Embed Size (px)

Citation preview

THE TAX IMPLICATIONS OF COVID-19

Published by Fast Forward Academy, LLChttps://fastforwardacademy.com(888) 798-PASS (7277)

© 2021 Fast Forward Academy, LLC

All rights reserved. No part of this publication may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written permission of the publisher.

1 Hour(s) - Other Federal Tax

CTEC Provider #: 6209CTEC Course #: 6209-CE-0146

IRS Provider #: UBWMFIRS Course #: UBWMF-T-00198-20-S

NASBA: 116347

The information provided in this publication is for educational purposes only, and does not necessarily reflect all laws, rules, or regulations for the tax year covered. This publication is designed to provide accurate and authoritative information concerning the subject matter covered, but it is sold with the understanding that the publisher is not engaged in rendering legal, accounting or other professional services. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.

To the extent any advice relating to a Federal tax issue is contained in this communication, it was not written or intended to be used, and cannot be used, for the purpose of (a) avoiding any tax related penalties that may be imposed on you or any other person under the Internal Revenue Code, or (b) promoting, marketing or recommending to another person any transaction or matter addressed in this communication.

CORONAVIRUS RELIEF......................................................................................................................................................... 7

Course Details ............................................................................................................................................................................... 7

CARES Act....................................................................................................................................................................................... 7

Families First Coronavirus Response Act ................................................................................................................................... 7

Relief for Individuals ..................................................................................................................................................................... 8

Relief for Businesses ..................................................................................................................................................................14

Working from Home...................................................................................................................................................................19

Course Details 7

•

•

•

•

•

•

CORONAVIRUS RELIEF

COURSE DETAILSINSTRUCTIONS

Read the information in this course one section at a time. You can navigate the course using the Table of Contents or by clicking the <Back Next> arrows on the bottom of the screen. You will encounter review questions at the end of the reading material for some sections. Your attempts on these questions are not scored, but you will receive evaluative feedback on your answers.

When you are finished with the reading material, select "Take Exam" to begin the final assessment for continuing education credit. There are 5 questions for each hour of credit, and you must achieve 70% or better to pass.

Note: Rules prevent us from sharing evaluative feedback for failed exams.

IMPORTANT: Upon successful completion, a certificate is generated for you automatically. If you would like to report the course to regulators you will have the option to enter your information to complete the reporting process. The reporting process is not complete until the course status indicates "Accepted" on the reporting dashboard.

COURSE DESCRIPTION AND LEARNING OBJECTIVES

The coronavirus (COVID-19) has had a huge impact on our lives. The Federal government introduced several new laws in response, many containing provisions that affect tax returns. This course is designed as a broad overview of important tax considerations related to both new and existing tax laws that impact both business and individual taxpayers.

Upon completion of this course you should be able to:

Explain the tax implications of the various COVID-19 provisions to the tax code.

Identify the major provisions of the CARES Act affecting individual tax returns.

Identify the changes to NOL limitations.

Recognize credits and other relief available to individuals and businesses.

Explain the deductibility of expenses used to qualify for PPP loan forgiveness.

CARES ACTThe Coronavirus Aid, Relief, and Economic Security Act (CARES Act), enacted on March 27, 2020, is designed to encourage eligible employers to keep employees on their payroll, despite experiencing economic hardship related to COVID-19, with an employee retention tax credit (Employee Retention Credit). The CARES Act also introduced several new loan programs available through the Small Business Administration (SBA) some of which can be forgiven if certain requirements are met. The Paycheck Protection Program (PPP) is one such loan program.

TIP: A taxpayer generally includes canceled debt in taxable income, unless an exception applies. A taxpayer does notinclude PPP loan forgiveness in taxable income.

FAMILIES FIRST CORONAVIRUS RESPONSE ACTThe Families First Coronavirus Response Act (FFCRA) requires certain employers to pay sick or family leave wages to employees who are unable to work or telework due to certain circumstances related to COVID-19. The following temporary provisions expire on December 31, 2020:

Emergency Paid Sick Leave Act (EPSLA) provides eligible employees up to two weeks of paid sick leave.

8 Coronavirus Relief

•

•

•

•

•

•

•

•

Emergency Family and Medical Leave Expansion Act (EFMLEA) amends the Family and Medical Leave Act of 1993 to provide eligible employees up to 12 weeks of family and medical leave, ten of which are paid.

TIP: An employee may be eligible for both types of leave—2 weeks of emergency paid sick leave and 10 weeks of paid emergency family leave, for a total of 12 weeks of paid leave.

Leave payments under the FFCRA are treated as taxable wages for income and employment tax purposes. Qualified sick leave wages and qualified family leave wages are not subject to the employer portion of social security tax.

Eligible employers are entitled to receive a credit in the full amount of the required sick leave and family leave, plus related health plan expenses and the employer’s share of Medicare tax on the leave, for the period of April 1, 2020, through December 31, 2020. The refundable credit is applied against certain employment taxes on wages paid to all employees.

TIP: The same wages do not count towards both credits.

Taxpayers may use Form 7200 to request an advance payment of the tax credits for qualified sick and qualified family leave wages and the employee retention credit. The advance payment does not apply if self-employed.

COVERED EMPLOYERS

Eligible employers are businesses and tax-exempt organizations with fewer than 500 full-time and part-time employees within the United States or any U.S. territory or possession and that have to meet employer-paid leave requirements. The law allows equivalent credits for self-employed individuals in similar circumstances.

RELIEF FOR INDIVIDUALSThere are several new benefits to help individuals and families affected by the novel coronavirus (COVID-19). Some of the recent developments include:

The deadlines to FILE and PAY federal income taxes are extended to July 15, 2020.

