Embed Size (px)

Citation preview

The World BankThe World Bank

Bank Insolvency Framework and the Global Bank Insolvency Initiative

Ernesto Aguirre, Manager of Banking RegulationJune 20, 2002

ContentsContents

Bank Insolvency Framework vs Corporate Insolvency - Definition- Concept of Bank Insolvency- Starting Point- Objectives

Importance of the Bank Insolvency Framework- Concept- Country Examples

The Bank Insolvency Initiative- Objectives- Participants- Work Program- Contents

I.I. What is the Bank Insolvency What is the Bank Insolvency Framework and how it differs Framework and how it differs from the general (corporate) from the general (corporate) insolvency framework.insolvency framework.

Bank Insolvency FrameworkBank Insolvency Framework

a) Definition

Set of measures that should (have to) be taken by the State Authorities to confront actual/potential bank insolvency.

Bank Insolvency FrameworkBank Insolvency Framework

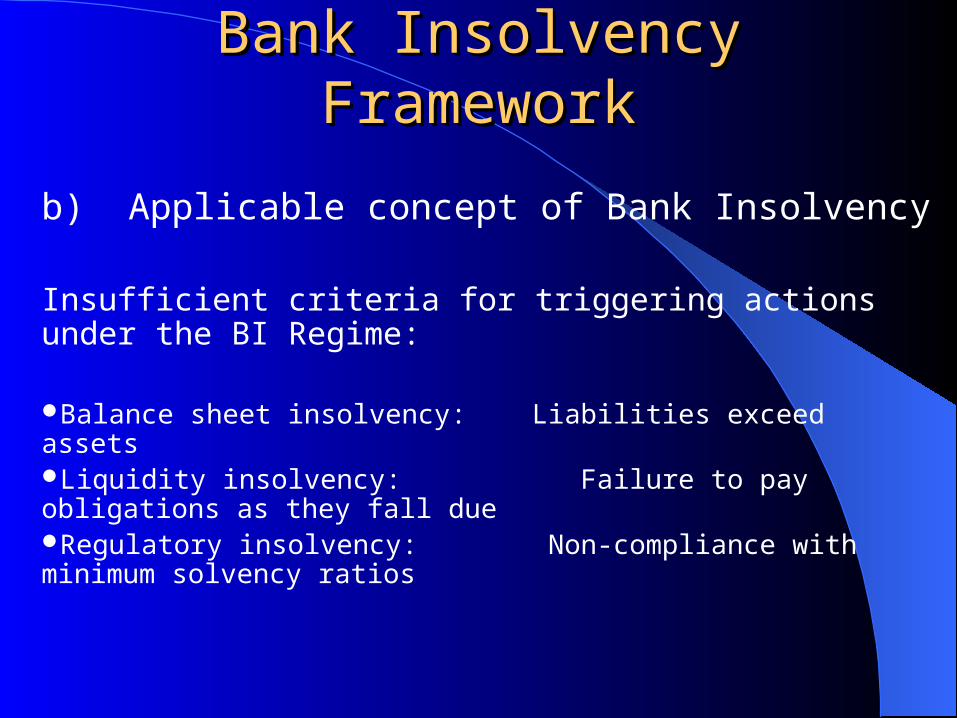

b) Applicable concept of Bank Insolvency

Insufficient criteria for triggering actions under the BI Regime:

Balance sheet insolvency: Liabilities exceed assetsLiquidity insolvency: Failure to pay obligations as they fall dueRegulatory insolvency: Non-compliance with minimum solvency ratios

Bank Insolvency FrameworkBank Insolvency Framework

b) Applicable concept of Bank Insolvency (cont.)

For banks the perception of the supervisor is key. “A bank is insolvent when the bank regulator says so...”

-Concept of insolvency as a trigger point:

Whenever a competent, independent regulator perceives the bank as potentially (imminent?) or actually insolvent measures under the BI regime should start to be taken.

