Embed Size (px)

DESCRIPTION

In Q2 of 2008 Spain officially announced its entrance in to what would come to be the worst recession of its economic history. Previously, the country had undergone nearly a decade of economic expansion, mainly stemming from a boom in real estate and construction. Ballooning housing prices created a severe accumulation of economic imbalances, making it vulnerable to shocks from that industry. Upon the bursting of the housing bubble, Spain underwent a vicious cycle of private debt problems; increasing unemployment levels, shrinking productivity, and a growing mistrust in the political system. This paper examines the different contributing factors in the evolution of the crisis, including deep economic, political, and banking flaws that were inherently present prior. It also examines the social consequences of the crisis, and analyzes how political authorities responded in their attempts to remedy the situation.

Citation preview

The Spanish Real Estate Crisis: A Historical Perspective

Christos Lycos1

1 Department of Finance at John Molson School of Business, Concordia University, 1450 Guy St., H3H-0A1, Montreal, QC, Canada Author’s E-mail: [email protected] UNIVERSIDAD CARLOS III DE MADRID c/ Madrid 126, 28903, Getafe

08 Fall

Working Paper: Spanish History January 2015

Universidad Carlos III de Madrid 2

The Spanish Real Estate Crisis: A Historical Perspective

Christos Lycos

Abstract

In Q2 of 2008 Spain officially announced its entrance in to what would come to be the worst recession of its economic history. Previously, the country had undergone nearly a decade of economic expansion, mainly stemming from a boom in real estate and construction. Ballooning housing prices created a severe accumulation of economic imbalances, making it vulnerable to shocks from that industry. Upon the bursting of the housing bubble, Spain underwent a vicious cycle of private debt problems; increasing unemployment levels, shrinking productivity, and a growing mistrust in the political system. This paper examines the different contributing factors in the evolution of the crisis, including deep economic, political, and banking flaws that were inherently present prior. It also examines the social consequences of the crisis, and analyzes how political authorities responded in their attempts to remedy the situation. Keywords: Housing bubble; corruption; private debt; mortgage crisis;

Universidad Carlos III de Madrid 3

The Spanish Real Estate Crisis: A Historical Perspective

Can a flap of a butterfly’s wings in Brazil be the root of a tornado in Texas? This is a popular analogy in economics that originated in the works of the famous American mathematician Edward Lorenz. It refers to the extreme case where a small and insignificant event in one point in time can trigger an unpredictable, and exponentially greater, outcome somewhere else down the line. This theory is often applied when studying the complexity and interconnectedness of financial markets and their tendency to behave in a chaotic fashion. Chaotic behavior is the result of a domino-like effect, where during the development of these small, inconspicuous events, their collective effect on a macro level is often overlooked until a drastic outcome occurs; at which point, in hindsight, it might then seem clear how it progressed, yet too late to bring it to a halt. Instead, if action is taken promptly, then it is sometimes possible to recourse towards a more desired outcome. Similarly, this is how crises develop, and for this reason although each crisis usually has a major causative factor that contributes to the overall distress, it is often accompanied by other unnoticed influences that either directly or indirectly have a role in the development of a crisis.

This paper will attempt to explore beyond the commonly blamed real estate sector, by looking at how other socio-political, macroeconomic, and banking factors together, and synchronically, contributed to unveiling the underlying weaknesses in the Spanish economy, bringing it to its ultimate halt in the fall of 2008.

Introduction From a global provider in fashion and textiles, to major contributor in the solar

and wind energy, and a market leader in the high-speed train industries; it is not by chance that Spain is now the fourth largest economy in Europe, and the 12th largest in the world, despite undergoing one of the most severe economic shocks during the global financial crisis of 2008 (Summers, 2012).

From and economic and political perspective, Spain’s rich history has led it to become one of the most important nations in the world. The sovereign state, located in the Iberian Peninsula, became a world power in the 16th century when it made overseas conquests and colonized a vast empire extending across a vast portion of Latin America (British Broadcasting Corporation, 2014). This empire lasted until the 19th century, where war became an opportunity for many of the transatlantic colonies to become independent from their mother country. It was at that point when Spain’s economy stagnated in comparison to the rest of Europe.

Although Spain had a substantial increase of income per capita by a factor of ten

over the last 160 years, up until 1990, this was considered mild compared to the real income growth experienced by other European nations (Prados de la Escosura, Sanches Daban and Oliva, 1992). A reason being that Spain was one of the last countries in the western world to become industrialized. The causes of this stagnation is something still

Universidad Carlos III de Madrid 4

argued by scholars today; however amongst some of the most prevailing explanations is that Spain had human and physical capital levels well below European standards, which widened the economic development gap (Prados de la Escosura, Sanches Daban and Oliva, 1992). This gap only began to shrink at the end of the Spanish Civil War in 1936 when General Francisco Franco came in to power as a dictator and led the country under autarky up until his death in 1975. His authoritarian leadership was unconventional given that although he didn’t endorse of democracy, he nevertheless promoted free-market capitalism, which was crucial for the economic expansion of Spain.

It was not until Franco’s death that the Spanish economy really took a leap forward towards becoming more robust. King Juan Carlos, Franco’s successor, transitioned the nation into democracy, which led to greater integration with its European neighbors. Historical Context

Following Spain’s transition towards democracy, another major milestone in its economic history was its entrance to the European Union in 1986, coupled with its adoption of the euro currency that was introduced on January 1st, 1999. The aim of this union was to solidify European nations by fostering economic growth and financial stability amongst members. This was to be done by eliminating trade barriers and tariffs and eventually introducing a single currency that would further establish a single integrated European market (Centre d'Études Prospectives et d'Informations Internationales, 2011).

