Embed Size (px)

Citation preview

THE USE OF CENTRAL BANK MONEY FORSETTL ING SECUR IT I E S TRANSACT IONS

MAY 2004

CURRENT MODELS ANDPRACTICES

In 2004 all ECB publications will feature

a motif taken from the

€100 banknote.

THE USE OF CENTRAL BANK MONEY FORSETTLING SECURIT IES TRANSACTIONS

MAY 2004

CURRENT MODELS AND

PRACTICES

© European Central Bank, 2004

AddressKaiserstrasse 2960311 Frankfurt am Main, Germany

Postal addressPostfach 16 03 1960066 Frankfurt am Main, Germany

Telephone+49 69 1344 0

Websitehttp://www.ecb.int

Fax+49 69 1344 6000

Telex411 144 ecb d

This Bulletin was produced under theresponsibility of the Executive Boardof the ECB.

All rights reserved. Reproduction foreducational and non-commercial purposesis permitted provided that the source isacknowledged.

ISBN 92-9181-507-1 (print)ISBN 92-9181-508-X (online)

3c ECB

The use o f Cent ra l bank money for se t t l ing secur i t i e s t ransac t ionsMay 2004

1 INTRODUCTION: AN OVERVIEW OFCURRENT MODELS 3

2 WHERE? – LOCATION OF ACCOUNTSUSED FOR CASH LEG SETTLEMENT 4

3 WHO? – GENERATING PAYMENTINSTRUCTIONS AND OPERATIONACCOUNTS ENTRIES 7

4 HOW? – FREQUENCY AND TYPE OF DVPINTERACTION: GROSS VERSUS NET DVPSETTLEMENT 8

5 WHEN? – TIMING OF INTERACTION:MODELS VARIANTS FOR PRE-OPENING/NIGHT-TIME PROCESSING OF NEXTVALUE DATE 9

6 THE COMPOSITION OF THE BALANCEAVAILABLE FOR CASH SETTLEMENT 14

ANNEX 1:REPLIES PROVIDED BY THE NATIONALCENTRAL BANKS OF THE ESCB 16

CONTENT S

4ECB cThe use of Central bank money for settling securities transactionsMay 2004

1 I N TRODUCT I ON : AN OV ERV I EWOF CURR ENT MODE L S

A securities trade typically results in anobligation for the seller to deliver securities(securities leg) and a corresponding obligationfor the buyer to deliver cash funds (cash leg).Central bank money settlement facilities enablesettlement of the cash leg of the trade in thebooks of the central bank. The balances of thesecash settlement accounts therefore represent anaccount holder’s claim on the national centralbank.

There are various ways of organising theinteraction of securities settlement systems(SSS) and payment systems (PS) to providecentral bank money settlement facilities. In theEuropean Union Member States ad hocsolutions have been developed that suit thespecific preferences of market participants andmeet the needs deriving from the design andorganisation of the settlement infrastructures.This note describes the various models in placein the European Union in 2003 taking accountof five main aspects:

1. The (technical) location of the cash accountsused for cash leg settlement, and the entitythat operates the accounts or makes theentries in the accounts of the central bank(these may be the same or different entities).

2. The entity that produces the funds transferinstructions on behalf of participants(normally the SSS; but, in some cases, aprevious transfer of liquidity on the initiativeof participants may be required).

3. The type and frequency of SSS-PSinteraction (for each business cycle).

4. The different operating hours of SSS andPS, and thus the timing of SSS-PSinteraction (daylight versus night-time orearly morning pre-opening processes).

5. The composition of the funds balanceavailable for cash settlement (which issometimes different in case of night-time/early morning processing compared tostandard daylight processing).

The models presented here summarise the maincharacteristics of the various national solutions,and do not claim to reproduce in detail all thesurveyed systems. The analysis is based on theanswers provided by the national central banks(NCBs) of the European System of CentralBanks (ESCB) to an ad hoc questionnaire inMarch and April 2003. The European CentralSecurities Depositories Association (ECSDA)also commented on the results of this survey.The ECB considers the survey a useful piece ofinformation for interested parties, e.g.practitioners in the field of payment andsettlement systems, infrastructures, otherservice providers, and therefore decided tomake it publicly available. A table summarisingthe answers from the NCBs is annexed to thisdocument.

5c ECB

The use of Central bank money for settling securities transactionsMay 2004

2

Where? – locationof accounts

used for cash legsettlement

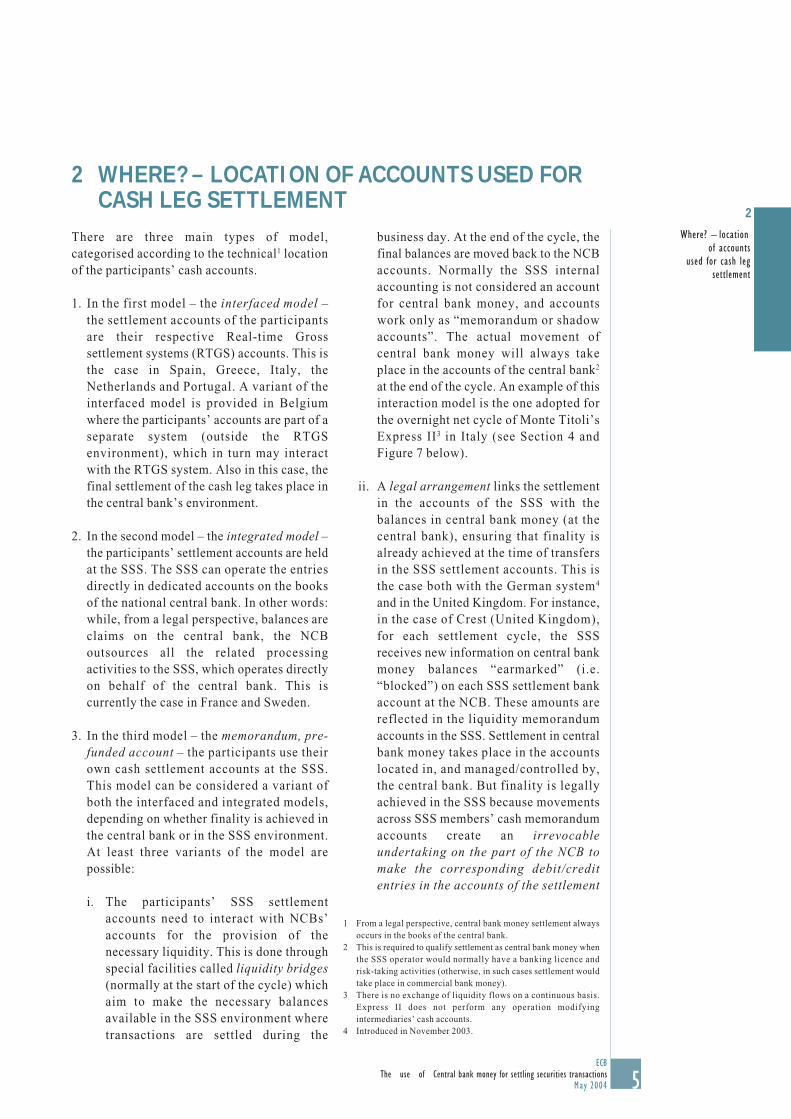

There are three main types of model,categorised according to the technical1 locationof the participants’ cash accounts.

1. In the first model – the interfaced model –the settlement accounts of the participantsare their respective Real-time Grosssettlement systems (RTGS) accounts. This isthe case in Spain, Greece, Italy, theNetherlands and Portugal. A variant of theinterfaced model is provided in Belgiumwhere the participants’ accounts are part of aseparate system (outside the RTGSenvironment), which in turn may interactwith the RTGS system. Also in this case, thefinal settlement of the cash leg takes place inthe central bank’s environment.

2. In the second model – the integrated model –the participants’ settlement accounts are heldat the SSS. The SSS can operate the entriesdirectly in dedicated accounts on the booksof the national central bank. In other words:while, from a legal perspective, balances areclaims on the central bank, the NCBoutsources all the related processingactivities to the SSS, which operates directlyon behalf of the central bank. This iscurrently the case in France and Sweden.

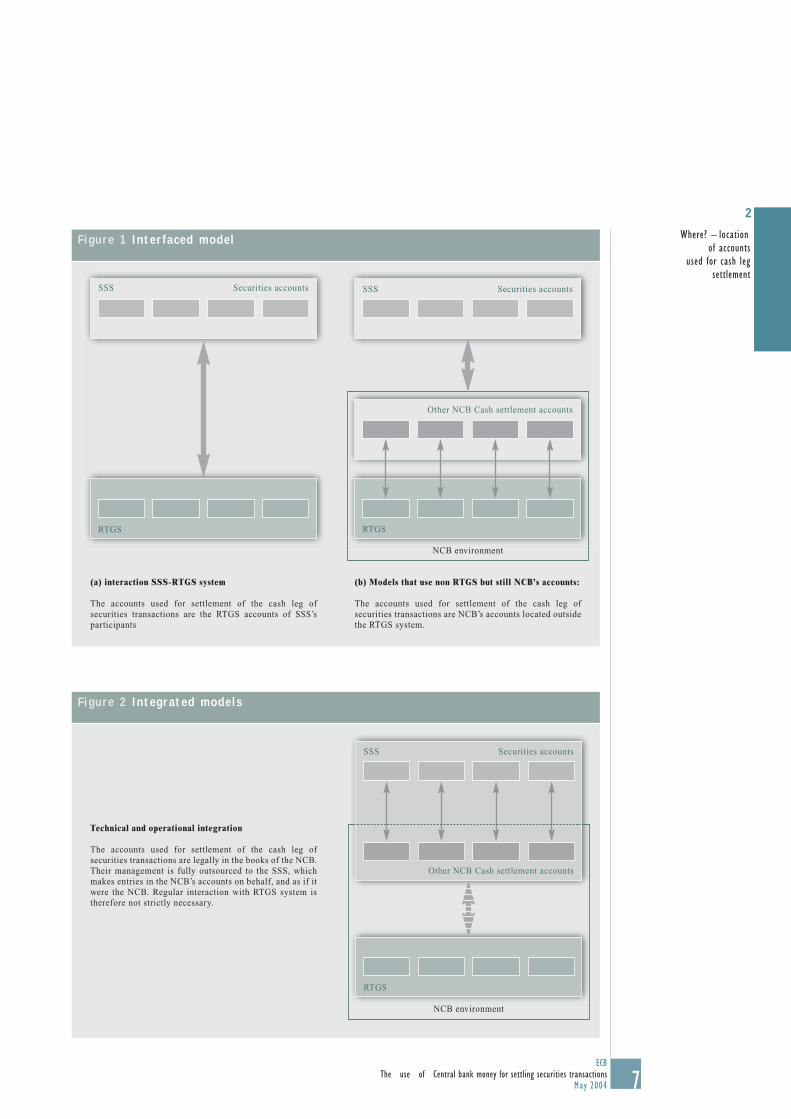

3. In the third model – the memorandum, pre-funded account – the participants use theirown cash settlement accounts at the SSS.This model can be considered a variant ofboth the interfaced and integrated models,depending on whether finality is achieved inthe central bank or in the SSS environment.At least three variants of the model arepossible:

i. The participants’ SSS settlementaccounts need to interact with NCBs’accounts for the provision of thenecessary liquidity. This is done throughspecial facilities called liquidity bridges(normally at the start of the cycle) whichaim to make the necessary balancesavailable in the SSS environment wheretransactions are settled during the

2 WHERE ? – L O C AT I ON O F A C COUNT S U S ED F ORC A SH L EG S E T T L EMENT

business day. At the end of the cycle, thefinal balances are moved back to the NCBaccounts. Normally the SSS internalaccounting is not considered an accountfor central bank money, and accountswork only as “memorandum or shadowaccounts”. The actual movement ofcentral bank money will always takeplace in the accounts of the central bank2

at the end of the cycle. An example of thisinteraction model is the one adopted forthe overnight net cycle of Monte Titoli’sExpress II3 in Italy (see Section 4 andFigure 7 below).

ii. A legal arrangement links the settlementin the accounts of the SSS with thebalances in central bank money (at thecentral bank), ensuring that finality isalready achieved at the time of transfersin the SSS settlement accounts. This isthe case both with the German system4

and in the United Kingdom. For instance,in the case of Crest (United Kingdom),for each settlement cycle, the SSSreceives new information on central bankmoney balances “earmarked” (i.e.“blocked”) on each SSS settlement bankaccount at the NCB. These amounts arereflected in the liquidity memorandumaccounts in the SSS. Settlement in centralbank money takes place in the accountslocated in, and managed/controlled by,the central bank. But finality is legallyachieved in the SSS because movementsacross SSS members’ cash memorandumaccounts create an irrevocableundertaking on the part of the NCB tomake the corresponding debit/creditentries in the accounts of the settlement

1 From a legal perspective, central bank money settlement alwaysoccurs in the books of the central bank.

2 This is required to qualify settlement as central bank money whenthe SSS operator would normally have a banking licence andrisk-taking activities (otherwise, in such cases settlement wouldtake place in commercial bank money).

