Embed Size (px)

Citation preview

The Smart Grid in China:

A Discussion Paper

Report of the Expert Policy Advisory Group led by

WU Jiandong China Center for International Economic Exchanges

Chinese Academy of Sciences and

WU Jiang Policy Research Office of

State Electricity Regulatory Commission to

State Electricity Regulatory Commission YU Yanshan, Deputy Director General

© Entri 2012

1

The Smart Grid In China: A Discussion Paper

Summary The Chinese government has taken the position that smart grid development represents a strategic choice closely aligned with development needs and could be an effective force to drive a transition to a low-carbon energy system. The government plans to make major investments in smart grid research and development during the 12th 5-Year Plan period, and has tasked the State Grid Corporation of China (State Grid) with early deployment efforts. State Grid has focused its efforts on construction of an ultra high voltage transmission network to serve as the backbone for a system that will incorporate large scale, intermittent, renewable power from remote sources. State Grid’s plans do not currently emphasize the potential role of the consumer in the electricity demand or supply chain, a shortcoming that threatens to limit the scope of demand side response and the depth of China’s smart grid development. The authors of this discussion paper, led by WU Jiandong, believe a more comprehensive approach to smart grid development will better serve China’s economic and environmental goals. They emphasize the importance of a fundamental shift from the current one-way flow of electricity to an interactive intelligent power system. They identify the key areas for research, demonstration, and policymaking that will encourage that shift.

China’s Smart Grid Vision China has undertaken an ambitious effort to provide the energy services required by its growing economy while mitigating China’s contribution to climate change. The Chinese government has committed to reduce the carbon intensity of its GDP in 2020 by 40-45 percent (compared with 2005 levels) and to increase non-fossil energy to 15 percent of primary energy consumption by 2020.1 Both of these commitments demand substantial changes in China’s electric power system. Achieving them will require incorporation of the advanced automation and information technologies essential to development of smart grids around the world.

The Chinese government has stated five objectives for deploying smart grid technologies:

• increasing the utilization of renewable energy; • improving grid assets utilization and management; • increasing efficiency of operations and return on investment with reduced losses • upgrading and renovating technology to support comprehensive and intelligent power

system development, including an integrated electricity management platform, smart meters and sensors, and an automated system for forecast, control, fault detection, monitoring, and recovery; and

• enabling demand-side interaction in optimizing the operation of the electricity system.2

In the near-term, State Grid, which will implement China’s smart grid, emphasizes the importance of a strong grid.3 It plans to construct an ultra high voltage transmission network as the backbone for a system that will incorporate large scale and/or intermittent power from remote

2

sources. In the longer term, the strong grid will also include technologies that enhance automation and interactivity, to make the system more robust.

State Grid’s plans do not currently emphasize the potential role of the consumer in the electricity demand or supply chain. Historical disinterest in the ability of the marketplace to influence electricity system development constitutes the main deviation of China’s smart grid planning efforts from those in North America and Europe. This difference threatens to limit the scope of demand side response and the depth of smart grid development.

Still, China’s broader vision of the necessary elements of a smart grid incorporates most of the features common to smart grid development programs internationally. These include:

• advanced automation and information systems; • interaction between information flows and power flows; • utilization of new, clean energy sources; • reduction of energy consumption; • consumer participation in system optimization; and • effective utilization of power equipment.

This technological scheme does not preclude incorporation of market reforms or transformation from the current one-way flow of electricity to a two-way flow. Such a change of focus could promote a shift in the operations of electricity system from a top-down vertical structure to a combination of multi-layered and distributed control structures. This type of smart grid structure holds the most potential to yield a transformed, intelligent, responsive, and flexible low carbon electricity system. The transition to a low carbon economy over the course of this century will entail major changes to the way China supplies and uses energy. A smart grid that encourages development and use of distributed sources of electric power, including the “negawatts” available from energy efficiency, will enhance the likelihood of success. Our research team, led by Professor WU Jiandong, has proposed a comprehensive integrated smart utility grid for further research during the 12th Five-Year Plan period. We believe the focus should be on transforming from the current concentrated energy structure towards four parallel systems comprising:

• a multi-layered energy production and transmission system; • advanced energy storage systems; • intelligent end-user systems; and • an intelligent energy service system.

