Embed Size (px)

Citation preview

The SEC’s Elimination of 20-F Reconciliation and the Cost of Bank Loans

Saiying Deng*, Southern Illinois University

Lucy Huajing Chen, Villanova University

Parveen P. Gupta, Lehigh University

Heibatollah Sami, Lehigh University

(Abstract)

We examine the impact of SEC’s elimination of 20-F reconciliation on cost of bank

loans. To the extent that information production is costly, the elimination of 20-F reconciliation

is associated with increased information collection costs. Consistent with such view, we find that

banks charge higher interest spread to IFRS firms after the elimination rule, to compensate for

the information loss. Furthermore, we document such effect is more pronounced in IFRS firms

borrowing from distant lenders such as foreign banks, and in IFRS firms with more opaque

financial reporting and less proprietary information. Our main results are robust to several

sensitivity checks.

First Draft: April 27, 2014

Preliminary draft, please do not quote.

JEL Classification: G31 and M48

Key Words: 20-F reconciliation; cost of bank loans; information loss; loan spread

* Corresponding author. Department of Finance, College of Business, Southern Illinois

University, Carbondale, IL 62901. Email: [email protected], phone: 618-453-1418.

1

1. Introduction

To respond to the global accounting convergence and especially the adoption of

International Financial Reporting Standards (IFRS) by the European Union, the U.S. Securities

and Exchange Commission (SEC) adopted a rule to accept financial statements from foreign

private issuers prepared in accordance with IFRS as issued by the International Accounting

Standards Board (IASB) without reconciliation to the U.S. Generally Accepted Accounting

Principles (GAAP) (SEC 2007) on December 21, 2007. This new rule became effective on

March 4, 2008, for all foreign private issuers with fiscal years ending on and after November 15,

2007. Prior to the adoption of this rule, foreign private issuers which prepared their financial

statements using accounting standards other than U.S. GAAP were required to file Form 20-F

reconciliation with the SEC.1

Prior studies document that reconciliation provides useful information to shareholders in

the U.S. equity market to assess the financial condition of the foreign private issuers and suggest

that the elimination of the reconciliation is “premature” (e.g., Harris and Muller 1999; Chen and

Sami 2008, 2013; Henry, Lin, and Yang 2009). On the other hand, more recent studies find

there are no significant economic consequences in the equity market associated with the

elimination of 20-F reconciliation (e.g., Kim, Li, and Li 2012; Jiang, Petroni, and Wang 2010).

However, there is scant empirical evidence on how the 20-F reconciliation information is used

by private lenders such as banks and the economic consequence of the elimination rule in private

debt market. In this paper, we attempt to fill this void by examining whether the elimination of

1 Form 20-F is an annual report filed by foreign private issuers with the SEC. Foreign firms were required to file

form 20-Fs within six months after fiscal year end. On Form 20-Fs, foreign firms reported the quantitative and

qualitative differences between their primary accounting standards, either home country GAAP or IFRS, and the

U.S. GAAP under item 17 or item 18.

2

20-F reconciliation is associated with cost of bank loans in the U.S. for foreign private issuers

that prepared their financial statements under IFRS as issued by the IASB.2

We focus on bank loans because they become the primary source of corporate debt

financing in the past decade (Sufi 2009). We argue that the impact of elimination of 20-F

reconciliation on the private debt market may differ from that of equity market for the following

reasons: First, banks act as delegated monitor (Diamond 1984) and are specialized in information

collection and processing. Banks collect borrower-specific information over time and across

multiple products, perform due diligence and act as delegated monitors to borrowers. This

information advantage makes lending relationship banks special (Fama 1985; James 1987;

Lummer and McConnell 1989; Gande and Saunders 2012;), compared to arm’s-length investors

such as stockholders.3 To the extent that information production is costly, the elimination of 20-F

reconciliation may result in higher information collection costs for banks.

Second, banks, if possible, collect both soft and hard information about borrowers to

help assess their credit quality and reduce information uncertainty (Petersen 2004). Soft

information comes from onsite visits, and face-to-face interactions, etc., while hard information

primarily comes from financial statements, including 20-F reconciliation. Although the U.S.

GAAP continues to converge with IFRS, understanding the differences between these two

accounting standards is informative when establishing debt covenants, especially in cross-border

transactions (PWC 2013). From this perspective, 20-F reconciliation provides valuable

supplemental information for lenders to better interpret the financial statements and confirm the

2 The standards developed and approved by the IASB since 2001 are IFRS. Before that, they were International

Accounting Standards (IAS). For convenience, we refer to IFRS as both IFRS and its predecessor IAS. 3 The information advantage may make banks less susceptible to the information loss associated with the

elimination of 20-F reconciliation, even if reconciliation can be value relevant to arm’s length investors as

documented in Harris et al. (2009), and Chen and Sami (2013).

3

accounting numbers. Unlike shareholders, banks have asymmetric payoff structure: they bear

substantial downside risk without the potential of reaping upside benefits (Watts 2003).

Accordingly, banks could be more sensitive to information risk engendered by the elimination of

20-F reconciliation.

Lastly, many cross-listed firms get syndicated loans in international loan market, of

which most of the lead arrangers are foreign banks. Lenders may find the cost of collecting soft

information about and monitoring borrowers at a great distance (i.e., foreign borrowers)

prohibitive, and may rely more on hard information to make loan decision. Therefore, we expect

the information loss associated with elimination of 20F reconciliation is more pronounced for

lenders that are at great distance from their borrowers. To sum up, the information loss

associated with elimination of 20-F reconciliation, coupled with greater information collection

and monitoring costs associated with geographic distance, may lead the banks to charge higher

interest rate to foreign private issuers after the elimination of 20-F reconciliation.

Based on the arguments presented above, we predict that banks charge higher interest

rates to IFRS firms after the elimination rule. We also predict that such effect is more

pronounced in IFRS firms that borrow from distant banks such as foreign banks, where the

borrower’s headquarters is located in a different country from the country of syndication of the

syndicated loan.

It is notable that there are alternative information sources such as corporate voluntary

disclosures that may aid a lender to evaluate its borrowers’ creditworthiness. The impact of

elimination of 20-F on information loss crucially depend on the usefulness of the alternative

information sources in assessing borrowers’ credit quality.

4

We also examine whether a firm’s financial reporting opacity affects the association

between the elimination of 20-F and cost of bank loans. According to Franco et al. (2012),

“because banks rely primarily on periodic financial accounting reports and disclosure, along with

private information, to assess the creditworthiness (Spiro 2007), if a firm’s financial reporting is

more opaque, then the demand for private information and other supplemental and

complementary information that help interpret financial statements will be greater.” We thus

expect that 20-F reconciliation provides more useful information for lenders to interpret financial

statements in more opaque reporting firms. Consequently, lenders may charge higher interest

spread in firms with more opaque financial reporting after the elimination of 20-F reconciliation.

We further investigate whether a firm’s proprietary information affect the cost of bank

loans after the elimination rule. Banks need to collect more soft information in firms with more

proprietary information to make prudential lending decision. On the contrary, banks rely more on

hard information in firms with less proprietary information to make wise lending decision.

Therefore, we postulate that 20-F reconciliation provides more useful information for firms with

less proprietary information. As a result lenders charge higher interest spread in firms with less

proprietary information after the elimination of 20-F reconciliation.

We test our hypotheses using foreign private issuers that borrow at least one bank loan

before and after the elimination rule during 2005─2012 sample period. Our test sample consists

of foreign firms that prepared financial statements under IFRS as issued by the IASB and did not

reconcile to U.S. GAAP after the elimination of 20-F reconciliation. Our control firms include

foreign firms that prepared financial statements under their home country GAAP or U.S. GAAP;

that is, firms that do not change their reconciling behavior after the no-reconciliation rule. We

5

use a difference-in-differences approach and cluster standard errors at firm level with industry

fixed effects.

Our findings are generally consistent with our predictions. We find that loan spread

increases significantly in the post-elimination period for the test firms vis-a-vis the control firms.

Our result is consistent with our conjecture that there is significant information loss associated

with the elimination rule to private lenders, and in turn banks charge higher loan spread to IFRS

firms. We also find that IFRS firms borrowing from foreign banks experience a significantly

higher loan spread after the elimination of 20-F reconciliation compared to the control firms,

while there is no association between loan spread and the elimination of 20-F reconciliation for

IFRS firms borrowing from domestic banks. The evidence is consistent with our predication that

the elimination of 20-F reconciliation is a significant information loss event for private lenders

especially foreign banks that are far away from borrowers. It also suggests that the increasing

geographic distance between the borrower and banks leads to a more pronounced information

loss due to the elimination of 20-F reconciliation, as a result lenders charge a higher loan spread.

Third, We further document foreign IFRS firms with greater financial reporting opacity and less

proprietary information experience higher loan spread after the elimination rule. The result is

consistent with our predication that 20-F reconciliation provides more useful information for

firms with more opaque financial reporting/less proprietary information; as a result lenders

charge higher interest spread to compensate for the greater information loss.

Our paper contributes to the literature in the following ways: first, to the best of our

knowledge, this is the first paper to examine the economic consequence of elimination of 20-F

reconciliation in private debt market. Banks are special, and have information collection and

monitoring advantages over dispersed arm’s-length investors (Rajan, 1992). The elimination of

6

20-F reconciliation may impose a significant information loss for lenders, especially

geographically distant ones, which rely more on hard information provided by financial

statements in their lending decisions. We find that the elimination of 20-F reconciliation is

associated with significant increase in loan spread, suggesting that there is a significant

information loss associated with the elimination of 20-F reconciliation in private debt market.

Second, our study is related to Kim et al. (2012) who find no evidence that the

elimination of 20-F reconciliation has a significant impact on market liquidity, probability of

informed trading, cost of equity, analyst forecasts, institutional ownership, and stock price

efficiency and synchronicity. Our results contrast with theirs as we document that banks charge

higher loan spread to IFRS borrowers after the elimination rule. Furthermore, we find a more

pronounced information loss effect for IFRS firms borrowing from distant banks such as foreign

banks, since great distance makes information collection and monitoring prohibitive and erodes

lenders’ information advantage. We do not find information loss when the IFRS firms borrow

from domestic lenders. We argue that banks are better at collecting and processing information,

compared to arm’s-length investors in the equity market. 20-F reconciliation provides important

supplemental information for banks to interpret the financial statements, while shareholders may

not rely on the 20-F reconciliation to assess the credit worthiness of borrowers, and therefore

there are no significant economic consequences associated with the elimination rule in the equity

market. 4

Third, our study complements existing studies on why banks are special (James 1987;

Lummer and McConnell 1989; Gande and Saunders 2012; etc.). We show that banks are

4 In addition, cross-listed firms possess much thinner trading volume than their underlying local markets

(Chakravarty, Chiyachantana, and Jiang 2011), which may make it harder to detect any price impact in these

markets using equity data.

7

different from shareholders or bondholders in the public market and experience significant

information loss due to the elimination of 20-F reconciliation, especially when the lender-

borrower distance increases.

Fourth, our study relates to an emerging stream of literature on how geography affects

important financial outcomes and how geographic proximity is related to information advantage

of being local. For example, Chen, Hong, Huang and Kubik (2004), Coval and Moskowitz

(1999 and 2001) document that mutual fund managers investing in geographically proximate

companies enjoy superior returns due to the informational advantage from selecting nearby

stocks. Francis, Hasan, and Waisman (2007) find that rural firms experience a higher cost of

debt than urban firms because of the difficultly associated with monitoring their activities.

