Embed Size (px)

Citation preview

1

The Time Value of Money

2

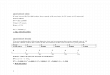

Inversement Options

Year: 1624 Property Traded: Manhattan Island Price : $24.00, FV of $24 @ 6%: FV = $24 (1+0.06)

388 = $158.08 billion

Option 1 0 1 2 3 4 5 t ($519.37) 0 0 0 0 $1,000 Option 2 0 1 2 3 4 5 t ($1,000) 150 150 150 150 150 1,000

3

1) Future Value – a single amount, a lump sum PV. i. 1 = PV(i) = I1 FV1 = PV + PVi = PV(1+i) [ PV(1+i)](i)(1) = I2 FV2 = [PV(1+i)] + [PV(1+i)i] FV2 = PV+PVi+PVi+PVi

2

= PV(1+I + i+ i2) = PV(1+ i)

2

FV3 = PV(1+ i) 3

........ ……. FVn = PV(1+ i)

n

Theorem: If PV(a lump sum) is deposited in an account at a rate of interest ,i, compounded annually, the account will accumulate a total of

FVn = PV(1+ i)

n

after n years. FVn is future value, ending amount, terminal value.

4

Example: What would the future value of $125 be after 8 years at 8.5% compound interest?

N 8 I/YR 8.5% PV $125 PMT $0 FV $240.08

FVn = PV(1+ i)

n =125(1+ 0.085)

8

= 125(1.920604) = $240.08 I = $240.08 – 125 = $115.08

in

n FVIFPViPVFV ,)()1(

where inFVIF ,)( is called “future value interest

factor” at n and i. FVIF

5

t where i1 < i2 < i3 < i4 < i5 < i6

Higher i => higher FV, n = constant

Higher n => higher FV, i = constant

2) Present Value – single amount, a lump sum

in

n FVIFPViPVFV ,)()1(

innnPVIFFV

iFV

i

FVPV ,)()

)1(

1(

)1(

where inPVIF ,)( is called “present value interest

factor” at n and i.

6

Example: Suppose a U.S. treasury bond will pay $2,500 five years from now. If the going interest rate on 5-year treasury bonds is 4.25%, how much is the bond worth today?

N 5 I/YR 4.25% PMT $0 FV $2,500.00 PV $2,030.30

2500 =PV(1+0.0425)

5 =>

PV =2500 / (1.0425)5

PV = 2500/1.231347 => PV = $2,030.30

Note: PVIF

7

t where i1 < i2 < i3 < i4 < i5

Higher i => lower PV, n = constant

Higher n => lower PV, i = constant Example: Suppose the U.S. Treasury offers to sell you a bond for $747.25. No payments will be made until the bond matures 5 years from now, at which time it will be redeemed for $1,000. What interest rate would you earn if you bought this bond at the offer price?

N 5 PV $747.25 PMT $0

8

FV $1,000.00 I/YR 6.00%

747.25 =1000/(1+i)5

(1+i)5 = 1000/747.25

(1+i) = (1.338240)0.2

=> i = (1.338240)0.2

-1 i = 1.060002 – 1 = 0.060002 = 6% Example: Last year Mason Corp's earnings per share were $2.50, and its growth rate during the prior 5 years was 9.0% per year. If that growth rate were maintained, how many years would it take for Mason’s EPS to double?

I/YR 9.0% PV $2.50 PMT $0 FV $5.00 N 8.04

FVn = PV(1+ i) n

2 =1(1+0.09)

n =(1.09)

n

Ln2 = nln 1.09 0.693147 = 0.086178n n= 0.693147 /0.086178 =8.04 years. Example: suppose two options are available: Option 1:

Bank One rate = 12% for a 5 year investment.

9

Option 2: Price = $519.37, n = 5, maturity value =$1000 Which one? 519.37 =1000/(1+i)

5

(1+i)

5 = 1000/519.37

(1+i) = (1.925)0.2

=> i = (1.925)0.2

-1 i = 1.14 – 1 = 0.14 = 14% Example: Ten years ago, Levin Inc. earned $0.50 per share. Its earnings this year were $2.20. What was the growth rate in Levin's earnings per share (EPS) over the 10-year period?

N 10 PV $0.50 PMT $0 FV $2.20 I/YR 15.97%

3) Annuity: an annuity is a set of periodic payments (or receipts) of equal amount at fixed intervals for a specified number of periods(years).

10

PMT PMT PMT PMT PMT 0 1 2 3 4 5 t for example a typical house mortgage repayment schedule is an annuity

If the PMT are made at the end of each period, the annuity is called an ordinary annuity or deferred annuity.