Bank Insolvency FrameworkBank Insolvency Framework

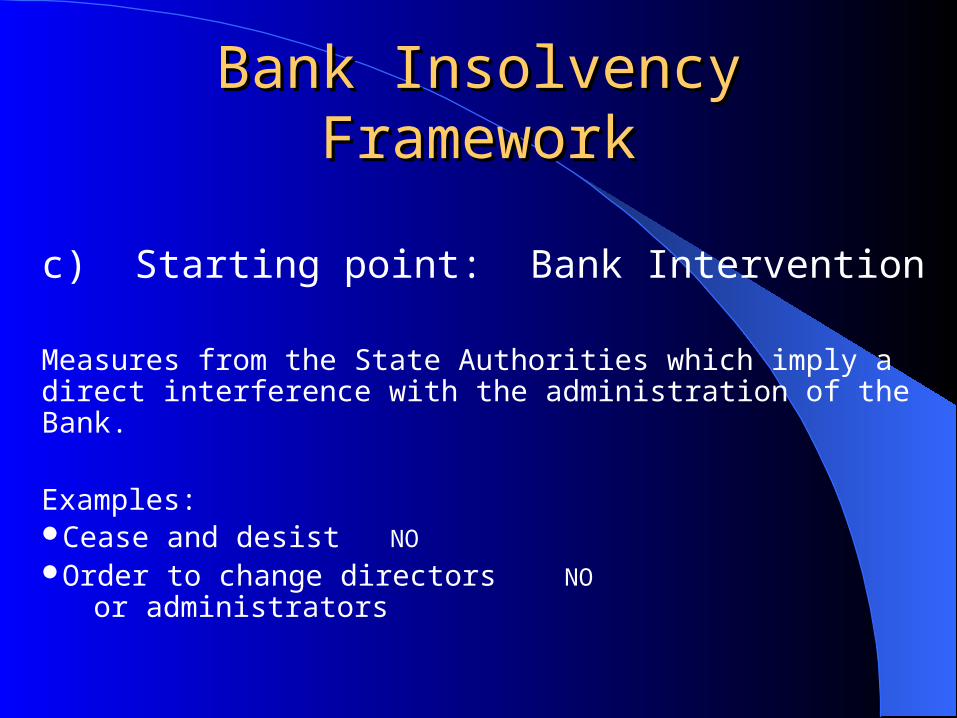

c) Starting point: Bank Intervention

Measures from the State Authorities which imply a direct interference with the administration of the Bank.

Examples: Cease and desist NOOrder to change directors NO or administrators

Bank Insolvency FrameworkBank Insolvency Framework

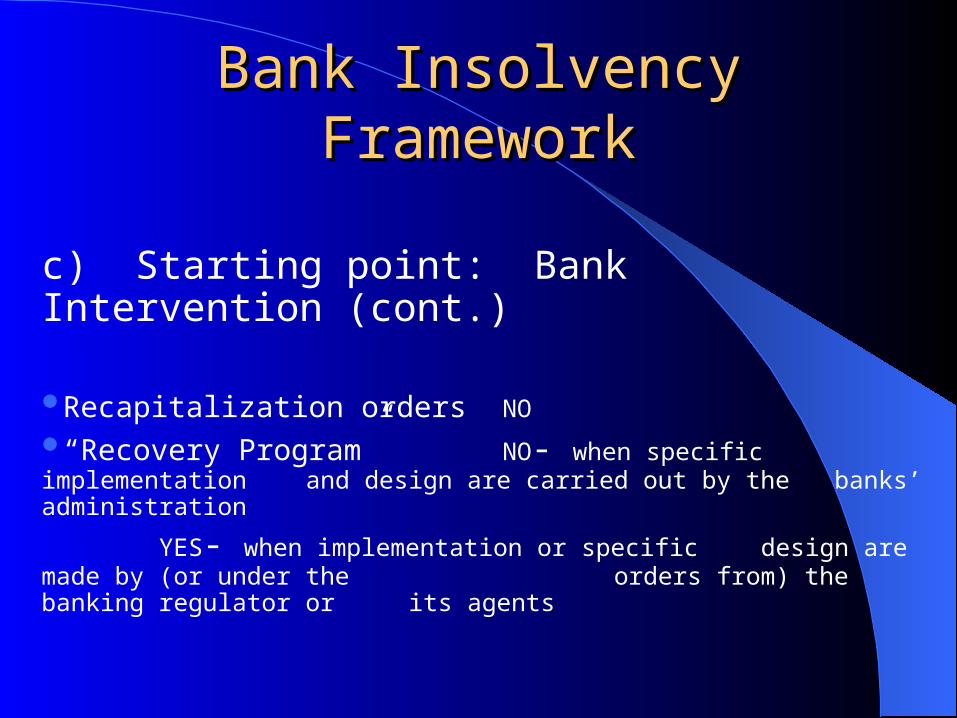

c) Starting point: Bank Intervention (cont.)

Recapitalization orders NO

“Recovery Program” NO- when specific implementation and design are carried out by

