Embed Size (px)

Citation preview

The Role of Social Partners in Pension Reforms in an Ageing Europe

Bernhard Ebbinghaus

School of Social Sciences & Mannheim Centre for

European Social Research (MZES),University of Mannheim, Germany

Pension reform – a hot topic for unions ….

I. Political dynamics of pension reform

Global paradigm shift:„Reforming pensions is one of the biggest challenges of the 21st century!“ (OECD)

• High expenditure, partly due to early exit from work

• Demographic problem of pay-as-you-go pensions!

Part II: Raising retirement age , phasing out early retirement options

Part III: Shift toward (pre)fundedpensions , the multipillar strategy

� What role for the interests of workers and retirees?

First: Political and membership strength

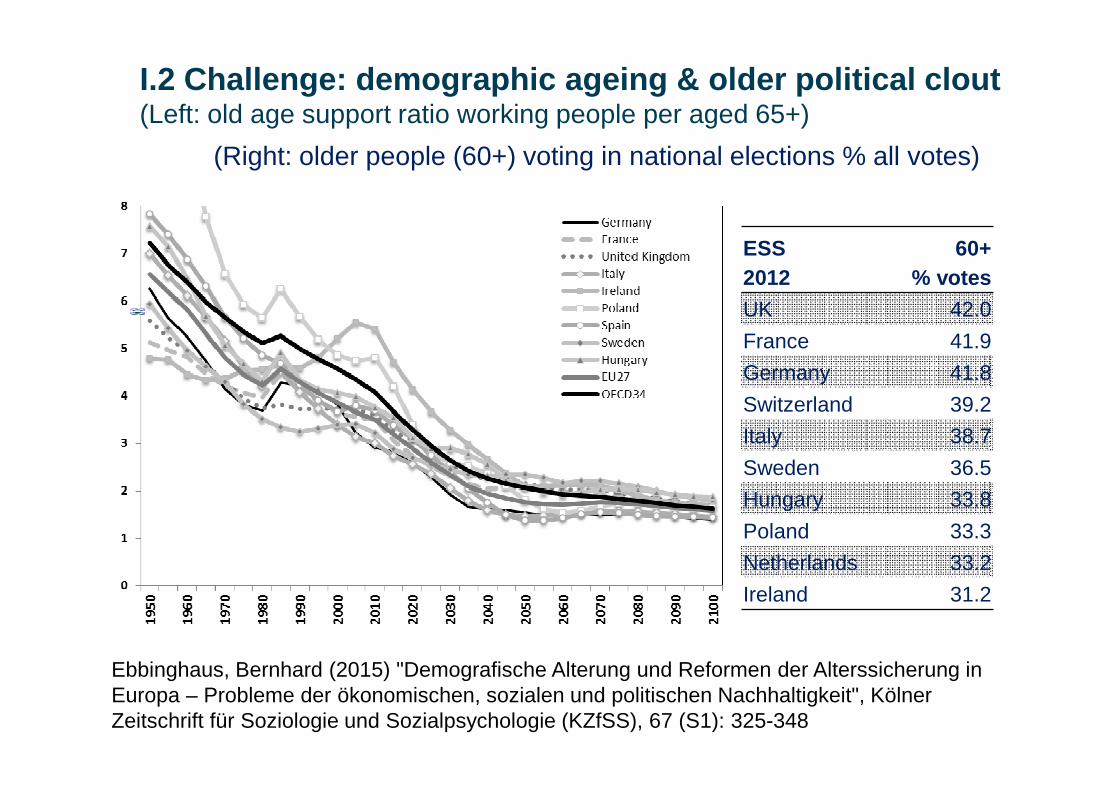

I.2 Challenge: demographic ageing & older political clout (Left: old age support ratio working people per aged 65+)

ESS 2012

60+ % votes

UK 42.0

France 41.9

Germany 41.8

Switzerland 39.2

Italy 38.7

Sweden 36.5

Hungary 33.8

Poland 33.3

Netherlands 33.2

Ireland 31.2

(Right: older people (60+) voting in national elections % all votes)

Ebbinghaus, Bernhard (2015) "Demografische Alterung und Reformen der Alterssicherung in Europa – Probleme der ökonomischen, sozialen und politischen Nachhaltigkeit", Kölner Zeitschrift für Soziologie und Sozialpsychologie (KZfSS), 67 (S1): 325-348

I.3 Union membership & votes in national elections

Source: European Social Survey (2012) 6, V2.1; weighted; own calculations.

