Embed Size (px)

Citation preview

Approved For Release 2007/04/10: CIA-RDP83M00914R00270Director ofCentralIntelligence

JUtiUU22-

The Soviet Gas Pipelinein Perspective

Special National Intelligence Estimate

SNIE 3-11/2-8221 September 1982

Copy 01 0

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060R-r 6S.

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

SNIE 3-11/2-82

THE SOVIET GAS PIPELINEIN PERSPECTIVE

Information available as of 16 September 1982 wasused in the preparation of this Estimate.

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

THIS ESTIMATE IS ISSUED BY THE DIRECTOR OF CENTRALINTELLIGENCE.

THE NATIONAL FOREIGN INTELLIGENCE BOARD CONCURS.The following intelligence organizations participated in the preparation of theEstimate:

The Central Intelligence Agency, the Defense Intelligence Agency, the National SecurityAgency, and the intelligence organizations of the Departments of State, the Treasury, andEnergy.

Also Participating:The Assistant Chief of Staff for Intelligence, Department of the Army

The Director of Naval Intelligence, Department of the Navy

The Assistant Chief of Staff, Intelligence, Department of the Air Force

The Director of Intelligence, Headquarters, Marine Corps

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

'Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

CONTENTS

Page

SCOPE NOTE 1

KEY JUDGMENTS 3

DISCUSSION 9

1, THE SOVIET ECONOMY: THE TIME OF TROUBLES 9

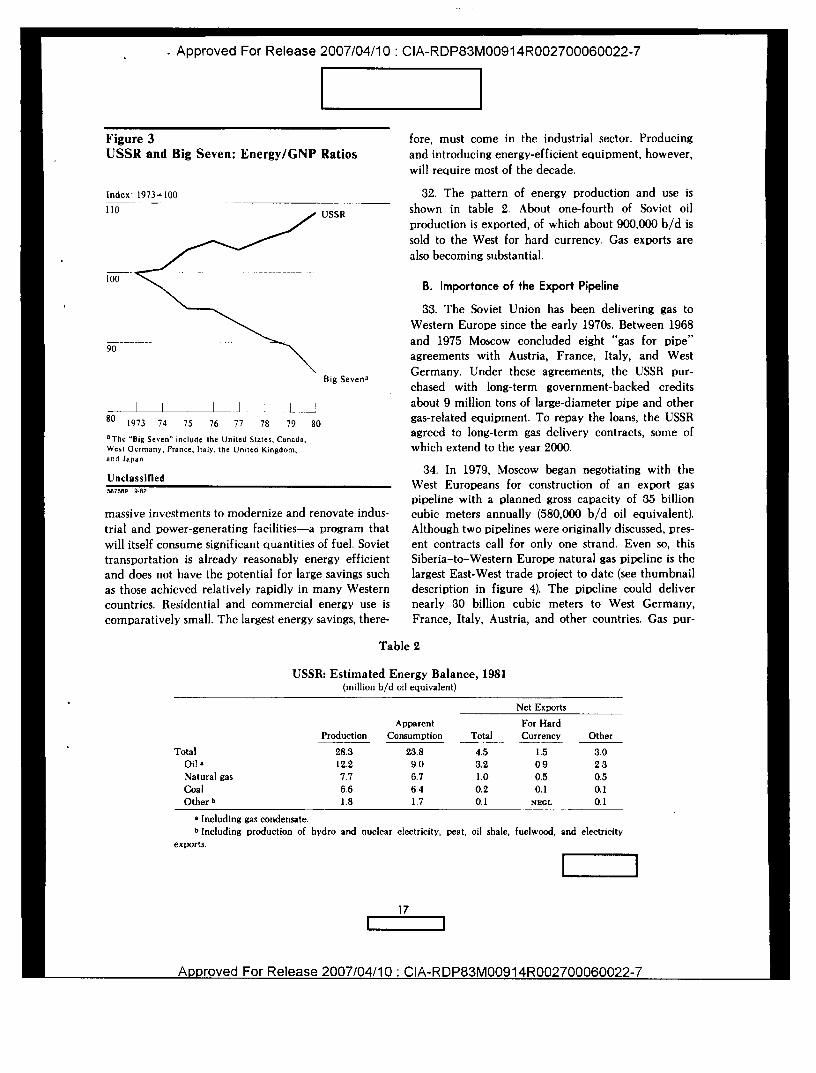

II. THE ROLE OF EAST-WEST TRADE 9A. East-West Economic Interaction 9B. Profile of Soviet Trade 9C. Soviet Gains From Trade 11D. Consequences for Soviet Military Power 11E. The Hard Currency Squeeze 13

III. OIL AND GAS: FUTURE KEY TO IMPORTS 16A. The Soviet Energy Problem 16B. Importance of the Export Pipeline 17C. Alternative Energy Sources 20D. Soviet Dependence on Western Oil Equipment 23

IV. OPPORTUNITIES FOR WESTERN GOVERNMENT POLICY 24A. Possible Restrictions 24B. Impact on the Gas Export Pipeline 24C. Impact on Oil Development 25D. Impact on Future Gas Export Deals 25E. Impact on the Soviet Economy and Military Capability 26

V. WEST EUROPEAN PERSPECTIVES 28A. Attitudes on East-West Trade and Trade Sanctions 28B. The Pipeline Deal in West European Eyes 28C. Possible Areas of Compromise 30

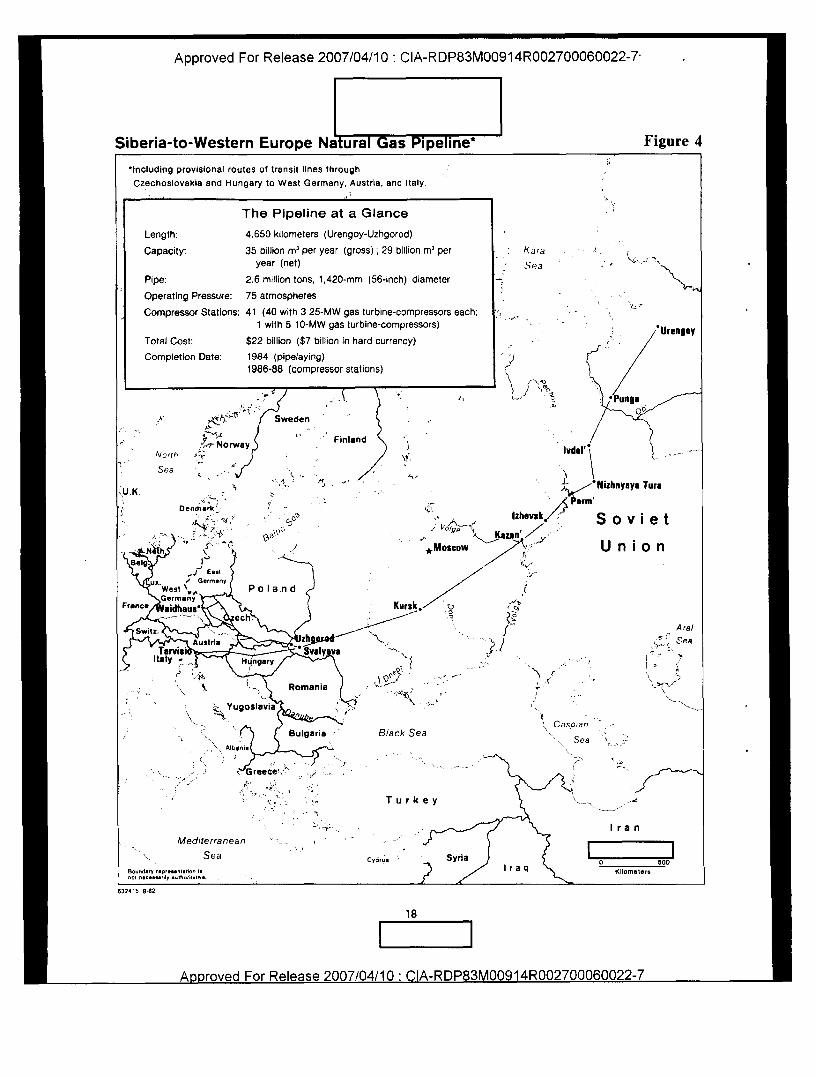

ANNEX: SOVIET DEPENDENCE ON US AND WESTERN OIL AND GASEQUIPMENT A-1

iii

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

i Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

SCOPE NOTE

This Special National Intelligence Estimate reviews the degree towhich Western trade, technology, and energy relationships have assist-ed—and can in the future assist—the USSR to increase its militarystrength and impose unwanted burdens on the Western nations. TheEstimate also assesses the potential impact on the USSR of the followingcourses of action:

— A strengthening of COCOM to assure that militarily sensitivetechnology is withheld from the Soviets.

— Avoidance of gas imports by the Europeans beyond the importsalready agreed to as part of the Soviet export pipeline project.

— An embargo on some energy equipment and technology.

