Embed Size (px)

Citation preview

Services Trade Protectionand Economic Isolation

Ingo Borchert1, Batshur Gootiiz2, Arti Grover Goswami2 and Aaditya Mattoo21University of Sussex, Brighton, UK and 2World Bank, Washington, DC, USA

1. INTRODUCTION

A country’s ability to benefit from flows of trade, tourism and knowledge depends on how

well connected it is, internally and internationally. Poor connectivity, in turn, is conven-

tionally blamed on difficult geography and low income. But economic isolation could also

result from policy choices in key ‘linking’ services such as air transportation and telecommu-

nications. A new services policy database reveals that many countries restrict trade and invest-

ment in these sectors. We show that these policies lead to more concentrated market

structures and more limited access to services, even after taking into account the constraining

influences of geography and low incomes, and the possibility that policies are endogenous.

To motivate the analysis, consider the example of three countries: Laos, Nepal and Zam-

bia. Each suffers the serious disadvantage of landlockedness, which is traditionally regarded

as the main reason for their economic isolation. Less attention has been focused on a self-in-

flicted handicap: their restrictive policies. Each country has at least until recently stifled com-

petition in telecommunications – primarily by restricting the conditions for new entry – and

in air transport – primarily by negotiating restrictive bilateral air service agreements (BASAs)

on key routes. In terms of access and quality of services, each of the three countries fairs

poorly. In Nepal, there are 2.5 telephone mainlines per 100 people, half the regional average

for South Asia; in Laos 1.5, one-seventh the regional average for East Asia; and in Zambia

0.75, one-quarter of the regional average for sub-Saharan Africa. In mobile telephony, the

gaps are slightly less stark but still significant; for example, Nepal had a mobile teledensity

(subscriptions per 100 people) of 12, which is about one-third of the South Asian regional

average. In air passenger transportation, Nepal Airlines, which has seen its fleet shrunk to two

Boeing 757 and four twin otters, occupies transport capacity agreed in BASAs that it is inca-

pable of exploiting. For instance, the number of seats is limited to 6,000 per week to the key

hub of Delhi, but Nepal Airlines uses only 1,300 seats of its allocated quota.

To what extent can concentrated markets and poor performance be attributed to poor pol-

icy? Or are they primarily attributable to other disadvantages? It is not easy to provide a con-

vincing answer to these questions because the policy information we have collected is only

for a single time period, making it difficult to control for all the possible sources of heteroge-

The authors would like to thank Nora Dihel, Ana M. Fernandes, Christopher Findlay, John Gibson,Hiau-Looi Kee, Charles Kunaka, Daniel Lederman, C�a�glar €Ozden, Gael Raballand, Martin Ravallion andBarry Reilly for helpful comments and discussions. This paper is part of a World Bank research projecton trade in services supported in part by the governments of Norway, Sweden and the United Kingdomthrough the Multidonor Trust Fund for Trade and Development, and by the UK Department for Interna-tional Development (DFID). The findings, interpretations and conclusions expressed in this paper areentirely those of the authors. They do not necessarily represent the views of the International Bank forReconstruction and Development/World Bank and its affiliated organisations, or those of the executivedirectors of the World Bank or the governments they represent, or any of the aforementioned individualsor institutions.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

1

The World Economy (2015)doi: 10.1111/twec.12327

The World Economy

neous performance across countries. Nevertheless, we are able to control for the most likely

determinants of poor performance: the adverse influences of geography and low incomes. We

show that poor policies lead to more concentrated market structures and to more limited

access to services than these countries would otherwise have. In addition, we recognise that

the commonly made assumption that trade policy is exogenous may not be entirely plausible,

and therefore also gauge robustness by employing an instrumental variable (IV) strategy. Even

though there are clear limitations to an IV exercise in a cross-country context, it leads to

broadly similar results.

Previous studies have looked at possible reasons for the transport sector’s poor perfor-

mance. Limao and Venables (2001) highlight the effect of infrastructure on trade costs and

trade flows but do not consider policy choices. Other studies recognise the role of policy, par-

ticularly in trucking. Raballand and Macchi (2009) find that market regulation is a critical

determinant of the price of trucking services, while market access restrictions and freight shar-

ing schemes hinder competitiveness and raise trade costs especially for landlocked countries

in Africa. Hallaert et al. (2011) do not find domestic transportation infrastructure to be an

important determinant of countries’ trade performance, pointing instead to the importance of

regulatory issues in the transport sector.1 The present study builds on this earlier work but is

broader in scope, both in terms of the range of countries and types of sectors and policies

covered. While previous studies acknowledge the importance of market structure, this paper

adds to that literature by illustrating how specific policies contribute to a concentrated market

structure. The dominant trend in trade facilitation projects under new ‘aid for trade’ initiatives

is increased investment in infrastructure, but this paper shows how such investments alone

may yield a low return as long as policies that restrict competition among service providers

remain in place.

2. POLICY DATA AND PATTERNS

A range of services link a country to the rest of the world. We focus on air transportation

and telecommunications, primarily because they are vital for connectivity but also because

countries’ policy choices could have a larger influence on performance in these sectors than

in other sectors such as road transportation, in which exogenous geographic factors play a

stronger role. In addition, better policy data are available for these services than for other rel-

evant services sectors such as trucking.

We focus on policies that affect market structure, particularly by influencing foreign entry.

The policy data come from the new World Bank Services Trade Restrictions Database, which

offers for the first time detailed information on actual or applied policies affecting foreign

presence in a number of services sectors (Borchert et al., 2014). In the telecommunications

sector, relevant policies include limits on the number of licences issued, restrictions on the

extent of foreign ownership in firms, nationality requirement for board of directors, restric-

tions on establishing an international gateway (IG) and the use of voice-over-IP (VOIP) tech-

nology. In the air transport sector, relevant policies include not just those affecting the ability

of foreign airlines to establish a local commercial presence, but also the BASAs that govern

international transport. To capture the restrictiveness of BASAs, we draw on the WTO’s

1 Raballand et al. (2008), Lall et al. (2009) and Arvis et al. (2010) also focus on road transport inAfrica.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

2 I. BORCHERT ET AL.

‘Quantitative Air Services Agreements Review’ (QUASAR) database which represents the

most comprehensive source currently available on bilateral air services agreements, covering

over 2,000 such agreements.

a. A Qualitative Picture of Policy in Selected Countries

To provide a country face to the subsequent empirical analysis, consider examples of

policies from the telecommunications sector in three landlocked countries: Nepal, Laos and

Zambia.2 In telecommunications, as much of the world is being transformed by the inter-

play between competition and new technologies, each of these countries has stifled compe-

tition in its own unique way. Nepal granted exclusive licences in the fixed-line segment

until 2009 to United Telecommunications Limited (with majority Indian Government own-

ership) and in mobile to Spice Telecom (with majority Kazakh ownership), effectively cre-

ating duopolies in each segment between these firms and the state-owned firm. Zambia set

a prohibitively high licence fee ($12 million) for establishing an independent international

gateway market (IGW), in order to give the incumbent state-owned operator, Zamtel,

a de facto monopoly in the international segment.3 Monopoly profits enabled Zamtel to

inhibit competition in other segments of the market through cross-subsidisation and did not

lead to a significant expansion of the rural network. In Laos, new entry is possible only

through direct negotiation with the government, and the government has in all cases

reserved its right to be a partial owner of the new undertakings (Millicom, Shinawatra,

Sky Communications and Veittel). In each of these countries, the regulatory authority is

not really independent and is widely reported to favour state-owned incumbent operators.

For example, since the regulator in Laos was unable or unwilling to induce the incumbent

firm to share its fibre-optic ‘backbone’ cable with rival firms, one of them has chosen to

create a parallel fibre-optic backbone at significant cost. Similar examples of policies

inhibiting competition and availability of services can be found in the air transport sector

of these three countries, primarily by maintaining restrictive BASAs. Schlumberger (2007)

has shown how both Zambia and South Africa have in the past denied fifth freedom rights

to other countries.4

b. Quantification of Survey Policy Information

It is hard to measure barriers to services trade.5 The most transparent approach would be

to include each policy variable separately as an explanatory variable, either as directly mea-

sured (e.g. the number of licences permitted) or as a binary indicator variable (e.g. whether

voice over internet protocol is allowed). The scope for such a strategy is, however,

constrained by the problem of collinearity between policy variables and limited degrees of

2 For an in-depth study of services sectors in Zambia, see Mattoo and Payton (2007).3 This licence fee has recently been reduced.4 Even though Zambia no longer has a national airline, it has denied Fifth Freedom rights to Ethiopia tofly the Addis Ababa-Lusaka-Johannesburg route, to Nigeria on the Lagos-Lusaka-Johannesburg route,and to Kenya on the Nairobi-Lusaka-Harare route.5 Non-tariff barriers, which are pervasive in services, have also proved hard to measure in goods trade.Existing methods in goods rely on inferring restrictiveness on the basis of the impact on trade flows(Kee et al., 2009), but the absence of disaggregated services trade data especially for developing coun-tries rules out such techniques.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

SERVICES PROTECTION AND ISOLATION 3

freedom. Therefore, we use a combination of methods. To the extent feasible, we assess the

impact of policy variables individually, but we also construct a summary measure of open-

ness in specific sectors.6 The latter approach conserves degrees of freedom in estimation, and

in addition enables us to address concerns about the possible endogeneity of policy through

an instrumental variable strategy.