Aside from Spain’s transition towards democracy, this period marks an important

step towards modernization since the Economic and Monetary Union (EMU) stimulated the country to further eradicate protectionist practices and open it to the outside world (Rojo, 2009). For Spain, the transition towards joining the EU presented its challenges given that despite its recent progress in the last couple of decades, it lacked the economic strength and stability due to structural imbalances compared to other EU members. Therefore its candidacy was contingent upon making several prompt structural reforms in order to meet the “Maastricht” criteria required to be part of the integration in 1999 (Rojo, 2009).

One of the adjustments included Banco de España becoming officially responsible

for independently executing monetary policy in 1994 in order to promote better price stability and help meet inflation targets. Furthermore, managing deficit levels, stimulating labor market reforms, and endorsing privatization were amongst some other prerequisite actions necessary in order to meet the EU’s high standards of flexibility and liberalization (Rojo, 2009).

In hindsight, it can be strongly argued that the benefits of Spain joining the EU far

outweigh the shortcomings that will later be discussed. Following Spain’s adoption of the euro, the country experienced almost a full decade of the sturdiest economic expansion in its history. One of the most important consequences of joining the single European

Universidad Carlos III de Madrid 5

currency was that small, weaker economies such as Spain’s were no longer dependent upon themselves; instead they were protected by the stability of the entire EMU. What this meant for Spain was that its risk of default was significantly reduced and therefore it experienced a virtually overnight double-digit reduction in borrowing costs. Its interest rates fell from 14% to a historical low of 4% within weeks of Spain’s adoption of the currency; this was abnomally low for its economy’s cyclical position (Chislett, 2013). With access to inexpensive credit, Spain and other European nations were now able to adjust their fiscal policies to increase spending to previously impossible levels (Daly, 2014). In addition, Spanish fiscal policy promoted acquisition of housing instead of renting, and also encouraged investing in real estate rather than pursuing other investment vehicles (Carballo-Cruz, 2011). Spanish politicians saw this as an opportunity to stimulate growth based on an economic model founded on construction, real estate, and property development activities as they righteously recognized it be a method to reduce unemployment, increase housing values, and thus generate tax revenue.

Indeed for the most part of the first decade following Spain’s adoption of the

euro, its economy experienced a colossal growth in productivity, breaking historical records and repositioning itself within the continent. Inevitably, there was an extraordinary demand for credit by households and enterprises looking to finance their investments. Between 1997 and 2007, private debt rose from 52.7% of disposable income to 132.1%. From a years of salary perspective, a borrower’s effort to acquire a home rose from 4.3 years to 9.1 years of salary by 2007 (Carballo-Cruz). People were quitting their jobs to take part in the real estate and construction boom; even foreigners had become aware of Spain’s flourishing economy, resulting in an enormous influx of 4.6 million immigrants during the first decade of the new millennium. It is estimated that one third of employment growth in the EU between 1999 and 2007 originated from Spain (Summers, 2012). The construction and real estate booms were so great that they accounted for 45% of all new construction in Europe; this figure is enormous when considering that the Spanish economy only accounted for 15% of the Eurozone’s GDP (Guillen, 2010).

The shockwave created by the collapse of Lehmann Brothers in 2008 reached

markets across the globe, putting the stability of the entire financial system under threat. Inevitably, after nearly a decade of unsustainable expansion in the housing and construction sectors in Spain, it resulted to enormous accumulation of private debt that generated significant economic imbalances, consequently driving the country into a deep recession, worse than that of 1975 and 1993.

Evolution of the Housing Bubble An Economic Perspective

In economics, a financial bubble occurs after a period of unsustainable and artificial growth in the price of an asset that creates a situation where the return of the overvalued asset fails to attract new investors resulting in a sudden and sharp drop in value. The development of the housing crisis in Spain grew in a similar fashion, fueled mostly by a sudden drop in interest rates upon the country’s entrance in the EMU, combined with financial deregulation, a rise in domestic incomes, and a drop in

Universidad Carlos III de Madrid 6

competitiveness (Euro Challenge, 2013). The burst of the housing bubble lead to what would be the worst recession in its economic history, more severe than that of U.S’.

Causes

As mentioned earlier, Spain’s adoption of the euro is often blamed for the recent recession. Becoming part of such a large union meant that the country was now bound by the same currency as the rest of its members, sharing the benefits of an integrated market, where default risks are spread amongst them. This gave each country access to credit amounts that were previously impossible to attain while sharing communal interest rates. This helps to explain why the benefits of being a member of the EMU outweigh the disadvantages, mainly a result of enhanced economic stability. Inevitably, Spanish households and enterprises seized the opportunity to borrow funds at the exceptionally low interest rates to finance their investments. The phenomenon was amplified as the country’s fiscal policy encouraged investments towards housing and construction developments. For almost ten years since 1999, Spain experienced enormous economic expansion, with a huge surge of employment levels ranging from 13 million in 1996, to 20 million by 2007. People quit their jobs and students dropped out of school to take part of the housing boom (Summers, 2012). Its success was not only seen in the private sector, but on the government level as well. By 2004, economic prosperity had also become evident through innovative infrastructure built across the country, notably upgraded highways and high-speed railway networks. Spain was becoming increasingly modernized with the development of new social infrastructures, including a more developed educational system, one of the best health care systems in Europe, and an enhanced consolidation of political organizations and institutions. The economy also became more open, better technologically equipped, with an abundance of internationally competitive financial and non-financial firms that were all well capitalized (Peñalosa, 2012).

