Embed Size (px)

DESCRIPTION

The Robin Report delivers the strategic and relevant information that you have come to expect from author and prognosticator Robin Lewis. You can subscribe to The Robin Report for free at TheRobinReport.com

Citation preview

Issue Seven 2011

h a t c h i n g n e w i n s i g h t s

www.TheRobinReport.com $10

Warnaco’s performance since CEO Joe Gromek arrived in 2003 has been spectacular. He inherited a company that was just coming out of bankruptcy, and had suffered a bottom line loss of almost $900 million in 2001 on sales of $1.6 billion and a loss of almost a billion dollars on sales of $1.4 billion in 2002. Starting with his first year, and every year thereafter, except for a negligible dip in income in 2008 and revenue in 2009, Warnaco enjoyed double digit growth on all key metrics. The company sailed through the Great Recession as though it didn’t happen. Sales now stand at about $2.3 billion, operating margin at 11.4%, and operating income at $262.7 million.

Q.���Joe,�can�you�give�us�some�back-ground�on�the�turnaround�efforts�put�in�place�before�the�recession,�and�highlights�of �how�you�were�able�to�get�through�the�recession�with�only�minor�hiccups�and�outperform�the�majority�of �play-ers�in�this�industry?�Was�there�something�about�your�business�that�“insulated”�Warnaco�from�the�full�impact�of �the�recession?

A. The real power behind Warnaco, even going back to 2003, is our portfolio of great brands, with Calvin Klein the jewel in the crown. We also had incredibly good people in the business. The middle management teams were sound, and we added a new senior management team to guide them. That made a big difference in the culture of the company.

&A

> Continued on Page 3 > Continued on Page 2 > Continued on Page 14

Now you see it. Now you don’t. This time I’m talking about the US economy falling into what may seem to be, and may feel like, inflation, but only for a nanosecond. Then, like sleight of hand, we will seem to be entering into stagfla-tion, (characterized by high inflation coupled with high unemployment and stagnant demand). But that too, will be for just a nanosecond. Then, abracadabra, the final unveiling toward the end of 2011 and early 2012 will reveal what the economy has really slipped into. And, that would be deflation, or a decrease in the general price level of goods and services, occurring when the annual inflation rate falls below 0%, driven by high unemploy-ment, stagnant demand and overcapacity.

FROM INFLATION TO STAGFLATION TO DEFLATION By Robin Lewis

I’m back onto economic issues, and how can I not be? What a mess we are in. I honestly do believe we have reached the highest point in our so-called recovery. Read “From Inflation to Stagflation to Deflation,” and “Tech Bubble II,” and you will find a lot of not so tasty food for thought, including the following points:

• “Free money” donated by the Fed that will neither get businesses to hire nor consumers to borrow and spend

• Inflating costs that cannot be passed

along to consumers through increasing prices

• A further decline in the value of housing

DEAR READER

Qwith Joseph Gromek

www.TheRobinReport.com2

DEAR READER > Continued from page 1 I N S I D E T h I S I S S u E

• DeaR ReaDeR ..........................1Robin Lewis

• FRom inFlaTion To sTagFlaTion To DeFlaTion.…………............1Robin Lewis

• Q&a wiTh Joseph gRomek.…………....... 1Robin Lewis

• waRnaco in bRieF ...............6Judith Russell

• pRicing pRessuRe: how highis Too high? .......9 Kurt Salmon

• looking ouT FoR numbeR one .........…...10 Herbert Mines Associates

• woRking 9 To—9?!!............12Dana Wood

• my DReam inTeRviewwiTh maRTha sTewaRT.........18 Warren Shoulberg

• sTaRbucks anD gReen mounTain.…………..20Robin Lewis

• posT scRipT claRiFicaTionsanD coRRecTions ..............21

• Tech bubble ii.…………..……22Robin Lewis

• QuoTes To RemembeR……...24

• Another technology “bubble” due to the trillions in capital with no- where else to invest, which simply adds to the never-ending stream of “more stuff than demand warrants” (overcapacity), including the thousands of new commercial websites launching every day

• The continuing “sclerosis” in

Washington and inability to get our country’s financial house in order

• The continuing debt crises in Europe.

I believe this combination of events will push us into another recession, and worse, a deflationary spiral. While I’m not basking alone in such “dark-ness,” most economists are somewhat less pessimistic. However, there is one whose theory (depending on how one interprets it), is darker and more permanent then mine. Globally respected Tyler Cowen, with a Ph. D in economics from Harvard University and currently the Holbert C. Harris Chair of Economics at George Mason University, has just published a new book The Great Stagnation.

As reviewed by BusinessWeek, Cowen’s book describes how the US has gone through 300 years of economic growth simply based on “low-hanging fruit,” as he calls it: “free land, technological breakthroughs and smart kids waiting to be educated.” Now, he claims there is no more “low-hanging fruit” in the developed countries, including Europe and Japan. However, they have developed political, social and commercial institutions based on the assumption of endless growth. Based on these dynamics, Cowen’s answer for the cause of the recent financial crisis was that “we thought we were richer than we were.” Cowen summarily dismisses some of the more commonly held views on the cause of the crisis like free credit, mortgage manipulations, flawed ratings, and questionable financial practices across the industry. His theory points to a deeper, more fundamental problem, one that cannot be fixed by more “free money,” bailouts, tax cuts and regulations.

With the “frontier” being used up, so to speak, having “educated all of the farm kids, and built a couple cars for every family,” Cowen believes we might be done growing for a while. I’d say that’s a pretty chilling assessment, yet one that if understood in a “big picture” way, is spot on, in my opinion.

So, if this economy is the “new, rather anemic normal” with no robust growth to look forward to, or worse, we get a deflationary setback, as I predict, what is a business to do? Domestically: think smaller; think quality over quantity; think more efficient productivity; think more profitability. Globally: think expansion into the developing countries.

Have a good read!

Robin Lewis has over forty years of strategic operating and consulting experience in the retail and related consumer products industries. He has held executive positions at DuPont, VF Corporation, Women’s Wear Daily (WWD), and Goldman Sachs,among others, and has consulted for Kohl’s Department Stores, and dozens of others. In addition to his role as Publisher and CEO of The Robin Report, he is a professor at the Graduate School of Professional Studies at The Fashion Institute of Technology.

Robin Lewis and Michael Dart, in their seminal study of modern US retailing, examine why and how the industry is quickly evolving — and what it will take

to be successful in this new world. Critics and industry leaders agree: The New Rules of Retail is a must-read for anyone interested in the industry. Available at Amazon.com in hard cover or Kindle form, and at a bookstore near you, or on our website at www.TheRobinReport.com.

h a t c h i n g n e w i n s i g h t s

Issue Seven 2011 3

A. The first thing we did when the recession started was focus on reducing our costs. We knew US revenue was going to head south. We focused on corporate SG&A. We started using video conferencing instead of traveling around the globe, and did some other things as well, which helped cut expenses about 10%. We didn’t stop the growth initiatives we had in place, though. In fact, we opened up more square footage than we ever thought we could, and our international retail business continued to grow dramatically. These businesses give us our highest margins - in some cases almost double those in the US - offsetting what was going on in the US and parts of Europe as well. Heritage plus CK in the US dropped 11%.

Q.��What�was�the�overriding�strategy�of �the�company�when�you�took�over?�

A. In 2003-2004, we focused on efficiency and execution, and made some large strategic moves. One was to exit

manufacturing. We had swimwear and intimate apparel manufacturing operations in Mexico and the DR, but felt that brick and mortar was not the right thing for us, so we sold those businesses at a cost to us. Putting 6,000 people out of work was not something we wanted to do, so we found management to sell those facilities to so they would continue to run and support us. The other thing we did was to integrate sourcing into the operation rather than use agents. I brought in two former sourcing colleagues, and within days we had a 200-person owned sourcing operation at Warnaco. Service improved and costs were cut almost in half.

Q.�How�did�the�brand�strategy�evolve?�A. We went through a strategic review of our brand

portfolio, and decided it made sense to exit certain businesses and focus on others, and to look at some strategic acquisitions as well. First, we tried to buy the assets of Speedo from the UK-based brand owners, but they had no interest in selling the brand, because it’s such a nice source of cash flow for them. Neither

were they interested in buying the business from us. So we decided okay, it’s a great brand, we’ll keep it. The second thing we did was buy the balance of the rights to the Calvin Klein Jeans business. That suddenly produced a very different Warnaco. It gave us the global rights to Calvin Klein Jeans, European and Asian rights to accessories, and rights to the bridge collection in Europe. We became a $300 million business with a 10% EBITDA almost overnight, and today that business has doubled, and we’re truly a global operation. We’ve been able to renew all licenses with Calvin Klein Inc. (owned by Phillips-Van Heusen) for 40 years.

Q.��So�what�part�of �this�new�strategy�helped�you�weather�the�recession�better�than�your��peer�group�guys?