Existing methods of constructing openness measures range from simple counts of

restrictive policies to more complex weighted averages, where weights reflect prior assess-

ments of the relatively restrictiveness of specific policy barriers (Francois and Hoekman,

2010). There is, however, a potentially serious problem with methods that treat all restric-

tions (entry, operational, regulatory) as additive. For instance, if foreign suppliers are not

allowed to enter in the first place, then the restrictions on operations and regulatory envi-

ronment simply do not matter. Similarly, a foreign equity limit of 49 per cent already pre-

cludes foreign corporate control and so adding to it a further (frequently encountered)

requirement that the majority of board of directors be nationals would amount to double

counting.

The measure of openness we construct is relatively transparent and avoids the pitfalls of

earlier additive approaches. Essentially, we assess policy regimes in their entirety and assign

them into five broad categories: completely open, that is, no restrictions at all; completely

closed, that is, no entry allowed at all; virtually open but with minor restrictions; virtually

closed but with very limited opportunities to enter and operate; and a final residual ‘middle’

category of regimes which allow entry and operations but impose restrictions that are nei-

ther trivial nor virtually prohibitive. We either represent each of these regimes by an indica-

tor variable or, when required for instrumental variables estimation, the regimes are

assigned a services trade restrictiveness index (STRI) on an openness scale from 0 to 1

with intervals of 0.25. When two or more measures are in place, the regime assignment

reflects the overall restrictiveness of the measures.7 More details about the methodology can

be found in Borchert et al. (2014).

For cross-border trade in air transport, we use the air liberalisation index (ALI) of the

QUASAR database created by the WTO Secretariat. The ALI ranges from 0 to 50 with

zero being the most restrictive. The ALI is calculated by selecting the provisions of

BASAs deemed to be particularly important for market access and assigning a score

between zero (most restrictive) and eight (least restrictive) to each restriction. These scores

are then averaged in consultation with a group of experts, using weights intended to reflect

the relative importance of each restriction. The scores attributed can also be altered to take

into account the specific situation of a country pair, in particular by giving more weight

to: fifth freedom traffic rights (e.g. for geographically remote countries such as Australia

and New Zealand); withholding, in particular, community of interest and principal place of

6 Notice that when the goal is to demonstrate how policies matter for outcome variables of interest, aswe endeavour in this paper, the restrictiveness of certain measures cannot be quantified econometricallyin a first step by estimating their effect on some outcome variable. In this case, the restrictiveness scoreneeds to be exogenous and must not be derived in a way that involves the quantity to be explained.7 Measures covered can be divided in two tiers. The first-tier measures include those that affect marketentry decisions most significantly, such as the limit on foreign ownership and the number of licencesallowed. The second-tier measures are those that affect operations of service providers, such as the boardof directors and repatriation of earnings etc. If the first-tier measures are prohibitive, the second-tiermeasures are not considered. But if the first-tier measures are not prohibitive, then the second-tier mea-sures are also considered to determine the overall restrictiveness.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

4 I. BORCHERT ET AL.

business; and multiple designation. For comparability, the scale of ALI is converted to the

STRI scale.8

c. Patterns of Policy and Performance

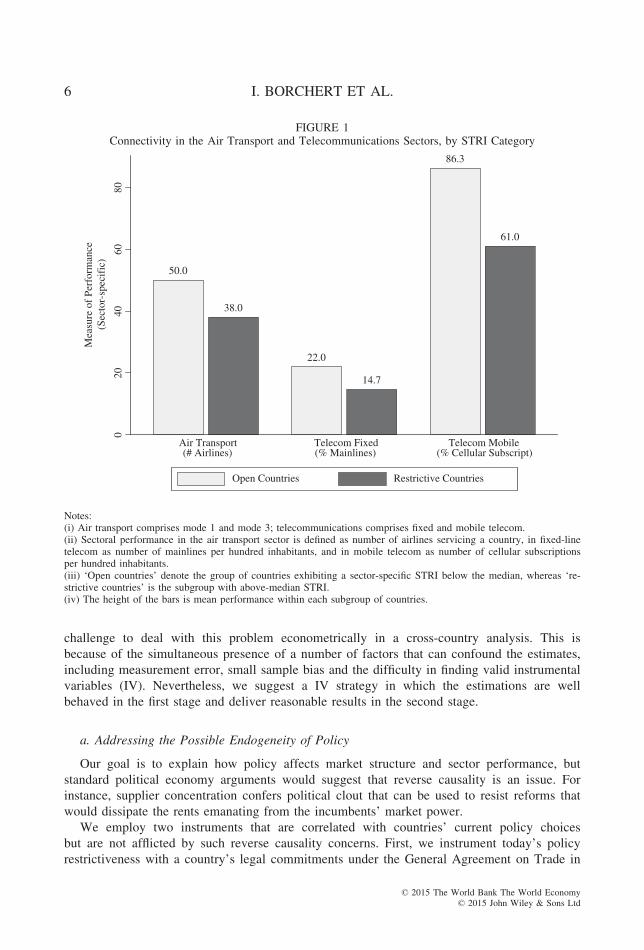

Before embarking on the econometric analysis, it is useful to compare sector performance

across groups of countries which differ in the level of policy restrictiveness. We take as indi-

cators of performance in the air transport sector the number of airlines servicing a country, in

fixed-line telecommunication the number of mainlines per hundred inhabitants, and in mobile

telecommunication the number of cellular subscriptions per hundred inhabitants. In Figure 1,

‘open countries’ denote the group of countries exhibiting a sector-specific STRI below the

median, whereas ‘restrictive countries’ is the subgroup with above-median STRI. The height

of the bars is mean performance within each subgroup of countries. The underlying differ-

ences in performance are in fact substantial; in each case, the performance indicator for the

open countries is about one-third higher than the indicator for restrictive countries. Annex 1

(published online as supplementary material) provides more detail on the patterns of policy at

the individual country level. More information about particular applied policy measures can

also be obtained from the Services Trade Restrictions Database website at http://iresearch.-

worldbank.org/servicetrade/home.htm. The relationship depicted in Figure 1 is likely to reflect

additional factors other than policy, but this distinctive pattern does suggest that policies

affect access to services. The next section therefore investigates the impact of policies

econometrically.

3. MARKET STRUCTURE AND PERFORMANCE – AN ECONOMETRIC ANALYSIS

We now investigate whether policy restrictions matter for market structure and perfor-

mance in the telecommunication and transportation sector, respectively. The effects of ser-

vices policy measures are not well studied especially in developing countries due to the

paucity of data on policy restrictiveness.9

The long-standing tradition in the trade literature, especially relating to services, is to treat

trade policy as exogenous and to study its effect on outcomes of interest (see e.g. the survey

by Francois and Hoekman, 2010). One part of our analysis follows this standard approach.

Even though we recognise that policy choices may be endogenously determined, it is a major

8 In Figure 1 presenting the overall STRI in air transport, the STRI for cross-border trade (BASAs) iscombined with the STRI for commercial presence using a weight of 0.7 and 0.3, respectively, becausecross-border supply is the primary mode of supply for air transport.9 Among the few studies in this area is Fink et al. (2003) who analyse the impact of policy reform inbasic telecommunications across 86 developing countries and find that both privatisation and competitionlead to significant improvements in performance. A study by the OECD (2009) is closest to ours, findingthat countries’ restrictiveness in telecommunications, as measured by a similar index, significantlyimpedes inward foreign direct investment (FDI) as well as domestic sales by foreign affiliates (FATS).Some studies provide index-type descriptive evidence on regulatory barriers in the telecom sector but donot proceed to a quantitative impact analysis, for example Holmes and Hardin (2000) on APEC coun-tries, Koyama and Golup (2006) on OECD and 13 non-OECD countries, Marouani and Munro (2009)on Egypt, Jordan and Morocco, and Golub (2009) on 73 developing and developed countries across theglobe. The latter focuses on a narrower definition of restrictiveness (only barriers to FDI) but demon-strates how FDI per capita decreases as the FDI restrictions index increases.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

SERVICES PROTECTION AND ISOLATION 5

challenge to deal with this problem econometrically in a cross-country analysis. This is

because of the simultaneous presence of a number of factors that can confound the estimates,

including measurement error, small sample bias and the difficulty in finding valid instrumental

variables (IV). Nevertheless, we suggest a IV strategy in which the estimations are well

behaved in the first stage and deliver reasonable results in the second stage.

a. Addressing the Possible Endogeneity of Policy

Our goal is to explain how policy affects market structure and sector performance, but

standard political economy arguments would suggest that reverse causality is an issue. For

instance, supplier concentration confers political clout that can be used to resist reforms that

would dissipate the rents emanating from the incumbents’ market power.