Similarly, Butler (2008) documents that local investment banks sell municipal bonds at lower

yields and charge lower fees than their non-local counterparts do. Such pricing advantage arises

from local investment banks’ soft information advantage. Using the elimination of 20-F

reconciliation as a unique setting, our study complements this stream of research by documenting

that distant lenders lose information advantage and charge a higher loan spread to foreign IFRS

firms after the elimination rule.

Finally, our paper contributes to the ongoing debate that challenges whether the SEC was

judicious in eliminating the 20-F reconciliation requirement. We document that eliminating the

20-F reconciliation requirement is associated with higher cost of bank debt for foreign IFRS

issuers. From this perspective, our result is more in line with Henry et al. (2009) and Chen and

Sami (2013) that reconciliation may provide some useful information to a subset of investors.

Overall, our findings shed some light on the economic consequences in the private debt market

8

associated with SEC’s decision to eliminate the 20-F reconciliation requirement for foreign

private issuers.

The remainder of the paper proceeds as follows: Section II presents related literature and

hypotheses development. Section III describes sample selection and research design. Section IV

presents the empirical results. Section V concludes.

II. Related literature and hypotheses development

2.1 Existing studies on 20-F reconciliation

There are split views about the economic consequences of elimination of 20-F

reconciliation in equity market. Hopkins et al. (2008), representing American Accounting

Association’s Financial Accounting and Reporting Section of the Financial Reporting Policy

Committee, argues that reconciliation provides useful information to assess the financial

condition of the foreign private issuers and suggests that the elimination of the reconciliation is

“premature” (Hopkins et al. 2008). Consistent with this view, prior literature provides empirical

evidence that reconciliation to U.S. GAAP contains some information content beyond IFRS.5 For

example, Harris and Muller (1999) find that earnings reconciliation from International

Accounting Standards (IAS) (forerunner to the current IFRS) to U.S. GAAP is value relevant in

the market valuation model, although earnings reconciliation per share is not associated with

price per share. In addition, Chen and Sami (2008) find that investors in the U.S. capital markets

trade on the earnings reconciliation from IAS to U.S. GAAP during the 1995-2004 period.

Henry, Lin, and Yang (2009) document that both net income reconciliation and book value

reconciliation from IFRS to U.S. GAAP are value relevant in the market valuation model but the

5 The standards developed and approved by the IASB since 2001 are IFRS. Before that, they were International

Accounting Standards (IAS). For convenience, we refer to IFRS as both IFRS and its predecessor IAS.

9

net income reconciliation is not value relevant in the long-term return model during the 2005-

2006 period. Also, Gordon, Jorgensen, and Linthicum (2008) show that accrual reconciliation

from IFRS to U.S. GAAP provides incremental information content beyond IFRS accruals from

2004 to 2006. Chen and Sami (2013) report that the relation between abnormal trading volume

and earnings reconciliation from IFRS to U.S. GAAP during the 2005-2006 period is driven by

first-time IFRS users with low institutional ownership.

On the other hand, Jamal et al. (2008), representing American Accounting Association’s

Financial Accounting Standards Committee, argue that the cost of preparing and auditing 20-F

reconciliation is substantial and “allowing foreign companies to use IFRS without costly

reconciliations to U.S. GAAP is likely to make U.S. stock exchanges more competitive and

provide useful feedback to U.S. accounting standard-setters about the efficacy of their standards”

(Jamal et al. 2008). There are also empirical studies echoing such view. For example, Kim et al.

(2012) compare foreign IFRS firms in the year before with the year after the no-reconciliation

rule. They find no evidence that removing the reconciliation has a negative impact on these

firms’ market liquidity, probability of informed trading, cost of equity, analyst forecasts,

institutional ownership, and stock price efficiency and synchronicity. Overall, their results do not

support information loss for equity investors. Similarly, Jiang et al. (2010) document no

abnormal trading volume, abnormal return volatility, or bid-ask spread during the short term

window around the release of 20-F in the year after the rule. In addition, Jiang et al. (2010) find

an accelerated filing of 20-F in the year after the rule compared to the year before, which they

interpret as an indication of the cost savings for these foreign IFRS firms.

2.2 Information, geographic distance, and bank lending

10

Banks collect borrower-specific information over time and across multiple products,

perform due diligence and act as delegated monitor to borrowers (Diamond 1984). This

information advantage makes lending relationship banks special (Fama 1985; Lummer and

McConnell 1989; Gande and Saunders 2012;). Banks can collect two types of borrower-specific

information: (i) Soft information, which is information loan officers collect through face-to-face

interaction with a potential borrower, onsite visits, and local contacts, etc., including

entrepreneur’s competence, honesty, management style, employee morale, etc.). Soft information

is hard to verify and credibly transfer within an organization hierarchy. (ii) Hard information,

which is information that is verifiable and can be credibly transferred (i.e. faxed or emailed)

within an organization hierarchy. The major sources of hard information are financial statements

and credit scoring, etc. 20-F reconciliation provides useful supplemental information about the

borrowers, which may help lenders especially lenders at a great distance from borrowers confirm

the accounting numbers. More specifically, reconciling to U.S. GAAP provides banks an

opportunity to confirm the IFRS-based accounting numbers, which potentially improves the

precision of information, provides additional assurance on the financial reporting quality, and

reduces information risk. Therefore the elimination of 20F reconciliation creates information loss

for lenders that rely on hard information to make loan decisions, for which lenders may charge

higher loan spread. Based on the above arguments, our first hypothesis is as follows:

H1: IFRS firms experience higher interest rates on bank loans after the elimination of 20-

F reconciliation.

However, there are alternative information sources such as corporate voluntary

disclosures that aid a lender to evaluate the borrowers’ creditworthiness. Those could become

countervailing forces against this prediction. IFRS firms may adopt voluntary disclosures to

11

make up the information loss associated with the elimination rule. Kim et al. (2012), Jiang et al.

(2010) find that none of their sample firms provide voluntary reconciliation after the rule. In

contrary, Yu (2011) find that IFRS firms significantly increase their overall voluntary disclosures

in annual financial reports and earnings announcement press releases after the elimination of 20-

F reconciliation. However, according to Cheng, Liao, and Zhang (2013), voluntary disclosure

does not serve as a credible commitment mechanism as mandatory disclosure.

Existing studies document that distance is related to information collection and

monitoring. Agarwal and Hauswald (2010) find that borrower proximity facilitates lenders to

collect soft information, thereby enhancing banks’ private information quality, and thus their

information advantage. Petersen and Rajan (2002) and Berger et al. (2005) document as the

physical distance between a lender and its borrowers increases, soft information collection

becomes more difficult and costly, eroding banks’ information advantage. Mian (2006)

document that foreign banks are willing to make transaction loans based on hard information, but

they are at a comparative disadvantage when making relational loans based on soft information.

Similarly, Hauswald and Marquez (2006) argue that lenders that are geographically

proximate to borrowers act as more effective monitors, and the quality of banks’ information

generation process is a decreasing function of lender-borrower distance. Along a similar vein,

Almazan (2002), and Sussman and Zeira (1995) indicate that a bank’s monitoring expertise is a

decreasing function of lender-borrower distance, and lenders’ monitoring costs are an increasing

function of distance. Hollander and Verriest (2011) find that distance erodes lenders’ ability to

collect and process borrower-specific information, as a result, lenders rely more on covenants to

resolve contracting frictions. Ayers, Ramalingegowda and Yeung (2011) posits that institutional

investor’s cost of acquiring monitoring information increases with the distance between a firm

12

and institutional investor, and find that local institutional investors lead to less financial reporting

discretion by the corporate managers.

Based on the above arguments, banks located closer to their borrowers enjoy significant

information advantage and more efficient monitoring, resulting in lower cost of information

collection and monitoring which the bank may pass on to borrowers in the form of lower interest

spread. On the other hand, banks may charge higher interest rates to distant borrowers due to the

greater information and monitoring costs. Therefore we propose the following hypothesis:

H2: IFRS firms that borrow from distant banks experience higher interest rates on bank

loans after the elimination of 20-F reconciliation.

2.3. Financial reporting opacity

We examine whether a firm’s financial reporting opacity may exacerbate the information

loss associated with the elimination rule. According to Franco et al. (2012), in a firm with more

opaque financial reporting, the demand for private information and other supplemental and

complementary information that may aid interpreting financial statements becomes greater. We

expect 20-F reconciliation provides more useful information in firms with more opaque financial

reporting. Therefore lenders may charge higher loan spread in firms with opaque financial

reporting after the elimination of 20-F, accordingly we propose the following hypothesis:

H3: IFRS firms that have more opaque financial reporting experience higher interest

rates on bank loans after the elimination of 20-F reconciliation.

2.4. Proprietary information

We investigate whether 20-F reconciliation provides more useful information in firms

with less proprietary information. In firms with more proprietary information, the demand for

banks collecting soft information is greater. In contrary, lenders rely more on hard information

13

(i.e., 20-F reconciliation) when making loans to firms with less proprietary information.

Therefore elimination of 20-F reconciliation leads to a greater information loss for banks that

lend to firms with less proprietary information. As a result, we expect cost of bank loan increase

more in firms with less proprietary information after the elimination of 20-F. Accordingly we

propose the following hypothesis:

H4: IFRS firms that have less proprietary information costs experience higher interest

rates on bank loans after the elimination of 20-F reconciliation.

III. Data and empirical methodology

3.1. Sample selection

We obtain syndicated loan data from the Dealscan database provided by the Loan Pricing

Corporation of Thomson Reuters, which contains detailed information on bank loans worldwide,

such as borrower and lender identities, loan amounts, LIBOR spread, issuing and maturity dates,

etc. We link the Dealscan and the Compustat database using a link file compiled by Chava and

Roberts (2008).6 Loan-specific, borrower-specific, and stock return information are obtained,

respectively, from Dealscan, Compustat, and CRSP databases. We hand collect the accounting

standard data from the SEC website. Since syndicate structure and loan contract terms (e.g., loan

amount, maturity, pricing) differ across different facilities in a deal, our analysis is conducted at

the loan facility level. Our sample spans from January 1, 2005 to December 31, 2012. We start

on January 1, 2005 as the European Union (EU) mandated all EU-listed companies adopt IFRS

beginning on January 1, 2005. As the elimination rule is effective for all foreign private issuers

with fiscal years ending on and after November 15, 2007, we classify the pre-elimination loan as

6 We would like to thank Michael R. Roberts for generously providing us the Dealscan-Compustat link file.

14

loan originated from January 1, 2005 to November 14, 2007 and the post-elimination loan as

loan originated from November 15, 2007 to December 31, 2012.

The sample selection process is as follows: We first hand collect accounting standard

information for 992 cross listed firms between January 1, 2005 and December 31, 2012. We

delete 147 firms which switch accounting standard before and after the elimination rule and

hence obtain 845 cross listed firms which use the same accounting standard during the entire

sample period. From these 845 firms, we extract Compustat data to construct firm-specific

variables and obtain 4,123 firm-year observations with 781 unique firms after deleting missing

values. We then merge these 4,123 observations with Dealscan dataset through Dealscan-

Compustat link file compiled by Chava and Roberts (2008). After deleting observations with

missing values, awe get 808 loan facilities for 179 unique cross listed firms over 2005~2012

sample period. There are 56 IFRS firms with 292 facilities, and 123 non-IFRS control firms with

516 facilities.

3.2. Research design

To investigate the effect of elimination of 20-F reconciliation on bank loan pricing, we

follow Graham, Li, and Qiu (2008) by controlling for firm-specific, loan-specific, and

macroeconomic factors that may affect loan pricing. We include industry fixed effects in all

models. We estimate the models with standard errors clustered at firm level.