Eventually, the over-specialization and unsustainable growth of construction and

housing sectors began unveiling imbalances2, slowly deteriorating the stability of the entire Spanish economy. For example, in 2006, there were 762,000 housing starts in Spain surpassing those of Germany, Italy, France, and the UK combined (Euro Challenge, 2012). What this meant for Spain is that it had exposed itself to excessive risk stemming from overreliance on investment making the entire economy vulnerable to shocks in the housing and construction sectors. For instance, by 2007 30.7% of its GDP stemmed from investment activities compared to the 20% Eurozone average. With the rise in housing prices over the course of the decade, Spaniards had become oblivious, believing house prices would continue to rise forever, consequently creating excessive demand despite the already strong supply of homes making their value triple by 2007. The seemingly massive increase in productivity over the decade eventually proved to be poor after all, given that it stemmed mostly from construction, which is characterized as low-skilled labor mostly in the form of fixed-term contracts (Laparra et al. 2012). In other words, there was little job security amongst Spaniards exposing the economy to another source of risk.

2 Economic imbalances occur when an economy relies excessively on certain sectors

Universidad Carlos III de Madrid 7

Another problem was that there was insufficient regulation that could have

minimized the impact of the shock when the crisis erupted. An example is the fact that “Cajas3 ” were able lend to everyone with flexible credit requirements, while the commercial banks began to slow down their lending when the bubble peaked in 2007. Finally, it was only a matter of time before Spain’s excessive imbalances would become problematic posing a threat to its economy. For most EU nations, many were suffering from excessive sovereign debt that threatened the financial stability of the euro. Like a domino effect, eventually Spain’s problems had surfaced as well, which unlike most distressed EU nations, Spain was faced with private debt problems rather than sovereign.

Consequences

Spain was on the headlines of news stations across the world when the financial crisis erupted in 2008. Having become such a large and important part of the European economy, there was panic in the markets stemming from concerns that Spain’s private debt may increase, leading to contagion4 that would threaten the entire EMU, and thus spread to the rest of the world. As mentioned earlier, Spain wasn’t struggling with sovereign debt like most countries during the outbreak of the crisis. In fact its public debt accounted for only 60% of its GDP, 25% lower than the Eurozone average. Its problem was private debt; with five times the debt growth from 2004 and onwards compared to most other countries, by 2008 it had reached 224% of its GDP. This was due to the excessive amounts of loans given to people and enterprises mostly for construction and real estate activities. Another reason why there was a lot of panic and pressure from the markets was due to the fact that 47% of Spanish debt was owned by foreign investors; an unusually high amount when compared to Italy, Japan, and Belgium’s debts that were mostly financed by domestic savings (Guillen, 2010).

This is where the complexities of markets comes in, given that everyone started becoming aware of what the potential effects of Spain’s housing bubble on its own economy and the rest of the world may be. Essentially, there was concern that if banks stopped lending, economic growth in Spain would come to a halt as its entire model was based on leveraged private investment. To make matters worse, the solvency of Spanish banks was threatened since many of them were at the verge of default. Banks were faced with massive liquidity5 problems that resulted from a large volume of people defaulting on their loans simultaneously. In addition, there was the concern that Spain’s private debt would turn in to sovereign eventually since the government would need to indebt itself to save its banking system from collapsing. Finally, another worry was that the drop in real estate and construction sectors would drive unemployment levels through the roof.

3 Cajas, also known as “Cajas de Ahorros” were Spain’s savings banks that were originally created to serve regional social and financial needs, however later evolved to becoming nationwide banks competing against traditional commercial banks. 4 A phenomenon where market disturbances in one place spread across sectors and other countries 5 Liquidity issues can appear in situations where financial institutions have insufficient funds to meet their short-term obligations, such as deposit withdrawals. This can occur from numerous loans defaulting at once rendering the bank at risk of being insolvent.

Universidad Carlos III de Madrid 8

It’s needless to say that concerns for Spain were serious as its position in 2008 looked frightening; and with the European market now so intertwined, a default in Spain’s economy would bankrupt other European nations that have served Spain’s borrowing needs over the years.

The Real-Estate Bubble

Ultimately, these concerns became reality by 2011. Although it is difficult to pinpoint what came first, there is a widespread agreement that the turning point for Spain was the burst its housing bubble. From that point on it became an exponentially growing downward spiral resulting from different sectors of the economy tumbling on one another. The burst of the bubble caused a halt in the housing sector due to an enormous drop in demand for homes. Simultaneously, as interest rates began to rise and 97% of Spanish mortgages being on variable rate contracts, it became increasingly hard for homeowners meet their loan payments, resulting to countless defaults and evictions (Fernández de Lis et al., 2013). In fact according to a report by “Save the Children Spain”, eviction rates had reached all time high with 82% of them being families with children; a shocking number when considering that there was more than 28% home vacancy (Sanchez, 2008). Some areas began to look like ghost towns; for example the Valdeluz development that was built for 30,000 people only had 700 people living in it in the midst of the crisis (Goldman and Lubin, 2011).

Employment Crisis

One of the most detrimental effects of the financial crisis was the record-breaking unemployment level that added enormous strain on the economy. Beginning of March 2008, unemployment levels doubled in the span of twelve months reaching a record-breaking four million people jobless (El Pais, 2009). By 2013, these levels peaked at 27%, with more than 50% jobless amongst people under the age of 25, excluding those pursuing studies (Ward, 2012). This was mainly a consequence of the burst of the housing bubble; the huge portion of construction jobs that were lost affected other construction-related industries, which further affected industries all over the country. Eventually the situation for Spaniards deteriorated driving many to flee the country in search for work elsewhere. In the 2012, the International Migration Outlook report by OECD found that emigration levels had officially surpassed immigration, making Spain a net emigrant country.

