Embed Size (px)

Citation preview

The World in 2050 -- Perspective on Global Economic Competition and the Role of China

John Hawksworth Head of Macroeconomics PricewaterhouseCoopers

Beijing, 16 May 2006

Date16 May 2006Page 2

PricewaterhouseCoopers LLP

Agenda

Methodology

- Growth model and key assumptions

- Market exchange rates vs PPPs

Key results: focus on China and India

Implications for OECD and Chinese companies

Public policy issues

Q&A

Date16 May 2006Page 3

PricewaterhouseCoopers LLP

Study covers the 17 largest economies in the world in 2004 based on GDP at PPPs (World Bank estimates)

G7 plus Spain, Australia and South Korea

E7 economies

- BRICs (Brazil, Russia, India and China)

- Indonesia, Mexico and Turkey

Note: methodology could easily be extended to other countries (though probably not small, very open economies like Ireland)

Date16 May 2006Page 4

PricewaterhouseCoopers LLP

Growth model structure

Each country modelled individually but with linkages via US productivity growth (the global technological frontier)

Cobb-Douglas production function with human capital included

Growth driven by:

- Investment in physical capital

- Working age population growth (UN projections)

- Investment in human capital (rising average education levels)

- Catch-up with US productivity levels (at varying rates: 0.5-1.5% per annum of the TFP gap closed each year)

Real exchange rates vary with relative productivity growth

Date16 May 2006Page 5

PricewaterhouseCoopers LLP

Figure 1: Relative GDP at market exchange rates and PPPs (2004)

0

20

40

60

80

100

120

Source: World Bank

Ind

ex r

elat

ive

to U

S =

10

0

GDP at market exchange rates

GDP at PPPs

China

India

US

Brazil RussiaUK

Date16 May 2006Page 6

PricewaterhouseCoopers LLP

How to compare GDP: Market exchange rates or PPPs?

GDP at PPPs a better indicator of:

- Relative living standards (GDP per capita)

- Volume of outputs or inputs (oil, carbon emissions etc)

GDP at market exchange rates better for assessing current market size for investors/exporters into emerging economies

- but need to allow for real exchange rate changes in longer term projections

Date16 May 2006Page 7

PricewaterhouseCoopers LLP

Projected real exchange rate changes: ratio of MERs to PPPs

0 20 40 60 80 100

India

China

Indonesia

Turkey

Brazil

Russia

Mexico

2005

MERs as % of PPPs

Date16 May 2006Page 8

PricewaterhouseCoopers LLP

Projected real exchange rate changes: ratio of MERs to PPPs

0 20 40 60 80 100

India

China

Indonesia

Turkey

Brazil

Russia

Mexico

2005

2050

MERs as % of PPPs

Date16 May 2006Page 9

PricewaterhouseCoopers LLP

Figure 3: Projected average growth rate of working age population: 2050-50

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

Source: UN

% c

han

ge p

er a

nnu

m

IndiaUS

UK

China

Brazil

Russia

Date16 May 2006Page 10

PricewaterhouseCoopers LLP

Figure 4: Human capital per worker relative to the US

0

20

40

60

80

100

120

Source: PwC estimates using base data from Barro and Lee (2001)

Ind

ex r

elat

ive

to U

S =

10

0

2050 estimate

2004 estimate

UKRussia

China India

Korea

Date16 May 2006Page 11

PricewaterhouseCoopers LLP

Key model results

GDP growth

Relative size of economies

GDP per capita levels

Sensitivity analysis

Date16 May 2006Page 12

PricewaterhouseCoopers LLP

Figure 6: Real GDP growth in US, Japan and the BRICs

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

% r

eal g

row

th

US

China

India

Brazil

Russia

Japan

India

China

Brazil

Russia

US

Japan

Date16 May 2006Page 13

PricewaterhouseCoopers LLP

Projected average real GDP growth: 2005-50

0 2 4 6 8

India

Indonesia

China

Turkey

Brazil

Mexico

Russia

US

UK

Germany

Japan

Domestic currency

% real GDP growth p.a.

Date16 May 2006Page 14

PricewaterhouseCoopers LLP

Projected average real GDP growth: 2005-50

0 2 4 6 8

India

Indonesia

China

Turkey

Brazil

Mexico

Russia

US

UK

Germany

Japan

Domestic currency

US $ terms

% real GDP growth p.a.