LoanSpread=α+β×IFRS+γ×After+ƥ×IFRS×After+¢×Firm-specific-factors+θ×Loan-specific-

factors+ρ×Macroeconomic-factors+ ε (1)

Since loan contract terms (e.g., loan amount, maturity, pricing) vary across different

facilities in a deal, we estimate model (1) using facility level data. Following Graham, Li, and

Qiu (2008), and Kim, Song, and Zhang (2011), we measure the interest rate spread using the all-

15

in-drawn spread (Spread) from Dealscan, the amount a borrower pays the lender each year in

basis points over LIBOR for each dollar borrowed, and take the log of Spread to proxy for

LoanSpread. IFRS is an indicator for firms which use IFRS accounting standard. After takes the

value of one for the post-elimination period loan, and zero for the pre-elimination period loan.

The post-elimination (pre-elimination) period loans consist of loans originate from November

15, 2007 to December 31, 2012 (from January 1, 2005 to November 14, 2007). Our variable of

interest is the interaction term between IFRS and After. If the elimination rule leads to

information loss to the test firms in private debt market, we expect the coefficient on the

interaction term positive.

Following prior studies (e.g., Graham, Li, and Qiu, 2008; Deng, Willis, and Xu, 2013),

we include the following firm-specific variables as control variables: firm size, market-to-book

ratio, Leverage, Profitability, Tangibility, cash flow volatility, and Z-Score. All variables are

defined in appendix A1. Larger firms usually have lower default risk and hence lower cost of

debt. Firms with more growth opportunities generally have lower default risk and are more likely

to have lower cost of debt. Firms with higher Leverage borrow more debt, resulting in higher

default risk and in turn a higher cost of debt. More profitable firms pay lower cost of debt as they

usually have lower default risk. Firms with more tangible assets pay lower cost of borrowing as

lenders may liquidate these assets when borrower defaults. Firms with higher cash flow volatility

have higher cost of debt because of the increased uncertainty for them to make timely debt

payments. Since higher Z-score implies lower insolvency risk, we expect an inverse relation

between Z-score and cost of borrowing.

We also control for loan-specific variables including loan size and maturity, etc. We

expect loan size to be negatively related to the cost of debt due to the economies of scale effect.

16

We expect maturity to be positively related to cost of debt. We include performance pricing, loan

type (e.g., term loan, revolving loan) and loan purpose (e.g., debt repayment, working capital

needs) dummies in the model. In addition, we include credit spread and term spread to control

for macroeconomic conditions.

3.3. Financial reporting opacity

Following Bharath et al. (2008), we construct our measure of financial reporting opacity

as the first principal component from three standard absolute abnormal operating accrual

measures that have been widely used in accounting literature (UAA1, UAA2, and UAA3). The

first measure is based on Dechow and Dichev (2002). We first define total current accrual TCA

as follow:

TCAit = − (∆ARit + ∆INVit + ∆APit + ∆TAXit + ∆OCAit) (2)

where ∆AR is the decrease (increase) in accounts receivable, ∆INV is the decrease (increase) in

inventory, ∆AP is the increase (decrease) in accounts payable, ∆TAX is the increase (decrease) in

taxes payable, and ∆OCA is the net change in other current assets.

We then estimate the following model based on Dechow and Dichev (2002) for each year

for each of the Fama and French (1997) industry groups:

where TCA is defined as above, CFO is the operating cash flows from continuing operations

from the statement of cash flows, and ATA is the average total assets. We obtain the coefficient

estimate from the above regression to compute the fitted value for the normal current accruals

and define the first accrual measure UAA1 as the absolute value of the residual from the

above regression.

17

For the second accrual measure UAA2, we estimate the following regression based on the

industry-year groups following Teoh et al. (1998).

where A is total assets, and ∆REV is the change in revenues from year t-1 to year t. We then use

the coefficient estimates from equation (4) to compute the normal current accruals (NCA) as:

where ∆AR is the change in accounting receivable between year t-1 and t for firm i. We then

compute our second accrual measure UAA2 as the absolute value of the difference between

TCAit/Ai,t-1 and NCAit.

Our third accrual measure UAA3 is based on the Jones model (Jones 1991) as modified

by Dechow et al. (1995). We first run the following regression for each of the industry-year

groups as:

where TA, total accrual, is defined as the difference between earnings before extraordinary items

and discontinued operations and the operating cash flows, and PPE is the gross value of property,

plant, and equipment. We then use the coefficient estimates from equation (6) to compute the

firm-specific normal accruals (NA) as follow:

Our third accrual measure UAA3 is the absolute value of the difference between total

accruals (TAit/Ai,t-1) and the fitted normal accruals NAit. We construct financial reporting opacity

as an indicator variable that equals one if the first principal component of three accrual measures

18

UAA1, UAA2, and UAA3 as discussed above is greater than the sample median and zero

otherwise.

3.4. Proprietary information

Following Franco et al. (2012), Ellis, Fee, and Thomas (2011), and Jones (2007), we use

two proxies for proprietary information. The first one is R&D expenditures. We construct a R&D

dummy which equals one if the research and development (R&D) expenditures of firm scaled by

lagged total assets are greater than the sample median, and zero otherwise. The second proxy for

proprietary information we employ is intangibility. We construct an intangibility dummy which

equals one if the one minus the sum of current assets and property, plant, and equipment scaled

by total assets are greater than the sample median, and zero otherwise. In firms with more

proprietary information, the need for banks to collect soft information is greater. In contrast,

lenders rely more on hard information including 20-F reconciliation in firms with less

proprietary information. We argue that there is a greater information loss associated with the

elimination of 20-F reconciliation in firms with less proprietary information. Therefore, we

expect firms with less proprietary information experience greater increase in interest spread

following the elimination rule.

IV. Empirical Results

4.1 Univariate analysis

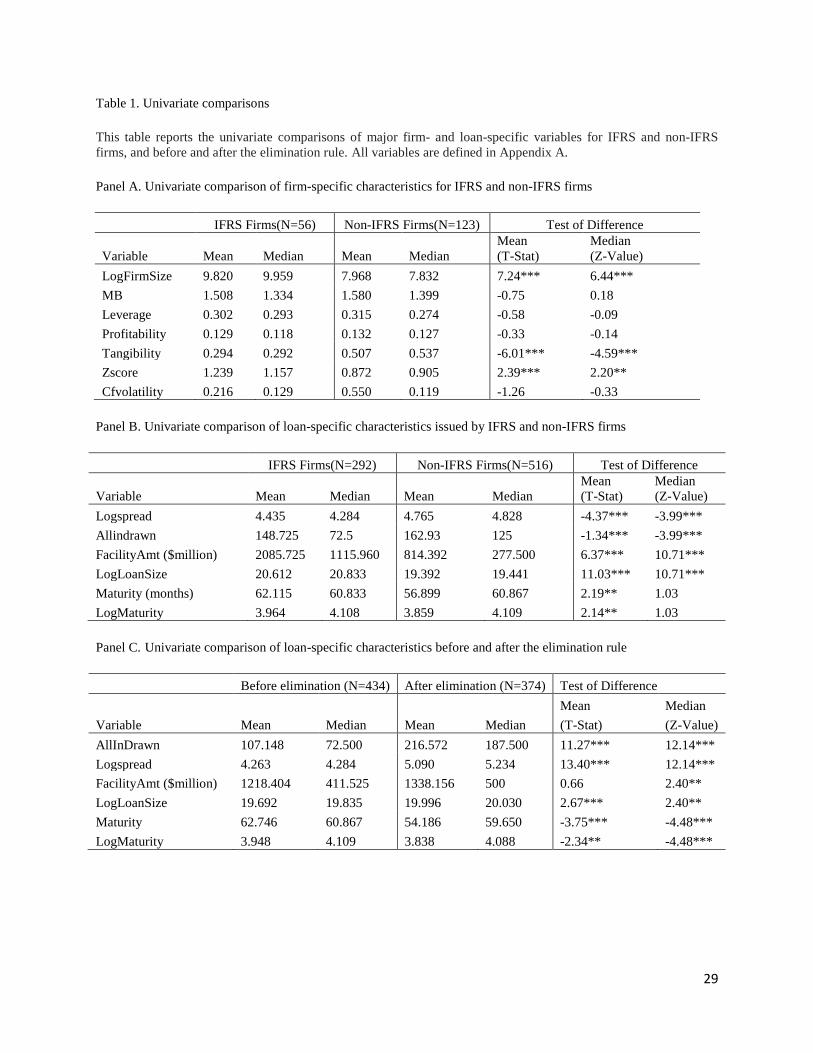

We present univariate comparison of the major control variables included in our

empirical model for both IFRS and non-IFRS firms in Table 1. Panels A and B contain firm-

level and loan level characteristics, respectively. Compared to non-IFRS firms, IFRS firms are

significantly larger in firm size, have fewer tangible assets, and are less likely to experience

financial distress. Compared to loans issued by non-IFRS firms, loans issued by IFRS firms are

19

significantly larger in loan size, have lower loan spread and longer maturity. Panel C presents the

univariate comparison of loan terms before and after the elimination of 20-F reconciliation rule.

Firms obtain loans with significantly shorter maturity, pay significantly higher loan spread after

the elimination of 20-F reconciliation. This provides support to our hypothesis that cost of bank

loans increases after the elimination of 20-F reconciliation.

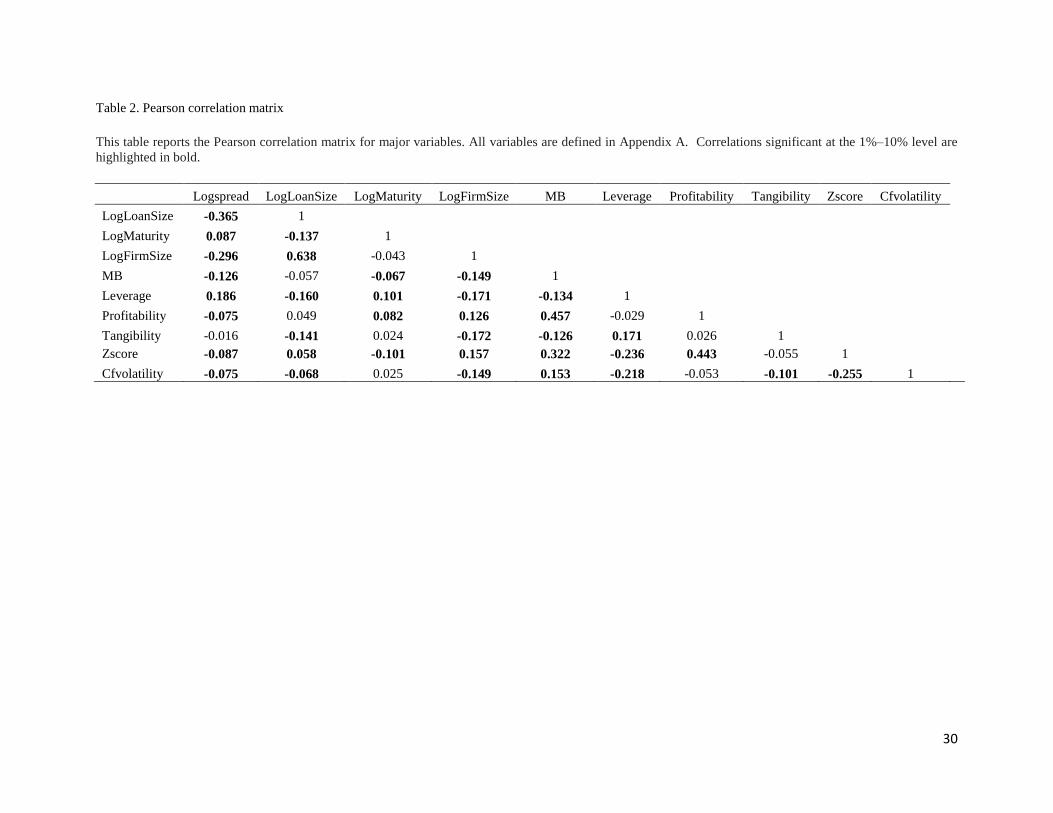

Table 2 presents the Pearson correlation matrix among the major variables. Logspread is

negatively and significantly correlated with firm size, MB, Profitability, Zscore, LogLoanSize,

and Cfvolatility, and positively and significantly correlated with Leverage and loan Maturity,

while insignificantly correlated with Tangibility.

