Embed Size (px)

Citation preview

MarinaGrahovar

PhD‐student School of Business, Economics and Law, Gothenburg University

Phone: +46 31 786 14 46 e‐mail :[email protected]

TheRoleofCorporatesocialdisclosure

Trust,reputationorfashiontool?

Script20101028

Keywords: corporate social reporting and communication, trust creation, reputationmanagement,accountability.

Abstract

Motivation: Corporate social responsibility (CSR) disclosure can be used as a device by companies to communicate accountability, by showing their vision for the future and account for past performances. If companies are able to communicate their social and environmental work they can receive advantages attached to a good reputation and build a relationship, based on trust, with the society in which they operate. Therefore it is in the interest of this thesis to examine what role CSR disclosure have or does not have in companies’ communication to their stakeholders.

Previous research has stated that quality of CSR disclosure, as it tends to be unaudited, is a possible explanation to users’ lack of interest for it. This study sees companies “attitude” towards CSR disclosure and lack of knowledge as another possible area where companies can improve to enhance users interest in CSR disclosure.

Problem statement: Previous researchers have pointed out possible roles CSR disclosure could have, which would benefit both companies and users. For example the report could be a communication device with which companies show accountability and performance to build trust for their company and at the same time provide stakeholders with information these can use to improve their decision- making.

The problem with CSR disclosure role seems to be that companies either “misuse” it or does not embrace the possibility to account for their good work. Critics of the CSR disclosure mean that it is used by companies to manage their reputation, and that it is rather reputation management than accountability that drives companies to engage in CSR accounting. Others points the problem of CSR disclosure role to that companies instead of taking advantage of it do not embrace the possibility to account for their good work through CSR disclosure, that is companies engage more in environmental and societal issues than they disclose in their CSR reports.

Approach: The starting point for this study is that companies do not seem to embrace the possibility of using CSR disclosure as a communication tool in which they can show accountability and build trust, but instead use it as a marketing tool or just produce disclosure because it is in “fashion”.

This thesis examines the role of CSR reports and companies use of the report as a communication tool to respond to external pressure and build trust and/or manage reputation. To examine the role of CSR reports knowledge about how companies use CSR reports for reputation management and/or trust building is acquired through a literature review, covering a number of well established journals’ articles regarding corporate social reporting. The purpose of such literature review and the focus of this paper are to start building an instrument which can be used to analyze companies’ use of CSR reports in order to explore the role of CSR reports.

1

1. Background–Aquestionaboutcompany’sroleinsociety

In the1960’s–1970’s itwasacknowledge that companies’ activitieshavean impacton

theirsurroundings,andassuchadiscussionaboutwhatresponsibilityacompanyshouldtake

for theiractionarose(Brownetal.2009).Thediscussionweredividedbetweentwo fieldson

onesideMiltonFriedmanandothersarguedthattheonlyresponsibilityacompanyshouldhave

was to be amarket playermaximizing shareholders profit. On the other side the discussants

arguedthatcompanies’responsibilityreachedbeyondtheirfinancialresponsibilities.

Scandals that occurred after the millennium such as Enron, WorldCom and Arthur

Andersen started a wave of mistrust against large companies driven by shareholder

maximization(Borglundetal.2009).FurtherthediscussionaboutCSRflourishedduetoreports

such as our common future orBrundtlandReport; where the relationship between economic

growthandenvironmentalissueswerediscussedandtheconceptsustainabledevelopmentwas

establish, Agenda 21; a sustainability program for sustainable development and Al Gore’s

documentary in2006“An inconvenient truth”discussingenvironmental issues.Externalactors

suchasgovernments,NGO:sandmediaengageinholdingcompaniesresponsiblefortheimpact

theiroperationhaveonsociety(PorterandKramer2007).CompaniessuchasNestlé,Shelland

Nike action were questioned by external actors and these companies had respond to the

externalpressurebyenhancingtheirresponsibilityengagementsinordertocontinueoperating

(Borglund et al. 2009). Media engage in reporting about what impact companies’ operations

haveontheirsurroundings,mostrecentlyBP:soilleakintheMexicangolfwereinthespotlight.

Investors’interestinCSRhasalsoincreasedandindexessuchasDowJonessustainabilityindex

and FTSE4Good have been established to give investors indication of which companies

operationsareethical.

Todaystakeholderstrustinacompany’soperationisconsideredtobeofimportancefor

companiesinorderforthemtocreatevalue(Borglundetal.2009).Thepurposeofthecurrent

paperistoexaminewhatroleCSRdisclosurehasordoesnothaveincompanies’communication

to respond to external pressure. KPMG’s international survey of corporate responsibility

reporting (2008) including approximately 2200 businesses in 22 countries showed that 80

percentofthesecompaniesincludedCSRintheirreporting.Thiswasanoticeableincreasefrom

thesurveyresultin2005when50percentofthecompaniesincludedCSRintheirreporting.(2008)

2

The increaseof sustainability reportingmaybean indicationof that companies regards

CSRdisclosureaspartoftheirstrategytobuildvaluebycreatingtrustamongtheirstakeholder

groups.DeegmanandUnderman(2006:312)statesthat:(DeeganandUnderman2006)

“the broader objective driving any particular organization to

undertake CSR and sustainability report can range from ethically

motivateddesire to ensure that theorganizationbenefits,ordoes

notnegativeimpactupon,societyandnaturalenvironmentthrough

toaneconomicallyfocusedmotivetousesocialandenvironmental

reportingandCSRtoprotectorenhanceshareholdervalue.”

Previous studies have found that what motivates companies to engage in CSR

communicationisthattheyreceiveadvantagesandresourceswhichhelpthemcreatedvaluefor

the company. For exampleWaddock andGraves (1997) found a positive connection between

companies work with sustainability and their financial results. In their article they refer to

Moskowitz (1972), Freeman and Gilbert (1988) Hamel and Prahlad (1989) and Bartlett and

Ghoshal (1994) which found that enhance social responsibility could lead to competitive

advantageshavingapositive impactoncompanies’ financial results.Coomb’s (1995)research

showedthatcompaniescommunicatingthattheyaresociallyandenvironmentallyresponsible

areabletorecoverfasterfromcompanycrisissincecustomerstendtokeepcompanieswitha

goodCSRreputationlessliable. O’Dwyer’s(2002)studyshowedthattheprimemotivationfor

adoptingsustainabilityreportingwastoenhancecorporatelegitimacy.Hestatesthatcompanies

seemtoreactandrespondtoexternalpressureespeciallyifitthreatenedcorporatereputation

and/ortheabilitytooperateunhindered.(WaddockandGraves1997)(O'Dwyer2002)

2. StartbuildingamodeltoexplorepossiblerolesforCSRdisclosure.

Thispapersuggeststhatcorporateresponsibilityreportingispartofcompanies’strategy

tocreatevaluebybuildingtrustormanagingtheirreputationamongtheirstakeholders.Itisin

theinterestofthestudytoexaminewhatroleCSRdisclosurehasordoesnothaveincompanies’

communicationtorespondtoexternalpressure.Inordertoachievethepurposeofthispaper;to

startbuildingamodelthatcanbeusedinordertodeterminetheroleofCSRcommunication,the

study’s starts from Carroll’s pyramid model from 1979 which divides the responsibility that

companies’stakeholderwantsthemtotakeinapyramid‐figure(Figure1)offeringaframework

“throughwhichacorporation’sstrategicresponsestoasocialissuecanbeidentifiedandassessed”

(Lee2008:60).(Lee2008)

3

The bottom and the largest part of the pyramid consist of company’s responsibility to

Economicmaximize the firm’svalue, thenextpieceof thepyramidconsistofcompaniesLegal

responsibility to comply with rules and regulations. At the next level companies’ Ethical

responsibilitytoactinawaythatsocietybelievedtobe“goodbehavior”isfoundandatthetop

ofthepyramidtheDiscretionaryorPhilanthropicresponsibilitytobeagoodcorporatecitizenis

found(SchwartzandCarroll2003,Carroll1979).

Figure 1 Carroll’s pyramid of CSR Source: Schwartz and Carroll 2003

Carroll’s pyramid is complemented with Elkington’s (1997) “Triple bottom line” that

suggestedthatsustainabilityaccountingshouldincludeinformationaboutcompanies’economic,

social and environmental impacts. The triple bottom line is often found in companies

sustainabilityreporting.(Elkington1997)

4

Inthetablebelowpresentsthecontentfromasmallsampleofcompanies’responsibility

reports and how such information can be sorted under the categorization of Carroll and

Elkington.

