Embed Size (px)

Citation preview

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 1

1. Introduction

Banking system plays a very important role in the economic life of the nation. The health of

the economy is closely related to the soundness of its banking system. In a developing

country like Bangladesh the banking system as a whole play a vital role in the progress of

economic development. A bank as a matter of fact is just like a heart in the economic

structure and the Capital provided by it is like blood in it. As long as blood is in circulation

the organs will remain sound and healthy. If the blood is not supplied to any organ then that

part would become useless. So if the finance is not provided to agriculture sector or industrial

sector, it will be destroyed. Loan facility provided by banks works as an incentive to the

producer to increase the production. Banking is now an essential part of our economic

system. Modern trade and commerce would almost be impossible without the availability of

suitable banking services. First of all, banking promotes savings. All manner of people, from

the ordinary laborers and workers to the rich land owners and businessmen, can keep their

money safely in banks and saving centers.

Secondly, banking promotes investments. Banks easily invest the money they get in industry,

agriculture and trade. They either invest it directly or advance loans to other investors.

Thirdly, it is most through banks that foreign trade is carried on. Whether we export or

import, it is through banks that money is transferred from one country to another. For

example, bills of exchange and letters of credit are the regular ways banks use to transfer

money. A number of recent studies, however, indicate that the banking sector plays a more

important role than it was believed earlier.

2. Objectives of the Study

The specific objectives of the study are as follows;

i) To evaluate the financial performance by the measurement techniques of private

commercial Banks of Bangladesh.

ii) To analyze the comparative study of financial performance of those Private

Commercial Banks of Bangladesh.

iii) To recommend remedial measures for the development of selected Private

Commercial Banks of Bangladesh.

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 2

3. Scope & Methodology of the study

The present study has been carried out to evaluate the performance of selected private

commercial banks of Bangladesh. The selected banks are

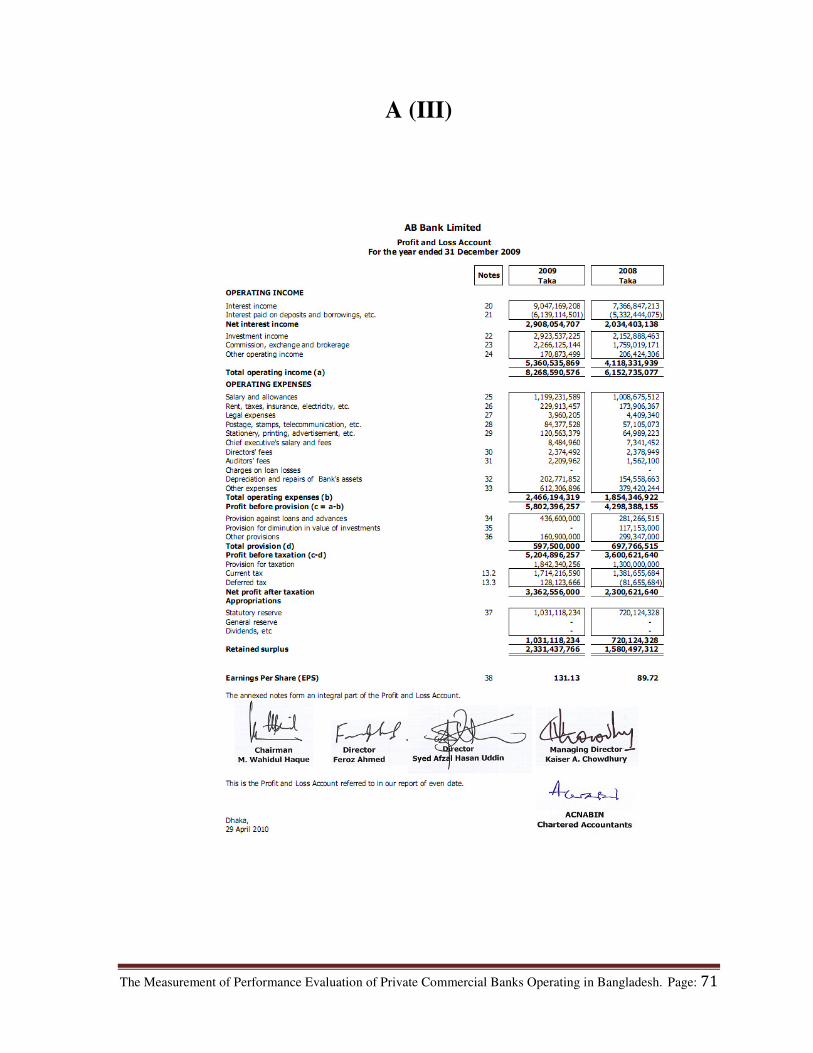

a) Arab Bangladesh Limited (AB Bank Limited),

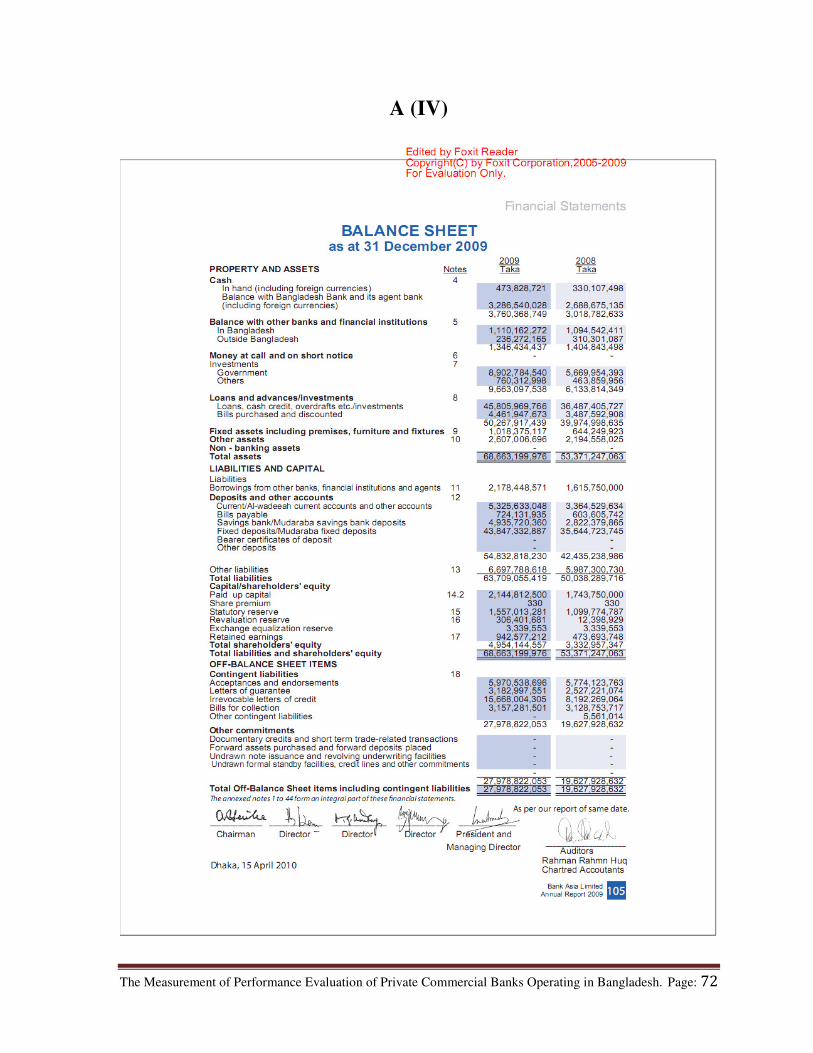

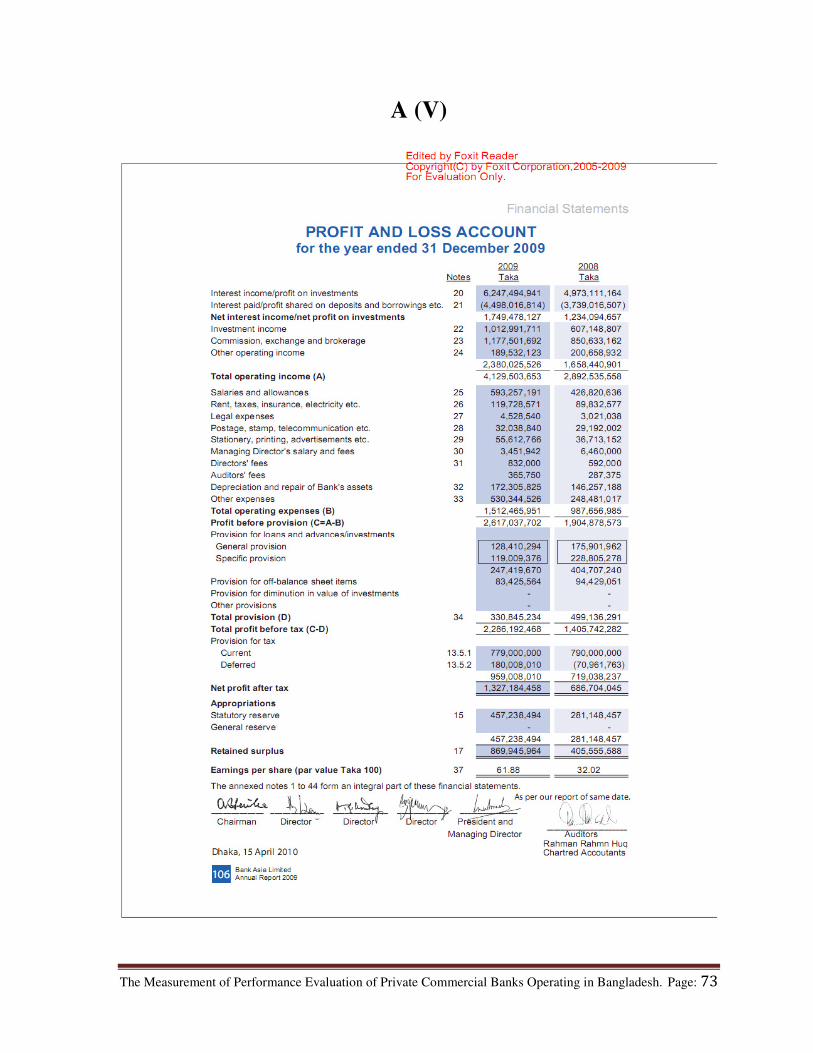

b) Bank Asia,

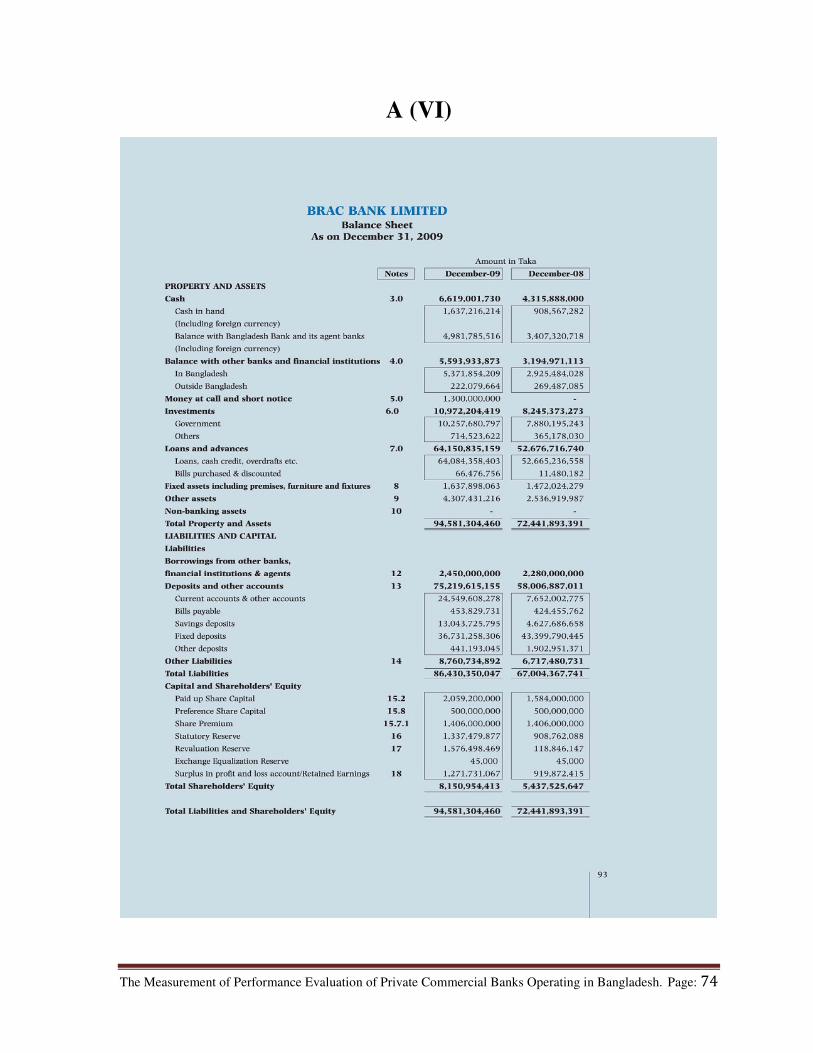

c) Brac Bank Limited,

d) Dutch Bangla Bank Limited (DBBL),

e) Mutual Trust Bank Limited (MTBL),

f) National Credit and Commerce Bank Limited (NCC Bank Limited),

g) The Prime Bank Limited,

h) Trust Bank Limited,

i) United Commercial Bank Limited (UCBL),

j) Uttara Bank Limited.

This study has been based mainly on data from secondary sources. The relevant data and

information were collected from Annual Reports of selected commercial banks of

Bangladesh, Relevant articles and literatures in this context have also been consulted. In this

article, banks are analyzed last two years data of selected private commercial banks of

Bangladesh. For evaluating the performance of selected private commercial banks of

Bangladesh data has been analyzed through the various financial measurement i.e, profit

ratios (return on equity, return on assets, net interest margin and earning per share of stocks

EPS), risk ratios (provision for loss ratio and loan ratio) and efficiency ratios (operating

efficiency ratio and employee productivity ratio). These ratios have been calculated by

financial equation and represent in table and bar chart. Both horizontal and vertical

comparison also represented by chart. In addition credit-risk rating of the selected private

commercial banks is shown which are measured by Credit Rating Agency of Bangladesh Ltd.

(CRAB) and Credit Rating Information and Service Ltd. (CRISL).

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 3

4. Function of Bangladesh Bank (BB)

Bangladesh Bank (BB) has been working as the central bank since the country's

independence. Its prime jobs include issuing of currency, maintaining foreign exchange

reserve and providing transaction facilities of all public monetary matters. Bangladesh Bank

(BB) regulates and supervises the activities of all banks. BB is also responsible for planning

the government's monetary policy and implementing it thereby. The BB has a governing

body comprising of nine members with the Governor as its chief. Apart from the head office

in Dhaka, it has nine more branches, of which two in Dhaka and one each in Chittagong,

Rajshahi, Khulna, Bogra, Sylhet, Rangpur and Barisal.

5. An overview of selected private commercial banks in Bangladesh

5.1. Arab Bangladesh Bank Limited

AB Bank Limited is one of the first generation private commercial banks (PCBs),

incorporated in Bangladesh on 31 December 1981 as a public limited company under the

Companies Act 1913, subsequently replaced by the Companies Act 1994, and governed by

the Banking Companies Act 1991. The Bank went for public issue of its shares on 28

December 1983 and its shares are listed with Dhaka Stock Exchange and Chittagong Stock

Exchange respectively. AB Bank Limited has 78 Branches including 1 Islami Banking

Branch, 1 Overseas Branch in Mumbai, India. The Bank has a subsidiary company, AB

International Finance Limited, incorporated in Hong Kong. The Bank through its Branches

and non-banking subsidiary provides a diverse range of financial services and products in

Bangladesh and in certain international markets. The Bank has expanded its capital market

oriented service horizon to its customers through Merchant Banking Wing.

5.2. Bank Asia Limited

Bank Asia Limited is one of the third generation private commercial banks (PCBs),

incorporated in Bangladesh on 28 September 1999 as a public limited company under the

Companies Act 1994, and governed by the Bank Companies Act 1991. The Bank went for

public issue of its shares on 23 September 2003 and its shares are listed with Dhaka Stock

Exchange Limited and Chittagong Stock Exchange Limited. At present the Bank has 41

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 4

branches, 30 own ATM booths and 33 shared ATM booths. Bank Asia Limited acquired the

business of Bank of Nova Scotia (incorporated in Canada), Dhaka, in the year 2001 and at

the beginning of the year 2002, the Bank also acquired the Bangladesh operations of Muslim

Commercial Bank Limited (MCBL), a bank incorporated in Pakistan, having two branches at

Dhaka and Chittagong. In taking over the Bangladesh operations, all assets and certain

specific liabilities of MCBL were taken over by Bank Asia Limited at book values.

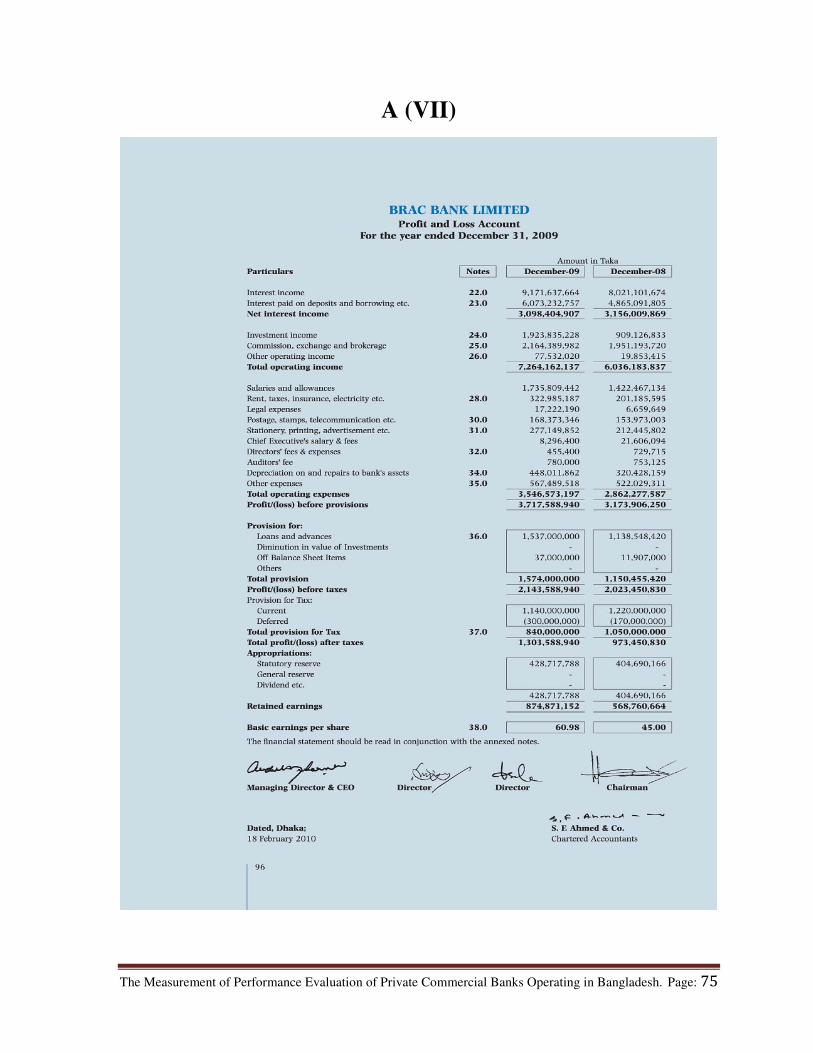

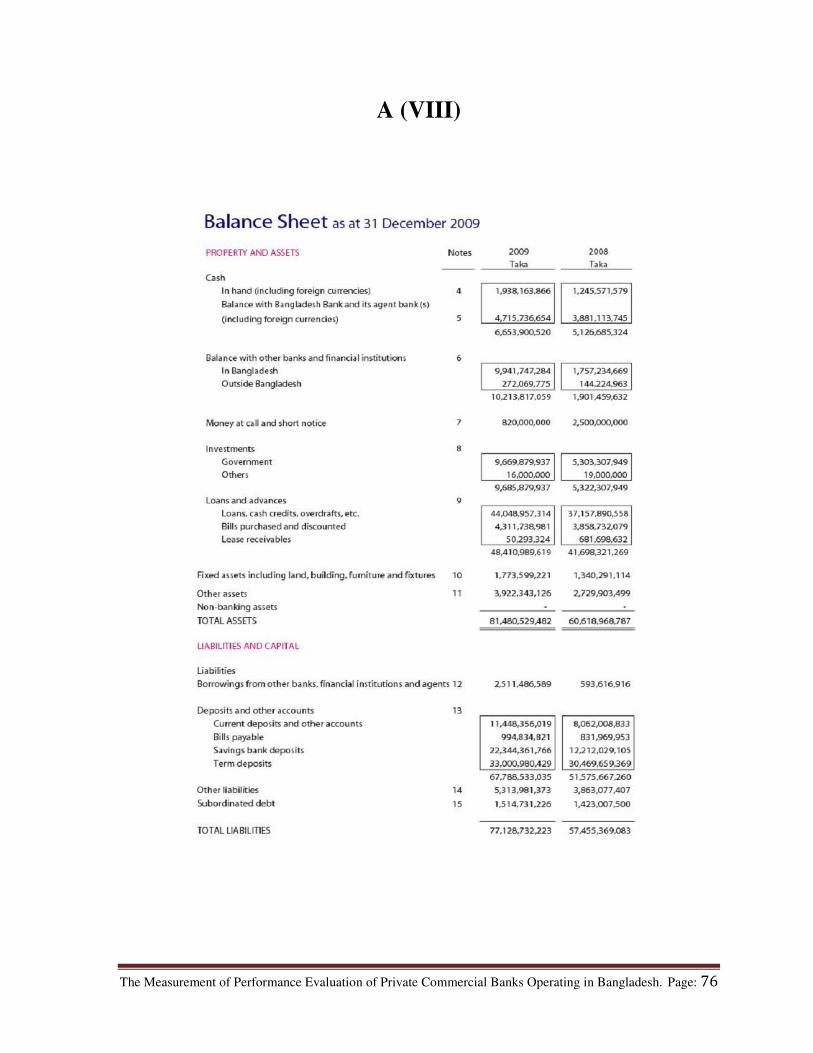

5.3. Brac Bank Limited

Brac Bank Limited is a scheduled commercial bank established under the Bank Companies

Act, 1991 and incorporated as a public company limited by shares on 20 May, 1999 under

the Companies Act, 1994 in Bangladesh. The primary objective of the bank is to carry on all

kind of banking businesses. The bank could not start its operations till 3 June, 2001 since the

activity of the Bank was suspended by the high Court of Bangladesh. Subsequently, the

judgment of the high court was set aside and dismissed by the Appellate Division of the

Supreme Court on 4 June, 2001 and accordingly, the Bank started its operations from 4 July,

2001. At Present the Bank has 69 (sixty nine) branches, 59 SME service centers, 145 zonal

offices and 429 unit offices of SME. The registered address of the Bank is 1, Gulshan

Avenue, Gulshan-1, Dhaka-1212, Bangladesh. BRAC bank is listed with Dhaka Stock

Exchange and Cittagong Stock Exchange as a publicly traded company on 28 January, 2007

and 24 January, 2007 respectively for its general class of shares. The principle activities of

the Bank are banking and related activities such as accepting deposits, personal banking,

trade financing, SME, Retail and Corporate credit, lease financing, project financing, issuing

debit and credit cards, SMS banking, internet banking, phone banking, call center, remittance

facilities, dealing in government securities etc. There have been no significant changes in the

nature of the principle activities of the Bank during the financial year under review.

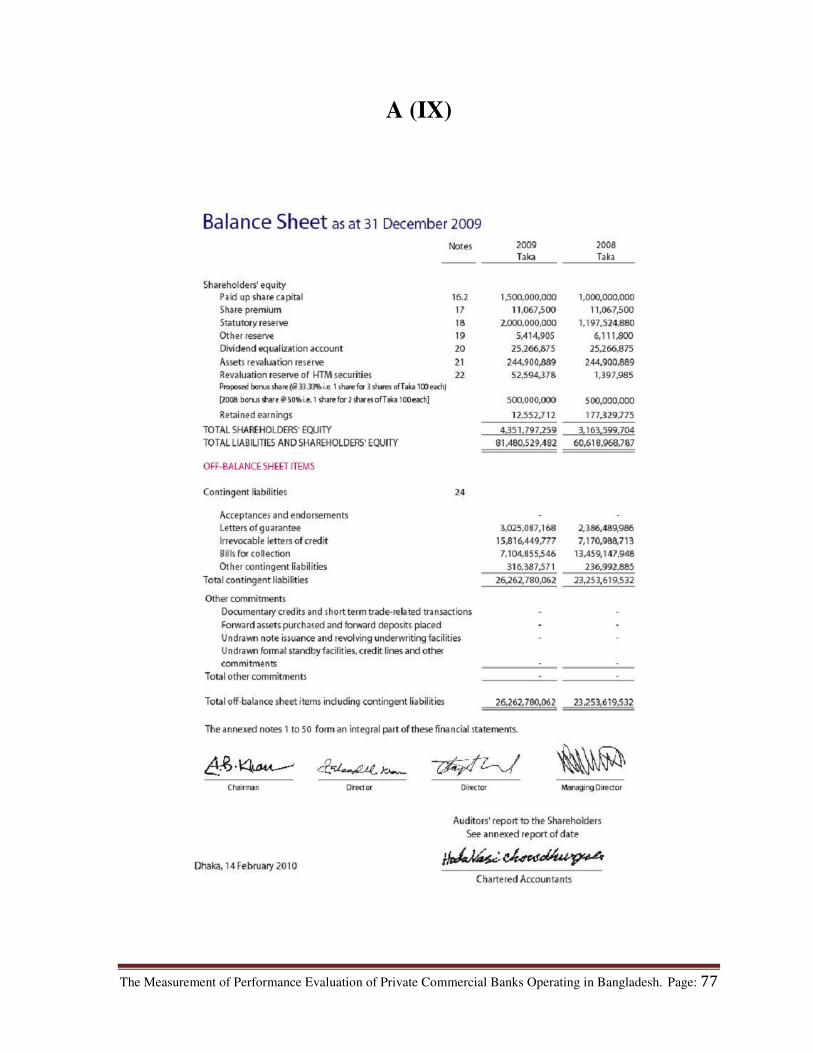

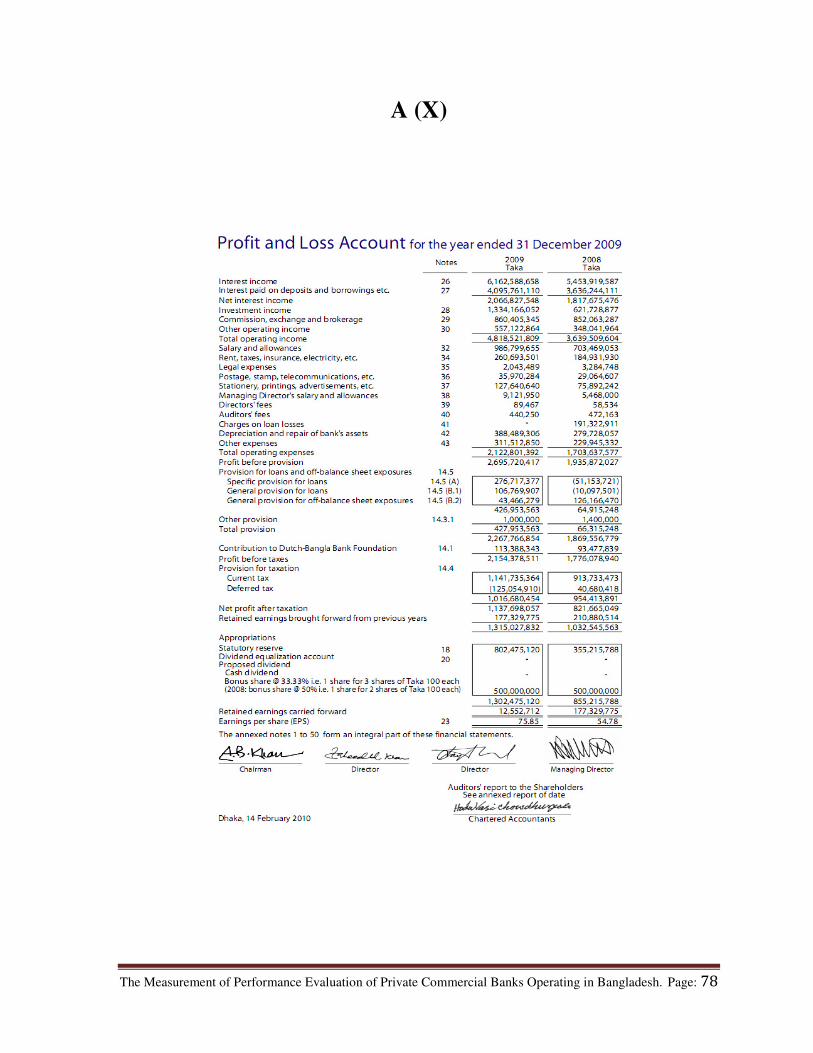

5.4. Dutch-Bangla Bank Limited

Dutch-Bangla Bank Limited (the Bank) is a scheduled commercial bank. The Bank was

established under the Bank Companies Act 1991 and incorporated as a public limited

company under the Companies Act 1994 in Bangladesh with the primary objective to carry

on all kinds of banking business in Bangladesh. The Bank is listed with Dhaka Stock

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 5

Exchange Limited and Chittagong Stock Exchange Limited. DBBL- a Bangladesh European

private joint venture scheduled commercial bank commenced formal operation from June 3,

1996.