Economic impact payments up to $1,200 ($2,400 MFJ) plus $500 for each qualifying child.

Up to $100,000 in penalty-free withdrawals for coronavirus-related distributions from retirement plans.

Waiver of required minimum distribution (RMD) rules for tax year 2020.

Up to 10 days paid sick leave, either to tend to your own health needs or to care for a family member.

Up to an additional 10 weeks of paid family and medical leave.

$300 above-the-line deduction for qualified charitable contributions.

CHANGES TO TAX DEADLINES

Notice 2020-23 extends additional key tax deadlines for individuals and businesses.

Extension of Deadline to File and Pay

The deadline to FILE and PAY is extended to July 15 for all taxpayers with returns due after April 1, 2020 and before July 15, 2020. Individuals, trusts, estates, corporations and other non-corporate tax filers qualify for the extra time. This means that anyone, including Americans who live and work abroad, can now wait until July 15 to file their 2019 federal income tax return and pay any tax due. No late-filing penalty, late-payment penalty or interest will be due.

Relief for Individuals 9

Additional Extension of Time to File

Individual taxpayers who need additional time to file beyond the July 15 deadline can file Form 4868 to request an extension to Oct. 15, 2020. A business taxpayer uses Form 7004 to request an extension.

NOTE: The extended deadline is for filing the tax return, it is not an extension to pay. A taxpayer should pay the tax owed by the July 15 filing deadline to avoid additional interest and penalties.

Estimated Tax Payments

Besides the April 15 estimated tax payment previously extended, relief extends to estimated tax payments due June 15, 2020. This means that any individual or corporation that has a quarterly estimated tax payment due on or after April 1, 2020, and before July 15, 2020, can wait until July 15 to make that payment, without penalty.

2016 Unclaimed Refunds Deadline

For 2016 tax returns, the normal April 15 deadline to claim a refund was extended to July 15, 2020. The law provides a three-year window of opportunity to claim a refund. If taxpayers do not file a return within three years, the money becomes property of the U.S. Treasury. The law requires taxpayers to properly address, mail, and ensure the tax return is postmarked by the July 15, 2020 date.

ECONOMIC IMPACT PAYMENT (RECOVERY REBATE)

Eligible taxpayers who filed tax returns for either 2019 or 2018 will automatically receive an economic impact payment (EIP) of up to $1,200 ($2,400 MFJ) and up to $500 for each qualifying child.

A qualifying child must be under age 17 and qualify as the dependent of the taxpayer (i.e., must meet the age, relationship, residency, and support tests).

Only children eligible for the Child Tax Credit qualify for the additional payment of up to $500 per child. To claim the Child Tax Credit, the taxpayer generally must be related to the child, live with them more than half the year and provide at least half of their support. Besides their own children, adopted children and foster children, eligible children can include the taxpayer's younger siblings, grandchildren, nieces and nephews if they can be claimed as dependents. In addition, any qualifying child must be a U.S. citizen, permanent resident or other qualifying resident alien. The child must also be under the age of 17 at the end of the year for the tax return on which the IRS bases the payment determination.

A qualifying child must have a valid Social Security number (SSN) or an Adoption Taxpayer Identification Number (ATIN). A child with an Individual Taxpayer Identification Number (ITIN) is not eligible for an additional payment.

Parents who are not married to each other and do not file a joint return cannot both claim their qualifying child as a dependent. The parent who claimed their child on their 2019 return may have received an additional Economic Impact Payment for their qualifying child. When the parent who did not receive an additional payment files their 2020 tax return next year, they may be able to claim up to an additional $500 per-child amount on that return if they qualify to claim the child as their qualifying child for 2020.

Pursuant to the CARES Act, dependent college students do not qualify for an EIP, and even though their parents may claim them as dependents, they normally do not qualify for the additional $500 payment.

EXAMPLE: A 20-year-old full-time college student claimed as a dependent on their mother's 2019 federal income tax return is not eligible for a $1,200 Economic Impact Payment. In addition, the student's mother will not receive an additional $500 Economic Impact Payment for the student because they do not qualify as a child younger than

10 Coronavirus Relief

•

•

•

•

•

•

17. This scenario could also apply if a parent's 2019 tax return hasn't been processed yet by the IRS before the payments were calculated, and a college student was claimed on a 2018 tax return.

However, if the student cannot be claimed as a dependent by their mother or anyone else for 2020, that student may be eligible to claim a $1,200 credit on their 2020 tax return next year.

TIP: In many instances, eligible taxpayers who did not receive a payment or received a smaller-than-expected payment may qualify to receive an additional amount early next year when they file their 2020 federal income tax return. The payment is technically an advance payment of a new temporary tax credit that eligible taxpayers can claim on their 2020 return.

This advance payment is not taxable income as it is a credit against tax. All taxpayers must have a valid Social Security Number (or ATIN for an adopted child) to qualify.

U.S. residents will receive the Economic Impact Payment of $1,200 for individual or head of household filers, and $2,400 for married filing jointly if they are not a dependent of another taxpayer and have a work-eligible Social Security number with adjusted gross income up to:

$75,000 for individuals (single or MFS)

$112,500 for head of household filers

$150,000 for married couples filing joint returns

Taxpayers will receive a 5% reduction in their payment for the amount their AGI is above these amounts, therefore, taxpayers will receive a reduced payment if their AGI is between:

$75,000 and $99,000 for individuals (single or MFS)

112,500 and $136,500 for head of household filers

$150,000 and $198,000 for married couples filing joint returns

The amount of the reduced payment will be based upon the taxpayer's specific adjusted gross income.