The four systems could be supported by a standardized, holistic information and communication network based on internet protocol version 6 (IPV 6). This would entail the construction of an entirely new energy operation system centered on IPV6 and its compatible energy facilities as the basis for energy information coordination and inter-exchange. By doing so, the utility facilities operating as islands could be easily transformed into flexible energy clusters and achieve substantial demand-side participation. The technological channels and sub-networks should be equipped with common interface standards and communication protocols to enable the

3

connection of both conventional and new facilities for inter-operability, and at the same time achieve unified data management. The interactive system between different energy networks should be optimized to facilitate smooth conversion and trading of different types of power, which could also be used for load adjustment and energy storage contributing to improved energy efficiency and emissions reduction.

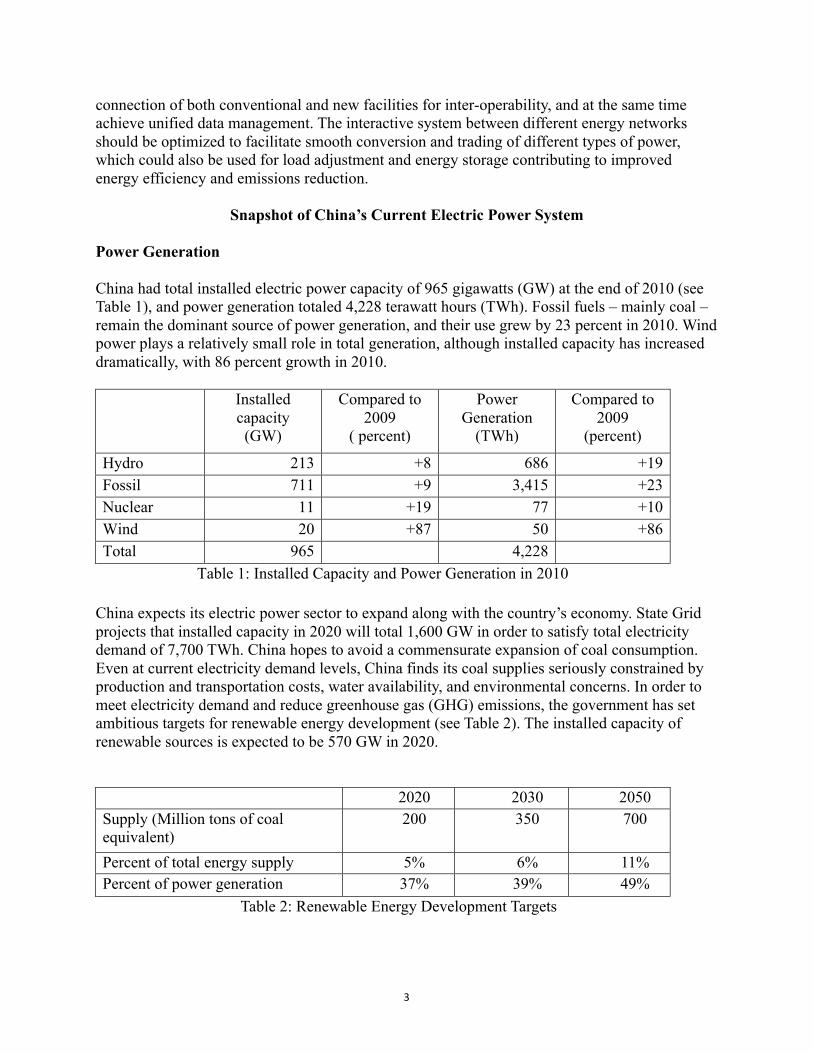

Snapshot of China’s Current Electric Power System

Power Generation China had total installed electric power capacity of 965 gigawatts (GW) at the end of 2010 (see Table 1), and power generation totaled 4,228 terawatt hours (TWh). Fossil fuels – mainly coal – remain the dominant source of power generation, and their use grew by 23 percent in 2010. Wind power plays a relatively small role in total generation, although installed capacity has increased dramatically, with 86 percent growth in 2010.