If the PMT are made at the beginning of each period, the annuity is called an annuity due.

4) Future Value of An Annuity(Sn)

a) Future Value of An Ordinary Annuity:

in

n

n FVIFAPMTi

iPMTordS ,)(

1)1(.)(

KnFVIFA ,)( is called “future value interest factor

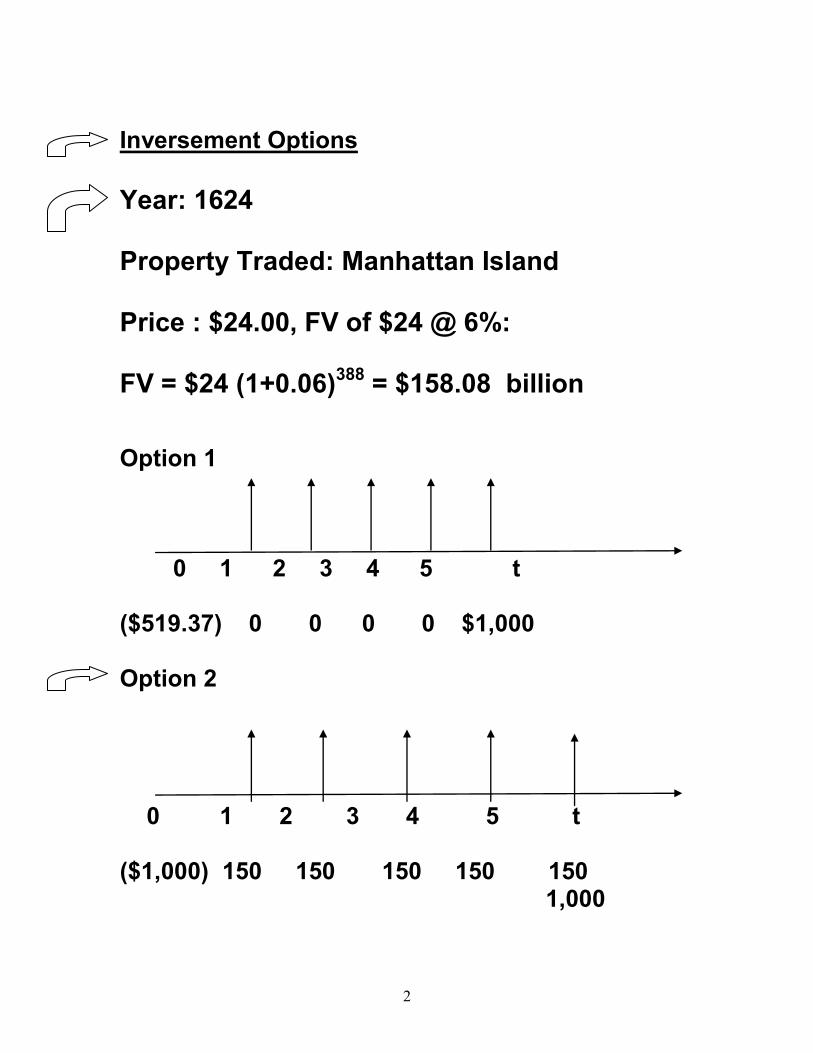

of annuity“ at n and i. Example: You want to buy a new sports car 3 years from now, and you plan to save $4,200 per year, beginning one year from today. You will

11

deposit your savings in an account that pays 5.2% interest. How much will you have just after you make the 3rd deposit, 3 years from now?

N 3 I/YR 5.2% PV $0.00 PMT $4,200 FV $13,266.56

$13,266.56

)158704.3(200,4052.0

1)052.01(200,4$.)(

3

ordSn

Example: Jack a movie star. Because of the failure of his recent movies at the box office, he feels his career will last only 4 years. To prepare for his future lack of popularity, he is planning to accumulate a sum of $5,864,636.00 at end of year 4 to retire in Florida. The account that he is looking at pays 6% interest compounded annually. How much payment of equal amount Jack has to deposits in that account at the end of each year in order to accumulate $5,864,636.00?

