Embed Size (px)

Citation preview

ON

BA

LA

NC

E

INSIDE THIS ISSUE

Case File . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Luxfer Gas Cylinders: Masteringthe Strategy–Operations Linkage

Luxfer Gas Cylinders, a global manu-facturer and distributor, provides an apt illustration of Kaplan andNorton’s six-stage management system (see On Balance story). A2006 BSC Hall of Fame winner, theU.K.-based company (with opera-tions in Europe, the Asia-Pacificregion, and North America), excelsat three stages: planning the strategy, aligning the organization,and planning operations—in partic-ular, at making the crucial linkbetween strategy and operations.Few organizations have achievedthe level of sophistication and rigorLuxfer has in managing by strategictheme and integrating its planningprocesses.This special extendedCase File offers rich detail aboutLuxfer’s approach.

Tools & Techniques ......................14Maximize Your “Return onInitiatives” with the InitiativePortfolio Review Process

In our continuing coverage of initiative management, consultantsKatz and Manzione explore a critical,but still widely overlooked, step ininitiative management: the ongoingmanagement and review process.Without systematic review, organi-zations inevitably put scarceresources at risk—and forgo untold opportunity.This four-step,portfolio-based approach ensuressystematic performance review ofinitiatives—individually and in theaggregate.This, in turn, helps organ-izations retain (and add) only thoseinitiatives that are strategically relevant—and, more important,optimize organizational resourcesfor maximum “return on initiatives.”

Continued on next page

T H E S T R A T E G Y E X E C U T I O N S O U R C E

M a y – J u n e 2 0 0 8 | V o l u m e 1 0 , N u m b e r 3

Special Book PreviewSpecial Book PreviewSpecial excerpt from the forthcoming book, The Execution Premium, due out in June.

Integrating Strategy Planning and Operational Execution:A Six-Stage System By Robert S. Kaplan and David P. Norton

This article, their January Harvard Business Review article, and their new book mark the next milestone in the evolution of Robert Kaplanand David Norton’s strategy execution movement: a comprehensivemanagement model that solves one of the greatest management challenges—linking strategy and operations.This powerful six-stagemodel incorporates the Balanced Scorecard, theme-based strategymaps, and the five Strategy-Focused Organization principles and practices. But it now also includes the most effective strategy develop-ment, planning, and management tools developed by leading experts.Collectively, these tools help companies not only plan and execute,but also monitor, learn, test, and adapt their strategic assumptions andpractices to achieve sustainable success.

Experts from Michael Porter to Michael Hammer concur: without excellent operational and governance processes, strategy—even the most visionary strategy—cannot be implemented. Conversely, without strategic vision and guidance,operational excellence is not sufficient to achieve, let alone sustain, success.1

A survey we conducted in 1996 revealed that few organizations link their systemsand align their employees to strategy. But a survey conducted in 2006 showedthat 54% of respondents were now using a formal strategy execution managementprocess. Of these, nearly 75% were outperforming their peer group. Conversely,among the organizations without a formal strategy execution process in place,75% were underperforming or, at most, matching the average performance oftheir peers. Having a formal strategy execution system apparently makes strategic success up to three times more likely.

A Six-Stage Management System

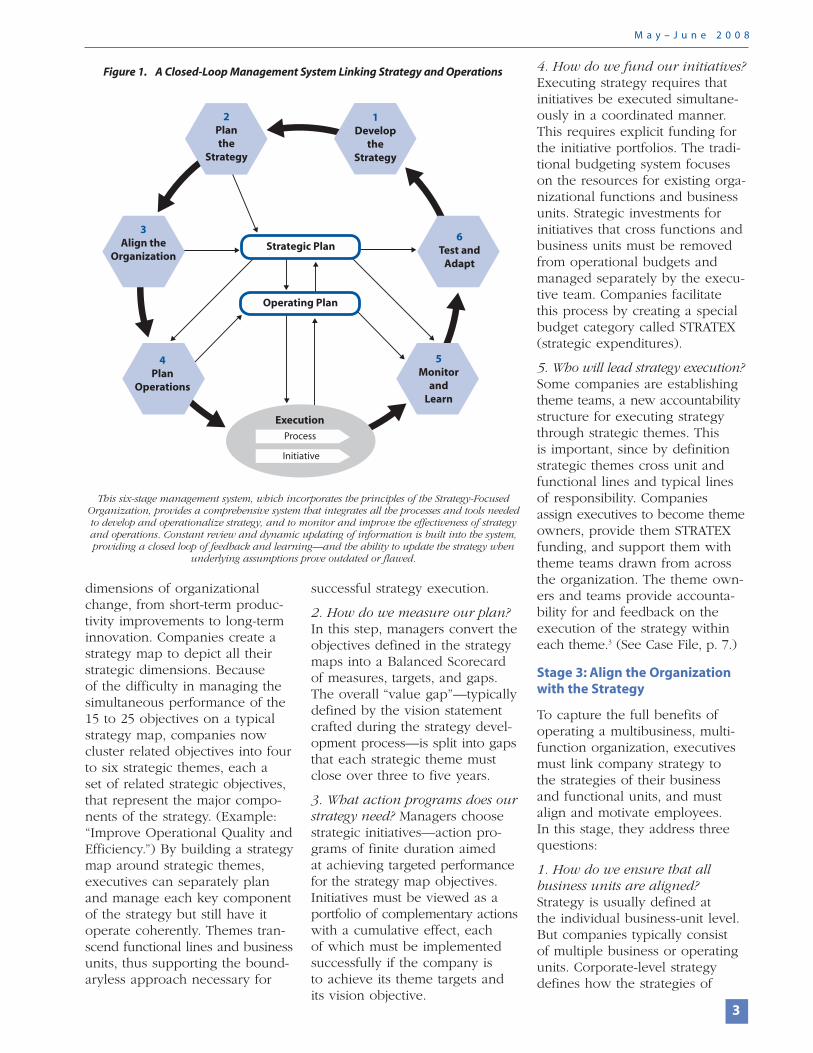

We have now formulated the architecture for a comprehensive and integrated management system that explicitly links strategy formulation and planning with operational execution. (See Figure 1, page 3.)

Stage 1: Develop the strategy using an array of strategy tools such as mission,values, and vision (MVV) statements; external competitive, economic, and environmental analyses; methodologies such as Michael Porter’s five forces andcompetitive positioning framework, the resource-based view of strategy, andblue ocean strategies, as well as scenario planning, dynamic simulations, andwar-gaming.

Stage 2: Plan the strategy usingsuch tools as strategy maps andBalanced Scorecards, along withtargets and strategic initiatives.

Stage 3: Align the organizationwith the strategy by cascadingstrategy maps and BalancedScorecards to all organizationalunits, by aligning employeesthrough a formal communicationsprocess, and by linking employees’personal objectives and incentivesto strategic objectives.

Stage 4: Plan operations usingtools such as quality and processmanagement, reengineering,process dashboards, rolling forecasts, activity-based costing,resource capacity planning, anddynamic budgeting.

Stage 5: Monitor and learn aboutproblems, barriers, and challenges.This process integrates informa-tion about operations and strategyinto a carefully designed structureof management review meetings.

Stage 6: Test and adapt the strategy, using internal operationaldata and new external environ-mental and competitive data—thus launching a new cycle ofintegrated strategy planning andoperational execution.

Stage 1: Develop the Strategy

The integrated management systembegins when executives developthe strategy. In this process,described at length in the January–February and March–April issues,2

companies address three questions:

1. What business are we in, andwhy? Executives begin strategydevelopment by affirming theorganization’s purpose (mission),the internal compass that guidesits actions (values), and its aspira-tion for future results (vision).These statements establish guide-lines for formulating and executingthe strategy.

2. What are the key issues we face?Managers conduct strategic analysisof their competitive and operating

environments, especially majorchanges that have occurred sincethey last crafted their strategy,using input from three sources:external environment analysis(PESTEL analysis—political,economic, social, technological,environmental, and legal or regu-latory factors); the internal envi-ronment (key processes, such asthe state of human capital, opera-tions, innovation, and technologydeployment); and the progress of the existing strategy (from BSC metrics). This environmentalassessment is summarized in aSWOT table of strengths, opportu-nities, weaknesses, and threats,which identifies a set of strategicissues that must be addressed bythe strategy.

From the outputs from questions(1) and (2), the executive teamdevelops and communicates astrategic change agenda thatexplains the need for the changesin the strategy.

3. How can we best compete? Inthe final step, executives formulatea strategy by addressing theseissues:

• In what niches will we compete?

• What customer value propositionwill differentiate us in thoseniches?

• What key processes will createour differentiation?

• What direction does the strategy require we take inhuman capital?

• What are the technologyenablers of the strategy?

Stage 2: Plan the Strategy

Managers plan the strategy bydeveloping strategic objectives,measures, targets, initiatives, andbudgets that guide action andresource allocation. Companiestypically address five questions inthis stage:

1. How do we describe our strategy?A strategy encompasses various

Balanced Scorecard Report

Editorial AdvisersRobert S. Kaplan

Professor, Harvard Business SchoolDavid P. Norton

Director and Founder, Palladium Group, Inc.

PublishersRobert L. Howie Jr.

Managing Director, Palladium Group, Inc.

Edward D. CrowleyGeneral Manager, Newsletters, HBS Publishing

Executive EditorRandall H. Russell

VP/Research Director, Palladium Group, Inc.

EditorJanice Koch

Palladium Group/Balanced Scorecard Collaborative

Circulation ManagerBruce Rhodes

Newsletters, HBS Publishing

DesignRobert B. Levers

Levers Advertising & Design

Letters and Reader FeedbackPlease send your comments and ideas to [email protected].

