Embed Size (px)

Citation preview

The Strategic Impact of 4K on the

Entertainment Value Chain

December 2012

© 2012 Futuresource Consulting Ltd

2

© 2012 Futuresource Consulting Ltd, all rights reserved

Reproduction, transfer, distribution or storage of part or all of the contents in this document in

any form without the prior written permission of Futuresource Consulting is prohibited.

Company Registration No: 2293034

For legal limitations, please refer to the rear cover of this report

© 2012 Futuresource Consulting Ltd

Section Page

1. Introduction: Defining 4K 4

2. Executive Summary 6

3. 4K in Digital Cinema 9

4. 4K in Broadcast 12

5. 4K Standards and Delivery to the Consumer 20

a) Pay TV 24

b) Blu-ray 25

c) OTT 26

6. Consumer Electronics: 4K Issues and Forecasts 27

a) USA 31

b) Western Europe 33

c) UK, Germany, France, Italy and Spain 35

7. 4K in Professional Displays Markets 37

8. Appendix – Company Overview 48

3

Contents

© 2012 Futuresource Consulting Ltd

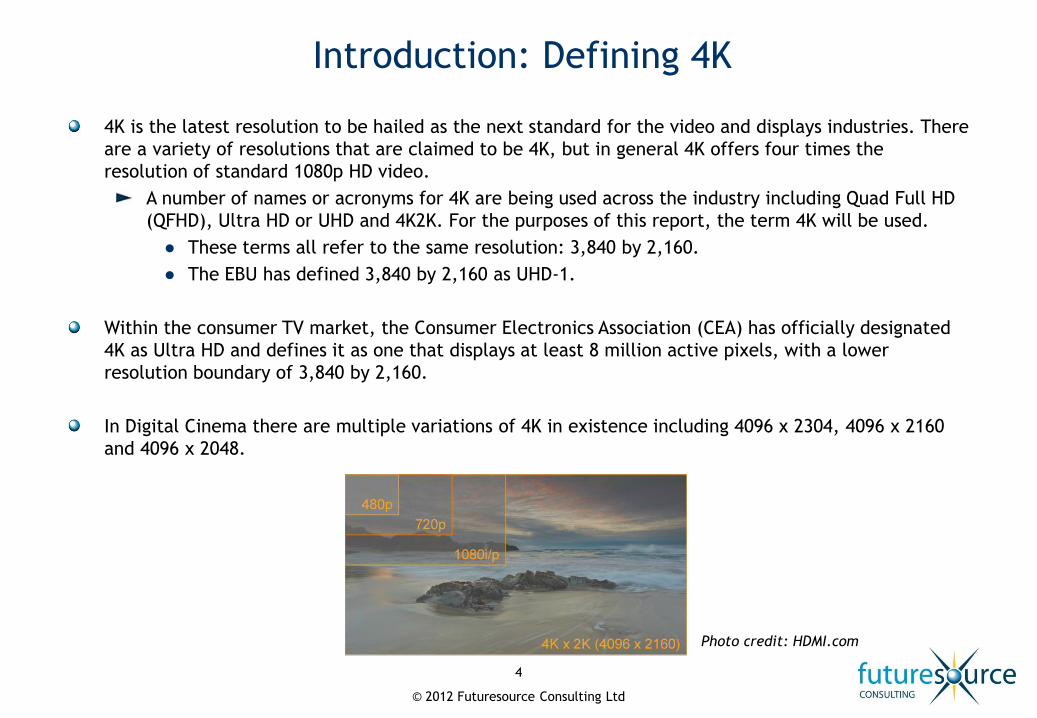

Introduction: Defining 4K

4K is the latest resolution to be hailed as the next standard for the video and displays industries. There

are a variety of resolutions that are claimed to be 4K, but in general 4K offers four times the

resolution of standard 1080p HD video.

A number of names or acronyms for 4K are being used across the industry including Quad Full HD

(QFHD), Ultra HD or UHD and 4K2K. For the purposes of this report, the term 4K will be used.

● These terms all refer to the same resolution: 3,840 by 2,160.

● The EBU has defined 3,840 by 2,160 as UHD-1.

Within the consumer TV market, the Consumer Electronics Association (CEA) has officially designated

4K as Ultra HD and defines it as one that displays at least 8 million active pixels, with a lower

resolution boundary of 3,840 by 2,160.

In Digital Cinema there are multiple variations of 4K in existence including 4096 x 2304, 4096 x 2160

and 4096 x 2048.

4

Photo credit: HDMI.com

2. Executive Summary

© 2012 Futuresource Consulting Ltd

Executive Summary (i) 4K is seen by many in the industry as a major new opportunity, but serious obstacles will need to be

overcome to enable development of the market. Most notable of these are the very limited supply of 4K

content, lack of distribution standards and the need for an installed base of 4K TV sets to create an

addressable audience.

As many elements of the broadcast equipment market become increasingly commoditised, manufacturers

continue to explore technological advancements that will capture the imagination and allow price points to

be stabilised. In addition, as global demand for TV displays starts to soften, LCD TV panel and set makers are

looking for the next value-add feature to kick-start a wave of consumer flat panel replacement. 3D in the

home was an attempt to achieve this and, while the technology hasn’t died away, it has yet to become the

solid success that many had hoped for. 4K represents a more natural progression for the industry, but one

that brings its own problems.

For the panel makers, the issues of producing 4K panels at higher yield rates are many, while prices for

commercialized sets are expected to remain out of the reach of mass market consumers for several years.

Furthermore, TV makers face the task of persuading consumers to upgrade to a higher resolution set at a

time when most consumers are just starting to recognize and enjoy the benefits of full HD. Despite these

barriers, Asian panel makers are moving forwards with the production of large screen 4K TVs and most major

TV brands will likely launch models over the next 12 months.

Looking to the broadcast industry and pay TV, the primary challenge is the increased bandwidth required to

transmit 4K. Providing four times the resolution of 1080p HD, 4K demands four times the data rate. In

addition, due to motion-blur being more visible at higher resolution, the frame rate should ideally be

doubled to counter this. This would mean the data rate would then also be doubled, hence the

uncompressed data rate of 4K would be eight times that of 1080p and 16 that of 1080i.

Clearly this has implications for the compression industry and while the new High Efficiency Video Codec

(HEVC) is due to be ratified in January, hardware-based, real-time encoding required for live transmission is

realistically at least two years away.

6

© 2012 Futuresource Consulting Ltd

Executive Summary (ii)

As with HD and more recently 3D, 4K consumer technology is ahead of the rest of the content chain and,

while 4K equipment is starting to emerge, there is currently no cross-platform 4K video source material

available for the market, meaning the TV or projector has to upscale the incoming signal to 4K resolution.

Sony is, however, bundling a 4K hard drive media player with its 84-inch 4K TV in the USA. The player

comes pre-loaded with 10 4K movies and some short-form content from Red Bull Media House. According

to Sony, the player will periodically be updated with new content.

The consumer electronics industry is showing willing to market 4K capable TVs and create an audience (as it

has previously done with ‘HD ready’ and ‘3D ready’ sets) but a sustained flow of 4K content will be critical to

its long term success.

Hollywood will be a key source of 4K content and will be keen to see the implementation of a Blu-ray 4K

standard in the near future. This will then usher in a new generation of 4K capable disc players.

A number of Pay TV operators have commenced testing of 4K acquisition and are expected to continue

investment in development technologies to enhance existing services and stave off competition.

With the backing of the consumer electronics, television and motion picture industries, Futuresource

believes that there is a positive commercial scenario for consumer 4K, although realistically this is likely to

take at least 5 to 6 years to develop.

7

3. 4K in Digital Cinema

© 2012 Futuresource Consulting Ltd

The digital cinema industry has been one of the pioneers of 4K video over the past few years, largely due to

the transition away from film.

Before 2007, there were a number of digital cinema cameras on the market, but the first camera that

made a real impact was the revolutionary Red One from Red Digital Cinema.

The launch of the Red One kick-started the digital revolution in the world of cinema, but also ushered in

the age of 4K.

The Red One can shoot in resolutions of up to 4.5k and so anyone opting to shoot digitally also had the

option to shoot in 4K from this point onwards.

Fast forward to 2012 and there are now a number of 4K digital cinema cameras on the market, at

varying price points and from various brands.

● In addition to the Red One, digital cinema cameras currently available include:

Red Epic

Red Scarlett

Sony F65

Sony F55

Sony F5

With 4K digital cinema equipment now ubiquitous, Hollywood is embracing 4K production. Many studios have

been acquiring movies in 4K for the past 18 months in order to future proof productions for the time when a

format is available for delivery to the consumer.

4K digital cinema productions are heavily centred on Hollywood or Hollywood-affiliated productions

currently. Other major film industries such as Bollywood have yet to make the transition to 4K,

although the move to digital is starting to gather pace.

In addition to this, existing titles are being scanned at 4K resolution to add to the 4K back catalogue.

● Titles so far given this treatment include Lawrence of Arabia, Jaws and Taxi Driver.

Digital Cinema – the 4K Pioneer (i)

9

© 2012 Futuresource Consulting Ltd

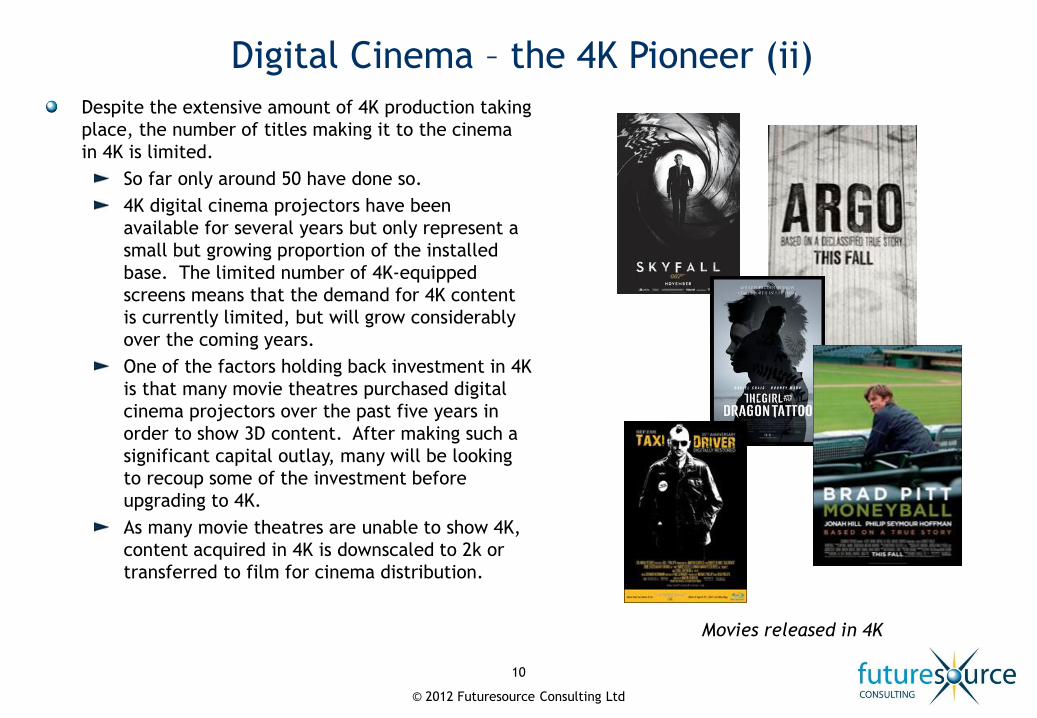

Despite the extensive amount of 4K production taking

place, the number of titles making it to the cinema

in 4K is limited.

So far only around 50 have done so.

4K digital cinema projectors have been

available for several years but only represent a

small but growing proportion of the installed

base. The limited number of 4K-equipped

screens means that the demand for 4K content

is currently limited, but will grow considerably

over the coming years.

One of the factors holding back investment in 4K

is that many movie theatres purchased digital

cinema projectors over the past five years in

order to show 3D content. After making such a

significant capital outlay, many will be looking

to recoup some of the investment before

upgrading to 4K.

As many movie theatres are unable to show 4K,

content acquired in 4K is downscaled to 2k or

transferred to film for cinema distribution.

Digital Cinema – the 4K Pioneer (ii)

10

Movies released in 4K

4. 4K in Broadcast

© 2012 Futuresource Consulting Ltd

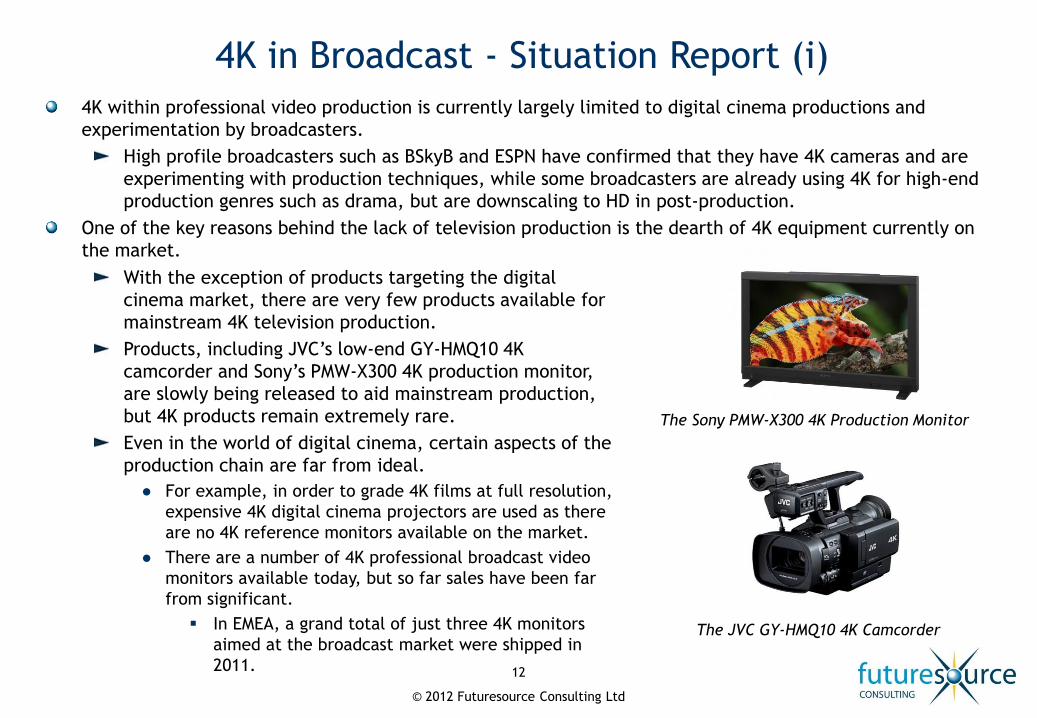

4K within professional video production is currently largely limited to digital cinema productions and

experimentation by broadcasters.

