Embed Size (px)

Citation preview

Hong Kong Economic Papers, No. 12, July, I9 78

THE SQUARE-ROOT FORMULA IN MONETARY THEORY

Y. C. JAO*

It is well known that in the classical monetary theory, whether of the Fisherian "equation of exchange” version or the Cambridge real-balance version, the demand for money was seen strictly as a demand for transactions purposes, which in turn was exogenously determined by institutional and technological factors.1 One of the innovations which Keynes introduced into monetary theory was his explicit recognition that the demand for money depends not only on income, but also on the yield on some alternative financial asset, typically a government bond. Keynes [42] dicho- tomized the demand for money into two parts: the first part, the transactions and precautionary demand depends, as in the classical model, on income, while the other part, the speculative demand, was treated as a function of the market rate of interest. Subsequently in the fifties, some economists began to argue that even the transactions demand for money is sensitive to the rate of interest, and that there are important economies of scale in the holding of cash for transactions purposes. This hypothesis, crystallized in the famous square-root formula, has dominated monetary thinking since the mid-fifties. Indeed, in some writings it has been referred to as the Square-Root Law. In recent years, however, this formulation of the transactions demand has been subjected to a critical re-examination from both the theoretical and empirical points of view. The relevant literature has grown to such an extent that a brief survey is called for.

The purpose of this paper is to re-appraise the inventory theoretic approach in general and the square-root formula in particular, in the light of recent theoretical discussions and empirical tests. Section I summarizes the formulation of the square- root hypothesis and its extensions. Section II reviews recent critiques and tests of the hypothesis. Section III then contains some concluding remarks.

I

Edgeworth [14, 15] is generally credited to be the first economist to anticipate the square-root formula. His interest was, however, confined to the application of

* Reader in Economics, University of Hong Kong. The author wishes to thank an anonymous referee for helpful comments, and Mr. S. K. Ma for drawing the figures

1 There have been some attempts by contemporary monetarists to establish the view that earlier quantity theorists, notably Fisher, Marshall and Pigou, explicitly recognized the influence of the interest rate on the demand for money. See especially Friedman [ 27] and Selden [ 63]. This view has however been disputed by Modigliani [50] and Patinkin [57]. In this paper, we subscribe to the "mainstream” view that the interest rate did not enter into the classical demand function for money.

38

probability theory to banking business only. In his two papers, Edgeworth argues, by invoking the law of error, that a bank's cash reserves against customers’ withdrawals vary, ceteris paribus, not in proportion to its deposit liabilities, but to the square-root of such liabilities. This theory of banking, though backed by a number of economists, notably Wicksell [75] and Fisher [22], did not appear to have attracted much attention. A somewhat different variant of the square-root formula was independently derived in the study of optimal inventory control, but this was a separate development in the field of management science that bore little or no relationship to the mainstream economic theory. Among the spate of expository writings following the publication of Keynes’ General Theory, Hansen [32] hypothesizes that even transactions balances will become interest-elastic at high enough interest rates. Apart from these occasional insights, however, the interest-elasticity and economizing of the transactions demand for money were not integrated into the corpus of monetary theory until the fifties, as a result of the seminal work by Baumol [7] and Tobin [70].

Baumol's paper in particular has been widely regarded as representing the new inventory approach because of the relative simplicity of his model and the explicit derivation of the square-root formula. The contents of his paper are so well known that only a very brief summary needs to be given. Assuming that transactions are perfectly foreseen and expenditures occur in a steady stream, Baumol's problem is how to minimize the cost of holding cash for transactions purposes. These costs are the interest opportunity cost of investing cash balances, transactions costs (brokerage fees) involved in switching from cash to interest-bearing securities and vice versa. In the simplest case, where the transactor "lives off’ his capital by steadily withdrawing cash from his investments to meet a predetermined value of transactions, the following formulas can be derived by the usual optimizing procedure:

c*= i J

2bT (1)

M*= % f-

(2)

where C* is the optimal evenly-spaced withdrawal of cash, M* is the optimal average cash balances, T is the money value of transactions, b is the fixed cost per transaction, and i is the market rate of interest. In the more general case, where the transactor retains part of his income in cash, R, and invests the rest in securities, I, the optimal cash retained, R*, is given by

R* = C* + T&w + k~) (3)

where kw is the variable cost of withdrawing funds and kd is the variable cost of investment. By definition R = T - I.

Differentiating logarithmically equation (2) with respect to T and i, it can readily be seen that the partial income elasticity of the transactions balances is 1/2, while the partial interest elasticity is - 1/2. These elasticities have been widely interpreted to mean that there are important economies of scale in the transactions demand for money, and that even this demand is fairly sensitive to changes in the interest rate. Furthermore, as long as the brokerage fee, b, (which can be regarded as a short-hand symbol for all kinds of transaction and conversion costs between cash and

39

other earning assets) is positive, the demand for transactions balances will also be positive, on the reasonable assumption that there is a finite limit to the rate of interest. Baumol's model thus provides a rational motivation for money demand in an uncertain world where information and other transaction costs are known to exist. Because of the economies of scale in cash holdings, the model also suggests that monetary policy might be more potent in unemployment situations than earlier thought, and that its effect in turn depends on the distribution of income, since a higher concentration implies larger economies of scale.

Tobin's 1956 paper is more concerned with the interest-elasticity of the demand for cash at any given volume of transactions. His problem is to find the optimal number of transactions that maximizes the transactor's net interest earnings, or given the number of transactions, to find the optimal timing and amounts of such transactions. Apart from stating that the optimal number of transactions and the optimal share of bonds vary directly with the interest rate, while the share of cash varies inversely with the interest rate, no square-root formula is explicitly presented. However, Tobin himself states that his equations will produce "essentially the same results” as Baumol's square-root formula. For this reason the square-root rule is often referred to in the literature as the Baumol-Tobin model. There are however some differences between the two authors. Firstly, Tobin permits the number of transactions between cash and interest-bearing securities to take on only positive integer values, while Baumol treats it as a continuous variable. Secondly, Tobin's paper rigorously proves what Baumol only assumes, namely that cash withdrawals should be equally spaced in time and equal in size. Thirdly, because Baumol's problem is formulated in terms of the minimization of the cost function, he overlooks the question whether interest earnings are high enough to justify any investment in bonds at all. By contrast, Tobin expressly considers four different solutions for the optimal number of transactions, depending on the relation between the interest rate and transactions costs. Under one of the solutions, a corner solution for example, the optimal number is zero, because transactions costs are assumed to be greater than interest earnings. As we shall see, these differences have a bearing on later theoretical developments.

The square-root formula has been developed implicitly in a closed economy context, but there is no logical reason why it should not be extended to the open economy case. A number of writers have in fact applied the rule to the field of international finance. Thus Heller [34] argues that the customary criterion used by national governments and international agencies to measure the adequacy of international reserves - the ratio of official reserves to imports - is unsatisfactory. This is because official international reserves held by the monetary authorities of various countries are for precautionary motives to finance temporary balance-of- payments deficits. They are not held for transactions purpose because the monetary authorities are not directly involved in day-today international payments. By contrast, commercial banks which are directly involved in financing such transactions do have a transactions demand for international means of payment. Thus in his view, the ratio of commercial banks’ foreign exchange holdings to imports constitutes a more meaning- ful index of the adequacy of international transactions balances. Furthermore, citing Baumol, he suggests that the commercial banks do not have to increase their foreign balances in exact proportion to the volume of international trade to maintain a given

degree of adequacy. If the banks’ foreign exchange holdings relative to the square root of imports are used as the criterion, then the coefficient of adequacy rose sharply from 12.6 in 1951 to 51.5 in 1966. The implication of this analysis is that the oft-repeated complaint in the sixties about the shortage of international liquidity was exaggerated.*

In an essay published in the same year, Swoboda [68] makes a straightforward application of Baumol's formula to a trader's transactions demand for a foreign currency. Assuming that the importer has a commitment to meet a stream of foreign currency payments over the relevant planning period, and that payments must be made continuously and at a constant rate, it will be to his advantage to invest his funds in domestic bonds, and convert them into foreign cash in lots of even size. The following formula is then derived:

(4)

where F* is the optimal average holding of foreign currency, M is the value of imports or commitments of foreign-currency payments, a is the fixed cost of converting domestic bonds into foreign cash, and r is the interest return on domestic bonds. The formula is the same as Baumol's with the terms appropriately redefined. Swoboda then goes on to use the result to show the savings from single-currency (or vehicle currency) denomination of international transactions. If there is no vehicle currency, the importer is required to hold n different foreign cash balances, or a total of

ZF*r = &GZJZ’ i = 1,2,..*n. (5)

If, on the other hand, there is a vehicle currency, then EMi =M, where the value of all expenditures is expressed in terms of one single currency. The importer's foreign currency cash balance is

F* = a% f 2r.

