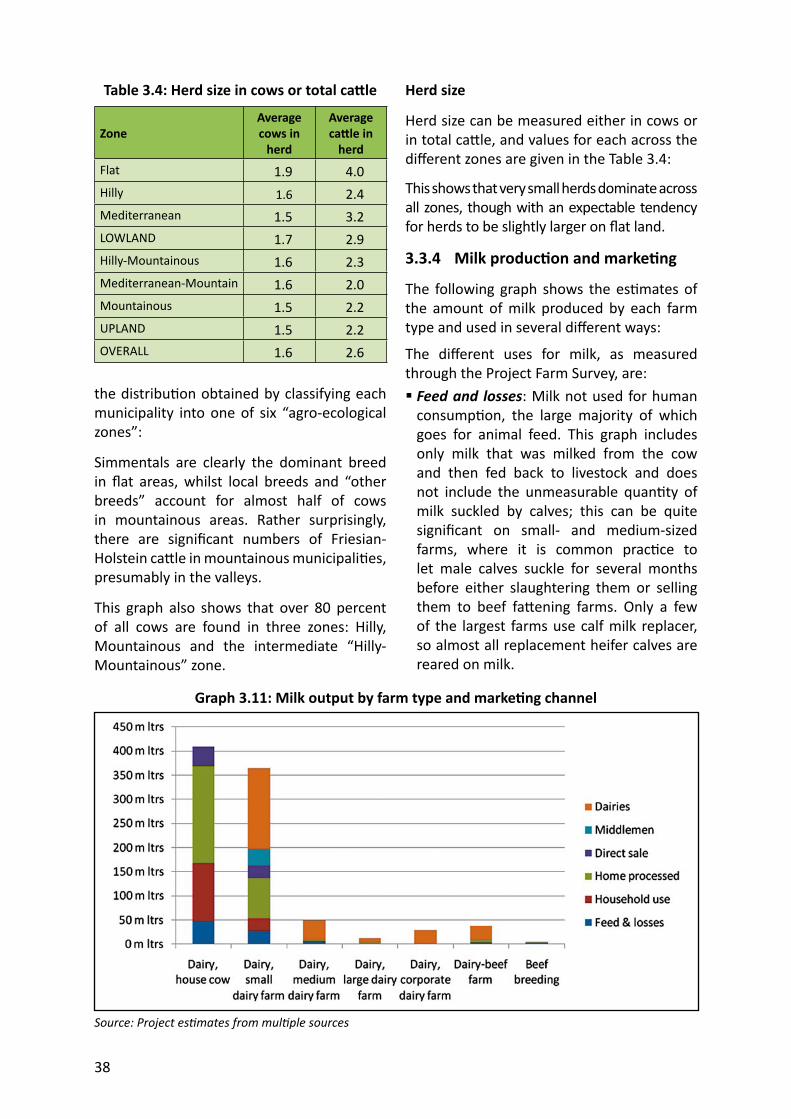

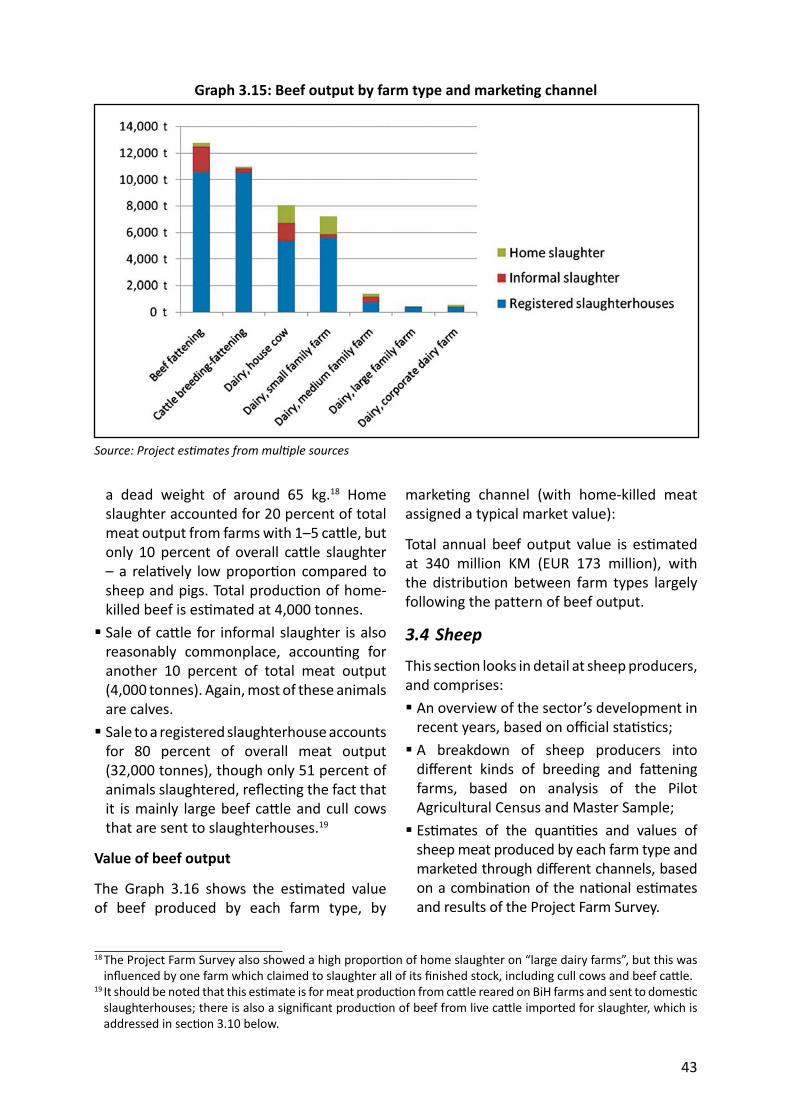

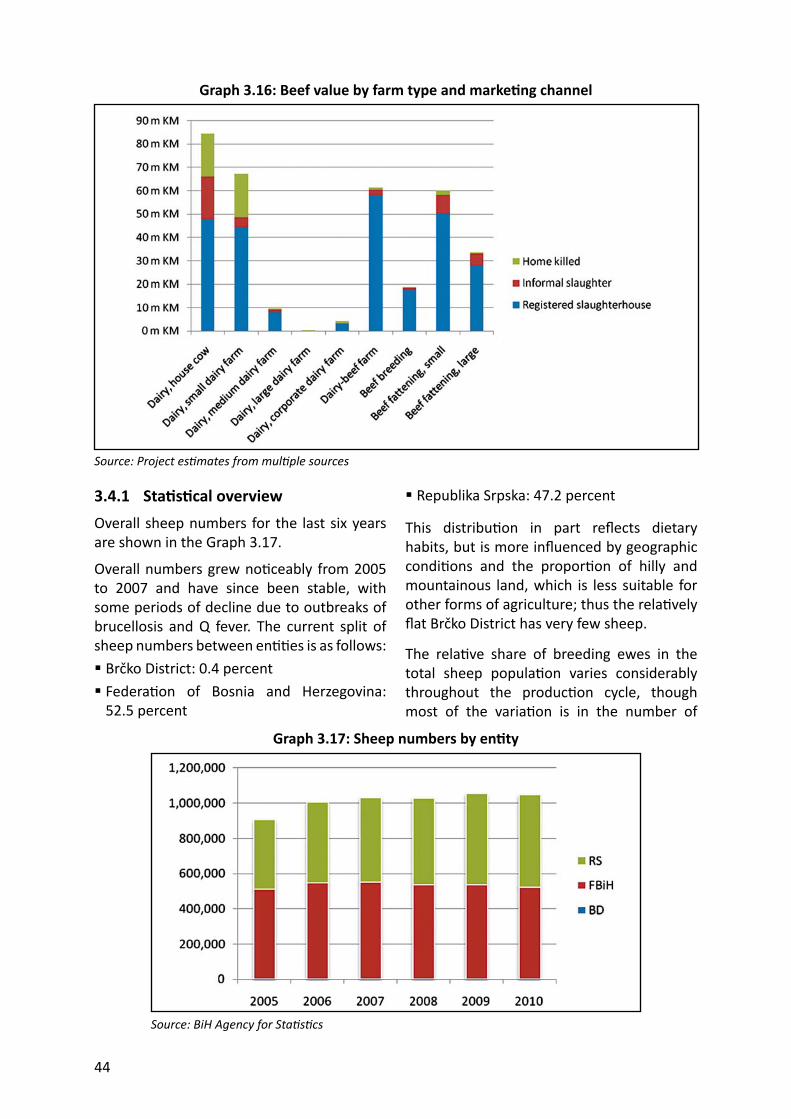

3.3 C 313.3.1 Sta s cal overview 313.3.2 Typology of ca le farms 323.3.3 Ca le breed and herd structure 373.3.4 Milk produc on and marke ng 383.3.5 Beef produc on and marke ng 42