Table 1 Carroll and Elkington's categorization

That is companies account for required responsibilities; that is what their economic

responsibilitiesareandwhattheeconomicimpact is.Furthermore,thismeansthatcompanies

accountforimpacttheireconomic,environmentalandsocialactionshavethatthelawrequires

them to account for. They also account for expected responsibilities; that is they account for

whatethicalresponsibilitytheytake,inthispaperthatmeansthattheyaccountfortheirsocial

andenvironmental impacts.Moreover, companiesdisclose informationaboutwhat theydo to

satisfyexternalsdesireforthemtotakeaphilanthropicresponsibility.(Elkington1997)

AquestionGray,OwenandAdams(1996)mightbeabletoansweriswhydocompanies

havetoaccountforthedifferentresponsibilitiesdiscussedabove?Theiranswerwouldprobably

be that in the struggle for sustainability the sustainability report could provide users with

information, which they could base their decision on. In their book Accounting and

Accountability they refer to Gray et al (1987:ix as cited in Gray et al 1996:3) defintion of

corporatesocialreportingas:(Grayetal.1996)

“ …the process of communicating the social and environmental

effects of organizations’ economic actions to particular interst

groupswithin society and to society at large. As such, it involves

extending the accountability of organizations (particularly

companies), beyond the traditional role of providing a financial

accounttotheownersofcapital,inparticular,shareholder.Suchan

extensionispredicatedupontheassumptionthatcompanieshaveto

Pages Carroll’sresponsibilitypyramid Philanthropic Ethical Legal Economical OtherTriplebottomline

Social Environmental Economic

AllianceOil

1 1 5 ‐ ‐

SCA 2 9 13 3 8 38SKF 5 4 7 1 4 5Husqvarna ‐1 2 6 ‐1 2 1HakonInvest

‐ ‐1 ‐1 ‐1 ‐1

SEB 4 8 4 5 27Ericsson 9 6 8 1 19

5

wider responsiblites than simply make money for their

shareholders”

In this paper the citation above is interpreted as that the purpose of responsibility

reportingistoprovidestakeholderswithinformationthatgoesbeyondstatinghowcompanies

managetheirfinancialobligations.AssuchCSRreportinginvolves“…extendstheaccountabilityof

organizations…”.Thewordaccountabilityincorporateaquestionregardingwhoshouldanswer

towho,forwhatandunderwhatrules(LernerandTetlock1999).Questionsuchaswhoshould

answertowhohas,asstatedinthebeginning,beendiscussedinthefieldofCSR,thatisshould

companiesonlyanswertoshareholdersoralsotostakeholders.Forwhathasalsobeenbrought

up,asstatedbefore,iswhatcompany’sextendedaccountabilityincorporate,andCarroll’shave

developed amodel todivide the responsibility of companies.Responsibility reporting ismost

oftenvoluntarybutasCarroll’sshowsexternalactorscanrequire,expectsordesirecompanies

toaccountfordifferentresponsibilities.Inordertogetahardergripaboutwhataccountability

meansintheCSRfiledsomepreviousresearchersfromtheCSRfielddefinitionofaccountability

willbepresented:

Gray et al. (1996:38) defined accountability as “The duty to provide an account (by no

means necessarilly a finacial account) or reckoning of those actions for which one is held

responsible”. ThiscitationlikeLearnerandTetlock(1999)statesthatsomeoneshouldoreven

mustprovideanaccountfortheirresponsiblities.

Adams (2004:732) demonstrate accountability as “corporate acceptance of its ethical,

socialandenvironmentalresponsiblity.Assuchthe”account”givenshouldreflectcorporateethical,

socialandenvironmentalperformance”.AdamscitationgivesanindicationofthatifCSRreports

is not only show performance (a bottom line result), but also stated what responsibility the

companyhasacceptedtotakeandworkwith.

Lozano (2004:102‐ 103)writes in the book edited by Brenkert (2004) that accountability

“definesthekindofcompanyonewantstobuildandthecontributiononewantsittomake…Inthis

respect,accountabilityinvolvesmuchmorethansimplyprovidinginformation;itinvolvesbuilding

acorporatelicensetooperatethroughinteractionwithothersocialactors…..Accountabilityisnot

aquestionofmetricsbutofvision.Thisvisionconcernshowacompanyseesitselfanditsroleinthe

world.”(Brenkert2004)

StealingthewordsofLozano(2004)accountability involvesbuildingacorporate license

to operation and one tool that is avaialble for companies to show their accountability are

6

corporate responsibility reports (Adams 2004). In order to show accountability and build a

licencetooperatethroughsuchreportspreviousresearchersstatedthatcompaniesshoulduse

ittodemonstratewhattheyaregoingtodosociallyandenvironmentally(vision&acceptanceof

responsiblity)andasloaccount forwhat theyhavedonesociallyandenvironmentally (record

actions). To sum up this means that the corporate responsibility report could be used by

companiestoshowaccountabilityandperformanceinordertobuilduptrustwhichhelpthem

togetaliciencetooperate.

Althoughcorporateresponsibilityreportinghavebeencriticizedforbeingusedasatoolto

managerepuation insteadof a tool to showaccountability.Previousresearchershavepointed

out that corporate social reports are used in order to manage repuation: As the corporate

responsibility report is a social construction (Morgan 1988, Hines 1988) established on

voluntary basis there is a risk that only certain aspects of the organizations operation is

visualized in thereports (Grayetal.1996).Assuchthecorporateresponsibilityreportinghas

been criticized for beingused as a reputationmanagement tool. For instance Schilizzi (2002)

criticizecorporatesocialreportsstatingthatitisonlyawayfororganizationstoenhancetheir

reputation.Adams (2004) complained that the reports lack completeness. She stated that the

reportswas not transparent enough, not covering positive aswell as negative aspects of the

company’s operation or showing the company’s acceptance of its responsibility by clearly

statingvaluesandcorresponding targets andexpectedachivementdates.Owen (2005) stated

thatitseemedtobeissuesofreputationandriskmanagementandcompetitiveadvantagesthat

drovecompaniestoengageincorporatesocialaccountingratherthanaccountability.Inastudy

made by Bebbington et al (2007) a connection between corporate social reporting and

reputationmanagementwas found.Bothexplicit and implicit evidence for reputationmanage

where found in theCSR reports examined. In some reports organization explicitly stated that

theysoughttogaingoodreputation.Inotherreportsexamplesofstrategiccommunicationwere

found. Furthermore, O’Dwyer (2002) found internal evidence for that companies use CSR

reports tomanage reputation.Managers interviewed in his study stated that corporate social

reports were used as symbolic tool rather than reflecting actual responsibility or activities

undertaken. Laufer (2002) referred to previous researchers to state that companies mislead

theirstakeholdersfromissuesthatmightconcernthemaboutthecompanyinordertomanage

their reputations, using communication practices misleading users’ perception about its

operations,suchasgreen‐washing,conductedbyQuirolaandSchlup(2001)andVogel(1989).

That is inorder tomanage their reputationcompaniesmayengage in complex strategies that

shiftattention fromthe firmandmisleadstakeholdersabout theirobjectivesorcommitments

(Laufer2003).(Bebbingtonetal.2007)(Owen2005)(Schilizzi2002,Adams2004,Morgan1988,Hines1988)

7

So far twodifferentpictureof theroleofCSRreportshavebeen introduced.On theone

handthereportsareusedbycompaniesinordertoaccountfortheirresponsibilityandassuch

buildtrustamongtheirstakeholders.Theotheroptioncompanieshaveistousethereportsto

manage reputation and in such tries tomislead their stakeholder about how theyworkwith

sustainabilityintheiroperations.Thispapersuggestathirdoption,thatisthatsomecompanies

useCSRreportingbecauseothersuccessfulcompaniesdoso.

Asanattempttounderstandwhyandhowcompaniesusetheirsustainabilityreportsthis

paper wants to continuing building on Carroll’s pyramid model by conducting a literature

reviewexaminingwhatpreviousresearchershavefoundaboutaboutwhyandhowcompanies

useCSRdisclosure,inorderbuildamodelthatcanbeusefordeterminingtheroleofcorporate

responsibilityreportinghaveincompaniesstrategiccommunicationtowardstheirstakholders.

3. Method

Thecurrentpaperis focusingonhowandwhycompaniescommunicateandaccount fortheir

responsibility through corporate responsibility reporting. The purpose is to contribute to the

CSR literaturebystarting tobuildamodel thatcanbeused forstudying theroleofcorporate

responsibility reports; that is how and why companies use these to respond to external

pressure.

Thequestionthispaperstartstoansweriswhy(whatcommunicationstrategyliesbehind

companiesuse)andhow(whattechniquesdoescompaniesusetoachievetheircommunication

strategy) companies use responsibility disclosure. This paper divides the role of corporate

responsibilitydisclosureintothreedifferentcategories;(1)trustbuildingdevise(2)reputation

managementtool(3)fashion‐followingdocument.Inthefirsttwocategoriesitisassumedthat

companiesembracethepossibilitytousethecorporateresponsibilitydisclosurestrategicallyto

receiveresources,althoughhowtheirattitudetowardshowtoreceiveresourcesdiffers.Inthe

thirdcategorycompaniesusethedisclosurebutdonotfullyembracetheirpossibilitytoaccount

fortheirgoodworkinordertocapturestakeholders’interestandtrustintheircompany.

