Embed Size (px)

Citation preview

16 The Moodie Report

ANALYSIS • The world’s top travel retailers May/June 2006

Publisher’s note: Drawing up a like-for-like evaluationof the world’s top travel retail companies is riddled withcomplexities. The various players report in different cur-rencies, across different periods, and often with differentdefinitions. What is included in ‘retail’ turnover? Dutyfree? Duty paid travel retail/Travel Value? Food & Bev-erage? Wholesale activity? Do the companies includethe turnover from joint ventures and other associateactivities (Aer Rianta International, for example, does;Gebr Heinemann does not)?

The Moodie Report has opted to focus on ‘land-based’retail operations (therefore excluding the likes ofSilja Line which Generation in its most recent rank-ing of individual locations says posted onboard rev-enues of over €235 million in 2004). Our definitionis direct retail activity to the travelling consumer.Apart from Gebr Heinemann, which declines to break

down its wholesale/retail split, the numbers here fitthat definition.

Differing reporting periods also pose a problem so wehave taken each company’s latest annual results (all datescontained in the report) or our/their best estimate as toannualised turnover.

We have chosen the Euro as our standard currency as itis the most reported currency among the various players.While currency fluctuations versus the US Dollar, theSwiss Franc and the Thai Baht respectively can and doalter the standardised values significantly, we believe thefigures contained in this chart and throughout the arti-cle offer a valid comparison of the relative scale of theindustry’s most important players. We have cross-checked numbers wherever we can and welcome feed-back from the industry.

THE WORLD’S TOPtravel retailers 2005With the focus of the investment community on the travel and transport sectors to an unprecedented extent, The Moodie Report presents a timely guide to the topplayers in the airport (and other land-based) duty free and travel retail industry.This includes a snapshot profile by ownership, turnover and retail portfolios.

The world’s top (airport and other land-based) travel retailers

Eur

os(b

illio

ns)

1.8

1.6

1.4

1.2

1.0

0.8

0.6

0.4

0.2

0

DFS

Nua

nce

Geb

rH

eine

man

n*

Duf

ry

Lotte

Dut

y Fr

ee

Ald

easa

Aer

Ria

nta

& A

RI

Wor

ld

Dut

y Fr

ee

Dub

aiD

uty

Free

Ael

ia

Kin

gP

ower

Hel

leni

c

Alp

ha

Brasif€242

million

* Includes wholesaleAll reported turnovers converted (where applicable) at rates as of 2 May 2006. Source: ©The Moodie Report

www.tissot.ch

Morethan a watchFounded in 1853, Tissot is proud to display the Swiss flag at the

heart of its logo. The Tissot , representing Tradition,

Technology, and Trend, combines with the Swiss flag and its

central sign to reflect the Tissot philosophy of giving its customers

MORE: the best materials– 316L stainless steel, titanium or

18K gold, scratchproof sapphire crystal, Swiss ETA manufacture

movement and minimum water resistance to 30m / 100ft - in a

watch that offers careful attention to details and “Gold value at

silver price”.

The Tissot T-Touch was created as a worldwide exclusivity in 2000.

Once the tactile sapphire crystal is activated, a light touch on the

glass will select the function - compass, altimeter, barometer,

thermometer alarm, or chrono - and provide the information in the

digital window.

MORE THAN A WATCH, T-Touch combines an innovative timepiece

with a precision instrument.

Tissot, Innovators by Tradition.

Michael Owen, International Football Player

CHRONO

ALTIMETER

COMPASS

METEO

THERMO

ALARM

Untitled-1 2 18/4/06 20:09:08 Untitled-1 3 18/4/06 20:09:11

Untitled-1 3 18/4/06 20:09:11

DFS GroupHeadquarters: Hong Kong

Ownership: Majority-owned (61.25%) by LVMH,France; the remainder by co-founder Bob Miller

Chairman: Ed Brennan

Turnover: Around US$2.2bill ion in 2005 (plusaround US$500 million forMiami Cruiseline Services)

Staff: Over 5,000

Comment: DFS is theworld’s largest travel retailer, thanks to a diverse interna-tional network of luxury downtown duty free stores, ledby the DFS Galleria chain. DFS is part of LVMH’s‘Selective Retailing’ division (which also includes domes-tic perfumery chain Sephora) which had a turnover of€3,648 million (up +11%) last year and Miami CruiselineServices, a thriving retail and miscellaneous businessworth around US$500 million in 2005. The division’sprofit leapt +46% to €347 million last year thoughLVMH declines to break out the performance of theindividual operations.

According to reports, 1997 was the best year for DFS sinceLVMH took over the group in 1996. In that year DFSposted duty free sales of US$2,299 million. Pre-LVMHDFS sales are believed to have peaked at US$3 billion.

It is fast getting back there. The Moodie Report under-stands that DFS volume is trending strongly at aroundUS$2.2 billion in sales, of which around 60% is down-town and the balance from airports. This is a big changefrom the recent past when the ratios would have beendirectly reversed – underlining the way the group hasmoved away from airport concessions that do not offer asustainable business model.

DFS Group’s operating divisions are clustered into twogeographic groups. The US Group is headquartered inHonolulu and includes Hawaii, Guam, Saipan, Palau andthe US Mainland. The Asia Group is headquartered inSingapore with operations in Tokyo, Hong Kong, Sin-gapore, Bali, New Zealand, Australia, Taiwan, Korea,Okinawa and New Caledonia. The group’s merchandis-ing team is based in San Francisco.

