Embed Size (px)

DESCRIPTION

The Weighted Average Cost of Capital and Company Valuation. Chapter 13 Fundamentals of Corporate Finance 2012 Linköpings universitet. Ivar Kreugers (1880-1932) Tändsticks imperium: debt can be bad. 1917 bildades Finanskoncernen Kreuger & Toll - PowerPoint PPT Presentation

Citation preview

1

The Weighted Average Cost of Capital and Company Valuation

Chapter 13 Fundamentals of Corporate Finance

2012 Linköpings universitet

2

Ivar Kreugers (1880-1932) Tändsticks imperium: debt can be bad.

1917 bildades Finanskoncernen Kreuger & Toll

Svenska Tändsticks AB, 1930 omfattade 60 % av världens tändsticksproduktion.

Kreuger & Toll Pris föll från sin högsta notering i mars 1929 på över 46 dollar till 4,5 dollar i slutet av 1931

1929 depression, och han fick likviditetskris Dock hans imperium blev grunden för

många svenska koncernen.

Ivar Kreuger omkring 1930 vid sitt skrivbord i Tändstickspalatset

3

Topics

Cost of CapitalWeighted Average Cost of Capital

(WACC)Measuring Capital StructureCalculating Required Rates of ReturnCalculating WACC Interpreting WACCValuing Entire Businesses

4

Concept: Cost of Capital

Most companies are financed by a mixture of securities. Including common stock, bonds, and other securities. These securities have different risks, therefore investors require different return on them.

Cost of Capital – required rate of return on investment.

It is the return the firm’s investors could expect to earn if they invested in other equally risky securities.

5

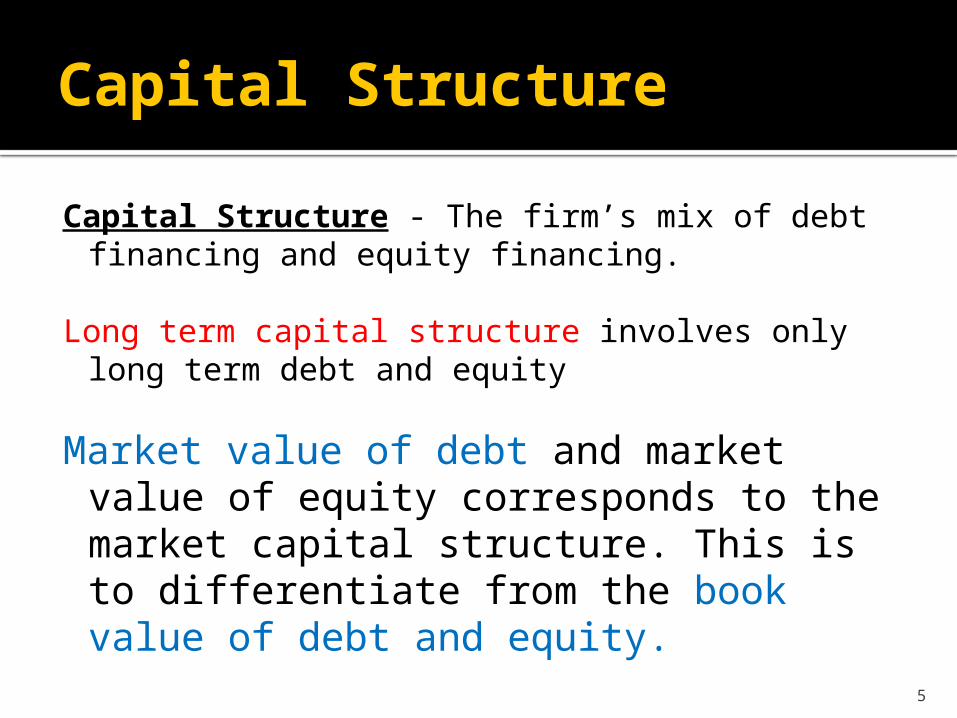

Capital Structure

Capital Structure - The firm’s mix of debt financing and equity financing.

Long term capital structure involves only long term debt and equity

Market value of debt and market value of equity corresponds to the market capital structure. This is to differentiate from the book value of debt and equity.

6

WACC

Taxes are an important consideration in the company cost of capital, because interest payments are tax deductible.

)-(1 x r=

rate)tax -(1cost x pretax =debt ofcost After tax

debt

7

WACC

Weighted Average Cost of Capital (WACC) The expected rate of return on a portfolio of all the firm’s securities, adjusted for tax savings due to interest payments.

