Embed Size (px)

Citation preview

The Australian Economic Review, vol. 32, no. 1, pp. 74–82

The University of Melbourne, Melbourne Institute of Applied Economic and Social Research 1999Published by Blackwell Publishers Ltd, 108 Cowley Road, Oxford OX4 1JF, UK and

350 Main Street, Malden, MA 02148, USA

1. Introduction

The inflationary surge of the 1970s and 1980sand the rising power of global financial inter-ests have been two important factors in ex-plaining a key shift in macroeconomic policyin western economies in the last two decades(Gourevitch 1986; Armstrong, Glyn & Harri-son 1991; Bell 1997). This has been the target-ing of low to very low inflation as anincreasingly important if not central policygoal. In this new context, increasingly indepen-dent central banks have climbed into the policycockpit, partly because monetary policy hastaken over as the key ‘swing instrument’, oneseen as having the ‘comparative advantage’and flexibility to fight inflation.

In Australia, from the early 1990s, the Re-serve Bank has guided short- to medium-termmonetary policy by explicitly targeting an in-flation rate of 2–3 per cent. There is some de-bate over how inflation-fixated the RBA hasbeen. Many other countries require their cen-tral banks to give priority or sole attention to‘price stability’ or very low inflation targets. InAustralia, the RBA’s legislative charter re-quires that it pay attention to two goals: ‘stabil-ity of the currency of Australia’ and ‘themaintenance of full employment in Australia’.This kind of goal ‘dualism’ reflects the Keyne-sian heritage of the Act. It is well known that,Bernie Fraser, the RBA’s previous Governor,actively championed dualism. Central banks,he argued, ‘should not be fixated solely withinflation, and we should not be loading the diceeven more in that direction’ (Fraser 1996, p.

17). Whether dualism (at least at the margins)made much difference to the conduct of mone-tary policy is difficult to assess (Bell 1997).What is clear, however, is that achieving verylow inflation has certainly been a central goalof the RBA (and other central banks) (Argy1998, pp. 41–4; Eatwell 1995; Luttwak 1996).Ian Macfarlane, the current Governor of theRBA, has admitted there was a willingness totake some ‘risks’ with unemployment in thename of fighting inflation in the depths of theearly 1990s recession (

Australian

22 May1992). More recently, the August 1996Howard Government/RBA joint

Statement onthe Conduct of Monetary Policy

appears to af-firm an inflation priority.

This paper asks whether pursuing the goal of‘very low inflation’ is a good idea. For our pur-poses, this level of inflation can be defined asthe RBA’s target range. The paper surveysmuch of the existing research on this question,particularly that which looks at the relationshipbetween inflation and other economic variablessuch as growth, productivity and unemploy-ment. It emerges from this survey that the costsof inflation only seem to appear when inflationis quite high. For ‘very low’ rates of inflation,costs appear elusive. Because the costs ofachieving very low inflation are widely ac-knowledged to have been high, it seems reason-able to call for debate on the efficacy of currentpolicy. Would we be better off taking a slightlymore relaxed approach to inflation, perhaps tar-geting a goal a few percentage points higherand thus leaving a bit more room for a lessinflation-constrained approach to growth?

Policy Forum: Should Inflation Be the Sole Target of Reserve Bank Monetary Policy?

The Scourge of Inflation? Unemployment and Orthodox Monetary Policy

Stephen BellSchool of GovernmentUniversity of Tasmania

Bell: Scourge of Inflation? 75

The University of Melbourne, Melbourne Institute of Applied Economic and Social Research

So far in Australia, despite some recent com-plaints from industry, the shift towards tightinflation targeting has largely gone unques-tioned. We briefly look at some political rea-sons as to why this is so. The paper concludesby noting some of the questions of policy ac-countability the RBA is likely to confront ifAustralia’s ‘low voltage’ monetary politicsever hots up.