(6)

Assuming for simplicity that Mr = M2, ... , = Mi, ... , = M,, the saving in cash balances, or the difference between (5) and (6), is positive. Thus

(ZF*l)-P = (n-fi)Jw = (n-fi)F:>O,forn> 1. (7)

Equation (7) states that economies of scale can be realized by denominating foreign currency payments in one single currency. These economies are directly related to the number of currencies pooled and the square-root of the value of imports.

While the above two papers are concerned with scale economies in foreign currency holdings that may be achieved by the private sector in international transactions, Olivera [52] argues that even the precautionary reserves held by monetary authorities are subject to the square-root rule. Such gold and foreign exchange reserves are held to even out transitory external disequilibrium, but not to finance transactions. He assumes that the monetary authorities choose a fixed "coefficient of security”, i.e., the probability that the excess demand for foreign

2 This analysis is indirectly linked to the author's later monetarist stance that the rapid accumu- lation of international reserves was responsible for the acceleration of world-wide inflation in the seventies. See Heller [ 35 ]

41

exchange reserves in any given time period will not exceed the amount of precautionary reserves, and further, that the excess demand is normally distributed. From this it is established that precautionary reserves must vary in proportion to the standard deviation of excess demand. Further assuming that the exchange market expands without any structural variation during the relevant time span, and making use of the well-known proposition in statistical theory that the standard deviation of a random sample from an infinite population is directly proportional to the square-root of the size of the sample, Olivera concludes that "the (precautionary) demand for reserves has an elasticity of 0.5 with respect to the volume of transactions”.3 This has been subsequently [53] generalized by the same author into what he calls "the square-root law of precautionary reserves” in a paper that synthesizes previous writings on the probabilistic estimates of safety stocks of commodities and liquid reserves for various purposes, including that of Edgeworth. One slight modification is that if expected excess demand is not zero, then the elasticity of the total reserve with respect to expected demand is between 0.5 and 1. The result follows from the assumption of "constant structure” of excess demand, and that total reserve is defined to be the sum of precautionary reserves and expected excess demand.

II

Since its explicit derivation in the fifties, the square-root rule has had a strong influence on the micro-theory of the demand for money, and it was only during the past decade or so that its underlying assumptions and empirical validity have been increasingly questioned. This section is devoted to a review of theoretical critiques and empirical findings.

We shall begin with a discussion of relatively minor criticisms or refinements which do not affect the substance of the theorem, In a very short note Johnson [38] observes that the Baumol-Tobin model assumes implicitly that any net interest earnings or withdrawal costs are either added to or subtracted from the transactor's stock of wealth, without affecting his current consumption. In other words, the model assumes that the transactor maximizes his end-of-period wealth subject to a consumption constraint. Johnson argues that a more acceptable approach is that the individual maximizes his consumption expenditure, subject to an end-of-period wealth constraint. On this alternative approach, a slightly different square-root formula is derived. The income elasticity of the transactions demand for cash is still 1/2 , but the interest elasticity is changed from - 1/2 to - [1/(2 + i)] . However, Johnson concedes that the change isnegligible, if the interest rate on earning assets per income-expenditure period is trivial, as it may realistically be assumed to be, so that the modified interest elasticity can be regarded as approximately equal to - 1/2 .

This approach has been criticized by Miller [49] who argues that the assumptions of both models are unduly restrictive. He maintains that it is more consistent with standard consumer theory to assume that the individual maximizes utility, which is a function of both consumption and wealth, subject only to the constraint that his choice is attainable. In terms of graphical analysis, a consumption-

3 An alternative method of finding the optimal international reserves is provided by applying the theory of Brownian motion. See Heller [ 33]1.

42

wealth frontier can be generated to the individual's opportunity set in the consumption and end-of-period wealth space. The optimal consumption-wealth pair is, as usual, determined by the tangency between the frontier and the individual's indifference map. The optimal cash holding is then that level associated with the utility maximization point. Algebraically, the individual seeks to maximize a utility function of the form U(c, W) subject to W = f(c; M,, r, b) where c is consumption expenditure over the planning period, W is the end-of-period stock of wealth, Mo is the initial cash balances, r is the rate of interest per period, and b is the fixed transactions cost in the bond market. More simply, the individual seeks to maximize the utility function with respect to consumption, His money demand function is then

M*= z J (8)

where M* is the optimal average holding of transactions balances and c* is the optimal consumption expenditure. As can be seen from this revised formula, optimal cash holdings vary with the square-root of consumption expenditure rather than with the volume of transactions. Moreover, the elasticity of transactions demand for cash with respect to any other parameter (Mo, r, and b) is now a linear function of the elasticity of consumption expenditure with respect to the same parameter. For instance, the interest elasticity of the transactions demand for money will be equal to -1/2 if and only if the interest elasticity of consumption is equal to zero.

The specification of the cost function in Baumol's paper has also been critically scrutinized lately. Morris [51] argues that Baumol's cost function for the general case where a part of income is withheld as cash balances is incorrect, as the implied saving in transactions costs involving the amount of cash so retained is not taken into account. A term equal to kd(T - I) should therefore be deducted from the opportunity costs of holding the retained income. When the cost function is thus corrected, the resulting solution of the optimal cash withdrawn remains the same as Baumol's, but the optimal cash initially withheld is higher. Morris’ note in turn has given rise to two "counter-corrections” by Grace [31] and Ahmad [1] , the former concluding that the optimal cash initially withheld should be even higher, while the latter supporting Baumol's original formulation, The present writer's sympathy is with Morris, though his result represents only a minor amendment.

We can now proceed to the discussion of more substantive objections and modifications to the Baumol-Tobin model. To facilitate exposition, the critics can be divided into two groups. The first group includes all those, while criticizing or modifying individual aspects of the model, nevertheless retain the overall deterministic framework in which the level of transactions is foreseen and cash disbursements occur in a steady stream. The other group approaches the problem in a stochastic context, with uncertainty in receipts and expenditures explicitly introduced. We shall discuss them in turn.

Within the first group, one important issue concerns the existence of economies of scale implied in the square-root formula. This has been sharply disputed by two well known monetarists, Brunner and Meltzer [9], on both theoretical and empirical grounds. They argue that, even accepting Baumol's assumptions, his model is not fully developed. Specifically, since in a general formulation, cash holdings consist of R, the initial amount withheld from investment, and C, the subsequent amount withdrawn

43

from investment, then the average holdings should be expressed as the weighted average of these two components, the weights being the respective lengths of time for which they are held, namely, (T - I)/T and I/T. The reformulated optimal weighted average cash holdings are then

M* = dm [l +(k, + k&/i] +T/2 [(k, + kd)/i12 (9)

where bw and kw are the fixed and variable costs of withdrawing cash from bonds respectively. From this, it can be shown that the elasticity of M with respect to T, denoted emt, is

[l t (k, + kd)/i] db,T/2i + t(kw + kd)lil 2T

emt =2[1 +(k, +kd)/i] db,T/2i + [(k, +kd)/il*T . (10)

The Baumol result that this elasticity equals 1/2 obtains only when T approaches zero, which is highly implausible.4 A more reasonable assumption is that bw is small while T can increase indefinitely especially when the number of transactors is large. In the limiting case, the elasticity in equation (10) approaches unity as T approaches infinity. This, denoting absence of economies of scale, is of course the value implied in the Quantity Theory of Money. Thus Brunner and Meltzer conclude that "the Baumol and Tobin models are not alternatives to the familiar quantity theory. They both imply it and as such perhaps furnish a firmer foundation for it”.

