Embed Size (px)

Citation preview

The Yo–Yo Yen

Also by Brendan Brown

THE FLIGHT OF INTERNATIONAL CAPITAL

MONETARY CHAOS IN EUROPE

ECONOMISTS AND FINANCIAL MARKETS

The Yo–Yo Yenand the Future of the Japanese Economy

Brendan Brown

Foreword by Robert Z. Aliber

© Brendan Brown 2002Foreword © Robert Z. Aliber 2002

All rights reserved. No reproduction, copy or transmission of this publication may be made without permission.

No paragraph of this publication may be reproduced, copied or transmitted save with written permission or in accordance with the provisions of the Copyright, Designs and Patents Act 1988, or under the terms of any licence permitting limited copying issued by the Copyright Licensing Agency, 90 Tottenham Court Road, London W1T 4LP.

Any person who does any unauthorised act in relation to this publication may be liable to criminal prosecution and civil claims for damages.

The author has asserted his right to be identified as the author of this work in accordance with the Copyright, Designs and Patent Act 1988.

First published 2002 byPALGRAVEHoundmills, Basingstoke, Hampshire RG21 6XS and 175 Fifth Avenue, New York, N.Y. 10010Companies and representatives throughout the world

PALGRAVE is the new global academic imprint of St. Martin’s Press LLC Scholarly and Reference Division and Palgrave Publishers Ltd (formerly Macmillan Press Ltd).

ISBN 0–333–92949–7

This book is printed on paper suitable for recycling and made from fully managed and sustained forest sources.

A catalogue record for this book is available from the British Library.

Library of Congress Cataloging-in-Publication DataBrown, Brendan, 1951–

The yo-yo yen: and the future of the Japanese economy/BrendanBrown.

p. cm.Includes bibliographical references and index.ISBN 0–333–92949–7

1. Yen, Japanese–History. 2. Money–Japan–History. 3. Monetary policy–Japan–History. I. Title.

HG1272.B76 2002332.4�952–dc21 2001059054

10 9 8 7 6 5 4 3 2 111 10 09 08 07 06 05 04 03 02

Printed and bound in Great Britain by Antony Rowe Ltd, Chippenham, Wiltshire

Contents

List of Figures vi

List of Tables ix

Acknowledgements x

Foreword by Robert Z. Aliber xii

Introduction 1

1 Historic Roots of the Yo–Yo Yen (1859–1949) 5

2 A Brief History of the Modern Yen (1960–87) 30

3 Who Pulls the String of the Yo–Yo Yen? 63

4 From Bubble Economy to Yen Bubble (1988–93) 116

5 Yen Opportunity Gained and Lost (1993–2000) 163

6 What To Do About the Yo–Yo Yen? 215

Bibliography 240

Index 244

v

List of Figures

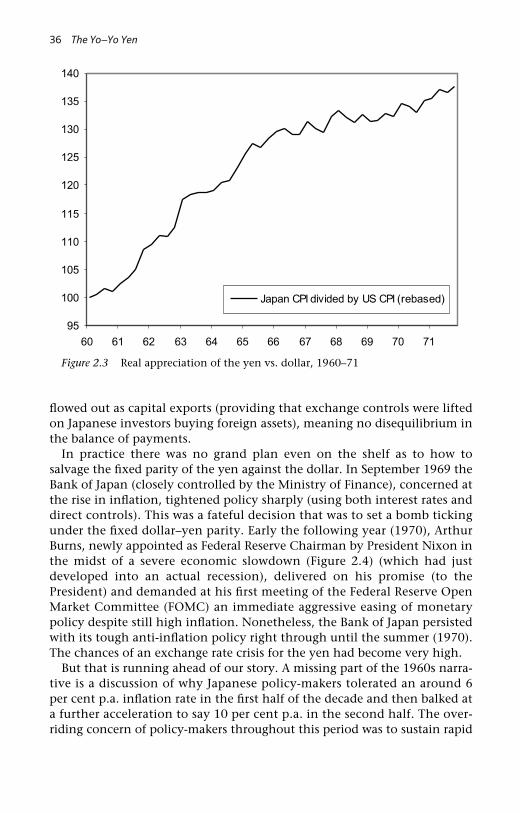

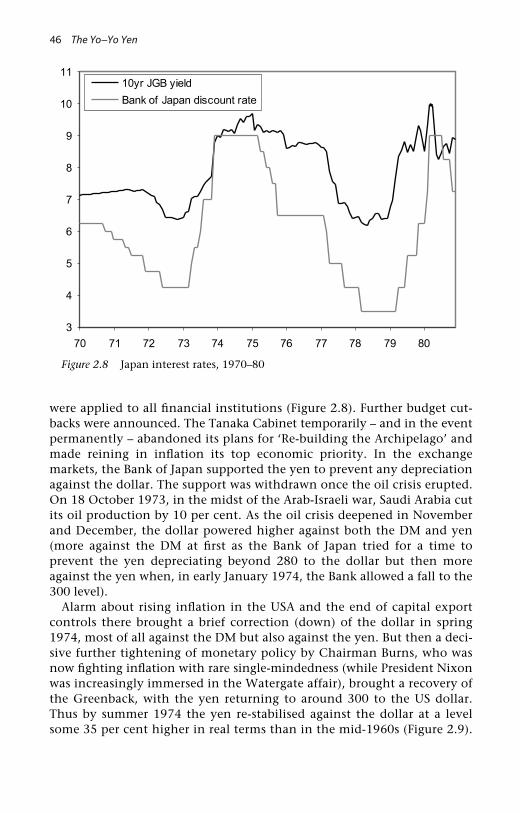

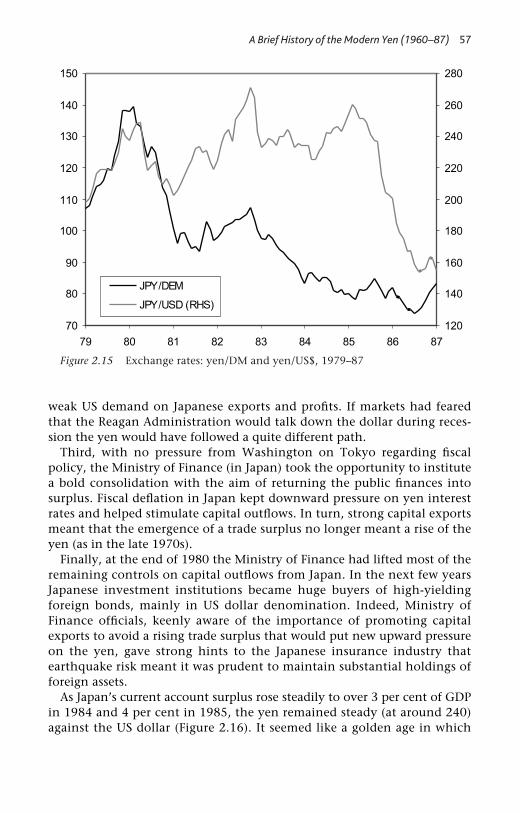

1.1 Gold–silver parity, 1868–94 121.2 US$/yen exchange rate, 1880–97 141.3 US$/yen exchange rate, 1918–25 222.1 Real effective exchange rate index of the yen, 1971–2001 322.2 Japan vs. Germany economic growth in the 1960s 342.3 Real appreciation of the yen vs. dollar, 1960–71 362.4 Japan vs. US economic growth, 1965–76 372.5 Yen exchange rate vs. US$ and DM, 1971–9 422.6 Japan budget deficit (per cent of GDP), 1960–2000 432.7 Japan vs. US business cycles, 1965–76 452.8 Japan interest rates, 1970–80 462.9 Real exchange rate index of the dollar against yen,