High profile broadcasters such as BSkyB and ESPN have confirmed that they have 4K cameras and are

experimenting with production techniques, while some broadcasters are already using 4K for high-end

production genres such as drama, but are downscaling to HD in post-production.

One of the key reasons behind the lack of television production is the dearth of 4K equipment currently on

the market.

4K in Broadcast - Situation Report (i)

12

With the exception of products targeting the digital

cinema market, there are very few products available for

mainstream 4K television production.

Products, including JVC’s low-end GY-HMQ10 4K

camcorder and Sony’s PMW-X300 4K production monitor,

are slowly being released to aid mainstream production,

but 4K products remain extremely rare.

Even in the world of digital cinema, certain aspects of the

production chain are far from ideal.

● For example, in order to grade 4K films at full resolution,

expensive 4K digital cinema projectors are used as there

are no 4K reference monitors available on the market.

● There are a number of 4K professional broadcast video

monitors available today, but so far sales have been far

from significant.

In EMEA, a grand total of just three 4K monitors

aimed at the broadcast market were shipped in

2011.

The Sony PMW-X300 4K Production Monitor

The JVC GY-HMQ10 4K Camcorder

© 2012 Futuresource Consulting Ltd

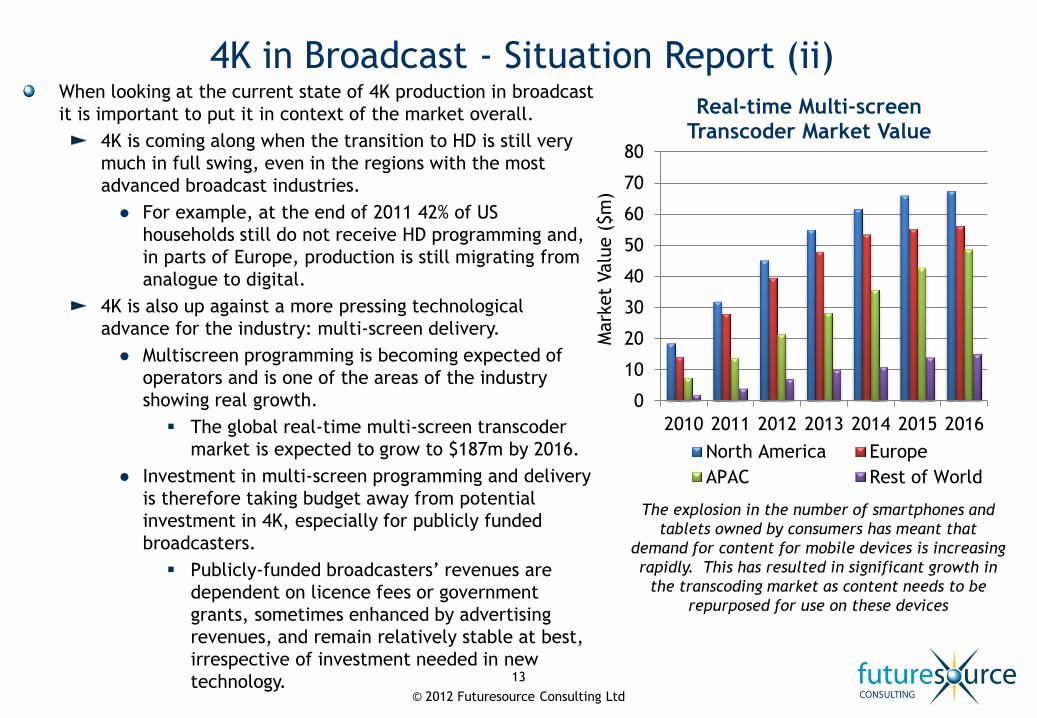

When looking at the current state of 4K production in broadcast

it is important to put it in context of the market overall.

4K is coming along when the transition to HD is still very

much in full swing, even in the regions with the most

advanced broadcast industries.

● For example, at the end of 2011 42% of US

households still do not receive HD programming and,

in parts of Europe, production is still migrating from

analogue to digital.

4K is also up against a more pressing technological

advance for the industry: multi-screen delivery.

● Multiscreen programming is becoming expected of

operators and is one of the areas of the industry

showing real growth.

The global real-time multi-screen transcoder

market is expected to grow to $187m by 2016.

● Investment in multi-screen programming and delivery

is therefore taking budget away from potential

investment in 4K, especially for publicly funded

broadcasters.

Publicly-funded broadcasters’ revenues are

dependent on licence fees or government

grants, sometimes enhanced by advertising

revenues, and remain relatively stable at best,

irrespective of investment needed in new

technology.

4K in Broadcast - Situation Report (ii)

13

0

10

20

30

40

50

60

70

80

2010 2011 2012 2013 2014 2015 2016

Real-time Multi-screen Transcoder Market Value

North America Europe

APAC Rest of World

Mark

et

Valu

e (

$m

)

The explosion in the number of smartphones and

tablets owned by consumers has meant that

demand for content for mobile devices is increasing

rapidly. This has resulted in significant growth in

the transcoding market as content needs to be

repurposed for use on these devices

© 2012 Futuresource Consulting Ltd

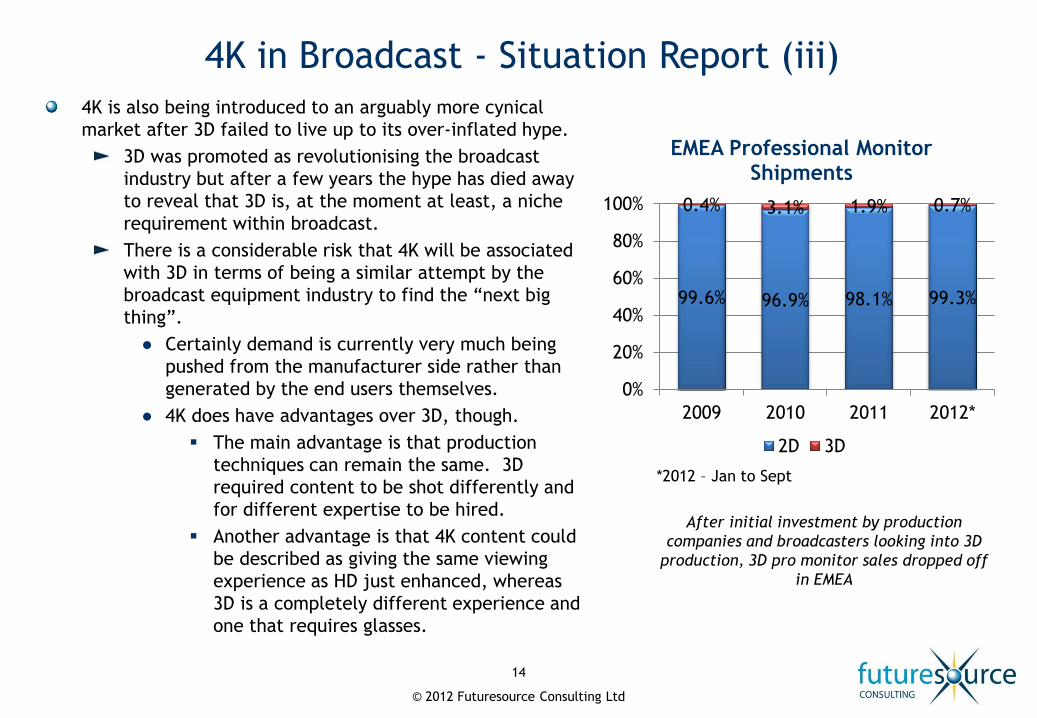

4K is also being introduced to an arguably more cynical

market after 3D failed to live up to its over-inflated hype.

3D was promoted as revolutionising the broadcast

industry but after a few years the hype has died away

to reveal that 3D is, at the moment at least, a niche

requirement within broadcast.

There is a considerable risk that 4K will be associated

with 3D in terms of being a similar attempt by the

broadcast equipment industry to find the “next big

thing”.

● Certainly demand is currently very much being

pushed from the manufacturer side rather than

generated by the end users themselves.

● 4K does have advantages over 3D, though.

The main advantage is that production

techniques can remain the same. 3D

required content to be shot differently and

for different expertise to be hired.

Another advantage is that 4K content could

be described as giving the same viewing

experience as HD just enhanced, whereas

3D is a completely different experience and

one that requires glasses.

4K in Broadcast - Situation Report (iii)

14

99.6% 96.9% 98.1% 99.3%

0.4% 3.1% 1.9% 0.7%

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012*

EMEA Professional Monitor Shipments

2D 3D

*2012 – Jan to Sept

After initial investment by production

companies and broadcasters looking into 3D

production, 3D pro monitor sales dropped off

in EMEA

© 2012 Futuresource Consulting Ltd

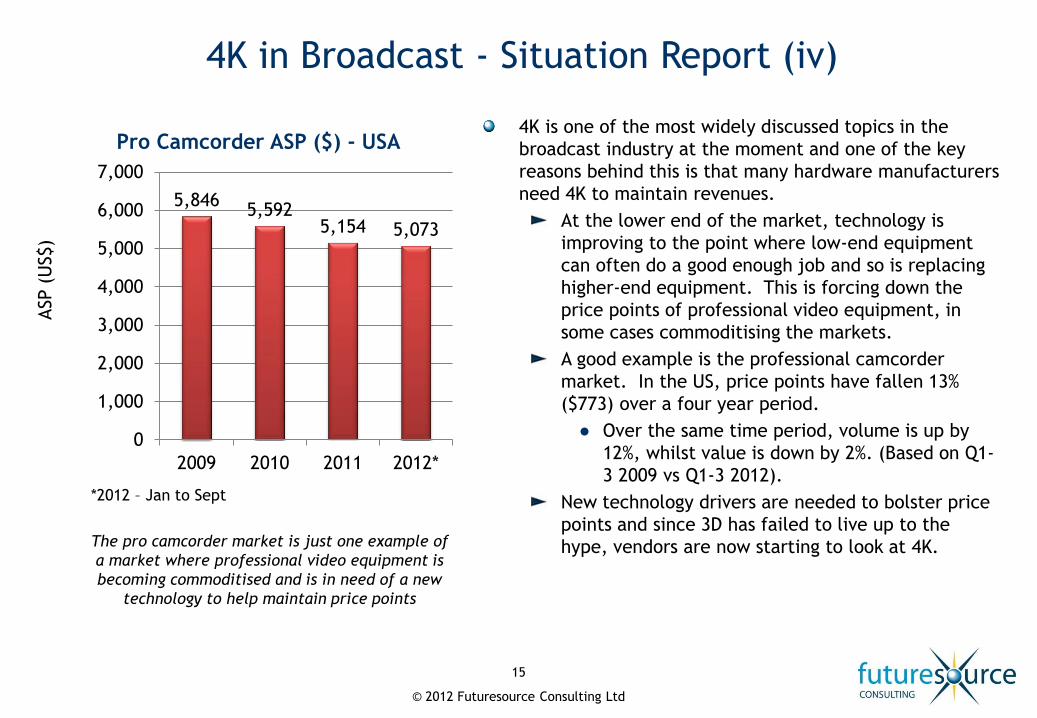

4K in Broadcast - Situation Report (iv)

4K is one of the most widely discussed topics in the

broadcast industry at the moment and one of the key

reasons behind this is that many hardware manufacturers

need 4K to maintain revenues.

At the lower end of the market, technology is

improving to the point where low-end equipment

can often do a good enough job and so is replacing

higher-end equipment. This is forcing down the

price points of professional video equipment, in

some cases commoditising the markets.

A good example is the professional camcorder

market. In the US, price points have fallen 13%

($773) over a four year period.

● Over the same time period, volume is up by

12%, whilst value is down by 2%. (Based on Q1-

3 2009 vs Q1-3 2012).

New technology drivers are needed to bolster price

points and since 3D has failed to live up to the

hype, vendors are now starting to look at 4K.

