Embed Size (px)

Citation preview

i

Document of

The World Bank

Report No: ICR00002649

IMPLEMENTATION COMPLETION AND RESULTS REPORT

(IDA-39030 TF-57844)

ON A

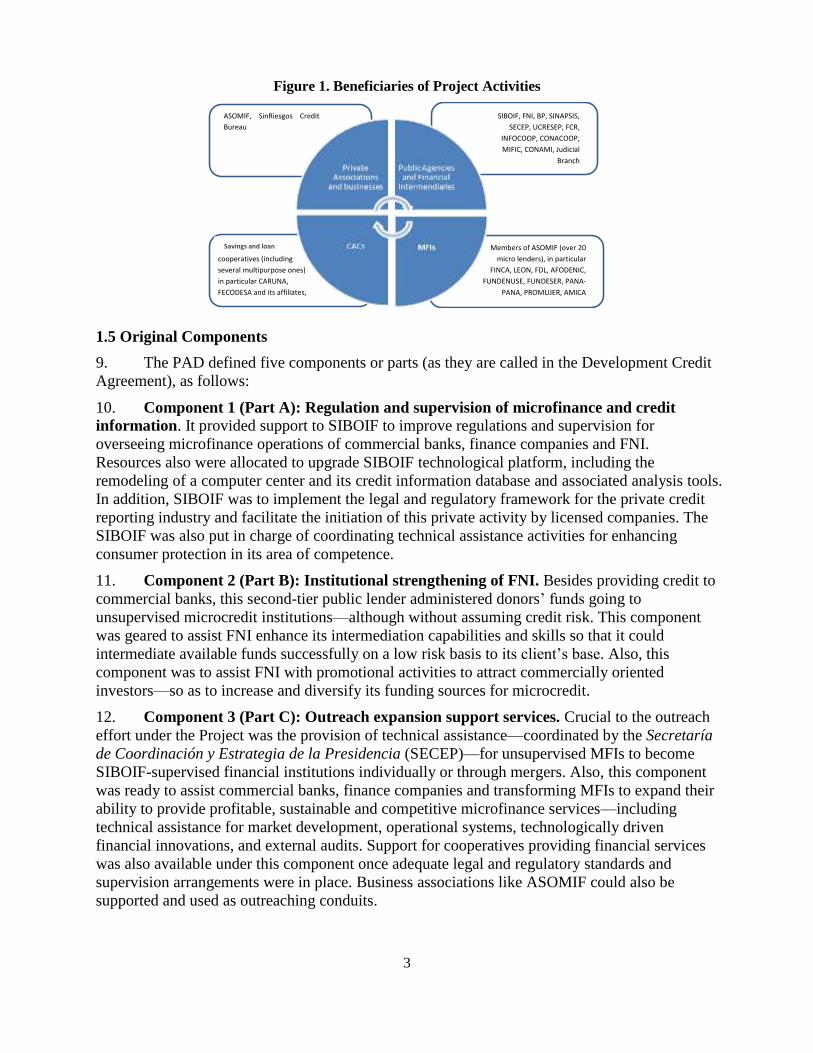

CREDIT

IN THE AMOUNT OF SDR 4.8 MILLION

(US$7.0 MILLION EQUIVALENT)

TO THE

REPUBLIC OF NICARAGUA

FOR A

BROAD BASED ACCESS TO FINANCIAL SERVICES PROJECT

June 27, 2013

Finance and Private Sector Development

Central America Country Management Unit

Latin America and the Caribbean Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

iii

CURRENCY EQUIVALENTS

(Exchange Rate Effective June 3, 2013)

Currency Unit = Cordoba

1.00 = US$ 0.04

US$ 1.00 = 24.63

FISCAL YEAR

January 1 – December 31

ABBREVIATIONS AND ACRONYMS

ASDI Swedish International Development Agency

ASOMIF Asociación Nicaragüence de Instituciones de Microfinanzas (Nicaraguan

Association of Microfinance Institutions)

BCN Central Bank of Nicaragua

BP Banco Produzcamos (a newly created state development bank, which

assumed FNI’s coordination and implementation responsibilities for the

Project)

CAC Cooperativa de Ahorro y Crédito (Savings and Loans Cooperative)

CAS Country Assistance Strategy

CPS Country Partnership Strategy

CONACOOP Consejo Nacional de Cooperativas (National Council of Cooperatives)

CONAMI Comisión Nacional de Microfinanzas (National Commission of

Microfinances)

COSUDE Swiss Development Corporation

DCA Development Credit Agreement

ECF Extended Credit Facility

FCR Fondo de Crédito Rural (Rural Credit Fund)

FI Financial institution

FNI Financiera Nicaragüense de Inversiones (the Borrower's second-tier

investment financial company)

FSAP Financial Sector Assessment Program

GoN Government of Nicaragua

IMF International Monetary Fund

IADB Inter American Development Bank

ISR Implementation Status and Results

INFOCOOP Instituto Nicaragüense de Fomento Cooperativo (Nicaraguan Institute of

Cooperative Promotion)

MEFCCA Ministerio de Economía Familiar, Comunitaria, Cooperativa y Asociativa

MFI Micro-finance institution

MIFIC Ministerio de Fomento, Industria y Comercio (Ministry of Development,

Industry and Commerce)

MUCCOOP Manual Unico de Cuentas Cooperativas (Cooperatives Manual of

iv

Accounts)

NDP National Development Plan

NGO Non-governmental organization

PAD Project Appraisal Document

PAGSF Proyecto de Acceso Generalizado a los Servicios Financieros (Cr. 3903-

NI) (Title of this Project in Spanish)

PCU Project Coordination Unit

PROMIFIN An agency of COSUDE

RAAN Región Autónoma del Atlántico Norte (North Atlantic Autonomous

Region)

RAAS Región Autónoma del Atlántico Sur (South Atlantic Autonomous Region)

SECEP Secretaría de Coordinación y Estrategia de la Presidencia (Secretariat of

Coordination and Strategy of the Presidency)

SETEC Secretaría Técnica de la Presidencia (Technical Secretariat of the

Presidency

SIBOIF Superintendencia de Bancos y de Otras Instituciones Financieras

(Superintendence of Banks and Other Financial Institutions)

SINASIP Sistema Nacional de Seguimiento de Pobreza (National System for

Monitoring Poverty)

TA Technical assistance

TAL

UCRESEP

UNICOOP

Technical assistance lending

Unidad de Coordinación del Programa de Reforma del Sector Público

(Public Sector Reform Program Coordination Unit)

Instituto Nicaragüense de Fomento Cooperativo (Nicaraguan Institute of

Cooperative Development)

Vice President: Hasan A. Tuluy

Country Director: Carlos Felipe Jaramillo

Sector Director:

Sector Manager:

Marialisa Motta

P. S. Srinivas

Project Team Leader: Patricia Caraballo

ICR Primary Author: Claudio A. Pardo

ii

v

NICARAGUA

Broad Based Access to Finance Project

CONTENTS

A. Basic Information

B. Key Dates

C. Ratings Summary

D. Sector and Theme Codes

E. Bank Staff

F. Results Framework Analysis

G. Ratings of Project Performance in ISRs

H. Restructuring (if any)

I. Disbursement Profile

1. Project Context, Development Objectives and Design ................................................... 1 1.1 Context at Appraisal ................................................................................................ 1

1.2 Original Project Development Objectives (PDO) and Key Indicators .................... 1 1.3 Revised PDO (as approved by original approving authority) and Key Indicators,

and reasons/justification…………………………………………………….……. 2

1.4 Main Beneficiaries ................................................................................................... 2 1.5 Original Components ............................................................................................... 3

1.6 Revised Components ............................................................................................... 4 1.7 Other significant changes ......................................................................................... 4

2. Key Factors Affecting Implementation and Outcomes .................................................. 5 2.1 Project Preparation, Design and Quality at Entry .................................................... 5

2.2 Implementation ........................................................................................................ 6 2.3 Monitoring and Evaluation (M&E) Design, Implementation and Utilization ......... 7 2.4 Safeguard and Fiduciary Compliance ...................................................................... 8

2.5 Post-completion Operation/Next Phase ................................................................... 9 3. Assessment of Outcomes ................................................................................................ 9 3.1 Relevance of Objectives, Design and Implementation ............................................ 9

3.2 Achievement of Project Development Objectives ................................................... 9 3.3 Efficiency ............................................................................................................... 13 3.4 Justification of Overall Outcome Rating ............................................................... 14 3.5 Overarching Themes, Other Outcomes and Impacts ............................................. 14

3.6 Summary of Findings of Beneficiary Survey and/or Stakeholder Workshops…...15

4. Assessment of Risk to Development Outcome……………………………………….15

5. Assessment of Bank and Borrower Performance ........................................................ .15

5.1 Bank Performance ................................................................................................. .15 5.2 Borrower Performance ........................................................................................... 16 6. Lessons Learned............................................................................................................ 17 7. Comments on Issues Raised by Borrower/Implementing Agencies/Partners............... 18

vi

Annex 1. Project Costs and Financing .............................................................................. 19 Annex 2. Outputs by Component...................................................................................... 21