Subscription Information To subscribe to Balanced Scorecard Report, call 800.668.6705. Outside the U.S., call 617.783.7474,or visit bsr.harvardbusinessonline.org. For group subscription rates, call the numbers above.

Services, Permissions, and Back IssuesBalanced Scorecard Report (ISSN 1526-145X) is published bimonthly. To resolve subscription service problems, please call 800.668.6705.Outside the U.S., call 617.783.7474.

Email: [email protected]

Copyright © 2008 by Harvard Business SchoolPublishing Corporation. Quotation is not permitted.Material may not be reproduced in whole or in part in any form whatsoever without permission from thepublisher.To order back issues or reprints of articles,please call 800.668.6705. Outside the U.S., call617.783.7474.

Harvard Business School Publishing is a not-for-profit, wholly owned subsidiary of Harvard University.The mission of Harvard Business School Publishing is to improve the practice of management and itsimpact on a changing world. We collaborate to createproducts and services in the media that best serve our customers—individuals and organizations thatbelieve in the power of ideas.

Palladium Group, Inc. helps its clients achieve an execution premium by linking strategy and operationsand enabling mission-critical links with timely, robustdata. Balanced Scorecard Collaborative (BSCol) isPalladium’s education and training division. Our productsand services in strategy, finance, and IT consulting,conferences, technology, training, research, publications,and communities are delivered globally from officesworldwide. BSCol also manages the Balanced ScorecardHall of Fame for Executing Strategy™ program. To learnmore, visit www.thepalladiumgroup.com, or call781.259.3737.

Explore the many resources available on the Balanced Scorecard and executing strategy at BSC Online. Join today—membership is free. For details, visitwww.thepalladiumgroup.com/bsconline.

Sign up for the electronic version of BSR—available only to subscribers—at www.bsronline.org/ereg.

2

B a l a n c e d S c o r e c a r d R e p o r t

dimensions of organizationalchange, from short-term produc-tivity improvements to long-terminnovation. Companies create astrategy map to depict all theirstrategic dimensions. Because of the difficulty in managing thesimultaneous performance of the15 to 25 objectives on a typicalstrategy map, companies nowcluster related objectives into fourto six strategic themes, each a set of related strategic objectives,that represent the major compo-nents of the strategy. (Example:“Improve Operational Quality andEfficiency.”) By building a strategymap around strategic themes,executives can separately planand manage each key componentof the strategy but still have itoperate coherently. Themes tran-scend functional lines and businessunits, thus supporting the bound-aryless approach necessary for

successful strategy execution.

2. How do we measure our plan?In this step, managers convert theobjectives defined in the strategymaps into a Balanced Scorecardof measures, targets, and gaps.The overall “value gap”—typicallydefined by the vision statementcrafted during the strategy devel-opment process—is split into gapsthat each strategic theme mustclose over three to five years.

3. What action programs does ourstrategy need? Managers choosestrategic initiatives—action pro-grams of finite duration aimed at achieving targeted performancefor the strategy map objectives.Initiatives must be viewed as aportfolio of complementary actionswith a cumulative effect, each of which must be implementedsuccessfully if the company is to achieve its theme targets andits vision objective.

4. How do we fund our initiatives?Executing strategy requires thatinitiatives be executed simultane-ously in a coordinated manner.This requires explicit funding forthe initiative portfolios. The tradi-tional budgeting system focuseson the resources for existing orga-nizational functions and businessunits. Strategic investments for initiatives that cross functions andbusiness units must be removedfrom operational budgets andmanaged separately by the execu-tive team. Companies facilitatethis process by creating a specialbudget category called STRATEX(strategic expenditures).

5. Who will lead strategy execution?Some companies are establishingtheme teams, a new accountabilitystructure for executing strategythrough strategic themes. This is important, since by definitionstrategic themes cross unit andfunctional lines and typical linesof responsibility. Companiesassign executives to become themeowners, provide them STRATEXfunding, and support them withtheme teams drawn from acrossthe organization. The theme own-ers and teams provide accounta-bility for and feedback on theexecution of the strategy withineach theme.3 (See Case File, p. 7.)

Stage 3: Align the Organizationwith the Strategy

To capture the full benefits ofoperating a multibusiness, multi-function organization, executivesmust link company strategy to the strategies of their businessand functional units, and mustalign and motivate employees.In this stage, they address threequestions:

1. How do we ensure that all business units are aligned?Strategy is usually defined at the individual business-unit level.But companies typically consist of multiple business or operatingunits. Corporate-level strategy defines how the strategies of

2Planthe

Strategy

1Develop

theStrategy

6Test and

Adapt

4Plan

Operations

5Monitor

andLearn

Operating Plan

Strategic Plan

Execution

Process

Initiative

3Align the

Organization

M a y – J u n e 2 0 0 8

Figure 1. A Closed-Loop Management System Linking Strategy and Operations

This six-stage management system, which incorporates the principles of the Strategy-FocusedOrganization, provides a comprehensive system that integrates all the processes and tools neededto develop and operationalize strategy, and to monitor and improve the effectiveness of strategyand operations. Constant review and dynamic updating of information is built into the system,providing a closed loop of feedback and learning—and the ability to update the strategy when

underlying assumptions prove outdated or flawed.

3

individual business units can beintegrated to create synergies not available to business unitsthat operate independently fromeach other. Corporate strategy isdescribed by a strategy map thatidentifies the specific sources ofsynergies. Managers then cascadethis map vertically to business

units, whose own strategy mapscan then reflect objectives relatedto their local strategies as well asthose objectives that integrate withthe corporate strategy and thestrategies of other business units.

2. How do we align support unitswith business-unit and corporatestrategies? Executives often treatsupport units and corporate staff functions as discretionaryexpense centers, that is, as over-head departments whose goalsare to minimize their operatingexpenses. As a result, the strate-gies and operations of supportunits do not align well with thoseof the company and the businessunits they are supposed to support.Successful strategy executionrequires that support units aligntheir strategies to the value-creatingstrategies of the company and its business units. Support unitsshould negotiate service-levelagreements with business units to define the set of services theywill provide. Creating support-unit strategy maps and scorecardsbased on the service-level agree-ments enables each unit to define and execute a strategy that enhances the strategies beingimplemented by business units.4

3. How do we motivate employeesto help us execute the strategy?Ultimately, employees are theones who improve the processes

and run the projects, programs,and initiatives required by thestrategy. They must know andunderstand the strategy if they are to successfully link their day-to-day work with the strategy.Formal communication programshelp employees understand the strategy and motivate them

to achieve it. Managers reinforce thecommunicationprogram by aligning employ-ees’ personalobjectives andincentives with

business-unit and company strate-gic objectives. Also, training andcareer development programshelp employees gain the compe-tencies they need for successfulstrategy execution.

Stage 4: Plan Operations

How do companies link long-termstrategy with day-to-day operations?Through an operational plan,which addresses these two keyquestions:

1. Which business processimprovements are most critical for executing the strategy? Theobjectives in a strategy map’sprocess perspective representhow strategy gets executed.Strategic themes originate in thesekey processes.5 For example, astrategic theme to “Grow ThroughInnovation” requires outstandingperformance from the new productdevelopment process; a theme to “Create Heightened LoyaltyAmong Targeted Customers”requires greatly improved cus-tomer management processes.Some process improvements are designed to deliver the finan-cial perspective’s cost reductionand productivity objectives,whereas others focus on excellingat regulatory and social objectives.These process improvements, dis-tinct from the short-term strategicinitiatives developed in Stage 2,

represent improvements to exist-ing, ongoing processes. Companiesmust focus their total quality man-agement, Six Sigma, and reengi-neering programs on enhancingthe performance of those processesdirectly related to the strategicobjectives that will yield desiredimprovements in the strategy’scustomer and financial objectives.Customized dashboards contain-ing key indicators of local processperformance provide focus andfeedback to employees’ processimprovement efforts.

2. How do we link strategy withoperating plans and budgets?The process improvement plansand the BSC’s high-level strategicmeasures and targets must beconverted into an annual operatingplan. An operating plan has threecomponents: a detailed sales fore-cast, a resource capacity plan, andbudgets for operating expensesand capital expenditures.

Sales forecast: Companies need to translate their strategic plan’srevenue targets into a sales fore-cast. The Beyond Budgeting move-ment6 advocates that companiescontinually respond to theirdynamic environments by refore-casting quarterly sales on a rollingbasis five to six quarters into the future. Whether developedannually or quarterly, the operatingplan is launched from a salesforecast, a task facilitated by analytic approaches such as driver-based planning. To provide thedetail necessary for the operatingplan, the sales forecast shouldincorporate the expected quantity,mix, and nature of individualsales orders, production runs,and transactions.

Resource capacity plan: Companiescan use time-driven activity-basedcosting (TDABC) to translatedetailed sales forecasts into esti-mates of the resource capacityrequired for the forecast periods.7

Activity-based costing is a tool for measuring the cost and prof-itability of processes, products,

B a l a n c e d S c o r e c a r d R e p o r t

4

Whether developed annually or quarterly,

the operating plan is launched from a sales

forecast, a task facilitated by analytic

approaches such as driver-based planning.

customers, channels, regions,and business units. But its “killerapp” is for resource planning andbudgeting. TDABC uses capacitydrivers (typically time) to mapresource expenses to the transac-tions, products, and customershandled by each process. It caneasily map forecast sales andprocess improvements to thequantity of resources—people,equipment, and facilities—required to fulfill the plan.