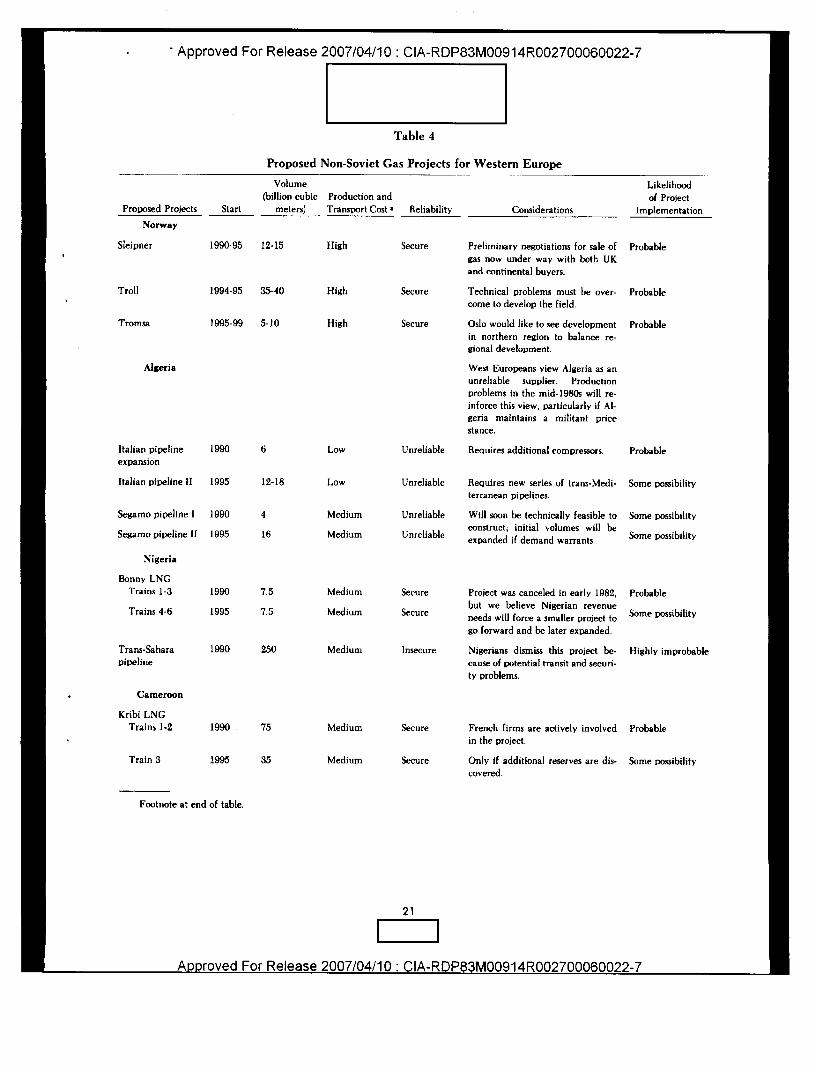

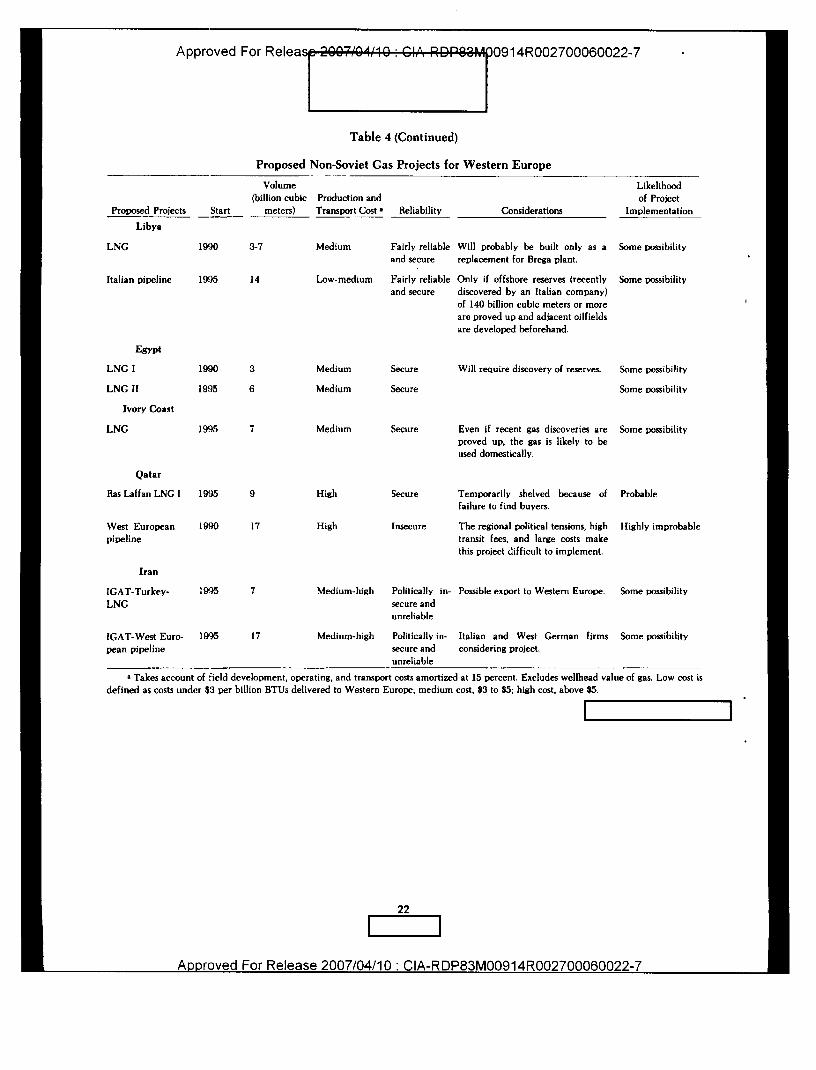

— An end to subsidized credits.

1

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

KEY JUDGMENTS

1. The USSR has used imports from the West to enhance itsmilitary capabilities:

— By obtaining goods and technology, legally and illegally, thatcontribute directly to the production and technical sophistica-tion of weapon systems.

— By expanding the base of industries of particular importance tomilitary production.

— And, more generally, by easing economic problems, therebyreducing the burden of defense.

2. The rapid increase in Soviet imports from the West in the 1970swas made possible by large windfall gains in export earnings due to thesurge in oil prices and the willingness of Western countries to providelarge credits, most of which were government guaranteed. The USSR isencountering growing economic difficulties, which will make it moredifficult for Moscow to increase its imports from the West in the future.The outlook for most Soviet exports, including oil, is not favorable, andWestern banks are unwilling to extend new long-term credits withoutgovernment guarantees.

3. Only the increase in gas exports through the Siberia-to-WesternEurope pipeline will prevent a marked decline in Soviet hard currencyimports in the 1980s. The USSR almost certainly will be able to meetscheduled deliveries of gas through the pipeline without diverting Sovietequipment from domestic uses. Enough equipment has already beendelivered, or soon will be, to enable the USSR to meet likely WestEuropean demand for gas until the late 1980s. By then, Moscow willprobably be able to produce enough modern turbines and compressorsto bring the line to full capacity, or will have found new sources ofequipment for any it may have lost as a result of US actions. Meetinggas delivery commitments and becoming self-sufficient in turbines andcompressors will impose costs on the Soviets in inefficiencies and shiftsin resources and effort.

4. While gas exports are the most promising future source of hardcurrency, oil exports still account for some 50 percent of Soviet exportearnings, and it is important for Moscow to minimize their future

3

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

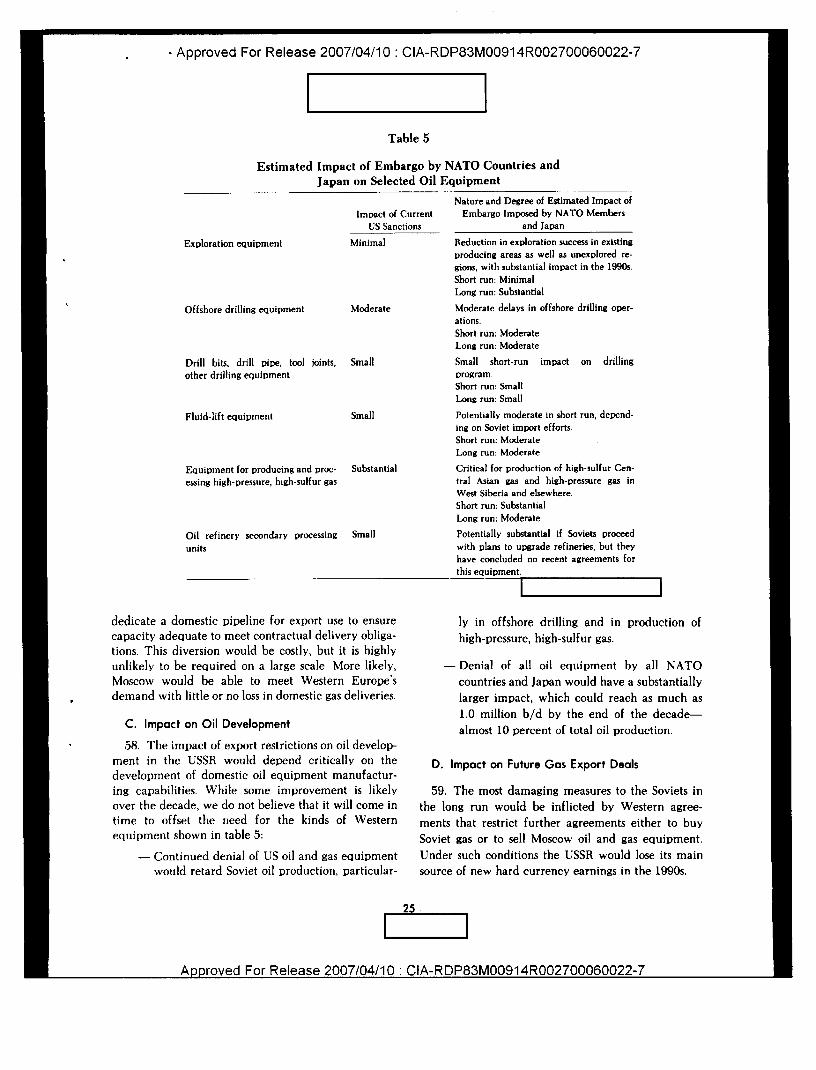

decline. The USSR depends on the West for specialized oil exploration,drilling, pumping, and processing equipment. As its deposits of high-quality, accessible oil are depleted, the Soviets are turning to moreremote oil and gas fields and more costly exploitation techniques. Butthey lag badly behind the West in the necessary technology. Withoutany access to Western equipment, the adverse impact on Soviet oilproduction could be as high as 10 percent of output by 1990.

5. Moscow's best hope of improving its strained hard currencyposit ion in the longer run is to secure the cooperation of WesternEurope in building large new pipelines for the delivery of additionalnatural gas in the late 1980s or in the 1990s, With enormous gas reservesand a powerful incentive to earn more hard currency , Moscow isprepared to sell as much gas as the West Europeans will accept. There ispotential uncovered gas demand in Western Europe to fill not only theSiberia–to–Western Europe pipeline now being built, but also a secondand third strand during the 1990s. Development of these large gasprojects currently requires Western pipe, equipment, and credit andmarkets as part of a package deal, although Soviet need for theseWestern products will diminish as Moscow develops its domestic gasequipment industry. Alternative sources of gas exist, notably in theNorwegian sector of the North Sea and in North Africa, although theyare in general relatively costly and some are considered insecure.

6. It will be difficult to enlist Allied cooperation in restrictingtrade with the USSR. Beyond economic incentives, there are politicalconsiderations that fuel the West Europeans' reluctance to acceptrestrictions on trade and credits to the USSR. These include:

— Their desire to restore the detente climate in Europe and toavoid exacerbating East-West strains.

— Their desire to maintain access to Eastern Europe.

— Their belief that economic and other ties with the USSR will in-fluence Soviet behavior.

