Embed Size (px)

Citation preview

The World Bank

FOR OFFICIAL USE ONLY

Report No: 40270-CL

PROJECT APPRAISAL DOCUMENT

O N A

PROPOSED L O A N

IN THE AMOUNT OF US$24.8 MILL ION

TO

THE REPUBLIC OF CHILE

FOR THE

SECOND PUBLIC EXPENDITURE MANAGEMENT PROJECT

August 3,2007

Poverty Reduction and Economic Management Argentina, Chile, Paraguay, Uruguay Country Management Unit Latin America and the Caribbean Region

This document has a restricted distribution and may be used by recipients only in the performance o f their official duties. I t s contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

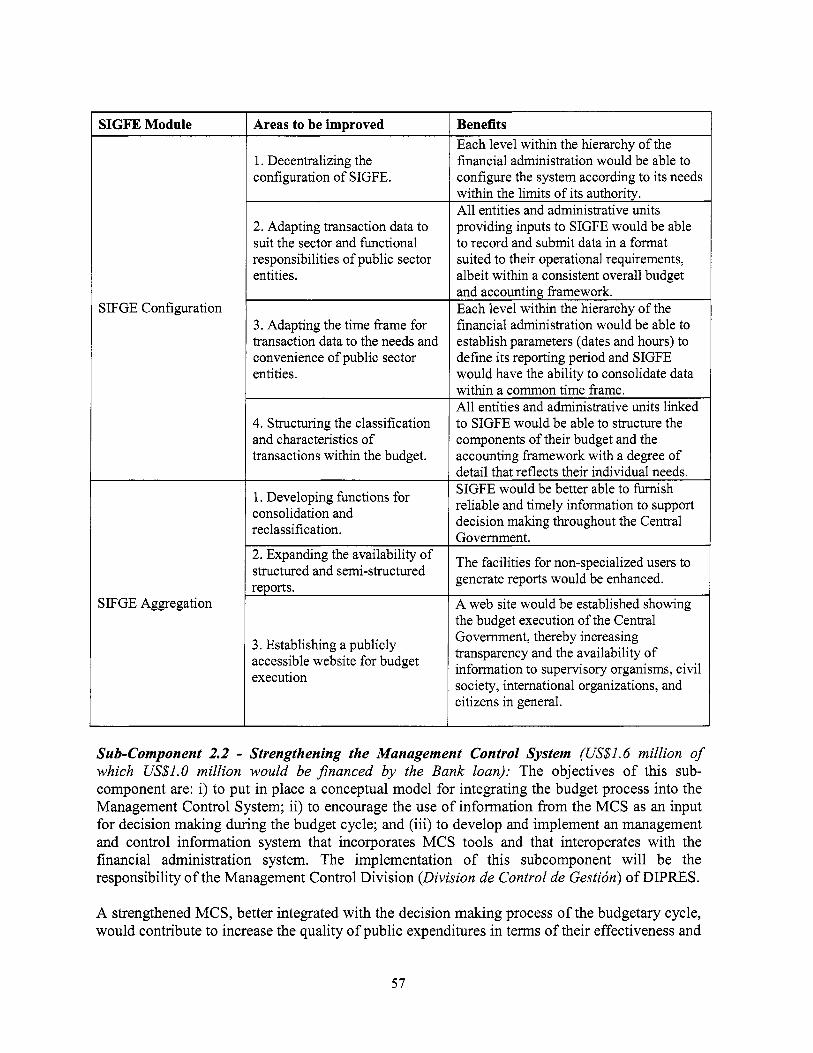

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS (Exchange Rate Effective January 28,2007)

Currency Unit = Chilean Peso (Ch$) Ch$l = US$O.O0184 US$1 = Ch$544.8

FISCAL YEAR January1 - December31

ABBREVIATIONS AND ACRONYMS (Spanish in parenthesis)

ACHM

BIP

BGI

CAS CFAA CGR

CLAD

CORFO

CONICYT

CPAR CPS DIPRES

ECLAC

F C M

GDP GFSM ICT IMF I T I L LAC MCS OECD PIU PROFIM

Chilean Association o f Municipalities (Asociacidn Chilena de Municipalidades) Public Investment Database (Banco Integrado de Proyectos) Integrated Balanced Management (Balance de Gestion Integral) Country Assistance Strategy Country Financial Accountability Assessment Office o f the Comptroller General (Contraloria General de la Republica) Latin American Center for Administration for Development (Centro Latinoamericano de Administracidn para el Desarrollo) Corporation for Production Development (Corporacidn de Foment0 de la Produccidn) National Commission for Scientific and Technological Research (Comisidn Nacional de Investigacidn CientFca y Tecnoldgica) Country Procurement Assessment Report Country Partnership Strategy Budget Directorate in the Ministry o f Finance (Direccidn de Presupuesto) Economic Commission on Latin America and the Caribbean (Comisibn Econdmica sobre Latinoame'rica y el Caribe) Common Municipal Fund (Fondo Comun Municipal) Gross Domestic Product Government Finance Statistics Manual Information and Communication Technology International Monetary Fund Information Technology Infrastructure Library Latin America and the Caribbean Management Control System Organization for Economic Co-operation and Development Project Implementation Unit Municipal Development Projects

11

FOR OFFICIAL USE ONLY

ROSC SIAP

SIAPER

SIGFE

S I L S I N I M

SOA SUBDERE

(Programa de Fortalecimiento Institucional Municipal) Report on the Observance o f Standards and Codes Budget Administration System (Sistema de Administracidn de Presupuesto) Human Resources Management System for the Civ i l Service (Sistema de Informacidn y Control del Personal de la Administracidn del Estado) Integrated Financial Management System (Sistema de Informacidn para la Gestidn Financiera del Estado) Specific Investment Loan National System o f Municipal Indicators (Sistema Nacional de Indicadores Municipales) Services Oriented Architect Sub-secretariat for Regional Development and Administration (Subsecretaria de Desarrollo Regional y Administracidn)

Vice President: Pamela Cox Country Director: Pedro Alba

Sector Director: Ernest0 M a y Sector Manager: Nicholas P. Manning

Sector Leader: James Parks Task Team Leader: Roberto Panzardi

I I

This document has a restricted distribution and may be used by recipients only in the performance o f their off icial duties. I t s contents may not be otherwise disclosed without Wor ld Bank authorization.

CHILE Second Public Expenditure Management Project

CONTENTS Page

A . STRATEGIC CONTEXT AND RATIONALE ............................................................................... 1 1 . 2 . 3 .

Country and sector issues ................................................................................................................ 1

Rationale for Bank Involvement ...................................................................................................... 8

Higher level objectives to which the project contributes ................................................................. 9

B . PROJECT DESCRIPTION ............................................................................................................. 10

1 . 2 . 3 . 4 . 5 .

Lending instrument ........................................................................................................................ 10

Project development objective and key indicators ......................................................................... 10

Project components ........................................................................................................................ 11

Lessons learned and reflected in the project design ....................................................................... 17

Alternatives considered and reasons for rejection ......................................................................... 19

C . IMPLEMENTATION .......................................................................................................................... 20 1 . 2.

3 . 4 . Sustainability 23

5 . 6 .

Partnership arrangements ............................................................................................................... 20

Institutional and implementation arrangements ............................................................................. 20

Monitoring and evaluation o f outcomes/results ............................................................................. 22

Critical r i sks and possible controversial aspects ............................................................................ 23

.................................................................................................................................

