Embed Size (px)

Citation preview

A report from the Economist Intelligence Unit

sponsored by SAP

Thinking bigMidsize retail firms and the challengesof growth

© The Economist Intelligence Unit 2006 1

Thinking big

Midsize retail firms and the challenges of growth

Thinking big: Midsize retail firms and the challenges of

growth is an Economist Intelligence Unit white paper,

sponsored by SAP.

The Economist Intelligence Unit bears sole

responsibility for the content of this report. The

Economist Intelligence Unit’s editorial team

conducted the interviews, executed the survey and

wrote the report. The findings and views expressed in

this report do not necessarily reflect the views of the

sponsor.

Our research drew on two main initiatives:

● We conducted a wide-ranging survey of 526

executives of midsize retail firms from October 2005

to January 2006, using both telephone and online

surveying techniques. This was part of the

Economist Intelligence Unit’s global survey, Midsize

companies, in which 3,722 executives took part.

● To supplement the survey results, we also

conducted in-depth interviews with several senior

executives of midsize retail firms.

The author of the report was James Watson and the

editor was Denis McCauley. Mike Kenny was

responsible for design and layout.

Our sincere thanks go to the interviewees and

survey participants for sharing their insights on this

topic.

March 2006

Preface

2 © The Economist Intelligence Unit 2006

Thinking big

Midsize retail firms and the challenges of growth

Executive summary

In markets dominated by large, powerful players

with enormous purchasing power, midsize

retailers face a difficult set of challenges. They are

decidedly growth-oriented, but they also find

themselves squeezed in a very tough competitive

environment, manifested in downward pressure on

prices and market saturation, not to mention

consolidation of competitors and suppliers. To cope

with these challenges while continuing to pursue

growth, they will take great pains over the next three

years to improve their operating efficiency.

This white paper, sponsored by SAP and based on

an Economist Intelligence Unit survey of 526 retail

executives from around the globe, suggests that

midsize retailers will focus on the following growth

priorities:

● Keep focused on the bottom line. Midsize retailers

plan to expand over the next three years, but always

with an eye on profitability. While half of retail firms in

the survey (50%) will pursue expansion of the

customer base as their primary means to secure

revenue growth, nearly as many (49%) say that

improving operating efficiency and reducing costs is a

central plank of growth strategy. Moreover, a majority

of retailers are oriented toward an optimal rate of

growth, suggesting a recognition that expanding too

fast can strain existing resources and structures.

● Growth from within. More than two-thirds of

midsize retailers (69%) plan to deliver profit and

revenue growth organically, using either their own

resources or a network of third parties. This internal

focus comes far ahead of any possible M&A-based

strategy, with companies preferring to partner where

necessary, rather than engage in the risky process of

taking control of other rivals.

● Stay nimble and responsive. Midsize firms

typically lack the muscle to compete effectively

against their larger rivals, a situation exacerbated by

the trend toward consolidation. Midsize retailers enjoy

the advantages of being closer to their customers, and

of being more flexible in strategy execution and

pricing. But survey respondents worry that these

attributes will erode as their firms expand.

● Good IT, good people. If used effectively,

information technology (IT) can help to stem the

erosion of speed, flexibility and customer intimacy

that usually comes with expansion. Indeed, two-thirds

of midsize retailers believe IT is critical to their firms’

ability to maintain flexibility as they grow.

Technology, however, is only as good as the people

who manage and use it. More than other types of

firms, midsize retailers struggle with a shortage of IT

expertise among their staff. Beyond deploying better

IT systems, they will need to improve their recruiting

and training practices in order to meet their growth

objectives.

© The Economist Intelligence Unit 2006 3

Thinking big

Midsize retail firms and the challenges of growth

Who took the survey?

A total of 3,722 executives from

around the world participated in the

Midsize companies survey,

conducted by the Economist

Intelligence Unit from October 2005

to January 2006. Of this number, 526

respondents hailed from the retail

industry. Of the latter group, 47%

were C-level executives such as CEOs,

CFOs and CIOs as well as owners, and

the other 53% were other senior

managers.

We have chosen to employ a

definition of midsize firms based on

revenue. Thus, 91% of the retail

firms in our survey have annual

global revenue of between US$20m

and US$500m. The other 9% range

slightly above or below these

thresholds. (For more detail on the

survey sample and results, please see

the Appendix to this report.)

In addition to our survey, we

conducted in-depth interviews with

senior executives of midsize retailers

in different regions, obtaining their

insights into the nature of the

growth challenges facing them over

the next three years and how they

plan to overcome them.

4 © The Economist Intelligence Unit 2006

Thinking big

Midsize retail firms and the challenges of growth

Midsize retail firms have an enormous appetite

for growth, but they currently find themselves

squeezed by the effects of an increasingly

tough global competitive environment. Downward

pressure on prices is the most troublesome

manifestation of this, as technology advances and

market liberalisation combine to lower entry barriers

to new competitors using traditional as well as online

channels.

Perhaps for this reason, leaders of most midsize

retailers also appear to appreciate the limits of

expansion. Over half, or 54%, of the executives in our

survey say that their firms are oriented toward an

optimal rate of growth. An even higher proportion

(57%) say that they have also identified an optimal

size. (Retailers in Asia-Pacific and the US are

considerably more likely than those in Europe to have

set optimal size and growth figures.) This suggests a

realisation on the part of midsize retailers that overly

rapid growth can strain the firm’s financial, human

and other resources.

