Embed Size (px)

Citation preview

The Skandia judgment: how to gain a competitive edge by using non-tax means

Prior to the summer of 2014, intra-company cross-border transactions were largely disregarded for VAT purposes within the EU (based on the FCE Bank principle1). As a result, businesses were neither obliged, nor motivated to identify intra-company costs on an item by item basis for VAT purposes.

Following the Skandia judgment2, financial services organizations with an establishment included in a VAT group in an EU Member State are faced with a new challenge. Intra-company supplies could, following Skandia, be subject to VAT. Considering that VAT rates range from 17% to 27% across the EU, and the fact that VAT is partly or fully irrecoverable for financial services organizations, this additional and unexpected VAT is a significant cost.

From an operational point of view, the challenge is to determine exactly which recharges and which amounts could be subject to VAT. In this analysis we demonstrate why financial services organizations can benefit from proper cost allocation methods and how they can utilize it to gain a competitive edge in the market by decreasing their VAT cost in compliance with the regulations on VAT and transfer pricing (“TP”).

The Skandia problemFinancial organizations have two major opportunities to minimize VAT on intra-group transactions.

• For cross-border recharges, they have the option to set up a branch structure, as according to the FCE Bank principle, transactions between a head office and its branches fall outside the scope of VAT.

• To mitigate VAT cost in relation to transactions being made between entities established in the same country, forming a VAT group may seem to be the holy grail as intra VAT group transactions are not subject to VAT.3

For cost-effective operations the above two structures are often applied in parallel. This structure created the “best of both worlds” solution, which does not trigger a VAT cost to any of the entities in the supply chain. In the pre-Skandia era this joint structure was not debated at an EU level other than in the Working Papers of the European Commission.4

However, in the Skandia judgment the ECJ held that if an EU branch is VAT grouped, its ‘VAT personality’ will be separated from its non-EU head office. As a result, where a head office supplies services to its VAT grouped branch, the supply should be regarded as if it is made to the VAT group. This VAT group is by virtue of the VAT grouping ‘fiction’, a separate taxable person. This means that, since the judgment in Skandia, intra-company supplies between a head office and its branches established in the EU that are members of a VAT group, could be subject to VAT.

The Skandia judgment: how to gain a competitive edge by using non-tax means

1 The ECJ ruled in its judgment (C-210/04) that services supplied by a head office to its branch, and vice versa, fall outside the scope of VAT by reason of the fact that they are one and the same taxable persons for VAT purposes, since (i) no legal relationship exists between a head office and its branch as they are the same legal entity and (ii) the branch cannot carry out independent economic activity on its own as it is economically bound to its head office.

2 Skandia America (USA) – 17 September 2014 (C-7/13) 3 A VAT group is a ‘fictitious’ single taxable person for VAT purposes, created by closely bound, but legally independent persons

established in a given Member State. Accordingly, by virtue of this ‘fiction’, supplies between VAT group members are treated as transactions performed within the same taxable person and are disregarded for VAT purposes.

4 To safeguard tax revenues (or avoid abusive practice), Member States may implement anti-avoidance measures with respect to their VAT grouping provisions. Some countries, such as the UK or Belgium, have implemented anti-avoidance rules on certain costs routed into a VAT group even before the Skandia judgment was released.

2

It is still debatable whether this judgment, which was based on the specific facts of the case, should be applied in a broader context. The application of the judgment needs to be reviewed in light of the specific facts of the case and whether it should be limited to cases where:

• the branch is part of an EU VAT group;• there is a non-EU head office and an EU branch; • the services falling within the scope of the Skandia judgment are limited to externally

purchased services; • supplies are made to a VAT group rather than by a VAT group; and • the supplies are of services and not goods.

Ostensibly, the positive aspect of the judgment could be where establishments (in practice mainly head offices) may achieve a higher recovery percentage. This would be due to supplies, previously outside the scope, being treated as taxable for recovery purposes.5

Implementation of Skandia across the EUIt is clear that the judgment itself creates an opportunity for EU Member States to tax transactions that were previously not subject to VAT. Given the limited right of financial organizations to recover this VAT, it is foreseeable that tax authorities will target this potential revenue. The question is, to what extent.