Eligible retirees and recipients of Social Security, Railroad Retirement, disability or veterans' benefits as well as taxpayers who do not make enough money to normally have to file a tax return will receive a payment. This also includes those who have no income, as well as those whose income comes entirely from certain benefit programs, such as Supplemental Security Income (SSI) benefits.

Retirees who receive either Social Security retirement or Railroad Retirement benefits will receive payments automatically.

Nonresident aliens, dependents of other taxpayers, estates and trusts are not eligible for the payment.

Social Security recipients and railroad retirees who are otherwise not required to file a tax return are also eligible and will not be required to file a return. The IRS will use SSA-1099 information they already have to automatically generate $1,200 economic impact payments to eligible Social Security beneficiaries who did not file tax returns in 2018 or 2019. Social Security Disability Insurance (SSDI) recipients are also part of this group who don't need to take action.

TIP: Supplemental Security Income (SSI) recipients are eligible to receive the economic impact payment. The Social Security Administration will not consider economic impact payments as income for SSI recipients, and the payments are excluded from resources for 12 months.

Relief for Individuals 11

$100,000 PENALTY-FREE CORONAVIRUS-RELATED DISTRIBUTIONS

The CARES Act waives the 10% early withdrawal penalty for up to $100,000 of coronavirus-related distributions from eligible retirement plans on or after January 1, 2020, and before December 31, 2020. The CARES Act also waives the 20% mandatory federal withholding requirement for qualified plan distributions.

The term eligible retirement plan is defined in 402(c)(8)(B) and includes defined contributions plans such as a 401(k), as well as 403(b), 457, and IRAs). No provision is made for defined benefit plans.

This treatment is available if a taxpayer, spouse, or dependent is diagnosed with COVID-19 or SARS by the Center for Disease Control and Prevention. It is also available to an individual who experiences adverse financial consequences as a result of quarantine, layoff or reduced hours, inability to work due to lack of childcare due to the virus, or business closure or reduced business hours due to the virus.

Contributions (up to the amount of the coronavirus-related distribution) made within 3 years to eligible retirement plans are treated as if the taxpayer made a direct trustee to trustee transfer within 60 days of the distribution. In other words, the taxpayer can contribute the money back into the plan for a period of 3 years beginning the day after the contribution without penalty or tax consequences.

Unless the taxpayer elects otherwise, any amount required to be included in gross income for a taxable year is spread over the 3-taxable-year period beginning with such taxable year.

TIP: We anticipate that taxpayers will need to file amended tax returns to claim a refund of the overpayment for years they recognize income and subsequently repay coronavirus-related distributions within the allowable 3-year period.

OTHER RETIREMENT PLAN PROVISIONS

In addition, the loan amount for certain qualified plans has increased to the lesser of $100,000 or 100% of the participant's account balance (from $50,000 / 50% previously). Participants may delay the repayment period for an existing loan with due dates in 2020 for 1 year.

Taxpayers generally must begin taking distributions from eligible retirement plans upon reaching age 72 (or 70.5 for years prior to 2020). The IRS waived the mandatory distribution requirement for taxpayers subject to the required minimum distribution (RMD) rules in 2020. The waiver applies to defined contribution plans and IRAs, as well as 403(b) and 457 plans.

CHARITABLE CONTRIBUTIONS

Individual taxpayers can claim an "above-the-line" deduction of up to $300 for cash donations made to charity during 2020. The special $300 deduction is designed especially for people who choose to take the standard deduction, rather than itemizing their deductions. Previously, charitable contributions could only be deducted if taxpayers itemized their deductions. Contributions of non-cash property do not qualify for this relief. Taxpayers may still claim non-cash contributions as a deduction, subject to the normal limits. Cash donations include those made by check, credit card or debit card. They don't include securities, household items or other property.

SICK AND FAMILY LEAVE

The Families First Coronavirus Response Act was signed by President Trump on March 18, 2020. Pursuant to the Act, for COVID-19 related reasons, employees receive up to 10 days (80 hours) of paid sick leave and expanded paid child care leave when employees' children's schools are closed or child care providers are unavailable.

12 Coronavirus Relief

1.

2.

3.

4.

5.

6.

•

•

•

•

EXCEPTION: Employers with more than 500 employees are not subject to the paid leave requirement, which is in effect through Dec. 31. Employers with fewer than 50 employees may qualify for an exemption from the requirement to provide paid leave due to school closings or the unavailability of child care if doing so would jeopardize the viability of the business as a going concern.

Paid Leave

An employee qualifies for paid family and medical leave if they’ve been on an employer’s payroll for 30 calendar daysor more. The employee receives 100% of the employee's pay where the employee is unable to work because the employee is quarantined, and/or experiencing COVID-19 symptoms, and seeking a medical diagnosis.

An employee who is unable to work because of a need to care for an individual subject to quarantine, to care for a child whose school is closed or child care provider is unavailable for reasons related to COVID-19, and/or the employee is experiencing substantially similar conditions as specified by the U.S. Department of Health and Human Services can receive two weeks (up to 80 hours for full-time employees, or the average hours the employee works over a 2-week period if part-time) of paid sick leave at 2/3 the employee's pay.

An employee who is unable to work due to a need to care for a child whose school is closed, or child care provider is unavailable for reasons related to COVID-19, may in some instances receive up to an additional ten weeks of expanded paid family and medical leave at 2/3 the employee's pay.

Under the FFCRA, an employee qualifies for paid sick time if the employee is unable to work (or unable to telework) due to a need for leave because the employee:

is subject to a Federal, State, or local quarantine or isolation order related to COVID-19;

has been advised by a health care provider to self-quarantine related to COVID-19;

is experiencing COVID-19 symptoms and is seeking a medical diagnosis;

is caring for an individual subject to an order described in (1) or self-quarantine as described in (2);

is caring for a child whose school or place of care is closed (or child care provider is unavailable) for reasons related to COVID-19; or

is experiencing any other substantially-similar condition specified by the Secretary of Health and Human Services, in consultation with the Secretaries of Labor and Treasury.