The DFS Galleria offers three distinct types of mer-chandise under one roof – luxury boutiques, contempo-

rary fashion and local destination products. The Galleriastores vary in size from about 175,000sq ft to less than20,000sq ft. There are nine large DFS Gallerias aroundthe world including Honolulu, Guam, Saipan, HongKong (2), Singapore, Sydney, Auckland and Okinawa.The next – and most ambitious to date – will open inMacau in 2007.

There are smaller Gallerias in several locations, and DFShas airport stores in Auckland, Bali, Cairns, Christchurch,NZ, Dallas, Guam, Hawaii Island, Hong Kong, Hon-olulu, Los Angeles, Maui, New Caledonia, New York(JFK), Okinawa, Saipan, San Francisco, San Jose, SeoulIncheon, Singapore and Tokyo.

Traditionally the company has been focused on the trav-elling Japanese, the nationality that drove the DFS empirefrom the 1960s on. Today DFS has an equally critical tar-get – the Chinese. The company relocated its headquar-ters from San Francisco to Hong Kong in 2003 so it coulddevote its attention to this fast-changing market.

“DFS is fortunate to be presented twice within its busi-ness life cycle with the opportunity to build a relationshipwith an emerging consumer,” Chairman Ed Brennantold The Moodie Report at the time.

Declared ‘non-core’ by LVMH Chairman BernardArnault in 2002, DFS Group’s performance hasimproved dramatically in recent years – and parentcompany LVMH’s attitude has changed with it. In mid-2005 Arnault said LVMH would not consider selling itsselective distribution business until the division achievesan operating margin of 10%, a figure it is now approach-ing – but don’t take it as read that divestment is now acertainty.

As recently as March 2006, on the back of what Arnaultcalled the “impressive growth trajectory” of the retaildivision, he dismissed the notion of a sale of his retailassets. Ever the pragmatist, the message from Arnault isclear: DFS will remain core to LVMH as long as it pro-duces double-digit growth in revenues and profits.

That drive for profitability is aided by DFS’s emphasis onhigh-end, high-margin brands and categories at its Gal-lerias, which are now at the core of its retail approach inAsia/Pacific. DFS’s Okinawa Galleria is now not just amagnet for shoppers but also for other travel retailerskeen to see the DFS approach for themselves.

As many of them readily admit, where DFS goes, theywill follow.

20 The Moodie Report

ANALYSIS • The world’s top travel retailers May/June 2006

Global Power

Masterfoods International Travel Retail

Untitled-1 2 18/4/06 20:38:01 Untitled-1 3 18/4/06 20:38:11

Untitled-1 3 18/4/06 20:38:11

The Nuance GroupHeadquarters: Zürich

Ownership: Co-owned (50% each) by GruppoPAM/GECOS and Stefanel, Italy

President: Roberto Graziani

Turnover: €1.3 billion in 2005 (including joint ventures)

Staff: 4,700

Comment: With opera-tions on five continentsNuance is the world’s topairport retailer byturnover. Its Italian co-owners are GECOS/Gruppo PAM, one of theleaders in Italian food

retailing, with an annual turnover of some €2.2 billionand more than 10,600 employees, and fashion chain andmanufacturer Stefanel. Acquired from former ownerSwissair in 2002, it also has a diverse inflight retail busi-ness with Edelweiss Air, European Air Express, Intersky,SATA, TAP Air Portugal and Yesair plus distribution toover 20 UK-based airlines.

The Nuance Group runs 320 stores or other retail out-lets in Angola, Austria, Australia, Canada, Denmark,Hong Kong, Ireland, the Netherlands, New Zealand,Portugal, Singapore, Sweden, Switzerland, Turkey, theUK and the US.

In February Nuance announced a financial restructuring,involving an agreement for a new CHF235 million(US$178 million) term and revolving credit facility. Thisreplaced the previous group financing and completedthe “process of financial restructuring of the group” thathas also included shareholder recapitalisation of CHF50million (US$40.6 million). President & CEO RobertoGraziani told The Moodie Report: “If one of our short-comings was financial instability in the past, we havecompletely resolved this issue.”

Graziani’s watchwords have been quality but profitableretailing, and much of his tenure as CEO has been spentdealing with ‘difficult’ contracts, notably those at Rome,Melbourne and Copenhagen airports. The retailer exit-ed its heavy loss-making Rome specialist business lastyear and Copenhagen, where Nuance is still incurringlosses, has been put out to tender. Melbourne though hasbeen constructively renegotiated. The surprise loss of

Vancouver in a tender last year hit hard and Nuance isup against a packed and eager field to retain its blue-rib-bon (at least in stature) though loss-making contract inSydney. Nuance faces the perennial problem of thisindustry's flawed model – bid only with sustainability inmind and you risk not winning at all, especially given thecurrent white-hot competitive environment. In Europe,Sweden is a healthy business and Nuance has struck a co-operation agreement with Cardiff landlord TBI thatoffers global potential. It also has real aspirations in Indiaand the US in addition to its strong European portfolio.

Most positively its Nuance-Watson businesses at Singa-pore Changi and Hong Kong International go fromstrength to strength, and have cemented Asia as Nuance’smost profitable division. Little wonder then that thecompany aims to stretch its legs into the wider Asian mar-ket from its Hong Kong base.

With the backing of partner AS Watson, part of theHutchison Whampoa Group, expect to see Nuance makea serious play for airport business in China, and soon.

