Embed Size (px)

Citation preview

THIS REPORT MAY NOT BE INDEPENDENT OF THE PROPRIETARY INTERESTS OF SBERBANK CIB USA, INC. OR ITS AFFILIATES (TOGETHER, “SBERBANK”). SBERBANK TRADES THE SECURITIES COVERED IN THIS REPORT FOR ITS OWN ACCOUNT AND ON A DISCRETIONARY BASIS ON BEHALF OF CERTAIN CLIENTS.

SUCH TRADING INTERESTS MAY BE CONTRARY TO THE RECOMMENDATION(S) OFFERED IN THIS REPORT.

In accordance with US SEC Regulation AC, important US regulatory disclosures and analyst certification can be found at https://research.sberbank-cib.com/group/guest/disclosure.

[email protected], http://research.sberbank-cib.com

INVESTMENT RESEARCHRUSSIA | STRATEGY

DECEMBER 10, 2018 | 13:15 MSK

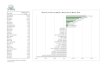

Russian sector performance 2018 YTD 20%

19%

�2%

�2%

�3%

�6%

�20%�20%

�21%

�22%

�23%

�26%

�28%

�38%

�60% �40% �20% 0% 20% 40%

GasOil

RTSSteel

Precious metalsMedia and IT

Real estateTelecomsFertilizersTransport

Base metalsBanks

UtilitiesConsumer

Source: Sberbank CIB Investment Research

Earnings revisions in Russian stocks

40

50

60

70

8080

95

110

125

140

Jan

’18

Feb

’18

Mar

’18

Apr

’18

May

’18

Jun

’18

Jul ’

18

Aug

’18

Sep

’18

Oct

’18

Nov

’18

Domestics Exporters USD/RUB (rhs, inverted) Note: 100 = January 1, 2018.

Source: Bloomberg, Sberbank CIB Investment Research

GEM EPS growth forecast over time

5%

10%

15%

20%

25%

Jan

’17

Mar

’17

May

’17

Jul ’

17

Sep

’17

Nov

’17

Jan

’18

Mar

’18

May

’18

Jul ’

18

Sep

’18

Nov

’18

2018 2019

Source: Bloomberg, Sberbank CIB Investment Research

Margin estimates in EM defensive and cyclical sectors

6.0%6.5%7.0%7.5%8.0%8.5%9.0%9.5%

Jan

’17

Mar

’17

May

’17

Jul ’

17

Sep

’17

Nov

’17

Jan

’18

Mar

’18

May

’18

Jul ’

18

Sep

’18

Nov

’18

Defensives Cyclicals Source: Bloomberg, Sberbank CIB Investment Research

The Russian Eagle 2019 Strategy: Standing Against the Headwinds █ One of the best performers in 2018. GEM equities have experienced a

tough year, with most deep in the red YTD. Meanwhile, Russian indexes are

set to close the year flat in dollar terms and deliver a total return of 5%.

Russia’s outperformance has been driven mainly by earnings upgrades, while

multiples have continued to fall and Russia now trades at a forward P/E of

5.3. However, most of the outperformance has come from exporters, while

domestic stocks have been beaten down heavily.

█ Global headwinds likely to extend into next year. The flattening of the US

yield curve points to a high risk of a cyclical slowdown. So far, we see no signs that

this factor is properly reflected in consensus estimates. Top�line numbers have not

seen any meaningful revisions in the developed world, while EM earnings

downgrades have primarily been driven by weaker currencies, staying unchanged

in real terms. Should a slowdown materialize, we would expect another wave of

earnings downgrades across the board. Alternatively, if US growth holds up, this

would leave more room for further Fed monetary tightening. In that case, the

dollar could strengthen further, putting more pressure on EMs.

█ Staying constructive on the Russian market. Despite global headwinds, Russia

has a certain valuation cushion. We argue that the equity risk premium (ERP)

expansion observed in 2018 is not fundamentally justified, and we expect it to

contract by some 200 bps. This could raise the market P/E from 5.3 to 6.3.

█ We set our end�2019 index target at 1,400. P/E expansion and modest

EPS growth translates into an RTS target of 1,400. This scenario does not

imply any meaningful improvement in geopolitical news flow. In an alternative

scenario in which new sanction fears evaporate, we could see much more

significant upside. Energy stocks fit for both scenarios – either they benefit

from the ruble staying weak, or they get rerated with the market. Banks are

likely to benefit the most from the optimistic outcome, as they are the highest

beta plays to Russia’s key risk.

█ Top picks. We like Lukoil for its high dividend yields and accelerating

buyback, Novatek in anticipation of further developments with Arctic LNG�2,

Norilsk Nickel for its double�digit dividend and decent development plan, TCS

Bank for its impressive ROE and EPS growth, and InterRAO for its deep value.

While global tech stocks are falling out of favor, we still like Yandex and

Mail.ru Group for fundamental reasons.

Andrey Kuznetsov Chief Equity Strategist+7 (495) 933 9868

Cole Akeson Equity Strategist+7 (495) 933 9851

The remaining contributors are listed after each respective section

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

2 SBERBANK CIB INVESTMENT RESEARCH

Contents

Standing Against the Headwinds...................................................................................................... 3

Oil and Gas: Keep “Maneuvering” the Macro Tailwinds .................................................................. 17

Metals and Mining: Coming off a Peak Year for Earnings ............................................................... 19

Financials: Looking to Avoid Repeat of 2018 Dichotomy................................................................ 22

TMT: Betting on the Digital Economy ............................................................................................. 24

Consumer: Headwinds to Abate in 2019 ....................................................................................... 26

Utilities: Modernization Further Postponed .................................................................................... 28

Transport: Mixed Outlook .............................................................................................................. 30

Global Context ............................................................................................................................... 32

Russian Macro Data ....................................................................................................................... 33

Stock Liquidity and Commodities ................................................................................................... 34

Note: All prices and performance figures based on November 30 close, unless noted otherwise.

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 3

Standing Against the Headwinds

GEM equities experienced a spectacular selloff in 2018. Although Russia outperformed all GEMs, we

expect the headwinds to continue. The flattening yield curve in the US suggests a fairly high probability

of a cyclical slowdown, which would likely lead to earnings downgrades. Against this trend, Russia has

a fairly large valuation cushion, which should help the market to continue outperforming, in our view.

We expect Russia’s ERP to compress by some 200 bps in 2019 and set our end�2019 RTS Index target

at 1,400. Within the market, we prefer exporters, primarily oil and gas stocks. We think the sector is

best placed to outperform amid any geopolitical backdrop, as the sector benefits from a weak ruble

when tensions escalate, and should they stay the same or ease, the whole market would likely rerate,

led by banks, while energy stocks would still deliver good results in absolute terms.

Flat is still good

This year has been a tough one for equities globally. Almost all equity markets are set to close the

year in the red. Against this backdrop, Russia’s flat performance is a fairly good result. Moreover,

given Russia’s solid dividend yield, the RTS Index has so far delivered a total return of 5%, making it

one of the best performing markets globally.

YTD equity market performance

2%

0%

�1%

�3%

�6%

�8%

�8%

�10%

�10%

�11%

�12%

�14%

�14%

�16%

�19%

�19%

�23%

�40%

�50% �40% �30% �20% �10% 0% 10%

S&P 500

Brazil

Russia (RTS)

MSCI World

Thailand

India

Japan

Malaysia

Taiwan

Indonesia

Europe

Poland

MSCI EM

China

Mexico

South Korea

South Africa

Turkey

Source: Bloomberg

Just a few weeks ago, it would have been easy to attribute Russia’s outperformance to soaring oil,

with Brent peaking at $86/bbl. However, it has since slid to around $60/bbl and is now trading

lower than it was at the beginning of the year. So the question is, why is Russia’s outperformance

holding up, and is it sustainable? The numbers suggest that the outperformance has been driven by

earnings upgrades, as its multiples have been sliding along with the rest of EM amid escalating

geopolitical tensions. Russia has become even cheaper, as its 2019E P/E has slid from already

depressed levels to just above 5. Meanwhile, the earnings upgrades have offset roughly 15% of the

slide in P/E in dollar terms.