1970–2000 472.10 Japan business investment and saving (per cent of GDP),

1960–80 482.11 Japan vs. US inflation, 1971–9 522.12 Japan vs. US economic growth, 1976–90 532.13 Japan vs. US government bond yields, 1975–80 542.14 Japan current account balance, 1970–80 552.15 Exchange rates: yen/DM and yen/US$, 1979–87 572.16 Japan current account balance, 1981–90 582.17 Japan vs. US government bond yields, 1985–6 602.18 Japan vs. US money market rates, 1985–6 613.1 Switzerland current account balance vs. real effective

exchange rate, 1980–2000 693.2 US Federal funds rate vs. Japan unsecured overnight

call rate, 1991–5 743.3 Euro corner, 1973–7 813.4 US dollar corner, 1973–7 823.5 Japanese yen corner, 1973–7 833.6 Euro corner, 1978–81 843.7 US dollar corner, 1978–81 853.8 Japanese yen corner, 1978–81 863.9 Euro corner, 1982–5 873.10 US dollar corner, 1982–5 883.11 Japanese yen corner, 1982–5 893.12 Euro corner, 1986–90 903.13 US dollar corner, 1986–90 913.14 Japanese yen corner, 1986–90 92

vi

3.15 Euro corner, 1991–4 933.16 US dollar corner, 1991–4 943.17 Japanese yen corner, 1991–4 953.18 Euro corner, 1995–7 963.19 US dollar corner, 1995–7 973.20 Japanese yen corner, 1995–7 983.21 Euro corner, 1998–2001 993.22 US dollar corner, 1998–2001 1003.23 Japanese yen corner, 1998–2001 1013.24 Sterling, 1995–2001 1103.25 Swiss franc, 1995–2001 1123.26 Singapore dollar, 1992–2001 1143.27 Taiwanese dollar, 1992–2001 1154.1 Japan, US and euro-area GDP per capita, 1990–5 1184.2 Japan, US and euro-area GDP per capita, 1995–2000 1194.3 Japan productivity growth, 1985–90 1224.4 Japan inflation, 1987–94 1244.5 Japan money supply, 1988–94 1254.6 Japan money rates, 1989–95 1284.7 US dollar vs. DM and yen, 1987–92 1294.8 Yen vs. US dollar and DM, 1987–92 1304.9 Japan vs. US money rates, 1986–91 1314.10 Japan vs. US equity markets, 1987–93 1344.11 Finnish mark real effective exchange rate, 1985–95 1364.12 British pound real effective exchange rate, 1988–95 1364.13 Japan, UK and Finland current account balances, 1987–95 1374.14 Switzerland real effective exchange rate, 1988–2001 1384.15 Switzerland inflation, 1988–2000 1384.16 Switzerland yield curve, 1988–2001 1394.17 Switzerland current account surplus vs. general

government balance, 1987–2000 1394.18 US$–DM–yen triangle – US dollar corner, 1987–92 1414.19 US$–DM–yen triangle – DM corner, 1987–92 1424.20 US$–DM–yen triangle – yen corner, 1987–92 1434.21 Japan vs. US leading indicators, 1986–92 1444.22 Japan 10-year JGB yield vs. overnight call rate, 1990–5 1454.23 Japan, US and (West) Germany real GDP, 1990–4 1474.24 3-month euro-yen, dollar and DM rates, 1990–3 1484.25 Japan vs. US current account balance as per cent of GDP,

1987–95 1514.26 Japan industrial production vs. real GDP, 1990–2001 1524.27 10-year JGB yields vs. 10-year T-bond yields, 1991–5 1594.28 Japan vs. US leading indicators, 1992–8 1604.29 Japan, US and euro-area real GDP, 1989–2001 161

List of Figures vii

5.1 Yen vs. US dollar and DM, 1993–8 1645.2 US dollar vs. yen and DM, 1993–8 1655.3 DM corner, 1993–8 1715.4 US dollar corner, 1993–8 1725.5 Yen corner, 1993–8 1735.6 10-year yield spreads, T-bond over JGB and Bund, 1993–5 1745.7 10-year JGB, T-bond and Bund yields, 1994–7 1745.8 Japan equity market vs. 10-year JGB yields, 1993–2001 1755.9 Japan private consumption deflator, 1985–2001 1775.10 Japan official discount rate vs. overnight call rate, 1993–7 1785.11 Yen vs. US dollar and DM, Feb–April 1995 1815.12 US dollar vs. yen and DM, Feb–April 1995 1815.13 10-year JGB vs. T-bond yields, 1996–9 1905.14 Japan, US and Germany real GDP growth, 1993–7 1915.15 Real GDP: Japan, US and euro-area, 1995–2000 1915.16 10-year bond spread (T-bond over JGB), 1996–2000 1935.17 3-month Japan CD rate vs. 3-month euro-dollar rate,

April–May 1997 1975.18 10-year JGB vs. T-bond yields, April–May 1997 1975.19 US$ vs. Yen and DM, April–May 1997 1995.20 Yen vs. US$ and DM, April–May 1997 1995.21 US dollar vs. Yen and DM, October 1998 2065.22 Japan yield curve, 1995–2001 2085.23 10-year JGB yield vs. 3-month CDs, June 1998–March 1999 2095.24 Euro currency corner, 1999–2001 2105.25 US$ currency corner, 1999–2001 2115.26 Yen currency corner, 1999–2001 212

viii List of Figures

List of Tables

3.1 Japan savings–investment balance, 1960–72 643.2 Japan savings–investment balance, 1974–82 653.3 Japan savings–investment balance, 1984–9 663.4 Japan savings–investment balance, 1990–9 673.5 Switzerland savings–investment balance, 1990–7 703.6 US savings–investment balance, 1982–90 773.7 US savings–investment balance, 1992–9 783.8 Euro-area savings–investment balance, 1991–8 793.9 Solo and axis movement in the US$–euro–yen triangle:

how frequent? 1033.10 US$, euro and yen: how long has each been in the limelight? 104

ix

Acknowledgements

On arrival at the University of Chicago’s Graduate School of Business, I hadno idea that my career would be in international finance and that my acad-emic source of inspiration would be Robert Z. Aliber. On departure, I wascertain about both points.

The era of floating exchange rates had just dawned. The Smithsonian fixbetween the yen, US dollar and DM had broken down. A new frontier – fullof danger and opportunity – had opened up for international business deci-sion-makers, whether as investors or borrowers. In his classes Bob Aliberintroduced us to the essential tools – Fisher Open, Fisher Closed, PPP, eco-nomic risk exposure (versus accounting) – for rational strategy-making inthe face of expected and unexpected exchange rate change.

I had some floating intention of immediately proceeding with doctoralstudy on these topics at the University of Chicago. But Bob was in nodoubt about the advantages of first engaging oneself in the real world of markets and offered me (jokingly!) a two-year forward contract of a place in his PhD programme. He must have known that once immersed in markets and in the European centre of action I would not exercise thecontract.

Just around the time when the contract would have matured, I had goneinto an art museum near the Bank for International Settlements. Suddenlya familiar voice called out my name. Bob had also been visiting the Bankand was travelling on the same plane to London that evening.

I do not recall whether we spoke about Japan, but that flight was the startof a continuous dialogue between us which has been a never-ending sourceof stimulus to my thinking about international financial developments. Myrecollection is that Japan became a big topic in our discussion by the early1980s. Huge Japanese capital inflows into the US were helping to sustain astrong dollar despite a record size US current account deficit.

Bob had no doubts about the driving force behind the new pattern ofglobal capital flows – the big private sector savings surplus in Japan whichhad emerged as its economic miracle faded away. He made the key compar-ison with Britain in the twenty years before the First World War.Unfortunately, policy-makers in Washington and Tokyo did not share BobAliber’s grasp of the essential problem – how Japan’s savings surplus wouldbe absorbed in the global economy.

Prophecy is a lonely business. And there is no doubt about Bob’sprophetic powers. His visits to my office in London were wake-up calls towhat lay ahead – whether the bursting of the Tokyo equity market bubble,the entry of the US economy into a low inflation era, the Asian crisis of

x

summer 1997, and most recently the bursting of the US bubble and subse-quent recession.

The one prediction where I can claim to have disagreed with Bob andbeen vindicated is about the future of floating exchange rates. Bob thoughtit possible that the end of the worldwide inflation storm which had ragedthrough the 1970s would bring a return to fixed exchange rates betweenthe major currencies.

As is so often the case, correct foresight was based on thinking which wasin fact incomplete. I failed to take full account of the Japanese-relatedfactors impeding a return to fixed rates. The focus of my argument (infavour of no return being likely) was too narrow and parochial. I took theBundesbank as the centre of the currency world.

That distortion of vision – too much importance to the DM and too littleto the yen – should have corrected itself during the many years I have hadthe deep privilege of being a member of the research team atTokyo–Mitsubishi International (and previously Mitsubishi Finance).Experience of talking to clients and to my colleagues about the outlook foryen markets in particular stretches back to the years of Japan’s bubbleeconomy.

Economic research activity at Tokyo–Mitsubishi International enjoyshigh respect from senior management and takes place in an environmentof total professional independence. The views expressed in this book arestrictly personal and in no way reflect those of my colleagues either indi-vidually or as a group.