12

90.605,340,1$

)374616.4(06.0

1)06.01($636,864,5$

4

PMT

PMTPMT

b) Future Value of An Annuity Due

)1()()1(1)1(

)( , iFVIFAPMTii

iPMTdueS in

n

n

Example: You want to buy a new sports car 3 years from now, and you plan to save $4,200 per year, beginning immediately. You will make 3 deposits in an account that pays 5.2% interest. Under these assumptions, how much will you have 3 years from today? Make sure to adjust your calculator for BEG

N 3 I/YR 5.2% PV $0.00 PMT $4,200 FV $13,956.42

13

$13,956.42

)322957.3(200,4)052.01(052.0

1)052.01(200,4)(

3

dueSn

Why FV of annuity due is higher? 5) Present Value of An Annuity (An)

a) PV of an Ord. Annuity

in

n

n PVIFAPMTi

iPMTA ,)(

)1(

11

Where inPVIFA ,)( is called “present value interest

factor of annuity” at n and i. Example: You have to make a set of payments of equal amount of $2000 at the end of each year for the next 3 years. 0 1 2 3 2,000 2,000 2,000 How much money you must deposit in an account today in order to be able to make these

14

payments? Account pay 5% interest compounded annually.

40.446,5$)7232.2(000,2$05.0

)05.01(

11

000,2$3

nA

note: 7232.2)( 3%,5 PVIFA

Example: You have a chance to buy an annuity that pays $1,200 at the end of each year for 3 years. You could earn 5.5% on your money in other investments with equal risk. What is the most you should pay for the annuity?

N 3 I/YR 5.5% PMT $1,200 FV $0.00 PV $3,237.52

3,237.52$)697933.2(200,1$055.0

)055.01(

11

200,1$3

nA

15

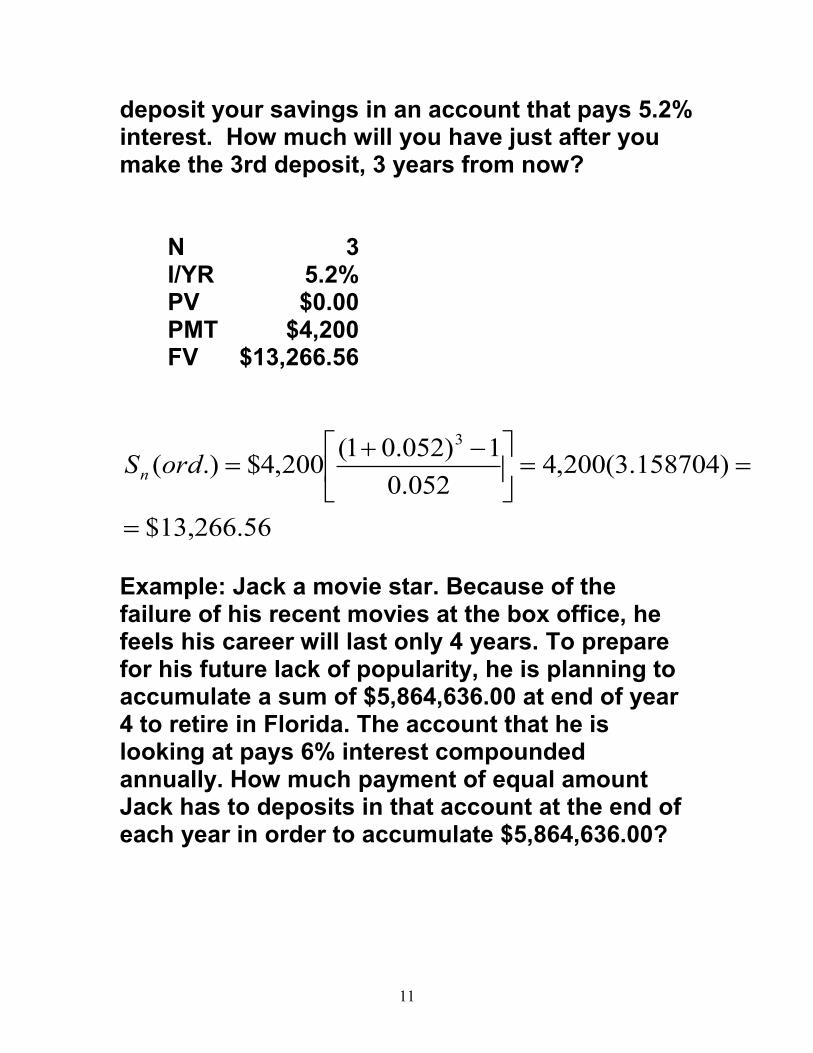

b) PV of an Annuity due.

)1()()1()1(

11

, iPVIFAPMTii

iPMTA in

n

n

Example: You have a chance to buy an annuity that pays $1,200 at the beginning of each year for 3 years. You could earn 5.5% on your money in other investments with equal risk. What is the most you should pay for the annuity? Make sure to adjust your calculator for BEG

N 3 I/YR 5.5% PMT $1,200 FV $0.00 PV $3,415.58

3,415.58$)055.1)(697933.2(200,1$

)055.01(055.0

)055.01(

11

200,1$3

nA

Why PV of annuity due is higher?

