Embed Size (px)

Citation preview

The Trilemma, International Currencies, Capital Controls and Financial Development

Menzie D. ChinnUniversity of Wisconsin, Madison

and NBER

Central German Doctoral Program Economics

Leipzig UniversitätDecember 17-22, 2015Rev 21.12.2015 18:30

2

Outline of Week

1. Trilemma2. Trilemma vs. Dilemma/Capital Controls3. Capital Controls/Financial

Development/Int’l Currencies4. International Currencies

The Next Reserve Currencies

Roles of an International Currency

Table 1:

Function of money Governments Private actors

Store of value International reserve holdings Currency substitution (private dollarization)

Medium of exchange Vehicle currency for foreign exchange intervention

Invoicing trade and financial transactions

Unit of account Anchor for pegging local currency

Denominating trade and financial transactions

Source: Kenen (1983)

Reserve Holdings, Homogeneous data

5

.0

.1

.2

.3

.4

.5

.6

.7

.8

1965 1970 1975 1980 1985 1990 1995 2000

USD

DEM EUR

JPYFFR SFRNLG

ECU

GBP

Reserve Holdings, Old + COFER

6

Determinants, again

(1)The pattern of output and trade.

(2)Financial markets (3)Confidence in the currency (4)Network externalities

7

Key Estimates, using Logit

8

Antecedents for Lower Tier Switches: UK and Germany

9

GDP

10

Geography of FX Trading(Proxy for Financial Development)

11

Financial Development

12

Financial Development

13

Financial Development

14

Institutional Development

15

Financial Openness (Chinn-Ito)

16

The RMB’s Prospects

RMB bonds and deposits in Hong Kong are small as a fraction of total RMB bonds and deposits (and of course Hong Kong is in any case part of China).

Development of China’s domestic financial market has just begun.

It is still very highly regulated, and the domestic system is “financially repressed.”

Cross-border capital flows are subject to heavy controls. Foreign companies still cannot borrow in mainland China.

- Frankel (2011)17

Eichengreen, Chitu, Mehl

18

Benefits

Seigniorage Lower government and private

borrowing costs Other nonpecuniary benefits

(prestige)

19

Costs Some countries might peg their currency

against the new reserve currency , mitigating the use of the own currency as macroeconomic shock absorber

Greater financial integration will make external shocks more easily transmitted to the reserve currency economy, above and beyond that associated with open capital markets.

Private investor shifts in and out of the reserve currency will force monetary authorities to respond to larger shocks in money demand.

20

Other Aspects of New International Currencies

Roles of an International Currency

Table 1:

Function of money Governments Private actors

Store of value International reserve holdings Currency substitution (private dollarization)

Medium of exchange Vehicle currency for foreign exchange intervention

Invoicing trade and financial transactions

Unit of account Anchor for pegging local currency

Denominating trade and financial transactions

Source: Kenen (1983)

0

4

8

12

16

20

24

1998 2000 2002 2004 2006 2008 2010 2012 2014

CNY

CHF

JPYShare offorex trading(out of 200%)

Source: BIS Triennial Survey (2013)

RMB in Foreign Exchange Trading

International Borrowing in own currency

24Source: Prasad (2015)

Payments in RMB

25Source: Prasad (2015)

Payments in RMB by location

26Source: Prasad (2015)

Trade Invoicing and RMB

Estimation of determinants Long tradition

27

Underused RMB?

United Kingdom

Austria

Belgium

Denmark

FranceItaly

Luxembourg

Netherlands

Norway SwedenFinland

GreeceIceland

IrelandPortugal

SpainAustralia

Cyprus

IndonesiaThailand

Slovak REstoniaLatvia

HungaryLithuania Slovenia

ChinaGermany

Japan

0.0

2.0

4.0

6.0

8.1

Exp

orts

sha

re in

the

wor

ld(%

), 20

07-1

1

0 .2 .4 .6 .8 1Share of exports invoicing in home currency (%), 2007-11

The Dollar Dominance

AUTBELDNK FRADEUITA NLD NORSWE FIN ISL

IRL

PRTESP CYP

IND

SVK ESTLVA HUNLTUSVNAustralia

IndoneThailandUnited KingdomEuro_Area

Japan

0.2

.4.6

.81

Exp

orts

to th

e U

nite

d S

tate

s(%

), 20

07-1

1

0 .2 .4 .6 .8 1Dollar share of export invoicing (%), 2007-11

Ito and Chinn (2015) Analyze the link between financial

liberalization and the potential path for RMB’s internationalization

Investigate how China’s liberalization efforts would affect the use of RMB invoicing