Dynamic operating and capitalbudgets: Once managers haveagreed on the quantity and mix of resources for a future period,they can easily calculate the financial implications of theseresource commitments. The company knows the cost of supplying each unit of resource.It multiplies the cost of eachresource type by the quantityof resources it has authorized,thereby obtaining the budgetedcost of supplying the resourcecapacity for the sales forecast and operating plan. Most of theresource capacity represents personnel costs and would beincluded in the operating expense(OPEX) budget. Increases inequipment resource capacitywould be reflected in the capitalbudget (CAPEX). The outputsfrom this process are dynamicoperating and capital budgets that have been derived quicklyand analytically from the salesand operating plans.

Because the company starts with detailed revenue forecastsand now has the resource costsassociated with delivering theseforecasts, simple subtractionyields a forecast and detailedprofit-and-loss statement for eachproduct, customer, channel, andregion. Companies that shift froman annual to a quarterly (rolling)budget process can follow thisprocess to get resource capacityplans for every period in whichthey have a sales forecast. Discre-tionary spending—such as pro-motional and advertising costs,

process improvement initiatives,and training—cannot yet be auto-mated through a model. Planningfor such costs is the last step inbudgeting.

Stage 5: Monitor and Learn

Once the strategy has been deter-mined, planned, and linked to acomprehensive operational plan,the company begins to execute its strategic and operational plans (represented by the ovalbetween stages 4 and 5 in Figure1), monitor the performanceresults, and act to improve operations and strategy based onnew information and learning.

At operational review meetings,companies examine departmentaland functional performance and address new or persistentproblems. They conduct strategyreview meetings to discuss theindicators and initiatives from the unit’s BSC and assess theprogress of and barriers to strategyexecution.8 By holding separateoperational and strategy reviewmeetings, companies avoid havingshort-term operational and tacticalissues displace discussions ofstrategy implementation andadaptation. The two meetingsaddress different questions:

1. Are our operations under control? At operational reviewmeetings companies examineshort-term performance andrespond to newly identified problems that need immediateattention. Operational reviewmeetings should correspond tothe frequency with which opera-tional data are generated and the speed at which managementwants to respond to sales andoperating data and the myriadother tactical issues that continu-ally emerge. Many companieshave weekly, twice-weekly, oreven daily meetings to reviewoperating dashboards of sales,bookings, and shipments and tosolve such short-term problems as complaints from important

customers, late deliveries, a near-term cash shortfall, or a new salesopportunity. Operational reviewmeetings are typically departmentaland function-based, bringingtogether the expertise and experi-ence of employees to solve day-to-day issues in such areas assales, purchasing, logistics,finance, and operations. Thesemeetings should be short, highlyfocused, data-driven, and action-oriented.

2. Are we executing our strategywell? Typically, companies sched-ule strategy review meetings oncea month to bring together theCEO and executive committeemembers to review the progressof the strategy. The leadershipteam discusses whether strategyexecution is on track, tracks thesource and causes of implementa-tion problems, recommends corrective actions, and assignsresponsibility for achieving thetargeted performance. If onethinks of strategy and problem-solving through the lens of theplan-do-check-act (PDCA) cycle,strategy review meetings are the“check” and “act” portions ofstrategy execution. If some of thesame people attend both reviewmeetings, meetings should beheld at different times and havedifferent agendas.

Because in-depth discussion ofevery BSC objective, measure,and initiative would require toomuch time at each monthly meeting, many companies noworganize their strategy reviewmeetings by strategic themes,covering one or two in depth at each meeting. Theme owners circulate BSC report data onmeasures and initiatives inadvance of the meeting so execu-tives can come prepared withideas and solutions. The meetingtime focuses on devising actionplans for new issues. (Meetingsshould also allow time for urgent“off theme” issues that cannotwait for the next meeting to be dealt with.)

M a y – J u n e 2 0 0 8

5

Each theme and objective is thusexamined carefully at least onceper quarter.

Stage 6: Test and Adapt the Strategy

A separate meeting is needed totest whether fundamental strategicassumptions remain valid. Sincethe previous major strategy reviewand update, the company has collected additional data from itsdashboards and monthly BSCmetrics, information on changesin the competitive and regulatoryenvironment, and new ideas(including new opportunities).The strategy testing and adaptingmeeting addresses the fundamen-tal question: Do we have the right strategy?

In this meeting, the executiveteam assesses the performance of its strategy and considers theconsequences of recent changesin the external environment.Testing and adapting the existingstrategy should be part of thestrategic analysis done as part of the first management systemstage. We treat it separatelybecause this process is designedfor modifying an existing strategyrather than for introducing a new,transformational strategy. The test-and-adapt meeting closes theloop on the integrated system ofstrategy planning and operationalexecution.

We believe every company shouldconduct such a meeting at leastannually, perhaps quarterly (ifcompetitive, technological, andconsumer dynamics warrant it),or whenever a major disruption or strategic opportunity arises.

This meeting should be informedby current external conditions (viaPESTEL analysis) and the competi-tive environment, as previouslydescribed. But the company nowhas, in addition, multiple inputsthat describe the actual perfor-mance of—the successes and failures of—the existing strategy.

Activity-based profitability reportssummarize profit-and-loss data by product line, customer, marketsegment, channel, and region.A second set of reports shows statistical analyses—summaries ofthe links among strategic metrics—that validate and quantify thehypothesized links on the compa-ny’s strategy map and strategicthemes; for example, the connec-tion between employee traininginitiatives and customer loyaltyand financial performance. Whenthe correlations are zero or oppo-site expectations, the executiveteam questions or rejects compo-nents of the existing strategy.Incremental improvements may be needed, or perhaps it’s time fora new, transformational strategy.

As the executive team updates its strategy, it also modifies theorganization’s strategy map andBSC and starts another cycle of strategy planning and opera-tional execution: new targets,new initiatives, the next period’ssales forecasts and operating plan,process improvement priorities,resource capacity requirements,and an updated financial plan.The strategic and operationalplans set the stage and establishthe information requirements fornext period’s schedule of opera-tional review, strategy review,and strategy testing and adaptingmeetings.

Balancing the demands of near-term operations with long-termstrategic goals and priorities hasalways been a major managementchallenge—and will remain so. Butdoing so is critical to successfulstrategy execution. This closed-loop system, which incorporatestime-tested approaches, not onlyhelps companies manage the two,but enables them to validate—andchallenge—their strategic hypothe-ses, and, if necessary, modify andchange in a timely, proactive way. �

1. Porter has said, “Operational effectiveness andstrategy are both essential to superior perform-ance…but they work in very different ways.”

See M. Porter, “What Is Strategy?” Harvard BusinessReview (November–December 1996). Similarly,Hammer noted that, “High performance operatingprocesses are necessary but not sufficient for enter-prise success.” See M. Hammer, “Redesigning thePractice of Management,” at Management: The LastProcess Frontier (Hammer & Company Conference,December 4, 2006).

2. See R. S. Kaplan and D. P. Norton, with E. A.Barrows, Jr., “Developing the Strategy: Vision, ValueGaps, and Analysis,” BSR January–February 2008(Reprint #B0801A); and R. S. Kaplan and D. P.Norton, with E. A. Barrows, Jr., “Formulating (andRevising) the Strategy,” BSR March–April 2008(Reprint #B0803A).

3. See R. S. Kaplan and C. Jackson, “Managing byStrategic Themes,” BSR September–October 2007(Reprint #B0709A).

4. See R. S. Kaplan, “The Demise of Cost and Profit Centers,” BSR January–February 2007 (Reprint #B0701A).

5. Horizontal strategic themes, such as for a collection of learning and growth or finance objec-tives, or for an entire perspective, are exceptionsand may not have originated within the processperspective.

6. A movement established by Jeremy Hope andRobin Fraser and an approach documented in their book Beyond Budgeting: How Managers CanBreak Free from the Annual Performance Trap(HBS Press, 2003) that calls for eliminating the static annual budget and replacing it with moredynamic tools such as rolling forecasts. Several BSCusers, including Hall of Fame organizations Borealis(2001) and Statoil (2007) are advocates. See “NewTools for a New Corporate Culture: The Budget-lessRevolution,” about Borealis, BSR January–February2002 (Reprint #B0201C); and “Statoil: ScorecardSuccess—the Second Time Around,” BSRJanuary–February 2008 (Reprint #B0801B).

7. R. S. Kaplan and S. P. Anderson, “Time-DrivenActivity-Based Costing,” Harvard Business Review(November 2004); and Kaplan and Anderson, Time-Driven Activity-Based Costing: A Simpler and MorePowerful Path to Higher Profits (HBS Press, 2007).

8. See D. P. Norton and J. R. Weiser, “The StrategyReview Process,” BSR November–December 2006(Reprint #B0611A).

“Mastering the ManagementSystem,” by Robert S. Kaplan andDavid P. Norton (Harvard BusinessReview, January 2008; Reprint#R0801D), offers further details onthe system described in this article,including a toolkit of concepts andframeworks related to each of thesix stages.

See also “Linking Strategy andPlanning to Budgets,” by David P. Norton (BSR May–June 2006;Reprint #B0605A); and “LinkingOperations to Strategy andBudgeting,” by David P. Nortonand Philip W. Peck (BSRSeptember–October 2006; Reprint#B0609A).

