Embed Size (px)

Citation preview

The “Shale Revolution” Myths and Realities

Trans-Atlantic Energy DialogueWashington, DC

December 10, 2013

J. David Hughes

Global Sustainability Research Inc.

Post Carbon Institute1

Conventional Wisdom

• The United States is on the verge of Energy Independence thanks to the “SHALE REVOLUTION”.

• Shale Gas production will continue to grow for the foreseeable future (2040 at least) and prices will remain below $4.50/mcf for the next 10 years and below $6.00/mcf for the next 20 years.

• The way is clear for U.S. LNG exports to monetize the shale bounty. Large scale LNG exports of shale gas from Canada will provide a bonanza.

• Tight Oil will allow U.S. production to exceed that of Saudi Arabia and U.S. imports will shrink to zero.

© Hughes GSR Inc, 2013

2

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

2040

0

5

10

15

20

25

30

35LNG Imports Canada Imports Shale GasAlaska Coalbed Methane Tight GasAssociated Conventional Offshore

Year

Tri

llio

n C

ub

ic F

ee

t p

er

Ye

ar

U.S. Natural Gas Supply Projection by Source, 2010-2040, EIA Reference Case 2013

Canadian Imports

Shale Gas(+105% 2012-2040)

Coalbed Methane

50% o

f 2040 Pro

du

ction

55% increase inproduction by 2040

Tight Gas

Conventional

Offshore

Associated

Alaska

U.S. domestic consumption

Exports

(data from EIA Annual Energy Outlook 2013, Tables 13 and 14, http://www.eia.gov/forecasts/aeo/er/excel/yearbyyear.xlsx)© Hughes GSR Inc, 2013

3

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

2040

0

1

2

3

4

5

6

7

8

9AlaskaOnshore EOROnshore Shale/Tight OilLower-48 Onshore Conventional Lower-48 Offshore

Year

Mil

lio

n B

arr

els

pe

r D

ay

Shale/Tight Oil

Lower-48 Offshore

Alaska

Lower-48 Onshore Conventional Production

Onshore EOR

32% o

f 2040 Su

pp

lyU.S. Crude Oil Production Projection by Source and

Region 2010-2040 (EIA 2013 Reference Case)

Peak Production 2019

© Hughes GSR Inc, 2013 (data from EIA Annual Energy Outlook 2013)

4

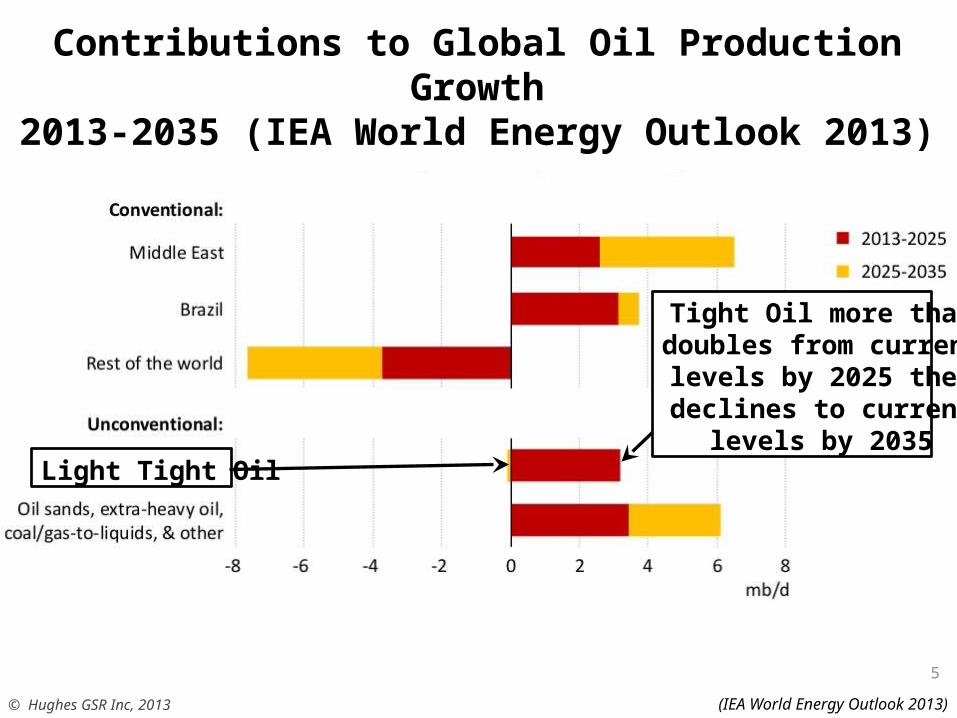

Contributions to Global Oil Production Growth2013-2035 (IEA World Energy Outlook 2013)

© Hughes GSR Inc, 2013 (IEA World Energy Outlook 2013)

Tight Oil more thandoubles from currentlevels by 2025 thendeclines to current

levels by 2035Light Tight Oil

5

2007 2008 2009 2010 2011 2012 20130

5

10

15

20

25

30

35

Marcellus (PA and WV)Bakken (ND)Eagle Ford (TX)Antrim (MI, IN, and OH)Rest of U.S.Woodford (OK)Fayetteville (AR)Haynesville (LA and TX)

Year

Gas

Pro

du

ctio

n (

Bil

lio

n c

ub

ic f

eet

per

day

)

Peak Excluding Marcellusoccurred August 2012

Now Down 5%

U.S. Shale Gas Production from EIA data, 2007 - June, 2013

(data from DI Desktop, HPDI, September, 2012)

© Hughes GSR Inc, 2013 (data from EIA, 2013, http://www.eia.gov/naturalgas/weekly/img/ShaleGas-201306.xlsx)

42% of U.S. Production

Peak Excluding Marcellusand tight oil plays

occurred November 2011Now Down 12% Marcellus

Haynesville

Barnett

Eagle Ford

6

2007 2008 2009 2010 2011 2012 20130

500

1000

1500

2000

2500

3000

3500

4000

Eagle FordBakkenHaynesvilleMarcellusPermianNiobrara

Year

Oil

Pro

du

ctio

n (

Th

ou

san

d B

arre

ls p

er D

ay)

Tight Oil, NG Liquids and Conventional Production from Six Plays, 2007- June, 2013 (EIA DPR Report, 2013)

© Hughes GSR Inc, 2013 (data from EIA DPR report December, 2012)