16

6) Perpetuity: Perpetuity is an annuity that is expected to continue forever (that is the life of

perpetuity is infinity i.e. n ). In this case the

present value of perpetuity )( perpetuityPV

is

calculated as follows:

i

PMTPVperpetuity

Example: If PMT =$100 (periodic payment) and i=8% then

250,1$08.0

100$

i

PMTPVperpetuity

What happens to PV if i increases (decreases)?

Example:

What’s the present value of a perpetuity that pays $250 per year if the appropriate interest rate is 5%?

I/YR 5.0% PMT $250 PV $5,000.00

17

000,5$05.0

250$

i

PMTPVperpetuity

7) Growing Annuity: this is a case in which all

variables in ordinary annuity formula are constant over time except payments(CFs) that grow at a constant rate per year over the life of the annuity.

gi

i

g

gPMTPVAn

n

g

)1(

)1(1

)1(

Graphical presentation: PMT PMT(1+g) PMT(1+g)2 PMT(1+g)3 PMT(1+g)4 0 1 2 3 4

Example: How much are you willing to pay for this gold

mining company? E(life) = 20 years, extract(production)= 5000 ounces/year. Current price of gold = $300/ounce

18

Expected rate of price increase=3%/year Our cost of capital (discount rate) (return on alternative investment)=10% The present owner is asking for $14,100,000. Is this company a bargain?

980,145,16$

03.010.0

)10.01(

)03.01(1

03.1)000,5)(300($20

20

gPVA

What is your decision? Example: Your father now has $1,000,000 invested in an account that pays 9.00%. He expects inflation to average 3%, and he wants to make annual constant dollar (real) beginning-of-year withdrawals over each of the next 20 years and end up with a zero balance after the 20th year. How large will his initial withdrawal (and thus constant dollar (real) withdrawals) be?

03.009.0

)09.01(

)03.01(1

)03.01(000,000,1$20

20

PMT

PMT = $85,951.76

19

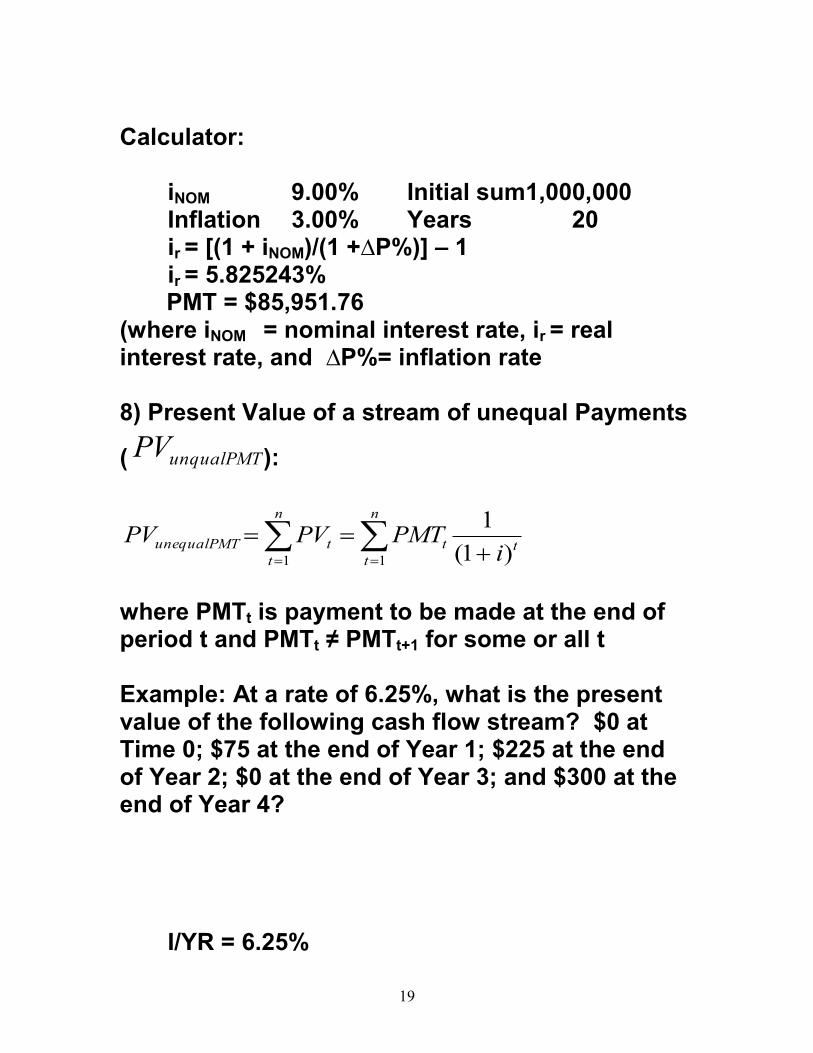

Calculator:

iNOM 9.00% Initial sum1,000,000 Inflation 3.00% Years 20 ir = [(1 + iNOM)/(1 +∆P%)] – 1 ir = 5.825243%

PMT = $85,951.76 (where iNOM = nominal interest rate, ir = real interest rate, and ∆P%= inflation rate 8) Present Value of a stream of unequal Payments

( unqualPMTPV ):

n

ttt

n

t

tunequalPMTi

PMTPVPV11 )1(

1

where PMTt is payment to be made at the end of period t and PMTt ≠ PMTt+1 for some or all t Example: At a rate of 6.25%, what is the present value of the following cash flow stream? $0 at Time 0; $75 at the end of Year 1; $225 at the end of Year 2; $0 at the end of Year 3; and $300 at the end of Year 4?

I/YR = 6.25%

20

0 1 2 3 4 CFs: $0 $75 $225 $0 $300 PV: $0 $71 $199 $0 $235

PVunequlaPMT = 0/(1.0625)

0 + 75/(1.0625)

1+

225/(1.0625)2 +0/(1.0625)

3 + 300/(1.0625)

4=

=0.0 + 70.59 + 199.31+ 0.0 + 235.40=$505.30 Calculator solution: 6.25 I/YR 0 CFj 75 CFj 225 CFj 0 CFj 300 CFj Yellow key : NPV 505.2956 Example: What is PV of the following unequal CFs @ 12% CF1 = $1, CF2 = $2,000, CF3 = $2,000, CF4 = $2,000, CF5 = $0, CF6= -$2,000 PVunequlaPMT = 1/(1.12) + 2000/(1.12)

2+ 2000/(1.12)

3

+2000/(1.12)4 + 0/(1.12)