T O L E A R N M O R E

B a l a n c e d S c o r e c a r d R e p o r t

6

Reprint #B0805A

With its all-encompassing focus on strategy management and execution, Luxfer has also madestrides in linking strategy andoperations management, providingan interesting case for illustratingthe management model put forthby Kaplan and Norton anddescribed in this month’s OnBalance article. Space constraintsprevent us from exploring all sixstages, so we will focus on the mostnoteworthy ones: Plan the Strategy,Align the Organization with theStrategy, and Plan Operations.

In 2001, Luxfer Gas Cylinders was by all appearances a success-ful, if decentralized, company.But CEO John Rhodes realizedoperational excellence alonecouldn’t sustain the company inan ostensible commodity market.He feared an inward focus would stifle competitiveness, andwas concerned about creeping“regionalism” throughout Luxfer’sEuropean, Asia-Pacific, and NorthAmerican operations. Rhodes thus decided to develop a new,transformational strategy andadopt a strategic framework thatwould galvanize employees andhelp implement the strategy. TheBalanced Scorecard is today thecentral mechanism guiding

Luxfer’s strategy management and execution, from initiative andresource allocation decisions tostrategy reporting and review.Let’s look at key managementstages at Luxfer and how the BSCrelates to them.

Planning the Strategy (Stage 2)

In 2002, 20 key managers con-vened at a weeklong offsite,where they forged a new strategyof customer focus and marketleadership. They developed thecompany’s “strategic road map”(its name for its Balanced Score-card), established targets, and prioritized initiatives and deter-mined their funding. Leaderssolicited manager feedback—now a regular practice before any changes are made to thestrategy map.

An Architecture for Managing by Theme

Luxfer’s strategy map reflects aninnovative architecture: verticalthemes that run throughout theperspectives, representing thecompany’s “management by theme”approach. To break away from a siloed, functional approach to managing and the unwanted

regionalism, Rhodes and his teamidentified key strategic themes—such as “Product Leadership,”“[Being] Market-led,” and“Customer Focus”—and assignedone of the seven divisional heads(the company’s top executives)ownership of each. Each themehas a team with representativesdrawn from different functionalareas and from all levels through-out Luxfer’s global operations.

This theme approach, conceivedat the beginning, prevails today inthe third iteration of the strategymap. As Jeff Riddell, theme team“coach” and reporting coordinator,explains, a theme “divvies up the objective among all the areas”—internal processes, people,customer—that will be involved in its execution. The learning andgrowth perspective is simultane-ously a perspective and a theme—the foundational theme of thecompany. The perspective “Market-led Organization” is also a foun-dational theme. These then feedinto other themes: Product Leader-ship, Customer Focus, and Opera-tional Excellence. Each theme permeates the internal process,customer, and financial perspec-tives. For example, in “internalprocess,” Product Leader-shipincludes the objective “Deliverinnovative SCBA1 products” and in the customer perspective, itincludes the objective “Provide mea medical product that enhancesmy profitability.” In the financialperspective, it includes the objec-tive “Grow our Global SCBA business to x £ per year.”

Devising Measures and Targets

Choosing the right measures hasbeen a long, ongoing, iterative—and arduous—process. Creating theright mix of lagging and leadingindicators “that show you whatmakes a difference in perform-ance…[is] a challenge for a company like ours with a lot of analytically minded people,”notes Riddell.

M a y – J u n e 2 0 0 8

7

CA

SE

FI

LE Luxfer Gas Cylinders:

Mastering the Strategy–Operations LinkageBy Randall H. Russell, VP and Director of Research, Palladium Group; and Janice Koch, Editor, Balanced Scorecard Report; with Jeff J. Riddell, Innovationand New Business Coordinator, Luxfer Gas Cylinders

Luxfer Gas Cylinders, a leading global producer and distributorof gas cylinders, used the Balanced Scorecard to transformitself from a high-volume, low-margin commodity provider toan innovator of high-tech, high-profit offerings that are moreclosely targeted to customer needs. To do so, the companycarried out an ambitious strategy management program that centered around moving from a functionally managedorganization to a cross-functionally managed one: that ofmanaging by strategic theme. It was a move that not onlyrevitalized the company but also yielded solid financialresults, and helped secure Luxfer a place in the 2006 BSC Hall of Fame for Executing Strategy.

B a l a n c e d S c o r e c a r d R e p o r t

8

Luxfer has been refining its meas-ures for the past several years.Theme teams come up with measures and initiatives, writethem up, and present them to the seven-person executive (divi-sional) team for approval. Leadindicators are critical, but asRiddell points out, “They’re hardto define. It’s difficult to put yourtrust in them. But lagging indica-

tors just report on current thinking.Just counting sales, for example,won’t make a change in the way we run our business.” Thecompany has learned that less ismore; that it’s important to focuson the critical few measures andmanage what is vital to their success.

Targets are linked across eachtheme (that is, through the relevantperspectives the theme perme-ates) and add up to an overallfinancial objective of targetedsales revenue with specific mini-mum return on sales by a givenyear. In other words, the overalltarget is decomposed into subtar-gets that are cascaded throughoutthe organization.2 Stretch targets,developed through a rigorousprocess, provide clarity about whatdrives and influences performanceand about what is expected ofeach team and individual.

Selecting and FundingInitiatives

Pre-BSC, Luxfer had dozens of initiatives—so many that thecompany was failing to deliver on most of them. Luxfer is not alarge company, and many of thesame faces, Riddell notes, wereon different initiative teams. “Theywere overwhelmed.”

Clearly, initiatives needed to bestreamlined, and more resourcesand attention needed to shift to the new growth strategy andthe customer focus and productleadership themes. Objectives inlearning and growth that wouldenable strategic success neededfunding, such as building projectand initiative management skills—skills then widely lacking through-

out the company.“It wasn’t untilwe identified thatthere are indeedright and wrongways to managea theme, an initiative, and a project that

performance began to improve,”Riddell says. To cultivate thesecompetencies, the company putabout 75 project managers andproject sponsors through a two-day course. It periodically offerssuch training for new managers.

Divisional leaders assembled aninitiative portfolio and cascadedinitiatives throughout the regions.Today, ongoing initiatives areassessed every quarter at the divisional level, and new initia-tives are rationalized on a yearlybasis. Luxfer also raised the bar in terms of asking hard questionsabout initiative progress, demand-ing that initiatives yield fruit andremain strategically relevant andworthy of resources. A checklist of higher-level issues related tothemes and objectives helps themeowners assess progress and therelevance of proposed initiatives.

To ensure strategic initiatives areincluded in the budget process,an initiative was assigned to theLearning and Growth theme teamback in 2002, after the first mapwas developed. It is part of theobjective “Provide the resourcesand structure necessary to imple-ment the divisional strategic priorities.” As the theme manage-ment system has evolved, themeowners are now responsible forensuring that budgeting is provided

for strategic initiatives. In theInitiative Definition form, a proj-ect charter for each new initiative,managers must specify underwhich operational budget the ini-tiative falls. Funding then occursthrough the annual budgetingprocess. If a problem arises, thetheme owner is responsible forbringing it to the attention of thedivisional leaders.

The Luxfer Innovation Manage-ment System (LIMS), developed in 2005, is an example of an initiative designed not only tohelp innovate new products (in support of the Market-LedOrganization objective “Provideprofitable solutions on time”) butalso to build product developmentcapabilities. Mirroring the thememanagement approach, LIMSinvolves a cross-functional teamto manage the innovation portfo-lio, from concept developmentthrough launch, coordinating allthe functional, managerial, andadministrative activities within a global team—and developingthe necessary competencies toproduce and launch each productthat is deemed commerciallyviable. Every member of the LIMSteam manages at least one projectteam, and emphasis is placed onproject management, timely exe-cution, and product developmentdisciplines. Each new initiative isnow aligned to the strategy mapand has a clear role and outcomein driving the strategy.

Who Will Lead StrategyExecution?

Luxfer pioneered the concept ofmanagement by theme, a wholenew way of managing that thecompany considers integral to its success. Theme “owners”drive divisional strategic prioritiesthroughout the company’sregions. Each one of the sevendivisional leaders is assignedownership of a strategy maptheme, although the theme ownerisn’t necessarily the seniormostfunctional executive. Themes

“It wasn’t until we identified that there

are indeed right and wrong ways to manage

a theme, an initiative, and a project that

performance began to improve.”

today include Product Leadership,Market-led Organization,Customer Focus, OperationalExcellence, and Learning andGrowth. Each theme has a team—an oversight committee thatensures execution of the themethroughout all of Luxfer. Eachtheme team—the people whomake strategy operational—reviews objectives, measures, andinitiatives and offers feedbackbefore actual implementationbegins, through a process knownas “cold toweling.” (The termrefers to a common treatmentfor migraines and hangovers,in which the person lies down in a dark, quiet room with a cold towel to the forehead.) Sowhile upper management createsstrategy, managers provide furtherinput. This fosters their buy-in—crucial since they are the oneswho will ultimately effect the necessary changes and must communicate them with convic-tion to their people.

The theme owner handpicks team members, and it’s consideredan honor to serve. The roster isgiven to Riddell, who, in his roleas theme team coach, reviews it with each candidate’s functionalhead to ensure the added respon-sibility will not overload the candidate. If it appears it will,a different candidate is invited.

Themes are cross-functional; theyare linked by core competenciesand activities, not by function.Themes span departments, facili-ties, and regions; so do their teammembers. Theme teams are globaland nonhierarchical. They do notsupersede departmental authority;they use influence and persuasion.Indeed, members are chosen inpart for having those very skills.Theme teams work within existingprocesses and the organizationalstructure, leading change fromwithin.

