Embed Size (px)

Citation preview

I)ocumlent ot

The World Balnk

M)R ()FIA(I A.l. I SF 0N

Report No. 9 39'X

PROJECT COMPL.ETION REPORT

THAI LAND

STRIKIT PETROLEUM PROJECT(LOAN 2639-TH)

FEBRUARY 28, 1991

Industrv and Energv Operations DivisionCotuntry Department Il

Asia Regional Office

This document hac a restricted distribution and ma! be used by recipients only in the performance oftheir official duties. Its contents rna! not othertAise be disclosed %ithout %Norld Bank authori,ation.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY l.QIJIVAI,EN'I.-S

At appraisal (1985): US$1 27 Baht

At complction (1989): US$I = 2( Baht

GLOSSARY

bbl - barrclBcf - billion cubic fcctBtu - British thermal ullitDMR - Departmcnt of Mincriil RcsourccsPTT - Pctrolcum Authority of ThailandPTTEP - PTF Exploration and Devclopmcnt

FOR OFFICIAL USE ONLYTHf WORLD BANK

Wd%hington D ( 20413US A

Ofe of DOtioi.Cene.alOpeqatmm tvaluatton

Yebruarv 28, 1!)91

MEMORANDUM TO THE EXECUTIVE DIRECTORS AND THE PRESIDENT

SUBJECT: Project Completion Report on ThailandSirikit Petroleum Project (Loan 2639-TH)

Attached. for information, is a copy of a report entitled "ProjectCompletion Report on Thailand - Sirikit Petroleum Project (Loan 2639-TH)"prepared by the Asia Regional Office with Part II of the report contributed bythe Borrower. No audit of this project has been made by the OperationsEvaluation Department at this time.

Attachment

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties Its contents may not otherwise be disclosed without World Bank authorization.

FOR OFFICtAL USE ONLY

PROJECT COMPLETION REPORT

THAIAND

SIRIKIT PETROLEUM PROJECT(Loan 2639-TH1)

Table of Contents

Page No.

Preface . ..........................................................Evaluation Summary ................................................

I. PROJECT REVIEW FROM THE BANK'S PERSPECTIVE .1

Project Identity .1Background. 2Project Objectives and Description. 3Project Design ............................................. 4Project Implementation ..................................... 4Project Results ............................................ 5Project Sustainability ..................................... 8Bank Performance ........................................... 8Borrower Performance ....................................... 9Project Relationships ...................................... 9Consulting Services ........................................ 9Project Documentation and Data ............................. 10

II. PROJECT REVIEW FROM BORROWER'S PERSPECTIVE ................. 11

Comments on Part I ......................................... 12Bank's Performance ......................................... 13Borrower's Performance ..................................... 14Relationship between Bank and Borrower ..................... 14Ad!quacy and Accuracy of Part III .......................... 14Noce on ERR Calculations ................................... 15

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties Its contents may not otherwise be disclosed without World Bank authorization

TABLE OF CONTENTS (Cvnit.)

III. STATISTICAL INFORMATION .................................... 22

Related Bank Loans ................... 23Project Timetable ................. 23Loan Disbursements ......................................... 24Project Implementation ..................................... 24Project Costs and Financing ................................ 25Project Results ............................................ 27Status of Covenants ........................................ 28Use of Bank Resources ...................................... 29

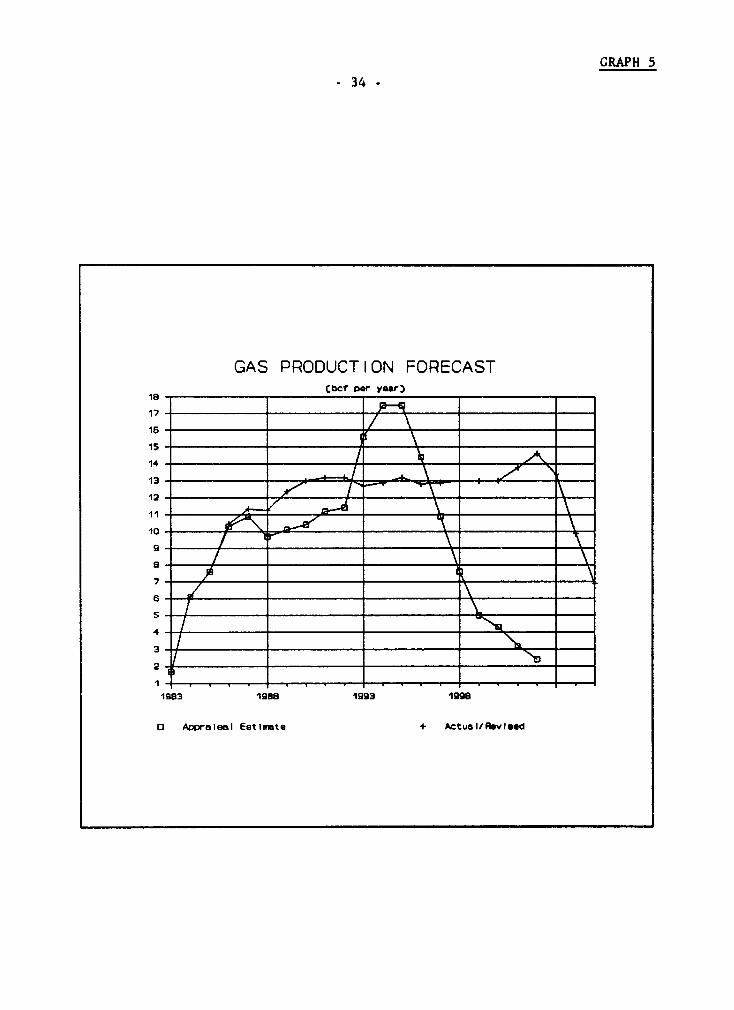

Graph 1: Sirikit Oil Prices (constant 1985 prices) .... .... 30Graph 2: Sirikit Oil Prices (current prices) .... .......... 31Graph 3: Estimated and Actual Investment Program .... ...... 32Graph 4: Sirikit Oil Production (Actual and Forecast) ..... 33Graph 5: Sirikit Gas Production (Actual and Forecast) ..... 34

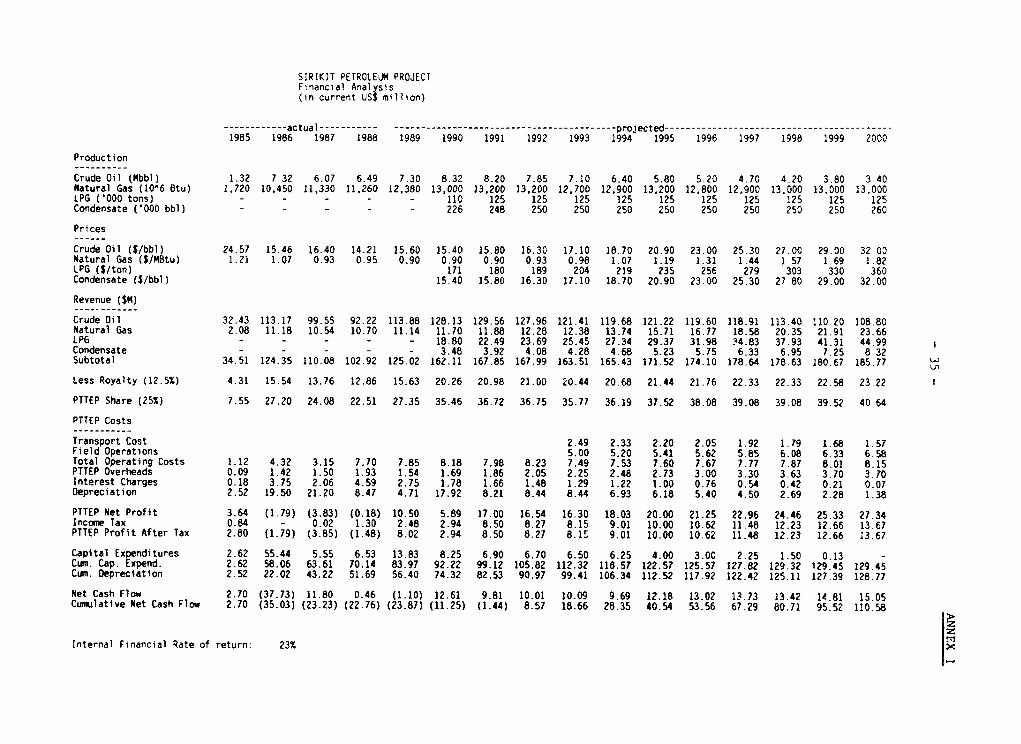

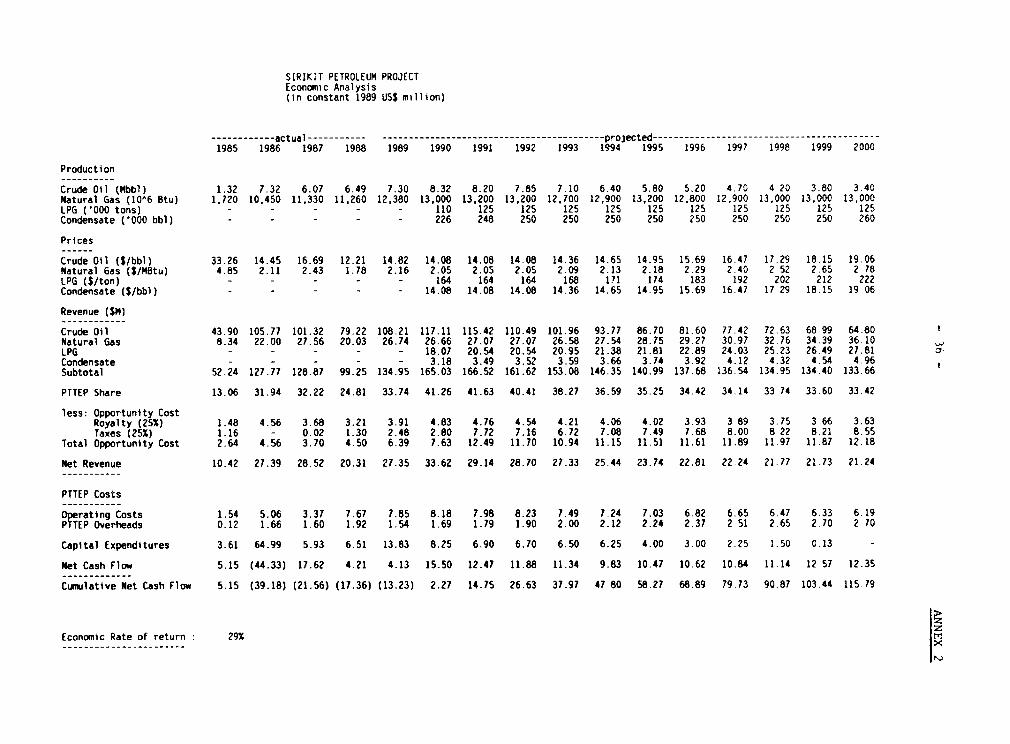

Annex 1: Financial Analysis ............................... 35Annex 2: Economic Analysis ................................ 36

PROJECT COMPLETION RlPORT

THAILAND

SRIKIT PETROLEUM PROJECT(Loan 2639-T1I)

Prcface

This is the Project Completion teport (PCR) for the SirikitPetroleum Project in Thailand, for which Loan 2639-TH to the PetroleumAuthority of Thailand in the amount of US$33 million was approved onDecember 3, 1985. The loan was closed undisbursed on August 29, 1989, oneyear ahead of schedule, following partial cancellations of U$S13.0 millionon July 1, 1986, and US$19 million on September 1, 1988.

The PCR was jointly prepared by the Industry and Energy OperationsDivision of Country Department II of the Asia Regional Office (Preface,Evaluation Summary, Parts I and III), and by the Borrower (Part II).

Preparation of this PCR was started during the Bank's finalsupervision of the project in October 198", and is based, inter alia, onthe President's Report; the Loan and Guarantee Agreements; supervisionreports; and internal Bank memoranda.

PROJECr COMPLETION REPORT

THlAHAND

SIRIKIT PETROLEUM PROJECr(Loan 2639-T

Evaluation Summary

The project was conceived in 1982-83 following the discovery by ThaiShell of the Sirikit oil field in central Thailand (Block S-1), which wasthe first significant domestic discovery of indigenous crude oil. TheSirikit discovery, together with other exploration results, had led to anupward revision in Thailand's oil production expectations. The possibilityof establishing a domestic oil production capability was an attractiveprospect for Thailand given its high dependence on impc.rted energy. Theproject was formulated with a view to optimizing Thailand's returns fromthe Sirikit discovery and promoting further exploration and development ofpetroleum resources. More generally, the project was intended to supportthe Government's strategy to strengthen domestic technical capabilities tomonitor the exploration and development ("upstream") activities ofinternational oil companies (IOCs) in Thailand, partly as a necessaryaccompanying measure to participation in joint-venture projects, a numberof which were on the horizon aside from the Sirikit venture.

The Government designated the state oil company, the PetroleumAuthority of Thailand (PTT), as its executing agency. To facilitate itsparticipation in upstream activities, PTT established a wholly-ownedsubsidiary, PTT Exploration and Production (PTTEP), to act as its operatingentity in the joint-venture with Thai Shell as well as in any otherupstream petroleum operations that could come about.

Proiect Obiectives

The project had three cajor objectives: (a) to build up thenecessary expertise for PTT to represent government interests in petroleumventures; (b) to increase the net revenues to Thailand from oil discoveriesin the Block S-1 concession; and (c) to strengthen government knowledge ofthe potential of other concessions so as to help expedite ongoingnegotiations with IOCs.

The project consisted of two components: (a) the establishment andinvestment program of the Sirikit joint venture; and (b) a technicalassistance and training component.

iU

Implementation Experience and Results

The project has been implemented succesfully, albeit with somevariance from original expectations. However, for a number of reasons, nouse was made of the Bank loan which was eventually cancelled in full onAugust 29, 1989,

While the project was prepared at a time when oil prices reachedtheir highest historical levels, subsequent investment decisions b; theoperator (Thai Shell) were to be severely affected by the drop in oilprices that ensued starting in 1985. This reduction in the investmentprogram had a disproportionate effect on the cash flow position of thejoint-venture, which remained positive in all single years thereafter,tlhereby precluding PTTEP's need to use the Bank loan to cover shortfalls infunds (cash calls). This development was exacerbated by a lack ofsignificant new oil discoveries after the loan was signed that would havejustified additional development investment. Yet, the results of theJoint-Venture Component met or exceeded appraisal expectations, both interms of production volumes and return on investment (Part I, paras 11 and13).

The Training and Technical Assistance Component of the project wasimplemented as planned but also without recourse to Bank financing, asPTTEP was able to identify grant funds for each of the items included inthe project scope or to finance the item out of its own resources as PTT'sfinances improved. The results of the component are mixed but generallypositive (Part I, para 14). In general, the institution building objectiveof the project was achieved, perhaps beyond appraisal expectations (Part I,para 15).