First things first—boost operating efficiency

In order to deliver the growth they desire, midsize

retailers will focus their attentions on a variety of

methods, although a consistent area of focus will be

on sharper operational efficiency. Half of all retailers

polled for this survey plan to cut costs through better

operating efficiencies, while also expanding their

customer base. Lori Schafer, a board member at a

US$500m speciality US retailer, says her firm needs to

entirely re-engineer its operational processes to

become more competitive. “We’re making significant

changes to the company, because for the first time in

our history, growth has completely stalled. We’ve hit a

plateau”, she says.

Retailers will pursue a number of strategies to

achieve revenue growth, but the priority of most firms

in the survey will be expansion of the customer base.

US retailers will pursue this path particularly

aggressively: 71% of American respondents cite new

customer acquisition as their top growth objective.

Beyond this, 34% of retailers surveyed will look to

diversify the products and services they provide.

TheFaceShop, a speciality cosmetics retailer based in

South Korea, will rely on an ever-expanding range of

products that fit within the brand’s value identity to

fuel its growth. “No products in our Korean market sell

for more than US$15”, says COO Tom Kim. “[Our range]

provides an attractive value proposition, and people

love the choice and availability of stock. We always

have about a thousand different products on the shelf

at any one point”.

Nearly a third of retailers polled will also focus on

squeezing more out of their existing customers. Some,

What are the most important ways in which your company will implement its growth strategy over the next three years? Top responses (% respondents)

Source: Economist Intelligence Unit

Expansion of the customer base

Cost reduction via better operating efficiency

Diversification of product/service portfolio

Further penetration of existing accounts

50

34

49

26

53

37

71

33

38

3126

4029

4948

60

Global Europe APAC US

Strategies for growth

© The Economist Intelligence Unit 2006 5

Thinking big

Midsize retail firms and the challenges of growth

such as the UK’s Phones4u, a High Street mobile

phone retailer, will achieve this through ongoing staff

training to deliver a superior customer service over

rivals. “The best way to grow is to train up people”,

says group managing director Tim Whiting. “It’s about

delivering on our sales process, in every store and on

every day. When we get it right, we take a very high

level of market share”.

Marshaling internal resources for growth

Larger midsize firms appear to be opportunistic about

acquisitions, but few midsize retailers will pursue

mergers or acquisitions (M&A) as a central plank of

growth strategy. Nearly seven out of ten survey

respondents believe their primary growth

opportunities will be based on organic expansion,

rather than through M&A or joint ventures. About 43%

of companies polled say they plan to rely on organic

growth via the use of wholly owned resources, while

more than one in five will use a network of third

parties for production and distribution to deliver

organic growth.

Phones4u plans to achieve organic growth in its

local market through an expansion of retail locations.

“The focus is on organic growth”, says Mr Whiting. “All

our growth occurs through this”. And those firms that

have gained a strong position in their local markets

will seek to expand abroad. “We are looking at markets

for growth outside of the UK, although the UK remains

our number one priority”, he adds.

By comparison, just one in ten retailers will use

M&A as a tool for expansion and 9% will engage in

joint ventures. In fact, some firms believe an

acquisition would actually hinder further progress,

especially for companies grappling with the transition

from a smaller niche player into a more substantial

midsize retailer. Ms Schafer says her organisation

needs to rebuild itself organically before considering

any possible acquisitions. “An acquisition wouldn’t

help; in fact it would probably compound our

problems”, she argues.

Expansion abroad will become a key driver for

growth for nearly a third of retailers. Clearly,

globalisation is not just for the big players. Midsize

companies are tapping into global markets to reap the

same benefits that multinationals are, including both

revenue growth and cost reduction. One in three

midsize retailers believe that tapping into new

geographic markets will be among the most important

ways that they’ll implement their growth strategy in

the coming three years.

As it approaches market saturation in its home

territory, TheFaceShop has moved aggressively beyond

its national borders into 14 different countries in the

space of just a few years. Its key targets include the

US, China and Japan. “They are the largest cosmetics

markets outside of South Korea, excluding Western

Europe”, says Mr Kim. Albert Béchet, CFO at France’s

Dexxon, a computer media and consumables

wholesaler, believes any firm unable to expand

internationally will suffer. “Those who can’t grow at an

international level will be in some trouble”, he says.

TheFaceShop is pursuing expansion by awarding

mass distribution licences to firms in local markets.

The agreements establish a franchise for the firm’s

trademark and products, as well as its technical

infrastructure and know-how. The rest is left to the

partner, who’s free to roll out stores in any location

In your company, what is viewed as the single most important measure of growth? Select one only.(% respondents)

Growth of total revenue 34

Growth of market share 18

Growth of profit 28

Growth in number of customers 16

Growth in number of employees 1

Growth in number of geographic markets reached 3

Source: Economist Intelligence Unit

6 © The Economist Intelligence Unit 2006

Thinking big

Midsize retail firms and the challenges of growth

they see opportunity. “We love the shopping malls and

department stores”, says Mr Kim. “In fact, in Korea

40% of our revenue come from these channels.

Wherever there’s the right traffic, that’s where we’re

going to be”.

