Embed Size (px)

Citation preview

Document of

The World Bank

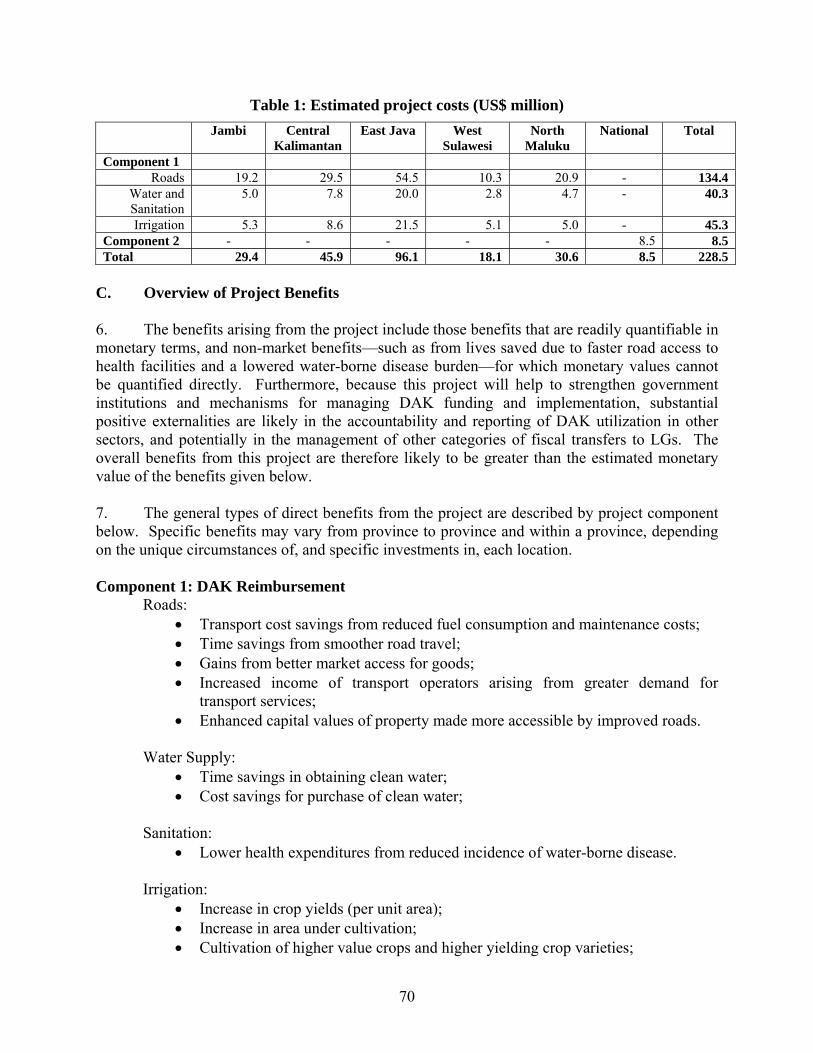

FOR OFFICIAL USE ONLY

Report No: 53613-ID

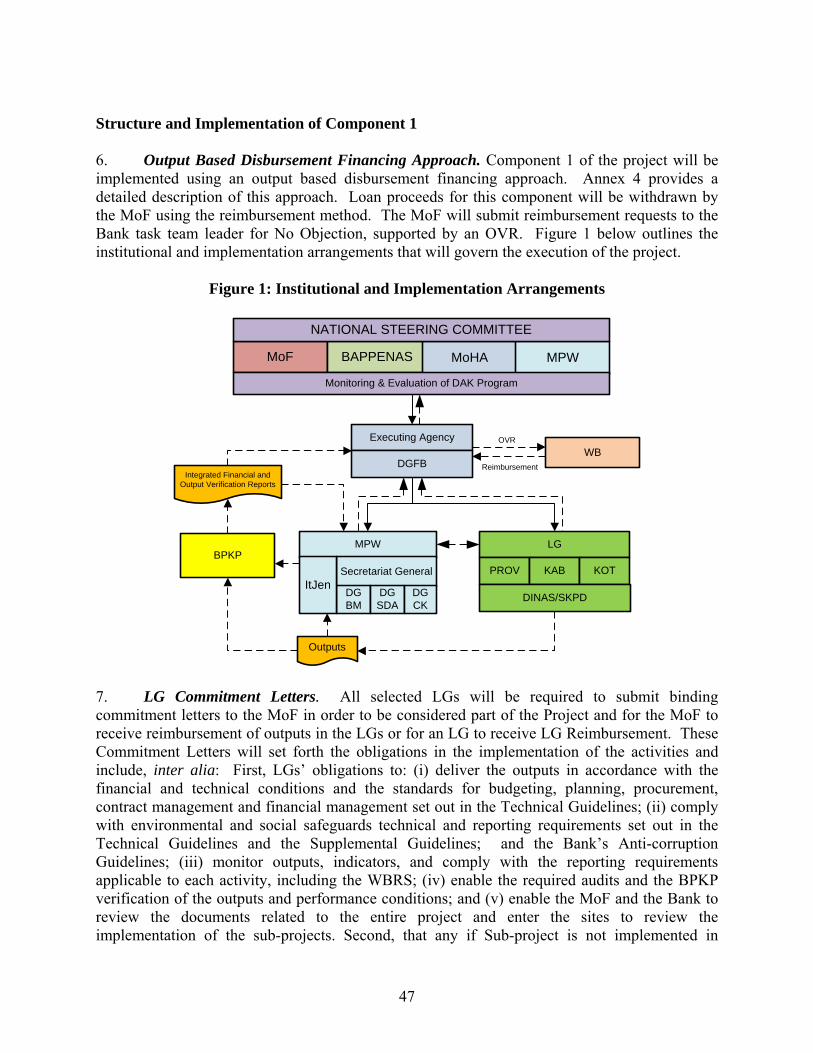

PROJECT APPRAISAL DOCUMENT

ON A

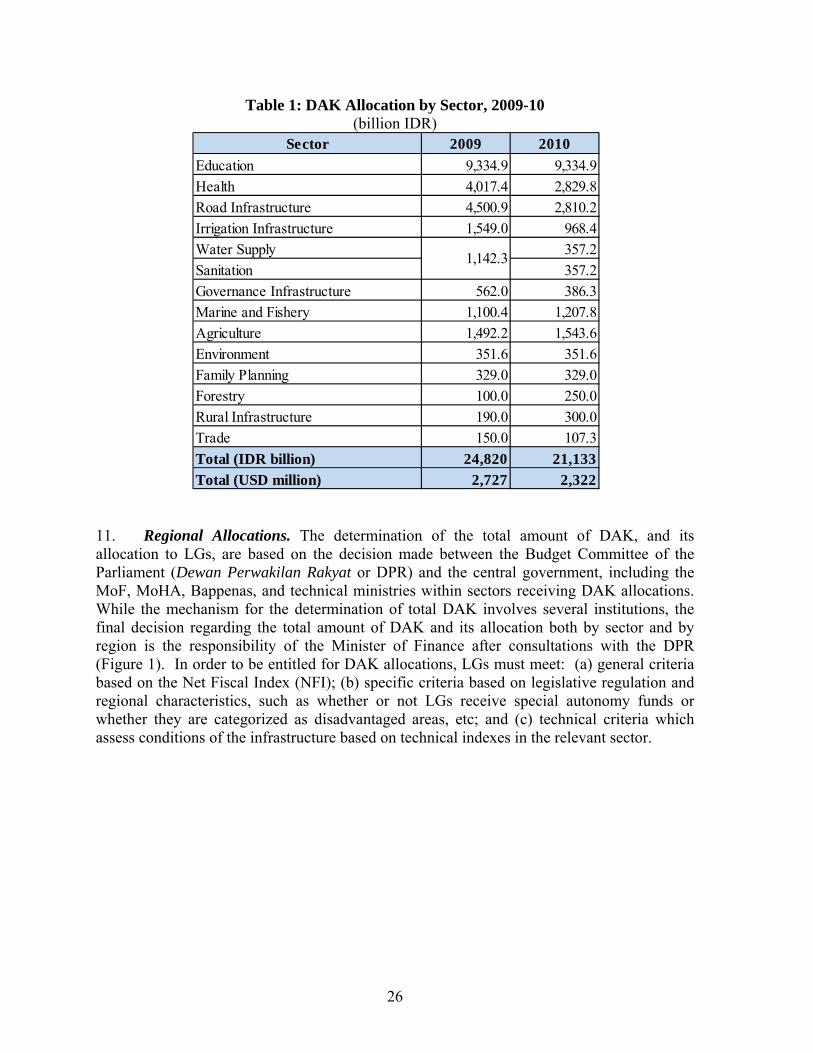

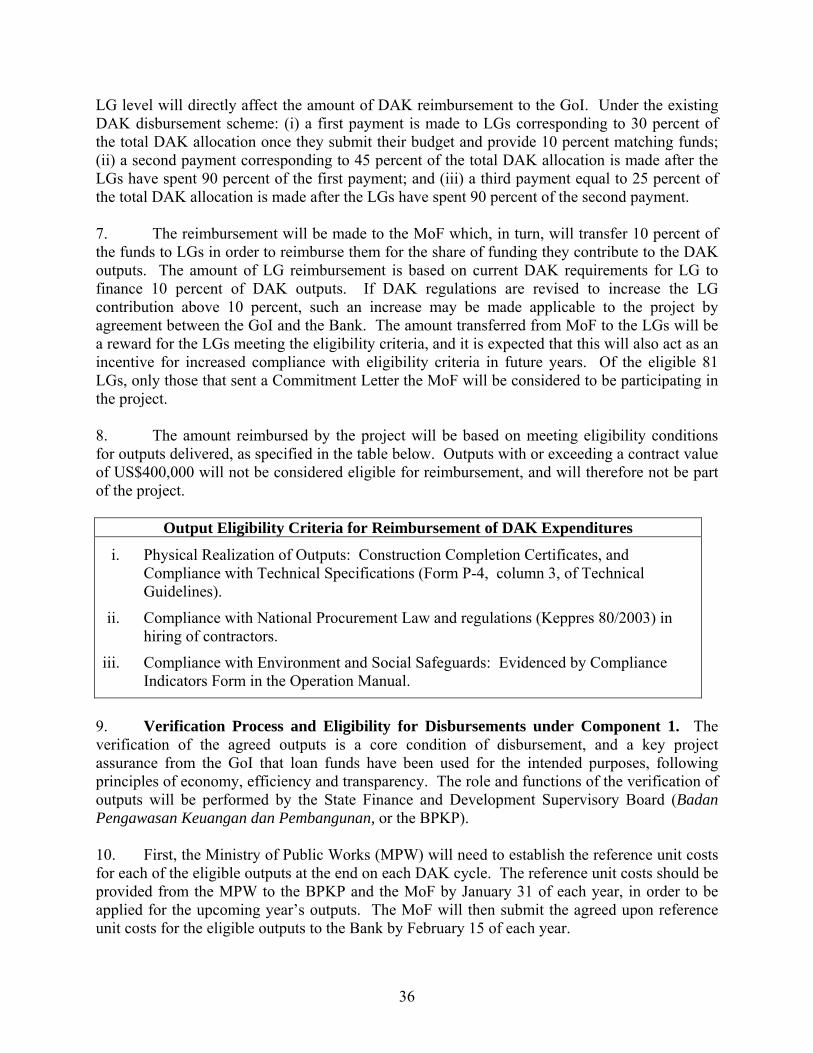

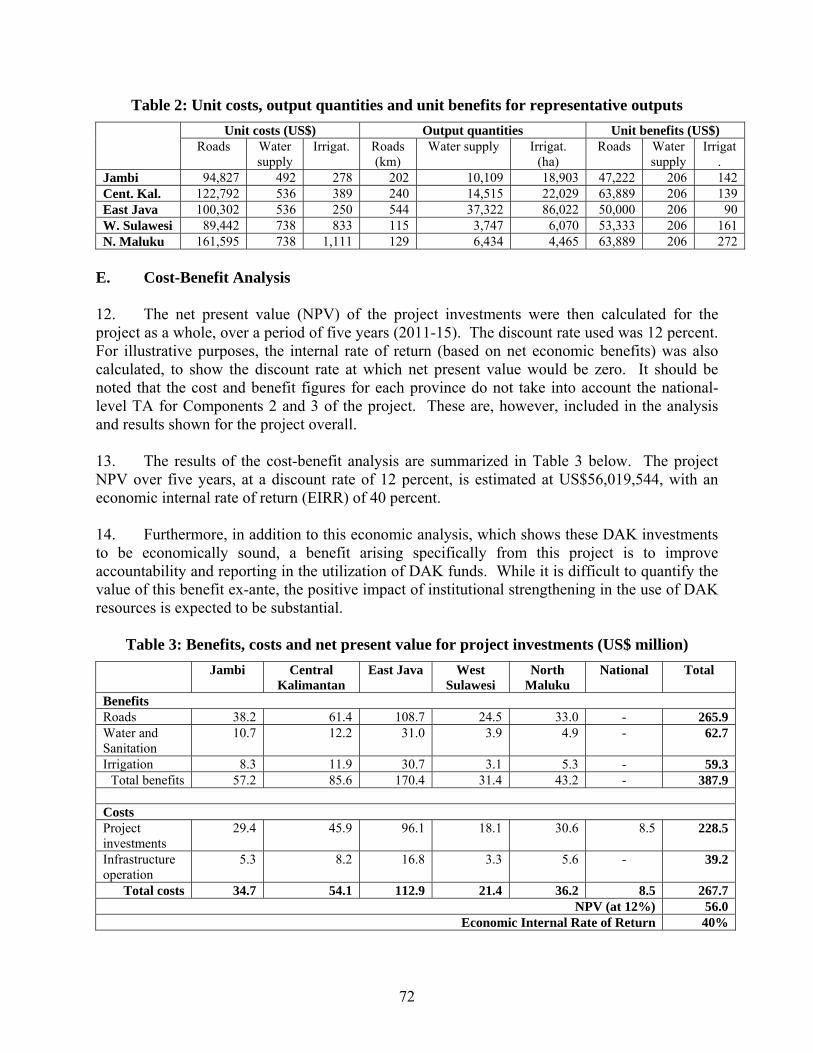

PROPOSED LOAN

IN THE AMOUNT OF US$ 220 MILLION

TO THE

REPUBLIC OF INDONESIA

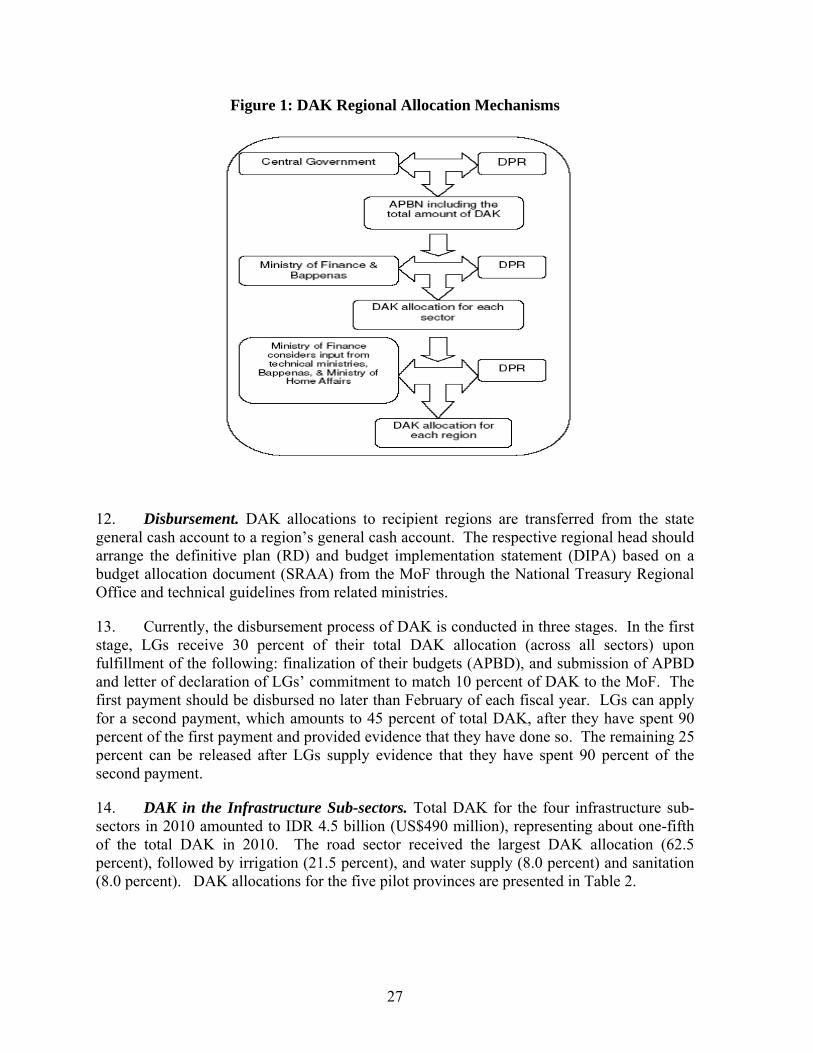

FOR A

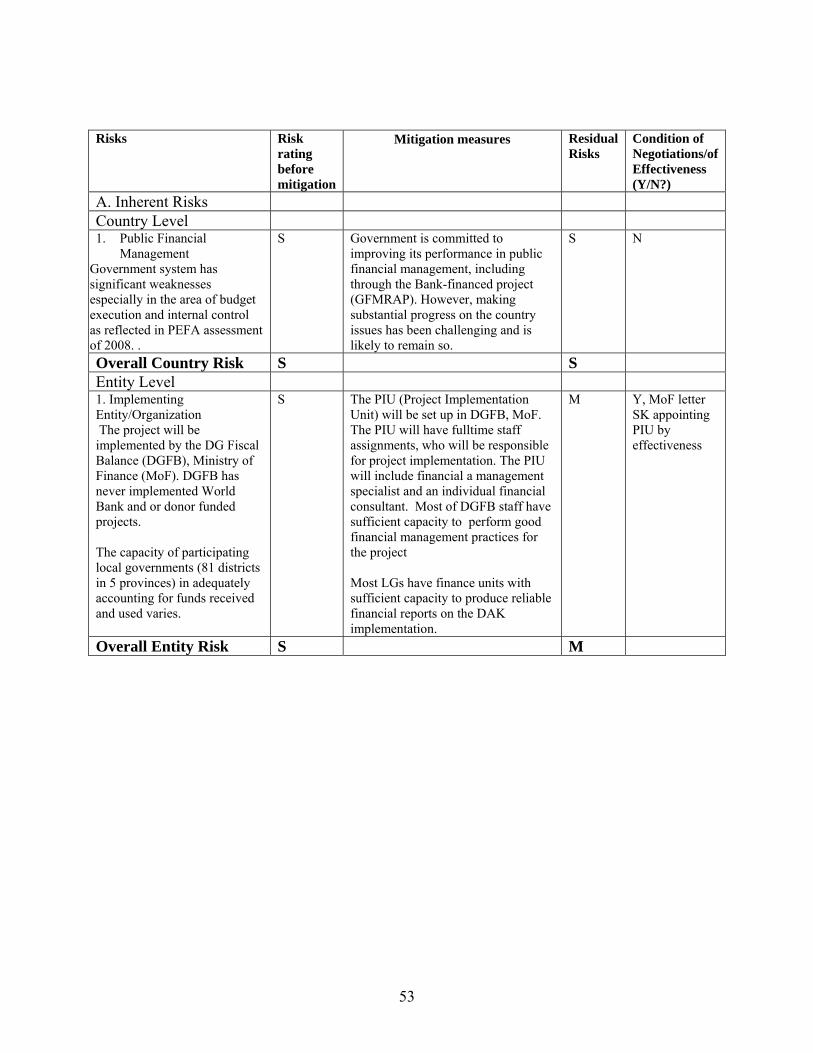

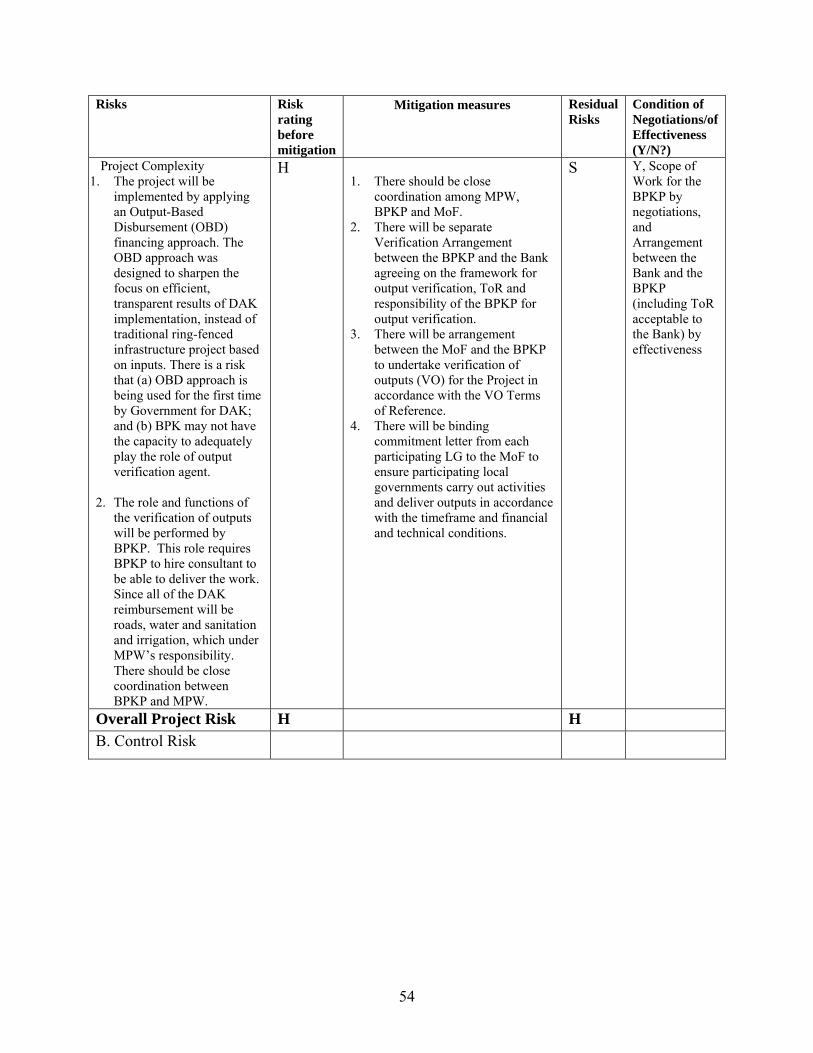

LOCAL GOVERNMENT AND DECENTRALIZATION PROJECT

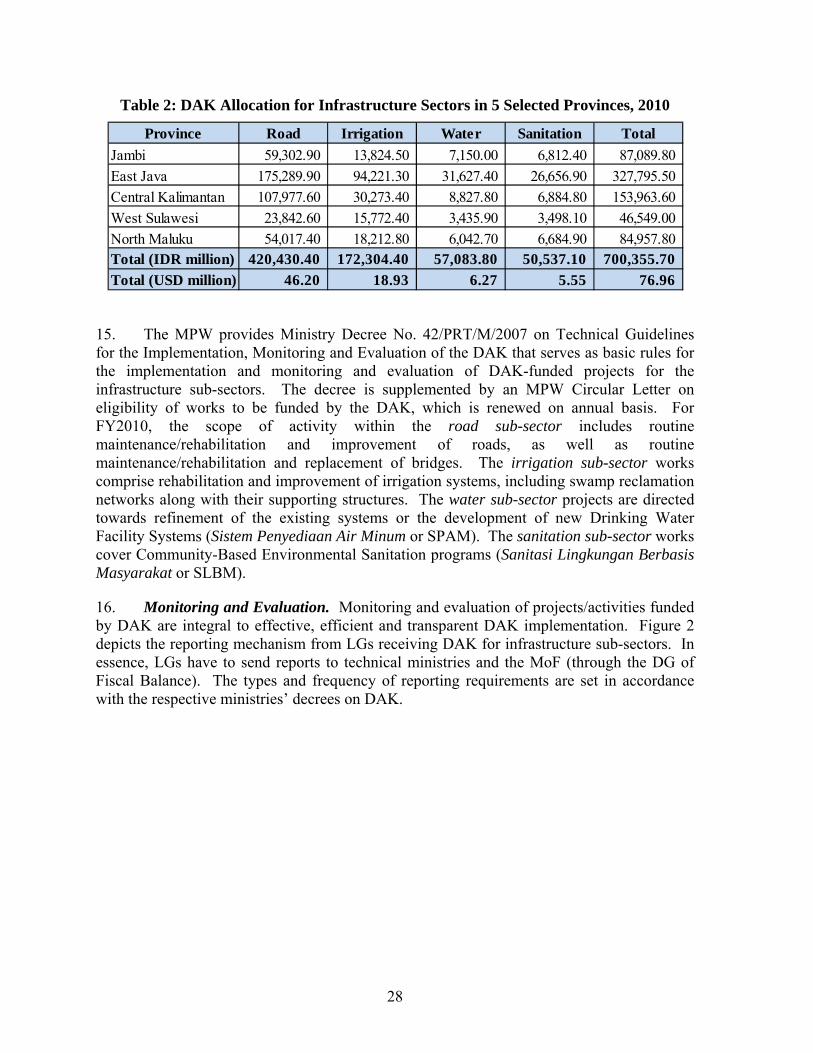

April 23, 2010

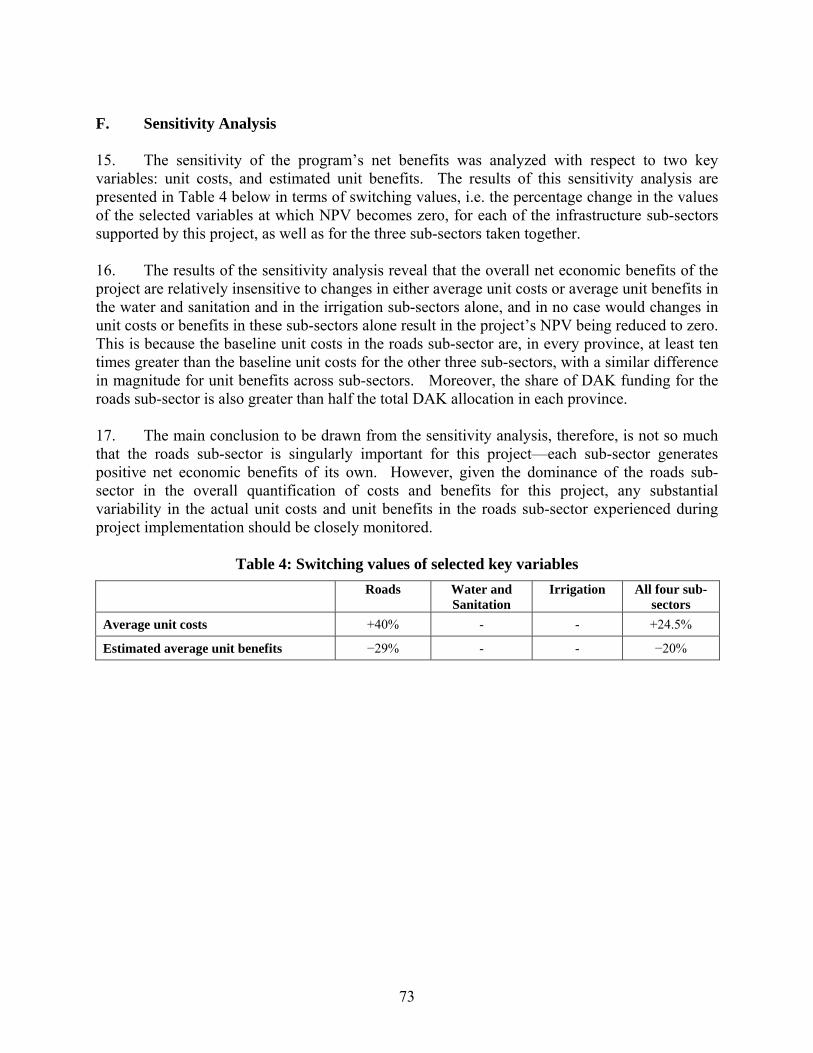

Indonesia Sustainable Development Unit East Asia and Pacific Region

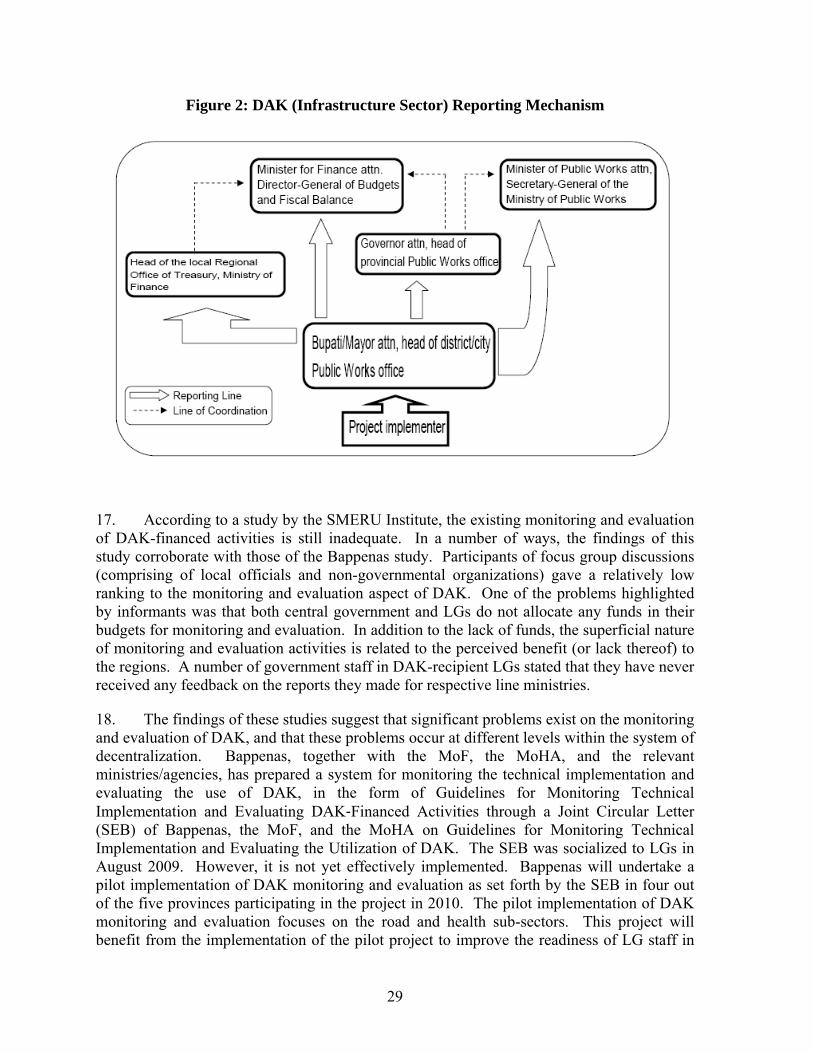

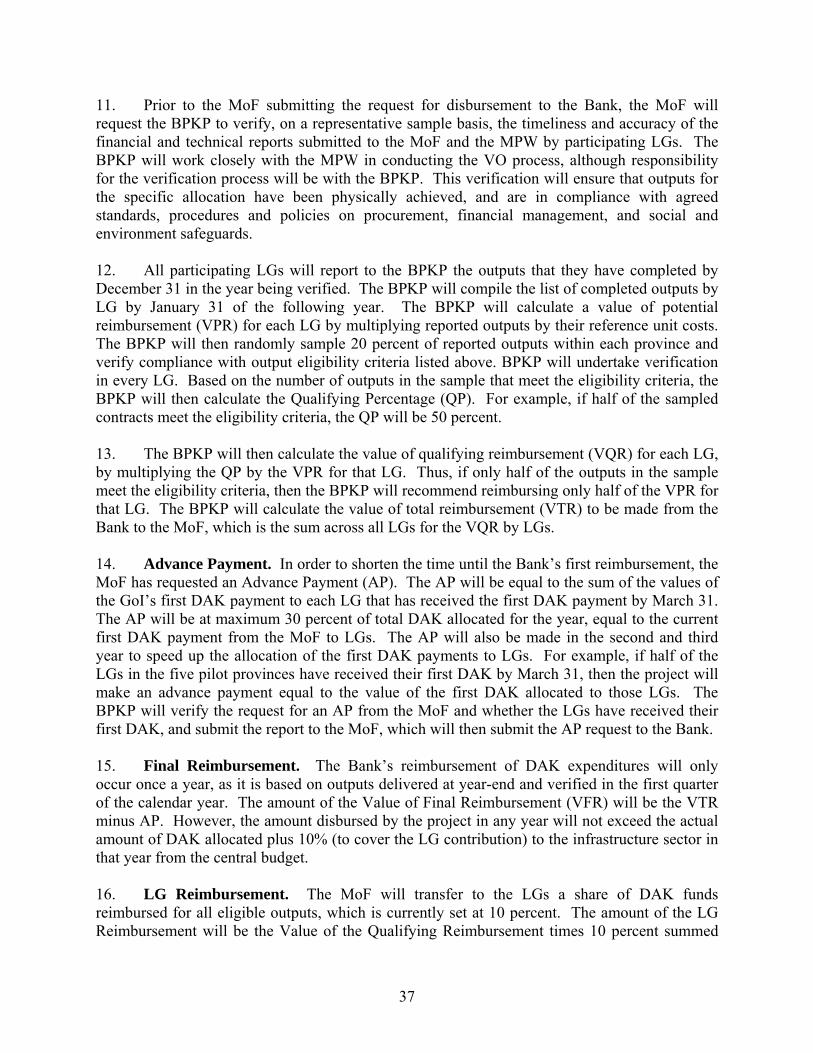

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

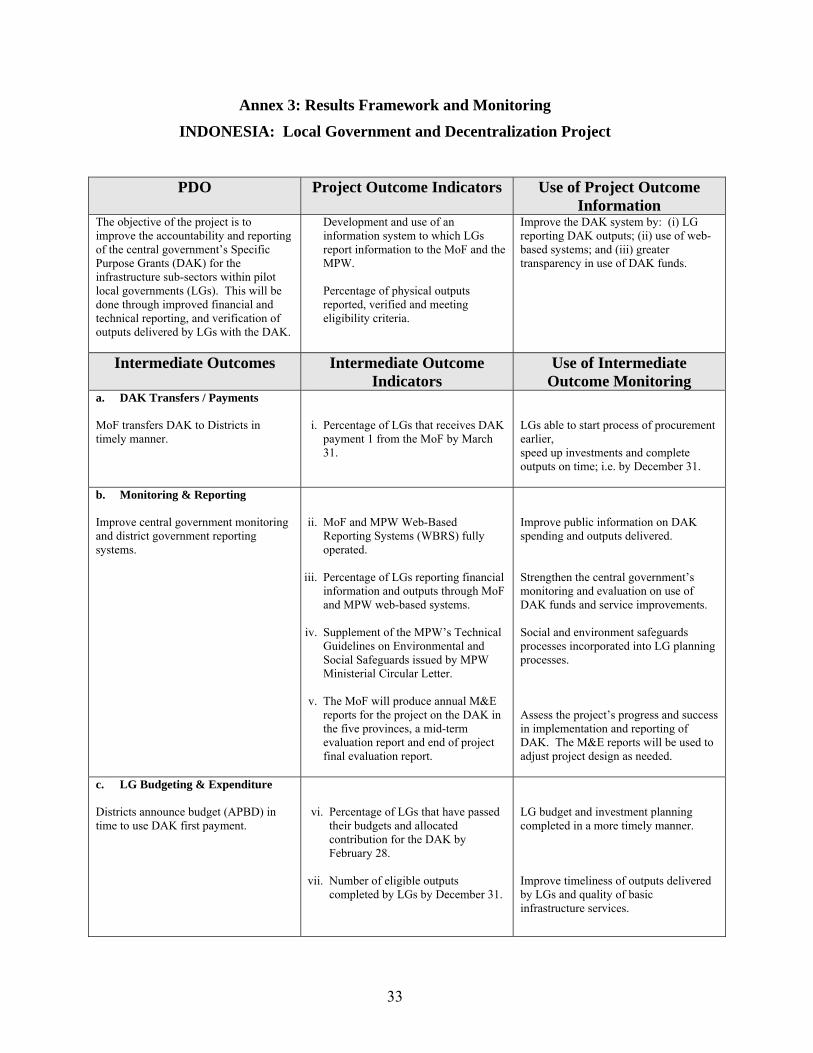

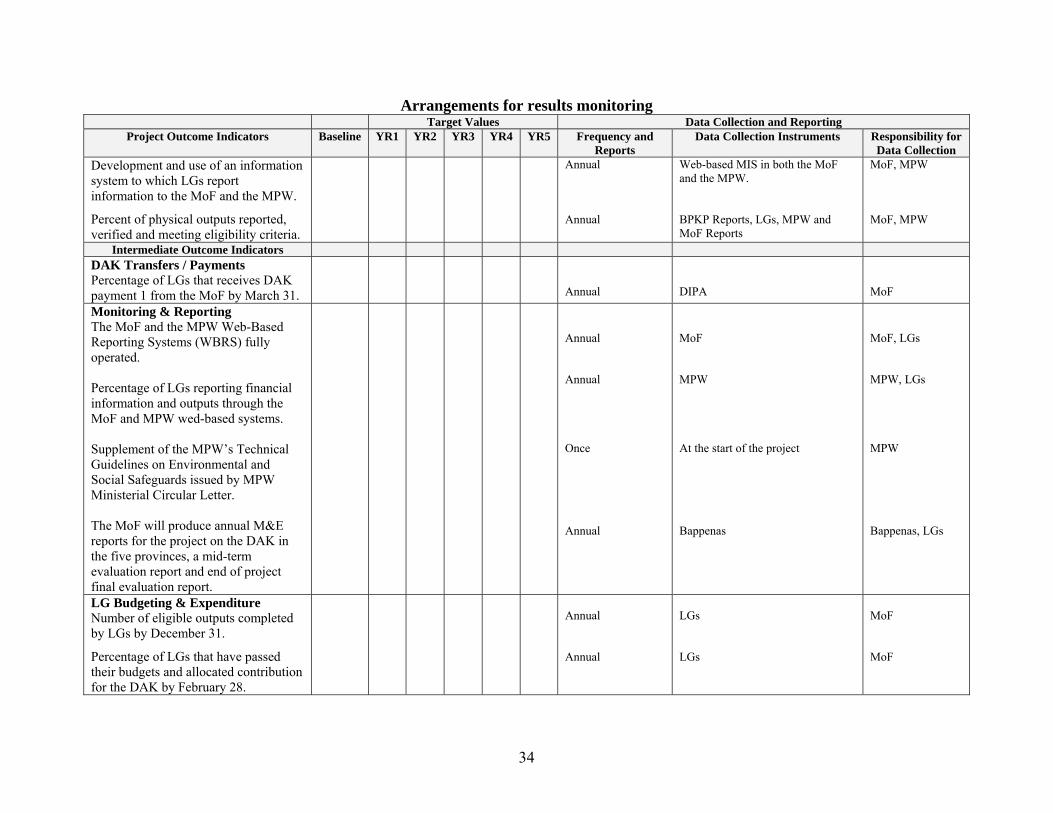

Pub

lic D

iscl

osur

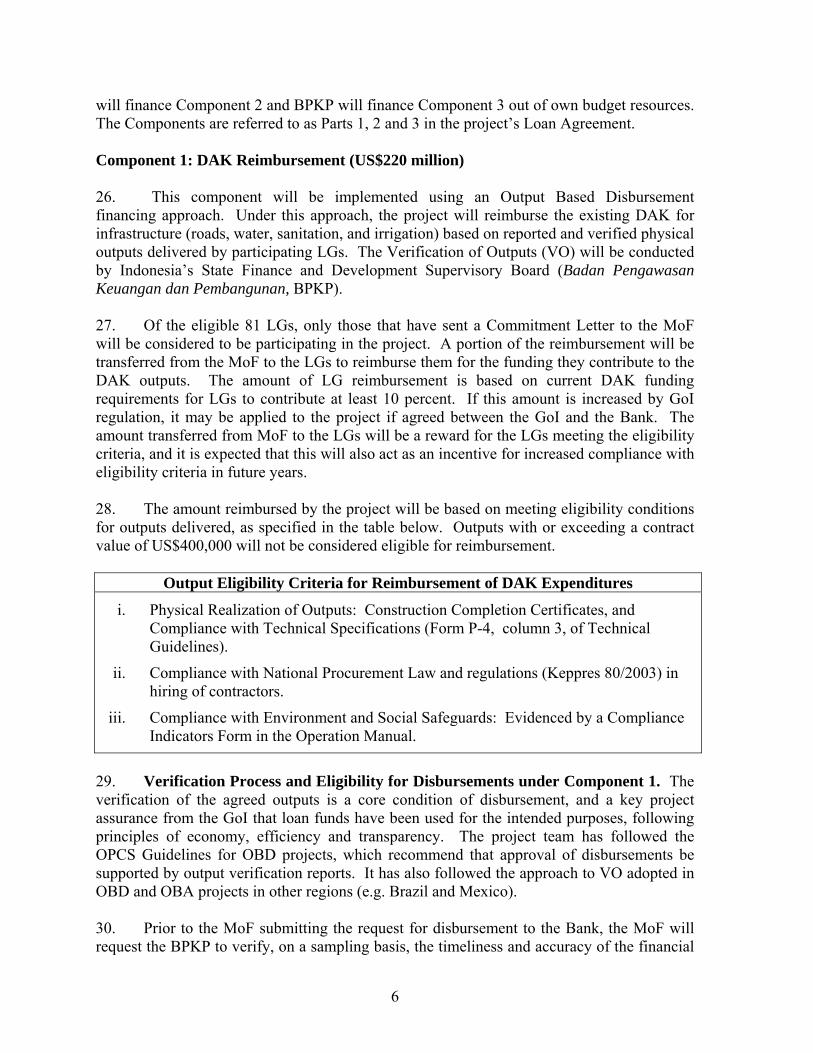

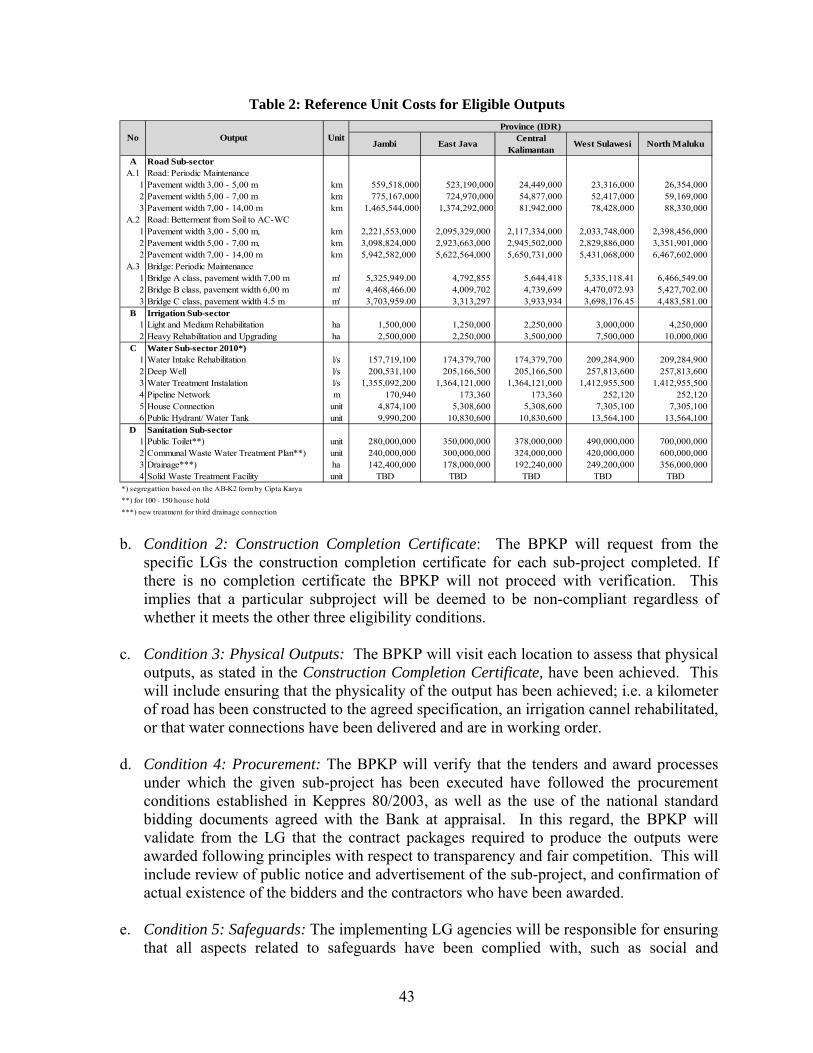

e A

utho

rized

Pub

lic D

iscl

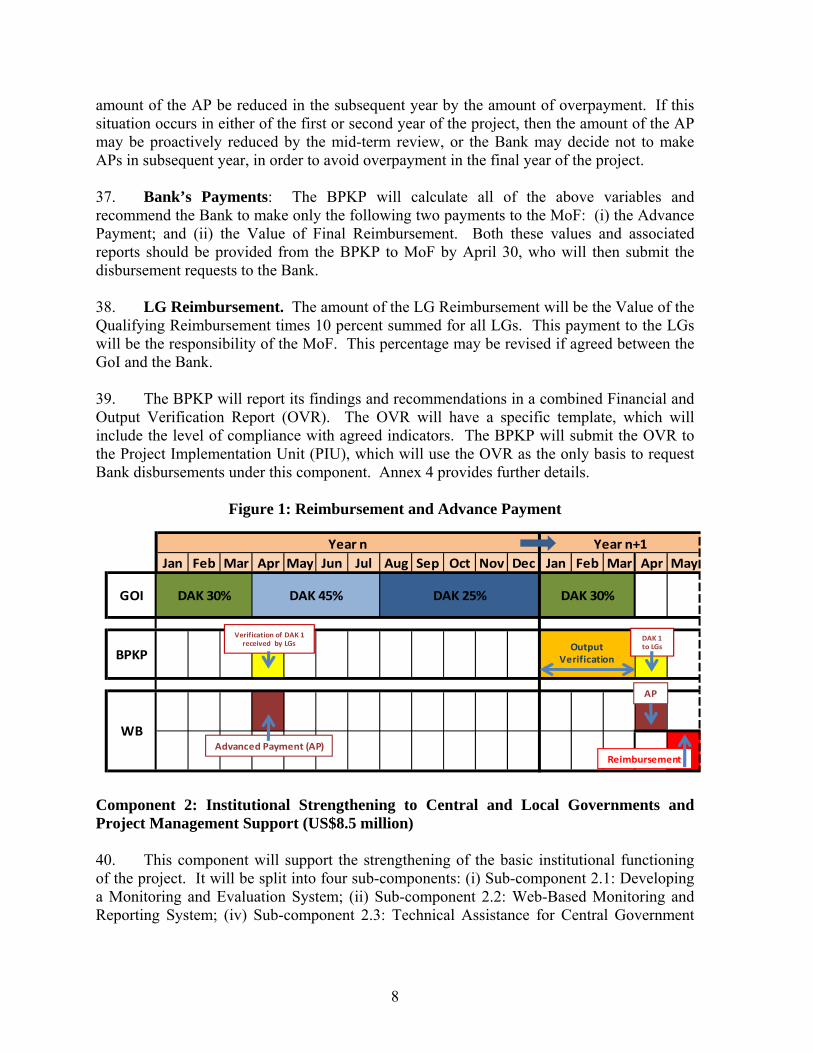

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS (Exchange Rate Effective April 23, 2010)

Currency Unit = Indonesian Rupiah (IDR) IDR 9,014 = US$1

US$ 1 = SDR 0.66

FISCAL YEAR January 1 – December 31

ABBREVIATIONS AND ACRONYMS

AMDAL AP APBD APBN Bappenas BPK BPKP

Environmental Impact Assessment Advance Payment Local Budget National / State Budget National Planning Agency State Audit Board State Finance and Development Supervisory Board

CPS COSU DAK

Country Partnership Strategy Central Operational Services Unit Specific Purpose Grants

DAU DBH DG DGFB DIPA DP DPR EIRR EMF EMP FMS FS FY GAC GFMRAP GoI GPOBA IBRD IDA IFR IFSA ILGRP IP IVP KDP Keppres

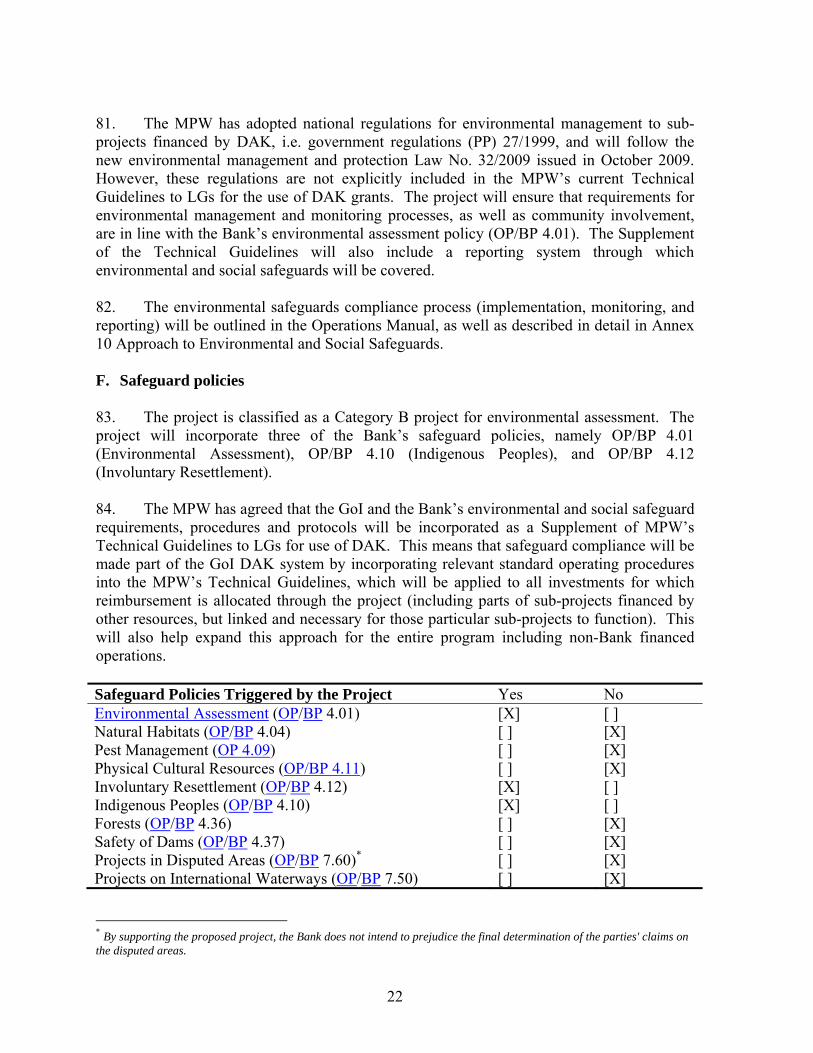

General Purpose Grants Revenue Sharing Directorate General Directorate General of Fiscal Balance Government Annual Budget Document Adjustment Fund Parliament Economic Internal Rate of Return Environmental Management Framework Environmental Management Plan Financial Management Specialist Fully Satisfactory Fiscal Year Government Anti-Corruption Plan Government Financial Management Reform Administration Project Government of Indonesia Global Partnership Output Based Aid International Bank for Reconstruction and Development International Development Association Interim Financial Report Integrated Fiduciary and Safeguards Assessment Initiatives for Local Governance Reform Project Indigenous People Isolated and Vulnerable People Kecamatan Development Program Presidential Decree