Theme teams provide multiplebenefits: they inject multiple perspectives, strengths, and talents

into decision making and execu-tion; they ensure buy-in andactive communication; they helpavoid power struggles; and theyprovide a healthy degree of diver-sity, which spurs creative thinking,challenges conventional thinking,and fortifies team-building.

“It’s important to not load themeteams with functional managers,”says Riddell. “While leaders aremanagers, managers are not alwaysleaders.” In the early days, a functional person might stop theconversation to check with his orher department, “as though theywere representing a constituency.”Functional areas are not con-stituencies, Riddell emphasizes.The team members’ job is to helpmake decisions for the companybased on their knowledge andexperience, not to represent theirfunctional area or power base.“Strategy is about change, whiledepartmental/functional thinking[tends to be] about control,”Riddell says. Strategic objectivesmust outweigh the concerns of current processes; otherwise,change will not take place. “Thatdoes not mean we’re free to ram-page like a bull in a china shop,but if we’re going to make anomelet, then eggs will be broken,”he adds.

Getting this idea across, andachieving the right team mix,took some time.It’s human naturefor functionalmanagers to feel protectiveabout their area.Cross-functionalthinking andnew relationshipbuilding is notnatural to manypeople; hierarchy is. Siloed behav-ior exists because it is powerfuland ingrained. And behavior isharder to change if the organiza-tion is successful with the statusquo. Despite being flatter thanmost organizations, Luxfer none-theless struggled to an extent with

promoting cross-functional behav-ior. “It’s also against our nature asa manufacturer,” Riddell observes.“We’re all about squeezing effi-ciency. Strategy involves theopposite approach—you need to involve more people to makechange happen.”

The new management approachalso required new ways to handlemany activities and procedures,from initiative sponsorship (forexample, who will now ensurethat resources are in place andprovide executive oversight?) to reporting (a new mechanismfor information flow had to beestablished), to coordinating andoversight (“How do I coordinatewith people who don’t report to me?”). Not all the right peoplewere in place, and some house-cleaning took place. Still, evenwith the right people, this newway of managing isn’t achievedeasily. It’s an ongoing challenge—“part of the journey,” Riddell notes.

Aligning the Organization (Stage 3)

The corporate strategy map is the cornerstone of organizationalalignment at Luxfer. After devel-oping the corporate map in 2002,each business unit in the U.S.went through a similar process tocreate its own strategy map. Thismultimap approach ultimatelyproved unwieldy to manage,

and Luxfer abandoned it, relyinginstead on just one map. But,leaders say, the exercise wasinvaluable in communicating theBSC. In going through the process,people saw how objectives wereformed and understood the cause-

M a y – J u n e 2 0 0 8

9

Theme teams are global and nonhierarchical.

They do not supersede departmental

authority; they use influence and persuasion.

Indeed, members are chosen in part for

having those very skills.

and-effect relationships, whichbolstered understanding of therationale behind the new manage-ment-by-theme approach.

Since the first corporate map,there have been two revisions,one in 2005 and the last in 2007. No radical changes weremade; for example, the earlierInnovation theme was consolidatedinto Product Leadership, andsome objectives were made morespecific. No changes are imple-mented without input from thebusiness units. In the cold towelingperiod, each theme team mullsover objectives, measures, and initiatives, offers feedback, anddevelops a commitment to thechanges. Cold toweling is a goodreality check after what Riddellcalls the “euphoria that people getwhen they’re put in a room totalk about what they can achieve.”The strategy map is presented to the entire management team in daylong sessions, and is laterpresented to staff at regularlyscheduled communication meetings.

Thus, through sharp strategicfocus, proper rollout, judiciousselection of theme team members,and effective theme manage-ment, Luxfer business units have become well aligned withenterprise strategy.

But the real mechanism for alignment is theme management.Besides holding theme teammeetings to review progress andfacilitate execution, theme teammembers serve as liaisonsbetween their teams and theirbusiness units. Each team works

differently. For example, becauseof variations in local labor lawsand culture, the Learning andGrowth team ensures that objec-tives, measures, and initiatives

are writtenbroadly to allowfor regional flexibility anddiscretion. TheOperationalExcellence(OpEx) theme is functional by

nature, and each business unit’splant managers report on initia-tives and measures directly to theOpEx team. Because all Luxfermanufacturing facilities are similarin nature and have extensivetraining in manufacturing via theLuxfer Production System (LPS),this highly structured team takes a straightforward approach toimplementing and executing the strategy. Less flexibility and discretion are needed, so quickeralignment and implementation are possible.

Do conflicts ever arise betweentheme owners or teams and func-tional leaders? Of course, saysRiddell. But team owners andfunctional-area heads must workout their differences. Strategy,he adds, is about change, andchange equals conflict. “Peoplehave different expectations andaspirations.” When you speak ofmaking major changes in yourcompany, “you must reassure yourpeople that you believe in sharinginformation—that you may nothave all the answers, but you cantell them what the rules will beand say ‘we’re going to worktogether to achieve them.’”

To align employees, Luxfer uses a variety of communication toolsand incentives ranging from quarterly updates and CEO lettersto interviews of divisional memberscirculated via email. An employeenewsletter provides strategicupdates, and the company also

has a communication network,established through its BusinessFocus Team implementation.Although Luxfer doesn’t tie com-pensation to strategic perform-ance, some awards are tied tocustomer service performance or to solving an important prob-lem, and the company highlightssignificant employee accomplish-ments in its internal communica-tions. Luxfer believes its vision for the future, expressed throughits strategy map, goes a long way toward fostering workforcemorale and unity of purpose,even amid temporary setbacks.

Supplier Alignment

Aligning with suppliers is critical,particularly in supply chain man-agement. For example, Luxferexecutives targeted compositeproducts as a significant contribu-tor to revenue growth. Producingcomposites requires a dependablesupply of carbon fiber, but just asthe new revenue-growth offensivewas being launched, a global carbon fiber shortage hit. Securinga supply was critical not only to the success of the new plan, butalso to Luxfer’s overall business.Despite intense competition, Luxferwas able to secure a new supplyfrom its vendor. This vendorchose to supply Luxfer over othermanufacturers because Luxfer was the only new customer thatcould clearly articulate its long-term strategy and show theimportance of carbon fiber to it.(Luxfer showed the vendor itsstrategy map.) The vendor sawhow well the two organizationscould fit as partners.

Planning Operations (Stage 4)

At Luxfer, linking strategy andoperations is enabled largelythrough theme management.Strategic efforts are pushed downthrough the organization tobecome integral parts of opera-tions. Through regular strategymeetings, team accountability,

B a l a n c e d S c o r e c a r d R e p o r t

10

Cold toweling is a good reality check

after the “euphoria that people get when

they’re put in a room to talk about what

they can achieve.”

and adherence to project manage-ment principles, the execution of strategic initiatives has becomeembedded within day-to-dayoperations.

According to Kaplan and Norton,this management stage—thenexus of linking strategy andoperations—involves two keyissues: improving key processesthat are critical for strategy execu-tion, and linking strategy with the operating plan and budgets.The operating plan includes adetailed sales forecast, budgets for operating expenses and capitalexpenditures, and a resourcecapacity plan.

Key Process Improvement

Two process improvement initiatives, integrated with theOperational Excellence themeobjectives, support a key elementof the strategy, “[Achieve] world-class manufacturing through the implementation of the LuxferProduction System.” LPS isLuxfer’s proprietary manufacturingmanagement system, which consists of elements of OliverWight3 performance improvementprinciples, along with those oflean manufacturing, Toyota, SixSigma, and other methodologies.The first strategy map at Luxferwas developed for the company’sSydney, Australia, plant in 2000.To align this initiative with thestrategy, the Asia-Pacific manage-ment team carefully mapped elements of the Wight system tothe Balanced Scorecard. Thus,the team knew that when it wasmanaging to a BSC objective, itwas also delivering on the OliverWight initiative targets. Today, theLPS initiative is embedded in thestrategy map as a universal goalof all of Luxfer’s plants.

In addition, within the effort toreduce cost of quality, Luxfer hasan initiative to obtain ISO 14001certification at all its facilities (allLuxfer facilities are ISO-certified).

Process improvements in this arearesult from the linkage to strategicinitiatives and have already yieldedtangible financial results.