No smooth sailing: a raft of challenges

But achieving growth will not come without

challenges. For midsize firms around the world,

downward pressure on prices is the most troublesome

manifestation of a tougher global competitive

environment, and the retail industry is no exception:

45% of survey respondents reckon that downward

price pressure will remain a hard fact of life over the

next three years. Technology advances are reducing

entry barriers to new competitors—in both traditional

and online channels—and big-box retailers with scale

economies are forcing many rivals to compete on

price. Margin squeeze is the result.

Mr Béchet says his firm now has to compete with

very aggressive rivals in France and other European

countries. “They’re not yet able to deliver high levels

of service, but can give some good prices”, he says.

“They’re low-cost organisations. They compete on

commodity products, but not on the whole range. This

hurts, because it puts pressure on the price, and

margins are very low already”.

As if price declines aren’t enough, 38% of midsize

retailers also see demand saturation in their markets

as a significant impediment to growth. One-third of

firms also believe they will encounter serious

difficulties in hiring sufficiently talented staff (a top

barrier to growth for the absolute majority of Asia-

Pacific retailers). And 34% cite the rising costs of

inputs as another issue to contend with.

What do you believe will be the most serious impediments to growth in your key markets over the next three years? Top responses (% respondents)

Source: Economist Intelligence Unit

Downward pressure on prices

Market saturation

Rising cost of raw materials and services

Shortage of talented staff

45

34

49

30

42

38

43

38

29

3319

5138

3833

50

Global Europe APAC US

© The Economist Intelligence Unit 2006 7

Thinking big

Midsize retail firms and the challenges of growth

The biggest competitive threat for most midsize

retailers comes from larger rivals in the same

market. And existing rivals aren’t the only

concern: nearly one in five midsize retailers are

concerned about larger organisations suddenly

entering their market and jostling for market share.

But there are some advantages involved with running

a smaller organisation. Survey respondents believe

their firms maintain deeper customer relationships

(46%), can implement changes in strategy more

rapidly (43%) and enjoy greater flexibility in setting

prices (42%).

Speed of execution in implementing strategy

resonates as a key competitive attribute of midsize

firms across industries. Ms Schafer says the

turnaround of her company will rely on a commitment

to change throughout the organisation. “The good

news for a company of our size is that it’s normally

much easier to achieve. We’re smaller, more willing to

change, more entrepreneurial. There are fewer layers

of bureaucracy”, she says.

But aggressive smaller rivals are also a worry,

nipping on the heels of midsize retailers and fighting

for market share. 31% of executives cite these firms as

their principle competitive threat. But as with larger

firms, midsize retailers hold key advantages. For

example, 40% say their firms can marshal resources

more effectively than smaller retailers to enter new

geographic markets. And they’re able to forge

stronger supplier relationships, something that 37%

of respondents see as a primary advantage over

smaller competitors.

In comparison with other industries such as

manufacturing, retail firms are considerably more

focused on local competition than the threat of

overseas entrants. For example, European

respondents view German and French retailers as the

principal threats to their position, whereas in the Asia-

Pacific region, expansion-minded Chinese retailers

pose the main worry, along with US and Japanese

retail rivals.

Growing pains

But as retailers grow, so their challenges evolve. The

company becomes harder to control as tightly as it did

before, and implementing change becomes tougher,

tending to get bogged down more frequently. When

asked which of their competitive attributes are most

likely to erode with growth, 37% of retail respondents

to the survey cite their ability to execute changes in

strategy quickly.

Just as serious a concern for executives of midsize

retailers is that their ability to maintain close

relationships with customers will deteriorate. Another

28% worry about the loss of pricing flexibility. And

about one in four think either the quality of their

products and services or their ability to specialise in

particular products and services will deteriorate.

Ms Schafer says that maintaining a strong brand

identity and close relationships with customers is

Staying one step ahead: Competitors, customers and suppliers

What types of firms are likely to pose the main competitive threat to your company over the next three years? Select one only.(% respondents)

Existing players in our market(s) larger than us in size 41

Existing players in our market(s) smaller or equivalent to us in size 31

New entrants to our market(s) larger than us in size 18

New entrants to our market(s) smaller or equivalent to us in size 10

Source: Economist Intelligence Unit

8 © The Economist Intelligence Unit 2006

Thinking big

Midsize retail firms and the challenges of growth

critical for midsize retailers as they expand.

Consequently, her firm is investing in customer

intelligence software, expanding loyalty programmes

and engaging in more closely targeted marketing.

“The challenge is being able to increase the customer

base, while also keeping the existing ones happy”, she

says. “It’s not just about discounting, but about

making a statement to specific categories of our

customers, such as teachers, children, camps,

churches and so on”.

Diversifying suppliers … and customers

Battling against large retailers with enormous scale is

tough enough, but midsize retailers also find

themselves having to deal with larger and more

powerful suppliers, another effect of consolidation. A

majority of executives (51%) believe there is a medium

or high level of risk that their firms will become overly

dependent on a few large suppliers for key inputs, and

16% consider the risk as high.

TheFaceShop’s Mr Kim says the key to his firm’s

success is being able to procure and manufacture

product at a sufficient scale, without disrupting

quality levels. Less than 0.5% of items returned by

customers are due to quality control failures. At the

same time, the company strives to attain a rapid time

to market to ensure that stock turnover times, and

related costs, are kept low. “We don’t hold too much

In your view, which of the following attributes is most likely to erode as your company expands in size? Top responses (% respondents)

Ability to execute quickly on changes in strategy

Deep customer relationships

Pricing flexibility

High quality of products/services

3731

4333

3737

3257

2824

325

26

2730

24

Global Europe APAC US

Source: Economist Intelligence Unit

Investing in people

Phones4u, a UK-based reseller of mobile

phones and services, has been one of the

country’s fastest growing retailers over the

past few years, even after entering the

market later than many of its rivals.

