Embed Size (px)

Citation preview

Chapter 4:

The Simple InterestSHMth1: General Mathematics

Accountancy, Business and

Management (ABM)

Mr. Migo M. Mendoza

Chapter 4: The Simple InterestLecture 14: Basic Concepts on Simple InterestLecture 15: Computing Simple Interest ProblemLecture 16: The Maturity Value and Present ValueLecture 17: Exact and Ordinary InterestsLecture 18: Time Between Two Dates

Lecture 14: Basic Concepts on Simple Interest

SHMth1: General Mathematics

Accountancy, Business and

Management (ABM)

Mr. Migo M. Mendoza

Classroom Task:

Family Activity 2: Views about Interest Rates

SSMth1: Precalculus

Science and Technology, Engineering

and Mathematics (STEM)

Mr. Migo M. Mendoza

Instructions:Gather your family members and discuss the following views about

interest rates. Please prepare a five-

minute presentation about it. The

presentation can be in a form of a family report, skit etc.

Grading System:Criteria Percentage

Content 40

Organization of Ideas 20

Communication Skills 15

Presentation and Aesthetic Consideration

15

Behavior during the Presentation

10

Views about the Interest Rates…

The lower the interest

rate the more people are

over-optimistic to borrow

money.

Views about the Interest Rates…

The higher the interest

rate the lesser people are

optimistic to borrow

money.

Views about the Interest Rates…

High interest rate

hurts seasonal

businesses.

Views about the Interest Rates…

The government

benefits from interest

rates.

Views about the Interest Rates…

Businesses and foreign

investors benefit from

interest rates.

Something to think about…

Lender vs. Borrower

The Three (3) Categories of Interest

1. Simple Interest2. Simple Discount

3. Compound Interest

The Simple Interest

SHMth1: General Mathematics

Accountancy, Business and

Management (ABM)

Mr. Migo M. Mendoza

The Simple Interest

Simple Interest is calculated only on the original principal amount and is paid at the end

of the loan period.

Take Note:

Interest is calculated only on the original principal

amount and is paid at the end of the borrowed money.

Three (3) Components of the Simple Interest

The Principal (P)The Rate of Interest (r)

The Time (t)

Principal (P)

The refers to the sum of money invested, deposited or borrowed. We will use P (majuscule letter P)

to denote or represent the principal.

Rate of Interest (r)

This refers to the percentage of the principal per year and is generally expressed in terms of percent. The rate of interest is usually represent

by r (minuscule letter r).

Take Note:

The rate of interest is the percentage of the principal that will

be charged for specified period of

time (e.g. daily, weekly, monthly, yearly, etc.).

Take Note:

Before computing rate in percent must be expressed

in decimal form.

Time (t)

This refers to the length of time between the date the loan is made

and the date the loan becomes payable to the lender. To denote time

we will use t (miniscule letter t).

Take Note:

Time is usually expressed in years. When t is given in months, then the number months is divided by 12.

Lecture 15: Computing Simple Interest Problems

SHMth1: General Mathematics

Accountancy, Business and

Management (ABM)

Mr. Migo M. Mendoza

Learning Expectation:

In this section we shall deal with the

computation of simple interest.

Formula 1: The Amount of Simple Interest

tI Pr

Formula 1: The Amount of Simple Interest

This shall be used in computing the amount of interest when principal amount (P), rate of

interest (r), and the duration of the term (t) are given.

Take Note:

In simple interest, the amount of interest

earned per annum is constant.

Explanation:

If the interest (I) for the first year is P100.00, then the value of I for the

succeeding years shall also be P100.00, assuming of course that the

Principal (P) and the interest rate are also constant.

