Embed Size (px)

Citation preview

10/23/2015

1

The world without oilThe world without oil

How the world will operate without fossil energy and when is this likely to

happen

1

10/23/2015

2

Conventional Wisdom• Oil and gas is a limited natural resource. We are finding hydrocarbon

resources in hard to reach and operate environments. That is why access to energy resources will continue to be more costly.

• Society is prepared to pay this high cost of energy because it has no real alternative.

• Alternatives that have been presented so far are too expensive, have fundamental technical limitations and will not be produced on a large enough scale to make a difference in the next 30-50 years.

• As nations like China and India continue to develop, they will replicate the same patterns of energy production and consumption as developed nations. That will continue to increase the demand for hydrocarbons for ground transportation, electricity generation and air travel.

• The oil and gas industry has unmatched intellectual, financial, political resources, and is well positioned to compete in the 21st century and will continue to prosper.

2

10/23/2015

3

“Its hard to make predictions. Especially about the future” h b d b l h– Danish proverb used by Niels Bohr

• Salt, was a “strategic resource used for centuries” and turned into an affordable commodity.y

• “Great horse manure crisis” ‐ never materialized.• “The great promise of nuclear energy” turned out to be too

expensive and too riskyexpensive and too risky.• “The limits to growth”. “Hubbard’s curve”. “Twilight in the

desert”. The world did not run out of fossil fuels, we are running out of fresh air to put CO2 into “Peak oil” for USA hasrunning out of fresh air to put CO2 into. Peak oil for USA has happened in the 1970’s based on per capita metric.

• Holditch “resource triangle” – essentially infinite hydrocarbon resourcesresources.

• “World will continue to use more fossil energy.” We see the decoupling of GDP and energy consumption in advanced economies (USA Germany others)economies (USA, Germany, others).

3

10/23/2015

4

Presentation OutlinePresentation Outline

• A little bit of history. The story of salt and the y ygreat environmental crisis at the beginning of the 20th century.

• Unconventional resources energy parity and the• Unconventional resources, energy parity and the era of great competition.

• How do we use oil? Do we expect changes?How do we use oil? Do we expect changes?– Automobiles and transportation– Heat and electric power generation– Aviation

• Where do we go from here?

4

10/23/2015

5

Salt Story• Today salt is a common and inexpensive substance. But, “Until about 100 years

ago, when modern geology revealed its prevalence, salt was one of the world's most sought‐after commodities. A substance so valuable it served as currency, l h i fl d h bli h f d d i i k d dsalt has influenced the establishment of trade routes and cities, provoked and

financed wars, secured empires and inspired revolutions.”• Salt has shaped civilizations from the very beginning. “Most Italian cities were

f d d i l k i i h R i h hill b hi d hfounded proximate to saltworks, starting with Rome in the hills behind the saltworks at the mouth of the Tiber”.

• Over the past several thousand years, humans have used salt to preserve food. Th R i d lt f it ldi d h At ti ldiThe Roman army required salt for its soldiers and horses. At times soldiers were even paid in salt, hence the words salary, “worth his salt”, soldier.

• Demand for salt established the earliest trade routes. The first of the great R d th Vi S l i S lt R d b ilt t b i thi lt t l tRoman roads, the Via Salaria, Salt Road, was built to bring this salt not only to Rome but across the interior of the peninsula.

• Salt has provoked and financed some wars, and been a strategic element in th h th A i R l ti d th Ci il W G dhi' lt h iothers, such as the American Revolution and the Civil War. Gandhi's salt march in

1930 began the overthrow of British rule in India.

Mark Kurlansky Salt: A World History. (2002), ISBN 0‐8027‐1373‐45

10/23/2015

6

Salt Industry InventionsSalt Industry Inventions

The salt industry invented drilling and pumping, and had the first recorded industrial use of natural gas “Few endeavors have inspired more ingenuity than salt making from theof natural gas. Few endeavors have inspired more ingenuity than salt making, from the natural gas furnaces of ancient China to the drilling techniques that led to the age of petroleum”.

6Mark Kurlansky Salt: A World History. (2002), ISBN 0‐8027‐1373‐4

10/23/2015

7

“The Great Horse Manure Crisis” • By the late 1800s, horse

pollution became a major problem. A public health and

it ti i i fsanitation crisis of “unimaginable dimensions” loomed. All transport of goods or people was drawn by horses. The horse had been the dominant mode of transportation for thousands of yearsof years.

• Horse population was growing faster than human city population. London (1900) had > 50,000 horses. In New York (1900) 100,000 horses produced 2.5 million pounds of horse manure per day More horses required more land to stable and feed themmanure per day. More horses required more land to stable and feed them.

• In 1894, the Times of London estimated that by 1950 every street in the city would be buried nine feet deep in horse manure. It was predicted that by 1930 the horse droppings in NYC would rise to Manhattan’s third‐story windows. “Vacant lots across America were

http://www.accessmagazine.org/articles/spring‐2007/ From Horse Power to Horsepower By Eric A. MorrisEdwin G. Burrows and Mike Wallace, Gotham: A History of New York City to 1898 New York: Oxford University Press, 1999.

piled high with manure; in New York these sometimes rose to forty and even sixty feet”.

7

10/23/2015

8

What Happened? Better Technology Better EconomicsBetter Technology, Better Economics

• Modern geology and drilling technology proved that salt resources are essentially infinite for practical purposes.

• The invention of refrigeration reduced the need for salt. Refrigeration is a better technology to preserve food. Also it led to increased productivity of farming and increased population of the western states.

• It took about 30 years for refrigeration to become prevalent. The timeline: – On February 15, 1882, the Dunedin sailed for London from New Zealand, what was the first commercially

successful refrigerated shipping voyage, and the foundation of the refrigerated meat industry.[*]

– By 1914, almost every location used artificial refrigeration. The big meat packers had purchased the most expensive units which they installed on train cars and in branch houses and storage facilities in the more remote distribution areas. [**]

• The great horse manure crisis vanished when millions of horses were replaced by motor vehicles.

• The price of horse‐drawn transport rose steadily as the cost of keeping cities clean, feeding and housing horses increased. This created strong incentives for people to find alternatives.

* Colin Williscroft (2007). A lasting Legacy ‐ A 125 year history of New Zealand Farming since the first Frozen Meat Shipment. NZ Rural Press Limited.** Freidberg, Susanne (2010). Fresh : a perishable history (1st Harvard University Press pbk. ed. ed.). Cambridge, Mass.: Belknap. p. 142. ISBN 0674057228.http://fee.org/freeman/detail/the‐great‐horse‐manure‐crisis‐of‐1894 09/ 01/2004 by Stephen Davies

8

10/23/2015

9

When The Transition Starts It Takes 30 to 45 Years

http://www.dtpli.vic.gov.au/__data/assets/pdf_file/0010/220402/Electric‐Vehicle‐trial‐mid‐term‐report.pdf

Technology adoption curves for a range of modern innovations. Theoretical take‐off point at 16% market penetration. (Rogers 1962)

9

10/23/2015

10

Unconventional Oil and Gas• Estimates of conventional vs. unconventional reserves and resources for North Americareserves and resources for North America.

• Worldwide projections for “unconventionals” show essentially unlimited resource.show essentially unlimited resource.

• Amazing technology advances led to drilling and completion efficiency gains.p y g

• EUR is not very attractive for low k oil.• What is the production activation index (PAI)?What is the production activation index (PAI)? How does it translate to cost of power $/W?