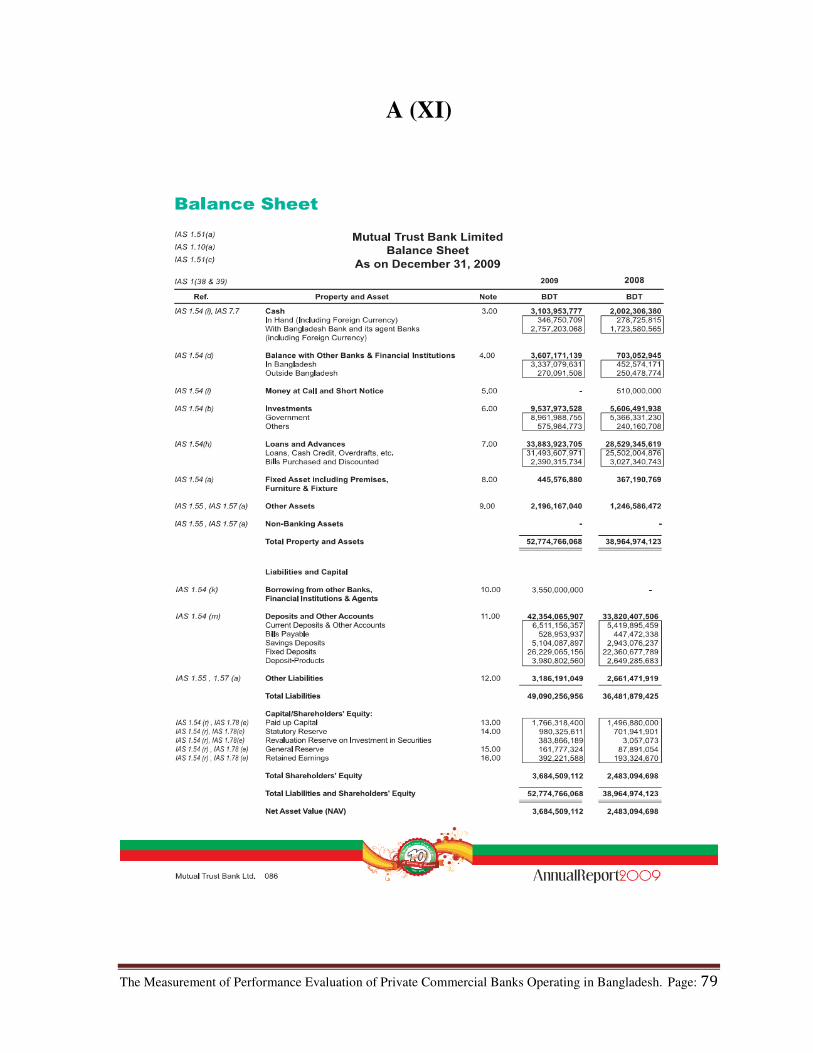

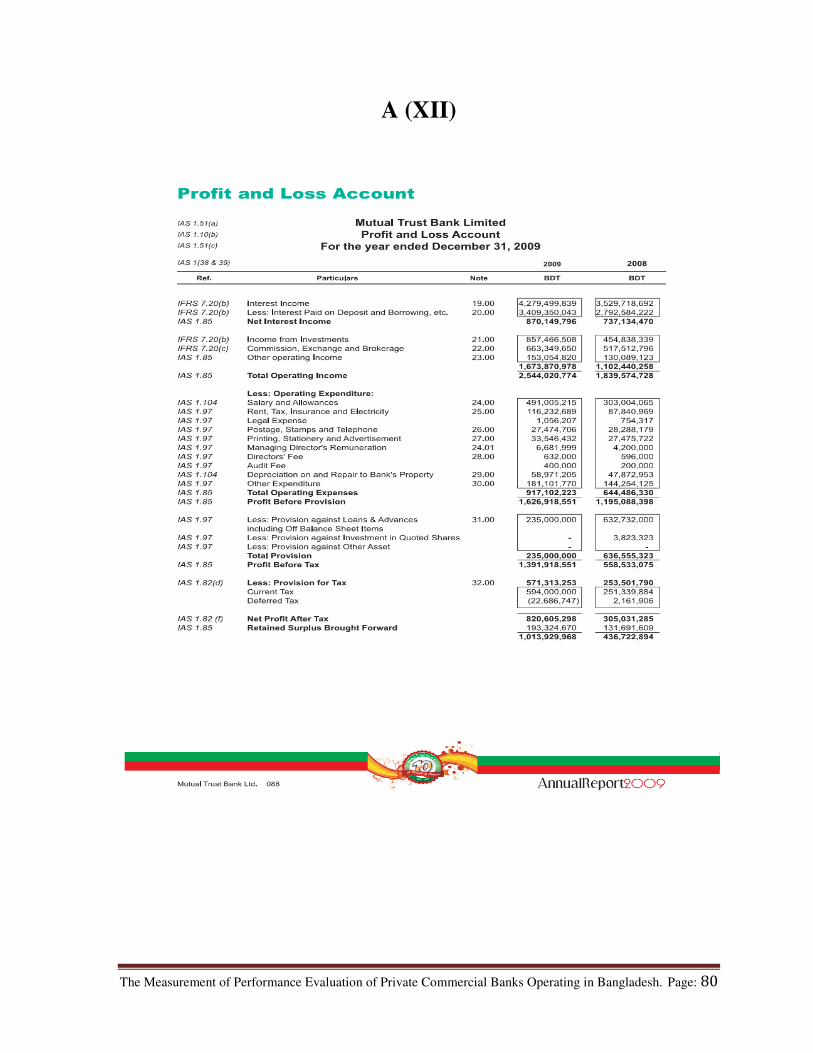

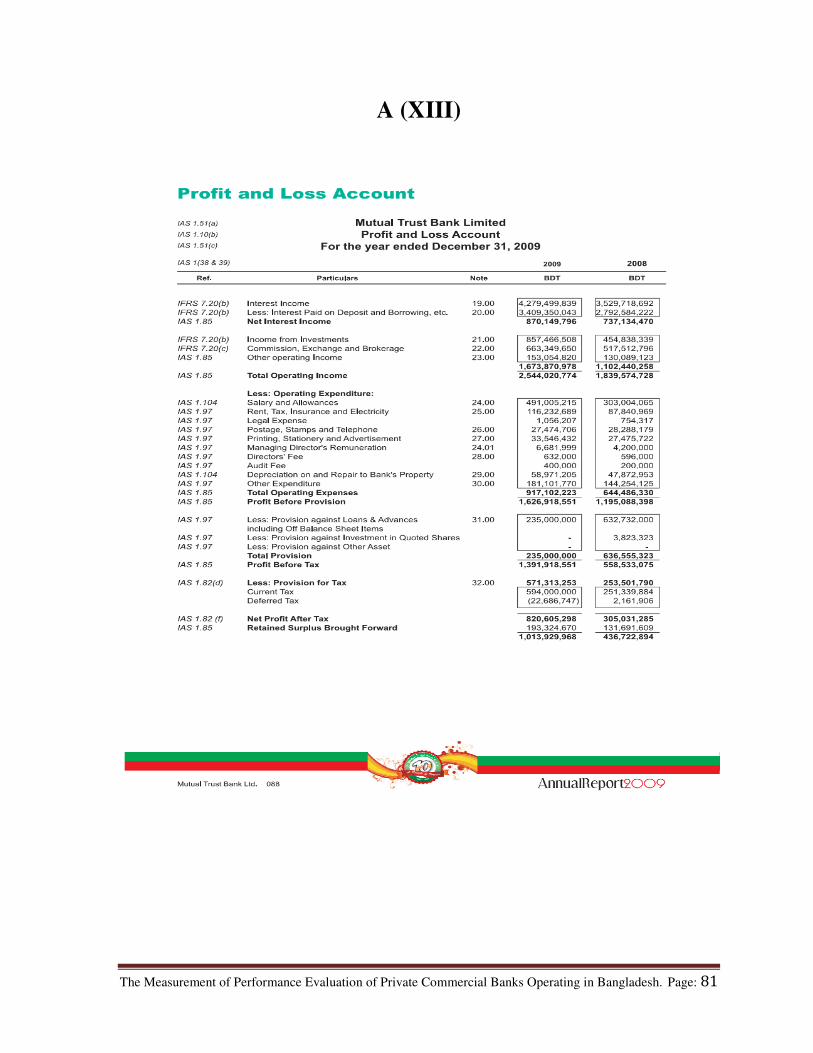

5.5. Mutual Trust Bank Limited

Mutual Trust Bank Limited was incorporated in Bangladesh in the year 1999 as a banking

company under the company Act, 1994. All types of commercial banking services are

provided by the bank within the stipulations laid down by the bank Companies Act, 1991 and

directive as received from Bangladesh Bank from time to time. The bank started its

commercial business from October 24, 1999. The shares of the bank are listed with the

Dhaka and Cittagong Stock Exchange, as a publicly quoted company for its shares. The bank

has 36 branches and 5 (Five) SME service centers, with no overseas branch as on December

31, 2009. The principle activities of the bank are to provide all kinds of commercial banking

services to its customers through its branches in Bangladesh.

5.6. National Credit and Commerce Bank Limited:

The National Credit and Commerce Bank Limited (NCCBL) was formed as a public limited

banking company incorporated in Bangladesh under the companies Act, 1994 with primary

objective to carry on all kind of banking business in and outside Bangladesh. The principle

place of business is the registered office at 7-8, Motijheel Commercial Area, Dhaka-1000. It

has 57 branches all over the Bangladesh. It carries out all banking activities through it

branches in Bangladesh. The bank went for initial public offering in 1999 and its share is

listed with Dhaka and Cittagong Stock Exchange Limited as a publicly traded company for

its general class of share. The commercial banking business activities of the bank encompass

a wide range of services including accepting deposits, making loans, discounting bills,

conducting money transfer, foreign exchange transaction and performing other related

services such as safekeeping collection, issuing guarantees, acceptance and latter of credit

through its branches in Bangladesh.

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 6

5.7. The Prime Bank Limited

The Prime Bank Limited ("the Bank") was incorporated as a public limited company in

Bangladesh under Companies Act, 1994. It commenced its banking business with one branch

from April 17, 1995 under the license issued by Bangladesh Bank. Presently the Bank has 84

branches, 5 (five) SME Centre all over Bangladesh, and a booth located at Dhaka Club,

Dhaka. The Bank had no overseas branches as at 31 December 2009. Out of the above 84

branches, 05 (five) branches are designated as Islamic Banking Branch complying with the

rules of Islamic Shariah, the modus operandi of which is substantially different from other

branches run on conventional basis. The Bank went for Initial Public Offering in 1999 and its

share is listed with Dhaka Stock Exchange Limited and Chittagong Stock Exchange Limited

as a publicly traded company for its general class of shares. The registered office of the

company is located at 119-120, Motijheel C/A, Dhaka-1000. The principal activities of the

Bank are to provide all kinds of commercial banking services to its customers through its

branches and SME centre in Bangladesh.

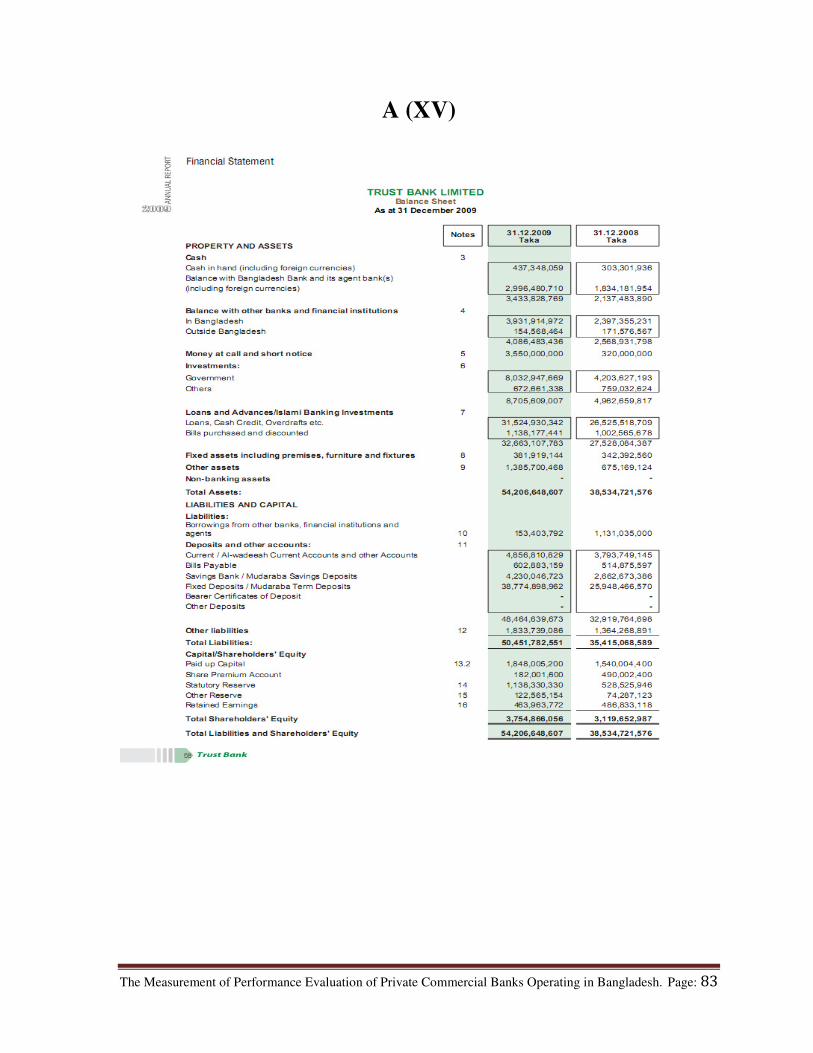

5.8. Trust Bank Limited

Trust Bank Limited is a scheduled commercial bank established under the Bank Companies

Act, 1991 and incorporated as a Public Limited Company under the Companies Act, 1994 in

Bangladesh on 17 September 1999 with the primary objective to carry on all kinds of

banking business in and outside Bangladesh. The Bank had Forty Two (42) branches and

Four (4) SME Service Centers are operating in Bangladesh as of 31 December 2009. The

Bank had no overseas branches as of 31 December 2009. The bank is listed with Dhaka

Stock Exchange Limited and Chittagong Stock Exchange Limited as a publicly traded

company for its general class of shares. The registered office of the Bank is located at 36,

Dilkusha Commercial Area, Dhaka – 1000 Initially the bank has started its operation in the

name of "The Trust Bank Limited" but on 12 November 2006 it was renamed as “Trust Bank

Limited” by the Registrar of Joint Stock Companies. The new name of the bank was

approved by Bangladesh Bank on 03 December 2006. Trust Bank Limited offers full range

of banking services that include deposit banking, loans & advances, export, import and

financing national and international remittance facilities etc.

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 7

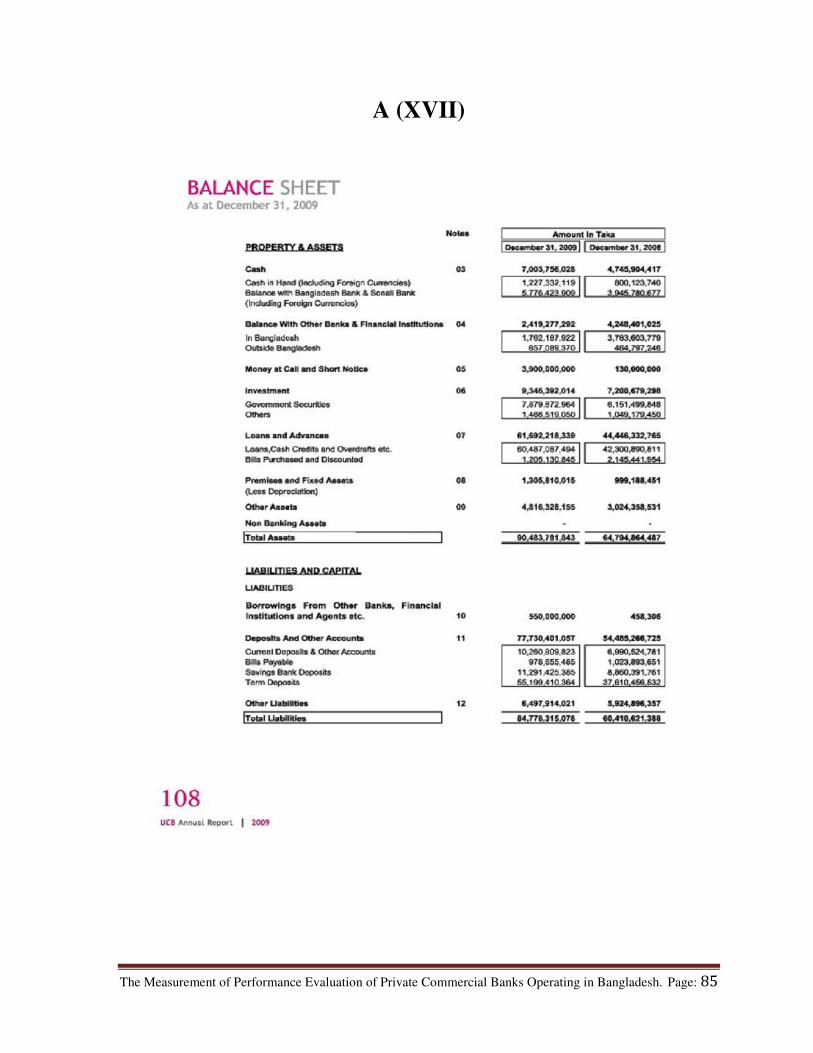

5.9. United Commercial Bank Limited

The United Commercial Bank Limited (UCBL) was incorporated in Bangladesh as public

limited company with limited liability as on 26 June, 1983 under Companies Act, 1913

(subsequently replaced by Companies Act, 1994) and commenced its operation immediately

after incorporation with due permission from Bangladesh Bank w.e.f. 13 November, 1983. It

has 98 branches all over the Bangladesh. The principle place of business and the registered

office were located at 60, Motijheel Commercial Area, Federation Bhaban, Dhaka-1000.

Principle place of business have been changed from January 2010 to Plot:CWS(A)1, Gulshan

Avenue, Dhaka1212. The principle activities carried out by the bank include all kinds of

commercial banking activities/services to its customers through its branches and electronic

delivery channels in Bangladesh.

5.10. Uttara Bank Limited

Uttara Bank Limited had been a nationalized bank in the name of Uttara Bank under the

Bangladesh Bank (Nationalization) order 1972, formally known as Eastern Banking

Corporation Limited which is started functioning on and from 28 Jan, 1965. Consequent

upon the amendment of the Bangladesh Bank (Nationalization) order 1972, the Uttara Bank

was converted into Uttara Bank Limited as a public limited company in the year 1983. The

Uttara Bank Limited was incorporated as a banking company on 29 Jun, 1983 and obtained

business commencement certificate on 21 Aug, 1983. The bank floated its share in the year

1984.

Uttara Bank Limited is one of the front ranking first generation private sector commercial

bank in Bangladesh. The bank has been carrying out business through its 211 branches

spreading all over the country. The management of the bank consists of a team lead by senior

bankers with vast experience in national and international markets. The bank’s operation has

achieved the confidence of its customers with sound fundamentals in respect to deposit

accumulation, loans and advances, import and export business. Overall performance of

Uttara Bank Limited has been improved for maintaining effective and constructive principles

of Bangladesh Bank.

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 8

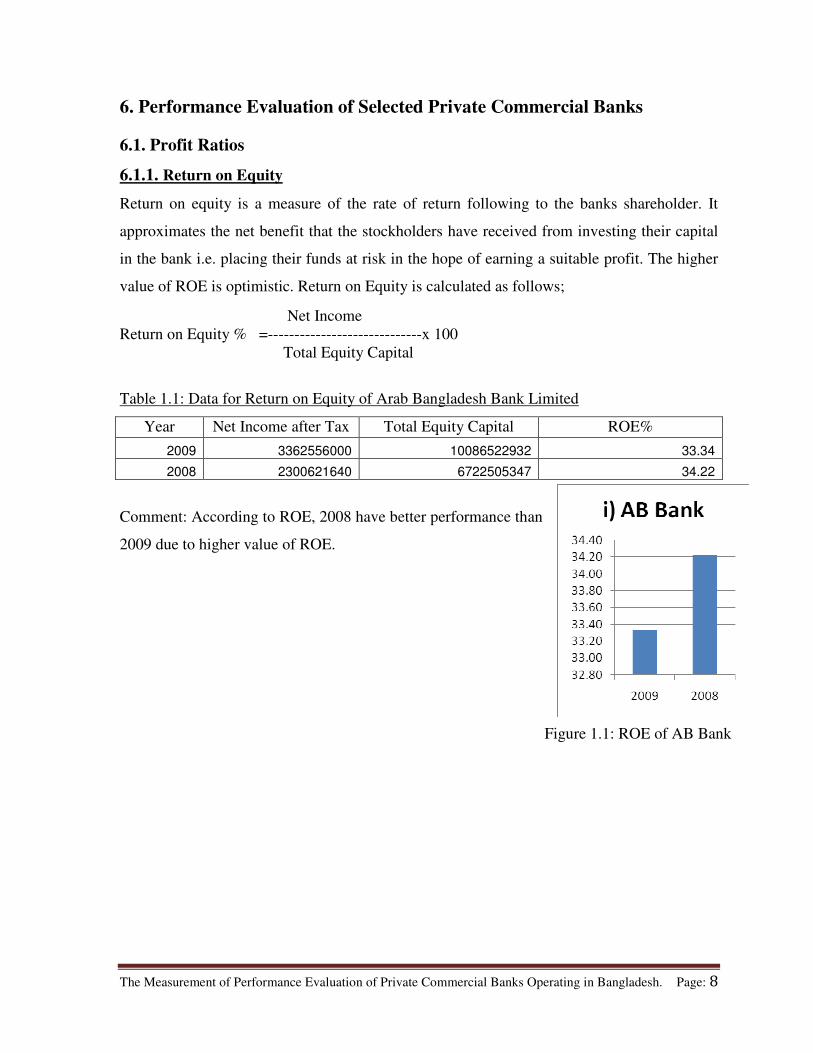

6. Performance Evaluation of Selected Private Commercial Banks

6.1. Profit Ratios

6.1.1. Return on Equity

Return on equity is a measure of the rate of return following to the banks shareholder. It

approximates the net benefit that the stockholders have received from investing their capital

in the bank i.e. placing their funds at risk in the hope of earning a suitable profit. The higher

value of ROE is optimistic. Return on Equity is calculated as follows;

Net Income

Return on Equity % =-----------------------------x 100

Total Equity Capital

Table 1.1: Data for Return on Equity of Arab Bangladesh Bank Limited

Year Net Income after Tax Total Equity Capital ROE%

2009 3362556000 10086522932 33.34

2008 2300621640 6722505347 34.22

Comment: According to ROE, 2008 have better performance than

2009 due to higher value of ROE.

Figure 1.1: ROE of AB Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 9

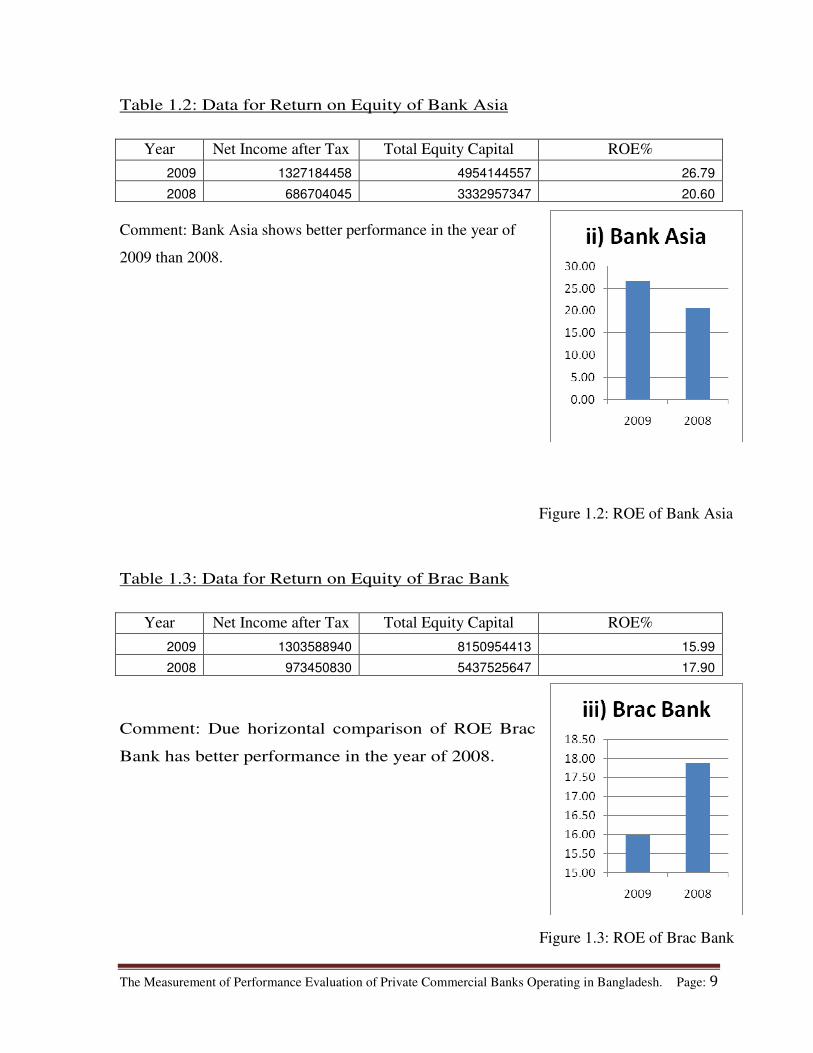

Table 1.2: Data for Return on Equity of Bank Asia

Year Net Income after Tax Total Equity Capital ROE%

2009 1327184458 4954144557 26.79

2008 686704045 3332957347 20.60

Comment: Bank Asia shows better performance in the year of

2009 than 2008.

Table 1.3: Data for Return on Equity of Brac Bank

Year Net Income after Tax Total Equity Capital ROE%

2009 1303588940 8150954413 15.99

2008 973450830 5437525647 17.90

Comment: Due horizontal comparison of ROE Brac

Bank has better performance in the year of 2008.

Figure 1.2: ROE of Bank Asia

Figure 1.3: ROE of Brac Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 10

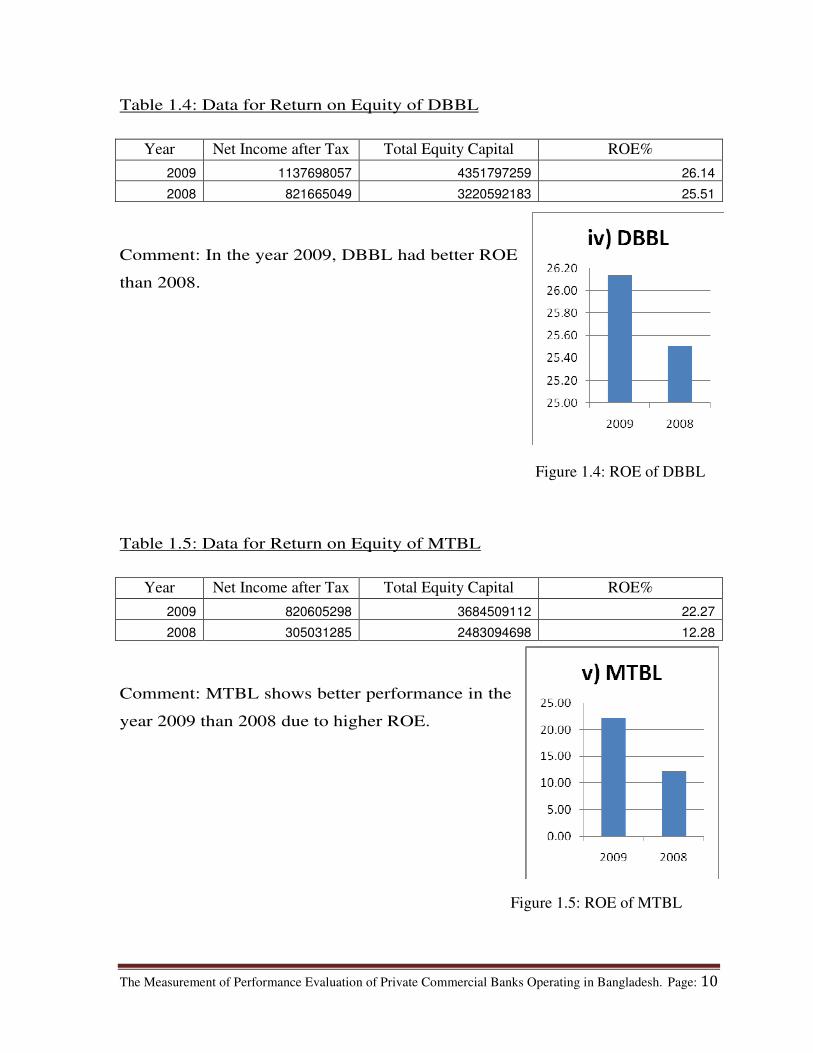

Table 1.4: Data for Return on Equity of DBBL

Year Net Income after Tax Total Equity Capital ROE%

2009 1137698057 4351797259 26.14

2008 821665049 3220592183 25.51

Comment: In the year 2009, DBBL had better ROE

than 2008.

Table 1.5: Data for Return on Equity of MTBL

Year Net Income after Tax Total Equity Capital ROE%

2009 820605298 3684509112 22.27

2008 305031285 2483094698 12.28

Comment: MTBL shows better performance in the

year 2009 than 2008 due to higher ROE.

Figure 1.4: ROE of DBBL

Figure 1.5: ROE of MTBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 11

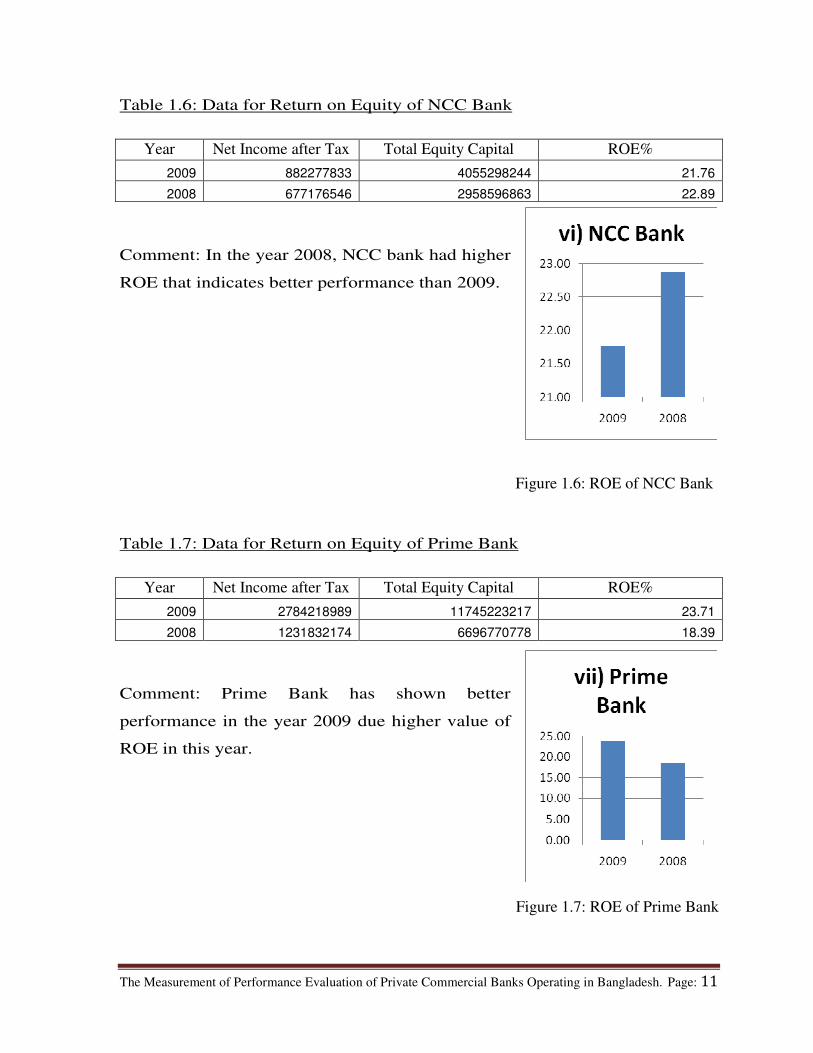

Table 1.6: Data for Return on Equity of NCC Bank

Year Net Income after Tax Total Equity Capital ROE%

2009 882277833 4055298244 21.76

2008 677176546 2958596863 22.89

Comment: In the year 2008, NCC bank had higher

ROE that indicates better performance than 2009.

Table 1.7: Data for Return on Equity of Prime Bank

Year Net Income after Tax Total Equity Capital ROE%

2009 2784218989 11745223217 23.71

2008 1231832174 6696770778 18.39

Comment: Prime Bank has shown better

performance in the year 2009 due higher value of

ROE in this year.