The challenging part of this study lies indefining the three categories. Although in this

paperthefocuswilllieonstudyingwhatpreviousstudieshavefoundregardingcompaniesuse

of the sustainability reporting. A literature review focusing on examining what previous

researchstatesabouthowandwhycompanieschoosetocommunicatetheirCSRresponsibilities

andactivitiestostakeholderswillbeconducted.TheaimistoextendCarroll’smodelinorderto

8

applyitforanalyzingcompanies’useofcorporatesocialdisclosureasstrategiccommunication

to theirstakeholders.For the future theaim is touse thismodel toanalyzecompanies’useof

CSRreportsempirically.

Firstsampleselection

Thesampleoftheliteraturereviewwaschosenbysearchingforthekeywords:corporatesocial

reporting+reputation,corporatesocialdisclosure+reputation,corporatesocialreporting+trust,

corporatesocialdisclosure+trust.Whentherewerelessthan20articlesintotalforthe

keywordscorporatesocialreportingorcorporatesocialdisclosureallarticlesinsuchjournal

willbereviewed.

HighlyrankedaccountingjournalsbyBallas&Theoharakis(2003)withdifferentfocuses(i.e.

moretheoretical,empirical,researchbased)wereselectedforthereview:(BallasandTheoharakis2003)

Keywords:Journals:

Reporting+reputation

Reporting+trust

Disclosure+reputation

Disclosure+trust

Accounting,organizations&society(AOS)

110 156 86 138

Accounting,auditingandAccountability(AAA)

110 156 77 99

ABACUS

135 204 37 60

JournalofAccountingandeconomics(JAE)

88 0 92 0

JournalofAccounting&publicpolicy(JAP)

42 41 37 13

TOTAL 443 516 292 297Accounting&Businessresearch(ABR)

16 7

EuropeanAccountingreview(EAR)

17 9

Table2FirstSelectionofarticlesbasedonkeywords(sortedafterhowmanyhitswherefoundineachjournal)

Thekeywordswerefirstselectedwiththehopetousearticlestobeabletodividebetweentrust

andreputationandassuchdistinguishthetwoconcepts,althoughsomearticlesarefoundboth

undertrustandreputationandthereforeeacharticlewillbeanalyzedandvaluedseparately.

9

Selectingarticles

Inordertoselectarticlesallabstractsfromthejournalsselectedwerereview.Atthisstage

some paper were excluded, that was paper focusing on auditing, performancemeasures (the

connectionbetweencorporatesocialreportingandcorporatefinancialperformance),webandon‐

line related questions, different sorts of accounting such as city accounting or compensation

accounting, pension incentive system, feminist theory, changed practice of financial institutions.

Insteadarticleswithabstractsindicatingthatthearticlefocusonhowandwhycompaniesuse

responsibilityreportswereselected.Afterthislimitation123articlesremained.

In the final stage of selecting articles the whole article is read and evaluated. If it is

believed that the article can contribute to the understanding of how andwhy companies use

corporatesocialdisclosure it isusedforbuilding themodel.Thethirdselectionprocess isnot

completedatthisstage;theliteraturereviewatthisstageisstillaworkinprogress.

Selectionofarticles Nr.ofarticlessecondselection

Nr.ofarticlesthirdselection

Accounting,organizations&society 36 21Accounting,auditingandAccountability 56 ?ABACUS 4 ?JournalofAccountingandeconomics 2 0JournalofAccounting&publicpolicy 9 ?Accounting&businessresearch 8 ?EuropeanAccountingreview 8 ?TOTAL 123 ?Table3Secondandthirdselectionofarticles

4. Literaturereview‐Companies’useofcorporateresponsibilitydisclosureasastrategiccommunicationtool

4.1Responsetoexternalpressure

Differenttheoreticalperspectiveshavebeenusedinordertoexplainthevoluntarydisclosure

practicethatexistsinsustainabilitydisclosure.Inseveralstudiesmorethanonetheoryhasbeen

usedas theories tend tooverlapandbe connected toeachother (Deegan2006). For instance

Greyetal. (1995)regards legitimacyandstakeholdertheoryastwosetofassumptionswithin

thepoliticaleconomictheory.Deegan(2006)alsostatesthatlegitimacytheoryarrivesfromthe

economic political theory but adds that legitimacy theory overlaps the institutional and

stakeholdertheory.AertsandCormier(2009)statesthatthelegitimacytheoryhasitsrootsin

both institutional theory and socio‐ political research. Furthermore, some assumptions in

impressionmanagement theory can be drawn back to the stakeholder theory and legitimacy

10

theory.Forinstanceimpressionmanagementliteraturestatesthatannualreportsnarrativesare

directedtowardsrelevantpublicincontrasttoothertextualdiscoursesthatmaybedirectedto

the general public (Neu et al. 1998). As such the power of a stakeholder affectswhat issue a

companychoosestodiscloseandthestrategychosenbyacompanytosendtherightmessageto

the relevant public (Neu et al. 1998). Furthermore, it is assumed in legitimacy theory that

managershavethepossibilitytocontrolinformationoutputinordertocreatecorrespondence

between social values and organizations activities. Impression management rest on the

assumption that managers will take this opportunity to provide a self‐ serving picture

(Hooghiemstra2000).(Grayetal.1995)

Different theories used in the CSR research have been influenced by each other and as

such come to share some convergent assumptions. A convergent assumption between some

theoriesisthatorganizations’existenceisaffectedbytheirexternalsurrounding’sperceptionof

them.Asexternalactorspossessresourcesfirm’saredependentofexternalactorsandassuch

needtorespondtoexternalexpectations(Molletal.2006).Onewayforcompaniestorespond

andaffectpublicopinionaboutthemistoengageinsocialdisclosure(Hooghiemstra2000).

Inaccordancetothetheoreticalassumptionsexpressedabovethisstudyisbasedonthe

assumption that companies use corporate responsibility disclosure in order to respond to

externalpressure.Assuchthefirstsectionofthisliteraturereviewwillexaminewhatprevious

researchershavefoundinregardstohowexternalexpectationsaffectaccountingpractice.

TherelationshipbetweenexternalpressureandsocialresponsiblereportingExternalpressuredependson:

Firmscharacteristicssuchas:Size,age,industry,ownership,profitabilityandcapitalintensityetc

AOS: Trotman&Bradley(1981);Roberts(1992);Aerts(1994)(2005);Cho,Roberts&Patten(2009);Aerts&Cormier(2009).AAAJ:O’Dwyer(2002);Laine(2010).

Thereisacorrelationbetweenfirms’characteristics andvisibilityandbetweenvisibilityandsocialresponsibledisclosure. Table 4: References to external pressures relationship with corporate social responsibility reporting

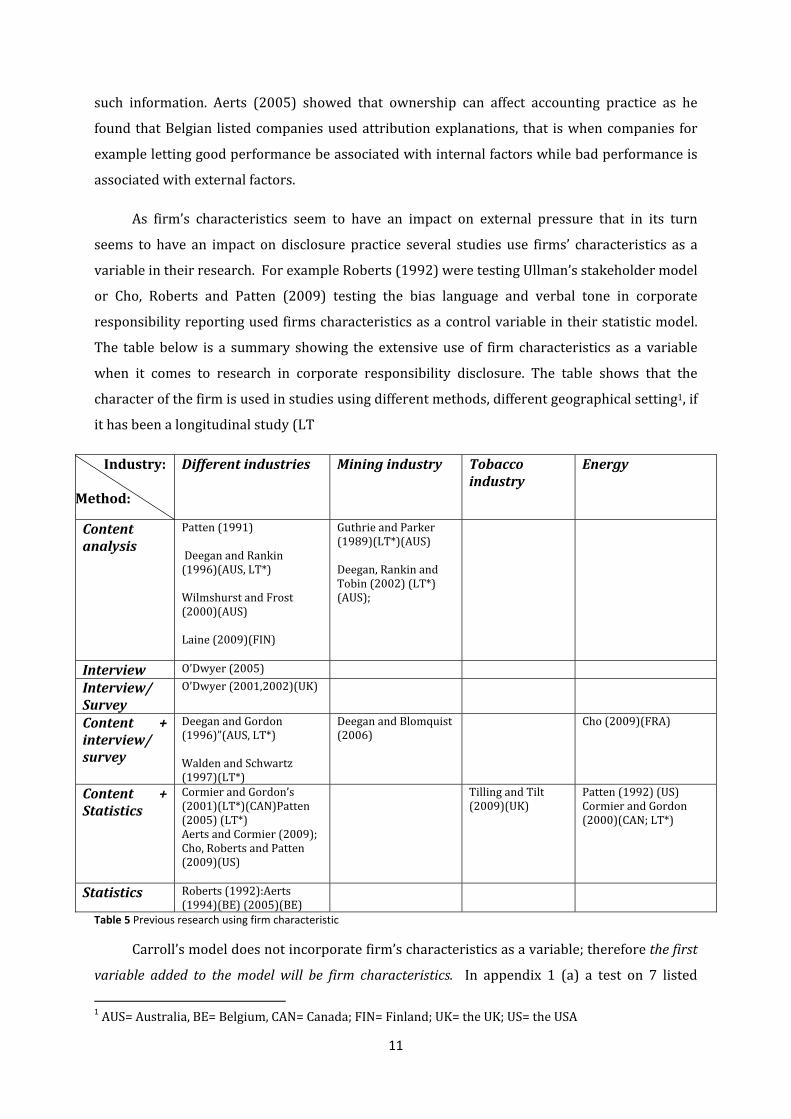

Ithasbeenrecognizedthatfirms’characteristicshaveanimpactonwhatexternalpressure

firmshavetodealwith,asfirmscharacteristicshaveanimpactonhowvisibleafirmis.O’Dwyer