3 There is no exchange of liquidity flows on a continuous basis.Express II does not perform any operation modifyingintermediaries’ cash accounts.

4 Introduced in November 2003.

6ECB cThe use of Central bank money for settling securities transactionsMay 2004

banks of the buying and sellingmembers5. The interaction with the cashaccounts located at the NCB throughliquidity bridges (initial, on demand, andat end-of-day) is similar (but notnecessarily identical) to that describedunder point (i).6

iii. Another variant of the pre-funded modelis the autonomous central bank moneymodel, which is in place in Finland. Inthis model, the SSS participates in theRTGS system, and its account is used forcash settlement of its participants.Participants in the SSS need to pre-fundthe SSS settlement by transferring therequired funds from their own RTGSaccount to the SSS’s RTGS account. TheSSS keeps a sub-accounting record ofsecurities-related cash transfers amongits participants. In practice thesetransfers are internal (sub-) transferstaking place inside the RTGS account ofthe SSS. However, the SSS’s sub-accounting is not considered central bankaccounting, and there is no effectivecontract outsourcing. Central bankmoney provision is made throughliquidity transfers (credit transfer by eachparticipant) to the SSS’s RTGS account.The main difference with other cases isthat the central securities depository(CSD) operating the SSS is strictlyspeaking a non-risk-taking entity,without any kind of banking licence. TheSSS is a “hermetically sealed” systemwith no other injection or leakage pointsapart from the RTGS account. The overallbalance of the SSS’s RTGS accountmatches the total of funds in SSS sub-accounting. Unrestricted use of theRTGS account balance is the irrevocableguarantee, as it is for all the other RTGSaccounts. A liquidity bridge “on demand”complements the initial provision ofliquidity to make additional fundsavailable whenever needed. At the end ofthe day, the SSS transfers back the sub-

5 The Crest system, as well as several other systems, has a two-tiermembership structure. Although this is not reported in detail inthe note, it is sufficient to state that the United Kingdom modelprovides central bank money settlement accounts to settlementbanks, and not to all SSS members. In other systems, although SSSmembers have central bank money settlement accounts, manyinvestors only have access to the SSS through these members.

6 For instance, in the German system, the SSS debits and credits the“home (NCB) accounts” of participants, and not the RTGSplusaccounts (which start and end the day with a zero-balance). Alsothe reservation of balances for night-time processing, and thesubsequent debiting, are done on these “home accounts”. Theproceeds of securities settlement can be used in the liquiditybridge to the RTGSplus system.

account balances to the RTGS accountsof the SSS participants.

The various solutions are described in Figures 1to 3. The list of the features does not claim to beexhaustive, and some simplifications inpresenting the main typology of interaction/models were necessary for the sake of clarity.As a result, the figures represent generalmodels rather than specific SSS.

7c ECB

The use of Central bank money for settling securities transactionsMay 2004

2

Where? – locationof accounts

used for cash legsettlement

F i g u re 1 I n t e r f a c ed mode l

SSS Securities accounts SSS Securities accounts

NCB environment

Other NCB Cash settlement accounts

RTGSRTGS

(a) interaction SSS-RTGS system

The accounts used for settlement of the cash leg of securities transactions are the RTGS accounts of SSS’s participants

(b) Models that use non RTGS but still NCB’s accounts:

The accounts used for settlement of the cash leg of securities transactions are NCB’s accounts located outsidethe RTGS system.

F i g u re 2 I n t eg r a t ed mode l s

SSS Securities accounts

NCB environment

Other NCB Cash settlement accounts

RTGS

Technical and operational integration

The accounts used for settlement of the cash leg of securities transactions are legally in the books of the NCB.Their management is fully outsourced to the SSS, whichmakes entries in the NCB’s accounts on behalf, and as if itwere the NCB. Regular interaction with RTGS system istherefore not strictly necessary.

8ECB cThe use of Central bank money for settling securities transactionsMay 2004

F i g u re 3 Mode l w i t h Memorandum /p re - f unded a c c oun t s

SSS Securities accounts

RTGS

Interfaced variant

The accounts used for settlement of the cash leg of securities transactions are in the SSS environments. SSS’saccounts movements are pre-funded or guaranteed by funds“reserved” (earmarked or blocked) in the RTGS system,where f inal cash settlement takes place. The SSS uses theinformation about the reserved balance available in theRTGS system.

* Alternatively, cash settlement f inalty may be achieved inthe SSS according to the variant described under 3 (ii).

Autonomous central bank variant

The SSS has an account in the RTGS system, which is pre-founded by SSS’s participants with transfers from theirrespective RTGS accounts. The SSS keeps an internal accounting reflecting the movements related to securitiessettlement. This internal accounting is not considered central bank accounting. The participants can fund andwithdraw cash whenever necessary. At the end of the day theoutstanding balances of the sub accounts are returned to theparticipants’ RTGS accounts.

SSS Securities accounts

SSS Cash settlement accounts

1. Information about“reserved amount”.

3. Final cash settlementtakes place in RTGS*

RTGS

SSS

2. settlement in the SSS sub-accounting

SSS Cash settlement (sub) accounts

Participants’RTGS accounts

9c ECB

The use of Central bank money for settling securities transactionsMay 2004

3

Who? – generatingpayment instructions

and operationaccounts entries

The SSS is normally in a better position than itsparticipants to calculate their respectiveobligations within the settlement process.Therefore it is the SSS that typically initiatesthe interaction with the payment system: inpractice, at the beginning and/or end of itssettlement cycle, the SSS sends a request forcash settlement to the funds transfer system. Itis therefore the SSS that produces the requiredcash settlement instructions on behalf of itsparticipants7.

In this context, the payment instruction requiredto transfer the funds can take three main forms:

– credit8 or debit transfer9, where the paymentinstructions are given, for each transfer,respectively, by the payer or the payee (i.e.by one of the SSS participants);

– direct debit ( i.e. the possibility of a pre-authorised debit on the payer’s account,upon instruction of the payee)10;

– mandated payment, i.e. a payment made onbehalf of a participant (securities buyer)upon instruction issued by a third party (inthis case the SSS). In practice, the SSS or thecentral bank is authorised to produce therequired transfer instructions on behalf ofthe account holders and to address them tothe relevant cash accounts manager/system.The system receiving the mandated paymentinstructions can recognise that the sendingparty is not the account holder; therefore, theaccount manager must be at least (i) aware ofthe agreement between the sending party(SSS) and the account holder (securitiesbuyer) and (ii) able to validate the message11.

3 WHO ? – G EN ER AT I NG PAYMENT I N S T RUC T I ON SAND OP ER AT I ON A C COUNT S EN TR I E S

7 In memorandum, pre-funded models, there may be a need for aprevious transfer of liquidity, on the initiative of the SSSparticipant, of the required liquidity from the RTGS accounts tothe SSS cash settlement accounts (e.g. Finland). Once funds havebeen recorded in the SSS sub-accounting system, settlement oftrades takes place automatically, i.e. the system credits anddebits cash and securities on its own. In the Finnish case, alsorepatriation of liquidity from the SSS takes place on the initiativeof the account holder (participants) using the SSS interface.

8 A credit transfer is an order by the part that has the obligation topay addressed to the manager of its account to debit its accountand transfer the funds in favour of the benef iciary.

9 A debit transfer is an order by the part that has the claim on thefunds addressed to its account manager to collect funds in itsfavour from the account manager of the part with the obligationto pay.

10 Direct debit is not allowed in the current TARGET system, whichis based on credit transfers.

11 In the case of the Netherlands, the scheme is based on a tripartiteagreement between commercial bank, the SSS and the NCB. TheDutch SSS (interfaced model) sends the payment instruction tothe NCB to pay out to the securities seller. The sender of themessage is not the ordering institution.

10ECB cThe use of Central bank money for settling securities transactionsMay 2004

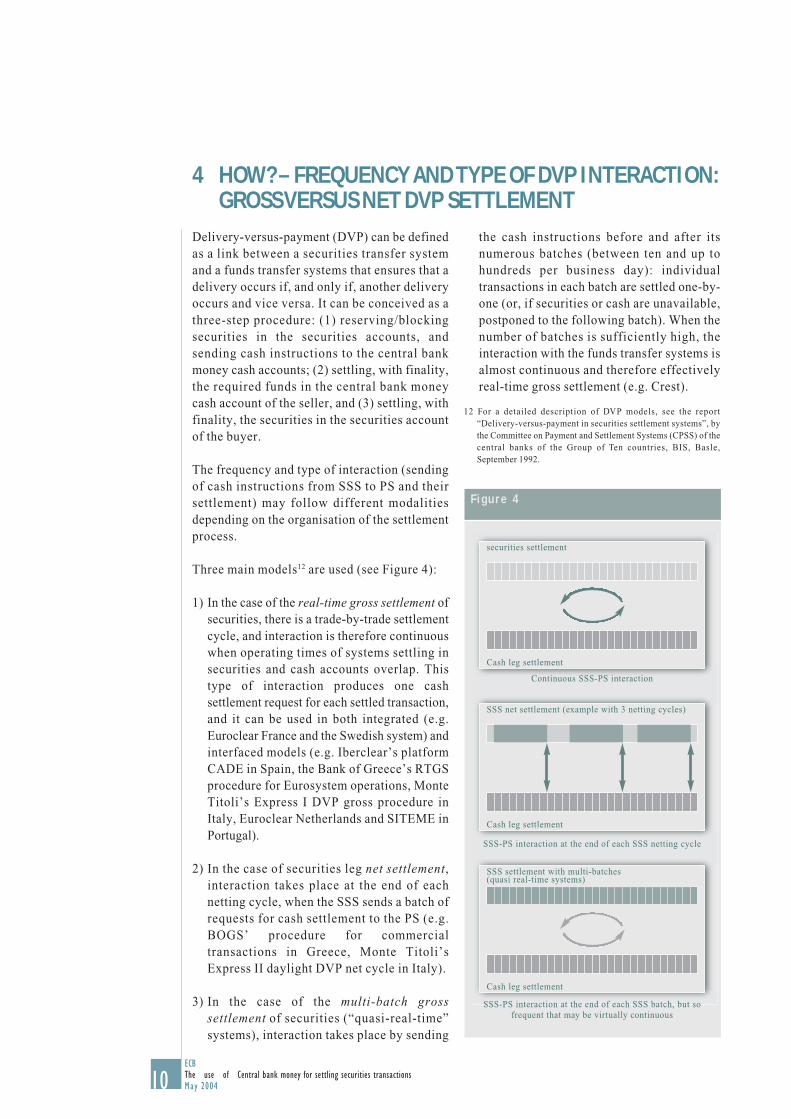

Delivery-versus-payment (DVP) can be definedas a link between a securities transfer systemand a funds transfer systems that ensures that adelivery occurs if, and only if, another deliveryoccurs and vice versa. It can be conceived as athree-step procedure: (1) reserving/blockingsecurities in the securities accounts, andsending cash instructions to the central bankmoney cash accounts; (2) settling, with finality,the required funds in the central bank moneycash account of the seller, and (3) settling, withfinality, the securities in the securities accountof the buyer.