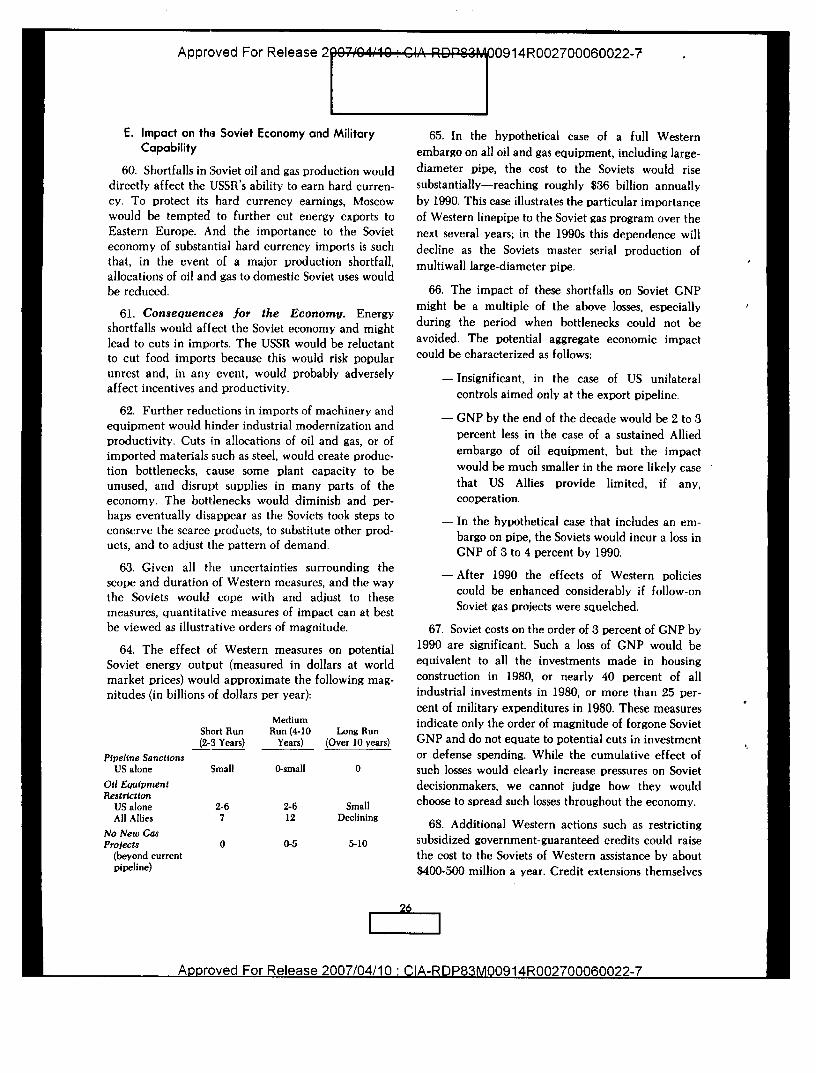

These political considerations, combined with the economic incentive,continue to limit West European cooperation with the United States inrestricting East-West trade.

7. The crux of the problem lies in developing with the WestEuropean countries a common understanding of the strategic implica-tions of East-West trade. Such an understanding has been notablyabsent, but the chances of achieving it may be better now that the WestEuropeans are becoming more aware of the issues and the depth of US

4

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

concern. Allied leaders have asserted that they will not conducteconomic warfare against the Soviet Union. But adequate analysis anddiscussion can lead to a common conclusion:

— That deficiencies in security policies among the Western Allieshave resulted in Soviet acquisition of militarily importanttechnology, financial subsidies, and, potentially, an importantrole in Western Europe's energy supply.

— That taking steps to withhold these benefits is merely prudentsecurity policy which Allies owe to each other, and can be seenas self-protection rather than economic warfare.

8. Accordingly, Western countries might be willing to cooperatein:

— Developing and implementing broader and tighter COCOMrestrictions.

— Agreeing to stricter limits on the terms and volume of govern-ment-supported credits.

— Developing other energy sources as an alternative to additionalSoviet pipelines.

9. Making Western military-related technology, subsidized credit,and locked-in gas markets available helps the Soviet military buildup.Western governments would then be under increased pressure to raisedefense costs, a move that requires heavy taxes, sometimes leads todeficit spending, and contributes to inflation and high interest rates.The United States is now committing some 6 percent of its economic ef-fort and the European Allies some 4 percent of theirs to defend againsta Soviet military threat that consumes 14 percent or more of their GNP.At the same time Western leaders are asking their citizens to carry aheavy defense burden they are pursuing policies that help the Sovietsmaintain a threat that adds to this burden.

10. This Estimate includes analysis of the potential impact ofWestern actions, including actions by Western Europe and Japan, onSoviet economic and military programs:

— The reduced availability of hard currency and energy wouldmake more difficult the decisions Moscow must make amongkey priorities in the 1980s—sustaining growth in militaryprograms, feeding the population, modernizing the civilianeconomy, supporting its East European clients, and expanding(or maintaining) its overseas involvements.

5

App roved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

While the cumulative impact of Western actions would clearlyincrease pressures on Soviet decisionmakers, we cannot judgehow they would choose to spread such losses throughout theeconomy.

— Because economic growth will be slow through the 1980s,annual additions to national output will be too small to simulta-neously meet the incremental demands that planners are plac-ing on the domestic economy. Even now, stagnation in theproduction of key industrial materials is retarding growth inmachinery output—the source of military hardware, investmentgoods, and consumer durables.

— Shortfalls in Soviet hard currency earnings due to Westernactions probably would force further cuts in imports of machin-ery and equipment. Moscow fears that reductions in foodimports would cause popular unrest and wants to avoid thebottlenecks that would be caused by cutting imports of industri-al materials, such as steel.

— In the longer term, cuts in machinery imports would retardprogress in modernizing a number of industrial sectors—steel,machine building, oil refining, robotics, microelectronics, trans-portation, and construction equipment—at a time when Mos-cow is counting on a strategy of limited investment growth andrelying instead on productivity growth.

— Placing controls on energy-related equipment and technologywould aggravate civilian industrial bottlenecks and, therefore,might cause civilian encroachment on defense production, suchas a reallocation of some military-oriented metallurgical andmachine-building facilities to produce the embargoed oil andgas equipment.

— The combination of enhanced COCOM controls and foreignexchange shortfalls would raise the cost of Soviet militarymodernization while at the same time weakening the industrialbase for military production.

11. The relative impact of Western economic measures on theUSSR can be estimated only as general orders of magnitude, as follows:

— Eschewing future gas projects—up to $10 billion a year in the1990s.

— Denying all oil equipment and technology—about $10 billion ayear for several years but then declining.

6

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

• Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

— Eliminating interest subsidies—less than $500 million a year.

In the long run, tighter COCOM restrictions on militarily sensitivetechnology (including technology and equipment that indirectly con-tributes to significant improvements in weapon systems) would perhapsbe the most valuable action for the West. Such action would retardmajor improvements in Soviet weaponry, which the West would beforced to counter. While the dollar value of such action is difficult to es-timate, the savings in terms of Western spending for defense annuallywould probably come to billions of dollars.

12. Moscow has the means to react to Western pressure by givingdefense needs an even greater priority than at present and by pursuinga more truculent foreign policy. The Soviets meet their fundamentalmilitary requirements from their own large industrial base. Militaryprograms, moreover, have great momentum and political support; theywould not easily be scaled back, although the rate of modernizationcould be slowed. Even so, Moscow could not escape the reality that itsbasic choices between military and economic programs would becomemore difficult, at a time when a change in leadership might also makethose choices less predictable.

7

I I

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

DISCUSSION

I. THE SOVIET ECONOMY:

THE TIME OF TROUBLES

1. The USSR is encountering increasingly severeand fundamental economic difficulties. Its rate ofeconomic growth has slowed to less than 2 percent andthe chances of any substantial improvement are slim.The causes of this slowdown are basically homegrown.Some of these—a drastic reduction in the growth ofpopulation of working age and the increasing diffi-culty of extracting and transporting energy and otherresources—were inevitable. Other causes of the slow-down, however, appear to have their roots in theSoviet bureaucratic, command-type system, whichseems to encounter great difficulty in coping with theincreasingly sophisticated problems of a modern econ-omy, and in the negative reaction of Soviet workers towhat they consider a weakening of their standard ofliving and inadequate rewards for hard work andinitiative within the system.

2. Although major systemic reforms could improveSoviet economic performance, at least in the longterm, none are in the offing because Soviet leaders andparty functionaries are unwilling to take any chanceswith an erosion of their political power and bureau-cratic control. Events in Poland have reinforced thisfear. Reform attempts have basically taken the form ofbureaucratic reorganizations that put new clothes onold problems. Any substantial political change afterBrezhnev is more likely to be in the direction oftightening controls and labor discipline than towardliberalization.

3. The slowdown in Soviet economic growth hasbeen characterized by a dramatic decline in theproductivity of investment and a much slower growthof labor productivity. Moreover, with some importantsectors and industries, notably steel and grain, actuallyexperiencing an absolute decline in output, majorshortages have developed. Given an unwillingness toundertake major economic reforms, the Soviet leader-ship has used imports from the West to ease itsproblems and will continue to do so.

II. THE ROLE OF EAST-WEST TRADE

A. East-West Economic Interaction

4. Throughout its history the USSR has exploitedeconomic interaction with the West both legally andillegally to expand its economic base, raise the techno-

logical level of its industry, relieve industrial bottle-necks, increase domestic food supplies, improve itsmilitary capability, and lessen the burden of defense.This exploitation reached its zenith in the 1970s asSoviet postwar productivity gains slowed and Moscowincreasingly turned to the West for equipment andtechnology to spur its industry, and for grain to offsetshortfalls in its inefficient farm sector. For its part, theWest encouraged expansion of East-West trade byloosening export controls and expanding the availabil-ity of credit, often at subsidized interest rates. More-over, the Soviets supplemented legal trade acquisitionsof Western goods with a well-organized and centrallydirected clandestine acquisitions program. The Sovietintelligence services and their East European surro-gates played a major role in acquiring US and otherWestern military technology, embargoed equipment,and manufacturing technology for Soviet military anddefense industrial needs.'

B. Profile of Soviet Trade

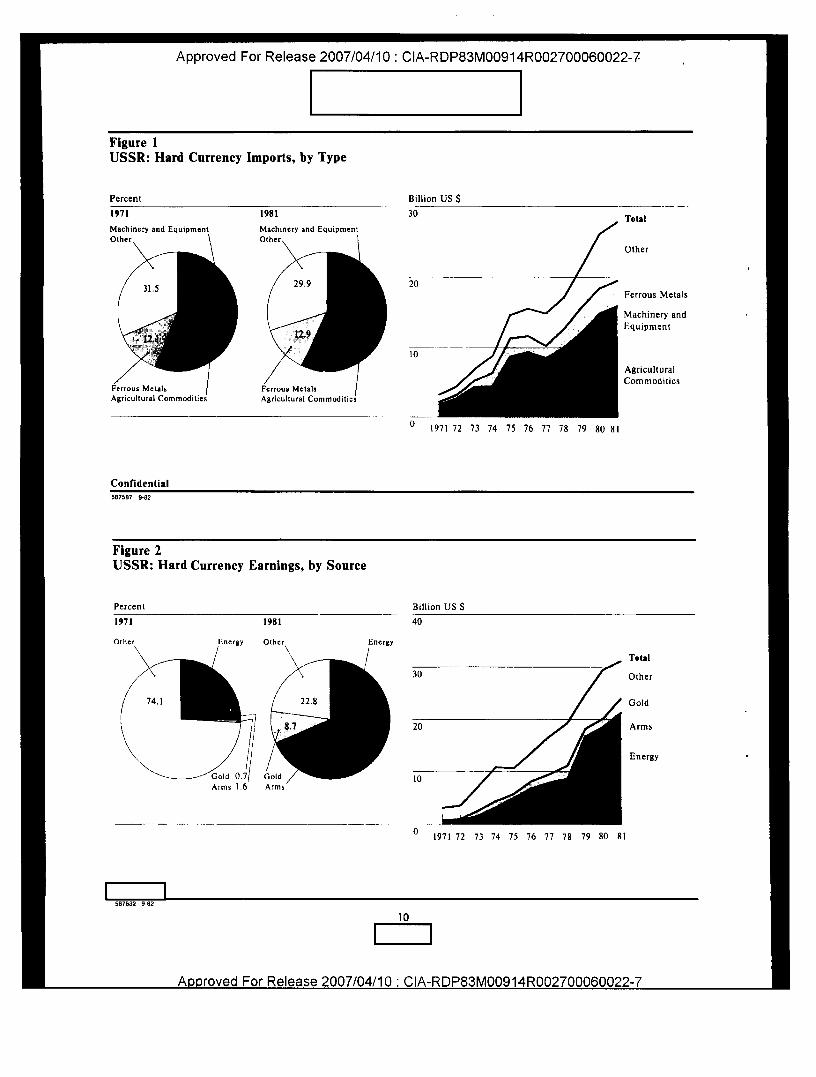

5. During the 1970s the value of Soviet hard cur-rency imports from the West increased more thanninefold in current prices (see figure 1) and more thantripled in constant prices. Although still small inrelation to gross national product (less than 4 to 5percent of GNP), Soviet hard currency imports—especially machinery, ferrous metals, and foodstuffs—have played a critical role in many high-priorityindustrial, agricultural, and military programs, includ-ing those for raising energy production and meat