A. Our business had suddenly changed – Calvin Klein became the growth vehicle of the company. We would grow through international expansion. The CK Jeans

and Underwear retail businesses were about 15% of total sales, but now are 30%. We used the heritage brands Speedo, Chaps, Warners, Olga and others, which at $600 million in sales were 30% of the business, to be the cash generators. That’s been our strategy for the past five years. We also became retailers. On average we’ve been growing our

retail footprint by over 20% per year – this year alone adding 150K sq. ft., last year 200K. Our stores do on average $800 per square feet. So if we grow by 200K sq. feet we add $160 million to revenue.

Q.�What�about�swimwear?�A. Swimwear has been a good business. The Speedo brand

has a 70% market share of the $70 million competitive swimwear market in the United States. It’s bounced back since the recession, and provides a good deal of cash to support our other businesses. We’ve tried to get Speedo out of the water, onto the shore, but we’ve stubbed our toe. Next year we’ll see a revenue spurt – we get one every four years from the Olympics.

Q.��Since�close�to�60%�of �your�business�is�interna-

tional,�and�the�fastest�growing�segment,�how��do�you�manage�through�currency�fluctuations?

A. As the recession was taking hold and the dollar experienced some strengthening, we got caught with our pants down in the UK and Europe. We brought

with Joseph Gromek Q&A > Continued from Page 1

“I brought in two former sourcing colleagues, and within days we had a 200-person owned sourcing operation at Warnaco. Service improved and costs were cut almost in half.”

www.TheRobinReport.com4

with Joseph Gromek Q&A > Continued from Page 3

in a new treasurer in 2009, whose sole job is to manage the currency risk, and developed a hedging program to reduce volatility. We do business in 112 different countries, and have 6 baskets of currencies that we pay close attention to. When 60% of your business is overseas, it becomes much more complex.

Q.��Do�you�run�your�own�international�stores?�

And�where�are�they? A. Of our 2,000 points of distribution, we operate 1,400

ourselves, and we have 600 that third parties operate. Our stores are in Europe, Asia and Latin America. Brazil is our fastest growing market. Money-wise our biggest growth market is China. China will be the largest country other than the US. As a region, Asia will surpass the US within another 4-5 years. For most of the world, what we’re selling is aspiration. Our brands are also the entry-level price for the luxury customer. In the emerging markets, where we do most of our business, the luxury consumer population is growing rapidly, and really fueling growth.

Q.��What�do�you�think�the�global�awareness�

of �the�Calvin�Klein�brand?�A. The awareness factor is incredible. Neilsen did an

awareness study in India, and Calvin Klein was the #2 brand in awareness, after Chanel. We hadn’t even sold one piece in India. CKI spends close to $300

million per year marketing its image of modern, sexy, minimalist, downtown - which works in all geographies. In emerging markets, they wear a pair of underwear that costs $30 to show it, to say “I’m successful, and I’m wearing Calvin Klein underwear.” That’s been the reason for our growth.

Q.��Where�are�we�in�the�economic�recovery,�and�

when�is�the�end�of �the�recession?A. This is as good as it gets right now in the US. This

is the new norm. Q.��That’s�a�major�statement.�Everybody’s�talking�

about�recovery,�recovery,�as�though�it’s�going�to�go�back�to�the�way�it�was.�Given�that�statement,�what�will�the�inflation�effect�have�on�everything�across�the�board?�With�denim�such�a�large�part�of �your�business,�will�you�offset�cotton�price�increases�or�try�to�pass�them�along?�Are�you�forecasting�a�decline�in�number�of �units?

A. Inflation is real, costs are rising rapidly. We will certainly attempt to pass some of it along, but “can we sell the same quantities?” becomes the issue. I think consumers will acquire and purchase less. The demand curve will contract. In our own Calvin Klein stores we have the best chance. The intrinsic value is understood in a very different way. I think where we will have a greater challenge is in the domestic market here, and in

h a t c h i n g n e w i n s i g h t s

Issue Seven 2011 5

Western Europe. Denim represents about 30% of the $800 million CK Jeans business, or $240 million in revenues, which is 10% of corporate sales.

Q.�How�many�stores�do�you�have�in�the�US?�A. One store. We don’t have the rights to the Calvin Klein

jeans stores in the US. In the bankruptcy those were given back to Phillips-Van Heusen. They operate 125 factory outlet stores that we provide the product for, which are very profitable for them.

�Q.�Are�you�looking�for�acquisition�candidates?A. Our company generates free cash flow of about

$300 million a year, so we have the ability to add to the portfolio. We’ve been very quietly acquiring businesses, in China, Taiwan, Singapore, and in parts of Europe, but they were Calvin Klein distributor businesses. There are still 600 stores that we don’t control, so there’s opportunity to acquire more. We cut out the middle man, and get the full retail revenue. In addition, we’re looking for brands that have the ability to be global lifestyle dual-gender brands using our unique global infrastructure. But we don’t need an acquisition to grow, and we believe that our margins will continue to expand. We have what could be considered the best global life-style apparel brand today, and we can grow in double-digit fashion today. It’s a high-class problem. We have to find the right thing. We can’t allow the money we have to burn a hold in our pockets, though we have to be very judicious about this thing.

�Q.�Any�pressure�from�retailers�for�exclusivity?�A. One of the best brands we have in the portfolio is

Chaps. We’ve had the sportswear license since 1978, and 50% of the business is Kohl’s – the balance are other department stores. I think most people think Kohl’s has an exclusive. The brand has done incredibly well during the recession. We create the product in the Polo image (Ralph Lauren is the licensor). Last year it grew 21% for us. It’s a great product, a great license, and for us a great opportunity.

�Q.��Do�you�think�at�some�point�in�time�it�would�

give�you�a�greater�opportunity�to�have�any�of �your�main�brands�exclusive�with�a�particular�store,�for�example?

A. The Calvin Klein brand performs at a very high level at Nordstrom, Bloomingdale’s, etc., so when you’ve got that kind of power – I’m sure a dominant retailer would love to have it, but I don’t think it’s in the brand’s best interest to make it exclusive to one retailer.

Q.���If �a�department�store�were�to�begin�leasing�space�to�outside�brands,�would�you�be��interested?�I�always�use�the�example�of �intimate�apparel,�because�the�department�stores�have�been�losing�share�for�some�time�there.�How��do�you�view�that�whole�thing�going�forward?�

A. We operate concessions in 800 locations around the world. We control everything – the inventory, sales staff, marketing, fixtures – and it’s incredibly profitable. We own everything except the space, but we pay rent and take advantage of the store’s traffic. We have history with it globally, and we’d like to see it in the US. I think we’d win big if we were to do that. We’ve broached the subject, but since the retailer would not get the full retail, it hasn’t gone anywhere. As time goes on that might change.

�Q.��Calvin�Klein�represents�three-quarters�

of �your�business.�What�does�the�future�hold? A. We’re on track to double the business in five years.

Most of the growth will come from international expansion and our own retail initiatives. We think we can get that to north of 5,000 Calvin Klein Jeans and Underwear stores.

Q.��Is�there�a�threat�beyond�your�control�from�

the�other�licensees�if �they�do�something�to�taint�the�brand?�Critics�have�said�that�some�of �the�women’s�product�sold�here�is�very�mainstream.�Also,�is�there�a�black�swan�out�there�that��could�pose�risks?

A. Calvin Klein Inc. has very good brand stewards, and they’ve done a very good job policing the brand. The women’s sportswear products which are very popularly priced here have been very successful. Quality require-ments are different in Europe and Asia than in the US. We’re selling a $50 women’s jean in the US, but a $160 pair in Asia, and the quality is different. In other parts of the world we’re offering a more premium operation. You play to the market. The propensity to pay more for apparel is higher in Europe. They’re very fashion conscious, and clothing represents a bigger part of their personal budget, and we like that. We’ve added $1.1 billion in retail sales to the total sales of Calvin Klein over the past 8 years, and the folks at CKI appreciate the way we’ve been doing it. We have an excellent relationship with Tom Murray, Bruce Klatsky, Manny Chirico, and others there. The total Calvin Klein business is now over $7 billion at retail, a huge business. However, if we were to approach $4 billion, we’d be an even more important part of it.