• Implications.p

10

10/23/2015

11

11Lecture on unconventional resources by SPE President 2002 Dr. S.A.Holditch

10/23/2015

12

Oil Price HistoryOil Price History

BP statistical review of world energy 201412

10/23/2015

13

Coal Price History, in $/short ton and $/MMbtu

70

2 586

3.103

50

60

70Nominal, $/mmbtu

1 552

2.069

2.586

30

40

50

short ton Real,

$/mmbtu

0 517

1.034

1.552

10

20

30

$ pe

r

0.000

0.517

0

10

49 52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 00 03 06 09

19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 20 20 20 20

13

10/23/2015

14

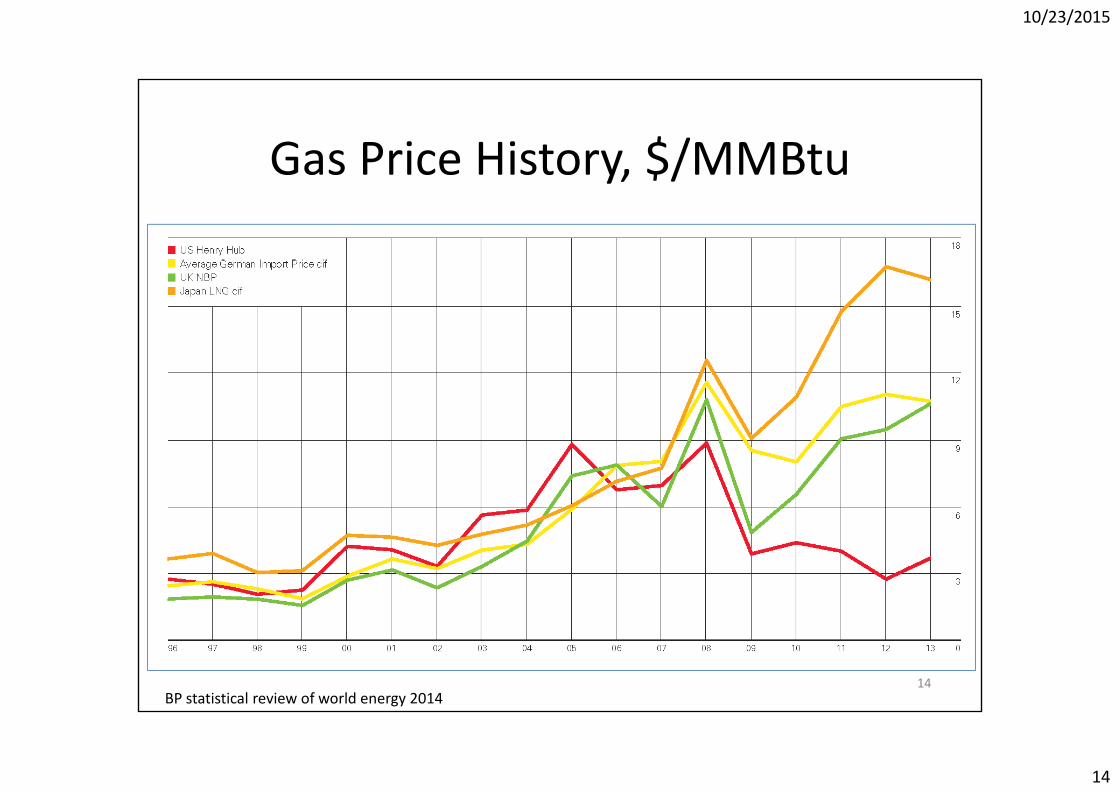

Gas Price History, $/MMBtuGas Price History, $/MMBtu

BP statistical review of world energy 201414

10/23/2015

15

Oil Industry Continues to Enjoy a Convenience Fee

70

High oil price $25/MMBtu vs gas $10/MMBtu vs. coal $1.5/MMBtu (2008)

60

70

40

50

hort to

n

20

30

$ pe

r sh

0

10

1949

1953

1957

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

2009

BP statistical review of world energy 201415

10/23/2015

16

Aggregate Technically Recoverable Resources (TRR) in N th A i A S ffi i t f 60 YNorth America Are Sufficient for 60+ Years

10000

1000

TRR Conventional, Tcfe

TRR Unconventional, Tcfe

Aggregate Resources (Tcfe)

10

100

1

16Cheng, K., Wu, W., Holditch, S. A., Ayers, W. B., & McVay, D. A. (2010, January 1). Assessment of the Distribution of Technically Recoverable Resources in North American Basins. Society of Petroleum Engineers. doi:10.2118/137599‐MS

10/23/2015

17

Worldwide Conventional And Unconventional Resources Are Essentially InfiniteResources Are Essentially Infinite

P10/P50/P90 correspond to 377, 219 and 146 years at current consumption

Unconventional OGIP Tcfe 1,000,000

100,000

1,000,000 Unconventional OGIP, Tcfe

P90

100,000

Total unconventional OGIP, Tcf

Conventional hydrocarbons (oil plus gas) in‐place, Tcfe

10,000

Tcfe

P90

P50

P10 10,000

1,000 CIS MET NAM AAO AFR LAM EUP World

1,000 CIS MET NAM AAO AFR LAM EUP World

“ConclusionsConclusionsFrom using published assessments of 26 North American basins, published global assessments, and resource-triangle-based methodology presented in this paper, we have developed a global estimate of unconventional gas in place with quantifying the uncertainty and conclude the following:1. Estimated global unconventional OGIP ranges from 83,300 Tcf(P90) to 184,200 Tcf(P10). The P50 of our global

17

unconventional OGIP assessments (125,700 Tcf) is 4 times greater than Rogner's estimate of 32,600 Tcf.”

Dong, Z., Holditch, S., McVay, D., & Ayers, W. B. (2012, October 1). Global Unconventional Gas Resource Assessment. Society of Petroleum Engineers. doi:10.2118/148365‐PA