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

4 SBERBANK CIB INVESTMENT RESEARCH

12m forward P/E

4

6

8

10

12

14

Jan ’18 Mar ’18 May ’18 Jul ’18 Sep ’18 Nov ’18

Russia MSCI EM

Source: Bloomberg

RTS Index earnings revisions

180

185

190

195

200

205

210

215

220

Jan ’18 Mar ’18 May ’18 Jul ’18 Sep ’18 Nov ’18

2018 2019 Source: Bloomberg

Decent headline index performance hides a substantial divergence between individual sectors. In

fact, Russia’s outperformance has been solely driven by the energy sector, which has been the only

one to post gains in 2018. Metals have essentially remained flat while domestic�oriented sectors

have dropped 20�40% in dollar terms. The weak ruble has been the key reason for this divergence.

The ruble has lost 13% YTD on the back of sanction fears and the fiscal rule, which prescribes the

CBR to effectively sterilize any increased current account surplus. Domestic sector earnings have

been revised downward along with the depreciating ruble, while exporters’ earnings have soared.

Given that exporters generate more than 70% of earnings for Russia’s publicly traded stocks, the

cumulative impact on index earnings has been positive.

Sector performance in 2018

20%19%

�2%�2%�3%

�6%�20%�20%�21%

�22%�23%

�26%�28%

�38%

�50% �40% �30% �20% �10% 0% 10% 20% 30%

GasOil

RTSSteel

Precious metalsMedia and IT

Real estateTelecomsFertilizersTransport

Base metalsBanks

UtilitiesConsumer

Source: Bloomberg, Sberbank CIB Investment Research

2018 earnings revisions

40

50

60

70

8080

95

110

125

140

Jan ’18 Mar ’18 May ’18 Jul ’18 Sep ’18 Nov ’18

Domestics Exporters USD/RUB (rhs, inverted)

Source: Bloomberg, Sberbank CIB Investment Research

GEM selloff

The GEM selloff has been one of the key events of 2018. Although Russia has managed to weather

this storm thanks to earnings upgrades, it cannot remain immune to adverse trends in this asset

class, as GEM funds are the largest group of investors in Russian equities. Flows in or out of these

funds do matter for market performance. So we need to delve a bit deeper into the GEM theme to

make a call on Russia.

The conventional explanation for the GEM selloff is that markets have been reacting to the Fed’s

tightening cycle and a potential slowdown in global growth. The Fed has raised rates by 75 bps so

far in 2018 and is expected to deliver another 25 bps at its December meeting. Ten�year US

Treasury yields have risen some 60 bps and the dollar has firmed 5% this year, which clearly looks

negative for EMs. The question is whether these interest rate increases will be sufficient to derail

global growth.

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 5

CONSENSUS ESTIMATES DO NOT FACTOR IN A SLOWDOWN

The IMF recently downgraded its global growth estimate by 0.2 pp, which does not look bad

enough to claim that we are heading into a cyclical slowdown. The IMF anticipates global growth

stabilizing at 3.6�3.7%. Of course, the IMF’s forecasts are not the best predictor for cyclical

slowdowns. Another option is to look at what is priced in by the market. It is hard to directly derive

real growth estimates from the available market data. However, we can take the evolution of

revenues estimates as a decent proxy. The data on consensus revenues revisions is depicted in the

two charts below. In DMs, revenue estimates have stayed pretty much unchanged throughout

2018, which suggests that markets are not pricing in any meaningful slowdown in global demand.

For EMs, revenues have been downgraded by around 7% from the top. This fact can be attributed

to EM currency depreciation: the index of EM currencies (weighted by MSCI EM country weights)

has fallen by the same 7%. So the downgrade does not reflect any material deterioration in the

demand outlook in real terms.

Consensus revenue forecast revisions, DMs

1,100

1,150

1,200

1,250

1,300

1,350

1,400

Jan

’17

Mar

’17

May

’17

Jul ’

17

Sep

’17

Nov

’17

Jan

’18

Mar

’18

May

’18

Jul ’

18

Sep

’18

Nov

’18

DM sales 2018 DM sales 2019

Source: Bloomberg

Consensus revenue forecast revisions, EMs

750

800

850

900

950

1,000

Jan

’17

Mar

’17

May

’17

Jul ’

17

Sep

’17

Nov

’17

Jan

’18

Mar

’18

May

’18

Jul ’

18

Sep

’18

Nov

’18

EM sales 2018 EM sales 2019 Source: Bloomberg

Meanwhile, earnings downgrades in the EM universe have been more material. EPS growth

estimates for 2018 have been revised down from 22% at the peak to 10%. This downgrade reflects

more than just revised revenue numbers. Margins have been hit as well. However, when we look at

sector�level margins in the GEM space, we see an interesting picture. Margins have been falling in

defensive sectors but have been more or less stable in cyclicals this year. For example, the biggest

margins revisions have been seen in the utilities space. This does not look like an anticipated cyclical

downturn. More likely, the downtrend in margins in defensive sectors reflects cost pressure from

rising commodities prices and weaker currencies.

EPS growth consensus forecasts in 2018 and 2019

5%

10%

15%

20%

25%

Jan

’17

Mar

’17

May

’17

Jul ’

17

Sep

’17

Nov

’17

Jan

’18

Mar

’18

May

’18

Jul ’

18

Sep

’18

Nov

’18

2018 2019

Source: Bloomberg, Sberbank CIB Investment Research

Estimated margins, consensus forecasts

9.0%

9.5%

10.0%

10.5%

11.0%

Jan

’17

Mar

’17

May

’17

Jul ’

17

Sep

’17

Nov

’17

Jan

’18

Mar

’18

May

’18

Jul ’

18

Sep

’18

Nov

’18

2018 2019

Source: Bloomberg, Sberbank CIB Investment Research

Margins in EM defensive and cyclical sectors, consensus for 2018

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

Jan

’17

Mar

’17

May

’17

Jul ’

17

Sep

’17

Nov

’17

Jan

’18

Mar

’18

May

’18

Jul ’

18

Sep

’18

Nov

’18

Defensives Cyclicals

Source: Bloomberg, Sberbank CIB Investment Research

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

6 SBERBANK CIB INVESTMENT RESEARCH

A divergence between margin trends in the defensive and cyclical sectors helps to explain another peculiar

phenomenon in GEMs in 2018. After several years of dismal performance, value stocks have finally started

outperforming. From what we have seen in client meetings, this has caught many investors by surprise, as

institutional investors tend to be overweight growth stocks in GEM. The changing value/growth

preference has been positive for Russia, and if persists, it will continue to support the market.

MSCI EM value relative to MSCI EM growth

80

85

90

95

100

105

Jan

’17

Mar

’17

May

’17

Jul ’

17

Sep

’17

Nov

’17

Jan

’18

Mar

’18

May

’18

Jul ’

18

Sep

’18

Nov

’18

Source: Bloomberg

OMINOUS SIGNALS FROM GLOBAL FI MARKETS

Our conclusion is therefore that the selloff in EM equities has been primarily driven by the strong

dollar rather than a weaker growth outlook. However, other indicators are sending the signal that a

cyclical slowdown is likely to materialize over the medium term. The US Treasury yield curve has

been flattening throughout 2H18. An inverting yield curve is considered a fairly reliable predictor of

economic recessions, and it is also associated with markets peaking, albeit with some lags. High�

yield bonds have started wobbling as well, with spreads jumping by more than 100 bps recently,

also pointing to a possible slowdown.

USD yield curve

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

0 5 10

End 2017 Mid�2018 Dec 2018

Source: Bloomberg

UST 2y10y spread and global equities performance

0

500

1,000

1,500

2,000

2,500

(1.0)

0.0

1.0

2.0

3.0

4.0

1990 1995 2000 2005 2010 2015

Yield curve slope, 10y minus 2yMSCI World (rhs)

Source: Bloomberg

US high�yield bond spreads, bps

2

4

6

8

10

2015 2016 2017 2018

Source: Bloomberg

If the fixed income markets are proved right in calling an imminent slowdown, we could see another

wave of earnings downgrades, this time on a global scale, based on revised revenue numbers.

However, the prospects for a slowdown mean that the dollar is unlikely to meaningfully appreciate

further. With the yield curve flattening, the Fed will exercise greater caution over rate hikes. After all,

US inflation remains under control and is not pressuring the Fed to tighten. The futures markets are

now pricing in only two rate hikes: one this month and another in 2019.

Alternatively, if “this time is different” and the flattening yield curve does not signify anything and

there is no slowdown, the Fed would be free to further tighten monetary policy. This would further

support the dollar, sending more shivers across emerging markets.