15

5,846 5,592

5,154 5,073

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2009 2010 2011 2012*

Pro Camcorder ASP ($) - USA

ASP (

US$)

*2012 – Jan to Sept

The pro camcorder market is just one example of

a market where professional video equipment is

becoming commoditised and is in need of a new

technology to help maintain price points

© 2012 Futuresource Consulting Ltd

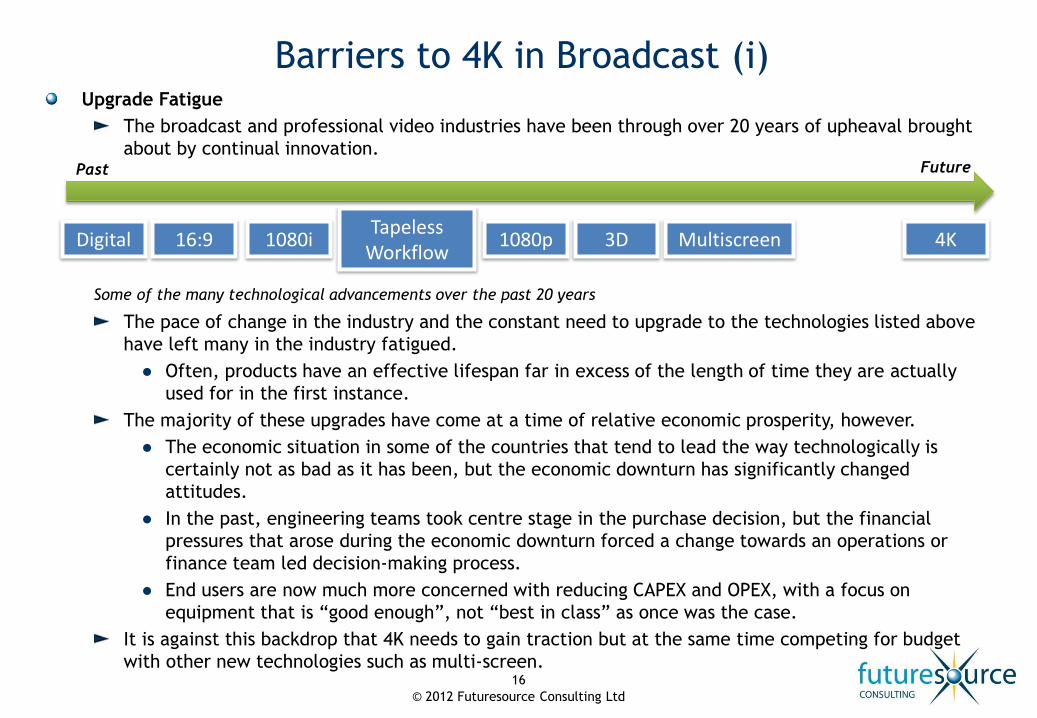

Barriers to 4K in Broadcast (i) Upgrade Fatigue

The broadcast and professional video industries have been through over 20 years of upheaval brought

about by continual innovation.

Some of the many technological advancements over the past 20 years

The pace of change in the industry and the constant need to upgrade to the technologies listed above

have left many in the industry fatigued.

● Often, products have an effective lifespan far in excess of the length of time they are actually

used for in the first instance.

The majority of these upgrades have come at a time of relative economic prosperity, however.

● The economic situation in some of the countries that tend to lead the way technologically is

certainly not as bad as it has been, but the economic downturn has significantly changed

attitudes.

● In the past, engineering teams took centre stage in the purchase decision, but the financial

pressures that arose during the economic downturn forced a change towards an operations or

finance team led decision-making process.

● End users are now much more concerned with reducing CAPEX and OPEX, with a focus on

equipment that is “good enough”, not “best in class” as once was the case.

It is against this backdrop that 4K needs to gain traction but at the same time competing for budget

with other new technologies such as multi-screen. 16

Digital 16:9 1080i 1080p Tapeless

Workflow 4K 3D

Past Future

Multiscreen

© 2012 Futuresource Consulting Ltd

Lack of Interfaces

There are currently no interfaces capable of coping with the extreme bandwidth demanded by

uncompressed 4K. There are a number of solutions available, though.

● 3G-SDI is the fastest real-time link available for the broadcast environment at the moment and so

the use of a quad 3G-SDI solution (four individual 3G-SDI interfaces used concurrently) is one

option.

● The second option is to use a fibre optic-based link that exists – 10GSDI, although this still may not

be enough to handle 4K unless a degree of compression is applied.

For 4K to be embraced throughout the production chain, an industry standard interface is essential.

Barriers to 4K in Broadcast (ii)

17

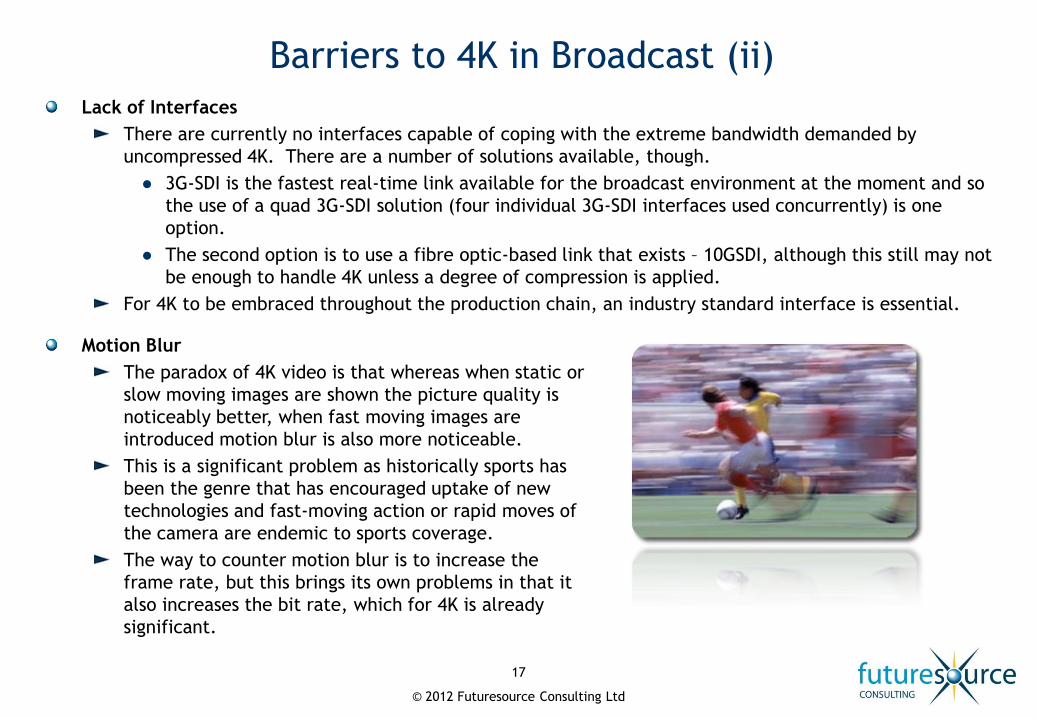

Motion Blur

The paradox of 4K video is that whereas when static or

slow moving images are shown the picture quality is

noticeably better, when fast moving images are

introduced motion blur is also more noticeable.

This is a significant problem as historically sports has

been the genre that has encouraged uptake of new

technologies and fast-moving action or rapid moves of

the camera are endemic to sports coverage.

The way to counter motion blur is to increase the

frame rate, but this brings its own problems in that it

also increases the bit rate, which for 4K is already

significant.

© 2012 Futuresource Consulting Ltd

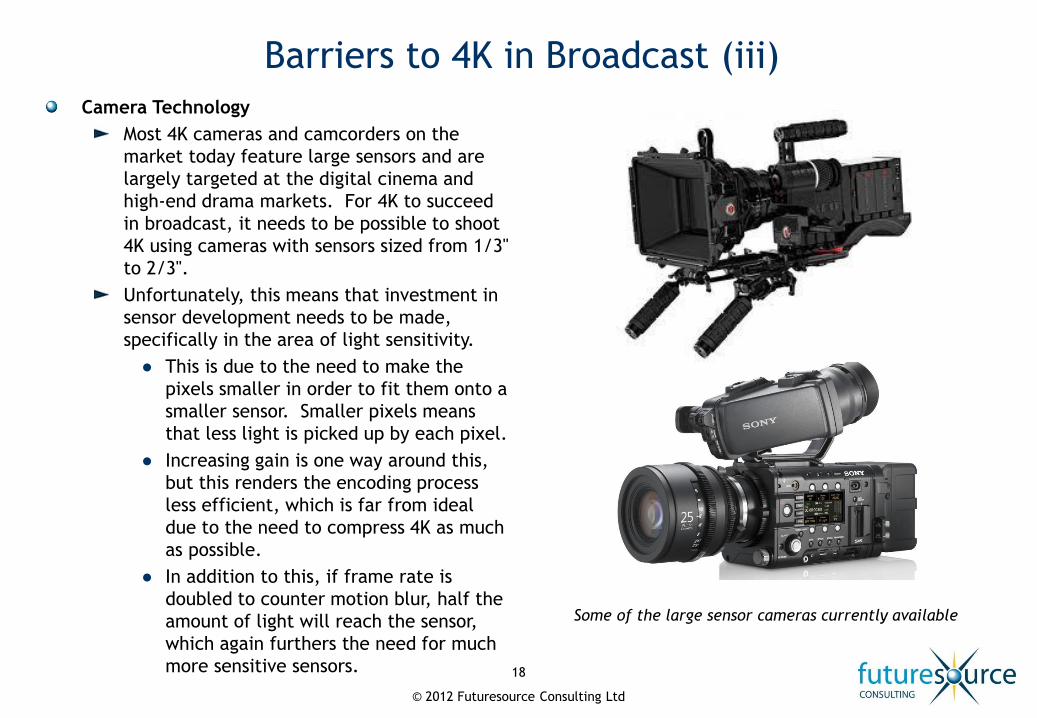

Camera Technology

Most 4K cameras and camcorders on the

market today feature large sensors and are

largely targeted at the digital cinema and

high-end drama markets. For 4K to succeed

in broadcast, it needs to be possible to shoot

4K using cameras with sensors sized from 1/3"

to 2/3".

Unfortunately, this means that investment in

sensor development needs to be made,

specifically in the area of light sensitivity.

● This is due to the need to make the

pixels smaller in order to fit them onto a

smaller sensor. Smaller pixels means

that less light is picked up by each pixel.

● Increasing gain is one way around this,

but this renders the encoding process

less efficient, which is far from ideal

due to the need to compress 4K as much

as possible.

● In addition to this, if frame rate is

doubled to counter motion blur, half the

amount of light will reach the sensor,

which again furthers the need for much

more sensitive sensors.

Barriers to 4K in Broadcast (iii)

18

Some of the large sensor cameras currently available

5. 4K Standards and Delivery to the Consumer

© 2012 Futuresource Consulting Ltd

HEVC (High Efficiency Video Codec) is the next generation compression standard that is due to be ratified in

January 2013.

It offers between 33% and 50% greater encoding efficiency when compared to H.264 (dependent on

vendor).

The high bandwidth required for 4K means that for many 4K and HEVC are intrinsically linked. When

bandwidth is tight, using HEVC brings the bit rate of 4K down to manageable levels.

● In tests, a bandwidth of 18 to 20Mbps for HEVC 4K is achievable, which is similar to the bit rate of

MPEG-2 HD, making 4K commercially viable.

● Luckily the higher resolution of 4K means that the encoding process can be completed a lot more

efficiently than with HD. Whilst uncompressed 4K requires four times the bandwidth of 1080p, this

does not equate to four times the compressed bandwidth.

HEVC is going to be particularly important for contribution and distribution over satellite as transponder

space is already at a premium. A sound business case will have to be built, though, as many will

question the economics of carrying one 4K channel in place of multiple SD channels.

Contribution and distribution of live content requires low-latency encoders but arguably the only way to

achieve this in real-time is to use hardware-based encoders and decoders.

Unfortunately, the dedicated silicon needed for such products is not yet available.

Expectations are that the first HEVC silicon will be available by the end of 2013 at the earliest,

indicating a likely launch of the first generation real-time HEVC encoders around NAB 2014, if not a little

earlier.

There is an argument that 4K does not depend on HEVC. Where bandwidth isn’t at a premium; where a cable

operator has invested heavily in a fibre optic network for example, then 4K can be distributed using H.264.

This would mean that 4K services would theoretically be viable much earlier than previously thought.

4K and the HEVC Standard

20

© 2012 Futuresource Consulting Ltd

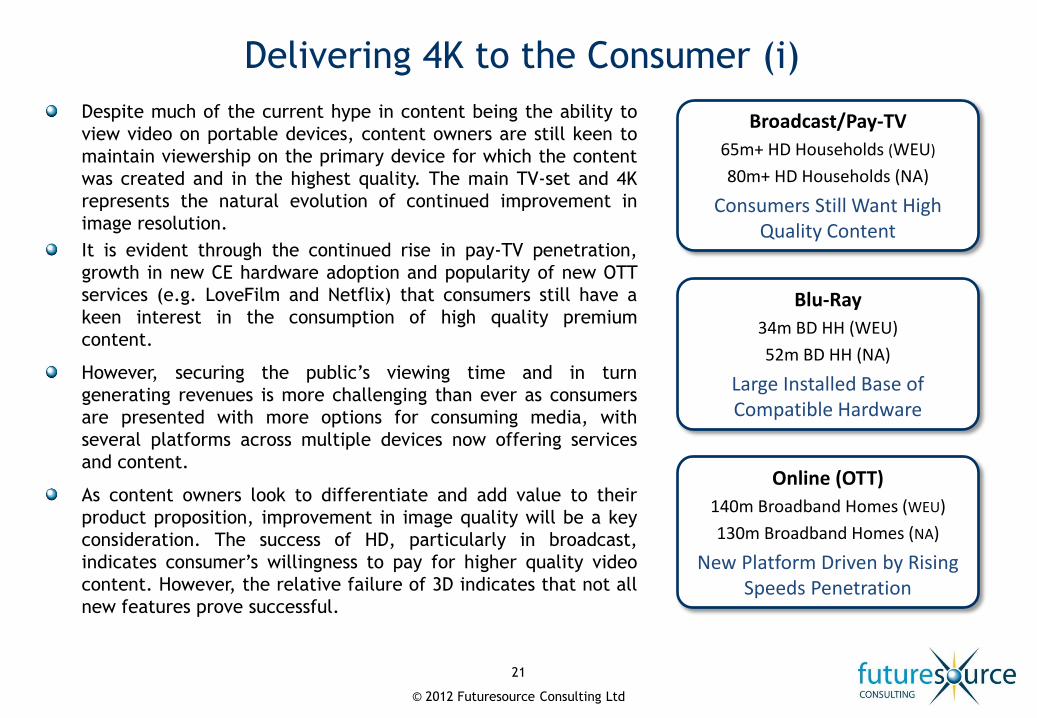

Delivering 4K to the Consumer (i)

Despite much of the current hype in content being the ability to

view video on portable devices, content owners are still keen to

maintain viewership on the primary device for which the content

was created and in the highest quality. The main TV-set and 4K

represents the natural evolution of continued improvement in

image resolution.