Operating in a fast-moving business with

constant pressure on prices and margins,

the company attempts to differentiate itself

from its High Street rivals with superior

customer service. Group managing director

Tim Whiting says his organisation is set up

to provide an entirely different experience

for customers. “This is a complicated market

and there’s a lot of anxiety with consumers

about what handset and tariff to get, so we

pride ourselves on giving a service to our

customers and the best advice”.

To get this right, the company has

invested more than £10m over the past year

in a major staff training campaign. Mr

Whiting firmly believes that the best way to

grow is to train people well. “We have a

bespoke national training academy, and

every person in does one week of training at

this facility before setting foot in our

stores”, he says. Retail locations are also

configured differently from rivals, with

more attention paid to how customers are

handled. “We’re very different from our

rivals; you’ll see that most of our floor space

is taken up not by display shelves, but by

desks”. According to Mr Whiting, staff

spend an average of an hour with every

client helping them complete a contract.

The result for customers is something

more of an appointment-based concept,

where they are led carefully through the

mass of available options to find one that

precisely suits their needs, rather than

simple self-service. “When we get it right,

we take a very high level of market share”,

says Mr Whiting. “So for us it’s not about

the generation of footfall, but the

conversion of that footfall”.

© The Economist Intelligence Unit 2006 9

Thinking big

Midsize retail firms and the challenges of growth

inventory. Typically less than three weeks turnover”,

says Mr Kim.

In her business, Ms Schafer says the focus is on an

increased reliance on IT to improve the company’s

supply chain and stock replenishment. She says the

firm currently relies on staff walking around stores

with scanners to manually update stock levels. “These

are the kinds of issues we’re bumping into. It’s the

classic type of issues for this size of business, in the

$300-$500m range”, she says.

Dependence on large customers is less of a concern,

but retailers of certain types of goods, such as office

suppliers or computer equipment, can generate large

chunks of revenue from corporate accounts, in

addition to individual consumers. A startlingly high

45% of survey respondents say there is a medium or

high degree of risk of becoming beholden for revenue

to such key customers.

10 © The Economist Intelligence Unit 2006

Thinking big

Midsize retail firms and the challenges of growth

Coping with competition from dominant big-box

retailers and nimble new entrants will require all

the speed, adaptability and responsiveness that

midsize retail firms can muster. Retaining some

measure of these attributes as they grow is a tall order,

but not impossible. One tool at their disposal in trying

to achieve this is a team of managers skilled in

adapting business processes. Another is IT.

Executives of midsize retail firms appear to

appreciate IT’s potential to pull this feat off. Although

they display marginally less enthusiasm than peers in

other industries, midsize retailers nonetheless put

great store in IT’s ability to help them grow and to do

so while retaining their best attributes, at least in

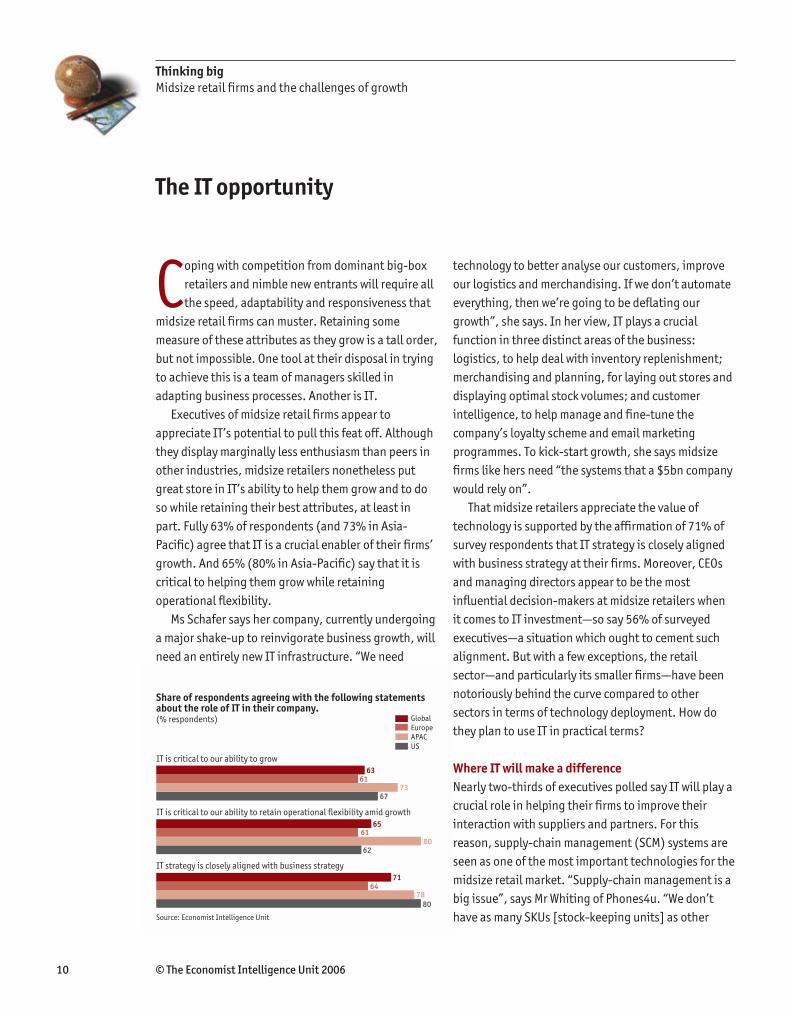

part. Fully 63% of respondents (and 73% in Asia-

Pacific) agree that IT is a crucial enabler of their firms’

growth. And 65% (80% in Asia-Pacific) say that it is

critical to helping them grow while retaining

operational flexibility.

