Embed Size (px)

Citation preview

Overbuilt?

The Seattle MD Apartment

Market Report

The question circulating around the

commercial real estate community as of late, has

been whether or not the Seattle-Bellevue-Everett

MD apartment market is becoming overbuilt. The

simple answer to this question is, it depends.

When looking at the Seattle-Bellevue-Everett

MD (King and Snohomish County) apartment

market as a whole, no, it is not being overbuilt,

but when the various submarkets are analyzed

individually, it is possible to conclude that some

areas may become overbuilt. (We will refer to

the Seattle-Bellevue-Everett MD as the Seattle

MD for the remainder of the newsletter.)

For instance, approximately 70% of all

units that are under construction in the Seattle

MD are located in the Seattle submarket. Even

within the Seattle submarket the units under

construction are relatively concentrated. In the

Seattle core there are 7 high-rise apartment

towers (approx. 4,000 units) under construction.

That represents nearly 35% of all apartment units

under construction in the Seattle MD. The other

areas with most of the construction activity are

Ballard and the University District. This implies

that the Eastside, Snohomish, and Southend

submarkets actually have a lack of supply in the

pipeline.

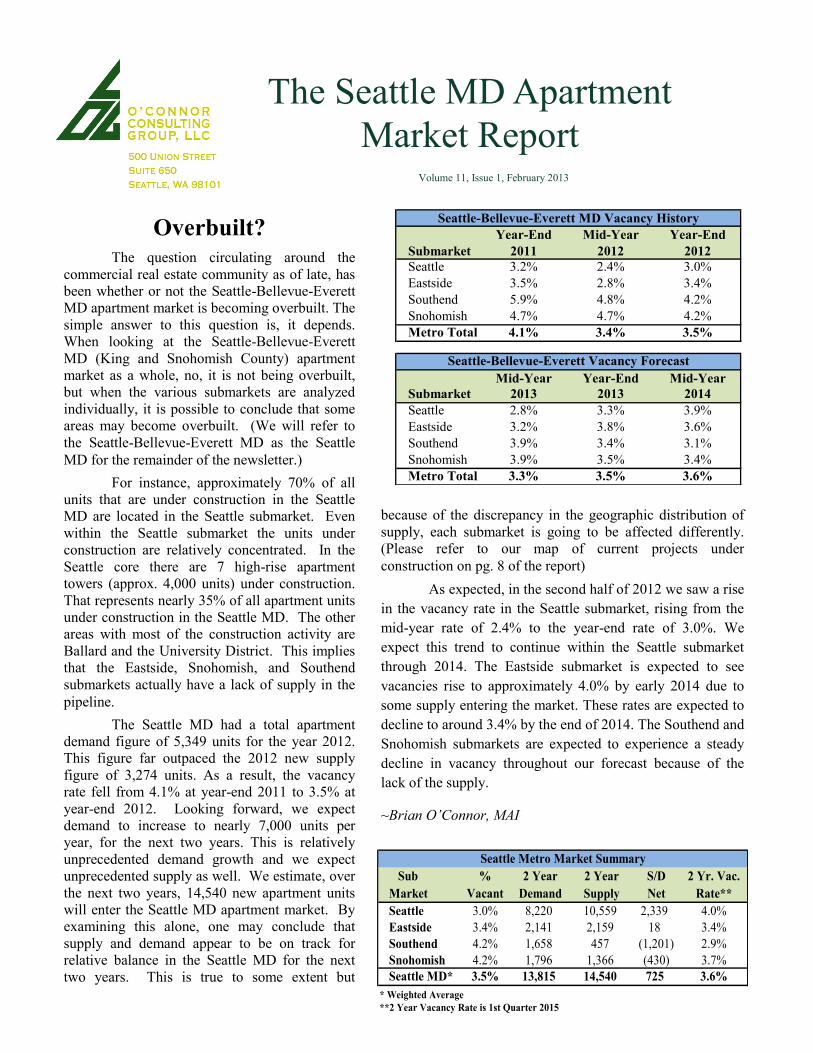

The Seattle MD had a total apartment

demand figure of 5,349 units for the year 2012.