(2002) found that companies in sensitive industries togetherwith size had an effect on how

visible a companywas in society. Aerts & Cormier (2009) tested and found support for that

companiesoperatinginenvironmentalsensitiveindustriesaremorevisible(inmedia)andthat

thesecompaniesdisclosemorecorporatesocialinformation.Trotman&Bradley(1981)showed

that companies providing social responsible information on average are larger in size, have

highersystematicriskandplacestrongeremphasisonlongtermthancompaniesnotdisclosing

11

such information. Aerts (2005) showed that ownership can affect accounting practice as he

foundthatBelgian listedcompaniesusedattributionexplanations, that iswhencompanies for

examplelettinggoodperformancebeassociatedwithinternalfactorswhilebadperformanceis

associatedwithexternalfactors.(O'Donovan2002,TrotmanandBradley1981,Aerts2005,AertsandCormier2009)

As firm’s characteristics seem to have an impact on external pressure that in its turn

seems to have an impact on disclosure practice several studies use firms’ characteristics as a

variableintheirresearch.ForexampleRoberts(1992)weretestingUllman’sstakeholdermodel

or Cho, Roberts and Patten (2009) testing the bias language and verbal tone in corporate

responsibilityreportingusedfirmscharacteristicsasacontrolvariableintheirstatisticmodel.

The table below is a summary showing the extensive use of firm characteristics as a variable

when it comes to research in corporate responsibility disclosure. The table shows that the

characterofthefirmisusedinstudiesusingdifferentmethods,differentgeographicalsetting1,if

ithasbeenalongitudinalstudy(LT).(Roberts1992,Choetal.2009)

Industry:Method:

Differentindustries Miningindustry Tobaccoindustry

Energy

Contentanalysis

Patten(1991)DeeganandRankin(1996)(AUS,LT*)WilmshurstandFrost(2000)(AUS)Laine(2009)(FIN)

Guthrieand Parker(1989)(LT*)(AUS)Deegan,RankinandTobin(2002)(LT*)(AUS);

Interview O’Dwyer(2005)

Interview/Survey

O’Dwyer(2001,2002)(UK)

Content +interview/survey

DeeganandGordon(1996)”(AUS,LT*)WaldenandSchwartz(1997)(LT*)

DeeganandBlomquist(2006)

Cho(2009)(FRA)

Content +Statistics

CormierandGordon’s(2001)(LT*)(CAN)Patten(2005)(LT*)AertsandCormier(2009);Cho,RobertsandPatten(2009)(US)

TillingandTilt(2009)(UK)

Patten(1992)(US)CormierandGordon(2000)(CAN;LT*)

Statistics Roberts(1992):Aerts(1994)(BE)(2005)(BE)

Table 5 Previous research using firm characteristic

Carroll’smodeldoesnotincorporatefirm’scharacteristicsasavariable;thereforethefirst

variable added to themodelwill be firm characteristics. In appendix 1 (a) a test on 7 listed

1 AUS=Australia,BE=Belgium,CAN=Canada;FIN=Finland;UK=theUK;US=theUSA

12

companies on the Stockholm Stock Exchange (large cap) is conducted in order to test the

differentvariablesincludedintheextendedmodel.Whatwasinterestinginthisrespectwasthat

Allianceoilwhichcouldbeconsideredasacompanyoperatinginasensitivebusinessonlyused

7pages toreport theirsustainabilitywhileSEBwhichoperate in thebanksector(notbeinga

sensitivebusiness)used48pages.Evenif it is interestingthisdifferencemaybeassociatedto

other firms’ characteristics that could have a greater impact on a firm’s visibility, more firm

specificcharactershavetobeconnectedtothetwocompanies.

4.2Whyandhowdocompaniesrespondtoexternalpressure

This sectionwill look at why andwho companies responds to external pressure. Aerts

(1994), which does not refer to environmental reporting specifically, states that narrative

accountingdisclosure,suchasresponsibilityreporting, isatoolcompaniescanuseinorderto

legitimacycompany’sactivitiesandoutcomes,asaccountinglanguagecanbeusedtoinfluence

thinking and behavior. Carruthers (1995) points out that new institutionalism regards

accounting practice as a tool companies can use to receive legitimacy by constructing an

appearanceofrationalityandefficiency.Hoopwood(2009:437)alsostatedthatcompaniesmay

be interested in engaging in environmental reporting in order to increase their legitimacy or

facilitate anewanddifferent imageof the company.As such the report “servesasacorporate

veil,simultaneouslyprovidinganewfacttotheoutsideworldwhileprotectingtheinnerworkings

oftheorganizationfromexternalview”.(Aerts1994,Carruthers1995)(Hopwood2009)

In the next sections knowledge about why and how companies use responsibility

reportingwillbecollectedfrompreviousresearch.

1. Respondtoexternalpressure–disclosureusedtocloselegitimacygap.

Accordingtothelegitimacytheoryacompany’sexistenceisdependentonifthesocietyinwhich

itoperaterecognizethatit’sactivitiesareinaccordancetothissociety’svaluesystem(Grayetal

1996).Dowling&Pfeffer(1975:122)statedthatorganizations:

“seek toestablishcongruencebetween thesocialvaluesassociatedwith or implied by their activities and the norms of acceptablebehaviorinthelargersocialsystemofwhichtheyarepart”.

If there is no correspondence between social values and organization’s activities, a

legitimacy gap may occur. The legitimacy gap may arise due to different reasons: company

changewhilesocietalexpectationremain thesame;societalexpectationschangebutcompany

performance remains the same; both organization and societal expectations change but in

13

opposite directions To reduce the legitimacy gap companiesmay adopt tactics and discloser

approaches(O'Donovan2002).Neu(1991)howexplorestheroleoftrustandstatesthattrust

depends on to expectations; on the onehand it depends on socialexpectation that is practice

takenforgrantedandacceptedasthecorrectwayofacting,tostoponcecareataredlightand

constructive expectation that is appropriate behavior for specific situation, this is learnt with

experienceandinteractions.Neu(1991)alsoexplainsthattrustisafundamentalingredientthat

isneededinorderforanexchangetooccur.(Neu, Neu 1991)

The next sectionwill explorewhat communication techniques previous research states

thatcompaniesinresponsibilityreportingtoreceivelegitimacyandtrust.Asmightbeexpected

previous researchhave looked at the rhetoric and categorization in companies’ responsibility

reportingtounderstandhowtheseareusedtobycompaniestobeperceivedaslegitimate.

Dowling & Pfeffer’s paper from 1975 provides a conceptual framework for analyzing

organizational legitimacy and process of legitimating. Dowling and Pfeffer (1975: 126‐127)

foundthatorganizationscaneitheradaptitsoutput,goalsandmethodsofoperationtowhatis

currentlyseenaslegitimate,throughcommunicationbecomeidentifiedwithsymbols,valuesor

institution that are associatedwith strong legitimacy or try tochange the definition of social

legitimacyinsuchawaythatitsuitspresentpracticeoftheorganization.

Some researchers have found that depending onwhat stakeholders’ present perception

are of a company, the company may choose different communication strategies in order to

acquire legitimacy. As such several previous researchers have looked at how companies use

rhetorictogain,thatistoestablishaperceptionofbeingalegitimatecompany,maintain,thatis

toholdontothecurrentperceptionofbeingalegitimatecompany,regain,thatisgetbackthe

perception of being legitimate for instance after a “scandal” has occurred or loss, that is to

reducetheperceptionofbeingalegitimacycompanyforinstancebecauseitrequirestoomuch

resourcestomaintaincurrentperceptionofthecompany.

Severalarticleshavealsolookedathowcompaniesuserhetorictogain,maintain,regain

or loss legitimacy. Ashford and Gibbs (1990) start the 1990’swith an article about symbolic

legitimacy. In theirarticle theauthorsexplainhowthe fieldexistsofdifferentactors trying to

maintain,extendanddefendlegitimacy.Thepurposeoftheirarticleistoexplainthedynamicsof

legitimacy. In Suchman’s article from 1995 he explains what strategies managers choose to

managetheirreputation,dependuponifacompanywantstogain,maintainorrepairlegitimacy.