Current & previous union membershipvaries considerable, Nordic on top

Current & previous union membersare voting block in Nordic countries

a) Union membership (net union density), 1990-2010

b) Union density and bargaining coverage, 1995-2005

I.4 Declining membership & bargaining coverage

erga omnesextension of collectiveagreements!

Sources: own calculations; adj.coverage & net density: Visser (ICTWSS 4.1) 2013

Nordic

decline

I.5 Social governance: influence of social partners

What influence do the social partners (unions and employers) exert

in welfare states? (here: pension reform )

Policy-making &Implementation

• Old politics thesis: organized labour � welfare state expansion • New politics thesis: policy feedback � blame avoidance for cuts• Veto power thesis: unions have quasi-veto power � concertation needed?

self-admin-

stration

consultation

bipartite

self-regulation

unilateral

STATE

EMPLOYER(S) UNION(S)

dele-gated

tripartite

concertation

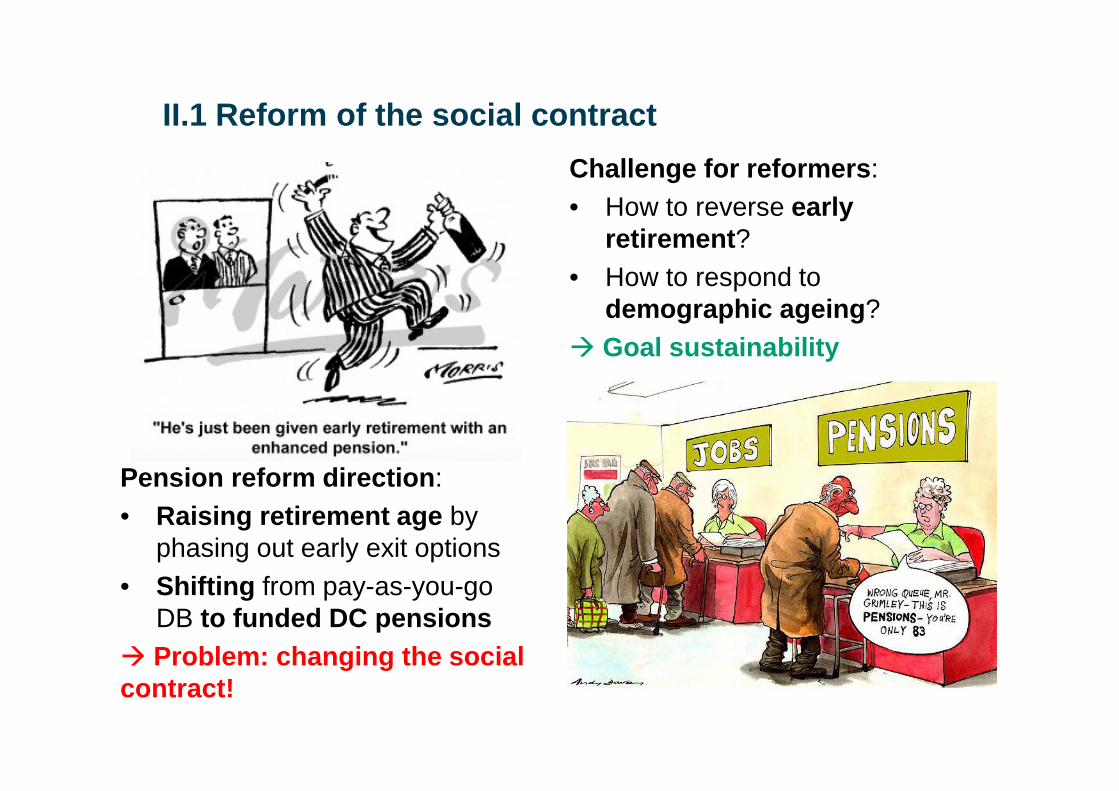

II.1 Reform of the social contract

Pension reform direction : • Raising retirement age by

phasing out early exit options• Shifting from pay-as-you-go

DB to funded DC pensions � Problem: changing the social contract!