Company cost of capital = Weighted average of debt and equity returns.

8

WACC

Weighted Average Cost of Capital = WACC

equitydebt r ED

E+)r-(1

ED

D=WACC

9

WACC

Three Steps to Calculating Cost of Capital

1. Calculate the proportion of firm´s debt and equity.

2. Determine the required rate of return on equity and debt.

3. Calculate a weighted average after tax return on the debt and equity.

10

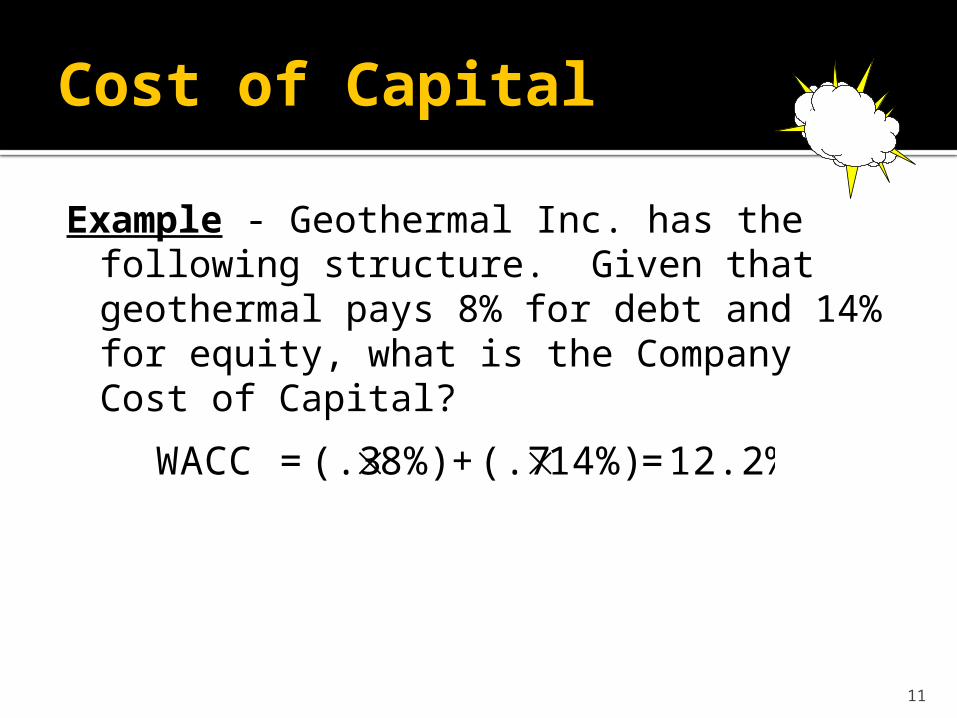

Cost of Capital

Example - Geothermal Inc. has the following structure. Given that geothermal pays 8% for debt and 14% for equity, what is the Company Cost of Capital?

100%$647Assets ValueMarket

70%$453 EquityValueMarket

30%$194 DebtValueMarket

11

Cost of Capital

Example - Geothermal Inc. has the following structure. Given that geothermal pays 8% for debt and 14% for equity, what is the Company Cost of Capital?

12.2%=14%)(.7+8%)(.3= WACC

12

Cost of Capital

Example - Geothermal Inc. has the following structure. Given that geothermal pays 8% for debt and 14% for equity, what is the Company Cost of Capital?

Interest is tax deductible. Given a 35% tax rate, debt only costs us 5.2% (i.e. 8 % x .65).

11.4%=14%)(.7+5.2%)(.3= WACC

12.2%=14%)(.7+8%)(.3=Return Portfolio

13

WACC

ED

r E+r D equitydebt

equityVE

debtVD

assets rr-1 r

sinvestment of valueincome total

assets =r

14

WACC

Weighted Average Cost of Capital with debt, equity and Preferred Stock

Preferred stock provides a specific dividend that is paid before any dividends are paid to common stock.

Preferredequitydebt r

V

P+r

V

E+)r-(1

V

D=WACC

Where D is the value of debt, E is the value of equity, P is preferred stock, τ is tax rate.