FromtheideasofDowling&Pfeffer(1975)thatcompaniesadoptorchangeperceptionof

what accepted as legitimate; Ashford & Gibbs (1990) and Suchman (1995) ideas about the

14

dynamicofcompanieslegitimacycreation,strategiclegitimacytheoryresearcherscontinuedto

examinehowcorporatesocialdisclosureisusedtocloselegitimacygaps.

ForinstanceLindblom(1994)(La‐cinthetablebelow)discusseshowcorporationsseek

toacquirelegitimacyandwhatdisclosurestrategiesanorganizationcantaketocloselegitimacy

gaps;(a)adjustorganizationoutputtoexternalpressureandcommunicatechangesinorderto

educateandinformtherelevantpublicsaboutthechangedperformance;(b)notadjustoutcome

to external pressure but inform and educate the public about the appropriateness of the

outcome; (c) not change outcome but be associated with symbols associated with high

legitimacystatus.(DowlingandPfeffer1975,AshforthandGibbs1990,TillingandTilt2009,Suchman1995,Lindblom1994)

O’Donovan(2002)(Oa‐dinthetablebelow)discussedwhatcommunicationstrategiesa

company could use to regain legitimacy; (a) avoid addressing the issue, (b) attempt to alter

social values, (c) attempt to shape perceptions of the organization, (d) conform to conferring

public’svalues.(O'Donovan2002)

Cho (2009) (C a‐c in the table below) took the ideas from Dowling & Pfeffer (1975),

Lindblom(1993)andO’Donovan(2002andcombined them into threenewclassifications: (a)

Image enhancement;where company link itself to positive values, (b) Avoidance/ deflection;

company redirect of deflect attention from social or environmental issue and (c)Disclaimer;

companyattempttolooklegitimatebydenyingitsresponsibilityinnegativeorharmfulactivity.

(Deegan2002,Cho2009)

BasedonCho’s(2009a)statementthatthereisaneedtobetterunderstandwhycompanies

engage in corporate social reporting and the rhetoric’s used in such, Laine (2009) started to

explorethelanguageusedbythreeFinishcompaniesintheirCSRreportsmoreindept.

Strategictacticsummary

Adapttosocialvalues(Dowling&Pfeffer,1975)

Changesocialvalues(Dowling&Pfeffer,1975)

Otheroptions

Gain(Suchman,1995)

L(a)Adaptand L(b) change L(c)Manipulateperceptions

15

(Tilling&Tilt,2009) communicate perceptionofoutcomebyeducation.

Maintain(Ashford&Gibbs,1990)(Suchman,1995)(Tilling&Tillt,2009)

L(a)Adaptandcommunicate

L(b) changeperceptionofoutcomebyeducation.

L(c)Manipulateperceptions

Regain(Ashford&Gibbs,1990)(Suchman,1995)(Tilling&Tilt,2009)

L(a)Adaptandcommunicate O(d)Conform

L(b) changeperceptionofoutcomebyeducation.O(b,c)changeperceptions

L(c)ManipulateperceptionsO(a)AvoidC(a)ImageenhancementC(b)Avoid/DeflectionC(c)Disclaimer

Loss(Tilling&Tilt,2009)

Table6Summarstrategictactics

L(a‐d)=Lindblom’s(1994)fourdifferentlegitimacystrategies. O(a‐d)=O’Donovan(2002)observationofmanagingreputationafteradisaster) C(a‐c)=Cho’s(2009)summaryofDowling&Pfeffer,LindblomandO’Donovan’sobservations.

O’Donovan(2002)alsousesOliver(1991)research,lookingatthephenomenaofcorporate

social disclosure (CSD) from an institutional and resource based theory, stating that effort

necessary tomaintain legitimacydependsonwhat legitimacy thecompanyhad tobeginwith.

BasedonthisO’Donovanstatesthatitisharderforacompanythatpromotesitselfasextremely

sociallyandenvironmentallyresponsible tomaintain legitimacy,as italwaysneed toperceive

publicexpectations.Although,maintaininglegitimacyiseasierthangainingorrepairingit,asthe

two latter activities requires proactive actions by the company (O'Donovan 2002). (O'Donovan 2002)(Oliver1991)

Tilling and Tilt (2009) study of Rothmans, an Australian tobacco company, result in an

expansionofAshford&Gibbs(1990)andSuchman(1995)modelofestablish,maintain,regain

withloss.Theynamedandexplainthedifferentphrasesoflegitimacy;establishingincludesearly

stageof firm’sdevelopmentwhere it ensures it canmeet itsobligations;maintaining includes

preserving itsroleandbecomeattachedtosymbolsaswellashandlingotherchallengesto its

legitimacy;extendingwherecompanyrealizeitsneedtochangeinaccordancetocircumstances;

defendingwherecompanyprovideresponsetoachallengedlegitimacyloss;insteadofdefending

itslegitimacyacompanymaychoosetolosssomeofitslegitimacyasitiseasiertomaintainless

legitimacy. At some point the company has to stop losing legitimacy and from that point the

company can either endup atdisestablishmentor start overwith establishment to gainmore

legitimacyagain.IntheirempiricalstudytheyfoundthatprevailingstrategyusedbyRothmans

to handle the smoking and health issue threat against its legitimacy, where to engage in

communityservicesandcharity.(DowlingandPfeffer1975,AshforthandGibbs1990,TillingandTilt2009,Suchman1995,Lindblom1994)

16

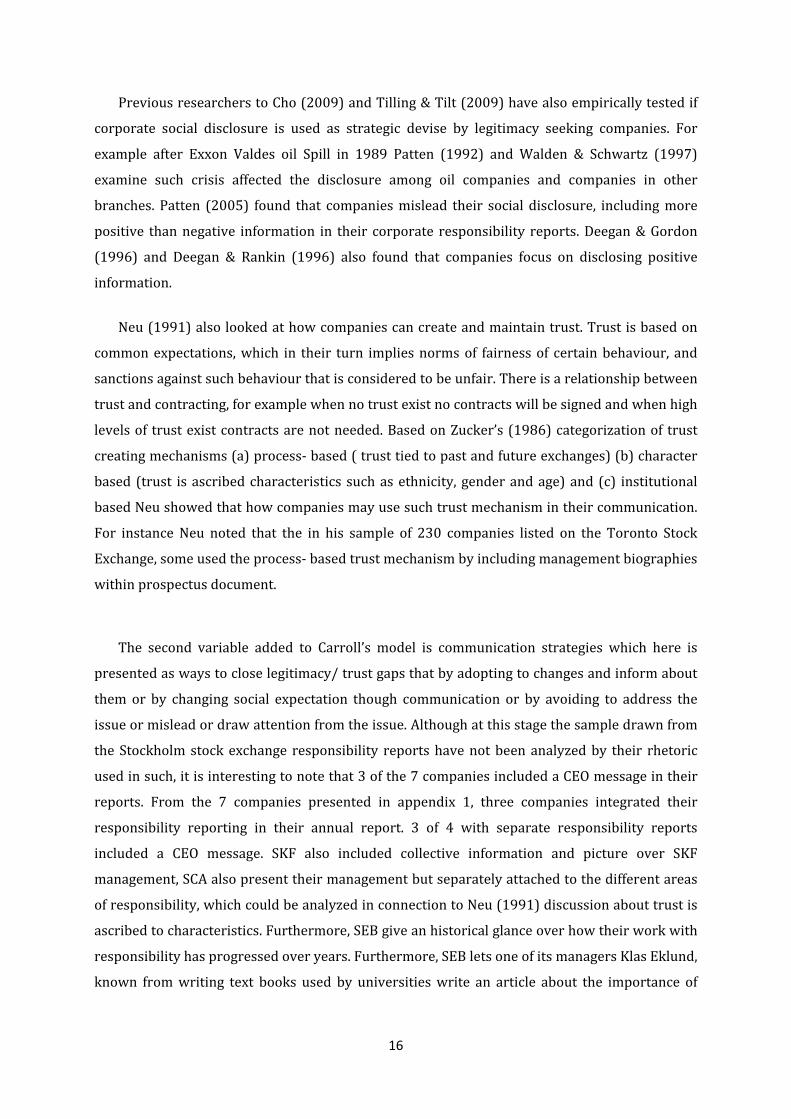

PreviousresearcherstoCho(2009)andTilling&Tilt(2009)havealsoempiricallytestedif

corporate social disclosure is used as strategic devise by legitimacy seeking companies. For

example after Exxon Valdes oil Spill in 1989 Patten (1992) and Walden & Schwartz (1997)

examine such crisis affected the disclosure among oil companies and companies in other

branches. Patten (2005) found that companiesmislead their social disclosure, includingmore

positive thannegative information in their corporate responsibility reports.Deegan&Gordon

(1996) and Deegan & Rankin (1996) also found that companies focus on disclosing positive

information.(Patten1992,WaldenandSchwartz1997,DeeganandGordon1996,DeeganandRankin1996,Patten2005)

Neu(1991)alsolookedathowcompaniescancreateandmaintaintrust.Trustisbasedon

commonexpectations,which in their turn impliesnormsof fairnessof certainbehaviour, and

sanctionsagainstsuchbehaviourthatisconsideredtobeunfair.Thereisarelationshipbetween

trustandcontracting,forexamplewhennotrustexistnocontractswillbesignedandwhenhigh

levelsof trustexistcontractsarenotneeded.BasedonZucker’s(1986)categorizationof trust

creatingmechanisms(a)process‐based(trusttiedtopastandfutureexchanges)(b)character

based (trust isascribedcharacteristics suchasethnicity,genderandage)and (c) institutional

basedNeushowedthathowcompaniesmayusesuchtrustmechanismintheircommunication.