Ms Schafer says her company, currently undergoing

a major shake-up to reinvigorate business growth, will

need an entirely new IT infrastructure. “We need

technology to better analyse our customers, improve

our logistics and merchandising. If we don’t automate

everything, then we’re going to be deflating our

growth”, she says. In her view, IT plays a crucial

function in three distinct areas of the business:

logistics, to help deal with inventory replenishment;

merchandising and planning, for laying out stores and

displaying optimal stock volumes; and customer

intelligence, to help manage and fine-tune the

company’s loyalty scheme and email marketing

programmes. To kick-start growth, she says midsize

firms like hers need “the systems that a $5bn company

would rely on”.

That midsize retailers appreciate the value of

technology is supported by the affirmation of 71% of

survey respondents that IT strategy is closely aligned

with business strategy at their firms. Moreover, CEOs

and managing directors appear to be the most

influential decision-makers at midsize retailers when

it comes to IT investment—so say 56% of surveyed

executives—a situation which ought to cement such

alignment. But with a few exceptions, the retail

sector—and particularly its smaller firms—have been

notoriously behind the curve compared to other

sectors in terms of technology deployment. How do

they plan to use IT in practical terms?

Where IT will make a difference

Nearly two-thirds of executives polled say IT will play a

crucial role in helping their firms to improve their

interaction with suppliers and partners. For this

reason, supply-chain management (SCM) systems are

seen as one of the most important technologies for the

midsize retail market. “Supply-chain management is a

big issue”, says Mr Whiting of Phones4u. “We don’t

have as many SKUs [stock-keeping units] as other

The IT opportunity

Share of respondents agreeing with the following statements about the role of IT in their company. (% respondents)

IT is critical to our ability to grow

IT is critical to our ability to retain operational flexibility amid growth

IT strategy is closely aligned with business strategy

6361

7367

6561

8062

7164

78

80

Global Europe APAC US

Source: Economist Intelligence Unit

© The Economist Intelligence Unit 2006 11

Thinking big

Midsize retail firms and the challenges of growth

retailers might have. However, if a new, fashionable

handset becomes available, then we need that to be

available. So SCM is very important”.

TheFaceShop’s Mr Kim says his firm tracks all stock

on a real-time basis in its home market, although it

has yet to achieve this level of control internationally.

“IT is very important to us. We would like to be able to

see all of our sales on a real-time basis and monitor

which product lines are doing well in different

markets”, he says. For a business like his, which also

produces the goods that it sells, SCM systems and

detailed sales forecasts are absolutely essential. “At

the end of the day”, adds Mr Kim, “we also make

manufacturing decisions on the products, and that

needs to be done at the right cost and volume and at

the right time. We don’t want to overproduce the

wrong product”.

For retailers that emphasize their strengths in

customer service, IT will play an increasingly vital role.

56% of firms polled say that IT is a critical tool for

maintaining tight customer relationships. Phones4u,

for example, aims to differentiate itself from local

rivals through superior customer service, with sales

staff spending as much as an hour with each customer

discussing their needs. In-store computers provide

sales staff with quick access to customer data via a CRM

application, which help staff to support their

interactions with individual customers. This is

focusing the firms’ IT spending accordingly. “The

biggest upgrade over the next 12-18 months will be in

our CRM systems”, says Mr Whiting.

Scaling up for growth

Midsize retailers point to a number of factors that will

drive investment in IT. First and foremost is the need

to accommodate the growth of the business, followed

by the need to replace existing systems and, not least

important, the overriding objective of boosting

Share of respondents agreeing with the following statements about the role of IT in their company. (% respondents)

IT is critical to our ability to improve customer relationships

IT is critical to our ability to interact with suppliers and partners more effectively

IT is critical to our ability to innovate continuously

5648

6848

6563

7286

6264

68

52

Global Europe APAC US

Source: Economist Intelligence Unit

What are likely to be the main drivers of IT investment in your company over the next three years? Top responses (% respondents)

47

39

36

29

23

23

22

18

18

6

15

Need to accommodate growth of the business

Inadequacy or obsolescence of current IT systems

Pressures on operating efficiency

Need to support company's competitiveness vis-à-vis larger firms

Need to enable adaptation of business model

Increasing concerns about information security

Need to support company's competitiveness in global markets

Increasing regulatory and reporting requirements

Need to create or maintain ability to innovate continuously

Mandates by key customers or suppliers (eg, on business processes, reporting standards)

Other

Source: Economist Intelligence Unit

12 © The Economist Intelligence Unit 2006

Thinking big

Midsize retail firms and the challenges of growth

operating efficiency. About one in three retailers

polled say their current infrastructure does not meet

their requirements for scaling up for growth.

France’s Dexxon has been investing heavily in

technology in recent years, including a new enterprise

resource planning (ERP) system. Its aim is to obtain a

real-time view of sales, profit and inventory details.