LG Local Government, comprising Provinces, Kabupaten and Kota MIS M&E MoF MoHA MPW NFI NPV OBA OBD OM OPCS

Management Information System Monitoring and Evaluation Ministry of Finance Ministry of Home Affairs Ministry if Public Works Net Fiscal Index Net Present Value Output Based Aid Output Based Disbursement Operations Manual Operations Policy & Country Services

OVR PDO PER

Output Verification Report Project Development Objective Public Expenditure Review

PFM PIU QP RD REOI RFP RKP RMR ROC SADC Satker SEB SIL SMERU SOP TA ToR ULP USDRP VFR VO VPR VQR VTR WBRS WBTMS WISMP

Public Financial Management Project Implementing Unit Qualifying Percentage Definitive Plan Request Expression of Interest Request for Proposal Government Work Plan Regional Management Review Regional Operation Committee Southern African Development Community Working unit Joint Circular Letter Specific Investment Loan Institution for Research and Public Policy Studies Standard Operating Procedure Technical Assistant Terms of Reference Procurement Service Unit Urban Sector Development Reform Project Value of Final Reimbursement Verification of Outputs Value of Potential Reimbursement Value of Qualifying Reimbursement Value of Total Reimbursement Web-Based Reporting System Web-Based Transfer Monitoring System Water Resources and Irrigation Sector Management Program

Vice President: James W. Adams

Country Director: Joachim von Amsberg Sector Director: John A. Roome Sector Manager: Sonia Hammam

Task Team Leader: Peter D. Ellis

INDONESIA

Local Government and Decentralization Project

CONTENTS

Page

I. STRATEGIC CONTEXT AND RATIONALE ................................................................. 1

A. Country and sector issues.................................................................................................... 1

B. Rationale for Bank Involvement ......................................................................................... 3

C. Higher level objectives to which the project contributes .................................................... 4

II. PROJECT DESCRIPTION ................................................................................................. 4

A. Lending Instrument ............................................................................................................. 4

B. Project Development Objective and Key Indicators ........................................................... 5