Insert Table 1 and Table 2 Here

4.2 Multivariate regression results

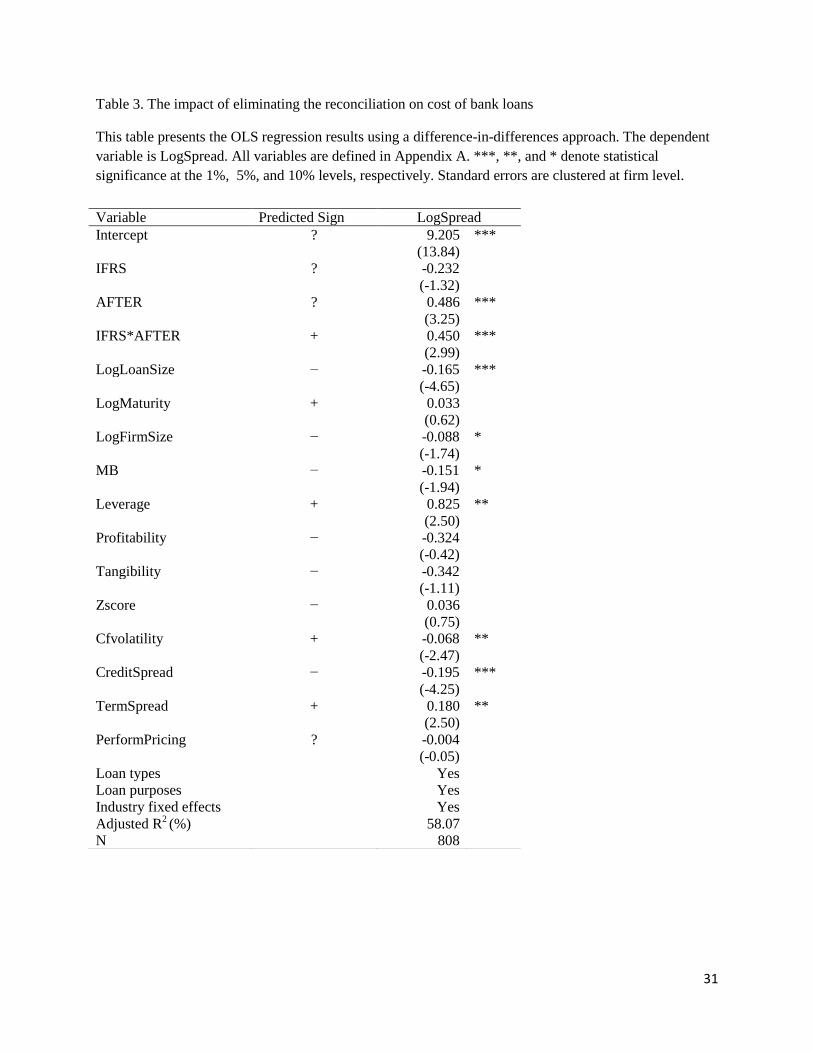

4.2.1 Baseline results

We report the regression result of the effect of eliminating the reconciliation on cost of

bank debt in Table 3. We cluster standard errors at firm level and include industry fixed effects.

The coefficient on IFRS is negative yet insignificant. The coefficient on After is positive and

significant (coefficient=0.486 , p-value<0.01), suggesting firms pay a 48.6% increase in loan

spreads after the elimination rule. The result is economically significant. The mean loan spread

of the sample firms is 107.148 basis points before the elimination rule. Therefore a 48.6%

increase implies, ceteris paribus, that the loan spread increases by approximately 52.074 basis

points after the elimination rule. Given the average loan issue size is $1338.156 million for the

sample firms after the elimination rule, the post- elimination increase of 52.074 basis points in

the loan spread implies an average increase of $6.968 million ($1338.156million × 0.0052074)

per loan in annual interest payments after elimination.

20

The variable of interest, IFRS*AFTER has a positive and significant coefficient

(coefficient=0.45, p-value<0.01). The result indicates that IFRS firms pay 45% higher loan

spread after the elimination of 20-F reconciliation, compared to non-IFRS firms. The result lends

support to hypothesis H1, and is consistent with our conjecture that there is a significant

information loss to private lenders after the elimination of 20-F reconciliation, and in turn banks

charge higher loan spread. The result is also economically significant. The mean loan spread of

the sample IFRS firms is 148.725 basis points before the elimination rule. Therefore a 45%

increase implies, ceteris paribus, that the loan spread increases by approximately 66.926 basis

points after the elimination rule. Given the average loan issue size is $2085.725 million for the

sample IFRS firms, the post- elimination increase of 66.926 basis points in the loan spread

implies an average increase of $13.959 million ($2085.725 million × 0.0066926) per loan in

annual interest payments after elimination.

The result contrasts with Kim et al. (2012) which documents insignificant economic

consequence in equity market, suggesting banks are special and different from public

shareholders in pricing the information risk associated with the elimination rule. Loan size, firm

size, cash flow volatility, and growth opportunity all have a negative and significant impact on

cost of bank debt, while Leverage has a positive and significant effect on cost of bank loans,

suggesting that larger firms with lower Leverage ratio and high growth opportunity, and firms

that borrow larger loans, pay lower interest rate on bank loans. The coefficient on credit spread is

negative and significant, which is consistent with our expectation that credit rating is inversely

related to loan spread. The coefficient on term spread is positive and significant, which is

consistent with our expectation that maturity is positively related to loan spread.

Insert Table 3 Here

21

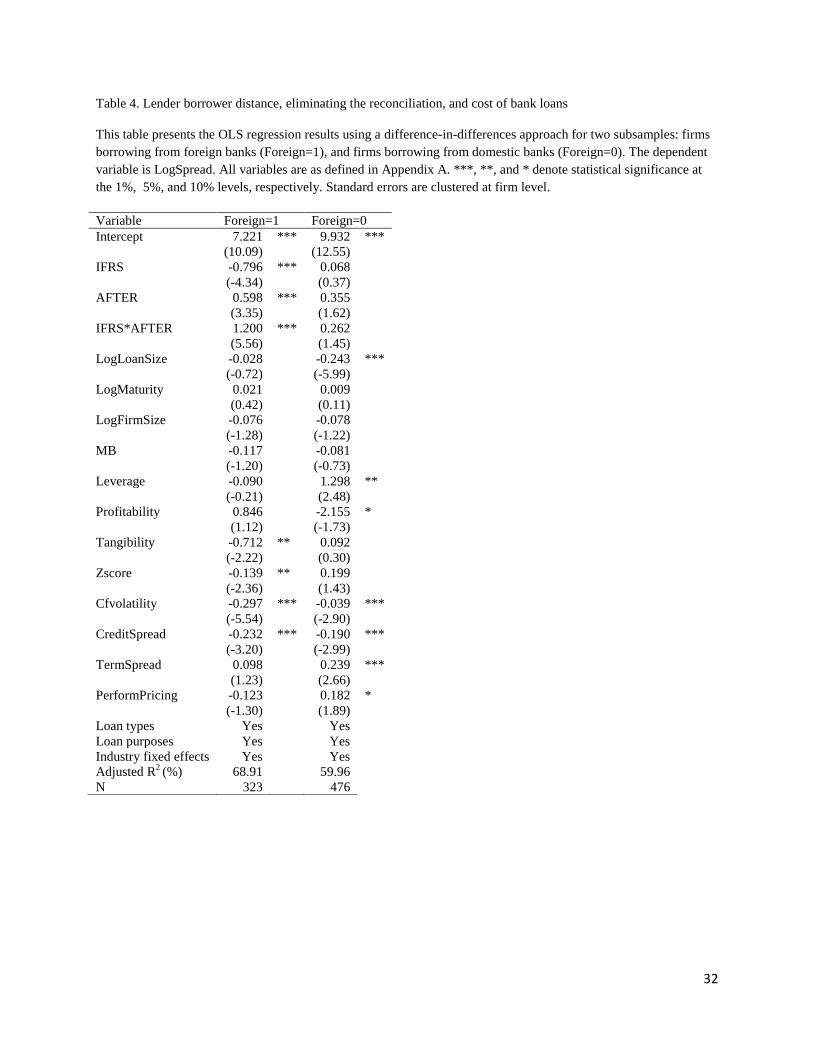

4.2.2 Lender-borrower distance

When partitioning the sample into two groups: firms borrowing from foreign banks, and

firms borrowing from domestic banks. We find that firms borrowing from foreign banks in

general pay a significantly lower loan spread before the elimination rule, and pay a higher loan

spread after the elimination rule. More interestingly, IFRS firms borrowing from foreign banks

pay a significantly higher loan spread after the elimination rule (p-value < 0.01), while we do not

find such evidence for IFRS firms borrowing from a domestic bank. The result is consistent with

hypothesis H2 in that foreign lenders which are more geographically distant from the borrowers,

rely more on hard information including the supplemental information provided by 20-F

reconciliation, charge a higher loan spread after the elimination rule to compensate for the

greater information loss. We also find both the magnitude and statistical significance of the

interaction term between IFRS and After are greater for IFRS firms borrowing from foreign

banks, compared to IFRS firms in the pooled sample. This evidence is consistent with the notion

that geographic distance matters in information collection and in turn in loan pricing.

Insert Table 4 Here

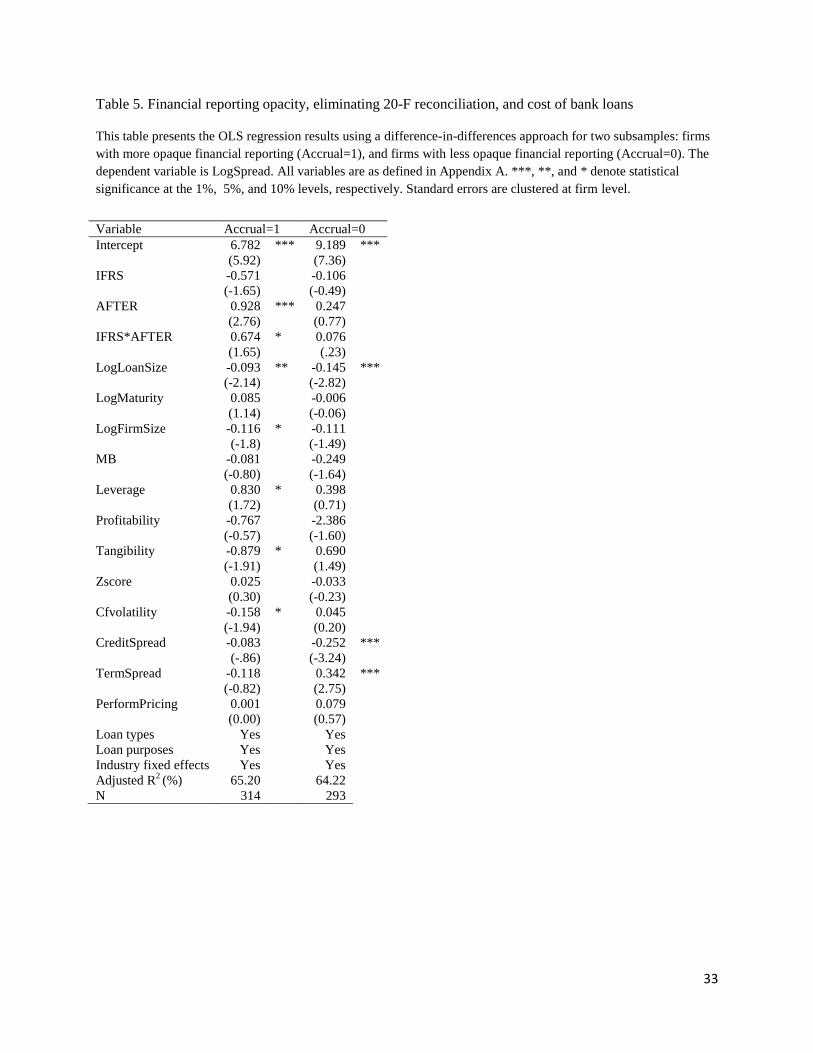

4.3 Financial reporting opacity

Partitioning results based on financial reporting opacity is reported in Table 4. We find

firms with more financial reporting opacity pay a higher loan spread after the elimination rule (p

value <0.10), while firms with lower financial reporting opacity do not pay a higher loan spread.