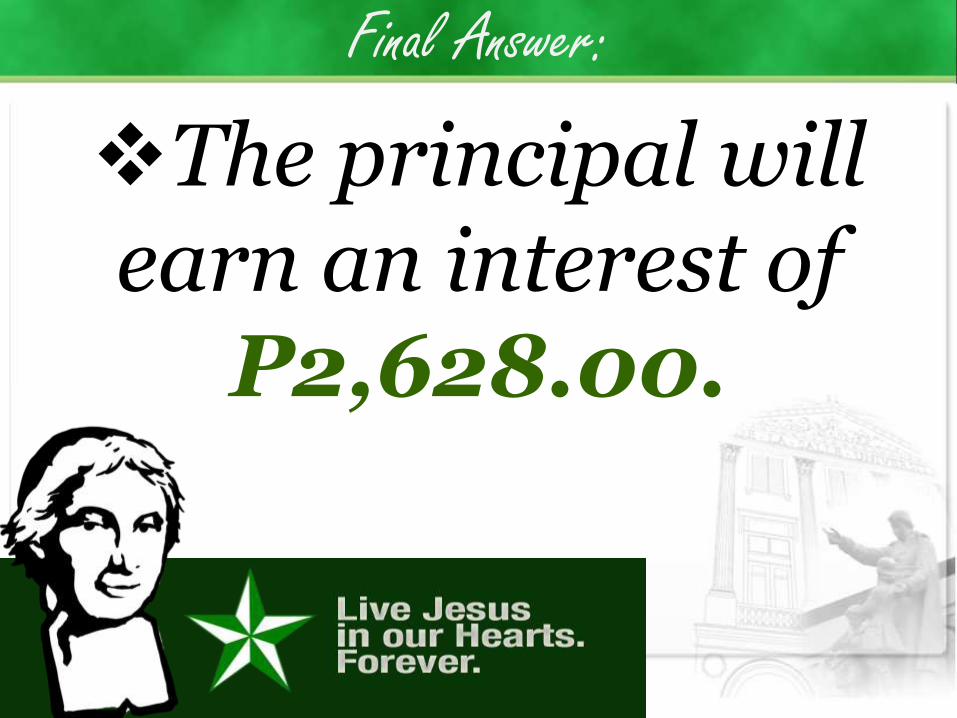

Example 68:

What amount of interest will be charged on the loan of Ms. Bea

Ky of P7,300.00 borrowed for 3years at a simple interest rate of

12% per annum?

Final Answer:

The principal will earn an interest of

P2,628.00.

Example 69:Nimfa Bebe deposited P5,000.00 in a

bank paying 6% simple interest for 5 years. Compute the:

a) amount of interest per annum; and

b) total amount of interest for the entire period.

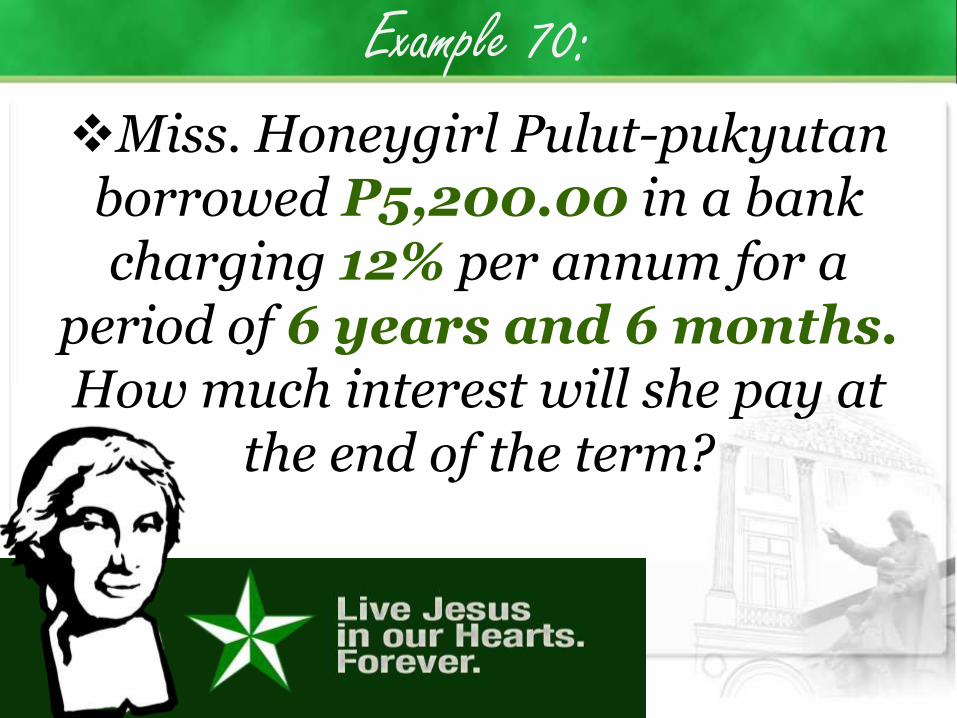

Example 70:

Miss. Honeygirl Pulut-pukyutanborrowed P5,200.00 in a bank charging 12% per annum for a

period of 6 years and 6 months.How much interest will she pay at

the end of the term?

Take Note:

What should we do when rate or percentage

of interest (r) is unknown?

Classroom Task :

Derive the formula for finding the rate

of interest.

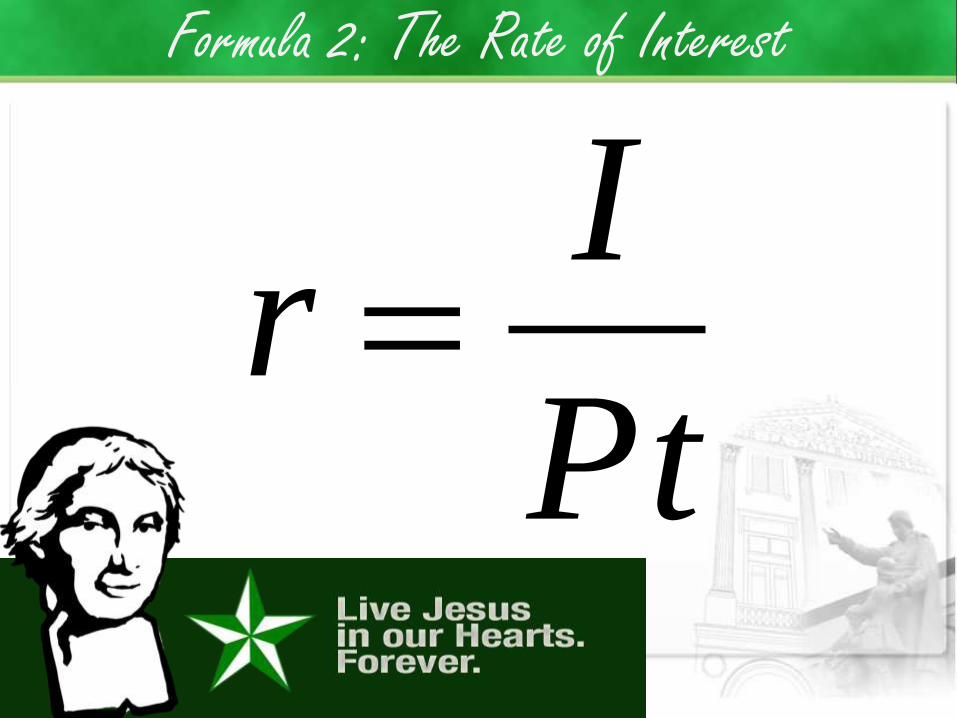

Formula 2: The Rate of Interest

Pt

Ir

Formula 2: The Rate of Interest

This formula shall be used when computing for the rate of interest

when amount of interest, principal amount, and time are

given.