When I mentioned to Bob some time ago that I was embarking on abook about the yen he had no doubts about the title. Back came the mail,crossing out my suggestion as too narrow, and replacing it with ‘Yo–Yo Yenand the Future of the Japanese Economy’. I know now from where the ideacame for the title of his bestseller The International Money Game.

A game suggests there are winners and losers, which there certainly are ininternational financial markets. The yo–yo yen has showered big gains andlosses on different groups both inside Japan and outside. On balance,though, the successive throws of the yo–yo have been a drag on Japaneseeconomic prosperity and exposed flaws in the international economicorder.

It is time to change the rules of the game.BRENDAN BROWN

Acknowledgements xi

Foreword

The economic developments in Japan in the last fifteen years present oneof the most interesting sets for economic analysis and one of the most chal-lenging for policy makers. The rate of economic growth has declined fromone of the most rapid in forty years prior to 1990 to one of the slowestamong the industrial countries. Japan is now experiencing its third eco-nomic contraction in the last ten years. The consumer price level is declin-ing by 1 per cent a year, and there is the prospect of a debt-deflation cycle;because prices are declining more rapidly than costs, profits are squeezedand the business failure rate has soared, which constrains the growth ofbank credit which leads to further downward pressure on prices. The banksand other financial institutions have been struggling under a mountain ofnon-performing loans as a result of the implosion of the asset price bubbleof the late 1980s and the recessions; because of the high rate of bankruptcy,banks have to dispose of old loans at an increasingly rapid rate to avoid anincrease in the number of non-performing loans on their balance sheets.The nominal interest rates on short term deposits and short term govern-ment securities are zero and real interest rates are slightly positive; thenominal interest rates on ten-year government bonds are below 2 per centand real interest rates are about 3 per cent. The fiscal deficit has been in therange of 8 to 10 per cent a year for each of the last four years, and the ratioof government debt in the hands of the public to GDP is much higher thanin any other large country. Either tax revenues must increase relatively togovernment expenditures by 6 per cent of GDP, or the government eventu-ally will default on its debt, either formally a, more likely, informally.

Still the cranes are back in Tokyo and the capital city is experiencinganother major construction boom. Despite the economic slowdown, thereremain fabulously successful Japanese firms – Toyota, Sony, Fuji Film, Fujitsu,Fanuc, Canon, DoCoMo, Honda, Nikon, Komatsu, Kubota and Toshiba.

Moreover Japanese-owned foreign assets are much larger than those of allother creditor countries combined; the ratio of these assets to the country’sGDP is twice the peak value for this same ratio for the United States.

In the last fifty years Japan has achieved the highest rate of growth of percapita income in any of the industrial countries. In the late 1940s percapita incomes had been at the equivalent of the proverbial $100 a year, aresult of the tremendous physical damage from the bombing during thelast several years of World War II, the loss of what had been its colonies,and limited ability to gain the advantage of international specialisationbecause of the lack of the ability to produce goods that could be sold inforeign markets.

xii

By the early 1990s per capita incomes in Japan were comparable to thosein other industrial countries. Japan now is a rich country, indeed a veryrich one even though many Japanese are still in a time warp and continuedto think that the country is poor.

The foreign exchange value of the yen had been set at 360 yen per USdollar in 1949 when Japan was still occupied by the US military forces; thisparity was viable only because a wide array of trade and exchange controlslimited payments for imports and foreign services and foreign securities. Ifmarket forces had been allowed to set the foreign exchange value of theyen on the basis of the competitiveness of Japanese goods in foreignmarkets, the Japanese yen price of the US dollar would have been in therange of 500 to 600 yen.

By the end of the 1970s, the yen traded at 150 yen to the US dollar andby 1995 the yen briefly had traded at 80 yen. Both the real appreciation ofthe Japanese yen and its variability around the trend were greater than forthe currency of any other industrial country.

The counter part of this remarkable appreciation of the currency is thatby the year 2001 the Bank of Japan had accumulated more than US$400billion of foreign exchange reserves, much larger than those of any othercountry.

The sharp appreciation and the remarkable increase in foreign exchangereserves resulted from the exceptionally rapid growth in the country’sexports and its foreign exchange earnings.

The 1990s was a devastating decade for Japanese expectations. In theearly 1970s ‘Japan: The First Super-state’ appeared; the successor volume inthe 1980s was ‘Japan as Number One’ to many in Tokyo. It seemed only amatter of a few years before Japan displaced the United States as the domi-nant super-power.

Until 1990 the rate of economic growth in Japan was higher than thecomparable rates in any other industrial country. In the 1950s and the1960s, the annual growth rate averaged 10 per cent; there were step-likereductions in the growth rate in each of the next two decades. Still in the1980s the rate of economic growth was higher than in most other indus-trial countries, at the same time asset prices were rising sharply, especiallyin the last three years of that decade.

There was a sharp unanticipated decline in the growth rate in the 1990s,and for most of the decade the country was in the economic doldrums,with a rate of economic growth substantially below that in the UnitedStates and the industrial countries in Western Europe, even below the ratein Great Britain, a country with a much lower saving rate, a much lessrobust industrial sector, an ageing capital stock and a much more truculentlabour force.

Throughout the 1990s domestic supply capabilities were increasing morerapidly than domestic demand; by the end of the decade the output gap

Foreword xiii

may have been in rage of 10 to 15 per cent. Nominal interest ratesdeclined, and the creditors who depended on interest receipts for a sub-stantial part of their income experienced a real decline in their incomes;they became increasingly sensitive to the differences in the prices ofsimilar goods. There was a surge in imports of competitive manufacturesfrom Korea, China, and other countries in the region, which contributedto the downward pressure on the price level. The ‘100 yen’ stores greatlyincreased their share of the domestic market with consumer goods pro-duced in China – often in Japanese-owned plants dedicated to producingfor the markets in Tokyo and Osaka – and there are 2000 such stores inJapan.

The prospect of ‘debt deflation’ cycle increased – a downward spiral inprices and bank capital. Excess supply resulted in downward pressure onprices. Profit rates and profit levels were squeezed because prices weredeclining more rapidly than costs. Many firms incurred losses, and somewent bankrupt; some of the losses were transferred to the bank lenders. Thevalue of bank capital declined and became more uncertain, and so itbecame more difficult for banks to raise capital. The banks were reluctant toexpand their loans to all except the most creditworthy borrowers, and thesluggish growth in credit meant that investment spending was not increas-ing and so excess supply continued to place downward pressure on theJapanese price level.

Japan continues to have the basic inputs that enabled it to achieve highrates of economic growth in the 1970s and the 1980s – the savings rate ishigh and the supply of capital is large, the labour force is skilled anddiligent and hard working, and firms are leaders in their ability to developnew technologies and to adapt those from other countries to the Japanesecircumstances.

The likelihood is high that the implosion of the asset price bubble of thelate 1980s derailed the economy. But why has the economy failed to moveback to its growth trajectory? Why has Say’s Law failed to operate in Japanfor a decade? Why hasn’t the remarkable supply capability created its owndemand? The central question is whether the tepid economic performanceof Japan in the last decades reflects the shortcomings of government policy– both the adoption of policies that were inappropriate following theimplosion of the asset price bubble and the failure to adopt policies thatwould have been appropriate – or whether instead there has been a ‘marketfailure’ and if so in which market and why?

The failure of government policy may reflect the delay in formally re-capitalising the banks after the large loan losses, or the increase in the con-sumption tax, or the efforts of the Bank of Japan to talk up the foreignexchange value of the yen, or the tepid approach to a more aggressivemonetary policy in the early 1990s, to cope with the effects of the implosionof a massive asset price bubble. To some extent the failure of government

xiv Foreword

policy might be attributed to the US authorities who at times were reluc-tant to see the yen depreciate and the trade surplus of Japan increase. The policy failure also might reflect that the ‘Japanese establishment’ wasreluctant to accept the financial losses and to accept the inevitable re-structuring of industry so that corporate Japan would be more profitable.The market failure would instead reflect that either the level of investmentor the level of saving are not sufficiently sensitive to the declines in interestrates. Thus the usual expectation is that as interest rates decline, invest-ment would increase and saving would decline until the amount thathouseholds wish to save, when the economy is fully employed, wouldcorrespond to the amount that business firms wish to invest.

Moreover, to what extent has the seemingly lost decade been anextended transient factor associated with the implosion of the bubble, andto what extent has the implosion revealed some permanent and underlyingstructural defects in the economy that had previously been obscured?