While Brunner and Meltzer are undoubtedly correct in asserting that the income elasticity of the transactions demand for money will approach unity in a properly specified model, they appear to have over-stated their case when they use this particular result to vindicate the "familiar quantity theory” rather than simply repudiate the square-root formula. For it can legitimately be asked whether unitary income elasticity is the only hallmark of the Quantity Theory. Such a unitary elasticity can indeed be unequivocably inferred from the Fisherian "equation of exchange” or the Cambridge cash-balance equation, but there is an influential school of thought within the quantity theorists themselves that money is a "luxury good”, with an income elasticity much higher than one. Friedman [25] for instance shows that the income elasticity of the demand for real balances was as high as 1.8 for the United States in 1870-1954.5 More important, the Quantity Theory is distinguished from the Keynesian theory principally by the fact that it regards the interest elasticity of the demand for money as either equal to or not significantly different from zero.6 But this is where the attempt by Brunner and Meltzer to vindicate the Quantity

4 The result can be obtained from equation (10) by using L'Hospital's Rules.

5 This high value of income elasticity is of course an empirical finding that is not necessarily implied by Friedman's monetary theory. Moreover, Friedman uses highly specialized definitions of money (M2) and income (permanent income) to reach this result, which remains a matter of unresolved controversy. Nevertheless, the point is that even among monetarists, there is no unanimity that income elasticity must be unity.

6 Zero interest elasticity can readily be inferred from classical Quantity Theory of either the Fisherian or Cambridge version. However, in the contemporary version of Friedman and others, the interest rate does enter as an argument in the money demand function, though its elasticity has been estimated to be very low. See Friedman [ 25 ; 26].

44

Theory gets them into trouble. As Ahmad [1] has shown, the interest elasticity that can be derived from equation (9) has a limiting value of -2.0 when T tends to infinity or bw tends to zero. The absolute value of this elasticity is much greater than that of the Baumol-Tobin model, which is - 1/2. In the words of Ahmad, while Brunner and Meltzer "have mended one flank of the quantity theory (even if only where income is received in cash in a creditless economy) by eliminating the economies of scale, they have, in the process, very much weakened its other flank by making the demand for money even more sensitive to the rate of interest”.

Criticisms of the square-root formula from the Quantity Theory perspective are therefore not entirely successful, and one must turn to other approaches that are not concerned with the vindication of the Quantity Theory as such. One problem of the Baumol model, to which we have briefly alluded earlier, is that the number of transactions is not explicitly restricted to integer values, so that transaction frequencies are assumed to react continuously to changes in such variables as interest rates, transactions costs and so forth. By ignoring integer constraints, Baumol is able to derive the various elasticities: the elasticities of money demand with respect to income and transactions costs are both1/2, the elasticity with respect to the interest rate is - 1/2 , and the elasticity with respect to the receipt interval is zero. Barro [4] has shown that if integer constraint is explicitly introduced, and assuming that the cross-sectional distribution of family income can be approximated by the first-order gamma density, then the elasticities predicted by the square-root formula would be close to those of the aggregated, integer-constrained solution if and only if the average number of transactions per payment period is above 1.6. Below that value, the square-root formula would understate the responsiveness of aggregate money demand to income and the receipt interval, and overstate the responsiveness to interest rates and transactions costs. Put another way, the income elasticity would be higher (hence economies of scale lower), the interest and transactions elasticities would be smaller, and the receipt interval elasticity would be positive. Barro's conclusion is that, although only a moderate value of the average number of transactions is required for the square-root formula to perform well in the presence of integer constraints, it also seems true from U.S. data that actual values of this number would be quite small. However, Barro's results follow from a very specialized form of income distribution, and it is not yet clear whether they would hold for more general forms.

An important refinement of the inventory theoretic approach is the incor- poration of the value of time, apparently made independently at about the same time by Barro and Santomero [6], Karni [40; 41], and Dutton and Gramm [12]. As the paper by Barro and Santomero is primarily an empirical one, we shall defer discussion of it until a later stage. In Karni's theoretical model, transactions costs consist of both financial costs (broker's fees, transportation etc.) and forgone earnings due to the loss of time in making conversions between cash and interest-bearing assets. The value of time thus lost can be represented by real wages. Moreover, the value of time, proxied by the real wage rate, is likely to change pari passu with real income. Once the influence of the real wage rate is taken into account, the rigid income elasticity implied by the Baumol-Tobin model is replaced by a wide range of possibilities, with the value of one-half representing only a lower limit. Specifically, only when no time is lost or the real wage rate is zero does the original Baumol-Tobin result hold. In all other cases, the elasticity would be higher, or in other words, the predicted economies

45

of scale would be smaller. Karni also argues that the interest elasticity of minus one-half neglects the possible effect of changes in the rate of interest on real income and consumption. Again when this is taken into account, the absolute value of the interest elasticity is normally smaller than one-half. Only when the proportion of property income is zero does the original value of minus one-half hold, In short, the validity of the square-root formula requires that the relevant variables - the volume of transactions or income, the rate of interest, and the costs of cash withdrawals and holdings are mutually independent. When the possible interdependence among the variables is allowed for, the predicted elasticities differ considerably from that implied in the formula. Dutton and Gramm also emphasize the fact that since the use of money saves transactions time, the consumer's valuation of time, i.e. the real wage rate, should be regarded as an additional determinant of the demand for money. Because income in turn depends on the wage rate, it follows that the demand for money is not determined by, but is simultaneously determined with the volume of transactions or the level of income. Unlike Karni, however, Dutton and Gramm are less concerned with the square-root formula than with the macroeconomic implications of the income and substitution effects of a change in the wage rate on the demand for money, In their analysis, for example, in a depression situation, consumers who are over-supplied with leisure time due to involuntary unemployment will have an incentive to reduce money balances, which have the generally accepted property of reducing transactions time and providing leisure. And if wages fall in response to excess labour supply, there will be a further reduction in the demand for money. The combined effects of such reductions will hardly fail to have a stabilizing influence on aggregate employment and output. Furthermore, their conclusion is much more charitable than Karni's concerning the economies of scale implied in the square-root formula. In their own words, "considering the net result of both the resource and leisure time valuation effects, if a rise in income, wage rate constant, produced a proportionate rise in the demand for money, then the total increase in the demand for money, produced by an increase in the wage rate associated with a rise in income, should be greater than proportionate to the increase in income due to the leisure valuation effect. Thus, an income elasticity (which includes both the resource and leisure valuation effects) of less than unity is not necessary for the confirmation of William Baumol's and James Tobin's models which predict economies of scale in the holding of transactions balances. If the leisure valuation effect is a significant determinant of the demand for money, an income elasticity of one would indicate economies of scale in transactions balances".7

The Baumol-Tobin analysis has also been criticized for treating bonds as the only alternative to money in the wealth-holder's portfolio - a feature no doubt strongly influenced by Keynes’ approach to monetary theory. Their model focuses attention on the costs of exchange between money and bonds only, but ignores the costs of exchange between money and commodities and hence neglects the holding of commodity inventory. Moreover, by implicitly following the Keynesian assumption of fixed prices, the model cannot deal with the effects of inflation on money and

7 In the quotation, "resource effect” is the income effect, while "leisure time valuation effect” is the substitution effect of a change in wage rate on the demand for money. Both effects are positive in the model.