Loan conditions and covenants ...................................................................................................... 25

D . APPRAISAL SUMMARY .................................................................................................................. 26

1 . Economic and financial analysis .................................................................................................... 26

2 . Technical ........................................................................................................................................ 27

3 . Fiduciary ............................ ........................................................................................................... 27

4 . Social ............................................................................................................................................. 27

5 . Environment ................................................................................................................................... 27

6 . Safeguard policies .......................................................................................................................... 27

7 . Policy Exceptions and Readiness ................................................................................................... 28

Annex 1: Country and Sector o r Program Background .................................................................. 29

Annex 2:

Annex 3:

Major Related Projects Financed by the Bank and/or other Agencies .......................... 36

Results Framework and Monitoring .................................................................................. 39

iv

Annex 4:

Annex 5:

Annex 6:

Annex 7:

Annex 8:

Annex 9:

Annex 10:

Annex 11 :

Annex 12:

Annex 13:

Annex 14:

Annex 15:

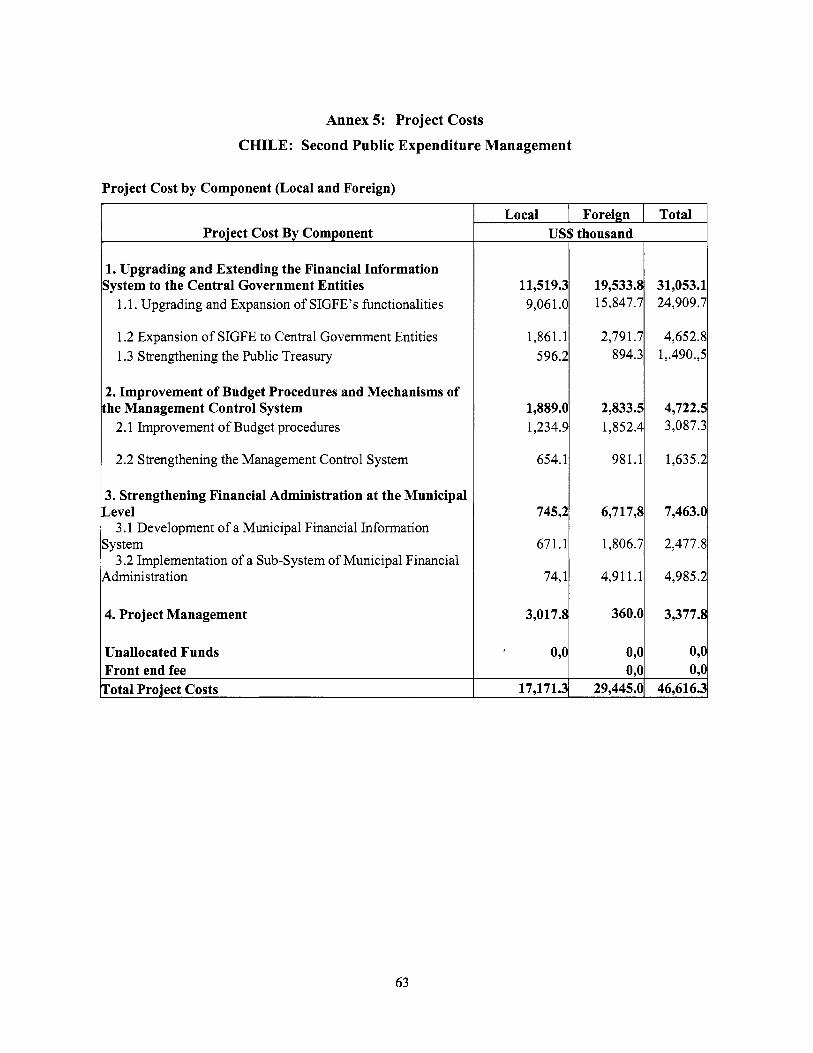

Detailed Project Description ............................................................................................... 51

Project Costs ........................................................................................................................ 63

Implementation Arrangements .......................................................................................... 65

Financial Management and Disbursement Arrangements .............................................. 68

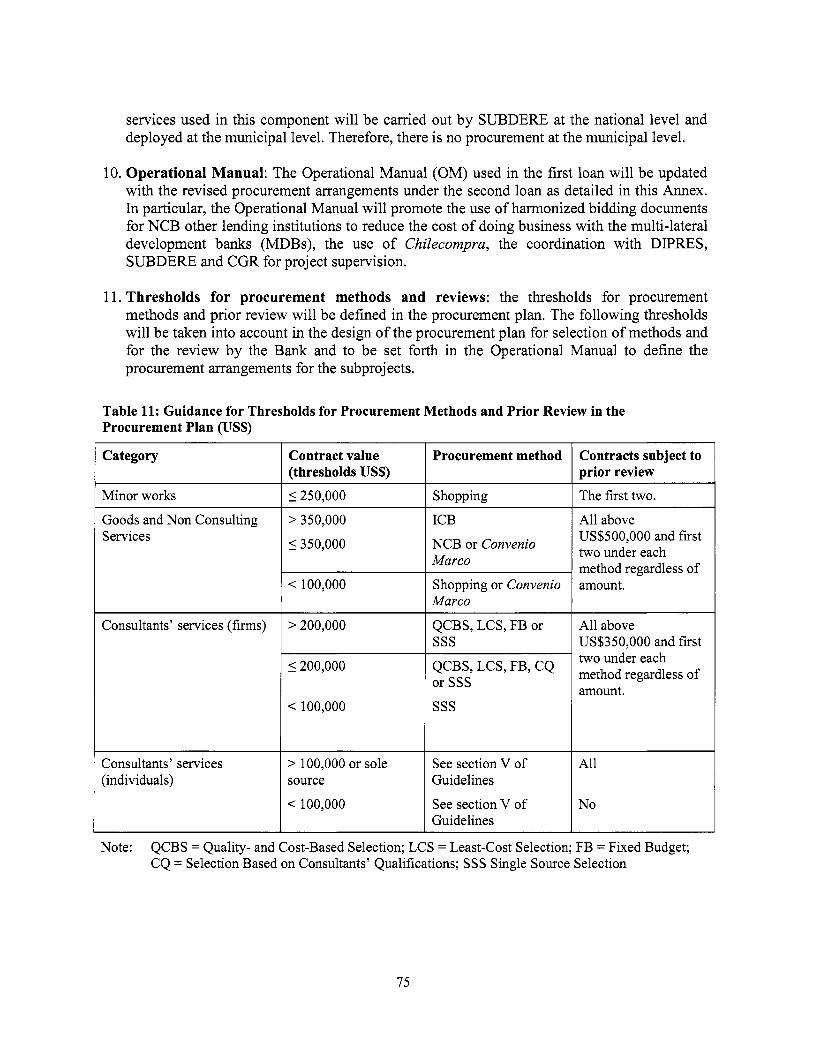

Procurement Arrangements ............................................................................................... 73

Economic and Financial Analysis ...................................................................................... 83

Safeguard Policy Issues ....................................................................................................... 84

Project Processing ................................................................................................................ 85

Documents in the Project Fi le ............................................................................................. 86

Statement of Loans and Credits ......................................................................................... 88

Country at a Glance ............................................................................................................ 89

Map - IBRD33386 ................................................................................................................ 91

V

CHILE

Source Borrower INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

SECOND PUBLIC EXPENDITURE MANAGEMENT

Local Foreign Total 21.8 0.00 21.8 0.00 24.8 24.8

PROJECT APPRAISAL DOCUMENT

L A T I N AMERICA AND CARIBBEAN

LCSPS

Total:

Date: August 3, 2007 Country Director: Pedro Alba Sector Director: Emesto May Sector Manager: Nicholas P.Manning

Team Leader: Roberto 0. Panzardi Sectors: Central government administration (70%); Information technology (30%) Themes: Public expenditure, financial management and procurement (P);Debt management and fiscal sustainability (P);Decentralization (S) Environmental screening category: Not Required

Project ID: P103441

Lending Instrument: Technical Assistance Loan

21.8 24.8 46.6

Project Financing Data [XI Loan [ ]Credit [ ] Grant [ ]Guarantee [ ]Other:

Borrower: REPUBLIC OF CHILE

Responsible Agency: Ministry o f Finance Calle Teatinos 120 Piso 12 Santiago, Chile Tel: (56) 2 473-25 17 mpv@dipres. c l

Estimated disbursements (Bank FY/US$m) I 2008 I 2009 I 2010 I 2011 I 2012 I 0 0 0 0

Project implementation period: October 1,2007 E1 Expected effectiveness date: September 28,2007 ExDected closing: date: December 31.2012

[]Yes [ X I N o

[ ]Yes [XINO

Does the project depart from the CAS in content or other significant respects? Re$ PAD A.3 Does the project require any exceptions from Bank policies? Re$ PAD D. 7 Have these been approved by Bank management? I s approval for any policy exception sought from the Board?

[ ]Yes [ IN0 [ ]Yes [ IN0 []Yes [ X ] N o

rv,v,, , hT,

Does the project include any critical r isks rated “substantial” or “high”? Re$ PAD C.5 Does the project meet the Regional criteria for readiness for implementation?

LAJ I C 3 J I Y U Re$ PAD D. 7 Project development objective Re$ PAD B.2, Technical Annex 3

The overall development objective would be to increase the efficiency o f operations regarding financial management, budget formulation, and budget execution, and the transparency o f public expenditure management at the central and municipal level through the implementation o f an updated, fbnctionally enhanced and expanded financial administration system (SIGFE).