10/23/2015

18

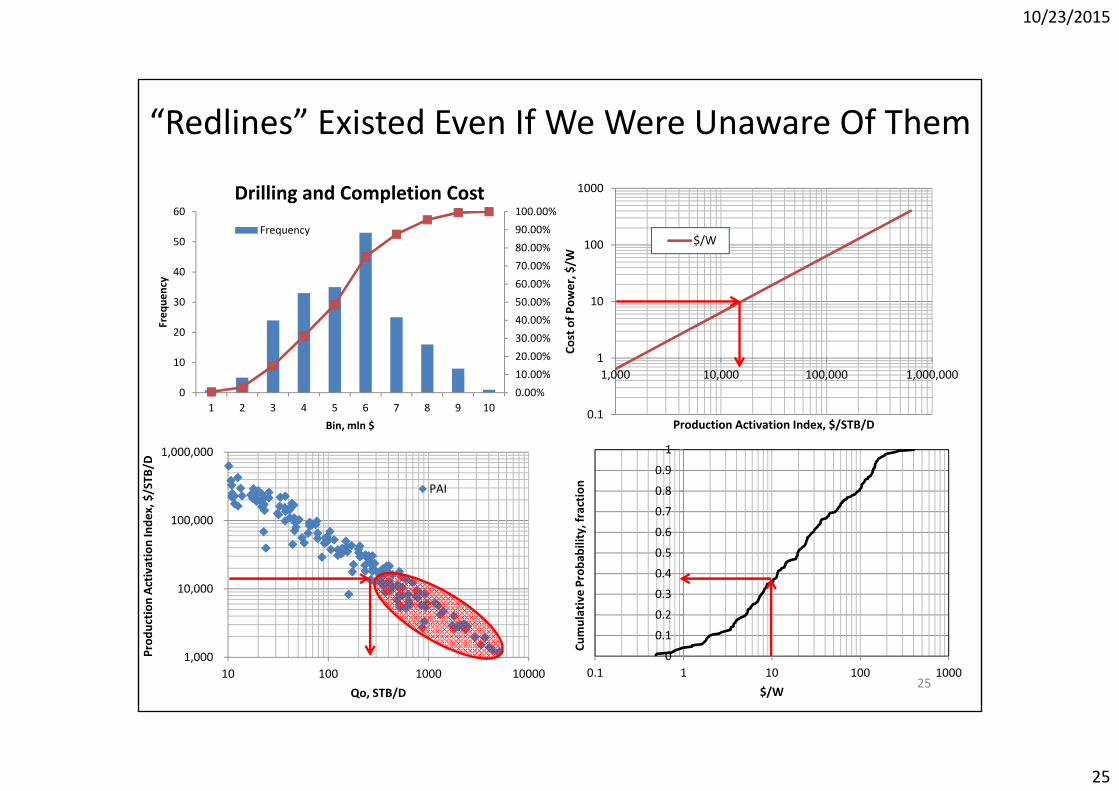

Comparing Different Sources of Energy• Oil production rate, Qo (STB/D), Energy/time => Power => W• Production activation index (PAI) = CAPEX/Qo => $/W • PAI correlated to EUR > CAPEX/Energy > c/kWh

Darcy’s Law for PSS Flow in oil field unitsDarcy’s Law for PSS Flow in oil field units

• PAI correlated to EUR => CAPEX/Energy => c/kWh

Darcy s Law for PSS Flow in oil field unitsDarcy s Law for PSS Flow in oil field units

ppkhQ wfr**00708.0 khT 00708.0

srrB

Qe

oo

fo

75.0ln

ppPB

khT

f

oo

00708.0

rw

J

ppP

D

wfr

1JPTQ **

s

rrw

e 75.0lnDo JPTQ **

10/23/2015

19

Comparison Between PAI In Different Areas

19SPE 108818 Diyashev 2005

10/23/2015

20

Typical EUR Per Well And PAI For Low k Oil Fields

1000.0

500 0

600.0

700.0

800.0

900.0

MSTB

EUR for 10 mln$ CAPEX, MSTB

100.0

200.0

300.0

400.0

500.0

EUR, M

0.0

• EUR per well is from about 180 M STB to 700 M STB • EUR per 10MMUSD CAPEX is in the range of about 400 M to 1 MM STB

PAI USD/STB/D i i th f 4000 t 14000 $/STB/D

20http://www.ogj.com/articles/print/vol‐110/issue‐12/exploration‐development/evaluating‐production‐potential‐of‐mature‐us‐oil.html 12/3/2012 by Rafael Sandrea

• PAI, USD/STB/D is in the range from 4000 to 14000 $/STB/D

10/23/2015

21

Amazing Efficiency Gains• Average oil and gas production rate per active drilling rig has improved by a factor of 3.5. • We use more efficient drilling process, pattern drilling, better technologies, and tools.

10000100

Permian

• Horizontal drilling and better completion/stimulation increased Qo.

1000

illing rig

, boe

/D Bakken Region

Eagle Ford Region

Haynesville Region g im

provem

ent

Permian Region

Niobrara Region

Eagle Ford Region

100

s produ

ction pe

r dr Haynesville Region

Marcellus Region

Niobrara Region

10

uctio

n rate per rig Region

Bakken Region

Haynesville Region

Marcellus

10

6 7 8 9 0 1 2 3 4 5 6Average oil an

d gas Permian Region

Utica Region

1Prod

u Marcellus Region

Utica Region

21

01/01/06

01/01/07

01/02/08

01/01/09

01/01/10

01/01/11

01/02/12

01/01/13

01/01/14

01/01/15

01/02/16A

Time

http://www.eia.gov/petroleum/drilling/ data from EIA drilling productivity report

10/23/2015

22

Smaller Efficiency Gains In The Larger Basins

1000

10000total rig count

100

Bakken Region

Eagle Ford Region

1000

average oil and gas rate per rig, BOE/D

100

Rig coun

t Haynesville Region

Marcellus Region100

05/28/05

10/10/06

02/22/08

07/06/09

11/18/10

04/01/12

08/14/13

12/27/14

05/10/16

10 Niobrara Region

Permian Region

Utica Region

100Q improvement

0 0 0 0 0 0

1

01/01/06

01/01/07

01/02/08

01/01/09

01/01/10

01/01/11

01/02/12

01/01/13

01/01/14

01/01/15

01/02/16

10

Q im

provem

ent

22

Time

110 100 1000

Q

Rig countData from EIA drilling productivity report

10/23/2015

23

Comparison Of The Production Profile For “Conventional” And “Unconventional” Oil WellConventional And Unconventional Oil Well

1 600100000

800

1,000

1,200

1,400

1,600

M STB

Qo, hyperbolic

Qo, STB/D

Conventional

200

400

600

800

EUR, M

10000

tion, STB

/mon

th

Conventional Qo

‐Np Conventional,

ExponentialNp Hyperbolic Np

Unconventional, Hyp+Exp 1000

Oil prod

uct

Qoi = 500 STB/D

1000 60 120 180 240 300 360 420

Conventional Di =12%, 1/yearDi, 1/year= 70%b = 1Dmin = 12%

23

0 60 120 180 240 300 360 420Time, months

Dmin = 12%Economic Limit = 10 STB/D

10/23/2015

24

Production Activation Index100

Economic AssumptionsUnconventional oilCombination of hyperbolic and

10

of cost, c/kW

h

cent/kWh

Combination of hyperbolic and exponential declineCFAT = 40%Di, year‐1 = 70%b = 1

11000 10000 100000

Fuel com

pone

nt

100

b = 1Dmin = 12%d (ROR) = 12%

0.1Production Activation Index, $/STB/D

10

EX

$50

$75For a given volume of investment

11000 10000 100000

Payout/CAP

$75

$100

For a given volume of investment $10 MM, for a value of PAI we can calculate EUR. Under the assumption of hyperbolic plus exponential decline

240.1Production Activation Index, $/STB/D

$150

PAI is related to EUR. Hence we have CAPEX/Energy => c/kWh

10/23/2015

25

“Redlines” Existed Even If We Were Unaware Of Them

80.00%90.00%100.00%

50

60Drilling and Completion Cost

Frequency100

1000

W

$/W

30.00%40.00%50.00%60.00%70.00%

20

30

40

Freq

uency

10

Cost of P

ower, $/W

0.00%10.00%20.00%

0

10

1 2 3 4 5 6 7 8 9 10Bin, mln $

0.1

11,000 10,000 100,000 1,000,000

C

Production Activation Index, $/STB/D

100,000

1,000,000

ndex, $/STB

/D

PAI

0 6

0.7

0.8

0.9

1

y, fractio

n10,000

ction Ac

tivation In

0.2

0.3

0.4

0.5

0.6

ulative Prob

ability

25

1,000 10 100 1000 10000

Prod

uc

Qo, STB/D

0

0.1

0.1 1 10 100 1000

Cumu

$/W

10/23/2015

26

About ¾ Of All Produced Oil Is Used As Gasoline Heating Oil And Jet FuelGasoline, Heating Oil And Jet Fuel

26Data from http://www.eia.gov/dnav/pet/pet_cons_psup_dc_nus_mbbl_m.htm

10/23/2015

27

API View “If It Ain’t Broke, Don’t Fix It.”API View If It Ain t Broke, Don t Fix It.• Transportation solutions are primarily oil driven. Natural gas still is the major source of energy for electric power.

h f d l bl i h hi i i i l ffi i I l• The fundamental problem with this mix is its low energy efficiency. Internal combustion engines have an energy efficiency of about 20%. Jet airplanes and power stations have an efficiency of about 30‐40%.