Annex 3. Economic and Financial Analysis ..................................................................... 24 Annex 3-A. The Faces of Microfinance: Beneficiaries’ Stories from Supported Micro

Lenders .................................................................................................................. 29 Annex 4. Bank Lending and Implementation Support/Supervision Processes ................. 34 Annex 5-A. Regulation and Supervision of Microfinance Institutions in Nicaragua ....... 36 Annex 5-B. Selected Median Performance Indicators for ASOMIF-associated MFIs .... 36 Annex 6. World Bank Financial Sector Engagement in Nicaragua .................................. 38

Annex 7. Summary of Borrower's ICR and/or Comments on Draft ICR ......................... 39 Annex 8. Project Revisions and Amendments .................................................................. 41 Annex 8-A: Revisions to Project Indicators .................................................................... 41 Annex 8-B: DCA Amendments and Level 2 Restructurings ........................................... 42 Annex 9. List of Supporting Documents and List of Institutions and People Interviewed

by the ICR Mission ............................................................................................... 48 Annex 9-B. List of Institutions and People Interviewed by the ICR Mission .................. 48

Map …………………………………………………………………………………….. 51

i

A. Basic Information

Country: Nicaragua Project Name: Broad-Based Access to

Financial Services

Project ID: P077826 L/C/TF Number(s): IDA-39030,TF-57844

ICR Date: 06/27/2013 ICR Type: Core ICR

Lending Instrument: TAL Borrower: GOVERNMENT OF

NICARAGUA

Original Total

Commitment: XDR 4.80M Disbursed Amount: XDR 3.56M

Revised Amount: XDR 3.56M

Environmental Category: C

Implementing Agencies:

Banco Produzcamos (Previously, Financiera Nicaraguense de Inversiones)

SIBOIF

Cofinanciers and Other External Partners:

Government of Japan

Government of Netherlands

IDB - Inter-American Development Bank

B. Key Dates

Process Date Process Original Date Revised / Actual

Date(s)

Concept Review: 03/19/2003 Effectiveness: 08/22/2005 08/22/2005

Appraisal: 11/03/2003 Restructuring(s):

11/27/2007

04/03/2009

09/15/2010

07/18/2011

Approval: 05/18/2004 Mid-term Review: 07/27/2009

Closing: 12/31/2009 12/31/2012

ii

C. Ratings Summary

C.1 Performance Rating by ICR

Outcomes: Moderately Satisfactory

Risk to Development Outcome: Moderate

Bank Performance: Moderately Satisfactory

Borrower Performance: Moderately Satisfactory

C.2 Detailed Ratings of Bank and Borrower Performance (by ICR)

Bank Ratings Borrower Ratings

Quality at Entry: Moderately Satisfactory Government: Moderately Satisfactory

Quality of Supervision: Moderately Satisfactory Implementing

Agency/Agencies: Moderately Satisfactory

Overall Bank

Performance: Moderately Satisfactory

Overall Borrower

Performance: Moderately Satisfactory

C.3 Quality at Entry and Implementation Performance Indicators

Implementation

Performance Indicators

QAG Assessments (if

any) Rating

Potential Problem Project

at any time (Yes/No): Yes

Quality at Entry

(QEA): None

Problem Project at any time

(Yes/No): Yes

Quality of Supervision

(QSA): None

DO rating before

Closing/Inactive status:

Moderately

Satisfactory

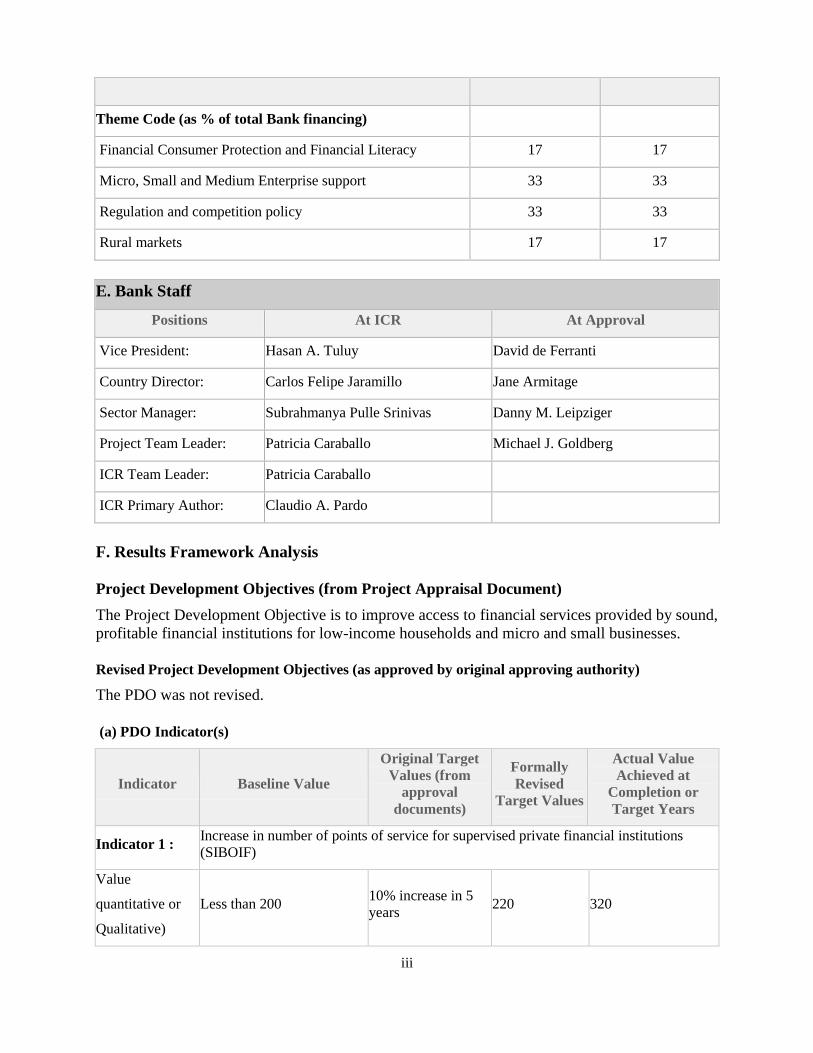

D. Sector and Theme Codes

Original Actual

Sector Code (as % of total Bank financing)

Credit Reporting and Secured Transactions 3 3

General finance sector 26 26

Microfinance 70 70

Other non-bank financial intermediaries 1 1

iii

Theme Code (as % of total Bank financing)

Financial Consumer Protection and Financial Literacy 17 17

Micro, Small and Medium Enterprise support 33 33

Regulation and competition policy 33 33

Rural markets 17 17

E. Bank Staff

Positions At ICR At Approval

Vice President: Hasan A. Tuluy David de Ferranti

Country Director: Carlos Felipe Jaramillo Jane Armitage

Sector Manager: Subrahmanya Pulle Srinivas Danny M. Leipziger

Project Team Leader: Patricia Caraballo Michael J. Goldberg

ICR Team Leader: Patricia Caraballo

ICR Primary Author: Claudio A. Pardo

F. Results Framework Analysis

Project Development Objectives (from Project Appraisal Document)

The Project Development Objective is to improve access to financial services provided by sound,

profitable financial institutions for low-income households and micro and small businesses.

Revised Project Development Objectives (as approved by original approving authority)

The PDO was not revised.

(a) PDO Indicator(s)

Indicator Baseline Value

Original Target

Values (from

approval

documents)

Formally

Revised

Target Values

Actual Value

Achieved at

Completion or

Target Years

Indicator 1 : Increase in number of points of service for supervised private financial institutions

(SIBOIF)

Value

quantitative or

Qualitative)

Less than 200 10% increase in 5

years 220 320

iv

Date achieved 04/19/2004 05/19/2004 12/31/2012 12/31/2012

Comments

(incl. %

achievement)

Achieved. Target value (220) grew by 45.5% (320). Indicator only includes branches of

commercial banks and finance companies. In addition, there were 145 MFIs offices

across the country at end-2012.

Indicator 2 : Increase in number of accounts in supervised financial institutions

Value

quantitative or

Qualitative)

310,300 (Baseline value

does not correspond with

actual values in 2004. The

total amount of deposit

(540k) and loan accounts

(593k) was actually 1.13

million at end-2004)

Number of savings

and loan accounts

increases 20% in

five years

400,000

Deposit (985,479)

and loan (918,566)

accounts for a total of

1,904,045

Date achieved 04/19/2004 05/19/2004 12/31/2012 12/31/2012

Comments

(incl. %

achievement)

Achieved, based on the original formulation in the PAD that required a 20 percent

increase in accounts. The sum of deposit and loan accounts grew 68.1 percent from

2004 to 2012.