Under the FFCRA, an employee qualifies for expanded family leave if the employee is caring for a child whose school or place of care is closed (or child care provider is unavailable) for reasons related to COVID-19.

Duration of Leave:

For reasons (1)-(4) and (6): A full-time employee is eligible for 80 hours of leave, and a part-time employee is eligible for the number of hours of leave that the employee works on average over a two-week period.

For reason (5): A full-time employee is eligible for up to 12 weeks of leave (two weeks of paid sick leave followed by up to 10 weeks of paid expanded family & medical leave) at 40 hours a week, and a part-time employee is eligible for leave for the number of hours that the employee is normally scheduled to work over that period.

Calculation of Pay:

For leave reasons (1), (2), or (3): employees taking leave are entitled to pay at either their regular rate or the applicable minimum wage, whichever is higher, up to $511 per day and $5,110 in the aggregate (over a 2-week period).

For leave reasons (4) or (6): employees taking leave are entitled to pay at 2/3 their regular rate or 2/3 the applicable minimum wage, whichever is higher, up to $200 per day and $2,000 in the aggregate (over a 2-week period).

Relief for Individuals 13

•

•

•

For leave reason (5): employees taking leave are entitled to pay at 2/3 their regular rate or 2/3 the applicable minimum wage, whichever is higher, up to $200 per day and $12,000 in the aggregate (over a 12-week period).

LOSS PROVISIONS

BACKGROUND

The Tax Cuts and Jobs Act of 2017 (TCJA) introduced substantial changes that limit the ability of a taxpayer to utilize losses on a tax return for taxable years beginning after December 31, 2017, and before January 1, 2026.

The TCJA introduced a new limitation that prevents taxpayers from claiming excess business losses in the current year. In 2020, the maximum net loss a taxpayer other than a corporation may deduct is $259,000 ($518,000 for a joint return). Any loss above this threshold is considered an excess business loss, and is nondeductible in the current year. A taxpayer treats any excess business loss as part of the taxpayer’s net operating loss carryforward in subsequent taxable years. Prior to the enactment of the TCJA a taxpayer could reduce taxable income to zero.

The TCJA eliminated the option for most taxpayers to carry a net operating loss (NOL) to a prior tax year and imposed an 80% of taxable income limitation on NOL deductions in future years. An exception applies to certain farming losses.

REPEAL OF EXCESS BUSINESS LOSS LIMITATION

The CARES Act temporarily removes the 80% taxable income limitation for deducting excess business loss for 2018, 2019, and 2020.

TIP: This means that taxpayers with business losses in tax years beginning prior to January 1, 2021 are no longer subject to the limitation and may utilize the entire loss to reduce taxable income. A taxpayer with previously filed returns which were subject to the limitation should file an amended return to claim previously disallowed losses.

EXAMPLE: In a previously filed 2019 tax return, a single taxpayer has $400,000 dividend income and $800,000 net business losses. Under prior law, the current year's business loss is limited to $255,000 and the taxpayer reports taxable income of $145,000 ($400,000 dividend – $255,000 business loss allowed). The taxpayer has an excess business loss of $545,000 ($800,000 net business losses – $255,000 business loss allowed), which is carried forward as an NOL to the next year. The taxpayer may deduct the entire NOL in the subsequent tax year, subject to the 80% of taxable income limitation.

Pursuant to the CARES Act, the 2019 tax return should be amended. This would reduce the taxpayer's 2019 taxable income to $0 as more of the loss is used to offset the $400,000 dividend income. The remaining $400,000 loss ($800,000 – $400,000) becomes part of the taxpayer's NOL, which also receives favorable treatment under the CARES Act.

NET OPERATING LOSS CARRYBACK

As authorized by the CARES Act, the IRS issued Revenue Procedure 2020-24 providing guidance on procedures for carrying back NOLs arising in 2018, 2019, or 2020 to each of the five preceding tax years. As a result of this amendment, taxpayers take into account such NOLs in the earliest taxable year in the carryback period, carrying forward unused amounts to each succeeding taxable year.