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 7

Neither option looks great for EMs, but it is worth noting that since derating this year, EMs do not look expensive, trading at a 2019E P/E of 10. This valuation cushion could somewhat soften the impact of earnings downgrades.

CHINA REMAINS THE BIGGEST RISK, BUT THIS IS UNLIKELY TO COME TO A HEAD IN 2019

Another large risk lies on the Chinese side. Markets have been living under a sword of Damocles for years in the form of China’s debt bubble. So far the Chinese authorities have managed to prevent this bubble from bursting by deploying new stimulus programs. However, the credit impulse is fading. In nominal terms, credit origination has faded by a quarter since late 2017. This shift appears to be even starker when considering that a substantial proportion of new loans is taken out simply to service existing debt.

China’s credit stimulus

6.0%

7.5%

9.0%

10.5%

12.0%

13.5%

15.0%

10,000

12,000

14,000

16,000

18,000

20,000

22,000

2014 2015 2016 2017 2018

New loans, CNY bln, annualizedNew loans origination, % of total debt stock, annualized (rhs)

Source: Bloomberg, BIS

We do not expect this bubble to burst in 2019, unless there is some external event such as a full�scale trade war. The Chinese government is keeping a tight grip and is clearly committed to holding growth to at least its targeted 6% rate, even if that means accumulating further imbalances. However, this risk remains something worth considering at all times.

Domestic backdrop: Solid and boring

The macro backdrop for Russian equities looks solid but unexciting. Investors long ago accepted that the Russian economy is unlikely to return to growth meaningfully above 2%. However, the country’s balance sheet looks exceptionally strong, with an impressive current account and fiscal surpluses, low debt and a cheap currency. Against this backdrop, the Russian market has loitered in deep�value territory for years. In 2018, this apparent value has been offset by sanction risks. As a result, the market has seen a further derate. P/Es have contracted across the board, although in some cases, such as the consumer or media space, it has been exacerbated by sector�specific or stock�specific negative developments.

RTS Index forward P/E

4.5

5.0

5.5

6.0

6.5

7.0

7.5

2016 2017 2018

Source: Bloomberg

P/E by sector

�30%

�25%

�20%

�15%

�10%

�5%

0%

0

5

10

15

20

25

30

RTS

Med

ia/

inte

rnet

Con

sum

er

Tele

com

s

Met

als

and

min

ing

Tran

spor

t

Oil

and

gas

Fina

ncia

ls

Util

ities

2017 average End 2018 P/E change (rhs) Source: Sberbank CIB Investment Research

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

8 SBERBANK CIB INVESTMENT RESEARCH

Investors cite two main arguments preventing them from increasing Russia exposure. First is

sanctions risk, to be discussed later. Another one is anemic GDP growth, which does not attract

growth�hungry GEM investors. However, as we have pointed out many times in the past, equity

investors do not have a claim on GDP growth; their claim is rather on EPS growth.

Over the past three years, Russia has managed to deliver double�digit EPS growth, despite

essentially stagnant GDP. This phenomenon does not only reflect strong commodity price

performance but also a change in the country’s economic model, which is transferring value from

consumers to corporates. We have previously pointed out that exporters are set to be the biggest

beneficiaries of this trend, and this call has proven to be right.

Another important thing about the current economic model is that it favors stability over growth. The

government demonstrates little appetite to risk macro stability in an attempt to boost growth, or to

engage in radical reforms that could shake up the political system. So investors complaining about

low growth should not forget that they also gain a higher degree of economic stability as a reward.

The macro stability and low valuations constitute another important feature of the Russian market: it

has become much less volatile in recent years. The fiscal rule and a number of other macro

developments have effectively decoupled the ruble and most other key macro indicators from the oil

price. Russia’s macro story has probably become the most transparent and predictable among all

EMs. Being boring and predictable is not the best option in more exciting times, but it helps to

weather any headwinds better than almost any other country.

There is no doubt that the Russian market offers deep value. However, this value can only

materialize once the geopolitical risk premium has dissipated. Until that time, Russian multiples are

set to stay low and the market will be primarily driven by earnings revisions. This is essentially the

pattern that has been observed in 2018.

A difficult international political backdrop in 2018�19

The key risk for the Russian market this year has arguably been international political developments

between Russia and the West. Arguably, these developments have played a more important role for

the market this year than they have had since 2014. Sadly, these events are more often than not

unpredictable, and neutral or negative for the market. Meanwhile, periods of reduced rhetoric have

allowed Russia’s good fundamentals (and sometimes, oil price strength) to shine through.

Two periods have been important for the market this year, in our view. The first was the April 6

announcement of US SDN sanctions on Rusal, En+ Group and others, after which the RTS fell some

12% in four sessions. The second was a combination of events in mid�July to mid�August, when the

Russian and US presidents held their summit in Helsinki, and in the aftermath US senators drafted

and submitted the Defending American Security from Kremlin Aggression Act (“DASKAA,” Senate

bill #3336). The day DASKAA was published in Kommersant coincided with an announcement that

the US would impose sanctions on Russia due to Russia’s alleged involvement in the attack on the

Skripals in March. The RTS ultimately sank 11% during the period, albeit in fits and starts, as shown

in the chart below, while the MSCI EM tumbled 4%.

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 9

Market performance and key international political events in 2018

900

950

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

Dec

29

, ’1

7Ja

n 5

, ’1

8Ja

n 1

2, ’

18

Jan

19

, ’1

8Ja

n 2

6, ’

18

Feb

2, ’

18

Feb

9, ’

18

Feb

16

, ’1

8Fe

b 2

3, ’

18

Mar

2, ’

18

Mar

9, ’

18

Mar

16

, ’1

8M

ar 2

3, ’

18

Mar

30

, ’1

8A

pr 6

, ’1

8A

pr 1

3, ’

18

Apr

20

, ’1

8A

pr 2

7, ’

18

May

4, ’

18

May

11

, ’1

8M

ay 1

8, ’

18

May

25

, ’1

8Ju

n 1

, ’1

8Ju

n 8

, ’1

8Ju

n 1

5, ’

18

Jun

22

, ’1

8Ju

n 2

9, ’

18

Jul 6

, ’1

8Ju

l 13

, ’1

8Ju

l 20

, ’1

8Ju

l 27

, ’1

8A

ug 3

, ’1

8A

ug 1

0, ’

18

Aug

17

, ’1

8A

ug 2

4, ’

18

Aug

31

, ’1

8Se

p 7

, ’1

8Se

p 1

4, ’

18

Sep

21

, ’1

8Se

p 2

8, ’

18

Oct

5, ’

18

Oct

12

, ’1

8O

ct 1

9, ’

18

Oct

26

, ’1

8N

ov 2

, ’1

8N

ov 9

, ’1

8N

ov 1

6, ’

18

Nov

23

, ’1

8N

ov 3

0, ’

18

RTS MSCI EM Events

"Oligarch report" and "debt report" published

Skripal attack

Sanctions on Rusaland EN+

1) Helsinki summit,2) DASKAA press release,3) DASKAA submission,4) DASKAA leak to Kommersantsame day as CBW sanctions announced CBW notification

that terms havenot been met

Kerch Straitincident

Source: US Library of Congress, OFAC, Kommersant, Bloomberg, Sberbank CIB Investment Research

Key political events of 2018 to date for the market Jan 16Jan 30Feb 2Mar 4Apr 6Jul 16Jul 24Aug 1Aug 8

Nov 6Nov 25

DETER formally submitted to Congress.Publication of the CAATSA "oligarch report."Publication of the CAATSA "debt report."Attack on Sergei and Yulia Skripal in the UK.Sanctions announced by US OFAC on Rusal, En+ and others.Helsinki summit between Russian and US presidents.US senators announce plan to submit bill now known as "DASKAA."DASKAA formally submitted to Congress, but not published.Kommersant publishes draft of DASKAA before official publication. The same day, US announces it sees Russia as culpable in Skripal attack and announces first chemical�weapons�related (a.k.a. "CBW") sanctions.

US State Department states that demands on Russia regarding CBW/Skripal case have not been metAltercation between Russian and Ukrainian navies at the Kerch Strait.