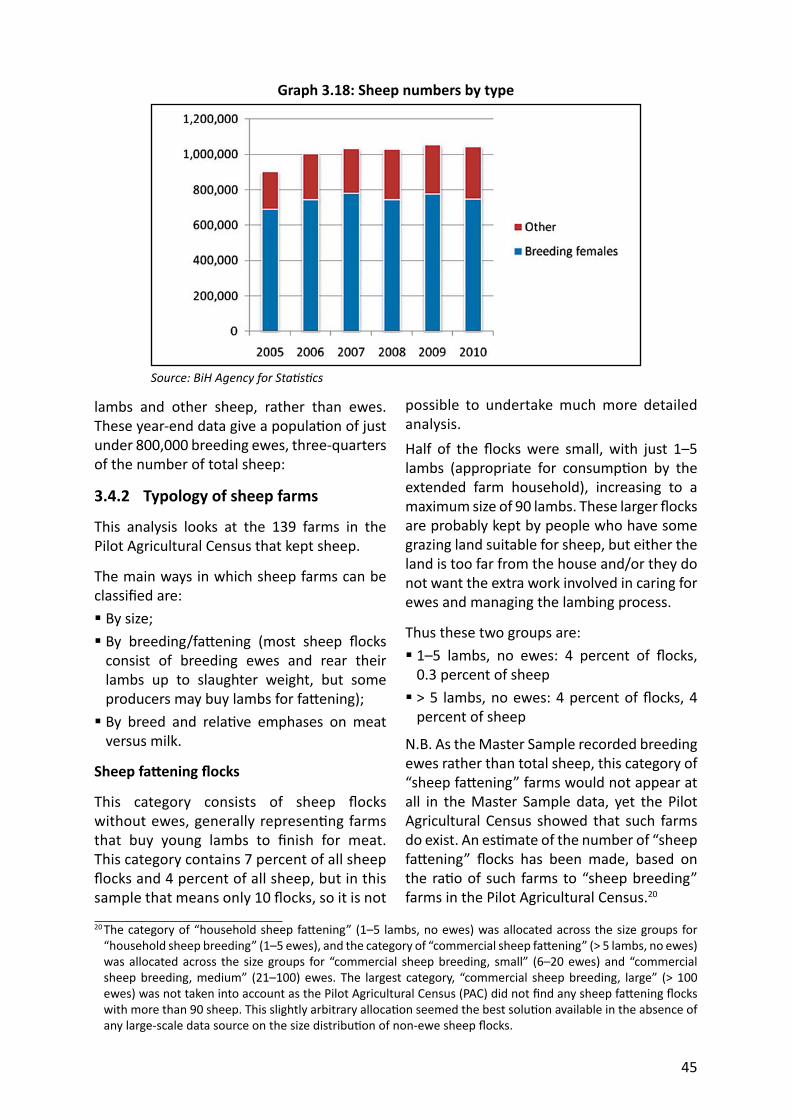

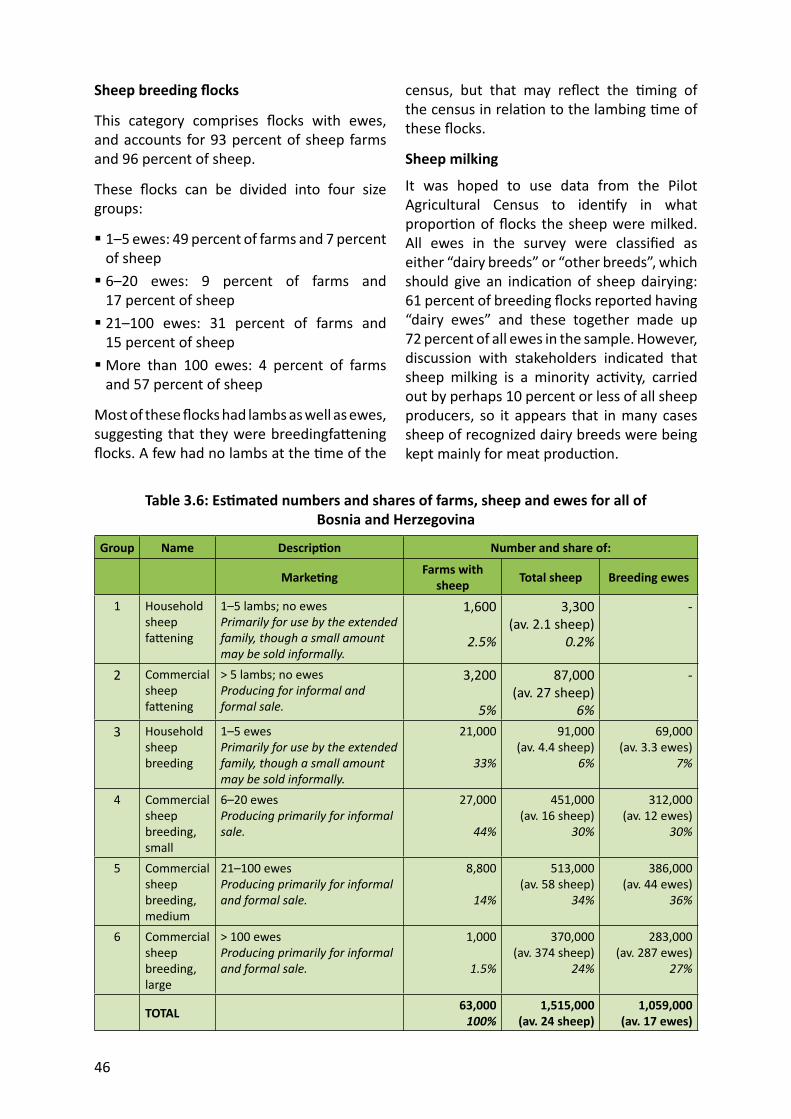

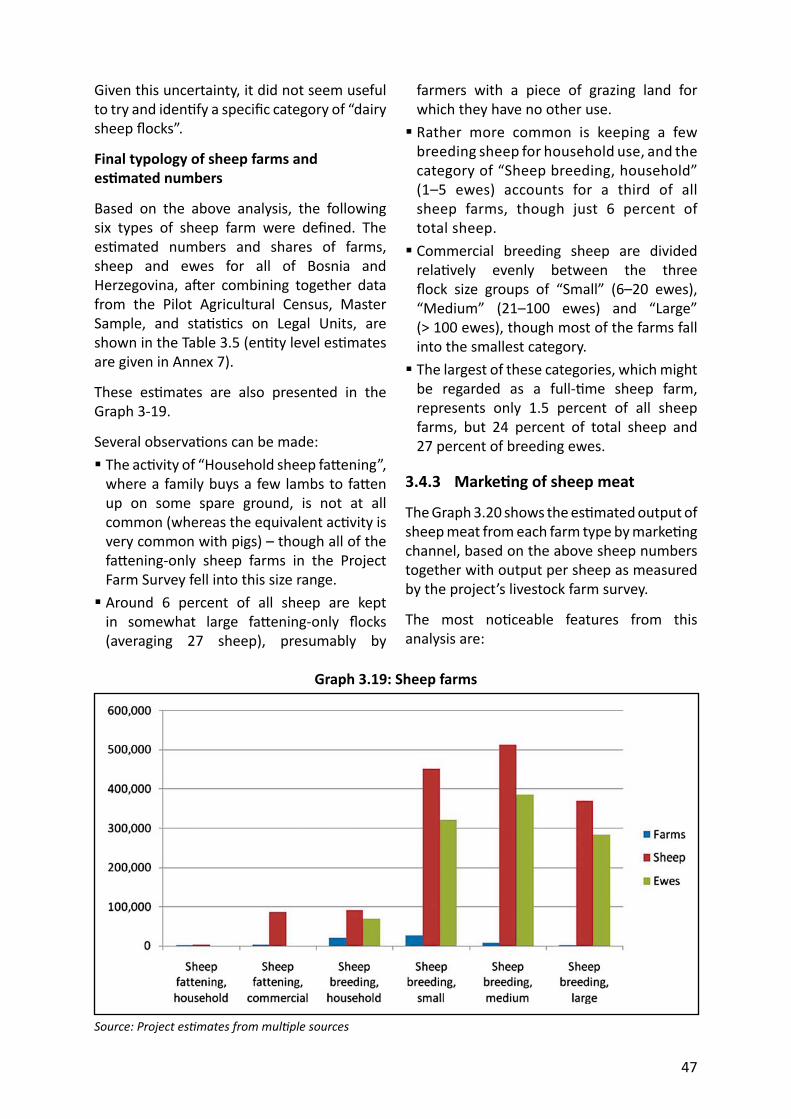

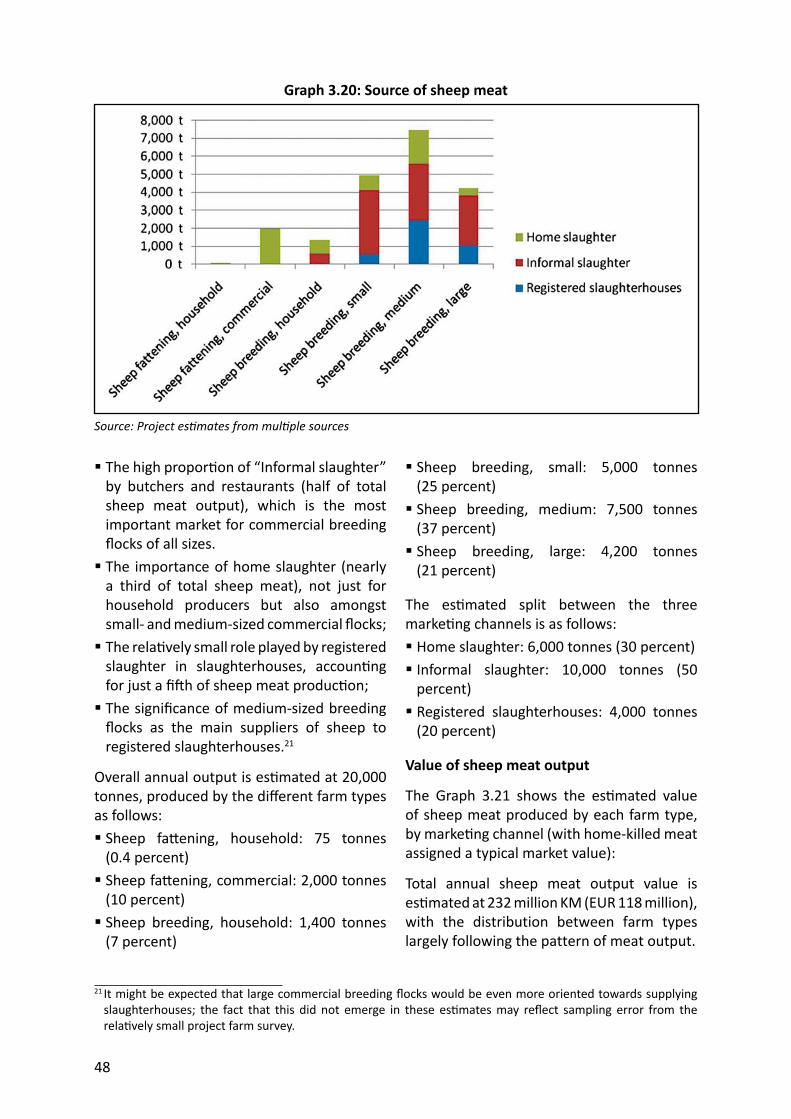

3.4 S 433.4.1 Sta s cal overview 443.4.2 Typology of sheep farms 453.4.3 Marke ng of sheep meat 47

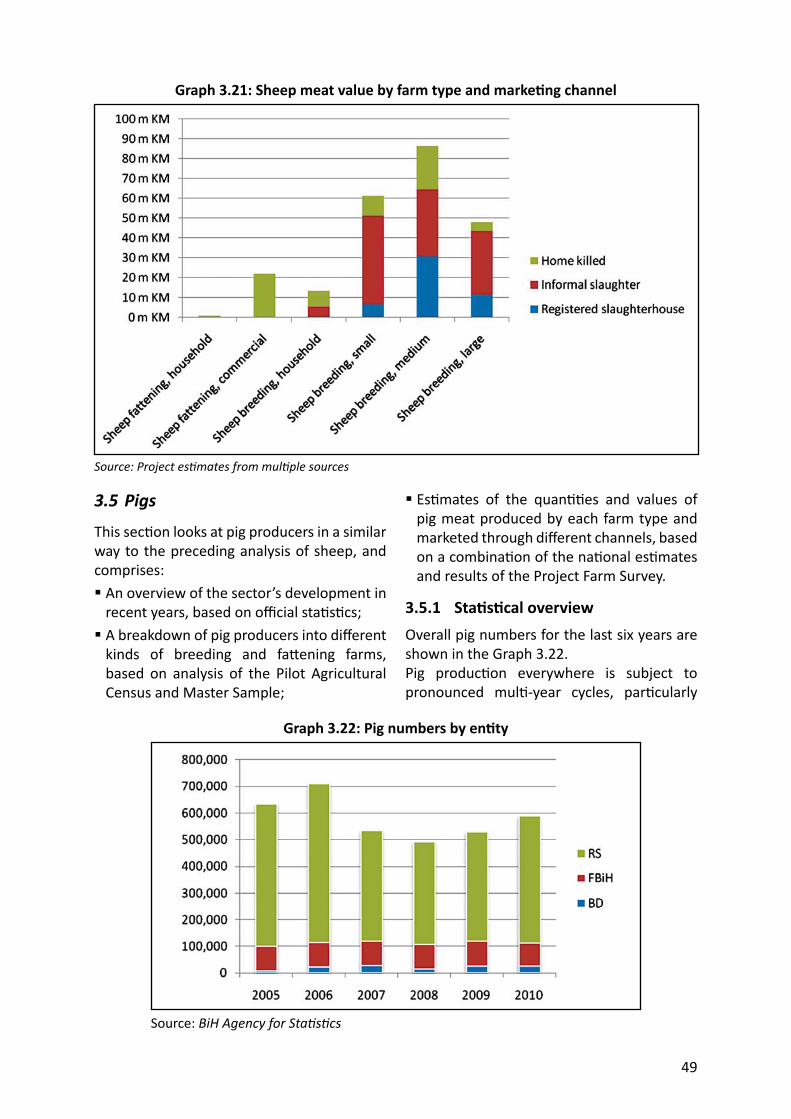

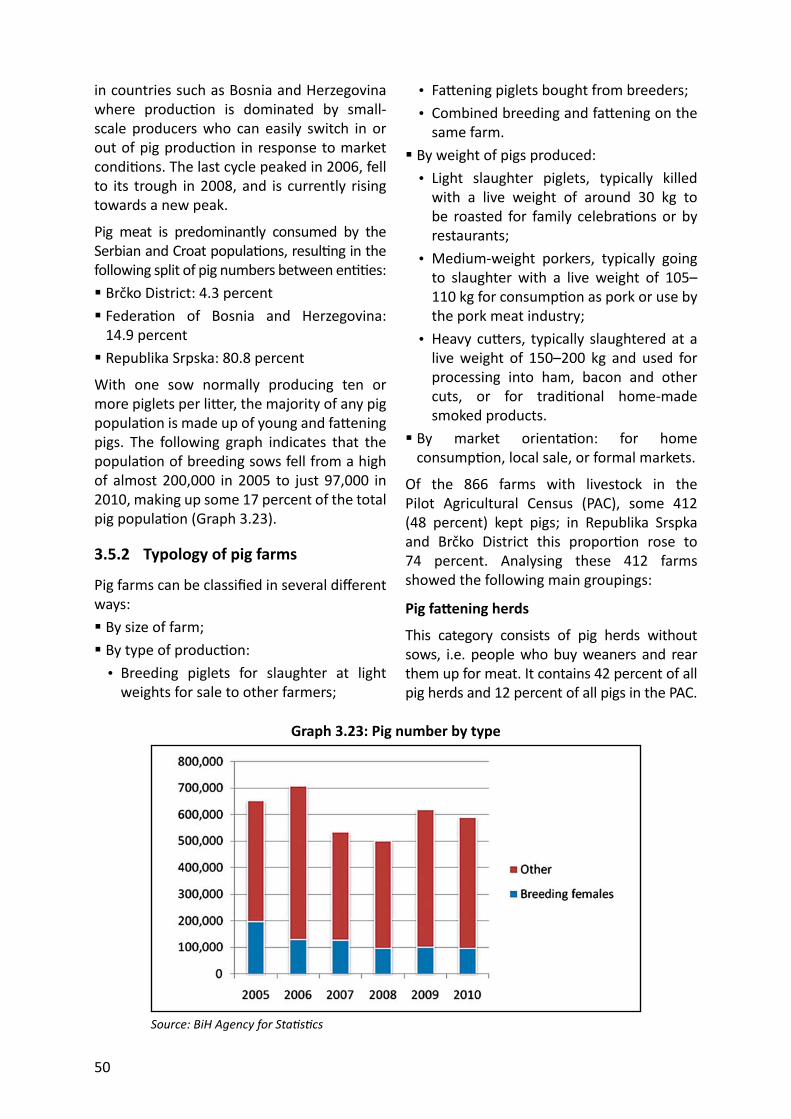

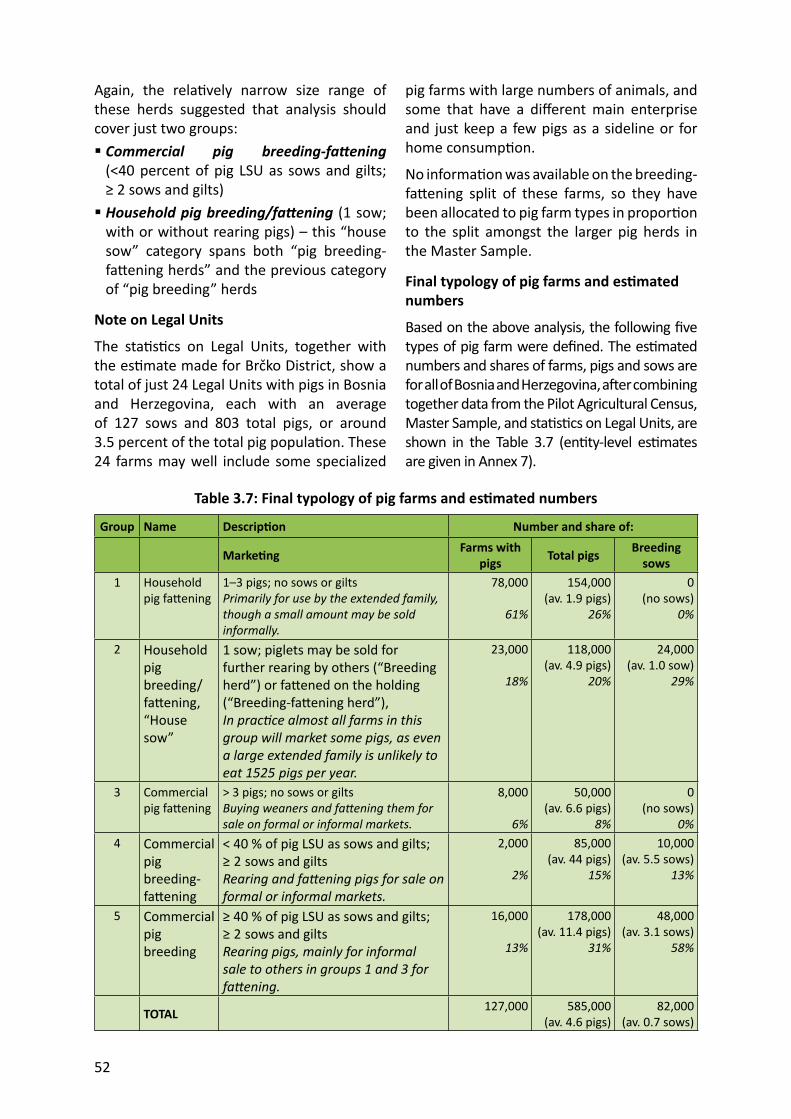

3.5 P 493.5.1 Sta s cal overview 493.5.2 Typology of pig farms 503.5.3 Marke ng of pig meat 53

ii

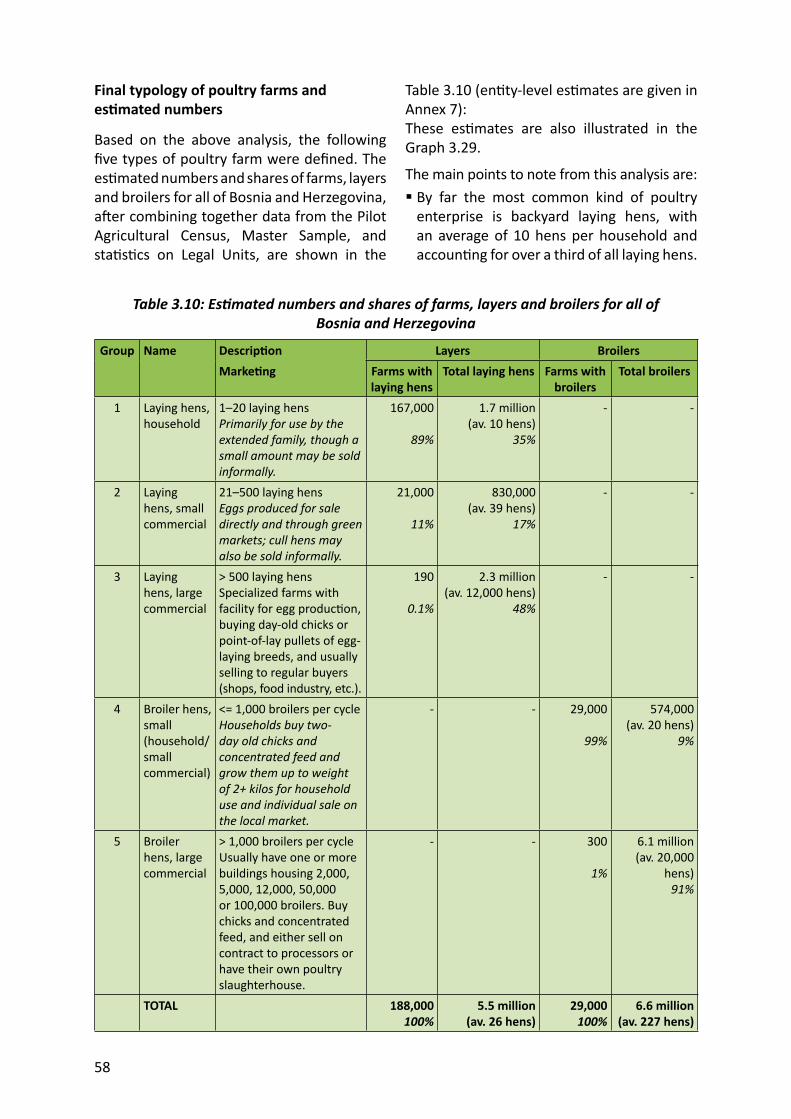

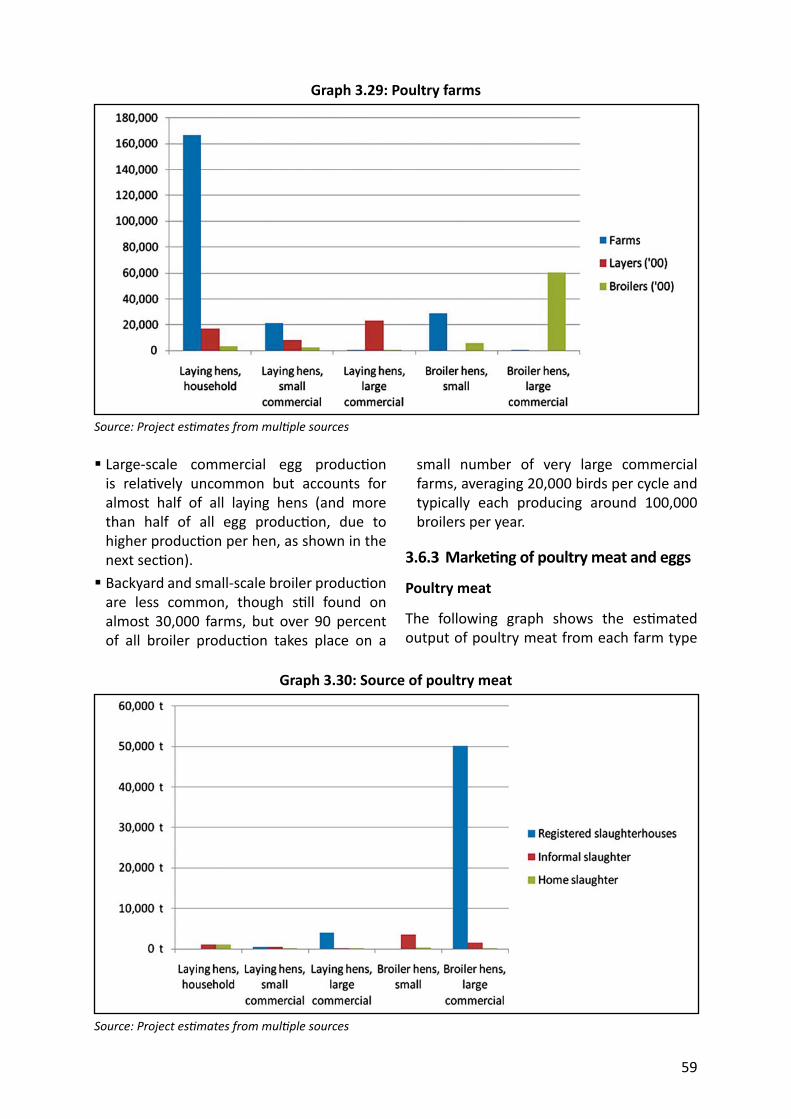

3.6 P 543.6.1 Sta s cal overview 543.6.2 Typology of poultry farms 563.6.3 Marke ng of poultry meat and eggs 59

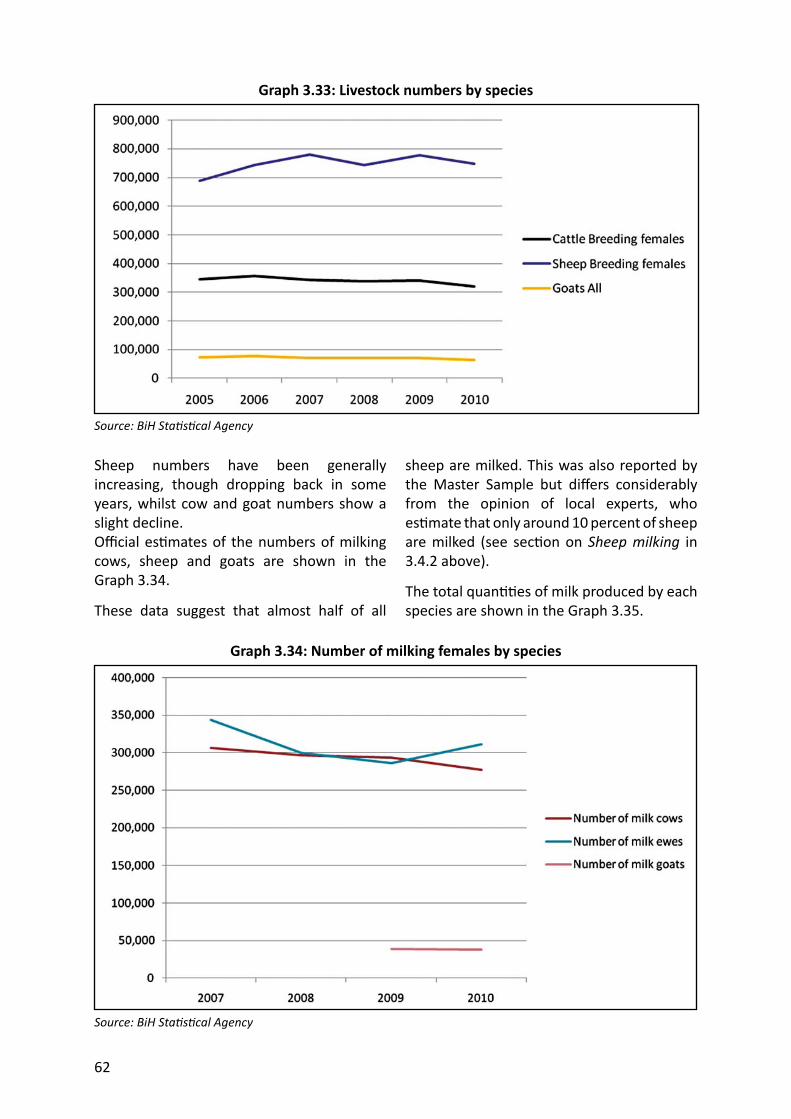

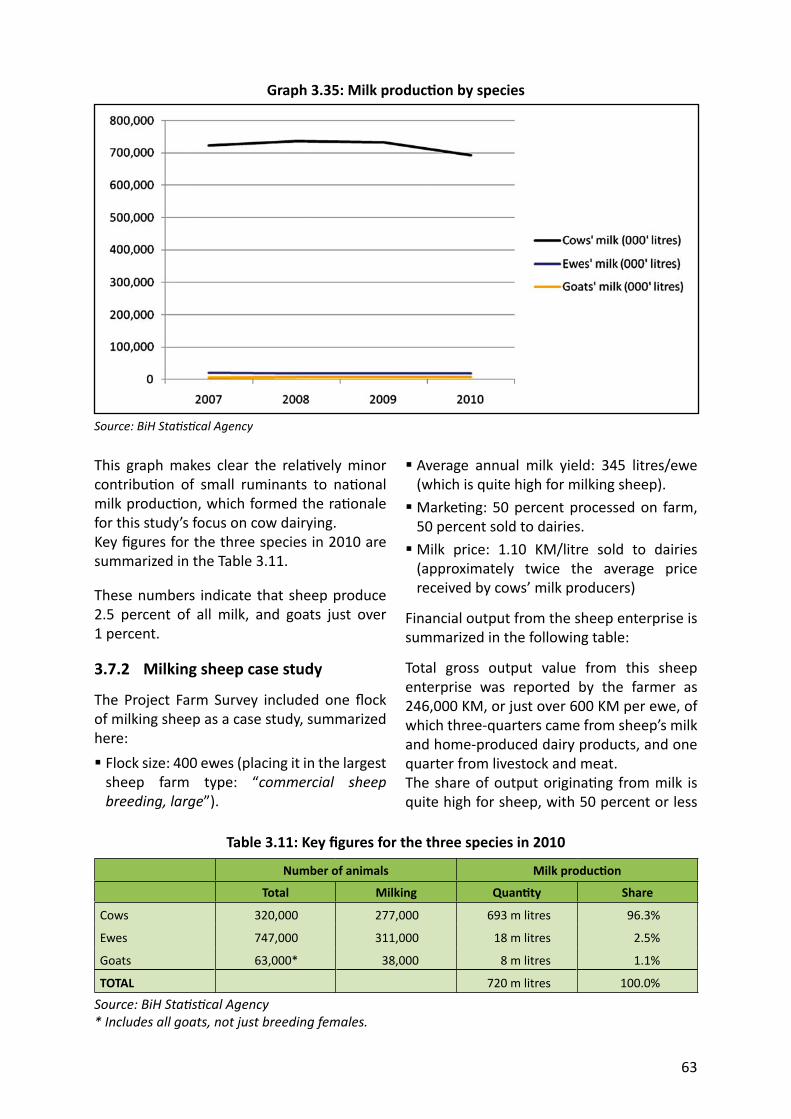

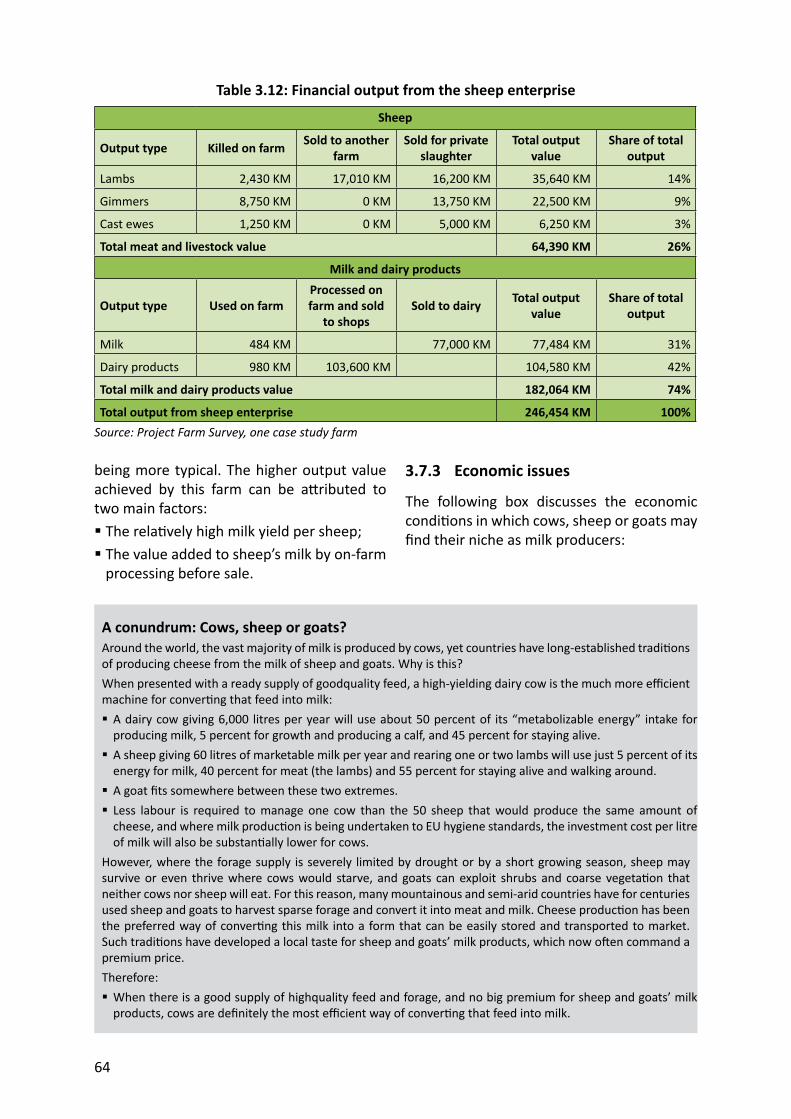

3.7 M 613.7.1 Sta s cs on animals and milk produc on by species 613.7.2 Milking sheep case study 633.7.3 Economic issues 64