14 Coronavirus Relief

•

•

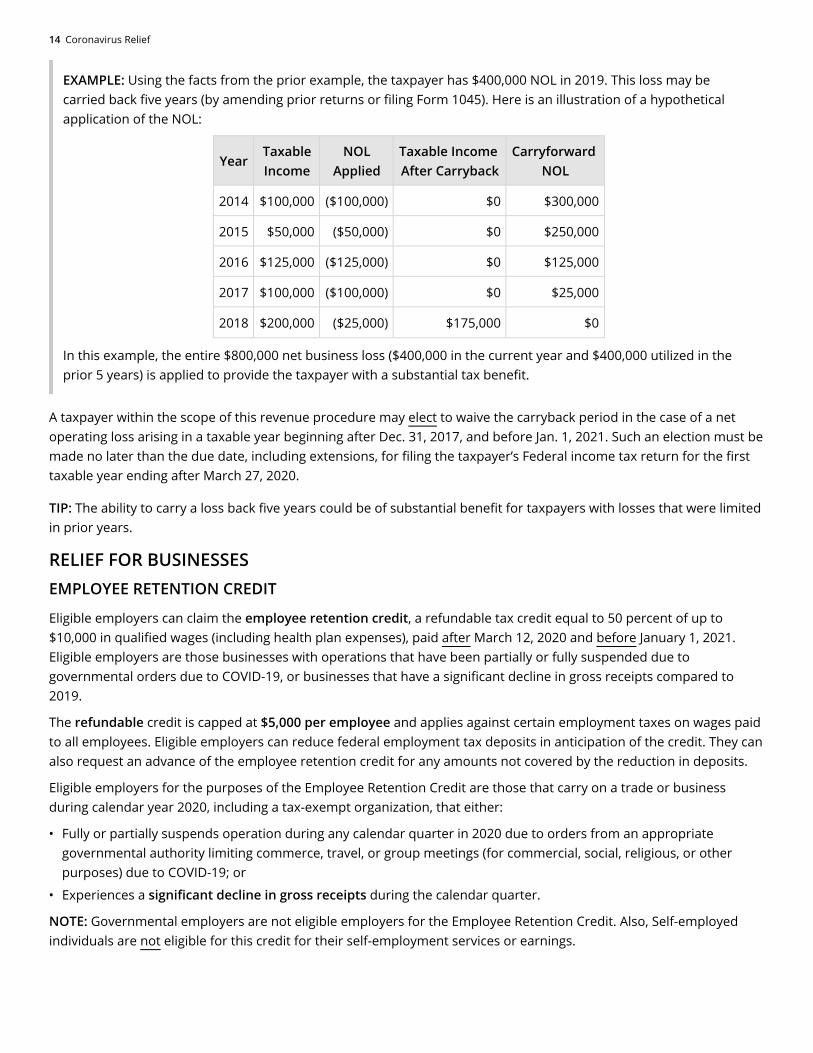

EXAMPLE: Using the facts from the prior example, the taxpayer has $400,000 NOL in 2019. This loss may be carried back five years (by amending prior returns or filing Form 1045). Here is an illustration of a hypothetical application of the NOL:

YearTaxableIncome

NOLApplied

Taxable Income After Carryback

Carryforward NOL

2014 $100,000 ($100,000) $0 $300,000

2015 $50,000 ($50,000) $0 $250,000

2016 $125,000 ($125,000) $0 $125,000

2017 $100,000 ($100,000) $0 $25,000

2018 $200,000 ($25,000) $175,000 $0

In this example, the entire $800,000 net business loss ($400,000 in the current year and $400,000 utilized in the prior 5 years) is applied to provide the taxpayer with a substantial tax benefit.

A taxpayer within the scope of this revenue procedure may elect to waive the carryback period in the case of a net operating loss arising in a taxable year beginning after Dec. 31, 2017, and before Jan. 1, 2021. Such an election must be made no later than the due date, including extensions, for filing the taxpayer’s Federal income tax return for the first taxable year ending after March 27, 2020.

TIP: The ability to carry a loss back five years could be of substantial benefit for taxpayers with losses that were limited in prior years.

RELIEF FOR BUSINESSESEMPLOYEE RETENTION CREDIT

Eligible employers can claim the employee retention credit, a refundable tax credit equal to 50 percent of up to $10,000 in qualified wages (including health plan expenses), paid after March 12, 2020 and before January 1, 2021. Eligible employers are those businesses with operations that have been partially or fully suspended due to governmental orders due to COVID-19, or businesses that have a significant decline in gross receipts compared to 2019.

The refundable credit is capped at $5,000 per employee and applies against certain employment taxes on wages paid to all employees. Eligible employers can reduce federal employment tax deposits in anticipation of the credit. They can also request an advance of the employee retention credit for any amounts not covered by the reduction in deposits.

Eligible employers for the purposes of the Employee Retention Credit are those that carry on a trade or business during calendar year 2020, including a tax-exempt organization, that either:

Fully or partially suspends operation during any calendar quarter in 2020 due to orders from an appropriate governmental authority limiting commerce, travel, or group meetings (for commercial, social, religious, or other purposes) due to COVID-19; or

Experiences a significant decline in gross receipts during the calendar quarter.

NOTE: Governmental employers are not eligible employers for the Employee Retention Credit. Also, Self-employed individuals are not eligible for this credit for their self-employment services or earnings.

Relief for Businesses 15

An eligible employer may not receive the Employee Retention Credit if he receives a Small Business Interruption Loan under the Paycheck Protection Program that is authorized under the CARES Act. An eligible employer that receives a paycheck protection loan should not claim Employee Retention Credits.

DECLINE IN GROSS RECEIPTS

A significant decline in gross receipts begins with the first quarter in which an employer’s gross receipts for a calendar quarter in 2020 are less than 50 percent of its gross receipts for the same calendar quarter in 2019. The significant decline in gross receipts ends with the first calendar quarter that follows the first calendar quarter for which the employer’s 2020 gross receipts for the quarter are greater than 80 percent of its gross receipts for the same calendar quarter during 2019.

EXAMPLE: An employer’s gross receipts were $100,000, $190,000, and $230,000 in the first, second, and third calendar quarters of 2020, respectively. Its gross receipts were $210,000, $230,000, and $250,000 in the first, second, and third calendar quarters of 2019, respectively. Thus, the employer’s 2020 first, second, and third-quarter gross receipts were approximately 48%, 83%, and 92% of its 2019 first, second, and third-quarter gross receipts, respectively. Accordingly, the employer had a significant decline in gross receipts commencing on the first day of the first calendar quarter of 2020 (the calendar quarter in which gross receipts were less than 50% of the same quarter in 2019) and ending on the first day of the third calendar quarter of 2020 (the quarter following the quarter for which the gross receipts were more than 80% of the same quarter in 2019). Thus the employer is entitled to a retention credit with respect to the first and second calendar quarters.