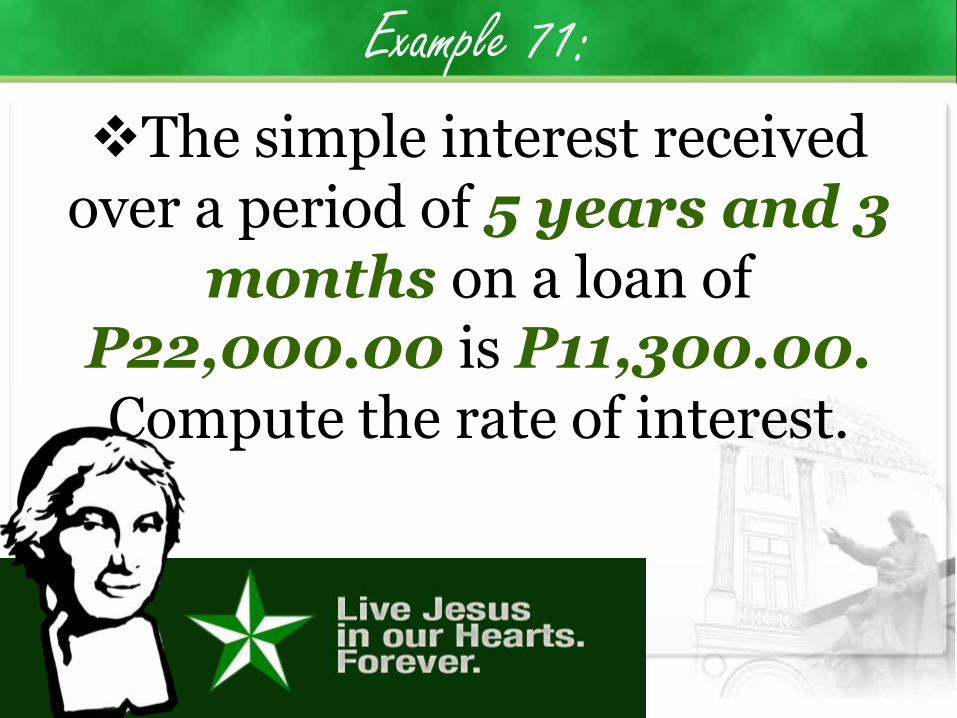

Example 71:

The simple interest received over a period of 5 years and 3

months on a loan of P22,000.00 is P11,300.00. Compute the rate of interest.

Something to think about…

What should we do when duration of the loan/ time

(t) is unknown?

Classroom Task :

Derive the formula for finding

the time.

Formula 3: The Duration of the Loan/ Time

Pr

It

Formula 3: The Duration of the Loan/ Time

This shall be used in computing the time given the principal, rate and the

amount of interest.

Example 72:Lhady_ZsUpFlaDeeTa borrowed P5,000.00 from a bank charging 12% simple interest. If she paid the

amount of interest equivalent to P1,200.00, for how long did she

use the money?

Example 73:

TrOuFHaNG_QOuLLheTszpaid an amount P13, 620.00

for a loan P25,600.00 at 10.5% interest rate. Find the

duration of the term?

Something to think about…

What should we do when Principal (P) is

unknown?

Classroom Task :

Derive the formula for finding the principal

amount.

Formula 4: The Principal Amount

rt

IP

Formula 4: The Principal Amount

This shall be used in computing the Principal when

amount of interest, rate of interest and time are given.

Example 74:

bHozSS_mHapA6mahAL paid

an interest of P2,800.00 on a

loan for 2 years at 9.5% interest rate. How much was

the original loan?

Performance Task 13:

Please download, print

and answer the “Let’s

Practice 13.” Kindly work

independently.

Lecture 16: The Maturity Value and the Present Value of the

Simple InterestSHMth1: General Mathematics

Accountancy, Business and

Management (ABM)

Mr. Migo M. Mendoza

The Maturity Value (F)

This refers to the sum of money at the end of the period

when a certain amount of money is deposited or

borrowed.

The Maturity Value (F)

Maturity Value denoted by Fis also called as the

“accumulated value,” “future value,” and “final

value.”

The Maturity Value (F)

In other words, maturity value is equal to the sum of the

amount of principal and the amount of interest.

Classroom Task :

Derive the formula for finding the maturity

value (F).

Formula 6: The Maturity Value (F)

)1( rtPF

Formula 6: The Maturity Value (F)

This shall be used in computing the maturity value given the amount

of principal and the amount of interest. Also, it can be computed

when original loan, rate of interest and time are given.

Example 75:

Miss Bea Bunda deposited an amount of P12,800.00 in a savings bank that

gives 6.5% simple interest for 8 years. How much would she have in her

account at the end of 8 years assuming that no withdrawals were made?

Example 76:

Mr. Hagardo Versoza paid an interest of P5,000.00 on a loan for 3 years at

8% simple interest. Compute the value of:

a) the original loan; andb) the amount Mr. Versosa paid

at the end of 3 years.