The Project Performance Indicators are:

Improve Efficiency of the Public Financial Management Administration: Time required for aggregating the financial data o f the central government i s to be reduced from 30 to 8 days. Increase EfJiciency of Operations regarding Budget Formulation and Execution: Time required to update SIGFE (execution) with the data generated by the SIAP system (formulation and administration) i s to be reduced from one week to one day. Improve Efficiency of Budget Execution: Processing capacity o f the SIGFE transaction module i s to be increased from 95,000 to 200,000 financial transactions per day, with a response time o f 8 seconds per transaction measured at the portal. Improve Efficiency of Financial Management Operations and Improve Effectiveness of Fiscal Control: Time for processing transactions within the Central Government Entities so that the information i s available in SIGFE i s to be reduced from 20 days to less than 3 days. Increase Transparency of Municipal Financial Information: Financial information and expenditures on at least 100 municipalities i s to be made available in the Municipal Financial Information System, which can aggregate the financial information o f a l l (presently 345) municipalities. Increase EfJiciency of Fiscal Monitoring of Municipal Finances: Information on aggregate municipal finances i s to be made available at the central level within 30 days instead o f presently up to 180 days. Increase Effectiveness of Budget Cycle Indicators: All monitoring indicators wil l be aligned

with the financial indicators and integrated in the budget formulation and execution. The new methodology wil l be adopted by al l Ministries covered by the M C S and wil l be integrated in the budget by 201 1.

0

Project description: Re$ PAD B.3, Technical Annex 4

Component 1 - Upgrading and Extending the Financial Information System to the Central Government Entities (US$31.1 million of which US$l7.1 million would be financed by the Bank loan):

This component would provide technical assistance, training, design and development o f software and equipment as wel l a procurement o f software licenses to upgrade SIGFE and install it in Central Government Entities. In particular, i t would support the further development and consolidation o f SIGFE by: (i) upgrading and optimizing the I C T and technical design o f SIGFE modules; (ii) improving i t s functionality, interoperability and reporting; and, (iii) implementing data standards issued by Normative Entities in al l agencies using the homologated systems.

Component 2: Improvement of Budget Procedures and Mechanisms o f the Management Control System (US$4.7 million of which US$2.8 million would be financed by the Bank loan):

This component would focus on enhancing the quality o f public expenditures by strengthening the Management Control System (MCS) and integrating them into the Budget Cycle. Specifically, this component would focus on developing and implementing: (i) a new conceptual model for the Budget Cycle, linking the budget classification and the MCS; (ii) a M C S information system; and (iii) a new version o f the budget formulation system used by DIPRES (SIAP). Innovative methods o f budget formulation would be developed for selected pol icy modules and the capacity o f DIPRES to undertake results-based monitoring and evaluation would be strengthened. This component consists o f two sub-components.

Component 3 - Strengthening Financial Administration at the Municipal Level (US$7.5 million of which US$4.5 million would be financed by the Bank loan):

This component would focus on: (i) improving the availability o f information on municipal budgets and on financial transfers; (ii) strengthening financial administration at the municipal level; (iii) Strengthening the capacity o f selected Municipalities to operate financial administration subsystems and the Municipal Financial Information System; and (iv) improving the effective use o f central government transfers to municipalities, for example within the Municipal Fund (Fond0 Comzin Municipal). The Office o f the Comptroller General in partnership with the Sub-secretariat for Regional Development within the Ministry o f the [nterior (Subsecretaria de Desarrollo Regional y Administracidn - SUBDERE) would implement this component. Finance would be provided for technical assistance, supplies and training within two sub-components.

Component 4 - Project Management (US$3.4 million of which US$0.4 million would be Gnanced bv the Bank loan):

This component would cover operating expenses, with the Borrower contributing US$3 .O mil l ion o f counterpart funds, related to the fol lowing activities: (i) Provision o f technical assistance to Central Government Entities as part o f the implementation o f SIFGE or SIGFE-compatible financial administration systems; (ii) Strengthening the Government’s capacity to monitor and supervise the overall implementation o f the Project. Which safeguard policies are triggered, if any? Re$ PAD D.6, Technical Annex 10 This project triggers none o f the Bank’s safeguard policies. Significant, non-standard conditions, if any: None

A. STRATEGIC CONTEXT AND RATIONALE

1. Country and sector issues

Country Issues

1. For almost three decades, Chile has been firmly committed to economic liberalization and free trade. Chile has had, by far, the most robust economic performance in Lat in America and it figures prominently among the list o f winners from globalization. Chile has averaged an annual per capita growth rate o f 4.1 percent over the fifteen years since the return to democracy in 1990. Due to the financial crises o f the late 1990s, growth between 1998 and 2003 decreased to an average o f only 1.3 percent per year. However Chile has recovered strongly over the past four years, with growth accelerating from 2-3 percent in 2002 to above 6 percent in each o f 2004 and 2005. Real growth fe l l to 4 percent in 2006. This deceleration i s attributable to the concerted anti-cyclical policy efforts o f the Government, the non-copper trade effects o f an appreciating peso, higher o i l prices and the natural slowing associated with an economy exhausting the “easy- wins” from earlier reforms. Several temporary factors, such as the copper strike in mid 2006, also contributed to slower growth during the year and the possibility o f similar labor actions cannot be discounted in the fbture. Chile’s economic success reflects past economic reforms, strong public institutions and the maintenance o f a solid macro-economic pol icy framework supported by high investment and savings rates, a strong financial sector with an autonomous central bank, stable fiscal management, and prudent monetary policy. Chile’s longstanding commitment to trade liberalization i s confirmed by recently signed free-trade agreements, such as those with the U.S. and China, together with numerous other trade deals signed with other nations and economic blocks.

2. Robust economic growth has helped reduce poverty and improve living conditions for the poor. Since 1990, poverty has been cut by more than half, from 40 percent to 13.7 percent in 2006. Likewise, social indicators such as enrollment in primary education, youth literacy, infant mortality and l i fe expectancy, also improved substantially as the result o f targeted social programs and strong economic growth, reaching levels close to those o f industrialized countries. However, despite advances in poverty reduction, Chile s t i l l faces serious challenges in the fight against poverty and income inequality. The poor st i l l account for approximately 2.2 mi l l ion o f the population and they remain highly vulnerable to adverse income shocks. Levels o f indigent poverty have fallen in recent years from 4.7 percent in 2003 to 3.2 percent in 2006. Income inequality i s also considerable, as shown by a gini-coefficient o f 0.54. The poorest tenth percentile o f the population accounts for just 1.2 percent o f overall consumption, compared to 47 percent for the wealthiest one. Moreover, economic growth has exacerbated regional differences. The copper-endowed northern region and the central valley are more prosperous than the rest o f the country and there are strong differences between living conditions in rural and urban areas.

3. The challenge now facing Chile i s to continue sustaining high levels o f Gross Domestic Product (GDP) growth and employment, while, at the same time, ensuring that a l l segments o f the population partake in the benefits o f economic prosperity. All four center-left administrations that have governed Chile since 1990, including the present administration o f Michel le Bachelet, have been firmly committed to seeking more balanced development without hampering economic growth. In this regard, the Bachelet administration campaigned on, and i s n o w

1

implementing, policies focused on the goal o f ‘Growth with Equity o f Opportunity’. The private sector continues to be seen as the primary driver o f employment and production, with the public sector facilitating and creating opportunities for private participation by maintaining a stable macro-economic framework as well as trade openness. At the same time, the new administration has pledged to improve a broad range o f social services including public health, education, social protection for the elderly, and an expansion o f opportunities for women to participate in economic and social progress.