www.TheRobinReport.com6

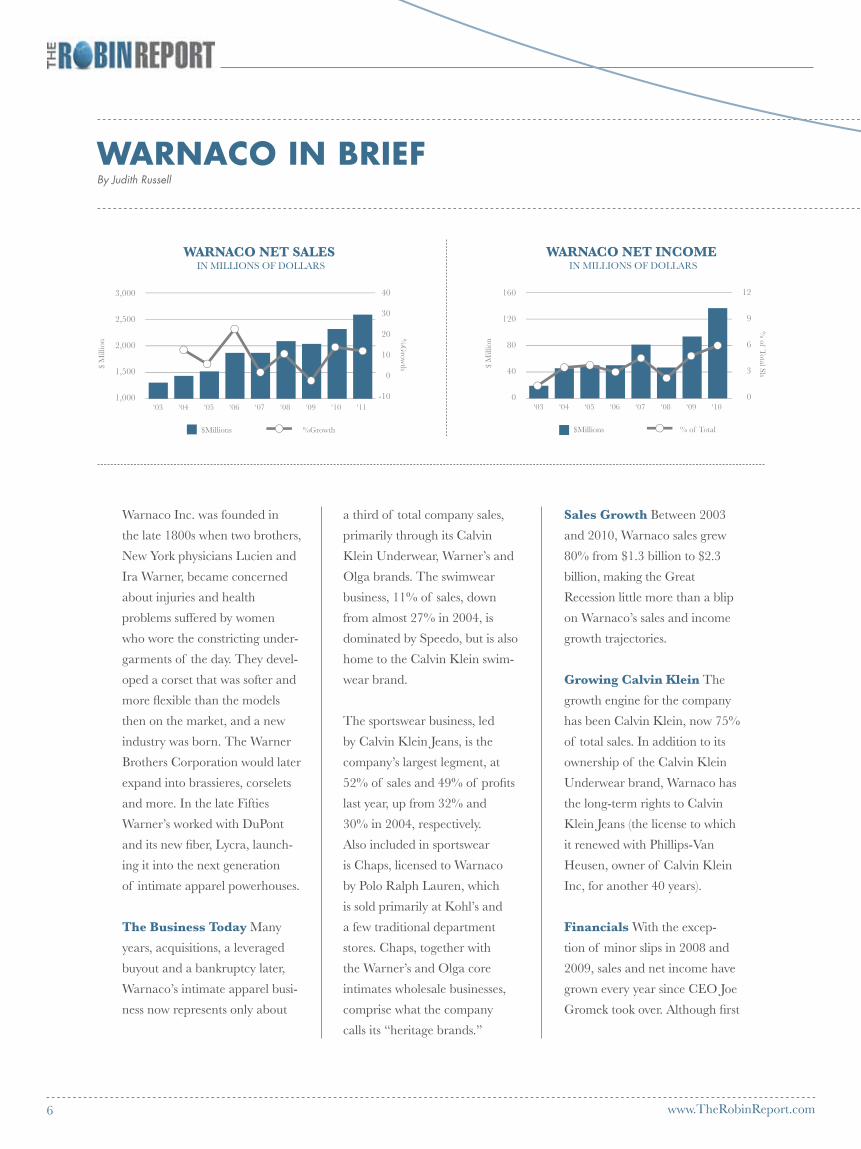

Warnaco Inc. was founded in

the late 1800s when two brothers,

New York physicians Lucien and

Ira Warner, became concerned

about injuries and health

problems suffered by women

who wore the constricting under-

garments of the day. They devel-

oped a corset that was softer and

more flexible than the models

then on the market, and a new

industry was born. The Warner

Brothers Corporation would later

expand into brassieres, corselets

and more. In the late Fifties

Warner’s worked with DuPont

and its new fiber, Lycra, launch-

ing it into the next generation

of intimate apparel powerhouses.

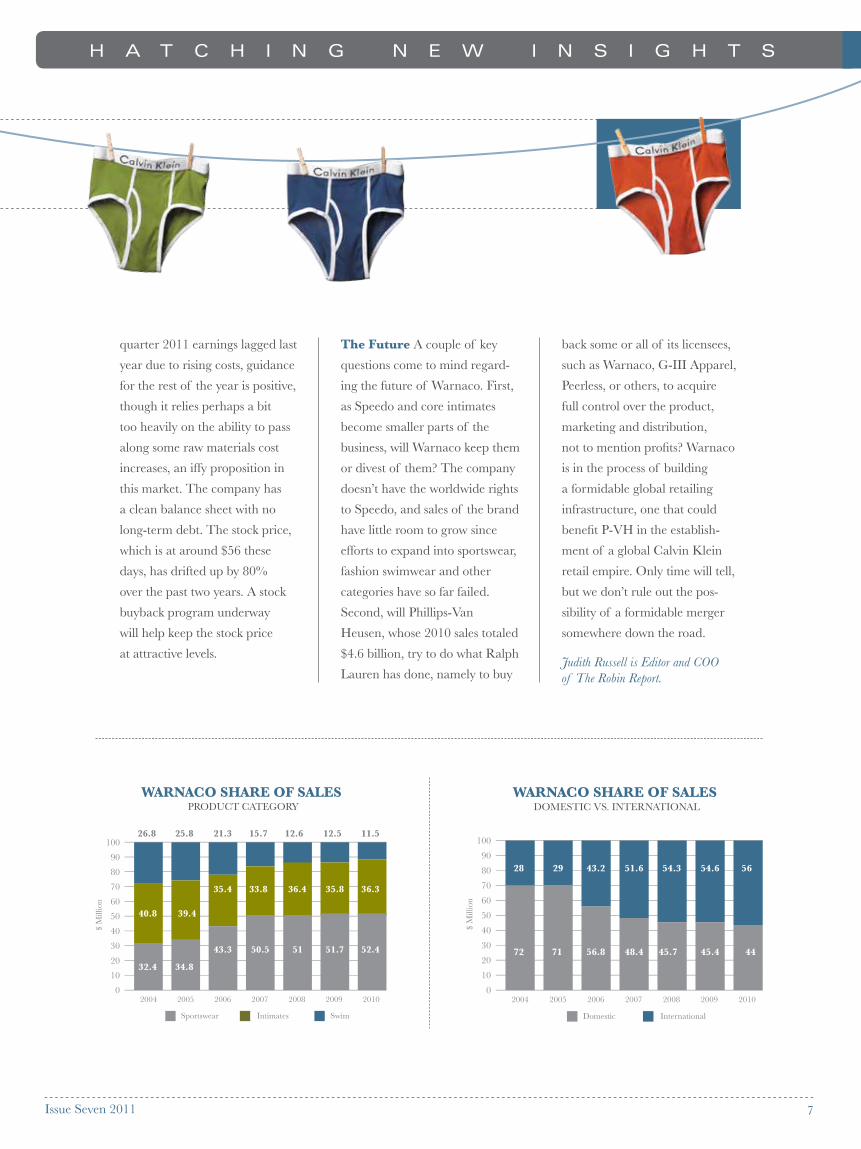

The Business Today Many

years, acquisitions, a leveraged

buyout and a bankruptcy later,

Warnaco’s intimate apparel busi-

ness now represents only about

a third of total company sales,

primarily through its Calvin

Klein Underwear, Warner’s and

Olga brands. The swimwear

business, 11% of sales, down

from almost 27% in 2004, is

dominated by Speedo, but is also

home to the Calvin Klein swim-

wear brand.

The sportswear business, led

by Calvin Klein Jeans, is the

company’s largest legment, at

52% of sales and 49% of profits

last year, up from 32% and

30% in 2004, respectively.

Also included in sportswear

is Chaps, licensed to Warnaco

by Polo Ralph Lauren, which

is sold primarily at Kohl’s and

a few traditional department

stores. Chaps, together with

the Warner’s and Olga core

intimates wholesale businesses,

comprise what the company

calls its “heritage brands.”

Sales Growth Between 2003

and 2010, Warnaco sales grew

80% from $1.3 billion to $2.3

billion, making the Great

Recession little more than a blip

on Warnaco’s sales and income

growth trajectories.

Growing Calvin Klein The

growth engine for the company

has been Calvin Klein, now 75%

of total sales. In addition to its

ownership of the Calvin Klein

Underwear brand, Warnaco has

the long-term rights to Calvin

Klein Jeans (the license to which

it renewed with Phillips-Van

Heusen, owner of Calvin Klein

Inc, for another 40 years).

Financials With the excep-

tion of minor slips in 2008 and

2009, sales and net income have

grown every year since CEO Joe

Gromek took over. Although first

WARNAcO IN BRIEF By Judith Russell

h a t c h i n g n e w i n s i g h t s

Issue Seven 2011 7

quarter 2011 earnings lagged last

year due to rising costs, guidance

for the rest of the year is positive,

though it relies perhaps a bit

too heavily on the ability to pass

along some raw materials cost

increases, an iffy proposition in

this market. The company has

a clean balance sheet with no

long-term debt. The stock price,

which is at around $56 these

days, has drifted up by 80%

over the past two years. A stock

buyback program underway

will help keep the stock price

at attractive levels.

The Future A couple of key

questions come to mind regard-

ing the future of Warnaco. First,

as Speedo and core intimates

become smaller parts of the

business, will Warnaco keep them

or divest of them? The company

doesn’t have the worldwide rights

to Speedo, and sales of the brand

have little room to grow since

efforts to expand into sportswear,

fashion swimwear and other

categories have so far failed.