2. Policy Orthodoxy

Central to the current orthodox view is thatKeynesian manipulation of the macroeconomyis likely to be ineffective and damaging. Rely-ing heavily on concepts of inflationary expec-tations, the new view is that in the medium tolong term we are now in a post-Phillips curveworld: that is, there is now no trade-off be-tween inflation and employment as there ap-peared to be in the postwar era. In the newview, once inflationary expectations adjust,any short-term employment gains throughstimulation will be neutralised through higherinflation. Don Brash (1997, p. 1), Governor ofthe Reserve Bank of New Zealand, has pro-vided a useful summary of this position:

there is in fact no evidence that monetary policycan, by tolerating a little more inflation, engineera sustainably higher rate of growth, or a sustain-ably higher level of employment . . . To be sure,monetary policy can engineer faster growth andhigher employment in the short term—by tolerat-ing a bit more inflation right now, there is not muchdoubt that growth and employment would be a lit-tle higher . . . than otherwise . . . Most of that fastergrowth and higher employment would be boughtat the cost of tricking working New Zealandersinto accepting a reduction in their real wages, asprices rose ahead of wages. However, it would notlast. Before too long, people would recognise thedeception and would demand compensation in theform of higher wages and salaries. Within a veryshort time, inflation would be rising, growthwould be back to its previous, lower level and wewould be left contemplating the cost of reducinginflation again . . . Not only is there no evidencethat tolerating more inflation can engineer a sus-tainable faster rate of growth, there is now over-whelming evidence that high inflation positivelydamages the way in which the economy works . . .

In current highly insecure labour marketsBrash’s claim that workers are able to ‘de-mand’ compensation in the form of higherwages is open to some debate. In any case themore interesting issue is his claim that ‘high in-flation positively damages the way in whichthe economy works’ (1997, p. 1). In the nextsection, evidence is presented which supportsthe claim that ‘high inflation’ is indeed damag-ing. However, there seems to be virtually noevidence that very low inflation, of the kindcurrently targeted by policy, is damaging.

3. Low Inflation?

The orthodox case against inflation is that itdistorts the price mechanism and leads to un-certainty about future prices which in turn dis-torts investment decisions and leads to aninefficient allocation of resources within theeconomy. Because of these distortions, and be-cause of heightened uncertainty in an inflation-ary environment, growth, investment andproductivity are said to suffer. ‘Many econo-mists’, as Sarel (1996, p. 200) argues, are thus‘convinced that inflation is undesirable andshould be avoided completely’.

Recent research, however, has cast somedoubt on these arguments (Fortin 1993; Brittan1995). In asking ‘is inflation harmful togrowth’, Bruno and Easterly (1998, p. 3) com-ment that ‘the ratio of fervent beliefs to tangi-ble evidence seems unusually high on thistopic’ (see also Krugman 1996). True, somestudies have found that inflation has a negativeimpact on growth (see Smyth 1994; De Grego-rio 1993; Fischer 1993; Bruno 1995; Barro1996). Fischer (1993), for example, found in astudy involving panel regressions for eightycountries for the period 1961–88, that a 10 per-centage point increase in inflation (from 5 percent to 15 per cent per annum) is correlatedwith a decline in output growth of 0.4 per centper annum. Another study by Barro (1996) ex-amined over 100 countries covering the period1960–90. Barro found that increasing inflationby 1 per cent is associated with a reduction inthe rate of economic growth by between 0.02and 0.03 per cent per annum.

1

What is strikingabout these studies is that the supposed effects

76 The Australian Economic Review March 1999

The University of Melbourne, Melbourne Institute of Applied Economic and Social Research

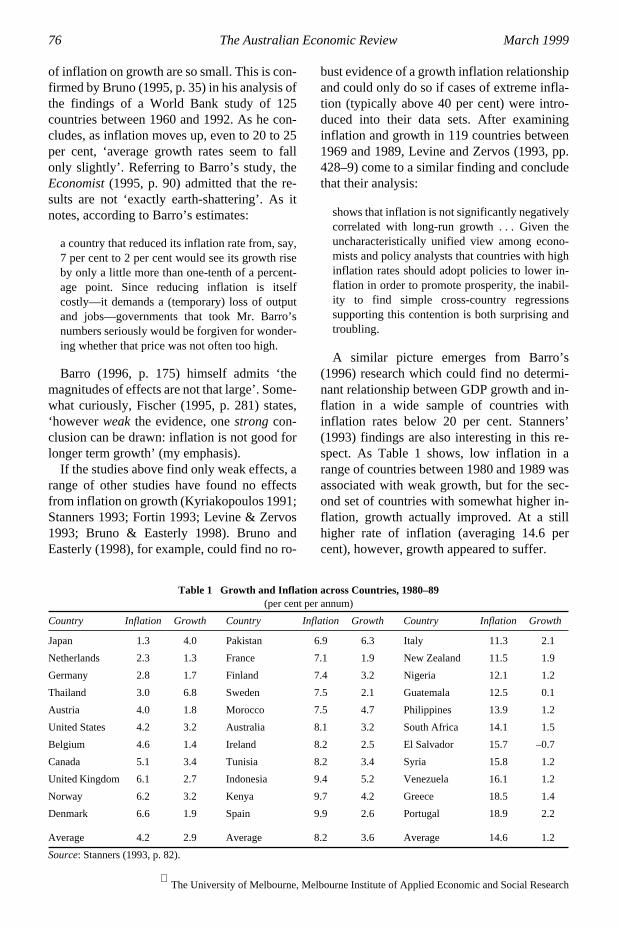

Table 1 Growth and Inflation across Countries, 1980–89

(per cent per annum)