4. Public sector modernization continues to be a top priority in Chile’s development agenda. President Bachelet recently announced her Transparency and Probity Agenda, aimed at further enhancing the probity, transparency, efficiency and modernization o f Chile’s public sector. With state modernization as one the central pillars, the transparency agenda will focus on enhancing management oversight to ensure not only accountability - that is, an appropriate use o f public funds - but also high standards o f public services. In addition, financial management would be increasingly decentralized. A system o f incentives and sanctions i s to be introduced so that municipalities can have more autonomy in financial management, based on a system o f r isk classification. Likewise, steps wil l be taken to improve the timely and accurate reporting o f municipal financial information

5. Enhancing municipal financial management i s o f particular importance given their prominent role in the provision o f services under the strategy o f decentralization. Over the past two decades, municipalities have become increasingly autonomous, while assuming responsibility for a wide range o f services and the management o f increased financial resources. N o t only are they responsible for traditional urban services - such as the paving o f urban and rural feeder roads, solid waste collection and disposal, public transportation, drainage, street lighting, parks and recreation, and public cemeteries - but they have also been delegated the responsibility for primary health care and basic (primary and secondary) education, as wel l as for administering a number o f poverty-relief programs. Municipal public education accounts for 57 and 49 percent o f the country’s enrollment in basic and intermediate education respectively. Municipal education i s even more important for the poor, providing education for 68 percent o f the poorest quintile. Likewise, 80 percent o f the overall population receives health care in municipal health centers. To match the newly assigned responsibilities, a larger mass o f funds is now being transferred to municipalities. The Common Municipal Fund (FCM), Chile’s largest source o f municipal finance has increased by a multiple o f 3.8 in real terms since i t s inception in 1982 and by a multiple o f 2.6 since 1990. Including both municipal budgets as wel l as transfers from the central government for municipal health, education and infrastructure, total municipal spending accounts for 14.2 percent o f the country’s total public expenditures. As the country moves ahead to even greater decentralization, increased autonomy and responsibilities must be accompanied by enhanced performance and accountability.

Sector Issues

6. Public sector modernization to increase efficiency in public sector management, reduce wasteful public spending, and enhance the targeting o f public services and social programs continues to be a central priori ty for Chile. Moreover, i t is widely recognized that Chile’s strong public institutions have been a key factor in the country’s economic success. A wide range o f governance indicators show that Chile ranks highest in Latin America and better than some

2

countries o f the Organization for Economic Co-operation and Development (OECD). Specifically, Chile stands out as a highly competitive country, ranking 23 out o f 117 countries in the 2005 Wor ld Economic Forum’s Global Competitiveness Report, far ahead o f the rest o f Lat in America. Similarly, Chile gets the top Lat in American ranking in the World Bank’s Doing Business in 2007. I t ranks 28th out o f 175 countries in terms o f ‘ease o f doing business,’ better than Spain and France. Out o f 163 countries assessed by the corruption perception index o f Transparency International in 2006, Chile was ranked 20 out o f out o f 158 countries, together with Belgium and the United States. The soundness o f Chile’s institutions and the rule o f law have been vital in instilling foreign investor confidence, thereby ensuring a steady f low o f foreign direct investment as wel l as access to international financial markets.

Previous Situation (Pre-SIGFE) Financial management systems were overly decentralized and inadequately integrated.

7. The modernization o f public expenditure management has been one o f the central pillars o f state reform in Chile. Although Chile’s budget procedures have been effective in yielding the fiscal surpluses critical to macroeconomic stability, by the f i rs t ha l f o f the 1990’s they were identified as an obstacle to the efficient allocation o f public resources. As opposed to more modem budget systems, Chile’s budget was characterized by a narrow focus o n controlling expenditures rather than on promoting the efficient and effective use o f resources, assessing the results o f spending, and hl ly accounting for the economic costs incurred. As a result o f a hierarchical structure with the Ministry o f Finance at the apex, l ine entities lacked financial and management sk i l ls and played only a minor role in planning and executing their operations. In addition, a lack o f adequate and t imely information together with insufficient capacity for planning and evaluation undermined service delivery. Finally, the legislature and the public saw the budget process in terms o f haggling about incremental annual changes in resource allocations rather than an opportunity for more informed debate o n strategic goals and trade-offs.

Current Situation (Post-SIGFE) SIGFE i s n o w operational in 349 out o f the 39 1 entities within the central government (equivalent to 90 percent coverage within the central government).

3

Previous Situation @re-SIGFE)

Financial management systems were unable to provide real time data and adequate information for performance monitoring.

The formulation and supervision o f macroeconomic policy and public investment suffered from organizational overlaps, gaps in information, and insufficient coordination especially between economic and social sector ministries and on inter-temporal decisions.

There was no modem human resource management information system linked to financial management.

There was no modern procurement system linked to financial management.

The financial and human resources units in public entities were weak.

The government lacked a broadly disseminated and robust system to evaluate budget execution.

Current Situation (Post-SIGFE) There are approximately 7,000 active users o f the system, who, on a typical day, use it to make more than 80,000 transactions. A t the sector level, information on budget execution i s available on the Internet in real time. Aggregated information on budget execution across the board i s made available to Congress and to the public with a lag o f only 30 days. Aggregated information from SIGFE i s being used increasingly to support not only reporting requirements but also decision making by various government entities, including the Ministry o f Finance, sector ministries and other government entities. The process o f implementing SIGFE has encouraged coordination between key government entities, particularly DPRES and CGR. For example, the CGR performed an overall evaluation o f SIGFE to identify problems encountered by users and to provide suggestions on how to resolve them. The development o f a Human Resources Information and Management System for the Civi l Service (Sistema de Informacidn y Administracidn de Personal-SIAPER) also received Bank support under the Public Expenditure Management Project. Although there have been some delays, i t i s anticipated that the system will be implemented in 20 institutions on a pilot basis by the end o f 2007. When completed, SIAPER will be fully integrated with SIGFE. SIGFE has been effectively linked to the newly implemented electronic system o f public procurement (ChileCompra) and to the data bank o f public sector investment projects. The implementation o f SIGFE has gone hand-in- hand with extensive technical support for entities within the central government. In addition to providing information and communication technology (ICT) equipment, SIGFE has been supported by an extensive training program, reaching over 9,000 public managers and government officials. The Evaluation Division o f DIPRES has developed B system o f program evaluation with qualitative and quantitative program indicators based on information from SIGFE. Program evaluations are now operational in 180 public sector institutions.

4

9. The more recent Reports on the Observance of Standards and Codes (ROSC) o f the International Monetary Fund provides an assessment o f fiscal transparency in Chile (International Monetary Fund - IMF 2003, 2005). I t reveals high level o f fiscal transparency in Chile, and documents the rapid progress made in recent years to close remaining gaps. In particular, the reports point to the Government’s success in constructing and disseminating a very clear view o f i t s objectives and targets, both at the macro level and for individual budget programs. According to the IMF report, the budget clearly articulates government priorities and there are well-developed tools for evaluating budget performance. In addition, Chile has completed the f i rs t stage o f adapting i t s fiscal statistics to the IMF’s Government Finance Statistics Manual (GFSM). The authorities also reformed the budgetary classification and introduced a new functional classification o f expenditures in l ine with the GFSM. In addition, the report points to the importance o f SIGFE in facilitating public financial management, addressing data gaps (e.g., o n arrears), as wel l as a reconciling fiscal and monetary accounts (IMF 2003, 2005).

10. Notwithstanding these advances, Chilean authorities are fully committed to further enhancing public expenditure management to help achieve s t i l l greater transparency, more efficient resource management, and more effective financial planning. International experience has shown that these objectives require continuous modernization in order to consolidate and deepen institutional reforms. Public-sector modernization should be regarded as a process o f progressive advances in basic management capabilities rather than as a one-time intervention. In that respect, there s t i l l remain challenges to be addressed as Chile continues to improve its public expenditure management.

11. Further consolidation of SIGFE i s needed: SIGFE faces a number o f technical challenges to process large numbers o f financial transactions more quickly and to extend i t s coverage to al l public entities. There i s a need to update the current technology o f SIGFE, to ensure i t s scalability and adaptability as wel l as its interoperability with other systems. There i s also a need to automate the core modules o f SIGFE, including the transaction module that records payments and receipts, the aggregation module that consolidates financial information, and the configuration module that enables the initial loading and subsequent changes o f the national budget, the chart o f accounts and other institutional or sector classifications. In addition, SIGFE has to be able to operate with other institutional or market-developed systems to comply with the Circular Conjunta CGR and DIPRES No. 646/45880 that requires that standardized institutional operational systems be certified. Furthermore, since DIPRES manages the Budget Administration System (SIAP), which is used for budget formulation and administration, the S I A P and the SIGFE systems need to be linked automatically to eliminate manual errors. It is equally important is to ensure that SIGFE i s institutionally sustainable and that the SIGFE team be mainstreamed into the governmental structure. Once SIGFE is fully adopted by al l l ine entities, the Ministry o f Finance will be able to further decentralize decisions for the allocation o f resources and wil l receive financial information to monitor and control the use o f public resources. Aggregated financial information will not only allow Congress and the public at large to be better informed about the status o f budget execution, i t wil l also help the budget decision making process by improved reporting, transparency and trust between government entities, including the Ministry o f Finance, Comptroller General Off ice and Congress.