Gebr HeinemannHeadquarters: Hamburg

Ownership: Family – the Heinemanns (4th generation)

Co-owners and Directors: Gunnar & Claus Heinemann

Turnover: €890 millionin Germany in 2005(includes wholesale, dutyfree and travel value butexcludes all foreign opera-tions in which the compa-ny is a retail partner – seeComment)

Staff: 1,800

Comment: Since the acquisition of its first concessions atKöln/Bonn Airport in 1970, Gebr Heinemann has beenoperating duty free and Travel Value shops. It pioneeredthe post intra-EU duty free abolition concept of TravelValue and continues to champion it. It is active as a retail-er in 14 countries and as a wholesaler in many more.

Gebr Heinemann runs 40 duty paid shops in airports, 80Travel Value and duty free shops and 15 ship boutiques.Main markets include Germany, Turkey, Norway, theformer CIS and other Central and Eastern Europeancountries.

24 The Moodie Report

ANALYSIS • The world’s top travel retailers May/June 2006

Untitled-6 Sec1:2 6/3/06 20:37:18

Sw

iss

ma

de

- H

arr

y C

on

nic

k J

r. b

y P

alm

a K

ola

ns

ky

L o n g i n e s e v i d e n z a

Untitled-6 Sec1:2 6/3/06 20:37:18

It is a much-admired company which continues to live bythe adage ‘out of debt, out of danger’. That philosophyhas meant Gebr Heinemann has largely avoided the bid-ding mania that has so undermined the industry’s prof-itability and exposed so many companies down the years.

Preferring to strike long-term alliances with airports andto enter new markets with trusted local partners, thecompany continues to focus mainly on Central andEastern Europe, following its highly-profitable exitfrom Duty Free International (subsequently WorldDuty Free Americas, now Duty Free Americas) in thelate 1990s.

However, benefiting from a more cost-effective supplychain than any of its rivals, it is prepared to moveaggressively for highly desirable locations. That was wit-nessed when a joint venture with a local partner won themid-2004 tender to operate duty free retail at OsloGardermoen and four regional airports in Norway.Expect a similarly compelling bid for CopenhagenAirport this year.

In recent times Gebr Heinemann has become a particularchampion of advancing new concepts in beauty retailing.Just before we went to press it unveiled an ambitious ‘Air-port Specials’ programme – a new and more consumer-friendly name for travel retail exclusive products.

As a privately-held company Gebr Heinemann guards itsnumbers jealously. It declines to break down its 2005sales of €890 million, which represented a +19% increaseover 2004. Gebr Heinemann has several thriving part-nerships abroad, notably in Turkey. With these factoredin, turnover would climb to well over €1 billion.

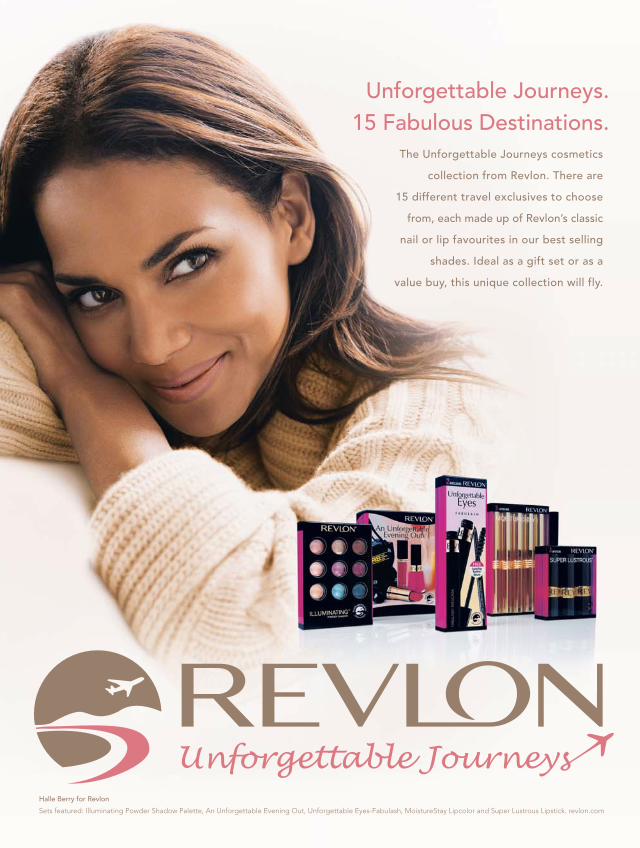

DufryHeadquarters: Basel

Ownership: Around 75% acquired by an Advent Inter-national-led consortium in February 2004; floated onthe Swiss Stock Exchange last December

CEO: Julián Díaz González

Turnover: Turnover forfiscal year 2005 grewby +12% to CHF949.8million (€608 million/US$768 million at theexchange rates of 2 May2006) from CHF850.5million for the 12 months

pro forma period 2004. In terms of profitability,EBITDA (before other operational results) amounted toCHF100.1 million (€64.1 million/US$81 million) for2005, compared to CHF83.8 million last time, repre-senting an increase of over +19%. EBITDA margin roseto 10.5% for the fiscal year 2005 from 9.9% for 2004. Netearnings before minorities surged by more than +70% toCHF52.7 million (€33.8 million/US$42.7 million).

Staff: About 6,000 employees worldwide

Comment: Thanks to its acquisitional approach Dufry isthe industry’s fastest-growing travel retailer and it will bedelighted with its 2005 results, unveiled on 28 April.Acquired in 2004 by a consortium led by private equitygiant Advent International, Dufry was listed on the Swissstock exchange on 5 December 2005. It vowed to makeacquisitions and, despite missing out on its number-one

26 The Moodie Report

ANALYSIS • The world’s top travel retailers May/June 2006

Source: Swiss Stock Exchange; The Moodie Report

Launching with style: Dufry’s share performance since debut 105

100

95

90

85

80

756 Dec 05 27 Apr 06

Sw

iss

Fran

cs

target Aldeasa last year, it delivered on that pledge in April2006 when it acquired Brasif, Brazil’s leading travelretailer. Based on combined 2005 turnover a US$1 billionforce has just been created. Brasif's turnover last year wasBRL637 million (€242 million/US$305 million).