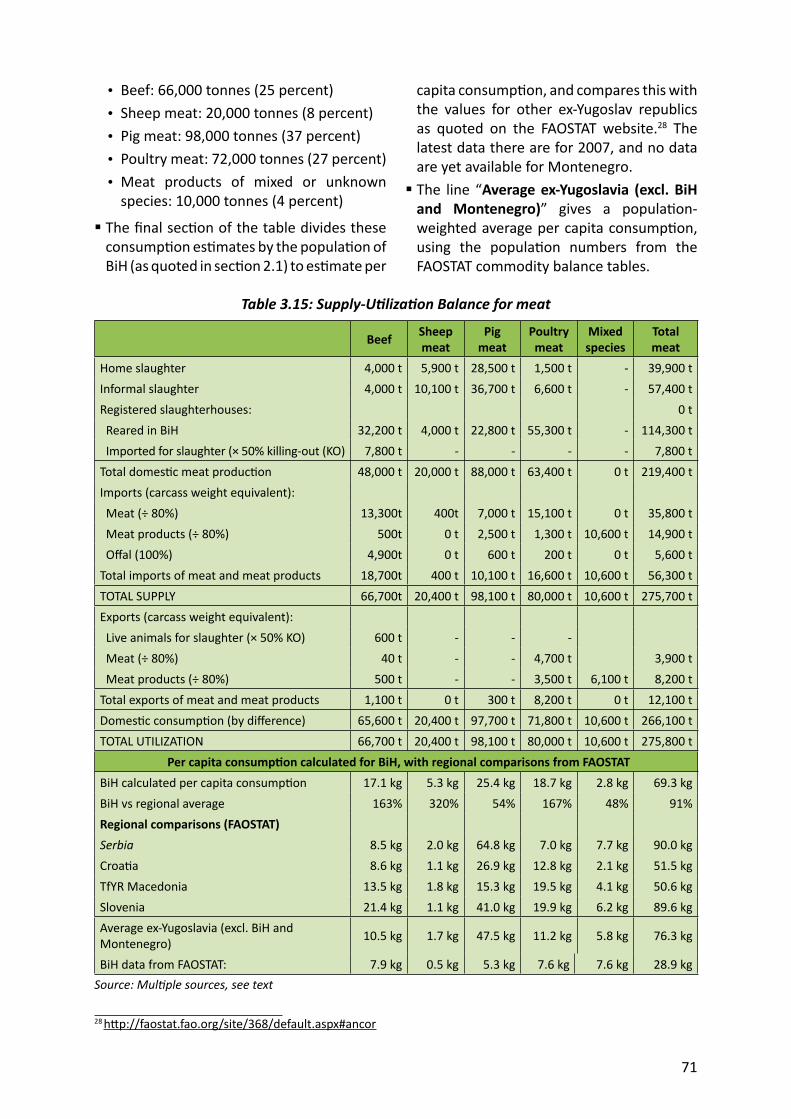

3.8 E G O 653.9 S 663.10 S -U B 70

4. PROCESSING 73

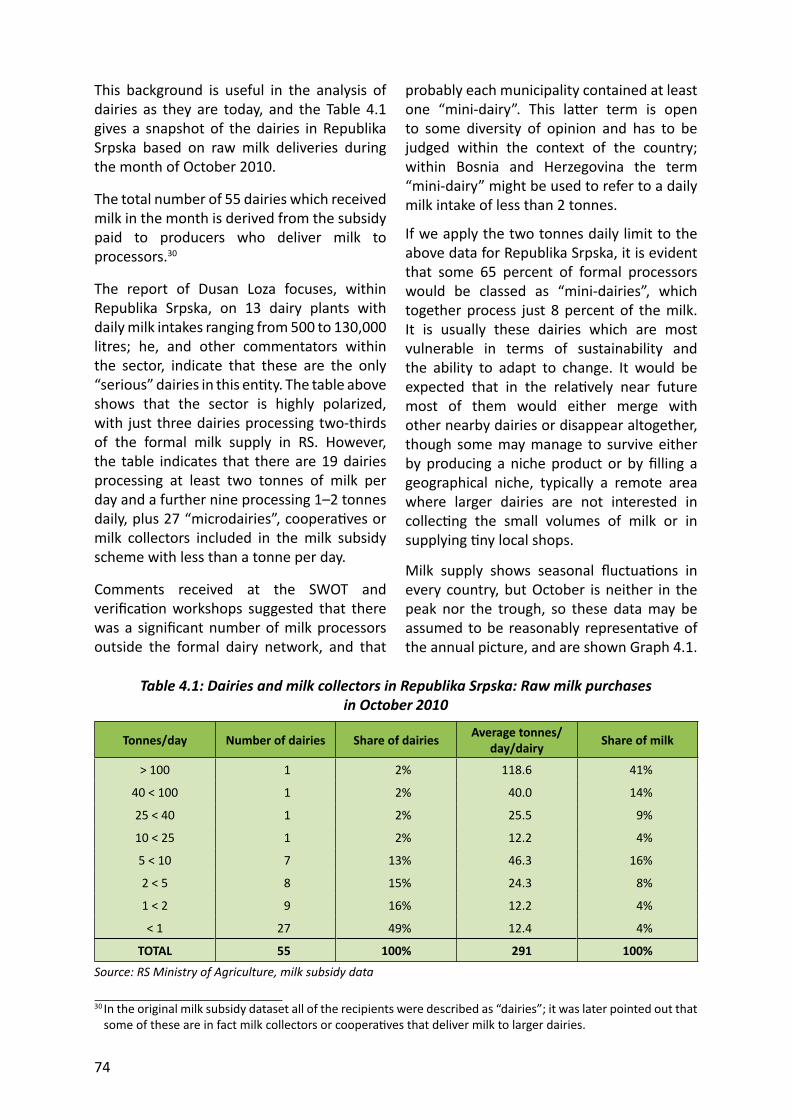

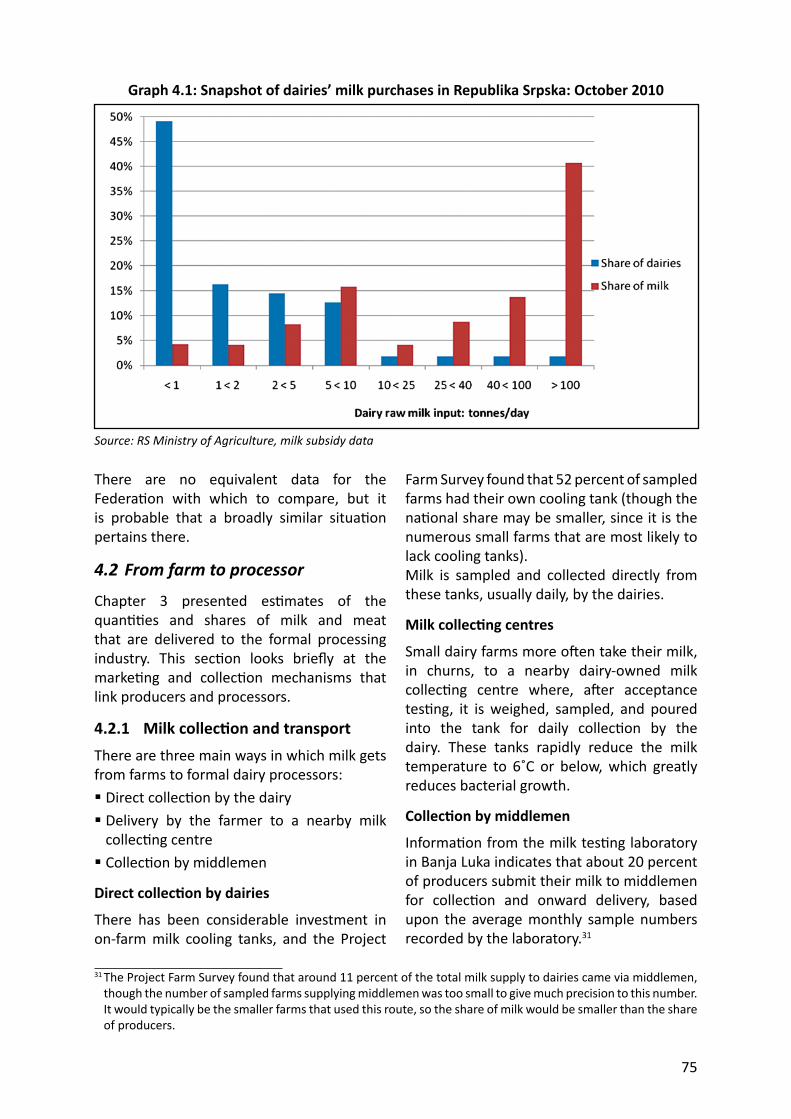

4.1 R 734.2 F 75

4.2.1 Milk collec on and transport 754.2.2 Livestock marke ng 77

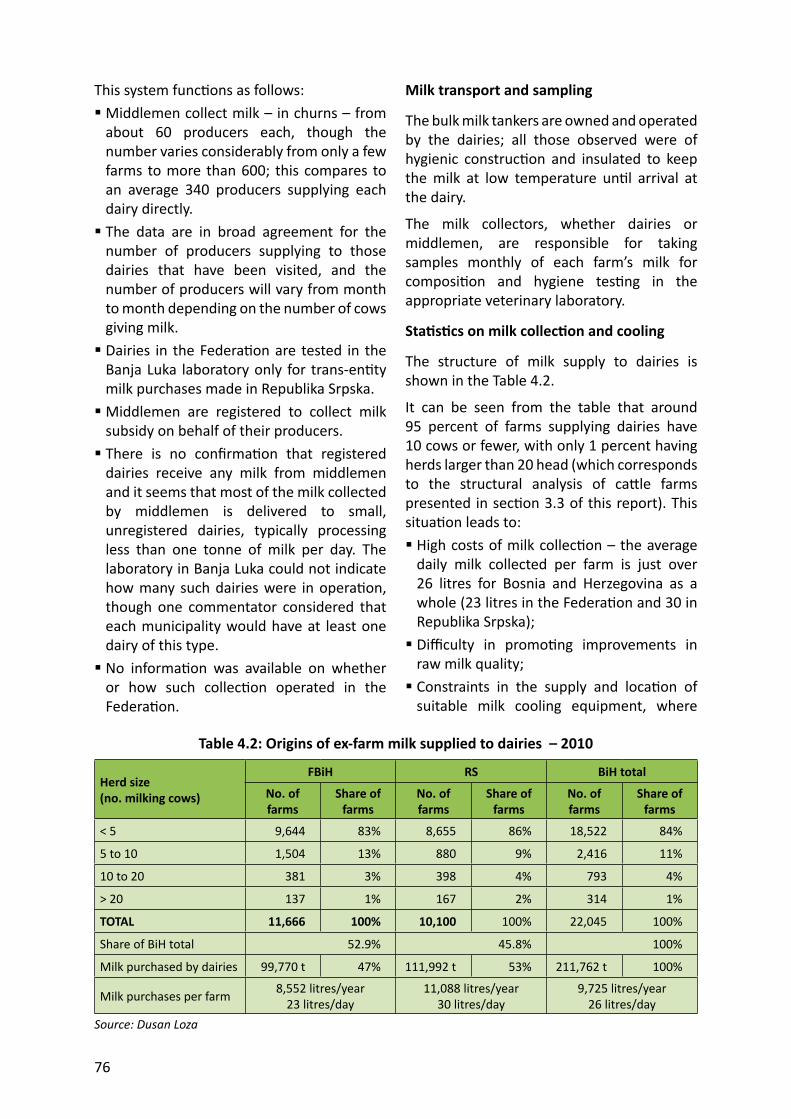

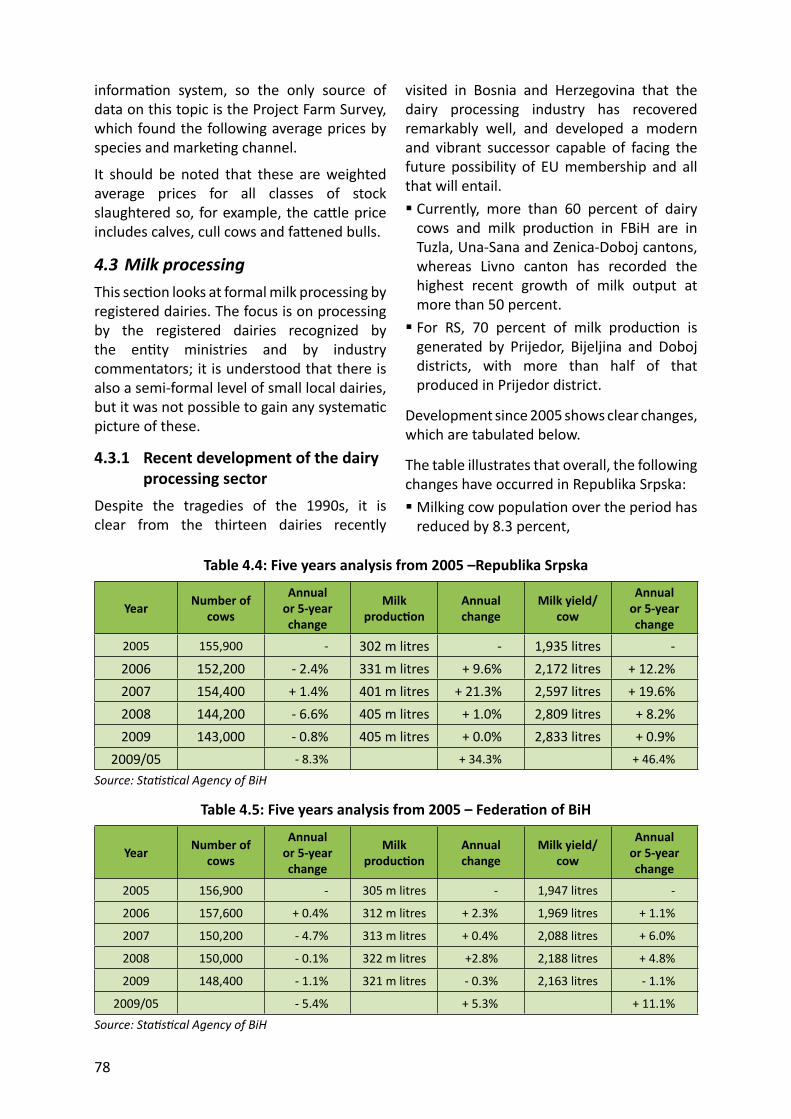

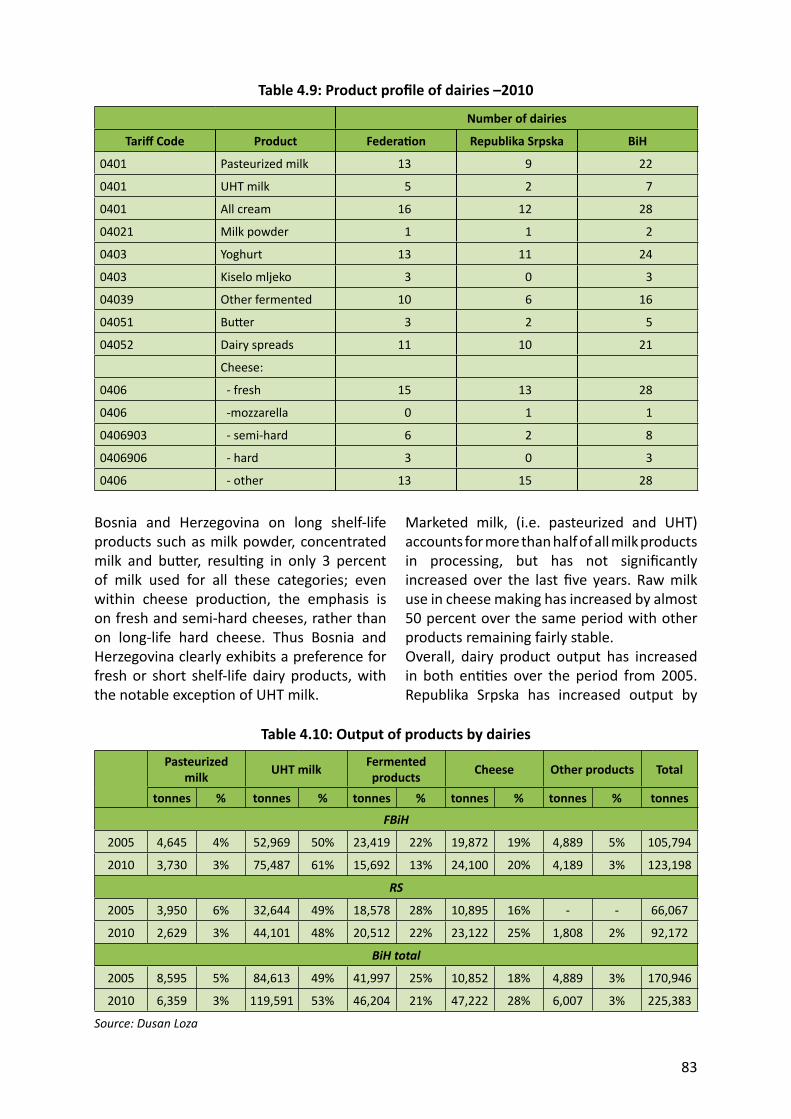

4.3 M 784.3.1 Recent development of the dairy processing sector 784.3.2 Current structure of the dairy processing industry 804.3.3 Raw milk deliveries for processing 814.3.4 Produc on profi les of dairies 814.3.5 Milk and dairy products manufactured 824.3.6 Assessment of visited dairies 844.3.7 Financial state of dairies 844.3.8 Interna onal comparisons 84

4.4 M 854.4.1 Background 854.4.2 Raw material sources 854.4.3 Slaughtering 864.4.4 Processing plants 874.4.5 Product range 884.4.6 The market 894.4.7 Management and fi nance 894.4.8 Meat processing survey 89

4.5 C 91

5. GOVERNMENT POLICY FOR THE SECTOR 93

5.1 P - 935.2 S 93

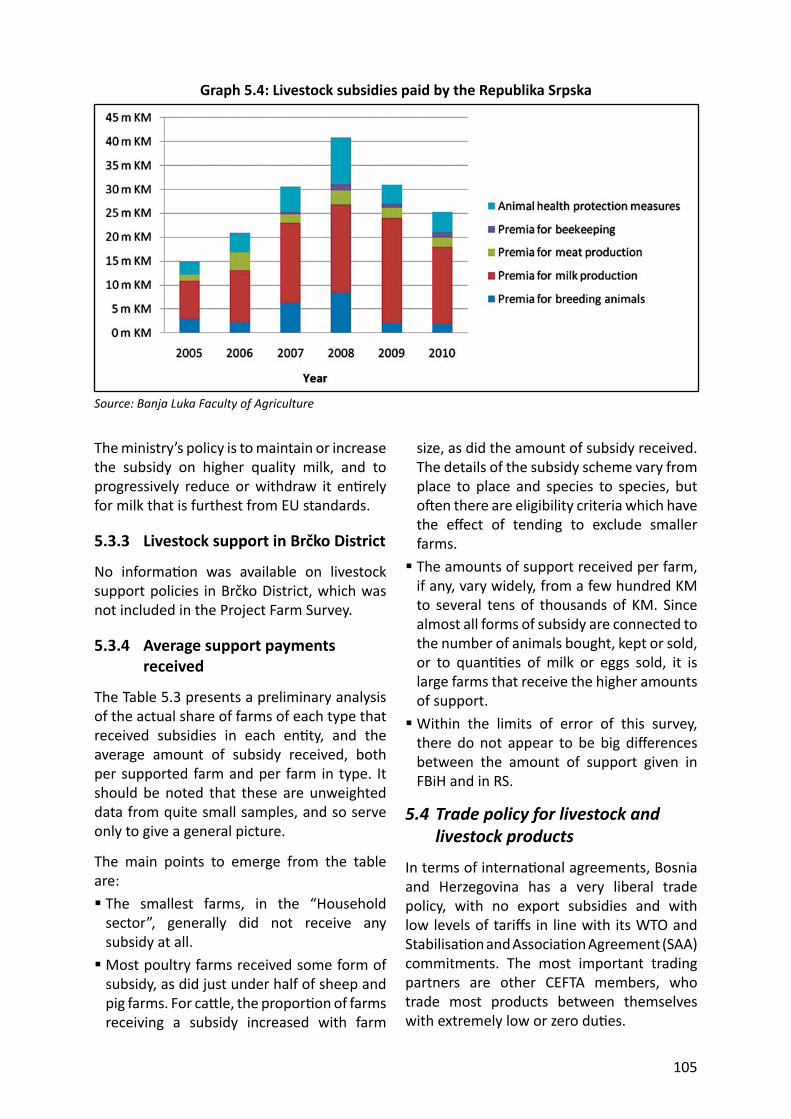

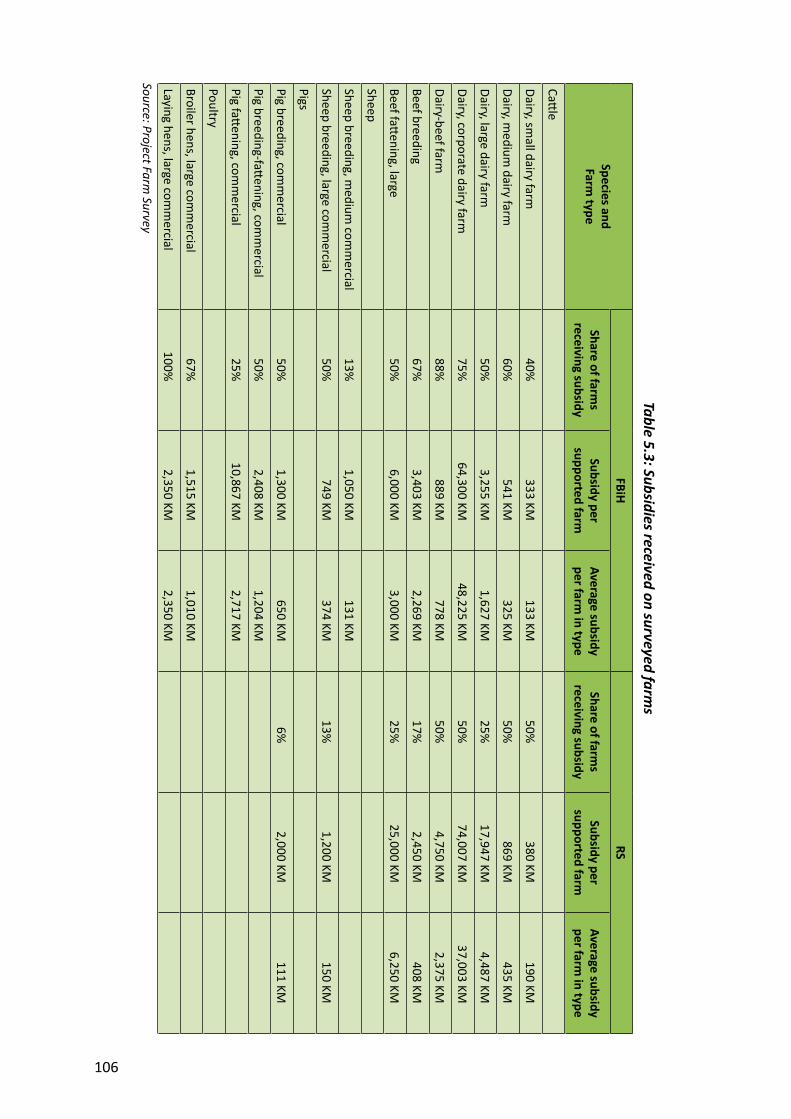

5.2.1 State level strategy 935.2.2 Strategy within the Federa on of Bosnia and Herzegovina 965.2.3 Strategy within Republika Srpska 975.2.4 Strategy within Brčko District 985.2.5 Conclusions on the strategic planning framework 99

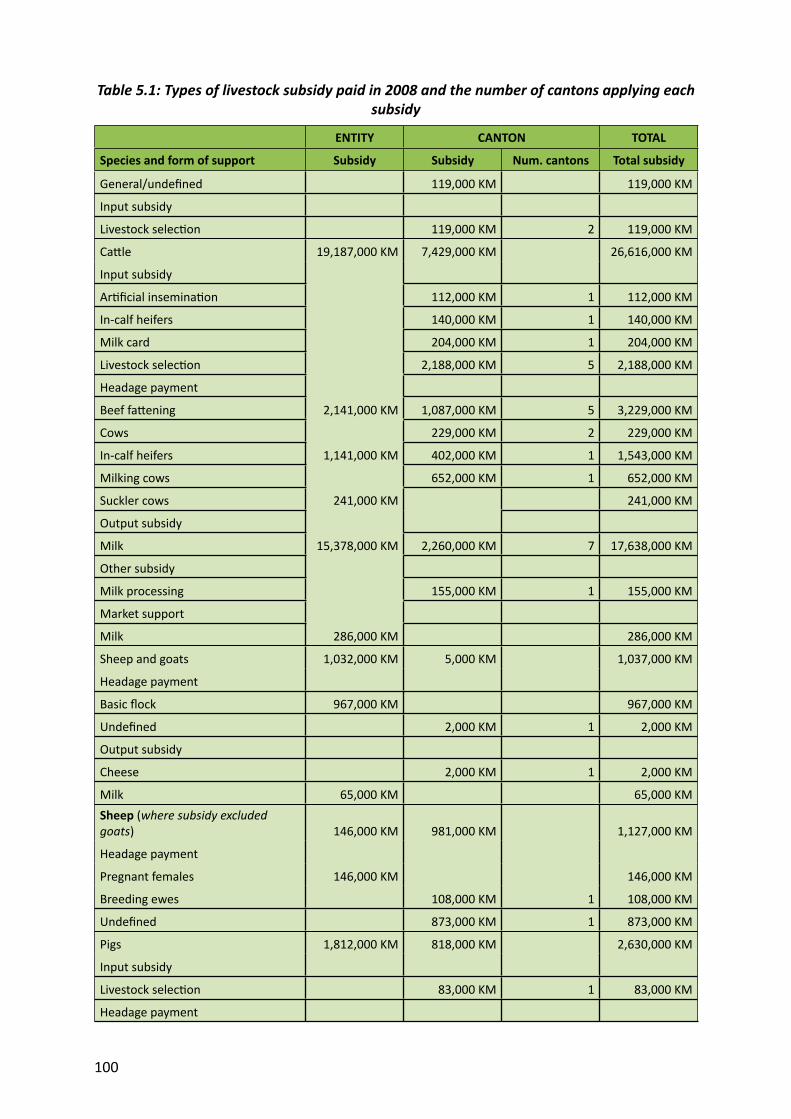

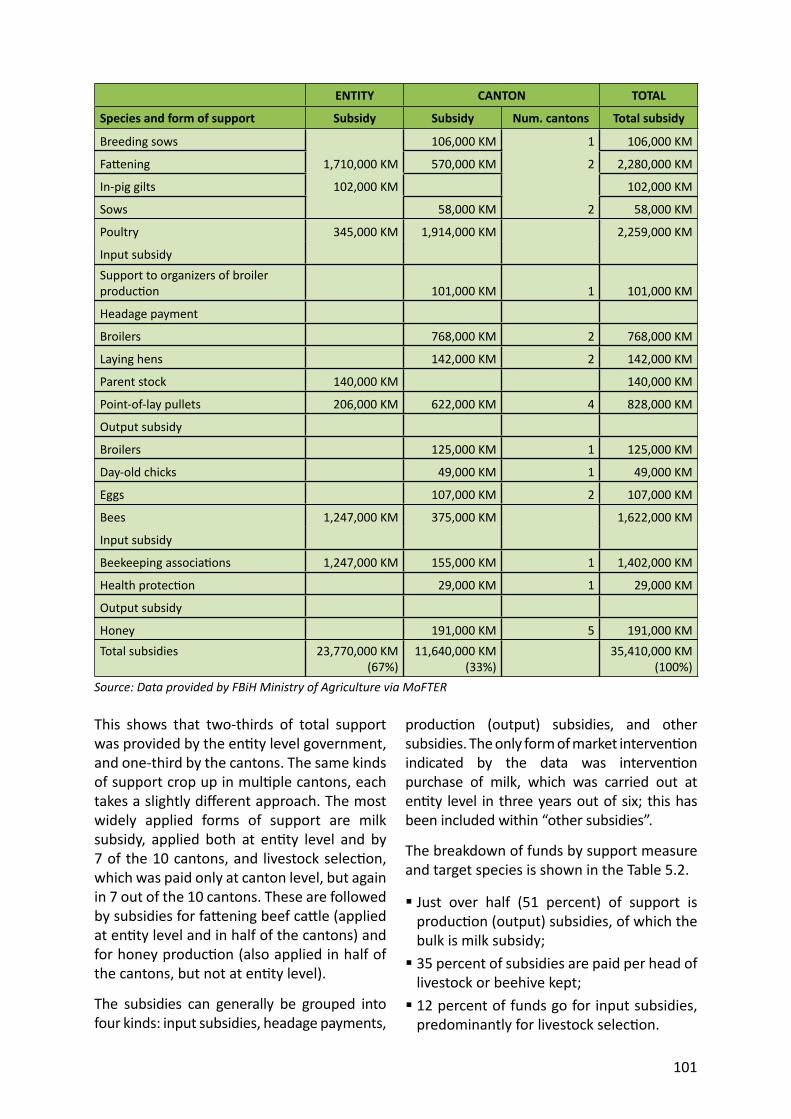

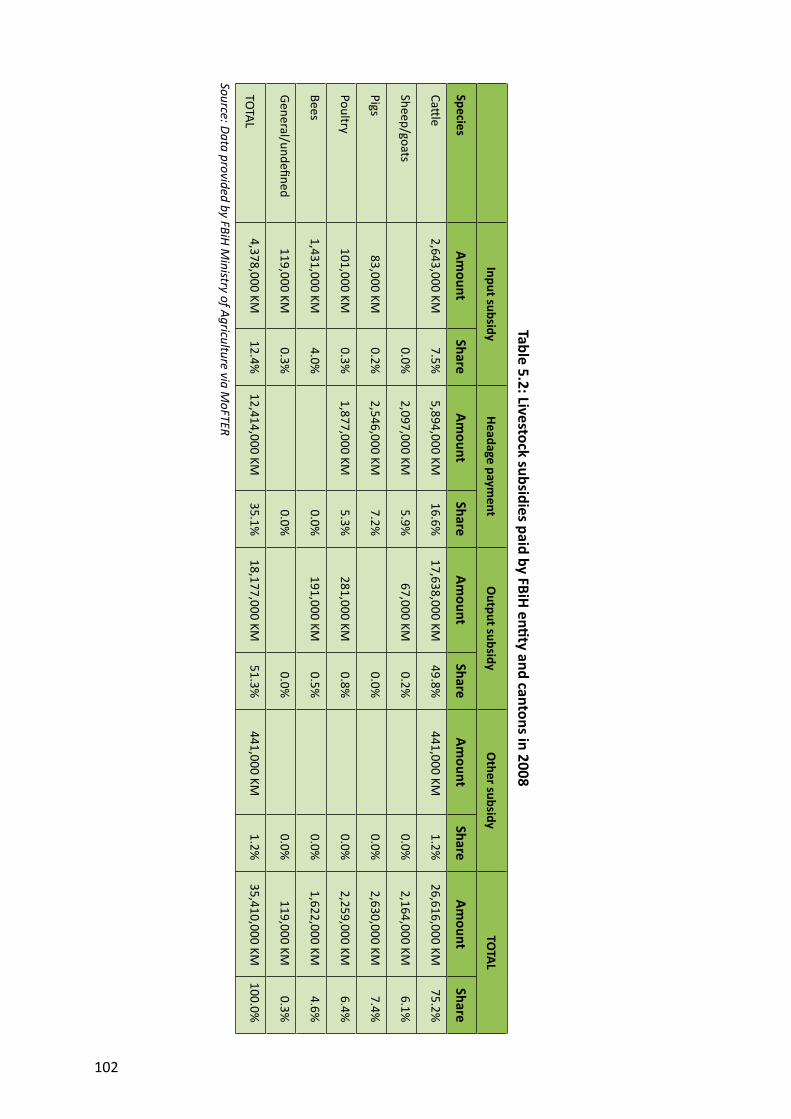

5.3 D 995.3.1 Livestock support in Federa on of Bosnia and Herzegovina 995.3.2 Livestock support in Republika Srpska 1045.3.3 Livestock support in Brčko District 1055.3.4 Average support payments received 105

iii

5.4 T 1055.5 R 1075.6 C 109

6. MARKETS AND TRADE 111

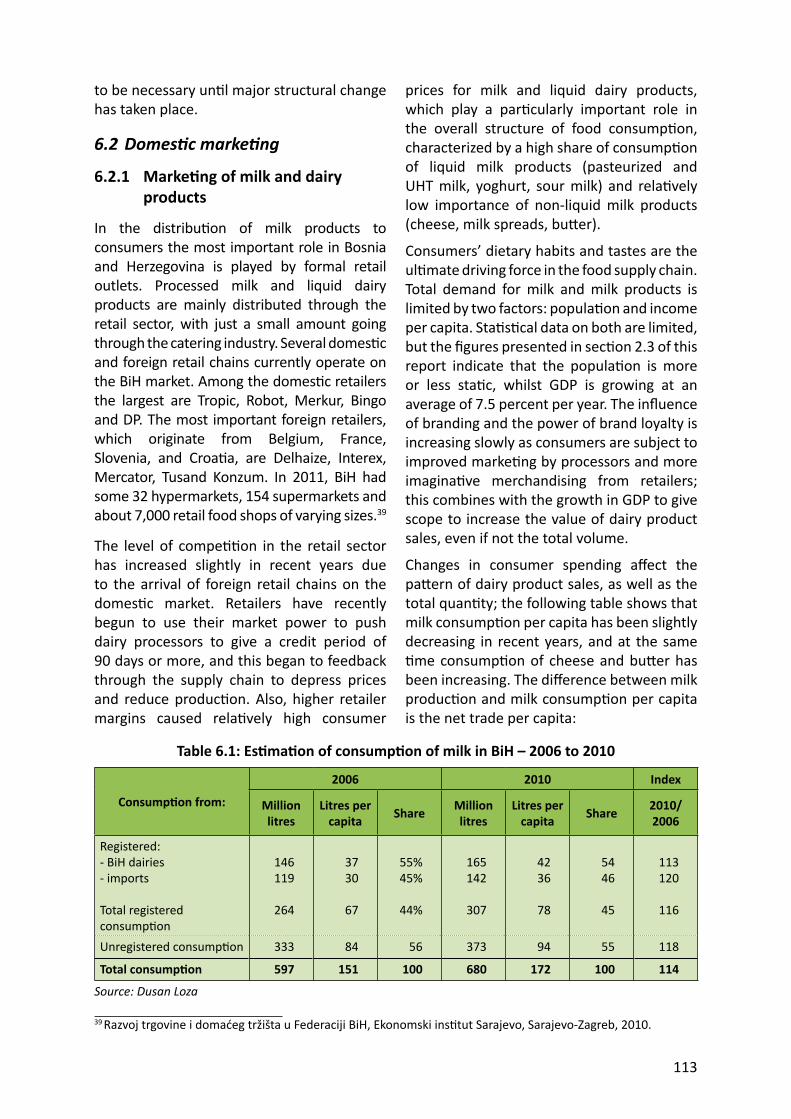

6.1 O 1116.1.1 Factors underlying the current situa on 111

6.2 D 1136.2.1 Marke ng of milk and dairy products 1136.2.2 The market for milk and dairy products 1146.2.3 Domes c market channels 114