Installed capacity (GW)

Compared to 2009

( percent)

Power Generation

(TWh)

Compared to 2009

(percent)

Hydro 213 +8 686 +19 Fossil 711 +9 3,415 +23 Nuclear 11 +19 77 +10 Wind 20 +87 50 +86 Total 965 4,228

Table 1: Installed Capacity and Power Generation in 2010 China expects its electric power sector to expand along with the country’s economy. State Grid projects that installed capacity in 2020 will total 1,600 GW in order to satisfy total electricity demand of 7,700 TWh. China hopes to avoid a commensurate expansion of coal consumption. Even at current electricity demand levels, China finds its coal supplies seriously constrained by production and transportation costs, water availability, and environmental concerns. In order to meet electricity demand and reduce greenhouse gas (GHG) emissions, the government has set ambitious targets for renewable energy development (see Table 2). The installed capacity of renewable sources is expected to be 570 GW in 2020.

2020 2030 2050

Supply (Million tons of coal equivalent)

200 350 700

Percent of total energy supply 5% 6% 11% Percent of power generation 37% 39% 49%

Table 2: Renewable Energy Development Targets

4

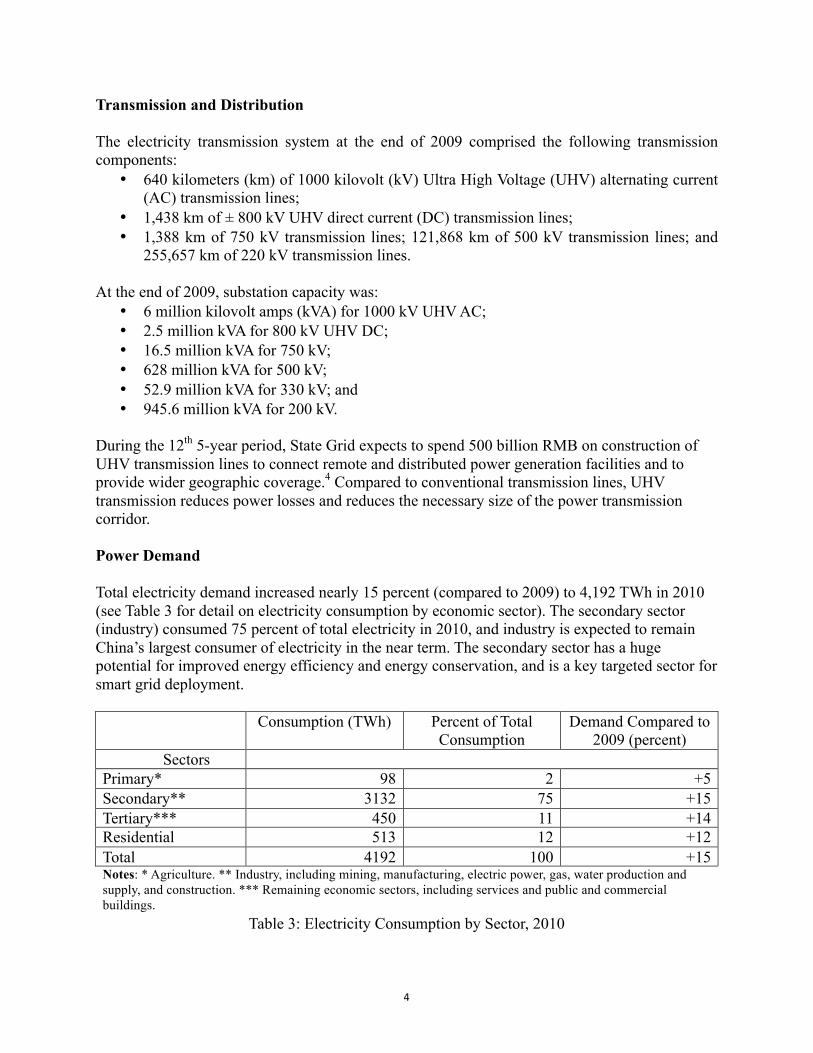

Transmission and Distribution The electricity transmission system at the end of 2009 comprised the following transmission components:

• 640 kilometers (km) of 1000 kilovolt (kV) Ultra High Voltage (UHV) alternating current (AC) transmission lines;

• 1,438 km of ± 800 kV UHV direct current (DC) transmission lines; • 1,388 km of 750 kV transmission lines; 121,868 km of 500 kV transmission lines; and

255,657 km of 220 kV transmission lines. At the end of 2009, substation capacity was:

• 6 million kilovolt amps (kVA) for 1000 kV UHV AC; • 2.5 million kVA for 800 kV UHV DC; • 16.5 million kVA for 750 kV; • 628 million kVA for 500 kV; • 52.9 million kVA for 330 kV; and • 945.6 million kVA for 200 kV.