46

commodity holdings. Feige and Parkin [18] break new ground by explicitly incorporating costly transactions between money and commodities into the inventory theoretic approach. However, they are more interested in the question of the payment of interest on cash balances (demand deposits) as a means of inducing society to hold the optimum quantity of money. Moreover, by abstracting from price changes they fail to analyze the impact of inflation. It remains for Santomero [59] to work out a more complete model that not only adds commodities as an alternative asset and analyzes the effects of inflation, but also disaggregates money holdings into demand deposits and currency in order to take into account their distinct characteristics. In this model, a household has the option of holding working balances in four forms: currency, demand deposits, savings deposits and commodities. An explicit rate of return on demand deposits is allowed to capture the provision of bank services or the remission of service charges in accordance with deposit balances.8 The rate of return on commodities is treated as the difference between the expected inflation rate and the rate of physical depreciation and storage costs. Given the respective yields on these assets and the transactions costs between them, the household tries to maximize the net return from its working balances over a given time period. The optimal average money holding, M*, (the sum of currency and demand deposits) derived from the solution of the model is:

M* = jm -G;F-G,* (11)

where Y is consumption expenditure, a, is transactions costs of using saving deposits, adc is transactions costs between demand deposits and currency, rs is the rate of return on savings deposits, rd is the rate of return on demand deposits (rs > rd), Gd* is goods purchased using demand deposits, and Gc is goods purchased using currency. These two optimal quantities of goods purchased can in turn be expressed as:

G; = J

a&Y(l -h) 2(‘d - ‘g>

(12)

G; = J

a,, Yh WC -rg)

(13)

where adg is transactions costs between demand deposits and goods, h is the fraction of expenditures made in currency, rg is the rate of return on commodities, rc is the rate of return on currency (assumed to be zero or negative in the model), and acg is transactions costs between currency and commodities.

The major differences between this model and the Baumol-Tobin model are that, by incorporating goods inventory as an alternative to money, an extra margin of substitution between money and commodities is added and the impact of expected inflation rate can be ascertained. Specifically, whereas in the square-root formula, a rise in the bond rate i (see equation 2) will result in a fall in the demand for money, in Santomero's model, the relevant variable is (rs - rd) so that a rise in rs will reduce the

8 A fuller explanation of allowing a nominal rate of interest on demand deposits, generally zero in most countries, and a derivation of a time-series of such a rate, are given in a joint paper by the same author and Barro. See Barro and Santomero [6]

demand for money if only rd is held constant. 9 A rise in the expected rate of inflation, represented by rg, will, ceteris paribus, reduce money holding without the need of a prior rise in the yield on financial assets. On the other hand, although money demand is inversely related to the differential (rs - rd), an equal rise in both rs and rd, with rc and rg constant, will have a positive effect on money demand. Another new dimension is that the demand for money is inversely related to the commodity transactions costs. The higher such costs, the less frequent will "shopping trips” be made, and hence larger commodity inventory, or lower money balances, will be held. Only under the restrictive condition that the costs of commodity transactions using either form of the medium of exchange are zero, i.e., adg = acg = 0, will money demand approximate the level suggested by the Baumol-Tobin analysis.

An alternative way of modifying the inventory approach to take account of the inflationary factor is to treat the payments period as a function of the rate of inflation. Barro [3] develops a model in which average cash holdings are reduced in response to a higher inflation rate via the reduction of the time period between transactions. The optimal payments period is derived as

T/n = dl(a/P)l [Y/Wp + r*)l (14)

where T is the given time horizon, n is the number of transactions, rp is the rate of inflation, Y is nominal income, P is the price level, r* is the rate of discount, and a is the costs of transactions. The corresponding optimal holding of real balances would then be:

M*/P = dz (15)

Clearly a high and accelerating rate of inflation rp would drastically reduce both the payments period T/n and real balances M*/P’. An additional mechanism by which cash holdings could be reduced involves the substitution of some alternative assets as medium of exchange (foreign currencies, gold bars, physical goods etc.)” The decision whether to employ money or its substitutes depends on the comparison of the inflationary costs of using money with the benefits of money as a transactions medium in terms of liquidity, convenience etc. However, once such substitutes are used, average cash holdings can be reduced even if transactions periods (velocity) remain constant.’ ’ The significance of this type of models is the demonstration that the income elasticity of the demand for money cannot be derived in a straightforward

9 In this model, the yield on financial assets is not represented by the usual bond rate, but by the yield on savings deposits, rs.

10 This situation normally occurs only in extreme conditions of accelerating inflation. In China during the late forties, for example, foreign currencies (mainly US and Hong Kong dollars) and gold bars were regularly used as both means of payment and store of value in major cities like Shanghai and Canton. Barro's own paper is devoted to a study of hyper-inflation in Austria, Germany, Hungary and Poland during the early twenties.

11 A related issue, which cannot be treated here, is the role of real balances as a factor. input. See Fischer [ 21]. Given a positive role of real balances in the production function, there is a finite limit to the reduction of real balances. This explains why, even under extreme conditions of inflation, the function of money as a transactions medium does not entirely disappear.

48

manner independently of the rate of inflation. Although the alternative definitions of money, M1, M2 , ... and so forth have

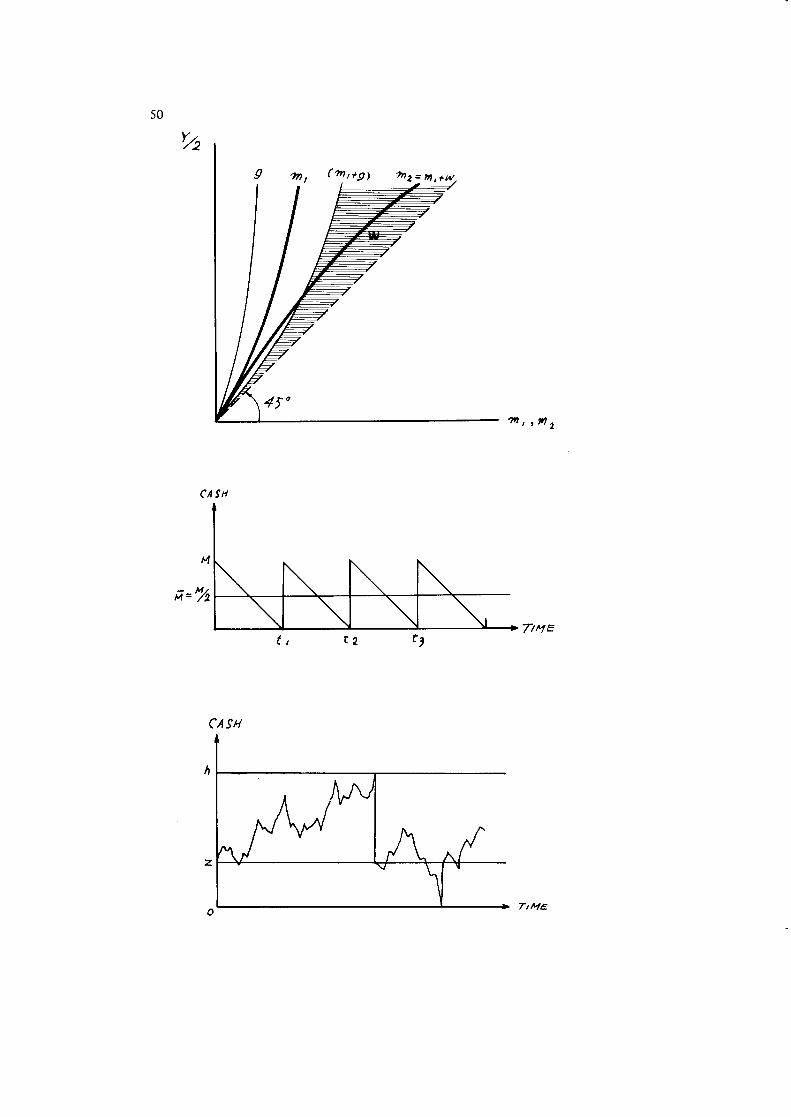

now been widely accepted in the statistical computation of money supply by monetary authorities as well as quantitative studies by economists, their separate treatment in the theory of demand for money has barely been developed. Santomero's study cited earlier distinguishes between two components of M1, namely currency and demand deposits, but not between M1 and M2. An important innovation in this respect has been made by Claassen [11], who explicitly works out optimal balances for both types of money. In his model, the economic unit can choose to hold its average real income y/2 among three assets: m1, the real balances of money defined in the narrow sense (demand deposits plus currency outside banks), w, liquid interest-bearing claims, including time deposits, and g, physical consumer goods. Note however that in his context, m2, real balances of money defined in the wider sense, is equal to the sum of ml and w. Thus, it covers a much wider ground than M2 as conventionally understood (M1 plus savings and time deposits at commercial banks).12 Because of the economies of scale in inventory holding, m1 and g rise less than proportionately with real income, while w rises more than proportionately with it. This can be shown graphically in Fig. 1, where the hatched area denotes investment in liquid claims w, which is equal to the difference between y/2 and (m1 + g).