Country Inflation Growth Country Inflation Growth Country Inflation Growth

Japan 1.3 4.0 Pakistan 6.9 6.3 Italy 11.3 2.1

Netherlands 2.3 1.3 France 7.1 1.9 New Zealand 11.5 1.9

Germany 2.8 1.7 Finland 7.4 3.2 Nigeria 12.1 1.2

Thailand 3.0 6.8 Sweden 7.5 2.1 Guatemala 12.5 0.1

Austria 4.0 1.8 Morocco 7.5 4.7 Philippines 13.9 1.2

United States 4.2 3.2 Australia 8.1 3.2 South Africa 14.1 1.5

Belgium 4.6 1.4 Ireland 8.2 2.5 El Salvador 15.7 –0.7

Canada 5.1 3.4 Tunisia 8.2 3.4 Syria 15.8 1.2

United Kingdom 6.1 2.7 Indonesia 9.4 5.2 Venezuela 16.1 1.2

Norway 6.2 3.2 Kenya 9.7 4.2 Greece 18.5 1.4

Denmark 6.6 1.9 Spain 9.9 2.6 Portugal 18.9 2.2

Average 4.2 2.9 Average 8.2 3.6 Average 14.6 1.2

Source

: Stanners (1993, p. 82).

of inflation on growth are so small. This is con-firmed by Bruno (1995, p. 35) in his analysis ofthe findings of a World Bank study of 125countries between 1960 and 1992. As he con-cludes, as inflation moves up, even to 20 to 25per cent, ‘average growth rates seem to fallonly slightly’. Referring to Barro’s study, the

Economist

(1995, p. 90) admitted that the re-sults are not ‘exactly earth-shattering’. As itnotes, according to Barro’s estimates:

a country that reduced its inflation rate from, say,7 per cent to 2 per cent would see its growth riseby only a little more than one-tenth of a percent-age point. Since reducing inflation is itselfcostly—it demands a (temporary) loss of outputand jobs—governments that took Mr. Barro’snumbers seriously would be forgiven for wonder-ing whether that price was not often too high.

Barro (1996, p. 175) himself admits ‘themagnitudes of effects are not that large’. Some-what curiously, Fischer (1995, p. 281) states,‘however

weak

the evidence, one

strong

con-clusion can be drawn: inflation is not good forlonger term growth’ (my emphasis).

If the studies above find only weak effects, arange of other studies have found no effectsfrom inflation on growth (Kyriakopoulos 1991;Stanners 1993; Fortin 1993; Levine & Zervos1993; Bruno & Easterly 1998). Bruno andEasterly (1998), for example, could find no ro-

bust evidence of a growth inflation relationshipand could only do so if cases of extreme infla-tion (typically above 40 per cent) were intro-duced into their data sets. After examininginflation and growth in 119 countries between1969 and 1989, Levine and Zervos (1993, pp.428–9) come to a similar finding and concludethat their analysis:

shows that inflation is not significantly negativelycorrelated with long-run growth . . . Given theuncharacteristically unified view among econo-mists and policy analysts that countries with highinflation rates should adopt policies to lower in-flation in order to promote prosperity, the inabil-ity to find simple cross-country regressionssupporting this contention is both surprising andtroubling.

A similar picture emerges from Barro’s(1996) research which could find no determi-nant relationship between GDP growth and in-flation in a wide sample of countries withinflation rates below 20 per cent. Stanners’(1993) findings are also interesting in this re-spect. As Table 1 shows, low inflation in arange of countries between 1980 and 1989 wasassociated with weak growth, but for the sec-ond set of countries with somewhat higher in-flation, growth actually improved. At a stillhigher rate of inflation (averaging 14.6 percent), however, growth appeared to suffer.