The frequency and type of interaction (sendingof cash instructions from SSS to PS and theirsettlement) may follow different modalitiesdepending on the organisation of the settlementprocess.

Three main models12 are used (see Figure 4):

1) In the case of the real-time gross settlement ofsecurities, there is a trade-by-trade settlementcycle, and interaction is therefore continuouswhen operating times of systems settling insecurities and cash accounts overlap. Thistype of interaction produces one cashsettlement request for each settled transaction,and it can be used in both integrated (e.g.Euroclear France and the Swedish system) andinterfaced models (e.g. Iberclear’s platformCADE in Spain, the Bank of Greece’s RTGSprocedure for Eurosystem operations, MonteTitoli’s Express I DVP gross procedure inItaly, Euroclear Netherlands and SITEME inPortugal).

2) In the case of securities leg net settlement,interaction takes place at the end of eachnetting cycle, when the SSS sends a batch ofrequests for cash settlement to the PS (e.g.BOGS’ procedure for commercialtransactions in Greece, Monte Titoli’sExpress II daylight DVP net cycle in Italy).

3) In the case of the multi-batch grosssettlement of securities (“quasi-real-time”systems), interaction takes place by sending

4 HOW? – FREQUENCY AND TYPE OF DVP INTERACTION:GROSS VERSUS NET DVP SETTLEMENT

the cash instructions before and after itsnumerous batches (between ten and up tohundreds per business day): individualtransactions in each batch are settled one-by-one (or, if securities or cash are unavailable,postponed to the following batch). When thenumber of batches is sufficiently high, theinteraction with the funds transfer systems isalmost continuous and therefore effectivelyreal-time gross settlement (e.g. Crest).

12 For a detailed description of DVP models, see the report“Delivery-versus-payment in securities settlement systems”, bythe Committee on Payment and Settlement Systems (CPSS) of thecentral banks of the Group of Ten countries, BIS, Basle,September 1992.

F i g u re 4

securities settlement

Cash leg settlement

Continuous SSS-PS interaction

SSS-PS interaction at the end of each SSS netting cycle

SSS-PS interaction at the end of each SSS batch, but sofrequent that may be virtually continuous

SSS net settlement (example with 3 netting cycles)

Cash leg settlement

SSS settlement with multi-batches (quasi real-time systems)

Cash leg settlement

11c ECB

The use of Central bank money for settling securities transactionsMay 2004

5

When? – timingof interaction:

models variants forpre-opening/night-time

processing of nextvalue date

Since settlement cycles for securities arenormally longer than T+0, participants may sendsecurities settlement instructions to the SSSbefore the settlement date. This also makes itpossible to pre-match securities instructions at anearly stage, thus both helping to reduce theincidence of settlement failures and reducing partof the participants’ operational risk and liquidityrisks in the SSS. Some SSSs that know abouttransactions before the settlement date find itconvenient to operate (gross or net) batchprocessing cycles overnight in addition to duringdaytime opening hours. The countries with night-time pre-opening processes are Germany, France,the Netherlands, Spain and Italy. In practice, thesystems simply bring forward to the earlymorning – or even to the late afternoon or thenight of the previous calendar day – a part of theprocessing for a certain value date. However, thisis not the standard organisation of large-valuepayment systems, which typically follow daytimeopening hours. Night-time DVP settlementcannot therefore be achieved using thestandard daytime processes in those models(e.g. the interfaced models) which requirecontemporaneous availability of RTGS or otherNCBs’ accounts. In the models with pre-funded/memorandum accounts night-time DVP requirescash pre-funding for the next value date.

Different solutions have been adopted to bypassthe inconvenient unavailability of the cashaccounts located in the payment systems:

1) to extend the opening hours of the paymentsystems, usually by pre-opening them for anearly morning slot overlapping with the SSSoperating hours, usually for activity limitedto facilitating the settlement of securitiessettlement systems (or other clearingsystems, e.g. retail payments). Thispossibility is explicitly envisaged by theTARGET Guideline, Annex V, 3 (i), whichstates that “(RTGS) early opening, before7.00 a.m., may take place after priornotification has been sent to the ECB: (i) fordomestic reason (e.g. in order to facilitatesettlement of securities transactions, tosettle balances of net settlement systems, or

5 WHEN ? – T IM I NG O F I N T E R A C T I ON : MODE L SVA R I AN T S F O R P R E - O P EN I NG / N I GH T- T IM EPROC E S S I NG O F N EX T VA LU E DAT E

to settle other domestic transactions, suchas batch transactions channelled by NCBsinto RTGS systems during the night); or (ii)for ESCB-related reasons (e.g. on dayswhen exceptional payment volumes areexpected, or in order to reduce foreignexchange settlement risk when processingthe euro leg of foreign exchange dealsinvolving Asian currencies)”.

This option has been followed by theNetherlands where there is continuousinteraction of the SSS and RTGS systemsduring the pre-opening of the RTGS system.

2) to reserve funds in the following value dayopening balances of the RTGS accounts (orother central bank settlement account). Inpractice these balances are “blocked” and areonly made available for settlement ofsecurities transactions. This means that theowner of these funds cannot use them forpurposes different from paying the cashobligations stemming from the securitiessettlement process. Thus, the RTGS balancesreserved for SSS settlement secure thesecurities settlement process. The amountswill then be actually debited in RTGSsystem/other NCBs’ accounts when thepayment systems open (e.g. as in Italy andGermany). This time may be the normalopening time (7:00 a.m., as in Italy) or anearlier time if the NCB has opted for theearly opening possibility under the TARGETGuideline (e.g. as in Germany), as describedin the previous point.

Where central banks books are accessibledirectly by the SSS in both technical andoperational terms (as in the French technicalintegrated model), or when the central bank isthe owner/manager of the SSS, thecontemporaneous availability of the RTGSsystem outside its normal operating hours is notnecessary. For instance, after the closing timeof 5:15 p.m., the French system is able to pre-open the following value date at 8:00 p.m. withall the required (dedicated) accounts availablefor final settlement.

12ECB cThe use of Central bank money for settling securities transactionsMay 2004

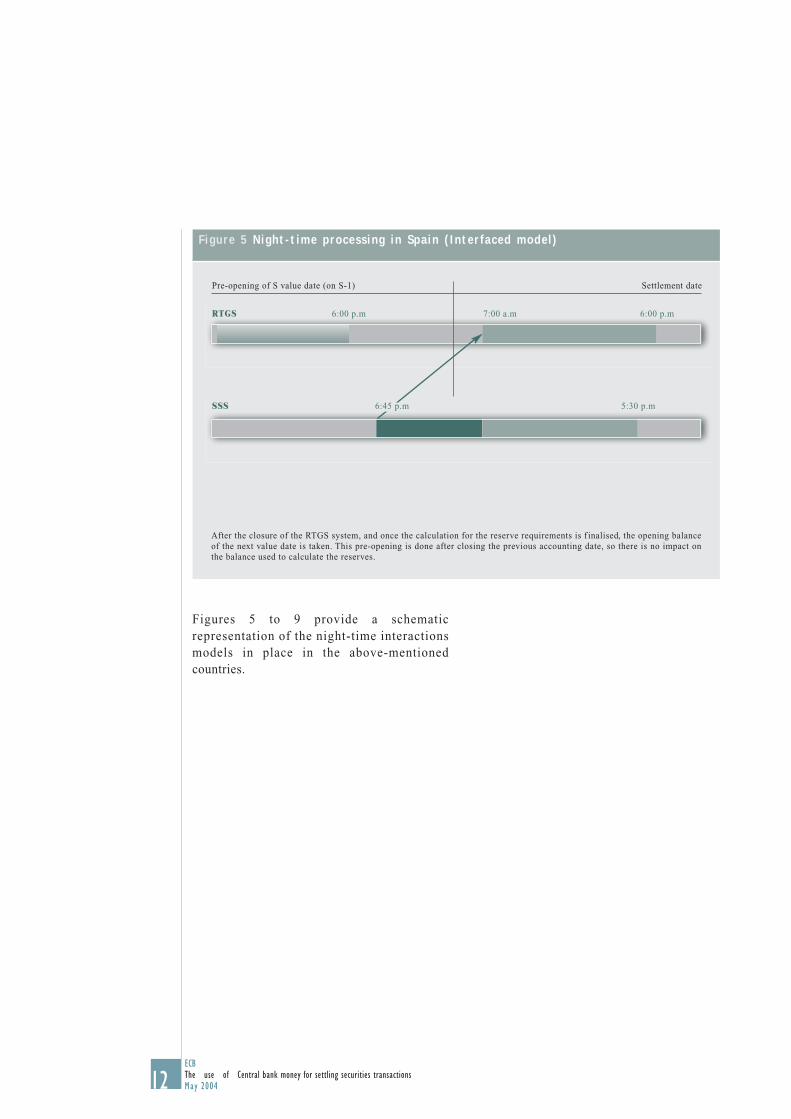

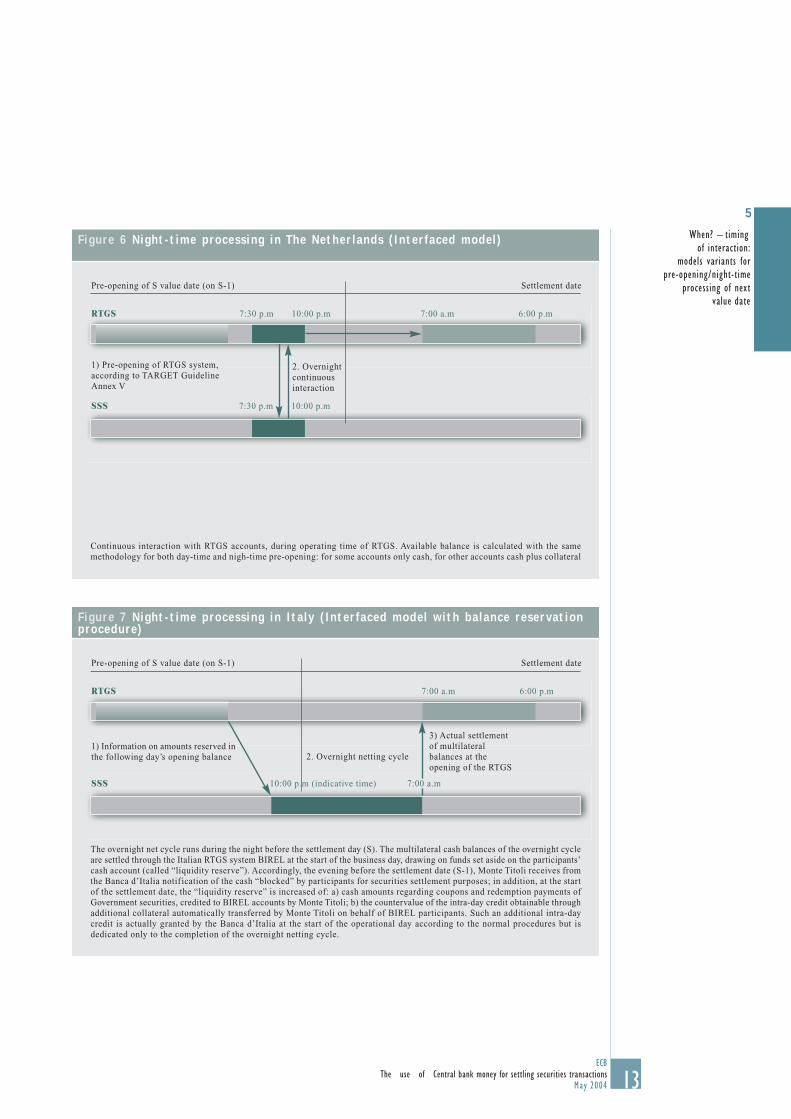

Figures 5 to 9 provide a schematicrepresentation of the night-time interactionsmodels in place in the above-mentionedcountries.