Source: US Library of Congress, OFAC, Kommersant, Bloomberg, Sberbank CIB Investment Research

WE ASSUME STATUS QUO FOR INTERNATIONAL RELATIONS IN 2019

To state the obvious, we can envisage three major scenarios for international relations next year: an

improvement, a continuation of the status quo, or a further decline.

At this time, the market appears to be pricing in that the status quo will prevail, and this includes an

assumption that the EU and their other partners will place no new sanctions on Russia that would

have a material impact on markets, and that Russia will also not place such measures against these

countries in turn. It would not be entirely accurate to describe this as a neutral scenario; rather it is a

mildly positive one, as the longer that no new negative events appear on this front, the more

investors will be able to return their focus to the decent fundamentals.

We acknowledge that there are several flashpoints to watch out for next year. Sadly, we see no

obvious forthcoming catalysts that could improve relations and drive the market to markedly reduce

the political discount for Russian assets.

POLITICAL DATES AND STORIES TO WATCH

Although international political developments tend to be unpredictable, there are a few known

dates to watch out for next year.

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

10 SBERBANK CIB INVESTMENT RESEARCH

█ New Congress in January. The newly elected US Congress will likely begin its session on January

3. Although support for CAATSA, the last Russia�related bill to become law, was widely

bipartisan, the shift of control in the House of Representatives to the Democrats and the regular

reconfiguration of committee assignments introduce some uncertainty (even all else being equal)

as to how the US’s legislative branch will address Russia. Also, the new Congress will almost

certainly have more pressing domestic issues to address early in its term, and even in foreign

affairs attention may be elsewhere than Russia, such as on the developing situations with China,

Saudi Arabia, Iran and Venezuela.

█ Continually delayed Rusal and En+ sanctions. On December 7, OFAC extended the deadlines

for Rusal and EN+ sanctions for the seventh time, this time until January 21. The track record of

this process suggests that delays will continue until a solution is finally found.

█ INF treaty developments by early February. Although the topic has been quite peripheral for

financial markets so far, the ongoing public debate between Russia and the US (with occasional

contributions from other European countries and NATO representatives) about who is or is not

complying with the Intermediate�Range Nuclear Forces (INF) Treaty is likely to come to a head

before the deadline imposed by the US for early February. While not too relevant for markets thus

far, rancor on this topic – like many others – could provoke yet more heated, negative rhetoric that

markets would have to consider. In particular, the debate could provoke remarks from members of

Congress seeking to weigh in, even if this is primarily an issue for the US executive at this time.

█ Skripal/CBW sanctions: Timing unknown. Two events that are due, but with no clear

timeframe, are the US decision on the next round of punitive measures related to accusations

against Russia in the Skripal case, and the outcome of the US special counsel’s investigation into

relations between Donald Trump’s 2016 presidential campaign and the Russian state.

Regarding the Skripal or “CBW” case, the most recent guidance from US State Department

representatives in November was that they have informed Congress that Russia has been

unwilling to meet the US’s demands, meaning that a second round of measures is technically due.

However, the representatives said that the administration’s legal view is that there is no specific

deadline for the next measures, and that the administration would consult with Congress before

making any decisions. The 1991 CBW law would require the US president to choose at least three

of the following six options:

More restrictions on US exports to Russia. Russian Federal Trade Service data show 5.5% of

annual imports, or $12.6 bln, coming from the US in 2017, with difficult to replace high�tech

goods for both business and consumers constituting a large share.

Restrictions on US imports from Russia, which could be written to include oil and oil products. In

2017, Russia exported $10.6 bln to the US, or 3.2% of total exports, with a concentration in

energy supplies, according to the Russian Federal Trade Service. Were the US to target imports

of Russian hydrocarbons, the event could be highly disruptive to global energy markets over the

short term. The US is always concerned with cost and supply of energy, and this administration

is more obviously concerned than most, with frequent remarks on the topic on Twitter, hence

we see the possibility of this measure as quite low.

Prohibition on US banks (not only the US state) extending credit to the Russian government.

The language of these rules is written for financial markets as they existed in the early 1990s,

and thus may be open to some more or less problematic interpretations for markets today. At

face value, the measures would appear to be insignificant.

Prohibitions on Russian state�owned airlines from US destinations, which could affect sentiment

toward Aeroflot but would have few meaningful financial implications.

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 11

US opposition to loans to Russia from multilateral development banks (i.e. the IMF and World

Bank). In the current environment, this would be of minimal relevance for markets, as Russia

has not taken out such loans for a long time and in most cases these are already banned or

highly frowned upon under existing sanctions.

Downgrade or suspension of diplomatic relations.

█ Mueller investigation results: Timing unknown, but more likely sooner than later. Headlines about US Special Counsel Robert Mueller’s investigation into the 2016 Trump

presidential campaign and its relations (if any) with the Russian state have been ongoing now for

more than 18 months, with just last week major releases of sentencing memos for three close

Trump associates who have agreed to provide testimony for the state.

Though any intention on Mueller’s part to wrap up the investigation soon and report back to the US

Justice Department and Congress is not publicly known, media sources have been claiming for

some time that the investigation’s full report will be due at the end of 2018 or very early in 2019.

To emphasize, there is no indication in public sources as to whether the investigation’s results will

directly blame the Russian state or Russian citizens for any criminal wrongdoing that could affect

relations. That said, until final results of the investigation are known, even lightly sourced media

speculation in the meantime is more likely to be negative than positive for sentiment. Hence, the

investigation remains a story to watch for Russia investors.

Summary of political events to watch through year end and into 2019 Dec 31Jan 3

Jan 21

Feb 2Mar 31?????? Any relevant outcomes from the US special counsel investigation.

Earliest date at which the newly elected Congress may convene the new session.

OFAC's SDN sanctions on Rusal and En+ scheduled to take effect. As of this text, the measures on securities and commercial transactions had each been delayed seven times since their initial announcement on April 6, 2018.

Theoretical 60�day deadline for US demand that Russia return to compliance with the INF treaty on threat of US pulling out. Based on US Secretary of State Mike Pompeo's speech on December 4, 2018.Ukrainian presidential electionImposition of second wave of CBW sanctions.

Ukrainian presidential campaign period formally begins

Source: OFAC, Bloomberg, Sberbank CIB Investment Research

UKRAINE: THE KERCH STRAIT AND THE MARCH PRESIDENTIAL ELECTION

On November 25, an altercation occurred between Russian and Ukrainian naval vessels that led to

Russia seizing three Ukrainian vessels and more than 20 Ukrainian soldiers. The RTS declined nearly

3% the following day but recovered shortly thereafter as it became clear that neither country would

escalate the situation into a full political or even military crisis immediately following the event.

However, as we write, the vessels and sailors remain in Russian custody, despite calls from Western

countries to return them. Media reports indicate that officials within the US and among EU member

states have discussed new punitive measures against Russia for this event and other developments

related to Ukraine and the Azov Sea, but that no decisions appear near at this time. President Petro

Poroshenko has been appearing on Western television channels frequently requesting support,

including calls to impose additional economic measures against Russia.

Moreover, tensions in Ukrainian domestic politics are currently heightened. The next presidential

election there is March 31, and the official campaign season starts on December 31. Recent polls

have shown incumbent Poroshenko in second or third place with 10�15% support, while the

consistent front�runner in recent months has been former Prime Minister Yulia Tymoshenko with

18�22%. At Poroshenko’s request, Ukraine’s Verkhovna Rada passed a declaration of martial law

lasting until December 27 in regions bordering Russia and Transdniestria; martial law in Ukraine

prevents formal political campaigning. To state a basic fact of international relations and geopolitics,

heightened domestic tensions can easily make international relations more volatile as well.

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

12 SBERBANK CIB INVESTMENT RESEARCH

Given that current sanctions on Russia from the US, EU and partners are largely based around the

developments in Ukraine since 2014, the combined story of the Azov Sea and the Ukrainian election

will remain key to watch for the market through 1Q19.

Market overview

While we see meaningful headwinds for global equity markets and GEMs in particular, we stay fairly

constructive on Russia. We expect cheap and boring Russian equities to continue outperforming

emerging markets, similar to what has happened this year. We set our 2019 year�end RTS Index

target at 1,400 points. This target may look ambitious given the uninspiring global economic

outlook. However, achieving this target would not require much, in our view. We base this forecast

on an assumption that implied ERP will come down from the current 10% to 8%. Our bottom�up

estimate for EPS growth in 2019 is 8% and flat in 2020. This is equivalent to P/E expansion from

5.3 to 6.3. Our base�case scenario assumes the status quo continues on international relations and

that Brent averages $65/bbl.