Something to think about…

Based on our previous example, what is now

the present value?

The Present Value (P)

The present value is the current worth of future sum of invested, borrowed, or deposited money given a specified rate of return.

The Present Value (P)

Since the present value is actually the principal, we

will denote it using majuscule letter P.

Classroom Task:

Derive the formula for finding the present

value (P).

Formula 6: The Present Value (P)

)1( rt

FP

Formula 6: The Present Value (P)

This shall be used in computing the present value given the maturity value, rate

and time.

Example 77:

Determine the present value of an investment which

accumulated to P48,600.00in 6 years at 6% simple

interest.

Example 78:

The maturity value paid on a loan is P72,000.00. If the loan was for 3 years at 9% simple interest, (a) how much was the original loan? (b)

Compute the total amount of interest.

Something to think about…

Based on our previous example, what is the easiest

way to compute the total amount of interest (I)?

Formula 7: The Total Interest

PFI

Formula 7: The Total Interest (I)

This shall be used in computing the total amount of

interest given the maturity value and the present value.

Performance Task 14:

Please download, print

and answer the “Let’s

Practice 14.” Kindly work

independently.

Lecture 17: The Exact and the Ordinary Interests

SHMth1: General Mathematics

Accountancy, Business and

Management (ABM)

Mr. Migo M. Mendoza

A Short Recap…

When the term of investment is expressed in days, what would be the approach in computing

for the amount of interest?

The Two ApproachesTwo Approaches in Computing for the Amount of

Interest Given the Time in Dates:

1. Exact Interest Method2. Ordinary Interest Method

The Exact Interest

This is used when interest is computed on the basis of 365 days a year or 366 days in a

leap year.

The Exact Interest

To denote Exact Interest we will use the symbol Ie

(majuscule letter I and subscript minuscule letter e).

Formula 8: The Exact Interest (Ie)

366

Pr

365

Pr torI

tI ee

Formula 8: The Exact Interest

This shall be used in computing for the exact

interest, given the principal amount, the rate of interest

and time per days.

The Ordinary Interest (Io)

This is used when interest is computed on the

basis of an assumed 30-day/month or 360-

day/year.

The Ordinary Interest (Io)

To denote Ordinary Interest we will use the symbol Io

(majuscule letter I and subscript minuscule letter o).

Formula 9: The Ordinary Interest (Io)

360

Pr tIo

Formula 9: The Ordinary Interest (Io)

This shall be used in computing for the ordinary interest, given the principal

amount, the rate of interest and time per days.

Example 79:Mr. Benny Bilang invested an amount of P28,100.00 at 7%

simple interest for 100 days. Compute the value of the:

1) exact interest; and2) ordinary interest.

Example 80:Miss Lily Mangipin deposited an amount of P12,800.00 in a time

deposit account at 8% simple interestfor 150 days. Compute the value of the:

exact interest; and the maturity valueat the end of the term.

Performance Task 15:

Please download, print

and answer the “Let’s

Practice 15.” Kindly work

independently.

Lecture 18:

Time between Two DatesSHMth1: General Mathematics

Accountancy, Business and

Management (ABM)

Mr. Migo M. Mendoza

Something to think about…

If two dates are given,

how can we determine

the number of days?

Example 81:

Determine the number of days from

September 21, 2017 to March 14, 2018.

Loan Date:

This is the first day the loan/ deposit/ investment was made. It is also called

as the “origin date.”

Hence,

In our previous example the loan date

or origin date is September 21, 2017.

Maturity Date

This is the last day of the loan/ deposit/ investment. It

is also called as the “due date.”

Hence,

In our previous example the loan date

or origin date is March

14, 2018.

Did you know?

There are two ways in

determining the

number of days given

two dates.

Two Ways in Determining Number of Days Given Two Dates

Two Ways in Determining the Number of Days Given Two Dates:

(1) Actual Time(2) Approximate Time

The Actual Time (Ac)

This refers to the exact number of days between two dates. It is

obtained by counting the actual number of days in each month

within the period of the transaction except the loan date.