' For a description of this activity and its contribution to Sovietacquisition of Western technology, see NI IIM 82-10006, TheTechnololy Acquisition Efforts of the Soviet Intelligence Services,June 198

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

10

Figure 1USSR: Hard Currency Imports, by Type

Percent

1971 1981

Machinery and EquipmentOther. OtherMachinery and Equipment

Billion US $

30

Ferrous Metals Ferrous MetalsAgricultural Commodities Agricultural Commodities

0 1971 72 73 74 75 76 77 78 79 80 81

Total

Other

Ferrous Metals

Machinery andEquipment

AgriculturalCommodities

Confidential587587 9-82

Figure 2USSR: Hard Currency Earnings, by Source

Percent Billion US $

1971

1981

40

587632 9-82

30

1971 72 73 74 75 76 77 78 79 80 81

10

Total

Other

Gold

Arms

Energy

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

• Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

consumption and improving missile performance.Moscow's ability to sustain growing imports of West-ern capital goods and foodstuffs was boosted sharplyby the runup in prices for oil and gold—two keysources of foreign exchange (see figure 2)—and aburgeoning market in the Third World for Sovietarms, the USSR's highest quality manufactu-ed goods.Spurred by overtures from Western businessmen hop-ing to sell equipment and technology from underuti-lized capital goods industries, Moscow successfullynegotiated a series of buyback deals with the West,involving purchases of Western plant and equipmentfinanced at favorable rates and long-term maturities.As payment for the equipment, Moscow was to sellraw materials and semimanufactures at prices thatgenerally reflected rising rates of inflation.

C. Soviet Gains From Trade

6. Imports from the West have contributed in anumber of important ways to Soviet economiccapabilities:2

— In the 1970s, imported chemical equipment,accounting for about one-third of all West-ern machinery purchased by the Soviets,was largely responsible for doubling theoutput of ammonia, nitrogen fertilizer, andplastics and for tripling synthetic fiberproduction.

— The Soviets could never have accomplishedtheir ambitious 15-year program of modern-ization and expansion in the motor vehicleindustry without Western help. The Fiat-equipped VAZ plant, for example, producedone-half of all Soviet passenger cars when itcame fully on stream in 1975; and the KamaRiver truck plant, which is based almostexclusively on Western equipment and tech-nology, now supplies nearly 50 percent ofSoviet output of heavy trucks.

— Grain imports have averaged about 25 mil-lion tons per year since 1975. Without West-ern grain, Soviet meat consumption wouldhave increased less in the early 1970s, and

2 For a more extensive survey of these gains, see CIA IntelligenceAssessment SOV 82-10012, Sopiet Ecoiwmic Dependence on theWest (A ppendix), January 1981 I

the fall in per capita consumption of meat inthe late 1970s would have been far worse.

— Large computer systems and minicomputersof Western origin have been imported inlarge numbers-1,300 systems since 1972—because they (a) have capabilities that theSoviets cannot match, (b) use complex soft-ware that the Soviets have not developed,and (c) often are backed up by experttraining and support that the Soviets cannotduplicate.

— Because of Soviet deficiencies in drill bits,pumps, and pipeline equipment, the USSRbought about $5 billion worth of oil and gasequipment alone in the 1970s, but thesepurchases have now largely ceased. Sub-mersible pumps purchased from the UnitedStates, for example, may have added asmuch as 2 million barrels a day of capacityto Soviet oil production in recent years.Similarly, the Soviet offshore explorationeffort would not be nearly as far along as itis without access to Western equipment andknow-how. Meanwhile, West Germany andJapan have provided most of the large-diameter pipe needed for gas pipelineconstruction.

D. Consequences for Soviet Military Power

7. Direct Benefits to Military Weapon Systems.Acquisition of goods and technology from the West,either by legal or illegal means, enhances Sovietmilitary programs in two principal ways: by makingavailable specific technologies that permit improve-ments in weapon and military support systems and theefficiency of military and civilian production technol-ogy and by providing economic gains from trade thatrelieve bottlenecks and improve the efficiency of theeconomy and thereby reduce the burden of defense.Soviet military power is based fundamentally on thelarge size and diversity of the Soviet economy and thebreadth of the Soviet technical and scientific base, onSoviet success in acquiring sophisticated technology inthe West, and on the longstanding preferred status ofthe military sector.

11

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

Approved For Release 914R002700060022-7

8. It has only been through an extraordinary alloca-tion of resources to defense that the Soviets haveattained their present military power. Soviet weaponsare designed to minimize the requirements for tech-nologies in which the USSR is deficient, but the Sovietshave turned to legal and illegal acquisitions of Westerntechnologies to make up for domestic shortcomings.

9. The Soviet armed forces are being modernized innearly every category of weapon system. Soviet mili-tary hardware, which was at one time distinguishedfor its rugged simplicity, has been qualitatively im-proved until it is in some instances the technologicalequal of—if not superior to—military hardware pro-duced in the West. Without Western technology,modernization and qualitative improvement of Sovietmilitary equipment would have proceeded at a slower

pace.

10. Through the acquisitions of Western technologyand hardware, the Soviets have been able to satisfycertain R&D and production objectives:

— The reduction of engineering risk by following orcopying proven Western designs.

— The reduction of R&D time by several yearsthrough the use of Western designs and technol-

ogy and equipment.

— The incorporation of countermeasures early inthe Soviet weapon development process.

In addition, the Soviets have been able to upgradecritical industrial sectors such as computers, microelec-tronics, and metallurgy, as well as to modernizeWarsaw Pact industrial manufacturing capabilities.This has also helped to limit the rise in military

production costs.

11. The Soviets commonly acquire even directlymilitary-related hardware under COCOM license, os-tensibly for commercial purposes. For example, ad-vanced acoustic signal analyzers, legally purchasedfrom Denmark in the middle 1970s, if used on theSoviets' own submarines, could significantly upgradetheir tactical passive sonar capability to detect andclassify Western submarines. In addition, two hugefloating drydocks purchased from the West for civilian

use have been diverted to strategic and tactical navalshipbuilding and repair.

12. Legal purchases of Western machinery, equip-ment, and manufacturing technologies have found awide range of applications in Soviet weapons produc-tion. (See inset below.)

Soviet Military Uses of Legal Imports

— US-origin gear-cutting machines were used toproduce military trucks, wheeled armored . vehi-cles, and components for missile transporters.

— Western gear-cutting machines were used in thedevelopment of the latest Soviet military heavy-lift helicopter, the MI-26.

— High-technology automatic lathes, milling ma-chines, and other machine tools from Sweden andWest Germany and two large rolling mills, oneJapanese and one West German, are probablyused in the construction of titanium hulls for theA-class nuclear attack submarine, the world'sfastest and deepest diving submarine.

— US-origin grinding machines were used in manu-facturing small, high-precision bearings suitablefor ballistic missile guidance operation.

— An electron beam drilling device of West Ger-man origin was used to improve the quality ofSoviet turbine blades.

— Austrian-origin hot and cold rotary forges (some26 in all) were used to produce artillery tubes andsmall-arms barrels.

— US blind riveting and French aerospace weldingtechnology equipment was used to produce ad-vanced Soviet interceptor aircraft.

— Western tungsten arc welders were used to fabri-cate armor plate for Soviet tanks.

— US technology acquired for the Cheboksary trac-tor plant was used to make a new 12-cylindertank engine.

13. The Soviets have historically relied on clandes-tine acquisitions of foreign technology to provide someof the most critical inputs needed in the developmentof their weapon systems. (See inset on next page.)Although they pay high premiums for illegal imports,the total value is small relative to total hard currencyimports of $30 billion.

12

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

• Approved For Release 2ee77,e47,1e-!-C-17k-FiePe3rviee91,1R002700060022-7

Soviet Military Uses of Illegal Imports

— Information on the US Redeye shoulder-firedsurface-to-air missile facilitated the developmentof the Soviet SA-7. During the prototype con-struction of the SA-7, bearings acquired fromJapan were used pending the subsequent develop-ment of indigenous bearings of suitable quality.

— In the mid-1960s the Soviets copied the TexasInstruments 7400 series monolithic integrated cir-cuit (IC) to produce the series 155 (Logika 2) ICThis IC was then used to develop the ES-1030computer, whose design and architecture werecopied from the IBM-360/40. The ES-1030 hasbeen used in a number of military applications.

— Materials acquired on the US TACAN navigationsystem were adapted for use in the MIG-25Foxbat navigation system.

Data acquired on the US C-5 transport haveapparently been used in the development of thenew AN-400 heavy transport under developmentat the Antonov Design Bureau in Kiev.

14. Other Benefits to Military Programs. West-ern technology and equipment also enable the Sovietsto improve industries that indirectly support weapondevelopments. Even though the defense industrialministries perform the bulk of weapons developmentand production, they rely on the nondefense industriesto supply specific products such as missile-handlingequipment, and to supply most of the basic tools ofweapons development and production—machinetools, sensors, and computer software. Because mostdefense industries also produce for the civilian econo-my, imports of Western machinery for the civiliansector also help to prevent greater encroachment ofcivilian requirements on defense production facilities.

15. Traditionally the Soviets have lagged behind theWest in their ability to produce modern electronicdevices—more so perhaps than in any other area ofmilitary technology. In particular, they have not beenable to produce the highly sophisticated precisionequipment they have needed in volume, and theirR&D methods are too ponderous and react too slowlyto stay current in a technology that moves withexpressway speed.

16. As a result, the Soviets undertook a major effortin the early 1970s to obtain Western equipment forthe manufacture of integrated circuits. They have now

acquired several hundred million dollars' worth ofmachinery that, if combined, would enable them toequip 16 to 20 medium-size production lines capableof producing advanced devices, including large-scaleintegrated circuitry with sufficient capacity to meetall current Soviet military requirements. This produc-tion base is known to be used to support developmentof military equipment such as strategic missiles, anti-ballistic missile systems, sensors and weapons for anti-submarine warfare, and computers for military appli-cations. It is also a key technological capability forcontinued advances in Soviet military electronics.