Sustainability

Output from the Sirikit field has proved sustainable and profitable.Moreover, the project has been instrumental in establishing PTTEP'scapability to analyze the benefits of future similar joint-venture options.Actually, a solid basis for Thai participation in upstream petroleumventures has been formed largely on the basis of the project experience(Part I, para 16).

Findings and Lessons-Learned

The project documentation probably was not sufficiently explicitabout the contingency nature of the proposed use of the loan proceeds andtherefore of the risk that the funds might not be utilized in full, shouldeconomic conditions change. In particular, the appraisal did not addressthe risk that a substantial reduction and stretch-out of the operator'sinvestment program would likely occur should a change in oil pricessubstantially affect the economics of field development, thereby affectingthe use of Bank funds. On the other hand, the justification for the loanremained, as it provided the necessary cushion to facilitate PTT'sinvestment decision at a time when its financial standing was not

iv

sufficiently strong to proceed with the investment. While the SAR did notclearly state the risk of the funds not being utilized, it is not clear howelse the Bank handles contingent financing needs.

Project Completion Report

THLILAND

SIRIKIT PETROLEUM PROJECT(Loan 2639-TE)

Part I: Project Review from the Bank's Persectve

A. Project Identity

1. Name: Sirikit Petroleum Project

2. Loan Number: 2639-TH

3. RVP Unit: Asia

4. Country: Thailand

5. Sector: Energy

6. Subsector: Petroleum

7. Loan Amount: US$33 million

-2-

B. lBackground

1. When the project was conceived, Thailand's identified petroleumendowment consisted essentially of a number of gas fields, located mostlyoffshore, some of which were already under development. Recent explorationresults had also led to an upward revision in oil production expectations.Particularly significant in this regard was the discovery by Shell of theSirikit oil field in central Thailand. The possibility of establishing adomestic oil production capability was an attractive prospect for Thailandgiven its high dependence on imported energy: at the time of project appraisalin October, 1984, imported petroleum accounted for 76% of commercial energyrequirements and 41% of total energy consumption. The petroleum import billamounted to 25% of total imports and absorbed 39% of foreign exchange earn-ings. The project was conceived as an instrument to surport Thailand'sobjectives of optimizing its returns from the Sirikit di. *very and promotingfurther exploration and development of petroleum resources.

2 The discovery made by Thai Shell (a wholly-owr,ed subsidiary of RoyalDutch Shell) in December 1981 on the S-1 license located in the PhitsanulokBasin onshore central Thailand was the first significant discovery of indige-nous crude oil. The S-1 license had been awarded to Thai Shell in 1979.Appraisal drilling had followed and the discovery which came to be known asthe Sirikit field was declared commercial and a production license awardedearly in 1983. Thai Shell started to implement an early production planimmediately thereafter.

3. The license agreement provided that Thai Shell, upon request from theGovernment, had the option to grant the Government a up to 25% workinginterest in the license. Prior to making such a request for participation,the Government designated the state oil company, the Petroleum Authority ofThailand (PTT), as its executing agency and requested the Bank to assist PTTin formulating a joint-venture project and to provide financing as required.

4. Thai Shell's terms for granting the option provided that: (a) PTTwould reimburse Thai Shell for 25% of all net past investment, i.e. capitalexpenditures and operating costs less accrued revenue from January 1, 1982onward; (b) ambiguities in the terms of the license regarding the pricing ofoil refined and sold domestically would be satisfactorily resolved; and (c)25% of all future cash shortfall would be paid promptly on a monthly basis(cash calls). PTT, with Bank assistance, determined that it was in theinterest of the Government to meet Thai Shell's conditions: the economic rateof return on investment was deemed attractive and the experience to be gainedfrom PTT's involvement advantageous.

5. More generally, the Bank supported the Government's and PTT'sstrategy to strengthen their technical capability to monitor the explorationand development ("upstream") activities of international oil companies (IOCs)in Thailand, partly as a necessary accompanying measure to participation injoint-ventures with IOCs, a number of which were on the horizon aside from theThai Shell venture. While the Department of Mineral Resources (DMR) of theMinistry of Industry remained the depository of government authority in

- 3 -

administering IOCs' licenses, PTT was to act as the operating arm of theGovernment for future public invest.ment in the sector. To facilitate itsparticipation in upstream activities, PTT established a wholly-owned subsid-iary, PTT Exploration and Production (PTTEP), to act as its operating entityin the joint-venture with Thai Shell as well as in any other upstreampetroleam operations that could come about. PTTEP was to be responsible forthe accrued buy-in cost of the joint-venture, which was determined to beUS$46.25 million and was financed from loans from the parent company PTT, the

Ministry of Finance, and Thai commercial banks.

C. Project Objectivcs and Dcscription

6. The project had three maior objectives: (a) through participation inthe S-1 joint-venture, to give PTT practical experience in oil and gasoperations so as to build up the necessary expertise for PTT to representgovernment interest as a minority partner in petroleum ventures; (b) toincrease the net revenues accruing to Thailand from the development ofdiscoveries in the Block S-1 concession; and (c) to strengthen governmentknowledge of the potential of other concessions so as to help expedite ongoingnegotiations with IOCs dealing with a number of undeveloped discoveries.

7. The project consisted of two components:

(a) Establishment and Investment Program of Sirikit Joint Venture

Anticipated investments (over and above PTT's buy-in cost) includedfurther geological and geophysical surveys, exploration anddevelopment drilling, production facilities at the field (including asmall liquefied petroleum gas (LPG) recovery facility) and any solerisk investments that may be prudent for PTTEP to undertake.

(b) Technical Assistance and Training

Consultancies and studies to strengthen PTT's (PTTEP's) technicalcapabilities in assessing other joint-venture options, includingstudies required to determine PTTEP's options in regards to the TexasPacific offshore "B" gas field, its possible participation in Esso'sKhorat Basin gas discovery, the scope for promoting foreign investorinterest in offshore Block 5/27 which had been granted to PTTfollowing relinquishment by Amoco, and such other technicalassistance and training as would be required to help build up PTTEPas an institution.

8. The Bank loan, which was made in an amount of US$33 million to PTTfor onlending to PTTEP, was expected to cover the cash calls occasionned byPTTEP's participation in the S-1 joint-venture (i.e., 25X of the net cash flow

- 4 -

of the joint venture) and the foreigni exchange cost of the techinicalassistance and training component.l/

D. Project Design and Organization

9. The project concept, which was clear and accepted by all parties,including Thai Shell, was rather innovative for the Bank in that the Bank loanwas not expected to finance a clearly defined investment program but rather tocover the Borrower's share of the net cash flow position of a venture whosefuture investment program, to be decided on an annual basis by the OperatingCommittee, could only be estimated at the time of appraisal (partly on thebasis of discussions with the operator). While participation in such adiscovery held the potential of additional benefits for the host country, itentailed some degree of financial uncertainty for the minority partner andplaced an additional burden on the country, two constraints which the loan wasintended to help alleviate.

E Project Implementation

10. The project has been implemented succesfully, albeit with somevariance from original expectations. However, for a number of reasonsdiscussed below, no use was made of the Bank loan which was eventuallycancelled in full on August 29, 1989.2/

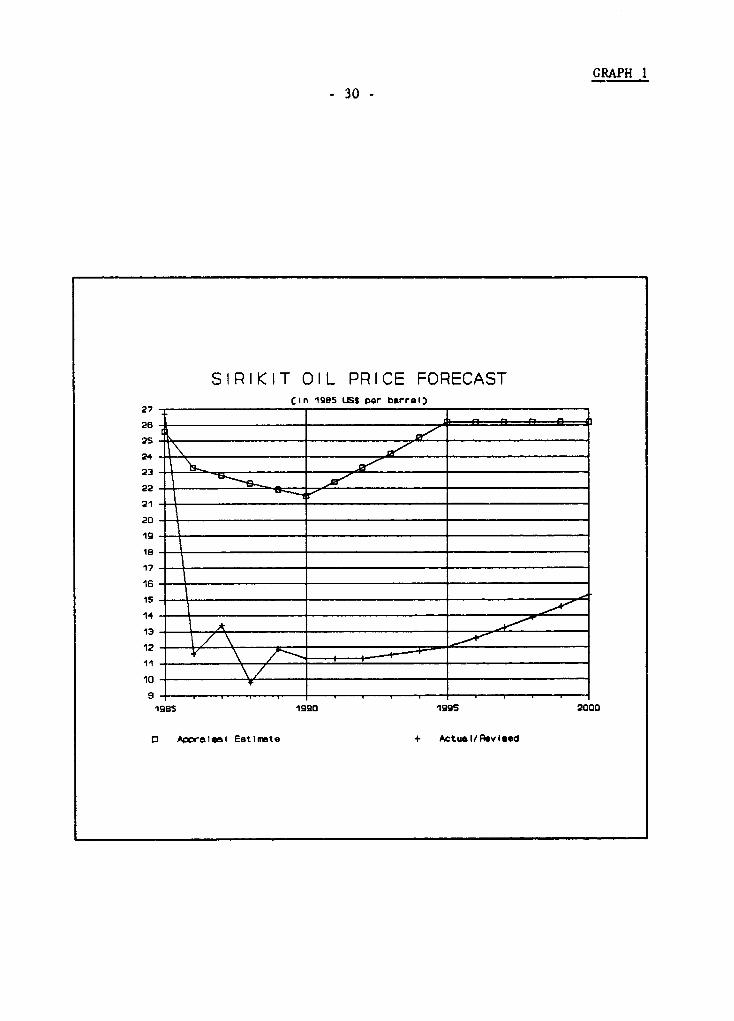

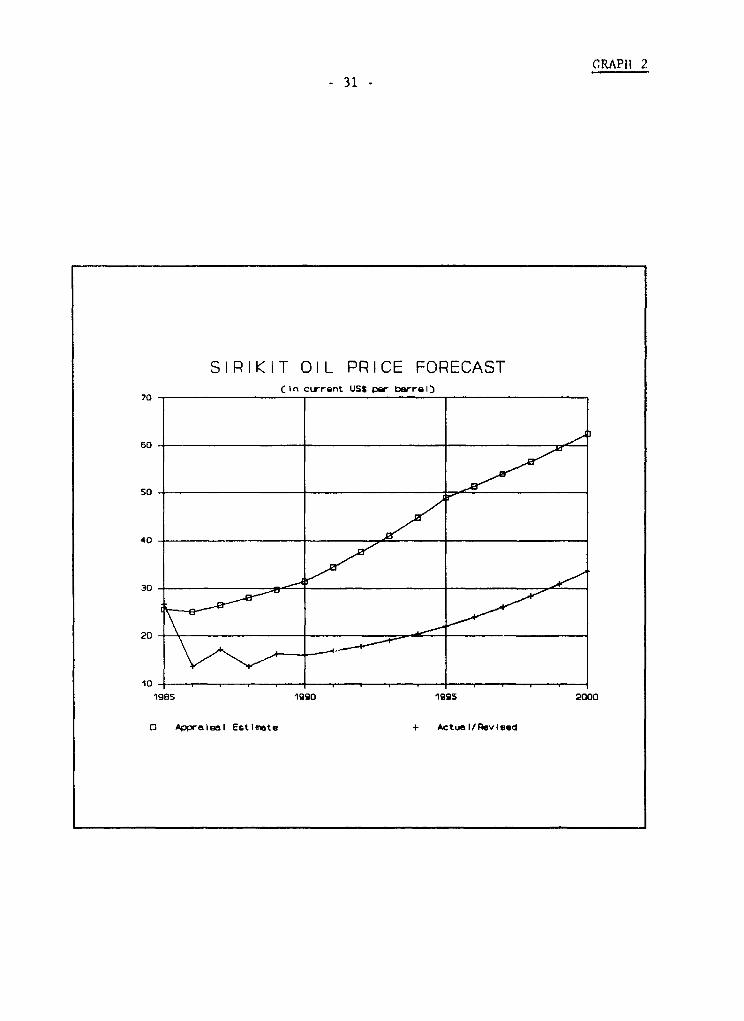

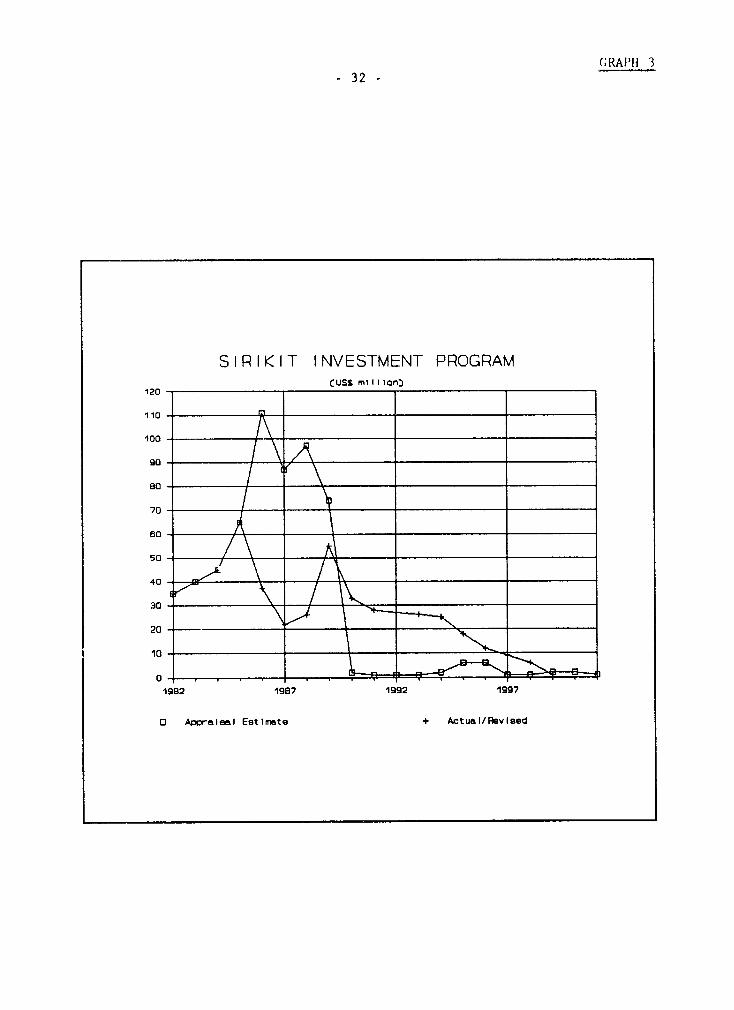

11. While the project was prepared at a time when oil prices reachedtheir highest historical levels, subsequent investment decisions by theoperator were to be severely affected by the drop in oil prices that ensuedstarting in 1985. Actually, almost immediately after the loan becameeffective, the price of Sirikit oil plummeted from US$24.50/barrel (bbl) in1985 to an average of US$15.4/bbl and a low of US$9.60/bbl in 1986 (see PartIII, Graphs 1 and 2). This sudden and unexpected price decline had a profoundeffect on Thai Shell's investment program, which was reduced from US$111million to US$37 million in 1986 and was to remain at low levels for the nextseveral years (see Part III, Graph 3). While this reduction in the investmentprogram proved prudent and was justified by the drastic change in oil priceconditions, it had a disproportionate effect on the cash flow position of thejoint-venture, which remained positive in all single years thereafter, therebyprecluding PTTEP's need to use the Bank loan to cover shortfalls in funds

i/ The Bank loan was expected to cover the financing gap for future cashcalls, estimated at US$25 million, and US$8 million of technical assistanceand studies.