As we have already mentioned, the ERP expansion in 2018 has not been driven by fundamental

changes. Sanction risks should be priced in on the cost of debt level, while ERP is responsible for

equity�specific risks like corporate governance and should not react to geopolitical news flow. We

treat ERP expansion as a temporary market dislocation caused primarily by a bout of sanction fears

in an environment of insufficient domestic demand. Assuming we do not see more significant

sanction moves, ERP should tend to compress, supporting valuations.

Implied cost of equity and cost of debt

6%

8%

10%

12%

14%

16%

18%

20%

Jul ’15 Jan ’16 Jul ’16 Jan ’17 Jul ’17 Jan ’18 Jul ’18

Implied cost of equity Corp bond yield, Cbonds Source: Cbonds, Sberbank CIB Investment Research

Implied equity risk premium

0%

2%

4%

6%

8%

10%

12%

Jul ’15 Jan ’16 Jul ’16 Jan ’17 Jul ’17 Jan ’18 Jul ’18

Source: Sberbank CIB Investment Research

Any bigger rerate would require a repricing of cost of debt and can only materialize once the fear of

new sanctions has disappeared from investors’ minds. Cost of debt of 7�8% could be considered

reasonable in this case, given the 4% inflation target. After all, we saw corporate bond yields

approaching 7% just before the April 2018 sanctions announcement. ERP in this case should

compress even more, to the historic mean of 5�6%. In this scenario, Russia’s P/E could move up to

around 8, or roughly 50% higher than now. While this is not our core scenario, this option is worth

considering to gain an idea of the magnitude of upside risk.

It is of course not realistic to forecast with certainty when the US (or the EU and partners) might

decide to again shift policy on Russia, be it in a bullish or bearish way for markets. Hence, it makes

the most sense to be overweight stocks that can outperform against any geopolitical backdrop.

Exporters give exactly that opportunity, in our view. If the backdrop for international relations does

not improve, foreign capital outflows are likely to continue. Moreover, the CBR is bound to resume

its FX interventions in January after having taken a pause in September. Adding the FX purchases to

ongoing capital outflows should weaken the ruble and benefit exporters.

If, on the other hand, sanction risks materially dissipate, the whole market could see a spectacular

rerating, including energy stocks. Of course, the ruble would be likely to appreciate in this scenario,

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 13

and exporters would underperform in relative terms, but in absolute terms they would do quite well

anyway, as a rising tide raises all boats.

Were market concerns that the US will consider more measures to dissipate (either from the simple

passage of time or via a policy shift, such as a focus shift to more pressing issues such as Saudi

Arabia or China), banks would be best set to perform in an overall improved outlook for the Russian

economy and market. The banking sector was beaten down the most in April and August. In fact,

banks are now the highest beta sector in an otherwise low�beta market, another reason they should

outperform if sentiment turns materially more positive.

Sector beta to RTS

0.0 0.5 1.0 1.5 2.0

Financials

Media/Internet

Metals&Mining

Utilities

Telecoms

Oil&Gas

Transport

Consumer

Source: Sberbank CIB Investment Research

Top picks for 2018

█ Lukoil. The company’s approach to dividend payouts promises the best dividend yield in the

sector, and its commitment to dividends is relatively strong. The management has also indicated

that buybacks will accelerate next year. This implies that the total return could improve by around

3 pp (or almost 50%) to 10% (including a 5% dividend yield).

█ Novatek. The company has stayed ahead of expectations and has continued to exhibit solid

execution on its LNG strategy throughout the year. It launched its Yamal LNG project well ahead

of schedule and signed up its first partner in the Arctic LNG�2 project. We expect key catalysts to

materialize for the stock next year, such as the announcement of the FID for Arctic LNG�2 and

new partners for projects. The first cash flow from Yamal LNG and SeverEnergia could lead to

discussion of a higher dividend payout toward the end of the year.

█ Norilsk Nickel. The stock is set to deliver a double�digit dividend yield next year. On top of this,

the company has finally drawn up a growth plan, including for the South Cluster, a project that

boasts rather attractive economics. This should help the company solidify its leadership in the

global palladium market.

█ TCS Bank. TCS Bank amply illustrates the share price�fundamentals dichotomy, with almost 40%

EPS growth expected and 60% ROE in 2018 but a share price that has been dragged down with

other Russian banks. We think another year of 20%+ EPS growth looks likely, while the overall

build�out of the ecosystem (8 mln customers) and non�credit card businesses are progressing

well.

█ InterRAO UES. The company’s combination of strong financial indicators and cheap valuation (a

current EV/EBITDA of 1.4, or 3.7 if the net cash position and treasury stake are not accounted

for) makes it an attractive investment opportunity. For the upside to materialize in this classic

deep�value story, the market will need to see the company start using the cash it has

accumulated, either via major M&A deals or dividend distributions.

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

14 SBERBANK CIB INVESTMENT RESEARCH

█ Yandex. Although we strategically prefer exporters and are wary of tech in the wider global

macro environment, we like Yandex as it is in its best ever fundamental shape given improved

visibility over the profitability of the taxi segment (which could make the plans for an IPO more

viable) and the monetization of new verticals, including Zen, Yandex.Auto and Yandex.Station.

We think the market should slowly but surely start to price in these factors.

█ Mail.ru Group. In general, we strategically prefer exporters. But within domestics, Mail.ru

Group’s outlook for ad and gaming revenues remains solid, and there are a number of positive

catalysts that we expect in 2019, including the closing of the AliExpress Russia JV deal and the

crystallization of the value of the O2O businesses.

[email protected], [email protected]

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 15

STRATEGY SUMMARY Sector performance

Gas

Oil

Russia � Exporters

RTS

Steel

Precious metals

Media and IT

Real estate

Telecoms

Fertilizers

Transport

Base metals

Russia � Domestics

Banks

Utilities

Consumer

7%

1%

3%

5%

�7%

9%

�4%

�4%

0%

1%

�6%

11%

5%

8%

�1%

�3%

20%

19%

9%

�2%

�2%

�3%

�6%

�20%

�20%

�21%

�22%

�23%

�25%

�26%

�28%

�38%

�40% �20% 0% 20%

3m YTD

Source: Bloomberg, Sberbank CIB Investment Research

RTS Index relative to peers, Dec ’17 = 100

80

90

100

110

120

Dec ’17 Feb ’18 Apr ’18 Jun ’18 Aug ’18 Oct ’18 Dec ’18

RTS Index Relative to MSCI EM Relative to MSCI World

Source: Sberbank CIB Investment Research

Russian sectors’ 2018E P/E as % of GEM peers

Media and ITReal estate

OilGas

TelecomsSteel

BanksBase metals

RetailRussia

TransportUtilities

0% 20% 40% 60% 80% 100% 120%

Source: Bloomberg, Sberbank CIB Investment Research

Forward P/E

0

5

10

15

20

2005 2007 2009 2011 2013 2015 2017

Russia EM DM Russia excl. oil and gas

Source: Thomson Reuters, Sberbank CIB Investment Research

Sector valuation ratios

MCap ADT P/BV Div yield Net debt/EBITDA$ mln $ mln 2018E 2019E 2018E 2019E 2018E 2019E 2018E 2018E 2018E

Financials 84,484 364 4.9 4.6 – – 1% 5% 1.1 8.8% –Oil 202,655 281 5.9 5.5 3.6 3.4 47% 6% 0.7 6.8% 56%Gas 108,516 165 5.0 4.3 3.9 3.8 43% 20% 0.5 3.8% 102%Media 23,693 147 23.9 17.9 13.6 9.7 14% 33% 3.3 0.0% �226%Base metals 37,132 63 5.3 4.8 5.4 4.8 66% 8% 2.8 11.6% 220%Precious metals 25,862 63 9.1 7.8 6.2 5.5 9% 12% 1.8 5.5% 123%Steel 43,127 60 6.4 7.7 4.1 4.6 32% �16% 2.1 12.3% 56%Telecoms 20,721 45 9.6 8.6 3.3 3.1 76% 11% 1.2 8.3% 140%Consumer 19,502 36 11.2 10.7 5.6 5.2 �1% 7% 1.7 4.2% 156%Utilities 12,800 16 2.8 3.1 3.1 3.3 �12% �9% 0.2 8.6% 143%Transport 6,079 15 7.4 5.8 5.2 4.3 �16% 31% 1.9 6.8% 156%Other 21,840 13 5.0 4.5 2.7 2.3 23% 12% 0.5 4.7% 81%Fertilizers 11,638 6 6.1 6.3 5.4 5.2 25% �5% 2.4 4.7% 206%Real Estate 5,419 2 5.7 5.7 4.2 4.3 72% 5% 1.2 9.0% 70%

