Embed Size (px)

Citation preview

The Second Aegon UK Readiness ReportIs the UK more ready for retirement since the 2014 Budget?November 2014

The Aegon UK Readiness Report

FOREWORD

The Government may have ripped up the rule book and cut through the red tape to give us greater freedom over how we spend the contents of our pension pot from next April, but when it comes to ‘how much’ is in there, it’s still down to each and every one of us to get saving.

Whether you retire with a comfortable amount or just enough to get by it’s down to you, and six months on from the first Aegon UK Readiness Report, the latest research shows we’re still not saving enough for our retirement.

In fact, we’re actually getting worse when it comes to keeping track of any existing pension savings, yet we expect a higher retirement income than we did six months ago!

Back in April, Aegon’s research found most people wanted to retire with an annual income of £35,000, yet were only on track to achieve a third of this at around £12,000.

Six months on, it seems our ‘expectations’ have grown as we now ‘want’ a target retirement income of £41,000 a year (nearly twice the average annual wage1). Yet the harsh reality is that 47% of us don’t make regular contributions to a pension scheme and 27% save under £100 a month so the harsh reality of our ‘dream’ retirement could well actually be a horrible nightmare.

Changing our financial habits won’t happen overnight. When you consider over 60% of us have never done something as simple as switching energy suppliers to save money, it’s easy to understand why tackling the task of retirement planning falls way down on our agenda.

That’s got to change. Taking small steps is the way forward and there are reassuring signs we’re moving in the right direction. According to Aegon’s report, the amount we’re saving in ISAs for our retirement is up by over 50% since April to nearly £13,000, but there’s still a long way to go.

Sue Hayward Personal Finance and Consumer Expert

1 Research was conducted by Watermelon on behalf of Aegon. Total sample size was 3983 adults. Fieldwork was undertaken in September 2014. The figures have been weighted and are representative of all GB adults (aged 18+). The research was then put through Aegon’s own unique methodology to create a readiness score. The income shortfall values referred to in the Aegon UK Readiness Report are shown in today’s value and not future inflated values. All figures quoted from this research unless otherwise stated.

NOVEMBER 2014

PAGE 3

Over the past six months, major changes to UK pensions have been announced. These will radically alter the way that people can access their savings from April 2015. We’re moving towards a more flexible system, thanks to the introduction of greater freedoms in how and when people can access their pension pots, and the new promise of free guidance. Now, no matter what your situation, there will be more freedom and choice when you reach retirement.

As I acknowledged in the first Aegon UK Readiness Report, these changes are also a great opportunity for the pensions industry to reconnect with customers. Alongside the expertise of financial advisers and other third parties, the pensions industry has a great responsibility to provide the information and tools people need in order to help them engage with their pensions and get ready for their retirement.

There is still some way to go in terms of helping people grow their savings – the new pensions changes focus on making it easier to access pensions, but we really need to ensure that people find it equally as easy to save for them. Auto-enrolment goes some way towards addressing this, but at the same time, I also know that we have a long road ahead of us. Through the launch of our Retiready service, Aegon is ahead of the competition in offering customers a way to save, check and change

their pension plans online. However, as an industry, we are still lagging behind – according to the Readiness data, at least 84% of people use technology to access their finances, yet only 11% manage their pension online.

Our second Aegon UK Readiness Report has also revealed that people are still not engaged enough in planning for their life after work. This may be down to the fact that the pension changes have caused “information overload”, but as people begin to see the actual impact the changes will have on them, the level of awareness will hopefully rise. However, in the meantime there are still issues. Even fewer people are tracking their retirement savings, even in key age groups – for instance, 45-54 year olds are the least likely to know exactly when they’ll access their pension. For a group not too far off retirement, this is worrying and should set alarm bells ringing for the industry.

This is particularly concerning as following next year’s changes, one in six people say they will access their pension at age 55, and one in six also want to access the full pot as a cash lump sum. While these options may make sense for a small number of people, the worry is that it won’t suit the majority, who can expect to live to 80 and may need their retirement savings to last 30 years if they begin accessing them at 55.

David Macmillan Managing Director, Aegon

In April this year, Aegon published its first UK Readiness Report. It contained key statistics, information and analysis based on a survey of over 4,000 people in the UK. Those who took part completed a series of questions designed to assess their behaviour, awareness and finances in relation to pensions and savings. And, most importantly, the study looked at people’s expectations about retirement against the plan they have in place now. Based on this information Aegon then applied its retirement readiness calculation to create a unique readiness score for the UK population. This score shows if people in the UK are on track to achieve the retirement they want, the higher their score the closer their expectations are to the reality of their situation – this is not about wealth.

The original report2 revealed that just 7% of the population was on track for the retirement they wanted.

Since the research for the first report was conducted, major changes to Britain’s pensions industry have been announced, which are expected to have a significant impact consumers. Six months on, Aegon has re-run this research, to gauge if the new pension freedoms brought about by the Chancellor’s Budget have focused people’s minds and behaviour on preparing for retirement.

2 Research was conducted by Watermelon on behalf of Aegon. Total sample size was 4,062 adults. Fieldwork was undertaken in February 2014. The figures have been weighted and are representative of all GB adults (aged 18+). The research was then put through Aegon’s own unique methodology to create a readiness score.

The lack of awareness about the potential dangers of the new pension changes may not yet have filtered through to people, but again, it’s our responsibility as an industry to provide customers with the help they need to make the right decisions and to fully understand the options available to them.

Despite the challenges that still face us, it’s encouraging to see that there are certain groups who are becoming more financially savvy, but I reiterate my comments from the first Readiness Report – we need to step up and educate people in the lead up to and throughout retirement; and technology is a key part of this.