F i g u re 5 N i gh t - t ime p ro c e s s i n g i n S p a i n ( I n t e r f a c ed mode l )

RTGS 6:00 p.m 7:00 a.m 6:00 p.m

Pre-opening of S value date (on S-1) Settlement date

After the closure of the RTGS system, and once the calculation for the reserve requirements is f inalised, the opening balanceof the next value date is taken. This pre-opening is done after closing the previous accounting date, so there is no impact onthe balance used to calculate the reserves.

SSS 6:45 p.m 5:30 p.m

13c ECB

The use of Central bank money for settling securities transactionsMay 2004

5

When? – timingof interaction:

models variants forpre-opening/night-time

processing of nextvalue date

F i g u re 6 N i gh t - t ime p ro c e s s i n g i n Th e Ne th e r l a nd s ( I n t e r f a c ed mode l )

RTGS 7:30 p.m 10:00 p.m 7:00 a.m 6:00 p.m

Pre-opening of S value date (on S-1) Settlement date

Continuous interaction with RTGS accounts, during operating time of RTGS. Available balance is calculated with the samemethodology for both day-time and nigh-time pre-opening: for some accounts only cash, for other accounts cash plus collateral

SSS 7:30 p.m 10:00 p.m

1) Pre-opening of RTGS system,according to TARGET GuidelineAnnex V

2. Overnightcontinuousinteraction

F i g u re 7 N i gh t - t ime p ro c e s s i n g i n I t a l y ( I n t e r f a c ed mode l w i t h b a l a n c e re s e r va t i o np ro c edu re )

RTGS 7:00 a.m 6:00 p.m

Pre-opening of S value date (on S-1) Settlement date

The overnight net cycle runs during the night before the settlement day (S). The multilateral cash balances of the overnight cycleare settled through the Italian RTGS system BIREL at the start of the business day, drawing on funds set aside on the participants’cash account (called “liquidity reserve”). Accordingly, the evening before the settlement date (S-1), Monte Titoli receives fromthe Banca d’Italia notif ication of the cash “blocked” by participants for securities settlement purposes; in addition, at the startof the settlement date, the “liquidity reserve” is increased of: a) cash amounts regarding coupons and redemption payments ofGovernment securities, credited to BIREL accounts by Monte Titoli; b) the countervalue of the intra-day credit obtainable throughadditional collateral automatically transferred by Monte Titoli on behalf of BIREL participants. Such an additional intra-daycredit is actually granted by the Banca d’Italia at the start of the operational day according to the normal procedures but isdedicated only to the completion of the overnight netting cycle.

1) Information on amounts reserved inthe following day’s opening balance 2. Overnight netting cycle

SSS 10:00 p.m (indicative time) 7:00 a.m

3) Actual settlementof multilateralbalances at theopening of the RTGS

14ECB cThe use of Central bank money for settling securities transactionsMay 2004

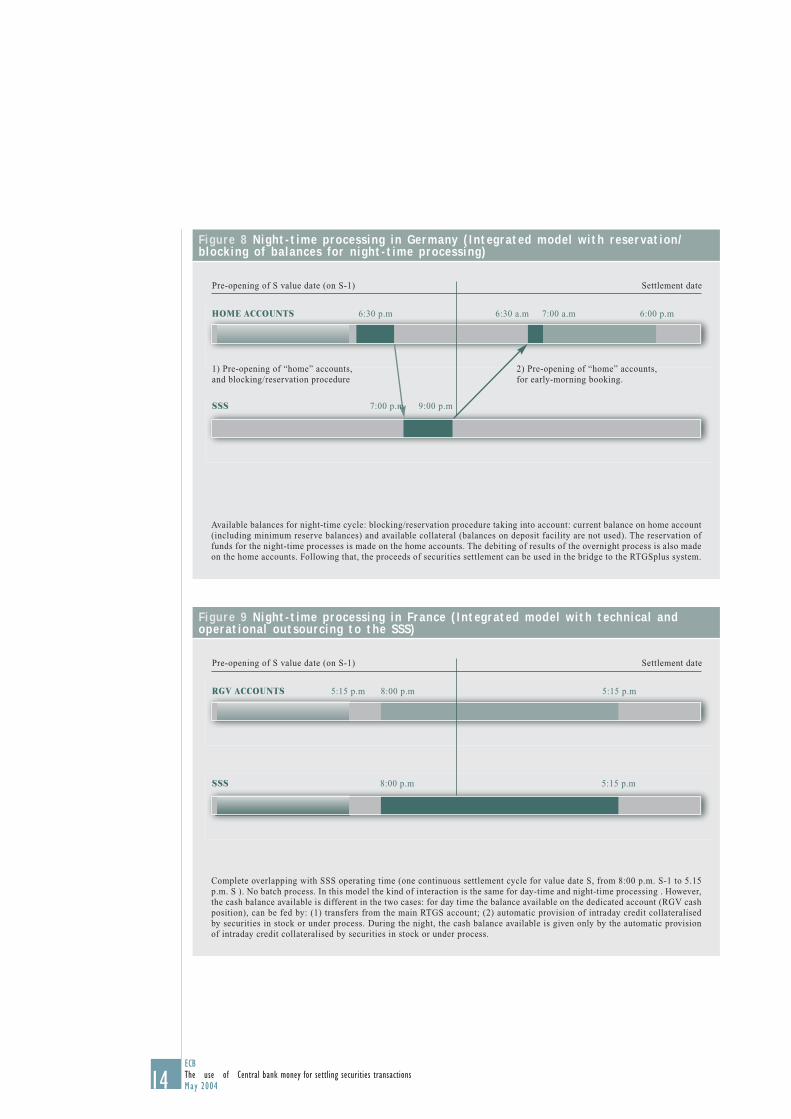

F i g u re 8 N i gh t - t ime p ro c e s s i n g i n G e rmany ( I n t eg r a t ed mode l w i t h re s e r va t i o n /b l o c k i n g o f b a l a n c e s f o r n i g h t - t ime p ro c e s s i n g )

HOME ACCOUNTS 6:30 p.m 6:30 a.m 7:00 a.m 6:00 p.m

Pre-opening of S value date (on S-1) Settlement date

Available balances for night-time cycle: blocking/reservation procedure taking into account: current balance on home account(including minimum reserve balances) and available collateral (balances on deposit facility are not used). The reservation offunds for the night-time processes is made on the home accounts. The debiting of results of the overnight process is also madeon the home accounts. Following that, the proceeds of securities settlement can be used in the bridge to the RTGSplus system.

1) Pre-opening of “home” accounts,and blocking/reservation procedure

2) Pre-opening of “home” accounts,for early-morning booking.

SSS 7:00 p.m 9:00 p.m

F i g u re 9 N i gh t - t ime p ro c e s s i n g i n F r an c e ( I n t eg r a t ed mode l w i t h t e c hn i c a l a ndope r a t i o n a l o u t s ou rc i n g t o t h e S S S )

RGV ACCOUNTS 5:15 p.m 8:00 p.m 5:15 p.m

Pre-opening of S value date (on S-1) Settlement date

Complete overlapping with SSS operating time (one continuous settlement cycle for value date S, from 8:00 p.m. S-1 to 5.15p.m. S ). No batch process. In this model the kind of interaction is the same for day-time and night-time processing . However,the cash balance available is different in the two cases: for day time the balance available on the dedicated account (RGV cashposition), can be fed by: (1) transfers from the main RTGS account; (2) automatic provision of intraday credit collateralisedby securities in stock or under process. During the night, the cash balance available is given only by the automatic provisionof intraday credit collateralised by securities in stock or under process.

SSS 8:00 p.m 5:15 p.m

15c ECB

The use of Central bank money for settling securities transactionsMay 2004

6

The compositionof the balance

available for cashsettlement

As described in Section 4, in the DVP three-step procedure, securities are finally deliveredonly after checks have been made to ensure thatthe cash transfer is possible, i.e. that theaccount has the required amount “available” andblocked for the settlement of the securitiestransaction.

The term “available amount” encompasses atleast two items:

1. The current balance of the account used forSSS settlement based on instructionsforwarded by participants, i.e. (i) the RTGSaccount balance in interfaced models, (ii) thebalance of another central bank account(where the RTGS is not directly used), or(iii) the balance of the participant’s (sub)accounts in the SSS environment pre-fundedwith central bank money, or assisted bycentral bank money balances guarantee13,depending on the model used.

2. Intraday credit available (when managedseparately from the RTGS account balance),which in turn depends on the amount ofavailable eligible collateral.

Two aspects are worth noting:

(i) Current balance is the cash balance at thetime of interaction with SSS.

(ii) In some systems, the amount of availablecollateral for the purpose of intraday-creditis calculated by also including in thecomputation the securities that the SSS istrying to deliver to the buyer in the samesettlement cycle for which the check of theavailable intraday credit is done.

The computation may be different in the case ofnight-time pre-opening of the followingbusiness day for the following reasons:

– It takes place after the payment systems andaccounting system end-of-day“housekeeping” procedures, therefore thecurrent RTGS or “home account” balance is

6 THE COMPO S I T I ON O F TH E B A L ANC EAVA I L A B L E F O R C A SH S E T T L EMENT

13 In this case the settlement may not be in central bank money.14 Monte Titoli works on the basis of the information received from

the Banca d’Italia based, in turn, on participants’ instructions.

in fact the opening balance of the followingbusiness day. This may include funds thathave been “released” by the central bankafter the closing of the previous dayaccounting date, for example the balancesthat may have been “blocked” for thefulfilment of the reserve requirement, andthat have therefore become free formobilisation at the opening of the followingbusiness day (e.g. in Germany, Italy andSpain). In principle, the same reasoningcould be applied to the funds for which thecounterparty has requested the activation ofthe deposit facility, which are automatically“returned” to the account holder on thefollowing morning. According to the survey,however, none of the responding NCBsfollows this practice.