27http://www.api.org/~/media/files/policy/soae‐2015/api‐2015‐soae‐report.pdf

10/23/2015

28

Disruptive TechnologiesDisruptive Technologies

• Gasoline fueled cars => electric carsGasoline fueled cars => electric cars• Electricity generated from fossil fuels => Solar

h l i i d d?• How much solar power generation is needed? • Airplanes => electric trains => magnetic levitation trains

• Efficiency and costs history and projectionsy y p j

28

10/23/2015

29

Number Of Electrified Models Available In The US MarketIn The US Market

Transportation consumes 46% of the oil in the US.

100hybrids

f l ll

1000

mod

els

10

fuel cell carEV 100

+Hyb

rid+FC m

in th

e USA

10

10

numbe

r of E

V+available i

total EV+Hybrid+FC

1

1998

2000

2002

2004

2006

2008

2010

2012

2014

1

1990

2000

2010

2020

2030

2040

2050

Total n

1 2 2 2 2 2 2 2 2 1 2 2 2 2 2 2

www.fueleconomy.gov data from annual fuel economy review by EPA and DOE 29

10/23/2015

30

By 2023 We Should See The Trajectory Of Market P t ti b El t i CPenetration by Electric Cars

16% of total current number of automobiles is 176 million2.5% of total number of automobiles is 27,5 million2.5% of total number of automobiles is 27,5 million

100,000,000

1,000,000,000

es

Global number of Plug‐Ins

Alternative projection

10,000,000

of Plug‐in veh

icle projection

100,000

1,000,000

Globa

l num

ber

10,000 2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

http://www.hybridcars.com/global‐plug‐in‐car‐sales‐now‐over‐600000/ by Jeff Cobb October 22, 2014http://cleantechnica.com/2015/09/21/1‐million‐evs‐sold‐worldwide/ by James Ayre September 21st, 2015

30

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

1/1/2

10/23/2015

31

USA Sales Numbers Indicate A Transition From Innovators To Early Adopters

100000

y p

10000

1000

s d d S af d lt d d d

Toyota Priu

ota Ca

mry Hybrid

ord Fusio

n Hy

brid

Tesla

Mod

el

Nissan

Le a

ord C‐max Hybrid

Chevy Vo

l

us CT200h Hy

brid

ota Avalon

Hybrid

da Accord Hy

brid

Toyo Fo Fo

Lexu

Toyo

Hond

USA sales over Jan‐May 2014. Estimated the year 2014 sales of 450000 units are about 2.5% of total USA sales.

Eric Schaal http://www.cheatsheet.com/automobiles/10‐best‐selling‐electric‐vehicles‐and‐hybrids‐in‐2014.html/?a=viewall http://en.wikipedia.org/wiki/Hybrid_electric_vehicles_in_the_United_States

Today there are 1.4% of EV of the total fleet of 256 MM

31

10/23/2015

32

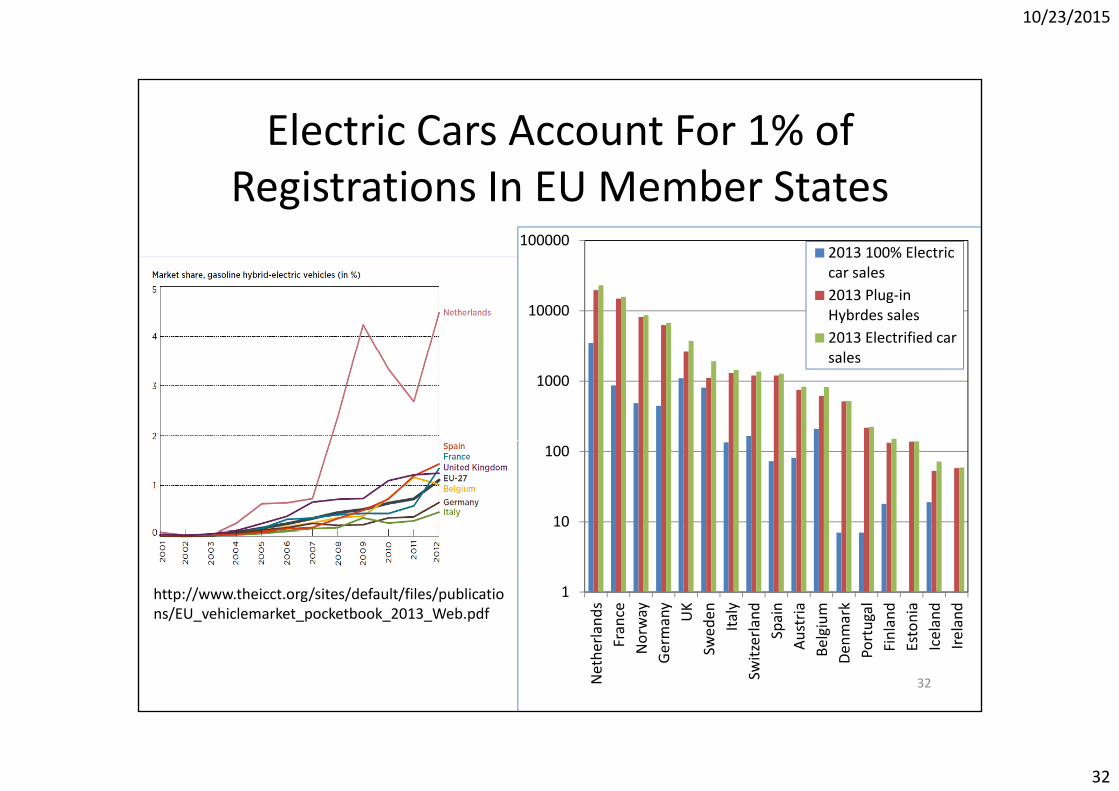

Electric Cars Account For 1% of bRegistrations In EU Member States

1000002013 100% Electric

10000

car sales2013 Plug‐in Hybrdes sales2013 Electrified car

1000sales

10

100

1nd

snce

way any

UK

den

aly

and

ain

tria um ark

gal

and

nia

and

and

http://www.theicct.org/sites/default/files/publications/EU_vehiclemarket_pocketbook_2013_Web.pdf

Nethe

rlan

Fran

Norw

Germa

Swed It

Switzerl a Spa

Aust

Belgiu

Denm

aPo

rtu

Finla

Esto

Icela

Irela

_ _p _ _ p

32

10/23/2015

33

Hybrids Break Through In The Japan kAuto Market

20 km/l = 47 miles/gallon

http://www.theicct.org/blogs/staff/hybrids‐break‐through‐japan‐auto‐marketPublished Fri, 2014.04.04 | By Dan Rutherford 33

10/23/2015

34

China EV Story Is Amazing In Two WaysPlug‐in EV Sales in China rose 37.9% to 17,600 in 2013. Overall sales in 2014 appear to have more than tripled as compared to 2013, with total market share climbing to 0.25%. All the top selling models are Chinese made except for the Tesla model S.