Pre-Brasif it had operations in 34 countries; 368 shopswith a total sales area of 66,603sq m. Brasif brings anoth-er 51 shops and 12,000sq m. Key markets include Sin-gapore, Sharjah, Mexico, South America, Switzerland,Italy, Eurasia and Russia.

Under the astute leadership of CEO Julián DíazGonzález the company is seeking to become a truly glob-al player, balanced in both sales and profitability acrossregions. The Brasif acquisition has accelerated that goal:both sales and return are now neatly split geographical-ly, with South America, North America/Caribbean andEurope each representing around 25% of the mix.

No-one doubts the depth of Dufry’s pockets nor thedetermination of its CEO, so future acquisitions seemcertain. Its bigger test though is whether it can raise itsqualitative game and become a truly great global retail-er, blending central disciplines with high-class localisedexecutions. Dufry is certainly the company to watch inthis business, and don’t count out an acquisition thatwould comparatively be off the Richter scale comparedwith that of Brasif.

Lotte Duty FreeHeadquarters: Seoul

Ownership: The Lotte Group (Lotte Shopping floated inearly 2006)

Sales & Marketing Director: YS Choi

Revenue: US$900 millionin 2005

Comment: Part of themassively powerful LotteGroup, Lotte Duty Free isthe biggest retailer inSouth Korea’s vibrant dutyfree market. It began oper-ations in 1980 on the 8th

floor of the Lotte Department Store in Sogong-dong indowntown Seoul and has flourished ever since.

Today Lotte is one of the industry’s top five retailers inturnover, having generated sales of around US$900 mil-lion last year from its two downtown locations in Seoul(Lotte Duty Free and Lotte World), a number of storesin Incheon International Airport, downtown Pusan,downtown Jeju and Jeju Airport.

This year it is on target to reach US$1.1 billion. One ofits stores at Incheon is believed to be the biggest-sellingcosmetics and fragrances outlets in travel retail.

Lotte’s duty free success has been built around an acuteknowledge of Japanese and South Korean consumers.The former account for around 60% of sales downtown

28 The Moodie Report

ANALYSIS • The world’s top travel retailers May/June 2006

Note: As at 31 December 2005

Source: Dufry; The Moodie Report

Dufry proforma product category mix (including Brasif)

� Perfumes & cosmetics 26% � Wine & spirits 19%� Tobacco goods 11% � Watches & jewellery 10%� Food 11% � Electronics 13% � Other 10%

Note: As at 31 December 2005

Source: Dufry; The Moodie Report

Dufry net sales split by duration of contracts

� 1-2 years 16% � 3-5 years 28%� 6-9 years 22% � 9+ years 34%

Untitled-6 1 20/4/06 17:08:36

Untitled-6 1 20/4/06 17:08:36

and around 20% at the airport. Lotte has alwayschampioned the stand-alone boutique concept forluxury brands and has played a pioneering role indeveloping some of the world’s greatest luxury nameswithin the South Korean market, including LouisVuitton, Chanel, Hermès, Prada and Bvlgari.

Although it once bid for the Honolulu Airport anddowntown duty free contract in the infamous tenderof 1988, Lotte Duty Free has preferred since toremain solely a Korean powerhouse. But that hasnow changed. The Lotte Group is in aggressivelyexpansionist mode, an approach accelerated by thisyear’s IPO of Lotte Shopping, said to be the biggestpublic float in global retail history.

Lotte was a notable inclusion in the line-up for theSydney Airport duty free tender currently beingassessed – and its expertise with the Asian consumerwill make it a strong candidate. The retailer is alsoeyeing opportunities throughout Asia Pacific includ-ing India, Indo-China, China and Australasia.

AldeasaHeadquarters: Madrid

Ownership: Co-owned since April 2005 by Italiancatering group Autogrill (which also owns travelretailer and caterer HMHost) and tobacco houseAltadis

Chairman: Javier Gomez Navarro

2005 revenue: Circa€660 million

Staff: Over 2,500

Comment: Since 1995Aldeasa has grownfrom the 12th-largestplayer in the travelretail market to top sixstatus, running over

230 stores covering more than 37,000sq m. Its mainmarkets are Spain, Jordan, Chile and Mexico. Itrecently made its debut in Kuwait after an ultra-aggressive and controversial US$20 million MAGand triumphantly won the hotly-contested Vancou-ver Airport tender in 2005 – it begins operationsthere next year.

The company has a long-term contract at flagship

30 The Moodie Report

ANALYSIS May/June 2006

location Madrid Barajas, but faces likely competition for itsother Spanish airport contracts as they progressively expirein the near future. This partly explains the company’sexpansionist strategy abroad. Around 82% of sales last yearwere generated from Spanish airports; 14% were fromnon-Spanish airports and 4% from other businesses. In2004 sales were €630 million and EBITDA €68 million.

Aldeasa has laid down three big markers to the industryin the past few months. Two came in the shape of theblockbuster financial bids that secured the Kuwait andVancouver contracts, though it should be noted that Van-

couver International Airport Authority was effusive in itspraise of the technical quality of Aldeasa’s offer.

Any doubts over the retailer’s ability to raise its qualita-tive game have surely been swept away by its fine newoffer at the new Madrid Barajas Terminal Four, an out-standing execution of a three-pronged (four if you countDestination Merchandise) offer.