The next section of this introduction summarises the unique aspects ofJapan’s industrial structure and the relation between this structure and thecomposition of the country’s foreign trade. The third section considers theimpacts of the implosion of the asset price bubble and on the relationshipbetween the banks and their affiliated firms. The fourth section developsthe major hypothesis that the dominant problem in Japan is that theamount that households wish to save, if the economy were growing atcapacity, is significantly larger than the amount that Japanese firms wouldwish to invest at home and can profitably invest at this rate of growth. Thefifth section evaluates the proposals for getting the Japanese economy togrow again in terms of this statement of the problem. The sixth section dis-cusses direct approaches to increase consumption spending relative toincome. The final section evaluates the major theme of the ‘The Yo-Yo Yen’.

Economic structure and the foreign exchange value of the yen

Japan is different from the other industrial countries. The domesticresource base is limited; virtually all raw materials, much of energy, andmany foodstuffs are imported. The surprising aspect of the Japanese econ-omy is that the ratio of imports to GDP is remarkably low, much belowthose of other industrial countries with much richer resource bases.

If this ratio had been more nearly similar to that of Germany or GreatBritain, then the ratio of exports to GDP also would have been higher, andJapan would have had to have grown its exports and increased its share ofthe domestic markets in most other industrial countries at more rapid rates.

For most of the period 1950 to 1990, Japan’s exports were increasingtwice as rapidly as world exports. At the beginning of the period, most ofthe exports were inexpensive commodity-like manufactures – textiles,apparel, toys, and bicycles – goods that were sold on the basis of a price

Foreword xv

advantage. Relatively few products then had recognisable brand names.The more rapid growth of Japanese exports than of world exports reflectedthat the Japanese firms were able to increase their share of foreign markets– despite many protectionist barriers – on the basis of declines in price andimprovements in quality and the development of a more favourable atti-tude in foreign countries toward Japanese brands.

The change in the composition of exports has been impressive. Therewas the move into steel and radios and then TVs and then motorcycles andthen small cars and then computers and sophisticated electronics. The ratioof Japanese value, added to the total price of the product, seemed to beincreasing exponentially; Japanese brand names became dominant in autosand electronics and photo-optics. Much of the growth in exports was ingoods that Japan had begun to produce relatively recently.

By the mid-1980s Japan had become an economic superpower, secondonly to the United States. Japanese firms had become dominant players inthe global markets for autos, steel, electronics, and photo-optics. Toyotawas one of the four or five major competitors in the global auto industry,while Honda had become one of the most innovative firms. Sony set thestandard for innovation and quality in the electronics industry – and therewere many firms like Matsushita and Sanyo with extensive product linesand others like Denon and Luxman and Yamaha and Nakamichi withmarket niches in quality components. Japanese financial institutions dom-inated the hit parades of the world’s largest firms. The assets of NomuraSecurities were larger than the combined assets of the five largest US invest-ment banks.

The rapid growth in Japanese exports was facilitated by its unique indus-trial structure that nurtured the development of new firms in new indus-tries. Most of the major industrial groups have organised around what hadbeen feudal families – the Mitsuis, the Yamamotos, the Sumitomos. Beforethe Second World War, each group had a bank holding company that con-trolled a trading company, a shipping line, an insurance company, and afirm in each of a large number of manufacturing and service industries.This zaibatsu arrangement was outlawed by the occupation, but its sub-stance was retained with significant cross-shareholdings between the banksand the firms, and among the firms. The cross-shareholdings accounted forabout two-thirds of the total share ownership of the relevant firms. (Not allfirms were part of one of these groups.)

Perhaps 30 per cent of the labour force was employed under ‘lifetimecontracts.’ The firm was a ‘village’ and the wage payment based onseniority meant that the residual owners were the employees. The stock-holders traded titles to ownership in a casino, but the managers of thefirms felt no commitment to enrich the anonymous shareholders. Becausewage rates were firm-specific, the less efficient firms could match the pricescharged by the more efficient by providing less rapid increases in wages

xvi Foreword

and bonuses. The first call on the firm’s revenues was the funds to expandand enrich its product line.

There were and are many more firms in each industry than in the UnitedStates and Western Europe; for example, for a long time there were ninefree-standing firms in the automobile industry (Toyota, Nissan, Honda,Mitsubishi, Mazda, Suzuki, Isuzu, Subaru, Daihatsu), more than the com-bined number for the United States and Western Europe. The flexibility inthe wage payment system meant that the smaller and less efficient firmscould continue to compete with the leaders in their industries.

Industrial policy captured by the motto ‘Japan Inc.’ facilitated economicgrowth. The domestic market was protected from imports until Japanesefirms had reduced their costs so that they were internationally competitive.Government financial regulations were extensive and led to high levels ofinvestments; the system was rigged so that household savers required sub-sidised industrial borrowers. Interest rate ceilings on bank deposits after wereat levels below the inflation rate, so the real rates of interest were negative.Initially loans were subject to interest rate ceilings. The demand for credit atthese low interest rates was larger than the supply, and some firms withaccess to credit profited by lending some of the funds at rates significantlyhigher than the regulated rates. Exchange controls prevented householdsavers and financial intermediaries from buying foreign securities.

Japan had a ‘dual economy’ or more of a dual economy than otherindustrial countries. Firms in a few industries were super internationalcompetitors, with output per worker per hour significantly higher than inother industrial countries. A typical statement might be was that it took 78worker-hours to produce an automobile in a Toyota factory in Japan, and110 worker-hours to produce an automobile in a Ford factory in the UnitedStates. These descriptive comparisons applied to perhaps 30 or 40 per centof the firms in various manufacturing industries. In the remaining sectorsof the economy – agriculture, the rest of manufacturing industry, and theservice sectors – productivity was much below that in the United States.Observers noticed the large numbers of service personnel in departmentstores and hotels. Most of the industries in the productive sector producedtradable goods, but not all the industries that produced these goods were inthe modern sector, the operative distinction appears to be between thosefirms that produce relatively new goods at those in traditional manufacturing.

The rapid growth of exports led to the secular appreciation of the yen; atthe same time the reduction in trade and exchange controls led to an increasein imports that limited the appreciation of the yen. Japanese foreign invest-ment began to surge in the early 1980s as exchange controls were relaxed;initially in the purchase of foreign securities and subsequently in the acquisi-tion of established firms in the United States and to a lesser extent in WesternEurope. The Japanese authorities apparently realized that domestic savingswere sufficiently large so that foreign investment would not significantly

Foreword xvii

‘crowd out’ domestic investment, and that the purchase of foreign securitiesand assets would limit the appreciation of the yen. Japanese investors wereattracted to the higher anticipated rates of return abroad.

By the end of the 1980s Japan had displaced the United States as theworld’s largest creditor country. This trend continued throughout the1990s, and at the end of that decade, Japanese net foreign assets were morethan $2,000 billion, larger than the net foreign assets of all other creditorcountries combined. Japan’s net foreign assets were one-third of its GDP.The country’s net foreign assets were increasing by about 2 per cent of itsGDP, or about $100 billion a year, and the investment income on the netforeign assets had increased to about one half the value of the tradesurplus.

The United States had become the world’s largest debtor, and its net lia-bilities were larger than the combined net foreign liabilities of all otherdebtor countries as a group. To a large extent, the development of the USinternational debtor position was the mirror-image of the changes in theJapanese external balance.

One of the major questions is whether the secular trend to a higherforeign exchange value of the Japanese yen resulted from the productivitysurge in autos and steel and electronics; the story is that continued highlevels of productivity growth led to declines in selling prices which led toincreases in foreign sales which led to increases in export earnings whichled to increases in the foreign exchange value of the yen.

The competing story is that the appreciation of the yen induced placedmany firms between the proverbial “rock and the hard place”; their profitson exports disappeared, and either they would have to reduce costs tomaintain the profitability on export sales or their market share would havedeclined.

Both stories are true for different industries at different times. When theproductivity gains in a particular industry were especially large, because ofthe rapid growth in production and sales, the firms in this industry reducedtheir selling prices and that led to increases in exports and the appreciationof the yen. Then five or ten years later, the rapid productivity gainsoccurred in a second group of industries, and the resulting appreciation ofthe yen led to a decline in the profitability of the firms in those industriesthat had experienced their most rapid productivity gains earlier, and so thefirms in these industries would experience a sharp decline in profits onexports unless they reduced their costs significantly.

As long as Japanese imports consisted primarily of foodstuffs and basicraw materials, the volume of Japanese imports was not sensitive to changesin their prices. Japanese exports did not appear especially sensitive tochange in the foreign exchange value of the yen; the caricature was thatJapanese firms would sell abroad at any price and that the profits on salesin the protected domestic markets were subsidising the losses on export

xviii Foreword

sales. Few firms would reduce their exports in response to the increase inthe foreign exchange value of the yen and the apparent decline in theprofitability of export sales.