This figure far outpaced the 2012 new supply

figure of 3,274 units. As a result, the vacancy

rate fell from 4.1% at year-end 2011 to 3.5% at

year-end 2012. Looking forward, we expect

demand to increase to nearly 7,000 units per

year, for the next two years. This is relatively

unprecedented demand growth and we expect

unprecedented supply as well. We estimate, over

the next two years, 14,540 new apartment units

will enter the Seattle MD apartment market. By

examining this alone, one may conclude that

supply and demand appear to be on track for

relative balance in the Seattle MD for the next

two years. This is true to some extent but

because of the discrepancy in the geographic distribution of

supply, each submarket is going to be affected differently.

(Please refer to our map of current projects under

construction on pg. 8 of the report)

As expected, in the second half of 2012 we saw a rise

in the vacancy rate in the Seattle submarket, rising from the

mid-year rate of 2.4% to the year-end rate of 3.0%. We

expect this trend to continue within the Seattle submarket

through 2014. The Eastside submarket is expected to see

vacancies rise to approximately 4.0% by early 2014 due to

some supply entering the market. These rates are expected to

decline to around 3.4% by the end of 2014. The Southend and

Snohomish submarkets are expected to experience a steady

decline in vacancy throughout our forecast because of the

lack of the supply.

~Brian O’Connor, MAI

Volume 11, Issue 1, February 2013

Sub % 2 Year 2 Year S/D 2 Yr. Vac.

Market Vacant Demand Supply Net Rate**

Seattle 3.0% 8,220 10,559 2,339 4.0%

Eastside 3.4% 2,141 2,159 18 3.4%

Southend 4.2% 1,658 457 (1,201) 2.9%

Snohomish 4.2% 1,796 1,366 (430) 3.7%

Seattle MD* 3.5% 13,815 14,540 725 3.6%

**2 Year Vacancy Rate is 1st Quarter 2015

* Weighted Average

Seattle Metro Market Summary

Year-End Mid-Year Year-End

Submarket 2011 2012 2012

Seattle 3.2% 2.4% 3.0%

Eastside 3.5% 2.8% 3.4%

Southend 5.9% 4.8% 4.2%

Snohomish 4.7% 4.7% 4.2%

Metro Total 4.1% 3.4% 3.5%

Seattle-Bellevue-Everett MD Vacancy History

Mid-Year Year-End Mid-Year

Submarket 2013 2013 2014

Seattle 2.8% 3.3% 3.9%

Eastside 3.2% 3.8% 3.6%

Southend 3.9% 3.4% 3.1%

Snohomish 3.9% 3.5% 3.4%

Metro Total 3.3% 3.5% 3.6%

Seattle-Bellevue-Everett Vacancy Forecast

Vacancy Forecast

The graphs below illustrate our

vacancy forecast for each of the four

primary Puget Sound markets.

Please note that these graphs reflect

physical vacancy, not economic

vacancy. Economic vacancies are

typically one or two points above

physical vacancies. Currently, we

estimate that there has been a shift

because of the new supply, and there

is now upward pressure on vacancy

rates in the Seattle submarket. All

other submarkets remain having

downward pressure in the near term.

T a b l e o f C o n t e n t s

Vacancy Forecast………………..1

Vacancy Forecast Charts……….2

V a c a n c y ………………………… . . 3

A b s o r p t i o n ……………………… . 4

Employ ment Fo reca st…………4

Population Forecast……………..4

Apartment Demand……………..5

Supply Forecast………………….5

Supply and Demand…………….6

Rental Rate Forecast……………7

C o n c l u s i o n ……………………… . 7

Under Construction Map…………...8

The Seattle Apartment Market

Report is a publication of the

O’Connor Consulting Group, a

Seattle-based real estate appraisal

and consulting firm specializing

in mixed-use multifamily and

commercial property valuation

and consultation.

For more information regarding

these services please contact

Brian O’Connor, MAI at

206-622-5100

The Seattle Apartment Market

Report is edited by:

Casey O’Connor, Associate.