The result is consistent with hypothesis H3. The demand for private information and other

supplemental information that may help interpret financial statements is greater in firms with

more opaque financial reporting. Therefore we expect 20-F reconciliation provides more useful

22

information in opaque reporting firms and its elimination results in greater information loss and

hence a higher cost of bank debt.

Insert Table 5 Here

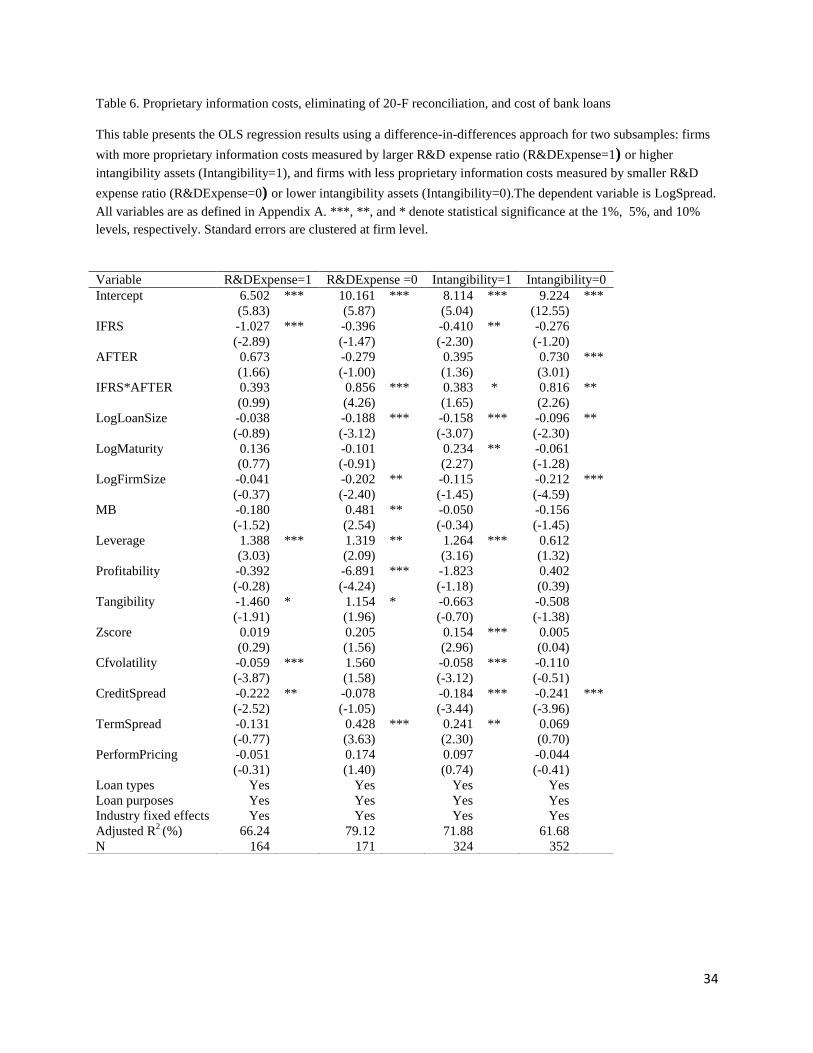

4.4 Proprietary information

Partitioning results based on proprietary information are reported in Table 5. We find

firms with lower proprietary information proxied by either R&D expenses (Column 1 and 2) or

Intangibility (Column 3 and 4) pay a higher loan spread after the elimination rule. The result

supports our hypothesis H4 in that in firms with less proprietary information banks rely more on

hard information such as 20-F reconciliation, and the elimination of 20-F results in more

information loss, and in turn lenders charge a higher loan spread.

Insert Table 6 Here

4.5 Robustness check

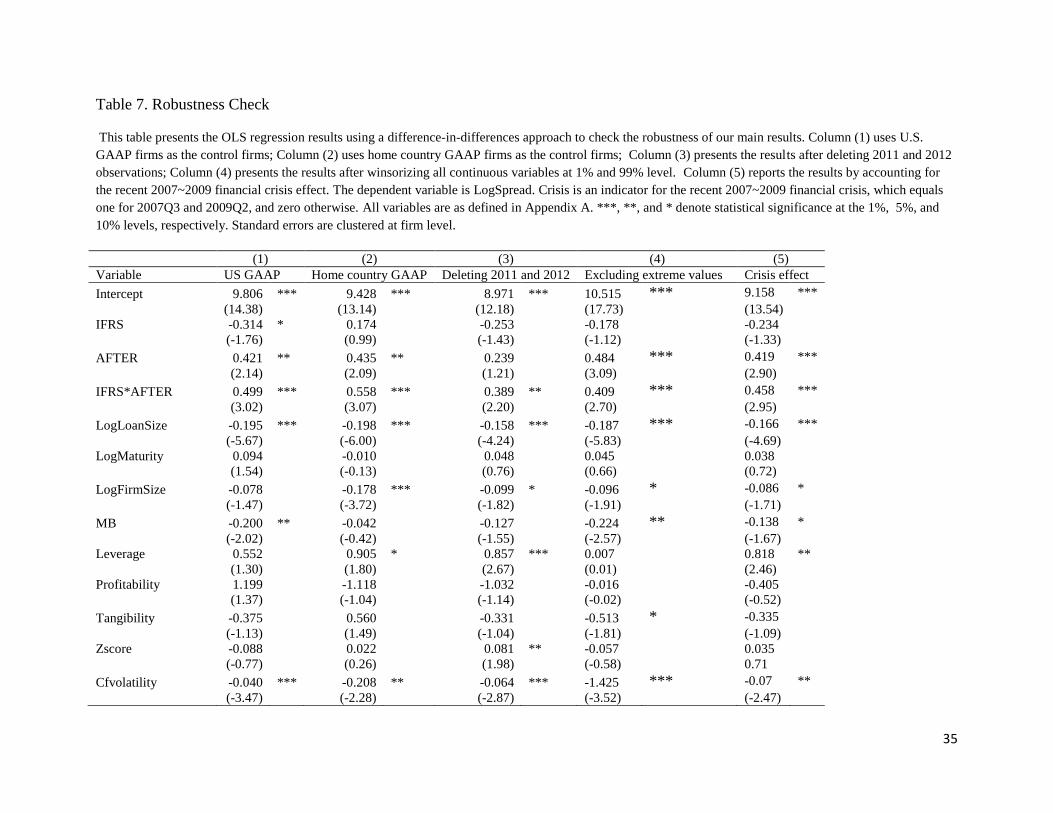

4.5.1 Alternative control sample

We include firms that use US GAAP or home country GAAP in the control sample.

There are likely systematic differences between the firms that use US GAAP from those that use

local GAAP. To address this concern, we separate these two groups of control firms and re-

estimate the models. Results are reported in Column 1 and 2 of Table 6. The results indicate that

our main results still hold, that IFRS firms experience higher cost of bank loans after the

elimination rule compared to US GAAP control firms (p-value <0.01), or home country GAAP

control firms (p-value < 0.01).

4.5.2 Constant pre- and post-elimination period

23

We also eliminate 2011 and 2012 data so that the post-elimination period is about three

years, similar to the pre-elimination period. Results are reported in Column 3 of Table 6. The

results show that our main results are robust, that IFRS firms experience higher cost of bank

loans after the elimination rule compared to non-IFRS control firms (p-value <0.05).

4.5.3 Influence of extreme values

Given the relatively small sample size, particularly for IFRS firms, we examine whether

our inferences are affected by extreme values by winsorizing all continuous variables at 1% and

99% and re-estimate the cost of bank loans model (1). Results are presented in Column 4 of

Table 7. We obtain qualitatively similar results, suggesting that our results are not driven by

extreme values.

4.5.4 Financial crisis effect

Since our sample period partially overlaps with the 2007-2009 financial crisis, we

investigate whether our results are driven by financial crisis effect by including a financial crisis

dummy in model (1). We define Crisis dummy equal one if the sample period falls between the

3rd

quarter of 2007 and the 2nd

quarter of 2009, and zero otherwise. Results are reported in

Column 5 of Table 7. The coefficient on Crisis is negative yet insignificant, while the coefficient

on IFRS*AFTER is still positive and significant, suggesting that our inferences are not affected

by financial crisis effect.

Insert Table 7 Here

V. Conclusion

24

In this study we examine how the elimination of 20-F reconciliation affects cost of bank

debt of foreign IFRS firms. Empirical evidence indicates that cost of bank debt increases after

the elimination rule for foreign IFRS firms. We also document that loan spread is higher for

firms borrowing from distant lenders (i.e., foreign banks), consistent with distant banks rely

more on hard information to make loan pricing decision. Furthermore we find that firms with

more opaque financial reporting pay higher loan spread after the elimination rule, consistent with

the demand for supplemental information is higher in such firms, and there is a more pronounced

information loss associated with the elimination rule in such firms. Lastly we find that firms with

less proprietary information costs pay higher loan spread after the elimination of 20-F

reconciliation, consistent with the conjecture that banks rely more on hard information (i.e., 20-F

reconciliation) when making loans to firms with less proprietary information costs. The

elimination of 20-F results in greater information loss and in turn banks charge a higher loan

spread.

The findings of this study are potentially important for several reasons: First, our study

sheds some light on private debt market consequences of SEC’s decision to eliminate the 20-F

reconciliation requirement for foreign private issuers. Our results suggest that the elimination

rule has a significant economic consequence in the private debt market, in that lenders charge

higher loan spread to compensate for the information loss. Second, our study complements prior

studies on the relationship between the elimination of 20-F reconciliation and the economic

consequences in equity market (e.g., Kim et al., 2012; Jiang et al., 2010). Third, our study

complements to existing studies on why banks are special. Fourth, our study relates to extant

studies on how geography affects important financial outcomes and how geographic proximity is

related to information advantage of being local. Using the elimination of 20-F reconciliation as a

25

unique setting, our study complements this stream of research by documenting that distant

lenders lose information advantage and charge a higher loan spread to foreign IFRS firms after

the elimination rule. Finally, our findings contribute to the ongoing debate whether the SEC was

judicious in eliminating the 20-F reconciliation requirement.

References

Agarwal, Sumit, and Robert Hauswald, 2010. Distance and private information in lending.

Review of Financial Studies 23 (7): 2757-2788.

Almazan, Andres, 2002. A model of competition in banking: bank capital vs. expertise. Journal

of Financial Intermediation 11, 87-121.

Altman, E., 1968. Financial Ratios, Discriminant Analysis and the Prediction of Corporate

Bankruptcy. The Journal of Finance 23, 589609.