We employ two instruments that are correlated with countries’ current policy choices

but are not afflicted by such reverse causality concerns. First, we instrument today’s policy

restrictiveness with a country’s legal commitments under the General Agreement on Trade in

50.0

38.0

22.0

14.7

86.3

61.0

020

4060

80

Mea

sure

of

Perf

orm

ance

(Sec

tor-

spec

ific

)

Air Transport(# Airlines)

Telecom Fixed(% Mainlines)

Telecom Mobile(% Cellular Subscript)

Open Countries Restrictive Countries

FIGURE 1Connectivity in the Air Transport and Telecommunications Sectors, by STRI Category

Notes:(i) Air transport comprises mode 1 and mode 3; telecommunications comprises fixed and mobile telecom.(ii) Sectoral performance in the air transport sector is defined as number of airlines servicing a country, in fixed-linetelecom as number of mainlines per hundred inhabitants, and in mobile telecom as number of cellular subscriptionsper hundred inhabitants.(iii) ‘Open countries’ denote the group of countries exhibiting a sector-specific STRI below the median, whereas ‘re-strictive countries’ is the subgroup with above-median STRI.(iv) The height of the bars is mean performance within each subgroup of countries.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

6 I. BORCHERT ET AL.

Services (GATS) made either in 1995 at the conclusion of the Uruguay Round or in 1997 at

the conclusion of the negotiations on basic telecommunications. These commitments vary

across services subsectors and countries and predate applied policies captured in the STRI by

more than a decade. The policy restrictiveness of GATS commitments has been quantified by

Borchert et al. (2011) using the same methodology as that used to derive the STRI scores.

Thus, even though policies may have evolved, GATS commitment scores provide a proxy for

policy choices that originate from within the same country, yet the variable is predetermined

with respect to today’s political economy forces and sector performance. One disadvantage of

this instrument is that ten countries in our sample did not make commitments under the GATS,

reducing the number of available observations down to 93 for this instrument.10 While the

fixed-line and mobile telecommunication sectors can be straightforwardly matched to GATS

commitments, air transportation services have always been outside the realm of the WTO. For

the latter, we therefore use an average of commitments made in the transportation sector (con-

sisting of maritime shipping, maritime auxiliary services, road transport and railway freight).

A second strategy for finding an instrument exploits the similarity of institutions across coun-

tries, in particular, is the extent to which they restrain rent-seeking.11 Specifically, the inclina-

tion of a government to favour vested interests is constrained by the extent to which it will be

held accountable for its decisions. Thus, political institutions that shape governance and the rule

of law appear to matter when policymakers decide on the level of openness.12 We use this

insight to instrument for a given country’s policy restrictiveness with the STRI score of another

country that is most similar in terms of institutional setup and stage of development. Yet the

matching country’s policymakers are insulated from any lobbying efforts that might exact an

influence on the STRI of the country for which we are seeking an instrument. We call the result-

ing variable a ‘nearest neighbour STRI’ which, in contrast to the GATS commitments variable,

can be constructed for all 103 countries in the sample (cf. Annex Table A.2.1). The approach is

implemented using the matching procedure incorporated in the Abadie and Imbens (2002) near-

est neighbour matching estimator. We match on per capita income as well as political institu-

tions such as the Polity IV Project’s political regime indicator, the Economist Intelligence

Unit’s democracy indicator and the Heritage Foundation’s Index of Economic Freedom.13

10 A list of those countries and further details are provided in Annex 2.11 Dihel and Shepherd (2007) show how policy barriers inflate firms’ price-cost margins. For commer-cial presence in fixed-line telecom, these estimates mostly range between 50 and 130 per cent, while thetax equivalents for the mobile segment in mode 3 are mostly in the single-digit range.12 Gasmi et al. (2009) find that in developing countries, the quality of the political process has a favour-able impact on performance in the telecom industry, though their measure of ‘accountability’ capturesinstitutions ranging from corruption to currency risk and is thus not directly comparable to our notion ofthis term. Gual and Trillas’s (2006, p. 263) search for determinants of telecom policy is inconclusive;they find that entry barriers are mainly a function of the inherited legal system, while the other institu-tional variables are insignificant. In addition, the size of the incumbent telecom firm, supposedly reflect-ing its political clout, is positively associated with the decision to create an independent regulator, a factthe authors themselves call ‘surprising’.13 The Polity IV Project’s political regime indicator locates countries along the range of being ‘stronglydemocratic’ to ‘strongly autocratic’ and summarises the opportunities available to citizens to expresstheir preferences over alternative policies and leaders, as well as the existence of institutionalized con-straints on the exercise of power by the executive branch. The Economist Intelligence Unit’s democracyindex is based on five categories: electoral process and pluralism; civil liberties; the functioning of gov-ernment; political participation; and political culture. The Heritage Foundation’s score measures fourbroad categories: rule of law, limited government, regulatory efficiency, and open markets.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

SERVICES PROTECTION AND ISOLATION 7

To the extent that instrument validity can be tested for, both variables perform very well.

The first-stage coefficients are always highly significant and correctly signed. Crucially, even

though using GATS commitments comes at a loss of observations, employing both instru-

ments allows an overidentifying restrictions test, which is comfortably passed across all

estimations.

b. Telecommunications

We estimate a non-structural linear model for each outcome variable of interest since there

is no established unified estimation framework for such diverse variables as market structure

and connectivity (in both telecommunications and transport sectors). In each specification, we

consider a core set of covariates as fundamental determinants of market structure and connec-

tivity, which reflect a country’s attractiveness to investors in telecommunications and trans-

port services sectors. These variables include GDP, GDP per capita, the percentage of urban

population and population density. We also include a dummy variable for landlocked and for

sub-Saharan African countries, respectively, to account for geography and to ensure that

results regarding policy choices are not driven solely by the Africa region. All these determi-

nants are closely related to gravity model variables that are known to affect goods trade

flows. In addition, the distribution and ‘lumpiness’ of demand, as proxied by the two popula-

tion variables, is important in services sectors because the fixed (often sunk) costs of sizable

investments in both telecommunications and transport must be covered by sufficiently high

(local) demand.

We start by looking at market structure in telecommunications, using data on the Herfind-

ahl index (HHI) of market concentration in the fixed-line and mobile segment.14 The model

including individual policy measures or the restrictiveness index (STRI) to be estimated is

given by

HHIi ¼ /0 þ /1Policyi þ /2Fundamentalsi þ /3Geographyi þ ei;

in which the vector of geographic controls includes a dummy for Africa and for landlocked-

ness, and fundamental determinants include GDP, income per capita, the share of urban popu-

lation and population density.15 We are interested in the conditional effect of policy variables.

Results are displayed in Table 1. Policy variables are first treated as exogenous in the col-

umns labelled ‘OLS.’ In the columns labelled ‘IV’, we instrument for the STRI variable as

discussed in the previous section. Before summarising a country’s policies in a single index

(see Section 2b on quantification), we explore directly the effects of individual elements of

policy. The relatively small sample size does not allow us to identify separately the effects

of the entire range of policy measures. We therefore focus on four aspects of the regulatory

regime, which were identified as salient in discussions with industry stakeholders and

14 We compute the HHI based on TeleGeography’s GlobalComms database as the sum of squared mar-ket shares of all firms in a market. A taxonomy commonly used by competition authorities would call amarket with HHI < 1,000 ‘unconcentrated’, 1,000 ≤ HHI < 1,800 ‘moderately concentrated’, and withHHI ≥ 1,800 ‘concentrated’. In the latter case, a market is usually no longer assumed to be competitive.A value of 10,000 would indicate a monopoly.15 The specification including GDP and GDP per capita follows from our interest in controlling fornotions of market size and stage of development. The marginal effects of GDP and population per secould, however, be easily computed from the two coefficient estimates in Table 1.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