15

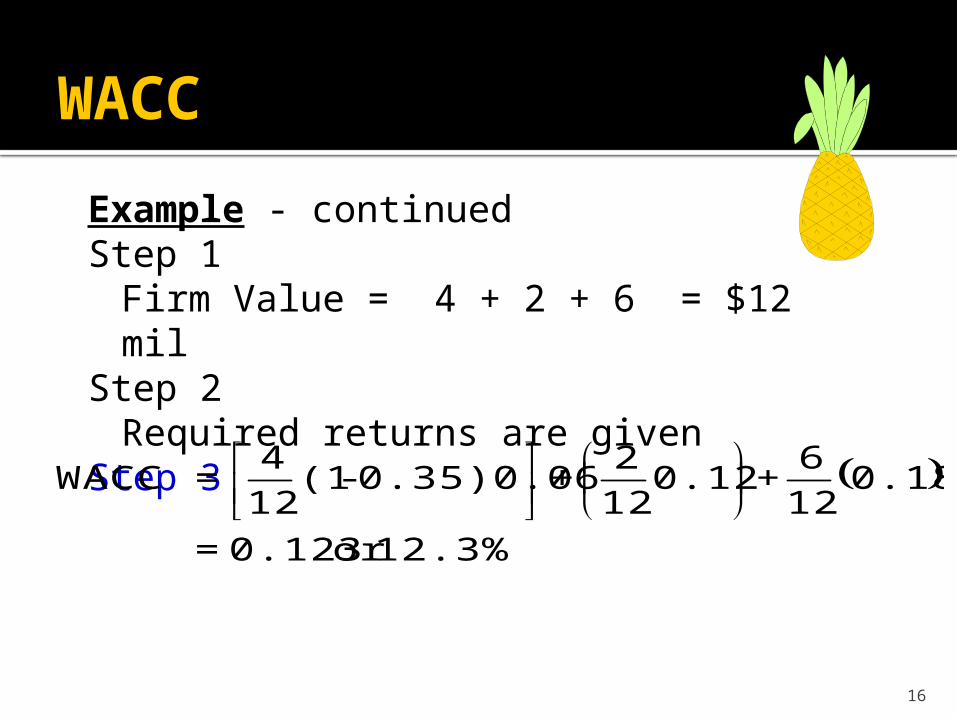

WACC

Example - Executive Fruit has issued debt, preferred stock and common stock. The market value of these securities are $4mil, $2mil, and $6mil, respectively. The required returns are 6%, 12%, and 18%, respectively.

Q: Determine the WACC for Executive Fruit, Inc.

16

WACC

Example - continuedStep 1

Firm Value = 4 + 2 + 6 = $12 milStep 2

Required returns are givenStep 3

12.3%or 0.123=

0.1812

6+0.12

12

2+0.35)0.06-(1

12

4=WACC

17

Measuring Market Capital Structure

Market Value of Bonds – Present Value of all coupons and par value discounted at the current yield to maturity, YTM.

Market Value of Equity - Market price per share multiplied by the number of outstanding shares.

18

Measuring Market Capital Structure

Book Value of Big Oil s Debt and Equity (mil)

Bank Debt 200$ 25,0%LongTerm Bonds 200$ 25,0%Common Stock 100$ 12,5%Retained Earnings 300$ 37,5%Total 800$ 100%

Page 374/5 Example: Suppose Long term bond has a coupon payment of 8%, 12 year to maturity. Common stocks 100 million shares valued at 12 $ each

19

Measuring Market Capital Structure

If the long term bonds pay an 8% coupon and mature in 12 years, market interest rate is 9%, what is the market value of the bonds?

70.185$09.1

216....

09.1

16

09.1

16

09.1

161232

PV

20

Measuring Capital Structure

Big Oil MARKET Value Debt and Equity (mil)

Bank Debt (mil) 200,0$ 12,6%LT Bonds 185,7$ 11,7%Total Debt 385,7$ 24,3%Common Stock 1 200,0$ 75,7%Total 1 585,7$ 100,0%

21

Cost of capital is the same as the Required Rates of Return

On Bondsr = YTMd

)r-(r+r=

CAPM=r

fmf

e

i

On Common Stock

That is, expected return on stock is equal to risk free return plus beta times market risk premium.