Its battle with Dufry, and perhaps Nuance, for the Span-ish airport contracts (other than long-term propertyMadrid) if they come up for tender promises to be one ofthe seminal industry contests of the future.

Aer Rianta Retail/Aer Rianta InternationalHeadquarters: Dublin (Aer Rianta Retail); Shannon,Ireland (Aer Rianta International)

Ownership: Subsidiaries of government-held Dublin Air-port Authority

Aer Rianta International Director General: EamonFoley

Aer Rianta Director of Retail: Frank O’Connell

Turnover: International retail operations posted man-aged turnover of €461 million in 2005, an impressive+63% rise year-on-year. The Moodie Report estimatesAer Rianta's retail turnover (duty free and Travel Value)at its three Irish airports, Cork, Shannon and Dublin,

32 The Moodie Report

ANALYSIS • The world’s top travel retailers May/June 2006

34.7 33.3 33.5 31.8 32.0

28.2

18.0

11.9

10.0

28.3

17.6

12.3

10.0

26.2

17.9

12.8

9.7

24.8

17.8

13.5

10.6

23.7

18.2

13.3

10.1

Source: Aldeasa

Aldeasa Spanish airport sales breakdown by product

2000 2001 2002 2003 2004

� Perfumes � Tobacco � Misc � Spirits � Food

100%

80%

60%

40%

20%

211

75

65

245

79

74

323

82

86

274

81

87

301

79

86

Note: *Including Canary Island sales under a special fiscal regime

Source: Aldeasa

Aldeasa Spanish airport sales2000–2004

2000 2001 2002 2003 2004

� Travel Value � Duty free � Duty paid*

500

400

300

200

100

Eur

os (m

illio

ns)

351

69

18

398

80

23

492

82

24

442

77

21

466

70

29

Source: Aldeasa

Aldeasa airport sales by region2000–2004

2000 2001 2002 2003 2004

� Spanish airports � Non-Spanish airports � Other income

600

500

400

300

200

100

Eur

os (m

illio

ns)

UP TO 12 XMORE VOLUME FOR YOUR LASHES.

DARE TO SHOCK!Aishwarya Rai dares to shock in Volume Shocking Black.

VOLUMESHOCKING

Two-step Volume Construction Mascara

NEW

Step 1 : The defining base coat arranges lashes into framework.

Step 2 : Revolutionary reservoir comb + Expansium top coat for explosive volume.4 years of research.16 patents. Scientifically provent results. BECAUSE YOU’RE WORTH IT.

Travel Retail L’ Oreal Paris - 7 rue Touzet - 93588 Saint Ouen - France - Tel : 33 1 58 61 75 51

36 The Moodie Report

ANALYSIS • The world’s top travel retailers May/June 2006

reached around €120 mil-lion last year. In 2005 theprofit contribution fromARI’s combined interests(retail and airports) rose to€17.4 million, up from€9.4 million the previousyear. No further details orturnover figures for 2005were disclosed.

Staff: Over 2,200 (ARI total including airports)

Comment: Aer Rianta International (ARI) is the greatglobe-trotter of duty free. It was formed in 1988 as a ded-icated international division of the Irish state-owned air-ports authority Aer Rianta, now known as the DublinAirport Authority. Aer Rianta established the world’s firstairport duty free facility at Shannon International Airportand the first international duty free operation in the for-mer Soviet Union (at Moscow Sheremetyevo Airport).

Since then, either as concessionaire, manager or oper-ations partner, ARI has evolved into an operationencompassing 20 retail operations in 11 countries,managed through a number of structures and businessmodels. The managed turnover referred to earlierincludes the total sales for all businesses in which ARIhas an interest whether by way of ownership, part own-ership, management or consultancy contracts.

Last year's impressive growth was driven by new busi-nesses such as Domodedevo and Vnukovo in Russiaand Aer Rianta International–Middle East’s (ARI-ME)fledgling though promising partnership in Egypt, plusstrong growth in existing businesses.

ARI-ME (see profile page 91) is a particularly buoyant,profitable and admired operation. With the advent ofthe Cyprus airport retail operations, the Bahrain-basedventure should generate annualised sales of overUS$500 million (€396 million). Cyprus is consideredpotentially a US$100 million-plus business.

ARI partnerships include:� Aer Rianta International Sardana (JFK), New York

(70%)� Aer Rianta International–Middle East, Bahrain (50%)� Aerofirst, Moscow (33%)� Lenrianta, St Petersburg, Russia (48.3%)

Aer Rianta Retail controls retail at Dublin, Shannon andCork airports. In theory this could change if the latter two

create autonomous airport authorities, as envisaged orig-inally by the government when it dissolved the formerAer Rianta. Today though, amid political tensions andunion intransigence, a split of the three Irish airports stilllooks a long way off.

Even if it were to happen the economies of scale that bulkbuying delivers to the group would make a compellingcase for retaining a retail division – one that would man-age business at all three state-owned airports.

Is ARI an acquisition target? Certainly. But would it be forsale? Interest has long been alerted in the international retailcommunity since the Irish government first hatched plansto break up Aer Rianta. Not least because of the profit con-tribution from its overseas assets, Dublin Airport Author-ity CEO Declan Collier (pictured left) says he remainscommitted to international and Irish travel retailing whilepreparing to sell fellow subsidiary Great Southern Hotels.

In the short term any sale is unlikely. In the longer term,if the political wind shifts – and as the privatisation ofstate-owned aviation assets picks up pace worldwide – thefuture could look very different.