– The RTGS current balance may not beavailable as such (because the RTGS systemis closed). Therefore, in the computation ofthe RTGS balance (available for SSSsettlement) it is possible that only the amountexplicitly devoted by RTGS participants isentered for the purpose of SSS night-timesettlement (e.g. Italy14).

– Alternatively, SSS cash accounts may havebeen adequately pre-funded via a liquiditybridge.

– Intraday refinancing possibilities for valuenext day could be counted as well, in a sortof night-time/early-morning provision ofcollateralised intraday credit. In the Frenchsystem, this facility is the only one availableduring the night-time processing.

1716ECB cThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ionsMay 2004

c ECBThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ions

May 2004

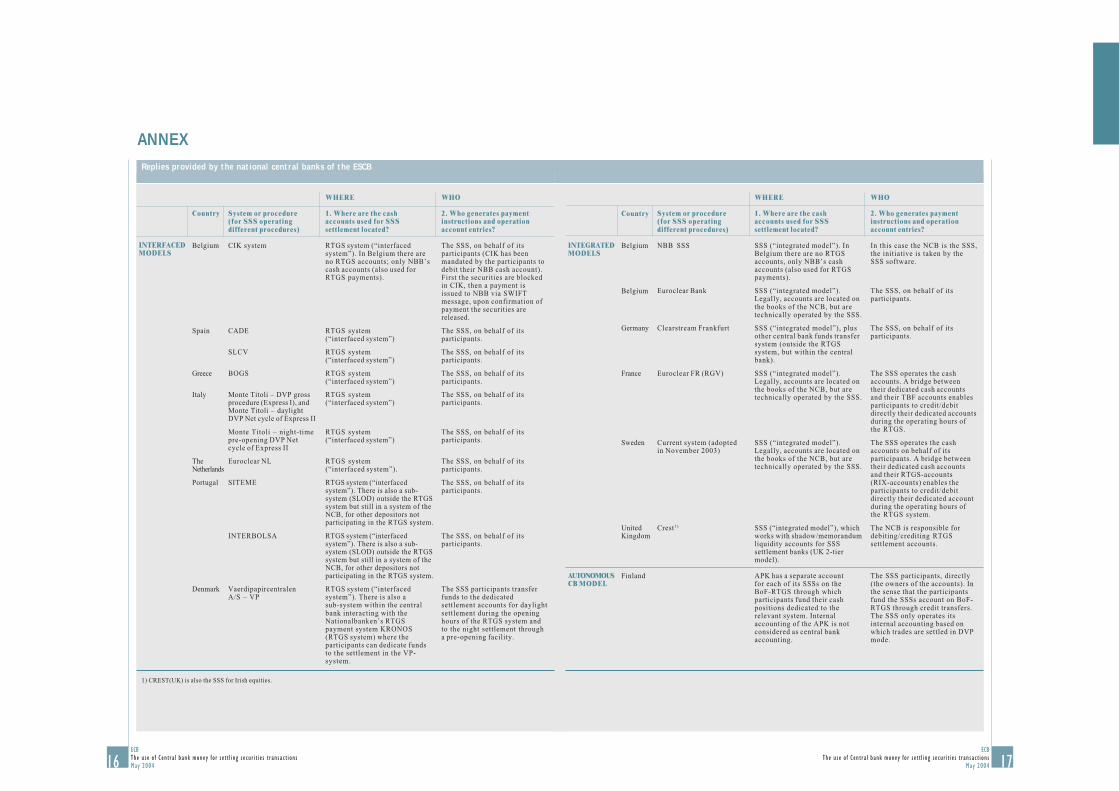

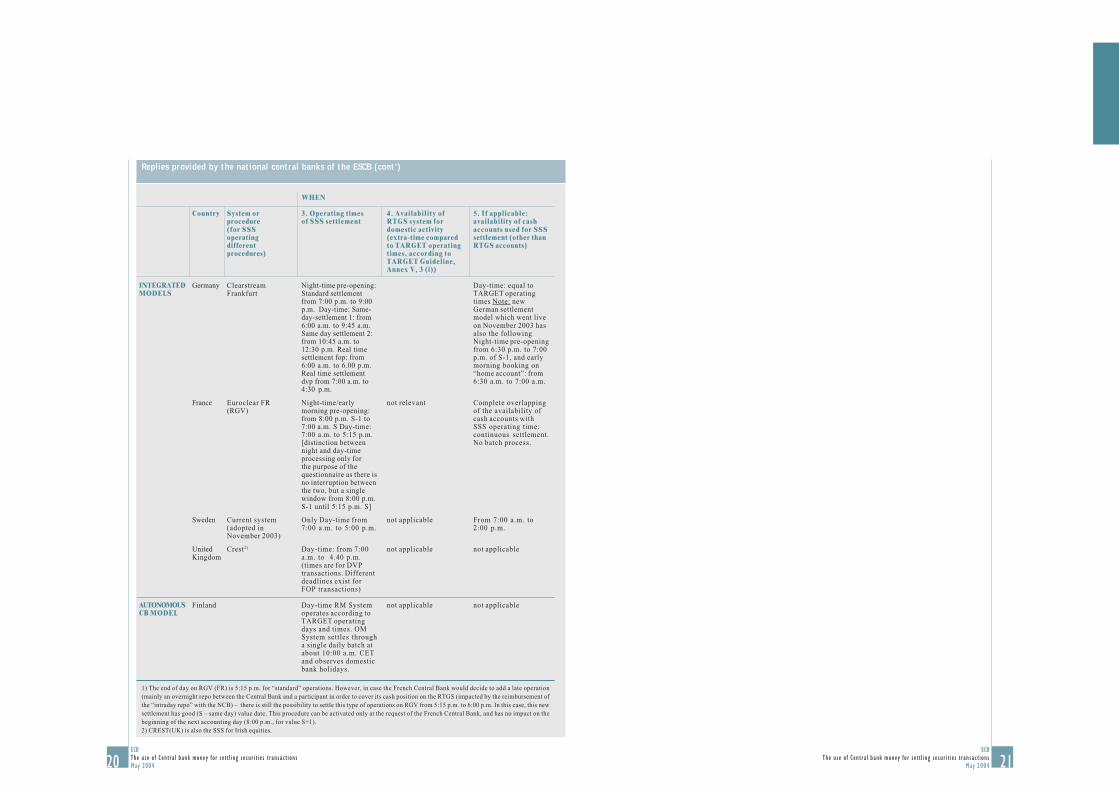

Replies provided by the national central banks of the ESCB

INTERFACEDMODELS

Country

Belgium

Spain

Greece

Italy

TheNetherlands

Portugal

Denmark

System or procedure(for SSS operatingdifferent procedures)

CIK system

CADE

SLCV

BOGS

Monte Titoli – DVP grossprocedure (Express I), andMonte Titoli – daylightDVP Net cycle of Express II

Monte Titoli – night-timepre-opening DVP Netcycle of Express II

Euroclear NL

SITEME

INTERBOLSA

VaerdipapircentralenA/S – VP

WHERE

1. Where are the cashaccounts used for SSSsettlement located?

RTGS system (“interfacedsystem”). In Belgium there areno RTGS accounts; only NBB’scash accounts (also used forRTGS payments).

RTGS system(“interfaced system”)

RTGS system(“interfaced system”)

RTGS system(“interfaced system”)

RTGS system(“interfaced system”)

RTGS system(“interfaced system”)

RTGS system(“interfaced system”).

RTGS system (“interfacedsystem”). There is also a sub-system (SLOD) outside the RTGSsystem but still in a system of theNCB, for other depositors notparticipating in the RTGS system.

RTGS system (“interfacedsystem”). There is also a sub-system (SLOD) outside the RTGSsystem but still in a system of theNCB, for other depositors notparticipating in the RTGS system.

RTGS system (“interfacedsystem”). There is also asub-system within the centralbank interacting with theNationalbanken’s RTGSpayment system KRONOS(RTGS system) where theparticipants can dedicate fundsto the settlement in the VP-system.

WHO

2. Who generates paymentinstructions and operationaccount entries?

The SSS, on behalf of itsparticipants (CIK has beenmandated by the participants todebit their NBB cash account).First the securities are blockedin CIK, then a payment isissued to NBB via SWIFTmessage, upon confirmation ofpayment the securities arereleased.

The SSS, on behalf of itsparticipants.

The SSS, on behalf of itsparticipants.

The SSS, on behalf of itsparticipants.

The SSS, on behalf of itsparticipants.

The SSS, on behalf of itsparticipants.

The SSS, on behalf of itsparticipants.

The SSS, on behalf of itsparticipants.

The SSS, on behalf of itsparticipants.

The SSS participants transferfunds to the dedicatedsettlement accounts for daylightsettlement during the openinghours of the RTGS system andto the night settlement througha pre-opening facility.

Country

Belgium

Belgium

Germany

France

Sweden

UnitedKingdom

Finland

System or procedure(for SSS operatingdifferent procedures)

NBB SSS

Euroclear Bank

Clearstream Frankfurt

Euroclear FR (RGV)

Current system (adoptedin November 2003)

Crest1)

WHERE

1. Where are the cashaccounts used for SSSsettlement located?

SSS (“integrated model”). InBelgium there are no RTGSaccounts, only NBB’s cashaccounts (also used for RTGSpayments).

SSS (“integrated model”).Legally, accounts are located onthe books of the NCB, but aretechnically operated by the SSS.

SSS (“integrated model”), plusother central bank funds transfersystem (outside the RTGSsystem, but within the centralbank).

SSS (“integrated model”).Legally, accounts are located onthe books of the NCB, but aretechnically operated by the SSS.

SSS (“integrated model”).Legally, accounts are located onthe books of the NCB, but aretechnically operated by the SSS.

SSS (“integrated model”), whichworks with shadow/memorandumliquidity accounts for SSSsettlement banks (UK 2-tiermodel).

APK has a separate accountfor each of its SSSs on theBoF-RTGS through whichparticipants fund their cashpositions dedicated to therelevant system. Internalaccounting of the APK is notconsidered as central bankaccounting.

WHO

2. Who generates paymentinstructions and operationaccount entries?

In this case the NCB is the SSS,the initiative is taken by theSSS software.

The SSS, on behalf of itsparticipants.

The SSS, on behalf of itsparticipants.

The SSS operates the cashaccounts. A bridge betweentheir dedicated cash accountsand their TBF accounts enablesparticipants to credit/debitdirectly their dedicated accountsduring the operating hours ofthe RTGS.

The SSS operates the cashaccounts on behalf of itsparticipants. A bridge betweentheir dedicated cash accountsand their RTGS-accounts(RIX-accounts) enables theparticipants to credit/debitdirectly their dedicated accountduring the operating hours ofthe RTGS system.

The NCB is responsible fordebiting/crediting RTGSsettlement accounts.

The SSS participants, directly(the owners of the accounts). Inthe sense that the participantsfund the SSSs account on BoF-RTGS through credit transfers.The SSS only operates itsinternal accounting based onwhich trades are settled in DVPmode.

INTEGRATEDMODELS

AUTONOMOUSCB MODEL

1) CREST(UK) is also the SSS for Irish equities.