5

12. Treasury functions can be improved: One particular area o f concern i s treasury operations, which are highly decentralized. Monthly cash allotments are transferred to ministries and entities and deposited in non-interest bearing accounts. Funds are deposited in more than 600 entities and approximately 7,000 accounts. A preliminary evaluation indicates that: (i) the Treasury has l imited capacity and there i s l i t t le interconnection between Treasury systems and SIGFE, (ii) most monthly and annual tax declarations o f individuals are handled manually (approximately 80 percent o f 1,000,000 tax declarations are processed manually); (iii) the accounting and budget norms are antiquated; (iv) the procedures and systems in place produce poor records and unreliable information on revenues and expenditures; (v) there are significant delays o f up to 20 days in the preparation o f monthly revenue reports; (vi) information regarding the administration o f financial assets (activos y pasivos Jinancieros), including debt instruments i s poor; (vii) inconsistencies between reports prepared by the Internal Revenue Services and the Treasury are reconciled manually so that monthly revenue reports are unreliable. Most o f these issues could be fixed with appropriate cash management devices such as a single electronic account and updated systems. They could be introduced at minimum cost without compromising financial decentralization.

13. The further integration of Management, Control and Evaluation System (MCS) into the Budget Cycle. As part o f a successful program o f public sector modernization, Chile has established a highly regarded system aimed at enhancing effectiveness and efficiency in the management and control o f public expenditures. The system encompasses management and control as wel l as ex-post monitoring and evaluation. Chile i s practically the only country in the region, which has succeeded in developing a M C S that f i l ly encompasses budget formulation, approval, execution, and monitoring and evaluation, along with mechanisms to provide feedback throughout the budget cycle. Furthermore, the methodologies and systems provide timely and reliable information, which, in turn, enable resources to be allocated o n the basis o f pol icy priorities. Some o f the tools are: (i) Strategic Definitions; (ii) the Evaluation Program o f Government Projects (PERG); (iii) Comprehensive Management Reports; (iv) the Government Competitive Fund; and, (v) Indicators and Performance Goals included in the budget to enhance the quality o f discussion about government programs among l ine entities, the Ministry o f Finance and Congress. These advances prepared the ground for the Structural Surplus Rule (Regla de Superavit EstructuraZ). The challenge ahead i s to integrate the systems developed by DPRES, so that budget classifications and the M C S classifications are effectively linked. That will enable the use o f financial and capital cost information to enhance monitoring and evaluation, to move forward an agenda to introduce an accrual accounting system and a better- integrated budget cycle.

14. SIGFE still does not cover all Central Government Entities (CGE): The expansion o f SIGFE since i t s inception in 2002 has been remarkable. Currently, SIGFE’s transaction module, which records budget and accounting data, commitments, and cash transactions, is now operational in 349 out o f the 391 entities within the CGE (equivalent to 90 percent coverage within the central government). This includes the totality o f the health sector with 192 public hospitals. Overall, there are close to 7,000 registered users in 1,3 13 financial management units (Unidades de Administracidn Financiera - U D A F s ) . They handle budget, accounting, and cash management operations using the standardized norms, procedures, and information software defined by SIGFE. However, there are st i l l 38 entities within the central government that do not

6

yet operate under SIGFE. Some o f these entities, such as the Treasury, do not have their own systems. Others, such as Public Minister and the Ministry o f Public Works, have their own financial management system and their financial records need to be standardized to allow them to be integrated within SIGFE. That is a challenging task.

15. The goal o f the Government project i s to implement SIGFE in al l Government entities, including Police, Armed Forces and Municipalities. This Government project wil l be financed through: (i) allocations made in the Chilean budget, and (ii) the Second Public Expenditure Management Project (SIGFE 11) - the proposed Bank operation - including Bank and counterpart fbnding. The Bank project does not finance activities within the Armed Forces or the Police.

16. Municipalities differ greatly in the quality of their financial administration: The weak financial administration o f many municipalities poses a serious challenge. They are being given greater responsible for the provision o f services and, consequently, they administer a larger share o f public expenditures. In general, management systems for controlling budgets and expenditures are inadequate. According to the results f i o m a 2005 survey o f the information and communication technology (ICT) infrastructure, roughly 25 percent o f the municipalities lack a treasury module, 17 percent do not have public accounting, and 68 percent do not have a budgetary planning and control system. O f those that have such systems, approximately 40 percent are not interconnected with the tax administration. Weaknesses in financial administration at the municipal level reflect not only a lack o f modern management tools, but also processes and practices that are not transparent and result in the inefficient allocation o f public resources. Municipal resources are allocated by elected officials and are based largely on perceptions and non-technical criteria. A lack o f understanding often leads to a ‘gauging’ o f fbture revenues, artificially inflating the budget and often generating deficits - usually covert ones. Technical capacity i s also weak, as there is very l i t t le training at the municipal level. On average, less than 2 percent o f municipal budget staff a year i s given training and i t i s usually in areas others than financial management.

17. Lack of timely financial information at the municipal level: Currently, there i s a lack o f aggregate financial data at the municipal level. Although municipalities report financial information to the CGR periodically as mandated by law, the logistics are cumbersome and inefficient, both for the CGR and for the municipalities themselves. Approximately one-third o f the municipalities provide their information using electronic formats Vorrnulario plano). The other two-thirds rely o n hard copies, which are later entered manually into the CGR database. Due to the complex logistics, there are substantial delays in processing the information and making i t available. For example, the 2005 Financial Administration Report (Informe de Gestidn Financiera del Estado) that i s published every March o f the fol lowing year by the CGR showed that only 48 percent o f municipalities had reported financial data corresponding to December 2005. In addition, a l l the available information relates to actual revenues and expenditures. That does not allow the central government to determine whether municipal budgets and their revenue forecasts are reasonable. Financial information collected through the National System o f Municipal Indicators (Sistema Nacional de Indicadores Municipales - SINIM) is also backward looking on an annual basis. The lack o f timely municipal financial information hinders the ability o f the central government to effectively take the pulse o f municipal finances and to detect early the prospective fiscal problems o f individual municipalities. In addition, there are loopholes in

7

the information system that caused municipal revenues to be under-reported, particularly those revenues that are to be shared with other municipalities through the FCM. It is estimated that approximately US$20 mi l l ion o f municipal revenues go unreported each year.

18. The state of municipal finances: The analysis o f aggregate municipal accounts for the period 2000-2005 reveals that, for Chile as a whole, municipal finances are strong. In general, this analysis o f municipal finances shows no deficits, a robust growth o f own-source revenues, as wel l as sound spending patterns for the municipal sector, with approximately equal spending on investment and o n personnel. However, upon closer examination, a more complex picture begins to emerge. Although municipal fiscal performance seems robust in the aggregate, there were a considerable number o f municipalities with a current-revenue deficit in 2005. Whi le only 10 percent o f municipalities have a budget deficit, 90 percent o f them experience cash f low problems in the course o f the fiscal year. Municipalities are not permitted to borrow, according to the IMF’s Fiscal ROSC, but there seem to be cases o f ad hoc financing through arrears. Specifically, there are substantial levels o f municipal floating debt - estimated at US$ l50 mi l l ion - much o f i t with private providers o f urban services, such as street cleaning and street lighting. Likewise, there are substantial arrears in contributions to health insurance and pensions for municipal teachers, estimated to amount to more than US$50 mil l ion. When needing cash, municipalities frequently sell some o f their assets, such as buildings or equipment, and then ‘lease’ them back, regardless o f the economic rationale. The Bachelet administration has recently announced i t s intention to give municipalities more financial autonomy, including more flexibility in contracting debt. To that effect, a municipal credit rating system i s being considered.

2. Rationale for Bank Involvement

19. The Bank i s wel l placed to support Chile as it continues to consolidate i t s financial administration system within the central administration and expand it to the municipal level. The following factors justify the Bank’s continued involvement:

(i) The Bank has already established a very effective working relationship with the Chilean authorities within the context o f the ongoing Public Expenditure Management Project. The Government has indicated i t s satisfaction with the broad international experience that the Bank has been able to bring to this cooperative endeavor.

i) As indicated above, the implementation o f SIFGE has already yielded significant benefits, including enhanced fiscal transparency, robust institution strengthening, improved inter-agency coordination, and enhanced financial planning. The further consolidation and expansion o f SIGFE wil l continue to strengthen Chile’s public expenditure management, thus ensuring increased efficiency and transparency in the allocation and use o f public resources. Moreover, by strengthening financial management at the municipal level, the Project will help improve the effective utilization o f municipal resources while promoting greater accountability.