It is evident through the continued rise in pay-TV penetration,

growth in new CE hardware adoption and popularity of new OTT

services (e.g. LoveFilm and Netflix) that consumers still have a

keen interest in the consumption of high quality premium

content.

However, securing the public’s viewing time and in turn

generating revenues is more challenging than ever as consumers

are presented with more options for consuming media, with

several platforms across multiple devices now offering services

and content.

As content owners look to differentiate and add value to their

product proposition, improvement in image quality will be a key

consideration. The success of HD, particularly in broadcast,

indicates consumer’s willingness to pay for higher quality video

content. However, the relative failure of 3D indicates that not all

new features prove successful.

21

Broadcast/Pay-TV

65m+ HD Households (WEU)

80m+ HD Households (NA)

Consumers Still Want High Quality Content

Blu-Ray

34m BD HH (WEU)

52m BD HH (NA)

Large Installed Base of Compatible Hardware

Online (OTT)

140m Broadband Homes (WEU)

130m Broadband Homes (NA)

New Platform Driven by Rising Speeds Penetration

© 2012 Futuresource Consulting Ltd

Delivering 4K to the Consumer (ii)

Several pay-TV operators have already begun to undertake evaluation and testing of 4K acquisition,

particularly on live events (predominantly sports). As operators are likely to apply premium pricing to 4K

channels/content, they can justify the financial outlay in light of the potential revenue stream.

Although no standard has yet been ratified by the Blu-ray Disc Association (BDA), Blu-ray is also expected to

become a distribution platform for 4K content. The uptake of hardware, although lower than anticipated,

has still secured a significant footprint, present in 86m households (inc. PS3) across North America and

Western Europe. Hollywood is expected to be keen to support 4K through Blu-ray in an effort to improve disc

sales, which to date have been relatively disappointing.

Improved broadband speeds are allowing the distribution of broadcast quality video content over IP, as a

result of which OTT video services now represent an alternative delivery platform for content owners to

deliver high quality video content to consumers.

With several significant players present in this space, including Amazon, Apple, Google and Microsoft all of

which are keen to exploit their respective video services, the launch of 4K content offers a new level of

quality and value to the customer base.

22

© 2012 Futuresource Consulting Ltd

Delivering 4K to the Consumer: Pay-TV

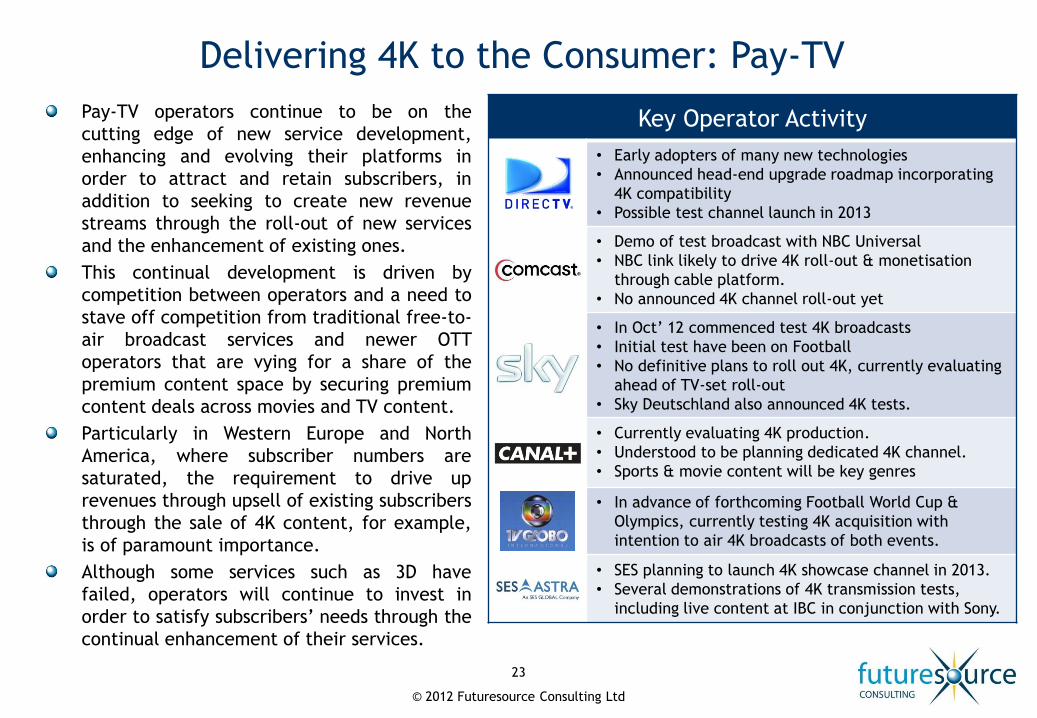

Pay-TV operators continue to be on the

cutting edge of new service development,

enhancing and evolving their platforms in

order to attract and retain subscribers, in

addition to seeking to create new revenue

streams through the roll-out of new services

and the enhancement of existing ones.

This continual development is driven by

competition between operators and a need to

stave off competition from traditional free-to-

air broadcast services and newer OTT

operators that are vying for a share of the

premium content space by securing premium

content deals across movies and TV content.

Particularly in Western Europe and North

America, where subscriber numbers are

saturated, the requirement to drive up

revenues through upsell of existing subscribers

through the sale of 4K content, for example,

is of paramount importance.

Although some services such as 3D have

failed, operators will continue to invest in

order to satisfy subscribers’ needs through the

continual enhancement of their services.

23

Key Operator Activity

• Early adopters of many new technologies

• Announced head-end upgrade roadmap incorporating

4K compatibility

• Possible test channel launch in 2013

• Demo of test broadcast with NBC Universal

• NBC link likely to drive 4K roll-out & monetisation

through cable platform.

• No announced 4K channel roll-out yet

• In Oct’ 12 commenced test 4K broadcasts

• Initial test have been on Football

• No definitive plans to roll out 4K, currently evaluating

ahead of TV-set roll-out

• Sky Deutschland also announced 4K tests.

• Currently evaluating 4K production.

• Understood to be planning dedicated 4K channel.

• Sports & movie content will be key genres

• In advance of forthcoming Football World Cup &

Olympics, currently testing 4K acquisition with

intention to air 4K broadcasts of both events.

• SES planning to launch 4K showcase channel in 2013.

• Several demonstrations of 4K transmission tests,

including live content at IBC in conjunction with Sony.

© 2012 Futuresource Consulting Ltd

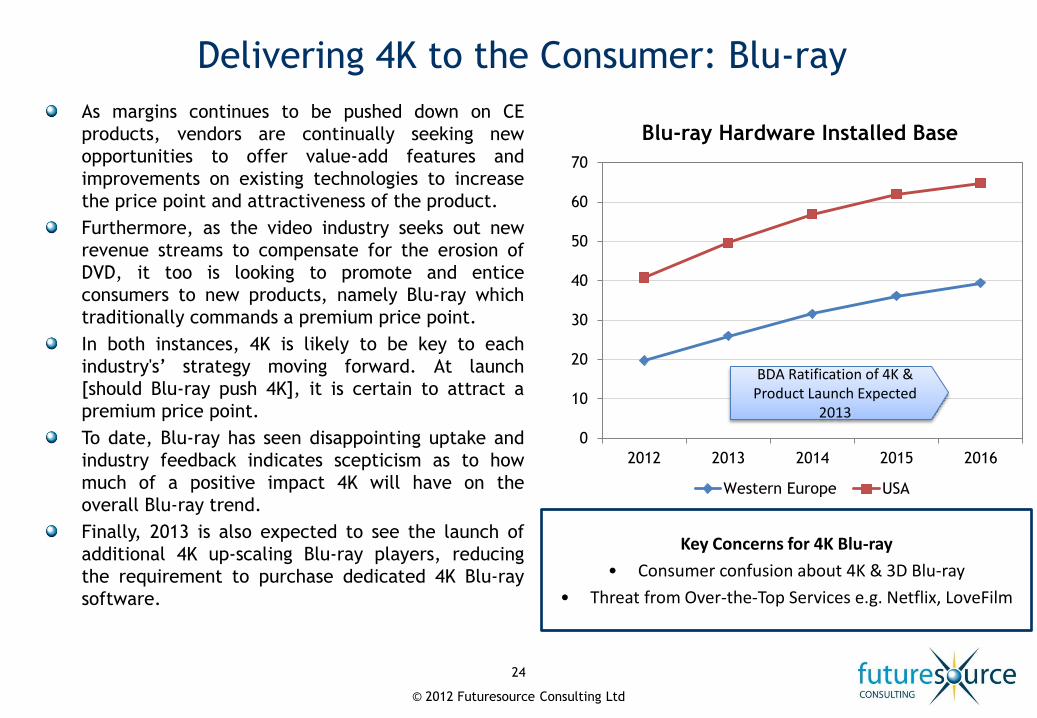

Delivering 4K to the Consumer: Blu-ray

As margins continues to be pushed down on CE

products, vendors are continually seeking new

opportunities to offer value-add features and

improvements on existing technologies to increase

the price point and attractiveness of the product.

Furthermore, as the video industry seeks out new

revenue streams to compensate for the erosion of

DVD, it too is looking to promote and entice

consumers to new products, namely Blu-ray which

traditionally commands a premium price point.

In both instances, 4K is likely to be key to each

industry's’ strategy moving forward. At launch

[should Blu-ray push 4K], it is certain to attract a

premium price point.

To date, Blu-ray has seen disappointing uptake and

industry feedback indicates scepticism as to how

much of a positive impact 4K will have on the

overall Blu-ray trend.

Finally, 2013 is also expected to see the launch of

additional 4K up-scaling Blu-ray players, reducing

the requirement to purchase dedicated 4K Blu-ray

software.

24

0

10

20

30

40

50

60

70

2012 2013 2014 2015 2016

Blu-ray Hardware Installed Base

Western Europe USA

BDA Ratification of 4K & Product Launch Expected

2013

Key Concerns for 4K Blu-ray

• Consumer confusion about 4K & 3D Blu-ray

• Threat from Over-the-Top Services e.g. Netflix, LoveFilm

© 2012 Futuresource Consulting Ltd

Delivering 4K to the Consumer: OTT

4K signifies new opportunities for OTT video platforms such as Netflix, LoveFilm and Apple, strengthening

their service proposition to include premium content, delivered in a comparable quality to that on offer from

traditional pay-TV platforms.

Furthermore, OTT platforms are expected to look to 4K in the future in order to create higher value

offerings and higher-priced subscription tiers, which will support continued revenue growth from increasingly

saturated subscriber bases.

4K is certain to place increased pressures on the IP infrastructure (which in many places is still struggling to

deliver HD). Therefore, in order to guarantee bandwidth and ensure no contention on the network, tie ups

between ISPs and video service providers are likely to ensure subscribers obtain a high quality of service.

The roll-out of Smart 4K TV-sets also presents an opportunity for OTT services to be delivered direct to the

TV-set and possible partnerships between CE manufacturers and content owners to promote 4K – particularly

in the early days.

25

6. Consumer Electronics: 4K Issues and Forecasts

© 2012 Futuresource Consulting Ltd

4K in the Consumer TV Market (i) The consumer TV market has been in a state of flux during the last few years. The traditional powerhouse

brands in Japan are struggling amid weak demand in developed markets and slowing growth rates in

emerging regions. Meanwhile, recent technology innovations such as 3D are not proving compelling enough to

consumers to warrant upgrading existing flat panels.

TV vendors are now looking to new display technologies and improvements to existing LED set designs to

drive replacement moving forwards. The two technologies that have been getting the most attention over

the past 12 months are OLED and 4K.

OLED is seen as a technology that will ultimately replace existing flat-panel display solutions, offering

significantly better picture quality, thinner form factors and perhaps most importantly much lower energy

consumption levels than today’s TVs.

However, despite the announcement of large-size OLED TVs from Samsung and LG in early 2012,

commercialization timescales of these sets have been put back to 2013 at the earliest following

difficulties in improving manufacturing yield.

Initially, OLED displays will have a resolution of 1080p although 4K versions will inevitably emerge as

production techniques improve.

4K, under its official consumer label of Ultra HD, is already beginning to be implemented into the home-

theatre environment via home-theatre receivers with either 4K pass-through and/or 4K video upscaling

capability, 4K home projectors, Blu-ray players with 4K video upscaling and 4K-capable TV displays.

4K LED TVs have rapidly emerged in 2012 thanks to the far simpler production process than for OLED

and most major TV brands are prioritising 4K over OLED in at least the short to mid-term.

There are currently no commercialized 4K Plasma TVs although it is technically possible to produce them

(Panasonic showed a 152” 4K Plasma set at CES 2010). However, producing 4K plasma panels at sizes under

60” will mean halving the cell size.

Plasma R&D is likely to start winding down moving forwards so it is likely that only extra large (100”+)

4K plasma panels will come to market.