Eagle Ford

Bakken

Permian Basin

7

2007 2008 2009 2010 2011 2012 20130

500

1000

1500

2000

2500

Eagle FordBakkenHaynesvilleMarcellusPermianNiobrara

Year

Oil

Pro

du

ctio

n (

Th

ou

san

d B

arre

ls p

er D

ay)

U.S. Tight OilProduction NowAbout 2.3 mbd

Tight Oil Production from Six Plays, 2007- June, 2013(EIA DPR Report, 2013) - Excludes NGLs and Conventional

© Hughes GSR Inc, 2013 (data from EIA DPR report December, 2013)

Eagle Ford

Bakken

8

9

Marcellus

Haynesville

Barnett

Eagle Ford

Fayetteville

Woodford

Bakken

Antrim

Rest of U

.S.0

1

2

3

4

5

6

7

8

9

10

Shale Play

Bil

lio

n C

ub

ic F

ee

t p

er

Da

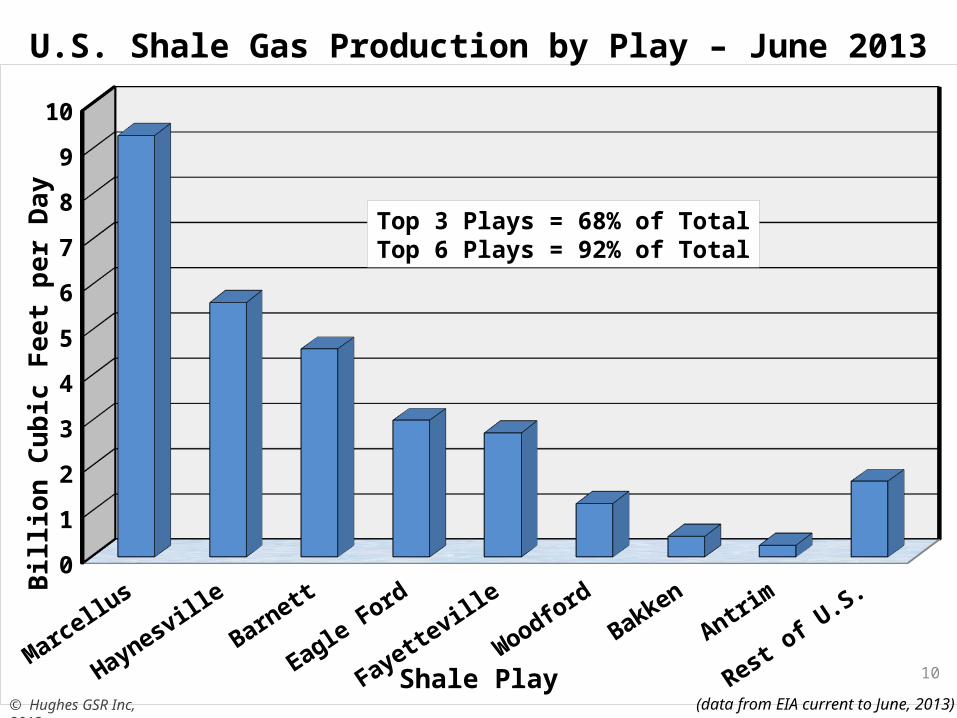

yU.S. Shale Gas Production by Play – June 2013

(data from EIA current to June, 2013)

Top 3 Plays = 68% of TotalTop 6 Plays = 92% of Total

© Hughes GSR Inc, 2013

10

Bakken

Eagle Ford

Permian Basin

Niobrara

Haynesville

Marcellus

Rest of U

.S.0

100

200

300

400

500

600

700

800

900

Shale Play

Th

ou

sa

nd

Ba

rre

ls p

er

Da

yU.S. Tight Oil Production by Play – June 2013

(data from EIA current to June, 2013 – excludes NGLs and conventional production)

Top 2 Plays = 74% of TotalTop 4 Plays = 85% of Total

© Hughes GSR Inc, 2013

11

The Shale Play Life Cycle

• Discovery followed by leasing frenzy.

• Drilling boom follows to meet “held-by-production” lease requirements.

• Sweet spots identified, targeted and drilled off.

• Production rises rapidly and is maintained for cash-flow despite potentially uneconomic full-cycle costs.

• Sweet spots become saturated and well quality and field production decline.

• Plays like the Haynesville become middle aged after just five years.

© Hughes GSR Inc, 2012

12

13

2006 2007 2008 2009 2010 2011 2012 20130

1

2

3

4

5

6

7

8

9

0

500

1000

1500

2000

2500

3000

3500

4000

Gas ProductionNumber of Wells

Year

Gas

Pro

du

ctio

n (

Bil

lio

n c

ub

ic f

eet

per

day

)N

um

ber o

f Op

erating

Wells

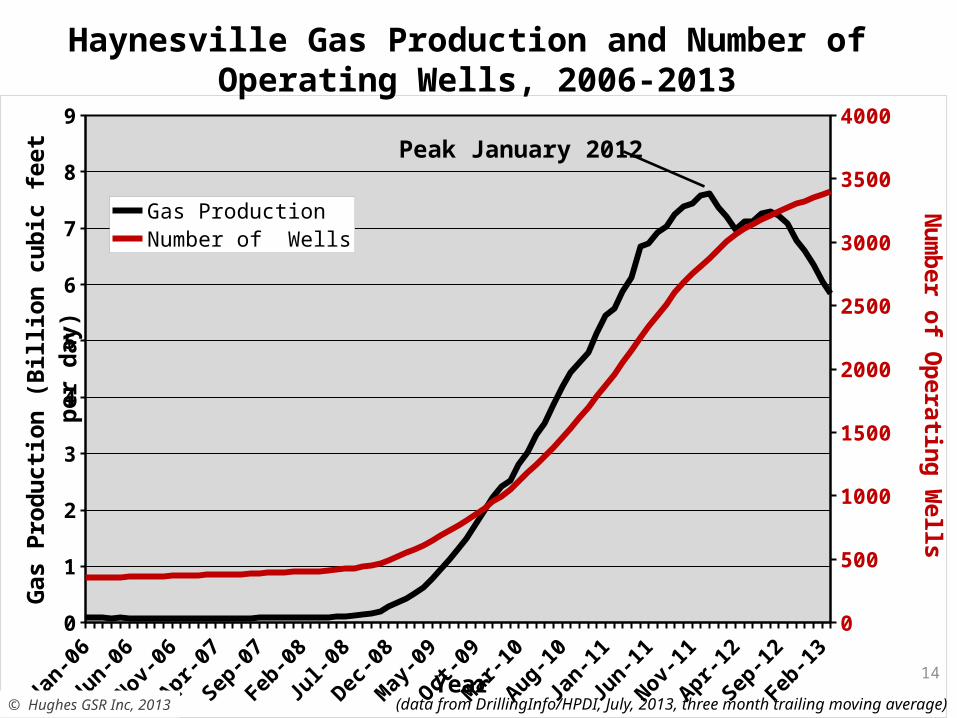

Haynesville Gas Production and Number of Operating Wells, 2006-2013

(data from DI Desktop, HPDI, September, 2012)