2/ While the reduced need for Bank financing became apparent as early as mid1986 (and partial cancellations were effected on July 1, 1986 (US$13 million)and September 1, 1988 (US$19 million)), the Borrower indicated it wished tokeep the loan in force so as to avail itself of regular supervision missionsby Bank staff.

(cash calls). This development was exacerbated by a lack of significant newoil discoveries after the loan was signed that would have justified additionaldevelopment investment. An additional factor was the delay in installing thel.PG recovery plant (utilizing associated gas production) which led to afurther reduction in investment during the critical first few years of projectimplementation when the cash flow position was expected to be the tig;itest.

12. The Training and Technical Assistance component of the project wasimplemented as planned but also without recourse to Bank financing as PTTEPwas able to identify grant funds for each of the items included in the projectdescription or to finance the item out of its own resources as PTT's financesimproved. These have included: (a) reservoir studies for simulation of theSirikit field (financed by PTTEP at a cost of approximately US$500,000); (b)consultant services to PTTEPI/ (financed by PTTEP at a cost to date ofUS$500,000); (c) consultancy study for reserve determination and developmentanalysis of the offshore "B" gas field, which was carried out by Statoil undergrant financing provided by the Norwegian Government at a cost ofapproximately US$5 million; (e) data gathering and processing to help promoteBlock 5/27 (initially licensed to PTT) to foreign partners, including apartial 3-D seismic survey and analysis, were undertaken with assistance fromPetro-Canada under grant financing provided by CIDA in an estimated amount ofUS$4 million; (f) training was provided by Petro Canada (under the abovegrant) in the form of in-house seminars and by Thai Shell in the form of on-site work exposure as provided under the joint venture contract; the cost ofstaff participation in international seminars was covered by PTTEP's ownfunds; and (g) the cost of computer hardware and software to build up PTTEP'sanalytical capabilities was also covered by PTTEP's internal funds. Anadditional study anticipated at the time of appraisal to help determine theextent of reserves at the (Esso) Namphong gas field in the Khorat basin andestablish or otherwise the economics of its development has not yet been donedue to delays in Esso's long-term testing program, the results of which willbe critical inputs in the analysis.

F. Project Results

13. The results of the Joint-Venture Compo,ient of the project met orexceeded appraisal expectations:

(a) Ultimate Oil and Gas Recovery from S-1 License Area. Recovery fromthe S-1 license was estimated at the time of appraisal at 80 millionbarrels (bbls). The current estimate is now between 100-120 millionbbls. Ultimate gas production was estimated to be about 300 billioncubic feet (Bcf) and this level is expected to be achieved. Oneshould note, however, that while about one third of the ultimate oiland gas recovery was expected to originate from new discoveries, the

3/ One full-time exploration consultant was recruited by PTTEP instead of twoas anticipated at appraisal (one for exploration and appraisal and one forproduction and reservoir engineering).

- 6 -

latter are now expected to contribute only 2% of total recovery.

Wlile growth in existing reserves more than made up for the lack of

new discoveries, the investmenit required to develop the reserves was

less than anticipated and the rate of return was correspondingly

increased.

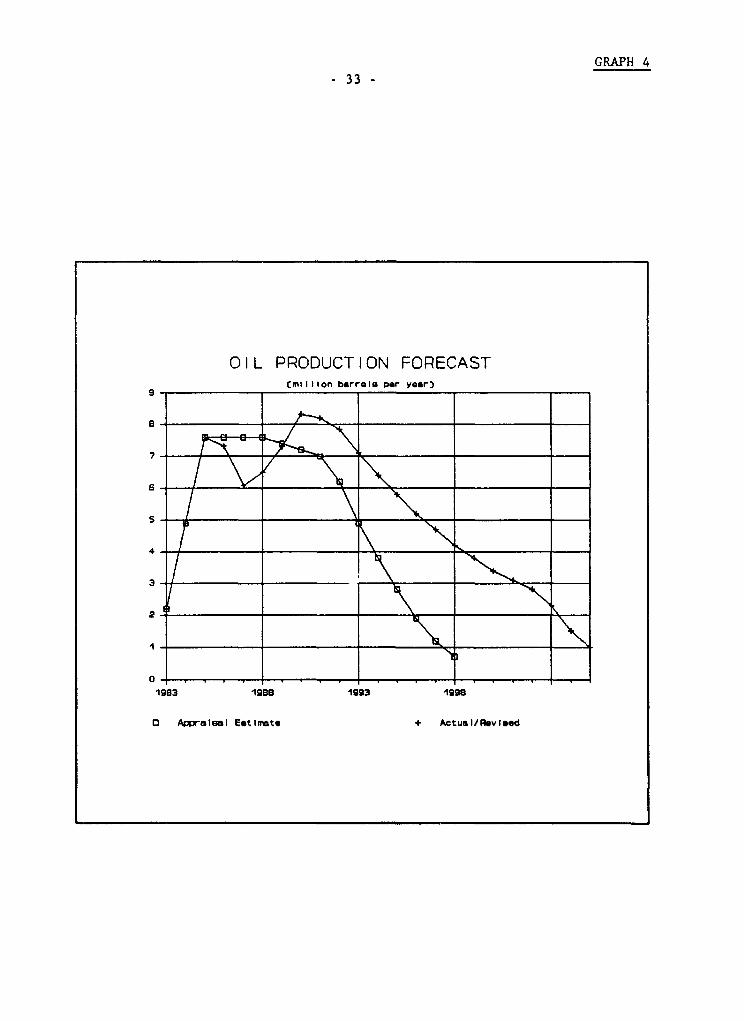

(b) Production. Due to the increase in reserves, peak pleteau production

is expected to continue through 1992 for oil and 2002 for gas (see

Part III, Graphs 4 and 5) while at appraisal oil production was

expected to start declining in 1990 and gas production in 1994. In

addition, some 125,000 tons/year of LPG and 226,000 bbl/year of

condensate are expected to be produced when the LPG recovery plant

comes on stream in 1990. These latter volumes were not included in

the appraisal estimate of benefits (because of the low priority given

to the LPG investment by the operator) although a notional US$35

million investment in LPG recovery was included in the project cost

estimate.

(c) Economic Rate of Return. The appraisal estimate of the economic

return on investment was 15%. The revised estimate is about 29% as

lower oil prices were more than offset by the larger volumes and the

reduced and extended investment profile (see Part III, Annex 2).

14. The results of the Technical Assistance and Training Component are

mixed but generally positive:

(a) S-1 Engineering Studies. At the time of appraisal, annual updates of

the reservoir studies for the S-1 license were expected to be

required. However, the consultant candidly determined following the

first update that the number and complexity of reservoirs made this

impractical. PTTEP and Bank staff concurred.

(b) In-house Consultancy. At the time of appraisal, it had been deemed

advisable for PTTEP to engage two highly experienced consultants to

provide full-time in-house assistance to interface with Thai Shell

(one advising on exploration and appraisal and one advising on

production and reservoir engineering). PTTEP eventually engaged only

one consultant whose experience was sufficiently broad to meet

PTTEP's needs satisfactorily. Bank staff concurred.

(c) Reserve and Development Study for the Offshore "B" Structure. At the

time of appraisal, it had been deemed advisable to engage an

international consulting firm to provide an independent analysis of

the "B" structure prospects (under license with Texas-Pacific and a

few other minority partners) since the possibility of buying out

Texas Pacific was considered as a possible option to expedite the

development of this gas resource. An earlier reserve determination

had already been made on behalf of Texas Pacific but the study was

considered deficient in several key areas. The study made under

Norwegian financing was considered an acceptable replacement even

though the lack of detailed background data provided in the study has

in effect precluded its critical review by Bank staff. PTTEP

ultimately purchased the Texas Pacific et al interest based on theStatoil findings; PTTEP is now in the final stage of acquiringoperating and non-operating partners to develop the field.

(d) Reserve and Development Study for the Nemphong Gas Field. It wasforeseen at appraisal that a detailed study would be beneficial priorto PTTEP's deciding on exercising its option to participate in thedevelopment of the field as a minority (20%) partner. However, thestudy required the results of a lengthy testing program by Esso toreach meaningful results. The testing program has been delayed and

is now expected to be conducted in 1990-92 and the study has yet tobe made. In the meanwhile PTTEP is in the process of concluding ajoint-venture agreement with Esso.

(e) 3-D Seismic Survey and Promotion of Offshore Block 5/27 to Industry.Prior to project appraisal, PTT had been granted exploration rightson Block 5/27 following its relinquishment by Amoco. Since Amoco had

produced oil at rates considered by them as noncommercial, activitiesrequired to pursue the evaluation of the block, i.e. a 3-D seismicsurvey, with a view to promoting it to IOCs were included in theproject scope. As indicated above, Petro Canada provided a 3-Dseismic survey on a limited area surrounding the Amoco discoveries.Bank staff assisted in the analysis of results. These were found tobe of average quality only and additional processing of the datawould be useful. However, due to subsequent discoveries offshore (byThai Shell and Premier Oil Co.) investor interest in Block 5/27 isnow fairly high and PTTEP plans to organize a promotion campaign onthe basis of available data.

(f) Training. The project provided for overseas training in the form ofshort courses, seminars, participation in international technicalmeetings and conventions, and interface with foreign consultants.PTTEP took some advantage of its staff's exposure to visiting

consultants and, more generally, substituted in-house courses and on-the-job training provided by Thai Shell in fulfillment of their jointventure contract for overseas training. Overall, this route provedsatisfactory although additional training would have been beneficial.The problem facing PTTEP at the outset of the project was theshortage of qualified staff and this has made it difficult tocomfortably accommodate the requirements of an intensive overseastraining.

(g) Computer Hardware and Software. At the time of appraisal theacquisition of greater computer capability was seen as a criticalneed for PTTEP. However, PTTEP was able to gradually andincrementally add to their computer capability without largeexpenditures. This need was probably overstated at appraisal andprobably should not have been highlighted as a specific loancomponent.

15. The institution building objective of the project was achieved,perhaps beyond appraisal expectations. At the outset PTTEP was thinly staffed

- 8 -

(eight professionals) with only limited experience, and building anorganization adequately staffed without prejudice to ongoing project activitywas considered a formidable challenge. However, through new hires ofexperienced personnel from oil companies and the government (particularly theDepartment of Mineral Resources), transfers from PTT as well as by hiringrecent graduates in petroleum specialties, PTTEP has been able to build up itsstaff to about 75 professionals with adequate support staff and superioroffice facilities. Both PTT and PTTEP are to be commended for thisdevelopment. While some need for further institutional strengthening remains,PTTEP can now face future new challenges with justified confidence.

G. Project Sustainabdity

16. Output from the Sirikit field has proved sustainable and profitable:production should continue until at least the year 2,000 and likely beyond.If at some future date Thai Shell decides to withdraw, PTTEP should be able tooperate the field on their own and should start preparing for this possibleeventuality. Moreover, the project has been instrumental in establishingPTTEP's capability to analyze the benefits of similar joint-venture options inthe future. Actually, a solid basis for Thai participation in upstreampetroleum ventures has been formed largely on the basis of the projectexperience.

IL Bank Performance

17. The Bank performed well, assisting the Borrower at all stages of theproject. In retrospect, the Bank's recommendation to PTT to go ahead with theSirikit investment and build up the institutional capability necessary tohandle such participations in upstream petroleum ventures was appropriate.Project supervision by Bank staff was also useful to smooth out the teethingproblems in the relationship between PTTEP and the operator during the initialperiod (in regards to such items as access to data, review of work program,etc). From the Bank standpoint, the project documentation probably was notsufficiently explicit about the contingency nature of the proposed use of loanproceeds and therefore of the risk that available funds might not be utilizedin full in the event of changes in economic conditions. In particular, theappraisal did not address the risk that a substantial reduction or stretch-outof the operator's investment program would likely occur, should a change inoil prices substantially affect the economics of field development. With thebenefit of hindsight, it appears that evaluation of investment requirementswere driven more by the geological potential of the venture perceived at thetime of appraisal rather than by considerations of expected financial returnto the operator. On the other hand, the justification for the loan remained,as it provided the necessary cushion to facilitate PTT's investment decisionat a time when its financial standing was not sufficiendly strong to proceedwith the investment. Moreover, while the SAR did not clearly state the riskof the funds not being utilized, it is not clear how else the Bank handlescontingent financing needs.

-9-

1. PBrrower Performance

18. The Borrower, PTT and indirectly its subsidiary PTTEP, allocated asubstantial proportion of their managerial resources to the success of theproject. Personnel performance, both managerial and technical, was always ofa high quality. Collaboration with the Bank was also always highlycooperative.

J. Project Relationships

19. The relationships between the Borrower, the Bank and Thai Shell wereboth smooth and cordial. Bank staff played a key role in maintaining goodrelations between the parties.

20. Thai Shell became disturbed with the Bank at the time of appraisalwhen the Bank recommended that an LPG recovery plant be included in theforecast investment program. Thai Shell feared that this would encouragePTTEP to force a decision upon them that they were not yet prepared totake.4/ Bank staff assured Thai Shell that this was not the Bank's intentbut that the Bank's intention was rather to make appropriate provisions forall likely future investments. Further, Bank staff persuaded PTTEP to workclosely with Thai Shell, and at their pace, on this investment component.Ultimately, the LPG recovery plant was included in the investment program andis expected to prove a particularly attractive project component with apayback period of about two years and a fifteen-year life.

K. Consulting Services

21. The Bank assisted PTTEP in obtaining high-quality consulting servicesfor assistance in their day-to-day contact with Thai Shell. The presence ofthe in-house consultant provided assurance to PTTEP that the joint venture wasconducted in a business-like and equitable manner; the services provided bythe consultant are considered highly satisfactory.

22. The Bank reviewed and commented on the various studies and surveysconducted by consultants under bilateral grant financing. On the whole, theseservices appear to have been conducted in a professional manner and to havebeen satisfactory and useful to PTTEP.

4/ This was largely due to the fact that Thai Shell had not officiallycredited associated gas cap reserves in one of the major reservoirs, whichthey were to do at a later stage.