For instance Neu noted that the in his sample of 230 companies listed on the Toronto Stock

Exchange,someusedtheprocess‐basedtrustmechanismbyincludingmanagementbiographies

withinprospectusdocument.

The second variable added to Carroll’s model is communication strategies which here is

presentedaswaystocloselegitimacy/trustgapsthatbyadoptingtochangesandinformabout

them or by changing social expectation though communication or by avoiding to address the

issueormisleadordrawattentionfromtheissue.Althoughatthisstagethesampledrawnfrom

theStockholmstockexchange responsibility reportshavenotbeenanalyzedby their rhetoric

usedinsuch,itisinterestingtonotethat3ofthe7companiesincludedaCEOmessageintheir

reports. From the 7 companies presented in appendix 1, three companies integrated their

responsibility reporting in their annual report. 3 of 4 with separate responsibility reports

included a CEO message. SKF also included collective information and picture over SKF

management,SCAalsopresenttheirmanagementbutseparatelyattachedtothedifferentareas

ofresponsibility,whichcouldbeanalyzedinconnectiontoNeu(1991)discussionabouttrustis

ascribedtocharacteristics.Furthermore,SEBgiveanhistoricalglanceoverhowtheirworkwith

responsibilityhasprogressedoveryears.Furthermore,SEBletsoneofitsmanagersKlasEklund,

known fromwriting text books used by universitieswrite an article about the importance of

17

sustainablework.Thisissomethingthatcouldbeconnectedtothesocalledprocess‐basedtrust

mechanism.

2. Respondtoexternalpressure–disclosureusedtopresentaself‐servingpicture.

AccordingtoHooghiemstra(2000)impressionmanagementstudieslookathowindividuals

representthemselvestocontroltheimpressionofothers.Neuetal.(1998)statesthatthetheory

rest on the assumption that the managers will provide a self‐ serving view of a company’s

performance.Cho,RobertsandPatten(2009)basedtheirresearchonMerkl‐Davies&Brennan

(2007) framework for analyzing corporate impressionmanagement strategies, assuming that

managerialself‐servingmotive“drivesbiasnarrativedisclosure”.Therearedifferentimpression

managementtechniquesavailable formanagerstoenhancegoodnewsanddiminishbadnews

(Hooghiemstra2000).(Neuetal.1998)

Previous researchers have tested companies’ use of communication techniques

companies’useforimpressionmanagementstrategieswhendisclosingcorporateresponsibility

information.Cho,RobertsandPatten(2009)lookedattherelationshipbetweendisclosureand

environmentalperformanceandmeasuredif“optimism”indisclosurewhererelatednegatively

tofirmsenvironmentalperformancewhile“certainty”indisclosurewhererelatedpositivelyto

firms performance. They found support for that companies rated as poorer environmental

performance by KLD (an independent rating firm) use impression management techniques.

Techniquesusedbymanagerswaseitherconceal information, that isemphasizinggoodnews

andcoverbadnews,orprovideinfluencingattributions,thatisattributingpositiveoutcometo

internalfactorsandnegativeoutcometoexternalfactors.IntheirstudyChoetal.(2009)looked

attherelationship.

Choetal.(2009)referstoAerts(1994)studywhichisabouthowcompaniesexplaintheir

performance in annual narrative reports. Aerts’ research is based on Schlenker (1980) and

Leary&Kowalski(1990)researchstatingthatthemoreacompany’srecentperformancediffers

fromwhat isdesired, themore likely it is thatmanagersbecomesconcernedwithwhat image

companiesactiongives thecompany.Accountingbias inAerts research is followingSchlenker

(1980), in the social psychology field, definition stating that an event can be interpreted

differently and as such an error may occur in the “objectivity” of the interpretation. Aerts’

(1994)researchalsoacknowledgesLeary&Kowalski (1990)statement that thevisibilityof a

companymayhaveanimpactoncompaniesawarenessofpublicopinionandassuch“encourage

verbalimpressionmanagementbehavior”(p.341).

18

Aerts (1994) found that companiesmostlyattributedpositiveeffects to internal factors;

theyfoundthat79%ofthepositiveperformancewasattributedtointernaleffect.Although,the

attributionofnegativeperformancewasnot inmajorityattributed toexternal factors, instead

Aerts research showed a more balanced picture with a small tendency to attribute negative

performancetoexternalfactorswereshown(53%ofthenegativeperformancewereattributed

toexternalfactors).Theresultsshowedthatnarrativeaccountinginformationtendstobebias,

although surprisingly the need to use accounting language to defend managers from

responsibility showed a lower result. Another interesting result Aerts (1994) found was in

opposition of the assumption that companieswith stable performancemight have less use of

defensive accounting narratives unstable firms might use such techniques more in order to

rationalize past experience and restore confidence in management capability. Aerts (1994)

resultshowedtheopposite:defensiveaccountinglanguagewasfoundonlyinstablecompanies

narratives.Hebelievesthatthiscouldbeanindicationofthatforstablecompaniesaccounting

explanations are used as “strategy for accountability predicaments”. In 2005 Aerts examines

accountingexplanationpractices’connectiontocontextualandmotivatinginfluences.Assuchhe

compared listed versus unlisted companies’ use of the attribution technique (that is how

performance is ascribed internal or external factors). They expected to find that listed

companies weremotivated to disclosemore accounting attributions and explanations due to

their public nature, incorporated with more pressure to show accountability. Examining the

explanatorybehaviorbetweenlistedandunlistedcompaniesfoundthat listedcompaniesused

more attribution statements than unlisted companies. Even so Aerts (2005) presented some

unexpectedresultssuchasthatunlisted,inoppositetotheexpectedlistedcompanies,disclosed

moreexplanationsperexplainedeffectthanlistedcompanies.

19

5. Concludingremarks

Inallregretsthisliteraturestudydoesnotprovidethereaderanyclearanswersastowhat

rolecompanies’responsibilityreportinghaveincompaniesstrategiccommunicationtorespond

toexternalpressure.Onereasonfornotbeingabletoprovidesuchanswerisbecauseithasbeen

hard to separate what is trust building and what is reputation management in the articles

reviewedsofar.Thismightbeexplainedbycompaniesownuseoftheconcepts,therearecases

werebothreputationandtrustisusedinthesamesentence.Forinstancethefollowingsentence

wasfoundonAstraZeneca’shomepage(accessed31ofOctober2010)“Ourreputationisbuilton

thetrustandconfidenceofallourstakeholdersandisoneofAstraZeneca'smostvaluableassets.”

WhatthispaperprovidesissomesuggestionsforvariablesthatcanbeattachedtoCarroll’s

and Elkington’s existing models which could help to understand the role of responsibility

reportingcouldhaveforcompanies’strategiccommunication.

First, it is suggested that what role the reporting get might depend on the firms’

characteristics.Asbeenstatedabovetheassumptionusedinmanytheoriesusedtodescribeand

understand corporate responsibility reporting, reports are provided to respond to external

pressure.Thecharacterofthefirmcanhaveanimpactoncompanies’“visible”forexamplesome

companies operation have a risk of causing high damage to their surroundings such as oil

companies.Therefore,stakeholdermayputmorepressureonandholdcompaniesaccountable

fortheiroperationspressuringthemtonotonlytaketheirfinancialresponsibilitybutalsotake

theirsocialandenvironmentalresponsibility.Aninterestingfindingwhencomparingthesmall

sampleof7companiesfromdifferentindustriescollectedonStockholmStockExchange(large

cap)wasthatAllianceoilwhichisoperatinginasensitiveindustryprovideslessinformationin

their sustainability report (7pages)while SEBoperating in thebank sectorprovides amore

extensive report (48 pages). Although the only character compared in my sample is their

industrybelongingandassuchotherfactorssuchasshareprice,ownershipstructureorother

characteristicscouldexplainthisfinding.

20

Secondly,theliteraturereviewstartstogivesomestructureastohowandwhycompanies

areusingCSRreportsforacertainpurpose.