ANNEX

1918ECB cThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ionsMay 2004

c ECBThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ions

May 2004

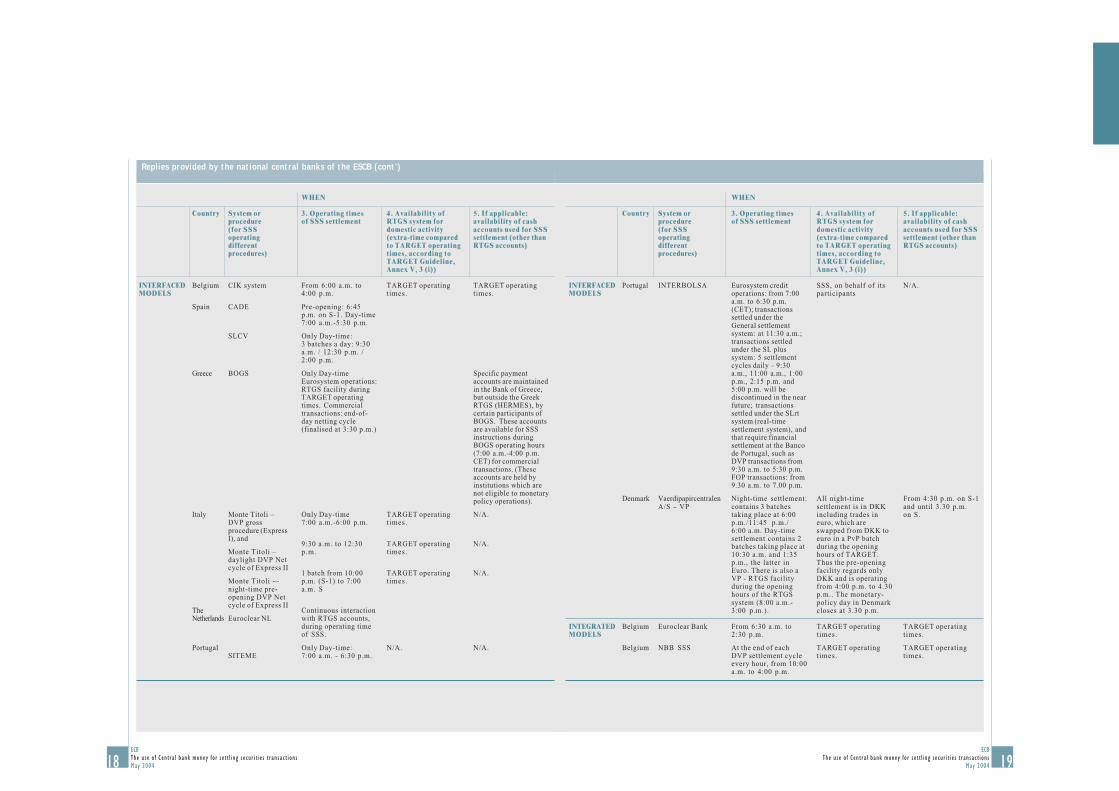

Replies provided by the national central banks of the ESCB (cont’)

INTERFACEDMODELS

Country

Belgium

Spain

Greece

Italy

TheNetherlands

Portugal

System orprocedure(for SSSoperatingdifferentprocedures)

CIK system

CADE

SLCV

BOGS

Monte Titoli –DVP grossprocedure (ExpressI), and

Monte Titoli –daylight DVP Netcycle of Express II

Monte Titoli -–night-time pre-opening DVP Netcycle of Express II

Euroclear NL

SITEME

WHEN

3. Operating timesof SSS settlement

From 6:00 a.m. to4:00 p.m.

Pre-opening: 6:45p.m. on S-1. Day-time7:00 a.m.-5:30 p.m.

Only Day-time:3 batches a day: 9:30a.m. / 12:30 p.m. /2:00 p.m.

Only Day-timeEurosystem operations:RTGS facility duringTARGET operatingtimes. Commercialtransactions: end-of-day netting cycle(finalised at 3:30 p.m.)

Only Day-time7:00 a.m.-6:00 p.m.

9:30 a.m. to 12:30p.m.

1 batch from 10:00p.m. (S-1) to 7:00a.m. S

Continuous interactionwith RTGS accounts,during operating timeof SSS.

Only Day-time:7:00 a.m. - 6:30 p.m.

4. Availability ofRTGS system fordomestic activity(extra-time comparedto TARGET operatingtimes, according toTARGET Guideline,Annex V, 3 (i))

TARGET operatingtimes.

TARGET operatingtimes.

TARGET operatingtimes.

TARGET operatingtimes.

N/A.

5. If applicable:availability of cashaccounts used for SSSsettlement (other thanRTGS accounts)

TARGET operatingtimes.

Specific paymentaccounts are maintainedin the Bank of Greece,but outside the GreekRTGS (HERMES), bycertain participants ofBOGS. These accountsare available for SSSinstructions duringBOGS operating hours(7:00 a.m.-4:00 p.m.CET) for commercialtransactions. (Theseaccounts are held byinstitutions which arenot eligible to monetarypolicy operations).

N/A.

N/A.

N/A.

N/A.

INTERFACEDMODELS

INTEGRATEDMODELS

Country

Portugal

Denmark

Belgium

Belgium

System orprocedure(for SSSoperatingdifferentprocedures)

INTERBOLSA

VaerdipapircentralenA/S – VP

Euroclear Bank

NBB SSS

WHEN

3. Operating timesof SSS settlement

Eurosystem creditoperations: from 7:00a.m. to 6:30 p.m.(CET); transactionssettled under theGeneral settlementsystem: at 11:30 a.m.;transactions settledunder the SL plussystem: 5 settlementcycles daily – 9:30a.m., 11:00 a.m., 1:00p.m., 2:15 p.m. and5:00 p.m. will bediscontinued in the nearfuture; transactionssettled under the SLrtsystem (real-timesettlement system), andthat require financialsettlement at the Bancode Portugal, such asDVP transactions from9:30 a.m. to 5:30 p.m.FOP transactions: from9.30 a.m. to 7.00 p.m.

Night-time settlement:contains 3 batchestaking place at 6:00p.m./11:45 p.m./6:00 a.m. Day-timesettlement contains 2batches taking place at10:30 a.m. and 1:35p.m., the latter inEuro. There is also aVP - RTGS facilityduring the openinghours of the RTGSsystem (8:00 a.m.-3:00 p.m.).

From 6:30 a.m. to2:30 p.m.

At the end of eachDVP settlement cycleevery hour, from 10:00a.m. to 4:00 p.m.

4. Availability ofRTGS system fordomestic activity(extra-time comparedto TARGET operatingtimes, according toTARGET Guideline,Annex V, 3 (i))

SSS, on behalf of itsparticipants

All night-timesettlement is in DKKincluding trades ineuro, which areswapped from DKK toeuro in a PvP batchduring the openinghours of TARGET.Thus the pre-openingfacility regards onlyDKK and is operatingfrom 4:00 p.m. to 4.30p.m.. The monetary-policy day in Denmarkcloses at 3.30 p.m.

TARGET operatingtimes.

TARGET operatingtimes.

5. If applicable:availability of cashaccounts used for SSSsettlement (other thanRTGS accounts)

N/A.

From 4:30 p.m. on S-1and until 3.30 p.m.on S.

TARGET operatingtimes.

TARGET operatingtimes.

2120ECB cThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ionsMay 2004

c ECBThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ions

May 2004

Replies provided by the national central banks of the ESCB (cont’)

INTEGRATEDMODELS

AUTONOMOUSCB MODEL

Country

Germany

France

Sweden

UnitedKingdom

Finland

System orprocedure(for SSSoperatingdifferentprocedures)

ClearstreamFrankfurt

Euroclear FR(RGV)

Current system(adopted inNovember 2003)

Crest2)

WHEN

3. Operating timesof SSS settlement

Night-time pre-opening:Standard settlementfrom 7:00 p.m. to 9:00p.m. Day-time: Same-day-settlement 1: from6:00 a.m. to 9:45 a.m.Same day settlement 2:from 10:45 a.m. to12:30 p.m. Real timesettlement fop: from6:00 a.m. to 6.00 p.m.Real time settlementdvp from 7:00 a.m. to4:30 p.m.

Night-time/earlymorning pre-opening:from 8:00 p.m. S-1 to7:00 a.m. S Day-time:7:00 a.m. to 5:15 p.m.[distinction betweennight and day-timeprocessing only forthe purpose of thequestionnaire as there isno interruption betweenthe two, but a singlewindow from 8:00 p.m.S-1 until 5:15 p.m. S]

Only Day-time from7:00 a.m. to 5:00 p.m.

Day-time: from 7:00a.m. to 4.40 p.m.(times are for DVPtransactions. Differentdeadlines exist forFOP transactions)

Day-time RM Systemoperates according toTARGET operatingdays and times. OMSystem settles througha single daily batch atabout 10:00 a.m. CETand observes domesticbank holidays.

4. Availability ofRTGS system fordomestic activity(extra-time comparedto TARGET operatingtimes, according toTARGET Guideline,Annex V, 3 (i))

not relevant

not applicable

not applicable

not applicable

5. If applicable:availability of cashaccounts used for SSSsettlement (other thanRTGS accounts)

Day-time: equal toTARGET operatingtimes Note: newGerman settlementmodel which went liveon November 2003 hasalso the followingNight-time pre-openingfrom 6:30 p.m. to 7:00p.m. of S-1, and earlymorning booking on“home account”: from6:30 a.m. to 7:00 a.m.

Complete overlappingof the availability ofcash accounts withSSS operating time:continuous settlement.No batch process.

From 7:00 a.m. to2:00 p.m.

not applicable

not applicable

1) The end of day on RGV (FR) is 5:15 p.m. for “standard” operations. However, in case the French Central Bank would decide to add a late operation(mainly an overnight repo between the Central Bank and a participant in order to cover its cash position on the RTGS (impacted by the reimbursement ofthe “intraday repo” with the NCB) – there is still the possibility to settle this type of operations on RGV from 5:15 p.m. to 6:00 p.m. In this case, this newsettlement has good (S – same day) value date. This procedure can be activated only at the request of the French Central Bank, and has no impact on thebeginning of the next accounting day (8:00 p.m., for value S+1).2) CREST(UK) is also the SSS for Irish equities.