© Hughes GSR Inc, 2013 (data from DrillingInfo/HPDI, July, 2013, three month trailing moving average)

Peak January 2012

14

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 460

1000

2000

3000

4000

5000

6000

7000

8000

Months on Production

Gas

Pro

du

ctio

n

(Th

ou

san

d c

ub

ic f

eet

per

Day

)Haynesville Type Gas Well Decline Curve

(data from DrillingInfo/HPDI, March, 2013)

Yearly DeclinesFirst year = 66%

Second year = 49%Third year = 41%

Fourth year = 49%

© Hughes GSR Inc, 2013

3-Year Decline = 89%

15

2007 2008 2009 2010 2011 20120

1

2

3

4

5

6

7

8

0

500

1000

1500

2000

2500

3000

3500

4000

Production from pre-2012 WellsNumber of pre-2012 Wells

Year

Gas

Pro

du

ctio

n (

Bil

lio

n c

ub

ic f

eet

per

Day

)N

um

ber o

f Op

erating

pre-2012 W

ellsOverall Field Decline for Haynesville Gas Production

based on Production Decline from pre-2012 Wells

(data from DI Desktop, HPDI, September, 2012)

Overall Field Decline = 47%

© Hughes GSR Inc, 2013 (data from DrillingInfo/HPDI, March, 2013)

16

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 460

1000

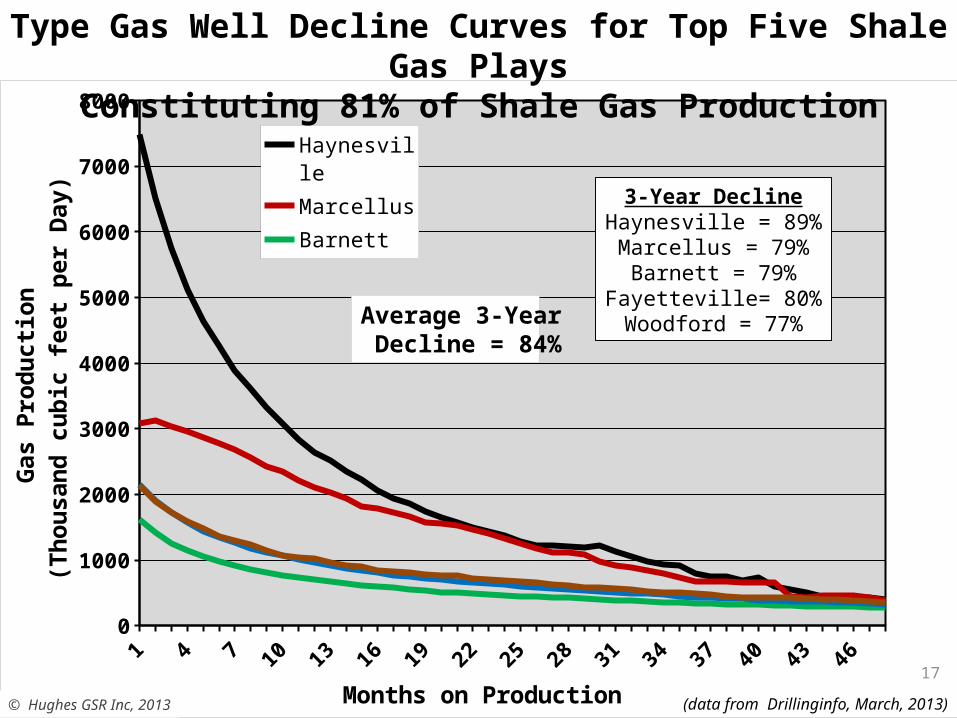

2000

3000

4000

5000

6000

7000

8000

HaynesvilleMarcellusBarnettFayettevilleWoodford

Months on Production

Gas

Pro

du

ctio

n

(Th

ou

san

d c

ub

ic f

eet

per

Day

)Type Gas Well Decline Curves for Top Five Shale Gas Plays

Constituting 81% of Shale Gas Production

(data from Drillinginfo, March, 2013)

3-Year DeclineHaynesville = 89%Marcellus = 79%Barnett = 79%

Fayetteville= 80%Woodford = 77%

© Hughes GSR Inc, 2013

Average 3-Year Decline = 84%

17

2008 2009 2010 2011 20120

1

2

3

4

5

6

7

8

HaynesvilleMarcellusBarnettFayettevilleWoodford

Year

Gas

Pro

du

ctio

n (

Bil

lio

n c

ub

ic f

eet

per

Day

)Overall Field Decline for Top Five Shale Gas Playsbased on Production Decline from pre-2012 Wells

(data from DI Desktop, HPDI, September, 2012)

Field Decline (per year)Haynesville = 47%Marcellus = 29%Barnett = 28%

Fayetteville = 35%Woodford = 44%

© Hughes GSR Inc, 2013 (data from Drillinginfo, March, 2013)