The Aegon UK Readiness Report

FOREWORD & OVERVIEW

Overview of the report

NOVEMBER 2014

PAGE 5

About the readiness score

There are three categories which make up the readiness score. Each of these are explained below.

• Financial – This gives us a picture of your financial situation and expectations in retirement and included questions like; in today’s money, what annual income would you like in retirement?

• Awareness – This assesses your awareness of what type of lifestyle you want in retirement and your understanding of the level of funding required to achieve your chosen lifestyle and included questions like; what is the current maximum Basic State Pension per week?

• Behaviour – This assesses the actions you’ve taken towards your retirement needs and to fund the income required to achieve the retirement you want and included questions such as; how much do you make in regular contributions to your ISAs each month? And - how recently have you checked the performance of your retirement savings?

Contents

The Readiness Report is divided into three sections, which clearly demonstrate how ready the UK is for retirement.

Section 1 – The national readiness profileLooks at how the UK is positioned as a whole when it comes to being ready for retirement

Section 2 – Why hasn’t the UK become more prepared? Highlights how the UK measures up in awareness, behaviour and financial capability

Section 3 – Expectations vs. realityExamines differences between gender, region and profession and discusses the key facts

Section 4 – The Impact of the Budget

The Aegon UK Readiness Report

SECTION 1 – THE NATIONAL READINESS PROFILE

The readiness score offers an objective indication of how on track people are for the retirement they want by taking into account factors like age, monthly savings, expected retirement age, guaranteed retirement income and broader understanding of saving. All of these factors combine to give a score out of 100. Scoring 70 and over indicates that people are on track for the retirement they would like or expect.

Using this measure, and despite the interest in pensions brought about by the Budget changes, the latest research shows that just 6% of the UK are on track for the retirement they want. This is marginally down from the first Readiness Report published earlier this year

which showed that just 7% had the right plans in place to meet their expectations in retirement. This leaves 94% of the UK population who remain unrealistic about their plans or who are simply not saving enough for the retirement they want. Most worrying is that those scoring below 30 increased by 9% from 4% to 13%, showing that the journey to get the UK ready for retirement still has some way to go.

There could be a number of reasons for this fall but it’s most likely that the reforms have yet to filter through, this paired with a long-standing disenchantment with saving for retirement and almost a decade of poor wage growth, means that the UK’s readiness score will not change overnight.

of the UK population are on track for the retirement they want

6%JUST

= 10% of UK population

Score of 30 or less4%

41%Score of 30-49

48%Score of 50-69

7%Score of 70 or more

Score of 30 or less13%

47%Score of 30-49

34%Score of 50-69

6%Score of 70 or more

Breakdown of figures VS H1 report, April 2014

PAGE 6

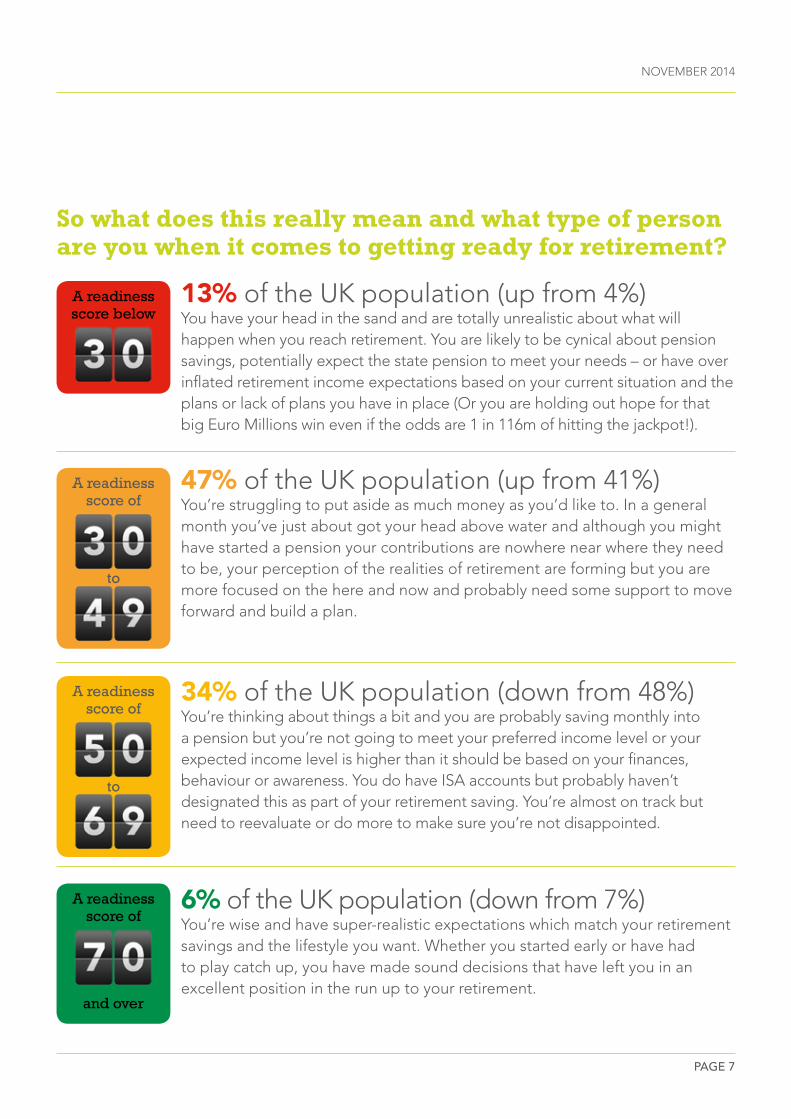

13% of the UK population (up from 4%)You have your head in the sand and are totally unrealistic about what will happen when you reach retirement. You are likely to be cynical about pension savings, potentially expect the state pension to meet your needs – or have over inflated retirement income expectations based on your current situation and the plans or lack of plans you have in place (Or you are holding out hope for that big Euro Millions win even if the odds are 1 in 116m of hitting the jackpot!).