Indicator 3 : Volume of Bank Support (US$ MM): Institutional Development - Microfinance

Value

quantitative or

Qualitative)

0

n.a. (indicator was

added during July

2011 restructuring)

3.89 3.64

Date achieved 04/19/2004 05/19/2004 12/31/2012 12/31/2012

Comments

(incl. %

achievement)

Largely achieved (93.6 percent). Indicator includes actual expenditures under

components 1, 2 and 3, which are compared with the PAD figures for these three

components.

Indicator 4 : Volume of Bank Support (US$ MM): Enabling Environment - Microfinance

Value

quantitative or

Qualitative)

0

n.a. (this indicator

formally added

during July 2011

restructuring)

2.14 0.49

Date achieved 04/19/2004 05/19/2004 12/31/2012 12/31/2012

Comments

(incl. %

achievement)

Not achieved (22.9%). Target value was the PAD amount for component 4—

Monitoring access to Financial Services/Implementing Financial Access Policy.

Implementation faced technical shortcomings in the absence of national household

financial surveys.

v

(b) Intermediate Outcome Indicator(s)

Indicator Baseline Value

Original Target

Values (from

approval

documents)

Formally

Revised Target

Values

Actual Value

Achieved at

Completion or

Target Years

Indicator 1 : Regulations, enforcement mechanisms and capacity to effectively supervise commercial

financial institutions with microfinance activities and second-tier institutions

Value

(quantitative

or Qualitative)

No functioning specialized

unit for supervision in place

(at SIBOIF)

Adequate regulatory

and supervision

framework for bank

and finance

companies engaged

in microfinance

Fully functional

system for in-

situ and extra-

situ inspections,

norms, reports

and on-line

tracking

Advanced

operational system in

place capable of

supervising in-situ

and via extra-situ

inspections (using

CAMELS-B-COR

model) all

microfinance

activities of SIBOIF-

supervised

institutions

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Largely achieved. The new tools put in place—partially with Project support—go far

beyond but certainly include micro financing activities. SIBOIF is currently in the latest

stages of implementation of a risk-based approach to supervision

Indicator 2 : Private credit registry established

Value

(quantitative

or Qualitative)

No system in place that

covers microfinance loans

Private credit

registry operating

under sound

regulatory controls

System

operating with

high degree of

microfinance

coverage

Two private credit

bureaus operate

actively in

Nicaragua:

SinRiesgos and

TransUnion

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Achieved. SinRiesgos was authorized in 08/2006 and received Project support. It started

as an ASOMIF initiative; its database includes most credit providers (250) sharing

positive and negative information and covering over 1.85 million debtors

Indicator 3 : SIBOIF has an automated credit information and analysis system in place

Value

(quantitative

or Qualitative)

No system in place

SIBOIF has

adequate staff and

systems in place to

monitor loan

portfolios for

commercial FIs with

microcredit

System

operating with

high degree of

microfinance

coverage

SIBOIF currently has

up-to-date IT systems

in place to receive,

store and analyze

micro credits and

other financial data

from supervised

vi

portfolio institutions on a

daily, weekly and

monthly basis

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Achieved. SIBOIF's risk unit and datacenter received Project support. The unit has the

ability to electronically receive, store and monitor on-site—and via an alternative

external site—transactions of banks and finance companies

Indicator 4 : Training on [BP] standards established, standards accepted by microcredit institutions

Value

(quantitative

or Qualitative)

No system in place; no

standards developed

Participating [in FNI

credit line]

unsupervised micro

credit and

microfinance

institutions will

voluntarily adopt the

accounting, external

auditing, credit

classification and

interest rate

disclosure and

reporting standards

established by the

SIBOIF

Standards in

place, training

offered, MFIs

qualified by BP

- BP credit policy and

procedures reflected

in a new manual. Its

credit review and

approvals have been

thoroughly upgraded

- MFIs and CACs

classified by risk

level and required to

fully collateralize BP

loans

- No systematic

training offered to

MFIs

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Partially achieved. Standards established but in need of revision since they rely mostly

on hard to meet collateral requirements —BP had 12 CONAMI-regulated MFIs and

audited CACs clients, for a portfolio of US$5.2 million at end-Jan 20

Indicator 5 : Participating MFIs will achieve improved efficiency and a higher degree of financial

sustainability

Value

(quantitative

or Qualitative)

No baseline data available

for financial sustainability

Participating MFIs

improve operational

(administrative

costs/average loan

portfolio) and

financial

sustainability

(adjusted operating

expenses/operating

income)

Improved

financial results

and outreach

compared to

baseline for

participating

MFIs

Average and median

operational

sustainability (as

defined) improved

steadily since end-

2004 for ASOMIF

members, with the

median going from

24.1% in 2004 to

18.1% in first half

2012. Data

unavailable for

quoted financial

sustainability ratio

vii

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Partially achieved. Project supported improvements in MFIs' loan portfolio

management, accounting systems and governance, contributing to better efficiency and

sustainability (the 4 solvency indicators published by ASOMIF have improved since

2007)

Indicator 6 : System of technical courses, technical assistance established and used by MFIs

Value

(quantitative

or Qualitative)

No system in place; no

quality training provided

System of technical

courses, technical

assistance in place,

used by MFIs

Training system

in place,

training offered

Project directly

supported and

promoted many

training initiatives

(mainly demand-

driven) for the

benefit of MFIs and

CACs by working

with industry

organizations (i.e.,

ASOMIF,

INFOCOOP, etc.)

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Partially achieved. PAD did not define a system but significant training took place

financed by the Project. Training is now dependent of funding from other donors.

Indicator 7 :

At least four MFIs have transformed or are in the process of transformation to regulated

supervised financial institutions

Value

(quantitative

or Qualitative)

0

n.a. (this indicator

was added following

the July 2011

restructuring)

4

Two previously

unsupervised MFIs

(FAMA in 2006 and

FINCA in 2011) are

now supervised and

operating under a

license granted by

SIBOIF. Two more,

FUNDESER and

FDL, are currently

advanced in their

process of

transformation

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Largely achieved. Two MFIs transformed and two are under the process of

transformation. Four others received various degrees of support. After the approval of

the new microfinance law 15 microfinance institutions registered with the new regulator

(CONAMI)

viii

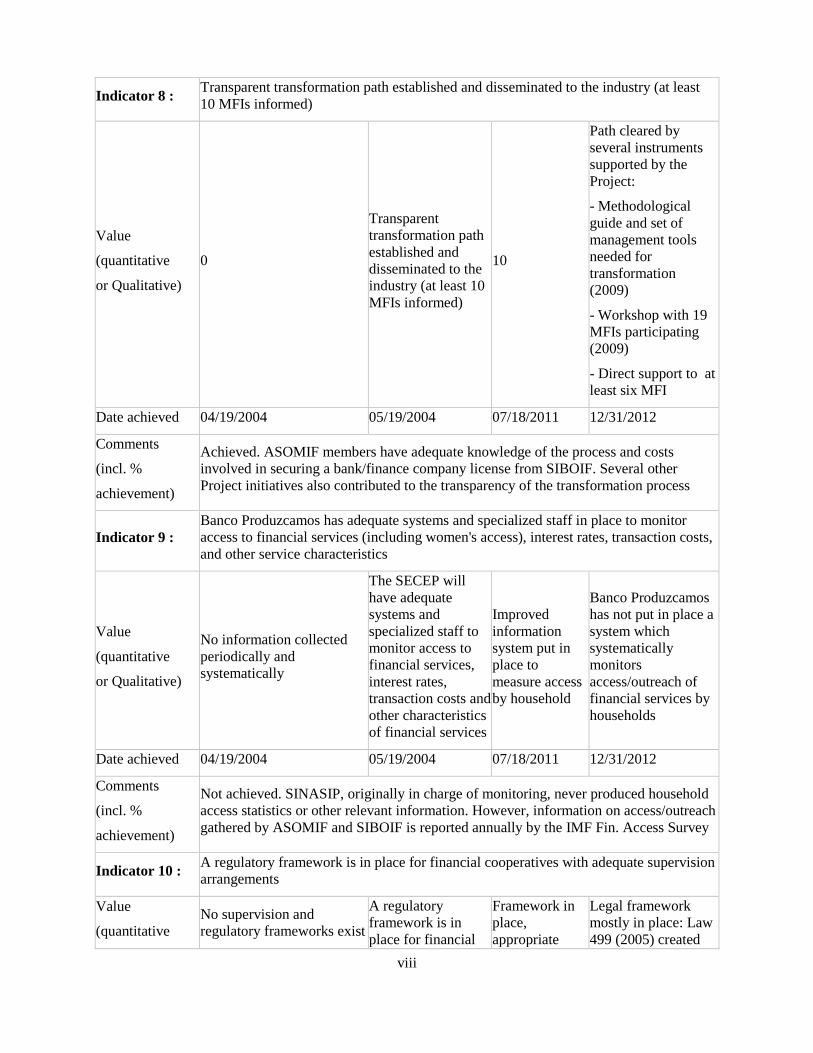

Indicator 8 : Transparent transformation path established and disseminated to the industry (at least