World Duty FreeHeadquarters: Near London Heathrow Airport

Ownership: 100% subsidiary of airports group BAA

Group Retail Director:Stephen Nelson

World Duty Free Manag-ing Director: Mark Riches

Turnover: £373 million inyear ended 31 March 2005

Staff: 2,000

Comment: World Duty Free is the powerhouse of UKduty free and travel retailing. The stand-alone organisa-tion, created by BAA in 1996, is one of the industry’s mostpowerful and respected retailers.

It is the leading retailer – domestic or airport – of fra-grances and cosmetics in the UK and pioneered the con-cept of ‘Summer fragrances’ which has become asub-category in its own right. The retailer claims to sell£3 million worth of fragrances a week, with HeathrowAirport alone generating almost 10% of all UK fra-grances sales.

38 The Moodie Report

ANALYSIS • The world’s top travel retailers May/June 2006

World Duty Free operates 65 stores across BAA’s sevenUK airports, with 15,000 square metres of retail spaceoffering over 12,500 products. UK airports are Heathrow,Gatwick, Stansted, Southamption, Edinburgh, Aberdeenand Glasgow. It has also created a range of specialistshops such as World of Whiskies, Chocolates, BeautyStudio, Perfume Gallery, The Cigar House, Sunglassesand For Men.

Turnover edged ahead in the year ended 31 March 2005to £373 million with operating profit up +4.2% to £25million. In March the group said it expected net retailincome per passenger to rise by around +2% this finan-cial year. Net UK retail income (including other retail)per passenger last year reached £4.16. For the six monthsto 30 September 2005 World Duty Free’s revenue grewby +1% to £200 million, with operating profit up by+7.7% year-on-year to £14 million. UK airports net retailincome rose +1.2%.

In 2005 it formed a joint venture with Crossbar Associ-ates, a business formed by three of travel retail’s mostexperienced retailers – Steve Franklin, Randy Emch andAdrian Murray. The partnership, Global Airport Ser-vices (GAS), is in turn seeking to create joint ventureswith airport companies to run their duty free activities,rather than using third-party concessionaires.

GAS certainly dominated the headlines but it has yet toland its first contract, though it has been close on sever-al occasions. Its future though is complicated by thecurrent saga involving BAA – the subject of intensetakeover interest as we went to press. Spanish transportand infrastructure group Ferrovial was leading thechase, heading a consortium that has offered 810 pencein cash for each BAA share, valuing the company at£8.75 billion. While rebuffed in no uncertain terms onthree occasions, Ferrovial is eminently capable of fund-ing an improved deal. Some pundits have predicted itwould ultimately help to offset any debt by sellingWorld Duty Free.

Dubai Duty FreeHeadquarters: Dubai

Ownership: Government

Managing Director: ColmMcLoughlin

Turnover: US$590 millionin 2005 (€467 million atcurrent exchange rates)

Staff: Over 1,500.

Comment: The third-biggest duty free retail location inthe world, from just two terminals – and despite beingonly the 11th biggest airport in the world, having just 23.9million passengers. Huge expansion plans at Dubai Inter-national Airport and then Jebel Ali Airport are expectedto see turnover rise to US$1 billion in the next few years.

Dubai Duty Free is unquestionably the most well-knowntravel retailer on the planet thanks partly to an extraor-dinary marketing, sponsorship and promotional pro-gramme. The retailer for example sponsors the mostacclaimed event on the men’s tennis ATP tour as well asthe counterpart women’s event, plus major horse-racingand golf events. It is also a major provider of leisure,entertainment and food & beverage activities in Dubai,all with a tourism emphasis.

Given its virtually unblemished growth record (saleswere flat during the first Gulf war) it’s hard to identifyany burning challenges for the company – other thanhow to sustain and manage growth. Buoyed by the ambi-tion of national carrier Emirates, traffic numbers areincreasing dramatically, and currently the airport isstruggling to cope with the resultant congestion. As aresult the retailer had to give up a considerable amountof space recently to ease passenger processing.

More routes always mean a changing customer profile.Dubai Duty Free will be keen to prove it is as adept atretailing to the fast-increasing North Asian passenger, forexample, as it is to those from the sub-continent.

Will privatisation rear its head as it has so recently inneighbouring Abu Dhabi? Airport development has to bepaid for, and the fact that the political capital of the UAEhas opted to part-privatise its airport and duty free activ-ities will not have gone unnoticed in Dubai.

AeliaHeadquarters: Paris

Ownership: Part of the Hachette Group, in turn ownedby Lagardère

President: Michel Perol

Turnover: Over €400 million in 2005

Staff: 1,300

Comment: Aelia operates at 14 airports in France and

Untitled-3 1 2/5/06 14:24:30

For information about opening a Bijoux Terner boutique contact:

Charles Pelegrin • + (1) 786 301 [email protected]

Rosa Terner • + (1) 305 266 [email protected]

Miami • Florida • United States • +(1) 305 266 9000

TFWA Asia Pacific • Singapore 16-19 May 2006Booth # E-8

Untitled-3 1 2/5/06 14:24:30

two in the UK/NorthernIreland. Its main marketsare France (where it is thedominant player), North-ern Ireland (Belfast) andthe UK (Luton). AIR, anAelia subsidiary, operatesin-flight sales for interna-tional and regional airlinecompanies such as Air

France, Royal Air Maroc and SWISS.

Aelia is clearly intent on international expansion, witnessits moves in Belfast and Luton and bidding interest inSydney and Copenhagen. It benefits from the stronginternational presence of owner Hachette DistributionServices (HDS), which claims to have specialised in trav-el retail since 1852 when it opened the first-ever shopslocated in a travel retail environment: the Bibliothèquesde Gare (Railway Bookshops).