- 10 -

L Project Documcntation and Data

23. Both the President's Report and Loan Documents provided adequateframework for project implementation. Supervision reports were complete andprovided adequate documentation of the progress of the project.

24. While much of the data gathered to prepare this PCR was obtained fromretained Bank information, details of physical activities and expenditureswere obtained from PTTEP during a completion mission in November 1989.

Project Completion Report

TILAILAND

SIRIT PETROLEUM PROJECT(Loan 2639-TH)

Part 11: Proect Review from Borrowers Perspective

- 12 -

A. Comments on Part I

The Sirikit Petroleum Project Completion Report is a

concise and clear presentation of the project, the

objectives and results. As stated in the report, we agree

that the objectives of the project were fully met.

PTTEP has markedly improved the expertise to represent

the government interest in petroleum joint ventures. The

company is now structured along the lines of an

international petroleum company, has been able to attract

new and experienced personnel and is growing rapidly. The

revenues generated for the government of Thaialnd has met

or exceeded all expectations. Further, having gained from

the experience of the project, PTTEP has now comfortably

entered into other concession agreements; the "B" Structure

development program with Total, British Gas and Statoil, and

the agreement with Esso for the development of the Nam Phong

gas field. In addition, PTTEP concluded a farm-out

agreement with British Gas for an exploration project over

offshore Block 5/27. Also, PTTEP has concluded a Joint

Venture Agreement with Unocal and their partner, Mitsui Oil

Exploration, for a 5 per cent interest in the Unocal II area

under terms of the Unocal III Gas Sales Agreement with PTT.

The most unique venture have been concluded is with

Unocal for a 10 per cent participation in their "F" Block in

Burma. This would represent the first experiment for PTTEP

to become engaged in activities outside the country in a

relatively unexplored area with some considerable risk

elements.

From the foregoing, it is clear the project of the Bank

initiated a series of events, allowing PTTEP to blossom into

genuine upstream institution. The technical advice from the

Bank was invaluable in directing PTTEP toward starting on

the right path and played a strong role in keeping PTTEP

going along that path. For this PTTEP is extremely

grateful.

- 1 3 -

There is concern expressed in the report over the fact

that the funds were not utilized. From our vantage point

the availability of the funds gave impetus to participation

in the joint venture and ultimately to the ensuing activity.

It is questionable that anyone in the petroleum industry

foresaw the sharp and dramatic reduction in petroleum

prices. The operator's investment program was an internal

decision and the lack of success in finding other

substantial petroleum reserves is part of the risks

associated with any upstream venture. Another factor which

affected utilization of the funds was in the area of

training and technical assistance. This part of the project

was not only affected by the factors described in the

report, including the internal constraints, but also to the

program granted bv the Petro-Canada International Assistance

Corporation (PCIAC) to PTT, for which PTTEP received

benefits through a significant training program of

concentrated classroom sessions and selected on-the-job

training in Canada.

B. Bank's Performance

The Bank's performance during the evaluation and

implementation must be classified as superior. A complete

assessment of the requirements of the Borrower was

conducted, which resulted in a set of meaningful objectives.

Representatives of the Bank were most helpful in the initial

stages of the project in assisting to establish a smooth

relationship between PTTEP and the Operator. Their

assistance in obtaining consultancy service was extremely

useful. The Bank's recommendation to include the LPG

recovery plant in the investment profile proved to be very

beneficial. Today the plant is in place and working. The

economics of the plant is anticipated to be extremely

favorable and should improve the overall economics of the

project.

- 14 -

C. Borrower's Performance

The Borrower's performance during evaluation and

implementation was primarily to learn as much as possible,

to maintian good relations with all parties involved in the

project and to work toward meeting the stated objectives.

PTTEP followed the Bank's recommendations to the extent

possible within the limits of a fluctuating business

environment. The relations with the Operator have continued

to improve over the years and PTTEP now enjoys a good

working relationship with Shell. The confidence gained

through the project by PTTEP is profound and this, compiled

with the favorable economics, is a measure of the success of

all of the parties involved in the project.

D. Relationship between Bank and Borrower

The effectiveness of the relationship between the Bank

and the Borrower has been touched on throughout this paper.

However, PTT believes the relationship during both the

evaluation and implementation phases of the project was

excellent.

E. Adequacy and Accuracy of Part III

With regard to Part III, details of activities and

expenditures were obtained from PTTEP during November 1989.

It has been impossible for us to ascertain exactly who

provided the figures. However, attached are six data sheets

provided by the PTTEP Finance and Accounting Sections.

These include the financial analysis for the project and

details of the projection from 1990 onward.

For the financial statement an explanation of the

Petroleum Tax is needed. Petroleum Tax is calculated as

0.50 (net Profit + Interest-Royalty). Interest is not

allowed as a deduction against tax and the income tax rate

is 50 percent of net profit less royalty.

- 15 -

The difference between the projections prepared by Bank staff (shownin Part I of the PCR) and those prepared by PTTEP (shown in Part II)results largely from:

(a) differences in oil production assumptions: PTTEP's projectionsare predicated on the operator's production plan for 1990-93with a declining trend thereafter, The Bank projections, whichwere developped during the PCR mission, are based on theexpectation of a probable upgrading of produced volumes by theoperator in future projections, as has happened historically,both in terms of reserve upgrading and increases in recoverablefraction; and

(b) differences in cost allocation between operating and capitalexpenditures.

The overall results, however, as encapsulated in ROR calculations,show a high degree of convergence between the two sets of calculations.

- 16 -

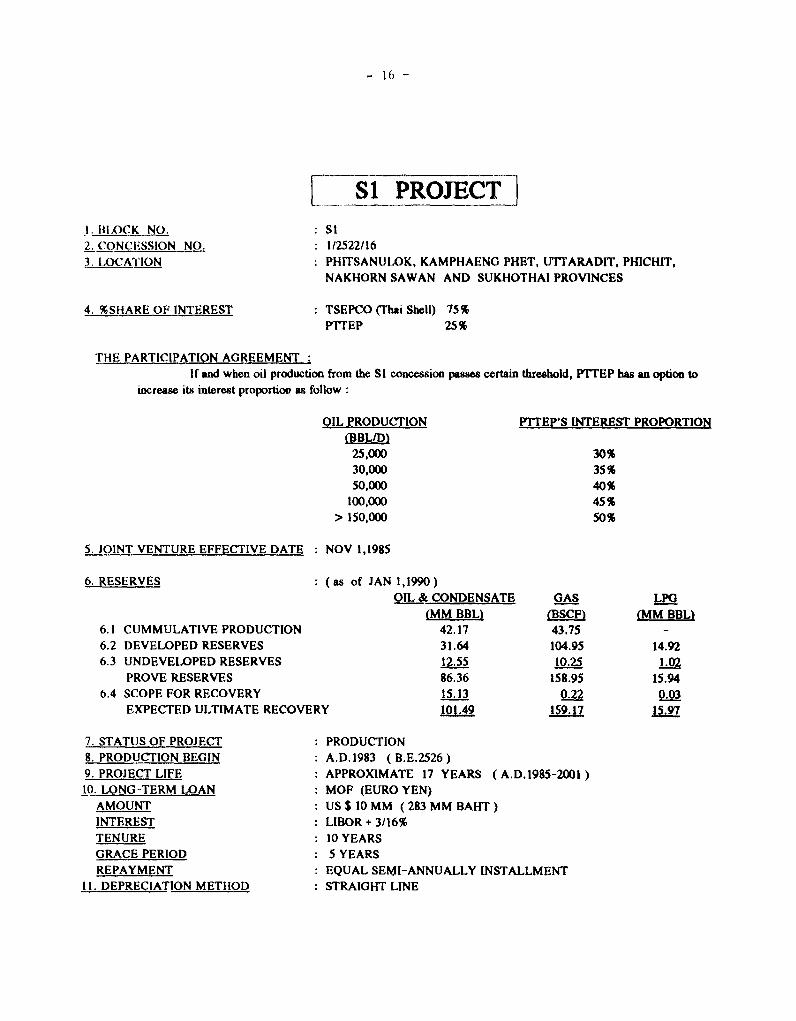

SI PROJECTI. IILOCK NO. SI2. CONCESSION NO. 1/2522/163. LOCATION : PHITSANULOK, KAMPHAENG PHET, UTTARADIT, PHICHIT,

NAKHORN SAWAN AND SUKHOTHAI PROVINCES

4. %SHARE OF INTEREST TSEPCO (Tbai Shell) 75%PTTEP 25%

THE PARTICIPATION AGREEMENTIf and when oil production ftom the Si concession passes certain threshold, PTTEP has an option to

increase its interest proportion as follow:

OIL PRODUCTION PTTEP'S INTEREST PROPORTION(BBLID)

25,000 30%30,000 35%50,000 40%

100,000 45%> 150,000 50%

5. JOINT VENTURE EFFECTIVE DATE NOV 1,1985

6. RESERVES . (as of JAN 1,1990)OIL & CONDENSATE GAS LPG

(MM BBL) (BSCF) (MM BBL)6.1 CUMMULATIVE PRODUCTION 42.17 43.75 -6.2 DEVELOPED RESERVES 31.64 104.95 14.926.3 UNDEVELOPED RESERVES 12.55 10.25 1.02

PROVE RESERVES 86.36 158.95 15.946.4 SCOPE FOR RECOVERY 15.13 0.22 0.03

EXPECTED ULTIMATE RECOVERY 1.49 159.17 15.97

7. STATUJS OF PROJECT : PRODUCTION8. PRODUCTION BEGIN A.D.1983 (B.E.2526)9. PROJECT LIFE : APPROXIMATE 17 YEARS (A.D.1985-2001)10. LONG-TERM LOAN : MOF (EURO YEN)

AMOUNT US$ 10 MM ( 283 MM BAHT)INTEREST : LIBOR + 3/16%TENURE : 10 YEARSGRACE PERIOD : 5 YEARSREPAYMENT : EQUAL SEMI-ANNUALLY INSTALLMENT

11. DEPRECIATION METHOD : STRAIGHT LINE

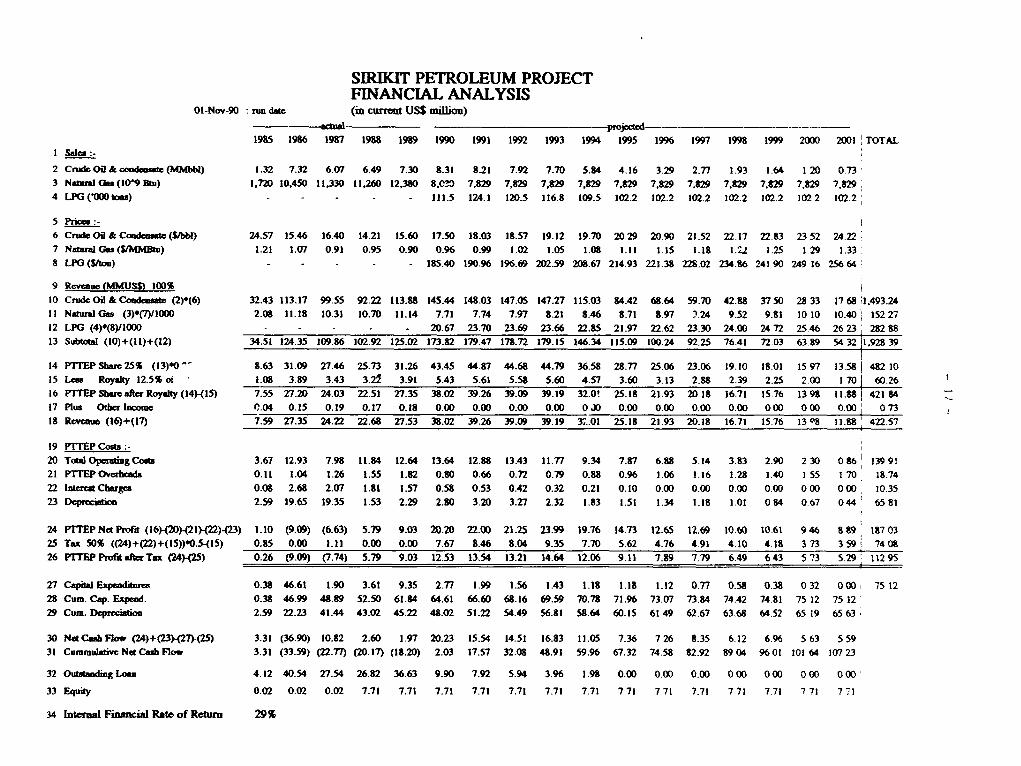

SIRIKIT PETROLEUM PROJECTFINANCIAL ANALYSIS

01-Nov-90: run date (in current US$ milion)pro.jetd -- -____ - -_

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 TOTAL

I Sales:-

2 Crde Oil & ondcate (MMbbl) 1.32 7.32 6.07 6.49 7.30 8.31 8.21 7.92 7.70 5.84 4.16 3.29 2.7 1.93 1.64 120 073

3 Naurl(lGas (109 Btu) 1,720 10,450 11,330 11,260 12,380 B.C?3 7,829 7,829 7,829 7829 7.829 7.829 7.829 7,829 7.829 7,829 7,829

4 LPG('00toas) - - - - 111.5 l24.1 120.5 116.8 109.5 102.2 102.2 102.2 102.2 102.2 1022 102.2

5 Prices: -6 CnrdeOil&Comdensaec(t$1bb) 24.57 15.46 16.40 14.21 15.60 17.50 18.03 18.57 19.12 19.70 20.29 20.90 21.52 22.17 22.83 2352 24.22

7 Naua Gas (VMM4to) 1.21 1.07 0.91 0.95 0.90 0.96 0.99 1.02 1.05 1.08 1.11 1.15 1.18 1.21 1.25 1.29 1.33

8 LPG (Shon) - - - - - 185.40 190.96 196.69 202.59 208.67 214.93 221.38 228.02 234.86 241 90 249 16 256 64

9 Rcvenur (MMUS$) 100%10 CnmdeOil&Cooda (2)0(6) 32.43 113.17 99.55 92.22 113.88 145.44 148.03 147.05 147.27 115.03 84.42 68.64 59.70 42.88 3750 2833 17681,493.24

II NauralGas (3)0(7)11000 2.08 11.18 10.31 10.70 11.14 7.71 7.74 7.97 8.21 8.46 8.71 8.97 2.24 9.52 9.81 10 10 10.40 15227

12 LPG (4)0(8)/1000 - - - - - 20.67 23.70 23.69 23.66 22.85 21.97 22.62 23.30 24.00 24 72 25.46 26 23 282 88

13 Subtoa (10)+(11)+(12) 34.51 124.35 109.86 102.92 125.02 17382 179.47 178.72 179.15 146.34 115.09 100.24 92.25 76.41 72.03 63.89 5432 31.92839