17. Western manufacturing technologies havehelped the USSR produce materials with critical mili-tary applications, especially in metallurgy. A US firmbuilt a turnkey plant to produce rock-drill bits thatincluded extensive tungsten-based powder metallurgytechnology. The US equipment and expertise providedhave enhanced the Soviets' ability to make the tung-sten powders needed to produce new and more lethaltungsten-alloy penetrators for their kinetic-energy,antitank projectiles. Sweden, Japan, and West Germa-ny also have sold the Soviets powder metallurgypressing technology similar to that used by Westernmanufacturers to make tungsten-alloy penetrators.The French firm Creusot-Loire is helping to build amassive steel plant in Novolipetsk, which will produceabout 7 million tons of specialty steel when operatingat full capacity in 1986. Much of the plant's outputwill be electroslag and vacuum-arc remelt steels of thekind used in submarine hulls, artillery tubes, and tankarmor.

E. The Hard Currency Squeeze

18. At a time when Soviet economic difficulties aregrowing, the USSR's hard currency earnings are de-clining. In the past few years, Moscow has used itshard currency earnings primarily to buy the goodsnecessary to cover major domestic shortages. As aresult of four bad grain crops in succession, foodimports have risen to about $12 billion, or about 40percent of total hard currency imports, reflecting thehigh priority the Soviet Government gives to at leastmaintaining supplies of major foods in the consumermarket. There has also been a large expansion of steelimports, especially large-diameter pipe and specialsteels, because the Soviet steel industry lacks the

13

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

diversity to support all the major Soviet economic andmilitary programs. These priority needs for hardcurrency imports have squeezed Soviet imports ofWestern machinery and equipment, which have fallenby about 40 percent in constant prices since 1977, withmost of the decline having occurred in the past twoyears.

19. During the past 18 months or so, the USSR hasexperienced a severe foreign exchange squeeze as aresult of a soft oil market, low prices for other Sovietexport commodities, and unexpected expenditures onimported grain and on aid to Poland. Although thecyclical causes of this deterioration are only tempo-rary, the longer term outlook for a rise in Soviet hardcurrency earnings in the 1980s is poor. Unlike the1970s, when enormous oil price increases financed thebulk of the threefold increase in the volume of Soviethard currency imports, the outlook for oil prices for atleast several years in the 1980s is for a decline in realterms, if not in nominal terms. At the same time, thevolume of Soviet oil exports is likely to be squeezed byat least slow growth in domestic consumption coupledwith stagnant or declining production. Market condi-tions for most other Soviet exports do not look verypromising either. In contrast to the 1970s, therefore,likely market conditions in the 1980s point to a declinein the purchasing power of Soviet hard currencyexports. (See inset below.)

Prospects for Major Hard Currency Exports

— The increase in gas exports now in train willessentially constitute an offset to the likely de-cline in oil exports.

— The dramatic decline of oil revenues of MiddleEast producers such as Libya makes it unlikelythat some major Soviet arms clients will be able tocontinue paying in hard currency.

— Exports of timber and wood products aresqueezed between rising domestic consumptionand the rising costs of exploiting timber in in-creasingly remote areas.

— Exports of minerals (platinum-group metals, nick-el, copper, aluminum, chromite, manganese, dia-monds, lead, and zinc) present a mixed picture—some trending up, others down.

Exports of Soviet manufacturers are not findingready acceptance in Western markets, and Mos-cow has not made the large investment requiredin quality control and marketing to make rapidprogress.

20. Role of Western Credit. Western credits to theUSSR, often government guaranteed, have been animportant factor in the rise in Soviet imports. Since theUSSR began large purchases of Western technology inthe early 1970s, Moscow has used official and official-ly backed credits to finance one-third of its imports ofplant, equipment, and large-diameter pipe from theWest. Annual Soviet drawings on government-backedcredits jumped from an average of $475 million in1971-73 to nearly $2 billion by 1975, but have held at$2.5 billion per year since 1978. The volume of newcommitments fell from a peak of nearly $4 billion in1975 to less than $2 billion by 1980, reflecting fallingSoviet orders for Western machinery and equipment.

21. The combination of rising debt service pay-ments and level drawings has steadily reduced the netresource inflow to the USSR on official credits from amaximum of $1.2 billion in 1976; by 1980-81 therewas a small net outflow from the USSR as debt serviceexceeded drawings.

22. Subsidized interest rates and lengthy maturitieson most government-backed credits have helped Mos-cow conserve some scarce hard currency. Interest ratesubsidies on new official loans reached a record levelin 1981—on the order of $300-400 million—as com-mercial rates in most Western countries averaged 5percentage points more than those charged on officialloans. Last October's increase in the OECD interestrate guidelines and a possible reclassification of theUSSR into the -rich country - category will reduce thesubsidy, but only slowly.

23. In 1977-80, contracts for sales of large-diameterpipe and chemical plants were the primary beneficia-ries of government-backed financing (see table 1). Pipecontracts backed by official financing totaled at least$2.5 billion, and approximately $300-500 million incontracts for other energy-related equipment alsoreceived official guarantees or credits. Officially guar-anteed credits covered $3 billion in contracts forcomplete plants; two-thirds of these commitmentswere for chemical plants, with the remainder goingmostly for steel mills ($170 million), aluminum plants($150 million), and factories for machinery and con-sumer goods ($690 million together). OECD datareport some $3 billion in official credit commitmentsfor machine tools and other plant and equipment in1977-80. Small amounts of credits have financed

14

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

• Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Table 1

Official Credit Commitments to the USSR in 1977-80, by Industrial Sector •(million US dollars)

Total CanadaWest

Germany France Italy bUnited

Kingdom Japan cTotal 8,992 208 2,673 2,683 775 728 1,450

Complete plants 2,993 718 1,184 423 300Steel 168 44 124Chemical 1,900 432 790 363 300Hydro and thermal power 44 37 7Wood, pulp, and paper 33Aluminum, copper, and zinc 162 162Other 686 205 101 60

Machinery and equipment 3,077 200 741 981 775 305Ships 32Telecommunications 87 87Road vehicles 2 2Oil and gas equipment 305 6 299Pipe 2,496 1,214 132 1,150

• Value of contracts supported by official credits with an original maturity of more than five yearsb presumably includes credits for pipe exports.

OECD reports for all countries except Ja pan. Data for Japan are based on announcements of credits backing specific contracts.

orders for telecommunications equipment, ships, andearthmoving vehicles.

24. France and Italy probably provide more thanhalf of the interest rate subsidies. In 1981, as a result ofthese subsidies, the Soviets saved an estimated $150million in interest payments to France and $110million in interest payments to Italy—or some 15 to 20percent of the value of the machinery exports of thesecountries to the USSR. If all official debt had beencontracted at commercial rates, the Soviets would havehad to pay $35 million more to the United Kingdomand perhaps $20 million more to Japan. Any WestGerman subsidy was undoubtedly quite small becauseonly 1 to 3 percent of exports to the USSR have beenfinanced through West Germany's AKA rediscountfacility. When the Soviets demand interest rates belowmarket levels on Hermes-guaranteed credits, the Ger-man exporter usually covers the financing cost bycharging higher prices. There is, however, an implicitsubsidy involved in providing government guaranteesfor private credits—namely, the interest premium theprivate lenders would require if there were noguarantee.

25. More recently, however, Moscow has had torecognize that it cannot count on a large increase in

Western credits to expand its hard currency imports.Although the Soviet hard currency position is stillrelatively strong (the debt service ratio is only about 17percent), the prospective stagnation in export volumemeans that any attempt to achieve a substantialincrease in imports would quickly push up hardcurrency debt to an unacceptable level. Indeed, alarge inflow of Western capital would be required justto maintain the current volume of imports, and thiswould result in a doubling of debt by 1985 and aquadrupling by 1990. The debt service ratio wouldapproach 30 percent by 1985—a level high enough tocause concern in financial circles—and reach danger-ous proportions (45 percent) by 1990.

26. Implications of Hard Currency Squeeze.Even a moderate fall in hard currency imports couldgreatly complicate Soviet economic problems andmake allocation decisions more painful. Large agricul-tural imports are essential to the growth of meatconsumption even in normal crop years. Expansion ofgas consumption and exports requires massive pur-chases of Western large-diameter pipe. Large importsof metals and chemicals are an integral part of Sovieteconomic plans. Orders of Western machinery andequipment have already been sharply curtailed; fur-

if=Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

ther cuts would certainly impinge on priority pro-grams in steel, transportation, agriculture, and heavymachine building.

III. OIL AND GAS:

FUTURE KEY TO IMPORTS

27. If Moscow is to avoid a severe squeeze on itshard currency import capacity, with painful repercus-sions in the economy, it must find new ways ofincreasing its exports to the West. This means develop-ing new capacity as well as finding new markets. Byfar the most promising potential for export expansionis in the massive resources of West Siberian naturalgas. Proved reserves of Siberian gas are ample to coverany likely increase in total energy consumption in theUSSR during the 1980s and 1990s as well as a largeexpansion in gas exports to the West. Although trans-port costs are high, production costs of Soviet gas arelow, and the USSR is willing to accept a low rate ofreturn on natural gas investment, making it likely thatSoviet gas can continue to be offered to WesternEurope at prices lower than those of most alternativesources. Moreover, while gas exports are the onlypromising future source of hard currency, oil exportsstill account for some 50 percent of Soviet exportearnings, and it is important for Moscow to minimizetheir future decline. An important factor affectingfuture oil production and exports will be the degree ofaccess to Western oil equipment and technology.

28. The dispute over the pipeline has occupiedmuch of the policy discussion of East-West interactionwithin the Western Alliance, partly because it involvesboth political and strategic considerations—US "politi-cal" export controls affect the pipeline, which theUnited States also opposes for "strategic" reasons.Some perspective on Soviet energy developments,problems, and prospects is necessary for an under-standing of the potential impact of Western actions.

A. The Soviet Energy Problem

29. Moscow is encountering rapidly rising costs inthe production and distribution of oil and coal:

— The USSR is running a race between decliningoil production in its older fields and increasingdevelopment of new ones. Requirements fordrilling and fluid lift are rising rapidly, andthe Soviets are moving to develop offshore

deposits and introduce more sophisticated re-covery techniques to prevent a decline in oiloutput.

— The coal industry is suffering from mine de-pletion, increasing mine depths, reduced seamthickness, and declining heat value per unit ofraw coal produced. Although the USSR pos-sesses enormous coal reserves in Siberia, theSoviets are ill prepared to exploit them—aresult of neglecting the coal industry since thelate 1960s, when Soviet policy put increasingemphasis on development of oil. Thus, devel-opment of coal deposits east of the Urals is nowconstrained by lack of progress on coal enrich-ment technology, unresolved technical prob-lems relating to transmission of electricity pro-duced at mine-mouth power stations, and lackof sufficiently developed transportation capac-ity in the east.