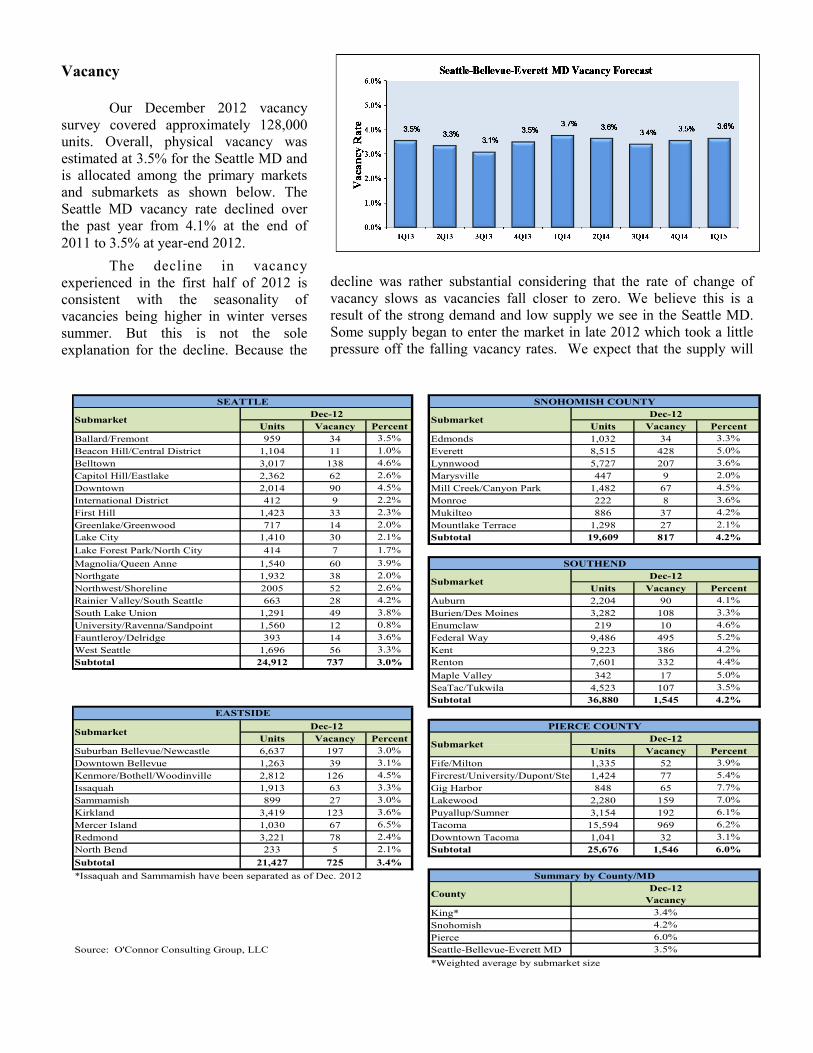

Vacancy

Our December 2012 vacancy

survey covered approximately 128,000

units. Overall, physical vacancy was

estimated at 3.5% for the Seattle MD and

is allocated among the primary markets

and submarkets as shown below. The

Seattle MD vacancy rate declined over

the past year from 4.1% at the end of

2011 to 3.5% at year-end 2012.

The decline in vacancy

experienced in the first half of 2012 is

consistent with the seasonality of

vacancies being higher in winter verses

summer. But this is not the sole

explanation for the decline. Because the

decline was rather substantial considering that the rate of change of

vacancy slows as vacancies fall closer to zero. We believe this is a

result of the strong demand and low supply we see in the Seattle MD.