Figure 1.6: ROE of NCC Bank

Figure 1.7: ROE of Prime Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 12

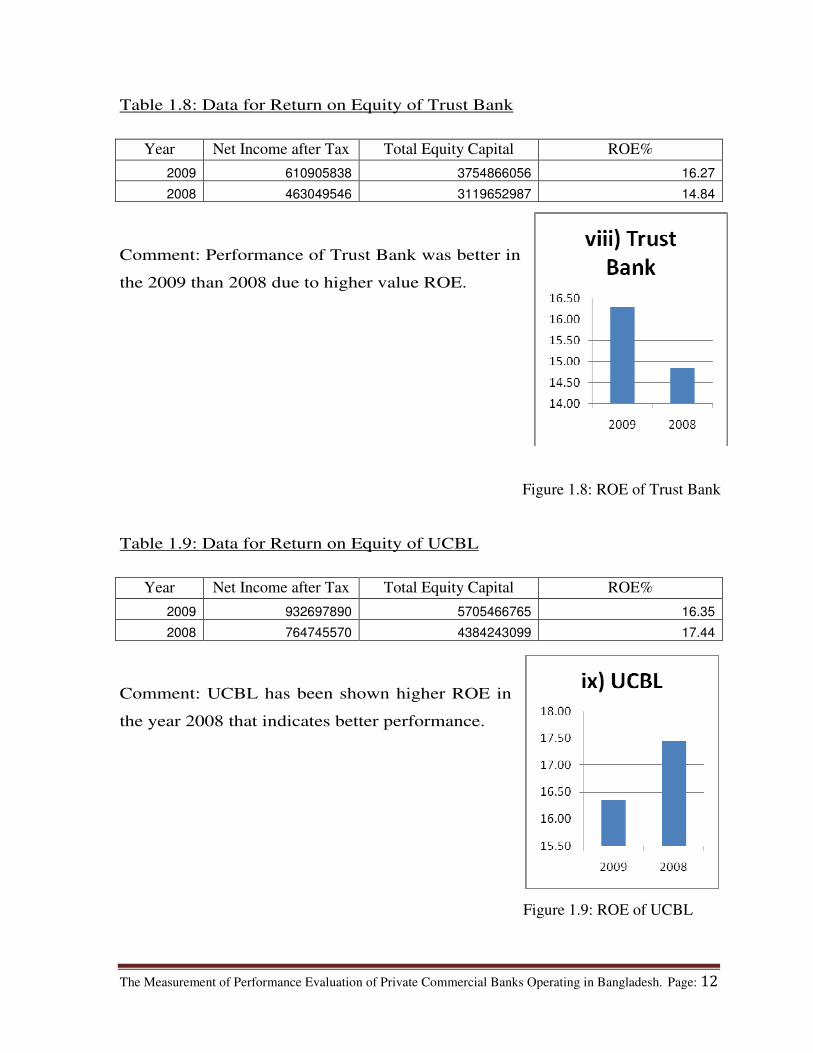

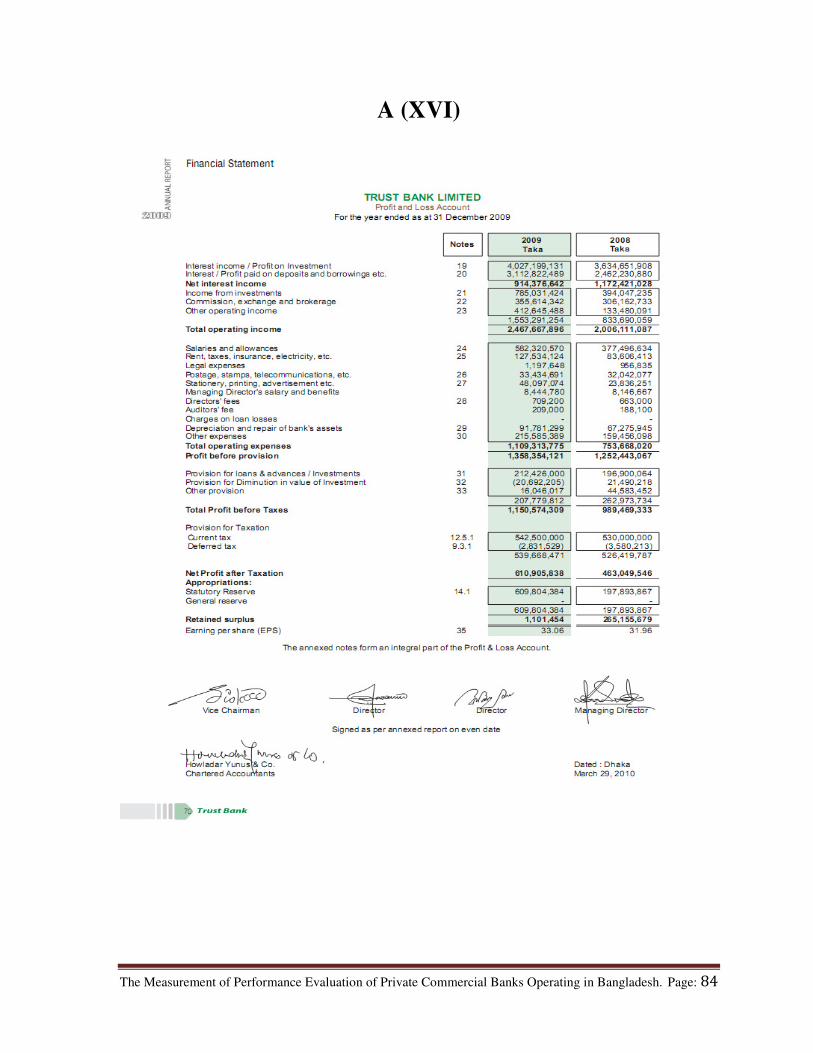

Table 1.8: Data for Return on Equity of Trust Bank

Year Net Income after Tax Total Equity Capital ROE%

2009 610905838 3754866056 16.27

2008 463049546 3119652987 14.84

Comment: Performance of Trust Bank was better in

the 2009 than 2008 due to higher value ROE.

Table 1.9: Data for Return on Equity of UCBL

Year Net Income after Tax Total Equity Capital ROE%

2009 932697890 5705466765 16.35

2008 764745570 4384243099 17.44

Comment: UCBL has been shown higher ROE in

the year 2008 that indicates better performance.

Figure 1.8: ROE of Trust Bank

Figure 1.9: ROE of UCBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 13

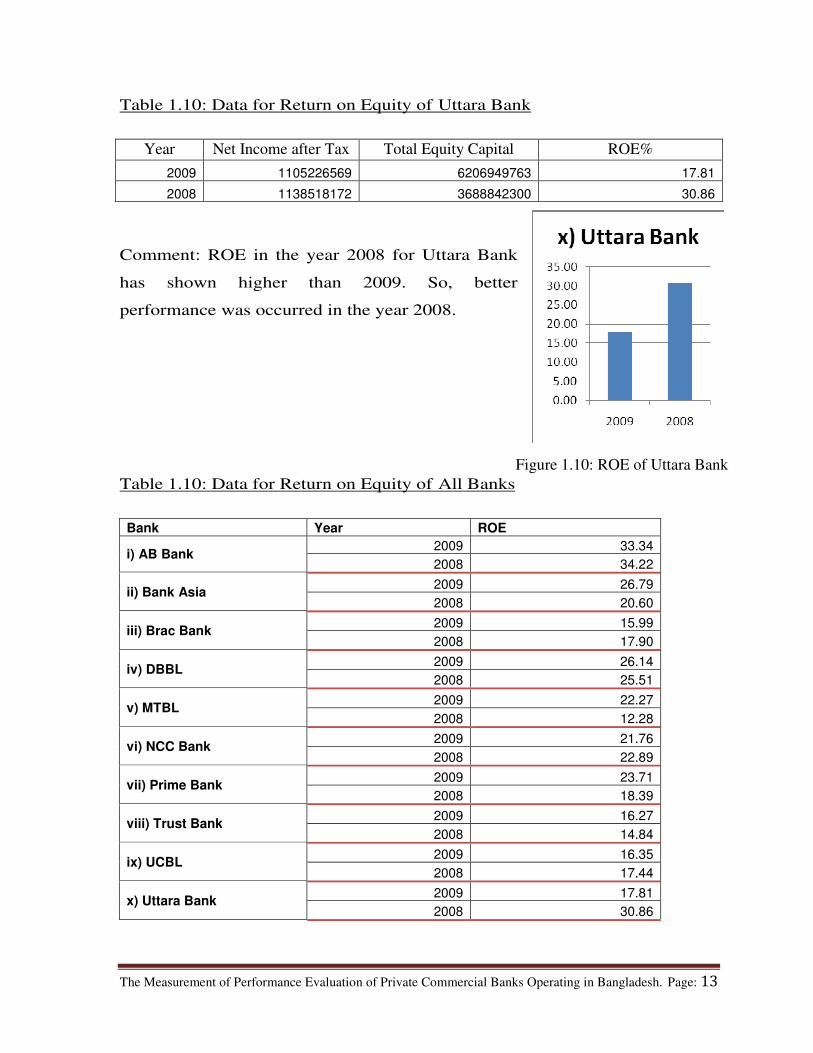

Table 1.10: Data for Return on Equity of Uttara Bank

Year Net Income after Tax Total Equity Capital ROE%

2009 1105226569 6206949763 17.81

2008 1138518172 3688842300 30.86

Comment: ROE in the year 2008 for Uttara Bank

has shown higher than 2009. So, better

performance was occurred in the year 2008.

Table 1.10: Data for Return on Equity of All Banks

Bank Year ROE

i) AB Bank 2009 33.34

2008 34.22

ii) Bank Asia 2009 26.79

2008 20.60

iii) Brac Bank 2009 15.99

2008 17.90

iv) DBBL 2009 26.14

2008 25.51

v) MTBL 2009 22.27

2008 12.28

vi) NCC Bank 2009 21.76

2008 22.89

vii) Prime Bank 2009 23.71

2008 18.39

viii) Trust Bank 2009 16.27

2008 14.84

ix) UCBL 2009 16.35

2008 17.44

x) Uttara Bank 2009 17.81

2008 30.86

Figure 1.10: ROE of Uttara Bank

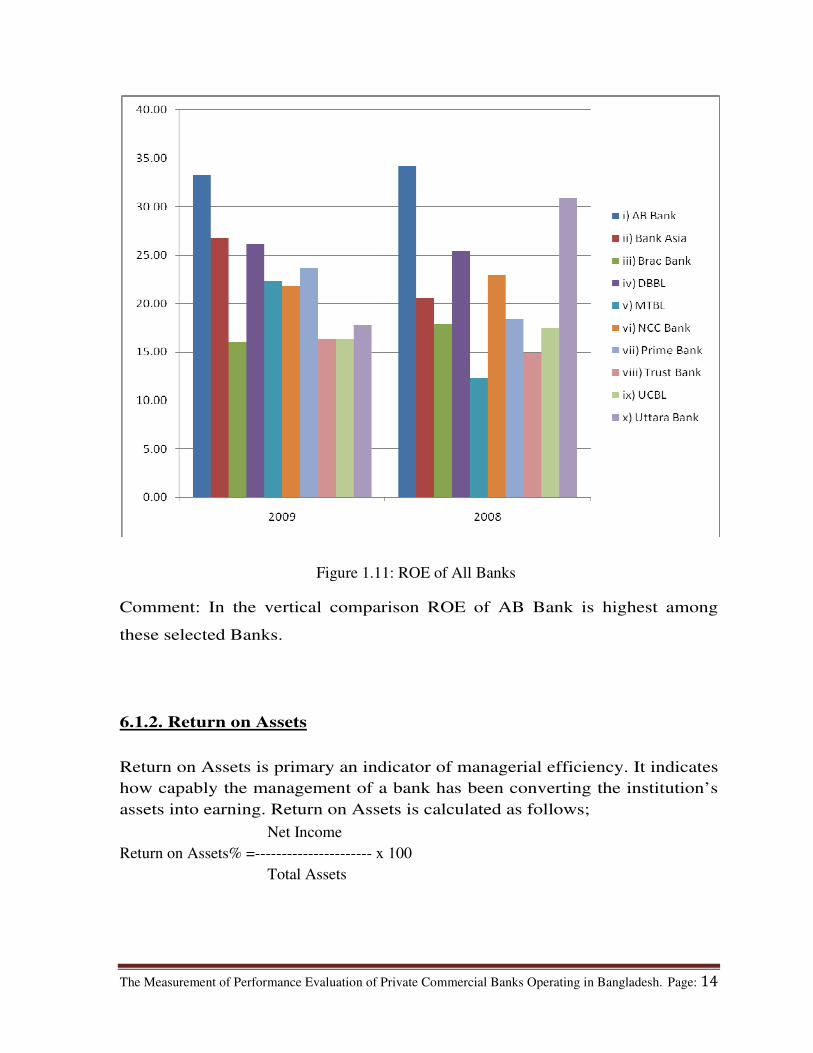

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 14

Comment: In the vertical comparison ROE of AB Bank is highest among

these selected Banks.

6.1.2. Return on Assets

Return on Assets is primary an indicator of managerial efficiency. It indicates

how capably the management of a bank has been converting the institution’s

assets into earning. Return on Assets is calculated as follows;

Net Income

Return on Assets% =---------------------- x 100

Total Assets

Figure 1.11: ROE of All Banks

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 15

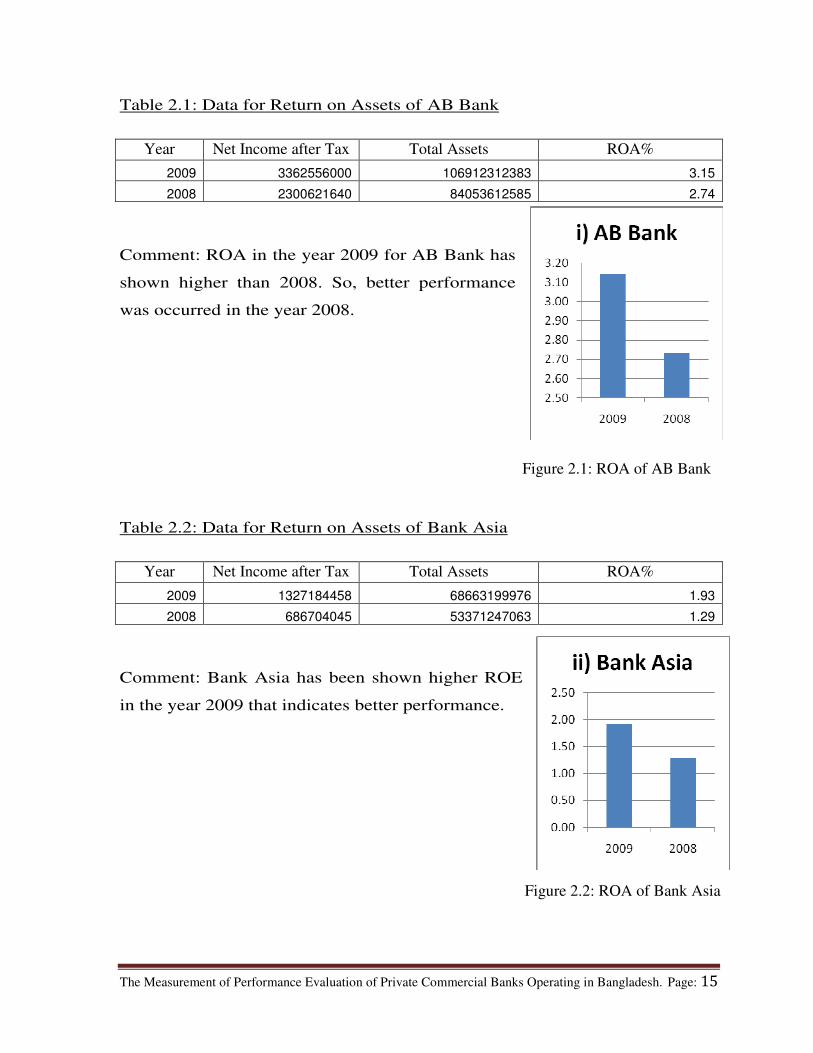

Table 2.1: Data for Return on Assets of AB Bank

Year Net Income after Tax Total Assets ROA%

2009 3362556000 106912312383 3.15

2008 2300621640 84053612585 2.74

Comment: ROA in the year 2009 for AB Bank has

shown higher than 2008. So, better performance

was occurred in the year 2008.

Table 2.2: Data for Return on Assets of Bank Asia

Year Net Income after Tax Total Assets ROA%

2009 1327184458 68663199976 1.93

2008 686704045 53371247063 1.29

Comment: Bank Asia has been shown higher ROE

in the year 2009 that indicates better performance.

Figure 2.1: ROA of AB Bank

Figure 2.2: ROA of Bank Asia

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 16

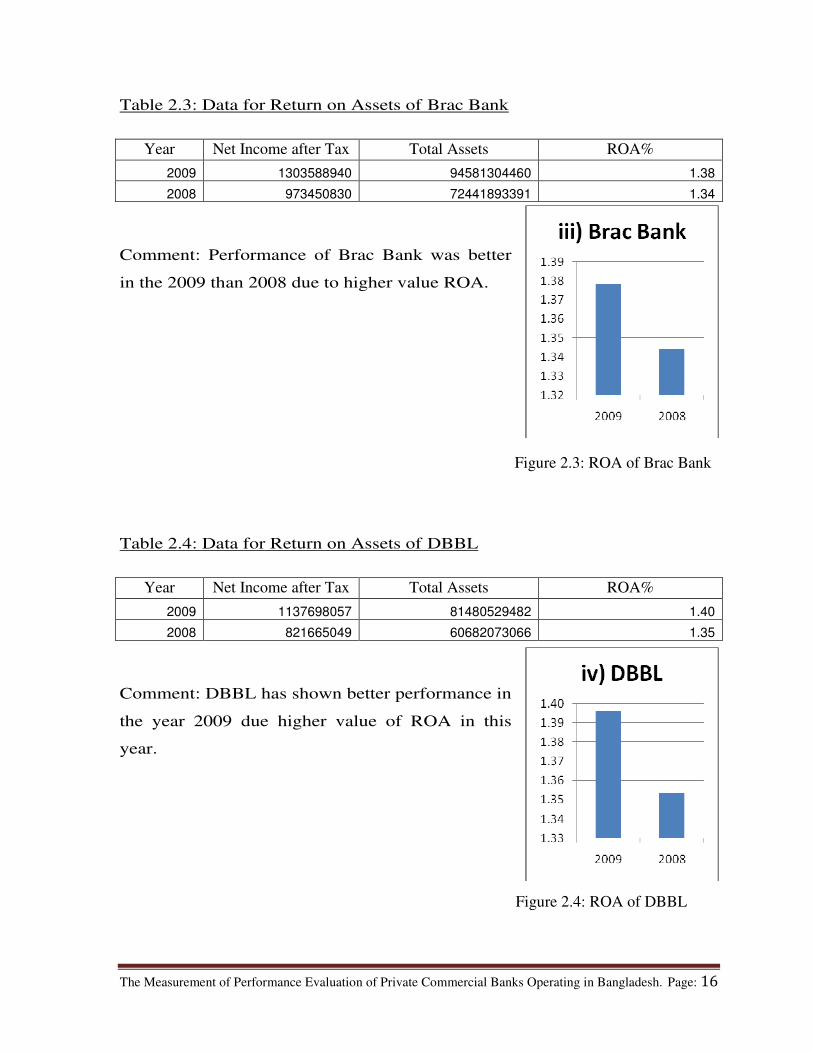

Table 2.3: Data for Return on Assets of Brac Bank

Year Net Income after Tax Total Assets ROA%

2009 1303588940 94581304460 1.38

2008 973450830 72441893391 1.34

Comment: Performance of Brac Bank was better

in the 2009 than 2008 due to higher value ROA.

Table 2.4: Data for Return on Assets of DBBL

Year Net Income after Tax Total Assets ROA%

2009 1137698057 81480529482 1.40

2008 821665049 60682073066 1.35

Comment: DBBL has shown better performance in

the year 2009 due higher value of ROA in this

year.

Figure 2.3: ROA of Brac Bank

Figure 2.4: ROA of DBBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 17

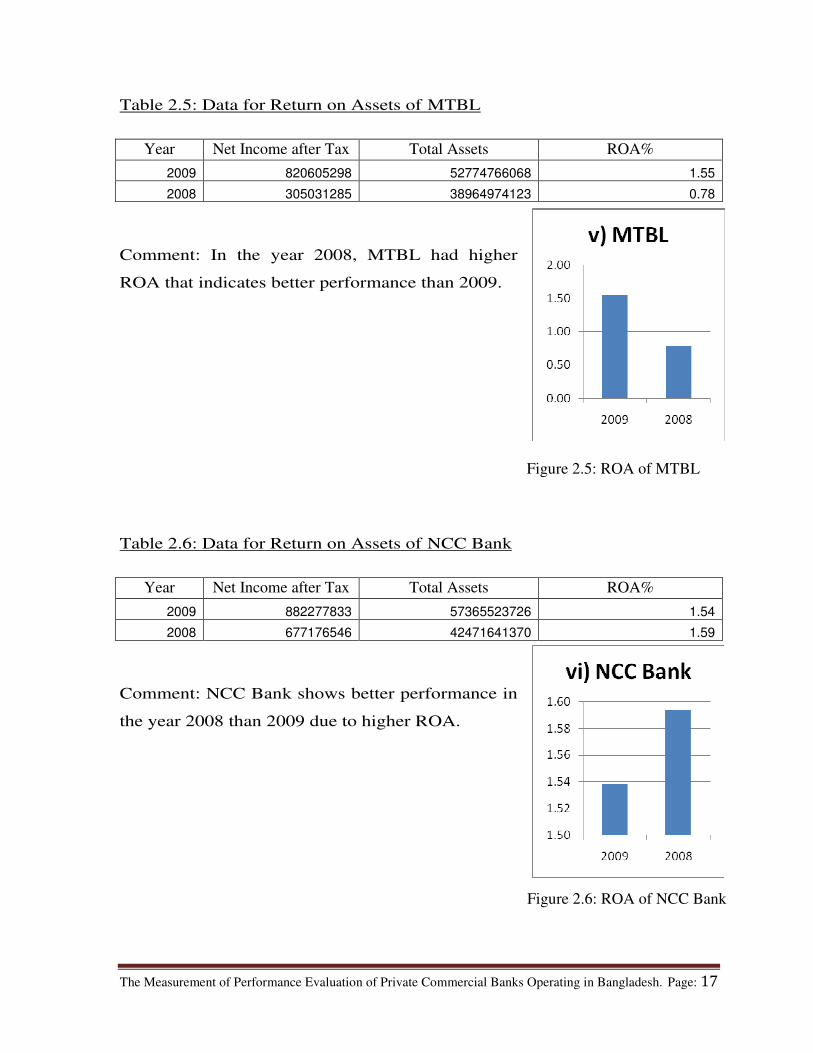

Table 2.5: Data for Return on Assets of MTBL

Year Net Income after Tax Total Assets ROA%

2009 820605298 52774766068 1.55

2008 305031285 38964974123 0.78

Comment: In the year 2008, MTBL had higher

ROA that indicates better performance than 2009.

Table 2.6: Data for Return on Assets of NCC Bank

Year Net Income after Tax Total Assets ROA%

2009 882277833 57365523726 1.54

2008 677176546 42471641370 1.59

Comment: NCC Bank shows better performance in

the year 2008 than 2009 due to higher ROA.

Figure 2.5: ROA of MTBL

Figure 2.6: ROA of NCC Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 18

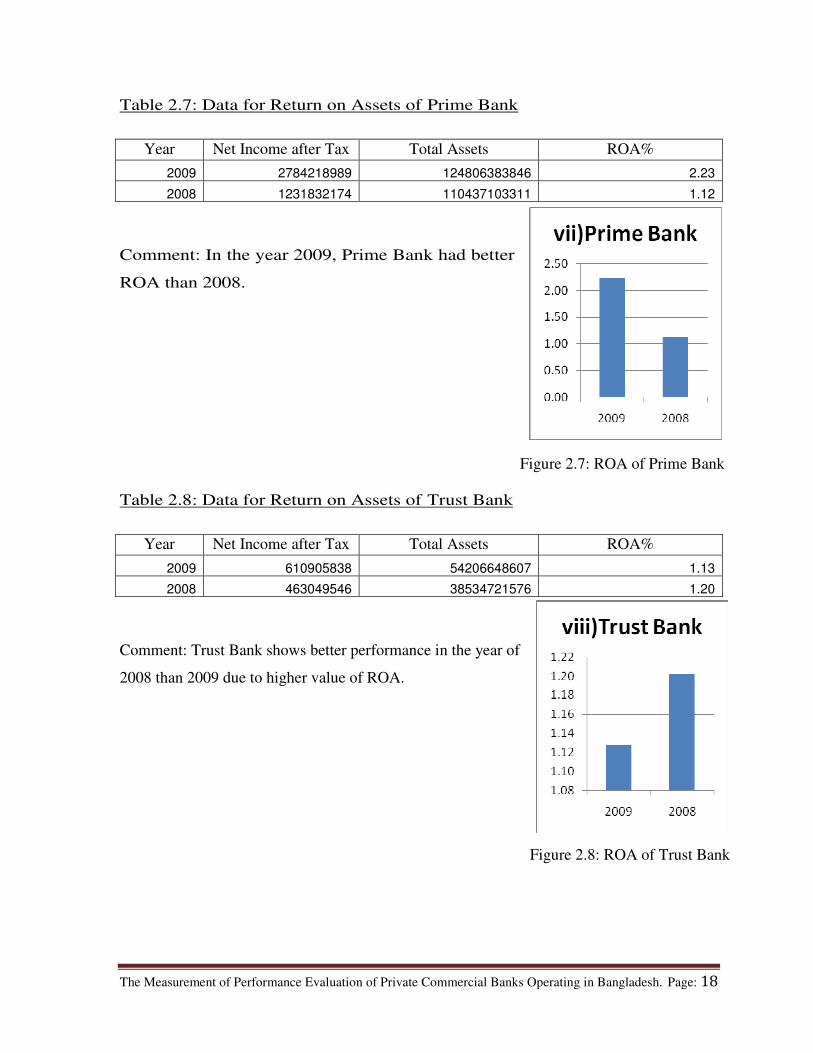

Table 2.7: Data for Return on Assets of Prime Bank

Year Net Income after Tax Total Assets ROA%

2009 2784218989 124806383846 2.23

2008 1231832174 110437103311 1.12

Comment: In the year 2009, Prime Bank had better

ROA than 2008.

Table 2.8: Data for Return on Assets of Trust Bank

Year Net Income after Tax Total Assets ROA%

2009 610905838 54206648607 1.13

2008 463049546 38534721576 1.20

Comment: Trust Bank shows better performance in the year of

2008 than 2009 due to higher value of ROA.

Figure 2.7: ROA of Prime Bank

Figure 2.8: ROA of Trust Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 19

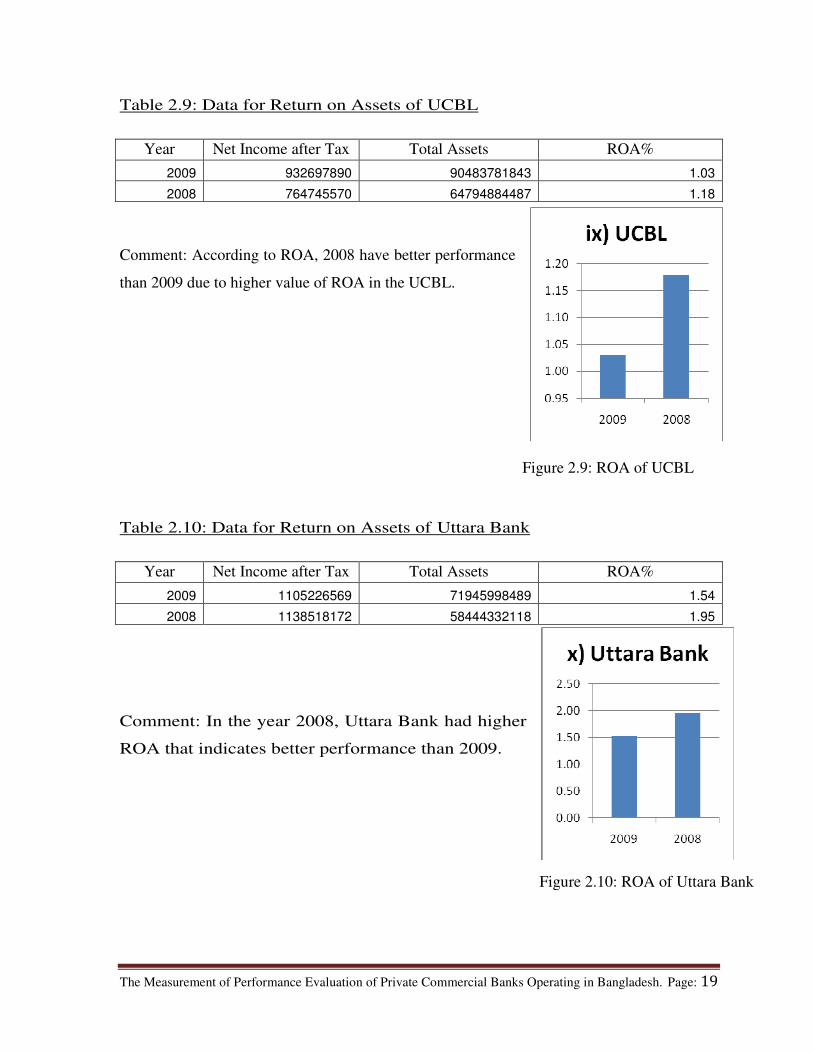

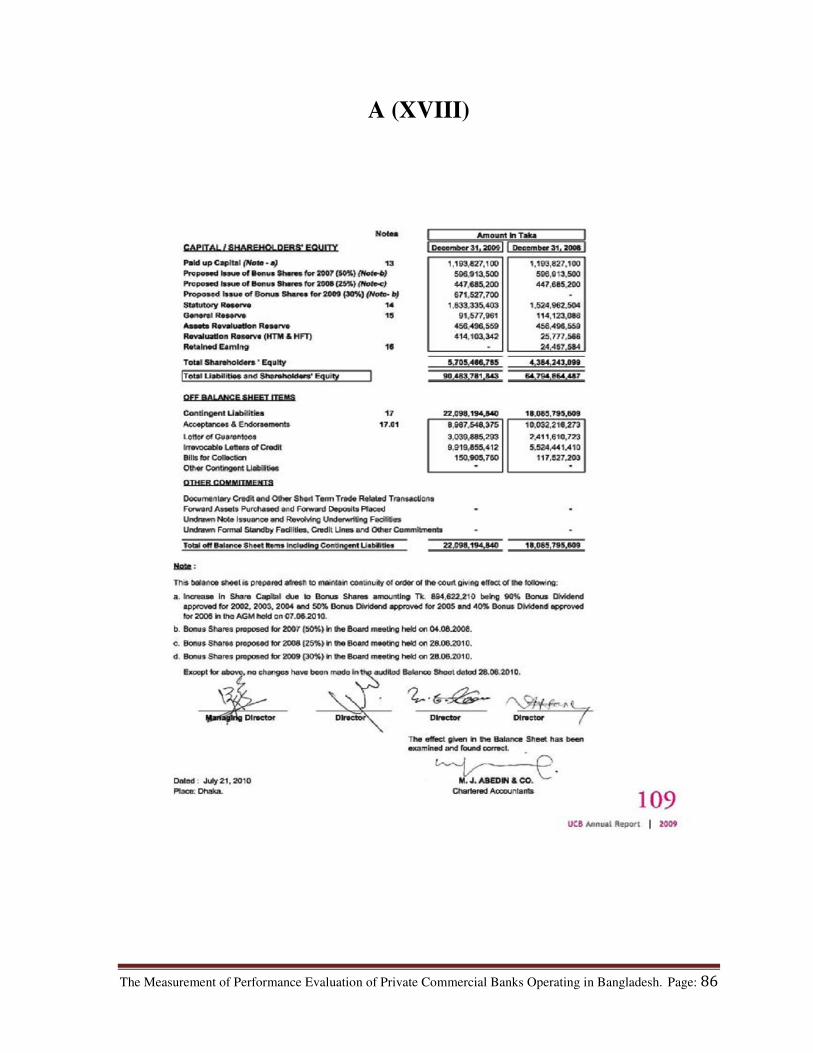

Table 2.9: Data for Return on Assets of UCBL

Year Net Income after Tax Total Assets ROA%

2009 932697890 90483781843 1.03

2008 764745570 64794884487 1.18

Comment: According to ROA, 2008 have better performance

than 2009 due to higher value of ROA in the UCBL.

Table 2.10: Data for Return on Assets of Uttara Bank

Year Net Income after Tax Total Assets ROA%

2009 1105226569 71945998489 1.54

2008 1138518172 58444332118 1.95

Comment: In the year 2008, Uttara Bank had higher

ROA that indicates better performance than 2009.

Figure 2.9: ROA of UCBL

Figure 2.10: ROA of Uttara Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 20

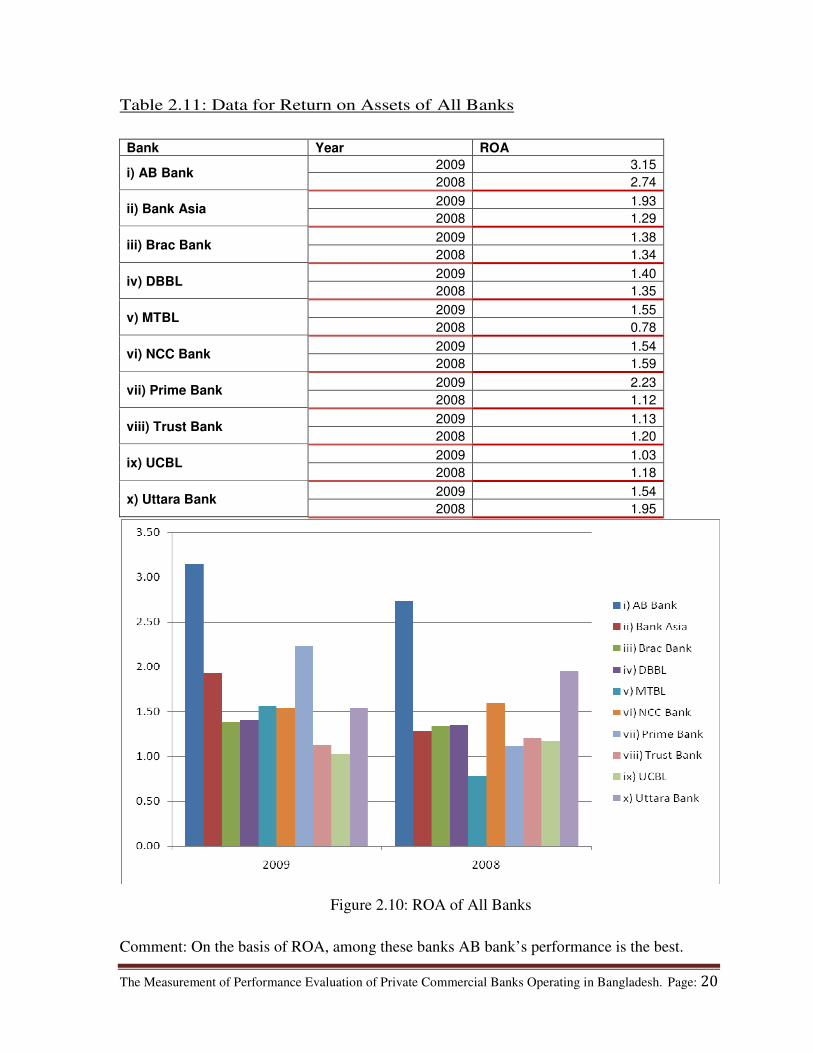

Table 2.11: Data for Return on Assets of All Banks

Bank Year ROA

i) AB Bank 2009 3.15

2008 2.74

ii) Bank Asia 2009 1.93

2008 1.29

iii) Brac Bank 2009 1.38

2008 1.34

iv) DBBL 2009 1.40

2008 1.35

v) MTBL 2009 1.55

2008 0.78

vi) NCC Bank 2009 1.54

2008 1.59

vii) Prime Bank 2009 2.23

2008 1.12

viii) Trust Bank 2009 1.13

2008 1.20

ix) UCBL 2009 1.03

2008 1.18

x) Uttara Bank 2009 1.54

2008 1.95

Comment: On the basis of ROA, among these banks AB bank’s performance is the best.