China car sales 2008-2014

http://chinaautoweb.com/2014/01/plug‐in‐ev‐sales‐in‐china‐rose‐37‐9‐to‐17600‐in‐2013/http://evobsession.com/china‐electric‐car‐sales‐estimates‐2014/ February 13th, 2015 by James Ayre

34

10/23/2015

35

Current State Of Battery TechnologyCurrent State Of Battery Technology

Tesla 85kWh battery has stored energy equivalent to the useful energy in 11 gallons of gas. 35

http://my.teslamotors.com/roadster/technology/battery

10/23/2015

36

Cost And Energy Density Of EV Batteriesgy y

If battery life is 1,000 cycles, then the extra cost of storage of kWh is 20c/kWh.If battery life is 10 000 then the extra cost is just 2c/kWh Storage of solar energy

http://energy.gov/sites/prod/files/2014/02/f8/eveverywhere_road_to_success.pdfEV everywhere – Grand Challenge, US DOE

36

If battery life is 10,000, then the extra cost is just 2c/kWh. Storage of solar energy becomes competitive.

10/23/2015

37

Principle Limitations Today Are Long Charging Times And Low Energy Densityg g gy y100.00

h/kg

1.00

10.00

nsity, kWh

ges in

cond

s

0.10

nergy de

n

Charg

16 se

0.01

total

gy useful

y y no

w

ne

citors

ne‐ hium

eries

E

Gasoline

energ

Gasoline u

energy

est b

attery

Graph

enup

ercapac

Graph

enrapp

ed lit

ulfur b

atte

G

Be su w su

5 October 2010. The Royal Swedish Academy of Sciences has decided to award the Nobel Prize in Physics for 2010 to Andre Geim and Konstantin Novoselov"for groundbreaking experiments regarding the two‐dimensional material graphene“. http://www.nobelprize.org/nobel_prizes/physics/laureates/2010/press.html

37

10/23/2015

38

Bernstein said “Welcome to Terrordome”Electric power generation and heating consumes 21% of the oil in the USA.

http://reneweconomy.com.au/wp‐content/uploads/2014/04/Bernstein‐solar.pdfBernstein Energy & Power Blast: Equal and Opposite… If Solar Wins, Who Loses; By Michael Parker, Hugh Wynne, Neil Beveridge, Oswald Clint, Bob Brackett, Scott Gruber, April 4, 201438

10/23/2015

39

Available Energy Resourcesgy

Solar Energy Perspectives © OECD/IEA, 2011

Technical potentials reported here represent the range of estimates for total worldwide potentials for annual RE supply and do not deduct any potential that is already being utilized. 1 exajoule (EJ) ≈ 278 terawatt hours (TWh).

39

10/23/2015

40

Price Learning Curve ‐ Swanson’s Law• Learning Rate: Each time the cumulative production doubled, the price went down by 20 %

for the last 33 years. Learning rate for Crystalline Technology (from Q2-2006 to Q4-2013) is 24.5 %. Learning rate for Thin Film Technology (from Q2-2006 to Q4-2013) is 20.9 %. I G i f t i l 10 t 100 kW PV ft t d 14 000• In Germany prices for a typical 10 to 100 kWp PV rooftop-system were around 14,000 €/kWp in 1990. At the end of 2013, such systems cost about 1,350 €/kWp. This is a net-price regression of 89 % over a period of 23 years and is equivalent to an annual compound average price reduction rate of 9 %.

all bulk PV Technologies

2

2

//$$

Wm

WUnitCost

c‐Si 121 GWpThin Film 18 GWp

2/ mWattWatt

40FRAUNHOFER INSTITUTE FOR SOLAR ENERGY SYSTEMS ISE “Photovoltaics Report”. Freiburg, 24 October 2014, www.ise.fraunhofer.de Dr. Simon Philipps (Fraunhofer ISE) [email protected] and Werner Warmuth (PSE AG) [email protected]

10/23/2015

41

41

10/23/2015

42

42

10/23/2015

43

Levelized Cost Of Energy Comparison—Sensitivity to Fuel PricesSensitivity to Fuel Prices

Unconventional

Conventional

Lazard‘s levelized cost of energy analysis — version 8.0 September 2014

Darkened areas in horizontal bars represent low end and high end levelized cost of energy corresponding with ±25% fuel price fluctuations.

43

10/23/2015

44

Average Price For 1 kWh In January Tripled Over 35 YearsTripled Over 35 Years

44

10/23/2015

45

Solar Is Affordable And CompetitiveTypical ranges and weighted averages for the total installed costs of utility‐scale renewable power generation technologies by region, 2013/2014.

Nuclear CAPEX = 10 USD/W

SOFC CAPEX = 7‐8 USD/W

SD/kW

2014

US

IRENA. Renewable power generation costs in 2014 http://www.irena.org/DocumentDownloads/Publications/IRENA_RE_Power_Costs_Summary.pdf

45

10/23/2015

46

254*254 km of Solar Panels In The Sahara C S l Th E ti W ld With ECan Supply The Entire World With Energy

46

10/23/2015

47

Pay Back Time for Multicrystalline Silicon PV R f S G hi l C iRooftop Systems ‐ Geographical Comparison

47

Data: M.J. de Wild‐Scholten 2013. Image: JRC European Commision. Graph: PSE AG 2014 (Modified scale with updated data from PSE AG and FraunhoferISE) FRAUNHOFER INSTITUTE FOR SOLAR ENERGY SYSTEMS ISE “Photovoltaics Report”. Freiburg, 24 October 2014, www.ise.fraunhofer.de Dr. Simon Philipps (Fraunhofer ISE) [email protected] and Werner Warmuth (PSE AG) [email protected]