During the 12th 5-year period, State Grid expects to spend 500 billion RMB on construction of UHV transmission lines to connect remote and distributed power generation facilities and to provide wider geographic coverage.4 Compared to conventional transmission lines, UHV transmission reduces power losses and reduces the necessary size of the power transmission corridor. Power Demand Total electricity demand increased nearly 15 percent (compared to 2009) to 4,192 TWh in 2010 (see Table 3 for detail on electricity consumption by economic sector). The secondary sector (industry) consumed 75 percent of total electricity in 2010, and industry is expected to remain China’s largest consumer of electricity in the near term. The secondary sector has a huge potential for improved energy efficiency and energy conservation, and is a key targeted sector for smart grid deployment.

Consumption (TWh) Percent of Total

Consumption Demand Compared to 2009 (percent)

Sectors Primary* 98 2 +5 Secondary** 3132 75 +15 Tertiary*** 450 11 +14 Residential 513 12 +12 Total 4192 100 +15 Notes: * Agriculture. ** Industry, including mining, manufacturing, electric power, gas, water production and supply, and construction. *** Remaining economic sectors, including services and public and commercial buildings.

Table 3: Electricity Consumption by Sector, 2010

5

The rapid increase in electricity demand in the tertiary and residential sectors has widened the difference in the maximum and minimum demands for electricity supply (the daily maximum peak/valley ratio). More frequent extreme weather events have affected this measurement. In 2008, 12 provinces had a daily maximum peak/valley difference of more than 50 percent, and only 6 provinces had a daily maximum peak/valley difference of less than 35 percent. Smart grid technologies should enable demand driven power supply and consumption, and improve peak load shifting. Pricing Policy China heavily regulates electricity prices. In the absence of a market, the government has introduced various pricing strategies to influence consumption. For example:

• Ladder-type pricing for residential users. The National Development and Reform Commission (NDRC) has piloted projects imposing ladder-type prices – prices that rise as electricity consumption increases – in Zhejiang, Sichuan, and Fujian provinces5.