8 I. BORCHERT ET AL.

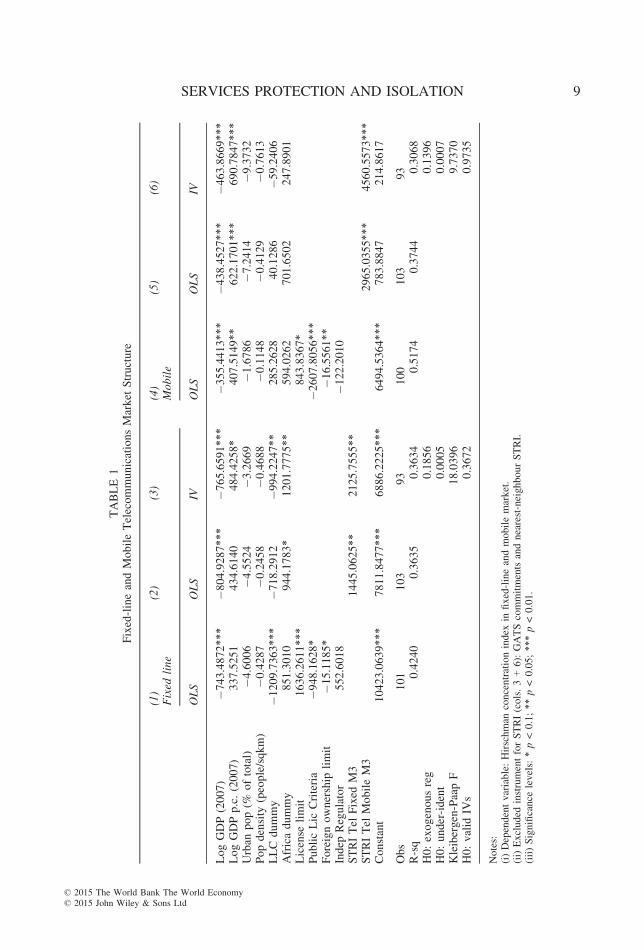

TABLE1

Fixed-lineandMobileTelecommunicationsMarket

Structure

(1)

(2)

(3)

(4)

(5)

(6)

Fixed

line

Mobile

OLS

OLS

IVOLS

OLS

IV

LogGDP(2007)

�743.4872**

*�8

04.9287**

*�7

65.6591**

*�3

55.4413**

*�4

38.4527**

*�4

63.8669**

*LogGDPp.c.(2007)

337.5251

434.6140

484.4258*

407.5149**

622.1701**

*690.7847**

*Urban

pop(%

oftotal)

�4.6006

�4.5524

�3.2669

�1.6786

�7.2414

�9.3732

Popdensity

(people/sqkm)

�0.4287

�0.2458

�0.4688

�0.1148

�0.4129

�0.7613

LLCdummy

�1209.7363**

*�7

18.2912

�994.2247**

285.2628

40.1286

�59.2406

Africadummy

851.3010

944.1783*

1201.7775**

594.0262

701.6502

247.8901

License

limit

1636.2611**

*843.8367*

PublicLic

Criteria

�948.1628*

�2607.8056**

*Foreignownership

limit

�15.1185*

�16.5561**

Indep

Regulator

552.6018

�122.2010

STRITel

Fixed

M3

1445.0625**

2125.7555**

STRITel

MobileM3

2965.0355**

*4560.5573**

*Constant

10423.0639**

*7811.8477**

*6886.2225**

*6494.5364**

*783.8847

214.8617

Obs

101

103

93

100

103

93

R-sq

0.4240

0.3635

0.3634

0.5174

0.3744

0.3068

H0:exogenousreg

0.1856

0.1396

H0:under-ident

0.0005

0.0007

Kleibergen-PaapF

18.0396

9.7370

H0:valid

IVs

0.3672

0.9735

Notes:

(i)Dependentvariable:Hirschman

concentrationindex

infixed-lineandmobilemarket.

(ii)Excluded

instrumentforSTRI(cols.3+6):GATScommitmentsandnearest-neighbourSTRI.

(iii)Significance

levels:*p<0.1;**

p<0.05;**

*p<0.01.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

SERVICES PROTECTION AND ISOLATION 9

regulators and which relate to whether: (i) there is a limit on the number of licences awarded;

(ii) licencing criteria are publicly available; (iii) there is a limit on the equity share foreign

investors are permitted to hold; and (iv) a regulatory authority exists that is independent of

the sector ministry.

The main result is a significant and quantitatively important effect of services policy

restrictiveness (columns 2 and 5), suggesting that – conditional on relevant country character-

istics – less open countries on average have a more concentrated market structure. The policy

effect remains strong and significant even after controlling for African and landlocked

countries.16 Moreover, the results remain fully robust when we account for the endogeneity of

policy choices (columns 3 and 6).17 If anything, the unbiased impact of restrictive policies on

market concentration seems to be even larger in magnitude.18

In terms of individual policies, the existence of a licence limit has a strong effect on fixed-

line operators and results in an average increase in market concentration by 1,636 index

points. Transparency of the licencing process reduces concentration, and the same is true of

more liberal foreign ownership rules. Overall, when all these (and other) policies are encapsu-

lated in a single index, a more restrictive policy stance – reflected in a higher STRI score – is

associated with significantly higher market concentration. The STRI coefficient in column 2

implies that a change in the index score by 25 points (which corresponds to one increment)

would on average be associated with a market that is less concentrated by about 361 HHI

points. The IV estimate in column 3 would raise this effect to about 531 HHI points. Thus,

the impact is sizable. In terms of scoring restrictiveness, the presence of a quota-like limit on

licences would ceteris paribus change a country’s STRI by 50 points, which corresponds to a

higher market concentration by 1,063 index points according to the column 3 coefficient; this

is somewhat lower than the effect inferred from model (1) but within the same ballpark, con-

sidering that the STRI is a composite index.

Similar findings emerge from the mobile telecommunications market, except that the quan-

titative impact of policy restriction tends to be higher (models 5 and 6). Transparency of

licencing criteria turns out to be more important than licence limits. This result is not surpris-

ing since the availability of radio spectrum imposes in principle exogenous limits on the num-

ber of mobile providers, and telecommunication authorities have often used discretion rather

than explicit licence limits to set licencing conditions.

In both market segments, the IV estimations with two instruments are based on slightly

fewer observations dictated by data availability. However, this loss of observations is

16 We always present robust standard errors which, in addition, include a correction for small samplesize. The findings are therefore designed to provide a conservative lower bound, in spite of the largerstandard errors associated with two-stage IV estimation.17 The IV estimation’s first-stage regression results are presented in Annex 2.2. The coefficient on theexcluded instruments is highly significant throughout and carries the expected sign. Shea’s (1997) partialR2 with respect to both instruments ranges between 28 and 35 per cent in telecommunications, and 14per cent in air transport. We are therefore confident to have strong and relevant instruments.18 A larger coefficient estimate under IV would be counterintuitive if one thought that the least squaresanalysis suffered from an upward bias due to reverse causality. However, this reasoning rests on asymp-totic behaviour of the estimators, whereas in small samples such as ours (about 100 observations) thedirection of bias is indeterminate. In addition, measurement error would induce an attenuation bias inthe OLS estimates, an effect that may dominate here. The phenomenon of OLS and IV coefficientsdiverging in an unexpected way has been a persistent feature in the literature on returns to education/schooling; see Card (2001) for an in-depth treatment of potential explanations.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

10 I. BORCHERT ET AL.

outweighed by the possibility of performing a test of overidentifying restrictions. The last

line of regression statistics in columns 3 and 6, respectively, reports the p-value associated

with Hansen’s J statistic. The joint null of the test is that the instruments are valid instru-

ments, that is uncorrelated with the error term, and that excluded instruments are correctly

excluded from the estimated equation. A rejection would cast doubt on the validity of the

instruments; however, the null cannot be rejected in any of the models (here or there-

after).

The effect of restrictive telecom policies on the sector’s market structure is robust to

other measures of market structure as well. In Annex Table A.3.1, we present results on

how restrictive policies affect the number of telecom operators active in a country, esti-

mated using a non-linear count data model. This approach yields qualitatively the same

results. Likewise, more restrictive policies are also associated with a significantly higher

market share of the largest provider in a given country, both in the fixed-line and the

mobile market. Apart from the main variables of interest, we also see that larger countries

are characterised by lower concentration, presumably because larger economies can sustain

more operators.19

Next we turn to an analysis of access to telecommunications services, for which we look

at the number of telephone main lines per hundred people (in fixed line) and the number of

mobile cellular subscriptions per hundred people (in mobile); data are taken from the World

Development Indicators for the year 2008. Estimating performance in the telecommunications

sector follows the approach taken in Ros (1999), Boylaud and Nicoletti (2000) and Fink et al.