2322ECB cThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ionsMay 2004

c ECBThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ions

May 2004

Replies provided by the national central banks of the ESCB (cont’)

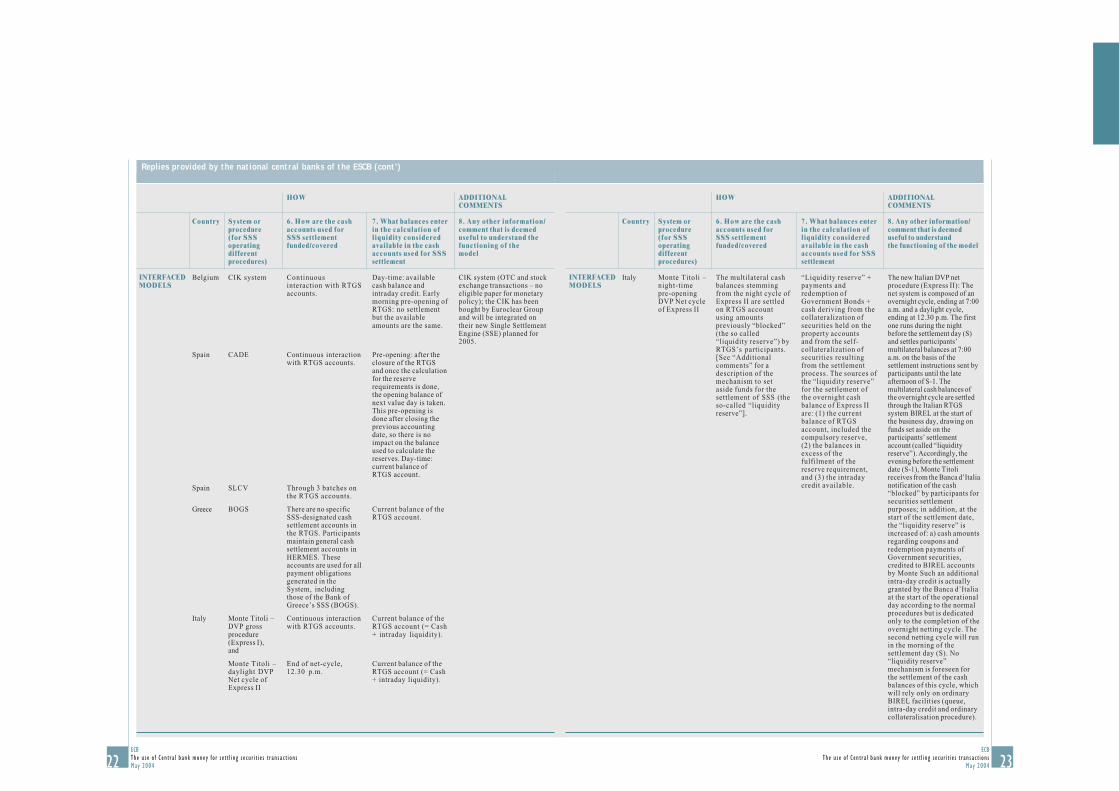

INTERFACEDMODELS

Country

Belgium

Spain

Spain

Greece

Italy

System orprocedure(for SSSoperatingdifferentprocedures)

CIK system

CADE

SLCV

BOGS

Monte Titoli –DVP grossprocedure(Express I),and

Monte Titoli –daylight DVPNet cycle ofExpress II

HOW

6. How are the cashaccounts used forSSS settlementfunded/covered

Continuousinteraction with RTGSaccounts.

Continuous interactionwith RTGS accounts.

Through 3 batches onthe RTGS accounts.

There are no specificSSS-designated cashsettlement accounts inthe RTGS. Participantsmaintain general cashsettlement accounts inHERMES. Theseaccounts are used for allpayment obligationsgenerated in theSystem, includingthose of the Bank ofGreece’s SSS (BOGS).

Continuous interactionwith RTGS accounts.

End of net-cycle,12.30 p.m.

7. What balances enterin the calculation ofliquidity consideredavailable in the cashaccounts used for SSSsettlement

Day-time: availablecash balance andintraday credit. Earlymorning pre-opening ofRTGS: no settlementbut the availableamounts are the same.

Pre-opening: after theclosure of the RTGSand once the calculationfor the reserverequirements is done,the opening balance ofnext value day is taken.This pre-opening isdone after closing theprevious accountingdate, so there is noimpact on the balanceused to calculate thereserves. Day-time:current balance ofRTGS account.

Current balance of theRTGS account.

Current balance of theRTGS account (= Cash+ intraday liquidity).

Current balance of theRTGS account (= Cash+ intraday liquidity).

ADDITIONALCOMMENTS

8. Any other information/comment that is deemeduseful to understand thefunctioning of themodel

CIK system (OTC and stockexchange transactions – noeligible paper for monetarypolicy); the CIK has beenbought by Euroclear Groupand will be integrated ontheir new Single SettlementEngine (SSE) planned for2005.

INTERFACEDMODELS

Country

Italy

System orprocedure(for SSSoperatingdifferentprocedures)

Monte Titoli –night-timepre-openingDVP Net cycleof Express II

HOW

6. How are the cashaccounts used forSSS settlementfunded/covered

The multilateral cashbalances stemmingfrom the night cycle ofExpress II are settledon RTGS accountusing amountspreviously “blocked”(the so called“liquidity reserve”) byRTGS’s participants.[See “Additionalcomments” for adescription of themechanism to setaside funds for thesettlement of SSS (theso-called “liquidityreserve”].

7. What balances enterin the calculation ofliquidity consideredavailable in the cashaccounts used for SSSsettlement

“Liquidity reserve” +payments andredemption ofGovernment Bonds +cash deriving from thecollateralization ofsecurities held on theproperty accountsand from the self-collateralization ofsecurities resultingfrom the settlementprocess. The sources ofthe “liquidity reserve”for the settlement ofthe overnight cashbalance of Express IIare: (1) the currentbalance of RTGSaccount, included thecompulsory reserve,(2) the balances inexcess of thefulfilment of thereserve requirement,and (3) the intradaycredit available.

ADDITIONALCOMMENTS

8. Any other information/comment that is deemeduseful to understandthe functioning of the model

The new Italian DVP netprocedure (Express II): Thenet system is composed of anovernight cycle, ending at 7:00a.m. and a daylight cycle,ending at 12.30 p.m. The firstone runs during the nightbefore the settlement day (S)and settles participants’multilateral balances at 7:00a.m. on the basis of thesettlement instructions sent byparticipants until the lateafternoon of S-1. Themultilateral cash balances ofthe overnight cycle are settledthrough the Italian RTGSsystem BIREL at the start ofthe business day, drawing onfunds set aside on theparticipants’ settlementaccount (called “liquidityreserve”). Accordingly, theevening before the settlementdate (S-1), Monte Titolireceives from the Banca d’Italianotification of the cash“blocked” by participants forsecurities settlementpurposes; in addition, at thestart of the settlement date,the “liquidity reserve” isincreased of: a) cash amountsregarding coupons andredemption payments ofGovernment securities,credited to BIREL accountsby Monte Such an additionalintra-day credit is actuallygranted by the Banca d’Italiaat the start of the operationalday according to the normalprocedures but is dedicatedonly to the completion of theovernight netting cycle. Thesecond netting cycle will runin the morning of thesettlement day (S). No“liquidity reserve”mechanism is foreseen forthe settlement of the cashbalances of this cycle, whichwill rely only on ordinaryBIREL facilities (queue,intra-day credit and ordinarycollateralisation procedure).

2524ECB cThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ionsMay 2004

c ECBThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ions

May 2004

Replies provided by the national central banks of the ESCB (cont’)

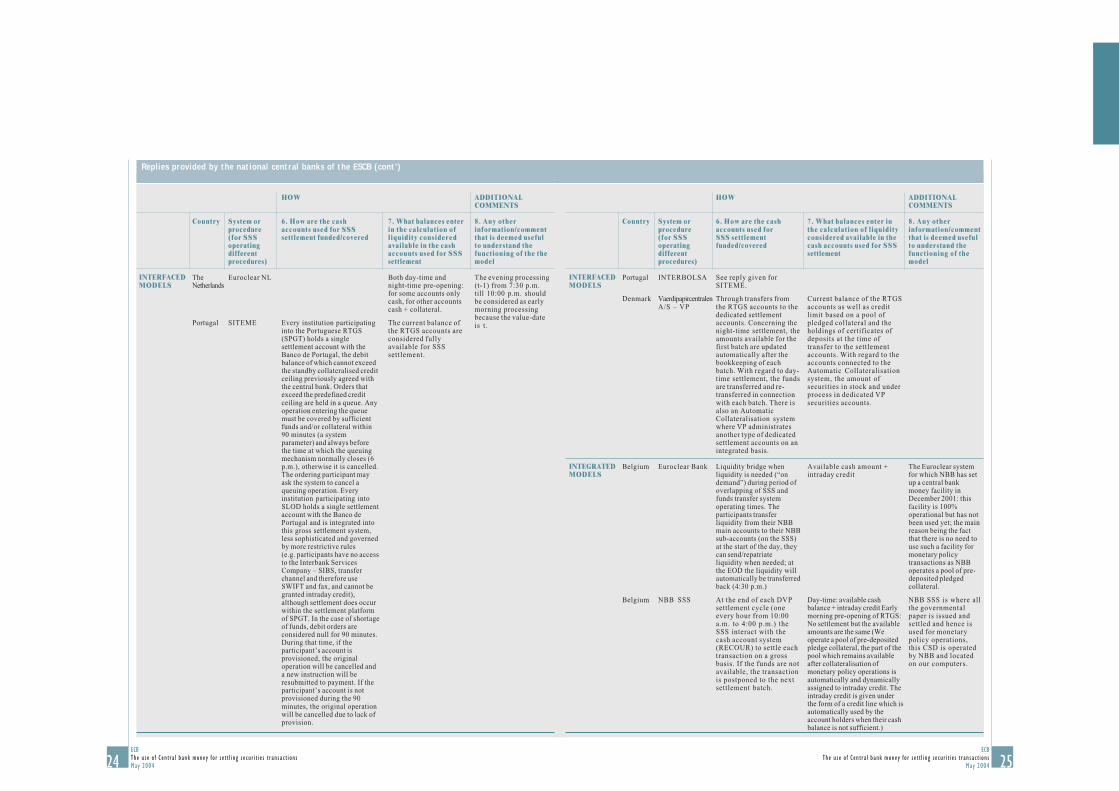

INTERFACEDMODELS

Country

TheNetherlands

Portugal

System orprocedure(for SSSoperatingdifferentprocedures)

Euroclear NL

SITEME

HOW

6. How are the cashaccounts used for SSSsettlement funded/covered

Every institution participatinginto the Portuguese RTGS(SPGT) holds a singlesettlement account with theBanco de Portugal, the debitbalance of which cannot exceedthe standby collateralised creditceiling previously agreed withthe central bank. Orders thatexceed the predefined creditceiling are held in a queue. Anyoperation entering the queuemust be covered by sufficientfunds and/or collateral within90 minutes (a systemparameter) and always beforethe time at which the queuingmechanism normally closes (6p.m.), otherwise it is cancelled.The ordering participant mayask the system to cancel aqueuing operation. Everyinstitution participating intoSLOD holds a single settlementaccount with the Banco dePortugal and is integrated intothis gross settlement system,less sophisticated and governedby more restrictive rules(e.g. participants have no accessto the Interbank ServicesCompany – SIBS, transferchannel and therefore useSWIFT and fax, and cannot begranted intraday credit),although settlement does occurwithin the settlement platformof SPGT. In the case of shortageof funds, debit orders areconsidered null for 90 minutes.During that time, if theparticipant’s account isprovisioned, the originaloperation will be cancelled anda new instruction will beresubmitted to payment. If theparticipant’s account is notprovisioned during the 90minutes, the original operationwill be cancelled due to lack ofprovision.

7. What balances enterin the calculation ofliquidity consideredavailable in the cashaccounts used for SSSsettlement

Both day-time andnight-time pre-opening:for some accounts onlycash, for other accountscash + collateral.

The current balance ofthe RTGS accounts areconsidered fullyavailable for SSSsettlement.

ADDITIONALCOMMENTS

8. Any otherinformation/commentthat is deemed usefulto understand thefunctioning of the themodel

The evening processing(t-1) from 7:30 p.m.till 10:00 p.m. shouldbe considered as earlymorning processingbecause the value-dateis t.

INTERFACEDMODELS

INTEGRATEDMODELS

Country

Portugal

Denmark

Belgium

Belgium

System orprocedure(for SSSoperatingdifferentprocedures)

INTERBOLSA

VaerdipapircentralenA/S – VP

Euroclear Bank

NBB SSS

HOW

6. How are the cashaccounts used forSSS settlementfunded/covered

See reply given forSITEME.