According to Mr Béchet: “We want information at our

fingertips across the business and across all of the

geographies we operate in. This is the backbone of the

company’s IT as a strategic asset and will remain so in

the future”. He is now working to make these systems

easily accessible by suppliers, partners and customers,

giving them a similar live view of the business. “We see

the need to improve the level of service that we can

provide our suppliers and customers, such as sales

reports, inventory lists, and so on. It’s a matter of

service and staying in the game”, he says.

But cost will restrain the IT spend of many midsize

retailers. Asked to list the top three barriers to their IT

investment over the next three years, a substantial

majority (61%) cite the cost of new systems and their

implementation ahead of all others. The limited IT

budgets typical of midsize firms, and fierce internal

competition for funds, also mean that other business

priorities will often take precedence over IT

investments.

This isn’t the only pitfall. Nearly a third of retail

respondents say that employees’ lack of adequate

technical skills is a major problem. Mr Béchet warns

that in businesses like his, with a total of about 20 IT

staff, everyone needs to be clued up on technology.

“We’ve all got to be experts, including people like the

chief accountant and myself”, he says.

What are likely to be the main impediments to IT investment in your company over the next three years? (% respondents)

61

34

31

24

23

23

22

20

14

7

Source: Economist Intelligence Unit

Cost of new systems and implementation

Other business priorities take precedence

Lack of employee technical skills to use technology

Employee resistance to change

Ineffective management of IT

Need to amortise existing technology investments

Technical shortcomings in IT systems and infrastructure

Lack of understanding of/confidence in technology benefits by senior management

Risk of business disruption from a failed IT project

Other

© The Economist Intelligence Unit 2006 13

Thinking big

Midsize retail firms and the challenges of growth

Midsize retailers face a unique challenge.

Although aggressively focused on growth and

expansion, they increasingly operate in

markets dominated by much larger rivals, but lack

their visibility, resources and influence. These

disadvantages often make it difficult to compete not

only for customers, but also for talent, finance and

sometimes even the attentions of suppliers,

weaknesses which are often magnified in foreign

markets.

Even as they grapple with larger competitors,

midsize retailers can usually rely on some advantages.

Execution is typically faster, they enjoy greater pricing

flexibility and often have deeper customer relations.

The key for growth-oriented retailers is to avoid or

mitigate the erosion of these attributes as they

expand.

Midsize retailers across the globe plan to invest in

IT and people to meet this challenge. “We’re a service-

based retailer, so having the best people and the best

skills will differentiate us going forward”, affirms Mr

Whiting of Phones4u. “This is all supported by IT, good

supply-chain management systems and strong

locations. But investing in people is absolutely key”.

Conclusion

14 © The Economist Intelligence Unit 2006

Appendix: survey resultsThinking big

Midsize retail firms and the challenges of growth

From October 2005 to January 2006, the Economist

Intelligence Unit conducted a survey of 526 executives

of midsize retail firms from 18 countries in Europe,

Asia-Pacific and the Americas. Our sincere thanks go to

all who took part in the survey.

Please note that not all answers add up to 100%,

because of rounding or because respondents were able

to provide multiple answers to some questions.

What is your firm’s ownership status? Select all that apply.(% respondents)

Privately owned 66

Publicly traded 18

Joint-venture ownership 11

50% or more state-owned 8

In which region are you personally based?(% respondents)

Asia-Pacific

Western Europe

Latin America

CIS (Commonwealth of Independent States)

North America

Eastern Europe

37

22

29

7

4

2

Which of the following titles best describes your job?(% respondents)

Manager

Head of department

CFO/Treasurer/Comptroller

CEO/COO/President/Managing director

Head of business unit

Owner

Other C-level executive

CIO/Technology director

SVP/VP/Director

Board member

Other

15

15

12

10

6

6

6

5

5

17

3

In which sector does your organisation belong?(% respondents)

Consumer goods & services retailFinancial services 100

© The Economist Intelligence Unit 2006 15

Appendix: survey results

Thinking big

Midsize retail firms and the challenges of growth

What is your company’s annual turnover in US dollars?(% respondents)

Under $10m

$10m to $20m

$20m to $40m

$40m to $50m

$50m to $100m

$100m to $200m

$200m to $300m

$300m to $500m

$500m to $600m

$600m to $700m

$700m to $1bn

More than $1bn

3

2

27

8

12

1

20

1

17

7

1

2

What are your main functional roles? Select up to three.(% respondents)

General management

Marketing and sales

Customer service

Finance

Strategy and business development

Human resources

IT

Procurement

Operations and production

Information and research

Risk

Legal

Supply-chain management

R&D

Other

32

28

24

22

16

13

12

10

8

5

5

7

2

7

5

Please characterise the primary type of growth strategy that your company will pursue over the next three years.(% respondents)

Organic growth via the use of wholly owned resources

Organic growth via a network of third parties for production and distribution

Mergers and acquisitions (M&A)

Joint ventures

Organic growth involving a public offering of equity

Other

43

21

11

8

4

12

In your company, what is viewed as the single most important measure of growth? Select one only.(% respondents)

Growth of total revenue 34

Growth of market share 18

Growth of profit 28

Growth in number of customers 16

Growth in number of employees 1

Growth in number of geographic markets reached 3

What are the most important ways in which your company will implement its growth strategy over the next three years? Select up to three.(% respondents)