(2003). We include the familiar set of covariates controlling for telecommunications market

attractiveness and estimate the following equation.20

logeðAccess to Telecom ServiceiÞ ¼ c0 þ c1STRIi þ c2Fundamentalsi þ c3Geographyi þ ni:

Table 2 presents the results for the fixed-line and mobile telecommunications sector,

respectively. For each sector, column 1 (column 4) estimates a model in which dummy vari-

ables capture the effect of intermediate and highly restrictive telecom policies, relative to

open countries.21 As an alternative, column 2 (column 5) treats the STRI as a quasi-continu-

ous variable.22 In general the results show a significant negative impact of restrictive policies

on a country’s teledensity. Column 3 (column 6) then applies the IV procedure to correct for

potential endogeneity and measurement error in the policy variable. Without placing too

much emphasis on the difference between OLS and IV coefficients–since the direction of the

bias in small samples is anyway indeterminate–we conclude that the adverse effect of more

restrictive policies on accessibility is confirmed. To the extent that the IV procedure reduces

attenuation bias, the true size of the effect might be stronger than indicated by the exogenous

policy model. Notice that in each segment the STRI coefficients are significant at the 1 per cent

19 This is confirmed by estimating the determinants of the number of operators with a Poisson model,the results of which can be found in the Annex.20 We continue to include log(GDP) but omit per capita income since the dependent variable in thisspecification is already normalised with respect to population. In addition, there exists a strong positivecorrelation between ICT access measures and stage of development (see World Bank 2009a, p. 136)which masks the effect of restrictive policies that is mainly behind this association.21 Open countries: STRI = 0; intermediate STRI = (25, 50); high STRI = (75, 100).22 In contrast to the dummy variable approach, this specification restricts the STRI to have a uniformlinear partial effect across all values of restrictiveness.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

SERVICES PROTECTION AND ISOLATION 11

TABLE2

Accessto

Telecom

Services

–Mainlines

andCellularSubscriptionsper

100Inhabitants

(1)

(2)

(3)

(4)

(5)

(6)

Fixed

line

Mobile

OLS

OLS

IVOLS

OLS

IV

LogGDP(2007)

3.9285**

*3.8478**

*3.1180**

*1.4323

1.5648

�0.5291

Urban

pop(%

oftotal)

0.3044**

*0.3196**

*0.3218**

*0.7333**

*0.7549**

*0.7806**

*Popdensity

(people/sqkm)

0.0054

0.0075

0.0143**

0.0037

0.0055

0.0199

Africadummy

�2.1596

�3.0254

�1.0841

�20.3490**

*�2

0.9946**

*�1

7.9575*

LLC

dummy

3.1080

4.4019**

3.2508

�7.4681

�4.4221

�6.9672

STRIinterm

ed�7

.3807**

*�2

0.0000**

*STRIhigh

�6.5709*

�22.6063**

*STRITelecom

M3

�8.2861**

�28.7561**

*�3

4.0787**

*�8

1.8148**

*Constant

�13.2371**

�16.1957**

*�8

.6152

47.5710**

*40.6288**

58.9118**

*

Obs

103

103

93

103

103

93

R-sq

0.6068

0.5870

0.5147

0.5916

0.5727

0.5192

H0:exogenousreg

0.0011

0.0149

H0:under-ident

0.0002

0.0002

Kleibergen-PaapF

22.0307

13.0442

H0:valid

IVs

0.7983

0.1932

Notes:

(i)Dependentvariables:Number

ofmainlines

(cols.1–3)andcellularsubscriptions(cols.4–6)per

100inhabitants.

(ii)STRIdenotesfixed-lineSTRIin

cols.1–3

andmobileSTRIin

cols.4–6,respectively.

(iii)Excluded

instrumentforSTRI(cols.3+6):GATScommitmentsandnearest-neighbourSTRI.

(iv)Significance

levels:*p<0.1;**

p<0.05;**

*p<0.01.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

12 I. BORCHERT ET AL.

level despite the higher standard errors typically associated with IV estimation. As before, the

instruments are strong and appear to be valid according to Hansen’s J test.

Comparing estimation results for the fixed-line market with the mobile segment suggests

that the application of restrictive measures has a significant effect in both markets; however,

the effect on fixed lines is quantitatively not as strong as the one on cellular subscriptions.

The coefficient estimates in columns 1–2 suggest that countries with restrictive policies have

on average 7 to 8 percentage points fewer fixed telephone mainlines than open countries. This

effect is highly significant. Given the much larger effect indicated by IV estimation, this esti-

mate probably constitutes a lower bound on the policy penalty. When policies are considered

one by one, it is the existence of an independent regulator as well as the prohibition of VoIP

and operation of own international gateways that stifles access to mainlines (see Annex

Table A.3.2). The absence of an independent regulator and restrictions on entrants ability to

use their own gateways and technology can inhibit competition which limits expansion of

mainlines.

Results for mobile telephony are qualitatively similar in that restrictive policies exert a

negative and highly significant effect on mobile cellular subscriptions. Compared with

fixed-line policies, the mobile STRI is more skewed towards openness; for example, there

are only four countries with high STRI values, which renders data support in the upper

tail thin. Thus, we mainly interpret the coefficient on the ‘intermediate STRI’ level in col-

umn 4 which, however, is quite large. The presence of major restrictions is associated

with about 20 percentage points fewer subscriptions, and all policy effects in columns 4–5are again highly significant.23 In terms of individual policy measures, apart from the exis-

tence of an independent regulator, publicly available licencing criteria are associated with

higher levels of per capita subscriptions (Annex Table A.3.3).24 The latter finding reflects

the positive effect of transparency already found in the mobile segment’s market structure

model.

In passing, we also note that the results confirm that the degree of urbanisation is a strong

determinant of access to telecom services, as we would expect. In the fixed-line segment,

absolute market size is also important, which plausibly reflects the high fixed costs associated

with setting up a fixed-line network. The large negative coefficient associated with the

sub-Saharan African region indicates that the level of wireless connectivity there is still

substantially lower than elsewhere, notwithstanding spectacular growth rates in cellular

subscriptions (from a low base) in many African countries.

c. Air Passenger Transportation

The number of international flights (inbound and outbound), as well as total seat capacity

serve as indicators for how well a country is connected in terms of air transport. We continue

to use the core set of gravity-type variables that determine a market’s attractiveness to foreign

providers, in this case airlines. GDP as a measure of economic size will control for the scale

23 We have checked whether observed market structure – itself a result of the first-round impact of pol-icy on entry decisions – directly influences access to telecommunication services. We find a small statis-tically significant effect in the mobile segment, but all results are qualitatively unchanged. Results areavailable upon request.24 It has proved difficult to include several policy measures simultaneously, which appears to be a prob-lem of insufficient degrees of freedom; see column 6 in Annex Tables A.3.2 and A.3.3, respectively.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

SERVICES PROTECTION AND ISOLATION 13

effect. In the following analysis, we limit our attention to air passenger transportation.25 Since

about half of global airborne cargo is transported in the belly of passenger aircraft, the results

in this section may be relevant beyond the narrowly defined air passenger sector (see also

World Bank 2009b).

Air passenger transport services are traded primarily on a cross-border basis. It is not

essential for airlines to establish a commercial presence in order to fly to a specific country,

but a commercial presence can facilitate operations. The key policy instruments affecting

air transport are governed by BASAs which stipulate conditions under which international

flights might be provided between the two contracting parties. However, the national invest-

ment regime, that is a set of rules for FDI in the airline sector, is also relevant. The type

and scope of relevant BASA provisions will be discussed in greater detail below. Due to

the predominance of cross-border trade in air services the number of airlines established in

a country is not a meaningful metric of market structure; airlines would rather compete to

provide flights between city pairs; that is, competition is defined on a route-specific basis.

