Embed Size (px)

Citation preview

The Smarter Loan For Your Home

CMG Financial, NMLS 1820Affinity Brochure

TM

2 3

It’s no secret that the price you buy your home for and the amount you end up paying are two very different figures. After factoring in your loan’s total interest costs, you will likely spend close to double your home’s original purchase price, which can impede other financial objectives.

Mortgages, however, are a “necessary evil” to many. Despite the cost of interest, they help provide an opportunity to own for those who cannot afford to pay with cash.

If you think about it, a mortgage is just a mere mathematical equation. So, why can’t a lender simply change the equation and create a more flexible and cost effective way to borrow? Well, that is exactly what CMG Financial has done.

Introducing the All In One™ Home Loan

Arguably, the United States is trailing behind other countries with the way we finance our homes. More efficient products have been developed and made available throughout Western Europe, Canada and Australia for decades.

The All In One™ was designed on the same principles as those products. Introduced in 2005, it can help you save hundreds of thousands of dollars in interest payments, accelerate the growth of accessible equity, and pay off your home sooner. It is indeed, The Smarter Loan for Your Home.

Introduction

After factoring in your loan’s total interest costs, you will likely spend close to double your home’s original purchase price, which can impede other financial objectives.

Borrowed Amount

Loan Term

Interest Rate

Interest Paid

Total Price

$ 300,000 30 Years 4.0 % $ 215,610 $ 515,610

Hypothetical example of a 30-year mortgage

4 5

The Smarter Loan

The All In One™ provides many benefits that reach beyond what a traditional mortgage can offer. But to begin your understanding, first consider how you manage the money you use to pay for your housing and other budgeted needs.

If you are like most Americans, you rely on a traditional checking account to temporarily store your income. From there, you withdraw and distribute those dollars to pay for your monthly expenses and debts – but not all at once.

In reality, a large sum of your earnings simply sit idle in your account, waiting to be spent. We refer to this money as your “lazy money,” due to the fact that while those dollars are not in use, they earn you low interest, or possibly none at all.

In comparison, you pay high interest on your mortgage. Wouldn’t it just make better sense to combine your “lazy money” with your mortgage debt in order to put those dollars to work?

Put Your “Lazy Money” To Work

That’s exactly what the All In One™ does by bundling the two together. Yes, borrowing and banking are combined so your deposits lower your mortgage balance, which lowers your monthly interest costs. It’s that simple.

The All In One™ can be used for home purchases and refinances and comes with 24/7 secure banking access including ATM cards, check writing and Online bill-pay.

Other ways to save with the All In One™

* Flow rental property income through the All In One™

* Flow small business income1 through the All In One™

* Flow tax withholdings and refunds through the All In One™

* Use outside rewards-cards to leverage your cash longer

1Consult a tax advisor for direction when considering leveraging small business income through the All In One™.

6 7

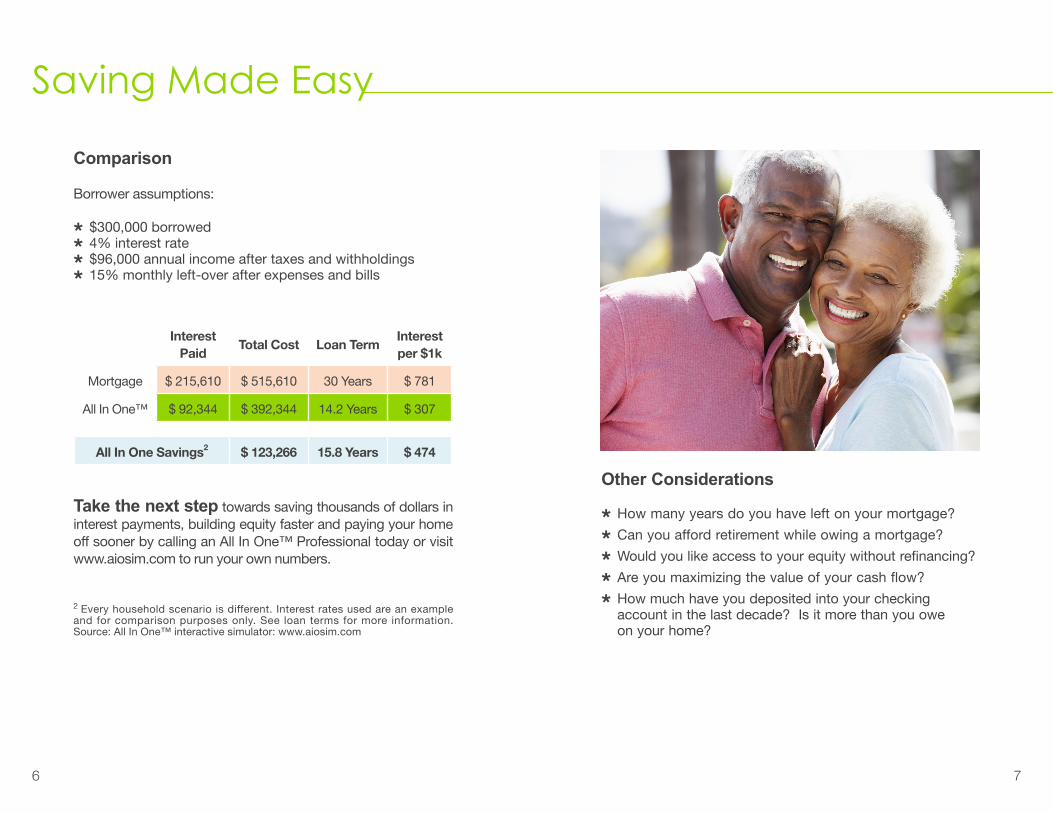

Saving Made Easy

Comparison

Borrower assumptions:

* $300,000 borrowed* 4% interest rate* $96,000 annual income after taxes and withholdings* 15% monthly left-over after expenses and bills

Interest Paid Total Cost Loan Term Interest

per $1k

Mortgage $ 215,610 $ 515,610 30 Years $ 781

All In One™ $ 92,344 $ 392,344 14.2 Years $ 307

All In One Savings2 $ 123,266 15.8 Years $ 474

Take the next step towards saving thousands of dollars in interest payments, building equity faster and paying your home off sooner by calling an All In One™ Professional today or visit www.aiosim.com to run your own numbers.