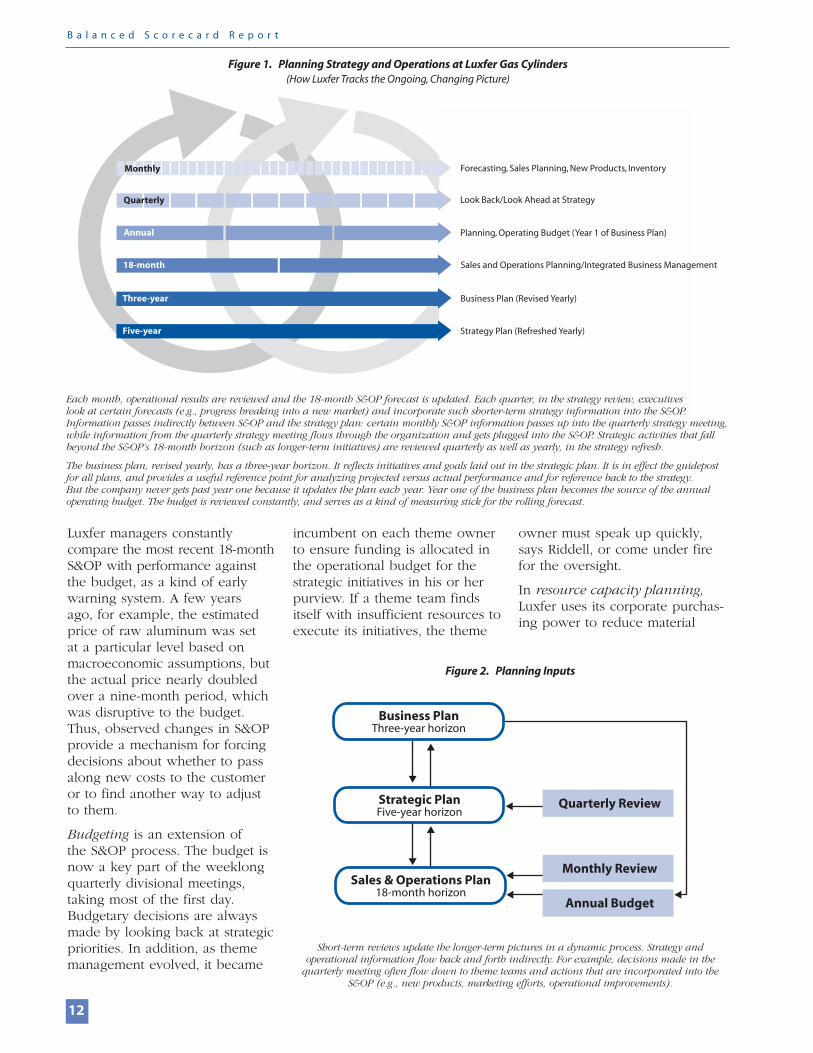

The Operating Plan

Long before adopting the BSCand theme management, Luxferhad a well-ingrained planningprocess. (See Figure 1, next page.)At its heart is Sales and OperationsPlanning (S&OP, known asIntegrated Business Managementor IBM in Luxfer’s European operations), which involves themonthly forecasting and planningof sales and operations (e.g., newproducts, inventory) all the waythrough to pro forma financials(financial statements accompany-ing the forecasts). The S&OPcycle runs monthly and extendsout 18 months. S&OP provides a tactical, near-term reading ofperformance, much as the instru-ment panel of a car provides analong-the-way view of a journey.In addition, it provides a linkbetween the strategy planningand management system, whichruns on a yearly and three-year basis, and the operationalmanagement system, which isreviewed and monitored daily,weekly, monthly, and quarterly.Inputs (i.e., actual performanceresults) from the shorter reviewcycles are fed into the longer-horizon plans to update themdynamically.

The S&OP system begins with areview of current demand, andthen incorporatesinformation onsales and long-term demand, byproduct, over an18-month rollingforecast. Thisinformation isfed to operationsto address capacity planning,helping answer the question,“How will we make these vol-umes in the time periods whenthey are needed?” In the third

week of each month, the produc-tion team reviews the supply/demand situation and provides anupdate of product developmentfor new products in the pipeline.Analysis is performed to ensuregoals are being hit for overall production (and for each productline), as well as for new productdevelopment, operational performance, and ultimately product profitability.

The strategic plan provides a five-year view that serves as a referencepoint for the S&OP’s 18-monthcycle. Updated every three years,the plan serves as the overallframework, but because it is constantly being reviewed andrevised with actual results, Luxfernever gets beyond the first year;at the end of each 12-month peri-od, a new five-year plan is created.Strategy guides the S&OP plansvia the annual budget cycle. Thetheme teams also provide input to make sure the theme-basedobjectives are accounted for.Specifically, the product leader-ship theme team, working withregional management, dissemi-nates divisional targets to regionsto build out the local S&OP plans.Thus, the two strategic inputs tothe S&OP process are the themeteams and the budget.

The business plan, written yearly,has a three-year horizon. It reflectsinitiatives and goals laid out inthe strategy, and is used for com-parison with strategic objectives.Around June each year, this plan

is “frozen” to become next year’soperating budget and year one of the next business plan. Figure2 (next page) shows key inputs to the plans and their relationships.

M a y – J u n e 2 0 0 8

11

Luxfer managers constantly compare

the most recent 18-month S&OP with

performance against the budget, as a kind

of early warning system.

Luxfer managers constantly compare the most recent 18-monthS&OP with performance againstthe budget, as a kind of earlywarning system. A few years ago, for example, the estimatedprice of raw aluminum was set at a particular level based onmacroeconomic assumptions, butthe actual price nearly doubledover a nine-month period, whichwas disruptive to the budget.Thus, observed changes in S&OP provide a mechanism for forcingdecisions about whether to passalong new costs to the customeror to find another way to adjustto them.

Budgeting is an extension of the S&OP process. The budget isnow a key part of the weeklongquarterly divisional meetings,taking most of the first day.Budgetary decisions are alwaysmade by looking back at strategicpriorities. In addition, as thememanagement evolved, it became

incumbent on each theme ownerto ensure funding is allocated inthe operational budget for thestrategic initiatives in his or herpurview. If a theme team findsitself with insufficient resources toexecute its initiatives, the theme

owner must speak up quickly,says Riddell, or come under firefor the oversight.

In resource capacity planning,Luxfer uses its corporate purchas-ing power to reduce material

B a l a n c e d S c o r e c a r d R e p o r t

12

Annual

18-month

Quarterly

Three-year

Monthly

Five-year

Forecasting, Sales Planning, New Products, Inventory

Sales and Operations Planning/Integrated Business Management

Look Back/Look Ahead at Strategy

Planning, Operating Budget (Year 1 of Business Plan)

Business Plan (Revised Yearly)

Strategy Plan (Refreshed Yearly)

Figure 1. Planning Strategy and Operations at Luxfer Gas Cylinders(How Luxfer Tracks the Ongoing, Changing Picture)

Each month, operational results are reviewed and the 18-month S&OP forecast is updated. Each quarter, in the strategy review, executives look at certain forecasts (e.g., progress breaking into a new market) and incorporate such shorter-term strategy information into the S&OP.Information passes indirectly between S&OP and the strategy plan: certain monthly S&OP information passes up into the quarterly strategy meeting,while information from the quarterly strategy meeting flows through the organization and gets plugged into the S&OP. Strategic activities that fallbeyond the S&OP’s 18-month horizon (such as longer-term initiatives) are reviewed quarterly as well as yearly, in the strategy refresh.

The business plan, revised yearly, has a three-year horizon. It reflects initiatives and goals laid out in the strategic plan. It is in effect the guidepostfor all plans, and provides a useful reference point for analyzing projected versus actual performance and for reference back to the strategy. But the company never gets past year one because it updates the plan each year. Year one of the business plan becomes the source of the annualoperating budget. The budget is reviewed constantly, and serves as a kind of measuring stick for the rolling forecast.

Sales & Operations Plan18-month horizon

Quarterly Review

Monthly Review

Annual Budget

Strategic PlanFive-year horizon

Business PlanThree-year horizon

Figure 2. Planning Inputs

Short-term reviews update the longer-term pictures in a dynamic process. Strategy and operational information flow back and forth indirectly. For example, decisions made in the

quarterly meeting often flow down to theme teams and actions that are incorporated into theS&OP (e.g., new products, marketing efforts, operational improvements).

costs. In the past, plants procuredmaterials independently; since the2005 strategy map revision, man-agers and purchasing departmentsacross regions collaborate to con-solidate purchases and, whereverpossible, negotiate with suppliersto lower prices.

A System with Results

Luxfer’s strategy transformation—a combination of rewriting thestrategy and implementing awhole new mechanism for man-aging it—has yielded powerfulresults. Before 2002, Luxfer waschiefly a low-margin, high-volumeenterprise, with 60% of its businessdriven by the operational excel-lence strategy. By 2005, more than60% of the business was drivenby the company’s new customer-focus strategy, underpinned by its emphasis on innovation andmarket leadership. Profits haveincreased year over year, and the product portfolio is now predominantly high-tech andhigh-margin. The restructuringaround theme ownership andvalue creation has put strategy

and strategy execution front and center.

The transformation has also fostered employee and unit align-ment and created a common language throughout this globalcompany. The workforce reflectsrenewed optimism and highermorale. And suppliers and strategiccustomers have shown greaterrespect and cooperation.

Luxfer’s leaders acknowledge that implementing the strategy—indeed, getting people to acceptall the new ways of doing business—has not happened overnight.Moreover, differences of opinionwill always exist; but such tension,they say, is natural and healthy,leading to constant improvement.At review meetings, for example,vigorous discussion is common,and divisional team members fre-quently challenge the conclusionsof theme owners. Change isn’talways comfortable or pretty, butit is integral to evolution—andcontinual strategy success. �

Besides serving as Luxfer’s Innovation and BusinessCoordinator, Jeff Riddell is responsible for assemblingall data, reports, and presentations for strategy reviews.

A member of all of Luxfer’s theme teams (exceptOperational Excellence), he also coaches teams onstrategy, processes, and best practices, and coacheseach theme owner individually. We thank Jeff for providing invaluable information and insights, andJohn Rhodes, CEO, for his support in publishing thisCase File.

1. Self-Contained Breathing Apparatus, which supplies breathing air to firefighters.

2. Kaplan and Norton describe the process ofdecomposing the value gap in “Developing the Strategy: Vision, Value Gaps, and Analysis,”BSR January–February 2008 (Reprint #B0801A).

3. Oliver Wight is a consulting firm that specializesin manufacturing management and processimprovement.

Luxfer Gas Cylinders, a 2006 BSC Hall of Fame winner, is profiled in the 2007 BSC Hall ofFame Report, available atwww.harvardbusiness.org. Also see “Managing by Theme,” an interview with Luxfer’s CEOJohn Rhodes, BSR November–December 2005 (Reprint #0511D);and “Managing by StrategicThemes,” by Robert S. Kaplan and Catherine (Kit) Jackson, BSR September–October 2007(Reprint #B0709A).