Figure 2.10: ROA of All Banks

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 21

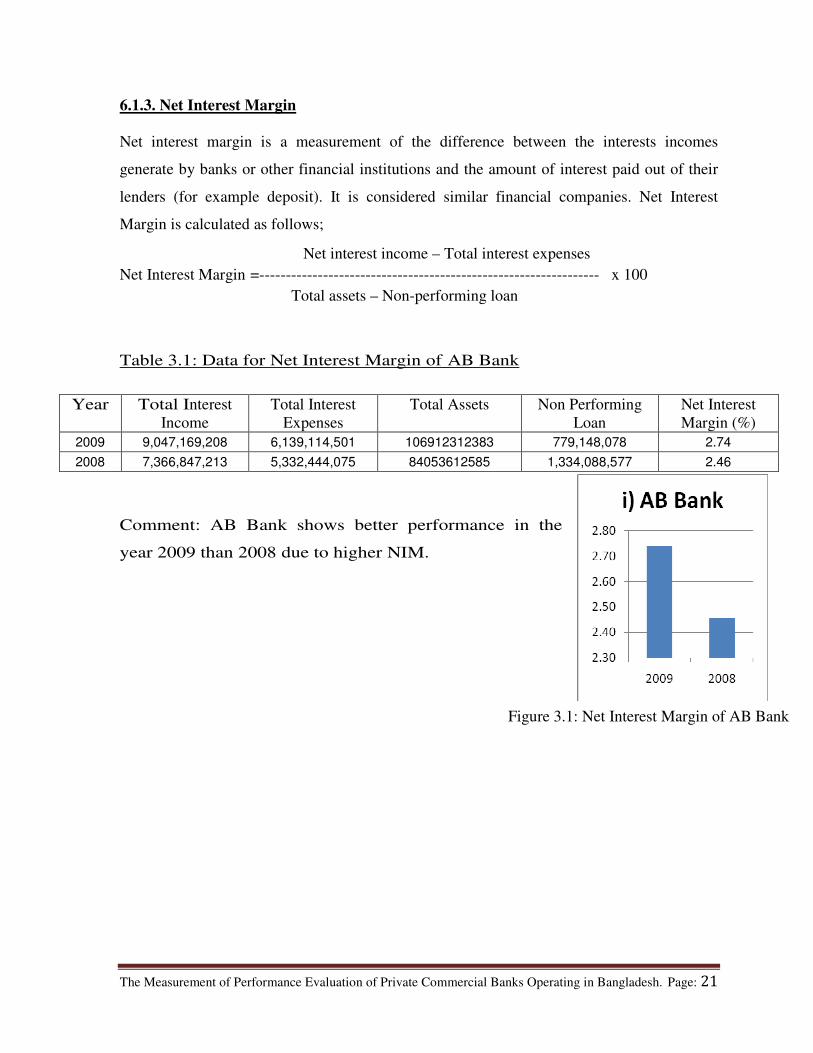

6.1.3. Net Interest Margin

Net interest margin is a measurement of the difference between the interests incomes

generate by banks or other financial institutions and the amount of interest paid out of their

lenders (for example deposit). It is considered similar financial companies. Net Interest

Margin is calculated as follows;

Net interest income – Total interest expenses

Net Interest Margin =---------------------------------------------------------------- x 100

Total assets – Non-performing loan

Table 3.1: Data for Net Interest Margin of AB Bank

Year Total Interest

Income

Total Interest

Expenses

Total Assets Non Performing

Loan

Net Interest

Margin (%)

2009 9,047,169,208 6,139,114,501 106912312383 779,148,078 2.74

2008 7,366,847,213 5,332,444,075 84053612585 1,334,088,577 2.46

Comment: AB Bank shows better performance in the

year 2009 than 2008 due to higher NIM.

Figure 3.1: Net Interest Margin of AB Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 22

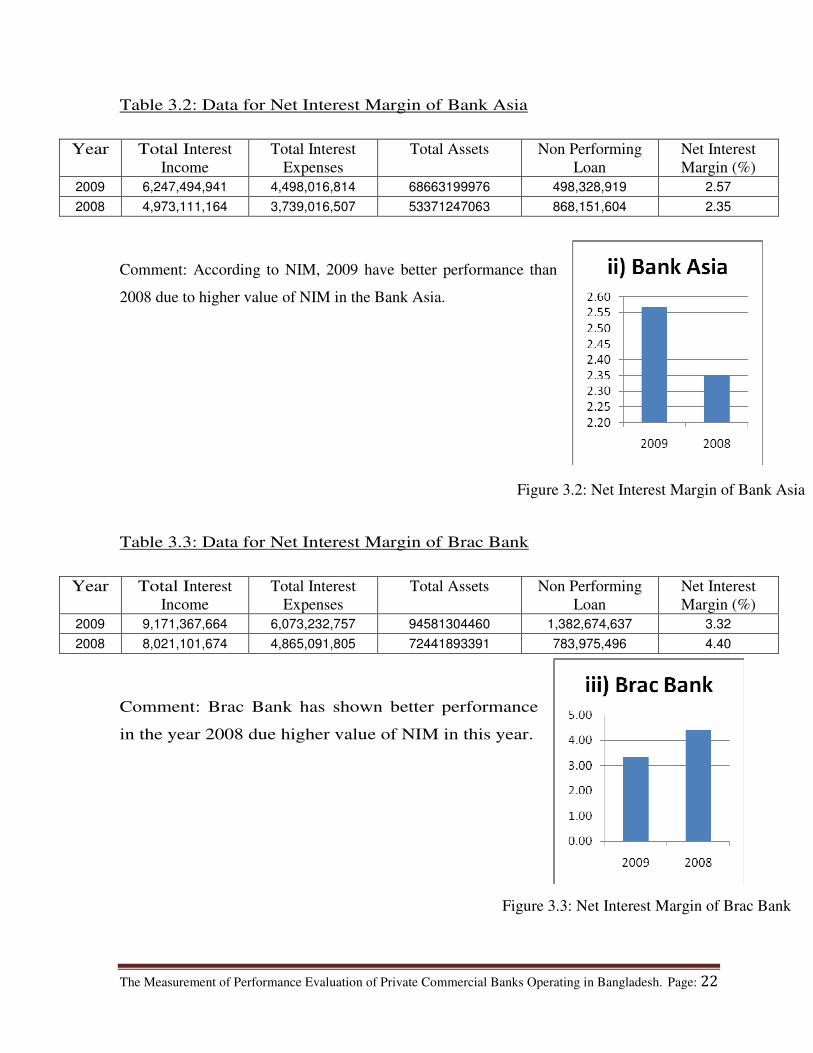

Table 3.2: Data for Net Interest Margin of Bank Asia

Year Total Interest

Income

Total Interest

Expenses

Total Assets Non Performing

Loan

Net Interest

Margin (%)

2009 6,247,494,941 4,498,016,814 68663199976 498,328,919 2.57

2008 4,973,111,164 3,739,016,507 53371247063 868,151,604 2.35

Comment: According to NIM, 2009 have better performance than

2008 due to higher value of NIM in the Bank Asia.

Table 3.3: Data for Net Interest Margin of Brac Bank

Year Total Interest

Income

Total Interest

Expenses

Total Assets Non Performing

Loan

Net Interest

Margin (%)

2009 9,171,367,664 6,073,232,757 94581304460 1,382,674,637 3.32

2008 8,021,101,674 4,865,091,805 72441893391 783,975,496 4.40

Comment: Brac Bank has shown better performance

in the year 2008 due higher value of NIM in this year.

Figure 3.2: Net Interest Margin of Bank Asia

Figure 3.3: Net Interest Margin of Brac Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 23

Table 3.4: Data for Net Interest Margin of DBBL

Year Total Interest

Income

Total Interest

Expenses

Total Assets Non Performing

Loan

Net Interest

Margin (%)

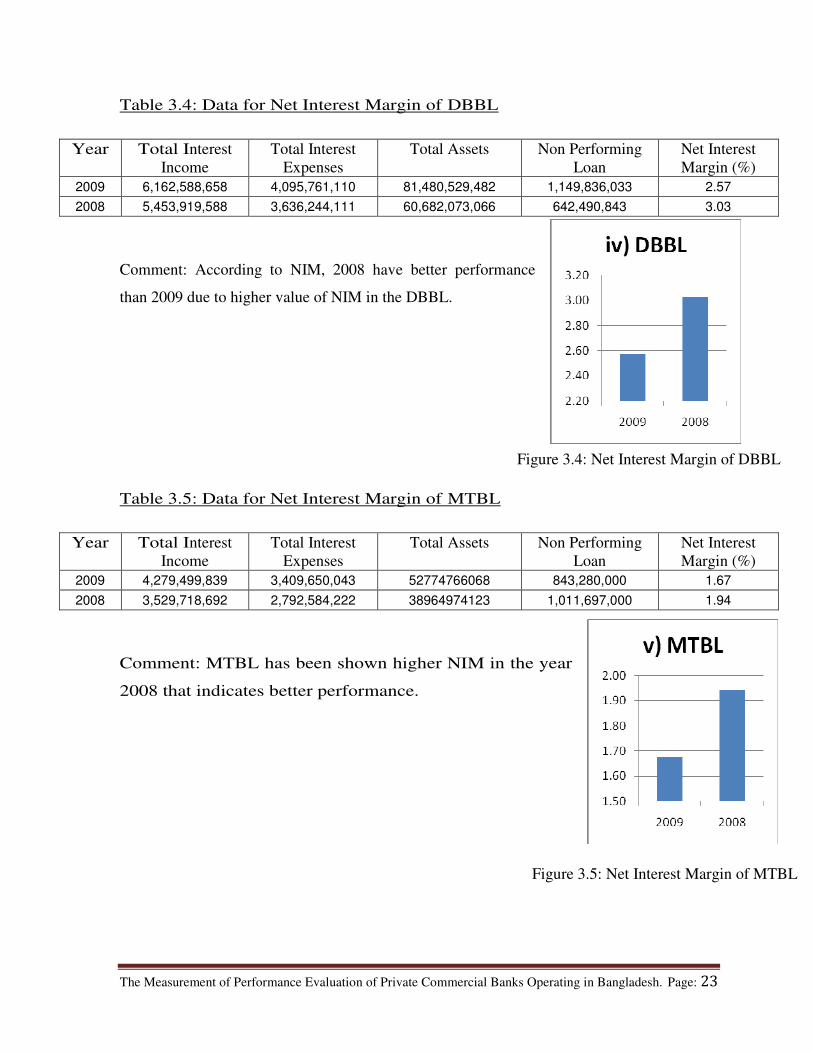

2009 6,162,588,658 4,095,761,110 81,480,529,482 1,149,836,033 2.57

2008 5,453,919,588 3,636,244,111 60,682,073,066 642,490,843 3.03

Comment: According to NIM, 2008 have better performance

than 2009 due to higher value of NIM in the DBBL.

Table 3.5: Data for Net Interest Margin of MTBL

Year Total Interest

Income

Total Interest

Expenses

Total Assets Non Performing

Loan

Net Interest

Margin (%)

2009 4,279,499,839 3,409,650,043 52774766068 843,280,000 1.67

2008 3,529,718,692 2,792,584,222 38964974123 1,011,697,000 1.94

Comment: MTBL has been shown higher NIM in the year

2008 that indicates better performance.

Figure 3.4: Net Interest Margin of DBBL

Figure 3.5: Net Interest Margin of MTBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 24

Table 3.6: Data for Net Interest Margin of NCC Bank

Year Total Interest

Income

Total Interest

Expenses

Total Assets Non Performing

Loan

Net Interest

Margin (%)

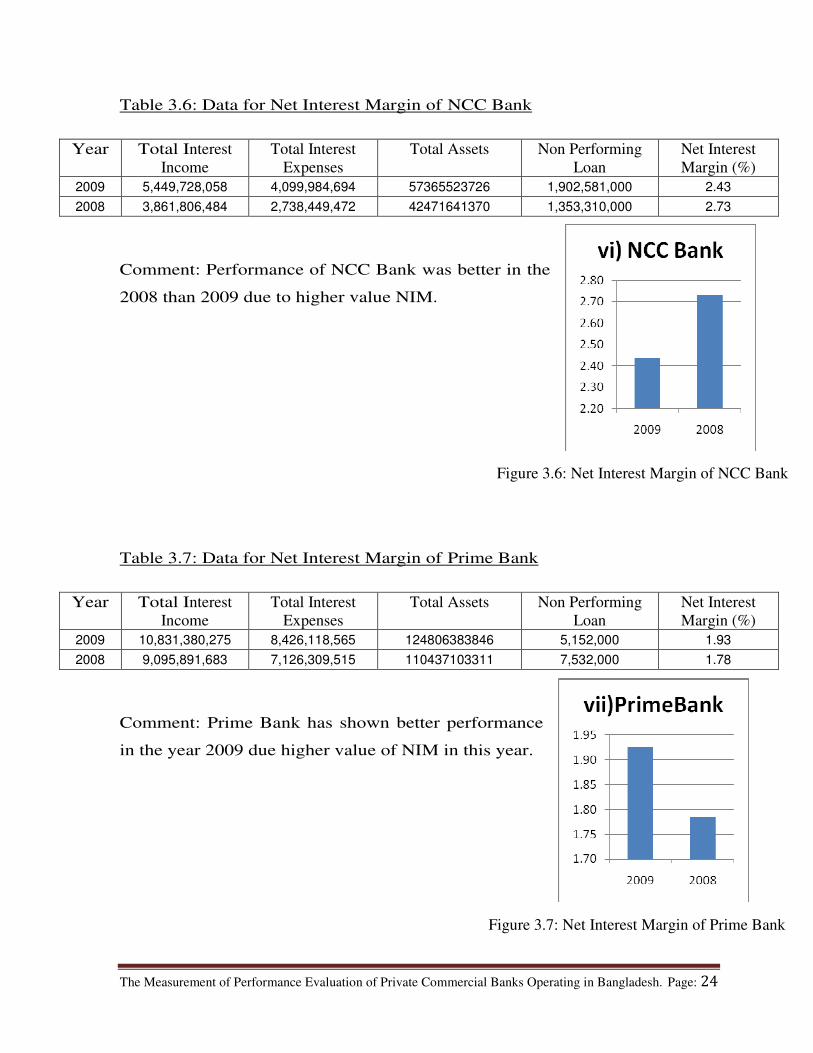

2009 5,449,728,058 4,099,984,694 57365523726 1,902,581,000 2.43

2008 3,861,806,484 2,738,449,472 42471641370 1,353,310,000 2.73

Comment: Performance of NCC Bank was better in the

2008 than 2009 due to higher value NIM.

Table 3.7: Data for Net Interest Margin of Prime Bank

Year Total Interest

Income

Total Interest

Expenses

Total Assets Non Performing

Loan

Net Interest

Margin (%)

2009 10,831,380,275 8,426,118,565 124806383846 5,152,000 1.93

2008 9,095,891,683 7,126,309,515 110437103311 7,532,000 1.78

Comment: Prime Bank has shown better performance

in the year 2009 due higher value of NIM in this year.

Figure 3.6: Net Interest Margin of NCC Bank

Figure 3.7: Net Interest Margin of Prime Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 25

Table 3.8: Data for Net Interest Margin of Trust Bank

Year Total Interest

Income

Total Interest

Expenses

Total Assets Non Performing

Loan

Net Interest

Margin (%)

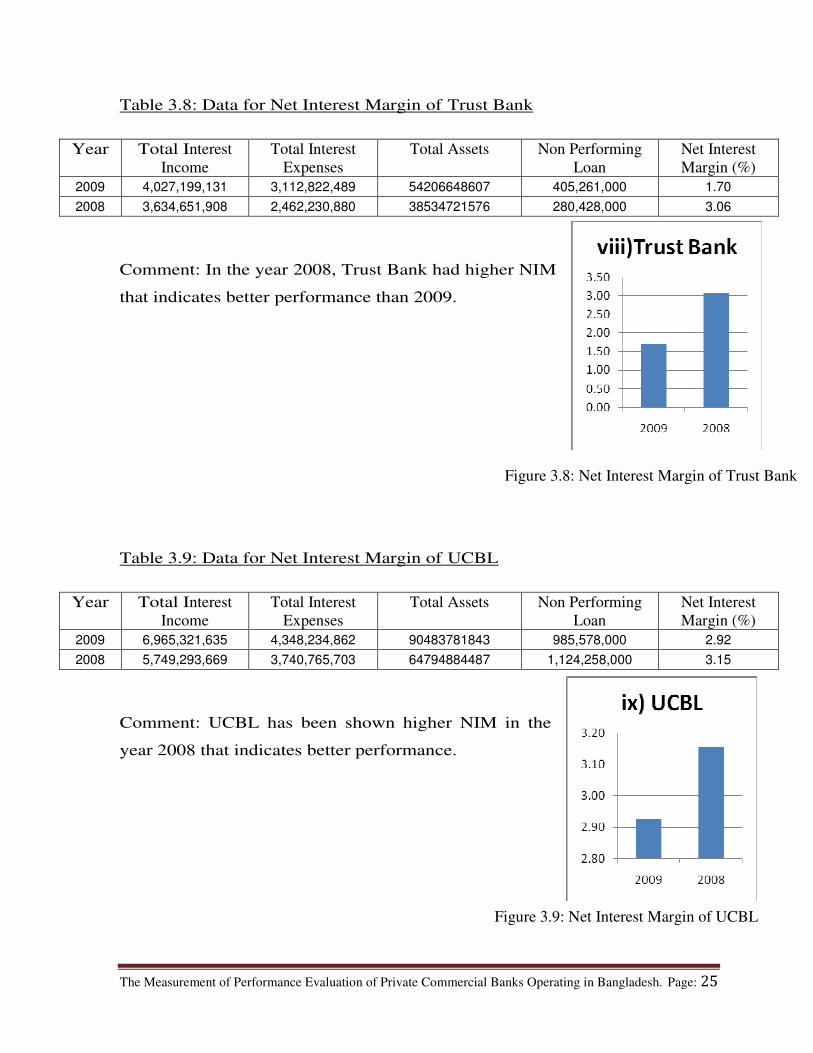

2009 4,027,199,131 3,112,822,489 54206648607 405,261,000 1.70

2008 3,634,651,908 2,462,230,880 38534721576 280,428,000 3.06

Comment: In the year 2008, Trust Bank had higher NIM

that indicates better performance than 2009.

Table 3.9: Data for Net Interest Margin of UCBL

Year Total Interest

Income

Total Interest

Expenses

Total Assets Non Performing

Loan

Net Interest

Margin (%)

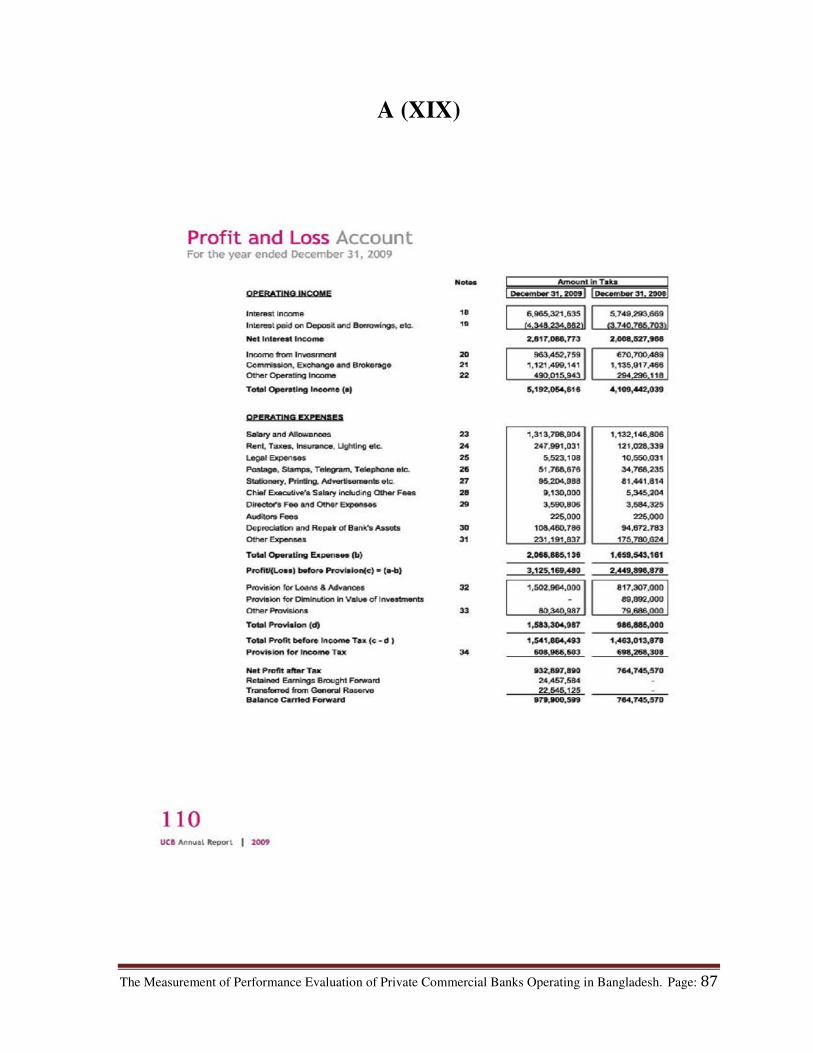

2009 6,965,321,635 4,348,234,862 90483781843 985,578,000 2.92

2008 5,749,293,669 3,740,765,703 64794884487 1,124,258,000 3.15

Comment: UCBL has been shown higher NIM in the

year 2008 that indicates better performance.

Figure 3.8: Net Interest Margin of Trust Bank

Figure 3.9: Net Interest Margin of UCBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 26

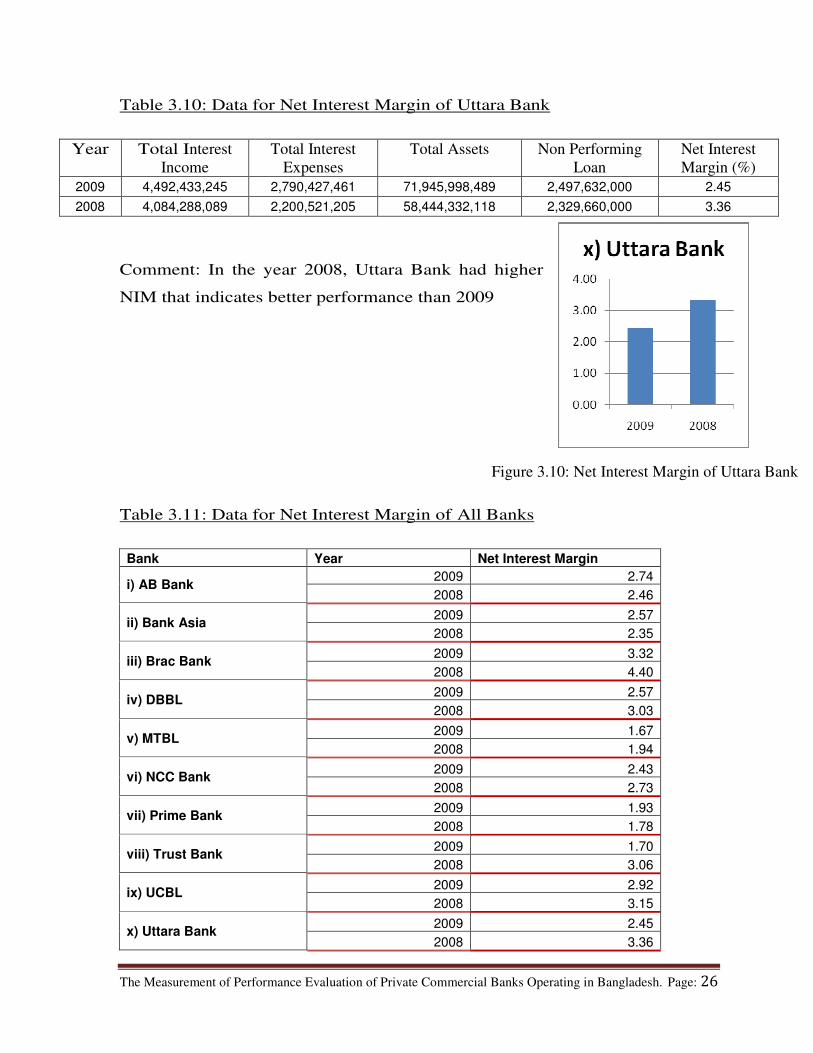

Table 3.10: Data for Net Interest Margin of Uttara Bank

Year Total Interest

Income

Total Interest

Expenses

Total Assets Non Performing

Loan

Net Interest

Margin (%)

2009 4,492,433,245 2,790,427,461 71,945,998,489 2,497,632,000 2.45

2008 4,084,288,089 2,200,521,205 58,444,332,118 2,329,660,000 3.36

Comment: In the year 2008, Uttara Bank had higher

NIM that indicates better performance than 2009

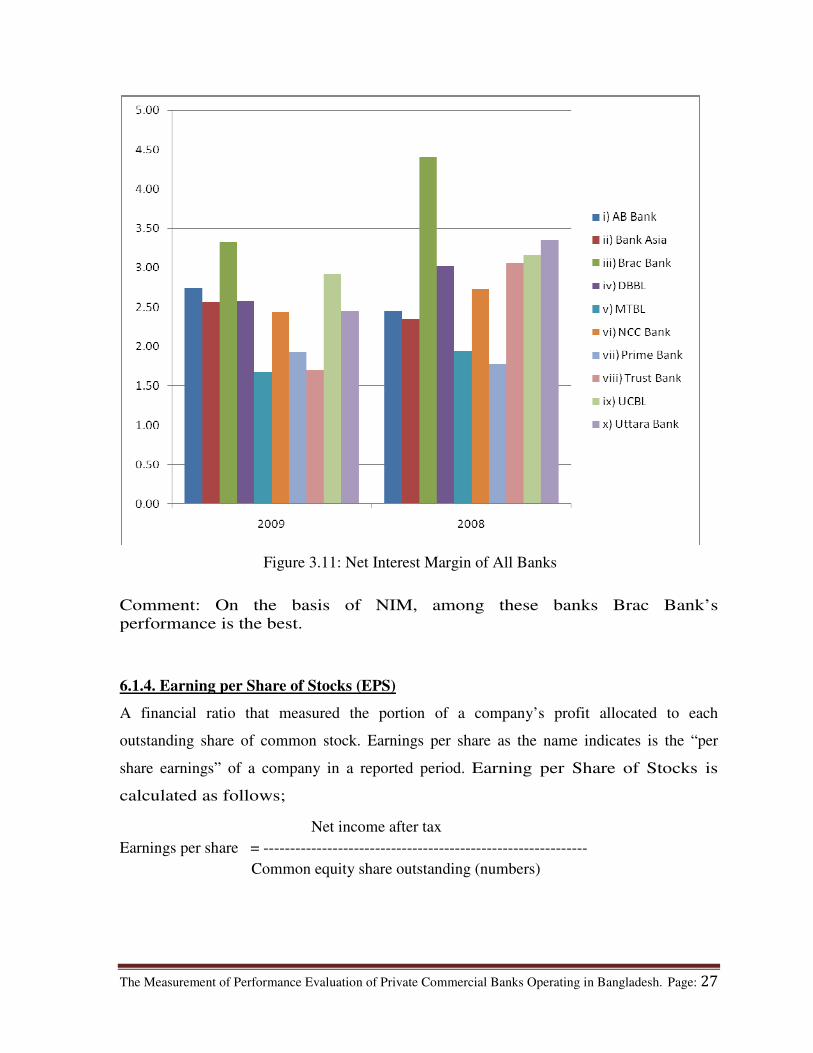

Table 3.11: Data for Net Interest Margin of All Banks

Bank Year Net Interest Margin

i) AB Bank 2009 2.74

2008 2.46

ii) Bank Asia 2009 2.57

2008 2.35

iii) Brac Bank 2009 3.32

2008 4.40

iv) DBBL 2009 2.57

2008 3.03

v) MTBL 2009 1.67

2008 1.94

vi) NCC Bank 2009 2.43

2008 2.73

vii) Prime Bank 2009 1.93

2008 1.78

viii) Trust Bank 2009 1.70

2008 3.06

ix) UCBL 2009 2.92

2008 3.15

x) Uttara Bank 2009 2.45

2008 3.36

Figure 3.10: Net Interest Margin of Uttara Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 27

Comment: On the basis of NIM, among these banks Brac Bank’s

performance is the best.

6.1.4. Earning per Share of Stocks (EPS)

A financial ratio that measured the portion of a company’s profit allocated to each

outstanding share of common stock. Earnings per share as the name indicates is the “per

share earnings” of a company in a reported period. Earning per Share of Stocks is

calculated as follows;

Net income after tax

Earnings per share = -------------------------------------------------------------

Common equity share outstanding (numbers)

Figure 3.11: Net Interest Margin of All Banks

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 28

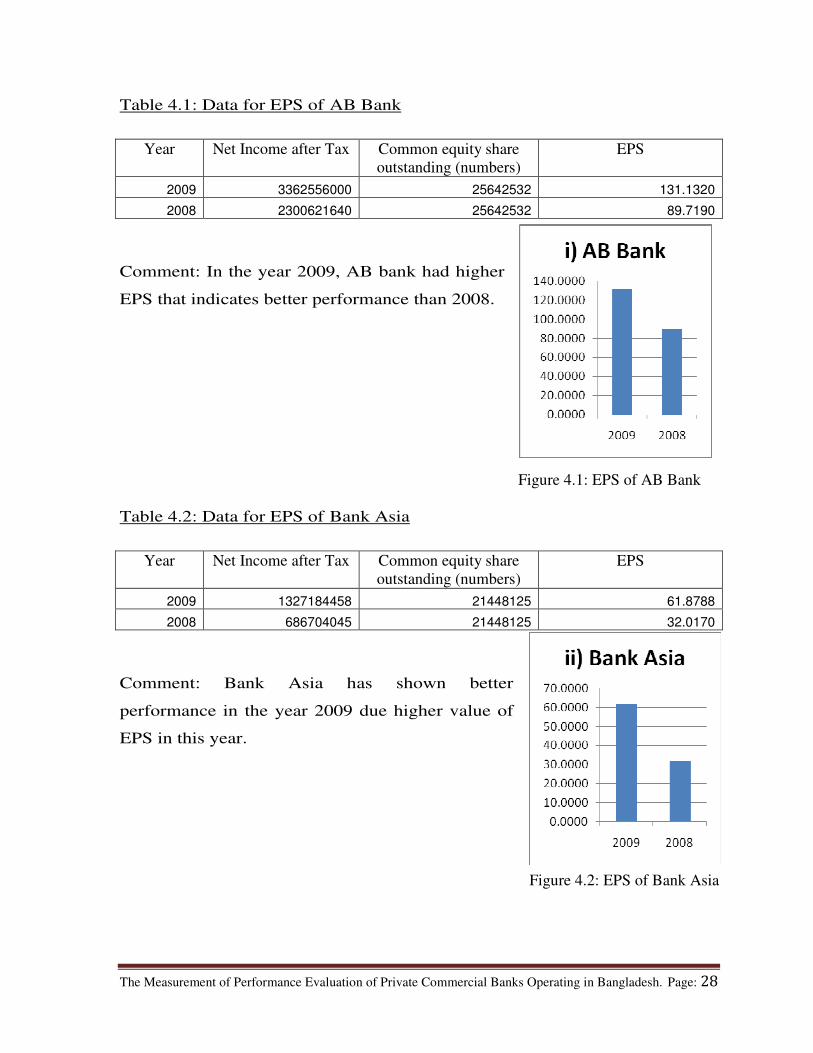

Table 4.1: Data for EPS of AB Bank

Year Net Income after Tax Common equity share

outstanding (numbers)

EPS

2009 3362556000 25642532 131.1320

2008 2300621640 25642532 89.7190

Comment: In the year 2009, AB bank had higher

EPS that indicates better performance than 2008.