Challenge for reformers :• How to reverse early

retirement ? • How to respond to

demographic ageing ?� Goal sustainability

Changing from generational contract to funded pensions?

� Status quo interests of contributors and beneficiaries – Electoral concern of politicians (blame avoidance)– Protests by unions (e.g. strikes in France 1995, 2010)– Concertation as consensual strategy to overcome reform blockage

No radical but smaller, gradual or long-term reforms : • Parametric , technical reforms, depolitisation (automatic adjustments)• Gradual reforms, exemptions for older cohorts (grandfathering)• Layering: supplementary pensions (e.g. German Riester pension)

II.2 Reform politics: changing the social contract

Pay-As-You-Go

Pensioners

Employees

Children

Double payer problem!

Savings Pension (returns)

Pensioners Pensioners

Employees Employees

Children Children

Bernhard Ebbinghaus: Reforming Early Retirement in Europe, Japan and the USA, Oxford University Press,

2006; pbk. 2008; and updates by Ebbinghaus & Hofäcker (Comparative Population Studies, 2013)

Rise of early retirement:• Early retirement common

since oil chocks in 1970sExternalization coalition of social partner• But less, yet cyclical exit in

liberal & Nordic (UK, S)

F

NL

D

I

S

UK

II.3 Early retirement: exit rate: men aged 60-64

Bernhard Ebbinghaus: Reforming Early Retirement in Europe, Japan and the USA, Oxford University Press,

2006; pbk. 2008; and updates by Ebbinghaus & Hofäcker (Comparative Population Studies, 2013)

Rise of early retirement:• Early retirement common

since oil chocks in 1970sExternalization coalition of social partner• But less, yet cyclical exit in

liberal & Nordic (UK, S)Reversal efforts:• Cut back on earl retirement

pathways since 1990s• Shift toward active ageing

(life long learning)• D, NL: significant reversal • but F, South & East belated

F

NL

D

I

S

UK

II.3 Early retirement: exit rate: men aged 60-64

Country ♂ ♀ Retirement age Special rulesBeveridge / Multipillar modelFinland 60.2 61.0 65 2005-: 63 (-0.4% p.m. (2005-);

62 <b.1952 -0.6% -63, 63+: -0%.

Sweden 66.0 63.6 Flexible NDC pension: 61-67 (basic pension -1972: 67, -1998: 65)

Flexible pension (NDC pension transferred into annuity based on unisex life expectancy), but guarantee pension only from age 65 (40 y.)

UK 64.3 62.1 ♂ 65 / ♀ 60 (2010-20: 60�65 b. 1950+); 65�66: 2018/20; 67: 2034/36; 68: 2044/36

gender difference will be phased out

Netherlands 62.1 62.6 65 (basic pension AOW) 2013-23: � 67

Phasing out of preretirement (1997-), reform of disability pensions 1990s

Bismarck / Dominant public pillar modelFrance 59.1 59.7 60 (b. 1956+ 2011-: �62 by 2017) 2010 pension reform: seniority (40 y.-

>41.5y),65 (b 1956+ 2011-: +2y. �67 by 2022) 2010 pension reform: without seniority

Germany 61.8 60.5 Public pension insurance:2012-29: 65 � 67

1992-: 63/60 pensions phased by 2010s; 2007 age reform; but partial reversal

Italy 61.1 58.7 2011: ♂61 / ♀56 (w/ 36 y.)� 65* (1996-: ♂ 60�65 / ♀ 55�60)

seniority / *gender equalization following ECJ 2008 ruling

♂ 65 / ♀ 60 � 65* (2010-18) without seniority / genderCzech Republic

62.0 59.0 1995-2016: ♂ 60�63 (2011: 62.4); 1995-2019: ♀ 57�63 (2011: 60.8, w/out, 56.8 with 5+)