Because of the combination of the composition of imports and themarket share orientation of exporting firms, relatively large changes in theforeign exchange value of the yen were necessary to effect a significantchange in Japan’s trade balance that might be associated with changes inthe price of imports like a change in the price of oil or changes in thevolume of capital outflows from Japan.

If the range of Japanese imports had been much broader – if a large pro-portion of these imports had been competitive with goods produced inJapan – then the shocks in the form of capital flows and changes in theimport prices would have had a smaller impact on the foreign exchangevalue of the yen. It is plausible that the economic planners in Tokyo fiftyyears ago asked the ‘Never Again’ question, ‘How can we minimise ourdependence on the rest of the world?’ Their answer might have been, ‘Tothe extent possible, minimise the dependence on imports – which also willhave the advantage that the protectionists and other problems that we willencounter in increasing our share of foreign markets will be minimised.’Initially the whole array of government controls facilitated the developmentof an industrial structure that was minimally dependent on imports. Theconsequence of this skewed structure is that the range of the movement inthe foreign exchange value of the yen in response to a share is much largerthan it would have been if there had been a significantly more diverse com-position of imports.

The asset price bubble and its implosion

In the 1980s Japan experienced a massive asset price bubble. Real estateprices increased by a factor of eight or nine, and the ratio of real estateprices to GDP increased by a factor of seven. The increase in the price ofreal estate led to an increase in the price of stocks by a factor of seven. Realestate was the primary collateral for bank loans, and as the value of realestate increased, individuals and firms borrowed more from the banks.There was a massive investment boom, and consumption spendingincreased at an above trend rate. Because banks and other financial institu-tions owned large amounts of both real estate and stocks, the increase inthe value of these assets led to large increases in bank capital and in theability of the banks to grow their loans.

It seemed like a perpetual motion machine. Increases in property pricesand stock prices meant that the value of the collateral of the borrowers wasincreasing at the same time that bank capital was increasing. Bank lendinghad some of the characteristics of ‘evergreen finance’ because the borrowerswere able to use the cash from new loans to pay the interest on outstand-

Foreword xix

ing loans. Loan losses were trivial because the increases in the value of realestate collateral were larger than the interest rates on bank loans.

It was too good to last and so it did not. Stock prices have fallen to onefourth of their value at the peak, and real estate prices have declined by acomparable amount. The Japanese financial community learned that theperpetual motion machine worked in reverse, and that the loan losses ofthe lenders and the value of their capital were highly correlated. TheJapanese banks and other financial institutions have been de-capitalised.

Still there were few ‘runs’ on banks; the Japanese savers believed that thebanks were ‘too big to fail’ – that in effect they had 100 per cent depositinsurance.

Until the 1980s the major function of the credit officers of the banks wasto ensure that the market value of the real estate pledged as collateral forloans more or less corresponded with the values stated by the borrowers intheir loan applications.

The de-capitalisation of the Japanese banks de-stabilised the relationshipbetween the main banks and their traditional borrowers. The credit officersin the banks were caught in a generational change – once real estate pricesbegan to decline, their algorithm for evaluating credit risk had becomeobsolete.

The de-capitalisation of the banks has doomed the keiritsu arrangement;the main bank is no longer able to act as lender of last resort to firms thathad been within its group. Twelve or so banks have been merged into fourmain groups, and the party lines among the feudal groups have beenshattered.

Now the credit officers in the banks must determine whether new loanswould have a positive impact on the cash flows of the borrowers. Once thebanks began to use financial data to scrutinise loan applications, the bor-rowers had to developed a capital budgeting approach to determinewhether potential projects would add to the firm’s market value. The likeli-hood is high that many firms needed to develop new accounting systemsbefore they could make this evaluation.

One policy innovation in the 1990s was that Japanese firms and bankswere required to unwind their cross-shareholdings. A notable objective forthe long run. This was like a massive initial public offering; the majorimpact was to reduce share prices and increase the cost of capital toJapanese firms.

As more Japanese firms began to apply the capital budgeting approach tocurrent and new proposed activities they found that many of their existingprojects were not earning their capital costs. The implication is that firmsmust raise the rates of return on these activities or exit the businesses. Theeconomic intuition is that many of the firms that first began to follow thisapproach have decided to shrink activities and for a while at least arepaying down bank loans.

xx Foreword

Eventually the Japanese banks will learn how to do credit analysis andcorporate Japan will develop an understanding of the usefulness of thecapital budgeting algorithm in evaluating the profitability of the plants andbranches of large firms with many subsidiaries and activities.

Identifying the problem – what went wrong?

There is a long tradition across the Pacific that countries with the successfultrack record for economic growth offer advice to the less successful ones toadopt ‘our types of policies’. In the 1980s Tokyo offered a lot of advice thatthe United States should increase both the national savings rate and theexpenditures on research and development and the policies to improvelabour-management relations. Washington offered a lot of industry-specificrecommendations that were grouped under the heading of the StrategicImpediments Initiative; most of these suggestions were intended to reducethe Japanese trade surplus.

There has been an extensive debate about the policies that the Japanesegovernment should adopt to get the ‘country moving again’. A distinctionshould be made between targets and instruments. For example financialrestructuring is an instrument that might be used to increase investmentspending (which is the target). But the story needed for the links betweenthis instrument and target often is vague.

In the best of all possible worlds, each proposal might be adopted, unlessthere were a conflict among them. Most proposals would impose costs onthe well-being of one or several groups if adopted. Proposals can be rankedin terms of their benefit-cost ratios – their ability to lead to an increase inthe rate of economic growth in terms of minimal cost in terms of welfarelosses to particular groups.

One set of proposals is macro and includes a more aggressive monetarypolicy for the Bank of Japan, for a while a more aggressive fiscal policy, anda more ambitious approval to reduce the foreign exchange value of theJapanese yen. The set of micro-policies include corporate restructuring andfinancial restructuring.

Those who advocate one of the macro policies believe that the majorproblem is that demand is too modest relative to the supply capabilities,and that either investment demand or consumption demand should beincreased.

One shortcoming in the debate is the failure to distinguish targets andinstruments. The targets are the output gap or the rate of growth of realincome, the instruments are the macro-policies and the micro-policies.Those who advance one of the micro-policies need to identify the linkagesbetween these policies and one of the targets.

There has been relatively little discussion of the features or attributes ofthe model of the Japanese economy at full employment. For example,

Foreword xxi

given the upper limit to the rate of potential growth of the Japaneseeconomy, what would be the ratio of investment to GDP and what wouldbe the household savings rate?

There was a minor debate about the upper limit to feasible rate ofJapanese economic growth. As the observed rate of economic growth haddeclined, estimates of the potential rate of economic growth have beenrevised downward. The prospective decline in the population growth rateseemed to be associated with the decline in the estimates of productivitygrowth, even though the economic intuition is that the prospectiveshortage of labour should lead to increases in the investment rate as capitalis substituted for labour.

The higher the rate of economic growth, the larger the share of domesticsaving that would be absorbed by investment in plant and equipment, andthe smaller the problem – if any – with insufficient aggregate demand.

Those who advocate one of the macro-policies believe that the majorproblem is that demand is too modest relative to the supply capabilities,and that either investment demand or consumption demand should beincreased.

The amount that Japanese households would wish to save if theeconomy were to grow at a rate consistent with the Japanese version of fullemployment is significantly larger than the amount that Japanese firmscould profitably invest at this rate of economic growth. If the potential rateof growth of GDP is 2.5 per cent a year and the marginal capital outputratio is 4, then the investment-GDP ratio would be 10 if the economy wereto grow at this capacity rate. If the potential rate of economic growth is3 per cent, then this ratio would be 12 per cent at the same marginalcapital output ratio. Japanese households save about 20 per cent of theirincome.

The core economic problem is that the amount that Japanese householdswould like to save if the economy were to operate at full employmentgrowth is substantially larger than the amount that Japanese firms wish toinvest at home. The savings rate in Japan is higher than in other industrialcountries, and one of the major questions is how the economy has adjustedto this rate in the previous five decades, and the policies that might beadopted now to use these savings efficiently.