— By 1990, gas will be the largest single source ofSoviet energy, with production at roughly 700billion cubic meters—the equivalent of 11.6million barrels a day (b/d) of oil. Reaching thislevel, however, will be a costly undertakingbecause it will require large amounts of West-ern pipe and equipment. The Soviets arebuilding an unprecedented six major 56-inch(1,420-millimeter) trunklines from Siberia—each one a larger undertaking than the Alas-kan oil pipeline—even though labor andequipment are already stretched thin. Themassive outlays for pipeline construction, andprovision of needed infrastructure—such asroads, all-weather ports, and electric powerfacilities—will strain Soviet investmentresources.

30. In contrast to the West, the Soviet record onenergy consumption has been abysmal. Soviet energyconsumption has continued to grow more rapidly thangross national product (see figure 3). If the relationshipbetween energy consumption and GNP in the USSRhad followed the trend in the "Big Seven" since 1973,the USSR's annual consumption of energy would beroughly 5 million b/d oil equivalent lower than it wasin 1980.

31. A major reason why conservation gains aredifficult in the USSR is that most of them require

16

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

. Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

Figure 3USSR and Big Seven: Energy/GNP Ratios

Index: 1973=100110 USSR

Big Sevena

i i I 1 80 1973 74 75 76 77 78 79 80a The "Big Seven" include the United States, Canada,West Germany, France, Italy, the United Kingdom,and Japan.

Unclassified587589 9-82

massive investments to modernize and renovate indus-trial and power-generating facilities-a program thatwill itself consume significant quantities of fuel. Soviettransportation is already reasonably energy efficientand does not have the potential for large savings suchas those achieved relatively rapidly in many Westerncountries. Residential and commercial energy use iscomparatively small. The largest energy savings, there-

fore, must come in the industrial sector. Producingand introducing energy-efficient equipment, however,will require most of the decade.

32. The pattern of energy production and use isshown in table 2. About one-fourth of Soviet oilproduction is exported, of which about 900,000 b/d issold to the West for hard currency. Gas exports arealso becoming substantial.

B. Importance of the Export Pipeline

33. The Soviet Union has been delivering gas toWestern Europe since the early 1970s. Between 1968and 1975 Moscow concluded eight "gas for pipe"agreements with Austria, France, Italy, and WestGermany. Under these agreements, the USSR pur-chased with long-term government-backed creditsabout 9 million tons of large-diameter pipe and othergas-related equipment. To repay the loans, the USSRagreed to long-term gas delivery contracts, some ofwhich extend to the year 2000.

34. In 1979, Moscow began negotiating with theWest Europeans for construction of an export gaspipeline with a planned gross capacity of 35 billioncubic meters annually (580,000 b/d oil equivalent).Although two pipelines were originally discussed, pres-ent contracts call for only one strand. Even so, thisSiberia-to-Western Europe natural gas pipeline is thelargest East-West trade project to date (see thumbnaildescription in figure 4). The pipeline could delivernearly 30 billion cubic meters to West Germany,France, Italy, Austria, and other countries. Gas pur-

Table 2

USSR: Estimated Energy Balance, 1981(million b/d oil equivalent)

ProductionApparent

Consumption

Net Exports

TotalFor HardCurrency Other

Total 28.3 23.8 4.5 1.5 3.0Oil a 12.2 9.0 3.2 0.9 2.3Natural gas 7.7 6.7 1.0 0.5 0.5Coal 6.6 6.4 0.2 0.1 0.1Other b 1.8 1.7 0.1 NECL 0.1

a Including gas condensate.b Including production of hydro and nuclear electricity, peat, oil shale, fuelwood, and electricity

exports.

17

App roved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

The Pipeline at a Glance

Length: 4,650 kilometers (Urengoy-Uzhgorod)

Capacity: 35 billion m' per year (gross); 29 billion m' per

year (net)

Pipe: 2.6 million tons, 1,420-mm (56-inch) diameter

Operating Pressure: 75 atmospheres

Compressor Stations: 41 (40 with 3 25-MW gas turbine-compressors each;1 with 5 10-MW gas turbine-compressors)

Total Cost:

$22 billion ($7 billion in hard currency)

Completion Date: 1984 (pipelaying)1986-88 (compressor stations)

Siberia-to-Western Europe Natural as Pipeline*

*Including provisional routes of transit lines throughCzechoslovakia and Hungary to West Germany, Austria, and Italy.

Figure 4

KaraSea

•Urengoy

•Punga

Finland

4"--, •DenMarki

EastGermany

WestGermanyaidhaus•

Nun,:

Sea

si-Norway

A._lzhevsk.

*Moscow

\

• Nizhrwaya Tura

WT.

Soviet

Union

Aral

Sea

Caspian

Sea

Iran

Sweden

SyriaIraq

0 500Kilometers

MediterraneanSea

Boundary repres4nlation itflat nee aaaaa p ly 1.Mo/it...P.c.

532415 8-82

18

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7.

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

• Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

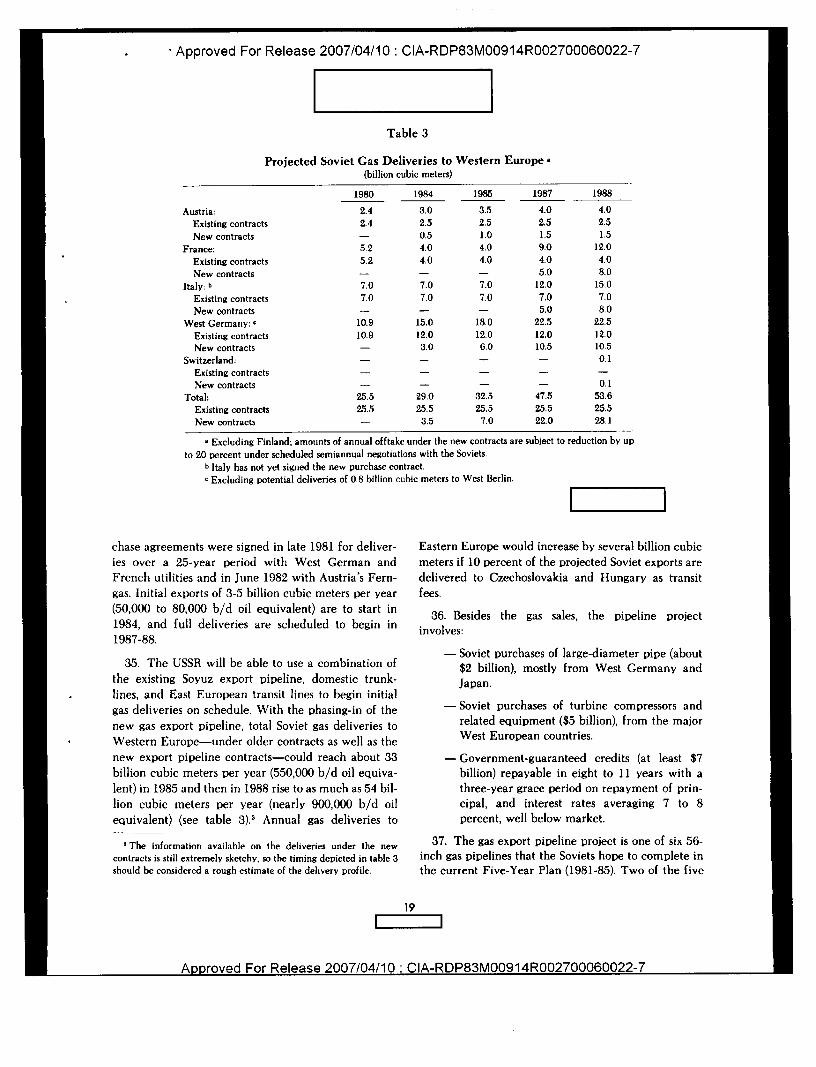

Table 3

Projected Soviet Gas Deliveries to Western Europe •(billion cubic meters)

1980 1984 1985 1987 1988

Austria: 2.4 3.0 3.5 4.0 4.0Existing contracts 2.4 2.5 2.5 2.5 2.5New contracts 0.5 1.0 1.5 1.5

France: 5.2 4.0 4.0 9.0 12.0Existing contracts 5.2 4.0 4.0 4.0 4.0New contracts 5.0 8.0

Italy : b 7.0 7.0 7.0 12.0 15.0Existing contracts 7.0 7.0 7.0 7.0 7.0New contracts 5.0 8.0

West Germany : c 10.9 15.0 18.0 22.5 22.5Existing contracts 10.9 12.0 12.0 12.0 12.0New contracts 3.0 6.0 10.5 10.5

Switzerland: 0.1Existing contractsNew contracts 0.1

Total: 25.5 29.0 32.5 47.5 53.6Existing contracts 25.5 25.5 25.5 25.5 25.5New contracts 3.5 7.0 22.0 28 1

• Excluding Finland; amounts of annual offtake under the new contracts are subject to reduction by upto 20 percent under scheduled semiannual negotiations with the Soviets.

b Italy has not yet signed the new purchase contract.c Excluding potential deliveries of 0.8 billion cubic meters to West Berlin.

chase agreements were signed in late 1981 for deliver-ies over a 25-year period with West German andFrench utilities and in June 1982 with Austria's Fern-gas. Initial exports of 3-5 billion cubic meters per year(50,000 to 80,000 b/d oil equivalent) are to start in1984, and full deliveries are scheduled to begin in1987-88.

35. The USSR will be able to use a combination ofthe existing Soyuz export pipeline, domestic trunk-lines, and East European transit lines to begin initialgas deliveries on schedule. With the phasing-in of thenew gas export pipeline, total Soviet gas deliveries toWestern Europe-under older contracts as well as thenew export pipeline contracts-could reach about 33billion cubic meters per year (550,000 b/d oil equiva-lent) in 1985 and then in 1988 rise to as much as 54 bil-lion cubic meters per year (nearly 900,000 b/d oilequivalent) (see table 3). 3 Annual gas deliveries to

3 The information available on the deliveries under the newcontracts is still extremel y sketch y, so the timing depicted in table 3should be considered a rough estimate of the delivery profile.

Eastern Europe would increase by several billion cubicmeters if 10 percent of the projected Soviet exports aredelivered to Czechoslovakia and Hungary as transitfees.

36. Besides the gas sales, the pipeline projectinvolves:

- Soviet purchases of large-diameter pipe (about$2 billion), mostly from West Germany andJapan.

- Soviet purchases of turbine compressors andrelated equipment ($5 billion), from the majorWest European countries.

- Government-guaranteed credits (at least $7billion) repayable in eight to 11 years with athree-year grace period on repayment of prin-cipal, and interest rates averaging 7 to 8percent, well below market.

37. The gas export pipeline project is one of six 56-inch gas pipelines that the Soviets hope to complete inthe current Five-Year Plan (1981-85). Two of the five

19

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

domestic lines have already been laid. In addition tothe export pipeline, Moscow hopes to lay by 1985three more lines from the Urengoy gasfield to theEuropean USSR, each 3,000 to 4,000 kilometers long.The six new trunklines from West Siberia account forroughly half of the total of 48,000 kilometers of gaspipelines planned for construction in 1981-85.

38. If the Soviets believe they cannot count onWestern imports a pipe and compressors, they willdevelop their own capability more rapidly. Certainlyby the 1990s they would be able to produce enough16- or 25-megawatt turbines to move gas through long-distance pipelines, such as the export line currentlybeing built. The Soviets would prefer to continue toimport some of this equipment from the West, howev-er, because it can be paid for with gas exports and itmaintains the commercial ties between Western Eu-rope and the USSR.