Techniquesusedcorporateresponsibilityreportingfoundbypreviousresearchers1. Respondtoexternalpressure– disclosureusedtocloselegitimacygap

ObtainMaintainRegainLoss

Adopt changes and inform about the adoption, change perceptions by educating (presenting facts), Avoid addressing the issue, draw attention from the issue, misleading.

AAAJ: Tilt and Tilling (2009);O’Donnovan(2002)ABR:Deegan&Gordon(1996)AOS:Patten(1992)EAR:Cho(2009a);Laine(2010).JAP:Walden&Schwarts(1997)

Focus on positiveinformation

AAAJ: Deegan&Rankin(1996)ABR:Deegan&Gordon(1996)JAP:Patten(2005)

Createtrust Process‐ Based; Character‐ based or institutional based

AOS: Neu(1991)

2. Respondtoexternalpressure–disclosureusedtopresentaself‐servingpicture.

BiaslanguageorvocaltoneinAccountingexplanationsused

Impressionmanagement:concealmentandattribution.

AOS: Cho,Roberts&Pattern(2009)2

Accountingattributionandperformanceexplanations.

AOS:Aerts(1994)3AOS:Aerts(2005)

Astherhetoricusedinthesamplewasnotanalyzedindepthandastheircurrentneedto

obtain,maintainorregainlegitimacyhasnotbeenconsidernoobservationcanbedrawnabout

theuseoftheirrhetoricdevice.

ThefashionfollowingsideofCSRreportshavenotbeendiscussedasmuchaswantedin

thispaperalthoughitisintheinterestofthisresearchtostudymoreresearchsuchastheone

conducted by Walden & Schwartz (1997) that examined how disclosure is affected among

companies after a crisis such Exxon Valdes oil Spill in 1989, that is does it lead to more

environmentaldisclosureinthecompany,inthecompany’sindustryorinallindustries.

TheresearchfromNeu(1991)abouttrustmechanismthatusedbycompaniesisbelieved

tobeofinterestandcontributiontoourmodel.Lookingatthesampletheinformationprovided 2 In order to measure ”optimism” and “certainty” in their samples environmental disclosure included in 10‐ K reports Cho et al. (2009) used a text analysis program developed by Hart, R.P. called DICTION; which is used for “lexical analysis through the analysis of five master variables: “certainty”, “optimism”, “activity”, “realism” and “commonality.”(p.6). In order to determine environmental performance an independent rating firm, KLD, results were used. 3 Attributions were coded according to an attribution‐ manual including the following dimensions 1) locus of causality (internal or external) 2)valence of the effect (positive or negative effect) 3) nature of explanation (based on technical‐ accounting terminology and logical or not)4) Expression of cause and effect (is it expressed in accounting terms or not) .

21

bythecompaniesthatliesoutsideCarroll’sandElkington’scategorizationsseemstobeableto

contributetotheunderstandingoftheroleofCSRreports.Forfutureresearchitisattemptedto

study if and how the information that falls outside can be connected to companies’ strategic

communicationstrategiesandtechniquestocreatetrustorbuildupareputation.

The table below shows examples of information that is considered to be outside the

categorizationofCarrollandElkington,anditissuchinformationthatwouldbeinterestingfor

thisstudytocontinueworkingtoanalyzeandconnecttocompanyuseandtheroleoftheCSR

report.

Information Trustbuilding

Reputationmanagement

Controlandassurance X Codeofconduct/principles/policy/Ourrole ? ?CEOMassage X Awardandrecognition Managementinformation/messages Memberships Audit Indexesbelonging

Asthisstudyhaveonlystartedtoreviewliteratureandorganizeinthefieldofcompanies’

useofsustainabilityreportingandhowandwhycompaniesusetorespondtoexternalpressure

thisprocesswillcontinueinordertobuildontoCarroll’sresponsibilitymodel.

22

References

2008. 'KPMG international survey of corporate responsiblity reporting 2008.' KPMG International. Adams, C. A. 2004. 'The ethical, social and environmental reporting‐performance portrayal gap.'

Accounting, Auditing & Accountability Journal, 17:5, 731‐57. Aerts, W. 1994. 'On the use of accounting logic as an explanatory category in narrative accounting

disclosures.' Accounting, Organizations and Society, 19:4‐5, 337‐53. Aerts, W. 2005. 'Picking up the pieces: impression management in the retrospective attributional

framing of accounting outcomes.' Accounting, Organizations and Society, 30:6, 493‐517. Aerts, W. & Cormier, D. 2009. 'Media legitimacy and corporate environmental communication.'

Accounting, Organizations & Society, 34:1, 1‐27. Ashforth, B. E. & Gibbs, B. W. 1990. 'The double‐edge of organizational legitmation ' Organization

Science, 1:2, 177‐94. Ballas, A. & Theoharakis, V. 2003. 'Exploring Diversity in Accounting through Faculty Journal

Perceptions.' Contemporary Accounting Research, 20:4, 619‐44. Bebbington, J., Larrinaga, C. & Moneva, J. M. 2007. 'Corporate social reporting and reputation risk

management.' Accounting, Auditing & Accountability Journal, 21:3, 337‐61. Borglund, T., De Geer, H. & Hallvarsson, M. 2009. 'Värdeskapande CSR. Hur företag tar socialt

ansvar.'. Sweden, Falun: Nordstedts akademiska förlag. Brenkert, G. 2004. 'Corporate intergrity and accountability.' Califonia: SAGE Publication. Brown, H. S., de Jong, M. & Levy, D. L. 2009. 'Building institutions based on information disclosure:

lessons from GRI's sustainability reporting.' Journal of Cleaner Production, 17:6, 571‐80. Carroll, A. B. 1979. 'A Three‐Dimensional Conceptual Model of Corporate Performance.' Academy of

Management Review, 4:4, 497‐505. Carruthers, B. G. 1995. 'Accounting, ambiguity, and the new institutionalism.' Accounting,

Organizations and Society, 20:4, 313‐28. Cho, C. H. 2009. 'Legitimation Strategies Used in Response to Environmental Disaster: A French Case

Study of Total SA's Erika and AZF Incidents.' European Accounting Review, 1, 33‐62. Cho, C. H., Roberts, R. W. & Patten, D. M. 2009. 'The language of US corporate environmental

disclosure.' Accounting, Organizations and Society, 35:4, 431‐43. Deegan, C. 2002. 'Introduction: The legitimising effect of social and environmental disclosures – a

theoretical foundation.' Accounting, Auditing & Accountability Journal, 15:3, 282‐ 311. Deegan, C. 2006. 'Legitimacy theory.' In Z. Hoque (Ed.) Methodological issues in accounting research:

theories and methods: 161‐205. London: Spiramus. Deegan, C. & Gordon, B. 1996. 'A Study of the Environmental Disclosure Practices of Australian

Corporations.' Accounting & Business Research, 26:3, 187‐99. Deegan, C. & Rankin, M. 1996. 'Do Australian companies report environmental news objectively? An

analysis of environmental disclosures by firms prosecuted successfully by the Environmental protection authority.' Accounting, Auditing & Accountability Journal, 9:2, 50‐ 67.

Deegan, C. & Underman, J. 2006. Financial Accounting Theory: European Edition. McGraw‐Hill Education.

Dowling, J. & Pfeffer, J. 1975. 'Organizational Legitimacy: Social Values and Organizational Behavior.' The Pacific Sociological Review, 18:1, 122‐36.

Elkington, J. 1997. Cannibals with forks : the triple bottom line of 21st century business. Oxford: Capstone.

23

Gray, R., Kouhy, R. & Lavers, S. 1995. 'Corporate social and environmental reporting. A review of the literature and a longitudinal study of UK disclosure.' Accounting, Auditing & Accountability Journal, 8:2, 47‐ 77.

Gray, R., Owen, D. & Adams, C. 1996. Accounting & accountability. Changes and challenges in corporate social and environmental reporting. Hertfordshire: Prentice Hall Europe.

Hines, R. D. 1988. 'Financial accounting: In commuicating reality, we construct reality. .' Accounting, Organizations & Society, 13:3, 251‐61.

Hooghiemstra, R. 2000. 'Corporate Communication and Impression Management ‐ New perspectives why companies engage in corporate social reporting.' Journal of Business Ethics:27, 55‐ 68.

Hopwood, A. G. 2009. 'Accounting and the environment.' Accounting, Organizations and Society, 34:3‐4, 433‐39.

Laufer, W. S. 2003. 'Social Accountability and Corporate Greenwashing.' Journal of Business Ethics, 43:3, 253‐61.

Lee, M.‐D. P. 2008. 'A review of the theories of corporate social responsibility: Its evolutionary path and the road ahead.' International Journal of Management Reviews, 10:1, 53‐73.

Lerner, J. S. & Tetlock, P. E. 1999. 'Accounting for the Effects of Accountability.' Psychological Bulletin, 125:2, 255‐75.

Lindblom, C. K. 1994. 'The implications of organizational legitimacy for corporate social performance and disclosure.' Critical perspectives on anncounting conference. New York, NY.