Two adjustments are necessary to the new financial environment inJapan. There needs to be a permanent adjustment so that there is a sustain-able relationship between savings and investment; either institutionalarrangements will develop so that savings can be used efficiently and prof-itably or the economy will fail to grow at its potential rate, much as in the1990s, and a non-trivial part of actual savings will be wasted – and therewill be foregone savings because income will not increase at the potentialrate. Then there is an extended transition from a time when the Japanesefinancial arrangements were effectively segmented from those in the

xxii Foreword

United States and other industrial countries; during this period there wasno systematic relation between the return on capital in Japan and theseother countries. During this transition – which has been on-going fornearly ten years – a large number of assets in Japan must be re-priced.

There are a limited number of ways in which Japan can adjust to itsmuch higher savings rate. The investment rate in Japan might be muchhigher than in other industrial countries; either because the growth rate ismuch higher while the marginal product of capital is comparable to thelevels in other countries or because the growth rate is similar to those inother industrial countries and capital is used much more inefficiently. Partor all of the excess of Japanese savings over Japanese domestic investmentmight be invested abroad – used to buy foreign securities and real assetsabroad. Part of the excess might be used to buy government securities andto finance the government’s fiscal deficit; the excess of government expen-ditures over tax revenues could be used to build roads and schools andhousing for the elderly and the poor and improve the water and sewageand transportation systems. Finally, if together these several measures arenot sufficient to absorb all of domestic saving, then Japan will adjust to theexcess of ex ante saving over ex ante investment by producing at a lowerlevel of output.

In the 1950s and the 1960s, the real rate of economic growth averaged10 per cent a year, and domestic investment was modestly greater thandomestic saving; the economy tended to become ‘over-heated’ and therewas a secular tendency toward current account deficits at least until the late1960s. The capital-output ratio was relatively low, and the rate of return oninvestment was high. In the 1970s the rate of economic growth declinedand so domestic saving began to exceed domestic investment; the capital-output ratio began to increase and there was a sharp decline in the rate ofreturn on domestic investments. Moreover, the Bank of Japan began topurchase US dollars to limit the appreciation of the yen and so foreigninvestment increased.

In the 1980s more of the excess saving was used to buy foreign securitiesand real assets including real estate; foreign investment increased to 2 percent of GDP. The combination of this level of investment and the rate ofeconomic growth of 4 per cent meant that the capital output ratio wasnearly 5 – the rate of return on investment had declined sharply, and a sig-nificant part of Japanese domestic investment was inefficient or wasteful.Because the economy was growing rapidly and household wealth wasincreasing at a rapid rate, the waste in the use of saving was not readilyapparent.

Domestic investment declined sharply in the 1990s. There was a modestincrease in foreign investment, in part because foreigners were borrowingin Tokyo to finance offshore activities. The major adjustment was theincrease in the fiscal deficit; the story or part of the story was that spending

Foreword xxiii

on public works increased sharply, and there were roads that went nowhere, airports without traffic, and parallel bridges across Tokyo Bay.Determining the value component and the waste component of thesepublic works expenditures is complex. The wasteful private investmentspending of the 1980s had been replaced by the wasteful public investmentspending of the 1990s. Finally, the rate of growth of income was modestbecause foreign investment and the fiscal deficit together were not suffi-ciently large to absorb all the saving that would have been available hadthe economy operated at full employment levels. One component of thewaste was that productive potential was underutilised.

In the long run, the rate of return on investment in Japan and thecapital-output ratio must be comparable to those in the United States andother industrial countries. The question then becomes the costs of thevarious adjustments to the higher ex ante savings in Japan, and whetherthese savings will be used efficiently.

Proposed solutions – restructuring and demand-expansion

The various proposals to solve the problem of the large and growingoutput gap in Japan can be evaluated in terms of the story that theamount that Japanese households would want to save if the economyoperated at its full employment level is significantly higher than theamount that Japanese households would want to invest. The challenge forthe proponents of individual measures to get the economy moving againis how the suggested measures will impact the relationship between savingand investment.

The dominant practice among analysts is to propose a modest number ofproposals – a more expansive monetary policy, a more expansive fiscalpolicy (at least until the ratio of government debt in the hands of thepublic begins to approach 150 per cent), re-capitalisation of the banks andother financial institutions, corporate re-structuring, and an increase inhousehold consumption. One reason that the policy makers may havebeen sluggish in adopting these measures is that almost always some groupwould become less well off if a particular measure were adopted.

An alternative approach is to endow the policy makers with ‘one thou-sand points.’ Their objective is to chose those policies which will be mosteffective in reducing the output gap in terms of the costs to different con-stituencies. The one thousand points is a metaphor for a budget constraint,the policy makers now have to choose among competing proposals. Thischoice now requires that they have a ‘production function’ for each ofthese proposals, so that they can be readily compared in terms of theireffectiveness in closing the output gap relative to their costs.

Each of the proposed policies that has been advocated to get theeconomy moving again can be evaluated in terms of how well the measures

xxiv Foreword

would enable the Japanese economy to begin to close the output gap byreducing the imbalance between saving and investment.

Corporate restructuring and financial restructuring often are viewed as‘twins’. Today financial restructuring might complicate or delay corporaterestructuring. Corporate restructuring is necessary for banks and otherfinancial institutions but it is distinct from financial restructuring.

The objective of the corporate re-structuring is to increase the profit rateon assets already on the ground. Those who advocate corporate re-structur-ing believe that the excess capacity is so extensive in some industries thatthe anticipated profit rate on new investments would be significantly belowthe cost of capital and that additional investments would depress themarket value of these firms.

Until the implosion of the bubble, most Japanese firms were interested inmarket share or in developing more sophisticated products; few were inter-ested in the relationship between the cost of capital – which was quite lowin the bubble years of the 1980s – and the anticipated rate of return oninvestment.

Now the cost of capital to Japanese firms is much higher than in the1980s as a result of the tumble in stock prices – a decline which has been intensified by the untimely decision to reduce and eliminate cross-holdings.

The implosion of the bubble and the financial stringency of Japanesefirms mean that money is no longer ‘free’ for Japanese firms, as it had beenin the 1980s and earlier decades, Now these firms have to convince bothlenders and investors that their investment projects will be profitable.

The required change in the investment behaviour of Japanese firmstoward the use of capital is seismic. These firms need to increase the rates ofreturn on the assets that are already on the ground so that they are compa-rable to the rates in the United States and other industrial countries.

Selling prices must be increased relative to costs. The managers mustrecognise and accept that the increases in selling prices may lead to adecline in sales and market share. If selling prices cannot be increased, thencosts must be reduced. Labour costs might be reduced by attrition of thenumber of employees.

Increasing the rate of return on the assets that are ‘already in the ground’requires that the owners of these assets revalue them downward – in effectto take a re-structuring charge and perhaps a large charge. These assets needto be priced so that their rates of return would be comparable to the ratesof return on new investments. Some assets might be scrapped.

The economic loss associated with the decline in the market value ofthese assets relative to their historic cost already has occurred. The ownersof these assets must recognise these losses.

The firms can shrink their non-profitable subsidiaries and activities, andstop, or at least sharply diminish, the cross-subsidisation from the prof-

Foreword xxv

itable to the non-profitable. The non-profitable activities and subsidiariescan be spun off, and allowed to sink or swim; swimming would likely meanthat the labour costs would be reduced, perhaps in part by reducing wagerates.

The Japanese government can encourage mergers to reduce excess capac-ity. The government might sponsor measures for labour retraining andearly retirement.

Increasing the rate of return on new investments is difficult as long asthere are many similar assets whose current market value is significantlybelow their reproduction costs.

The objective of financial re-structuring is to encourage banks to be moreaggressive lenders. Those who advocate financial re-structuring believe thatbanks would make a larger number of loans and investment spendingwould be significantly larger if banks were more adequately capitalised.

As a result of loan losses, the market value of the assets of many banksand financial institutions has declined below their liabilities; these institu-tions have levels of capital below the required level. Nevertheless therehave been very few runs on Japanese banks; the Japanese public believedthat their deposits were fully guaranteed by the government.

As long as there was substantial uncertainty about the value of many ofthe loans held by the Japanese banks, there was substantial uncertaintyabout the value of their capital, and it was virtually impossible for thebanks to raise additional capital in private markets. As long as banks arenot confident that they are adequately capitalised, they are likely to be cau-tious in extending new loans. The cliché that ‘they would lend only tothose firms that didn’t need to borrow’ is relevant. Private investors werereluctant to buy ‘a pig in a poke’; the insiders generally believed that thevalue of bank capital after recognition of these losses was much higherthan the outside investors. It was only in1997 that the Japanese govern-ment developed a programme that would enable the banks to becomeformally re-capitalised.