Ayers, Benjamin c., Santhosh Ramalingegowda, and P. Eric Yeung, 2011. Hometown advantage:

the effects of monitoring institution location on financial reporting discretion. Journal of

Accounting and Economics 52, 41-61.

Berger, Allen N., Nathan H. Miller, Mitchell A. Petersen, Raghuram G. Rajan, and Jeremy

C. Stein, 2005. Does function follow organizational form? Evidence from the lending

practices of large and small banks. Journal of Financial Economics 76, 237–69.

Bharath, S., Sunder, J., Sunder, S., 2008. Accounting quality and debt contracting. Accounting

Review 23, 1–28.

Butler, Alexander, 2008. Distance still matters: evidence from municipal bond underwriting.

Review of Financial Studies 21, 763-784.

Chava, S., and M. Roberts, 2008. How Does Financing Impact Investment? The Role of Debt

Covenants. The Journal of Finance 63, 20852121.

Chen, Joseph, Harrison Hong, Ming Huang, and Jeffrey D. Kubik, 2004, Does fund size erode

mutual fund performance? American Economic Review 94, 1276-1302.

Chen, L. H., Sami, H., 2008. Trading volume reaction to the earnings reconciliation from IAS to U.S.

GAAP. Contemporary Accounting Research 25 (1), 1553.

Chen, L, H., Sami, H., 2013. The impact of firm characteristics on trading volume reaction to the earnings

reconciliation from IFRS to U.S. GAAP. Contemporary Accounting Research 30 (2), 697-718.

26

Cheng, Lin, Scott Liao, and Haiwen Zhang, 2013. The commitment effect versus information

effect of disclosure─Evidence from smaller reporting companies. The Accounting Review

88(4): 1239-1263.

Coval, Joshua D., and Tobias J. Moskowitz, 1999, Home bias at home: Local equity preference

in domestic portfolios. Journal of Finance 104, 2045-2073.

Coval, Joshua D., and Tobias J. Moskowitz, 2001, The geography of investment: Informed

trading and asset prices. Journal of Political Economy 109, 811-841.

Dechow, P. M., R. Sloan, and A. Sweeney. 1995. Detecting earnings management. The

Accounting Review 70 (2), 193–225.

Dechow, P. M., and I. Dichev. 2002. The quality of accruals and earnings: The role of accrual

estimation errors, The Accounting Review 77, 35–59.

Deng, S., R. Willis, and L. Xu, 2013. Shareholder Litigation, Reputational Loss, and Bank Loan

Contracting. Journal of Financial and Quantitative Analysis, forthcoming.

Diamond, D. 1984. Financial Intermediation and Delegated Monitoring. Review of Economic

Studies 51: 393-414.

Ellis, J., C. E. Fee, AND S. E. Thomas. 2010. Proprietary costs and the disclosure of information

about customers. University of Pittsburgh, Working Paper.

Fama, Eugene, 1985. What’s different about banks? Journal of Monetary Economics 15 (1), 29-

39.

Focarelli, D., Casolaro, L., Pozzolo, A.F., 2008. The pricing effect of certification on

syndicated loans. Journal of Monetary Economics 55, 335-349.

Francis, Bill, Iftekhar Hasan, and Maya Waisman, 2007, Does geography matter to

bondholders?, Federal Reserve Bank of Atlanta Working Papers Series (Federal Reserve

Bank of Atlanta, Atlanta, GA).

Franco, Gus De, Alexander Edwards, and Scott Liao, 2012. Banks’ Competitor-Specific

Knowledge in Loan Markets. Working paper, University of Toronto.

Gande, A. and A. Saunders. 2012. Are banks still special when there is a secondary market for

loans? Journal of Finance 67 (5): 1649-1684.

Gordon, E. A., Jorgensen, B. N., Linthicum, C. L., 2008. Could IFRS replace US GAAP? A comparison

of earnings attributes and informativeness in the US market. Working paper, Temple University,

Columbia University, and University of Texas – San Antonio.

27

Graham, J., and S. Li, and J. Qiu. “Corporate Misreporting and Bank Loan Contracting.” Journal

of Financial Economics, 89 (2008), 4461.

Harris, M.S., Muller, K. A., 1999. The market valuation of IAS versus US-GAAP accounting measures

using Form 20-F reconciliations. Journal of Accounting and Economics 26 (1-3), 285-312.

Hauswald, Robert, and Robert Marquez, 2006. Competition and strategic information acquisition

in credit markets. Review of Financial Studies 19 (3), 967-1000.

Henry, E., Lin, S., Yang, Y., 2009. The European-U.S. “GAAP Gap”: IFRS to U.S. GAAP Form 20-F

reconciliations. Accounting Horizons 23 (2), 121150.

Hollander, Stephan, and Arnt Verriest, 2011. Location and Debt Contracts. Working paper,

Tilburg University.

Hopkins, P. E., Botosan, C. A., Bradshaw, M. T., Callahan, C. M., Ciesielski, J., Farber, D. B., Hodder,

L. D., Kohlbeck, M. J., Laux, R., Stober, T. L., Stocken, P. C., Yohn, T. L., 2008. Response to the

SEC release, “Acceptance from foreign private issuers of financial statements prepared in accordance

with international financial reporting standards without reconciliation to U.S. GAAP File No. S7–13–

07.” Accounting Horizons 22 (2), 223–40.

Jamal, K., Benston, G. J., Carmichael, D. R., Christensen, T. E., Colson, R. H., Moehrle, S. R.,

Rajgopal, S., Stober, T. L., Sunder, S., Watts, R. L., 2008. A perspective on the SEC’s

proposal to accept financial statements prepared in accordance with international financial

reporting standards (IFRS) without reconciliation to U.S. GAAP. Accounting Horizons 22

(2), 241–48.

James, C., 1987. Some evidence on the uniqueness of bank loans. Journal of Financial

Economics 19, 217–36.

Jiang, J. X., Petroni, K. R., Wang, I. Y., 2010. Did eliminating the 20-F reconciliation between IFRS and

US GAAP matter? Working Paper, Michigan State University.

Jones, J., 1991. Earnings management during import relief investigations. Journal of Accounting

Research 29, 193–228.

Jones, D. A. 2007. Voluntary disclosure in R&D-intensive industries. Contemporary Accounting

Research 24, 489–522.

Kim, J., B. Song, and L. Zhang. “Internal Control Weakness and Bank Loan Contracting:

Evidence from SOX Section 404 Disclosures.” The Accounting Review, 86 (2011), 1157–

1188.

28

Kim, Y., Li, H., Li, S., 2012. Does eliminating the Form 20-F reconciliation from IFRS to U.S. GAAP

have capital market consequences? Journal of Accounting and Economics 53 (1-2), 249−270.

Lummer and McConnell, 1989. Further evidence on the bank lending process and the capital-

market response to bank loan agreements. Journal of Financial Economics 25 (1), 99-122.

Mian, A., 2006. Distance constraints: the limits of foreign lending in poor economies. Journal of

Finance 61(3): 1465-1505.

Petersen, M., 2004. Information: Hard and Soft. Working Paper, Northwestern University.

Petersen, M., and R. Rajan, 2002. Does distance still matter? The information revolution in small

business lending. Journal of Finance 57, 2533-2570.

Rajan, R.G., 1992. Insiders and outsiders: the choice between informed and arm’s-length debt.

Journal of Finance 47 (4): 1367-1400.

Securities and Exchange Commission (SEC), 2007. Final Rule: Acceptance from Foreign Private

Issuers of Financial Statements Prepared in Accordance with International Financial

Reporting Standards without Reconciliation to U.S. GAAP. Washington, D.C.: SEC,

December 21.

Securities and Exchange Commission (SEC), 2008. Final Rule: Foreign issuer reporting

enhancements. Washington, D. C.: SEC, September 23.

Spiro, A. 2007. The architecture of information distribution in the loan market. In A. Taylor and A.

Sansone’s, The Handbook of Loan Syndications & Trading (186-207). New York: McGraw-Hill.

Sufi, A., 2009. Bank Lines of Credit in Corporate Finance: An Empirical Analysis. Review of

Financial Studies 22(3): 1057-1088.

Sussman, O., and J. Zeira, 1995. Banking and development. CEPR, London.

Teoh, S. H., I. Welch, and T. J. Wong. 1998. Earnings management and the underperformance of

seasoned equity offerings. Journal of Financial Economics 50: 63–99.

Watts, R. L., 2003. Conservatism in accounting Part I: Explanations and implications.

Accounting Horizons 17 (3), 207−221.

Yu, Julia, 2011. The Interaction of Voluntary and Mandatory Disclosures: Evidence from the

SEC’s Elimination of the IFRS-U.S. GAAP Reconciliation. Working Paper, University of

Georgia.

29

Table 1. Univariate comparisons

This table reports the univariate comparisons of major firm- and loan-specific variables for IFRS and non-IFRS

firms, and before and after the elimination rule. All variables are defined in Appendix A.

Panel A. Univariate comparison of firm-specific characteristics for IFRS and non-IFRS firms

IFRS Firms(N=56) Non-IFRS Firms(N=123) Test of Difference

Variable Mean Median Mean Median

Mean

(T-Stat)

Median

(Z-Value)

LogFirmSize 9.820 9.959 7.968 7.832 7.24*** 6.44***

MB 1.508 1.334 1.580 1.399 -0.75 0.18

Leverage 0.302 0.293 0.315 0.274 -0.58 -0.09

Profitability 0.129 0.118 0.132 0.127 -0.33 -0.14

Tangibility 0.294 0.292 0.507 0.537 -6.01*** -4.59***

Zscore 1.239 1.157 0.872 0.905 2.39*** 2.20**

Cfvolatility 0.216 0.129 0.550 0.119 -1.26 -0.33

Panel B. Univariate comparison of loan-specific characteristics issued by IFRS and non-IFRS firms

IFRS Firms(N=292) Non-IFRS Firms(N=516) Test of Difference

Variable Mean Median Mean Median

Mean

(T-Stat)

Median

(Z-Value)

Logspread 4.435 4.284 4.765 4.828 -4.37*** -3.99***

Allindrawn 148.725 72.5 162.93 125 -1.34*** -3.99***

FacilityAmt ($million) 2085.725 1115.960 814.392 277.500 6.37*** 10.71***

LogLoanSize 20.612 20.833 19.392 19.441 11.03*** 10.71***

Maturity (months) 62.115 60.833 56.899 60.867 2.19** 1.03

LogMaturity 3.964 4.108 3.859 4.109 2.14** 1.03

Panel C. Univariate comparison of loan-specific characteristics before and after the elimination rule

Before elimination (N=434) After elimination (N=374) Test of Difference

Mean Median

Variable Mean Median Mean Median (T-Stat) (Z-Value)

AllInDrawn 107.148 72.500 216.572 187.500 11.27*** 12.14***

Logspread 4.263 4.284 5.090 5.234 13.40*** 12.14***

FacilityAmt ($million) 1218.404 411.525 1338.156 500 0.66 2.40**

LogLoanSize 19.692 19.835 19.996 20.030 2.67*** 2.40**

Maturity 62.746 60.867 54.186 59.650 -3.75*** -4.48***

LogMaturity 3.948 4.109 3.838 4.088 -2.34** -4.48***

30

Table 2. Pearson correlation matrix

This table reports the Pearson correlation matrix for major variables. All variables are defined in Appendix A. Correlations significant at the 1%–10% level are

highlighted in bold.