the banks’ administration

YES- when implementation or specific design are made by (or under the

orders from) the banking regulator or its agents

Bank Insolvency FrameworkBank Insolvency Framework

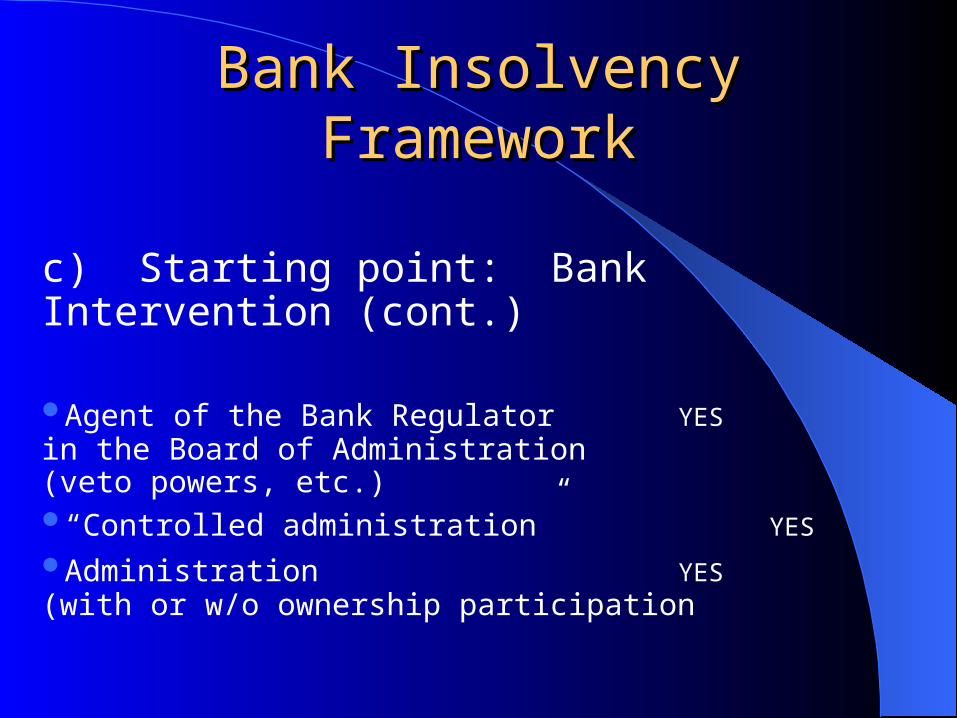

c) Starting point: Bank Intervention (cont.)

Agent of the Bank Regulator YES in the Board of Administration(veto powers, etc.)“Controlled administration” YES

Administration YES(with or w/o ownership participation

Bank Insolvency FrameworkBank Insolvency Framework

d) Objectives

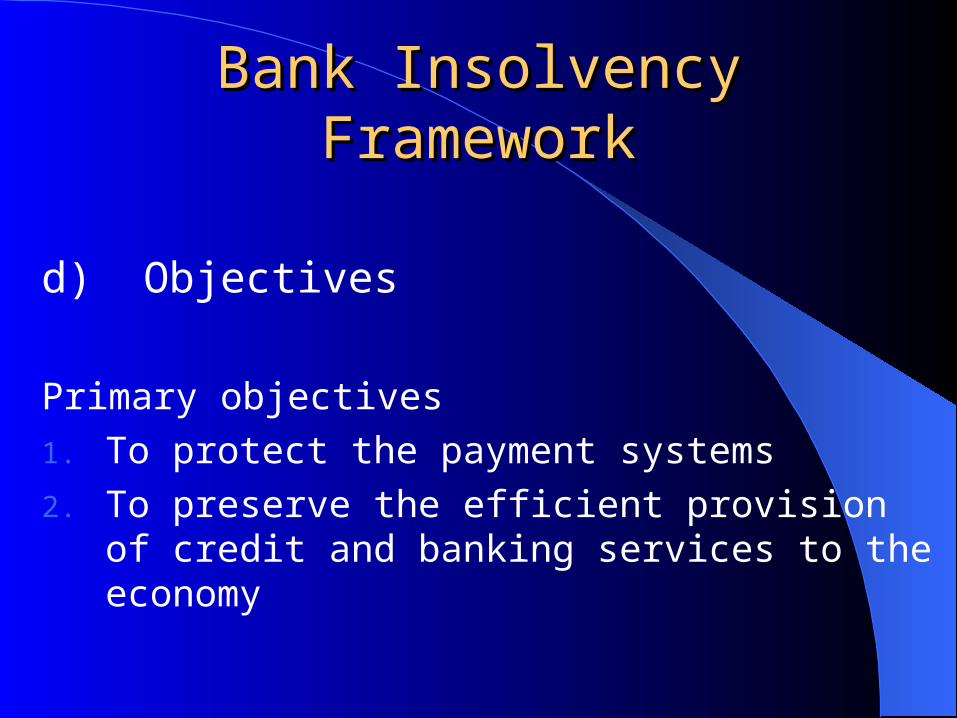

Primary objectives

1. To protect the payment systems

2. To preserve the efficient provision of credit and banking services to the economy

Bank Insolvency FrameworkBank Insolvency Framework

d) Objectives (cont.)

Preconditions:

1. Public confidence in the Banking System

2. Technical capability of the Banking System

Bank Insolvency FrameworkBank Insolvency Framework

d) Objectives (cont.)