Some supply began to enter the market in late 2012 which took a little

pressure off the falling vacancy rates. We expect that the supply will

Units Vacancy Percent Units Vacancy Percent

Ballard/Fremont 959 34 3.5% Edmonds 1,032 34 3.3%

Beacon Hill/Central District 1,104 11 1.0% Everett 8,515 428 5.0%

Belltown 3,017 138 4.6% Lynnwood 5,727 207 3.6%

Capitol Hill/Eastlake 2,362 62 2.6% Marysville 447 9 2.0%

Downtown 2,014 90 4.5% Mill Creek/Canyon Park 1,482 67 4.5%

International District 412 9 2.2% Monroe 222 8 3.6%

First Hill 1,423 33 2.3% Mukilteo 886 37 4.2%

Greenlake/Greenwood 717 14 2.0% Mountlake Terrace 1,298 27 2.1%

Lake City 1,410 30 2.1% Subtotal 19,609 817 4.2%

Lake Forest Park/North City 414 7 1.7%

Magnolia/Queen Anne 1,540 60 3.9%

Northgate 1,932 38 2.0%

Northwest/Shoreline 2005 52 2.6% Units Vacancy Percent

Rainier Valley/South Seattle 663 28 4.2% Auburn 2,204 90 4.1%

South Lake Union 1,291 49 3.8% Burien/Des Moines 3,282 108 3.3%

University/Ravenna/Sandpoint 1,560 12 0.8% Enumclaw 219 10 4.6%

Fauntleroy/Delridge 393 14 3.6% Federal Way 9,486 495 5.2%

West Seattle 1,696 56 3.3% Kent 9,223 386 4.2%

Subtotal 24,912 737 3.0% Renton 7,601 332 4.4%

Maple Valley 342 17 5.0%

SeaTac/Tukwila 4,523 107 3.5%

Subtotal 36,880 1,545 4.2%

Units Vacancy Percent

Suburban Bellevue/Newcastle 6,637 197 3.0% Units Vacancy Percent

Downtown Bellevue 1,263 39 3.1% Fife/Milton 1,335 52 3.9%

Kenmore/Bothell/Woodinville 2,812 126 4.5% Fircrest/University/Dupont/Steilacoom1,424 77 5.4%

Issaquah 1,913 63 3.3% Gig Harbor 848 65 7.7%

Sammamish 899 27 3.0% Lakewood 2,280 159 7.0%

Kirkland 3,419 123 3.6% Puyallup/Sumner 3,154 192 6.1%

Mercer Island 1,030 67 6.5% Tacoma 15,594 969 6.2%

Redmond 3,221 78 2.4% Downtown Tacoma 1,041 32 3.1%

North Bend 233 5 2.1% Subtotal 25,676 1,546 6.0%

Subtotal 21,427 725 3.4%

*Issaquah and Sammamish have been separated as of Dec. 2012

King*

Snohomish 4.2%

Pierce 6.0%

Source: O'Connor Consulting Group, LLC Seattle-Bellevue-Everett MD 3.5%

*Weighted average by submarket size

SEATTLE SNOHOMISH COUNTY

SubmarketDec-12

SubmarketDec-12

SOUTHEND

EASTSIDE

SubmarketDec-12 PIERCE COUNTY

SubmarketDec-12

SubmarketDec-12

County

Summary by County/MD

Dec-12

Vacancy

3.4%

Employment Forecast

National economic conditions

have begun to improve, though at a pace

that is frustratingly slow for most

metropolitan areas. Thankfully, the

Seattle MD remains an uncommon gem

among the national scene with

unemployment trending downward and

healthy job growth in forward-looking

industries being estimated for the area.

As of December 2012, national

unemployment was at 7.8%, Washington

state was at 7.6%, and the Seattle MD

was at 6.5%.

To gain a little perspective on

the current employment forecast, it is

worth rewinding a couple years to give

the reader some context. The year 2009

was a difficult year for the Seattle MD.,

with a total annual loss of approximately

76,500 jobs. A loss of this magnitude

implied a negative growth rate of 5.5%

for that year. A further 26,100 jobs were

lost in 2010. However, most of these

loses occurred in January of that year,

with generally positive gains thereafter.

The year 2011 marked a turn-

around for Seattle MD job seekers.

According to the most recent data, the

Seattle MD increased employment by

33,200 new jobs in 2011, which

represents a healthy 2.4% growth rate.

Th e ye a r 2 0 1 2 w a s

characterized by positive job growth,

with an over-the-year percent

employment increase of 2.8%. This

represents the addition of approximately

39,600 jobs for the year 2012.