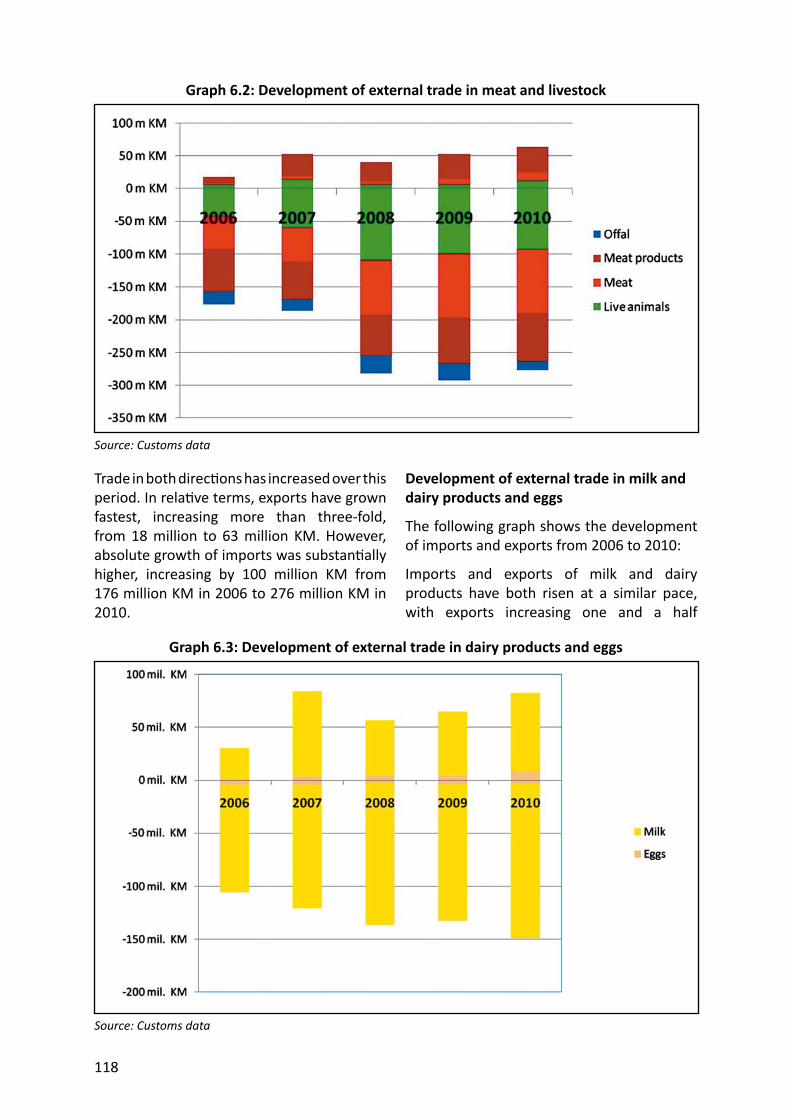

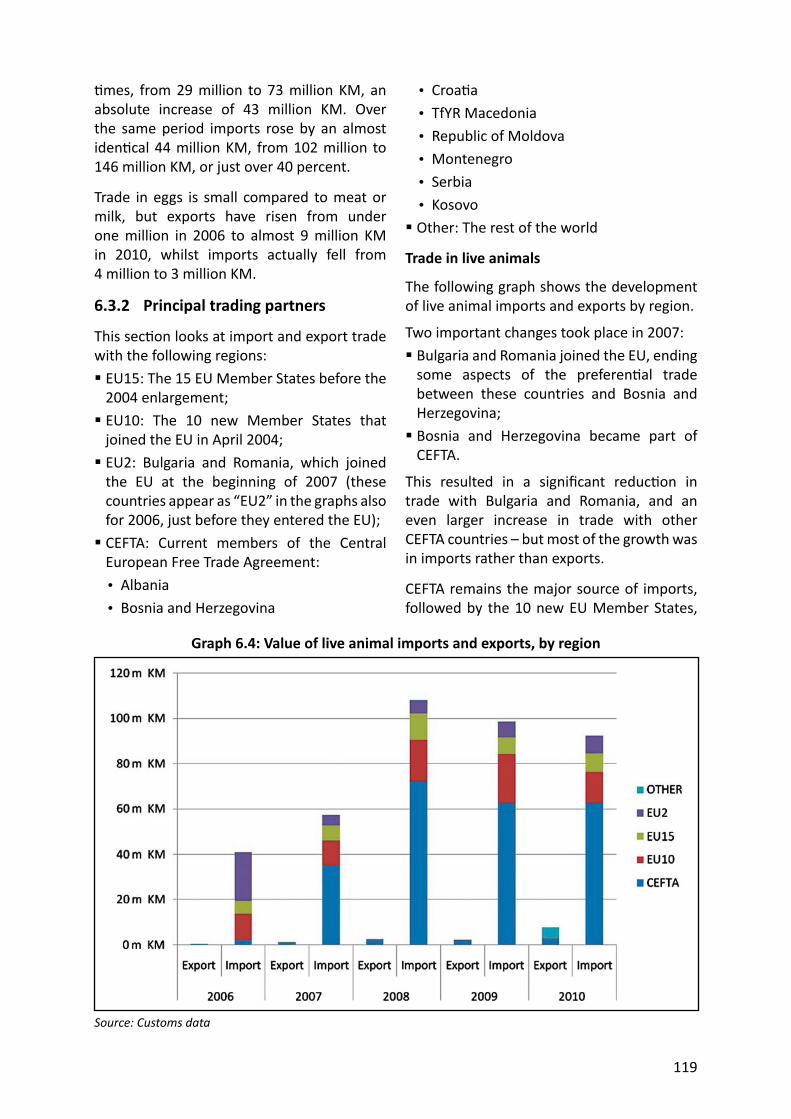

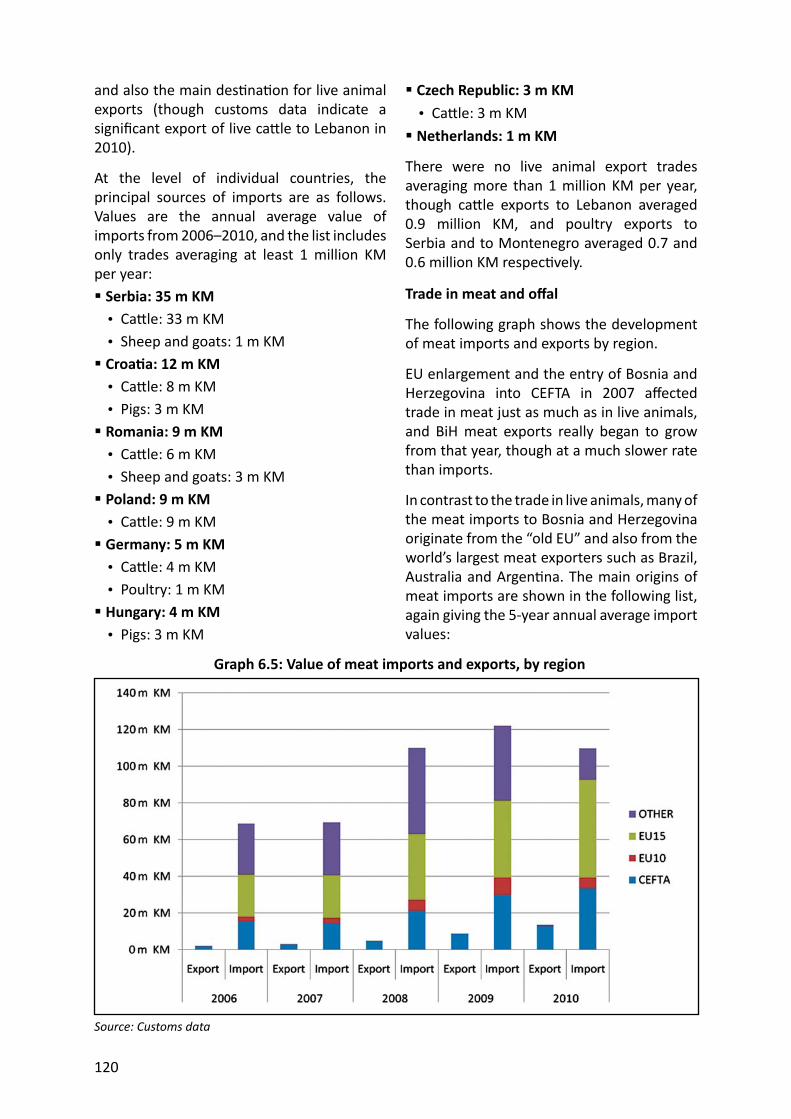

6.3 I 1166.3.1 Trade balance by product 1176.3.2 Principal trading partners 1196.3.3 The threat of EU enlargement 124

6.4 S 1256.5 T - 1256.6 S 129

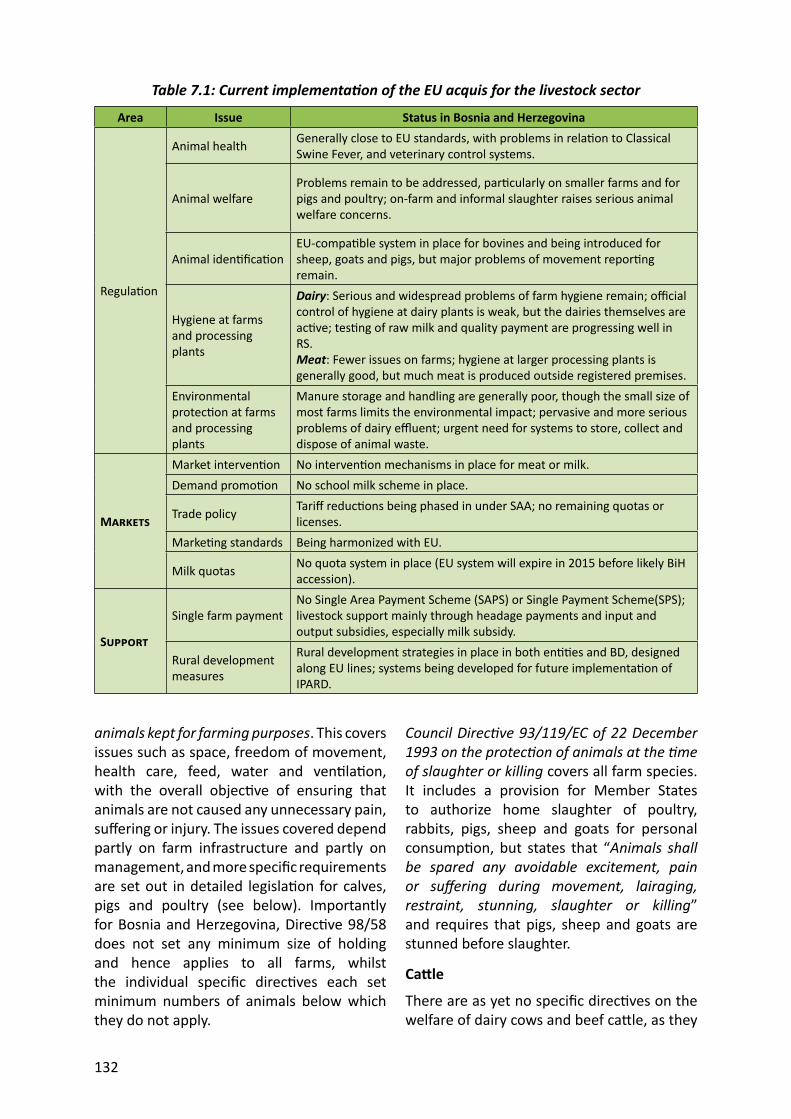

7. LEVEL OF ATTAINMENT OF RELEVANT EU STANDARDS 131

7.1 EU 1317.2 S 131

7.2.1 Animal health 1317.2.2 Animal welfare 1317.2.3 Animal iden fi ca on 134

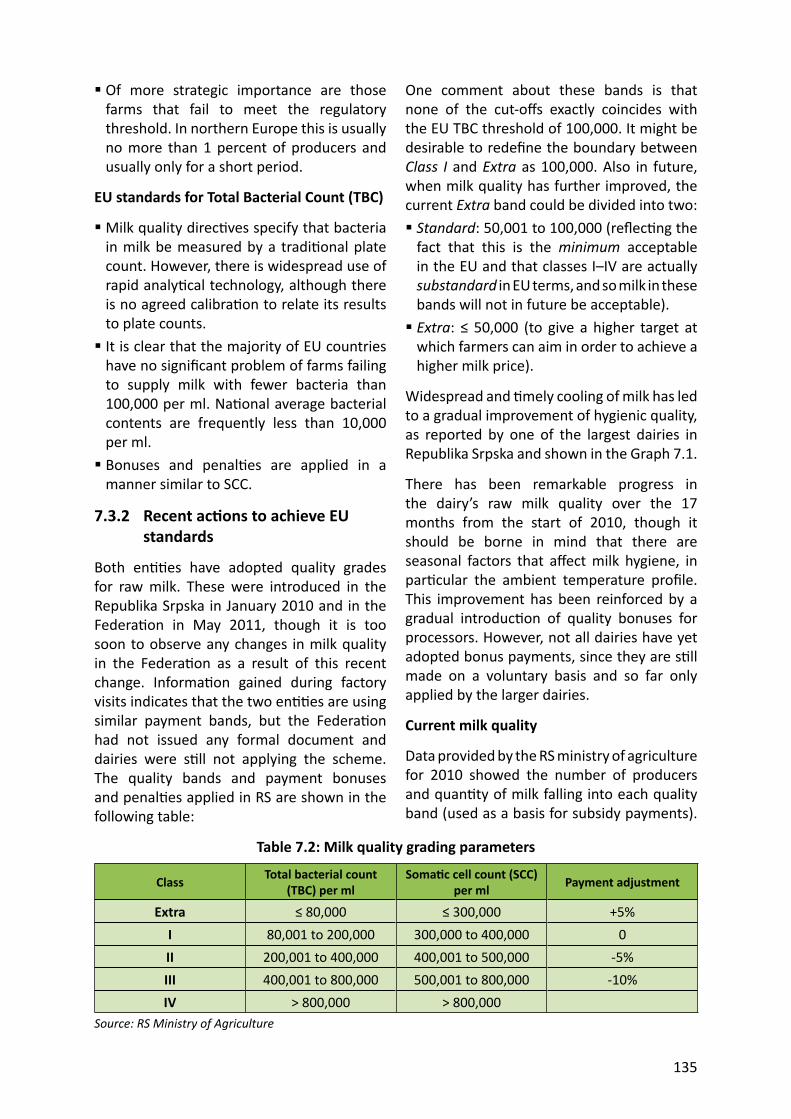

7.3 M 1347.3.1 EU standards in force 1347.3.2 Recent ac ons to achieve EU standards 1357.3.3 Factors aff ec ng milk quality 137

7.4 S 1387.4.1 Dairy processors 1387.4.2 Meat processors 138

7.5 E EU 1397.6 C EU 139

8. INVESTMENT TRENDS AND FUTURE DEVELOPMENTS 141

8.1 R 1418.1.1 Investments on farms 1418.1.2 Investments in processing 141

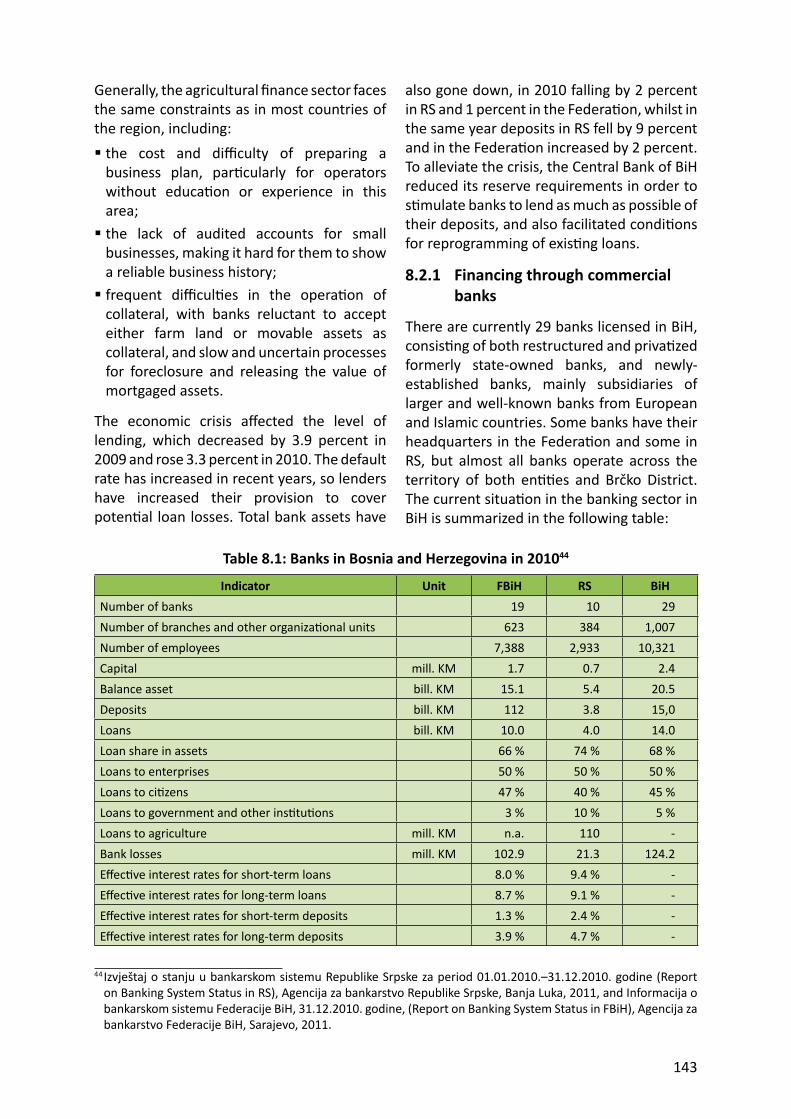

8.2 T B H 1428.2.1 Financing through commercial banks 1438.2.2 Lending through microcredit organiza ons and companies 1468.2.3 Lending through savings and credit organiza ons 1488.2.4 Guarantee Funds 1498.2.5 Leasing 150

8.3 P 1508.4 C 151

9. IDENTIFICATION OF POTENTIAL AND NEEDS OF THE SECTOR 153

9.1 M 153

iv

9.2 S , W , O T (SWOT) 1539.2.1 Strengths 1549.2.2 Weaknesses 1549.2.3 Opportuni es 1559.2.4 Threats 156

9.3 SWOT 1579.4 I 158

9.4.1 Infrastructure on ca le farms 1589.4.2 Infrastructure on sheep farms 1599.4.3 Infrastructure on pig farms 1599.4.4 Infrastructure on poultry farms 159

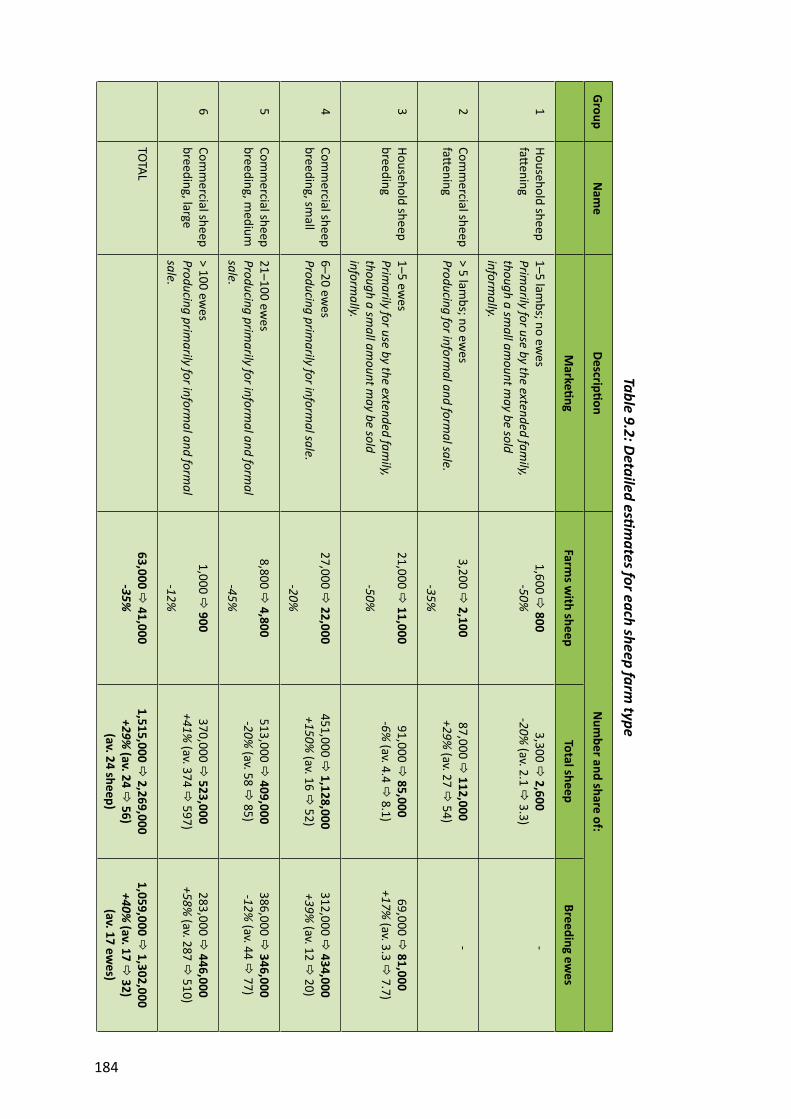

9.5 T EU 1599.5.1 Ca le 1599.5.2 Sheep 1649.5.3 Pigs 1659.5.4 Poultry 1679.5.5 Processors 168

9.6 B 1689.6.1 Ca le 1699.6.2 Sheep 1739.6.3 Pigs 1759.6.4 Poultry 1779.6.5 Livestock farm structures 180

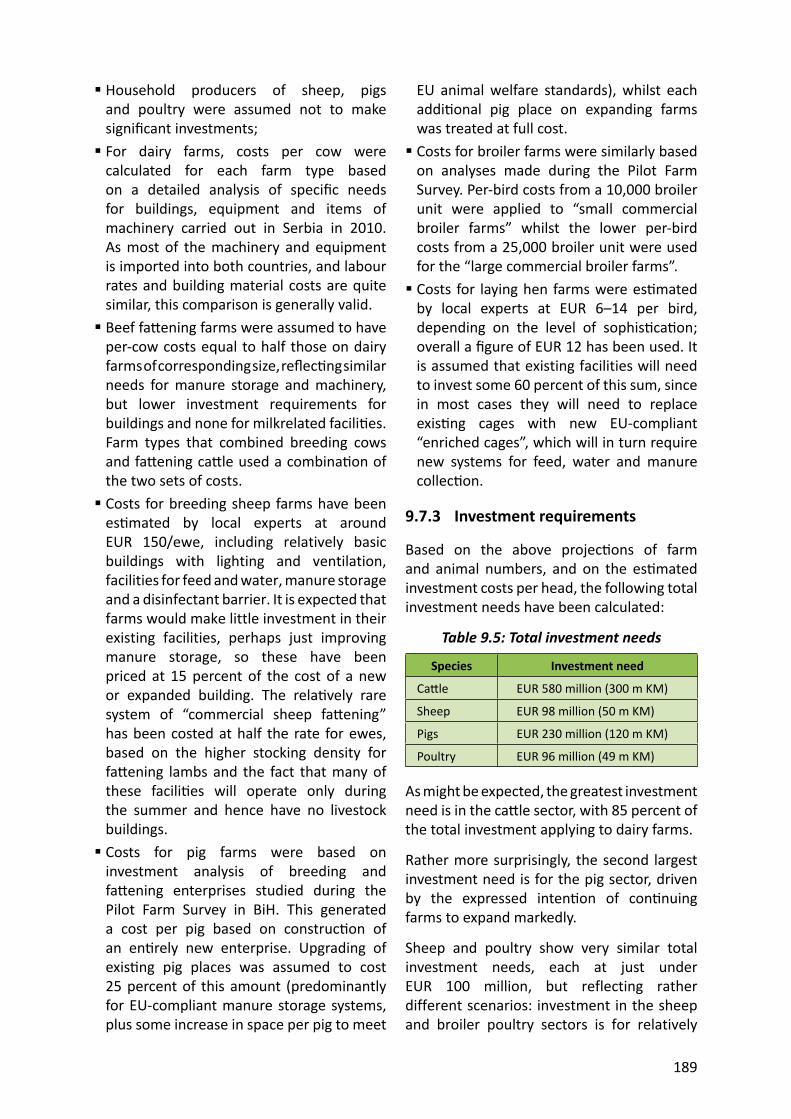

9.7 E - 1809.7.1 Poten al changes in farm structures 1819.7.2 Investment costs 1879.7.3 Investment requirements 189

9.8 C : I 1909.8.1 Priority investments on farms 1919.8.2 Priority investments in processing 192

10. IDENTIFICATION OF TRAINING NEEDS IN THE SECTOR 193

10.1 C , 19310.2 G EU 19410.3 T 19410.4 T 19610.5 T 19810.6 C 198

11. OUTCOMES 199

11.1 S 19911.1.1 Key investment needs 19911.1.2 Key constraints 19911.1.3 Farm size distribu on 199

11.2 P IPARD 20011.2.1 Measure 101/1: Improvement and enlargement of agricultural holdings 20011.2.2 Measure 101/2: Manure storage and disposal 20111.2.3 Measure 101/3: Forage machinery 20211.2.4 Measure 103/1: Improvement of processing facili es 20211.2.5 Measure 103/2: Dairy effl uent storage and treatment 202

v

11.2.6 Measure 103/3: Animal waste collec on and processing 20211.2.7 Measures considered but rejected 202

11.3 S EU 20311.3.1 Improving the policy and regulatory environment 20311.3.2 Improving effi ciency through extension and training 203