10/23/2015

48

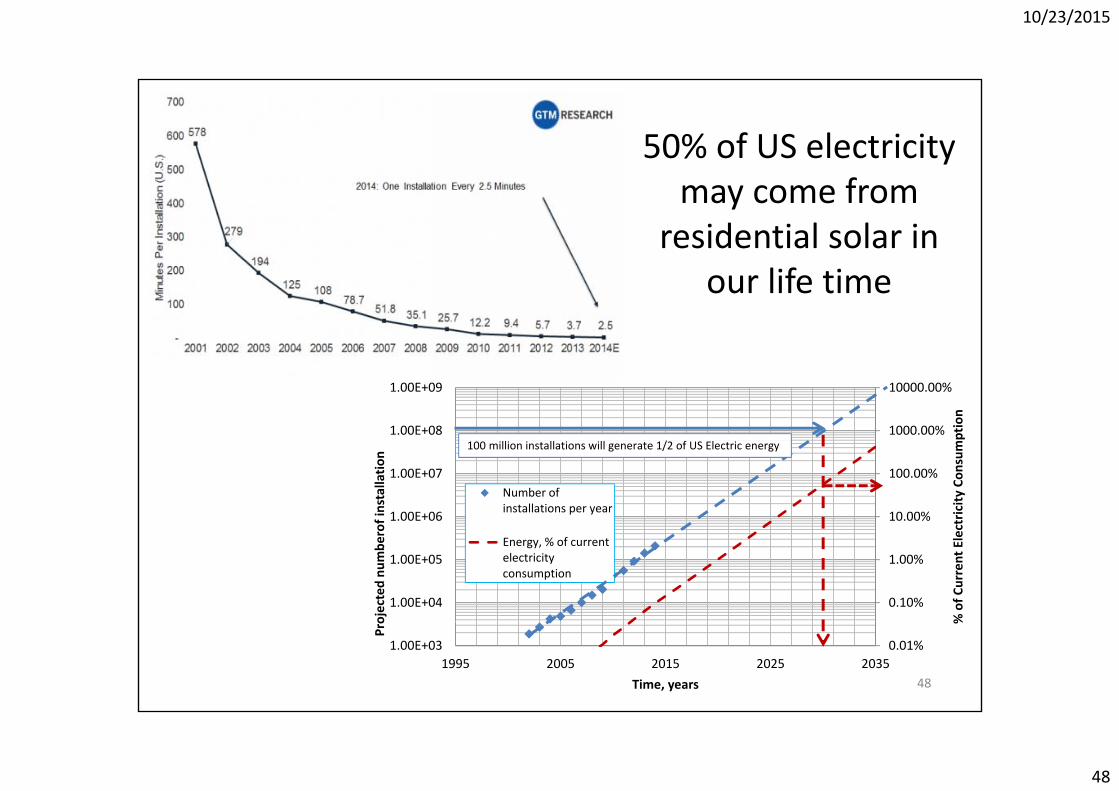

50% of US electricity may come from

residential solar in our life time

1000.00%

10000.00%

1.00E+08

1.00E+09

ption

/

10.00%

100.00%

1.00E+06

1.00E+07

ectricity

Con

sum

of in

stallatio

n

Number of installations per year

100 million installations will generate 1/2 of US Electric energy

0.10%

1.00%

1.00E+04

1.00E+05

% of C

urrent Ele

ojected nu

mbe

r

Energy, % of current electricity consumption

0.01%1.00E+031995 2005 2015 2025 2035

%

Pro

Time, years 48

10/23/2015

49

Transforming Parking Lots Into Power Plants

BakersfieldCollegeCollege

Number of Parking spots in the USA 800,000,000Area (8.5*21 ft) 16.58Share of parking spots under the sun 50%Share of parking spots under the sun 50%Total area that can be harvested, m2 6,633,277,056Annual Global Horizontal Irradiation, kW*h/m2 (Average in USA) 1600Conversion efficiency, % 20A l ti t ti l kW*h 2 1E 12

Photo credit http://solairegeneration.com/

Annual energy generation potential, kW*h 2.1E+12Electric power consumption (kWh) in the United States 4.1E+12Share of electric power consumption 51% 49

10/23/2015

50

World Total Energy Demand ProjectionWorld Total Energy Demand Projection

900 30.1

800

Qua

ds

World: New Policies Scenario, Quads

Current Policies Scenario, Quads

450 Scenario, Quads

26.8

r

600

700

Projectio

n, Q

23.4

20.1 power

500

gy Dem

and P

16.7

TW

300

400

Total Ene

rg

13.4

10 03001980 1990 2000 2010 2020 2030 2040 2050

Years

10.0

© 2014 OECD/IEA Source: World Energy Outlook 201450

10/23/2015

51

Total World Energy Demand in 2007 Was 465 Quads Q

Energy efficiency = 45.65%Most energy is wasted in electricity generation 63.2% and transportation 75.6% 51

10/23/2015

52

Solar Will Probably Overtake Fossil Fuels In Power Generation In Our Life TimePower Generation In Our Life Time

100000Wh

10000

ation, TW

1000

wer gen

era

CoalGasOil

100

Globa

l pow

OilSolar

102000 2010 2020 2030 2040 2050

G

Time, yearsSource: World Energy Outlook 2014 New Policies ScenarioHistorical data by Hanergy Research Team, Bloomberg New Energy Finance

52

10/23/2015

53

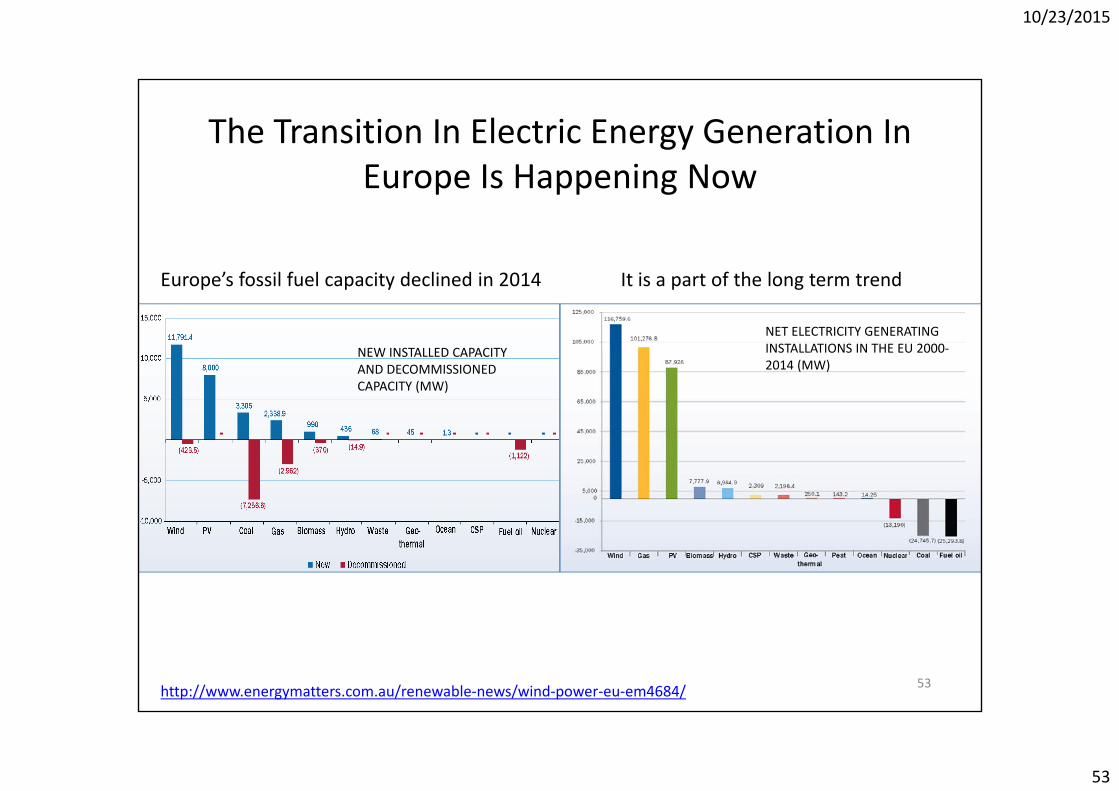

The Transition In Electric Energy Generation In E I H i NEurope Is Happening Now

NEW INSTALLED CAPACITY

Europe’s fossil fuel capacity declined in 2014 It is a part of the long term trend

NET ELECTRICITY GENERATING INSTALLATIONS IN THE EU 2000‐NEW INSTALLED CAPACITY

AND DECOMMISSIONED CAPACITY (MW)

INSTALLATIONS IN THE EU 20002014 (MW)

http://www.energymatters.com.au/renewable‐news/wind‐power‐eu‐em4684/ 53

10/23/2015

54

A Vision Of A Future Euro‐Mediterranean GridInterconnecting sites with large renewable electricity sources and sites with high demand for clean energy .

http://www.menarec.org/resources/Trieb_EUMENA_Whitebook_02.pdfSustainable electricity and water for Europe Middle East and North Africa By Franz Trieb and Hans Müller‐Steinhagen

54

10/23/2015

55

DCHV Transmission Is a KeyDCHV Transmission Is a Key• “War of Currents” competition (end of 19th century) between the direct

current (DC) system of Thomas Edison and the AC system of Georgecurrent (DC) system of Thomas Edison and the AC system of George Westinghouse. AC transmission became the de facto standard.