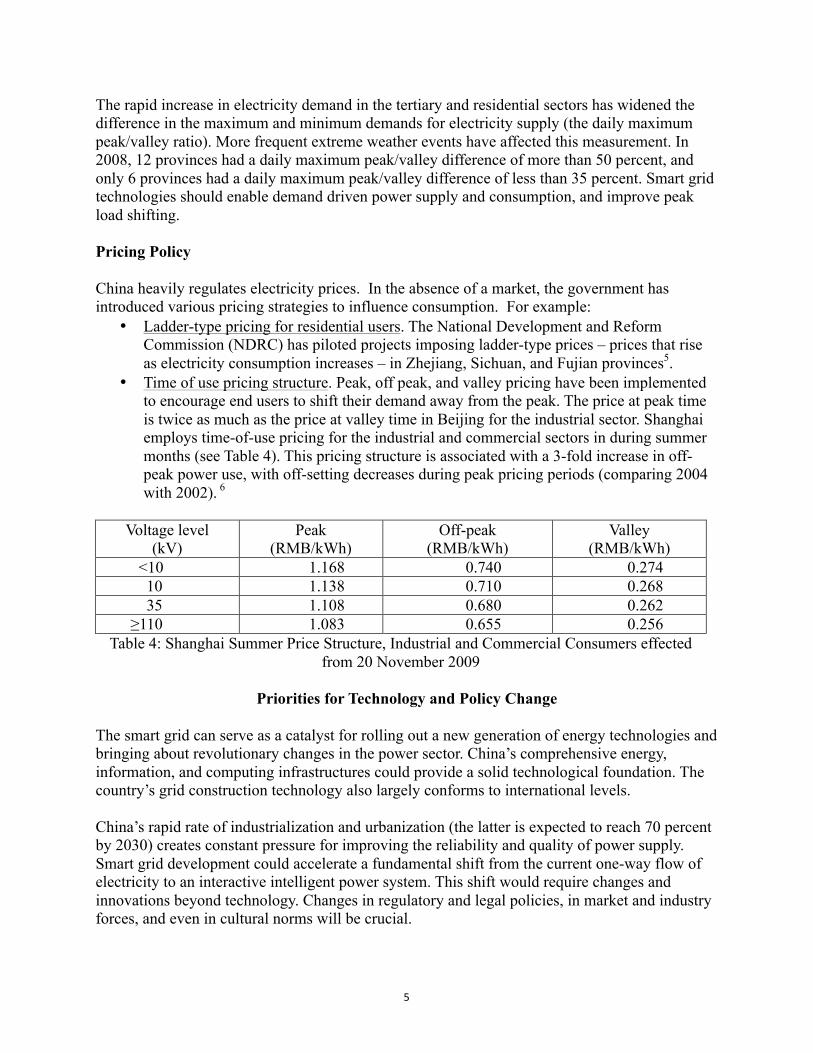

• Time of use pricing structure. Peak, off peak, and valley pricing have been implemented to encourage end users to shift their demand away from the peak. The price at peak time is twice as much as the price at valley time in Beijing for the industrial sector. Shanghai employs time-of-use pricing for the industrial and commercial sectors in during summer months (see Table 4). This pricing structure is associated with a 3-fold increase in off-peak power use, with off-setting decreases during peak pricing periods (comparing 2004 with 2002). 6

Voltage level

(kV) Peak

(RMB/kWh) Off-peak (RMB/kWh)

Valley (RMB/kWh)

<10 1.168 0.740 0.274 10 1.138 0.710 0.268 35 1.108 0.680 0.262

≥110 1.083 0.655 0.256 Table 4: Shanghai Summer Price Structure, Industrial and Commercial Consumers effected

from 20 November 2009

Priorities for Technology and Policy Change

The smart grid can serve as a catalyst for rolling out a new generation of energy technologies and bringing about revolutionary changes in the power sector. China’s comprehensive energy, information, and computing infrastructures could provide a solid technological foundation. The country’s grid construction technology also largely conforms to international levels. China’s rapid rate of industrialization and urbanization (the latter is expected to reach 70 percent by 2030) creates constant pressure for improving the reliability and quality of power supply. Smart grid development could accelerate a fundamental shift from the current one-way flow of electricity to an interactive intelligent power system. This shift would require changes and innovations beyond technology. Changes in regulatory and legal policies, in market and industry forces, and even in cultural norms will be crucial.

6

At the technical level, automated interactive and control technologies make a smart grid more complex than a conventional grid. China has made progress in large-scale power grid offline simulation and control technologies and has demonstrated world class UHV transmission systems. However, a large number of facilities cannot be fully digitized or meet the requirements of complete automation and interactive information flow. Some core technologies for building a smart grid infrastructure have not been fully mastered yet, and the technologies for certain components are still lagging behind. China needs a set of unified standards to guide the implementation of smart grid transmission technologies, information and computer technologies, sensing technologies, power electronic technologies and power storage technologies. Optimum deployment of smart grid technologies will require changes in China’s current legal and regulatory systems as well as increased utilization of market mechanisms. The smart grid has the potential to rectify the distortion of energy resources allocation, electricity pricing, and distribution of benefits inherent in the current system. Introduction of a smart grid could effectively leverage the construction of the first ever locally managed end-user network, through which electricity pricing can be made based on varied local market circumstances.7 A more responsive system will enable more effective handling of renewable power’s intermittent availability, better coordination of peak-shifting, and large-scale introduction of distributed generation through enhanced network utilization. In addition to sending the appropriate pricing signals to end users, a smart grid can also overlay the market architecture for carbon trading and tradable energy quotas in the long term. China will need policies that encourage policies for technological innovation and demonstration of smart grid development. Preferential taxes and government subsidies could be put in place. New financing modalities to encourage public and private partnerships could be provided to ensure sufficient level of commercial interest and investment. Awareness-raising activities can also be carried out across the various end-use sectors to give voice to disparate interests, which would help in reaching a usable roadmap for smart grid development in China.