Expansion of the customer base

Cost reduction through improvement of operating efficiency

Diversification of product/service portfolio

Further penetration of existing customer accounts

Tapping new geographic markets

Establishment/expansion of distributor network

More aggressive pricing

Establishment/expansion of marketing alliances with third parties

Establishment/expansion of licensing or franchising agreements

Outsourcing of production to third parties

Other

50

49

34

31

31

18

18

14

12

6

5

16 © The Economist Intelligence Unit 2006

Appendix: survey results

Thinking big

Midsize retail firms and the challenges of growth

Please indicate whether you agree with the following statements about your company’s size and growth.(% respondents)

Owners and senior management have identified an optimal rate of growth for our company 54 30 16

Owners and senior management have identified an optimal size (in revenue or other terms) for our company 57 24 18

Agree Disagree Don’t know

What do you believe will be the most serious impediments to growth in your key markets over the next three years? Select up to three.(% respondents)

45

38

34

33

25

21

18

15

12

10

7

Downward pressure on prices

Market saturation

Rising cost of raw materials and services

Shortage of talented staff

Consolidation among competitors

High labour costs vis-à-vis competitors in other countries

Tight availability of financing

Increased regulatory pressures

Customer-driven mandates (eg, on product standards, business processes, reporting standards)

Consolidation among customers

Other

What types of firms are likely to pose the main competitive threat to your company over the next three years? Select one only.(% respondents)

Existing players in our market(s) larger than us in size 41

Existing players in our market(s) smaller or equivalent to us in size 31

New entrants to our market(s) larger than us in size 18

New entrants to our market(s) smaller or equivalent to us in size 10

Competitors from which country are likely to present the biggest threat to your company in your existing market(s)? Select one only.(% respondents)

China

United States of America

Germany

France

Japan

Brazil

Argentina

Australia

Italy

Other

18

17

12

11

6

4

3

3

3

24

© The Economist Intelligence Unit 2006 17

Appendix: survey results

Thinking big

Midsize retail firms and the challenges of growth

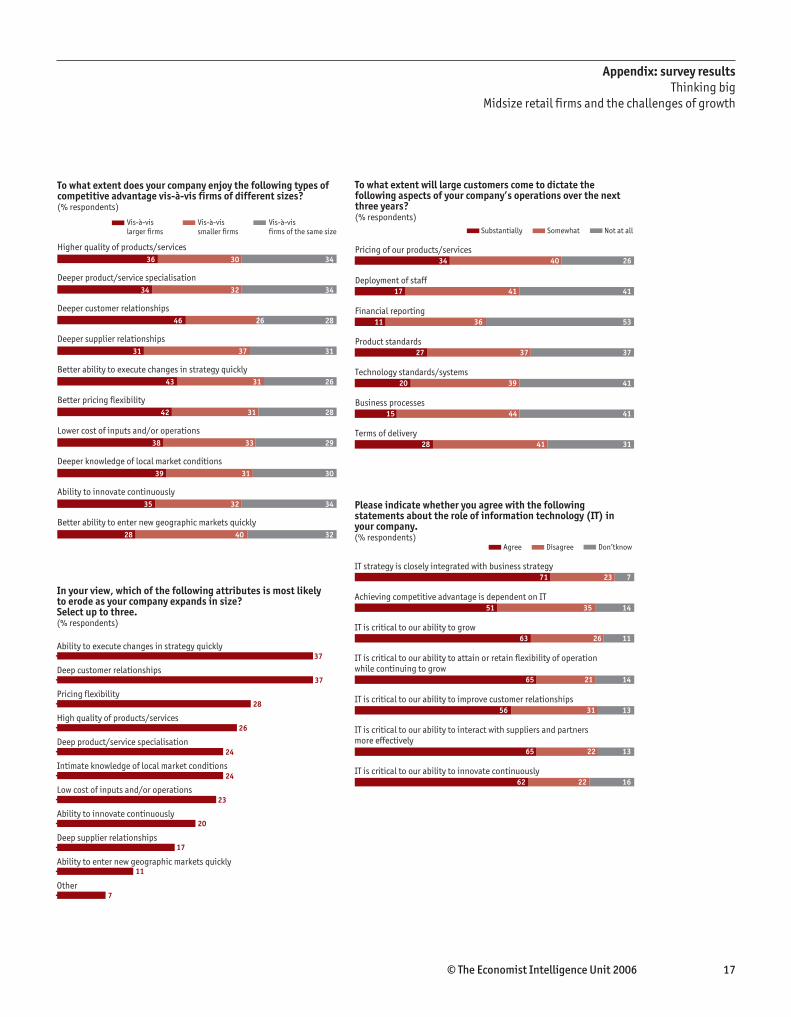

To what extent does your company enjoy the following types of competitive advantage vis-à-vis firms of different sizes?(% respondents)

Higher quality of products/services

36 30 34

Deeper product/service specialisation

34 32 34

Deeper customer relationships

46 26 28

Deeper supplier relationships

31 37 31

Better ability to execute changes in strategy quickly

43 31 26

Better pricing flexibility

42 31 28

Lower cost of inputs and/or operations

38 33 29

Deeper knowledge of local market conditions

39 31 30

Ability to innovate continuously

35 32 34

Better ability to enter new geographic markets quickly

28 40 32

Vis-à-vis Vis-à-vis Vis-à-vis larger firms smaller firms firms of the same size

To what extent will large customers come to dictate the following aspects of your company’s operations over the next three years?(% respondents)