We therefore focus directly on the impact of air transport policies on the availability of air

transport services, for which the number of airlines flying to a given country matters as

well.26

Information on the number of airlines, the number of international flights and available seat

kilometres for each country is obtained from Air Transport Intelligence’s (ATI) Flight Global

database. We consider the total number of international flights (or, alternatively, the total seat

capacity of such flights) as the dependent variable. In addition to the core set of gravity-type

variables already introduced, the provision of flights is also linked to two additional character-

istics. From a supply-side perspective, airport infrastructure matters and is, at least in the short

run, exogenous to the number of flights. Second, from the demand side, a country’s attractive-

ness to tourism is an important determinant of flights and seats offered. Therefore, we also

control for the number of airports with a paved runway per country and for tourist arrivals as

a share of domestic population.27

In terms of policies affecting air connectivity, the appropriate measure of policy restrictive-

ness needs to take into account both air traffic rights and foreign investment rules. The former

is summarised by the WTO’s ALI, whereas information on the latter comes from the World

Bank’s newly developed policy database (see footnote 8 on the construction of the combined

STRI). We estimate the following model:

25 The chief reason for limiting our analysis to passenger transportation is inadequate data availability interms of both policies that specifically apply to air cargo transportation as well as cargo volume, someof which travels as belly cargo in scheduled passenger flights and some on dedicated cargo flights. Onewould need to concord the fraction of belly cargo to the corresponding BASA provisions applicable topassenger traffic, and the remainder to specific provisions governing dedicated cargo traffic, which maybe scheduled or charter flights. Current data availability do not allow for this matching.26 We regard the evidence of policy impact on air movements offered in this paper as complementary torelated work that has studied the effect of aviation policies on bilateral goods trade flows. For example,Geloso Grosso (2008), Piermartini and Rousov�a (2008), and Geloso Grosso and Shepherd (2009) havedirectly included the ALI in the trade cost function of gravity model of goods trade.27 For instance, Dresner et al. (2002) show that constrained access to gates may constitute a barrier toentry (and increase the cost of airline service for incumbents). Similarly, Brueckner (2002) uses a Cour-not duopoly model to show how incumbent duopolists may restrict runway capacity such that no thirdparty can enter the market. These studies strongly suggest that airport infrastructure matters.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

14 I. BORCHERT ET AL.

LogðNo:of FlightsiÞ ¼ b0 þ b1STRIi þ b2Infrastri þ b3Tourismi þ b4Fundamentalsiþ b5Geographyi þ ni:

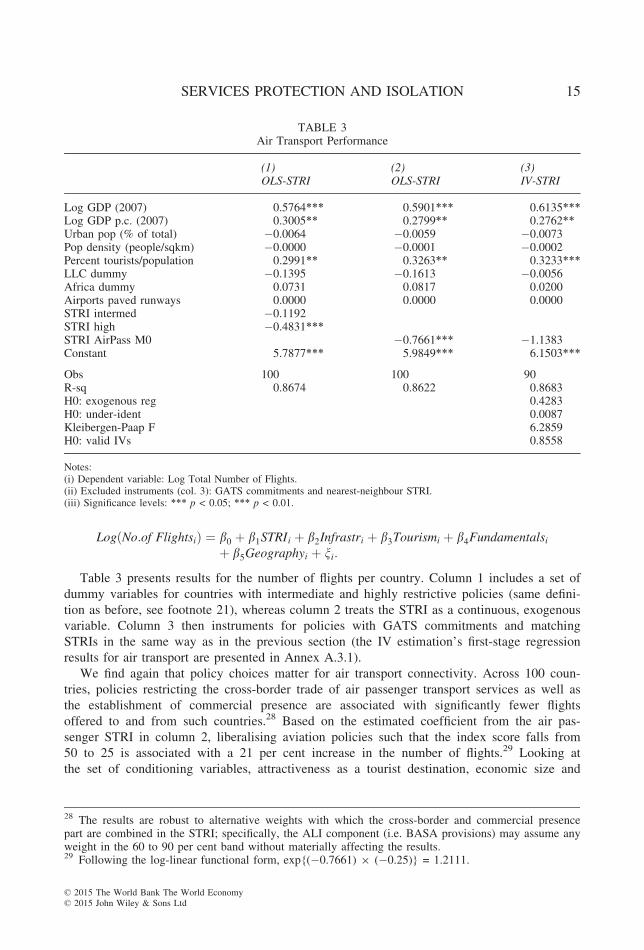

Table 3 presents results for the number of flights per country. Column 1 includes a set of

dummy variables for countries with intermediate and highly restrictive policies (same defini-

tion as before, see footnote 21), whereas column 2 treats the STRI as a continuous, exogenous

variable. Column 3 then instruments for policies with GATS commitments and matching

STRIs in the same way as in the previous section (the IV estimation’s first-stage regression

results for air transport are presented in Annex A.3.1).

We find again that policy choices matter for air transport connectivity. Across 100 coun-

tries, policies restricting the cross-border trade of air passenger transport services as well as

the establishment of commercial presence are associated with significantly fewer flights

offered to and from such countries.28 Based on the estimated coefficient from the air pas-

senger STRI in column 2, liberalising aviation policies such that the index score falls from

50 to 25 is associated with a 21 per cent increase in the number of flights.29 Looking at

the set of conditioning variables, attractiveness as a tourist destination, economic size and

TABLE 3Air Transport Performance

(1) (2) (3)OLS-STRI OLS-STRI IV-STRI

Log GDP (2007) 0.5764*** 0.5901*** 0.6135***Log GDP p.c. (2007) 0.3005** 0.2799** 0.2762**Urban pop (% of total) �0.0064 �0.0059 �0.0073Pop density (people/sqkm) �0.0000 �0.0001 �0.0002Percent tourists/population 0.2991** 0.3263** 0.3233***LLC dummy �0.1395 �0.1613 �0.0056Africa dummy 0.0731 0.0817 0.0200Airports paved runways 0.0000 0.0000 0.0000STRI intermed �0.1192STRI high �0.4831***STRI AirPass M0 �0.7661*** �1.1383Constant 5.7877*** 5.9849*** 6.1503***

Obs 100 100 90R-sq 0.8674 0.8622 0.8683H0: exogenous reg 0.4283H0: under-ident 0.0087Kleibergen-Paap F 6.2859H0: valid IVs 0.8558

Notes:(i) Dependent variable: Log Total Number of Flights.(ii) Excluded instruments (col. 3): GATS commitments and nearest-neighbour STRI.(iii) Significance levels: *** p < 0.05; *** p < 0.01.

28 The results are robust to alternative weights with which the cross-border and commercial presencepart are combined in the STRI; specifically, the ALI component (i.e. BASA provisions) may assume anyweight in the 60 to 90 per cent band without materially affecting the results.29 Following the log-linear functional form, exp{(�0.7661) 9 (�0.25)} = 1.2111.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

SERVICES PROTECTION AND ISOLATION 15

income per capita all exert a positive and significant effect on flights, as expected. Overall,

the model fits the data very well, explaining about 86 per cent of the cross-country

variation in the number of international flights. The same qualitative results obtain when we

look at total seat capacity rather than flights. These estimations are therefore not shown to

conserve space but are available upon request. In both cases – number of flights and seat

capacity as dependent variables – the results are robust to using the ALI alone as a measure

of policy openness.

When aviation policies are instrumented for, the magnitude of the coefficient on policy

increases but ceases to be significant. However, this result based on total seat capacity hides that

fact that policies do have an effect along a certain dimension, as we will show in the next step.

In Table 3, the number of flights is an ‘absolute’ measure of connectivity in that it is not

scale-invariant. As such, a given number of flights, say 400, could be the result of 40 airlines

offering 10 flights each or a single airline offering 400 flights, or of course any other combina-

tion. In analogy to the goods trade literature, in which a distinction is commonly made between

‘trade in more product categories’ and ‘more trade of a given product’, we may think of the

number of airlines serving a country as the ‘extensive margin’ and of the number of flights per

airline as the ‘intensive margin’, Individual BASA provisions may either primarily affect the

number of airlines or the frequency and/or size of carriers’ operations, respectively.30 On the

one hand, air traffic rights, in particular fifth and higher freedom rights, as well as the type of

designation and withholding clauses, are likely to affect the number of airlines able (or willing)

to service a country. On the other hand, the range of provisions relating to airfares, number of

flights per route and maximum seat capacity directly affect the frequency and capacity of

flights for a given (designated) airline.

In order to disentangle the channel through which aviation rules affect air connectivity, we

split the total number of flights (F) into the average number of flights per airline (F/A) and

the number of airlines (A), which allows us to study the intensive and extensive margin sepa-

rately. We take advantage of the property of OLS estimation that under these circumstances,

the estimated coefficients on the policy variable in the flights-per-airline and in the number-

of-airline estimations will exactly add up to the policy coefficient in the total number of

flights regression. This allows for a convenient decomposition of the overall policy effect into

one working through the intensive and extensive margin, respectively.

Fi ¼ ðF=AÞi � Ai

logðFiÞ ¼ log ðF=AÞi þ logðAiÞ+

b̂F

STRI ¼ b̂ðF=AÞSTRI þ b̂

A

STRI

:

Table 4 presents the decomposition results; the first three columns refer to OLS estimations

assuming the STRI is an exogenous variable, whereas the last three columns employ IV

30 Bilateral air service agreements contain four types of provisions that regulate the possibility and theextent of bilateral flight connections: (i) traffic rights; (ii) ownership rules; (iii) fares/tariffs; and (iv)capacity. For a comprehensive overview of regulatory aspects of the air transport services sector, andhow the restrictiveness of market access provisions is quantified in the QUASAR database, see WTOdocument S/C/W/270/Add.1, Volume I, of November 2006. A detailed exposition of the ‘Freedoms ofthe Skies’ can be found on page I.15.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

16 I. BORCHERT ET AL.

estimation. Looking at the STRI coefficients, it is evident that aviation policies affect

predominantly the average number of flights per airline. In column (2), the effect of policy is

highly significant at the 1 per cent level and increasing in magnitude as restrictiveness moves

from an intermediate to a high level. The partial effect of an intermediate STRI value is a

reduction in the number of flights per airline by 25 per cent, whereas highly restrictive polices

reduce flights per airline by another 15 per cent, that is by almost 40 per cent compared with

the reference point of liberal policies.31 The decomposition thus reveals that the number of

flights per airline is the primary margin of adjustment in response to restrictive aviation

policies. The IV estimation in column 5 corroborates this finding.