Table 4.2: Data for EPS of Bank Asia

Year Net Income after Tax Common equity share

outstanding (numbers)

EPS

2009 1327184458 21448125 61.8788

2008 686704045 21448125 32.0170

Comment: Bank Asia has shown better

performance in the year 2009 due higher value of

EPS in this year.

Figure 4.1: EPS of AB Bank

Figure 4.2: EPS of Bank Asia

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 29

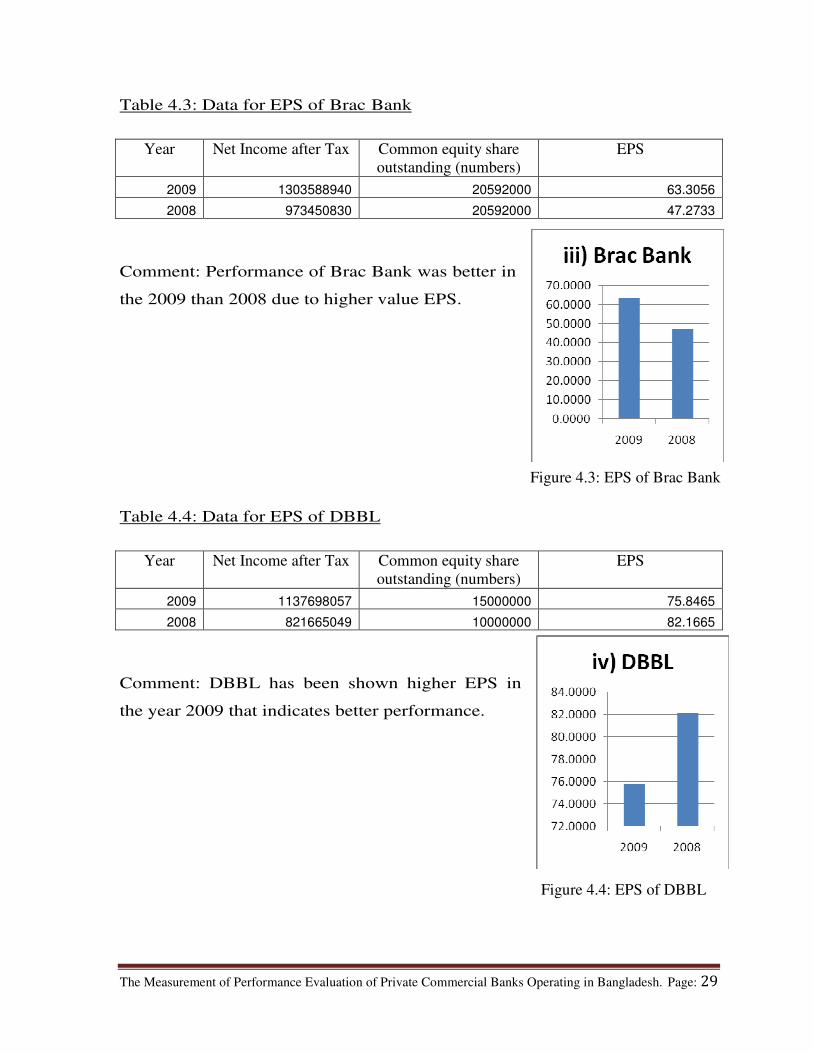

Table 4.3: Data for EPS of Brac Bank

Year Net Income after Tax Common equity share

outstanding (numbers)

EPS

2009 1303588940 20592000 63.3056

2008 973450830 20592000 47.2733

Comment: Performance of Brac Bank was better in

the 2009 than 2008 due to higher value EPS.

Table 4.4: Data for EPS of DBBL

Year Net Income after Tax Common equity share

outstanding (numbers)

EPS

2009 1137698057 15000000 75.8465

2008 821665049 10000000 82.1665

Comment: DBBL has been shown higher EPS in

the year 2009 that indicates better performance.

Figure 4.3: EPS of Brac Bank

Figure 4.4: EPS of DBBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 30

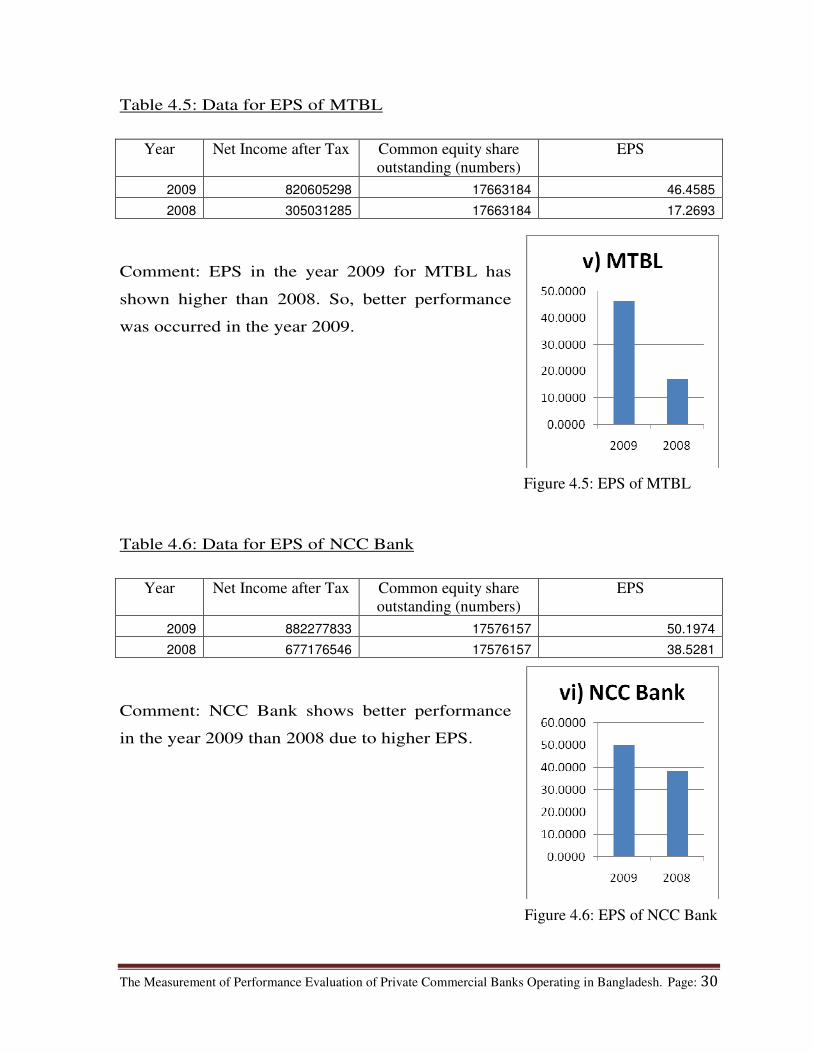

Table 4.5: Data for EPS of MTBL

Year Net Income after Tax Common equity share

outstanding (numbers)

EPS

2009 820605298 17663184 46.4585

2008 305031285 17663184 17.2693

Comment: EPS in the year 2009 for MTBL has

shown higher than 2008. So, better performance

was occurred in the year 2009.

Table 4.6: Data for EPS of NCC Bank

Year Net Income after Tax Common equity share

outstanding (numbers)

EPS

2009 882277833 17576157 50.1974

2008 677176546 17576157 38.5281

Comment: NCC Bank shows better performance

in the year 2009 than 2008 due to higher EPS.

Figure 4.5: EPS of MTBL

Figure 4.6: EPS of NCC Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 31

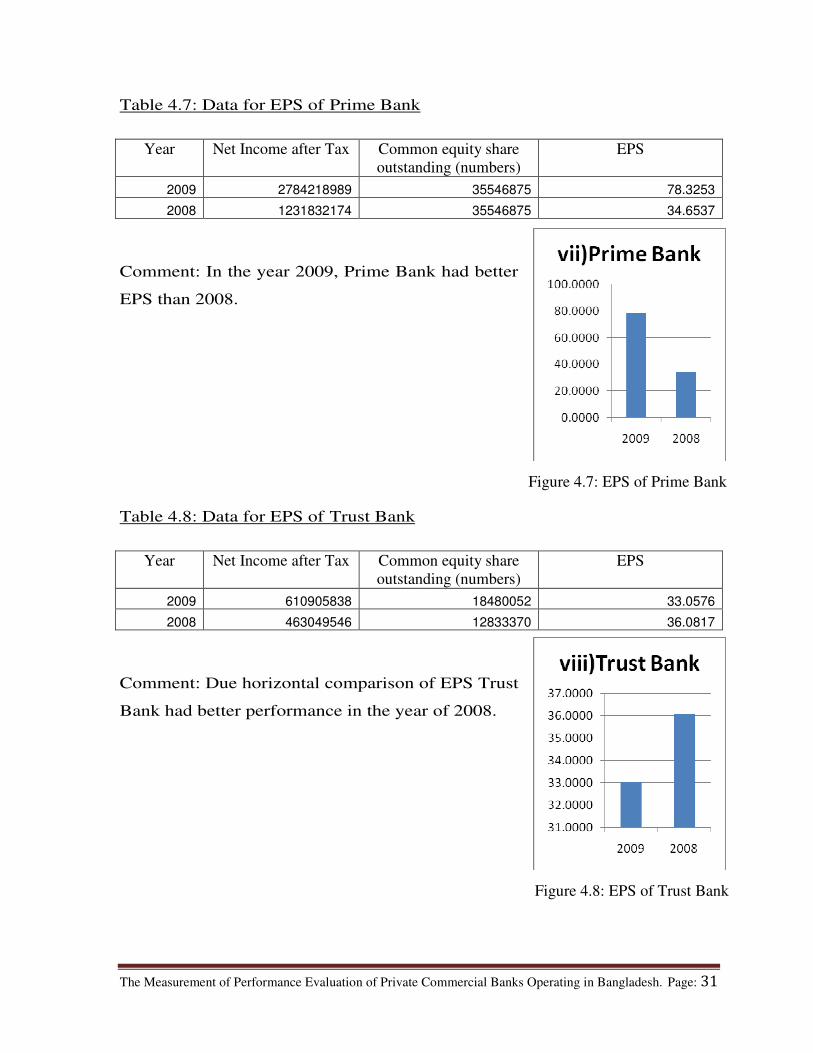

Table 4.7: Data for EPS of Prime Bank

Year Net Income after Tax Common equity share

outstanding (numbers)

EPS

2009 2784218989 35546875 78.3253

2008 1231832174 35546875 34.6537

Comment: In the year 2009, Prime Bank had better

EPS than 2008.

Table 4.8: Data for EPS of Trust Bank

Year Net Income after Tax Common equity share

outstanding (numbers)

EPS

2009 610905838 18480052 33.0576

2008 463049546 12833370 36.0817

Comment: Due horizontal comparison of EPS Trust

Bank had better performance in the year of 2008.

Figure 4.7: EPS of Prime Bank

Figure 4.8: EPS of Trust Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 32

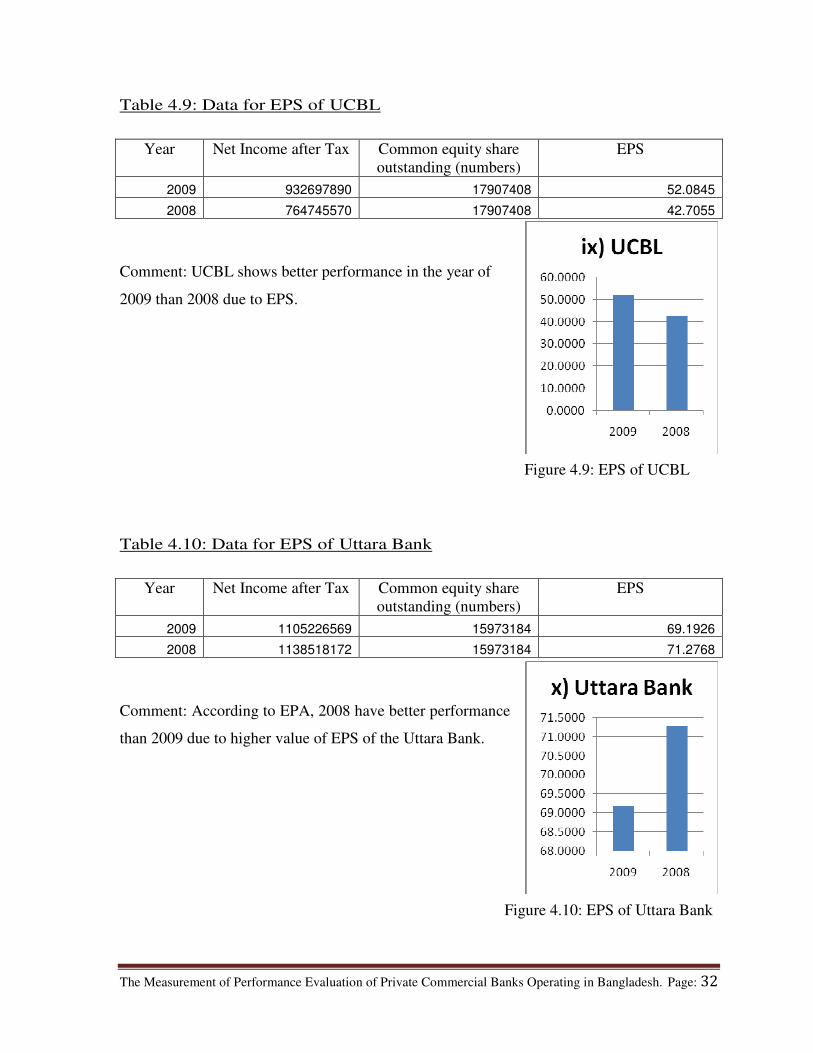

Table 4.9: Data for EPS of UCBL

Year Net Income after Tax Common equity share

outstanding (numbers)

EPS

2009 932697890 17907408 52.0845

2008 764745570 17907408 42.7055

Comment: UCBL shows better performance in the year of

2009 than 2008 due to EPS.

Table 4.10: Data for EPS of Uttara Bank

Year Net Income after Tax Common equity share

outstanding (numbers)

EPS

2009 1105226569 15973184 69.1926

2008 1138518172 15973184 71.2768

Comment: According to EPA, 2008 have better performance

than 2009 due to higher value of EPS of the Uttara Bank.

Figure 4.9: EPS of UCBL

Figure 4.10: EPS of Uttara Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 33

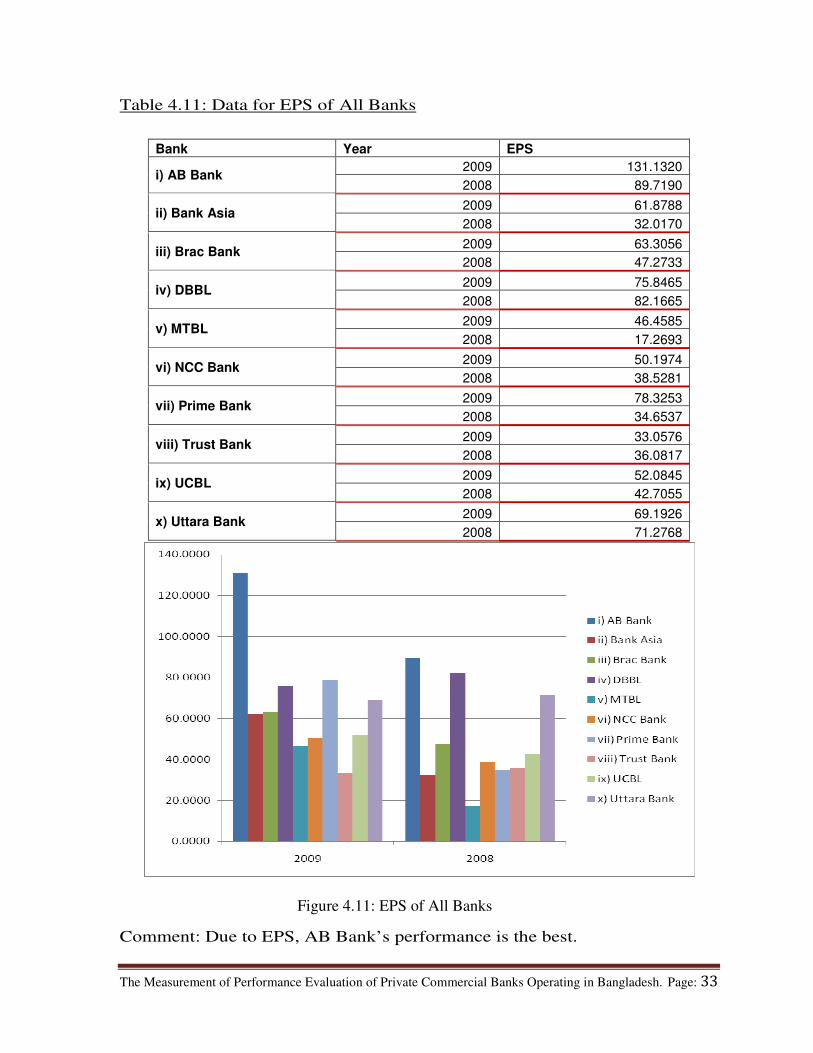

Table 4.11: Data for EPS of All Banks

Bank Year EPS

i) AB Bank 2009 131.1320

2008 89.7190

ii) Bank Asia 2009 61.8788

2008 32.0170

iii) Brac Bank 2009 63.3056

2008 47.2733

iv) DBBL 2009 75.8465

2008 82.1665

v) MTBL 2009 46.4585

2008 17.2693

vi) NCC Bank 2009 50.1974

2008 38.5281

vii) Prime Bank 2009 78.3253

2008 34.6537

viii) Trust Bank 2009 33.0576

2008 36.0817

ix) UCBL 2009 52.0845

2008 42.7055

x) Uttara Bank 2009 69.1926

2008 71.2768

Comment: Due to EPS, AB Bank’s performance is the best.

Figure 4.11: EPS of All Banks

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 34

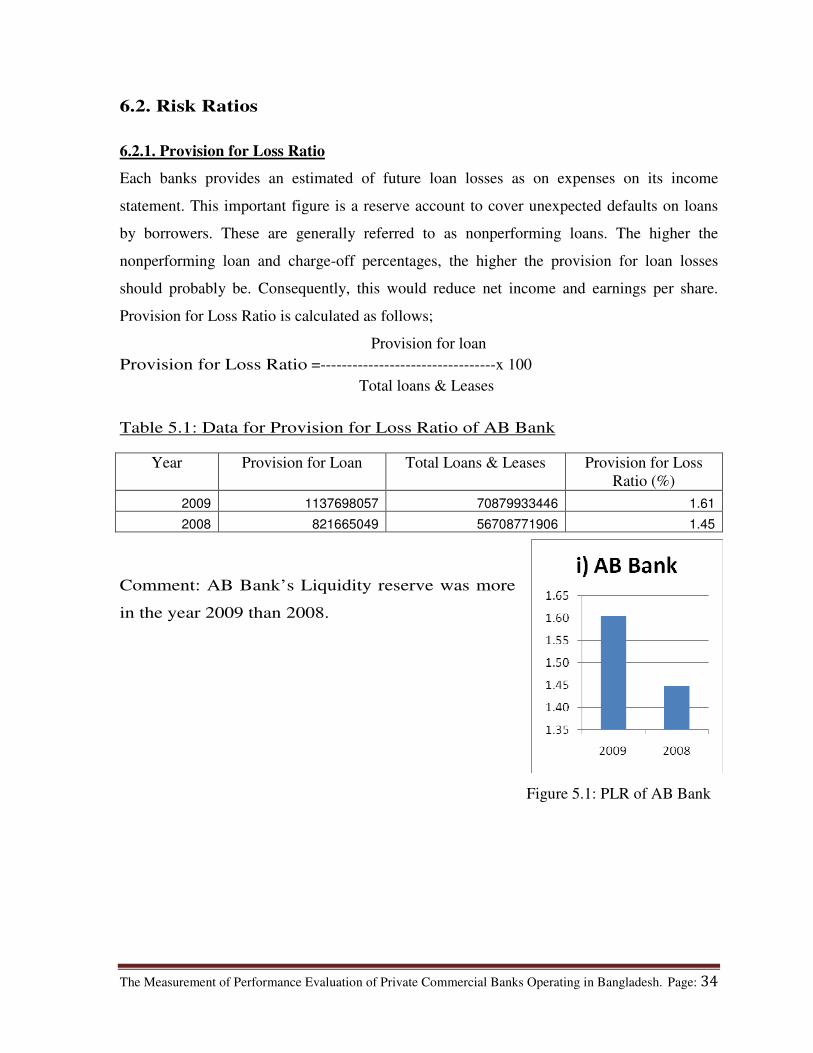

6.2. Risk Ratios

6.2.1. Provision for Loss Ratio

Each banks provides an estimated of future loan losses as on expenses on its income

statement. This important figure is a reserve account to cover unexpected defaults on loans

by borrowers. These are generally referred to as nonperforming loans. The higher the

nonperforming loan and charge-off percentages, the higher the provision for loan losses

should probably be. Consequently, this would reduce net income and earnings per share.

Provision for Loss Ratio is calculated as follows;

Provision for loan

Provision for Loss Ratio =---------------------------------x 100

Total loans & Leases

Table 5.1: Data for Provision for Loss Ratio of AB Bank

Year Provision for Loan Total Loans & Leases

Provision for Loss

Ratio (%)

2009 1137698057 70879933446 1.61

2008 821665049 56708771906 1.45

Comment: AB Bank’s Liquidity reserve was more

in the year 2009 than 2008.

Figure 5.1: PLR of AB Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 35

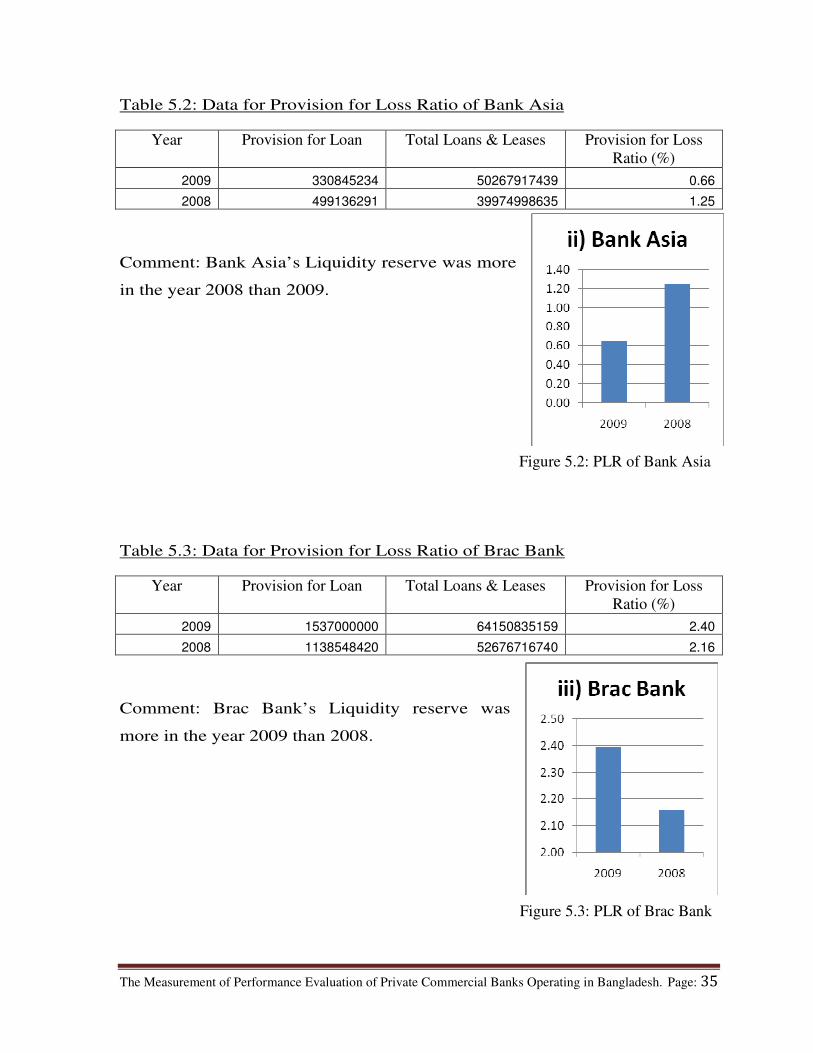

Table 5.2: Data for Provision for Loss Ratio of Bank Asia

Year Provision for Loan Total Loans & Leases

Provision for Loss

Ratio (%)

2009 330845234 50267917439 0.66

2008 499136291 39974998635 1.25

Comment: Bank Asia’s Liquidity reserve was more

in the year 2008 than 2009.

Table 5.3: Data for Provision for Loss Ratio of Brac Bank

Year Provision for Loan Total Loans & Leases

Provision for Loss

Ratio (%)

2009 1537000000 64150835159 2.40

2008 1138548420 52676716740 2.16

Comment: Brac Bank’s Liquidity reserve was

more in the year 2009 than 2008.

Figure 5.2: PLR of Bank Asia

Figure 5.3: PLR of Brac Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 36

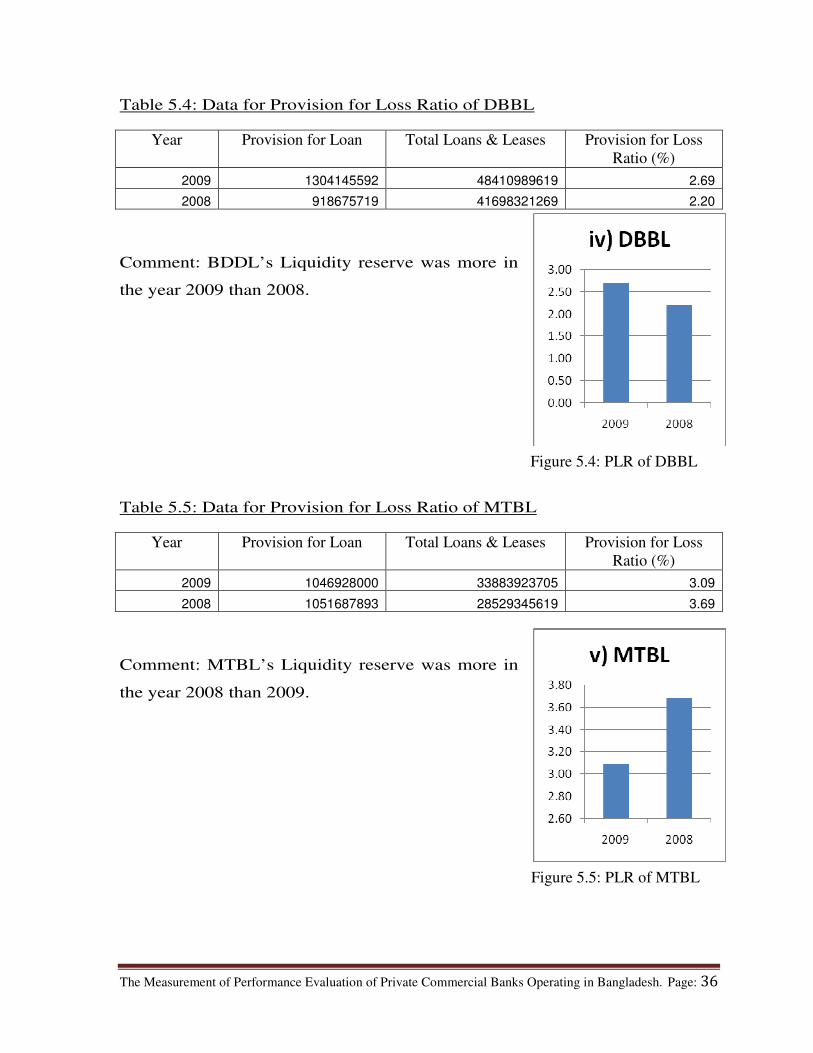

Table 5.4: Data for Provision for Loss Ratio of DBBL

Year Provision for Loan Total Loans & Leases

Provision for Loss

Ratio (%)

2009 1304145592 48410989619 2.69

2008 918675719 41698321269 2.20

Comment: BDDL’s Liquidity reserve was more in

the year 2009 than 2008.

Table 5.5: Data for Provision for Loss Ratio of MTBL

Year Provision for Loan Total Loans & Leases

Provision for Loss

Ratio (%)

2009 1046928000 33883923705 3.09

2008 1051687893 28529345619 3.69

Comment: MTBL’s Liquidity reserve was more in

the year 2008 than 2009.

Figure 5.4: PLR of DBBL

Figure 5.5: PLR of MTBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 37

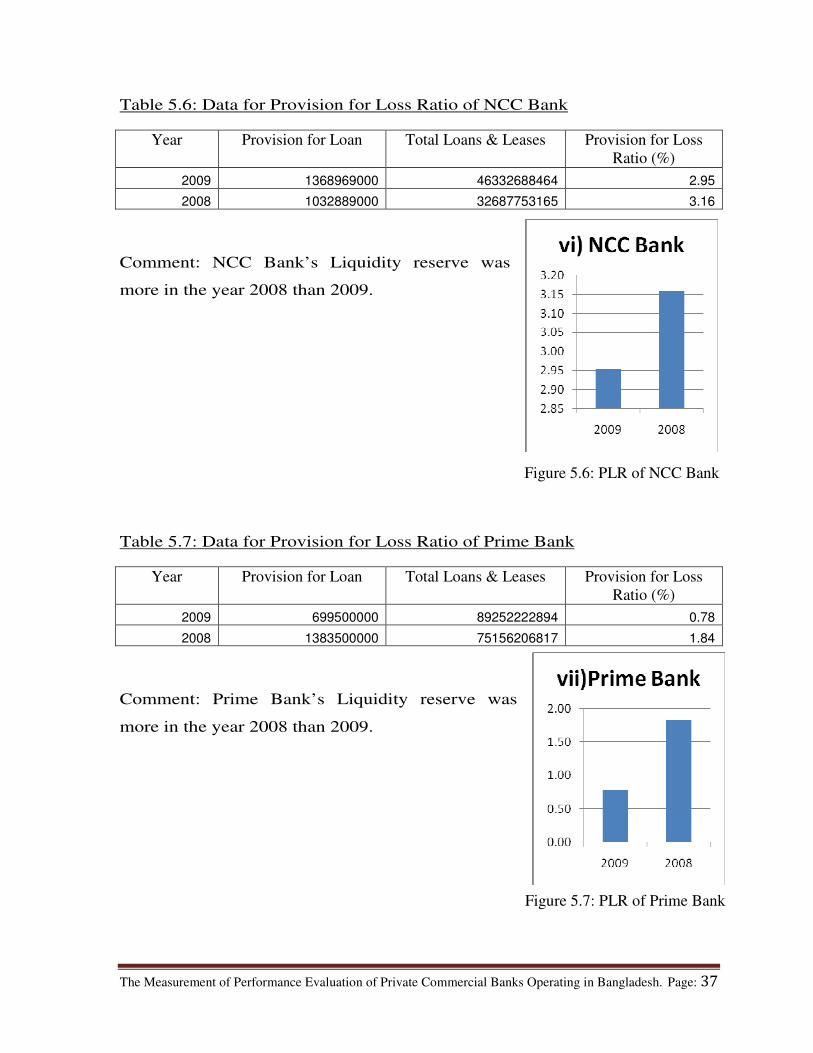

Table 5.6: Data for Provision for Loss Ratio of NCC Bank

Year Provision for Loan Total Loans & Leases

Provision for Loss

Ratio (%)

2009 1368969000 46332688464 2.95

2008 1032889000 32687753165 3.16

Comment: NCC Bank’s Liquidity reserve was

more in the year 2008 than 2009.

Table 5.7: Data for Provision for Loss Ratio of Prime Bank

Year Provision for Loan Total Loans & Leases

Provision for Loss

Ratio (%)

2009 699500000 89252222894 0.78

2008 1383500000 75156206817 1.84

Comment: Prime Bank’s Liquidity reserve was

more in the year 2008 than 2009.