27

© 2012 Futuresource Consulting Ltd

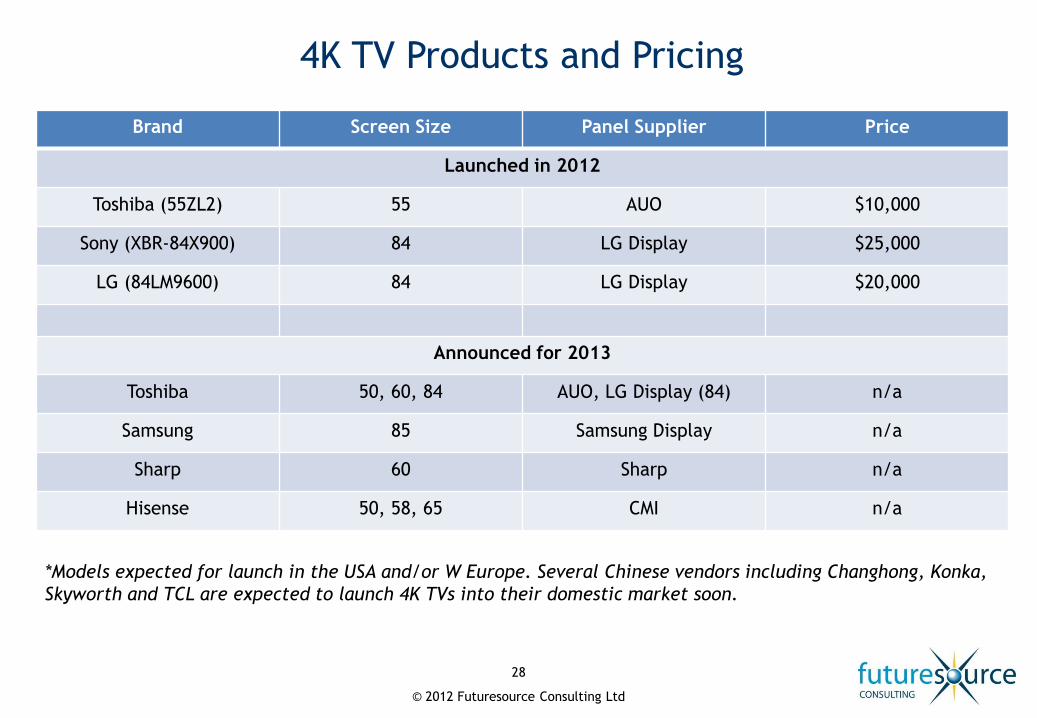

4K TV Products and Pricing

Brand Screen Size Panel Supplier Price

Launched in 2012

Toshiba (55ZL2) 55 AUO $10,000

Sony (XBR-84X900) 84 LG Display $25,000

LG (84LM9600) 84 LG Display $20,000

Announced for 2013

Toshiba 50, 60, 84 AUO, LG Display (84) n/a

Samsung 85 Samsung Display n/a

Sharp 60 Sharp n/a

Hisense 50, 58, 65 CMI n/a

28

*Models expected for launch in the USA and/or W Europe. Several Chinese vendors including Changhong, Konka,

Skyworth and TCL are expected to launch 4K TVs into their domestic market soon.

© 2012 Futuresource Consulting Ltd

4K in the Consumer TV Market (ii):

Key Drivers and Inhibitors

29

The large screen 50”+ TV market is set for strong growth. At today’s best resolution of 1080p, individual pixels

can become noticeable at large screen sizes (particularly those upwards of 60”). 4K resolution provides such a

high level of visual data that pixels on large screen displays are virtually unnoticeable.

The higher resolution of 4K will also benefit current 3D solutions. Passive 3D cuts the horizontal resolution in

half to create a 3D image and so a 1080p 3D movie seen with passive glasses is actually viewed at 540p. By

doubling the horizontal resolution, a Full HD 3D image delivered to each eye is achieved. Most first generation

4K sets are expected to include Passive 3D technology.

4K is also expected to be a key enabler of auto-stereoscopic (glasses-free) 3D technology as 4K will allow

resolution to be regained on multiview lenticular displays.

4K resolution can produce a level of reality that surpasses 3D.

Good 4K up-scaling can provide noticeable picture quality improvements in the absence of true 4K source

material. All 4K TVs are expected to include up-conversion engines, enabling the TV to deliver higher detail

from current SD and HD sources.

Native 4K content is virtually non-existent today. There is no 4K standard for Blu-ray yet. Broadcasters are still

in very early trial phases while delivery over the Internet is dependent upon significant improvements in

average broadband speeds within the home.

The benefits of 4K only start to become visible on very large displays (60”+) under common viewing distance

conditions. In order to benefit from 4K on smaller screen sizes, viewing distance would have to be closer than

typical consumers are used to.

The rapid shift to 720p and 1080p resolutions was driven by the unprecedented boom in TV sales over the last

10 years – a result of dramatically shortened replacement cycles during the transition from CRT to Digital HD

Flat Panel displays. TV upgrade cycles are extending out to previous levels of 8-9 years while most markets are

contracting to more natural sales levels.

© 2012 Futuresource Consulting Ltd

4K in the Consumer TV Market (iii)

The 4K TV forecasts for the USA and Western Europe set out on the following pages assume that a steady

flow of native 4K content will emerge over the next 2-3 years. Despite this, Futuresource expects 4K TV sales

to remain relatively low for at least the next 4-5 years.

4K is not expected to penetrate the TV market as rapidly as the 720p and 1080p high definition resolutions

did, as many TV viewers will struggle to justify paying a premium for a set on which they may find it difficult

to see a noticeable difference in picture quality.

The rapid growth in demand for 720p and 1080p coincided with the transition from CRT to flat panel as

well as the shift in broadcasting standards to digital and HD and there do not appear to be any similar

upgrade drivers on the horizon that could facilitate a more rapid build up.

Many TV viewers actually struggle to see a difference between 720p and 1080p on 40” or 50” sets and

so TV vendors may find it difficult to convince consumers of the benefits of upgrading to 4K.

With this in mind, Futuresource expects 4K to be restricted to large screen displays (50” and upwards) for

the next 2-3 years with demand coming from wealthy home-cinema enthusiasts.

In the USA, 4K is expected to reach just 4% of all TV sales by 2017 (13% of 50” and larger TVs). After this

time, price points for 4K will fall to more affordable levels and a wider range of models will emerge

including smaller screen sizes below 50”. By 2020 4K will account for 13% of total TV sales (31% of 50”+

sets).

Europe will lag behind the USA due to European customers favouring smaller screens. However, large

screen TV sales will experience strong growth across the region moving forwards making it a market

with high potential for 4K equipment and content.

30

© 2012 Futuresource Consulting Ltd

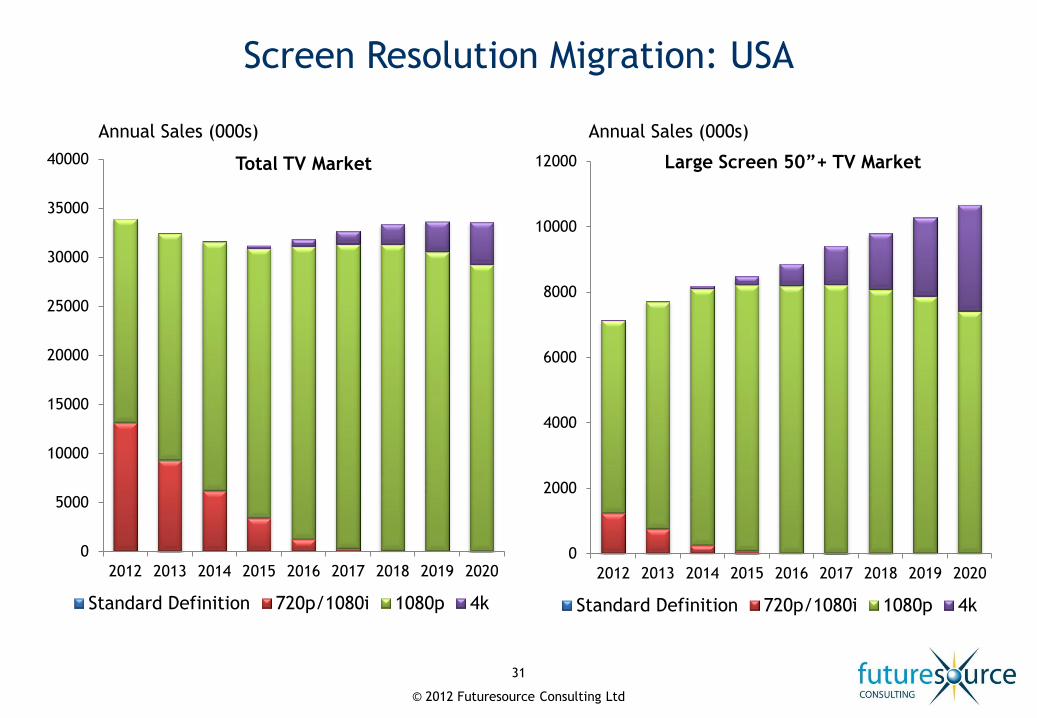

Screen Resolution Migration: USA

0

5000

10000

15000

20000

25000

30000

35000

40000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Standard Definition 720p/1080i 1080p 4k

Annual Sales (000s)

31

Total TV Market

0

2000

4000

6000

8000

10000

12000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Standard Definition 720p/1080i 1080p 4k

Large Screen 50”+ TV Market

Annual Sales (000s)

© 2012 Futuresource Consulting Ltd

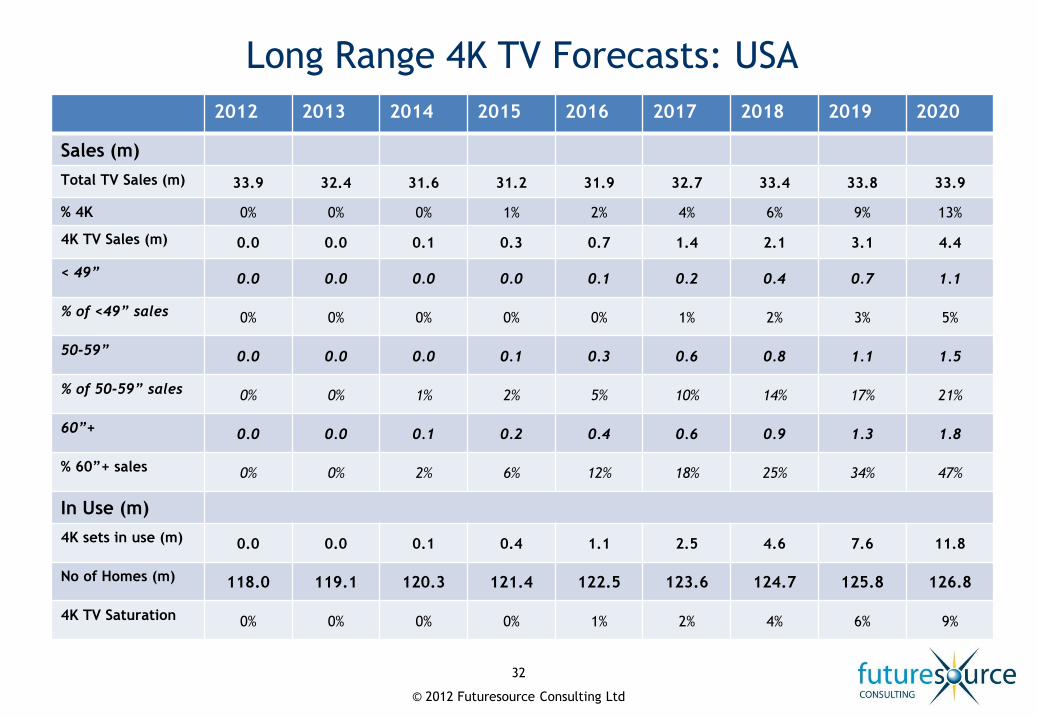

Long Range 4K TV Forecasts: USA

32

2012 2013 2014 2015 2016 2017 2018 2019 2020

Sales (m)

Total TV Sales (m) 33.9 32.4 31.6 31.2 31.9 32.7 33.4 33.8 33.9

% 4K 0% 0% 0% 1% 2% 4% 6% 9% 13%

4K TV Sales (m) 0.0 0.0 0.1 0.3 0.7 1.4 2.1 3.1 4.4

< 49” 0.0 0.0 0.0 0.0 0.1 0.2 0.4 0.7 1.1

% of <49” sales 0% 0% 0% 0% 0% 1% 2% 3% 5%

50-59” 0.0 0.0 0.0 0.1 0.3 0.6 0.8 1.1 1.5

% of 50-59” sales 0% 0% 1% 2% 5% 10% 14% 17% 21%

60”+ 0.0 0.0 0.1 0.2 0.4 0.6 0.9 1.3 1.8

% 60”+ sales 0% 0% 2% 6% 12% 18% 25% 34% 47%

In Use (m)