Emerging Priorities for R&D in the 12th 5-Year Plan Period

The 12th Five-Year Plan has set goals for research and development (R&D) of a smart grid, which has also been identified as an emerging strategic industry. The smart grid is expected to be a driver for further increasing the utilization of renewable energy sources and improving the efficiency of power generation, grid transmission and distribution, power dispatch, and power consumption. The government anticipates investing 430 billion Yuan during the 2011-2020 period for the deployment of intelligent components8 of smart grid alone. The rationale for this investment includes environmental and economic benefits. Environmental benefits: The government estimates that renovation of the traditional grid to function as a smart grid could avoid a total of 220 million tons of standard coal consumption during 2011-2020 in comparison with the “no-smart grid function” scenarios.9 Economic benefits: The government estimates that its planned 430 billion RMB investment in smart grid could ultimately yield total economic output of 1.7 trillion RMB and generate 3 million new jobs10. It expects to recoup 420 billion RMB by 2020 through reduced power

7

generation investment and improved utilization of grid and power generation assets. Total economic benefits by 2020 should be in the range of 675 billion RMB. The government has taken the position that smart grid development represents a strategic choice closely aligned with development needs and could be an effective force to drive a transition to a low-carbon energy system in China. Medium- and long- term development objectives are summarized below. Medium-term Objectives (during the 12th Five-Year Plan Period)

• Master the core smart grid technologies. • Develop Relatively comprehensive smart grid national standards developed by 2015,

with certain standards closely aligned with the international smart grid standards. • Construct initial high voltage grids across provinces as the basic infrastructure for

nationwide smart grid development. • Establish electric vehicle charging network with scale and geographic coverage. • Accelerate the contribution of smart community districts and smart buildings to engage end-users.

• Promote utilization of fiber optic communication to enable integration of power and communications networks.

Long Term Goals

• Develop a strong and robust structure for close coordination with grids at different levels based on information flow, automation, and interaction.

• Maintain a stable and secure power supply to enable the connection and distribution of diversified power sources, particularly focusing on environmental protection and clean energy resources.

• Optimize resource allocation while meeting end-users’ varied service needs. • Establish international advanced comprehensive standards for smart grid by 2020.

Opportunities for International Cooperation

The research team foresees several opportunities for cooperation, particularly on key technologies and on standardization. Key technologies for potential cooperation include the following:

• Large capacity storage technology, in particular flow batteries and electromagnetic storage.

• Grid control technology, in particular WAN monitoring technology and real time communication technology.

• Analysis and decision support technology, with an emphasis on optimization of grid capacity and allocation of resources.

• Intelligent metering technology, to enable provision of real-time power consumption data, which will allow customers to alter power use based on the actual prices.

• Sensing and communication technology, to facilitate construction of an optical network, with Automatically Switched Optical Network (ASON), Fiber to the Home (FTTH), Power Line Communication (PLC) and wireless.

8

One of the major challenges for smart grid construction will be to solve the massive information collection and data exchange problems. If a smart grid is to flourish, it will need unified semantics (data modeling), a unified grammar (protocols), and a compatible network to build up the architecture for highly efficient, centralized power system information. China’s Standardization Administration (SAC) and National Energy Administration (NEA) have established a National Smart Grid Standardization task force to deepen research on uniform standards development in China. State Grid has also issued a smart grid standards system development plan. A total of 22 standards such as the integration of distributed electric resources, solar and wind, on-grid online monitoring technology and substation have been identified as the priorities for domestic standards development. Deepening research and joint R&D on internationally compatible smart grid standards development is one of the near-term priorities for international cooperation.

The Energy Transition Research Institute (Entri) would like to thank the Blue Moon Fund for its support of this project, in particularly its Vice President of Programs, Zhang Ji-Qiang. Entri supported the preparation of this discussion paper to provide an introduction to its broader research on smart grid development in China. We have developed a China Electric Grid Modeling System that will enable policymakers and energy experts to project the economic and environmental costs and benefits of deploying a range of electric power technologies. We plan to issue a series of reports on specific technologies and policy measures based on the modeling system.