47% of the UK population (up from 41%)You’re struggling to put aside as much money as you’d like to. In a general month you’ve just about got your head above water and although you might have started a pension your contributions are nowhere near where they need to be, your perception of the realities of retirement are forming but you are more focused on the here and now and probably need some support to move forward and build a plan.

34% of the UK population (down from 48%)You’re thinking about things a bit and you are probably saving monthly into a pension but you’re not going to meet your preferred income level or your expected income level is higher than it should be based on your finances, behaviour or awareness. You do have ISA accounts but probably haven’t designated this as part of your retirement saving. You’re almost on track but need to reevaluate or do more to make sure you’re not disappointed.

6% of the UK population (down from 7%)You’re wise and have super-realistic expectations which match your retirement savings and the lifestyle you want. Whether you started early or have had to play catch up, you have made sound decisions that have left you in an excellent position in the run up to your retirement.

NOVEMBER 2014

PAGE 7

So what does this really mean and what type of person are you when it comes to getting ready for retirement?

A readiness score below

A readiness score of

to

to

A readiness score of

A readiness score of

and over

The Aegon UK Readiness Report

SECTION 2 – WHY HASN’T THE UK BECOME MORE PREPARED?

Once again, people scored least favourably in the financial section, followed by awareness and behaviour.

A readiness score of

A readiness score of

A readiness score of

Financial • On average people wanted an income of £41k in retirement, an increase of

£6k from the April report, but in reality people reported that they only have an average guaranteed income of £18k per year.

• 46% reported that they had a guaranteed income between £1k and £10k per year and 33% that they had no guaranteed income during retirement.

Awareness

• Across the UK there is a very low awareness of how to set and achieve retirement goals, only 6% received a readiness score over 70.

• Over a quarter of people overestimate the amount of the maximum state pension they will receive.

• The average age people in the UK expect to retire has remained the same at 63, signaling that most will require their retirement savings to last for around 20 years according to the average life expectancy; 78.7 years for men and 82.6 for women1.

Behaviour • 50% of the UK population claims never to have checked the performance

of their retirement savings indicating low engagement levels or that people simply don’t have easy access to review their pension savings.

• 47% of the UK do not make any regular contributions to a pension and a further 27% are currently saving under £100 per month.

• Over half of the UK adult population does not have any savings in an ISA meaning that over £20m2 people may not be using their tax free savings allowance. Between the age of 18 and 60 this could amount to tax-free savings of £630 if the full £15k annual allowance were to be used and excludes the possibility of investment growth or interest.

1ONS Life Expectancy Statistics March 2014 2Source: Table 1 2011 Census: Usual resident population by five-year age group and sex, United Kingdom and constituent countries

3 Research conducted through the State Pension Calculator. https://www.gov.uk/calculate-state-pension

SECTION 3 – EXPECTATIONS VS. REALITY NOVEMBER 2014

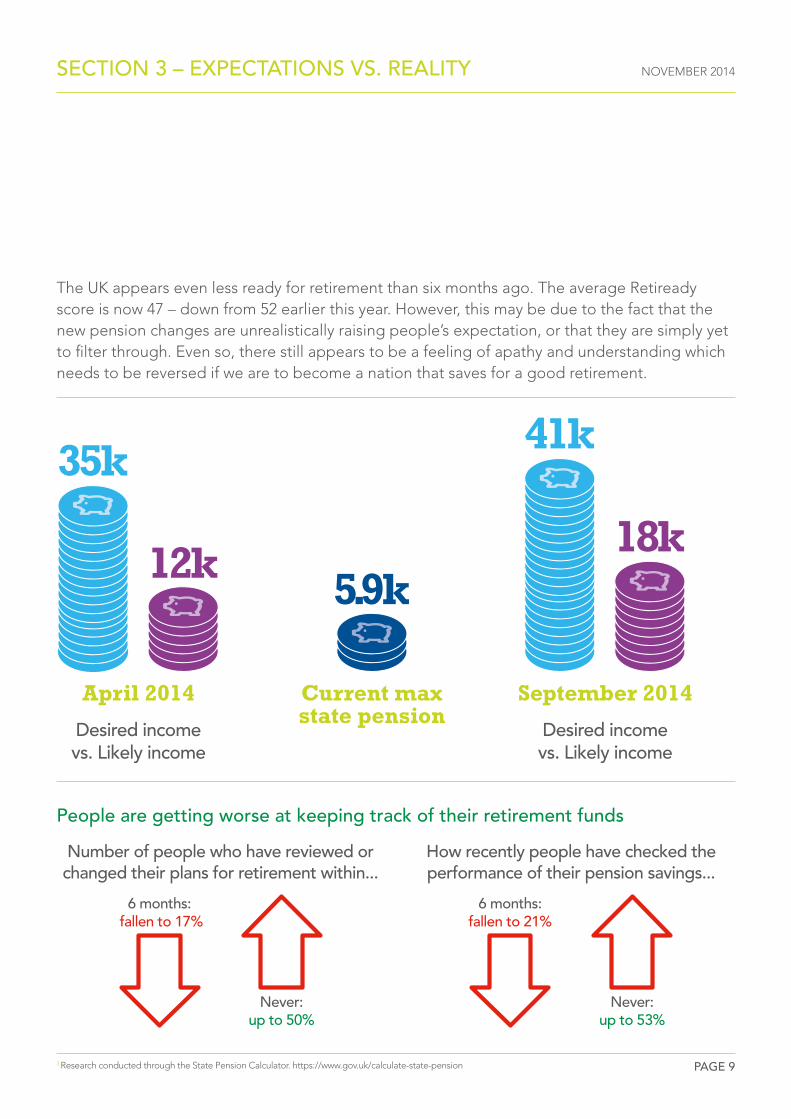

The UK appears even less ready for retirement than six months ago. The average Retiready score is now 47 – down from 52 earlier this year. However, this may be due to the fact that the new pension changes are unrealistically raising people’s expectation, or that they are simply yet to filter through. Even so, there still appears to be a feeling of apathy and understanding which needs to be reversed if we are to become a nation that saves for a good retirement.