Logspread LogLoanSize LogMaturity LogFirmSize MB Leverage Profitability Tangibility Zscore Cfvolatility

LogLoanSize -0.365 1

LogMaturity 0.087 -0.137 1

LogFirmSize -0.296 0.638 -0.043 1

MB -0.126 -0.057 -0.067 -0.149 1

Leverage 0.186 -0.160 0.101 -0.171 -0.134 1

Profitability -0.075 0.049 0.082 0.126 0.457 -0.029 1

Tangibility -0.016 -0.141 0.024 -0.172 -0.126 0.171 0.026 1

Zscore -0.087 0.058 -0.101 0.157 0.322 -0.236 0.443 -0.055 1

Cfvolatility -0.075 -0.068 0.025 -0.149 0.153 -0.218 -0.053 -0.101 -0.255 1

31

Table 3. The impact of eliminating the reconciliation on cost of bank loans

This table presents the OLS regression results using a difference-in-differences approach. The dependent

variable is LogSpread. All variables are defined in Appendix A. ***, **, and * denote statistical

significance at the 1%, 5%, and 10% levels, respectively. Standard errors are clustered at firm level.

Variable Predicted Sign LogSpread

Intercept ? 9.205 ***

(13.84)

IFRS ? -0.232

(-1.32)

AFTER ? 0.486 ***

(3.25)

IFRS*AFTER + 0.450 ***

(2.99)

LogLoanSize − -0.165 ***

(-4.65)

LogMaturity + 0.033

(0.62)

LogFirmSize − -0.088 *

(-1.74)

MB − -0.151 *

(-1.94)

Leverage + 0.825 **

(2.50)

Profitability − -0.324

(-0.42)

Tangibility − -0.342

(-1.11)

Zscore − 0.036

(0.75)

Cfvolatility + -0.068 **

(-2.47)

CreditSpread − -0.195 ***

(-4.25)

TermSpread + 0.180 **

(2.50)

PerformPricing ? -0.004

(-0.05)

Loan types Yes

Loan purposes Yes

Industry fixed effects Yes

Adjusted R2 (%) 58.07

N 808

32

Table 4. Lender borrower distance, eliminating the reconciliation, and cost of bank loans

This table presents the OLS regression results using a difference-in-differences approach for two subsamples: firms

borrowing from foreign banks (Foreign=1), and firms borrowing from domestic banks (Foreign=0). The dependent

variable is LogSpread. All variables are as defined in Appendix A. ***, **, and * denote statistical significance at

the 1%, 5%, and 10% levels, respectively. Standard errors are clustered at firm level.

Variable Foreign=1 Foreign=0

Intercept 7.221 *** 9.932 ***

(10.09) (12.55)

IFRS -0.796 *** 0.068

(-4.34) (0.37)

AFTER 0.598 *** 0.355

(3.35) (1.62)

IFRS*AFTER 1.200 *** 0.262

(5.56) (1.45)

LogLoanSize -0.028 -0.243 ***

(-0.72) (-5.99)

LogMaturity 0.021 0.009

(0.42) (0.11)

LogFirmSize -0.076 -0.078

(-1.28) (-1.22)

MB -0.117 -0.081

(-1.20) (-0.73)

Leverage -0.090 1.298 **

(-0.21) (2.48)

Profitability 0.846 -2.155 *

(1.12) (-1.73)

Tangibility -0.712 ** 0.092

(-2.22) (0.30)

Zscore -0.139 ** 0.199

(-2.36) (1.43)

Cfvolatility -0.297 *** -0.039 ***

(-5.54) (-2.90)

CreditSpread -0.232 *** -0.190 ***

(-3.20) (-2.99)

TermSpread 0.098 0.239 ***

(1.23) (2.66)

PerformPricing -0.123 0.182 *

(-1.30) (1.89)

Loan types Yes Yes

Loan purposes Yes Yes

Industry fixed effects Yes Yes

Adjusted R2 (%) 68.91 59.96

N 323 476

33

Table 5. Financial reporting opacity, eliminating 20-F reconciliation, and cost of bank loans

This table presents the OLS regression results using a difference-in-differences approach for two subsamples: firms

with more opaque financial reporting (Accrual=1), and firms with less opaque financial reporting (Accrual=0). The

dependent variable is LogSpread. All variables are as defined in Appendix A. ***, **, and * denote statistical

significance at the 1%, 5%, and 10% levels, respectively. Standard errors are clustered at firm level.

Variable Accrual=1 Accrual=0

Intercept 6.782 *** 9.189 ***

(5.92) (7.36)

IFRS -0.571 -0.106

(-1.65) (-0.49)

AFTER 0.928 *** 0.247

(2.76) (0.77)

IFRS*AFTER 0.674 * 0.076

(1.65) (.23)

LogLoanSize -0.093 ** -0.145 ***

(-2.14) (-2.82)

LogMaturity 0.085 -0.006

(1.14) (-0.06)

LogFirmSize -0.116 * -0.111

(-1.8) (-1.49)

MB -0.081 -0.249

(-0.80) (-1.64)

Leverage 0.830 * 0.398

(1.72) (0.71)

Profitability -0.767 -2.386

(-0.57) (-1.60)

Tangibility -0.879 * 0.690

(-1.91) (1.49)

Zscore 0.025 -0.033

(0.30) (-0.23)

Cfvolatility -0.158 * 0.045

(-1.94) (0.20)

CreditSpread -0.083 -0.252 ***

(-.86) (-3.24)

TermSpread -0.118 0.342 ***

(-0.82) (2.75)

PerformPricing 0.001 0.079

(0.00) (0.57)

Loan types Yes Yes

Loan purposes Yes Yes

Industry fixed effects Yes Yes

Adjusted R2 (%) 65.20 64.22

N 314 293

34

Table 6. Proprietary information costs, eliminating of 20-F reconciliation, and cost of bank loans

This table presents the OLS regression results using a difference-in-differences approach for two subsamples: firms

with more proprietary information costs measured by larger R&D expense ratio (R&DExpense=1) or higher

intangibility assets (Intangibility=1), and firms with less proprietary information costs measured by smaller R&D

expense ratio (R&DExpense=0) or lower intangibility assets (Intangibility=0).The dependent variable is LogSpread.

All variables are as defined in Appendix A. ***, **, and * denote statistical significance at the 1%, 5%, and 10%

levels, respectively. Standard errors are clustered at firm level.

Variable R&DExpense=1 R&DExpense =0 Intangibility=1 Intangibility=0

Intercept 6.502 *** 10.161 *** 8.114 *** 9.224 ***

(5.83) (5.87) (5.04) (12.55)

IFRS -1.027 *** -0.396 -0.410 ** -0.276

(-2.89) (-1.47) (-2.30) (-1.20)

AFTER 0.673 -0.279 0.395 0.730 ***

(1.66) (-1.00) (1.36) (3.01)

IFRS*AFTER 0.393 0.856 *** 0.383 * 0.816 **

(0.99) (4.26) (1.65) (2.26)

LogLoanSize -0.038 -0.188 *** -0.158 *** -0.096 **

(-0.89) (-3.12) (-3.07) (-2.30)

LogMaturity 0.136 -0.101 0.234 ** -0.061

(0.77) (-0.91) (2.27) (-1.28)

LogFirmSize -0.041 -0.202 ** -0.115 -0.212 ***

(-0.37) (-2.40) (-1.45) (-4.59)

MB -0.180 0.481 ** -0.050 -0.156

(-1.52) (2.54) (-0.34) (-1.45)

Leverage 1.388 *** 1.319 ** 1.264 *** 0.612

(3.03) (2.09) (3.16) (1.32)

Profitability -0.392 -6.891 *** -1.823 0.402

(-0.28) (-4.24) (-1.18) (0.39)

Tangibility -1.460 * 1.154 * -0.663 -0.508

(-1.91) (1.96) (-0.70) (-1.38)

Zscore 0.019 0.205 0.154 *** 0.005

(0.29) (1.56) (2.96) (0.04)

Cfvolatility -0.059 *** 1.560 -0.058 *** -0.110

(-3.87) (1.58) (-3.12) (-0.51)

CreditSpread -0.222 ** -0.078 -0.184 *** -0.241 ***

(-2.52) (-1.05) (-3.44) (-3.96)

TermSpread -0.131 0.428 *** 0.241 ** 0.069

(-0.77) (3.63) (2.30) (0.70)

PerformPricing -0.051 0.174 0.097 -0.044

(-0.31) (1.40) (0.74) (-0.41)

Loan types Yes Yes Yes Yes

Loan purposes Yes Yes Yes Yes

Industry fixed effects Yes Yes Yes Yes

Adjusted R2 (%) 66.24 79.12 71.88 61.68

N 164 171 324 352

35

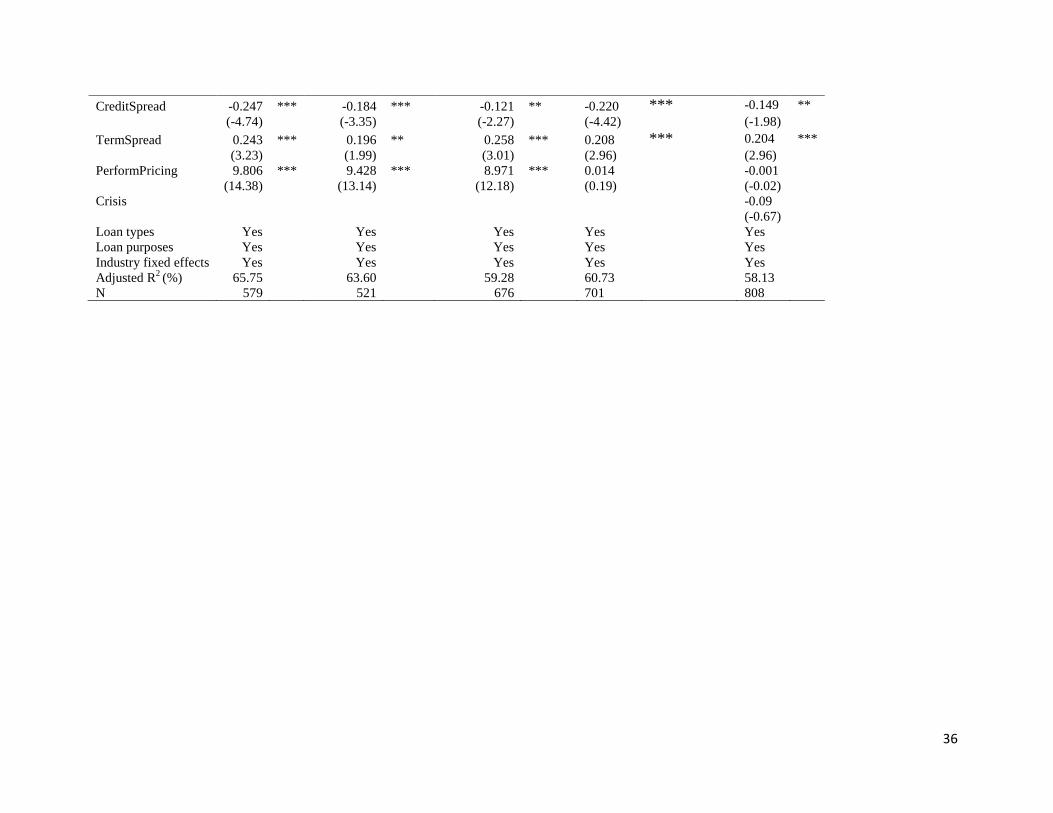

Table 7. Robustness Check

This table presents the OLS regression results using a difference-in-differences approach to check the robustness of our main results. Column (1) uses U.S.

GAAP firms as the control firms; Column (2) uses home country GAAP firms as the control firms; Column (3) presents the results after deleting 2011 and 2012

observations; Column (4) presents the results after winsorizing all continuous variables at 1% and 99% level. Column (5) reports the results by accounting for

the recent 2007~2009 financial crisis effect. The dependent variable is LogSpread. Crisis is an indicator for the recent 2007~2009 financial crisis, which equals

one for 2007Q3 and 2009Q2, and zero otherwise. All variables are as defined in Appendix A. ***, **, and * denote statistical significance at the 1%, 5%, and

10% levels, respectively. Standard errors are clustered at firm level.