Moll, J., Burns, J. & Major, M. 2006. 'Institutional theory.' In Z. Hoque (Ed.) Methodological issues in accounting research: theories and methods: 161‐205. London: Spiramus.

Morgan, G. 1988. 'Accounting as reality construction: Towards a new epistemology for accounting practice.' Accounting, Organizations & Society, 13:5, 477‐85.

Neu, D. 'The social construction of positive choices.' Accounting, Organizations and Society, 17:3‐4, 223‐37.

Neu, D. 1991. 'Trust, contracting and the prospectus process.' Accounting, Organizations and Society, 16:3, 243‐56.

Neu, D., Warsame, H. & Pedwell, K. 1998. 'Managing public impressions: environmental disclosures in annual reports ' Accounting, Organizations & Society, 23:3, 265‐82.

O'Donovan, G. 2002. 'Environmental disclosures in the annual report. Extending the applicability and predictive power of legitmacy theory.' Accounting, Auditing & Accountability Journal, 15:3, 344‐ 71.

O'Dwyer, B. 2002. 'Managerial perceptions of corporate social disclosure. An Irish story.' Accounting, Auditing & Accountability Journal, 15:3, 406‐ 36.

Oliver, C. 1991. 'Strategic responses to institutional processes.' Academy of Management Review, 16:1, 145‐79.

Owen, D. 2005. 'CSR after Enron: A Role for the academic accounting profession?' European Accounting Review, 14:2, 395‐404.

Patten, D. M. 1992. 'Intra‐ industry environmental disclosures in response to the alaskan oil spill: A note on legitimacy theory.' Accounting, Organizations & Society, 17:5, 471‐75.

Patten, D. M. 2005. 'The accuracy of financial report projections of future environmental capital expenditures: a research note.' Accounting, Organizations & Society, 30:5, 457‐68.

Porter, M. E. & Kramer, M. R. 2007. 'Strategy and Society: The Link Between Competitive Advantage and Corporate Social Responsibility.' Harvard Business Review: 136‐37. Harvard Business School Publication Corp.

Roberts, R. W. 1992. 'Determinants of corporate social responsibility disclosure: An application of stakeholder theory.' Accounting, Organizations and Society, 17:6, 595‐612.

Schilizzi, S. 2002. 'Triple Bottom Line Accounting: How serious is it?' Connetions. A joint publication of the agribusiness association of austraila and the australian agriculturaland resource economics society. Australia.

Schwartz, M. S. & Carroll, A. B. 2003. 'Corporate social responsiblity: a three‐ domain approach ' Business Ethics Quarterly, 13:4, 503‐30.

24

Suchman, M. C. 1995. 'Managing Legitimacy: Strategic and Institutional Approaches.' The Academy of Management Review, 20:3, 571‐610.

Tilling, M. V. & Tilt, C. A. 2009. 'The edge of legitimcy. Voluntary social and environmental reporting in Rothmans' 1956‐ 1999 annual reports.' Accounting, Auditing & Accountability Journal, 23:1, 55‐81.

Trotman, K. T. & Bradley, G. W. 1981. 'Associations between social responsibility disclosure and characteristics of companies.' Accounting, Organizations and Society, 6:4, 355‐62.

Waddock, S. A. & Graves, S. B. 1997. 'THE CORPORATE SOCIAL PERFORMANCE‐ FINANCIAL PERFORMANCE LINK.' Strategic Management Journal, 18:4, 303‐19.

Walden, W. D. & Schwartz, B. N. 1997. 'Environmental Disclosures and Public Policy Pressure.' Journal of Accounting & Public Policy, 16:2, 125‐54.

25

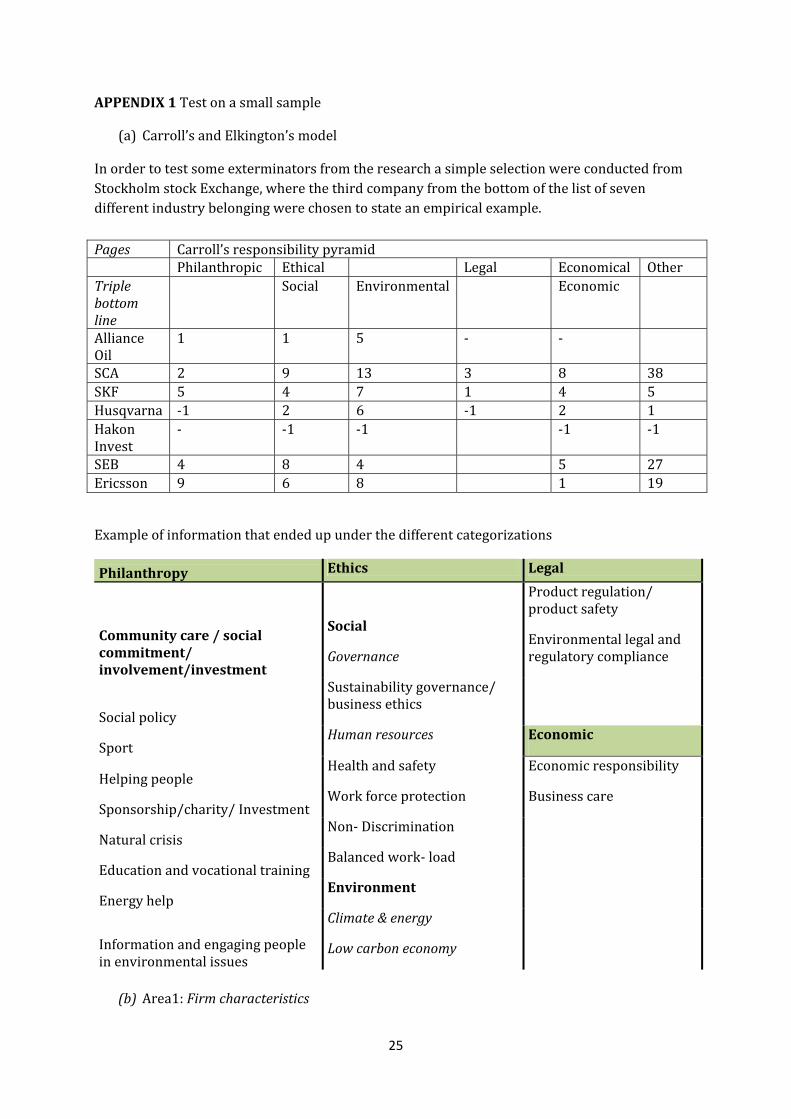

APPENDIX1Testonasmallsample

(a) Carroll’sandElkington’smodel

InordertotestsomeexterminatorsfromtheresearchasimpleselectionwereconductedfromStockholmstockExchange,wherethethirdcompanyfromthebottomofthelistofsevendifferentindustrybelongingwerechosentostateanempiricalexample.

Exampleofinformationthatendedupunderthedifferentcategorizations

Philanthropy Ethics Legal

Communitycare/socialcommitment/involvement/investment

Social

Governance

Productregulation/productsafety

Environmentallegalandregulatorycompliance

Socialpolicy

Sustainabilitygovernance/businessethics

SportHumanresources Economic

HelpingpeopleHealthandsafety Economicresponsibility

Sponsorship/charity/InvestmentWorkforceprotection Businesscare

NaturalcrisisNon‐ Discrimination

EducationandvocationaltrainingBalancedwork‐ load

EnergyhelpEnvironment

Informationandengagingpeopleinenvironmentalissues

Climate&energy

Lowcarboneconomy

(b) Area1:Firmcharacteristics

Pages Carroll’sresponsibilitypyramid Philanthropic Ethical Legal Economical OtherTriplebottomline

Social Environmental Economic

AllianceOil

1 1 5 ‐ ‐

SCA 2 9 13 3 8 38SKF 5 4 7 1 4 5Husqvarna ‐1 2 6 ‐1 2 1HakonInvest

‐ ‐1 ‐1 ‐1 ‐1

SEB 4 8 4 5 27Ericsson 9 6 8 1 19

26

Company Industry CSRreport Separatereport(S)Integratedreport(I)

AllianceOil Energy 7pages SSCA Material 73pages SSKF Industry 26pages IHusqvarna Consumer

Discretionary12pages I

HakonInvest ConsumerStaples 3pages ISEB Finance 48pages SEricsson IT 43pages S

Separatereport,meansthatthecompanyhasanownreportfordisclosingCSRactivities.IntegratedreportmeansthatthecompanyhasincludedCSRactivitydisclosureinitsannualreport.

(c) Area2:Why–strategiccommunication&How–communicationtechniques

FirmcharacteristicsFirmsneedtoobtain,maintainorregainlegitimacy Trust Reputation FashionWhy

How How How

Closelegitimacygap Adapttoexpectationandinformaboutthechange Changeperceptionbyeducation Drawattentionfrom

issue

Avoidtoaddressanissue

Process‐basedmechanism Character‐ based“ Institutional‐ based“ Self‐servingimage Attribution Concealment Explanations