Desired income vs. Likely income

Desired income vs. Likely income

5.9k

35k

12k

41k

18k

PAGE 9

April 2014 September 2014 Current max state pension

People are getting worse at keeping track of their retirement funds

Number of people who have reviewed or changed their plans for retirement within...

How recently people have checked the performance of their pension savings...

6 months: fallen to 17%

Never: up to 50%

6 months: fallen to 21%

Never: up to 53%

The Aegon UK Readiness Report

SECTION 3 – EXPECTATIONS VS. REALITY

There’s also been a significant drop in the number of people who know what the basic state pension is. The fact that more people were aware of this figure back in April than the figure now, may be down to the fact that the maximum weekly state pension changed in April but again could be an indication that pension changes are not getting through to people.

Auto-enrollment, although two years old, is one of the few measures brought in that will actually help people in the lead up to retirement – rather than when they reach retirement age. While 31% of people are unsure whether they are eligible to be auto-enrolled, a further 32.1% say they have already opted into a scheme with just 8% saying they chose or intend to opt out of the scheme.

Readiness 2 data October 2014

Knew the basic state pension in April was £110.15

Know the renewed basic state pension is £113.10

44% 30%

NOVEMBER 2014

PAGE 11

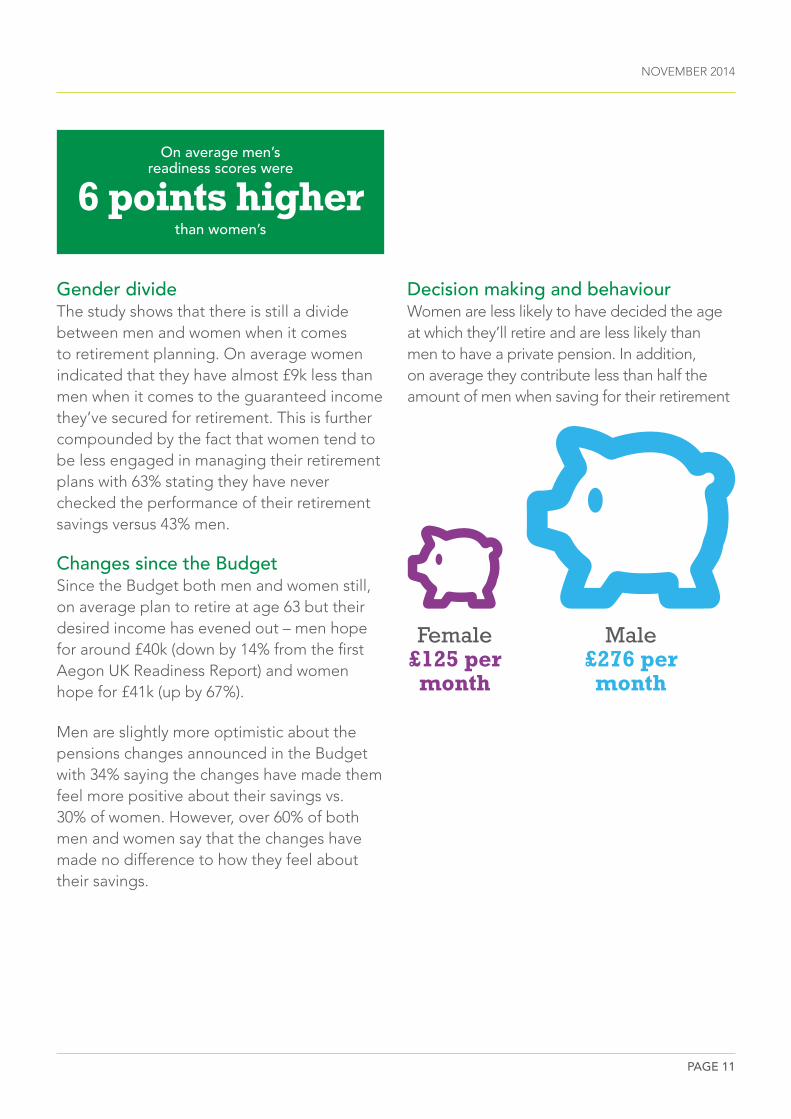

Gender divideThe study shows that there is still a divide between men and women when it comes to retirement planning. On average women indicated that they have almost £9k less than men when it comes to the guaranteed income they’ve secured for retirement. This is further compounded by the fact that women tend to be less engaged in managing their retirement plans with 63% stating they have never checked the performance of their retirement savings versus 43% men.

Changes since the Budget Since the Budget both men and women still, on average plan to retire at age 63 but their desired income has evened out – men hope for around £40k (down by 14% from the first Aegon UK Readiness Report) and women hope for £41k (up by 67%).

Men are slightly more optimistic about the pensions changes announced in the Budget with 34% saying the changes have made them feel more positive about their savings vs. 30% of women. However, over 60% of both men and women say that the changes have made no difference to how they feel about their savings.