One of the buzz-words for financial re-structuring is the ‘sale of non-per-forming loans’. This term is generic and has several different meanings.Usually banks allocate part of each year’s income to a loan-loss reserve onthe assumption that loan losses are episodic and that it is desirable tosmooth reported income from the occasional losses. When loan losses arefirst recognised, the value of the loan-loss reserve (an entry in the bank’scapital account) and the loan are reduced. Subsequently the banks can sellthe loans or they can sell the collateral that they might have acquired inthe settlement of the loan; if the funds received from the sale are largerthan the value of the loan on their balance sheet, the banks have a capitalgain.

The view that financial restructuring might occur at a more rapid pacemight mean that the amounts that the banks were adding to their loan loss

xxvi Foreword

reserves were too small or that the banks were too slow in writing down thevalue of the loans or that the banks were too slow in selling the loans thatwere in default or the collateral acquired from the borrowers that defaulted.

The sluggishness in re-capitalising banks could have two impacts. One isthat the banks were reluctant to lend to many firms because they were souncertain about the value of their own capital; the implication is that if thebanks had been better capitalised, they would make a larger volume ofsomewhat riskier loans, and the level of business investment would behigher.

The second way in which the sluggishness of banks in selling non-performing loans affects the real economy is that the overhang of theseassets on the market would depress the prices of these assets. Firms would bereluctant to invest because of the concern that a more rapid sale of the non-performing loans would lead to a decline in the value of real estate assets.

Both factors may operate at the same time. If the dominant factor is thatbanks are sluggish lenders, then the interest rates spread between govern-ment securities and securities of commercial borrowers should be excep-tionally large. If the dominant factor is that the borrowers are reluctant toincrease their loans because of the concern that the sale of non-performingloans will depress asset values, then the interest rate spread should beexceptionally low.

If both factors are operating, then the relation of interest rates on bankloans to interest rates on government debt would provide the basis forinferring which factor was relatively more important.

Even if the banks had sold all their non-performing loans and had beenfully re-capitalised Japan would still face the problem that the amount thathouseholds would like to save, if the economy were operating at fullemployment, would exceed the amount that firms would like to investdomestically. Moreover, domestic investment might still be significantlybelow the level associated with full employment because many Japanesefirms still had not been able to increase the anticipated rate of return ontheir investments to correspond with their cost of capital.

The Japanese banks eventually will be re-capitalised and they will selltheir non-performing assets. Still these measures should receive priorityonly after a much larger number of firms have been successful in increasingthe profit rates on their current investments.

The necessary condition for believing that financial restructuring shouldbe a priority for the government is evidence that there are significantnumbers of firms with profitable investment projects that cannot obtainfinance. That seems unlikely.

The decline in the rate of business investment in the late 1990s is evi-dence that more and more firms realise that they must raise the rate ofreturn on their investments to their cost of capital. The decision to requirethat banks and firms reduce their cross shareholdings has increased the cost

Foreword xxvii

of capital by depressing share prices. The firms that are among the first intheir industries to understand the importance of increasing the rate ofreturn to match the cost of capital will be capturing market share from theslow learners. The banks – at least some of the banks – understand the newfinancial environment and now are reluctant to lend to those firms whohave failed to learn the lesson.

Those who favoured macro-policies believed that the dominant problemwas that aggregate demand was inadequate – that the amount thatJapanese households would want to save if the economy were operating atits full potential is significantly higher than the sum of the amounts thatJapanese firms can invest profitably domestically and the amount thatfirms and individuals can and want to invest abroad. This type of compari-son leads to the conclusion that measures should be adopted to increaseconsumption – in effect to reduce saving.

One of the objectives in most countries is to increase the savings rate sothat the consumption levels in the future will increase more rapidly. Thesavings rate in Japan is significantly higher than in virtually every otherindustrial country. But Japan is different from other countries, and the keyquestion is whether the households are myopic and are saving too much.Assume that the objective of saving is to smooth consumption over the lifecycle, so that spending to maintain the living standards in the post-retirement period will be comparable to the standards in the working years.The wealth of Japanese households is in the range of three to four timestheir incomes; assume that this same ratio is in the range of six to eight onthe eve of retirement. Assume that the life expectancy of individualJapanese at age 65 is twenty five years. Finally, assume that the real rate ofreturn on household wealth is zero.

During each of the retirement years the individual Japanese would sellsome of the assets acquired while in the active labour force to get the fundsto finance current consumption. If the spending is constant during thetwenty five years of retirement, then the individual Japanese would be ableto spend twenty four per cent of pre-retirement income if the wealth toincome ratio is six on the eve of retirement and thirty two per cent of thepre-retirement income if this ratio is eight. If consumption had been 80 percent of personal income, then the consumption spending in retirementwould be 30 per cent and 40 per cent with the two different values for thewealth-income ratio on the eve of retirement. In addition many Japanesewould have corporate pensions and government pensions, but in generalthese pensions are modest.

The funds available to finance consumption from the depletion of capitalmust be adjusted for the real rate of return on household saving. Duringmost of the period since 1950, the real rate of return to household saverswas not significantly above zero, since the inflation rate more or less cor-responded with the nominal interest rate.

xxviii Foreword

The higher the real interest rate on household savings, the larger theincome of the retired. Moreover, the higher the real interest rate, the morerapidly the stock of saving would increase. At some stage, the increase inthe stock of saving from a higher real rate of return on the previously accu-mulated savings would be so large so that households could achieve theirwealth targets with a lower level of saving from current income.

The conclusion, from the comparison of the amount available for con-sumption in the post-retirement years with the pre-retirement years, is thatJapanese households have not been saving too much. Many households arelikely to experience a sharp decline in the funds available for consumptionin the retirement years.

The reason that Japanese households may have such a high savings rate isthat they have responded rationally – and inadequately – to the very low realinterest rate on their household savings. (In a curious way this is the ‘saver’srevenge – for decades the mandarins in the Ministry of Finance used interestrate ceilings to ‘tax’ savers to subsidise business investment.) Householdsresponded by increasing the amount they saved out of current income.

Hence there are two somewhat overlapping transitions. The first transi-tion is that Japanese firms are adjusting to the requirement that theyinvested only in those projects that will prove sufficiently profitable thatthey ‘earn their cost of capital.’ Japanese savers are adjusting – slowly andcautiously – to the increase in the real rate of return on their savings. Theimplication is that the most effective approach that the Japanese policymakers might adopt to reduce the savings rate is to facilitate an increase inthe real rate of return to the savers.

Nevertheless, there is likely to be an extended period in which theamount that Japanese households wish to save will be significantly larger than the amount that Japanese firms can and want to investdomestically.

A more expansive fiscal policy would stimulate final demand; to theextent that tax rates were reduced, consumption spending and investmentspending would increase since after-tax incomes would be higher.Otherwise government expenditures would be increased. A more expansivemonetary policy would stimulate business investment and household con-sumption spending. The exchange rate policy would lead to a lower foreignexchange value for the Japanese yen.

During the 1990s Japan adopted a large number of programmes to stimu-late government spending. By the late 1990s the fiscal deficit had increasedto the range of 7 to 10 per cent of GDP; the government debt outstandinghad increased to 130 per cent of GDP and government debt in the hands ofthe public had increased to 100 per cent of GDP. These ratios increase by20 percentage points after adjustment is made for the increase in govern-ment expenditures required to formally re-capitalise the banks and otherfinancial institutions.

Foreword xxix

The persistence of a large output gap despite the large fiscal deficits hasbeen interpreted to mean that the increase in the fiscal deficit has not ledto a decline in the output gap. The alternative interpretation is that theoutput gap would have been significantly larger if the fiscal deficit hadbeen significantly smaller.

The Japanese government is on a non-sustainable fiscal trajectory; debtcannot continue to increase relative to GDP without leading to a reductionin the willingness of the public to hold government debt. The credit ratingagencies already have begun to downgrade government debt. If the ratio ofdebt to GDP continues to increase, these agencies will continue to reducethe credit ratings.

It is arguable that the agencies are mistaken in down-rating Japanesegovernment debt, since the government can always rely on the bankingsystem to finance the maturing debt. At some stage however that processwould lead to a depreciation of the yen, and the purchasing power of theyen securities would decline. As the ratio of debt in the hands of the publicto GDP increases, an increasingly large number of investors might shiftmore of their wealth into foreign securities and the yen would depreciate.Interest rates on yen securities will increase, and the interest component ofgovernment payments would increase.

At some stage and probably in the not-too-distant future, the Japanesegovernment must reduce the primary fiscal deficit from its current level of6 per cent to 5 per cent to 4 per cent; eventually the government musthave a primary fiscal surplus. The investors and the credit rating agenciesmust be convinced that the fiscal policy is on a sustainable trajectory.