Bell: Scourge of Inflation? 77

The University of Melbourne, Melbourne Institute of Applied Economic and Social Research

This points to the possibility of non-linearityand to the possibility of a structural break in theeffects of inflation. As indicated above, Barro(1996, p. 159) could not find a statistically sig-nificant relationship between growth and infla-tion for rates of inflation below 20 per cent.Stanners’ (1993) findings also suggest thatthings may start going wrong when inflationstarts to average around 14 or 15 per cent. Sarel(1996), however, detects a structural break atabout 8 per cent inflation. In a study of 87countries in the period from 1970 to 1990,Sarel (1996, p. 200) found that:

When inflation is low, it has no significant nega-tive effect on economic growth; the effect mayeven be positive. But when inflation is high, it hasa powerful negative effect on growth. The struc-tural break is estimated to occur where the aver-age annual rate of inflation is 8 per cent.

Other studies have looked for a connectionbetween growth and productivity (which ana-lysts generally see as partly driving any nega-tive links between inflation and growth).Fischer (1993) found that a 10 per cent increasein inflation was associated with a decline inproductivity growth of 0.18 per cent per an-num. Again the estimated effects are small. Inanother study, on US data, Rudebusch and Wil-cox (1994) found the relationship betweeninflation and productivity growth to be insig-nificant, if corrections are made for cyclical ef-fects (see also Fortin 1993; Seccareccia &Lavoie 1996). More recently, Chowdhury andMallik (1999) could only find a ‘fragile’ rela-tionship between inflation and productivitygrowth using Australian and New Zealanddata. On the question of the effects of inflationon investment, McClain and Nichols (1993–94) recently found not a negative link but apositive link between (moderate) inflation andinvestment. As these authors conclude, ‘Thissurprising finding casts some doubt upon pol-icy judgements that moderate inflation is morecostly to an economy than increasing unem-ployment’ (McClain & Nichols 1993–94, p.218).

It is also important to note that the studiesabove explore correlations and not causation.Here, and at a somewhat more fundamental

level, there is, as Fischer (1995) admits,

no

ev-idence of any causal relationships that wouldsupport the orthodox anti-inflation case, what-ever the correlations. The problem is thatgrowth and productivity are driven by a widerange of factors, making it difficult to untanglecause and effect. There are even claims thatany causation at work might be ‘reverse causa-tion’; wherein, for example, growth and pro-ductivity are stymied not by inflation but bydisinflationary policy (Fortin 1993, p. 5; Sec-careccia & Lavoie 1996, p. 537).

The conclusions from the above seem clear.The evidence supporting any policy targetingof very low inflation is, at best, mixed, and, atworst, weak.

4. The Costs of Disinflation

Doubts about the orthodox targeting of verylow inflation are strengthened if we considerthe costs of disinflationary policy. Notwith-standing orthodox arguments about relation-ships in the long term, analysts generally agreethat in the short term there

is

a trade-off be-tween inflation, on the one hand, and growthand unemployment, on the other. Thus, periodsof disinflationary policy will help drive up un-employment. Witness the way in which thepolicy-induced recessions of the early 1980sand early 1990s ratcheted up unemployment.

Beside being only short term, orthodox ana-lysts argue that the costs of disinflation will bemore than compensated for by a more sustain-able pattern of growth once inflation is purgedfrom the system. Yet a more cautious assess-ment is possible. The policy strike against in-flation has not been a short, sharp shock, but along and costly battle. In the last twenty yearsdisinflationary policy has helped produce ratesof economic growth in Australia and theOECD that have averaged only half thatachieved during the postwar era (Bell 1997, pp.88–9; Mathews 1996). The tough monetarypolicy response of the late 1980s, although aking hit against inflation, helped produce theworst recession since the 1930s. Nevertheless,in late 1994 the RBA moved decisively todamp down a minor recovery in the name offighting an inflationary surge that was nowhere

78 The Australian Economic Review March 1999

The University of Melbourne, Melbourne Institute of Applied Economic and Social Research

visible (Wright 1995). For Australia, there areestimates of very large GDP losses arisingfrom restrictionist policy (Langmore & Quig-gin 1994, p. 30; Australian Chamber of Com-merce and Industry 1997). In the United States,Krugman (1996, p. 16) estimates that disinfla-tionary policy in the 1980s produced a cumula-tive loss of output of more than a trilliondollars.