AMOUNT OF CREDIT

The credit equals 50 percent of the qualified wages (including qualified health plan expenses) that an eligible employer pays in a calendar quarter (paid after March 12, 2020, and before January 1, 2021). The maximum amount of qualified wages taken into account with respect to each employee for all calendar quarters is $10,000 so that the maximum credit for qualified wages paid to any employee is $5,000.

EXAMPLE 1: Eligible employer pays $10,000 in qualified wages to Employee A in Q2 2020. The Employee Retention Credit available to the eligible employer for the qualified wages paid to Employee A is $5,000.

EXAMPLE 2: Eligible Employer pays Employee B $8,000 in qualified wages in Q2 2020 and $8,000 in qualified wages in Q3 2020. The credit available to the eligible employer for the qualified wages paid to Employee B is equal to $4,000 in Q2 and $1,000 in Q3 due to the overall limit of $10,000 on qualified wages per employee for all calendar quarters.

QUALIFIED WAGES

The definition of qualified wages depends on how many employees an eligible employer has.

If an employer averaged more than 100 full-time employees during 2019, qualified wages are generally those wages, including certain health care costs, (up to $10,000 per employee) paid to employees that are not providing services because operations were suspended or due to the decline in gross receipts. These employers can only count wages up to the amount that the employee would have been paid for working an equivalent duration during the 30 days immediately preceding the period of economic hardship.

16 Coronavirus Relief

•

•

•

•

If an employer averaged 100 or fewer full-time employees during 2019, qualified wages are those wages, including health care costs, (up to $10,000 per employee) paid to any employee during the period operations were suspended or the period of the decline in gross receipts, regardless of whether or not its employees are providing services.

CLAIMING THE CREDIT

In order to claim the new Employee Retention Credit, eligible employers will report their total qualified wages and the related health insurance costs for each quarter on their quarterly employment tax returns, which will be Form 941 for most employers, beginning with the second quarter of 2020.

The credit is allowed against the employer portion of social security taxes, and the portion of taxes imposed on railroad employers under the Railroad Retirement Tax Act (RRTA) that corresponds to the social security taxes.

The credits are fully refundable because the eligible employer may get a refund if the amount of the credit is more than certain federal employment taxes the eligible employer owes. That is, if for any calendar quarter the amount of the credit the eligible employer is entitled to exceeds the employer portion of the social security tax on all wages (or on all compensation for employers subject to RRTA) paid to all employees, then the excess is treated as an overpayment and refunded to the employer (after offsetting other tax liabilities on the employment tax return and subject to any other offsets under section 6402(a) of the Code).

EXAMPLE: Eligible Employer pays $10,000 in qualified wages to Employee A in Q2 2020. The Employee Retention Credit available to the eligible employer for the qualified wages paid to Employee A is $5,000. This amount may be applied against the employer share of social security taxes that the eligible employer is liable for with respect to all employee wages paid in Q2 2020. Any excess over the employer’s share of social security taxes is treated as an overpayment and refunded to the eligible employer.

IMPACT OF OTHER CREDIT AND RELIEF PROVISIONS

An eligible employer's ability to claim the Employee Retention Credit is impacted by other credit and relief provisions as follows:

If an employer receives a Small Business Interruption Loan under the Paycheck Protection Program, authorized under the CARES Act, then the employer is not eligible for the Employee Retention Credit.

Wages for this credit do not include wages for which the employer received a tax credit for paid sick and family leave under the Families First Coronavirus Response Act.

Wages counted for this credit can't be counted for the credit for paid family and medical leave.

Employees are not counted for this credit if the employer is allowed a Work Opportunity Tax Credit for the employee.

SMALL BUSINESS ADMINISTRATION (SBA) LOANS

The CARES Act established several new temporary programs through the Small Business Administration (SBA) to address the COVID-19 outbreak. There was a rush for the door on April 3, 2020 as many "small" businesses raced to secure funding through two new forgivable loan programs intended to help main street businesses—the Paycheck Protection Program (PPP) and the Economic Injury Disaster Loan (EIDL) Advance.

PAYCHECK PROTECTION PROGRAM (PPP)

The Paycheck Protection Program is a loan designed to provide a direct incentive for small businesses to keep their workers on the payroll during the COVID-19 crisis. The loan is fully forgiven if—over the 8 week period after the loan is made—the funds are used for payroll costs (at least 60% of the forgiven amount must have been used for payroll), interest on mortgages, rent, and utilities. The funds are intended to cover costs on obligations in place before February

Relief for Businesses 17

•

1.

2.

3.

4.

•

•

•

•

•

•

15, 2020. Costs incurred as a result of a subsequent mortgage, rental, or utility service do not count towards forgiveness.

Payroll costs include:

Salary, wages, commissions, or tips (capped at $100,000 on an annualized basis for each employee);

Employee benefits including costs for vacation, parental, family, medical, or sick leave; allowance for separation or dismissal; payments required for the provisions of group health care benefits including insurance premiums; and payment of any retirement benefit;

State and local taxes assessed on compensation; and

For a sole proprietor or independent contractor: wages, commissions, income, or netearnings from self-employment (capped at $100,000 on an annualized basis for eachemployee).

Forgiveness is based on the employer maintaining or quickly rehiring employees and maintaining salary levels. Forgiveness will be reduced if full-time headcount declines, or if salaries and wages decrease.

This loan has a maturity of 2 years and an interest rate of 1%. Loan payments will be deferred for 6 months.

Deduction for Expenses

The Consolidated Appropriations Act, 2021 overturned prior IRS guidance provided in Notice 2020-32 preventing a taxpayer from deducting expenses paid with PPP loan proceeds that are excluded from income. The new law provides that "no amount shall be included in the gross income of the eligible recipient by reason of forgiveness of indebtedness..." and furthermore "no deduction shall be denied, no tax attribute shall be reduced, and no basis increase shall be denied, by reason of the exclusion..."