On average men’s readiness scores were

than women’s

6 points higher

Decision making and behaviour Women are less likely to have decided the age at which they’ll retire and are less likely than men to have a private pension. In addition, on average they contribute less than half the amount of men when saving for their retirement

Male £276 per month

Female £125 per month

The Aegon UK Readiness Report

SECTION 3 – EXPECTATIONS VS. REALITY

Key facts

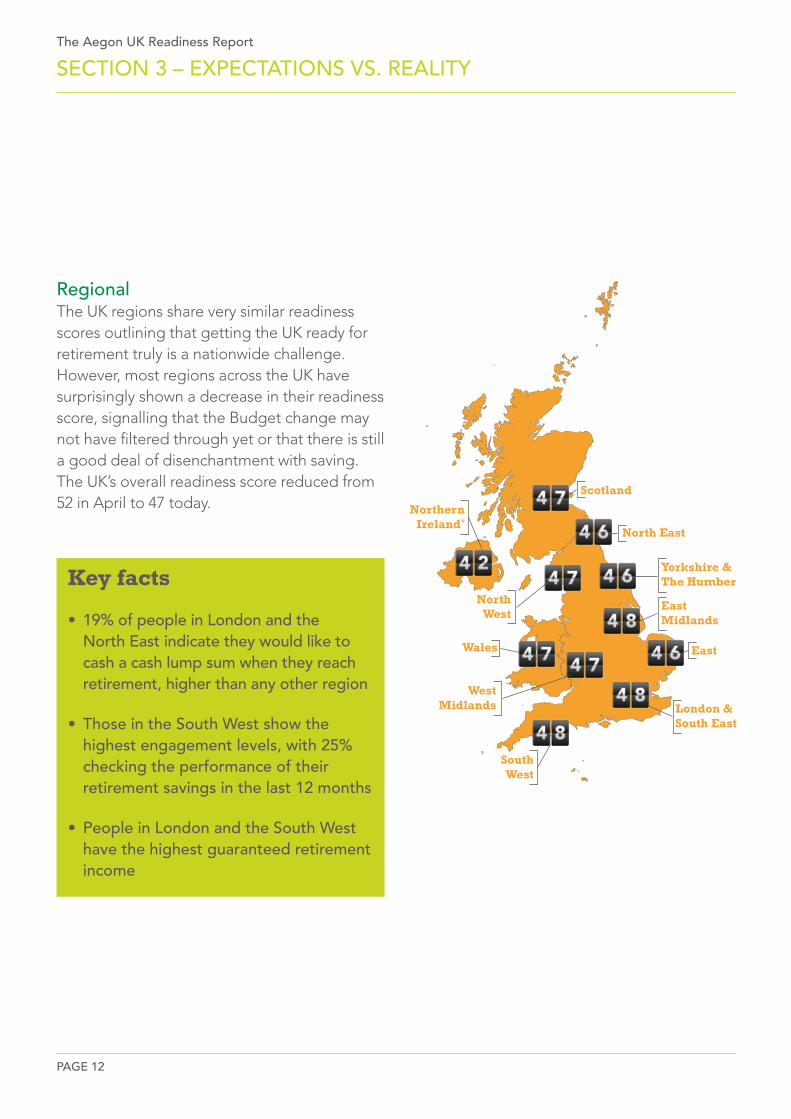

• 19% of people in London and the North East indicate they would like to cash a cash lump sum when they reach retirement, higher than any other region

• Those in the South West show the highest engagement levels, with 25% checking the performance of their retirement savings in the last 12 months

• People in London and the South West have the highest guaranteed retirement income

Scotland

North East

Yorkshire & The Humber

East Midlands

East

London & South East

South West

West Midlands

Wales

North West

Northern Ireland*

RegionalThe UK regions share very similar readiness scores outlining that getting the UK ready for retirement truly is a nationwide challenge. However, most regions across the UK have surprisingly shown a decrease in their readiness score, signalling that the Budget change may not have filtered through yet or that there is still a good deal of disenchantment with saving. The UK’s overall readiness score reduced from 52 in April to 47 today.

PAGE 12

* Based on a very small sample.

NOVEMBER 2014

PAGE 13

Key facts

• People who work in advertising, media, the performing arts and Retail buying are among the least engaged in their retirement planning – 50% of each group report having never checked their retirement savings

• Those in scientific services are most astute when it comes to taking advantage of tax free savings with an average ISA balance of over £30k

• Those in Banking and financial management are one of the most ready groups with an overall readiness score of 55

ProfessionsThe study shows some marked differences between the retirement readiness of different professions and highlights the important role of pensions in the workplace. Those in the IT sector boast an average pension pot of over £40k, a huge gap when compared to those in healthcare who have on average £22k saved for their retirement.

Banking & financial£382

Healthcare£304Creative arts & design£150Social care & guidance£256

Ave. Monthly Pension contributions

Despite the promising signs shown by the value of the average monthly contribution it’s important to remember that the second UK Readiness Report identified that nearly 50% of the UK population make no regular contributions to their pension.

The Aegon UK Readiness Report

SECTION 4 – THE IMPACT OF THE BUDGET

PAGE 14

Impact of the BudgetThe changes to pensions announced at this year’s Budget mean people will have far greater flexibility over how they access their pension and they’ll be able to start accessing savings from age 55.

There has been a renewed interest in pensions in recent month as a result and while 64% of people say they are unmoved by the changes, 32% believe they are a change for the better while just 4% view them as a change for the worse.

Everyone will be able to access their pension from age 55 next year, but only around one in six people intend to do so. This may be a wise choice given average life expectancy and savings may need to last 30 or more years if accessed at the earliest point.