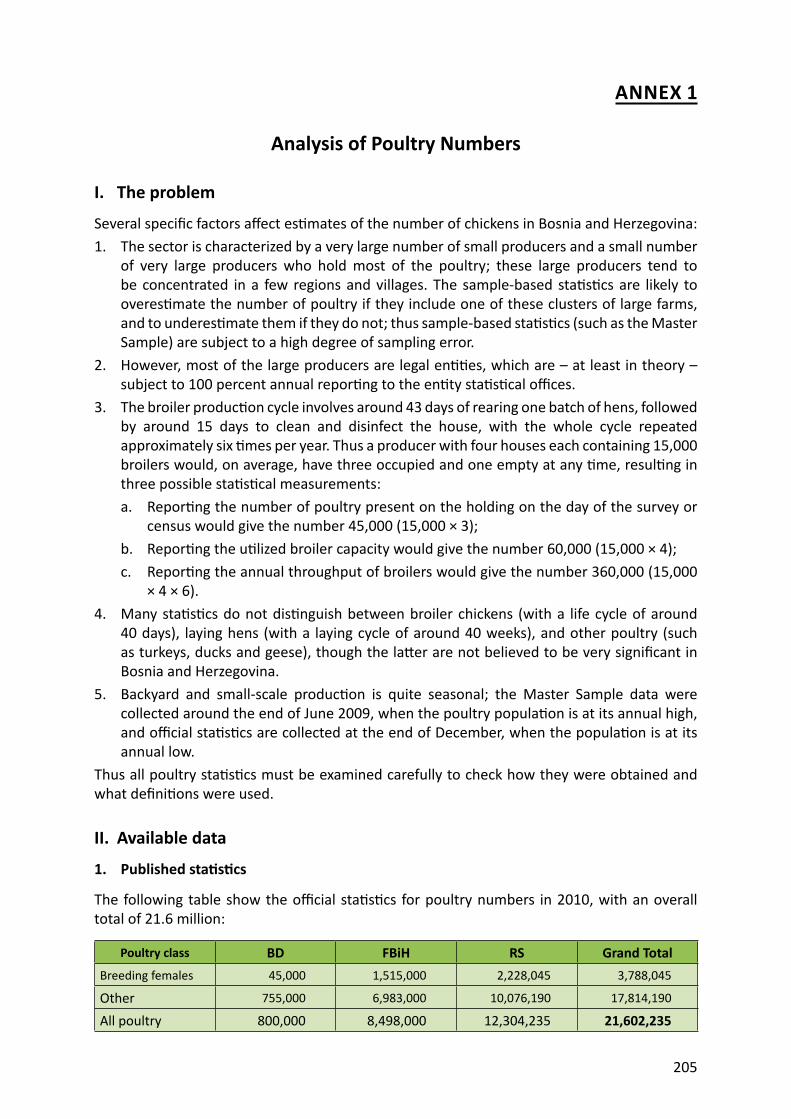

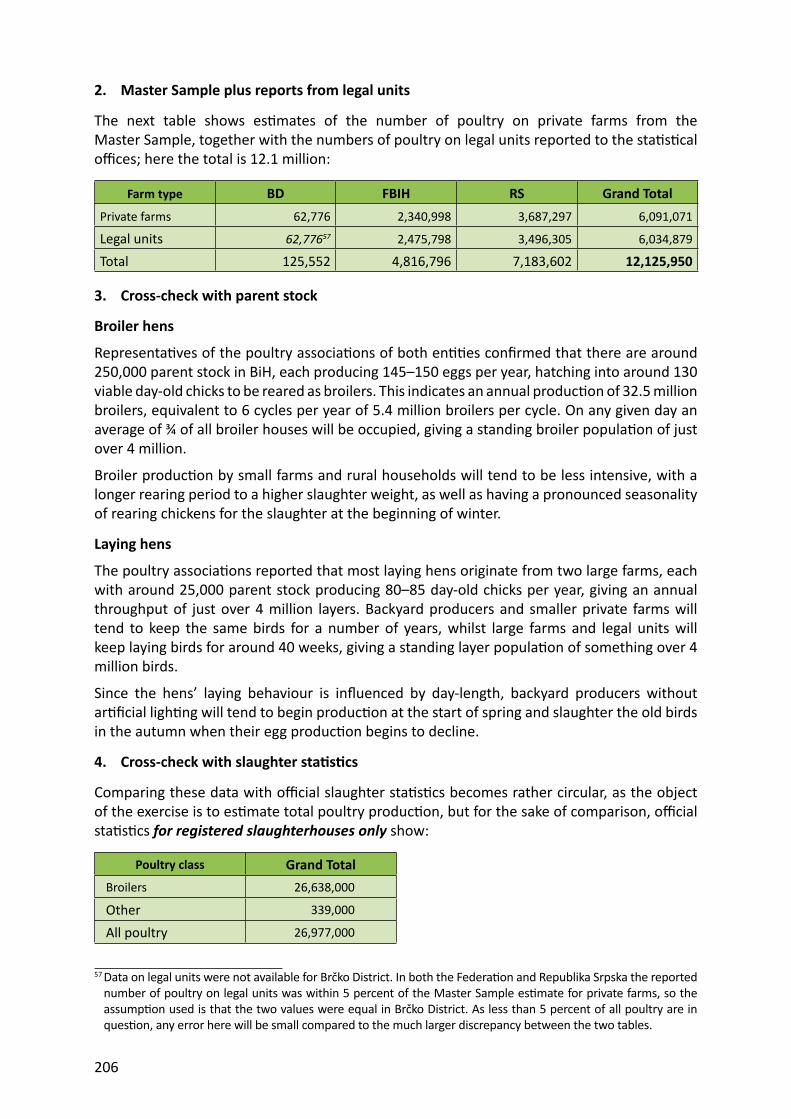

ANNEX 1: ANALYSIS OF POULTRY NUMBERS 205

ANNEX 2: SWOT WORKSHOP CONCLUSIONS 209

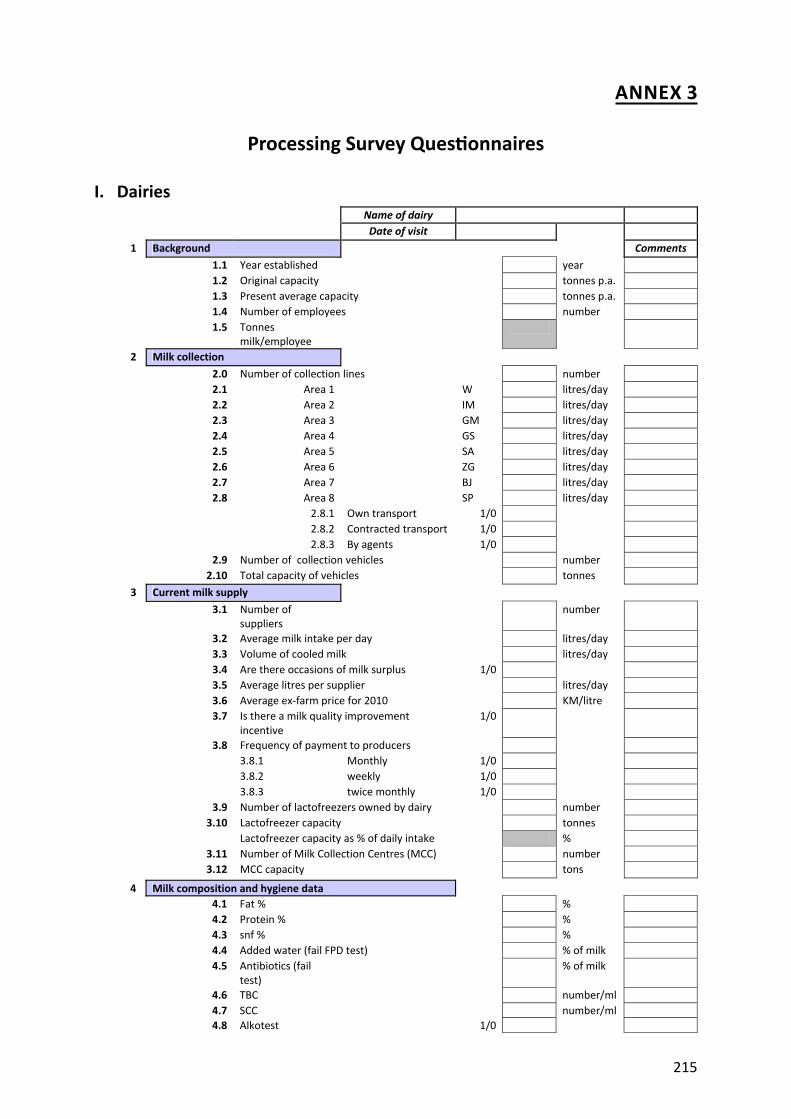

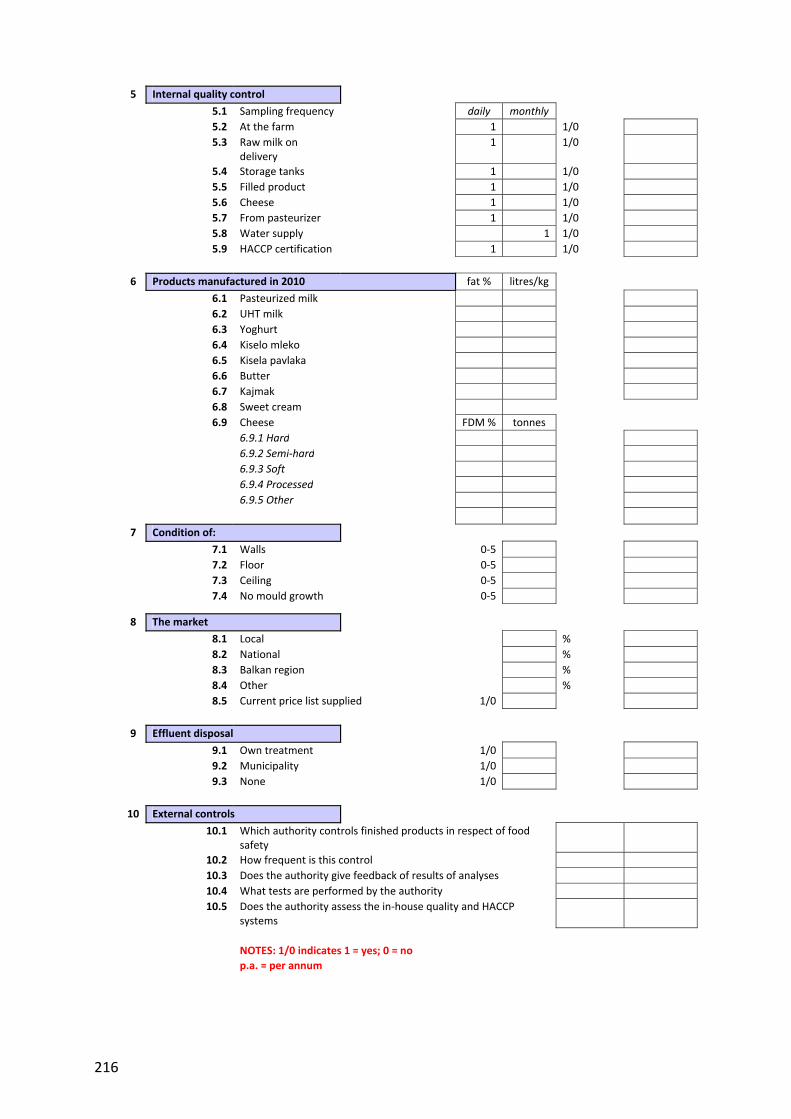

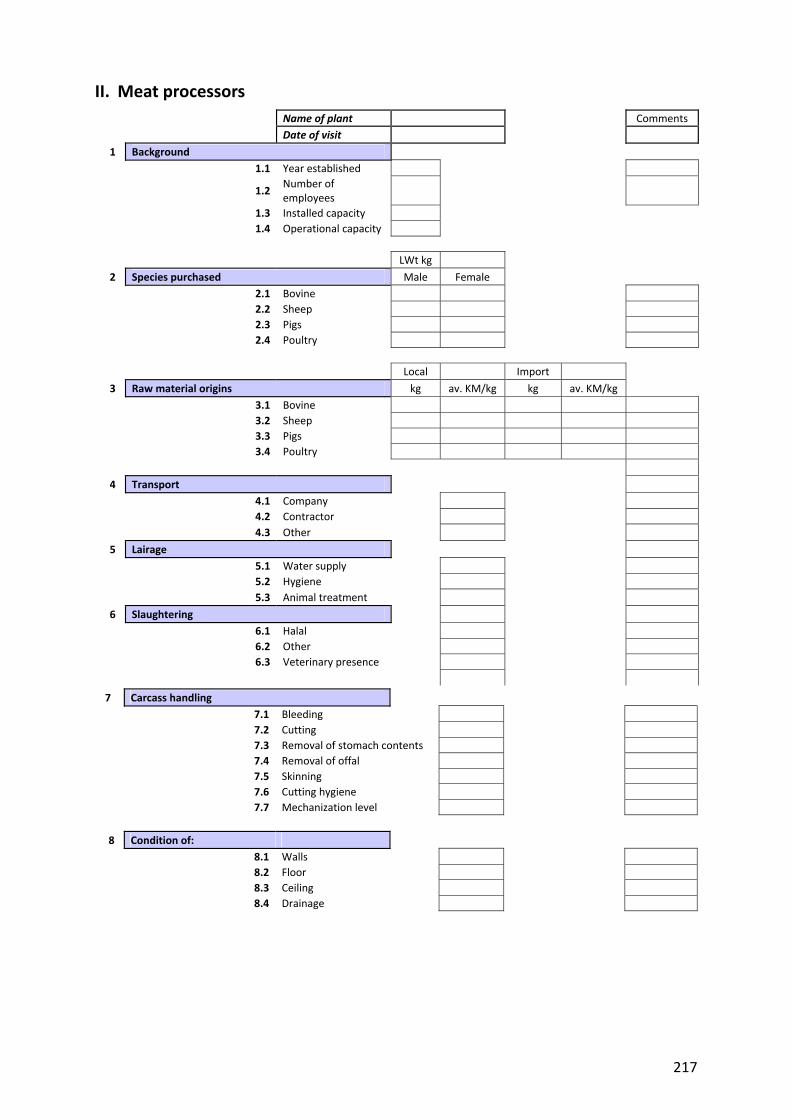

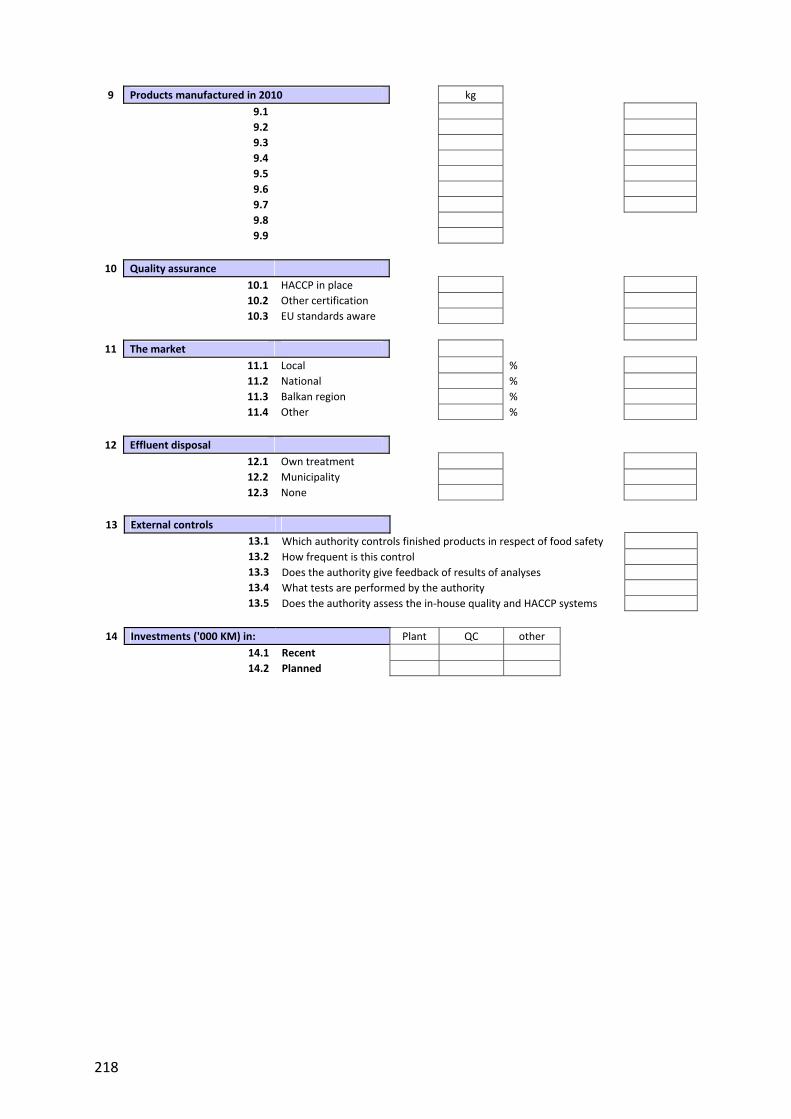

ANNEX 3: PROCESSING SURVEY QUESTIONNAIRES 215

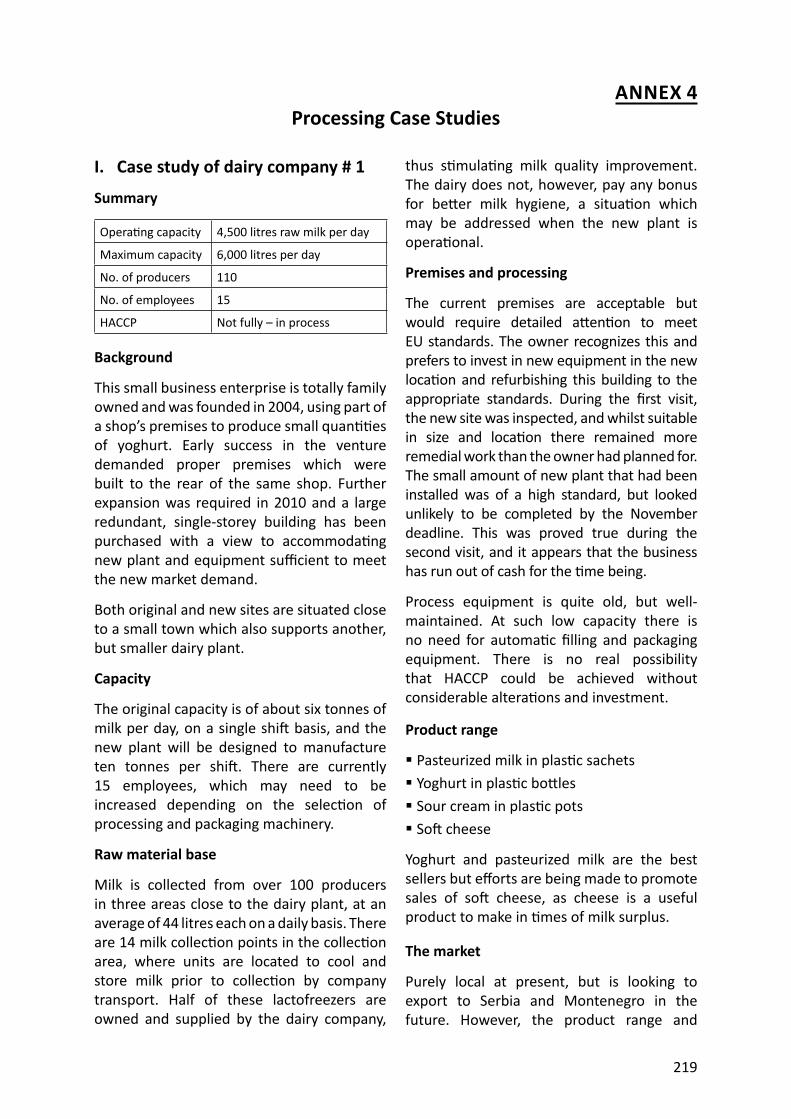

ANNEX 4: PROCESSING CASE STUDIES 219

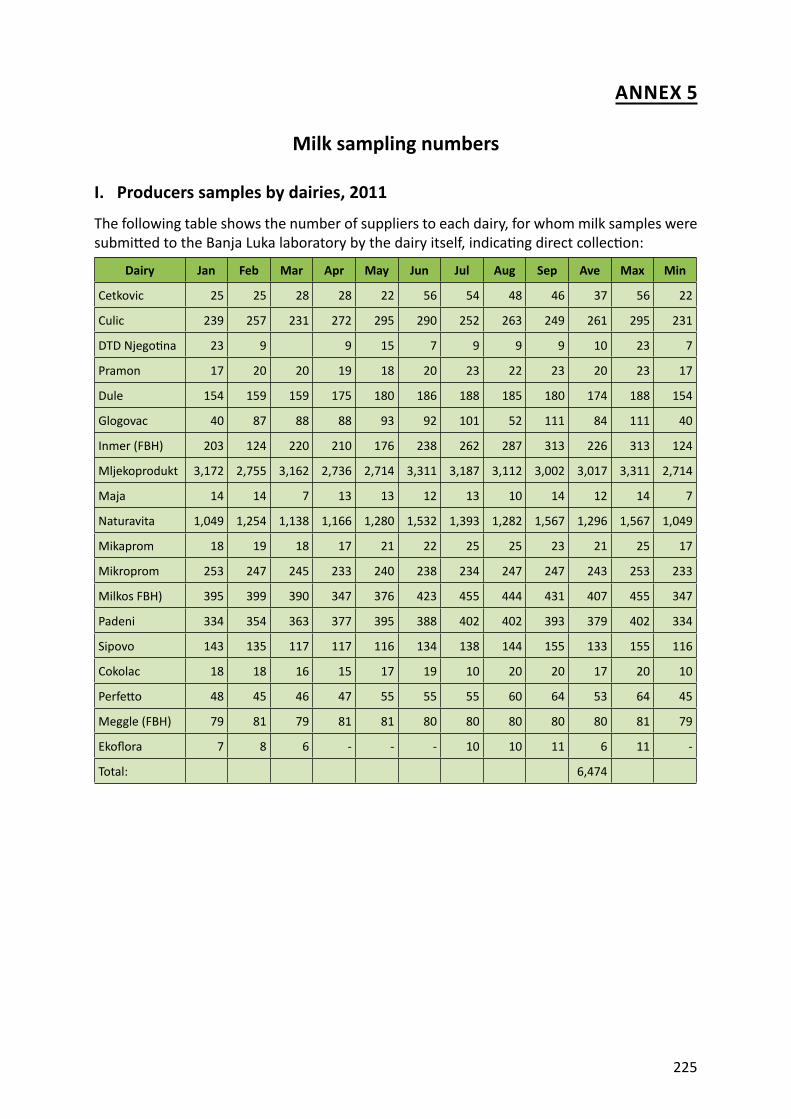

ANNEX 5: MILK SAMPLING NUMBERS 225

ANNEX 6: CHECKLIST FOR AN EU STANDARD DAIRY FARM 229

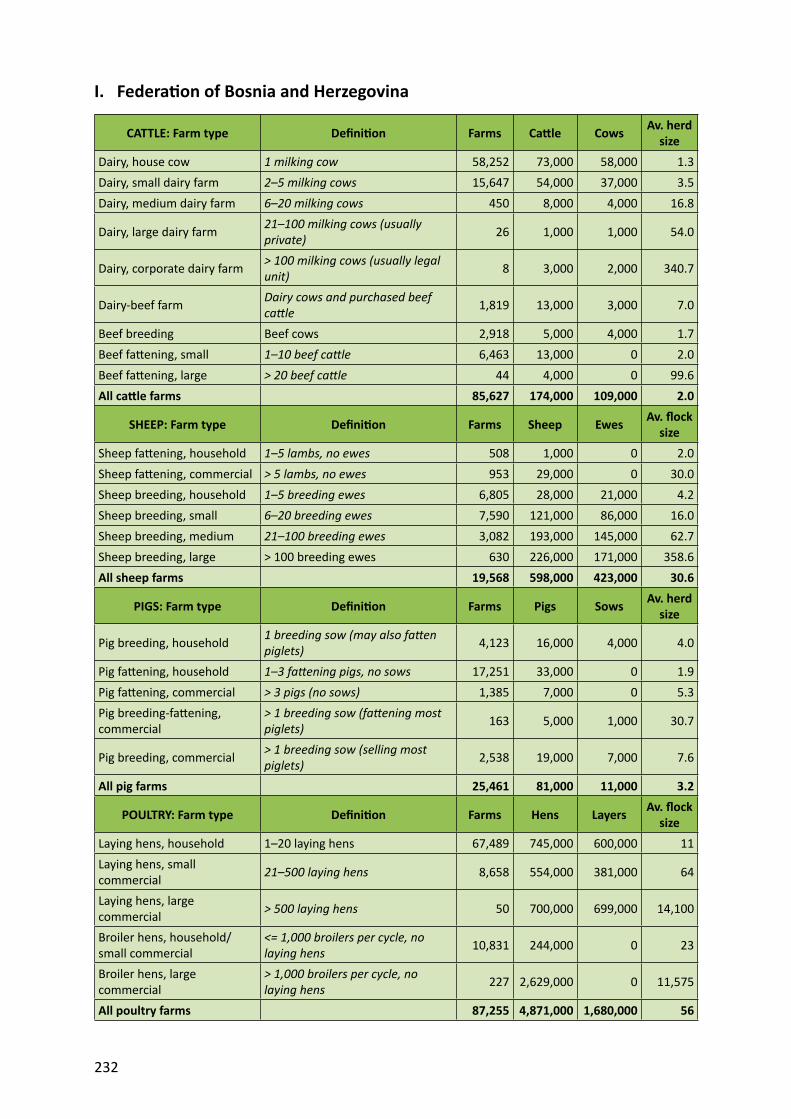

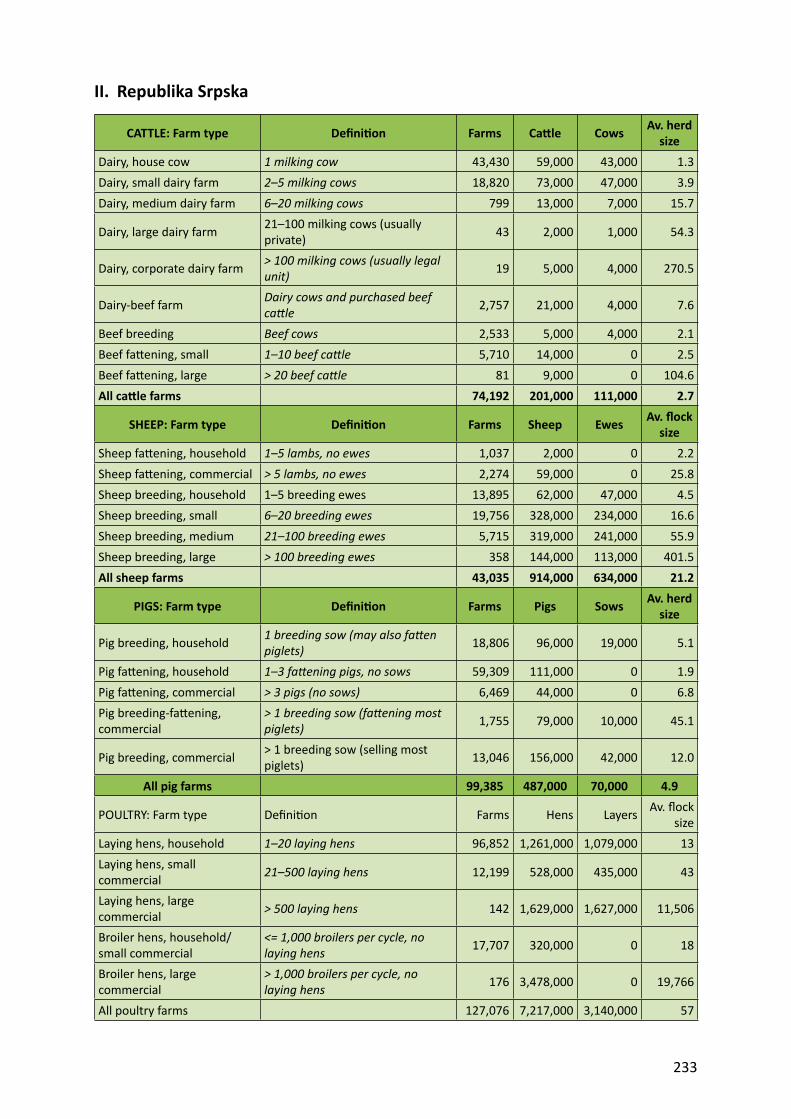

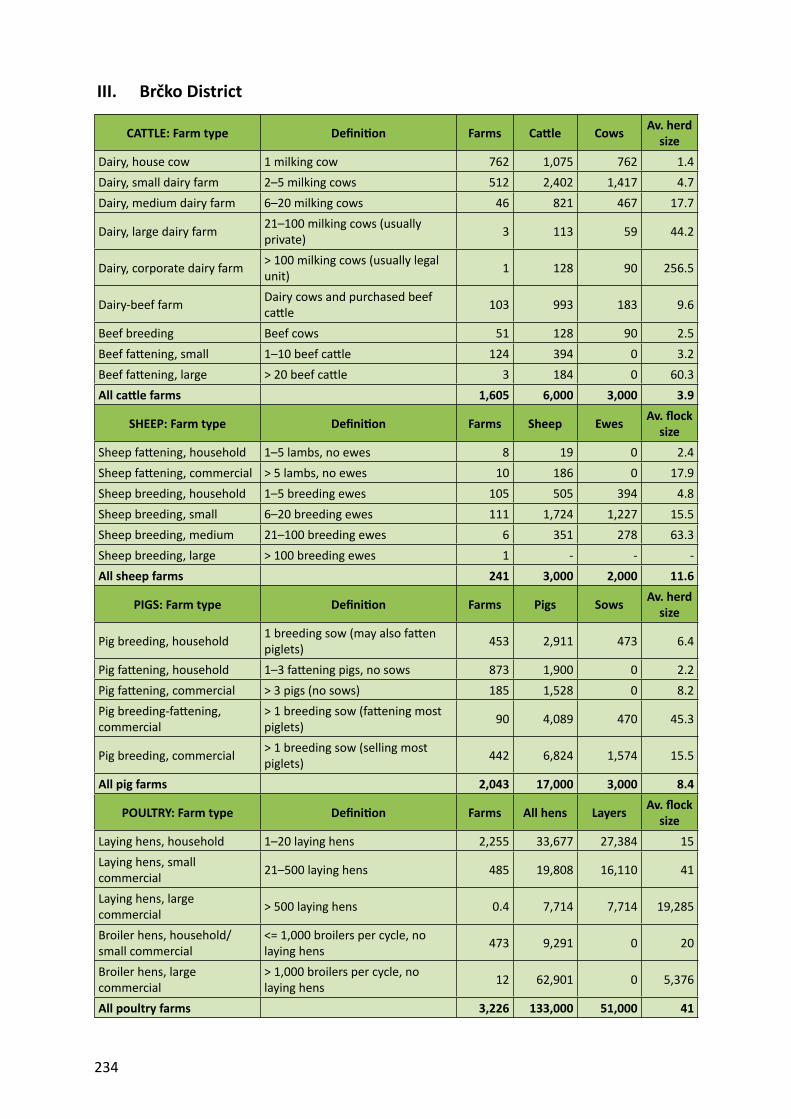

ANNEX 7: ESTIMATED FARM AND ANIMAL NUMBERS BY ENTITY 231

vi

vii

Abbrevia ons and Acronyms

AMIS Agricultural Market Informa on SystemBAM BiH currency; 1 EUR = 1.9558 BAMBD Brčko DistrictBHAS Bosnia and Herzegovina Agency for Sta s csBHMAC Bosnia and Herzegovina Mine Ac on CentreBiH Bosnia and HerzegovinaCAP Common Agricultural Policy CEFTA Central European Free Trade AgreementEU European UnionEUD Delega on of the European Union to Bosnia and HerzegovinaEUR EuroFADN Farm Accountancy Data NetworkFAO Food and Agriculture Organiza on of the United Na onsFBiH Federa on of Bosnia and Herzegovina FSA Food Safety Agency FVO Food and Veterinary Offi ceGAECs Good Agricultural and Environmental Condi onsGAEP Good Agricultural and Environmental Prac ceGAP Good Agricultural Prac ceGDP Gross Domes c ProductGoBiH Government of BiHGVA Gross Value AddedHa hectareHACCP Hazard Analysis Cri cal Control PointsI&R Iden fi ca on and Registra on (system)IDB Investment Development BankIFAD Interna onal Fund for Agricultural DevelopmentIFS Interna onal Food StandardIPARD Instrument for Pre-Accession Assistance for Rural DevelopmentIPHC Interna onal Plant Health Conven onISO Interna onal Organiza on for Standardiza onKg kilogramLSU livestock unitLU Legal UnitMCO microcredit organiza onMoFTER Ministry of Foreign Trade and Economic Rela onsMS Master SampleNGO non-governmental organiza onNVA Net Value AddedPAC Pilot Agricultural CensusPHPA Plant Health Protec on Administra onPPP Power Point Presenta onRASFF Rapid Alert System for Food and FeedRS Republika SrpskaSAA Stabilisa on and Associa on AgreementSAFFRD Sector for Agriculture, Food, Forestry and Rural DevelopmentSAPARD Special Accession Programme for Agriculture and Rural Development

viii

SAPS Single Area Payment SchemeSCC Soma c Cell CountSESMARD Support for Establishment of the State Ministry of Agriculture and Rural

DevelopmentSIDA Swedish Interna onal Development Coopera on AgencySPS Single Payment SchemeSWOT Strengths, Weaknesses, Opportuni es and Threats (analysis)TBC total bacterial countUNDP United Na ons Development ProgrammeUPOV Interna onal Union for the Protec on of New Varie es of PlantsVAT Value Added TaxWB World BankWTO World Trade Organiza on

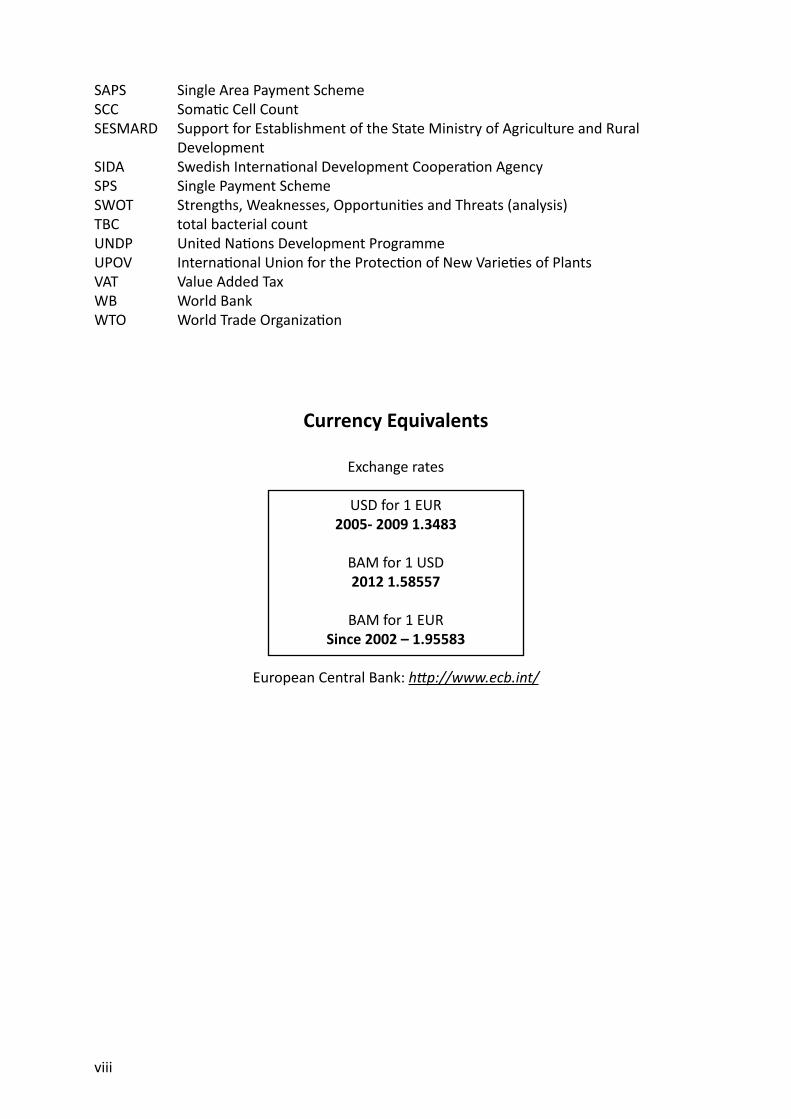

Currency Equivalents

Exchange rates

USD for 1 EUR2005- 2009 1.3483

BAM for 1 USD2012 1.58557

BAM for 1 EURSince 2002 – 1.95583

European Central Bank: h p://www.ecb.int/

ix

Introduc on

Survey fi eldwork:• Agricultural extension service, Republika

Srpska• Team of assistants from the Sarajevo

Faculty of Agriculture and Food Science Support:• Vlado Pijunović, background papers• Zorica Jovanović, desk research

The report was reviewed by Gerold Boedeker, Magali Herranz, Raimund Jehle, Andriy Rozstalnyy and Dmitry Zvyagintsev (all FAO). Valuable support regarding language edi ng was provided by Tom Hunter and Valerie Guidi.