Figure 5.6: PLR of NCC Bank

Figure 5.7: PLR of Prime Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 38

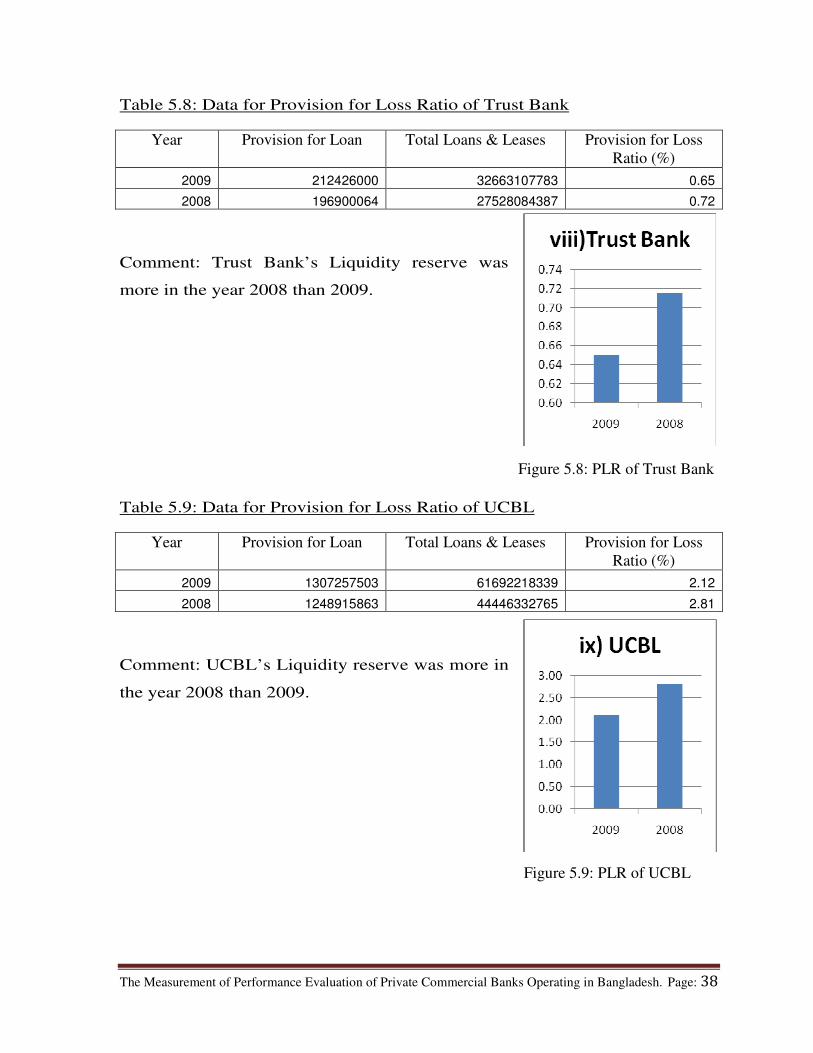

Table 5.8: Data for Provision for Loss Ratio of Trust Bank

Year Provision for Loan Total Loans & Leases

Provision for Loss

Ratio (%)

2009 212426000 32663107783 0.65

2008 196900064 27528084387 0.72

Comment: Trust Bank’s Liquidity reserve was

more in the year 2008 than 2009.

Table 5.9: Data for Provision for Loss Ratio of UCBL

Year Provision for Loan Total Loans & Leases

Provision for Loss

Ratio (%)

2009 1307257503 61692218339 2.12

2008 1248915863 44446332765 2.81

Comment: UCBL’s Liquidity reserve was more in

the year 2008 than 2009.

Figure 5.8: PLR of Trust Bank

Figure 5.9: PLR of UCBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 39

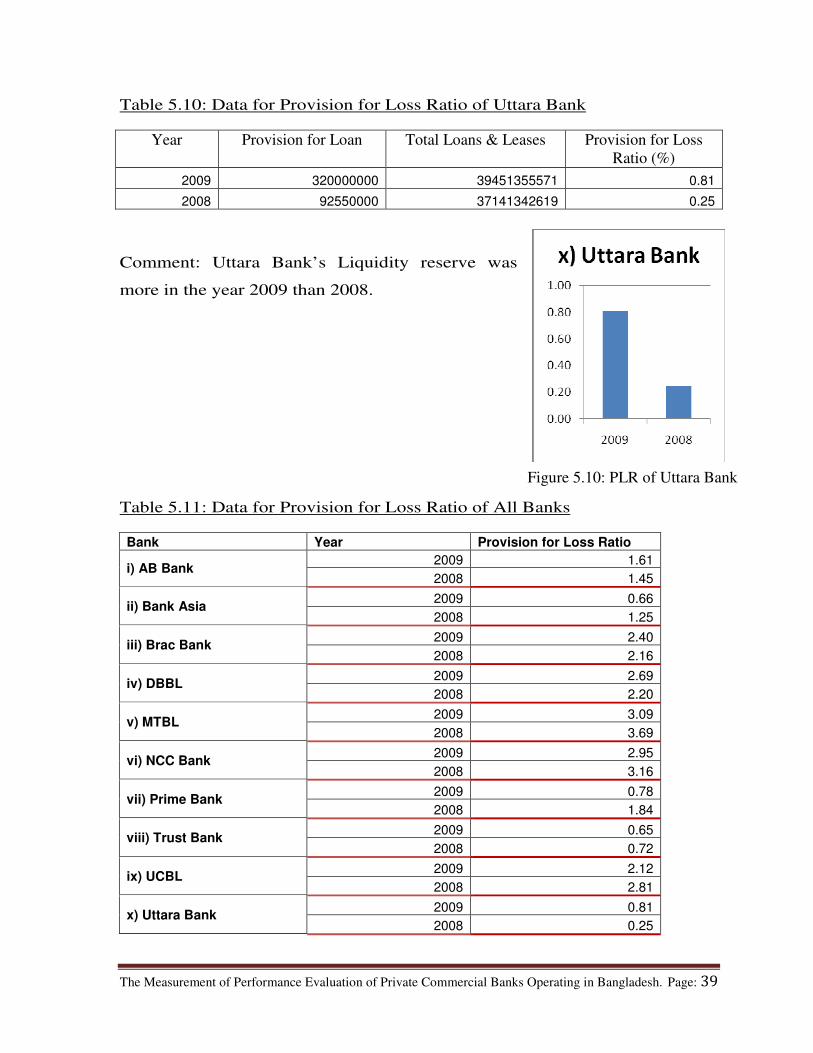

Table 5.10: Data for Provision for Loss Ratio of Uttara Bank

Year Provision for Loan Total Loans & Leases

Provision for Loss

Ratio (%)

2009 320000000 39451355571 0.81

2008 92550000 37141342619 0.25

Comment: Uttara Bank’s Liquidity reserve was

more in the year 2009 than 2008.

Table 5.11: Data for Provision for Loss Ratio of All Banks

Bank Year Provision for Loss Ratio

i) AB Bank 2009 1.61

2008 1.45

ii) Bank Asia 2009 0.66

2008 1.25

iii) Brac Bank 2009 2.40

2008 2.16

iv) DBBL 2009 2.69

2008 2.20

v) MTBL 2009 3.09

2008 3.69

vi) NCC Bank 2009 2.95

2008 3.16

vii) Prime Bank 2009 0.78

2008 1.84

viii) Trust Bank 2009 0.65

2008 0.72

ix) UCBL 2009 2.12

2008 2.81

x) Uttara Bank 2009 0.81

2008 0.25

Figure 5.10: PLR of Uttara Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 40

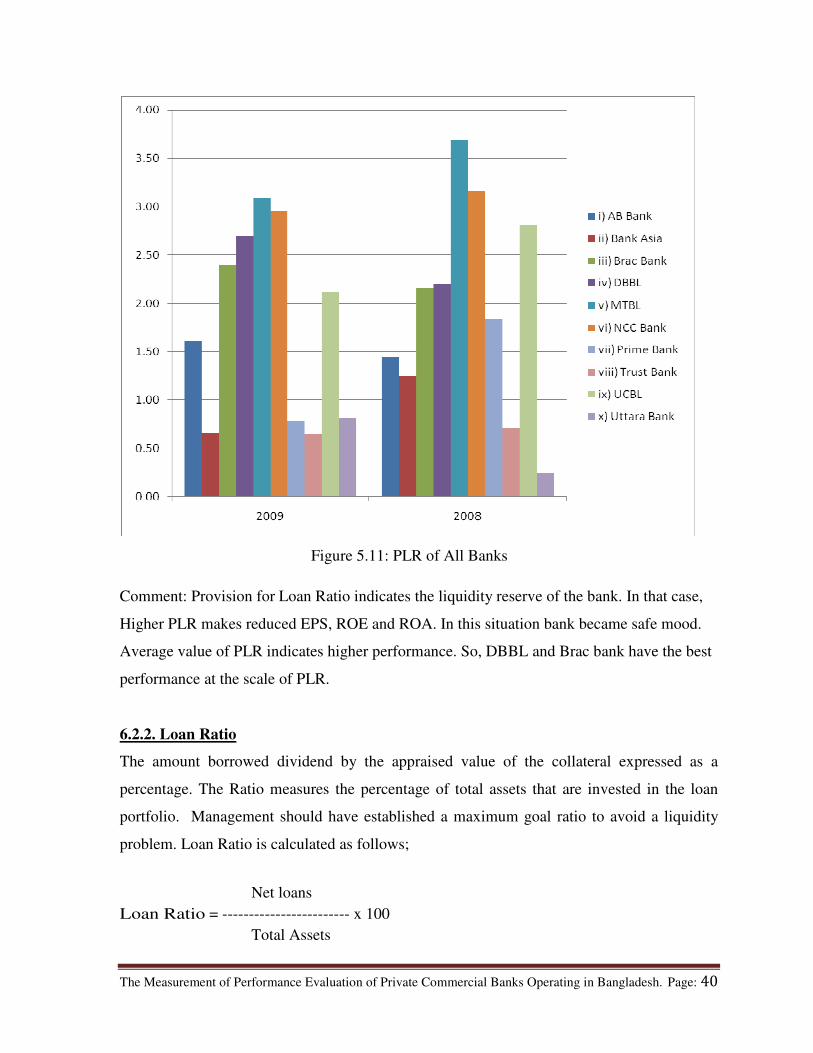

Comment: Provision for Loan Ratio indicates the liquidity reserve of the bank. In that case,

Higher PLR makes reduced EPS, ROE and ROA. In this situation bank became safe mood.

Average value of PLR indicates higher performance. So, DBBL and Brac bank have the best

performance at the scale of PLR.

6.2.2. Loan Ratio

The amount borrowed dividend by the appraised value of the collateral expressed as a

percentage. The Ratio measures the percentage of total assets that are invested in the loan

portfolio. Management should have established a maximum goal ratio to avoid a liquidity

problem. Loan Ratio is calculated as follows;

Net loans

Loan Ratio = ------------------------ x 100

Total Assets

Figure 5.11: PLR of All Banks

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 41

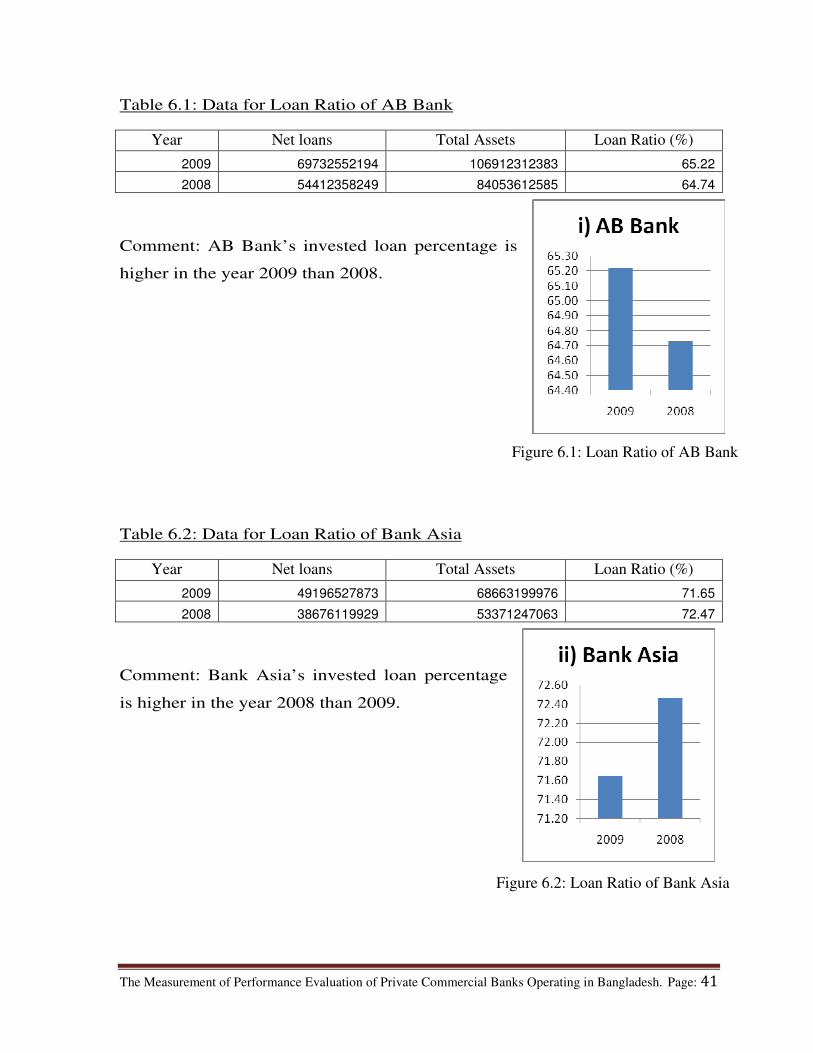

Table 6.1: Data for Loan Ratio of AB Bank

Year Net loans Total Assets Loan Ratio (%)

2009 69732552194 106912312383 65.22

2008 54412358249 84053612585 64.74

Comment: AB Bank’s invested loan percentage is

higher in the year 2009 than 2008.

Table 6.2: Data for Loan Ratio of Bank Asia

Year Net loans Total Assets Loan Ratio (%)

2009 49196527873 68663199976 71.65

2008 38676119929 53371247063 72.47

Comment: Bank Asia’s invested loan percentage

is higher in the year 2008 than 2009.

Figure 6.1: Loan Ratio of AB Bank

Figure 6.2: Loan Ratio of Bank Asia

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 42

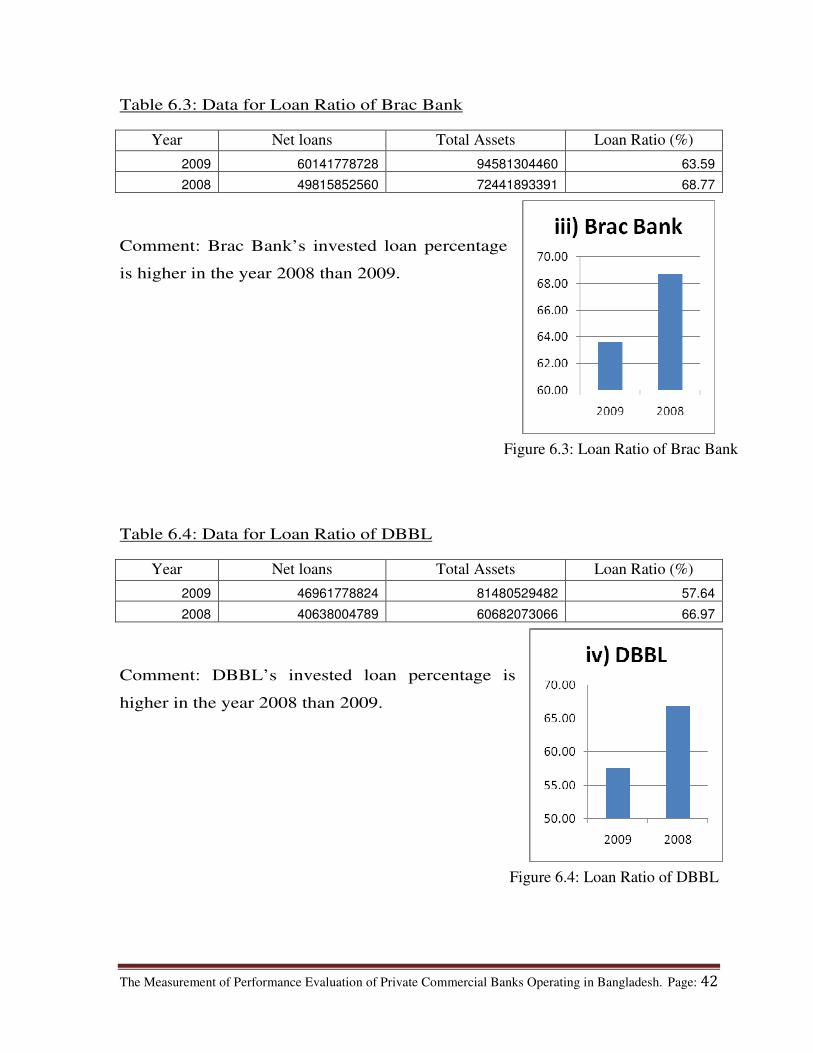

Table 6.3: Data for Loan Ratio of Brac Bank

Year Net loans Total Assets Loan Ratio (%)

2009 60141778728 94581304460 63.59

2008 49815852560 72441893391 68.77

Comment: Brac Bank’s invested loan percentage

is higher in the year 2008 than 2009.

Table 6.4: Data for Loan Ratio of DBBL

Year Net loans Total Assets Loan Ratio (%)

2009 46961778824 81480529482 57.64

2008 40638004789 60682073066 66.97

Comment: DBBL’s invested loan percentage is

higher in the year 2008 than 2009.

Figure 6.3: Loan Ratio of Brac Bank

Figure 6.4: Loan Ratio of DBBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 43

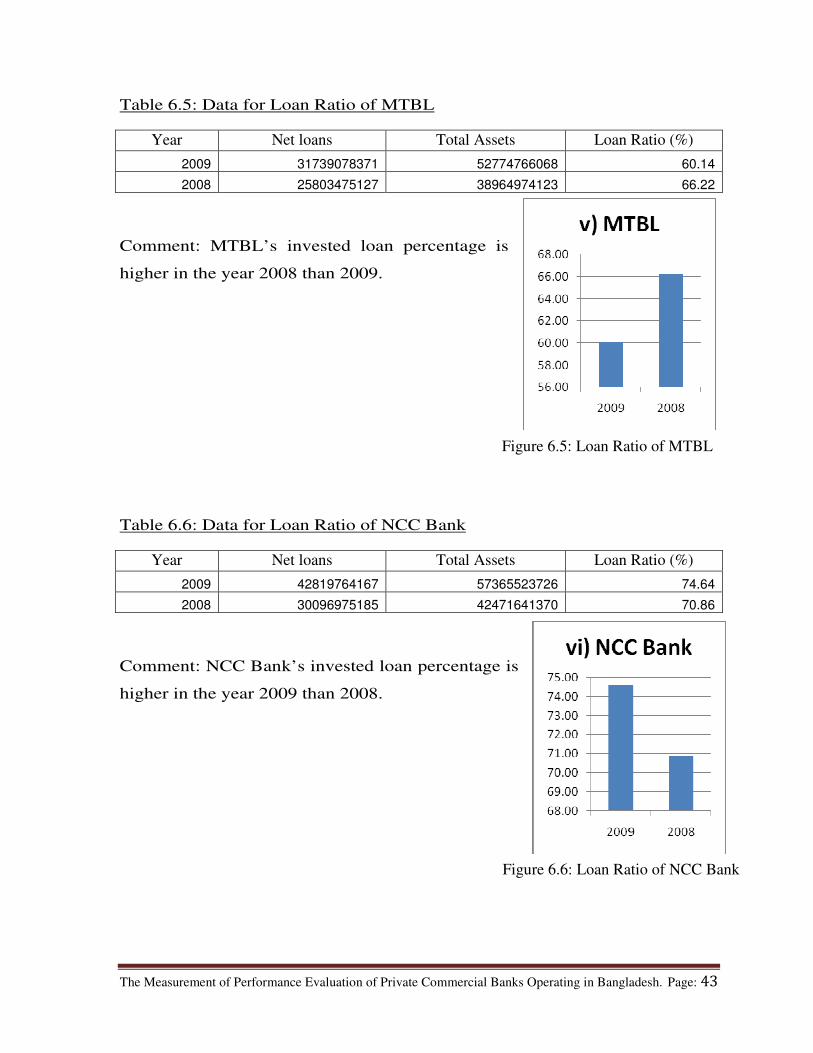

Table 6.5: Data for Loan Ratio of MTBL

Year Net loans Total Assets Loan Ratio (%)

2009 31739078371 52774766068 60.14

2008 25803475127 38964974123 66.22

Comment: MTBL’s invested loan percentage is

higher in the year 2008 than 2009.

Table 6.6: Data for Loan Ratio of NCC Bank

Year Net loans Total Assets Loan Ratio (%)

2009 42819764167 57365523726 74.64

2008 30096975185 42471641370 70.86

Comment: NCC Bank’s invested loan percentage is

higher in the year 2009 than 2008.

Figure 6.5: Loan Ratio of MTBL

Figure 6.6: Loan Ratio of NCC Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 44

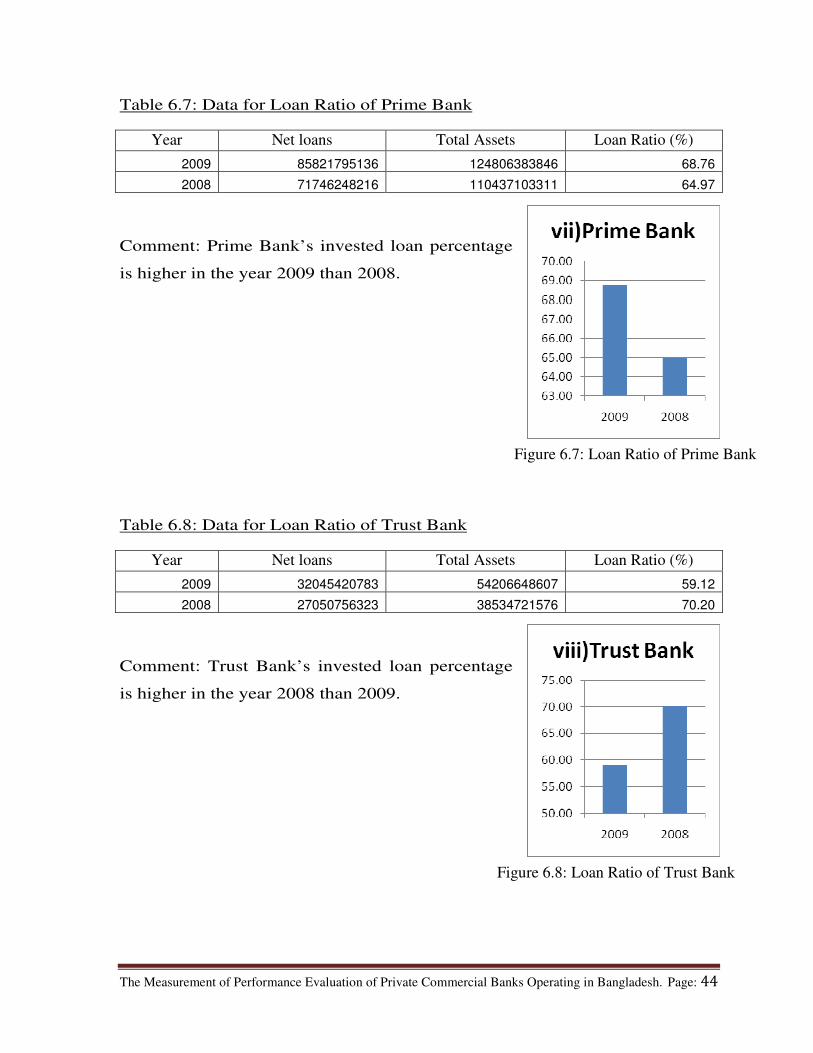

Table 6.7: Data for Loan Ratio of Prime Bank

Year Net loans Total Assets Loan Ratio (%)

2009 85821795136 124806383846 68.76

2008 71746248216 110437103311 64.97

Comment: Prime Bank’s invested loan percentage

is higher in the year 2009 than 2008.

Table 6.8: Data for Loan Ratio of Trust Bank

Year Net loans Total Assets Loan Ratio (%)

2009 32045420783 54206648607 59.12

2008 27050756323 38534721576 70.20

Comment: Trust Bank’s invested loan percentage

is higher in the year 2008 than 2009.

Figure 6.7: Loan Ratio of Prime Bank

Figure 6.8: Loan Ratio of Trust Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 45

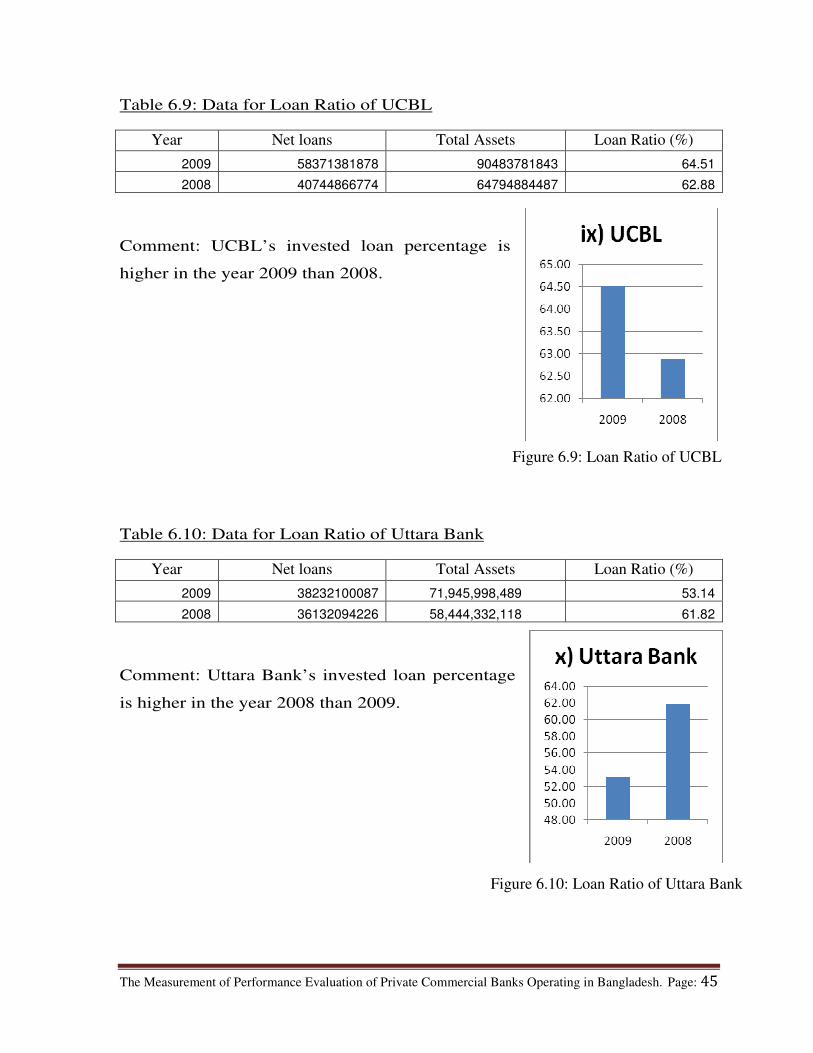

Table 6.9: Data for Loan Ratio of UCBL

Year Net loans Total Assets Loan Ratio (%)

2009 58371381878 90483781843 64.51

2008 40744866774 64794884487 62.88

Comment: UCBL’s invested loan percentage is

higher in the year 2009 than 2008.

Table 6.10: Data for Loan Ratio of Uttara Bank

Year Net loans Total Assets Loan Ratio (%)

2009 38232100087 71,945,998,489 53.14

2008 36132094226 58,444,332,118 61.82

Comment: Uttara Bank’s invested loan percentage

is higher in the year 2008 than 2009.

Figure 6.9: Loan Ratio of UCBL

Figure 6.10: Loan Ratio of Uttara Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 46

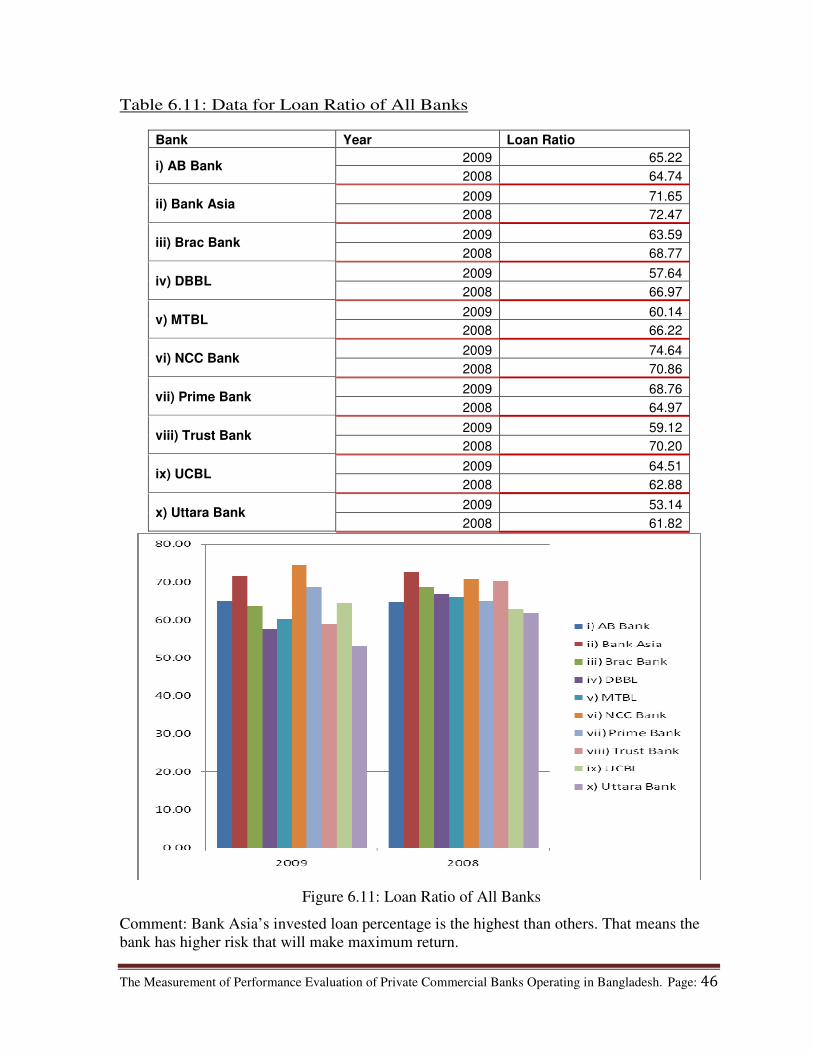

Table 6.11: Data for Loan Ratio of All Banks

Bank Year Loan Ratio

i) AB Bank 2009 65.22

2008 64.74

ii) Bank Asia 2009 71.65

2008 72.47

iii) Brac Bank 2009 63.59

2008 68.77

iv) DBBL 2009 57.64

2008 66.97

v) MTBL 2009 60.14

2008 66.22

vi) NCC Bank 2009 74.64

2008 70.86

vii) Prime Bank 2009 68.76

2008 64.97

viii) Trust Bank 2009 59.12

2008 70.20

ix) UCBL 2009 64.51

2008 62.88

x) Uttara Bank 2009 53.14

2008 61.82

Comment: Bank Asia’s invested loan percentage is the highest than others. That means the

bank has higher risk that will make maximum return.

Figure 6.11: Loan Ratio of All Banks

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 47

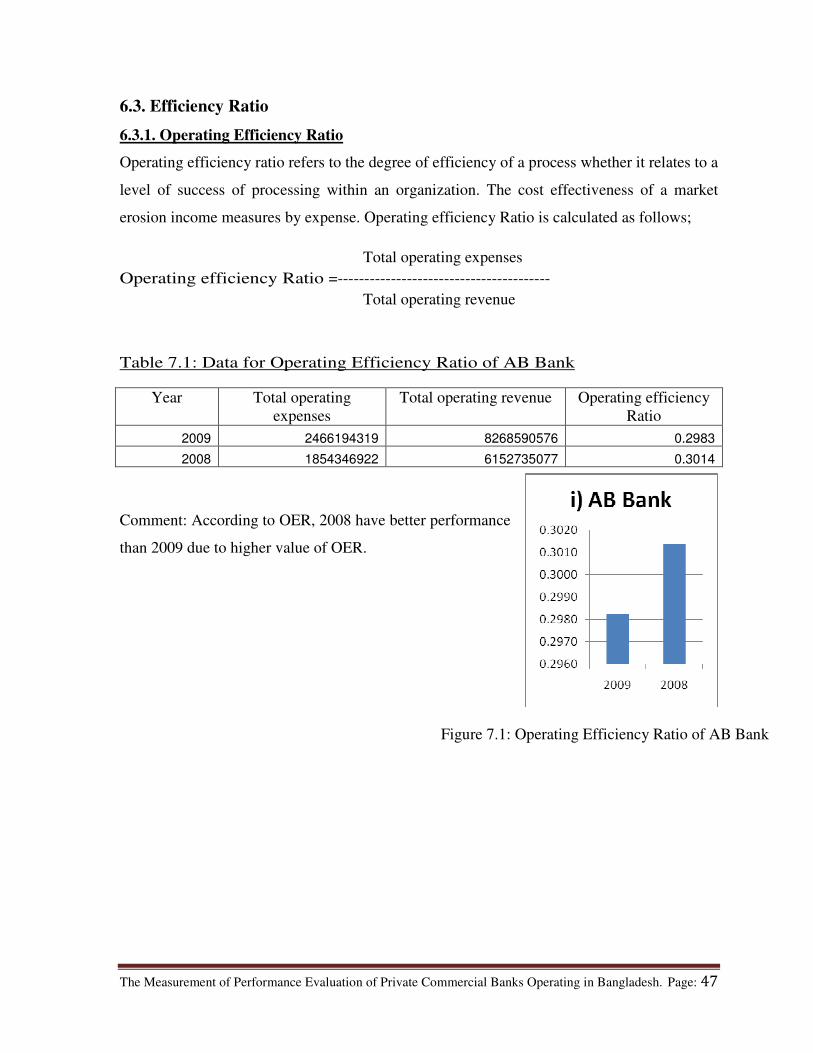

6.3. Efficiency Ratio

6.3.1. Operating Efficiency Ratio

Operating efficiency ratio refers to the degree of efficiency of a process whether it relates to a

level of success of processing within an organization. The cost effectiveness of a market

erosion income measures by expense. Operating efficiency Ratio is calculated as follows;

Total operating expenses

Operating efficiency Ratio =----------------------------------------

Total operating revenue

Table 7.1: Data for Operating Efficiency Ratio of AB Bank

Year Total operating

expenses

Total operating revenue Operating efficiency

Ratio

2009 2466194319 8268590576 0.2983

2008 1854346922 6152735077 0.3014

Comment: According to OER, 2008 have better performance

than 2009 due to higher value of OER.