Second, will Phillips-Van

Heusen, whose 2010 sales totaled

$4.6 billion, try to do what Ralph

Lauren has done, namely to buy

back some or all of its licensees,

such as Warnaco, G-III Apparel,

Peerless, or others, to acquire

full control over the product,

marketing and distribution,

not to mention profits? Warnaco

is in the process of building

a formidable global retailing

infrastructure, one that could

benefit P-VH in the establish-

ment of a global Calvin Klein

retail empire. Only time will tell,

but we don’t rule out the pos-

sibility of a formidable merger

somewhere down the road.

Judith Russell is Editor and COO of The Robin Report.

www.TheRobinReport.com8

h a t c h i n g n e w i n s i g h t s

Issue Seven 2011 9

PRIcING PRESSuRE: How HigH is Too HigH?By John B. R. Long III

Best Practices from Kurt Salmon

The industry knows consumer prices will have to rise this year. Now the question is: by how much? Thanks mostly to a dramatic rise in input costs, retailers are being forced to rework their pricing strategies, shifting focus from permanent markdowns to initial and temporary promotional pricing. But the current economic landscape — rising commodity and labor costs against a sharply falling dollar, tight credit, sluggish housing markets and cautious consumers — means retailers are particu-larly wary of passing along any significant price increases to consumers, especially on discretionary items. The challenge then is how to deliver acceptable margins and stave off competition while still maintaining brand position and retaining core customers. In short, retailers are overhauling the very core of their pricing strategies, asking: 1. Will my customers accept higherretail prices? If so, in which categories and by how much?Successful retailers will not assume they instinctively know the answers to these questions; instead, they will leverage multiple data sources to determine their customers’ likely attitudes and behaviors toward prices. For example, while it’s a fair assumption that wealthier customers with larger disposable incomes will be less impacted by price increases, retailers catering to this segment can still use data to understand the point at which these customers feel the impact of rising prices and which items create important price impressions on the rest of a retailer’s offerings. These insights can be gained through a combination of focus groups, historic elasticity curves, competitive intelligence, and a deep understanding of each category’s role in the overall assortment and price tests. These price tests may have surprising results — many retailers with whom we’ve worked report conducting selective price increases over the past several months and not one

reported a greater-than-expected drop in demand.

2. How can we ensure to continuallymaintain our price positioning relative to our competitors?The best way for retailers to maintain their relative price positioning is to leverage a series of processes and robust tools that continually monitor competi-tors’ pricing across all channels and enable quick adjustments to meaningful disparities. Leading retailers will also gather customer feedback to ensure that, in addition to these tactical maneuvers, they maintain their desired overall relative market positioning. Retailers often overlook market positioning, failing to recognize that customers can be influenced by effective branding and marketing campaigns that use emotion to overcome facts. 3. How do we determine prices at each stage — initial prices, temporary promotions and permanent markdowns — to optimize realized margin dollars?Each stage of the pricing continuum is addressed individually, yet within the context of an overall set of financial objectives. Of the three pricing stages, initial pricing likely offers most retailers the greatest opportunity for enhanced precision and margin improvement. Making this stage more thoughtful, scientific and consistent by incorporating a fact set of customer insights, competi-tive intelligence, historic analytics and category strategy will help achieve greater efficiency and precision. As retailers seek to protect margins, they may reduce the depth or length of promotional discounts; as a tactic, this may fail to stimulate sufficient demand from customers who’ve become accustomed to discounts of 50% or more. For permanent markdowns, many retailers have shifted to optimiza-tion tools that apply scientific algorithms to achieve specific margin results. In these last two pricing stages, retailers must not only monitor the effects of their price changes on customer demand, but must

also carefully monitor any price changes taken by their competitors across all relevant channels. Thankfully, some new monitoring tools can make this process more “real time,” consistent and fact-based.Once these questions are explored and answered, creating a singular, integrated pricing strategy with a defined process and specific owners for each step will help ensure these new pricing decisions are implemented correctly. This proactive process must establish objectives and align incentives across the organization (including merchandising, planning, marketing and store operations) to create and capture value most profitably. It is this cross-functional integration and orchestration that forms the essential backbone of any pricing strategy and ensures that every part of the organiza-tion shares a common set of goals.

As these pricing strategies are implemented, they may require:

• Visible and continuous sponsorship from senior leadership to ensure that everyone in the organization will embrace the changes

• Rethinking long-held pricing practices and organizational structures (such as the roles and responsibilities of those who manage pricing)

• New capabilities and tools to continually monitor, measure and manage the effectiveness of the strategy

• Mid-course corrections to address com-petitors’ moves and customer feedback

• An intense focus on change manage-ment at all levels

Above all, leading retailers will make a long-term commitment to building a strategic pricing capability, a likely mandate as retailing grows increasingly complex and competitive.

John Long has more than 20 years of deep experience in all facets of the retail and consumer products industry and leads Kurt Salmon’s strategic pricing practice. He can be reached at [email protected].

www.TheRobinReport.com10

Q���What kind of activity are you seeing right now in the executive ranks?

A Companies who had been averse to making changes when times were tough are now free to assess the level and effectiveness of their talent pool, so we have been seeing a lot of movement at the very top. As the retail environment has improved, and they can no longer blame the market, companies are taking a long, hard look at their executives.

Q��During the recession, executives were hunkering-down and not looking to change jobs. Do you find that executives are more willing to consider new opportunities now?

A Executives are beginning to move on from being happy just to have a job, a mindset of risk aversion, to considering new opportunities. The difficult housing market has made relocation more challenging. However, there is a lot of great opportunity right now for the person who is willing to consider change.

Q��What is the most effective way for executives to manage their internal promotability?

A Internal promotability is very specific to each company. The best thing you can do is prove yourself by doing your job well. However, if you want to broaden your

skills, the easiest place to do so is in your existing company. Ask for new tasks to broaden your horizons.

If you are in a finance role and you’d like to take on operations, ask for some new responsibilities that will round out your skill set and give you the opportunity to prove to your employer that you are capable of handling more.

Q��What about external marketability? A Of course, I am biased, but it seems absurd not to

at least take a look at what else is out there. Our job as recruiters is not just to convince people to make a move but to present them with a compelling reason to move — for a bigger, better job. You won’t know what is out there if you don’t look and listen. Also, part of being a professional manager is managing your own career, creating alliances with search firms, and learn-ing what’s going on in the competitive environment.

Q��What are the signs that an executive is ready for his or her next position? What advice would you give people who are ready for change?

A The worst thing you can do from a performance perspective is to allow yourself to be bored. If you feel like you’ve stopped learning, and are no longer excited about the job, maybe it’s time to make a change. Managing your career means taking on new challenges time and again. They’re out there – the business is not a static one. You need to constantly stay ahead of your game and ask yourself if you are growing.

ReFlecTions FRom The coRneR oFFice FRom heRbeRT mines associaTes

As the economic outlook has improved in the retail sector, so has the hiring landscape. We talked to Heidi Rustin, a Managing Director of Herbert Mines Associates, about the personal side of careerism, and what professionals should be doing to ensure promotability and maximize marketability in this fast-changing business landscape.

looking ouT FoR numbeRBy Heidi Rustin One

h a t c h i n g n e w i n s i g h t s

Issue Seven 2011 11

Q��Who bears the burden for grooming and growing executives – the company or the individual?

A It depends. There are some companies – particularly larger ones - that have a very specific track and a succession plan and are mindful of grooming their executives. If you work in one of those companies, make sure you understand how the track works. Work with the HR executive or your direct supervisor and really get your arms around what the metrics are to perform. If you work in a smaller company that does not have a track, you need to assume more responsibility for your own destiny.

Q���If you are not looking for a job and you don’t want to put your name in play, why should you take a call from a recruiter?

A Again, I’m biased! You might be well paid, happy and productive but there could be an even better opportunity out there but you will never know unless you listen. One of the reasons people are reluctant to cultivate relationships with the search community is they believe it sends a signal to the universe of being disloyal. But listening to what’s happening in your area of the job market is not a disloyal act. Also, and this is really important, you shouldn’t wait until you don’t have a job to look for one. People are more marketable when gainfully employed.

Q���Will you still pursue conversation with an executive who says “I’m not looking but I will listen”?

A Absolutely. We would have no practice if we didn’t have open-ended conversations. A high percentage of our placements were happy in their previous jobs.

Q���What advice would you give to someone who has been with the same company for a while and is thinking that because they haven’t moved, they may not be as well paid as they could be?

A The truth is if you have a long track record with one company, there’s a good chance that you maybe a bit salary suppressed. A move can provide you with economic opportunity, because most people won’t make a financially lateral move. At the senior level, you can do your own research by looking into company proxies for what executives make.

Q���Have there been instances where the candidate was reluctant but you knew that it was a great match and persevered?

A That happens a lot because people have preconceived ideas about what a company represents. I’ve had people say to me “I’m not an off-price retailer kind of guy” or “I’m a luxury exec” or “I don’t want to go contemporary.” And, in most cases when they further assessed the opportunity and got rid of these prejudices, they were pleasantly surprised and made a move.