Local economists Dick

Conway and Doug Pederson predict

strong job growth in the Seattle MD of

2.8% in 2013, 2.5% in 2014, and 2.3%

in 2015. These increases in job growth

would represent approximately 115,600

new jobs over the next three years.

Population Forecast

Our forecast of vacancy and

rental changes are driven primarily by

anticipated population growth in the

region. The chart below displays the

historical relationship between net

migration and net employment growth in

the Seattle metropolitan area.

As is evident in the chart

below, net migration is heavily

dependent upon net employment

growth.. Migration rates are sensitive to

both local economic conditions as well

as economic conditions elsewhere. The

pattern of future job growth will

determine the pattern of net migration

and thus population growth and

household growth.

Based on the April 1, 2012,

population increase of 20,300 people, we

had a net migration figure -1,996 people

in 2011, and an estimated 3,300 in 2012.

Net migration averaged 11,363 people

from 2001 to 2012.

It is fascinating that despite

historically lower net migration figures,

the Seattle MD continues to absorb a

healthy amount of apartment units. We

believe that this is due in large part to a

shift in household tenureship. We are

currently experiencing a significant shift

away from ownership and toward the

rental market. Despite historically low

interest rates, there are a multitude of

factors that are currently acting upon

potential buyers that make renting a

more attractive option. We believe that

this trend may be the most significant

factor acting upon the Seattle MD

apartment market today and strongly

encourage the reader to download our

PDF on Housing Tenure, which can be

found on the same download page as this

newsletter.

Despite the hiccup in net

migration experienced in 2010/2011,

Seattle remains one of the healthier

regional economies in the nation. Due to

this factor, we believe net migration will

be pos i t ive moving fo rward

(approximately 8,700-13,800 per annum)

despite the notably slow national

recovery.

Apartment Demand

Despite the economic turmoil

of years past, the Seattle MD is one of

the most economically attractive regions

in the nation, regularly receiving

attention in nation-wide publications due

to the area’s strong base with forward-

looking industries such as aerospace,

biotechnology, and software design.

Given the area’s strong fundamentals,

expected net positive migration, and the

recent employment forecast by Dick

Conway and Doug Pederson, we believe

that positive growth will continue, on an

annual basis, through 2015.

The year 2012 went as

expected for the most part. We

witnessed vacancy rates drop

significantly in the first half but began to

level off in the second half due to some

new supply entering the market. As

strong as the demand was in 2012 (5,349

units), we predict even stronger demand

in 2013 and 2014. However, the

relationship between supply and demand

may vary greatly depending on the

submarket. For instance, Eastside

demand is tending to shift to the

Southend and Snohomish submarkets as

rent rates increase on the Eastside.

Looking forward, our positive

expectations have resulted in healthy

es timates of fu ture demand.

Historically, an approximate average of

35% of all new households have been

expected to choose apartments. We

expect that the proportion of new

households that will choose rental

housing is currently hovering around

50% to 55%. Please see the PDF on our

website titled Housing Tenure for more

on this topic.

Supply Forecast

Our estimate of new multi-

family supply is derived from a survey of

all units currently in lease-up, projects

under construction, and known projects

in their pre-development stage. To

gauge the number of units in the

pipeline, we track all multifamily

building permits, physically inspect the

permitted sites, and reconfirm the

number of units and the property type

(apartment or condominium). This

information was calculated for each of

the four major markets within the Seattle

metropolitan area.

As of our year 2012 survey, the

Seattle MD has a total of 11,932

apartment units under construction, and

another 2,382 new units currently in the

lease-up phase. The majority of those

units under construction will be

impacting the Seattle MD in our two year

forecast. The Seattle submarket deserves

special mention as approximately 75% of

all region wide construction is centered

in Seattle. More specifically, 4,103 of

those units, or 35% of all units under

construction throughout the Seattle MD,

are located within the Seattle core.