VAT grouping is a ‘may’ provision in the VAT Directive and Member States have discretion to introduce additional measures for the purposes of mitigating tax avoidance. Member States that have implemented VAT grouping have done so differently (e.g. narrow or broad territorial interpretation of the VAT group6, use of anti-avoidance measures). This has led in itself to a discrepancy in the interpretation and implementation of Skandia across the EU.

The debate around the scope of Skandia and its potential implementation and implications has not reached a conclusion, even on an international level. Both the European Commission and the VAT Expert Group7 published papers on this topic, but their arguments and recommendations seem to profoundly contradict each other.8

From a practical point of view, the tax authorities in the EU have also not aligned their implementation of Skandia. Some Member States have published official guidelines regarding their standpoint (e.g. whether there is a need for change the law and, if so, when this change will take effect), while others – mainly where the VAT grouping regime has not been implemented – remain silent on the topic. As a result, the VAT risk associated with higher VAT costs to a structure deriving from the Skandia judgment varies from low to high across the Member States.

5 In such a situation, e.g. where a head office provides IT services to its foreign branch which is VAT grouped, the supply of the head office would be seen as taxable, meaning that the head office may improve its pro-rata and deduct proportionally more input VAT than before Skandia. To make things work in a reverse scenario, where the supplier is VAT grouped, the local VAT grouping provisions in the Member State of the VAT group should limit such grouping to local establishments.

6 Some Member States include foreign establishments of entities in a local VAT group, 7 The VAT Expert Group assists and advises the European Commission on VAT matters, especially with regard to the preparation of

legislative acts and other policy initiatives, as well as provides insights regarding the practical implementation of legislatives acts and other EU policy initiative in the field of VAT. The group is composed of acknowledged organisations and individuals with the requisite expertise in the area of VAT.

8 The Commission has taken the view that the Skandia judgment should be interpreted in a broader context (e.g. applicable for supply of goods and internally generated supplies of services as well), while the VAT Expert Group has articulated that, in their view, there is a need for a limited interpretation of Skandia.

3

The decision to makeThe majority of international financial services organizations have operated a branch-VAT group structure. Since the judgment in Skandia, we know that head office recharges, previously disregarded for VAT purposes, are now subject to VAT in some jurisdictions.

These organizations affected by the judgment must make a decision. They either:

• Bear the cost of non-recoverable VAT on all of the group recharges they receive9 from HQ; or• Start looking at those recharges in a greater level of detail to identify opportunities to mitigate

the VAT cost to the extent possible.

Essentially, financial services organizations should look at the recharges and determine if there are alternatives that would offer a cost efficient solution. It is also worth noting that the latter exercise would provide other benefits driven by enhanced transparency besides pure cost saving.

However, before one would start to do this, we have to review the practical challenges to be able to come up with an efficient solution for how businesses can leverage from a multidisciplinary approach.

Cost allocation a zero-sum game?Cost allocation has traditionally been a management control method which was being used to measure profitability in different dimensions (e.g. branches, customers, distribution channels, etc.). The objectives of cost allocation have expanded over time. Nowadays, cost allocation is being used for a wide range of purposes including transfer pricing, individual performance measurement & incentivization, regulatory reporting and risk management. As a result of the Skandia judgment, cost allocation can now also serve a VAT purpose.

Traditionally, a broad percentage of expenses may have arbitrarily been added to direct costs to account for indirect (overhead) costs. However, as the percentages of indirect costs rose, this technique has become increasingly inaccurate. Indirect costs are not caused equally by all the products or services. Consequently, when multiple products share common costs, there is a danger of one product subsidizing another.

Activity Based Costing (ABC) is a methodology that measures cost and performance of activities, resources and cost objects, assigns resources to activities and activities to cost objects based on their use, and recognizes causal relationships of cost drivers to activities. ABC aims to answer the simple question: what do things (activities, products, services, customers, channels, etc.) cost. This methodology (looking at what is done in terms of activities) differs from a traditional view on costing (looking at what is spent) in the assumption that activities consume costs, and products and services consume activities.

The Skandia judgment: how to gain a competitive edge by using non-tax means

9 If the recipient of the recharges performs both VAT taxable and exempt supplies as part of its business operation, it may recover a portion of the VAT due on these recharges via the reverse charge mechanism.