RMB’s becoming a major invoicing currency is not a sufficient condition for the RMB internationalization

But focus on this issue because:o Data are limitedo RMB’s becoming an invoicing currency is

an important first step

Three Questions1. What factors, including capital account

liberalization, affect the use of currencies in terms of invoicing in international trade?

2. How does the RMB’s recent experience differ from that of other currencies in terms of their use for invoicing exports?

3. How would foreseeable capital account liberalization China may implement affect the level of use of the RMB in international trade?

Empirical Analysis

Investigate the determinants of the use of three currencies, the U.S. dollar, the Euro, and the home country’s currency for export invoicing by using the dataset that encompasses 50 countries

Show the implied share of RMB based on the model estimation

Predict the (out-of-period) path of RMB shares for different scenarios of CA liberalization

Data on the Shares of Currencies in Trade Invoicing

The empirical literature on trade invoicing is thin, esp. in terms of the cross-country analysis, due to data limitations

Exceptions: Goldberg and Tille (2008) and Kamps (2006)

Augment the Kamps dataset by resorting to past and recent papers and gov’t reports on trade invoicing Expand the data coverage from 43

countries for 1990s through 2004 to 50 countries for 1970s through 2012

The dataset is probably the most comprehensive one

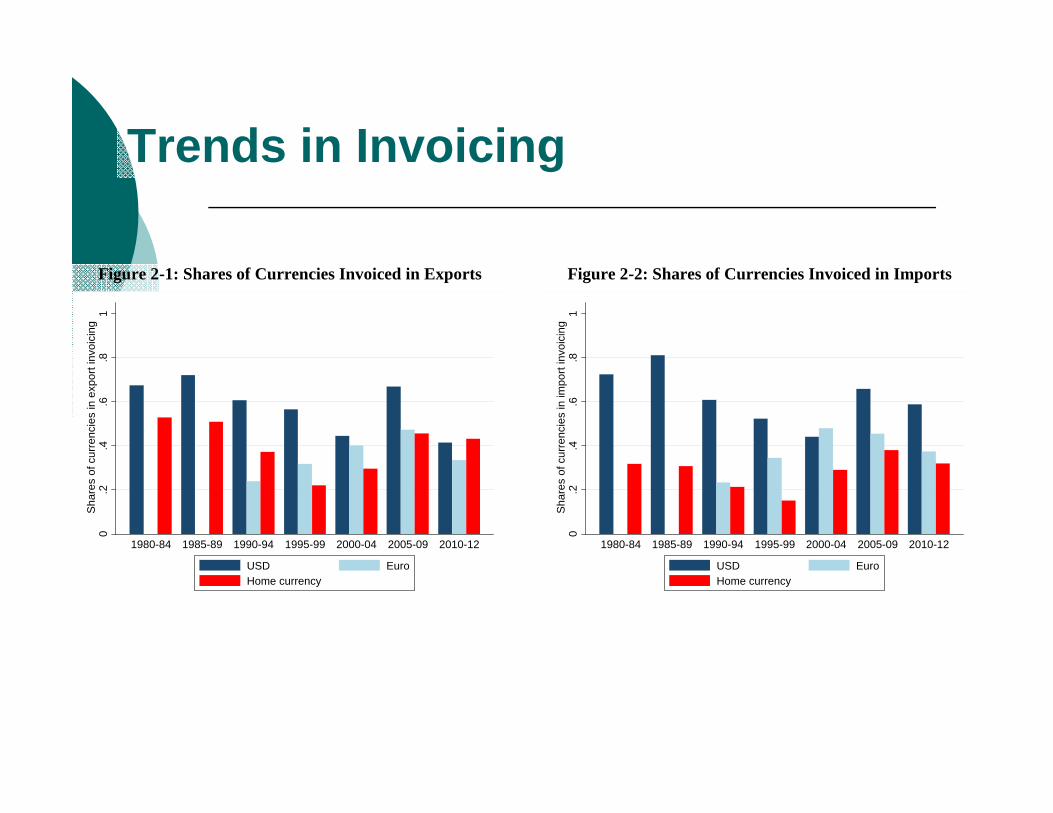

Trends in Invoicing

Figure 2-1: Shares of Currencies Invoiced in Exports

Figure 2-2: Shares of Currencies Invoiced in Imports

0.2

.4.6

.81

Sha

res

of c

urre

ncie

s in

exp

ort i

nvoi

cing

1980-84 1985-89 1990-94 1995-99 2000-04 2005-09 2010-12

USD EuroHome currency

0.2

.4.6

.81

Sha

res

of c

urre

ncie

s in

impo

rt in

voic

ing

1980-84 1985-89 1990-94 1995-99 2000-04 2005-09 2010-12

USD EuroHome currency

Trends in Invoicing - Groups

Figure 3-1: Shares of Currencies in Export Invoicing – EU Countries

Note: The countries in the EU subsample are: Austria, Belgium, Bulgaria, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Poland, Portugal, Romania, Slovak Republic, Slovenia, Spain, Sweden, and the United Kingdom.

Figure 3-2: Shares of Currencies Invoiced in Exports – ex-Japan Asian and Pacific Countries

Note: The countries in this subsample are: Australia, China, India, Indonesia, Korea, Malaysia, Pakistan, and Thailand.