5+

(-2000)/(1.12)6

=0.89 + 1594.40 + 1423.60+ + 1271.0 + 0 -1013.2 = $3276.69 Example 3

21

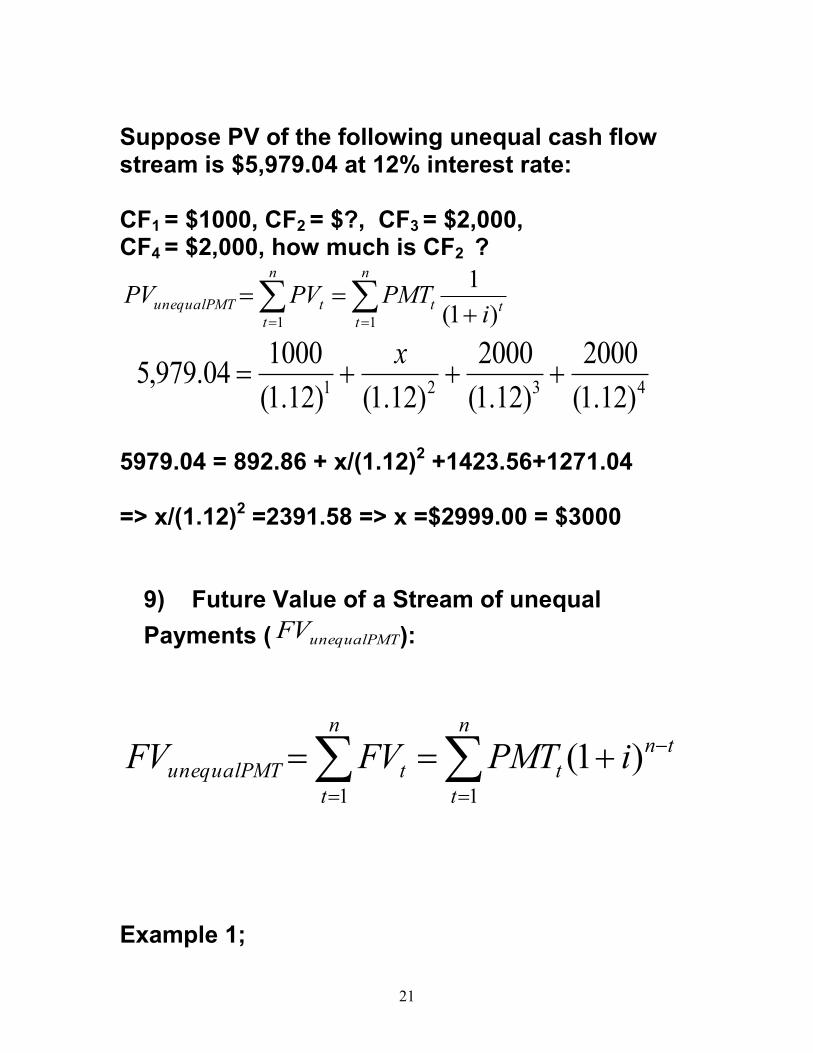

Suppose PV of the following unequal cash flow stream is $5,979.04 at 12% interest rate: CF1 = $1000, CF2 = $?, CF3 = $2,000, CF4 = $2,000, how much is CF2 ?

n

ttt

n

t

tunequalPMTi

PMTPVPV11 )1(

1

4321 )12.1(

2000

)12.1(

2000

)12.1()12.1(

100004.979,5

x

5979.04 = 892.86 + x/(1.12)

2 +1423.56+1271.04

=> x/(1.12)

2 =2391.58 => x =$2999.00 = $3000

9) Future Value of a Stream of unequal

Payments ( unequalPMTFV ):

tnn

t

t

n

t

tunequalPMT iPMTFVFV

)1(11

Example 1;

22

Suppose a firm plans to deposit $2,000 today and $1,500 one year from now in a bank account with no other future deposit or withdrawal. The bank pays 10% interest compounded annually. What is the future value of the account at the end of 4 years?

70.4924

50.199620.2928)10.01(0

)10.01(0)10.01(0

)10.01(500,1)10.01(000,2

)1(

44

3424

1404

1

tnn

t

tunequalPMT iPMTFV

Example: You just graduated, and you plan to work for 10 years and then to leave for the Australian. You figure you can save $1,000 a year for the first 5 years and $2,000 a year for the next 5 years. These savings cash flows will start one year from now. In addition, your family has just given you a $5,000 graduation gift. If you put the gift now, and your future savings when they start, into an account which pays 8 percent compounded annually, what will your financial "stake" be when you leave for Australia 10 years from now?

23

96.619,8$)08.1(08.0

1)08.01(000,1.)(1 5

5

ordSFV n

20.733,11$08.0

1)08.01(000,2.)(2

5

ordSFV n

62.794,10$)08.01(50003 10 FV

FV = 8,619.96 + 11,733.20 + 10,794.62 =31,147.78 OR

FV = $1,000(FVIFA8%,10)+ $1,000(FVIFA8%,5) + $5,000(FVIF8%,10)

= $1,000((1.0810

-1)/.08) + $1,000((1.085-1)/.08) +

$5,000(1.0810

)

= $1,000(14.487) + $1,000(5.866) + $5,000(2.1589) = $14,487 + $5,866 + $10,794.50 = $31,148.

24

10) Determining Interest Rate: You just won the state lottery, and you have a choice between receiving $3,500,000 today or a 10-year annuity of $500,000, with the first payment coming one year from today. What rate of return is built into the annuity?

N 10 PV $3,500,000 PMT $500,000 FV $0.00 I/YR 7.07%

Example:

FV = $1,610.50 PV = $1000 and n = 5 so FV = PV (1 + i)

n => 1,610.50 = 1000 (1 + i)

5

or (1 +i)

5 = 1,610.50 = 1.610

hence 1 + i = (1.610)

1/5 = (1.610)

0.20 = 1.10

or i = 1.10 – 1 = .10 = 10%

25

Suppose you sign a loan contract that calls for annual payment of $2,545.16 over 25 years (at the end of each year) and the amount that you borrow is $25,000. The question is what interest rate the bank is charging you?