R&D Priorities Standardized Systems • Monitoring and controls for grid integration and power consumption; • Online fault detection and forecasting; • Automation of distribution and dispatch; and • Adaptation of demand response to the requirements of “smart” communities and electric vehicles. Key Supporting Technologies • Modeling, forecasting and application technologies for large scale integration of renewables and

distributed energy; • Self-diagnosis and recovery of transmission faults; and • End-user data collection and control technologies. Key Areas for Pilot and Demonstration: • Demonstrations of storage and transmission technologies for wind and solar power systems; • Pilot testing of advanced automated power distribution in economically viable regions; • Establishing a provincial level power dispatch support system to test forecasting technology for wind

power and other new energy sources, on-grid operations risk management, and wide area phasor measurement;

• Deployment of smart meters in municipalities by the end of 12th Five-Year Plan; • Demonstrations of electric vehicle charging stations; • Demonstrations of applying electrical vehicle battery storage and load adjustment capabilities to utility

load management requirements; and • Pilot testing of unified meter reading of electricity, water and gas services.

9

1 Carbon intensity is defined as the amount of carbon emitted per unit of GDP. The Chinese government announced this and related goals on 26 November 2009 as the nation’s commitment to reducing the risk of global climate change. 2 State Electricity Regulatory Commission (SERC): Smart Grid Development Situation Analysis, page 3, Beijing, Feb 2011. [Note: This report is an internal report of the Chinese government and is not available for public inspection. The report is the basis for the authors’ assertions regarding government forecasts, plans, and budgets, unless such assertions are otherwise referenced.] 3 State Grid Corporation of China was formed in 2002 when the Chinese government separated the State Power Corporation into generation, transmission, and service units. State Grid controls investment, construction, and management of electricity transmission and distribution in all of China’s provinces except for Guangzhou, Guangxi, Yunnan, Guizhou, and Hainan. State Grid ranks seventh among the Fortune Global 500. 4 State Grid Cooperation of China, Prospectus of Ultra-short-term Financing Bond, Phase II of 2011, Page 31, April 2011 5 NDRC, NDRC conference about Ladder-pricing for Residential Users, October 2010 http://www.sdpc.gov.cn/xwfb/t20101009_374288.htm NDRC Guidance on Ladder-‐pricing for Residential Users, Draft for Discussion, October 2010: http://www.sdpc.gov.cn/jtdjyj/qwll/t20101008_374091.htm 6Interpret the Characteristic of the New Model Electricity Structure in Shanghai, June 2005 http://finance.eastday.com/eastday/finance/node39294/node39304/node39308/userobject1ai1204409.html 7 State Electricity Regulatory Commission (SERC): Smart Grid Development Situation Analysis, page 14, Beijing, Feb 2011 8 WU Jiang, State Electricity Regulatory Commission (SERC): Smart Grid Research Report, page21. Beijing, January 2011 9 WU Jiang, State Electricity Regulatory Commission (SERC): Smart Grid Research Report, page 21, Beijing, January 2011. 10 WU Jiang, State Electricity Regulatory Commission (SERC): Smart Grid Research Report, page 21, Beijing, January 2011.

![[Smart Grid Market Research] South Korea: Smart Grid Revolution, Zpryme Smart Grid Insights, July 2011](https://img.pdfslide.us/doc/110x75/5414026d8d7f727d698b47c7/smart-grid-market-research-south-korea-smart-grid-revolution-zpryme-smart-grid-insights-july-2011.jpg)

![[Smart Grid Market Research] Smart Grid Hiring Trends Study (Part 2 of 2)- Zpryme Smart Grid Insights](https://img.pdfslide.us/doc/110x75/5414021c8d7f7284698b47a9/smart-grid-market-research-smart-grid-hiring-trends-study-part-2-of-2-zpryme-smart-grid-insights.jpg)

![[Smart Grid Market Research] India: Smart Grid Legacy, Zpryme Smart Grid Insights, September 2011](https://img.pdfslide.us/doc/110x75/541402518d7f7294698b47d4/smart-grid-market-research-india-smart-grid-legacy-zpryme-smart-grid-insights-september-2011.jpg)

![[Smart Grid Market Research] The Optimized Grid - Zpryme Smart Grid Insights](https://img.pdfslide.us/doc/110x75/541402188d7f7294698b47d2/smart-grid-market-research-the-optimized-grid-zpryme-smart-grid-insights.jpg)