The Four Key Ages People Intend to Access their Pension

16% 5%

21% 20%

24% 14%

Age 55 Age 70

Age 60 Other

Age 65 Don’t know

Change for the

Change for the

by changes

32%64%

4%

better

worse

Unmoved

PAGE 15

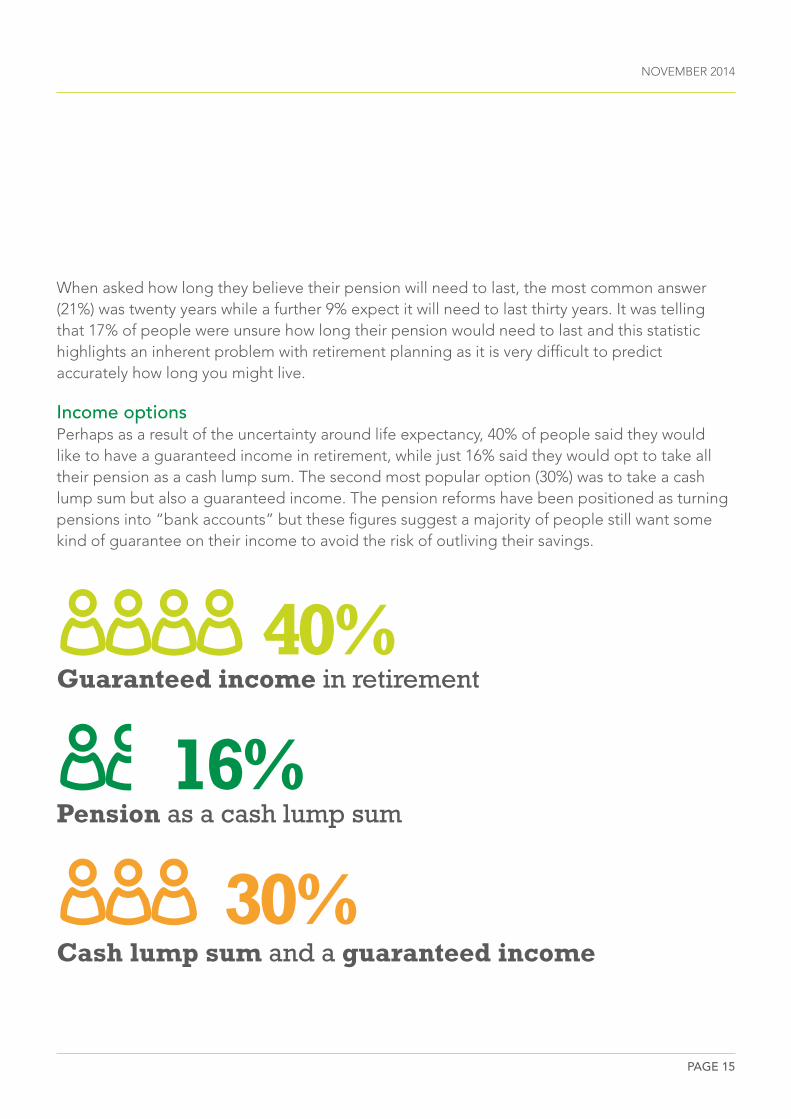

When asked how long they believe their pension will need to last, the most common answer (21%) was twenty years while a further 9% expect it will need to last thirty years. It was telling that 17% of people were unsure how long their pension would need to last and this statistic highlights an inherent problem with retirement planning as it is very difficult to predict accurately how long you might live.

Income optionsPerhaps as a result of the uncertainty around life expectancy, 40% of people said they would like to have a guaranteed income in retirement, while just 16% said they would opt to take all their pension as a cash lump sum. The second most popular option (30%) was to take a cash lump sum but also a guaranteed income. The pension reforms have been positioned as turning pensions into “bank accounts” but these figures suggest a majority of people still want some kind of guarantee on their income to avoid the risk of outliving their savings.

NOVEMBER 2014

40%

30%

Guaranteed income in retirement

Cash lump sum and a guaranteed income

Pension as a cash lump sum16%

PAGE 16

TaxTax tends to be a complicated topic and the amount owed to the tax man when you access your pension is no different. It will vary depending on an individual’s circumstances and how they choose to access their pension, but our research suggests many people are unclear on how much they can access without paying tax.

41% admit they are not sure what percentage of their pension they could access tax free as a lump sum while 8% believe they can take

100%. As a rule of thumb, most people are able to access 25% of their pension tax free and a 18% of people said they thought this was the amount they could take.

ISAsAs part of this year’s Budget, the ISA limit was increased to £15,000. Encouragingly, it would appear many people are trying to take advantage of this tax efficient savings option as the amount people say they have saved in an ISA has increased from £8,200 to £12,700 since April.