Figure 7.1: Operating Efficiency Ratio of AB Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 48

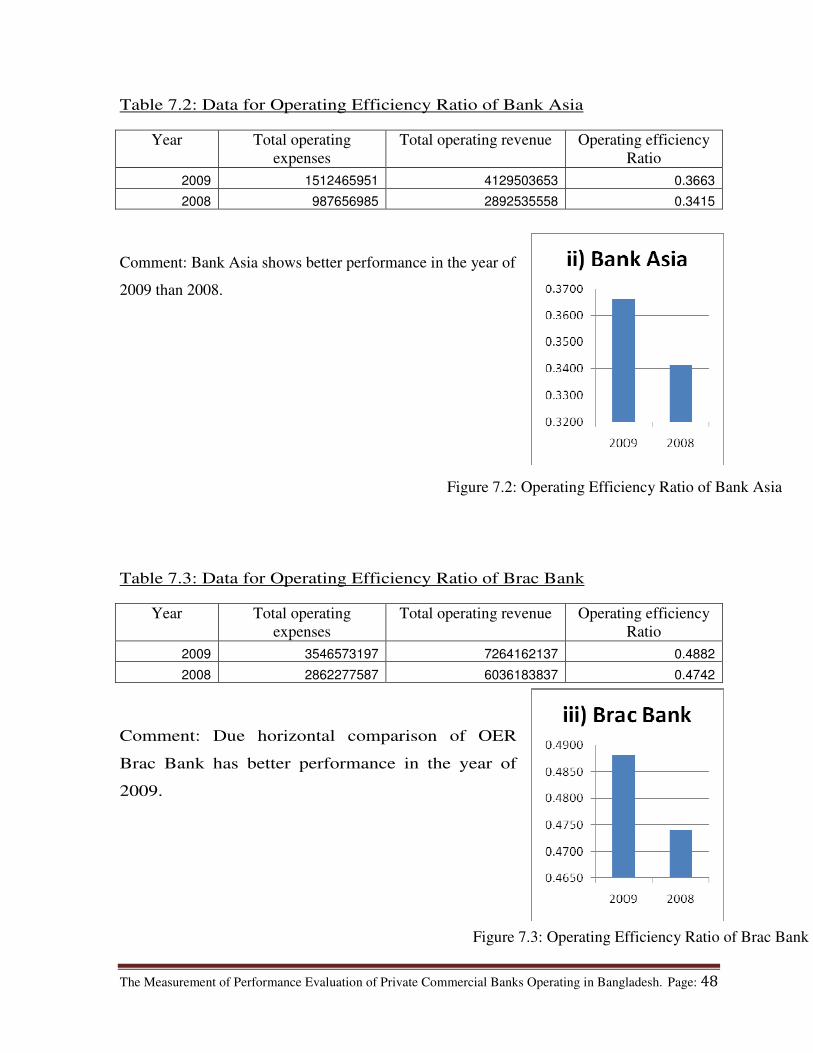

Table 7.2: Data for Operating Efficiency Ratio of Bank Asia

Year Total operating

expenses

Total operating revenue Operating efficiency

Ratio

2009 1512465951 4129503653 0.3663

2008 987656985 2892535558 0.3415

Comment: Bank Asia shows better performance in the year of

2009 than 2008.

Table 7.3: Data for Operating Efficiency Ratio of Brac Bank

Year Total operating

expenses

Total operating revenue Operating efficiency

Ratio

2009 3546573197 7264162137 0.4882

2008 2862277587 6036183837 0.4742

Comment: Due horizontal comparison of OER

Brac Bank has better performance in the year of

2009.

Figure 7.2: Operating Efficiency Ratio of Bank Asia

Figure 7.3: Operating Efficiency Ratio of Brac Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 49

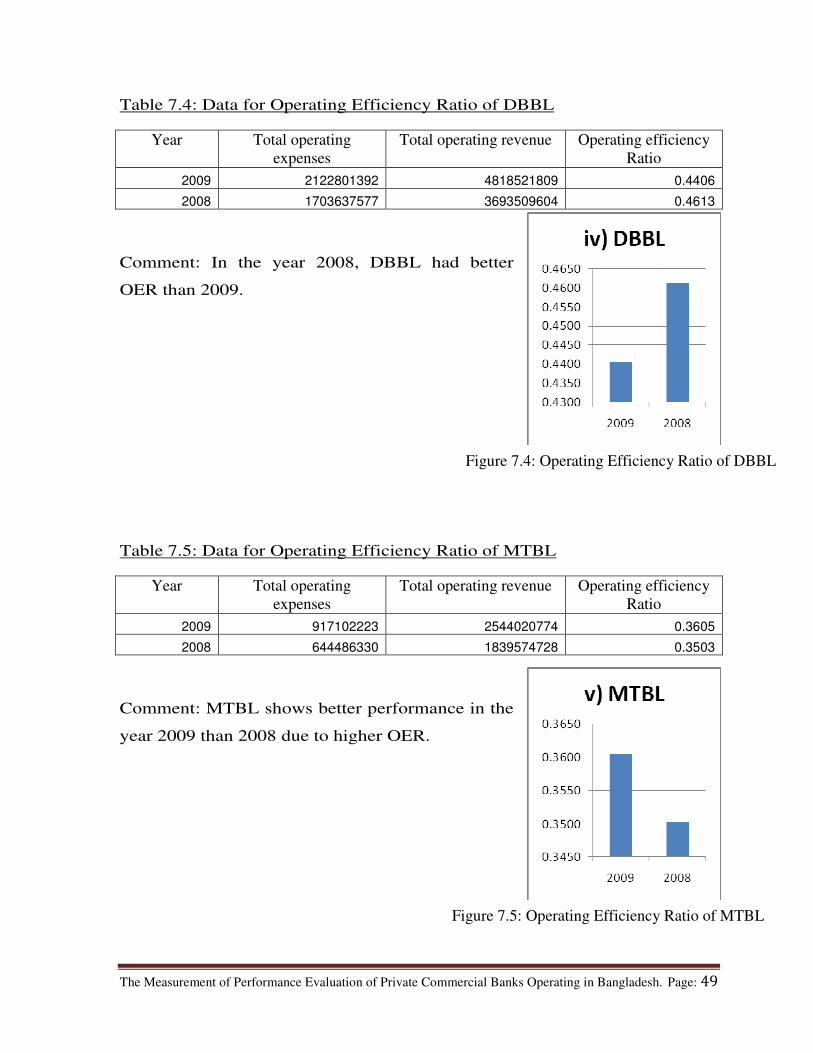

Table 7.4: Data for Operating Efficiency Ratio of DBBL

Year Total operating

expenses

Total operating revenue Operating efficiency

Ratio

2009 2122801392 4818521809 0.4406

2008 1703637577 3693509604 0.4613

Comment: In the year 2008, DBBL had better

OER than 2009.

Table 7.5: Data for Operating Efficiency Ratio of MTBL

Year Total operating

expenses

Total operating revenue Operating efficiency

Ratio

2009 917102223 2544020774 0.3605

2008 644486330 1839574728 0.3503

Comment: MTBL shows better performance in the

year 2009 than 2008 due to higher OER.

Figure 7.4: Operating Efficiency Ratio of DBBL

Figure 7.5: Operating Efficiency Ratio of MTBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 50

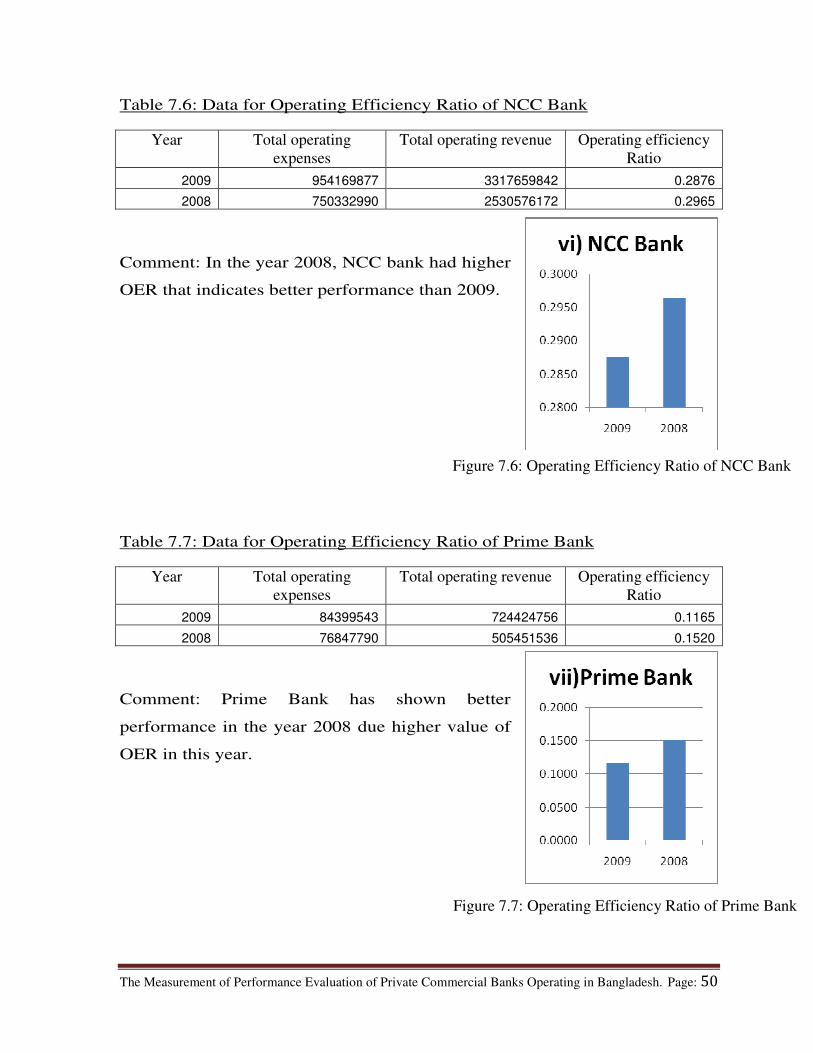

Table 7.6: Data for Operating Efficiency Ratio of NCC Bank

Year Total operating

expenses

Total operating revenue Operating efficiency

Ratio

2009 954169877 3317659842 0.2876

2008 750332990 2530576172 0.2965

Comment: In the year 2008, NCC bank had higher

OER that indicates better performance than 2009.

Table 7.7: Data for Operating Efficiency Ratio of Prime Bank

Year Total operating

expenses

Total operating revenue Operating efficiency

Ratio

2009 84399543 724424756 0.1165

2008 76847790 505451536 0.1520

Comment: Prime Bank has shown better

performance in the year 2008 due higher value of

OER in this year.

Figure 7.6: Operating Efficiency Ratio of NCC Bank

Figure 7.7: Operating Efficiency Ratio of Prime Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 51

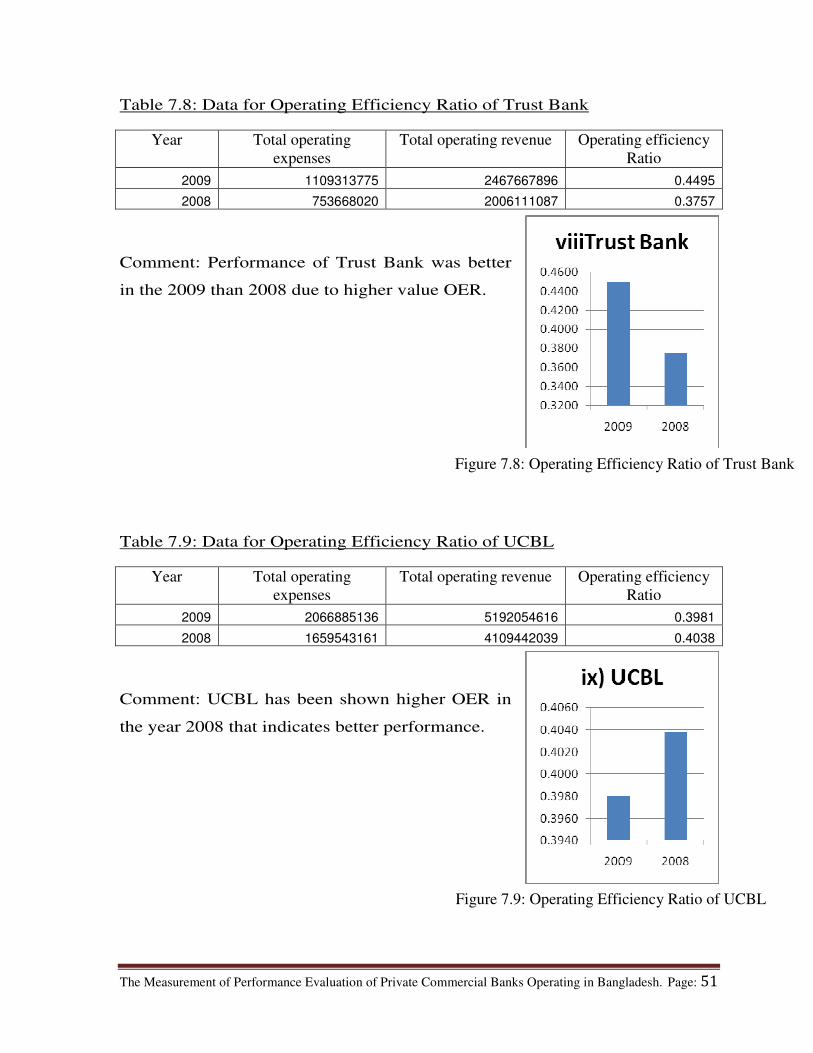

Table 7.8: Data for Operating Efficiency Ratio of Trust Bank

Year Total operating

expenses

Total operating revenue Operating efficiency

Ratio

2009 1109313775 2467667896 0.4495

2008 753668020 2006111087 0.3757

Comment: Performance of Trust Bank was better

in the 2009 than 2008 due to higher value OER.

Table 7.9: Data for Operating Efficiency Ratio of UCBL

Year Total operating

expenses

Total operating revenue Operating efficiency

Ratio

2009 2066885136 5192054616 0.3981

2008 1659543161 4109442039 0.4038

Comment: UCBL has been shown higher OER in

the year 2008 that indicates better performance.

Figure 7.8: Operating Efficiency Ratio of Trust Bank

Figure 7.9: Operating Efficiency Ratio of UCBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 52

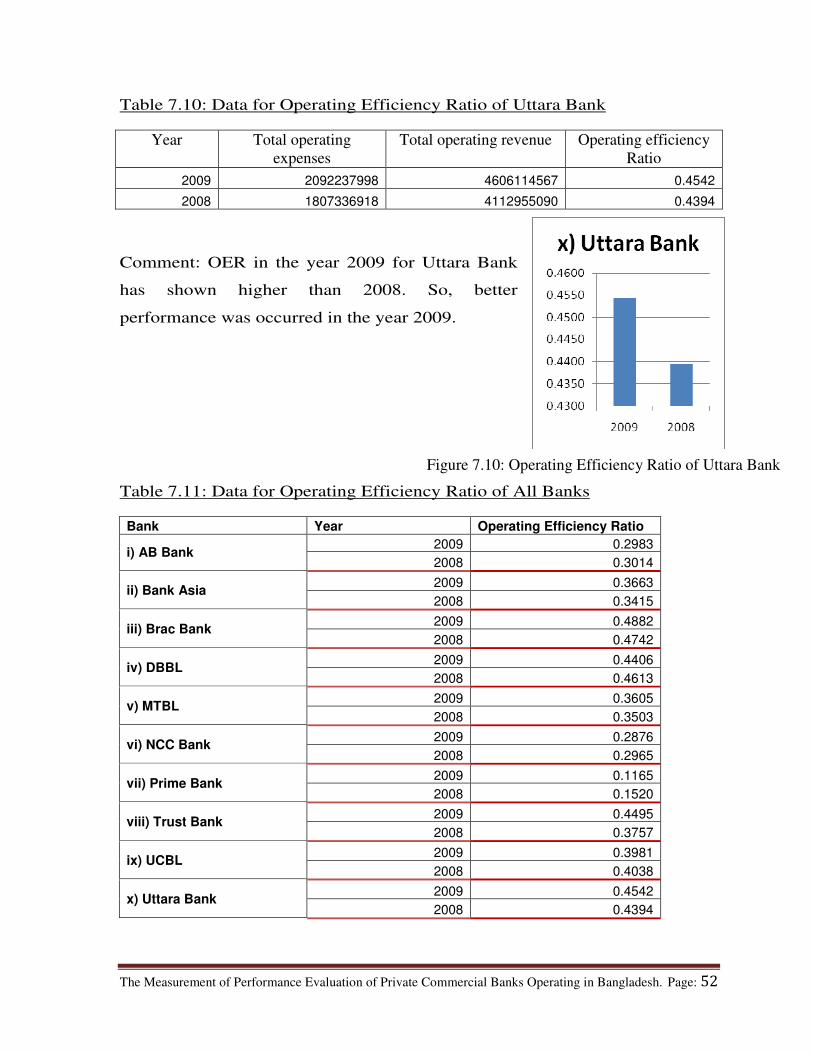

Table 7.10: Data for Operating Efficiency Ratio of Uttara Bank

Year Total operating

expenses

Total operating revenue Operating efficiency

Ratio

2009 2092237998 4606114567 0.4542

2008 1807336918 4112955090 0.4394

Comment: OER in the year 2009 for Uttara Bank

has shown higher than 2008. So, better

performance was occurred in the year 2009.

Table 7.11: Data for Operating Efficiency Ratio of All Banks

Bank Year Operating Efficiency Ratio

i) AB Bank 2009 0.2983

2008 0.3014

ii) Bank Asia 2009 0.3663

2008 0.3415

iii) Brac Bank 2009 0.4882

2008 0.4742

iv) DBBL 2009 0.4406

2008 0.4613

v) MTBL 2009 0.3605

2008 0.3503

vi) NCC Bank 2009 0.2876

2008 0.2965

vii) Prime Bank 2009 0.1165

2008 0.1520

viii) Trust Bank 2009 0.4495

2008 0.3757

ix) UCBL 2009 0.3981

2008 0.4038

x) Uttara Bank 2009 0.4542

2008 0.4394

Figure 7.10: Operating Efficiency Ratio of Uttara Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 53

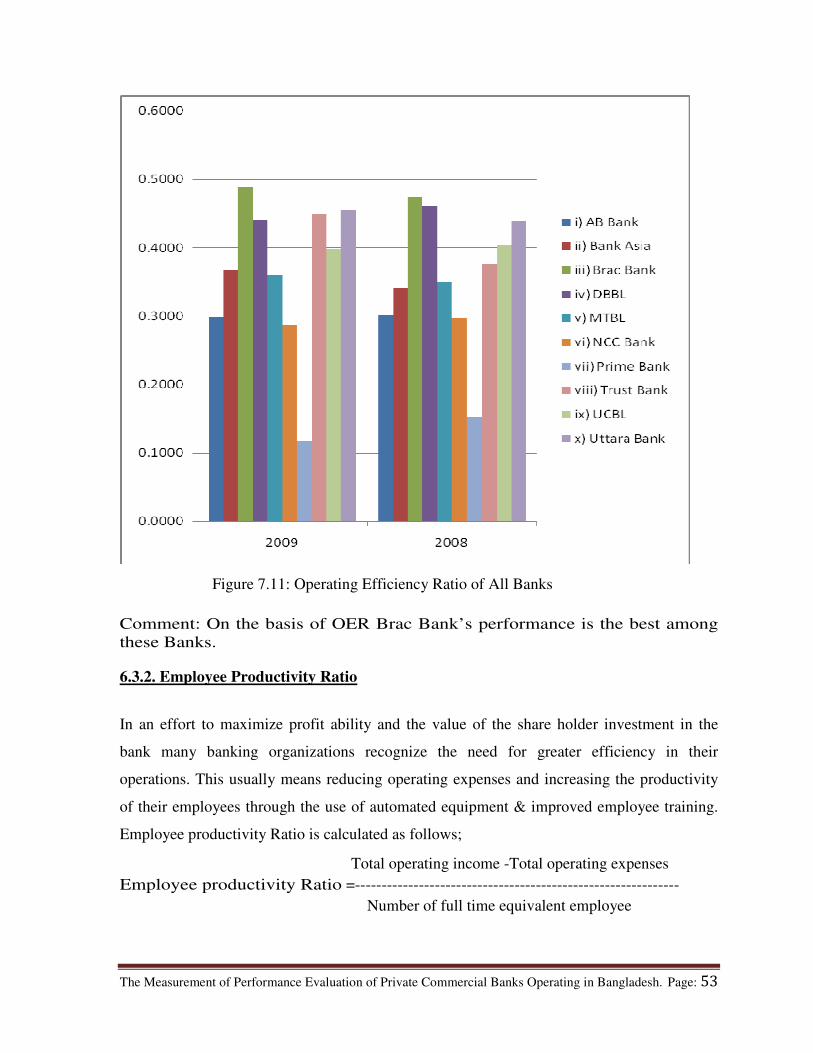

Comment: On the basis of OER Brac Bank’s performance is the best among

these Banks.

6.3.2. Employee Productivity Ratio

In an effort to maximize profit ability and the value of the share holder investment in the

bank many banking organizations recognize the need for greater efficiency in their

operations. This usually means reducing operating expenses and increasing the productivity

of their employees through the use of automated equipment & improved employee training.

Employee productivity Ratio is calculated as follows;

Total operating income -Total operating expenses

Employee productivity Ratio =-------------------------------------------------------------

Number of full time equivalent employee

Figure 7.11: Operating Efficiency Ratio of All Banks

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 54

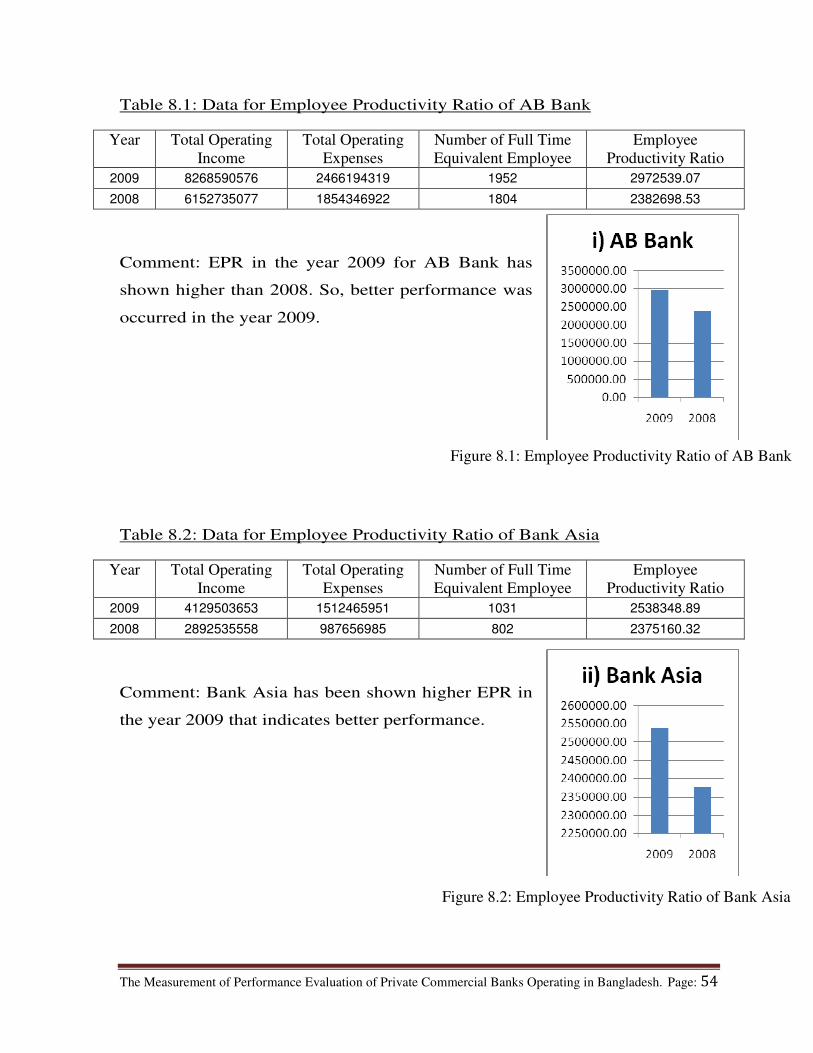

Table 8.1: Data for Employee Productivity Ratio of AB Bank

Year Total Operating

Income

Total Operating

Expenses

Number of Full Time

Equivalent Employee

Employee

Productivity Ratio

2009 8268590576 2466194319 1952 2972539.07

2008 6152735077 1854346922 1804 2382698.53

Comment: EPR in the year 2009 for AB Bank has

shown higher than 2008. So, better performance was

occurred in the year 2009.

Table 8.2: Data for Employee Productivity Ratio of Bank Asia

Year Total Operating

Income

Total Operating

Expenses

Number of Full Time

Equivalent Employee

Employee

Productivity Ratio

2009 4129503653 1512465951 1031 2538348.89

2008 2892535558 987656985 802 2375160.32

Comment: Bank Asia has been shown higher EPR in

the year 2009 that indicates better performance.

Figure 8.1: Employee Productivity Ratio of AB Bank

Figure 8.2: Employee Productivity Ratio of Bank Asia

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 55

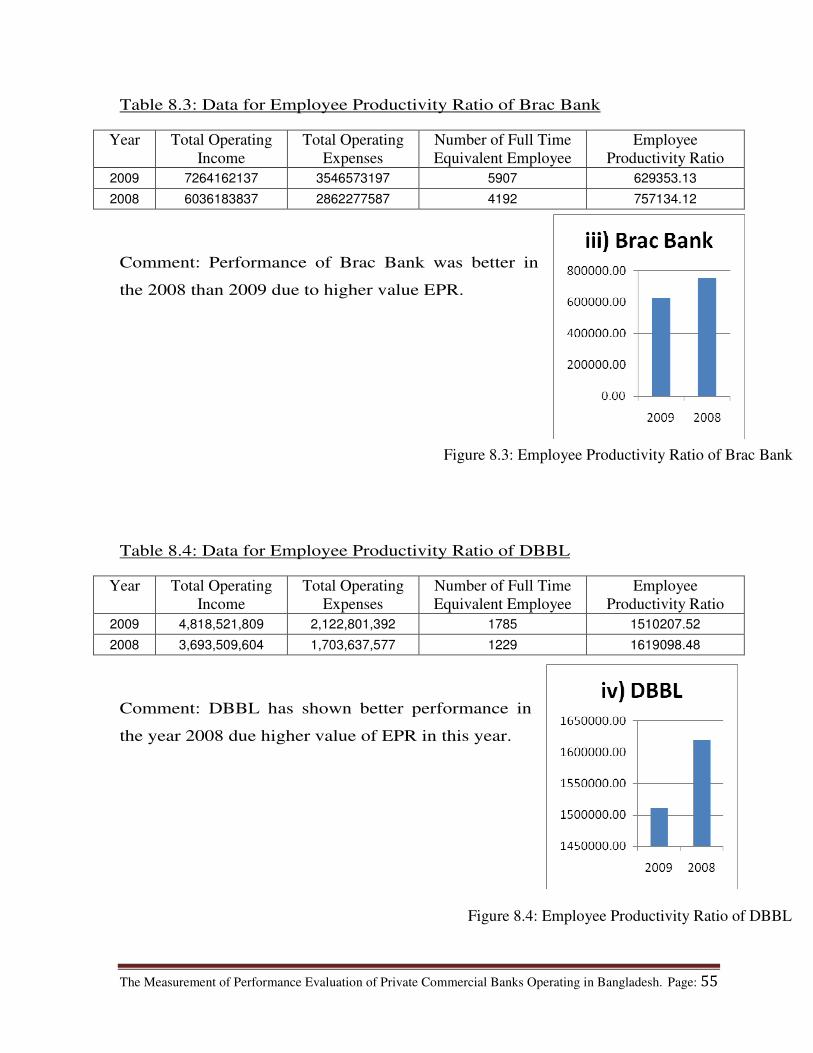

Table 8.3: Data for Employee Productivity Ratio of Brac Bank

Year Total Operating

Income

Total Operating

Expenses

Number of Full Time

Equivalent Employee

Employee

Productivity Ratio

2009 7264162137 3546573197 5907 629353.13

2008 6036183837 2862277587 4192 757134.12

Comment: Performance of Brac Bank was better in

the 2008 than 2009 due to higher value EPR.

Table 8.4: Data for Employee Productivity Ratio of DBBL

Year Total Operating

Income

Total Operating

Expenses

Number of Full Time

Equivalent Employee

Employee

Productivity Ratio

2009 4,818,521,809 2,122,801,392 1785 1510207.52

2008 3,693,509,604 1,703,637,577 1229 1619098.48

Comment: DBBL has shown better performance in

the year 2008 due higher value of EPR in this year.

Figure 8.3: Employee Productivity Ratio of Brac Bank

Figure 8.4: Employee Productivity Ratio of DBBL

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 56

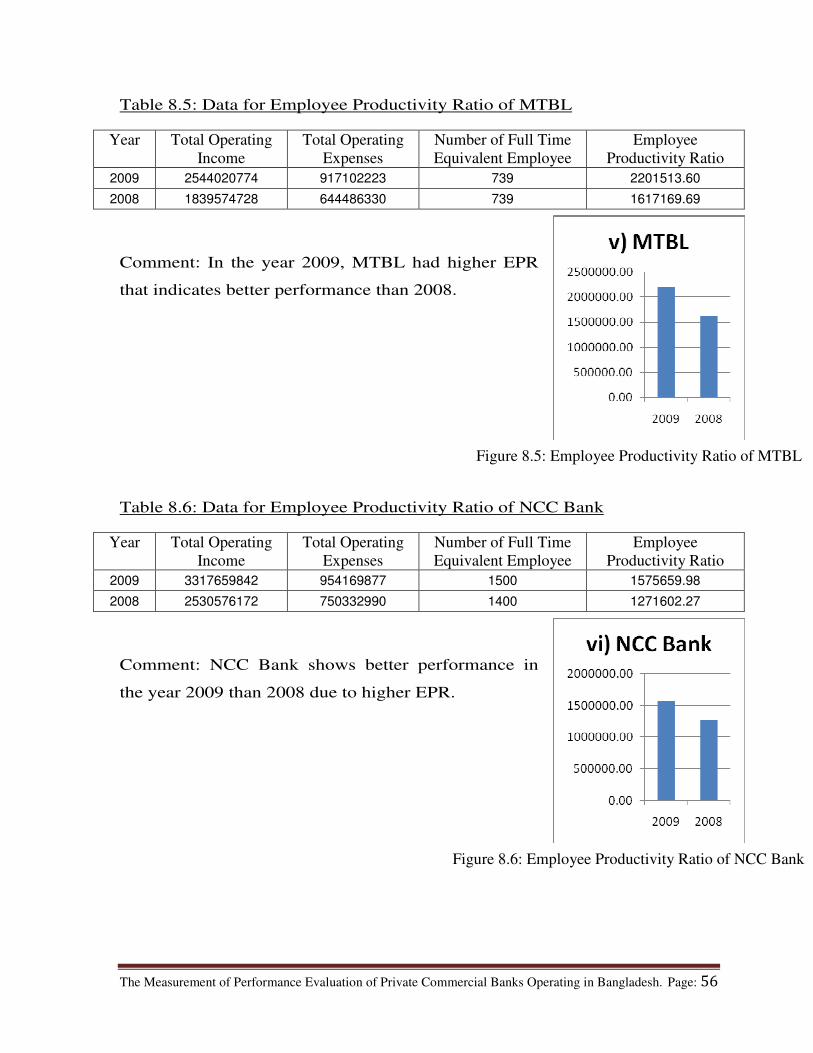

Table 8.5: Data for Employee Productivity Ratio of MTBL

Year Total Operating

Income

Total Operating

Expenses

Number of Full Time

Equivalent Employee

Employee

Productivity Ratio

2009 2544020774 917102223 739 2201513.60

2008 1839574728 644486330 739 1617169.69

Comment: In the year 2009, MTBL had higher EPR

that indicates better performance than 2008.