In Europe the situation is worse (Palley1998). There, economies lie in a state of rigourmortis as unemployment climbs above 10 percent and the number out of work in the Euro-pean Union approaches twenty million. InGermany, traditionally Europe’s Hawk onmonetary policy, growth averaged only 2.3 percent per annum between 1981 and 1994, and inthe five years to September 1996, Germangrowth averaged a meagre 1.2 per cent. Overthe same period, France’s growth averaged 1.3per cent, Italy averaged 1.1 per cent and theUnited Kingdom 1.9 per cent. Orthodox analy-sis ascribes this situation to a high NAIRUrooted in labour market inflexibility and ex-pensive welfare entitlements for workers andthe unemployed (

Economist

5 April 1997).One problem with such an explanation is thatEuropean labour market and welfare condi-tions have if anything become more ‘flexible’.Yet this is the same period in which unemploy-ment has increased fourfold. As Krugman(1994, pp. 25–6) states: ‘If the welfare state isso bad for employment, why were Europeancountries able to achieve such low unemploy-ment rates before 1970?’.

Reviewing the Australian evidence ongrowth–inflation trade-offs and the costs andbenefits of disinflation, Junor (1995) citesMcTaggart’s (1992) estimate of a gain in out-put of 0.25 per cent per year as a result of a 1per cent reduction in inflation. Set against this,studies by Ball (1993) and Stevens (1992) esti-mate a 1 per cent reduction in inflation will in-duce a cumulative loss of real output ofbetween 1 and 2.7 per cent (Ball) or 1.5 and 3per cent of GDP (Stevens). As Junor (1995, p.59) comments, on this evidence:

it is likely that for output losses at the upper endof the range, the present value of these transition-

ary losses would exceed that of the permanentoutput gains. This suggests that anti-inflation pol-icy is likely to impose net output losses, which isnot consistent with the consensus view that acost–benefit analysis would always favour lowerinflation.

As Junor adds, ‘this conclusion is given fur-ther support’ if we take account of the findingsin a study by Junankar and Kapuscinskiu(1992) which lifts the estimate of potential out-put losses to as much as 7.7 per cent of GDPper annum. Junor further adds that if we acceptthere is significant hysteresis in the labour mar-ket, and that the output or employment lossesfrom a restrictionist policy are thus unlikely tobe temporary, then the case against such a pol-icy is further strengthened (see also Fortin1993).

5. Is Inflation Good for the Economy?

Some analysts have argued that moderate ratesof inflation (say in the range of 4–5 per cent)might actually be good for the economy. Tobin(1972) has argued that a little inflation helps oilthe wheels of the economy, especially in termsof assisting labour market adjustment. Thiskind of adjustment is central to the process ofstructural economic change and requires wagesto fall in some areas and to rise in others. Yet ina context of very low inflation, wage declineswill usually involve actual reductions in

nomi-nal

wages. Akerlof, Dickens and Perry (1996a,1996b) show, however, that even in the UnitedStates, wages display a marked downward ri-gidity and that ‘employers almost never [di-rectly] cut wages’ (1996a, p. 13). Akerlof andhis co-authors then run a series of simulationsof the effects of low inflation policy in a con-text of downward wage rigidity and detect per-manent unemployment losses. As they explain:

As expected, unemployment rises at low rates ofinflation. This is a permanent cost to pursuing lowinflation. The employment losses are permanentbecause the churning of the economy always pro-duces some firms that need to cut relative wagesto preserve employment. When inflation is verylow, they cannot do this, because as we have seen,nominal wages are rigid downward. Unemploy-ment rises instead. Not only are these losses

Bell: Scourge of Inflation? 79

The University of Melbourne, Melbourne Institute of Applied Economic and Social Research

permanent, we find that they are also much largerthan any reasonable estimate of the gains of tar-geting low inflation.[Akerlof et al. 1996a, p. 15]

The discussion above suggests that the ortho-dox approach to inflation is open to dispute andthat positive assessments of the benefits of verylow inflation may be misplaced. Beyond this,the costs of deflationary policy, costs that arequite possibly more than short term, plus thehints above that moderate inflation might insome respects be good for the economy, sug-gest it is time for a wider debate on the efficacyof current policy. If there is a structural breakbeyond which the costs of inflation rapidlymount, then policy should aim to keep inflationbelow that level. As noted above, even the mostconservative estimate, by Sarel (1996), sug-gests this level may be around an inflation rateof 8 per cent. Fortin’s (1993, p. 15) conclusionsfor Canada may well be applicable to Australia:

The minimal implication of these results is thatthe present monetary strategy in Canada is proba-bly much more costly than the policy authoritiesare ready to admit, and that the benefits are muchmore uncertain than they want to acknowledge. Inother words, the problem with the strategy is notthat it is so hard to sell to the Canadian public, butthat it is an imprudent strategy to start with.