-Always remember the amount that you borrow, and you want to repay it in a set of equal periodic payments over a given number of years, is present value of an annuity Here: Present value of this annuity (An) is $25,000, n = 25 and PMT = $2545.16 so we use the following formula:

An = PMT

1-1

(1+ i)n

i

é

ë

êêêê

ù

û

úúúú

then

25,000 = $2545.16

1-1

(1+ i)25

i

é

ë

êêêê

ù

û

úúúú

26

Calculator solution:

N 25 PV $25,000 PMT $2,545.16 FV $0.00 I/YR 9.00%

11) Semiannual and other Compounding Period: So far we have assumed that interest is compounded once a year, however, if interest is compounded more than once a year; we have to adjust all the formulas that we have discussed so for to reflect this fact. For example:

If PV dollars is deposited in an account that pays i percent interest compounded m times a year, the account will contain a total of

nm

m

iPVFV )1(

dollars after n years. Example: What is the future value of $1000 at 8% compounded quarterly after 6 years? Here PV = 1000, i = 8%, n = 6, and m = 4 (4 quarters in one year) so

27

Example: What’s the future value of $1,500 after 5 years if

the appropriate interest rate is 6%, compounded semiannually?

Years 5 Periods/Yr 2 Nom. I/YR 6.0% ===================== N = Periods 10 PMT $0 I = I/Period 3.0% PV $1,500

FV $2,015.87

We can make the above type of adjustments for all the formulas that we discussed in case of interest being compounded annually. For instance, to calculate future value of an ordinary annuity with a life of n years in which interest is compounded m times a year( PMTs are made m times a year), we use the following adjusted formula:

m

im

i

PMTS

nm

n

1)1(

44.608,1$)4

08.01(1000$ )6)(4( FV

28

Example: Suppose you deposit $1000 every month in an account that pays 8% for 35 years. How much will your account contain after 35 years? Here, m = 12, n = 35, i = 8%, and PMT = $1000. The future value of this annuity will be:

880,293,2$

)88.293,2)(000,1(

12

08.0

1)12

08.01(

000,1$

1)1(

)35)(12(

m

im

i

PMTS

nm

n

For present value of annuity, the adjusted formula is:

29

m

im

i

PMTA

mn

n

)1(

11

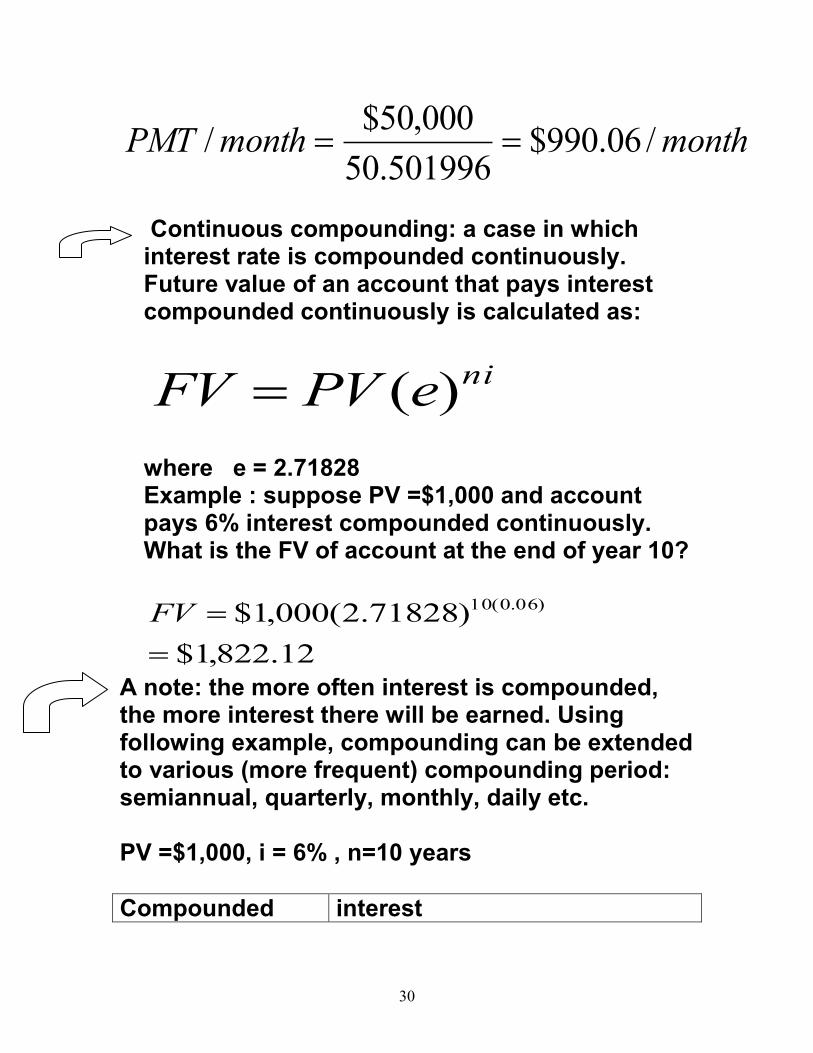

Example: Suppose you want to buy a car that is priced $110,000, you put $60,000 down payment and borrow the rest at 7%. You want to pay off the loan in 5 years. What is your monthly car payment? Amount borrowed = $110,000 –$ 60,000= $50,000.