Acknowledgements

The FAO team would like to extend its sincere thanks for the assistance and close collabora on in the implementa on of the project to the following organiza ons and individuals: BiH Ministry of Foreign Trade and Economic Rela ons (MoFTER):• Dušan Nešković, Assistant Minister• Melisa Ljuša, Expert Advisor, Policy

Analysis, and key daily contact• Ms Jelena Prorok, Expert Advisor Federa on of BiH (FBiH), Ministry of Agriculture, Water Management and Forestry:• Contact point, Kasbašić Azijada Republika Srpska (RS), Ministry of Agriculture, Forestry and Water Management:• Contact point, Marko Srdić Brčko District, Department of Agriculture, Forestry and Water Management:• Contact point, Abdulah Ribić

1 The fi nal concept for pre-accession assistance to agriculture and rural development a er 2013 is not yet known, and it may be diff erent from the current IPARD model. As a ma er of simplicity, reference is made to IPARD throughout the sector analyses.

2 The University of Sarajevo team managed the farm survey and SWOT workshops in FBiH but did not par cipate in the analysis or dra ing of the report. Dra s of the report were submi ed to them for comment before being fi nalised.

This is one of fi ve sector analyses (Meat and Dairy; Fruit and Vegetables; Cereals; Wine; Diversifi ca on) prepared between spring 2011 and spring 2012 for the agricultural authori es in Bosnia and Herzegovina (BiH) at state, en ty and Brčko District level. The sector analyses are inputs for use during the design of measures to be fi nanced under the European Union (EU) Instrument for Pre-accession Assistance for Rural Development (IPARD).1 They are also for use during the design of en ty level interven ons in general. The analyses were commissioned by the EU and monitored by task manager Ms Timea Makra, EU Delega on in Sarajevo. The analyses were coordinated by Mr Morten Kvistgaard, Interna onal Team Leader under the overall management of Mr Gerold Boedeker, Budget Holder and Mr Raimund Jehle, Lead Technical Offi cer, Regional Offi ce for Europe and Central Asia of the Food and Agriculture Organiza on of the United Na ons (FAO) in Budapest.

Further informa on on the studies themselves and on the IPARD planning process is provided in Chapter 2 of this report.

Study team

This study was conducted by the following team: Core team:• Dr Steve Goss• John Howells (processing)• Dr Željko Vaško, Dr Ljiljana Drinić and

Dr Gordana Rokvić, University of Banja Luka, Ins tute of Agricultural Economics

• Dr Aleksandra Nikolić and Dragan Ognjenović, Faculty of Agriculture and Food Science, University of Sarajevo2

x

BiH Agency for Sta s cs FBiH Federal Offi ce of Sta s cs RS Ins tute of Sta s cs BiH Agency for Animal Iden fi ca on EU-funded project on “Agricultural Informa on Systems”, led by Colin Sco Vlado Cirko, for wide-ranging logis cal support

1

1. Execu ve summary

This document follows the standard format of an IPARD sectoral study, with the analysis developing progressively through the chapters as follows:

1.1 Background and key fi gures

Chapter 1 provides a general introduc on to Bosnia and Herzegovina and its livestock sector, prepared for each of the fi ve sectoral studies on the basis of published sta s cs.

– Key fi nding 1: Livestock is the most important sector in BiH agriculture

Total GDP: € 12.7 billion Agriculture GDP: € 930 million (7 percent) Livestock output: € 900 million (farm-gate value)

– Key fi nding 2: Over 300,000 agricultural holdings keep some kind of livestock, which makes a signifi cant contribu on to household income

On the surveyed farms: Milk and dairy products contributed 20 percent of household income Meat and livestock contributed 50 percent of household income

1.1 Farmers Chapter 2 presents the key sta s cal data and then develops a quan ta ve descrip on and typology of livestock farms in Bosnia and Herzegovina; and brings together sta s cal data and the fi ndings of a farm survey conducted for this study to create

comprehensive es mates of fl ock and herd numbers, animal numbers, and milk and meat produc on and marke ng for each farm type, with es mates of value and volume.

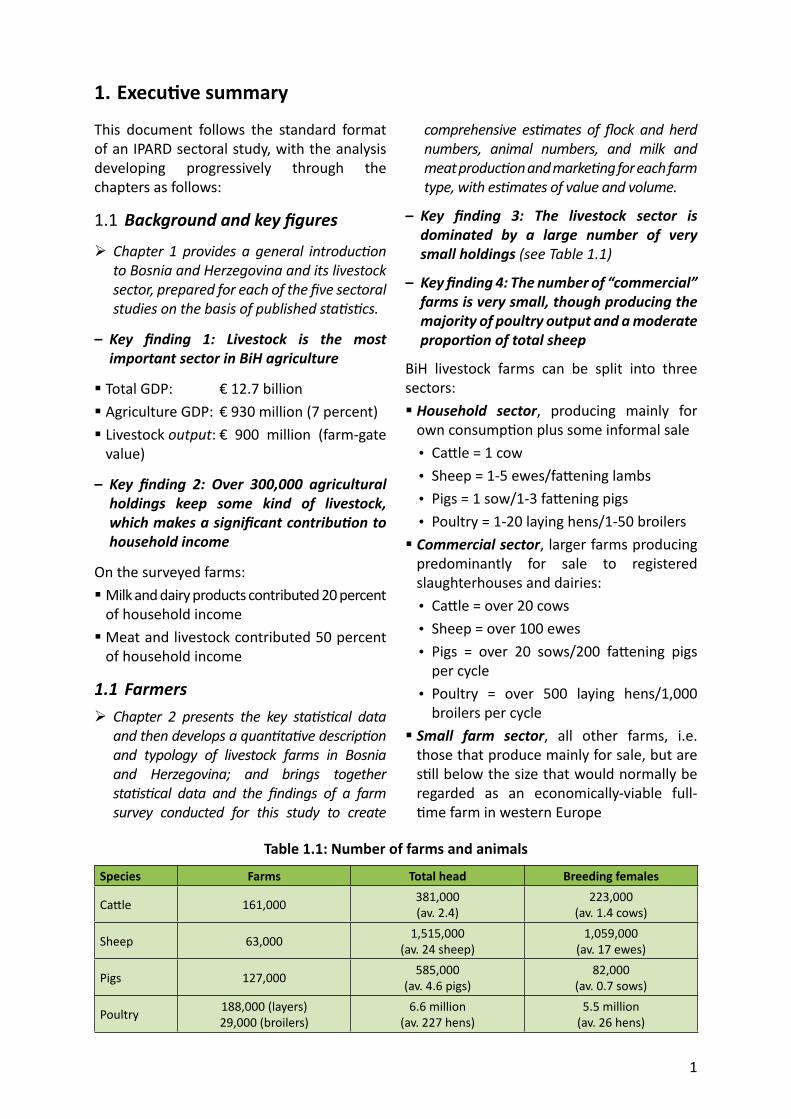

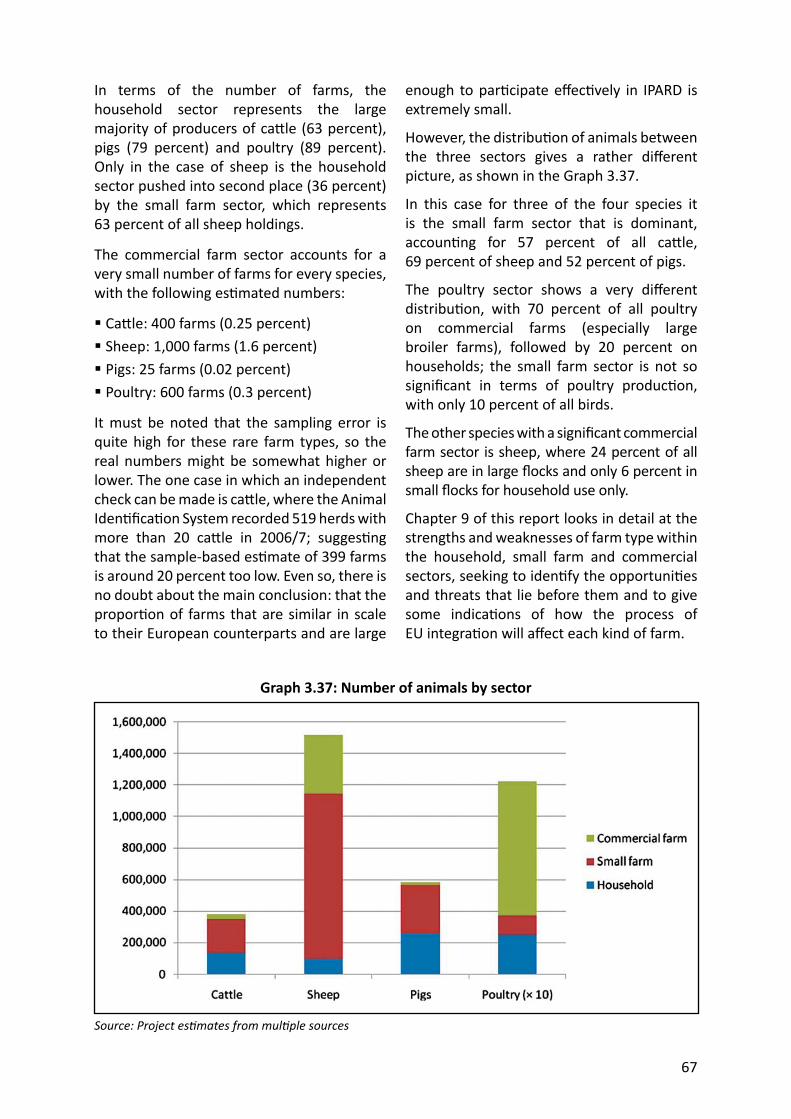

– Key fi nding 3: The livestock sector is dominated by a large number of very small holdings (see Table 1.1)

– Key fi nding 4: The number of “commercial” farms is very small, though producing the majority of poultry output and a moderate propor on of total sheep

BiH livestock farms can be split into three sectors: Household sector, producing mainly for own consump on plus some informal sale• Ca le = 1 cow• Sheep = 1-5 ewes/fa ening lambs• Pigs = 1 sow/1-3 fa ening pigs• Poultry = 1-20 laying hens/1-50 broilers Commercial sector, larger farms producing predominantly for sale to registered slaughterhouses and dairies:• Ca le = over 20 cows• Sheep = over 100 ewes• Pigs = over 20 sows/200 fa ening pigs

per cycle• Poultry = over 500 laying hens/1,000

broilers per cycle Small farm sector, all other farms, i.e. those that produce mainly for sale, but are s ll below the size that would normally be regarded as an economically-viable full- me farm in western Europe

Table 1.1: Number of farms and animals

Species Farms Total head Breeding females

Ca le 161,000 381,000(av. 2.4)

223,000(av. 1.4 cows)

Sheep 63,000 1,515,000(av. 24 sheep)

1,059,000(av. 17 ewes)

Pigs 127,000 585,000(av. 4.6 pigs)

82,000(av. 0.7 sows)

Poultry 188,000 (layers)29,000 (broilers)

6.6 million(av. 227 hens)

5.5 million(av. 26 hens)

2

The commercial farm sector accounts for a very small number of farms for every species, with the following es mated numbers: Ca le: 400 farms (0.25 percent) Sheep: 1,000 farms (1.6 percent) Pigs: 25 farms (0.02 percent) Poultry: 600 farms (0.3 percent)

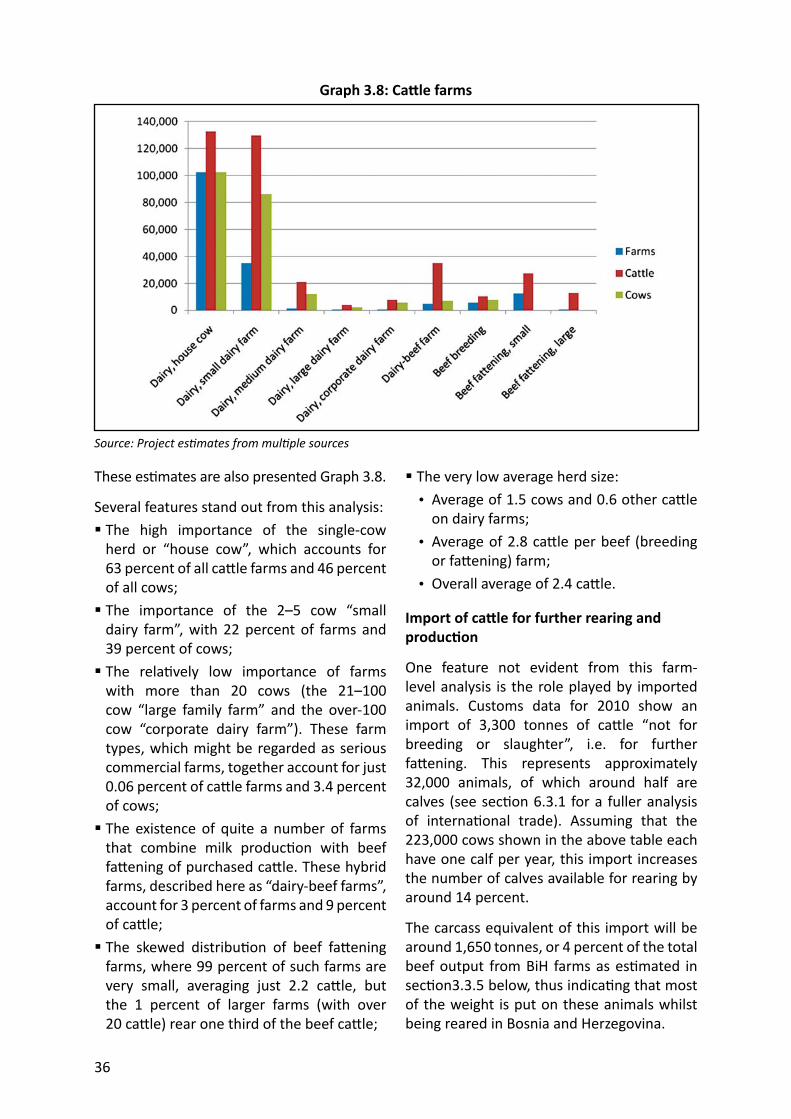

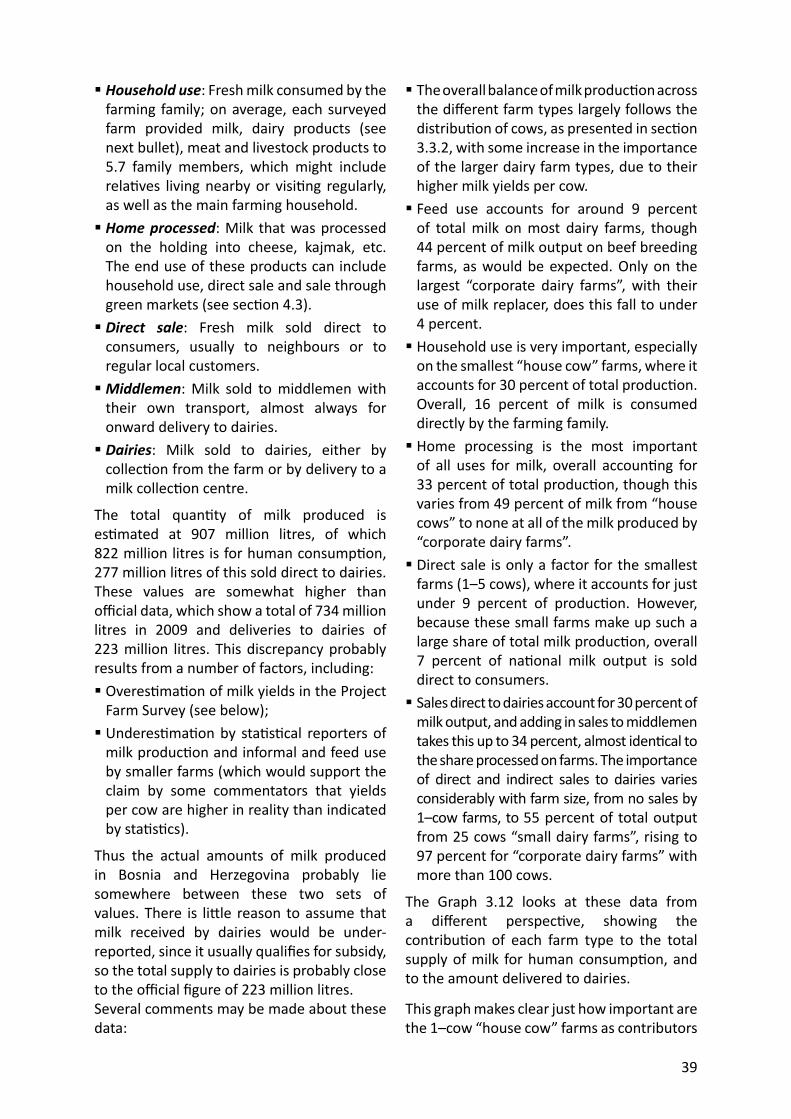

– Key fi nding 5: Farms with 1-5 cows produce 85 % of the total milk supply and 60 % of the supply to dairies

– Key fi nding 6: Household use and informal marke ng are very important, especially for milk, sheepmeat and pigmeat

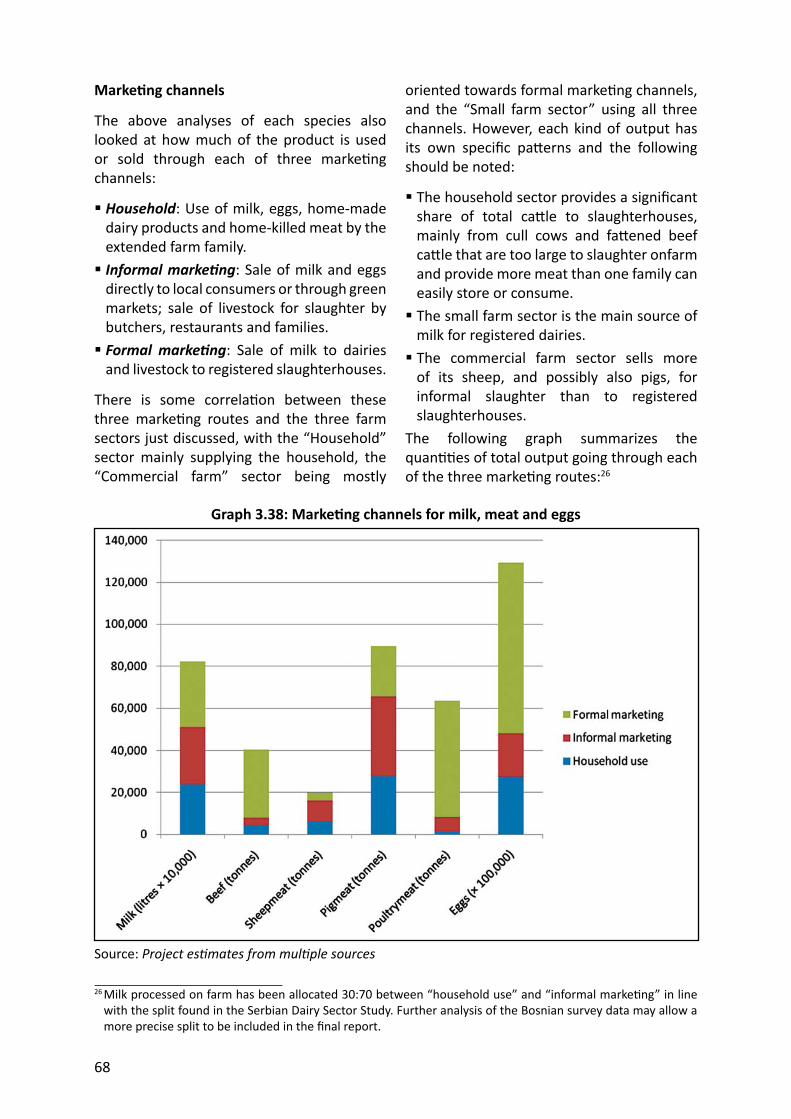

Livestock products are marketed through three main channels:

Household: Use of milk, eggs, home-made dairy products and home-killed meat by the extended farm family. Informal marke ng: Sale of milk and eggs direct to local consumers or through green

Graph 1.1: Number of farms by sector

Graph 1.2: Number of animals by sector

3

markets; sale of livestock for slaughter by butchers, restaurants and families. Formal marke ng: Sale of milk to dairies and livestock to registered slaughterhouses.

– Key fi nding 7: Per capita meat consump on is typical for the region, with the balance between species refl ec ng local condi ons and preferences

Graph 1.3: Marke ng channels for milk, meat and eggs

Graph 1.4: Annual meat consump on per capita

4

CONCLUSION 1: Farm structures will change, but slowly, and BiH should plan on entering the EU with a livestock sector dominated by small farms

CONCLUSION 2: The number of farms large enough to compete successfully for IPARD grants is small, and most farms will require other sources of investment

1.2 Processors

Chapter 3 provides a systema c descrip on of formal milk and meat processing in Bosnia and Herzegovina, based heavily on a face-to-face survey of processors carried out by the project team.

– Key fi nding 8: The processing sector has recovered a er the war, in some cases managing to “leap-frog” past neighbouring countries

– Key fi nding 9: Milk collec on is diverse, including collec ng centres and middlemen as well as direct collec on by dairies, and some raw milk is not yet cooled

– Key fi nding 10: Daily milk collec on per farm is small (av. 26 litres), increasing unit cost

– Key fi nding 11: Raw milk tes ng works well in RS but not yet in FBiH

– Key fi nding 12: Milk processing is bimodal

More than 75 % of collected milk is processed by 7 dairies Around 50 dairies, plus an unknown number of micro-dairies, process the other 25 % – Key fi nding 13: Most dairies concentrate on established regional products, with larger dairies also producing UHT milk

– Key fi nding 14: Most dairies are in good technical and fi nancial condi on, and almost all have HACCP cer fi ca on

– Key fi nding 15: Major needs are in-house laboratories and, especially, proper effl uent disposal

– Key fi nding 16: Meat processing combines local supplies with cheaper imports

Processors report that: Local meat is up to 30 % more expensive than imports Quality of imported meat is quite adequate for processing They would like to use more imported meat

– Key fi nding 17: The range of meat products is tradi onal, targe ng the local and CEFTA markets, with good quality control and packaging

– Key fi nding 18: Meat processing plants are generally in good condi on, but red meat slaughterhouses need considerable investment

– Key fi nding 19: BiH has no adequate system to dispose of slaughterhouse waste and fallen stock

CONCLUSION 3: Dair ies and meat processors will need to diversify their product range to penetrate EU markets – but have li le incen ve to innovate without market access

CONCLUSION 4: As E U integra on increases access to cheaper imported meat, it will benefi t processors but increase pressure on producers

CONCLUSION 5: The top investment priority in processing relevant to IPARD is effl uent treatment and waste disposal

1.3 Policy

Chapter 4 outlines the na onal support, regulatory and trade policies aff ec ng the livestock farm and processing sectors; includes a common introduc on on state- and en ty-level strategies, developed for all fi ve sectoral studies.