The Aegon UK Readiness Report

SECTION 4 – THE IMPACT OF THE BUDGET

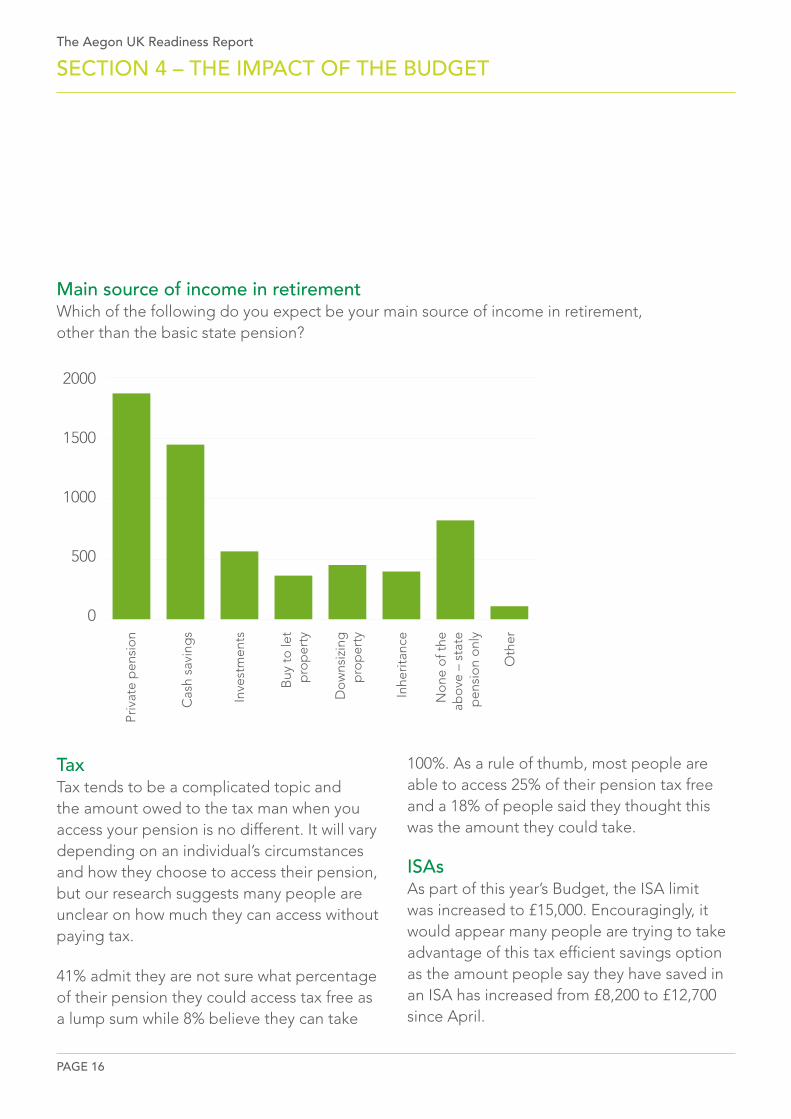

Main source of income in retirementWhich of the following do you expect be your main source of income in retirement, other than the basic state pension?

2000

1500

1000

500

0

Priv

ate

pen

sio

n

Cas

h sa

ving

s

Inve

stm

ents

Buy

to

let

pro

per

ty

Do

wns

izin

g

pro

per

ty

Inhe

ritan

ce

No

ne o

f the

ab

ove

– s

tate

p

ensi

on

onl

y

Oth

er

NOVEMBER 2014

CONCLUSION

ConclusionThe second Aegon UK Readiness Report has found that the majority of people are still not confident or engaged in saving for their retirement despite the recent pension reforms. Over 60% of the UK population say that the changes have made no difference to how they feel about their pension savings and over 50% admit to never having checked the performance of their pension pots.

Reflecting on the 2014 Budget, perhaps one of the most interesting statistics is that two in five (40%) would choose a guaranteed regular income, as opposed to any other combined or cash-only option. This signals that a significant number of people value security over a one off lump sum.

While, on the face of it, the UK appears even less ready for retirement than six months ago, with the UK’s readiness score falling from 52 in April to 47, there is hope that a broader level of awareness will develop, once the implications of the new pension changes filter through. Perhaps what we are seeing now is that things won’t change overnight and that they may get worse before they get better.

Alongside this, there are certain areas in which the industry has a role to play in raising awareness. In particular, it’s key that pensions are made accessible and that the internet is used to ensure the 38 million adults who use it every day can manage and track their pension pots (currently just 11% do). In addition, it is also very important that we address the gender divide, 63% of women said they had never checked the performance of their pension savings vs. 43% of men, despite in most cases living longer.

The report raises clear questions about the UK’s attitudes towards saving, the industry’s current approach and the recent government interventions. Does the fact that people are putting off looking at their pensions, suggest that at the moment it feels like an unachievable goal? Is legislation that only affects people at retirement unlikely to improve savings behaviour in the lead up? And does more need to be done to build on and complement pre-retirement initiatives like auto-enrolment, to really boost the UK’s readiness score?

PAGE 17

The Aegon UK Readiness Report

CONCLUSION

PAGE 18

Aegon’s proposition following the Budget This report has largely focused on the challenges facing the UK in saving up to retirement, but the changes brought about by the Budget relate to how people take their income in retirement. Through our online service, Retiready Aegon is helping non-advised customers to accumulate savings but the business is also very focused on providing a range of options for people looking to draw an income.

From next April, Aegon will be offering a wide range of services for customers looking take an income and many of these are already in place. Through Aegon Retirement Choices and One Retirement platform the business will offer drawdown services and access to a range of investments that can be used to grow savings or take an income such as the Aegon High Income fund.

As these changes come into place, the business is likely to launch further services but Aegon is well placed to deliver these with its unique platform offering that allows individuals, advisers and employers to manage their pensions and income online.

PAGE 19

What next?While the industry is moving towards better serving customers, people can start to make small changes which will help support this:

Tips to improve your readiness score:

1. Use Retiready to find out your current readiness score, and use the coaching facility to find out the steps you can take to improve on this if needed

2. Get clued up on what the new pension changes mean for you, and how this can complement your lifestyle (especially if you’re approaching or at retirement) there is lots of useful information at www.pensionsadvisoryservice.org.uk

3. Use this knowledge to start thinking realistically about what changes you could make in the long term. It needn’t be seen as sacrifices to be made today, rather gradual changes that will ultimately make a big difference tomorrow

4. And, as always, if you think that you need more help, seek professional advice

Below 30:

• Start thinking about how much you could put away each month

• Be proactive. Open a cash ISA and start putting away a little bit every month – this will get you into the rhythm of saving regularly

30 – 49:

• Think how you could change your spending habits to put a little bit away each month – every penny counts

• Remember that your pension contributions qualify for tax relief and so just putting away a little but often could help you feel more comfortable during your retirement

50 – 69

• Be mindful that ISA savings can be a key part of your retirement income – especially with the revised limits

• Review your savings – if you haven’t checked their performance in a long time, now is the perfect chance to speak to an adviser or review them yourself online

70 and over:

• You are on track but you can still look for more ways to maximise your retirement by using the coaching tool on the Retiready app

Resist the temptation to dip into savings you have outside your pension pot such as your ISA. Keep separate savings aside for extras and emergencies.