(iii) With extensive experience in the Chile’s municipal sector, the Bank i s well positioned to help the Government extend its public expenditure modernization agenda to municipalities. The Bank has played an active role supporting Chile’s decentralization

8

efforts since the reestablishment o f democratic rule. The Chile: Sub-National Government Finance study (Report No. 10583; October 13, 1992) outlined a sector strategy to support improvements in sub-national government finances. Subsequently, the First and Second Municipal Development Projects (Programa de Fortalecimiento Institucional Municipal; PROFIM-I and 11; Loans No. 3668-CH and 4429-CL) supported the Government’s policies for gradual decentralization and for strengthening and modernizing municipal governments. Particularly relevant to this project was the Bank’s experience in supporting the development o f a National System o f Municipal Indicators (SINIM), which received Bank financing under the two municipal operations.

One o f the Bank’s assets i s i t s ability work across entities within the central administration and at various levels o f government - i.e., central government and municipalities - which will help foster the coordination needed for the successfbl implementation o f the next phase o f financial management modernization.

The Project is f i l ly consistent with the Bank’s overall strategy o f assistance to Chile. Specifically, the Project directly supports a strategic objective o f the Country Partnership Strategy Report No. 38691-CL, April 24, 2007), which aims at accelerating sustainable growth by, inter alia, strengthening public sector management. Likewise, the Project’s objectives are in l ine with the findings o f the latest Development Pol icy Review (Report No. 33501-CL; June 2006), which concluded that the utilization o f revenues and transfers could be improved by giving more discretion to municipalities along with greater accountability, as well as by strengthening institutional capabilities at the local level in preparation for further decentralization. The Project i s also consistent with the findings o f a study undertaken by the Bank o n a fee-for-service basis, which evaluated the effectiveness o f the Government’s own system o f program evaluation (Report No. 34589- CL, December 30, 2005). In addition, Project wil l generate synergies with other components o f the Bank’s analytic work, including a Country Procurement Assessment Report (CPAR) and fol low up o n the Country Financial Accountability Assessment (CFAA, Report No. 32630-CL June 27,2005)

3. Higher level objectives to which the project contributes

20. The project would improve public expenditure management by furnishing Congress and the Executive with more effective tools for budget formulation and budget execution. Better public expenditure management would, in turn, ensure increased efficiency and transparency in the allocation and use o f public resources. Congress, the Executive and the public at large would have access to financial information that i s more accurate, timelier and more complete, thereby supporting the Transparency and Probity Agenda o f the Bachelet administration as well as the objectives o f the World Bank Country Partnership Strategy (CPS) for 2007-2010. The expansion and strengthening o f SIGFE is one o f the Government’s key initiatives incorporated in the 2007 Budget law.

9

B. PROJECT DESCRIPTION

1. Lending instrument

21. (SIL) to support technical assistance during FY 2008-2012.

2. Project development objective and key indicators

22. The overall development objective would be to increase the efficiency o f operations regarding financial management, budget formulation, and budget execution, and the transparency o f public expenditure management at the central and municipal level through the implementation o f an updated, hnct ional ly enhanced and expanded financial administration system (SIGFE).

The Government o f Chile has requested a US$24.8 mi l l ion Specific Investment Loan

The indicators for the aforementioned PDO outcomes would be as follows:

Improve EfJiciency of the Public Financial Management Administration: Time required for aggregating the financial data o f the central government i s to be reduced from 30 to 8 days. Increase Efficiency of Operations regarding Budget Formulation and Execution: Time required to update SIGFE (execution) with the data generated by the SIAP system (formulation and administration) i s to be reduced from one week to one day. Improve Efficiency of Budget Execution: Processing capacity o f the SIGFE transaction module is to be increased from 95,000 to 200,000 financial transactions per day, with a response time o f 8 seconds per transaction measured at the portal. Improve Efficiency of Financial Management Operations and Improve Effectiveness of Fiscal Control: Time for processing transactions within the Central Government Entities so that the information i s available in SIGFE is to be reduced f rom 20 days to less than 3 days. Increase Transparency of Municipal Financial Information: Financial information and expenditures o n at least 100 municipalities i s to be made available in the Municipal Financial Information System, which can aggregate the financial information o f a l l (presently 345) municipalities. Increase EfJiciency of Fiscal Monitoring of Municipal Finances: Information on aggregate municipal finances i s to be made available at the central level within 30 days instead o f presently up to 180 days. Increase Effectiveness of Budget Cycle Indicators: All monitoring indicators wil l be aligned with the financial indicators and integrated in the budget formulation and execution. The new methodology will be adopted by al l Ministries covered by the M C S and wil l be integrated in the budget by 201 1.

The PDO would be achieved through upgrading and expanding the financial administration system (SIGFE) and by developing and implementing a new municipal financial information system. The new SIGFE system for Central Government Entities would adopted by al l CGE. I t would be compatible with other systems used by government entities and levels o f government not adopting the upgraded SIGFE system for significant technical reasons. On the municipal level the project would strengthen the financial administration capacity and on

10

the central level a new municipal financial information system would be developed and implemented that would be capable o f aggregating information from al l municipalities.

Intermediate outcome indicators would be as follows:

Improve Efficiency of Public Financial Management: SIGFE would be upgraded by enhancing functionality and increased usability as wel l as the upgrading i t s technological platform, which wil l reduce processing time. Improve Efficiency of Budget Execution: SIGFE would be upgraded and technically enhance the link with SIAP. Linking both systems will ensure the consistency o f budget data, and wil l improve the updating o f the systems in case o f changes if necessary. Improve EfJiciency of Financial Management Operations and Improve Effectiveness of Fiscal Control: The upgraded and expanded system wil l allow users to monitor and execute transactions through a single operation in real time. At present, transactions must fol low a number o f steps including: verify the budget approval, confirm funds allocation, validate account balances, assign invoice numbers and execute financial transactions individually. Increase Transparency of Municipal Financial Information: The new municipal financial information system wil l allow the Government to have complete information about the municipal finances through an aggregation system. At present, municipalities have different accounting systems o f varying quality. This slows down reporting o f the municipal financial data to the central government. Increase Efficiency of Municipal Financial Information: The new municipal financial information system will ensure interoperability with SIGFE. Increase effectiveness of Budget Cycle Indicators: The upgraded and expanded system wil l incorporate monitoring and evaluation indicators from the MCS, which are aligned with budget data, and budget indicators. During budget formulation, the DIPRES and Congress will have al l necessary projects and programs data available allowing for an analysis o f the services o f the entities taking into consideration financial information and performance. At present, M C S information i s not fully consistent with financial indicators for projects and programs. Increase Transparency of public expenditure: The upgrading o f SIGFE and interoperability o f SIGFE with M C S wil l improve the quality o f budget information and improve the quality o f information disseminated.

3. Project components

26. The operation would consist o f four components: Component 1 - Upgrading and Expansion o f SIGFE; Component 2 - Improvement o f Budget Procedures and Mechanisms o f the Management Control System; Component 3 - Strengthening Financial Administration at the Municipal Level; and Component 4 - Project Management. Table 2 shows the financing for each component:

11

Component

Component 1

Total World Bank Financing Local Financing

31.1 17.1 I 55.0% 14.0 45.0% (US$ Mil l ion) (US$ Mil l ion) % (US$ Mi l l ion) %

Component 2 Component 3 Comoonent 4

27. Component 1 - Upgrading and Extending the Financial Information System to the Central Government Entities (US$31.1 million of which US$l7. I million would be financed by the Bank loan): This component would provide technical assistance, training, design and development o f software and equipment as wel l a procurement o f software licenses to upgrade SIGFE and install it in Central Government Entities. In particular, i t would support the further development and consolidation o f SIGFE by: (i) upgrading and optimizing the I C T and technical design o f SIGFE modules; (ii) improving i t s finctionality, interoperability and reporting; and, (iii) implementing data standards issued by Normative Entities in al l entities using the homologated systems. There would be three sub-components as follows:

4.7 2.8 60.0% 1.9 40.0% 7.5 4.5 60.0% 3 .O 40.0% 3.4 0.4 11.8% 3.0 88.2%

28. Sub-Component 1.1: Upgrading and Expanding SIGFE Functions (US$22.3 million of which US$13.4 million would be financed by the Bank loan): This sub-component would provide assistance to transform SIGFE into a modern integrated web-based system by: (i) eliminating redundant and outdated operations, increasing processing capacity and better integrating the transaction, aggregation and configuration modules; (ii) updating the software to improve budget programming and budget execution as well as accounting and treasury hnctions; (iii) strengthening the interoperability o f SIGFE with other systems; (iv) optimizing the reporting capacity o f SIGFE for the benefit o f internal and external users, including public sector entities, Congress, and Normative Entities; and (v) mainstreaming the organization and the functions o f SIGFE within DPRES and establishing financial management units within Central Government Entities.