14 PTTEPSbam2s% (13)00 8.63 31.09 27.46 25.73 31.26 43.45 44.87 44.68 44.79 36.58 2877 25.06 23.06 19.10 18.01 15 97 13.58 | 482 10

15 Low Royalty 12.5% ot 1.08 3.89 3.43 3.22 3.91 5.43 5.61 5.58 5.60 4.57 3.60 3.13 2.88 2.39 2.25 2.00 1 70 60.26

16 PTTEP Sbareafr Royalty (14)-(15) 7.55 27.20 24.03 22.51 27.35 38.02 39.26 39.09 39.19 32.0! 25.18 21.93 20.18 16.71 15.76 1398 11.88 421 84

17 Plus Otber income 0.04 0.15 0.19 0.17 0.18 o.o0 0.00 0.00 o.o0 0JD0O.0 0.00 0.00 0.0 000 0o 0 0.00 0 73

18 Reveau (16)+(17) 7.59 27.35 24.22 22.68 27.53 38.02 39.26 39.09 39.19 3. 01 25.18 21.93 20.18 16.71 15.76 13Q8 11.88 422.57

19 PTrEP Costs20 Tot OperatingCosts 3.67 12.93 7.98 11.84 12.64 13.64 12.88 13.43 11.77 9.34 7.87 6.88 5.14 3.83 2.90 230 086 13991

21 PrTEPOverbcads 0.11 1.04 1.26 1.55 1.82 0.80 0.66 0.72 0.79 0.88 0.96 1.06 1.16 1 28 1.40 1 55 1 70 18.74

22 CbatChargcs 0.08 2.68 2.07 1.81 1.57 0.58 0.53 0.42 0.32 0.21 0.10 0.00 0.00 0.00 0.00 000 000 10.35

23 Dqerciatio 2.59 19.65 19.35 1.53 2.29 2.80 3.20 3.27 2.32 1.83 1.51 1.34 1.18 1.01 0 4 0.67 044 65 81

24 PMTEP Not Porot (16)20)M-21(222)(23) 1.10 (9.0) (6.63) 5.79 9.03 20.20 22.00 21.25 23.99 19.76 14.73 12.65 12.69 10.60 10.61 9 46 8 89 187 03

25 Tax 50% ((24)+(22)+(15))*0.5-lS5) 0.85 0.00 1.11 0.00 0.00 7.67 8.46 8.04 9.35 7.70 5.62 4.76 4.91 4.10 4.18 3 73 3 59 7408

26 PITEPProfitafterTax (24)(25) 0.26 (9.09) (7.74) 5.79 9.03 12.53 13.54 13.21 14.64 12.06 9.11 7.89 7.79 6.49 643 573 5.29 11295I-

27 Capt Expeoditus 0.38 46.61 1.90 3.61 9.35 2.77 1.99 156 1.43 1.18 1.18 1.12 0.77 0.58 0.38 0 32 0 00 7512

28 Cum. Cap. Expend. 0.38 46.99 48.89 52.50 61.84 64.61 66.60 68.16 69.59 70.78 71.96 73.07 73.84 74.42 74.81 75 12 75 12

29 Cum. D _reciation 2.59 22.23 41.44 43.02 45.22 48.02 51.22 54.49 56.81 58.64 60.15 61 49 62.67 63.68 64.52 65 19 65 63

30 NotCash Flow (24)+ (327)-(5 3.31 (36.90) 10.82 2.60 1.97 20.23 15.54 14.51 16.83 11.05 7.36 726 8.35 6.12 6.96 563 559

31 Cummulativc Nd Cash Flow 3.31 (33.59) (22.77) (20.17) (18.20) 2.03 17.57 32.08 48.91 59.96 67.32 74.58 82.92 89 04 9601 101 64 107 23

32 Outstanding Loan 4.12 40.54 27.54 26.82 36.63 9.90 7.92 5.94 3.96 1.98 0.00 0.00 0.00 0 00 0 00 0 00 0 00

33 Equity 0.02 0.02 0.02 7.71 7.71 7.71 7.71 7.71 7.71 7.71 7.71 7 71 7.71 771 7.71 7 71 7 71

34 Internal Finwial Rate of Return 29%

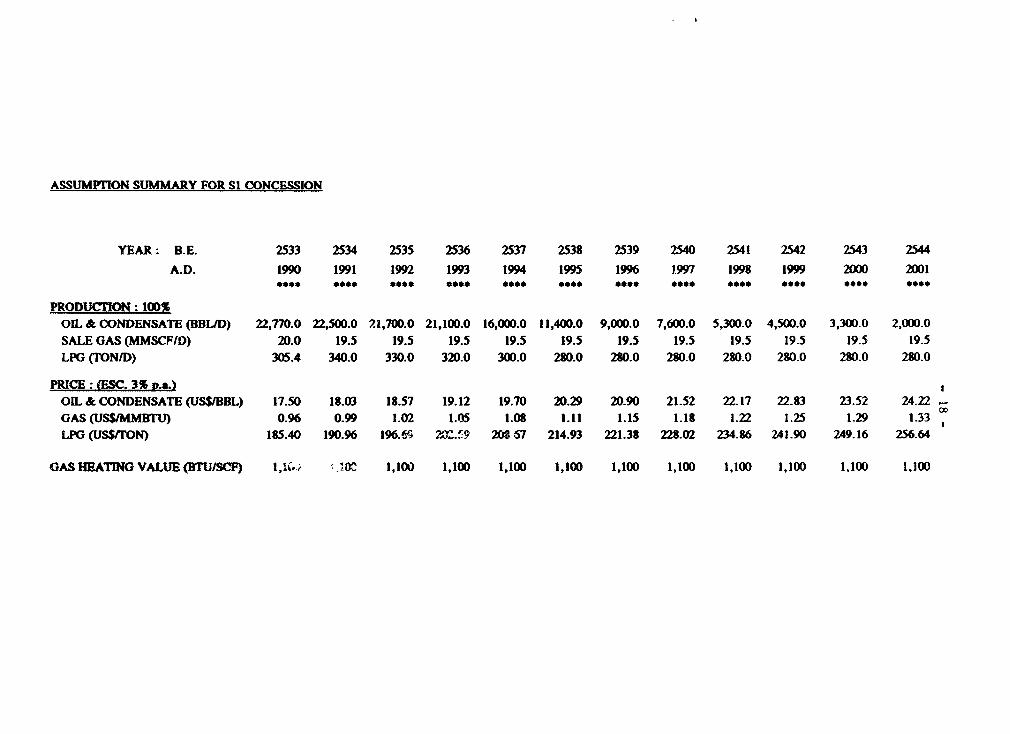

ASSUMPTION SUMMARY FOR Si CONCESSION

YEAR: B.E. 2533 2534 2535 2536 2537 2538 2539 2540 2541 2542 2543 2544

A.D. 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001X*** .*.e .*. *.** **. . * ***. *.. **.. ***. .**. S... 5*5*

PRODUCTION: 100%OIL & CONDENSATE (BBUD) 22,770.0 22,500.0 21,700.0 21,100.0 16,000.0 11,400.0 9,000.0 7,600.0 5,300.0 4,500.0 3,300.0 2,000.0SALE GAS (MMSCF/D) 20.0 19.5 19.5 19.5 19.5 19.5 19.5 19.5 19.5 19.5 19.5 19.5LPG (TON/D) 305.4 340.0 330.0 320.0 300.0 280.0 280.0 280.0 280.0 280.0 280.0 280.0

PRICE : (ESC. 3% P.a) OIL & CONDENSATE (US$IBBL) 17.50 18.03 18.57 19.12 19.70 20.29 20.90 21.52 22.17 22.83 23.52 24.22GAS (US$/MMBTU) 0.96 0.99 1.02 1.05 1.08 1.11 1.15 1.18 1.22 1.25 1.29 1.33LPG (US$/TON) 185.40 190.96 196.64 2-)Z. 9 20857 214.93 221.38 228.02 234.86 241.90 249.16 256.64

GAS HEATING VALUE (BTUSCF) I,lC ' 1,10 1,100 1,100 1,100 1,100 1,100 1,100 1,100 1,100 1,100

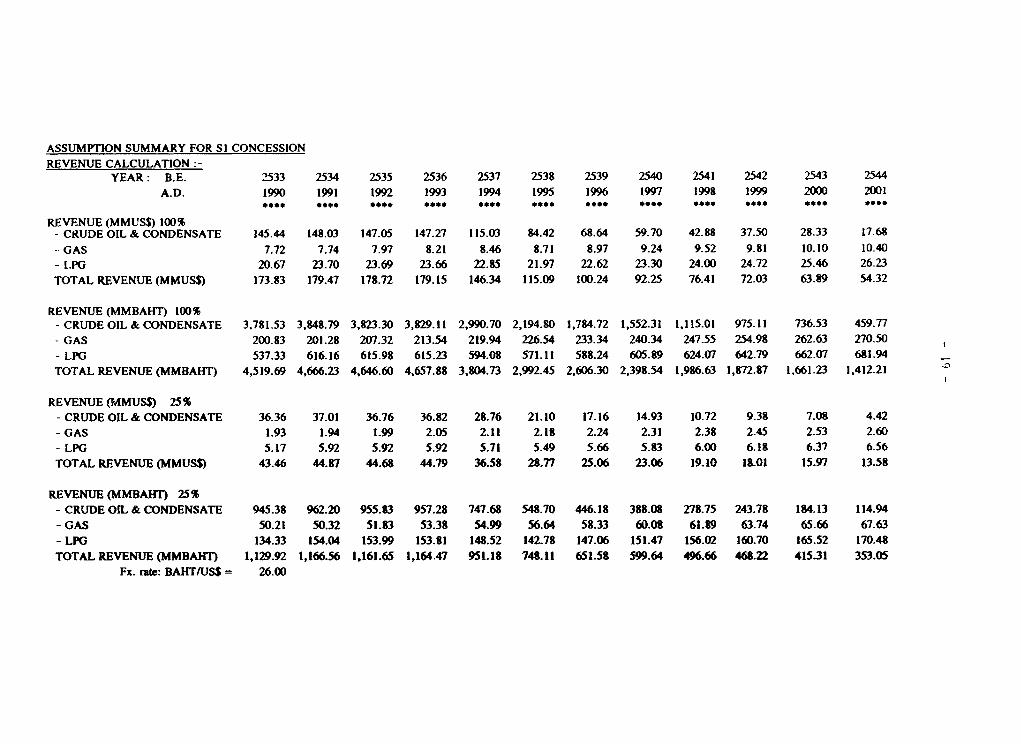

ASSUMPTION SUMMARY FOR Si CONCESSIONREVENUE CALCULATION:-

YEAR: B.E. 2533 2534 2535 2536 2537 2538 2539 2540 2541 2542 2543 2544A.D. 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

* **** *** *** **** **** **** **** 4. ** *4*4 *4*4 *4*4 4*,,

REVENUE (MMUSS) 100%- CRUDE OIL & CONDENSATE 145.44 148.03 147.05 147.27 115.03 84.42 68.64 59.70 42.88 37.50 28.33 17.68- GAS 7.72 7.74 7.97 8.21 8.46 8.71 8.97 9.24 9.52 9.81 10.10 10.40- I.PG 20.67 23.70 23.69 23.66 22.85 21.97 22.62 23.30 24.00 24.72 25.46 26.23TOTAL REVENUE (MMUS$) 173.83 179.47 178.72 179.15 146.34 115.09 100.24 92.25 76.41 72.03 63.89 54.32

REVENUE (MMBAHT) 100%- CRUDE OIL & CONDENSATE 3,781.53 3,848.79 3,823.30 3,829.11 2,990.70 2,194.80 1,784.72 1,552.31 1,115.01 975.11 736.53 459.77- GAS 200.83 201.28 207.32 213.54 219.94 226.54 233.34 240.34 247.55 254.98 262.63 270.50- LPG 537.33 616.16 615.98 615.23 594.08 571.11 588.24 605.89 624.07 642.79 662.07 681.94TOTAL REVENUE (MMBAHT) 4,519.69 4,666.23 4,646.60 4,657.88 3,804.73 2,992.45 2,606.30 2,398.54 1,986.63 1,872.87 1,661.23 1,412.21

REVENUE (MMUS$) 25%- CRUDE OIL & CONDENSATE 36.36 37.01 36.76 36.82 28.76 21.10 17.16 14.93 10.72 9.38 7.08 4.42- GAS 1.93 1.94 1.99 2.05 2.11 2.18 2.24 2.31 2.38 2.45 2.53 2.60- LPG 5.17 5.92 5.92 5.92 5.71 5.49 5.66 5.83 6.00 6.18 6.37 6.56TOTAL REVENUE (MMUS$) 43.46 44.87 44.68 44.79 36.58 28.77 25.06 23.06 19.10 18.01 15.97 13.58

REVENUE (MMBAHT) 25%- CRUDE OIL & CONDENSATE 945.38 962.20 955.83 957.28 747.68 548.70 446.18 388.08 278.75 243.78 184.13 114.94- GAS 50.21 50.32 51.83 53.38 54.99 56.64 58.33 60.08 61.89 63.74 65.66 67.63- LPG 134.33 154.04 153.99 153.81 148.52 142.78 147.06 151.47 156.02 160.70 165.52 170.48TOTAL REVENUE (MMBAHT) 1,129.92 1,166.56 1,161.65 1,164.47 951.18 748.11 651.58 599.64 496.66 468.22 415.31 353.05