The Approximate Time (Ap)This refers to the assumption that each

month has 30 days. The number of days is obtained therefore by counting

each day of each month within the period of the transaction except the

loan date.

Something to think about…

How can we determine

which are 30-day month

and which are not?

The Knuckle Months MethodThe knuckle and the space between them are consecutively given the names

of the months, each knuckle corresponds to months with 31 days

and each space corresponds to a short month.

The Knuckle Months Method

Example 81: Determine the number of days

from September 21, 2017 to

March 14, 2018 using actual and approximate time

methods.

Did you know?

There are certain steps to follow in order to determine

the number of days when loan date and maturity date

are given.

Steps in Determining the Number of Days Given Two Dates

Step 1:

Identify the number of days remaining in the first month

excluding the loan date.

Steps in Determining the Number of Days Given Two Dates

Step 2:

Write the number of days in each succeeding month.

Steps in Determining the Number of Days Given Two Dates

Step 3:

Identify the number of days in the last month including the

maturity date.

Steps in Determining the Number of Days Given Two Dates

Step 4:

Add the days from the first month to the last month.

Example 82:Determine the actual and

approximate time from February 1, 2016 to December 25, 2016.

Did you know?When dealing with transactions

where the loan and maturity dates are given, we have four

possible ways of computing the period t.

Four Methods for Computing the Amount of Interest Given Two Dates

Four Methods for Computing the Amount of Interest Given Two Dates:

1.Actual Time, Ordinary Interest Method2.Actual Time, Exact Interest Method

3.Approximate Time, Ordinary Interest Method

4.Approximate Time,Exact Interest Method

Formula 10: Actual Time, Ordinary Interest Method

360

Pr co

AI

Formula 10: Actual Time, Ordinary Interest Method

This shall be used in computing for the ordinary

interest when amount of principal, rate of interest and

actual time are given.

Formula 11: Actual Time, Exact Interest Method

365

Pr ce

AI

Formula 10: Actual Time, Exact Interest Method

This shall be used in computing for the exact interest when amount of

principal, rate of interest and actual time are given.

Formula 12: Approximate Time, Ordinary Interest Method

360

Pr p

o

AI

Formula 12: Approximate Time, Ordinary Interest Method

This shall be used in computing for the ordinary interest given the amount of

principal, rate of interest and approximate time.

Formula 13: Approximate Time, Exact Interest Method

365

Pr p

e

AI

Example 83:An amount of P18,000.00 was invested

to McDollibee at 8% simple interest on May 25, 2016. How much shall be the

amount of interest earned on October 12, 2016 using the four methods of

computing period t?

Banker’s Rule: This is the common commercial

practice and is the most favorable of all methods to the lender. This rule is an advocate of “Actual Time, Ordinary

Interest” method.

Something to think about…

Why do you think most

of the lenders or banks

love to use banker’s

rule?

Did you know?Since ordinary interest is greater than

exact interest and actual time is greater than approximate time. Actual time with ordinary

interest method yields the highest amount. Therefore, more money!

More profit! Yehey!

Example 84:On December 25, 2011, LIBING Things

Funeral Parlor deposited an amount of P15,800.00 in a bank that pays 6.5% simple

interest. Compute the maturity value on August 8, 2012, using the:

1) Banker’s Rule; and

2) Approximate time, Exact Interest method.

Performance Task 16:

Please download, print

and answer the “Let’s

Practice 16.” Kindly work

independently.

![120+ Simple interest & Compound Interest … Simple interest & Compound Interest Questions With Solution GovernmentAdda.com Daily Visit : [GOVERNMENTADDA.COM] GovernmentAdda.com |](https://img.pdfslide.us/doc/110x75/5adc5eab7f8b9ae1408b7ca2/120-simple-interest-compound-interest-simple-interest-compound-interest-questions.jpg)

![120+ Simple interest & Compound Interest Questions With … · 120+ Simple interest & Compound Interest Questions With Solution GovernmentAdda.com . Daily Visit : [GOVERNMENTADDA.COM]](https://img.pdfslide.us/doc/110x75/5e7b9ad23f4ca3416d59c1c7/120-simple-interest-compound-interest-questions-with-120-simple-interest.jpg)