Average Field Decline = 37%

18

2006 2007 2008 2009 2010 2011 2012 20130

1

2

3

4

5

6

7

8

9

Barnett

Fayetteville

Woodford

Haynesville

PA Marcellus

WV Marcellus

Year

Gas

Pro

du

ctio

n (

Bil

lio

n c

ub

ic f

eet

per

day

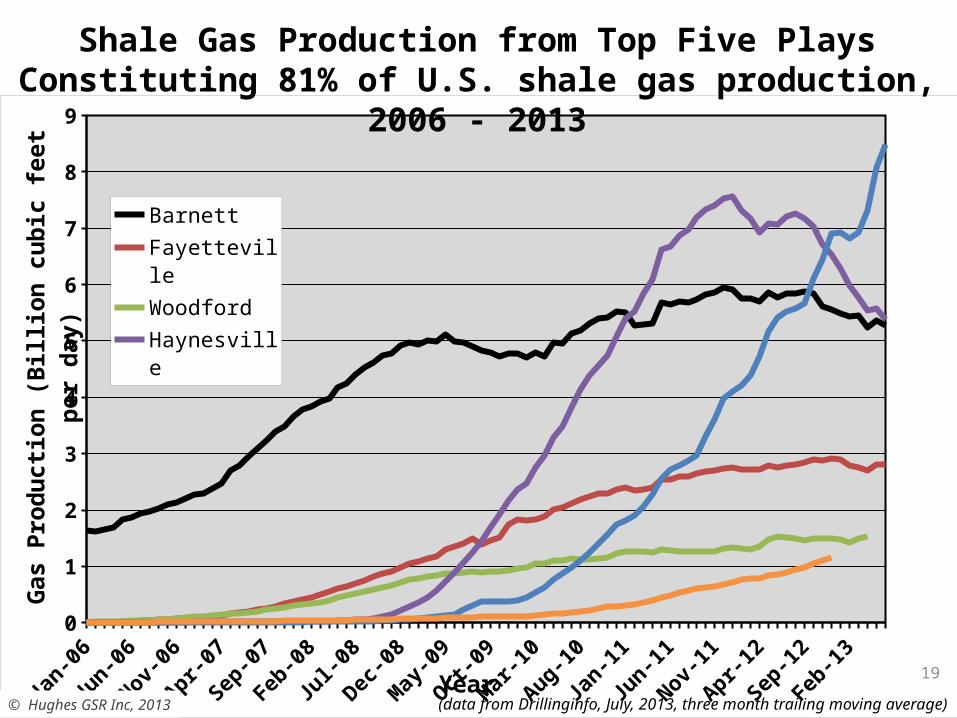

)Shale Gas Production from Top Five Plays Constituting

81% of U.S. shale gas production, 2006 - 2013

(data from DI Desktop, HPDI, September, 2012)

© Hughes GSR Inc, 2013 (data from Drillinginfo, July, 2013, three month trailing moving average)

19

2006 2007 2008 2009 2010 2011 2012 20130

5

10

15

20

25

30

PA Marcellus

WV Marcellus

Woodford

Fayetteville

Haynesville

Barnett

Year

Gas

Pro

du

ctio

n (

Bil

lio

n c

ub

ic f

eet

per

day

)

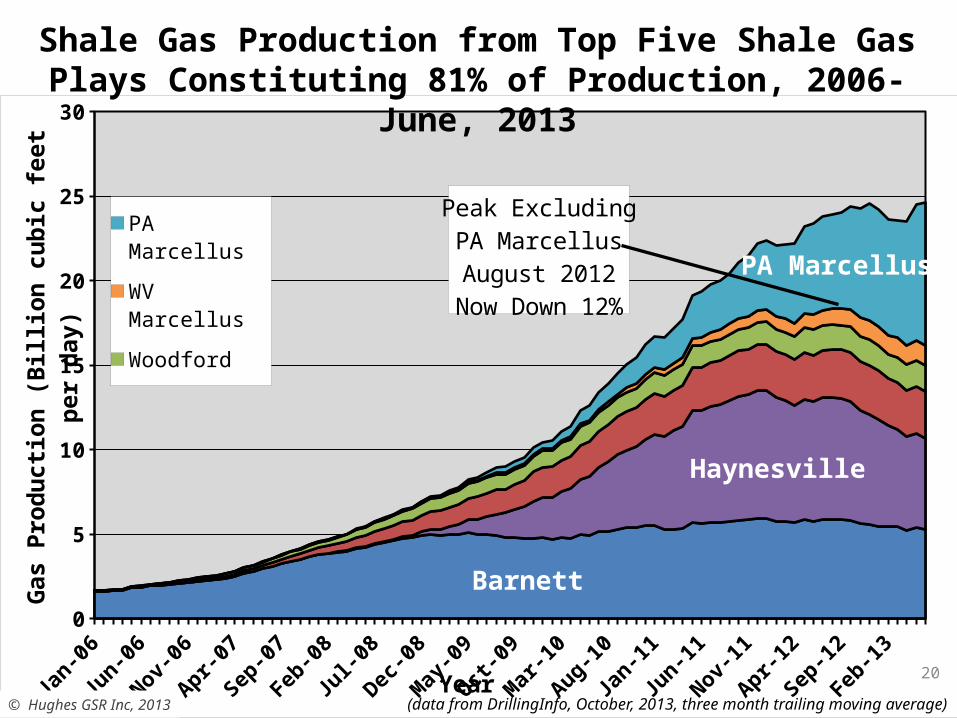

Peak ExcludingPA MarcellusAugust 2012

Now Down 12%

Shale Gas Production from Top Five Shale Gas Plays Constituting 81% of Production, 2006-June, 2013

© Hughes GSR Inc, 2013 (data from DrillingInfo, October, 2013, three month trailing moving average)