C. Project Components ............................................................................................................ 5

D. Lessons Learned and Reflected in the Project Design ........................................................ 9

E. Alternatives Considered and Reasons for Rejection ......................................................... 12

III. IMPLEMENTATION .................................................................................................... 13

A. Partnership Arrangements ................................................................................................. 13

B. Institutional and Implementation Arrangements .............................................................. 13

C. Monitoring and Evaluation of Results .............................................................................. 14

D. Sustainability..................................................................................................................... 14

E. Critical risks and possible controversial aspects ............................................................... 15

F. Loan/Credit Conditions and Covenants ............................................................................ 17

IV. APPRAISAL SUMMARY ............................................................................................. 17

A. Economic and Financial Analysis ..................................................................................... 17

B. Technical ........................................................................................................................... 18

C. Fiduciary ........................................................................................................................... 18

D. Social................................................................................................................................. 20

E. Environment ...................................................................................................................... 21

F. Safeguard policies ............................................................................................................. 22

G. Policy Exceptions and Readiness...................................................................................... 23

Annex 1: Country and Sector or Program Background ......................................................... 24

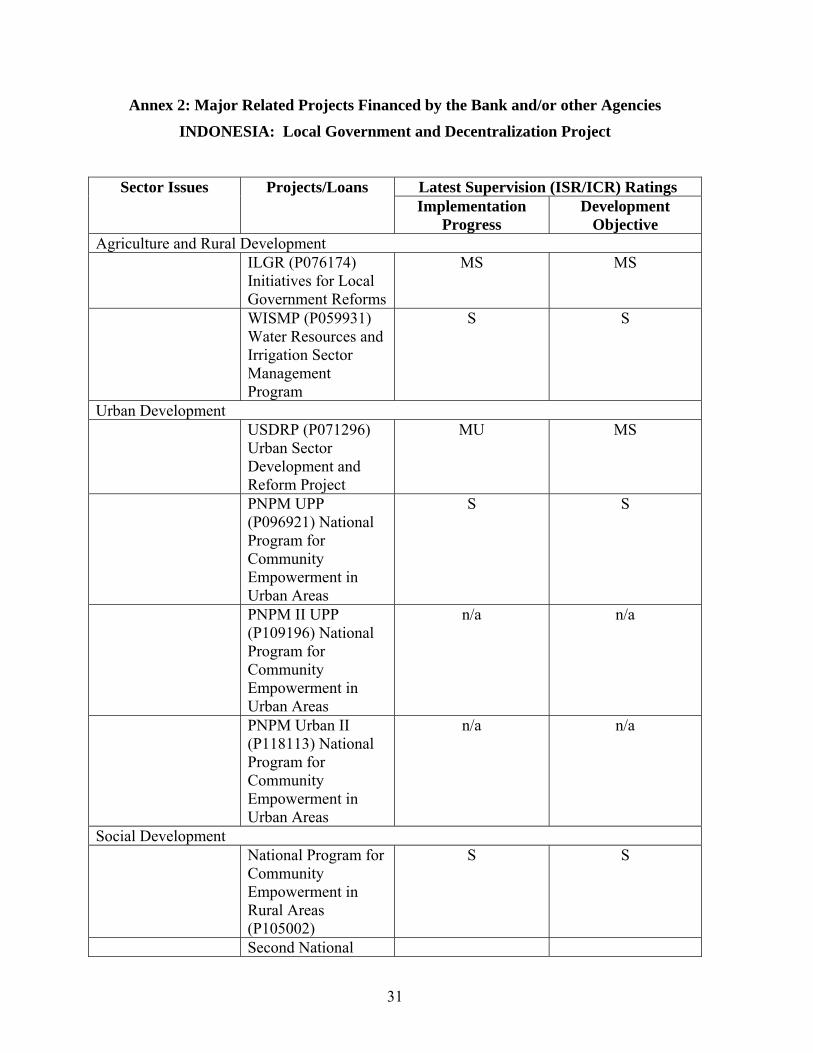

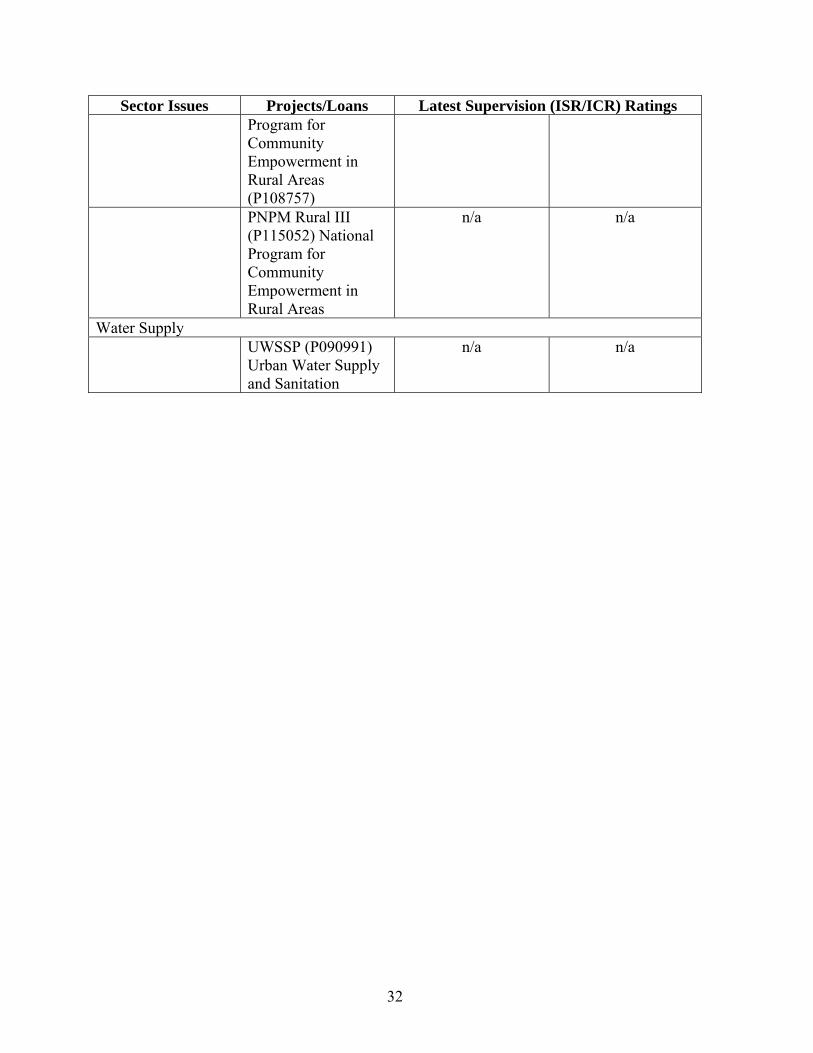

Annex 2: Major Related Projects Financed by the Bank and/or other Agencies ................. 31