Q���What are the biggest mistakes or pitfalls executives make in managing their careers?

A The first mistake is job hopping or, as we jokingly call it, “Job ADD.” It is hard to point to success when you haven’t stayed long enough to see your success through. Of course, sometimes you land in a job and it’s not what you expected, so you leave after a short time. It happens. When it’s recurring, however, it could be a problem. For example, if someone leaves after a short time when business gets tough, that’s not exactly evidence that you’re going to help your new company through good times and bad. The second biggest mistake is not to trust your gut. Make sure you allow your instincts to kick in wherever you consider moving and make sure it is a great cultural fit.

Q���One last question: When you send a candidate into a retail position, should he or she wear that company’s key designer?

A I actually think it can seem contrived unless you already wear it. But if you are going to interview at a contemporary brand, wear something contemporary. Don’t wear a buttoned down suit to a jeans culture company. Retail is an image-driven business and you need to convey the right physical presence and a sense that you “get it.” Although experience, skills and business acumen are most important, fitting into the corporate culture can be a critical element to success.

Heidi Rustin joined Herbert Mines Associates in 2003 and became a Managing Director in 2008. Her executive search practice is focused on the fashion, luxury and retail sectors with senior level placements in a broad range of disciplines including CEOs, Sales, Finance and Operations, Design, Creative Services, Marketing and Merchandising. She can be reached at [email protected].

www.TheRobinReport.com12

en years ago, the young women who would eventually band together and form the public relations firm DNA, planting their flag in the

‘burbs in Rye, NY, were hard-charging Manhattan beauty publicists, toiling for the big-league agencies. Though they worked hard, there was a basic framework around their days. Hitting the office at 9-ish, they dove into a round of press release-writing, calling magazines to pitch the latest miracle crème or hotshot hairstylist, and wooing the marquée-name editors over fancy lunches at the happening restaurant du jour. Save for the occasional evening press event, they could pretty much call it quits by 6.

Circa 2011, their day-to-day is very different, and not because they went the entrepreneurial route. Business is booming (roughly 30 accounts across all sectors of the beauty and wellness markets), so it’s not as if the founding partners - Dana Epstein and Lauren Kahn – are lying awake at night worrying whether they’ll make payroll.

But they just might be up at 3 a.m. for an altogether different reason: combing the internet for breaking news they can post to their clients’ blogs, Facebook pages and Twitter accounts. Oh – and can’t forget Flick’r and YouTube.

“The digital world works at warp speed,” says Kahn. “Not immediately capitalizing on a story that hits the Web positions our clients as ‘me too’ rather than cutting-edge. So we scour the internet, linking, hashtagging and tagging our clients’ products and services.”

Clearly, this is now an almost 24/7 gig. “There are no 9 to 5 publicists anymore,” says Kahn. “If someone tells you otherwise, they simply aren’t doing their job.”

Although DNA clients possess varying levels of tech-savvy, each and every one is positively convinced they need to have a social media presence. So to that end, there is now a digital component to every pitch and brand-building plan DNA presents.

And thanks to this broadened portfolio of client expecta-tions, DNA has found itself firmly entrenched in the customer service game. Yes, in addition to strategizing public relations – a big-enough chunk of a business to claim, one might think – DNA is now on tap to interact

directly with consumers. Basically, this is an entirely new layer of service publicists are routinely delivering, one that didn’t exist in the pre-digital days.

Let’s take DNA’s biggest social-media success story to date – Hard Candy - as an example of this shift. When the agency first came on board to do publicity for the edgy and beloved makeup brand, Facebook and Twitter hadn’t even been hatched. But within one year of putting a digital program in place, Hard Candy now has well north of 17,000 Facebook fans, many of whom interact frequently with the page, commenting and posting. (Occasionally complaining, too, which we’ll get to in a minute.)

The general hubbub on the Hard Candy page is the surest sign, says Kahn, that DNA has scored a home run for its client. “On many, many Facebook brand pages you’ll see tens of thousands of fans but very little interaction, from ‘likes’ to commenting on updates or links,” she notes. “That means people are hiding or ignoring the news.’”

But since it prides itself on responding to virtually every chirp and peep from Hard Candy’s fans, no matter how seemingly mundane and un-important (I’m sorry, but that applies to a good 90 percent of the chirping and peeping on Facebook), that means DNA has to monitor the page constantly.

On a recent Wednesday, for instance, there were multiple comments and postings on the page, and DNA, posing as Hard Candy, got right in there, feed-backing on just about every one, including this punctuation-challenged request:

Katie Burns Gq: “You should have coupons for birthdays mine is coming up this friday and nothing can get better than using a coupon on ur fav product.”

Hard Candy: “Working on coupons as we speak Katie! We’ll keep everyone posted. Won’t happen by Friday but Happy early Birthday anyway!”

For the record, “Katie” wrote in at 3:53 pm. “Hard Candy” responded at 5:02 pm. That’s pretty solid customer service.

T

WORKInG 9 TO – 9?!!Publicists in the Digital Age Get no Beauty SleepBy Dana Wood

h a t c h i n g n e w i n s i g h t s

Issue Seven 2011 13

While they don’t list it in the “Services” section of their own website, DNA is essentially providing what SEM (Search Engine Management) company Anvil Media calls Online Reputation Management. To hear Anvil tell it, companies that don’t have a similar type of technology watchdog in place can be in for serious brand erosion. “Just because your company isn’t actively involved in social media communities doesn’t mean your customers and constituents aren’t,” reads an ominous entry on the Anvil website. “In fact, industry research tells us that quite the opposite is true: your Web-savvy customers own your brand online. So if you’re not getting in on the conversation, you expose yourself to tremendous risk.” But isn’t Kahn pining for those long-ago Luddite days, when round-the-clock account maintenance wasn’t part of the equation, and she could consider a two-hour editor schmooze-a-thon over lunch at the Four Seasons a smashing success?

It certainly doesn’t sound like it. “A running theme for each of our clients is that they’ve heard from customers that their service is impeccable,” she says with pride, and not an ounce of disgruntlement at how much the game has changed since the world became welded to its hand-held devices and Twitter feeds. “Opportunities happen all the time, and I want to make sure my clients jump on them. I’m driven to provide the highest ROI possible. It’s safe to say we all are.”

Dana Wood has served as Beauty Director for both W and Cookie magazines, has written for numerous national publications including Glamour, InStyle, Harper’sBazaar and Self, and spent several years in the Luxury Products division of L’Oreal as Assistant Vice President, Strategic Development. Her first book, Momover: The new Mom’s Guide to Getting It Back Together, was published in 2010 by Adams Media.

Clearly, this is now an almost 24/7 gig. “There are no 9 to 5 publicists anymore,” says Kahn. “If someone tells you otherwise, they simply aren’t doing their job.”

www.TheRobinReport.com14

This can turn into a spiraling cycle of price declines ultimately resulting in the feared “double dip” recession, if not worse.

Following is a scenario of how this journey unfolds.

ThE ILLuSION OF INFLATIONThe Producer Price Index (PPI) has been increasing at accelerating rates for the past several months, rising 7.3% in May, excluding services and falling home prices. Intermediate goods prices rose an annualized 10.3% in the most recent month. Further, the broad retail sector, including most consumer goods wholesalers, have been rail- ing for months about the rising cost of manufacturing, ingredient products, oil, food, international labor, transportation and distribu-tion. All combined, cost increase

estimates range anywhere from 10-20% across the board.

So, let the debates begin, about whether retailers should increase consumer prices, and/or about how much and in what categories to pare back on purchasing, in anticipation that consumers will buy less.

As of this writing and going into the last half of the year, retailers have made a combination of selective price increases and unit reductions based on lower forecasts for consumption.

In a true inflationary environment, characterized by too many dollars chasing too few goods and spawned by the Fed unleashing billions of newly minted dollars, buying back treasury bills and keeping the federal funds rate near zero, the theory goes that with all of this “free” money in the hands of consumers, they would not only accept higher prices, but buy two of something instead of one, anticipating that prices would increase even further. Accordingly, they would demand higher wages, driving businesses to raise prices again. Consumers and businesses would borrow more, ultimately driving government to increase interest rates, etc. and so forth. This is the upward inflationary spiral.

Well, the inflation theory doesn’t work in today’s reality. Of each dollar spent by the Fed, (of the

total of $684 billion of new funds injected to-date into the banking system to jump-start lending and economic growth) less than 50 cents is making its way into the “real” economy. The current reality is that roughly 9% of the eligible workforce is still not employed, many having homes foreclosed upon (with home prices still dropping), and still trying to pay down debt while also increas-ing their savings rate. Businesses are sitting on close to $2 trillion in cash because they don’t see consumer demand justifying an investment in expansion and growth, (including

hiring). So, this inflation won’t make it to anything that even looks like an upward spiral.