4K sets in use (m) 0.0 0.0 0.1 0.4 1.1 2.5 4.6 7.6 11.8

No of Homes (m) 118.0 119.1 120.3 121.4 122.5 123.6 124.7 125.8 126.8

4K TV Saturation 0% 0% 0% 0% 1% 2% 4% 6% 9%

© 2012 Futuresource Consulting Ltd

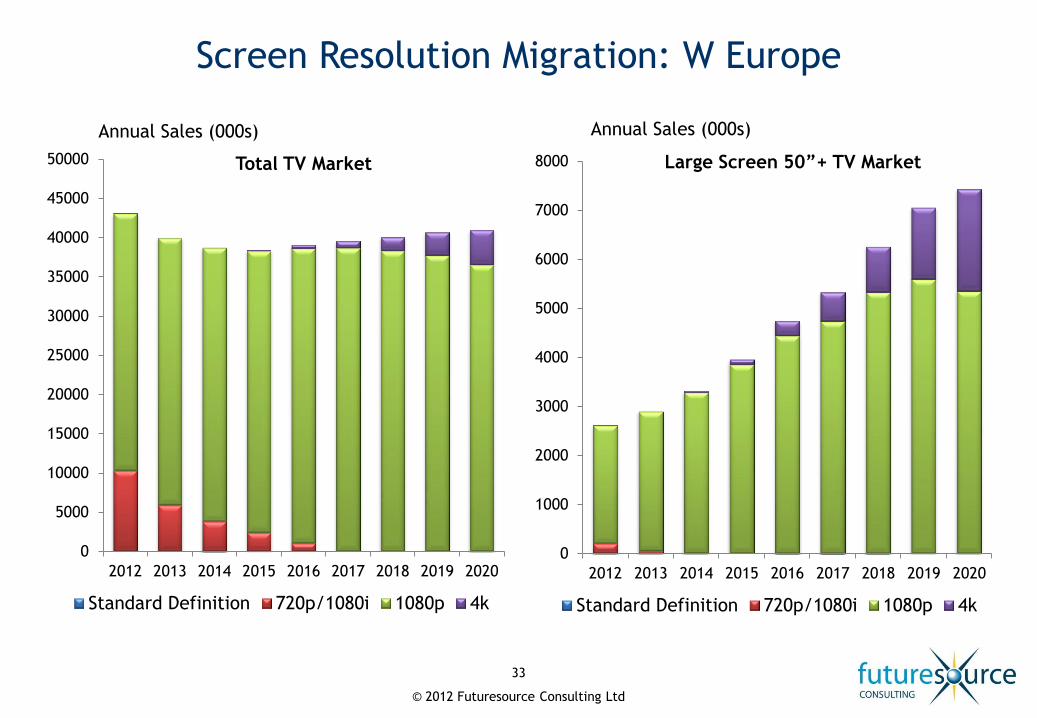

Screen Resolution Migration: W Europe

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Standard Definition 720p/1080i 1080p 4k

Annual Sales (000s)

33

Total TV Market

0

1000

2000

3000

4000

5000

6000

7000

8000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Standard Definition 720p/1080i 1080p 4k

Large Screen 50”+ TV Market

Annual Sales (000s)

© 2012 Futuresource Consulting Ltd

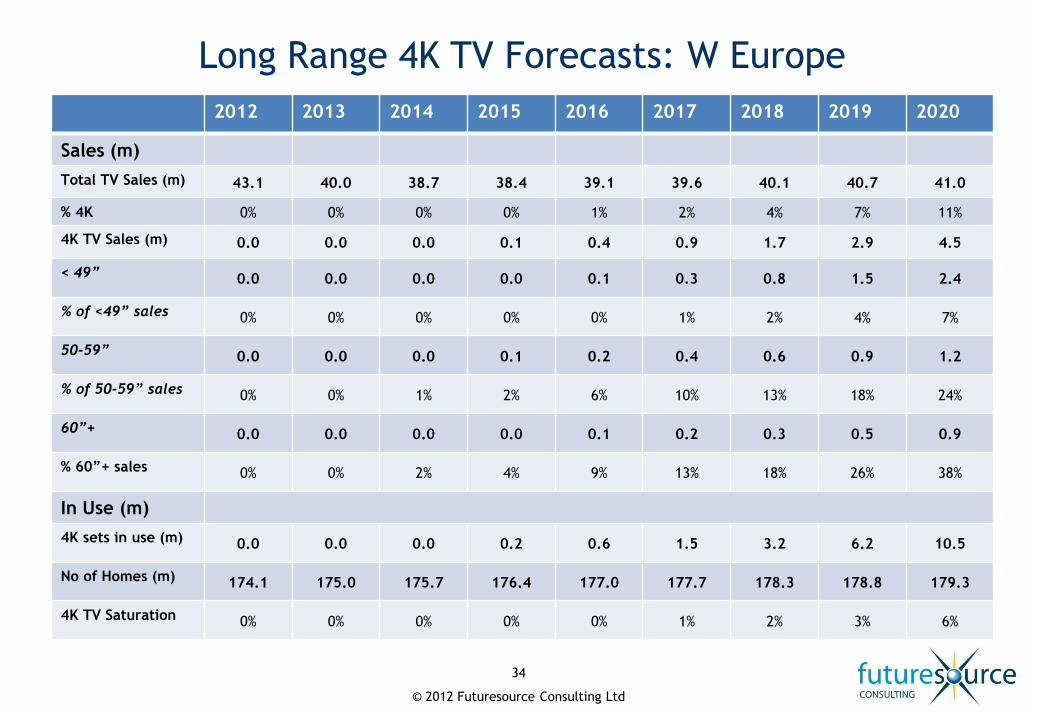

Long Range 4K TV Forecasts: W Europe

34

2012 2013 2014 2015 2016 2017 2018 2019 2020

Sales (m)

Total TV Sales (m) 43.1 40.0 38.7 38.4 39.1 39.6 40.1 40.7 41.0

% 4K 0% 0% 0% 0% 1% 2% 4% 7% 11%

4K TV Sales (m) 0.0 0.0 0.0 0.1 0.4 0.9 1.7 2.9 4.5

< 49” 0.0 0.0 0.0 0.0 0.1 0.3 0.8 1.5 2.4

% of <49” sales 0% 0% 0% 0% 0% 1% 2% 4% 7%

50-59” 0.0 0.0 0.0 0.1 0.2 0.4 0.6 0.9 1.2

% of 50-59” sales 0% 0% 1% 2% 6% 10% 13% 18% 24%

60”+ 0.0 0.0 0.0 0.0 0.1 0.2 0.3 0.5 0.9

% 60”+ sales 0% 0% 2% 4% 9% 13% 18% 26% 38%

In Use (m)

4K sets in use (m) 0.0 0.0 0.0 0.2 0.6 1.5 3.2 6.2 10.5

No of Homes (m) 174.1 175.0 175.7 176.4 177.0 177.7 178.3 178.8 179.3

4K TV Saturation 0% 0% 0% 0% 0% 1% 2% 3% 6%

© 2012 Futuresource Consulting Ltd

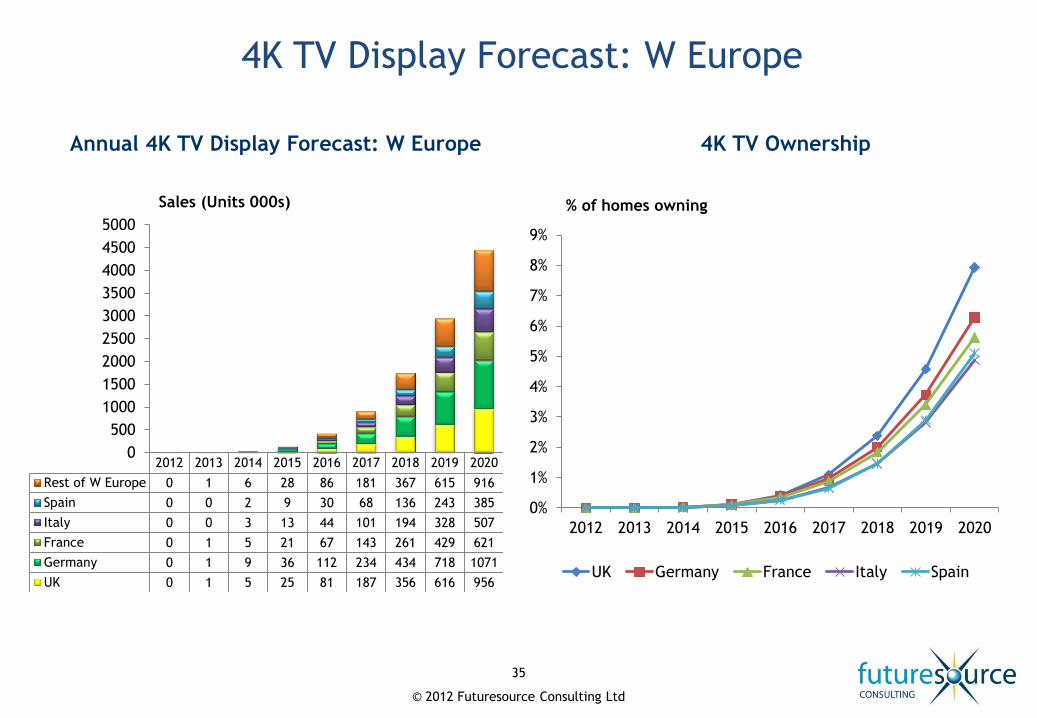

2012 2013 2014 2015 2016 2017 2018 2019 2020

Rest of W Europe 0 1 6 28 86 181 367 615 916

Spain 0 0 2 9 30 68 136 243 385

Italy 0 0 3 13 44 101 194 328 507

France 0 1 5 21 67 143 261 429 621

Germany 0 1 9 36 112 234 434 718 1071

UK 0 1 5 25 81 187 356 616 956

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

4K TV Display Forecast: W Europe

35

Annual 4K TV Display Forecast: W Europe 4K TV Ownership

Sales (Units 000s) % of homes owning

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2012 2013 2014 2015 2016 2017 2018 2019 2020

UK Germany France Italy Spain

7. 4K in Professional Displays Markets

© 2012 Futuresource Consulting Ltd

4K displays are gradually entering the professional market, but with sales limited to very specific niche markets where

ultra high definition is specifically required.

Most of these markets have very specific requirements and often need dedicated sku’s in order to ensure suitability.

These high-end commercial markets are likely to act as product innovators for 4K solutions (and effective markets to drive

R&D) as the usage requirements are extremely demanding.

Vendors such as Sony, Christie and Barco have leveraged their digital cinema platforms to offer high-end 4K

projection-based solutions. Many of these 4K models are also 3D and are used in verticals seeking advanced graphics

such as simulation, visualisation, planetariums etc.

While the transition to high resolution displays has happened rapidly in the consumer sector, the projector market has

seen an extremely slow uptake.

The majority of projector sales (over 95%) are into corporate meeting rooms or the education sector where the main

usage is for presentation purposes.

With PowerPoint/Excel still the main content shown on presentation devices, the sales argument for high definition

projectors has not been compelling for ‘mainstream’ market verticals.

The use of high definition video however is becoming more common within corporates, especially as large corporates

develop their own internal communication channels.

Large format flat panels have transitioned at a much faster rate, in part driven by developments at factory level (where

the consumer market is rapidly driving the transition towards high definition).

Panel vendors are developing 4K solutions and beginning to seek opportunities for 4K in commercial markets.

4K in Professional Display Markets - Situation Report (i)

37

© 2012 Futuresource Consulting Ltd

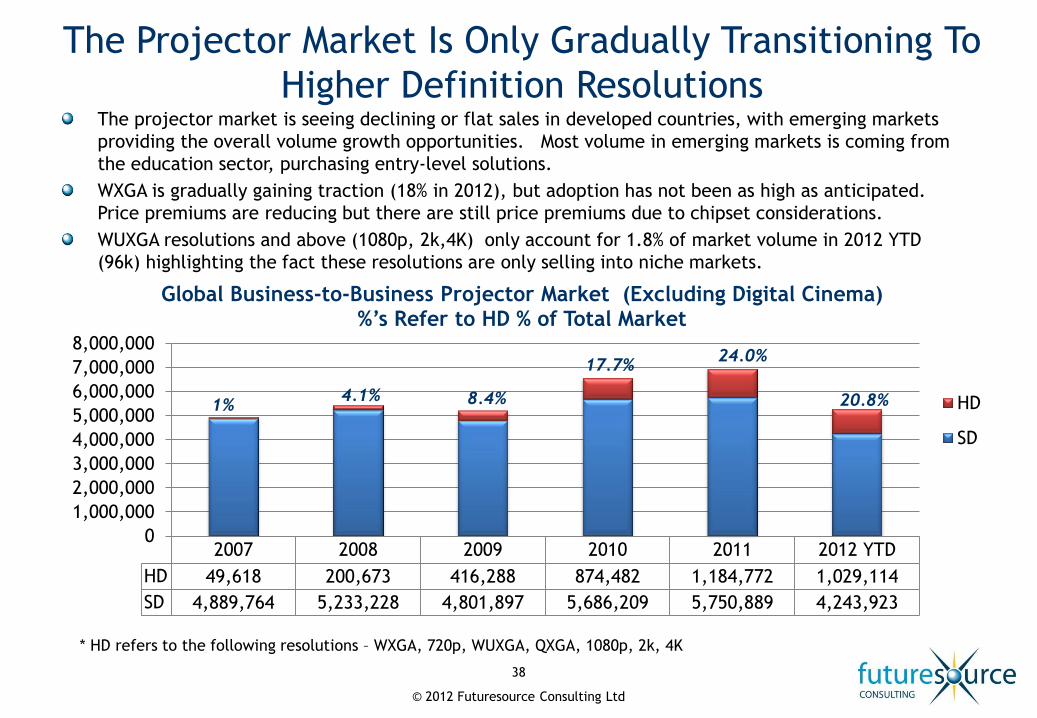

The Projector Market Is Only Gradually Transitioning To

Higher Definition Resolutions

38

2007 2008 2009 2010 2011 2012 YTD

HD 49,618 200,673 416,288 874,482 1,184,772 1,029,114

SD 4,889,764 5,233,228 4,801,897 5,686,209 5,750,889 4,243,923

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Global Business-to-Business Projector Market (Excluding Digital Cinema) %’s Refer to HD % of Total Market

HD

SD

1% 4.1% 8.4%

17.7% 24.0%

20.8%

* HD refers to the following resolutions – WXGA, 720p, WUXGA, QXGA, 1080p, 2k, 4K

The projector market is seeing declining or flat sales in developed countries, with emerging markets

providing the overall volume growth opportunities. Most volume in emerging markets is coming from

the education sector, purchasing entry-level solutions.

WXGA is gradually gaining traction (18% in 2012), but adoption has not been as high as anticipated.

Price premiums are reducing but there are still price premiums due to chipset considerations.

WUXGA resolutions and above (1080p, 2k,4K) only account for 1.8% of market volume in 2012 YTD

(96k) highlighting the fact these resolutions are only selling into niche markets.