Russia 618,152 1,274 5.8 5.4 4.0 3.8 30% 8% 0.8 6.8% 94%Russia � Domestics 179,445 580 5.8 5.4 3.7 3.5 4% 6% 0.8 7.0% 118%Russia � Exporters 438,707 694 5.8 5.4 4.0 3.9 44% 8% 0.8 6.7% 87%EM – – 11.0 9.9 6.5 5.9 18% 11% 1.4 3.6% 109%DM – – 15.5 14.4 9.7 8.9 14% 9% 2.2 2.7% 150%

P/E EV/EBITDA EPS growth

Source: Bloomberg, Sberbank CIB Investment Research

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

16 SBERBANK CIB INVESTMENT RESEARCH

STOCK SUMMARY Top performers, Q�o�Q

PolymetalPolyus

Mail.ru GroupNorilsk Nickel

GazpromX5 Retail Group

SberbankSberbank pref

QIWILukoil

RaspadskayaTransneft prefBashneft prefRaven Russia

RosSetiLenenergo prefGazprom Neft

UniproBank of St Petersburg

Rusagro

21%

16%

16%

14%

12%

12%

11%

9%

7%

6%

29%

22%

11%

10%

10%

9%

9%

7%

7%

7%

0% 5% 10% 15% 20% 25% 30% Source: Bloomberg

Biggest underperformers, Q�o�Q

TCSYandex

VEONSeverstal

TatneftEPAM Systems

EvrazMagnit

RusHydroLuxoft

Global PortsPIK GroupLSR Group

MechelMosenergo

PetropavlovskO`Key

GlobaltransLentaTMK

�5%

�5%

�6%

�7%

�9%

�10%

�13%

�15%

�16%

�29%

�3%

�3%

�4%

�5%

�5%

�10%

�12%

�15%

�17%

�21%

�30% �25% �20% �15% �10% �5% 0%

Source: Bloomberg

Highest dividend yields

NLMKSeverstal

MTSRusHydro

MMKNorilsk Nickel

VEONSurgutneftegaz pref

Moscow ExchangeVTB

BashneftEnel Russia

Federal Grid CompanyGlobaltrans

Gazprom NeftUnipro

RostelecomDetsky Mir

O`KeyPhosAgro

14.9%

13.1%

12.5%

12.5%

11.9%

11.8%

11.4%

10.0%

9.6%

9.6%

16.8%

12.6%

11.0%

10.7%

9.2%

8.6%

7.5%

7.2%

6.7%

6.5%

0% 5% 10% 15% 20% Source: Sberbank CIB Investment Research

Lowest and highest P/BV

PolyusNorilsk Nickel

EPAM SystemsTCS

YandexSeverstalNovatek

MTSPIK Group

EvrazSistema

RostelecomObuv Rossii

Transneft prefBank of St Petersburg

RusHydroGazprom

SurgutneftegazFederal Grid Company

Rosseti

7.9

6.4

5.9

4.7

4.4

3.5

3.3

3.3

3.2

3.0

0.6

0.6

0.5

0.5

0.3

0.3

0.3

0.3

0.2

0.1

0 2 4 6 8 10

Source: Sberbank CIB Investment Research

Major upgrades this quarter

ChangeFrom To From To in TP

Aeroflot SELL HOLD 1.61 1.56 �3%Enel Russia HOLD BUY 0.0255 0.0206 �19%Polyus BUY BUY 38.53 44.00 14%Polymetal HOLD HOLD 9.64 10.60 10%

Recommendation Target price, $

Source: Sberbank CIB Investment Research

Major downgrades this quarter

ChangeFrom To From To in TP

Lenta BUY BUY 8.00 5.50 �31%O`Key SELL SELL 2.10 1.50 �29%Obuv Rossii BUY BUY 2.85 2.09 �27%Luxoft BUY BUY 61.89 47.68 �23%VTB HOLD HOLD 2.00 1.60 �20%X5 Retail Group BUY BUY 38.00 31.00 �18%Magnit HOLD HOLD 20.00 17.00 �15%

Rec Target price, $

Source: Sberbank CIB Investment Research

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 17

Oil and Gas: Keep “Maneuvering” the Macro Tailwinds

KEY DEVELOPMENTS

The Russian energy sector has gained 17% this year, outperforming the MSCI EM Energy Index by

10% and Brent by circa 30%. Brent had been rising steadily for most of the year, peaking at

$86/bbl in October (up around 30% YTD). However, since then it has dropped back to a low of

$59/bbl (down 12% YTD).

As we had anticipated, Novatek has been the best performer this year, up 42% YTD. The call we

made in February and reiterated in July returned 25% versus the sector YTD. Novatek is followed by

Tatneft commons, Gazprom Neft and Lukoil, which saw 26�28% gains. All of these names have

substantially improved their distribution of cash flow to shareholders. Transneft prefs,

Surgutneftegaz and Bashneft commons lagged the sector.

STRATEGIC VIEW

The sector demonstrated solid improvement in its financial performance this year on the back of the

oil price recovery and the still�weak ruble. Current market conditions and the macro outlook suggest

a still relatively favorable outlook for Russian oil and gas producers, with the oil price in ruble terms

almost flat y�o�y despite the recent correction. That said, our preference in the sector is for the

names where we can still see further material improvement in the payout to shareholders.

The so�called “tax maneuver” approved for the oil sector in 2019�24 replaces downstream export

duty�related subsidies with a direct recoverable excise. The impact on the integrated oil companies

would seem to be fairly limited at first glance. However, the domestic product market, a big part of

their business, will effectively become regulated. This is not something that has been fully

acknowledged by the market, but the effects could become visible if oil prices move significantly

from the current levels. We expect the oil companies to be more careful in budgeting for their

downstream projects and focus more on greenfield opportunities in the upstream, where the

government could be more generous with tax incentives.

TOP PICKS

█ Lukoil. The company’s approach to dividend payouts promises the best dividend yield in the

sector, and its commitment to dividends is relatively strong. Although the dividend is unlikely to

increase by more than 10% y�o�y on a per�share basis, the management has indicated that

buybacks will accelerate next year. This implies that the total return could improve by around 3 pp

(or almost 50%) to 10% (including a 5% dividend yield).

█ Novatek. The company stayed ahead of expectations and continued to exhibit solid execution on

its LNG strategy throughout the year. It launched its Yamal LNG project well ahead of schedule

and signed up its first partner in the Arctic LNG�2 project. We expect key catalysts to materialize

for the stock next year, such as the announcement of the FID for Arctic LNG�2 and new partners

for projects. The first cash flow from Yamal LNG and SeverEnergia could lead to discussion of a

higher dividend payout toward the end of the year.