Instead, consumers are going to take money from their clothing, entertainment, “eating out” budgets, or other discretionary parts of their wallet, to pay for the rising prices of food, gas and other essential goods and services. And, the makers and sellers of all the non-essential stuff, who have selectively increased prices, will end up putting that stuff on sale and taking the hit to their bottom lines. And, they will buy fewer units going forward. Some retailers, like Dollar General, will not raise prices, publicly stating they would take the hit on gross margin growth to maintain or hopefully gain share of market.

So, what this situation might feel and look like is stagflation.

ThE ILLuSION OF STAGFLATIONStagflation, as named by British politician Iain McLeod in 1965, is characterized by high inflation coupled with high unemployment and stagnant demand. The US experienced a serious bout with it in the late 1970s, and many economists believe it was triggered by OPEC drastically increasing the price of oil.

The same triggers that lead to inflation - a flood of easy money, low interest rates and rising prices - can also drive stagflation. However, stagnant demand, accentuated by high unemployment, is also a required ingredient. So, in our current economic environment, it would seem that we are more likely to be entering a period of stagflation.

Professor Ronald McKinnon at Stanford University, who is also a senior fellow at the Stanford Institution for Economic Policy Research, takes us a step further

FROM INFLATION TO STAGFLATION TO DEFLATION > Continued from Page 1

This can turn into a spiraling cycle of price declines ultimately resulting in the feared “double dip” recession, if not worse.

h a t c h i n g n e w i n s i g h t s

Issue Seven 2011 15

in understanding the stagflation scenario. He believes global monetary fluctuations, and the US failure to adopt an exchange rate objective, has caused the surge in inflation in emerging markets which ultimately loops around to a rising CPI in the US.

Secondly, he refers to the huge increase in excess reserves or “base money” in the US banking system, which has virtually tripled since 2008 as a result of the Fed’s spewing dollars into the system with the two stimulus packages, QE1 and QE2 (named from “quantitative easing,”) which were expected to be used for consumption and business investment and, ultimately, increased employment.

McKinnon specifically emphasizes the fact that the primary engine for increasing employment in economic recoveries has been the small and medium-sized business employers, or SME’s. And, their main source for working capital and credit lines is from the banks.

Well, as stated, along with the nearly $2 trillion of cash sitting in the coffers of large corporations not being invested in growth or hiring, the banks are also sitting on billions of “base money” reserves, and they are not lending. Neither has seen a return to consumption; indeed, they must be seeing stagnant demand.

So, stagflation it must be?

Not so fast. Don’t touch that dial. Do not be lulled into the belief that stagflation is the new normal, or reality. Reality will come in the form of deflation.

ThE REALITy OF DEFLATION Deflation can be driven by (or at least exacerbated by) high unemployment, stagnant demand and overcapacity. Its effect is economically catastrophic, and

its vicious spiral of feeding on itself, ever-downward, makes it almost impossible to reverse, as demon-strated by Japan’s past two decades of struggling along the bottom.

My prediction, amidst the chatter and predictions of many economists about the dangers of inflation or stagflation, and as put forth in Issue 3 of The Robin Report late last year, is that many economists and business leaders will be confused by what I believe will be erratic cost and pricing dynamics going into the last half of 2011. And, the confusion will be heightened by the consumer response, which will ultimately lead to a clear understanding of the fact that we are not heading into inflation or stagflation, but caught in a deflation-ary cycle, similar to the one that housing is currently experiencing.

And, I have some not too shabby support for this prediction. Supply-side economics pioneer and Nobel Laureate Robert Mundell, as reported in the Wall Street Journal, said that dollar weakness (caused by QE1 and QE2, and leading to higher oil and commodity prices – a precursor to broader more damaging inflation), is not his main concern. Instead, he fears a return to recession later this year when

QE2 ends and the dollar begins its inevitable rise. He states that deflation, not inflation, should be the greater concern.

The key point regarding his deflation prediction is that exchange rates transmit inflation or deflation into economies by raising or lowering prices for imported items and commodities. So, when the dollar declines significantly against the world’s second leading currency, the euro, commodity prices rise, which in turn creates US inflation-ary pressure. Conversely, when the dollar appreciates significantly against the euro, commodity prices fall, which leads to deflat- ionary pressure.

So, just as the dollar declined against the euro from 2001-2007, due to the Fed’s suppression of the federal funds rate to pull us out of a recession, the same dynamics are occurring now, only with greater force (including QE1 and QE2), due to the severity of this recession.

Mundell tracks the monetary events to make his point. In response to the dollar’s decline during 2001-2007, investors diverted capital into inflation hedges, notably real estate, leading to the housing bubble and the horrific leveraging of global

www.TheRobinReport.com16

debt. He claims the bubble burst in 2007, followed by the Fed quickly reducing short-term interest rates, further lowering the dollar. How-ever, as severe as the subprime crisis was, with looser money the economy seemed to be stabilizing in the sec-ond quarter of 2008. But then in the summer of 2008, Mundell says the Fed made one of the worst mistakes in its history: in the middle of the real estate crunch – made worse by “mark-to-market” accounting rules requiring banks to cover short-term losses, the Fed paused in lowering the federal funds rate. The result: in a few short weeks the dollar shot up 30% against the euro.

This dollar scarcity, according to Mundell, broke the economy’s back, led to the economic collapse and financial meltdown.

So, back to tried and true tactics goes the Fed. In March of 2009, they enact QE1, lowering the dollar against the euro, and we begin to feel a recovery. But, again, it’s another illusion, proven by the fact that in November of 2009, they ended QE1, and, again, the dollar soars over the euro pushing us back toward recession. So, what does the Fed do? They enact QE2, and again, it lowers the dollar and we are led to believe we are once again headed to recovery.

Then, I ask, if we are to believe Mundell’s prediction, what will happen when the Fed ends QE2 as they are expected to do in June?

Like a yo-yo, is not the dollar going to soar beyond the euro, just as it did twice before? And, if so, will we slip back into recession, including the dreaded deflation?

And, if we do fall backward again, will the Fed play a QE3 yo-yo? With the political pressure on our country’s debt and deficit, I don’t think so.

Mundell says that even if the Fed plays the loose money game again, it will just remain a band-aid, without curing the cancer. His solution: have the US Treasury fix the exchange rate between the dollar and the euro to maintain an upper and lower limit on the euro price, say between $1.30 and $1.40. He says over time the band would narrow to a given rate, and such a fixed exchange rate would allow prices to move free from the scourge of sudden deflation and inflation, allowing investment and planning timelines to expand along with pro-duction levels in Europe and the US.

BuT ThIS TIME IT’S DIFFERENT AND WORSEAs much as I respect Robert Mundell and appreciate his brilliant view, and particularly because it adds great weight to my own prediction, I do believe there are a couple of additional and major points to be made about a difference between the recovery from the recession in the early 2000’s and the one we are currently “recovering” from. And, I believe they simply intensify Mundell’s prediction.

One big difference between then and now is that when the Fed loosened the money supply in 2003, the government, with the help of the “financial engineers” on Wall Street,

found a new bubble to inflate to get the economy growing again: hous-ing. And, as we now know, ‘growing’ was an understatement. As I have said before, it was more like a legal Ponzi scheme on steroids. Thus, the effects of its collapse were apocalyptic.

So, Ben Bernanke is left with a bigger mess than his mentor had faced. And, worse, do you see any new growth bubbles forming that Wall Street can work its alchemy to spread the risk and outsized profits around the world? I don’t think so.

There are some murmurings among economists that a new tech bubble is inflating once again, this time in its third iteration, with a focues on consumer markets, every pricing and promotional gimmick you might conjure up, social networking, etc. and so forth.

However big the potential of this bubble might be, I do not believe it has the leveraging power or the capacity for global finance to cata-pult entire economies around the world, as did the housing bubble.

The second major difference: overcapacity marches on; too many stores; too much stuff; and now a million web-site stores popping up on the Internet every day, all of which will drive deflation deeper and faster and longer.

OuR “MANAGED” AND FLAWED FREE MARkET SySTEMAs opposed to focusing on the demand side for consumption growth (where we have been since WWII), I suggest that we are, and have been for some time, facing a supply side problem that reveals a major flaw in our now somewhat ‘managed’ free market system.

Overcapacity is being perpetuated through new business entrants

FROM INFLATION TO STAGFLATION TO DEFLATION > Continued from Page 15

h a t c h i n g n e w i n s i g h t s

Issue Seven 2011 17

adding to the supply side at a faster rate than those leaving, and all of it compounded by slow and slower growth on the demand side. If this is so, it’s possible that no amount of stimulus to increase consumption will stop deflating prices, simply because a new paradigm now exists, with an eternal disequilibrium of too much supply driving an unre-lenting downward pricing spiral.

As I’ve stated many times, every-thing is on sale all the time and shipped for free. Retailers have shifted their pricing structures (good, better, best), down. Outlet stores are growing faster than full price stores, even in the luxury sector. ‘Flash sales’ and ‘Groupon’ and all other kinds of on-sale online models are proliferating at the speed of light. What’s more, if you wait for two seconds, your smart phone will beep with an ad or a friend telling you where you can get whatever it is you’re thinking of buying, cheaper.