Annex 3: Results Framework and Monitoring ........................................................................ 33

Annex 4: Detailed Project Description ...................................................................................... 35

Annex 5: Project Costs ............................................................................................................... 45

Annex 6: Implementation Arrangements ................................................................................. 46

Annex 7: Financial Management and Disbursement Arrangements ..................................... 49

Annex 8: Procurement Arrangements ...................................................................................... 62

Annex 8.1: Anti-Corruption Action Plan.................................................................................. 67

Annex 9: Economic and Financial Analysis ............................................................................. 69

Annex 10: Approaches in Environmental and Social Safeguards .......................................... 74

Annex 11: Project Preparation and Supervision ..................................................................... 83

Annex 12: Documents in the Project File ................................................................................. 85

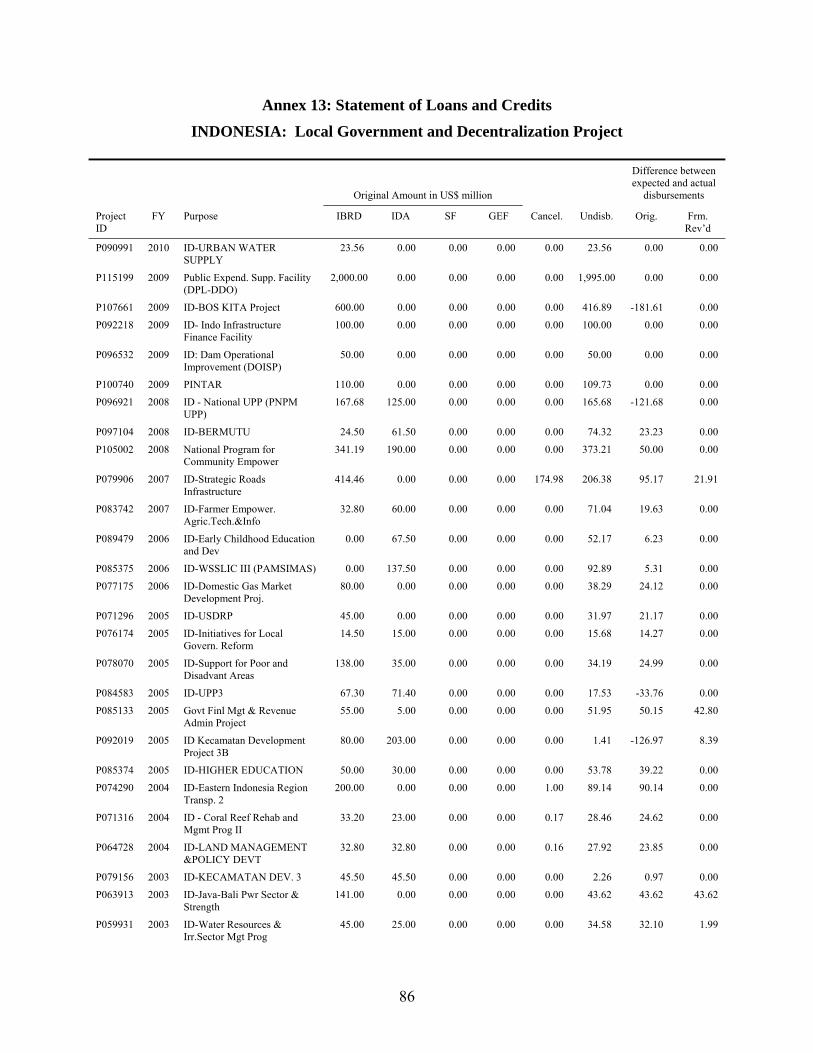

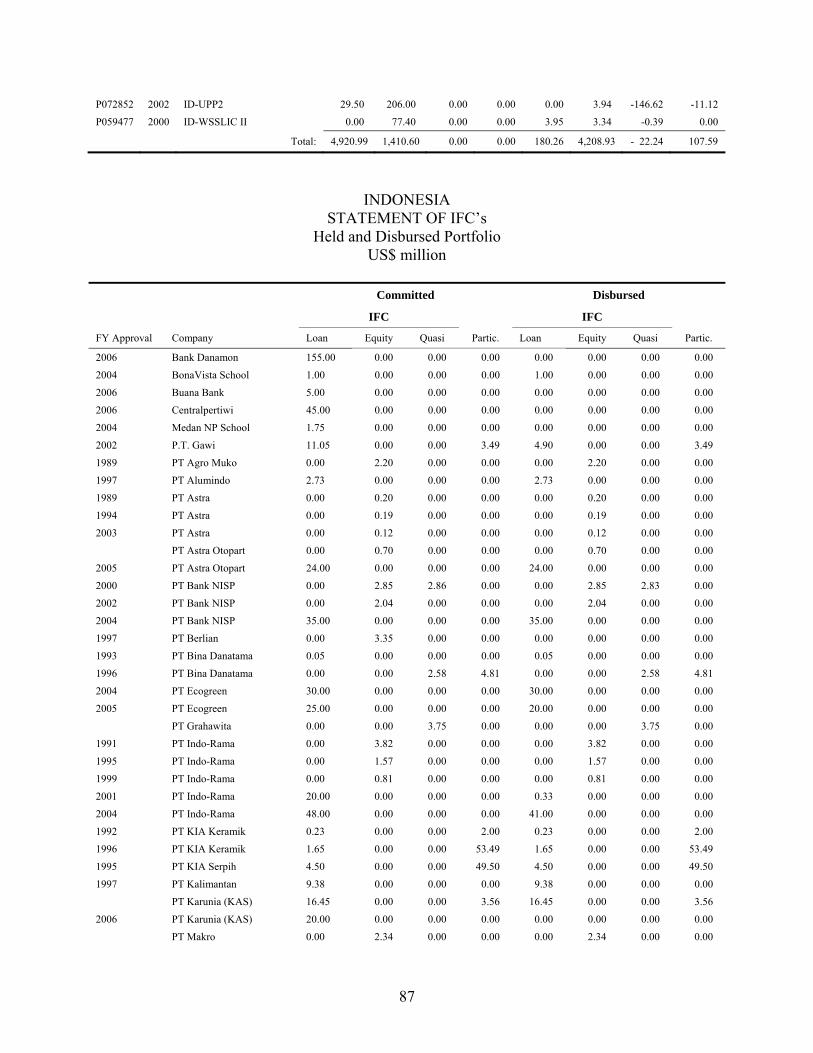

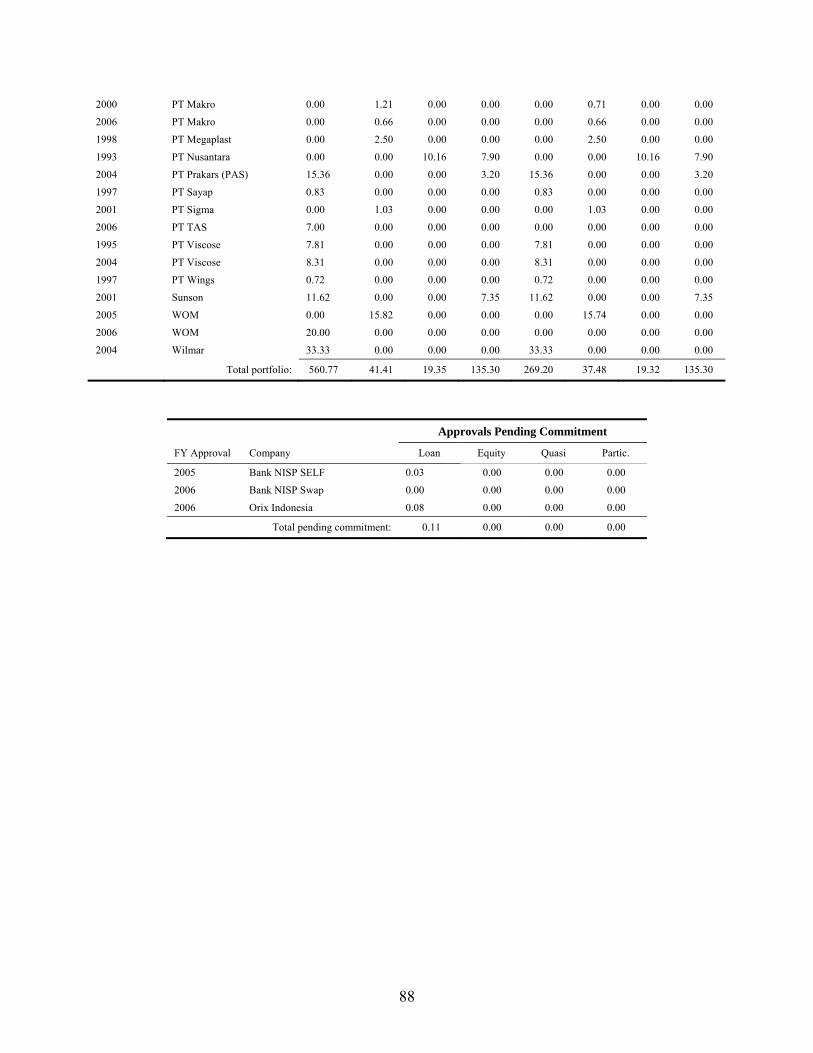

Annex 13: Statement of Loans and Credits .............................................................................. 86

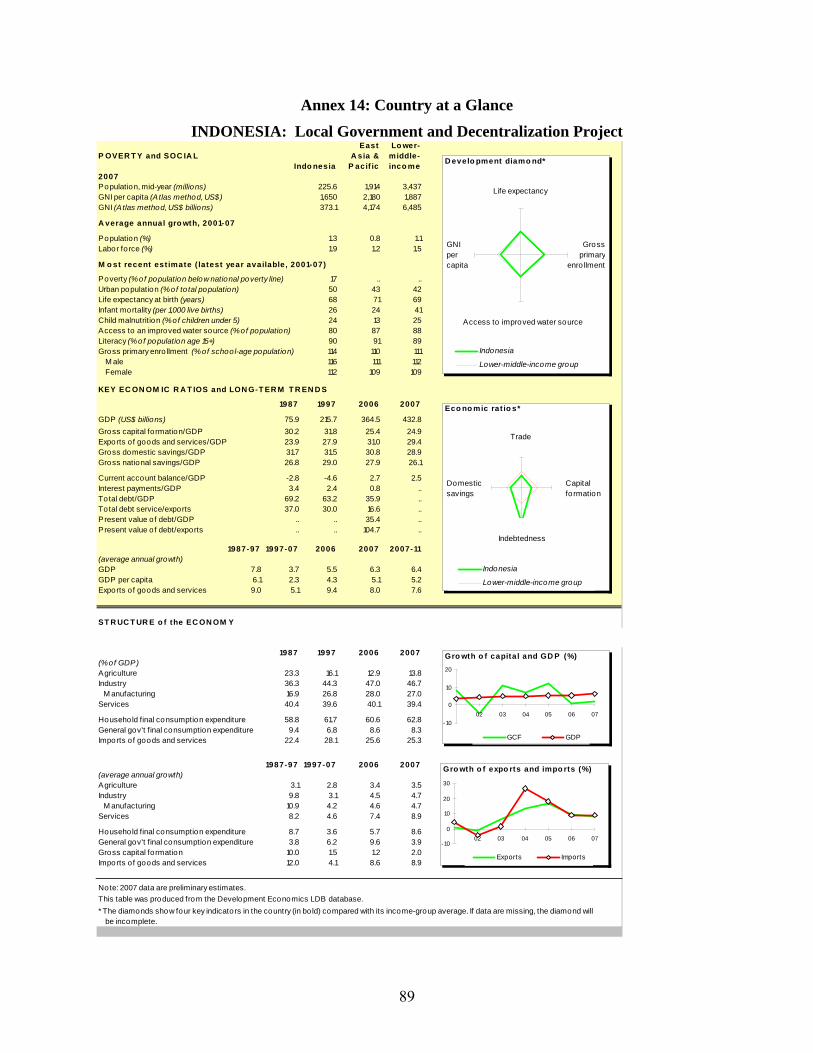

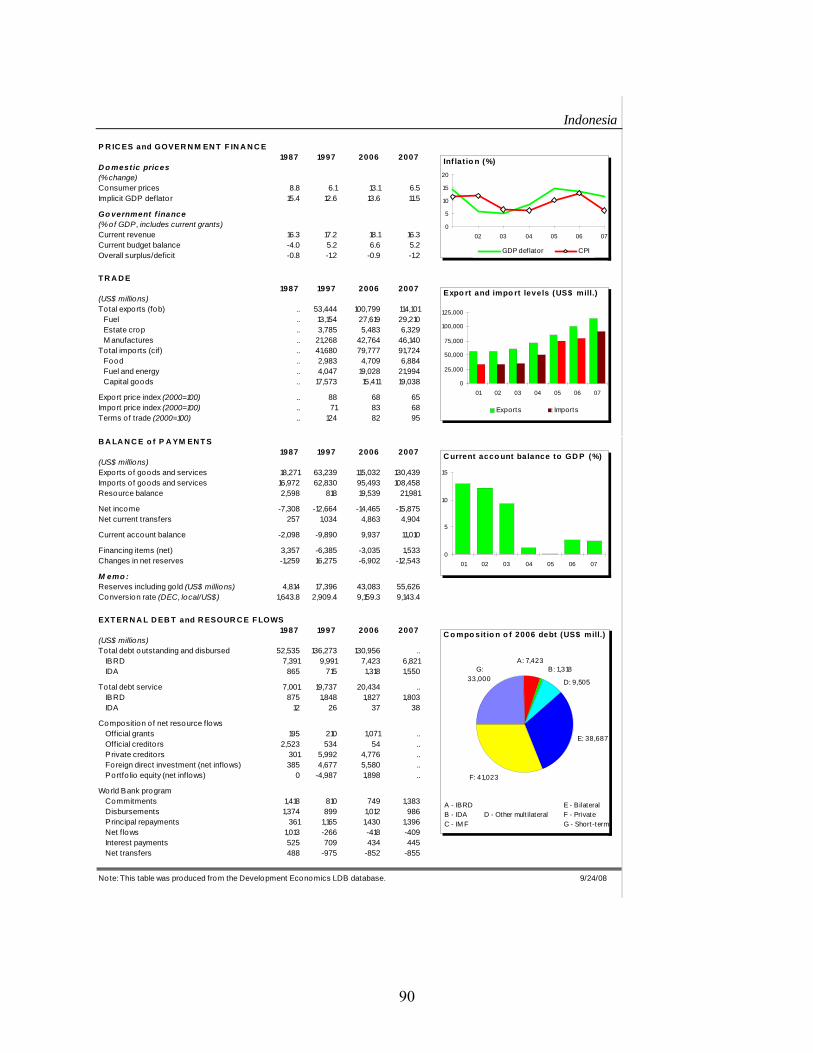

Annex 14: Country at a Glance ................................................................................................. 89

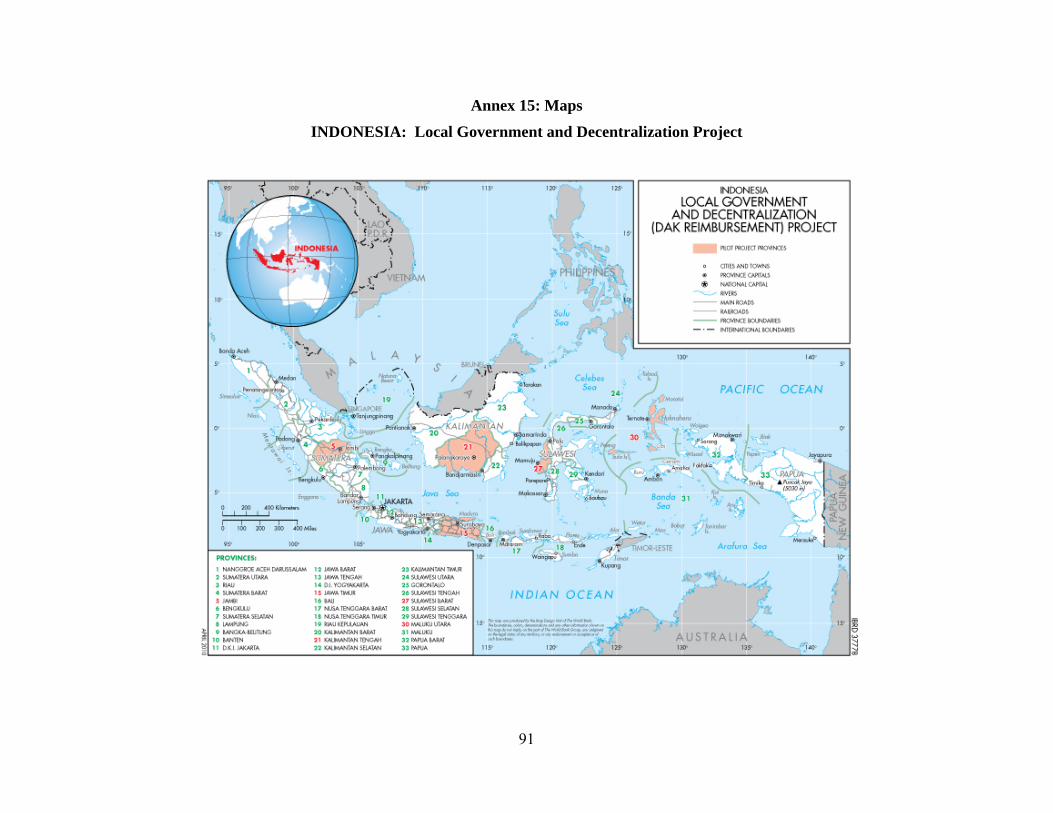

Annex 15: Maps IBRD 37778 ..................................................................................................... 91