39. Because of the weak export prospects outlinedabove, the pipeline is vital to Moscow's prospects forearning sufficient hard currency beyond the mid-1980s to avoid a major drop in its import capacity.Annual revenues from the pipeline deal alone shouldreach $51/2 billion (:.n 1981 dollars) in the early 1990swhen all credits are repaid, and total gas earnings(including existing contracts) could be roughly $101/2billion.

40. The USSR also calculates that the increasedfuture dependence of the West Europeans on Sovietgas deliveries will make them more vulnerable toSoviet coercion and will become a permanent factor intheir decisionmaking on East-West issues. The Soviets,moreover, have used the pipeline issue to create andexploit divisions between Western Europe and theUnited States. In the past, the Soviets have used WestEuropean interest in expanding East-West commerceto undercut US sanctions, and they believe successfulpipeline deals will reduce European willingness tosupport future US economic actions against the USSR.

41. Follow-On Gas Projects. The factors that ledthe Soviets to conclude the recent Siberia–to–WesternEurope gas deal—huge gas reserves and continuedneed for hard currency earnings—almost certainlywill lead to a proposal for new export contracts thatwill require additional export pipelines. If a secondstrand of the new export pipeline were built, Soviet

revenues from gas sales would rise in the 1990s tomore than $15 billion per year (1981 prices). Sovietbehavior in negotiating the first contracts suggests thatadditional gas supplies would be offered at a baseprice near the low end of the market. By accepting arelatively low price initially, the Soviets would be ableto increase their market penetration and still securehard currency earnings.

42. Indeed, potential demand in Western Europecould support purchases of at least an additional 60billion cubic meters (about 1 million b/d oil equiva-lent) of Soviet gas by the year 2000—enough for twoadditional pipelines of the magnitude of the one nowbeing built. This potential will be realized, of course,only if alternative new sources of gas for WesternEurope are not developed.4

C. Alternative Energy Sources

43. The development of such alternative Westernenergy sources—particularly the large gas resources ofthe North Sea—will take too long to have much effecton the West European demand for Soviet gas in the1980s but could determine whether Western Europeseeks additional Soviet gas in the 1990s. At best, anadditional 9-15 billion cubic meters of new suppliescould be delivered by 1990 through increased Dutchand Norwegian production; estimated Norwegian gasreserves are by themselves sufficient to permit a largeexpansion of production in the 1990s. Several Africanand Middle Eastern countries also have the potentialto increase gas exports during the 1990s.

44. Continental gas import requirements are ex-pected to increase by about 70-80 billion cubic metersin the 1990s as demand grows and domestic produc-tion declines. Under favorable circumstances, NorthSea and Dutch gas could meet about 80 percent ofthese requirements, or about 60 billion cubic meters.North African gas could provide about 45-60 billioncubic meters. Supplies from the Middle East andNorth Africa would be substantially less secure fromdisruption than would gas from West Europeansources. Moreover, the likely investment costs of devel-oping and transporting this gas would be extremelyhigh. (See table 4.)

'See SNIE 3/11-82, Western Alternatives to Soviet Natural Gas:Prospects and Implications, 28 May 1981

20

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Likelihoodof Project

Considerations

Implementation

Preliminary negotiations for sale ofgas now under way with both UKand continental buyers.

Technical problems must be over-come to develop the field.

Oslo would like to see developmentin northern region to balance re-gional development.

Probable

Probable

Probable

West Europeans view Algeria as anunreliable supplier. Productionproblems in the mid-1980s will re-inforce this view, particularly if Al-geria maintains a militant pricestance.

Requires additional compressors. Probable

Requires new series of trans-Medi- Some possibilityterranean pipelines.

Will soon be technically feasible toconstruct; initial volumes will beexpanded if demand warrants.

Some possibility

Some possibility

Project was canceled in early 1982, Probablebut we believe Nigerian revenueneeds will force a smaller project togo forward and be later expanded.

Nigerians dismiss this project be- Highly improbablecause of potential transit and securi-ty problems.

Some possibility

French firms are actively involved Probablein the project.

Only if additional reserves are dis- Some possibilitycovered

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Table 4

Proposed Non-Soviet Gas Projects for Western Europe

Volume(billion cubic Production and

Proposed Projects Start meters) Transport Cost a Reliability

Norway

Sleipner 1990-95 12-15 High Secure

Troll 1994-95 35-40 High Secure

Tromsa 1995-99 5-10 High Secure

Algeria

Italian pipelineexpansion

1990 6 Low Unreliable

Italian pipeline II 1995 12-18 Low Unreliable

Segamo pipeline I 1990 4 Medium Unreliable

Segamo pipeline II 1995 16 Medium Unreliable

Nigeria

Bonny LNGTrains 1-3 1990 7.5 Medium Secure

Trains 4-6 1995 7.5 Medium Secure

Trans-Saharapipeline

1990 250 Medium Insecure

Cameroon

Kribi LNGTrains 1-2 1990 75 Medium Secure

Train 3 1995 35 Medium Secure

Footnote at end of table.

21

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Approved For Releas 0914R002700060022-7

Table 4 (Continued)

Proposed Non-Soviet Gas Projects for Western Europe

Likelihoodof Project

ReliabilityConsiderations Implementation

Fairly reliable Will probably be built only as a Some possibilityand secure replacement for Brega plant.

Fairly reliable Onl y if offshore reserves (recently Some possibilityand secure discovered by an Italian company)

of 140 billion cubic meters or moreare proved up and adjacent oilfieldsare developed beforehand.

Secure Will require discovery of reserves. Some possibility

Secure Some possibility

Secure Even if recent gas discoveries are Some possibilityproved up, the gas is likely to beused domestically.

Secure Temporarily shelved because of Probablefailure to find buyers.

Insecure The regional political tensions, high Highly improbabletransit fees, and large costs makethis project difficult to implement.

Politically in- Possible export to Western Europe. Some possibilitysecure andunreliable

Politically in- Italian and West German firms Some possibilitysecure and considering project.unreliable

• Takes account of field develo pment, operating, and transport costs amortized at 15 percent. Excludes wellhead value of gas. Low cost isdefined as costs under $3 per billion BTUs delivered to Western Europe; medium cost, $3 to $5; high cost, above $5.

Proposed Projects Start

Volume(billion cubic Production and

meters) Transport Cost •

Libya

LNG 1990 3-7 Medium

Italian pipeline 1995 14 Low-medium

Egypt

LNG 1 1990 3 Medium

LNG II 1995 6 Medium

Ivory Coast

LNG 1995 7 Medium

Qatar

Ras Laffan LNG I 1995 9 High

West Europeanpipeline

1990 17 High

Iran

IGAT-Turkey- 1995 7 Medium-highLNG

IGAT-West Euro- 1995 17 Medium-highDean pipeline

22

I I

App roved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

45. Multinational cooperation will be critical ifsizable new volumes of North Sea gas are to bebrought to the Continent by the early 1990s. Projectsto boost North Sea gas exports will require enormouscapital investments—$15-20 billion may be needed todevelop Norway's Troll gasfield alone—and will haveto compete with other North Sea oil and gas projectsfor a share of the development funds to be spentduring the next decade. Interest rate subsidies similarto those offered for the construction of the Sovietpipeline could substantially speed development ofNorth Sea gas reserves; an interest rate subsidy ofabout 2 percentage points could cut 15 percent fromtotal investment costs.

46. Cooperative agreements to transport gas to themarketplace will be equally important. A gas swapagreement, for example, would involve increased Nor-wegian gas deliveries to the United Kingdom inexchange for delivery of equal volumes of British gasto the European Continent. This could save $1-2billion in facilities investments and could shortenleadtimes by two to three years. Similarly, Dutchparticipation in a coordinated gas marketing strategycould vastly simplify Norway's efforts to increasefuture gas sales.

47. Although the commercial advantages of sucharrangements are sizable, numerous political obstaclesmust still be overcome, including Norwegian reluc-tance to become overly dependent on hydrocarbondevelopment. Other critical factors determining thetiming and size of new North Sea projects include:

— Tax policies. The current UK tax regime is aserious deterrent to the development of smallfields. Norway's petroleum taxes are also high,and development has been slowed further byshort drilling seasons and generally cautiousgovernment policies.

Market prospects. An unprecedented declinein West European gas consumption during thelast two years has clouded the outlook for thefuture size of the European gas market. Pres-ent uncertainties could cause North Sea pro-ducers to hesitate before launching new proj-ects, especially in view of the possibility ofbeing undercut by cheaper Soviet gas.

— Revenue needs of producing countries. Ifthe budget crisis in the Netherlands worsens,

pressures to increase gas sales will increase.Similarly, Norway may be inclined to speedgas development because of lowered expecta-tions of future oil revenues.

D. Soviet Dependence on Western Oil Equipment

48. The USSR faces increasing dependence on theWest in developing and processing its oil resources inthe 1980s. The Soviets already have drilled most of therelatively shallow, easily located, accessible oil depos-its. They specifically need Western seismic and well-logging technology to bolster their ability to explorefor oil reserves in the 1980s (see annex). The Sovietsplan to nearly double the amount of drilling for oiland gas in 1981-85 and to increase it further in the late1980s, but their drilling productivity is poor by inter-national standards. Thus, Western rigs, drill pipe, tooljoints, drill bits, blowout preventers, and drilling-fluidtechnology could substantially aid Soviet drillingefforts.

49. The Soviet oil industry faces rising fluid-liftrequirements in the 1980s, as the amount of waterproduced along with oil increases. According to Sovietplans, a large additional volume of fluid—well over 6million barrels a day—must be lifted in 1985 simply tomaintain production of oil at the 1980 level of 12million b/d. To handle the high volume of fluid, theSoviets plan to double the number of wells producingoil with the help of submersible pumps and gas-liftequipment. Imported equipment could boost the pro-ductivity of this effort because the capacity andquality of Soviet-made submersible pumps and gas-liftequipment are low.

50. The Soviets' least explored prospective areas fornew petroleum discoveries are offshore, and explora-tion and development of the continental shelf willcontribute to their oil production in the 1990s. TheUSSR already has received substantial assistance fromthe West, and continued assistance could speed devel-opment in the Caspian Sea and Arctic areas.

51. The United States is the preferred supplier ofmost types of oil and gas equipment throughout theworld because it is by far the largest producer, withthe most experience, the best support network, andoften the best technology. In some products—forexample, large-capacity down-hole pumps—the UnitedStates has a world monopoly. The position of most

23

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Approved For Release ?007/O1/10: CIA mrsam000i 1 002700060022-7r

US suppliers in the changing world market has beenpreserved by establishing overseas subsidiary firmsand licensees during the past decade. These offshoreoperations deterred new competition from "wedgingin'' to overcrowded markets. Up to now, the learningcurve for new competitors has been very steep andentrance has been too costly in a highly cyclicalmarket. Booms in demand often trigger new invest-ment in additional capacity, often only to be followedby a drying up of the market when production begins18 to 24 months later. Risk is high for any newcomerbecause the period following the boom is marked byfierce price competition until the excess capacity isworked off. Nonetheless, in recent years the US shareof the market decreased, even before the US embargowas imposed.