0.2

.4.6

.81

Shar

es o

f cur

renc

ies

in e

xpor

t inv

oici

ng

1995-99 2000-04 2005-09 2010-12

USD EuroHome currency

0.2

.4.6

.81

Shar

es o

f cur

renc

ies

in e

xpor

t inv

oici

ng

1985-89 1990-94 1995-99 2000-04 2005-09 2010-12

USD EuroHome currency

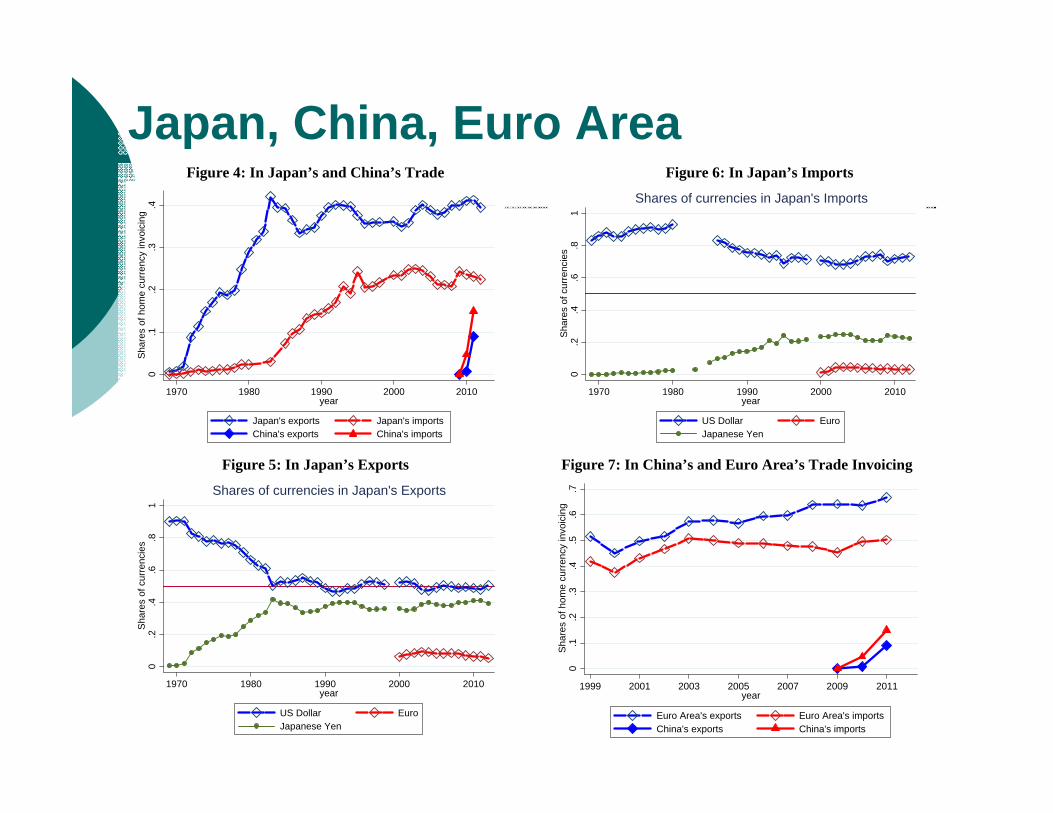

Japan, China, Euro AreaFigure 4: In Japan’s and China’s Trade

Figure 5: In Japan’s Exports

Figure 6: In Japan’s Imports

Figure 7: In China’s and Euro Area’s Trade Invoicing

0.1

.2.3

.4S

hare

s of

hom

e cu

rren

cy in

voic

ing

1970 1980 1990 2000 2010year

Japan's exports Japan's importsChina's exports China's imports

0.2

.4.6

.81

Sha

res

of c

urre

ncie

s

1970 1980 1990 2000 2010year

US Dollar EuroJapanese Yen

Shares of currencies in Japan's Exports

0.2

.4.6

.81

Sha

res

of c

urre

ncie

s

1970 1980 1990 2000 2010year

US Dollar EuroJapanese Yen

Shares of currencies in Japan's Imports

0.1

.2.3

.4.5

.6.7

Sha

res

of h

ome

curr

ency

invo

icin

g

1999 2001 2003 2005 2007 2009 2011year

Euro Area's exports Euro Area's importsChina's exports China's imports

Formal Empirical Analysis

Conduct panel data analysis to investigate the determinants of export invoicing

We use the augmented trade invoicing data that encompass 50 countries for 1970s through 2012 (though very unbalanced)

The model follows Kamps (2006)Cit

Cit

Cit

Cit

CEXit FLDX 1321

XCit Share of exports to the US or Euro area to total

exports, or to the world trade Commodity exports as a percentage of total

exports Relative income Exchange rate volatility and inflation

differentials Financial Development = Fin_Size = PCGDP x

Priv_sizeFLC

it = Financial openness, Chinn-Ito index (i.e., de jure index based on IMF’s AREAER)DC