The optimal balances for both types of money, expressed in nominal terms, are given by:

MT = Pm 1 = py+[(&)+ - ( 21 2(sdP*))tl

M*2=Pm2=py/2-P( ay 2(s - p*) )

’

(16)

(17)

where y is real income, P is general price level, a is transactions costs of commodities, b is transactions costs of interest-bearing securities, i is interest on liquid assets, s is storage costs of commodities, and p* is the expected rate of inflation. In comparison with the Baumol-Tobin model, the optimal balance for M1 is smaller by the amount of Pg because of the addition of physical commodities. The income elasticity of M1 remains equal to 1/2, but its interest elasticity is variable and no longer equal to -1/2 , M2 has an income elasticity of greater than one and an interest elasticity equal to zero.13 Furthermore, the holding of both types of money is shown to vary inversely with the expected rate of inflation, an effect ignored in the traditional inventory model. In particular, the decrease in M1 in an inflationary situation results from two substitution effects: one coming from w due to higher market rate of interest, and another coming from g due to higher level of prices.

A forceful critique of the square-root formula, based mainly on the institutional

12 Thus the Federal Reserve System now has five definitions of money stock, but even the widest one, M5, covers only M2 plus deposits at non-bank financial intermediaries and negotiable Certificates of Deposits of large denominations. Claassen's definition of M2 in this paper therefore approximates the "Radcliffe view”. See Meyer [461, Claassen [10], and Kwon [43].

13 This result follows from Claassen's rather special definition of M2 so that any income that is not spent on consumer goods is necessarily invested in M2.9

49

characteristics of the modern banking and monetary system, has been made by Sprenkle [64; 66; 67]. The formula is generally regarded as more relevant for large economic units, but even this is disputed by Sprenkle. First, he points out that the Baumol-Tobin model rests on the assumption that there is no pecuniary return on money held in the form of demand deposits. This is by no means universally true; as in many countries, banks still pay explicit interest on such deposits. Even in the United States, where such a practice is legally prohibited, there are ample opportunities to pay implicitly for such deposits by offering depositors a wide range of services, by providing loans at favourable terms, and by remitting service charges, etc. This is a point made also by a number of other economists. If a positive interest rate is allowed on demand deposits, and if this rate is an increasing function of the total volume of deposits (i.e., banks compete heavily for the largest deposit accounts) as well as the yield on short-term securities, then the income elasticity and the absolute value of the interest elasticity of optimal cash balances will both be substantially greater than that implied in the square-root formula. Secondly, he shows that differences in decentrali- zation of cash management and timing of receipts/expenditures can lead to enormous disparity in optimal cash holdings. The Baumol-Tobin model implicitly assumes that the economic unit has complete centralization of its cash management: all receipts and payments flow in and out of the head office only without passing through any other branch or office. Such an assumption is obviously unrealistic with respect to the modern corporation. If a large economic unit has J branches or separate accounts, and the jth branch or account receives xj per cent of total receipts T, then it can be shown that optimal cash holdings under complete decentralization will be greater than that under complete centralization by a factor equal to J, the square root of the number of branches or accounts. Clearly if J is large, the difference will be considerable: a firm with 25 branches and complete decentralization will have to keep 5 times as much cash holdings as that of another firm identical in all respects except having complete centralization in cash management. Both are of course extreme cases, but as a general statement it is still true that optimal cash balances vary directly with the degree of decentralization and inversely with the degree of centralization. Thirdly, Sprenkle also demonstrates that the minimal size of yearly transactions T for profitable switchings between cash and securities to take place depends on the frequency of income receipts during the year. The larger the frequency, the larger T will have to be. Thus taking the parameters of a = $20, r = 0.05, where a is the fixed costs of switching between cash and securities, and r is the annual interest rate on such securities, it can be shown that for yearly receipts, T need only be equal to or greater than $3,200 for profitable switchings to take place; but for weekly receipts, T will have to be equal to or greater than $8.65 million. Even with a large economic unit, its cash balances for transactions may well be held in relatively small accounts for which switchings hardly occur. The implication of all these considerations is that by ignoring such institutional characteristics, the square-root formula grossly underestimates the income elasticity of the transactions demand for money and somewhat overestimates its interest elasticity.

The criticisms and modifications of the square-root rule so far reviewed still retain the deterministic framework of cash flows assumed in the model, i.e., cash expenditures and balances follow a smooth “saw-tooth” pattern as depicted in Fig. 2. The other group of critiques denies this deterministic framework and replaces it with a stochastic one. Cash flows in the approach are assumed to behave as if they were generated by a trendless random walk.

CASH

t, t2

CASH

t

51

The first model developed in this direction appears to be that of Orr and Mellon [55] which specifically explores the effects of uncertainty in the cash flows of banks on the expansion of bank credit. Taking a cue from the "banking game” proposed by Edgeworth [15], they examine the problem of how far a profit-maximizing bank should expand its credit, given the random nature of its cash flows and the reserve requirement it must meet in order to avoid penalty loss. Their conclusion is that optimal credit creation under uncertainty will generally be less than that postulated in traditional static multiplier analysis where such an effect is not allowed for, or in other words, that banks will tend to hold larger excess reserves. However, their model does not explicitly criticize the square-root formula.

Much more explicit in its criticism and also much better known in the literature is the stochastic model developed by Miller and Orr [47; 48]. In this model, the random and driftless behaviour of the cash flows are assumed to conform to the Bernoulli process, with the variance of daily changes in cash balances equal to m2 t, where m is the change in cash balances (positive or negative), and t is the number of operating cash transactions per day. The economic unit allows its cash balances to fluctuate freely until they reach either the lower bound, zero, or an upper bound, h, at which point a portfolio switch will be undertaken to restore the balances to a level of z. This is a (h, z) cash management policy which requires that when the upper bound is hit, there will be a lump-sum transfer from cash of (h - z) dollars, while when the lower limit is reached, a transfer to cash of z dollars. This is shown in Fig. 3. The economic unit's objective is then to minimize its expected costs (the sum of transfer costs and opportunity costs) with respect to the control variables: the upper bound on cash holdings h, and the intermediate return point, z. The solution of the model gives the optimal average cash balances as:

where b is the fixed costs of transfer and i is the yield on securities. As in the Baumol-Tobin model, the demand for transactions balances is an

increasing function of the costs of transferring funds to and from the earning portfolio, and a decreasing function of the interest rate or opportunity costs of cash.14 The novel feature is the fact that optimal cash balances vary positively, not with the total volume of transactions, but with its variance, m2 t. Miller and Orr justify this by saying "that there is a relation between total sales and the variance of changes in the cash balance is clear enough since total sales are approximately the positive changes in the cash balance summed over a time interval”. But they also point out that "the relation is a loose one, and no precise value can be established for the elasticity of the demand for cash with respect to sales that is implied by our model”. Specifically, if the increase in sales or income is due to the increase in the size of each transaction but the frequency of transactions remains constant, then the income elasticity will be in the order of 2/3. On the other hand, if transactions frequency increases with sales or

14 M* is defmed by Miller and Orr as the "discretionary” transactions balances (net of the minimum balances agreed with the bank) to capture an important institutional characteristic of the American banking system. It is of course applicable also to other banking regimes where there are various requirements for compensating balances.