6. Conclusions

Dissatisfaction with the pursuit of very low in-flation in Australia has mainly emerged by wayof sporadic complaints about deflationary pol-icy by industry. In the late 1970s, for example,the Victorian Chamber of Manufactures (1977)complained that ‘it would indeed be a tragedyif the battle against inflation were won only tofind industry had died fighting the battle’.More recently, the Australian Chamber ofCommerce and Industry has similarly com-plained ‘that the economy is being held backbecause of a phantom concern about inflation’,and that ‘Reserve Bank policy over the past de-cade has cost the economy billions in lost pro-duction in a quixotic attempt to containinflation’ (Australian Chamber of Commerceand Industry 1996, p. 1).

Overall, however, the shift to a low inflationregime has gone surprisingly smoothly interms of elite and public acceptance. Hibbs(1987) emphasises that aversion to inflationrises with income and this helps create a pow-erful low inflation constituency amongstwealth holders. It is also true that Australia,with its high foreign debt and heavily tradedcurrency, is particularly exposed to financialmarket sentiment. Also, central bank and or-thodox fiscal authorities in Australia dominatethe state institutionally and provide strongbacking for targeting very low inflation.Industry–financial sector linkages are alsoweak and the financial sector is not closely tiedto the (potentially more expansionary) interestsof domestic industry. Industry itself has also insome ways benefited from a higher unemploy-ment/low inflation mix, especially in terms ofongoing efforts to discipline labour and pro-mote labour market reform. These factors helpexplain why the politics of monetary policy inAustralia has been a low voltage affair.

Yet high and continuing unemployment po-tentially remains the Achilles heel of very lowinflation targeting. Michl (1995, p. 54) is cor-rect to point out that ‘the danger of inflation isperhaps the most common excuse for policieswhich shrink from aggressively reducing un-employment’. Official endorsement of theNAIRU framework, whereby rates of unem-ployment estimated to be as high as 6 to 8 percent (RBA 1993, p. 7) can be regarded as effec-tive ‘full employment’, establishes a veryconservative bias in attempts to reduce unem-ployment through macroeconomic policy. Butwhat if the evils of inflation have been over-stated and the costs of disinflationary policiesunderstated? This question frames the responseof Phillip Holt (1997, p. 20) of the AustralianBusiness Chamber when he states that the RBAshould ‘come clean’ and explain its thinkingmore clearly on the ‘costs/benefits of low infla-tion vis-a-vis the costs/benefits of high unem-ployment and exactly how and when lowinflation will lead to low unemployment’. Holtadds that the RBA should also explain ‘why a2–3 per cent inflation target is necessary, ratherthan say a 1–2 per cent target or a 3–4 per centtarget’.

80 The Australian Economic Review March 1999

The University of Melbourne, Melbourne Institute of Applied Economic and Social Research

The

Economist

(1997b, p. 98) has stated that‘allowing inflation to rise in order to curb un-employment may not always be undesirable’.Perhaps we should take this idea more seri-ously. Nor, contrary to orthodoxy, is inflationlikely to

accelerate

away under a slightly moreexpansionary policy. As Stiglitz (1997, p. 9) ar-gues:

Contrary to the accelerationist view, not only doesthe economy not stand on a precipice—with aslight dose of inflation leading to ever-increasinglevels of inflation—but the magnitude by whichinflation rises does not increase when the unem-ployment rate is held down for a prolonged periodof time . . . [This] suggests that even risk-aversepolicymakers might want to engage in moderateexperiments with . . . unemployment . . .[see also Galbraith 1997]

This is especially so, if, as various analystsargue, there has been a structural weakening ininflationary pressures, both domestically andinternationally (Thurow 1996, pp. 189–90;Bootle 1996). Perhaps, then, Stiglitz is rightwhen he argues that the costs of higher infla-tion incurred in driving unemployment belowthe NAIRU are likely to be small compared tothe gains. He modestly proposes that in:

testing the waters, we do not risk drowning. Ifneed be, we can always reverse course. But by ex-perimenting, and showing some hesitation aboutrestraining the economy through higher interestrates . . . as the NAIRU draws nigh, we mightlearn a little more about the depth of the watersand possibly become better swimmers . . .[Stiglitz 1997, p. 10]

January 1999

Endnote

1. It should be pointed out that much of this ef-fect is achieved by including many third worldcountries with high to very high inflation rates.