it = Dummies for Monetary union and pegs to USD or Euro

Cit

Cit

Cit

Cit

CEXit FLDX 1321

Extended Analyses Tested w/ de facto measure of financial openness

using the Lane and Milesi-Ferretti data ??

Tested w/ post-1996 disaggregated AREAER data Capital market securities Money market instruments Collective investment securities Derivatives and other instruments Commercial credits Financial credits Guarantees, sureties, and financial backup facilities Direct investment Repatriation of profits or liquidation of direct investment Real estate transactions Personal capital movements Provisions specific to commercial banks and other credit institutions Provisions specific to institutional investors:

Extended Analyses When the average of 13

disaggregated categories is included ?? Significantly negative for both

USD and HOME eqs. When each of the disaggregated

categories is included: Significantly positive:

liquidation of direct investmentpersonal capital transactionsinstitutional investorscommercial credit

Extended Analyses What about the impact of legal

development? Use LEGAL = principal component of LAO, BQ, and CORRUPT

Insignificantly negative for the U.S. dollar share estimation, significantly negative for the Euro share estimation, and insignificantly positive for the home currency share estimation

Extended Analyses What about financial crisis? We include the dummy for

currency, banking, or debt crisis individually Countries that experience a banking crisis tend to

increase the share of the U.S. dollar for their export invoicing by 2.8 percentage points while they also tend to decrease the share of the Euro by 2.3 percentage points

The effect of banking crisis on the home currency share or that of other types of crises turn out to be insignificant