10 MFIs informed)

Value

(quantitative

or Qualitative)

0

Transparent

transformation path

established and

disseminated to the

industry (at least 10

MFIs informed)

10

Path cleared by

several instruments

supported by the

Project:

- Methodological

guide and set of

management tools

needed for

transformation

(2009)

- Workshop with 19

MFIs participating

(2009)

- Direct support to at

least six MFI

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Achieved. ASOMIF members have adequate knowledge of the process and costs

involved in securing a bank/finance company license from SIBOIF. Several other

Project initiatives also contributed to the transparency of the transformation process

Indicator 9 :

Banco Produzcamos has adequate systems and specialized staff in place to monitor

access to financial services (including women's access), interest rates, transaction costs,

and other service characteristics

Value

(quantitative

or Qualitative)

No information collected

periodically and

systematically

The SECEP will

have adequate

systems and

specialized staff to

monitor access to

financial services,

interest rates,

transaction costs and

other characteristics

of financial services

Improved

information

system put in

place to

measure access

by household

Banco Produzcamos

has not put in place a

system which

systematically

monitors

access/outreach of

financial services by

households

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Not achieved. SINASIP, originally in charge of monitoring, never produced household

access statistics or other relevant information. However, information on access/outreach

gathered by ASOMIF and SIBOIF is reported annually by the IMF Fin. Access Survey

Indicator 10 : A regulatory framework is in place for financial cooperatives with adequate supervision

arrangements

Value

(quantitative

No supervision and

regulatory frameworks exist

A regulatory

framework is in

place for financial

Framework in

place,

appropriate

Legal framework

mostly in place: Law

499 (2005) created

ix

or Qualitative) for cooperatives cooperatives

(CACs), with

adequate

supervision

arrangements

staff in place,

reports on

financial

cooperatives

generated

INFOCOOP; its

Resolution 04-2011

norms cooperatives

financial statements

- Law 804 (2012)

created MEFCCA

with oversight over

cooperatives

- Regulation has

started; supervision is

still incipient

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Partially achieved. Standard financial reporting rules supported by the Project are in

place, but CACs figures are not publicly available. New legal framework (Law 804)

requires updating to make it fully compatible with Law 499 on INFOCOOP

Indicator 11 : The microfinance regulatory framework is in place, with adequate supervision

arrangements

Value

(quantitative

or Qualitative)

No supervision and

regulatory framework in

place

The microfinance

regulatory

framework is in

place, with adequate

supervision

arrangements

System

operating with

high degree of

microfinance

coverage

Legal framework

established by Law

769 (2011) which

created CONAMI

with oversight over

MFIs. End-2012, 15

MFIs had registered

with CONAMI, as

required by the law.

Active work

continues on

supervision

arrangements and

supporting

regulations

Date achieved 04/19/2004 05/19/2004 07/18/2011 12/31/2012

Comments

(incl. %

achievement)

Largely achieved. The passage of the microfinance law in 2011 which established

CONAMI was a major Project achievement. Project also supported the drafting of

regulatory/supervisory framework for CONAMI. The IADB is currently providing

additional support

x

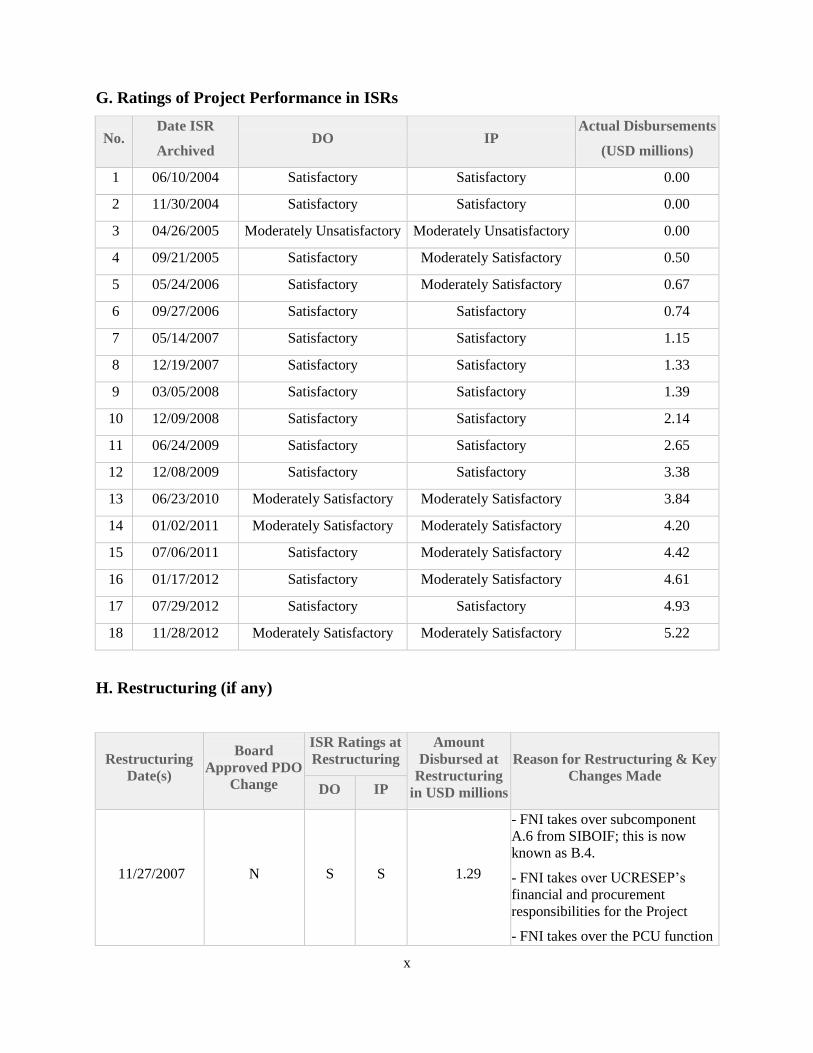

G. Ratings of Project Performance in ISRs

No. Date ISR

Archived DO IP

Actual Disbursements

(USD millions)

1 06/10/2004 Satisfactory Satisfactory 0.00

2 11/30/2004 Satisfactory Satisfactory 0.00

3 04/26/2005 Moderately Unsatisfactory Moderately Unsatisfactory 0.00

4 09/21/2005 Satisfactory Moderately Satisfactory 0.50

5 05/24/2006 Satisfactory Moderately Satisfactory 0.67

6 09/27/2006 Satisfactory Satisfactory 0.74

7 05/14/2007 Satisfactory Satisfactory 1.15

8 12/19/2007 Satisfactory Satisfactory 1.33

9 03/05/2008 Satisfactory Satisfactory 1.39

10 12/09/2008 Satisfactory Satisfactory 2.14

11 06/24/2009 Satisfactory Satisfactory 2.65

12 12/08/2009 Satisfactory Satisfactory 3.38

13 06/23/2010 Moderately Satisfactory Moderately Satisfactory 3.84

14 01/02/2011 Moderately Satisfactory Moderately Satisfactory 4.20

15 07/06/2011 Satisfactory Moderately Satisfactory 4.42

16 01/17/2012 Satisfactory Moderately Satisfactory 4.61

17 07/29/2012 Satisfactory Satisfactory 4.93

18 11/28/2012 Moderately Satisfactory Moderately Satisfactory 5.22

H. Restructuring (if any)

Restructuring

Date(s)

Board

Approved PDO

Change

ISR Ratings at

Restructuring

Amount

Disbursed at

Restructuring

in USD millions

Reason for Restructuring & Key

Changes Made DO IP

11/27/2007 N S S 1.29

- FNI takes over subcomponent

A.6 from SIBOIF; this is now

known as B.4.

- FNI takes over UCRESEP’s

financial and procurement

responsibilities for the Project

- FNI takes over the PCU function

xi

Restructuring

Date(s)

Board

Approved PDO

Change

ISR Ratings at

Restructuring

Amount

Disbursed at

Restructuring

in USD millions

Reason for Restructuring & Key

Changes Made DO IP

and SECEP’s remaining

implementing responsibilitie under

Parts D and E.1 (SECEP is out)

- Requirement to hire a single

management firm (Sec 3.01 of

Credit Agreement) to manage

provision of TA under Parts C.1

and C.2 deleted

- Works category can now be

financed 100 percent out of credit

proceeds, up from 87 percent

04/03/2009 N S S 2.45

Reallocation of proceeds in

Schedule 1 of DCA:

- Substantial increases in Works

and Goods categories

- A reallocation of Consulting

Services shifting resources away

from Part C

- A major reduction on proceeds

reserved for training

09/15/2010 N MS MS 3.95

- Closing Date extended two years,

to 12/31/2012. This was the

second date extension of the

Project.