Apart from the main findings pertaining to policy, results for other covariates are also of

interest. For instance, and unlike aviation policies, attractiveness for tourists increases the num-

ber of flights mainly through more airlines (two-thirds of the effect) and only to a smaller but

still significant extent through more flights. Given that different airlines bring in tourists from

TABLE 4Air Transport Performance – Number of Flights, Flights per Airline and Number of Airlines

(1) (2) (3) (4) (5) (6)OLS IV

F-STRI F/A-STRI A-STRI F-STRI F/A-STRI A-STRI

Log GDP (2007) 0.5764*** 0.1975*** 0.3789*** 0.6135*** 0.2213*** 0.3955***Log GDP p.c.(2007)

0.3005** 0.2546*** 0.0459 0.2762** 0.2401*** 0.0342

Urban pop (% oftotal)

�0.0064 �0.0044 �0.0020 �0.0073 �0.0042 �0.0030

Pop density(people/sqkm)

�0.0000 �0.0001 0.0001 �0.0002 �0.0000 �0.0002

Percent tourists/Population

0.2991** 0.1060* 0.1931* 0.3233*** 0.0865 0.2388***

LLC dummy �0.1395 0.0460 �0.1854 �0.0056 0.1970 �0.1947Africa dummy 0.0731 0.2500* �0.1771 0.0200 0.2166 �0.1982Airports pavedrunways

0.0000 0.0001** �0.0000 0.0000 0.0001** �0.0001*

STRI intermed �0.1192 �0.2830*** 0.1637STRI high �0.4831*** �0.5104*** 0.0273STRI AirPass M0 �1.1383 �1.4688** 0.3534Constant 5.7877*** 4.5629*** 1.2250* 6.1503*** 4.8239*** 1.3143

Obs 100 100 100 90 90 90R-sq 0.8674 0.7208 0.7491 0.8683 0.7233 0.7585H0: exogenous reg 0.4283 0.2278 0.9216H0: under-ident 0.0087 0.0087 0.0087Kleibergen-Paap F 6.2859 6.2859 6.2859H0: valid IVs 0.8558 0.7408 0.8561

Notes:(i) Dependent variable: Total flights (F); Flights per airline (F/A); Number of airlines (A).(ii) Excluded instruments for STRI (cols. 4–6): GATS commitments and nearest-neighbour STRI.(iii) Significance levels: * p < 0.1; ** p < 0.05; *** p < 0.01.

31 Using the coefficient estimates of column (2), one obtains exp{�0.2803} � 1 = �0.2465 andexp{�0.5104} � 1 = �0.3997, respectively, the difference of which is �0.1533.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

SERVICES PROTECTION AND ISOLATION 17

their respective national markets, this result and the relative size of both margins are quite plau-

sible. Likewise, a country’s ‘absorptive capacity’ as measured by airports with paved runways

affects the number of flights per airline rather than the number of airlines.

The findings in Table 4 suggest that the adverse impact on air transport connectivity is

mainly driven by BASA provisions that affect frequency and capacity of air traffic, for example

designation clauses, weekly flight limitations and perhaps also traffic rights. A more detailed

analysis of the differential impact of various BASA provisions would require much richer data.

4. CONCLUSIONS AND POLICY IMPLICATIONS

Drawing on a new data set of applied policies affecting services trade, we are able to iso-

late the effect of policies on market structure and performance from other country characteris-

tics. Our results suggest that a country’s own policy reform can contribute to a more

competitive market structure and to improved access to telecommunications and air transport

services. We find that in the telecommunications sector, moving from an intermediate level of

restrictiveness to an open regime would result on average in an increase in cellular teledensity

by 20 percentage points and an increase in fixed-line teledensity by 7 percentage points.

Within the STRI scoring framework applied in this paper, such a step could for instance be

achieved by abolishing a licence limit or by allowing majority foreign ownership. In the air

transport sector, a reform of aviation policies from a similar level of intermediate restrictive-

ness is estimated to be associated with a 25 per cent increase in the number of flights per air-

line. The effect of aviation policies works mainly through reducing the average number of

flights per airline, rather than reducing the number of airlines flying to and from a country.

Countries with highly restrictive aviation policies have on average almost 40 per cent fewer

flights per airline than liberal countries.

The importance of services policies for market structure and performance, therefore, has

two implications for policymaking. First, international assistance for transport and telecommu-

nications infrastructure needs to be complemented by policy reform. Second, in transport ser-

vices, there is a strong case for multilateral negotiations because there are limits to what

unilateral reform can achieve. We address each aspect in turn.

Our results suggest that access to key ‘linking’ services is determined not only by the state of

infrastructure (see Francois and Manchin, 2007; Portugal-Perez and Wilson, 2008) but also by

competition in those sectors. However, current trade facilitation and trade-related aid have

placed a heavy emphasis on infrastructure projects, especially so in transportation but also in

telecommunication. Moreover, studies which evaluate the effectiveness of aid for trade (see e.g.

Cali and TeVelde, 2010) do not explicitly specify the role of restrictive policies as constraints to

trade performance. Our findings indicate that international assistance for infrastructure invest-

ment is likely to earn a low return where policies restrict competition between service providers.

Apart from policy reform within a country, progress in transport liberalization requires

stronger international cooperation. First, the reason is that a particularly country, say Zambia,

is limited in what it can achieve on its own in the air transport sector because introducing

competition on any international route requires the consent of other countries involved.32

32 While Zambia is engaging in restrictive BASA policies itself (see footnote 4), South Africa has alsodenied Fifth Freedom rights to other countries such as Egypt to fly the vital Cairo-Lusaka-Johannesburgroute, out of a desire to protect its national airline’s interests on routes between Zambia and SouthAfrica.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

18 I. BORCHERT ET AL.

Second, Borchert et al. (2014) show that air transport services are also restricted in other

developing and industrial countries, many of which are either important destination and

source countries, or transit or hub countries for connecting flights to landlocked economies.

Third, even though the mercantilistic quid pro quo logic may not be particularly suited to

services negotiations, regional or multilateral negotiations with strong demandeurs may some-

times help overcome entrenched domestic interests, as the example of Costa Rica shows,

which opened one of its most sensitive services sectors (telecommunications) under the aus-

pices of the CAFTA-DR agreement (Robert and Stephenson, 2008). Finally, the beneficial

effect on specific countries’ connectivity of policy reforms in other (transit or final destina-

tion) countries constitutes a positive externality that is unlikely to be fully internalised by

policymakers in those partner countries. This externality could be addressed in international

negotiations.

The WTO would be a natural platform for multilateral negotiations, but its contribution

to liberalising the transport sector has so far been limited. Air traffic rights are explicitly

excluded from the scope of services negotiations, and maritime transport has never been

seriously negotiated. In the Uruguay Round, many countries, including OECD countries,

did not make full commitments on cross-border road and rail transport services. Regional

agreements like the Yamoussoukro Decision, which entered into force in 2000, also

offer scope for regional policy reform, but they have, however, so far seen only limited

implementation.

There is no doubt that transport and telecommunications services are critical to a coun-

try’s overall economic performance. However, connectivity requires not just good infras-

tructure but also an appropriate national policy regime and international regulatory

cooperation. International assistance for infrastructure investment, therefore, needs to be

complemented by national and multilateral reform in order to yield full benefits. To insist

on such reform as a condition for assistance is now anathema. At the same time, mecha-

nisms to ensure participation by country governments and other stakeholders in processes

to determine country needs, such as ‘poverty reduction strategy papers’, are noticeably

short on reform proposals and long on lists of required investments.33 Perhaps the way for-

ward is to ask countries to present proposals that specify both intended reforms and

required investments, and to allocate assistance competitively to maximise the expected

social rate of return.

SUPPORTING INFORMATION

Additional Supporting Information may be found in the online version of this

article:

Annex A1. Restrictiveness of services trade policies.

Annex A2. Instrumental variables.

Annex A3. Additional estimation results.

Annex A4. Data sources and description.