When including a dummy for the GFC Countries on average increase the share of dollar

invoicing by 4.1 percentage points, although the crisis does not affect other currency shares

Extended Analyses Do appreciation expectations of the home

currency lead to more use of the currency for export invoicing? We include in the time trend of the exchange rate Significantly positive for the U.S. dollar

share estimation = Appreciation trend of the home currency leads to less use of the USD for export invoicing

Extended Analyses Does net investment position matter? We

include the NIP variable based on the Lane and Milesi-Ferretti dataset Significantly positive for the home

currency share estimation = Countries with better net investment positions tend to be able to invoice their exports in their own currency

Endogeneity issues?: Countries with int’l currencies often turn into debtor countries

Methodological Robustness Checks

Tobit estimation Seemingly Unrelated Regression (SUR)

Estimation The estimates are mostly robust,

including the financial openness variable While financial development continues

to be a negative contributor to USD invoicing, it also becomes a significantly negative contributor to home currency invoicing

Predicted vs. Actual Currency Shares

(a) RMB in Chinese Exports

(c) USD in Japan’s Exports

(b) Japanese Yen in Japan’s Exports

(d) Euro Share in Euro Area’s Exports

0.1

.2.3

.4.5

.6.7

.8.9

1S

hare

of Y

uan

expo

rt in

voic

ing

2004 2005 2006 2007 2008 2009 2010years

Prediction Actual

0.1

.2.3

.4.5

.6.7

.8.9

1S

hare

of U

SD

exp

ort i

nvoi

cing

1970 1980 1990 2000 2010years

Prediction Actual

0.1

.2.3

.4.5

.6.7

.8.9

1S

hare

of Y

en e

xpor

t inv

oici

ng

1970 1980 1990 2000 2010years

Prediction Actual

.5.6

.7.8

.91

Sha

re o

f Eur

o in

exp

ort i

nvoi

cing

2000 2002 2004 2006 2008 2010years

Prediction Actual

Forecasting of the RMB Share in China’s Exports

0.0

5.1

.15

.2.2

5.3

.35

Sha

re o

f RM

B in

exp

ort i

nvoi

cing

2008 2010 2012 2014 2016 2018years

Optimistic Pessmistic Prediction Out-of-sample forecasting Actual

The baseline assumption: KAOPEN=0.35 for 2015 (c.f., the current level of 0.16), but not as high as the level of Brazil, Columbia, and Indonesia (0.41). 0.50 for 2018, more financially open than Turkey (0.45).

Under the pessimistic scenario: no change in KAOPEN in 2015 (i.e., 0.16). 0.25 In 2018

Under the optimistic scenario, 0.60 in 2015 and to 0.80 in 2018

Concluding Remarks The U.S. dollar still plays an important role as

the vehicle currency Asian countries in particular have relied heavily

on the U.S. dollar The share of the RMB use for trade

transactions has been rapidly rising Interestingly, the Chinese RMB has been more

used for import invoicing rather than for export invoicing

Countries with more developed financial markets tend to invoice less in the U.S. dollar

Countries with a more open capital account tend to invoice in either the Euro or their home currency

Concluding Remarks (Ito Chinn, 2015)

A currency with expected appreciation tends to be used for export invoicing

The use of the RMB in export invoicing should have been higher, around low to mid-20s as a percentage of total exports

The underperformance of the RMB export invoicing can be attributed to the inertia of the choice of currency for trade invoicing

The share of RMB invoicing for China’s exports may rise up to 27.5% in 2015 and 33.5% in 2018

Summing Up

On its present trajectory, China will have a nearly fully open capital account in the nextfew years, allowing the RMB to play an increasingly prominent role in global trade and finance. The RMB already plays a significant role in the denomination and settlement of international trade transactions that involve China. The RMB is also making inroads into the global financial system and is starting to appear in the reserve portfolios of certain emerging market central banks.