07/18/2011 N S MS 4.42

- BP replaces FNI and assumes its

coordination, procurement and

implementation responsibilities

- Project’s monitoring and

evaluation indicators updated to

reflect restructurings and new

institutions—several added,

revised or deleted

- Part D.1 (b) is redefined as the

“Implement the Inclusion Policy”

subcomponent

- Proceeds reallocated: Goods,

Consultants’ Services and

Operational Costs go up, and

Works and Training down

xii

I. Disbursement Profile

1

1. Project Context, Development Objectives and Design

1.1 Context at Appraisal

1. In 2002 the Office of the Presidency of Nicaragua requested a project to increase

financial access, particularly of those poorly served at the lower end of the income scale. Access was scarce especially in rural areas, and the authorities were concerned with the high cost

of credit, transfers and payments incurred by small and micro businesses and households. The

Government of Nicaragua (GoN) saw an efficient, competitive financial sector with strong

outreach as an additional instrument for poverty reduction and alleviation—poverty was around

45 percent and inequality was high. International donors shared the Government’s view and had

been supporting the microfinance sector in Nicaragua with funding and expertise for years,

mainly for the benefit of microcredit.1

2. The proliferation of donor initiatives, however, contributed to considerable market

fragmentation, undermining the efficiency and viability of the financial system. At the

government level there was lack of transparency in microcredit provision and a large number of

conflicting programs. All this presented the final beneficiary with a chaotic menu of options.

3. In mid-2003, the Government announced a new policy for access to financial

services to address these challenges. The policy aimed at increasing market transparency,

strengthening financial intermediaries and establishing a more robust legal and regulatory

framework for microfinance activities.2 On the supply side, the policy sought sound,

commercially oriented financial institutions dealing in a fair and vigorously competitive

marketplace. This vision included the gradual transformation of unsupervised private providers

into supervised financial institutions and the restructuring of three state agencies: a) Financiera

Nicaragüense de Inversiones (FNI), a second-tier bank; b) Fondo de Crédito Rural (FCR), and c)

Instituto de Desarrollo Rural (IDR).

4. At the time of appraisal, the Project fit well with a Country Assistance Strategy

(CAS) focused on the Poverty Reduction Strategy Program (PRSP). This Project met the

CAS objectives by supporting two of its four strategic pillars: a) broad-based economic growth

and rural development, and b) good governance and institutional development.

1.2 Original Project Development Objectives (PDO) and Key Indicators

5. The Project Development Objective was: “to improve access to financial services

provided by sound, profitable financial institutions for low-income households and micro

and small businesses.” Two key indicators were originally defined to gauge outcome

achievement under the PDO: a) a 20 percent increase in the number of savings and loan accounts

in supervised financial institutions in five years, and b) a 10 percent increase in the number of

points of service of supervised financial institutions in five years. Additionally, the Project

Appraisal Document (PAD) defined five key performance indicators aimed at tracking

1 See CGAP’s Nicaragua: Country-Level Effectiveness and Accountability Review, July 2005, for a broad view of the

microfinance industry. Briefly, micro lenders, principally NGO microfinance institutions (MFIs) and savings and loans

cooperatives (CACs) had seen a sharp increase in the number of clients—approximately 26 percent per year from 1999 to 2004.

The CGAP review indicates that there were approximately 300 organizations serving 470,000 clients supplying some US$240

million in microcredit at end-2004—this made of Nicaragua the leading market for microcredit in Central America. 2 The referred policy is in the National Development Plan of September 2003.

2

intermediate results of four of the Project’s components (or Parts, as referred to in the

Development Credit Agreement or DCA)—a fifth component supported project coordination and

administration. These key intermediate result indicators were:

A private credit registry will be established

The Superintendence of Banks and Other Financial Institutions (SIBOIF) will have a fully

automated credit information and analysis system in place

Participating [in FNI credit line] unsupervised micro credit and microfinance institutions

will voluntarily adopt the accounting, external auditing, credit classification and interest

rate disclosure and reporting standards established by the SIBOIF

FNI will gradually develop a second-tier risk-based credit line for micro-finance

institutions (MFIs) of about US$15 million, with an acceptable level of portfolio at risk

Participating MFIs will achieve improved efficiency (as measured by administrative costs

as a portion of the average loan portfolio) and a higher degree of financial sustainability (as

measured by adjusted operating expenses as a portion of operating income)

1.3 Revised PDO (as approved by original approving authority) and Key Indicators, and

reasons/justification

6. The PDO was not revised. This was originally a five year Project which was extended

twice for a total of three and a half additional years in response to institutional changes and

external events. Nevertheless, the PDO was not revised during project life. Two core indicators

were formally added in 2011, to comply with Bank guidelines which require that MSME finance

core indicators should be reported for all World Bank lending operations supporting micro, small

and medium enterprises. In addition, the July 2011 Restructuring Paper presented a complete list

of revised intermediate result indicators. Three of the original intermediate result indicators were

dropped, two experienced a material change, and a new one was added to the original list in the

PAD (see Annex 8 for detailed information).

1.4 Main Beneficiaries

7. The primary target groups identified in the PAD were low-income households and

micro and small businesses, especially those in rural areas where access to financial

services was the weakest. However, broadening sustainable financial access and achieving

substantially higher levels of financial inclusion among targeted groups first required a major

structural reform in the supply of micro financial services. This was a precondition for achieving

a material change in the situation existing at the time of project appraisal.

8. Thus, the Project design made several public and private agencies and

organizations—including private micro lenders—the direct and indirect beneficiaries of

Project activities and resources. The aim was to significantly upgrade financial intermediation

and improve access of low income people and other vulnerable groups in the Nicaraguan society.

Many secondary beneficiaries were identified in the PAD or added later during project

implementation (see Figure 1). (Also see Annex 5 - Regulation and Supervision of Microfinance

Institutions in Nicaragua).

3

Figure 1. Beneficiaries of Project Activities

1.5 Original Components

9. The PAD defined five components or parts (as they are called in the Development Credit

Agreement), as follows:

10. Component 1 (Part A): Regulation and supervision of microfinance and credit

information. It provided support to SIBOIF to improve regulations and supervision for

overseeing microfinance operations of commercial banks, finance companies and FNI.

Resources also were allocated to upgrade SIBOIF technological platform, including the

remodeling of a computer center and its credit information database and associated analysis tools.

In addition, SIBOIF was to implement the legal and regulatory framework for the private credit

reporting industry and facilitate the initiation of this private activity by licensed companies. The

SIBOIF was also put in charge of coordinating technical assistance activities for enhancing

consumer protection in its area of competence.

11. Component 2 (Part B): Institutional strengthening of FNI. Besides providing credit to

commercial banks, this second-tier public lender administered donors’ funds going to

unsupervised microcredit institutions—although without assuming credit risk. This component

was geared to assist FNI enhance its intermediation capabilities and skills so that it could

intermediate available funds successfully on a low risk basis to its client’s base. Also, this

component was to assist FNI with promotional activities to attract commercially oriented

investors—so as to increase and diversify its funding sources for microcredit.

12. Component 3 (Part C): Outreach expansion support services. Crucial to the outreach

effort under the Project was the provision of technical assistance—coordinated by the Secretaría

de Coordinación y Estrategia de la Presidencia (SECEP)—for unsupervised MFIs to become

SIBOIF-supervised financial institutions individually or through mergers. Also, this component

was ready to assist commercial banks, finance companies and transforming MFIs to expand their

ability to provide profitable, sustainable and competitive microfinance services—including

technical assistance for market development, operational systems, technologically driven

financial innovations, and external audits. Support for cooperatives providing financial services

was also available under this component once adequate legal and regulatory standards and

supervision arrangements were in place. Business associations like ASOMIF could also be

supported and used as outreaching conduits.

Members of ASOMIF (over 20

micro lenders), in particular

FINCA, LEON, FDL, AFODENIC,

FUNDENUSE, FUNDESER, PANA-

PANA, PROMUJER, AMICA

Over 20 savings and loan

cooperatives (including

several multipurpose ones)

in particular CARUNA,

FECODESA and its affiliates,

LA CENTRAL, WASLALA

ASOMIF, SinRiesgos Credit

Bureau

SIBOIF, FNI, BP, SINAPSIS,

SECEP, UCRESEP, FCR,

INFOCOOP, CONACOOP,

MIFIC, CONAMI, Judicial

Branch

Savings and loan

4

13. Component 4 (Part D): Monitoring access to financial services and implementing

the financial services access policy. This component was designed to provide support to four

closely related activities.3 First, it was to assist SECEP to expand the SINAPSIP, a statistical

platform that was being developed to generate poverty-monitoring indicators at the national level,

so that it could also monitor the demand and supply of microfinance services. Second, this

component was to assist SECEP coordinate efforts geared to advance the formulation and

implementation of the government’s Financial Services Access Policy. Third, this component

included support for the enhancement and strengthening of the legal/regulatory framework and

supervision arrangements covering MFIs, cooperatives providing financial services, NGOs and

other micro credit institutions. Finally, the component would assist SECEP with the design of the

monitoring unit.