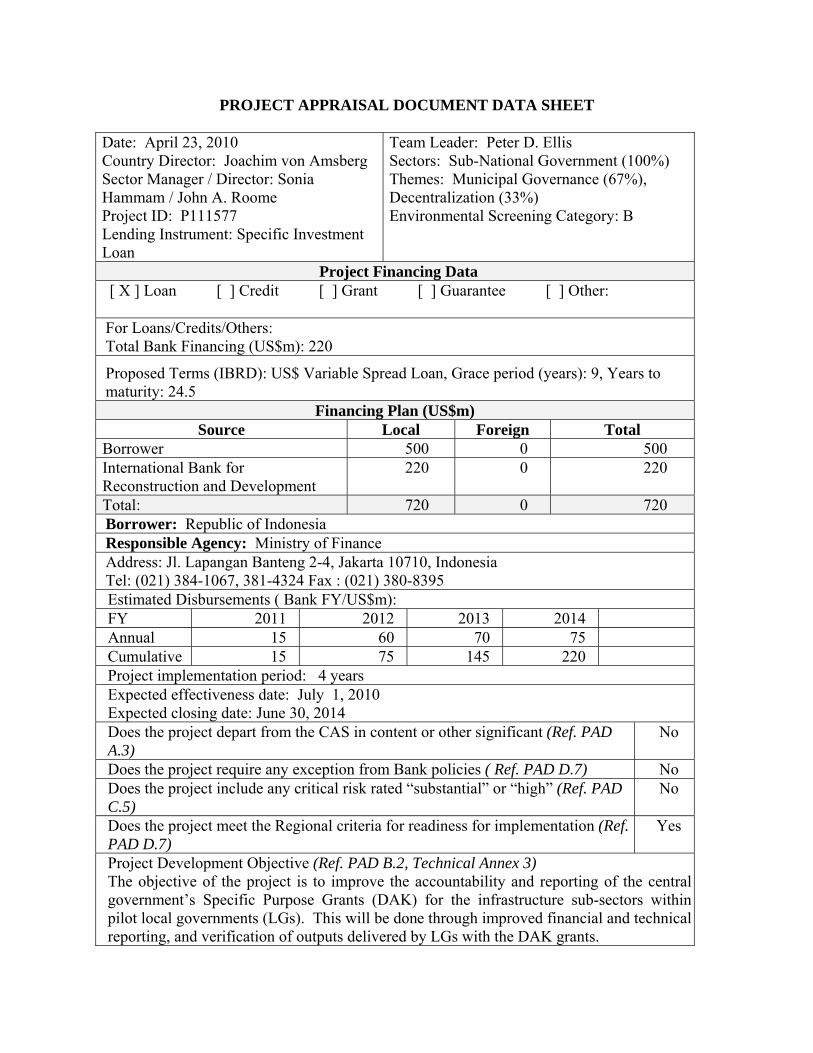

PROJECT APPRAISAL DOCUMENT DATA SHEET

Date: April 23, 2010 Country Director: Joachim von Amsberg Sector Manager / Director: Sonia Hammam / John A. Roome Project ID: P111577 Lending Instrument: Specific Investment Loan

Team Leader: Peter D. Ellis Sectors: Sub-National Government (100%) Themes: Municipal Governance (67%), Decentralization (33%) Environmental Screening Category: B

Project Financing Data [ X ] Loan [ ] Credit [ ] Grant [ ] Guarantee [ ] Other: For Loans/Credits/Others: Total Bank Financing (US$m): 220

Proposed Terms (IBRD): US$ Variable Spread Loan, Grace period (years): 9, Years to maturity: 24.5

Financing Plan (US$m) Source Local Foreign Total

Borrower 500 0 500 International Bank for Reconstruction and Development

220 0 220

Total: 720 0 720 Borrower: Republic of Indonesia Responsible Agency: Ministry of Finance Address: Jl. Lapangan Banteng 2-4, Jakarta 10710, Indonesia Tel: (021) 384-1067, 381-4324 Fax : (021) 380-8395 Estimated Disbursements ( Bank FY/US$m): FY 2011 2012 2013 2014 Annual 15 60 70 75 Cumulative 15 75 145 220 Project implementation period: 4 years Expected effectiveness date: July 1, 2010 Expected closing date: June 30, 2014 Does the project depart from the CAS in content or other significant (Ref. PAD A.3)

No

Does the project require any exception from Bank policies ( Ref. PAD D.7) No Does the project include any critical risk rated “substantial” or “high” (Ref. PAD C.5)

No

Does the project meet the Regional criteria for readiness for implementation (Ref. PAD D.7)

Yes

Project Development Objective (Ref. PAD B.2, Technical Annex 3) The objective of the project is to improve the accountability and reporting of the central government’s Specific Purpose Grants (DAK) for the infrastructure sub-sectors within pilot local governments (LGs). This will be done through improved financial and technical reporting, and verification of outputs delivered by LGs with the DAK grants.

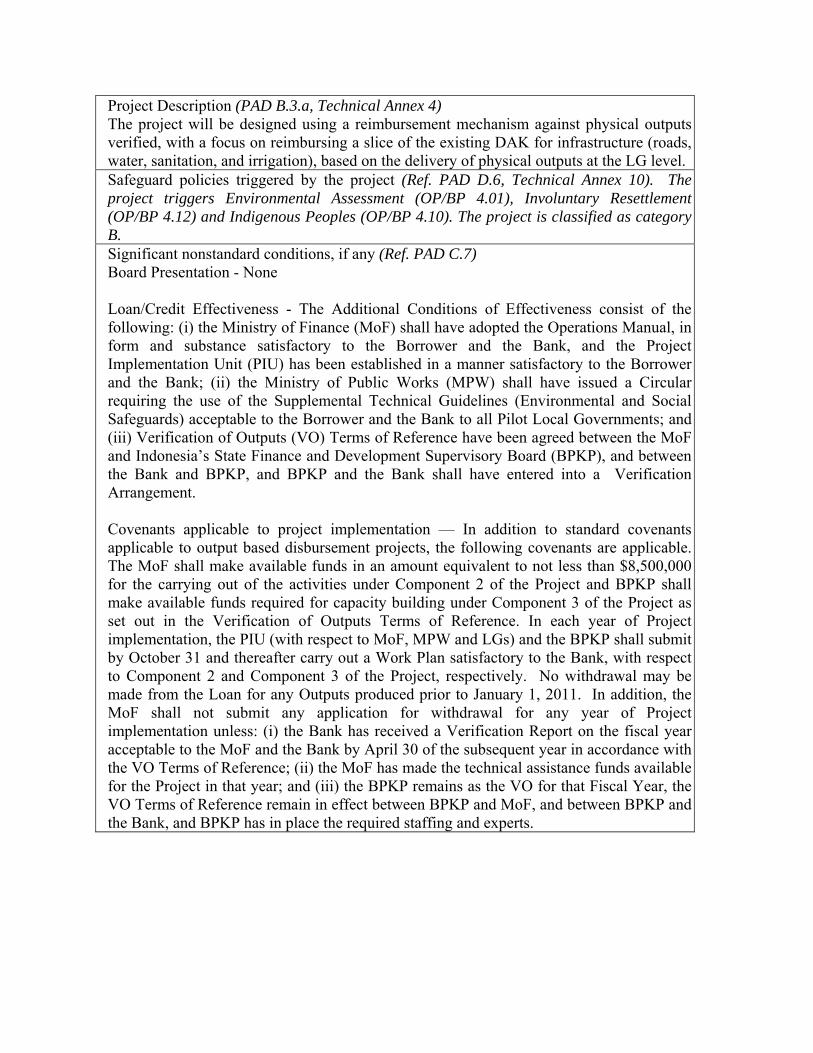

Project Description (PAD B.3.a, Technical Annex 4) The project will be designed using a reimbursement mechanism against physical outputs verified, with a focus on reimbursing a slice of the existing DAK for infrastructure (roads, water, sanitation, and irrigation), based on the delivery of physical outputs at the LG level. Safeguard policies triggered by the project (Ref. PAD D.6, Technical Annex 10). The project triggers Environmental Assessment (OP/BP 4.01), Involuntary Resettlement (OP/BP 4.12) and Indigenous Peoples (OP/BP 4.10). The project is classified as category B. Significant nonstandard conditions, if any (Ref. PAD C.7) Board Presentation - None Loan/Credit Effectiveness - The Additional Conditions of Effectiveness consist of the following: (i) the Ministry of Finance (MoF) shall have adopted the Operations Manual, in form and substance satisfactory to the Borrower and the Bank, and the Project Implementation Unit (PIU) has been established in a manner satisfactory to the Borrowerand the Bank; (ii) the Ministry of Public Works (MPW) shall have issued a Circular requiring the use of the Supplemental Technical Guidelines (Environmental and Social Safeguards) acceptable to the Borrower and the Bank to all Pilot Local Governments; and (iii) Verification of Outputs (VO) Terms of Reference have been agreed between the MoFand Indonesia’s State Finance and Development Supervisory Board (BPKP), and between the Bank and BPKP, and BPKP and the Bank shall have entered into a Verification Arrangement. Covenants applicable to project implementation — In addition to standard covenants applicable to output based disbursement projects, the following covenants are applicable. The MoF shall make available funds in an amount equivalent to not less than $8,500,000 for the carrying out of the activities under Component 2 of the Project and BPKP shall make available funds required for capacity building under Component 3 of the Project as set out in the Verification of Outputs Terms of Reference. In each year of Project implementation, the PIU (with respect to MoF, MPW and LGs) and the BPKP shall submit by October 31 and thereafter carry out a Work Plan satisfactory to the Bank, with respect to Component 2 and Component 3 of the Project, respectively. No withdrawal may be made from the Loan for any Outputs produced prior to January 1, 2011. In addition, the MoF shall not submit any application for withdrawal for any year of Project implementation unless: (i) the Bank has received a Verification Report on the fiscal year acceptable to the MoF and the Bank by April 30 of the subsequent year in accordance with the VO Terms of Reference; (ii) the MoF has made the technical assistance funds available for the Project in that year; and (iii) the BPKP remains as the VO for that Fiscal Year, the VO Terms of Reference remain in effect between BPKP and MoF, and between BPKP and the Bank, and BPKP has in place the required staffing and experts.

1

I. STRATEGIC CONTEXT AND RATIONALE

A. Country and sector issues

1. Fiscal decentralization. With the “big bang” decentralization of 2001, Indonesia went from being one of the most centralized countries in the world in administrative, fiscal and political terms, to one of the most decentralized. Under Law 32/2004 (on Regional Autonomy) and Law 33/2004 (on Fiscal Balance), local governments (LGs) have assumed new responsibilities that were previously covered by the central government, as well as managing new financial resources that have been transferred from the central government or raised within their own localities. LGs have therefore experienced substantial increases in financial resources, mostly through increased transfers from the central level.

2. Transfers from the central government are currently the main source of LG finance. LGs now manage 38 percent of total public expenditure and carry out more than half of all public investment. However, Public Expenditure Reviews (PER) conducted at the LG level show that they are experiencing difficulty in managing and spending their resources. Some LGs have accumulated significant financial reserves, although reserves were not found to be excessive in general. Given the high investment needs in basic services, greater reserve accumulation can be seen as symptomatic of an inability to spend financial resources effectively. Fiscal decentralization in Indonesia still faces a number of major challenges, such as how to improve and speed up spending, and reduce LG dependency on central government transfers.

3. Capital investment after the onset of regional autonomy. Following the decentralization process of 2001, the responsibility for investment in most services was transferred to LGs. Indonesia’s more than 500 LGs (provincial, kabupaten and kota) are now in charge of delivering education, health and infrastructure services. When capital investment needs are taken into account, LGs have insufficient financial resources to meet their investment needs for basic services, which far exceed their revenues and surpluses.

4. LGs lack significant own-source revenue, which accounts for only about 15 percent on average of total revenues. This causes great reliance on central government transfers for capital expenditure purposes. In order to increase investments over time, LGs will need to have access to larger financial flows and the central government will need to strengthen its transfer mechanisms, especially its grants for investments. In terms of management of expenditure assignments, LGs have great autonomy, so strengthening the intergovernmental capital grant transfer system will not weaken decentralization, but will strengthen LGs’ ability to deliver services.

5. Intergovernmental transfers in Indonesia. The bulk of the intergovernmental transfers to LGs are constituted by the General Purpose Grants (Dana Alokasi Umum, DAU) and the Specific Purpose Grants (Dana Alokasi Khusus, DAK). In 2010, the DAU share of total intergovernmental transfers was 63 percent, while the share of DAK was around 7 percent. DAU is mainly used to fund salaries and other administrative costs. DAK funds investment expenditures that are also considered a national government priority. The total DAK allocation for 2010 is about US$2.3 billion.

2

6. The Public Expenditure Review (2008) reported that public expenditure for infrastructure has been relatively under-funded compared with other sectors, such as education and health. The central government has tried to compensate by allocating significant amounts of its DAK transfers to infrastructure. There are currently 14 sectors eligible for DAK funds, including four infrastructure sectors of roads, irrigation, water supply, and sanitation. Total DAK among the four infrastructure sectors amounted to IDR 4.5 billion (US$490 million), representing about one-fifth of the total DAK in 2010. Within infrastructure, the road sector received the largest DAK allocation (62.5 percent), followed by irrigation (21.5 percent), and water supply (8.0 percent) and sanitation (8.0 percent).

7. Specific Purpose Grants (DAK). DAK is a grant from the national budget allocated to LGs with the purpose of financing specified activities that are aligned to national priorities and conducted under the jurisdiction of LGs. The amount of DAK allocation is determined on an annual basis within the national budget. There are three types of criteria that LGs must be satisfied in order to receive DAK, namely: general, specific, and technical criteria. General criteria refer to LGs’ net fiscal capacity. Specific criteria relate to whether LGs receive special autonomy funds or are categorized as disadvantaged areas, etc. Technical criteria assess conditions of the infrastructure, for example, the total road length and condition. These three criteria are used in a formula for determining the DAK allocation by sector and district.

8. The DAK allocation has been growing very rapidly, increasing from IDR 2.2 billion in 2003 to IDR 24.8 billion in 2009, and accounting for 0.7 percent to 2.4 percent of the national budget, respectively. In 2010, however, total DAK declined by 17.4 percent compared with 2009 as a result of global financial turmoil. Eligible recipient LGs are required to provide a 10 percent LG contribution (dana pendamping) for each DAK sector. Exceptions to this rule are allowed where regions have low fiscal capacity. 9. The MoF allocates the DAK to each sector and within the sectors LGs have the flexibility to determine which subprojects they invest in. The Ministry of Public Works (MPW) provides Ministry Decree No. 42/PRT/M/2007 for Technical Guidelines on the Implementation, Monitoring and Evaluation of the DAK for each infrastructure sector. MPW’s Technical Guidelines clearly specify the outputs on which the DAK grants can be spent, and these are mostly limited to maintenance, rehabilitation, and the upgrading or improvement of existing infrastructure. 10. Challenges in DAK implementation. Since the implementation of the fiscal decentralization policy in 2001, policies regarding DAK have been well established, although the monitoring and verification of use of funds, especially with regard to physical outputs, remains a challenge. A recent study undertaken by the National Planning Agency (Bappenas), Options for Improving DAK (2009), assesses DAK management over the past five years. The study reveals that improvements are needed in the financial, technical, institutional and governance areas. With regard to the financial aspect, the main problem is the mismatch between the amounts of DAK funds allocated and local needs. Financial reporting on the DAK from LGs to the Ministry of Finance (MoF) has improved significantly since the MoF started to impose sanctions by withholding future DAK in 1998. On technical issues, LGs formulate DAK investments as part of their annual planning and budgeting

3

process. However, the link between longer-term development planning and annual DAK expenditures is still weak. Institutional issues revolve around the lack of coordination between the central and local governments on priorities for the DAK, and the lack of appropriate reporting and monitoring of DAK utilization, particularly on the verification of outputs delivered. These weaknesses in financial, technical, and institutional aspects all combine to impact the overall governance of the DAK in terms of transparency and accountability.

11. Monitoring and evaluation of DAK‐financed activities is still inadequate, according to a study by the SMERU Institute, The Specific Purpose Grants (DAK): Mechanisms and Uses (2008). In a number of ways, the findings of this study corroborate those of the Bappenas study. Focus group discussion participants (comprising local officials and non-governmental organizations) gave a relatively low ranking to the monitoring and evaluation aspect of DAK. One of the problems highlighted by participants was that both central and LGs do not allocate any funds in their budgets for monitoring and evaluation.

B. Rationale for Bank Involvement 12. The Bank’s engagement with LGs to date has focused on providing investments to districts across many provinces, and analytical work largely in the form of PERs in selected provinces. The proposed project would focus the Bank’s engagement on a selected few LGs, and allow the Bank to build strong partnerships, while strengthening LG institutions that deliver key basic services. The project would also strengthen government mechanisms, as it is designed to work with GoI systems for delivering DAK funds and monitoring the use of the delivery of outputs. 13. The MoF requested that the World Bank support LGs in improving their use of DAK, while strengthening GoI’s systems for reporting and monitoring of utilization of DAK. This will provide a concrete means for the Bank to engage in-depth at the LG level on issues related to improving planning, budgeting and investment execution, and the monitoring and verification of results.

14. Currently, the governance systems covering DAK fund utilization are weak. Reporting systems of the financial aspects of the DAK from LGs to the MoF are manual, with every LG submitting a summary of the DAK disbursement to the MoF in hard copy. Financial reporting requirements are complied with by all LGs, since the MoF is able to withhold scheduled DAK transfers should a LG fail to submit the required financial reports. The reporting systems from LGs to the line ministries, such as MPW, in terms of physical outputs resulting from spending the DAK, are also manual, and with minimal technical or physical output information. This means that the line ministries are unable to fully verify that outputs have actually been delivered. 15. In 2009, the MoF developed a Web-Based Transfer Monitoring Systems (WBTMS) for financial reporting, which LGs will start using in 2010. The system will monitor all transfers from the MoF to LGs, comprising revenue sharing (DBH), DAU, DAK, the Special Autonomy Fund (Otsus) and the Adjustment Fund (DP). With respect to DAK, the system will also monitor LG funds contributed to DAK-funded projects (dana pendamping), as well

4

as disbursements. This initiative shows that the GoI is beginning to strengthen its governance system related to intergovernmental transfers to LGs, including the DAK. However, there are still no appropriate reporting systems on physical outputs, which ideally should include information on project location, GPS coordinates, technical data, physical progress and visual (picture) of the projects. The MoF, in collaboration with the MPW, intends to develop a web-based system of technical reporting of outputs. Notably, this project will build upon these systems and enhance, where appropriate, reporting methodologies especially related to the tracking of pre-defined outputs.

C. Higher level objectives to which the project contributes 16. The Bank’s current Country Partnership Strategy (CPS) for Indonesia FY 2009-2012 outlines a strategy whereby the Bank will develop a framework of engagement with the GoI in order to “support Indonesia in the implementation of its own programs and (provide) solutions in addressing its development challenges” (CPS, page 10). The two cross-cutting engagements in the CPS are to develop both national and LG institutions and systems. At the LG level, the CPS seeks to “support local governments by promoting well-targeted and sustainable public spending through the co-financing of sub-national expenditure programs” (CPS, page 17). 17. The Bank currently supports both cross-cutting engagements of the CPS by strengthening existing GoI and LG institutions, in order to increase the effectiveness of planning processes and the impact of budget expenditures. The proposed project will focus on improving the utilization of intergovernmental the DAK fund at both the central and local government levels. The project will contribute to the improvement of the current intergovernmental transfer mechanism, and work to strengthen LG systems for reporting and monitoring of DAK grants. The project will also support the development of one of the core engagements of the CPS, namely developing a program with LGs, while also strengthening central government institutions.

18. A key concern of the GoI is improvement of the functioning of the DAK system overall, especially with regard to utilization of funds at the LG level. Associating the DAK with defined outputs, if appropriately documented and verified, could allow the GoI to assess the development impacts of DAK expenditures over time. Strengthening the verification of outputs could therefore be an important element in creating a dataset for budget and development planning of both central and local governments. Improved monitoring and verification of outputs will allow the GoI to assess the effectiveness of DAK expenditures and could support systematic reform of the entire system.

II. PROJECT DESCRIPTION

A. Lending Instrument 19. The project will be designed as a Specific Investment Loan (SIL), with a proposed size of IBRD financing of US$220 million to be implemented over four years. It will be implemented using an Output Based Disbursement (OBD) approach supported by capacity building and technical assistance activities to strengthen the framework for improving the

5

reporting and monitoring of DAK expenditures. The project will reimburse a slice of the existing DAK for infrastructure (roads, water, sanitation and irrigation) based on delivery of verified physical outputs by selected LGs. Technical assistance will finance activities in support of the institutional strengthening both at the central government and LG levels. 20. The project will be piloted in five provinces and all of their districts/LGs (Jambi, East Java, Central Kalimantan, West Sulawesi, and North Maluku). These provinces were selected by the GoI based on geographic diversity, and performance criteria related to current compliance with reporting, ability to absorb DAK, and success in delivering outputs financed by their DAK. These five provinces in total received DAK allocation for their infrastructure sub-sectors of US$110 million in 2009 and US$75 million 2010, which was reduced due the impacts of the global financial crisis. For these five provinces, DAK allocations for infrastructure are expected to be at least US$100 million per year over the next four years, although it figure is likely to increase significantly.