Fx. rate: BAHT/US$ = 26.00

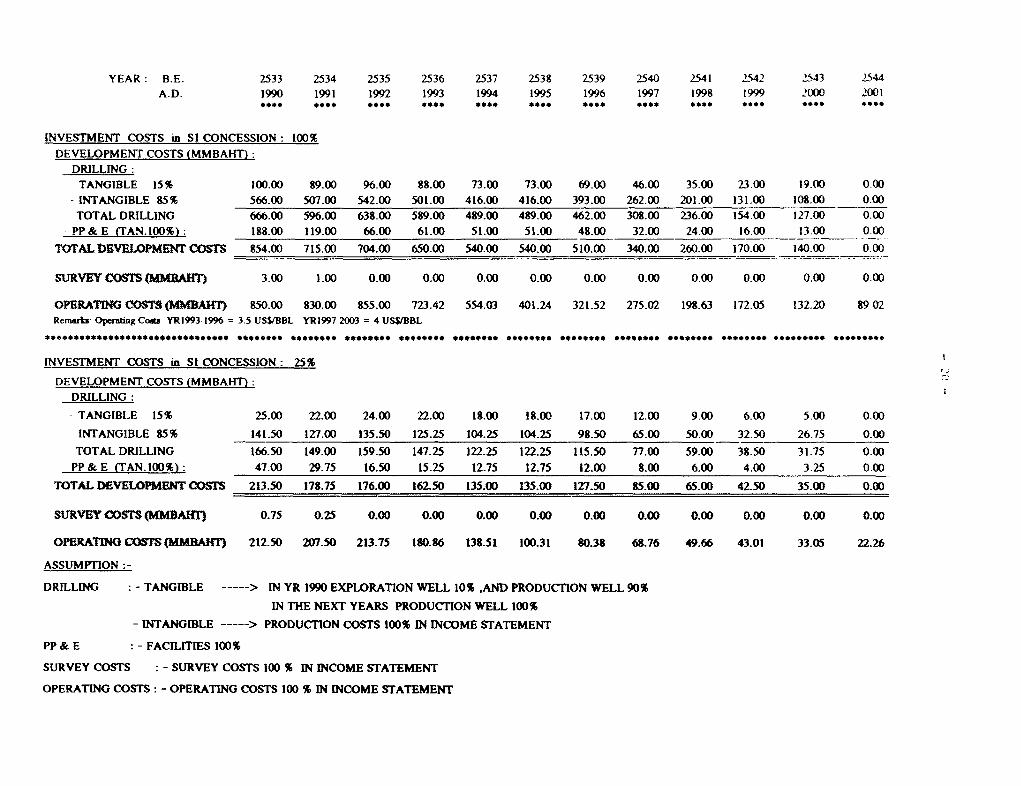

YEAR: B.E. 2533 2534 2535 2536 2537 2538 2539 2540 2541 >542 2543 2544

A. D. 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001** * **** **.* *.** **** **** *a** **.* *..* .... ....

INVESTMENT COSTS in SI CONCESSION: 100%

DEVELOPMENr COSTS (MMBAHT):DRILLING:

TANGIBLE 15% 100.00 89.00 96.00 88.00 73.00 7300 69.00 46.00 35.00 23.00 19.00 0.00

- INTANGIBLE 85% 566.00 507.00 542.00 501.00 416.00 416.00 393.00 262.00 201.00 131.00 108.00 0.00

TOTAL DRILLING 666.00 596.00 638.00 589.00 489.00 489.00 462.00 308.00 236.00 154.00 127.00 0.00

PP&E (TAN.I00%): 188.00 119.00 66.00 61.00 51.00 51.00 48.00 32.00 24.00 1600 13.00 0.00

TOAL DEVELPMENT COSTS 854.00 715.00 704.00 650.00 540.00 540.00 510.00 340.00 260.00 170.00 140.00 0.00

SURVEY COSTS(MMRAT 3.00 1.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

OPERATING COSTS (MId 850.00 830.00 855.00 723.42 554.03 401.24 321.52 275.02 198 63 172.05 132.20 89 02

Rcmarb Opernting Cons YR1993 1996 = 3.5 USVIBBL YR1997 2003 = 4 USVBBL

.. ,,.*..************s *s*.*.*.*.*e*** ****e********* 0....*** *ss.s* ........ ******** ******. ******** ******** *0*.... *** 00** *...*-** *.

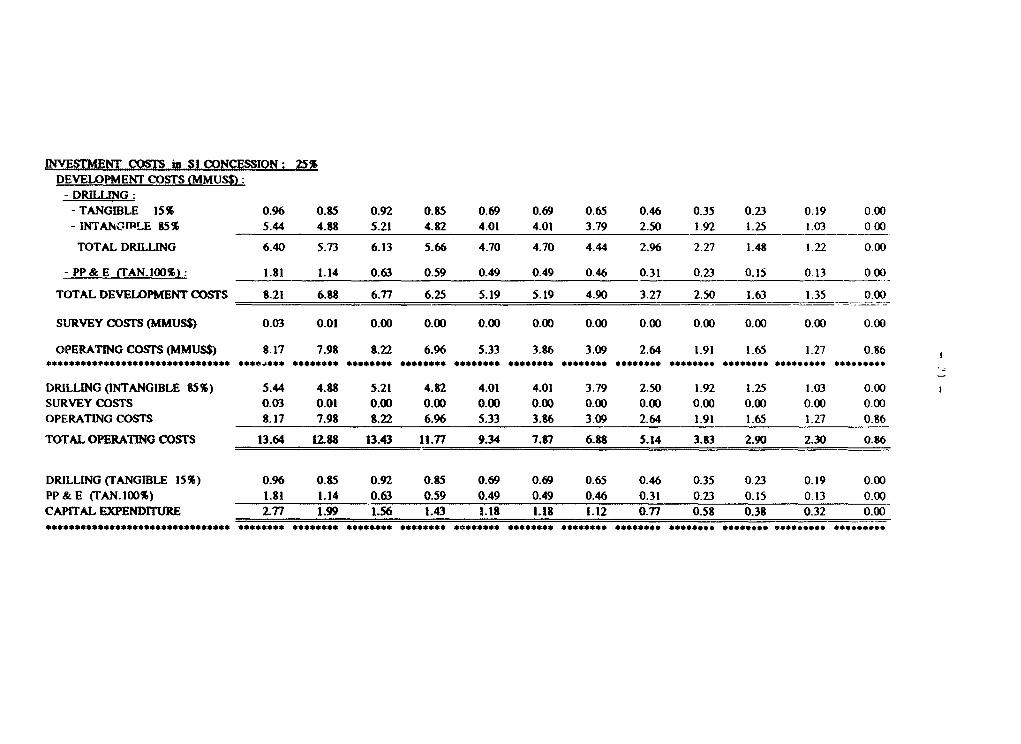

INVESTMENT COSTS in SI CONCESSION: 25%

DEVELOPMENT COSTS (MMBAHT):DRILLING:

.TANGIBLE 15% 25.00 22.00 24.00 22.00 18.00 18.00 17.00 12.00 9.00 6.00 5.00 0.00

INTANGIBLE 85% 141.50 127.00 135.50 125.25 104.25 104.25 98.50 65.00 50.00 32.50 26.75 0.00

TOTAL DRILLING 166.50 149.00 159.50 147.25 122.25 122.25 115.50 77.00 59.00 38.50 31.75 0.00

PP & E (TAN.100%L. 47.00 29.75 16.50 15.25 12.75 12.75 12.00 8.00 6.00 4.00 3.25 0.00

TOTAL DEVELOPMENT COSTS 213.50 178.75 176.00 162.50 135.00 135.00 127.50 85.00 65.00 42.50 35.00 0.00

SURVEY CODS (NMBAHT) 0.75 0.25 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

OPERATING COST (UM AHT) 212.50 207.50 213.75 180.86 138.51 100.31 80.38 68.76 49.66 43.01 33.05 22.26

ASSUMPTION:-

DRILLING : - TANGIBLE ----- > IN YR 1990 EXPLORATION WELL 10% ,AND PRODUCTION WELL 90%

IN THE NEXT YEARS PRODUCTION WELL 100%

- INTANGIBLE ----- > PRODUCTION COSTS 100% IN INCOME STATEMENT

PP & E : - FACILITIES 100%

SURVEY COSTS : - SURVEY COSTS 100 % IN INCOME STATEMENT

OPERATING COSTS: - OPERATING COSTS 100 % IN INCOME STATEMENT

VESTMMNT COSTS m Sl CONCE .ION 2%DEVELOPMENT COSTS (MMUS$):

- DRILLING:- TANGIBLE 15% 0.96 0.85 0.92 0.85 0.69 0.69 0.65 0.46 0.35 0.23 0.19 0.00

- INTANCI1PLE 85% 5.44 4.88 5.21 4.82 4.01 4.01 3.79 2.50 1.92 1.25 1.03 _ 000

TOTAL DRILLING 6.40 5.73 6.13 5.66 4.70 4.70 4.44 2.96 2.27 1.48 1.22 0.00

- PP& E (TAN.100%): 1.81 1.14 0.63 0.59 0.49 0.49 0.46 0.31 0.23 0.15 0.13 0.00

TOTAL DEVELOPMENT COSTS 8.21 6.88 6.77 6.25 5.19 5.19 4.90 3.27 2.50 1.63 1.35 0.00

SURVEY COSTS (MMUSS) 0.03 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

OPERATING COSTS (MMUSS) 8.17 7.98 8.22 6.96 5.33 3.86 3.09 2.64 1.91 1.65 1.27 0.86

*********+***.*****e******.******* ****4*** *******e ******** ********e ******** *****.*** ****e*** ****e*** ****e**** ******** ********* *********

DRILLING (INTANGIBLE 85%) 5.44 4.88 5.21 4.82 4.01 4.01 3.79 2.50 1.92 1.25 1.03 0.00

SURVEY COSTS 0.03 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 000 0.00

OPERATING COSTS 8.17 7.98 8.22 6.96 5.33 3.86 3.09 2.64 1.91 1.65 1.27 0.86

TOTAL OPERATING COSTS 13.64 12.88 13.43 11.77 9.34 7.87 6.88 5.14 3.83 2.90 2.30 0.86

DRILLING (TANGIBLE 15%) 0.96 0.85 0.92 0.85 0.69 0.69 0.65 0.46 0.35 0.23 0.19 0.00

PP & E (TAN.100%) 1.81 1.14 0.63 0.59 0.49 0.49 0.46 0.31 0.23 0.15 0.13 0.00

CAPITAL EXENDITURE 2.77 1.99 1.56 1.43 1.18 1.18 1.12 0.77 0.58 0.38 0.32 0.00

*e*¢*************************** ******* ********** ******** ******** ******** ****Ooo* ******** ******** ... **. *....... ........ ....... ** **0000...

Project Completion Rcport

THAILAND

SIRIKT PEIvROLEUM PROJECr(Loan 2639-TH)

Part m: Statistical Information

- 23 -

Project Completion Rcport

THAILAND

SIRIKIT PETROLEUNI PROJECIr

Part HI: Summary of Statistical Data

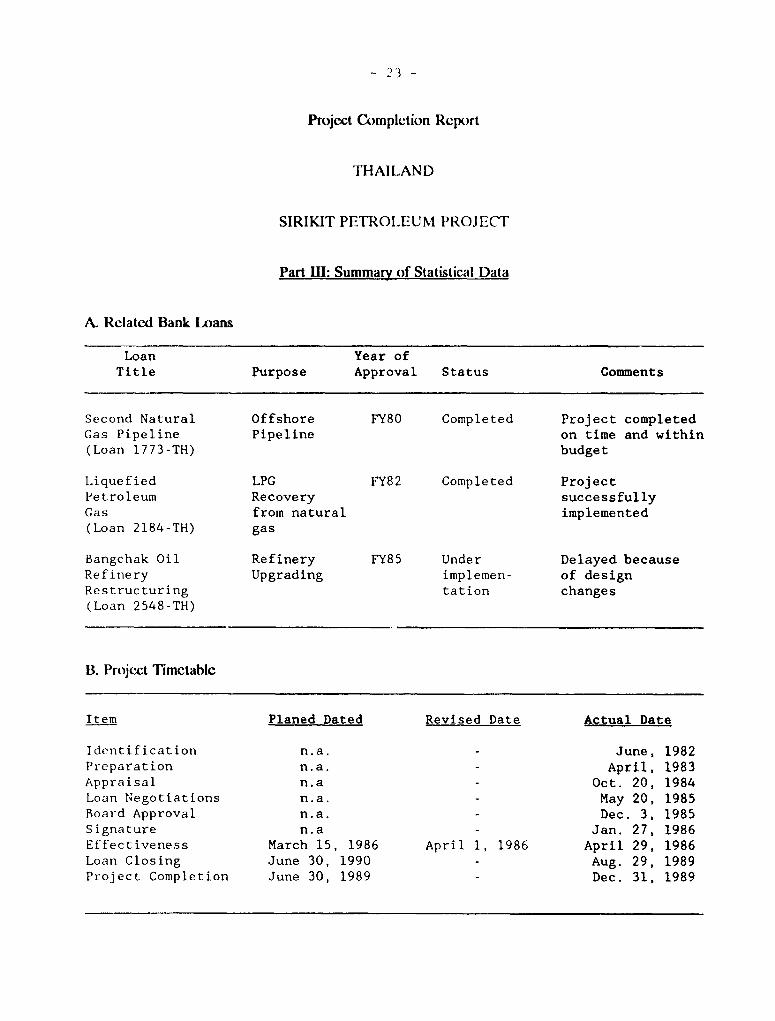

N Related Bank Loans

Loan Year ofTitle Purpose Approval Status Comments

Second Natural Offshore FY80 Completed Project completedGas Pipeline Pipeline on time and within(Loan 1773-TH) budget

Liquefied LPG FY82 Completed ProjectPetroleum Recovery successfullyGas from natural implemented(Loan 2184-TH) gas

Bangchak Oil Refinery FY85 Under Delayed becauseRefinery Upgrading implemen- of designRestructuring tation changes(Loan 2548-TH)

B. Project Timetable

Item Planed Dated Revised Date Actual Date

Identification n.a. - June, 1982Preparation n.a. - April, 1983Appraisal n.a - Oct. 20, 1984Loan Negotiations n.a. - May 20, 1985Board Approval n.a. - Dec. 3, 1985Signature n.a - Jan. 27, 1986Effectiveness March 15, 1986 April 1, 1986 April 29, 1986Loan Closing June 30, 1990 - Aug. 29, 1989Project Completion June 30, 1989 Dec. 31, 1989

- 24 -

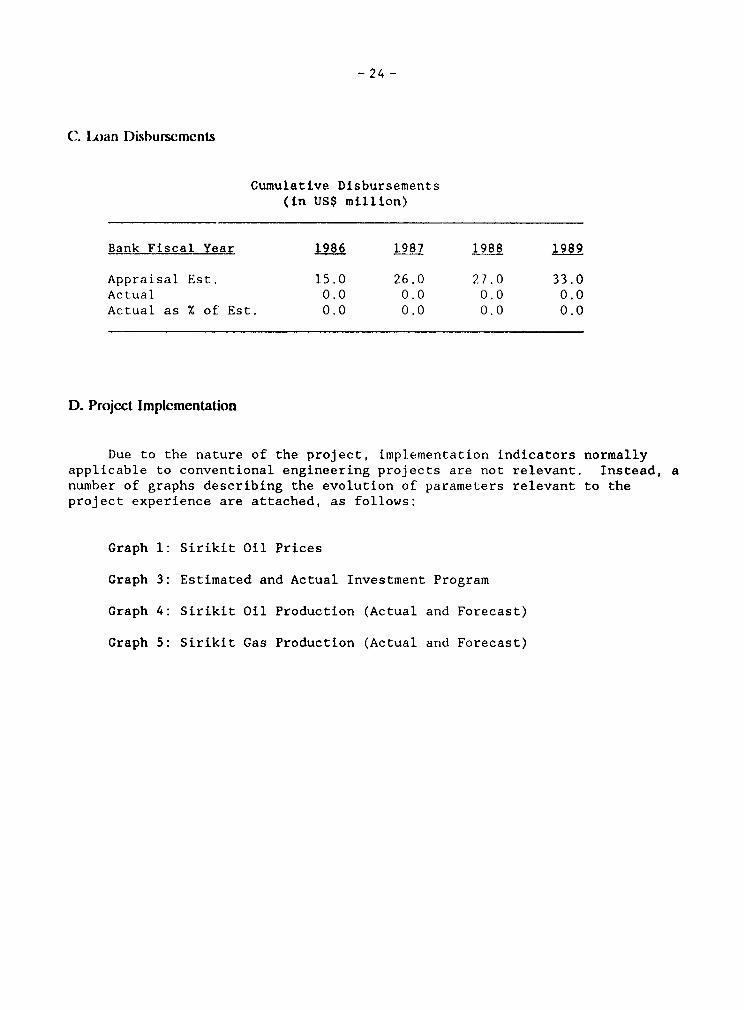

C. IL)an Dsburscmcnts

Cumulative Disbursements(in US$ million)