Political Perspective

Spain was caught in a downward spiral of debt problems, low productivity, and unemployment, which resulted to public mistrust in their political system. Although the public acknowledged that they were dealing with a multifaceted problem, politicians were often the ones blamed for the misfortunes of their economy. Particularly, they were outraged that regulators had not taken adequate measures to prevent the crisis from

Universidad Carlos III de Madrid 9

developing. Eventually, public reaction worsened when numerous corruption scandals and reckless spending cases were being discovered. By 2011, the situation had deteriorated further as unemployment rates had tripled and social welfare was continuously being deprived, creating a need for a radical change. As financial problems were developing, restructuring in Spain’s political framework was crucial for the sake of addressing economic issues that had surfaced from the housing bubble and imprudent political governing. This meant that social-democratic and conservative parties were faced with many political changes (Laparra et al., 2012). In essence, a clash had arisen from ultra right-wing parties promoting national economic protection with a strict stance against immigration and corruption, with left-wing parties and social movements that were opposing strict budgetary cuts, which were critical in remedying the economic crisis (Laparra et al., 2012). For example, socialist leader of the PSOE party, José Luis Rodriguez Zapatero, announced a government-spending cut of €15 billion in response to control financing costs in 2010 (Roberts, 2012). Nevertheless, the complexity of the situation called for early elections in November 2011, in which PSOE’s seven-year rule came to an end when center-right wing Mariano Rajoy from People’s Party (PP) took the place as prime minister. Following PP’s successful election, the party worked closely with European authorities to implement a financial restructuring program, predominately one that encompassed further budgetary cuts of €45 billion and new labor reforms (Roberts, 2012). These changes that were adopted in February 2012 encompassed making it easier and less costly to dismiss workers, including those in the public sector. In addition, they increased the legal retirement age from 65 to 67, and implemented many liberalization measures, such as, unrestricting store-opening hours by allowing businesses to choose freely (Powell, 2012). Essentially the goal was to prescribe an internal devaluation strategy that would promote exports and reduce imports, which would help the economy remain competitive. This is different from the conventional strategy, which involves a country devaluing its own currency to get the same effect. However this was no longer an option for Spain, as it no longer had control over its currency ever since its adoption of the euro. Instead, the objective was to stimulate growth by raising unemployment levels through labor reforms as a way to eventually reduce prices and wages, and thus making it more attractive to foreign markets.

It is also important to note that there was lot of history that unfolded in Spain’s politics at the time, given that beyond the housing and European debt crisis, a constitutional crisis nearly broke out as well. After the Franco regime in 1975, there was devolution of power from Madrid to some to regions like Basque and Catalonia. Those regions each struck their own deal, for example the Basque region got a better deal than the Catalonians in terms of getting control of their own financing. In 2013, a lot of tension manifested between the center and the regional governments about budgets; in fact the worst debt problems in Spain were not on the national level, but on a regional one (Jubak, 2013). So Catalonia, Valencia, and Andalusia requested financial assistance from the €23 billion bailout package the central government of Madrid had set aside. The reason this is important is because at the regional level, politicians were resisting to cut budget spending, which created problems for the central government to bail them out. In addition, regional governments were exploiting the situation by trying to devolve a little more. For instance, the Catalonian governments called snap elections in November 2013,

Universidad Carlos III de Madrid 10

which then turned in to a referendum on Catalan independence. The center government in Madrid made statements announcing its aversion to the situation. This situation put Spain in the risk of adding a constitutional crisis on top of its economic problems (Jubak, 2013).

Corruption

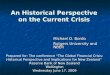

There were numerous corruption scandals at all levels of government that further eradicated public’s confidence in politics. For instance, in 2013, newspaper El Pais documented more than 800 corruption cases over the decade that led to over 2000 arrests (Gomez, 2013). A frequent pattern in these cases involved large companies channeling money to political parties in return for favorable permit grants, amplifying the housing boom even more. Other common cases included politicians exploiting the banking sector. For instance, savings bank CAM granted a loan of €200 million to the financially distressed Valencia government run by PP, just two days before it collapsed. This bank was also responsible for employing inexperienced board members including a supermarket cashier, a designer, and a college psychologist; all who took generous compensations, numerous trips, and discounted loans despite their little expertise and inability to perform tasks (Cardenas, 2013). Amongst other things, regional governments, savings banks, and construction developers had established a system where they each profited. For example, regional governments granted attractive zoning permits, developers would buy the land with loans from savings banks, while at the same time these banks were managed by local politicians and their friends (Lopez and Rodriguez, 2011). The most critical crucial effect of political corruption is however the loss of public confidence in its politics. In Figure 1 we see the sharp rise in public concerns for corruption and fraud by the year 2013, coming only second place after unemployment; a sign that the Spaniards had lost confidence in its politics.

Fig. 1. Main Concerns amongst the Spanish public between 2005 and 2013 (The Barcelona Centre for International Affairs Brief, 2013).