And, of course, the biggest undertow of them all is housing. As of this writing, home prices have dropped to the level they were in 2002, which essentially means that a decade of home equity just disappeared. As homes are consum-ers’ biggest investment in life, and a major source for spending dollars, the effect this continuing decline is having on the recovery is devastating. Worse, roughly 25% of homes were mortgaged at a higher value than the homes are now worth, and still falling. And, experts don’t see an end to this downward spiral. Sounds like a deflationary sector to me.

Across the entire marketplace, value is being recalibrated – down. And, it will continue, even as businesses

“selectively” raise their prices to pass along inflating costs. They will not stick.

ThE PERPETuATING OvERcAPAcITyI maintain that even if demand were to increase, excesses on the supply side will continue to proliferate, because marginal players are not disappearing from the supply side quickly enough. The immutable theories from “Economics 101” are being reversed and we have no tracking or measuring devices to see such a fundamental transformation. The free market forces that have historically eliminated excess are impeded by: • The liberal and “strategic”use (or misuse) of bankruptcy during which businesses shed debt, renegotiate contracts and emerge as new low cost competitors. Over-capacity is preserved and the new company drives another round of price decreases • An endless pool of invest-ment capital willing to “prop up” the losers or ostensibly to turn them around. In many cases they act as “vultures” whose ultimate goals are purely financial • An immeasurable and increasing global flow of new businesses adding to the supply side while consumption demand is either slowing or at least not balanced against supply, exacer-bated by the two previous points

• Finally, of course, the un-relenting acceleration of ecommerce,with virtually no barri-

ers to entry, including financial. This is an unprecedented phenomenon, and there are no measures that indi-cate these enormous additions to the supply side are being offset by cor-responding declines in the ‘brick and mortar ‘ or any other retail sector.

Can lower interest rates or extra dollars in the pocketbook stimulate consumer purchases in such an environment? I think not, at least not enough to absorb the relentlessly growing and excessive amounts of stuff being tossed into the market-place, which has many markdowns built into it before it even hits the shelves, and tomorrow, and the next day, and the next, even lower.

And today’s consumer knows it, and doesn’t need it, and eventually will wait for tomorrow and the next day and the next. They are already behaving this way in the housing market, as it continues to plum- met. Owning a home used to be considered an investment. Now it’s considered a risk.

So, the potential, and in my view, probability for deflation exists. However, it will be driven by infinitely growing overcapacity on the supply side.

What happens next? The hope is that the demand-side stimulants will elevate demand in tandem with some rationalization on the supply side, a shedding of the excess, so to speak. The result: a relative equilibrium of supply and demand, poised for a new round of healthy growth.

Don’t bet the bank on it.

Across the entire marketplace, value is being recalibrated – down. And, it will continue, even as businesses “selectively” raise their prices to pass along inflating costs.

www.TheRobinReport.com18

Warren: So, Martha – you don’t mind if I call you Martha, do you? You recently announced you were putting your namesake company into play, making several executive changes, and seemingly taking on a larger role in management. Your business has been caught in the twin vortex of both the retailing and media meltdowns of the past few years. Can you tell the readers of The Robin Report why exactly you’re putting the company up for sale?

mega media merchandising mother martha (mmmmm): Robin, hmmmmm? You know, Robin’s Egg Blue is one of my favorite colors - I use it all the time when I decorate. It’s particularly great on walls, on ribbons, and, of course,

on egg shells. But you seem to be flesh-colored. Would you like my people to dye you the color I know you should be?

Warren: No, but thanks anyway. And my name’s Warren. Anyway, why now to be putting the company up for sale?

mmmmm: Well, you see -- I’m sorry, what was your name again? – I believe the stock market is undervaluing the company which I own and manage and which is, by the way in case you hadn’t noticed, named after me. And rightly so, since let’s face it, I am the company. More chamomile? I had my people grow it on my estate in Bedford.

Last night I had the craziest dream, where I was actually interviewing Martha Stewart herself. Of course it was all just a dream and it never actually happened, but it seemed so real! (Must have been a damn Rachael Ray recipe that made me dream this; I knew I should stick with Martha’s.) I asked her a lot of questions I’ve been dying to know the answers to, and, well…here’s what I remember from the dream:

my Dream interview with maRTha sTewaRTBy Warren Shoulberg

h a t c h i n g n e w i n s i g h t s

Issue Seven 2011 19

Warren: But you have to admit your business is not what it used to be. Your big Kmart merchandising deal is over and all the smaller ones you’ve cobbled together with Macy’s, Home Depot and even Pet Smart, they’re just not the same. You used to have your TV show on the big networks, even a prime time reality series, but now you’ve got to search the really, really high numbers on cable to find your show.

mmmmm: Would you mind moving over here to this other table? I just had my people hand-stencil those placemats in a Pennsylvania Dutch motif, and they’re not quite dry. Warren: Huh? Oh, sure. Anyway, your flagship Martha Stewart Living magazine has suffered like all the rest of the home and shelter magazines, but it’s not really feeling much of the rebound some of them are having this year. You’ve got a lot of competition, now. It’s not a great story to take to a potential buyer, is it? mmmmm: Would you like to try one of these Meyer lemon squares? I had my people make them themselves. Notice the evenly sprinkled powdered sugar, and how they’re perfectly shaped. Warren: But what about the shape your company is in? mmmmm: Listen, I invented the entire idea of integrating media and merchandising. All of these websites combining content and product – like Gilt Groupe - think they’re so smart, but I’ve been doing that since 1995. Nobody else understood you could use media to promote your merchandise, which would promote your media, which would promote your merchandise.

It’s not my fault that that putz Eddie Lampert came along and bought Kmart. He wouldn’t know the difference between a spatula and a spittoon. He thought he didn’t need me. Everyone needs Martha.

So, who’s he left with, Jaclyn Smith? Pleeeese. Maybe she was a Charlie’s Angel, but my people could make an angel food cake she would die for. Oh, and have you seen the Christmas tree angels I had my people carve out of real aspen wood from Aspen and embellish with glittered wire-framed tulle wings?

Warren: What about the Macy’s program for home you have? It’s not doing badly, though the volume can’t be producing anywhere near the royalty checks you used to get from Kmart.

mmmmm: That’s a lovely notebook you have, but did you know my people can make paper out of rutabaga and prune waste, and press it with rosemary blossoms? It’s eco-friendly, long lasting and very tasty.

Warren: Macy’s? mmmmm: I sat down with Terry Lundgren and told him, “Don’t screw this up like Eddie did.” As a result, Macy’s is a good program. And if a lot of the designs look pretty close to what we did for Kmart, hey, that’s my people who did that, not me. I told Macy’s they should open another 1,500 stores so we could do the volume we did with Kmart, but they don’t seem to be listening. I don’t know why they don’t listen to me. I’m never wrong.

Warren: Not everything is working the way it should with your licensing. Your deal with Bernhardt for furniture has ended and there’s no replacement licensee in place yet that we know about. mmmmm: Would you like to try one of these credenzas? I had my people make them themselves. You know, I could have my people make all my furniture themselves, that’s how good I am. Maybe that’s why I’ll do. Warren: So, what’s next? Anything you can share with us? Any new recipes? Gardening tips? mmmmm: I’m thinking if Rupert Murdoch or Si Newhouse buys me, I can give them lots of tips, help them straighten out their companies. Lord knows they could use my help. Conde Stewart? I like the sound of that. But they won’t get me cheap.

Warren: Throughout your entire merchandising career, you’ve been one of the most successful names ever to segment the marketplace and place your brand at multiple levels and into multiple channels of distribution. Hardly anybody has been able to pull that off. How do you do it?

mmmmm: Well, I am, after all, me.

Warren Shoulberg has been reporting on Martha Stewart since the early 1990s and is now editorial director of several Sandow Media business titles. He is working on his new book, Stupid Business. As is the case with this interview, neither Martha nor her people are in it.

my Dream interview with maRTha sTewaRTBy Warren Shoulberg

www.TheRobinReport.com20

STARBuckS AND GREEN MOuNTAIN SInGle-Serve deAl IS PreemPTIve dISTrIBuTIon on roCKeT Fuel By Robin Lewis

Out of the starting gate, it appeared that Starbucks understood preemptive distribu-tion until they didn’t, which resulted in a near death experience that finally jolted them awake like a strong cup of Java. Not that the misunderstanding of preemptive distribution alone brought them to near death, but it was a major factor.