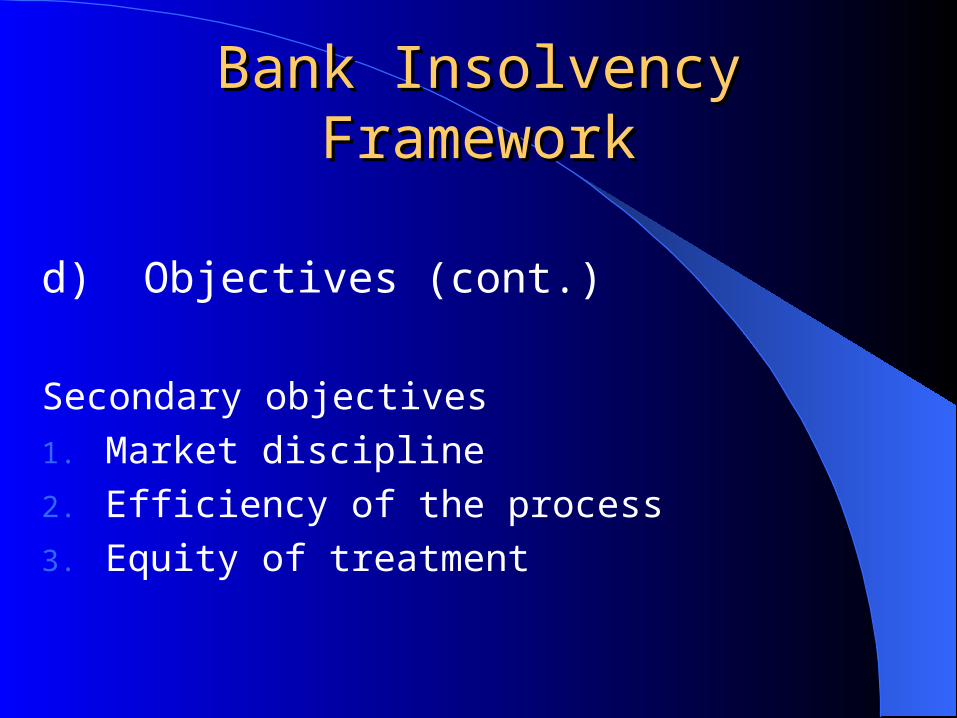

Secondary objectives

1. Market discipline

2. Efficiency of the process

3. Equity of treatment

Bank Insolvency FrameworkBank Insolvency Framework

Secondary Objectives (cont.)

The secondary objectives become the paramount ones when the bank has been closed (Banking Liquidation) and it is only in this context that all principles applicable to Corporate insolvency apply equally to the two processes. ( i.e. The 3 secondary objectives, plus all principles reflected in Principle 6 of the Legal Framework for Corporate Insolvency)

Bank Insolvency FrameworkBank Insolvency Framework

Conclusion

The scope of the BI regime is:

Very wide, and Different from the scope of the CI Regime

(similar only in the context of Bank Liquidation)

II. Importance of the Institutional, legal and II. Importance of the Institutional, legal and regulatory framework to deal with bank regulatory framework to deal with bank

insolvency, including in the context of systemic insolvency, including in the context of systemic crisiscrisis

Strategy- - - - - - -Framework- - - - -Implementation

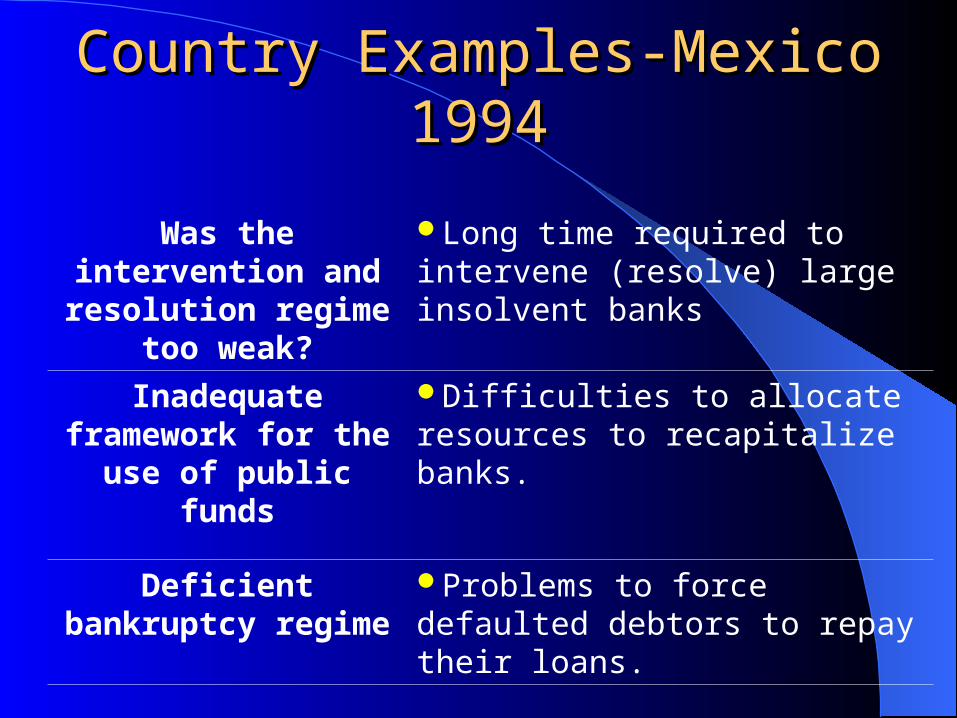

Country Examples-Mexico 1994Country Examples-Mexico 1994

Was the intervention and resolution regime

too weak?

Long time required to intervene (resolve) large insolvent banks

Inadequate framework for the use of public

funds

Difficulties to allocate resources to recapitalize banks.

Deficient bankruptcy regime

Problems to force defaulted debtors to repay their loans.