Universidad Carlos III de Madrid 11

Wasteful Government Spending Another strain on the economy was the uncontrolled budgetary spending that regional governments engaged in. It had become a vicious cycle, given that an economic model based on real estate and construction generated increased tax revenue, which then created incentives to promote investment forming a feedback loop. For Spanish authorities, this illusionary effect of increased tax revenue translated to more leeway for public expenditures. For example, some of the controversial projects included the countless construction of toll roads during the boom years. Eventually so many were built that Spain positioned itself in third place after U.S. and China for having the most toll roads in the world (Cardenas, 2013). Regional governments invested substantial amounts in airports as well. In fact, ever since the economic expansion, Spain had become the country with the most airports in Europe. Spain’s 49 airports seemed excessive when compared to UK’s, Italy’s, Germany’s, and France’s, who each only had 33, 31, 24, and 21 respectively; ironically Spain had the smallest population amongst these countries. To make matters worst, one airport became insolvent, and nine were unprofitable. Not only were some not generating revenue, but a government subsidy of €250 million had to be granted to airlines servicing routes to unprofitable airports in order to keep them solvent. Another case that describes the country’s political binge spending includes a subsidy made available by mayor, Maria Victoria Pinilla, to residents of a small town “La Muella” for vacation around 11 different destination including Brazil, Mexico, and the Caribbean beaches of Santo Domingo (Cardenas, 2013). Apart from intensifying the construction bubble, these spending cases were responsible for putting the entire economy in a deficit position, and for creating large amount of debt at the regional levels. Social Consequences

One of the most detrimental consequences of the crisis is the impact it had on people’s lives. At the forefront, the most prevailing suspects blamed were the politicians due to irresponsible governing, reckless spending, and corruption scandals mentioned above. Spaniards were also outraged for having to pay for banks’ irresponsible lending practices, as well as the enormous inflow of immigrants throughout the decade. Eventually this contributed to the emergence of populist, anti-immigrant, and anti-EU politics resulting to xenophobia, and discrimination (Laparra, Eransus and Lasheras, 2012). Emergence of Anti-Establishment Parties

The Spanish began directing their frustration towards their two-party system6, given that for a long time they had two prevailing parties dominating elections. Specifically, it was a common belief that the strong similarities between left-wing PSOE and right-wing PP’s had become a hindrance to Spain’s need for radical change. It became clear that Spain began moving away from this system when “Podemos” party came to rise in early 2014, gaining radical popularity in just months. Its creation can be traced back to social movements that took place in city squares around the country in 6 A two-party system is one where two political parties consistently dominate nearly all elections, resulting to almost all members of each party being part of the regime.

Universidad Carlos III de Madrid 12

2011. This anti-establishment party was the reason both majority parties lost five million votes combined; totaling to only 49% from a high of 81% of shared votes in 2009. The reason for such a surge in popularity is a result of the public’s loss of confidence in politics; as well the need for a more progressive-thinking party that contributes new ideas. For example, unlike other anti-establishment parties in the Eurozone, Podemos is not anti-EU. Instead, its policies stand for actions that address economic troubles, liberty and equality, as well as “green” initiatives such as: renewable energy, endorsement of public transport, and reduction of fuel consumption to name a few (Podemos, 2014).

Movimiento 15-M

An important day, the Spanish public protested against the problems the crisis had brought upon them was on May 15, 2011. Some dared to call it “the most interesting political development since the death of General Franco in 1975” (Beas, 2011); since its impact achieved in bringing over 300,000 people to city squares around 84 different Spanish cities. Even people from 50 foreign cities worldwide came out to support the revolution (Nieto, 2011). The initiative was held for people to publicly demonstrate their dissatisfaction against the severe austerity measures that were being imposed, the massive unemployment rates, including the unpopular two-party system, and the widespread political corruption (Glhermine, 2011). The credit for the initiation of the movement is due to online activists who created a platform on social networks five months prior. The platform became a tool to coordinate the entire revolution, which they called it the 15-M movement. It began on May 15, in Madrid’s central “Puerta del Sol”; some demonstrators decided to camp outside which signaled to the rest of the country the graveness of the situation. By the 18th of May, the situation gained national and international momentum in response to the police attempting to disperse campers from the center (Varsavsky, 2011). The protests lasted a week, up until elections took place on the 22nd of May with encouraging results. PP’s victory over the previously-ruling socialist party PSOE seemed to give hope to the people, particularly for those upset with PSOE’s poor handling of the recession coupled with the enormous unemployment levels. The election also demonstrated people’s loss of confidence in politics, since the amount of people that voted for alternative parties or no party at all grew by one million from the previous election (Varsavsky, 2011).

Another notable social consequence of the crisis is the growing appearance of an

underground economy in Spain. It seems that when people are under difficult circumstances, such as the deprived social welfare from lack of employment and increased austerity, they become more willing to engage in illegal activities to make ends meet. For example, according to a report at the end of 2012 by Spain’s ministry of finance, the underground economy soared to 24.6% of Spain’s GDP; up from 17.8% in 2008. Besides the record-breaking jobless numbers, the increase in personal income tax rates can be another explanation for the growing underground economy. As a measure to control its budget deficit, the Spanish government raised income tax to the highest rates in Europe, contributing to more incentives to work off the books (Mount, 2014). Corruption however also sometimes works like a self-fulfilling prophecy. For example, in 2014 the European Commission found that 95% of Spaniards believed that corruption

Universidad Carlos III de Madrid 13

was common and part of their everyday lives, just behind Italy and Greece at 97% and 99% respectively (European Commission, 2014). In other words, people had become more prone to engage in illicit activities justified by the perception that everyone else is corrupt as well.

Evolution of the Banking Crisis

Before unveiling the Spanish banking system’s role in the evolution of the financial crisis it is important to first understand its framework. Specifically, how savings banks, also known as “cajas de ahorros” have developed over time to become what they are today. They were historically associated with charitable organizations; a model influenced by Italy in the 15th century where the institutions would grant interest-free loans (Cardenas, 2013). Eventually, as this model seemed to be unsustainable due to its low profitability, they began to charge interest in 1836, which resulted to the creation of the first official savings bank two years later in Madrid. Ultimately the new savings bank and the original charitable institutions merged three decades later creating the “Caja de Ahorros y Montes de Piedad de Madrid”; a pioneer in the modern day Spanish savings bank system (Cardenas, 2013).