Pricing of our products/services 34 40 26

Deployment of staff 17 41 41

Financial reporting 11 36 53

Product standards 27 37 37

Technology standards/systems 20 39 41

Business processes 15 44 41

Terms of delivery 28 41 31

Substantially Somewhat Not at all

Please indicate whether you agree with the following statements about the role of information technology (IT) in your company.(% respondents)

IT strategy is closely integrated with business strategy 71 23 7

Achieving competitive advantage is dependent on IT 51 35 14

IT is critical to our ability to grow 63 26 11

IT is critical to our ability to attain or retain flexibility of operation while continuing to grow 65 21 14

IT is critical to our ability to improve customer relationships 56 31 13

IT is critical to our ability to interact with suppliers and partners more effectively 65 22 13

IT is critical to our ability to innovate continuously 62 22 16

Agree Disagree Don’tknow

In your view, which of the following attributes is most likely to erode as your company expands in size? Select up to three.(% respondents)

Ability to execute changes in strategy quickly

Deep customer relationships

Pricing flexibility

High quality of products/services

Deep product/service specialisation

Intimate knowledge of local market conditions

Low cost of inputs and/or operations

Ability to innovate continuously

Deep supplier relationships

Ability to enter new geographic markets quickly

Other

37

37

28

26

24

24

23

20

17

11

7

18 © The Economist Intelligence Unit 2006

Appendix: survey results

Thinking big

Midsize retail firms and the challenges of growth

How would you characterise the risk of your company becoming, over the next three years, overly dependent on a few large customers or suppliers?(% respondents)

A few large customers, for revenue 14 30 51 4

A few large suppliers, for key inputs 16 35 44 5

High risk Medium risk Low risk We’re already overly dependent

What are likely to be the main drivers of IT investment in your company over the next three years? Select up to three.(% respondents)

47

39

36

29

23

23

22

18

18

6

15

Need to accommodate growth of the business

Inadequacy or obsolescence of current IT systems

Pressures on operating efficiency

Need to support company's competitiveness vis-à-vis larger firms

Need to enable adaptation of business model

Increasing concerns about information security

Need to support company's competitiveness in global markets

Increasing regulatory and reporting requirements

Need to create or maintain ability to innovate continuously

Mandates by key customers or suppliers (eg, on business processes, reporting standards)

Other

Please indicate whether your company’s current IT infrastructure and systems meet business requirements in the following areas.(% respondents)

Scaling up to accommodate growth of business

52 34 14

Conforming to business process requirements set by customers or suppliers

54 30 17

Conforming to government-mandated reporting and other standards

60 18 21

Meet requirements Do not meet requirements Don’tknow

How influential are the following executives in key decisions your company makes on IT?(% respondents)

Owner/board members

54 27 14 6

Chief executive/managing director

56 29 8 6

CIO/CTO

40 33 15 12

CFO

34 44 11 11

IT manager

41 36 13 10

Line-of-business managers

19 44 26 11

Very influential Somewhat influential Not influential Don’t know

To whom does your company typically turn for external assistance on IT matters? Select all that apply.(% respondents)

IT consulting firm/value-added reseller

Software/hardware/telecommunications equipment vendor

IT specialist with supplier(s)

Management consultant

Accountant

Industry analyst

Legal counsel/solicitor

Other

49

43

40

20

15

12

10

9

© The Economist Intelligence Unit 2006 19

Appendix: survey results

Thinking big

Midsize retail firms and the challenges of growth

In your view, what will be the most effective ways that government can help mid-size companies grow over the next three years? Select up to three.(% respondents)

Offer more favourable tax incentives for investment

Reduce “red tape” (procedures for approvals, licenses, etc.)

Develop more innovative financing support mechanisms

Introduce more flexible labour laws

Provide better information about foreign market conditions and opportunities

Negotiate favourable trade agreements

Invest directly in companies

Expand export credit schemes

Other

63

51

47

41

24

19

14

14

7

What are likely to be the main impediments to IT investment in your company over the next three years? Select up to three.(% respondents)

61

34

31

24

23

23

22

20

14

7

Cost of new systems and implementation

Other business priorities take precedence

Lack of employee technical skills to use technology

Employee resistance to change

Ineffective management of IT

Need to amortise existing technology investments

Technical shortcomings in IT systems and infrastructure

Lack of understanding of/confidence in technology benefits by senior management

Risk of business disruption from a failed IT project

Other

Whilst every effort has been taken to verify the

accuracy of this information, neither The

Economist Intelligence Unit Ltd. nor the sponsor

of this report can accept any responsibility or

liability for reliance by any person on this white

paper or any of the information, opinions or

conclusions set out in the white paper.

LONDON

26 Red Lion Square

London

WC1R 4HQ

United Kingdom

Tel: (44.20) 7576 8000

Fax: (44.20) 7576 8476

E-mail: [email protected]

NEW YORK

111 West 57th Street

New York

NY 10019

United States

Tel: (1.212) 554 0600

Fax: (1.212) 586 1181/2

E-mail: [email protected]

HONG KONG

60/F, Central Plaza

18 Harbour Road

Wanchai

Hong Kong

Tel: (852) 2585 3888

Fax: (852) 2802 7638

E-mail: [email protected]