Date16 May 2006Page 15

PricewaterhouseCoopers LLP

Figure 7: Relative size of G7 and E7 economies

0

20000

40000

60000

80000

100000

120000

140000

2005 MER 2050 MER 2005 PPP 2050 PPP

$ bi

llio

n (

2004

rea

l va

lues

)

G7 GDP

E7 GDP

Date16 May 2006Page 16

PricewaterhouseCoopers LLP

Relative size of E7 vs G7 economies: 2005, 2025 and 2050

0

20

40

60

80

100

120

140

160

180

200

GDP at MERs GDP at PPPs

2005

2025

2050

Index: G7 GDP = 100

Date16 May 2006Page 17

PricewaterhouseCoopers LLP

China and India vs US GDP in 2050

0

20

40

60

80

100

120

140

160

China at MERs China at PPPs India at MERs India at PPPs

2005

2025

2050

Index: US = 100

Date16 May 2006Page 18

PricewaterhouseCoopers LLP

China and India dominate E7 economies (relative GDP at MERs)

0

20

40

60

80

100

120

2005

2025

2050

Index: US = 100

Date16 May 2006Page 19

PricewaterhouseCoopers LLP

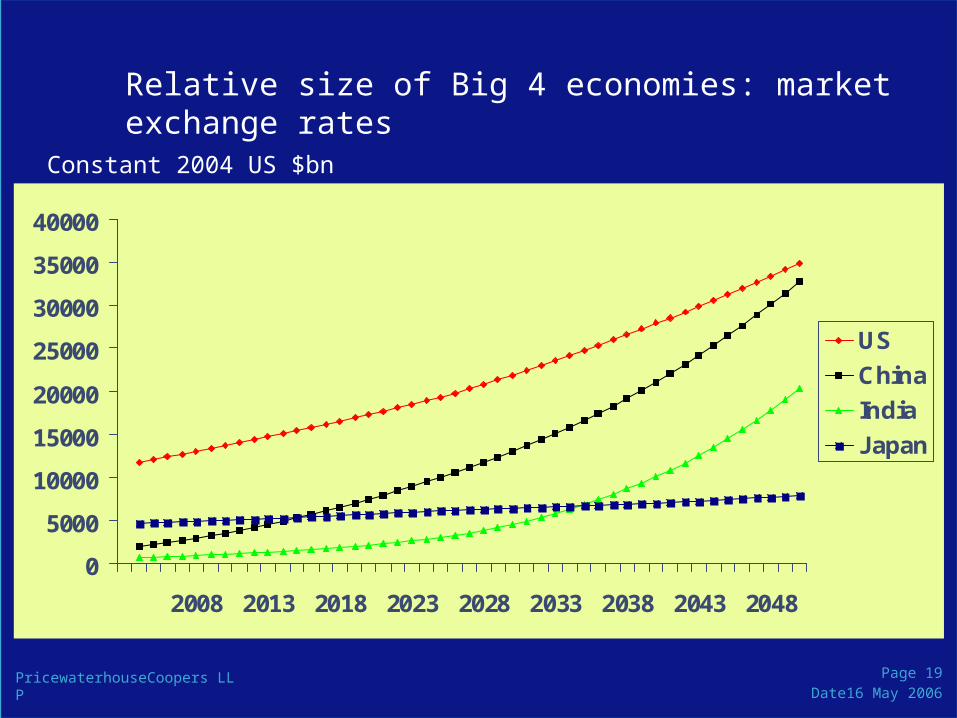

Relative size of Big 4 economies: market exchange rates

0

5000

10000

15000

20000

25000

30000

35000

40000

2008 2013 2018 2023 2028 2033 2038 2043 2048

US

China

India

Japan

Constant 2004 US $bn

Date16 May 2006Page 20

PricewaterhouseCoopers LLP

Relative size of Big 4 economies: PPP exchange rates

0

10000

20000

30000

40000

50000

60000

2006

2009

2012

2015

2018

2021

2024

2027

2030

2033

2036

2039

2042

2045

2048

US

China

India

Japan

Constant 2004 US $bn at PPPs

Date16 May 2006Page 21

PricewaterhouseCoopers LLP

Figure 8: Projected GDP per capita in PPP terms

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2004

$ p

er

cap

ita a

t P

PP

s

2005

2050

US

UK

Russia

Brazil China

India

Germany

Korea

E7 still well below G7 onincome per capita at PPPs

Date16 May 2006Page 22

PricewaterhouseCoopers LLP

Sensitivity analysis

Results are particularly sensitive to assumptions on:

- investment rates

- education level trends

- catch-up rates for E7 economies

- real exchange rate relationship to productivity (for GDP at MERs)

Perfectly possible that China relative to US could be 30% higher or lower than base case in 2050 – but would not alter the broad direction of change

Model allows effect of alternative assumptions to be explored

Date16 May 2006Page 23

PricewaterhouseCoopers LLP

What might derail growth in China and India?

Macroeconomic instability:

- Overheating in China

- Fiscal deficit in India

Energy, water and transport infrastructure constraints

Over-investment without proper capital allocation mechanisms (c.f. Japan in 1980s/1990s)

Protectionism in key export markets (US/EU)

Political instability

Environmental crises

Date16 May 2006Page 24

PricewaterhouseCoopers LLP

How can the OECD economies compete with China, India and other E7 economies?