– Key fi nding 20: BiH’s unique administra ve structure creates special challenges in policy making, implementa on and enforcement

– Key fi nding 21: Livestock subsidies in both en es favour larger farms and mainly pursue social rather than development goals

5

CONCLUSION 6: BiH will struggle to achieve EU export approval for livestock products without a more unifi ed veterinary control system

CONCLUSION 7: Both en es should re-direct their livestock support to help smaller farms prepare for EU accession

1.4 Marke ng

Chapter 5 reviews the variety of domes c marke ng channels employed for livestock and their products; presents a systema c

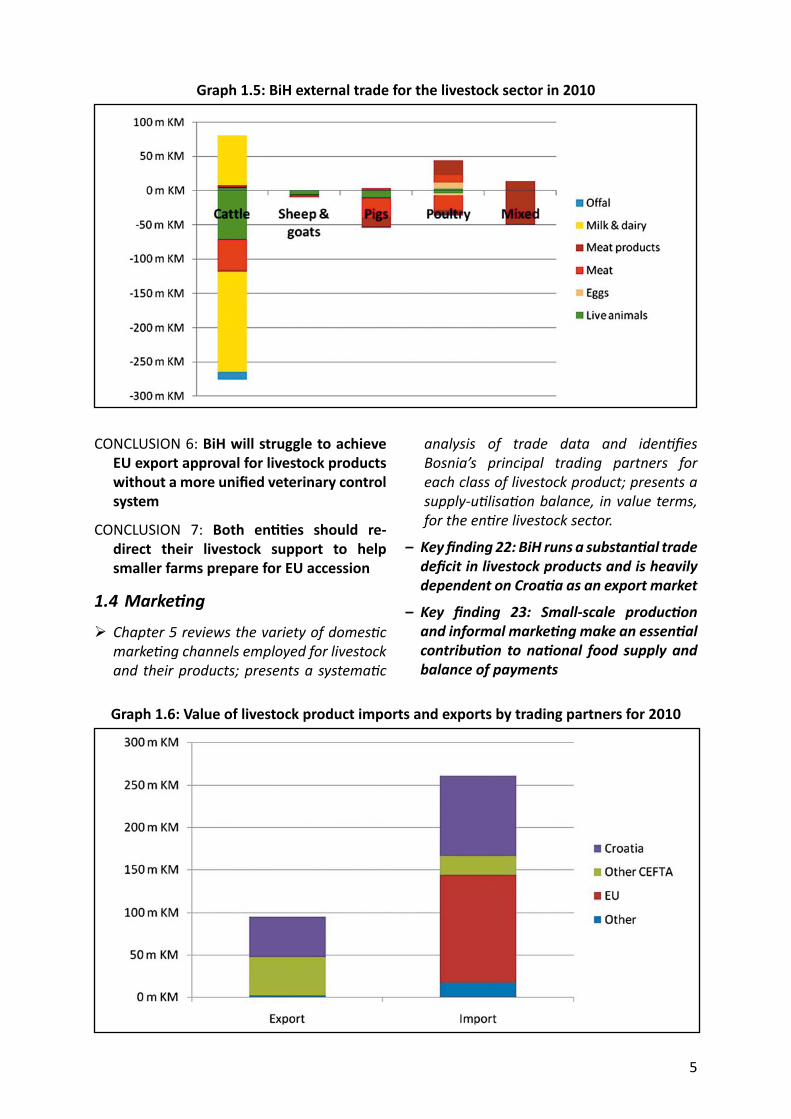

Graph 1.5: BiH external trade for the livestock sector in 2010

analysis of trade data and iden fi es Bosnia’s principal trading partners for each class of livestock product; presents a supply-u lisa on balance, in value terms, for the en re livestock sector.

– Key fi nding 22: BiH runs a substan al trade defi cit in livestock products and is heavily dependent on Croa a as an export market

– Key fi nding 23: Smal l-scale produc on and informal marke ng make an essen al contribu on to na onal food supply and balance of payments

Graph 1.6: Value of livestock product imports and exports by trading partners for 2010

6

CONCLUSION 8: Croa a ’s accession to the EU will give a serious shock to the BiH livestock sector, with a drama c drop in exports

1.5 EU standards Chapter 6 provides an overview of where Bosnia and Herzegovina currently stands in rela on to each element of the acquis communautaire for the livestock sector; notes that Bosnia and Herzegovina does not as yet have EU approval to export any farmed livestock or their products.

– Key fi nding 24: Livestock farms fall short of EU standards in three main areas: manure storage & handling, animal welfare, and milk hygiene

– Key fi nding 25: Processors fall short of EU standards in four main areas: red meat slaughtering, slaughterhouse waste disposal, liquid effl uent treatment, and raw milk tes ng

1.6 Investment Chapter 7 reviews recent investments in livestock farms and processing plants; discusses the availability of commercial credit, ins tu onal credit and government subsidies; presents a comprehensive picture of the agricultural fi nance sector prepared for all fi ve sector studies.

Graph 1.7: Poten al eff ect on trade balance of curtailing informal marke ng and household use of livestock products

– Key fi nding 26: Access to credit is a signifi cant constraint for livestock producers, par cularly small farms

CONCLUSION 9: Despite the achievements of investment banks and micro-credit organisa ons, and the promise of IPARD funding, there is a massive shor all between credit supply and farm investment needs

1.7 Iden fi ca on of poten als and needs of the sector

Chapter 8 presents SWOT analyses for both livestock farms and processors, based on stakeholder workshops held in Sarajevo and Banja Luka; presents the fi ndings of the project farm survey on the current status of infrastructure on livestock farms and their investment needs; assesses how EU integra on will impact on each livestock farm type; establishes benchmarks to put the BiH livestock sector in a European and regional context; predicts the future structure of the sector based on survey responses and es mates total investment requirements; summarises investment priori es for livestock farms and processors.

– Key fi nding 27: Investment priori es refl ect the shor alls from EU standards, plus

7

the need to increase scale and technical effi ciency

Producers:• Herd/fl ock enlargement (esp. dairy; but

note that livestock purchases are not eligible for IPARD funding)

• Buildings & equipment (esp. dairy)• Machinery (esp. forage)• Manure storage & handling (esp. ca le &

pigs) Dairy processors:• Plant upgrading to improve opera ng

effi ciency & product range• In-house laboratories to improve product

quality• Effl uent storage & treatment to meet

environmental standards Meat processors:• Plant upgrading to improve opera ng

effi ciency• Animal waste storage, transport &

disposal

1.8 Iden fi ca on of training needs in the sector

Chapter 9 outlines the exis ng structures to provide training, advice and informa on to the livestock sector; presents a short summary of the key training priori es for diff erent groups of benefi ciaries, including farmers, processors and inspectors.

– Key fi nding 28: Current extension services are inadequate to help 300,000 livestock farmers meet EU standards and improve technical effi ciency, management & marke ng

CONCLUSION 10: Develop ing an eff ec ve mass extension system is a top priority

1.9 Outcomes

Chapter 10 summarises the key factors to be taken into account when designing investment measures for the BiH livestock sector; presents proposals for six specifi c measures to be funded under the IPARD programme.

– Key fi nding 29: The implica ons of EU accession for livestock farms stem directly from their structure

Ca le (160,000 holdings)◊ Major structural problem in dairy

produc on, with a need to help smaller farms adapt to the changing situa on; less serious situa on in beef produc on.

Sheep (50,000 holdings)◊ Less serious structural problem, as even

smaller farms can be EU-compliant and commercially viable, though only the larger farms are likely to par cipate in IPARD.

Pigs (130,000 holdings)◊ Big problem of compe veness, which is

likely to see many small pig farms cease produc on; only the larger farms are likely to have a long-term commercial future, and these could benefi t greatly from IPARD assistance.

Poultry (220,000 holdings)• Laying hens:◊ Current bi-modal structure is sustainable,

as the numerous small farms are essen ally non-commercial; many large commercial farms will require substan al assistance to adapt to EU standards.

• Broilers:◊ Smaller broiler farms have li le

commercial future; IPARD investment should focus on helping large broiler farms to adapt to EU standards, increase effi ciency and con nue to expand.

– Key fi nding 30: Three IPARD measures are proposed for livestock producers, and three for processors

Modernisa on of agricultural holdings (101):a. 101/1: Improvement & enlargement of

agricultural holdingsb. 101/2: Manure storage & disposalc. 101/3: Forage machinery Processing and marke ng of agricultural products (103):d. 103/1. Improvement of processing facili ese. 103/2: Dairy effl uent storage & treatmentf. 103/3: Animal waste collec on &

processing

8

R IPARD – F M (101)

101/1: Improvement & enlargement of agricultural holdings

Objec ves: Achieving EU standards for hygiene, animal welfare & environment Increasing compe veness through herd/fl ock enlargement and improving effi ciency

Eligible expenditure: Construc on & reconstruc on of buildings Construc on of manure stores Purchase of machinery and equipment

Eligible enterprise size at end of investment: 20 – 200 cows 100 – 5,000 breeding ewes 20-500 sows 200-5,000 fa ening pigs per cycle 500-50,000 laying hens 1,000 – 100,000 broilers per cycle

Es mated number of poten al applicants: Ca le: 230 current farms (+ up to 300 expanding) Sheep: 1,000 current farms (low applica on rate expected) Pigs: 25 current farms (+ up to 4,000 expanding) Poultry: 390 current farms (+ up to 300 expanding)

101/2: Manure storage & disposal

Objec ves: Reducing pollu on from manure & silage (simplifi ed measure for farms that are too large or too small to apply under 101/1)

Eligible expenditure: Construc on of manure stores Purchase of machinery for handling & spreading manure & slurry

Eligible enterprise size at end of investment: 10+ cows 10+ sows 20+ fa ening pigs per cycle 500+ laying hens 1,000 + broilers per cycle

Es mated number of poten al applicants: Approx. 50 farms too large for 101/1 Up to 2,000 ca le & 2,000 pig farms if procedure kept simple

9

101/3: Forage machinery

Objec ve: Specifi c measure to provide machinery for making and handling big-bale silage and other kinds of forage, to anyone who will cover a reasonable area, e.g. machinery rings, farmers’ associa ons and private contrac ng services (individual farmers would apply under measure 101/1).

Eligible expenditure: Forage-handling machinery and associated tractors & trailers

Eligible size by end of investment: Demonstrated capacity & business plan to harvest at least 100 ha of forage for mul ple holdings

10

R IPARD – P P (103)

103/1. Improvement of processing facili es

Objec ves:General investment with the aim of helping dairies & meat plants to: Meet EU hygiene, welfare &/or environmental standards Increase compe veness through increased size, more effi cient opera on and increased product range.

Eligible expenditure: (Re)construc on of buildings Purchase of machinery and fi xed equipment Construc on/upgrading of effl uent storage & treatment facili es Construc on/upgrading of in-house laboratories for rapid tes ng of incoming milk and for checking fi nal products

Eligible size by end of investment: Dairies opera ng regularly at more than fi ve tonnes daily milk intake. Meat processors producing at least fi ve tonnes of products per day.

Es mated number of poten al applicants: Five dairies and four meat processors are known to be within this size range.

103/2: Dairy effl uent storage & treatment

Objec ve: Simplifi ed measure specifi cally to reduce pollu on aimed at processors that are too large to apply under 103/1.

Eligible expenditure: Construc on/upgrading of effl uent storage & treatment facili es

Eligible size by end of investment: At least 20 tonnes of waste water per day.

Es mated number of poten al applicants: Approximately eight processors.

11

103/3: Animal waste collec on & processing

Objec ve: Investment for the safe collec on & disposal of animal waste in line with EU standards for public & animal health and the environment

Eligible expenditure: Construc on of rendering plant or incinerator Vehicles for transport of animal waste (Storage at plants is eligible under 103/1)

Eligible size by end of investment: Not applicable – would probably be one or two central facili es to serve many operators.

Es mated number of poten al applicants: Depends on poli cal choices between private and public investment, with the la er approach like to generate either one na onal or two regional rendering plants or incinerators.

S C CONCLUSION 1: Farm structures will

change, but slowly, and BiH should plan on entering the EU with a livestock sector dominated by small farm s

CONCLUSION 2: The number of farms large enough to compete successfully for IPARD grants is small, and most farms will require other sources of investm ent

CONCLUSIO N 3: Dairies and meat processors will need to diversify their product range to penetrate EU markets – but have li le incen ve to innovate without market a ccess

CONCLUS ION 4: As EU integra on increases access to cheaper imported meat, it will benefi t processors but increase pressure on pr oducers

CONCL USION 5: The top investment priority in processing relevant to IPARD is effl uent treatment and waste disposal

CON CLUSION 6: BiH will struggle to achieve EU export approval for livestock products without a more unifi ed veterinary con trol system

C ONCLUSION 7: Both en es should re-direct their livestock support to help smaller farms prepare for EU accession

CONCLUSION 8: Croa a’s accession to the EU will give a serious shock to the BiH livestock sector, with a drama c drop in expor ts

CONCLUSION 9: Despite the achievements of investment banks and micro-credit organisa ons, and the promise of IPARD funding, there is a massive shor all between credit supply and farm investment ne eds

CONCLUSION 10: Developing an eff ec ve mass extension system is a top priority

12

13

2. Background and key fi gures

This sec on provides a general background to Bosnia and Herzegovina and its economy and agriculture, developed for all fi ve of the sectoral studies. Sec on 2.1 presents general informa on about t he country. Sec on 2.2 explains the context and objec ve of the sec tor studies. Sec on 2.3 gives some further informa on on the BiH econom y as a whole. Sec on 2.4 reviews the main agricultural indicators and sta s cs.

2.1 General informa on about Bosnia and Herzegovina

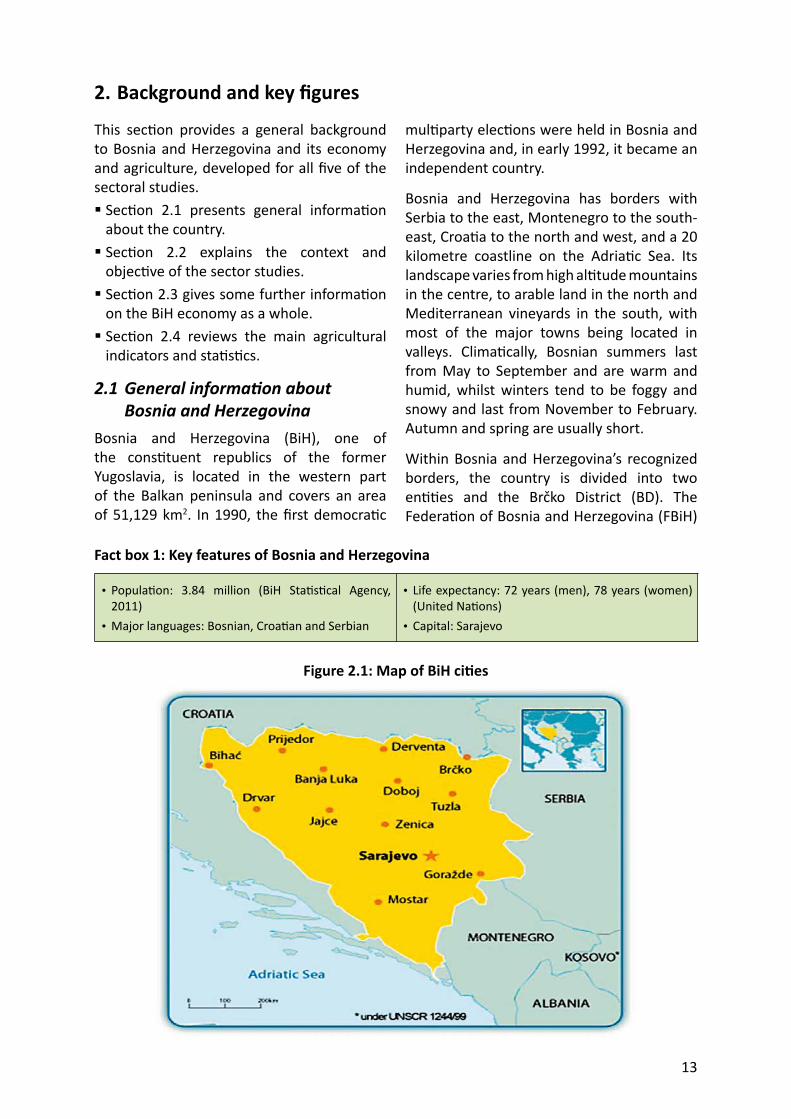

Bosnia and Herzegovina (BiH), one of the cons tuent republics of the former Yugoslavia, is located in the western part of the Balkan peninsula and covers an area of 51,129 km2. In 1990, the fi rst democra c

mul party elec ons were held in Bosnia and Herzegovina and, in early 1992, it became an independent country.

Bosnia and Herzegovina has borders with Serbia to the east, Montenegro to the south-east, Croa a to the north and west, and a 20 kilometre coastline on the Adria c Sea. Its landscape varies from high al tude mountains in the centre, to arable land in the north and Mediterranean vineyards in the south, with most of the major towns being located in valleys. Clima cally, Bosnian summers last from May to September and are warm and humid, whilst winters tend to be foggy and snowy and last from November to February. Autumn and spring are usually short.

Within Bosnia and Herzegovina’s recognized borders, the country is divided into two en es and the Brčko District (BD). The Federa on of Bosnia and Herzegovina (FBiH)

Fact box 1: Key features of Bosnia and Herzegovina

• Popula on: 3.84 million (BiH Sta s cal Agency, 2011)

• Major languages: Bosnian, Croa an and Serbian

• Life expectancy: 72 years (men), 78 years (women) (United Na ons)

• Capital: Sarajevo

Figure 2.1: Map of BiH ci es

14

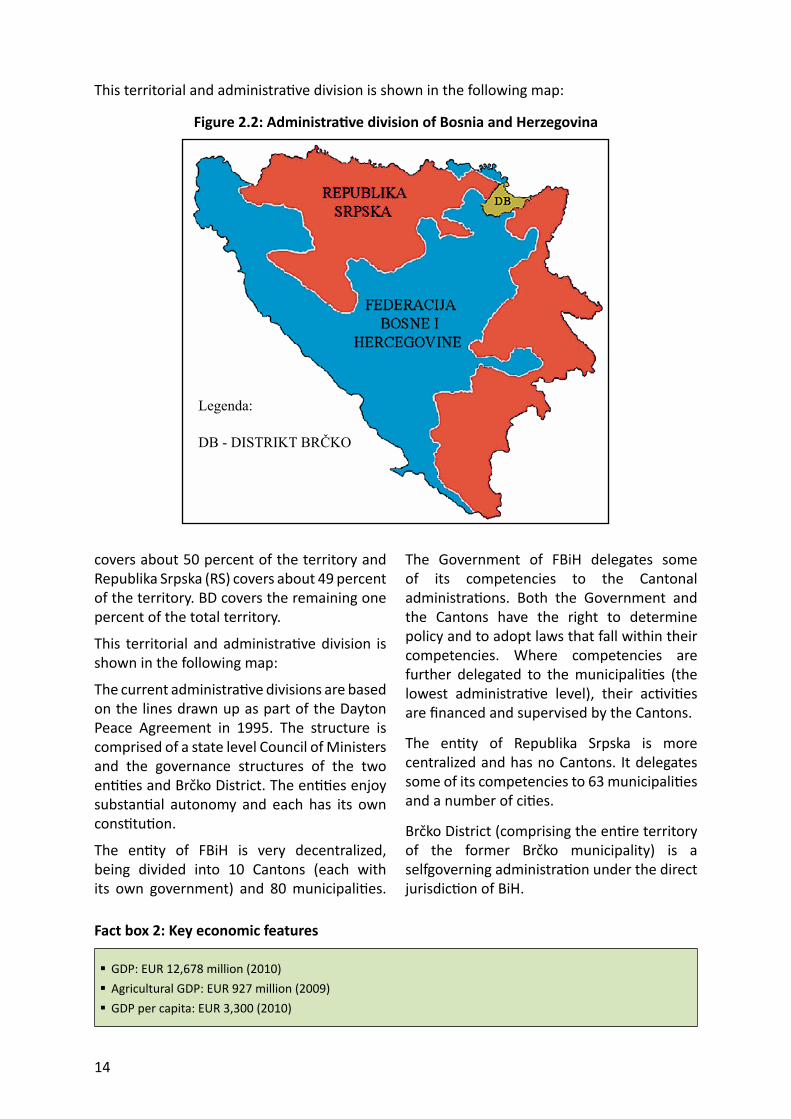

covers about 50 percent of the territory and Republika Srpska (RS) covers about 49 percent of the territory. BD covers the remaining one percent of the total territory.

This territorial and administra ve division is shown in the following map:

The current administra ve divisions are based on the lines drawn up as part of the Dayton Peace Agreement in 1995. The structure is comprised of a state level Council of Ministers and the governance structures of the two en es and Brčko District. The en es enjoy substan al autonomy and each has its own cons tu on.

The en ty of FBiH is very decentralized, being divided into 10 Cantons (each with its own government) and 80 municipali es.

This territorial and administra ve division is shown in the following map:

Figure 2.2: Administra ve division of Bosnia and Herzegovina

The Government of FBiH delegates some of its competencies to the Cantonal administra ons. Both the Government and the Cantons have the right to determine policy and to adopt laws that fall within their competencies. Where competencies are further delegated to the municipali es (the lowest administra ve level), their ac vi es are fi nanced and supervised by the Cantons.

The en ty of Republika Srpska is more centralized and has no Cantons. It delegates some of its competencies to 63 municipali es and a number of ci es.

Brčko District (comprising the en re territory of the former Brčko municipality) is a selfgoverning administra on under the direct jurisdic on of BiH.

Fact box 2: Key economic features

GDP: EUR 12,678 million (2010) Agricultural GDP: EUR 927 million (2009) GDP per capita: EUR 3,300 (2010)

Legenda:

DB - DISTRIKT BRČKO

15

Since the Dayton Peace Agreement, the country has made remarkable progress in postconfl ict reconstruc on, social integra on and state building.3 Based on its economic recovery and sustained social stability, which have been supported by high levels of interna onal assistance, the country is now working towards accession to the European Union and membership in the World Trade Organiza on.

The popula on is es mated at a li le less than 4 million, but a precise fi gure is not available, since there has been no recent census. The last popula on census was carried out in 1991 and major popula on movements have taken place since then, par cularly during the confl ict of the early 1990s.The offi cial fi gure of 3.8 million, given by the BiH Sta s cal Agency, is used in FAO sta s cs and for calcula ons in this report.

2.2 Context and objec ve of the sector analyses

2.2.1 General context of the sector analyses: Prepara on for EU accession

Bosnia and Herzegovina is a poten al candidate country for EU accession following the Thessaloniki European Council of June 2003. In June 2008, the EU and Bosnia and Herzegovina signed a “Stabilisa on and Associa on Agreement” (SAA). An “Interim Agreement on Trade and Trade-related Issues” entered into force on 1 July 2008 and a new European partnership with Bosnia and Herzegovina was adopted by the Council on 18 February 2008.4

Bosnia and Herzegovina has benefi ted from EU autonomous trade measures since 2000. A er the Interim Agreement came into force on 1 July 2008, EU access to products from Bosnia and Herzegovina has expanded, and

EU exports to the country have been granted trade preferences.

It was a milestone on Bosnia and Herzegovina’s road to Europe that it and the EC signed the Financing Agreement for the “Instrument for Pre-accession Assistance” (IPA) 2007 Na onal Programme on 31 July 2008. The total fi nancial alloca on within IPA is EUR 11.47 billion (current prices) over the 2007–2013 period.

As a pre-candidate country, Bosnia and Herzegovina cannot yet take full advantage of IPA support, as certain aspects of the support only apply to Candidate Countries. However, prepara ons are already being made to implement the full IPA programme, including IPARD support for agricultural and rural development, once BiH receives Candidate Country status.

2.2.2 Sector context

In order for Bosnia and Herzegovina to benefi t from the pre-accession assistance under the IPARD, it must: Achieve candidate country status Have an IPARD Programme adopted by the European Commission Conclude the Framework and Sectoral Agreements Establish IPARD opera onal structure and receive na onal accredita on Receive accredita on and conferral of management decisions from the Commission Conclude a Mul -annual Financing Agreement

The IPA Implemen ng Regula on (718/2007) (Ar cle 184, Paragraph “2.b”) indicates that the IPARD Programme should be based on an analysis of the current situa on in rural areas and on in-depth analysis of the sectors concerned.5 Among other things, the IPARD programme should include a quan fi ed

3 Ministry for Human Rights and Refugees in BiH4 See EU Delega on Website for Bosnia and Herzegovina: h p://www.delBIH.ec.europa.eu/5 The fi nal concept for pre-accession assistance to agriculture and rural development a er 2013 is not yet known,

and it may be diff erent from the current IPARD model, and the new regula on might diff er from the current IPA Implemen ng Regula on (718/2007). As a ma er of simplicity reference is made to IPARD in the sector analyses.

16

descrip on of the current situa on, showing dispari es, shortcomings and poten al for development. The programme should also include quan fi ed objec ves. The analyses of the situa on and priori za onof the areas for poten al interven on should be made with the help of independent exper se.

Bearing this in mind, the main objec ve of the sector analyses is to provide a solid input to the prepara on of the IPARD Programme and provide the grounds for jus fi ed and appropriate targe ng of the measures included in the IPARD Programme. Therefore, the sector studies are not a part of the IPARD Programme as such, but rather cons tute a basic input to the programming process.

Furthermore, it should be emphasized that the na onal authori es may use the sector studies as inputs for the prepara on of any interven on targe ng the agricultural and rural sectors. As such the sector studies do not exclusively contribute to the prepara on of the IPARD Programme.

IPARD support will, if so decided, address the weaker links in the produc on and supply chains. The objec ves of the IPARD interven on are to contribute towards upgrading to EU standards, strengthening overall compe veness and performance as well as fostering the sustainable development of the sector in the context of EU accession. In this respect, the sector analyses have been undertaken for the most demanding sectors in terms of the costs of mee ng the standards, for which the highest poten al and added-value of the interven on is an cipated.

The agricultural sector analyses carried out in Bosnia and Herzegovina have been selected based on a consulta on process with local authori es and are based on EU standard relevance as well as economic relevance. Analyses have been prepared for: Meat, including rendering, and Dairy Fruits and Vegetables Cereals (wheat and maize) Wine Diversifi ca on

The sector analyses provide a comprehensive analysis of the current state of the sectors. They iden fy the weaknesses and sector concerns to be addressed by the IPARD interven on and by other state, en ty and district level interven ons. Where appropriate the sector analyses take into account specifi c regional development needs.

Report structure

This sector analysis follows a standard structure applied in all sectors and pre-candidate countries, and covers: Background and key fi gures for the sector Structural characteris cs of the sector: Producers and processing industry Government policy for the sector at state and en ty level Markets and trade Level of a ainment of relevant EU standards Past trends and future developments in terms of investment Iden fi ca on of poten als and needs of the sector Iden fi ca on of training needs in the sector Outcome: As an outcome, the analysis of the sector provides:• A transparent overview of the sector

containing a quan ta ve and qualita ve descrip on of the situa on;

• Detailed analysis of poten al and obstacles in the produc on and marke ng chain;

• Recommenda ons for targe ng of specifi c IPARD investments, primarily focusing on the weakest links in supply chain.

2.3 General economic indicators for Bosnia and Herzegovina

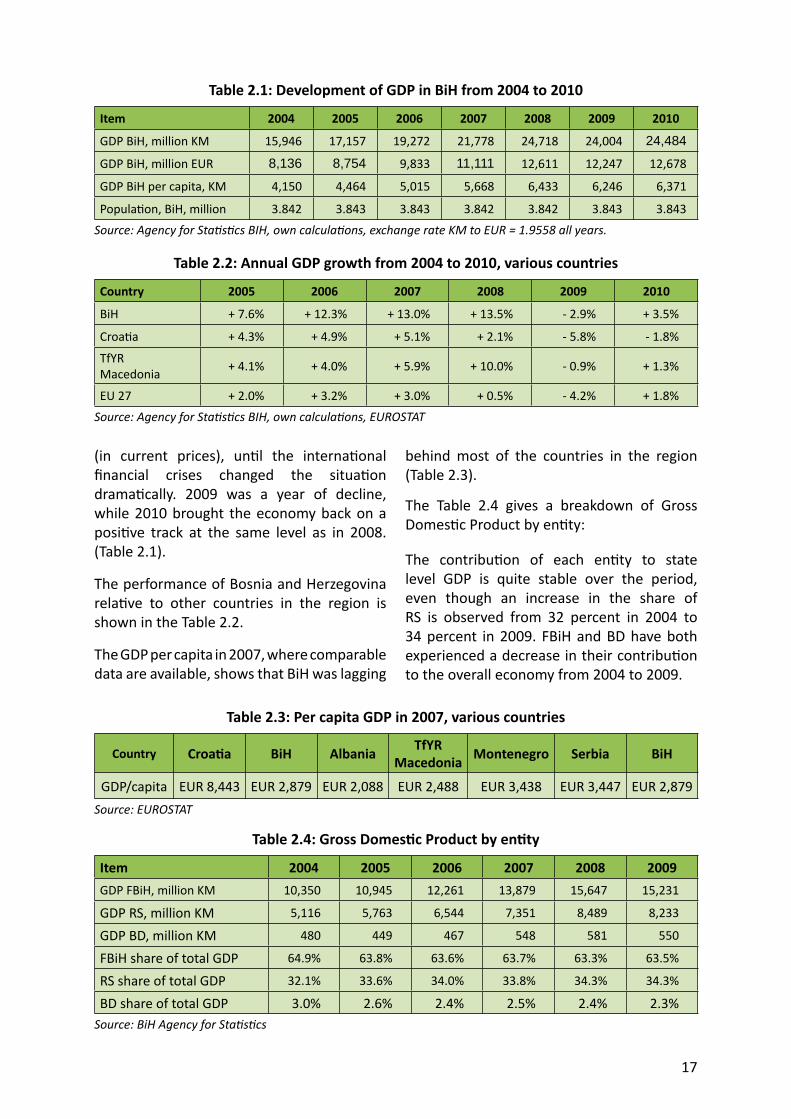

This sec on of the report provides basic economic informa on about the development of the BiH economy.