12

07.0

)12

07.01(

11

000,50$

)12)(5(

PMT

then, $50,000 = PMT (50.501996) so

30

monthmonthPMT /06.990$501996.50

000,50$/

Continuous compounding: a case in which interest rate is compounded continuously. Future value of an account that pays interest compounded continuously is calculated as:

niePVFV )(

where e = 2.71828 Example : suppose PV =$1,000 and account pays 6% interest compounded continuously. What is the FV of account at the end of year 10?

12.822,1$

)71828.2(000,1$ )06.0(10

FV

A note: the more often interest is compounded, the more interest there will be earned. Using following example, compounding can be extended to various (more frequent) compounding period: semiannual, quarterly, monthly, daily etc. PV =$1,000, i = 6% , n=10 years

Compounded interest

31

Not at all(simple interest

1,000 x0.06x10=$600

yearly 85.790$000,1)

1

06.01(000,1 10 I

semi-annually 11.806$000,1)

2

06.01(000,1 20 I

quarterly 02.814$000,1)4

06.01(000,1 40 I

monthly 40.819$000,1)

12

06.01(000,1 120 I

daily exercise

hourly exercise

Continuously 1,822.12-1,000=822.12

Look at the pattern: increasing the frequency of compounding makes smaller and smaller difference in the amount of interest earned.

12) Nominal or Stated Interest rate: Stated(nominal) interest rate is rate of interest stated in the loan contract. Let $1,000 be compounded monthly at a 12% for one year.

83.1126$)12

12.01(1000 12 FV

32

What interest rate would give us the same future value if interest is compounded annually for one year? That is what is equivalent annual interest rate? 1,126.83 = 1,000(1+x) => (1+x) = 1.12683

x = 0.1268 = 12.68% 12.68% is called Effect Annual Rate(EAR) That is annual interest rate that would generate the same future value under more frequent compounding(monthly in the above example). In general one can prove that:

1)1( mnom

m

iEAR

using for above example:

%68.121268.01)12

12.01( 12 EAR

For continuous compounding:

1 nomieEAR

33

if inom= 10% and interest is compounded continuously, then EAR = (2.71828)

0.10 – 1 = 0.1052 = 10.52%

We do need EAR because different investment (deposits, bonds, stock etc) use different compounding period. If we want to compare securities with different compounding periods, we need to put them is a common basis, i.e. returns on yearly basis. For example: State Bank CD rate = 6.5%, annual compounding National Bank: MMDA rate = 6.0%, daily compounding If two banks are equally risky, which bank do you choose? EARCD = 6.5% (why?) EARMMDA = [1 + (0.06/365)

365 ] - 1 = 6.18%

Example

34

East Coast Bank offers to lend you $25,000 at a nominal rate of 7.5%, compounded monthly. The loan (principal plus interest) must be repaid at the end of the year. Midwest Bank also offers to lend you the $25,000, but it will charge an annual rate of 8.3%, with no interest due until the end of the year. What is the difference in the effective annual rates charged by the two banks?

Nominal rate, East Coast Bank 7.5% Nominal rate, Midwest Bank 8.3% Periods/yr, East Coast 12 Periods/yr, Midwest 1 EFF% East Coast 7.76% EFF% Midwest 8.30% Difference 0.54%

EAREast Coast bank = [1 + (0.075/12)

12 ] - 1 = 7.763

Amortized Loan: is a loan which is repaid in equal periodic amounts.

Suppose a small firm takes a 5-year- loan of $40,000 from a bank to be repaid in 5 years in equal payment at the end of each year. The bank charges 8% interest on outstanding balance in each year, prepare loan amortization schedule for this firm: First, we got to find PMT for each year:

35

)99271.3(08.0

)08.01(

11

000,40$)5(

PMTPMT

PMT = $10,018.26/ year

Amortization Schedule

year payment interest repayment of principal

remaining balance

1 10,018.26 3,200.00 6,818.26 33,181.74

2 10,018.26 2,654.54 7,363.72 25,818.02

3 10,018.26 2,065.44 7,952.82 17,865.20

4 10,018.26 1,429.22 8,589.04 9,276.16

5 10,018.26 742.10 9,276.16 0.00

5 50,091.30 10,091.30 40,000

Cost to the borrower: $50,091.30 – $40,000 =$10,091.30