NOVEMBER 2014

CONCLUSION

The Aegon UK Readiness Report

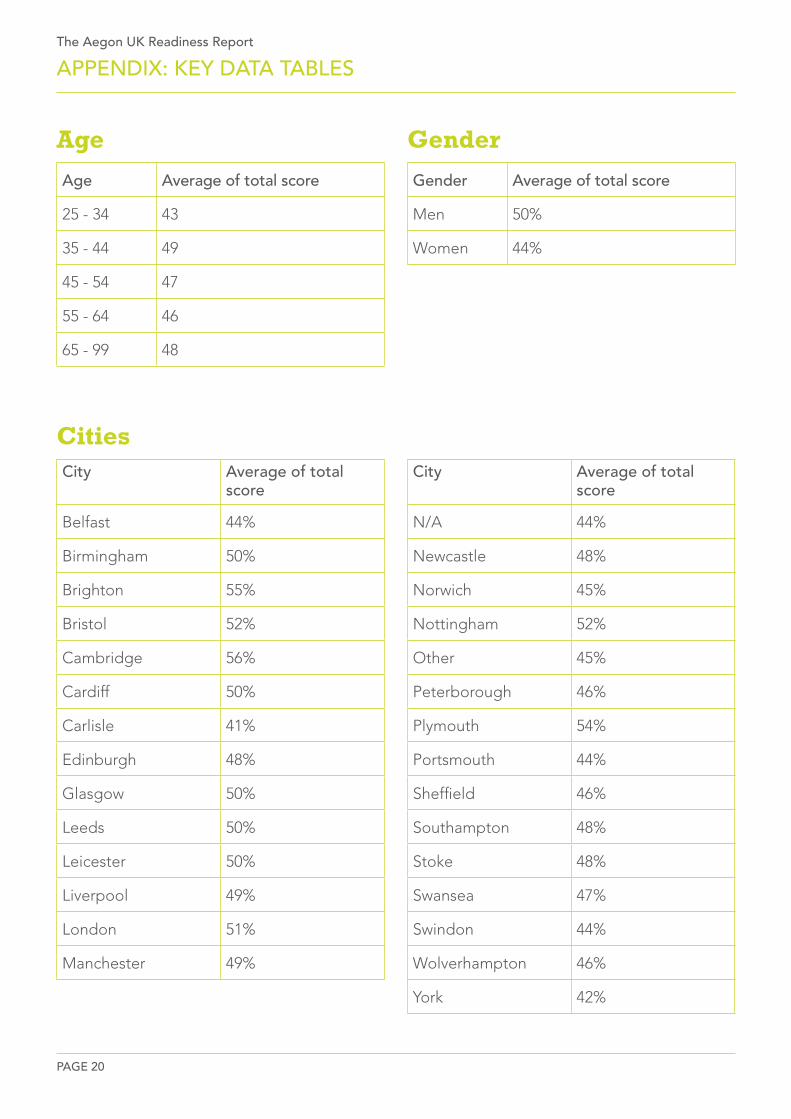

APPENDIX: KEY DATA TABLES

PAGE 20

Gender Average of total score

Men 50%

Women 44%

City Average of total score

Belfast 44%

Birmingham 50%

Brighton 55%

Bristol 52%

Cambridge 56%

Cardiff 50%

Carlisle 41%

Edinburgh 48%

Glasgow 50%

Leeds 50%

Leicester 50%

Liverpool 49%

London 51%

Manchester 49%

Age Average of total score

25 - 34 43

35 - 44 49

45 - 54 47

55 - 64 46

65 - 99 48

Gender

Cities

Age

City Average of total score

N/A 44%

Newcastle 48%

Norwich 45%

Nottingham 52%

Other 45%

Peterborough 46%

Plymouth 54%

Portsmouth 44%

Sheffield 46%

Southampton 48%

Stoke 48%

Swansea 47%

Swindon 44%

Wolverhampton 46%

York 42%

Profession Average of total score

Administration 50%

Advertising, marketing and PR 51%

Animal and plant resources 59%

Banking, financial management and accountancy

55%

Charity and voluntary work 48%

Construction and property 52%

Creative arts and design 48%

Education 50%

Engineering, manufacturing and production

53%

Environment 49%

Healthcare 49%

Hospitality and events management 47%

Human resources and employment 54%

I am unemployed n/a

Information services 57%

ProfessionsProfession Average of

total score

Information technology 58%

Insurance and pensions 53%

Law enforcement and protection 55%

Legal profession 56%

Leisure, sport and tourism 48%

Management and statistics 62%

Media and broadcasting 44%

Mining and land surveying 55%

Other n/a

Performing arts 41%

Publishing and journalism 51%

Retailing, buying and selling 47%

Scientific services 57%

Social care and guidance work 52%

Transport, logistics and distribution 50%

References1. Pg 8 – [1] ONS Life Expectancy Statistics March 2014 – (78.7 years for men and 82.6 for women [1])

2. Pg 8 [2] Source: Table 1 2011 Census: Usual resident population by five-year age group and sex, United Kingdom and constituent countries – (over £20m [2] people

3. Pg15 – ONS Internet Access – Households and Individuals 2014 – (38 million adults who use the internet every day )

NOVEMBER 2014

APPENDIX: KEY DATA TABLES

PAGE 21

Retiready and Aegon are brand names of Scottish Equitable plc (No. SC144517) and Aegon Investment Solutions Ltd (No. SC394519) registered in Scotland, registered office: Edinburgh Park, Edinburgh, EH12 9SE. Both are Aegon companies. Scottish Equitable plc is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Aegon Investment Solutions Ltd is authorised and regulated by the Financial Conduct Authority. Their Financial Services Register numbers are 165548 and 543123 respectively. © 2014 Aegon UK plc

C 288130 RETR 00272443 10/14