Unlike commercial banks whose sole objective is to maximize profits, savings banks on the other hand kept their core model they had adopted five centuries ago: to redistribute profits in to cultural and social projects; sometimes they even provided more funding than the government (Burgen, 2012). Another difference amongst the two was that savings banks also didn’t have shareholders, and neither were they publicly traded. Instead the institutions were governed with a board of directors, often made up of depositors, employees, politicians, and public founders. In fact, a significant portion of the board members was put in place by regional governments, making political ties with these institutions inheritably intertwined.

Historically these banks were very territorial by law; however this began to

change in 1977 when it was announced that savings banks would become liberalized. Despite their business model of servicing local communities’ social needs, these banks were also required to invest at least 60% of depositors’ money in public Spanish funds, including federal bonds. In return the state would provide support in situations where the banks are faced with financial difficulties, consequently establishing a partnership between political institutions and savings banks (Cardenas, 2013).

Eventually, following the liberalization, these banks began a period of

geographical expansion to neighboring provinces, until 1988 where barriers were completely stripped away across Europe; leading to an extraordinary expansion in savings banks throughout the country. A study looking at a period between 1992 and 2004, found that during that period savings banks expanded their branches by over 300% while commercial banks had actually contracted by 20% (Illueca, Norden and Udell, 2011). A possible explanation for the rapid growth was that savings banks were more closely involved with their territorial client base compared to traditional foreign commercial banks, which led them to become the preferred choice amongst Spaniards.

Universidad Carlos III de Madrid 14

Another study by the same researchers found that the rapid geographical expansions were linked with significant risk-taking behavior, and thus suggesting that savings banks had moved to more aggressive lending practices compared to their previous safe business model. For example, they discovered that these banks were lending excessively to housing and construction developments. The same study also revealed that regional governments who were board member of these banks promoted expansion to territories where the same party was governing. They concluded that these politically intertwined banks, which had politicians as board members in fact underperformed in terms of loan performance and profit generation, exposing them to high default risks (Illueca, Norden and Udell, 2011). This can be explained by the fact that politicians had little banking experience as well as the fact that their decision-making may have been in-line with political motives instead of bank solvency and profit generation. It was a dangerous phenomenon when considering that bank stability is so systemically important to the overall economy.

Eventually the repercussions of political entanglement with financial institutions

became clear as corruption scandals and wasteful government spending at the regional level surfaced. The 17 autonomous governments were €185 billion in debt by 2013, mainly a result of lavish spending in more roads and airports than any other nation in Europe, despite its lower population than the average in the Eurozone (Cardenas, 2013). The spending was financed by the nationwide 45 savings banks driving an almost nine-fold increase in debt in only eight years since the year 2000 (Mauldin, 2009).

Spain’s economic model based on property developments and construction was the root cause of the problem as in created enormous imbalances making Spanish banks, and the entire economy vulnerable to shocks in these sectors. Aside from savings banks engaging in over-extensive lending practices to the real estate sectors, these banks were often becoming direct owners of real estate developments firms as well. A study conducted by Ernst & Young in 2013 found that Spain was one of the countries with the most non-performing loans adding up to €190 billion. Banking Crisis Resolution

By 2009, the enormous amounts of non-performing loans created serious liquidity issues threatening their solvency. Premier Luis Rodriguez Zapatero, leader of the socialist PSOE party at the time, announced that they needed to implement a nationwide bank-restructuring program in order to safeguard from banks defaulting. They created a three-phase program that would help distressed banks merge with more stable ones as a way to pool resources, reduce costs, and remain competitive. They also created Fondo de Reestructaració Ordenada Bancaria (FROB); a government body that would act as bailout fund with €9 billion to help distressed banks. By 2011 they entered in the second phase, where they focused their energies on improving bank solvency. In this stage, FROB injected an additional €5.7 billion to four distressed banks, coupled with an industry wide

Universidad Carlos III de Madrid 15

increase in capital requirements7 (Fondo de Reestructuracion Ordenada Banacaria, 2014). In the final stage, their efforts were focused on further cleaning up toxic assets from the balance sheets of distressed banks. They also passed two new laws in 2012 that were intended to improve banking regulation in order to prevent this situation from happening again. The same year, the Spanish government reached out to the European Central Bank (ECB) in request for a loan of €100 billion to fix its internal problems and to further provide stability to its banking system. Some of the requirements of ECB included conducting ongoing stress tests on its banks, improving the regulatory framework, as well as increased transparency laws, and solidifying the independence of the Banco de España (Bank of Spain) (Fondo de Reestructuracion Ordenada Banacaria, 2014).

The restructuring of the Spain’s banking sector was so effective, that they

successfully reduced the amount of savings banks from 45 institutions to only two in the span of three years since 2010. For better or for worse, this doesn’t mean that the restructuring didn’t have its consequences. For instance, by 2013, there was a 22.7% reduction in offices and a 20.4% reduction in banking personnel, which deepened Spain’s unemployment issues (Cardenas, 2013). In addition there was a substantial reduction in social welfare programs in a time where they were needed the most. Finally, by consolidating the banking industry, they created fewer and larger institutions that were now considered “too big to fail8”, exposing the economy to a new source of risk.

Conclusion

In 2008, Spain underwent one of the deepest recessions in its history. From being an economy that stagnated for the most part of the 20th century, the country managed to catch up to European standards by becoming a more modernized economy; this happened particularly upon its transition to democracy after the Franco era and its entrance in the EU. Adopting the Euro was also a major turning point as it gave Spaniards access to large amounts of inexpensive credit.