During its explosive growth phase bet- ween 1995 and 2009, Starbucks grew from under a thousand stores to almost seventeen thousand. One could literally be spotted on just about every corner. And, Starbucks was not shy about its long-term goal, to reach twenty-five to thirty thousand stores. The company was so committed to this frenzied expansion that it was distracted away from its histori-cal focus on the brand’s signature experi-ence, that connection with consumers that had them hopelessly hooked and willing to pay premium prices (which, incidentally,

earned the brand the nickname “four-bucks.”) At the point in their accelerated growth trajectory at which they opened one too many Starbucks locations, they verged on becoming ubiquitous. What consumer wants a watered down Starbucks experience on every corner?

Preemptive distribution does not mean ubiquitous distribution (everywhere, all the time). It means being precisely where your consumer wants you, when they want you, and how often they want you. And, it means being there ahead of (preempt-ing) the hundreds of other equally compelling brands. It’s not buckshot distribution. It’s surgical, laser-like and in-stantaneous distribution. Therefore, it also means distribution through every elec-tronic and physical distribution medium available that connects with the brand’s core consumers, and, it potentially means that a brand may distribute through

a competitor’s medium. So, ubiquity and the loss of the brand’s “soul,” began the meltdown, luring former CEO, Howard Schultz, out of retirement in 2008 to fix it. In an internal memo he criticized the loss of some of the “romance and theater” along its growth trajectory. Schultz’s assessment of the decisions he made in favor of growth was stated in the memo: “Over the past ten years, in order to achieve growth, development, and scale necessary to go from less than 1,000 stores to 13,000 and beyond, we have had to make a series of decisions that, in retrospect, have led to the watering down of the Starbucks experience and what some might call the commoditization of our brand. Many of these decisions were probably right at the time, and on their own merit would not have created the dilution of experience; but in this case, the sum is much greater and, unfor-tunately, much more damaging than the individual pieces.”

From uBIQuITy To PreemPTIve dISTrIBuTIon Recovering Starbucks experiential DNA was job #1 for Schultz upon his return. And, simultaneous with this effort, during 2009, some 1500 stores were closed. Schultz’s efforts in reestablishing Starbucks as the “third place” unique experience has been paying off, and is becoming the biggest competitive preemptor of all for the brand. Simply, a Starbucks “addict” will travel across town for his or her “fix” when a competi-tive coffee shop might be right across the street, which has debunked the original thesis that a Starbucks on every corner was a preemptive advantage.

Schultz further expanded and strength-ened the brand by means of social media, implementating e-and-mobile commerce initiatives like a Starbucks Card eGift and creating a variety of apps, like the My Starbucks iPhone app, Rewards Program, and others.

h a t c h i n g n e w i n s i g h t s

Issue Seven 2011 21

And, most recently, Starbucks is pursuing what my co-author and I have defined in our book The New Rules of Retail as part of the Third Wave of preemptive distribution: pursuing synergy-creating third party distribution mediums.

With a strategy to diversify into multi-channels and multi-brands, Starbucks launched into supermarkets with the Starbucks brand, then added its VIA Ready Brew instant coffee, Frappuccino beverages and the Tazo tea brand. These were followed by an expansion of its strategy for its subsidiary Seattle’s Best Coffee into 40,000 locations worldwide.

A meTeorIC SynerGy WITH Green mounTAInNow Starbucks could be latching onto a rocket-fueled ride to co-dominate the fastest growing coffee distribution model: single-cup brewing. Green Mountain Coffee Roasters, with its Keurig system, owns an 80% share of the single-cup brewing market in North America, and has agreed to partner with Starbucks. Both will integrate their distribution and product portfolios in what investors have voted will be a win-win synergy and a meteoric growth opportunity.

In the single-cup market, while Green Mountain owns an 80% share, Starbucks research indicated that 80% of its customers do not yet own a single-cup brewer. Further research points out that in 2010, 86% of coffee drinkers made coffee at home, up 4% from 2009.

On top of this “low hanging fruit” Starbucks will sell the Keurig system and its own K-cup coffee packs in its over 11,000 shops in North America. Green Mountain projects sales of seven million brewing machines in 2012, and expects to be in 30% of US homes over the next three years.

One analyst predicted the partnership will yield an additional one million brewer sales for Green Mountain and 600 million Starbucks K-cups in the first year.

SynerGy-CreATInG PreemPTIve dISTrIBuTIonWe will begin to see an acceleration of this type of synergy-creating preemptive distribution. We have provided numerous examples in recent articles of The Robin

Report where the combining of brands such as Sephora, Mango and JC Penney, Sun Glass Hut and Macy’s, Whole Foods and Forever 21 and Sears, drives fundamentally new traffic.

Recently, I’ve noticed that Kroger will be selling Bombay home furnishings in 180 of its stores. The Gilt Groupe is about to launch gourmet foods for sale on its site, (not as flash sales, but 24/7). Radio Shack is referring to itself as an “agnostic, multi-carrier” provider of prepaid and subscription cell phone services, featuring T-Mobile kiosks in its own stores. Target will have Verizon kiosks in its stores.

For those of you who are making this strategy a priority, and are proactively (vs. opportunistically) pursuing its imple-mentation, the win will be enormous.

In this worsening “share wars” environment, topline organic growth is near impossible. You need to steal a consumer from a competitor or get your customers to buy more from you, and more often. By combining two different, but compatible brands and/ or product categories, a business can accomplish both. It’s happening.

Now it’s your turn - just do it!

After the original version of Issue Six’s feature article, “Is the Liz Claiborne Board Missing in Action?” was posted on our website (www.therobinreport.com), Liz Claiborne Inc. CEO Bill McComb responded with a message on the Liz Claiborne corporate website that took issue with some of the points made in the article. Following are excerpts of his message (in italics), with corresponding clarifications of some of the statements made and opinions offered in the article that we realize might be potentially confusing and not completely accurate in certain particulars. Both the online and print articles have been revised to include these clarifications. “Throughout our turnaround, we have consistently hired industry veterans – skewing toward leadership experience in vertical retailing as opposed to wholesale alone. These include senior executives such as Craig Leavitt, Deborah Lloyd, LeAnn nealz, Peter Warner, and Thomas Grote, among literally dozens more at various levels throughout the Company...” Despite his claims of hiring industry veterans, including the five executives listed, several key experienced direct reports (referred to in the article as “an entire layer of seasoned manage-ment”) were released within months of his arrival, and were not replaced. He also hired many people without industry experience. It should be noted that a key thesis of this article was that Mr. McComb, who clearly lacked industry experience, would have perhaps benefitted from an experienced staff, early on, to help him navigate his new business. In my opinion, this point was successfully made and supported in the article. “… [The] blog refers to our Lucky Brand CEO Dave DeMattei as a former Williams Sonoma executive in an effort to discredit his experience, failing to reference his more than 10 years of experience at Coach, J. Crew, Banana Republic and the Gap.”

The article omitted the executive’s prior experi-ence, implying that he had no apparel experience, which is not the case. Accordingly we’ve revised both the online and “hard copy” articles. “Again, contrary to reports, the Liz Claiborne brand was always considered part of “partnered brands” under the current management and was noted as such in our first presentation in July, 2007.”

The March 2007 issue of WWD stated of McComb’s new strategy: “Although McComb will not unveil his full plan until July, he has said he will focus on Claiborne’s five “power brands”: Juicy Couture, Lucky Brand, Kate Spade, Mexx and Liz Claiborne.” Certainly one could be confused when his official unveiling of the new strategy in July, Liz Claiborne was no longer included as a “power brand” (re-named “direct brands”).

“The report misrepresents our strategy for the Liz Claiborne brand and provides an inaccurate timeline of events. The original JC Penney relationship for Liz & Co. was formed and announced under the previous manage-ment. In 2009, it became clear that the Macy’s-Liz Claiborne brand relationship no longer made sense given the challenges faced by the department store channel. Given Liz & Co.’s success at JC Penney we made the decision to exclusively license the brand to JC Penney.”

The fact that Liz & Co. was licensed exclusively to JC Penney by Mr. McComb’s predecessor was never refuted, nor was it implied in the article to have taken place under McComb’s watch.

The Robin Report is an opinion blog dedicated to publishing the views of its editors. These views are intended to be thought- provoking and even controversial: we see the blog’s role as getting people in our industry to think critically about the business. Our mission is to provide knowledge, strategic insights and opinions on industry events, companies and trends. The article in question clearly meets these criteria.

POST ScRIPT cLARIFIcATIONS AND cORREcTIONS

www.TheRobinReport.com22

TEch BuBBLE IIBy Robin Lewis

Is it “here we go again?” Or, is it “this time is different”? Is it “irrational exuberance”? Or, is it a brilliant investment strategy?

Is this a new bubble that floats? Or, is this a “same old, same old” bubble that explodes, and quite possibly at a time when the fragile and hardly recovering economy can least absorb it.

So, the question is not whether there will be a technology “bubble.” There is one. And, its inflation will accelerate given all the free money sloshing around in pursuit of investment nirvana. The only question is: will the bubble’s seemingly insane valuation, in fact, turn out to be accu-rately valued with long term sustainable growth, like railroads a century ago? Or, something like that.