© 2012 Futuresource Consulting Ltd

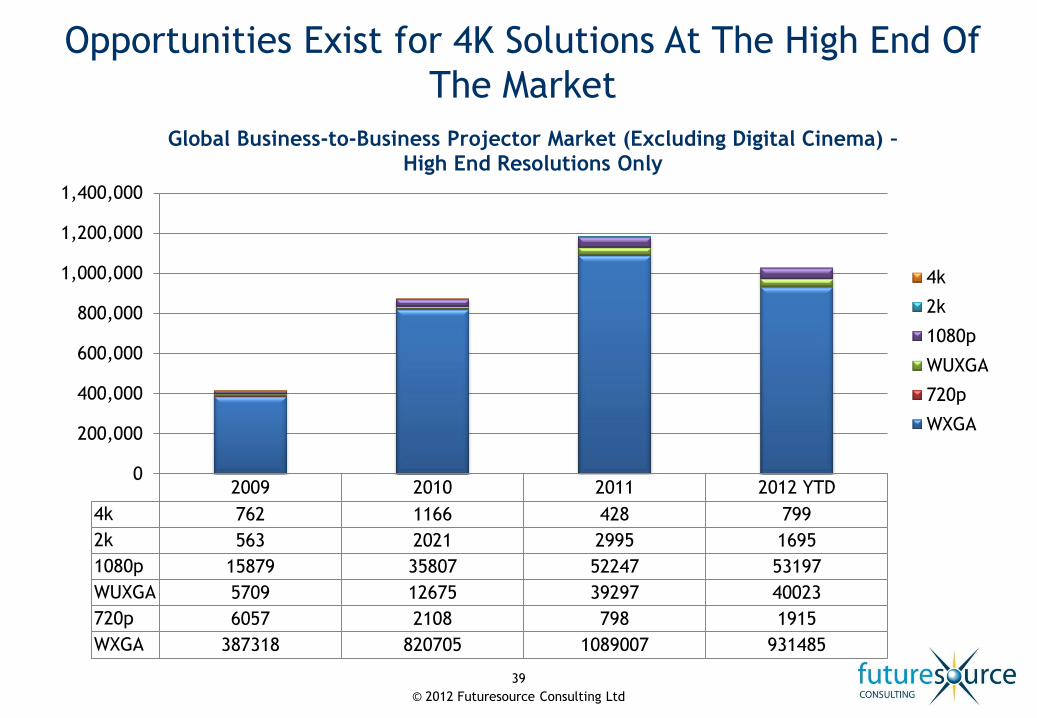

Opportunities Exist for 4K Solutions At The High End Of

The Market

39

2009 2010 2011 2012 YTD

4k 762 1166 428 799

2k 563 2021 2995 1695

1080p 15879 35807 52247 53197

WUXGA 5709 12675 39297 40023

720p 6057 2108 798 1915

WXGA 387318 820705 1089007 931485

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

Global Business-to-Business Projector Market (Excluding Digital Cinema) – High End Resolutions Only

4k

2k

1080p

WUXGA

720p

WXGA

© 2012 Futuresource Consulting Ltd

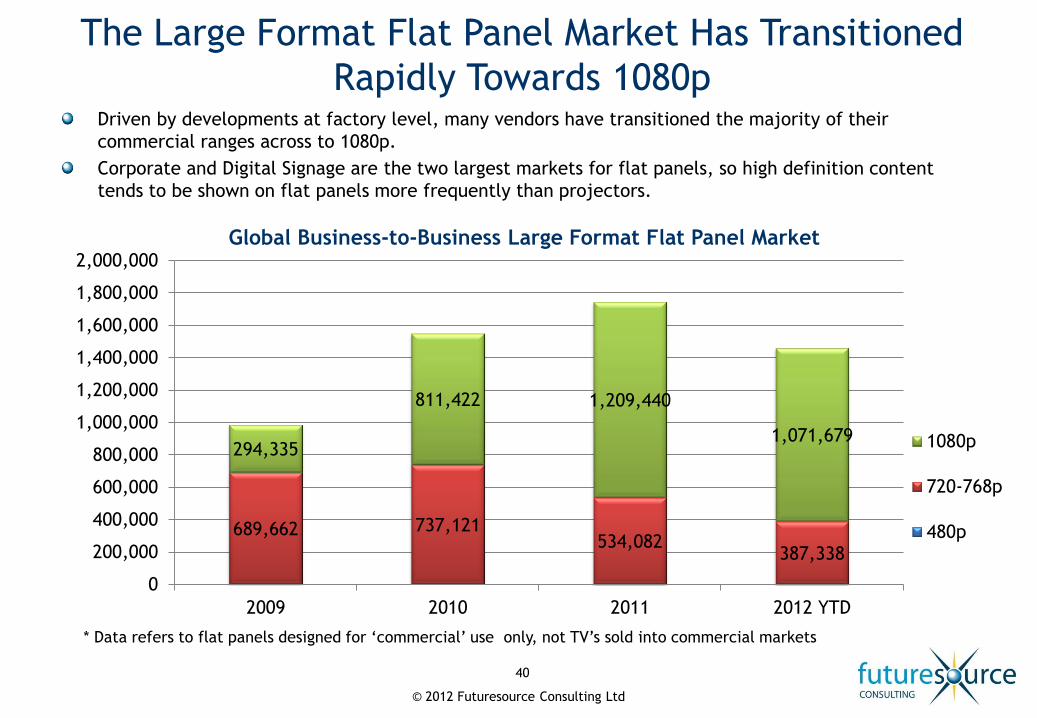

The Large Format Flat Panel Market Has Transitioned

Rapidly Towards 1080p

40

689,662 737,121 534,082

387,338

294,335

811,422 1,209,440

1,071,679

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2009 2010 2011 2012 YTD

Global Business-to-Business Large Format Flat Panel Market

1080p

720-768p

480p

* Data refers to flat panels designed for ‘commercial’ use only, not TV’s sold into commercial markets

Driven by developments at factory level, many vendors have transitioned the majority of their

commercial ranges across to 1080p.

Corporate and Digital Signage are the two largest markets for flat panels, so high definition content

tends to be shown on flat panels more frequently than projectors.

© 2012 Futuresource Consulting Ltd

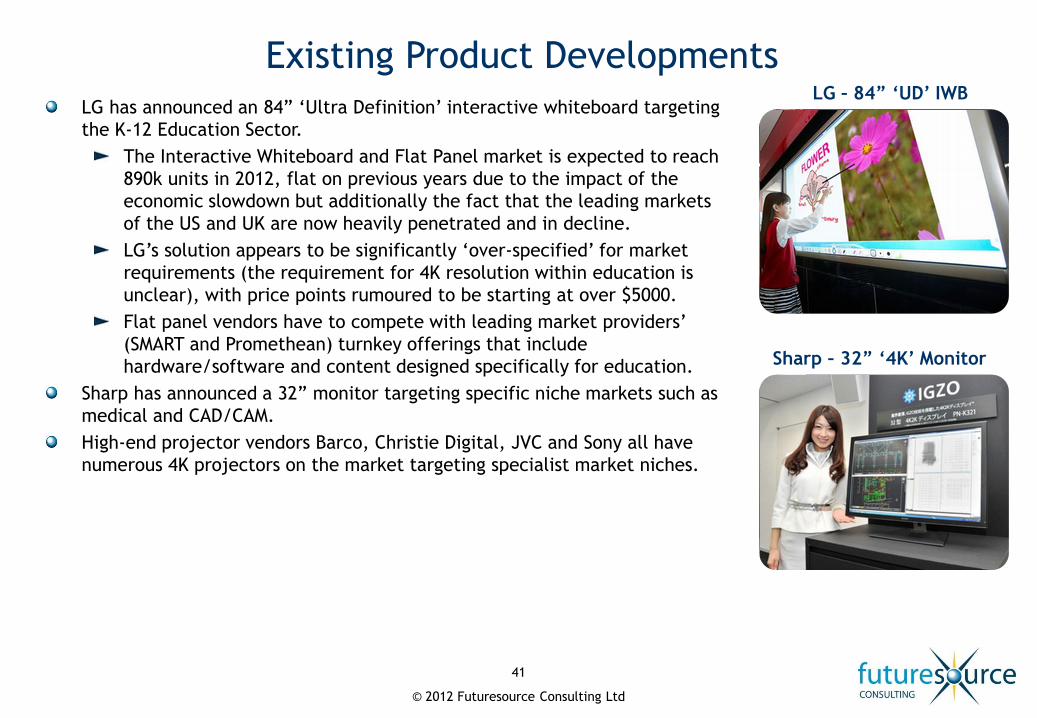

LG has announced an 84” ‘Ultra Definition’ interactive whiteboard targeting

the K-12 Education Sector.

The Interactive Whiteboard and Flat Panel market is expected to reach

890k units in 2012, flat on previous years due to the impact of the

economic slowdown but additionally the fact that the leading markets

of the US and UK are now heavily penetrated and in decline.

LG’s solution appears to be significantly ‘over-specified’ for market

requirements (the requirement for 4K resolution within education is

unclear), with price points rumoured to be starting at over $5000.

Flat panel vendors have to compete with leading market providers’

(SMART and Promethean) turnkey offerings that include

hardware/software and content designed specifically for education.

Sharp has announced a 32” monitor targeting specific niche markets such as

medical and CAD/CAM.

High-end projector vendors Barco, Christie Digital, JVC and Sony all have

numerous 4K projectors on the market targeting specialist market niches.

Existing Product Developments

41

LG – 84” ‘UD’ IWB

Sharp – 32” ‘4K’ Monitor

© 2012 Futuresource Consulting Ltd

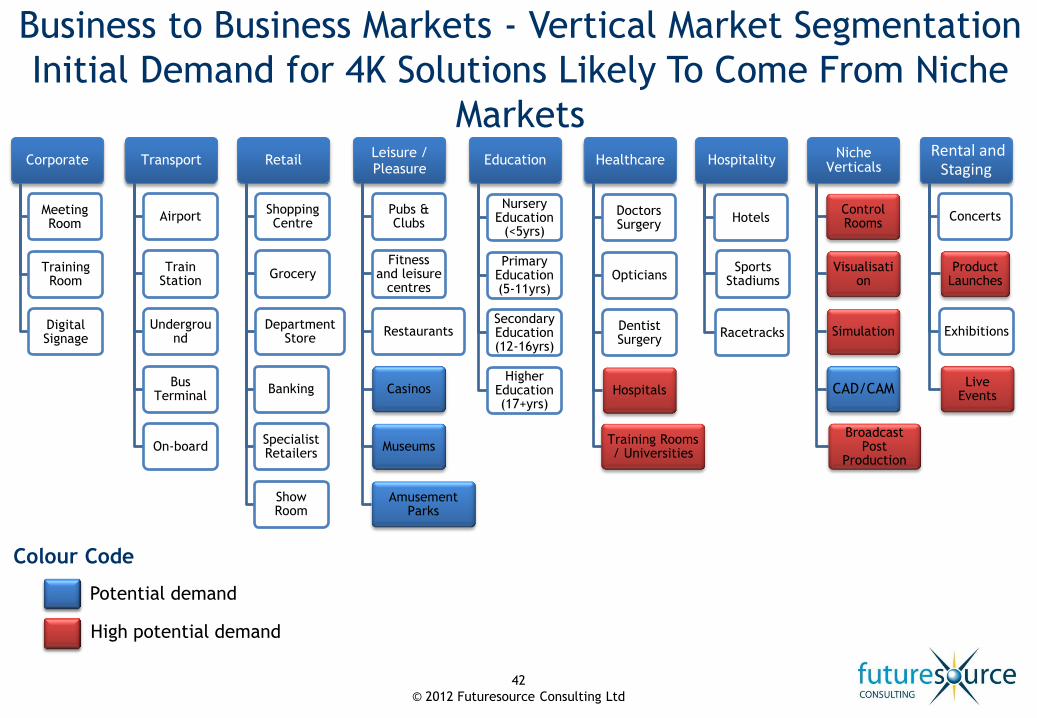

Transport

Airport

Train Station

Underground

Bus Terminal

On-board

Retail

Shopping Centre

Grocery

Department Store

Banking

Specialist Retailers

Show Room

Leisure / Pleasure

Pubs & Clubs

Fitness and leisure

centres

Restaurants

Casinos

Museums

Amusement Parks

Corporate

Meeting Room

Training Room

Digital Signage

Education

Nursery Education

(<5yrs)

Primary Education (5-11yrs)

Secondary Education (12-16yrs)

Higher Education (17+yrs)

Healthcare

Doctors Surgery

Opticians

Dentist Surgery

Hospitals

Training Rooms / Universities

Hospitality

Hotels

Sports Stadiums

Racetracks

Niche Verticals

Control Rooms

Visualisation

Simulation

CAD/CAM

Broadcast Post

Production

Rental and Staging

Concerts

Product Launches

Exhibitions

Live Events

Business to Business Markets - Vertical Market Segmentation

Initial Demand for 4K Solutions Likely To Come From Niche

Markets

Colour Code

Potential demand

High potential demand

42

© 2012 Futuresource Consulting Ltd

Opportunities for 4K in Niche Markets (i)