Absorption

The Seattle absorbed 3,274

new units and 2,075 existing units in

2012. Important to take note, out of the

3,274 new units absorbed, the Seattle

submarket captured 70% of the 2012

new unit demand. For reference, the

Seattle submarket historical captures

approximately 45% of the demand.

Also worth mentioning, the Eastside

submarket captured only 8.6% of

demand in 2012. Historically, the

Eastside’s capture rate is usually around

25%-30%.

Submarket 2010 2011 2012

Vacancy Rate 4.2% 4.1% 3.5%

Market Size 358,128 360,278 363,552

Occupied Units 343,177 345,419 350,768

New Units Absorbed 4,443 2,150 3,274

Existing Units Absorbed 4,988 92 2,075

Total Demand 9,431 2,242 5,349

Submarket 2013 2014

Seattle 4,289 3,932

Eastside 899 1,242

Southend 830 828

Snohomish 899 897

Metro Total 6,917 6,897

New Units New Units Abs. Average

Submarket in 2012 in 2012 Absorption/Mo.

Seattle 3,060 2,282 18.8

Eastside 628 383 8.9

Southend 260 358 10.4

Snohomish 386 351 14.3

Metro Total 4,334 3,374 13.2

2012 Absorption Summary

Multifamily Demand Forecast by Submarket (in Units)

Metro Area Market Demand Summary

December Average Vacant Units Total

Sub 2012 Absorption Units In Under Two Year

Market % Vacant Complex/Mo. Lease-Up Construction Pipeline

Seattle 3.0% 18.8 1,771 9,019 10,790

Eastside 3.4% 8.9 68 1,879 1,947

Southend 4.2% 10.4 129 140 269

Snohomish 4.2% 14.3 414 894 1,308

Seattle MD * 3.5% 13.2 2,382 11,932 14,314

* Weighted Average

Seattle Metro Supply Survey

Supply and Demand Summary

The table below illustrates our

forecast for both apartment supply and

demand within each major submarket in

the Metropolitan area. Vacancies are

expected to stabilize over the next two

years as supply steadily catches up with

demand.

As opposed to years past, the

Seattle MD apartment market in 2012 is

best characterized by analyzing the

individual submarkets within the Seattle

MD. It is because of the events of the

previous years, such as the recession,

lack of available financing, and pent up

demand that has lead to this supply

boom that the Seattle MD is now

entering. The vast majority of the

supply entering the market in the next

two

years is going to be in the Seattle

submarket. The Seattle submarket can

expect 10,559 new units over the next

two years. The next closest submarket is

the Eastside with 2,159 new units over

the next two years. In the Southend, we

expect only 457 new units to enter the

market. The Snohomish submarket will

see 1,366 new units over our forecast

period.

The discrepancies in the

geographic distribution of supply

mentioned above have caused some

interesting patterns in demand to occur.

In the Eastside submarket, we have seen

some of the demand shift to the

Southend and Snohomish submarkets

because of lack of new supply and rising

rents. This is a trend we expect to

continue throughout our forecast period.

As the reader can see, we

expect the Southend and Snohomish

submarkets to see a significant drop in

their vacancy rates, while the Eastside

vacancy rate will largely remain

unchanged over the next two years.

In the table below, we can see

that our in-house supply/demand models

predict vacancies at 3.6% in the Seattle

MD. Demand is expected to peak at

approximately 6,900 in 2013, decreasing

to 5,500 units incrementally by 2016,

Supply is expected to respond to this

healthy demand as the national economy

continues to improve.

Sub Market % No. 2 Year 2 Year S/D 2 Yr. Mkt 2 Yr. Vac. Total

Market Size Vacant Vacant Demand Supply Net Size Rate** Vacant

Seattle 154,977 3.0% 4,585 8,220 10,559 2,339 165,536 4.0% 6,695

Eastside 65,069 3.4% 2,202 2,141 2,159 18 67,228 3.4% 2,281

Southend 81,680 4.2% 3,422 1,658 457 -1,201 82,137 2.9% 2,366

Snohomish 61,826 4.2% 2,576 1,796 1,366 -430 63,192 3.7% 2,345

Metro * 363,552 3.5% 12,784 13,815 14,540 725 378,092 3.6% 13,693

**Two-Year Vacancy rate is end of 1st quarter 2015

Seattle Metro Market Summary

* Weighted Average

Apartment Data

Net Apartments Year End Average

Total Percent Total Percent Total Percent Total New Under Vacancy Rent

Year Persons Change Jobs Change Households Change Units Absorp. Construction Rates Change