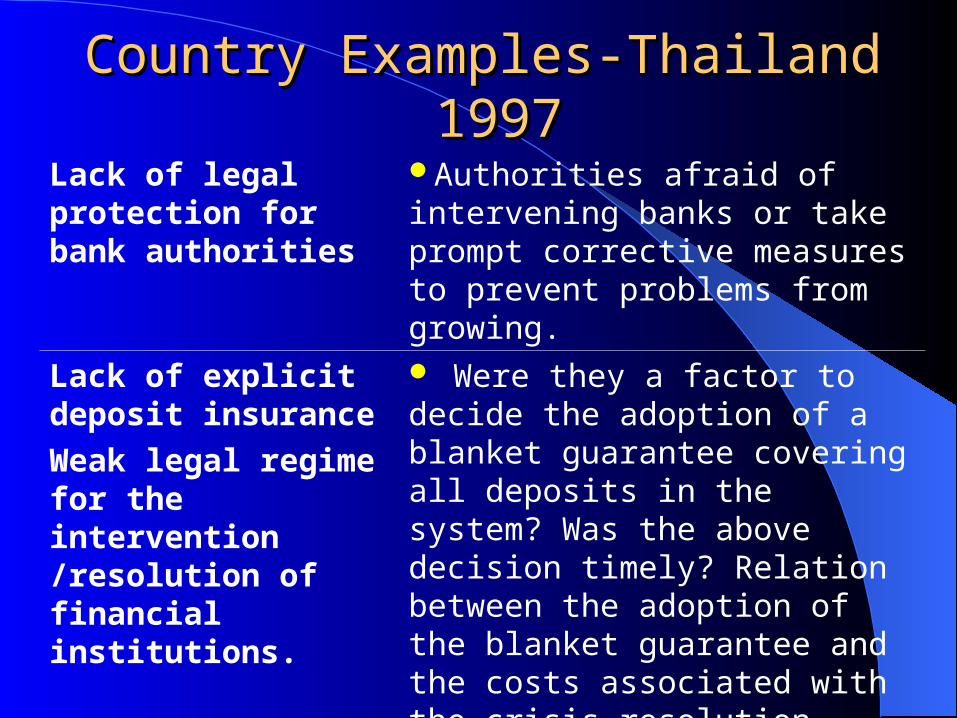

Country ExamplesCountry Examples--ThailandThailand 199 19977

Lack of legal protection for bank authorities

Authorities afraid of intervening banks or take prompt corrective measures to prevent problems from growing.

Lack of explicit deposit insurance

Weak legal regime for the intervention /resolution of financial institutions.

Were they a factor to decide the adoption of a blanket guarantee covering all deposits in the system? Was the above decision timely? Relation between the adoption of the blanket guarantee and the costs associated with the crisis resolution.

Deficient bankruptcy regime

Problems to force debtors to repay or renegotiate their loans.

Country Examples-Korea 1997Country Examples-Korea 1997

Excessive constraints to entry of foreign

investors

Delays to sell large intervened banks

Fragmented financial sector legislation

Authorities dealt rapidly with banks’ problems, but failed to recognize and rapidly solve problems of other non-bank financial institutions.

Deficient bankruptcy regime

Problems to force defaulted debtors to repay their loans.

Country Examples-Ecuador 1998Country Examples-Ecuador 1998

Lack of legal protection to bank authorities

Authorities afraid to intervene banks or take appropriate corrective measures before a bank collapses.

Weak institutional arrangements

High Turnover of senior government officials.Main decisions revoked by courts or the legislative.

Deficient bankruptcy regime

Problems to force defaulted debtors to repay their loans or restructure their debts..