2 Every household scenario is different. Interest rates used are an example and for comparison purposes only. See loan terms for more information. Source: All In One™ interactive simulator: www.aiosim.com

Other Considerations

* How many years do you have left on your mortgage?

* Can you afford retirement while owing a mortgage?

* Would you like access to your equity without refinancing?

* Are you maximizing the value of your cash flow?

* How much have you deposited into your checking account in the last decade? Is it more than you owe on your home?

8 9

Loan Terms

Lien Position

Lien Type

HELOC Limit

Interest Rate Term - KPCU3

--

Fixed Margin Options

Index

Floor Rate

Lifetime Cap

Loan Purpose

Loan Amount Maximum

Access Features

First Position

30 Year Draw Home Equity Line of Credit (HELOC)

Level for 10 years then reduces 1/240th monthly

3 Year Fixed then monthly adjustable for 27 years

--

3.000%, 3.250% or 3.500%

One Month LIBOR4

3.500%

6% over start rate or floor rate, which ever is greater

Purchase and Refinance transactions

$ 2,000,000

ATM Cards, Check Writing, Online Bill Pay, ACH

3 Eligibility limitations may apply. Call for details4 London Inter-Bank Offered Rate

10 11

Eligibility

The All In One™ Home Loan is available through CMG Financial, partner of Ameriprise Financial and developers of the loan product, and KeyPoint Credit Union as the service provider and investor. Your loan will be sold and serviced by KeyPoint Credit Union.

Interested applicants are eligible, providing they become a new member or are currently a member of KeyPoint Credit Union. The membership application will be presented to you as part of the loan document signing process. CMG Financial has agreed to pay for your $35.00 membership fee.

KeyPoint Credit Union began in 1979 as AEA Credit Union by serving people with their banking needs in the technology industry, specifically companies who were members of the organization formerly called the American Electronics Association. The AEA is a nationwide, non-profit trade association that has represented all segments of the technology industry for more than 60 years.

Membership Criteria:

You live, work, attend school or worship in one of the following California counties:

* Santa Clara County * Alameda County* El Dorado County * Placer County* San Mateo County* Sacramento County* Santa Barbara County* Contra Costa County* Ventura County

Call CMG Financial for more information

12 13

CMG Financial

CMG Financial is an established privately held mortgage banking firm, headquartered in San Ramon, California, and Preferred Lending Provider for Ameriprise Financial.

NMLS 1820

“This was the least complicated mortgage process I’ve ever experienced. Thank you CMG.”

- Brett, Seattle WA

As a Direct Seller-Servicer to Fannie Mae and Freddie Mac as well as an approved Ginnie Mae Issuer, CMG Financial is widely known for responsible lending practices, product innovation, consumer advocacy and operational agility.

The President and CEO, Christopher M. George, currently serves as (2012 - 2014) President of the California Mortgage Bankers Association (CMBA) and is also on the Board of Directors for the Mortgage Bankers Association (MBA).

Company Philosophy

At CMG Financial, we understand that no two households are the same and the needs of each household are as unique as a fingerprint. Delivering the right loans, for the right reasons, in a way that exceeds all expectations is our business.

CMG Financial | 3160 Crow Canyon RoadSan Ramon, CA 94583 | 925-983-3000

14 15

Questions

Is CMG Financial a reputable company?

Who takes my loan application?

If my budget is tight, is this the right loan for me?

Does this loan require Mortgage Insurance?

Can I access home equity without refinancing?

What happens if I pay my home off early?

Is the mortgage interest deductible?

Won’t I lower my deductible amount if I pay less interest?

What access features does the All In One™ provide?

Isn’t access to home equity a bit dangerous?

Should I close my old checking accounts?

Answers

Yes, CMG Financial is a well known and established firm.

A CMG Financial Mortgage Consultant will work with you.

The All In One™ is suitable for cash flow positive households.

No. The maximum you can borrow is 80% loan-to-value.

With the All In One™, yes. With a conventional mortgage, no.

You can close your account or keep it open for use.

Yes it is, but you should always consult your tax advisor first.

Yes. Paying financing fees is not in your best interest.

The loan comes with POS Cards, check writing and online bill-pay.

For irresponsible borrowers, yes. This loan isn’t for everyone.

No. You may need to use those other accounts in the future.

FAQ’s

1-888-CMG-HOME | www.cmgfi.com/am Ask to speak to an Ameriprise Financial dedicated Mortgage Consultant or

have your Advisor refer you directly.

© 2013 CMG Financial, All Rights Reserved. ©“All-In-One Home Loan™” and the All-In-One logo are trademarks of CMG Financial. CMG Financial is a registered trade name of CMG Mortgage, Inc., NMLS #1820 in most, but not all states. CMG Mortgage, Inc. is an equal opportunity lender. Offer of credit is subject to credit approval. For information about our company, please visit us at www.cmgfi.com. To verify our state licensing, please visit www.nmlsconsumeraccess.org. This presentation is not intended to serve as a business solicitation for residents in the following states: Louisiana, Massachusetts, New York, Rhode Island, Vermont, and West Virginia.

E x p e r i e n c e E x t r a o r d i n a r y

247668 A (8/13)