This created an opportunity to build on economy founded on construction and real estate, as this would produce tax revenue, increase house prices, and most importantly, create jobs. Eventual, low borrowing costs coupled with government support for real estate investment created a huge demand for credit, both on a personal and corporate level, which led to nearly a decade of ample economic expansion which helped Spain reposition itself within the continent. The turning point for the Iberian economy was in September 2008, when the Lehman Brothers collapse was announced. A shockwave spreading across markets induced a global credit crunch9. A sudden halt in bank lending created a significant drop in real-estate demand driving prices to all-time lows. The

7 Capital requirement is a minimum amount of capital a bank must hold in order to buffer against financial shocks. Spanish banking regulators raised it form 8% to 9% as of January 1st, 2013 as a measure to ensure furthure stability in their financial institutions 8 “Too big to fail” is a situation where a financial institution becomes so large that it becomes a systemically important part of the economy. Consequently this creates a moral hazard problem where its implicit belief that governments will save them in the case of failures creates increased incentives for excess risk-taking. 9A sudden halt in bank lending

Universidad Carlos III de Madrid 16

raging fall in home prices meant that construction and other related industries were affected as well, eventually driving the economy in to recession.

Many were left jobless and felt like the politicians were the ones to blame. Over the years political actions have revealed to be more inline with real estate and construction activities, fuelling the bubble even more instead of taking measures to prevent it. Along with numerous corruption cases that were uncovered, politicians were also engaging in excessive public spending in unnecessary infrastructure, which at the time was justified by the artificial extra tax revenue that was generated mainly from private expenditures in real estate. At the same time, despite their lack of experience in the banking industry, politicians were also heavily involved in daily operations at financial institutions. This created moral hazard issues, as bank incentives became more aligned with political motives rather than profitability and soundness.

As Spanish banks were intertwined with politics and real estate, this inevitably produced a severe banking crisis as well. The excessive amount of loans given to real-estate developments exposed banks to significant risks related to that sector. In addition, Spanish savings banks, cajas de ahorros, were much less regulated than traditional commercial banks, which created moral hazard issues as they were able to grant loans and mortgages to individuals with flexible credit requirements. Consequently, an enormous strain was put on the banking system when many loans were defaulting at once. The banks’ collective distressed position eventually became a systemic issue threatening the entire economy. This led to massive restructuring programs aimed to merge small distressed banks with more stable ones as a way to pool their resources and reduce their costs. Eventually the Spanish government had to request additional financial assistance from the ECB, as it was no longer able to save its banking system on its own. Essentially this made Spain become a victim of sovereign debt along with its private debt problems.

The most detrimental effect of the crisis was on people’s lives. Many lost their

homes and jobs, and were affected by the severe austerity measures imposed by the government. The Spanish public’s outrage was seen in the streets of Madrid with the 15-M movement, which spread nationally and internationally within days. The collective desperation explains why there has also been a growing underground economy, putting the nation in third place after Greece and Italy’s levels of corruption.

Economies sometimes behave like ecosystems, where many organisms come

together to create a harmonious and balanced structure. This means that they’re complex by nature, and there’s never a one-sided story to how and why crises evolve since there’s usually a combination of factors contributing to their development. There’s also the irrational human behavior factor that leads to an unpredictable effect. For example, economic models seen in textbooks and applied to the real world can sometimes be oversimplified, in the sense that they are based on people being rational decision-makers. In other words, they assume that borrowers always borrow within their means, lenders always lend responsibly, and regulators (politicians) always act diligently and in good faith. However, time after time we’ve seen how this black and white approach doesn’t

Universidad Carlos III de Madrid 17

work, and perhaps we need to change our perspective to allow greater control of unforeseeable events.

Universidad Carlos III de Madrid 18

References Beas, Diego. How Spain's 15-M movement is redefining politics. 15 October 2011. 19

Decemeber 2014 <http://www.theguardian.com/commentisfree/2011/oct/15/spain-15-m-movement-activism>.

British Broadcasting Corporation . Spain profile. 14 October 2014. 19 December 2014 <http://www.bbc.com/news/world-europe-17941641>.

Burgen, Staphen. "Spanish culture industry becomes bank collapse casualty." 29 June 2012. The Guardian. 23 December 2014 <http://www.theguardian.com/world/2012/jun/29/spanish-culture-industry-bank-collapse-casualty>.

Caminal, Ramon, Jordi Gual and Xavier Vives. Competition in Spanish Banking . Working Paper. University of Navarra . Barcelona : IESE Business School , 1990.

Carballo-Cruz, Francisco. Causes and Consequences of the Spanish Economic Crisis: Why the Recovery is Taken so Long? . Research . University of Minho. Mingo: Panoeconomicus, 2011.

Cardenas, Amalia. The Spanish Savings Banks Crisis: History, Causes, and Responses . Working Paper. Barcelona: Internet Interdiscipliary Institute , 2013.

Centre D'éTudes Prospectives Et D'informations Internationales. "Lettre du CEPII." 316 (2011): 6.

Chislett, William. Is Spain different? The political, economic and social consequences of its crisis. 4 September 2014. 2 January 2015 <http://www.williamchislett.com/2014/09/is-spain-different-the-political-economic-and-social-consequences-of-its-crisis/>.

—. Spain: What Everyone Needs to Know . New York : Oxford University Press, 2013. El Pais. El paro supera los cuatro millones de personas por primera vez en la historia. 24

Apri 2009. 3 January 2014 <http://economia.elpais.com/economia/2009/04/24/actualidad/1240558374_850215.html>.

Euro Challange. "An Overview of Spain's Economy." Euro Challenge (2012): 2. Fernández de Lis, Santiago, et al. Some international trends in the regulation of mortgage

markets: Implications for Spain. Working Paper. BBVA Bank. Madrid: BBVA Research , 2013.