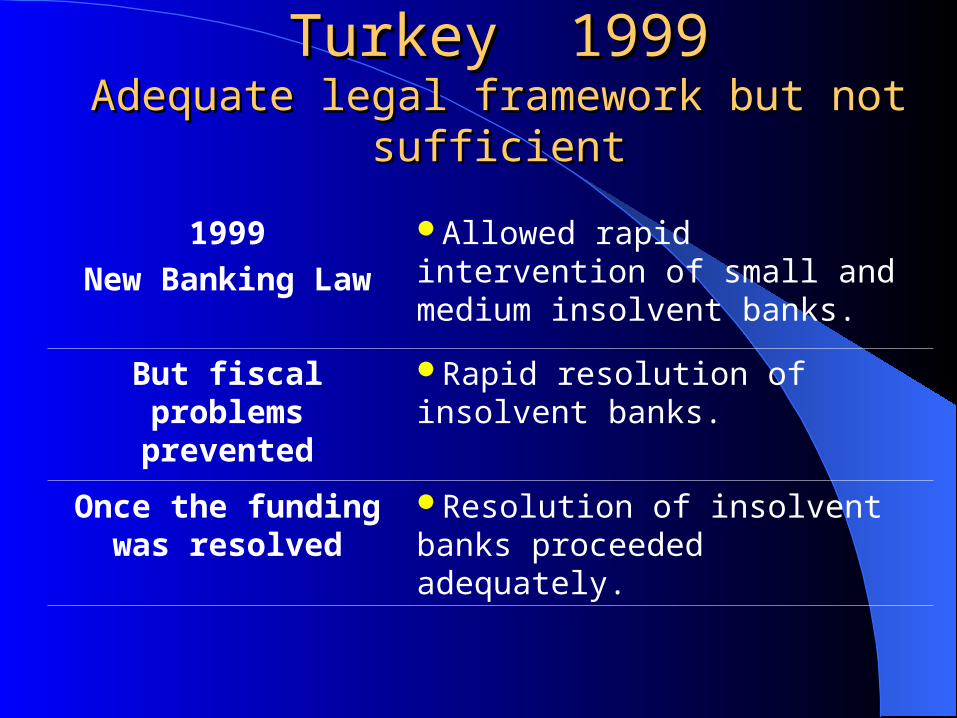

Turkey 1999Turkey 1999Adequate legal framework but not sufficientAdequate legal framework but not sufficient

1999

New Banking Law

Allowed rapid intervention of small and medium insolvent banks.

But fiscal problems prevented

Rapid resolution of insolvent banks.

Once the funding was resolved

Resolution of insolvent banks proceeded adequately.

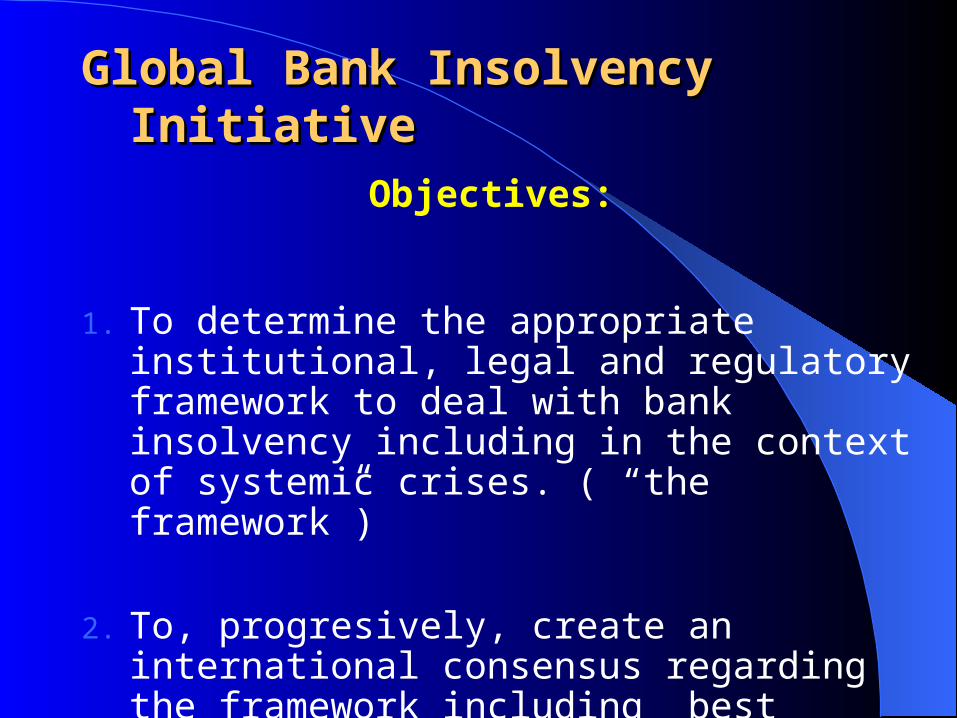

Global Bank Insolvency InitiativeGlobal Bank Insolvency InitiativeObjectives:

1. To determine the appropriate institutional, legal and regulatory framework to deal with bank insolvency including in the context of systemic crises. ( “the framework”)

2. To, progresively, create an international consensus regarding the framework including best practices and alternatives to deal with bank insolvency.