2003 2428024 0.88% 1,322,825 -1.12% 977,671 0.89% 347,423 3,947 4,976 6.57% 0.1%

2004 2449561 0.89% 1,334,983 0.92% 987,860 1.04% 348,343 396 6,507 6.72% 1.9%

2005 2476345 1.09% 1,370,925 2.69% 1,004,035 1.64% 347,155 4,648 4,902 5.06% 2.0%

2006 2521335 1.82% 1,416,017 3.29% 1,020,257 1.62% 345,185 3,959 4,853 3.37% 13.0%

2007 2560412 1.55% 1,460,300 3.13% 1,033,178 1.27% 347,625 2,021 5,944 3.47% 8.5%

2008 2590455 1.17% 1,478,283 1.23% 1,043,575 1.01% 350,105 -3,035 6,931 5.02% 1.4%

2009 2615099 0.95% 1,399,900 -5.30% 1,054,885 1.08% 353,989 1,202 2,856 5.72% -10.3%

2010 2644584 1.13% 1,376,850 -1.65% 1,062,338 0.71% 358,128 9,435 3,320 4.18% 4.0%

2011 2659600 0.57% 1,405,475 2.08% 1,069,930 0.71% 359,996 2,086 3,114 4.12% 7.70%

2012 2679900 0.76% 1,450,456 3.20% 1,081,455 1.08% 363,552 3,274 11,932 3.52% 5.43%

5 Yr. Avg. 0.9% -0.1% 0.9% 2592 5631 4.5% 1.6%

Total Percent Total Percent Total Percent Total Total Vacancy Rent

Year Persons Change Jobs Change Households Change Units Demand Rates Change

2013 2,711,551 1.18% 1,492,281 2.88% 1,095,290 1.28% 370,697 6,917 3.5% 4.8%

2014 2,747,117 1.31% 1,530,239 2.54% 1,109,085 1.26% 378,092 6,897 3.6% 4.5%

2015 2,781,245 1.24% 1,566,044 2.34% 1,121,230 1.10% 384,404 6,072 3.6% 3.4%

2016 2,810,351 1.05% 1,597,281 1.99% 1,132,377 0.99% 389,204 5,574 3.3% N/A

2017 2,837,806 0.98% 1,623,420 1.64% N/A N/A N/A N/A N/A N/A

5 Yr. Avg. 1.2% 2.3% 1.16% 5,747 3.5% 4.2%

10 Yr. Avg. 1.0% 1.1% 1.0% 4,044 4.0% 2.6%

O'CONNOR CONSULTING GROUP,LLC: Brian R. O'Connor, MAI

Employment Forecast Household Forecast Apartment Demand Forecast

(1) Population as of April 1st.

(2) Excludes Military & Self-Employed

Metropolitan Area is King & Snohomish Counties

Sources: WA State Employment Security & WA State Office of Financial Management

(3) Total households are estimates

Apartment Demand Forecast

Seattle MD, 2013-2017

Population Forecast

Seattle Metropolitan Apartment Market Data & ForecastApartment Trend Analysis

Seattle MD, 2003-2012

Population Estimates (1) Employment (2) Households (3)

Rental Rate Forecast

The two tables to the right illustrate the

recent history and our forecast of

changes in rental rates for each

submarket of the Seattle MD. During

2010 Seattle MD vacancies were

continuing to decline, which lead to an

increase of 6.8% in rents. Responding to

a rapid drop in vacancies, Seattle MD

rents grew by 9.1%% in 2011. In 2012,

as some supply entered the market, rents

stabilized somewhat yet we still saw an

increase of 5.4%. Based upon our

estimates of new apartment supply and

demand, we estimate healthy rent

growth going forward. As new supply

enters the market, we expect rents to

stabilize.