4

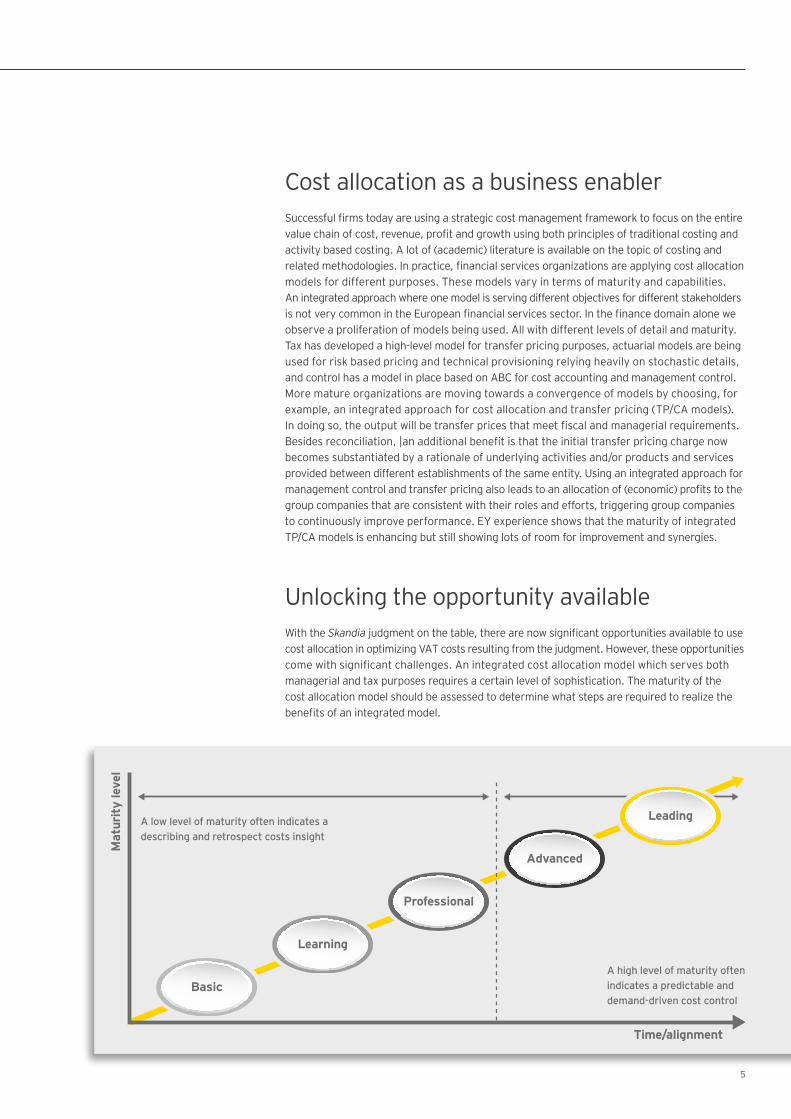

Cost allocation as a business enablerSuccessful firms today are using a strategic cost management framework to focus on the entire value chain of cost, revenue, profit and growth using both principles of traditional costing and activity based costing. A lot of (academic) literature is available on the topic of costing and related methodologies. In practice, financial services organizations are applying cost allocation models for different purposes. These models vary in terms of maturity and capabilities. An integrated approach where one model is serving different objectives for different stakeholders is not very common in the European financial services sector. In the finance domain alone we observe a proliferation of models being used. All with different levels of detail and maturity. Tax has developed a high-level model for transfer pricing purposes, actuarial models are being used for risk based pricing and technical provisioning relying heavily on stochastic details, and control has a model in place based on ABC for cost accounting and management control. More mature organizations are moving towards a convergence of models by choosing, for example, an integrated approach for cost allocation and transfer pricing (TP/CA models). In doing so, the output will be transfer prices that meet fiscal and managerial requirements. Besides reconciliation, |an additional benefit is that the initial transfer pricing charge now becomes substantiated by a rationale of underlying activities and/or products and services provided between different establishments of the same entity. Using an integrated approach for management control and transfer pricing also leads to an allocation of (economic) profits to the group companies that are consistent with their roles and efforts, triggering group companies to continuously improve performance. EY experience shows that the maturity of integrated TP/CA models is enhancing but still showing lots of room for improvement and synergies.