Reprint #B0805B

T O L E A R N M O R E

M a y – J u n e 2 0 0 8

13

C O M I N G U P I N B S R

• Is your OSM on track? Kaplan and

Norton on the three key roles of the

Office of Strategy Management

• Author Adrian Slywotzsky on turning

strategic risks into growth opportunities

• Using Strategy Maps for Competitor

Analysis

• Achieving the execution premium

at Nemours, the nation’s leading

children’s healthcare system (and a

2007 inductee to the BSC Hall of

Fame for Executing Strategy)

• How Experience Co-Creation can help

shape (and sharpen) customer strategy

• Building a sustainable strategy execution

program: findings from our follow-up

survey of Hall of Fame winners

The Balanced Scorecard Hall of Fame Report 2008

Learn the secrets to the breakthrough

performance of the 16 newest inductees to

the BSC Hall of Fame for Executing Strategy—

a roster that includes Statoil, Infosys, and

Lockheed Martin Enterprise Services. Visit

www.bsrhof.org to order.

Sharpen Your Strategic Skillswith the latest publications from Balanced Scorecard Report

BSR ReadersCheck out the newest releases: Setting

Measures and Targets that Drive Performance,

Managing Innovation, and The Strategy-

Focused IT Organization. Visit bsr.harvard-

businessonline.org and download the free

BSR Index for a full listing of all BSR

Readers and other publications. Or go to

www.harvardbusiness.org and search

Readers by title.

In “Initiative Management: PuttingStrategy into Action (BSRNovember–December 2007) Peter LaCasse and Travis Manzioneoutlined a comprehensive,four-step process for managinginitiatives: (1) identifying and collecting initiative ideas; (2) evaluating and prioritizing ideas;(3) planning and approvingimplementation; and (4) institut-ing project management and portfolio management practices.Each step is equally important;one weak link can undermine the entire process. While we’veseen widespread improvement in prioritizing and selecting initia-tives, organizations still have along way to go in reporting andmanaging them. This ongoingstep is not only critical for assess-ing the progress of each initiative,but also for demonstrating thereturn each initiative is yielding(“ROI,” or Return on Initiative).It ensures the initiative’s ongoingvalue relative to the organization’saggregate initiatives, providing adynamic cost/benefit assessmentthat tracks each initiative’s impacton funding and resources.

First, let’s reiterate our definitionof initiative. An initiative is a proj-ect of finite duration that supports

a strategic objective. Because ofits strategic tie, and because itfalls outside of day-to-day opera-tions, it is funded with resourcesthat fall outside of the operatingbudget. Some organizations actu-ally segregate this portion ofstrategic expenditures into aSTRATEX (strategic expenditures)budget. In this article, “funding”initiatives refers not only to supporting their tangible, directcosts, but also providing the full-time employees they require.

All too often, initiatives continueto receive funding, even in theabsence of a clearly identified“owner” with performanceaccountability. Sometimes theyextend long beyond their pro-posed life, incurring cost overrunsand failing to provide theirintended benefit. Unanticipatedobstacles and barriers can pushan initiative off track. A change inorganizational strategy can rendera once-worthy initiative strategi-cally irrelevant. In every case,the lack of sufficient informationand oversight prevents leadersfrom making informed investmentdecisions.

Resources are, of course, finite,and not all strategically relevant

initiatives can be funded. Hardchoices must be made to priori-tize those that promise the moststrategic payoff. Each resourcedecision affects not only the fund-ed initiative, but also all proposedinitiatives that are vying for theorganization’s limited resources.In other words, every investmentcarries an associated opportunitycost to the organization, as it displaces resources that mightotherwise be available for otherinitiatives. For that reason, it isimperative that an organizationmonitor initiatives to maximizetheir individual and collectiveimpact on organizational perform-ance—and monitor them regularly.

A regular, formal review processhelps organizations keep track ofthe costs and benefits, obstacles,and strategic shifts that can radi-cally alter an initiative’s value and progress. But it does more: it enables organizations to captureimportant opportunities as theyarise. Good ideas do not emergejust once a year during the strate-gic planning process. When organi-zations relegate initiative review to a once-a-year strategic planningperiod, they lose the ability todynamically allocate resources to capture new opportunities as they emerge—or to replaceunderperforming initiatives withmore promising ones, or evensimply to adjust to existing initia-tives’ actual performance. So it’snot enough to institute a formalannual review; organizationsshould schedule regular reviews,at least two a year.

Take a Portfolio View

Initiatives have “standalone”value—their inherent value—aswell as their value as a componentof a larger portfolio supporting astrategic theme. Managing initia-tives within portfolios providesaccretive value; it recognizes thatthe sum of a cluster of initiativesis more than the sum of individualinitiatives.

B a l a n c e d S c o r e c a r d R e p o r t

14

TO

OL

S

&

TE

CH

NI

QU

ES Maximize Your “Return on

Initiatives” with the InitiativePortfolio Review Process By Keith Katz, Consultant, and Travis Manzione, former Senior Consultant,Palladium Group, Inc.

More and more organizations are instituting a formal initia-tive management process. Such a process ensures that newand ongoing initiatives are aligned with strategic goals andthat the value of each initiative is maximized. It also ensuresthat organizational resources are being properly allocated.Yet many of these organizations do not manage all four stepsof the initiative management process with equal rigor, put-ting the entire management process at risk. One step that isstill woefully lacking is reporting and managing the total ini-tiative portfolio. Katz and Manzione offer guidelines to helpyou sharpen this critical step and ensure your organization’s“Return on Initiatives.”

Initiative Portfolio Managementconsists of four steps. In informa-tion collection, the organizationgathers essential informationabout the initiative’s performance,including progress against mile-stones, variance from anticipatedbudget, and projected deviationsfrom Return on Initiative. Thisinformation is entered into a standardized reporting templatethat includes space for a high-level,qualitative analysis of performanceas well as for recommendations.The information on each individ-ual initiative is consolidated into a master report. A summaryreview is added, to create theInitiative Portfolio Analysis. Thisdocument (step two) is the pri-mary document supporting theInitiative Portfolio Review (stepthree). In step four, leaders com-municate their decisions aboutongoing, as well as funded but not yet launched, initiatives to all affected parties. These include initiative sponsors and projectteams, as well as those whowould use the initiative’s deliver-ables—for example, customerservice reps awaiting a new CRMsoftware implementation.

The Initiative Portfolio AnalysisDocument

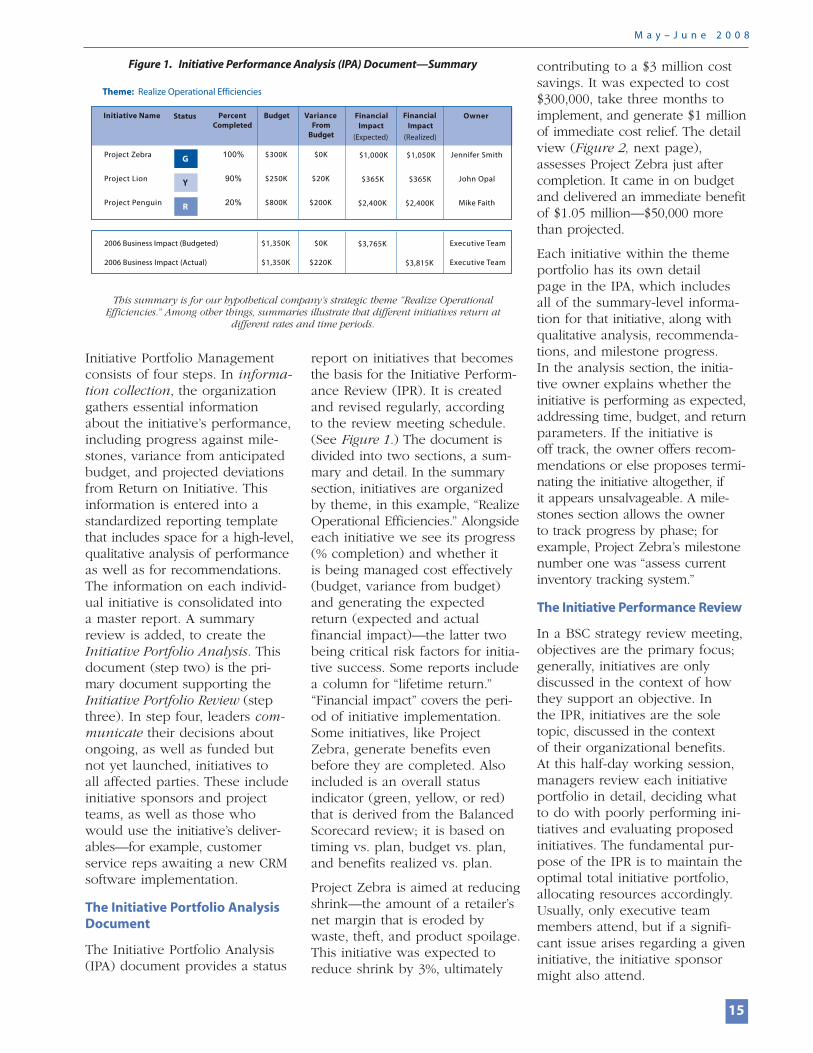

The Initiative Portfolio Analysis(IPA) document provides a status

report on initiatives that becomesthe basis for the Initiative Perform-ance Review (IPR). It is createdand revised regularly, accordingto the review meeting schedule.(See Figure 1.) The document isdivided into two sections, a sum-mary and detail. In the summarysection, initiatives are organizedby theme, in this example, “RealizeOperational Efficiencies.” Alongsideeach initiative we see its progress(% completion) and whether it is being managed cost effectively(budget, variance from budget)and generating the expectedreturn (expected and actual financial impact)—the latter twobeing critical risk factors for initia-tive success. Some reports include a column for “lifetime return.”“Financial impact” covers the peri-od of initiative implementation.Some initiatives, like ProjectZebra, generate benefits evenbefore they are completed. Alsoincluded is an overall status indicator (green, yellow, or red)that is derived from the BalancedScorecard review; it is based ontiming vs. plan, budget vs. plan,and benefits realized vs. plan.