ER: -3 y. °6-7%p.a. child credits (1:-1;2:-2;3:-3;5+:-4)

Poland 61.4 57.7 ♂ 65 (2013-20: +3m.p.a. �67); ♀ 60 (2013-40: +3m.p.a. �67);

(ER for sp. grps & ♀ <b.1949) 2009-: bridging pens. for sp.grps

II.4 Raising retirement age & phasing out early exi t

III.1 Pension system architecture: One or multi-pil lars?

Multipillar strategy to maintain financial sustainabilityPillar I: public pay-as-you go pension not sustainable in

ageing societiesPillar II: workplace-related funded pensions,

traditionally defined benefit (DB), increasingly DCPillar III: individual savings - defined contributions (DC) Pension system legacies:• Bismarck-type pensions: public earnings-related

pension with only belated private funded pension • Beveridge-type pensions: multipillar systems with

public basic pension & private pensions � Different developmental space and timing

for private funded pensions!� Self-regulatory role for social partners in private

pensions?Lord Beveridge Chancellor von Bismarck(*1879-1963) (*1815-1898)

III.2 Public-private pension mix in Europe before t he crisis

Total private pension assets (% GDP), OECD 2007

Public and private pension expenditure (% GDP), OECD 2006

1,1

4,8

5,4

6,7

7,5

7,7

8,1

11,7

11,9

12,0

9,2

4,2

3,6

5,5

3,1

1,1

10,3

9,0

9,0

12,1

10,5

8,9

9,5

11,9

12,2

12,2

0 2 4 6 8 10 12

Finland

Denmark

Netherlands

Switzerland

United Kingdom

Sweden

Belgium

Germany*

France**

Italy

Public expenditure Private expenditure

78

141

149

152

96

57

14

18

7

4

0 50 100 150

Finland

Denmark

Netherlands

Switzerland

United Kingdom

Sweden

Belgium

Germany

France

Italy

Source: OECD Pensions Outlook 2008, own calculations.

Bism

arck dom

inant publicB

everidge multipillar

State pensions crowded out private funded pensions

III.3 The scope of (private) funded pensions

Table 5: Pension assets, coverage, contributions and expendi ture in Europe

Pension expenditure

(%GDP) 2012

Private coverage

2011

Assets (%GDP) 2010

Private pensions (%GDP) 2012

Total Private (%) {%} All

funds Public funds

Contri-butions Benefits

Beveridge UK 9.4 3.2 (34.2) {43.3} 88.7

d2.9 d3.2 Netherlands 9.4 4.3 (46.0) {88.0} 128.5 5.5 4.3 Finland 10.5 0.6 (5.9) *{74.2} *91.0 10.2 *11.2 Sweden 9.5 1.3 (14.0) {>90.0} 84.1 27.2 Bismarck France 14.1 0.4 (2.5) v{20.9} 13.1 4.6 c0.6 c0.4 Germany 11.4 0.2 (1.8) {71.3} 5.4 0.3 0.2 Italy 15.8 0.3 (1.8) {14.0} 5.3 0.6 0.3 Poland 11.8 0.0 (0.1) {56.5} 16.6 0.7 0.5 0.0 Sources: own calculations; expenditure (2012): Pension Market in Focus 2013; coverage: OECD Pension Outlook 2012, Tab. 4.1, p. 105; Public pension funds: OECD (2011): Table 4; Private pension funds: OECD Global Pension Statistics database. Notes: (%) % of Total; {*} occupational and personal pension coverage in % of working age population; > underestimated; includes mandatory occupational pensions (partly funded private schemes);

III.4 Governance & regulation of private pensions

Conflicts of interests in supplementary pensions:• Vertical conflicts = principal-agent problem (sponsor/financial agent)• Horizontal conflicts : sponsor (employer) vs. beneficiary (worker)