[email protected]; [email protected]

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

18 SBERBANK CIB INVESTMENT RESEARCH

OIL AND GAS

Performance

Novatek

Tatneft

Gazprom Neft

Lukoil

Rosneft

Tatneft pref

Bashneft pref

Russian oil and gas

Surgutneftegaz pref

MSCI EM Energy

Gazprom

MSCI World Energy

Surgutneftegaz

Transneft pref

Bashneft

1%

�9%

9%

6%

�2%

�4%

11%

4%

4%

0%

12%

�12%

�2%

22%

0%

42%

28%

28%

26%

24%

19%

17%

17%

15%

7%

6%

�9%

�16%

�16%

�27%

�40% �20% 0% 20% 40% 60% 80%

3m YTD

Source: Bloomberg, Sberbank CIB Investment Research

Sector performance versus peers and RTS

90

100

110

120

130

140

Dec ’17 Feb ’18 Apr ’18 Jun ’18 Aug ’18 Oct ’18 Dec ’18

Russian oil and gas Relative to MSCI World Energy Relative to RTS Source: Sberbank CIB Investment Research

Forward P/E

0

5

10

15

20

25

30

35

2005 2007 2009 2011 2013 2015 2017

Russia EM DM Source: Bloomberg, Sberbank CIB Investment Research

Oil and gas prices

0

3

6

9

12

0

30

60

90

120

2014 2015 2016 2017 2018

$/m

mbt

u

Brent, $/bbl Gas, Henry Hub (rhs) Gas, UK spot (rhs)

Source: Bloomberg

Valuation ratios

Price Target price MCap ADT P/BV Div yield Net debt/EBITDA$ $ $ mln $ mln Rec 2018E 2019E 2018E 2019E 2018E 2019E 2018E 2018E* 2018E

Lukoil 72.92 85.00 62,022 147 BUY 4.9 5.1 47% �4% 3.5 3.3 0.8 4.9% 11%Gazprom 2.40 3.25 56,868 126 BUY 3.1 2.8 48% 12% 2.9 2.9 0.3 6.1% 113%Rosneft 6 – 66,784 70 UR 10.9 6.6 150% 18% 5.7 5.1 1.0 6.8% 284%Novatek 170.10 185.00 51,648 37 BUY 16.3 10.0 18% 64% 12.8 11.6 3.3 1.9% 0%Tatneft 10.61 10.00 24,242 36 HOLD 8.1 8.3 40% �3% 5.3 5.3 1.7 9.1% �30%Surgutneftegaz** 0.41 0.50 18,883 23 HOLD 2.9 3.3 83% �13% neg neg 0.3 17.5% �659%Transneft 2,612 3,000 18,552 6 HOLD 5.0 4.5 13% 12% 2.7 2.3 0.5 5.0% 32%Gazprom Neft 5.41 7.00 25,647 3 BUY 3.8 4.1 55% 2% 3.4 3.8 0.8 8.3% 73%Bashneft 28.80 45.00 5,076 1 HOLD 3.0 2.7 �19% 0% 1.8 1.6 0.7 9.8% 25%

Russia – – 329,724 450 – 5.5 5.0 43% 11% 3.7 3.5 0.6 5.7% 70%EM – – – – – 9.2 8.5 60% 9% 4.1 3.7 1.0 4.8% 79%DM – – – – – 12.7 11.0 69% 17% 5.2 4.5 1.4 4.5% 75%

P/E EPS growth EV/EBITDA

Note: *Dividend yields updated for the factual announcements of interim dividends.

**Surgutneftegaz dividend is for preferred shares.

Source: Bloomberg, IBES, Sberbank CIB Investment Research

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 19

Metals and Mining: Coming off a Peak Year for Earnings

KEY DEVELOPMENTS

Average commodity prices for 2018 look set to come in above the 2017 averages nearly across the board, with silver and platinum being the key exceptions, averaging 7�8% below last year’s levels. As we had expected, steel prices were nicely supported by production restrictions in China and still�healthy demand in key markets. Evraz, one of our top picks, has outperformed the whole Russian metals and mining sector, up almost 30% YTD. Copper prices were fairly volatile during the year, responding sharply to escalations in the US/China trade dispute and to signs of a slowdown in the Chinese economy. Nickel and cobalt (metals widely used in the production of batteries for electric vehicles) are both on track to post price averages well above the 2017 levels this year. Gold has been relatively flat versus the beginning of the year, constrained by ongoing monetary policy tightening in the US but supported by heightened geopolitical uncertainty stemming in part from the mounting tensions between the US and China. The diamond market has been in good shape, while Alrosa finally cheered up investors with a meaningful improvement to its dividend policy. As we expected, the phosphate market has been strong thanks to good demand, rising production costs in China (a marginal producer) and a slower than planned ramp�up of new capacity in Saudi Arabia and Morocco. In general, we think that sector earnings and cash flows will likely have picked up in 2018, translating into an above 10% dividend yield in most cases.

STRATEGIC VIEW

While average prices in 2018 will be higher than last year’s averages in most cases, the recent market correction has wiped out nearly all of the price growth – spot prices have fallen below the 2017 average levels. Although the recent 90�day truce in the US�China trade war brings some relief, Chinese macro data shows that domestic demand is slowing down, which has been primarily reflected in a cooling property market and slower credit growth. Since we think the Chinese government values economic stability over growth, we expect its monetary stimulus to become less and less aggressive (if compared with 2016, for instance), which could eventually result in a slowdown in global commodity demand. Therefore, we believe that prices on steel and most other commodities will decline y�o�y in 2019, though there may be a few bright spots, such as nickel (supported by the electric vehicle story) and palladium (due to the tight market). Since most Russian metals and mining companies were able to bring their financial leverage to record low levels and have had decent support from the weak ruble, we think that they will be able to continue distributing nearly 100% of free cash flow as dividends. Therefore, the dollar dividend yields in the sector may remain attractive, especially compared with Russian domestic stories.

TOP PICKS

█ Norilsk Nickel. As believers in the electric vehicle story, we think nickel sulfide prices should take

off at some point. Meanwhile, the company’s commodity basket is fairly diversified, and the

prospects of palladium look strong, as there is not enough visible supply to cover the current

deficit. Apart from the decent outlook for nickel and palladium prices, Norilsk Nickel has finally

drawn up a growth plan, including South Cluster, a project that boasts rather attractive

economics. This should help the company solidify its leadership in the global palladium market. As

the shareholder agreement is still in place, the company should continue to pay dividends yielding

more than 10�12% per year even in years when capex is elevated.

[email protected], [email protected]

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

20 SBERBANK CIB INVESTMENT RESEARCH

FERROUS METALS

Performance

Evraz

Raspadskaya

Russia

Severstal

NLMK

MMK

EM

DM

TMK

Ferrexpo

Mechel

�13%

29%

�7%

�7%

�3%

�4%

�13%

�18%

�22%

9%

�3%

26%

21%

�2%

�4%

�8%

�8%

�21%

�25%

�28%

�44%

�52%

�60% �40% �20% 0% 20% 40% 60% 80%

3m YTD Source: Bloomberg, Sberbank CIB Investment Research

Sector performance versus peers and RTS Index

90

100

110

120

130

140

Dec ’17 Feb ’18 Apr ’18 Jun ’18 Aug ’18 Oct ’18 Dec ’18

Russia Relative to global steel Relative to RTS Source: Bloomberg, Sberbank CIB Investment Research

Forward P/E

0

5

10

15

20

25

2005 2007 2009 2011 2013 2015 2017

Russia EM DM Source: Bloomberg, Sberbank CIB Investment Research

Valuation ratios

Price Target price MCap ADT P/BV Div yield Net debt/EBITDA$ $ $ mln $ mln Rec 2018E 2019E 2018E 2019E 2018E 2019E 2018E 2018E 2018E

Evraz 5.79 8.05 8,221 19.4 HOLD 5.3 7.8 35% �32% 3.4 4.3 3.0 7.5% 96%Severstal 14.69 19.06 12,306 19.1 HOLD 7.3 8.0 23% �9% 4.5 4.8 3.5 13.1% 40%NLMK 23.54 29.77 14,108 12.6 HOLD 6.7 8.0 45% �16% 4.5 5.3 1.9 14.9% 6%MMK 8.92 10.84 7,667 8.2 HOLD 6.7 7.8 14% �14% 3.6 4.0 1.3 11.9% �5%

Russia – – 43,127 59.7 – 6.4 7.7 32% �16% 4.1 4.6 2.1 12.3% 56%EM – – – – – 6.9 6.8 31% 1% 4.6 4.4 0.9 6.5% 170%DM – – – – – 6.1 6.7 32% �8% 4.5 4.4 0.7 2.6% 159%

P/E EPS growth EV/EBITDA

Source: Bloomberg, Sberbank CIB Investment Research

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 21

NON�FERROUS METALS

Performance

ALROSA

Acron

Norilsk Nickel

Polyus

PhosAgro

DM

EM

Polymetal

Russia

Petropavlovsk

KAZ Minerals

1%

2%

14%

16%

�2%

�11%

�6%

21%

10%

�13%

15%

14%

2%

1%

�7%

�13%

�15%

�19%

�20%

�20%

�25%

�42%

�60% �40% �20% 0% 20% 40%

3m YTD Source: Bloomberg, Sberbank CIB Investment Research

Sector performance versus peers and RTS Index

70

80

90

100

110

120

Dec ’17 Feb ’18 Apr ’18 Jun ’18 Aug ’18 Oct ’18 Dec ’18

Russian non�ferrous Relative to global Relative to RTS Source: Bloomberg, Sberbank CIB Investment Research