43

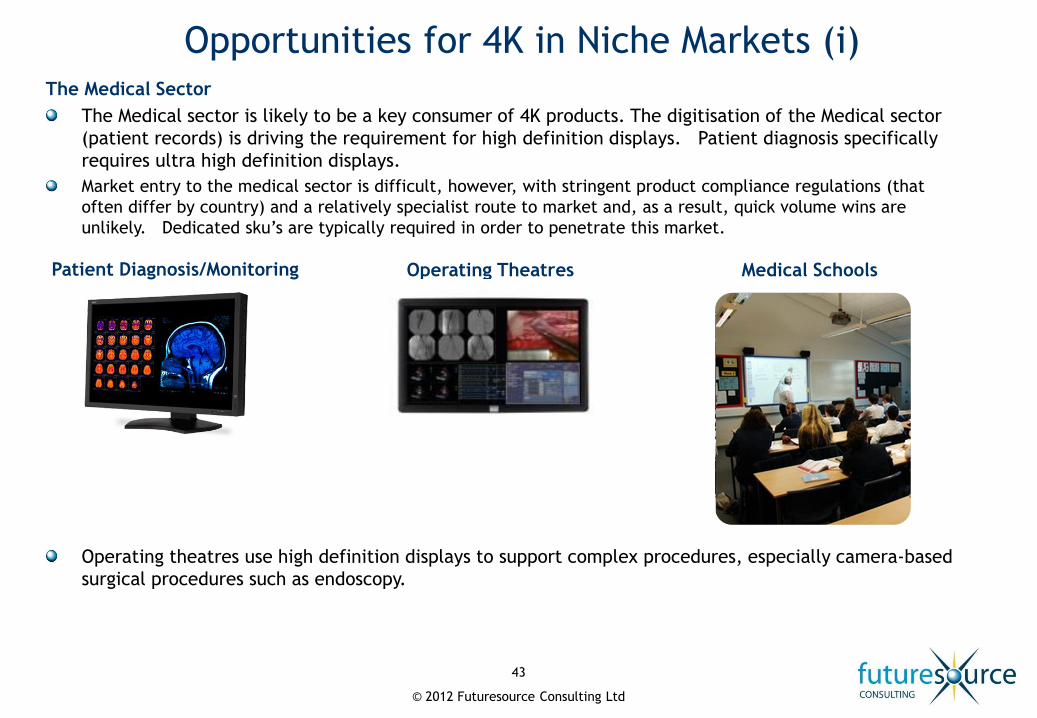

The Medical Sector

The Medical sector is likely to be a key consumer of 4K products. The digitisation of the Medical sector

(patient records) is driving the requirement for high definition displays. Patient diagnosis specifically

requires ultra high definition displays.

Market entry to the medical sector is difficult, however, with stringent product compliance regulations (that

often differ by country) and a relatively specialist route to market and, as a result, quick volume wins are

unlikely. Dedicated sku’s are typically required in order to penetrate this market.

Patient Diagnosis/Monitoring Operating Theatres Medical Schools

Operating theatres use high definition displays to support complex procedures, especially camera-based

surgical procedures such as endoscopy.

© 2012 Futuresource Consulting Ltd

Opportunities for 4K in Niche Markets (ii)

44

CAD/CAM & Visualisation

Advanced visualisation markets require extremely high resolution displays. At present projectors are

often blended to develop high resolution large screen displays. This can, however, lead to loss in screen

size and shifts in brightness/colour. It is also costly and time consuming to run/align/maintain multiple

displays.

High resolution, immersive displays (often using 3D and where 4K has the benefit of allowing full 1080p

per eye) can be used in the product design phase to speed up time-to-market of a concept product.

Visualisation is also used heavily in the science industry (especially by oil and gas providers).

CAD/CAM & Visualisation

© 2012 Futuresource Consulting Ltd

Opportunities for 4K in Niche Markets (iii)

45

Simulation

The military, police, army and aviation industry all use

high-end simulators to train their staff.

4K displays increase the immersive nature of the display

and, as with visualisation, have obvious benefits when

utilised in conjunction with 3D.

Displays are sold as part of a very advanced solution and a

very small number of specialist channel providers per

country control access to the end user.

Broadcast Post Production

4K projectors are typically used within post

production applications such as colour grading and in

pre-release screenings.

Simulation

Control Room Control Rooms

Video wall cube technology remains the dominant

technology in control rooms due to reliability and

colour reproduction needs.

Super narrow bezel flat panel displays gradually gaining

traction, however, and 4K displays both projector and flat

panel-based could penetrate the control room market.

The majority of growth in the control room sector is

coming from emerging markets and significant investments

into the monitoring of their natural resources (oil and gas

industries etc).

© 2012 Futuresource Consulting Ltd

Opportunities for 4K in Niche Markets (iv)

46

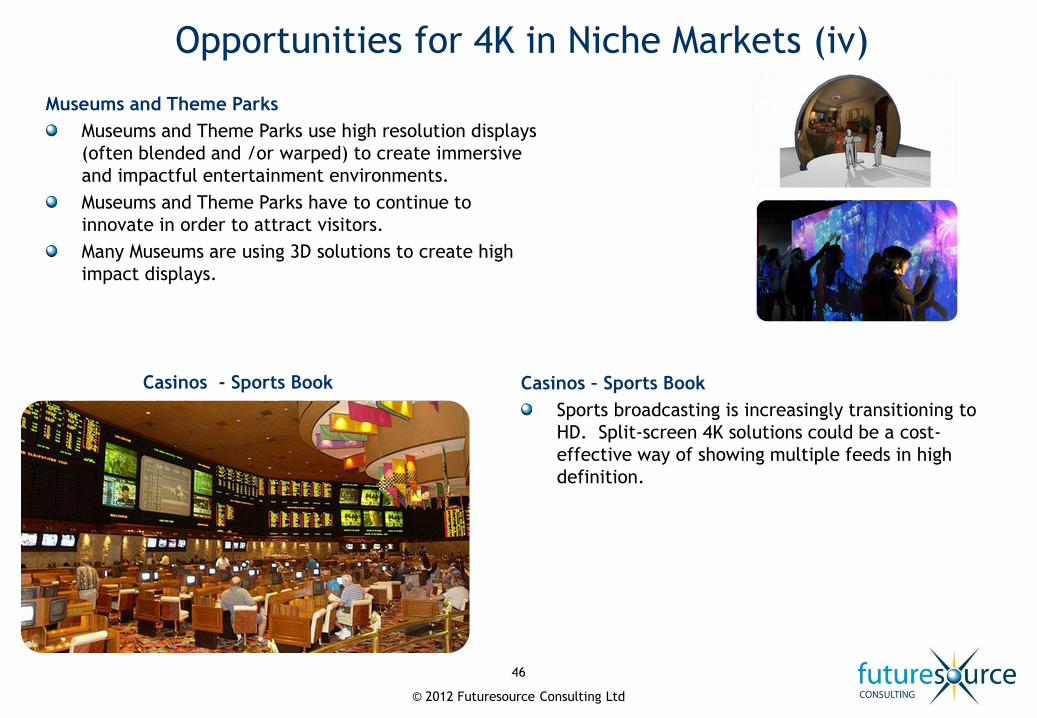

Museums and Theme Parks

Museums and Theme Parks use high resolution displays

(often blended and /or warped) to create immersive

and impactful entertainment environments.

Museums and Theme Parks have to continue to

innovate in order to attract visitors.

Many Museums are using 3D solutions to create high

impact displays.

Casinos – Sports Book

Sports broadcasting is increasingly transitioning to

HD. Split-screen 4K solutions could be a cost-

effective way of showing multiple feeds in high

definition.

Casinos - Sports Book

© 2012 Futuresource Consulting Ltd

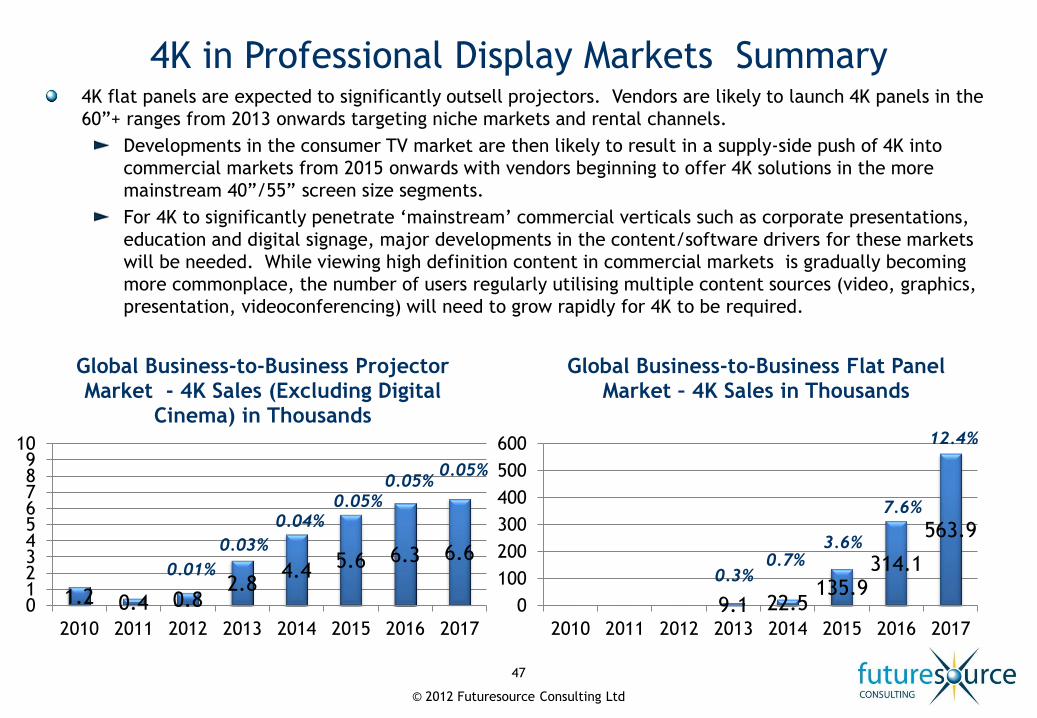

4K flat panels are expected to significantly outsell projectors. Vendors are likely to launch 4K panels in the

60”+ ranges from 2013 onwards targeting niche markets and rental channels.

Developments in the consumer TV market are then likely to result in a supply-side push of 4K into

commercial markets from 2015 onwards with vendors beginning to offer 4K solutions in the more

mainstream 40”/55” screen size segments.

For 4K to significantly penetrate ‘mainstream’ commercial verticals such as corporate presentations,

education and digital signage, major developments in the content/software drivers for these markets

will be needed. While viewing high definition content in commercial markets is gradually becoming

more commonplace, the number of users regularly utilising multiple content sources (video, graphics,

presentation, videoconferencing) will need to grow rapidly for 4K to be required.

4K in Professional Display Markets Summary

47

1.2 0.4 0.8 2.8

4.4 5.6 6.3 6.6

0123456789

10

2010 2011 2012 2013 2014 2015 2016 2017

Global Business-to-Business Projector Market - 4K Sales (Excluding Digital

Cinema) in Thousands

9.1 22.5 135.9

314.1

563.9

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015 2016 2017

Thousa

nds

Global Business-to-Business Flat Panel Market – 4K Sales in Thousands

0.3% 0.7%

3.6%

7.6%

12.4%

0.01%

0.03%

0.04% 0.05%

0.05% 0.05%

8. Appendix

© 2012 Futuresource Consulting Ltd

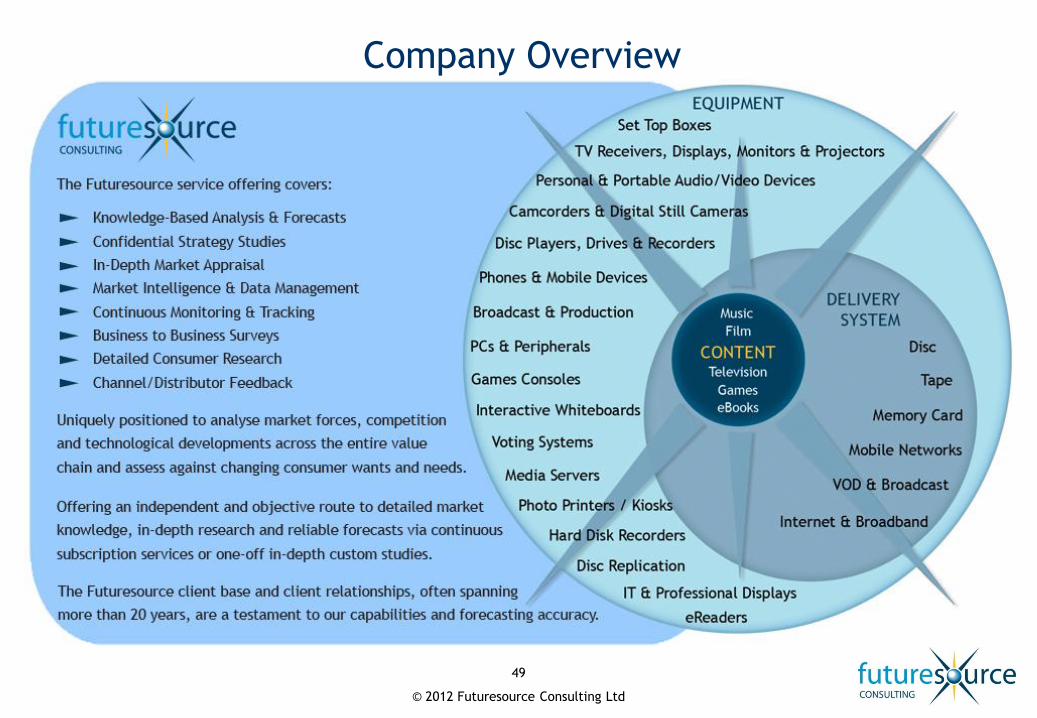

Company Overview

49

© 2012 Futuresource Consulting Ltd 50

While every effort is made by Futuresource Consulting Ltd to provide accurately researched information and

carefully supported conclusions and recommendations to its client, in no event will the company or its

professionals be liable for information, analysis, advice or recommendations provided to the client at any stage

of the project, or be liable for actions and decisions taken as a result of this report.

talk to us…

Futuresource Consulting +44 (0)1582 500 100

www.futuresource-consulting.com