Fondo de Reestructuracion Ordenada Banacaria . Fund for Orderly Bank Restructuring . Report . Madrid: FROB, 2014.

Glhermine. Spain 2011. 23 May 2011. 22 December 2014 <https://welections.wordpress.com/2011/05/23/spain-2011/>.

Goldman, Leah and Gus Lubin. Amazing Satellite Images Of Spanish Ghost Towns -- Abandoned Since The Crash. 27 May 2011. 22 December 2014 <http://www.businessinsider.com/spain-ghost-towns-satellite-2011-4?op=1>.

Universidad Carlos III de Madrid 19

Gomez, Luis. La corrupción sumó 800 casos y casi 2.000 detenidos en una década. 17 June 2013. 8 January 2015 <http://politica.elpais.com/politica/2013/06/16/actualidad/1371400129_702560.html>.

Guillen, Mauro. The Pain in Spain: An Economy in Crisis Stephen Sherretta. 17 March 2010.

Illueca, Manuel, Lars Norden and Gregory F. Udell. Liberalization, Bank Governance, and Risk Taking . Working Paper. Chicago: Social Science Research Network , 2011.

Laparra, Miguel, et al. Crisis and Social Fracture in Europe: Causes and Effects in Spain. Vol. 35. Barcelona: "la Caixa" Welfare Projects, 2012.

Lopez, Isidro and Emmanuel Rodriguez. "The Spanish Model." June 2011. New Left Review . 2 January 2014 <http://newleftreview.org/II/69/isidro-lopez-emmanuel-rodriguez-the-spanish-model>.

Martín-Aceña, Pablo, Angeles Pons and Concepcion Betran. Financial Crises and Financial Reforms in Spain: What Have We Learned? Working Paper . Universidad Carlos III de Madrid . Madrid: Instituto Figuerola de Historia y Ciencias Sociales , 2010.

Mauldin, John. Spain: The Hole In Europe's Balance Sheet. Investors Insight. 31 August 2009 . 10 January 2015 <http://www.investorsinsight.com/blogs/john_mauldins_outside_the_box/archive/2009/08/31/spain-the-hole-in-europe-s-balance-sheet.aspx>.

Organization for Economic Co-Operation and Development. "International Migration Outlook 2012." Research. OECD, 2012.

Peñalosa, Eloísa Ortega and Juan. THE SPANISH ECONOMIC CRISIS: KEY FACTORS AND GROWTH CHALLENGES IN THE EURO AREA. Documentos Ocasionales. Banco de España. Madrid: Banco de España, 2012.

Podemos. Documento Final Del Programa Colaborativo . Madrid: Podemos , 2014. Powell, Charles. The pain in Spain: political, social and foreign policy implications of the

European economic crisis. 31 December 2012. 22 December 2014 <http://www.realinstitutoelcano.org/wps/portal/web/rielcano_en/contenido?WCM_GLOBAL_CONTEXT=/elcano/elcano_in/zonas_in/image+of+spain/powell_pain_spain_europe_trouble_oct12#.VLbKPou4lPN>.

Prados de la Escosura, Leandro, Teresa Sanches Daban and Jorge C. Sanz Oliva. Long-Run Economic Growth in Spain Since the Nineteenth Century: An International Perspective. Research. Universidad Carlos III de Madrid. Mdrid: Universidad Carlos III de Madrid, 1992.

Roberts, Martin. Debt crisis: where did it all go wrong in Spain? 24 July 2012. Telegraph Media Group Limited. 6 January 2014 <http://www.telegraph.co.uk/finance/financialcrisis/9423143/Debt-crisis-where-did-it-all-go-wrong-in-Spain.html>.

Universidad Carlos III de Madrid 20

Rojo, Luis Angel. "Spain's Membership of EMU: lessons for 2009." Spain and The Euro . Ed. Jaun F. Jimeno. Madrid: Banco de Espana, 2009. 290.

Sanchez, Carlos. Más de 900.000 viviendas construidas en los años del ‘boom’ inmobiliario están vacías. 28 August 2008. 5 January 2014 <http://www.elconfidencial.com/mercados/archivo/2008/08/28/noticias_50_900000_viviendas_construidas_inmobiliario_estan.html>.

Spanish Politics and the Euro Crisis. Perf. Jim Jubak. 2013. Spanish revolution-15M, "It´s time to fly". By Pablo Nieto. Dir. Pablo Nieto. Perf. David

Icke. 2011. Summers, Graham. The Secrets of the Spanish Banking System That 99% of Analysts

Fail to Grasp. Charlottesville: Phoenix Capital Research , 12 April 2012. The Barcelona Centre for International Affairs Brief. "The End of the Spanish Two-Party

System? Vote Drain and no one’s Gain." 10 July 2013. The Barcelona Centre for International Affairs. 22 December 2014 <http://www.cidob.org/en/publications/articulos/spain_in_focus/july_2013/the_end_of_the_spanish_two_party_system_vote_drain_and_no_one_s_gain>.

The European Debt Crisis Visualized . By Jonathan Jarvis & Cullen Daly. Dir. Jonathan Jarvis & Theo Alexopoulos. Perf. John Levoff. Prod. Cullen Daly, Chris Berend Heather Hartnett. Bloomberg, 2014.

Varsavsky, Martin. "Spanish Revolution" of 2011 Explained. 5 Mat 2011. 22 Decemeber 2014 <http://www.huffingtonpost.com/martin-varsavsky/spanish-revolution-of-201_b_867156.html>.

Ward, Clarissa. Desperation, anger grows for Spanish youth, with 51 percent unemployed . 7 June 2012. 3 January 2014 <http://www.cbsnews.com/news/desperation-anger-grows-for-spanish-youth-with-51-percent-unemployed/>.

-