Forward P/E

0

5

10

15

20

2005 2007 2009 2011 2013 2015 2017

Russia EM DM Source: Bloomberg, Sberbank CIB Investment Research

Base metal prices

0

500

1,000

1,500

2,000

2,500

3,000

0

5,000

10,000

15,000

20,000

25,000

30,000

2010 2011 2012 2013 2014 2015 2016 2017 2018

Nickel, $/tonne Copper, $/tonneAluminum,$/tonne (rhs) Gold, $/oz (rhs)

Source: Bloomberg

Valuation ratios

Price Target price MCap ADT P/BV Div yield Net debt/EBITDA$ $ $ mln $ mln Rec 2018E 2019E 2018E 2019E 2018E 2019E 2018E 2018E 2018E

Norilsk Nickel 18.84 22.20 29,813 60.8 BUY 8.0 7.5 75% 7% 6.4 6.0 6.4 11.8% 127%Polymetal 10.01 10.60 4,563 35.9 HOLD 11.4 8.0 �4% 43% 7.9 5.9 2.9 4.0% 199%ALROSA 1.48 1.59 10,928 20.1 BUY 7.8 8.7 3% �10% 4.9 5.0 2.0 6.3% 10%Polyus 35.55 44.00 9,496 6.3 BUY 8.1 6.5 18% 26% 7.0 5.5 7.9 5.8% 172%PhosAgro 13.32 16.66 5,175 5.0 BUY 7.7 8.3 76% �7% 5.7 5.7 2.4 6.5% 150%

Russia – – 63,703 112.2 – 6.1 5.5 49% 9% 5.7 5.1 2.4 8.8% 216%EM – – – – – 9.8 9.0 28% 5% 6.0 5.5 1.6 4.7% 124%DM – – – – – 13.7 13.3 7% 4% 7.0 6.7 1.8 3.6% 106%

P/E EPS growth EV/EBITDA

Source: Bloomberg, Sberbank CIB Investment Research

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

DECEMBER 10, 2018 THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS

22 SBERBANK CIB INVESTMENT RESEARCH

Financials: Looking to Avoid Repeat of 2018 Dichotomy

KEY DEVELOPMENTS

This year was a good one for the fundamentals of Russian banks, with record earnings for many

names, but a bad one for their stocks, which have largely had a dismal year. Russia’s two largest

banks (Sberbank and VTB) underperformed the Russian market by 25% and more despite

increasing earnings to record levels. The cases of Bank of St Petersburg and TCS were similar.

Meanwhile, Moscow Exchange both underperformed the Russian market, by about 30%, and showed

lacking fundamental performance, with annual earnings heading for a third consecutive decline.

This is all despite the fact that the landscape for banks has been much calmer in 2018 than 2017,

when the CBR took over three large failing banks. What has of course hurt banks’ share price

performance, however, are sanctions – both action and talk. Indeed, prior to new US sanctions in

early April, Sberbank’s share price was up 13% and nicely outperforming the market.

STRATEGIC VIEW

How sanctions play out is inevitably likely to dominate stock performance in the early months of 2019.

But the fundamental outlook again looks supportive, marked by stability (we expect) in terms of

economic growth, interest rates (with a flat key rate inked in for 1H19 and maybe 50 bps worth of cuts

in 2H) and the ruble. We anticipate credit growth of around 10% in 2019. Retail will continue to drive

overall loan growth, albeit at a slower pace than in 2018 (about 14% versus 22%), pressured by a

combination of rising consumer leverage, higher interest rates, weak real disposable income growth and

tighter regulation. Corporate lending, as well as retail and corporate deposits, should see growth in the

mid�to�high single digits, in our view. Meanwhile, asset quality should remain broadly benign, margins

should be more or less stable as asset repricing takes some of the heat out of higher deposit rates, and

the ongoing shift to digital banking and payments should help maintain decent fee income growth for

the more technologically savvy names.

As for risks, we see rising consumer leverage as one, though it is in better shape than in 2014�15,

with a slower pace of growth, the CBR on the front foot and more secured lending. Another is ruble

weakness, which has pressured capital ratios and sparked some debate about postponing the final

steps to Basel 3, but we do not see any risk of imminent state�backed recapitalizations. We expect a

mixed picture for dividends from state banks, with VTB looking more constrained than its larger peer.

The final piece of the jigsaw is valuations: they bode well for a good year for Russian banks in 2019

if they can get through the sanctions risks relatively unscathed. Russia’s bellwether Sberbank trades

on a consensus 2019 P/E of 4.8 with a 2018 dividend yield of 8.5%.

TOP PICKS

█ TCS. Tinkoff amply illustrates the share price�fundamentals dichotomy, with almost 40% EPS growth

expected and 60% ROE in 2018 but a share price that has been dragged down with other Russian

banks. It remains a top pick for us in 2019, even as some risks are set to increase. We think another

year of 20% or higher EPS growth looks likely, while the overall build�out of the ecosystem (8 mln

customers) and non�credit card businesses are progressing well. As for those risks, higher consumer

leverage means core credit card lending will slow, but we think the increasing diversification of its

business better insulates Tinkoff against cycle risks, which are also being mitigated by CBR policy.

[email protected] [email protected]

This document is being provided for the exclusive use of [email protected] document is being provided for the exclusive use of [email protected]

THE RUSSIAN EAGLE – 2019 STRATEGY: STANDING AGAINST THE HEADWINDS DECEMBER 10, 2018

SBERBANK CIB INVESTMENT RESEARCH 23

FINANCIALS

Performance

Halyk Bank

MSCI EM Banks

TCS

MSCI World Banks

TBC Bank

Bank of St Petersburg

Russia � Financials

Sberbank

Moscow Exchange

VTB

Bank of Georgia

4%

2%

�5%

�8%

�8%

7%

8%

11%

�5%

�2%

�20%

15%

�7%

�8%

�13%

�19%

�22%

�26%

�26%

�30%

�32%

�64%

�80% �60% �40% �20% 0% 20%

3m YTD Source: Bloomberg, Sberbank CIB Investment Research

Sector performance versus peers and RTS

60

80

100

120

140

Dec ’17 Feb ’18 Apr ’18 Jun ’18 Aug ’18 Oct ’18 Dec ’18

Russian banks Relative to EM banks Relative to RTS

Source: Bloomberg, Sberbank CIB Investment Research

Trailing P/BV

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2008 2010 2012 2014 2016 2018

Russia financials EM DM Source: Bloomberg, Companies

Russian banks loan portfolio, R bln

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2012 2013 2014 2015 2016 2017 2018

Corporate loans Loans to households

Source: CBR

Valuation ratios

Price Target price MCap ADT$ $ $ mln $ mln Rec 2018E 2019E 2017 2018E 2018E 2019E 2018E 2019E

Sberbank 2.89 – 64,889 329 – 5.1 4.7 1.0 1.1 22% 21% �6% 9%VTB 1.25 1.60 8,074 16.4 HOLD 4.0 4.3 0.6 0.7 16% 14% 44% �8%Moscow Exchange 1.33 1.88 3,038 13.0 BUY 9.7 9.1 1.4 1.7 18% 18% �11% 7%TCS 17.34 26.00 3,167 2.4 BUY 8.3 7.2 4.3 4.7 57% 49% 16% 15%Bank of Georgia 17.47 25.83 690 1.4 HOLD 6.4 5.2 0.7 1.2 19% 21% �26% 22%TBC Bank 19.08 24.55 955 0.5 HOLD 6.2 5.8 1.4 1.2 20% 19% 16% 6%Halyk Bank 11.40 17.50 3,134 0.3 BUY 4.8 4.6 1.2 1.2 25% 24% 24% 2%Bank of St Petersburg 0.73 1.33 323 0.2 BUY 2.9 2.6 0.3 0.3 12% 12% �4% 12%

FSU – – 84,484 363.1 – 4.9 4.6 1.0 1.1 21% 20% 0% 7%EM – – – – – 7.9 7.1 1.0 1.0 13% 13% 5% 10%DM – – – – – 15.5 14.4 2.3 2.2 14% 14% 14% 9%

EPS growthP/E P/BV ROE

Source: Bloomberg, Sberbank CIB Investment Research