ECONOMIC INJURY DISASTER LOAN (EIDL)

In response to the Coronavirus (COVID-19) pandemic, small business owners, including agricultural businesses, and nonprofit organizations in all U.S. states, Washington D.C., and territories can apply for an Economic Injury Disaster Loan. The EIDL program is designed to provide economic relief to businesses that are currently experiencing a temporary loss of revenue due to coronavirus (COVID-19).

TIP: Unlike the EIDL Advance, the standard EIDL Loan is not forgivable and is generally repaid over a 30 year period. For tax purposes, treat interest paid on an EIDL loan the same as a traditional business loan.

EIDL Advance

EIDL Advance was a grant program offered together with the economic injury loan program. The EIDL Advance does not have to be repaid. The amount of the grant was determined by the number of employees indicated on the EIDL application: $1,000 per employee, up to a maximum of $10,000.

Recipients did not have to be approved for an EIDL loan to receive the EIDL Advance.

The amount of the loan Advance was deducted from total loan eligibility.

Businesses who received an EIDL Advance in addition to the Paycheck Protection Program (PPP) loan will have the amount of the EIDL Advance subtracted from the forgiveness amount of their PPP loan.

All available funds for the EIDL Advance program have been allocated.

TIP: The Consolidated Appropriations Act, 2021 clarified the tax treatment of the EIDL Advance. Like forgivable PPP loans, the EIDL advance will not generate any taxable income, and any associated expenses paid are fully deductible.

18 Coronavirus Relief

•

•

•

•

EMPLOYER CREDITS FOR PAID LEAVE

The Families First Coronavirus Relief Act (FFCRA) provides that all American businesses with fewer than 500 employeesshall provide employees with paid leave, either for the employee's own health needs or to care for family members.

EXCEPTION: Employers with fewer than 50 employees are eligible for an exemption from the requirements to provide leave to care for a child whose school is closed, or child care is unavailable in cases where the viability of the business is threatened.

Employers receive 100% reimbursement for paid leave pursuant to the Act.

Health insurance costs are also included in the credit.

Employers face no payroll tax liability.

Self-employed individuals receive an equivalent credit to offset their federal self-employment tax for any taxable year equal to their “qualified sick leave equivalent amount” or “qualified family leave equivalent amount.”

Eligible employers report their total qualified leave wages and the related credits for each quarter on their federal employment tax return, usually Form 941, Employer’s QUARTERLY Federal Tax Return. They can receive the benefit of the credits by reducing their federal employment tax deposits for that quarter by the amount of the qualified leave wages, allocable qualified health plan expenses, and the employer’s share of Medicare tax on the wages. They’ll account for the reduction in deposits due to the leave credits on the Form 941 they file at the end of the quarter.

If employers don’t have enough federal employment taxes to cover the amount of the credits, after they have deferred deposits of employer Social Security taxes under the CARES Act, they may request an advance payment of the credits from the IRS by submitting Form 7200, Advance Payment of Employer Credits Due to COVID-19. They may fax their completed forms to 855-248-0552.

PAID SICK LEAVE CREDIT

For an employee who is unable to work because of Coronavirus quarantine or self-quarantine or has Coronavirus symptoms and is seeking a medical diagnosis, eligible employers may receive a refundable sick leave credit for sick leave at the employee's regular rate of pay, up to $511 per day and $5,110 in the aggregate, for a total of 10 days.

For an employee who is caring for someone with Coronavirus, or is caring for a child because the child's school or child care facility is closed, or the child care provider is unavailable due to the Coronavirus, eligible employers may claim a credit for two-thirds of the employee's regular rate of pay, up to $200 per day and $2,000 in the aggregate, for up to 10 days. Eligible employers are entitled to an additional tax credit determined based on costs to maintain health insurance coverage for the eligible employee during the leave period.

EXAMPLE: An eligible employer is entitled to a credit of $5,000 for paying qualified sick leave wages and qualified family leave wages (and allocable health plan expenses) and is otherwise required to deposit $8,000 in federal employment taxes withheld from all of its employees for wage payments made during the same quarter as the $5,000 in qualified leave wages. The employer may keep up to $5,000 of the $8,000 of taxes it was going to deposit, and it will not owe a penalty for keeping the $5,000. The eligible employer will claim the credit and reflect the reduced liability for the $5,000 when it files Form 941.

CHILD CARE LEAVE CREDIT

In addition to the sick leave credit, for an employee who is unable to work because of a need to care for a child whose school or child care facility is closed or whose child care provider is unavailable due to the Coronavirus, eligible employers may receive a refundable child care leave credit. This credit is equal to two-thirds of the employee's regular pay, capped at $200 per day or $10,000 in the aggregate. Up to 10 weeks of qualifying leave can be counted towards

Working from Home 19

•

•

•

the child care leave credit. Eligible employers are entitled to an additional tax credit determined based on costs to maintain health insurance coverage for the eligible employee during the leave period.

EXAMPLE: An employee’s child-care provider is unavailable indefinitely due to the COVID-19 outbreak, leaving the employee unable to work or telework because of the need to care for their child. For up to the first 80 hours of any period of leave to care for their child, the employee is entitled to qualified sick leave wages, up to $200 per day and $2,000 in total. After that, the employee is entitled to qualified family leave wages for up to 10 weeks of additional leave needed, up to $200 per day and $10,000 in total.