(1) (2) (3) (4) (5)

Variable US GAAP Home country GAAP Deleting 2011 and 2012 Excluding extreme values Crisis effect

Intercept 9.806 *** 9.428 *** 8.971 *** 10.515 *** 9.158 ***

(14.38) (13.14) (12.18) (17.73) (13.54)

IFRS -0.314 * 0.174 -0.253 -0.178 -0.234

(-1.76) (0.99) (-1.43) (-1.12) (-1.33)

AFTER 0.421 ** 0.435 ** 0.239 0.484 *** 0.419 ***

(2.14) (2.09) (1.21) (3.09) (2.90)

IFRS*AFTER 0.499 *** 0.558 *** 0.389 ** 0.409 *** 0.458 ***

(3.02) (3.07) (2.20) (2.70) (2.95)

LogLoanSize -0.195 *** -0.198 *** -0.158 *** -0.187 *** -0.166 ***

(-5.67) (-6.00) (-4.24) (-5.83) (-4.69)

LogMaturity 0.094 -0.010 0.048 0.045 0.038

(1.54) (-0.13) (0.76) (0.66) (0.72)

LogFirmSize -0.078 -0.178 *** -0.099 * -0.096 * -0.086 *

(-1.47) (-3.72) (-1.82) (-1.91) (-1.71)

MB -0.200 ** -0.042 -0.127 -0.224 ** -0.138 *

(-2.02) (-0.42) (-1.55) (-2.57) (-1.67)

Leverage 0.552 0.905 * 0.857 *** 0.007 0.818 **

(1.30) (1.80) (2.67) (0.01) (2.46)

Profitability 1.199 -1.118 -1.032 -0.016 -0.405

(1.37) (-1.04) (-1.14) (-0.02) (-0.52)

Tangibility -0.375 0.560 -0.331 -0.513 * -0.335

(-1.13) (1.49) (-1.04) (-1.81) (-1.09)

Zscore -0.088 0.022 0.081 ** -0.057 0.035

(-0.77) (0.26) (1.98) (-0.58) 0.71

Cfvolatility -0.040 *** -0.208 ** -0.064 *** -1.425 *** -0.07 **

(-3.47) (-2.28) (-2.87) (-3.52) (-2.47)

36

CreditSpread -0.247 *** -0.184 *** -0.121 ** -0.220 *** -0.149 **

(-4.74) (-3.35) (-2.27) (-4.42) (-1.98)

TermSpread 0.243 *** 0.196 ** 0.258 *** 0.208 *** 0.204 ***

(3.23) (1.99) (3.01) (2.96) (2.96)

PerformPricing 9.806 *** 9.428 *** 8.971 *** 0.014 -0.001

(14.38) (13.14) (12.18) (0.19) (-0.02)

Crisis -0.09

(-0.67)

Loan types Yes Yes Yes Yes Yes

Loan purposes Yes Yes Yes Yes Yes

Industry fixed effects Yes Yes Yes Yes Yes

Adjusted R2 (%) 65.75 63.60 59.28 60.73 58.13

N 579 521 676 701 808

37

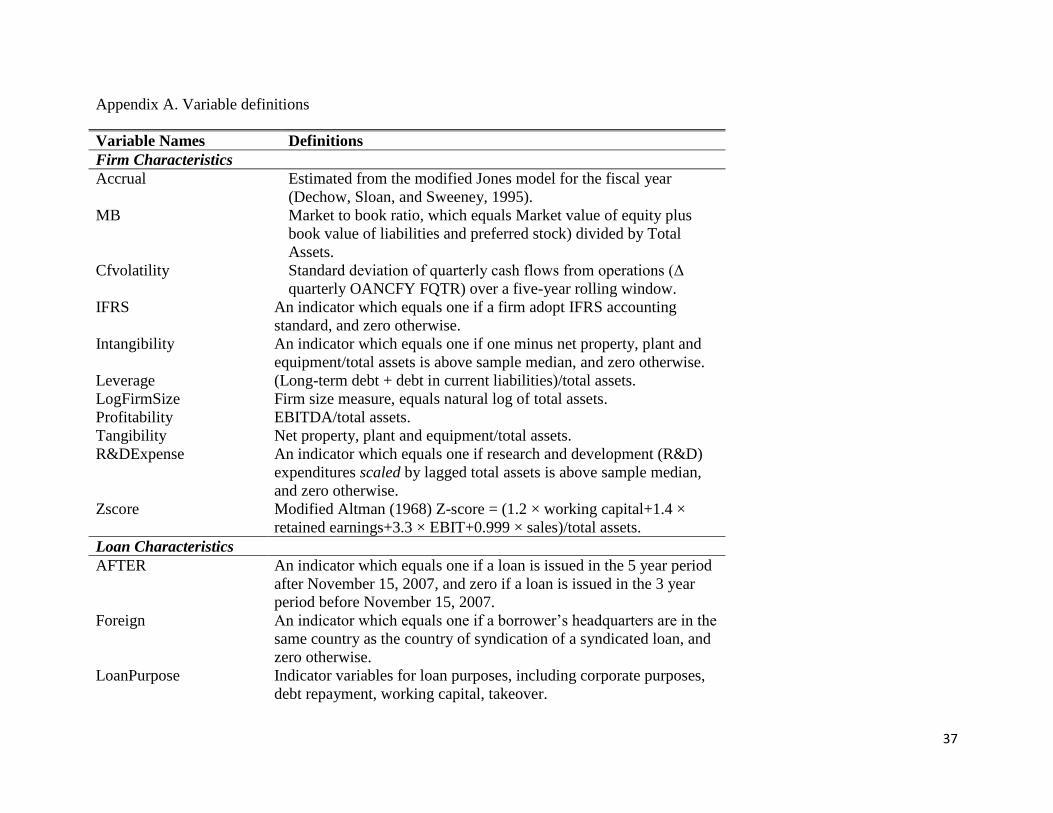

Appendix A. Variable definitions

Variable Names Definitions

Firm Characteristics

Accrual Estimated from the modified Jones model for the fiscal year

(Dechow, Sloan, and Sweeney, 1995).

MB Market to book ratio, which equals Market value of equity plus

book value of liabilities and preferred stock) divided by Total

Assets.

Cfvolatility Standard deviation of quarterly cash flows from operations (Δ

quarterly OANCFY FQTR) over a five-year rolling window.

IFRS An indicator which equals one if a firm adopt IFRS accounting

standard, and zero otherwise.

Intangibility An indicator which equals one if one minus net property, plant and

equipment/total assets is above sample median, and zero otherwise.

Leverage (Long-term debt + debt in current liabilities)/total assets.

LogFirmSize Firm size measure, equals natural log of total assets.

Profitability EBITDA/total assets.

Tangibility Net property, plant and equipment/total assets.

R&DExpense An indicator which equals one if research and development (R&D)

expenditures scaled by lagged total assets is above sample median,

and zero otherwise.

Zscore Modified Altman (1968) Z-score = (1.2 × working capital+1.4 ×

retained earnings+3.3 × EBIT+0.999 × sales)/total assets.

Loan Characteristics

AFTER An indicator which equals one if a loan is issued in the 5 year period

after November 15, 2007, and zero if a loan is issued in the 3 year

period before November 15, 2007.

Foreign An indicator which equals one if a borrower’s headquarters are in the

same country as the country of syndication of a syndicated loan, and

zero otherwise.

LoanPurpose Indicator variables for loan purposes, including corporate purposes,

debt repayment, working capital, takeover.

38

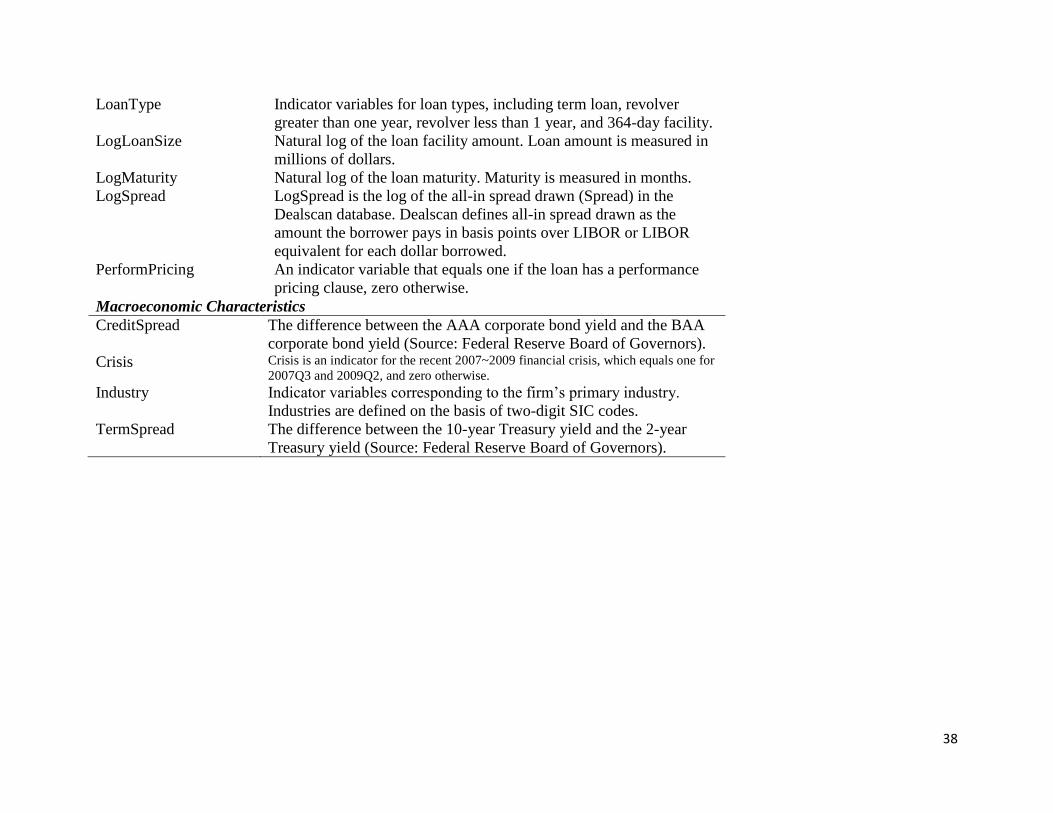

LoanType Indicator variables for loan types, including term loan, revolver

greater than one year, revolver less than 1 year, and 364-day facility.

LogLoanSize Natural log of the loan facility amount. Loan amount is measured in

millions of dollars.

LogMaturity Natural log of the loan maturity. Maturity is measured in months.

LogSpread LogSpread is the log of the all-in spread drawn (Spread) in the

Dealscan database. Dealscan defines all-in spread drawn as the

amount the borrower pays in basis points over LIBOR or LIBOR

equivalent for each dollar borrowed.

PerformPricing An indicator variable that equals one if the loan has a performance

pricing clause, zero otherwise.

Macroeconomic Characteristics

CreditSpread The difference between the AAA corporate bond yield and the BAA

corporate bond yield (Source: Federal Reserve Board of Governors).

Crisis Crisis is an indicator for the recent 2007~2009 financial crisis, which equals one for

2007Q3 and 2009Q2, and zero otherwise. Industry Indicator variables corresponding to the firm’s primary industry.

Industries are defined on the basis of two-digit SIC codes.

TermSpread The difference between the 10-year Treasury yield and the 2-year

Treasury yield (Source: Federal Reserve Board of Governors).