HDS is present at 75 airports and travel terminals in 14countries across the world, with a travel retail turnover of€1.4 billion. HDS has a diversified portfolio of brandsand logos, including RELAY (newspapers, magazines &gifts) and Virgin (electronics and multimedia).

HDS is established in 15 countries and is the world’slargest retailer of newspapers and magazines, with aninternational network deployed across fifteen countries inEurope, Asia and North America. In turn HDS is ownedby Lagardère, a company listed on the Paris StockExchange and a leader in the media and high-technologydomains.

Is Aelia, astutely led by Michel Perol (pictured), seriousabout becoming a truly global player? It certainly has theparenthood, the geographic synergies and an establishedinternational airport network through Hachette.

King Power International Group

Headquarters: Bangkok

Ownership: Owned by a group of shareholders led byVichai Raksriaksorn who took the group private in 2003(it had formerly been listed in the US).

Chairman & CEO: Vichai Raksriaksorn

Turnover: Sales of the King Power group last year totalledTHB12.65 billion (US$333 million) with a net profit ofTHB700 million (US$18.5 million). Sales this year are

expected to grow by +31% to THB16.64 billion (US$439million) with a net profit of at least THB1 billion (US$26.4million). Sales are expected to reach THB30 billion(US$791 million) in 2007, the first full calendar year for thenew operations at Si Ayutthaya [downtown Bangkok] andthe capital’s new airport Suvarnabhumi.

Comment: King PowerInternational may be aone-market player, butwhat a market it is.Despite a muted 2005caused by the impact ofthe December 2004 tsuna-mi on Thailand’s tourisminfrastructure, the compa-ny’s retail business across

Thailand’s airports is in vibrant shape. It has long-termsecurity of tenure at all its key locations but crucially atBangkok’s new Suvarnabhumi International Airport,which is expected to finally open in late 2006.

Suvarnabhumi forms one part of the retailer’s two biggestprojects to date – the duty free and food & beverage offerat the new airport, and the King Power Downtown com-plex located in the heart of Bangkok at Sri AyutthyaRoad, adjacent to Makkasa station, the new internation-al airport train terminal. The 12-acre plot there will bethe future site of the group’s headquarters, a new flagshipdowntown duty free shop, a 400-room hotel and anentertainment and restaurant complex.

Vichai Raksriaksorn (pictured) says he is preparing towind down his career after 17 years of building his com-pany into a “king of duty free” in Asia.

Thailand’s tourism industry shows solid growth projec-tions with particularly good prospects for Chinese trav-ellers. The retailer is more scientific than most insegmenting its offer by nationality, and further work in thisarea will be crucial to the success of its new operations.

Hellenic Duty Free ShopsHeadquarters: Athens

Ownership: Privatised in1993. Greek companiesFolli Follie and Germanoscollectively own a 49.4%stake; the balance is public

General Director: GeorgeVelentzas

40 The Moodie Report

ANALYSIS • The world’s top travel retailers May/June 2006

Untitled-3 1 2/5/06 14:25:14

For information about opening a Bijoux Terner boutique contact:Charles Pelegrin • + (1) 786 301 0190 • [email protected]

Rosa Terner • + (1) 305 266 9000 • [email protected] • Florida • United States / + (1) 305 266 9000

TFWA Asia Pacific • Singapore 16-19 May 2006 • Booth # E-8

ALLITEMS

INOUR

STOREARE

Untitled-3 1 2/5/06 14:25:14

BELGIAN CHOCOLATES, TRUFFLES AND SEASHELLS

I r r e s i s t i b l e J ewe l s

Meet us at: TFWA Asia/Pacifi c Stand G10

www.ducdo.com

DUC_01023_13_TFWA_Asia_225x170.indd 1 18-04-2006 15:07:48

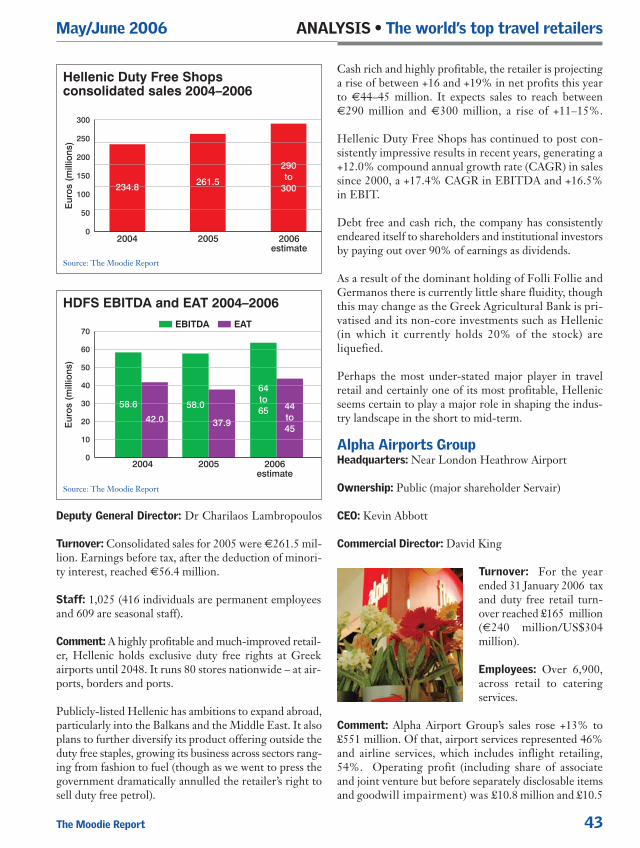

Deputy General Director: Dr Charilaos Lambropoulos

Turnover: Consolidated sales for 2005 were €261.5 mil-lion. Earnings before tax, after the deduction of minori-ty interest, reached €56.4 million.