Unlocking the opportunity availableWith the Skandia judgment on the table, there are now significant opportunities available to use cost allocation in optimizing VAT costs resulting from the judgment. However, these opportunities come with significant challenges. An integrated cost allocation model which serves both managerial and tax purposes requires a certain level of sophistication. The maturity of the cost allocation model should be assessed to determine what steps are required to realize the benefits of an integrated model.

5

In a recent EY publication “Effective cost management and profitability analysis for the financial services sector” the different stages of this maturity model are described. Typical challenges include definition of a set of products and services which are provided both internally as well as to external clients. Additionally, the appropriate level of detail in the definition of activities which are being executed to deliver these products and services is a challenge. One should bear in mind that the costs of costing should not exceed the benefits. An approach which is based on the principle “better be approximately right, then precisely wrong” is therefore advised.

EY experience demonstrates that in building cost allocation models, organizations struggle in the distinction between activities and products/services and defining the appropriate activity drivers. This is exactly the area which, from a VAT perspective, the opportunities reside.

More mature cost allocation models have a clear distinction between activities and products / services but also a sound set of activity drivers. These are often agreed upon within the organization using a product/service catalog. Organizations which are also capable of breaking down the nature of the costs of a product / service (i.e. provide the insight into which part of the costs are fixed, and which are variable) have an additional benefit from a VAT perspective.

The Skandia judgment: how to gain a competitive edge by using non-tax means

Cost Alloccation Model (CAM)

2. Products/services

The products of services delivered are the cost objects to wich te final costs are allocated

1. Customers

Cost- and commercial prices for the customer to which products and/or services are deleverd

3. Activities

The operational activities wich are required to go through a proces step

4. Activities

The resources (costs) distributed by costs pools based on the general ledger

7. Resource drivers

The amount of recources (eg. hours, sqaure meters) required for carrying out an activity

5. Transaction volumes

Transaction volumes are the amount (quantity) of products and/or services clients purchase

6. Activity drivers

The frequency and intesity of an activity required to generate a product/service (eg. volumes)

6

Where do we go from here?In being able to distinguish the type of activities resulting in an allocation of costs, the VAT treatment of the specific activities can be determined, thereby leading to a more precise analysis of the VAT treatment of group costs that are recharged. This in turn can minimize VAT costs that are incurred as a result of the Skandia judgment particularly if any costs can benefit from VAT exemption. Furthermore, the true costs can be oncharged rather than arbitrary costs, with added internal labour costs, that merely drive up the VAT costs to the organization.

The Skandia judgment has resulted in international organizations reviewing the costs allocated between their VAT groups and establishments in other Member States in order to quantify VAT costs to the business and to minimize penalties or non-compliance. In doing so, such organizations would be wise to revisit their cost allocation methodologies, to refine them in a way that the activities relating to each recharge can be isolated. This allows the tax specialists to allocate the correct VAT treatment to these costs, thereby possibly excluding certain costs from the charge to VAT. This can only be beneficial for organizations in a sector where VAT is generally an irrecoverable cost.

The starting point for gaining this competitive advantage is an integrated approach towards cost management. A review of the current cost allocation model (from both a management accounting and a tax perspective) could give the organization insight into what steps can be taken to realize the benefits. These quick wins bring immediate benefit to the organization. It is likely that these quick wins trigger improvements to the Finance and Tax function as a whole. An integrated approach towards Cost Management and Profitability Analysis can maxiamize value and can bring Finance and Tax to the next level.

Bas BreimerPartner Tel: +31 (0)88 407 87 73Mobile: +31 (0)6 29 08 39 37Email: [email protected]

Financial Services Tax Financial Services Advisory

Rianne VedderPartner Tel: +31 (0)88 407 08 56Mobile: +31 (0)6 21 25 28 94Email: [email protected]

Shima HeydariSenior Manager Tel: +31 (0)88 407 14 15Mobile: +31 (0)6 55 44 21 41Email: [email protected]

Diederik LigtenbergSenior Manager Tel: +31 (0)88 407 08 56Mobile: +31 (0)6 52 46 59 27Email: [email protected]

Contact details EY

7

EY | Assurance | Tax | Transactions | Advisory

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate Legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2016 Ernst & Young Accountants LLP.All Rights Reserved.

ED None155010228

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com/nl