Sub-Total 46.6 24.8 Fee 0 0 Total 46.6 24.8

29. The activities to be financed within this sub-component include:

53.1% 21.8 46.9% 0% 0 0%

53.1% 21.8 46.9%

Updating o f software to improve and optimize SIGFE hnctions, especially with respect to budget programming, budget execution, and accounting and treasury f i c t i o n s . Upgrading software and hardware to overcome operational problems, increase processing capacity, facilitate the integration o f a l l modules, and increase automatic l i n k s between different budget, commitment and accounting classifications. Strengthening the capacity o f SIGFE to prepare reports for internal and external users, such as other public entities, Congress, and the Normative Entities. Improving SIGFE to allow interconnectivity with other systems such as ChileCompra (Chile’s e-procurement system), MIDEPLAN’s public investment database (Banco Integrado de Proyectos - BP) and other systems aimed at improving the decision-making process, including fixed asset and cash management.

12

Strengthening the capacity o f financial units within Central Government Entities and diagnostic o f the improvement needs o f key processes within the financial administration and o f the normative framework related to the access and processing o f data. Supporting the integration o f SIGFE as an operational unit within D P R E S on the basis o f best international practice. Implementation o f a system for aggregation and consolidation o f financial information o f the general government with financial and accounting information provided by the Central Government Entities and municipalities.

0

30. Sub-Component 1.2 - Extending S IGFE to Central Government Entities (US$4.7 million of which US$2.8 million would be financed by the Bank loan): This sub-component would finance the expansion o f the transaction module o f SIGFE or, alternatively, the certification o f agency-developed or market-developed systems to fully integrate financial information o f a l l Central Government Entities into the existing system. Central Government Entities are al l entities at the central government level. The Project will not finance activities within the Armed Forces or the Police. Although the transaction module o f SIGFE has been adopted by 90 percent o f a l l CGE, the remaining 10 percent represent a large share o f the budget. These entities include: the National Treasury, the Ministry o f Public Works, the Legislature and the Judiciary. This sub-component would support the integration o f existing independent systems into SIGFE though assimilation or certification (homologation). Further this component would finance the integration o f SIGFE into the National Pension Administration (Instituto Nacional de Previsidn).

3 1. The activities to be financed within this sub-component include: Definit ion o f reporting standards consistent with the norms issued by the Normative Entities for the Central Government Entities, which have financial information systems other than SIGFE. Analysis and evaluation o f the results o f the implementation process o f market products used in Central Government Entities, e.g., the Corporation for Production Development (Corporacidn de Foment0 de la Produccidn - CORFO). Implementation o f one such market products on a pi lot basis in one institution such as the Ministry o f Public Works or the Tax Revenue Services. Diagnostic o f the improvement needs o f the financial management processes in Central Government Entities so that they may be integrated into SIGFE. Installation o f SIGFE or alternative systems in the Borrower’s Pension Administration Agency (Instituto de Normalizacidn Previsional) or its successors. Provision o f hardware for the implementation o f SIAPER in Central Government Entities.

32. Sub-Component 1.3 - Strengthening the Public Treasury (US$1.5 million of which US0.9 million would be financed by the Bank loan): This sub-component would focus on modernizing the Treasury and the treasury functions to improve the recording o f accounting and budget transactions.

33. e

Activities to be financed include: Revision and updating o f the conceptual module, including norms and procedures, to update accounting and budget records o f the Public Treasury.

13

0

0

Revision o f norms and procedures used in the recording and administration o f financial assets and liabilities. Design and implementation o f improvements to the Public Treasury accounting and budget records system Review o f the interconnection between such improved accounting and budget systems with other information and management subsystems o f the Public Treasury, consistent with the norms and procedures approved by the Normative Entities.

34. Component 2: Improvement of Budget Procedures and Mechanisms of the Management Control System (US$4.7 million of which US$2.8 million would be financed by the Bank loan):

This component would focus on supporting efforts to enhance the quality o f public expenditures by strengthening the Management Control System (MCS) and integrating i t into the Budget Cycle. Specifically, this component would focus on developing and implementing: (i) a new conceptual model for the Budget Cycle, linking the budget classification with the information categories o f the MCS; (ii) a M C S information system; and (iii) a new version o f the budget formulation system (SIAP) used by DIPRES. Innovative methods o f budget formulation would be developed for selected pol icy modules and the capacity o f DIPRES to undertake results-based monitoring and evaluation would be strengthened. This component consists o f two sub- components : Figure 1: Budget Cycle

35. Sub-Component 2.1 - Improvement of Budget Procedures (US$3.1 million of which US$1.9 million would be financed by the Bank loan): This subcomponent would support the development o f new budget processes and techniques to enhance the overall quality o f budget design. Whi le Chile’s budget systems are wel l developed, there i s additional room for further improvement, particularly in terms o f linking resource allocations to measurable results. The incentives for client entities to participate in SIGFE would be enhanced by demonstrating how performance-based management can help them improve their own effectiveness and efficiency.

14

36. The activities to be financed include: Developing a conceptual model for integrating information f rom the Borrower’s MCS into the Borrower’s budget formulation process, including linking the budget classification with the information categories o f the MCS.

0 Developing new budget techniques such as budget formulation by pol icy areas and performance-based-budgeting.

0 Developing and implementation o f an improved version o f the budget formulation system (SIAP) in DIPRES interconnected with SIGFE and the MCS.

0 Studies to improve the borrower’s budget process, including public treasury functions and cash management. Strengthening DIPRES’ capacity to generate information to be provided to Congress.

37. Sub-component 2.2 - Strengthening the Management Control System (US$l. 6 million of which US$l million would be financed by the Bank loan): The objectives o f this sub- component are: (i) applying the conceptual model to integrate the budgetary process with the Management Control System; (ii) using information from the M C S as an input for decision making during the budget cycle; and (iii) developing a management and control information system that integrates the various M C S tools and that interacts with the financial administration systems (SIGFE and SIAP). Implementation o f this subcomponent will be the responsibility o f the Management Control Division (Divisidn de Control de Gestidn) o f DIPRES.

38. A strengthened MCS, better integrated with the decision-making processes o f the budgetary cycle, would contribute to increase the quality o f public expenditures in terms o f their effectiveness and their efficiency. In addition, the linkage between the M C S information system and the financial administration system would result in an integrated system.

39.

0

The activities to be financed within this sub-component include: Strengthening the existing information technology instruments used by the M C S and integrating them better. Developing and implementing an M C S information system that interoperates with SIGFE and SIAP, as defined in the conceptual model described under sub-component 2.1. Strengthening the institutional capacities o f the M C S so that it may operate along the l ines envisaged by the conceptual module described under sub-component 2.1. Developing a new methodology to quantify a ‘coverage indicator’ o f the MCS. This new indicator wil l measure the relative weight o f public sector programs included under the M C S as a percentage o f the public sector programs in the overall budget. Improve processes to enable decision makers in government entities and in Congress to make more efficient use o f information generated by the MCS. Reporting formats would be adapted to the specific needs o f users.

40. (US$7.5 million of which US$4.5 million would be financed by the Bank loan):

Component 3 - Strengthening Financial Administration at the Municipal Level

This component would focus on: (i) improving the availability o f information on municipal budgets and on financial transfers; (ii) strengthening financial administration at the municipal

15

level; and (iii) improving the effective use o f central government transfers to municipalities, for example within the Municipal Fund (Fond0 Comun Municipal). The Off ice o f the Comptroller General in partnership with the Sub-secretariat for Regional Development within the Ministry o f the Interior (Subsecretaria de Desarrollo Regional y Administracidn - SUBDERE) would implement this component. Finance would be provided for technical assistance, supplies and training within two sub-components, as follows:

41. Sub-Component 3.1 - Development of a Municipal Financial Information System (US$2.5 million of which US$1.5 million would be financed by the Bank loan): This sub- component would support the development o f a Municipal Financial Information System that includes al l Chilean municipalities. The system would be capable to aggregate financial information f rom all, presently 345, municipalities, according to the normative framework - e.g., budget classifications and accounting framework (Plan de Cuentas) - defined by the responsible Normative Entities (organismos rectores). It would record financial information corresponding to areas o f municipal responsibility - e.g., municipal management, health, education, and cemeteries.