The eligible employer is entitled to a fully refundable tax credit equal to the required paid family leave wages. Eligible employers can also get an additional credit for the employer’s share of Medicare tax imposed on those wages and its cost of maintaining health insurance coverage for the employee during the family leave period. The eligible employer isn’t subject to the employer portion of Social Security tax on those wages.

CORPORATE CHARITABLE CONTRIBUTIONS

For the tax year 2020 only, a corporation may deduct qualified contributions of up to 25% (previously the limit was 10%) of its taxable income. Contributions that exceed that amount can carry over to the next tax year.

To qualify, the contribution must be:

a cash contribution

made to a qualifying organization

made during the calendar year 2020

Contributions of non-cash property do not qualify for this relief. Taxpayers may still claim non-cash contributions as a deduction, subject to the normal limits.

WORKING FROM HOME

Due to COVID, the home office deduction is more relevant than ever. Unfortunately, the Tax Cuts and Jobs Act of 2017 eliminated the home office deduction for W-2 employees, who previously could deduct unreimbursed employee expenses as a miscellaneous itemized deduction. The home office deduction remains available for self-employed taxpayers.

Generally, no deduction is allowed for the taxpayer’s business use of his or her own home. This general prohibition, however, does not apply to the extent an expense is allocable to a portion of the taxpayer’s home that is exclusivelyused on a regular basis as either: (1) the principal place of business for any trade or business of the taxpayer; or (2) a place of business which is used by patients, clients, or customers in meeting or dealing with the taxpayer in the normal course of his or her trade or business. Additionally, a deduction may be taken in the case of a separate structure which is not attached to the dwelling unit, if it is used in connection with the taxpayer’s trade or business even if it is not the taxpayer's principal place of business.

To qualify under the trade-or-business-use test, the taxpayer must use part of your home in connection with a trade or business. If you use your home for a profit-seeking activity that is not a trade or business, you cannot take a deduction for its business use.

EXAMPLE: You use part of your home exclusively and regularly to read financial periodicals and reports, clip bond coupons, and carry out similar activities related to your own investments. You do not make investments as a

20 Coronavirus Relief

•

•

•

•

•

•

•

•

•

•

•

•

•

•

broker or dealer. So, your activities are not part of a trade or business and you cannot take a deduction for the business use of your home.

Principal Place of Business

A taxpayer can have more than one business location, including a home, for a single trade or business. To qualify to deduct the expenses for the business use of the home under the principal place of business test, the home must be the taxpayer's principal place of business for that trade or business. To determine whether the home is your principal place of business, you must consider:

The relative importance of the activities performed at each place where you conduct business, and

The amount of time spent at each place where you conduct business.

TIP: Taxpayers who work from home two days of the week, but go into the office the other three days may be unable to claim the deduction, but it will depend on the nature of activities performed at each location.

A home office will qualify as the principal place of business if the taxpayer meets the following requirements:

The home is used exclusively and regularly for administrative or management activities of the trade or business.

The taxpayer does not conduct substantial administrative or management activities of the trade or business from any other fixed location.

TIP: If, after considering all business locations, the home cannot be identified as a principal place of business, you cannot deduct home office expenses.

Administrative or management activities.

There are many activities that are administrative or managerial in nature. The following are a few examples.

Billing customers, clients, or patients.

Keeping books and records.

Ordering supplies.

Setting up appointments.

Forwarding orders or writing reports.

Administrative or management activities performed at other locations.

The following activities will not disqualify a home office from being a principal place of business:

The taxpayer has others conduct administrative or management activities at locations other than the home. (For example, another company does billing from its place of business.)

The taxpayer conducts administrative or management activities at places that are not fixed locations of the business, such as in a car or a hotel room.

The taxpayer occasionally conducts minimal administrative or management activities at a fixed location outside the home.

The taxpayer conducts substantial nonadministrative or non-management business activities at a fixed location outside the home. (For example, the taxpayer meets customers, clients, or patients at a fixed location of the business outside the home.)

The taxpayer has suitable space to conduct administrative or management activities outside the home, but chooses to use the home office for those activities instead.

Working from Home 21

•

•

Place To Meet Patients, Clients, or Customers

A taxpayer can deduct expenses for the part of their home used exclusively and regularly for business if meeting boththe following tests:

The taxpayer physically meets with patients, clients, or customers at the home.

Their use of the home is substantial and integral to the conduct of the taxpayer's business.

TIP: A taxpayer meeting these tests can deduct expenses even if the taxpayer also conducts business at another location.

Doctors, dentists, attorneys, and other professionals who maintain offices in their homes generally will meet this requirement.

Using a home for occasional meetings and telephone calls will not qualify the taxpayer to deduct expenses for the business use of your home.

The part of the home used exclusively and regularly to meet patients, clients, or customers does not have to be the principal place of business.

EXAMPLE: June Quill, a self-employed attorney, works 3 days a week in her city office. She works 2 days a week in her home office used only for business. She regularly meets clients there. Her home office qualifies for a business deduction because she meets clients there in the normal course of her business.

Amount of the Deduction

The law provides taxpayers with two options for determining the amount of the home office deduction. Under the traditional method, the taxpayer must substantiate each expense that is allocated to the home office, such as utilities, mortgage interest, depreciation, etc. Revenue Procedure 2013-13 provides a second, safe harbor method. The safe harbor amount is $5 per square foot of qualified use up to 300 square feet, resulting in a maximum deduction for $1,500. Other than being limited to the income generated by the trade or business income of the taxpayer, the traditional method is not subject to any specific dollar limitation.

When claiming a deduction for a home office under either the safe harbor or the traditional method the taxpayer must substantiate the fact that the home office is actually used for business. While there is no specific time requirement, there should be some documentary support that business activities are being conducted there on a regular basis.