52

income, while the size of each transaction remains constant, then the predicted value of the income elasticity will be only 1/3. In the words of the authors, "the existence of such a wide range for the sales elasticity in our (h, z) model is in sharp contrast to the prediction of the Baumol model where the elasticity of average cash holdings with respect to sales (assuming constant prices) is always and precisely 1/2". The attractiveness of their model therefore lies in the wider range of elasticity val es, and 21 as such offers a more plausible and testable explanation for the observed systematic interindustry differences in cash holdings.15 At the same time, the predicted interest elasticity is - 1/3, implying that the demand for transactions balances is much less sensitive to changes in interest rates than assumed by the square-root formula if uncertainty is incorporated into the model.

In their 1966 paper, Miller and Orr still retain the two-asset framework, the only alternative asset to cash being a separately managed portfolio of short-term liquid assets. In their 1968 paper, a third asset, long-term securities with less liquidity but higher return, is introduced. However, they demonstrate that the money demand predictions of their earlier paper are not significantly affected by this modification.16 They do admit however that negotiated compensating balances may distort estimates of the relevant income and interest elasticities, and the practice of maintaining numerous cash accounts may similarly obscure the presence of significant scale economies. The first point has been taken up by Frost [29], who develops a model that incorporates both the Miller-Orr stochastic structure as well as an explicit demand for banking services in the form of minimum compensating balances. In contrast to Miller and Orr, who regard minimum compensating balances in lieu of service charges as completely exogenous to the model, Frost shows that such compensating balances and transactions balances should not be treated independently if the bank takes into account the firm's average deposit level or the range over which the firm allows its deposits to vary in determining the supply of bank services. Only when the bank supplies services in proportion to the minimum cash balances maintained by the firm do the original Miller-Orr results remain unscathed. If however the supply of bank services is a function of both the minimum balances and the average balances, then complications arise and the original results may not hold.

Tsiang [72] argues that both the inventory theoretic approach to the transactions demand for money of Baumol and Tobin, and the portfolio theoretic approach to the asset demand for money of Tobin [71] and Hicks [36] neglect the precautionary demand for money. Moreover, in a society with highly developed money markets, there are always some very liquid assets that "dominate” cash in the sense that they are virtually riskless and yet have a positive yield.” Thus, the asset or

15 This variable range in elasticity values should be stressed. Thus, the interpretation by Barro and Fischer [ 21] that "the differences between the Miller and Orr elasticities and the Baumol elasticities involve a substitution of l/3 for 1/2" is not strictly correct.

16 The 1968 paper by Miller and Orr also contains an elaborate defence of the symmetric Bernoulli process that underlies their 1966 paper. A formal proof of the (h, z) decision rule is given by Eppen and Fama [17] who, however, treat transactions costs as proportional rather than as a fixed lump sum.

17 This point is also made by Hicks [ 37 ] and Modigliani [ 50].

53

speculative demand is likely to be less important than precautionary demand in explaining cash holdings. Precautionary cash balances are defined as those held in order to meet contingencies which are not expected to happen in the normal course of events, but which, if they should occur, would call for cash payment. In Tsiang's model, the expenditure rate is assumed to be stochastic, while the income receipt pattern is still lumpy and deterministic. There are two assets other than cash: short-term bills and long-term bonds. Any delay in the receipt of funds from forced liquidation of such assets to meet contingencies will involve penalty costs. The expected yield of holding precautionary balances, in addition to transactions balances, is the avoidance or reduction in such costs. Tsiang's conclusions are that the optimal number of cash replenishments during the income receipt period is fairly insensitive to moderate changes in planned expenditure. Given the short-term interest rate and the number of cash replenishments, the optimum precautionary cash balances would then vary roughly with the square-root of the expected rate of expenditure.‘* However, if the sum of the initial holdings of short-term assets and precautionary cash balances is not a sufficiently large multiple of the square-root of the minimum required cash replenishments, then the economies of scale in holding precautionary balances would be less. The effect of a change in interest rate on the demand for precautionary cash balances is even less straightforward. For an increase in interest rate would, on the one hand, increase the opportunity cost of holding precautionary balances, but on the other hand also raise the marginal yield on such balances by increasing the penalty for running out of cash. In normal situations, however, a rise in interest rate would probably reduce the demand for precautionary reserves. The major difference between Tsiang's model and the Baumol-Tobin model is therefore that in the former, where the rate of expenditure flow is uncertain, no precise predicted values of income and interest elasticities can be inferred. Note that although Tsiang distinguishes con- ceptually between transactions and precautionary demand for cash, he recognizes that they are not independent of each other: as a matter of fact, his model provides for a joint determination of the optimal quantities of the two.

Incidentally, this joint determination of transactions and precautionary cash balances also raises a more fundamental issue in monetary theory. The square-root formula rests on the implicit assumption that transactions balances, or at least the sum of transactions and precautionary balances, can be neatly separated from the asset or speculative balances. Many economists, of both monetarist and Keynesian persuasion, have questioned whether this dichotomy is valid. Thus Friedman, in his famous 1956 restatement of the Quantity Theory, explicitly rejects this dichotomy. More recently, Hicks [37], Modigliani [SO], Borch [8] , Feldstein [20], Tsiang [73] and Thorn [69] have expressed dissatisfaction with Tobin's [71] risk-aversion or mean-variance analysis of the demand for money. The gist of the critics’ argument is that the mean-variance indifference curve does not necessarily have the convexity property ascribed to it, and that transactions costs and unforeseen requirements for cash expenditures provide a surer foundation on which to rationalize the holding of cash balances than risk-aversion. This controversy is however beyond the scope of this

18 A similar conclusion is reached in Dvoretzky [ 13] where the increased volume of transactions is generated by an increase, not in the average value of each contract, but in their number. The precautionary reserves then vary positively with the square-root of the number of transactions.

54

paper. For our purpose, we shall continue to assume that it is conceptually convenient to distinguish between money held for transactions and other purposes, in order to meet the square-root theorem on its own ground.

We now turn to a brief review of the results of empirical testings of the square-root hypothesis. Since the Baumol-Tobin analysis is generally regarded as being more relevant to large economic units, most direct tests relate to the observed cash behaviour of business firms. Attention is focused on the estimated values of income and interest elasticities, particularly the former.

One of the best-known tests is Meltzer's [45] study of cash balances of 126 business firms in 14 American industries for the period 1938-57. Meltzer uses sales as a proxy for income and experiments with several alternative estimating equations. His main finding is that the income elasticity of the demand for cash by firms is approximately unity, thus implying neither economies nor diseconomies of scale. For particular industries, he finds that in each of the nine years and in twelve of the fourteen industries, the mean value of the income elasticity is greater than unity. The 26 cases in which this elasticity is smaller than unity are largely concentrated in only a couple of industries. He thus concludes that "these data give little evidence of economies of scale and little support to the Baumol-Tobin model as an explanation of the demand for money by firms”. However, apart from asserting the importance of interest rate as a determinant of the firms’ demand for money, no precise estimate of the interest elasticity is given. Whalen [74] makes a cross-section study of 109 non-financial corporations in 8 American industries during the fiscal year 1958-59. In the first test, the firms’ cash holdings are adjusted for investment balances, so that they represent money held for transactions and precautionary purposes only. Using a linear equation that treats the ratio of cash balances to total monetary assets as the dependent variable, and the ratios of sales as well as the square-root of sales respectively to total monetary assets as the independent variables, the author concludes that no systematic economies of scale in cash management can be found, though he is cautious enough to add a proviso that "required for this cross-section approach is the assumption that firms in the same industry are homogeneous in all respects except for the size of their business operations”. In the second test, he uses a modified form of Meltzer's log-linear equation, but without adjusting for investment balances. The results are similar to Meltzer's, but the omission of interest rates in the money demand function, and the failure to adjust for investment balances are acknowledged to be possible sources of bias. Frazer [23] also makes a cross-section analysis of manufacturing corporations during 1956-61, but his paper is not strictly a test of the square-root hypothesis, since he is concerned with precautionary cash balances only. His main finding is that the larger-sized firms have smaller precautionary cash balances, larger non-cash liquid assets, and less bank borrowings, all relative to total assets, than smaller-sized firms, thus indicating some economies of scale with respect to money held for precautionary purposes, though no elasticities are given. Sprenkle [66] studies the actual cash holdings at the end of 1966 of 475 of the largest 500 American industrial firms as listed by the Fortune magazine. He finds that, for the largest 50 firms, on the average only 1% of their cash balances is explained by the square-root formula, and the greatest amount explained is 3.7%. For all the firms, the median amount explained is only 2.5%, and for only 2 firms is more than 20% explained. Thus, on the average, 97.5% of the actual cash holdings of these large firms

55

is unexplained by the model. Nor can allowance for decentralization of cash management and the timing of receipts fully explain such observed balances. In Sprenkle's view, the only convincing rationale for these excess balances is that they are held to pay for bank services in the U.S. institutional setting. Aronson [2] finds that cash balances held by American State and local governments in 1962 are grossly in excess of that implied by the square-root formula, though he attributes this more to mismanagement or decentralization of cash management than inadequacy of the model.