42. The activities to be financed within this sub-component include: Develop and implement a Municipal Financial Information System, which wil l be linked to the Municipal Financial Administration Sub-Systems, and i s capable to aggregate and integrate financial information from the sub-systems o f a l l municipalities. This system would be both flexible and dynamic and, thus, able to respond to the changing needs o f the users. The conceptual model wil l be based on the aggregation module o f SIGFE I. Develop an interface linking the Municipal Financial Information Sub-systems to the new Municipal Financial Information System within SUBDERE. Def ine norms to standardize the financial information o f individual municipalities according to requirements specified by the Normative Entities to meet the needs o f internal and external users; and streamline the reporting required from municipalities by CGE. Strengthening the Government’s capacity, in particular DIPRES and SUBDERE, for analyzing and monitoring o f the financial situation o f municipalities. Disseminate information about the Municipal Financial Information System to municipalities and the Chilean Association o f Municipalities (Asociacidn Chilena de Municipalidades ACHM). Training users in the use o f the system.

43. Sub-Component 3.2 - Installation of a Sub-System of Municipal Financial Administration (US$5 million of which US$3 million would be financed by the Bank loan): This sub-component would strengthen financial administration at the municipal leve l by developing a simplified sub-system o f financial management in municipalities that lack adequate systems, and by upgrading others to ensure that they meet the homologation standards defined under the Municipal Information System. This component would cover about one hundred municipalities. The financial administration sub-system would cover budget, accounting and treasury functions. I t would be consistent with the normative framework established by Normative Entities. I t would incorporate the budget classifications jo int ly determined by CGR, DIPRES and SUDBERE, and the accounting processes (Plan de Cuentas) established by the CGR. This subsystem would comply with the homologation standards defined under the Municipal

16

Financial Information System. Special emphasis would be placed on training municipal authorities and officials not only in the operation o f the financial administration sub-system but also in the use o f information. Implementation at the municipal level would build on the lessons learned during the introduction o f Chile’s electronic procurement system (ChileCompra) at the municipal level.

Lessons Learned Leadership, clear strategic direction, and commitment are critical for success.

Coordination i s critical.

Training and technical support during the

44. The activities to be financed within this sub-component include: Diagnosis o f the information technology and communication capacity at the municipal level, based on a survey o f the technological infrastructure currently available in the Municipalities, including internet access and broad-band connection. Diagnosis o f the financial administration systems available in the market, their capabilities and the cost o f installation and operation o f such systems. Strengthening the capacity o f selected Municipalities to operate financial administration subsystems and the Municipal Financial Information System. Strengthening o f financial administration o f selected Municipalities, including, inter alia, the provision o f equipment and the introduction o f a system o f financial administration in those municipalities that currently lack one, including data assembly, testing, and equipment, data migration and implementation o f the Technology Upgrading Plans, as applicable. Provision o f training programs for municipal authorities and staff, focusing on the operation o f the new financial administration sub-system and the use o f information f rom it.

0

0

0

Project Design Inter-agency coordination i s critical to the success o f the Project and DIPRES will assume a leadership role during project implementation, as it did during the f i r s t stage o f SIGFE’s development. The CGE need to coordinate both their message and their actions in order to avoid codusion and in order to maximize their effectiveness. The responsibilities and prerogatives o f other key actors-Le., SUBDERE and CGR-will be clearly defined. A critical mass o f officials at the managerial and operational level

45. financed by the Bank loan):

Component 4 - Project Management (US$3.4 million of which US$0.4 million would be

This component would cover operating expenses, with the Borrower contributing US$3 .O mil l ion o f counterpart funds, related to the fol lowing activities: 0 Provision o f technical assistance to Central Government Entities as part o f the

0 Strengthening the Government’s capacity to monitor and supervise the overall implementation o f SIFGE or SIGFE-compatible financial administration systems.

implementation o f the Project.

4. Lessons learned and reflected in the project design

17

Lessons Learned implementation o f SIGFE and beyond are critical.

I t i s critical to provide timely and sufficient support to users during implementation.

Need to establish an inclusive and integrated framework for systems development and replication.

A mature information system i s best conceived as a system with multiple actors, including those who provide input data and those who use it.

Need to include municipalities early on in the design process.

Need to limit the scope o f the project.

Need to identify a ‘champion o f reform’ in each government agency project leadership and political coordination. There should be close, continuous dialogue with counterparts at the national and sub- national levels.

Need for political commitment to modernization.

The technical soundness o f municipal counterpart has to be ensured, particularly in small- and medium-sized municipalities where weak technical capacity has been a bottleneck.

Local information systems should be Conceived as a dynamic process. They should allow for periodic revisions, and also set in place processes and mechanisms to

Project Design has to be trained in the use o f the new tools. Implementation has to be flexible enough to accommodate unanticipated needs in terms o f time and resources. As in the previous operation, there wil l be progress reports and training programs from basic computer use to specific sk i l l s such as accounting or treasury. A help desk will continue to operate to solve urgent p rob lem on the spot and thereby facilitate project implementation. An e-government framework for policy, interoperability, integration and replication w i l l be sought as part o f the consolidation o f SIGFE and the development o f the Municipal Financial Information System Early in the design process, an inventory o f the needs o f users-e.g. entities within the central administration, Congress, regional and municipal governments, non-government associations, and academia-will be made and used to design the new version o f SIGFE and the Municipal Financial Information System. After a failed f i r s t attempt as a result o f resistance from municipalities, the SINIM was successfully implemented largely due to the participatory process that was adopted subsequently. Individual municipalities as well as the A C H M w i l l be invited to participate in the design o f the Municipal Financial Information System. The A C H M has already indicated its support for the development o f such an information system. As opposed to the Municipal Development Projects, which tackled financial management as one component o f a more complex municipal agenda, this project w i l l focus exclusively on financial management, working joint ly wi th al l critical stakeholders at the central level-including, not only SUBDERE but also DIPRES and CGR. Each participating government agency and municipality will be expected to designate a counterpart responsible and accountable for the project. Chile’s municipalities are extremely heterogeneous and r e w i r e - individual (rather than wholesale) implementation arrangements. SUBDERE’s strong ties to municipalities-both individual municipalities and the ACHM-wil l facilitate the dialogue. Thus, the SUBDERE w i l l be responsible for the implementation o f Component 3, There i s strong political support f rom the highest authorities for the expansion o f SIGFE at the central level and the development o f a Municipal Financial Information System. A demand-based approach w i l l be adopted for municipal strengthening to ensure the participation o f those with a w i l l to participate. Component 3, which focuses on municipal financial management, w i l l have a strong focus on training in basic I C T ski l ls as well as financial administration and budget processes with an emphasis on newly adopted budget classifications and accounting procedures. Municipalities w i l l also be provided with basic working tools- such as computers and communication technology-as needed. A steering committee with representatives from the major stakeholders-DIPRES, CGR, SUBDERE and representatives from the municipalities-will be established to oversee the Municipal Financial Information System. Annual and five-year evaluations

18

Lessons Learned foster change and innovation.

Making local information systems accessible to the general public enables citizens to effectively monitor the performance o f local governments and, in turn, increases the credibility o f the overall system.

5. Alternatives considered and reasons for rejection

Project Design w i l l be conducted to ensure that the f i anc ia l information as well as the processes o f collection, aggregation, and distribution corresponds to the needs o f users. Information about the Municipal Financial Information System wi l l be made available to the public.

47. Develop a new SIGFE in house vs. purchasing a commercial product. The project team has evaluated the pros and cons o f commercial products that could replace SIGFE. I t was decided that the new version o f SIGFE will operate with open standards based on J2EE specification, with minimal proprietary elements, at the database engine level. In addition, to ensure scalability and adaptability, a modular application development strategy i s envisaged on the basis o f a services oriented architecture (SOA). This approach allows for the incremental development o f applications; the integration o f the system into a Web environment, and interoperability with different SIGFE modules and with the applications o f other entities (e.g. Chile-Compra). The fol lowing tasks wil l be outsourced: (i) the detailed IT design and construction o f the application; (ii) the process o f conformity testing; and (iii) the evaluation o f the application’s user friendliness. The SIGFE team proposal wil l hire local and international f i rms, based on international and national competitive bidding. The objective wi l l be to have the SIGFE application developed during 2008 and to begin implementation in 2009. DIPRES i s considering contracting an external data center and using the current DIPRES data center as a backup.