Competitive advantage vs comparative advantage

- Some commentators focus on the former -> relative pessimism

- Economists tend to focus on the latter -> relative optimism (though there will be winners and losers)

- recent PwC survey suggest multinational CEOs also mostly positive about opportunities in BRICs

Date16 May 2006Page 25

PricewaterhouseCoopers LLP

Figure 9: Accessing new customers is the key driver for doing business in emerging economies

12

48

82

28

18

35

46

74

35

39

22

50

75

38

48

11

56

76

30

20

0 20 40 60 80 100

Accessing a highlyskilled talent pool

Serving existingcustomers

Accessing newcustomers

Increasing capacity

Reducing costs

%

Brazil

China

IndiaRussia

Ref: Q5. Which of the following business objectives are driving your decision to do business in………………..?

Source: PricewaterhouseCoopers’ 9th Annual Global CEO Survey. All respondents, except Brazil, China, India and Russia (331-674)

China ranks higheston cost reduction

India ranks higheston skilled talent pool

Date16 May 2006Page 26

PricewaterhouseCoopers LLP

Figure 10: Main actions that CEOs are taking/planning to take inemerging economies

11

28

53

22

48

13

17

11

32

52

26

44

28

30

10

40

62

27

54

33

34

32

47

26

35

15

19

12

0 10 20 30 40 50 60 70 80

Making charitable donations/performing other pro-bono work

Developing unique products for this market

Forming alliances with partners

Engaging in mergers and acquisitions

Opening new offices

Offshoring manufacturing activities or supportservices within your own company

Outsourcing manufacturing activities or supportservices to a third party

%

Brazil

China

India

Russi a

Ref: Q6. Which of the following actions is your organization taking or planning to take in………………..?

Source: PricewaterhouseCoopers’ 9th Annual Global CEO Survey. All respondents, except Brazil, China, India and Russia (331-674)

China is toppriority on mostmeasures

Date16 May 2006Page 27

PricewaterhouseCoopers LLP

China and India have different comparative advantages

India has strengths in:

- IT skills and technologies

- low cost English speaking staff for offshoring services

- younger population

China has advantages in:

- low cost manufacturing

- higher average education levels

- higher savings and investment rates

Should create potential for mutually beneficial trade

But: also competing for resources to support growth

Date16 May 2006Page 28

PricewaterhouseCoopers LLP

Relative competitiveness rankings: China vs India

5731Business competitiveness index

5033- Macroeconomics environment sub-index

5256- Public institutions sub-index

5564- Technology sub-index

5049Overall global competitiveness index

IndiaChinaCountry rankings (out of 117)

Source: World Economic Forum Global Competitiveness Report 2005

Date16 May 2006Page 29

PricewaterhouseCoopers LLP

Potential impact on OECD companies over next 10 years

Winners

Retailers

Global brand owners

Business and financial services

Creative industries

Healthcare and education providers

Niche high value added manufacturers

Losers

Mass market manufacturers (both low tech and increasingly hi-tech)

Financial services companies not able to penetrate E7 markets who become vulnerable at home to E7 entrants

Companies that over-commit to E7 without right local partners and business strategies

Date16 May 2006Page 30

PricewaterhouseCoopers LLP

Potential longer term challenges for Chinese companies

Gradual loss of cost advantages to other emerging markets

Rising input costs (energy, metals etc)

Competition from OECD companies in domestic market as effects of WTO membership continue to feed through

Overseas investments: choosing the right targets and not overpaying for them (c.f. Japan)

Moving from technological imitation to innovation

Developing domestic capital markets

Adapting to an ageing labour force

Date16 May 2006Page 31

PricewaterhouseCoopers LLP

Public policy issues for China (and other countries)

Danger of protectionist response from US/Europe

Capital market development and banking sector reform

Rural-urban income inequalities (land reform?)

Energy and water supply

Education

Environmental issues

- Domestic: air and water quality, soil erosion, deforestation etc

- Global: challenge of climate change

Date16 May 2006Page 32

PricewaterhouseCoopers LLP

Rise of China and India will push up C02 emissions unless offsetting measures taken to reduce energy/carbon intensity

0

5

10

15

20

25

2005 2025 2050

A2 world (low energyefficiency)

A1 world (moderateenergy efficiency)

B1 world (high energyefficiency)

Source: IPCC scenarios (2000), preliminary PwC model estimates

GtC

Date16 May 2006Page 33

PricewaterhouseCoopers LLP

Summary

The E7 are coming!

- US, China and India to be three major economies by 2050

- India could actually grow faster than China beyond c.2015

- Brazil, Russia, Indonesia, Mexico and Turkey smaller but also potentially significant

Potential win-win for the UK and other OECD economies if they can remain open, flexible and focused on human capital

China and India potential partners as well as rivals

Major public policy challenges … not least climate change