Empirical tests of the hypothesis with respect to household demand for cash have been relatively few. Barro and Santomero [6] use a modified form of the square-root formula for their test, where the relevant interest variable is not the usual yield on bonds, but the differential between the interest rate on deposits of savings and loan associations and the interest rate on commercial bank demand deposits. Barro and Santomero argue that remission of service charges and provision of various services as a function of average balances should be regarded as a form of positive imputed return on demand deposits. A novel feature of their study is the derivation of a time- series of such yield for 1950-68 through a private survey of American commercial banks. They find that the income elasticity is close to unity, though they do not regard this as necessarily inconsistent with the square-root hypothesis, since the time value of transactions costs is typically neglected. To quote the authors, "as transaction volume increases, economies-of-scale are realized only to the extent that transactions costs rise less than transactions volume. Since transaction costs depend largely on value of time, and since value of time may increase even faster than transactions volume, diseconomies-of-scale (money being a "luxury”) is quite compatible with the inventory approach”. As regards interest elasticity, if the differential between savings deposit rate and demand deposit rate is taken as the relevant variable, the coefficient is -0.549, strikingly close to the predicted value of the Baumol-Tobin model. On the other hand, if savings deposit rate alone is used as the interest rate measure, the coefficient becomes -1.092. The conclusion is therefore that a reconstructed inventory model is more robust to empirical testing than the simple Baumol-Tobin version. The Tobin formulation of the model also predicts that, if the average receipt interval is one month, the maximum average holding of cash would be two weeks’ income. Barro and Fischer [5] however report that "this figure substantially under-estimates household money holdings in the United States, which are about 1 1/2 months’ income in 1973”.

Aggregate money demand functions have also been used to test directly or indirectly the hypothesis. Khan [39] employs the average real wage rate as a surrogate for transactions costs in testing the model for the period 1900-65 in the United States. He concludes that "although the coefficients of current income and the rate of interest were found to differ significantly from the 0.5 value predicted by the theory, the model was found to yield marginally better results than the Friedman-Laidler and Keynesian models”. Liebermann [44] in his very recent study departs from the usual procedure by treating debits to demand deposits rather than income as the measure of transactions, and incorporating time as a crude estimate of the mean rate of technological change, for the period 1947-73 in the United States. The main finding is that there are very substantial economies of scale, as the debits elasticities tend to fall in the 0.33 to 0.37 range. However, the interest elasticities tend to have a very small absolute value, varying between -0.051 and -0.098. A potentially important metho-

56

dological issue has been raised in the author's observation that "previously published transactions demand for money studies may have been misspecified”.

Most of the empirical studies reviewed above are apparently unfavourable to the square-root hypothesis. Even when the results appear to be more favourable, they are derived from modified or reconstructed models. At the same time, one must acknowledge that the empirical evidence is by no means final and conclusive. One important conceptual and methodological issue is that the Baumol-Tobin model explicitly confines itself to the transactions demand for money. Observed cash balances, whether held by firms, households or other economic agents may well include balances held for other purposes - precautionary and speculative purposes for example. Only if the observed cash balances are held entirely for transactions purposes will the empirical findings be strictly relevant for evaluating the hypothesis. However, in the studies cited above, only Whalen has adjusted the observed cash holdings for investment balances (i.e., balances held for speculative purposes) in one of his tests. The failure or inability to segregate transactions balances (or at least the sum of transactions and precautionary balances) would seem to cast doubt on the validity of much of the evidence. Nevertheless, critics of the Baumol-Tobin hypothesis have defended their estimating procedure on the following grounds. Firstly, they argue that in advanced contemporary economies where money markets are highly developed and virtually riskless liquid assets (with respect to nominal capital value) with positive yields are readily available, speculative balances can be regarded as trivial, if not zero. Thus Modigliani [50] writes, "the proposition that people will flee from long-term bonds when the price of bonds is deemed to be untenably high, seems valid enough, but the obvious abode for funds accruing from moving out of long-term bonds should be short-term ones, not cash”. Secondly, precautionary balances can also be treated as negligible, particularly with respect to large economic units. Thus Sprenkle [66] asserts that "the only uncertainty involved in a precautionary demand for money is the uncertainty of payments and receipts between the present and next planned purchase or sale of short-term assets. For a large economic unit this period can be as little as one day. The amount of uncertainty over such a short period is apt to be small indeed, and thus the precautionary demand for money should also be very low”. In another paper [65], he argues that the precautionary demand might conceivably be negative under certain circumstances. Consequently, observed cash balances are still regarded as a good proxy for transactions balances.

The other reservation about empirical studies concerns the role of transactions costs. It is being increasingly realized that these costs, which are nothing but the costs of factor inputs, are not independent of the volume of transactions or income. As real income rises, real wage rate representing these costs tends to rise puri passu. Hence there will be an incentive to hold more real balances to save costs. As emphasized by Barro and Santomero [6] and Dutton and Gramm [12] , when the value of time is recognized, a measured income elasticity of money demand in excess of unity is not necessarily inconsistent with the inventory theory. At the same time, as Enzler, Johnson and Paulus [16] have pointed out, recent innovations in banking and finance, such as overdraft credit lines, money-market mutual funds, third-party transfers from savings accounts, bank-managed accounts etc. have the effect of reducing costs of switching between cash and interest-bearing instruments. These developments work in opposite directions on the demand for money, and the net effect is by no means clear.

57

Apart from the direct tests of the Baumol-Tobin hypothesis, there is of course a vast empirical literature on the aggregate demand function for money. These studies are however not concerned with the square-root formula as such, but with wider macroeconomic issues such as the stability of the money demand function, the efficacy of monetary policy, the substitutability of money and near-monies and so forth. Again, no attempt has been made in such studies to isolate the transactions balances as a component of total money holdings. Nevertheless, one useful by-product of these investigations is the information on the range of income and interest elasticities, which could serve as an approximate frame of reference for our more specialized purpose. A convenient survey has recently been provided by Feige and Pearce [19]. In summarizing the time-series studies, they report that "the mean income elasticity is 0.57, consistent with the inventory theoretic prediction of economies of scale in money holdings”. This statement seems to us to be unwarranted. For a closer look at the data reveals that the standard deviation of these estimates is quite high, with the coefficients ranging from a low value of 0.117 to a high value of 1.219. It is highly doubtful whether a crude arithmetic average can be taken to be a valid confirmation of the square-root hypothesis. Moreover, when we turn to temporal cross-section studies, we find that the mean becomes 0.887, ranging from a low value of 0.62 to a high value of 1.12. Although some economies of scale are indicated, they hardly provide a sufficient basis for vindicating the hypothesis. As to the interest elasticities, results vary greatly, depending on which rate of return is chosen as the relevant variable. The best performance is shown by the Treasury bill rate, with a mean of -0.57, which is very close to the value predicted by the square-root formula. Unfortunately, the standard deviation is again very high, with the estimates ranging from a low value of -0.15 to a high value of -0.006. Furthermore, apart from the fact that money demand in these studies relate to total demand rather than transactions demand only, comparatively little work has been done to disaggregate money demand by ownership category. In those few studies that do, it is found that elasticities may differ significantly across sectors. In a recent important study by Goldfeld [30], for example, while the income elasticity is estimated to be around 0.7 in the aggregate money demand function, that of the household sector is found to be well above unity. Goldfeld however finds himself unable to make sense of the money demand behaviour of the business sector and the state and local government sector. As an aside, he remarks that “this evidence suggests that a simple transactions model (especially if couched in real terms) will have a hard time explaining money holding by business and by state and local governments”.