14. Component 5 (Part E): Project coordination. This component funded the Project’s

Coordination Unit (PCU) at SECEP and the procurement, financial management and accounting

support functions at UCRESEP, the Public Sector Reform Coordinating Unit.

1.6 Revised Components

15. Although the PAD components remained unchanged, they were updated in scope

and scale during the life of the Project. The DCA was modified five times. Changes were

introduced under the DCA amendments and restructurings—including two Closing Date

extensions and changes of the implementing agencies —and are summarized in section H of the

Data Sheet.4 Annex 8 elaborates on the rationale behind the changes agreed with the Borrower.

1.7 Other significant changes

16. Project financing reallocations took place in association with the restructurings.

Table 1 shows the history of credit proceeds for different expenditure categories, as stated in

Schedule 1 of the DCA. New country financing parameters adopted in 2005 reduced the need for

GoN’s counterpart funding, explaining the changes in the last two columns:

Table 1. Reallocations (in SDRs '000s)

Category Schedule 1 of CDA Bank funding

06/2004 05/2005 11/2007 04/2009 07/2011 Beginning End

Works 8.0 197.7 197.7 434.9 331.6 87% 100%

Goods 350.0 638.3 638.3 828.5 1,059.8 100% foreign;

87% local 100%

Consultants 3,780.0 2,170.1 2,170.1 2,323.2 2,523.6 100% foreign;

91% local 100%

- Part C 900.0 137.1 137.4 41.6 48.4 id.

- Other 2,880.0 2,033.0 2,033.0 2,281.6 2,475.2 id.

Training 235.0 1,728.7 1,728.7 1,151.6 817.6 100% 100%

Operational

costs 65.0 65.3 65.3 61.9 67.4 100% 100%

Unallocated 362.0 0.0 0.0 0.0 0.0

Total 4,800.0 4,800.0 4,800.0 4,800.0 4,800.0

3 Schedule 2 of the DCA consolidates those six subcomponents in the PAD into four subparts (Parts 4.1 to 4.4). 4 The main changes agreed with the Borrower include: (i) reallocation of credit proceeds, (ii) replacement of the SECEP and

UCRESEP with FNI as implementing agency for both programmatic and fiduciary responsibilities, (iii) replacement of FNI by

BP as the implementing agency mandated by law, (iv) two closing date extensions, and (v) update of the indicators in the results

framework. See Data Sheet and Annex 8 for additional information.

5

2. Key Factors Affecting Implementation and Outcomes

2.1 Project Preparation, Design and Quality at Entry

17. A TAL was the appropriate instrument in 2004 to support government policy and

better organize and coordinate the robust agenda for the microfinance sector. Project

preparation and design relied on analytical work5, including background papers

6 such as the

institutional strengthening of FNI under component 2 and the 2005 CGAP paper “Nicaragua:

Country-Level Effectiveness and Accountability Review”. The Project design was also closely

attuned to the objectives and policy strategies for financial services in the 2003 National

Development Plan (NDP)7 and the recommendations from the 2003-2004 Financial Sector

Assessment Program (FSAP). While there was limited Bank experience with financial reform in

Nicaragua on which to draw for the design of this TAL, the Project took into account lessons

learned from other initiatives.8

18. Commitment to the Project agenda was high. In 2002, the Office of the Presidency of

Nicaragua created a microfinance working group for the development of a more sustainable

microfinance sector. The fact that the PCU was incorporated into the SECEP and that the

management of components 3 and 4 was added to its list of responsibilities indicates that there

was ownership and commitment to the Project’s agenda at the highest levels of the Executive

Branch. Commitment was also high at SIBOIF, as shown by the satisfactory implementation of

component 1 under its management. Less clear was the commitment of FNI to the Project

objectives. FNI was less prepared to address the challenge of upgrading its intermediation skills

and the creation of a strong new line of business lending to unregulated MFIs. Although there

was general political consensus on the Project’s PDO and its components, there was less

consensus on the details of Project design in the National Assembly when the Board-approved

version went for ratification. As a result, the DCA had to be amended prior to effectiveness and

congressional approval (i.e., moving component 3 from the SECEP to FNI9), which led to delays

in implementation.

19. Macroeconomic stability was rightly identified in the PAD as a critical risk for a

smooth Project implementation. While the probability of macro instability was seen as

moderate, severe draught and the unexpected global financial crisis meant that this risk

materialized with severe consequences for the Nicaraguan financial sector and the microfinance

industry (MFIs and CACs alike). Furthermore, the situation for the microfinance sector was

aggravated by the “No pago” movement and the “Moratoria” Law in 2010. In addition, the

operational risk of the large number of stakeholders in a technical assistance loan was fully

5 As illustrated by the long list of documents on microfinances listed in Annex 9 of the PAD. 6 See footnote 4 in page 35 of the PAD. 7 For example, measures in the NDP to promote financial access, such as the establishment of a new legal and supervisory

framework for microfinance activities, the enhancement of consumer protection, a normative framework for credit bureaus or the

provision of TA to microfinance institutions—among others. 8 The experience of the Rural Financial Services component of the Agricultural Technology and Land Management project in

Nicaragua (1997-2000) appears to have been useful in this respect, in particular that “the legal and regulatory framework greatly

affects incentives for outreach expansion”. 9 While not the best, there were few options left since SIBOIF did not see that its mission of oversight over regulated institutions

fit well with the promotional activities in the agenda of component 3. On the other hand, there was opposition at the Economic

Commission of the National Assembly to the idea of mixing the responsibilities of the Office of the Presidency over the

formulation of the financial inclusion policy with the outreach function which was going to benefit specific private MFIs for their

transformation using public funds—the President’s office was expected to manage component 3 via SECEP.

6

recognized in the PAD. SECEP had to work smoothly with SIBOIF, FNI, UCRESEP and a

management firm (under the outreach component 3), to successfully integrate various donors and

other public and private parties with vested interest on the proposed agenda. These operational

and coordination risks did materialized during implementation and played a significant role in

the delays and slow pace of disbursement.

2.2 Implementation

20. Project restructurings created delays, but were necessary to adapt to changes in the

national institutional framework and to respond to unexpected external events.10

One of the

initial challenges for the Project was the long delay for effectiveness – one year after its expected

original date. In addition, following the 2006 Presidential election, some aspects of Project

execution were delayed due to significant policy changes, a more centralized process of decision

making, as well as a rotation of senior officials. Furthermore, external events outside Project

control also caused delays in implementation and affected Project output and outcome. In

particular, the ‘no-pago’ movement, which surfaced following the rising beneficiary

indebtedness after the 2008 global financial crisis, hindered MFI expansion. Thus, the Project

had to be restructured to adjust the work plan, provide additional time for Project execution and

facilitate implementation, while reallocating Project resources toward activities with the greatest

potential for impact. Most of the adjustments came in response to a changing political climate

and severe hardship in the macroeconomic environment that called for corrective measures and

structural reforms in the microfinance sector and its business model.

21. Although the IDA credit was not fully spent, the Project played an important

catalytic role and attracted a good deal of complementary donor support. Given

interruptions during implementation due to restructurings and the ambitious work program in a

poor country with large policy swings, disbursements were unevenly paced from year to year.

Frequent institutional adjustments—for example, the long transition from FNI to BP in 2010 and

2011, required an extended period of due diligence. Disbursements finally recovered in 2012

with the launch of the National Commission of Microfinances (CONAMI), a pickup in training

(i.e., postgraduate course for civil judges) and the equipment purchases at SIBOIF and BP. Still

some resources remained unutilized. On November 19, 2012, as per the request of the GoN,

SDR 933.5 thousand of the IDA credit was cancelled. This is due, in part, to the fact the IDA

credit helped Nicaragua attract and access co-financing for US$1.33 million in complementary

donations from third parties, which were not in the original funding plan and were given

disbursement priority. Besides the contribution by the Dutch government since 2006, a Japanese

grant and key donations from the Inter-American Development Bank (IADB)11

were received.

22. Despite challenges, most components produced a rich output and numerous

achievements (see section 3.2)12

. Successful implementation can be attributed to the

commitment of the implementing agencies to execute an ambitious Project agenda with

numerous intertwined and complex tasks, and the close Bank supervision during implementation.

The use of IDA credit was highest under component 1 executed by SIBOIF, where the

10 See Annex 8–B for details on Project revisions and amendments caused by a changing environment. 11 IADB has been particularly active in its support to CONAMI. It is also supplying fresh funding and technical assistance to BP. 12 Also see Annex 1 for more details on Project costs and financing, Annex 2 for Project activities by component and Annex 3 for

more details on achievements.

7

counterpart agenda and ownership was strong.13

Project implementation was the weakest under

component 4 since the system to monitor financial access by the poor proposed under that

component suffered from a combination of over-ambitious goals and implementing agency’s

shortcomings—first under SECEP and later on under FNI and BP.