21. Should the MoF wish to change or add any provinces during project implementation, the substitution will have to be agreed between the MoF and the Bank. In addition, the change or addition in provinces will have to be made before January 1 in the year they will participate, so that all the requirements for the project will then be applied to the new province.

B. Project Development Objective and Key Indicators 22. The objective of the project is to improve the accountability and reporting of the central government’s Specific Purpose Grants (DAK) for the infrastructure sub-sectors within pilot local governments (LGs). This will be done through improved financial and technical reporting, and the verification of outputs delivered by LGs with the DAK. 23. The project will work with the existing mechanisms used for the transfer of the DAK. Existing GoI and LG systems for monitoring and reporting will provide baseline information and criteria for evaluating project performance. However, physical outputs and reporting on use of DAK funds are the benchmarks to measure project achievement. 24. Annex 3 contains the detailed intermediate outcome indicators for monitoring the project’s progress during implementation and achieving the Project Development Objective (PDO) during project implementation. The PDO will be monitored using the two Key Performance Indicators below:

i. Development and use of an information system to which LGs report information to the MoF and corresponding line ministries.

ii. Percentage of physical outputs reported, verified and meeting eligibility criteria. C. Project Components 25. The project consists of three components, namely: Component 1: DAK Reimbursement; Component 2: Institutional Strengthening for the Central Government and LGs, and Project Management Support; and Component 3: Verification of Outputs. The GoI

6

will finance Component 2 and BPKP will finance Component 3 out of own budget resources. The Components are referred to as Parts 1, 2 and 3 in the project’s Loan Agreement. Component 1: DAK Reimbursement (US$220 million) 26. This component will be implemented using an Output Based Disbursement financing approach. Under this approach, the project will reimburse the existing DAK for infrastructure (roads, water, sanitation, and irrigation) based on reported and verified physical outputs delivered by participating LGs. The Verification of Outputs (VO) will be conducted by Indonesia’s State Finance and Development Supervisory Board (Badan Pengawasan Keuangan dan Pembangunan, BPKP). 27. Of the eligible 81 LGs, only those that have sent a Commitment Letter to the MoF will be considered to be participating in the project. A portion of the reimbursement will be transferred from the MoF to the LGs to reimburse them for the funding they contribute to the DAK outputs. The amount of LG reimbursement is based on current DAK funding requirements for LGs to contribute at least 10 percent. If this amount is increased by GoI regulation, it may be applied to the project if agreed between the GoI and the Bank. The amount transferred from MoF to the LGs will be a reward for the LGs meeting the eligibility criteria, and it is expected that this will also act as an incentive for increased compliance with eligibility criteria in future years.

28. The amount reimbursed by the project will be based on meeting eligibility conditions for outputs delivered, as specified in the table below. Outputs with or exceeding a contract value of US$400,000 will not be considered eligible for reimbursement.

Output Eligibility Criteria for Reimbursement of DAK Expenditures

i. Physical Realization of Outputs: Construction Completion Certificates, and Compliance with Technical Specifications (Form P-4, column 3, of Technical Guidelines).

ii. Compliance with National Procurement Law and regulations (Keppres 80/2003) in hiring of contractors.

iii. Compliance with Environment and Social Safeguards: Evidenced by a Compliance Indicators Form in the Operation Manual.

29. Verification Process and Eligibility for Disbursements under Component 1. The verification of the agreed outputs is a core condition of disbursement, and a key project assurance from the GoI that loan funds have been used for the intended purposes, following principles of economy, efficiency and transparency. The project team has followed the OPCS Guidelines for OBD projects, which recommend that approval of disbursements be supported by output verification reports. It has also followed the approach to VO adopted in OBD and OBA projects in other regions (e.g. Brazil and Mexico). 30. Prior to the MoF submitting the request for disbursement to the Bank, the MoF will request the BPKP to verify, on a sampling basis, the timeliness and accuracy of the financial

7

and technical reports submitted to the MoF and the MPW by participating LGs. The BPKP will work closely with the MPW in conducting the process of output verification. This verification will ensure that outputs for the specific allocation have been physically achieved, and are in compliance with agreed procedures and policies on procurement, financial management, and social and environmental safeguards.

31. First, the MPW will need to establish the reference unit costs (RUCs) for each of the eligible outputs at the beginning of the year; i.e. prior to the start of the DAK cycle. The RUCs should be provided from the MPW to the BPKP and the MoF by January 31 of each year, in order for the RUCs to be applied for the upcoming year’s outputs once completed. The MoF will then submit the agreed upon reference unit costs for the eligible outputs to the Bank by February 15 of each year.

32. All participating LGs will report to the BPKP the outputs that they have completed by December 31. BPKP will compile a list of completed outputs by LG by January 31 of the following year. The BPKP will calculate a value of potential reimbursement (VPR) for each LG by multiplying reported outputs by their reference unit costs. The BPKP will then randomly sample 20 percent of reported outputs in each province and verify compliance with the output eligibility criteria listed above. BPKP will conduct sampling in every LG. Based on the number of outputs in the sample that meet the eligibility criteria, the BPKP will then calculate the Qualifying Percentage (QP). For example, if half of the sampled contracts meet the eligibility criteria, the QP will be 50 percent.

33. The BPKP will then calculate the value of qualifying reimbursement (VQR) for each LG, by multiplying the QP by the VPR for that LG. Thus, if only half of the outputs in the sample meet the eligibility criteria, the BPKP will recommend reimbursing only half of the VPR for that LG. The BPKP will also calculate the value of total reimbursement (VTR) to be made from the Bank to the MoF, which is the sum across all LGs for the VQR by LGs. 34. Advance Payment. In order to shorten the time until the Bank’s first reimbursement, the MoF has requested an Advance Payment (AP). The AP will be equal to the sum of the values of the GoI’s first DAK payment to each LG that has received the first DAK payment by March 31. The AP would be at maximum 30 percent of total DAK allocated for the year, and equal to the current first DAK payment from the MoF to LGs. The AP will also be made in the second and third years to speed up the allocation of the first DAK payments to LGs. 35. Final Reimbursement. The Bank’s reimbursement of DAK expenditures will only occur once a year, as it is based on outputs delivered at year-end and verified in the first quarter of the calendar year. The amount of the Value of Final Reimbursement (VFR) will be the VTR minus the AP. However, the amount disbursed by the project in any year will not exceed the actual amount of DAK allocated by the MoF plus 10% (to cover LG contribution) to the infrastructure sector in that year. 36. In the event that the amount of the AP in a given year exceeds the total amount of DAK that can be reimbursed (i.e. the VTR) for that year based on the verification review by the BPKP, the Bank will not reimburse anything for the VFR. This will also require that the

8

amount of the AP be reduced in the subsequent year by the amount of overpayment. If this situation occurs in either of the first or second year of the project, then the amount of the AP may be proactively reduced by the mid-term review, or the Bank may decide not to make APs in subsequent year, in order to avoid overpayment in the final year of the project. 37. Bank’s Payments: The BPKP will calculate all of the above variables and recommend the Bank to make only the following two payments to the MoF: (i) the Advance Payment; and (ii) the Value of Final Reimbursement. Both these values and associated reports should be provided from the BPKP to MoF by April 30, who will then submit the disbursement requests to the Bank.

38. LG Reimbursement. The amount of the LG Reimbursement will be the Value of the Qualifying Reimbursement times 10 percent summed for all LGs. This payment to the LGs will be the responsibility of the MoF. This percentage may be revised if agreed between the GoI and the Bank.

39. The BPKP will report its findings and recommendations in a combined Financial and Output Verification Report (OVR). The OVR will have a specific template, which will include the level of compliance with agreed indicators. The BPKP will submit the OVR to the Project Implementation Unit (PIU), which will use the OVR as the only basis to request Bank disbursements under this component. Annex 4 provides further details.

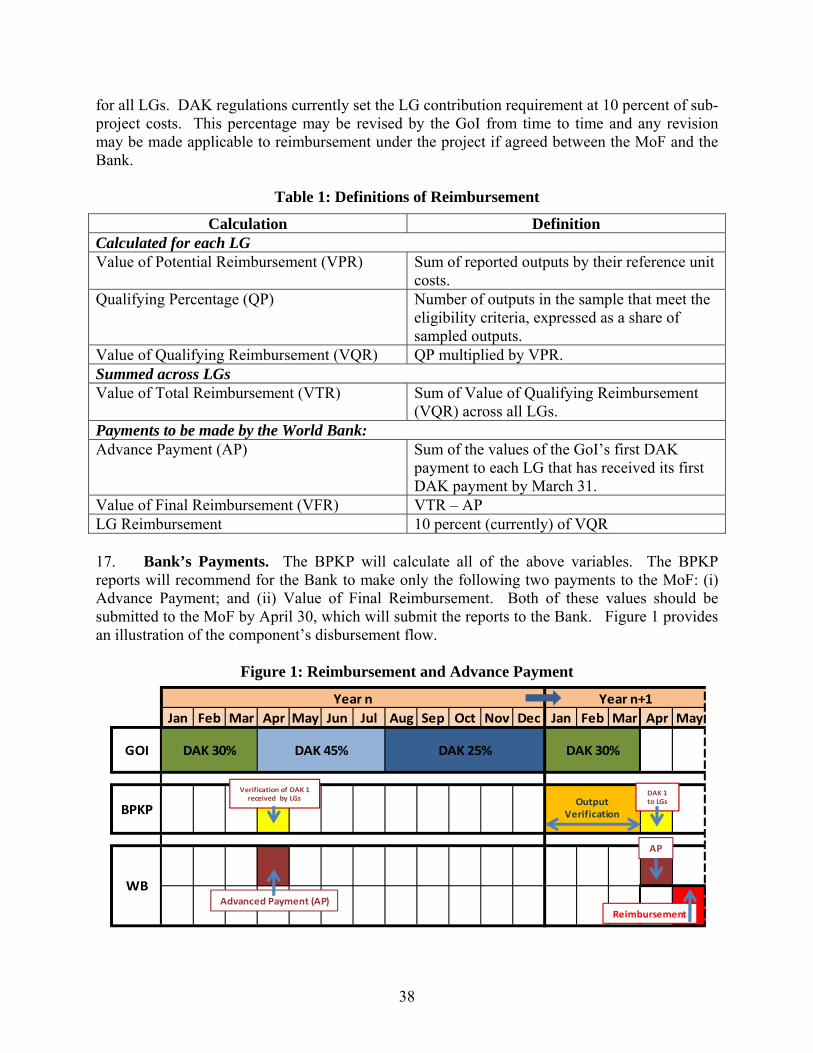

Figure 1: Reimbursement and Advance Payment

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May

GOI

BPKP

DAK 30%

Year n+1

WB

Year n

DAK 30% DAK 45% DAK 25%

Advanced Payment (AP)Reimbursement

Verification of DAK 1received by LGs Output

Verification

AP

DAK 1 to LGs

Component 2: Institutional Strengthening to Central and Local Governments and Project Management Support (US$8.5 million) 40. This component will support the strengthening of the basic institutional functioning of the project. It will be split into four sub-components: (i) Sub-component 2.1: Developing a Monitoring and Evaluation System; (ii) Sub-component 2.2: Web-Based Monitoring and Reporting System; (iv) Sub-component 2.3: Technical Assistance for Central Government

9

and LGs; and Sub-component 2.4: Project Management Support to implement and monitor the project. 41. Component 2 will be financed from the GoI’s national budget. The MoF will provide not less than US$8,500,000 equivalent from its budget to finance the activities under Component 2 of the project. The provision of these resources is a condition of DAK reimbursement under Component 1 of the project. Each year during project implementation, each participating agency—Bappenas, the MoF, and the MPW (including capacity building for LGs from MoF and MPW)—will submit a work plan for technical assistance (TA) to the Bank to support the planning, technical, procurement, financial management, social and environmental safeguards, and improve reporting capacity of both central agencies and LGs. BPKP will similarly submit a work plan and budget under Component 3.

42. In order to ensure adequate funding is available and that the TA is delivered, the following will be conditions for each year’s DAK to be eligible for reimbursement: (i) adequate funds are allocated in the national budget for the TA; and (ii) the work-plan is prepared and agreed upon with the Bank. In the event that the GoI does not provide the required documentation for the funds and the annual work plan for TA for any fiscal year by October 31 in the preceding GoI fiscal year, then the Bank has the right to not provide any Advance Payment or Reimbursement for that year. The TA funding and work plan for July – December 2010 is due 30 days after project effectiveness. Component 3: Verification of Outputs (US$ 4.5 million) 43. This component will constitute BPKP’s verification of outputs. BPKP will finance the VO function, plus any needed hiring of new staff and capacity enhancement from their own budget. An assessment of BKPK’s ability to do the VO function shows that they currently do technical audits for selected infrastructure outputs in LGs. However, in order to do the VO at the scale required for the project, the BPKP will require additional financial and human resources. BPKP will prepare an annual work plan to be discussed with the Bank regarding its VO tasks for the upcoming year. In the event that the BPKP fails to provide the required documentation for the budget and the work plan for any fiscal year by October 31 in the preceding fiscal year, then the Bank has the right to not make any Advance Payment or Reimbursement for that year. D. Lessons Learned and Reflected in the Project Design 44. Lessons learned for this project are drawn from three areas: (i) experience in Indonesia with two pilot local governance projects; (ii) pilot projects funded by the Global Partnership for Output-Based Aid; and (iii) Output Based Disbursement approaches in recent programs in Mexico and Brazil. 45. Indonesia Local Governance Projects. Two pilot projects on local governance in Indonesia are the Initiative for Local Government Reform Project (ILGRP) and the Urban Sector Development Reform Project (USDRP). Both the ILGRP and the USDRP were designed to support kabupaten and kota in improving transparency, accountability and public

10

participatory practices in order to undertake reforms in financial management and procurement. The ILGRP worked with the on-granting mechanism from the central government to LGs, while the USDRP was designed to promote on-lending to improve urban services. Both projects were designed to promote reform using parallel mechanisms to the GoI’s existing system, and this becomes an important lesson learned in designing successful reform projects.

46. In the case of the ILGRP, the on-granting mechanism could not be utilized fully work, as appropriate GoI decrees were not in place and the mechanism was not operational. The project thus became co-managed by the Ministry of Home Affairs (MoHA) and the LGs. The ILGRP invested in creating assets through investment sub-projects that are similar in nature to those funded by the DAK for infrastructure, especially roads and irrigation. With the USDRP, the process of sub-loan agreements proved complicated and GoI regulations limiting on-lending to revenue-generating projects limited the project’s ability to fund investments with public goods characteristics, such as roads, sanitation and irrigation.

47. More general lessons from LG projects were taken into account as the current project was designed. These lessons also reflect the result of the Integrated Fiduciary and Safeguards Assessment (IFSA) that was carried by the Central Operational Services Unit (COSU) for Indonesia’s LG projects.

(a) The geographic scope of the project was too vast, while the number of LGs covered were too few—nine and six provinces, and 14 and 11 LGs across these provinces in the ILGRP and the USDRP, respectively. The DAK project will be focused in five provinces and include all 81 of their LGs. This will give the project geographic concentration and scalability in the number of LGs covered, while also allowing some diversity across Indonesia’s regions.

(b) The complex reforms implemented by the LGs took a significant amount of time. Both projects adopted a staged approach, with restructuring at the mid-term review (MTR) to simplify reforms so that they remained manageable and implementable. The lesson is to start simple, show some improvements and results, then increase the complexity over time as LGs improve their ability to implement reforms and the investments required. (c) Greater reliance on government-driven reforms that also strengthen government systems was important in the sustainability of reforms. As reforms shifted increasingly to those that the GoI were also promoting and emphasis was placed more on LGs implementing reforms, rather than consultants, LGs started to internalize the reforms into their own processes. For example, in the ILGRP and the USDRP the projects support the GoI’s initiative to create procurement service units (ULPs) in all LGs. This also means aligning the Bank’s project with strengthening the GoI’s systems, such as procurement. (d) The bulk of investments made as part of the ILGRP, especially, were relatively small-scale, in the range of US$100,000 to US$500,000. Most contracts

11

fell within the Bank’s post-review limit, and very few contracts were subjected to prior review. Post review reports typically found a limited number of issues with the contracts. The contract management process between LGs and their contractors thus appear to be working reasonably well. This provides greater comfort on contracting for DAK funded infrastructure projects, which are typically less than US$400,000. (e) As LGs improve their capacity to implement programs, the central government should support decentralization by moving more intergovernmental transfers to LGs on-budget and on-treasury, rather than using line ministries to continue large-scale implementation at the LG level. Central government should therefore help LGs by improving the rules and regulations in the contract management process, strengthening compliance with the national procurement law (Keppres 80/2003), and safeguarding laws and regulations. The role of central government should transition from implementation to monitoring and evaluation.

48. Output Based Aid Projects. Important lessons were drawn from the methodology and experience in the design and implementation of Output-Based Aid (OBA) schemes to increase direct access of services to the poor from pilot projects funded by the Global Partnership on Output-Based Aid (GPOBA).

OBA Schemes in Bank Operations

The Bank’s knowledge and experience in structuring OBA schemes has grown in recent years. Since 2002, when OBA schemes were introduced in Bank operations, the Bank has developed 131 OBA projects (40 projects in the past two years), with a total value of about US$3.8 billion (US$2.6 billion Bank and US$1.1 billion government). Despite its growing use, Bank-financed OBA schemes in the WSS sector are currently limited, with a total of 33 OBA projects, 24 projects focused on water supply, three on sanitation, and six on providing both water and sanitation. The majority of projects identified tend to be small, as they are still in a pilot stage. The majority of projects involve piped water and one-off access fund schemes, with access usually defined as the delivery of working connections as demonstrated through a paid water bill. One project under implementation and another under design also involve wastewater connection, and two projects involve on-site sanitation facilities. Furthermore, thus far, OBA approaches have been tested mostly with private contracts that allocate the full risks to the private sector, including the responsibility to bear financing risks. Note that the 131 projects reported are OBA schemes in the sense that they target the poor.

Source: GPOBA/IDA-IFC Secretariat. 2009. Output Based Aid: A Compilation of Lessons Learned and Best Practice Guidance (Draft for discussion). Washington DC: GPOBA/IDA-IFC Secretariat.

49. Output Based Disbursement Operations. The project’s output based disbursement financing approach was designed to sharpen the focus on efficient, transparent results that move the risk to the LGs responsible for the implementation and operation of the corresponding DAK allocation. Instead of the traditional, ring-fenced infrastructure project based on inputs, the proposed project is focused on the broader concerns of achieving results, ensuring effective public expenditure and strengthening institutions. Lessons learned and incorporated in the specific design of the project’s OBD approach come from previously Bank-financed projects in the LAC region. 50. Mexico’s Decentralization Infrastructure Reform Project. During project preparation the team studied the experience of Mexico’s Decentralized Infrastructure Reform and Development Project (State of Guanajuato Project). In studying the Guanajuato project, the

12

project team also considered the guidance provided to the team by the Financial Management Operations Review Committee (FMORC). FMORC guidance for the Guanajuato project has been followed consistently in the proposed project, allowing a more accurate assessment and control of the overall risk.