IV. OPPORTUNITIES FOR WESTERNGOVERNMENT POLICY

A. Possible Restrictions

52. Western governments, at considerable cost tothemselves, could increase Soviet economic difficultiesby:

— Restricting Soviet access to Western oil and gasequipment and technology.

— Eliminating subsidies, including governmentguarantees, on credits to the USSR.

— Using their influence to discourage Westernfirms from entering into large-scale energyprojects with the USSR.

— Taking steps to shrink the potential Westernenergy market for Soviet gas by developingalternative energy sources.

53. The effectiveness of such steps depends onmany factors, including the scope of the action, thedegree of cooperation among the Western Allies, andthe duration of the Testriction. It is highly unlikely, forexample, that US Allies will participate in an exportembargo, except in response to specific politicalevents, with the result that such an embargo is likely tobe partial and/or short-lived. On the other hand, theremay be a better chance of gaining Allied cooperationon credit policy and on development of alternativeenergy sources, especially if common ground can befound on a "strategic" policy concerning East-Westeconomic relations.

54. The following sections consider the impact ofpossible Western measures on:

— The construction of the export pipeline andthe planned Soviet gas deliveries to WesternEurope.

'For a detailed survey of the export pipeline's status, see CIAIntelligence Assessment SOV 82-10120/EUR 82-10078, Outlook forthe Siberia-to-Western Europe Natural Gas Pipeline, August 1982

shipped from Western Europe, or about to be shipped,turbines built with the GE-made rotors already

and by operating compressor stations without standbyunits, Moscow could deliver through the new pipelineabout 70 percent of the planned annual throughput of

additional 40 rotors—the number Alsthom-Atlantiquecontracted before the US embargo to build for theSoviet Union under GE license—could boost through-put to more than 90 percent of capacity. For reliabil-ity of pipeline operation and periodic maintenance,

somewhat.

equip the pipeline using either imported or domesticequipment. By then they will probably be able to

nearly 30 billion cubic meters. Turbines using an

however, the Soviets might use some of the availableturbines as standby units, thereby reducing throughput

needed until near the end of the decade, because WestEuropean gas demand is lagging substantially. Beforethe end of the 1980s the Soviets will be able to fully

produce 25-megawatt turbines, in spite of a history oftroubles. If necessary, the USSR could divert construc-tion crews and compressor-station equipment fromnew domestic pipelines to the export pipeline or even

57. It is highly unlikely that full capacity will be

•

— The development of Soviet oil production.

— The development of new gas export projects.

B. Impact on the Gas Export Pipeline

55. We believe that the USSR will succeed inmeeting its gas delivery commitments to WesternEurope through the 1980s and will do so withoutsignificant diversion of domestic resources from othersectors. Deliveries could begin in late 1984, as sched-uled, by using existing pipelines, which have excesscapacity of at least 10 billion cubic meters annually.

56. The Soviets probably can begin deliveriesthrough the new pipeline in 1985 or 1986. With the 22

24

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

Drill bits, drill pipe, tool joints, Smallother drilling equipment

Fluid-lift equipment Small

- Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

Table 5

Estimated Impact of Embargo by NATO Countries andJapan on Selected Oil Equipment

Impact of CurrentUS Sanctions

Exploration equipment Minimal

Offshore drilling equipment Moderate

Equipment for producing and proc- Substantialessing high-pressure, high-sulfur gas

Oil refinery secondar y processing Smallunits

Nature and Degree of Estimated Im pact ofEmbargo Imposed by NATO Members

and Japan

Reduction in exploration success in existingproducing areas as well as unex plored re-gions, with substantial impact in the 1990s.Short run: MinimalLong run: Substantial

Moderate delays in offshore drilling oper-ations.Short run: ModerateLong run: Moderate

Small short-run impact on drillingProgram.Short run: SmallLong run: Small

Potentially moderate in short run, depend-ing on Soviet import efforts.Short run: ModerateLong run: Moderate

Critical for production of high-sulfur Cen-tral Asian gas and hi gh-pressure gas inWest Siberia and elsewhere.Short run: SubstantialLong run: Moderate

Potentiall y substantial if Soviets proceedwith plans to upgrade refineries, but theyhave concluded no recent agreements forthis equipment.

dedicate a domestic pipeline for export use to ensurecapacity adequate to meet contractual delivery obliga-tions. This diversion would be costly, but it is highlyunlikely to be required on a large scale. More likely,Moscow would be able to meet Western Europe'sdemand with little or no loss in domestic gas deliveries.

C. Impact on Oil Development

58. The impact of export restrictions on oil develop-ment in the USSR would depend critically on thedevelopment of domestic oil equipment manufactur-ing capabilities. While some improvement is likelyover the decade, we do not believe that it will come intime to offset the need for the kinds of Westernequipment shown in table 5:

— Continued denial of US oil and gas equipmentwould retard Soviet oil production, particular-

ly in offshore drilling and in production ofhigh-pressure, high-sulfur gas.

— Denial of all oil equipment by all NATOcountries and Japan would have a substantiallylarger impact, which could reach as much as1.0 million b/d by the end of the decade—almost 10 percent of total oil production.

D. Impact on Future Gas Export Deals

59. The most damaging measures to the Soviets inthe long run would be inflicted by Western agree-ments that restrict further agreements either to buySoviet gas or to sell Moscow oil and gas equipment.Under such conditions the USSR would lose its mainsource of new hard currency earnings in the 1990s.

25

Approved For Release 2007/04/10 : CIA-RDP83M00914R002700060022-7

Approved For Release 2 0914R002700060022-7

E. Impact on the Soviet Economy and MilitaryCapability

60. Shortfalls in Soviet oil and gas production woulddirectly affect the USSR's ability to earn hard curren-cy. To protect its hard currency earnings, Moscowwould be tempted to further cut energy exports toEastern Europe. And the importance to the Sovieteconomy of substantial hard currency imports is suchthat, in the event of a major production shortfall,allocations of oil and gas to domestic Soviet uses wouldbe reduced.

61. Consequences for the Economy. Energyshortfalls would affect the Soviet economy and mightlead to cuts in imports. The USSR would be reluctantto cut food imports because this would risk popularunrest and, in any event, would probably adverselyaffect incentives and productivity.

62. Further reductions in imports of machinery andequipment would hinder industrial modernization andproductivity. Cuts in allocations of oil and gas, or ofimported materials such as steel, would create produc-tion bottlenecks, cause some plant capacity to beunused, and disrupt supplies in many parts of theeconomy. The botl lenecks would diminish and per-haps eventually disappear as the Soviets took steps toconserve the scarce products, to substitute other prod-ucts, and to adjust the pattern of demand.

63. Given all the uncertainties surrounding thescope and duration of Western measures, and the waythe Soviets would cope with and adjust to thesemeasures, quantitative measures of impact can at bestbe viewed as illustrative orders of magnitude.

64. The effect of Western measures on potentialSoviet energy output (measured in dollars at worldmarket prices) would approximate the following mag-nitudes (in billions of dollars per year):

MediumShort Run Run (4-10 Long Run(2-3 Years) Years) (Over 10 years)

Pipeline SanctionsUS alone Small 0-small 0

Oil EquipmentRestriction

US alone 2-6 2-6 SmallAll Allies 7 12 Declining

No New GasProjects

(beyond currentpipeline)

0 0-5 5-10

65. In the hypothetical case of a full Westernembargo on all oil and gas equipment, including large-diameter pipe, the cost to the Soviets would risesubstantially—reaching roughly $36 billion annuallyby 1990. This case illustrates the particular importanceof Western linepipe to the Soviet gas program over thenext several years; in the 1990s this dependence willdecline as the Soviets master serial production ofmultiwall large-diameter pipe.

66. The impact of these shortfalls on Soviet GNPmight be a multiple of the above losses, especiallyduring the period when bottlenecks could not beavoided. The potential aggregate economic impactcould be characterized as follows:

— Insignificant, in the case of US unilateralcontrols aimed only at the export pipeline.

— GNP by the end of the decade would be 2 to 3percent less in the case of a sustained Alliedembargo of oil equipment, but the impactwould be much smaller in the more likely casethat US Allies provide limited, if any,cooperation.

— In the hypothetical case that includes an em-bargo on pipe, the Soviets would incur a loss inGNP of 3 to 4 percent by 1990.

After 1990 the effects of Western policiescould be enhanced considerably if follow-onSoviet gas projects were squelched.

67. Soviet costs on the order of 3 percent of GNP by1990 are significant. Such a loss of GNP would beequivalent to all the investments made in housingconstruction in 1980, or nearly 40 percent of allindustrial investments in 1980, or more than 25 per-cent of military expenditures in 1980. These measuresindicate only the order of magnitude of forgone SovietGNP and do not equate to potential cuts in investmentor defense spending. While the cumulative effect ofsuch losses would clearly increase pressures on Sovietdecisionmakers, we cannot judge how they wouldchoose to spread such losses throughout the economy.

68. Additional Western actions such as restrictingsubsidized government-guaranteed credits could raisethe cost to the Soviets of Western assistance by about$400-500 million a year. Credit extensions themselves

26

Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

- Approved For Release 2007/04/10: CIA-RDP83M00914R002700060022-7

would probably fall sharply if government guaranteeswere withheld, as most bankers are reluctant to extendlarge long-term credits without government guaran-tees.

69. In the long run, tighter COCOM restrictions onmilitarily sensitive technology (including technologyand equipment that indirectly contributes to signifi-cant improvements in weapon systems) would perhapsbe the most valuable action for the West. Such actionwould retard major improvements in Soviet weaponry,which the West would be forced to counter. While thedollar value of such action is difficult to estimate, thesavings in terms of Western spending for defenseannually would probably come to billions of dollars.

70. Consequences for Military Programs. Thereduced availability of hard currency and energywould also make more difficult the decisions Moscowmust make among key priorities in the 1980s—sustain-ing growth in military programs, feeding the popula-tion, modernizing the civilian economy, supporting itsEast European clients, and expanding (or maintaining)its overseas involvements. Because economic growthwill be slow through the 1980s, annual additions tonational output will be too small to simultaneouslymeet the incremental demands that planners areplacing on the domestic economy. Even now, stagna-tion in the production of key industrial materials isretarding growth in machinery output—the source ofmilitary hardware, investment goods, and consumerdurables.

71. If growing resource stringencies and hard cur-rency shortages prompt Soviet leaders to cut back onimports, it seems likely that, in true bureaucratictradition, initial efforts would be implemented in abroad-brush fashion affecting a number of Sovietministries across the board. The very top-priorityprograms no doubt would be spared, but many rela-tively high-priority ones, including some military pro-grams, could be hurt at least indirectly.

72. Even in the longer term, cuts in machineryimports would retard progress in modernizing a num-ber of industrial sectors—steel, machine building, oilrefining, robotics, microelectronics, transportation,and construction equipment—at a time when Moscowis counting on a strategy of limited investment growthand relying instead on productivity growth.