Through transfers fromthe RTGS accounts to thededicated settlementaccounts. Concerning thenight-time settlement, theamounts available for thefirst batch are updatedautomatically after thebookkeeping of eachbatch. With regard to day-time settlement, the fundsare transferred and re-transferred in connectionwith each batch. There isalso an AutomaticCollateralisation systemwhere VP administratesanother type of dedicatedsettlement accounts on anintegrated basis.

Liquidity bridge whenliquidity is needed (“ondemand”) during period ofoverlapping of SSS andfunds transfer systemoperating times. Theparticipants transferliquidity from their NBBmain accounts to their NBBsub-accounts (on the SSS)at the start of the day, theycan send/repatriateliquidity when needed; atthe EOD the liquidity willautomatically be transferredback (4:30 p.m.)

At the end of each DVPsettlement cycle (oneevery hour from 10:00a.m. to 4:00 p.m.) theSSS interact with thecash account system(RECOUR) to settle eachtransaction on a grossbasis. If the funds are notavailable, the transactionis postponed to the nextsettlement batch.

7. What balances enter inthe calculation of liquidityconsidered available in thecash accounts used for SSSsettlement

Current balance of the RTGSaccounts as well as creditlimit based on a pool ofpledged collateral and theholdings of certificates ofdeposits at the time oftransfer to the settlementaccounts. With regard to theaccounts connected to theAutomatic Collateralisationsystem, the amount ofsecurities in stock and underprocess in dedicated VPsecurities accounts.

Available cash amount +intraday credit

Day-time: available cashbalance + intraday credit Earlymorning pre-opening of RTGS:No settlement but the availableamounts are the same (Weoperate a pool of pre-depositedpledge collateral, the part of thepool which remains availableafter collateralisation ofmonetary policy operations isautomatically and dynamicallyassigned to intraday credit. Theintraday credit is given underthe form of a credit line which isautomatically used by theaccount holders when their cashbalance is not sufficient.)

ADDITIONALCOMMENTS

8. Any otherinformation/commentthat is deemed usefulto understand thefunctioning of themodel

The Euroclear systemfor which NBB has setup a central bankmoney facility inDecember 2001: thisfacility is 100%operational but has notbeen used yet; the mainreason being the factthat there is no need touse such a facility formonetary policytransactions as NBBoperates a pool of pre-deposited pledgedcollateral.

NBB SSS is where allthe governmentalpaper is issued andsettled and hence isused for monetarypolicy operations,this CSD is operatedby NBB and locatedon our computers.

2726ECB cThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ionsMay 2004

c ECBThe use of Cent ra l bank money for se t t l ing secur i t i e s t ransac t ions

May 2004

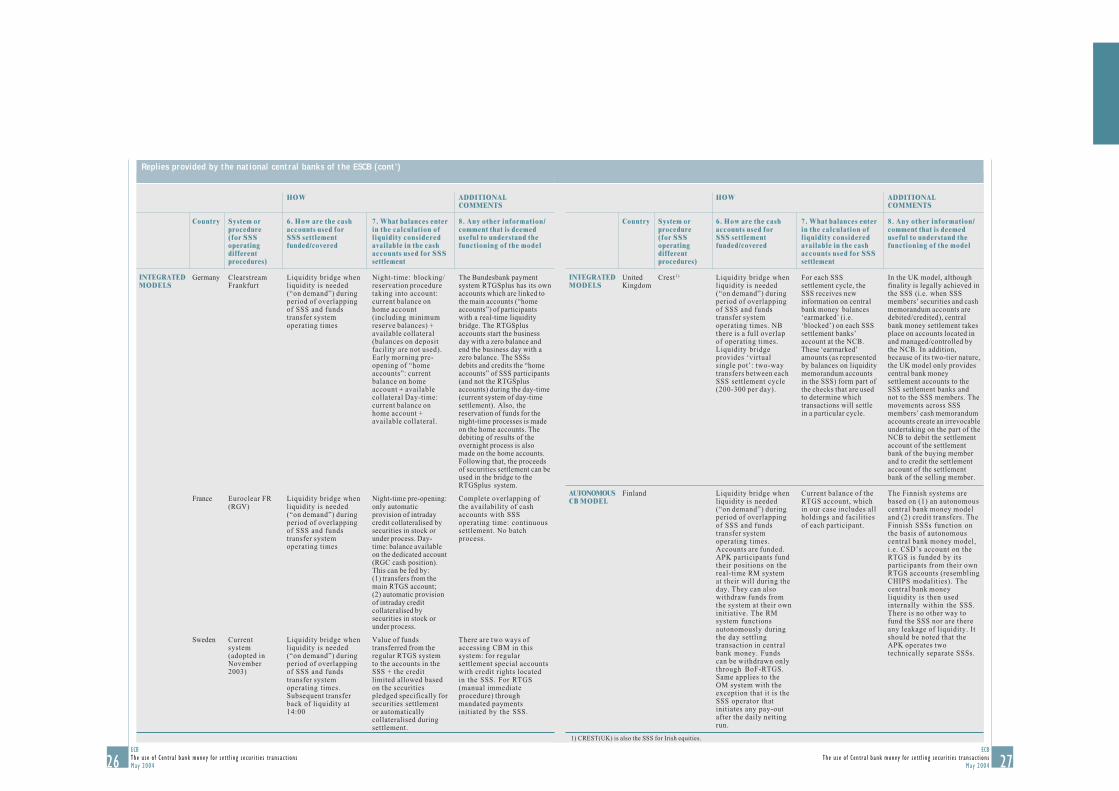

Replies provided by the national central banks of the ESCB (cont’)

INTEGRATEDMODELS

Country

Germany

France

Sweden

System orprocedure(for SSSoperatingdifferentprocedures)

ClearstreamFrankfurt

Euroclear FR(RGV)

Currentsystem(adopted inNovember2003)

HOW

6. How are the cashaccounts used forSSS settlementfunded/covered

Liquidity bridge whenliquidity is needed(“on demand”) duringperiod of overlappingof SSS and fundstransfer systemoperating times

Liquidity bridge whenliquidity is needed(“on demand”) duringperiod of overlappingof SSS and fundstransfer systemoperating times

Liquidity bridge whenliquidity is needed(“on demand”) duringperiod of overlappingof SSS and fundstransfer systemoperating times.Subsequent transferback of liquidity at14:00

7. What balances enterin the calculation ofliquidity consideredavailable in the cashaccounts used for SSSsettlement

Night-time: blocking/reservation proceduretaking into account:current balance onhome account(including minimumreserve balances) +available collateral(balances on depositfacility are not used).Early morning pre-opening of “homeaccounts”: currentbalance on homeaccount + availablecollateral Day-time:current balance onhome account +available collateral.

Night-time pre-opening:only automaticprovision of intradaycredit collateralised bysecurities in stock orunder process. Day-time: balance availableon the dedicated account(RGC cash position).This can be fed by:(1) transfers from themain RTGS account;(2) automatic provisionof intraday creditcollateralised bysecurities in stock orunder process.

Value of fundstransferred from theregular RTGS systemto the accounts in theSSS + the creditlimited allowed basedon the securitiespledged specifically forsecurities settlementor automaticallycollateralised duringsettlement.

ADDITIONALCOMMENTS

8. Any other information/comment that is deemeduseful to understand thefunctioning of the model

The Bundesbank paymentsystem RTGSplus has its ownaccounts which are linked tothe main accounts (“homeaccounts”) of participantswith a real-time liquiditybridge. The RTGSplusaccounts start the businessday with a zero balance andend the business day with azero balance. The SSSsdebits and credits the “homeaccounts” of SSS participants(and not the RTGSplusaccounts) during the day-time(current system of day-timesettlement). Also, thereservation of funds for thenight-time processes is madeon the home accounts. Thedebiting of results of theovernight process is alsomade on the home accounts.Following that, the proceedsof securities settlement can beused in the bridge to theRTGSplus system.

Complete overlapping ofthe availability of cashaccounts with SSSoperating time: continuoussettlement. No batchprocess.

There are two ways ofaccessing CBM in thissystem: for regularsettlement special accountswith credit rights locatedin the SSS. For RTGS(manual immediateprocedure) throughmandated paymentsinitiated by the SSS.

INTEGRATEDMODELS

AUTONOMOUSCB MODEL

Country

UnitedKingdom

Finland

System orprocedure(for SSSoperatingdifferentprocedures)

Crest1)

HOW

6. How are the cashaccounts used forSSS settlementfunded/covered

Liquidity bridge whenliquidity is needed(“on demand”) duringperiod of overlappingof SSS and fundstransfer systemoperating times. NBthere is a full overlapof operating times.Liquidity bridgeprovides ‘virtualsingle pot’: two-waytransfers between eachSSS settlement cycle(200-300 per day).

Liquidity bridge whenliquidity is needed(“on demand”) duringperiod of overlappingof SSS and fundstransfer systemoperating times.Accounts are funded.APK participants fundtheir positions on thereal-time RM systemat their will during theday. They can alsowithdraw funds fromthe system at their owninitiative. The RMsystem functionsautonomously duringthe day settlingtransaction in centralbank money. Fundscan be withdrawn onlythrough BoF-RTGS.Same applies to theOM system with theexception that it is theSSS operator thatinitiates any pay-outafter the daily nettingrun.

7. What balances enterin the calculation ofliquidity consideredavailable in the cashaccounts used for SSSsettlement

For each SSSsettlement cycle, theSSS receives newinformation on centralbank money balances‘earmarked’ (i.e.‘blocked’) on each SSSsettlement banks’account at the NCB.These ‘earmarked’amounts (as representedby balances on liquiditymemorandum accountsin the SSS) form part ofthe checks that are usedto determine whichtransactions will settlein a particular cycle.

Current balance of theRTGS account, whichin our case includes allholdings and facilitiesof each participant.

ADDITIONALCOMMENTS

8. Any other information/comment that is deemeduseful to understand thefunctioning of the model

In the UK model, althoughfinality is legally achieved inthe SSS (i.e. when SSSmembers’ securities and cashmemorandum accounts aredebited/credited), centralbank money settlement takesplace on accounts located inand managed/controlled bythe NCB. In addition,because of its two-tier nature,the UK model only providescentral bank moneysettlement accounts to theSSS settlement banks andnot to the SSS members. Themovements across SSSmembers’ cash memorandumaccounts create an irrevocableundertaking on the part of theNCB to debit the settlementaccount of the settlementbank of the buying memberand to credit the settlementaccount of the settlementbank of the selling member.

The Finnish systems arebased on (1) an autonomouscentral bank money modeland (2) credit transfers. TheFinnish SSSs function onthe basis of autonomouscentral bank money model,i.e. CSD’s account on theRTGS is funded by itsparticipants from their ownRTGS accounts (resemblingCHIPS modalities). Thecentral bank moneyliquidity is then usedinternally within the SSS.There is no other way tofund the SSS nor are thereany leakage of liquidity. Itshould be noted that theAPK operates twotechnically separate SSSs.

1) CREST(UK) is also the SSS for Irish equities.

![SECURITIES CONTRACTS (REGULATION) ACT, 1956 · SECURITIES CONTRACTS (REGULATION) ACT, 1956 [42 OF 1956] An Act to prevent undesirable transactions in securities by regulating the](https://img.pdfslide.us/doc/110x75/5e0b22521f39f236845e8071/securities-contracts-regulation-act-1956-securities-contracts-regulation-act.jpg)