The implication is that the reduction in the fiscal deficit will lead to adecline in aggregate demand, and so the excess of household saving overdomestic investment will increase.

One inference from the combination of the short term interest rateshovering about zero and the large level of bank reserves is that the Bank ofJapan has followed an expansive monetary policy. Some economists haveargued that the Bank of Japan should be even more expansive and adopt aprice level target, perhaps an increase of 1 or 2 per cent a year. The Bank ofJapan would buy assets as well as securities until the annual price leveltarget had been achieved.

One rationale for the price level target is that the more expansive mone-tary policy would lead to an increase in investment spending. The implicitassumption is that real interest rates would decline because the increase inthe inflation rate would be larger than the increase in nominal interestrates. Thus the cost of capital to Japanese firms would decline relative tothe anticipated profit rate on domestic investments. The alternative resultis that the increase in the inflation rate would be smaller than the increasein nominal interest rates because investors would want to maintain thepurchasing power of their interest income and principal.

xxx Foreword

The Bank of Japan’s monetary policy might be able to forestall theincrease in short term interest rates, but it is not likely that conventionalmonetary policies could prevent an increase in nominal and real interestrates on longer term securities.

A second rationale for the more expansive monetary policy is that con-sumption spending would increase because households would be con-cerned that the purchasing power of their time and saving deposits woulddecline, and so they would increase their spending to forestall or dampenthe decline in their purchasing power of these balances.

The competing view is that household saving would increase as the realpurchasing power of the money balances declined.

One possible result is that investment spending would increase if theBank of Japan were to follow a policy of price level targeting while house-hold spending would decline and partially or fully offset the increase ininvestment spending. That result may seem a bit paradoxical, since one ofthe motivation for the increase in investment spending would be a morerapid increase in consumption spending. Moreover, even if the householdspending increases, it is not clear that the increase in spending will make asignificant dent in reducing the output gap.

The more expansive monetary policy is likely to lead to a decline in theforeign exchange value of the yen as Japanese investors adjust to theincrease in inflationary expectations by reducing their holding of yen secu-rities. The counterpart of the increase in the capital outflow would be anincrease in the current account surplus; the increase in Japan’s net exportswould close part of the output gap. Moreover the increase in the yen priceof the US dollar would lead to an increase in the profit rate on the produc-tion of exports and import competing goods, which in turn would lead to ahigher level of investment.

The alternative approach to increasing the Japanese trade surplus is forthe Bank of Japan to buy US dollar securities – in effect the Bank of Japanwould conduct its open market operations in US dollar securities.

A major difference between these two approaches is that the yen rate ofreturn on Japanese foreign investments has been significantly smaller thanthe rate of return measured in the foreign currencies because of the seculartendency toward the appreciation of the yen. The revaluation losses thatJapanese investors have encountered on their foreign investments varieswith the choice of holding periods; this loss has been in the range of 3 to4 per cent for most extended holding periods involving the purchase of USdollar securities.

The Bank of Japan might be more willing to incur the revaluation lossesthan private investors because of the positive externalities for the countryof a larger trade surplus.

One question is the relation between the increase in the capital outflowfrom Japan, and the decline in the foreign exchange value of the yen.

Foreword xxxi

Japan’s major trading partners and particularly the United States mayconclude that attempting to reduce the output gap by significantlyincreasing net exports and the current account surplus, smacks of a‘beggar-thy-neighbor’ policy. In part the US reaction to the increase inthe Japanese trade surplus of a given amount will depend on the changein the foreign exchange value of the yen associated with the increase inthe Japanese trade surplus. The smaller the decline in the foreignexchange value of the yen associated with the increase in the Japanesetrade surplus, the less likely is an adverse or hostile reaction from USpolicy makers.

One of the empirical concerns is how much of the output gap in Japanmight be closed by an increase in the trade surplus.

The second factor limiting the reduction in the output gap that might beassociated with the increase in the Japanese trade surplus is that at somestage Japan must move from being a young creditor country to a maturecreditor; then Japan would have a trade deficit that would be fully financedfrom the income on its foreign investments. That transition is likely to beassociated with a real appreciation of the yen. In the past Japaneseinvestors who have purchased foreign securities have experienced revalua-tion losses as the Japanese yen has appreciated; the nominal appreciationhas absorbed most of the excess of interest rates on US dollar securities overthe interest rates on comparable yen securities.

If the yen were pegged to the US dollar, then Japanese investors mightconclude that the likelihood of a revaluation loss would be smaller and theamount of this loss would be smaller. In the short run, say for a year ortwo, Japanese purchases of foreign securities would be smaller because theywould lack confidence in the stability of the parity. As their confidenceincreases, their purchases of foreign securities would increase.

The review of the menu of alternatives available to the Japanese gov-ernment is complete. Corporate restructuring with the intent to increasethe profit rate on new investments and hence on old investments is toppriority. Financial restructuring in contrast is low priority because theproblem is not the shortage of funds available for lending – and the saleof assets would depress the rate of return on new investments. (At somestage these assets must be sold, but the sale should wait until the rate ofeconomic growth has increased toward the rate of growth of output.)Fiscal policy must move into a less expansive stance. Monetary policy ishighly risky. Exchange rate policy may be successful in closing part of theoutput gap, but the window for a potent increase in the trade surplusbegan to narrow rapidly when the United States moved into a recession.Japan’s competitors in the export markets are unlikely to accept a signifi-cant decline in their own competitive position, and the United States is notlikely to accept a major increase in its trade deficit with Asian countries as agroup.

xxxii Foreword

Adjusting the savings gap

One of the central questions noted at the beginning of this introduction iswhether the increase in the output gap in Japan should be attributed to thefailure of government policy or to a market failure. The companion ques-tion is whether the surge in the output gap is more nearly a transientphenomenon or whether instead the increase is permanent.

There have been failures in Japanese policy – errors because of the fail-ures of economic analysis and of an appreciation in Tokyo and inWashington about the major changes in the financial environmenteffected by the implosion of the bubble. The major policy errors were theeffort to ‘talk up’ the foreign exchange value of the yen and the timid andbelated efforts to formally re-capitalise the banks. The major problem isthat a great deal of time would have been required for those involved infinance at the corporate level and the banking level to recognise the impli-cations of the need for the rates of return on assets in Japan to adjust toworld levels.

The adjustment has been complicated because there is a strong presump-tion that there has been a market failure – that Japanese savers as a groupwill not reduce the amount they want to save as interest rates decline inconformance with the usual textbook model. So a non-trivial componentof saving has been ‘wasted’. During the 1980s the waste involved an exces-sively high level of private investment; in the 1990s the waste involved theexcessive expenditures on public works and an increasingly high levelunderemployment. ‘Saving is a private virtue and a public vice’, at least forthe last twenty years in Japan.

The implosion of the bubble effectively de-capitalised the banks, with theconsequence that Japanese firms now for the first time must satisfy a cost-of-capital test comparable to the one faced by firms headquartered in mostother industrial countries. Many Japanese multinational firms already arecomfortable in dealing with this global standard.

The seismic shift is that for the first time the managers are being requiredto be concerned with the profitability of the firm’s subsidiaries and otheractivities. The task of increasing profitability is immensely more difficultbecause of the commitment to lifetime employment.

The attention to financial restructuring is misplaced. There is relativelylittle evidence tha the sluggishness in investment has resulted because thebanks were tepid lenders; the dominant factor has been that firms havebeen adjusting their investment spending downward as they strive toincrease the rate of return on existing assets.

The dominant economic problem of a large and growing output gap inJapan reflects that the domestic saving rate at the full employment level ofoutput growth would be significantly larger than the amount that businessfirms wish to invest at this output level. In the 1980s the primary adjust-

Foreword xxxiii

ment to this imbalance involved an excessively high level of private invest-ment. Some of this investment was wasteful, and ongoing adjustments tothis level of investment continue to depress investment spending.

In the 1990s and especially in the second half of the decade, the growingand large fiscal deficit absorbed some of the excess saving; part of thepublic works spending and perhaps a large part was frivolous. The secondadjustment was that the output gap continued to increase.

The government’s fiscal policy now is on an unsustainable trajectory. Aslong as the annual fiscal deficit continues to increase much more rapidlythan GDP, the credit rating agencies will lower the ranking of governmentdebt. At some stage the government will be obliged to reduce the primarydeficit; initially the government may place a ceiling on the interest rate onthis debt. This interest rate ceiling will reduce the nominal and real rate ofreturn to Japanese savers.