The development from 2004 to 2010 in Gross Domes c Product (GDP) is presented in the table below. The economy demonstrated very posi ve performance from 2004 to 2008 with an average yearly growth of 13 percent

17

(in current prices), un l the interna onal fi nancial crises changed the situa on drama cally. 2009 was a year of decline, while 2010 brought the economy back on a posi ve track at the same level as in 2008. (Table 2.1).

The performance of Bosnia and Herzegovina rela ve to other countries in the region is shown in the Table 2.2.

The GDP per capita in 2007, where comparable data are available, shows that BiH was lagging

Table 2.1: Development of GDP in BiH from 2004 to 2010

Item 2004 2005 2006 2007 2008 2009 2010

GDP BiH, million KM 15,946 17,157 19,272 21,778 24,718 24,004 24,484

GDP BiH, million EUR 8,136 8,754 9,833 11,111 12,611 12,247 12,678

GDP BiH per capita, KM 4,150 4,464 5,015 5,668 6,433 6,246 6,371

Popula on, BiH, million 3.842 3.843 3.843 3.842 3.842 3.843 3.843Source: Agency for Sta s cs BIH, own calcula ons, exchange rate KM to EUR = 1.9558 all years.

behind most of the countries in the region (Table 2.3).

The Table 2.4 gives a breakdown of Gross Domes c Product by en ty:

The contribu on of each en ty to state level GDP is quite stable over the period, even though an increase in the share of RS is observed from 32 percent in 2004 to 34 percent in 2009. FBiH and BD have both experienced a decrease in their contribu on to the overall economy from 2004 to 2009.

Table 2.2: Annual GDP growth from 2004 to 2010, various countries

Country 2005 2006 2007 2008 2009 2010

BiH + 7.6% + 12.3% + 13.0% + 13.5% - 2.9% + 3.5%

Croa a + 4.3% + 4.9% + 5.1% + 2.1% - 5.8% - 1.8%

TfYRMacedonia + 4.1% + 4.0% + 5.9% + 10.0% - 0.9% + 1.3%

EU 27 + 2.0% + 3.2% + 3.0% + 0.5% - 4.2% + 1.8%Source: Agency for Sta s cs BIH, own calcula ons, EUROSTAT

Table 2.3: Per capita GDP in 2007, various countries

Country Croa a BiH Albania TfYRMacedonia Montenegro Serbia BiH

GDP/capita EUR 8,443 EUR 2,879 EUR 2,088 EUR 2,488 EUR 3,438 EUR 3,447 EUR 2,879Source: EUROSTAT

Table 2.4: Gross Domes c Product by en ty

Item 2004 2005 2006 2007 2008 2009GDP FBiH, million KM 10,350 10,945 12,261 13,879 15,647 15,231

GDP RS, million KM 5,116 5,763 6,544 7,351 8,489 8,233

GDP BD, million KM 480 449 467 548 581 550

FBiH share of total GDP 64.9% 63.8% 63.6% 63.7% 63.3% 63.5%

RS share of total GDP 32.1% 33.6% 34.0% 33.8% 34.3% 34.3%

BD share of total GDP 3.0% 2.6% 2.4% 2.5% 2.4% 2.3%Source: BiH Agency for Sta s cs

18

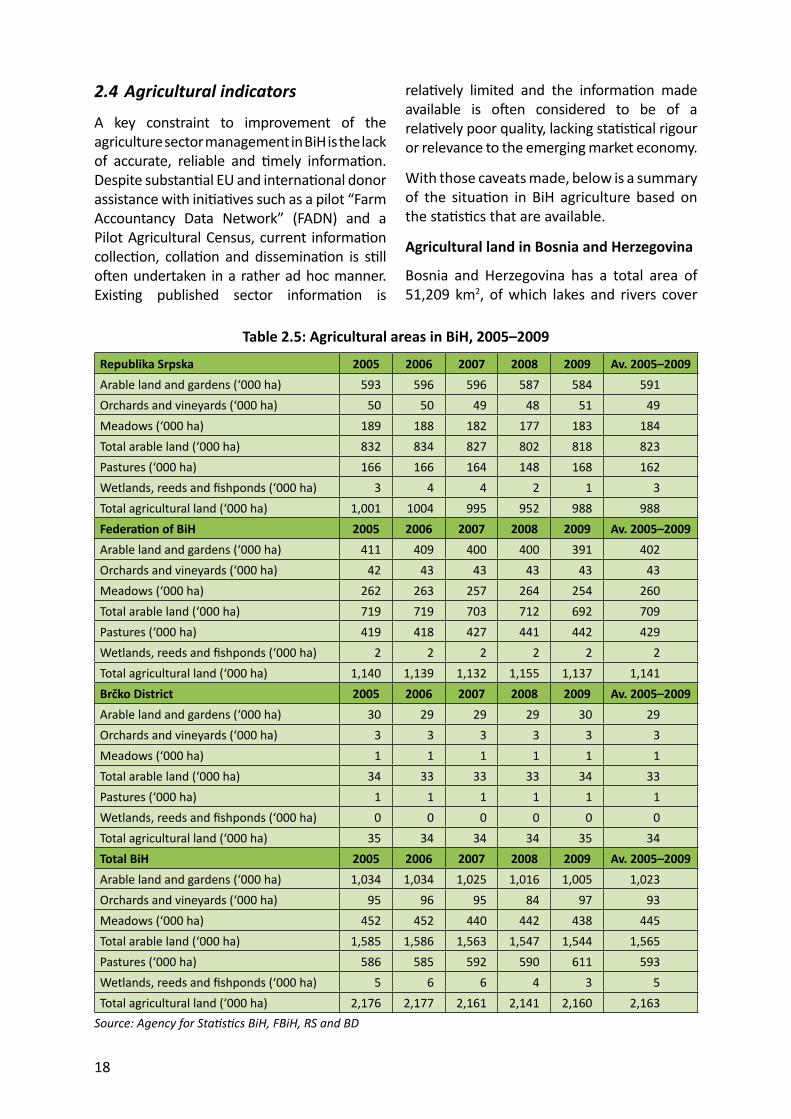

2.4 Agricultural indicators

A key constraint to improvement of the agriculture sector management in BiH is the lack of accurate, reliable and mely informa on. Despite substan al EU and interna onal donor assistance with ini a ves such as a pilot “Farm Accountancy Data Network” (FADN) and a Pilot Agricultural Census, current informa on collec on, colla on and dissemina on is s ll o en undertaken in a rather ad hoc manner. Exis ng published sector informa on is

Table 2.5: Agricultural areas in BiH, 2005–2009

Republika Srpska 2005 2006 2007 2008 2009 Av. 2005–2009Arable land and gardens (‘000 ha) 593 596 596 587 584 591Orchards and vineyards (‘000 ha) 50 50 49 48 51 49Meadows (‘000 ha) 189 188 182 177 183 184Total arable land (‘000 ha) 832 834 827 802 818 823Pastures (‘000 ha) 166 166 164 148 168 162Wetlands, reeds and fi shponds (‘000 ha) 3 4 4 2 1 3Total agricultural land (‘000 ha) 1,001 1004 995 952 988 988Federa on of BiH 2005 2006 2007 2008 2009 Av. 2005–2009Arable land and gardens (‘000 ha) 411 409 400 400 391 402Orchards and vineyards (‘000 ha) 42 43 43 43 43 43Meadows (‘000 ha) 262 263 257 264 254 260Total arable land (‘000 ha) 719 719 703 712 692 709Pastures (‘000 ha) 419 418 427 441 442 429Wetlands, reeds and fi shponds (‘000 ha) 2 2 2 2 2 2Total agricultural land (‘000 ha) 1,140 1,139 1,132 1,155 1,137 1,141 Brčko District 2005 2006 2007 2008 2009 Av. 2005–2009Arable land and gardens (‘000 ha) 30 29 29 29 30 29Orchards and vineyards (‘000 ha) 3 3 3 3 3 3Meadows (‘000 ha) 1 1 1 1 1 1Total arable land (‘000 ha) 34 33 33 33 34 33Pastures (‘000 ha) 1 1 1 1 1 1Wetlands, reeds and fi shponds (‘000 ha) 0 0 0 0 0 0Total agricultural land (‘000 ha) 35 34 34 34 35 34Total BiH 2005 2006 2007 2008 2009 Av. 2005–2009Arable land and gardens (‘000 ha) 1,034 1,034 1,025 1,016 1,005 1,023Orchards and vineyards (‘000 ha) 95 96 95 84 97 93Meadows (‘000 ha) 452 452 440 442 438 445Total arable land (‘000 ha) 1,585 1,586 1,563 1,547 1,544 1,565Pastures (‘000 ha) 586 585 592 590 611 593Wetlands, reeds and fi shponds (‘000 ha) 5 6 6 4 3 5Total agricultural land (‘000 ha) 2,176 2,177 2,161 2,141 2,160 2,163

Source: Agency for Sta s cs BiH, FBiH, RS and BD

rela vely limited and the informa on made available is o en considered to be of a rela vely poor quality, lacking sta s cal rigour or relevance to the emerging market economy.

With those caveats made, below is a summary of the situa on in BiH agriculture based on the sta s cs that are available.

Agricultural land in Bosnia and Herzegovina

Bosnia and Herzegovina has a total area of 51,209 km2, of which lakes and rivers cover

19

6 A report of the Agriculture Sector in Bosnia and Herzegovina 2007, Ministry of Foreign Trade and Economic Rela ons. 2008. p. 6

7 Ac on Plan for Environmental Protec on BiH (Na onal Environmental Ac on Plan of Bosnia and Herzegovina), Ministry of Urbanism, Housing and Services, Civil Engineering and Ecology and the Federa on Ministry of Spa al Planning and Environment. 2003. p. 10

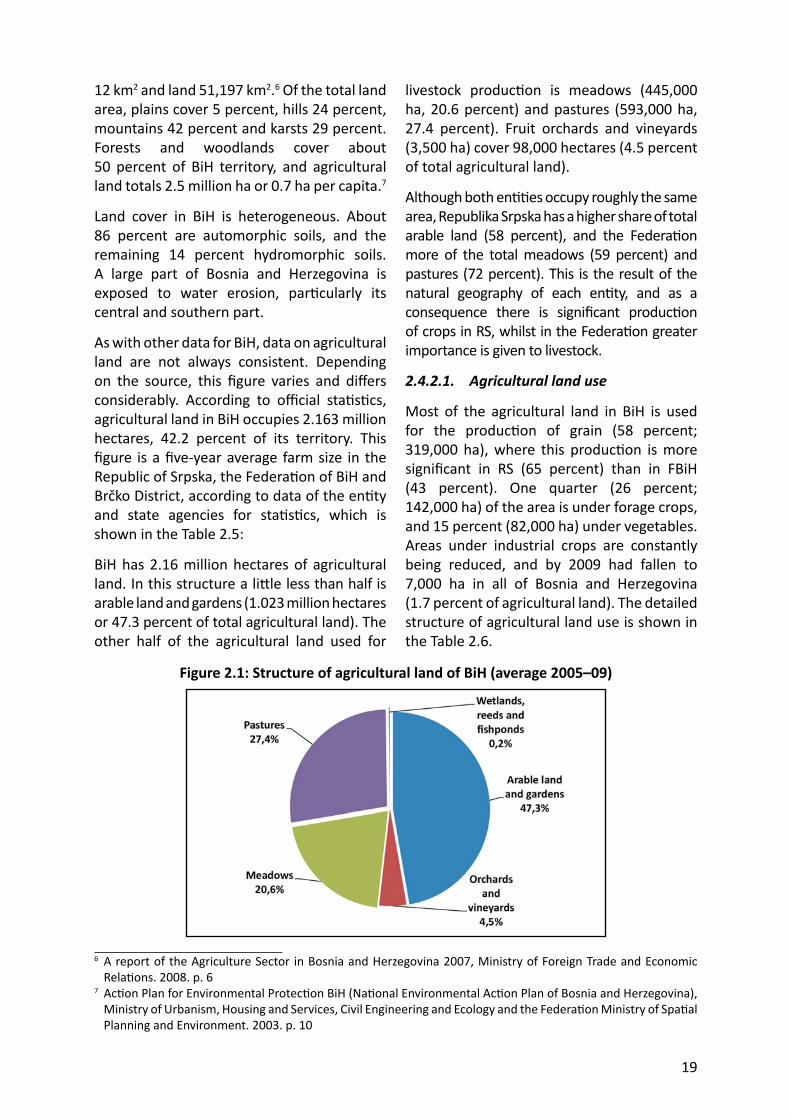

Figure 2.1: Structure of agricultural land of BiH (average 2005–09)

12 km2 and land 51,197 km2.6 Of the total land area, plains cover 5 percent, hills 24 percent, mountains 42 percent and karsts 29 percent. Forests and woodlands cover about 50 percent of BiH territory, and agricultural land totals 2.5 million ha or 0.7 ha per capita.7

Land cover in BiH is heterogeneous. About 86 percent are automorphic soils, and the remaining 14 percent hydromorphic soils. A large part of Bosnia and Herzegovina is exposed to water erosion, par cularly its central and southern part.

As with other data for BiH, data on agricultural land are not always consistent. Depending on the source, this fi gure varies and diff ers considerably. According to offi cial sta s cs, agricultural land in BiH occupies 2.163 million hectares, 42.2 percent of its territory. This fi gure is a fi ve-year average farm size in the Republic of Srpska, the Federa on of BiH and Brčko District, according to data of the en ty and state agencies for sta s cs, which is shown in the Table 2.5:

BiH has 2.16 million hectares of agricultural land. In this structure a li le less than half is arable land and gardens (1.023 million hectares or 47.3 percent of total agricultural land). The other half of the agricultural land used for

livestock produc on is meadows (445,000 ha, 20.6 percent) and pastures (593,000 ha, 27.4 percent). Fruit orchards and vineyards (3,500 ha) cover 98,000 hectares (4.5 percent of total agricultural land).

Although both en es occupy roughly the same area, Republika Srpska has a higher share of total arable land (58 percent), and the Federa on more of the total meadows (59 percent) and pastures (72 percent). This is the result of the natural geography of each en ty, and as a consequence there is signifi cant produc on of crops in RS, whilst in the Federa on greater importance is given to livestock.

2.4.2.1. Agricultural land use

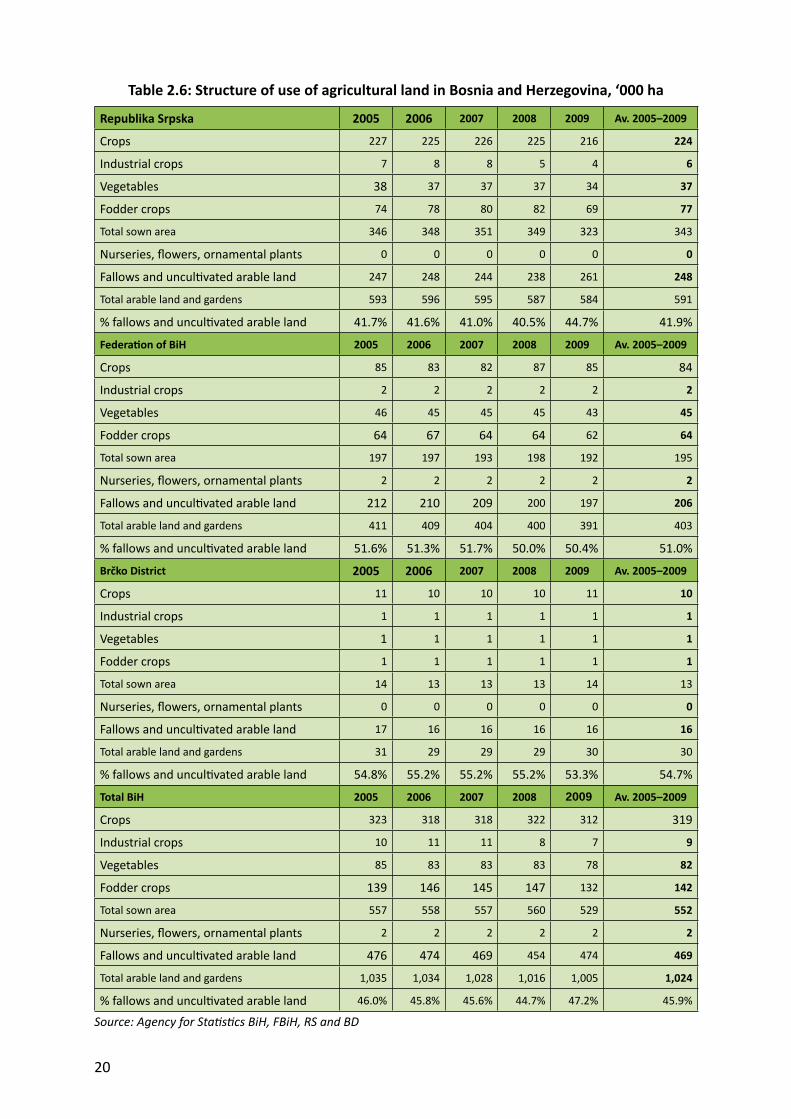

Most of the agricultural land in BiH is used for the produc on of grain (58 percent; 319,000 ha), where this produc on is more signifi cant in RS (65 percent) than in FBiH (43 percent). One quarter (26 percent; 142,000 ha) of the area is under forage crops, and 15 percent (82,000 ha) under vegetables. Areas under industrial crops are constantly being reduced, and by 2009 had fallen to 7,000 ha in all of Bosnia and Herzegovina (1.7 percent of agricultural land). The detailed structure of agricultural land use is shown in the Table 2.6.

20

Table 2.6: Structure of use of agricultural land in Bosnia and Herzegovina, ‘000 ha

Republika Srpska 2005 2006 2007 2008 2009 Av. 2005–2009

Crops 227 225 226 225 216 224

Industrial crops 7 8 8 5 4 6

Vegetables 38 37 37 37 34 37

Fodder crops 74 78 80 82 69 77

Total sown area 346 348 351 349 323 343

Nurseries, fl owers, ornamental plants 0 0 0 0 0 0

Fallows and uncul vated arable land 247 248 244 238 261 248

Total arable land and gardens 593 596 595 587 584 591

% fallows and uncul vated arable land 41.7% 41.6% 41.0% 40.5% 44.7% 41.9%

Federa on of BiH 2005 2006 2007 2008 2009 Av. 2005–2009

Crops 85 83 82 87 85 84

Industrial crops 2 2 2 2 2 2

Vegetables 46 45 45 45 43 45

Fodder crops 64 67 64 64 62 64

Total sown area 197 197 193 198 192 195

Nurseries, fl owers, ornamental plants 2 2 2 2 2 2

Fallows and uncul vated arable land 212 210 209 200 197 206

Total arable land and gardens 411 409 404 400 391 403

% fallows and uncul vated arable land 51.6% 51.3% 51.7% 50.0% 50.4% 51.0%

Brčko District 2005 2006 2007 2008 2009 Av. 2005–2009

Crops 11 10 10 10 11 10

Industrial crops 1 1 1 1 1 1

Vegetables 1 1 1 1 1 1

Fodder crops 1 1 1 1 1 1

Total sown area 14 13 13 13 14 13

Nurseries, fl owers, ornamental plants 0 0 0 0 0 0

Fallows and uncul vated arable land 17 16 16 16 16 16

Total arable land and gardens 31 29 29 29 30 30

% fallows and uncul vated arable land 54.8% 55.2% 55.2% 55.2% 53.3% 54.7%

Total BiH 2005 2006 2007 2008 2009 Av. 2005–2009

Crops 323 318 318 322 312 319

Industrial crops 10 11 11 8 7 9

Vegetables 85 83 83 83 78 82

Fodder crops 139 146 145 147 132 142

Total sown area 557 558 557 560 529 552

Nurseries, fl owers, ornamental plants 2 2 2 2 2 2

Fallows and uncul vated arable land 476 474 469 454 474 469

Total arable land and gardens 1,035 1,034 1,028 1,016 1,005 1,024

% fallows and uncul vated arable land 46.0% 45.8% 45.6% 44.7% 47.2% 45.9%

Source: Agency for Sta s cs BiH, FBiH, RS and BD

21

Close to half of the arable land in BiH is not cul vated (450–480,000 hectares). There are many contribu ng factors, including the presence of mines,8 the absence of economic mo va on of producers to be involved in agricultural produc on, the ageing of rural households, and the number of proper es s ll remaining vacant a er the war.

Household and farm structure

During the period of the Socialist Federal Republic of Yugoslavia, the size of private farms was limited to 10 ha on fl at and hilly land, whilst in mountain regions farmers were allowed to own up to about 30 ha. Moreover, private proper es and farms were not much favoured by the government during that me, and full a en on was paid only to state farms, which worked about 5 percent of all agricultural land.9

In 2006, it was es mated that there were over 500,000 agricultural holdings in BiH. More than 50 percent of these agricultural holdings are es mated to be less than 2 ha, and over 80 percent are less than 5 ha. These small farms are o en further divided into 7–9 small parcels crea ng major problems for produc vity and overall effi ciency. Although the size of land areas actually cul vated by individual farms may be larger, the extent of land fragmenta on restricts the adop on of more modern agricultural systems.

Recent surveys indicate that subsistence and semi-subsistence farms, which consume the majority of their produc on and produce only li le marketable surplus, remain the dominant form of farm structure in BiH. However, in recent years, there is increasing evidence of more farmers producing for the market. Most commercially oriented farms tend to be larger, though they are o en

restricted in their development due to their status as par ally priva zed en es, which limits their access to and use of modern management and investment capital; consequently many have leased parts of their lands to smaller private farmers. Overall, the need for consolida on of fragmented farm holdings into more viable economic units is recognized as one of the most pressing agricultural policy issues in BiH today.

The general problem of inadequate and uncoordinated data extends also to cadastral and land ownership data, much of which have not been updated since the war and so do not refl ect the current situa on. There is as yet no comprehensive farm or sta s cal register, so no offi cial data are available on the numbers of landowners or agricultural households. In the immediate post-war period there was evidence that the number of landowners was growing and the average size of holdings contrac ng, in marked contrast to the pa erns shown in almost every country of Europe;10 as the economy returns to a more normal condi on, a progressive migra on to the towns (shown consistently in Yugoslavia throughout its existence) may be expected to resume.

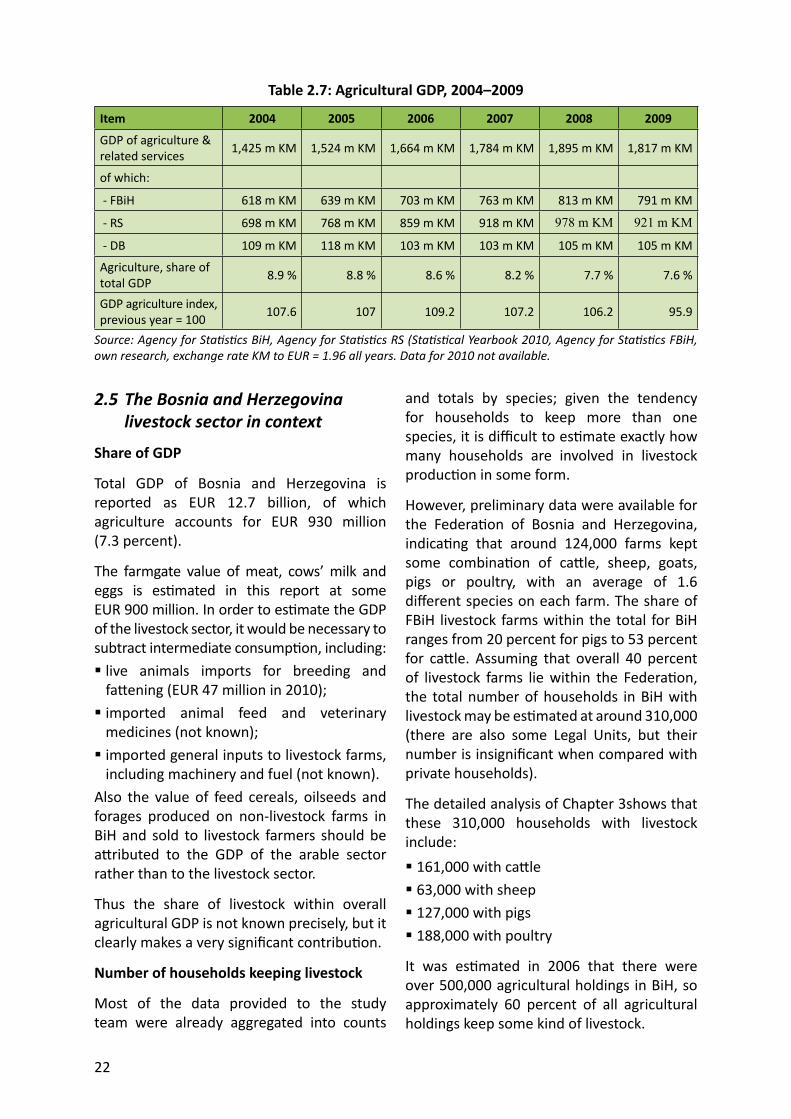

Agricultural GDP

The recent development of agricultural GDP is presented in the Table 2.7.

The share of agriculture in overall GDP has decreased steadily from 2004 to 2009, and is rela vely low compared with other coun es in the region. In 2004, FBiH generated 43 percent of agricultural GDP, RS 49 percent and BD the remaining 8 percent. In 2009, FBiH generated 43.5 percent, RS 50.7 percent and BD 5.8 percent, represen ng a rela vely stable distribu on.

8 According to the BiH Mine Ac on Strategy (2009–2019), the Council of Ministers BiH, 2008, p. 6, BiH at the end of 2008, had suspected 1,573 km2 (mined) areas, which is slightly more than 3 percent of the territory. According to the Managing Director of the Bosnia and Herzegovina Mine Ac on Centre (BHMAC), the suspected area is today (June 2012) 1,544 km2 equal to 3.04 percent of the territory, see Atlan c Ini a ve Newsle er, June 2012. The capacity of demining is 35–40 km2 per year from 2012 to 2019, if fully opera onal. Recent data from the EUD indicate a suspected area of 1,442 km2 equal to 2.81 percent of the BiH territory.

9 Čustović, H. & Ljuša, M. Par cipatory Land Use Development in Bosnia and Herzegovina.p. 1.10 Čustović, H. & Ljuša, M. Par cipatory Land Use Development in Bosnia and Herzegovina. p.3.

22

2.5 The Bosnia and Herzegovina livestock sector in context

Share of GDP