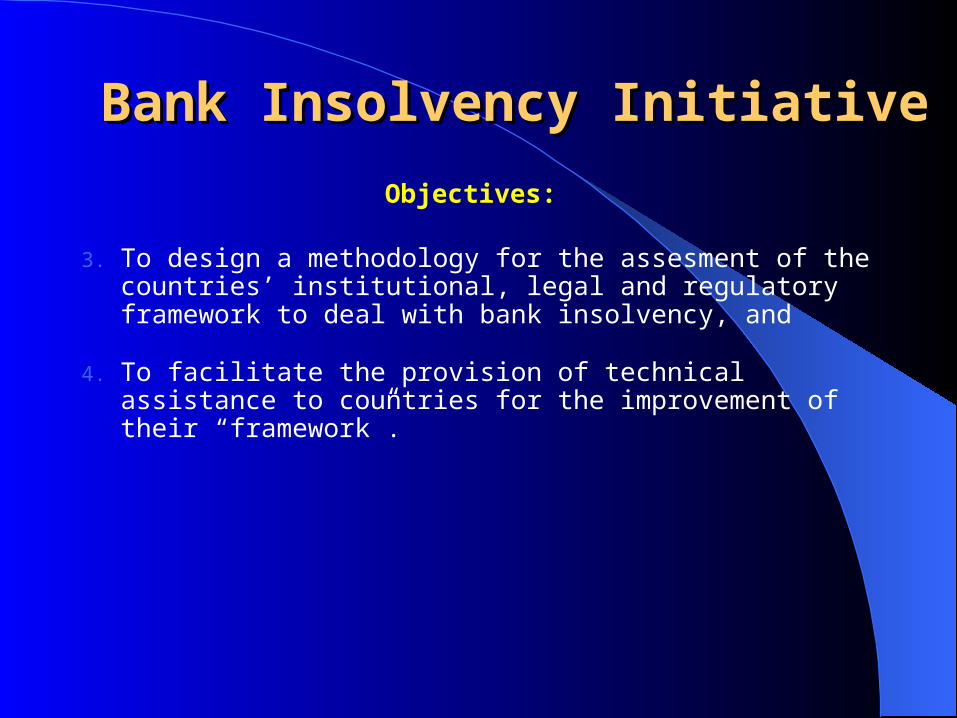

Bank Insolvency InitiativeBank Insolvency Initiative

Objectives:

3. To design a methodology for the assesment of the countries’ institutional, legal and regulatory framework to deal with bank insolvency, and

4. To facilitate the provision of technical assistance to countries for the improvement of their “framework”.

Participating InstitutionsParticipating Institutions

Coordination WB (leading institution)IMF (main partner)

Participants

(International Institutions)

BIS, FSI, BCBSRegional Development Banks

Participants

(Countries)

All countries through:Bank Supervisory AgencyCentral BankDeposit Insurance Agency

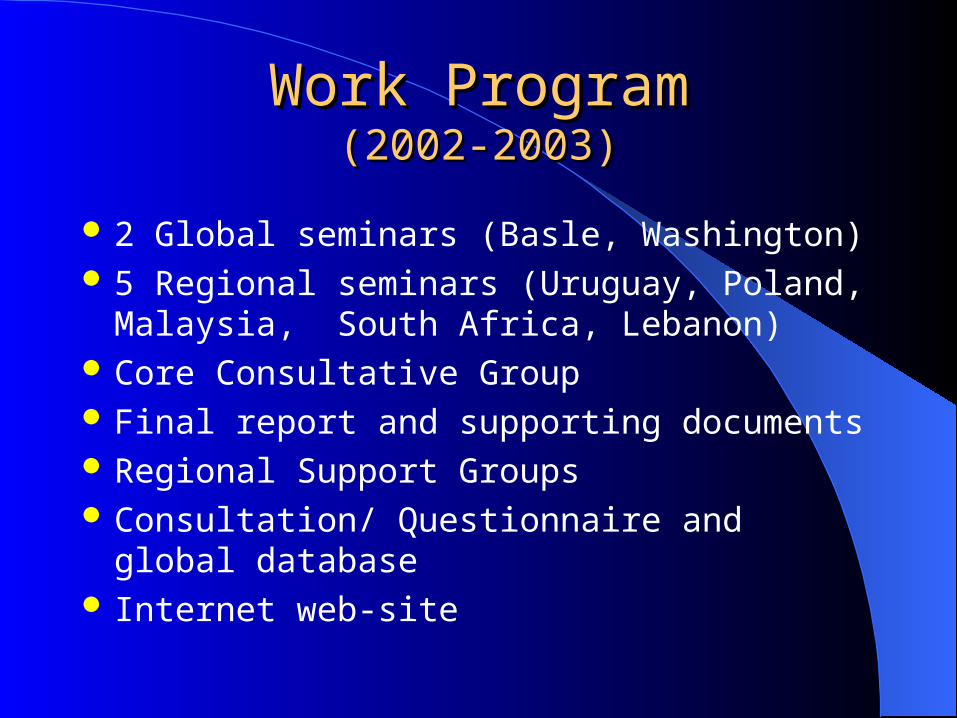

Work ProgramWork Program(2002-2003)(2002-2003)

2 Global seminars (Basle, Washington) 5 Regional seminars (Uruguay, Poland, Malaysia,

South Africa, Lebanon) Core Consultative Group Final report and supporting documents Regional Support Groups Consultation/ Questionnaire and global database Internet web-site