Haynesville

Barnett

PA Marcellus

20

Feb, 11 Jun, 11 Oct, 11 Feb, 12 Jun, 12 Oct, 12 Feb, 13 Jun, 13 Oct, 130

100

200

300

400

500

600

700

800

900

1,000 OtherMarcellusBarnettHaynesville

Haynesville

Other

(data from Baker-Hughes, November, 2013)© Hughes GSR Inc, 2013

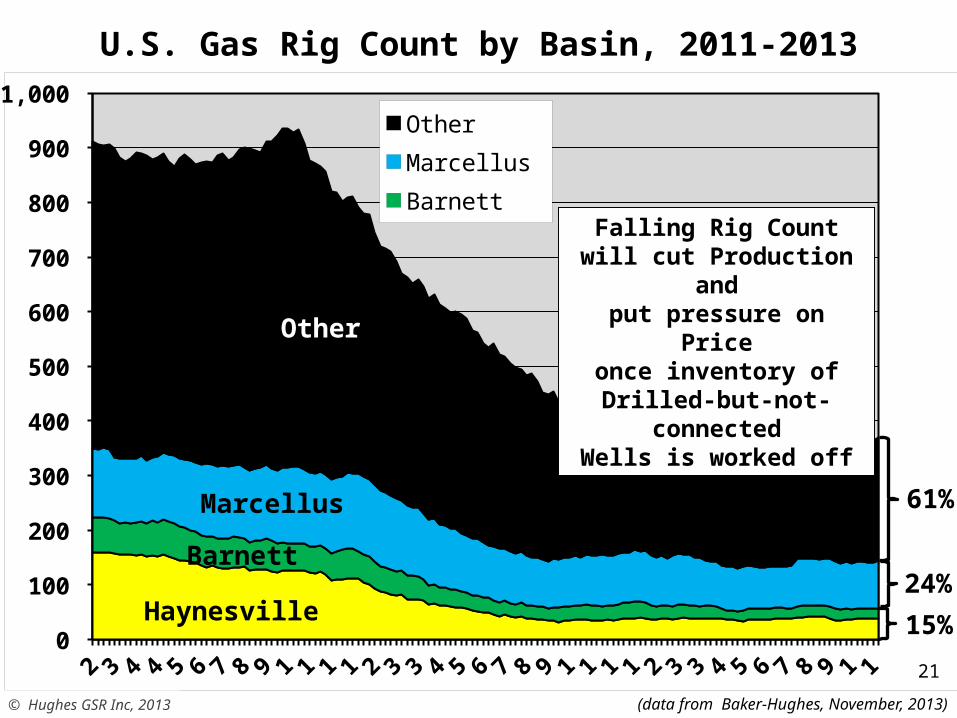

U.S. Gas Rig Count by Basin, 2011-2013

Barnett

Marcellus 61%

24%

15%

Falling Rig Countwill cut Production andput pressure on Price

once inventory ofDrilled-but-not-connected

Wells is worked off

21

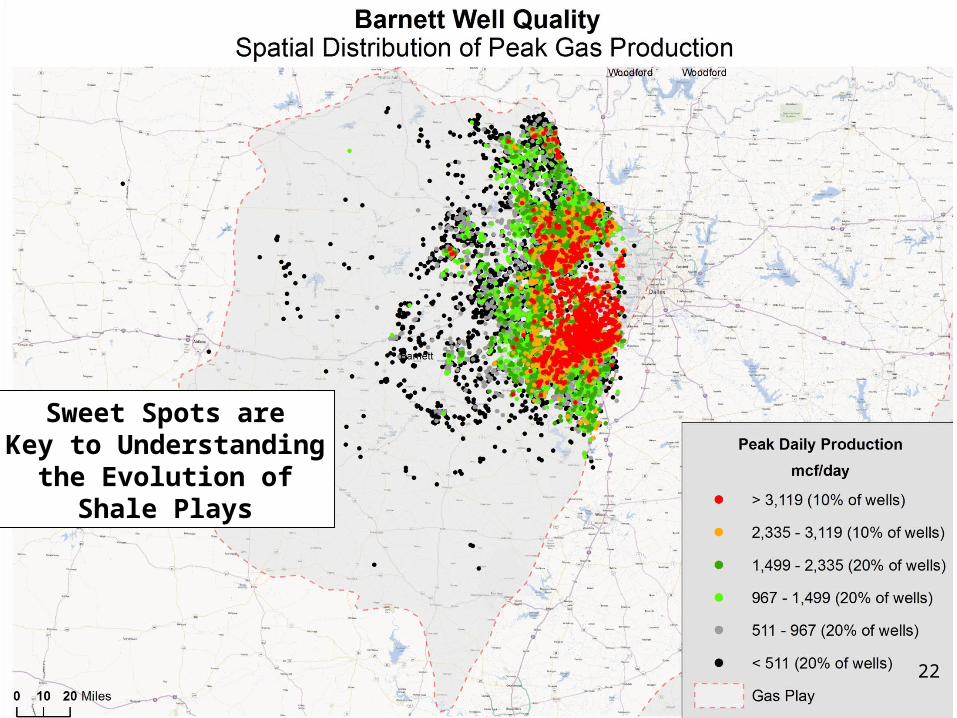

Sweet Spots areKey to Understanding

the Evolution ofShale Plays

22

2008 2009 2010 2011 20120

0.2

0.4

0.6

0.8

1

1.2

MarcellusHaynesvilleBarnettFayettevilleWoodford

Year

Ave

rag

e In

tial

Pro

du

ctiv

ity

per

Wel

lIn

dex

ed t

o 2

010

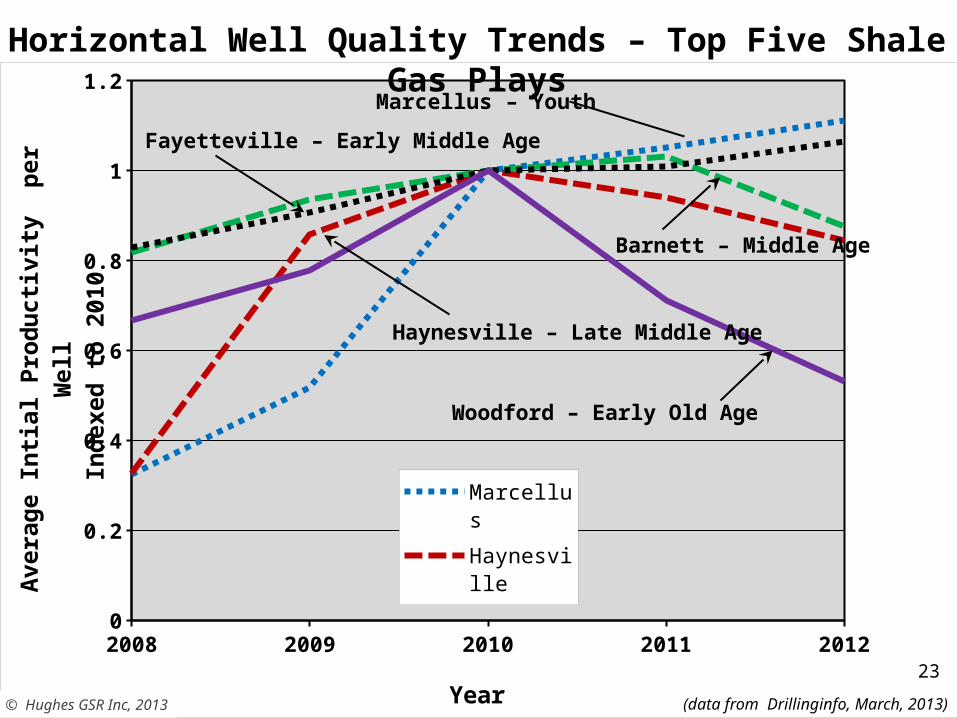

Marcellus – Youth

Horizontal Well Quality Trends – Top Five Shale Gas Plays

(data from DI Desktop, HPDI, September, 2012)

© Hughes GSR Inc, 2013 (data from Drillinginfo, March, 2013)