Project Zebra is aimed at reducingshrink—the amount of a retailer’snet margin that is eroded bywaste, theft, and product spoilage.This initiative was expected toreduce shrink by 3%, ultimately

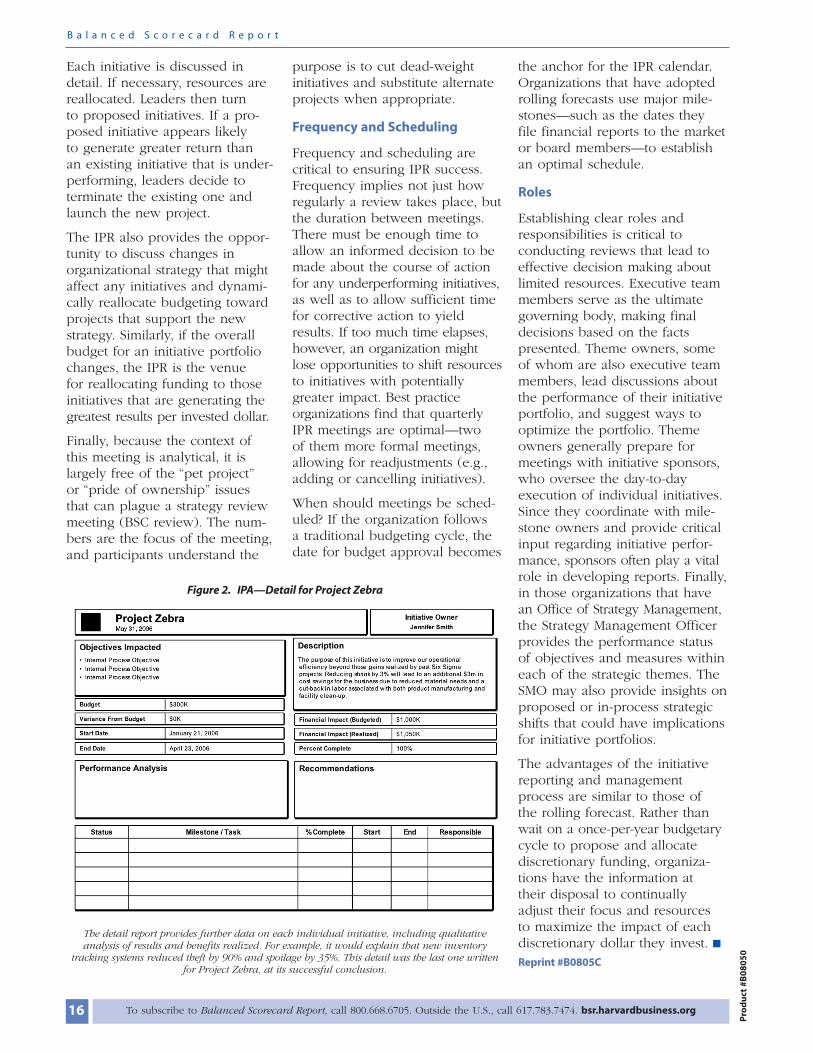

contributing to a $3 million costsavings. It was expected to cost$300,000, take three months toimplement, and generate $1 millionof immediate cost relief. The detailview (Figure 2, next page),assesses Project Zebra just aftercompletion. It came in on budgetand delivered an immediate benefitof $1.05 million—$50,000 morethan projected.

Each initiative within the themeportfolio has its own detail page in the IPA, which includesall of the summary-level informa-tion for that initiative, along withqualitative analysis, recommenda-tions, and milestone progress.In the analysis section, the initia-tive owner explains whether theinitiative is performing as expected,addressing time, budget, and returnparameters. If the initiative is off track, the owner offers recom-mendations or else proposes termi-nating the initiative altogether, if it appears unsalvageable. A mile-stones section allows the owner to track progress by phase; forexample, Project Zebra’s milestonenumber one was “assess currentinventory tracking system.”

The Initiative Performance Review

In a BSC strategy review meeting,objectives are the primary focus;generally, initiatives are only discussed in the context of howthey support an objective. In the IPR, initiatives are the soletopic, discussed in the contextof their organizational benefits.At this half-day working session,managers review each initiativeportfolio in detail, deciding whatto do with poorly performing ini-tiatives and evaluating proposed initiatives. The fundamental pur-pose of the IPR is to maintain theoptimal total initiative portfolio,allocating resources accordingly.Usually, only executive teammembers attend, but if a signifi-cant issue arises regarding a giveninitiative, the initiative sponsormight also attend.

M a y – J u n e 2 0 0 8

15

20%

90%

100%

PercentCompleted

$2,400K

$365K

$1,000K

FinancialImpact

(Expected)

$3,765K

$2,400K

$365K

$1,050K

FinancialImpact

(Realized)

$3,815K

$200K

$20K

$0K

VarianceFrom

Budget

$220K

$0K

$800K

$250K

$300K

Budget

$1,350K

$1,350K

Mike Faith

John Opal

Jennifer Smith

Owner

Executive Team

Executive Team

Project Penguin

Project Lion

Project Zebra

Initiative Name

2006 Business Impact (Actual)

2006 Business Impact (Budgeted)

Status

G

Y

R

Theme: Realize Operational Efficiencies

This summary is for our hypothetical company’s strategic theme “Realize OperationalEfficiencies.” Among other things, summaries illustrate that different initiatives return at

different rates and time periods.

Figure 1. Initiative Performance Analysis (IPA) Document—Summary

Each initiative is discussed indetail. If necessary, resources arereallocated. Leaders then turn to proposed initiatives. If a pro-posed initiative appears likely to generate greater return than an existing initiative that is under-performing, leaders decide to terminate the existing one andlaunch the new project.

The IPR also provides the oppor-tunity to discuss changes in organizational strategy that mightaffect any initiatives and dynami-cally reallocate budgeting towardprojects that support the newstrategy. Similarly, if the overallbudget for an initiative portfoliochanges, the IPR is the venue for reallocating funding to thoseinitiatives that are generating thegreatest results per invested dollar.

Finally, because the context ofthis meeting is analytical, it islargely free of the “pet project”or “pride of ownership” issuesthat can plague a strategy reviewmeeting (BSC review). The num-bers are the focus of the meeting,and participants understand the

purpose is to cut dead-weight initiatives and substitute alternateprojects when appropriate.

Frequency and Scheduling

Frequency and scheduling arecritical to ensuring IPR success.Frequency implies not just howregularly a review takes place, butthe duration between meetings.There must be enough time toallow an informed decision to bemade about the course of actionfor any underperforming initiatives,as well as to allow sufficient timefor corrective action to yieldresults. If too much time elapses,however, an organization mightlose opportunities to shift resourcesto initiatives with potentiallygreater impact. Best practiceorganizations find that quarterlyIPR meetings are optimal—two of them more formal meetings,allowing for readjustments (e.g.,adding or cancelling initiatives).

When should meetings be sched-uled? If the organization follows a traditional budgeting cycle, thedate for budget approval becomes

the anchor for the IPR calendar.Organizations that have adoptedrolling forecasts use major mile-stones—such as the dates they file financial reports to the marketor board members—to establishan optimal schedule.

Roles

Establishing clear roles andresponsibilities is critical to conducting reviews that lead toeffective decision making aboutlimited resources. Executive teammembers serve as the ultimategoverning body, making finaldecisions based on the facts presented. Theme owners, someof whom are also executive teammembers, lead discussions aboutthe performance of their initiativeportfolio, and suggest ways tooptimize the portfolio. Themeowners generally prepare formeetings with initiative sponsors,who oversee the day-to-day execution of individual initiatives.Since they coordinate with mile-stone owners and provide criticalinput regarding initiative perfor-mance, sponsors often play a vitalrole in developing reports. Finally,in those organizations that havean Office of Strategy Management,the Strategy Management Officerprovides the performance statusof objectives and measures withineach of the strategic themes. TheSMO may also provide insights onproposed or in-process strategicshifts that could have implicationsfor initiative portfolios.

The advantages of the initiativereporting and managementprocess are similar to those of the rolling forecast. Rather thanwait on a once-per-year budgetarycycle to propose and allocate discretionary funding, organiza-tions have the information at their disposal to continually adjust their focus and resources to maximize the impact of eachdiscretionary dollar they invest. �

Reprint #B0805C

B a l a n c e d S c o r e c a r d R e p o r t

16 To subscribe to Balanced Scorecard Report, call 800.668.6705. Outside the U.S., call 617.783.7474. bsr.harvardbusiness.org

Pro

du

ct #

B0

80

50

The detail report provides further data on each individual initiative, including qualitative analysis of results and benefits realized. For example, it would explain that new inventory

tracking systems reduced theft by 90% and spoilage by 35%. This detail was the last one writtenfor Project Zebra, at its successful conclusion.

Figure 2. IPA—Detail for Project Zebra