Bank Fiscal Year 1986 1987 1988 1989

Appraisal Est. 15.0 26.0 27.0 33.0Actual 0.0 0.0 0.0 0.0Actual as % of Est. 0.0 0.0 0.0 0.0

D. Projcct Implcmentation

Due to the nature of the project, implementation indicators normallyapplicable to conventional engineering projects are not relevant. Instead, anumber of graphs describing the evolution of parameters relevant to theproject experience are attached, as follows:

Graph 1: Sirikit Oil Prices

Graph 3: Estimated and Actual Investment Program

Graph 4: Sirikit Oil Production (Actual and Forecast)

Graph 5: Sirikit Gas Production (Actual and Forecast)

- 25 -

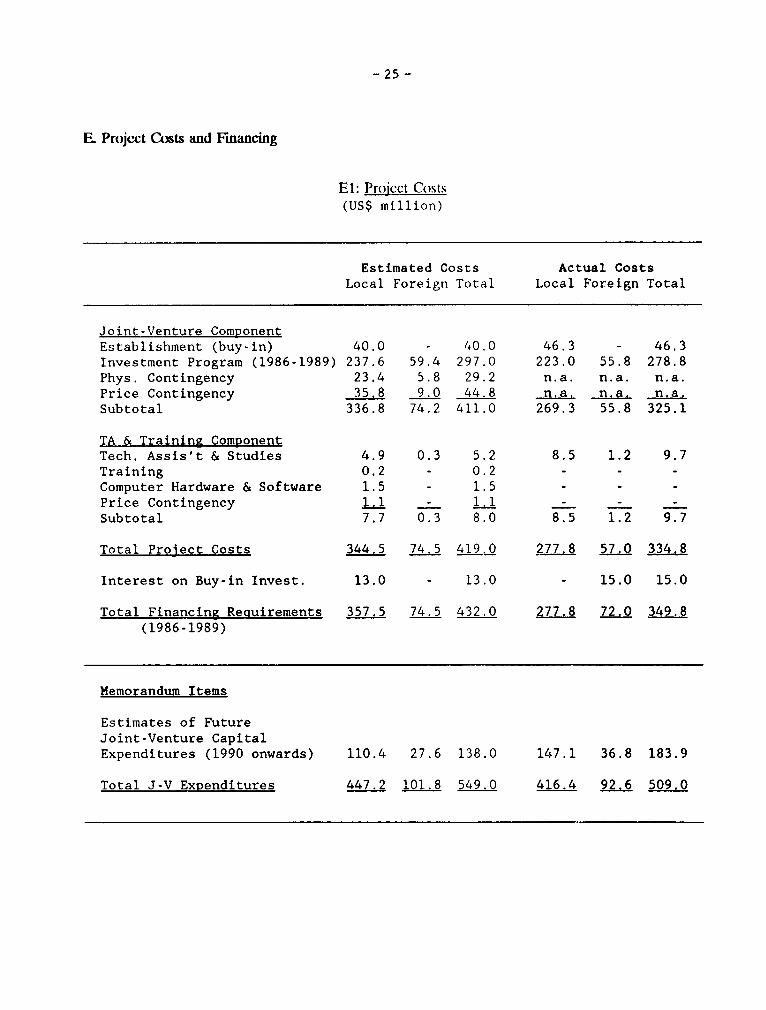

FE Project Costs and Financing

El: Project Costs(US$ million)

Estimated Costs Actual CostsLocal Foreign Total Local Foreign Total

Joint-Venture ComponentEstablishment (buy-in) 40.0 - 40.0 46.3 - 46.3Investment Program (1986-1989) 237.6 59.4 297.0 223.0 55.8 278.8Phys. Contingency 23.4 5.8 29.2 n.a. n.a. n.a.Price Contingency 35.8 9.0 44.8 n.a. n.a. n.a,Subtotal 336.8 74.2 411.0 269.3 55.8 325.1

TA & Training ComponentTech. Assis't & Studies 4.9 0.3 5.2 8.5 1.2 9.7Training 0.2 - 0.2 - - -Computer Hardware & Software 1.5 - 1.5 - - -

Price Contingency 1.1 - 1.1 - - -

Subtotal 7.7 0.3 8.0 8.5 1.2 9.7

Total Project Costs 344.5 74.5 419.0 277.8 57.0 334.8

Interest on Buy-in Invest. 13.0 - 13.0 - 15.0 15.0

Total Financing Reguirements 357,5 74.5 432.0 277.8 72.0 349.8(1986-1989)

Memorandum Items

Estimates of FutureJoint-Venture CapitalExpenditures (1990 onwards) 110.4 27.6 138.0 147.1 36.8 183.9

Total J-V Expenditures 447.2 101.8 549.0 416.4 92.6 509.0

- 26 -

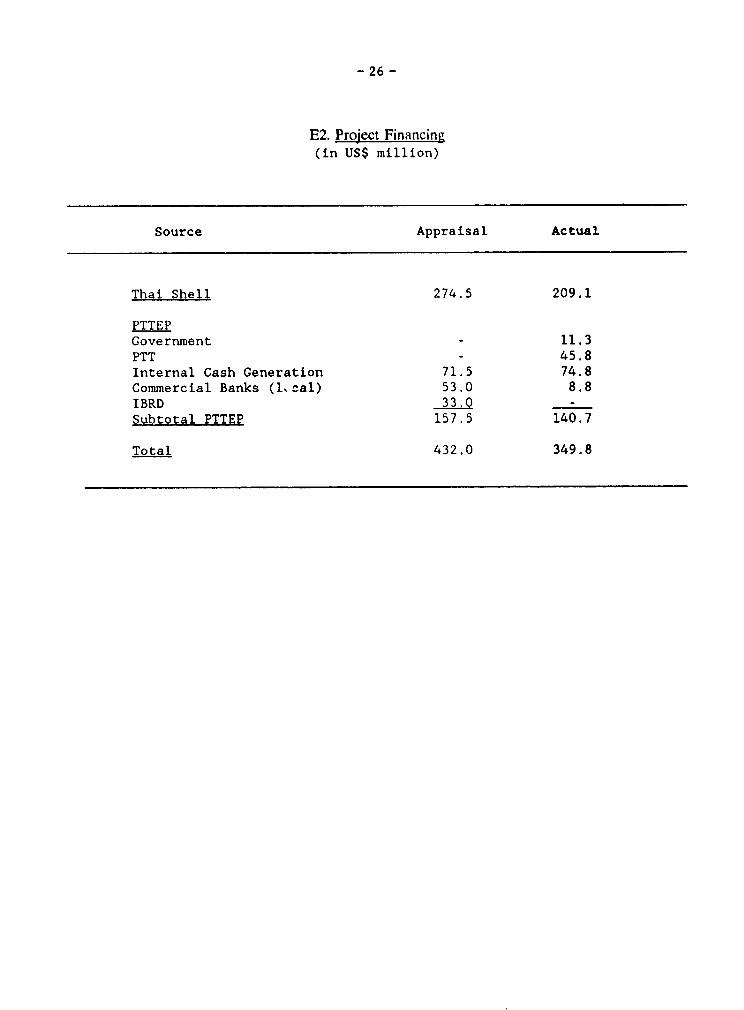

E2. Project Financing(in US$ million)

Source Appraisal Actual

Thai Shell 274.5 209.1

PTTEPGovernment - 11.3PTT - 45.8Internal Cash Generation 71.5 74.8Commercial Banks (l,cal) 53.0 8.8IBRD 330 -

Subtotal PTTEP 157.5 140.7

Total 432.0 349.8

- 27 -

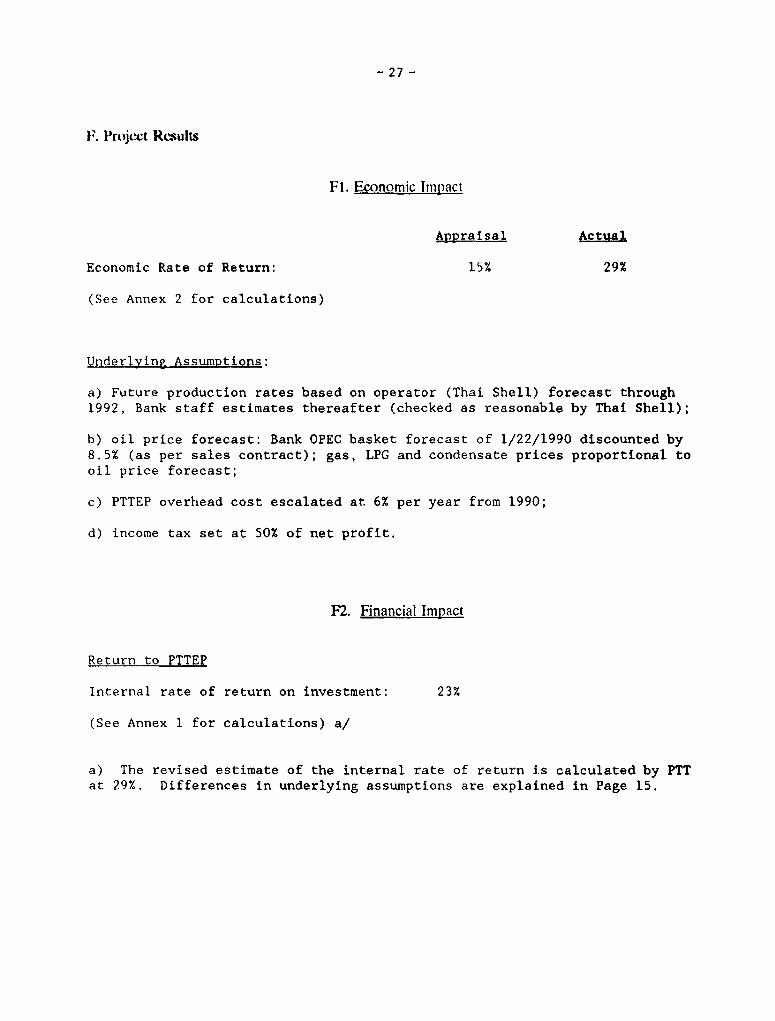

F. Project Results

Fl. Economic Impact

Appraisal Actual

Economic Rate of Return: 15% 29%

(See Annex 2 for calculations)

Underlying AssumDtions:

a) Future production rates based on operator (Thai Shell) forecast through

1992, Bank staff estimates thereafter (checked as reasonable by Thai Shell);

b) oil price forecast: Bank OPEC basket forecast of 1/22/1990 discounted by

8.5% (as per sales contract); gas, LPG and condensate prices proportional to

oil price forecast;

c) PTTEP overhead cost escalated at 6% per year from 1990;

d) income tax set at 50% of net profit.

F2. Financial Impact

Return to PTTEP

Internal rate of return on investment: 23%

(See Annex 1 for calculations) a/

a) The revised estimate of the internal rate of return is calculated by PTTat 29%. Differences in underlying assumptions are explained in Page 15.

- 28 -

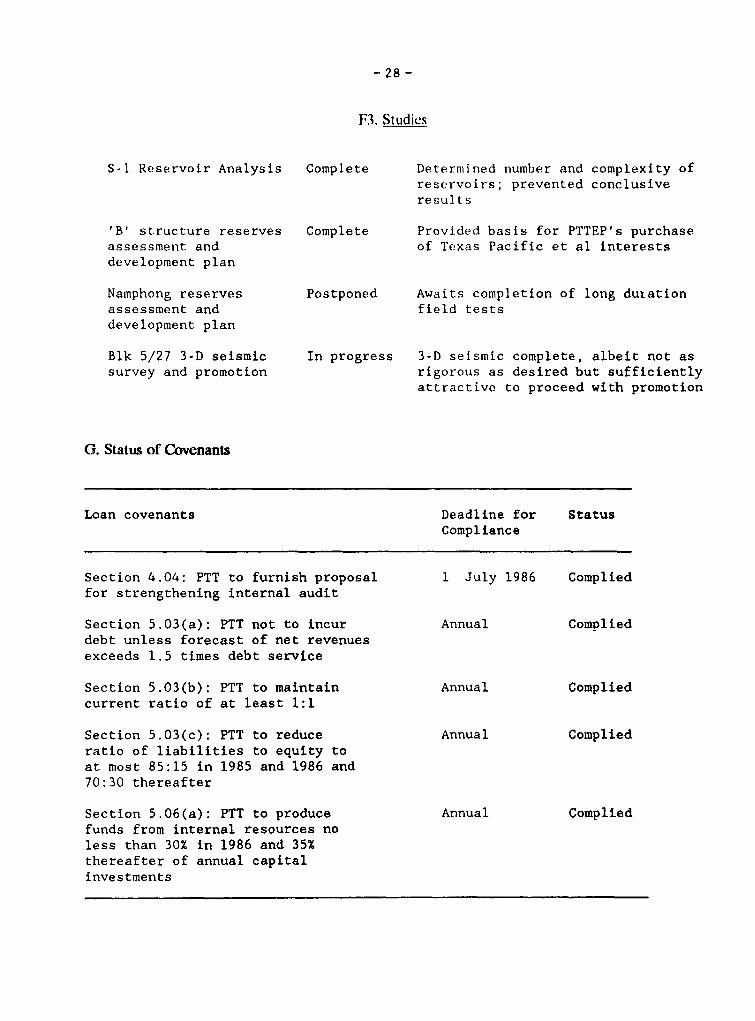

F3. Studies

S-1 Reservoir Analysis Complete Determined number and complexity ofreservoirs; prevented conclusiveresults

'B' structure reserves Complete Provided basis for PTTEP's purchaseassessment and of Texas Pacific et al interestsdevelopment plan

Namphong reserves Postponed Awaits completion of long duiationassessment and field testsdevelopment plan

Blk 5/27 3-D seismic In progress 3-D seismic complete, albeit not assurvey and promotion rigorous as desired but sufficiently

attractive to proceed with promotion

G. Status of Covenants

Loan covenants Deadline for StatusCompliance

Section 4.04: PTT to furnish proposal 1 July 1986 Compliedfor strengthening internal audit