2.3 Monitoring and Evaluation (M&E) Design, Implementation and Utilization

23. Although the Project was relevant to country needs, it was difficult to aggregate

impacts and to assess progress toward achievement of the PDO. The original list of key

performance indicators was to a certain extent appropriate for monitoring progress on

sustainability of micro lenders, given the PAD’s emphasis on rapidly transforming unsupervised

micro lenders into SIBOIF-regulated intermediaries. However the remaining unsupervised micro

lenders were also expected to voluntarily submit themselves to much more rigorous standards in

order to access FNI’s US$15 million new credit line. Unfortunately, this did not materialize as

expected. As previously mentioned, the Project was restructured often to meet the new political

and market realities; however, the performance indicators were not, ultimately affecting the

M&E implementation and utilization. The major revision of indicators in the last restructuring of

July 2011 improved partially the capacity to measure results although it did not go far enough to

improve the adequacy of the indicators. For example, in the case of the PDO Indicator 1 the

number of point of service remained limited to those financial institutions supervised by SIBOIF.

The original results framework was not successful in monitoring progress on financial access by

the poor and their micro and small businesses. Also, the two core indicators (Indicators 3 and 4)

added in July 2011 were not the best measure of specific PDO achievements.

24. Monitoring the TAL was based on continuous dialogue with Government

counterparts. Implementing agencies and the Bank staff did not systematically report on key

indicators. However, the Bank, SIBOIF and FNI (later BP) had sufficient data from alternative

sources to make decisions, including the rich information generated by the Project many

activities and intense supervision efforts. It is notable that ISRs tracked only a limited number of

performance indicators, conveying a narrow view of progress toward PDOs and intermediate

objectives. Nonetheless, the Bank team supervised Project execution closely, registering over

two supervision mission per year during implementation, having rated the Project performance

eighteen times in an equal number of ISR reports. The Bank made a concerted effort to obtain

information on all performance indicators by the time of the mid-term review and close to the

end of the Project’s implementation.

25. Of four PDO indicators, two were achieved, one was largely achieved and only one

fell short. The sharp increase in deposit and loan accounts and the much larger number of points

of service of intermediaries under SIBOIF oversight, the two main PDO indicators, were

particularly encouraging for financial access. Of the Project’s eleven intermediate result

indicators, six were achieved or largely achieved, four were partially achieved and one was not

achieved by the closing date. The intermediate results of indicators associated with component 1,

13 With the help of the Project and others, the SIBOIF has developed strong oversight capacities and capabilities over financial

institutions under its watch, adopting an integrated risk analysis approach whereby each supervised financial intermediary will

have to measure and assess the integral risk it faces in the marketplace. SIBOIF now has systems in place with the ability to

electronically receive, store and monitor on-site—and via an alternative external site— transactions of banks and finance

companies. SIBOIF is currently working on the implementation of an early warning system based on the risk profile of each

supervised institution. SIBOIF also provides online credit reports on clients of supervised institutions to banks and finance

companies, complementing the information provided by private credit bureaus.

8

as well as the indicators related to stronger MFI oversight, speak well of the efforts made to have

more financially sustainability and sounder MFIs coming out of the prolonged recent financial

crisis. Implementation issues in component 4 did not help in the monitoring of developments

related to financial inclusion.14

2.4 Safeguard and Fiduciary Compliance

26. Financial fiduciary performance by the Borrower (at UCRESEP, FNI and BP) was

adequate. Most audit opinions on the Project’s financial statements were unqualified, although

they highlighted moderate shortcoming in the internal control systems, which were generally

corrected to meet the audit recommendations. In general, these shortcomings did not prevent the

timely and reliable provision of information required to manage and monitor the implementation

of the Project. There were some financial management and operational capacity constraints at the

PCU, which with the adoption of timely corrections could have resulted in a more intensive

utilization of available Project resources.

27. The PCU management of procurement processes was mostly satisfactory, except in

the final year when it was rated moderately satisfactory. Procurement plans were adjusted

often to meet the demands of the several Project amendments, but processes were generally well

managed. The last procurement rating suffered due to shortcomings in the Borrower’s

procurement processes of major outputs and poor coordination between BP and SIBOIF.

Particularly, the Bank procurement staff observed in the last year a moderate overall risk in the

bidding processes and in the administration of contracted activities. No fraud or corruption issues

were found during Project execution.

28. Overall compliance with safeguard policies was satisfactory. The Project triggered the

Indigenous Peoples Policy (O.P. 4.10). As outlined in the Project’s Indigenous Peoples Inclusion

Plan, the objective was to actively pursue the PDO for the benefit of indigenous groups living in

the North and South Atlantic Autonomous Regions (RAAN and RAAS), where large

concentrations of indigenous people live. An open dialogue was established with indigenous

groups and communities in these two regions early on the implementation of the Project, leading

to extensive and focused provision of technical assistance.

29. In August 2007, the Caribbean coast was devastated by Hurricane Felix to which

the Bank responded with an emergency credit. This made Project assistance even more urgent.

A Bank mission visited the RAAN in early 2008, confirming the very limited supply of financial

services.15

There were just eight microcredit institutions with very limited funding access, poor

record in credit recovery and only serving small entrepreneurs around the three main urban

centers. Their reach in rural areas was undermined by costly and limited transportation and

communication means. Because indigenous lands are generally community owned, the lending

14 SECEP first and then FNI and BP were unable to assist with the development of a monitoring system for measuring access to

financial services. In its original formulation at appraisal, the responsibility to generate household access to financial services

data was placed in SINASIP within SECEP—in charge of monitoring a broad spectrum of poverty/access indicators. However,

the SINASIP initiative never materialized and was cancelled, together with discontinuation of SECEP, when the Ortega

Administration came into office. Several indicators of social outreach and coverage are published semiannually by ASOMIF—as

illustrated in Annex 5-B. These indicators, however, point in the direction of deterioration in financial access among the poor and

micro and small businesses since the onset of the global crisis in 2008, which has imposed a heavy burden on the most vulnerable

groups of the Nicaraguan society (see Annex 3). 15 BANPRO, the only bank operating in the region with one office in Puerto Cabezas, offered loans of at least US$3,500, too high

to be within reach of the majority of the indigenous population.

9

modalities of these financial intermediaries were mainly through solidarity groups and

communal banks.

30. The Project provided extensive technical assistance and training to assist micro

lenders in the Caribbean coast to improve their performance and reach. Project activity

focused on local intermediaries and community groups while the financial support was delivered

mainly via the Rural Credit Fund (FCR), a second-tier state institution also providing technical

assistance to agribusinesses across the country. Project funding helped improve accounting and

financial management processes and procedures, and provided training of local consultants (see

Annex 2 for a sample of Project activities in the Caribbean coast; also, Annex 3-A illustrates

micro lending in the RAAN). However, the sustainability of these investments was undermined

by lenders’ very low absorption capacity and the limited market size. Despite the extensive

technical assistance and training provided to micro lenders in the Caribbean coast, financial

access by indigenous people remains low. MFIs’ loan portfolios have continued to deteriorate

and never recovered after Hurricane Felix. The contrast between financial access in Managua

versus the RAAN and RAAS remains stark.

2.5 Post-completion Operation/Next Phase

31. Currently, the 2012-2017 CPS is following this TAL with a series of smaller

technical assistance grants and closer collaboration with IFC and MIGA. So far, three new

FIRST grants have been approved for different aspects of the financial sector – payment systems,

consumer protection and support to CONAMI. Meanwhile, MIGA recently approved a

guarantee for one microcredit lending and IFC is exploring re-entering the sector. No other IDA

credit is planned at this time. A follow up FSAP is also programmed for FY2015.

3. Assessment of Outcomes

3.1 Relevance of Objectives, Design and Implementation

32. The objectives of the Project are relevant to Government priorities and aligned with

Bank assistance strategies. Improving the low levels of financial access remains relevant for

reducing poverty and inequality in Nicaragua, and important for enhancing competitiveness and

exports by small producers, especially in rural areas.

33. The Project’s design correctly placed the emphasis on institutional strengthening,

which remains a priority for the microfinance sector of Nicaragua even today. As stressed

throughout this document, this operation contributed substantially to key issues in the

microfinance agenda. While responsive to government needs, this TAL had the ambitious goal of

reforming microfinances at all levels to advance financial inclusion on a more solid basis. This

meant that financial access had to reach rural areas, including indigenous people, and promote

the addition of a substantial number of new points of service by financial intermediaries. Key to

sustainability was the need of a major financial reform, which the Project promoted and assisted

with direct financing (see Annex 3).

3.2 Achievement of Project Development Objectives

34. The Project contributed to the development objectives, with gains made in several

areas. Project contribution is now broadly recognized and well appreciated by practically all

stakeholders. There were significant advances in PDO outcomes:

10

The number of financial (deposit and loan) accounts has had an impressive expansion

(68.1%) since 2004, even after netting out the impact of the financial crisis. Points of service

also have increased significantly from around 200 to 320, mostly among intermediaries under

SIBOIF oversight—the incorporation of MFIs FAMA and FINCA to this oversight certainly

helped16

.