(Prasad, 2015)51

Roles of an International Currency

Table 1:

Function of money Governments Private actors

Store of value International reserve holdings Currency substitution (private dollarization)

Medium of exchange Vehicle currency for foreign exchange intervention

Invoicing trade and financial transactions

Unit of account Anchor for pegging local currency

Denominating trade and financial transactions

Source: Kenen (1983)

RMB as Anchor Currency

Do other currencies peg or manage against the RMB instead of USD or EUR?

53

RMB as Anchor (I)

-.20

-.15

-.10

-.05

.00

.05

.10

.15

2006 2007 2008

China Malaysia

Singapore

Taiwan

Thailand

Log SDRexchange rates,2005M06=0

Indonesia

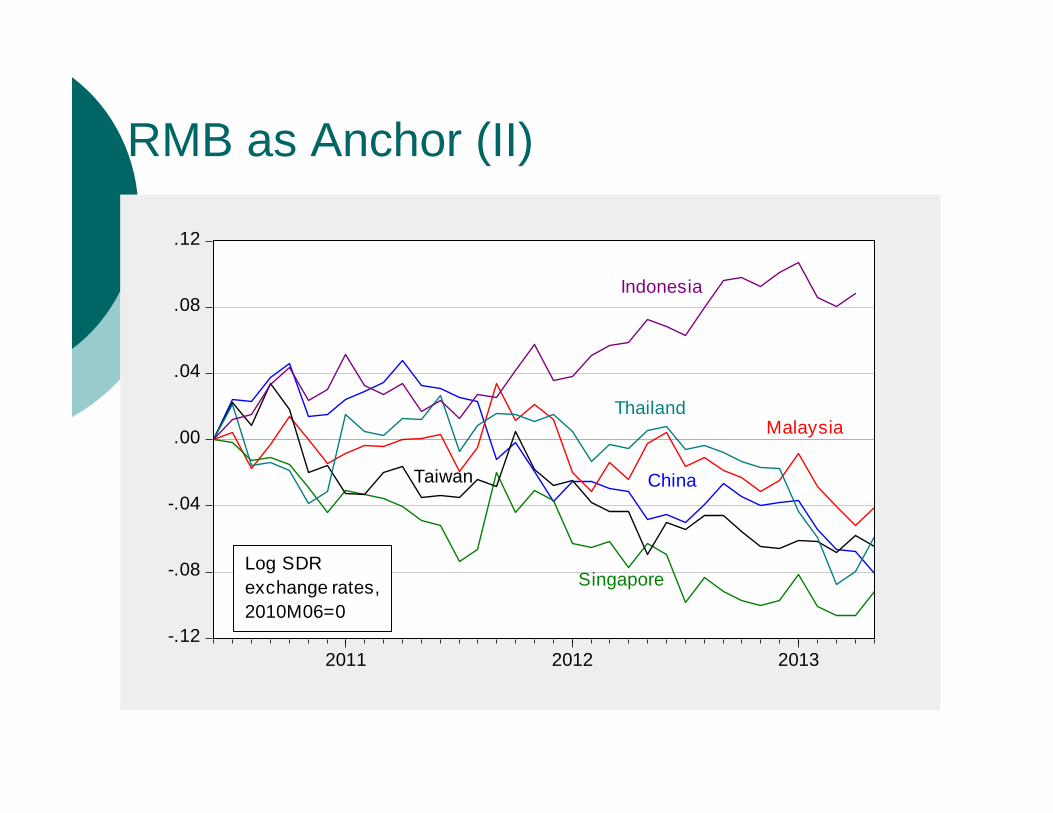

RMB as Anchor (II)

-.12

-.08

-.04

.00

.04

.08

.12

2011 2012 2013

China

Malaysia

Singapore

Taiwan

Thailand

Log SDRexchange rates,2010M06=0

Indonesia

Exchange Rate Factors

Formalize using Frankel-Wei approach to infer weights

Exchange Rate Factors & Long Run

Need a specification allows for both short and long run dynamics

Estimated with monthly data Allows for the effects of financial stress

Source: Chinn (2015)

The RMB Zone: Findings

In the pre-2005 period, little evidence of long run relationships between CNY, USD, JPY and respective currencies

Post-2005, there is greater evidence of cointegration

And more anchoring on the CNY Exception: KRW