Table 8.6: Data for Employee Productivity Ratio of NCC Bank

Year Total Operating

Income

Total Operating

Expenses

Number of Full Time

Equivalent Employee

Employee

Productivity Ratio

2009 3317659842 954169877 1500 1575659.98

2008 2530576172 750332990 1400 1271602.27

Comment: NCC Bank shows better performance in

the year 2009 than 2008 due to higher EPR.

Figure 8.5: Employee Productivity Ratio of MTBL

Figure 8.6: Employee Productivity Ratio of NCC Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 57

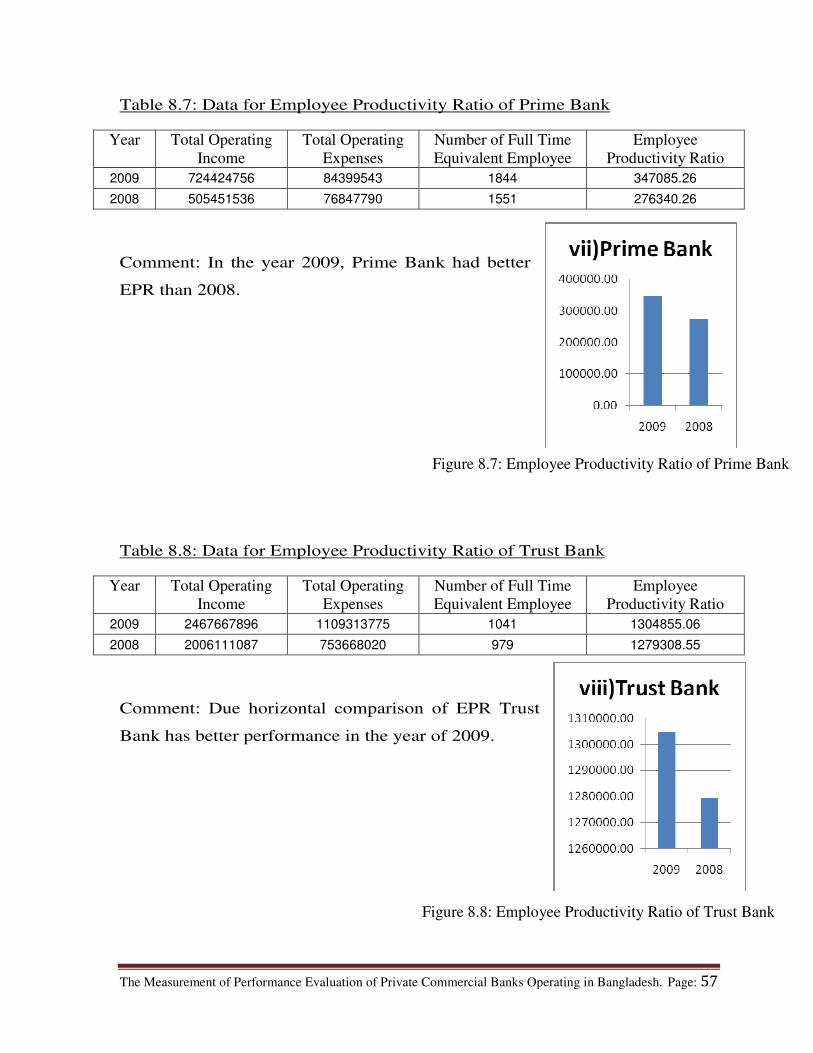

Table 8.7: Data for Employee Productivity Ratio of Prime Bank

Year Total Operating

Income

Total Operating

Expenses

Number of Full Time

Equivalent Employee

Employee

Productivity Ratio

2009 724424756 84399543 1844 347085.26

2008 505451536 76847790 1551 276340.26

Comment: In the year 2009, Prime Bank had better

EPR than 2008.

Table 8.8: Data for Employee Productivity Ratio of Trust Bank

Year Total Operating

Income

Total Operating

Expenses

Number of Full Time

Equivalent Employee

Employee

Productivity Ratio

2009 2467667896 1109313775 1041 1304855.06

2008 2006111087 753668020 979 1279308.55

Comment: Due horizontal comparison of EPR Trust

Bank has better performance in the year of 2009.

Figure 8.7: Employee Productivity Ratio of Prime Bank

Figure 8.8: Employee Productivity Ratio of Trust Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 58

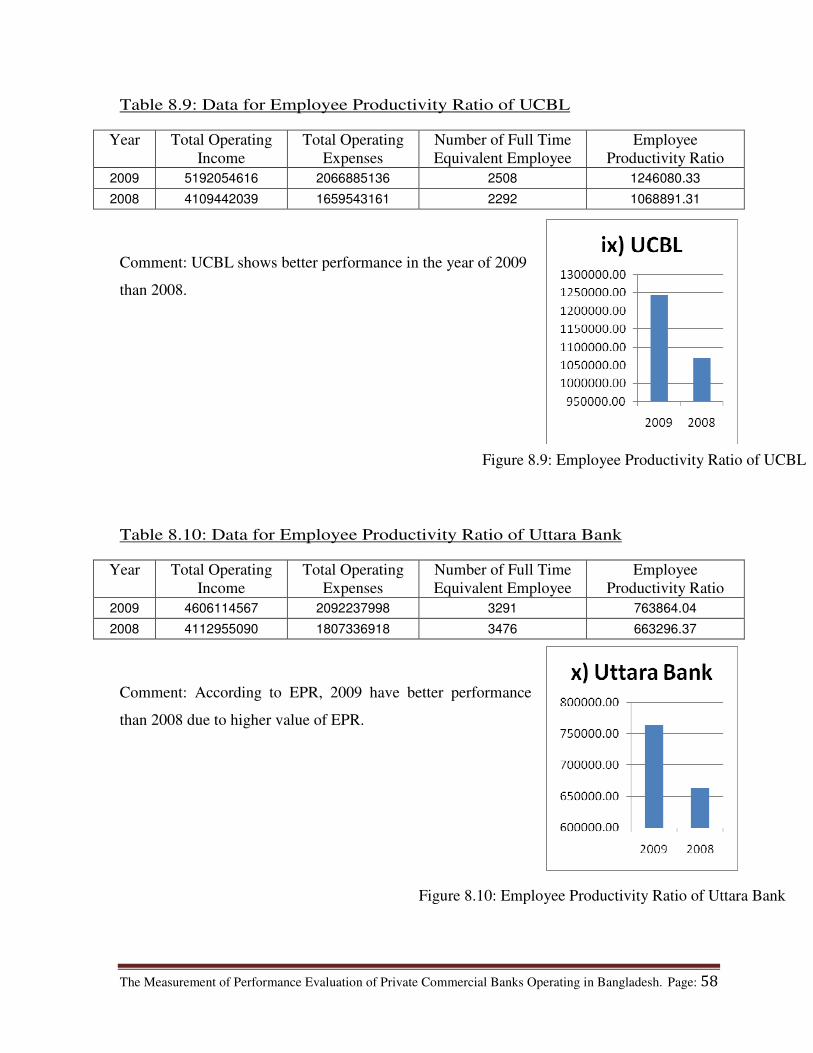

Table 8.9: Data for Employee Productivity Ratio of UCBL

Year Total Operating

Income

Total Operating

Expenses

Number of Full Time

Equivalent Employee

Employee

Productivity Ratio

2009 5192054616 2066885136 2508 1246080.33

2008 4109442039 1659543161 2292 1068891.31

Comment: UCBL shows better performance in the year of 2009

than 2008.

Table 8.10: Data for Employee Productivity Ratio of Uttara Bank

Year Total Operating

Income

Total Operating

Expenses

Number of Full Time

Equivalent Employee

Employee

Productivity Ratio

2009 4606114567 2092237998 3291 763864.04

2008 4112955090 1807336918 3476 663296.37

Comment: According to EPR, 2009 have better performance

than 2008 due to higher value of EPR.

Figure 8.9: Employee Productivity Ratio of UCBL

Figure 8.10: Employee Productivity Ratio of Uttara Bank

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 59

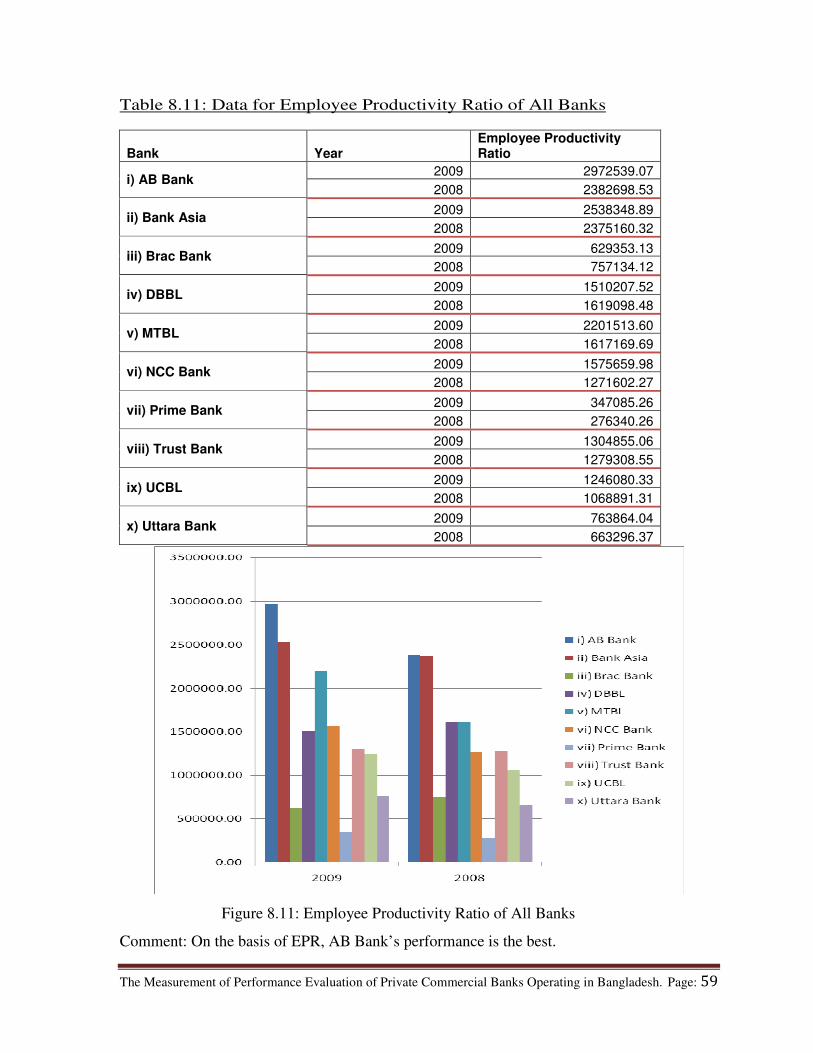

Table 8.11: Data for Employee Productivity Ratio of All Banks

Bank Year Employee Productivity Ratio

i) AB Bank 2009 2972539.07

2008 2382698.53

ii) Bank Asia 2009 2538348.89

2008 2375160.32

iii) Brac Bank 2009 629353.13

2008 757134.12

iv) DBBL 2009 1510207.52

2008 1619098.48

v) MTBL 2009 2201513.60

2008 1617169.69

vi) NCC Bank 2009 1575659.98

2008 1271602.27

vii) Prime Bank 2009 347085.26

2008 276340.26

viii) Trust Bank 2009 1304855.06

2008 1279308.55

ix) UCBL 2009 1246080.33

2008 1068891.31

x) Uttara Bank 2009 763864.04

2008 663296.37

Comment: On the basis of EPR, AB Bank’s performance is the best.

Figure 8.11: Employee Productivity Ratio of All Banks

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 60

7. Credit Rating of the Selected Banks by CRAB and CRISL

7.1. Credit Rating agency of Bangladesh Ltd. (CRAB)

Credit Rating agency of Bangladesh Ltd. (CRAB) was established in 2003 at the initiative of

some leading personalities in private sector and institutions of the country with the

commitment to contribute to the development of the capital market by providing quality

ratings and comprehensive research services. CRAB was incorporated as a public limited

company in 2003 and received its Certificate for Commencement of Business in the same

year. In 2004, CRAB was granted license by the Securities & Exchange Commission (SEC)

of Bangladesh (under the Credit Rating companies Rules 1996) for operating as a Credit

Rating Company. In 2009 CRAB has been accredited as an External Credit Assessment

Institution (ECAI) by Bangladesh Bank, to provide rating of Bank Clients under Basel II

regime. CRAB has established its reputation as a reliable source of independent opinion on

risks based on systematic and standardized analysis done by professionals.

CRAB has a Technical Collaboration Agreement with ICRA Ltd. of India, one of the leading

credit rating agencies of the region. This collaboration has provided CRAB with facility for

development of rating methodologies, for performing rating assignments and for training of

its professionals. ICRA-CRAB collaboration facilitates sharing of resources and information

base and professional expertise between the two organizations, much to the advantage of

CRAB. ICRA Limited (an Associate of Moody's Investors Service, USA) was incorporated

in 1991 as an independent and professional company. ICRA is a leading provider of

investment information and credit rating services in India. ICRA's major shareholders

include Moody's Investors Service and leading Indian financial institutions and banks. With

the growth and globalization of the Indian capital markets leading to an exponential surge in

demand for professional credit risk analysis, ICRA has been proactive in widening its service

offerings, executing assignments including credit ratings, equity grading, and specialized

performance grading and mandated studies spanning diverse industrial sectors. In addition to

being a leading credit rating agency with expertise in virtually every sector of the Indian

economy, ICRA has broad-based its services for the corporate and financial sectors, both in

India and overseas.

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 61

CRAB has developed highly standardized rating methodologies for different instruments and

entities. The methodologies have been developed considering all the relevant factors

affecting the future cash generation capacity of the issuers. These factors include industry

characteristics, competitive position of the issuer, operational efficiency, management

quality, commitment to new projects and other associate companies, and future funding

policies of the issuer. A detailed analysis of the past financial statements is made to assess

the actual business performance. Analysis considers the estimated future earnings under

various sensitivity scenarios are drawn up and evaluated against the future obligations that

require servicing over the tenure of the instrument being rated. CRAB rating methodology

intends to assess the relative comfort level of the issuers to service the obligations and this is

reflected in the rating of a debt instrument. In case of equity instruments, the rating reflects

the future earning capabilities with reference to the resilience to perform in adverse

situations.

7.1.1. Rating Definition

A) Long Term

AAA (Triple A): Have extremely strong capacity to meet financial commitments,

maintains highest quality, with minimal credit risk.

AA1, AA2, AA3 (Double A): Have very strong capacity to meet financial commitments,

maintains very high quality, with very low credit risk.

A1, A2, A3 (Single A): Have strong capacity to meet financial commitments, maintains

high quality, with low credit risk, but susceptible to adverse changes in circumstances

and economic conditions.

BBB1, BBB2, BBB3 (Triple B): Have adequate capacity to meet financial commitments

but are susceptible to moderate credit risk. Adverse changes in circumstances and

economic conditions are more likely to impact capacity to meet financial commitments.

BB1, BB2, BB3 (Double B): Have inadequate capacity to meet financial commitments

and possess substantial credit risk, with major ongoing uncertainties and exposure to

adverse business, financial, or economic conditions.

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 62

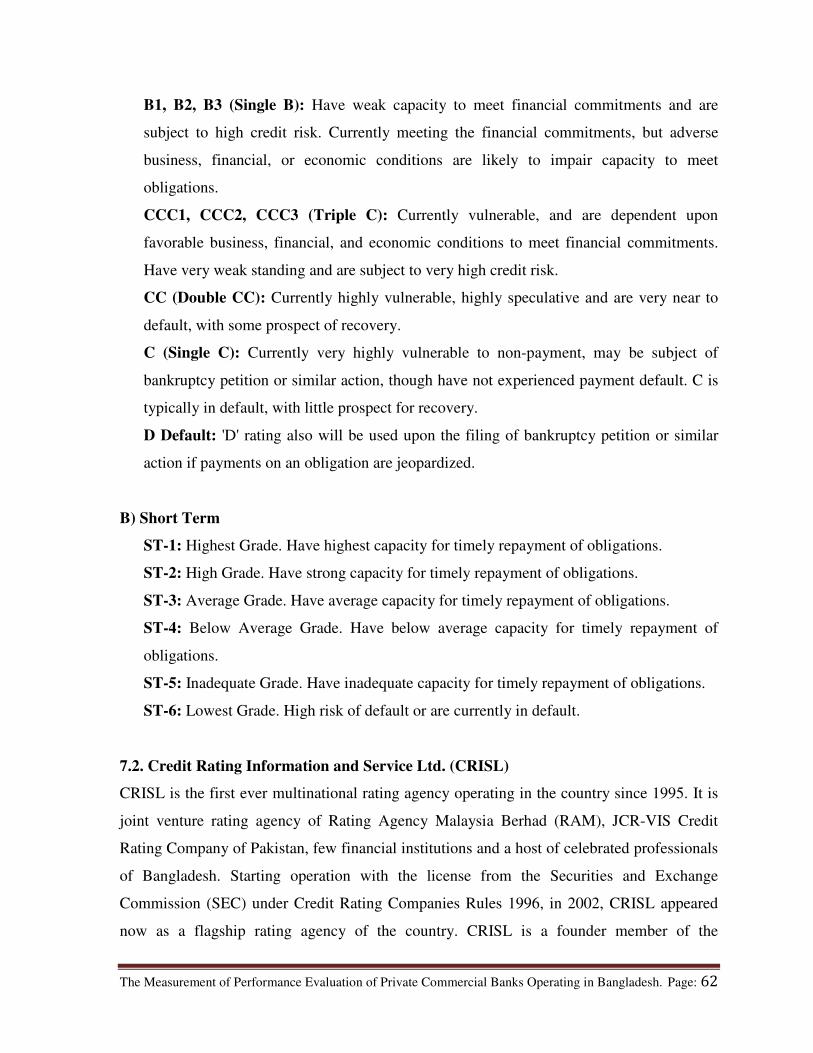

B1, B2, B3 (Single B): Have weak capacity to meet financial commitments and are

subject to high credit risk. Currently meeting the financial commitments, but adverse

business, financial, or economic conditions are likely to impair capacity to meet

obligations.

CCC1, CCC2, CCC3 (Triple C): Currently vulnerable, and are dependent upon

favorable business, financial, and economic conditions to meet financial commitments.

Have very weak standing and are subject to very high credit risk.

CC (Double CC): Currently highly vulnerable, highly speculative and are very near to

default, with some prospect of recovery.

C (Single C): Currently very highly vulnerable to non-payment, may be subject of

bankruptcy petition or similar action, though have not experienced payment default. C is

typically in default, with little prospect for recovery.

D Default: 'D' rating also will be used upon the filing of bankruptcy petition or similar

action if payments on an obligation are jeopardized.

B) Short Term

ST-1: Highest Grade. Have highest capacity for timely repayment of obligations.

ST-2: High Grade. Have strong capacity for timely repayment of obligations.

ST-3: Average Grade. Have average capacity for timely repayment of obligations.

ST-4: Below Average Grade. Have below average capacity for timely repayment of

obligations.

ST-5: Inadequate Grade. Have inadequate capacity for timely repayment of obligations.

ST-6: Lowest Grade. High risk of default or are currently in default.

7.2. Credit Rating Information and Service Ltd. (CRISL)

CRISL is the first ever multinational rating agency operating in the country since 1995. It is

joint venture rating agency of Rating Agency Malaysia Berhad (RAM), JCR-VIS Credit

Rating Company of Pakistan, few financial institutions and a host of celebrated professionals

of Bangladesh. Starting operation with the license from the Securities and Exchange

Commission (SEC) under Credit Rating Companies Rules 1996, in 2002, CRISL appeared

now as a flagship rating agency of the country. CRISL is a founder member of the

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 63

Association of Credit Rating Agencies in Asia (ACRAA) sponsored by Asian Development

Bank where it is positive contribution towards the development of the profession of credit

rating in the Asian region. CRISL is public limited company dedicated for credit rating and

related services and being recognized by Bangladesh Bank as The external Credit

Assessment Institution (ECAI) to offer its services to the banking community for client

rating. CRISL provides its services with high business and ethical standard as approved by

the International Organization of securities Commission (IOSCO), Securities and Exchange

Commission of Bangladesh and Bangladesh Bank ECAI recognition criteria.

7.2.1. Credit Rating Definition

A) Long Term

AAA (Triple A): To offer highest safety and having highest credit quality.

AA+, AA, AA- (Double A): To offer higher safety and having higher credit quality.

A+, A, A- (Single A): To offer adequate safety for timely repayment of financial

obligations.

BBB+, BBB, BBB- (Triple B): To offer moderate degree of safety for timely repayment

of financial obligations.

BB+, BB, BB- (Double B): Lack of key protection factors which result in an inadequate

safety.

B+, B, B-(Single B): Timely repayment of financial obligations is impaired by serious

problem which the entity is faced with.

CCC+, CCC, CCC- (Triple C): This rating indicates that the degree of certainty

regarding timely payment of financial obligations is quit lower unless overall

circumstances are favorable or requirement of high degree external support.

C+, C, C- (Single C): In this category are adjusted to be with near to default in timely

repayment of financial obligations. This type rating may be use to cover a situation where

an insolvency position has been field.

D (Default): This category are adjusted to be either currently in default or expected to be

in default. This level of rating indicates that the entities are unlikely to meet maturing

financial obligations are call for immediate support of a high order.

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 64

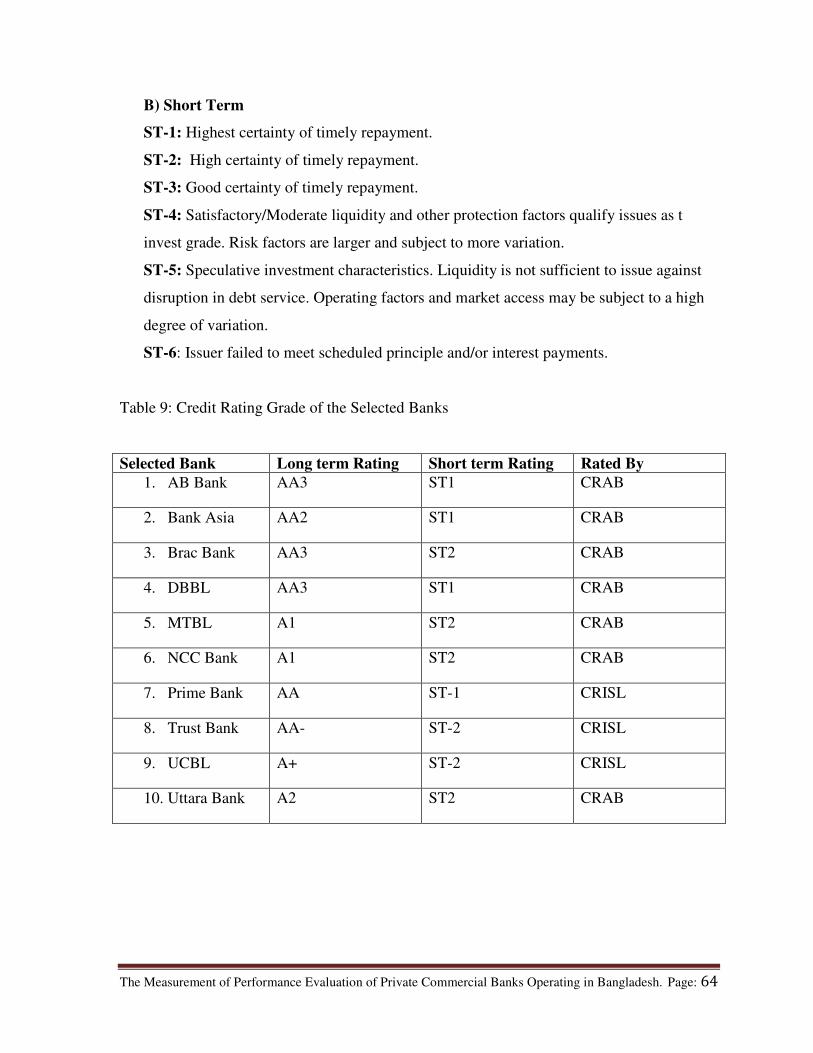

B) Short Term

ST-1: Highest certainty of timely repayment.

ST-2: High certainty of timely repayment.

ST-3: Good certainty of timely repayment.

ST-4: Satisfactory/Moderate liquidity and other protection factors qualify issues as t

invest grade. Risk factors are larger and subject to more variation.

ST-5: Speculative investment characteristics. Liquidity is not sufficient to issue against

disruption in debt service. Operating factors and market access may be subject to a high

degree of variation.

ST-6: Issuer failed to meet scheduled principle and/or interest payments.

Table 9: Credit Rating Grade of the Selected Banks

Selected Bank Long term Rating Short term Rating Rated By

1. AB Bank AA3 ST1 CRAB

2. Bank Asia AA2 ST1 CRAB

3. Brac Bank AA3 ST2 CRAB

4. DBBL AA3 ST1 CRAB

5. MTBL A1 ST2 CRAB

6. NCC Bank A1 ST2 CRAB

7. Prime Bank AA ST-1 CRISL

8. Trust Bank AA- ST-2 CRISL

9. UCBL A+ ST-2 CRISL

10. Uttara Bank A2 ST2 CRAB

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 65

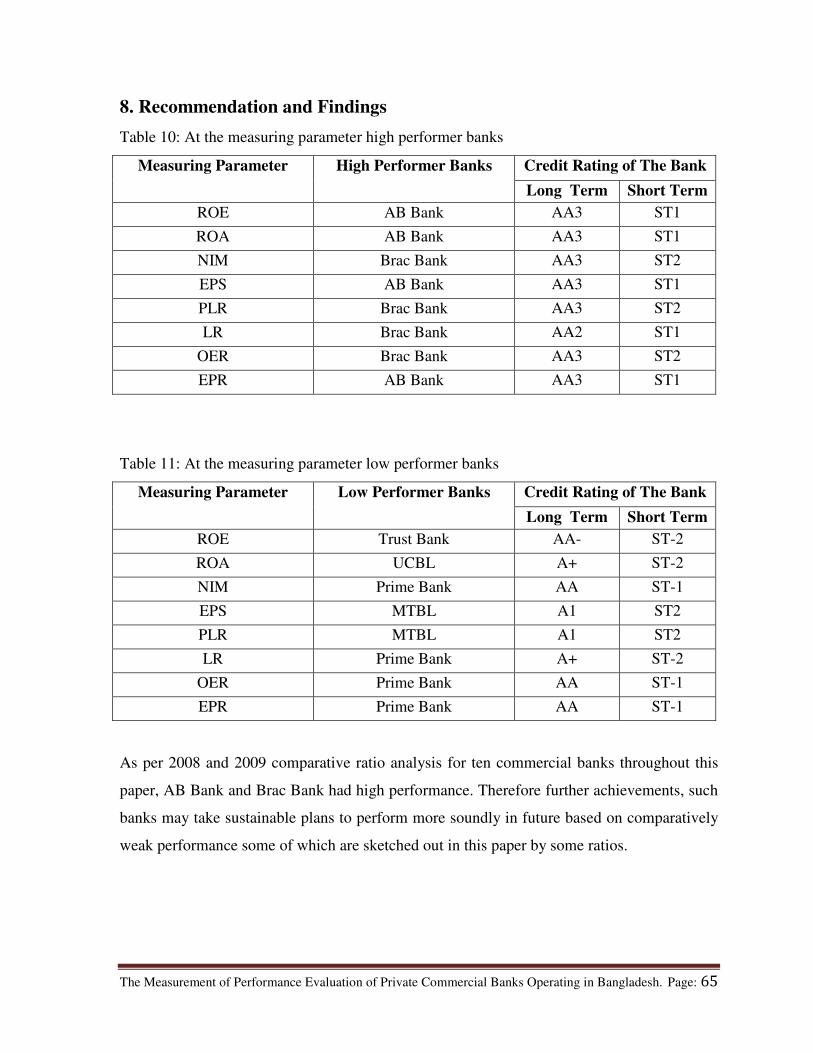

8. Recommendation and Findings

Table 10: At the measuring parameter high performer banks

Measuring Parameter High Performer Banks Credit Rating of The Bank

Long Term Short Term

ROE AB Bank AA3 ST1

ROA AB Bank AA3 ST1

NIM Brac Bank AA3 ST2

EPS AB Bank AA3 ST1

PLR Brac Bank AA3 ST2

LR Brac Bank AA2 ST1

OER Brac Bank AA3 ST2

EPR AB Bank AA3 ST1

Table 11: At the measuring parameter low performer banks

Measuring Parameter Low Performer Banks Credit Rating of The Bank

Long Term Short Term

ROE Trust Bank AA- ST-2

ROA UCBL A+ ST-2

NIM Prime Bank AA ST-1

EPS MTBL A1 ST2

PLR MTBL A1 ST2

LR Prime Bank A+ ST-2

OER Prime Bank AA ST-1

EPR Prime Bank AA ST-1

As per 2008 and 2009 comparative ratio analysis for ten commercial banks throughout this

paper, AB Bank and Brac Bank had high performance. Therefore further achievements, such

banks may take sustainable plans to perform more soundly in future based on comparatively

weak performance some of which are sketched out in this paper by some ratios.

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 66

Trust Bank and UCBL had lowest ROE and ROA respectively and MTBL had lowest EPS

which indicated that the banks need to increase their return or earning and take strategic

measures and healthy management. Again, Prime Bank performed with lowest NIM, OER

and EPR which suggested proper nursing of employees with overall skills and improvement

of employment system. So that it can make better operating profit and interest income.

Medium category with mediocre ratios like Bank Asia, DBBL, NCC Bank and Uttara Bank

should emphasize on their overall operation and maintenance to ensure brighter future

performance. Even, to prevent possible crises, they should at least take care to minimize the

obstructive and temporary bad factors which are liable for comparative lower ratios.

Financial ratios are contracted by forming ratios of accounting data contained in the bank’s

Annual Report of Income (i.e., profit and loss account) and Condition (i.e., balance sheet). A

wide variety of financial ratios can be calculated to assess different characteristics of

financial performance. It is beneficial to track the ratio over time relative to other banks.

Even without comparison with other banks, ratio trends over time may provide valuable

information about the bank’s performance.

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 67

9. Conclusion

A potential shortfall of financial ratio analysis is that other factors are held constant. To

overcome this problem, various financial ratios should be calculated that provide a broader

understanding of the bank’s financial condition. Most of the remainder of this discusses key

ratios commonly used by bank analysts to evaluate different dimensions of financial

performance. It is quite optimistic that if the given suggestions of this paper are implemented

then the Banking sector may be able to overcome its present problems and may contribute in

the rapid development of the economy of Bangladesh.

The Measurement of Performance Evaluation of Private Commercial Banks Operating in Bangladesh. Page: 68

Bibliography

Al Shammari, M., and Salimi, M. (1998). Modeling the operating efficiency of banks, A

parametric methodology. Journal of Logistic Information Management, Vol. 11.

Avkiran, N. K. (1997). Models of retail performance for bank branches: predicting the level

of key business drivers. International Journal of Bank Marketing, Vol. 15, No. 6.

Bhatt, P. R., and Ghosh, R. (1992). Profitability of Commercial Banks in India. Indian

Journal of Economics, India.

Chowdhury, A., (2002). Politics, Society and Financial Sector Reform in Bangladesh.

International Journal of Social Economies, 29(12), 963 – 988. Vol. 4, No. 4

International Journal of Business and Management 92.

Chowdhury, H. A., and Islam, M. S. (2007). Interest Rate Sensitivity of Loans and Advances:

A Comparative Study between Nationalized Commercial Banks (NCBs) and

specialized Banks (SBs). ASA University Review, Vol.1, No.1.

CPD Dialogue Report 49, (2002). Financial Sector Reforms in Bangladesh: The Next Round.

Center for Policy Dialogue, Dhaka.

Hossain, M. K., and Bhuiyan, R. H. (1990). Performance Dynamics of Nationalized