Sustainability of the microfinance industry coming out of the crisis is more robust, under the

umbrella of a far stronger oversight by specialized public agencies and with MFIs showing

stronger coverage and outreach indicators (according to ASOMIF17

and SIBOIF data).

35. The strengthening of the legal, regulatory and supervisory framework of the

microfinance industry was a major Project achievement and central to PDO sustainability.

SIBOIF’s primary responsibility under the Project was to improve microfinance regulations and

supervision practices for commercial banks, finance companies and FNI, which are its direct

responsibility. Clearly, SIBOIF did that and component 1 provided substantial support to that

effect. The May 2005 restructuring added to SIBOIF the responsibility of also having to work

on strengthening the framework for MFIs and CACs. By 2006, SIBOIF was otherwise moving

forcefully ahead with its work of developing prudential norms for microfinance activities of

regulated intermediaries. In 2007, Project restructuring moved the responsibility to assist with

the strengthening of a similar framework for CACs and MFIs to FNI—as a new subcomponent

under the institutional strengthening component 2.18

At the end, SIBOIF did a satisfactory job

and currently has a comprehensive in-situ and extra-situ protocol for supervision of microfinance

activity of regulated entities.19

36. In 2011, with Project support, a new microfinance law created CONAMI as the

oversight body for MFIs. When the Bank approved the Project the general concept of the

Special Law on Microfinance had already been approved in first instance by the National

Assembly. In 2011, after the microfinance sector crisis and a new microfinance law was enacted

with the support of the Bank, the International Monetary Fund (IMF), and the Central Bank of

Nicaragua and created CONAMI as the regulator for the sector. It was particularly helpful in

this respect that the IMF included the passage of this law as one of the Structural Benchmarks

under its 2010-2011 Extended Credit Facility (ECF).20

In 2012, the Project was able to actively

support the launching of CONAMI (see Annexes 2 and 3) and the drafting of its regulatory and

supervisory framework. SIBOIF also has been contributing to CONAMI’s effort, which is

essential for the establishment of harmonized rules and practices for the oversight of

microfinances. Since its formal establishment in October 2012 until December 2012, there were

fifteen MFIs registered with CONAMI, with around US$134 million in loan portfolios. As of

today, all eighteen MFIs that were required by law to register have done so and other smaller

16 The incorporation of MFIs FAMA and FINCA to the SIBOIF oversight explained 10.9 percent of the points of sale under its

supervision at end-2012. FAMA and FINCA explained 8.2 percent of the loans accounts under SIBOIF supervision at end-2012.

As finance companies, these two MFIs do not take deposits from the public.

17 See Annex 5-A on performance indicators.

18 See table in Annex 8 for a detailed history of this subcomponent. 19 According to the Annual IMF Financial Access Survey Data, commercial banks had 91,389 SME loan accounts at end-2011,

while regulated MFIs (finance companies) had 242,688 borrowers in total (households and SMEs). 20 The effort to comply with the Fund’s conditionality benefited from the previous work done under this TAL operation to

improve microfinance regulation, supervision and enforcement under the SIBOIF. Fund-imposed conditionality to make

mandatory the use of the MUCCOOP—“Manual de Unico de Cuentas Cooperativas” was facilitated also by the assistance

provided by this Project to UNICOOP in the preparation of that manual.

11

MFIs have started to register. Now the challenge for CONAMI is to attract other unregulated

financial intermediaries to register and to enforce a sound and effective supervisory function.

37. The transformation of MFIs into regulated, deposit-taking institutions was a key

Project goal; however, a combination of external events and lack of targeted funding for

the effort reduced the Project’s efficacy in this area. Initially, MFIs did not see much

advantage in becoming regulated intermediaries. Until mid-2008, abundant foreign funding was

coming into Nicaragua, while the attraction of being able to take deposits from the public

required their transformation into commercial banks, a demanding undertaking in terms of

capital and management overhauling21

. The desire to transform on the part of MFIs became more

pronounced with the onset in 2008 of the global financial crisis, which sharply limited foreign

credit and imposed the need to upgrade operations and attract capital investors. However, the

financial support that the Project could offer at that time to assist with MFI transformations was

limited following cuts at the Borrower’s request.22

The Project nonetheless contributed to a better

understanding of the transformation process involved in securing a bank/finance company

license from SIBOIF. Also, with the Project’s assistance ASOMIF was able to: a) gather data via

a market survey to learn about MFIs feasibility of becoming regulated finance companies, b)

prepare a standardized set of financial accounts for its affiliates, and c) revise existing MFIs

manuals and accounting practices bringing them closer to SIBOIF requirements.

38. The Project made a significant effort to improve CACs’ prudential regulations and

supervision (see Annex 2). Since 2005 the responsibility to supervise cooperatives had been

with the Instituto Nicaragüense de Fomento Cooperativo (INFOCOOP), an autonomous state

agency, and the Project actively supported the development of its oversight function. However,

in July 2012 a new ministry (MEFCCA) was created and assumed oversight of cooperatives,

including CACs. The INFOCOOP was placed under its umbrella, with responsibilities limited to

the promotion and development of the cooperative model. While the separation of the

supervisory function from the other two functions INFOCOOP used to have is a step in the right

direction, there may be some risks inherent in the move. However, the impression of the ICR

mission was that much of the progress at INFOCOOP will be able to be of benefit to the new

regulator of cooperatives. In addition, the Project contributed with abundant TA targeted directly

to CACs under component 3.23

39. In addition, the Project’s agenda had important achievements consistent with the

objective of enhancing financial access by the poor and other vulnerable groups. In

particular:

SIBOIF prudential regulations and supervision practices and capacities benefited across the

board from Project assistance. This important achievement was extended to microcredit

21 Experience has shown that the direct cost of transformation can range from US$3 to 5 million, an amount hard to assemble

even for the biggest MFIs; much higher capital levels are also required. 22 In fact, the 2005 Assembly-led Project restructuring had deeply cut the availability of consulting funds for the outreach

component 3 (see consulting services, Part C in Table 1) geared for assisting with MFIs transformations. When the Ortega

Administration came into office in early 2007, it also showed little desire to dedicate great sums of IDA funding for this purpose.

Although, the Dutch grant was quite helpful in this respect and was used to this effect. 23 For example, over 100 CACs and over 20 MFIs received training: a) 24 courses (postgraduate level and certificate programs)

about finance, accounting, credit risk, financial planning, internal controls, risk management and systems, etc; b) 3 seminars in

the Caribbean coast, related to financial management and internal controls; c) 5 workshops related to "Manual Unico de Cuentas”

(MUC) and financial sector technology.

12

transactions of regulated banks and finance companies—which already have an important

share of microcredit.

Advances in consumer protection for financial services, the education of civil judges on

financial issues and the impact of licensed private credit bureaus in the mitigation of over

indebtedness of MFIs’ clients have had a social impact and favored those micro borrowers

with limited financial sophistication.

A clear path and renewed interest by leading MFIs (i.e Fundeser, FDL and others) to be

regulated under the SIBOIF umbrella. Moreover, direct and indirect MFI support contributed

to a strong industry response for establishing its regulatory and supervisory framework (see

Annex 2). All this is creating a better environment for a more sustainable sector.

The Project planted important seeds in terms of better accounting and management practices,

which were incorporated into new legislation and regulation. Substantial progress was made

on information management systems and technology used by the industry as a whole.

Although less advanced, important legal and regulatory steps have been taken to bring

prudential regulation and supervision to cooperatives providing financial services.

The Project also contributed training, studies, direct technical assistance and in-house experts

for the benefit of intermediaries and public agencies. Sustainability of Project achievements

in this area depends largely on continued support from the international donor community.

The work with the indigenous communities along the Caribbean coast (RAAN and RAAS),

was intensive. It now provides a more solid basis for future efforts in the region. Additional

support is needed from the low point left by the devastation caused by Hurricane Felix in

2007. Nonetheless, as mentioned in section 2.4, the work done to include indigenous groups

advanced the objective of reaching the poorest with financial services.

40. However, after a prolonged period of rapid expansion, the onset of the global

financial turmoil in late 2008 and the microfinance sector crisis that followed caused a

sharp reversal in credit access. The decline was generalized and affected clients of regulated

and unregulated micro lenders and it is still being felt strongly today. The number of loans of

small and medium-sized enterprises (SMEs) in commercial banks fell by 43.6 percent, from over

162,000 at the end of 2008 to over 91,000 at the end of 2011, a decline much more pronounced

than that of their overall portfolio. For MFIs members of ASOMIF, the number of clients

dropped by 36.3 percent between June 2008 and June 2012, to 225,966.24

An even bigger

concern has been the more pronounced decline in microfinance number of loans and clients in

municipalities with high poverty (i.e., RAAN and RAAS). ASOMIF results show a drop of 63.3

percent in the number of clients and of 60.7 percent in the size of the associated loan portfolio

from June 2008 to June 2012 (to US$45 million versus US$147 million for the MFI total

portfolio).

41. The recent deterioration in financial inclusion among the poor should not invalidate