Staff: 1,025 (416 individuals are permanent employeesand 609 are seasonal staff).

Comment: A highly profitable and much-improved retail-er, Hellenic holds exclusive duty free rights at Greekairports until 2048. It runs 80 stores nationwide – at air-ports, borders and ports.

Publicly-listed Hellenic has ambitions to expand abroad,particularly into the Balkans and the Middle East. It alsoplans to further diversify its product offering outside theduty free staples, growing its business across sectors rang-ing from fashion to fuel (though as we went to press thegovernment dramatically annulled the retailer’s right tosell duty free petrol).

Cash rich and highly profitable, the retailer is projectinga rise of between +16 and +19% in net profits this yearto €44–45 million. It expects sales to reach between€290 million and €300 million, a rise of +11–15%.

Hellenic Duty Free Shops has continued to post con-sistently impressive results in recent years, generating a+12.0% compound annual growth rate (CAGR) in salessince 2000, a +17.4% CAGR in EBITDA and +16.5%in EBIT.

Debt free and cash rich, the company has consistentlyendeared itself to shareholders and institutional investorsby paying out over 90% of earnings as dividends.

As a result of the dominant holding of Folli Follie andGermanos there is currently little share fluidity, thoughthis may change as the Greek Agricultural Bank is pri-vatised and its non-core investments such as Hellenic(in which it currently holds 20% of the stock) are liquefied.

Perhaps the most under-stated major player in travelretail and certainly one of its most profitable, Hellenicseems certain to play a major role in shaping the indus-try landscape in the short to mid-term.

Alpha Airports GroupHeadquarters: Near London Heathrow Airport

Ownership: Public (major shareholder Servair)

CEO: Kevin Abbott

Commercial Director: David King

Turnover: For the yearended 31 January 2006 taxand duty free retail turn-over reached £165 million(€240 million/US$304million).

Employees: Over 6,900,across retail to cateringservices.

Comment: Alpha Airport Group’s sales rose +13% to£551 million. Of that, airport services represented 46%and airline services, which includes inflight retailing,54%. Operating profit (including share of associateand joint venture but before separately disclosable itemsand goodwill impairment) was £10.8 million and £10.5

The Moodie Report 43

May/June 2006 ANALYSIS • The world’s top travel retailers

Source: The Moodie Report

Hellenic Duty Free Shops consolidated sales 2004–2006

2004 2005 2006estimate

234.8 261.5

290to

300

Eur

os(m

illio

ns)

300

250

200

150

100

50

0

HDFS EBITDA and EAT 2004–2006

Eur

os(m

illio

ns)

Source: The Moodie Report

2004 2005 2006estimate

58.6

42.0

58.0

37.9

64to65 44

to45

70

60

50

40

30

20

10

0

� EBITDA � EAT

million respectively. No further split was published butfor the previous year airport-based retail sales reached£219.3 million (with profits of £11.7 million).

The group has over 200 retailing and catering outlets,in 83 airports in 15 countries across five continents. Mainmarkets for duty free and airport retail are the UK, theUS, Italy, Sri Lanka, the Maldives and India. Alpha claimsto be the world’s biggest independent supplier of retailand catering services, mainly to airlines and airports.

Alpha has three main shareholders: Servair, SchroderInvestment Management and Aberforth Partners. Servairis the major shareholder. A subsidiary of Air France, Ser-vair and its subsidiaries have 34 units and realise aturnover of more than €489 million. Its network is com-posed of Servair and its partners (Alpha, Flying FoodGroup, Servair Air Chef and Eurest Servair). Despiteinternational diversification UK business still represents82% of turnover, but 41% of profit. Alpha has stated oneof its business priorities for 2006 is to improve operatingmargin in its UK and Ireland businesses.

It is aiming for a 5% return on sales in the mediumterm, a tough task given the often very thin margins onwhich it operates across retail and especially catering inthe UK, where the return on sales was 2% last year. Thereturn on sales in overseas businesses was 12%, whichdwarfs the high-volume, lower-yield UK operations.The acquisition strategy laid down over the past 18months looks likely to be a key platform for expansion.And overseas opportunities will be core to this: interna-tional operations accounted for 18% of sales and 59% ofprofit in 2005/06.

Internationally, Alpha will aim to boost its airport pres-ence from Sri Lanka, India and Jordan into the wider sub-continent and Middle East markets – a job that will beeasier said than done in some highly competitive markets.

The company recently unveiled a major review of itsbusiness, meaning the loss of several senior managers.One of the key challenges the review identified was thepressure on penetration rates caused by capacity pressuresin congested UK airports. The company will he hopingthat the suspension of its shares in late April after theauditors refused to sign off the preliminary annual results(due to concerns over an unspecified contract award) isnothing more than a nasty blip.

Widely acknowledged as one of the sector’s most inno-vative retailers – its new Birmingham and ManchesterAirport (pictured) executions are among the industry’sbest – it will need every ounce of that creativity to helpchallenge the much deeper pockets of highly ambitiousand fast globalising players such as Dufry and Aldeasa. �

The Moodie Report 45

May/June 2006 ANALYSIS • The world’s top travel retailers

Note: Alpha shares were temporarily suspended on 25 April.Source: The Moodie Report

Alpha Airports Group share performance November 2005 to 1 May 06100

90

80

70

60Nov 05 May 06

Pen

ce