Fayetteville – Early Middle Age

Barnett – Middle Age

Haynesville – Late Middle Age

Woodford – Early Old Age

23

Feb, 11 Jun, 11 Oct, 11 Feb, 12 Jun, 12 Oct, 12 Feb, 13 Jun, 13 Oct, 130

200

400

600

800

1,000

1,200

1,400

1,600 OtherPermianEagle FordWilliston (Bakken)

Williston (Bakken)

Other

(data from Baker-Hughes, November, 2013)© Hughes GSR Inc, 2013

U.S. Oil Rig Count by Basin, 2011-2013

Permian Basin

Eagle Ford

40%

33%

14%

13%

24

2005 2006 2007 2008 2009 2010 2011 2012 20130

100

200

300

400

500

600

700

800

900

0

1000

2000

3000

4000

5000

6000

7000

Oil ProductionNumber of Wells

Year

Oil

Pro

du

ctio

n (

Th

ou

san

d B

arre

ls/d

ay)

Nu

mb

er of P

rod

ucin

g W

ellsBakken/Three Forks Oil Production and Number of

Operating Wells, 2005- June 2013

© Hughes GSR Inc, 2013 (data from Drillinginfo, October, 2013, three month trailing moving average)

25

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 470

100

200

300

400

500

600

Oil Production

Months on Production

Oil

Pro

du

ctio

n (

Bar

rels

per

Day

)Bakken/Three Forks Type Oil and Barrels of Oil Equivalent Well Decline Curves Including Montana and North Dakota

(data from Drillinginfo, October, 2013)© Hughes GSR Inc, 2013

Oil DeclineFirst Year = 70%

Second Year = 34%Third Year = 23%

Fourth Year = 21%

3-Year Decline = 84%

26

2007 2008 2009 2010 2011 2012 20130

100

200

300

400

500

600

700

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Total Oil ProductionNumber of pre-2012 Wells

Year

Oil

Pro

du

ctio

n (

Th

ou

san

d B

arre

ls/d

ay)

Nu

mb

er of P

rod

ucin

g W

ells

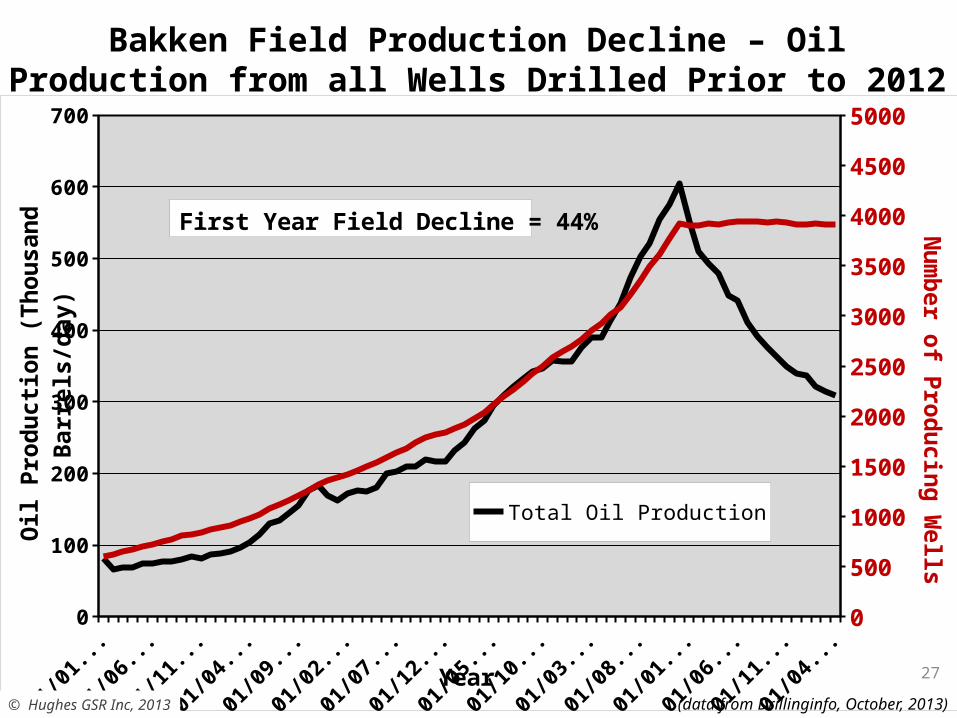

First Year Field Decline = 44%

Bakken Field Production Decline – Oil Production from all Wells Drilled Prior to 2012

© Hughes GSR Inc, 2013 (data from Drillinginfo, October, 2013)

27

28

0

50

100

150

200

250

County

Pro

du

ctio

n (

Th

ou

san

d B

arre

ls

per

day

)Bakken/Three Forks Production By County,

North Dakota and Montana, June, 2013

Total Production = 787 Kbbls/dayTop 2 counties = 52% of productionTop 4 counties = 85% of production

© Hughes GSR Inc, 2013 (data from Drillinginfo, October, 2013)