References

Akerlof, G., Dickens, W. & Perry, G. 1996a,‘Low inflation or no inflation: Should theFederal Reserve pursue complete price sta-bility?’, vol. 39, no. 5, pp. 11–17.

Akerlof, G., Dickens, W. & Perry, G. 1996b,‘The macroeconomics of low inflation’,

Brookings Papers on Economic Activity

, no.1, pp. 1–76.

Argy, F. 1998,

Australia at the Cross Roads

,Allen & Unwin, Sydney.

Armstrong, P., Glyn, A. & Harrison, J. 1991,

Capitalism since 1945

, Blackwell, Oxford.

Australian

1992, ‘Recession our fault, ReserveDeputy says’, 22 May, pp. 1, 4.

Australian Chamber of Commerce and Indus-try 1996,

Pre-Budget Submission

, February,Canberra.

Australian Chamber of Commerce and Indus-try 1997,

Pre-Budget Submission

, February,Canberra.

Ball, L. 1993, ‘How costly is disinflation?:The historical evidence’,

Federal ReserveBank of Philadelphia

Business Review

,November–December, pp. 17–28.

Barro, R. J. 1996, ‘Inflation and growth’,

Fed-eral Reserve Bank of St. Louis

Review

, vol.78, no. 3, pp. 153–69.

Bell, S. 1997,

Ungoverning the Economy: ThePolitical Economy of Australian Econ-omic Policy

, Oxford University Press, Mel-bourne.

Bootle, R. 1996,

The Death of Inflation: Sur-viving and Thriving in the Zero Era

, Nicho-las Brealy, London.

Brash, D. 1997, ‘The new inflation target andNew Zealanders’ expectations about in-flation and growth’, address to CanterburyEmployers’ Chamber of Commerce,Christchurch, 23 January.

Brittan, S. 1995, ‘Elusive case for stableprices’,

Financial Times

, 18 May, p. 9.Bruno, M. 1995, ‘Does inflation really lower

growth’,

Finance and Development

, vol. 32,no. 3, pp. 35–8.

Bruno, M. & Easterly, W. 1998, ‘Inflation cri-ses and long-run growth’,

Journal of Mone-tary Economics

, vol. 41, pp. 3–26.Chowdhury, A. & Mallik, G. 1999, ‘A land

locked into low inflation: How far is thepromised land?’,

Economic Analysis andPolicy

, forthcoming.De Gregorio, J. 1993, ‘Inflation, taxation and

long-run growth’,

Journal of Monetary Eco-nomics

, vol. 31, pp. 271–98.

Bell: Scourge of Inflation? 81

The University of Melbourne, Melbourne Institute of Applied Economic and Social Research

Eatwell, J. 1995, ‘The international origins ofunemployment’, in

Managing the GlobalEconomy

, eds J. Michie & J. Grieve Smith,Oxford University Press, Oxford.

Economist

1995, ‘The cost of inflation’, 13May, p. 90.

Economist

1997a, ‘The politics of unemploy-ment’, 5 April, pp. 17–19.

Economist

1997b, ‘Up the NAIRU without apaddle’, 8 March, p. 98.

Fischer, S. 1993, ‘The role of macroeconomicfactors in growth’,

Journal of Monetary Eco-nomics

, vol. 32, pp. 485–512.Fischer, S. 1995, ‘Modern central banking’, in

The Future of Central Banking

, eds F. Capie,C. Goodhart & N. Schmidt, Cambridge Uni-versity Press, Cambridge.

Fortin, F. 1993, ‘The unbearable lightness ofzero-inflation optimism’,

Canadian Busi-ness Economics

, vol. 1, pp. 3–18.Fraser, B. W. 1996, ‘Reserve Bank indepen-

dence’,

Reserve Bank of Australia Bulletin

,September, pp. 14–20.

Galbraith, J. 1997, ‘Time to ditch the NAIRU’,

Journal of Economic Perspectives

, vol. 11,no. 1, pp. 93–108.

Gourevitch, P. 1986,

Politics in Hard Times

,Cornell University Press, Ithaca.

Hibbs, D. A. 1987,

The American PoliticalEconomy: Macroeconomics and ElectoralPolitics

, Harvard University Press, Cam-bridge, Massachusetts.

Holt, P. M. 1997, ‘RBA must lay it on line’,

Australian Financial Review

, Letters, 30April, p. 20.

Junankar, P. N. & Kapuscinskiu, C. A. 1992,

The Costs of Unemployment in Australia,

EPAC Background Paper no. 24, AGPS,Canberra.