Mexico Decentralization Infrastructure Reform and Development Loan Project

The proposed project represents an improvement from the pioneer Guanajuato project on five accounts. First, while the Guanajuato project financed strategies in multiple sectors, the proposed project will finance specific WSS investment activities. Second, discussions with the Guanajuato project team revealed that reference unit costs were not pre-defined and had to be revised during project implementation. For the proposed project, the reference unit costs of outputs are based on historical contract prices. Third, unlike the Guanajuato project, there will be a mid-term review to assess the reference unit costs to ensure that they are in-line with actual costs (in a way resembling the regulatory agencies periodic assessment of the K factor). Fourth, the Guanajuato project revealed that the most important by-product of the use of an output-based financing mechanism was the establishment of a clear results framework. Under the proposed project, the results will be clearly defined in the performance agreements signed between SSE and the selected service providers. Fifth, to avoid the double accounting problems faced by the Guanajuato project, the proposed project will disburse funds not against individual expenditures on the input side, but against agreed outputs. However, to ensure that expenditures are eligible and that the funds are used for the intended purposes in line with the principles of economy, efficiency, transparency and competition, one of the initial concerns in the Guanajuato project, the BPKP will verify the outputs delivered by LGs.

Source: Performance-Based Budgeting in the Water Sector: The Case of Guanajuato. Mexico: Quality of Public Expenditure, Note No. 5, September 2008.

51. Brazil’s São Paulo Water Recovery Project (REAGUA). The project also builds upon the lessons from Brazil’s REAGUA project. The REAGUA Project, an initiative of the State of Sao Paulo, builds upon an OBD approach to partially subsidize wastewater treatment plants by paying for outputs. The proposed DAK project draws upon and will expand on this experience. Relevant lessons from REAGUA that have been incorporated in the design of the project include: (i) decentralizing responsibility of investments to the lowest level possible, such as provincial or local providers of WSS services, in order to increase accountability and improve investment quality; (ii) linking disbursement of loan proceeds to outputs to increase the efficiency of both executing agencies and public expenditure; and (iii) estimating reference unit costs of outputs, and defining and measuring appropriate standards and performance indicators for disbursements. Consistent with this lesson, the project team worked extensively with the MPW on clearly defining and simplifying outputs and unit costs using the REAGUA design model. REAGUA’s verification of outputs has also been incorporated into the project design. E. Alternatives Considered and Reasons for Rejection 52. Two options were considered for the delivery of this operation. First, a traditional stand alone input-based project was considered, whereby the GoI would finance specific inputs/capital investments based on completion of physical milestones. This option was rejected as the number of LGs targeted would be limited and the Bank would not be able to work with and strengthen the GoI’s DAK system of grants. Second, a DPL was considered. This option was rejected as it would only focus on higher level reforms and not provide the incentives and support needed by LGs to improve reporting and monitoring systems.

13

53. Based on extensive discussions with the GoI, it was agreed that a project to support strengthening the GoI’s systems at both central and LG levels should be based on the achievement of results. The OBD approach, based on the achievement of results and delivery of outputs, is responsive to the GoI’s request to use this operation to make its own DAK system more effective. The project will therefore seek to make the current input-based financing model of DAK responsive to incentives based on the achievement of outputs. 54. The use of an OBD financing approach for the proposed project would allow: (i) working with the GoI’s inter-government finance and LG expenditure systems; (ii) focusing on the explicit definition of outputs against which funds would be disbursed would sharpen the targeting of results in a more transparent and accountable way than under a traditional input-based operation, and have a major impact on improving the performance of LGs; (iii) payments based on outputs that would shift financial and operational risks of service delivery to LGs, who would be considered best positioned to manage such risks and decide how to best reach performance targets; (iv) verification of outputs prior to disbursement of payments, which provides a critical fiduciary safeguard on the accurate targeting of funds, as well as evidence that public funding is being well spent; and (v) the potential of the scheme to be replicated in other sectors and other provinces. 55. The GoI expects that the use of an OBD financing approach will increase accountability at the LG level, as there will be greater transparency in reporting and verification of outputs delivered. Over time, this can support reforms focused more specifically on improving service quality through better planning by LGs. This understanding is aligned with the Bank’s current interest in eliminating the disconnect between the programmatic engagements in Indonesia, as reflected in the CPS, and the static stages of the basic project cycle. The current project supports the CPS as it directly ties disbursements with results (outputs and reports) and facilitates a programmatic engagement with the country by financing a share of an important LG program.

III. IMPLEMENTATION

A. Partnership Arrangements Not applicable. B. Institutional and Implementation Arrangements 56. The MoF will implement the project. The MPW will also be a key supporting agency for the implementation of the project. The operational execution and coordination of the project will be managed by the PIU, which will be formally established under the Directorate General of Fiscal Balance (DGFB) within the MoF. The PIU will report to Director of Balancing Funds and will be composed of career staff and supported by a group of specialized consultants. The structure and specific responsibilities of the PIU are defined in the Operations Manual. The DGFB will coordinate the project’s implementation. The DGFB has conducted, and will continue to conduct, consultations with potential LGs for the selection of activities to be financed by the project.

14

Figure 2: Institutional Arrangements

MoF BAPPENAS MoHA MPW

NATIONAL STEERING COMMITTEE

Executing Agency

DGFB

MPW

Secretariat General

LG

PROV KAB KOT

BPKP

WB

Integrated Financial and Output Verification Reports

Outputs

DINAS/SKPDDGBM

DGSDA

DGCK

OVR

Reimbursement

ItJen

Monitoring & Evaluation of DAK Program

C. Monitoring and Evaluation of Results 57. The Results Framework for the project is outlined in Annex 3. The project will rely on one key report submitted to the Bank as part of the process of determining eligibility of expenditures incurred at the LG level, namely the combined Financial and Output Verification Report (OVR) produced by the BPKP in collaboration with the MPW. The OVR will be submitted to the DG Fiscal Balance in the MoF, which will then submit a report to the Bank for consideration regarding the amount to reimburse. 58. The MPW, in consultation with the PIU and Bappenas, will be responsible for continuous monitoring of the program and for conducting evaluation reports on the performance of the DAK program in the five provinces. The MPW will prepare annual monitoring and evaluation reports based on end-of-year outputs delivered, which should be finalized in the first quarter of the calendar year. The PIU, on behalf of the GoI, will conduct a mid-term review (MTR) of the project by the end of 2012. The annual M&E reports and MTR will form the basis for assessing any changes in the project design, implementation, and possible restructuring, if needed. D. Sustainability 59. The project is designed to work with the GoI system of inter-governmental transfers and strengthen the central government’s monitoring of funds, while also improving the effective delivery of outputs at the LG level. The project builds on the GoI’s existing mechanisms for monitoring and reporting, and will strengthen these structures, along with the enhanced verification of outputs delivered by LGs. The project presents a shift away from

15

financing individual investment sub-projects in a small number of LGs and focuses instead on improving the government framework within which investments take place. This places the emphasis on the achievement of results through the delivery of outputs, the verification of outputs, and compliance with GoI laws and regulations. 60. As part of the Project, the GoI will implement a capacity building program to improve the internal controls of LGs, including the planning process, project preparation and supervision, monitoring and reporting of outputs through web-based systems, and strengthening procurement and financial management. Such capacity enhancement of LG systems is expected to be sustained after the Project is completed.

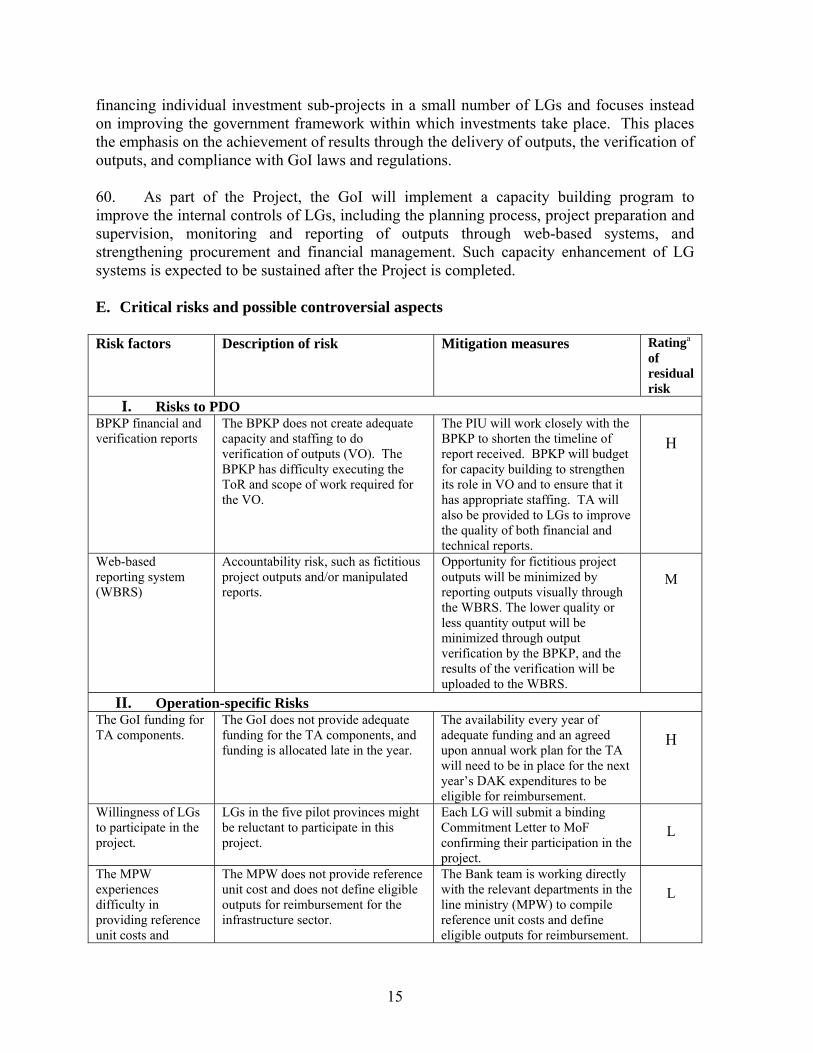

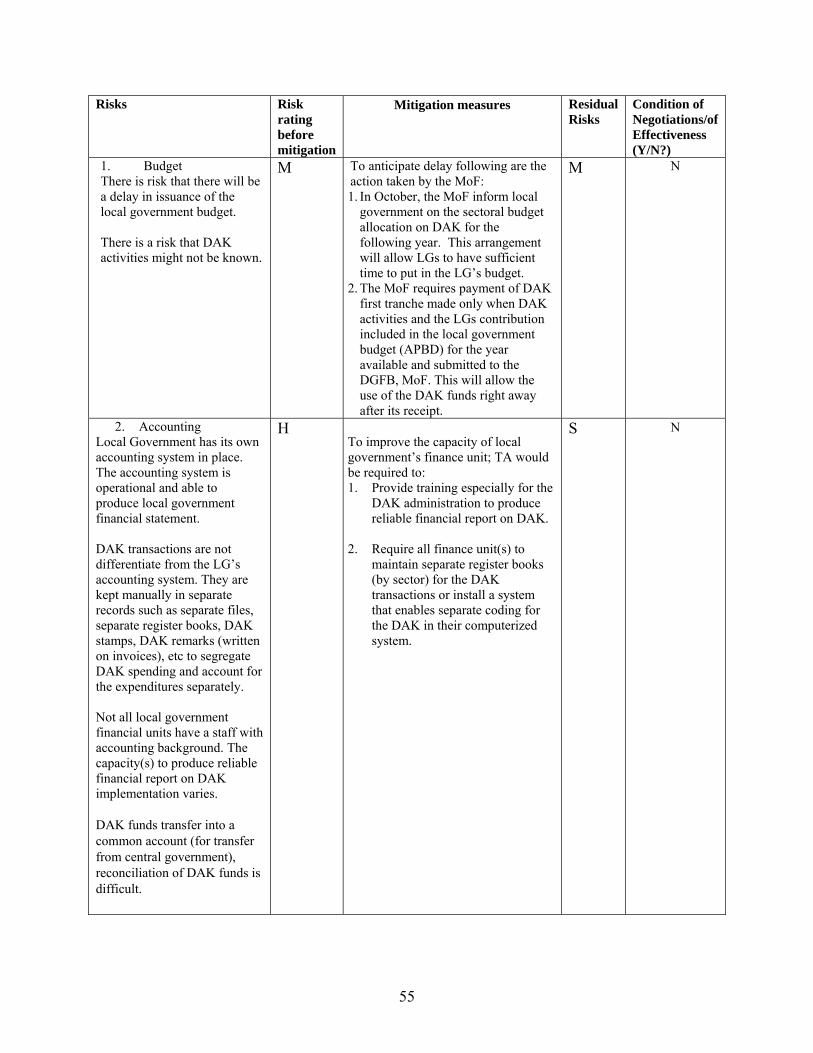

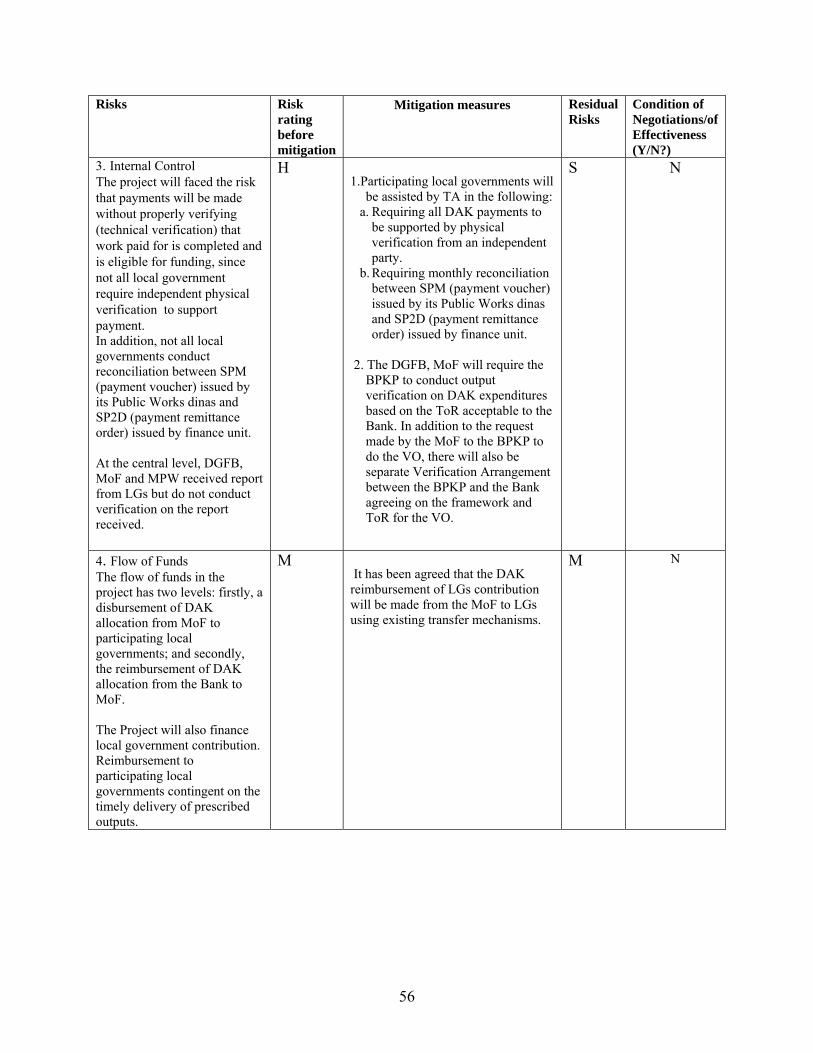

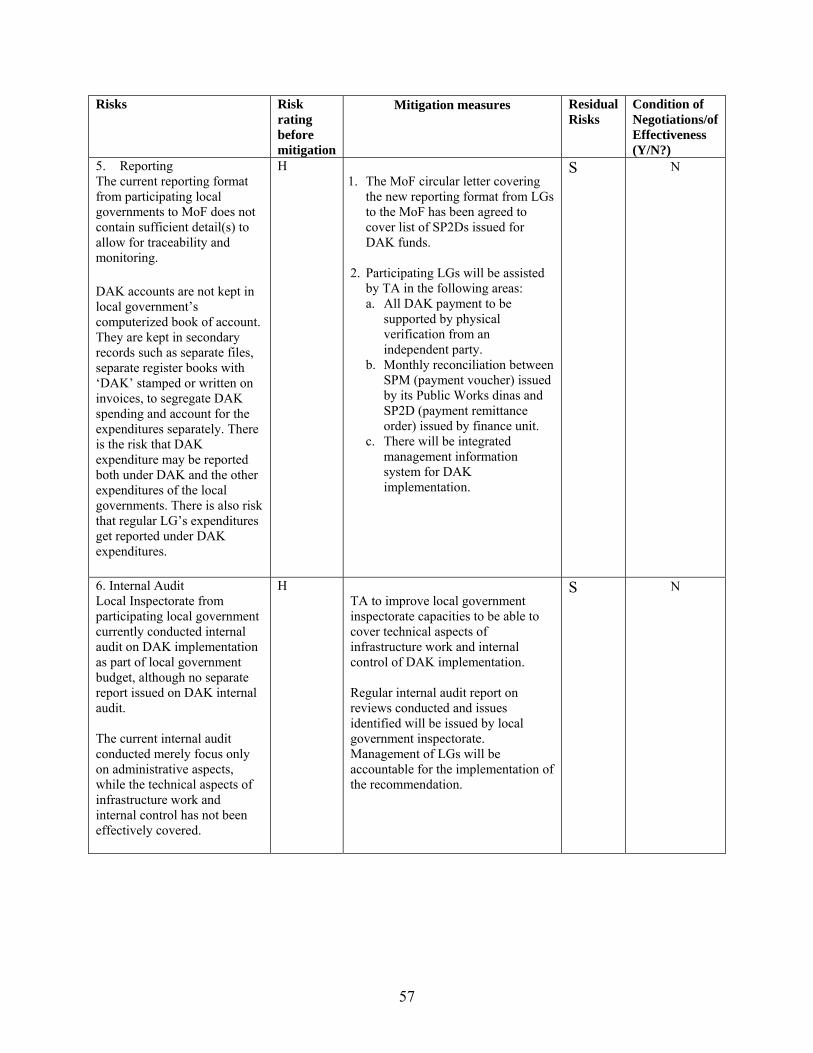

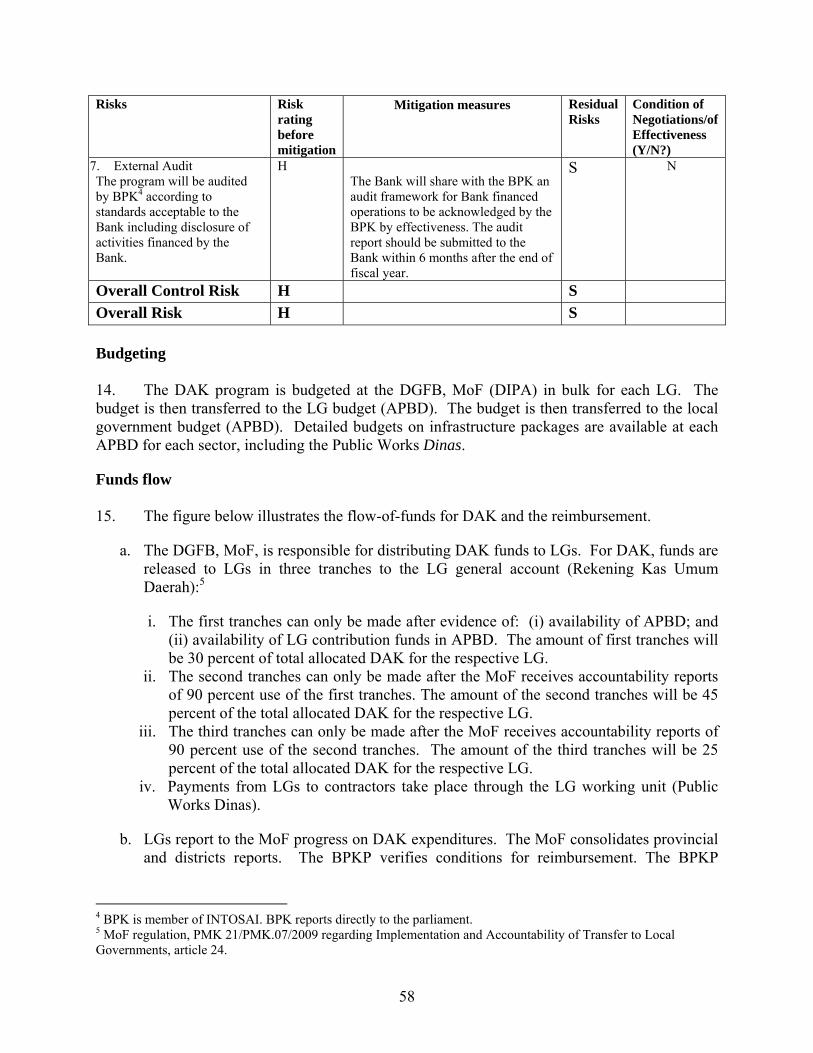

E. Critical risks and possible controversial aspects Risk factors Description of risk Mitigation measures Ratinga

of residual risk

I. Risks to PDO BPKP financial and verification reports

The BPKP does not create adequate capacity and staffing to do verification of outputs (VO). The BPKP has difficulty executing the ToR and scope of work required for the VO.