• Technology mainly developed in Sweden and Germany in the 1930’s. One of the first large scale trials in USSR in 1950.

• Now the longest HVDC link in the world is currently the Xiangjiaba–Shanghai 2,071 km (1,287 mi), ±800 kV, 6400 MW link connecting the Xiangjiaba Dam to Shanghai in China.

• This is roughly equivalent to 24” gas transmission pipeline operating at• This is roughly equivalent to 24” gas transmission pipeline operating at 250 bars (about 3700 psia) of pressure.

• HVDC link Ekibastuz – Tambov (USSR, Kaz‐Rus) 2414 km line 750 kV 6000 MW was abandoned around 1990 due to the collapse of the USSR.6000 MW was abandoned around 1990 due to the collapse of the USSR.

• The principle advantage of DCHV is minimal energy losses of about 3% at 1000 km in transmission of vast quantities of energy at large distances.

http://new.abb.com/systems/hvdc/references/xiangjiaba‐‐‐shanghaihttp://en.wikipedia.org/wiki/List_of_HVDC_projects 55

10/23/2015

56

In Europe Transition Seems To Be Accelerating

What are the reasons? Prices? Environmental concerns? Politics?

100.0%

Share of energy from renewable sources for electricity

2000 2010 2020 2030 2040 2050

56

10.0%

Data from http://ec.europa.eu/eurostat/statistics‐explained/index.php/Energy_from_renewable_sources

10/23/2015

57

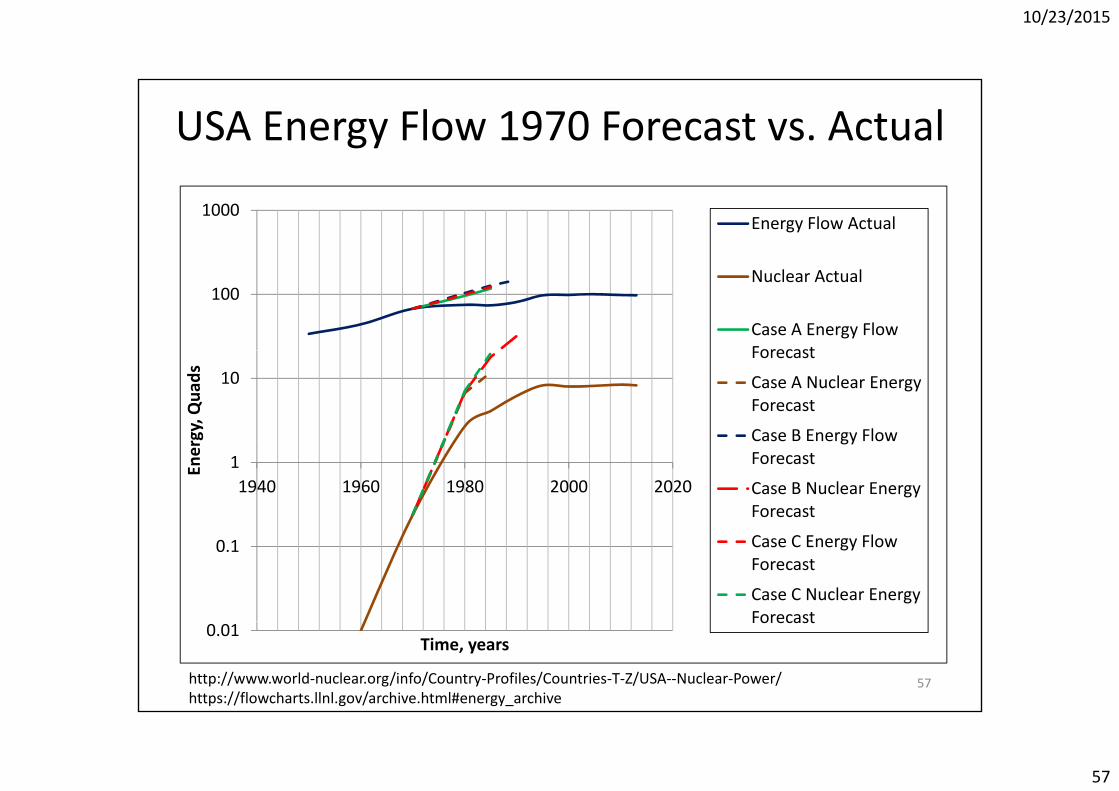

USA Energy Flow 1970 Forecast vs. Actual

1000Energy Flow Actual

100Nuclear Actual

Case A Energy Flow Forecast

10

rgy, Qua

ds

Forecast

Case A Nuclear Energy Forecast

Case B Energy Flow11940 1960 1980 2000 2020

Ener

Case B Energy Flow Forecast

Case B Nuclear Energy Forecast

0.1 Case C Energy Flow Forecast

Case C Nuclear Energy Forecast

57

0.01Time, years

Forecast

http://www.world‐nuclear.org/info/Country‐Profiles/Countries‐T‐Z/USA‐‐Nuclear‐Power/https://flowcharts.llnl.gov/archive.html#energy_archive

10/23/2015

58

Energy efficiency = 39.43%

58

10/23/2015

59

Nuclear Is NOT The Solution, And Perhaps Should Not Be A Part Of The Solution

The Historic Crossover

Should Not Be A Part Of The Solution

Solar and Nuclear Costs — The Historic Crossover: Solar Energy is Now the Better BuyBy John O. Blackburn and Sam Cunningham. July 2010. Prepared for NC WARN: Waste Awareness & Reduction Network, PO Box 61051, Durham, NC 27715‐1051 • 919‐416‐5077, www.ncwarn.org

http://www.ucsusa.org/sites/default/files/legacy/assets/documents/nuclear_power/nuclear‐economics‐fact‐sheet.pdf by Union of Concerned Scientists August 2009 Nuclear Power: A Resurgence We Can’ t Affordhttp://npolicy.org/article_file/New_Nuclear‐The_Economics_Say_No.pdf New Nuclear – The Economics Say No Pan‐Europe Utilities (Citi) by Peter Atherton, Andrew M Simms, Sofia Savvantidou, Stephen B Hunt

59

10/23/2015

60

Nuclear Is NOT The Solution, And Perhaps Sho ld Not Be A Part Of The Sol tion

• Safety record is not very good. To date, there have been around 440 reactors constructed The following 9 have melted down to some degree:

Should Not Be A Part Of The Solution

reactors constructed. The following 9 have melted down to some degree:3 reactors at Fukushima1 reactor at Chernobyl1 reactor at 3-Mile Island1 reactor in Saint-Laurent, France, 19691 reactor at Lucens, Switzerland, 19691 reactor KS 150 in Czech Republic Feb. 22, 19771 reactor NRX Ontario Canada in 19521 reactor NRX Ontario Canada in 1952

• Gap of 15 TW will require to build 15000 nuclear reactors of 1GW each over next 30 years. Potentially dozens of major accidents, nuclear terrorism danger, unsolved and (potentially unsolvable) nuclear waste problem and g , (p y ) pabout 150 trillion USD in CAPEX.