29

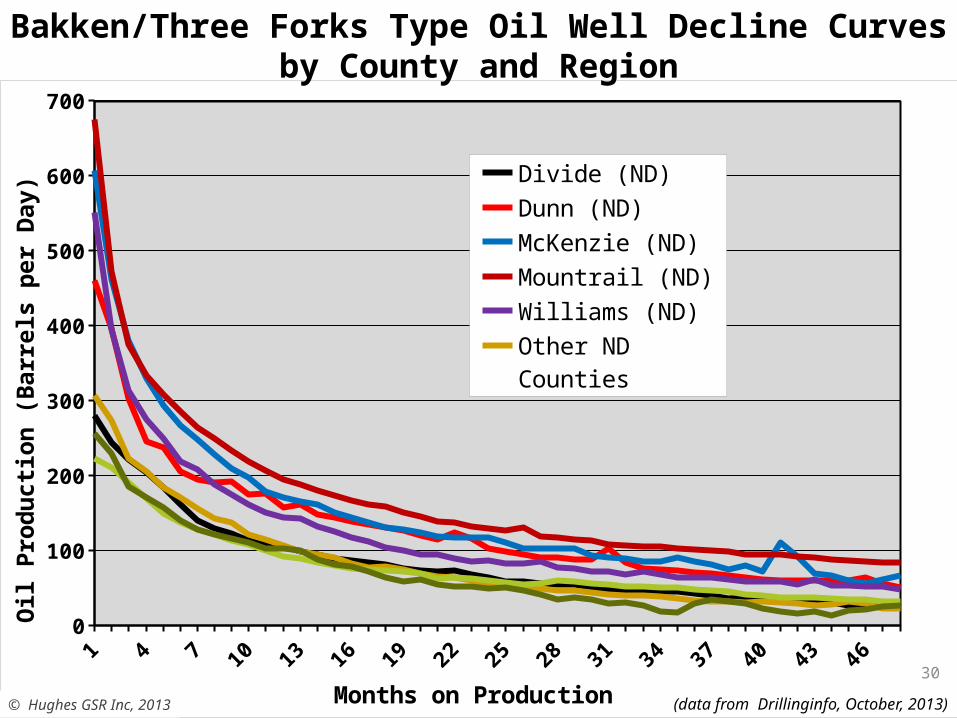

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 470

100

200

300

400

500

600

700

Divide (ND)Dunn (ND)McKenzie (ND)Mountrail (ND)Williams (ND)Other ND CountiesRichland (MT)Other MT Counties

Months on Production

Oil

Pro

du

ctio

n (

Bar

rels

per

Day

)Bakken/Three Forks Type Oil Well Decline Curves

by County and Region

(data from Drillinginfo, October, 2013)© Hughes GSR Inc, 2013

30

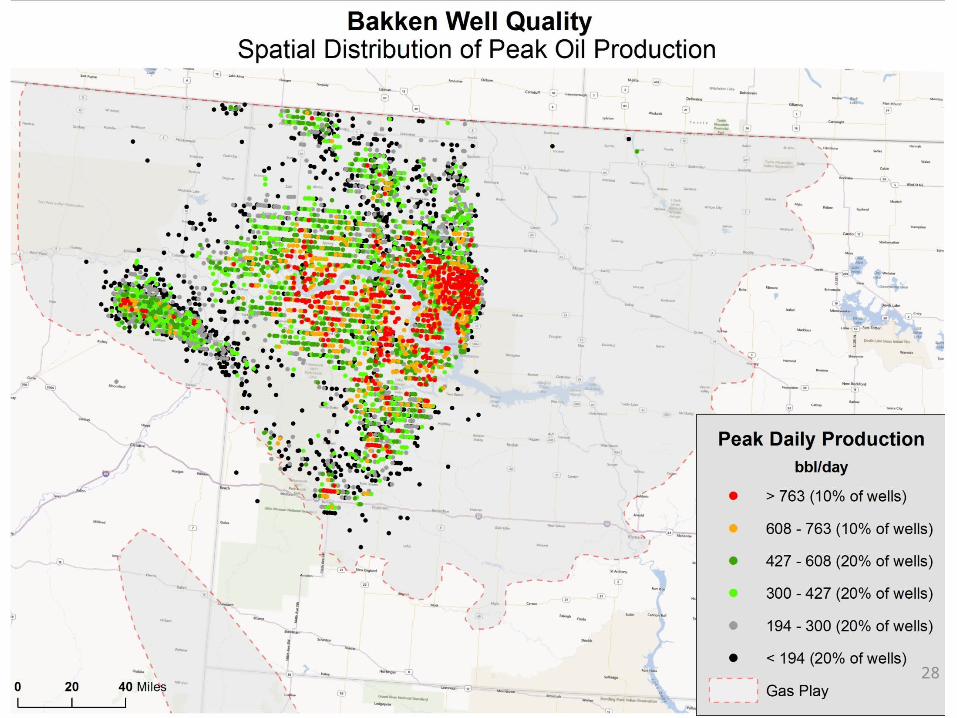

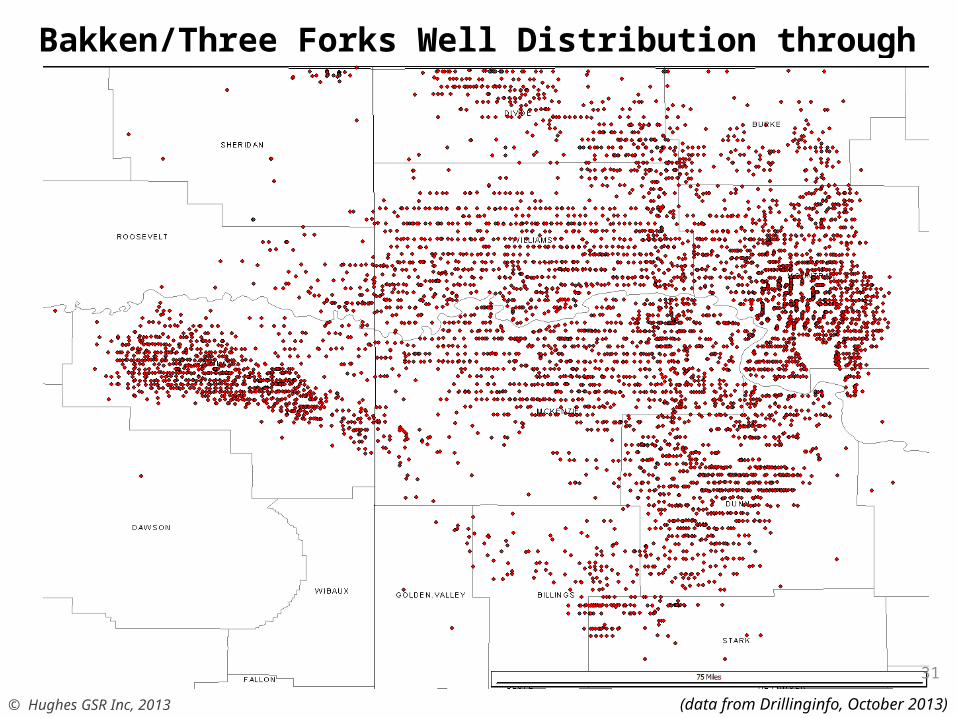

Bakken/Three Forks Well Distribution through mid-2013

© Hughes GSR Inc, 2013 (data from Drillinginfo, October 2013)