33 Poverty Reduction Strategy Papers (PRSPs) were introduced in 1999 by the World Bank and the IMFas a new framework to enhance domestic accountability for poverty reduction reform efforts; a means toenhance the coordination of development assistance between governments and development partners;and a precondition for access to debt relief and concessional financing from both institutions.

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

SERVICES PROTECTION AND ISOLATION 19

REFERENCES

Abadie, A. and G. W. Imbens (2002), ‘Simple and Bias-Corrected Matching Estimators for AverageTreatment Effects’, NBER Technical Working Paper 0283 (Cambridge, MA: National Bureau ofEconomic Research).

Arvis, J.-F., G. Raballand and J.-F. Marteau (2010), ‘The Cost of Being Landlocked: Logistics Costsand Supply Chain Reliability’, Directions in Development – Trade No. 55837 (Washington, DC:The World Bank).

Borchert, I., B. Gootiiz and A. Mattoo (2011), ‘Services in Doha: What’s on the Table?’, in W. Martinand A. Mattoo (eds.), Unfinished Business? The WTO’s Doha Agenda (London: CEPR and WorldBank), 115–43.

Borchert, I., B. Gootiiz and A. Mattoo (2014), ‘Policy Barriers to International Trade in Services:Evidence from a New Database’, World Bank Economic Review, 28, 1, 162–88.

Boylaud, O. and G. Nicoletti (2000), ‘Regulation, Market Structure and Performance in Telecommunica-tions’, OECD Economics Department Working Paper No. 237 (Paris: OECD).

Brueckner, J. K. (2002), ‘Airport Congestion When Carriers Have Market Power’, American EconomicReview, 92, 5, 1357–75.

Cali, M. and D. W. TeVelde (2010), ‘Does Aid for Trade Really Improve Trade Performance?’, WorldDevelopment, 39, 5, 725–40.

Card, D. (2001), ‘Estimating the Return to Schooling: Progress on Some Persistent EconometricProblems’, Econometrica, 69, 5, 1127–60.

Dihel, N. and B. Shepherd (2007), ‘Modal Estimates of Services Barriers’, OECD Trade Policy WorkingPaper 51, TD/TC/WP(2005)36/FINAL (Paris: OECD).

Dresner, M., R. Windle and Y. Yao (2002), ‘Airport Barriers to Entry in the US’, Journal of TransportEconomics and Policy, 36, 2, 389–405.

Fink, C., A. Mattoo and R. Rathindran (2003), ‘An Assessment of Telecommunications Reform inDeveloping Countries’, Information Economics and Policy, 15, 4, 443–66.

Francois, J. and B. Hoekman (2010), ‘Services Trade and Policy’, Journal of Economic Literature, 48,3, 642–92.

Francois, J. and M. Manchin (2007), ‘Institutions, Infrastructure, and Trade’, World Bank PolicyResearch Working Paper 4152 (Washington, DC: World Bank).

Gasmi, F., P. Noumba Um and L. Recuero Virto (2009), ‘Political Accountability and Regulatory Perfor-mance in Infrastructure Industries: An Empirical Analysis’, World Bank Economic Review, 23, 3,509–31.

Geloso Grosso, M. (2008), ‘Liberalising Air Passenger Services in APEC’, Working Paper, Grouped’�Economie Mondiale, Sciences Po, November 2008 (Paris: Groupe d’ �Economie Mondiale).

Geloso Grosso, M. and B. Shepherd (2009), ‘Liberalising Air Cargo Services in APEC’, MPRA WorkingPaper 17781 (Munich: University Library of Munich).

Goldberg, P. K. and G. Maggi (1999), ‘Protection for Sale: An Empirical Investigation’, AmericanEconomic Review, 89, 5, 1135–55.

Golub, S. S. (2009), ‘Openness to Foreign Direct Investment in Services: An International ComparativeAnalysis’, The World Economy, 32, 8, 1245–68.

Grossman, G. M. and E. Helpman (1994), ‘Protection for Sale’, American Economic Review, 84, 4,833–50.

Gual, J. and F. Trillas (2006), ‘Telecommunications Policies: Measurement and Determinants’, Reviewof Network Economics, 5, 2, 249–72.

Hallaert, J.-J., R. C. Cepeda and G. Kang (2011), ‘Estimating the Constraints to Trade of DevelopingCountries’, OECD Trade Policy Working Paper 116 (Paris: OECD).

Holmes, L. and A. Hardin (2000), ‘Assessing Barriers to Services Sector Investment’, in C. Findlay andT. Warren (eds.), Impediments to Trade in Services – Measurements and Policy Implications(London: Routledge), 52–70.

Kee, H. L., A. Nicita and M. Olarreaga (2009), ‘Estimating Trade Restrictiveness Indices’, EconomicJournal, 119, 534, 172–99.

Koyama, T. and S. Golup (2006), ‘OECD’s FDI Regulatory Restrictiveness Index: Revision and Exten-sion to More Economies’, OECD Working Papers on International Investment 2006/4 (Paris: OECD).

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

20 I. BORCHERT ET AL.

Lall, S. V., H. Wang and T. Munthali (2009), ‘Explaining High Transport Costs within Malawi’, WorldBank Policy Research Working Paper 5133 (Washington, DC: World Bank).

Limao, N. and A. J. Venables (2001), ‘Infrastructure, Geographical Disadvantage, Transport Costs andTrade’, World Bank Economic Review, 15, 3, 451–79.

Marouani, M. A. and L. Munro (2009), ‘Assessing Barriers to Trade in Services in the MENA Region’,OECD Trade Policy Working Paper 84, TAD/TC/WP(2008)25/FINAL (Paris: OECD).

Mattoo, A. and L. Payton (eds) (2007), ‘Services Trade and Development: The Experience of Zambia’,(Basingstoke: co-publication of Palgrave Macmillan and the World Bank).

OECD (2009), ‘Testing the Services Trade Restrictiveness Index: Gravity Regressions and Trade CostsAnalysis’, paper presented at the OECD Experts Meeting on the Services Trade Restrictiveness Index(STRI), 2–3 July 2009 (Paris: OECD).

Piermartini, R. and L. Rousov�a (2008), ‘Liberalisation of Air Transport Services and Passenger Traffic’,Staff Working Paper Economic Research and Statistics Division, ERSD-2008-06 (Geneva: WorldTrade Organisation).

Portugal-Perez, A. and J. S. Wilson (2008), ‘Trade Costs in Africa: Barriers and Opportunities forReform’, World Bank Policy Research Working Paper 4619 (Washington, DC: World Bank).

Raballand, G. and P. Macchi (2009), ‘Transport Prices and Costs: The Need to Revisit Donors’ Policiesin Transport in Africa’, BREAD Working Paper 190 (Washington, DC: Bureau for Research andEconomic Analysis of Development).

Raballand, G., C. Kunaka and B. Giersing (2008), ‘The Impact of Regional Liberalization and Harmo-nization in Road Transport Services: A Focus on Zambia and Lessons for Landlocked Countries’,World Bank Policy Research Working Paper 4482 (Washington, DC: World Bank).

Robert, M. and S. Stephenson (2008), ‘Opening Services Markets at the Regional Level Under theCAFTA-DR: The Cases of Costa Rica and the Dominican Republic’, in J. A. Marchetti and M. Roy(eds.), Opening Markets for Trade in Services: Countries and Sectors in Bilateral and WTONegotiations (Cambridge: Cambridge University Press), 537–72.

Ros, A. J. (1999), ‘Does Ownership or Competition Matter? The Effects of Telecommunications Reformon Network Expansion and Efficiency’, Journal of Regulatory Economics, 15, 1, 65–92.

Schlumberger, C. E. (2007), ‘Air Transport: Revitalizing Yamoussoukro’, in A. Mattoo and L. Payton(eds.), Services Trade and Development: The experience of Zambia (Basingstoke: co-publication ofPalgrave Macmillan and the World Bank), 191–211.

World Bank (2009a), Information and Communications for Development 2009: Extending Reach andIncreasing Impact (Washington, DC: The World Bank Group).

World Bank (2009b), ‘Air Freight: A Market Study with Implications for Landlocked Countries’,Transport Papers TP-26 (Washington, DC: The World Bank Group).

© 2015 The World Bank The World Economy© 2015 John Wiley & Sons Ltd

SERVICES PROTECTION AND ISOLATION 21

本文献由“学霸图书馆-文献云下载”收集自网络,仅供学习交流使用。

学霸图书馆(www.xuebalib.com)是一个“整合众多图书馆数据库资源,

提供一站式文献检索和下载服务”的24 小时在线不限IP

图书馆。

图书馆致力于便利、促进学习与科研,提供最强文献下载服务。

图书馆导航:

图书馆首页 文献云下载 图书馆入口 外文数据库大全 疑难文献辅助工具