Section 5.03(a): PTT not to incur Annual Complieddebt unless forecast of net revenuesexceeds 1.5 times debt service

Section 5.03(b): PTT to maintain Annual Compliedcurrent ratio of at least 1:1

Section 5.03(c): PTT to reduce Annual Compliedratio of liabilities to equity toat most 85:15 in 1985 and 1986 and70:30 thereafter

Section 5.06(a): PTT to produce Annual Compliedfunds from internal resources noless than 30% in 1986 and 35%thereafter of annual capitalinvestments

- 29 -

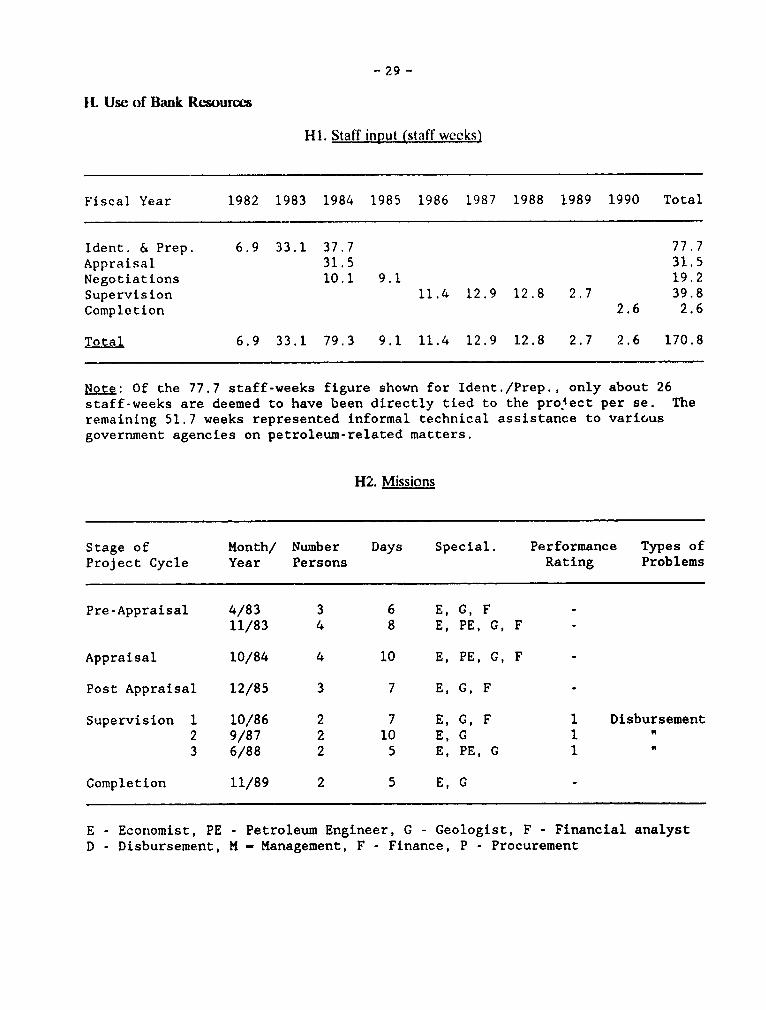

[L Use of Bank Resources

HI. Staff input (staff weeks)

Fiscal Year 1982 1983 1984 1985 1986 1987 1988 1989 1990 Total

Ident. & Prep. 6.9 33.1 37.7 77.7Appraisal 31.5 31.5Negotiations 10.1 9.1 19.2Supervision 11.4 12.9 12.8 2.7 39.8Completion 2.6 2.6

Total 6.9 33.1 79.3 9.1 11.4 12.9 12.8 2.7 2.6 170.8

Note: Of the 77.7 staff-weeks figure shown for Ident./Prep., only about 26staff-weeks are deemed to have been directly tied to the projiect per se. Theremaining 51.7 weeks represented informal technical assistance to variousgovernment agencies on petroleum-related matters.

H2. Missions

Stage of Month/ Number Days Special. Performance Types ofProject Cycle Year Persons Rating Problems

Pre-Appraisal 4/83 3 6 E, G, F -11/83 4 8 E, PE, G, F -

Appraisal 10/84 4 10 E, PE, G, F -

Post Appraisal 12/85 3 7 E, G, F -

Supervision 1 10/86 2 7 E, G, F 1 Disbursement2 9/87 2 10 E,G 13 6/88 2 5 E, PE, G 1

Completion 11/89 2 5 E, G

E - Economist, PE - Petroleum Engineer, G - Geologist, F - Financial analystD - Disbursement, M - Management, F - Finance, P - Procurement

GRAPH I

- 30 -

SIRIKIT OIL PRICE FORECASTCin 1985 US$ per barrael

27.

25 ........ 9

23 Et,t + AC_U_ _ _ _

22r

20t

19l

17

12 -

10 /. . . .

91985 ~~~~1991Z 1995 201X1

O Appraisal Estiffete + Actual/ Nvised

CRAPH 2

- 31

SIRIKIT OIL PRICE FORECASTc In CLrront USS per barrQi)

70-

80

40-

30

20J -.

1985 1990 1995 2000

O Appriesl Estimnte + Actusl/Revlsed

2GRAPH 3

- 32 -

SIRIKIT INVESTMENT PROGRAMCUSS mil Ilon)

110-

100 -<$ -

30 ' - --

1902 19S719297

O Apy n l l Est lrnete + AC t uel / evil ed

GRAPH 4- 33 -

OIL PRODUCTION FORECAST(ml Ilion barralo per year)

9

g9B3 t988 1993 1998

0 AppreleAl Eetimate + Actual/Rgvlged

GRAPH 534 -

GAS PRODUCTION FORECASTCbct pcr year)

is

1?

Is

14

13

12

11

10

7.

6

1983 191 1993 9

Cl Apporeell Estl mte + ActuXl/IRvgl.d

SIRIKIT PETROLEUM PROJECTFinancial Analysis(in current USS million)

------------actual----------- ---------- -----------------------projected------------------------------------------1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Production

Crude Oil (Mbbl) 1.32 7 32 6.07 6.49 7.30 8.32 8.20 7.85 7.10 6.40 5.80 5.20 4.70 4.20 3.80 3 40Natural Gas (10^6 8tu) 1,720 10,450 11,330 11,260 12,380 13,000 13,200 13.200 12,700 12,900 13.200 12.800 12,900 13,000 13,000 13.000LPG ('000 tons) - - - - - 110 125 125 125 125 125 125 125 125 125 125Condensate ('000 bbl) - - - - - 226 248 250 250 250 250 250 250 250 250 260

Prices

Crude Oil (S/bbl) 24.57 15.46 16.40 14.21 15.60 15.40 15.80 16.30 17.10 18.70 20.90 23.00 25.30 27.OC 29.00 32 00Natural Gas (S/MBtu) 1.21 1.07 0.93 0.95 0.90 0.90 0.90 0.93 0.98 1.07 1.19 1.31 1.44 1 57 1.69 1.82LPG (S/ton) 171 180 189 204 219 235 256 279 303 330 360Condensate (S/bbl) 15.40 15.80 16.30 17.10 18.70 20.90 23.00 25.30 27.80 29.00 32.00

Revenue ($M)

Crude Oil 32.43 113.17 99.55 92.22 113.88 128.13 129.56 127.96 121.41 119.68 121.22 119.60 118.91 113.40 110.20 108.80Natural Gas 2.08 11.18 10.54 10.70 11.14 11.70 11.88 12.28 12.38 13.74 15.71 16.77 18.58 20.35 21.91 23.66LPG - - - - - 18.80 22.49 23.69 25.45 27.34 29.37 31.98 34.83 37.93 41.31 44.99Condensate - - - - - 3.48 3.92 4.08 4.28 4.68 5.23 5.75 6.33 6.95 7.25 8.32Subtotal 34.51 124.35 110.08 102.92 125.02 162.11 167.85 167.99 163.51 165.43 171.52 174.10 178.64 178.63 180.67 185.77 w

Less Royalty (12.5%) 4.31 15.54 13.76 12.86 15.63 20.26 20.98 21.00 20.44 20.68 21.44 21.76 22.33 22.33 22.58 23.22 l

PTTEP Share (25%) 7.55 27.20 24.08 22.51 27.35 35.46 36.72 36.75 35.77 36.19 37.52 38.08 39.08 39.08 39.52 40.64

PTTEP Costs

Transport Cost 2.49 2.33 2.20 2.05 1.92 1.79 1.68 1.57Field Operations 5.00 5.20 5.41 5.62 5.85 6.08 6.33 6.58Total Operating Costs 1.12 4.32 3.15 7.70 7.85 8.18 7.98 8.23 7.49 7.53 7.60 7.67 7.77 7.87 8.01 8.15PTTEP Overheads 0.09 1.42 1.50 1.93 1.54 1.69 1.86 2.05 2.25 2.48 2.73 3.00 3.30 3.63 3.70 3.70Interest Charges 0.18 3.75 2.06 4.59 2.75 1.78 1.66 1.48 1.29 1.22 1.00 0.76 0.54 0.42 0.21 0.07Depreciation 2.52 19.50 21.20 8.47 4.71 17.92 8.21 8.44 8.44 6.93 6.18 5.40 4.50 2.69 2.28 1.38

PTTEP Net Profit 3.64 (1.79) (3.83) (0.18) 10.50 5.89 17.00 16.54 16.30 18.03 20.00 21.25 22.96 24.46 25.33 27.34Income Tax 0.84 - 0.02 1.30 2.48 2.94 8.50 8.27 8.15 9.01 10.00 10.62 11.48 12.23 12.66 13.67PTTEP Profit After Tax 2.80 (1.79) (3.85) (1.48) 8.02 2.94 8.50 8.27 8.15 9.01 10.00 10.62 11.48 12.23 12.66 13.67

Capital Expenditures 2.62 55.44 5.55 6.53 13.83 8.25 6.90 6.70 6.50 6.25 4.00 3.00 2.25 1.50 0.13 -Cum. Cap. Expend. 2.62 58.06 63.61 70.14 83.97 92.22 99.12 105.82 112.32 118.57 122.57 125.57 127.82 129.32 129.45 129.45Cum. Depreciation 2.52 22.02 43.22 51.69 56.40 74.32 82.53 90.97 99.41 106.34 112.52 117.92 122.42 125.11 127.39 128.77

Net Cash Flow 2.70 (37.73) 11.80 0.46 (1.10) 12.61 9.81 10.01 10.09 9.69 12.18 13.02 13.73 13.42 14.81 15.05Cumulative Net Cash Flow 2.70 (35.03) (23.23) (22.76) (23.87) (11.25) (1.44) 8.57 18.66 28.35 40.54 53.56 67.29 80.71 95.52 110.58

Internal Financial Rate of return: 23%

SIRIKIT PETROLEUM PROJECTEconomic Analysis(in constant 1989 uSS million)

------------actual----------- ------------------------------------------projected-------------------------------------------1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Production

Crude 011 (Mbbl) 1.32 7.32 6.07 6.49 7.30 8.32 8.20 7.85 7.10 6.40 5.80 5.20 4.70 4 20 3.80 3.40Natural Gas (1O06 Btu) 1.720 10,450 11.330 11.260 12,380 13.000 13,200 13,200 12,700 12,900 13,200 12,800 12.900 13.000 13,000 13.000LPG ('000 tons) - - - - - 110 125 125 125 125 125 125 125 125 125 125Condensate ('000 bbl) - - - - - 226 248 250 250 250 250 250 250 250 250 260

Prices

Crude 011 (S/bbl) 33.26 14.45 16.69 12.21 14.82 14.08 14.08 14.08 14.36 14.65 14.95 15.69 16.47 17.29 18.15 19.06Natural Gas ($/MBtu) 4.85 2.11 2.43 1.78 2.16 2.05 2.05 2.05 2.09 2.13 2.18 2.29 2.40 2 52 2.65 2 78LPG (S/ton) - - - - - 164 164 164 168 1?1 174 183 192 202 212 222Condensate (S/bbl) - - - - - 14.08 14.08 14.08 14.36 14.65 14.95 15.69 16.47 17 29 18.15 19 06

Revenue ($M)

Crude 011 43.90 105.77 101.32 79.22 108.21 117.11 115.42 110.49 101.96 93.77 86.70 81.60 77.42 72.63 68 99 64.80Natural Gas 8.34 22.00 27.56 20.03 26.74 26.66 27.07 27.07 26.58 27.54 28.75 29.27 30.97 32.76 34.39 36.10LPG - - - - - 18.07 20.54 20.54 20.95 21.38 21.81 22.89 24.03 25.23 26.49 27.81Condensate - - - - - 3.18 3.49 3.52 3.59 3.66 3.74 3.92 4.12 4.32 4.54 4.96Subtotal 52.24 127.77 128.87 99.25 134.95 165.03 166.52 161.62 153.08 146.35 140.99 137.68 136.54 134.95 134.40 133.66

PTTEP Share 13.06 31.94 32.22 24.81 33.74 41.26 41.63 40.41 38.27 36.59 35.25 34.42 34.14 33 74 33.60 33.42

less: Opportunity CostRoyalty (25%) 1.48 4.56 3.68 3.21 3.91 4.83 4.76 4.54 4.21 4.06 4.02 3.93 3 89 3.75 3 66 3.63Taxes (25%) 1.16 - 0.02 1.30 2.48 2.80 7.72 7.16 6.72 7.08 7.49 7.68 8.00 8 22 8.21 8.55

Total Opportunity Cost 2.64 4.56 3.70 4.50 6.39 7.63 12.49 11.70 10.94 11.15 11.51 11.61 11.89 11.97 11.87 12.18

Net Revenue 10.42 27.39 28.52 20.31 27.35 33.62 29.14 28.70 27.33 25.44 23.74 22.81 22.24 21.77 21.73 21.24

PTTEP Costs

Operating Costs 1.54 5.06 3.37 7.67 7.85 8.18 7.98 8.23 7.49 7.24 7.03 6.82 6.65 6.47 6.33 6.19PTTEP Overheads 0.12 1.66 1.60 1.92 1.54 1.69 1.79 1.90 2.00 2.12 2.24 2.37 2 51 2.65 2.70 2 70

Capital Expenditures 3.61 64.99 5.93 6.51 13.83 8.25 6.90 6.70 6.50 6.25 4.00 3.00 2.25 1.50 0.13 -

Net Cash Flow 5.15 (44.33) 17.62 4.21 4.13 15.50 12.47 11.88 11.34 9.83 10.47 10.62 10.84 11.14 12 57 12.35

Cumulative Net Cash Flow 5.IS (39.18) (21.56) (17.36) (13.23) 2.27 14.75 26.63 37.97 47 80 58.27 68.89 79.73 90.87 103.44 115.79

zEconomiic Rate of return : 29%