31

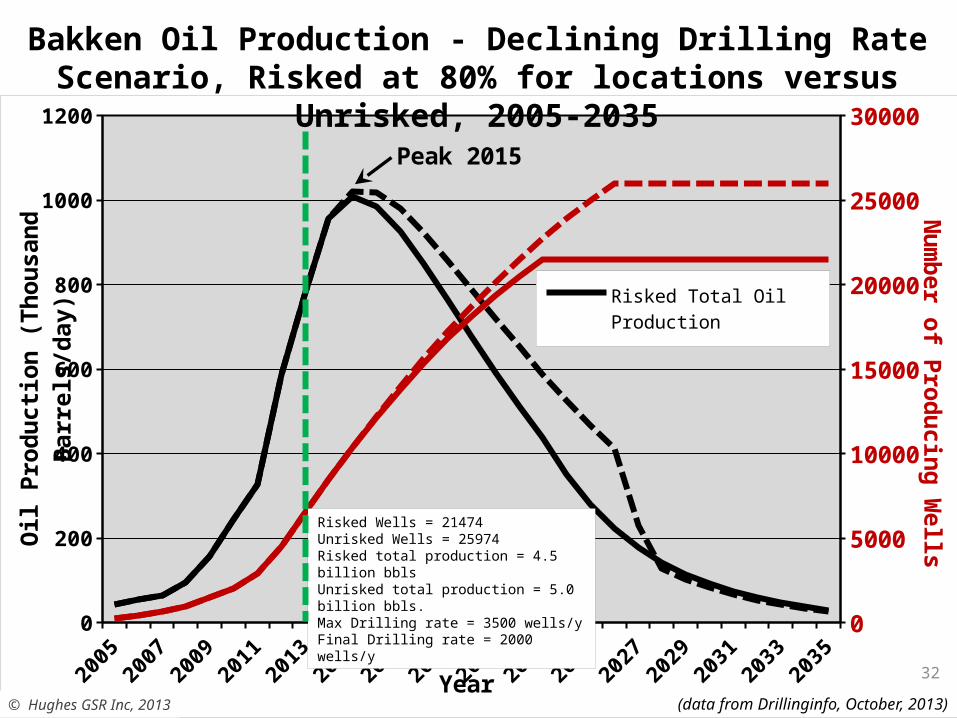

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

0

200

400

600

800

1000

1200

0

5000

10000

15000

20000

25000

30000

Risked Total Oil Produc-tion

Year

Oil

Pro

du

ctio

n (

Th

ou

san

d B

arre

ls/d

ay)

Nu

mb

er of P

rod

ucin

g W

ells

Peak 2015

Bakken Oil Production - Declining Drilling Rate Scenario, Risked at 80% for locations versus Unrisked, 2005-2035

© Hughes GSR Inc, 2013 (data from Drillinginfo, October, 2013)

Risked Wells = 21474Unrisked Wells = 25974Risked total production = 4.5 billion bblsUnrisked total production = 5.0 billion bbls.Max Drilling rate = 3500 wells/yFinal Drilling rate = 2000 wells/y

32

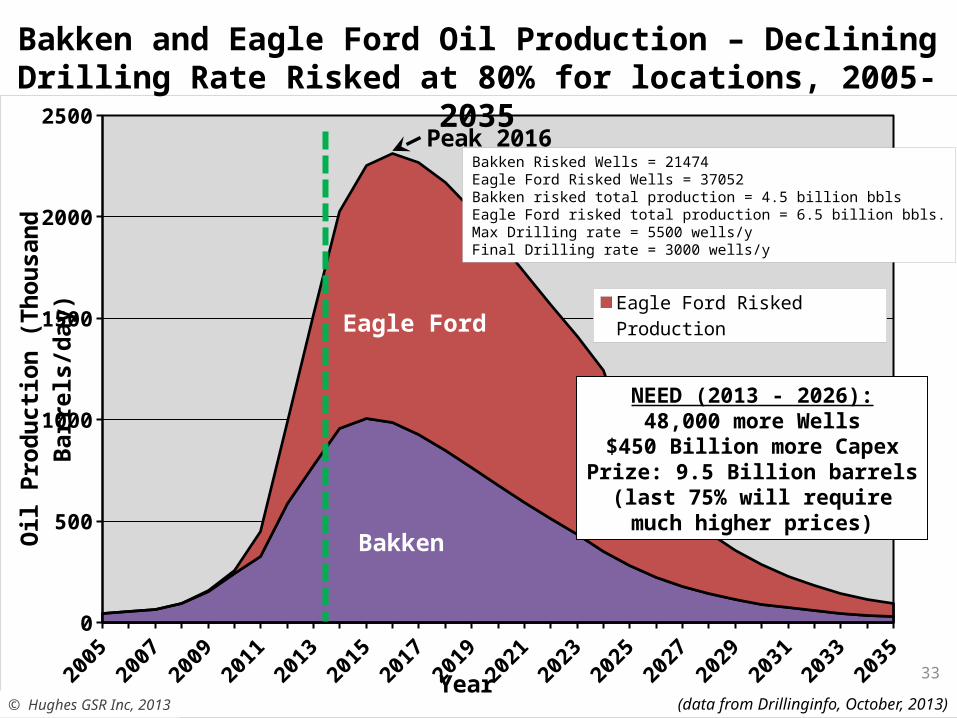

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

0

500

1000

1500

2000

2500

Eagle Ford Risked ProductionBakken Risked Production

Year

Oil

Pro

du

ctio

n (

Th

ou

san

d B

arre

ls/d

ay)

Peak 2016

Bakken and Eagle Ford Oil Production – Declining Drilling Rate Risked at 80% for locations, 2005-2035

© Hughes GSR Inc, 2013 (data from Drillinginfo, October, 2013)

Bakken Risked Wells = 21474Eagle Ford Risked Wells = 37052Bakken risked total production = 4.5 billion bblsEagle Ford risked total production = 6.5 billion bbls.Max Drilling rate = 5500 wells/yFinal Drilling rate = 3000 wells/y

Eagle Ford

Bakken

NEED (2013 - 2026):48,000 more Wells

$450 Billion more CapexPrize: 9.5 Billion barrels

(last 75% will requiremuch higher prices)

33

• Shale gas production in several top plays is declining and tight oil production from the top two plays is likely to peak in the 2016-2017 timeframe

• High well- and field-decline rates mandate sustained high levels of drilling to maintain production.

• Sweet spots become exhausted early on in field development hence drilling rates must continually escalate to maintain production levels.

• Liquids production with associated gas has allowed gas production to remain stable – for now – but long term sustainability is questionable.

• High quality shale plays are not ubiquitous:

• 68% of shale gas production comes from 3 plays.

• 74% of tight oil production comes from 2 plays.

• Environmental concerns with fracking are widespread and will likely escalate with the escalating drilling treadmill needed to maintain, let alone grow, shale gas and oil production.

Shale Takeaways

© Hughes GSR Inc, 2013

34