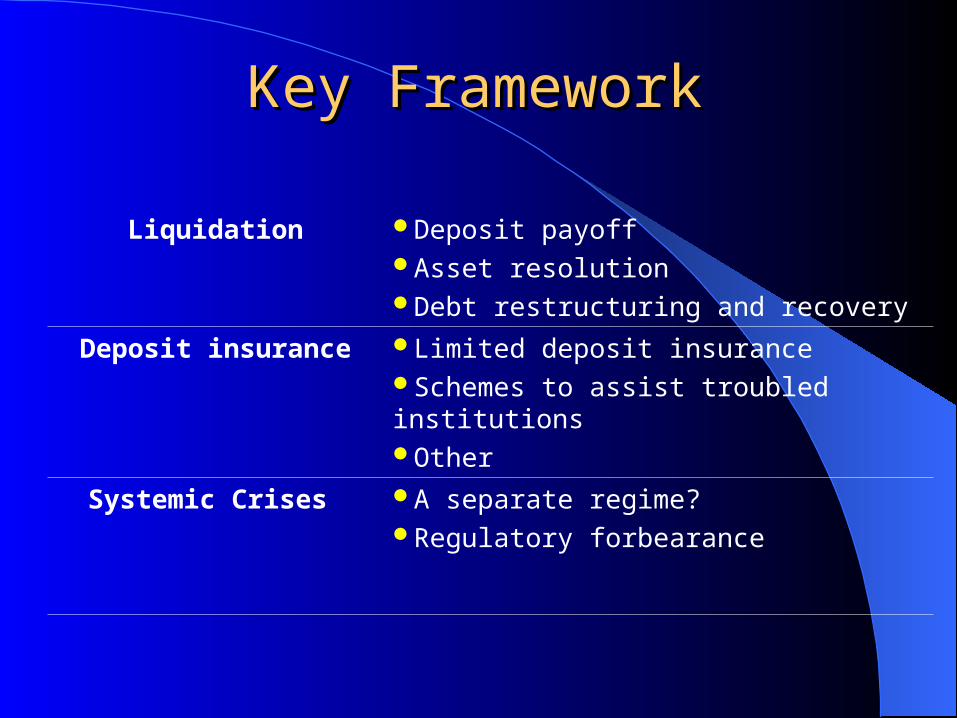

Key FrameworkKey Framework

Institutional aspects Who decidesWho implementsNeed to avoid gaps and duplications of responsibilitiesEliminate uncertainty as to which authority is in charge

Legal protection and accountability

Bank regulator/bank restructuring authorityAccountability to whom?

Principles and mechanisms for the use of public funds

Least-cost solutions TransparencyFairness

Key FrameworkKey Framework

Bank Intervention Clear rules for bank interventionFlexibility to carry out an intervention whenever the bank authority deems it necessary.

Entry Rules New foreign and domestic investors“Fit and proper” rules

Mechanisms for bank restructuring and resolution

Mergers and acquisitions “Purchase and assumption” transactionsBridge banksGood bank-bad bank Other

Liquidation Deposit payoffAsset resolutionDebt restructuring and recovery

Deposit insurance Limited deposit insuranceSchemes to assist troubled institutionsOther

Systemic Crises A separate regime?Regulatory forbearance

Key FrameworkKey Framework

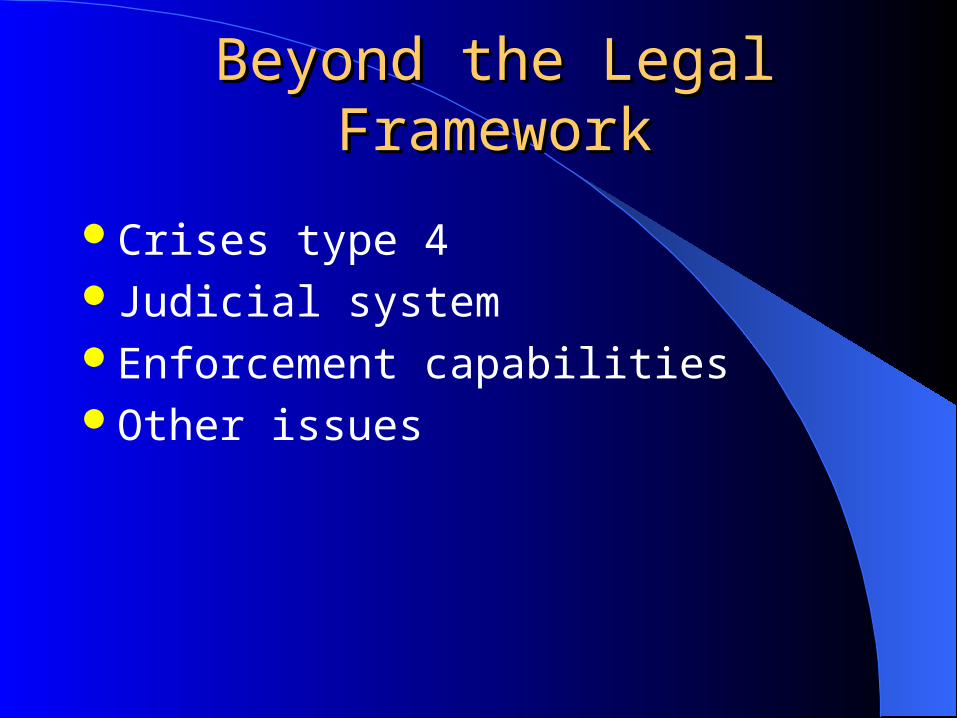

Beyond the Legal FrameworkBeyond the Legal Framework

Crises type 4Judicial systemEnforcement capabilitiesOther issues

The World BankThe World Bank

Bank Insolvency and the Global Bank Insolvency Initiative

Ernesto Aguirre, Manager of Banking Regulation, June 20, 2002