Prof. Mark Jacobson, Stanford University 60

10/23/2015

61

Will There Be More Air Travel and More Demand For Jet Fuel As China and India Develop?For Jet Fuel As China and India Develop?

Jet fuel accounts for 8% of US oil consumption.

61Radius of this circle is about 3000 km.

10/23/2015

62

R = 3000 kmR 3000 kmTotal length of TAR network is about 117000 km.

62

10/23/2015

63

63"Rail map of China" by Howchouhttp://commons.wikimedia.org/wiki/File:Rail_map_of_China.svg#/media/File:Rail_map_of_China.svg

10/23/2015

64

Proven Concept, Technology And l bl lAvailable Capital

• “Just five years after China’s high-speed rail system opened, it is carrying l t i h th th t ’ d tinearly twice as many passengers each month as the country’s domestic

airline industry. With traffic growing 28 percent a year for the last several years, China’s high-speed rail network will handle more passengers by early next year than the 54 million people a month who board domestic y y p pflights in the United States”. (NY Times)

• The Mid-to-Long Term Railway Network Plan adopted in 2004, and updated in 2008, laid out such a railway development plan through 2020, including the connection of all provincial capitals and cities aboveincluding the connection of all provincial capitals and cities above 500,000 people to a rapid rail network of 45,000 km, including about 16,000 km of dedicated high speed rail lines. This program was subsequently accelerated to achieve most of these objectives by 2015.

• Asian Infrastructure Investment Bank established for major infrastructure projects. All of the important Asian and European economic powers have joined this effort.

64http://qz.com/116190/high‐speed‐rail‐is‐at‐the‐foundation‐of‐chinas‐growth‐strategy/http://www.nytimes.com/2013/09/24/business/global/high‐speed‐train‐system‐is‐huge‐success‐for‐china.html?_r=0

10/23/2015

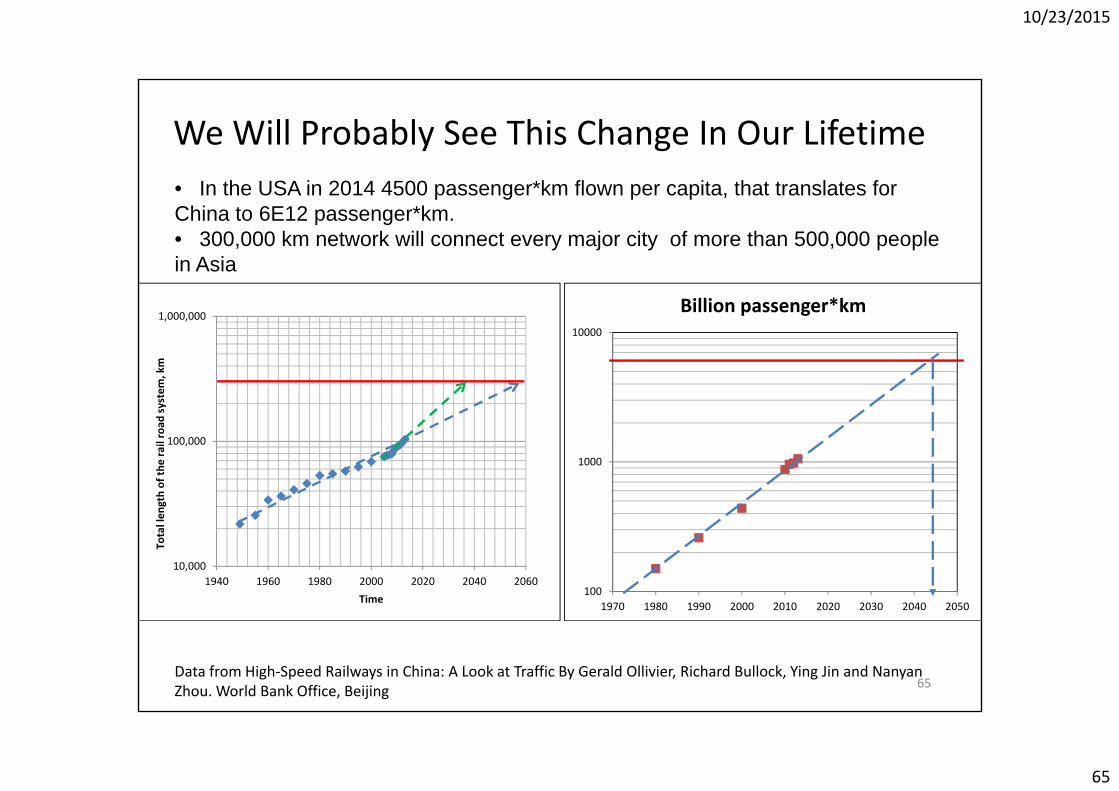

65

We Will Probably See This Change In Our Lifetime• In the USA in 2014 4500 passenger*km flown per capita, that translates for China to 6E12 passenger*km.• 300,000 km network will connect every major city of more than 500,000 people i A i

1,000,00010000

Billion passenger*km

in Asia

100 000road

system

, km

100,000

al length of the

rail

1000

10,0001940 1960 1980 2000 2020 2040 2060

Tota

Time100

1970 1980 1990 2000 2010 2020 2030 2040 2050

65Data from High‐Speed Railways in China: A Look at Traffic By Gerald Ollivier, Richard Bullock, Ying Jin and NanyanZhou. World Bank Office, Beijing

10/23/2015

66

Energy Efficiency by Transport ModeIn Barrels of Oil or Oil Equivalent Per 10,000 Passenger*Miles

Oil fueled autos, trucks, & airplanes dominated 20th century transport. Electrically powered automobiles and MagLev will dominate 21st century transportpowered automobiles and MagLev will dominate 21st century transport.

66Energy Efficiency and Economics of Maglev Transport By James Powell and Gordon Danbyhttp://www.aertc.org/conference/AEC_Sessions%5CCopy%20of%20Session%201%5CTrack%20E‐%20Innovation%5CIntelligent%20Advanced%20Transport%5C3.%20Dr.%20James%20Powell%5CJames%20Powell%20presentation.pdf

10/23/2015

67

Conclusions

• Our industry during the “unconventional revolution” had the same rate of improvement as high tech industries. Is this rate of innovation sustainable for the petroleum industry?

• Innovations in material sciences challenge the high energy density advantage of our product.

• Competitive technologies are likely to erode the “convenience premium” for oil. Electric cars will be just as convenient as gasoline powered cars. Electric powered trains may be more convenient then airplanes.

• For the first time in history we are in direct competition with industries (transportation and power generation) that used to be our customers.

67

10/23/2015

68

So what do we have to do now?So what do we have to do now? • Production activation index of 20000 USD/STB/D or more is a sign

of great danger to the prosperous existence of our industryof great danger to the prosperous existence of our industry.• We must keep innovating and improving drilling efficiency. We must

continue to focus on recovery efficiency in developed basins. High capital cost projects like Arctic offshore may never be developedcapital cost projects like Arctic offshore may never be developed.

• Innovate, develop new products and materials based on natural gas and petroleum chemistry. W h ld b f l ll t h l f di t ib t d• We should embrace fuel cell technology for distributed power generation.

• We should embrace every type of technology where solar energy t i i h i l b dstorage is in chemical bonds.

• Young petroleum engineers must be trained to be much more adaptable to changing business environment. We should be more like energ engineers rather than j st petrole m engineerslike energy engineers rather than just petroleum engineers.

68