– employer commitment: employer sponsors ‘trust’ fund, implicit contract – collective agreement: delegated to employer/union negotiations

horizontal labour-capital

conflict

principal-agent

relations

Individual: mainly “exit” option

some “voice” less “exit” option

“voice” through collective action / institutionalized power

III.5 Private pension governance: pros & cons

Collective (= employer/unions co-manage collective scheme):� Pooling of risks, broader coverage, lower administrative costs � Balancing interests between sponsors & beneficiaries, informed decisions o But less personal choice , less attractive for higher income groups� Collective funds are more like public pensions, consensus necessary

Employer-led (= employer-sponsored pension fund or on the book reserves):o Limited representation of beneficiary interestso Risk of bankruptcy of firm: reinsurance neededo Underfunding problem for sponsors but also who owns surpluses?� Employer interest in binding employees but higher costs & lower mobility� Employer-funds can lead to conflicts of interests , thus requiring regulation

Individual :� Individual decision to save for old age: freedom of choiceo Individual savings depends on financial literacy, foresight , and liquidity� Individual responsibility but individualization of risks , regulation needed

III.6 Post-crash rethinking of multipillar pensions

• Financial market crisis 2008+ & Great Recession

• Low net returns • Acute problem for

DC pensioners • Underfunding in DB funds

Source: return on pension fund investment (%) in OECD Pensions in Focus, July 2010, Paris: 2010

III.7 Post-crash governance & regulatory issues

The financial crisis has revealed major governance & regulatory gaps:• Netherlands:

– DB underfunding: <105%, but time frame extendable by ministry – Short-/long-term plans need approval, benefits cuts are possible

• United Kingdom: – Protection fund premiums increase due to bankruptcy– Public sector pensions (DB) under political pressure to change

• Switzerland– Nominal interest rate set by Federal government, easing in crisis– Conflict over who owns surpluses / deficits of pension funds!

• Germany– Voluntary (Riester) pension: zero return guarantee but front fees– Occupational pensions with book reserves under pressure– Rising premiums for protecting book reserves or DB schemes

See country chapters in Bernhard Ebbinghaus (Ed.), Varieties of Pension Governance, OUP 2011

IV. Conclusion & Outlook

• Social governance: – Consultation & self-administration have become less important– Successful concertation on pension reforms is highly contingent– More self-regulation by social partners in collective pensions

• Social partners :– Membership decline challenges representativeness– Unions ability to negotiate pensions depends on bargaining power – Social partners face difficult decisions in private DB pensions– Employers move away from DB to DC: individualization of risks?

• Social contract:– Pension is a deferred wage , (implicit) part of wage negotiations – Raising retirement age needs concerted action (also of firms) – Workers, employers and retirees have to adapt to new norms– Political sustainability of pension policy requires trust in reforms

Further readings

Monographs :• B. Ebbinghaus (ed.): The Varieties of Pension Governance. Pension

Privatization in Europe. Oxford: OUP 2011.Journal publications :• B. Ebbinghaus: The Privatization and Marketization of Pensions in Europe:

A Double Transformation Facing the Crisis, European Policy Analysis 1, 2015.• B. Ebbinghaus: "Demografische Alterung und Reformen der Alterssicherung

in Europa – Probleme der ökonomischen, sozialen und politischen Nachhaltigkeit", Kölner Zeitschrift für Soziologie und Sozialpsychologie (KZfSS), 67 (S1) 2015: 325-348.

• B. Ebbinghaus & D. Hofäcker: "Reversing Early Retirement in Advanced Welfare Economies: A Paradigm Shift to Overcome Push and Pull Factors", Comparative Population Studies (CPoS), 2013 38(4): 807-840

• B. Ebbinghaus & T. Wiß : Taming pension fund capitalism in Europe: collective & state regulation in times of crisis Transfer 17/1, 2011: 15-28.

• B. Ebbinghaus & N. Whiteside : Shifting responsibilities in Western European pension systems, Global Social Policy, 12(3) 2012: 266 –282.