Junor, B. 1995, ‘Inflation’, in

The AustralianEconomy

, ed. P. Kriesler, Allen & Unwin,Sydney.

Krugman, P. 1994, ‘Europe jobless, Americapenniless?’,

Foreign Policy

, no. 95, pp. 19–34.

Krugman, P. 1996, ‘Stable prices and fastgrowth: Just say no’,

Economist

, 31 August,pp. 15–18.

Kyriakopoulos, J. 1991, ‘Does moderate infla-tion affect economic growth?’, in

Contempo-

rary Issues in Australian Economics

, ed. M.R. Johnson, Macmillan, Melbourne.

Langmore, J. & Quiggin, J. 1994,

Work for All:Full Employment in the Nineties

, MelbourneUniversity Press, Melbourne.

Levine, R. & Zervos, S. 1993, ‘What have welearned about policy and growth from cross-country regressions?’,

American EconomicReview

, vol. 83, pp. 426–30.Luttwak, E. 1996, ‘Central bankism’,

LondonReview of Books

, 14 November, pp. 3, 6–7.McClain, K. T. & Nichols, L. M. 1993–94, ‘On

the relation between investment and infla-tion: Some results from cointegration, causa-tion, and sign tests’,

Journal of Post-Keynesian Economics

, vol. 16, pp. 205–20.McTaggart, D. 1992, ‘The cost of inflation in

Australia’, in

Inflation, Disinflation andMonetary Policy

, ed. A. Blundell-Wignall,Reserve Bank of Australia, Sydney.

Mathews, R. L. 1996, ‘Financial markets andfailed economic policies’, in

Dialogues onAustralia’s Future

, eds P. Sheehan, B. Gre-wal & M. Kumnick, Centre for StrategicEconomic Studies, Victoria University, Mel-bourne.

Michl, T. 1995, ‘Assessing the costs of infla-tion and unemployment’, in

The PoliticalEconomy of Full Employment

, eds P. Arestis& M. Marshall, Edward Elgar, London.

Palley, T. I. 1998, ‘Restoring prosperity: Whythe US model is not the answer for theUnited States or Europe’,

Journal of Post-Keynesian Economics

, vol. 20, pp. 337–53.Reserve Bank of Australia 1993, ‘Towards full

employment’, Occasional Paper no. 12,RBA, Sydney.

Reserve Bank of Australia 1996,

AustralianEconomic Statistics 1949–50 to 1994–95

,RBA, Sydney.

Rudebusch, G. D. & Wilcox, D. W. 1994,

Pro-ductivity and Inflation: Evidence and In-terpretations

, Federal Reserve Board,Washington, DC.

Sarel, M. 1996, ‘Nonlinear effects of inflationon economic growth’,

IMF Staff Papers

, vol.43, pp. 199–215.

Seabright, P. 1996, ‘Down with deflation’,

London Review of Books

, 12 December, pp.30–1.

82 The Australian Economic Review March 1999

The University of Melbourne, Melbourne Institute of Applied Economic and Social Research

Seccareccia, M. & Lavoie, M. 1996, ‘Centralbank austerity policy, zero-inflation targetsand productivity growth in Canada’,

Journalof Economic Issues

, vol. 30, pp. 533–43.Smyth, D. J. 1994, ‘Inflation and growth’,

Journal of Macroeconomics

, vol. 16, pp.261–70.

Stanners, W. 1993, ‘Is low inflation an impor-tant condition for high growth?’,

CambridgeJournal of Economics

, vol. 17, pp. 79–107.Stevens, G. 1992, ‘Inflation and disinflation in

Australia: 1950–91’, in

Inflation, Disinfla-tion and Monetary Policy

, ed. A. Blundell-Wignall, Reserve Bank of Australia, Sydney.

Stiglitz, J. 1997, ‘Reflections on the naturalrate hypothesis’,

Journal of Economic Per-spectives

, vol. 11, no. 1, pp. 3–10.Thurow, L. C. 1996,

The Future of Capitalism

,Allen & Unwin, Sydney.

Tobin, J. 1972, ‘Inflation and unemployment’,

American Economic Review

, vol. 62, pp. 1–18.

Victorian Chamber of Manufactures 1977,‘1977—Crucial time for manufacturing’,

VCM File

, vol. 22, no. 1.Wright, L. 1995, ‘Post-monetarism at the

Reserve Bank’,

Current Affairs Bulletin

,February–March, pp. 13–22.