Finally, all empirical tests of the square-root hypothesis, whether direct or indirect, are based on domestic (predominantly American) money demand data. The extension of the square-root formula to international transactions and/or pre- cautionary reserves has so far not been formally tested, although Heller [34] has made some ad hoc observations on the trend of official reserves and commercial banks’ foreign exchange holdings relative to imports during the period 1951-66. On purely a priori grounds however, there are reasons to believe that the deterministic inventory model is even less able to assess the adequacy of international reserves, since they are held not only to accommodate systematic and random fluctuations in current account receipts and payments as well as capital flows, but also to cope with unpredictable and often irrational speculative attacks, a need that is not obviated by the present makeshift system of "managed floating”.

58

III

The inventory theoretic approach to the transactions demand for money marks a new departure in the evolution of monetary theory by treating such demand, not as a constant exogenously determined by institutional and technological factors (system and customs of receipts and payments, degree of market specialization and industrial concentration, efficiency in communications and transportation and so forth) but as a result of voluntary choice by cost-minimizing or utility-maximizing wealth-holders. It also represents a seminal attempt to demonstrate that positive transactions costs are a necessary and sufficient condition for the holding of money balances.19 That it constitutes an important innovation and contribution to the micro-foundations of monetary theory can hardly be gainsaid.

This inventory approach, as pioneered by Baumol and Tobin, gives rise to the famous square-root formula which purports to show that there are important economies of scale and interest elasticity in the transactions demand for cash. The simple though somewhat mechanical way in which the formula is presented undoubtedly has considerable intuitive and heuristic appeal which explains its popularity and influence for well over two decades. However, it is symptomatic of the pace of developments in monetary economics that this simplistic model has in recent years been increasingly challenged on both theoretical and empirical grounds. From the theoretical point of view, it is clear from our survey that alternative inventory models, based on more plausible assumptions, can yield quite different results. Perhaps the greatest weakness of the square-root formula lies in the rigid predicted values of income and interest elasticities, which to a large extent explain the poor performance of the formula in empirical studies. Granted that these studies are by no means conclusive due to the conceptual and methodological difficulties already described, it nevertheless remains true that no study has come up with any firm support of the model in its original form .20

In spite of these strictures, we canot concur with Sprenkle's [66] blanket condemnation of all transactions models as being "useless”. A distinction needs to be drawn between the inventory approach to monetary theory in general and the particular forms which it might take, e.g. the square-root formula. In our judgment, the inventory approach is still a fruitful and suggestive way of tackling the issue of money demand with potentially rich rewards. The square-root formula, on the other hand, is at best a tentative and unconfirmed hypothesis. It certainly does not deserve the title of "law” given to it by some of its more enthusiastic supporters. We therefore agree with Orr's recently expressed view and hope [54] that "the combination of a more appropriately specified model and a more directly relevant data base will yield sharply improved, albeit still improvable, predictions”.

19 For a formal discussion of this point, see Savings [ 60; 6 1; 62].

20 Some writers tend to regard a measured unitary income elasticity as the dividing line for supporting or rejecting the square-root hypothesis. This seems to be somewhat misleading. For the hypothesis predicts substantial, not just some economies of scale, in the transactions demand for money.

REFERENCES

1.

2.

3.

4.

5.

6.

1:

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

Ahmad, S., "Transactions demand for money and the quantity theory”, Quarterly Journal of Economics, May 1977, pp. 327-335.

Aronson, J.R., "The idle balances of State and local governments: an economic problem of national concern”, Journal of Finance, June 1968, pp. 499-508.

Barro, R. J., "Inflation, the payments period, and the demand for money”, Journal of Political Economy, Nov./Dec. 1970, pp. 1228-1263.

Barro, R. J., "Integral constraints and aggregation in an inventory model of money demand”, Journal of Finance, March 1976, pp. 17-88.

Barre, R. J. and Fischer, S., "Recent developments in monetary theory”, Journal of Monetary Economics, April 1976, pp. 133-167.

Barro, R. J. and Santomero, A.M., "Household money holdings and the demand deposit rate”, Journal of Money, Credit and Banking, May 1972, pp. 397-413.

Baumol, W., "The transactions demand for cash: an inventory theoretic approach”, Quarterly Journal of Economics, Nov. 1952, pp. 545-556.

Borch, K., "A note on uncertainty and indifference curves”, Review of Economic Studies, Jan. 1969, pp. 14.

Brunner, K. and Meltzer, A.H., "Economies of scale in cash balances reconsidered”, Quarterly Journal of Economics, August 1967, pp. 422-436.

Claassen, E.-M., "Die Definitionskriterien der Geldmenge: M1, M2 ... oder Mx?'', Kredit und Kapital, 7 Jahrgang, 1974, pp. 273-290.

Claassen, E.-M., "Die optimale Transaktionskasse vom Typ M1 und M2", Kredit und Kapital, 9 Jahrgang, 1976, pp. 101-122.

Dutton, D.S. and Gramm, W. P., "Transactions costs, the wage rate, and the demand for money”, American Economic Review, September 1973, pp. 652-665.

Dvoretzky, A., "The probability distribution generated by the random payment process”, in [56], pp. 450-456.

Edgeworth, F.Y., “Problems in probabilities”, London Edinburgh and Dublin Philosophical Magazine, Oct. 1886, pp. 371-384.

Edgeworth, F.Y., "The mathematical theory of banking”, Journal of the Royal Statistical Society, Vol. LI, 1888, pp, 113-127.

Enzler, J., Johnson, L., and Paulus, J., "Some problem of money demand”, Brookings Papers on Economic Activity, Vol. 1, 1976, pp. 26 1-281.

Eppen, G.D. and Fama, E.F., "Cash balance and simple dynamic portfolio problems with proportional costs”, International Economic Review, June 1969, pp. 119-133.

Feige, E. L. and Parkin, M., "The optimal quantity of money, bonds, commodity inventories, and capital”, American Economic Review, June 1971, pp. 335-349.

60

19. Feige, E L. and Pearce, D. K., "The substitutability of money and near-monies: a survey of the thne-series evidence”, Journal of Economic Literature, June 1977, pp. 439-469.

20. Feldstein, MS., "Mean-variance analysis in the theory of liquidity preference and portfolio selection”, Review of Economic Studies, Jan. 1969, pp, 5-12.

21. Fischer, S., "Money and the production function”, Economic Enquiry, Dec. 1974, pp. 517-533.

22. Fisher, I., The Purchasing Power of Money, New York, 1912.

23. Frazer, W. J., "The financial structure of manufacturing corporations and the demand for money”, Journal of Political Economy, April 1964, pp. 176-183.

24. Friedman, M., (ed.), Studies in the Quantity Theory of Money, Chicago, 1956.

25. Friedman, M., "The demand for money: some theoretical and empirical results”, Journal of Political Economy, August 1959, pp. 327-351.

26. Friedman, M., "Interest rates and the demand for money”, Journal of Law and Economics, October 1966, reprinted as chapter 7 in [28].

27. Friedman, M., "Money - II: Quantity Theory”, International Encyclopaedia of Social Sciences, Vol. 10, 1968, pp. 432-441.

28. Friedman, M., The Optimum Quantity of Money and Other Essays, Chicago, 1969.

29. Frost, P.A., "Banking services, minimum cash balances, and the firm’s demand for money”, Journal of Finance, Dec. 1970, pp. 1029-1039.

30. Goldfeld, S.M., "The demand for money revisited”, Brookings Papers on Economic Activity, 1973, pp. 577-638.