22

Required Rates of Return can also be obtained from DDM

Dividend Discount Model (DDM) Constant Dividend Growth Model =

solve for re

P =Div

r - g01

e

r =Div

P+ ge

1

0

23

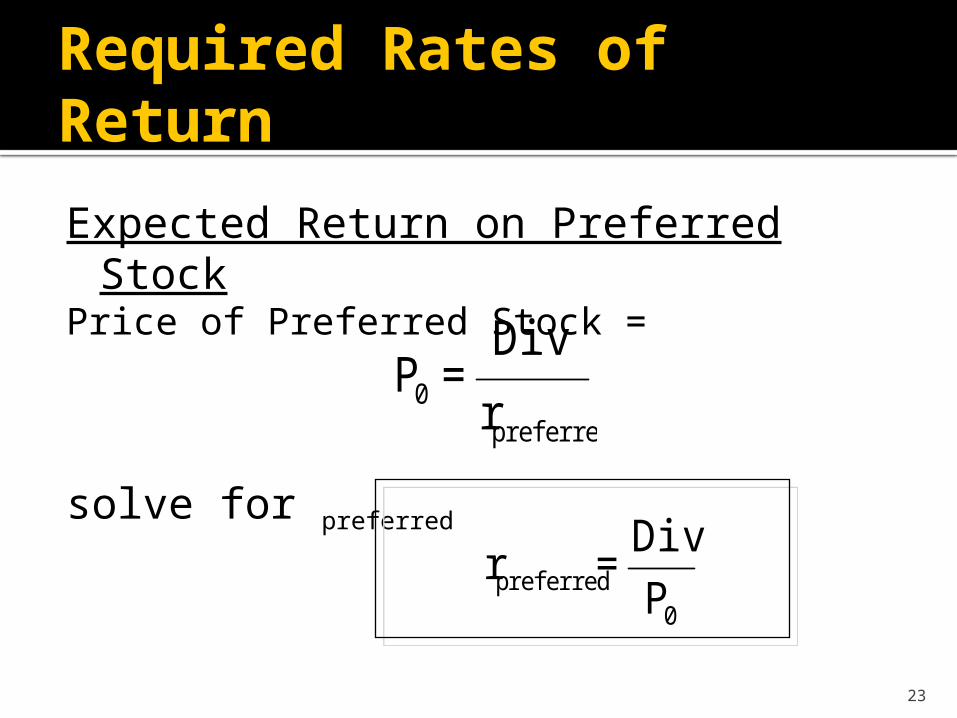

Required Rates of Return

Expected Return on Preferred StockPrice of Preferred Stock =

solve for preferredpreferred

0 r

Div=P

0preferred P

Div=r

24

WACC for Selected Firms

Expected return Interest rate Proportion of Proportion of

on equity (%) on debt (%) Equity (E/V) Debt (D/V) WACC (%) Mkt Cap Totl debtAmazon.com 19.8 7.3 0.96 0.04 19.3 33.8 1.2Ford 20.2 7.7 0.07 0.93 6.1 12.2 163.2Newmont Mining 8.9 6.5 0.89 0.11 8.4 24.2 3.0Intel 14.1 5.8 0.98 0.02 13.9 111.2 2.0Microsoft 10.3 na 1.00 0.00 10.3 311.7 0.0Dell Computer 11.9 6.0 0.99 0.01 11.8 47.8 0.7Boeing 11.6 5.8 0.88 0.12 10.7 62.4 8.6McDonalds 13.1 5.9 0.89 0.11 12.1 62.5 7.8Pfizer 7.7 5.3 0.95 0.05 7.5 159.3 8.7Dupont 11.7 6.0 0.81 0.19 10.2 38.9 9.0Disney 10.0 6.0 0.78 0.22 8.7 55.5 15.5ExxonMobil 8.7 5.3 1.00 0.00 8.7 465.0 0.0IBM 10.9 5.8 0.80 0.20 9.5 140.7 35.3Wal-Mart 4.7 5.7 0.80 0.20 4.5 190.0 47.4Campbell Soup 6.2 6.0 0.82 0.18 5.8 12.6 2.8GE 8.3 5.3 0.41 0.59 5.4 344.0 491.0Heinz 7.1 6.7 0.73 0.27 6.4 14.3 5.3

Notes: 1. Expected return on equity is taken from Table 12-2

2. Interest rate on debt is calculated from yields on similarly rated bonds

3. D is the book value of the firm's debt,and E is the market value of equity

4. WACC = (1 - .35) x rdebt x (D/V) + requity x (E/V)

25

Interpreting WACC

The WACC is an appropriate discount rate only for a project that is the same of the firm's existing business

There are two costs of debt financing. The explicit cost of debt is the rate of interest bondholders demand. The implicit cost is the increased required return from equity due to increased bankruptcy probability.