Submarket 2010 2011 2012

Seattle 6.5% 9.0% 6.0%

Eastside 7.3% 12.6% 8.0%

Southend 2.4% 5.3% 3.9%

Snohomish 4.6% 10.8% 3.3%

Seattle MD Total* 6.8% 9.1% 5.4%

Submarket 2013 2014 2015

Seattle 4.0% 3.0% 2.0%

Eastside 6.0% 7.0% 4.0%

Southend 5.0% 5.0% 5.0%

Snohomish 5.0% 5.0% 4.0%

Seattle MD Total* 4.8% 4.5% 3.4%

*Weighted Average

Seattle-Bellevue-Everett MD Rental Rate History

*Weighted Average

Seattle-Bellevue-Everett MD Rental Rate Forecast

Employment in Core Areas

The “Seattle Core” consists of

(Downtown, South Lake Union, and

parts of Capitol Hill, First Hill, Queen

Anne, and the International District).

The “Bellevue Core” consists of the

Downtown Bellevue area.

Within the Seattle MD, the

Seattle Core deserves special attention

with regards to employment. Over the

last decade, the Seattle Core has aver-

aged over a 14% (or approx. 200,00

jobs) share of the total employment in

the Seattle MD (1,450,456 jobs in 2012).

This has made it an attractive place for

commercial real estate investment fol-

lowing turbulent economic times. As a

result, approximately 35% of all apart-

ment units currently under construction

are located in the Seattle Core.

The Bellevue Core is smaller

geographically and in total population

than the Seattle Core, yet still contrib-

utes a significant amount of the overall

employment for the Seattle MD. Over

the past decade, the Bellevue Core has

averaged a 2.6% (or approx. 38,000

jobs) share of total employment in the

Seattle MD. In 2010 and 2011 the

Bellevue Core has had a 3.1% (or

45,000 jobs) share of total employment.

35,704 35,652

32,08231,111

29,85632,117

37,50838,440 38,929

35,893

42,78943,743

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Bellevue Core Total Jobs 2000-2011

Source: Wa State Employment Security Dept., PSRC

216,097

203,815

198,667

194,466

190,987192,217

197,015

202,629

209,165

198,148

189,358

194,603

175000

180000

185000

190000

195000

200000

205000

210000

215000

220000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Seattle Core Total Jobs 2000-2011

Source: WA State Employment Security Dept., PSRC

The following map is of the Seat-

tle-Bellevue-Everett MD that consists of

every apartment project currently under

construction . By mapping the locations of

each project clearly illustrates the geo-

graphic distribution of supply.

When looking at the map of the

entire Seattle MD, the reader can see that

the vast majority of projects currently un-

der construction are in the Seattle submar-

ket. Within the Seattle submarket, the pro-

jects are focused in the “Seattle Core” ,

Ballard, and the University District .

The map as a whole represents an

astounding 11,932 units currently under

construction. The Seattle submarket has

approximately 75% or 9,000 of those

units. The Seattle core has approxi-

mately 35% or 4,000 of all the units

under construction.

One noteworthy company is

the internet based retailer, Amazon,

who is rapidly expanding in the Seattle

Core. They currently employ 10,000

people in the Seattle Downtown area

and currently have three major blocks

in South Lake Union under contract to

build an additional three million square

feet of office space. That amount of

square footage will support approxi-

mately 12,000 new employees.

Map of Apartment Projects Under Construction

As this map illustrates,

apartment construction is almost en-

tirely focused in centrally located

Seattle neighborhoods. The centrally

located distribution is not a coinci-

dence. As we were coming out of the

recession, developers were able to

finance their projects in the areas with

the least amount of risk. Many of

those projects happened to be in the

Seattle Core, where many of the jobs

are located.

This trend that we have seen

for the last few years, will likely tran-

sition to more projects developed

outside of the Seattle Core.

For more information on services offered by the

O’Connor

Consulting

Group, LLC

please contact Brian O’Connor, MAI at (206) 622-5100 or visit

our website at: www.ocgp.com