The PIU will work closely with the BPKP to shorten the timeline of report received. BPKP will budget for capacity building to strengthen its role in VO and to ensure that it has appropriate staffing. TA will also be provided to LGs to improve the quality of both financial and technical reports.

H

Web-based reporting system (WBRS)

Accountability risk, such as fictitious project outputs and/or manipulated reports.

Opportunity for fictitious project outputs will be minimized by reporting outputs visually through the WBRS. The lower quality or less quantity output will be minimized through output verification by the BPKP, and the results of the verification will be uploaded to the WBRS.

M

II. Operation-specific Risks The GoI funding for TA components.

The GoI does not provide adequate funding for the TA components, and funding is allocated late in the year.

The availability every year of adequate funding and an agreed upon annual work plan for the TA will need to be in place for the next year’s DAK expenditures to be eligible for reimbursement.

H

Willingness of LGs to participate in the project.

LGs in the five pilot provinces might be reluctant to participate in this project.

Each LG will submit a binding Commitment Letter to MoF confirming their participation in the project.

L

The MPW experiences difficulty in providing reference unit costs and

The MPW does not provide reference unit cost and does not define eligible outputs for reimbursement for the infrastructure sector.

The Bank team is working directly with the relevant departments in the line ministry (MPW) to compile reference unit costs and define eligible outputs for reimbursement.

L

16

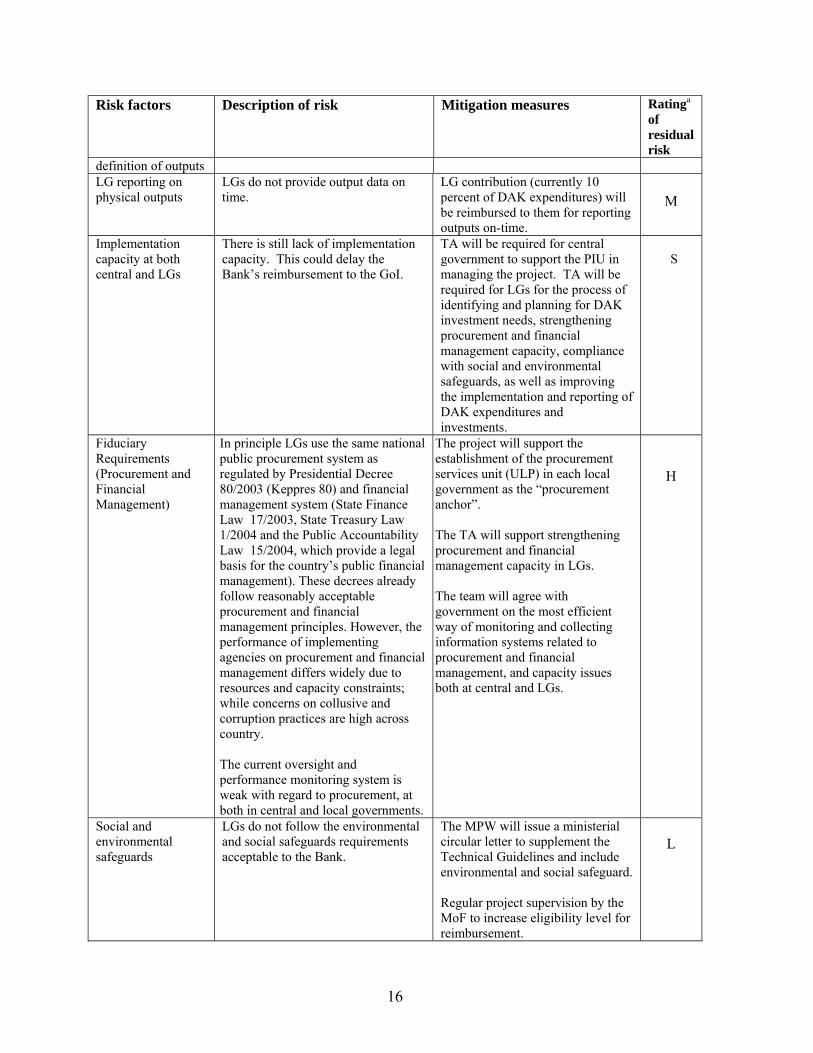

Risk factors Description of risk Mitigation measures Ratinga of residual risk

definition of outputs LG reporting on physical outputs

LGs do not provide output data on time.

LG contribution (currently 10 percent of DAK expenditures) will be reimbursed to them for reporting outputs on-time.

M

Implementation capacity at both central and LGs

There is still lack of implementation capacity. This could delay the Bank’s reimbursement to the GoI.

TA will be required for central government to support the PIU in managing the project. TA will be required for LGs for the process of identifying and planning for DAK investment needs, strengthening procurement and financial management capacity, compliance with social and environmental safeguards, as well as improving the implementation and reporting of DAK expenditures and investments.

S

Fiduciary Requirements (Procurement and Financial Management)

In principle LGs use the same national public procurement system as regulated by Presidential Decree 80/2003 (Keppres 80) and financial management system (State Finance Law 17/2003, State Treasury Law 1/2004 and the Public Accountability Law 15/2004, which provide a legal basis for the country’s public financial management). These decrees already follow reasonably acceptable procurement and financial management principles. However, the performance of implementing agencies on procurement and financial management differs widely due to resources and capacity constraints; while concerns on collusive and corruption practices are high across country. The current oversight and performance monitoring system is weak with regard to procurement, at both in central and local governments.

The project will support the establishment of the procurement services unit (ULP) in each local government as the “procurement anchor”. The TA will support strengthening procurement and financial management capacity in LGs. The team will agree with government on the most efficient way of monitoring and collecting information systems related to procurement and financial management, and capacity issues both at central and LGs.

H

Social and environmental safeguards

LGs do not follow the environmental and social safeguards requirements acceptable to the Bank.

The MPW will issue a ministerial circular letter to supplement the Technical Guidelines and include environmental and social safeguard. Regular project supervision by the MoF to increase eligibility level for reimbursement.

L

17

Risk factors Description of risk Mitigation measures Ratinga of residual risk

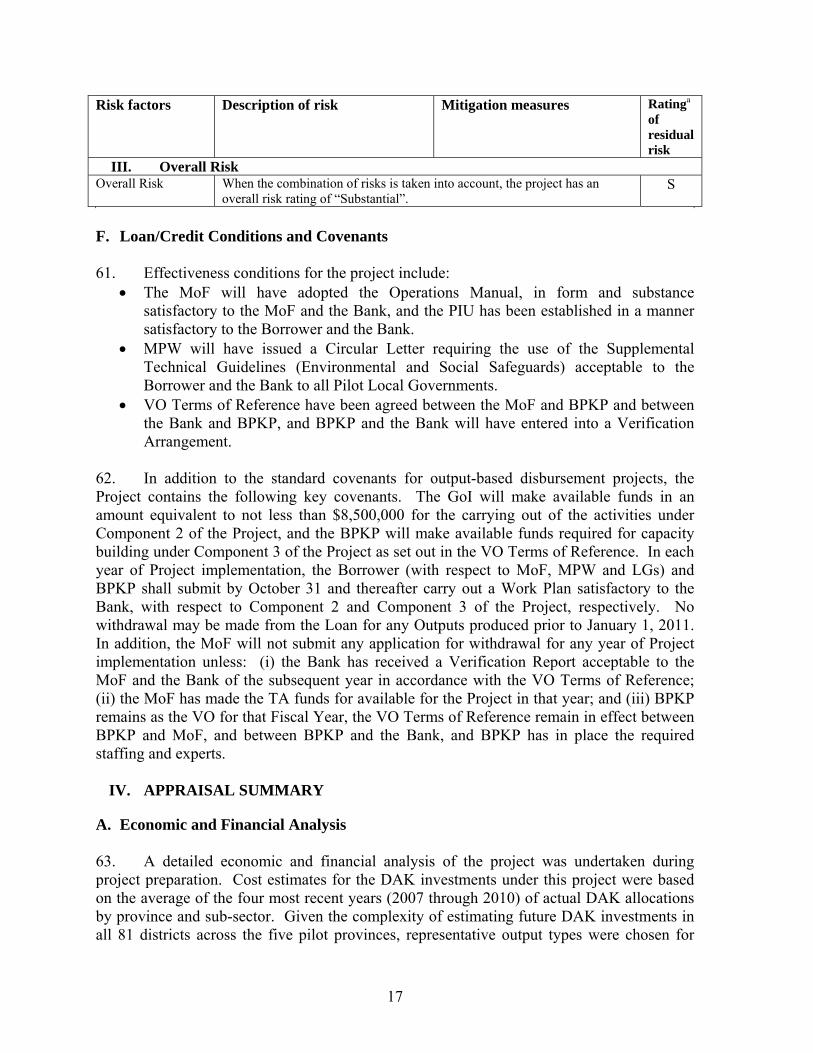

III. Overall Risk Overall Risk When the combination of risks is taken into account, the project has an

overall risk rating of “Substantial”. S

F. Loan/Credit Conditions and Covenants 61. Effectiveness conditions for the project include:

The MoF will have adopted the Operations Manual, in form and substance satisfactory to the MoF and the Bank, and the PIU has been established in a manner satisfactory to the Borrower and the Bank.

MPW will have issued a Circular Letter requiring the use of the Supplemental Technical Guidelines (Environmental and Social Safeguards) acceptable to the Borrower and the Bank to all Pilot Local Governments.

VO Terms of Reference have been agreed between the MoF and BPKP and between the Bank and BPKP, and BPKP and the Bank will have entered into a Verification Arrangement.

62. In addition to the standard covenants for output-based disbursement projects, the Project contains the following key covenants. The GoI will make available funds in an amount equivalent to not less than $8,500,000 for the carrying out of the activities under Component 2 of the Project, and the BPKP will make available funds required for capacity building under Component 3 of the Project as set out in the VO Terms of Reference. In each year of Project implementation, the Borrower (with respect to MoF, MPW and LGs) and BPKP shall submit by October 31 and thereafter carry out a Work Plan satisfactory to the Bank, with respect to Component 2 and Component 3 of the Project, respectively. No withdrawal may be made from the Loan for any Outputs produced prior to January 1, 2011. In addition, the MoF will not submit any application for withdrawal for any year of Project implementation unless: (i) the Bank has received a Verification Report acceptable to the MoF and the Bank of the subsequent year in accordance with the VO Terms of Reference; (ii) the MoF has made the TA funds for available for the Project in that year; and (iii) BPKP remains as the VO for that Fiscal Year, the VO Terms of Reference remain in effect between BPKP and MoF, and between BPKP and the Bank, and BPKP has in place the required staffing and experts.

IV. APPRAISAL SUMMARY

A. Economic and Financial Analysis 63. A detailed economic and financial analysis of the project was undertaken during project preparation. Cost estimates for the DAK investments under this project were based on the average of the four most recent years (2007 through 2010) of actual DAK allocations by province and sub-sector. Given the complexity of estimating future DAK investments in all 81 districts across the five pilot provinces, representative output types were chosen for

18

each of the sub-sectors, based on outputs most commonly funded by DAK investments in these provinces. Unit costs for each output type in each province were obtained, based on actual unit cost data from the MPW. Expected output quantities were derived by dividing the planned investments by the unit costs. Annual operating costs for the resulting infrastructure were included in the analysis, assuming a service life of at least five years. 64. Expected benefits deriving from each unit of representative output were then estimated for this project using data from the 2009 study of the economic benefits arising from investments delivered under the Initiatives in Local Governance Reform Project (ILGRP). Annex 9 provides greater detail on the unit costs, calculated output quantities, and estimated benefits for the representative output types in each province. 65. The net present value (NPV) of the net economic benefits from the Project is thus estimated to be US$56.0 million, over a period of five years, using a discount rate of 12 percent. The internal rate of return, based on net economic benefits, is 40 percent, this being the discount rate at which NPV would be zero. B. Technical 66. Based on extensive discussions with the GoI, it was agreed that a project to support the strengthening of the GoI’s systems at both central and LG levels should be based on achievement of results. Through the DAK mechanism, the GoI and LGs finance outputs, which will be subject to Bank reimbursement, based upon delivery and verification of physical outputs. The GoI expects that the use of an OBD financing approach will increase accountability at the LG level, thereby leading to improved service quality by allowing LGs to use the information in their planning processes and by improving oversight by the central government. Furthermore, in addition to this economic analysis that shows these DAK investments to be economically sound, a benefit arising specifically from this project is the accountability and reporting in the use of DAK funds. While it is difficult to quantify the value of this benefit ex-ante, the positive impact of institutional strengthening in the use of DAK resources is expected to be substantial, particularly if there are positive spillover effects in other sectors and for other fiscal transfers.

C. Fiduciary 67. The arrangements for the project will focus on ensuring that the selected LGs have the capacity to procure, supervise, track expenditures, and report on agreed outputs. The Bank team conducted capacity assessments on selected LGs to verify that financial management and procurement systems ensure that: (i) expenditure on works and goods takes place in line with the principles of economy, efficiency, transparency, and competition; (ii) expenditure is productive; (iii) expenditure contributes to solutions within a fiscally sustainable framework; and (iv) acceptable internal oversight arrangements are in place. 68. Procurement. The procurement under sub-projects will be carried out by the participating LGs via the procurement services unit/ULP. The MoF, through its TA for Institutional Strengthening (not Bank financed), will provide the support and capacity building as required to ensure that procurement follows the agreed procedures. The

19

procurement includes small works (below US$400,000 equivalent) for minor repairs, maintenance or rehabilitation of facilities/services, and output-based disbursement will be used. Despite the weaknesses in implementation, the national procurement procedures under Keppres 80/2003 generally have the elements of good international practice and have the minimum requirements that make them acceptable for this type of operation. In addition, the fact that no international bidders will be involved and that the project is using an output-based mechanism makes this the most reasonable approach for the project. The procurement for the proposed project would be carried out in accordance with Section 1 (excluding paragraph 1.16) and paragraphs 3.14 and 3.15 of the World Bank’s "Guidelines: Procurement Under IBRD Loans and IDA Credits" dated May 2004 revised October 2006; and the provisions stipulated in the Legal Agreement. Since the project will be using an output-based approach and will finance outputs and not specific contracts, and due to the straightforward and simple nature of the expected procurement, consistent with paragraph 3.14 of the Bank’s Procurement Guidelines, the procurement procedures for sub-projects under LGs will follow competitive procurement methods of Keppres 80/2003 acceptable to the Bank.

69. Under output-based disbursement, where payment is made based on outputs rather than inputs, the Bank neither reviews the procurement plans nor individual procurement. However, prior to the MoF submitting the request for reimbursement from the Bank, the BPKP will review the procurement process and contract documents on a sampling basis, in order to verify that agreed procurement procedures are strictly followed and that the national standard bidding documents are adopted. Samples will include all participating LGs at 20 percent of the total number of contracts in each Province in the particular review period. If the verification report shows non-compliance of reviewed contracts in a particular review period, then the respective LG outputs will not be eligible for Bank reimbursements. By the end of this project, covenants will need to be met by each participating LG with respect to improving its procurement management system and capacity, as follows: (i) improved procurement planning system and reporting; and (ii) establish and improve the capacity of the ULP. 70. The procurement of TA for Institutional Strengthening to support LGs in managing the sub-projects (including improving their procurement management system and capacity), as well as the TA for improving the capacity of BPKP are not Bank financed. GoI will ensure that adequate funds are made available for the TA. Since the GoI is financing the TA Component, the Bank’s Consultant Guidelines do not apply. 71. Financial Management. The financial management assessment concludes that the current DAK arrangements satisfy the Bank’s requirements for financial management as stipulated in OP/BP 10.02. The risk at the LG level is high given that payment verification mechanisms vary significantly across LGs. While the segregation of duties is in place, not all LGs have requested third party consultant(s) to verify payments made for infrastructure. At the central level, the DGFB (MoF) receives accountability reports on the use of DAK funds. However, the DGFB does not conduct verification on the use of the funds reported, hence the report is too general and does not provide enough information for traceability purposes. On the technical side, LGs send technical progress reports on DAK

20

implementation, although the reporting requirement to the MPW has low compliance and the MPW also does not conduct output verification on the reports received.

72. There is currently no integrated management information system in place for the DAK program. The financial management risk is similar to the overall risk of the project, which is considered ‘High Risk’ before mitigation and ‘Substantial’ after mitigation. In order to overcome the risks regarding financial management, the mitigation measures include: (i) establishing an improved reporting format and integrated management information system for DAK, which provides better traceability on the use of DAK funds; (ii) conducting output verification on the reports received; (iii) and agreement between the BPKP and the Bank on the ToR for the BPKP as the output verifier for the project; (iv) a binding Commitment Letter from each participating LG to MoF; (v) TA to improve LG administration and internal audit of DAK; and (vi) improving the external audit arrangements for the DAK program.

73. Governance and Anti-Corruption (GAC). The project disbursement will be made based on the outputs of DAK at the LG level instead of on the process to produce outputs. Therefore, it will be very important to obtain reasonable assurance of the existence of the outputs. Higher assurance will be achieved through direct verification of the outputs by the BPKP. However, the BPKP will only reach some of the outputs depending on the number of samples. Therefore, an appropriate reporting system, one that will allow the assessment of the existence, quality, quantity, and timeliness in completion of the outputs, is required. Since the existing DAK reporting system does not have these capabilities, the WBRS will be developed. On the other hand, understanding fraud and corruption by DAK stakeholders, as well as the consequences of fraud and corruption if and when these occur, will contribute to preventing fraud and corruption in DAK funded projects. Therefore, the Bank guidelines on Preventing and Combating Fraud and Corruption will be socialized to officers and stakeholders of the DAK. D. Social 74. The DAK funds will mainly be used by LGs to finance the maintenance, rehabilitation and improvement of existing infrastructure. In some cases, however, there will be investments for new civil works but the scale will be relatively small. The project will only reimburse small civil works, with an investment size up to US$400,000, which is also the prior review threshold under some existing Bank LG projects (e.g. ILGRP).

75. The project is expected to positively impact the social and economic living standards of its beneficiaries, particularly those in poor communities, by improving existing infrastructure and other facilities serving these communities. Remote villages will have better access to other villages and towns/cities; agricultural productivity levels will increase through better access to markets; people will enjoy improved health through better access to water supply services and sanitation facilities; and improved infrastructure and other facilities will generally save costs and time for beneficiaries.

76. Past and ongoing DAK for the roads, water, sanitation and irrigation sub-sectors, have shown that the potentially adverse social risks have been minimized, as sub-project

21

proposals were developed through participatory planning process using a “Musrenbang” mechanism that involved various stakeholders from the village level up to the central level. Land acquisition is likely to be insignificant, as the project will mainly finance the maintenance, rehabilitation and improvement of existing infrastructure and facilities. The expansion and extension of current networks and facilities will be limited. As the nature of the project is consistent with past and ongoing DAK in the four sub-sectors, it is likely that potentially adverse social risks will remain insignificant. The project design will ensure that the potential adverse social risks of sub-projects, including parts financed by other funding sources, will be better managed and addressed than in the past.