26

WACC

Issues in Using WACC

Debt has two costs. 1)return on debt and 2)increased cost of equity demanded due to the increase

in risk of bankruptcy Betas may change with capital structure

Corporate taxes complicate the analysis and may

change our decision

equityVE

debtVD

assets +-1 =

27

FCF and PV

Free Cash flow is cash flow that is available to investors,

FCF= operating cash flow - investment expenditures. FCF is a more accurate measurement of PV

than either Dividend or Earnings per share EPS.

Free Cash Flows (FCF) should be the theoretical basis for all PV calculations.

When valuing a business for purchase, always use FCF.

28

Capital BudgetingValuing a Business

The value of a business or project is usually computed as the discounted value of FCF out to a valuation horizon (H).

The valuation horizon is sometimes called the terminal value and is calculated like present value of growth opportunity (PVGO).

HH

HH

WACC

PV

WACC

FCF

WACC

FCF

WACC

FCFPV

)1()1(...

)1()1( 22

11

29

Capital Budgeting

Valuing a Business or Project

PV (free cash flows) PV (horizon value)

HH

HH

WACC

PV

WACC

FCF

WACC

FCF

WACC

FCFPV

)1()1(...

)1()1( 22

11

30

Capital Budgeting

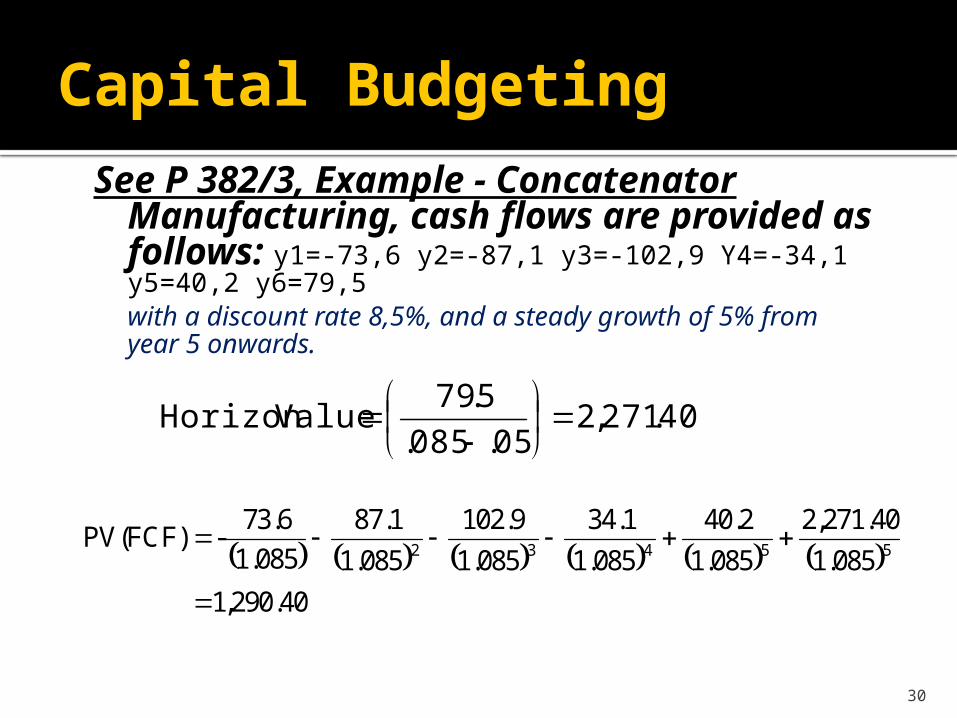

See P 382/3, Example - Concatenator Manufacturing, cash flows are provided as follows: y1=-73,6 y2=-87,1 y3=-102,9 Y4=-34,1 y5=40,2 y6=79,5with a discount rate 8,5%, and a steady growth of 5% from year 5 onwards.

40.271,205.085.

5.79ValueHorizon

40.290,1

085.1

40.271,2

085.1

2.40

085.1

1.34

085.1

9.102

085.1

1.87

085.1

73.6-PV(FCF) 55432

![Evolution of Valuation in Bankruptcy - 2017 NCBJ … symp Simkovic...[The] weighted average method of valuation . . . shall no longer exclusively control such proceedings. We believe](https://img.pdfslide.us/doc/110x75/5b356ca57f8b9a5f288b8b7c/evolution-of-valuation-in-bankruptcy-2017-ncbj-symp-simkovicthe-weighted.jpg)